Embed Size (px)

Citation preview

Classification and quantification of the

key stakeholders

Alan MatthewsTrinity College Dublin

Presentation to Joint UCD/DAFF/Teagasc initiative“Driving a sustainable agri-food sector: the new roadmap for

education, research and innovation”Dublin, 29 November 2007

Feedback to: [email protected]

• Identification of stakeholders

• The agricultural context

• Future trends for main stakeholders

• Some implications for research and education system

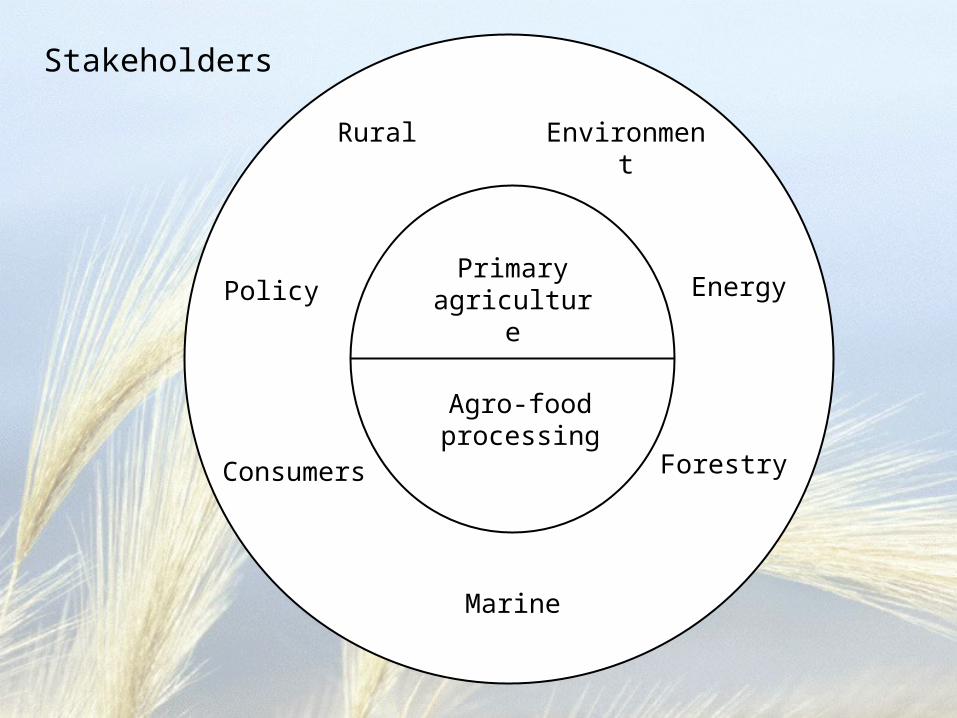

Primary agriculture

Agro-food processing

Environment

Energy

Forestry

Marine

Consumers

Policy

Rural

Stakeholders

40.0

50.0

60.0

70.0

80.0

90.0

100.0

110.0

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

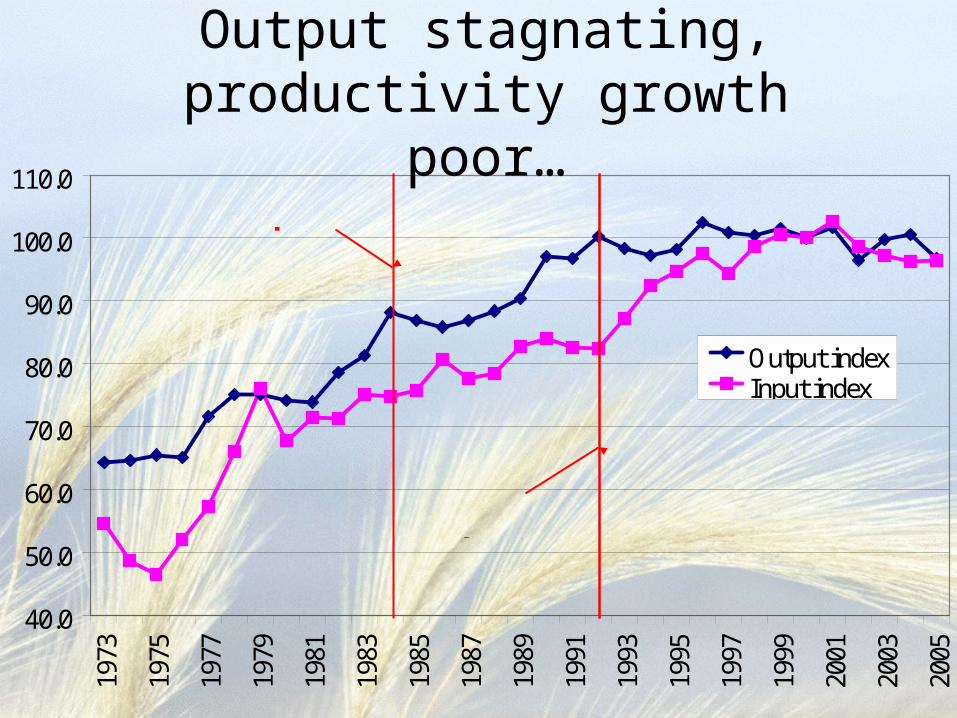

Output indexInput index

MacSharry reform

Milk quota

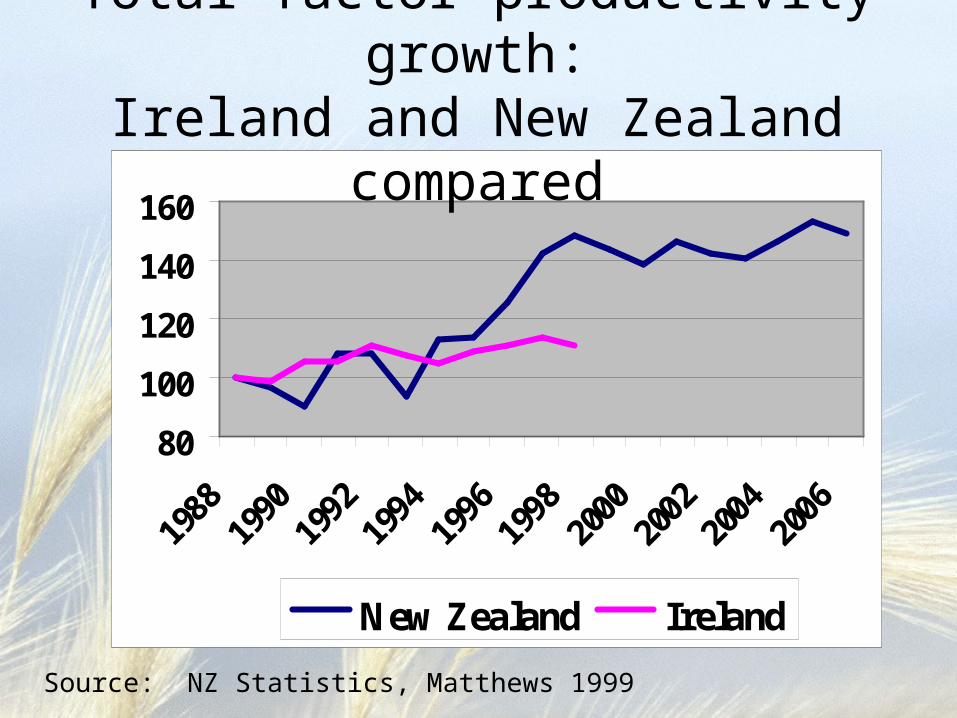

Output stagnating, productivity growth poor…

80

100

120

140

160

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

New Zealand Ireland

Total factor productivity growth:Ireland and New Zealand compared

Source: NZ Statistics, Matthews 1999

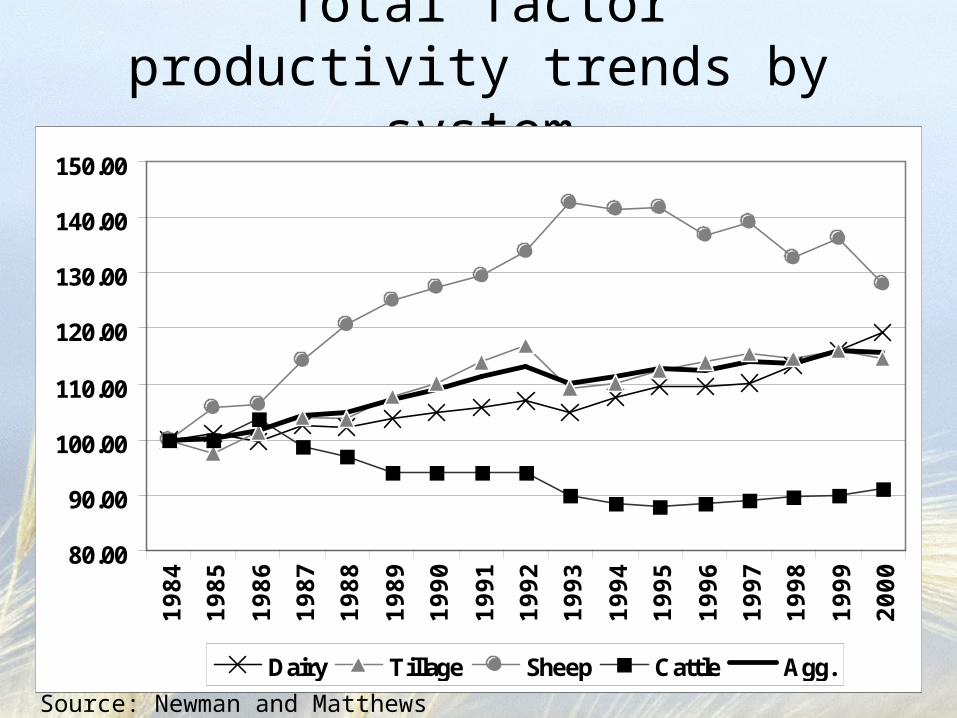

Total factor productivity trends by system

80.00

90.00

100.00

110.00

120.00

130.00

140.00

150.0019

84

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

Dairy Tillage Sheep Cattle Agg.

Source: Newman and Matthews

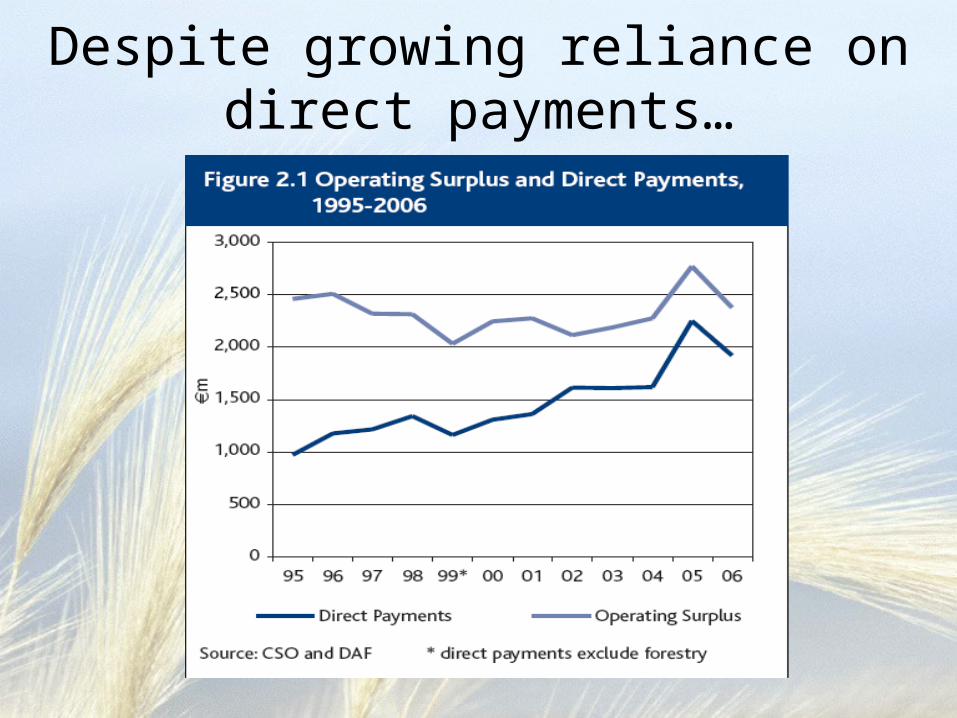

Despite growing reliance on direct payments…

Source: Teagasc NFS 2006

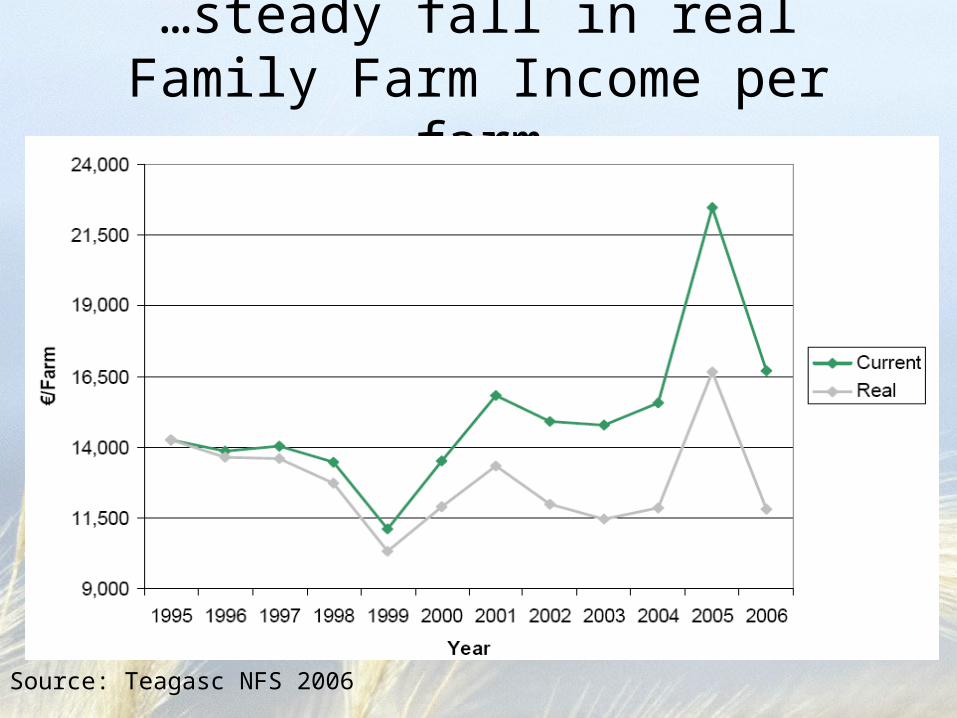

…steady fall in real Family Farm Income per farm

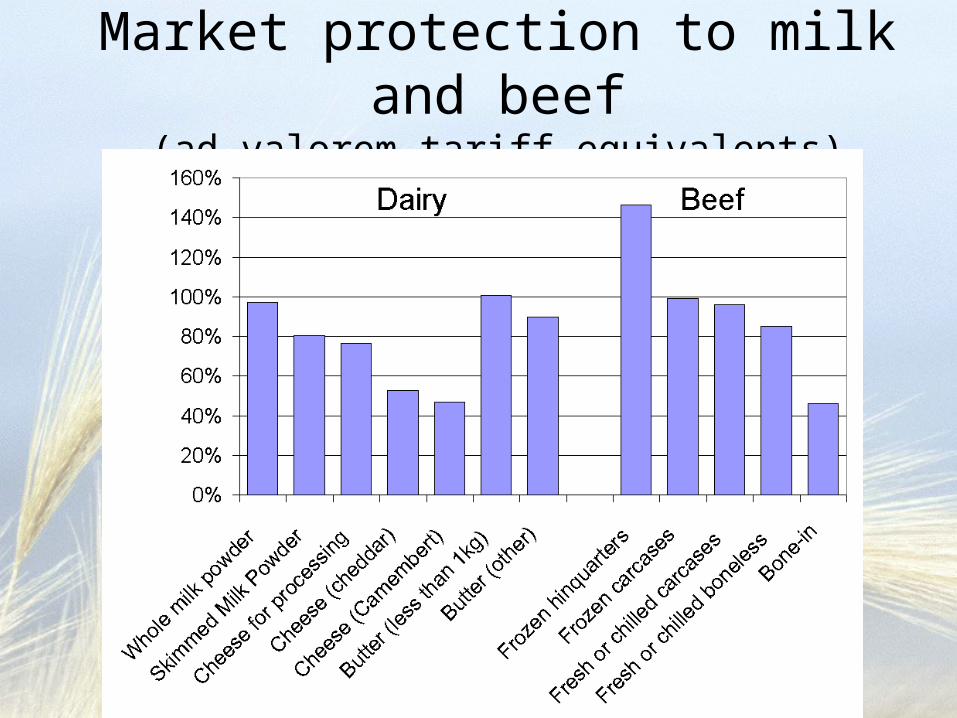

Market protection to milk and beef(ad valorem tariff equivalents)

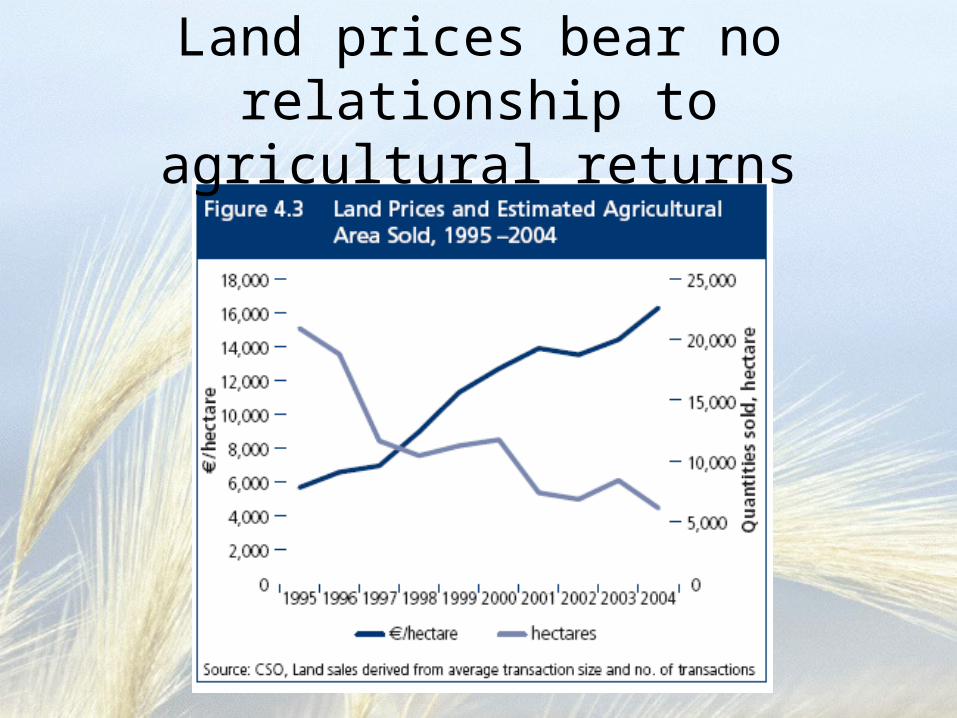

Land prices bear no relationship to agricultural returns

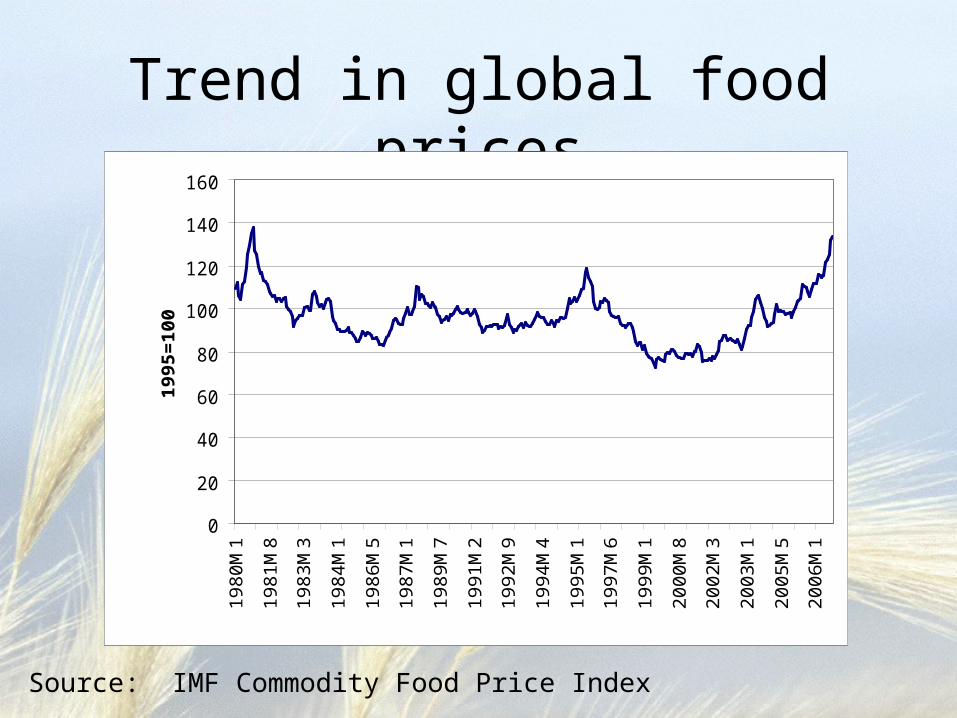

Trend in global food prices

0

20

40

60

80

100

120

140

160

19

80

M1

19

81

M8

19

83

M3

19

84

M1

19

86

M5

19

87

M1

19

89

M7

19

91

M2

19

92

M9

19

94

M4

19

95

M1

19

97

M6

19

99

M1

20

00

M8

20

02

M3

20

03

M1

20

05

M5

20

06

M1

19

95

=1

00

Source: IMF Commodity Food Price Index

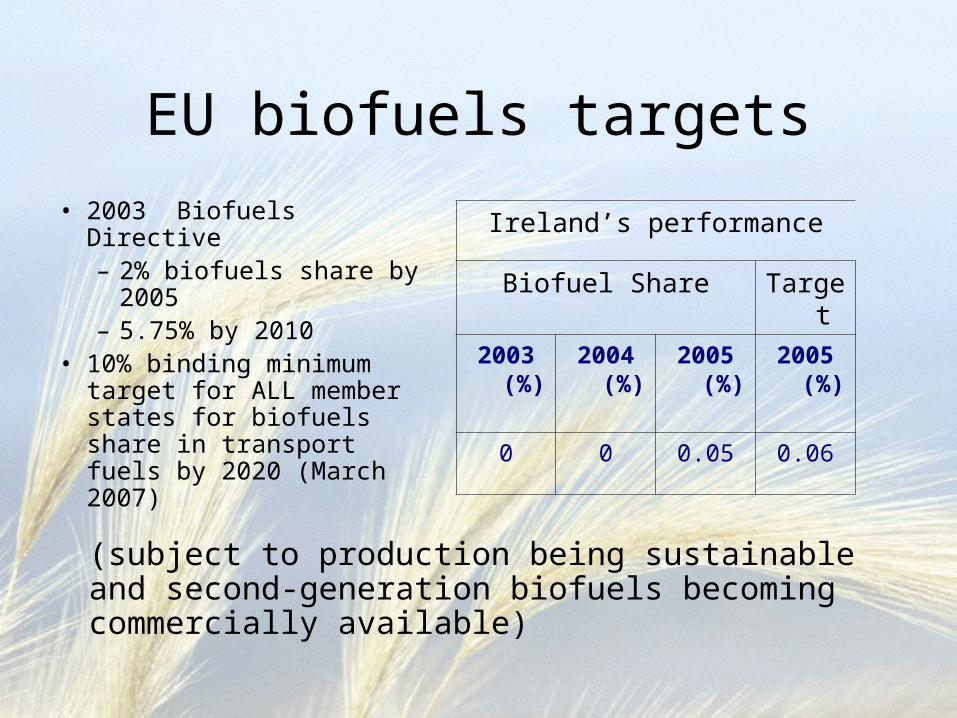

EU biofuels targets

• 2003 Biofuels Directive– 2% biofuels share by

2005– 5.75% by 2010

• 10% binding minimum target for ALL member states for biofuels share in transport fuels by 2020 (March 2007)

Ireland’s performance

Biofuel Share Target

2003 (%)

2004 (%)

2005 (%)

2005 (%)

0 0 0.05 0.06

(subject to production being sustainable and second-generation biofuels becoming commercially available)

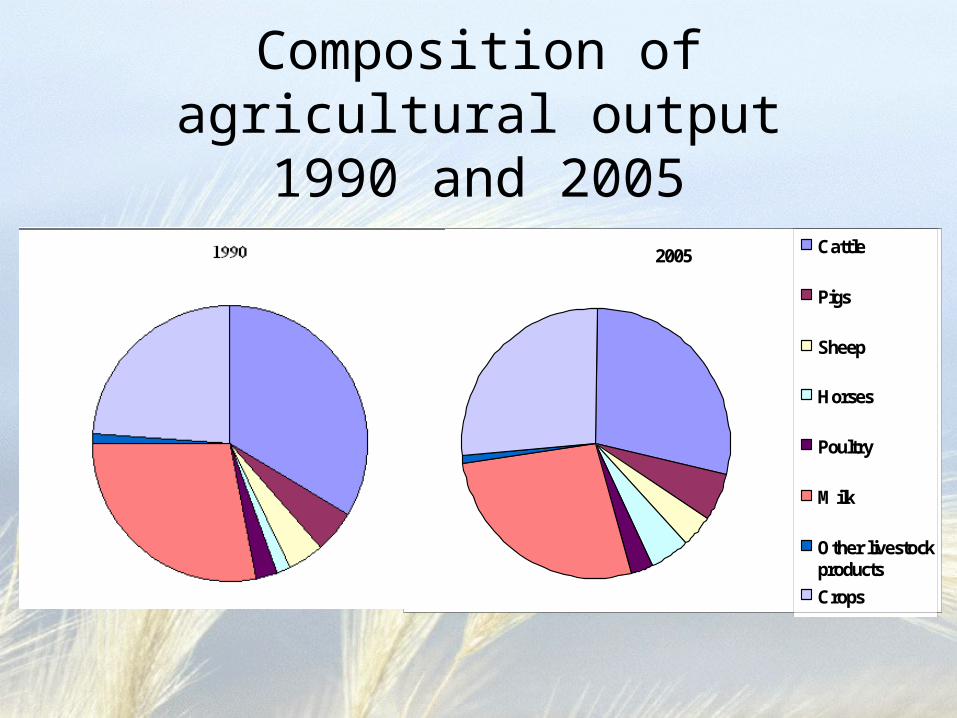

Composition of agricultural output1990 and 2005

2005 Cattle

Pigs

Sheep

Horses

Poultry

Milk

Other livestockproducts

Crops

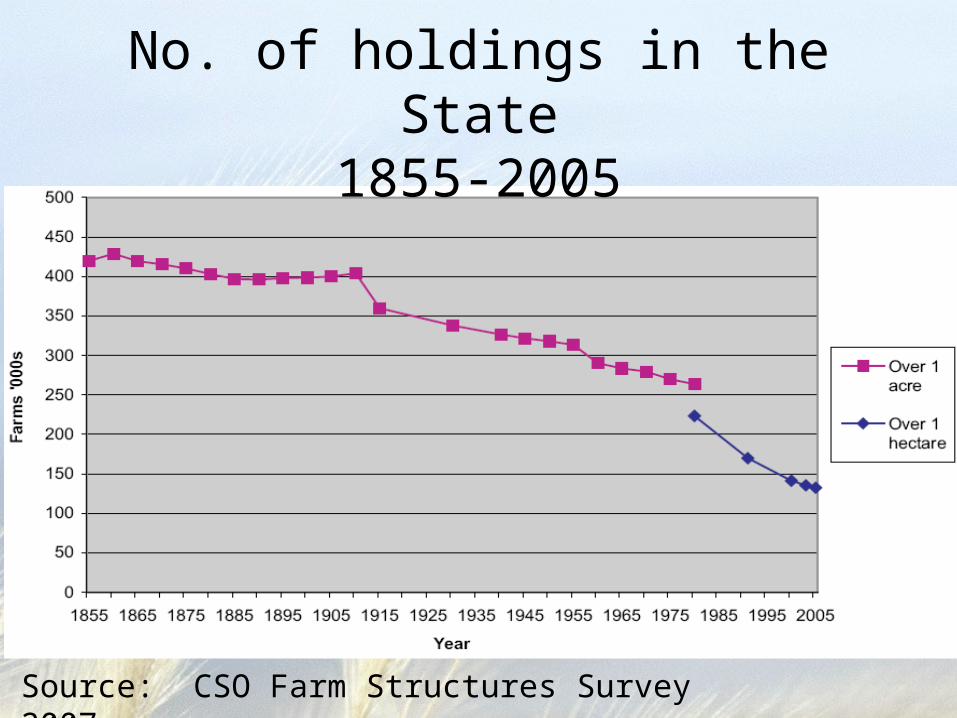

No. of holdings in the State1855-2005

Source: CSO Farm Structures Survey 2007

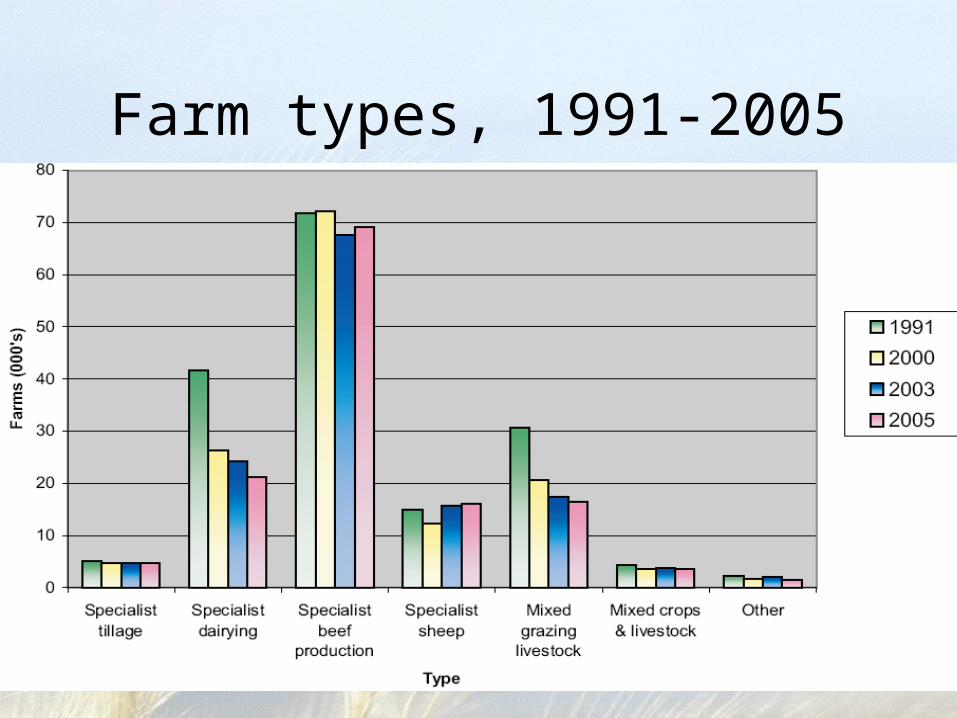

Farm types, 1991-2005

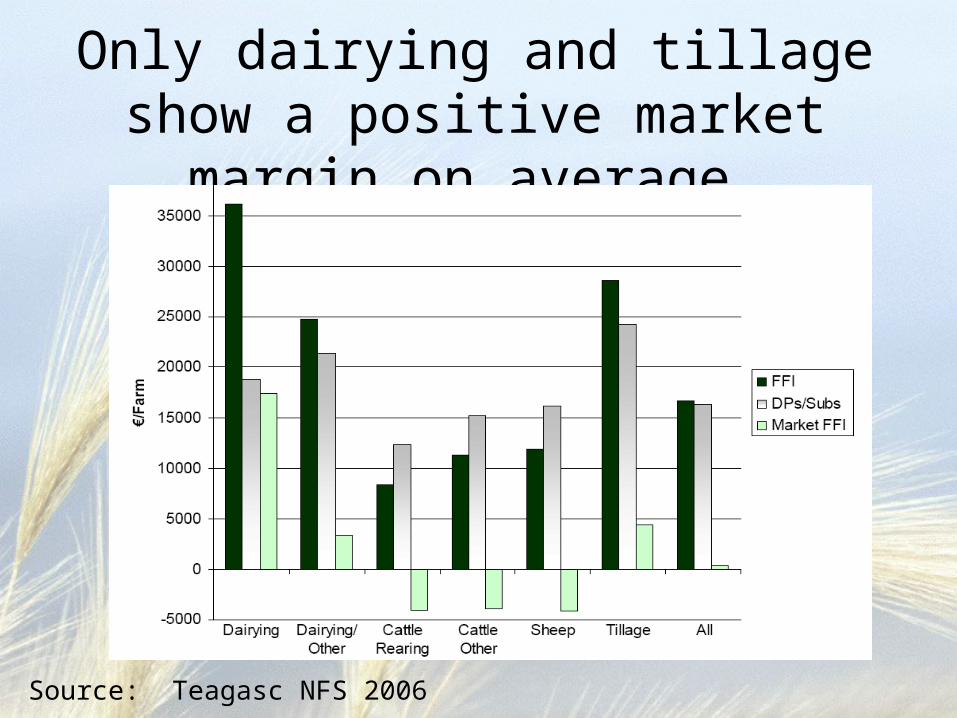

Only dairying and tillage show a positive market margin on average…

Source: Teagasc NFS 2006

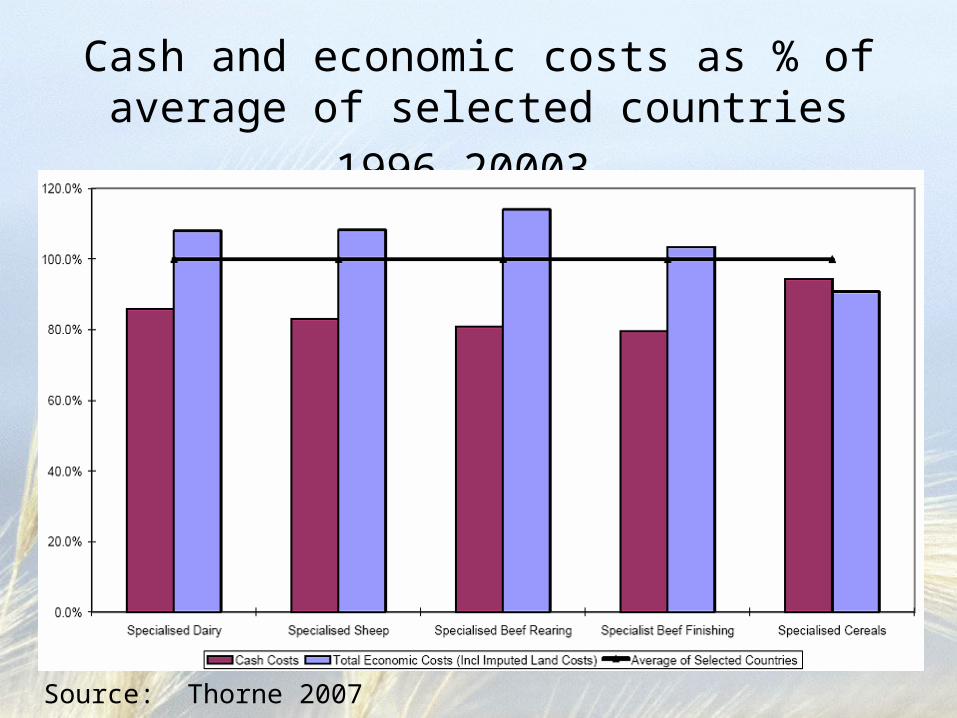

Source: Thorne 2007

Cash and economic costs as % of

average of selected countries 1996-20003

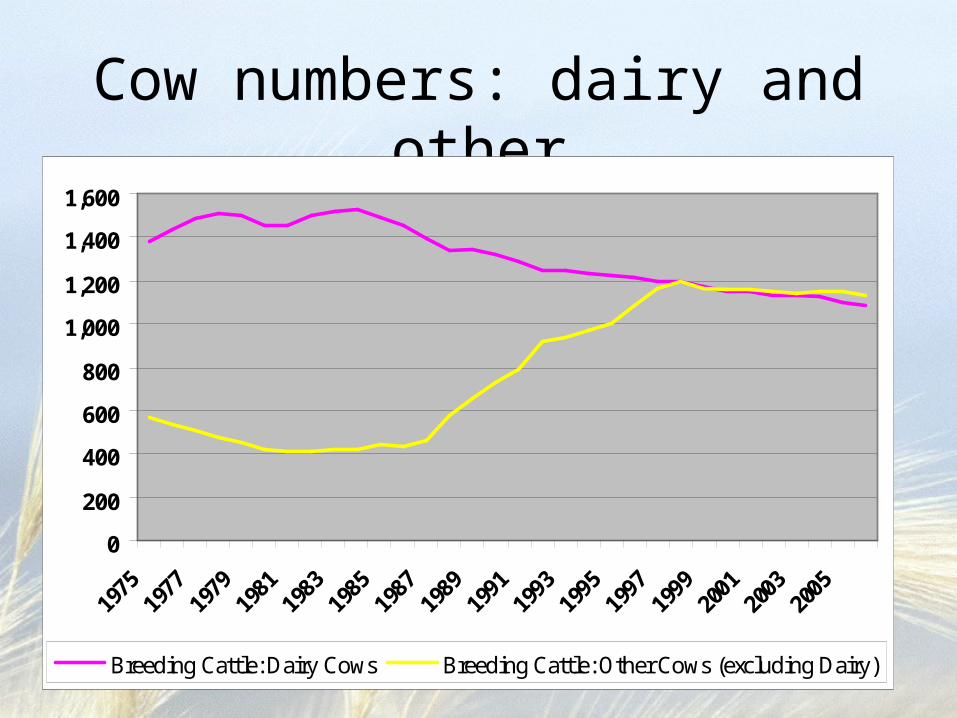

Cow numbers: dairy and other

0

200

400

600

800

1,000

1,200

1,400

1,600

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

Breeding Cattle: Dairy Cows Breeding Cattle: Other Cows (excluding Dairy)

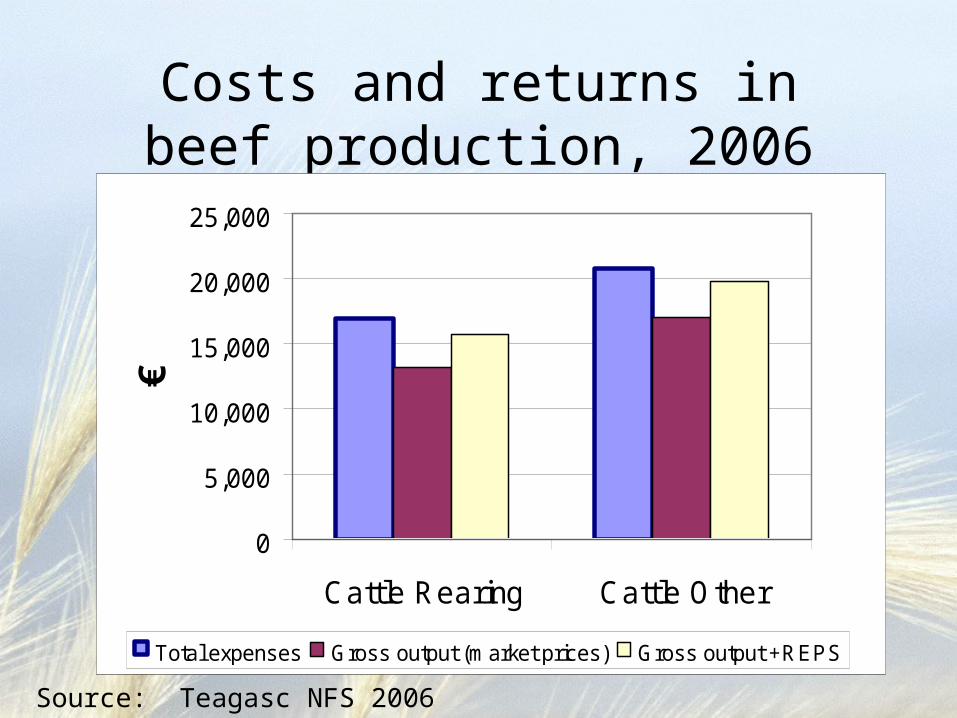

Costs and returns in beef production, 2006

0

5,000

10,000

15,000

20,000

25,000

Cattle Rearing Cattle Other

€

Total expenses Gross output (market prices) Gross output +REPS

Source: Teagasc NFS 2006

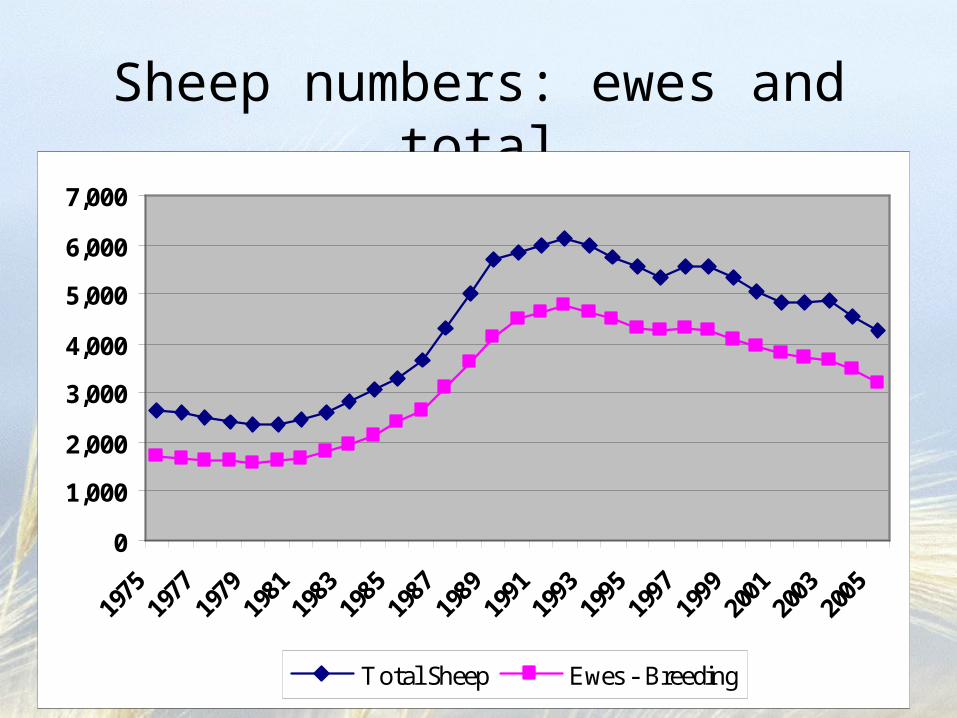

Sheep numbers: ewes and total

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

Total Sheep Ewes - Breeding

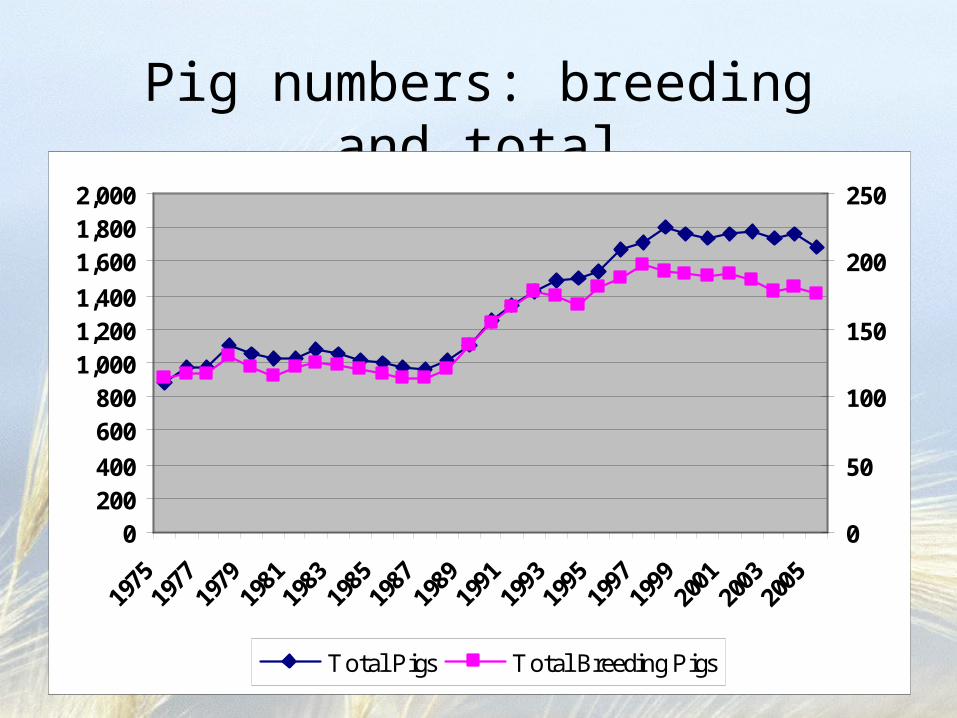

Pig numbers: breeding and total

0200400

600800

1,0001,2001,400

1,6001,8002,000

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

0

50

100

150

200

250

Total Pigs Total Breeding Pigs

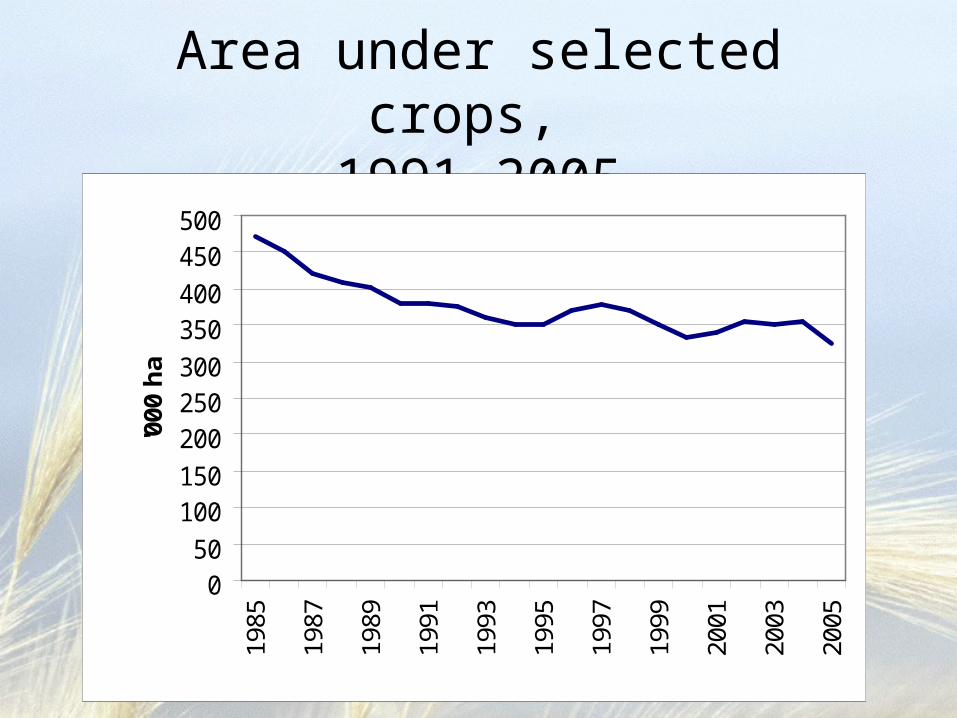

Area under selected crops, 1991-2005

050

100150

200250300

350400

450500

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

'000

ha

Other stakeholders• Agri-food industry

• Forestry

• Rural

• Bioenergy

• Consumers

• Environment

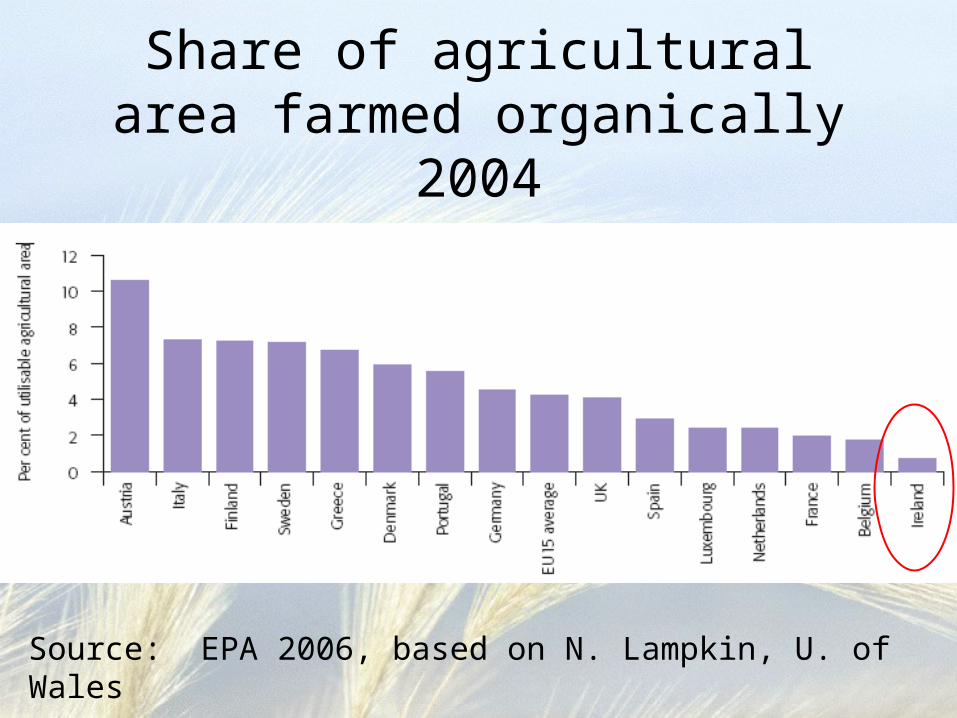

Share of agricultural area farmed organically 2004

Source: EPA 2006, based on N. Lampkin, U. of Wales

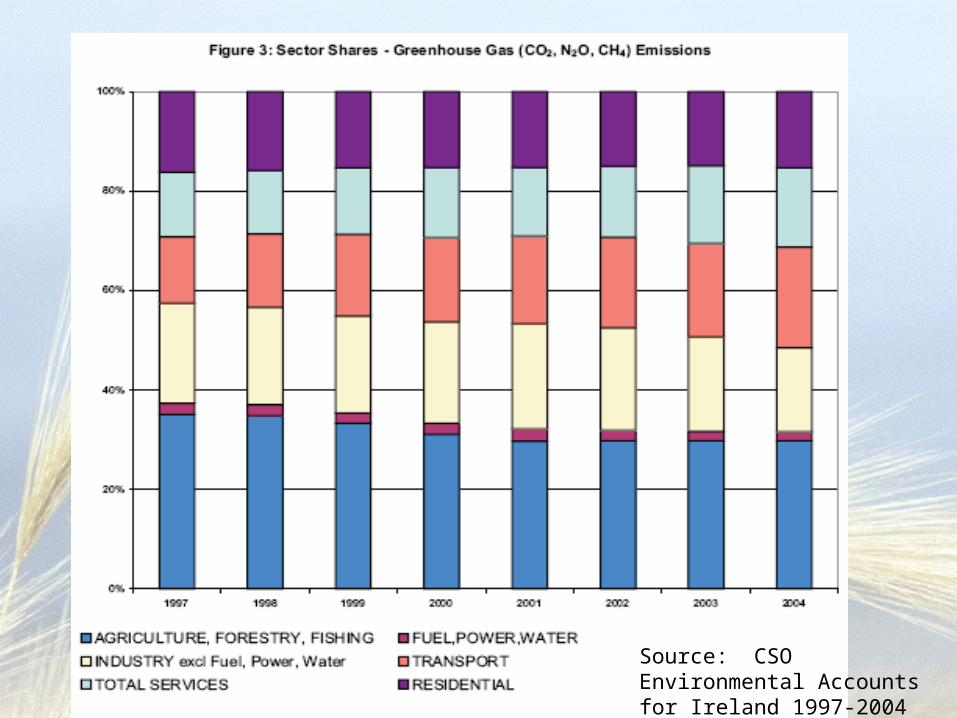

Source: CSO Environmental Accounts for Ireland 1997-2004

Implications for research and education

• Importance of agreeing long term strategic objectives to inform research/education

• High rates of return to public investment in agri-food R&D

• Importance of certainty in research funding– core vs competitive grants– own initiative vs demand driven research– economies of scale at fourth level