Embed Size (px)

Citation preview

Cassava in Asia: Exposing the drivers and trajectories of the hidden ingredient in global supply chains

Dr Jonathan Newby CIAT Asia, Hanoi

World Congress on Roots and Tubers 18th – 22nd January 2016 Nanning, China

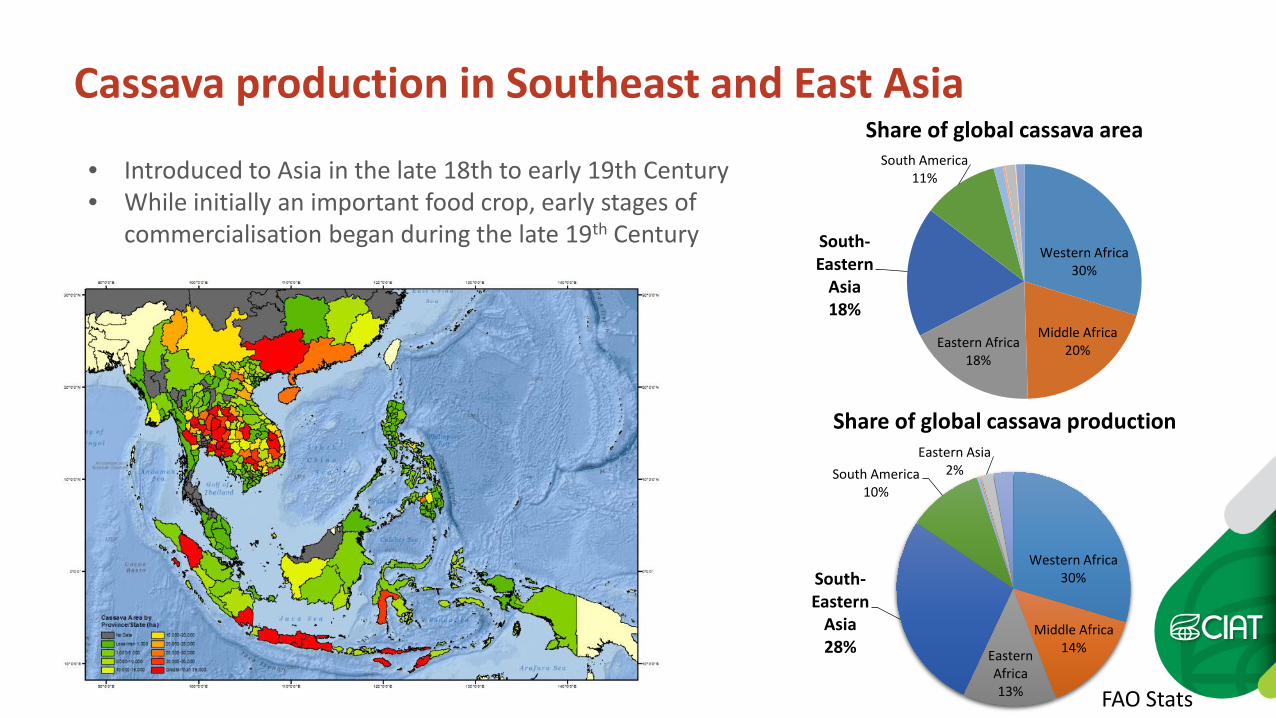

Cassava production in Southeast and East Asia

Western Africa 30%

Middle Africa 14% Eastern

Africa 13%

South-Eastern

Asia 28%

South America 10%

Eastern Asia 2%

Western Africa 30%

Middle Africa 20% Eastern Africa

18%

South-Eastern

Asia 18%

South America 11%

Share of global cassava area

Share of global cassava production

• Introduced to Asia in the late 18th to early 19th Century • While initially an important food crop, early stages of

commercialisation began during the late 19th Century

FAO Stats

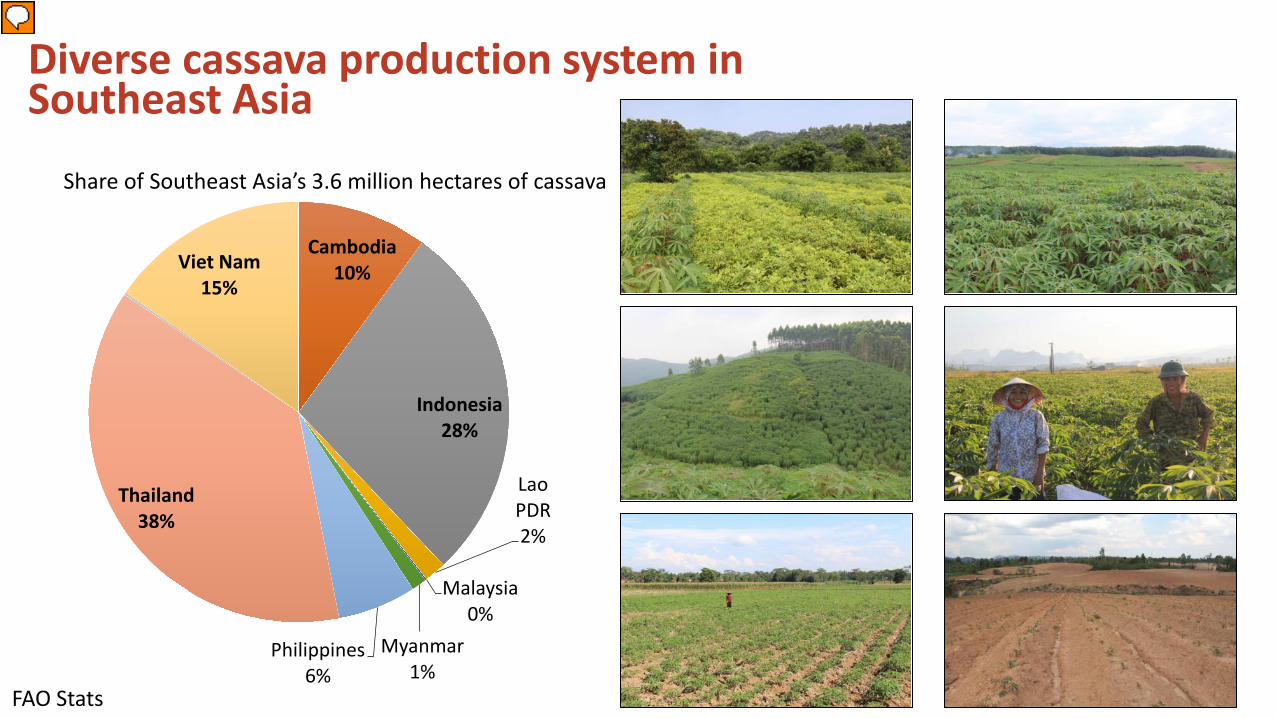

Diverse cassava production system in Southeast Asia

Cambodia 10%

Indonesia 28%

Lao PDR 2%

Malaysia 0%

Myanmar 1%

Philippines 6%

Thailand 38%

Viet Nam 15%

Share of Southeast Asia’s 3.6 million hectares of cassava

FAO Stats

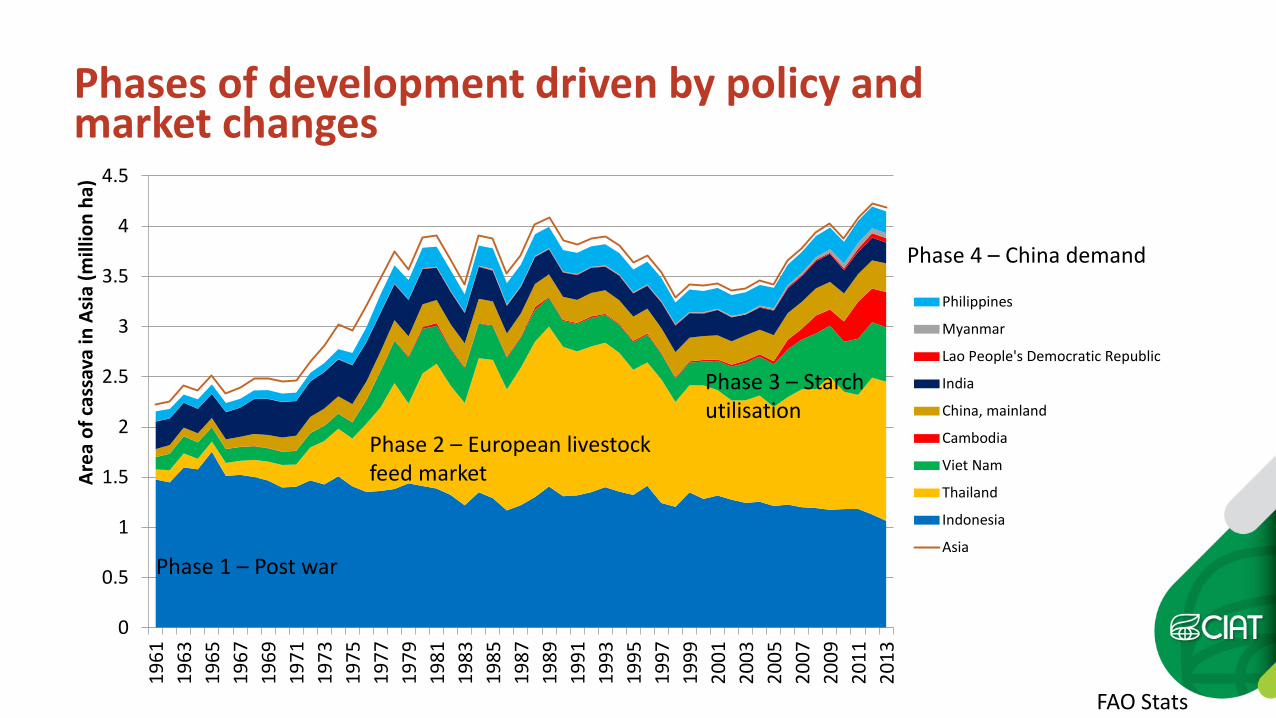

Phases of development driven by policy and market changes

0

0.5

1

1.5

2

2.5

3

3.5

4

4.519

6119

6319

6519

6719

6919

7119

7319

7519

7719

7919

8119

8319

8519

8719

8919

9119

9319

9519

9719

9920

0120

0320

0520

0720

0920

1120

13

Area

of c

assa

va in

Asi

a (m

illio

n ha

)

Philippines

Myanmar

Lao People's Democratic Republic

India

China, mainland

Cambodia

Viet Nam

Thailand

Indonesia

AsiaPhase 1 – Post war

Phase 2 – European livestock feed market

Phase 3 – Starch utilisation

Phase 4 – China demand

FAO Stats

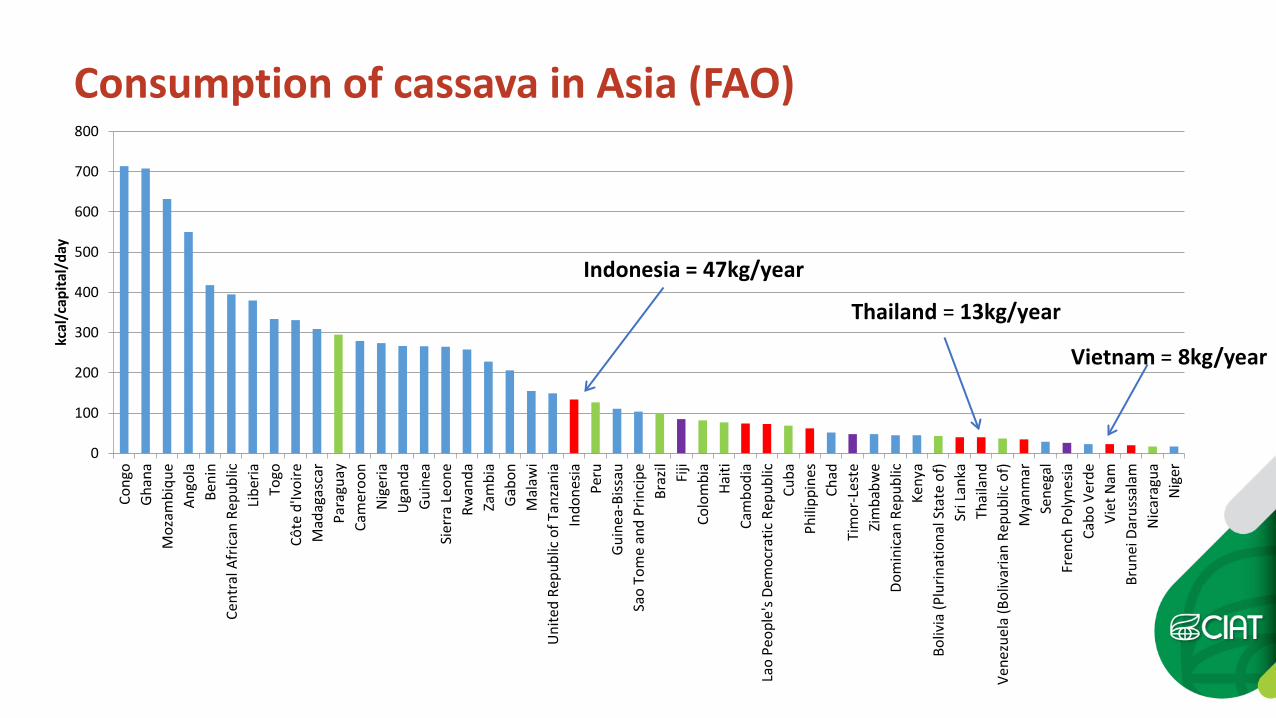

Consumption of cassava in Asia (FAO)

0

100

200

300

400

500

600

700

800Co

ngo

Ghan

aM

ozam

biqu

eAn

gola

Beni

nCe

ntra

l Afr

ican

Rep

ublic

Libe

riaTo

goCô

te d

'Ivoi

reM

adag

asca

rPa

ragu

ayCa

mer

oon

Nig

eria

Uga

nda

Guin

eaSi

erra

Leo

neRw

anda

Zam

bia

Gabo

nM

alaw

iU

nite

d Re

publ

ic o

f Tan

zani

aIn

done

siaPe

ruGu

inea

-Biss

auSa

o To

me

and

Prin

cipe

Braz

ilFi

jiCo

lom

bia

Haiti

Cam

bodi

aLa

o Pe

ople

's De

moc

ratic

Rep

ublic

Cuba

Phili

ppin

esCh

adTi

mor

-Les

teZi

mba

bwe

Dom

inic

an R

epub

licKe

nya

Boliv

ia (P

lurin

atio

nal S

tate

of)

Sri L

anka

Thai

land

Vene

zuel

a (B

oliv

aria

n Re

publ

ic o

f)M

yanm

arSe

nega

lFr

ench

Pol

ynes

iaCa

bo V

erde

Viet

Nam

Brun

ei D

arus

sala

mN

icar

agua

Nig

er

kcal

/cap

ital/

day

Indonesia = 47kg/year

Thailand = 13kg/year

Vietnam = 8kg/year

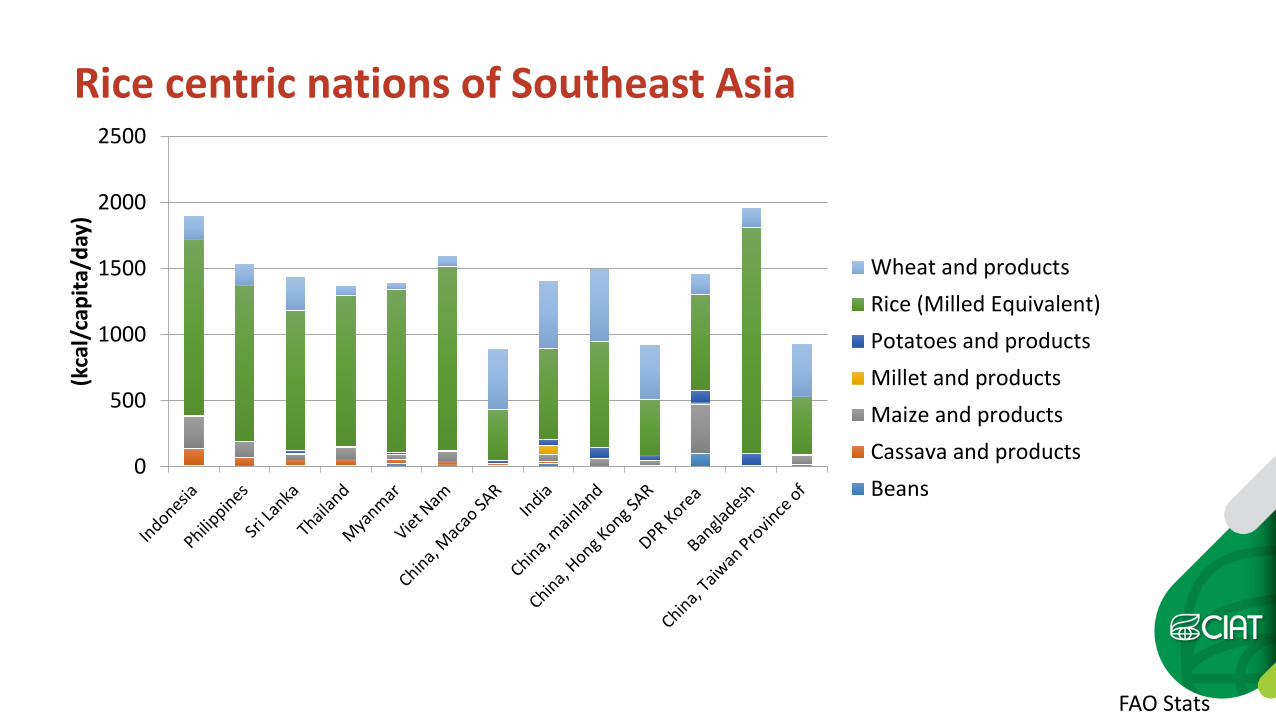

Rice centric nations of Southeast Asia

0

500

1000

1500

2000

2500

(kca

l/ca

pita

/day

)

Wheat and productsRice (Milled Equivalent)Potatoes and productsMillet and productsMaize and productsCassava and productsBeans

FAO Stats

Cassava food value chains in Southeast Asia

Over 306,000 cassava households in Nusa Tenggara Timur – 85% sell no cassava

Still plays an important role in the upland subsistence oriented livelihoods

Percent of households not marketing any cassava production

G.Smith

Remains a hidden ingredient in global supply chains • Cassava still has a reputation of being grown as a

secondary refuge crop grown by poor upland farmers

• Little appreciation of its modern application, with consumers unaware of their consumption and interactions with cassava starch

• Historically, a low priority of national governments

• Largely off the donor radar

• Limited private sector investment beyond the processing industry

Population, economic growth and demand in Asia

0%

10%

20%

30%

40%

50%

60%

Chin

a

Indi

a

Indo

nesia

Bang

lade

sh

Japa

n

Phili

ppin

es

Viet

nam

Thai

land

Mya

nmar

Kore

a, R

ep.

Mal

aysia

Nep

al

Kore

a, D

em. R

ep.Cu

mul

ativ

e sh

are

of g

loba

l pop

ulat

ion

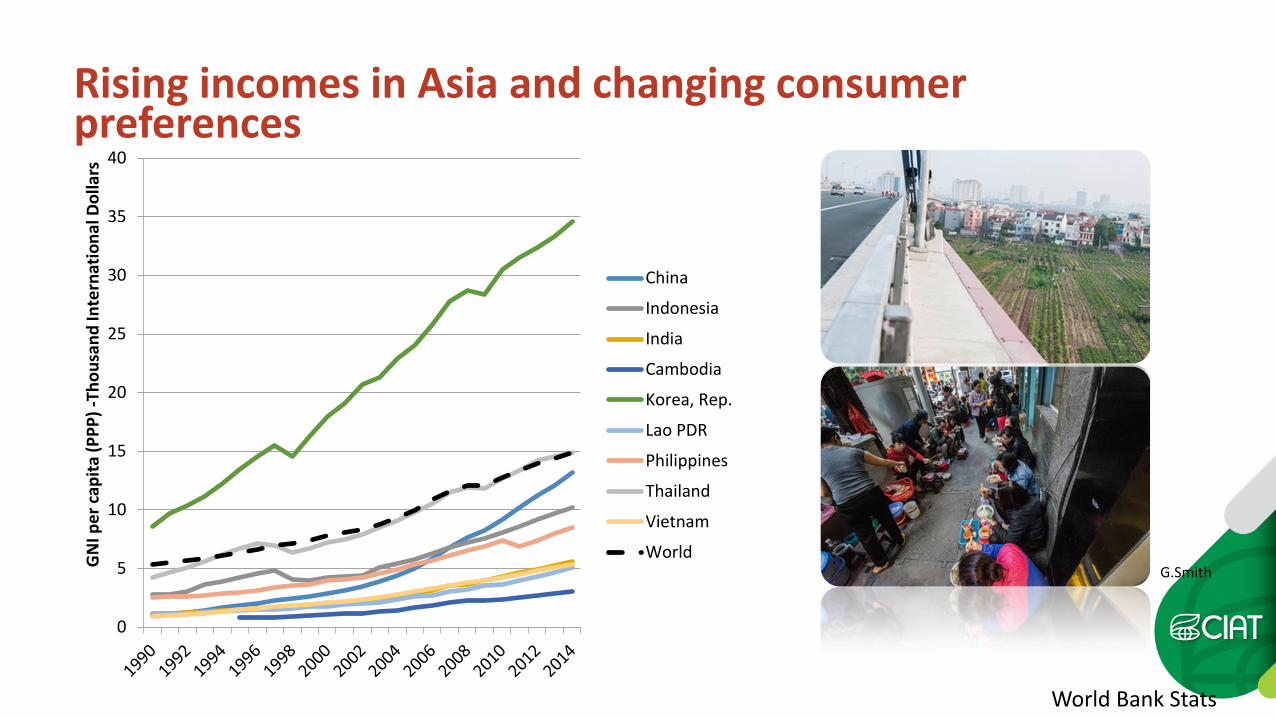

Rising incomes in Asia and changing consumer preferences

0

5

10

15

20

25

30

35

40

GN

I per

capi

ta (P

PP) -

Thou

sand

Inte

rnat

iona

l Dol

lars

China

Indonesia

India

Cambodia

Korea, Rep.

Lao PDR

Philippines

Thailand

Vietnam

World

World Bank Stats

G.Smith

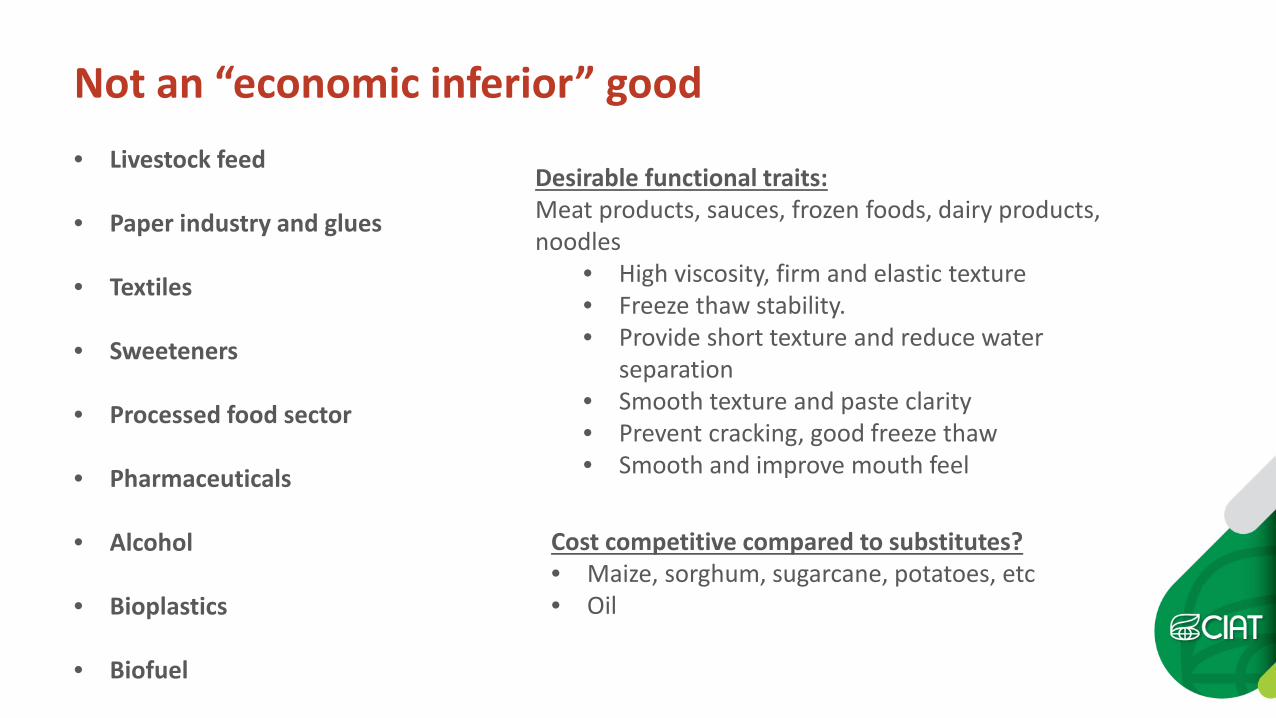

Not an “economic inferior” good • Livestock feed

• Paper industry and glues

• Textiles

• Sweeteners

• Processed food sector

• Pharmaceuticals

• Alcohol

• Bioplastics

• Biofuel

Desirable functional traits: Meat products, sauces, frozen foods, dairy products, noodles

• High viscosity, firm and elastic texture • Freeze thaw stability. • Provide short texture and reduce water

separation • Smooth texture and paste clarity • Prevent cracking, good freeze thaw • Smooth and improve mouth feel

Cost competitive compared to substitutes? • Maize, sorghum, sugarcane, potatoes, etc • Oil

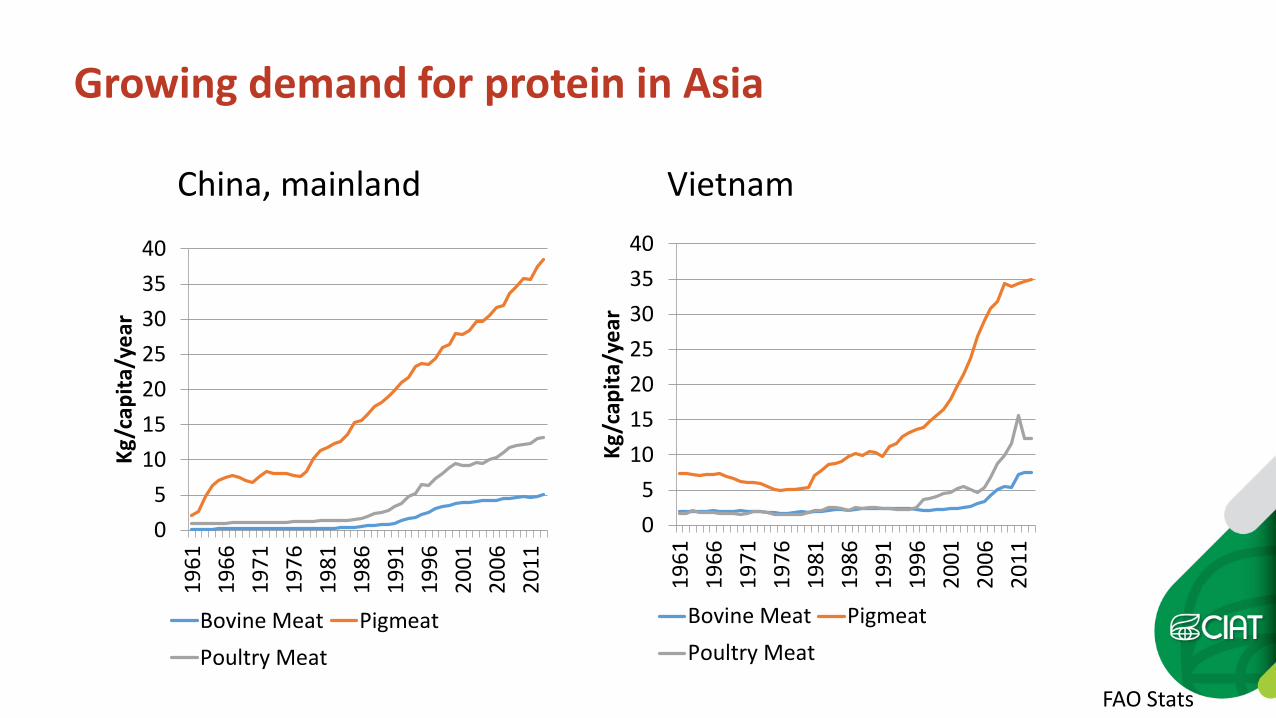

Growing demand for protein in Asia

China, mainland

05

10152025303540

1961

1966

1971

1976

1981

1986

1991

1996

2001

2006

2011

Kg/c

apita

/yea

r

Bovine Meat PigmeatPoultry Meat

Vietnam

05

10152025303540

1961

1966

1971

1976

1981

1986

1991

1996

2001

2006

2011

Kg/c

apita

/yea

r Bovine Meat PigmeatPoultry Meat

FAO Stats

0

0.5

1

1.5

2

2.5

3

3.5

4

4.520

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Valu

e of

exp

orts

(Bill

ion

USD

)

Cassava (fresh and dried) Cassava Starch

Multi-billion dollar export industry

Comtrade

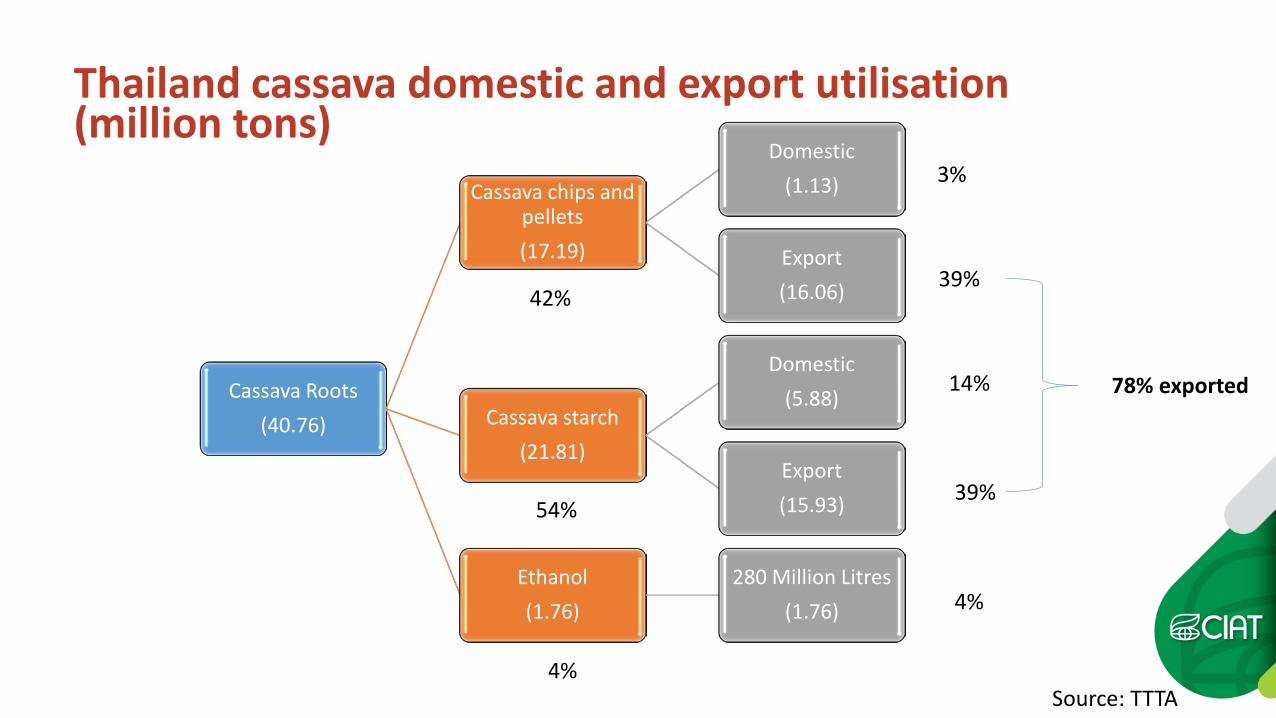

Cassava Roots (40.76)

Cassava chips and pellets (17.19)

Domestic (1.13)

Export (16.06)

Cassava starch (21.81)

Domestic (5.88)

Export (15.93)

Ethanol (1.76)

280 Million Litres (1.76)

42%

54%

4%

3%

39%

39%

4%

14%

Thailand cassava domestic and export utilisation (million tons)

78% exported

Source: TTTA

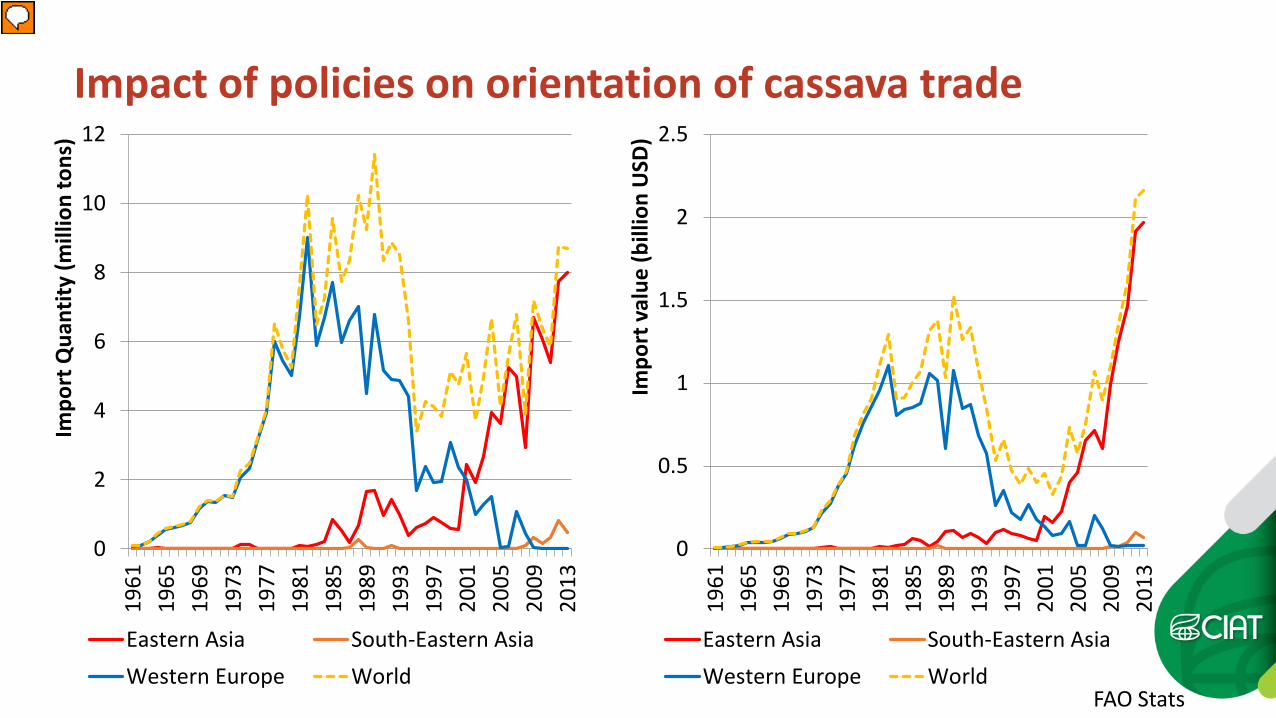

0

2

4

6

8

10

1219

6119

6519

6919

7319

7719

8119

8519

8919

9319

9720

0120

0520

0920

13

Impo

rt Q

uant

ity (m

illio

n to

ns)

Eastern Asia South-Eastern AsiaWestern Europe World

0

0.5

1

1.5

2

2.5

1961

1965

1969

1973

1977

1981

1985

1989

1993

1997

2001

2005

2009

2013

Impo

rt v

alue

(bill

ion

USD

) Eastern Asia South-Eastern AsiaWestern Europe World

Impact of policies on orientation of cassava trade

FAO Stats

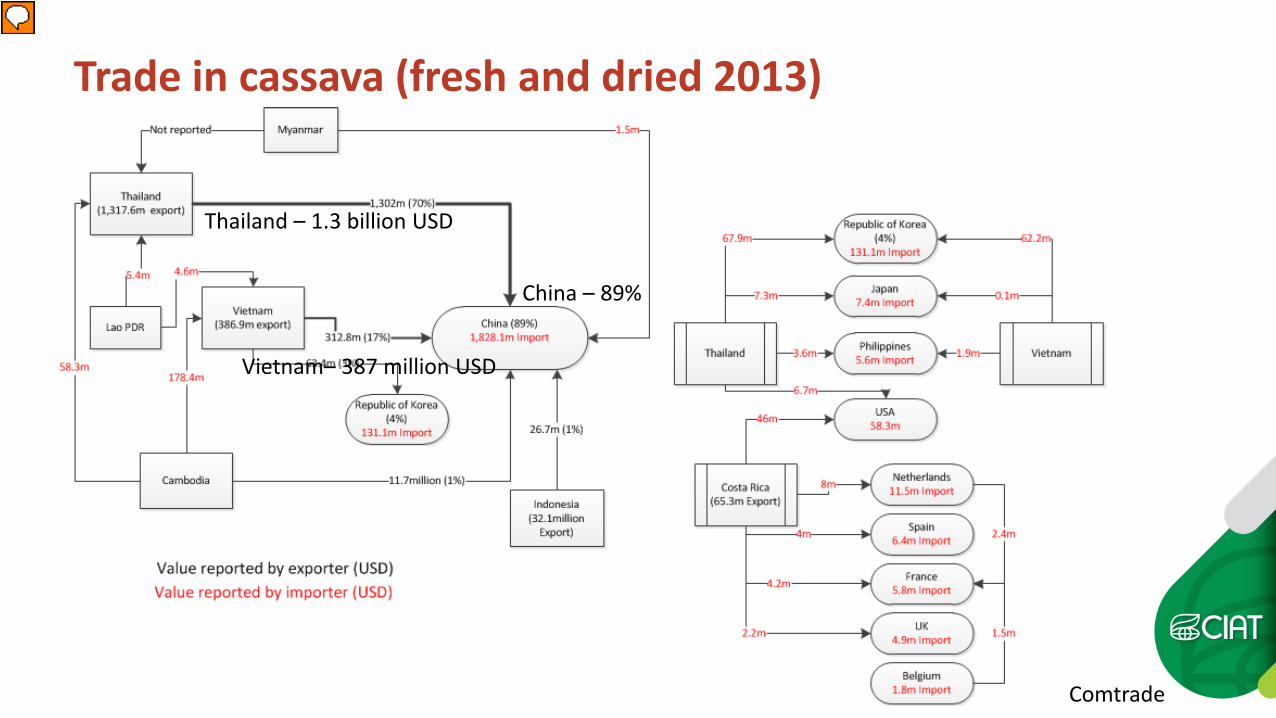

Trade in cassava (fresh and dried 2013)

Comtrade

China – 89%

Thailand – 1.3 billion USD

Vietnam– 387 million USD

0

50

100

150

200

250

300

350

40019

90

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Cass

ava

Area

(tho

usan

d ha

)

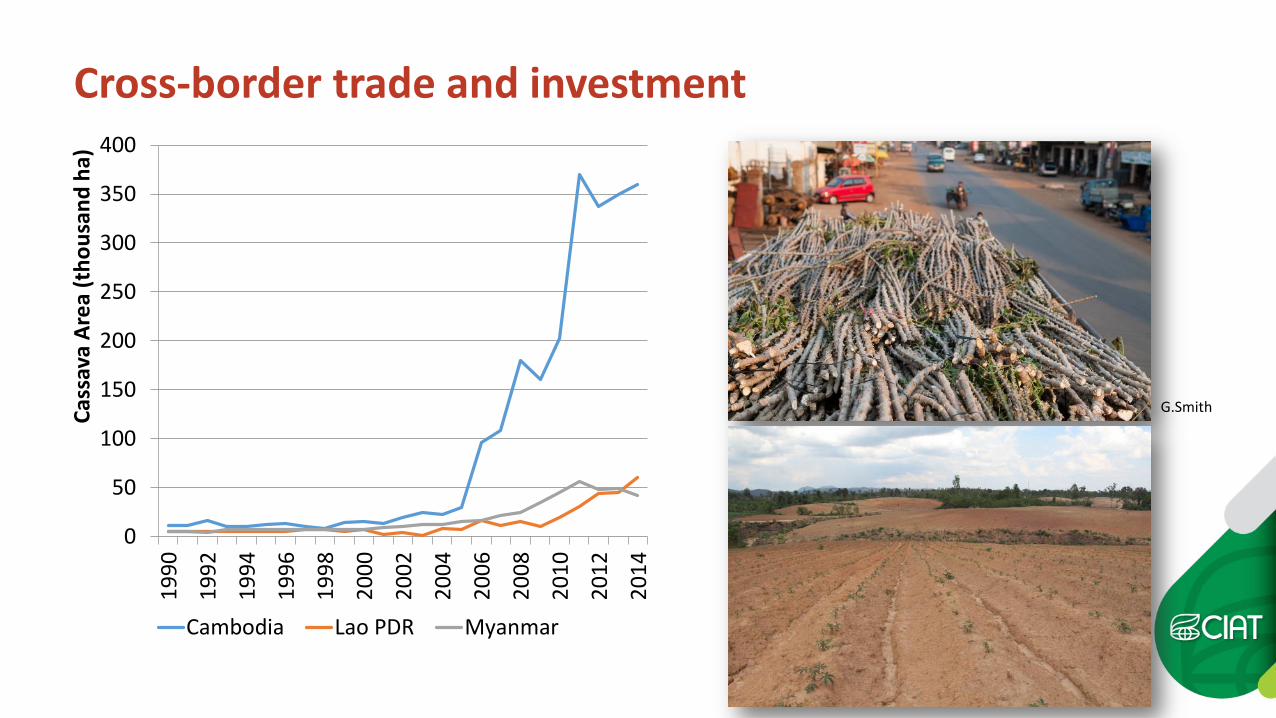

Cambodia Lao PDR Myanmar

Cross-border trade and investment

G.Smith

00.5

11.5

22.5

33.5

44.5

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Expo

rt V

alue

(Bill

ion

USD

)

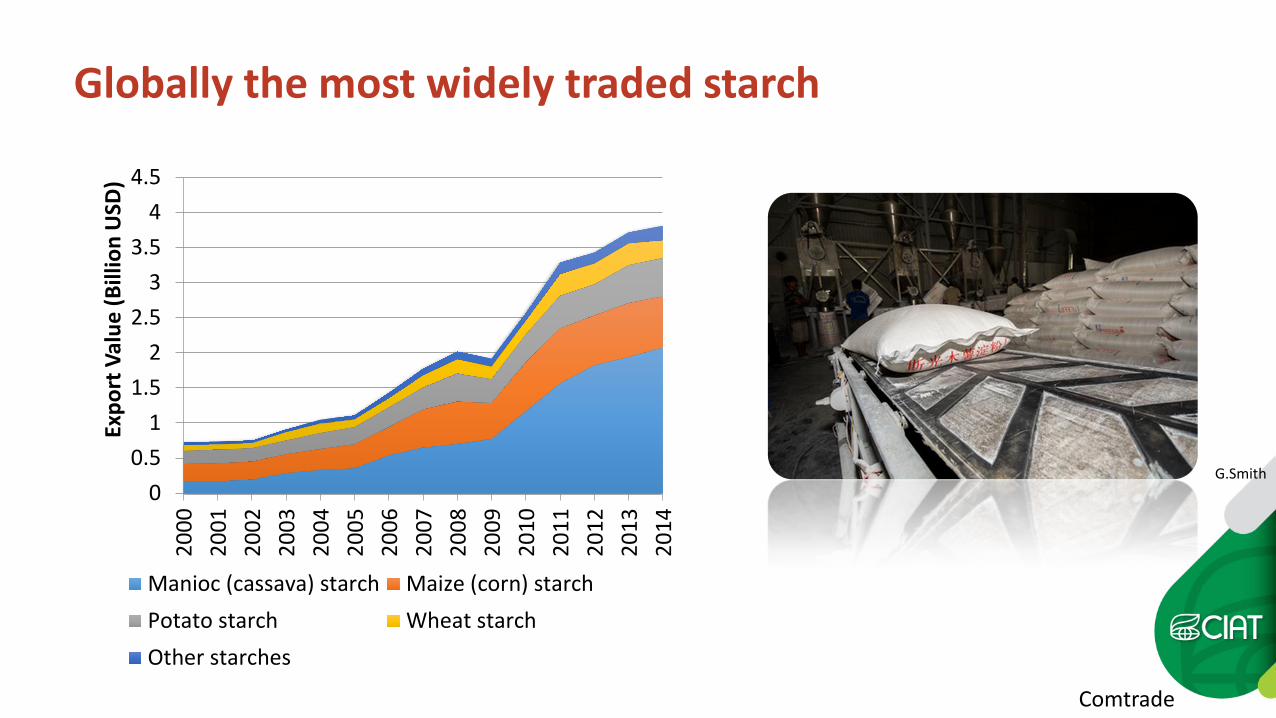

Manioc (cassava) starch Maize (corn) starchPotato starch Wheat starchOther starches

Globally the most widely traded starch

Comtrade

G.Smith

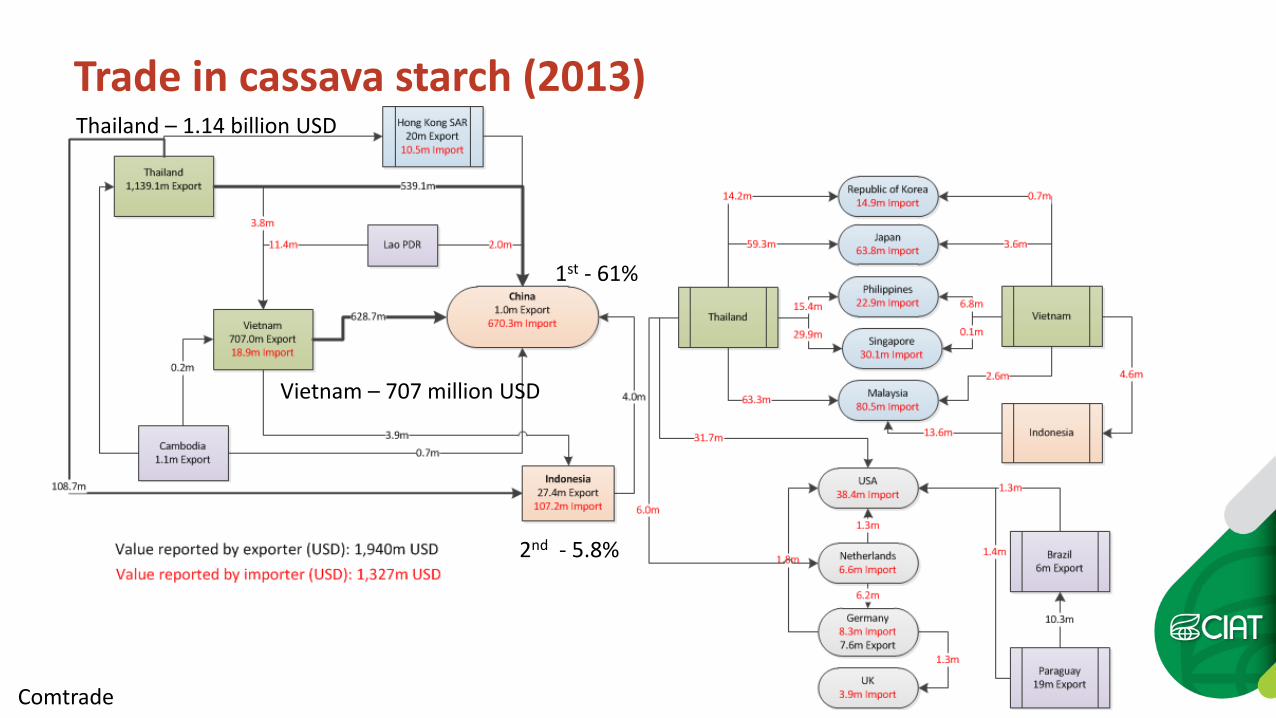

Trade in cassava starch (2013)

1st - 61%

2nd - 5.8%

Comtrade

Vietnam – 707 million USD

Thailand – 1.14 billion USD

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

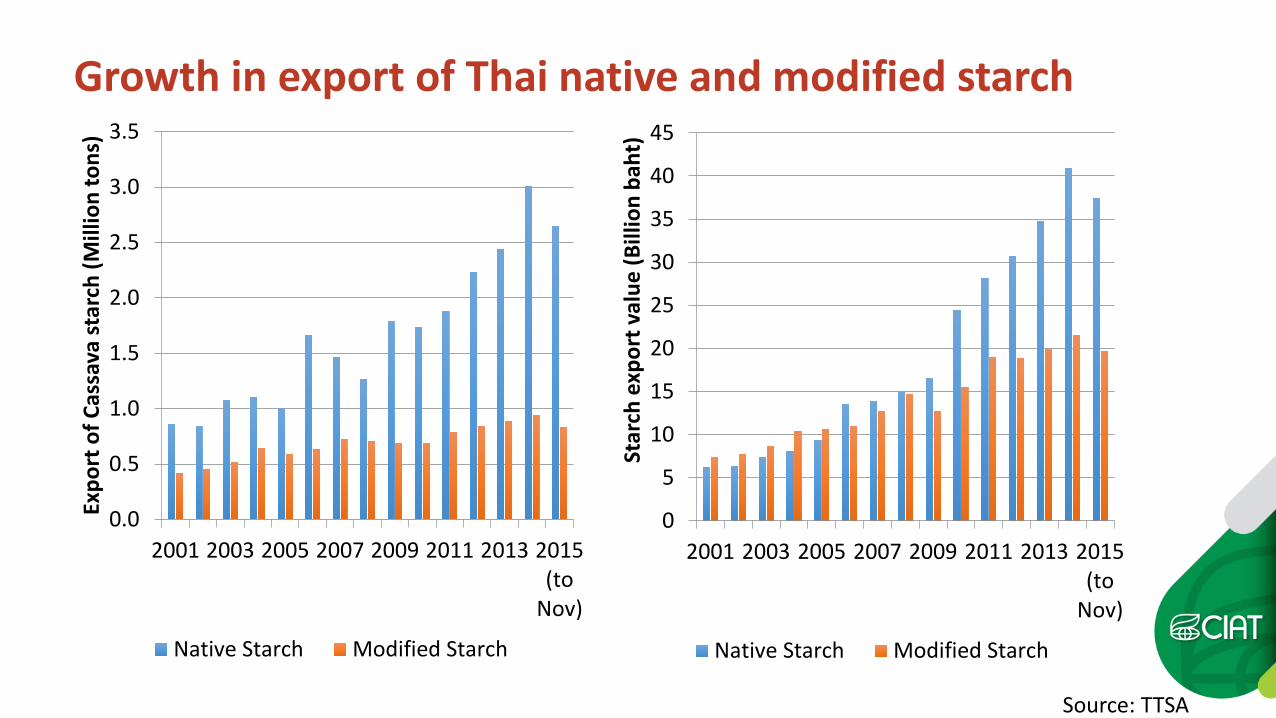

2001 2003 2005 2007 2009 2011 2013 2015(to

Nov)

Expo

rt o

f Cas

sava

star

ch (M

illio

n to

ns)

Native Starch Modified Starch

0

5

10

15

20

25

30

35

40

45

2001 2003 2005 2007 2009 2011 2013 2015(to

Nov)St

arch

exp

ort v

alue

(Bill

ion

baht

) Native Starch Modified Starch

Growth in export of Thai native and modified starch

Source: TTSA

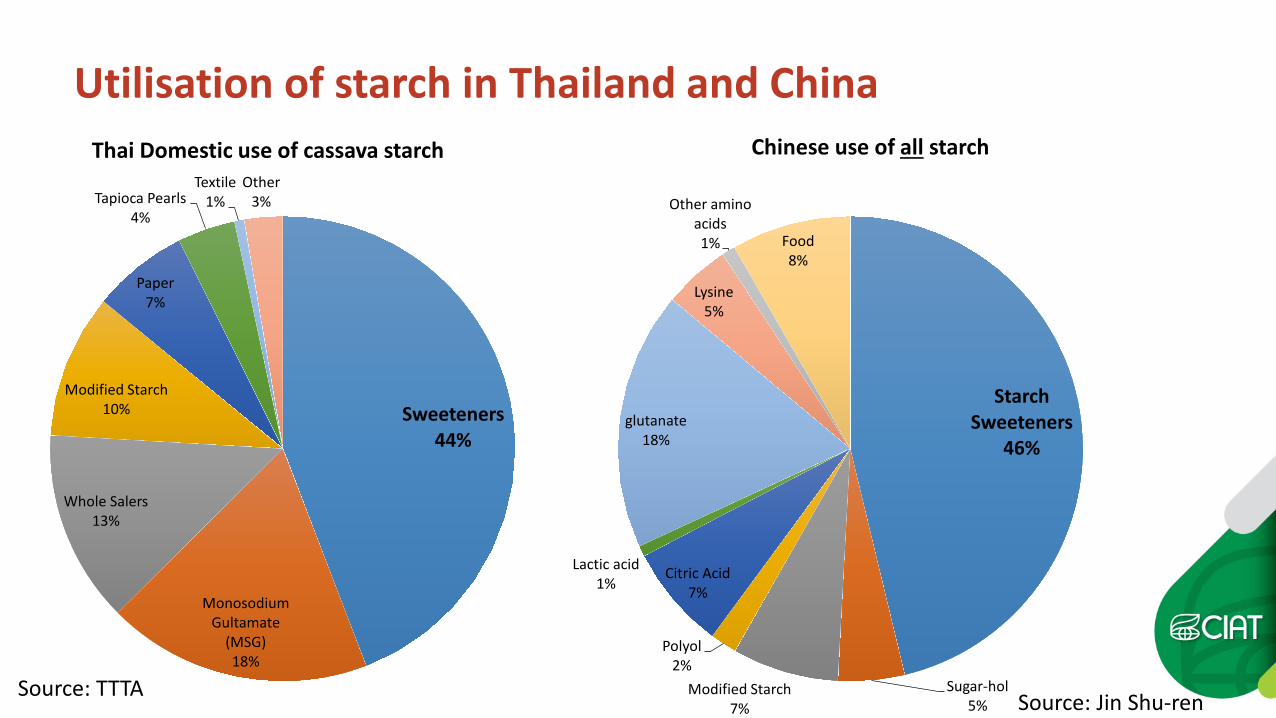

Sweeteners 44%

Monosodium Gultamate

(MSG) 18%

Whole Salers 13%

Modified Starch 10%

Paper 7%

Tapioca Pearls 4%

Textile 1%

Other 3%

Starch Sweeteners

46%

Sugar-hol 5%

Modified Starch 7%

Polyol 2%

Citric Acid 7%

Lactic acid 1%

glutanate 18%

Lysine 5%

Other amino acids 1% Food

8%

Utilisation of starch in Thailand and China Thai Domestic use of cassava starch Chinese use of all starch

Source: TTTA Source: Jin Shu-ren

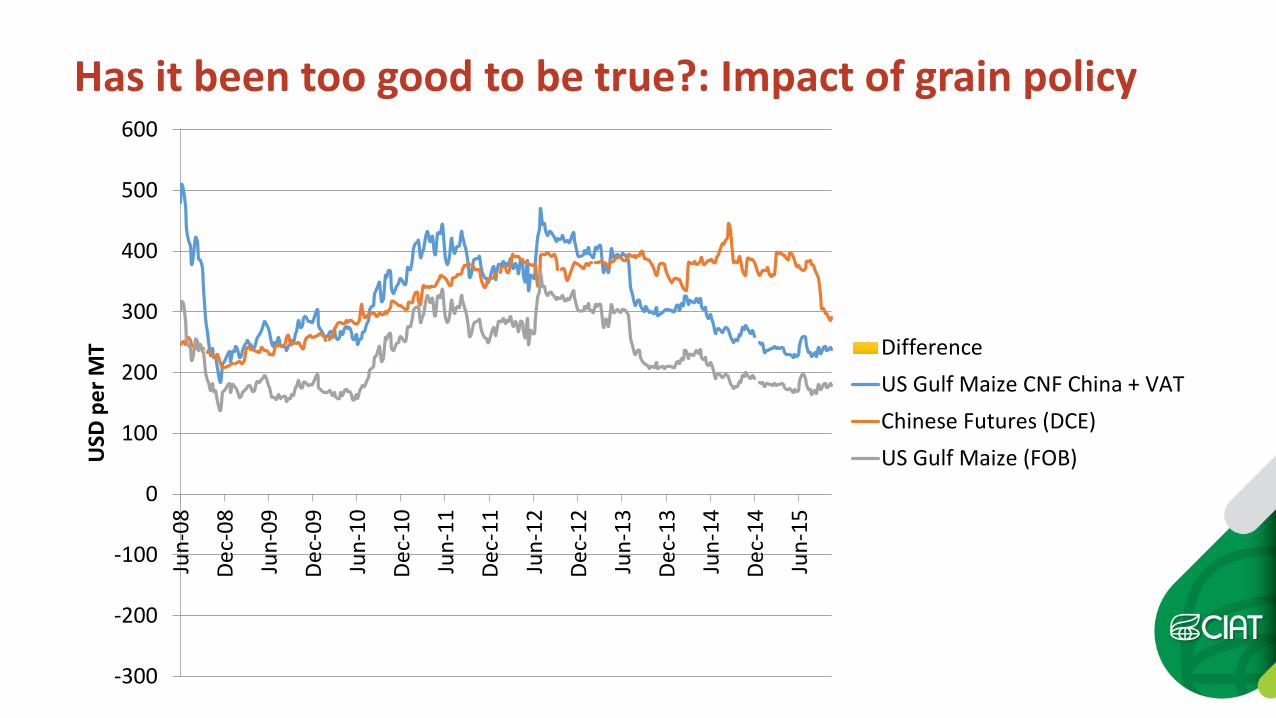

-300

-200

-100

0

100

200

300

400

500

600

Jun-

08

Dec-

08

Jun-

09

Dec-

09

Jun-

10

Dec-

10

Jun-

11

Dec-

11

Jun-

12

Dec-

12

Jun-

13

Dec-

13

Jun-

14

Dec-

14

Jun-

15

USD

per

MT Difference

US Gulf Maize CNF China + VATChinese Futures (DCE)US Gulf Maize (FOB)

Has it been too good to be true?: Impact of grain policy

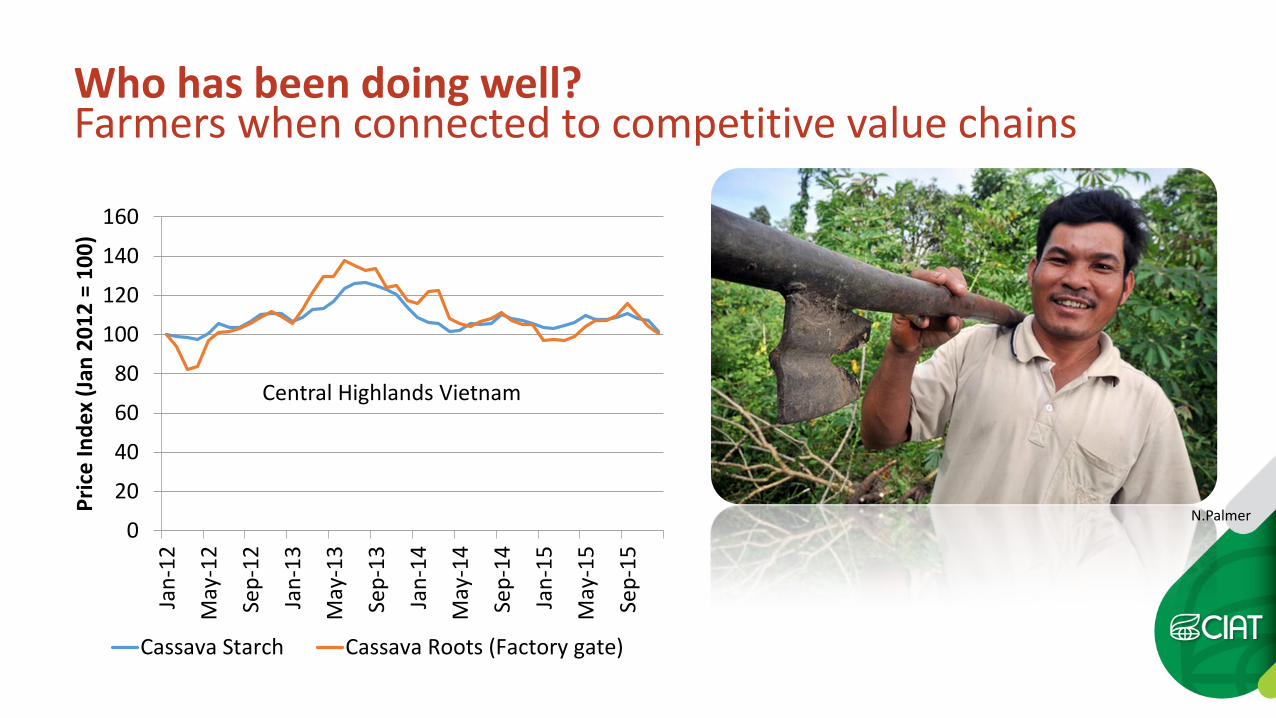

Who has been doing well? Farmers when connected to competitive value chains

0

20

40

60

80

100

120

140

160

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Jan-

14

May

-14

Sep-

14

Jan-

15

May

-15

Sep-

15

Pric

e In

dex

(Jan

201

2 =

100)

Cassava Starch Cassava Roots (Factory gate)

Central Highlands Vietnam

N.Palmer

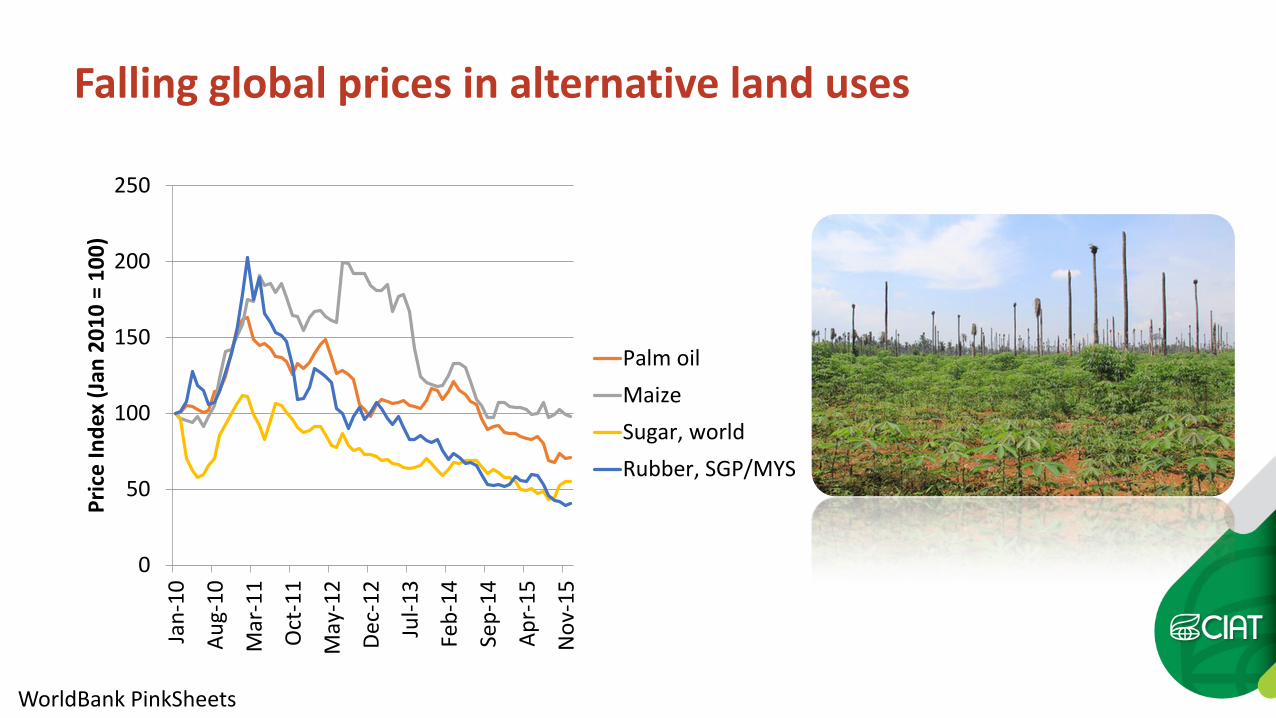

Falling global prices in alternative land uses

0

50

100

150

200

250Ja

n-10

Aug-

10

Mar

-11

Oct

-11

May

-12

Dec-

12

Jul-1

3

Feb-

14

Sep-

14

Apr-

15

Nov

-15

Pric

e In

dex

(Jan

201

0 =

100)

Palm oilMaizeSugar, worldRubber, SGP/MYS

WorldBank PinkSheets

0

100

200

300

400

500

600

700

0

100

200

300

400

500

600

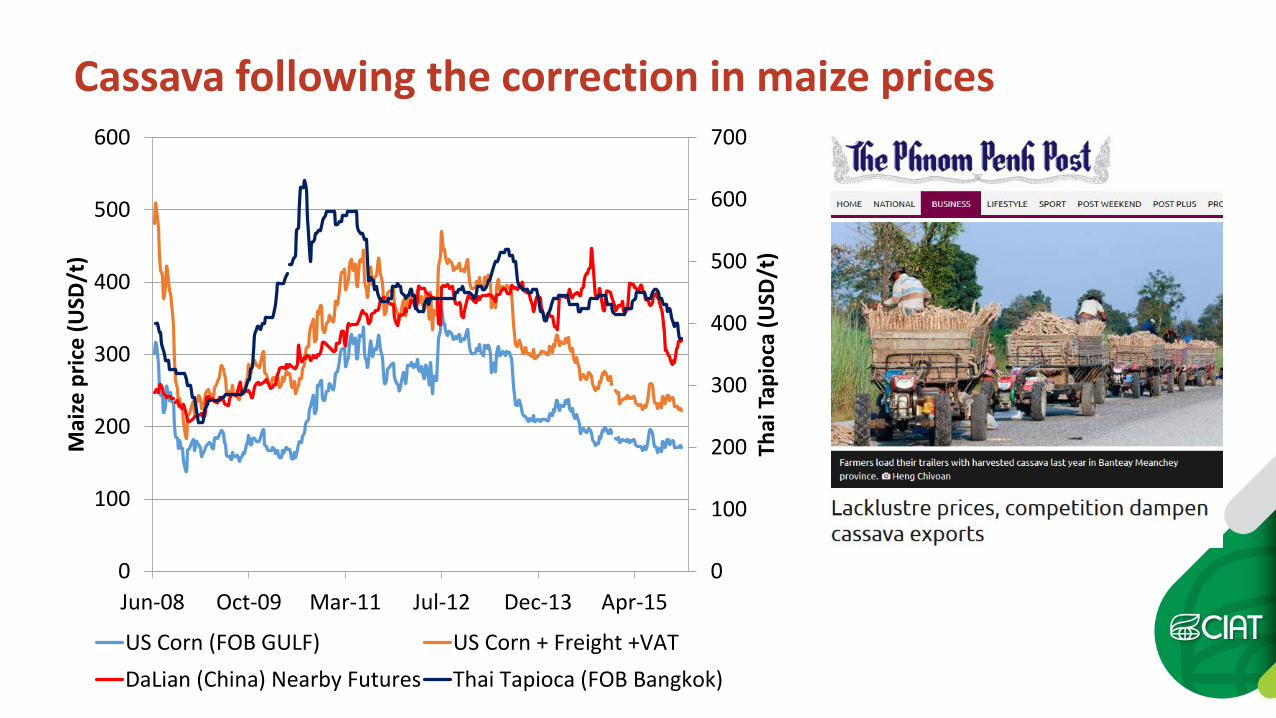

Jun-08 Oct-09 Mar-11 Jul-12 Dec-13 Apr-15

Thai

Tap

ioca

(USD

/t)

Mai

ze p

rice

(USD

/t)

US Corn (FOB GULF) US Corn + Freight +VATDaLian (China) Nearby Futures Thai Tapioca (FOB Bangkok)

Cassava following the correction in maize prices

• Small-scale labor intensive starch processors have found it difficult to compete for raw material unless they have a niche market • E.g. Small-scale processors in Cambodia

closed as they struggled to compete for roots

• Large processors of raw material, but not linked to Chinese market • E.g. Biofuel industry in Vietnam

• Deep processors depending on cassava starch,

but competing against maize based products • E.g. Glucose, sorbitol producers

• Limited utilisation in domestic livestock sector

Who has been doing it tough?

G.Smith

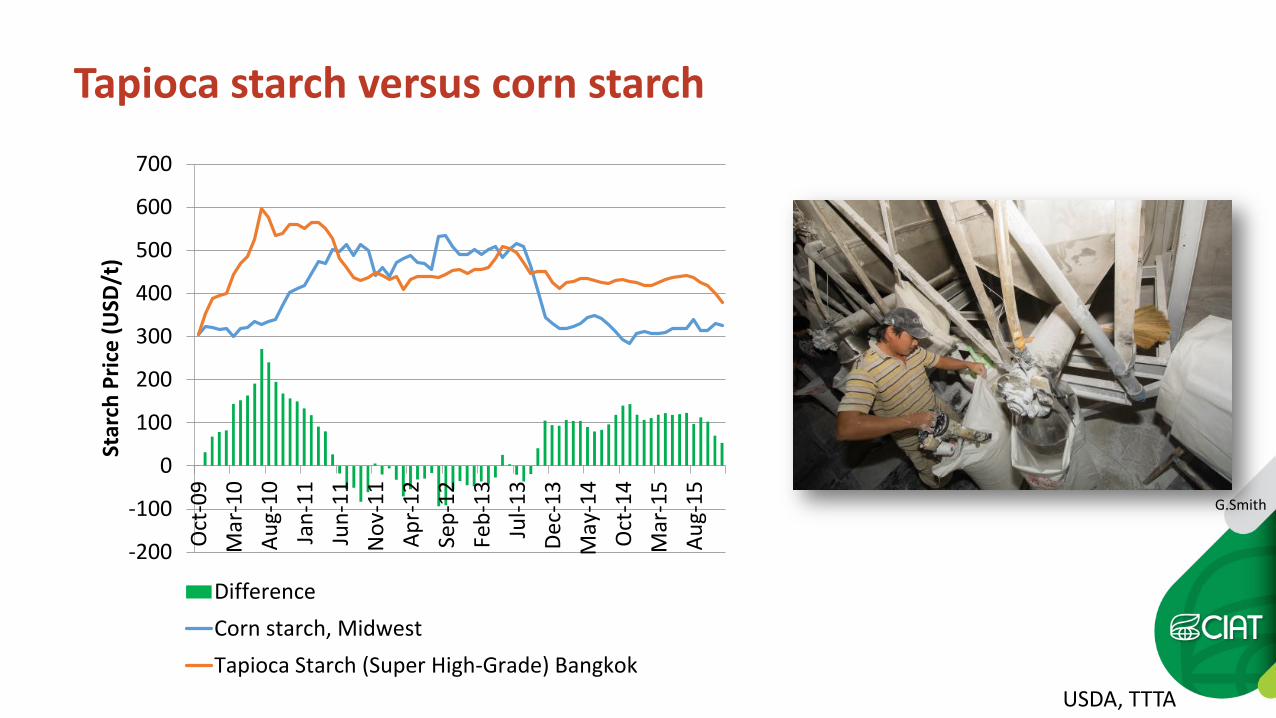

-200

-100

0

100

200

300

400

500

600

700O

ct-0

9M

ar-1

0Au

g-10

Jan-

11Ju

n-11

Nov

-11

Apr-

12Se

p-12

Feb-

13Ju

l-13

Dec-

13M

ay-1

4O

ct-1

4M

ar-1

5Au

g-15

Star

ch P

rice

(USD

/t)

DifferenceCorn starch, MidwestTapioca Starch (Super High-Grade) Bangkok

Tapioca starch versus corn starch

USDA, TTTA

G.Smith

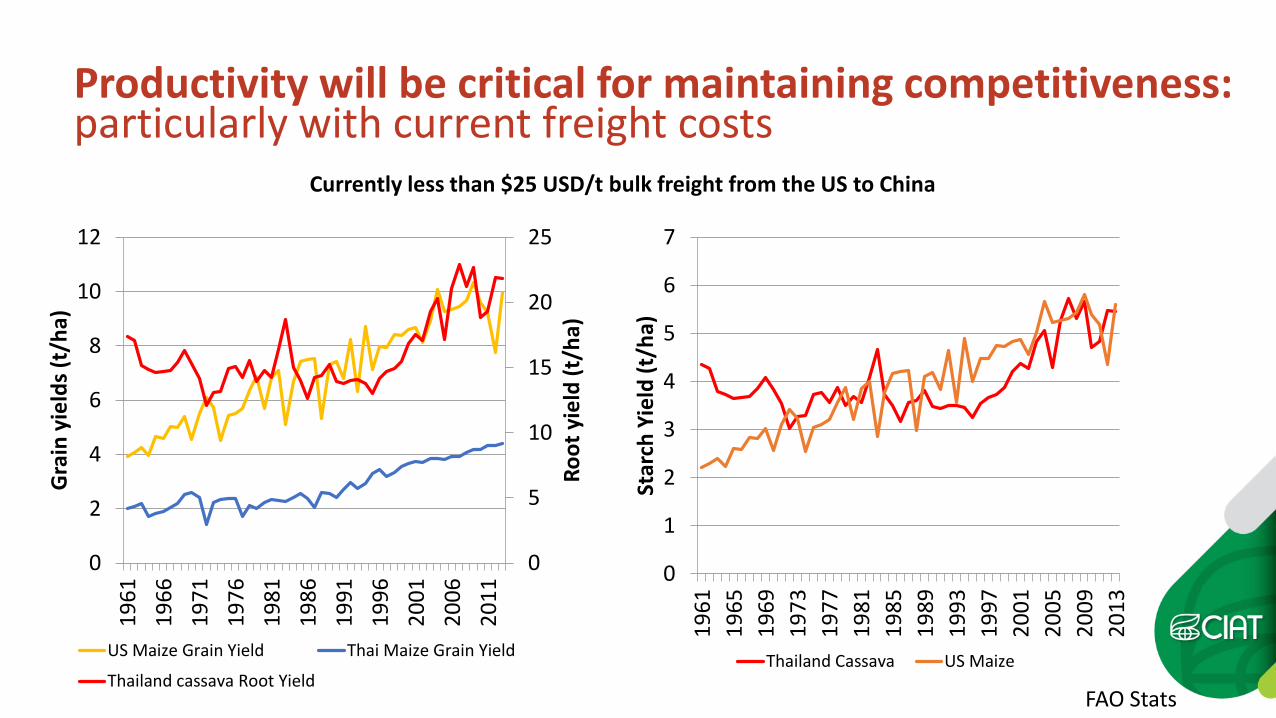

Productivity will be critical for maintaining competitiveness: particularly with current freight costs

0

5

10

15

20

25

0

2

4

6

8

10

12

1961

1966

1971

1976

1981

1986

1991

1996

2001

2006

2011

Root

yie

ld (t

/ha)

Gra

in y

ield

s (t/

ha)

US Maize Grain Yield Thai Maize Grain Yield

Thailand cassava Root Yield

0

1

2

3

4

5

6

7

1961

1965

1969

1973

1977

1981

1985

1989

1993

1997

2001

2005

2009

2013

Star

ch Y

ield

(t/h

a)

Thailand Cassava US Maize

Currently less than $25 USD/t bulk freight from the US to China

FAO Stats

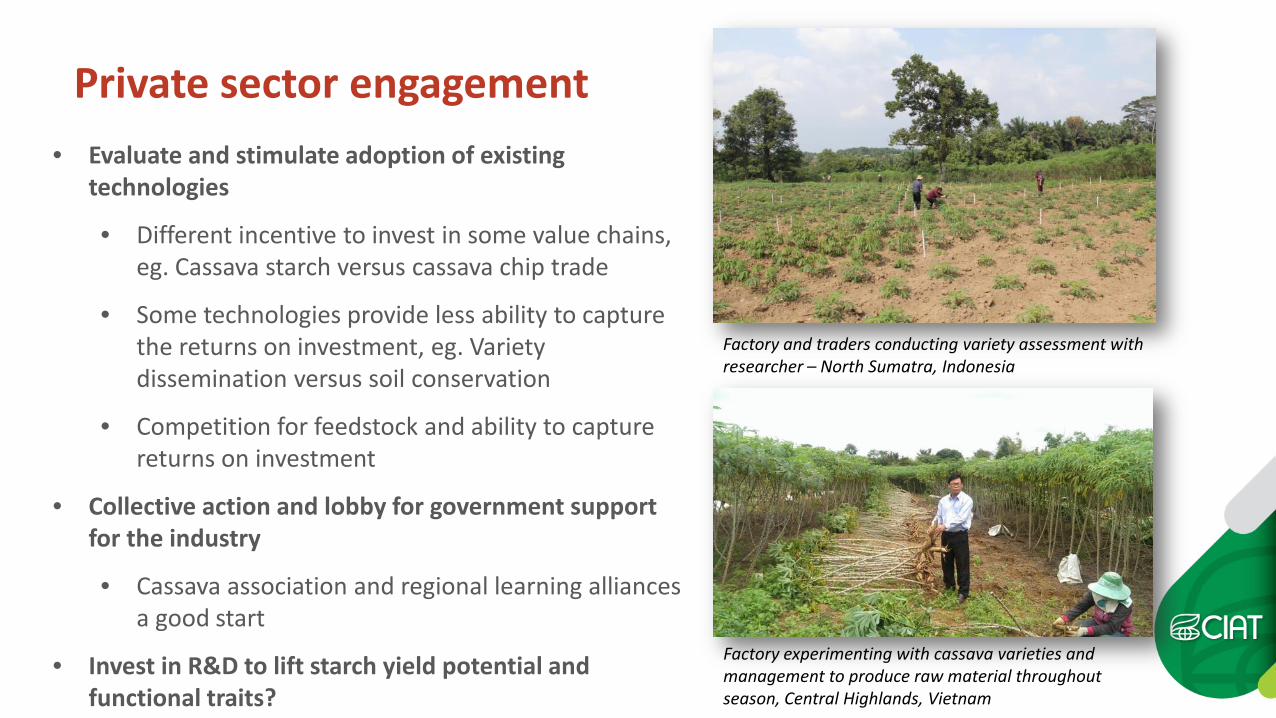

Private sector engagement

• Evaluate and stimulate adoption of existing technologies

• Different incentive to invest in some value chains, eg. Cassava starch versus cassava chip trade

• Some technologies provide less ability to capture the returns on investment, eg. Variety dissemination versus soil conservation

• Competition for feedstock and ability to capture returns on investment

• Collective action and lobby for government support for the industry

• Cassava association and regional learning alliances a good start

• Invest in R&D to lift starch yield potential and functional traits?

Factory and traders conducting variety assessment with researcher – North Sumatra, Indonesia

Factory experimenting with cassava varieties and management to produce raw material throughout season, Central Highlands, Vietnam

Public sector support • Private sector involvement not a panacea

• Recognise that there are treats to productivity on the horizon that need public sector leadership • Land degradation • Emerging pests and diseases in Asia

• Opportunity for national governments to deliver

both improve rural livelihoods for smallholders and economic development • Conditions for inclusive development

• Be proactive rather than let the trajectory of the cassava sector oscillate based on developments in substitute commodities

• Strengthen linkages and partnerships between research, industry, governments and farmers

G.Smith

![CraftConf [Preview] "Empathy - The Hidden Ingredient of Good Software Development"](https://img.pdfslide.net/doc/110x75/58efd73c1a28abd22a8b45fd/craftconf-preview-empathy-the-hidden-ingredient-of-good-software-development.jpg)