Embed Size (px)

Citation preview

CORPORATES

CREDIT OPINION21 April 2020

Update

RATINGS

Petroleos MexicanosDomicile Mexico City, Ciudad de

Mexico, Mexico

Long Term Rating Ba2

Type LT Corporate FamilyRatings

Outlook Negative

Please see the ratings section at the end of this reportfor more information. The ratings and outlook shownreflect information as of the publication date.

Contacts

Nymia Almeida +52.55.1253.5707Senior Vice [email protected]

Marianna Waltz, CFA +55.11.3043.7309MD-Corporate [email protected]

Petroleos MexicanosUpdate following downgrade to Ba2 and negative outlook

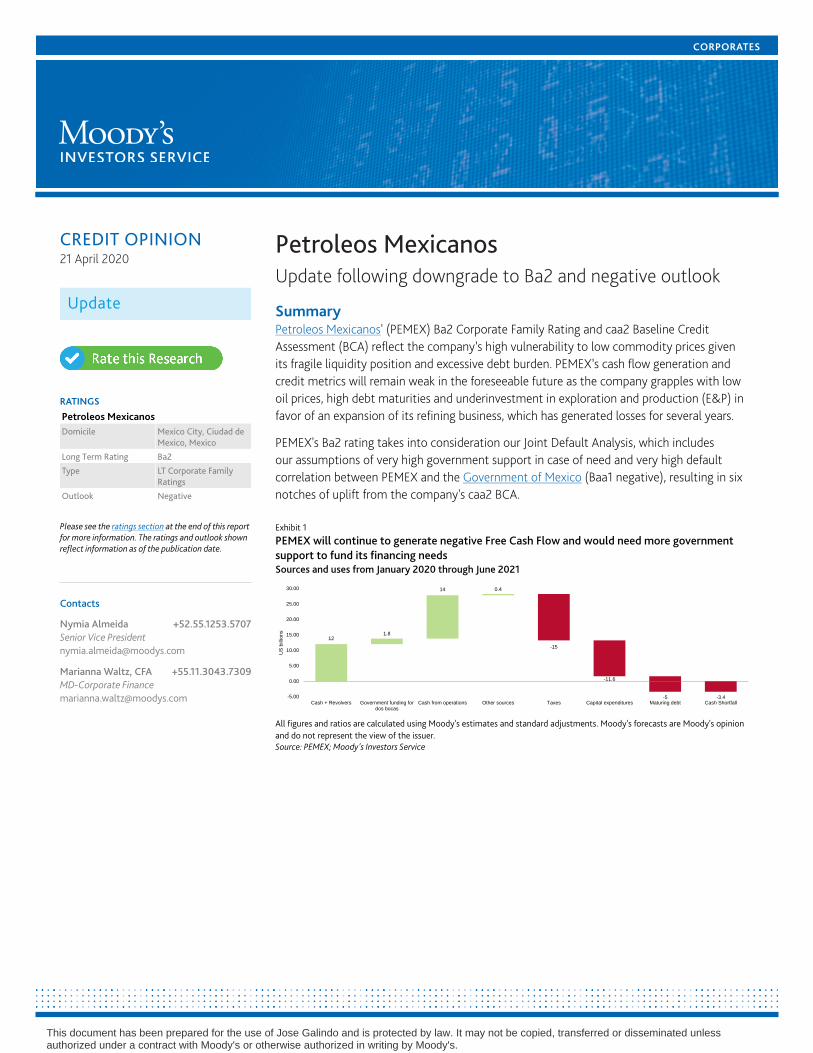

SummaryPetroleos Mexicanos' (PEMEX) Ba2 Corporate Family Rating and caa2 Baseline CreditAssessment (BCA) reflect the company’s high vulnerability to low commodity prices givenits fragile liquidity position and excessive debt burden. PEMEX’s cash flow generation andcredit metrics will remain weak in the foreseeable future as the company grapples with lowoil prices, high debt maturities and underinvestment in exploration and production (E&P) infavor of an expansion of its refining business, which has generated losses for several years.

PEMEX's Ba2 rating takes into consideration our Joint Default Analysis, which includesour assumptions of very high government support in case of need and very high defaultcorrelation between PEMEX and the Government of Mexico (Baa1 negative), resulting in sixnotches of uplift from the company's caa2 BCA.

Exhibit 1

PEMEX will continue to generate negative Free Cash Flow and would need more governmentsupport to fund its financing needsSources and uses from January 2020 through June 2021

121.8

14 0.4

-15

-11.6

-5 -3.4-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

Cash + Revolvers Government funding fordos bocas

Cash from operations Other sources Taxes Capital expenditures Maturing debt Cash Shortfall

US

billion

s

All figures and ratios are calculated using Moody's estimates and standard adjustments. Moody's forecasts are Moody's opinionand do not represent the view of the issuer.Source: PEMEX; Moody's Investors Service

This document has been prepared for the use of Jose Galindo and is protected by law. It may not be copied, transferred or disseminated unlessauthorized under a contract with Moody's or otherwise authorized in writing by Moody's.

MOODY'S INVESTORS SERVICE CORPORATES

Credit strengths

» Large-scale reserves and production with access to developable resources

» Government-related issuer, with very high government support assumed

Credit challenges

» Weak intrinsic liquidity and credit metrics

» High debt amount vis-à-vis cash generation

» High tax and interest burden

Rating outlookThe negative outlook on PEMEX’s Ba2 rating coincides with the negative outlook on Mexico's Baa1 rating given the importance of thesovereign's credit strength and ongoing support to the company's ratings. In addition, the negative outlook on PEMEX's rating takesinto account our expectation of an increase in debt to fund negative free cash flow (FCF) and the company’s limited ability to improveits business results given the mature stage of oil fields; shortage of capital to sufficiently invest in E&P, with negative consequences inproduction and reserve replacement; and the mandate to expand the refining business.

Factors that could lead to an upgrade

» An upgrade is unlikely given the negative outlook on PEMEX's and Mexico's ratings as well as our expectation of continued negativeFCF at PEMEX.

Factors that could lead to a downgrade

» A downgrade of Mexico's Baa1 rating would likely result in a downgrade of PEMEX's rating.

» For an affirmation of PEMEX’s Ba2 rating following a sovereign downgrade, the company’s BCA would have to substantiallyimprove. Factors that could lead to a much higher BCA would be the company's ability to strengthen its liquidity position andideally internally fund sufficient capital reinvestment to fully replace reserves and deliver modest production growth, and generateFCF for debt reduction.

» Because PEMEX's rating is highly dependent on support from the Government of Mexico, a change in our assumptions aboutgovernment support and its timeliness could lead to a downgrade of PEMEX's rating.

» A lowering of the BCA could also lead to a downgrade of PEMEX's rating. Factors that could lead to a lower BCA include materialincreases in net debt, an operating performance worse than forecasted, reserves declines and decreases in reserves life.

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 21 April 2020 Petroleos Mexicanos: Update following downgrade to Ba2 and negative outlook

This document has been prepared for the use of Jose Galindo and is protected by law. It may not be copied, transferred or disseminated unlessauthorized under a contract with Moody's or otherwise authorized in writing by Moody's.

MOODY'S INVESTORS SERVICE CORPORATES

Key indicators

Exhibit 2

Petroleos Mexicanos

US Millions Dec-14 Dec-15 Dec-16 Dec-17 Dec-18 Dec-19 2020-proj. 2021-proj.

Average Daily Production (MBOE / Day) 3,432.4 3,174.0 2,950.8 2,661.6 2,440.6 2,179.0 2,200.8 2,222.8

Total Proved Reserves (MBOE) 12,101.8 9,412.0 8,383.0 7,525.8 6,848.7 6,453.3 6,101.2 5,743.2

Crude Distillation Capacity (mbbls/day) 1,602.0 1,640.0 1,602.0 1,627.0 1,640.0 1,640.0 1,640.0 1,640.0

Downstream EBIT/Total Throughput Barrels ($17.7) ($11.0) ($10.3) ($13.3) ($14.2) ($15.5) ($13.9) ($13.7)

EBIT / Avg. Book Capitalization -3% 13% 19% 28% 25% 11% 26%

EBIT / Interest Expense 6.5x -0.4x 1.4x 2.1x 2.7x 1.4x 0.6x 1.3x

RCF / Net Debt 3% -1% -1% 5% 2% -2% -1% 1%

Debt / Book Capitalization 142% 195% 164% 186% 188% 274% 299% 294%

All figures and ratios are calculated using Moody’s estimates and standard adjustments. Moody's Forecasts (f) or Projections (proj.) are Moody's opinion and do not represent the views ofthe issuer. Periods are Financial Year-End unless indicated. LTM = Last Twelve Months. Total Proved Reserves for 2019 are our estimates as we do not have final certification report for 2019.Sources: Moody’s Financial Metrics™ and Moody's Investors Service (estimates)

ProfileFounded in 1938, PEMEX is Mexico's productive state-owned oil and gas enterprise. The company is the main energy company in thecountry, with fully integrated operations in oil and gas including exploration and production (E&P), refining, distribution and retailmarketing, as well as petrochemicals.

PEMEX is a leading crude oil exporter; around 65% of its crude is exported to various countries, mainly to the US and Canada (about60%). In 2019, the company posted $74.4 billion in revenue and had $100.3 billion in assets; in the same period, PEMEX produced anaverage of 1,703 thousand barrels of per day (mbpd) of crude oil (excluding partners). In 2019, PEMEX's royalties, tax, duties and otherpayments to the government amounted to around $22.6 billion. In 2018, PEMEX had total proved reserves of 6.8 billion barrels of oilequivalent (boe), with a reserve life of 7.7 years at 2018 production levels.

Exhibit 3

Revenue breakdown by business segmentExhibit 4

Operating income breakdown by business segment

Exploration and Production29%

Industrial Transformation57%

Others1%

Commercial entities13%

Industrial Transformation refers mostly to refining and marketing. Others includefertilizers, ethylene, and other operating subsidiaries. Revenue includes only sales toexternal clients.Data as of December 2019.Sources: PEMEX's fourth quarter Mexican Stock Exchange financial report

-40%

-20%

0%

20%

40%

60%

80%

100%

2016 2017 2018 2019

E&P TRI Trading companies Logistics Others

Industrial Transformation refers mostly to refining and marketing. Others includefertilizers, ethylene, perforation, logistics and other operating subsidiaries.Source: PEMEX's 20-F reports and fourth quarter Mexican Stock Exchange financial report

3 21 April 2020 Petroleos Mexicanos: Update following downgrade to Ba2 and negative outlook

This document has been prepared for the use of Jose Galindo and is protected by law. It may not be copied, transferred or disseminated unlessauthorized under a contract with Moody's or otherwise authorized in writing by Moody's.

MOODY'S INVESTORS SERVICE CORPORATES

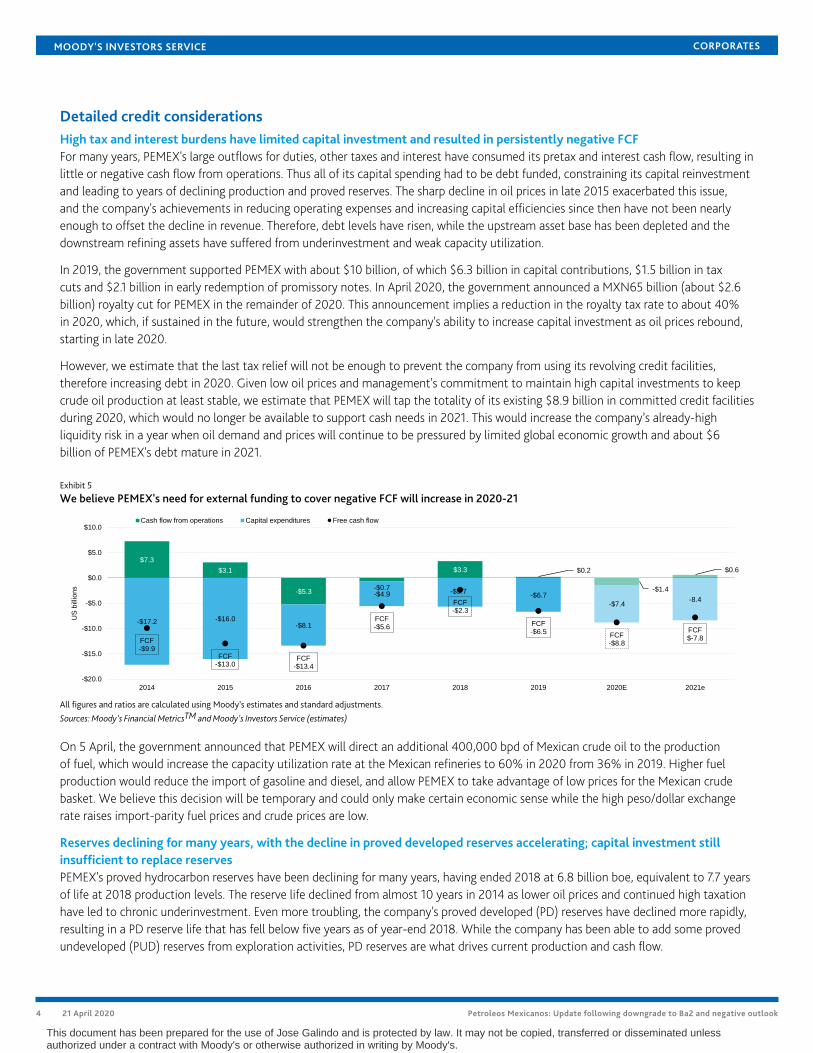

Detailed credit considerationsHigh tax and interest burdens have limited capital investment and resulted in persistently negative FCFFor many years, PEMEX's large outflows for duties, other taxes and interest have consumed its pretax and interest cash flow, resulting inlittle or negative cash flow from operations. Thus all of its capital spending had to be debt funded, constraining its capital reinvestmentand leading to years of declining production and proved reserves. The sharp decline in oil prices in late 2015 exacerbated this issue,and the company's achievements in reducing operating expenses and increasing capital efficiencies since then have not been nearlyenough to offset the decline in revenue. Therefore, debt levels have risen, while the upstream asset base has been depleted and thedownstream refining assets have suffered from underinvestment and weak capacity utilization.

In 2019, the government supported PEMEX with about $10 billion, of which $6.3 billion in capital contributions, $1.5 billion in taxcuts and $2.1 billion in early redemption of promissory notes. In April 2020, the government announced a MXN65 billion (about $2.6billion) royalty cut for PEMEX in the remainder of 2020. This announcement implies a reduction in the royalty tax rate to about 40%in 2020, which, if sustained in the future, would strengthen the company's ability to increase capital investment as oil prices rebound,starting in late 2020.

However, we estimate that the last tax relief will not be enough to prevent the company from using its revolving credit facilities,therefore increasing debt in 2020. Given low oil prices and management's commitment to maintain high capital investments to keepcrude oil production at least stable, we estimate that PEMEX will tap the totality of its existing $8.9 billion in committed credit facilitiesduring 2020, which would no longer be available to support cash needs in 2021. This would increase the company’s already-highliquidity risk in a year when oil demand and prices will continue to be pressured by limited global economic growth and about $6billion of PEMEX's debt mature in 2021.

Exhibit 5

We believe PEMEX's need for external funding to cover negative FCF will increase in 2020-21

$7.3

$3.1

-$5.3-$0.7

$3.3 $0.2

-$1.4

$0.6

-$17.2 -$16.0-$8.1

-$4.9 -$5.7-$6.7

-$7.4-8.4

FCF-$9.9

FCF-$13.0

FCF-$13.4

FCF-$5.6

FCF-$2.3

FCF-$6.5

FCF-$8.8

FCF$-7.8

-$20.0

-$15.0

-$10.0

-$5.0

$0.0

$5.0

$10.0

2014 2015 2016 2017 2018 2019 2020E 2021e

US

billion

s

Cash flow from operations Capital expenditures Free cash flow

All figures and ratios are calculated using Moody’s estimates and standard adjustments.

Sources: Moody's Financial MetricsTM and Moody's Investors Service (estimates)

On 5 April, the government announced that PEMEX will direct an additional 400,000 bpd of Mexican crude oil to the productionof fuel, which would increase the capacity utilization rate at the Mexican refineries to 60% in 2020 from 36% in 2019. Higher fuelproduction would reduce the import of gasoline and diesel, and allow PEMEX to take advantage of low prices for the Mexican crudebasket. We believe this decision will be temporary and could only make certain economic sense while the high peso/dollar exchangerate raises import-parity fuel prices and crude prices are low.

Reserves declining for many years, with the decline in proved developed reserves accelerating; capital investment stillinsufficient to replace reservesPEMEX's proved hydrocarbon reserves have been declining for many years, having ended 2018 at 6.8 billion boe, equivalent to 7.7 yearsof life at 2018 production levels. The reserve life declined from almost 10 years in 2014 as lower oil prices and continued high taxationhave led to chronic underinvestment. Even more troubling, the company's proved developed (PD) reserves have declined more rapidly,resulting in a PD reserve life that has fell below five years as of year-end 2018. While the company has been able to add some provedundeveloped (PUD) reserves from exploration activities, PD reserves are what drives current production and cash flow.

4 21 April 2020 Petroleos Mexicanos: Update following downgrade to Ba2 and negative outlook

This document has been prepared for the use of Jose Galindo and is protected by law. It may not be copied, transferred or disseminated unlessauthorized under a contract with Moody's or otherwise authorized in writing by Moody's.

MOODY'S INVESTORS SERVICE CORPORATES

PEMEX’s management believes that the company was able to replace proved reserves at a rate of 120% in 2019; however, it is unlikelythat the company will be able to replace reserves at a rate equal or close to 100% in 2020-21 given weak cash generation and limitedaccess to capital. The Reserve Report, with related certifications, is available at the end of April, annually, in conjunction with auditedfinancial statements.

The current administration installed a new senior management team at PEMEX in December 2018 and increased the capital budget(including non-capitalizable maintenance) to around $11.6 billion for 2020, a 20% increase from the 2019 budget. In 2019, PEMEX'sIFRS capital spending amounted to $6.7 billion, about 40% lower than expected. For 2020, the company reduced its capital spendingbudget by 15%, or $1.2 billion (MXN30,000 million in IFRS) to protect its liquidity amid the current oil price shock. We expect thecompany to invest a total of $7.4 billion in capital in 2020, of which close to 90% will be allocated to the E&P business. The $1.8 billionto be invested in the new refinery will be funded by the Ministry of Energy.

We believe that PEMEX's need for external funding to cover negative FCF will increase as a consequence of the company's limitedability to improve its business results due to the mature stage of oil fields; shortage of capital to sufficiently invest in E&P, with negativeconsequences in production and reserve replacement; and the mandate to expand the refining business, which we expect will continueto post operating losses and be vulnerable to the oil and gas industry medium-term demands trends.

In 2019, PEMEX demonstrated good progress on its primary objective of stabilizing oil production. We expect the company'sproduction to hover around 780,000 million barrels per year in 2020-21.

The company announced several discoveries in 2019, including the Quesqui field in Tabasco, which is estimated to have 500 millionboe of 3P (proved, possible and probable) reserves, and the Uchukil project (located in the Gulf of Mexico near Tabasco), which hasthree wells with preliminary 3P reserves of 94 million boe. These discoveries support longer-term reserve replacement, but they requiremore capital investment to become proved reserves and to eventually migrate to proved developed producing reserves.

While the amount required for reserve replacement is not necessarily the same as the amount needed to maintain or grow production,they are correlated over time and therefore we believe PEMEX will need to meaningfully increase its exploration and developmentspending to achieve the production growth targets the government has established. This would require further support from thegovernment.

New refinery adds to PEMEX's capital spending burden with doubtful returns on investment and cost overrun risksA key objective of the current administration's energy agenda is for PEMEX to build a new refinery and improve the operationalperformance of the existing refineries to make Mexico more self-sufficient in refined products. Given ample refining capacity, bothglobally and in North America, even before the Coronavirus pandemic, we believe the economic returns from this investment are likelyto be low. In addition, if the new refinery is completed and the existing refineries' operational capacity is increased as planned, thiswill add exposure to lower-margin fuel production and reduce PEMEX's crude exports and therefore its US dollar revenue generation,increasing its credit risk.

However, the more near-term challenges are the risks of cost overruns and delays on completion of the new refinery. In May 2019 thegovernment announced the cancellation of the private tender process with major international construction firms to build the newrefinery. Bids came in between $10 billion and $12 billion, with a timeline for completion in excess of three years. But the governmentbelieves that the project should cost $8 billion and take no more than three years to complete and mandated PEMEX to construct thenew refinery.

We believe that the project could end up costing more than the $10 billion-$12 billion suggested by the tenders given thegovernment's and PEMEX's limited know-how of refinery building. Over time, this will place a greater burden on the company'smanagement resources and will ultimately require more sovereign support to fund the capital investment.

The risks in building the new refinery are akin to those of Petroleo Brasileiro (Petrobras, Ba2 stable), which began construction ofthe new RNEST refinery with two units planned. Construction of the second unit was stopped in the fourth quarter of 2014 and thecompany has cumulatively recorded impairment charges of $4.8 billion through 31 December 2018 and the second unit remainsunfinished. Petrobras is now in the process of selling half of its refining business, which it expects to complete before 2021.

5 21 April 2020 Petroleos Mexicanos: Update following downgrade to Ba2 and negative outlook

This document has been prepared for the use of Jose Galindo and is protected by law. It may not be copied, transferred or disseminated unlessauthorized under a contract with Moody's or otherwise authorized in writing by Moody's.

MOODY'S INVESTORS SERVICE CORPORATES

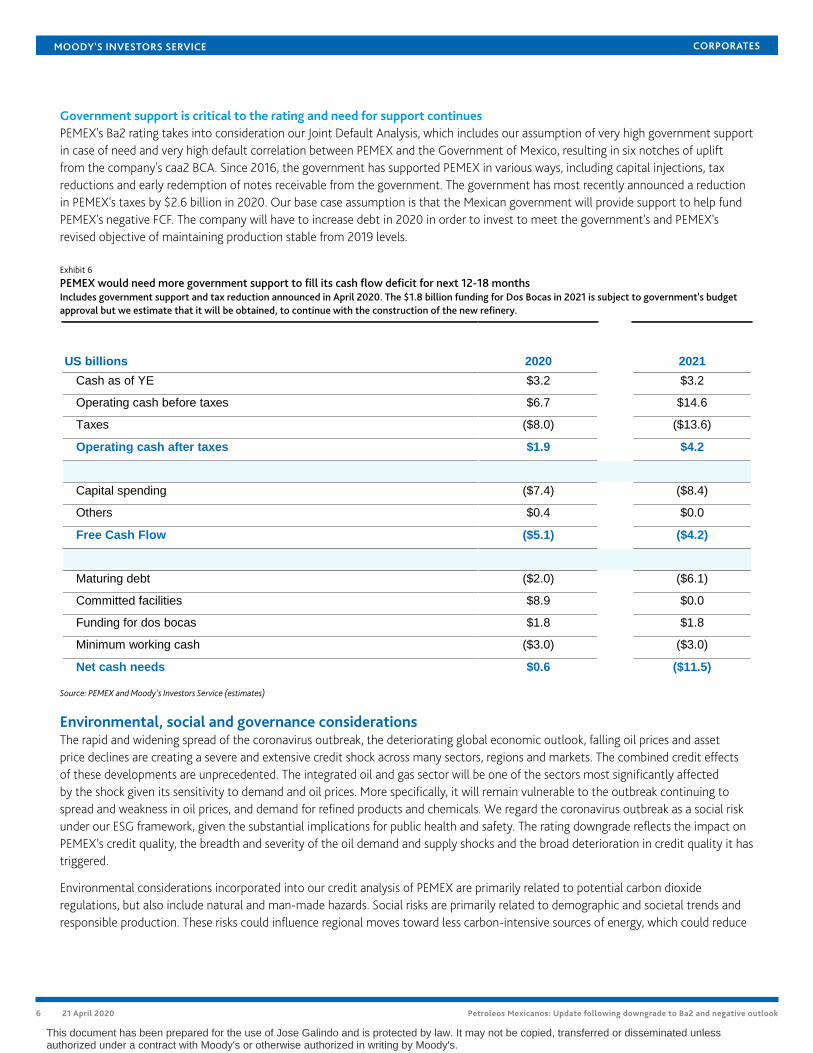

Government support is critical to the rating and need for support continuesPEMEX's Ba2 rating takes into consideration our Joint Default Analysis, which includes our assumption of very high government supportin case of need and very high default correlation between PEMEX and the Government of Mexico, resulting in six notches of upliftfrom the company's caa2 BCA. Since 2016, the government has supported PEMEX in various ways, including capital injections, taxreductions and early redemption of notes receivable from the government. The government has most recently announced a reductionin PEMEX's taxes by $2.6 billion in 2020. Our base case assumption is that the Mexican government will provide support to help fundPEMEX's negative FCF. The company will have to increase debt in 2020 in order to invest to meet the government's and PEMEX'srevised objective of maintaining production stable from 2019 levels.

Exhibit 6

PEMEX would need more government support to fill its cash flow deficit for next 12-18 monthsIncludes government support and tax reduction announced in April 2020. The $1.8 billion funding for Dos Bocas in 2021 is subject to government's budgetapproval but we estimate that it will be obtained, to continue with the construction of the new refinery.

US billions 2020

Colu

mn2 2021

Cash as of YE $3.2 $3.2

Operating cash before taxes $6.7 $14.6

Taxes ($8.0) ($13.6)

Operating cash after taxes $1.9 $4.2

Capital spending ($7.4) ($8.4)

Others $0.4 $0.0

Free Cash Flow ($5.1) ($4.2)

Maturing debt ($2.0) ($6.1)

Committed facilities $8.9 $0.0

Funding for dos bocas $1.8 $1.8

Minimum working cash ($3.0) ($3.0)

Net cash needs $0.6 ($11.5)

Source: PEMEX and Moody's Investors Service (estimates)

Environmental, social and governance considerationsThe rapid and widening spread of the coronavirus outbreak, the deteriorating global economic outlook, falling oil prices and assetprice declines are creating a severe and extensive credit shock across many sectors, regions and markets. The combined credit effectsof these developments are unprecedented. The integrated oil and gas sector will be one of the sectors most significantly affectedby the shock given its sensitivity to demand and oil prices. More specifically, it will remain vulnerable to the outbreak continuing tospread and weakness in oil prices, and demand for refined products and chemicals. We regard the coronavirus outbreak as a social riskunder our ESG framework, given the substantial implications for public health and safety. The rating downgrade reflects the impact onPEMEX’s credit quality, the breadth and severity of the oil demand and supply shocks and the broad deterioration in credit quality it hastriggered.

Environmental considerations incorporated into our credit analysis of PEMEX are primarily related to potential carbon dioxideregulations, but also include natural and man-made hazards. Social risks are primarily related to demographic and societal trends andresponsible production. These risks could influence regional moves toward less carbon-intensive sources of energy, which could reduce

6 21 April 2020 Petroleos Mexicanos: Update following downgrade to Ba2 and negative outlook

This document has been prepared for the use of Jose Galindo and is protected by law. It may not be copied, transferred or disseminated unlessauthorized under a contract with Moody's or otherwise authorized in writing by Moody's.

MOODY'S INVESTORS SERVICE CORPORATES

the demand for oil, gas and refined products. Given the company's weak credit profile captured in its caa2 BCA, the emerging risksrelated to future laws and regulations that could accelerate the rate of energy transition were not material factors in PEMEX's ratings.

PEMEX aims to continuously improve its environmental performance through efficient use of energy and water resources whileminimizing the effects from its operations on human health and ecosystems where the company carries out its activities. Throughexternal environmental audits, PEMEX ensures that its business lines comply with legal and other environmental requirements thatenable greater eco-efficiency in hydrocarbon exploitation and transformation processes. In the same way, the response plans toenvironmental emergencies are evaluated, decreasing the likelihood of accidents with adverse impacts on the environment.

In terms of social responsibility, PEMEX continuously strengthens the capacities of its staff and communication with the communitiesnear its operations. In addition, the company develops an effective and independent dispute resolution mechanism; ensures that itsplanning processes incorporate social and environmental externalities associated with them; to identify and map the non-technicalrisks associated with its operation to anticipate and manage them more effectively; and, in general, to consolidate a clean operationthat generates real and tangible benefits for them.

The primary governance considerations incorporated into our analysis of PEMEX is its 100% ownership and direct control by theGovernment of Mexico. Therefore, the company's management and budget are subject to both fiscal and public policy considerationsand not solely commercial considerations. The government has implemented the Petroleos Mexicanos Law, under which PEMEX isgoverned by a 10-member board of directors composed by the Ministry of Energy, the Ministry of Finance, the Mexican government’srepresentatives appointed by the president of Mexico and five independent members (not public officials and not former/currentPEMEX employees) appointed by the president of Mexico, subject to ratification by the Senate. PEMEX has to comply with local(Mexican Stock Exchange) and international regulations (Securities and Exchange Commission) in terms of compliance and reporting.

Liquidity analysisPEMEX's intrinsic liquidity is weak and highly dependent on government support, although its liquidity improved from earlier 2019.As of December 31, 2019, PEMEX had $3.2 billion in cash and, as of April 6, 2020, it had $8.9 billion in unused committed revolvingfacilities, which mature between 2021 and 2024, to cover over $8 billion in debt maturities through December 2021, besides ourestimated negative FCF of over $9 billion in the period. During 2019, PEMEX refinanced most of its 2020 debt maturities, reducingthem to $2 billion in January 2020 from $9.6 billion as of year-end 2018.

Exhibit 7

Debt maturity profile

$3.2 $8.9 $2.0 $6.1 $5.6 $6.3

$78.6

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

$70.0

$80.0

$90.0

Sources 2020 2021 2022 2023 +2024

US

billion

s

Cash & Eq. Revolver LT maturities

Cash as of December 31, 2019. Revolver facilities as of April 2020 and LT maturities as of February 2020.Source: PEMEX

7 21 April 2020 Petroleos Mexicanos: Update following downgrade to Ba2 and negative outlook

This document has been prepared for the use of Jose Galindo and is protected by law. It may not be copied, transferred or disseminated unlessauthorized under a contract with Moody's or otherwise authorized in writing by Moody's.

MOODY'S INVESTORS SERVICE CORPORATES

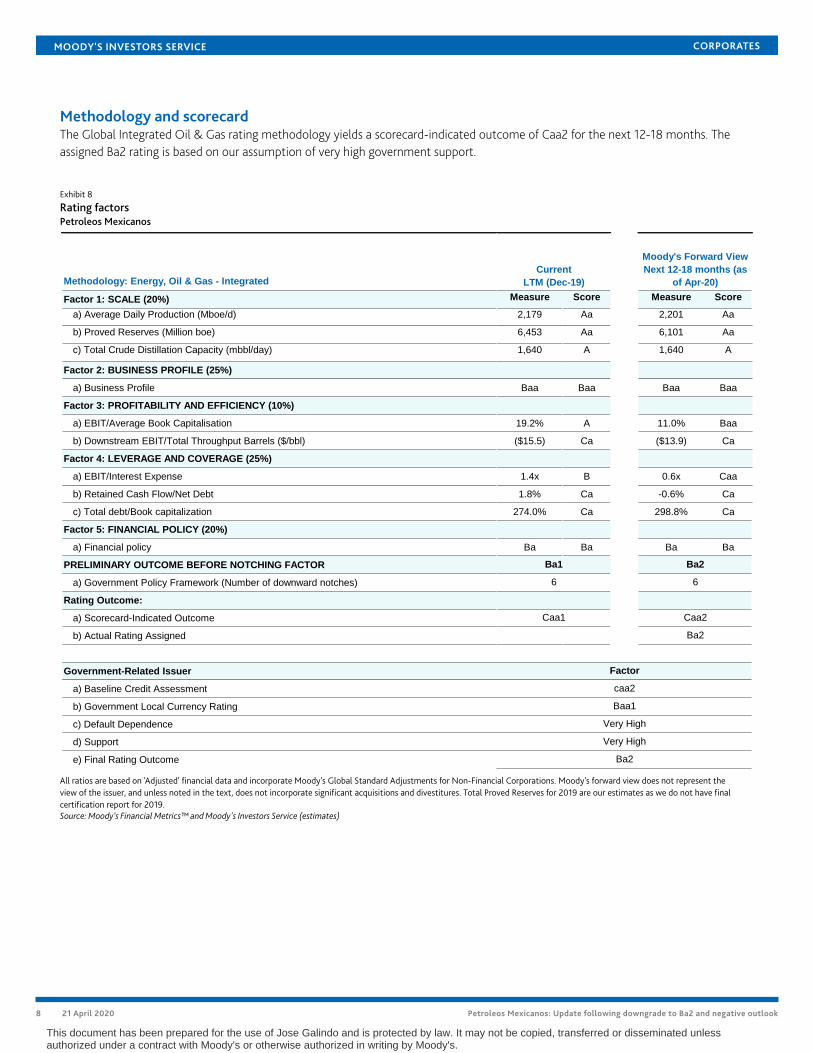

Methodology and scorecardThe Global Integrated Oil & Gas rating methodology yields a scorecard-indicated outcome of Caa2 for the next 12-18 months. Theassigned Ba2 rating is based on our assumption of very high government support.

Exhibit 8

Rating factorsPetroleos Mexicanos

Methodology: Energy, Oil & Gas - Integrated

Factor 1: SCALE (20%) Measure Score Measure Score

a) Average Daily Production (Mboe/d) 2,179 Aa 2,201 Aa

b) Proved Reserves (Million boe) 6,453 Aa 6,101 Aa

c) Total Crude Distillation Capacity (mbbl/day) 1,640 A 1,640 A

Factor 2: BUSINESS PROFILE (25%)

a) Business Profile Baa Baa Baa Baa

Factor 3: PROFITABILITY AND EFFICIENCY (10%)

a) EBIT/Average Book Capitalisation 19.2% A 11.0% Baa

b) Downstream EBIT/Total Throughput Barrels ($/bbl) ($15.5) Ca ($13.9) Ca

Factor 4: LEVERAGE AND COVERAGE (25%)

a) EBIT/Interest Expense 1.4x B 0.6x Caa

b) Retained Cash Flow/Net Debt 1.8% Ca -0.6% Ca

c) Total debt/Book capitalization 274.0% Ca 298.8% Ca

Factor 5: FINANCIAL POLICY (20%)

a) Financial policy Ba Ba Ba Ba

PRELIMINARY OUTCOME BEFORE NOTCHING FACTOR

a) Government Policy Framework (Number of downward notches)

Rating Outcome:

a) Scorecard-Indicated Outcome

b) Actual Rating Assigned

Government-Related Issuer

a) Baseline Credit Assessment

b) Government Local Currency Rating

c) Default Dependence

d) Support

e) Final Rating Outcome

Very High

Very High

Ba2

Caa1 Caa2

Ba2

Factor

caa2

Baa1

Current

LTM (Dec-19)

Moody's Forward View

Next 12-18 months (as

of Apr-20)

6 6

Ba1 Ba2

All ratios are based on 'Adjusted' financial data and incorporate Moody's Global Standard Adjustments for Non-Financial Corporations. Moody's forward view does not represent theview of the issuer, and unless noted in the text, does not incorporate significant acquisitions and divestitures. Total Proved Reserves for 2019 are our estimates as we do not have finalcertification report for 2019.Source: Moody’s Financial Metrics™ and Moody's Investors Service (estimates)

8 21 April 2020 Petroleos Mexicanos: Update following downgrade to Ba2 and negative outlook

This document has been prepared for the use of Jose Galindo and is protected by law. It may not be copied, transferred or disseminated unlessauthorized under a contract with Moody's or otherwise authorized in writing by Moody's.

MOODY'S INVESTORS SERVICE CORPORATES

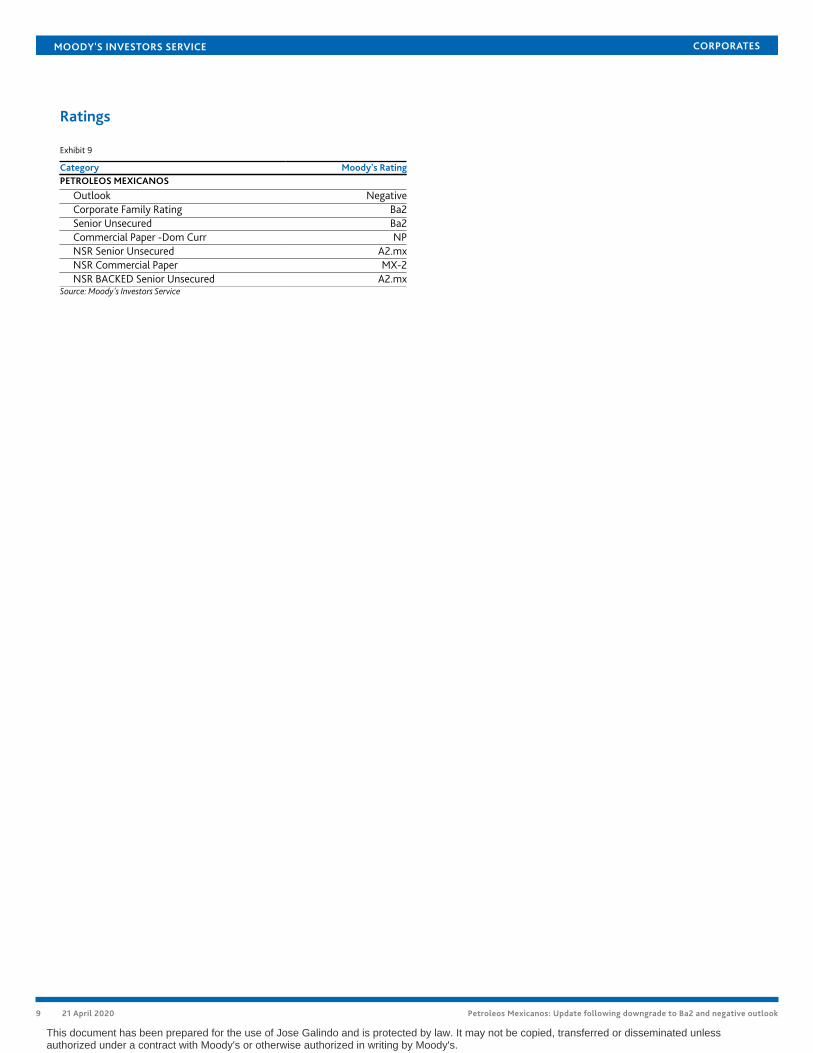

Ratings

Exhibit 9

Category Moody's RatingPETROLEOS MEXICANOS

Outlook NegativeCorporate Family Rating Ba2Senior Unsecured Ba2Commercial Paper -Dom Curr NPNSR Senior Unsecured A2.mxNSR Commercial Paper MX-2NSR BACKED Senior Unsecured A2.mx

Source: Moody's Investors Service

9 21 April 2020 Petroleos Mexicanos: Update following downgrade to Ba2 and negative outlook

This document has been prepared for the use of Jose Galindo and is protected by law. It may not be copied, transferred or disseminated unlessauthorized under a contract with Moody's or otherwise authorized in writing by Moody's.

MOODY'S INVESTORS SERVICE CORPORATES

© 2020 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND/OR ITS CREDIT RATINGS AFFILIATES ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURECREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MATERIALS, PRODUCTS, SERVICES AND INFORMATION PUBLISHED BY MOODY’S(COLLECTIVELY, “PUBLICATIONS”) MAY INCLUDE SUCH CURRENT OPINIONS. MOODY’S INVESTORS SERVICE DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAYNOT MEET ITS CONTRACTUAL FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT OR IMPAIRMENT. SEEMOODY’S RATING SYMBOLS AND DEFINITIONS PUBLICATION FOR INFORMATION ON THE TYPES OF CONTRACTUAL FINANCIAL OBLIGATIONS ADDRESSED BY MOODY’SINVESTORS SERVICE CREDIT RATINGS. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, ORPRICE VOLATILITY. CREDIT RATINGS, NON-CREDIT ASSESSMENTS (“ASSESSMENTS”), AND OTHER OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTSOF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS ORCOMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. AND/OR ITS AFFILIATES. MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS DONOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS ARE NOTAND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS ANDPUBLICATIONS DO NOT COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS, ASSESSMENTS ANDOTHER OPINIONS AND PUBLISHES ITS PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDYAND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS, AND PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESSAND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS OR PUBLICATIONS WHEN MAKING AN INVESTMENTDECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BYLAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHERTRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANYFORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A BENCHMARK AS THAT TERM ISDEFINED FOR REGULATORY PURPOSES AND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing its Publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY CREDITRATING, ASSESSMENT, OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any credit rating,agreed to pay to Moody’s Investors Service, Inc. for credit ratings opinions and services rendered by it fees ranging from $1,000 to approximately $2,700,000. MCO and Moody’sinvestors Service also maintain policies and procedures to address the independence of Moody’s Investors Service credit ratings and credit rating processes. Information regardingcertain affiliations that may exist between directors of MCO and rated entities, and between entities who hold credit ratings from Moody’s Investors Service and have also publiclyreported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Investor Relations — Corporate Governance —Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as tothe creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any credit rating, agreed to pay to MJKK or MSFJ (as applicable) for credit ratings opinions and servicesrendered by it fees ranging from JPY125,000 to approximately JPY250,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1223548

10 21 April 2020 Petroleos Mexicanos: Update following downgrade to Ba2 and negative outlook

This document has been prepared for the use of Jose Galindo and is protected by law. It may not be copied, transferred or disseminated unlessauthorized under a contract with Moody's or otherwise authorized in writing by Moody's.