Embed Size (px)

Citation preview

Cognitive Economics and Cognitive Economics and Financial Choices:Financial Choices:

Explaining Portfolio Choice and Explaining Portfolio Choice and Total SavingTotal Saving

Miles KimballMiles Kimball

Tyler ShumwayTyler Shumway

Robert WillisRobert Willis

Cognitive Economics:Cognitive Economics:The Economics of The Economics of What is in People’s What is in People’s

MindsMinds

33

Named by Analogy to Named by Analogy to “Cognitive Psychology”“Cognitive Psychology”

• Cognitive Psychology = the area of psychology that examines internal mental processes such as problem solving, memory and language.

• Cognitive Psychology was a departure from Behaviorism--the idea that only outward behavior is a legitimate object of study.

• Milton Friedman famously advocated behaviorism in Economics.

44/65/65

Areas of Economics by Areas of Economics by Distinctive Data TypeDistinctive Data Type

• Standard Economics (including “Mindless” Psychological Economics a la Gul and Pesendorfer): actual market choices only.

• Experimental Economics: choices in artificial situations but with real stakes.

• Neuroeconomics: FMRI, saccades, skin conductance, …

• Bioeconomics: genes, hormones• Cognitive Economics: mental contents (based

on tests and self-reports) and hypothetical choices.

55/65/65

Four Themes of Cognitive Four Themes of Cognitive EconomicsEconomics

1. New Types of Data

2. Heterogeneity

3. Finite and Scarce Cognition

4. Welfare Economics Revisited

66/65/65

3. Finite and Scarce Cognition3. Finite and Scarce Cognition

• Finite cognition=the reality that people are not infinitely intelligent.

• Scarce cognition=some decisions required by our modern environment—at work and in private lives—can require more intelligence for full-scale optimization than an individual has

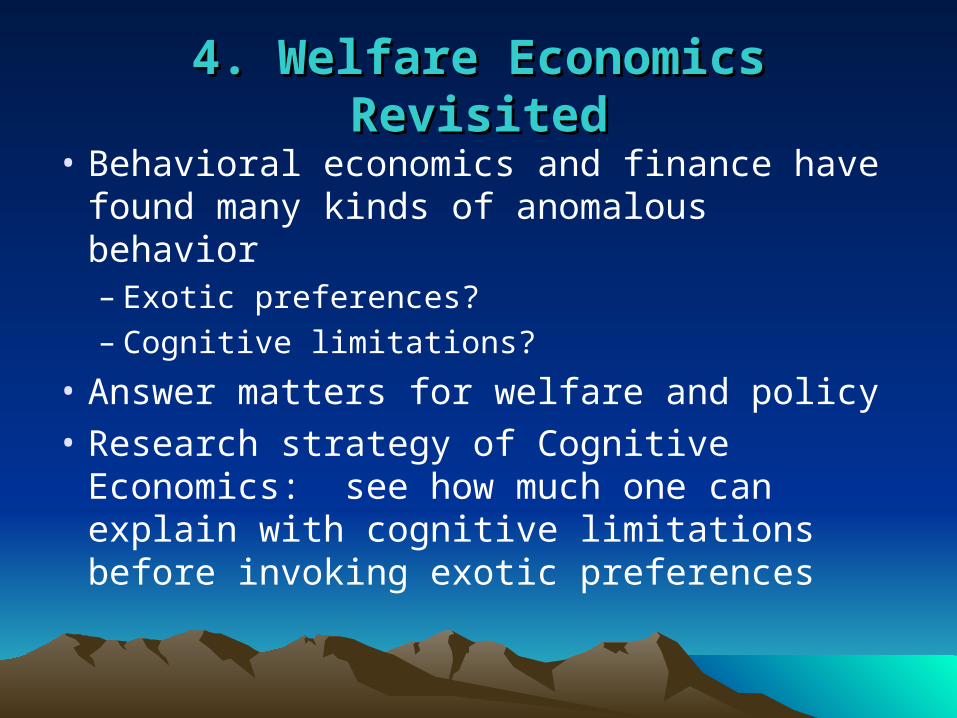

4. Welfare Economics Revisited4. Welfare Economics Revisited

• Behavioral economics and finance have found many kinds of anomalous behavior– Exotic preferences?– Cognitive limitations?

• Answer matters for welfare and policy• Research strategy of Cognitive Economics:

see how much one can explain with cognitive limitations before invoking exotic preferences

Dimensions of CognitionDimensions of Cognition

• Sophistication (some say literacy)– Distance from truth

• Overconfidence– Awareness of distance from truth

• Folk theories– Direction of departure from truth

Financial SophisticationFinancial Sophistication

• We hypothesize that the common explanation of lack of financial sophistication can account for many behavioral anomalies (“Investor Sophistication and the Home Bias, Diversification and Employer Stock Puzzles”)

• The alternative has been a separate explanation for each anomaly.

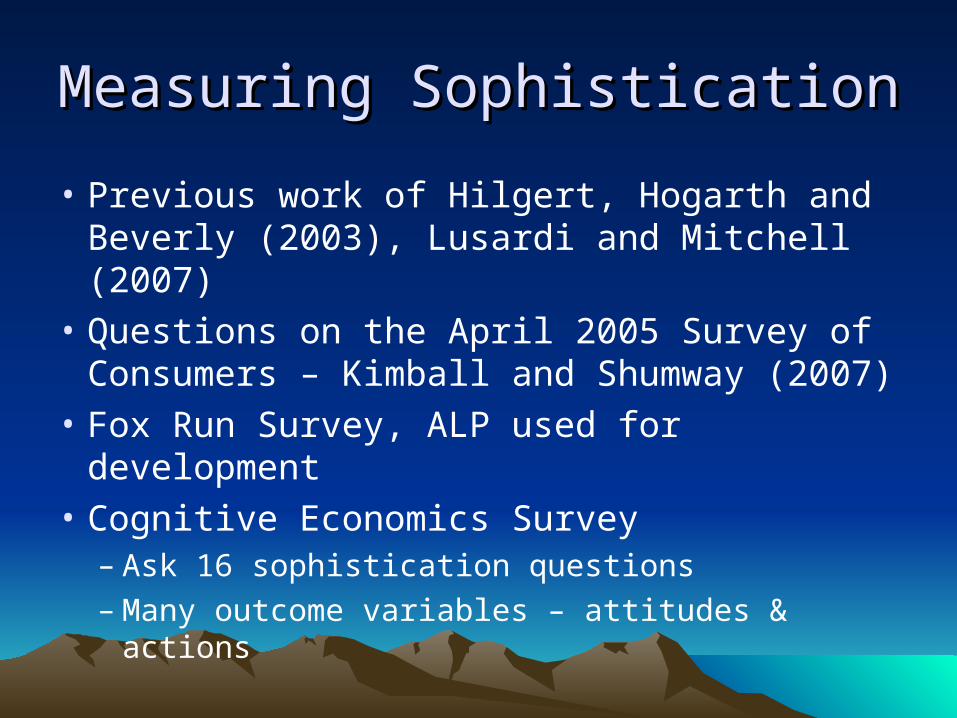

Measuring SophisticationMeasuring Sophistication

• Previous work of Hilgert, Hogarth and Beverly (2003), Lusardi and Mitchell (2007)

• Questions on the April 2005 Survey of Consumers – Kimball and Shumway (2007)

• Fox Run Survey, ALP used for development

• Cognitive Economics Survey– Ask 16 sophistication questions– Many outcome variables – attitudes & actions

Measuring SophisticationMeasuring Sophistication

• We count “correct” answers to sophistication questions to form an index

• Correct answers are verified by factor analysis and average response

• This index is extremely highly correlated with the first component in the factor analysis

T/F Questions with 12-point ScaleT/F Questions with 12-point Scale

An example of a true-false statement is the following: Example Statement: A savings bank never offers a checking account.

Most Likely False Most Likely True Surely False

Guess False

Guess True Surely

True

100% 90% 80% 70% 60% 50%

50% 60% 70% 80% 90% 100%

Please Circle One Number If you think that this statement is most likely to be true, please choose a number in the right half of the box above. If you think that the statement is surely true circle “100%”. If you think it is only 60% likely to be true, please circle 60%.

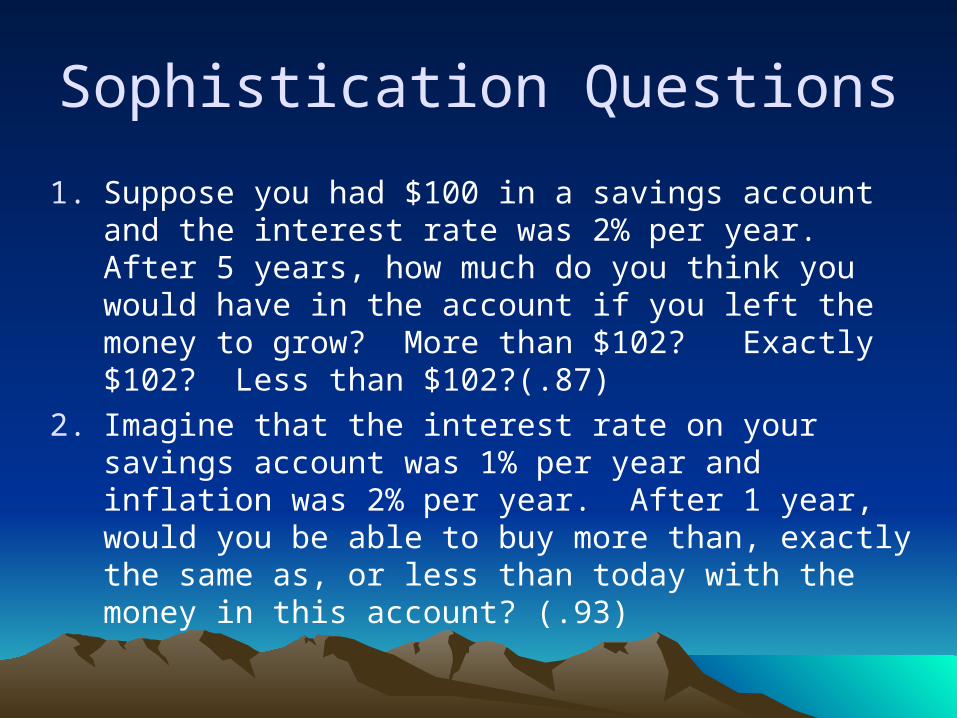

Sophistication Questions

1. Suppose you had $100 in a savings account and the interest rate was 2% per year. After 5 years, how much do you think you would have in the account if you left the money to grow? More than $102? Exactly $102? Less than $102?(.87)

2. Imagine that the interest rate on your savings account was 1% per year and inflation was 2% per year. After 1 year, would you be able to buy more than, exactly the same as, or less than today with the money in this account? (.93)

Sophistication Questions (T/F)

3. An investment advisor tells a 30-year-old couple that $1000 in an investment that pays a certain, constant interest rate would double in value to $2000 after 20 years. If so, that investment would be worth $4000 in less than 45 years. (.80)

4. When an investor spreads money between 20 stocks rather than 2, the risk of losing a lot of money increases. (.83)

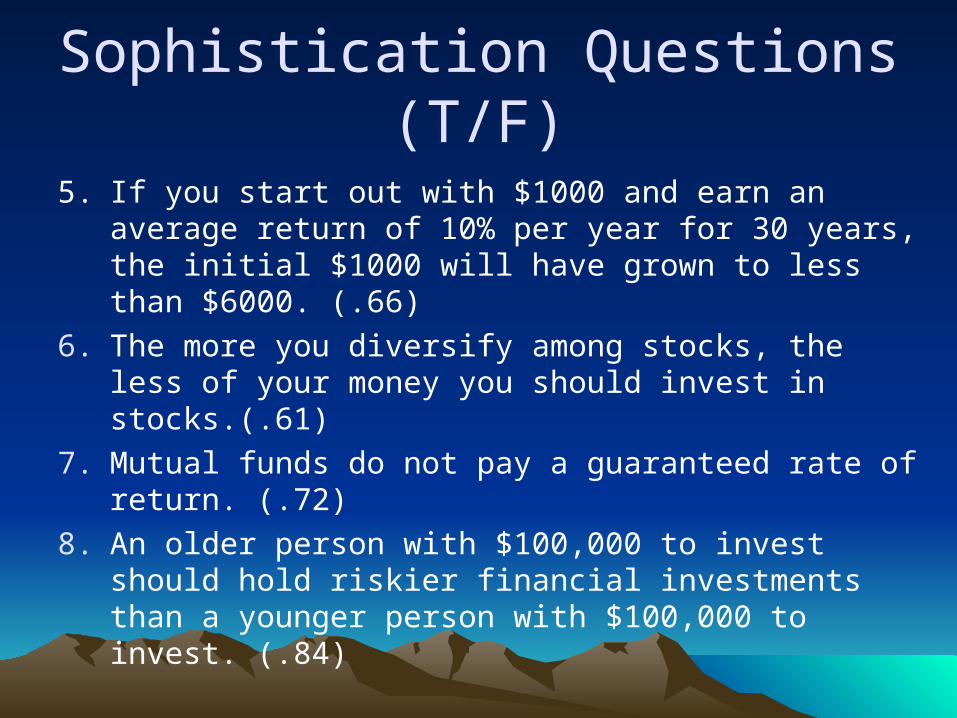

Sophistication Questions (T/F)

5. If you start out with $1000 and earn an average return of 10% per year for 30 years, the initial $1000 will have grown to less than $6000. (.66)

6. The more you diversify among stocks, the less of your money you should invest in stocks.(.61)

7. Mutual funds do not pay a guaranteed rate of return. (.72)

8. An older person with $100,000 to invest should hold riskier financial investments than a younger person with $100,000 to invest. (.84)

Sophistication Questions (T/F)

9. It is hard to find mutual funds that have annual fees of less than one percent of assets. (.57)

10. Using money in a bank savings account to pay off credit card debt is usually a good idea. (.74)

11. You could save money in interest costs by choosing a 30-year rather than a 15-year mortgage. (.90)

12. If the interest rate falls, bond prices will fall. (.60)

13. Taxes affect how you should invest your money. (.78)

Foreign Stock HoldingForeign Stock Holding

Logit Regression, N = 359, Pseudo R2 = 0.1596------------------------------------------------------------------------------

| Coef. Std. Err. z P>|z|

-------------+-------------------------------------------

fin sophist | 2.508706 1.129884 2.22 0.026 ln(income) | -.0028919 .0882921 -0.03 0.974

ln(fin wealth) | .4421791 .0960877 4.60 0.000

age | -.2720059 .1587194 -1.71 0.087

age2 | .0019148 .001196 1.60 0.109

use the web | 1.162134 .3712195 3.13 0.002

female | -.0374495 .2566188 -0.15 0.884

education | .1065741 .071805 1.48 0.138

econ classes | -.0417273 .054217 -0.77 0.442

married | -.390569 .3198808 -1.22 0.222

number series | -.1275469 .2467387 -0.52 0.605

number series2 | .0001152 .0002339 0.49 0.622

risk tolerance | .1699616 .0620871 2.74 0.006

constant | 34.0129 65.04428 0.52 0.601

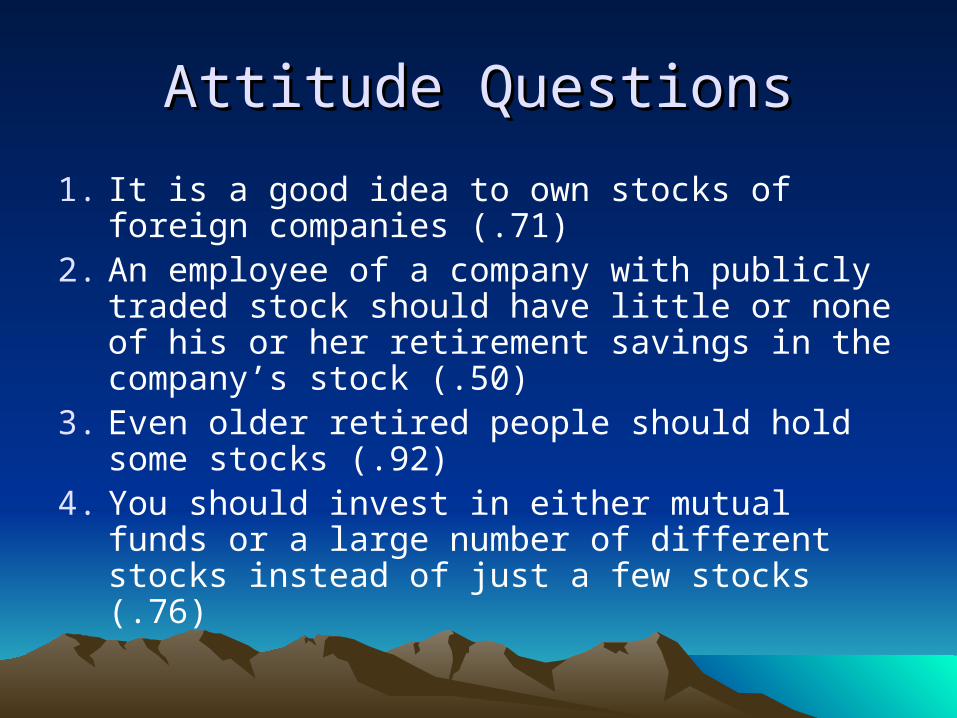

Attitude QuestionsAttitude Questions

1. It is a good idea to own stocks of foreign companies (.71)

2. An employee of a company with publicly traded stock should have little or none of his or her retirement savings in the company’s stock (.50)

3. Even older retired people should hold some stocks (.92)

4. You should invest in either mutual funds or a large number of different stocks instead of just a few stocks (.76)

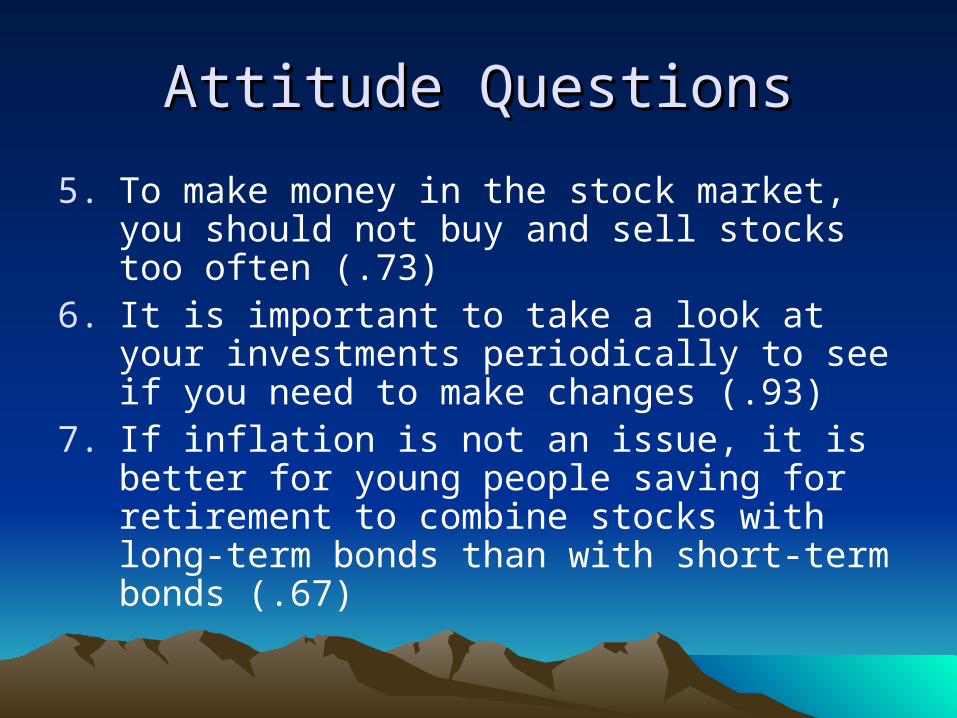

Attitude QuestionsAttitude Questions

5. To make money in the stock market, you should not buy and sell stocks too often (.73)

6. It is important to take a look at your investments periodically to see if you need to make changes (.93)

7. If inflation is not an issue, it is better for young people saving for retirement to combine stocks with long-term bonds than with short-term bonds (.67)

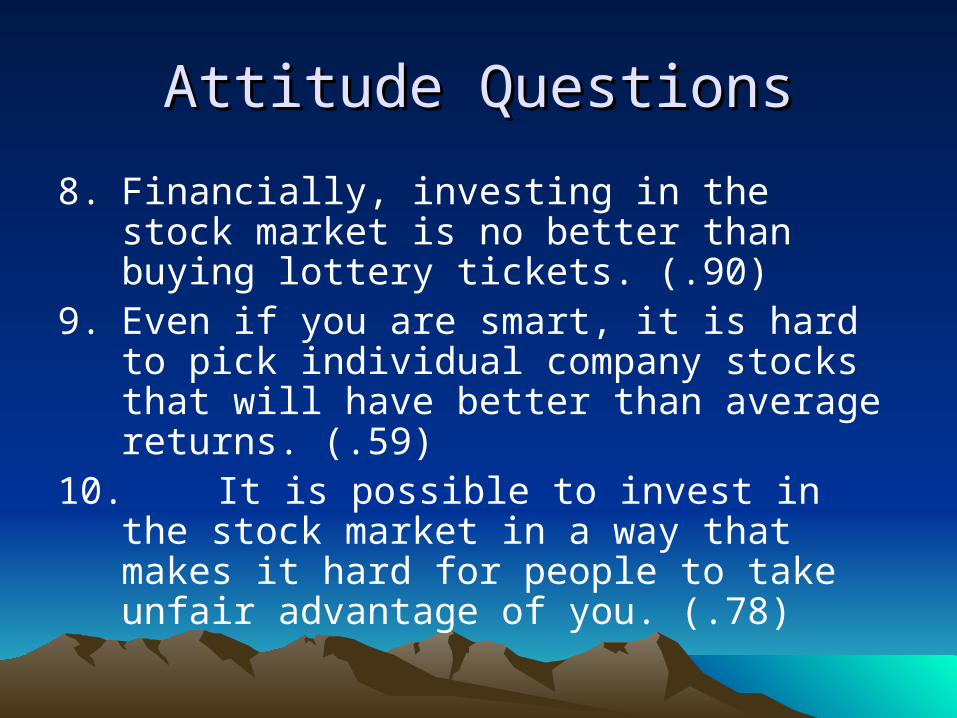

Attitude QuestionsAttitude Questions

8. Financially, investing in the stock market is no better than buying lottery tickets. (.90)

9. Even if you are smart, it is hard to pick individual company stocks that will have better than average returns. (.59)

10. It is possible to invest in the stock market in a way that makes it hard for people to take unfair advantage of you. (.78)

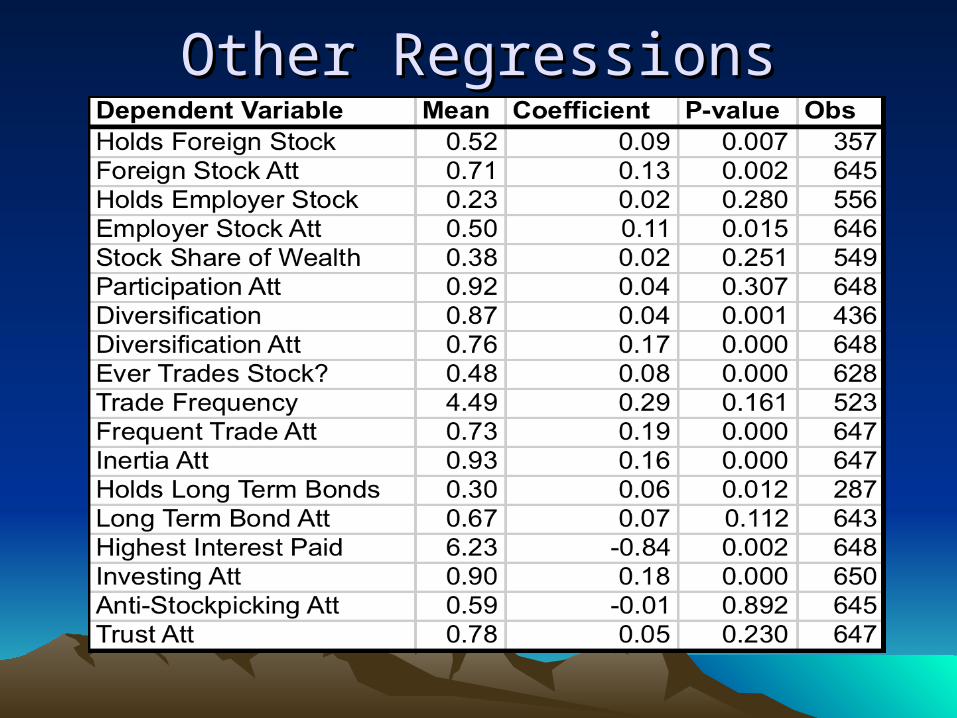

Other RegressionsOther Regressions

Sophistication and ChoiceSophistication and Choice

• Portfolio choice appears to be significantly affected by sophistication

• Less sophisticated people make mistakes

• Causality may be an issue for some of these, but not for all of them

• Education may help to remedy this, or better policy (defaults, etc)

OverconfidenceOverconfidence

• Overconfidence is thought to be a significant factor in financial decisions

• Typically not measured very well– Gender (Barber and Odean, 2001)– Excessive trading– Old military records (Grinblatt and Keloharju,

2008)

Overconfidence QuestionsOverconfidence Questions

An example of a true-false statement is the following: Example Statement: A savings bank never offers a checking account.

Most Likely False Most Likely True Surely False

Guess False

Guess True Surely

True

100% 90% 80% 70% 60% 50%

50% 60% 70% 80% 90% 100%

Please Circle One Number If you think that this statement is most likely to be true, please choose a number in the right half of the box above. If you think that the statement is surely true circle “100%”. If you think it is only 60% likely to be true, please circle 60%.

Measuring OverconfidenceMeasuring Overconfidence

• Accuracy Overconfidence: The difference between the average probability of a correct answer and the actual fraction

• Self-Rated Overconfidence: Residual of regression of percent correct on self-rating variables, math score, demographics

• Return Overconfidence: Return I can get – return average individual can get

Overconfidence Regressions 1Overconfidence Regressions 1Dependent Variable Overconf Coeff P-value Obs

Accuracy 0.284 0.622 63Self-Rated 3.299 0.018 62Return -0.007 0.899 62Accuracy 0.060 0.620 357Self-Rated 0.034 0.913 356Return 0.004 0.618 358Accuracy 0.091 0.443 444Self-Rated 0.234 0.448 439Return -0.006 0.479 441Accuracy -1.311 0.053 72Self-Rated -1.691 0.411 72Return -0.042 0.399 72Accuracy 0.026 0.770 545Self-Rated 0.388 0.107 532Return 0.010 0.140 543Accuracy -0.500 0.004 545Self-Rated -1.390 0.002 532Return -0.026 0.054 543Accuracy 0.316 0.065 382Self-Rated 0.575 0.203 372Return 0.022 0.101 382

Momentum Trader?

Bonds Fraction

Cash Fraction

LT Bonds Fraction

Stock Fraction (w/o Empl)

Foreign Stock Fraction

Diversification

Overconfidence Regressions 2Overconfidence Regressions 2Dependent Variable Overconf Coeff P-value Obs

Accuracy 6.999 0.102 53Self-Rated 2.080 0.833 53Return -0.190 0.585 53Accuracy 0.558 0.005 623Self-Rated 2.317 0.000 605Return 0.017 0.294 619Accuracy 0.392 0.883 651Self-Rated -8.944 0.192 632Return -0.086 0.694 646Accuracy 263.747 0.013 574Self-Rated 297.316 0.282 560Return -2.058 0.810 568Accuracy 0.334 0.106 628Self-Rated 1.425 0.007 610Return 0.015 0.370 624Accuracy -0.002 0.993 625Self-Rated -0.134 0.752 607Return 0.000 1.000 621Accuracy -0.512 0.019 624Self-Rated -1.737 0.002 607Return -0.073 0.000 621

Ever Trades?

At least 1/3 Cash

Trade Frequency

Highest Interest Paid

Debt to Income Ratio

At least 1/3 Stocks

At least 1/3 Bonds

Overconfidence and ChoiceOverconfidence and Choice

• Overconfidence is clearly related to a number of portfolio choices– Stock and cash holdings– Trading frequency

• Contrary to other findings, not significantly related to gender or momentum trading

Total SavingTotal Saving

• We looked for a wide range of psychological factors that might affect total saving

–Survey Practicum course

–Focus groups

• Savings questions on the June, 2008 Survey of Consumers

Measuring Propensity to Save Measuring Propensity to Save

Measuring consumption etc. would take more survey time than we had. Instead

• Make an index of many “outcome variables”• 79% of variance is explained with responses to

two hypothetical questions:– Suppose you got a (new) job that has a 401(k)

retirement savings plan. You can contribute up to 10% of your pay. For every dollar you put in, your (new) employer will put in a dollar. What percentage of your pay would you choose to contribute?

– Same question with a twenty-five cent match

Responses to HypotheticalsResponses to HypotheticalsMatch 1 Dollar 25 Cent

Percent Match Match0 3 141 1 52 6 103 10 224 1 85 39 526 7 127 9 88 6 89 0 110 275 221Total 357 361

Factor Loadings:Factor Loadings:

• Factor | Eigenvalue Difference Proportion Cumulative

• Factor1 | 3.64046 2.02111 0.4410 0.4410

• Factor2 | 1.61935 0.24951 0.1962 0.6372

• Factor3 | 1.36984 0.57893 0.1659 0.8031

• Factor4 | 0.79091 0.07968 0.0958 0.8989

• Factor5 | 0.71123 0.05788 0.0862 0.9851

Other Savings Questions: Other Savings Questions:

• (.4097) Compared to people who are similar to you in age, income, and family size, do you think you have more retirement savings, about the same amount of retirement savings, or less retirement savings? [.43]

• (.0223) Is your current level of spending higher than it should be, about right,or lower than it should be? [.32]

• (.1894) How much have you thought about retirement –- would you say a lot, some, a little, or hardly at all? [-2.05]

• *(Factor Loadings) [Raw Mean]

Other Savings Questions: Other Savings Questions:

• (-.4015) Suppose that the government decided that in addition to current Social Security taxes, everyone under sixty-five who is working would be required to put an additional ten percent of their pre-tax income into a personal retirement account. How hard would it be for you to adjust to your (and your spouse/partner’s) lower take-home pay –- would you say it would be extremely hard, quite hard, somewhat hard, not so hard, or not Hard at all? [-.16]

• (-.1603) Would you vote for such a program? [.63]

Other Savings Questions: Other Savings Questions: • Participation in 401K: (.3447) Does your employer offer a

retirement plan where the money is yours and you can take it with you even if you quit, such as a 401K or another defined contribution plan? [.72] Could you have chosen to participate? [.86] Could you have chosen not to participate? [.83]

• Participation interacted with match rate: (.3361) If you contributed some of your pay to your retirement account, would your employer match or partially match your contribution? [7.62]

• As a percentage of your pay, what percent do you contribute to your retirement account? (.1976)

[8.22]

Other Savings Questions: Other Savings Questions:

• Contribution level interacted with match rate: (.1248) Could you contribute more of your pay to your account? [.66] If you contributed more of your pay to your retirement account, would your employer also contribute more? [.21] For each extra dollar that you put into your retirement account, how much would your employer put in? [.86]

• Participation in defined benefit plan: (.0736) Does your employer offer a pension plan, also referred to as a defined benefit plan, that works like Social Security -- that is, there is a set of rules that determine how much you will get per month after you retire? [.32] Could you have chosen not to participate? [.26] Could you have chosen to participate? [.86]

Other Savings Questions: Other Savings Questions:

• (.3345) Other than employer retirement plans from current or past employers, do you have anything saved for retirement? [.57]

• (.3085) What is the total amount you have saved up for retirement, including what you have in retirement accounts such as 401K’s and IRA’s? [$150,642]

• (.1957) The last time you (and your family living there) refinanced your mortgage, did you take away money from the closing that you could use for whatever you wanted to use it for? [.47]

Other Savings Questions: Other Savings Questions:

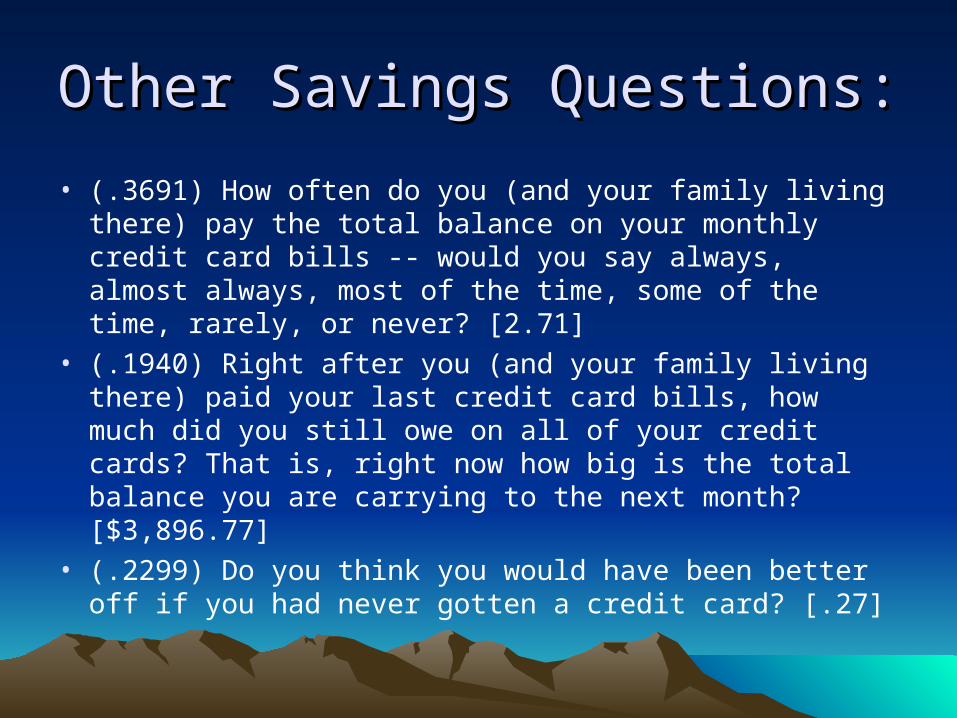

• (.3691) How often do you (and your family living there) pay the total balance on your monthly credit card bills -- would you say always, almost always, most of the time, some of the time, rarely, or never? [2.71]

• (.1940) Right after you (and your family living there) paid your last credit card bills, how much did you still owe on all of your credit cards? That is, right now how big is the total balance you are carrying to the next month? [$3,896.77]

• (.2299) Do you think you would have been better off if you had never gotten a credit card? [.27]

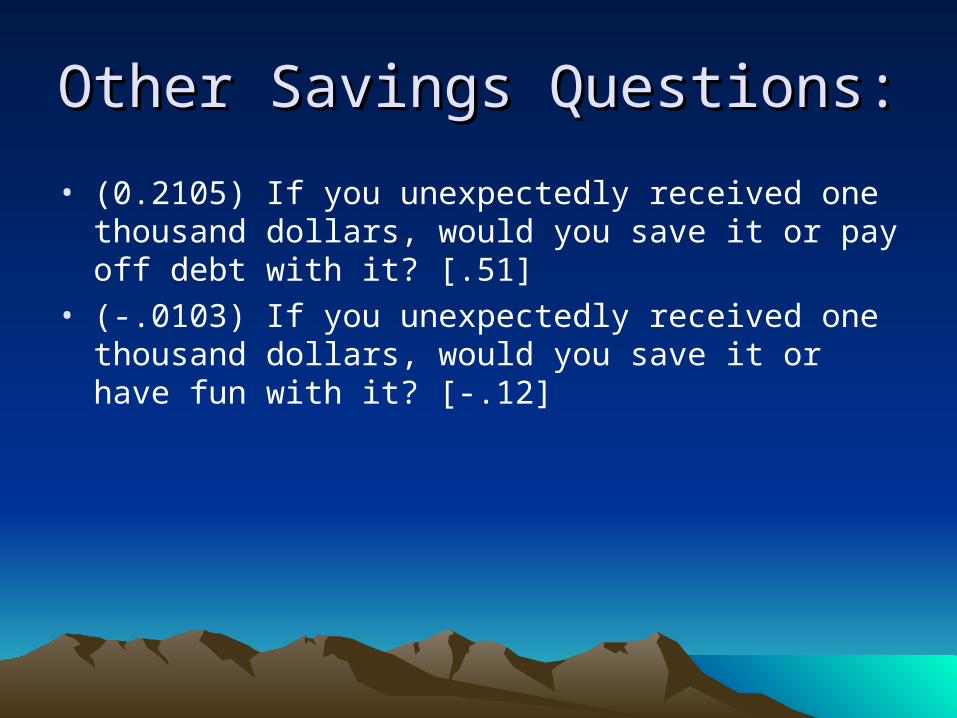

Other Savings Questions: Other Savings Questions:

• (0.2105) If you unexpectedly received one thousand dollars, would you save it or pay off debt with it? [.51]

• (-.0103) If you unexpectedly received one thousand dollars, would you save it or have fun with it? [-.12]

Folk Theories and Cognitive and Folk Theories and Cognitive and Psychological Factors We ExaminePsychological Factors We Examine

• Trust in institutions and others• Planning• Others will take care of me• Saving is good vs. thinking about money is bad• Fatalism• Social pressure• Psychological tricks to encourage saving• Self control• Budgeting skill• Locus of Control

Controls:Controls:

• All regressions use a savings index as the dependent variable with standard controlsSaveIndex Coef. Std. Err. T P-value

Log Income .4769 .1052 4.53 0.000

Education .0003 .0582 0.01 0.995

Age .0108 .0051 2.11 0.036

Spouse Ed. -.0041 .0494 -0.08 0.933

Sex -.0996 .1140 -0.87 0.384

Race 0.0606 .0479 1.26 0.208

Married -0.0231 0.0887 -0.26 0.795

Institutional TrustInstitutional Trust

• If I try to save through financial institutions, someone is likely to figure out a way to cheat me out of the money.

• Coefficient = -.15, t-stat = -2.44

PlanningPlanning

• I enjoy planning for activities like vacations well in advance. (strongly agree ..)

• Coefficient = .07, t-stat = 1.44

• Thinking about money stresses me out.

• Coefficient = -.15, t-stat = -3.07

• I am good at seeing the big picture

• Coefficient = 0.03, t-stat = .56

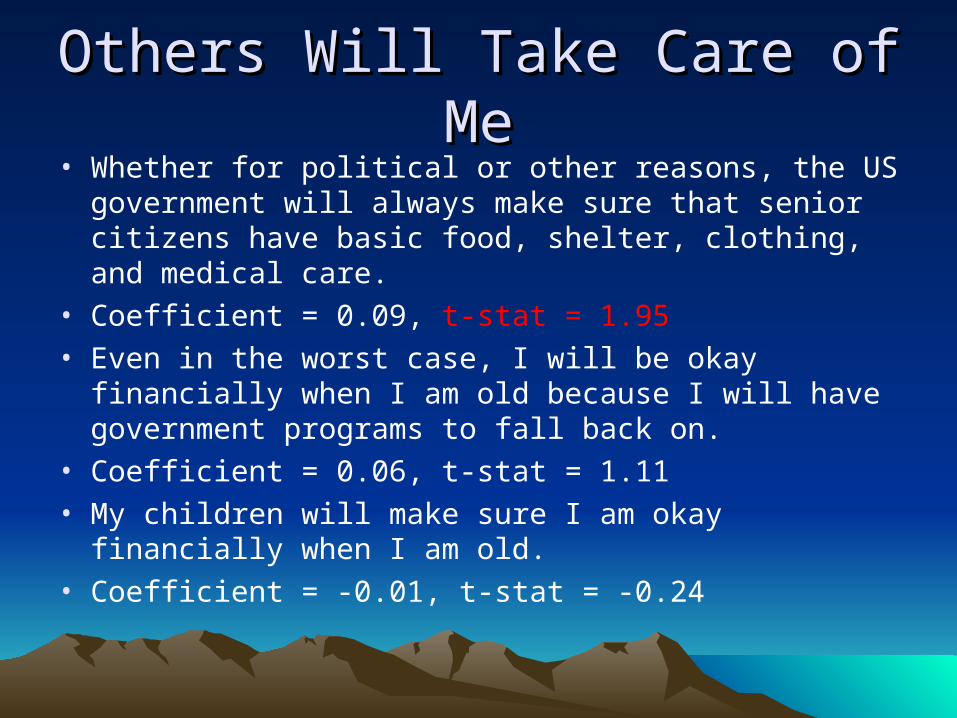

Others Will Take Care of MeOthers Will Take Care of Me• Whether for political or other reasons, the US

government will always make sure that senior citizens have basic food, shelter, clothing, and medical care.

• Coefficient = 0.09, t-stat = 1.95• Even in the worst case, I will be okay financially when I

am old because I will have government programs to fall back on.

• Coefficient = 0.06, t-stat = 1.11• My children will make sure I am okay financially when I

am old.• Coefficient = -0.01, t-stat = -0.24

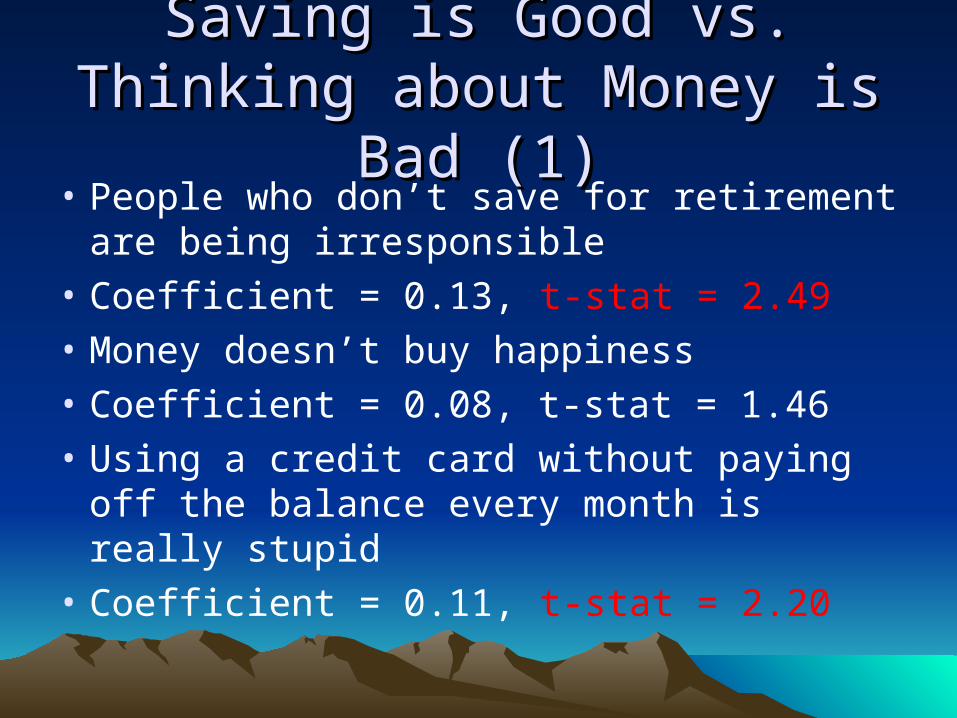

Saving is Good vs. Thinking Saving is Good vs. Thinking about Money is Bad (1)about Money is Bad (1)

• People who don’t save for retirement are being irresponsible

• Coefficient = 0.13, t-stat = 2.49

• Money doesn’t buy happiness

• Coefficient = 0.08, t-stat = 1.46

• Using a credit card without paying off the balance every month is really stupid

• Coefficient = 0.11, t-stat = 2.20

Saving is Good vs. Thinking Saving is Good vs. Thinking about Money is Bad (2)about Money is Bad (2)

• Thinking about money all the time, even when you have enough, is a terrible way to live

• Coefficient = 0.06, t-stat = 1.23

• Most Americans save too little

• Coefficient = 0.05, t-stat = 0.87

• Most Americans borrow too much

• Coefficient = 0, t-stat = -0.06

Saving is Good vs. Thinking Saving is Good vs. Thinking about Money is Bad (3)about Money is Bad (3)

• I really respect people who have managed to save a lot of money

• Coefficient = -0.10, t-stat =-1.98 (wrong sign)

• It is nice to have money saved up, but you have to live

• Coefficient = -0.06, t-stat = -1.28

FatalismFatalism

• If you don’t let yourself get too worried, everything tends to work out in the end.

• Coefficient = -0.10, t-stat = -2.09

• No one can predict the future, so trying to save doesn’t do much good.

• Coefficient = -0.22, t-stat = -4.71

Social Pressure (1)Social Pressure (1)

• My parents or guardians encouraged me to save.• Coefficient = 0.04, t-stat = 0.85• I would hate to have people think I am careless

with money.• Coefficient = -0.09, t-stat = -1.72• I would feel guilty about going bankrupt, even if I

had to.• Coefficient = -0.01, t-stat = -0.24

Social Pressure (2)Social Pressure (2)

• When I was growing up, my parents were good at saving their money.

• Coefficient = -0.02, t-stat = -0.33

• I would hate to have someone think that I am stingy with my money.

• Coefficient = -0.03, t-stat = -0.67

Psychological Tricks to Psychological Tricks to Encourage SavingEncourage Saving

• Before I buy something, I ask myself if I am really going to use it.

• Coefficient = 0.03, t-stat = 0.62• Pretending to yourself that you have less money

than you really do is a good idea.• Coefficient = 0.01, t-stat = 0.21• Before I buy something, I think twice to make

sure it is something I really need.• Coefficient = -0.002, t-stat = -0.05

Self Control (1)Self Control (1)

• I often make impulse purchases.

• Coefficient = -0.09, t-stat = -1.93

• Breaking a rule gives me a feeling of freedom.

• Coefficient = -0.03, t-stat = -0.62

• I have problems with self control.

• Coefficient = -0.06, t-stat = -1.09

Self Control (2)Self Control (2)

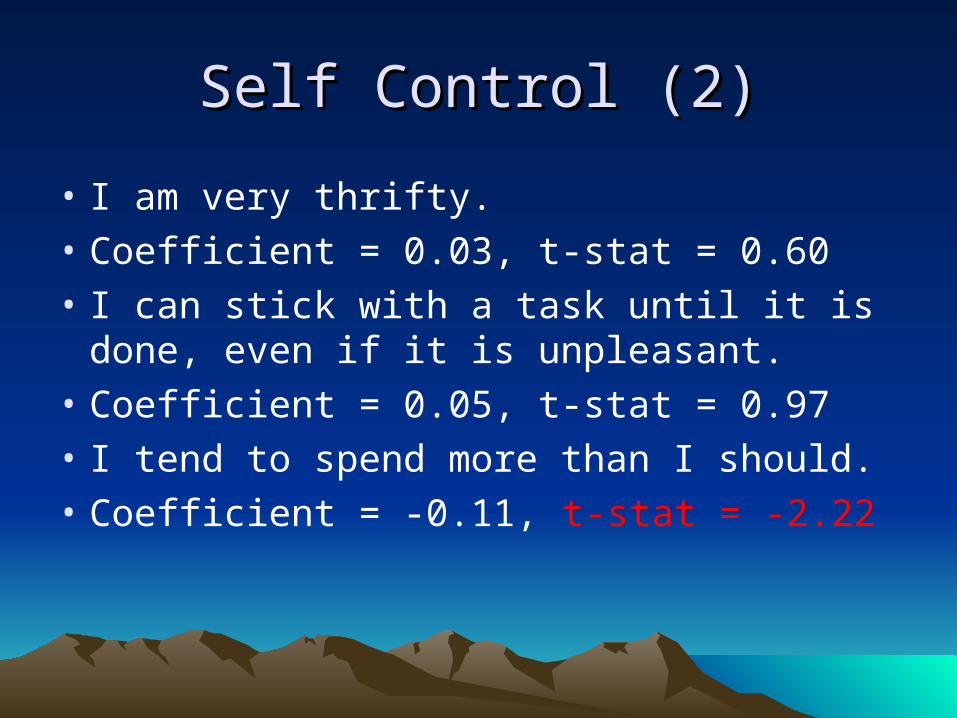

• I am very thrifty.

• Coefficient = 0.03, t-stat = 0.60

• I can stick with a task until it is done, even if it is unpleasant.

• Coefficient = 0.05, t-stat = 0.97

• I tend to spend more than I should.

• Coefficient = -0.11, t-stat = -2.22

Budgeting SkillBudgeting Skill

• I often wonder, “Where did all my money go?”

• Coefficient = -0.14, t-stat = -2.83

Locus of ControlLocus of Control

• It is difficult to stay ahead financially because of the things my family members want to buy.

• Coefficient = -0.15, t-stat = -3.12

• Many of the things that keep me from saving more money are out of my control.

• Coefficient = -0.17, t-stat = -3.33

Summary: Low Correlation with Summary: Low Correlation with Propensity to SavePropensity to Save

• Others will take care of me• Mild statements about desirability of saving• Social pressure• Psychological tricks to encourage saving• Many of the measures of self-control• Some measures of planning propensity:

– vacation planning– seeing the big picture

Summary: Promising Questions Summary: Promising Questions for Further Investigation (1)for Further Investigation (1)

• If I try to save through financial institutions, someone is likely to figure out a way to cheat me out of the money.

• Thinking about money stresses me out.

• Judgmental Statements:– People who don’t save for retirement are being

irresponsible– Using a credit card without paying off the

balance every month is really stupid

Summary: Promising Questions Summary: Promising Questions for Further Investigation (2)for Further Investigation (2)

• Fatalism– If you don’t let yourself get too worried,

everything tends to work out in the end.– No one can predict the future, so trying to

save doesn’t do much good.

• I tend to spend more than I should.

• I often wonder, “Where did all my money go?”

Summary: Promising Questions Summary: Promising Questions for Further Investigation (2)for Further Investigation (2)

• Fatalism– If you don’t let yourself get too worried,

everything tends to work out in the end.– No one can predict the future, so trying to

save doesn’t do much good.

• I tend to spend more than I should.

• Budgeting skill: I often wonder, “Where did all my money go?”

Summary: Promising Questions Summary: Promising Questions for Further Investigation (3)for Further Investigation (3)

• Locus of Control:

–It is difficult to stay ahead financially because of the things my family members want to buy.

–Many of the things that keep me from saving more money are out of my control.

ConclusionConclusion

• In a rudimentary R2 sense, Economics has not been very successful in explaining portfolio choice or high vs. low saving.

• Measuring what is in people’s minds provides insight into what kinds of additional factors might help explain portfolio choice and total saving.

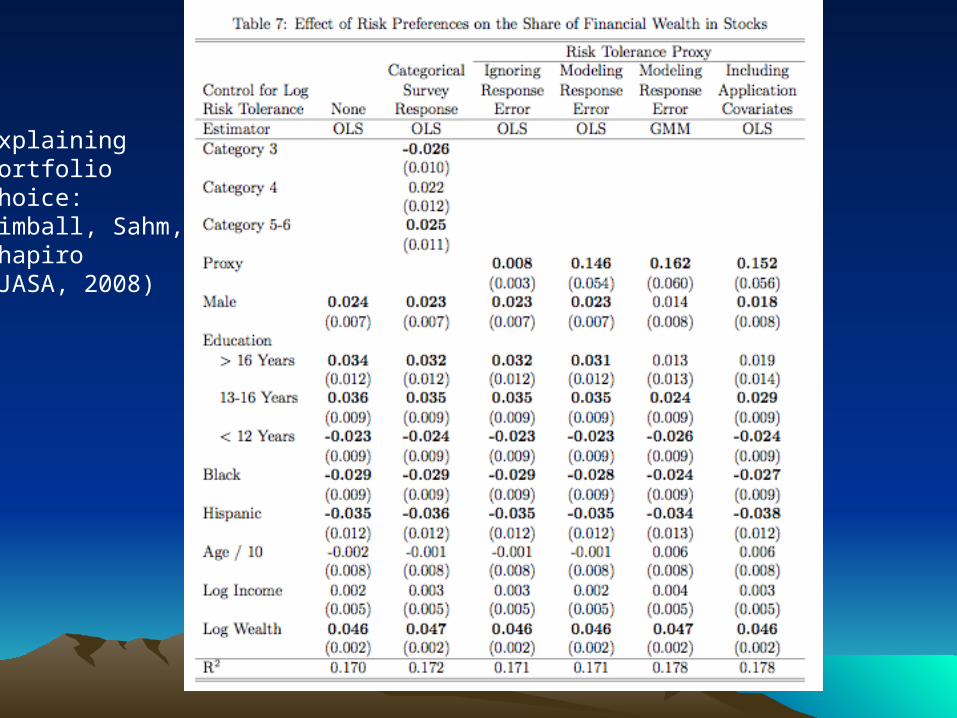

ExplainingPortfolio Choice:Kimball, Sahm, Shapiro(JASA, 2008)

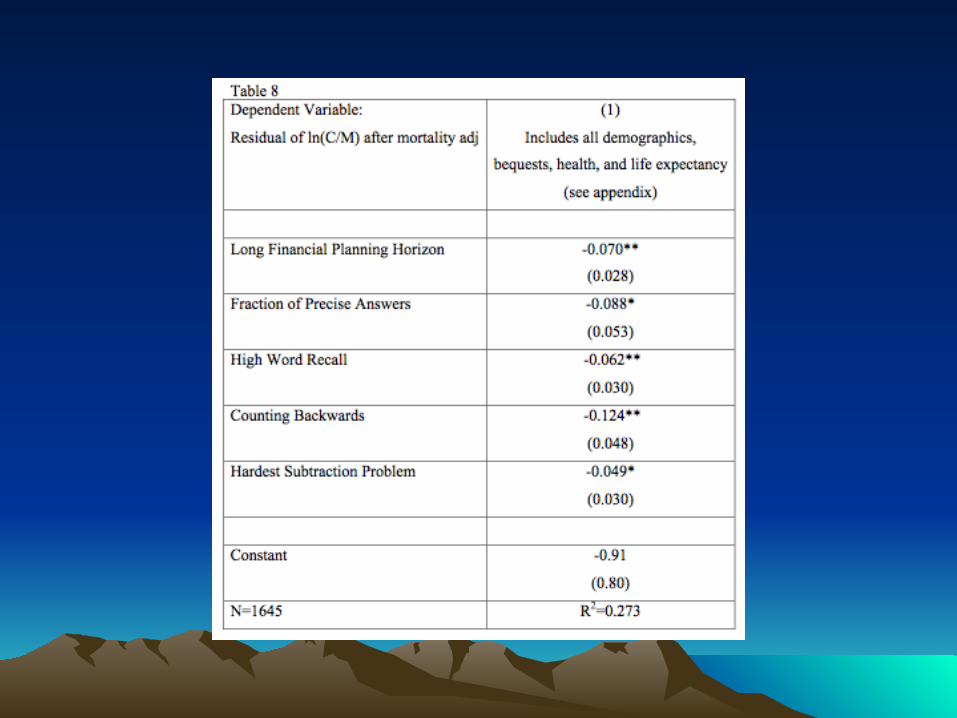

Laurie Pounder (2006): High and Low Savers? Laurie Pounder (2006): High and Low Savers? Circumstances, Patience and Cognition Circumstances, Patience and Cognition

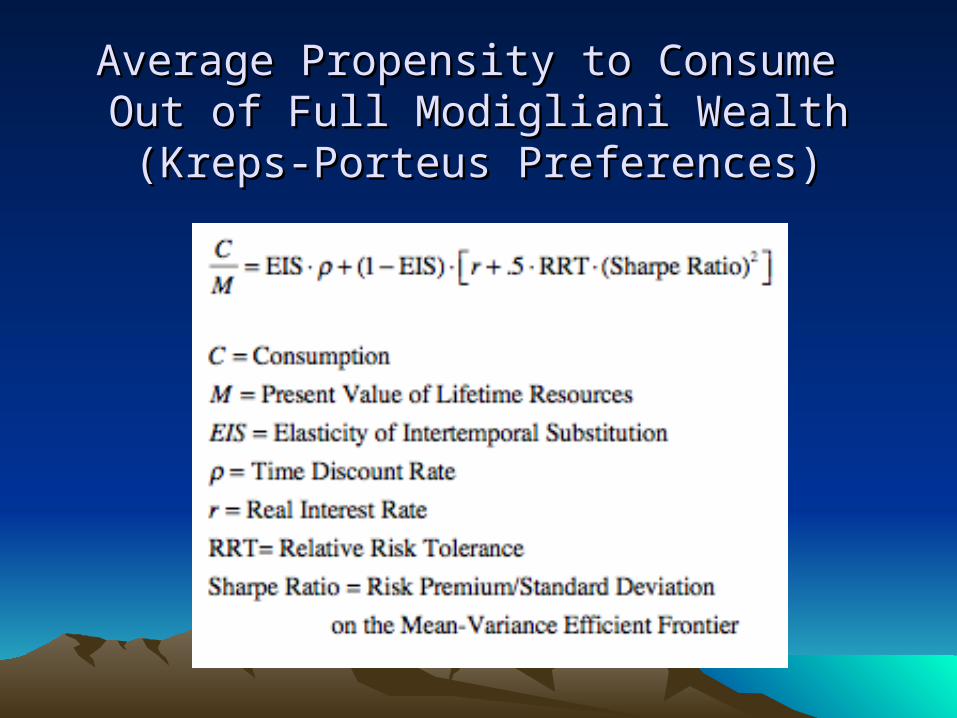

Average Propensity to Consume Average Propensity to Consume Out of Full Modigliani WealthOut of Full Modigliani Wealth(Kreps-Porteus Preferences)(Kreps-Porteus Preferences)