Embed Size (px)

Citation preview

INDUSTRIAL MARKETS

Benchmarking the Automotive Industryin Central & Eastern Europe: Creating and Preserving Value

for the Long-term

KPMG IN CENTRAL & EASTERN EUROPE

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Contents

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Introduction 4

Executive Summary 5

Methodology 7

Financial Performance – Determining the 8High Performers

Regulation and Compliance 10

Risk 17

Entering New Markets 29

Generating Value Through Managing 34Performance

Conclusion 43

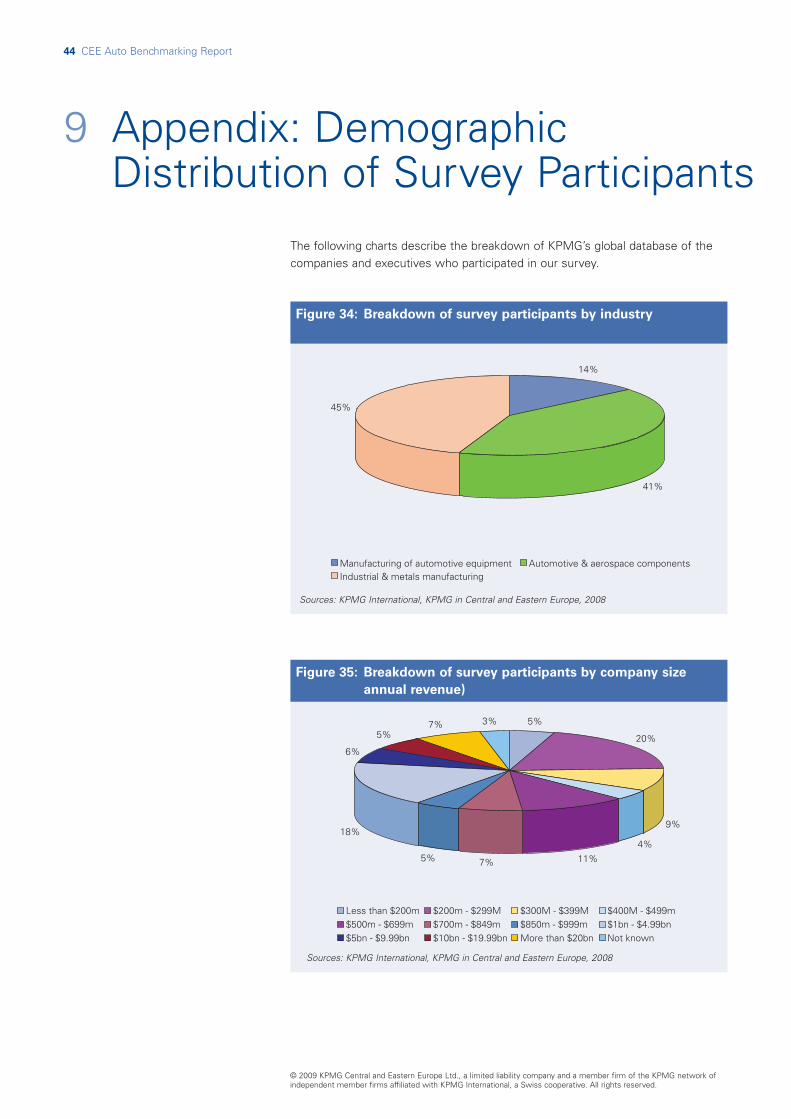

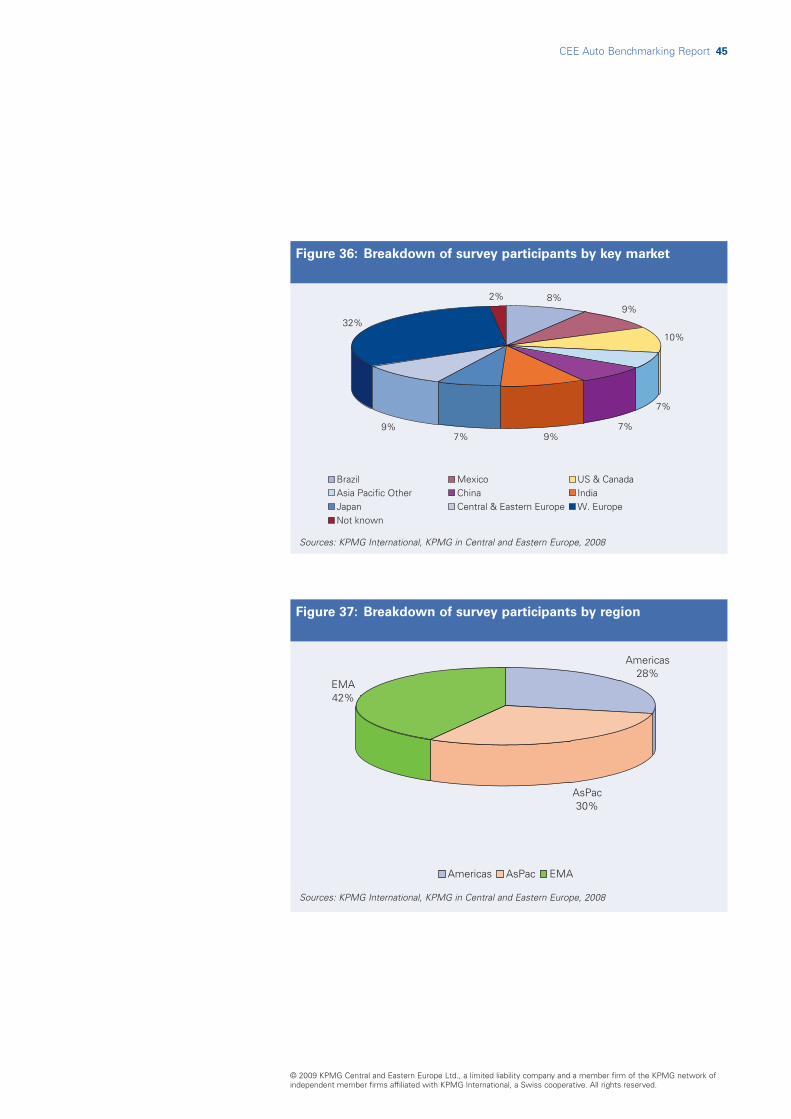

Appendix: Demographic Distribution of 44Survey Participants

KPMG Information 46

1

2

3

4

5

6

7

8

9

10

The automotive sector in Central and Eastern Europe (CEE) has experiencedunprecedented expansion during much of the last decade, enjoying the benefitsof both growth and investment. Without doubt, the global financial and economicdownturn, which has unfolded during the past six months, will have a majorimpact on the region. The significant decline in consumer demand forautomobiles is causing manufacturers to scale back production with acorresponding effect on the supply chain. Manufacturers and suppliers havealready announced job reduction programs in the region and it is likely that thiswill continue throughout much of 2009. However, CEE's reputation as a cost-effective and productive manufacturing location means that the medium-termoutlook is broadly positive and the issue of value remains forefront in the mindsof the region's automotive executives.

Considering the current environment, executives are no doubt focused onpreserving the value they have created over many years during an era ofsignificant change in one of the world's most dynamic regions. This requiresmany tasks, for example conserving and maintaining cash while simultaneouslyretaining highly skilled human resources. It also mandates the ability to identifyand manage numerous risks, often originating outside the regions’ borders, yetlanding squarely on the door step of local economies with frightening speed.

But executives are equally concerned with creating value. So while risksconfronting the automotive sector and the region may indeed be increasing,some players will likely consider industry upheaval an opportunity to find newplatforms for medium- and long-term growth in both profits and revenue.

To assist executives in the region's automotive sector in gaining insights intovalue creation and value preservation strategies this survey seeks to benchmarka sample of automotive sector companies operating in key countries of Central &Eastern Europe, including the Czech Republic, Hungary, Poland, Romania andSlovakia against their global manufacturing peers. We benchmarked this sampleboth against the automotive sector and again against a wider sample of industrialmanufacturing organizations.

To our readers, we believe, and hope you agree, that the knowledge provided inour survey is beneficial, whatever your role in the organization or the sector as awhole. To the executives who participated in the survey our heartfelt thanks foryour time and efforts to assist this endeavor.

Andrew Sutherland

Head of Automotive Sector for KPMG in Central & Eastern Europe

Introduction

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

CEE Auto Benchmarking Report 5

The emerging markets of Central &Eastern Europe (CEE) are

sometimes considered undersizedmarkets, especially relative to the oftenmentioned BRIC countries: Brazil,Russia, India & China. However, whenit comes to the automotive industry,the region is increasingly oversized, as“original equipment manufacturers”(OEMs) and suppliers continuerelocating to the region for a broadrange of factors including the cost andquality of the workforce; its ideallocation at the nexus between eastand west; as well as an increasinglyfavorable tax environment.

But as suppliers and OEMs continue toset up new facilities and newoperations – either through greenfields, acquisitions or joint ventures –the array of management challengesare increasingly complex. Therefore, inthis survey we have asked automotiveexecutives for their key insights intoissues that cause the most concern aswell as their approach to solving theseproblems.

We have also attempted to go onestep further. To assist executives intheir decision making we havebenchmarked those insights fromexecutives in the region and comparedtheir approach to three separategroups:

� Global industrial manufacturers – ourproprietary database of over 260industrial manufacturing companies

� Global automotive manufacturers – asubset of our database comprisingover 130 vehicle manufacturers andcomponent suppliers

� High performing companies – thosecompanies who met our criteria foroutsized financial performance,representing approximately 5% ofcompanies in the database (pleasesee our sidebar below: Making thegrade).

In a global economy where emergingmarkets and industrialized economiesoften follow divergent paths, it issomewhat of a surprise that one of themain themes to emerge from oursurvey is the continuing integration ofthe CEE region into the globaleconomy, and these countries’continued convergence with thedeveloped economies in WesternEurope and the US.

As an overall message we see this islargely positive, and to some extent theregion is enjoying the best of bothworlds. For example, as with the moreestablished EU states in Western Europe,the region and the industry are starting toachieve a critical mass of infrastructureafter almost two decades of extensiveinvestment. Also, the stability of EUmembership has substantially reducedrisks typically associated with emergingmarkets, where a lack of transparencyaround financial, legal and environmentalregulations can cloud a company’s trueperformance.

At the same time, these countries arealso achieving outsized growth asmarkets are still far from saturated. The Czech Republic, for example - thecountry in the region with the highestlevels of car ownership - still has lessthan 80% the ownership levels of the UK and Germany, while Romania’sownership is barely 45% of theselevels.

1 Executive Summary

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The Czech Republic, forexample - the country inthe region with the highestlevels of car ownership -still has less than 80% theownership levels of the UKand Germany, whileRomania’s ownership isbarely 45% of these levels.

6 CEE Auto Benchmarking Report

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

There are however, several key caveatsto this generally rosy picture. Forinstance the overall growth andprofitability profiles are beginning tomatch the less-than astoundingnumbers found in mature economies.While the majority of surveyrespondents from the CEE automotivesector were able to post double digitrevenue growth and profit margins, thefinancial performance profile of thethese companies tended to match thatof participants in the global industry.

Nevertheless some key differencesbetween emerging and maturemarkets come to light in this survey,and from which automotive executivesand their organizations can learn keylessons. These differences were mostpronounced in the areas of Risk andOperational Efficiency, as companies inthe region experience inflation, strongcurrencies, rising wages and increasedoperational and supply chain risk.

Hopefully, executives and theircompanies can benefit from theseinsights when tailoring their strategiesand executing their plans across allrealms of the organization includingStrategic Development; RiskManagement; Operations & SupplyChain; and Regulation & Compliance.Key highlights of our findings are asfollows:

� When it comes to spending on keyregulatory and compliance issues,companies operating in the CEEregion fell very much in line with theglobal averages across all industries,as well as with the automotivesector. One difference however, wasspending on environmentalcompliance, which was less forregional automotive companies.

Overall, high performing companiesare spending more and applyingmore capacity towards complianceissues.

� The approach of the CEE automotivesector to regulatory and complianceissues was also very similar to thetypical global participant in oursurvey in that most companiestended to integrate compliance intocompany processes. This differshowever from the approach taken byhigh performing companies, who aremore likely to add on moreresources for compliance issues,make greater use of third partyproviders, and tailor their approachspecifically to each country, ratherthan have a standardized, one-size-fits all solution.

� There appear to be stark differencesin how the regional automotivecompanies perceive Risk in severalkey areas, most notably financialrisk, operational and supply chainrisk, and labor risk. These are verylikely driven by conditions on theground in CEE which includeinflation, strengthening currencies (adanger for exporters), rising wagesand an increasingly tight labormarket, particularly for skilled labor.High performers see financial,macroeconomic, regulatory, IT, andtax risk to be greater, relative to theaverage CEE company, than riskssuch as the supply chain.

� And supply chains, althoughincreasingly global, are neverthelessperceived as fragile. With manysmall players the market is stillfragmented, implying that reliabilityand quality of supply are notnecessarily at the levels of the more

developed markets. This is wreakinggreater havoc for automotivecompanies where JIT systems aremore common place, as companiesare finding it more difficult toaccurately forecast demand andtherefore efficiently scheduleproduction.

� In terms of strategic decisions thatdrive growth, automotive companiesin the CEE region differ from theirglobal counterparts as they arerelatively more likely to seek growththrough new markets. Both highperformers and average companiespreferred to capture new customersin existing markets as a growthstrategy. This may be driven by thesmall size and structural elements ofthe countries in the region,positioning them as largely exportmarkets. Also, high performers tendto enter new markets throughacquisitions rather then JVs orgreenfield operations.

� Preferred corporate structures forcompanies in the CEE region differfrom their global counterparts in thatjoint ventures appear relatively morepopular, and outsourcing operationsas a way to enter new markets isnot a strategy any of the companiesin the region pursued. Companies inthe region also appear more hesitantabout acquiring brown fields as amarket entry strategy. Regional andglobal players appear similar,however, when it comes to buildinggreen field operations, as this isslightly more popular for regionalcompanies than the average globalplayer, although still in-line.

� Auto companies in CEE are facingrising labor costs at a much higher

CEE Auto Benchmarking Report 7

This report, which focuses on theautomotive industry in Central &Eastern Europe, is an extension of anearlier study on global automotive andindustrial product manufacturers. Theoriginal research for this study includesa questionnaire which was answeredby 25 companies in five countrieswithin the Central and Eastern Europeregion (The Czech Republic, Hungary,Poland, Romania and Slovakia) during asix-month period from October 2007 toMarch 2008. The questionnaire usedfor the Central & Eastern European

study was based on the questionnaireused in KPMG’s Global ManufacturingBenchmark Survey, where 269interviews were carried out betweenlate Spring and early Summer 2007.

Our final analysis and interpretationsare based on the combined data set ofsurveys conducted in the region andglobally. Additionally a select numberof supplementary, qualitativeinterviews were carried by the authorwith regional automotive executivesand industry analysts. Finally, publically

available data from market researchfirms, the media and KPMGInternational were used to assist inevaluating the proprietary data andprovide qualitative examples in supportof the quantitative analysis. We wouldalso note that our research wasconducted prior to the full scaleunfolding of the financial and economicdownturn of 2008. This is a potentiallylimiting factor to our survey.

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

rate compared to the average globalplayer in our survey. This issueappears to be a double-edged swordfor companies as they try to havethe best of both emerging andindustrialized markets. Unfortunately,development and stability come at aprice which in the automotiveindustry is clearly a cost squeezedue to a severe shortage of labor, inthe industry, and rising wages,generally. The good news is theregion is also posting productivitygains that are generally trendingabove inflation, meaning that in realterms wages are actually steady oreven declining. The question iswhether the automotive sector isenjoying this benefit to the sameextent.

� When it comes to sourcing from lowcost countries, companies in theregion appear a bit behind the curverelative to their global counterparts,and are less engaged compared tothe other peer groups. However theyare more likely to be consideringsourcing from low cost countries,particularly for raw material andcomponents. This may be a result ofrising wages and inflation in theregion as many countries, onceconsidered low cost countries, areincreasingly less so, and hence arelooking further east for cost savings.Surprisingly, high performers werenot taking advantage of low costcountry sourcing options but didappear to be getting advantagesfrom leveraging their IT infrastructureand tax planning.

� Tax optimization strategies appear tobe an area where the automotivesector in the region is less likely tohave fully leveraged potential savingopportunities. On balance,companies in the region are lesslikely than their global counterpartsto have achieved their optimal taxrate, and at the same timecompanies are more likely to beplanning to improve their taxliabilities in the near future. Thisoutlook is potentially driven byalready low tax rates and an increasein flat taxes in the region. Theexception to this is Hungary wherepersonal and social taxes onemployees are having a negativeeffect for many companies.

2 Methodology

8 CEE Auto Benchmarking Report

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Making the GradeWhat constitutes high performancecan be a tricky question. There aremany different measures for gaugingperformance and every executive andanalyst has their preferred method formeasuring the health and value of anorganization. Market share, marketcapitalization, return on equity, totalassets, and so on are all validmeasures and tell similar stories - sohow to pick the correct measure?

In the final analysis there tend to bethree measures upon which mostothers rest, and which fundamentallydrive underlying asset values for anorganization. These are the annualgrowth rate of the firm’s revenues; therelative profitability of the company, orits profit margin; and the sustainabilityof these margins and growth ratesover time, or its risk profile.

In this survey we have chosen to focuson the first two elements as the bestway to compile a current snap shot ofcompany performance. While realizing

that profits in the future are moreimportant than profits from the past oreven today, establishing accurateforecasts for the companies in thissurvey was beyond the scope of thisstudy.

Likewise obtaining data about eachcompany’s past earnings and revenuewas prohibitive, such that we wereunable to obtain a reliable indicator forearnings’ volatility and accuratelyincorporate risk in any quantifiable wayinto our measure of a high performingcompany.

Nevertheless, our criteria werestringent enough such that only about5% of the companies were able toclaim the mantle of “high performing”in our survey. To achieve this statuscompanies were required to reportboth annual revenue growth and pre-tax profit margins greater than 15%.

This elite group proved to be quitediverse, but one that well representedour sample. Some facts about thedemographic breakdown include:

� Both large and small companieswere represented, with sizes rangingfrom total revenues of just over USD200 million, to over USD 20 billion.The median annual revenue for thehigh performing per group wasbetween USD 300 and 400 mln.

� All main global geographic regionswere well represented including30% of companies coming fromEurope; 60% coming from theAmericas; and 10% from Asia.

� Automotive companies made upalmost one-third of the highperformers (30%) with industrialmanufactures representing slightlymore of this peer group (40%), withmetals producers (10%) and otherindustries (20%) making up theremaining share.

� Major emerging markets were alsowell represented as 50% of the highperforming peer group came fromthe BRIC countries (Brazil, Russia,India, and China).

3 Financial Performance – Determining the High Performers

Only about 5% of the companies were able to claimthe mantle of “high performing” in our survey. To achieve this status companies were required toreport both annual revenue growth and pre-tax profitmargins greater than 15%.

CEE Auto Benchmarking Report 9

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%N

egat

ive

Bre

ak e

ven

Less

tha

n 5%

5 to

10%

11 t

o 15

%

16 t

o 25

%

Gre

ater

tha

n25

%

Don

’tkn

ow/r

efus

ed

All

Industry

High performers

CEE

Figure 1: In terms of pre-tax profit margins, in approximate terms

what is your company’s current profitability?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Rev

enue

will

decl

ine

Zero

/mar

gina

lgr

owth

Up

to 5

%

5 to

10%

11 t

o 15

%

16 t

o 20

%

Mor

e th

an20

%

Don

’tkn

ow/r

efus

ed

All

Industry

High performers

CEE

Figure 2: What is your company’s forecasted annual

revenue growth over the next three years?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

10 CEE Auto Benchmarking Report

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

4 Regulation and Compliance

In a post-Enron world, the regulatoryand compliance environment for

business across the globe is morecomplex than ever before. Perhaps morefrightening, is the ever increasing rate ofchange of regulation. Take for exampleone European Auto supplier grapplingwith International Financial ReportingStandards (IFRS): “It would not be anissue if you didn’t have any changes tothe regime – the problem is there arecontinual changes”1. And while it’s truethat the impact will vary across differentindustries and geographies, in manyrespects the automotive industry in CEEappears to be feeling the impact, andresponding, in very similar measure asother automotive and industrialmanufacturers across the globe.

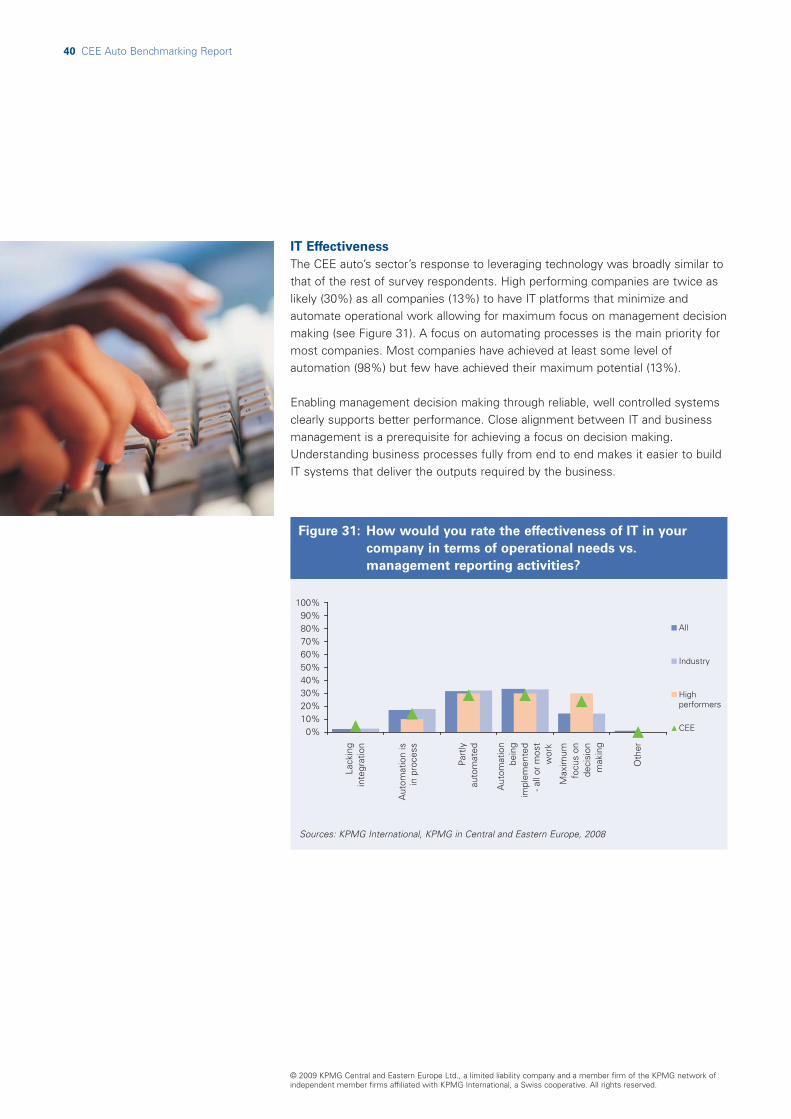

The typical response for mostcompanies in our survey is to integratecompliance processes into existingprocesses. This has largely proven aneffective method from a cost point ofview. While the costs can besignificant, they are largelymanageable with companies typicallyestimating costs on the order of 1%for both financial and environmentalcompliance costs. This appears to begood news for the auto sector in CEE.According to Gartner Group, anintegrated approach is in line with bestpractices which suggest thatcompanies who take individualsolutions for each regulatory challengecan potentially face costs many timesover compared to companies who takean integrated approach2.

It’s also important to point out that lookingat cost alone can be deceiving, as the

burden of management time can imposesignificant costs in terms of lostopportunities which are impossible tocalculate. As one executive at a leadingauto parts manufacturer puts it, “for us,compliance is more an issue ofmanagement discipline than it is a costissue.”3 This appears to be even truer forthe auto sector in CEE due to thesignificant strain on resources thesecompanies are experiencing. Virtually allrespondents who viewed regulatoryissues as a significant risk found nothaving enough resources to be asignificant challenge (please see figure 3).

Interestingly the high performingcompanies in our survey were morelikely to take a different approach andspend more money than the typicalcompany we interviewed. Thesecompanies were more likely to set upstand alone processes, outsourcecompliance activities to third partiesand use different approaches fordifferent countries. While this mayseem counter intuitive, it may be thecase these companies are moreforward looking and treatingcompliance costs as much as aninvestment for the future than a one-off cost in the current period.

According to one analyst, JohnHaggerty at AMR Research Inc., costsincurred now can bring future benefits.“The way I look at it, you have to spendmoney now to save money in thefuture. In order to make compliance arepeatable and sustainable process,companies should automate as much asthey can so that human-related costscan drop over time.4”

1 KPMG International, Global ManufacturingBenchmark Survey: How manufacturingcorporations preserve and create value. 2007, p. 12.

2 John Bace et al, Understanding the costs ofcompliance. Gartner, Inc. 7 July 2006. p. 1.

3 KPMG International, Global ManufacturingBenchmark Survey: How manufacturingcorporations preserve and create value. 2007, p 12.

4 John Haggerty, Compliance spending savesmoney. AMR Research. 10 March 2006.http://searchstoragechannel.techtarget.com/generic/0,295582,sid98_gci1218086,00.html#

“The way I look at it, youhave to spend money nowto save money in thefuture. In order to makecompliance a repeatableand sustainable process,companies shouldautomate as much as theycan so that human-relatedcosts can drop overtime.4”

CEE Auto Benchmarking Report 11

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

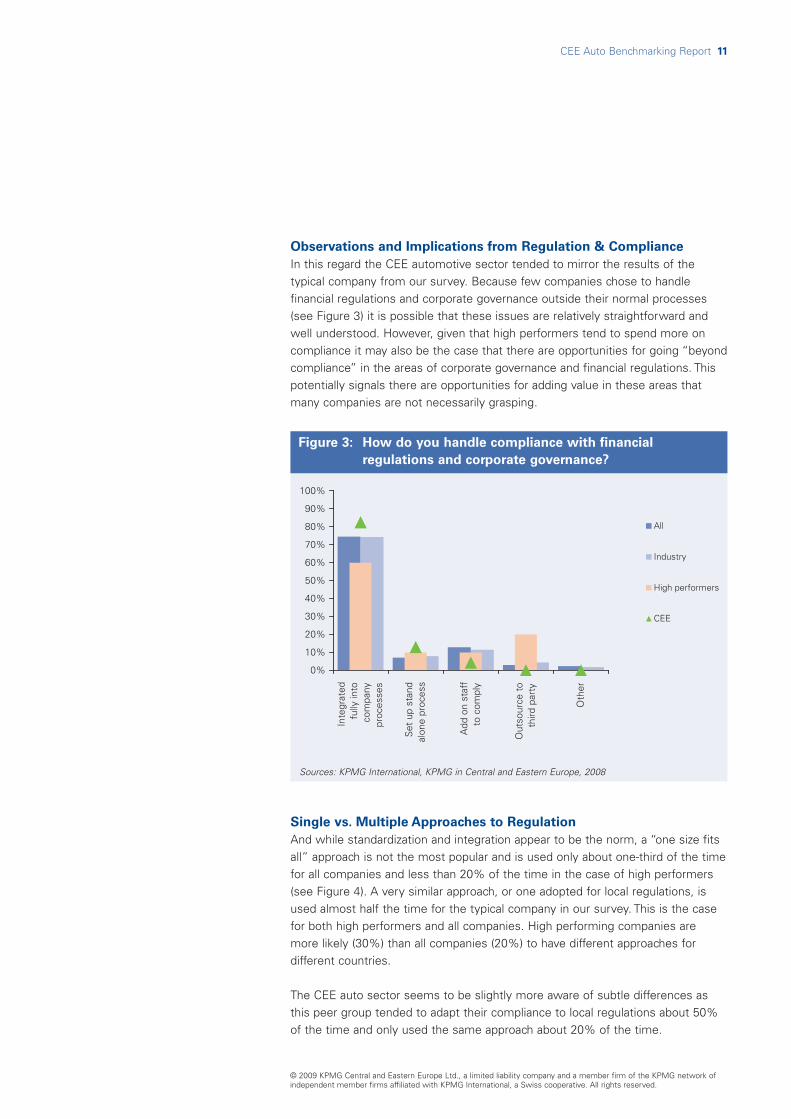

Observations and Implications from Regulation & Compliance

In this regard the CEE automotive sector tended to mirror the results of thetypical company from our survey. Because few companies chose to handlefinancial regulations and corporate governance outside their normal processes(see Figure 3) it is possible that these issues are relatively straightforward andwell understood. However, given that high performers tend to spend more oncompliance it may also be the case that there are opportunities for going “beyondcompliance” in the areas of corporate governance and financial regulations. Thispotentially signals there are opportunities for adding value in these areas thatmany companies are not necessarily grasping.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Inte

grat

edfu

lly in

toco

mpa

nypr

oces

ses

Set

up

stan

dal

one

proc

ess

Add

on

staf

fto

com

ply

Out

sour

ce t

oth

ird p

arty

Oth

er

All

Industry

High performers

CEE

Figure 3: How do you handle compliance with financial

regulations and corporate governance?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

Single vs. Multiple Approaches to Regulation

And while standardization and integration appear to be the norm, a “one size fitsall” approach is not the most popular and is used only about one-third of the timefor all companies and less than 20% of the time in the case of high performers(see Figure 4). A very similar approach, or one adopted for local regulations, isused almost half the time for the typical company in our survey. This is the casefor both high performers and all companies. High performing companies aremore likely (30%) than all companies (20%) to have different approaches fordifferent countries.

The CEE auto sector seems to be slightly more aware of subtle differences asthis peer group tended to adapt their compliance to local regulations about 50%of the time and only used the same approach about 20% of the time.

12 CEE Auto Benchmarking Report

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

At least some degree of customization appears either necessary or desirable fordealing with regulations and corporate governance across all companies. Highperforming companies are possibly able to see the value in customizing how theydeal with financial regulations and corporate governance issues in the differentlocations in which they operate.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Sam

eap

proa

ch

Sim

ilar

appr

oach

es

App

roac

hsi

mila

r bu

tad

apte

d to

loca

l reg

s

Diff

eren

tap

proa

ches

for

diff

eren

tco

untr

ies

All

Industry

High performers

CEE

Figure 4: Do you use a single approach worldwide to comply

with financial regulations & corporate governance?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

Global vs. Local Approach for Tax Compliance

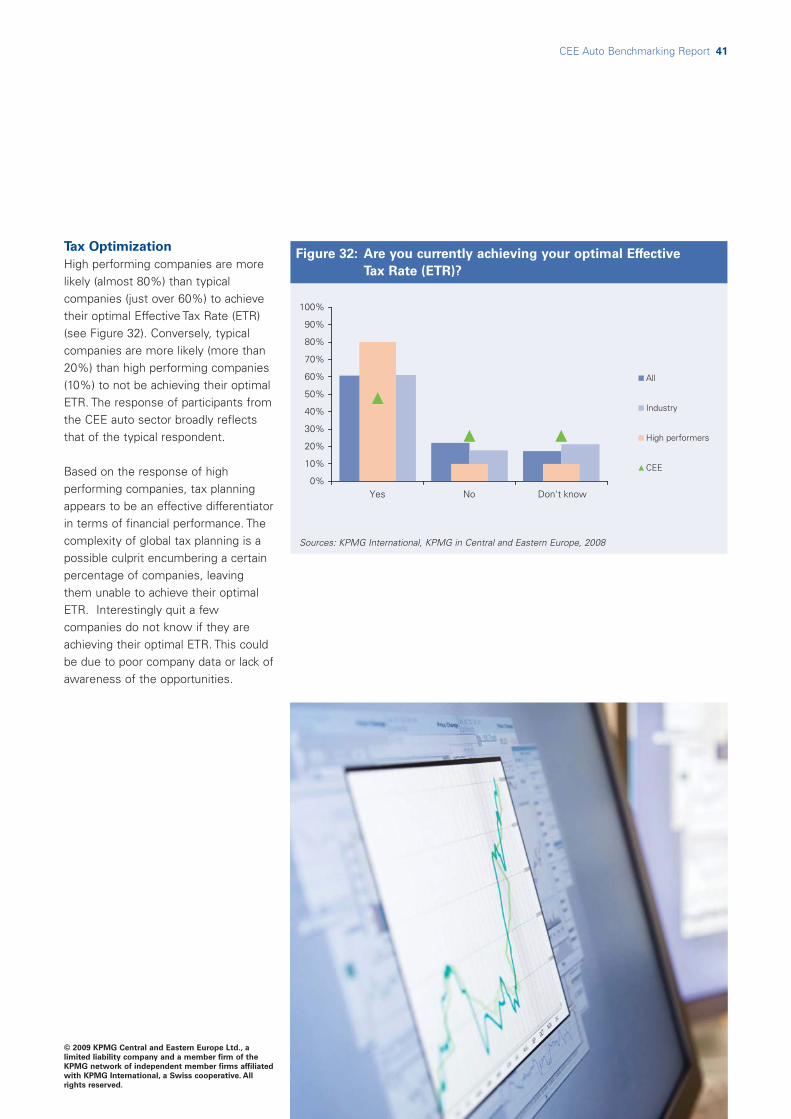

Survey participants from the CEE auto sector by-and-large used a local approach(60%) when addressing tax issues, although a significant portion (40%) took aglobal approach (see Figure 5). This is interesting in light of comments later in thesurvey indicating there is some opportunity for better optimizing tax rates.

High performing companies (50%) are more likely than all companies (about33%) to approach tax compliance from a global perspective. Interestingly, a largepercentage of high performers nonetheless tend to handle compliance locally.

Taking a global approach to tax compliance is a relatively recent trend, arisingfrom the increased regulatory responsibilities of finance and tax officers. Manymultinational companies (MNCs) have more or less completely out-sourced taxcompliance outside their home country to reduce (or shift) regulatory reportingrisks. Benefits of doing so include better information (provided by thesophisticated software used by outsourcing vendors), lower process risk, andlower regulatory compliance risks.

CEE Auto Benchmarking Report 13

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

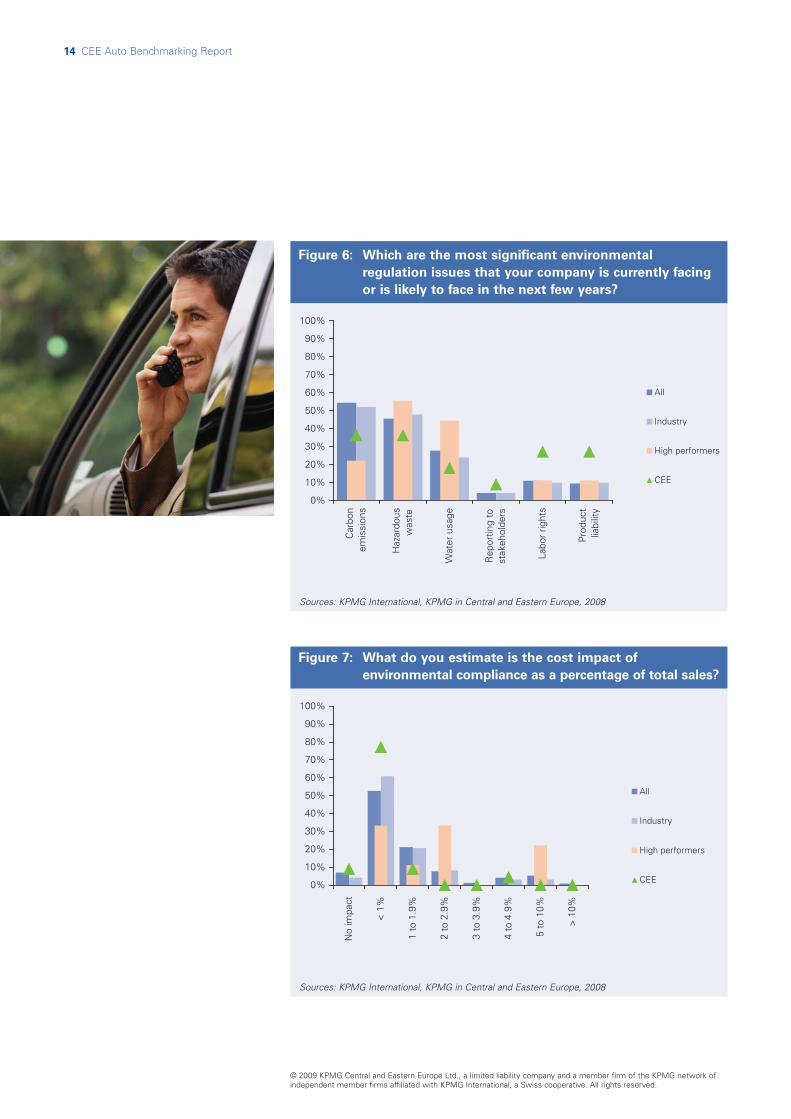

Environmental Regulations

The biggest concerns for the CEE auto sector are issues relating to worker’shealth and safety – a response in line with the overall competitiveness of thelabor market and a general concern for local regulations over global regulations.High performers were more likely to view hazardous waste (55%) and waterusage (45%) as significant issues than were all companies (49% and 29%,respectively), but less likely (23%) than all participants (54%) to view carbonemissions as a significant issue (see Figure 6).

In terms of the regulatory impacts of climate change this may indicate somedoubts as to the degree of government intervention. It may be the case that theimpact of carbon emissions on financial performance is limited, despite its beinghigh profile in the media and public perception. Nevertheless companies need tobe aware of the significant likelihood that environmental issues related to climatechange will be regulated through market-based policies rather than traditionalcontrol and command legislation. It may be the case that the impact of carbonemissions on financial performance is limited, despite its being high profile in themedia and public perception.

Given the attention paid by high performers to waste and water, it is possible thatpressure to manage these costs is coming as much from clients and supply chainpartners as from government/regulation. This could be due to the immediate andvisible nature of these costs and represent an opportunity to save money.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Ent

irely

glo

bal

Mai

nly

glob

al,

som

e as

pect

slo

cally

Mai

nly

glob

al,

som

e as

pect

sre

gion

ally

Mai

nly

loca

l,so

me

aspe

cts

glob

ally

Mai

nly

loca

l,so

me

aspe

cts

regi

onal

ly

Ent

irely

loca

l

All

Industry

High performers

CEE

Figure 5: Do you approach tax compliance from a global or

local perspective?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

Nevertheless companiesneed to be aware of thesignificant likelihood thatenvironmental issuesrelated to climate changewill be regulated throughmarket-based policiesrather than traditionalcontrol and commandlegislation.

14 CEE Auto Benchmarking Report

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Car

bon

emis

sion

s

Haz

ardo

usw

aste

Wat

er u

sage

Rep

ortin

g to

st

akeh

olde

rs

Labo

r rig

hts

Pro

duct

liabi

lity

All

Industry

High performers

CEE

Figure 6: Which are the most significant environmental

regulation issues that your company is currently facing

or is likely to face in the next few years?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No

impa

ct

< 1

%

1 to

1.9

%

2 to

2.9

%

3 to

3.9

%

4 to

4.9

%

5 to

10%

> 1

0%

All

Industry

High performers

CEE

Figure 7: What do you estimate is the cost impact of

environmental compliance as a percentage of total sales?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

CEE Auto Benchmarking Report 15

Compliance Costs for Finance

and Corporate Governance

Again, the CEE auto sector alsoappears to be paying less incompliance costs for financial andcorporate governance relatedcompliance than the rest of the surveyparticipants. If this is indeed the resultof laxer regulations rather than moreefficient compliance processes, thencompanies probably need to considerhow this might change in the nearfuture.

Overall, more than 60% of allcompanies estimate financial andcorporate governance compliancecosts to be less than 1% of total sales(see Figure 8). About 20% of allcompanies estimate costs at between1 and 2%, and less than 15% ofcompanies at greater than 3%. Incontrast, about 60% of highperforming companies estimate thecost of financial and corporategovernance to be more than 1% oftotal sales and more than one-third ofhigh performers estimate costs atgreater than 3%.

As with environmental compliance,high performing companies clearlyestimate the cost of financial andcorporate governance compliance tobe more significant than do allcompanies.

The question seems to emerge as towhether compliance is just a cost or isin fact an investment. This is furtherevidence of a ‘beyond compliance’theme continuing to emerge in thissurvey.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No

impa

ct

< 1

%

1 to

1.9

%

2 to

2.9

%

3 to

3.9

%

4 to

4.9

%

5 to

10%

> 1

0%

All

Industry

High performers

CEE

Figure 8: What do you estimate is the cost impact of

financial/corporate governance compliance as a

percentage of total sales?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network

of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

16 CEE Auto Benchmarking Report

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

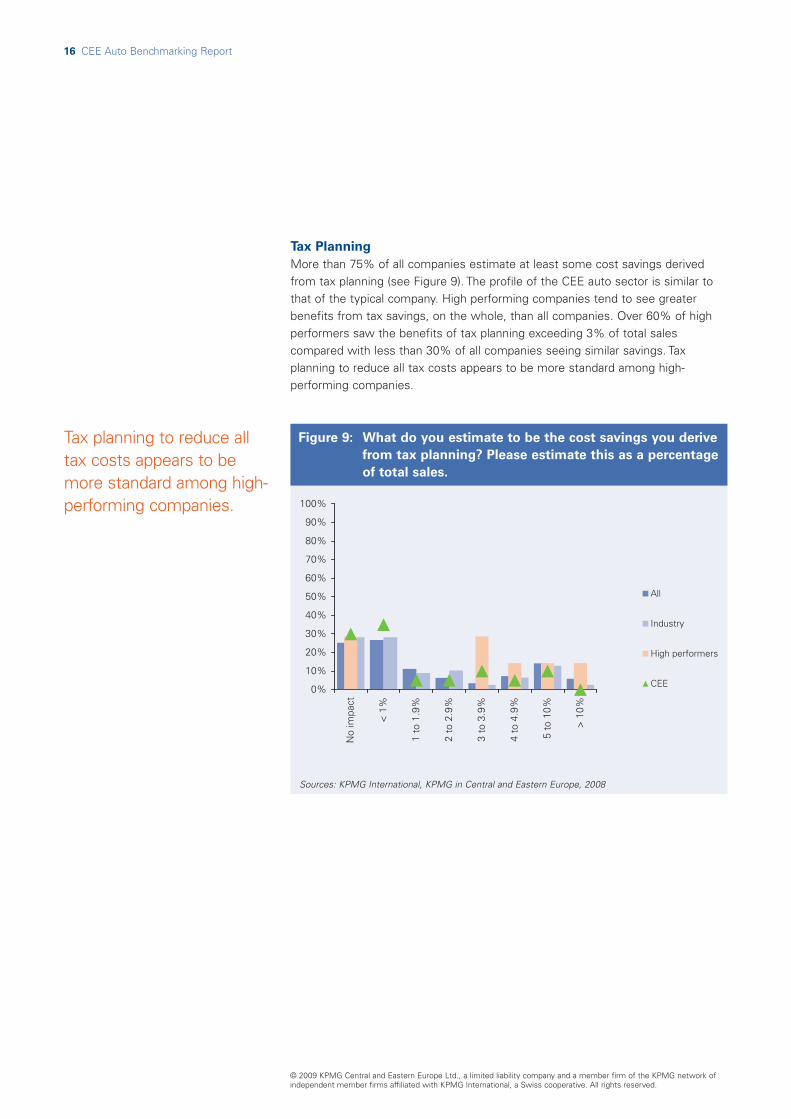

Tax Planning

More than 75% of all companies estimate at least some cost savings derivedfrom tax planning (see Figure 9). The profile of the CEE auto sector is similar tothat of the typical company. High performing companies tend to see greaterbenefits from tax savings, on the whole, than all companies. Over 60% of highperformers saw the benefits of tax planning exceeding 3% of total salescompared with less than 30% of all companies seeing similar savings. Taxplanning to reduce all tax costs appears to be more standard among high-performing companies.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No

impa

ct

< 1

%

1 to

1.9

%

2 to

2.9

%

3 to

3.9

%

4 to

4.9

%

5 to

10%

> 1

0%All

Industry

High performers

CEE

Figure 9: What do you estimate to be the cost savings you derive

from tax planning? Please estimate this as a percentage

of total sales.

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

Tax planning to reduce alltax costs appears to bemore standard among high-performing companies.

CEE Auto Benchmarking Report 17

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

5 Risk

5 Dr. Daniel Thorniley, The “Fat Boxer” story turned out to be true: Reasons why the CEE region is stilldoing so well - The Economist Intelligence Unit. December 2007. p. 4.

6 Dr. Daniel Thorniley, The “Fat Boxer” story turned out to be true: Reasons why the CEE region is stilldoing so well - The Economist Intelligence Unit. December 2007. p. 5.

In today’s climate, Risk is truly a four letter word. The housing crisis whichstarting heating up a year ago in the US appears to have found firm footing in

the UK and pockets of the European continent. At the same time auto sales inthe US have plummeted to depths not seen in decades with annual salesdeclines in the double digits. Europe as a whole appears to be following suit. Thelatter, of course, is driven by high gas prices while the former is more complex,apparently a combination of speculation, lax regulation and plain old fashionedgreed, from Main Street to Wall Street. The net result, of course, is both the USand the largest European economies are entering into a recession, with no end insight, with the potential to bring the global economy along with it.

Yet, it would seem that many companies and industries in the CEE region aresuccessfully skirting the potential disasters that seem to be just abouteverywhere. To explain this phenomenon, Dr. Daniel Thorniley of the EconomistIntelligence Unit likens the CEE region to a “fat boxer”. “Whenever the going getstough, the CEE markets have several layers of fat protecting them from globaldownturns”5, explains Thorniley.

The key advantages for many countries in CEE - which are protecting the regionas a whole – include:

� Strong GDP growth;

� EU accession; political stability;

� A strong and growing SME sector;

� High productivity levels;

� A restructured and well functioning banking sector;

� Low inflation; and

� Strong currencies.

All of the above imply that should the global credit crunch manifest itself in theregion the downside could be limited by these buffers6.

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

7 Based on KPMG interviews carried out by theauthor of this report.

Many of these advantages are indeed proving to be beneficial for the region’sautomotive sector, as well. For example, Foreign Direct Investment in the region’sautomotive sector has been booming for years and appears to be going strong.Nevertheless, companies would certainly benefit from heeding the hard lessonsthat many companies are learning in the US and elsewhere.

For the region’s automotive sector, financial risk, operational & supply chain risk,and human resource-related risks all stand out as the most significant dangersthreatening financial performance. Looking deeper into the issues aroundfinancial risks, inflation and strong currencies are clearly perceived as the biggestthreats.

The effect of strong currencies potentially has a very different impact on the autosector than the economy as a whole, for most of the counties in the region.Strong currencies are generally good for the purchasing power of households,who depend on many imports for basic necessities such as food and clothing aswell as more durable purchases such as white goods and automobiles. This isincreasingly so as rising real wages in the region mean a strong and growingdemand for pricier and higher quality imports.

For the automotive sector, however, which is mostly export driven - with manysuppliers being paid in Euros and most costs in local currency - the impact issignificant. For example, according to a tier one auto parts manufacturer, “Thestrength of the Czech koruna has caused us to completely revise our financialresult for the fiscal year.”7

Inflation pressures are also taking their toll on the automotive sector. With oilprices spiking upwards, commodities in general are at an all time high, includingmany of the key inputs needed for the sector including aluminum, steel, alloys,glass and petro-based chemicals for inputs to plastics. But the trouble hardlystops there. Both strong FDI and surging GDP growth have left unemploymentlevels at an all time low meaning wage inflation - which is happening anyways - isespecially fierce in the automotive sector. In many countries, especially in theCzech Republic and Slovakia, but even in Hungary, some manufacturers areresorting to immigrant workers to keep production lines fully manned. Eventhough the benefits of a highly productive work force are offering some relief, itis impacting the sector and it’s overall business performance. For this reason,executives are concerned not only with rising wages but even more so withrecruiting and retaining staff.

For the region’s automotivesector financial risk,operational & supply chainrisk, and human resource-related risks all stand outas the most significantdangers threateningfinancial performance.

“The strength of the Czechkoruna has caused us tocompletely revise ourfinancial result for thefiscal year.”7

CEE Auto Benchmarking Report 19

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Rep

utat

iona

l ris

k

Reg

ulat

ory

Fina

ncia

l

Liqu

idity

Ope

ratio

nal/

supp

ly c

hain IT

Tax

Inte

llect

ual

prop

erty

Labo

r

Mac

ro e

cono

mic

Non

e

Oth

ers

All

Industry

High performers

CEE

Figure 10: Which areas of risk are top of mind for your company

and most critical for the industry?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

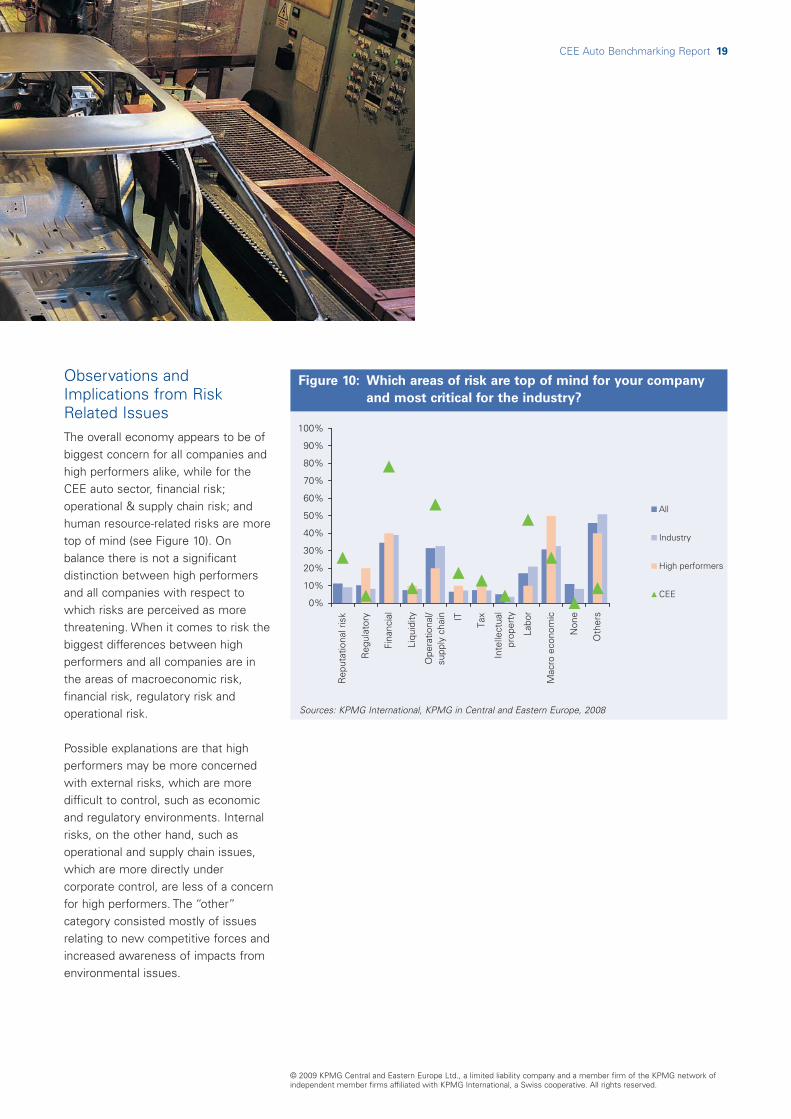

Observations andImplications from RiskRelated IssuesThe overall economy appears to be ofbiggest concern for all companies andhigh performers alike, while for theCEE auto sector, financial risk;operational & supply chain risk; andhuman resource-related risks are moretop of mind (see Figure 10). Onbalance there is not a significantdistinction between high performersand all companies with respect towhich risks are perceived as morethreatening. When it comes to risk thebiggest differences between highperformers and all companies are inthe areas of macroeconomic risk,financial risk, regulatory risk andoperational risk.

Possible explanations are that highperformers may be more concernedwith external risks, which are moredifficult to control, such as economicand regulatory environments. Internalrisks, on the other hand, such asoperational and supply chain issues,which are more directly undercorporate control, are less of a concernfor high performers. The “other”category consisted mostly of issuesrelating to new competitive forces andincreased awareness of impacts fromenvironmental issues.

20 CEE Auto Benchmarking Report

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Cris

is

Mar

kets

Med

ia

Oth

erst

akeh

olde

rs

CS

R is

sues

Oth

ers

All

Industry

High performers

CEE

Figure 11: Which elements of reputational risk are particularly

challenging?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

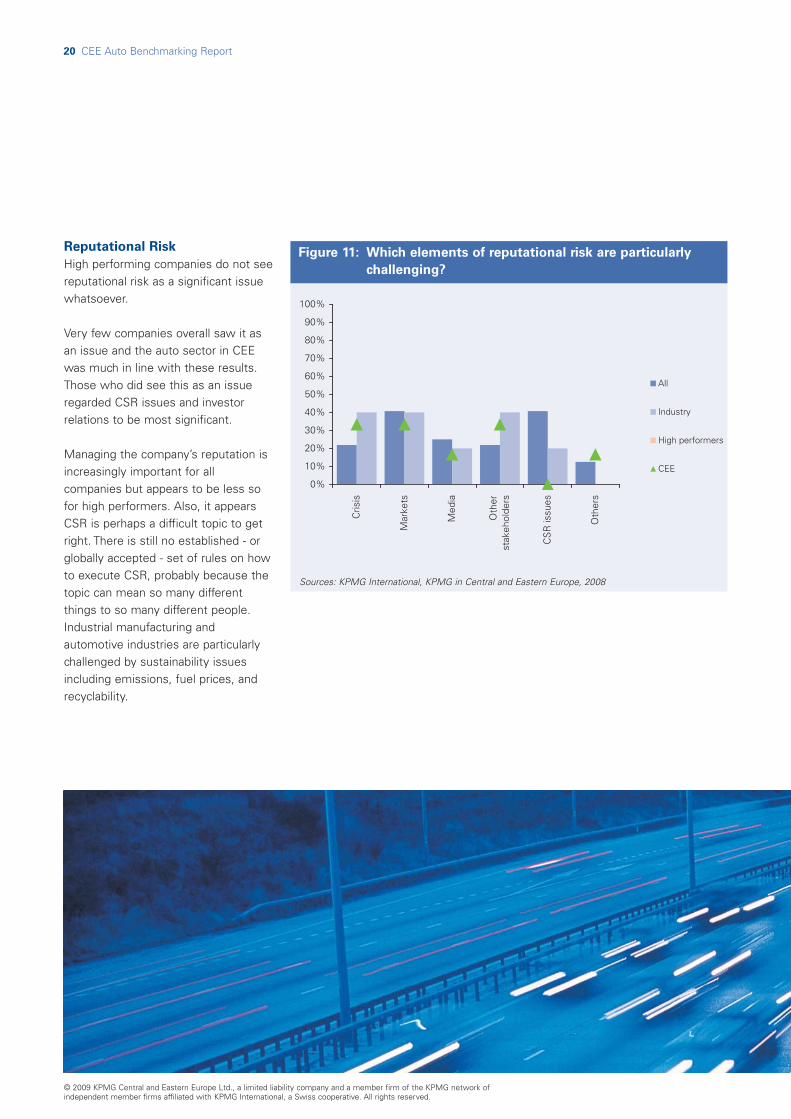

Reputational Risk

High performing companies do not seereputational risk as a significant issuewhatsoever.

Very few companies overall saw it asan issue and the auto sector in CEEwas much in line with these results.Those who did see this as an issueregarded CSR issues and investorrelations to be most significant.

Managing the company’s reputation isincreasingly important for allcompanies but appears to be less sofor high performers. Also, it appearsCSR is perhaps a difficult topic to getright. There is still no established - orglobally accepted - set of rules on howto execute CSR, probably because thetopic can mean so many differentthings to so many different people.Industrial manufacturing andautomotive industries are particularlychallenged by sustainability issuesincluding emissions, fuel prices, andrecyclability.

CEE Auto Benchmarking Report 21

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

0%10%20%30%40%50%60%70%80%90%

100%

Lack

SO

Ps

Func

tiona

l ba

rrie

rsH

igh

leve

ls o

f m

anua

l act

iviti

esN

ot e

noug

h de

cisi

on-s

uppo

rtD

iffic

ulty

usi

ng

info

rmat

ion

Com

petin

g pr

iorit

ies

for

reso

urce

sN

ot e

noug

h re

sour

ces

Lack

of

clar

ity in

co

de o

f co

nduc

tC

omm

unic

atin

g w

ith

key

stak

ehol

ders

Man

agin

g ch

ange

No

cohe

sive

vie

w

of t

he o

rgan

izat

ion

Lack

of

inte

grat

ed IT

Lack

of

optim

ized

proc

esse

s

Oth

ers

All

Industry

Highperformers

CEE

Figure 12: Which elements of regulatory risk are particularly

challenging?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

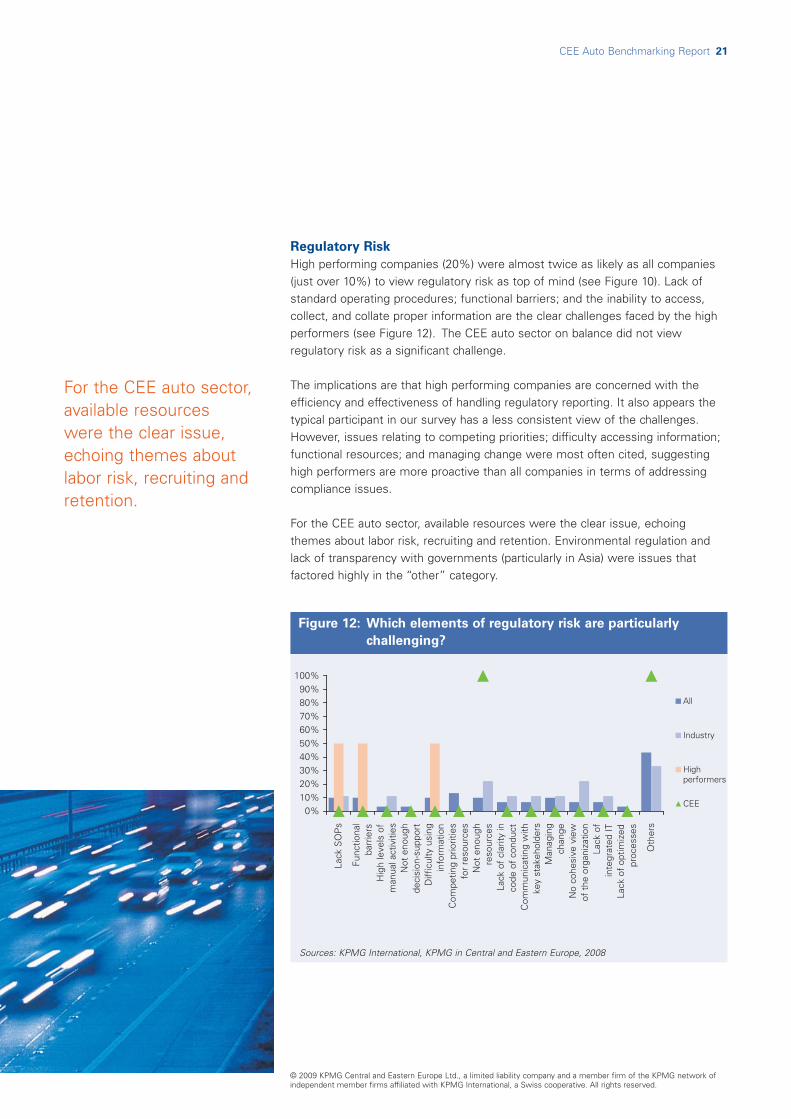

Regulatory Risk

High performing companies (20%) were almost twice as likely as all companies(just over 10%) to view regulatory risk as top of mind (see Figure 10). Lack ofstandard operating procedures; functional barriers; and the inability to access,collect, and collate proper information are the clear challenges faced by the highperformers (see Figure 12). The CEE auto sector on balance did not viewregulatory risk as a significant challenge.

The implications are that high performing companies are concerned with theefficiency and effectiveness of handling regulatory reporting. It also appears thetypical participant in our survey has a less consistent view of the challenges.However, issues relating to competing priorities; difficulty accessing information;functional resources; and managing change were most often cited, suggestinghigh performers are more proactive than all companies in terms of addressingcompliance issues.

For the CEE auto sector, available resources were the clear issue, echoingthemes about labor risk, recruiting and retention. Environmental regulation andlack of transparency with governments (particularly in Asia) were issues thatfactored highly in the “other” category.

For the CEE auto sector,available resources were the clear issue,echoing themes aboutlabor risk, recruiting andretention.

22 CEE Auto Benchmarking Report

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

0%10%20%30%40%50%60%70%80%90%

100%

Invo

icin

gau

tom

atio

n &

accu

racy

Cre

dit

risk

man

agem

ent

Incr

ease

dfin

ance

cos

ts

Oth

ers

All

Industry

Highperformers

CEE

Figure 13: Which elements of financial risk or liquidity risk are

particularly challenging?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

Financial Risk

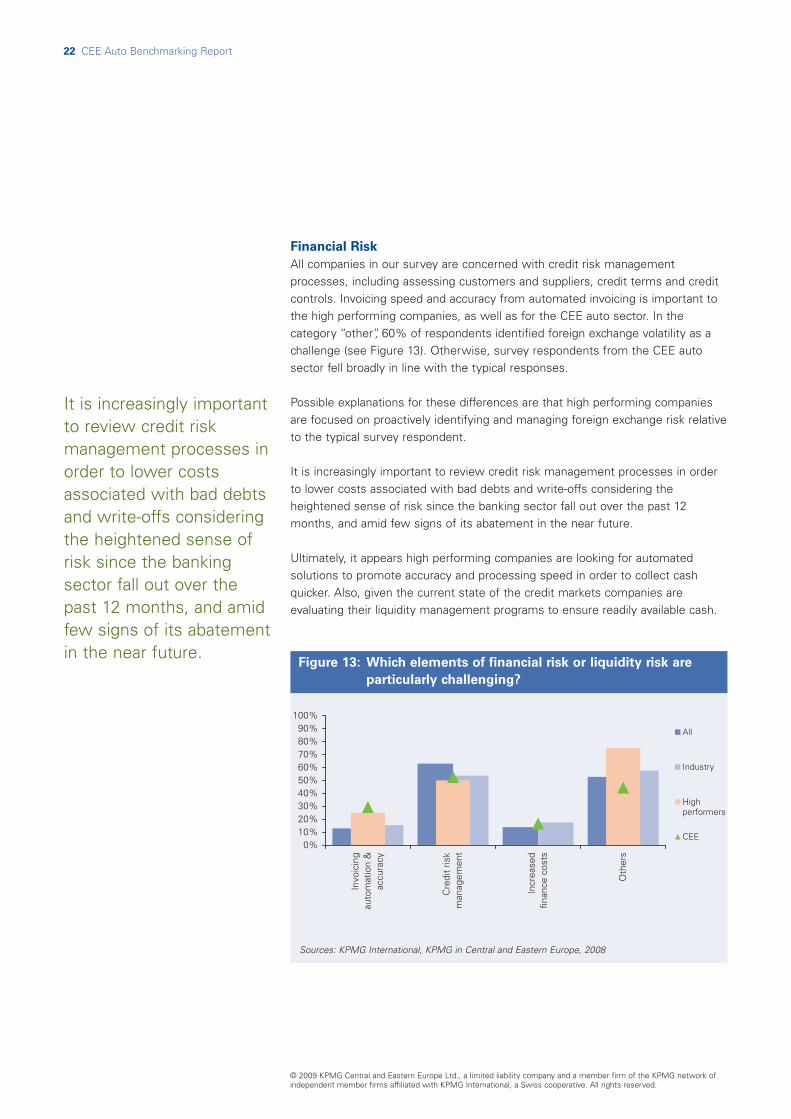

All companies in our survey are concerned with credit risk managementprocesses, including assessing customers and suppliers, credit terms and creditcontrols. Invoicing speed and accuracy from automated invoicing is important tothe high performing companies, as well as for the CEE auto sector. In thecategory “other”, 60% of respondents identified foreign exchange volatility as achallenge (see Figure 13). Otherwise, survey respondents from the CEE autosector fell broadly in line with the typical responses.

Possible explanations for these differences are that high performing companiesare focused on proactively identifying and managing foreign exchange risk relativeto the typical survey respondent.

It is increasingly important to review credit risk management processes in orderto lower costs associated with bad debts and write-offs considering theheightened sense of risk since the banking sector fall out over the past 12months, and amid few signs of its abatement in the near future.

Ultimately, it appears high performing companies are looking for automatedsolutions to promote accuracy and processing speed in order to collect cashquicker. Also, given the current state of the credit markets companies areevaluating their liquidity management programs to ensure readily available cash.

It is increasingly importantto review credit riskmanagement processes inorder to lower costsassociated with bad debtsand write-offs consideringthe heightened sense ofrisk since the bankingsector fall out over thepast 12 months, and amidfew signs of its abatementin the near future.

CEE Auto Benchmarking Report 23

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

0%10%20%30%40%50%60%70%80%90%

100%

Inte

grity

of

supp

ly

Fore

cast

vs.

pro

duct

ion

sche

dule

s

Nat

ural

dis

aste

r

Coo

rdin

atio

n

Third

par

ties

Sys

tem

s co

mpa

tibili

ty

Labo

r re

latio

ns

Mar

ket

risk

Pol

itica

l ins

tabi

lity

Reg

ulat

ory

risk

Fina

ncia

l ris

k

Ris

k of

fra

ud

Oth

ers

All

Industry

Highperformers

CEE

Figure 14: Which elements of operational & supply chain risk are

particularly challenging?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

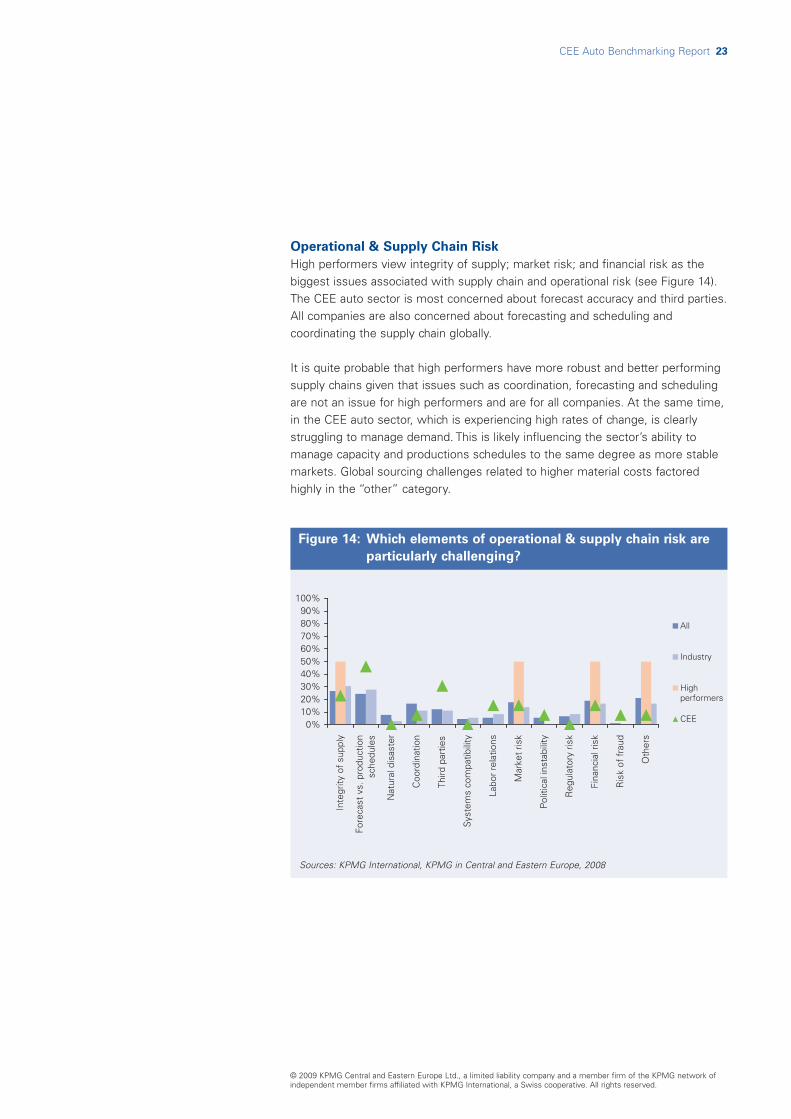

Operational & Supply Chain Risk

High performers view integrity of supply; market risk; and financial risk as thebiggest issues associated with supply chain and operational risk (see Figure 14).The CEE auto sector is most concerned about forecast accuracy and third parties.All companies are also concerned about forecasting and scheduling andcoordinating the supply chain globally.

It is quite probable that high performers have more robust and better performingsupply chains given that issues such as coordination, forecasting and schedulingare not an issue for high performers and are for all companies. At the same time,in the CEE auto sector, which is experiencing high rates of change, is clearlystruggling to manage demand. This is likely influencing the sector’s ability tomanage capacity and productions schedules to the same degree as more stablemarkets. Global sourcing challenges related to higher material costs factoredhighly in the “other” category.

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Dat

a in

tegr

ity

Tim

elin

ess

ofre

port

ing

Sys

tem

dow

ntim

e

Sec

urity

Leve

l of

inte

grat

ion

Lack

of

inte

rnal

know

-how

Tran

sfor

mat

ion

toin

sour

cing

Oth

ers

All

Industry

High performers

CEE

Figure 15: Which elements of IT risk are particularly challenging?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

IT Risk

High performing companies take security risks more seriously (100%) than allcompanies (slightly less than 50%) (see Figure 15). Generally, all companies weremore concerned with data integrity and system down time, which were notissues for high performers. The CEE auto sector on the other hand was mostconcerned with data integrity – an issue which possibly related to both the highlydynamic environment in the region, as well as the chronic lack of resources inCEE reported elsewhere in the survey.

Possible explanations are that high performers are more likely to have integratedsystems in place. High performers may also be recognizing the link betweengreater global integration of business systems and higher security managementstandards. In a more integrated environment, the weakest link in securitybecomes a weakness for the whole business; therefore the issue of security ismore likely to be on the radar screen. Investment in good security management(people, process and technology) is required to address these risks.

CEE Auto Benchmarking Report 25

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Una

ble

to

estim

ate

taxe

s

Exc

ess

cust

oms

Non

-co

mpl

ianc

e on

re

gula

tions

Lack

of

prop

er

plan

ning

Com

plex

ity o

fre

gs

Lack

of

fam

iliar

ityw

ith r

egs

Oth

ers

All

Industry

High performers

CEE

Figure 16: Which elements of tax risk are particularly challenging?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

Tax Risk

Regulatory complexity is the most challenging risk area for typical companies inour survey (see Figure 16).

And, when combined with the similar “lack of familiarity” category, this group ofissues presented the most challenges. For the CEE auto sector, non-compliancewas the biggest concern, again echoing earlier comments that CEE is both ahighly dynamic environment and one that suffers from a chronic lack ofresources.

The proliferation of tax rules and regulations, in all major markets, which are oftentimes conflicting, appears to be a major area of difficulty for survey respondentsincluding those from the CEE auto sector. It is possible that the tax regulatoryenvironment is changing faster than the resources that companies have availableto devote to the issue. We would expect companies coping with this complexityto seek simplicity and uniformity in tax-related structuring. The degree and paceof changes in regulation (especially in China) featured highly in the “other”category.

26 CEE Auto Benchmarking Report

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

0%10%20%30%40%50%60%70%80%90%

100%

Mai

ntai

ning

up

to d

ate

IPpo

rtfo

lio

Und

erst

andi

ng IP

pro

tect

ion

Und

erst

andi

ng t

ools

to

safe

guar

d IP

Und

erst

andi

ng h

ow IP

isle

vera

ged

Col

labo

ratin

g w

ith e

xter

nal

agen

cies

Form

ulat

ing

IP p

rote

ctio

n

Oth

ers

All

Industry

High performers

CEE

Figure 17: Which elements of intellectual property risk are

particularly challenging?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

Intellectual Property Risk

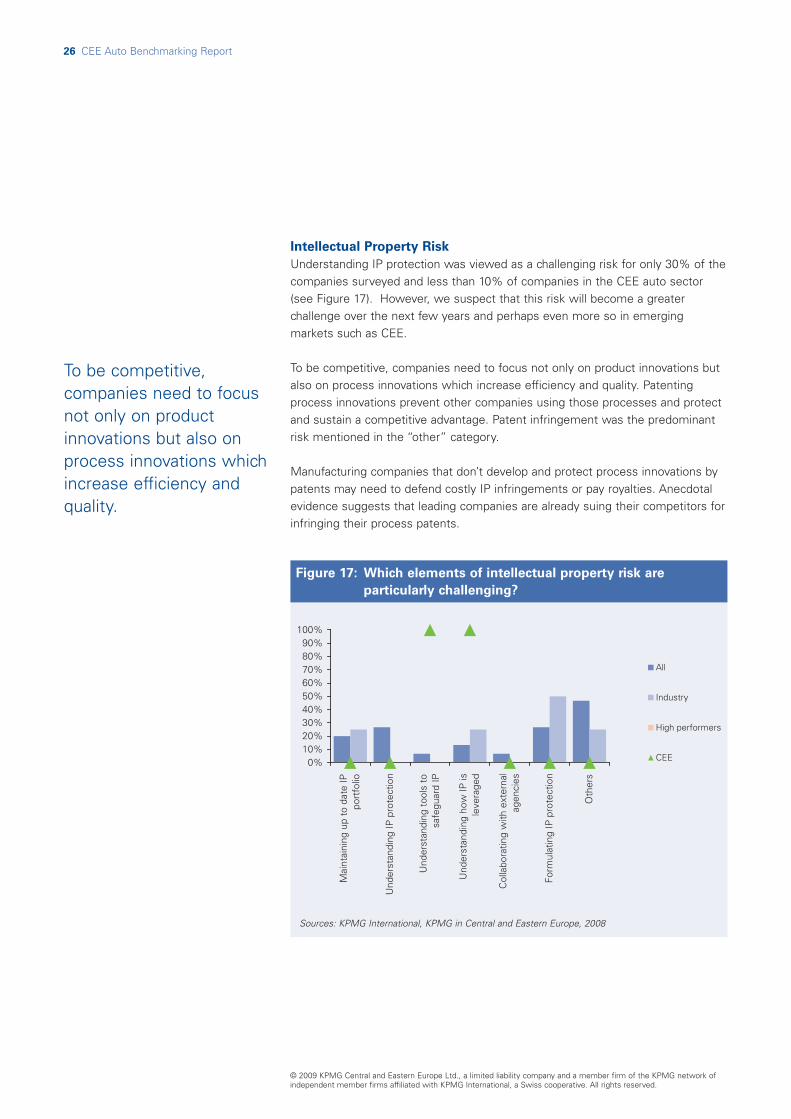

Understanding IP protection was viewed as a challenging risk for only 30% of thecompanies surveyed and less than 10% of companies in the CEE auto sector(see Figure 17). However, we suspect that this risk will become a greaterchallenge over the next few years and perhaps even more so in emergingmarkets such as CEE.

To be competitive, companies need to focus not only on product innovations butalso on process innovations which increase efficiency and quality. Patentingprocess innovations prevent other companies using those processes and protectand sustain a competitive advantage. Patent infringement was the predominantrisk mentioned in the “other” category.

Manufacturing companies that don’t develop and protect process innovations bypatents may need to defend costly IP infringements or pay royalties. Anecdotalevidence suggests that leading companies are already suing their competitors forinfringing their process patents.

To be competitive,companies need to focusnot only on productinnovations but also onprocess innovations whichincrease efficiency andquality.

CEE Auto Benchmarking Report 27

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Pot

entia

l for

str

ike

Rec

ruiti

ng/r

etai

ning

peop

le

Cos

t of

wor

kfor

ce

Pen

sion

cos

ts

Rel

atio

ns w

ithun

ions

Oth

ers

All

Industry

High performers

CEE

Figure 18: Which elements of labor risk are particularly

challenging?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

Labor Risk

Surprisingly all high performing companies – but only 5% of companies overall –emphasized relations with unions while typical companies are finding recruitmentand retention difficult (see Figure 18). This is especially true for the CEE autosector, which also emphasized the cost of workforce as an issue. Few companiesare worried about pension costs. Also, labor regulations and worker flexibilitywere concerns frequently mentioned in the “other” category.

A possible explanation for the high performers focus on relations with unionscould be their attempts to squeeze workers while unions respond negatively.However, it seems more likely that fast-growing companies must work closelywith unions to ensure workforce flexibility needed for growth. Other companiesmay be more concerned about recruitment, retention, and wage costs becausethey haven’t invested into training and motivational programs. In the case for theCEE auto sector, it seems very clear that the influx of investment in relation tothe available work force is the main driver. Meanwhile, pension costs may havereceded as an issue due to strong financial markets in previous years, however,current market volatility is again throwing valuation into question.

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

GD

P

Inte

rest

Rat

e

Infla

tion

FX P

olic

y

Nat

iona

lizat

ion

Oth

er

All

Industry

High performers

CEE

Figure 19: Which element of macro economic risk is the most

challenging?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

Macro-economic Risk

High performing companies are less concerned about GDP risk than othercompanies, while all companies (but especially high performers, and even moreso the CEE auto sector) cited exchange rate exposure as a challenge (see Figure19). Typical survey respondents do not seem particularly concerned about othermacro risks such as interest rates and inflation. This is in stark contrast to theCEE auto sector, where inflation was a significant risk within the macro economy.Economic volatility and political stability were mentioned often in the “other”category, especially in emerging markets.

High performing companies may have reduced dependence on overall growth by,for example, taking market share from competitors. Also, high performers maybe more exposed to FX risk as they explore new, less mature markets.Ultimately, while the business environment has been benign for a number ofyears until now (e.g., strong growth and low interest rates), turmoil in financialmarkets imply that macro risks are rising sharply as fundamental weakness feedsinto the global economy.

Ultimately, while thebusiness environment hasbeen benign for a numberof years until now (e.g.,strong growth and lowinterest rates), turmoil infinancial markets implythat macro risks are risingsharply as fundamentalweakness feeds into theglobal economy.

CEE Auto Benchmarking Report 29

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

6 Entering New Markets

When it comes to expansion opportunities, the countries of Central &Eastern Europe are unique. In many respects they are not like their more

easterly cousins including Russia, China and India, as they have much smallerpopulations, and are more developed with higher living standards. While thisenvironment has its advantages, it also presents business challenges. Forexample, companies cannot always rely on their home market to continually grow– as these markets are often not big enough to support the revenuerequirements of an expanding business. At the same time companies operatingin the region are constantly under threat from cheaper imports, typically fromChina or other parts of Asia.

The CEE region also faces difficulties in relation to its more westerly neighbors.For example, despite a steady track record of almost 20 years, manufacturers inthe region are not necessarily at levels of manufacturing capability as those ofthe EU 15 or the US. This is exemplified in terms of many measures ranging fromGDP per capita and levels of infrastructure. One implication of these differentlevels of development is that customers are not always willing to pay the sameprices for products that are perceived as coming from a “low-cost” country.

This means manufacturers in the CEE region must continually reinventthemselves. Fortunately, the region is well placed to do this. For example,although labor costs in the region are increasing, companies are more thanoffsetting this cost by constantly increasing value. Consider the thoughts of anexecutive from Rieter Automotive, a Swiss concern with operations in the CzechRepublic and Poland: “Costs are rising but you have to factor in productivityimprovements in low-cost countries which outweigh direct cost increases. Plusyou have more labor flexibility and often a superior work ethic.”8

Another clear advantage for CEE companies is their apparent flexibility in enteringnew markets. Although strategies cited by the region’s auto sector are similar tothose cited by survey participants elsewhere across the globe, on balance,companies from the CEE are more likely to choose a new market entry strategyto drive growth rather than relying on existing customers or existing markets. Twoissues are likely driving this: On one hand, the size of markets is pushingcompanies in CEE to be more proactive in looking outside their own borders. Onthe other hand, the ideal location of many countries from the region –sandwiched in between lower cost regions to the east, and higher cost marketsto the west - give these companies a unique geographical advantage.

“Costs are rising but youhave to factor inproductivity improvementsin low-cost countries whichoutweigh direct costincreases. Plus you havemore labor flexibility andoften a superior workethic.”8

8 KPMG International, Global ManufacturingBenchmark Survey: How manufacturingcorporations preserve and create value. 2007, p. 24.

30 CEE Auto Benchmarking Report

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

9 KPMG International, Global Manufacturing Benchmark Survey: How manufacturing corporationspreserve and create value. 2007, p. 24.

10 Based on KPMG interviews carried out by the author of this report.

Flexibility appears the main benefit from the regional sector’s geographicaladvantage as evidenced by their relative preference to enter into joint ventures,rather than acquisition or greenfield operations. These choices are generally moreexpensive but often preferred by western companies, as they often come withless day-to-day risk. According to a US executive in the automotive componentssector, “The difficult part is not running the manufacturing; it is establishing andmaintaining the relationship. You have to be there, you have to know people byname, and it is the only way to make it work.”9 Given the location and culturalsimilarity of the region it is very likely that companies are more fluid in theirability to be “on the ground” and this reduces the risks perceived by respondentsfrom other geographic locales.”

Observations and Implications from Entering New Markets

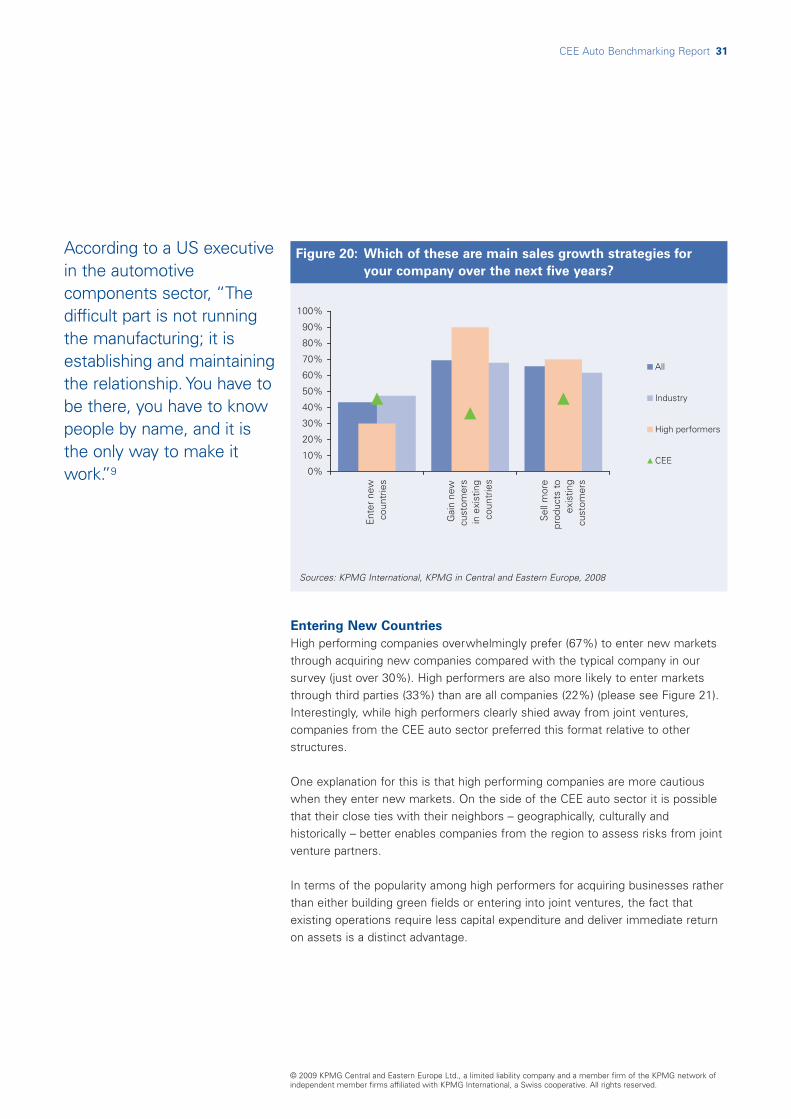

The majority of companies in our survey rated gaining new customers in existingmarkets as their key growth strategy, with international expansion less of apriority. Relatively speaking, this was not the case for companies in the CEE autosector, which were more likely to look abroad than at home. High-performingcompanies are more likely to expand upon their existing foothold (90%) bywinning new customers in existing markets (see Figure 20). Overall, winning newcustomers was seen as more important than selling more products to existingcustomers. And while this was also the, view of survey participants from theauto sector in CEE, it appears less pronounced.

By all appearances high performing companies tend to take a more consideredapproach to international expansion. Says one KPMG partner who has advisedcompanies on their expansion strategies, “Growth requires focus – it is a longterm effort, its not just about placing flags”10. A slower paced geographicexpansion could potentially help companies by allowing them more time toassess the appropriate level of risk and reward.

Also, for companies located in the CEE region, expansion abroad may be a higherpriority for at least two reasons: one being that many countries in CEE are smalland are quickly saturated; and two, the critical success drivers in the autoindustry, such as adherence to JIT schedules, means auto suppliers will locatequickly to wherever their customers go. This latter phenomenon is known as“clustering”.

CEE Auto Benchmarking Report 31

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Entering New Countries

High performing companies overwhelmingly prefer (67%) to enter new marketsthrough acquiring new companies compared with the typical company in oursurvey (just over 30%). High performers are also more likely to enter marketsthrough third parties (33%) than are all companies (22%) (please see Figure 21).Interestingly, while high performers clearly shied away from joint ventures,companies from the CEE auto sector preferred this format relative to otherstructures.

One explanation for this is that high performing companies are more cautiouswhen they enter new markets. On the side of the CEE auto sector it is possiblethat their close ties with their neighbors – geographically, culturally andhistorically – better enables companies from the region to assess risks from jointventure partners.

In terms of the popularity among high performers for acquiring businesses ratherthan either building green fields or entering into joint ventures, the fact thatexisting operations require less capital expenditure and deliver immediate returnon assets is a distinct advantage.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Ent

er n

ewco

untr

ies

Gai

n ne

wcu

stom

ers

in e

xist

ing

coun

trie

s

Sel

l mor

epr

oduc

ts t

oex

istin

gcu

stom

ers

All

Industry

High performers

CEE

Figure 20: Which of these are main sales growth strategies for

your company over the next five years?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

According to a US executivein the automotivecomponents sector, “Thedifficult part is not runningthe manufacturing; it isestablishing and maintainingthe relationship. You have tobe there, you have to knowpeople by name, and it isthe only way to make itwork.”9

32 CEE Auto Benchmarking Report

Joint Ventures

While for the typical company there appears no clear priority as to whycompanies do JVs, for the CEE auto sector several issues seem to stand outincluding: the increased speed in gaining market access; learning from the localpartner; and meeting regulatory requirements.

For players in the region’s auto sector regulatory issues are cited elsewhere inthe survey as a challenge and therefore JVs may be seen as one strategy forovercoming these challenges. Otherwise, technical challenges and operationalchallenges, which often have higher thresholds in the auto sector, may proveeasier with help from JV partners.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Who

llyow

ned

oper

atio

n –

gree

n fie

ld

Who

llyow

ned

oper

atio

n –

acqu

isiti

on

Join

tve

ntur

e

Thro

ugh

ath

ird p

arty

All

Industry

High performers

CEE

Figure 21: How do you generally enter new countries or plan to

enter new countries - which of these would be your

business model?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMGnetwork of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

CEE Auto Benchmarking Report 33

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

JV Challenges

In terms of the key challenges, identifying partners and establishing sharedobjectives appear to be the key challenges companies face when participating inJVs. For the CEE auto sector, effective control and managing day-to-dayoperations is also a challenge.

Again these issues are possibly linked to the short supply of labor and thedynamism of the region and the sector, where development has been rapid. Thesector in many countries of the region, especially in Hungary and Romania, hasgone from almost non-existent to serious global players, in just over a decade.

0%10%20%30%40%50%60%70%80%90%

100%

Reg

ulat

ory

requ

irem

ents

Mar

ket

acce

ss

Red

uced

cost

s

Incr

ease

dsp

eed

Lear

n fr

omlo

cal p

artn

er

Und

erst

andi

ngof

loca

l pr

actic

e

Sha

ring

tech

nolo

gy

Oth

er

All

Industry

High performers

CEE

Figure 22: What are your primary motivations for undertaking the

joint venture operations?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Iden

tifyi

ng r

ight

part

ner

Est

ablis

hing

sha

red

obje

ctiv

es

Sha

red

prac

tices

Man

agin

g da

y-to

-day

Eff

ectiv

e co

ntro

ls

Info

rmat

ion

tran

spar

ency

Dev

elop

ing

trus

t

Res

olvi

ng is

sues

Com

mun

icat

ion

Bre

ach

of li

cens

es/

agre

emen

ts

Oth

ers

All

Industry

Highperformers

CEE

Figure 23: What do you see as the top three challenges in

participating in, and successfully operating, joint ventures?

Sources: KPMG International, KPMG in Central and Eastern Europe, 2008

34 CEE Auto Benchmarking Report

© 2009 KPMG Central and Eastern Europe Ltd., a limited liability company and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

11 KPMG International, Global Manufacturing Benchmark Survey: How manufacturing corporationspreserve and create value. 2007, p. 24.

7 Generating Value Through Managing Performance

While the auto sector in CEE is increasingly willing to look outside itsborders to drive growth and find new customers, these companies are

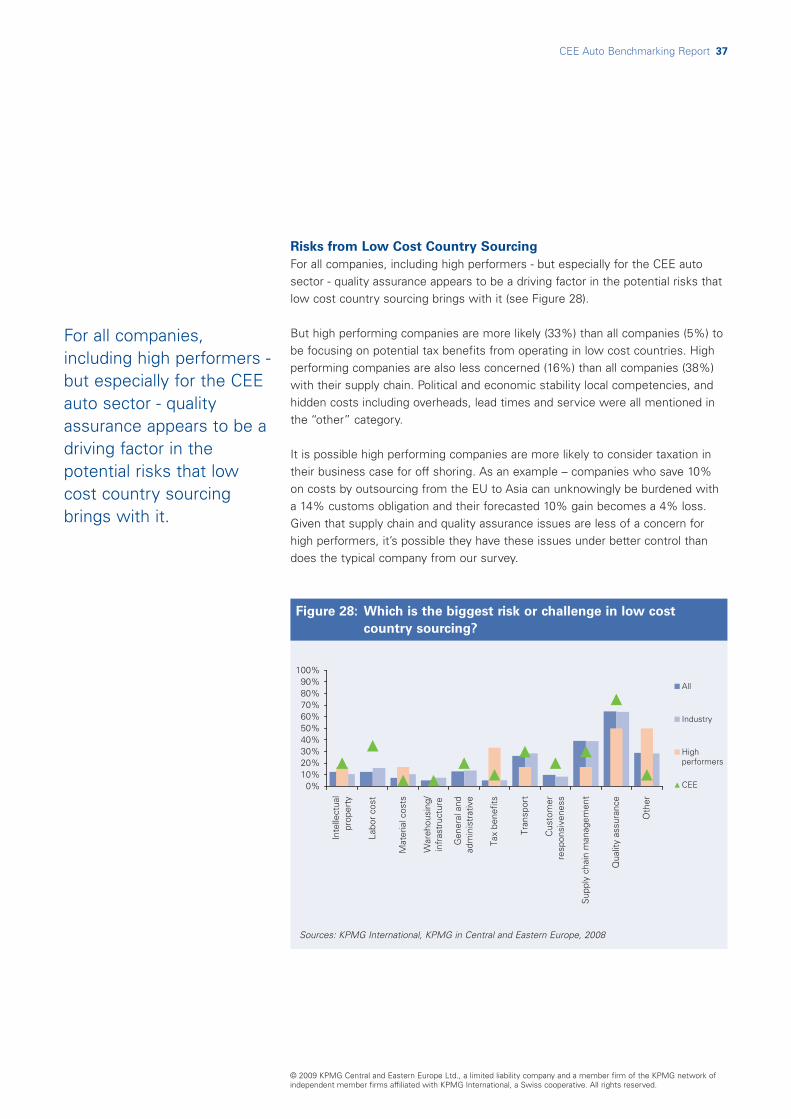

less likely to look to low cost countries for cheaper labor; this is despite repeatedconcerns about rising wage costs. One of the apparent drivers of this reluctanceappears to be potential concerns about quality coming from these regions.

Based on what executives are telling us there appears to be a definite distinctionbetween so-called middle cost locations, like the CEE region, and truly low costlocations such as China. For example one executive from Europe states, “wehave more quality issues in high cost locations, than [medium]-cost. We make allour critical components in places such as the Czech Republic... where we havelow-cost and the highest quality.”11

Manufacturing in places such as China and elsewhere in Asia is generally seen asmore problematic. Ultimately, however, it boils down to management issues.According to several executives, it’s about being on the ground and establishingappropriate controls and communication. “Achieving quality from low costmarkets is entirely dependent on how long you have had to manage the issue,”says one executive.

In terms of what low-cost countries appear to offer regions like CEE there seemsto be a clear pecking order whereby companies in the auto sector are most likelyto consider sourcing raw materials, with components coming next in line.Companies from CEE are least likely to consider sourcing manufacturingoperations in lower cost geographies.

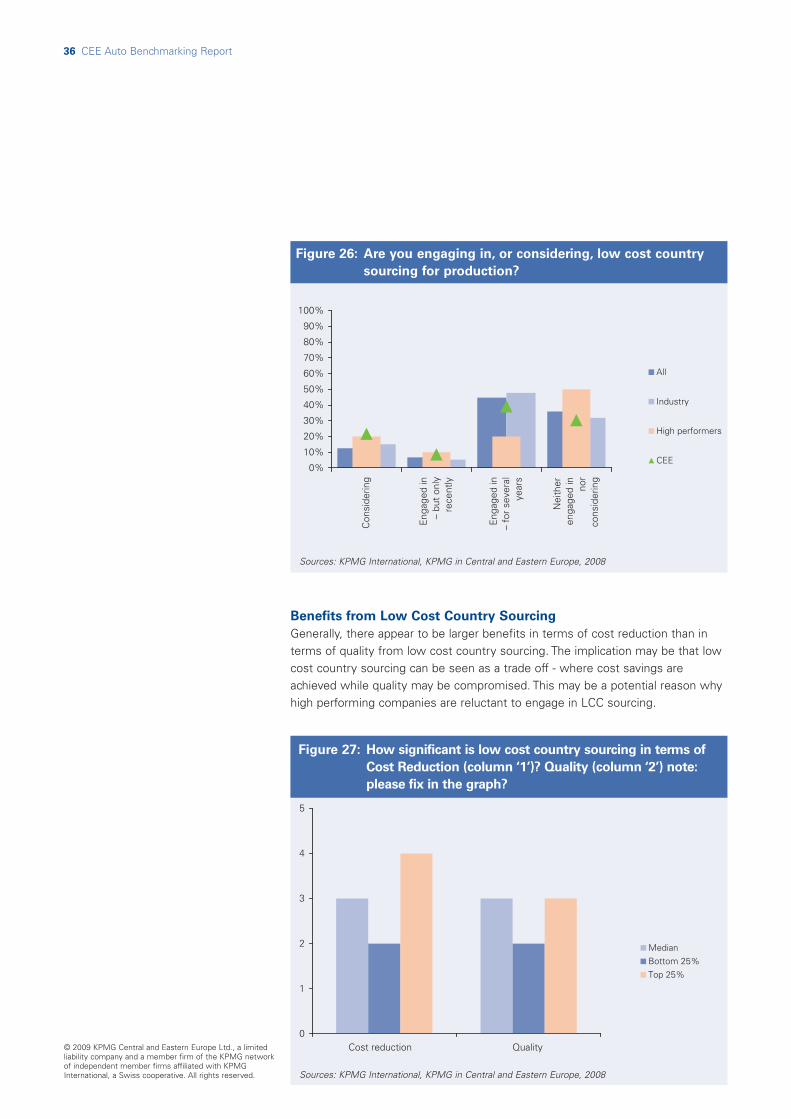

Observations & Implications from Managing Performance

Surprisingly high performing companies are not big fans of low cost countrysourcing. A larger percentage of this group (40 to 60% - depending on what wassourced) did not employ low cost country strategies for a variety of sourcingneeds including raw materials, components, and manufacturing (see Figures 24-26). The typical company who took our survey was more apt to employ low costcountry strategies, or at least to be considering them, than to be whole-heartedlyagainst them.