Embed Size (px)

Citation preview

COLLIERS INTERNATIONALTownsville Residential Research Report

Quarter 3, 2007Residential year in review 2007

2007 was the year Townsville was named Best Australian Regional Investment hotspot by Colliers International at their annual Regional Expo in Sydney and Brisbane. Townsville is the largest population centre in North Queensland and in 2007 a robust economy, strong jobs growth, solid household incomes and a tight residential vacancy rate, helped the Townsville region produce a scintillating median house price growth rate. This was despite two interest raterises late in 2007.

Multiple factors have encouraged investors, upgraders and national developers to the Australian Mediterranean in 2007.

www.colliers.com/townsville

Houses 2007

The combination of a wealth and incomes effect saw minor impact at the top end of the market. Upgraders, those that invested even as late as last year, benefited from this wealth effect and have remained active in the market. According to REIQ annualised Median House prices have grown by around 25% for the year to September 2007. Strong growth occurred in the CBD fringe suburbs of South Townsville (36%), West End (34%) and Hyde Park (31%). In Thuringowa median prices grew by around 20% with the tree change suburbs of Black River (34.6%) and Bluewater (33%) benefiting most. Kirwan remained the dominant suburb for total sales in Greater Townsville.

Units 2007

The Joh economic prosperity index (cranes on buildings) is alive in Townsville with multiple cranes working the local skyline. Mirvac entered the Townsville market in August and reportedly sold 93 units over one weekend. Annual Median Unit prices have grown, driven by increased construction costs and investors capacity to afford increased prices.

Land 2007

Castle Hill exploded onto the market in July with the BMD offer selling out in nine hours. Annual Median land prices have grown, driven by tight supply conditions and demand for prestige locations. Price growth occurred strongly in the first part of the year especially for those localities that represented good value such as the new development in Deeragun.

All the local property researchers’ picked the growth potential in the Townsville market at the start of 2007 although the level of growth was unexpected. It will be interesting to see if next year can maintain the same stellar growth of 2007.

Residential Outlook 2008

Property in Greater Townsville had an amazing 2007 and the good news, if you own property, is that the trend should continue in 2008 although at a slower pace. The bad news is rental vacancy rates are probably going to tighten further in early 2008 and the Reserve Bank of Australia looks likely to maintain a tightening bias on interest rates in 2008. Continuing economic and population growth, incomes growth, employment opportunities and tight vacancy rates are expected to drive the residential property market in 2008.

Generally median house prices should trend up by the end of 2008, fuelled by demand and supply side pressures. Unit prices should also rise, fuelled mainly by supply side pressures, and land prices should experience some growth depending on quality, availability and location.

We expect prestigious and well positioned homes to outperform the market, fuelled by continued wealth and incomes growth and affordable Unit and Land developments close to new facility impact zones to also perform well.

COLLIERS INTERNATIONALTownsville Residential Research Report

Quarter 3, 2007

www.colliers.com/townsville

Indicator Expected growth range

Total number of sales -10% to -15%

Median House Prices 7% to10%

Median Unit Prices 4% to 10%

Land Prices 4% to 10%

Gross Residential Yields 0.0% to 0.5%

Population growth 1.7% to 2.5%

Economy 7.5% to 10%

With a tight residential rental vacancy rate in Townsville, rental yields are likely to remain solid. Some University students will potentially struggle to find lodgings, with the closure of Western Halls. JCU Students will start to exert pressure on the rental market by mid to late January and place pressure on an already tight rental market. At Colliers International Residential Rentals our vacancy rate is below 1% and our arrears rate is also below 1%.

Interest rates are likely to maintain a dominant position on the economic landscape in 2008 and although there is a chance of interest rates increasing; international financial markets are still accounting for the US sub prime fallout. Some economists suggest the RBA may adopt a more cautious approach to further rate rises. The Greater Townsville property market is likely to adopt more of a solid performance in 2008 with some sectors performing better than others.

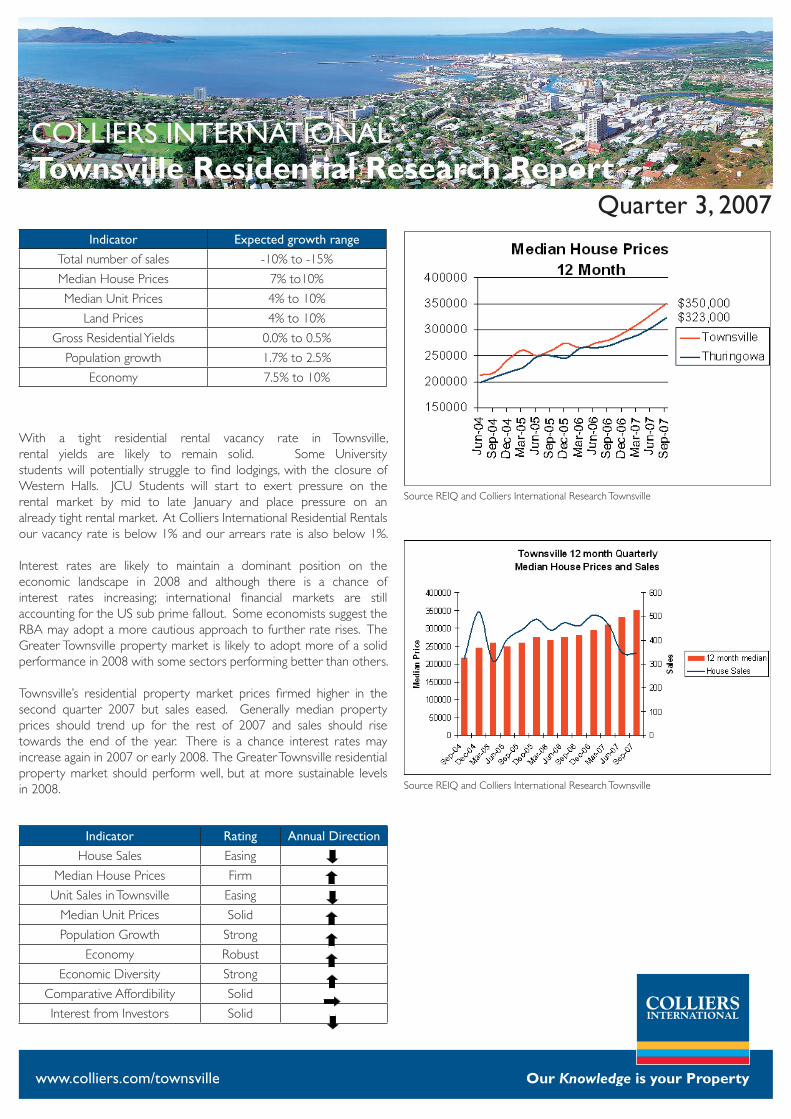

Townsville’s residential property market prices firmed higher in the second quarter 2007 but sales eased. Generally median property prices should trend up for the rest of 2007 and sales should risetowards the end of the year. There is a chance interest rates may increase again in 2007 or early 2008. The Greater Townsville residential property market should perform well, but at more sustainable levelsin 2008.

Indicator Rating Annual Direction

House Sales Easing

Median House Prices Firm

Unit Sales in Townsville Easing

Median Unit Prices Solid

Population Growth Strong

Economy Robust

Economic Diversity Strong

Comparative Affordibility Solid

Interest from Investors Solid

Source REIQ and Colliers International Research Townsville

Source REIQ and Colliers International Research Townsville

COLLIERS INTERNATIONALTownsville Residential Research Report

Quarter 3, 2007

www.colliers.com/townsville

House Prices

The median price paid for houses in Townsville in the 12 months to September 2007 was $350,000, up 25% for the year. In Thuringowa the median house price was $323,000, up 20% for the year.

Source REIQ and Colliers International Research Townsville

Tree Change

Official September Quarter 2007 annual median prices for acreage properties in Thuringowa continue to soar, 20.5% for the year. According to official data, for September Quarter 2007, Thuringowa acreage property has achieved solid growth over the year. Those suburbs that have performed well in annual median house prices terms include Blue Water Park (33%), Black River (34.6%) and Kelso (27.4%).

Tree Change suburbs median house price growth

SuburbMedian house Price Annualised

Sept Qtr 2007

ALICE RIVER ~ $ 412,500

BLACK RIVER ~ $ 379,500

KELSO ~ $ 414,000

Source REIQ and Colliers International Research Townsville~Varying quality of stock

House Demand

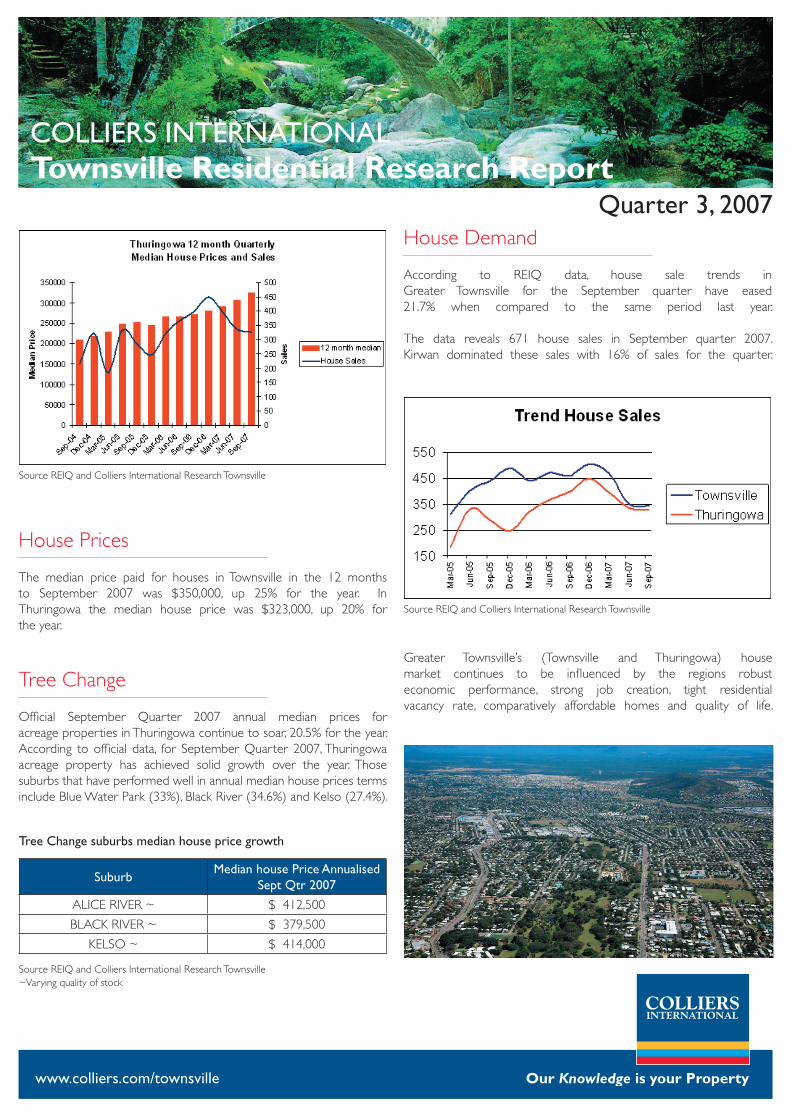

According to REIQ data, house sale trends in Greater Townsville for the September quarter have eased 21.7% when compared to the same period last year.

The data reveals 671 house sales in September quarter 2007. Kirwan dominated these sales with 16% of sales for the quarter.

Source REIQ and Colliers International Research Townsville

Greater Townsville’s (Townsville and Thuringowa) house market continues to be influenced by the regions robust economic performance, strong job creation, tight residential vacancy rate, comparatively affordable homes and quality of life.

COLLIERS INTERNATIONALTownsville Residential Research Report

Quarter 3, 2007Units

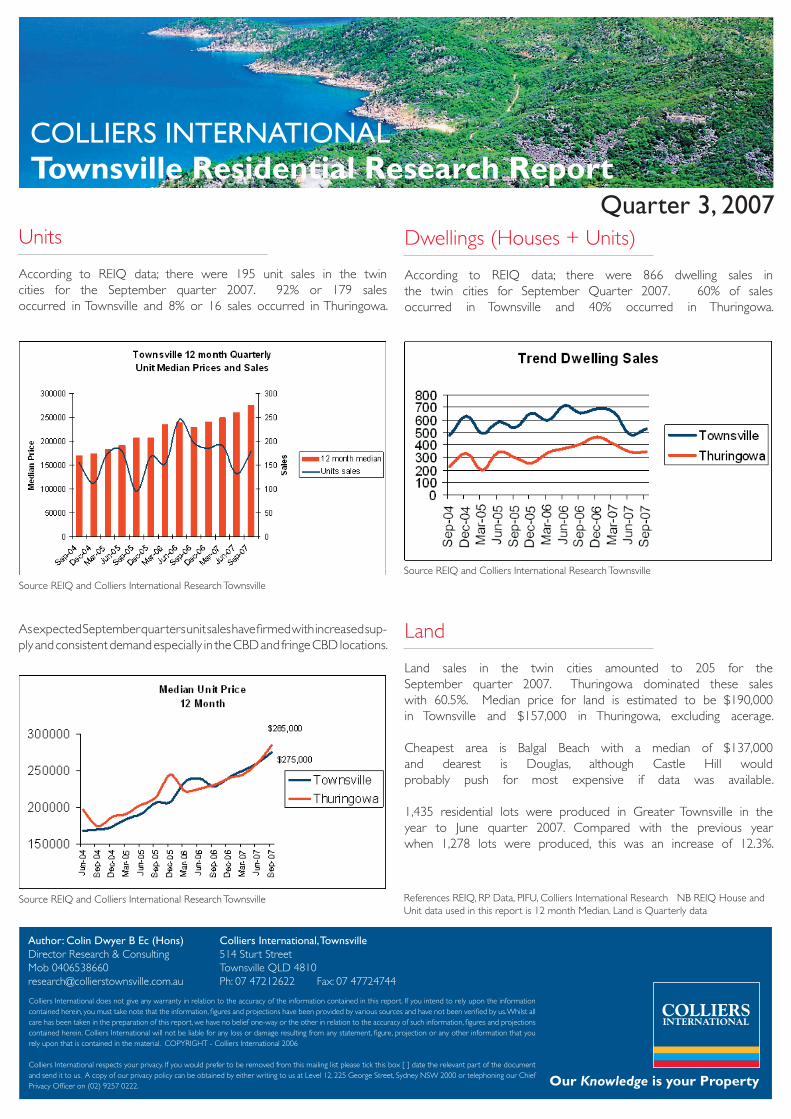

According to REIQ data; there were 195 unit sales in the twin cities for the September quarter 2007. 92% or 179 sales occurred in Townsville and 8% or 16 sales occurred in Thuringowa.

Source REIQ and Colliers International Research Townsville

As expected September quarters unit sales have firmed with increased sup-ply and consistent demand especially in the CBD and fringe CBD locations.

Source REIQ and Colliers International Research Townsville

Dwellings (Houses + Units)

According to REIQ data; there were 866 dwelling sales in the twin cities for September Quarter 2007. 60% of sales occurred in Townsville and 40% occurred in Thuringowa.

Source REIQ and Colliers International Research Townsville

Land

Land sales in the twin cities amounted to 205 for the September quarter 2007. Thuringowa dominated these sales with 60.5%. Median price for land is estimated to be $190,000 in Townsville and $157,000 in Thuringowa, excluding acerage.

Cheapest area is Balgal Beach with a median of $137,000 and dearest is Douglas, although Castle Hill would probably push for most expensive if data was available.

1,435 residential lots were produced in Greater Townsville in the year to June quarter 2007. Compared with the previous year when 1,278 lots were produced, this was an increase of 12.3%.

References REIQ, RP Data, PIFU, Colliers International Research NB REIQ House and Unit data used in this report is 12 month Median. Land is Quarterly data

Author: Colin Dwyer B Ec (Hons) Colliers International, Townsville Director Research & Consulting 514 Sturt StreetMob 0406538660 Townsville QLD [email protected] Ph: 07 47212622 Fax: 07 47724744

Colliers International does not give any warranty in relation to the accuracy of the information contained in this report. If you intend to rely upon the information contained herein, you must take note that the information, figures and projections have been provided by various sources and have not been verified by us. Whilst all care has been taken in the preparation of this report, we have no belief one-way or the other in relation to the accuracy of such information, figures and projections contained herein. Colliers International will not be liable for any loss or damage resulting from any statement, figure, projection or any other information that you rely upon that is contained in the material. COPYRIGHT - Colliers International 2006

Colliers International respects your privacy. If you would prefer to be removed from this mailing list please tick this box [ ] date the relevant part of the document and send it to us. A copy of our privacy policy can be obtained by either writing to us at Level 12, 225 George Street, Sydney NSW 2000 or telephoning our Chief Privacy Officer on (02) 9257 0222.