Embed Size (px)

Citation preview

The Heart of Oregon

Payroll Conference

Oct 2010

Canadian Payroll . . .not as “alien” as you may

think.

Presented by

Natasha Smyth BSc (Agr), CPM

The Heart of Oregon

Payroll Conference

Oct 2010

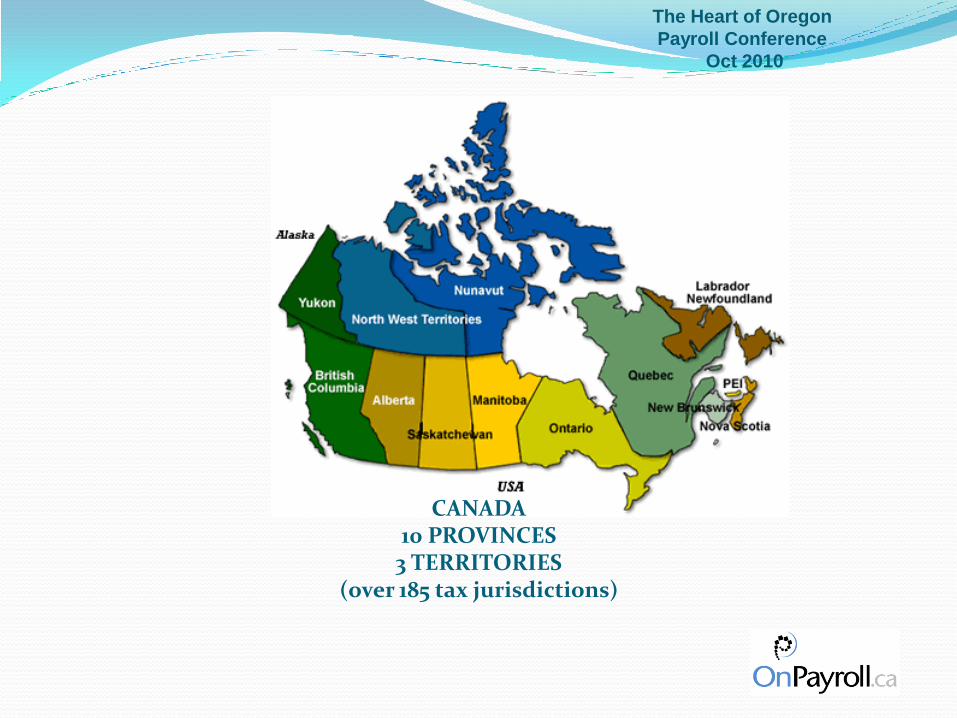

CANADA10 PROVINCES

3 TERRITORIES(over 185 tax jurisdictions)

The Heart of Oregon

Payroll Conference

Oct 2010

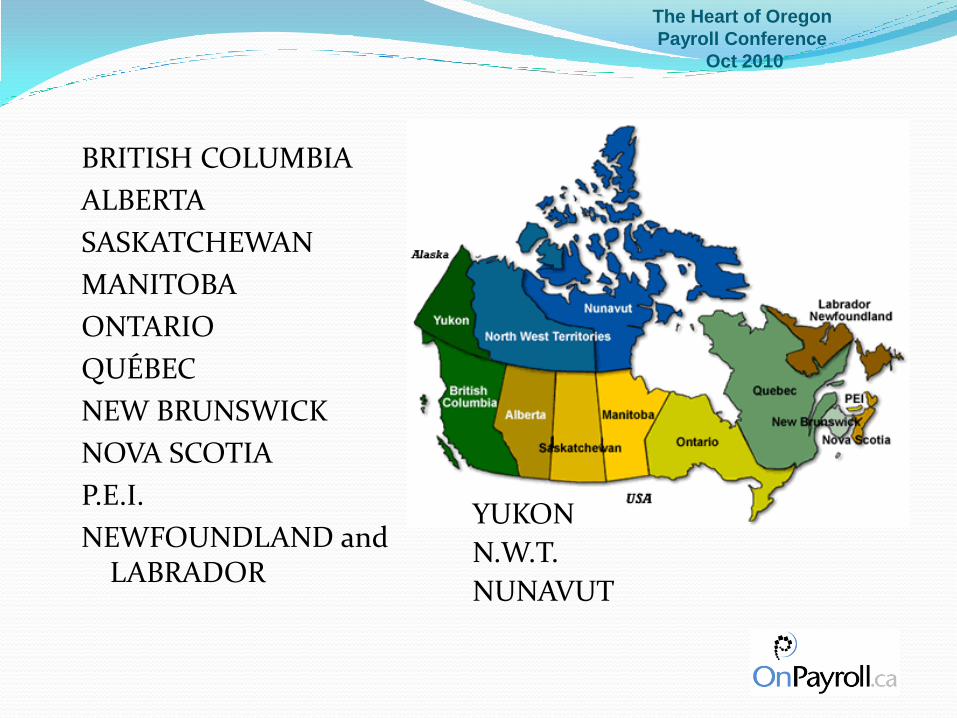

BRITISH COLUMBIA

ALBERTA

SASKATCHEWAN

MANITOBA

ONTARIO

QUÉBEC

NEW BRUNSWICK

NOVA SCOTIA

P.E.I.

NEWFOUNDLAND and LABRADOR

YUKON

N.W.T.

NUNAVUT

The Heart of Oregon

Payroll Conference

Oct 2010

Canadian Government Agencies

Canada Revenue Agency (CRA)

The Ministere du Revenu du Québec (MRQ)

Service Canada

Statistics Canada

Canada Labour Code

Provincial and territorial employment standards

Workers’ Compensation Boards

The Heart of Oregon

Payroll Conference

Oct 2010

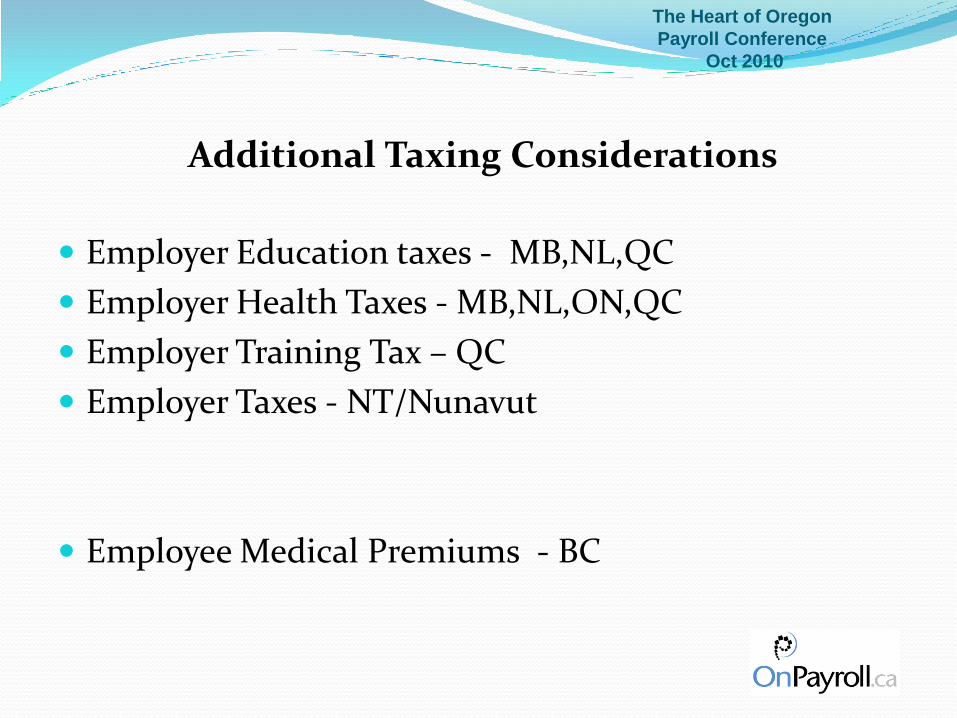

Additional Taxing Considerations

Employer Education taxes - MB,NL,QC

Employer Health Taxes - MB,NL,ON,QC

Employer Training Tax – QC

Employer Taxes - NT/Nunavut

Employee Medical Premiums - BC

The Heart of Oregon

Payroll Conference

Oct 2010

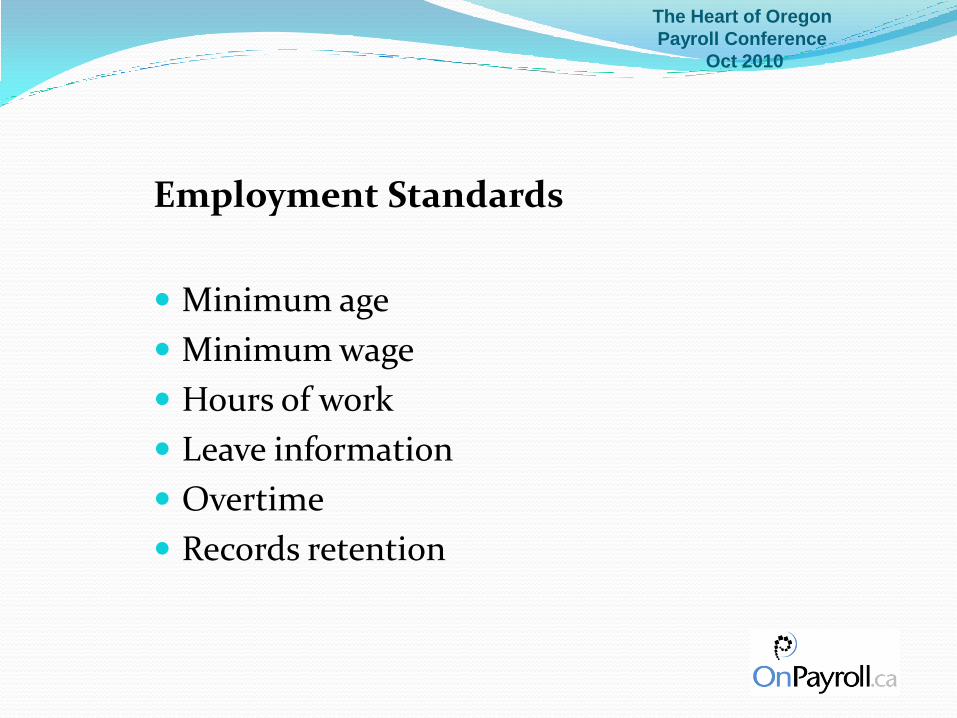

Employment Standards

Minimum age

Minimum wage

Hours of work

Leave information

Overtime

Records retention

The Heart of Oregon

Payroll Conference

Oct 2010

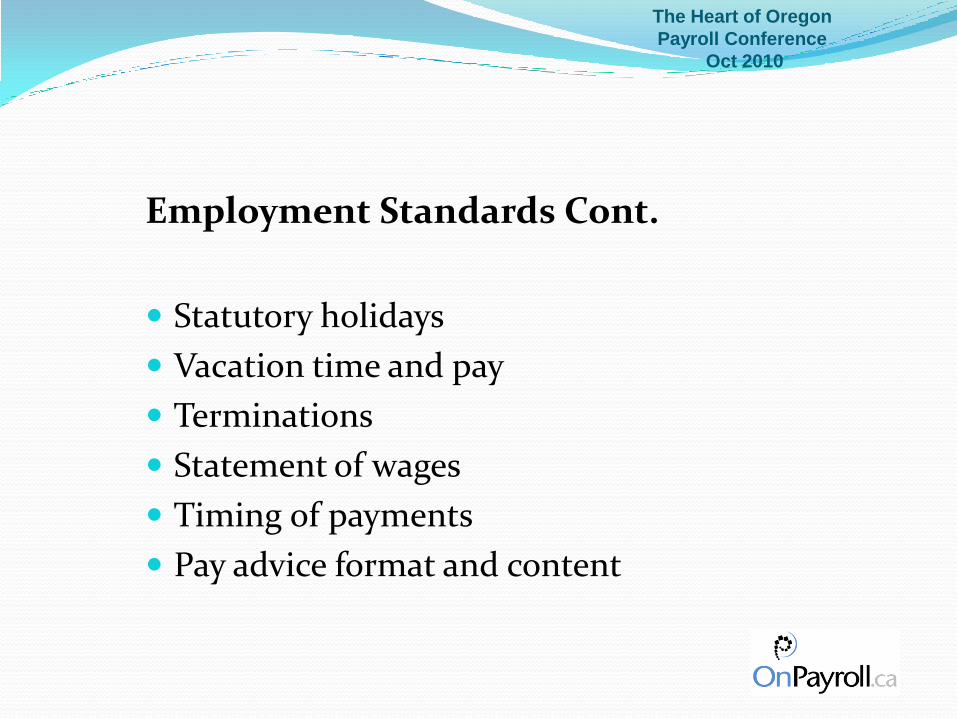

Employment Standards Cont.

Statutory holidays

Vacation time and pay

Terminations

Statement of wages

Timing of payments

Pay advice format and content

The Heart of Oregon

Payroll Conference

Oct 2010

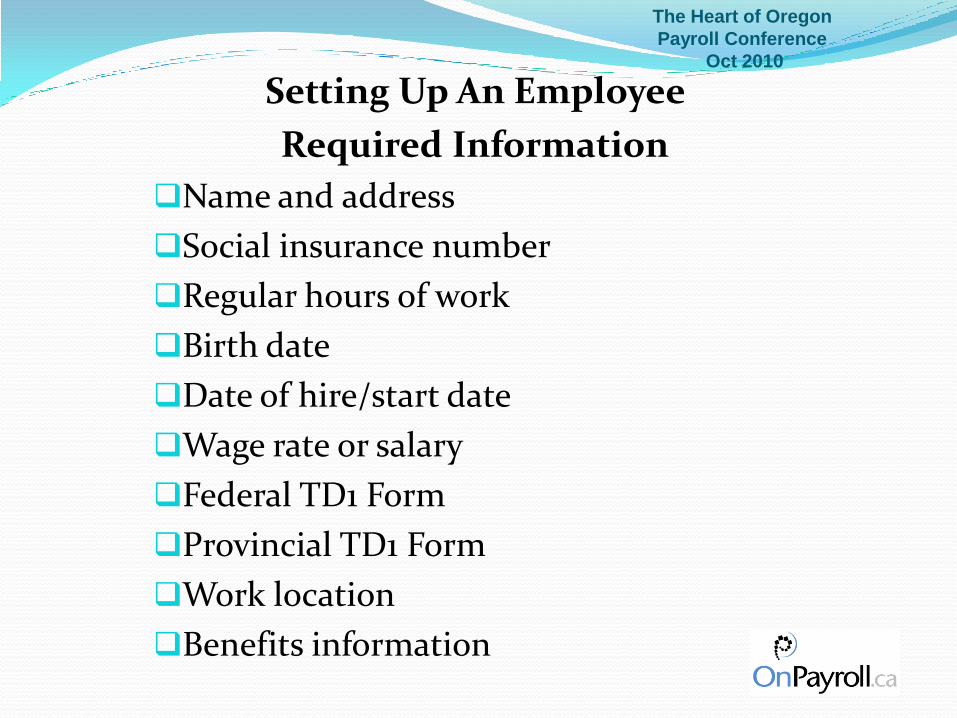

Setting Up An Employee

Required Information

Name and address

Social insurance number

Regular hours of work

Birth date

Date of hire/start date

Wage rate or salary

Federal TD1 Form

Provincial TD1 Form

Work location

Benefits information

The Heart of Oregon

Payroll Conference

Oct 2010

3 Types of Deductions

Statutory

Mandatory

Voluntary

The Heart of Oregon

Payroll Conference

Oct 2010

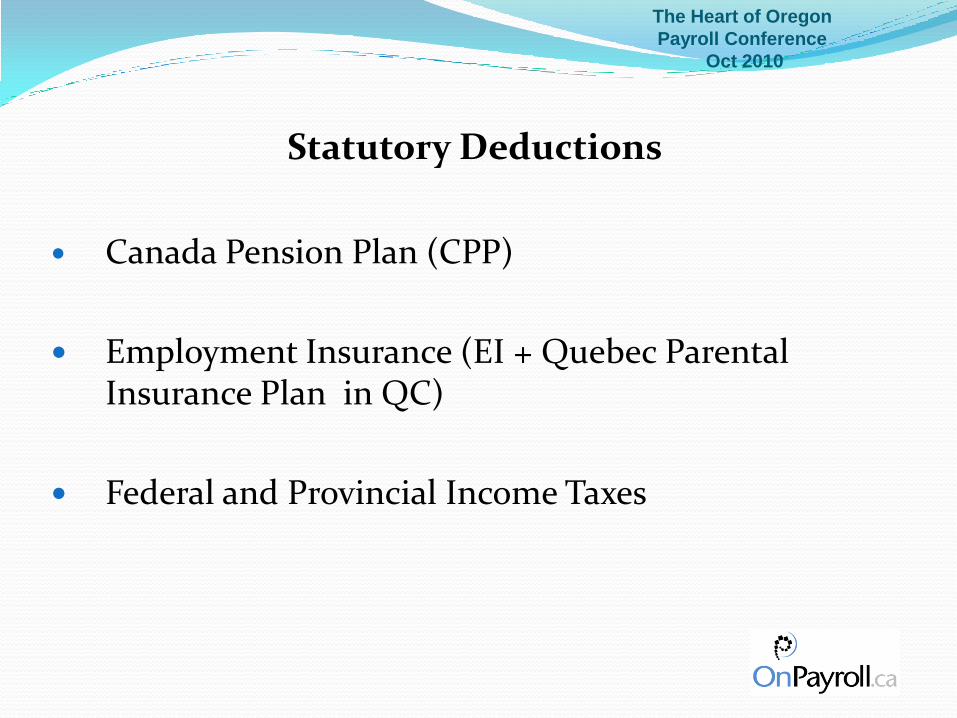

Statutory Deductions

Canada Pension Plan (CPP)

Employment Insurance (EI + Quebec Parental Insurance Plan in QC)

Federal and Provincial Income Taxes

The Heart of Oregon

Payroll Conference

Oct 2010

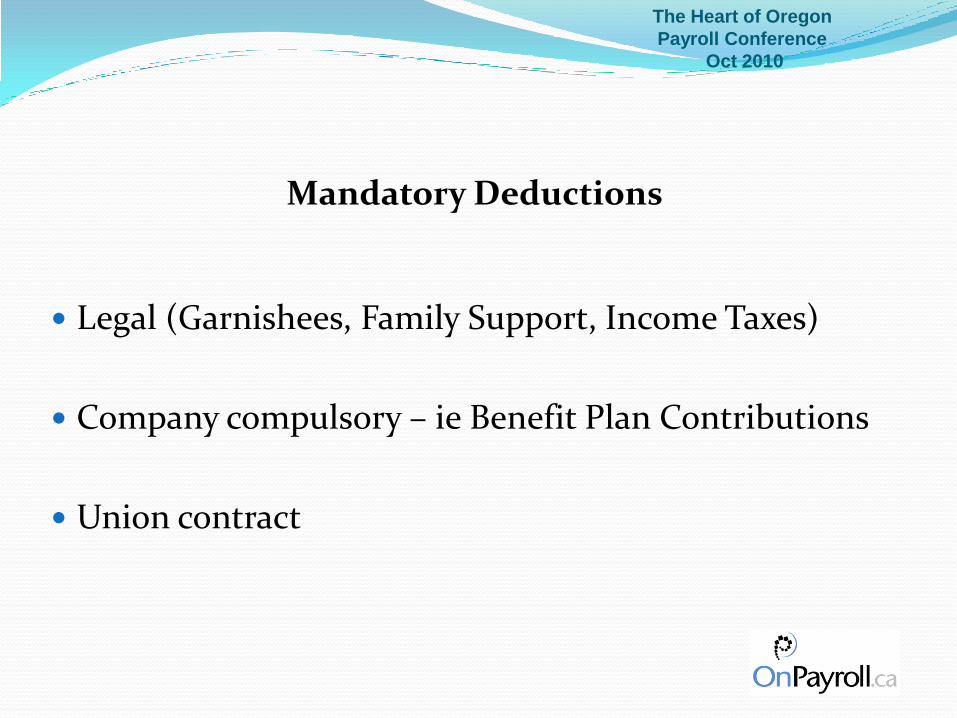

Mandatory Deductions

Legal (Garnishees, Family Support, Income Taxes)

Company compulsory – ie Benefit Plan Contributions

Union contract

The Heart of Oregon

Payroll Conference

Oct 2010

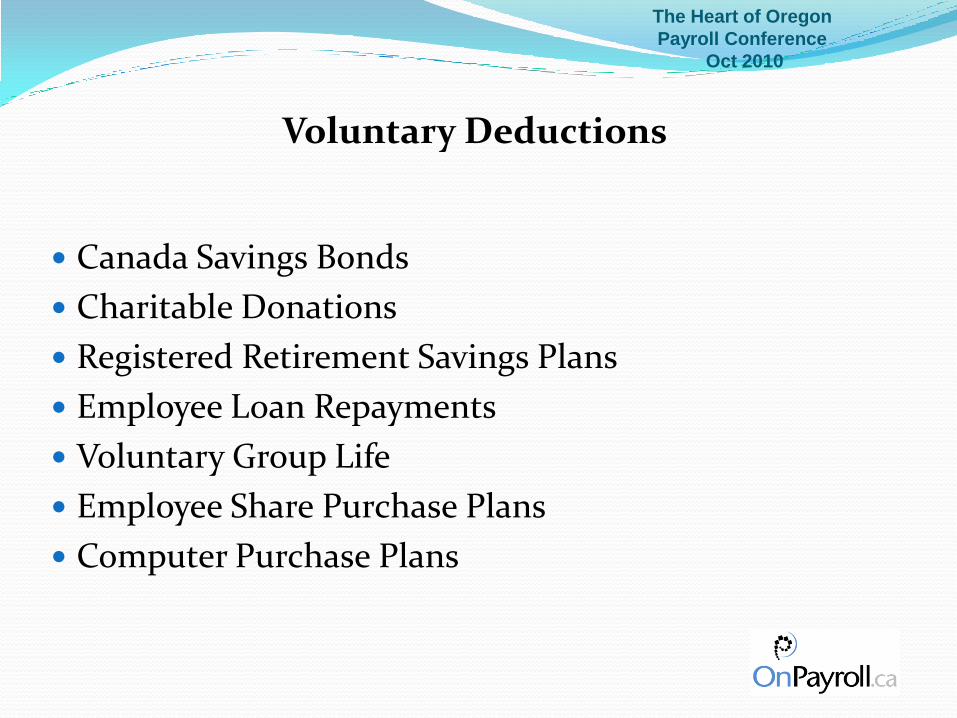

Voluntary Deductions

Canada Savings Bonds

Charitable Donations

Registered Retirement Savings Plans

Employee Loan Repayments

Voluntary Group Life

Employee Share Purchase Plans

Computer Purchase Plans

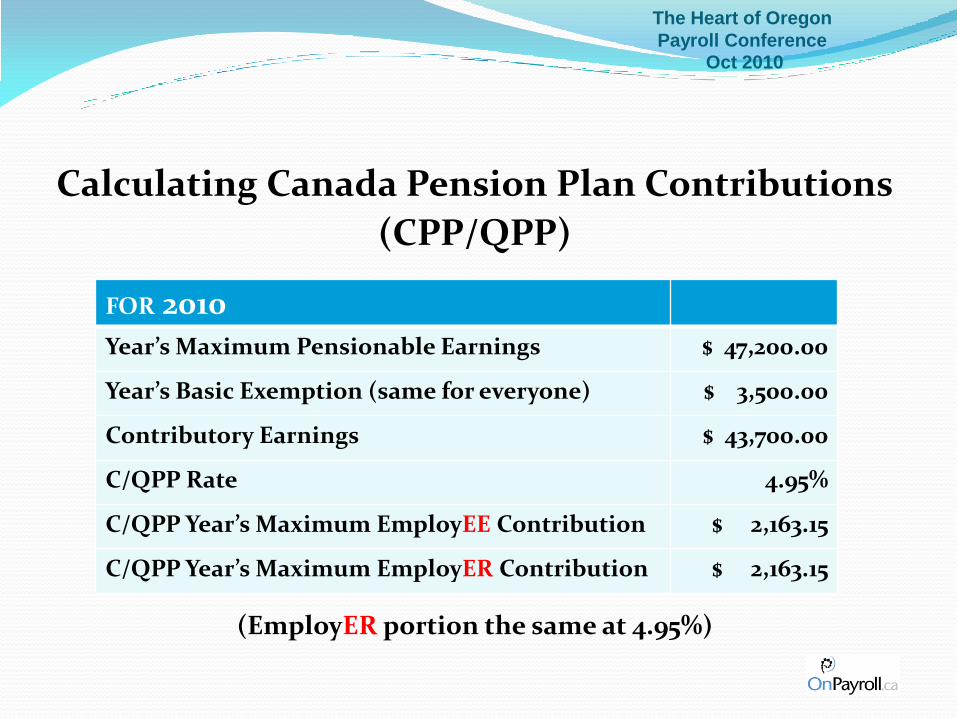

Calculating Canada Pension Plan Contributions

(CPP/QPP)

(EmployER portion the same at 4.95%)

FOR 2010

Year’s Maximum Pensionable Earnings $ 47,200.00

Year’s Basic Exemption (same for everyone) $ 3,500.00

Contributory Earnings $ 43,700.00

C/QPP Rate 4.95%

C/QPP Year’s Maximum EmployEE Contribution $ 2,163.15

C/QPP Year’s Maximum EmployER Contribution $ 2,163.15

The Heart of Oregon

Payroll Conference Oct 2010

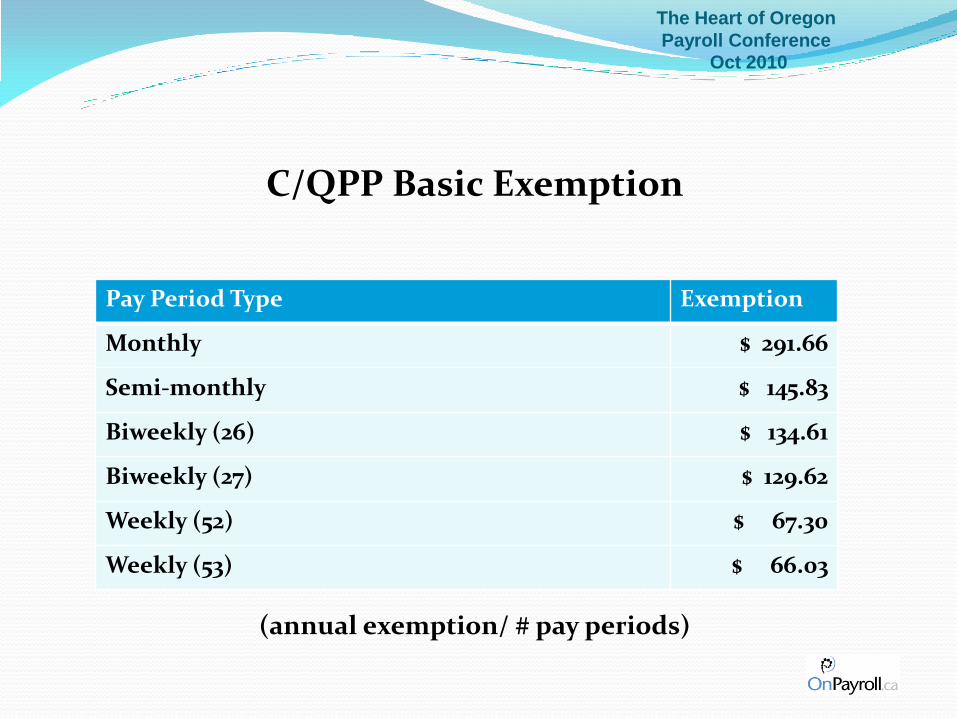

C/QPP Basic Exemption

(annual exemption/ # pay periods)

Pay Period Type Exemption

Monthly $ 291.66

Semi-monthly $ 145.83

Biweekly (26) $ 134.61

Biweekly (27) $ 129.62

Weekly (52) $ 67.30

Weekly (53) $ 66.03

The Heart of Oregon

Payroll Conference Oct 2010

The Heart of Oregon

Payroll Conference

Oct 2010

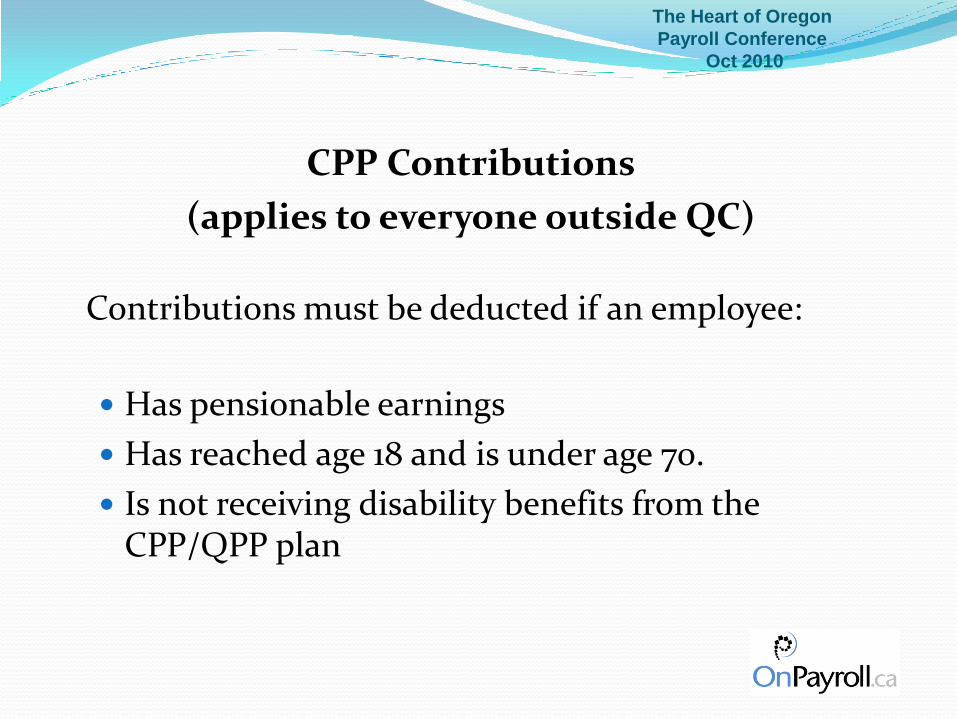

CPP Contributions

(applies to everyone outside QC)

Contributions must be deducted if an employee:

Has pensionable earnings

Has reached age 18 and is under age 70.

Is not receiving disability benefits from the CPP/QPP plan

The Heart of Oregon

Payroll Conference

Oct 2010

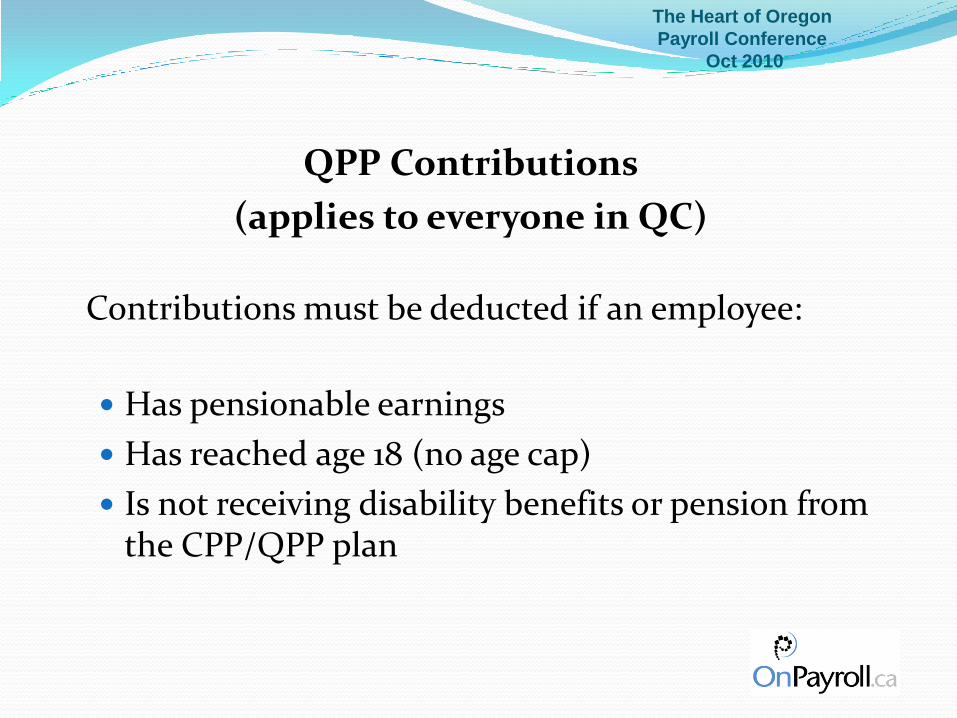

QPP Contributions

(applies to everyone in QC)

Contributions must be deducted if an employee:

Has pensionable earnings

Has reached age 18 (no age cap)

Is not receiving disability benefits or pension from the CPP/QPP plan

The Heart of Oregon

Payroll Conference

Oct 2010

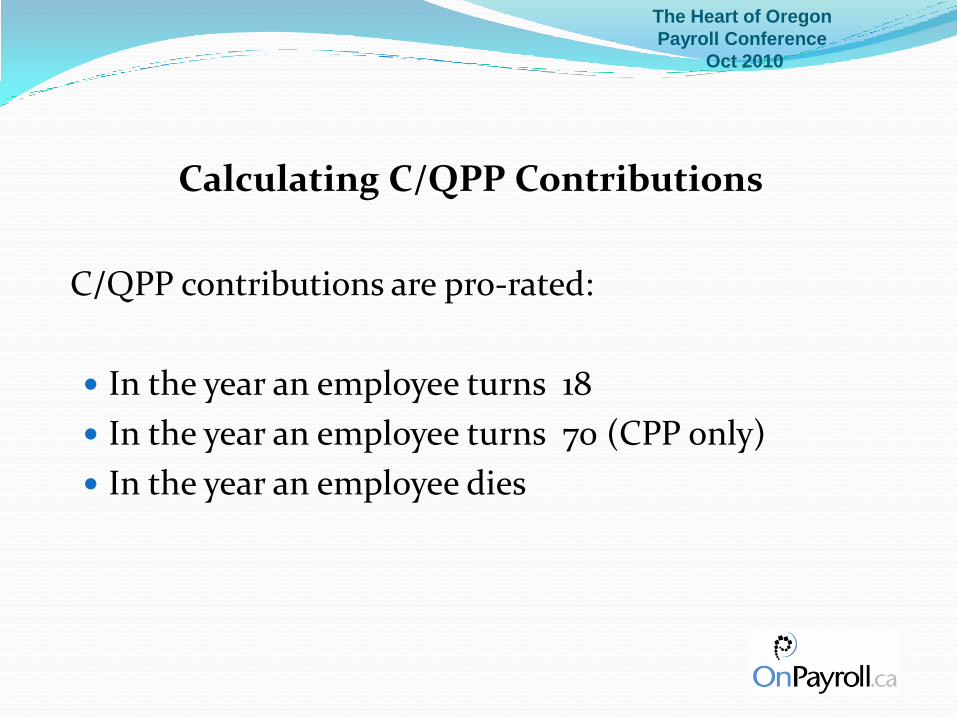

Calculating C/QPP Contributions

C/QPP contributions are pro-rated:

In the year an employee turns 18

In the year an employee turns 70 (CPP only)

In the year an employee dies

The Heart of Oregon

Payroll Conference

Oct 2010

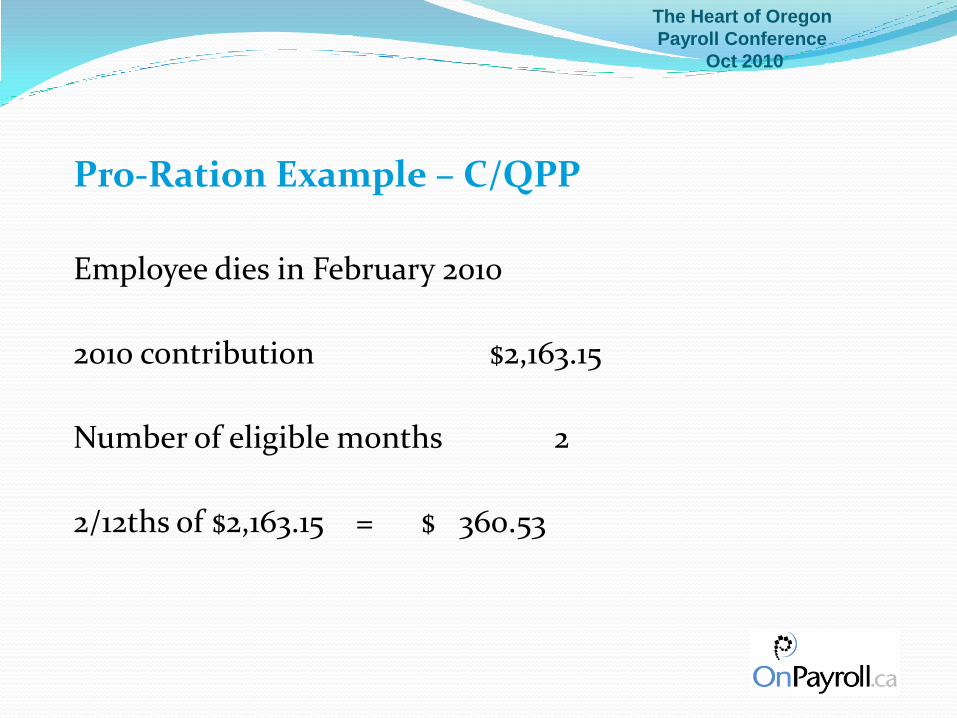

Pro-Ration Example – C/QPP

Employee dies in February 2010

2010 contribution $2,163.15

Number of eligible months 2

2/12ths of $2,163.15 = $ 360.53

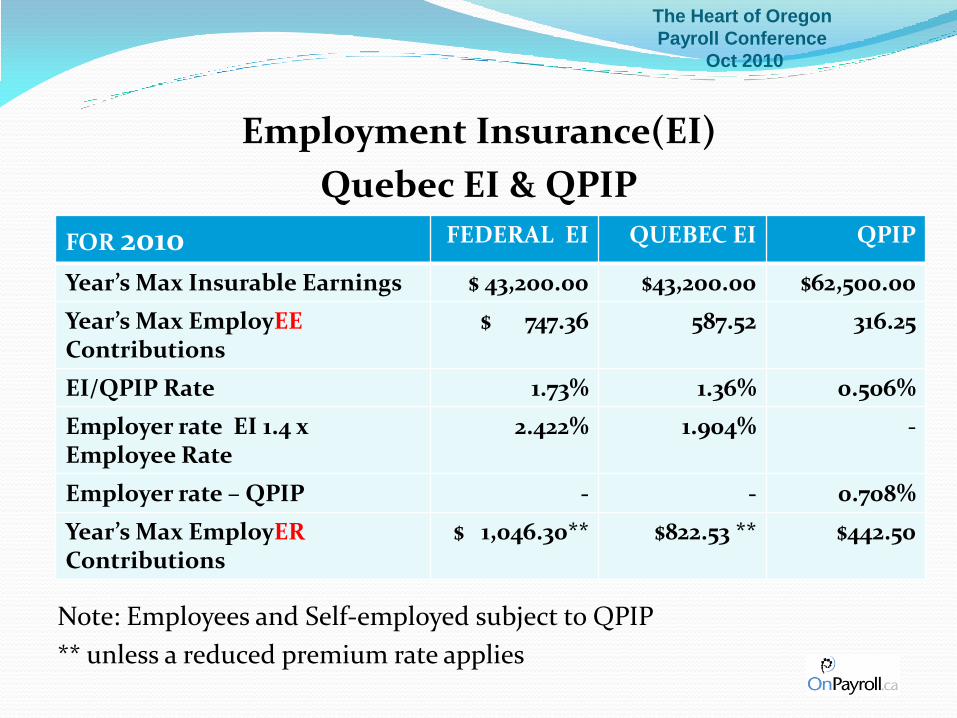

Employment Insurance(EI)

Quebec EI & QPIP

Note: Employees and Self-employed subject to QPIP

** unless a reduced premium rate applies

FOR 2010 FEDERAL EI QUEBEC EI QPIP

Year’s Max Insurable Earnings $ 43,200.00 $43,200.00 $62,500.00

Year’s Max EmployEEContributions

$ 747.36 587.52 316.25

EI/QPIP Rate 1.73% 1.36% 0.506%

Employer rate EI 1.4 x Employee Rate

2.422% 1.904% -

Employer rate – QPIP - - 0.708%

Year’s Max EmployERContributions

$ 1,046.30** $822.53 ** $442.50

The Heart of Oregon

Payroll Conference

Oct 2010

The Heart of Oregon

Payroll Conference

Oct 2010

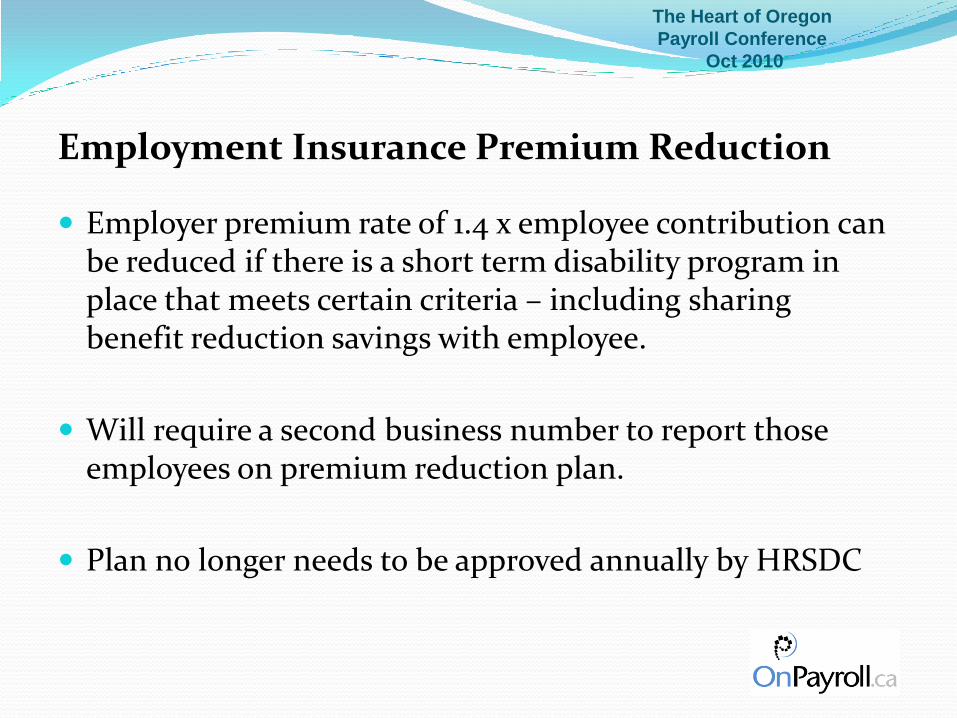

Employment Insurance Premium Reduction

Employer premium rate of 1.4 x employee contribution can be reduced if there is a short term disability program in place that meets certain criteria – including sharing benefit reduction savings with employee.

Will require a second business number to report those employees on premium reduction plan.

Plan no longer needs to be approved annually by HRSDC

The Heart of Oregon

Payroll Conference

Oct 2010

Quebec Parental Insurance Plan (QPIP)

• provides temporary financial maternity, paternity, parental, and adoption benefits to eligible Québec residents who take time off work and have an interruption of earnings.

• For Québec residents only, QPIP coverage only applies to the above benefits rather that EI. EI continues to cover other benefits such as regular, sickness and compassionate care.

The Heart of Oregon

Payroll Conference

Oct 2010

Calculating Employment Insurance for Record of Employment Purposes

Québec has assumed weekly numbers can be obtained from ROE for QPIP program

Earnings that are not subject to EI and therefore not reported on the ROE are reported on a separate form

The Heart of Oregon

Payroll Conference

Oct 2010

Calculating Employment Insurance for Record of Employment Purposes

INSURABLE EARNINGS

Non Cash taxable benefits are not Insurable

Retirement Allowances are not Insurable

Self employment – and related parties are not insurable

The Heart of Oregon

Payroll Conference

Oct 2010

Calculating Employment Insurance for Record of Employment Purposes

INSURABLE HOURS

Hours worked and paid

Deemed hours

Paid leave hours

The Heart of Oregon

Payroll Conference

Oct 2010

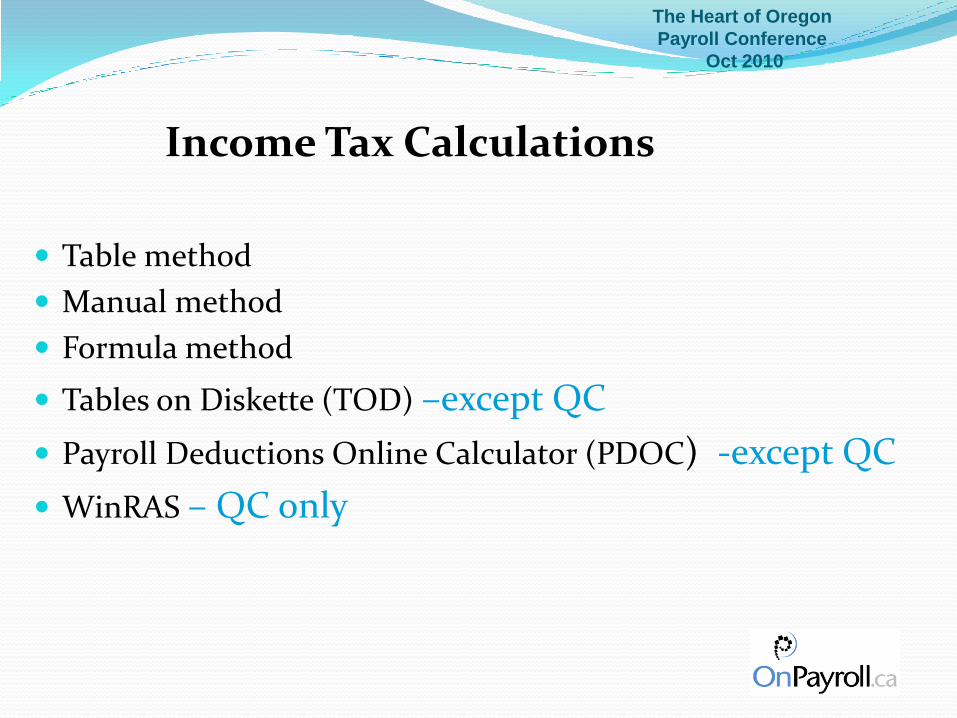

Income Tax Calculations

Table method

Manual method

Formula method

Tables on Diskette (TOD) –except QC

Payroll Deductions Online Calculator (PDOC) -except QC

WinRAS – QC only

The Heart of Oregon

Payroll Conference

Oct 2010

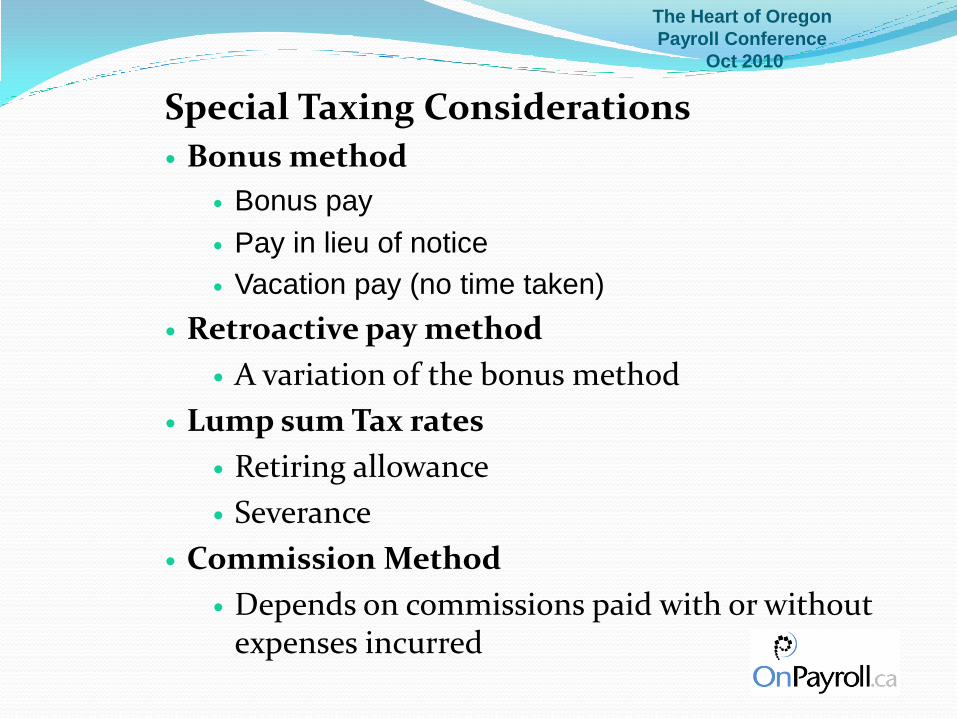

Special Taxing Considerations

Bonus method

Bonus pay

Pay in lieu of notice

Vacation pay (no time taken)

Retroactive pay method

A variation of the bonus method

Lump sum Tax rates

Retiring allowance

Severance

Commission Method

Depends on commissions paid with or without expenses incurred

The Heart of Oregon

Payroll Conference

Oct 2010

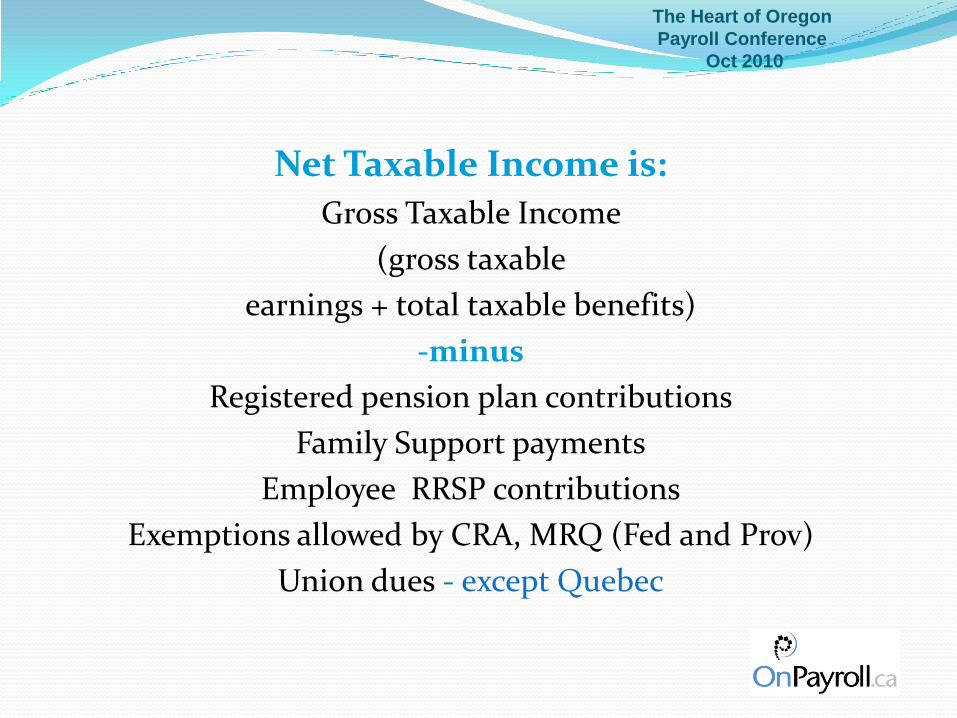

Net Taxable Income is:

Gross Taxable Income

(gross taxable

earnings + total taxable benefits)

-minus

Registered pension plan contributions

Family Support payments

Employee RRSP contributions

Exemptions allowed by CRA, MRQ (Fed and Prov)

Union dues - except Quebec

The Heart of Oregon

Payroll Conference

Oct 2010

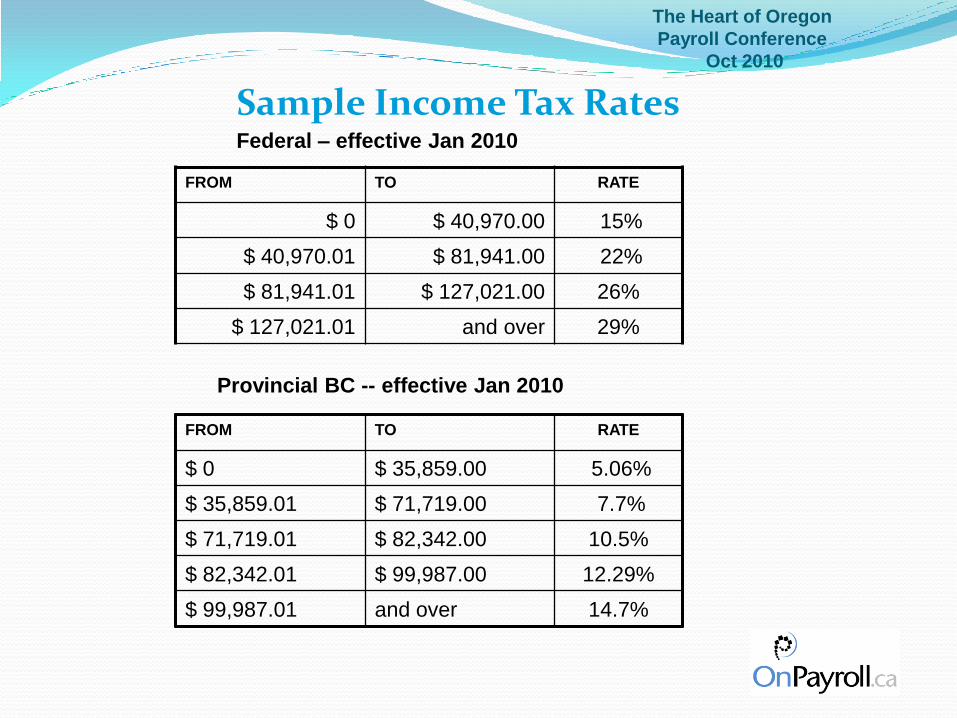

Provincial BC -- effective Jan 2010

Sample Income Tax RatesFederal – effective Jan 2010

FROM TO RATE

$ 0 $ 35,859.00 5.06%

$ 35,859.01 $ 71,719.00 7.7%

$ 71,719.01 $ 82,342.00 10.5%

$ 82,342.01 $ 99,987.00 12.29%

$ 99,987.01 and over 14.7%

FROM TO RATE

$ 0 $ 40,970.00 15%

$ 40,970.01 $ 81,941.00 22%

$ 81,941.01 $ 127,021.00 26%

$ 127,021.01 and over 29%

The Heart of Oregon

Payroll Conference

Oct 2010

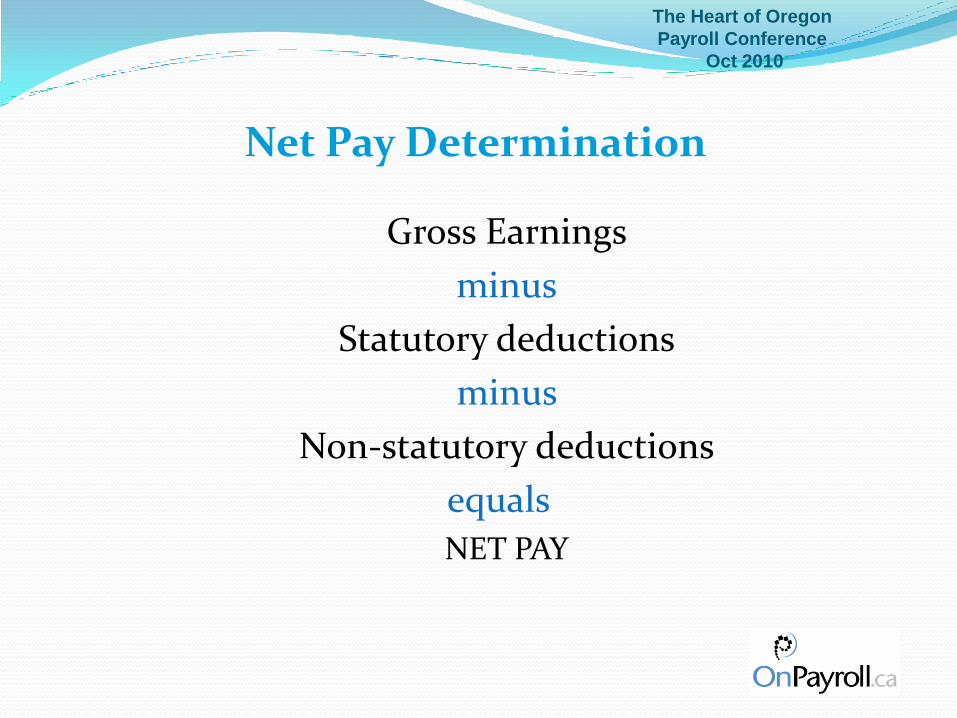

Net Pay Determination

Gross Earnings

minus

Statutory deductions

minus

Non-statutory deductions

equals

NET PAY

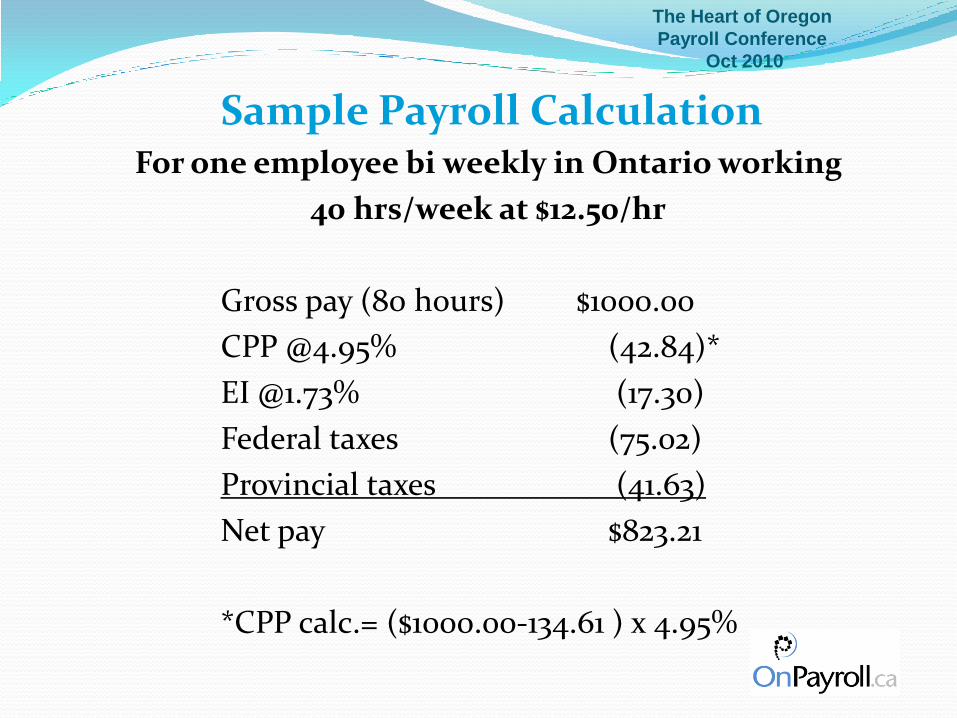

Sample Payroll CalculationFor one employee bi weekly in Ontario working

40 hrs/week at $12.50/hr

Gross pay (80 hours) $1000.00

CPP @4.95% (42.84)*

EI @1.73% (17.30)

Federal taxes (75.02)

Provincial taxes (41.63)

Net pay $823.21

*CPP calc.= ($1000.00-134.61 ) x 4.95%

The Heart of Oregon

Payroll Conference

Oct 2010

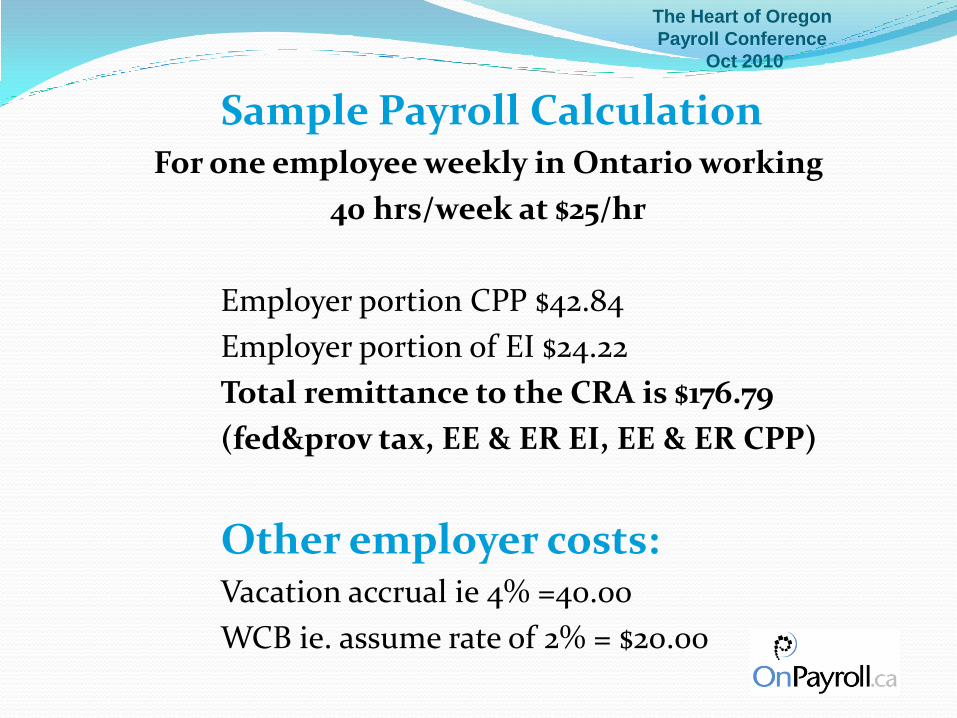

Sample Payroll CalculationFor one employee weekly in Ontario working

40 hrs/week at $25/hr

Employer portion CPP $42.84

Employer portion of EI $24.22

Total remittance to the CRA is $176.79

(fed&prov tax, EE & ER EI, EE & ER CPP)

Other employer costs:Vacation accrual ie 4% =40.00

WCB ie. assume rate of 2% = $20.00

The Heart of Oregon

Payroll Conference

Oct 2010

The Heart of Oregon

Payroll Conference

Oct 2010

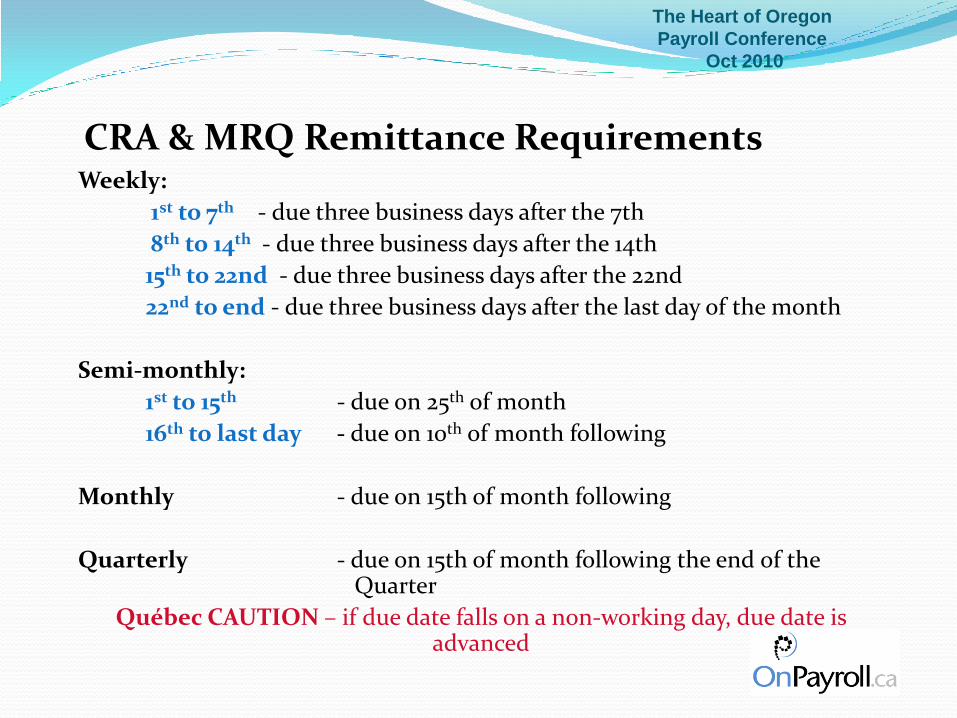

CRA & MRQ Remittance RequirementsWeekly:

1st to 7th - due three business days after the 7th

8th to 14th - due three business days after the 14th

15th to 22nd - due three business days after the 22nd

22nd to end - due three business days after the last day of the month

Semi-monthly:

1st to 15th - due on 25th of month

16th to last day - due on 10th of month following

Monthly - due on 15th of month following

Quarterly - due on 15th of month following the end of the Quarter

Québec CAUTION – if due date falls on a non-working day, due date is advanced

The Heart of Oregon

Payroll Conference

Oct 2010

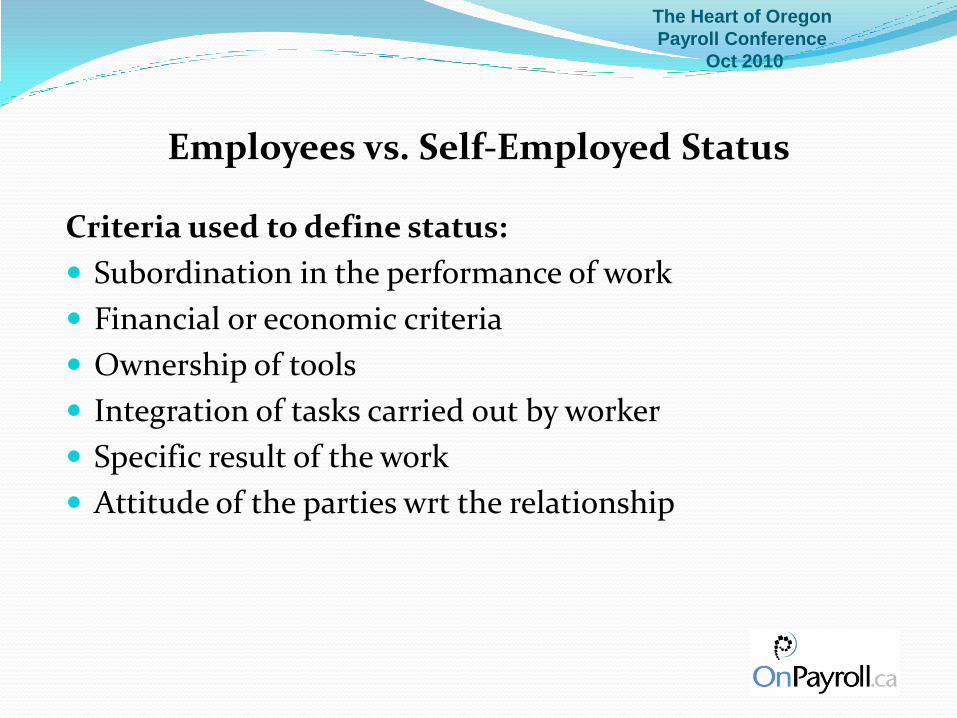

Employees vs. Self-Employed Status

Criteria used to define status:

Subordination in the performance of work

Financial or economic criteria

Ownership of tools

Integration of tasks carried out by worker

Specific result of the work

Attitude of the parties wrt the relationship

The Heart of Oregon

Payroll Conference

Oct 2010

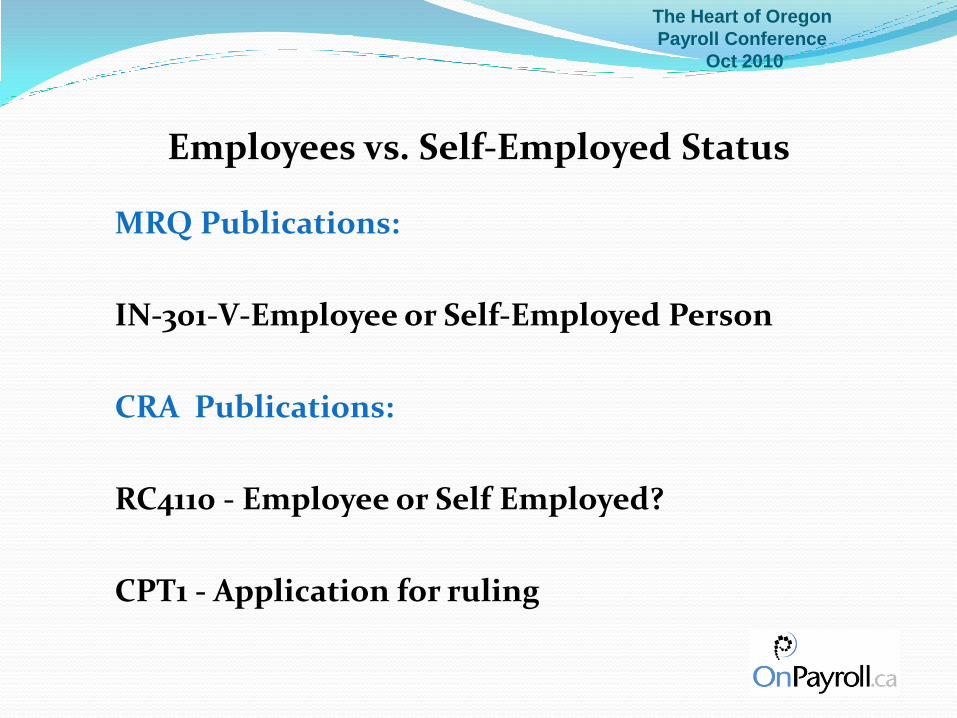

Employees vs. Self-Employed Status

MRQ Publications:

IN-301-V-Employee or Self-Employed Person

CRA Publications:

RC4110 - Employee or Self Employed?

CPT1 - Application for ruling

The Heart of Oregon

Payroll Conference

Oct 2010

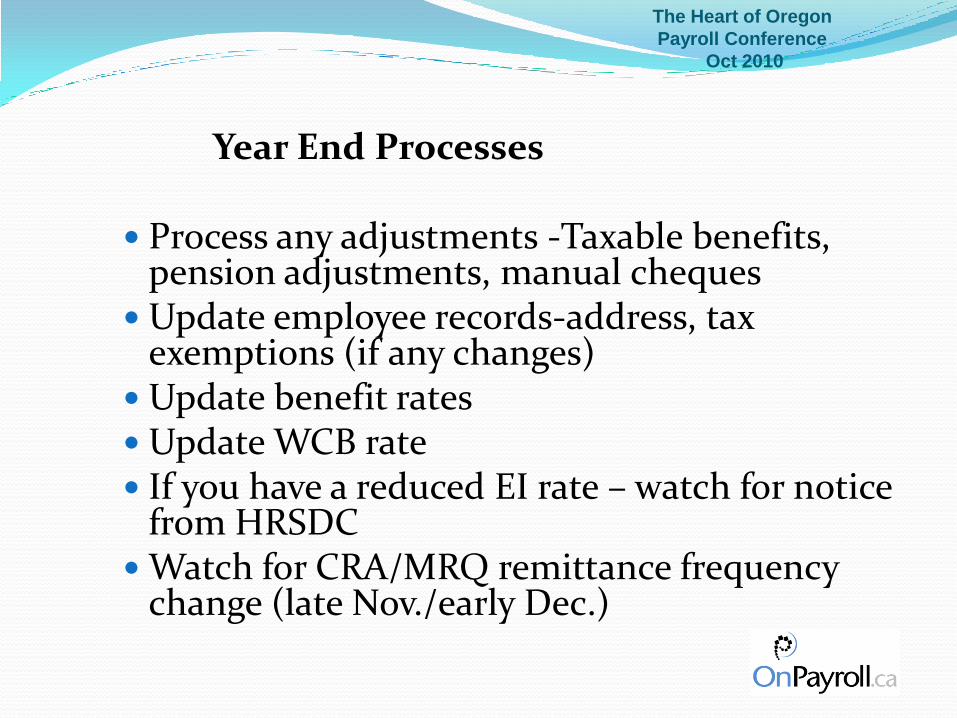

Year End Processes

Process any adjustments -Taxable benefits, pension adjustments, manual cheques

Update employee records-address, tax exemptions (if any changes)

Update benefit rates Update WCB rate If you have a reduced EI rate – watch for notice

from HRSDCWatch for CRA/MRQ remittance frequency

change (late Nov./early Dec.)

The Heart of Oregon

Payroll Conference

Oct 2010

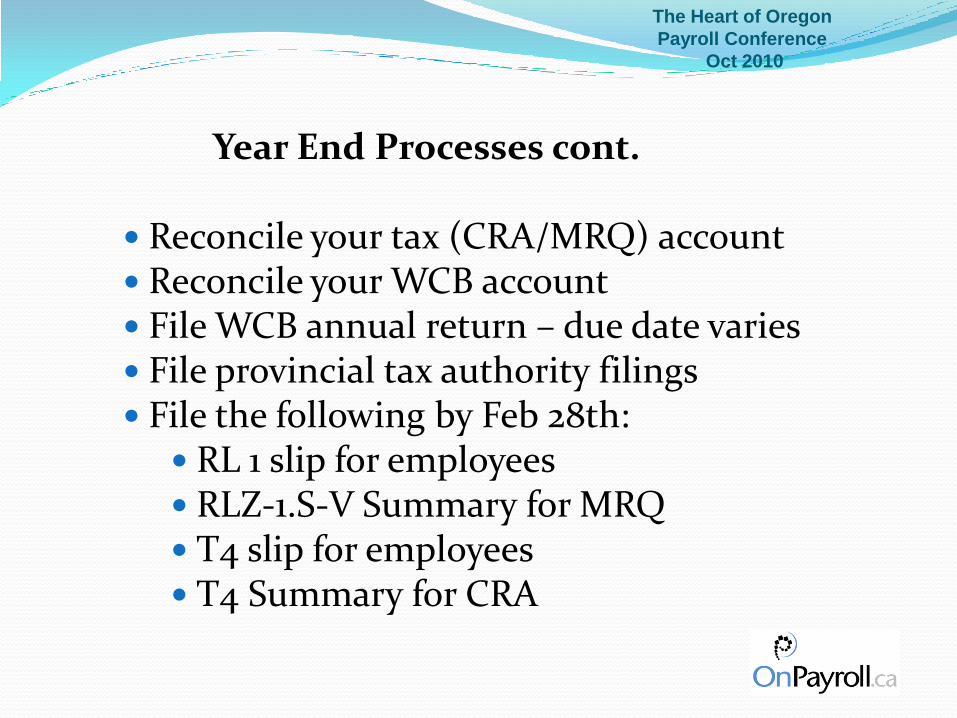

Year End Processes cont.

Reconcile your tax (CRA/MRQ) account Reconcile your WCB account File WCB annual return – due date varies File provincial tax authority filings File the following by Feb 28th: RL 1 slip for employees RLZ-1.S-V Summary for MRQ T4 slip for employees T4 Summary for CRA

The Heart of Oregon

Payroll Conference

Oct 2010

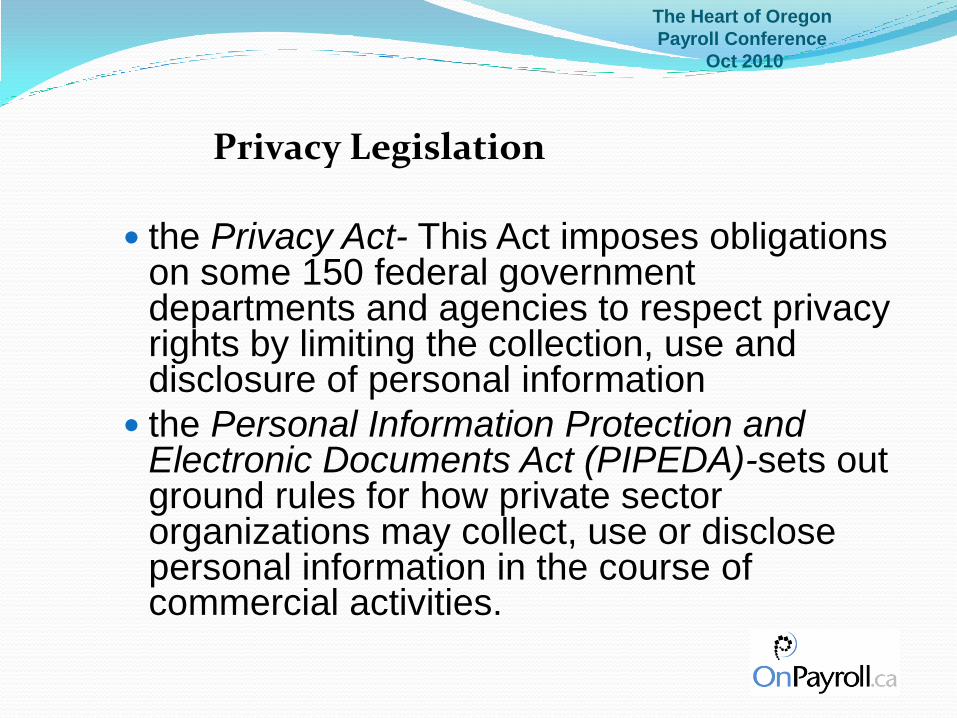

Privacy Legislation

the Privacy Act- This Act imposes obligations on some 150 federal government departments and agencies to respect privacy rights by limiting the collection, use and disclosure of personal information

the Personal Information Protection and Electronic Documents Act (PIPEDA)-sets out ground rules for how private sector organizations may collect, use or disclose personal information in the course of commercial activities.

The Heart of Oregon

Payroll Conference

Oct 2010

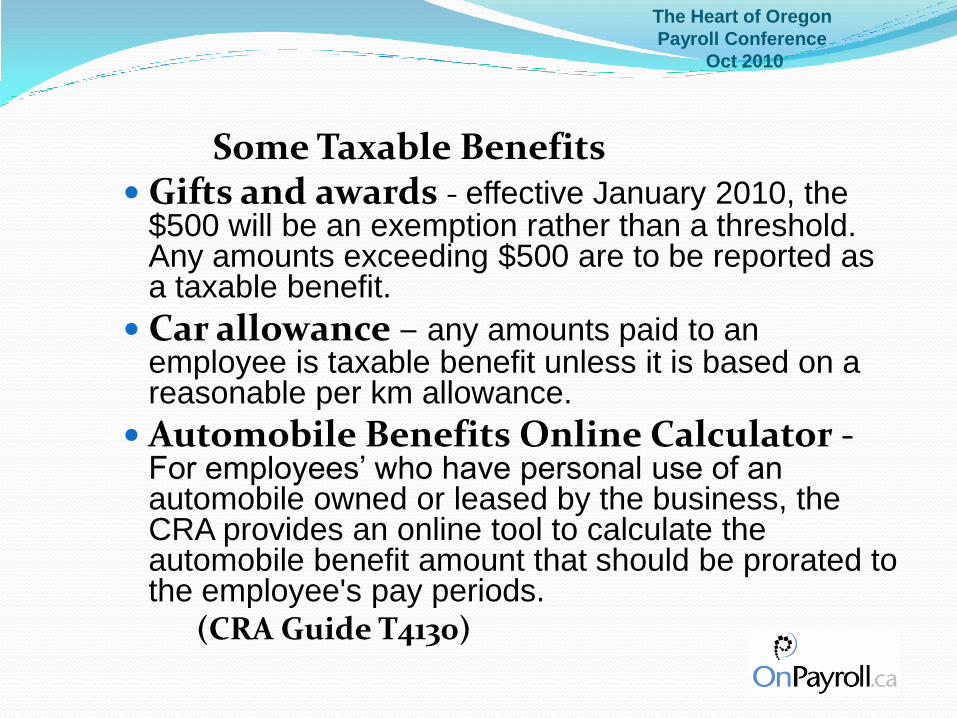

Some Taxable Benefits Gifts and awards - effective January 2010, the

$500 will be an exemption rather than a threshold. Any amounts exceeding $500 are to be reported as a taxable benefit.

Car allowance – any amounts paid to an employee is taxable benefit unless it is based on a reasonable per km allowance.

Automobile Benefits Online Calculator -For employees’ who have personal use of an automobile owned or leased by the business, the CRA provides an online tool to calculate the automobile benefit amount that should be prorated to the employee's pay periods.

(CRA Guide T4130)

The Heart of Oregon

Payroll Conference

Oct 2010

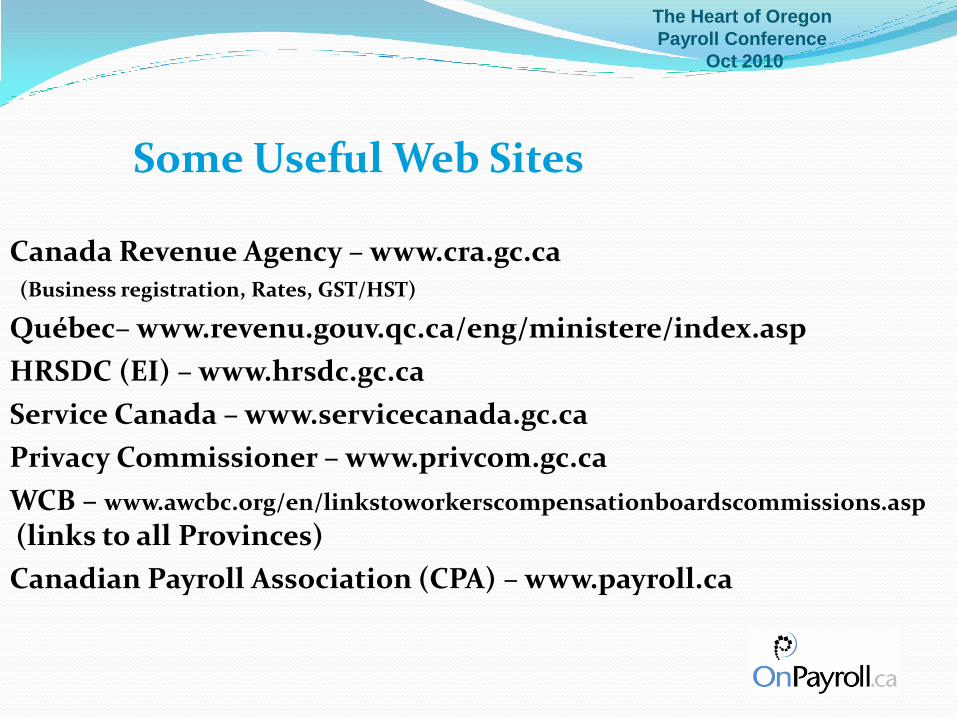

Some Useful Web Sites

Canada Revenue Agency – www.cra.gc.ca(Business registration, Rates, GST/HST)

Québec– www.revenu.gouv.qc.ca/eng/ministere/index.asp

HRSDC (EI) – www.hrsdc.gc.ca

Service Canada – www.servicecanada.gc.ca

Privacy Commissioner – www.privcom.gc.ca

WCB – www.awcbc.org/en/linkstoworkerscompensationboardscommissions.asp

(links to all Provinces)

Canadian Payroll Association (CPA) – www.payroll.ca

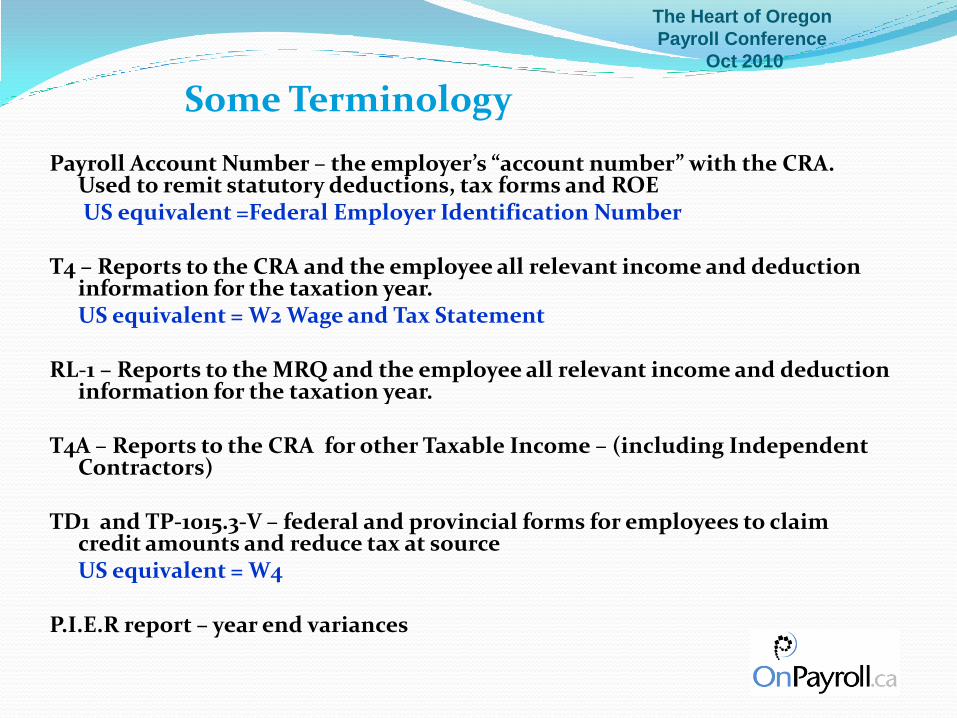

Some Terminology

Payroll Account Number – the employer’s “account number” with the CRA. Used to remit statutory deductions, tax forms and ROEUS equivalent =Federal Employer Identification Number

T4 – Reports to the CRA and the employee all relevant income and deduction information for the taxation year. US equivalent = W2 Wage and Tax Statement

RL-1 – Reports to the MRQ and the employee all relevant income and deduction information for the taxation year.

T4A – Reports to the CRA for other Taxable Income – (including Independent Contractors)

TD1 and TP-1015.3-V – federal and provincial forms for employees to claim credit amounts and reduce tax at sourceUS equivalent = W4

P.I.E.R report – year end variances

The Heart of Oregon

Payroll Conference

Oct 2010

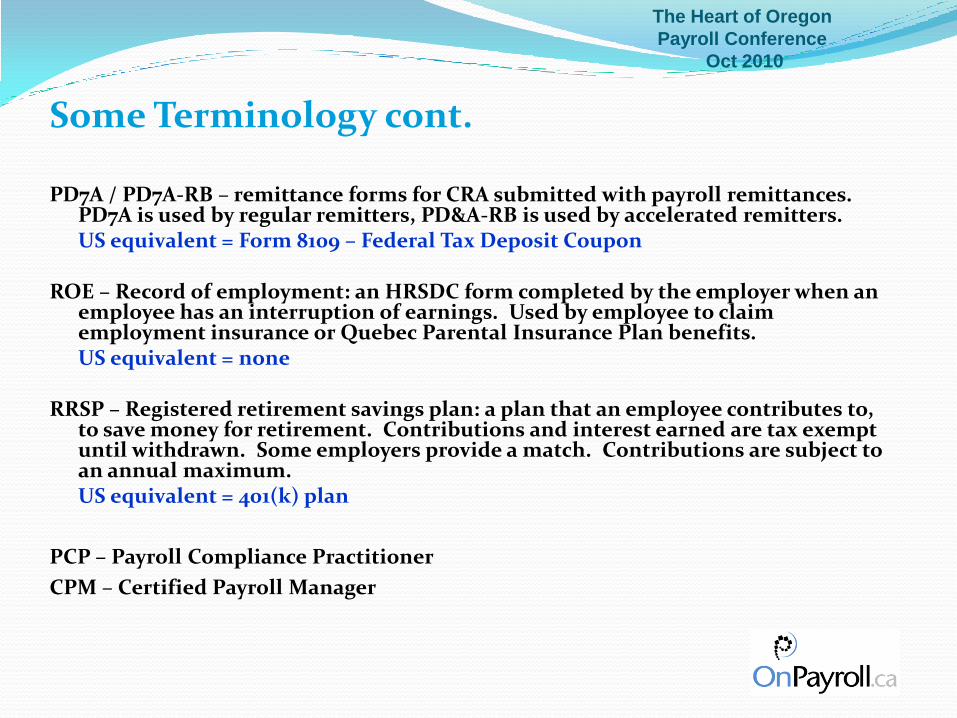

Some Terminology cont.

PD7A / PD7A-RB – remittance forms for CRA submitted with payroll remittances. PD7A is used by regular remitters, PD&A-RB is used by accelerated remitters. US equivalent = Form 8109 – Federal Tax Deposit Coupon

ROE – Record of employment: an HRSDC form completed by the employer when an employee has an interruption of earnings. Used by employee to claim employment insurance or Quebec Parental Insurance Plan benefits. US equivalent = none

RRSP – Registered retirement savings plan: a plan that an employee contributes to, to save money for retirement. Contributions and interest earned are tax exempt until withdrawn. Some employers provide a match. Contributions are subject to an annual maximum.US equivalent = 401(k) plan

PCP – Payroll Compliance Practitioner

CPM – Certified Payroll Manager

The Heart of Oregon

Payroll Conference

Oct 2010

The Heart of Oregon

Payroll Conference

Oct 2010

Canadian Payroll

Presented by Natasha Smyth, CPM

Vice PresidentOnPayroll.ca Corp

1-800-955-0806 [email protected]

North Vancouver, BCCANADA

The Heart of Oregon

Payroll Conference

Oct 2010

Canadian Payroll

BONUS MATERIAL

The Heart of Oregon

Payroll Conference

Oct 2010

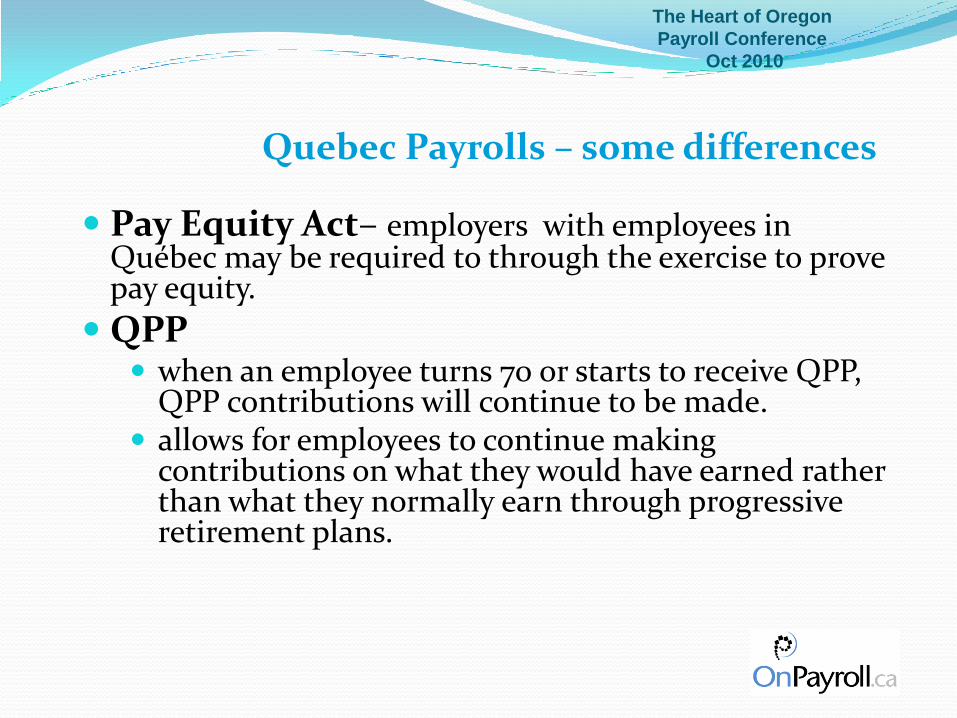

Quebec Payrolls – some differences

Pay Equity Act– employers with employees in Québec may be required to through the exercise to prove pay equity.

QPP when an employee turns 70 or starts to receive QPP,

QPP contributions will continue to be made. allows for employees to continue making

contributions on what they would have earned rather than what they normally earn through progressive retirement plans.

The Heart of Oregon

Payroll Conference

Oct 2010

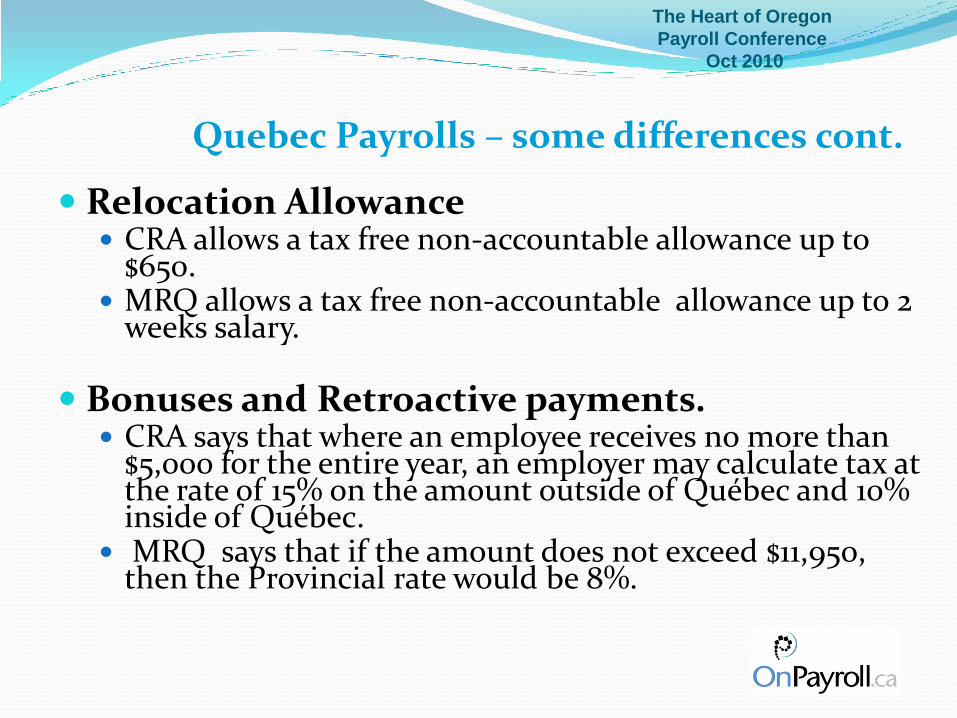

Quebec Payrolls – some differences cont.

Relocation Allowance CRA allows a tax free non-accountable allowance up to

$650. MRQ allows a tax free non-accountable allowance up to 2

weeks salary.

Bonuses and Retroactive payments. CRA says that where an employee receives no more than

$5,000 for the entire year, an employer may calculate tax at the rate of 15% on the amount outside of Québec and 10% inside of Québec.

MRQ says that if the amount does not exceed $11,950, then the Provincial rate would be 8%.

The Heart of Oregon

Payroll Conference

Oct 2010

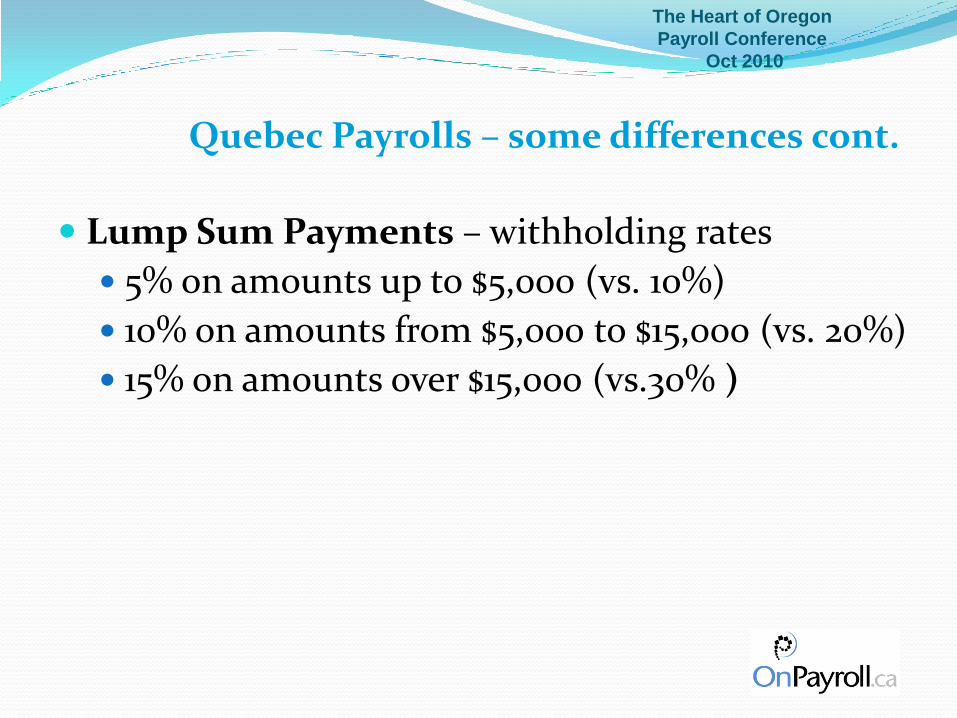

Quebec Payrolls – some differences cont.

Lump Sum Payments – withholding rates

5% on amounts up to $5,000 (vs. 10%)

10% on amounts from $5,000 to $15,000 (vs. 20%)

15% on amounts over $15,000 (vs.30% )

The Heart of Oregon

Payroll Conference

Oct 2010

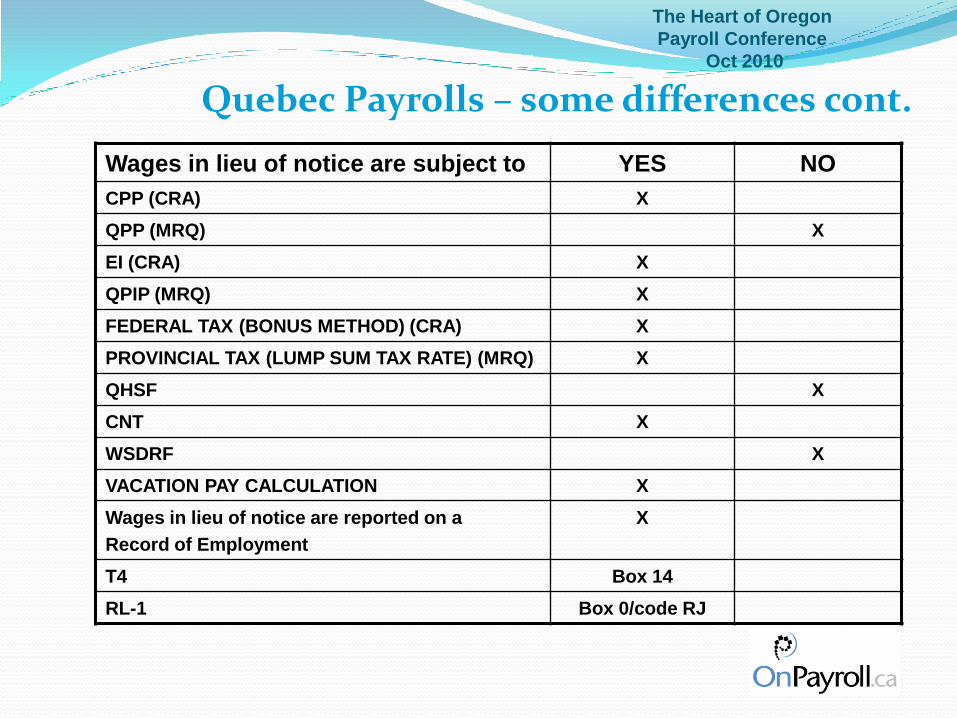

Wages in lieu of notice are subject to YES NO

CPP (CRA) X

QPP (MRQ) X

EI (CRA) X

QPIP (MRQ) X

FEDERAL TAX (BONUS METHOD) (CRA) X

PROVINCIAL TAX (LUMP SUM TAX RATE) (MRQ) X

QHSF X

CNT X

WSDRF X

VACATION PAY CALCULATION X

Wages in lieu of notice are reported on a

Record of Employment

X

T4 Box 14

RL-1 Box 0/code RJ

Quebec Payrolls – some differences cont.

The Heart of Oregon

Payroll Conference

Oct 2010

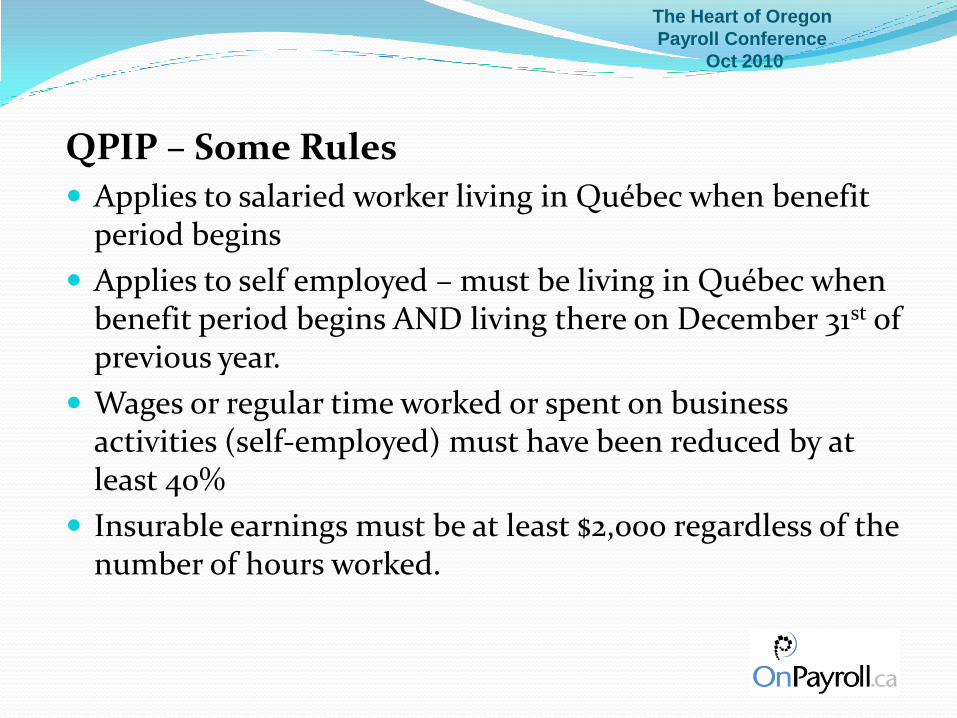

QPIP – Some Rules

Applies to salaried worker living in Québec when benefit period begins

Applies to self employed – must be living in Québec when benefit period begins AND living there on December 31st of previous year.

Wages or regular time worked or spent on business activities (self-employed) must have been reduced by at least 40%

Insurable earnings must be at least $2,000 regardless of the number of hours worked.

The Heart of Oregon

Payroll Conference

Oct 2010

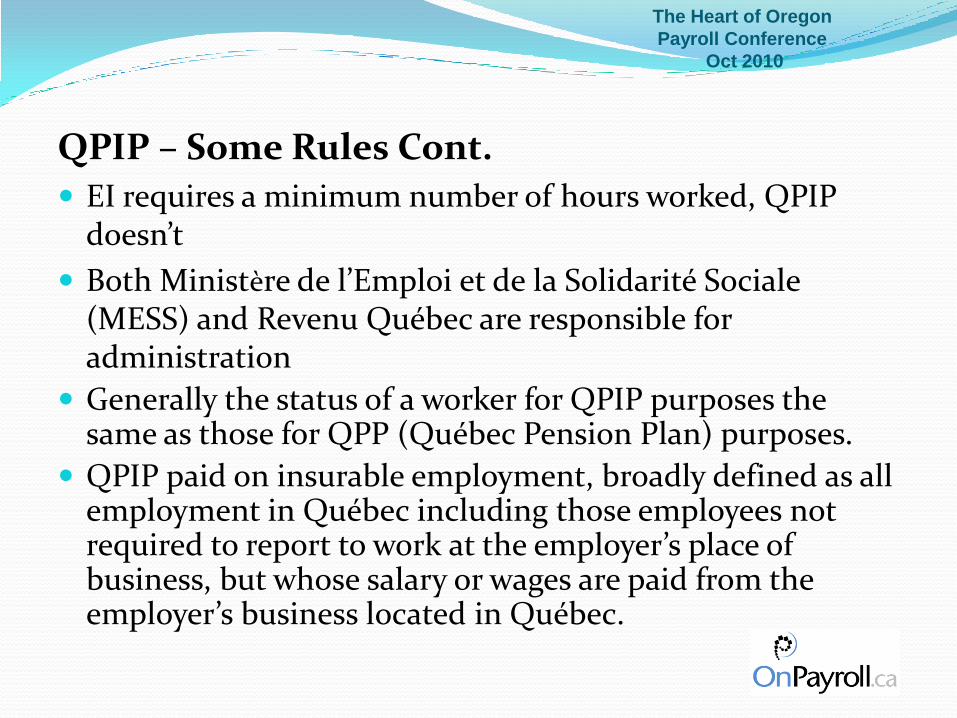

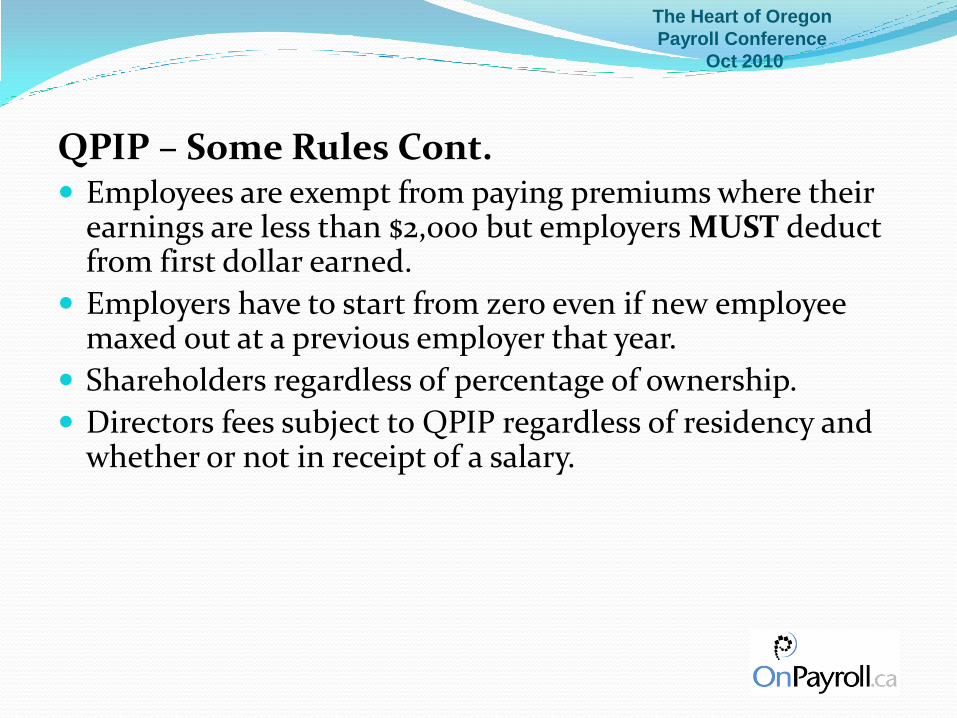

QPIP – Some Rules Cont.

EI requires a minimum number of hours worked, QPIP doesn’t

Both Ministѐre de l’Emploi et de la Solidarité Sociale (MESS) and Revenu Québec are responsible for administration

Generally the status of a worker for QPIP purposes the same as those for QPP (Québec Pension Plan) purposes.

QPIP paid on insurable employment, broadly defined as all employment in Québec including those employees not required to report to work at the employer’s place of business, but whose salary or wages are paid from the employer’s business located in Québec.

The Heart of Oregon

Payroll Conference

Oct 2010

QPIP – Some Rules Cont. Employees are exempt from paying premiums where their

earnings are less than $2,000 but employers MUST deduct from first dollar earned.

Employers have to start from zero even if new employee maxed out at a previous employer that year.

Shareholders regardless of percentage of ownership.

Directors fees subject to QPIP regardless of residency and whether or not in receipt of a salary.

The Heart of Oregon

Payroll Conference

Oct 2010

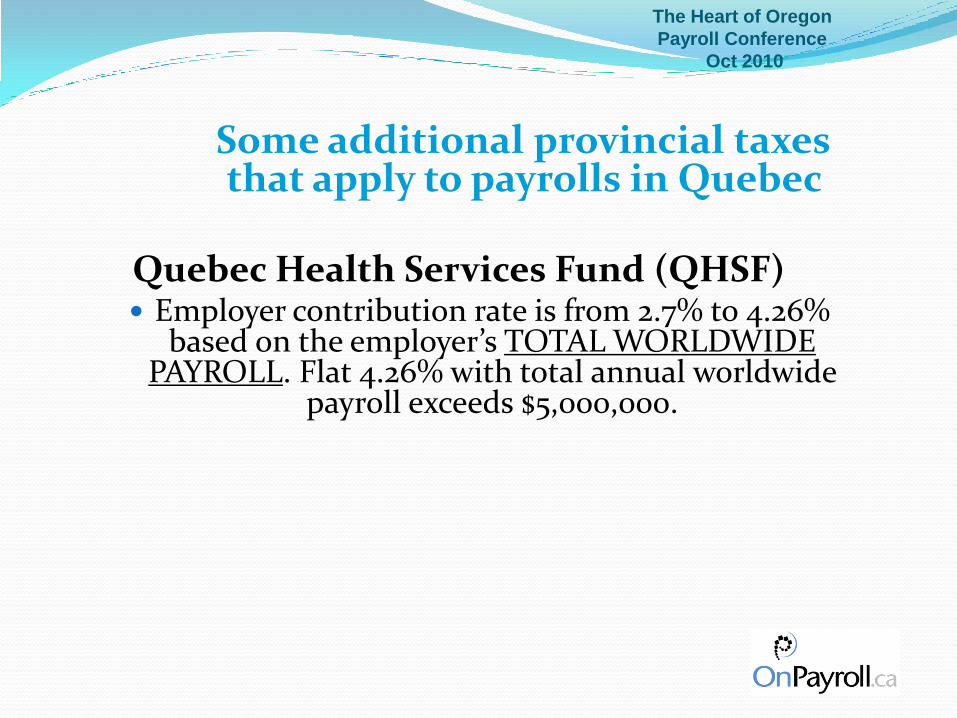

Some additional provincial taxes that apply to payrolls in Quebec

Quebec Health Services Fund (QHSF) Employer contribution rate is from 2.7% to 4.26%

based on the employer’s TOTAL WORLDWIDE PAYROLL. Flat 4.26% with total annual worldwide

payroll exceeds $5,000,000.

The Heart of Oregon

Payroll Conference

Oct 2010

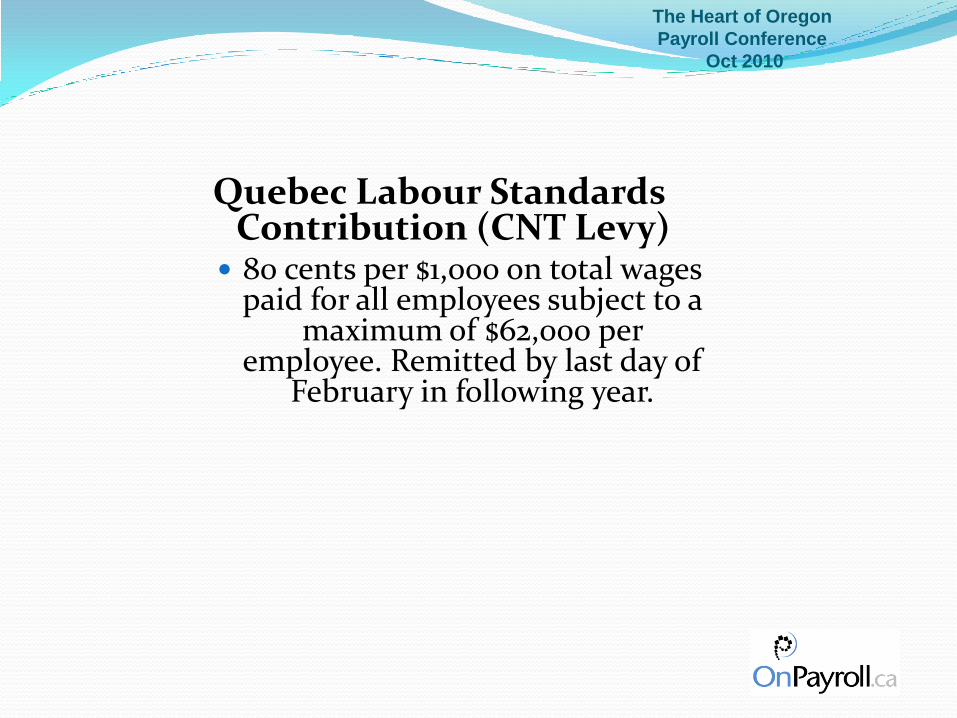

Quebec Labour Standards Contribution (CNT Levy) 80 cents per $1,000 on total wages

paid for all employees subject to a maximum of $62,000 per

employee. Remitted by last day of February in following year.

The Heart of Oregon

Payroll Conference

Oct 2010

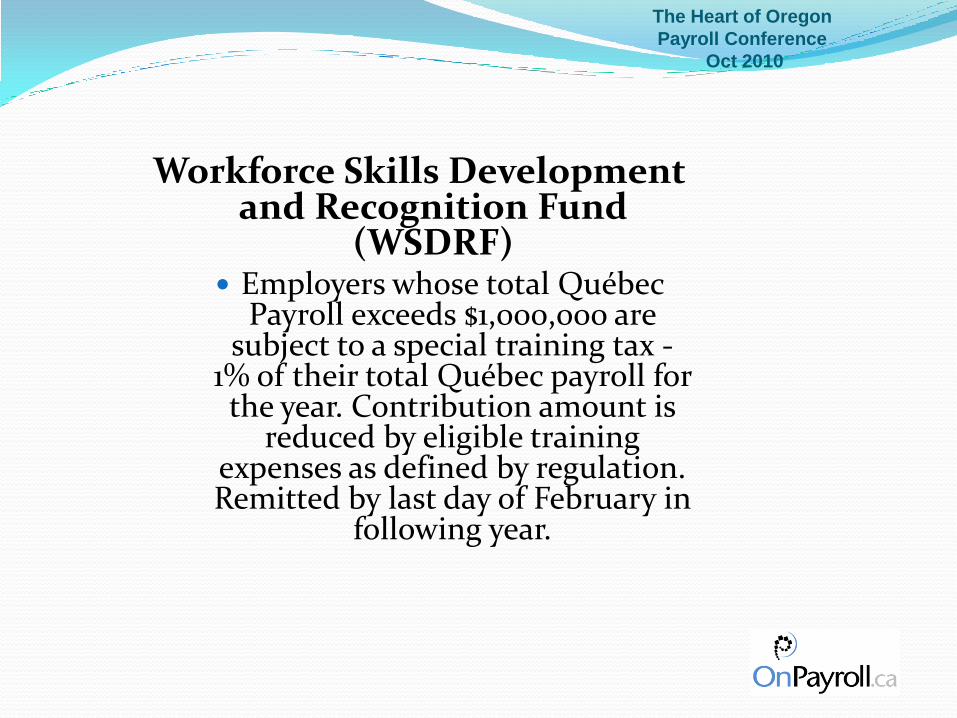

Workforce Skills Development and Recognition Fund

(WSDRF) Employers whose total Québec

Payroll exceeds $1,000,000 are subject to a special training tax -

1% of their total Québec payroll for the year. Contribution amount is

reduced by eligible training expenses as defined by regulation. Remitted by last day of February in

following year.

![JD Edwards EnterpriseOne Applications Canadian Payroll ... · [1]JD Edwards EnterpriseOne Applications Canadian Payroll Implementation Guide Release 9.1 E15127-05 July 2019](https://img.pdfslide.net/doc/110x75/5f7a45016ccd8f3ab16c47d7/jd-edwards-enterpriseone-applications-canadian-payroll-1jd-edwards-enterpriseone.jpg)