Embed Size (px)

DESCRIPTION

MIF Appraisal Worksheet

Citation preview

AppraiseVersion 1

"Getting Started" provides a quick step-by step guide to set up options and data input.

"About Appraise" provides version information about Appraise.xls

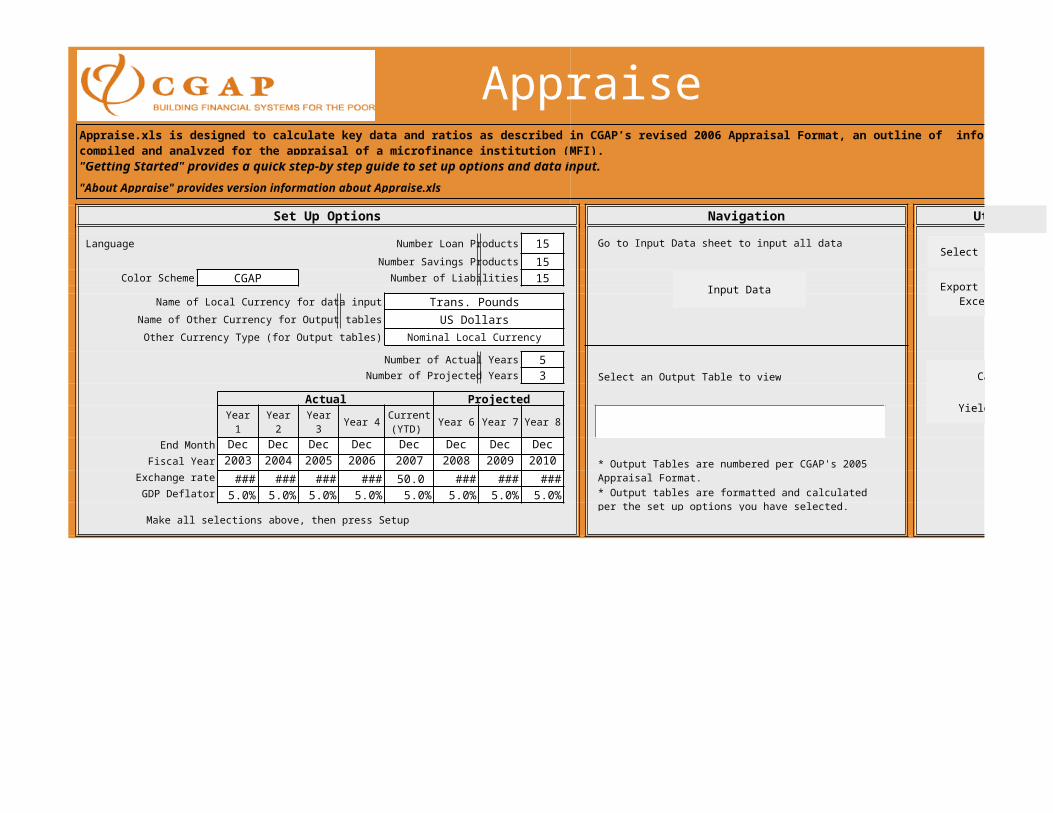

Set Up Options Navigation Utilities

Language Number Loan Products 15 Go to Input Data sheet to input all data

Number Savings Products 15Color Scheme CGAP Number of Liabilities 15

Name of Local Currency for data input Trans. Pounds

Name of Other Currency for Output tables US Dollars

Other Currency Type (for Output tables) Nominal Local Currency

Number of Actual Years 5Number of Projected Years 3 Select an Output Table to view

Actual Projected

Year 1 Year 2 Year 3 Year 4 Year 6 Year 7 Year 8

End Month Dec Dec Dec Dec Dec Dec Dec Dec

Fiscal Year 2003 2004 2005 2006 2007 2008 2009 2010

Exchange rate 50.0 50.0 50.0 50.0 50.0 48.0 48.0 48.0 GDP Deflator 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0%

Make all selections above, then press Setup

Appraise.xls is designed to calculate key data and ratios as described in CGAP’s revised 2006 Appraisal Format, an outline of information to be compiled and analyzed for the appraisal of a microfinance institution (MFI).

Current (YTD)

* Output Tables are numbered per CGAP's 2005 Appraisal Format.

* Output tables are formatted and calculated per the set up options you have selected.

Input Data

Select sheets to print

Export all data to an Excel .csv file

Calculator

Yield Calculator

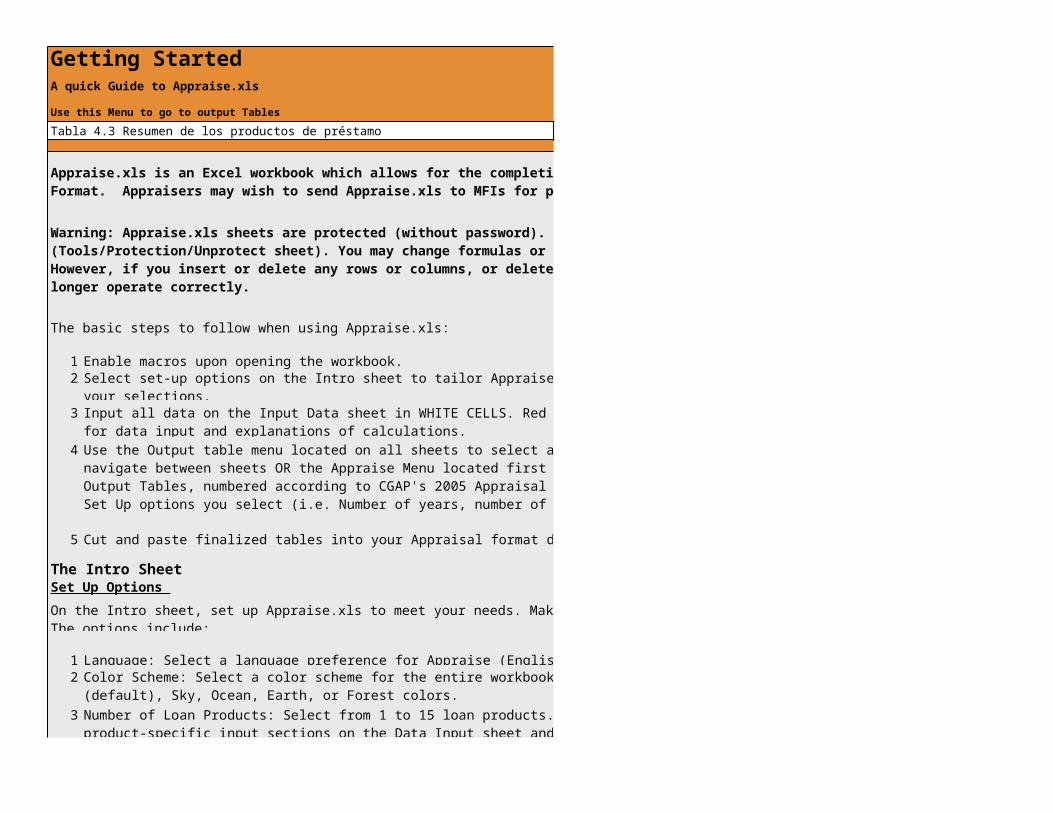

Getting StartedA quick Guide to Appraise.xls

Use this Menu to go to output Tables

Tabla 4.3 Resumen de los productos de préstamo

The basic steps to follow when using Appraise.xls:

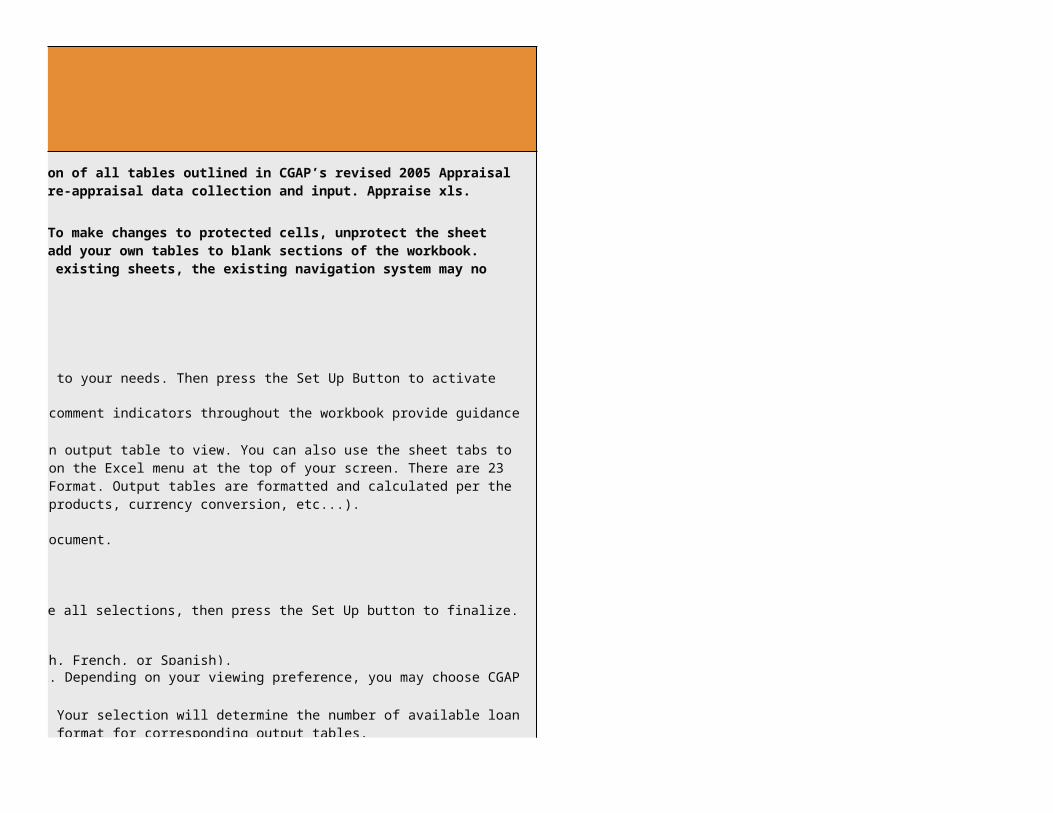

1 Enable macros upon opening the workbook.2 Select set-up options on the Intro sheet to tailor Appraise to your needs. Then press the Set Up Button to activate your selections.

3

4

5 Cut and paste finalized tables into your Appraisal format document.

The Intro Sheet Set Up Options

On the Intro sheet, set up Appraise.xls to meet your needs. Make all selections, then press the Set Up button to finalize. The options include:

1 Language: Select a language preference for Appraise (English, French, or Spanish).2

3

Appraise.xls is an Excel workbook which allows for the completion of all tables outlined in CGAP’s revised 2005 Appraisal Format. Appraisers may wish to send Appraise.xls to MFIs for pre-appraisal data collection and input. Appraise xls.

Warning: Appraise.xls sheets are protected (without password). To make changes to protected cells, unprotect the sheet (Tools/Protection/Unprotect sheet). You may change formulas or add your own tables to blank sections of the workbook. However, if you insert or delete any rows or columns, or delete existing sheets, the existing navigation system may no longer operate correctly.

Input all data on the Input Data sheet in WHITE CELLS. Red comment indicators throughout the workbook provide guidance for data input and explanations of calculations.

Use the Output table menu located on all sheets to select an output table to view. You can also use the sheet tabs to navigate between sheets OR the Appraise Menu located first on the Excel menu at the top of your screen. There are 23 Output Tables, numbered according to CGAP's 2005 Appraisal Format. Output tables are formatted and calculated per the Set Up options you select (i.e. Number of years, number of products, currency conversion, etc...).

Color Scheme: Select a color scheme for the entire workbook. Depending on your viewing preference, you may choose CGAP (default), Sky, Ocean, Earth, or Forest colors.

Number of Loan Products: Select from 1 to 15 loan products. Your selection will determine the number of available loan product-specific input sections on the Data Input sheet and format for corresponding output tables.

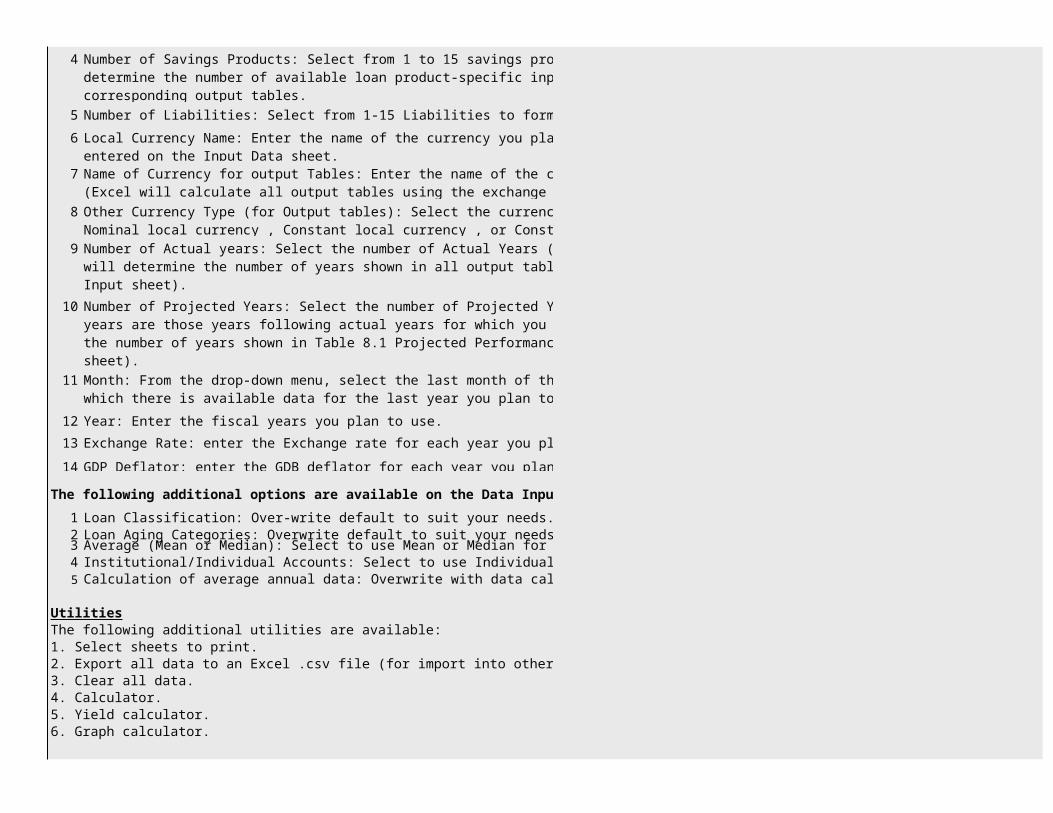

4

5 Number of Liabilities: Select from 1-15 Liabilities to format your Composition of Liabilities table.

6

7

8

9

10

11

12 Year: Enter the fiscal years you plan to use.

13 Exchange Rate: enter the Exchange rate for each year you plan to use.

14 GDP Deflator: enter the GDB deflator for each year you plan to use.

The following additional options are available on the Data Input Sheet:

1 Loan Classification: Over-write default to suit your needs.2 Loan Aging Categories: Overwrite default to suit your needs.3 Average (Mean or Median): Select to use Mean or Median for Average calculations.4 Institutional/Individual Accounts: Select to use Individual Accounts, Institutional Accounts, or both.5 Calculation of average annual data: Overwrite with data calculated from monthly entries.

UtilitiesThe following additional utilities are available:1. Select sheets to print.2. Export all data to an Excel .csv file (for import into other programs).3. Clear all data.4. Calculator.5. Yield calculator.6. Graph calculator.

Number of Savings Products: Select from 1 to 15 savings products from the drop-down menu provided. Your selection will determine the number of available loan product-specific input sections on the Data Input sheet and format for corresponding output tables.

Local Currency Name: Enter the name of the currency you plan to use to enter all data. Your input data will remain as entered on the Input Data sheet.

Name of Currency for output Tables: Enter the name of the currency you want for Financial Statements output tables. (Excel will calculate all output tables using the exchange rate you specify).

Other Currency Type (for Output tables): Select the currency type to show financial statements output tables in: Nominal local currency , Constant local currency , or Constant other currency.

Number of Actual years: Select the number of Actual Years (from 1 to 5) you wish to input and show data. This selection will determine the number of years shown in all output tables (but all input years will remain visible on the Data Input sheet).

Number of Projected Years: Select the number of Projected Years (from 0-3) you wish to input and show data. Projected years are those years following actual years for which you wish to show projected data. This selection will determine the number of years shown in Table 8.1 Projected Performance (All input years will remain visible on the Data Input sheet).

Month: From the drop-down menu, select the last month of the fiscal year for all full years, and the last month for which there is available data for the last year you plan to use.

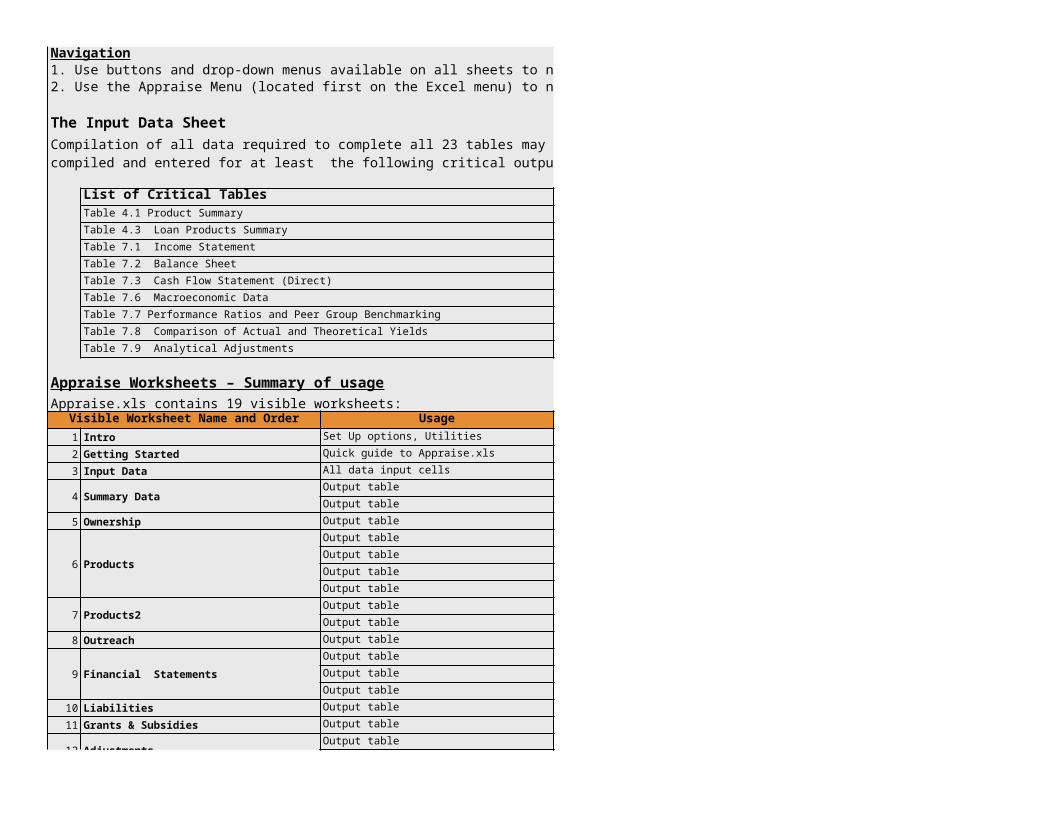

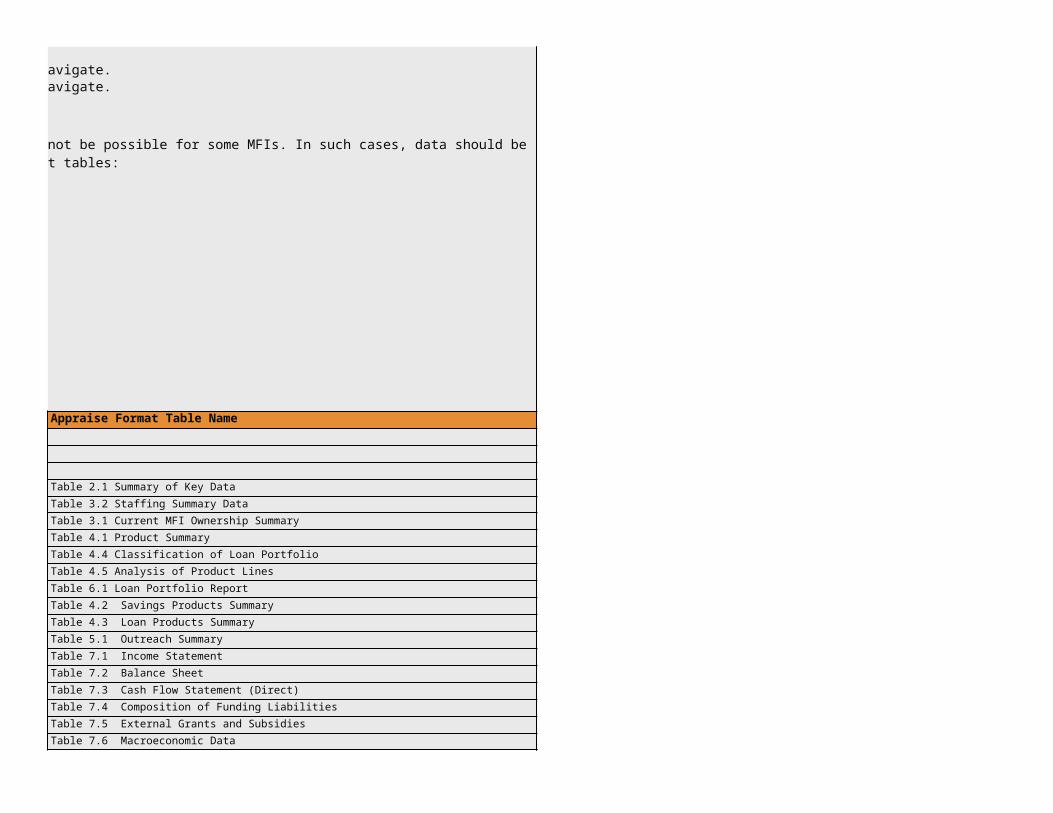

Navigation1. Use buttons and drop-down menus available on all sheets to navigate.2. Use the Appraise Menu (located first on the Excel menu) to navigate.

The Input Data Sheet

List of Critical Tables

Table 7.1 Income Statement

Table 7.2 Balance Sheet

Table 7.3 Cash Flow Statement (Direct)

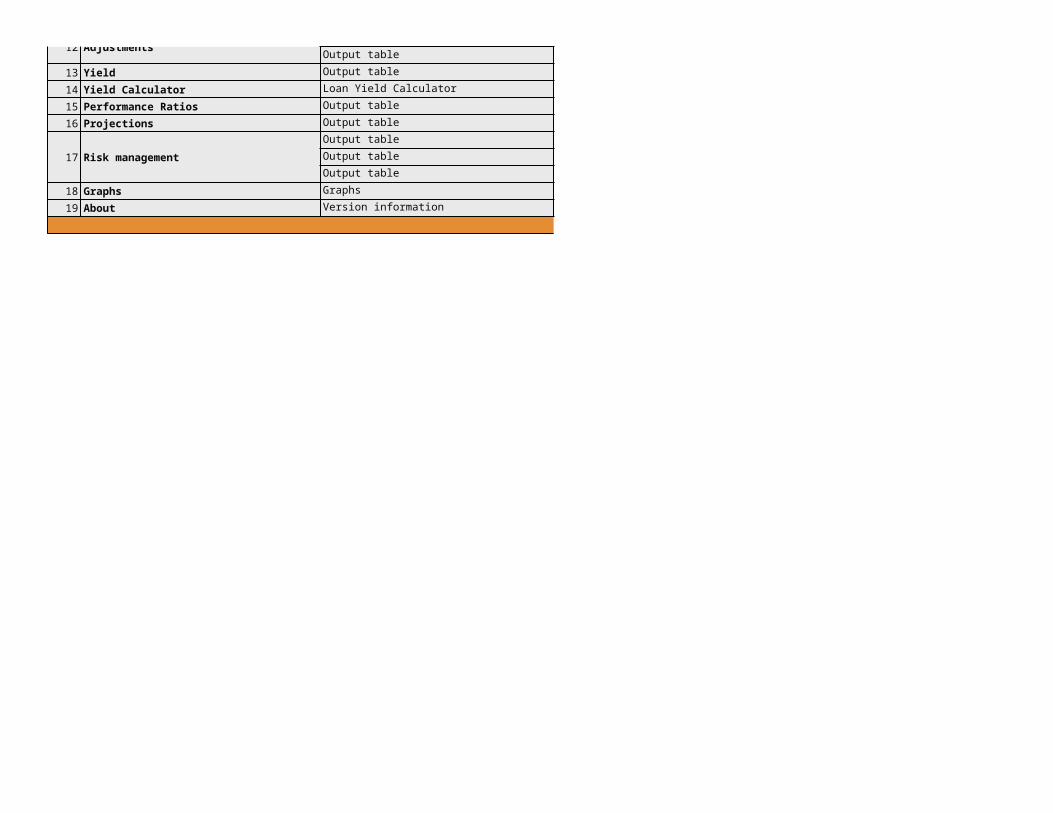

Appraise Worksheets – Summary of usageAppraise.xls contains 19 visible worksheets:

Visible Worksheet Name and Order Usage Appraise Format Table Name

1 Intro Set Up options, Utilities

2 Getting Started Quick guide to Appraise.xls

3 Input Data All data input cells

4 Summary DataOutput table Table 2.1 Summary of Key Data

Output table Table 3.2 Staffing Summary Data

5 Ownership Output table Table 3.1 Current MFI Ownership Summary

6 Products

Output table

Output table

Output table

Output table Table 6.1 Loan Portfolio Report

7 Products2Output table

Output table

8 Outreach Output table

9 Financial Statements

Output table Table 7.1 Income Statement

Output table Table 7.2 Balance Sheet

Output table Table 7.3 Cash Flow Statement (Direct)

10 Liabilities Output table

11 Grants & Subsidies Output table

12 AdjustmentsOutput table

Compilation of all data required to complete all 23 tables may not be possible for some MFIs. In such cases, data should be compiled and entered for at least the following critical output tables:

Table 4.1 Product Summary

Table 4.3 Loan Products Summary

Table 7.6 Macroeconomic Data

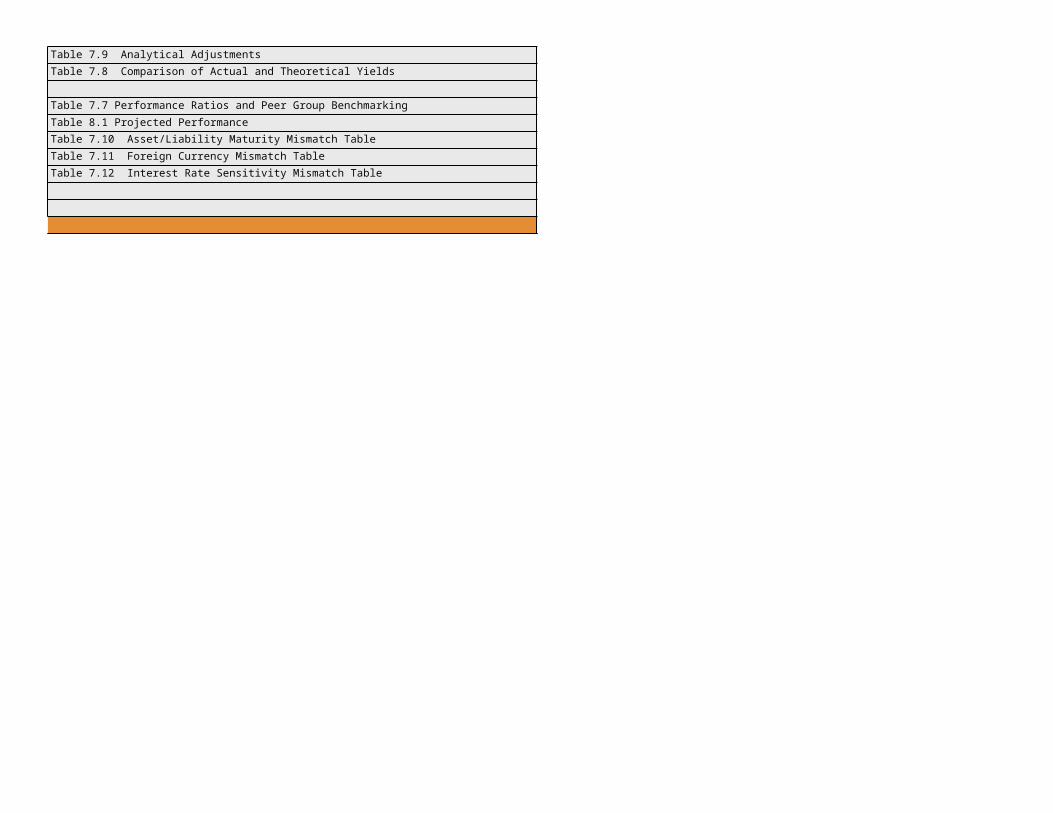

Table 7.7 Performance Ratios and Peer Group Benchmarking

Table 7.8 Comparison of Actual and Theoretical Yields

Table 7.9 Analytical Adjustments

Table 4.1 Product Summary

Table 4.4 Classification of Loan Portfolio

Table 4.5 Analysis of Product Lines

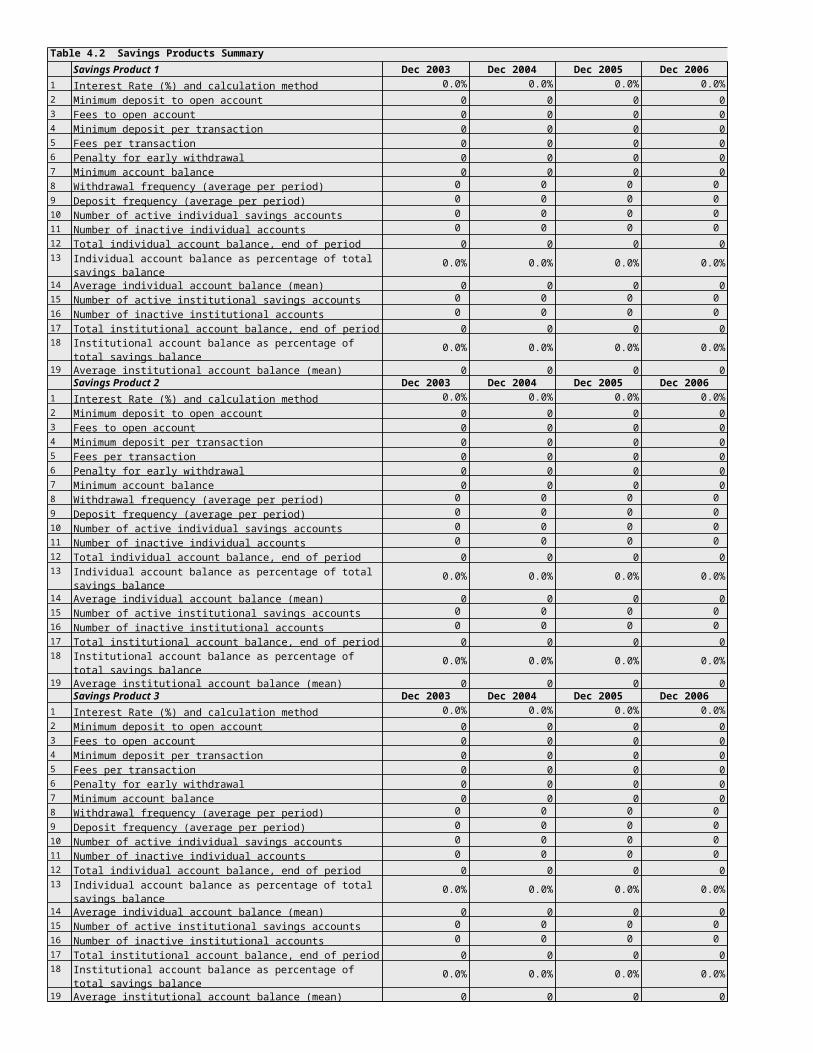

Table 4.2 Savings Products Summary

Table 4.3 Loan Products Summary

Table 5.1 Outreach Summary

Table 7.4 Composition of Funding Liabilities

Table 7.5 External Grants and Subsidies

Table 7.6 Macroeconomic Data

12 AdjustmentsOutput table

13 Yield Output table

14 Yield Calculator Loan Yield Calculator

15 Performance Ratios Output table

16 Projections Output table Table 8.1 Projected Performance

17 Risk management

Output table

Output table

Output table

18 Graphs Graphs

19 About Version information

Table 7.9 Analytical Adjustments

Table 7.8 Comparison of Actual and Theoretical Yields

Table 7.7 Performance Ratios and Peer Group Benchmarking

Table 7.10 Asset/Liability Maturity Mismatch Table

Table 7.11 Foreign Currency Mismatch Table

Table 7.12 Interest Rate Sensitivity Mismatch Table

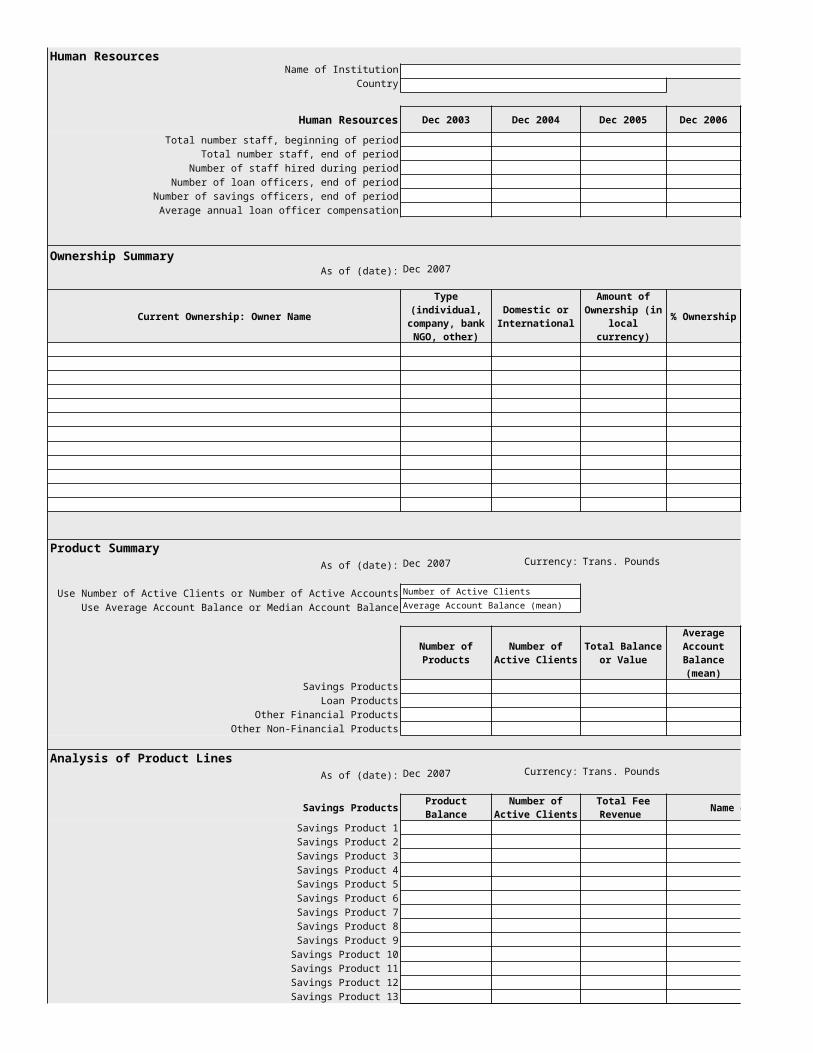

Human ResourcesName of Institution

Country

Human Resources Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Total number staff, beginning of period

Total number staff, end of period

Number of staff hired during period

Number of loan officers, end of period

Number of savings officers, end of period

Average annual loan officer compensation

Ownership SummaryAs of (date): Dec 2007

Current Ownership: Owner Name % Ownership

Product SummaryAs of (date): Dec 2007 Currency: Trans. Pounds

Use Number of Active Clients or Number of Active Accounts Number of Active Clients

Use Average Account Balance or Median Account Balance Average Account Balance (mean)

Savings Products

Loan Products

Other Financial Products

Other Non-Financial Products

Analysis of Product LinesAs of (date): Dec 2007 Currency: Trans. Pounds

Savings Products Product Balance Name of Savings Product

Savings Product 1

Savings Product 2

Savings Product 3

Savings Product 4

Savings Product 5

Savings Product 6

Savings Product 7

Savings Product 8

Savings Product 9

Savings Product 10

Savings Product 11

Savings Product 12

Savings Product 13

Type (individual, company, bank

NGO, other)

Domestic or International

Amount of Ownership (in local currency)

Number of Products

Number of Active Clients

Total Balance or Value

Average Account Balance (mean)

Number of Active Clients

Total Fee Revenue

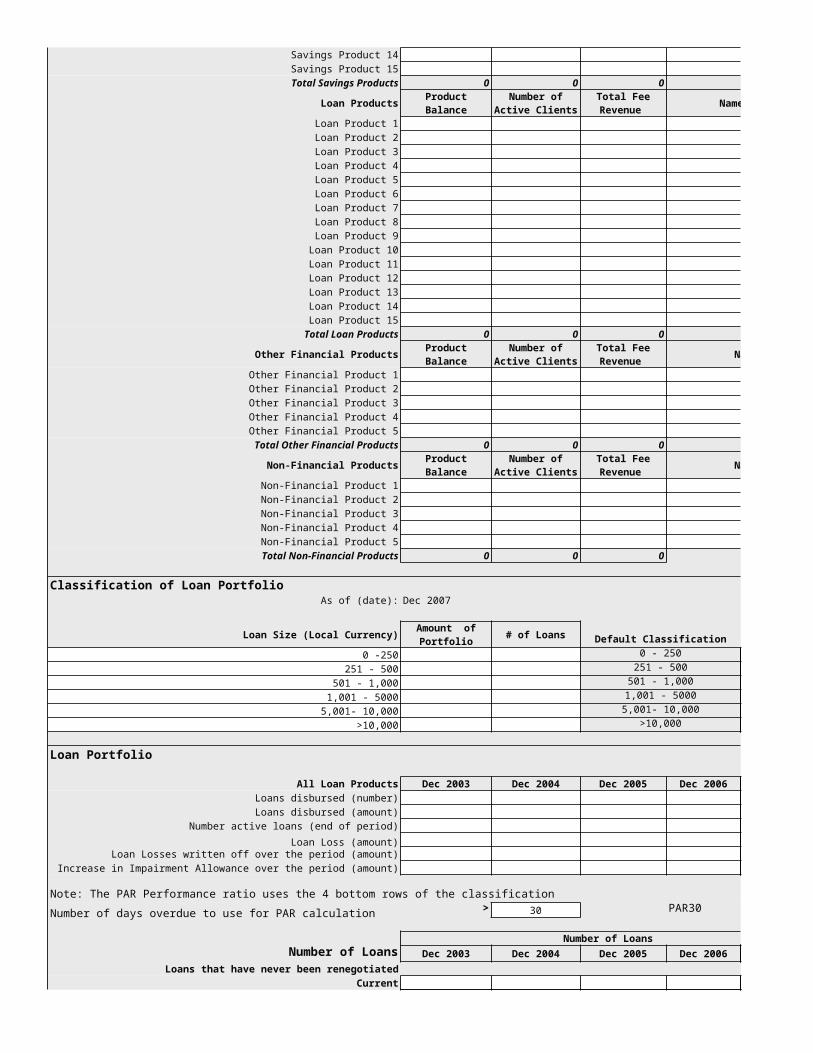

Savings Product 14

Savings Product 15

Total Savings Products 0 0 0

Loan Products Product Balance Name of Loan Product

Loan Product 1

Loan Product 2

Loan Product 3

Loan Product 4

Loan Product 5

Loan Product 6

Loan Product 7

Loan Product 8

Loan Product 9

Loan Product 10

Loan Product 11

Loan Product 12

Loan Product 13

Loan Product 14

Loan Product 15

Total Loan Products 0 0 0

Other Financial Products Product Balance Name of Product

Other Financial Product 1

Other Financial Product 2

Other Financial Product 3

Other Financial Product 4

Other Financial Product 5

Total Other Financial Products 0 0 0

Non-Financial Products Product Balance Name of Product

Non-Financial Product 1

Non-Financial Product 2

Non-Financial Product 3

Non-Financial Product 4

Non-Financial Product 5

Total Non-Financial Products 0 0 0

Classification of Loan PortfolioAs of (date): Dec 2007

Loan Size (Local Currency) # of Loans Default Classification

0 -250 0 - 250

251 - 500 251 - 500

501 - 1,000 501 - 1,000

1,001 - 5000 1,001 - 5000

5,001- 10,000 5,001- 10,000

>10,000 >10,000

Loan Portfolio

All Loan Products Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Loans disbursed (number)

Loans disbursed (amount)

Number active loans (end of period)

Loan Loss (amount)Loan Losses written off over the period (amount)

Increase in Impairment Allowance over the period (amount)

Note: The PAR Performance ratio uses the 4 bottom rows of the classification

Number of days overdue to use for PAR calculation > 30 PAR30

Number of Loans

Number of Loans Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Loans that have never been renegotiated

Current

Number of Active Clients

Total Fee Revenue

Number of Active Clients

Total Fee Revenue

Number of Active Clients

Total Fee Revenue

Amount of Portfolio

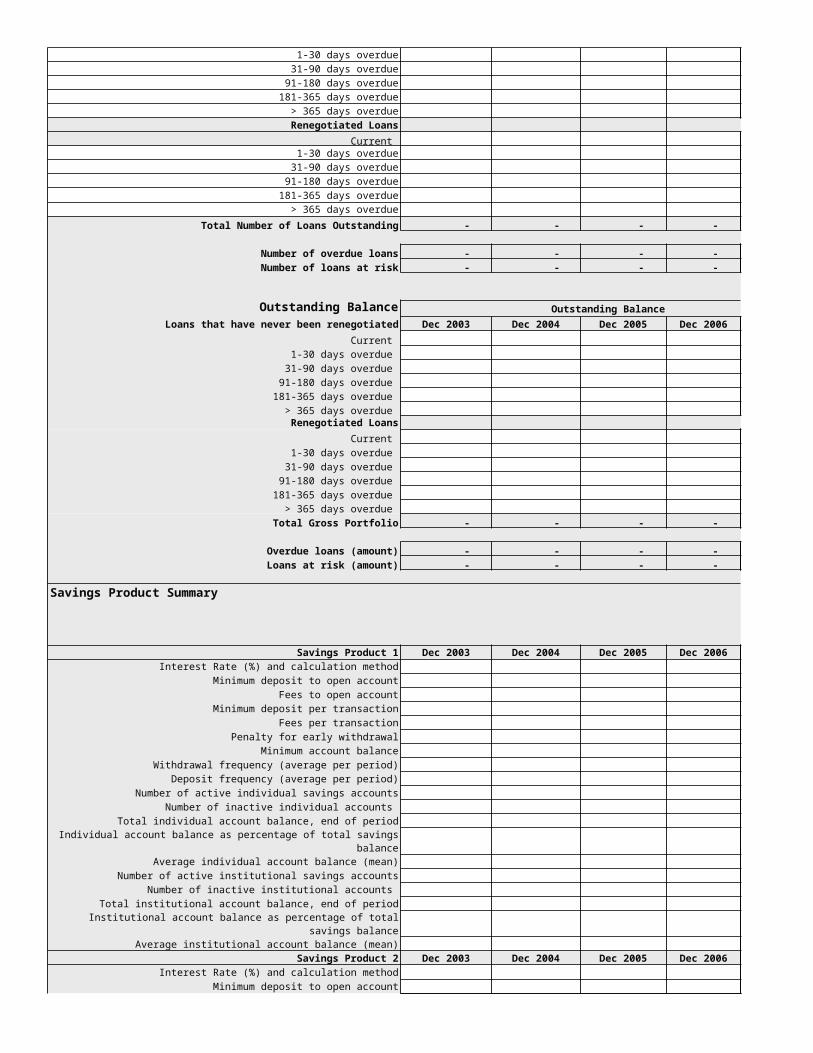

1-30 days overdue

31-90 days overdue

91-180 days overdue

181-365 days overdue

> 365 days overdue

Renegotiated Loans

Current 1-30 days overdue

31-90 days overdue

91-180 days overdue

181-365 days overdue

> 365 days overdue

Total Number of Loans Outstanding - - - - -

Number of overdue loans - - - - -

Number of loans at risk - - - - -

Outstanding Balance Outstanding Balance

Loans that have never been renegotiated Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Current

1-30 days overdue

31-90 days overdue

91-180 days overdue

181-365 days overdue

> 365 days overdue Renegotiated Loans

Current

1-30 days overdue

31-90 days overdue

91-180 days overdue

181-365 days overdue

> 365 days overdue

Total Gross Portfolio - - - - -

Overdue loans (amount) - - - - -

Loans at risk (amount) - - - - -

Savings Product Summary

Savings Product 1 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Interest Rate (%) and calculation method

Minimum deposit to open account

Fees to open account

Minimum deposit per transaction

Fees per transaction

Penalty for early withdrawal

Minimum account balance

Withdrawal frequency (average per period)

Deposit frequency (average per period)

Number of active individual savings accounts

Number of inactive individual accounts

Total individual account balance, end of period

Individual account balance as percentage of total savings balance

Average individual account balance (mean)

Number of active institutional savings accounts

Number of inactive institutional accounts

Total institutional account balance, end of period

Institutional account balance as percentage of total savings balance

Average institutional account balance (mean)

Savings Product 2 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Interest Rate (%) and calculation method

Minimum deposit to open account

Fees to open account

Minimum deposit per transaction

Fees per transaction

Penalty for early withdrawal

Minimum account balance

Withdrawal frequency (average per period)

Deposit frequency (average per period)

Number of active individual savings accounts

Number of inactive individual accounts

Total individual account balance, end of period

Individual account balance as percentage of total savings balance

Average individual account balance (mean)

Number of active institutional savings accounts

Number of inactive institutional accounts

Total institutional account balance, end of period

Institutional account balance as percentage of total savings balance

Average institutional account balance (mean)

Savings Product 3 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Interest Rate (%) and calculation method

Minimum deposit to open account

Fees to open account

Minimum deposit per transaction

Fees per transaction

Penalty for early withdrawal

Minimum account balance

Withdrawal frequency (average per period)

Deposit frequency (average per period)

Number of active individual savings accounts

Number of inactive individual accounts

Total individual account balance, end of period

Individual account balance as percentage of total savings balance

Average individual account balance (mean)

Number of active institutional savings accounts

Number of inactive institutional accounts

Total institutional account balance, end of period

Institutional account balance as percentage of total savings balance

Average institutional account balance (mean)

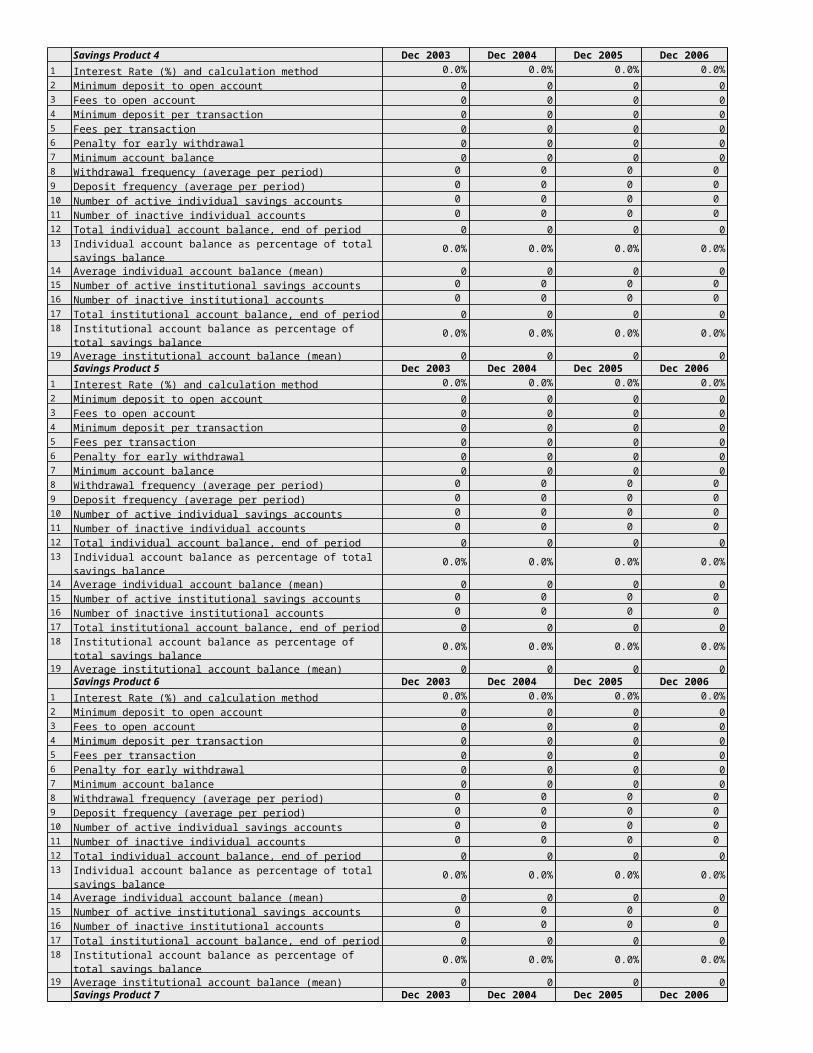

Savings Product 4 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Interest Rate (%) and calculation method

Minimum deposit to open account

Fees to open account

Minimum deposit per transaction

Fees per transaction

Penalty for early withdrawal

Minimum account balance

Withdrawal frequency (average per period)

Deposit frequency (average per period)

Number of active individual savings accounts

Number of inactive individual accounts

Total individual account balance, end of period

Individual account balance as percentage of total savings balance

Average individual account balance (mean)

Number of active institutional savings accounts

Number of inactive institutional accounts

Total institutional account balance, end of period

Institutional account balance as percentage of total savings balance

Average institutional account balance (mean)

Savings Product 5 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Interest Rate (%) and calculation method

Minimum deposit to open account

Fees to open account

Minimum deposit per transaction

Fees per transaction

Penalty for early withdrawal

Minimum account balance

Withdrawal frequency (average per period)

Deposit frequency (average per period)

Number of active individual savings accounts

Number of inactive individual accounts

Total individual account balance, end of period

Individual account balance as percentage of total savings balance

Average individual account balance (mean)

Number of active institutional savings accounts

Number of inactive institutional accounts

Total institutional account balance, end of period

Institutional account balance as percentage of total savings balance

Average institutional account balance (mean)

Savings Product 6 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Interest Rate (%) and calculation method

Minimum deposit to open account

Fees to open account

Minimum deposit per transaction

Fees per transaction

Penalty for early withdrawal

Minimum account balance

Withdrawal frequency (average per period)

Deposit frequency (average per period)

Number of active individual savings accounts

Number of inactive individual accounts

Total individual account balance, end of period

Individual account balance as percentage of total savings balance

Average individual account balance (mean)

Number of active institutional savings accounts

Number of inactive institutional accounts

Total institutional account balance, end of period

Institutional account balance as percentage of total savings balance

Average institutional account balance (mean)

Savings Product 7 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Interest Rate (%) and calculation method

Minimum deposit to open account

Fees to open account

Minimum deposit per transaction

Fees per transaction

Penalty for early withdrawal

Minimum account balance

Withdrawal frequency (average per period)

Deposit frequency (average per period)

Number of active individual savings accounts

Number of inactive individual accounts

Total individual account balance, end of period

Individual account balance as percentage of total savings balance

Average individual account balance (mean)

Number of active institutional savings accounts

Number of inactive institutional accounts

Total institutional account balance, end of period

Institutional account balance as percentage of total savings balance

Average institutional account balance (mean)

Savings Product 8 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Interest Rate (%) and calculation method

Minimum deposit to open account

Fees to open account

Minimum deposit per transaction

Fees per transaction

Penalty for early withdrawal

Minimum account balance

Withdrawal frequency (average per period)

Deposit frequency (average per period)

Number of active individual savings accounts

Number of inactive individual accounts

Total individual account balance, end of period

Individual account balance as percentage of total savings balance

Average individual account balance (mean)

Number of active institutional savings accounts

Number of inactive institutional accounts

Total institutional account balance, end of period

Institutional account balance as percentage of total savings balance

Average institutional account balance (mean)

Savings Product 9 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Interest Rate (%) and calculation method

Minimum deposit to open account

Fees to open account

Minimum deposit per transaction

Fees per transaction

Penalty for early withdrawal

Minimum account balance

Withdrawal frequency (average per period)

Deposit frequency (average per period)

Number of active individual savings accounts

Number of inactive individual accounts

Total individual account balance, end of period

Individual account balance as percentage of total savings balance

Average individual account balance (mean)

Number of active institutional savings accounts

Number of inactive institutional accounts

Total institutional account balance, end of period

Institutional account balance as percentage of total savings balance

Average institutional account balance (mean)

Savings Product 10 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Interest Rate (%) and calculation method

Minimum deposit to open account

Fees to open account

Minimum deposit per transaction

Fees per transaction

Penalty for early withdrawal

Minimum account balance

Withdrawal frequency (average per period)

Deposit frequency (average per period)

Number of active individual savings accounts

Number of inactive individual accounts

Total individual account balance, end of period

Individual account balance as percentage of total savings balance

Average individual account balance (mean)

Number of active institutional savings accounts

Number of inactive institutional accounts

Total institutional account balance, end of period

Institutional account balance as percentage of total savings balance

Average institutional account balance (mean)

Savings Product 11 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Interest Rate (%) and calculation method

Minimum deposit to open account

Fees to open account

Minimum deposit per transaction

Fees per transaction

Penalty for early withdrawal

Minimum account balance

Withdrawal frequency (average per period)

Deposit frequency (average per period)

Number of active individual savings accounts

Number of inactive individual accounts

Total individual account balance, end of period

Individual account balance as percentage of total savings balance

Average individual account balance (mean)

Number of active institutional savings accounts

Number of inactive institutional accounts

Total institutional account balance, end of period

Institutional account balance as percentage of total savings balance

Average institutional account balance (mean)

Savings Product 12 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Interest Rate (%) and calculation method

Minimum deposit to open account

Fees to open account

Minimum deposit per transaction

Fees per transaction

Penalty for early withdrawal

Minimum account balance

Withdrawal frequency (average per period)

Deposit frequency (average per period)

Number of active individual savings accounts

Number of inactive individual accounts

Total individual account balance, end of period

Individual account balance as percentage of total savings balance

Average individual account balance (mean)

Number of active institutional savings accounts

Number of inactive institutional accounts

Total institutional account balance, end of period

Institutional account balance as percentage of total savings balance

Average institutional account balance (mean)

Savings Product 13 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Interest Rate (%) and calculation method

Minimum deposit to open account

Fees to open account

Minimum deposit per transaction

Fees per transaction

Penalty for early withdrawal

Minimum account balance

Withdrawal frequency (average per period)

Deposit frequency (average per period)

Number of active individual savings accounts

Number of inactive individual accounts

Total individual account balance, end of period

Individual account balance as percentage of total savings balance

Average individual account balance (mean)

Number of active institutional savings accounts

Number of inactive institutional accounts

Total institutional account balance, end of period

Institutional account balance as percentage of total savings balance

Average institutional account balance (mean)

Savings Product 14 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Interest Rate (%) and calculation method

Minimum deposit to open account

Fees to open account

Minimum deposit per transaction

Fees per transaction

Penalty for early withdrawal

Minimum account balance

Withdrawal frequency (average per period)

Deposit frequency (average per period)

Number of active individual savings accounts

Number of inactive individual accounts

Total individual account balance, end of period

Individual account balance as percentage of total savings balance

Average individual account balance (mean)

Number of active institutional savings accounts

Number of inactive institutional accounts

Total institutional account balance, end of period

Institutional account balance as percentage of total savings balance

Average institutional account balance (mean)

Savings Product 15 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Interest Rate (%) and calculation method

Minimum deposit to open account

Fees to open account

Minimum deposit per transaction

Fees per transaction

Penalty for early withdrawal

Minimum account balance

Withdrawal frequency (average per period)

Deposit frequency (average per period)

Number of active individual savings accounts

Number of inactive individual accounts

Total individual account balance, end of period

Individual account balance as percentage of total savings balance

Average individual account balance (mean)

Number of active institutional savings accounts

Number of inactive institutional accounts

Total institutional account balance, end of period

Institutional account balance as percentage of total savings balance

Average institutional account balance (mean)

Loan Products Summary

Loan Product 1 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Initial amount

Increment / Maximum

Term

Repayment frequency

Interest rate

Commissions and fees

Guarantees and collateral

Theoretical interest yield (APR)

Savings requirement (if any)

Number of active loans (clients), end of period

Average principle balance per client

Median principal balance per client

Average principal balance outstanding, over period

Total principal balance outstanding, end of period

Percentage of total loan balance

Total outstanding balance associated with loans that are:

On time (and never renegotiated)

Overdue 1 to 30 days (and never renegotiated)

Overdue 31 to 90 days (and never renegotiated)

Overdue 91 to 180 days (and never renegotiated)

Overdue 181 to 365 days (and never renegotiated)

Overdue over 365 days (and never renegotiated)

Renegotiated loans - On time

Renegotiated loans - overdue 1 to 30 days

Renegotiated loans - overdue 31 to 90 days

Renegotiated loans - overdue 91 to 180 days

Renegotiated loans - overdue 181-365 days

Renegotiated loans - overdue over 365 days

Loan Product 2 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Initial amount

Increment / Maximum

Term

Repayment frequency

Interest rate

Commissions and fees

Guarantees and collateral

Theoretical interest yield (APR)

Savings requirement (if any)

Number of active loans (clients), end of period

Average principle balance per client

Median principal balance per client

Average principal balance outstanding, over period

Total principal balance outstanding, end of period

Percentage of total loan balance

Total outstanding balance associated with loans that are:

On time (and never renegotiated)

Overdue 1 to 30 days (and never renegotiated)

Overdue 31 to 90 days (and never renegotiated)

Overdue 91 to 180 days (and never renegotiated)

Overdue 181 to 365 days (and never renegotiated)

Overdue over 365 days (and never renegotiated)

Renegotiated loans - On time

Renegotiated loans - overdue 1 to 30 days

Renegotiated loans - overdue 31 to 90 days

Renegotiated loans - overdue 91 to 180 days

Renegotiated loans - overdue 181-365 days

Renegotiated loans - overdue over 365 days

Loan Product 3 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Initial amount

Increment / Maximum

Term

Repayment frequency

Interest rate

Commissions and fees

Guarantees and collateral

Theoretical interest yield (APR)

Savings requirement (if any)

Number of active loans (clients), end of period

Average principle balance per client

Median principal balance per client

Average principal balance outstanding, over period

Total principal balance outstanding, end of period

Percentage of total loan balance

Total outstanding balance associated with loans that are:

On time (and never renegotiated)

Overdue 1 to 30 days (and never renegotiated)

Overdue 31 to 90 days (and never renegotiated)

Overdue 91 to 180 days (and never renegotiated)

Overdue 181 to 365 days (and never renegotiated)

Overdue over 365 days (and never renegotiated)

Renegotiated loans - On time

Renegotiated loans - overdue 1 to 30 days

Renegotiated loans - overdue 31 to 90 days

Renegotiated loans - overdue 91 to 180 days

Renegotiated loans - overdue 181-365 days

Renegotiated loans - overdue over 365 days

Loan Product 4 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Initial amount

Increment / Maximum

Term

Repayment frequency

Interest rate

Commissions and fees

Guarantees and collateral

Theoretical interest yield (APR)

Savings requirement (if any)

Number of active loans (clients), end of period

Average principle balance per client

Median principal balance per client

Average principal balance outstanding, over period

Total principal balance outstanding, end of period

Percentage of total loan balance

Total outstanding balance associated with loans that are:

On time (and never renegotiated)

Overdue 1 to 30 days (and never renegotiated)

Overdue 31 to 90 days (and never renegotiated)

Overdue 91 to 180 days (and never renegotiated)

Overdue 181 to 365 days (and never renegotiated)

Overdue over 365 days (and never renegotiated)

Renegotiated loans - On time

Renegotiated loans - overdue 1 to 30 days

Renegotiated loans - overdue 31 to 90 days

Renegotiated loans - overdue 91 to 180 days

Renegotiated loans - overdue 181-365 days

Renegotiated loans - overdue over 365 days

Loan Product 5 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Initial amount

Increment / Maximum

Term

Repayment frequency

Interest rate

Commissions and fees

Guarantees and collateral

Theoretical interest yield (APR)

Savings requirement (if any)

Number of active loans (clients), end of period

Average principle balance per client

Median principal balance per client

Average principal balance outstanding, over period

Total principal balance outstanding, end of period

Percentage of total loan balance

Total outstanding balance associated with loans that are:

On time (and never renegotiated)

Overdue 1 to 30 days (and never renegotiated)

Overdue 31 to 90 days (and never renegotiated)

Overdue 91 to 180 days (and never renegotiated)

Overdue 181 to 365 days (and never renegotiated)

Overdue over 365 days (and never renegotiated)

Renegotiated loans - On time

Renegotiated loans - overdue 1 to 30 days

Renegotiated loans - overdue 31 to 90 days

Renegotiated loans - overdue 91 to 180 days

Renegotiated loans - overdue 181-365 days

Renegotiated loans - overdue over 365 days

Loan Product 6 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Initial amount

Increment / Maximum

Term

Repayment frequency

Interest rate

Commissions and fees

Guarantees and collateral

Theoretical interest yield (APR)

Savings requirement (if any)

Number of active loans (clients), end of period

Average principle balance per client

Median principal balance per client

Average principal balance outstanding, over period

Total principal balance outstanding, end of period

Percentage of total loan balance

Total outstanding balance associated with loans that are:

On time (and never renegotiated)

Overdue 1 to 30 days (and never renegotiated)

Overdue 31 to 90 days (and never renegotiated)

Overdue 91 to 180 days (and never renegotiated)

Overdue 181 to 365 days (and never renegotiated)

Overdue over 365 days (and never renegotiated)

Renegotiated loans - On time

Renegotiated loans - overdue 1 to 30 days

Renegotiated loans - overdue 31 to 90 days

Renegotiated loans - overdue 91 to 180 days

Renegotiated loans - overdue 181-365 days

Renegotiated loans - overdue over 365 days

Loan Product 7 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Initial amount

Increment / Maximum

Term

Repayment frequency

Interest rate

Commissions and fees

Guarantees and collateral

Theoretical interest yield (APR)

Savings requirement (if any)

Number of active loans (clients), end of period

Average principle balance per client

Median principal balance per client

Average principal balance outstanding, over period

Total principal balance outstanding, end of period

Percentage of total loan balance

Total outstanding balance associated with loans that are:

On time (and never renegotiated)

Overdue 1 to 30 days (and never renegotiated)

Overdue 31 to 90 days (and never renegotiated)

Overdue 91 to 180 days (and never renegotiated)

Overdue 181 to 365 days (and never renegotiated)

Overdue over 365 days (and never renegotiated)

Renegotiated loans - On time

Renegotiated loans - overdue 1 to 30 days

Renegotiated loans - overdue 31 to 90 days

Renegotiated loans - overdue 91 to 180 days

Renegotiated loans - overdue 181-365 days

Renegotiated loans - overdue over 365 days

Loan Product 8 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Initial amount

Increment / Maximum

Term

Repayment frequency

Interest rate

Commissions and fees

Guarantees and collateral

Theoretical interest yield (APR)

Savings requirement (if any)

Number of active loans (clients), end of period

Average principle balance per client

Median principal balance per client

Average principal balance outstanding, over period

Total principal balance outstanding, end of period

Percentage of total loan balance

Total outstanding balance associated with loans that are:

On time (and never renegotiated)

Overdue 1 to 30 days (and never renegotiated)

Overdue 31 to 90 days (and never renegotiated)

Overdue 91 to 180 days (and never renegotiated)

Overdue 181 to 365 days (and never renegotiated)

Overdue over 365 days (and never renegotiated)

Renegotiated loans - On time

Renegotiated loans - overdue 1 to 30 days

Renegotiated loans - overdue 31 to 90 days

Renegotiated loans - overdue 91 to 180 days

Renegotiated loans - overdue 181-365 days

Renegotiated loans - overdue over 365 days

Loan Product 9 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Initial amount

Increment / Maximum

Term

Repayment frequency

Interest rate

Commissions and fees

Guarantees and collateral

Theoretical interest yield (APR)

Savings requirement (if any)

Number of active loans (clients), end of period

Average principle balance per client

Median principal balance per client

Average principal balance outstanding, over period

Total principal balance outstanding, end of period

Percentage of total loan balance

Total outstanding balance associated with loans that are:

On time (and never renegotiated)

Overdue 1 to 30 days (and never renegotiated)

Overdue 31 to 90 days (and never renegotiated)

Overdue 91 to 180 days (and never renegotiated)

Overdue 181 to 365 days (and never renegotiated)

Overdue over 365 days (and never renegotiated)

Renegotiated loans - On time

Renegotiated loans - overdue 1 to 30 days

Renegotiated loans - overdue 31 to 90 days

Renegotiated loans - overdue 91 to 180 days

Renegotiated loans - overdue 181-365 days

Renegotiated loans - overdue over 365 days

Loan Product 10 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Initial amount

Increment / Maximum

Term

Repayment frequency

Interest rate

Commissions and fees

Guarantees and collateral

Theoretical interest yield (APR)

Savings requirement (if any)

Number of active loans (clients), end of period

Average principle balance per client

Median principal balance per client

Average principal balance outstanding, over period

Total principal balance outstanding, end of period

Percentage of total loan balance

Total outstanding balance associated with loans that are:

On time (and never renegotiated)

Overdue 1 to 30 days (and never renegotiated)

Overdue 31 to 90 days (and never renegotiated)

Overdue 91 to 180 days (and never renegotiated)

Overdue 181 to 365 days (and never renegotiated)

Overdue over 365 days (and never renegotiated)

Renegotiated loans - On time

Renegotiated loans - overdue 1 to 30 days

Renegotiated loans - overdue 31 to 90 days

Renegotiated loans - overdue 91 to 180 days

Renegotiated loans - overdue 181-365 days

Renegotiated loans - overdue over 365 days

Loan Product 11 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Initial amount

Increment / Maximum

Term

Repayment frequency

Interest rate

Commissions and fees

Guarantees and collateral

Theoretical interest yield (APR)

Savings requirement (if any)

Number of active loans (clients), end of period

Average principle balance per client

Median principal balance per client

Average principal balance outstanding, over period

Total principal balance outstanding, end of period

Percentage of total loan balance

Total outstanding balance associated with loans that are:

On time (and never renegotiated)

Overdue 1 to 30 days (and never renegotiated)

Overdue 31 to 90 days (and never renegotiated)

Overdue 91 to 180 days (and never renegotiated)

Overdue 181 to 365 days (and never renegotiated)

Overdue over 365 days (and never renegotiated)

Renegotiated loans - On time

Renegotiated loans - overdue 1 to 30 days

Renegotiated loans - overdue 31 to 90 days

Renegotiated loans - overdue 91 to 180 days

Renegotiated loans - overdue 181-365 days

Renegotiated loans - overdue over 365 days

Loan Product 12 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Initial amount

Increment / Maximum

Term

Repayment frequency

Interest rate

Commissions and fees

Guarantees and collateral

Theoretical interest yield (APR)

Savings requirement (if any)

Number of active loans (clients), end of period

Average principle balance per client

Median principal balance per client

Average principal balance outstanding, over period

Total principal balance outstanding, end of period

Percentage of total loan balance

Total outstanding balance associated with loans that are:

On time (and never renegotiated)

Overdue 1 to 30 days (and never renegotiated)

Overdue 31 to 90 days (and never renegotiated)

Overdue 91 to 180 days (and never renegotiated)

Overdue 181 to 365 days (and never renegotiated)

Overdue over 365 days (and never renegotiated)

Renegotiated loans - On time

Renegotiated loans - overdue 1 to 30 days

Renegotiated loans - overdue 31 to 90 days

Renegotiated loans - overdue 91 to 180 days

Renegotiated loans - overdue 181-365 days

Renegotiated loans - overdue over 365 days

Loan Product 13 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Initial amount

Increment / Maximum

Term

Repayment frequency

Interest rate

Commissions and fees

Guarantees and collateral

Theoretical interest yield (APR)

Savings requirement (if any)

Number of active loans (clients), end of period

Average principle balance per client

Median principal balance per client

Average principal balance outstanding, over period

Total principal balance outstanding, end of period

Percentage of total loan balance

Total outstanding balance associated with loans that are:

On time (and never renegotiated)

Overdue 1 to 30 days (and never renegotiated)

Overdue 31 to 90 days (and never renegotiated)

Overdue 91 to 180 days (and never renegotiated)

Overdue 181 to 365 days (and never renegotiated)

Overdue over 365 days (and never renegotiated)

Renegotiated loans - On time

Renegotiated loans - overdue 1 to 30 days

Renegotiated loans - overdue 31 to 90 days

Renegotiated loans - overdue 91 to 180 days

Renegotiated loans - overdue 181-365 days

Renegotiated loans - overdue over 365 days

Loan Product 14 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Initial amount

Increment / Maximum

Term

Repayment frequency

Interest rate

Commissions and fees

Guarantees and collateral

Theoretical interest yield (APR)

Savings requirement (if any)

Number of active loans (clients), end of period

Average principle balance per client

Median principal balance per client

Average principal balance outstanding, over period

Total principal balance outstanding, end of period

Percentage of total loan balance

Total outstanding balance associated with loans that are:

On time (and never renegotiated)

Overdue 1 to 30 days (and never renegotiated)

Overdue 31 to 90 days (and never renegotiated)

Overdue 91 to 180 days (and never renegotiated)

Overdue 181 to 365 days (and never renegotiated)

Overdue over 365 days (and never renegotiated)

Renegotiated loans - On time

Renegotiated loans - overdue 1 to 30 days

Renegotiated loans - overdue 31 to 90 days

Renegotiated loans - overdue 91 to 180 days

Renegotiated loans - overdue 181-365 days

Renegotiated loans - overdue over 365 days

Loan Product 15 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Initial amount

Increment / Maximum

Term

Repayment frequency

Interest rate

Commissions and fees

Guarantees and collateral

Theoretical interest yield (APR)

Savings requirement (if any)

Number of active loans (clients), end of period

Average principle balance per client

Median principal balance per client

Average principal balance outstanding, over period

Total principal balance outstanding, end of period

Percentage of total loan balance

Total outstanding balance associated with loans that are:

On time (and never renegotiated)

Overdue 1 to 30 days (and never renegotiated)

Overdue 31 to 90 days (and never renegotiated)

Overdue 91 to 180 days (and never renegotiated)

Overdue 181 to 365 days (and never renegotiated)

Overdue over 365 days (and never renegotiated)

Renegotiated loans - On time

Renegotiated loans - overdue 1 to 30 days

Renegotiated loans - overdue 31 to 90 days

Renegotiated loans - overdue 91 to 180 days

Renegotiated loans - overdue 181-365 days

Renegotiated loans - overdue over 365 days

OutreachUse Mean or Median account balances Average Account Balance (mean)

Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Population of region(s) covered

Market size (if available)

Total number of active clients (end of period)

Total number new clients(over period)

Total number of loan clients

Total number of savings clients (voluntary)

Percentage of clients who are women

Percentage of clients located in rural areas

Percentage of recent clients living below the national poverty line

Percentage of clients living on less than PPP adjusted US$1 per day

Mean loan balance as % of national poverty line or GNI

Mean voluntary savings balance as % of national poverty line or GNI

Macroeconomic Data Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Inflation rate

GDP Deflator 5.0% 5.0% 5.0% 5.0% 5.0%

Market Rate for Borrowings (IMF statistics)

90-day certificate of deposit rate

Prime rate paid by commercial bank borrowers

Marginal commercial rate available to the MFI

Per capita GDP

Per capita GNI

Exchange rate (Local currency/Other currency) 50.0 50.0 50.0 50.0 50.0

National Poverty Line

Financial Statements

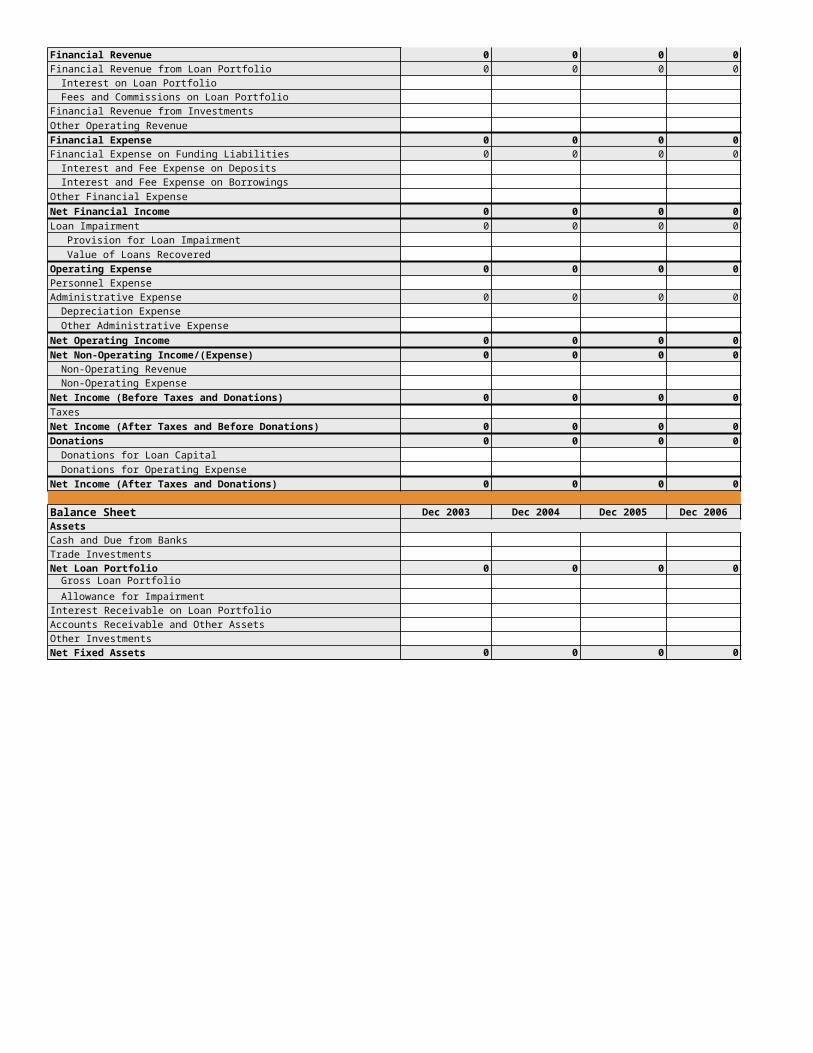

Income Statement Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Financial Revenue 0 0 0 0 0

Financial Revenue from Loan Portfolio 0 0 0 0 0

Interest on Loan Portfolio

Fees and Commissions on Loan Portfolio

Financial Revenue from Investments

Other Operating Revenue

Financial Expense 0 0 0 0 0

Financial Expense on Funding Liabilities 0 0 0 0 0

Interest and Fee Expense on Deposits

Interest and Fee Expense on Borrowings

Other Financial Expense

Net Financial Income 0 0 0 0 0

Loan Impairment 0 0 0 0 0

Provision for Loan Impairment

Value of Loans Recovered

Operating Expense 0 0 0 0 0

Personnel Expense

Administrative Expense 0 0 0 0 0

Depreciation Expense

Other Administrative Expense

Net Operating Income 0 0 0 0 0

Net Non-Operating Income/(Expense) 0 0 0 0 0

Non-Operating Revenue

Non-Operating Expense

Net Income (Before Taxes and Donations) 0 0 0 0 0

Taxes

Net Income (After Taxes and Before Donations) 0 0 0 0 0

Donations 0 0 0 0 0

Donations for Loan Capital

Donations for Operating Expense

Net Income (After Taxes and Donations) 0 0 0 0 0

Balance Sheet Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Assets

Cash and Due from Banks

Trade Investments

Net Loan Portfolio 0 0 0 0 0Gross Loan Portfolio

Allowance for Impairment

Interest Receivable on Loan Portfolio

Other Investments

0 0 0 0 0

Accounts Receivable and Other Assets

Net Fixed Assets

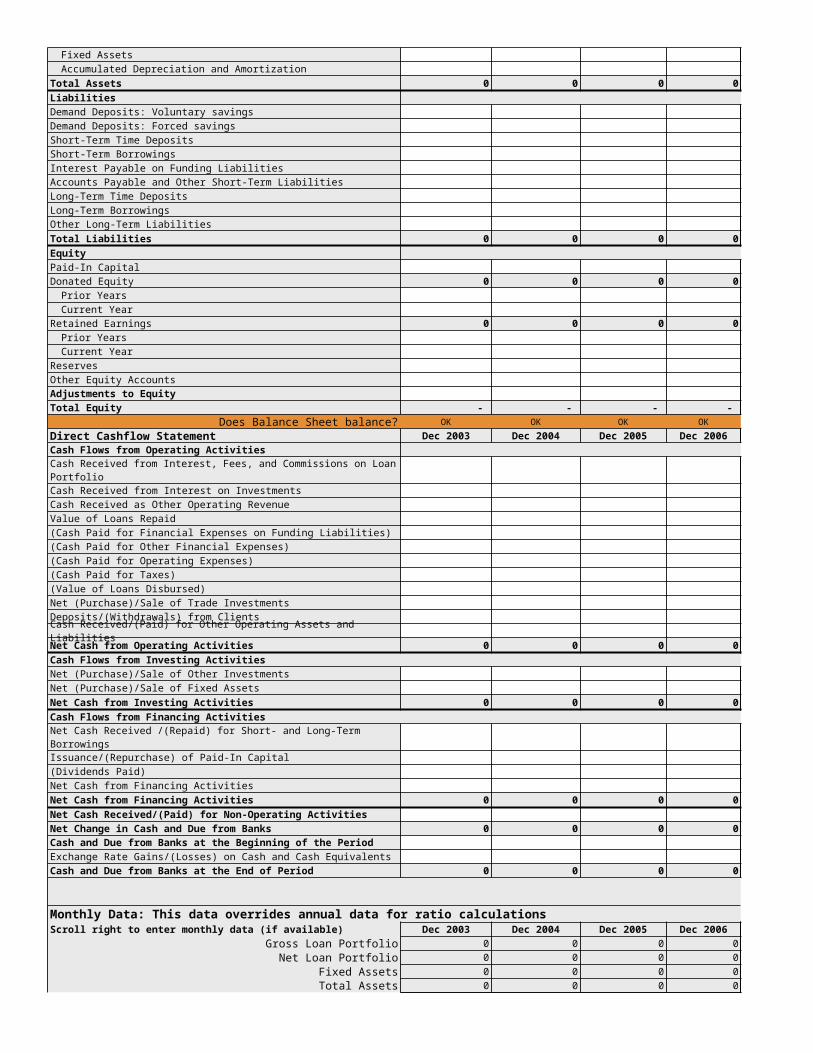

Fixed Assets

Accumulated Depreciation and Amortization

Total Assets 0 0 0 0 0

Liabilities

Demand Deposits: Voluntary savings

Demand Deposits: Forced savings

Short-Term Time Deposits

Short-Term Borrowings

Interest Payable on Funding Liabilities

Accounts Payable and Other Short-Term Liabilities

Long-Term Time Deposits

Long-Term Borrowings

Other Long-Term Liabilities

Total Liabilities 0 0 0 0 0

Equity

Paid-In Capital

Donated Equity 0 0 0 0 0

Prior Years

Current Year

Retained Earnings 0 0 0 0 0

Prior Years

Current Year

Reserves

Other Equity Accounts

Adjustments to Equity

Total Equity - - - - -

Does Balance Sheet balance? OK OK OK OK OK

Direct Cashflow Statement Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Cash Flows from Operating Activities

Cash Received from Interest, Fees, and Commissions on Loan Portfolio

Cash Received from Interest on Investments

Cash Received as Other Operating Revenue

Value of Loans Repaid

(Cash Paid for Financial Expenses on Funding Liabilities)

(Cash Paid for Other Financial Expenses)

(Cash Paid for Operating Expenses)

(Cash Paid for Taxes)

(Value of Loans Disbursed)

Net (Purchase)/Sale of Trade Investments

Deposits/(Withdrawals) from Clients

Cash Received/(Paid) for Other Operating Assets and Liabilities

Net Cash from Operating Activities 0 0 0 0 0

Cash Flows from Investing Activities

Net (Purchase)/Sale of Other Investments

Net (Purchase)/Sale of Fixed Assets

Net Cash from Investing Activities 0 0 0 0 0

Cash Flows from Financing Activities

Net Cash Received /(Repaid) for Short- and Long-Term Borrowings

Issuance/(Repurchase) of Paid-In Capital

(Dividends Paid)

Net Cash from Financing Activities

Net Cash from Financing Activities 0 0 0 0 0

Net Cash Received/(Paid) for Non-Operating Activities

Net Change in Cash and Due from Banks 0 0 0 0 0

Cash and Due from Banks at the Beginning of the Period

Exchange Rate Gains/(Losses) on Cash and Cash Equivalents

Cash and Due from Banks at the End of Period 0 0 0 0 0

Monthly Data: This data overrides annual data for ratio calculationsScroll right to enter monthly data (if available) Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Gross Loan Portfolio 0 0 0 0 0

Net Loan Portfolio 0 0 0 0 0

Fixed Assets 0 0 0 0 0

Total Assets 0 0 0 0 0

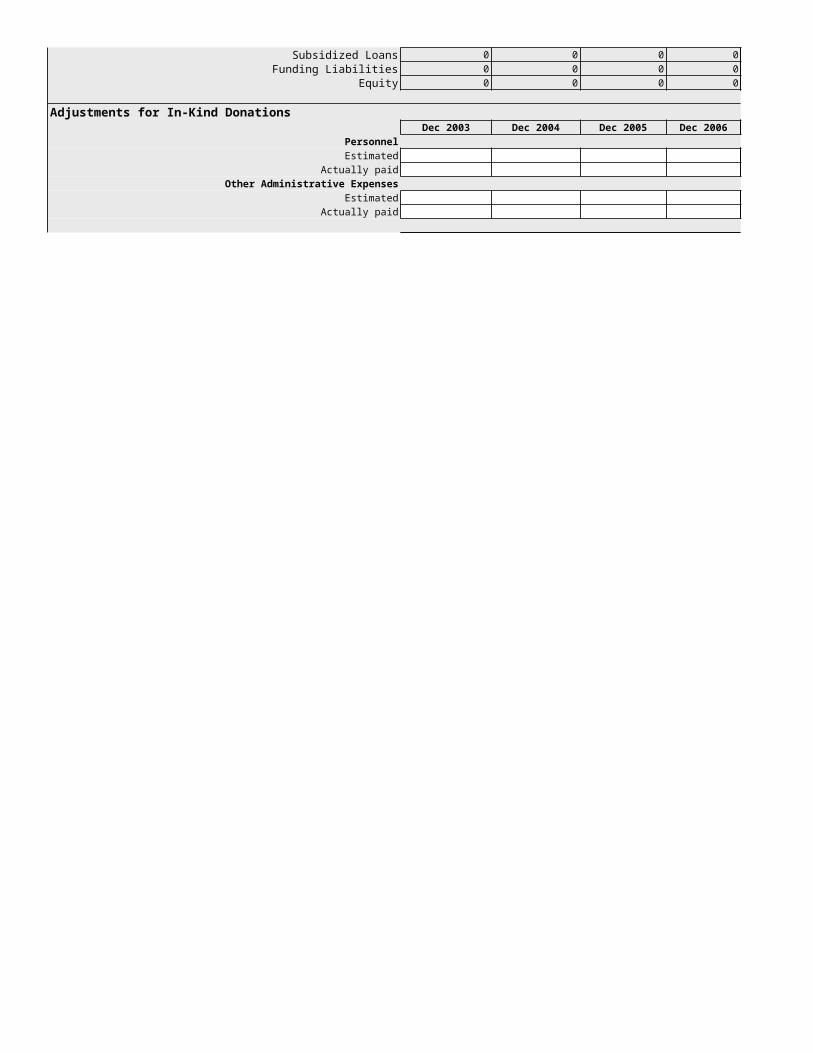

Subsidized Loans 0 0 0 0 0

Funding Liabilities 0 0 0 0 0

Equity 0 0 0 0 0

Adjustments for In-Kind DonationsDec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Personnel

Estimated

Actually paid

Other Administrative Expenses

Estimated

Actually paid

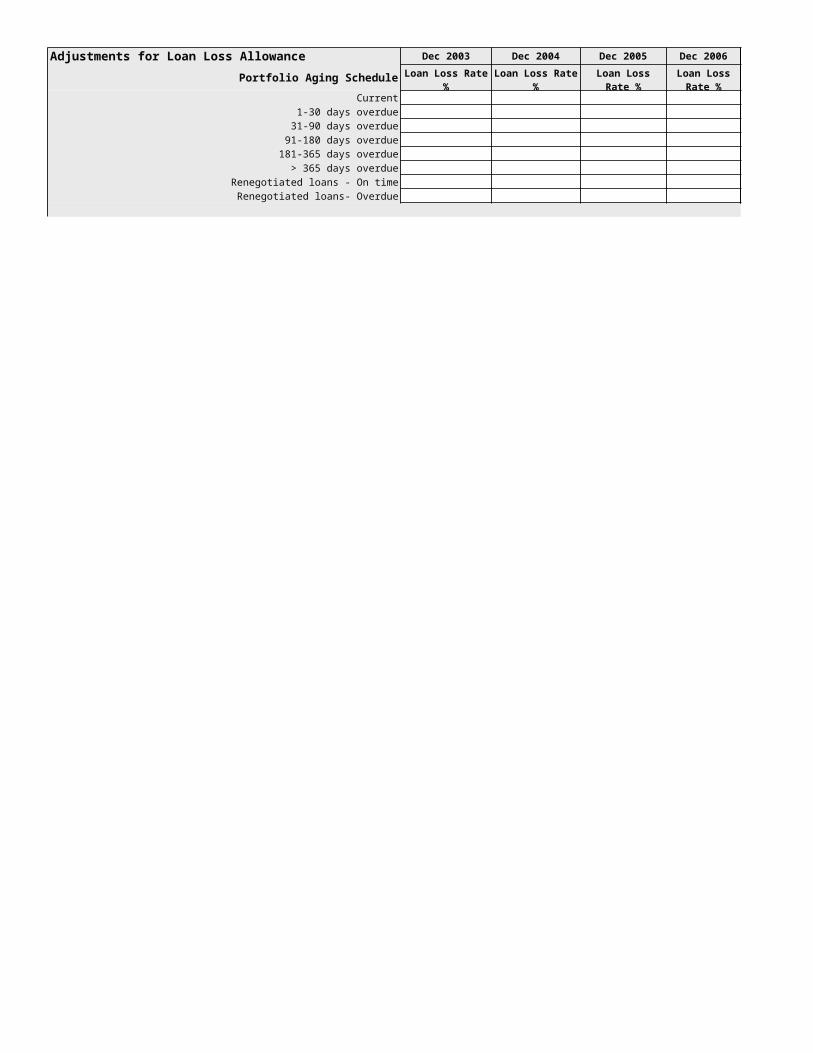

Adjustments for Loan Loss Allowance Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Portfolio Aging Schedule

Current

1-30 days overdue

31-90 days overdue

91-180 days overdue

181-365 days overdue

> 365 days overdue

Renegotiated loans - On time

Renegotiated loans- Overdue

Loan Loss Rate %

Loan Loss Rate %

Loan Loss Rate %

Loan Loss Rate %

Loan Loss Rate %

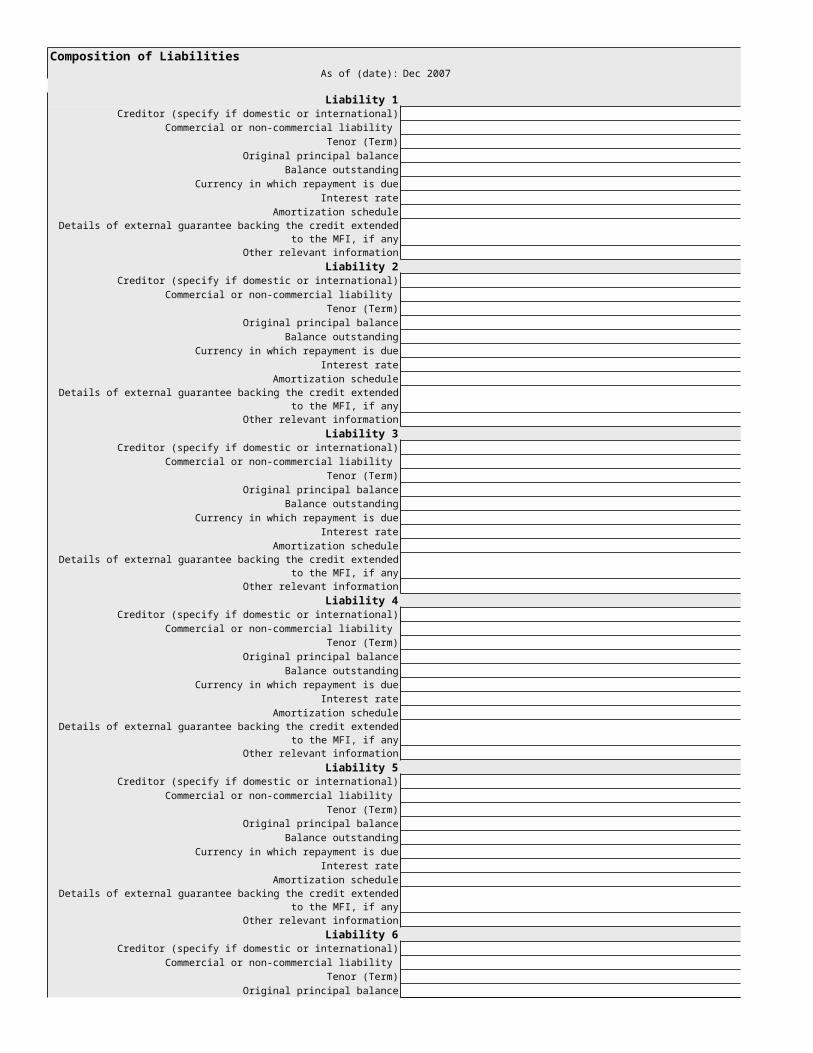

Composition of LiabilitiesAs of (date): Dec 2007

Liability 1Creditor (specify if domestic or international)

Commercial or non-commercial liability

Tenor (Term)

Original principal balance

Balance outstanding

Currency in which repayment is due

Interest rate

Amortization schedule

Other relevant information

Liability 2Creditor (specify if domestic or international)

Commercial or non-commercial liability

Tenor (Term)

Original principal balance

Balance outstanding

Currency in which repayment is due

Interest rate

Amortization schedule

Other relevant information

Liability 3Creditor (specify if domestic or international)

Commercial or non-commercial liability

Tenor (Term)

Original principal balance

Balance outstanding

Currency in which repayment is due

Interest rate

Amortization schedule

Other relevant information

Liability 4Creditor (specify if domestic or international)

Commercial or non-commercial liability

Tenor (Term)

Original principal balance

Balance outstanding

Currency in which repayment is due

Interest rate

Amortization schedule

Other relevant information

Liability 5Creditor (specify if domestic or international)

Commercial or non-commercial liability

Tenor (Term)

Original principal balance

Balance outstanding

Currency in which repayment is due

Interest rate

Amortization schedule

Other relevant information

Liability 6Creditor (specify if domestic or international)

Commercial or non-commercial liability

Tenor (Term)

Original principal balance

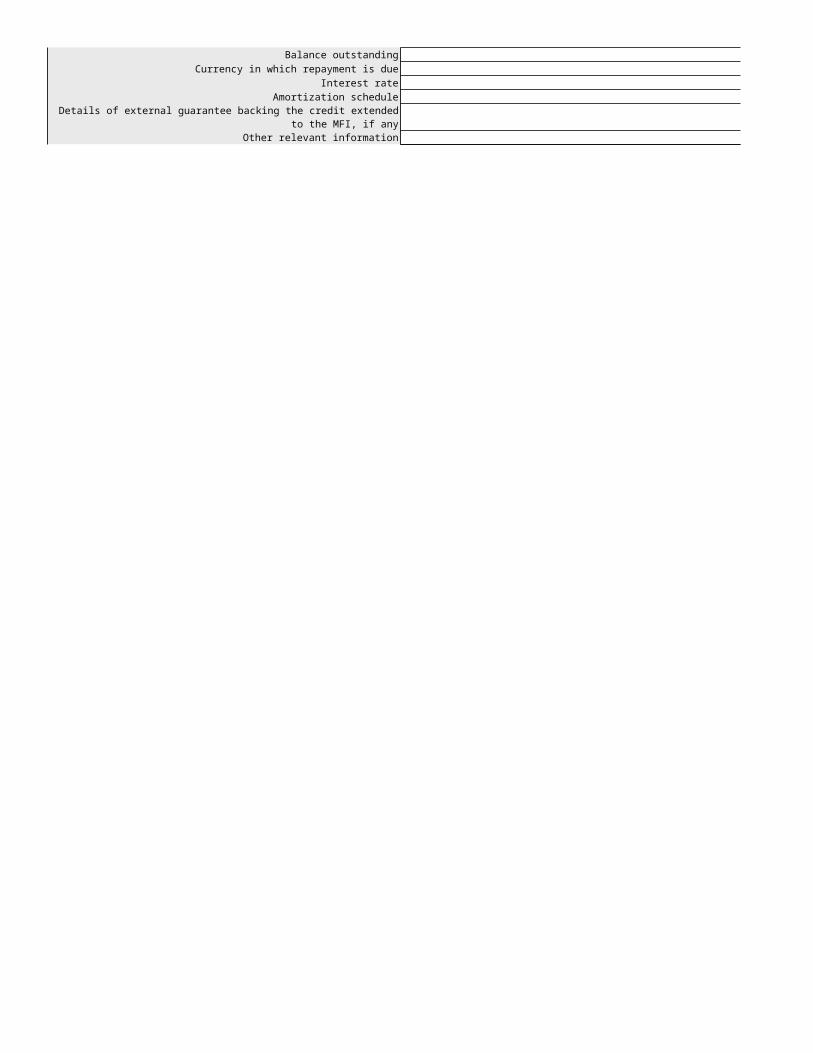

Details of external guarantee backing the credit extended to the MFI, if any

Details of external guarantee backing the credit extended to the MFI, if any

Details of external guarantee backing the credit extended to the MFI, if any

Details of external guarantee backing the credit extended to the MFI, if any

Details of external guarantee backing the credit extended to the MFI, if any

Balance outstanding

Currency in which repayment is due

Interest rate

Amortization schedule

Other relevant information

Details of external guarantee backing the credit extended to the MFI, if any

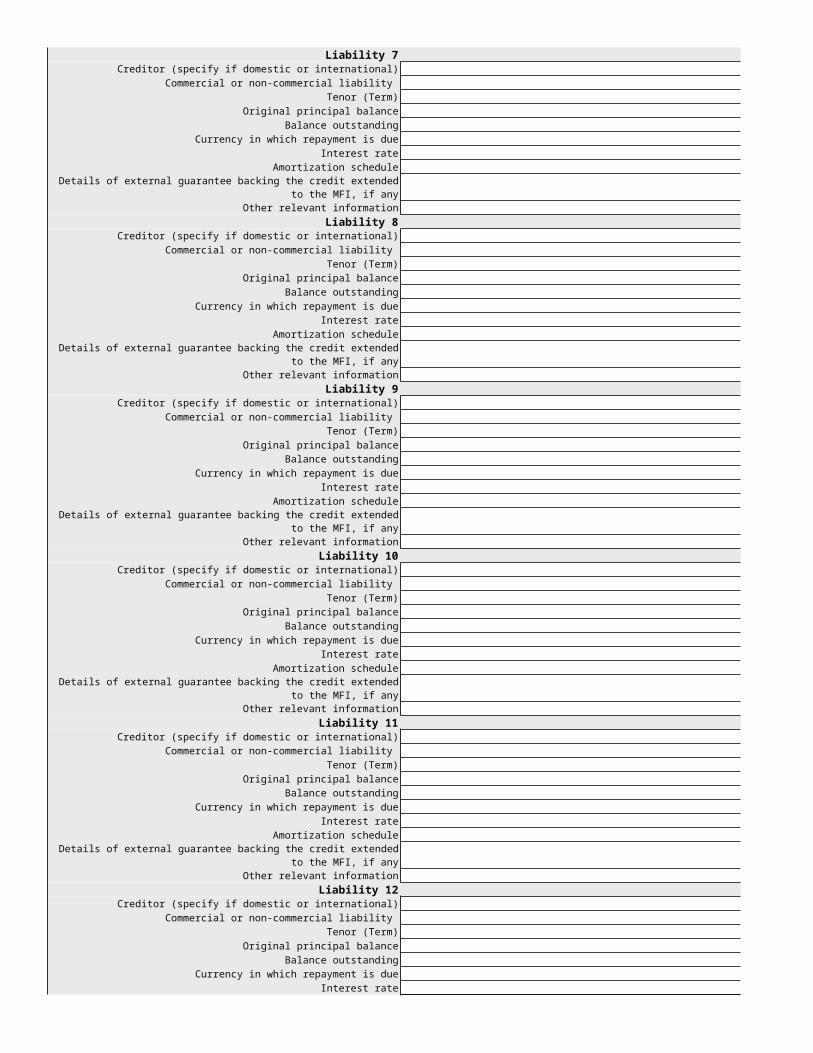

Liability 7Creditor (specify if domestic or international)

Commercial or non-commercial liability

Tenor (Term)

Original principal balance

Balance outstanding

Currency in which repayment is due

Interest rate

Amortization schedule

Other relevant information

Liability 8Creditor (specify if domestic or international)

Commercial or non-commercial liability

Tenor (Term)

Original principal balance

Balance outstanding

Currency in which repayment is due

Interest rate

Amortization schedule

Other relevant information

Liability 9Creditor (specify if domestic or international)

Commercial or non-commercial liability

Tenor (Term)

Original principal balance

Balance outstanding

Currency in which repayment is due

Interest rate

Amortization schedule

Other relevant information

Liability 10Creditor (specify if domestic or international)

Commercial or non-commercial liability

Tenor (Term)

Original principal balance

Balance outstanding

Currency in which repayment is due

Interest rate

Amortization schedule

Other relevant information

Liability 11Creditor (specify if domestic or international)

Commercial or non-commercial liability

Tenor (Term)

Original principal balance

Balance outstanding

Currency in which repayment is due

Interest rate

Amortization schedule

Other relevant information

Liability 12Creditor (specify if domestic or international)

Commercial or non-commercial liability

Tenor (Term)

Original principal balance

Balance outstanding

Currency in which repayment is due

Interest rate

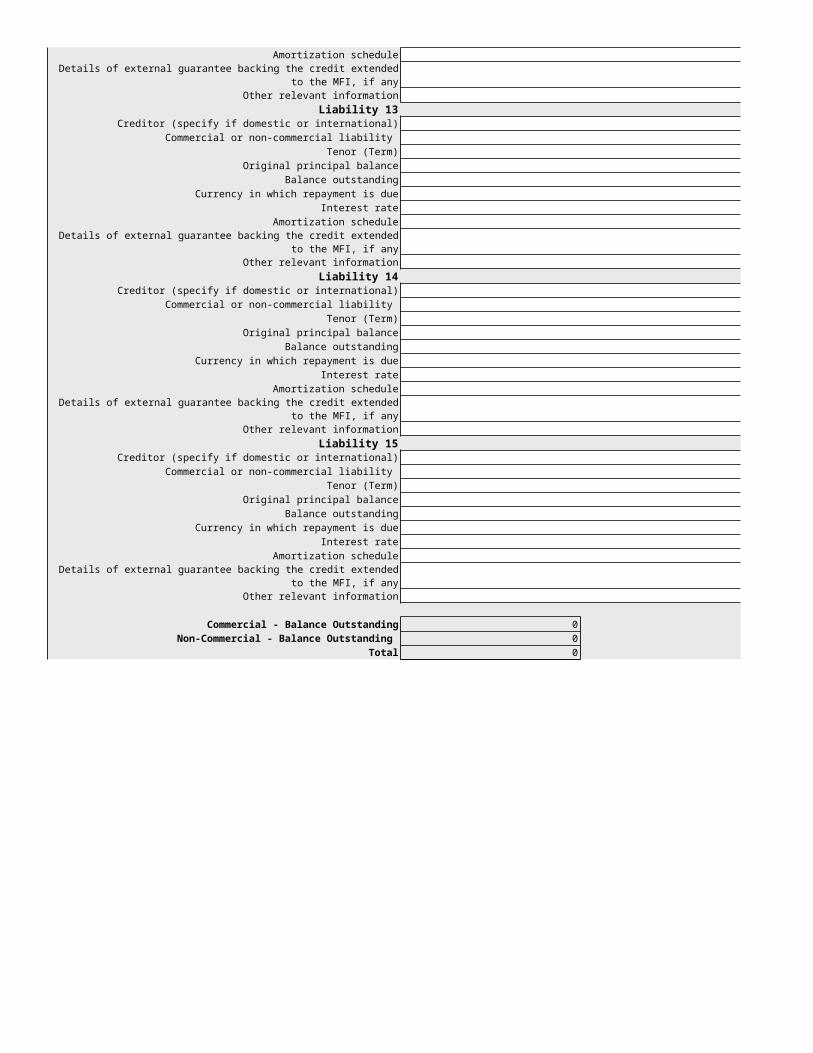

Details of external guarantee backing the credit extended to the MFI, if any

Details of external guarantee backing the credit extended to the MFI, if any

Details of external guarantee backing the credit extended to the MFI, if any

Details of external guarantee backing the credit extended to the MFI, if any

Details of external guarantee backing the credit extended to the MFI, if any

Amortization schedule

Other relevant information

Liability 13Creditor (specify if domestic or international)

Commercial or non-commercial liability

Tenor (Term)

Original principal balance

Balance outstanding

Currency in which repayment is due

Interest rate

Amortization schedule

Other relevant information

Liability 14Creditor (specify if domestic or international)

Commercial or non-commercial liability

Tenor (Term)

Original principal balance

Balance outstanding

Currency in which repayment is due

Interest rate

Amortization schedule

Other relevant information

Liability 15Creditor (specify if domestic or international)

Commercial or non-commercial liability

Tenor (Term)

Original principal balance

Balance outstanding

Currency in which repayment is due

Interest rate

Amortization schedule

Other relevant information

Commercial - Balance Outstanding 0

Non-Commercial - Balance Outstanding 0

Total 0

Details of external guarantee backing the credit extended to the MFI, if any

Details of external guarantee backing the credit extended to the MFI, if any

Details of external guarantee backing the credit extended to the MFI, if any

Details of external guarantee backing the credit extended to the MFI, if any

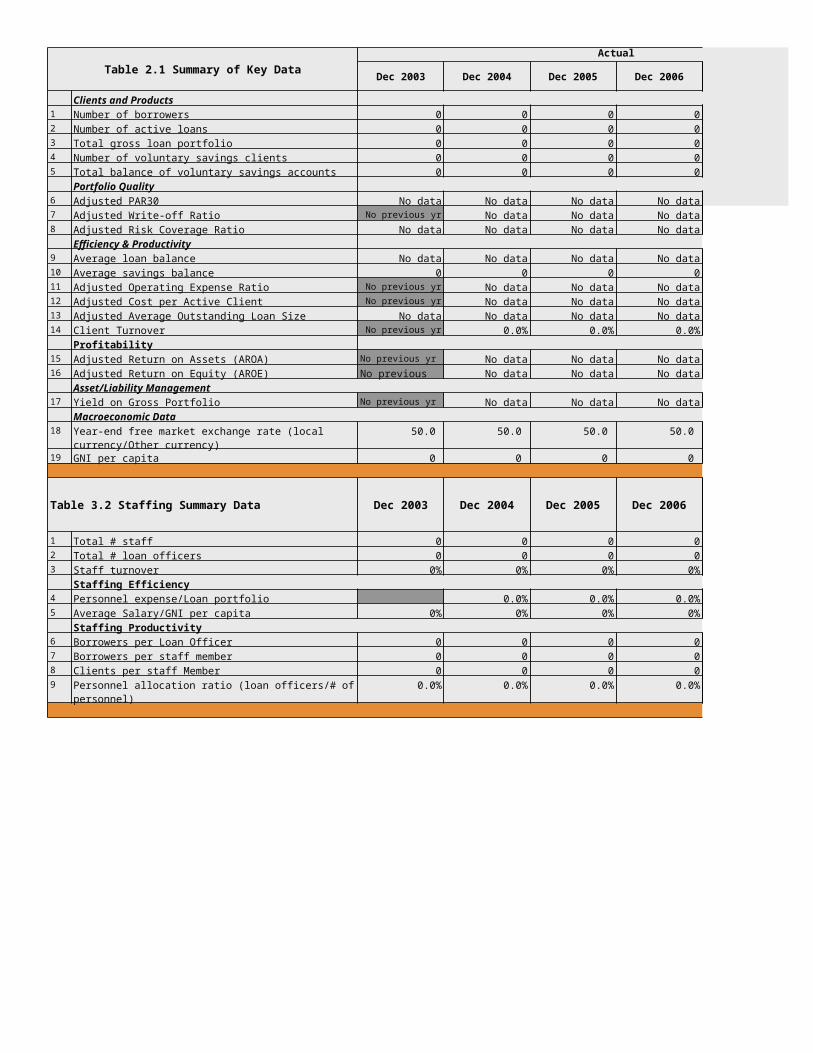

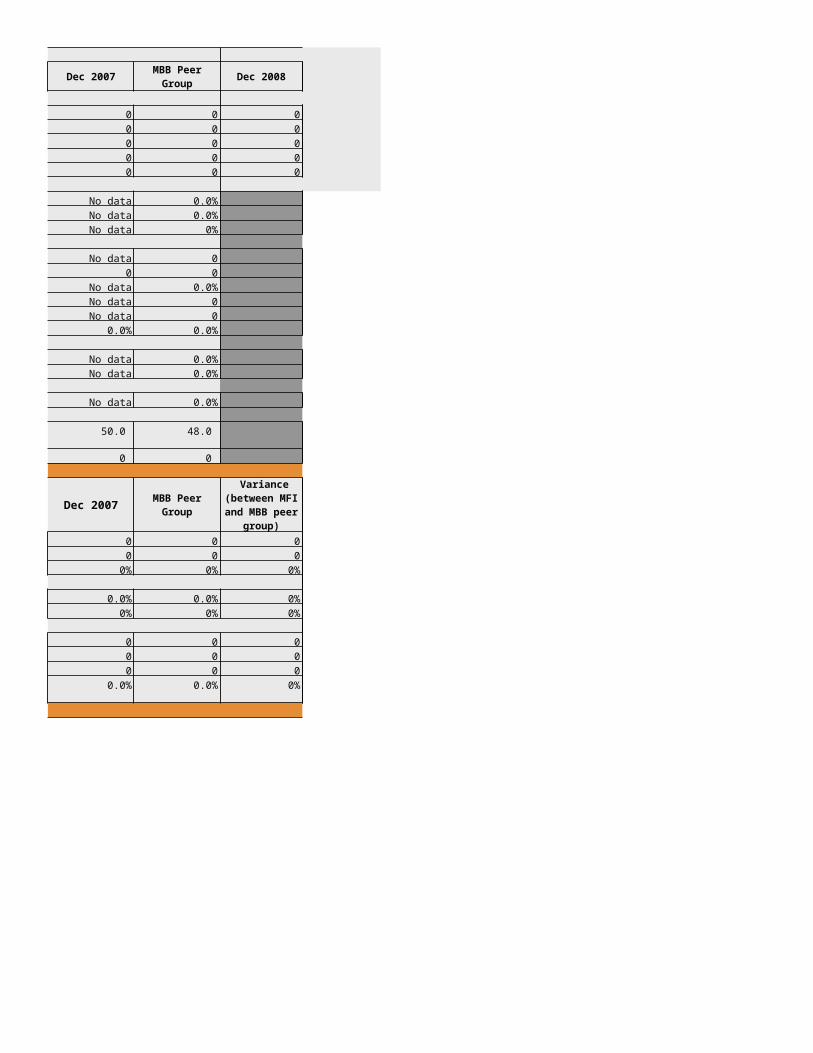

Table 2.1 Summary of Key DataActual

Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Clients and Products1 Number of borrowers 0 0 0 0 02 Number of active loans 0 0 0 0 03 Total gross loan portfolio 0 0 0 0 04 Number of voluntary savings clients 0 0 0 0 05 Total balance of voluntary savings accounts 0 0 0 0 0

Portfolio Quality6 Adjusted PAR30 No data No data No data No data No data7 Adjusted Write-off Ratio No previous yr No data No data No data No data8 Adjusted Risk Coverage Ratio No data No data No data No data No data

Efficiency & Productivity9 Average loan balance No data No data No data No data No data10 Average savings balance 0 0 0 0 011 Adjusted Operating Expense Ratio No previous yr No data No data No data No data12 Adjusted Cost per Active Client No previous yr No data No data No data No data13 Adjusted Average Outstanding Loan Size No data No data No data No data No data14 Client Turnover No previous yr 0.0% 0.0% 0.0% 0.0%

Profitability15 Adjusted Return on Assets (AROA) No previous yr No data No data No data No data16 Adjusted Return on Equity (AROE) No previous yr No data No data No data No data

Asset/Liability Management17 Yield on Gross Portfolio No previous yr No data No data No data No data

Macroeconomic Data 18 50.0 50.0 50.0 50.0 50.0

19 GNI per capita 0 0 0 0 0

Table 3.2 Staffing Summary Data Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

1 Total # staff 0 0 0 0 02 Total # loan officers 0 0 0 0 03 Staff turnover 0% 0% 0% 0% 0%

Staffing Efficiency4 Personnel expense/Loan portfolio 0.0% 0.0% 0.0% 0.0%5 Average Salary/GNI per capita 0% 0% 0% 0% 0%

Staffing Productivity6 Borrowers per Loan Officer 0 0 0 0 07 Borrowers per staff member 0 0 0 0 08 Clients per staff Member 0 0 0 0 09 Personnel allocation ratio (loan officers/# of personnel) 0.0% 0.0% 0.0% 0.0% 0.0%

Year-end free market exchange rate (local currency/Other currency)

Actual Projected

Dec 2008

0 0

0 0

0 0

0 0

0 0

0.0%

0.0%

0%

0

0

0.0%

0

0

0.0%

0.0%

0.0%

0.0%

48.0

0

0 0

0 0

0% 0%

0.0% 0%

0% 0%

0 0

0 0

0 0

0.0% 0%

MBB Peer Group

MBB Peer Group

Variance (between MFI and MBB peer

group)

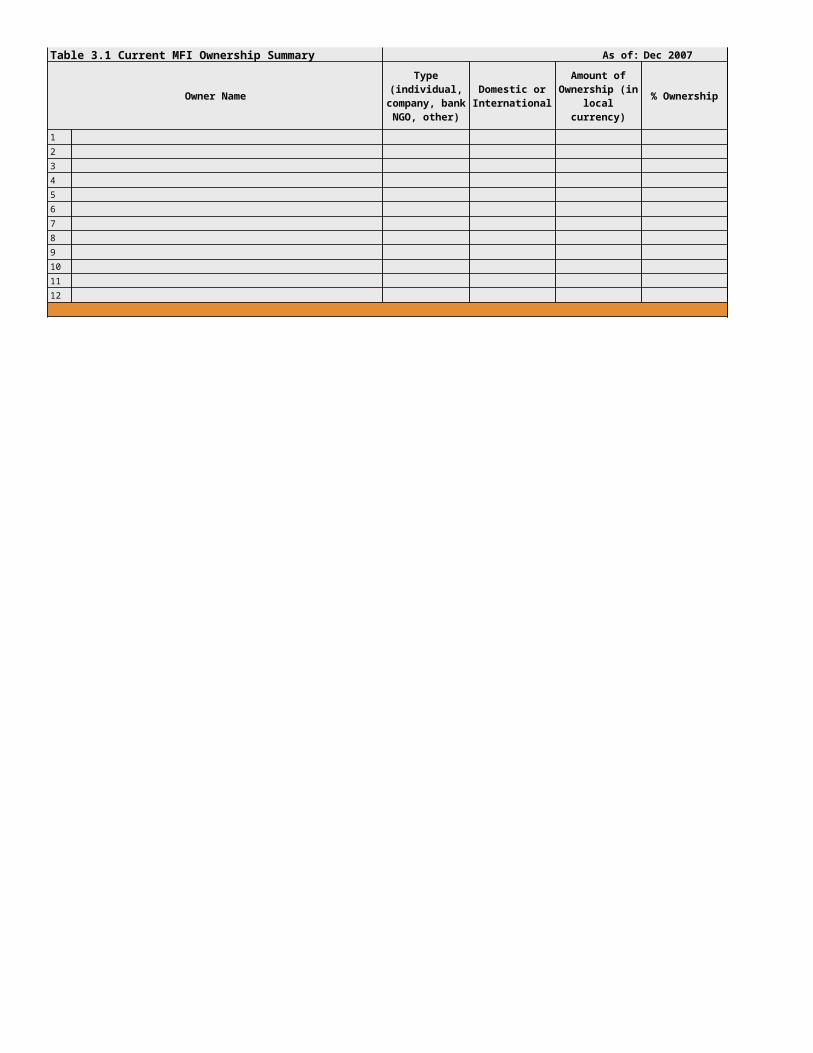

Table 3.1 Current MFI Ownership Summary As of: Dec 2007

Owner Name % Ownership

1 2 3 4 5 6 7 8 9 10 11 12

Type (individual,

company, bank NGO, other)

Domestic or International

Amount of Ownership (in local currency)

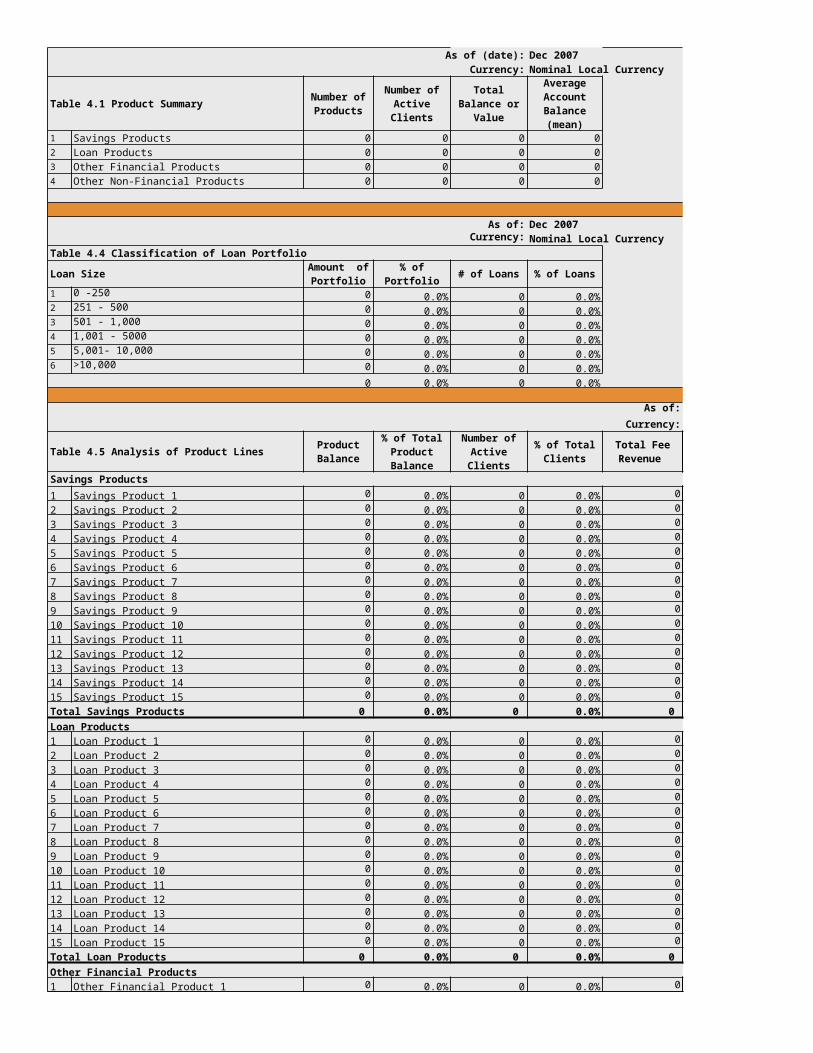

As of (date): Dec 2007

Currency: Nominal Local Currency

1 Savings Products 0 0 0 02 Loan Products 0 0 0 03 Other Financial Products 0 0 0 04 Other Non-Financial Products 0 0 0 0

As of: Dec 2007Currency: Nominal Local Currency

Loan Size % of Portfolio # of Loans % of Loans

1 0 -250 0 0.0% 0 0.0%2 251 - 500 0 0.0% 0 0.0%3 501 - 1,000 0 0.0% 0 0.0%4 1,001 - 5000 0 0.0% 0 0.0%5 5,001- 10,000 0 0.0% 0 0.0%6 >10,000 0 0.0% 0 0.0%

0 0.0% 0 0.0%

As of: Dec 2007

Currency: Nominal Local Currency

Savings Products

1 Savings Product 1 0 0.0% 0 0.0% 0 0.0%

2 Savings Product 2 0 0.0% 0 0.0% 0 0.0%

3 Savings Product 3 0 0.0% 0 0.0% 0 0.0%

4 Savings Product 4 0 0.0% 0 0.0% 0 0.0%

5 Savings Product 5 0 0.0% 0 0.0% 0 0.0%

6 Savings Product 6 0 0.0% 0 0.0% 0 0.0%

7 Savings Product 7 0 0.0% 0 0.0% 0 0.0%

8 Savings Product 8 0 0.0% 0 0.0% 0 0.0%

9 Savings Product 9 0 0.0% 0 0.0% 0 0.0%

10 Savings Product 10 0 0.0% 0 0.0% 0 0.0%

11 Savings Product 11 0 0.0% 0 0.0% 0 0.0%

12 Savings Product 12 0 0.0% 0 0.0% 0 0.0%

13 Savings Product 13 0 0.0% 0 0.0% 0 0.0%

14 Savings Product 14 0 0.0% 0 0.0% 0 0.0%

15 Savings Product 15 0 0.0% 0 0.0% 0 0.0%

Total Savings Products 0 0.0% 0 0.0% 0 0.0%

Loan Products

1 Loan Product 1 0 0.0% 0 0.0% 0 0.0%

2 Loan Product 2 0 0.0% 0 0.0% 0 0.0%

3 Loan Product 3 0 0.0% 0 0.0% 0 0.0%

4 Loan Product 4 0 0.0% 0 0.0% 0 0.0%

5 Loan Product 5 0 0.0% 0 0.0% 0 0.0%

6 Loan Product 6 0 0.0% 0 0.0% 0 0.0%

7 Loan Product 7 0 0.0% 0 0.0% 0 0.0%

8 Loan Product 8 0 0.0% 0 0.0% 0 0.0%

9 Loan Product 9 0 0.0% 0 0.0% 0 0.0%

10 Loan Product 10 0 0.0% 0 0.0% 0 0.0%

11 Loan Product 11 0 0.0% 0 0.0% 0 0.0%

12 Loan Product 12 0 0.0% 0 0.0% 0 0.0%

13 Loan Product 13 0 0.0% 0 0.0% 0 0.0%

14 Loan Product 14 0 0.0% 0 0.0% 0 0.0%

15 Loan Product 15 0 0.0% 0 0.0% 0 0.0%

Total Loan Products 0 0.0% 0 0.0% 0 0.0%

Other Financial Products

1 Other Financial Product 1 0 0.0% 0 0.0% 0 0.0%

Table 4.1 Product Summary Number of Products

Number of Active Clients

Total Balance or Value

Average Account Balance (mean)

Table 4.4 Classification of Loan Portfolio

Amount of Portfolio

Table 4.5 Analysis of Product Lines Product Balance

% of Total Product Balance

Number of Active Clients

% of Total Clients

Total Fee Revenue

% of Total MFI Fee Revenue

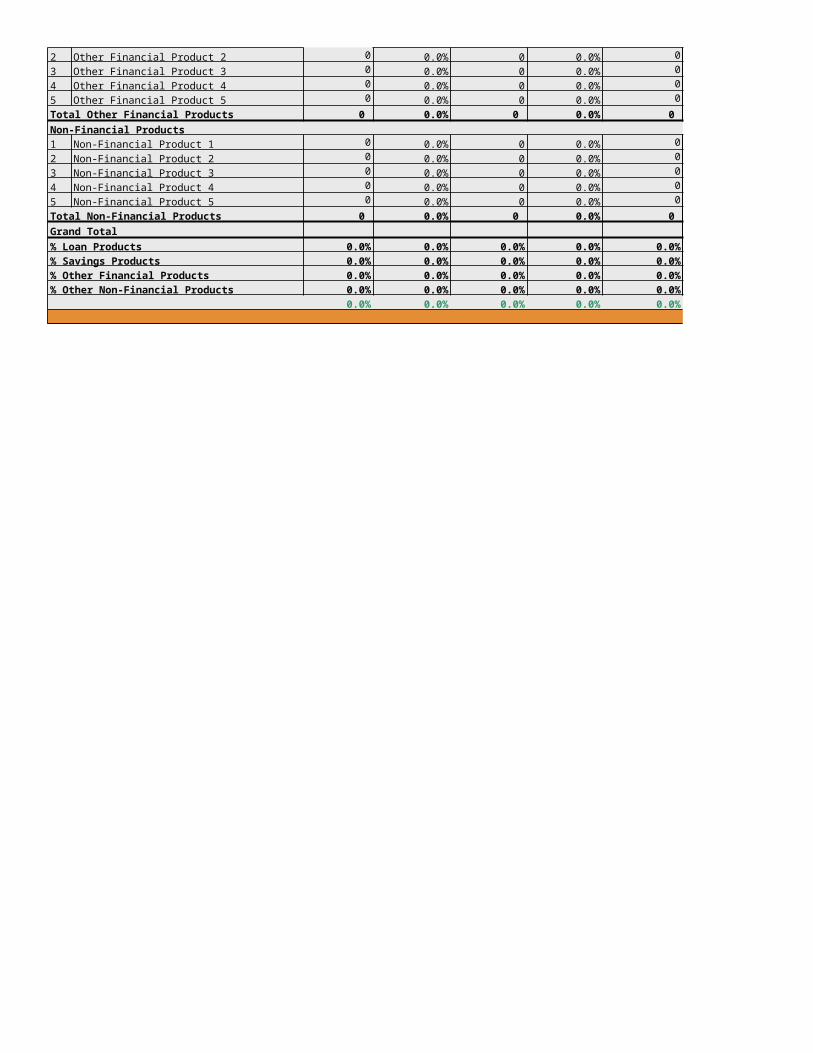

2 Other Financial Product 2 0 0.0% 0 0.0% 0 0.0%

3 Other Financial Product 3 0 0.0% 0 0.0% 0 0.0%

4 Other Financial Product 4 0 0.0% 0 0.0% 0 0.0%

5 Other Financial Product 5 0 0.0% 0 0.0% 0 0.0%

Total Other Financial Products 0 0.0% 0 0.0% 0 0.0%

Non-Financial Products

1 Non-Financial Product 1 0 0.0% 0 0.0% 0 0.0%

2 Non-Financial Product 2 0 0.0% 0 0.0% 0 0.0%

3 Non-Financial Product 3 0 0.0% 0 0.0% 0 0.0%

4 Non-Financial Product 4 0 0.0% 0 0.0% 0 0.0%

5 Non-Financial Product 5 0 0.0% 0 0.0% 0 0.0%

Total Non-Financial Products 0 0.0% 0 0.0% 0 0.0%

Grand Total

% Loan Products 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

% Savings Products 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

% Other Financial Products 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

% Other Non-Financial Products 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Nominal Local Currency

Savings Product 1 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 20071 Interest Rate (%) and calculation method 0.0% 0.0% 0.0% 0.0% 0.0%2 Minimum deposit to open account 0 0 0 0 03 Fees to open account 0 0 0 0 04 Minimum deposit per transaction 0 0 0 0 05 Fees per transaction 0 0 0 0 06 Penalty for early withdrawal 0 0 0 0 07 Minimum account balance 0 0 0 0 08 Withdrawal frequency (average per period) 0 0 0 0 0 9 Deposit frequency (average per period) 0 0 0 0 0 10 Number of active individual savings accounts 0 0 0 0 0 11 Number of inactive individual accounts 0 0 0 0 0 12 Total individual account balance, end of period 0 0 0 0 013

0.0% 0.0% 0.0% 0.0% 0.0%

14 Average individual account balance (mean) 0 0 0 0 015 Number of active institutional savings accounts 0 0 0 0 0 16 Number of inactive institutional accounts 0 0 0 0 0 17 Total institutional account balance, end of period 0 0 0 0 018

0.0% 0.0% 0.0% 0.0% 0.0%

19 Average institutional account balance (mean) 0 0 0 0 0Savings Product 2 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

1 Interest Rate (%) and calculation method 0.0% 0.0% 0.0% 0.0% 0.0%2 Minimum deposit to open account 0 0 0 0 03 Fees to open account 0 0 0 0 04 Minimum deposit per transaction 0 0 0 0 05 Fees per transaction 0 0 0 0 06 Penalty for early withdrawal 0 0 0 0 07 Minimum account balance 0 0 0 0 08 Withdrawal frequency (average per period) 0 0 0 0 0 9 Deposit frequency (average per period) 0 0 0 0 0 10 Number of active individual savings accounts 0 0 0 0 0 11 Number of inactive individual accounts 0 0 0 0 0 12 Total individual account balance, end of period 0 0 0 0 013

0.0% 0.0% 0.0% 0.0% 0.0%

14 Average individual account balance (mean) 0 0 0 0 015 Number of active institutional savings accounts 0 0 0 0 0 16 Number of inactive institutional accounts 0 0 0 0 0 17 Total institutional account balance, end of period 0 0 0 0 018

0.0% 0.0% 0.0% 0.0% 0.0%

19 Average institutional account balance (mean) 0 0 0 0 0Savings Product 3 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

1 Interest Rate (%) and calculation method 0.0% 0.0% 0.0% 0.0% 0.0%2 Minimum deposit to open account 0 0 0 0 03 Fees to open account 0 0 0 0 04 Minimum deposit per transaction 0 0 0 0 05 Fees per transaction 0 0 0 0 06 Penalty for early withdrawal 0 0 0 0 07 Minimum account balance 0 0 0 0 08 Withdrawal frequency (average per period) 0 0 0 0 0 9 Deposit frequency (average per period) 0 0 0 0 0 10 Number of active individual savings accounts 0 0 0 0 0 11 Number of inactive individual accounts 0 0 0 0 0 12 Total individual account balance, end of period 0 0 0 0 013

0.0% 0.0% 0.0% 0.0% 0.0%

14 Average individual account balance (mean) 0 0 0 0 015 Number of active institutional savings accounts 0 0 0 0 0 16 Number of inactive institutional accounts 0 0 0 0 0 17 Total institutional account balance, end of period 0 0 0 0 018

0.0% 0.0% 0.0% 0.0% 0.0%

19 Average institutional account balance (mean) 0 0 0 0 0

Table 4.2 Savings Products Summary

Individual account balance as percentage of total savings balance

Institutional account balance as percentage of total savings balance

Individual account balance as percentage of total savings balance

Institutional account balance as percentage of total savings balance

Individual account balance as percentage of total savings balance

Institutional account balance as percentage of total savings balance

Savings Product 4 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 20071 Interest Rate (%) and calculation method 0.0% 0.0% 0.0% 0.0% 0.0%2 Minimum deposit to open account 0 0 0 0 03 Fees to open account 0 0 0 0 04 Minimum deposit per transaction 0 0 0 0 05 Fees per transaction 0 0 0 0 06 Penalty for early withdrawal 0 0 0 0 07 Minimum account balance 0 0 0 0 08 Withdrawal frequency (average per period) 0 0 0 0 0 9 Deposit frequency (average per period) 0 0 0 0 0 10 Number of active individual savings accounts 0 0 0 0 0 11 Number of inactive individual accounts 0 0 0 0 0 12 Total individual account balance, end of period 0 0 0 0 013

0.0% 0.0% 0.0% 0.0% 0.0%

14 Average individual account balance (mean) 0 0 0 0 015 Number of active institutional savings accounts 0 0 0 0 0 16 Number of inactive institutional accounts 0 0 0 0 0 17 Total institutional account balance, end of period 0 0 0 0 018

0.0% 0.0% 0.0% 0.0% 0.0%

19 Average institutional account balance (mean) 0 0 0 0 0Savings Product 5 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

1 Interest Rate (%) and calculation method 0.0% 0.0% 0.0% 0.0% 0.0%2 Minimum deposit to open account 0 0 0 0 03 Fees to open account 0 0 0 0 04 Minimum deposit per transaction 0 0 0 0 05 Fees per transaction 0 0 0 0 06 Penalty for early withdrawal 0 0 0 0 07 Minimum account balance 0 0 0 0 08 Withdrawal frequency (average per period) 0 0 0 0 0 9 Deposit frequency (average per period) 0 0 0 0 0 10 Number of active individual savings accounts 0 0 0 0 0 11 Number of inactive individual accounts 0 0 0 0 0 12 Total individual account balance, end of period 0 0 0 0 013

0.0% 0.0% 0.0% 0.0% 0.0%

14 Average individual account balance (mean) 0 0 0 0 015 Number of active institutional savings accounts 0 0 0 0 0 16 Number of inactive institutional accounts 0 0 0 0 0 17 Total institutional account balance, end of period 0 0 0 0 018

0.0% 0.0% 0.0% 0.0% 0.0%

19 Average institutional account balance (mean) 0 0 0 0 0Savings Product 6 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

1 Interest Rate (%) and calculation method 0.0% 0.0% 0.0% 0.0% 0.0%2 Minimum deposit to open account 0 0 0 0 03 Fees to open account 0 0 0 0 04 Minimum deposit per transaction 0 0 0 0 05 Fees per transaction 0 0 0 0 06 Penalty for early withdrawal 0 0 0 0 07 Minimum account balance 0 0 0 0 08 Withdrawal frequency (average per period) 0 0 0 0 0 9 Deposit frequency (average per period) 0 0 0 0 0 10 Number of active individual savings accounts 0 0 0 0 0 11 Number of inactive individual accounts 0 0 0 0 0 12 Total individual account balance, end of period 0 0 0 0 013

0.0% 0.0% 0.0% 0.0% 0.0%

14 Average individual account balance (mean) 0 0 0 0 015 Number of active institutional savings accounts 0 0 0 0 0 16 Number of inactive institutional accounts 0 0 0 0 0 17 Total institutional account balance, end of period 0 0 0 0 018

0.0% 0.0% 0.0% 0.0% 0.0%

19 Average institutional account balance (mean) 0 0 0 0 0Savings Product 7 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

Individual account balance as percentage of total savings balance

Institutional account balance as percentage of total savings balance

Individual account balance as percentage of total savings balance

Institutional account balance as percentage of total savings balance

Individual account balance as percentage of total savings balance

Institutional account balance as percentage of total savings balance

1 Interest Rate (%) and calculation method 0.0% 0.0% 0.0% 0.0% 0.0%2 Minimum deposit to open account 0 0 0 0 03 Fees to open account 0 0 0 0 04 Minimum deposit per transaction 0 0 0 0 05 Fees per transaction 0 0 0 0 06 Penalty for early withdrawal 0 0 0 0 07 Minimum account balance 0 0 0 0 08 Withdrawal frequency (average per period) 0 0 0 0 0 9 Deposit frequency (average per period) 0 0 0 0 0 10 Number of active individual savings accounts 0 0 0 0 0 11 Number of inactive individual accounts 0 0 0 0 0 12 Total individual account balance, end of period 0 0 0 0 013

0.0% 0.0% 0.0% 0.0% 0.0%

14 Average individual account balance (mean) 0 0 0 0 015 Number of active institutional savings accounts 0 0 0 0 0 16 Number of inactive institutional accounts 0 0 0 0 0 17 Total institutional account balance, end of period 0 0 0 0 018

0.0% 0.0% 0.0% 0.0% 0.0%

19 Average institutional account balance (mean) 0 0 0 0 0Savings Product 8 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

1 Interest Rate (%) and calculation method 0.0% 0.0% 0.0% 0.0% 0.0%2 Minimum deposit to open account 0 0 0 0 03 Fees to open account 0 0 0 0 04 Minimum deposit per transaction 0 0 0 0 05 Fees per transaction 0 0 0 0 06 Penalty for early withdrawal 0 0 0 0 07 Minimum account balance 0 0 0 0 08 Withdrawal frequency (average per period) 0 0 0 0 0 9 Deposit frequency (average per period) 0 0 0 0 0 10 Number of active individual savings accounts 0 0 0 0 0 11 Number of inactive individual accounts 0 0 0 0 0 12 Total individual account balance, end of period 0 0 0 0 013

0.0% 0.0% 0.0% 0.0% 0.0%

14 Average individual account balance (mean) 0 0 0 0 015 Number of active institutional savings accounts 0 0 0 0 0 16 Number of inactive institutional accounts 0 0 0 0 0 17 Total institutional account balance, end of period 0 0 0 0 018

0.0% 0.0% 0.0% 0.0% 0.0%

19 Average institutional account balance (mean) 0 0 0 0 0Savings Product 9 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

1 Interest Rate (%) and calculation method 0.0% 0.0% 0.0% 0.0% 0.0%2 Minimum deposit to open account 0 0 0 0 03 Fees to open account 0 0 0 0 04 Minimum deposit per transaction 0 0 0 0 05 Fees per transaction 0 0 0 0 06 Penalty for early withdrawal 0 0 0 0 07 Minimum account balance 0 0 0 0 08 Withdrawal frequency (average per period) 0 0 0 0 0 9 Deposit frequency (average per period) 0 0 0 0 0 10 Number of active individual savings accounts 0 0 0 0 0 11 Number of inactive individual accounts 0 0 0 0 0 12 Total individual account balance, end of period 0 0 0 0 013

0.0% 0.0% 0.0% 0.0% 0.0%

14 Average individual account balance (mean) 0 0 0 0 015 Number of active institutional savings accounts 0 0 0 0 0 16 Number of inactive institutional accounts 0 0 0 0 0 17 Total institutional account balance, end of period 0 0 0 0 018

0.0% 0.0% 0.0% 0.0% 0.0%

19 Average institutional account balance (mean) 0 0 0 0 0Savings Product 10 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

1 Interest Rate (%) and calculation method 0.0% 0.0% 0.0% 0.0% 0.0%

Individual account balance as percentage of total savings balance

Institutional account balance as percentage of total savings balance

Individual account balance as percentage of total savings balance

Institutional account balance as percentage of total savings balance

Individual account balance as percentage of total savings balance

Institutional account balance as percentage of total savings balance

2 Minimum deposit to open account 0 0 0 0 03 Fees to open account 0 0 0 0 04 Minimum deposit per transaction 0 0 0 0 05 Fees per transaction 0 0 0 0 06 Penalty for early withdrawal 0 0 0 0 07 Minimum account balance 0 0 0 0 08 Withdrawal frequency (average per period) 0 0 0 0 0 9 Deposit frequency (average per period) 0 0 0 0 0 10 Number of active individual savings accounts 0 0 0 0 0 11 Number of inactive individual accounts 0 0 0 0 0 12 Total individual account balance, end of period 0 0 0 0 013

0.0% 0.0% 0.0% 0.0% 0.0%

14 Average individual account balance (mean) 0 0 0 0 015 Number of active institutional savings accounts 0 0 0 0 0 16 Number of inactive institutional accounts 0 0 0 0 0 17 Total institutional account balance, end of period 0 0 0 0 018

0.0% 0.0% 0.0% 0.0% 0.0%

19 Average institutional account balance (mean) 0 0 0 0 0Savings Product 11 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

1 Interest Rate (%) and calculation method 0.0% 0.0% 0.0% 0.0% 0.0%2 Minimum deposit to open account 0 0 0 0 03 Fees to open account 0 0 0 0 04 Minimum deposit per transaction 0 0 0 0 05 Fees per transaction 0 0 0 0 06 Penalty for early withdrawal 0 0 0 0 07 Minimum account balance 0 0 0 0 08 Withdrawal frequency (average per period) 0 0 0 0 0 9 Deposit frequency (average per period) 0 0 0 0 0 10 Number of active individual savings accounts 0 0 0 0 0 11 Number of inactive individual accounts 0 0 0 0 0 12 Total individual account balance, end of period 0 0 0 0 013

0.0% 0.0% 0.0% 0.0% 0.0%

14 Average individual account balance (mean) 0 0 0 0 015 Number of active institutional savings accounts 0 0 0 0 0 16 Number of inactive institutional accounts 0 0 0 0 0 17 Total institutional account balance, end of period 0 0 0 0 018

0.0% 0.0% 0.0% 0.0% 0.0%

19 Average institutional account balance (mean) 0 0 0 0 0Savings Product 12 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

1 Interest Rate (%) and calculation method 0.0% 0.0% 0.0% 0.0% 0.0%2 Minimum deposit to open account 0 0 0 0 03 Fees to open account 0 0 0 0 04 Minimum deposit per transaction 0 0 0 0 05 Fees per transaction 0 0 0 0 06 Penalty for early withdrawal 0 0 0 0 07 Minimum account balance 0 0 0 0 08 Withdrawal frequency (average per period) 0 0 0 0 0 9 Deposit frequency (average per period) 0 0 0 0 0 10 Number of active individual savings accounts 0 0 0 0 0 11 Number of inactive individual accounts 0 0 0 0 0 12 Total individual account balance, end of period 0 0 0 0 013

0.0% 0.0% 0.0% 0.0% 0.0%

14 Average individual account balance (mean) 0 0 0 0 015 Number of active institutional savings accounts 0 0 0 0 0 16 Number of inactive institutional accounts 0 0 0 0 0 17 Total institutional account balance, end of period 0 0 0 0 018

0.0% 0.0% 0.0% 0.0% 0.0%

19 Average institutional account balance (mean) 0 0 0 0 0Savings Product 13 Dec 2003 Dec 2004 Dec 2005 Dec 2006 Dec 2007

1 Interest Rate (%) and calculation method 0.0% 0.0% 0.0% 0.0% 0.0%2 Minimum deposit to open account 0 0 0 0 0

Individual account balance as percentage of total savings balance