Embed Size (px)

Citation preview

revised 1/2012

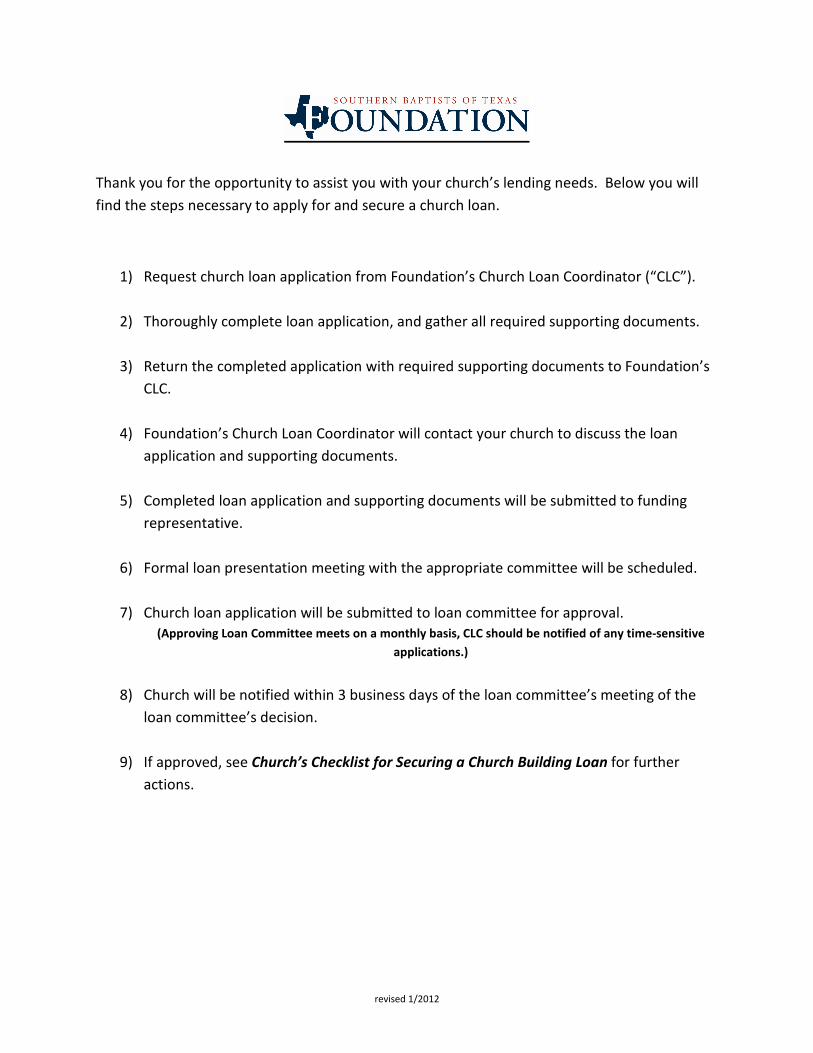

Thank you for the opportunity to assist you with your church’s lending needs. Below you will

find the steps necessary to apply for and secure a church loan.

1) Request church loan application from Foundation’s Church Loan Coordinator (“CLC”).

2) Thoroughly complete loan application, and gather all required supporting documents.

3) Return the completed application with required supporting documents to Foundation’s

CLC.

4) Foundation’s Church Loan Coordinator will contact your church to discuss the loan

application and supporting documents.

5) Completed loan application and supporting documents will be submitted to funding

representative.

6) Formal loan presentation meeting with the appropriate committee will be scheduled.

7) Church loan application will be submitted to loan committee for approval.

(Approving Loan Committee meets on a monthly basis, CLC should be notified of any time-sensitive

applications.)

8) Church will be notified within 3 business days of the loan committee’s meeting of the

loan committee’s decision.

9) If approved, see Church’s Checklist for Securing a Church Building Loan for further

actions.

revised 3/2013

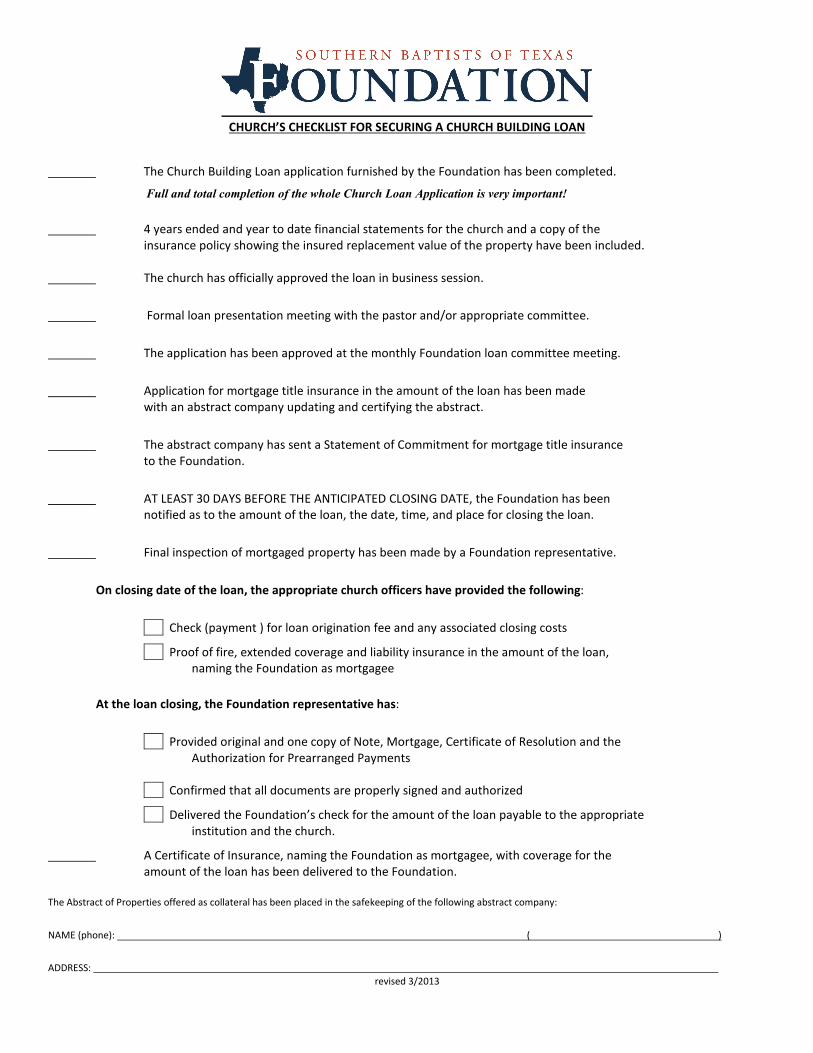

CHURCH’S CHECKLIST FOR SECURING A CHURCH BUILDING LOAN

The Church Building Loan application furnished by the Foundation has been completed.

Full and total completion of the whole Church Loan Application is very important!

4 years ended and year to date financial statements for the church and a copy of the

insurance policy showing the insured replacement value of the property have been included.

The church has officially approved the loan in business session.

Formal loan presentation meeting with the pastor and/or appropriate committee.

The application has been approved at the monthly Foundation loan committee meeting.

Application for mortgage title insurance in the amount of the loan has been made

with an abstract company updating and certifying the abstract.

The abstract company has sent a Statement of Commitment for mortgage title insurance

to the Foundation.

AT LEAST 30 DAYS BEFORE THE ANTICIPATED CLOSING DATE, the Foundation has been

notified as to the amount of the loan, the date, time, and place for closing the loan.

Final inspection of mortgaged property has been made by a Foundation representative.

On closing date of the loan, the appropriate church officers have provided the following:

Check (payment ) for loan origination fee and any associated closing costs

Proof of fire, extended coverage and liability insurance in the amount of the loan,

naming the Foundation as mortgagee

At the loan closing, the Foundation representative has:

Provided original and one copy of Note, Mortgage, Certificate of Resolution and the

Authorization for Prearranged Payments

Confirmed that all documents are properly signed and authorized

Delivered the Foundation’s check for the amount of the loan payable to the appropriate

institution and the church.

A Certificate of Insurance, naming the Foundation as mortgagee, with coverage for the

amount of the loan has been delivered to the Foundation.

The Abstract of Properties offered as collateral has been placed in the safekeeping of the following abstract company:

NAME (phone): ( )

ADDRESS:

1

For Foundation Use Only

Date Received Application Number Loan Amount Requested

Interest Rate Desired

Loan Term in Years

Loan Application

(To be completed by Borrowing Church)

Name of Church: Year Organized:

Street Address:

City: State: Zip:

Mailing Address (if different):

County: Association: Is Church Incorporated:

Church Phone: ( ) Church Fax: ( ) Church Email:

Contact Person: Home Phone: ( ) Work Phone: ( )

Contact Email:

Pastoral Information

Name: Home Phone: ( ) Email:

Date Called to Church: Date of Ordination: Total Years in Ministry:

Education (list schools attended, dates attended and degree earned):

Previous Ministries (list churches and dates served):

Other Building Projects:

Authorization Information

This application is submitted for a loan in the amount of $ _____________________________ and was duly

authorized in a business meeting held on the ___________ day of ___________________________ / 20 __

and is hereby submitted on the ________ day of ________ _______________________ / 20 __ to the

SBT Foundation.

Clerk of Applicant Church Signature _____________________________________________________

Moderator of Applicant Church Signature ___________________________________________________ _

2

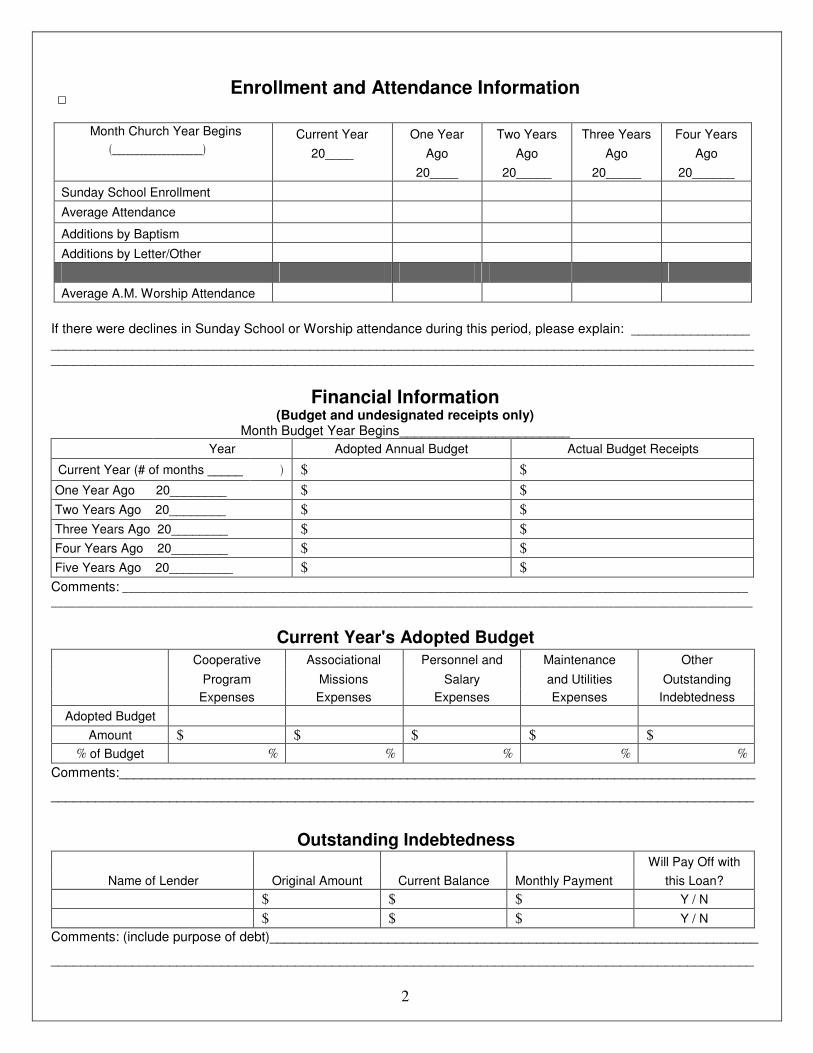

Enrollment and Attendance Information □

Month Church Year Begins

(____________________) Current Year

20____

One Year

Ago

20____

Two Years

Ago

20_____

Three Years

Ago

20_____

Four Years

Ago

20______

Sunday School Enrollment

Average Attendance

Additions by Baptism

Additions by Letter/Other

Average A.M. Worship Attendance

If there were declines in Sunday School or Worship attendance during this period, please explain: ________________ ______________________________________________________________________________________________________________________________________________________________________________________________

Financial Information

(Budget and undesignated receipts only) Month Budget Year Begins_______________________

Year Adopted Annual Budget Actual Budget Receipts

Current Year (# of months _____ ) $ $

One Year Ago 20________ $ $

Two Years Ago 20________ $ $

Three Years Ago 20________ $ $

Four Years Ago 20________ $ $

Five Years Ago 20_________ $ $ Comments: ___________________________________________________________________________________________________ _______________________________________________________________________________________________________________

Current Year's Adopted Budget Cooperative Associational Personnel and Maintenance Other

Program Missions Salary and Utilities Outstanding

Expenses Expenses Expenses Expenses Indebtedness

Adopted Budget

Amount $ $ $ $ $

% of Budget % % % % % Comments:______________________________________________________________________________________

_______________________________________________________________________________________________

Outstanding Indebtedness

Will Pay Off with

Name of Lender Original Amount Current Balance Monthly Payment this Loan?

$ $ $ Y / N

$ $ $ Y / N Comments: (include purpose of debt)__________________________________________________________________

_______________________________________________________________________________________________

3

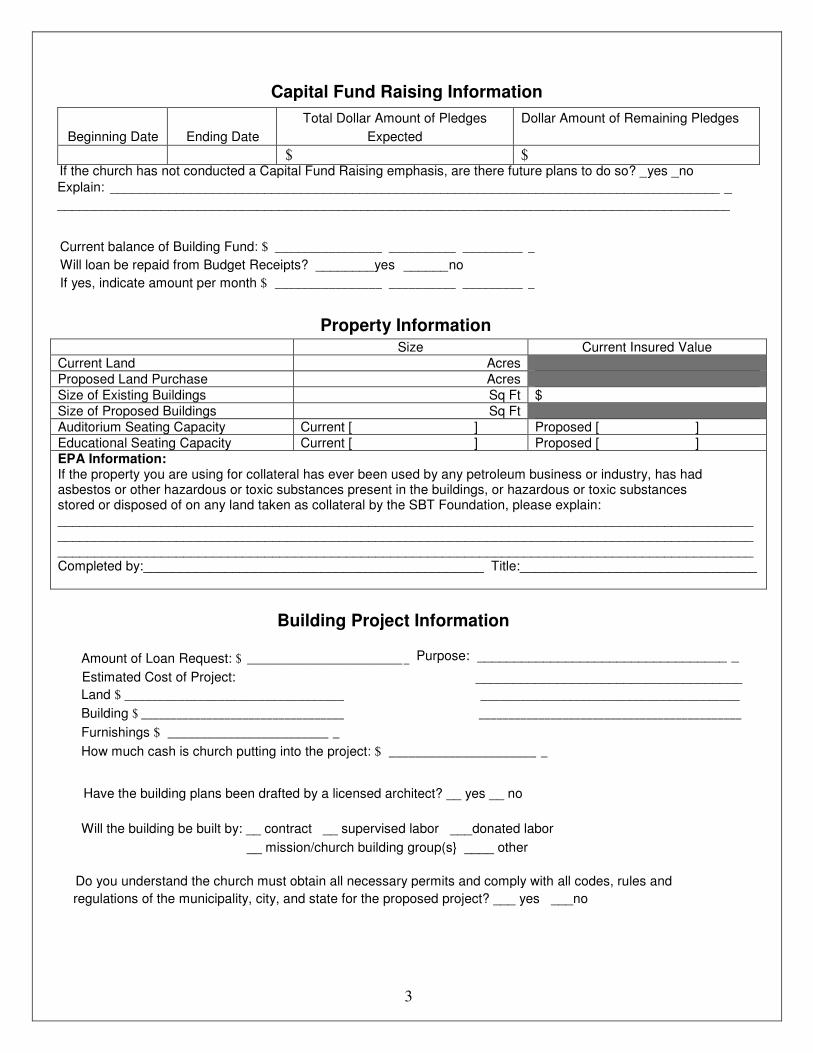

Size Current Insured Value Current Land Acres Proposed Land Purchase Acres Size of Existing Buildings Sq Ft $ Size of Proposed Buildings Sq Ft Auditorium Seating Capacity Current [ ] Proposed [ ] Educational Seating Capacity Current [ ] Proposed [ ] EPA Information: If the property you are using for collateral has ever been used by any petroleum business or industry, has had asbestos or other hazardous or toxic substances present in the buildings, or hazardous or toxic substances stored or disposed of on any land taken as collateral by the SBT Foundation, please explain: __________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________ Completed by:______________________________________________ Title:________________________________

If the church has not conducted a Capital Fund Raising emphasis, are there future plans to do so? _yes _no Explain: ___________________________________________________________________________________ _

___________________________________________________________________________________________

Capital Fund Raising Information

Total Dollar Amount of Pledges Dollar Amount of Remaining Pledges

Beginning Date Ending Date Expected

$ $

Current balance of Building Fund: $ ________________ __________ _________ _

Will loan be repaid from Budget Receipts? ________yes ______ no

If yes, indicate amount per month $ ________________ __________ _________ _

Property Information

Building Project Information

Amount of Loan Request: $ ___________________________ _

Estimated Cost of Project: ____________________________________

Land $ _________________________________ _______________________________________

Building $ __________________________________ ____________________________________________

Furnishings $ ________________________ _

How much cash is church putting into the project: $ ______________________ _

Purpose: __________________________________ _

Have the building plans been drafted by a licensed architect? __ yes __ no

Will the building be built by: __ contract __ supervised labor ___donated labor

__ mission/church building group(s} ____ other

Do you understand the church must obtain all necessary permits and comply with all codes, rules and

regulations of the municipality, city, and state for the proposed project? ___ yes ___no

4

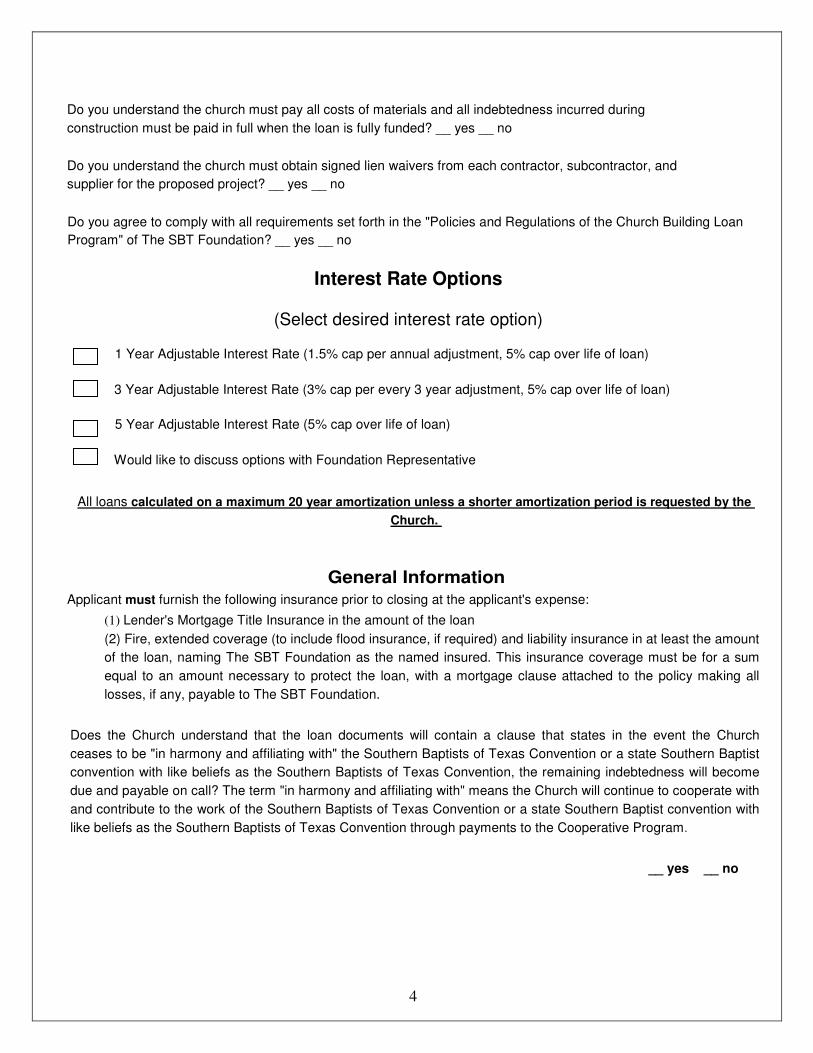

Do you understand the church must pay all costs of materials and all indebtedness incurred during

construction must be paid in full when the loan is fully funded? __ yes __ no

Do you understand the church must obtain signed lien waivers from each contractor, subcontractor, and

supplier for the proposed project? __ yes __ no

Do you agree to comply with all requirements set forth in the "Policies and Regulations of the Church Building Loan

Program" of The SBT Foundation? __ yes __ no

Interest Rate Options

(Select desired interest rate option)

□ 1 Year Adjustable Interest Rate (1.5% cap per annual adjustment, 5% cap over life of loan)

3 Year Adjustable Interest Rate (3% cap per every 3 year adjustment, 5% cap over life of loan)

5 Year Adjustable Interest Rate (5% cap over life of loan)

Would like to discuss options with Foundation Representative

All loans calculated on a maximum 20 year amortization unless a shorter amortization period is requested by the

Church.

General Information

Applicant must furnish the following insurance prior to closing at the applicant's expense:

(1) Lender's Mortgage Title Insurance in the amount of the loan

(2) Fire, extended coverage (to include flood insurance, if required) and liability insurance in at least the amount

of the loan, naming The SBT Foundation as the named insured. This insurance coverage must be for a sum

equal to an amount necessary to protect the loan, with a mortgage clause attached to the policy making all

losses, if any, payable to The SBT Foundation.

Does the Church understand that the loan documents will contain a clause that states in the event the Church

ceases to be "in harmony and affiliating with" the Southern Baptists of Texas Convention or a state Southern Baptist

convention with like beliefs as the Southern Baptists of Texas Convention, the remaining indebtedness will become

due and payable on call? The term "in harmony and affiliating with" means the Church will continue to cooperate with

and contribute to the work of the Southern Baptists of Texas Convention or a state Southern Baptist convention with

like beliefs as the Southern Baptists of Texas Convention through payments to the Cooperative Program.

__ yes __ no

5

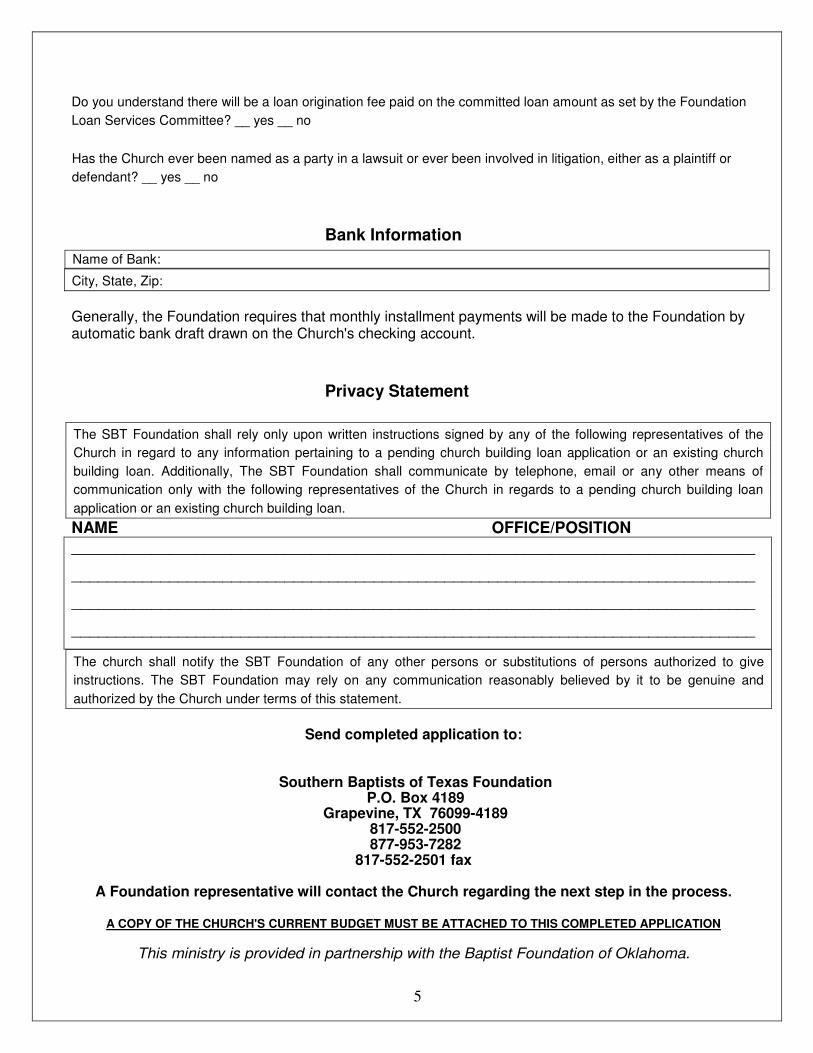

Do you understand there will be a loan origination fee paid on the committed loan amount as set by the Foundation

Loan Services Committee? __ yes __ no

Has the Church ever been named as a party in a lawsuit or ever been involved in litigation, either as a plaintiff or

defendant? __ yes __ no

Bank Information

Name of Bank:

City, State, Zip:

Generally, the Foundation requires that monthly installment payments will be made to the Foundation by automatic bank draft drawn on the Church's checking account.

Privacy Statement

The SBT Foundation shall rely only upon written instructions signed by any of the following representatives of the

Church in regard to any information pertaining to a pending church building loan application or an existing church

building loan. Additionally, The SBT Foundation shall communicate by telephone, email or any other means of

communication only with the following representatives of the Church in regards to a pending church building loan

application or an existing church building loan.

NAME OFFICE/POSITION _____________________________________________________________________________

_____________________________________________________________________________

_____________________________________________________________________________

_____________________________________________________________________________

The church shall notify the SBT Foundation of any other persons or substitutions of persons authorized to give

instructions. The SBT Foundation may rely on any communication reasonably believed by it to be genuine and

authorized by the Church under terms of this statement.

Send completed application to:

Southern Baptists of Texas Foundation

P.O. Box 4189 Grapevine, TX 76099-4189

817-552-2500 877-953-7282

817-552-2501 fax

A Foundation representative will contact the Church regarding the next step in the process.

A COPY OF THE CHURCH'S CURRENT BUDGET MUST BE ATTACHED TO THIS COMPLETED APPLICATION

This ministry is provided in partnership with the Baptist Foundation of Oklahoma.

CHURCH BUILDING LOAN PROGRAM

POLICIES AND REGULATIONS

In Partnership with The Baptist Foundation of Oklahoma

PURPOSE

The Southern Baptists of Texas Foundation makes church building loans available to SBTC churches through a partnership with The Baptist Foundation of Oklahoma. The Church Building Loan Program is a credit assistance program for the benefit of the churches and ministry partners of the Southern Baptists of Texas Convention. First mortgage loans are made to qualifying members for equity loans, building projects and the acquisition of additional properties and buildings. As funds are available, consideration will be given to applications for refinancing qualifying member indebtedness or other member institutions building or property indebtedness as defined by this policy. The funds are not the property of either Foundation, but are held in trust for the benefit of Baptist causes designated by the donors. The earnings and interest received from loans are distributed to the designated causes through the Fixed Income Pool. The program is administered by the SB Texas Foundation and the Baptist Foundation of Oklahoma Loan Services Committee, composed of members of the Board of Directors of The Baptist Foundation of Oklahoma. In discharging its duties of approving loans to churches and other Baptist entities, the Loan Services Committee is guided by the following policies and regulations.

MINIMUM ELIGIBILITY FOR A LOAN APPLICATION

1. DENOMINATIONAL LOYALTY. Churches and Ministry Partners applying for loans must be loyal to the denomination. Such loyalty shall be evidenced by affiliation with the Southern Baptists of Texas Convention, and by regular and substantial contributions to mission causes through the Cooperative Program.

2. WRITTEN BUDGET. Members applying for loans must have a written budget plan which is adopted

at least annually by congregational action and must give evidence of a consistent pattern of church finance.

3. LOCATION AND NEED. Members applying for loans shall be located in communities which

represent opportunities for building and maintaining a church. Members shall provide ample parking space and shall comply with city, county and state fire codes and building regulations.

4. INCORPORATION. Churches applying for loans must be incorporated in the state in the state of Texas

INTEREST RATES AND METHOD FOR PAYMENT ON A LOAN 5. Interest rates are established as market conditions dictate. The interest rate charged to churches shall be

the rate in effect when the loan documents are executed. Members shall have the option of choosing one of three (3) adjustable rates of interest within a twenty (20) year amortization.

6. The interest rate shall be immediately adjustable or fixed for one (1), three (3), five (5) years, depending

on the adjustable interest rate chosen by the church at the time of closing and the following conditions shall be in effect:

The 1 year adjustable interest rate will be adjusted to the Foundation's annual adjustable interest rate on each anniversary date of the original loan agreement. The interest rate may not be raised or lowered over the life of the loan more than one arid one-half (1 ½) percent (150 basis points) in any one year, or more than five (5) percent (500 basis points) above or below the interest rate effective at the beginning of the loan. The 3 year adjustable interest rate will be adjusted to the Foundation's three year adjustable interest rate on the third (3rd), sixth (6th), ninth (9th), twelfth (12th), fifteenth (15th), and eighteenth (18) year anniversary dates of the original loan agreement. The interest rate may not be raised or lowered over the life of the loan more than three (3) percent (300 basis points) at any three year adjustment time, or more than five (5) percent (500 basis points) above or below the interest rate effective at the beginning of the loan. The 5 year adjustable interest rate will be adjusted to the Foundation's five year adjustable interest rate on the fifth (5th), tenth (10th), and fifteenth (15th) year anniversary dates of the original loan agreement. The interest rate may not be raised or lowered over the life of the loan more than five (5) percent (500 basis points) above or below the interest rate effective at the beginning of the loan.

7. Loans with the 1, 3, or 5 year adjustable interest rate will be amortized at the time of closing and again at the anniversary date of each 1, 3, 5 or year period respectively. Monthly installment payments shall include accrued interest on the unpaid principal balance and a monthly principal reduction to retire the loan within the remaining term of the loan.

8. No loan shall be made for more than twenty (20) years.

9. Prepayment of the principal may be made at any time without penalty.

10. Monthly loan installment payments shall be accomplished by automatic bank draft by The Baptist

Foundation of Oklahoma on the member's account on the first (1st or fifteenth (15th) day of each month or the first business day thereafter.

11. If payment is not received on the due date, accrued interest on the unpaid balance shall be included in

the amount required to bring the loan current.

12. In the event a member ceases to be affiliated with Southern Baptists of Texas Convention, as described under DENOMINATIONAL LOYALTY, the remaining indebtedness shall become due and payable on call.

APPLICATION PROCESS FOR A LOAN

13. All applications for loans shall be made on forms provided by the SB Texas Foundation. 14. Information submitted by the member on the application forms must be current and complete.

15. When applications have been received and evaluated, a representative of the Foundation shall contact

the member to arrange a meeting with the appropriate committees and/or with the church body, as required, at a regularly scheduled or called meeting of the congregation. The purpose of such meetings shall be to discuss the member's loan request, the proper legal action required by the member to make loans and to mortgage property, and the Foundation's purposes and obligations in the administration of the Church Building Loan Program.

16. A Baptist Foundation representative will, prior to the approval of any loan, inspect the real property and

improvements that are to be used as collateral for the loan. The purpose of this inspection is to determine the possibility of contamination of the land or buildings by toxic or hazardous substances. This inspection is not to be construed as approval by SB Texas Foundation or The Baptist Foundation of Oklahoma or that the premises are in compliance with laws, rules and regulations dealing with environmental matters. If this inspection reveals the possibility of such contamination, the Baptist Foundation may require that a professional environmental study be conducted at borrower's expense. If the professional environmental study reveals the presence of toxic or hazardous substances, the Baptist Foundation shall have the right to reject the loan request.

17. Final approval or denial of loan applications shall be made by the Loan Services Committee or by the

Board of Directors of The Baptist Foundation of Oklahoma at any regular or special meeting.

18. A mortgage title insurance policy is required on loans in excess of $50,000.00 on land used as collateral. A mortgage title report is required on loans up to $50,000.00 on land used as collateral. The mortgage title insurance underwriter may require affidavits from builders and/ or suppliers showing all construction debts and liens have been satisfied or paid from the loan proceeds.

19. When a loan has been approved, the member shall be provided a formal letter of approval by the Foundation specifying terms of the loan. On loans in excess of $50,000.00 a mortgage title insurance policy commitment must be received before a closing date can be set. On loans up to $50,000.00 a mortgage title report must be received before a closing date can be set. The loan closing must take place no more than six months from the date of the Foundation Loan Services Committee approval.

(l)An equity loan is closed when fees are paid, a mortgage title insurance policy commitment letter or mortgage title report is furnished to the Baptist Foundation and an agreement, promissory note and

mortgage are signed and filed for the full amount approved. Approximate monthly drafts will be funded until the project is complete, not to exceed 24 months. (2) Monthly interest only payments shall be required during construction. The interest payments will be based on the daily-accrued interest for the current principal balance. The interest rate during construction shall be the same interest rate chosen by the borrower for long term financing. (3)A loan, not requiring interim financing, is closed when fees are paid, a mortgage title insurance policy commitment letter or mortgage title report is furnished to the Baptist Foundation and a certificate of resolution, promissory note and mortgage are signed, and filed.

GUIDELINES FOR A LOAN

20. The total amount loaned to a single church shall not exceed $2,500,000.00 unless approved by the Board of Directors. The Foundation may participate with other lenders in loans that exceed this limit.

21. The Baptist Foundation's representative will perform a market value analysis for property used as

collateral.

22. No loan shall be made in excess of fifty (50) percent of the fair market value of the property offered as collateral. The value of new construction shall be included in the market value.

(1) Exception to policy #22 shall be made when the member is borrowing funds for purchase, construction or renovation of a parsonage. The member shall be allowed to borrow up to 75% of the current market value of the parsonage. (2)The Foundation Loan Services Committee may make an exception to policy #22 for land purchases on a case-by-case basis for growth or expansion.

23. No loan shall be made where installment payments on indebtedness, including payments on the Foundation loan, exceeds twenty-five (25) percent of the average annual budget receipts for the past two (2) years. Members receiving loans from the Foundation must agree not to increase indebtedness beyond the twenty-five (25) percent debt limit without written permission from the Foundation Loan Services Committee. Failure to secure such written permission may result in the loan becoming due and payable on call.

(1) Exception to the "debt ratio" policy set forth in policy #23 may be made by the Foundation Loan Services Committee when a member has completed a pledge program that will raise cash, within a three (3) year period, toward payment of the project. In such cases a loan amount equal to a 25% debt service amount may be loaned to the member along with an additional amount of up to one-half (½) the total outstanding pledges.

(2) A member approved under this exception shall agree to pay the required minimum monthly payment by automatic bank draft from their general undesignated budget receipts during the first 36 months of the loan. They shall further agree to pay all monies received for the payment of pledges directly to the Foundation as principal reduction of the loan. The required monthly payment will be adjusted at the end

of the thirty-six (36) month period by reamortizing the principal balance at that time for the remaining term of the note at the effective interest rate chosen by the borrower at the beginning of the loan and adjusted according to the interest rate policy.

24. Church building loans shall be secured by a first mortgage on real estate owned by the member.

Construction, renovation or purchase of a cabin on leased Southern Baptist campgrounds will require the main church property as collateral.

25. The Baptist Foundation shall fund an approved loan to a member purchasing land and/or buildings after

all terms and provisions for purchase of the property have been fulfilled by both the member and the seller.

26. Members receiving loans shall, at their own expense, furnish to the Foundation a Mortgage Title

Insurance Policy on loans in excess of $50,000.00 issued by a title insurance underwriter approved by the Foundation. This policy insures that no loss shall be sustained by the lender by reason of defects in the mortgage given as security for the loan. When the loan is approved and a letter of commitment has been issued, the borrower shall make application for such mortgage title policy. Members receiving loans up to $50,000.00 shall, at their own expense, furnish to the Foundation a Mortgage Title Report issued by an abstract company approved by the Foundation.

27. Construction Financing. When property market value is sufficient, an Equity Loan may be established

before the project is begun and these funds may be used for construction. Upon completion of the project or up to 24 months, whichever is earlier, fully amortized payments begin with monthly principal and interest payments required. If present property market value is below policy guidelines, construction financing may be obtained from a local financial institution and the Foundation will give a commitment letter for long term financing when the project is complete.

28. There shall be a loan origination fee calculated on the loan amount committed to the borrower.

(1) This fee shall be scaled based on the amount and conditions of the loan. (2) This fee shall be disclosed prior to the closing of the loan. (3) This fee shall be paid when the loan is closed.

28. A loan shall be closed only after final inspection is made and approved by a Baptist Foundation representative, title policy requirements are satisfied, and proof of insurance coverage is provided as outlined in paragraph 32.

29. The Foundation shall pay the mortgage tax. The member shall pay for the recording of the mortgage and

other expenses involved in completing the transaction.

30. The abstract of the real estate offered by the member as security for the loan shall be stored off the borrower's premises for safekeeping during the term of the loan.

31. Members shall maintain insurance on properties mortgaged to the Baptist Foundation. Coverage shall

include fire and extended coverage (including flood insurance, if in flood zone) during the existence of the loan, for a sum equal to an amount necessary to protect the loan. The policy shall also contain a loss

payable clause to The Baptist Foundation of Oklahoma. A certificate of insurance shall be provided to the Foundation at the time of loan closing and during the term of the loan.

FUTURE ADDITIONAL ADVANCE CLAUSE

32. The Future Additional Advance ("Advance") clause would permit a church building loan customer

("borrower"), on written request and approval of The Baptist Foundation of Oklahoma ("Foundation"), to draw amounts or re-advance prepayments of principal. The prepayments that could be drawn upon would generally be limited to principal prepayments in excess of regularly scheduled payments of principal and interest. The Foundation would have sole discretion over approval of the Advance.

33. Following church approval, the borrower will submit a written request along with current financial

information, stating the amount of the Advance. The amount of the Advance shall not exceed the amount of prepayment of principal and could, in some instances, be an amount less than the prepayment of principal.

34. The amount of the Advance would be subject to the applicable amortization schedule in effect at the

point in time the request is made and approved. If the amount requested would jeopardize the remaining amortization of the loan based on the current monthly payment, the amount of the monthly payment would increase so as to fully amortize the loan for the remaining term of the loan. However, the increase in the monthly payment based on the Advance and the new principal balance of the loan shall not exceed the 25% debt service ratio of the borrower, based on current financial information of the borrower, as outlined in the Policies and Procedures of the Church Building Loan program.

35. There will be a fee of .25% for each Advance under the terms of this clause. 36. The approval of any Advance will be at the sole discretion of the Foundation, whether or not the

borrower meets the conditions of the Future Additional Advance Clause.

37. Exceptions to the above stated policies must have the approval of The Baptist Foundation of Oklahoma Board of Directors.

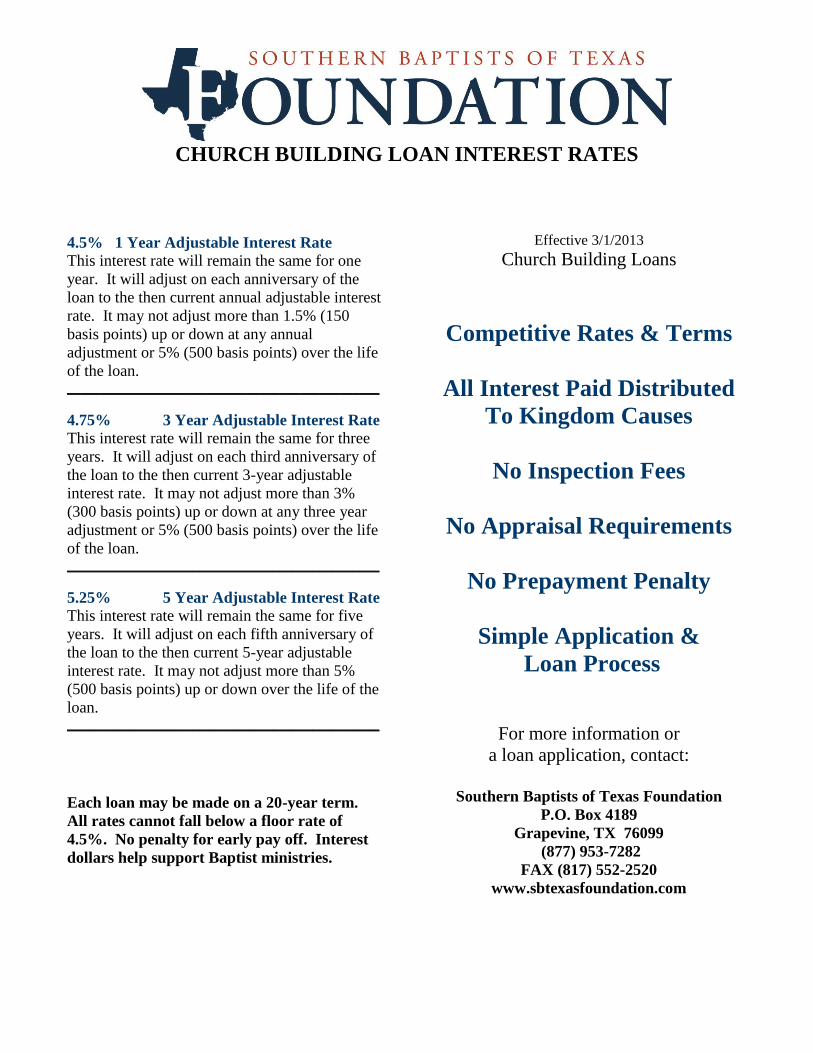

CHURCH BUILDING LOAN INTEREST RATES

4.5% 1 Year Adjustable Interest Rate

This interest rate will remain the same for one

year. It will adjust on each anniversary of the

loan to the then current annual adjustable interest

rate. It may not adjust more than 1.5% (150

basis points) up or down at any annual

adjustment or 5% (500 basis points) over the life

of the loan. _______________________________________________

4.75% 3 Year Adjustable Interest Rate

This interest rate will remain the same for three

years. It will adjust on each third anniversary of

the loan to the then current 3-year adjustable

interest rate. It may not adjust more than 3%

(300 basis points) up or down at any three year

adjustment or 5% (500 basis points) over the life

of the loan. _______________________________________________

5.25% 5 Year Adjustable Interest Rate

This interest rate will remain the same for five

years. It will adjust on each fifth anniversary of

the loan to the then current 5-year adjustable

interest rate. It may not adjust more than 5%

(500 basis points) up or down over the life of the

loan. _______________________________________________

Each loan may be made on a 20-year term.

All rates cannot fall below a floor rate of

4.5%. No penalty for early pay off. Interest

dollars help support Baptist ministries.

Effective 3/1/2013

Church Building Loans

Competitive Rates & Terms

All Interest Paid Distributed

To Kingdom Causes

No Inspection Fees

No Appraisal Requirements

No Prepayment Penalty

Simple Application &

Loan Process

For more information or

a loan application, contact:

Southern Baptists of Texas Foundation

P.O. Box 4189

Grapevine, TX 76099

(877) 953-7282

FAX (817) 552-2520

www.sbtexasfoundation.com

![How Church's Make Decisions [Part 2]](https://img.pdfslide.net/doc/110x75/5576ce59d8b42ae3108b5334/how-churchs-make-decisions-part-2.jpg)