Embed Size (px)

Citation preview

Chapter Twenty

Understanding Personal Finances and Investments

Copyright © Cengage Learning. All rights reserved.

Learning Objectives

1. Explain why you should manage your personal finances and develop a personal investment program.

2. Describe how the factors of safety, risk, income, growth, and liquidity affect your investment decisions.

3. Understand how securities are bought and sold.4. Identify the advantages and disadvantages of

savings accounts, bonds, stocks, mutual funds, and real estate.

5. Describe high-risk investment techniques.6. Use financial information to evaluate investment

alternatives.

20 | 2

Chapter 20 Outline

– Preparing for an Investment Program• Managing Your Personal Finances• Investment Goals• A Personal Investment Program• Important Factors in Personal Investment

– How Securities Are Bought and Sold• The Primary Market• The Secondary Market• The Role of an Account Executive• Regulation of Securities Trading

Copyright © Cengage Learning. All rights reserved. 20 | 3

Chapter 20 Outline (cont’d)

– Traditional Investment Alternatives• Portfolio Management• Asset Allocation, the Time Factor, and Your

Age• Bank Accounts• Corporate and Government Bonds• Common Stock• Preferred Stock• Mutual Funds• Real Estate

Copyright © Cengage Learning. All rights reserved. 20 | 4

Chapter 20 Outline (cont’d)

– High-Risk Investment Techniques• Selling Short• Buying Stock on Margin• Other High-Risk Investments

– Sources of Financial Information• The Internet• Financial Coverage of Securities Transactions• Other Sources of Financial Information• Security Averages

Copyright © Cengage Learning. All rights reserved. 20 | 5

Copyright © Cengage Learning. All rights reserved.

Preparing for an Investment Program

• Managing Your Personal Finances– The use of your personal funds to earn a financial

return– Personal budget is a specific plan for spending

income

• Investment goals– Personal investment goals must be

• Specific and measurable

• Tailored to individual needs

• Focused on the future

• Realistic in terms of economic conditions and opportunities

20 | 6

Copyright © Cengage Learning. All rights reserved.

Preparing for an Investment Program (cont’d)

• Questions to consider when establishing goals– What financial goals do you want to achieve?

– How much money will you need, and when?

– What will you use the money for?

– Is it reasonable to assume that you can obtain the amount of money you will need to meet your investment goals?

– Do you expect your personal situation to change in a way that will affect your investment goals?

– What economic conditions could alter your investment goals?

– Are you willing to make the necessary sacrifices to ensure that your investment goals are met?

– What are the consequences of not obtaining your investment goals?

20 | 7

Copyright © Cengage Learning. All rights reserved.

Preparing for an Investment Program (cont’d)

• A personal investment program– Involves a careful evaluation of different

investment opportunities

– Financial planner

– Begin by accumulating an emergency fund

– Invest funds according to your plan

– Monitor the plan

20 | 8

Copyright © Cengage Learning. All rights reserved.

Preparing for an Investment Program (cont’d)

• Suggestions to help you accumulate the money needed to fund an investment plan

– Learn to balance your budget

– Make savings a higher priority

– Take advantage of employer-sponsored retirement programs

– Participate in an elective savings program

– Make a special savings effort one or two months each year

– Take advantage of gifts, inheritances, and windfalls

Source: Jack R. Kapoor, Les R. Dlabay, and Robert J. Hughes, Personal Finance, 9th ed. Copyright © 2009 by The McGraw Hill Companies, Inc. . 20 | 9

Copyright © Cengage Learning. All rights reserved.

Important Factors in Personal Investment

• Match potential investments with your goals in terms of several factors

– Safety and risk

– Investment income

– Investment growth

– Investment liquidity

20 | 10

Copyright © Cengage Learning. All rights reserved.

Surviving a Financial Crisis

• To survive a financial crisis, many experts recommend that you take action before the crisis to make sure your financial affairs are in order

• Seven steps you can take– Establish a larger than usual emergency fund– Know what you owe– Reduce spending– Pay off credit cards– Apply for a line of credit at your bank, credit union, or

financial institution– Notify credit card companies and lenders if you are unable

to make payments– Monitor the value of your investment accounts

20 | 11

Copyright © Cengage Learning. All rights reserved.

How Securities Are Bought and Sold

• Securities are usually exchanged with the help of an account executive or stockbroker

• The primary market– A market in which an investor purchases financial

securities (via an investment bank) directly from the issuer of those securities

• Investment banking firm

• High-risk investment

20 | 12

Copyright © Cengage Learning. All rights reserved.

How Securities Are Bought and Sold (cont’d)

• The secondary market– A market for existing financial securities that

are traded between investors

– Securities exchange

– Over-the-counter (OTC) market

• Nasdaq

20 | 13

Copyright © Cengage Learning. All rights reserved.

How Securities Are Bought and Sold (cont’d)

• The role of an account executive– An individual, sometimes called a stockbroker or

registered representative, who buys and sells securities for clients

• Full-service broker

• Discount broker

20 | 14

Copyright © Cengage Learning. All rights reserved.

How Securities Are Bought and Sold (cont’d)

• The mechanics of a transaction

– Market order

– Limit order

– Discretionary order

20 | 15

Copyright © Cengage Learning. All rights reserved.

How Securities Are Bought and Sold (cont’d)

• Online security transactions– Software can help investors evaluate potential

investments, manage investments, monitor value, and place buy and sell orders online

– Investors must still analyze the information and make decisions

– Online trading generally has lower costs

– Program trading—a computer-driven program that monitors the market value of particular stocks and enters buy or sell orders when those stocks reach specified prices

20 | 16

Copyright © Cengage Learning. All rights reserved.

How Securities Are Bought and Sold (cont’d)

• Commissions– Most brokerage firms have a minimum

commission– Additional commission charges are based on the

number of shares and the value of stock bought and sold

– Generally, online transactions are less expensive when compared to trading through a full-service brokerage firm

– Full-service brokerages charge a percentage of the transaction amount (as much as 1.5 to 2.0%)

– Commissions for bonds, commodities, and options are lower than for stocks

20 | 17

Copyright © Cengage Learning. All rights reserved.

Regulation of Securities Trading

• A regulatory pyramid of four different levels exists to make sure investors are protected– 1st level: Federal regulation by the U.S.

Congress

– 2nd level: Securities and Exchange Commission (SEC)

– 3rd level: State regulation

– 4th level: Self-regulation by securities exchanges and brokerage firms

20 | 18

Copyright © Cengage Learning. All rights reserved.

Traditional Investment Alternatives

• Portfolio management• Asset allocation, the time factor, and your age

– Asset allocation

– The time factor

– Age

20 | 19

Copyright © Cengage Learning. All rights reserved.

Traditional Investment Alternatives (cont’d)

• Bank accounts– Advantages

– Disadvantage

• Corporate bonds

• Convertible bonds

20 | 20

Copyright © Cengage Learning. All rights reserved.

Traditional Investment Alternatives (cont’d)

• Government bonds– Considered risk free; pay low interest– Treasury bills

– Treasury notes

– Treasury bonds

– Savings bonds

– Municipal bonds

20 | 21

Copyright © Cengage Learning. All rights reserved.

Traditional Investment Alternatives (cont’d)

• Common stock– Dividend income

• Stock dividend

• Dividend payments

– Increase in dollar value• Capital gain

• Market value

– Stock splits

20 | 22

Copyright © Cengage Learning. All rights reserved.

Traditional Investment Alternatives (cont’d)

• Preferred stock– Stock in a corporation that has a claim on the

dividends that supersedes common stock

– Cumulative preferred stock

– Convertible preferred stock

20 | 23

Copyright © Cengage Learning. All rights reserved.

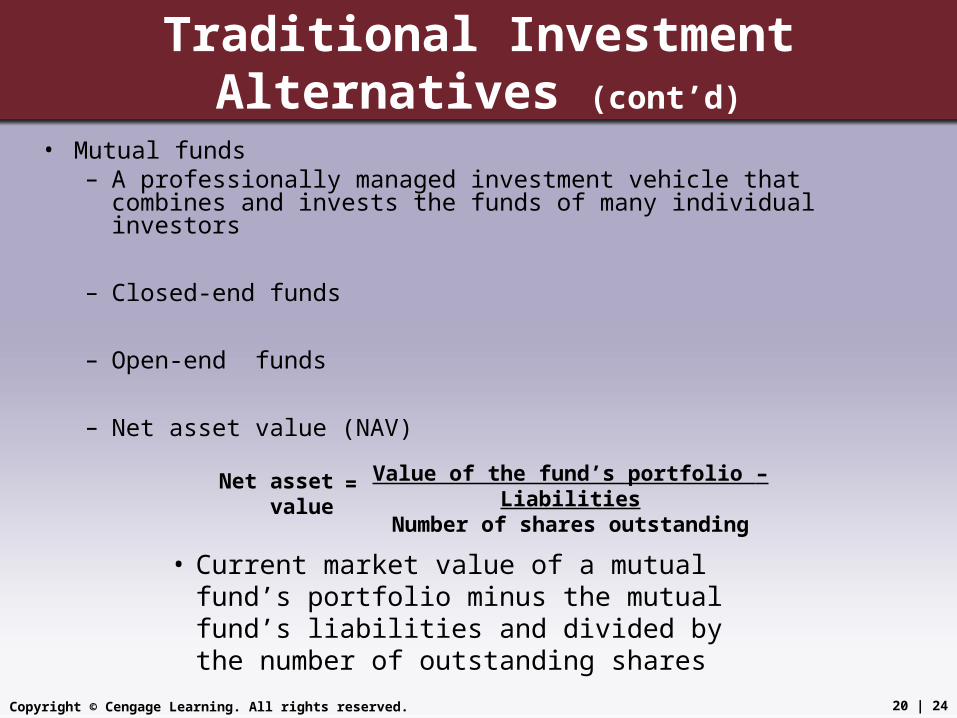

Traditional Investment Alternatives (cont’d)

• Mutual funds– A professionally managed investment vehicle that combines

and invests the funds of many individual investors

– Closed-end funds

– Open-end funds

– Net asset value (NAV)

Net asset value Value of the fund’s portfolio – LiabilitiesNumber of shares outstanding

=

• Current market value of a mutual fund’s portfolio minus the mutual fund’s liabilities and divided by the number of outstanding shares

20 | 24

Copyright © Cengage Learning. All rights reserved.

Traditional Investment Alternatives (cont’d)

• Mutual funds (cont.)– Load funds

– No-load funds

– Yearly management fee

– Managed funds

– Index funds

– Family of funds

20 | 25

Copyright © Cengage Learning. All rights reserved.

Traditional Investment Alternatives (cont’d)

• Types of mutual fund investments– Aggressive growth stock funds

– Global stock funds

– Growth stock funds

– High-yield (junk) bond funds

– Income stock funds

– Index funds

– Long-term U.S. bond funds

– Sector stock funds

– Small-cap stock funds

20 | 26

Copyright © Cengage Learning. All rights reserved.

Traditional Investment Alternatives (cont’d)

• Real estate– Advantages

– Disadvantages

20 | 27

Copyright © Cengage Learning. All rights reserved.

High-Risk Investment Techniques

• Buying long– Buying stocks expected to increase in value,

which can then can be sold at a profit

• Selling short– The process of selling stock that an investor does

not actually own but has borrowed from a brokerage firm and will repay at a later date

• Buying stock on margin– Buying stock by borrowing part of the purchase

price, usually from a stock brokerage firm• Margin requirement

20 | 28

Copyright © Cengage Learning. All rights reserved.

High-Risk Investment Techniques (cont’d)

• Other high-risk investments– Stock options

– Commodities

– Precious metals

– Gemstones

– Coins

– Antiques and collectibles

20 | 29

Copyright © Cengage Learning. All rights reserved.

Sources of Financial Information

• The Internet– www.bloomberg.com

– http://money.cnn.com

– www.fool.com

– www.quicken.com

– www.sec.gov

– http://finance.yahoo.com

• Newspaper coverage of securities transactions– Common and preferred stocks

– Bonds

– Mutual funds

20 | 30

Copyright © Cengage Learning. All rights reserved.

Sources of Financial Information

• Other sources of financial information– Investors’ services

• Moody’s, Standard & Poor’s, Mergent, Value Line, Morningstar, Lipper Analytical Services, Wiesenberger Investment Companies

– Brokerage firm analysts’ reports• UBS PaineWebber, Smith Barney, Merrill Lynch

– Business periodicals• Business Week, Fortune, Forbes• Advertising Age, Business Insurance• U.S. News & World Report, Time, Newsweek• Money, Kiplinger’s Personal Finance Magazine, Consumer Reports

– Corporate reports

• A security average (security index) is an average of the current market prices of selected securities

20 | 31

Copyright © Cengage Learning. All rights reserved.

Sources of Financial Information (cont’d)

• Security averages– An average of the current market prices of

selected securities

– Dow Jones Industrial Average

– Standard & Poor’s 500 Stock Index

– New York Stock Exchange Composite Index

– American Stock Exchange Index

– Nasdaq Composite Index

20 | 32