Embed Size (px)

Citation preview

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Presenting a live 90-minute webinar with interactive Q&A

Construction Contract Waivers of

Subrogation, Indemnity and Contribution Navigating the Complexities and Pitfalls of Waiver Provisions for Contractors, Owners and Insurers

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, JULY 6, 2017

William E. Kelley, Jr., Partner, Drewry Simmons Vornehm, Carmel, Ind.

Peter Martin, Partner, Martin & Martin Law, Dallas

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-871-8924 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can

address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 35.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

WAIVERS OF

SUBROGATION Presented by: William E. Kelly and Peter Martin

Prepared by: Stephen Palley

Palley Law, PLLC

Waivers of Subrogation

• Basic principles:

• Common feature in commercial contracts.

• Often ignored until after all a claim arises.

• Scope can be broader than anyone realizes.

• They are WAIVERS • (“of subrogation”)

• State law varies widely

• Different rules may apply where litigated between

insurers, as opposed to insured v. insured.

6

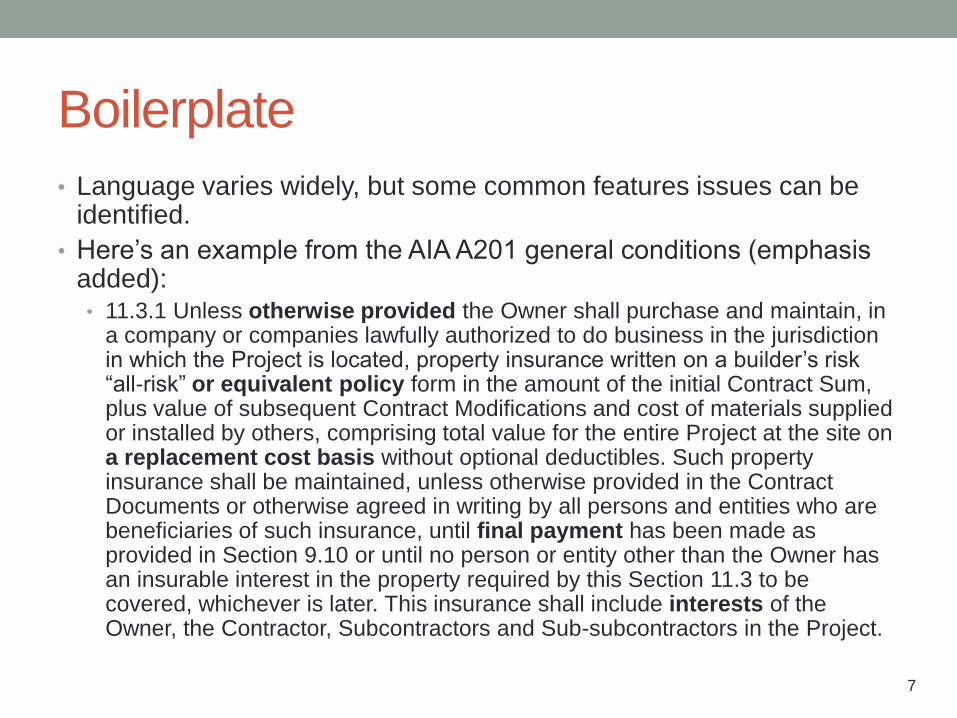

Boilerplate

• Language varies widely, but some common features issues can be identified.

• Here’s an example from the AIA A201 general conditions (emphasis added): • 11.3.1 Unless otherwise provided the Owner shall purchase and maintain, in

a company or companies lawfully authorized to do business in the jurisdiction in which the Project is located, property insurance written on a builder’s risk “all-risk” or equivalent policy form in the amount of the initial Contract Sum, plus value of subsequent Contract Modifications and cost of materials supplied or installed by others, comprising total value for the entire Project at the site on a replacement cost basis without optional deductibles. Such property insurance shall be maintained, unless otherwise provided in the Contract Documents or otherwise agreed in writing by all persons and entities who are beneficiaries of such insurance, until final payment has been made as provided in Section 9.10 or until no person or entity other than the Owner has an insurable interest in the property required by this Section 11.3 to be covered, whichever is later. This insurance shall include interests of the Owner, the Contractor, Subcontractors and Sub-subcontractors in the Project.

7

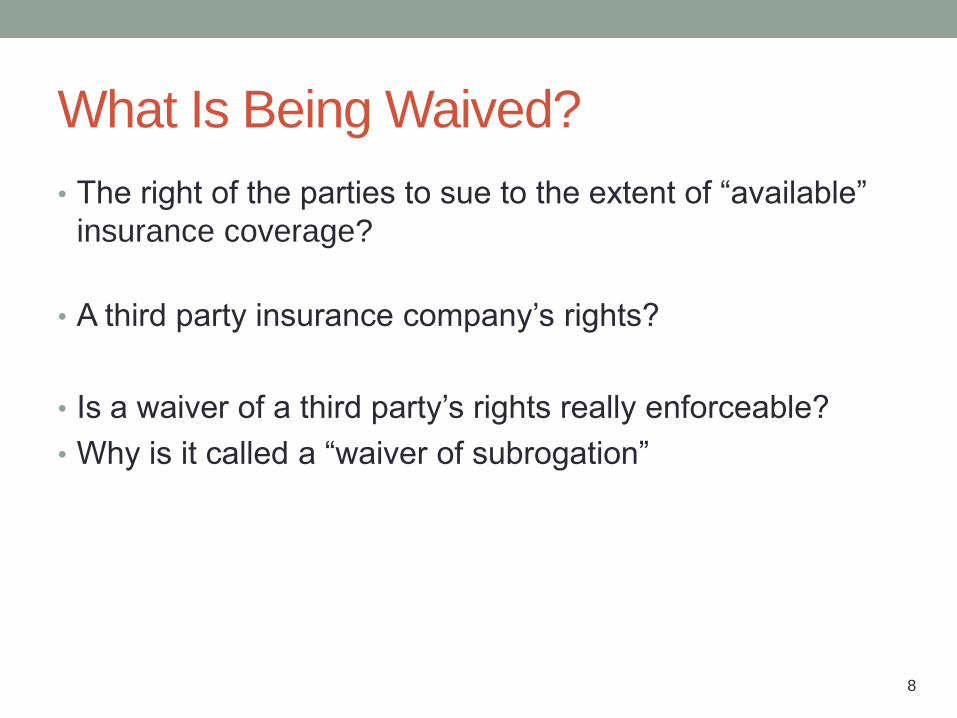

What Is Being Waived?

• The right of the parties to sue to the extent of “available”

insurance coverage?

• A third party insurance company’s rights?

• Is a waiver of a third party’s rights really enforceable?

• Why is it called a “waiver of subrogation”

8

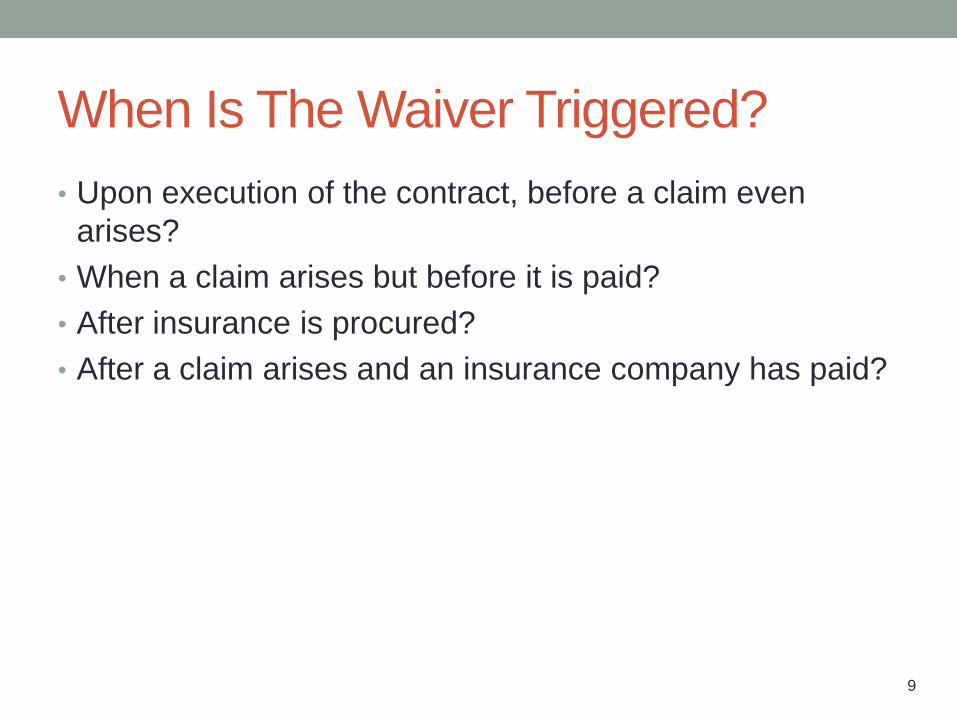

When Is The Waiver Triggered?

• Upon execution of the contract, before a claim even

arises?

• When a claim arises but before it is paid?

• After insurance is procured?

• After a claim arises and an insurance company has paid?

9

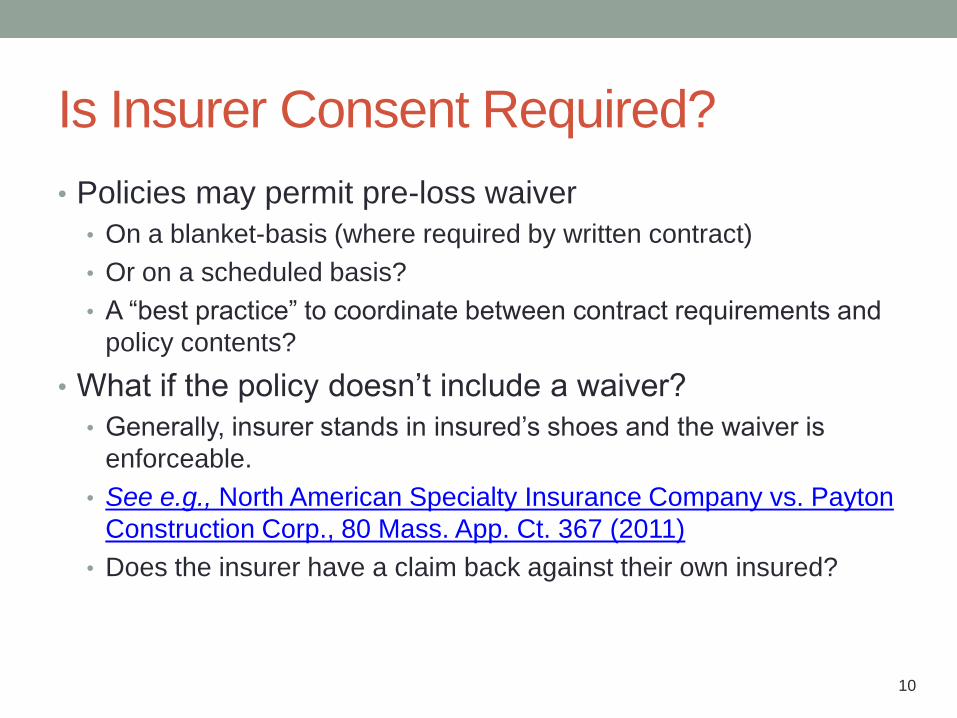

Is Insurer Consent Required?

• Policies may permit pre-loss waiver

• On a blanket-basis (where required by written contract)

• Or on a scheduled basis?

• A “best practice” to coordinate between contract requirements and

policy contents?

• What if the policy doesn’t include a waiver?

• Generally, insurer stands in insured’s shoes and the waiver is

enforceable.

• See e.g., North American Specialty Insurance Company vs. Payton

Construction Corp., 80 Mass. App. Ct. 367 (2011)

• Does the insurer have a claim back against their own insured?

10

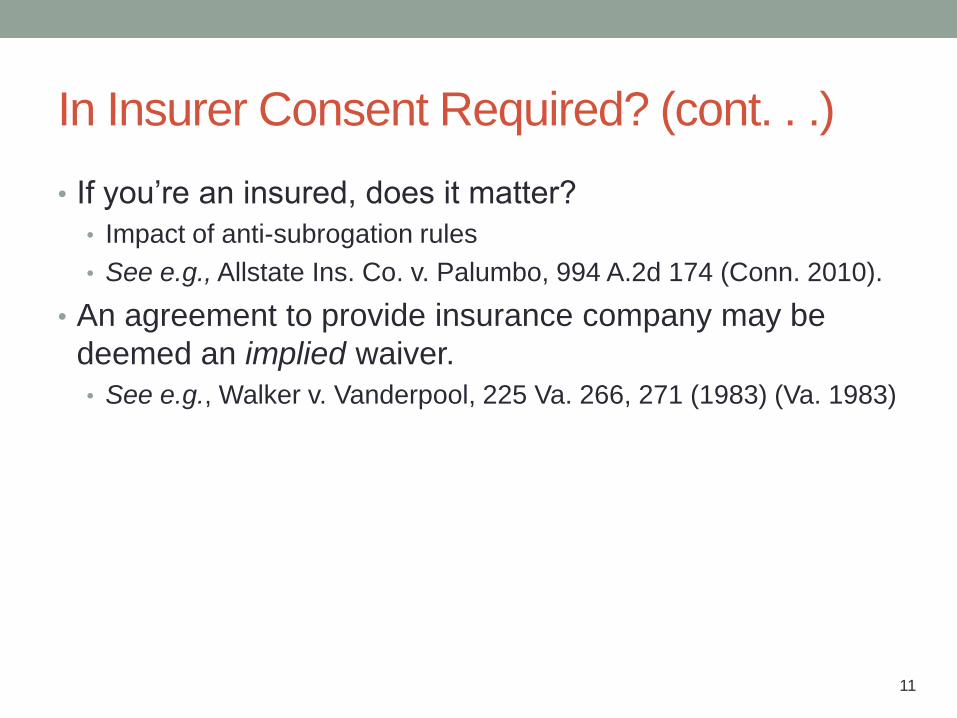

In Insurer Consent Required? (cont. . .)

• If you’re an insured, does it matter?

• Impact of anti-subrogation rules

• See e.g., Allstate Ins. Co. v. Palumbo, 994 A.2d 174 (Conn. 2010).

• An agreement to provide insurance company may be

deemed an implied waiver.

• See e.g., Walker v. Vanderpool, 225 Va. 266, 271 (1983) (Va. 1983)

11

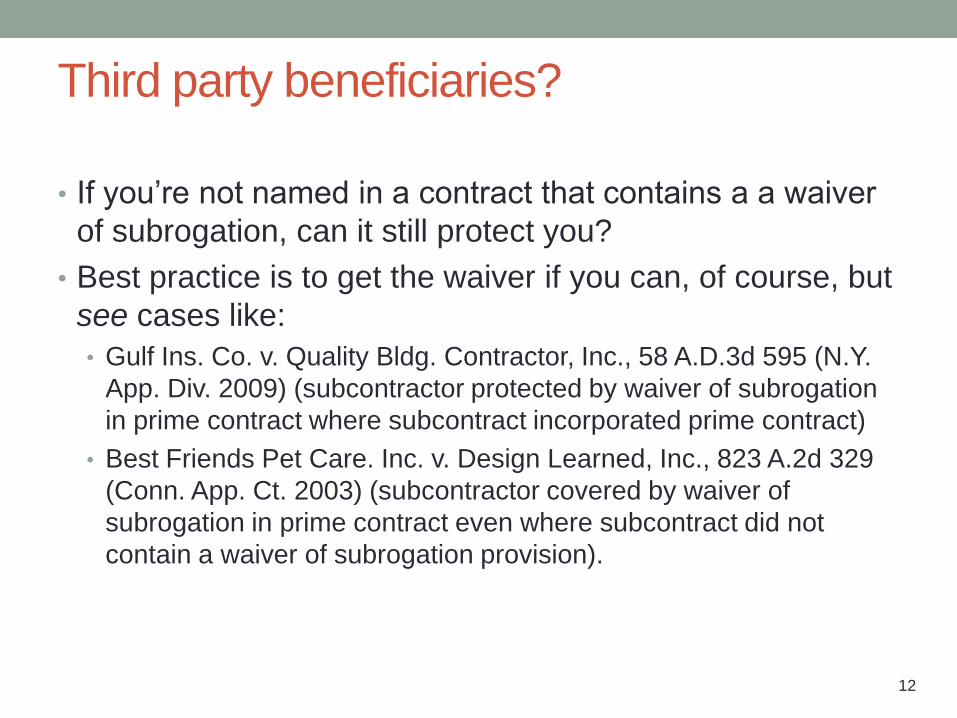

Third party beneficiaries?

• If you’re not named in a contract that contains a a waiver

of subrogation, can it still protect you?

• Best practice is to get the waiver if you can, of course, but

see cases like:

• Gulf Ins. Co. v. Quality Bldg. Contractor, Inc., 58 A.D.3d 595 (N.Y.

App. Div. 2009) (subcontractor protected by waiver of subrogation

in prime contract where subcontract incorporated prime contract)

• Best Friends Pet Care. Inc. v. Design Learned, Inc., 823 A.2d 329

(Conn. App. Ct. 2003) (subcontractor covered by waiver of

subrogation in prime contract even where subcontract did not

contain a waiver of subrogation provision).

12

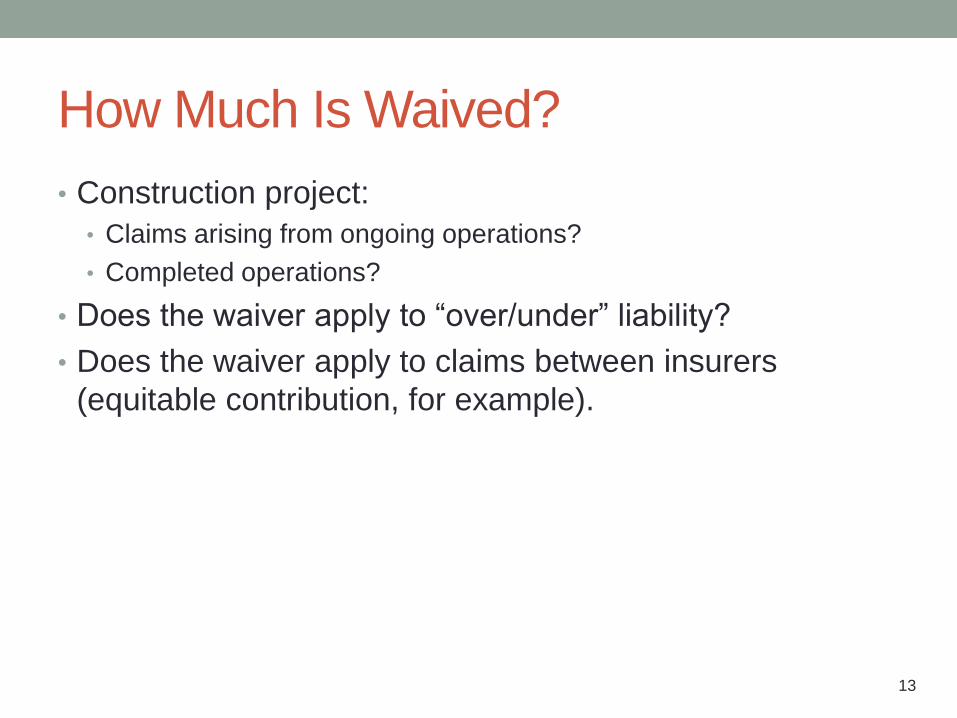

How Much Is Waived?

• Construction project:

• Claims arising from ongoing operations?

• Completed operations?

• Does the waiver apply to “over/under” liability?

• Does the waiver apply to claims between insurers

(equitable contribution, for example).

13

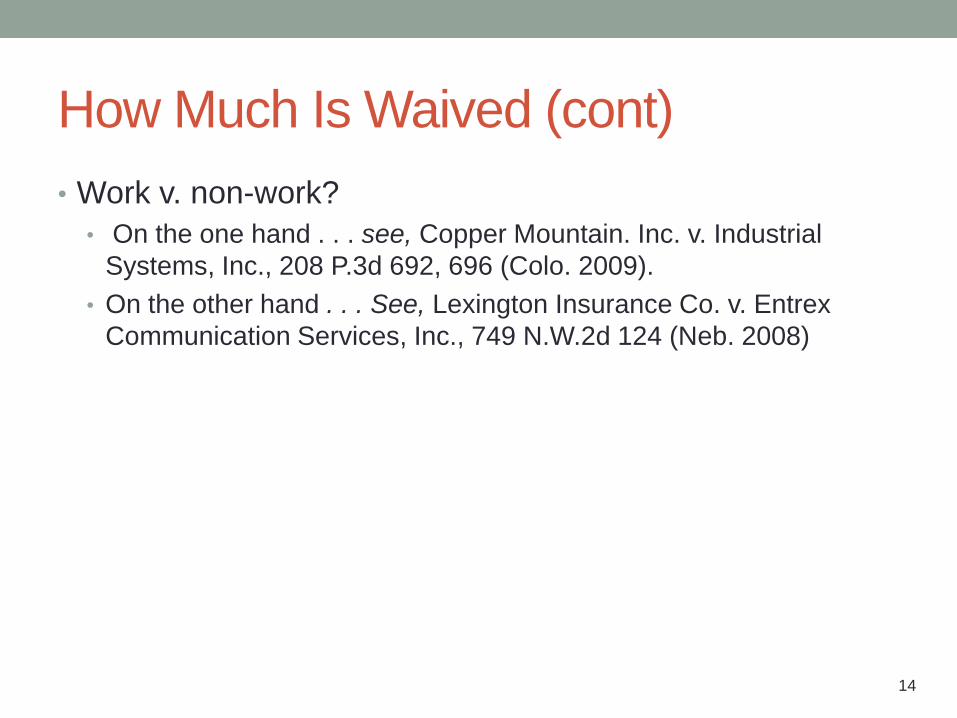

How Much Is Waived (cont)

• Work v. non-work?

• On the one hand . . . see, Copper Mountain. Inc. v. Industrial

Systems, Inc., 208 P.3d 692, 696 (Colo. 2009).

• On the other hand . . . See, Lexington Insurance Co. v. Entrex

Communication Services, Inc., 749 N.W.2d 124 (Neb. 2008)

14

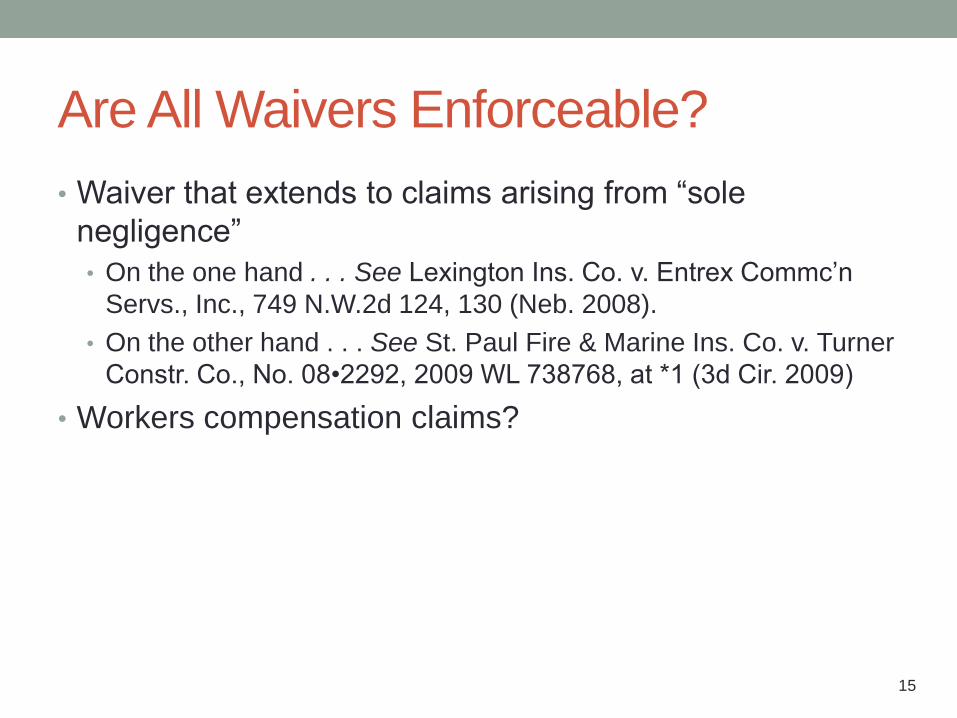

Are All Waivers Enforceable?

• Waiver that extends to claims arising from “sole

negligence”

• On the one hand . . . See Lexington Ins. Co. v. Entrex Commc’n

Servs., Inc., 749 N.W.2d 124, 130 (Neb. 2008).

• On the other hand . . . See St. Paul Fire & Marine Ins. Co. v. Turner

Constr. Co., No. 08•2292, 2009 WL 738768, at *1 (3d Cir. 2009)

• Workers compensation claims?

15

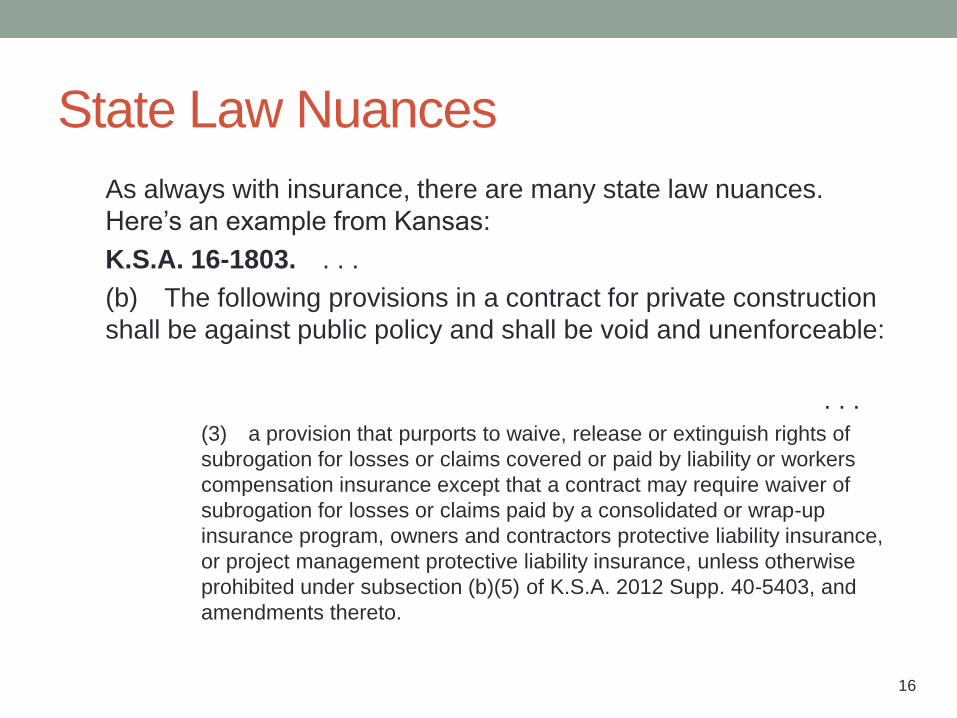

State Law Nuances

As always with insurance, there are many state law nuances.

Here’s an example from Kansas:

K.S.A. 16-1803. . . .

(b) The following provisions in a contract for private construction

shall be against public policy and shall be void and unenforceable:

. . .

(3) a provision that purports to waive, release or extinguish rights of

subrogation for losses or claims covered or paid by liability or workers

compensation insurance except that a contract may require waiver of

subrogation for losses or claims paid by a consolidated or wrap-up

insurance program, owners and contractors protective liability insurance,

or project management protective liability insurance, unless otherwise

prohibited under subsection (b)(5) of K.S.A. 2012 Supp. 40-5403, and

amendments thereto.

16

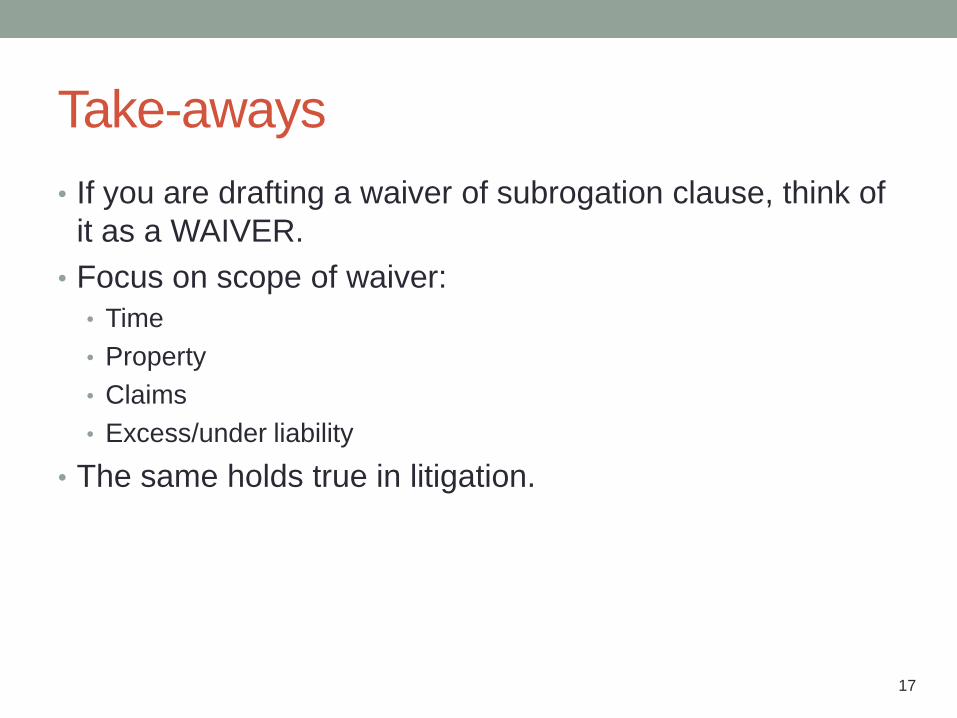

Take-aways

• If you are drafting a waiver of subrogation clause, think of

it as a WAIVER.

• Focus on scope of waiver:

• Time

• Property

• Claims

• Excess/under liability

• The same holds true in litigation.

17

Construction Contract Waivers of Subrogation, Indemnity and Contribution

WILLIAM E. KELLEY, JR. DREWRY SIMMONS VORNEHM, LLP

C A R M E L / I N D I A N A P O L I S / C R O W N P O I N T , I N D I A N A

E - M A I L : W K E L L E Y @ D S V L A W . C O M

T W I T T E R : @ W I L L K E L L E Y J R

J U L Y 6 , 2 0 1 7

WAIVER OF SUBROGATION CLAUSE

VS.

OTHER CONTRACTUAL RISK TRANSFER PROVISIONS

19

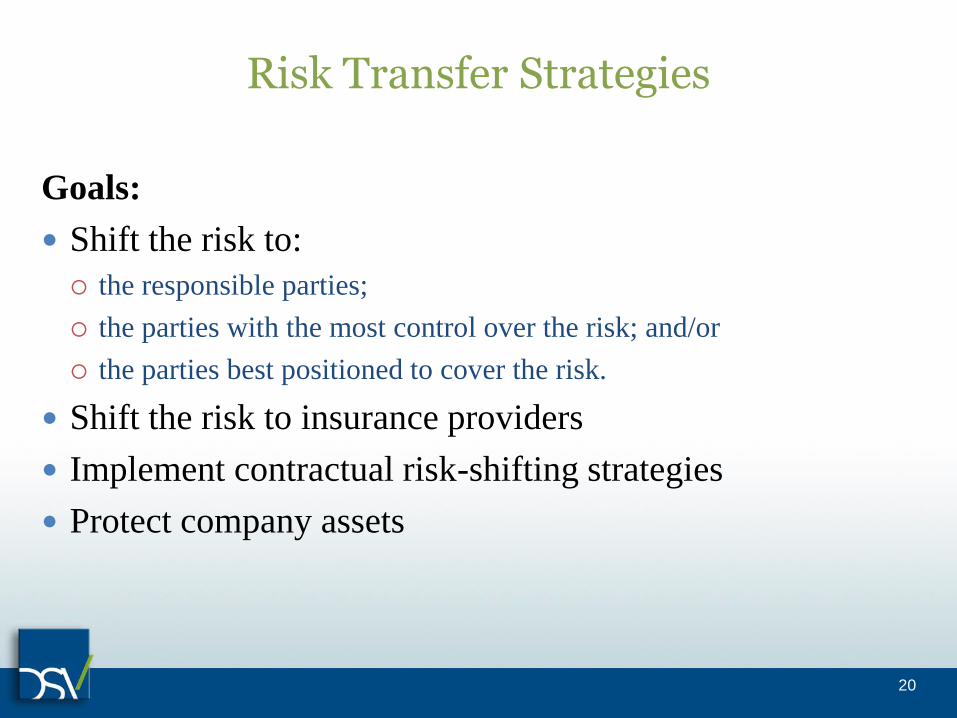

Risk Transfer Strategies

Goals:

Shift the risk to:

the responsible parties;

the parties with the most control over the risk; and/or

the parties best positioned to cover the risk.

Shift the risk to insurance providers

Implement contractual risk-shifting strategies

Protect company assets

20

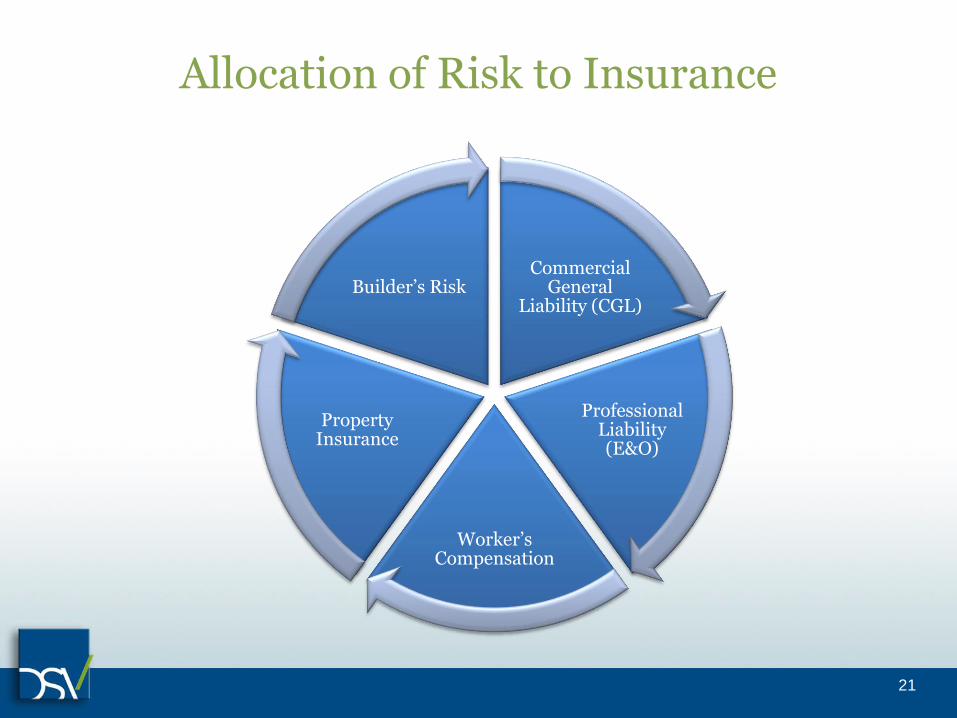

Allocation of Risk to Insurance

Commercial General

Liability (CGL)

Professional Liability (E&O)

Worker’s Compensation

Property Insurance

Builder’s Risk

21

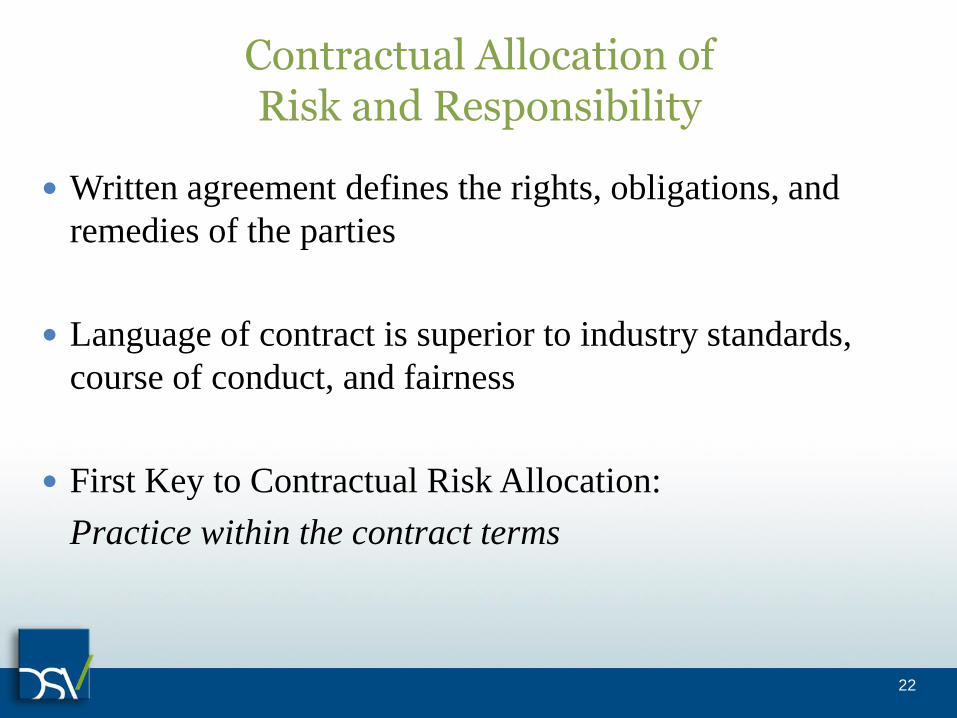

Contractual Allocation of Risk and Responsibility

Written agreement defines the rights, obligations, and

remedies of the parties

Language of contract is superior to industry standards,

course of conduct, and fairness

First Key to Contractual Risk Allocation:

Practice within the contract terms

22

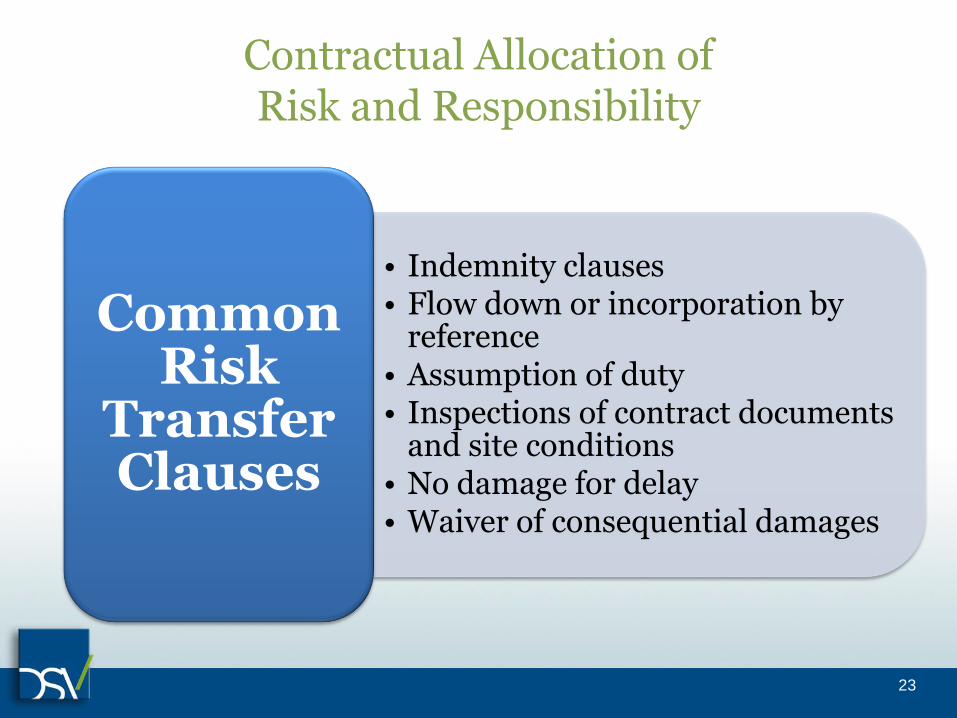

Contractual Allocation of Risk and Responsibility

• Indemnity clauses • Flow down or incorporation by

reference • Assumption of duty • Inspections of contract documents

and site conditions • No damage for delay • Waiver of consequential damages

Common Risk

Transfer Clauses

23

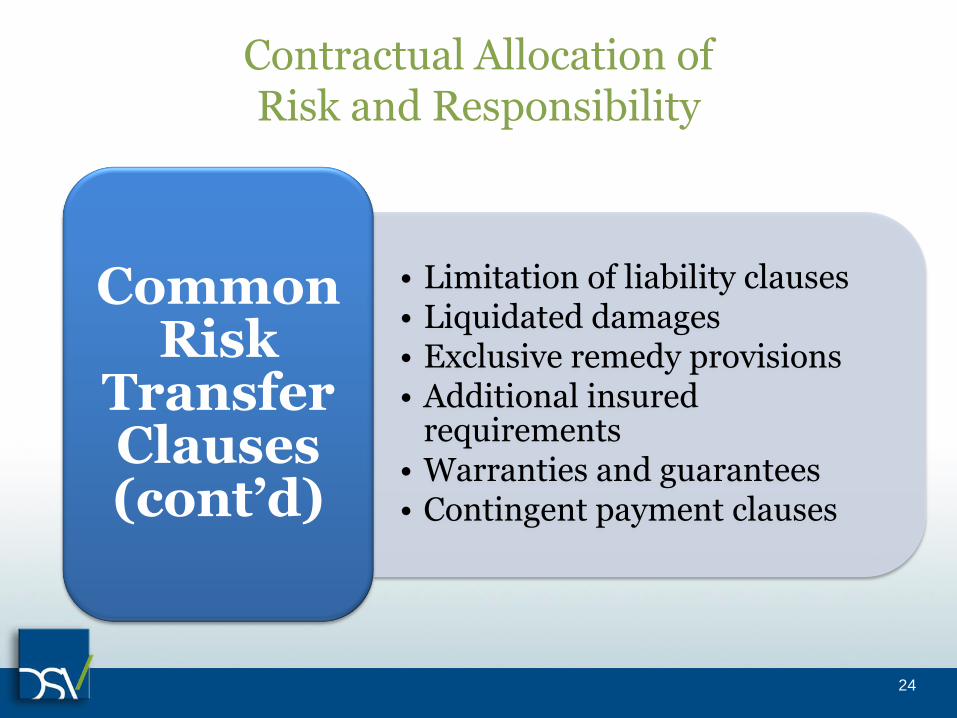

Contractual Allocation of Risk and Responsibility

• Limitation of liability clauses • Liquidated damages • Exclusive remedy provisions • Additional insured

requirements • Warranties and guarantees • Contingent payment clauses

Common Risk

Transfer Clauses (cont’d)

24

IMPACT TO THE PARTIES TO THE

CONTRACT

25

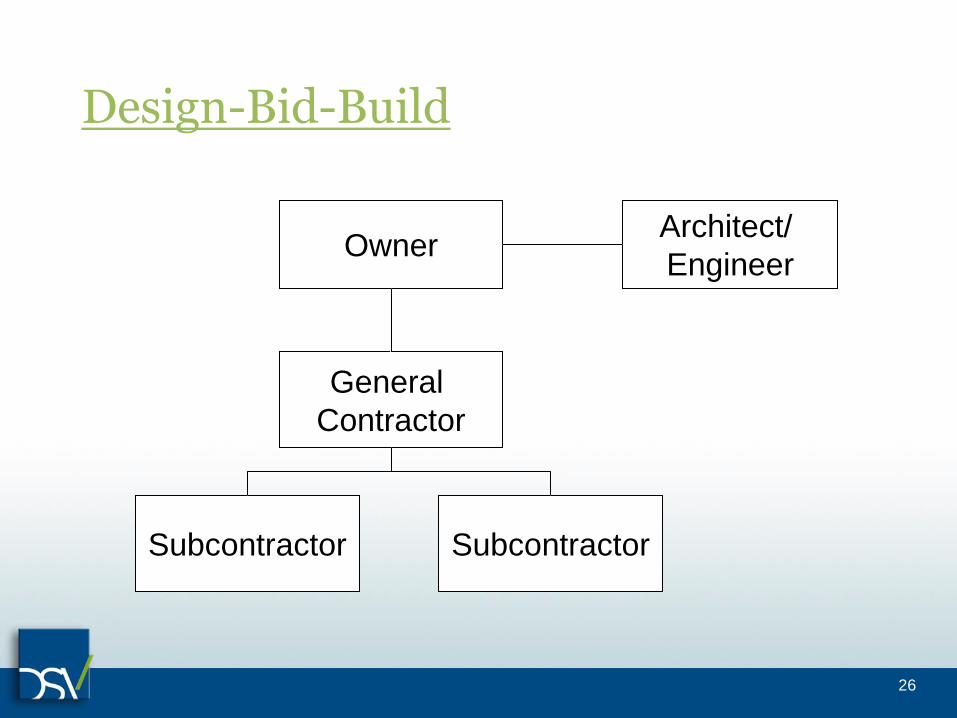

Design-Bid-Build

Owner

General

Contractor

Subcontractor

Architect/

Engineer

Subcontractor

26

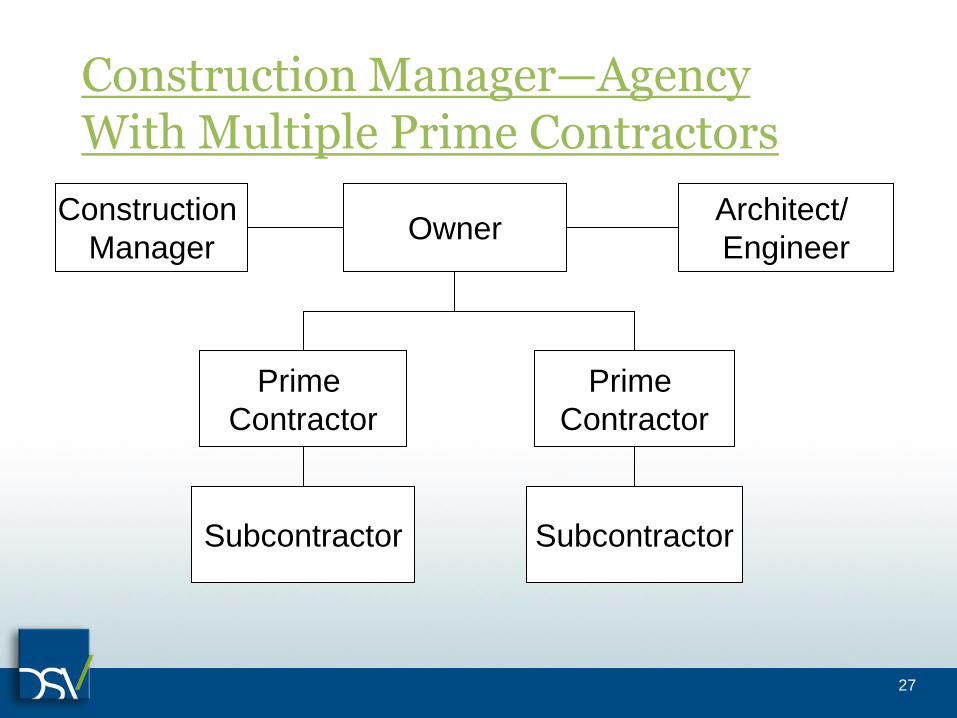

Construction Manager—Agency With Multiple Prime Contractors

Owner

Prime

Contractor

Prime

Contractor

Architect/

Engineer

Subcontractor

Construction

Manager

Subcontractor

27

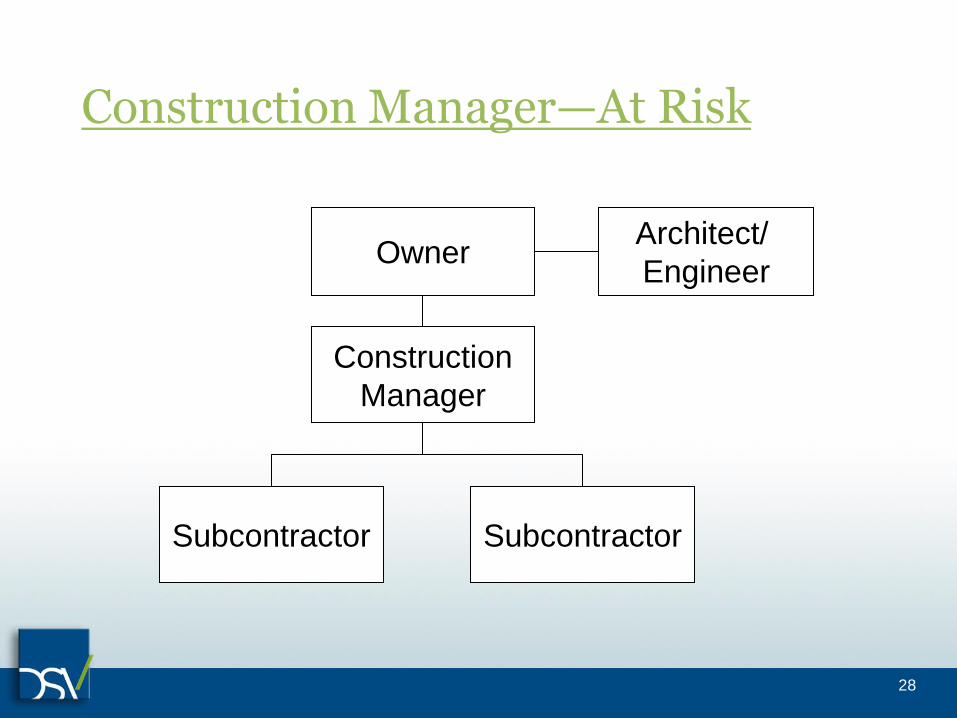

Construction Manager—At Risk

Owner

Construction

Manager

Subcontractor

Architect/

Engineer

Subcontractor

28

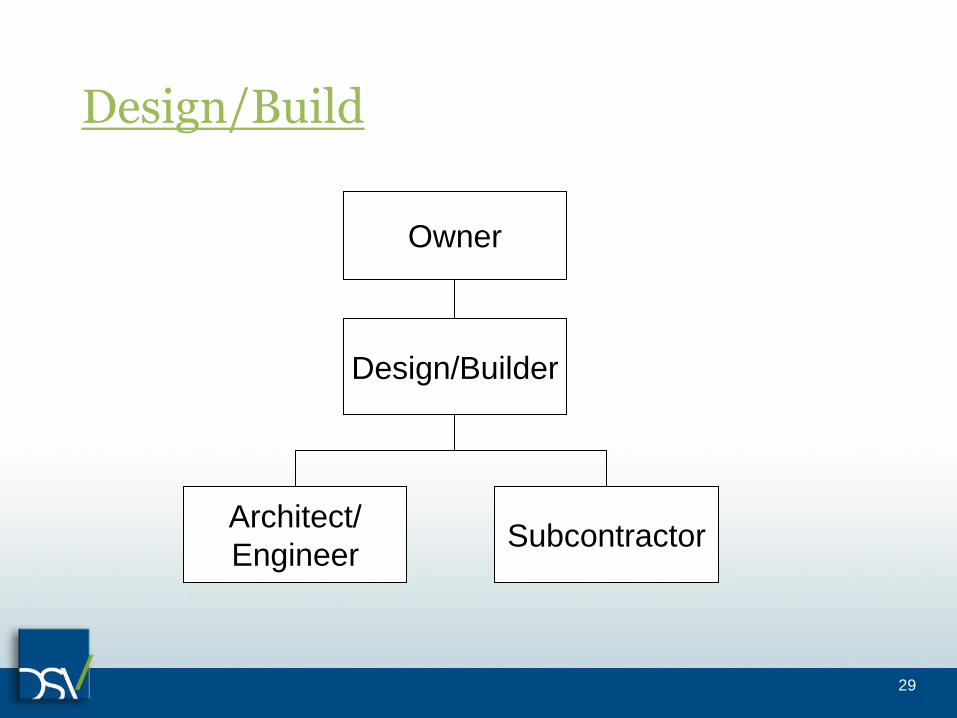

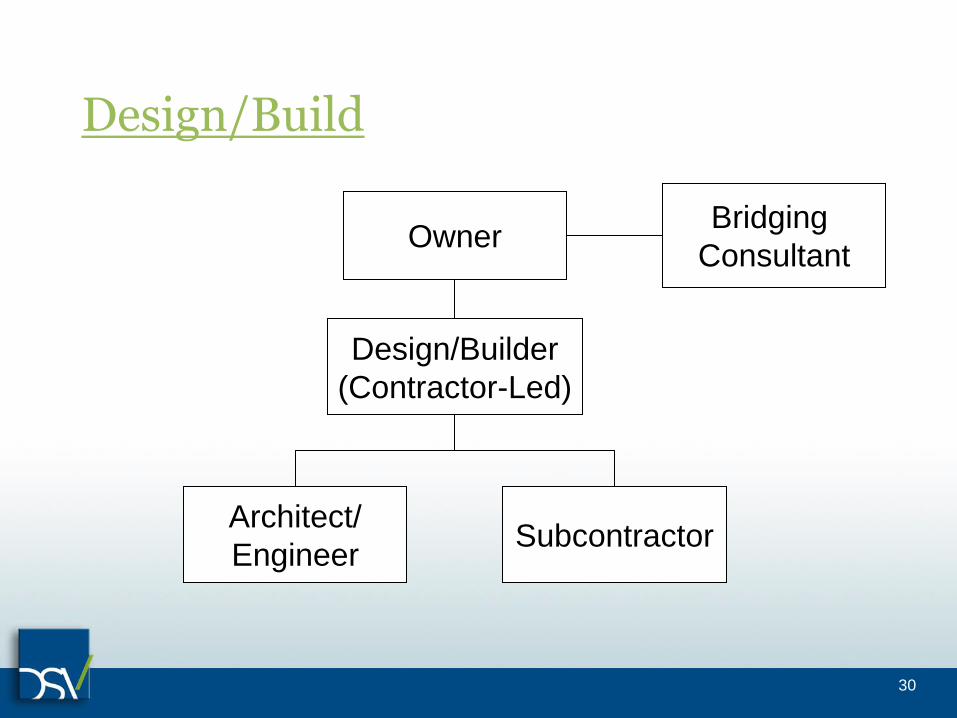

Design/Build

Owner

Design/Builder

Architect/

Engineer Subcontractor

29

Design/Build

Owner

Design/Builder

(Contractor-Led)

Architect/

Engineer Subcontractor

Bridging

Consultant

30

Who Is Covered?/What Is Covered?

The Owner and the Contractor waive all rights against each other and Subcontractors and sub-subcontractors of the Contractor, for damages caused by perils covered by insurance provided under Sections ABC, DEF, and GHI, except such rights as they may have to the proceeds of such insurance held by the Owner and the Contractor as trustees. The Contractor shall require similar waivers from its Subcontractors.

31

Who Is Covered?/What Is Covered?

The Owner and the Contractor waive all rights against each other and their design professionals and subcontractors for damages caused by perils covered by insurance under Sections ABC, DEF and GHI, except such rights as they may have to the proceeds of such insurance. The Contractor shall require similar waivers from its Subcontractors.

Post-Completion and Adjacent Property. The Owner waives subrogation against the Contractor and its' Subcontractors and sub-subcontractors on all property and consequential loss policies, on adjacent structures and properties and under property and consequential loss policies purchased for the Project after Substantial Completion.

32

Who Is Covered?/What Is Covered?

To the extent damages are covered by property insurance during construction, Owner and the Architect waive all rights against each other and against the contractors, consultants, agents and employees of the other for damages, except such rights as they may have to the proceeds of such insurance as set forth in the Construction Contract for the Project. Owner or the Architect, as appropriate, shall require of the contractors, consultants, agents and employees of any of them similar waivers in favor of the other parties enumerated herein.

33

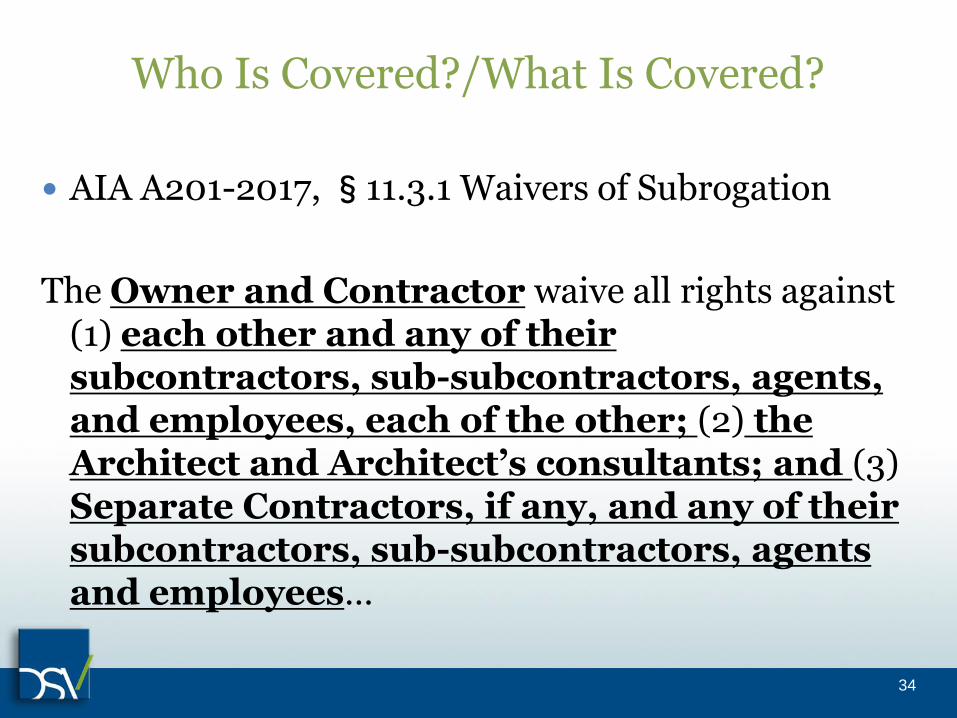

Who Is Covered?/What Is Covered?

AIA A201-2017, §11.3.1 Waivers of Subrogation

The Owner and Contractor waive all rights against (1) each other and any of their subcontractors, sub-subcontractors, agents, and employees, each of the other; (2) the Architect and Architect’s consultants; and (3) Separate Contractors, if any, and any of their subcontractors, sub-subcontractors, agents and employees…

34

Who Is Covered?/What Is Covered?

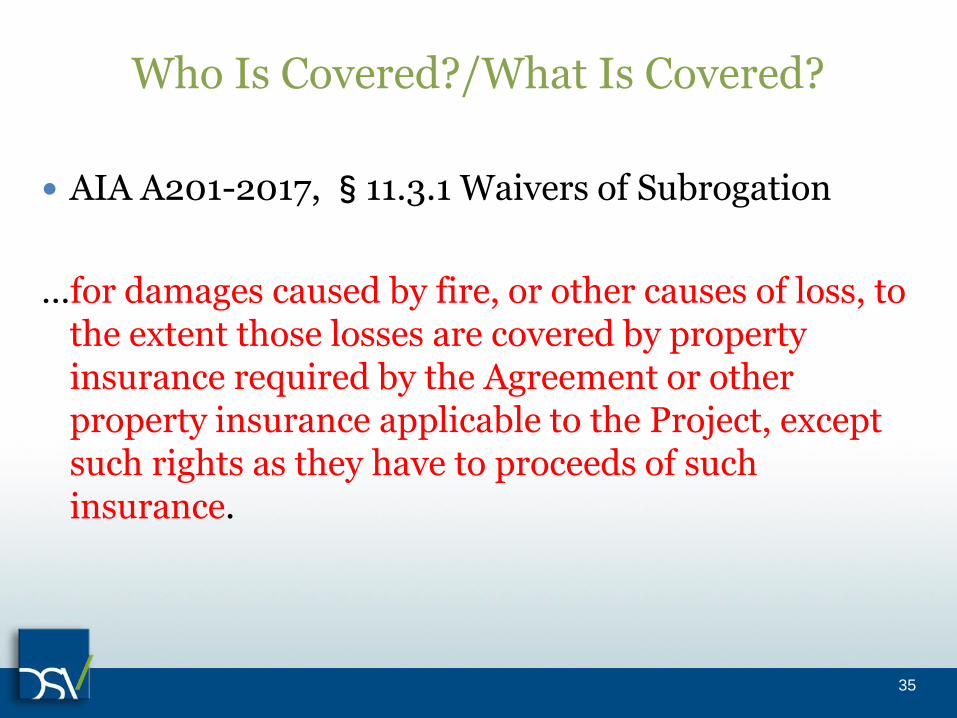

AIA A201-2017, §11.3.1 Waivers of Subrogation

…for damages caused by fire, or other causes of loss, to the extent those losses are covered by property insurance required by the Agreement or other property insurance applicable to the Project, except such rights as they have to proceeds of such insurance.

35

Who Is Covered?/What Is Covered?

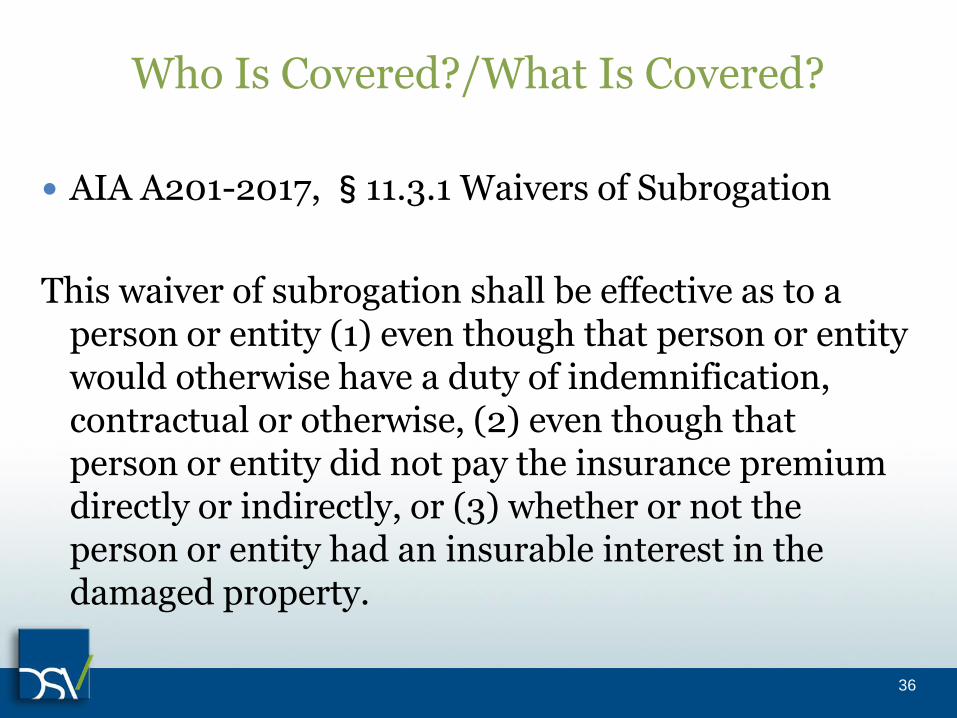

AIA A201-2017, §11.3.1 Waivers of Subrogation

This waiver of subrogation shall be effective as to a person or entity (1) even though that person or entity would otherwise have a duty of indemnification, contractual or otherwise, (2) even though that person or entity did not pay the insurance premium directly or indirectly, or (3) whether or not the person or entity had an insurable interest in the damaged property.

36

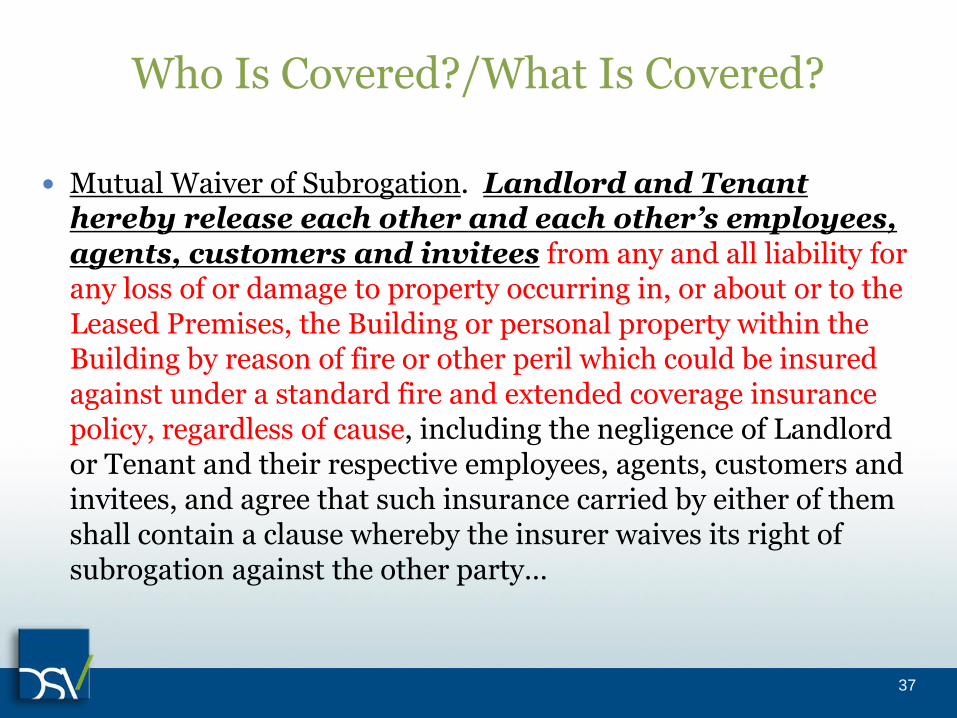

Who Is Covered?/What Is Covered?

Mutual Waiver of Subrogation. Landlord and Tenant hereby release each other and each other’s employees, agents, customers and invitees from any and all liability for any loss of or damage to property occurring in, or about or to the Leased Premises, the Building or personal property within the Building by reason of fire or other peril which could be insured against under a standard fire and extended coverage insurance policy, regardless of cause, including the negligence of Landlord or Tenant and their respective employees, agents, customers and invitees, and agree that such insurance carried by either of them shall contain a clause whereby the insurer waives its right of subrogation against the other party…

37

Waivers of Subrogation in Construction Contracts: Recent Cases

Peter T. Martin

Martin & Martin Law, P.C.

Dallas, Texas

Work vs. Non-Work: A Matter of Contract Interpretation

A casualty loss occurs on a construction contract and causes damages to property not part of the scope of Work. Does the waiver of subrogation apply only to claims associated with the Work under the contract, or does the waiver apply to non-work areas as well? The question here is when a loss occurs, is whether the waiver of subrogation determined by the description of the Work under the contract, or is it determined by the extent of the coverage obtained by the Owner.

40

Overview of Owner’s WOS for Property Insurance Covering Non-work under the A201:

If an Owner obtains coverage for non-work related property damage:

Majority view: Owner waives its insurance carrier’s right to subrogation for damages to the non-work portions of the property. (Conn., Neb., Ind.)

Minority view: Distinguishes between work and non-work property damages and applies the waiver only to property damages related to the work. (Co.)

41

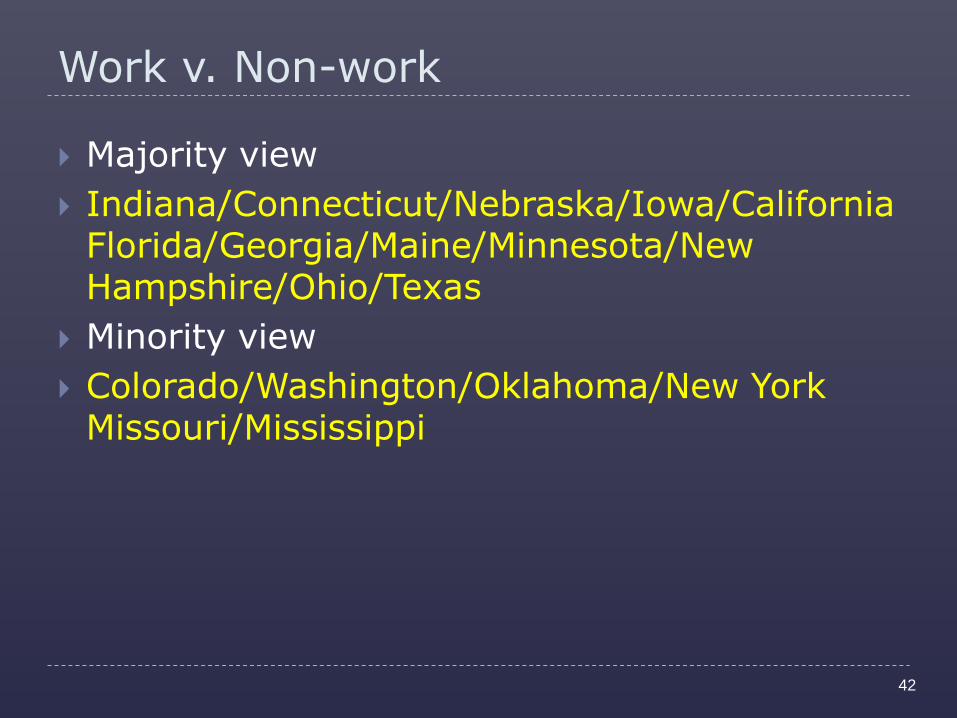

Work v. Non-work

Majority view

Indiana/Connecticut/Nebraska/Iowa/CaliforniaFlorida/Georgia/Maine/Minnesota/New Hampshire/Ohio/Texas

Minority view

Colorado/Washington/Oklahoma/New York Missouri/Mississippi

42

Key Language AIA A201

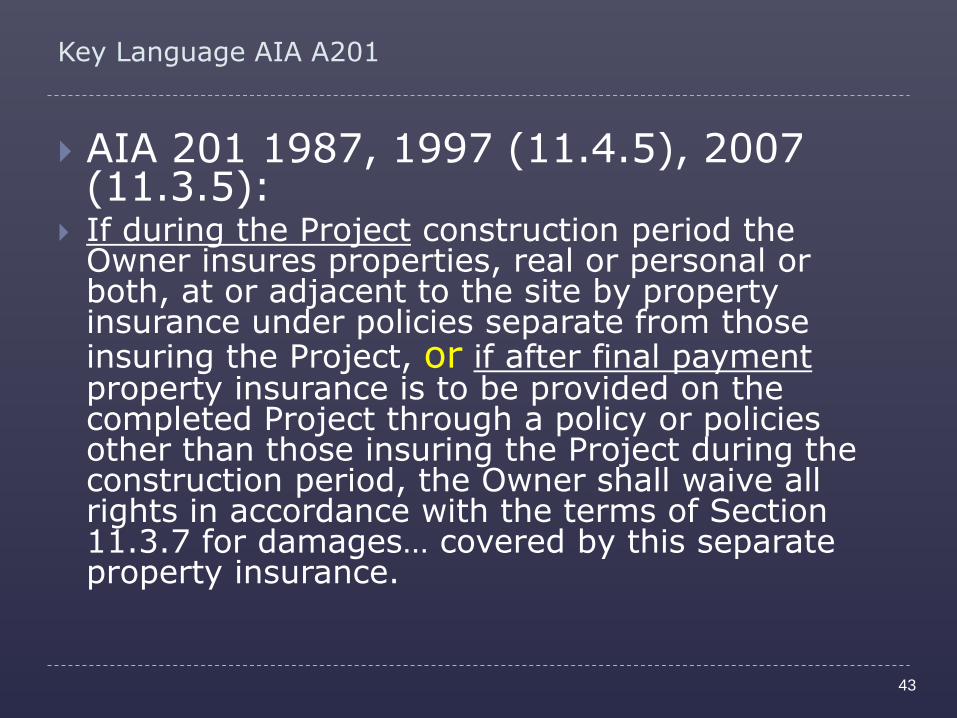

AIA 201 1987, 1997 (11.4.5), 2007 (11.3.5):

If during the Project construction period the Owner insures properties, real or personal or both, at or adjacent to the site by property insurance under policies separate from those insuring the Project, or if after final payment property insurance is to be provided on the completed Project through a policy or policies other than those insuring the Project during the construction period, the Owner shall waive all rights in accordance with the terms of Section 11.3.7 for damages… covered by this separate property insurance.

43

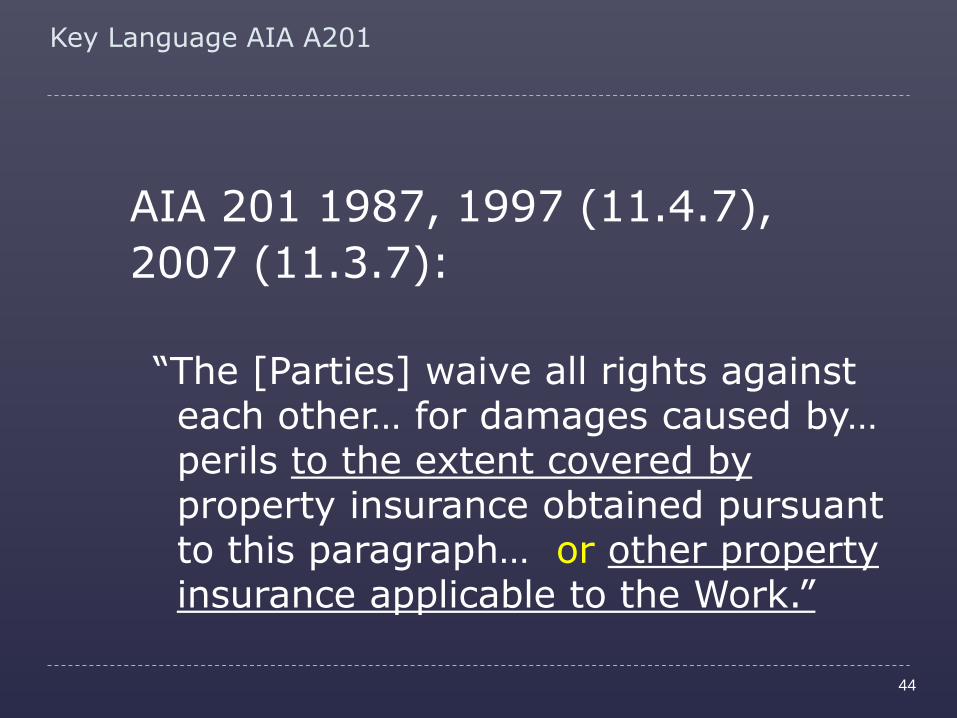

Key Language AIA A201

AIA 201 1987, 1997 (11.4.7),

2007 (11.3.7):

“The [Parties] waive all rights against each other… for damages caused by… perils to the extent covered by property insurance obtained pursuant to this paragraph… or other property insurance applicable to the Work.”

44

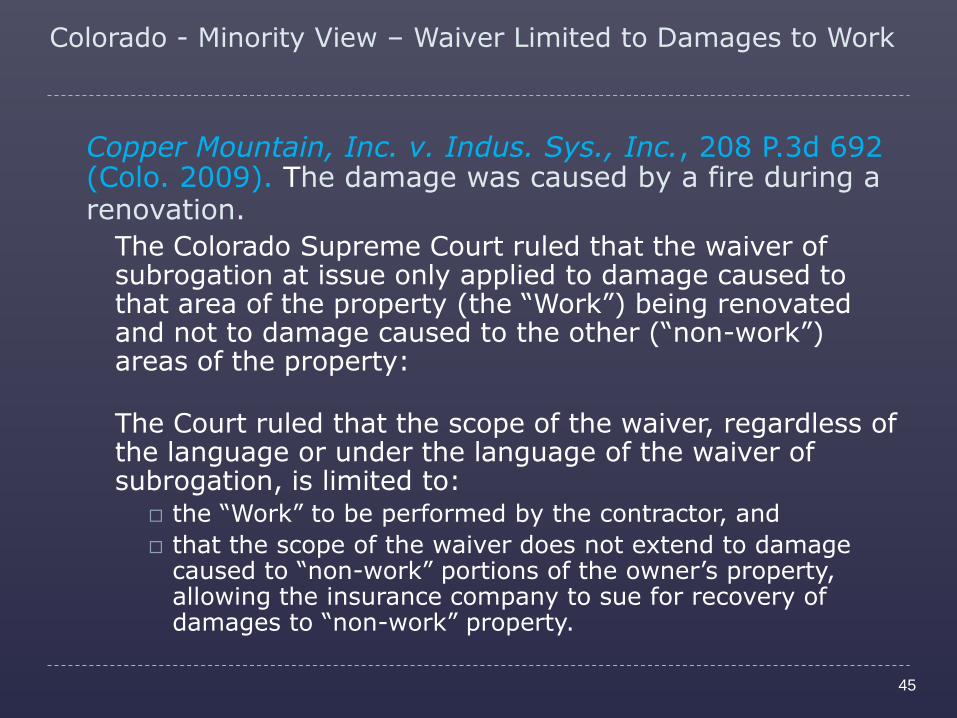

Colorado - Minority View – Waiver Limited to Damages to Work

Copper Mountain, Inc. v. Indus. Sys., Inc., 208 P.3d 692 (Colo. 2009). The damage was caused by a fire during a renovation.

The Colorado Supreme Court ruled that the waiver of subrogation at issue only applied to damage caused to that area of the property (the “Work”) being renovated and not to damage caused to the other (“non-work”) areas of the property:

The Court ruled that the scope of the waiver, regardless of the language or under the language of the waiver of subrogation, is limited to:

the “Work” to be performed by the contractor, and

that the scope of the waiver does not extend to damage caused to “non-work” portions of the owner’s property, allowing the insurance company to sue for recovery of damages to “non-work” property.

45

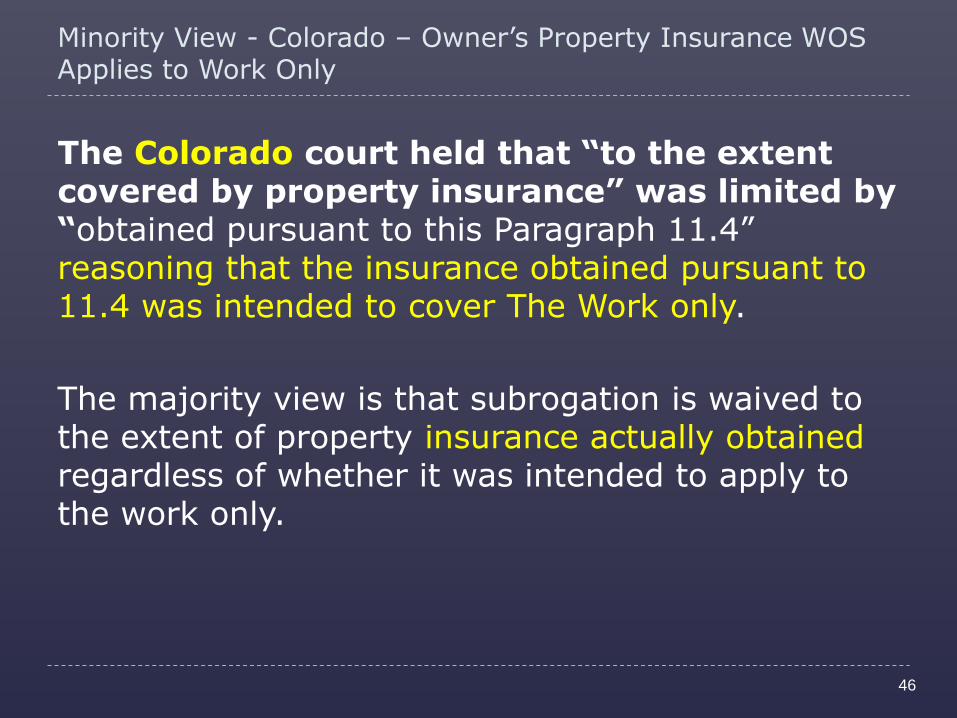

Minority View - Colorado – Owner’s Property Insurance WOS Applies to Work Only

The Colorado court held that “to the extent covered by property insurance” was limited by “obtained pursuant to this Paragraph 11.4” reasoning that the insurance obtained pursuant to 11.4 was intended to cover The Work only.

The majority view is that subrogation is waived to the extent of property insurance actually obtained regardless of whether it was intended to apply to the work only.

46

Majority View - Indiana

Bd. of Comm'rs of Cnty. of Jefferson v. Teton Corp., 30 N.E.3d 711 (Ind. 2015): The Indiana Supreme Court ruled that the distinction between damage caused by a contractor to areas of a building that were “work” and areas not being renovated “non-work” was irrelevant and that the waiver of subrogation applied to the entirety of the building in question:

A subcontractor caused significant damage to a courthouse during a renovation, including areas that were not part of the renovation and arguably not covered by the “work” definition in the contract.

Insurer argued that the waiver of subrogation should not apply to the “non-work” areas of the courthouse that had been damaged.

The Supreme Court of Indiana declined to adopt the “Work versus non–Work” approach to scope of waivers of subrogation.

Therefore, any damage caused (in this case by a subcontractor on courthouse renovation) that was covered by owner’s property insurance fell under the scope of the waiver.

47

Majority View - Nebraska

Lexington Ins. Co. v. Entrex Communication Services, Inc., supra, at 749 N.W.2d 124 AIA interpreted to mean that waiver covers work and non-work.

“the waiver of subrogation is subject to only one reasonable interpretation ... that the contract is not ambiguous and that here, the waiver applies to damages to both the Work and the non-Work property.” Id., at 132.

“We understand [Section 11.4.5] to mean that if the owner acquires a separate property insurance policy to cover non-Project property—a policy that did not cover the Project or Work property—and the non-Project property is damaged, the owner waives subrogation rights for the insurer as to those damages. So even though the damage occurred to non-Work property, the owner waived subrogation rights because the damages were insured.

48

Majority view - Nebraska

We see no reason why the parties would intend a different result when, instead of purchasing two separate policies, the owner relied on one policy covering both the Work and the non-Work property ...

“[This] approach furthers the policy underlying the use of waiver of subrogation clauses in construction contracts ... because it avoids disrupting the project and eliminates the need for lawsuits.” (Footnote omitted.) Id., at 734–35.1

The AIA [11.3.5] stating that “Owner shall waive all rights in accordance with the terms of Section 11.3.7 for damages … covered by this separate property insurance” means that the parties intended Owner to waive damages to work or non-work.

49

Majority View – Connecticut 2016

Connecticut Interlocal Risk Mgmt. Agency v. Silktown Roofing, Inc., 2016 WL 1444111, at *2 (Conn. Super. Ct. 2016) Summary Judgment granted by trial court.

Facts:

The plaintiff paid a claim to Naugatuck under a general liability policy for extensive damages suffered by Naugatuck as a result of fireproofing material being dislodged from the underside of the metal decking of a roof at Naugatuck High School.

The plaintiff paid Naugatuck for the damages and treated “the matter as a general property claim and did not pay damages based on a builder's risk policy.”

Issue:

The defendant filed this motion for summary judgment on the ground that the language of the contract with Naugatuck prohibits the plaintiff from bringing this subrogation claim. The plaintiff counters that, because the loss it covered was to property that was not related to the work the defendant was contracted to perform, the contract permits this subrogation action to be maintained.

50

Majority View - Connecticut

Holding: “This court adopts the reasoning of Lexington (Neb.) and finds that the paragraphs in question are subject to only one reasonable interpretation, namely that no right of subrogation exists for damages to non-Work property when payment for those damages has been made through a single insurance policy which covers damages to both Work and non-Work property.”

The Connecticut Court analyzed the minority view set forth in the Copper Mountain case and the majority view set forth in the Lexington case and followed the majority view.

51

Empress – Illinois App Court 2016 on 5 WOS issues

Facts: $81 million fire damage subrogation case – standard AIA A201

Insurers appeal from summary judgement granted enforcing WOS

Reversed and remanded for consideration of non-signatory subcontractor

Insurer’s arguments

1) WOS only applies to builder’s risk policy, and not to general property insurance policies

2) Work/Non-work

3) Material breach / willful and wanton misconduct by contractors of construction contract barred enforcement of WOS

4) No waiver by insurers of right to recover deductibles of $2.5 million by at least some of the insurers

5) Waiver does not apply to action of owner’s separate contractors

52

Empress – Illinois App Court 2016 on 5 WOS issues

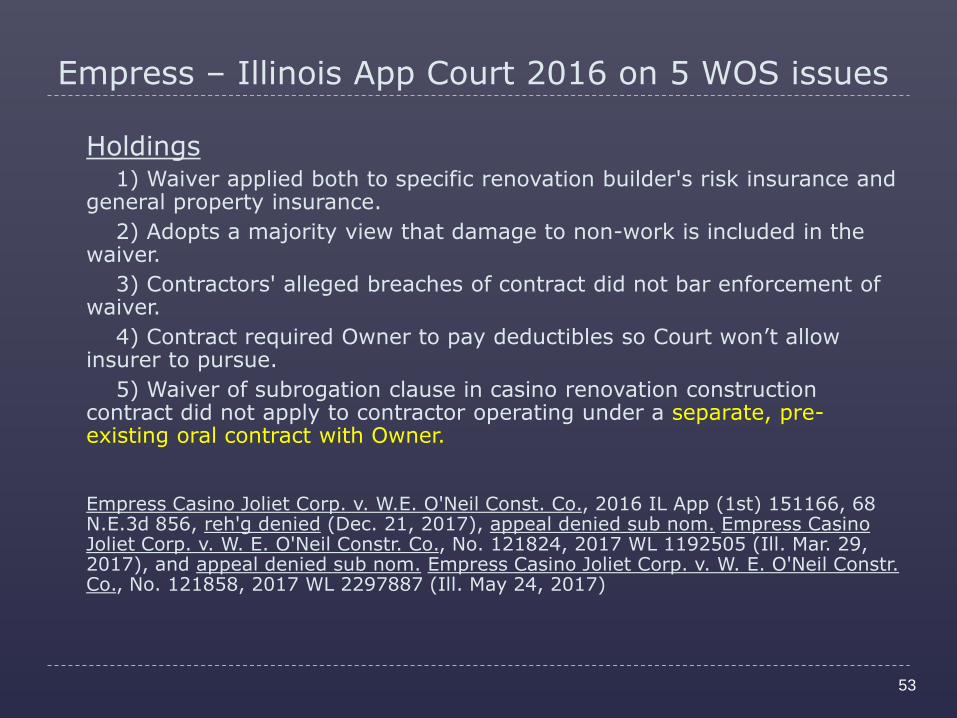

Holdings 1) Waiver applied both to specific renovation builder's risk insurance and general property insurance.

2) Adopts a majority view that damage to non-work is included in the waiver.

3) Contractors' alleged breaches of contract did not bar enforcement of waiver.

4) Contract required Owner to pay deductibles so Court won’t allow insurer to pursue.

5) Waiver of subrogation clause in casino renovation construction contract did not apply to contractor operating under a separate, pre-existing oral contract with Owner.

Empress Casino Joliet Corp. v. W.E. O'Neil Const. Co., 2016 IL App (1st) 151166, 68 N.E.3d 856, reh'g denied (Dec. 21, 2017), appeal denied sub nom. Empress Casino Joliet Corp. v. W. E. O'Neil Constr. Co., No. 121824, 2017 WL 1192505 (Ill. Mar. 29, 2017), and appeal denied sub nom. Empress Casino Joliet Corp. v. W. E. O'Neil Constr. Co., No. 121858, 2017 WL 2297887 (Ill. May 24, 2017)

53

Work/Non-work Take Away

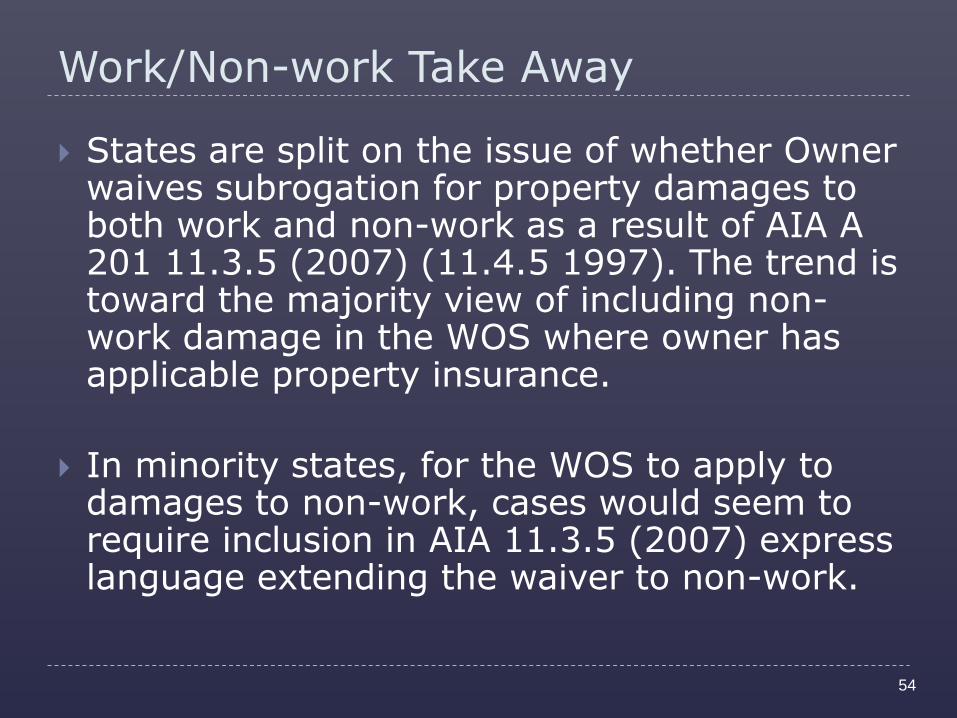

States are split on the issue of whether Owner waives subrogation for property damages to both work and non-work as a result of AIA A 201 11.3.5 (2007) (11.4.5 1997). The trend is toward the majority view of including non-work damage in the WOS where owner has applicable property insurance.

In minority states, for the WOS to apply to damages to non-work, cases would seem to require inclusion in AIA 11.3.5 (2007) express language extending the waiver to non-work.

54

Applicability of WOS to Liability Insurance

The majority of cases discussing waivers of subrogation involve first party property insurance. On occasion, however, an insurer issuing a liability policy may seek subrogation. A question can arise as whether “other property insurance” referenced in a WOS applies to liability insurers. Some courts look at only whether the insurance paid or was applicable to property damage.

55

Applicability of WOS to Liability Insurance

Scottsdale Ins. Co. v. Heritage Gen. Contractors, LLC, 2015 WL 2260714 (Conn. Super. Ct. Apr. 17, 2015):

The defendants tried to argue that a waiver of subrogation clause that extended the waiver to damages paid by “other property insurance applicable to the work,” should be held to include amounts paid by the owner’s liability insurance and the court remanded for consideration of this issue.

The Connecticut Superior Court considered this a fact issue and remanded, but compare the Indiana Supreme Court, which unequivocally held that waiver depended on the extent of coverage of “property insurance” not liability insurance. (See Bd. of Commissioners of Jefferson County cited above.)

56

Waiver of Subrogation not a bar to Owner’s suit for damages amounts not covered by insurance.

Allen Cnty. Pub. Library v. Shambaugh & Son, L.P., 2 N.E.3d 132 (Ind. Ct. App. 2014): The Indiana Court of Appeals ruled that even with a WOS, an Owner can sue its contractor to recover for those damages not covered by the owner’s insurance policy:

Facts. A contractor and subcontractor caused damage to a library building that caused a large diesel fuel leak under the building with the cleanup cost in excess of $490,000.

Clean-up costs. The insurance policy purchased pursuant to the contract by the library, provided only $5,000 for such pollutant cleanup costs.

The Indiana Court of Appeals ruled that “however one reads the AIA standard contract waiver of subrogation the parties had agreed that the library could sue the defendants for all cleanup costs not covered by their insurance as the waiver only applied to “damages covered by owner’s insurance.”

See also: Garden City Apartments, LLC v. Xcel Plumbing of N.Y., Inc. 2017 WL 193151, at *2 (E.D.N.Y. 2017) (barred claims for damage to the work only insofar as insurance compensated that loss)

57

Waiver for damages over Insurance Deductible Amount limited to value of Insurance deductible amount.

Affiliated FM Ins. Co. v. Slack, 2015 WL 5023089 (W.D. La. Aug. 24, 2015): Enforcing the plain language of the WOS, the court applying Louisiana law held that the WOS barred the insurer from suing the contractor for any damages (in excess of the deductible):

August 2015 pre-trial Federal District Court Summary Judgment.

Less than 2 years after the building had been opened, the insurance company alleged that construction defects in the roof and drainage system caused a partial roof collapse resulting in $2,591,821 in damage.

The district court ruled that a waiver of subrogation provision in the building lease applied to extinguish claims against the GC arising from any cause covered by any insurance was valid.

58

Waiver for damages over Insurance Deductible Amount limited to value of Insurance deductible amount.

Affiliated (cont.)

The Carrier also argued that it had no notice of the waiver of subrogation clause.

No notice to the insurer of the WOS in the construction or lease contract was required and the court enforced the WOS as written. Beware of insurance policy provisions which prohibit the insured from doing anything to impact the carrier’s right of subrogation. There may be a separate cause of action by the insurer against the insured for breach of contract when the insured agrees to a waiver of subrogation without notice in some states. Most large construction companies purchase a “blanket waiver” for their insurance policy which allows them to waive subrogation as long as the underlying contract requires a waiver of subrogation.

Also, the general contractor argued here that it was a third party beneficiary to the WOS contained in the Lease Agreement. The court used both the construction agreement and the lease agreement to determine intent of the Owner.

59

Scope of Waiver – Waiver not applicable to negligence

cause of action.

Cmty. Ass'n Underwriters of Am. v. Rhodes Dev. Grp., Inc., 488 F. App'x 547 (3d Cir. Penn 2012): The Court ruled that the waiver of subrogation did not bar suit against contractor and subcontractor by the insurer where the insurer alleged that damage caused was a result of contractor/subcontractor negligence:

Fire was caused by the negligent placement and handling of propane heaters during the installation by drywall subcontractor.

Insurers only asserted negligence claims against contractor and subcontractor.

Owner’s insurer was bound by waiver-of-subrogation only to the extent that insurer asserted claims arising under construction contract. (breach of contract)

As such, the waiver of subrogation clause didn’t bar insurer’s subrogation claims against contractor and subcontractors that were based on alleged negligence by defendants.

60

Waiver applicable to cause of actions for breach of contract but not for negligence cause of action.

Economic Loss Doctrine:

Compare Rhodes above with courts and states enforcing the economic loss doctrine (i.e. Great American Insurance vs. Superior). In Rhodes, the insurer was barred from bringing a breach of contract claim by the terms of the WOS. In an economic loss state, the result of Rhodes would presumably be different as the insurer is barred by economic loss doctrine from bringing a negligence action to the extent the claim involves property damage to the “subject of the contract”.

61

Texas Enforces Waiver for Any Claims Covered by Owner’s Policy, Including Negligence

Am. Zurich Ins. Co. v. Barker Roofing, L.P., 387 S.W.3d 54 (Tex. App.-Amarillo 2012): The fire originated

in the exterior roof covering ignited by a subcontractor’s torch.

The Texas Court of Appeals upheld a waiver of subrogation clause and ruled that the waiver protected the contractor, subcontractor,

and barred all claims asserted by the insurer: damages “covered by property insurance” barred insurer’s

subrogation claim;

subcontractor was entitled to enforce project owner's waiver as a third-party beneficiary;

indemnity clause in subcontract did not apply to damages covered by property insurance;

waiver of claims for damages covered by property insurance included business interruption damages; and

subrogation provision of property policy did not grant insurer a claim to recover uninsured losses or deductible.

62

Texas Enforces Waiver for Any Claims Covered by Owner’s Policy, Including Negligence

Zurich (cont.)

Waiver provision.

“[t]he Owner and Contractor waive all rights against each other and the Architect, Architect's consultants, separate contractors, and any of their Subcontractors, sub-subcontractors, agents and employees, for damages caused by fire or other perils to the extent covered by property insurance obtained pursuant to this Article or any other property insurance applicable to the Work,”

Negligence claim included in waiver.

WOS construed under rules of contract construction.

As long as the owner's property insurance covers the damages to the structure, whether completed or not, the waiver applies.

the plain meaning of “other property insurance applicable to the Work,” is property insurance other than that required to be purchased by the owner under the construction contract.

Scope of a waiver provision in a standard AIA contract is determined by whether the owner's policy provided coverage for the losses arising from the damage to the property.

63

Subcontractors

64

Subcontractors

“Recklessness” by subcontractors not sufficient to defeat waiver of subrogation.

Ace Am. Ins. Co. v. Keystone Const. & Maint. Servs., Inc., 2012 WL 4483913 (D. Conn. 2012): Even though the subcontractors had acted recklessly, the waiver of subrogation was held to apply as the WOS did not exclude recklessness.

In February of 2010, there was a natural gas explosion resulting in deaths, injuries and significant property damage. Temporary natural gas piping which was to be directed vertically had been directed horizontally into an area with numerous sources of ignition, including welding and other activities.

Insurer brought subrogation action against subcontractors and others after paying $200 million for damages.

The construction contract specifically waived subrogation claims against the subcontractors; however, the insurer argued that the subcontractors who caused the accident were reckless and that public policy consideration dictated that the waiver of subrogation should be voided.

The District Court found that nothing in the construction contracts excepted or excluded reckless conduct even though the subcontractors were, in fact, reckless. Because the owners had been compensated, the court held that there was no public policy concern.

65

Failure To Secure Waivers of Subrogation from All Subcontractors Does Not Constitute Material Breach of Contract, Enabling Waiver of Subrogation to Remain In Effect.

N. Am. Specialty Ins. Co. v. Payton Const. Corp., 953 N.E.2d 233 (2011): The general contractor’s failure to obtain a waiver of

subrogation from one of the subcontractors did not void the WOS in the prime contract, despite contract language requiring contractor to obtain waivers from all subcontractors:

Insurer paid $1.2 million to owners of guest house for fire damage caused during renovation.

The AIA conditions included a mutual waiver of subrogation, and

The Insurer argued the GC’s failure to obtain the WOS from a subcontractor was a material breach of the prime contract and as such, GC had forfeited the right to enforce the WOS in the Contract.

The trial and appeals courts disagreed with the insurer and ruled that the failure to obtain the one subcontractor waiver was not a material breach of the AIA A201 general provisions.

66

Subcontractor not Protected by Waiver of Subrogation Between Owner and General Contractor.

St. Paul Fire and Marine Ins. Co. v. FD Sprinkler Inc., 76 A.D.3d 931, 908 N.Y.S.2d 637 (1st Dep't 2010): The waiver of

subrogation did not apply to a subcontractor because the contract was clear that the only insurance applicable to the subcontractor was for personal property (ex. tools) and that the subcontractor would have to repair any damage the subcontractor caused.

On appeal, the court reversed the trial court and held that the subcontractor was not shielded by the waiver-of-subrogation provision in the Owner/GC contract.

An insurer cannot usually subrogate against its insured including its additional insureds. This rule did not apply in this case because the insurance in question was limited to coverage for the subs own tools not the property. Also, the contract was clear that the subcontractors would have to repair any damage they caused.

The subcontractors were not parties to the prime contract and thus could not avail themselves of the waiver of subrogation provision.

67

Completed Construction Projects

68

Inapplicability of Waivers of Subrogation After Completion of Construction if Parties Deleted Express Requirement in Contract.

Great Am. Ins. Co. of New York v. Superior Contracting Corp., No. 2:14-CV-00055-PPS, 2014 WL 5597272, (N.D. Ind. Nov. 4, 2014):

Insurance company sued the GC and two subcontractors for failing to properly insulate sprinkler pipes which burst the winter following completion and caused damages some of which were insured against and some of which were not.

The construction contract contained a waiver of subrogation clause that applied only to the time of performance under the contract.

The contract also contained a separate clause extending the waiver to the period after the project had been completed, but that provision had been struck out/deleted by the parties.

69

Economic Loss Doctrine Eliminates Tort Claims only if they were the Subject of the Contract

Great Am. Ins. (cont.)

Negligence. The court applied the economic loss doctrine to damages which were the subject of the contract. This is a breach of contract claim. “Defendant is right that plaintiff has no claim in tort for damages to the subject of the contract.”

However, court would not apply the economic loss doctrine to other property such as personal property in the building at the time of the occurrence as it was not a subject of the contract.

70

Waiver of Subrogation clause extended beyond completion of construction when insurance was purchased after completion unless the clause does not expressly exclude post-completion claims.

Travelers Indem. Co. v. Crown Corr Inc., 589 F. App'x 828 (9th Cir. 2014): The Court ruled that a waiver of subrogation against

the Owner’s insurer applied to an occurrence after the completion of construction.

The subrogation waiver was enforceable against an insurer whose policy had been purchased by Owner years after the stadium at issue had been completed and opened.

Affirming the district court below, the 9th Circuit ruled that insurer did not prove that the subrogation waiver referred only to the stadium before substantial completion. There were references in the contract to the contrary.

Parole evidence was not allowed because the WOS was not ambiguous.

71

Waiver of Subrogation clause extended beyond completion of construction when insurance was purchased after completion unless the clause does not expressly exclude post-completion claims.

Middleoak Ins. Co. v. Tri-State Sprinkler Corp., 77 Mass. App. Ct. 336, 931 N.E.2d 470 (2010): The property owner obtained property insurance after the completion of construction. The waiver of subrogation clause in the construction contract was held to continue to prevent the insurer from suing the contractor:

Middleoak, insurer of apartment complex constructed by a GC and subcontractor. Fire damaged one of the buildings after completion.

A Massachusetts district court ruled and Court of Appeals affirmed that an AIA waiver of subrogation clause in the contract between Owner and contractor barred insurer from suing contractor for recovery of damages that occurred after construction had been completed because the owner had obtained property insurance on the completed building.

72

Remand for Ambiguity: In the absence of express inclusion of post-completion claims in waiver of subrogation clause, burden is on contractor/subcontractor to prove applicability of clause after completion.

John L. Mattingly Const. Co. v. Hartford Underwriters Ins. Co., 415 Md. 313, 999 A.2d 1066 (2010): The waiver of subrogation language was vague as to whether or not the waiver would apply after construction had been completed. On remand, the burden of showing that the waiver applied after the construction period would be on the contractor/subcontractor:

Months after an Arby’s restaurant had been completed and opened, defective wiring installed by a subcontractor caused an electrical fire and significant damage. Final payment was made. Insurer sued contractor and subcontractor for negligence and breach of warranty.

Waiver provision was silent as to claims following completion.

The Court of Appeals of Maryland overruled the Court of Special Appeals and held that the language in the construction contract was impermissibly vague as to applicability after completion, when the WOS was read in tandem with the definition of the Work.

73

Non AIA WOS Creates a Fact Issue as to Application of WOS to Completed Projects

Mattingly (cont.)

This case contains an exhaustive review of opinions from around the country dealing with the question of the applicability of WOS to occurrences after completion and the evidence which may be used to determine the intent of the parties.

The issue is whether the property insurance secured after completion of the restaurant comes within the phrase “other property insurance applicable to the Work.”

Court determines the meaning of the “Work,” but “whether completed or partially completed” could indicate that the “Work” includes completed Work.

Court distinguished AIA contracts which have express provisions pertaining to completion.

In the absence of express provision, the intent of the parties must be determined, which is a fact issue for the lower court.

74

Ambiguity in Non-AIA Contract defeats SJ

Facts: Six years after final completion, pipe broke flooding the building. Owner had BI purchased after substantial completion.

Motion for SJ against insurer based on WOS; non AIA WOS

WOS: “The Owner waives subrogation against the Contractor ... under property and consequential loss policies purchased for the “Project” after its “substantial completion.”

Dispute about meaning of “Project.” Conflicting interpretations of the WOS raised an ambiguity in the WOS and the parties’ intent concerning the WOS.

Holding: Summary judgment was denied because of a genuine issue of material fact regarding the resolution of the ambiguity in the WOS. Cont'l W. Ins. Co. v. Opechee Const. Corp., 2015 WL 5838408, at *5 (USDC D.N.H. 2015)

75

Thank You for Listening

Peter T. Martin

Martin & Martin Law, P.C.

Dallas, Texas

76