Embed Size (px)

DESCRIPTION

Community Bankers of Iowa monthly newsletter

Citation preview

OFF

ICIA

L P

UB

LIC

ATI

ON

OF

THE

CO

MM

UN

ITY

BA

NK

ERS

OF

IOW

AD

ECEM

BER

201

5

2 COMMUNITY BANKER UPDATE | DECEMBER 2015

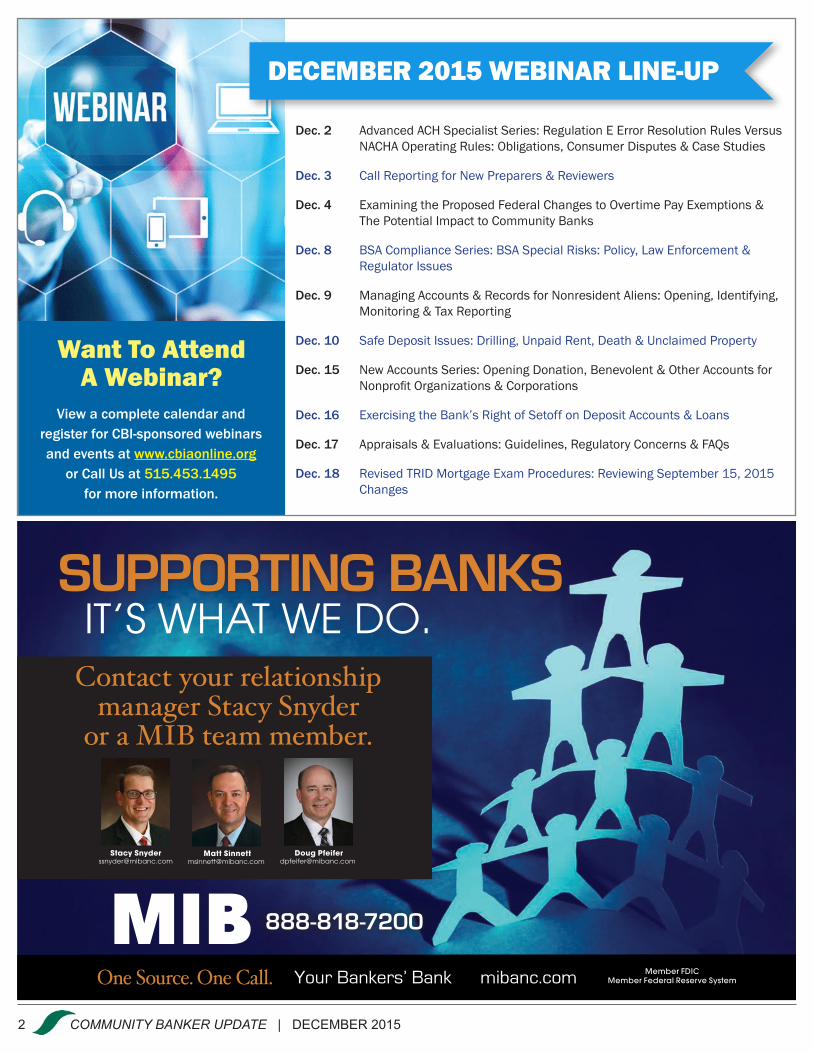

Want To AttendA Webinar?

View a complete calendar andregister for CBI-sponsored webinarsand events at www.cbiaonline.org

or Call Us at 515.453.1495for more information.

Member FDIC Member Federal Reserve SystemOne Source. One Call.

SUPPORTING BANKSIT’S WHAT WE DO.

Your Bankers’ Bank mibanc.com

888-818-7200

Matt [email protected]

Doug [email protected]

Stacy [email protected]

Contact your relationship manager Stacy Snyder

or a MIB team member.

Dec. 2 AdvancedACHSpecialistSeries:RegulationEErrorResolutionRulesVersus NACHAOperatingRules:Obligations,ConsumerDisputes&CaseStudies

Dec. 3 CallReportingforNewPreparers&Reviewers

Dec. 4 ExaminingtheProposedFederalChangestoOvertimePayExemptions& ThePotentialImpacttoCommunityBanks

Dec. 8 BSAComplianceSeries:BSASpecialRisks:Policy,LawEnforcement& RegulatorIssues

Dec. 9 ManagingAccounts&RecordsforNonresidentAliens:Opening,Identifying, Monitoring&TaxReporting

Dec. 10 SafeDepositIssues:Drilling,UnpaidRent,Death&UnclaimedProperty

Dec. 15 NewAccountsSeries:OpeningDonation,Benevolent&OtherAccountsfor NonprofitOrganizations&Corporations

Dec. 16 ExercisingtheBank’sRightofSetoffonDepositAccounts&Loans

Dec. 17 Appraisals&Evaluations:Guidelines,RegulatoryConcerns&FAQs

Dec. 18 RevisedTRIDMortgageExamProcedures:ReviewingSeptember15,2015 Changes

DECEMBER 2015 WEBINAR LINE-UP

COMMUNITY BANKER UPDATE | DECEMBER 2015 3

Community Bankers of Iowa1603 22nd St, Suite 102

West Des Moines, Iowa 50266Phone: [email protected]

In This IssueDecember2015WebinarLineup.................................2

CommunityBankersforComplianceProgram............4

2016CBIWebinars.......................................................5

IsYourInvestmentProgramSuccessful?....................6

ICBA&DellAnnouncePurchasingProgram................7

FromtheTop..................................................................8

FinePoints.....................................................................9

RuralMainstreetSurvey.......................................10-12

ValuingtheValue........................................................ 13

HAPPY HOLIDAYSThe Board of Directors of Community Bankers of Iowa,

Community Bankers Services and Insurance, the Community Bankers Education Foundation and the Community Bankers Political Action Committee would like to wish each and every

one of you a Happy Holiday season and a great 2016.

Your association has steadfastly defended and advocated for the unique needs of community banks since it’s inception, and

2015 was no exception. Thousands of community bankers attended your networking meetings, education, compliance

and certification seminars, webinars and Annual Management Conference, reinforcing the desire of community bankers to

keep the community banking model intact and alive.

2016 will present new challenges no doubt. But working together we will not only survive; we will prosper. Your CBI staff will be

ready, willing and enthusiastic. Again, Happy Holidays!

Don HoleEVP/CEO

Jackie HaleyMembership Services Director

Krissy LeeCommunications Director

Pretty PatelOperations Manager

Adrenaline

Welcome NewCBI Member!

The Community Bankers of Iowawould like to welcome the following

company to the association, and thank them for their support:

4 COMMUNITY BANKER UPDATE | DECEMBER 2015

Robb Nielsen (717) 369-0139 • [email protected]

www.protectmybank.com

• InformationSecurityAudit

• DesignedExclusivelyforBanks

• SimilarScope&ApproachasBankRegulators

• DeterminesAdequacyofSecurityControls

• FreeAccesstoanAutomatedRemediationTrackingTool

• VerifiesCompliancewithExistingBankPolicyandProcedures

• Savemoneybybundlingtheseservices

InformationSecurity Audit Bundle

• Penetration Test

• Vulnerability Assessment

• Social Engineering

Endorsed by:

Partner with us.Our correspondent bankers will get you clear answers and fast decisions. As your partner, we will help you enhance your customer relationships. As your bank grows, we’ll help you meet your needs.

Together,let’s make it happen.

bellbanks.com

Call me at 605.201.1864

Member FDIC

1090

7

Commercial and ag participation loans | Bank stock & ownership loans | Bank building financing | Business & personal loans for bankers

10907 CORR AD Community Bankers of Iowa.indd 1 9/15/15 11:03 AM

Today’scommunitybankcomplianceofficerischargedwithstayingcurrentwithallthecompliancerulesandregulationsandmakingsuretheyarebeingusedeffectivelywithinthebank.For13years,theCommunityBankersofIowahaspartneredwithYoung&AssociatestoofferCommunityBankersforCompliance(CBC),aprogramthatoffersthetoolsandinformationneededtoimplementcompliancethroughoutyourbank.Thecomplexityofregulatorychangesmakesitcriticalthatyourcomplianceofficerisreadytodealwiththesechangesastheyoccur.

TheCBCprogramisthemostsuccessfulandlongestrunningcompliancetrainingprograminthecountryandprovidesup-to-dateinformationoncomplianceissuesanddevelopmentsinbankregulations,aswellasproventechniquesformaintainingyourin-bankcomplianceprogram.Havingreceivedapprovalfromregulatoryagencies,theprogramhasbeeninstrumentalinhelpingover2,000communitybankersacrossthenationdevelopanincreasedunderstandingandabilitytodealwithregulatoryissues.

AnnualmembershiptotheCBCProgramincludesfiveinter-relatedcomplianceservices:

1. Live Regulatory Seminars.Twoliveseminarsareprovidedthroughouttheyear.Adetailedmanualisprovidedtoeachparticipant.

2. Webcasts - Regulatory Update.Fourregulatoryupdate

sessionsarepresentedinwebcastformatonseparatedays.Eachwebcastdiscussescurrentnewsandregulatorychangesthatmayhaveanimpactoncommunitybanks.Eachwebcastwillbe1.5hours,includingquestionsandanswers.Adetailedmanual,writteninfullnarrative,willbeprovided.

3. Monthly Newsletter.TheComplianceUpdatenewsletterissenttoprogrammemberseachmonth.Itprovidesanupdateofcomplianceissuesthatimpactcommunitybanks.

4. Compliance Hotline.MembersoftheprogrammayvisitYoung&Associates’websiteorcalltheirtoll-freenumberforcomplianceofficerquestionsthatariseonadailybasis.Thisserviceensuresthatyourbankisjustaphonecallawayfromtheinformationyouneedinordertoansweryourcompliancequestions.

5. CBC Members-Only Web Page.ThisdedicatedwebpageisreservedforbanksthatareregisteredmembersoftheCommunityBankersforComplianceProgram.Inityouwillfindspecialandtimelyinformationandtoolsthatcanbeusedtoenhancetheregulatorycompliancefunctionatyourbank.

FormoreinfoortoregisterfortheCommunityBankersforComplianceprogram,visitourwebsiteatcbiaonline.orgorcontactPrettyPatelat515.453.1495orppatel@cbiaonline.org.

Be Prepared for Upcoming Compliance Changes:Enroll in the Community Bankers for Compliance Program

COMMUNITY BANKER UPDATE | DECEMBER 2015 5

CBI Offers Over 120 Webinars, New Series for 2016Get Affordable, Professional Training When and Where You Choose

CBIoffersover120webinarsannuallythathavebecomeoneofthemostpopulartrainingdeliverysystemsamongcommunitybankers.Coveringcriticalissuesforeverylevelofthefinancialinstitution,industryexpertswithlong-term,real-life,hands-onexperiencedeliverhighqualitywebinarsthatareexclusivelytailoredforcommunitybankers.Topicsrangefromauditing&accounting,collections,compliance,HR,lendingandmore.Alsoofferedarespecializedseriesfordirectors,emergingleaders,callreportsandcybersecuritytonameafew.

In2016CBIwillofferfiveNEWwebinarseriesinadditiontothepopularDirectorsSeriesandEmergingLeadersSeriesofwebinars!Theseinclude:AuditComplianceSeries,CallReportSeries,CyberSeris,DebtCollectionSeriesandHRSeries.VisittheWebinarssectionatwww.cbiaonline.org/webinars.htmlformoredetailsoneachoftheseinformativewebinartopics.

CBIwebinarshavethreeregistrationoptions:1. LIVE WEBINAR.Thelivewebinaroptionallowsyoutohaveone

Internetconnectionfromasinglecomputerterminal.Youmayhaveasmanypeopleasyoulikelistenandwatchfromyourofficecomputer.Registrantsreceiveawebsiteaddressandpasscodethatwillallowentrancetotheseminar.Thesessionwillbeapproximately90minutes,includingquestionandanswersessions.Seminarmaterials,includinginstructions,passcode,andhandoutswillbeemailedtoyoupriortothebroadcast.Youwillneedthemost-currentversionofAdobeReader,availablefreeatwww.adobe.com.

2. ARCHIVED WEBINAR.Can’tattendthelivewebinar?Thearchivedwebinarisarecordingoftheliveevent,includingaudio,visuals,andhandouts.Weevenprovidethepresenter’semailaddresssoyoumayaskfollow-upquestions.Approx.oneweekpriortothewebinar,youwillreceiveanemailwiththearchivedwebinarlink.Thiswebinarlinkcanbeviewedanytime24/7,beginning6businessdaysafterthewebinarandwillexpire6monthsaftertheliveprogramdate.Youwillalsoreceiveinstructionsonhowtodownloadadigitalcopyofthewebinarwhichyoumaykeepanduseindefinitely.Thearchivedwebinar/digitaldownloadmayONLYbeorderedfor6monthsfollowingthewebinar.Itwillnotbeavailableafterthistime.YoucanalsolistentoarchivedwebinarsonyouriPad,iPhone,orAndroiddevice!

3. BOTH LIVE WEBINAR & ARCHIVED WEBINAR LINK.Options1and2describedabove.

NEW IN 2016,archivedwebinarswillnowbeavailableonarchivedlinksandnolongerbeofferedonCD-ROMs.CDswillnotbeavailableforany2015archivedwebinarsorderedafter12/31/15.

Formoreinformationandtoviewcurrentwebinarofferings,visitourEventsCalendaratwww.cbiaonline.org.Toviewall2016offeringsvisittheWebinarssectionatwww.cbiaonline.org/webinars.htmlanddownloadaschedule.Acompletesetoflistingscanalsobefoundinthe2016CBIAnnualPlannerandResourceGuide,comingtoCBImembersinlateDecember.

Plan Your 2016 Online Education Program!

Visit the Webinars section at cbiaonline.org for current listings, or to view and download a scheduled of all

2016 CBI webinar offerings. Find it at:

www.cbiaonline.org/webinars.html

6 COMMUNITY BANKER UPDATE | DECEMBER 2015

Thequestionissimpleenough,buttheanswerisalittlemorecomplex.Howdoesacommunityfinancialinstitutiontrulyknowhowtheirin-houseinvestment

programfaresagainstitscompetitors?Thisneed-to-knowquestionisbecomingmoreandmoreimportanttocommunitybankersasthebankinglandscaperemainshighlycompetitiveandcontinuestoconsolidate.Thesearchformorenoninterestincomeisasimportantasithaseverbeen,whichmakesmeasuringyourprogramandensuringitisimpactingyourbottomlinesignificantlyiskey.Whilegrossrevenuesandpre-taxcontributionsareobviousmeasuresofperformance,thesefiguresdonotalwaysrepresentthefullpictureofinvestmentprogramsuccessorlackthereof.Oneofthemostwidelyacceptedandprovenmethodologiestomeasurethesuccessofyourinvestmentprogramisbasedonabank’sdepositbase.Calculatingtherevenuesgeneratedfromanin-housebrokerageprogrampermillionofretailbankdepositscreatesaperformancemetricthatallowscommunitybanksofvariedsizetobeevaluatedonalevelplayingfield.Incombinationwithgrossrevenueandpretaxcontributions,thiscalculationisafull-scope,accuratewayofknowingwhetherornotyourinvestmentprogramiscompetitive.

AnalysisofSeptember2015callreportdataforthosebanksbetween$100millionand$10billionintotalassetsshowsthatbanksthatreportedmorethan$10,000inbrokerageandannuityrevenuesovertheprior12monthsaveraged$835ofbrokeragerevenuepermillionindeposits1.Inotherwords,aninstitutionwith$250millioninretaildepositsgenerated,onaverage,$208,750ininvestmentprogramrevenue.

Topquartilebanksinthesamecategorygenerated$2,119ofbrokeragerevenuepermillionofdeposits1,or$529,750inaverageprogramrevenueifusingthepreviouslymentioned$250millionbankcase.

Notsurprisingly,thedatasetofbanksreportingmorethan$10,000inbrokerageandannuityrevenuesgeneratesignificantlymoreinnoninterestincomethanthosewithlittleornorevenuesfromaninvestmentprogram.Thesebanksreportmorethan16percenthighernoninterestincomenumbersthanbankswithoutbrokeragerevenues.

Howmuchshouldthepre-taxcontributionbefromtheserevenues?WithfirmslikeInvestmentProfessionals,Inc.offeringprogramstructuremodelsallowingbankstoearnaflatpercentageofrevenues,withlittleoverhead,itisreasonabletoprojectanetequaltoapproximately25percentofgrossrevenues.

Thequestioncommunitybankersshouldbeaskingthenbecomes,“Ismyprogramsuccessful,anddoesourbroker-dealer’sprogramstructureallowustogainmaximumrevenue?”

Broker-dealersthatspecializeinworkingwithcommunitybanksshouldnotonlyhavethecapabilitytoprovidethisinformationtotheirpartners,ideallywithbothinternalandnationalbenchmarks,theyshouldalsoreportittotheirpartnersregularlytoensurethebarisbeingmetandraised.

Since 1992, CBI Endorsed Member Investment Professionals, Inc. has assisted community banks with implementing profitable investment programs. For more information about how your investment program should perform, or the nondeposit income potential you could gain, contact Tara Tagle at (800) 679-1237.

Provided by Investment Professionals, Inc.

Is Your Investment Program Successful?The Answer May Surprise You!

Bank Architecture

& ConstructionPre-design

Master PlanningSite Development

ArchitectureProject Management

ConstructionPost-project SupportSecurity & Signage

TrustPersonalityExperienceIntegrityTeamwork

Steph Weiand (L) Suzanne Meyers (C) Jim Christensen (R)

112 W. Park Lane, Waterloo319-232-6554

Brokerage Revenues per $ million of Deposits

$835

Average

$2,119

Top QuartileSource: SNL Financial

COMMUNITY BANKER UPDATE | DECEMBER 2015 7

ICBAandDellhaveannouncedanagreementprovidingbenefitstocommunitybanks.Throughthisrelationship,CommunityBankersofIowamemberbankswillbeabletotakeadvantageofexclusive,preferredpricingoncomputerequipmentsuchasworkstations,laptops,printers,accessoriesandmore.“ItisimportanttohavetechnologyinplacethateffectivelyhelpsIowacommunitybanksandcustomersthrive,”saidCBIExecutiveVicePresident&CEODonHole.“Byhavingcurrentcomputerequipmentintheirbanks,communitybankerscontinuetomeettheneedsoftheircustomersandbetterservetheirlocalcommunities.Throughthepurchasingagreement,CBImemberbankscanhaveconfidenceknowingtheyreceivedthebestpossiblepricingonvitalbusinessequipment.”Hardwarecoveredundertheagreementincludesworkstations,laptops,ultrabooks,desktops,servers,printers,electronicsandaccessoriesaswellasservicesandsoftware.CBImemberswillalsohaveaccesstoadedicatedaccountexecutivefamiliarwithICBA’sprogramwhowilladvocateforthemwithappropriateDellteams,includingtechnicalexpertsfromallofDell’sbrandsandproductlines.“Likeanybusiness,communitybanksrelyonqualitycomputinghardware,”saidICBAExecutiveVicePresidentofServicesDan

Clancy.“Thelaunchofthisprogramistimelybecausemanycommunitybanksmakefourth-quarterITandcomputerpurchases,andwiththeupcomingholidayseason,employeescanalsotakeadvantageoftheprogramfortheirpersonalpurchases.”“Accesstonewtechnologysolutionsthatsupportfuturegrowthiscriticaltocompaniesofallsizes,”saidDellExecutiveDirectorofGlobalMarketingGeraldineTunnell.“DellispleasedtoworkwithorganizationssuchasICBAandCBItohelpprovideanaffordableandconvenientwaytoacquirethetechnologysolutionstheyneedtogrowtheirbusinesses.”Formoreinformationandtotakeadvantageoftheprogram,visitwww.Dell.com/ICBA.Needhelp?CalltheMemberservicelineat1-800-757-8442tospeakwithaDellrepresentative.Whetherorderingonlineoroverthephone,remembertousetheuniqueCBI/ICBAMemberID#141351622.

IowaTIB Ad1/2 pg.April 2015

ICBA, CBI and Dell Announce Member Purchasing PlanGroup Buying Power Benefits Iowa’s Community Banks

8 COMMUNITY BANKER UPDATE | DECEMBER 2015

Go Local HolidaysWritten By: Jack Hartings, Chairman of ICBA

Ascommunitybankers,supportinglocalsmallbusinessissecondnature.Eventhoughweascommunitybankerssupportsmallbusinesseseverydayoftheyear,theholidaysprovideuswithauniqueopportunitytoputsmallbusinessesandourcommunitiesfrontandcenter.

ICBAmakesiteasyforyoutosharethepositivestoryofcommunitybanksandsmallbusinesseswithitsannualGoLocalHolidayscampaign.Thiscampaignoffersturnkeycommunicationsandmarketingmaterialsthatcanhelpyourteamspreadthemessageinyourcommunity.Withalocalpressrelease,op-ed,samplesocialmediapostsandmarketingideas,there’snostoppingtheGoLocalHolidaysmessagefromreachingsmallbusinesses,consumersandmediafromcoasttocoast.

ThinkofwhatwecoulddoifeverycommunitybankinthecountrygotintotheGoLocalHolidaysspirit?

That’swhyIencourageyourbanktoparticipateinGoLocalWednesdayonDec.16.Throughouttheday,ICBAemployees,communitybankersandconsumersfromacrossthenationwillvisitlocallyownedandoperatedbusinessesandrestaurantstosupportcommunityentrepreneursthisholidayseason.ICBAcontinuestohostGoLocalWednesdayonthethirdWednesdayofeverymonth,sothespiritofGoLocalcarriesthroughallyearlong.

ThisrangtrueformeasIwastalkingwithourmarketingdirectoraboutourplansforGoLocalHolidays.Withinminutes,shesentoverpicturesfrompastyearswhereweencouragedouremployeestovisitsmallbusinessesthroughoutthearea.WealwayspostourGoLocalHolidaysphotosonourFacebookpagetoshowcaseoursupportforsmallbusinessesduringtheseasonandalsoshowareaconsumersthattheycandothesame.It’sagreatwaytoengagewithourcustomersandthecommunity.

Wehavebranchesinsixdifferentcommunities.What’ssointerestingaboutourbank’sfootprintisthatwehavesuchawidevarianceincommunitycensusfrom500tomorethan10,000.Whileeachareaisunique,thesmallbusinesspresenceisalwaysthereandthriving.Asacommunitybank,wetakegreatprideinthat.

Sotoallmyfellowcommunitybanks,enjoytheholidaysandspreadthecheer.Ascommunitybankers,wehavesomuchtobethankfulfor,solet’scontinuetogivebacktoourcustomersandcommunitiesbyspreadingtheGoLocalmessagenowandthroughout2016.

Jack Hastings is Chairman of ICBA, and President and CEO of The People’s Bank in Coldwater, Ohio.

TOPFrom the

“Think of what we could do if every community bank in the country got into the Go Local Holidays spirit?”

Get more tips on Going Local, for the Holiday

Season and all year long!Visit our website for marketing

ideas and social media tips.Find Go Local resources at:

cbiaonline.org/go-local.html

COMMUNITY BANKER UPDATE | DECEMBER 2015 9

Everyindustryandmarketplaceisfacingsomemeasureofparadigm-shakingdigitaldisruptionthesedays.Amongthenewestfinancialindustrydisruptorsareonlinemarketplacelenders,thedeceptivelybenignnameforpotentiallypredatorynonbanklendingplatformsproliferatingontheInternet.Manyofthesetechnology-basedlendersaredigitallyslicked-upcreditprovidersofleastandlastresort.Noneofferaglimmerofrelationshipbankingwhatsoever.

Forseveralreasons,ICBAisconcernedabouttheriskstheseemergingcreditproviderscouldbespreading.Theirrisky,virtuallyunregulatedandrapidlyexpandinglendingistroubling—forborrowers,foroureconomy,forourfinancialsystem.ScionsofSiliconValleyandWallStreet,onlinemarketplacelendersareacreationoftoday’steemingpetridishofso-calledFinTechtechnologyinnovation.ThesenonbankfirmsrelyonpowerfulBigDatasoftwareenginestominetheInternetforinformationthatfeedblack-boxalgorithmstojustifytheirhigh-costloansandnearlyinstantaneouscreditapprovals.Speedistheirnoveltyandallure.Formanyconsumers,thecredittheyofferistooeasilyobtained—andtooeasilymisunderstood.

Oftentargetingthemostunsophisticatedanddesperateborrowers,onlinemarketplacelendersoffercaveatemptorcreditthatisunbridledbyanymainstreamregulatoryoversightorconstraints.Somesolelyserveconsumers.Otherscaterexclusivelytosmallbusinesses.Somespecializeinpayday,purchase-finance,educationormerchantcash-advancefinancing.VirtuallyallaredrivenbyWallStreetandhedgefundinvestorsimpatientlyseekingthebiggest,mostimmediateinvestmentreturns.Aborrower’sabilitytounderstandorrepaytheseloansistheleastmotivationforthesecompanies.

Moreover,theinherentrisksonlinemarketplacelenderscarryhaveanominouslyfamiliarpattern.Higherdefaultsarehardwiredintotheirassumptions.Theircomputer-generatedlendingtypicallyinvolveslittletonounderwriting.Nocollateralisinvolved.Thecreativelydisparate

datathesecompaniesrelyonhaveneverbeforesupportedwidespreadcreditdecisions.Theirobscurelendingpracticesareuntestedbyanyreasonablemeasureoftimeoreconomicstress.Andmirroringactivitiesduringthefinancialcrisis,somemarketplacelendersareaggressivelyoffloadingtheirloansintosecuritizedinvestmentvehiclesonWallStreet.

Yetdespitetheirtroublingcharacteristics,theselendersareproliferatinglikedigitaldandelions.Becauseofalloftheirrealdangers,ICBAissoundingawarningbell,andwemayaskcommunitybankerstohelpusinthefuture.Incommentlettersandindustryforums,wehaveencouragedTreasuryandotherpublicofficialstostudytheproducts,businessespracticesandrisksoftheselenders.Weareaskingthemtoconsiderwhateverregulationsarenecessarytoprotectconsumersandouroveralleconomy.Moreover,asanalternativetotheselenders,wearealsoaskingTreasuryofficialstoworkwithICBAtoeasetheconsiderableregulatoryburdensofcommunitybanksthatarediscouragingtheirtrulyproductive,responsiblelending.

Technologyandinnovationshouldbringprogressandsolveproblems,notspreadnewdangersorharm.Westillfeeltherecentpainbroughtbyactivitiestrumpetedasfinancialprogressthatsoonbecamefinancialscourges.Forourstill-recoveringcitizens,economyandcountry,ICBAemphaticallysaysneveragain.

A Digital DangerWrittenBy:CamdenFine,PresidentandCEOofICBA

FINEPOINTS

“For many consumers, thecredit [online lenders] offer is

too easily obtained -- andtoo easily misunderstood.”

Following Mr. FineMorethan1,000peoplearefollowingCamdenFine’stweets@Cam_Fine—areyou?Visitwww.twitter.com/cam_fine.

10 COMMUNITY BANKER UPDATE | DECEMBER 2015

November Survey Results at a Glance:• Forathirdstraightmonth,theRuralMainstreetIndexfell

belowgrowthneutral.• Retailsalescontinuetofallashousingpurchasesremain

healthy.• BankersestimatethatDodd-Frankhasincreasedcompliance

costsby34percentsince2010.• Approximately17percentofbankersindicatedthatnew

regulationshavecausedtheirbanktoeitherabandonorcutbackoncertaintypesofloans.

OMAHA,Neb.–TheCreightonUniversityRuralMainstreetIndexforNovemberfellfromOctober’sweakreading,accordingtoamonthlysurveyofbankCEOsinruralareasofa10-stateregiondependentonagricultureand/orenergy.

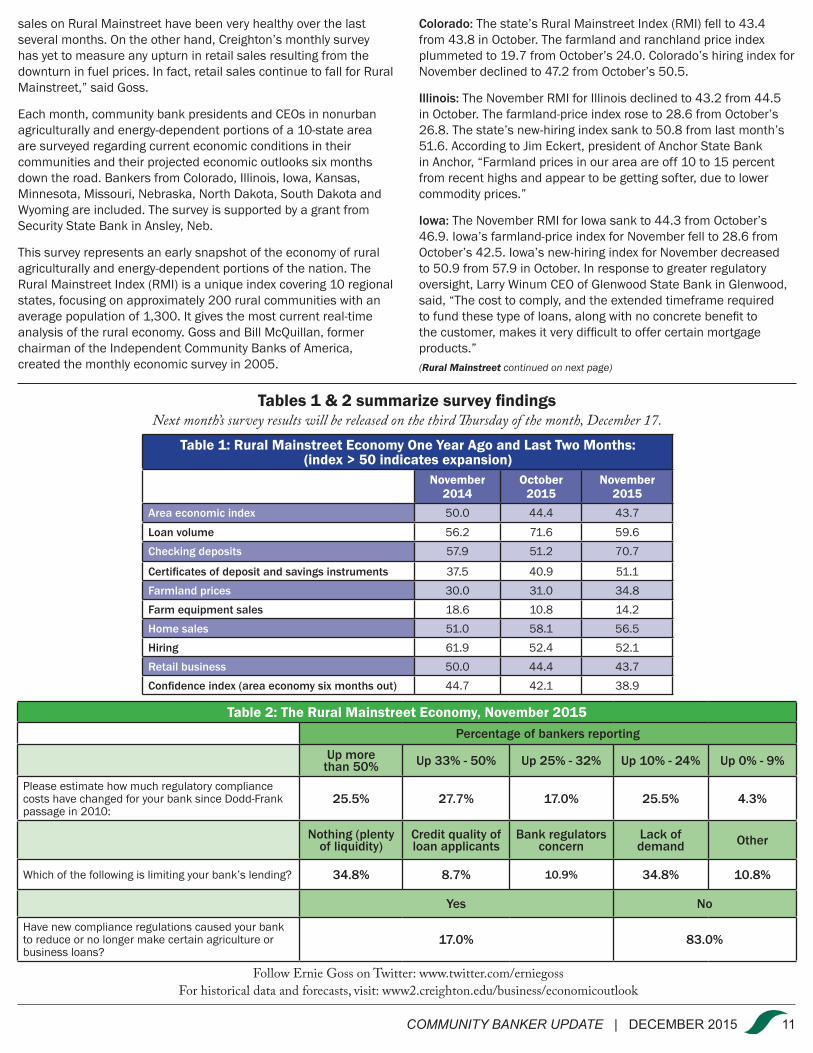

Overall:TheRuralMainstreetIndex(RMI),whichrangesbetween0and100,sankto43.7fromOctober’sweak44.4.

“Thisisthefourthstraightmonththeoverallindexhasdeclined,reflectingweaknessstemmingfromloweragricultureandenergycommoditypricesandfromdownturnsinmanufacturing,”saidErnieGoss,JackA.MacAllisterChairinRegionalEconomicsatCreightonUniversity’sHeiderCollegeofBusiness.

Farming and Ranching:ThefarmlandandranchlandpriceindexforNovemberroseto34.8from31.0inOctober.“Thisisthe24thstraightmonththeindexhasmovedbelowgrowthneutral.But,asinpreviousmonths,thereisagreatdealofvariationacrosstheregioninthedirectionandmagnitudeoffarmlandpriceswithpricesgrowinginsomeportionsoftheregion,”saidGoss.

Evenwithlowerfarmlandprices,morethanone-third,or34.8percent,ofbankersindicatedtheirbankshavesufficientliquidityandcontinuetolendtofarmersasdemanded.ThisproportiondifferslittlefromNovember2014.

TheNovemberfarmequipment-salesindexadvancedtoaveryweak14.2fromOctober’srecordlow10.8.“ThestrengtheningU.S.dollarandglobaleconomicweaknesshavepushedfarmcommoditypricesdownby14.1percentoverthepast12months.Theseweakerpriceshavediscouragedfarmersfrombuyingmoreagricultureequipmentandhavenegativelyaffectedtheagricultureequipmentdealersandmanufacturersintheregion.BankersremainpessimisticabouttheshortandintermediateprospectsforagricultureequipmentdealersandproducersonRuralMainstreet,”saidGoss.

Banking:TheNovemberloan-volumeindexsankto59.6fromlastmonth’s71.6.Thechecking-depositindexexpandedto70.7from

October’s51.2,whiletheindexforcertificatesofdepositandothersavingsinstrumentsdippedto38.9from40.9inOctober.

Thismonthbankerswereaskedtoassesstheimpactofthe2010Dodd–FrankWallStreetReformandConsumerProtectionActonthecompliancecostsfortheirbanksince.BankCEOsestimateDodd-Frankpushedupcompliancecostsbyanaverageof34percent.ThisisupfromNovember2014,whenbankersestimatedanincreaseof29.4percent.

ClarkLehr,presidentofFirstNebraskaBankinColumbus,Nebraska,said,“Compliancecostsamounttoabout20-25basispoints(quarterofapercentagepoint)ofournetinterestmargin.Wemadeabusinessdecisiontonotletitlimitourlendingopportunities.”

Approximately17percentindicatednewregulationshadcausedtheirbankstoreduce,ornolongermake,certaintypesofagricultureandbusinessloans.

AccordingtoPeteHaddeland,CEOoftheFirstNationalBankinMahnomen,Minnesota,“Thebankingbusinessisatthebreakingpointwithnewrulesandregulations.Itiscausingthesmallbankstoconsolidate.”

Manyofthebankersidentifiedhowregulations,whilewellintended,havegoneastray.LarryWinumCEOofGlenwoodStateBankinGlenwood,Iowasaid,“Insteadofbeingmoreunderstandable(i.e.regulations)tothecustomer,theyaremoreconfused.Fortunately,mostcommunitybankswillcontinuetodowhattheyalwaysdo–findawaytotakecareoftheircustomersbytreatingthemfairly,despitealltheadditionalregulatoryburden.”

Hiring:Despiteweakercroppricesandpullbacksfrombusinesseswithclosetiestoagricultureandenergy,RuralMainstreetbusinessescontinuetoaddworkerstotheirpayrollsbutataslightlylowerpace.Thehiringindexfelltoastill52.1from52.4inOctober.“RuralMainstreetbusinessescontinuetohireadditionalworkers,butatamuchslowerpacewithjoblossesforsomeareasintheregion,”saidGoss.

Confidence:Theconfidenceindex,whichreflectsexpectationsfortheeconomysixmonthsout,slidto38.9from42.1inOctober.“WeakerenergyandagriculturecommoditypricesstemmingfromthestrongU.S.dollarandglobaleconomicweaknesspushedbankers’economicoutlooklowerforthemonth,”saidGoss.

Home and Retail Sales:TheNovemberhome-salesindexslippedtoahealthy56.5from58.1inOctober.TheNovemberretail-salesindexdecreasedto43.7from44.4lastmonth.“Home

Main Street Economic Survey

C r e i g h t o nU N I V E R S I T Y

Rural Mainstreet Index Falls Below Growth Neutral for Third Straight Month: Retail Sales Fall, Home Sales Healthy

Ernie Goss

COMMUNITY BANKER UPDATE | DECEMBER 2015 11

salesonRuralMainstreethavebeenveryhealthyoverthelastseveralmonths.Ontheotherhand,Creighton’smonthlysurveyhasyettomeasureanyupturninretailsalesresultingfromthedownturninfuelprices.Infact,retailsalescontinuetofallforRuralMainstreet,”saidGoss.

Eachmonth,communitybankpresidentsandCEOsinnonurbanagriculturallyandenergy-dependentportionsofa10-stateareaaresurveyedregardingcurrenteconomicconditionsintheircommunitiesandtheirprojectedeconomicoutlookssixmonthsdowntheroad.BankersfromColorado,Illinois,Iowa,Kansas,Minnesota,Missouri,Nebraska,NorthDakota,SouthDakotaandWyomingareincluded.ThesurveyissupportedbyagrantfromSecurityStateBankinAnsley,Neb.

Thissurveyrepresentsanearlysnapshotoftheeconomyofruralagriculturallyandenergy-dependentportionsofthenation.TheRuralMainstreetIndex(RMI)isauniqueindexcovering10regionalstates,focusingonapproximately200ruralcommunitieswithanaveragepopulationof1,300.Itgivesthemostcurrentreal-timeanalysisoftheruraleconomy.GossandBillMcQuillan,formerchairmanoftheIndependentCommunityBanksofAmerica,createdthemonthlyeconomicsurveyin2005.

Colorado:Thestate’sRuralMainstreetIndex(RMI)fellto43.4from43.8inOctober.Thefarmlandandranchlandpriceindexplummetedto19.7fromOctober’s24.0.Colorado’shiringindexforNovemberdeclinedto47.2fromOctober’s50.5.

Illinois:TheNovemberRMIforIllinoisdeclinedto43.2from44.5inOctober.Thefarmland-priceindexroseto28.6fromOctober’s26.8.Thestate’snew-hiringindexsankto50.8fromlastmonth’s51.6.AccordingtoJimEckert,presidentofAnchorStateBankinAnchor,“Farmlandpricesinourareaareoff10to15percentfromrecenthighsandappeartobegettingsofter,duetolowercommodityprices.”

Iowa:TheNovemberRMIforIowasankto44.3fromOctober’s46.9.Iowa’sfarmland-priceindexforNovemberfellto28.6fromOctober’s42.5.Iowa’snew-hiringindexforNovemberdecreasedto50.9from57.9inOctober.Inresponsetogreaterregulatoryoversight,LarryWinumCEOofGlenwoodStateBankinGlenwood,said,“Thecosttocomply,andtheextendedtimeframerequiredtofundthesetypeofloans,alongwithnoconcretebenefittothecustomer,makesitverydifficulttooffercertainmortgageproducts.”(Rural Mainstreet continued on next page)

Tables 1 & 2 summarize survey findingsNext month’s survey results will be released on the third Thursday of the month, December 17.

Table 1: Rural Mainstreet Economy One Year Ago and Last Two Months: (index > 50 indicates expansion)

November2014

October2015

November2015

Area economic index 50.0 44.4 43.7

Loan volume 56.2 71.6 59.6Checking deposits 57.9 51.2 70.7

Certificates of deposit and savings instruments 37.5 40.9 51.1Farmland prices 30.0 31.0 34.8Farm equipment sales 18.6 10.8 14.2Home sales 51.0 58.1 56.5Hiring 61.9 52.4 52.1Retail business 50.0 44.4 43.7Confidence index (area economy six months out) 44.7 42.1 38.9

Table 2: The Rural Mainstreet Economy, November 2015Percentage of bankers reporting

Up morethan 50% Up 33% - 50% Up 25% - 32% Up 10% - 24% Up 0% - 9%

PleaseestimatehowmuchregulatorycompliancecostshavechangedforyourbanksinceDodd-Frankpassagein2010:

25.5% 27.7% 17.0% 25.5% 4.3%

Nothing (plenty of liquidity)

Credit quality of loan applicants

Bank regulators concern

Lack of demand Other

Whichofthefollowingislimitingyourbank’slending? 34.8% 8.7% 10.9% 34.8% 10.8%

Yes No

Havenewcomplianceregulationscausedyourbanktoreduceornolongermakecertainagricultureorbusinessloans?

17.0% 83.0%

Follow Ernie Goss on Twitter: www.twitter.com/erniegossFor historical data and forecasts, visit: www2.creighton.edu/business/economicoutlook

12 COMMUNITY BANKER UPDATE | DECEMBER 2015

(Rural Mainstreet continued from previous page)

Kansas:TheKansasRMIforNovemberincreasedto43.9fromOctober’s42.5.Thestate’sfarmland-priceindexforNovemberadvancedtoaveryweak28.8fromOctober’s21.8.Thenew-hiringindexforthestateclimbedto50.9from49.7inOctober.

Minnesota:TheNovemberRMIforMinnesotaslumpedto43.3fromOctober’s44.0.Minnesota’sfarmland-priceindexslumpedto28.5from34.2inOctober.Thenew-hiringindexforthestatedeclinedto50.8fromlastmonth’s52.9.

Missouri:TheNovemberRMIforMissouridippedto39.4from45.5inOctober.Thefarmland-priceindexexpandedto30.9fromOctober’s18.8.Missouri’snew-hiringindexexpandedto51.7fromOctober’s48.4.

Nebraska:TheNebraskaRMIforNovemberslumpedto40.1from45.2inOctober.Thestate’sfarmland-priceindexslippedto20.8fromOctober’s21.8.Nebraska’snew-hiringindexdeclinedto47.7from49.7inOctober.

North Dakota:TheNorthDakotaRMIforNovemberdecreasedtoaregionallowof31.3from34.8inOctober.Thefarmland-priceindexadvancedto37.0from17.8inSeptember.NorthDakota’snew-hiringindexdeclinedto31.0fromOctober’s37.7.

South Dakota:TheNovemberRMIforSouthDakotafellto46.9,aregionalhigh,fromOctober’s47.9.Thefarmland-priceindexsankto49.2from50.0inOctober.SouthDakota’snew-hiringindexinchedlowertoastillhealthy59.0fromOctober’s60.9.

Wyoming:TheNovemberRMIforWyomingslumpedto42.3fromOctober’s46.3.TheNovemberfarmlandandranchland-priceindexslippedto30.2from29.7inOctober.Wyoming’snew-hiringindexdippedto51.4fromOctober’s52.8.

“CBI’s LOT has been very beneficial to me, not only as a banker, but also as an individual. The group has shown me the ins and outs of the banking industry, but also has allowed me to grow as a leader in my bank, community and family. I can honestly tell you this has been oneof the most beneficial groups for me.”

LOT Member Matt MuellerThe State Bank, Spirit Lake

Leaders of Tomorrow

MaxiMize YourPotentialwithCBi’s

leadersoftoMorrow

Visit cbiaonline.org or call 515.453.1495 for information on becoming a member of CBI’s LOT program.

COMMUNITY BANKER UPDATE | DECEMBER 2015 13

Everyonehasadviceforcommunitybankersthesedays.Embracechange,betechforwardorlookmodern,somesay.Offerproductsandservicesonthecustomer’sterms,othersadvise,orperhapsmoreobscurely,beonewithyourcustomer.Befaster,cheaper,betterat(fillinalmostanyoperationoractivityhere).

Onemightwonderhowwe’vesurvivedasanindustrythislong.Withmorethanhalfofcommunitybanksoperatingformorethan100years,wemustbedoingsomethingright.Orisourindustrytrulyatatippingpointoftransformation?

Thecustomerenvironmenthasshiftedsignificantlyinthelastfiveyears.First,ourbestcustomersstartedaskingformorebecauseotherfinancialprovidersareaggressivelycourtingthem.Second,withmarginstight,spendingfordatamining,boldermarketinginitiativesandnewcustomeracquisitionisn’talwaysreadilyavailable.Third,it’stoughertodifferentiateourselvesinamarketplaceburgeoningwithunfairlyadvantagedcompetitors.

Thegoodnewsisthatbykeepingacloseeyeonotherindustries,smartcommunitybankmarketersareleadingthewaywithoutreinventingthewheel.Withallthisinmind,herearethreescenariosandquestionstoconsider.

Scenario:Youknowyourcustomersbyname—eventheirchildren’snames!Yourextendedservicehoursaccommodatetheirworkschedules.Yousupportlocalcausesthatarehighlyvisibleyetmeaningful.Yourlendingratesarecompetitiveandpostedwhereeveryonecanseethem.Yet,yourcustomersdrivecarsyoudidn’tfinance,liveinhousesyoudon’tholdthemortgageonanduseacreditcardthatdoesn’tincludeyourbank’slogo.

(Valuing the Value continued on next page)

Valuing the Value:Three questions about the changing customer environment

Written By: Chris LorenceEVP and Chief Marketing Officer, ICBA

14 COMMUNITY BANKER UPDATE | DECEMBER 2015

(Valuing the Value continued from previous page)

Ask yourself:Did you ask for their business or wait to be asked? It’sneveramistaketoremindallyourcustomers,evenfrequently,thatyouwantalltheirbusiness,nottojustholdtheircheckingaccount.Yes,sometimesyouneedtosayitverballyandnotassumetheyknow.

Scenario:Youplacelocalnewspaperadspromotingyourcompetitivelendingrates.You’vepurchasedradiospotswithcreatedcatchyjinglesthatpeoplerecognizeandsingalongtointhecar.Yourhighwaybillboardscan’tbemissed.Yet,youaren’tseeingabigboostinnewaccountsorlendingnumbers,atleastnotenoughtojustifythemarketingcosts.

Ask yourself:Is your marketing campaign aimed at the people you want to attract?Asmallercampaignwithaclearlydefinedaudiencewilllikelybringtheresultsyouseek.It’smoreimportantthanever

tohaveyourcampaignbecomprehensive,includingvisualsanddirect-mailmessagingthatresonatewithyourtargetcustomer.

Scenario:Youfindyourselfcompetingforbusinessyou’vealwaysthoughtwasneverupforgrabs.Creditunions,out-of-townbanks,FarmCreditSysteminstitutionsandevenonlinelendersaremakingitallabouttheinterestrate,andthat’swreakinghavoconyourbottomline.

Ask yourself: Are your customers valuing your value?Whatmightappeartobeabouttheinterestratemayactuallybeaboutconvenience,accessibility,termsorbecomingmoreanonymouswiththeirfinances.Yourcustomers’needsmayhaveshifted,socommunicatingthevalueofwhatyou’reofferingmighttoo.

Chris Lorence ([email protected]) is ICBA’s executive vice president and chief marketing officer.

CBI Members:Your 2016 Annual Planner & Resource Guide Is Coming Soon!

The2016CBIAnnualPlannerandResourceGuideisapowerfulreference,filledwithusefulfeaturesandinformationlikeCBImemberbenefits,ServicesandInsuranceproviders,Iowa

legislativecontacts,2016educationandwebinarlistings,aplanningcalendarwithascheduleofupcomingCBIevents,andmore!

AlsocontainedintheGuideisanInformationRequest/Updateform.PleaseusethisformtorequestinformationonCBIprograms,committees,peergroupsandmore,orjustupdate

yourCBIMembercontactinformation.Findtheformonpage15oftheGuide.

Watch your mailboxes for the 2016 Annual Planner and Resource Guide, arriving mid December 2015.

Call SHAZAM today.

Delivering Unlimited Possibilities

855-314-1212 | shazam.net | @SHAZAMNetwork

We believe community financial institutions must stay in control of their

future. Since 1976, we’ve been providing community financial institutions

with choice and innovation to compete in the market. From debit cards

to core processing to marketing services and more, we deliver.

SHAZAM is a financial services company offering you choice and flexibility to use the products and services that meet YOUR needs.

MET