Embed Size (px)

Citation preview

Consumer Protection Rules & Regulations

________________________________________________Duncan Douglass

Partner, Retail and Corporate Payment SystemsAlston & Bird LLP

Agenda

2

• Refresher overview of payment types and laws• EFTA/Regulation E

• Subpart A – “Old Reg. E”• Subpart B – “New Reg. E”

• TILA/Regulation Z• EFAA/Regulation CC• Other relevant laws/regulations• Application of existing laws/regulations to new

payment types• Recent developments and the CFPB

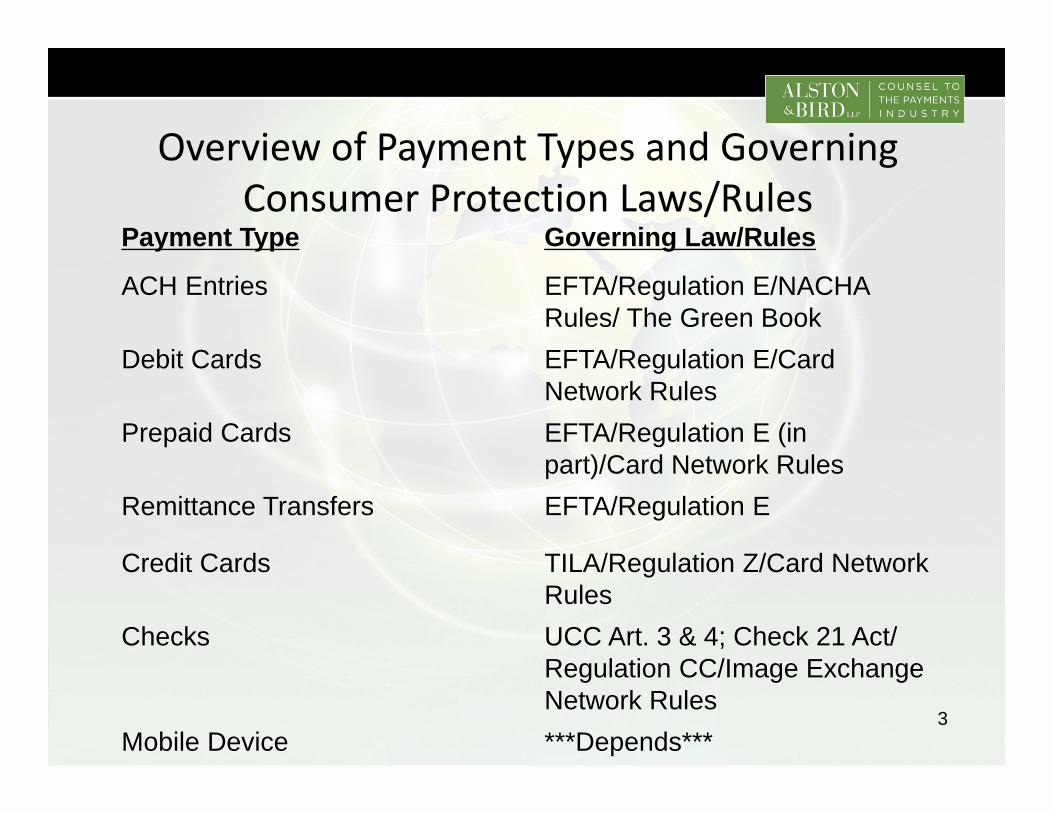

Overview of Payment Types and Governing Consumer Protection Laws/Rules

3

Payment Type Governing Law/Rules

ACH Entries EFTA/Regulation E/NACHA Rules/ The Green Book

Debit Cards EFTA/Regulation E/Card Network Rules

Prepaid Cards EFTA/Regulation E (in part)/Card Network Rules

Remittance Transfers EFTA/Regulation E

Credit Cards TILA/Regulation Z/Card Network Rules

Checks UCC Art. 3 & 4; Check 21 Act/ Regulation CC/Image Exchange Network Rules

Mobile Device ***Depends***

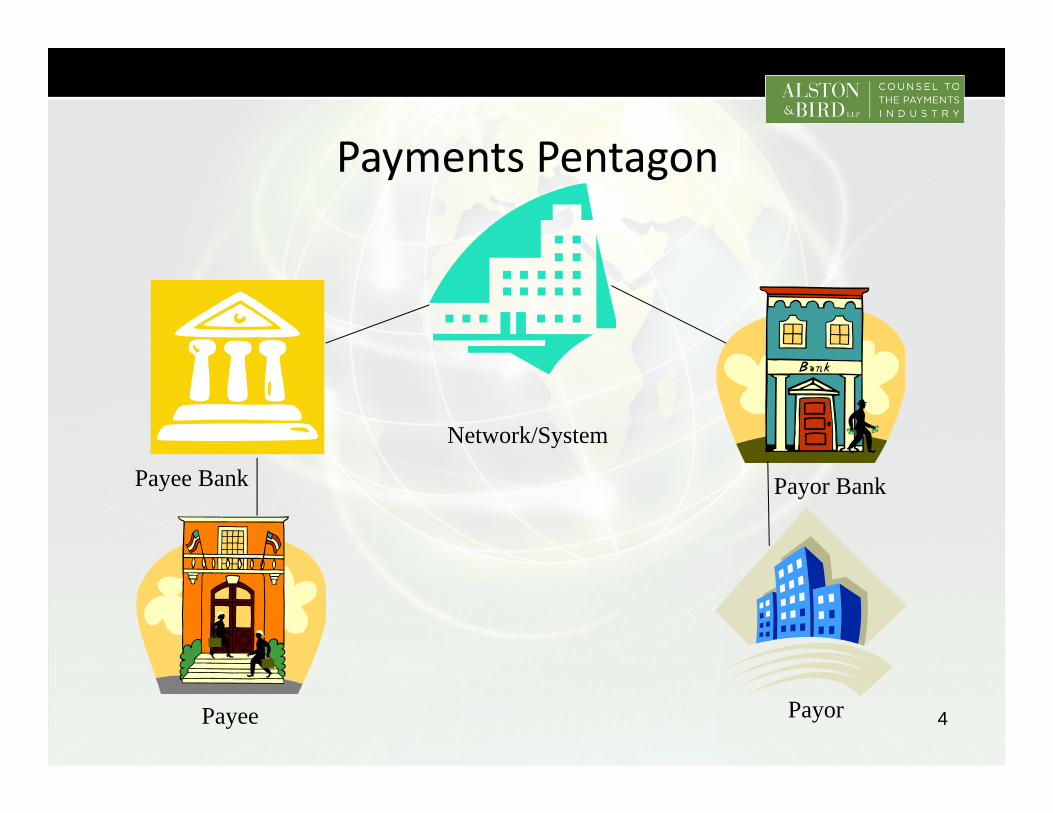

Payments Pentagon

Payee Bank

Payee

Network/System

Payor Bank

Payor 4

Electronic Fund Transfer Act / Regulation E

5

Overview• Electronic Fund Transfer Act (EFTA) was enacted in 1978, when consumer electronic fund transfers were limited

• Regulation E implements EFTA• EFTA/Regulation E provides the framework for establishing the rights, liabilities and responsibilities of consumers and providers of EFT services to consumers

• Sole Purpose: Consumer Protection –EFTA/Regulation E sets the floor for consumer rights/protections in connection with EFTs

6

Regulation E, Subpart A

7

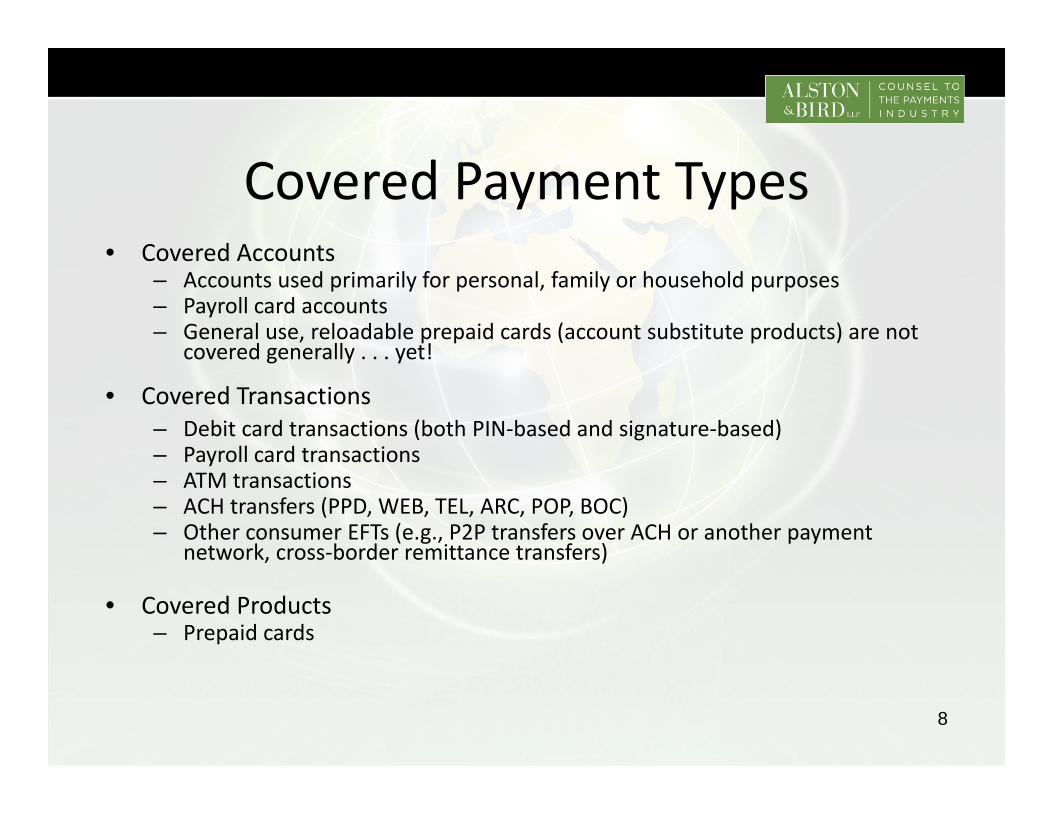

Covered Payment Types• Covered Accounts

– Accounts used primarily for personal, family or household purposes– Payroll card accounts– General use, reloadable prepaid cards (account substitute products) are not

covered generally . . . yet!

• Covered Transactions– Debit card transactions (both PIN‐based and signature‐based)– Payroll card transactions– ATM transactions– ACH transfers (PPD, WEB, TEL, ARC, POP, BOC)– Other consumer EFTs (e.g., P2P transfers over ACH or another payment

network, cross‐border remittance transfers)

• Covered Products– Prepaid cards

8

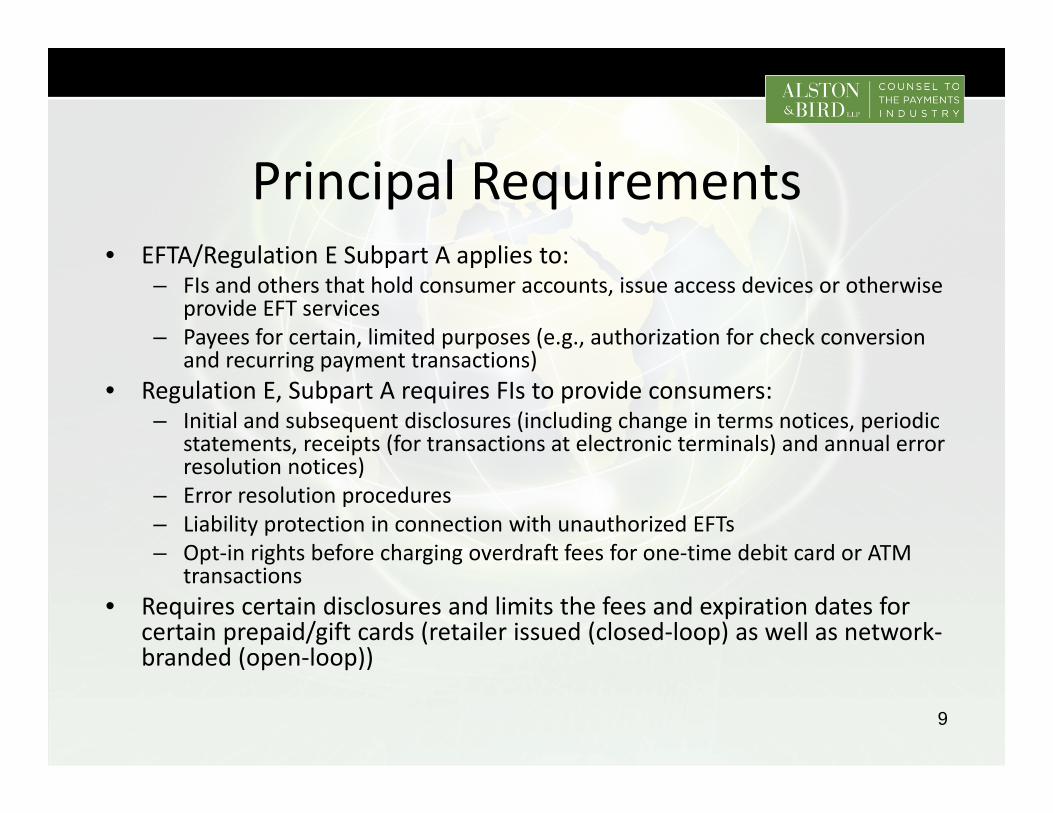

Principal Requirements• EFTA/Regulation E Subpart A applies to:

– FIs and others that hold consumer accounts, issue access devices or otherwise provide EFT services

– Payees for certain, limited purposes (e.g., authorization for check conversion and recurring payment transactions)

• Regulation E, Subpart A requires FIs to provide consumers:– Initial and subsequent disclosures (including change in terms notices, periodic

statements, receipts (for transactions at electronic terminals) and annual error resolution notices)

– Error resolution procedures– Liability protection in connection with unauthorized EFTs– Opt‐in rights before charging overdraft fees for one‐time debit card or ATM

transactions• Requires certain disclosures and limits the fees and expiration dates for

certain prepaid/gift cards (retailer issued (closed‐loop) as well as network‐branded (open‐loop))

9

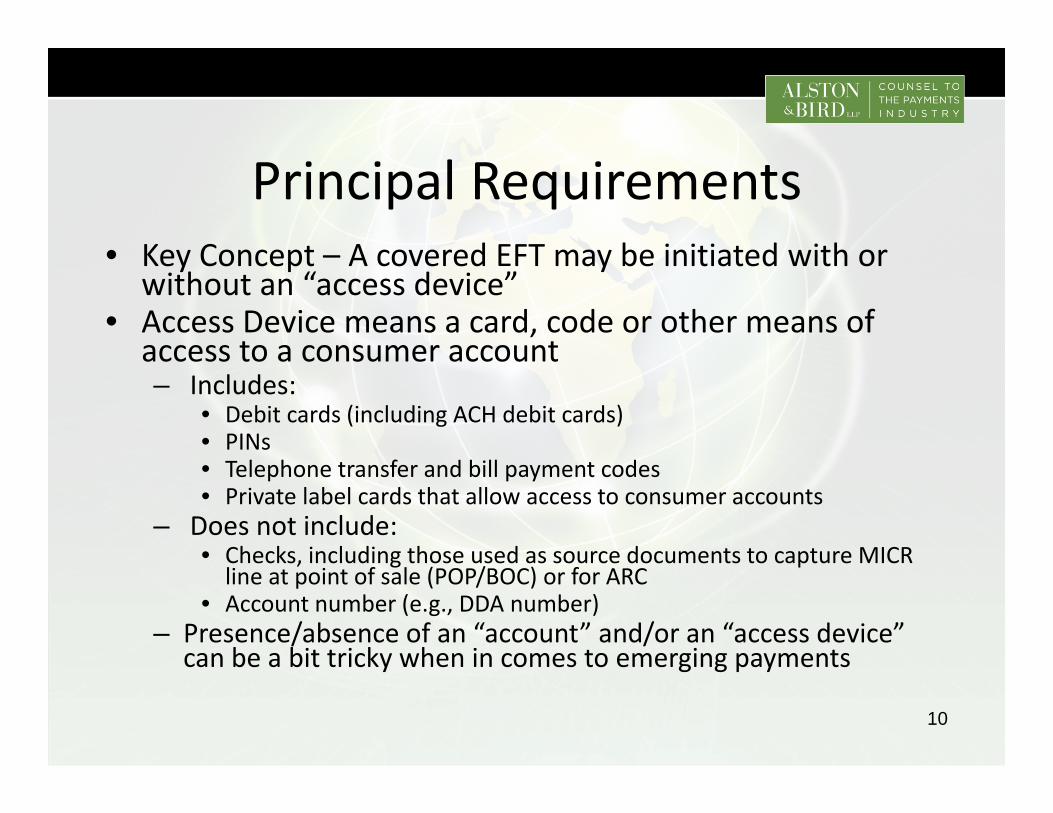

Principal Requirements• Key Concept – A covered EFT may be initiated with or

without an “access device”• Access Device means a card, code or other means of

access to a consumer account– Includes:

• Debit cards (including ACH debit cards)• PINs• Telephone transfer and bill payment codes• Private label cards that allow access to consumer accounts

– Does not include:• Checks, including those used as source documents to capture MICR line at point of sale (POP/BOC) or for ARC

• Account number (e.g., DDA number)– Presence/absence of an “account” and/or an “access device”

can be a bit tricky when in comes to emerging payments

10

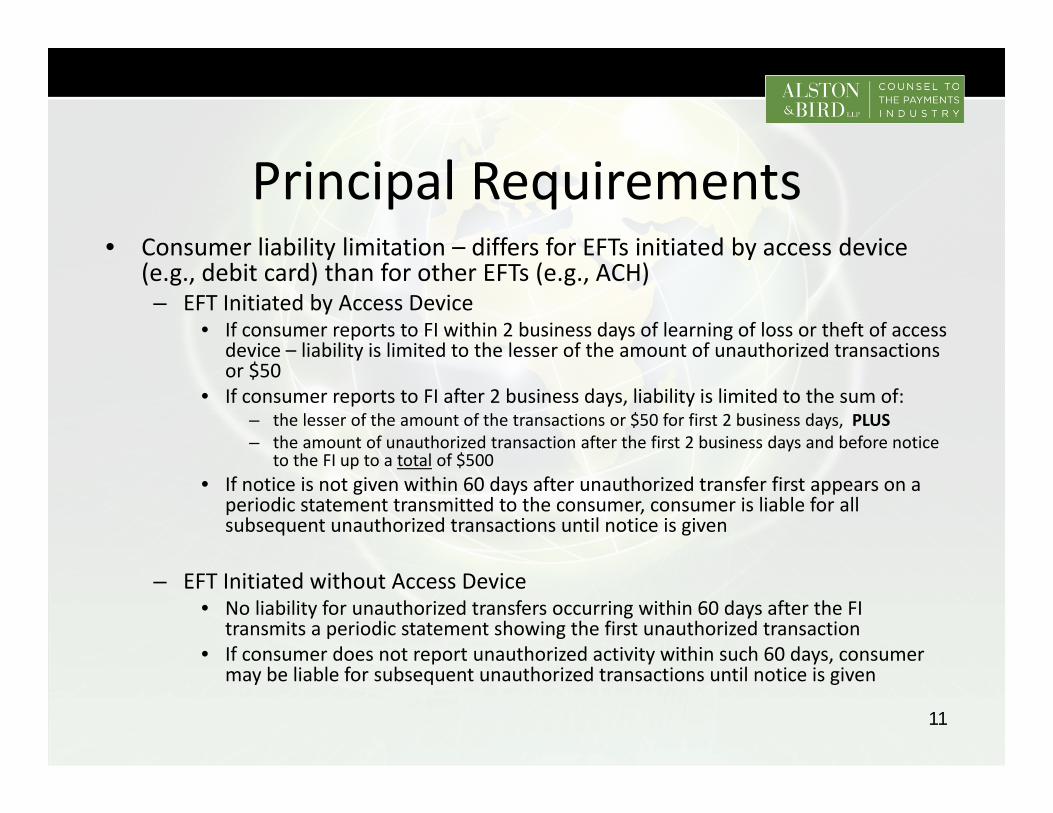

Principal Requirements• Consumer liability limitation – differs for EFTs initiated by access device

(e.g., debit card) than for other EFTs (e.g., ACH)– EFT Initiated by Access Device

• If consumer reports to FI within 2 business days of learning of loss or theft of access device – liability is limited to the lesser of the amount of unauthorized transactions or $50

• If consumer reports to FI after 2 business days, liability is limited to the sum of:– the lesser of the amount of the transactions or $50 for first 2 business days, PLUS– the amount of unauthorized transaction after the first 2 business days and before notice

to the FI up to a total of $500• If notice is not given within 60 days after unauthorized transfer first appears on a

periodic statement transmitted to the consumer, consumer is liable for all subsequent unauthorized transactions until notice is given

– EFT Initiated without Access Device• No liability for unauthorized transfers occurring within 60 days after the FI

transmits a periodic statement showing the first unauthorized transaction• If consumer does not report unauthorized activity within such 60 days, consumer

may be liable for subsequent unauthorized transactions until notice is given

11

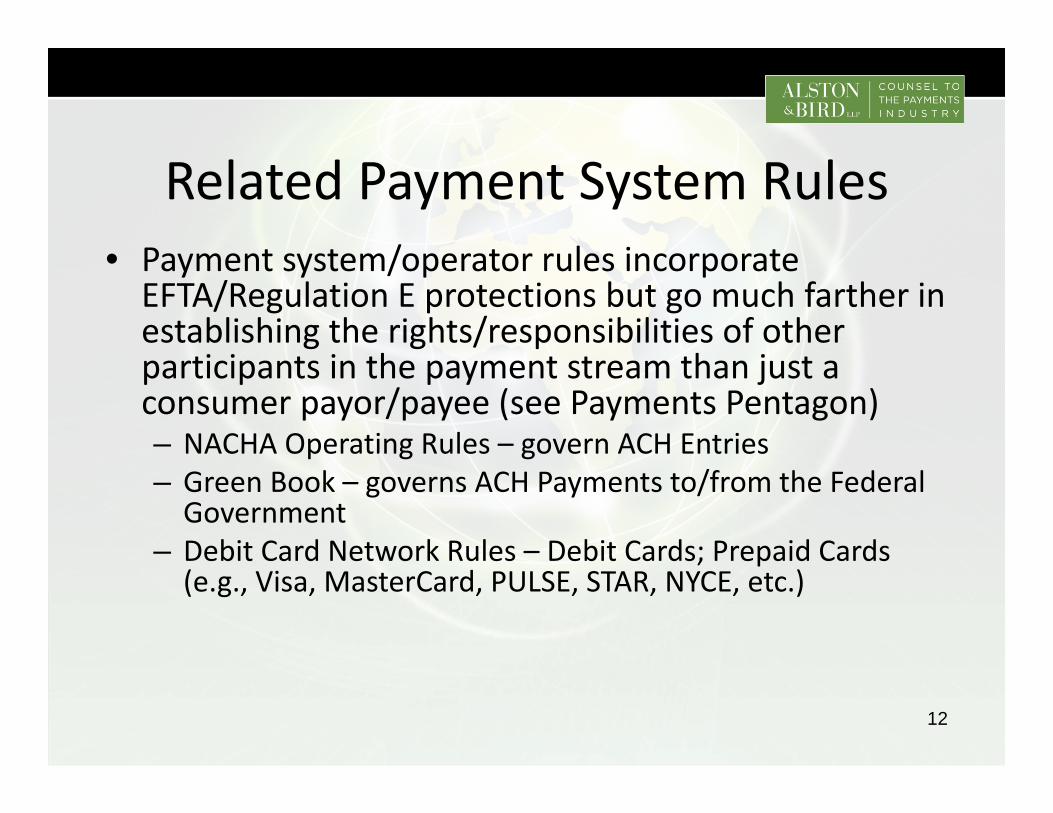

Related Payment System Rules• Payment system/operator rules incorporate EFTA/Regulation E protections but go much farther in establishing the rights/responsibilities of other participants in the payment stream than just a consumer payor/payee (see Payments Pentagon)– NACHA Operating Rules – govern ACH Entries– Green Book – governs ACH Payments to/from the Federal Government

– Debit Card Network Rules – Debit Cards; Prepaid Cards (e.g., Visa, MasterCard, PULSE, STAR, NYCE, etc.)

12

Related Payment System Rules – NACHA Operating Rules – govern ACH Entries

• Governs, as a matter of contract, the relative rights and responsibilities of financial institutions that use the ACH network

• Financial institutions pass down certain of these requirements to their customers (i.e., originators and receivers) by contract

– Green Book – governs ACH Payments to/from the Federal Government• A guide for financial institutions that receive ACH payments from or send ACH

payments to the Federal government (based in large part on 31 CFR 210 – Federal Government Participation in the Automated Clearing House)

• The Federal government generally follows the NACHA Operating Rules (with some exceptions), so most of the same requirements apply to Federal government ACH transactions as apply to other ACH transactions

– Debit Card Network Rules – Debit Cards; Prepaid Cards• Govern, as a matter of contract law, the relative rights and responsibilities of

financial institutions that use the applicable payment card network (issuers and acquirers)

• Financial institutions further pass down certain of these requirements to their customers (i.e., cardholders and merchants) by contract

• Some debit card networks increase by rule consumer protections required under EFTA/Regulation E (“Zero Liability”) for unauthorized transactions

13

Recent Developments• Credit CARD Act amended EFTA and Regulation E Subpart A to prohibit issuance/sale of retailer and network‐branded prepaid cards that do not meet expiration date and fee requirements

• CFPB ANPR to extend Regulation Subpart A of Regulation E to General‐use Reloadable Prepaid Cards

14

Regulation E, Subpart B

15

Overview• Section 1073 of the Dodd‐Frank Wall Street Reform and Consumer

Protection Act (“Dodd‐Frank”) amended the Electronic Fund Transfer Act (“EFTA”) by adding a new section entitled “Remittance Transfers.”

• New Section 919 of the EFTA:– Requires disclosure of certain information prior to and at the time of the transfer;– Creates new consumer protections, including the right cancel a transfer and the

right to a refund in certain circumstances; – Establishes a new error resolution scheme to which remittance transfer providers

must adhere; and– Establishes standards of liability for remittance transfer providers and their agents.

• Was to be effective on February 7th, 2013, but CFPB temporarily delayed effective date on December 21, 2012 until 90 days after CFPB issues certain revisions to its final rule implementing EFTA Section 919

16

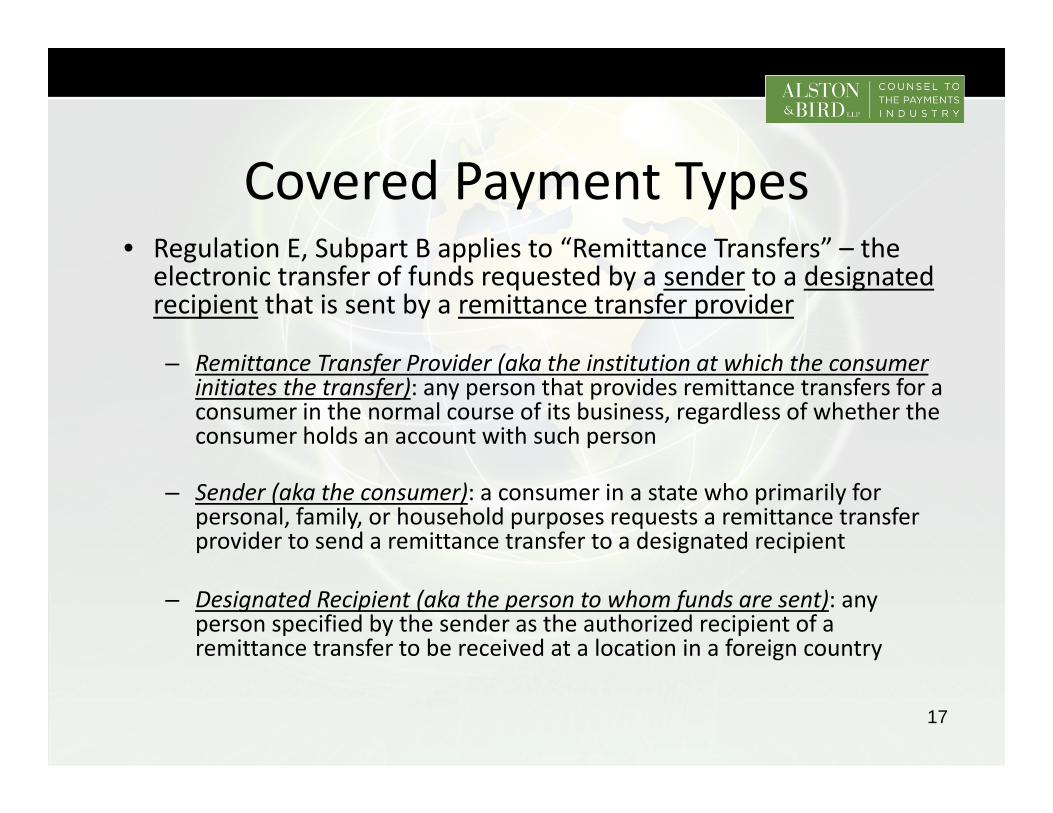

Covered Payment Types• Regulation E, Subpart B applies to “Remittance Transfers” – the

electronic transfer of funds requested by a sender to a designated recipient that is sent by a remittance transfer provider

– Remittance Transfer Provider (aka the institution at which the consumer initiates the transfer): any person that provides remittance transfers for a consumer in the normal course of its business, regardless of whether the consumer holds an account with such person

– Sender (aka the consumer): a consumer in a state who primarily for personal, family, or household purposes requests a remittance transfer provider to send a remittance transfer to a designated recipient

– Designated Recipient (aka the person to whom funds are sent): any person specified by the sender as the authorized recipient of a remittance transfer to be received at a location in a foreign country

17

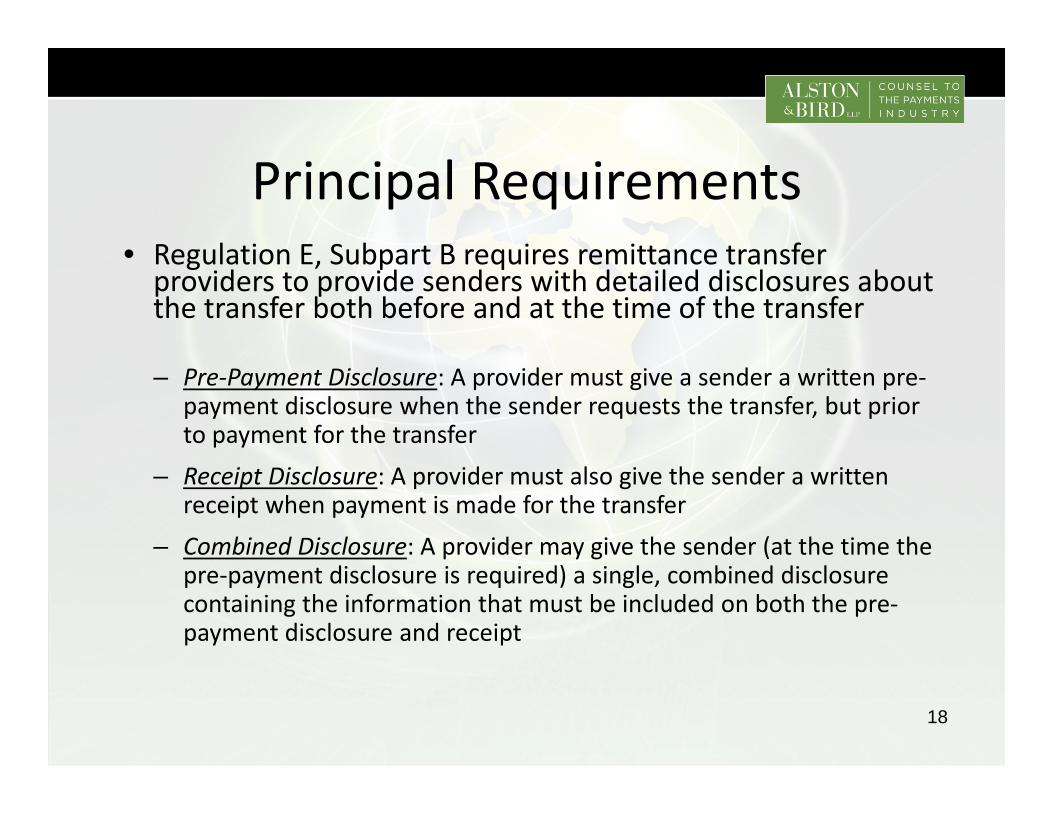

Principal Requirements• Regulation E, Subpart B requires remittance transfer providers to provide senders with detailed disclosures about the transfer both before and at the time of the transfer

– Pre‐Payment Disclosure: A provider must give a sender a written pre‐payment disclosure when the sender requests the transfer, but prior to payment for the transfer

– Receipt Disclosure: A provider must also give the sender a written receipt when payment is made for the transfer

– Combined Disclosure: A provider may give the sender (at the time the pre‐payment disclosure is required) a single, combined disclosure containing the information that must be included on both the pre‐payment disclosure and receipt

18

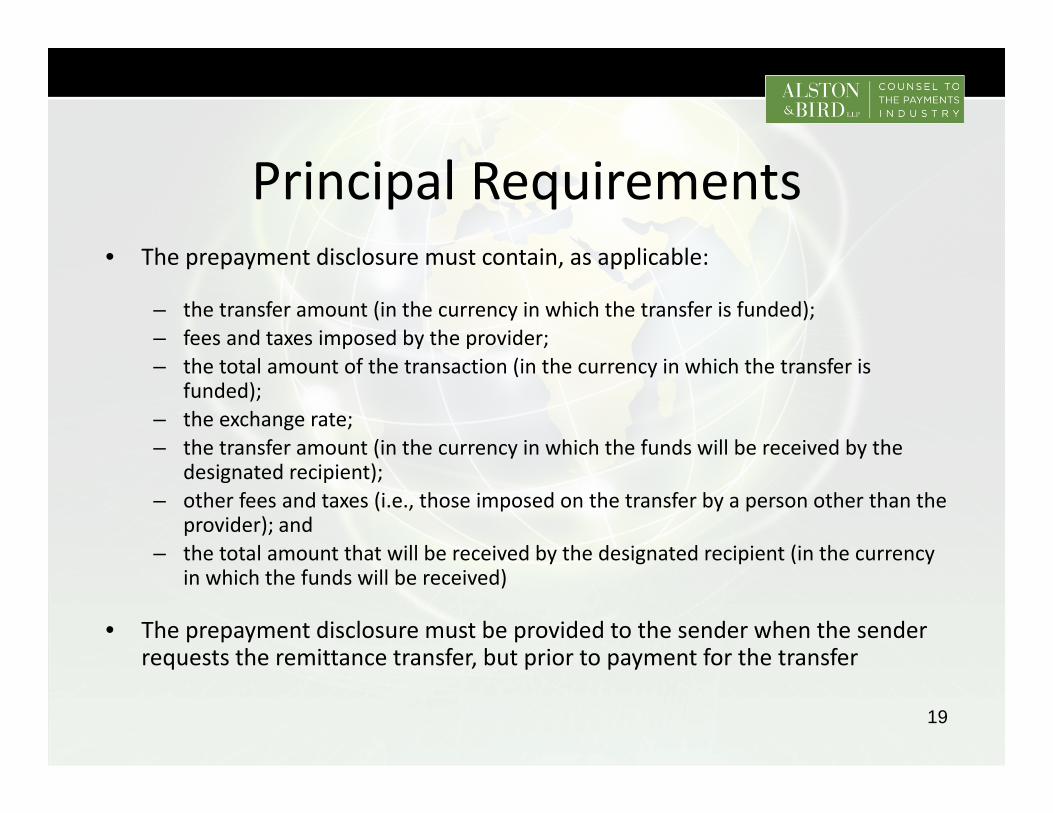

Principal Requirements• The prepayment disclosure must contain, as applicable:

– the transfer amount (in the currency in which the transfer is funded);– fees and taxes imposed by the provider;– the total amount of the transaction (in the currency in which the transfer is

funded);– the exchange rate;– the transfer amount (in the currency in which the funds will be received by the

designated recipient);– other fees and taxes (i.e., those imposed on the transfer by a person other than the

provider); and– the total amount that will be received by the designated recipient (in the currency

in which the funds will be received)

• The prepayment disclosure must be provided to the sender when the sender requests the remittance transfer, but prior to payment for the transfer

19

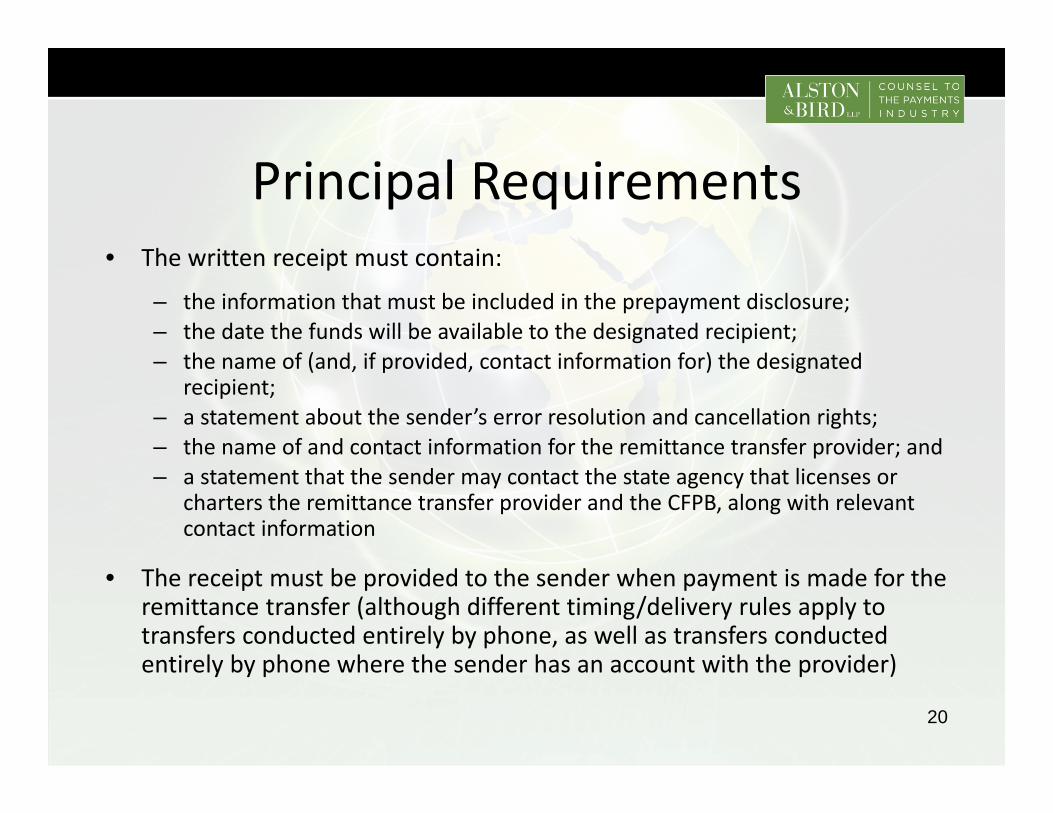

Principal Requirements• The written receipt must contain:

– the information that must be included in the prepayment disclosure;– the date the funds will be available to the designated recipient;– the name of (and, if provided, contact information for) the designated

recipient; – a statement about the sender’s error resolution and cancellation rights;– the name of and contact information for the remittance transfer provider; and– a statement that the sender may contact the state agency that licenses or

charters the remittance transfer provider and the CFPB, along with relevant contact information

• The receipt must be provided to the sender when payment is made for the remittance transfer (although different timing/delivery rules apply to transfers conducted entirely by phone, as well as transfers conducted entirely by phone where the sender has an account with the provider)

20

Principal Requirements• The Final Rule generally provides consumers the right to cancel a

transfer within 30 minutes of making payment for the transfer – For transfers scheduled at least 3 days in advance, the cancellation period is 3

days

• If the following two conditions are satisfied, providers are required to refund to the sender the total amount provided by the sender in connection with the remittance transfer:– the sender’s oral or written request to cancel enables the provider to identify

the sender and the particular transfer to be cancelled; and – the transferred funds have not been picked up by or deposited into the

account of the designated recipient

• Providers must make this refund at no additional cost to the sender and must do so within 3 business days of receiving the request

21

Principal Requirements• A provider is required to investigate and remedy an error if it receives notice

of the error no later than 180 days after the disclosed date of funds availability

• The provider must investigate and determine whether an error occurredwithin 90 days of receiving a notice of error and report the results to thesender within 3 business days after completing its investigation

• A provider is also required to correct the error as designated by the sender inaccordance with the remedy provisions contained in the Final Rule. Theseremedies include:– refunding to the sender the amount of funds provided by the sender in connection with

a transfer that was not properly transmitted (or the amount appropriate to resolve theerror); or

– making available to the designated recipient, without additional cost to the sender ordesignated recipient, the amount appropriate to resolve the error. This means that insome circumstances a provider may be required to resend the transfer at no additionalcost to the sender or the designated recipient

22

Related Payment System Rules• Section 1073 and new Subpart B to Regulation E define the term “remittance

transfer” very broadly to include the vast majority of electronic fund transfers (including wire and ACH transactions) sent by U.S. consumers to consumers and businesses in foreign countries, and the term is not limited by rule or statute to remittance transfers as traditionally understood

• UCC Article 4A historically governed all wire transfers, including consumer wire transfers (and such transfers were excluded from EFTA/Regulation E coverage)

• New Subpart B of Regulation E undermines this existing framework, making cross‐border consumer wire transfers subject to EFTA/Regulation E, thereby making UCC Article 4A inapplicable– FIs will no longer be able to rely on security procedure agreement and related loss

allocation/liability rules

– Fed/CFPB acknowledged this conundrum in issuing rules, but left resolution to state law (i.e., amend UCC Article 4A in all 50 states)

23

Related Payment System Rules• Many financial institutions use open networks to send transfers to

unaffiliated institutions in foreign countries with which they have no contractual relationship

• A provider that sends an “open network” transfer often has limited control over and information regarding the transaction – the funds are transferred from the sending institution to a recipient institution through a network of intermediary institutions

• The CFPB has acknowledged that it is aware that “a number of providers likely do not currently possess or have easy access to the information needed to satisfy the new disclosure requirements for every transaction” and “for these providers, as well as their operating partners, compliance may require modification of current systems, protocols, and contracts.”

24

Recent Developments• On December 21, 2012, the CFPB issued a proposed rule to

temporarily delay the effective date of its remittance transfer rules and to modify 3 aspects of the prior rule:• Easing of requirements for accurate disclosure of foreign taxes and

receiving institution fees;• Elimination of requirement to disclose regional, state, provincial or

local foreign (subnational) taxes; and• Softening of sending institution liability for “error” resulting when

sender provides incorrect recipient account information.• Issuance of a final version of the December 21 revisions is

expected imminently, which will begin the 90 “shot clock” on effectiveness

25

Truth in Lending Act / Regulation Z

26

Overview• Truth in Lending Act (TILA) was enacted in 1968 to promote

the informed use of credit by consumers• Regulation Z implements TILA• The purpose of TILA/Regulation Z is to assure accurate

disclosure of credit terms to consumers– Allow for comparison of terms– Inform consumers about the costs of credit– Protect against inaccurate/unfair credit billing and credit card

practices• TILA/Regulation Z entitles consumers/cardholders to certain

protections in connection with credit transactions– Right to cancel certain transactions– Mechanism for timely resolution of credit billing disputes

27

Covered Payment Types• Types of credit subject to Regulation Z

– Open‐End Credit – revolving credit like credit cards, lines of credit– Closed‐End Credit – any extension of credit that is not open‐end credit (e.g.,

retailer‐financed purchase)• Not covered by Regulation Z

– Business, commercial, agricultural or organizational credit (i.e., non‐consumer credit, unless a credit card is involved)

– Credit over $25,000 ($50,000 as of July 21, 2011, $53,000 as of January 1, 2013 due to annual CPI adjustment) unsecured by real property/consumer dwelling

– Public utility credit (e.g., financing of public utility service charges)– Extensions of credit in securities/commodities accounts (e.g., margin loans)– Student loans made, insured or guaranteed pursuant to Title IV of the Higher

Education Act– Employer‐sponsored retirement plans

28

Principal Requirements• TILA/Regulation Z generally applies to persons/business that,

on a regular basis, extend consumer credit subject to a finance charge or payable in installments (i.e., creditors)

• Requires creditors to provide consumers:– Detailed account‐opening and subsequent disclosures regarding the

terms and conditions of credit (including information about finance charges/interest rates, fees, available credit, payoff estimates, changes in terms, periodic statements, and statements of billing error rights)

– Billing error rights and resolution procedures– Liability protection in connection with unauthorized transactions

involving credit cards

29

Principal Requirements• A “credit card” is any “card, plate or other single credit device that may be used from time to time to obtain credit”– Certain special provisions of Regulation Z apply to credit cards even if associated credit is not subject to a finance charge (e.g., a charge card) or is not consumer credit

– Credit obtained through use of a credit card entitles the user to enhanced protections and rights

• Limitation of liability for unauthorized transactions• Right to assert claims or defenses against the card issuer

30

Principal Requirements• Cardholder liability for unauthorized use of a credit card may not exceed the lesser of $50 or the amount of unauthorized transactions that occurs before the cardholder notifies the issuer of the loss, theft or unauthorized use of the credit card

• A cardholder that has a dispute with a merchant related to a credit card transaction may, after attempting to resolve the dispute with the merchant, bring the claim against the card issuer (subject to geography and amount limitations)

31

Related Payment System Rules• Payment card network rules incorporate TILA/Regulation Z protections but go much farther in establishing the rights/responsibilities of other participants in the payment stream than just a creditor (see Payments Pentagon)

• Payment card network rules (Visa, MasterCard, Discover, Amex) require card issuing and transaction acquiring participants in their networks (usually financial institutions) to abide by common risk allocation/compliance requirements as a condition to network participation

32

Recent Developments• Credit Card Accountability, Responsibility and Disclosure Act of 2009 (Credit CARD Act) – expanded on TILA/Regulation Z’s historical scope (disclosure) by prohibiting a number of credit card industry practices– Limit interest rate changes and advance notice requirements

– Enhance disclosures– Cap penalty fees for cardholder agreement non‐compliance (e.g., late payments)

– Regulate promotional/teaser rates

33

Expedited Funds Availability Act / Regulation CC

34

Overview• Expedited Funds Availability Act (EFAA) – enacted in 1987 to standardize hold periods on deposits

• Regulation CC consists of 4 Subparts– Subpart A – General– Subpart B – Availability of Funds and Disclosure of Funds Availability Policy (implementing the EFAA)

– Subpart C – Collection of Checks (governing transfer and payment of checks)

– Subpart D – Substitute Checks (implementing Check 21)

35

Covered Payment Types• EFAA/Regulation CC – Subpart B

– Specifies the availability schedule for all different types of deposits to transaction accounts

– Requires that financial institutions provide transaction account customers with disclosures regarding availability of deposited funds

• Applies to cash, electronic deposits and checks of various types (with different availability applying depending on the type/risk of instrument)

36

Principal Requirements• Certain deposits are required to be made available for withdrawal on the

first business day following the banking day of deposit – Cash deposited in person, second business day if deposited remotely (e.g., at

ATM)– Electronic payments (when collected funds are received by the FI)– Certain types of checks and money orders (PMOs, FRB and FHLB checks,

government checks, cashiers and certified checks, on‐us checks and first $100 of other checks)

• Other deposits generally must be made available for withdrawal in accordance with the schedule specified in Regulation CC– After first $100, full amount of standard check must be made available for

withdrawal on second business day (Remember: all checks local)• Large deposit exception – for both next day and delayed availability items

(other than cash and electronic payments), if total deposit in a day exceeds $5,000, only the first $5,000 needs to be made available on the above availability schedules

• New account exception

37

Recent Developments• Dodd‐Frank Act – Expanded $100 next day availability for checks to $200 (subject to adjustment) effective July 21, 2011

• Proposed amendments to Regulation CC (released March 3, 2011)– Would reduce hold time for deposit of checks at nonproprietary ATMs from 5 to 4 business days

– Safe harbor for reasonable hold extension for non‐on‐us checks reduced to 2 business days

38

Other Relevant Laws/Regulations

39

Other Relevant Consumer Protection Laws/Regulations

• Truth in Savings Act/Regulation DD – requires that depository institutions provide disclosures to enable consumers to meaningfully compare deposit accounts

• Gramm‐Leach‐Bliley Act/Regulation P – requires financial institutions to provide notice of their privacy policies and the opportunity to opt out of certain information sharing arrangements

• Equal Credit Opportunity Act/Regulation B – prohibits creditors from using demographic characteristics such as age, marital status, race, religion, natural origin or sex when evaluating credit applications or extending credit

• Federal Trade Commission Act/Regulation AA – Prohibits unfair or deceptive acts or practices by banks in connection with extensions of credit to consumers

40

Considering Applicability of Existing Federal

Laws/Regulations to New Payment Types

41

Application of Existing Laws/ Regulations to New Payment Types

• Mobile Payments– New access device (e.g., phone as debit card)– New network (e.g., wireless carrier as issuer and network operator)

• Person‐to‐Person transfers– Use of FIs as endpoints to transfers– Dedicated “accounts” on new network/operator (e.g., PayPal)

42

Bureau of Consumer Financial Protection – The New Consumer Protection

Watchdog

43

CFPB: Overview• Bureau of Consumer Financial Protection (CFPB) – created out

of the Dodd‐Frank Act to administer and enforce all federal consumer financial protection laws

• CFPB has authority over “covered persons” – anyone who engages in offering or providing a consumer financial product or service

• CFPB assumed responsibility for federal consumer protection laws on July 21, 2011 (the “designated transfer date”). Since then it has:– Issued final Remittance Transfer Rules (Regulation E)– Issued an ANPR on Prepaid Cards (Regulation E)– Initiated non‐bank supervision/examination program

44

CFPB: Authority• Consumer financial products or services include many traditional consumer financial products and services “for use by consumers primarily for personal, family, or household purposes”

• Generally includes an extension of credit, deposit‐taking activity, funds transmission, check cashing, data processing services and providing certain financial advice

• Unfair, deceptive, or abusive practices – CFPB has broad, catchall authority to reach even acts/practices not specifically prohibited by another consumer protection regulation

45

CFPB: Tools • CFPB is authorized to administer, enforce and implement

consumer financial protection laws and carry out its Dodd Frank authorities by – prescribing regulations– issuing orders– publishing guidance– responding to consumer complaints– carrying out its examination & supervision authority

• Non‐FI providers (all participants in residential mortgage, private education lending, and payday lending markets; larger participants in other markets designated by CFPB; nonbanks designated by CFPB (regardless of market) deemed to pose risk to consumers due to offering of covered products/services

• Large FIs with assets >$10 billion

46

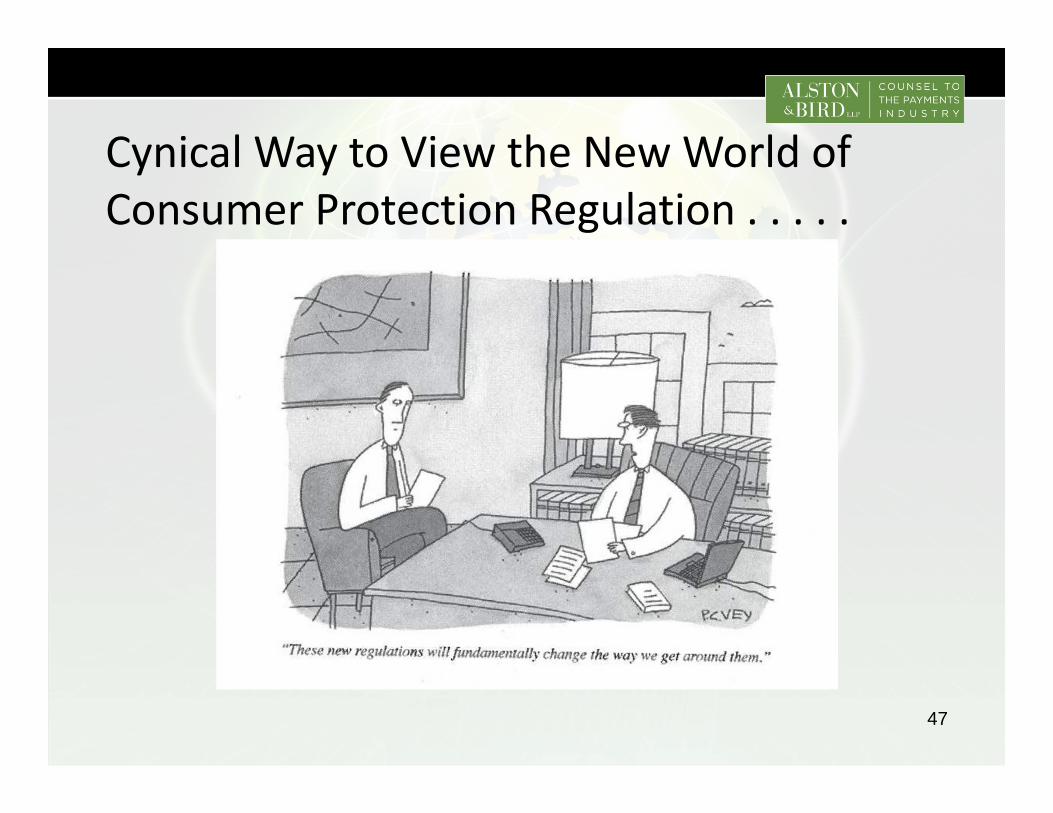

Cynical Way to View the New World of Consumer Protection Regulation . . . . .

47

Questions?Thank You!

Duncan B. DouglassAlston & Bird LLP

One Atlantic Center1201 West Peachtree StreetAtlanta, GA 30309‐3424

Telephone: (404) 881‐7768Fax: (404) 253‐8297

Email: [email protected]

48