Embed Size (px)

Citation preview

Slide 12.1

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Principles of Auditing: An Introduction to

International Standards on Auditing

Chapter 12 – Audit Reports and

Communication

Rick Hayes, Hans Gortemaker

and Philip Wallage

Slide 12.2

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Management responsibility for audit report – SOX

SOX Requires that the principal executive officer or officers and the principal financial officer or officers, certify in each report filed with the SEC the following:

the signing officer has reviewed the report;

the report does not contain any untrue statement of a material fact or omit to state a material fact;

the financial statements, and other financial information, fairly present in all material respects the financial condition of the company;

the signing officers:

• are responsible for establishing and maintaining internal controls;

• have evaluated the effectiveness of the company’s internal controls;

• have presented in the report their conclusions about the effectiveness of their internal controls based on their evaluation.

Slide 12.3

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Management responsibility for audit

report under SOX (Continued)

Requires that the principal executive officer or officers and the principal financial officer or officers, certify in each report filed with the SEC the following:

the signing officers have disclosed to the company’s auditors and the audit committee of the board of directors:

• all significant deficiencies in the design or operation of internal controls which could adversely affect the company’s ability to record, process, summarise and report financial data and have identified for the company’s auditors any material weaknesses in internal controls;

• any fraud, whether or not material, that involves management or other employees who have a significant role in the company’s internal controls.

Slide 12.4

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

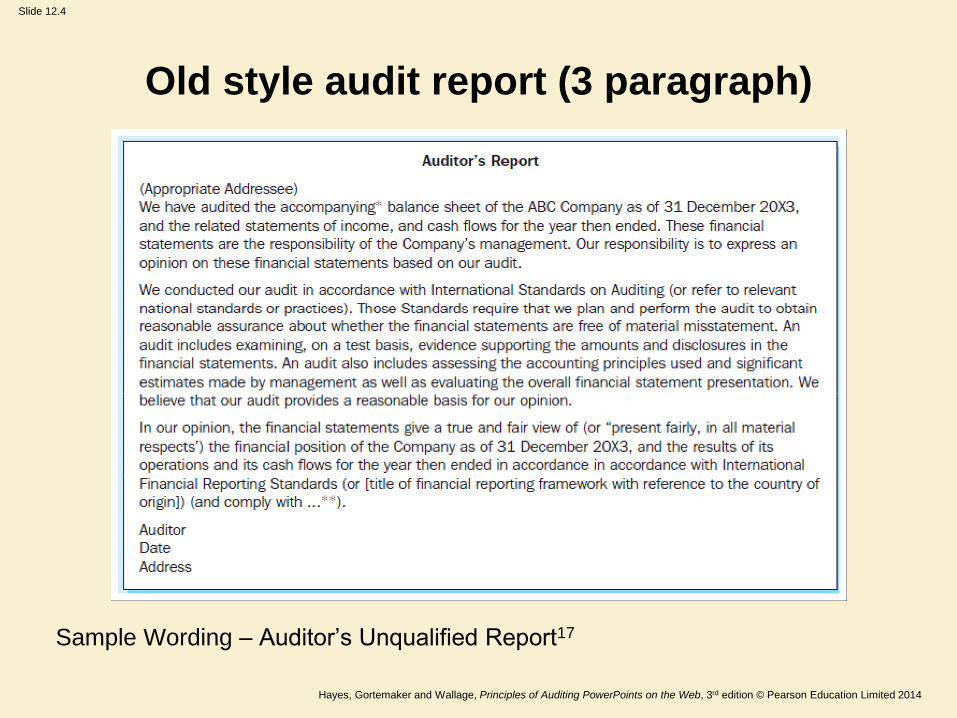

Old style audit report (3 paragraph)

Sample Wording – Auditor’s Unqualified Report17

Slide 12.5

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

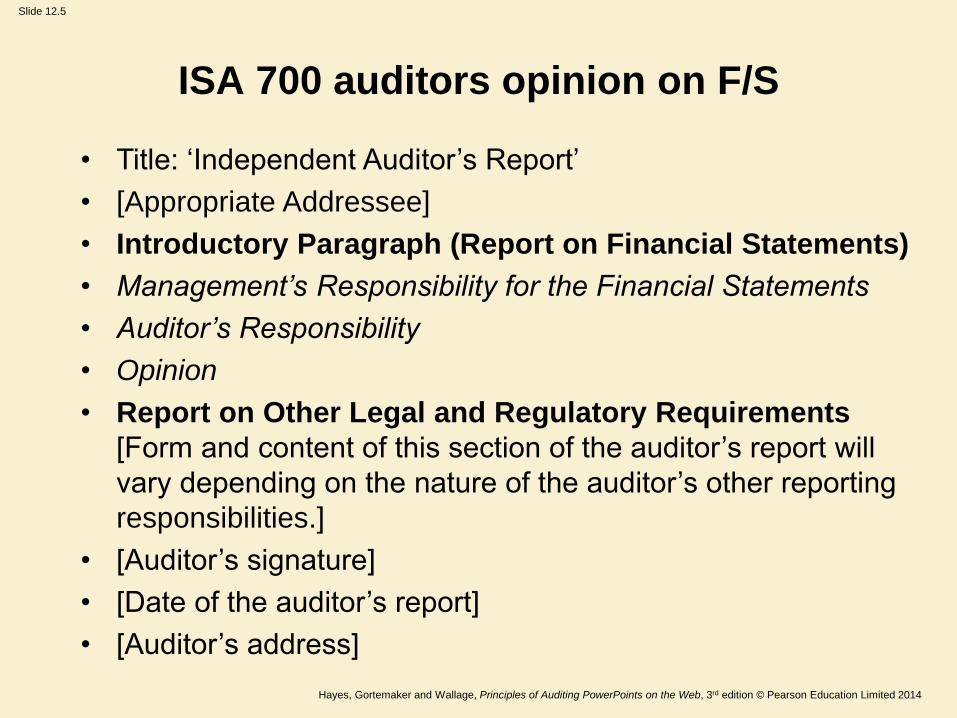

ISA 700 auditors opinion on F/S

• Title: ‘Independent Auditor’s Report’

• [Appropriate Addressee]

• Introductory Paragraph (Report on Financial Statements)

• Management’s Responsibility for the Financial Statements

• Auditor’s Responsibility

• Opinion

• Report on Other Legal and Regulatory Requirements

[Form and content of this section of the auditor’s report will

vary depending on the nature of the auditor’s other reporting

responsibilities.]

• [Auditor’s signature]

• [Date of the auditor’s report]

• [Auditor’s address]

Slide 12.6

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

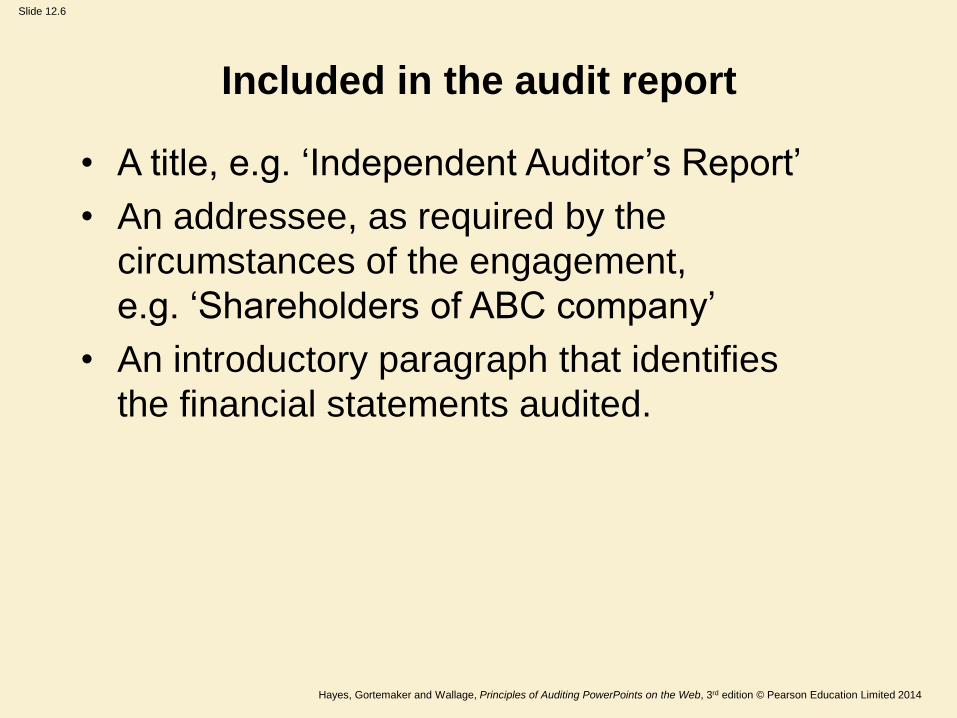

Included in the audit report

• A title, e.g. ‘Independent Auditor’s Report’

• An addressee, as required by the

circumstances of the engagement,

e.g. ‘Shareholders of ABC company’

• An introductory paragraph that identifies

the financial statements audited.

Slide 12.7

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

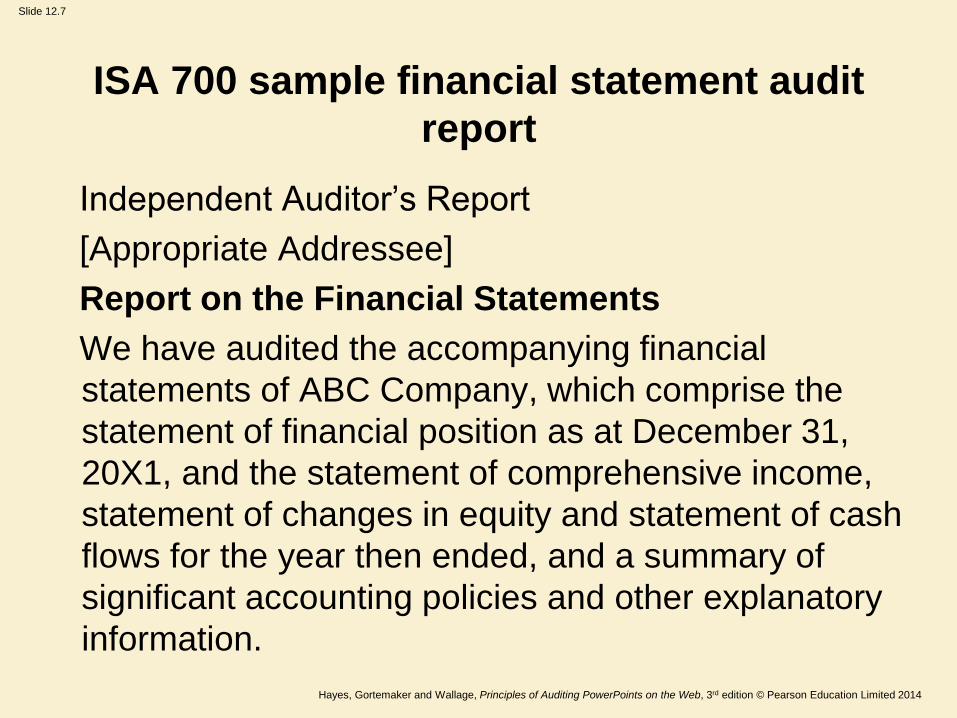

ISA 700 sample financial statement audit

report

Independent Auditor’s Report

[Appropriate Addressee]

Report on the Financial Statements

We have audited the accompanying financial

statements of ABC Company, which comprise the

statement of financial position as at December 31,

20X1, and the statement of comprehensive income,

statement of changes in equity and statement of cash

flows for the year then ended, and a summary of

significant accounting policies and other explanatory

information.

Slide 12.8

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

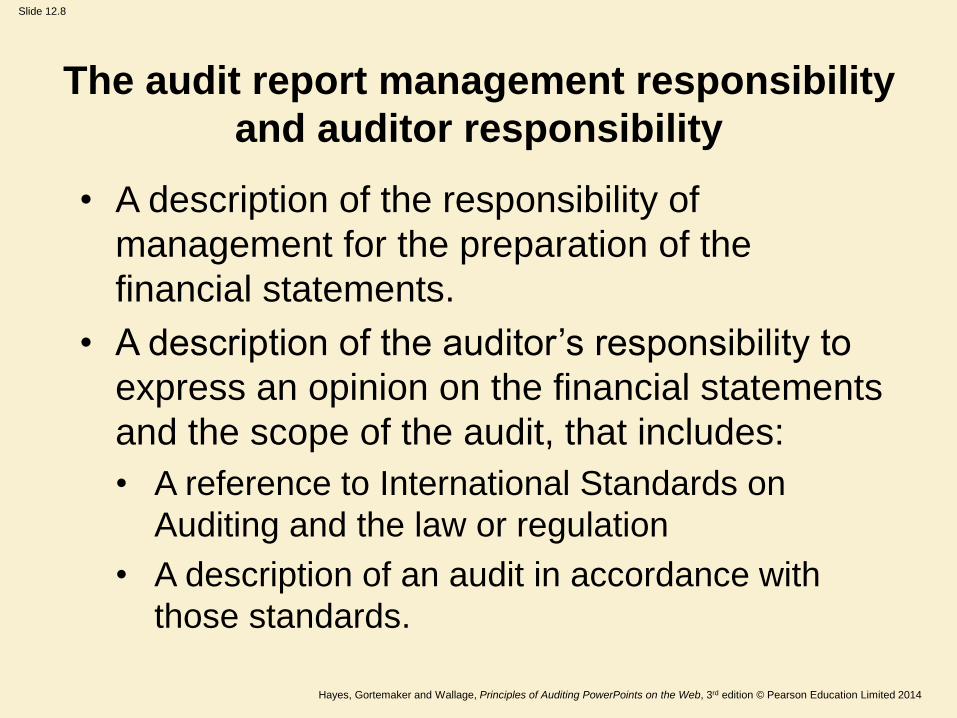

• A description of the responsibility of

management for the preparation of the

financial statements.

• A description of the auditor’s responsibility to

express an opinion on the financial statements

and the scope of the audit, that includes:

• A reference to International Standards on

Auditing and the law or regulation

• A description of an audit in accordance with

those standards.

The audit report management responsibility

and auditor responsibility

Slide 12.9

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

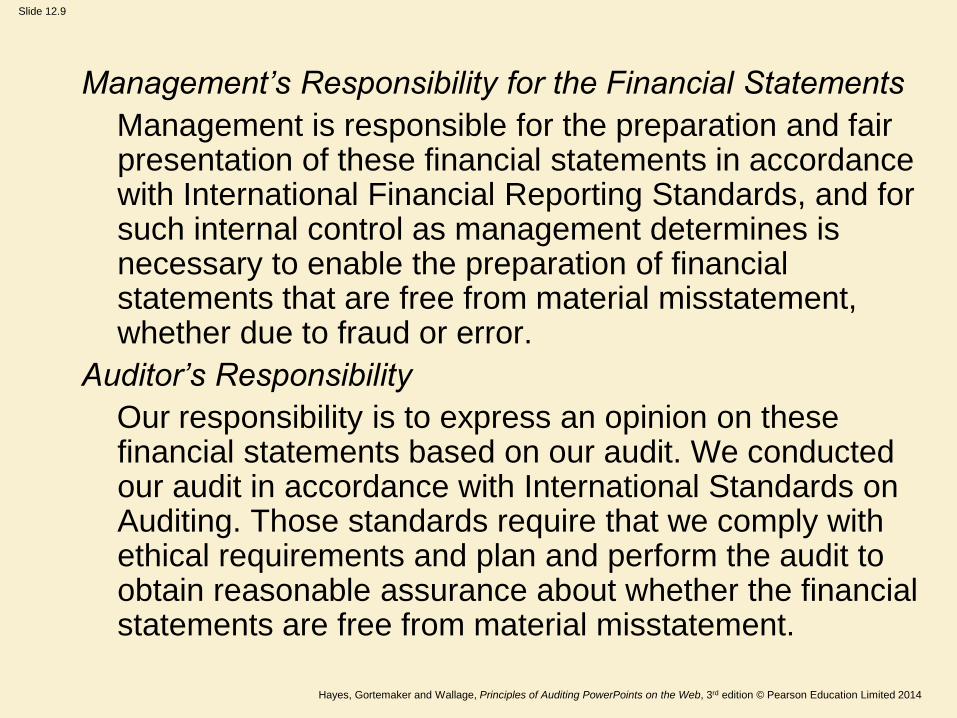

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

Slide 12.10

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

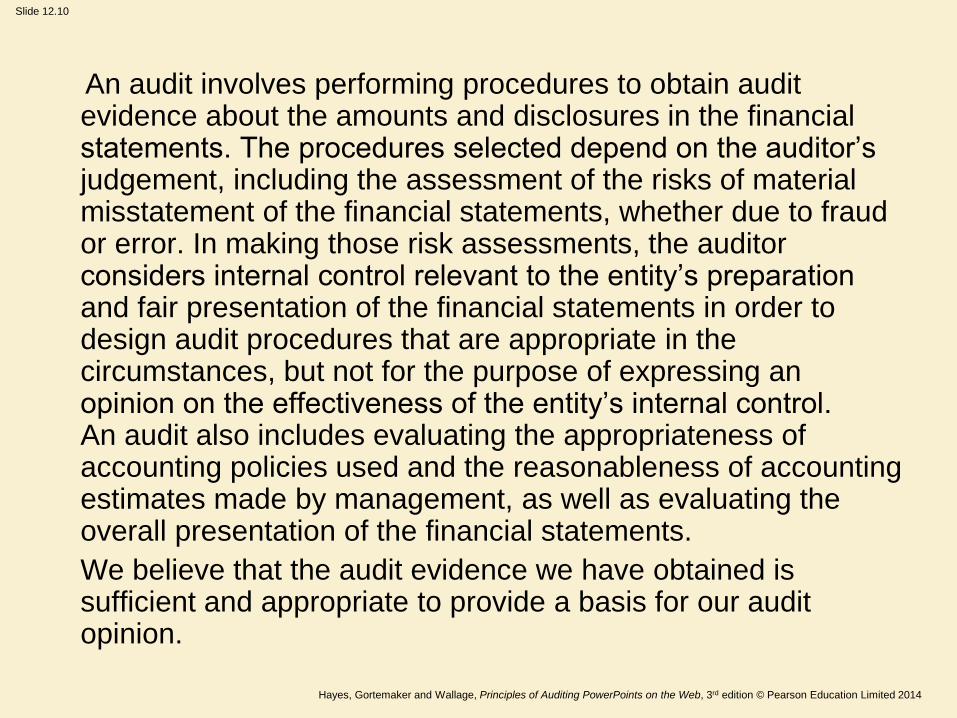

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Slide 12.11

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

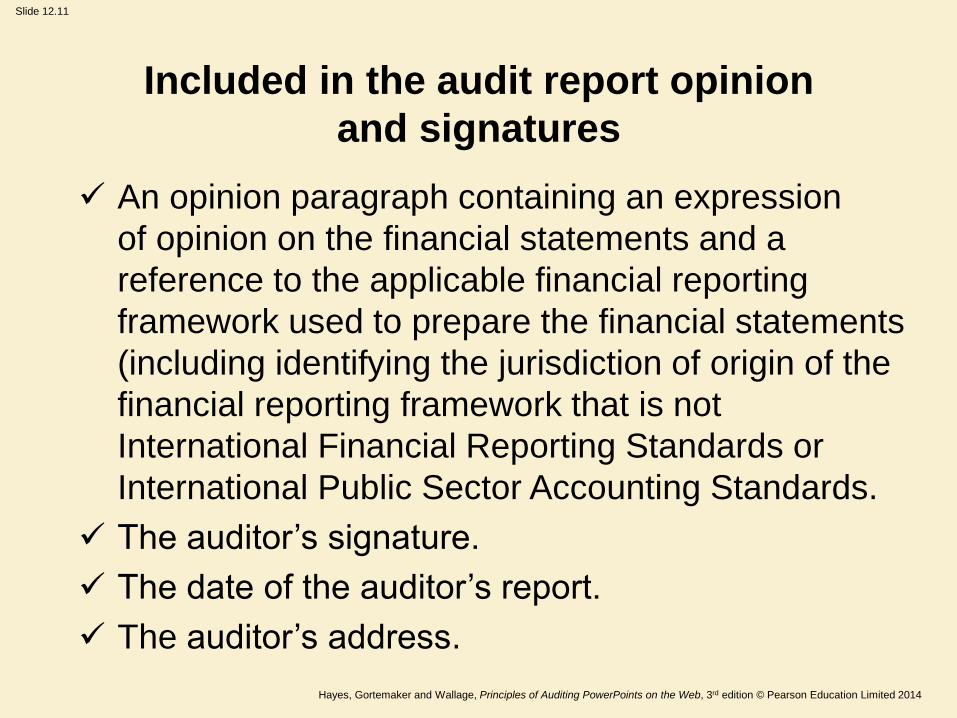

An opinion paragraph containing an expression

of opinion on the financial statements and a

reference to the applicable financial reporting

framework used to prepare the financial statements

(including identifying the jurisdiction of origin of the

financial reporting framework that is not

International Financial Reporting Standards or

International Public Sector Accounting Standards.

The auditor’s signature.

The date of the auditor’s report.

The auditor’s address.

Included in the audit report opinion

and signatures

Slide 12.12

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

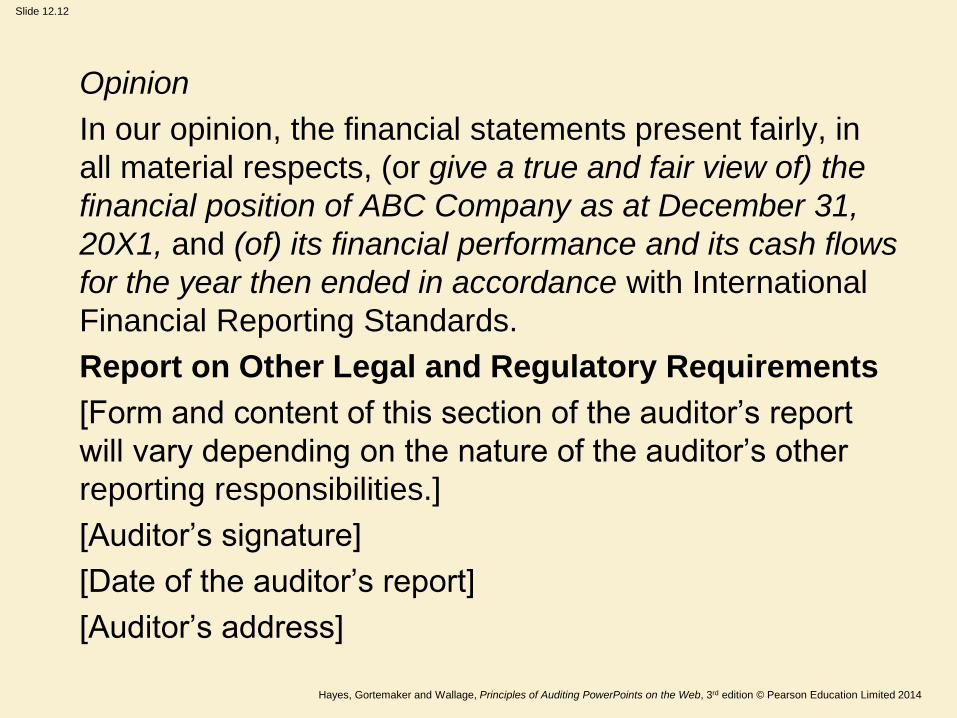

Opinion

In our opinion, the financial statements present fairly, in

all material respects, (or give a true and fair view of) the

financial position of ABC Company as at December 31,

20X1, and (of) its financial performance and its cash flows

for the year then ended in accordance with International

Financial Reporting Standards.

Report on Other Legal and Regulatory Requirements

[Form and content of this section of the auditor’s report

will vary depending on the nature of the auditor’s other

reporting responsibilities.]

[Auditor’s signature]

[Date of the auditor’s report]

[Auditor’s address]

Slide 12.13

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

The report must be dated

The auditor shall date the report no earlier than

the date on which the auditor has obtained

sufficient appropriate audit evidence on which to

base the auditor’s opinion on the financial

statements including evidence that: (a) all the

statements that comprise the financial statements,

including the related notes, have been prepared;

and (b) those with recognised authority have

asserted that they have taken responsibility for

those financial statements.

Slide 12.14

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

The opinion expressed in the auditor’s report

may be one of four types:

Unmodified

(unqualified), Three Modified Opinions:

qualified,

adverse or

disclaimer of

opinion

Q U A D

Slide 12.15

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Unqualified audit opinion – also called

unmodified opinion

• Unmodified (unqualified) opinion – The opinion

expressed by the auditor when the auditor concludes

that the financial statements are prepared, in all

material respects, in accordance with the applicable

financial reporting framework.

• Most common type of audit report.

• Called ‘clean opinion’.

• Used for more than 90 per cent of all audit reports.

• Other audit reports are referred to as ‘modified opinion (adverse opinion, disclaimer of opinion and qualified opinion).

Slide 12.16

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Evaluation of the compliance to the reporting framework

include consideration of these qualitative aspects

• Whether the financial statements adequately disclose the

significant accounting policies selected and they are consistent

and appropriate.

• Accounting estimates made by management are reasonable.

• Information presented in the financial statements is relevant,

reliable, comparable and understandable.

• Disclosures to enable the intended users to understand the effect

of material transactions and events on the information conveyed in

the financial statements.

• Terminology used in the financial statements, including the title

of each financial statement, is appropriate.

• Whether the financial statements achieve fair presentation. If they

are prepared in accordance with a fair presentation framework.

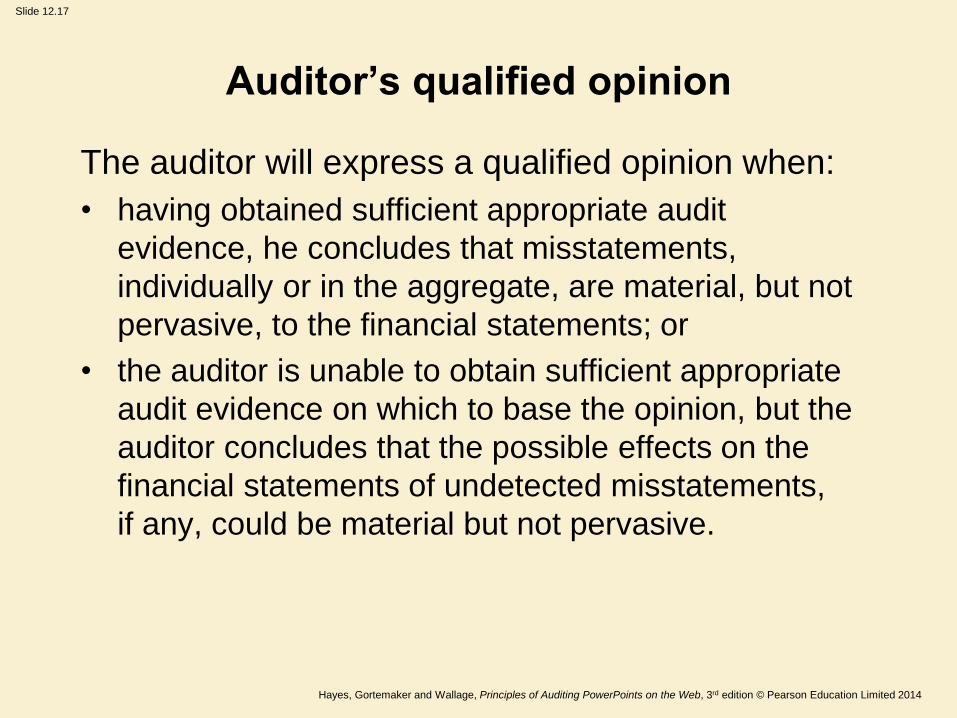

Slide 12.17

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Auditor’s qualified opinion

The auditor will express a qualified opinion when:

• having obtained sufficient appropriate audit

evidence, he concludes that misstatements,

individually or in the aggregate, are material, but not

pervasive, to the financial statements; or

• the auditor is unable to obtain sufficient appropriate

audit evidence on which to base the opinion, but the

auditor concludes that the possible effects on the

financial statements of undetected misstatements,

if any, could be material but not pervasive.

Slide 12.18

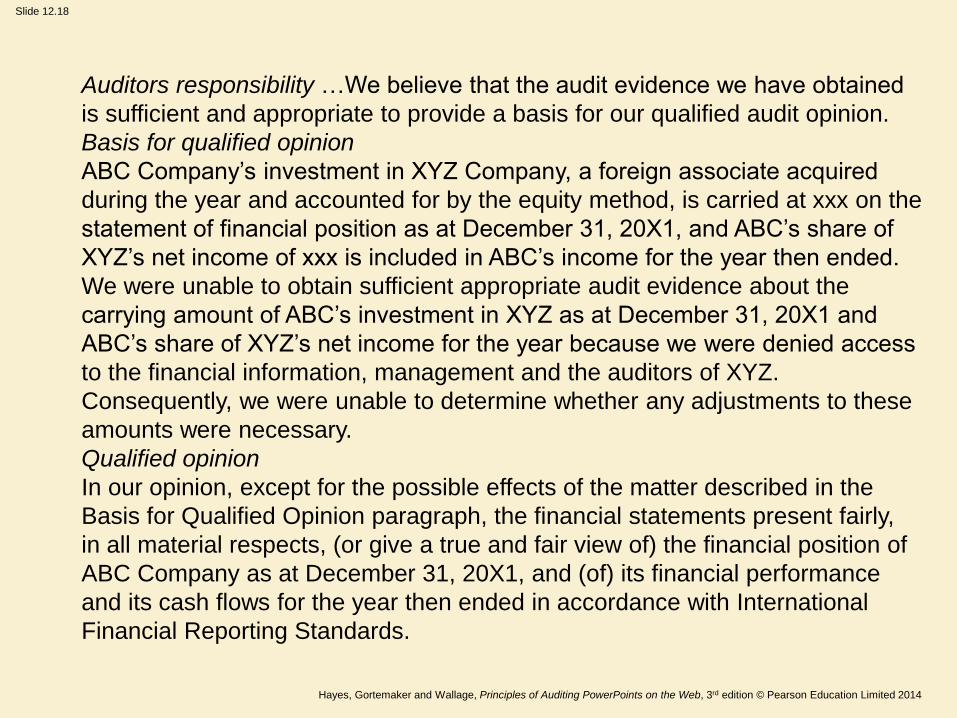

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Auditors responsibility …We believe that the audit evidence we have obtained

is sufficient and appropriate to provide a basis for our qualified audit opinion.

Basis for qualified opinion

ABC Company’s investment in XYZ Company, a foreign associate acquired

during the year and accounted for by the equity method, is carried at xxx on the

statement of financial position as at December 31, 20X1, and ABC’s share of

XYZ’s net income of xxx is included in ABC’s income for the year then ended.

We were unable to obtain sufficient appropriate audit evidence about the

carrying amount of ABC’s investment in XYZ as at December 31, 20X1 and

ABC’s share of XYZ’s net income for the year because we were denied access

to the financial information, management and the auditors of XYZ.

Consequently, we were unable to determine whether any adjustments to these

amounts were necessary.

Qualified opinion

In our opinion, except for the possible effects of the matter described in the

Basis for Qualified Opinion paragraph, the financial statements present fairly,

in all material respects, (or give a true and fair view of) the financial position of

ABC Company as at December 31, 20X1, and (of) its financial performance

and its cash flows for the year then ended in accordance with International

Financial Reporting Standards.

Slide 12.19

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

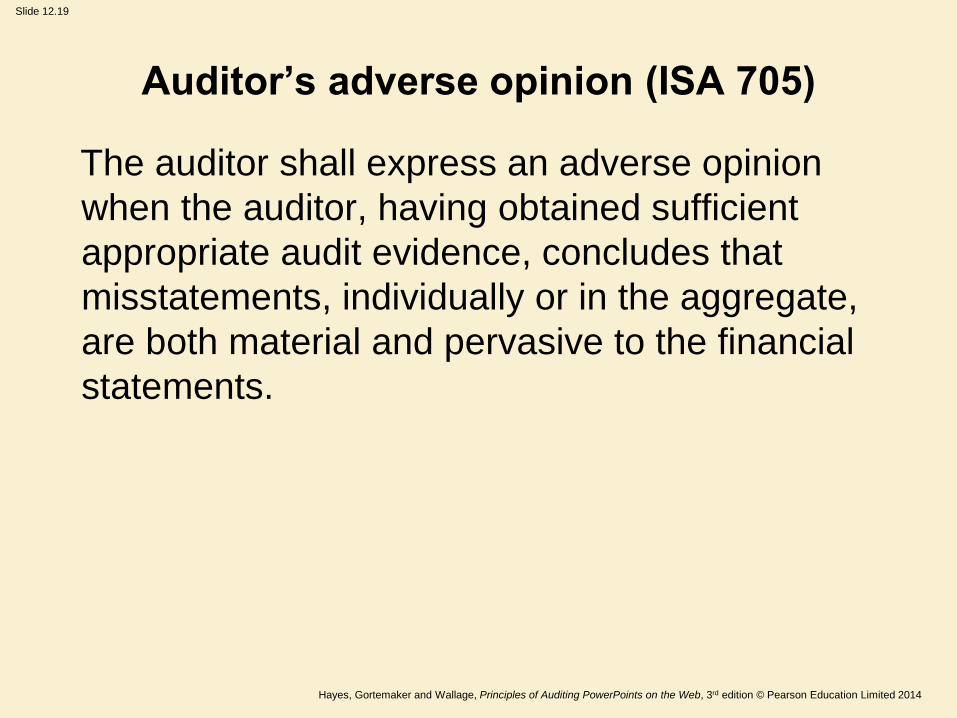

Auditor’s adverse opinion (ISA 705)

The auditor shall express an adverse opinion

when the auditor, having obtained sufficient

appropriate audit evidence, concludes that

misstatements, individually or in the aggregate,

are both material and pervasive to the financial

statements.

Slide 12.20

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

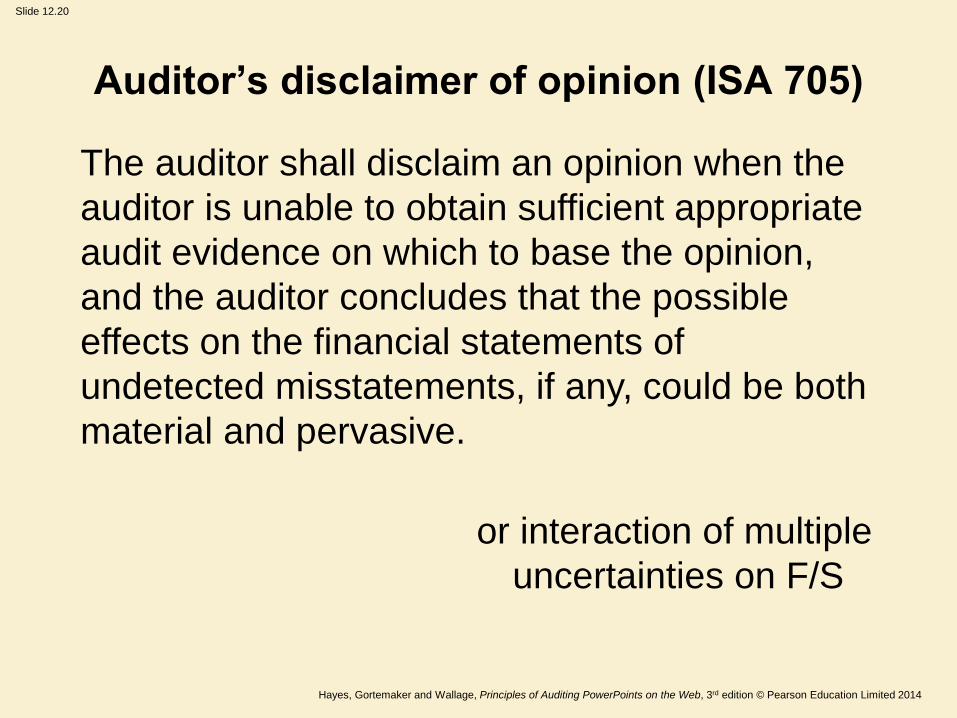

Auditor’s disclaimer of opinion (ISA 705)

The auditor shall disclaim an opinion when the

auditor is unable to obtain sufficient appropriate

audit evidence on which to base the opinion,

and the auditor concludes that the possible

effects on the financial statements of

undetected misstatements, if any, could be both

material and pervasive.

or interaction of multiple

uncertainties on F/S

Slide 12.21

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Basis for modification paragraph

When the auditor modifies the opinion on the

financial statements, the auditor shall, in addition to

the specific elements required by ISA 700, include

a paragraph in the auditor’s report that provides a

description of the matter giving rise to the

modification. The auditor shall place this paragraph

immediately before the opinion paragraph in the

auditor’s report and use the heading ‘Basis for

Qualified Opinion’, ‘Basis for Adverse Opinion’ or

‘Basis for Disclaimer of Opinion’, as appropriate.

Slide 12.22

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

When the auditor includes an Emphasis of Matter

paragraph in the auditor’s report, the auditor shall:

a. include it immediately after the Opinion paragraph

in the auditor’s report;

b. use the heading ‘Emphasis of Matter’;

c. include in the paragraph a clear reference to the

matter being emphasised and to where relevant

disclosures that fully describe the matter can be

found in the financial statements;

d. indicate that the auditor’s opinion is not modified

in respect of the matter emphasised.

Slide 12.23

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

An auditor might write an emphasis of

a matter paragraph:

• If there is a significant uncertainty which may affect the financial statements, the resolution of which is dependent upon future events.

• Examples of uncertainties that might be emphasised include:

• the existence of related party transactions;

• important accounting matters occurring subsequent to the balance sheet date;

• matters affecting the comparability of financial statements with those of previous years (e.g. change in accounting methods);

• litigation, long-term contracts, recoverability of asset values, losses on discontinued operations.

• To highlight a material matter regarding a going concern problem.

Slide 12.24

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

The going concern disclosure should:

• describe the principal conditions that raise doubt;

• state that there are doubts about going concern; therefore the entity may be unable to realise its assets and discharge its liabilities in the normal course of business;

• state that the financial statements do not include any adjustments relating to the recoverability and classification of recorded asset amounts or to amounts and classification of liabilities that may be necessary should the entity be unable to continue as a going concern.

ISA 570

Slide 12.25

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

1. A limitation in scope

2. The auditor’s judgement about the pervasiveness

of the effects or possible effects of the matter

on the financial statements.

The circumstances described in 1 – scope

limitation – could lead to a modified opinion

or a disclaimer of opinion. The circumstances

described in 2 – disagreement with

management – could lead to a modified opinion

or an adverse opinion.

Circumstances that may result in other

than an unmodified opinion

Slide 12.26

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Limitation on scope

• Scope limitations arise when the auditors are

unable for any reason to obtain the

information and explanations considered

necessary for the audit

– limited by the inability to carry out a procedure

the auditors consider necessary

– the absence of proper accounting records

• The audit report should describe the

limitation.

Slide 12.27

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Modification of opinion results from

disagreement with management on

• the acceptability of the accounting policies

selected;

• the method of policy application, including

the adequacy of valuations and disclosures

in the financial statements; or

• the compliance of the financial statements

with relevant regulations and statutory

requirements.

Slide 12.28

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Uncertainties leading to qualification

of opinions

Certain uncertainties may lead to an auditor’s report

containing a qualification of opinion in many

countries. These uncertainties include:

• material uncertainties;

• lack of consistency;

• independence of auditor;

• reports in reference to an expert;

• fraud.

Slide 12.29

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Materiality, lack of consistency, independence

• If the amounts of a misstatement in the financial statements are so significant that the financial statements are materially affected as a whole, it is necessary to issue either a qualified or an adverse opinion.

• Lack of consistency in the application of accounting principles in the current period in relation to the preceding period may require a modification to an unmodified opinion based on standards in many countries.

• ISA auditing standards do not require a modified opinion or a disclaimer of opinion if the auditor is not independent, although this is the case in several countries (including US).

Slide 12.30

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Reports involving other auditors and experts

ISA 620 suggests that when expressing an unmodified

(unqualified) opinion the auditor should not refer to the

work of an expert in her report as such a reference might

be misunderstood to be a qualification of the auditor’s

opinion or a division of responsibility. If the auditor, as a

result of the other auditor’s or expert’s work, issues an

opinion other than unmodified, he may in some

circumstances describe the work of the expert.

Slide 12.31

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

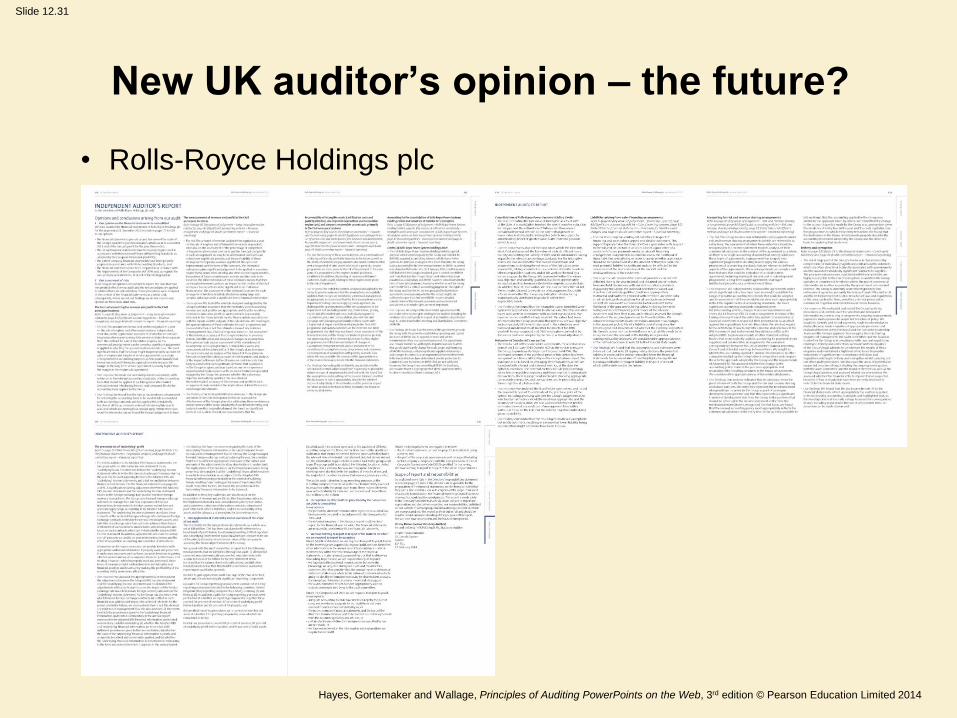

New UK auditor’s opinion – the future?

• Rolls-Royce Holdings plc

Slide 12.32

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

New UK auditor’s opinion – the future?

(Continued)

• The risk

• Our response

• Our findings

• Our testing identified weaknesses in the design and operation of controls. In response to this

we assessed the effectiveness of the Group’s plans for addressing these weaknesses and

we increased the scope and depth of our detailed testing and analysis from that originally

planned. We found no significant errors in calculation. Overall, our assessment is that the

assumptions and resulting estimates (including appropriate contingencies) resulted in mildly

cautious profit recognition.

• Our testing did not identify any deviation in the operation of controls which would have

required us to amend the nature or scope of our planned detailed test work. We found that

the assumptions and resulting estimates were balanced and that the disclosures in note 9

appropriately describe the inherent degree of subjectivity in the estimates and the potential

impact on future periods of revisions to these estimates. We found no errors in calculations.

• We found that the resulting estimate was acceptable but mildly optimistic resulting in a

somewhat lower liability being recorded than might otherwise have been the case.

Slide 12.33

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

New UK auditor’s opinion – the future?

(Continued)

May 8, 2014

Holding Auditors Accountable

Rolls-Royce – the jet engine maker, not the car company – used estimates and assumptions in its

financial results that resulted in ‘mildly cautious profit recognition’ in an important part of its

business. On the other hand, the company was ‘mildly optimistic’ in other assumptions, ‘resulting in

a somewhat lower liability being recorded than might otherwise have been the case’.

Coming from almost anyone else, such observations might not be particularly notable. But those

comments came from Jimmy Daboo, the lead audit partner on the Rolls-Royce account at KPMG,

and are included in the company’s new annual report.

Until now, auditors’ letters have been among the least interesting parts of annual reports. If the

opinions said the accounting was proper – and virtually all did – and did not voice concern about

whether a company could stay in business, the letters were basically the same. There was no

reason for an investor to read them. In the United States, that is still the case.

Slide 12.34

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Auditor communications to governance entity

Audit matters of governance interest to be communicated by the auditor to the board or audit committee ordinarily include:

• Material weaknesses in internal control

• Non-compliance with laws and regulations

• Fraud involving management

• Questions regarding management integrity

• The general approach and overall scope of the audit

• The selection of, or changes in, significant accounting policies and practices that have a material effect on the financial statements.

Slide 12.35

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Communications of deficiencies in

internal control

The auditor must communicate to management in

writing significant deficiencies in internal control

that are of sufficient importance to merit

management’s attention. The communication

should include:

A description of the deficiencies and an explanation

of their potential effects

Sufficient information to enable those charged with

governance and management to understand the

context of the communication.

Slide 12.36

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Governance structures

• The structures of governance vary from country

to country reflecting cultural and legal

backgrounds.

• In some countries, the supervision function, and

the management function are legally separated

into different bodies, such as a supervisory

(wholly or mainly non-executive) board and a

management (executive) board.

• In other countries, such as the US, both functions

are the legal responsibility of a single, unitary

board.

Slide 12.37

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Reporting fraud and error

• When the auditor encounters circumstances

that may indicate that there is a material

misstatement in the financial statements

resulting from fraud or error, the auditor should

perform procedures to determine whether the

financial statements are materially misstated.

• The auditor’s duty of confidentiality would

ordinarily preclude reporting fraud or error to a

third party. However, in certain circumstances,

statute or law overrides this duty.

Slide 12.38

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Long-form audit report

• In many countries it is customary for the auditor to prepare a ‘long-form’ report to the Audit Committee of an entity’s board of directors in addition to the publicly published ‘short-form’ report discussed in this chapter.

• A long-form report ordinarily includes:

• Overview of the Audit Engagement

• Analysis of Financial Statements

• Risk Management and Internal Control

• Optional Topics

• Auditor independence and quality control

• Fees.

Slide 12.39

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Management letter

The management letter identifies issues not

required to be disclosed in the Annual Financial

Report but represent the auditors concerns

and suggestions noted during the audit.

An evaluation is made of the present system,

pointing out problem areas. Recommendations

for improvement are cited. Also included is a

discussion of any problem which may require

immediate action to correct.

Slide 12.40

Hayes, Gortemaker and Wallage, Principles of Auditing PowerPoints on the Web, 3rd edition © Pearson Education Limited 2014

Thank you for your attention

Any Questions?