Embed Size (px)

Citation preview

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 1/23

PTR Restaurant

Group – 7

Saurabh raj –

12202156

Saurav Shaisesh – 12202157

Sheelpam dhar – 12202158

Shiv kumar singh – 12202159

Shreyansh agrawal –

12202160Shreyanshi Das - 12202161

RAISING LONG TERM FINANCE

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 2/23

An Introduction A venerable restaurant in Bangalore set-up decades ago. Successful business

Owner unwilling to open new branches due to risk of

dilution in quality New business opportunities and competitive

compulsions led to the opening of branches inBangalore & Chennai.

Newest endeavor financed by “ internal accruals “ Successful attempt led to plans for opening nation-wide

chain of PTR restaurants , hence to raise capitalthrough IPO.

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 3/23

KEY ISSUES in the minicase

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 4/23

What are the pros of going public ? Access to capital- A company that doesn’t tap the public financial market

may find it difficult to grow beyond a certain point for want of capital.

Respectability-Many entrepreneurs believe that they have “arrived “ in somesense if their company goes public because a public company may command greater respectability

Investor recognition- In Robert Merton’s pricing model it is shown thatother things being equal ,stock prices are higher , the larger the number of investor who are aware of the securities of the firm.

Window of opportunity-When a non-public company recognises that othercompanies in its industry are over-priced , it has an incentive to go publicand exploit that opportunity.

Benefits of diversification-When a firm goes public those who have investedin it-original owners ,investors , managers and others-can cash out of thefirm.

Signals from the market-Stock prices represent useful information for

managers.

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 5/23

ublic ?

Dilution-When a company issues shares to public , existingshareholders suffer dilution of their proportionateownership in the firm.

Loss of flexibility-the affairs of a public company are

subject to fairly comprehensive regulations. Disclosures-A company cannot maintain a strict veil of

secrecy over its expansion plans and product marketstrategies as its non public counterpart can do.

Accountability-the degree of accountability of a publiccompany is higher.

Public pressure-Because of its greater visibility , a publiccompany may be pressurized to do things that it may not

otherwise do.

i f k

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 6/23

company satisfy to make an

IPO ? A company has to satisfy at least one of the following

conditions to make an IPO:-

1) Track record

The company should have net tangible assets of at leastRs 3 crore, net worth of at least Rs 1 crore, &

distributable profits

for at least three out of the preceeding five years.

The issue size should not exceed 5 times the pre-issue net worth.

2) QIB Participation

The issue is made through the book building process, withat least

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 7/23

Continued …. 3. ) Appraisal & Participation by Financial

Institutions or Commercial Banks

Company’s project should have been appraised by

financial institutions or scheduled commercial banks &the appraisers should provide at least 10% of thefinancing.

The post-issue capital has to be at least Rs 10 crore ,failing which has to be compulsory market making for 2 yrs.

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 8/23

What is book building ? - Book building is actually a price discovery method. Inthis method, the company doesn't fix up a particularprice for the shares, but instead gives a price range, e.g.Rs 80-100.

In book building,The company announces a price band within whichpotential investors are required to bid for the shares. Thelowest price of the range is called the floor price and the

highest price is called as cap price.During the bidding process, investors can change theirbids.

After the bidding is over, the cut-off price is determinedbased on the demand for the share. Cut off price is the

Wh h i i l i

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 9/23

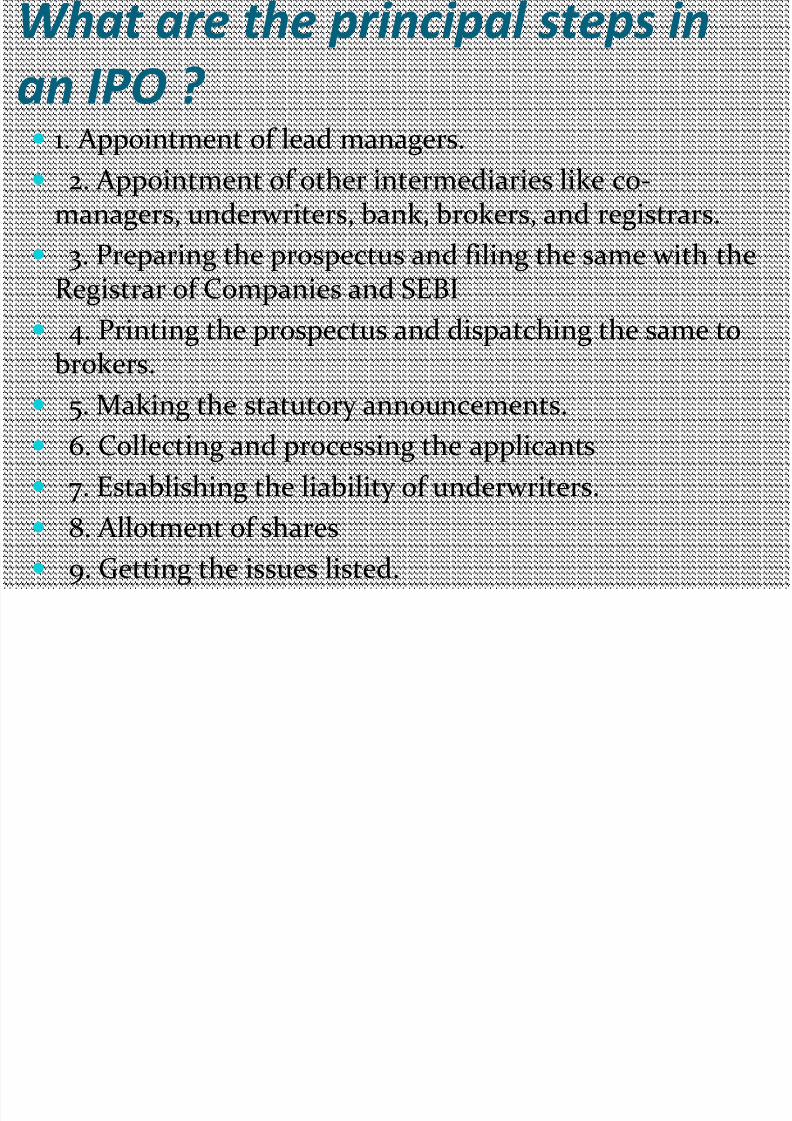

What are the principal steps in

an IPO ? 1. Appointment of lead managers. 2. Appointment of other intermediaries like co-

managers, underwriters, bank, brokers, and registrars.

3. Preparing the prospectus and filing the same with theRegistrar of Companies and SEBI

4. Printing the prospectus and dispatching the same tobrokers.

5. Making the statutory announcements. 6. Collecting and processing the applicants

7. Establishing the liability of underwriters.

8. Allotment of shares

9. Getting the issues listed.

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 10/23

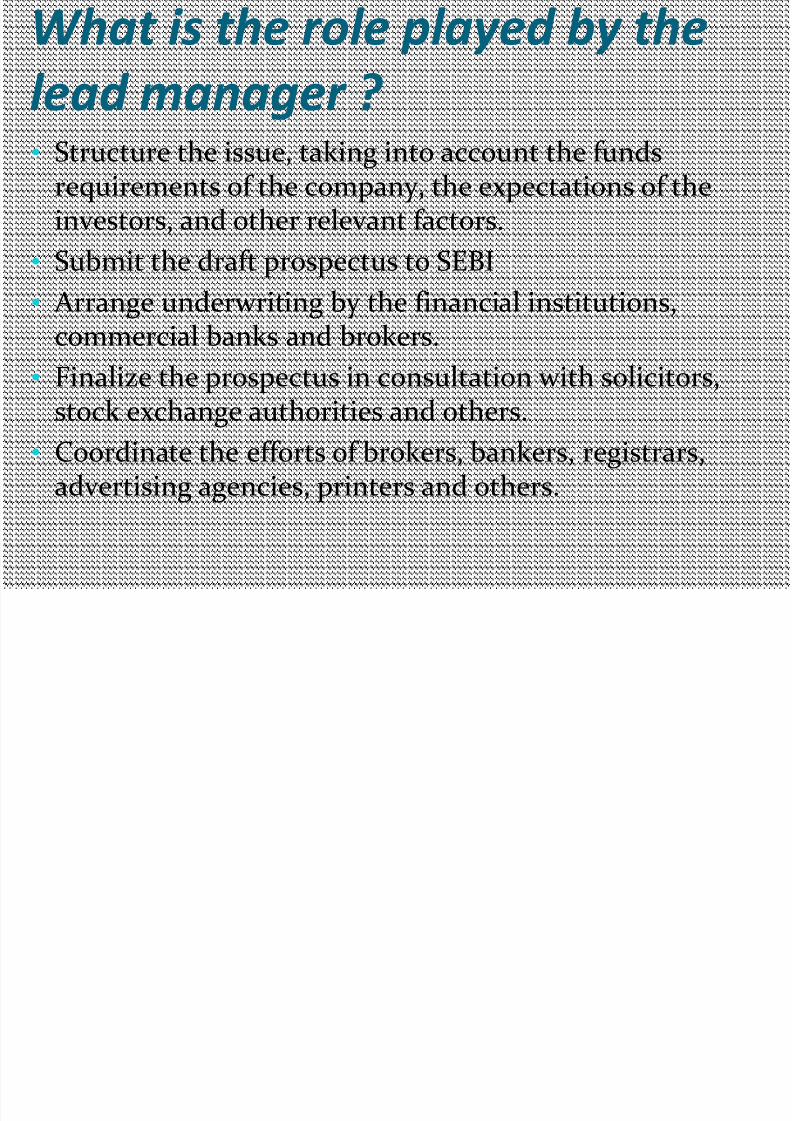

What is the role played by the

lead manager ? • Structure the issue, taking into account the funds

requirements of the company, the expectations of theinvestors, and other relevant factors.

•

Submit the draft prospectus to SEBI• Arrange underwriting by the financial institutions,

commercial banks and brokers.

• Finalize the prospectus in consultation with solicitors,

stock exchange authorities and others.• Coordinate the efforts of brokers, bankers, registrars,

advertising agencies, printers and others.

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 11/23

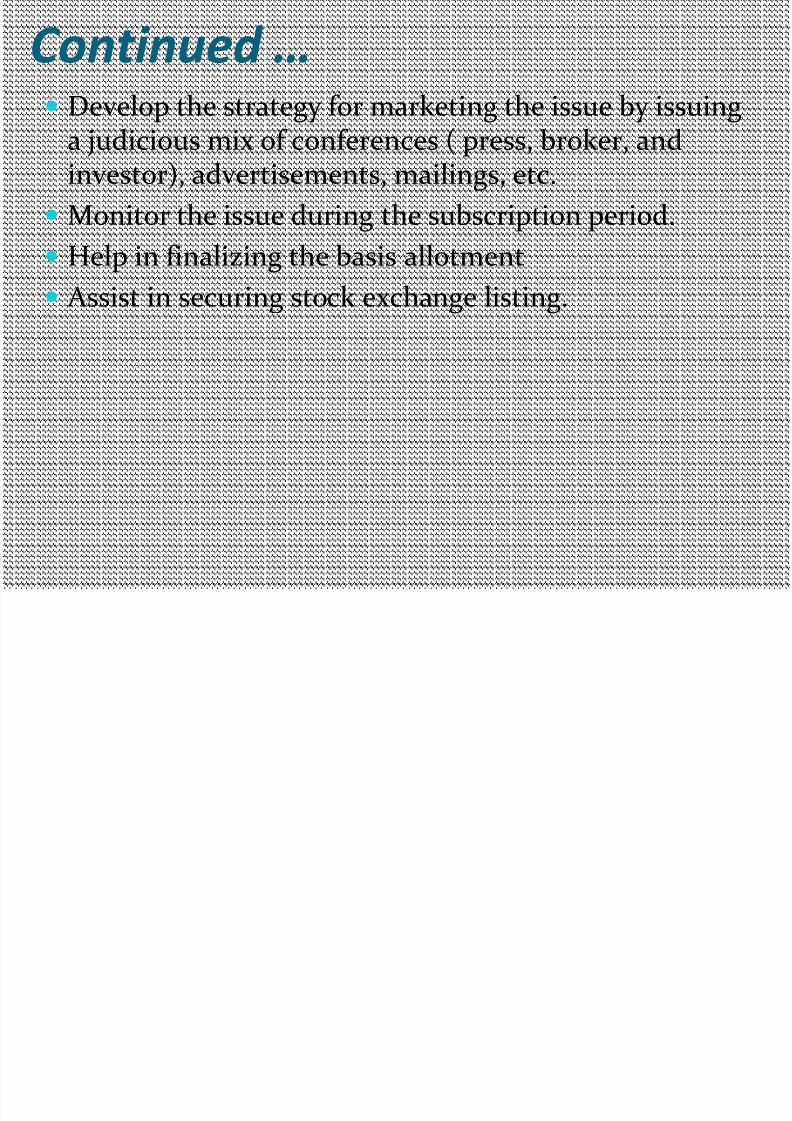

Continued … Develop the strategy for marketing the issue by issuing

a judicious mix of conferences ( press, broker, andinvestor), advertisements, mailings, etc.

Monitor the issue during the subscription period.

Help in finalizing the basis allotment

Assist in securing stock exchange listing.

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 12/23

What are the costs of a public

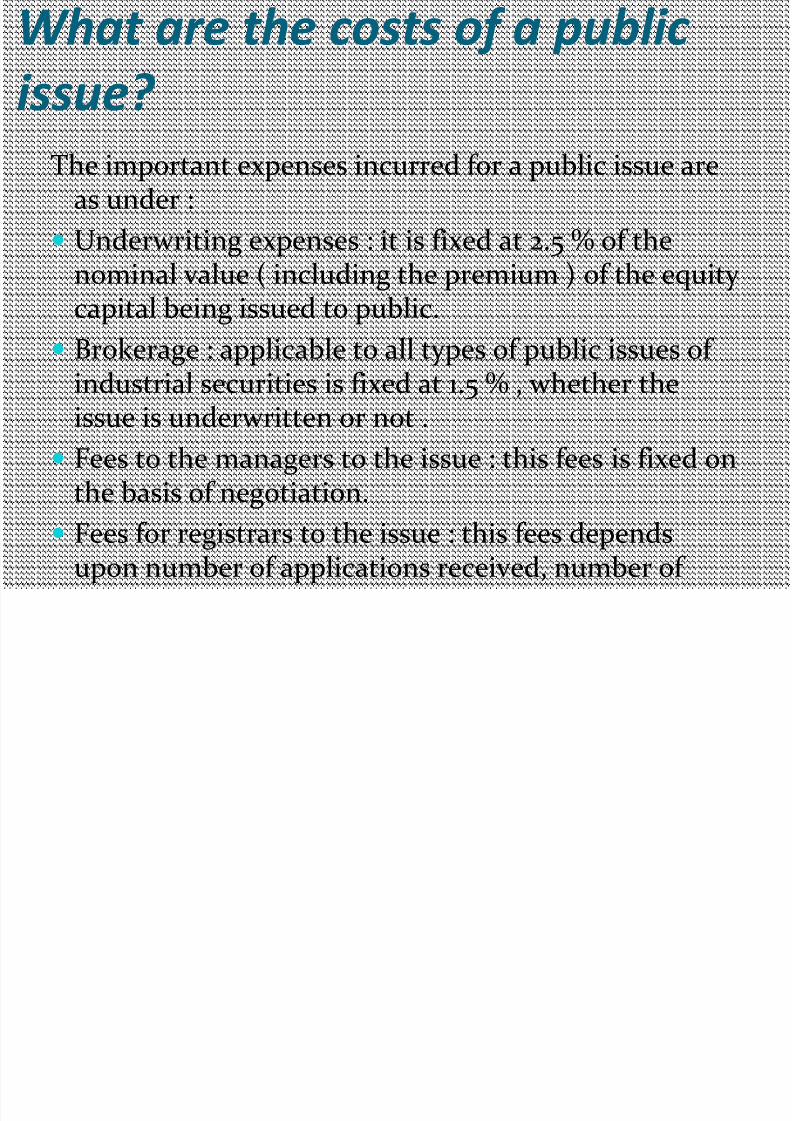

issue? The important expenses incurred for a public issue are

as under :

Underwriting expenses : it is fixed at 2.5 % of the

nominal value ( including the premium ) of the equity capital being issued to public.

Brokerage : applicable to all types of public issues of industrial securities is fixed at 1.5 % , whether the

issue is underwritten or not . Fees to the managers to the issue : this fees is fixed on

the basis of negotiation.

Fees for registrars to the issue : this fees dependsupon number of applications received, number of

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 13/23

Continued …. Printing expenses : relates to the printing of

prospectus, application forms, brochures, sharecertificates, allotment/ refund letters, envelopes, etc.

Postage expenses : these pertain to the mailing of application letters by ordinary posts and allotment /

refund letters by registered post. Advertising and publicity expenses : these are

incurred primarily toward statutory announcements,PC’s and investor conferences.

Listing fees : the fees payable to concerned stockexchanges where the securities are listed.

Stamp duty : this is the duty payable on share

certificates issued by the company.

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 14/23

an a company ma ng a pu c issue freely price its shares ? As per the present SEBI disclosure and investor

protection guidelines 2000 ( DIP guidelines ) , every company whether listed or unlisted, which is eligible tomake a public issue can freely price its shares. However

the issuing company has to make the followingdisclosures.

Adjusted EPS ( past 3 years )

P / E ratio in relation to issue

Return on net worth

Minimum return on the total net worth after the issueneeded to maintain EPS

Net asset value

f ’

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 15/23

15

Why is under- pricing of IPO’s a

universal phenomenon ? Under pricing of IPO is termed as a universal phenomenon

due to the following explanations –

Winner’s curse : investors are of 2 types : informed &

uninformed . In general the FI are informed and theindividual investors are uninformed. So the individualinvestors tend to become victims of winners curse . When they receive allotment of shares for which they

have applied in for in an IPO , it may be because theshares are overpriced and informed investors have stayedaway from the issue. Hence the uninformed investors will need an incentive in the form of a substantial under-

pricing of the IPO to remain in the market .

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 16/23

16

Continued …. Bait for future offerings : a company making an IPO

would like the investors to have a rewarding experience,to create loyalty, which helps in raising capital in futureat a higher price.

Informational asymmetry : the merchant bankers

know the market better than the issuing company .They may exploit this superior knowledge to under-pricing issues.

Regulatory constraints : during the days of controllerof capital issues , the issue price in India was governed

by a very conservative formula. Political goals : companies may deliberately under-

price their issues and allot them to people in power.( Eg: recruitment company in Japan )

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 17/23

A right issue is an issue of capital to the existing share

holders of the company through a ‘ letter of order ‘ madein the 1st instance to the existing shareholders on a pro-rata basis.

Characteristics of rights :

The issuing firm decides on the number of rights sharesto be issued.

Based on the proposition , rights entitlement of theexisting shareholders are determined .

The price / share for additional equity called thesubscription price is left to discretion of the company.

Rights are negotiable. Holder can sell them

Rights can be exercised only during a fixed period ,

usually about 30 days .

What is a right issue ?

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 18/23

Continued …. Conditions : the conditions that have to be satisfied for

obtaining the approval for rights issues are as under : Existing shareholders , exercising their full rights are given

opportunities to apply for additional shares.

Existing shareholders , who renounce their rights wholly or

partially are not entitled to do the above . Shares which become available , due to non exercise of

rights by some shareholders, are allotted to shareholders who have applied for additional shares in proportion to

their shareholding. Any balance shares , left after meeting requests for

additional shares by the existing shareholders, are disposedof at the ruling market price or the issue price , whicheveris higher .

Wh t th diff t ki d f

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 19/23

What are the different kinds of

dilution ? There are 3 kinds of dilution : -

Control dilution Earnings dilution

Value dilution

Control Dilution :- Control dilution describes the reduction in ownership percentage

or loss of a controlling share of an investment's stock. Many venture capitalcontracts contain an anti-dilution provision in favor of the original investors, toprotect their equity investments. One way to raise new equity without diluting voting control is to give warrants to all the existing shareholders equally. They canchoose to put more money in the company, or else lose ownership percentage. When employee options threaten to dilute the ownership of a control group, the

company can use cash to buy back the shares issued.

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 20/23

Continued …. The measurement of this percent dilution is made at a point intime. It will change as market values change, and cannot be

interpreted as a measure of the impact of dilutions.

1. Presume that all convertible securities are convertible at thedate.

2. Add up the number of new shares that will be issued as a result.3. Add up the proceeds that would be received on these

conversions and issues (The reduction of debt is a 'proceed').

4. Divide the total proceeds by the current market price of the

stock to determine the number of shares the proceeds canbuyback.

5. Subtract the number bought-back from the new sharesoriginally issued

6. Divide the net increase in shares by the starting shares

outstanding.

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 21/23

4/10/2013

Continued ….

Earnings dilution :- Earnings dilution describes thereduction in amount earned per share in an investment dueto an increase in the total number of shares. The calculationof earnings dilutions derives from this same process as

control dilution. The net increase in shares (steps 1-5) isdetermined at the beginning of the reporting period, andadded to the beginning number of shares outstanding. TheNet Income for the period is divided by this increased

number of shares. Notice that the conversion rates aredetermined by market values at the beginning, not theperiod end. The returns to be realized on the reinvestmentof the proceeds are not part of this calculation

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 22/23

4/10/2013

Continued …. Value dilution :- Value dilution describes the reduction in the current price

of a stock due to the increase in the number of shares. This generally

occurs when shares are issued in exchange for the purchase of a business,and incremental income from the new business must be at least theReturn on equity (ROE) of the old business. When the purchase priceincludes goodwill, this becomes a higher hurdle to clear.

The theoretical diluted price, i.e. the price after an increase in the number of shares, can be calculated as : -

Theoretical Diluted Price = ((O x OP) +(N x IP)) / (O + N) where

O = original number of shares , OP = Current share price,N = number of newshares to be issued , IP = issue price of new shares

For example if there is a 3-for-10 issue, the current price is $0.50, the issue price $0.32, we have

O = 10, OP = $0.50, N = 3, IP = $0.32 and TDP = ((10x0.50)+(3x0.32))/(10+3) =

$0.4585

7/28/2019 CF final(1) on ptr restaurant mini case

http://slidepdf.com/reader/full/cf-final1-on-ptr-restaurant-mini-case 23/23