Embed Size (px)

Citation preview

Copyright

by

James Stephen Doran

2004

The Dissertation Committee for James Stephen Dorancertifies that this is the approved version of the following dissertation:

On the Market Price of Volatility Risk

Committee:

Ehud Ronn, Supervisor

Stephen Magee

Ramesh Rao

Stathis Tompaidis

Li Gan

On the Market Price of Volatility Risk

by

James Stephen Doran, B.A.

DISSERTATION

Presented to the Faculty of the Graduate School of

The University of Texas at Austin

in Partial Fulfillment

of the Requirements

for the Degree of

DOCTOR OF PHILOSOPHY

THE UNIVERSITY OF TEXAS AT AUSTIN

May 2004

Dedicated to my wife Heather, my parents Charles and Elaine, and to my

son Jackson.

Acknowledgments

I wish to thank the multitudes of people who helped me.

I would like to single out especially my advisor, Ehud Ronn, my parents,

Charles and Elaine, and my wife Heather

This work would never have to come to fruition without the guidance and

support of my advisor and friend Ehud Ronn. His persistence and belief in me

was the necessary and sufficient condition required for successful completion

of this document.

Without the words of wisdom and teaching of my parents, I would never have

persisted in the pursuit of my goals, from the smallest task to the largest

achievement.

Finally, if it had not been for my wife, with which all things begin and end, I

would never have been at this stage in life that I am at today. It is our lives

together that allow us individually to succeed.

. . .

v

On the Market Price of Volatility Risk

Publication No.

James Stephen Doran, Ph.D.

The University of Texas at Austin, 2004

Supervisor: Ehud Ronn

This work examines the extent of the bias between Black-Scholes (1973)/Black

(1976) implied volatility and realized term volatility, estimation of the market

price of volatility risk, and option model fit in the natural gas market. To

examine this bias I institute a stochastic volatility data generating process,

and demonstrate the bias through Monte Carlo simulation of the underlying

parameters. This provides a numerical justification for testing the importance

of a risk premia for volatility. I implement empirical tests for the market

price of volatility risk by analyzing at-the-money options on the S&P 500 and

S&P 100. Further, I extend the study by considering options on natural gas

contracts by examining option model fit for a variety of parametric candi-

dates. Using risk-neutral parameter estimates I re-estimate the market price

of volatility risk using the full cross-section of option prices. The findings

demonstrate a negative market price of volatility risk, and show that this risk

is a significant component of the bias between Black-Scholes/Black implied

volatility and realized term volatility.

vi

Table of Contents

Acknowledgments v

Abstract vi

List of Tables x

List of Figures xiii

Chapter 1. Introduction 1

1.1 Evidence on the Market Price of Volatility Risk . . . . . . . . 9

Chapter 2. The Bias in Black-Scholes/BlackImplied Volatility 14

2.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

2.2 The Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

2.2.1 Stochastic Volatility . . . . . . . . . . . . . . . . . . . . 14

2.3 Estimation of the Bias in BSIV/BIV . . . . . . . . . . . . . . . 19

2.3.1 Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

2.3.1.1 Measurement Error . . . . . . . . . . . . . . . . 21

2.3.2 Estimating the bias . . . . . . . . . . . . . . . . . . . . 22

2.3.2.1 Equity Bias . . . . . . . . . . . . . . . . . . . . 22

2.3.2.2 Modeling of the TSOV . . . . . . . . . . . . . . 26

2.3.2.3 Gas Bias . . . . . . . . . . . . . . . . . . . . . . 30

2.4 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

Chapter 3. Monte Carlo Simulation and Estimation of the Mar-ket Price of Volatility Risk 36

3.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

3.2 Monte Carlo Simulation . . . . . . . . . . . . . . . . . . . . . . 37

vii

3.2.1 Stochastic Volatility Simulation . . . . . . . . . . . . . . 41

3.2.1.1 Perfect and Zero Correlation Cases . . . . . . . 41

3.2.1.2 Equity . . . . . . . . . . . . . . . . . . . . . . . 42

3.2.1.3 Commodities . . . . . . . . . . . . . . . . . . . 45

3.2.2 Jump Model Simulation . . . . . . . . . . . . . . . . . . 47

3.2.2.1 Results of Pure Jump Model-Equity . . . . . . 50

3.2.2.2 Results of Pure Jump Model-Commodities . . . 52

3.2.2.3 Results of Proportional Jump Model- Equity . . 54

3.2.2.4 Results of Proportional Jump Model-Commodities 55

3.2.2.5 Results of Jump Models with Negative MarketPrice of Volatility Risk- Equity . . . . . . . . . 56

3.2.2.6 Results of Jump Models with Negative MarketPrice of Volatility Risk- Commodities . . . . . . 57

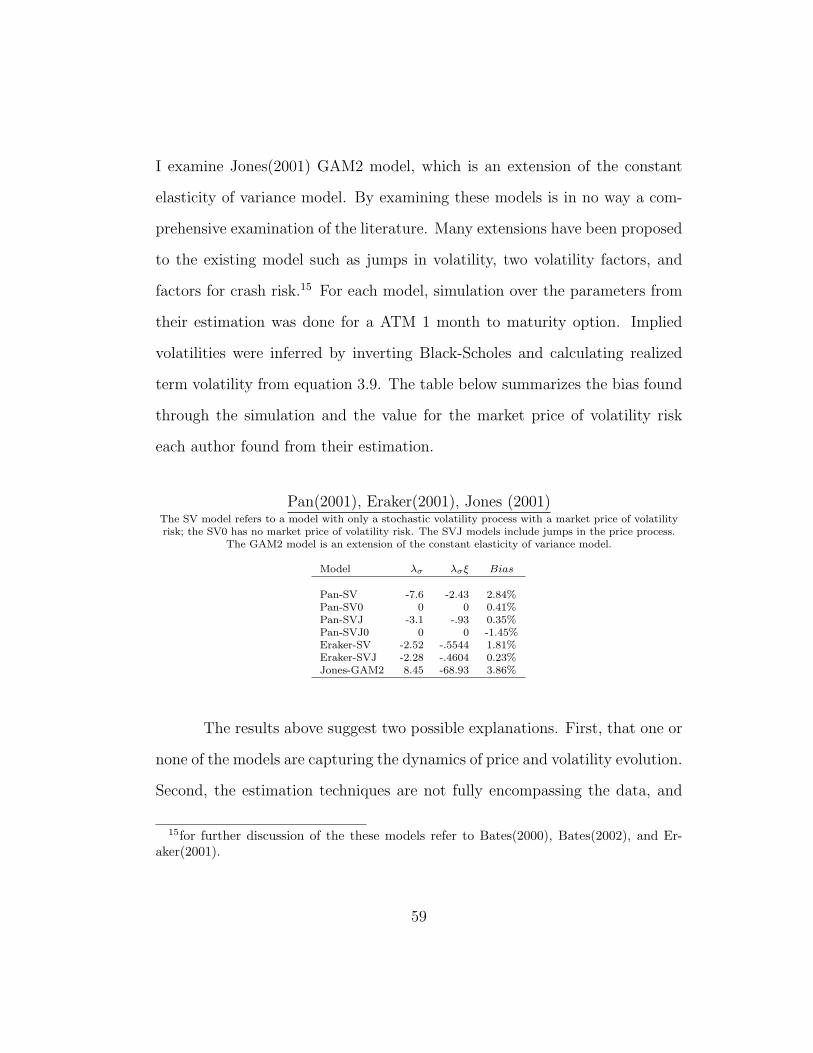

3.2.3 Results of Prior Parameter Estimates . . . . . . . . . . 58

3.3 Estimation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

3.3.1 Simulation within a Simulation . . . . . . . . . . . . . . 61

3.3.2 Estimation Using Mean Reverting Framework . . . . . . 65

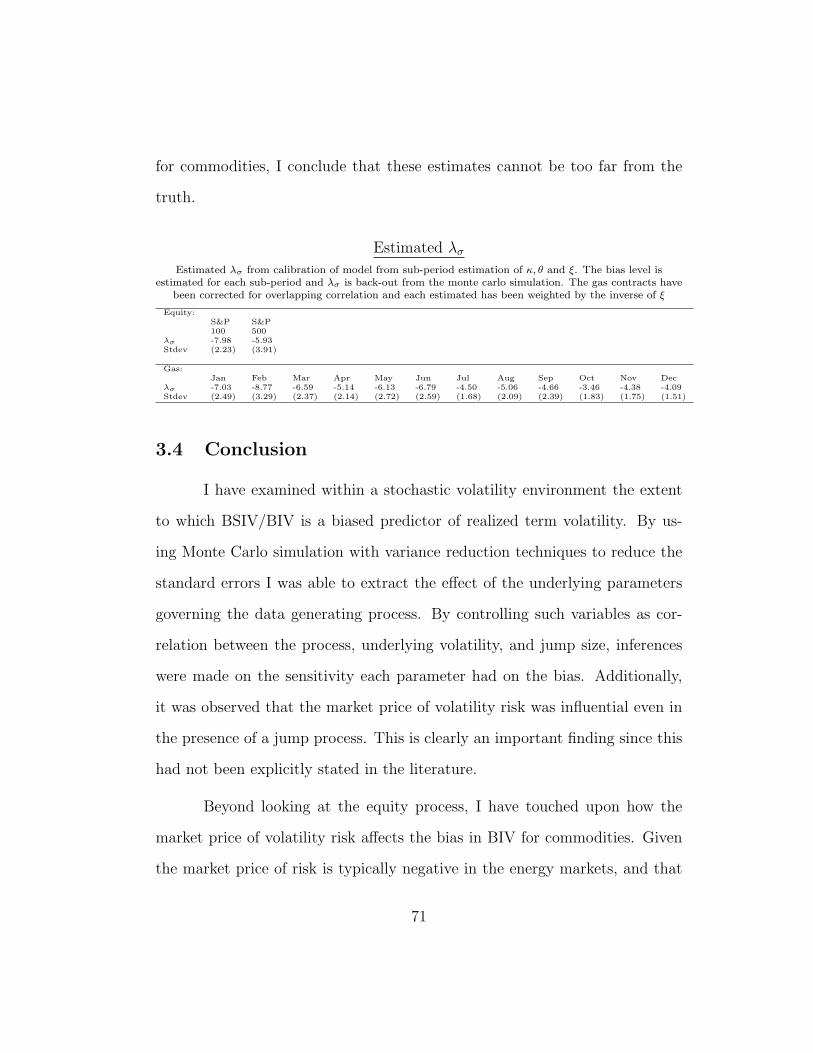

3.3.3 Estimation of λσ . . . . . . . . . . . . . . . . . . . . . . 66

3.4 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

Chapter 4. Empirical Performance of Option Models for Nat-ural Gas and Estimation of the Market Price(s) ofRisk 74

4.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74

4.2 Modeling Issues . . . . . . . . . . . . . . . . . . . . . . . . . . 80

4.2.1 Data Generating Process for the Double Jump Model . 80

4.2.2 Double Jump Option Model . . . . . . . . . . . . . . . . 83

4.2.3 Independent Double Jumps and TSOV considerations . 85

4.3 Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

4.3.1 Understanding the volatility in gas markets . . . . . . . 89

4.4 Model Estimation . . . . . . . . . . . . . . . . . . . . . . . . . 90

4.4.1 Estimation Technique . . . . . . . . . . . . . . . . . . . 92

4.4.2 Structural Parameter Estimation and Model Performance 94

4.4.3 Out of sample pricing performance . . . . . . . . . . . . 101

viii

4.5 Mean-Reversion in Stochastic Volatility . . . . . . . . . . . . . 103

4.6 Proposed Algorithms . . . . . . . . . . . . . . . . . . . . . . . 106

4.6.1 Parameter Estimation, including Market Price of Risk . 106

4.6.2 Results . . . . . . . . . . . . . . . . . . . . . . . . . . . 108

4.7 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 110

Tables and Figures 113

Appendices 176

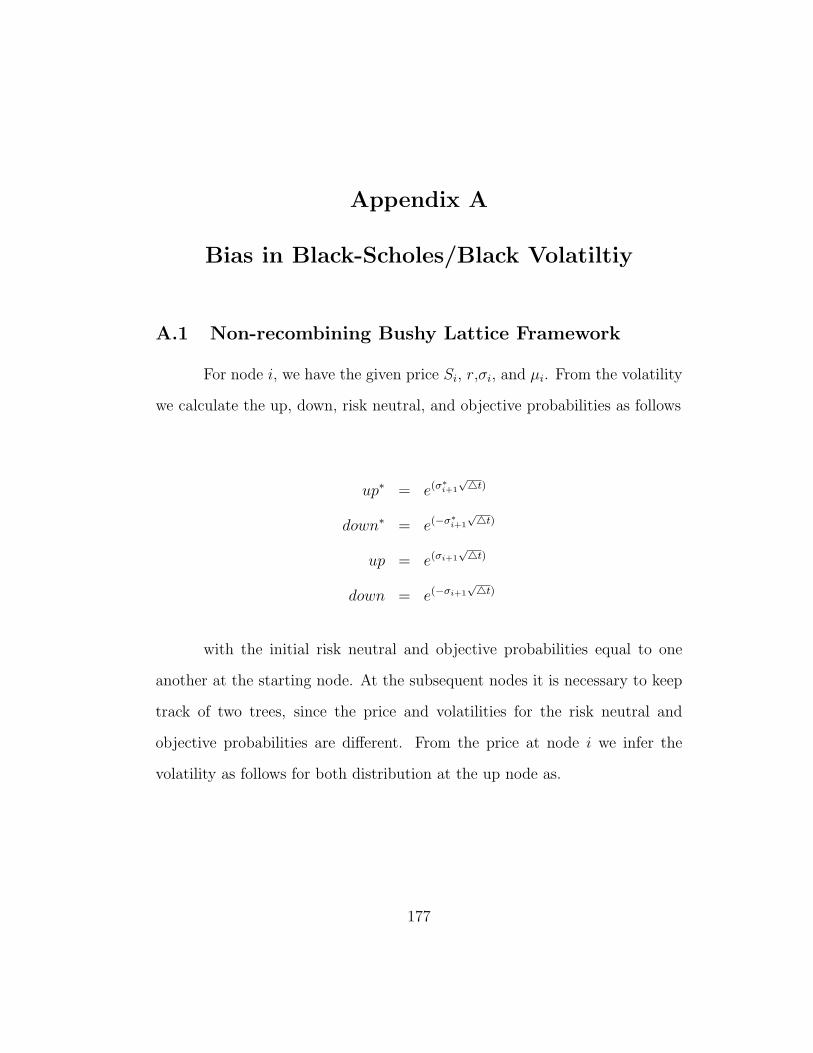

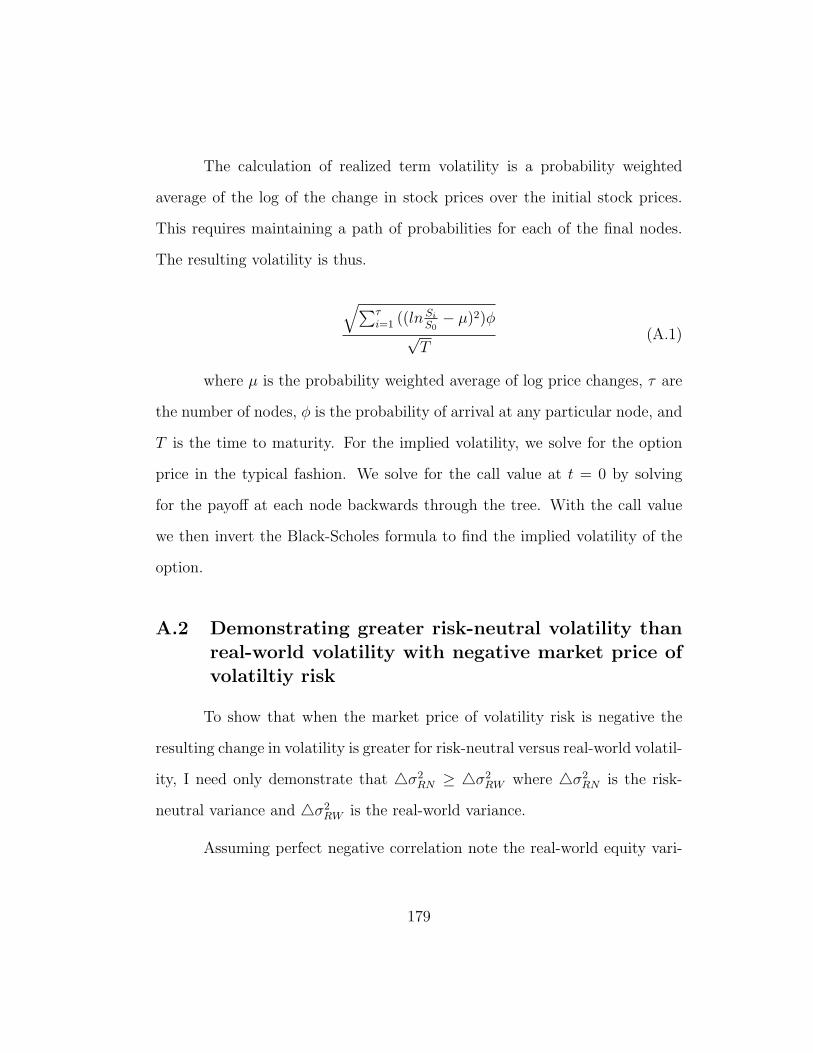

Appendix A. Bias in Black-Scholes/Black Volatiltiy 177

A.1 Non-recombining Bushy Lattice Framework . . . . . . . . . . . 177

A.2 Demonstrating greater risk-neutral volatility than real-world volatil-ity with negative market price of volatiltiy risk . . . . . . . . . 179

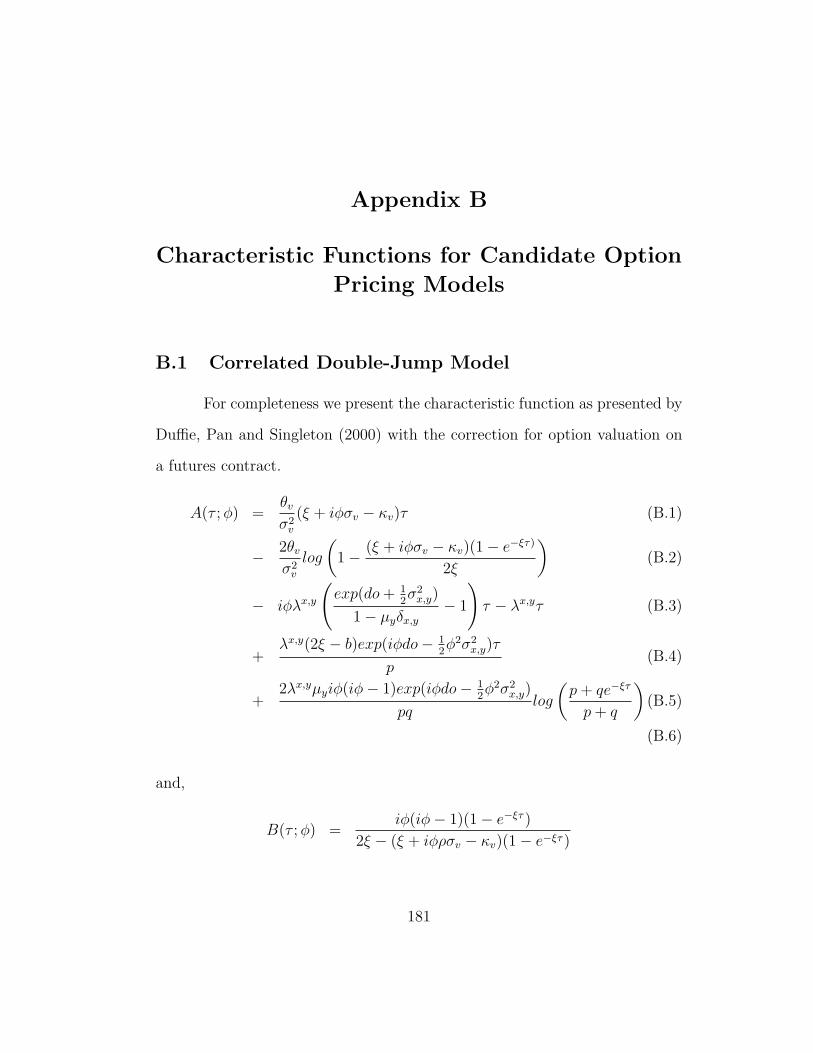

Appendix B. Characteristic Functions for Candidate Option Pric-ing Models 181

B.1 Correlated Double-Jump Model . . . . . . . . . . . . . . . . . 181

B.2 Independent Double-Jump Model . . . . . . . . . . . . . . . . 182

B.3 Barone-Adesi and Whaley Analytical Approximation for Amer-ican Option Prices . . . . . . . . . . . . . . . . . . . . . . . . . 183

Index 186

Bibliography 187

Vita 195

ix

List of Tables

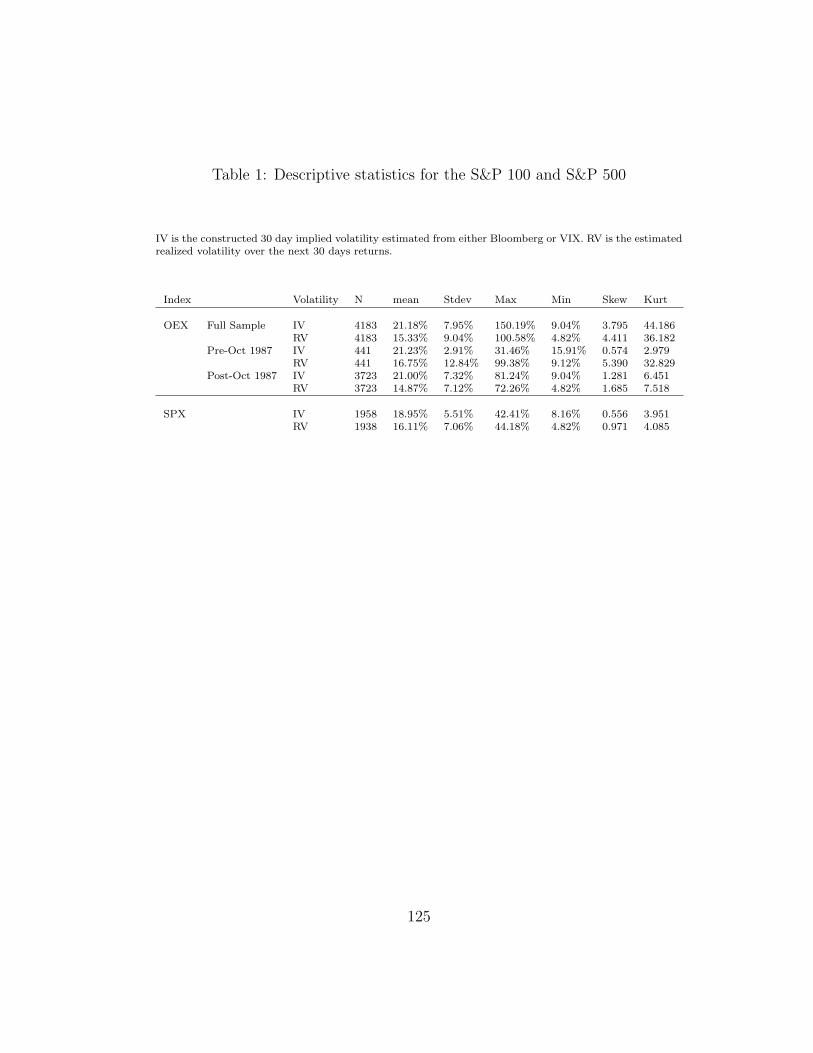

1 Descriptive statistics for the S&P 100 and S&P 500 . . . . . . 125

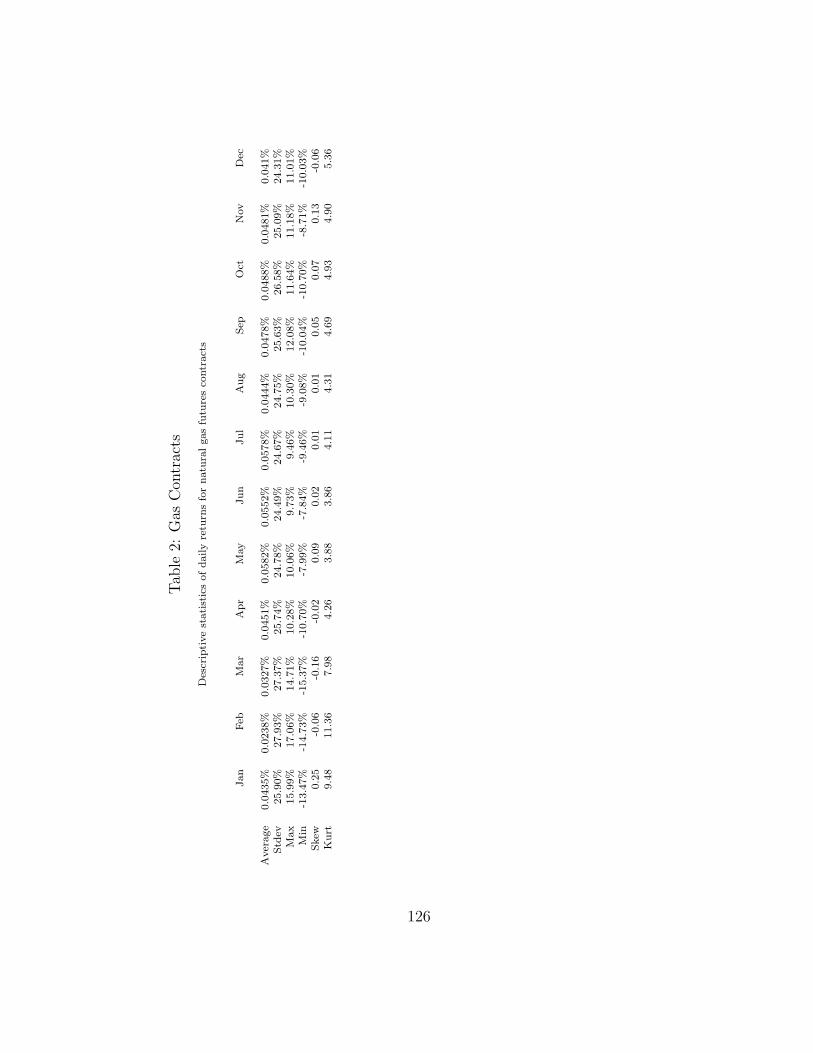

2 Gas Contracts . . . . . . . . . . . . . . . . . . . . . . . . . . . 126

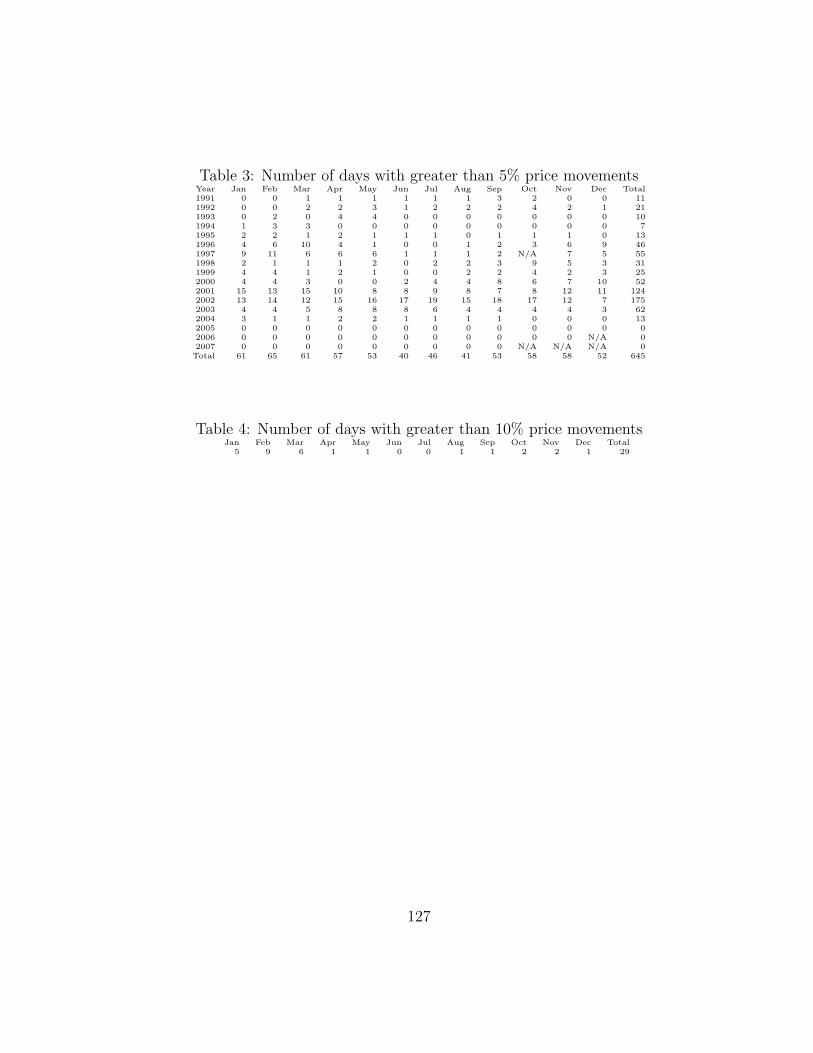

3 Number of days with greater than 5% price movements . . . . 127

4 Number of days with greater than 10% price movements . . . 127

5 Bias in BSIV in S&P 100 contracts . . . . . . . . . . . . . . . 128

6 Bias in BSIV in S&P 500 contracts . . . . . . . . . . . . . . . 129

7 TSOV Specification Fit . . . . . . . . . . . . . . . . . . . . . . 130

8 Bias in BIV in Natural Gas Futures . . . . . . . . . . . . . . . 131

9 Perfect and Zero Correlation Case . . . . . . . . . . . . . . . . 132

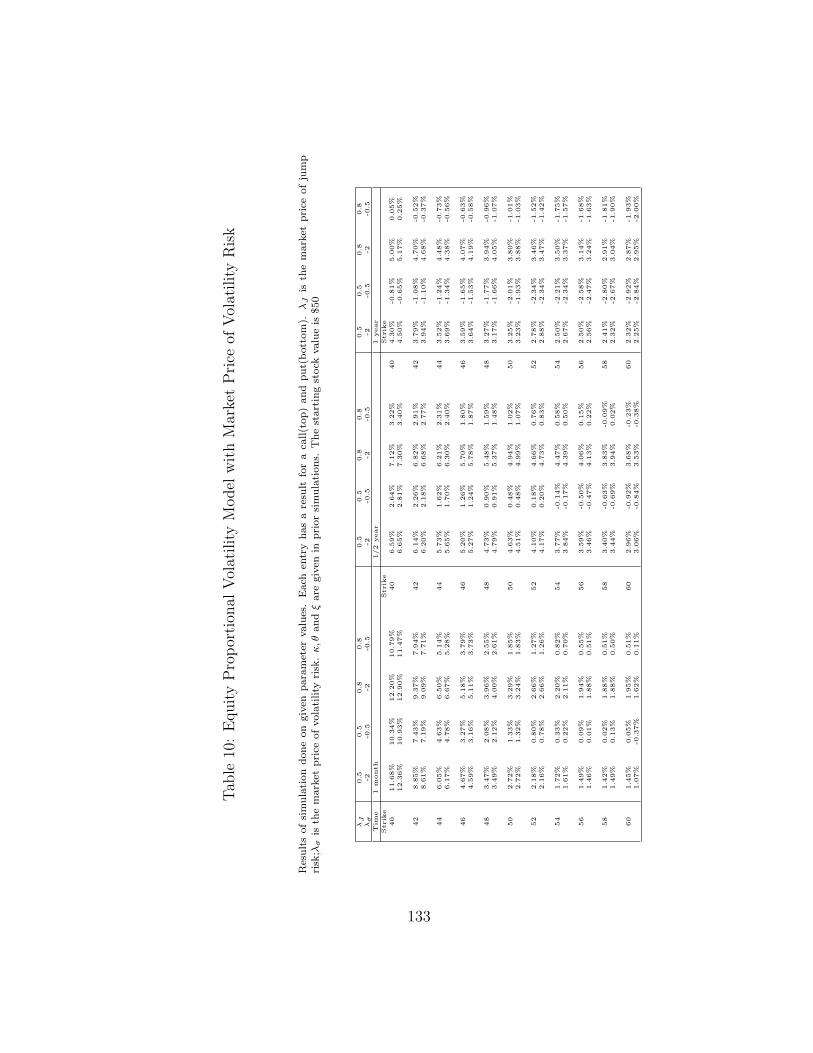

10 Equity Proportional Volatility Model with Market Price of Volatil-ity Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 133

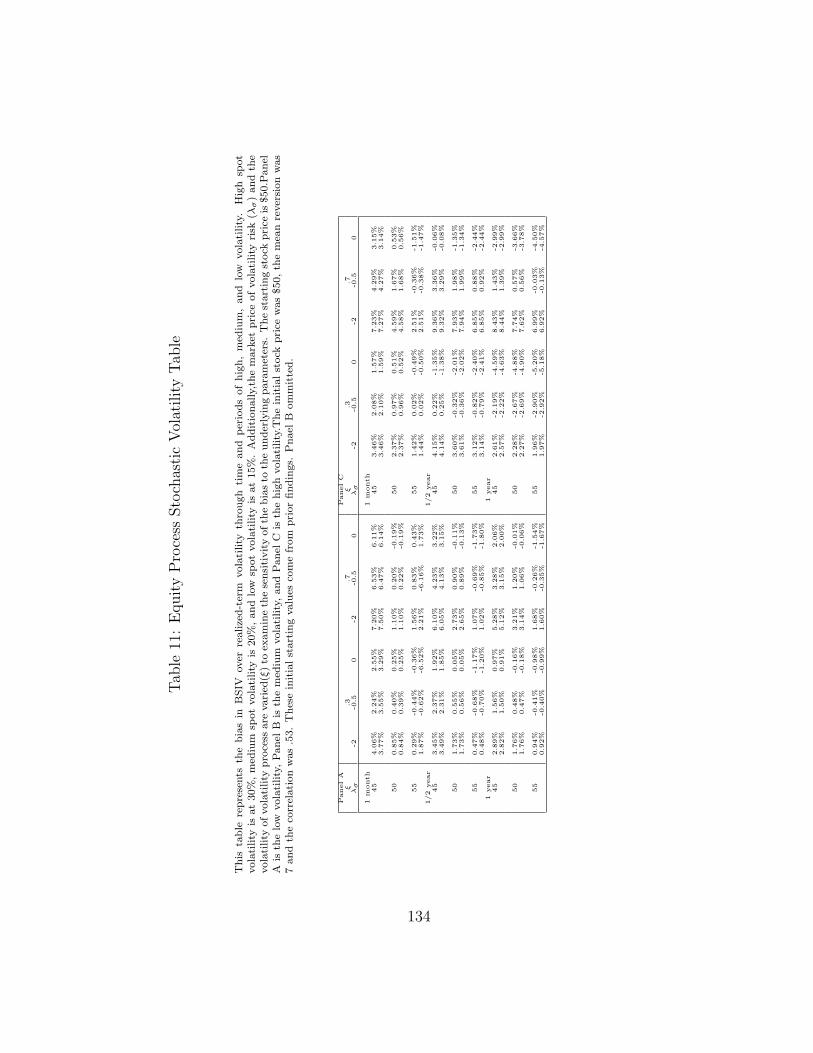

11 Equity Process Stochastic Volatility Table . . . . . . . . . . . 134

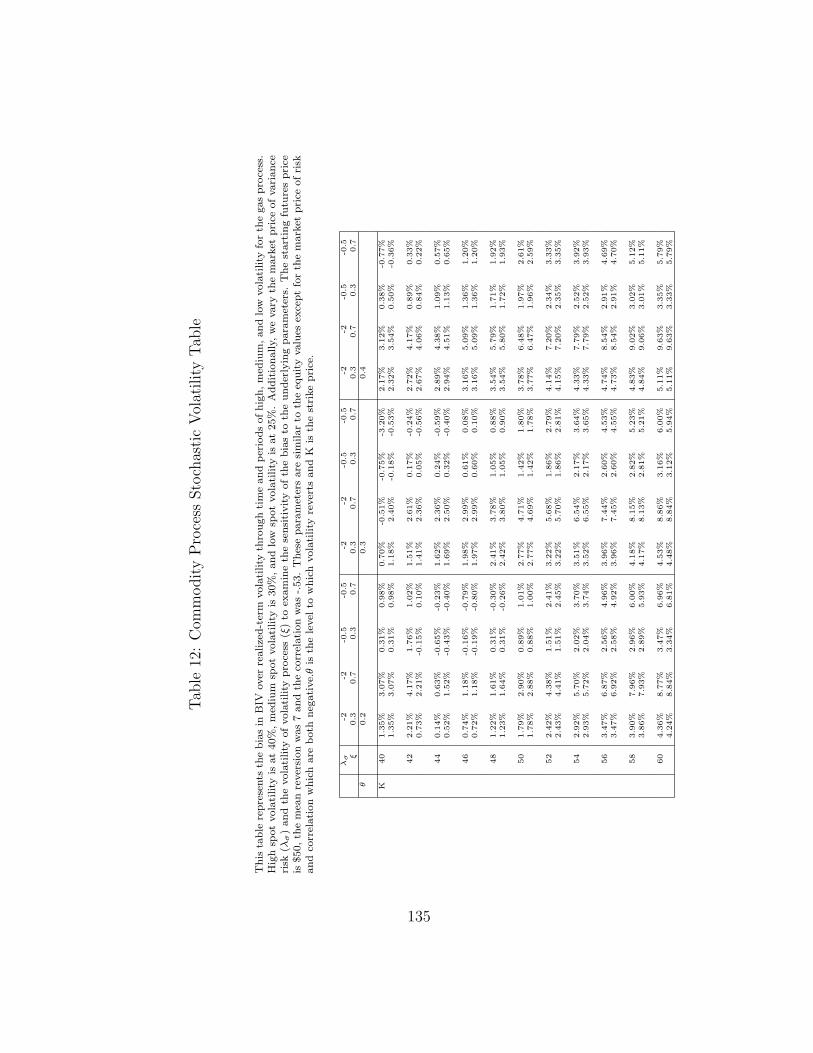

12 Commodity Process Stochastic Volatility Table . . . . . . . . 135

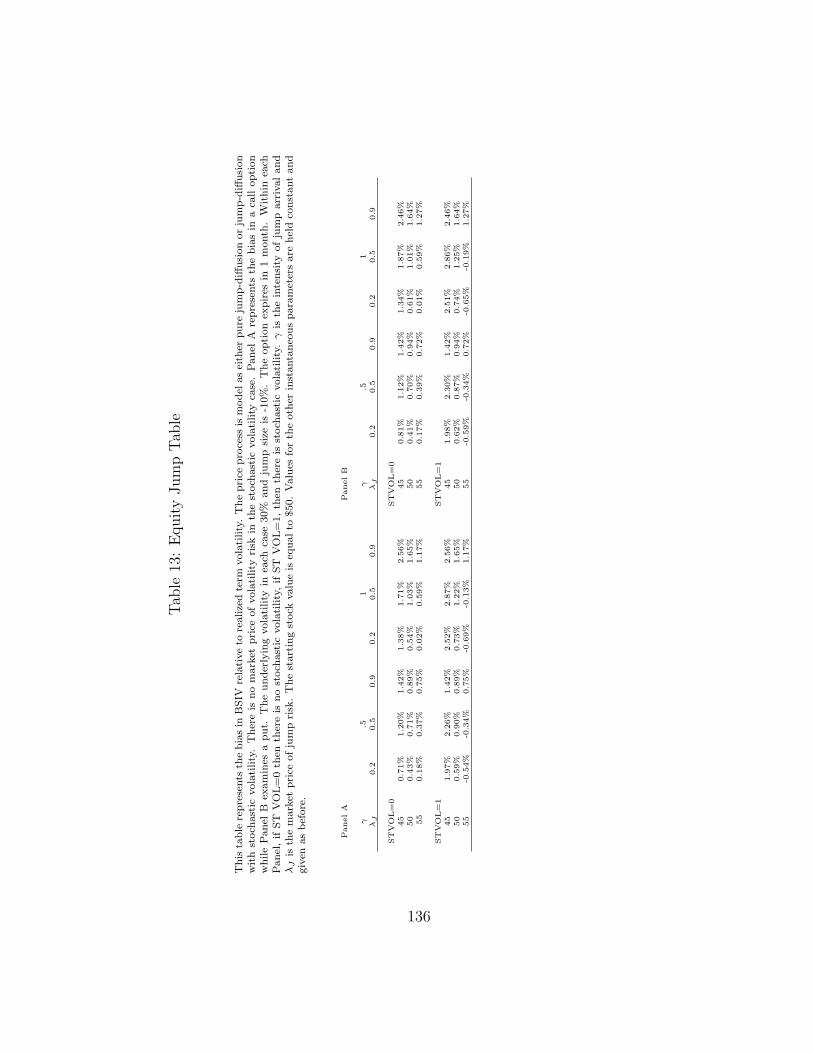

13 Equity Jump Table . . . . . . . . . . . . . . . . . . . . . . . . 136

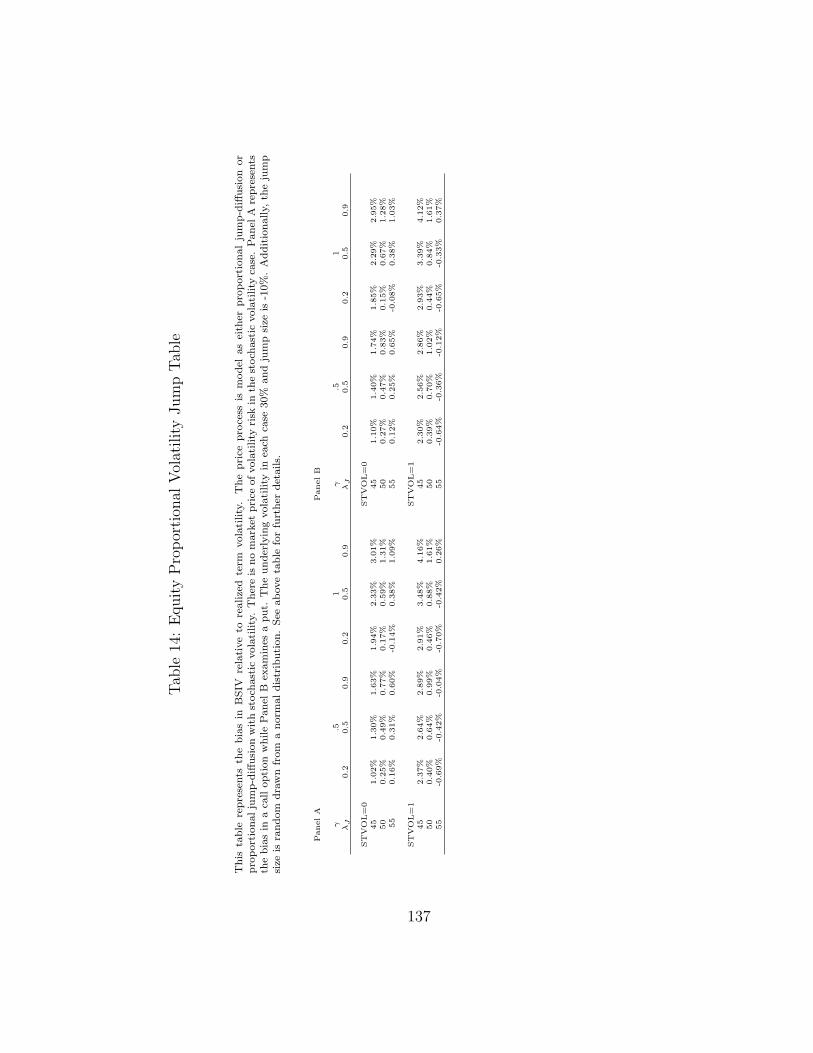

14 Equity Proportional Volatility Jump Table . . . . . . . . . . . 137

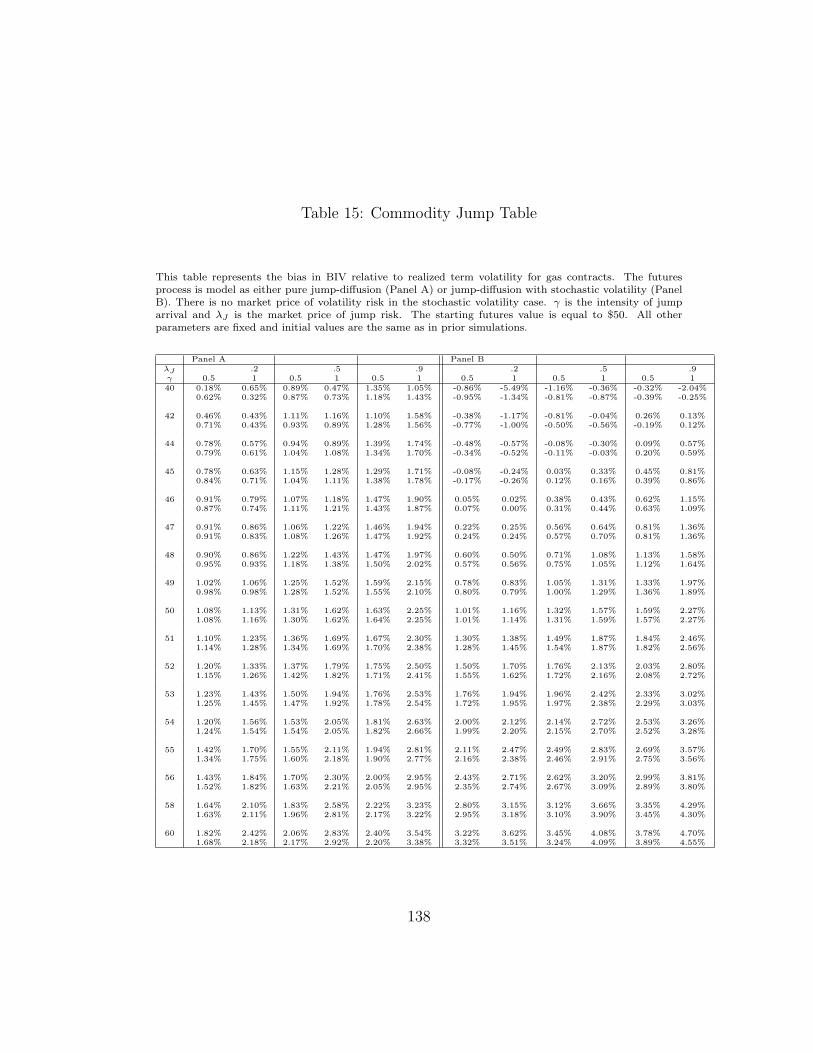

15 Commodity Jump Table . . . . . . . . . . . . . . . . . . . . . 138

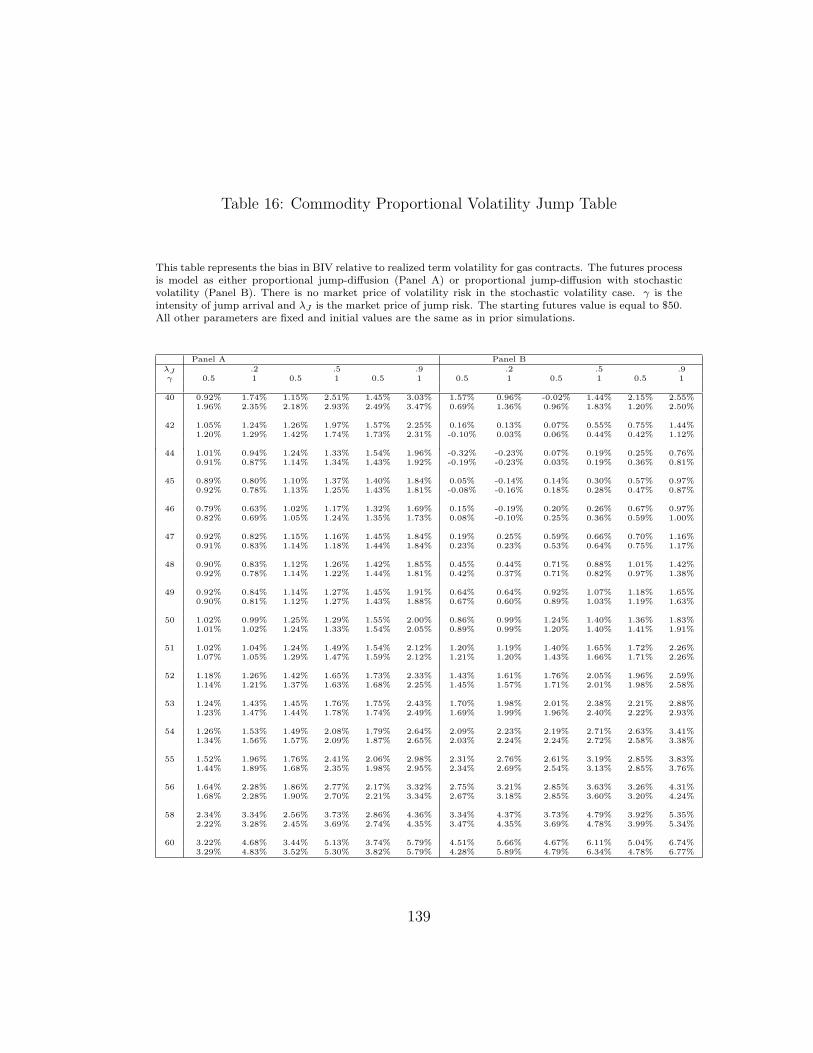

16 Commodity Proportional Volatility Jump Table . . . . . . . . 139

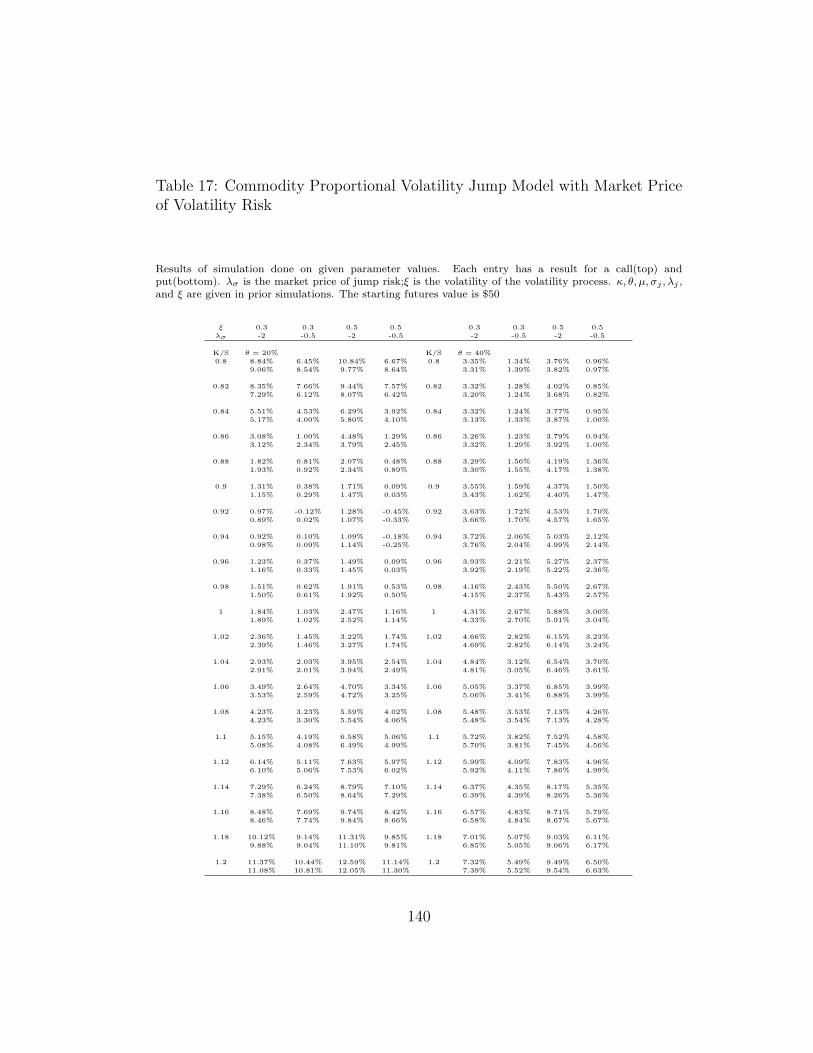

17 Commodity Proportional Volatility Jump Model with MarketPrice of Volatility Risk . . . . . . . . . . . . . . . . . . . . . . 140

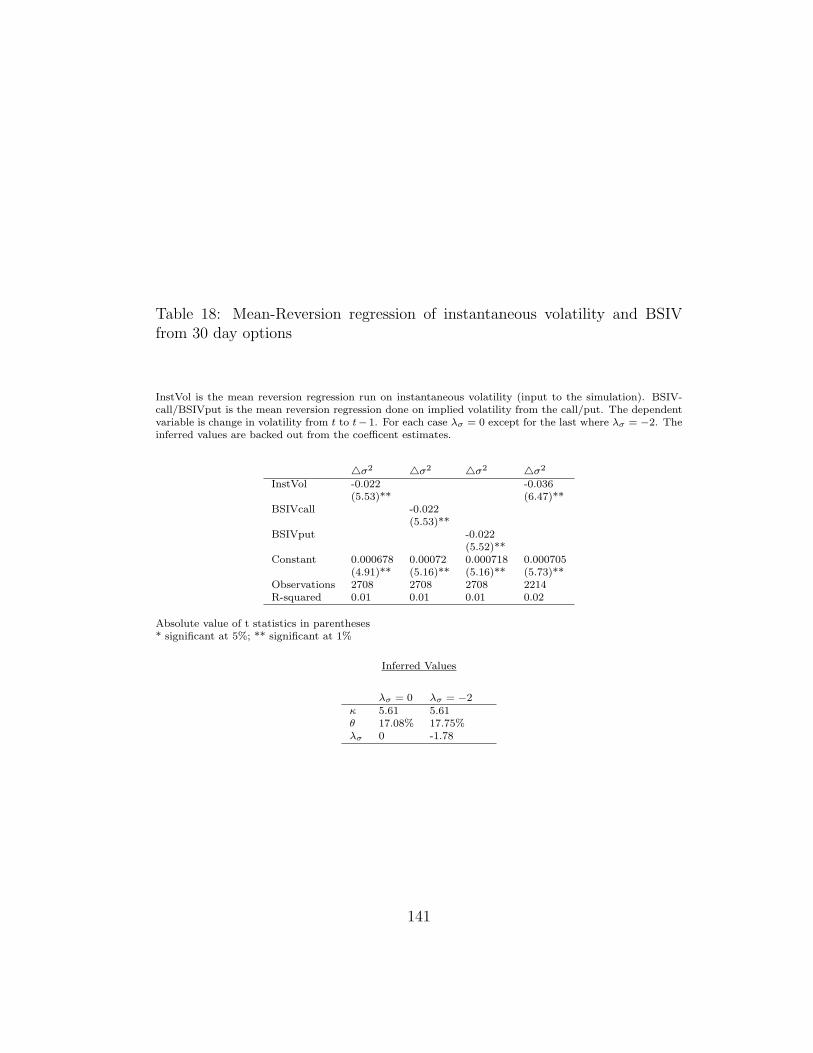

18 Mean-Reversion regression of instantaneous volatility and BSIVfrom 30 day options . . . . . . . . . . . . . . . . . . . . . . . . 141

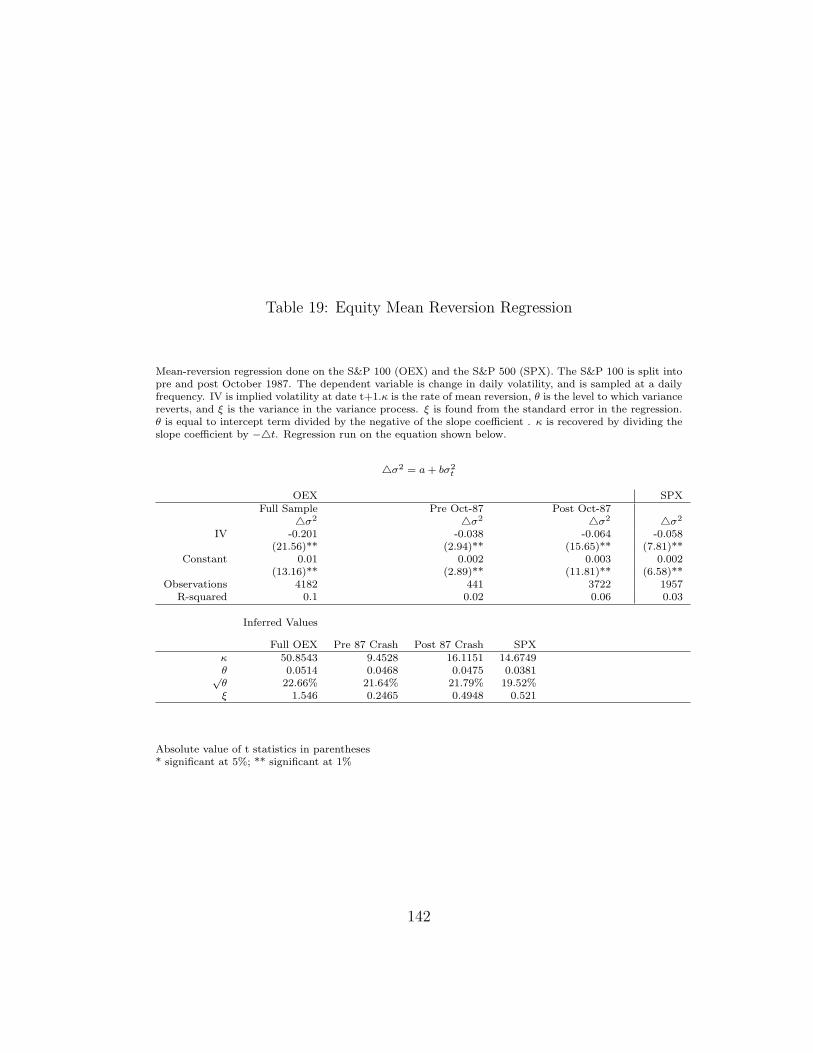

19 Equity Mean Reversion Regression . . . . . . . . . . . . . . . 142

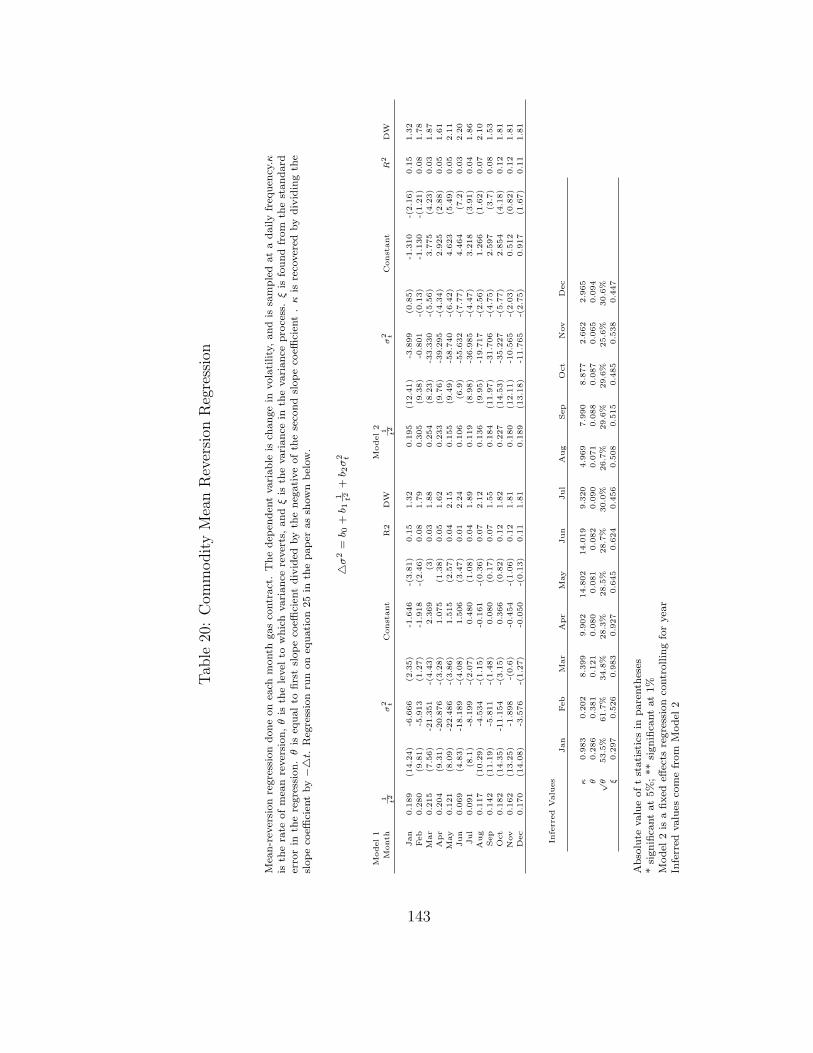

20 Commodity Mean Reversion Regression . . . . . . . . . . . . . 143

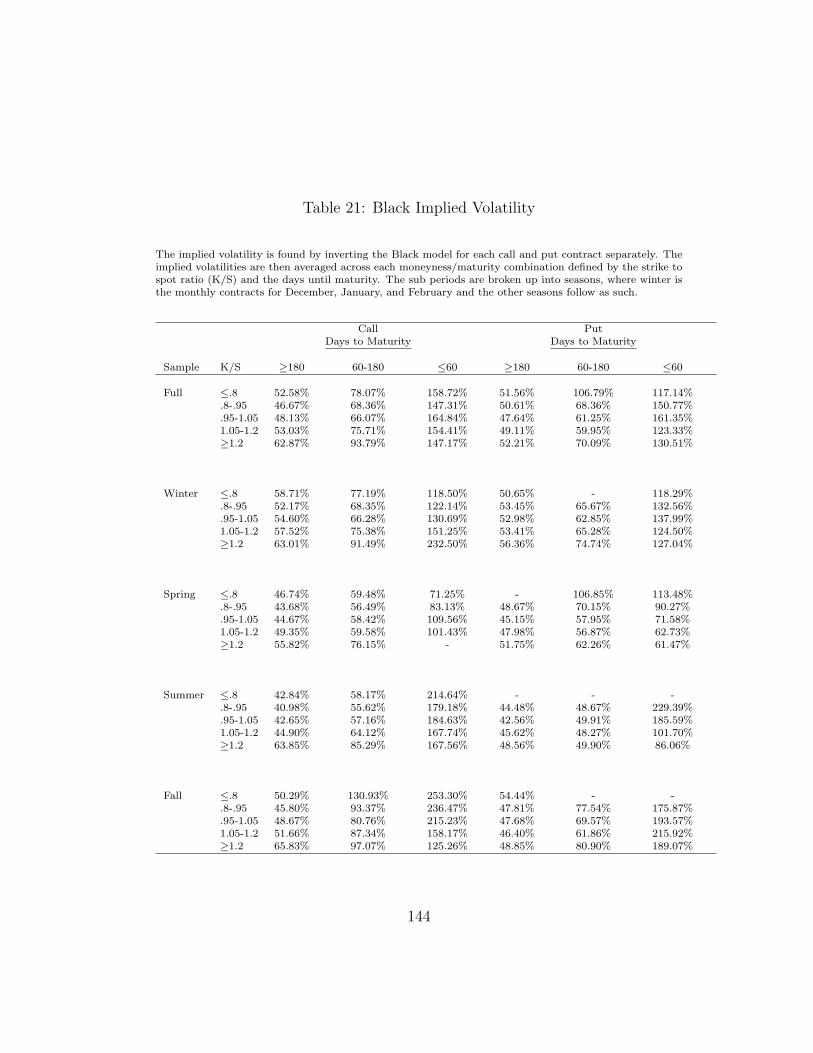

21 Black Implied Volatility . . . . . . . . . . . . . . . . . . . . . 144

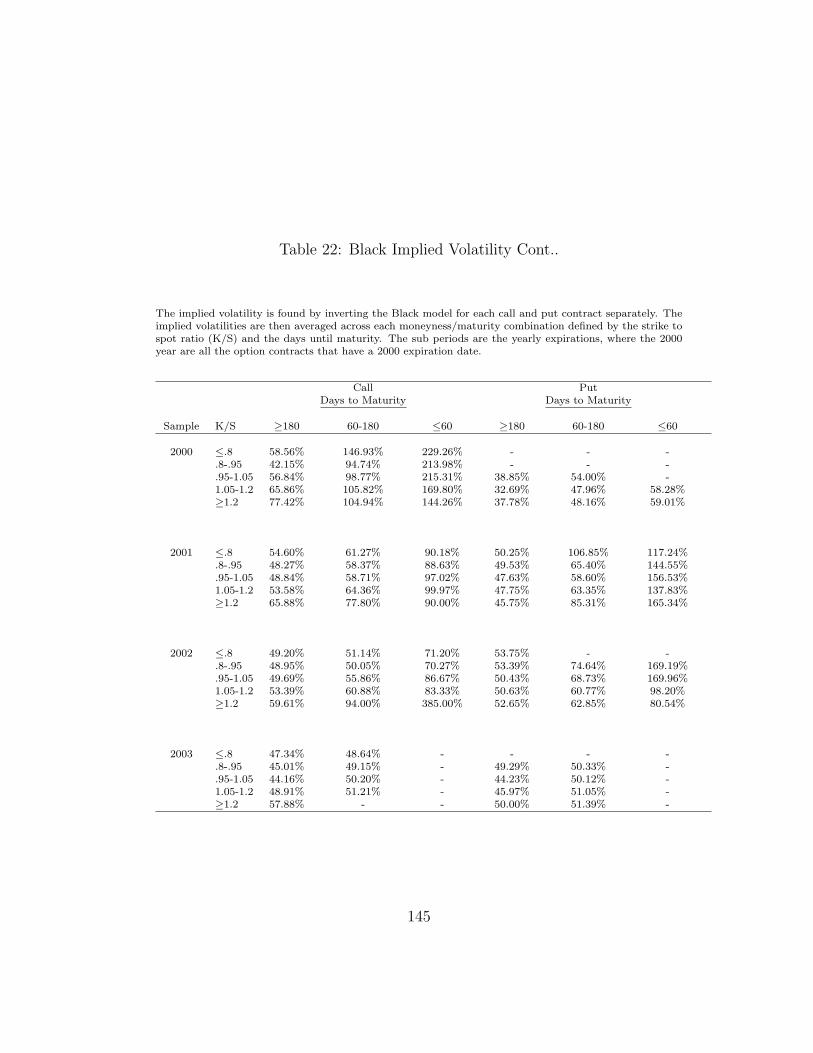

22 Black Implied Volatility Cont.. . . . . . . . . . . . . . . . . . . 145

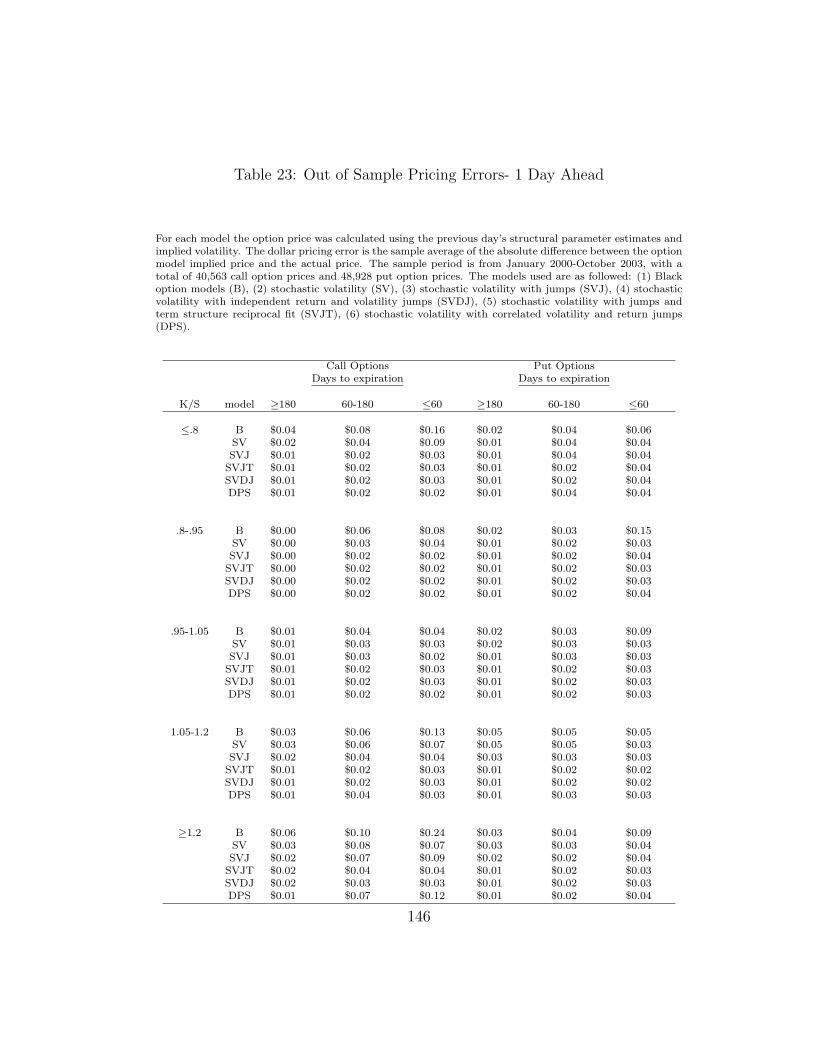

23 Out of Sample Pricing Errors- 1 Day Ahead . . . . . . . . . . 146

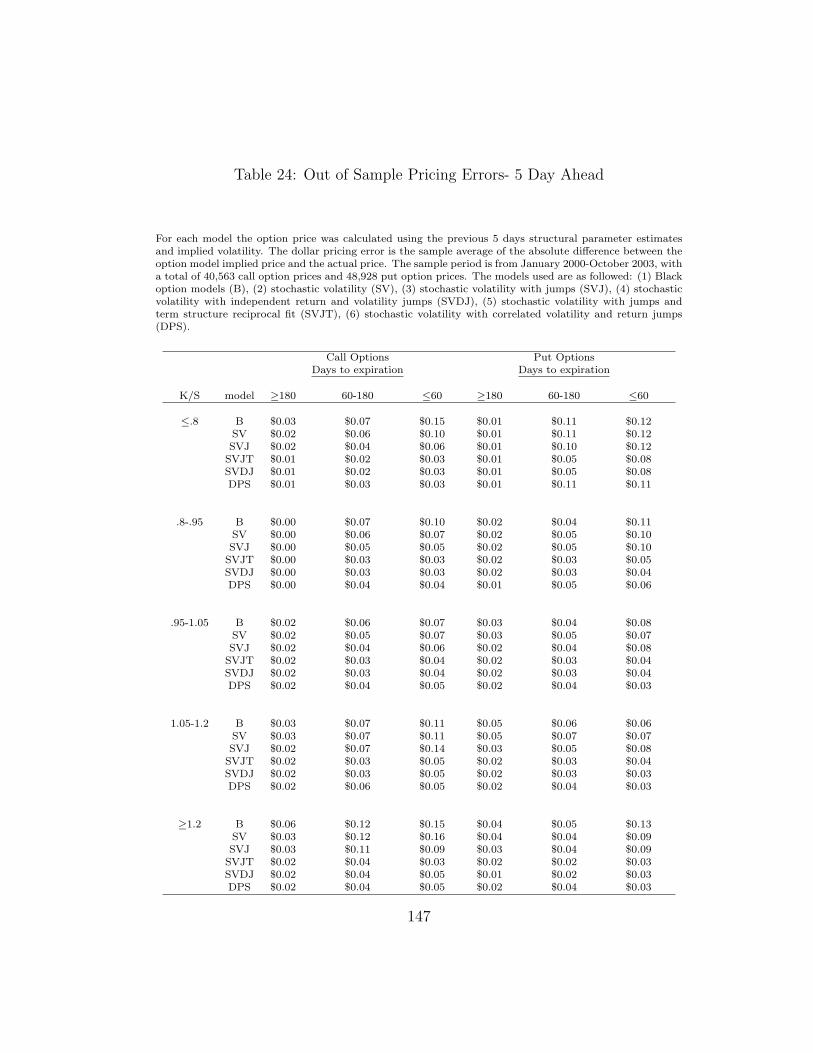

24 Out of Sample Pricing Errors- 5 Day Ahead . . . . . . . . . . 147

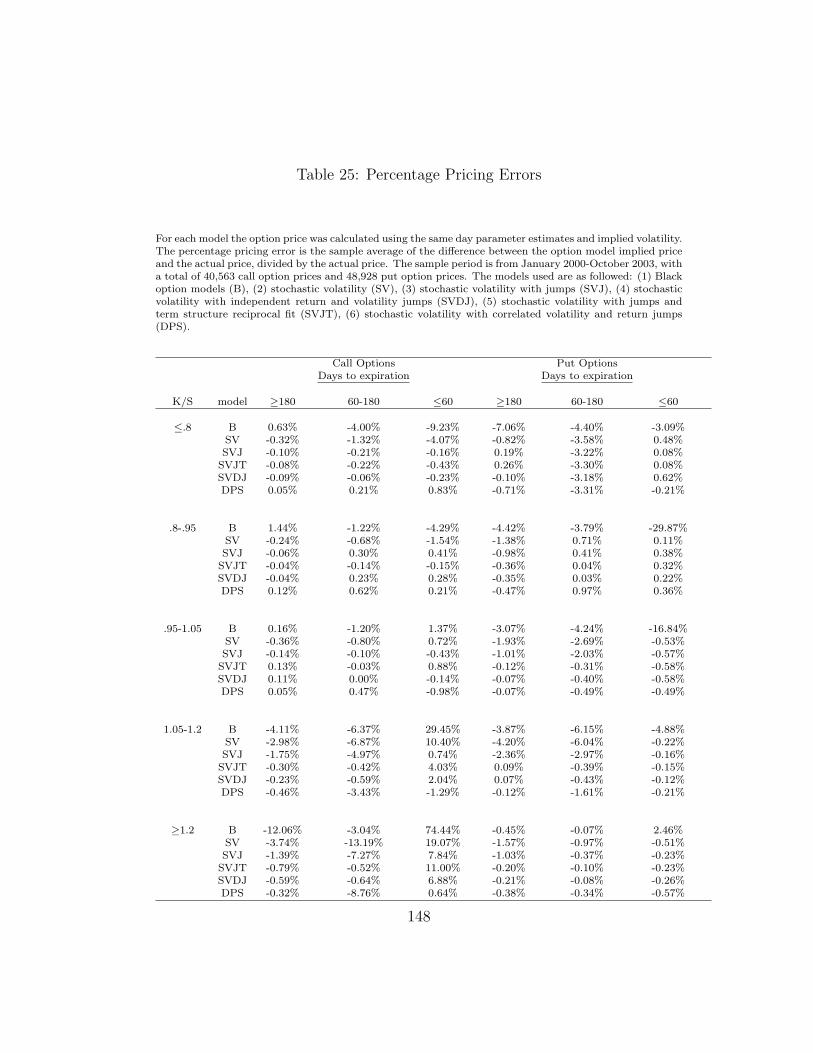

25 Percentage Pricing Errors . . . . . . . . . . . . . . . . . . . . 148

x

26 In Sample Parameter Estimation and Fit of Gas Price Process 149

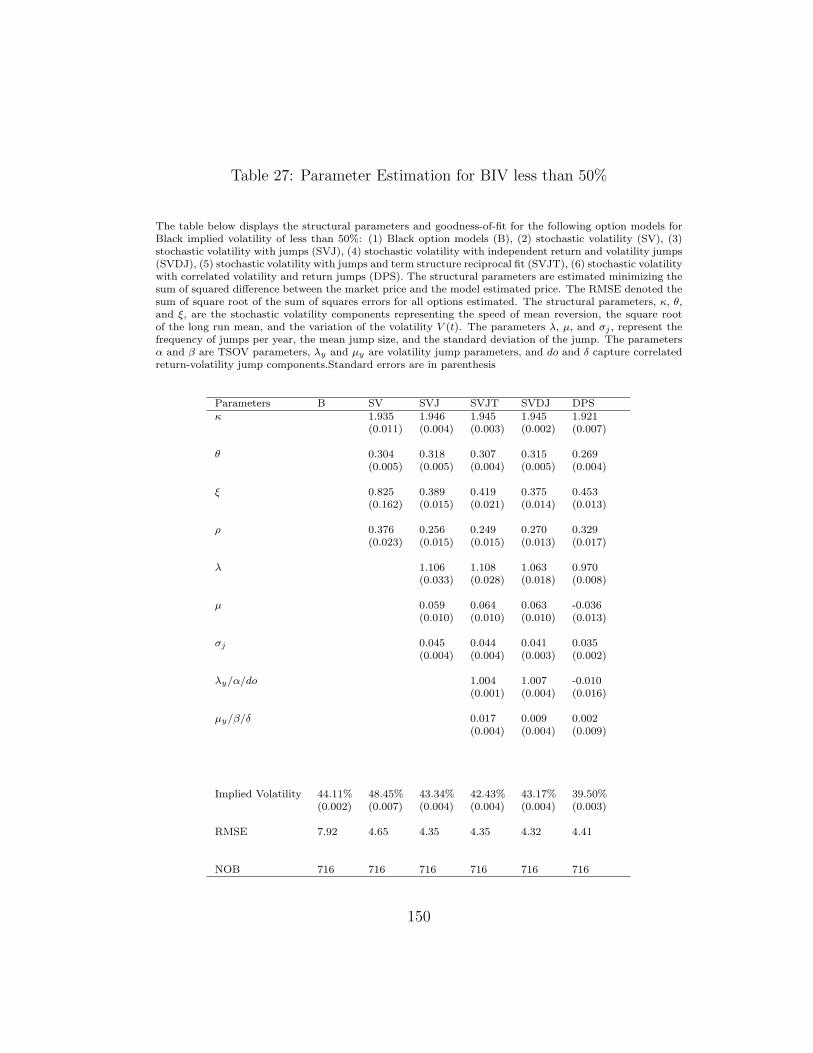

27 Parameter Estimation for BIV less than 50% . . . . . . . . . . 150

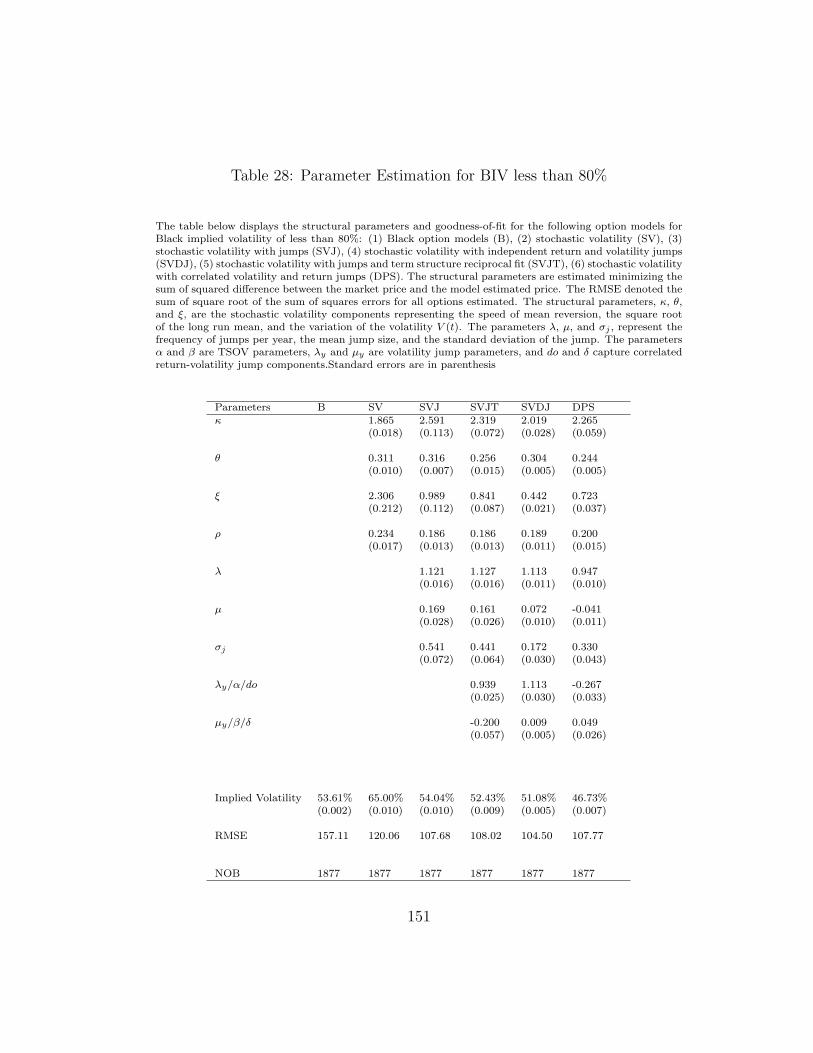

28 Parameter Estimation for BIV less than 80% . . . . . . . . . . 151

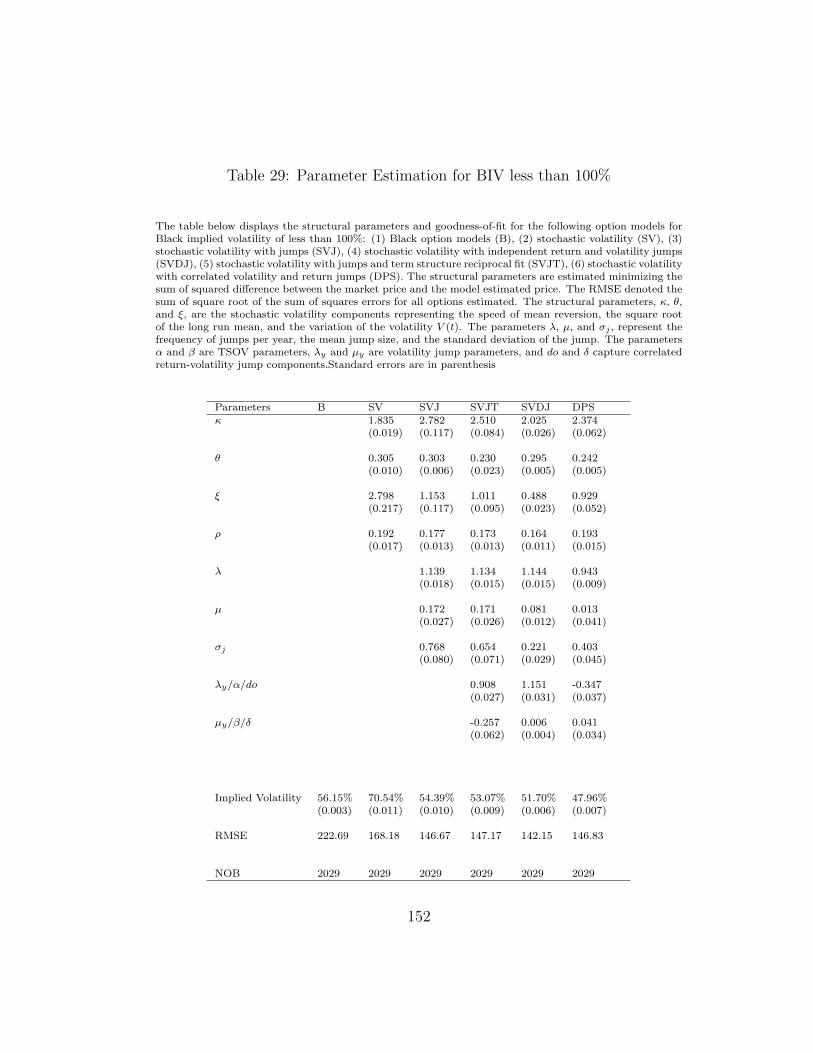

29 Parameter Estimation for BIV less than 100% . . . . . . . . . 152

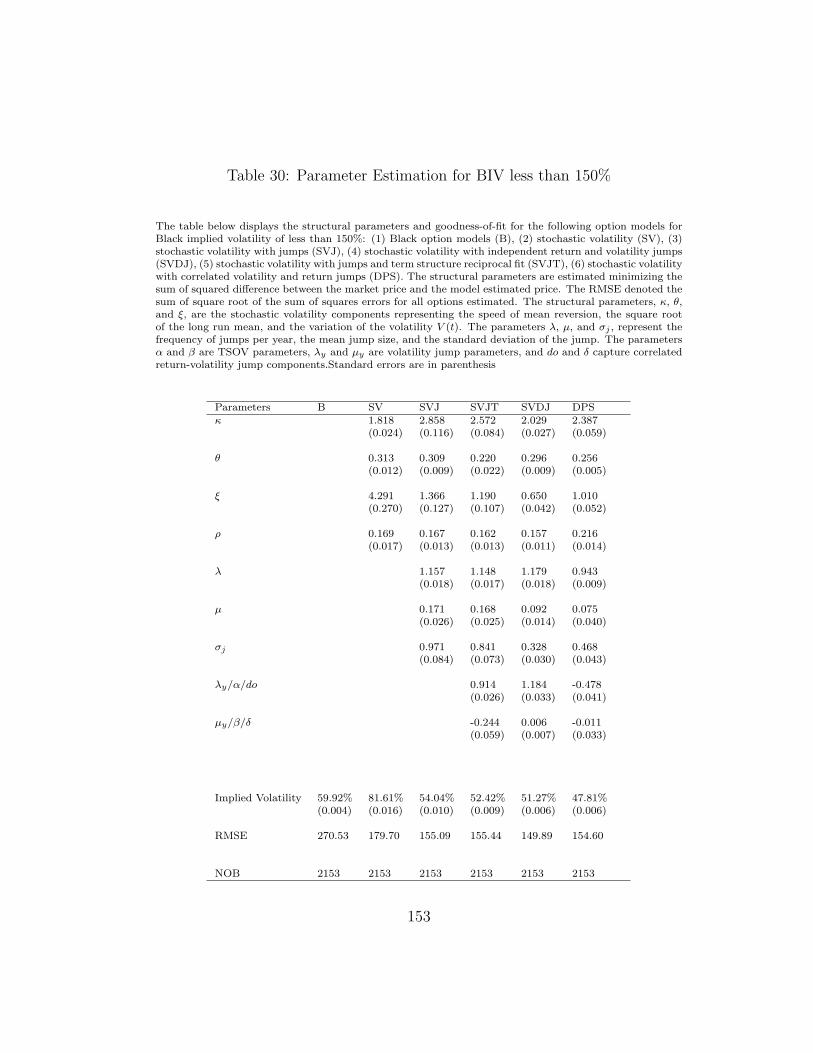

30 Parameter Estimation for BIV less than 150% . . . . . . . . . 153

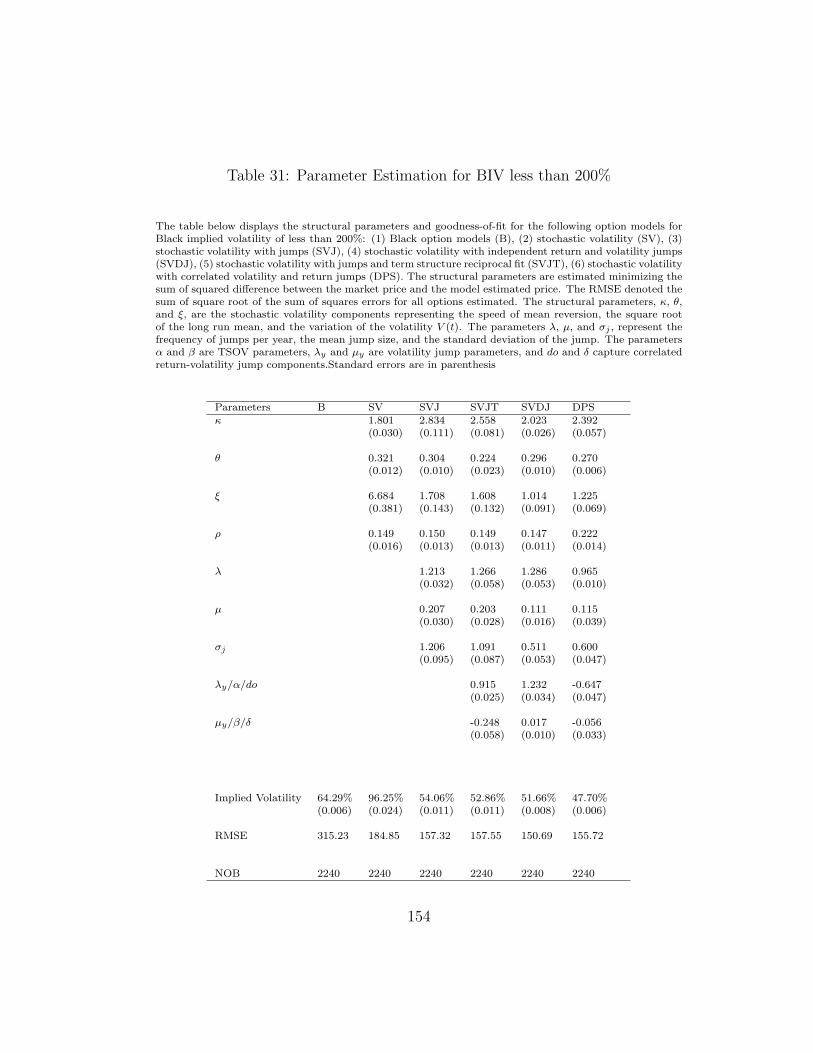

31 Parameter Estimation for BIV less than 200% . . . . . . . . . 154

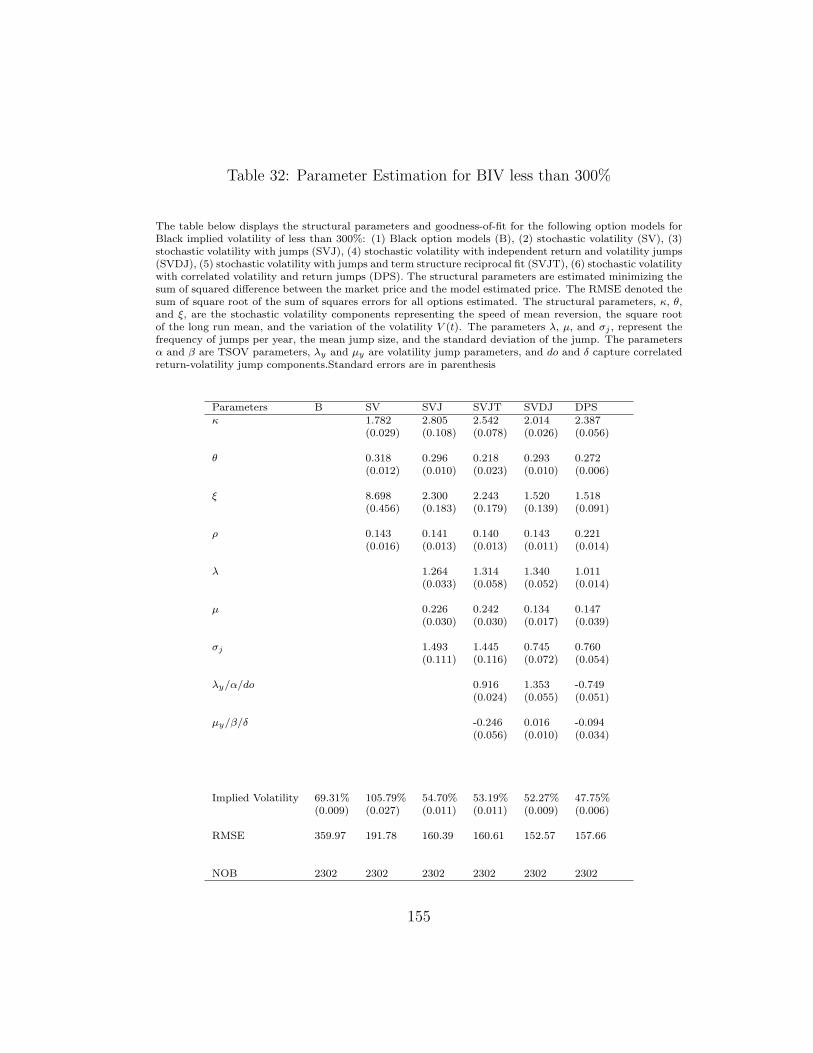

32 Parameter Estimation for BIV less than 300% . . . . . . . . . 155

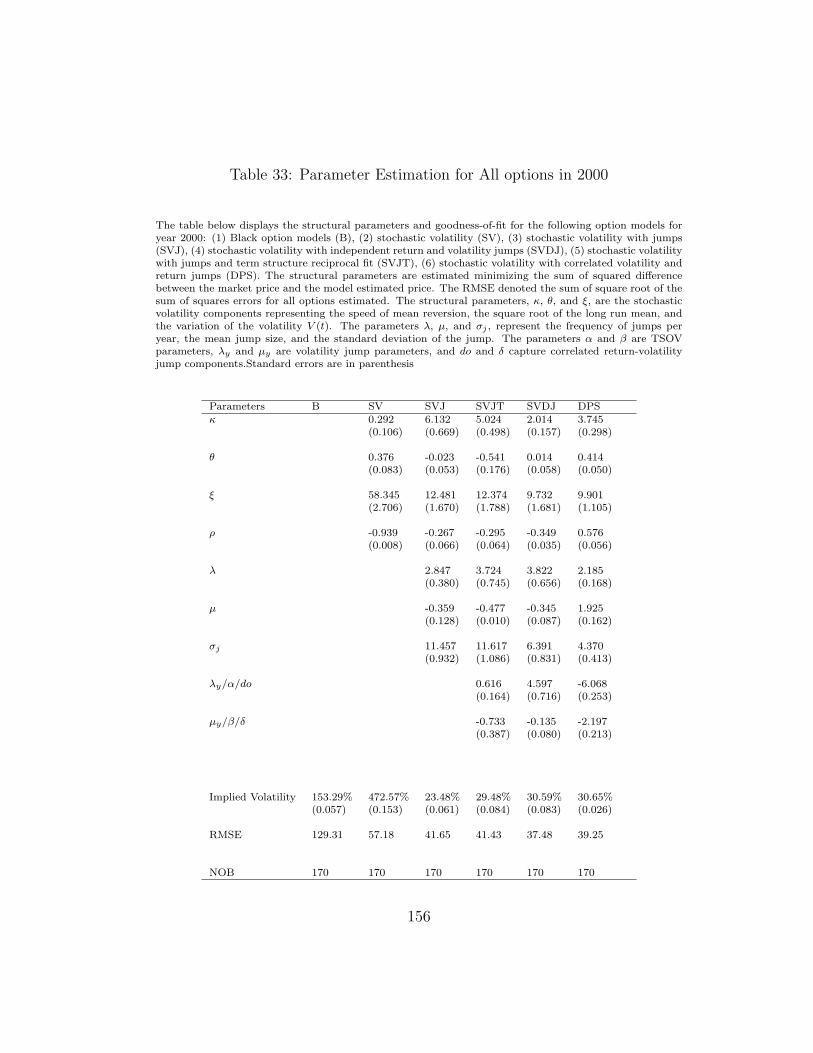

33 Parameter Estimation for All options in 2000 . . . . . . . . . . 156

34 Parameter Estimation for All options in 2001 . . . . . . . . . . 157

35 Parameter Estimation for All options in 2002 . . . . . . . . . . 158

36 Parameter Estimation for All options in 2003 . . . . . . . . . . 159

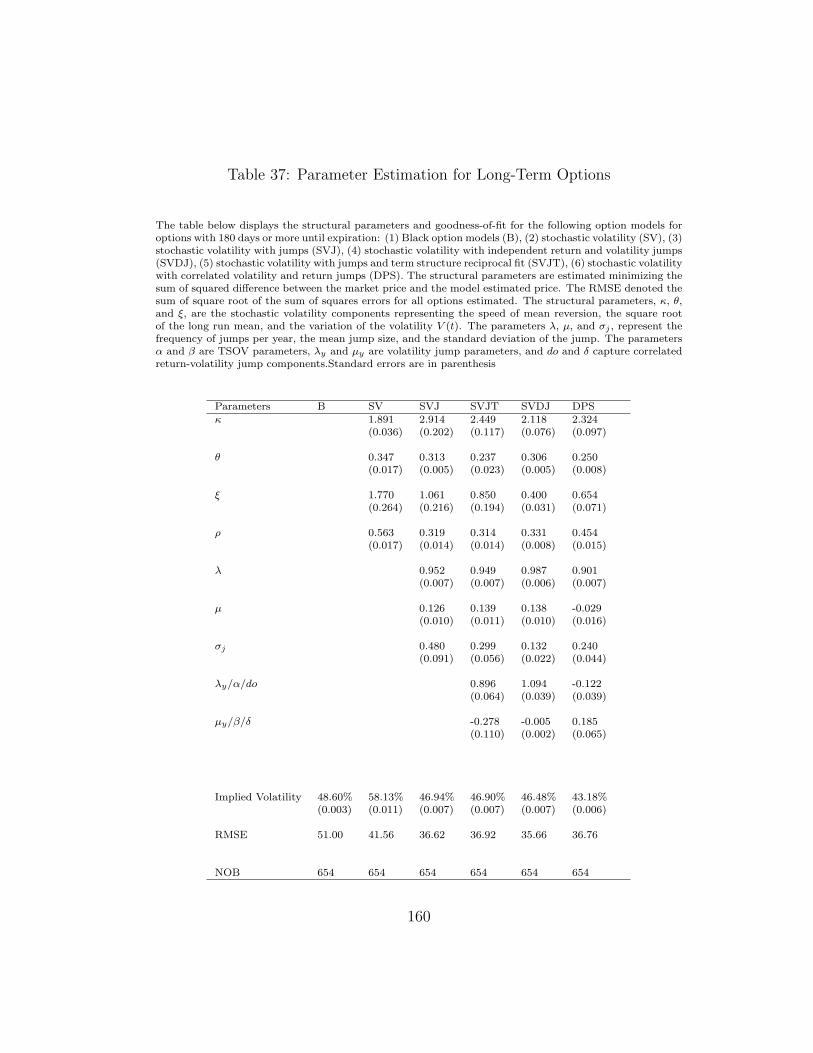

37 Parameter Estimation for Long-Term Options . . . . . . . . . 160

38 Parameter Estimation for Medium-Term Options . . . . . . . 161

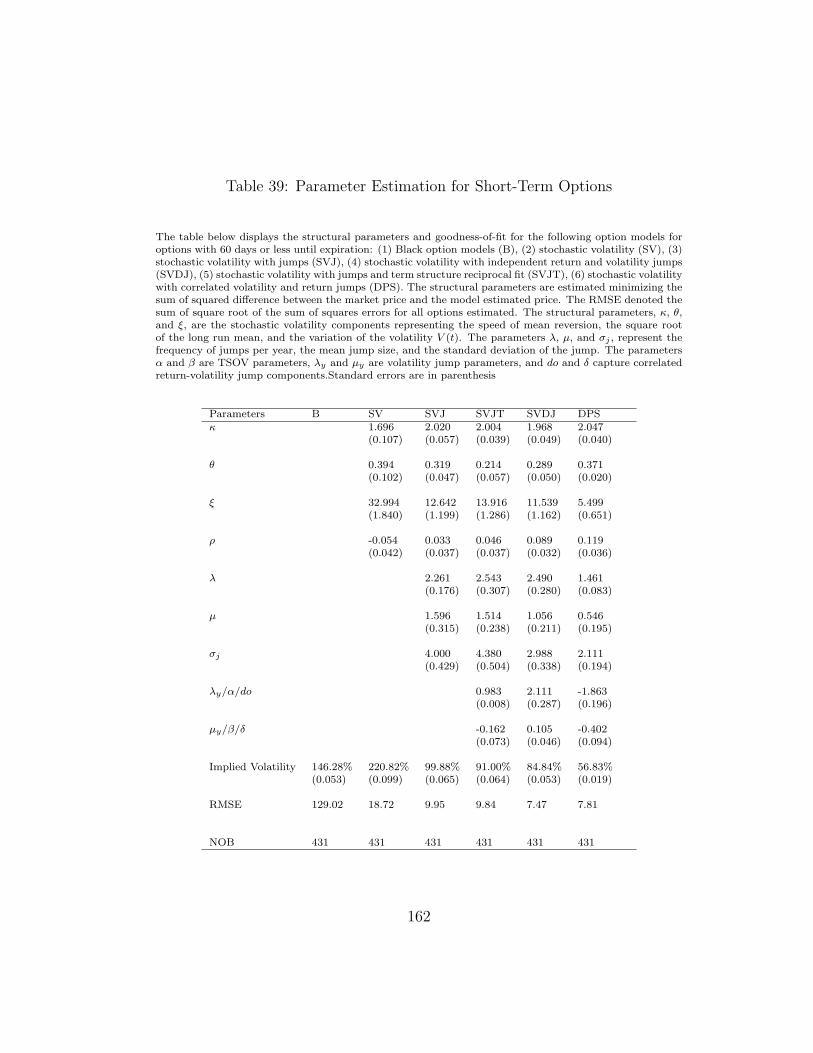

39 Parameter Estimation for Short-Term Options . . . . . . . . . 162

40 Parameter Estimation for Long-Term Options in the WinterMonths . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 163

41 Parameter Estimation for Medium-Term Options in the WinterMonths . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 164

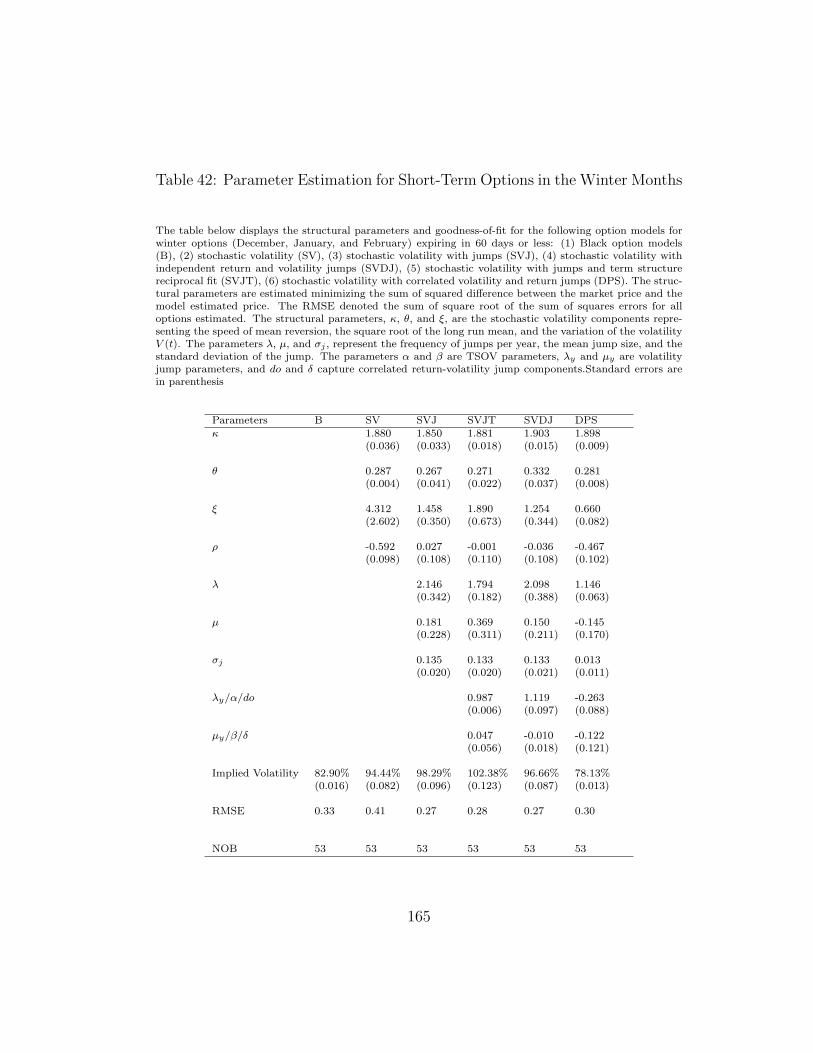

42 Parameter Estimation for Short-Term Options in the WinterMonths . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 165

43 Parameter Estimation for Long-Term Options in the SpringMonths . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 166

44 Parameter Estimation for Medium-Term Options in the SpringMonths . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 167

45 Parameter Estimation for Short-Term Options in the SpringMonths . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 168

46 Parameter Estimation for Long-Term Options in the SummerMonths . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 169

47 Parameter Estimation for Medium-Term Options in the Sum-mer Months . . . . . . . . . . . . . . . . . . . . . . . . . . . . 170

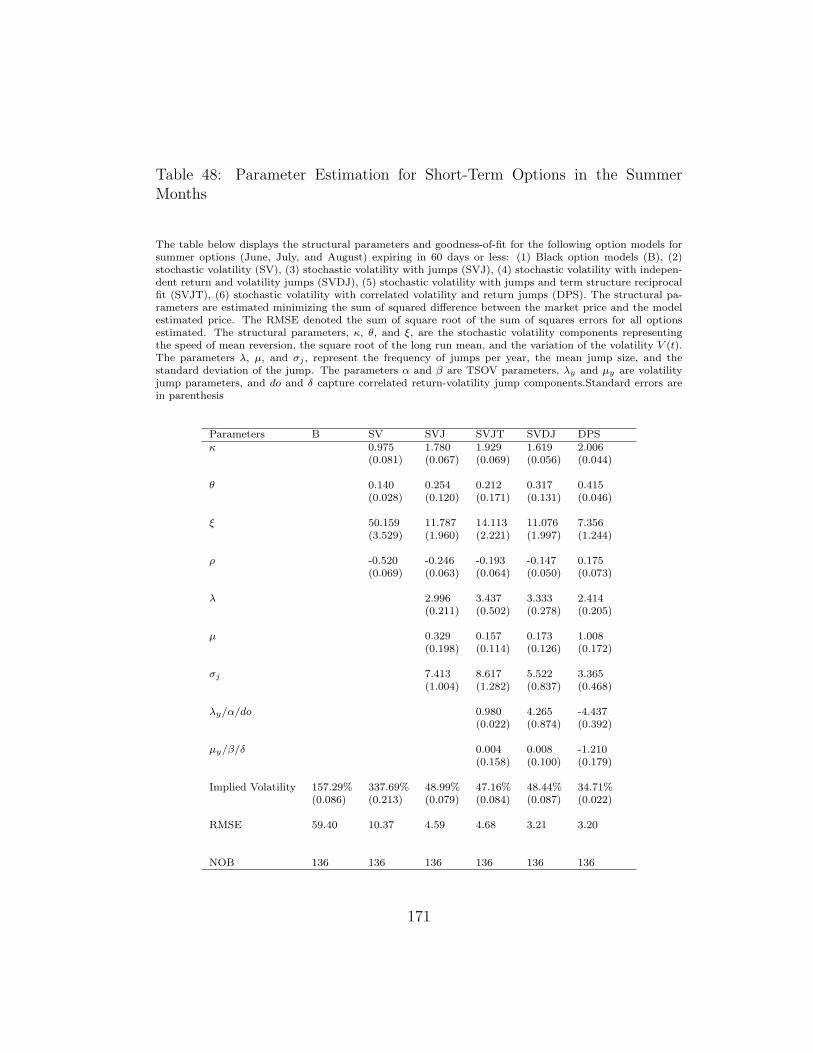

48 Parameter Estimation for Short-Term Options in the SummerMonths . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 171

49 Parameter Estimation for Long-Term Options in the Fall Months172

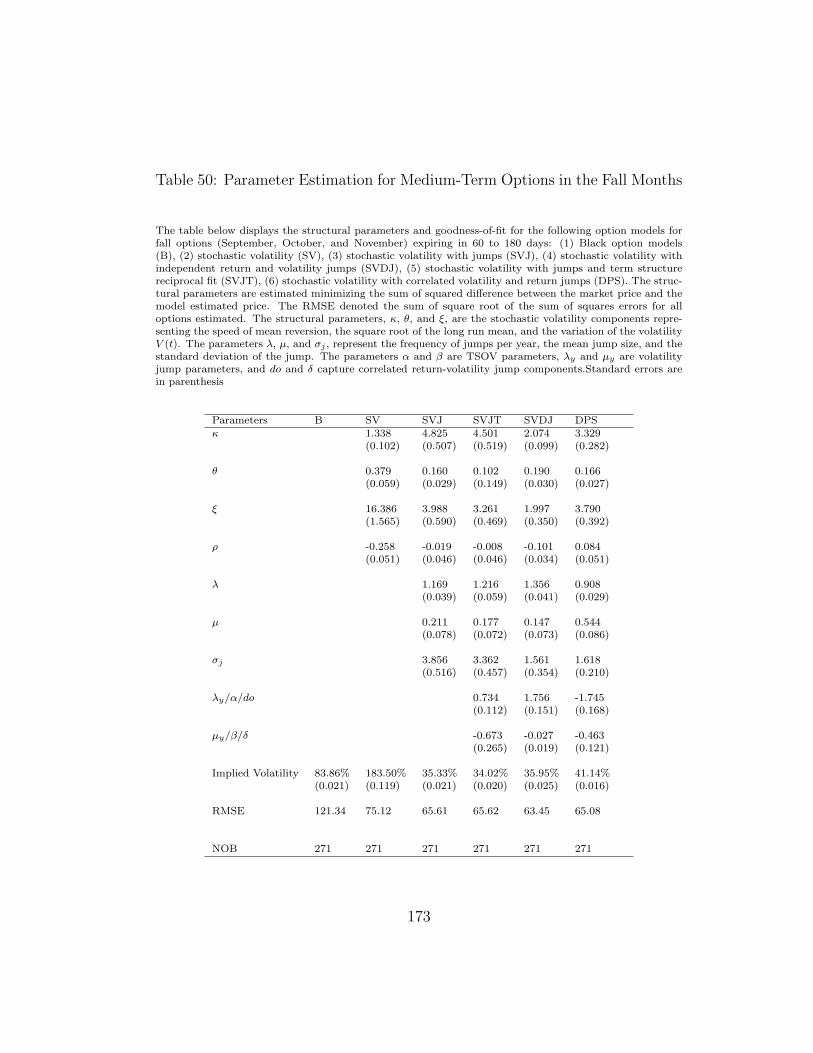

50 Parameter Estimation for Medium-Term Options in the FallMonths . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 173

xi

51 Parameter Estimation for Short-Term Options in the Fall Months174

52 Market Price(s) of Risk . . . . . . . . . . . . . . . . . . . . . . 175

xii

List of Figures

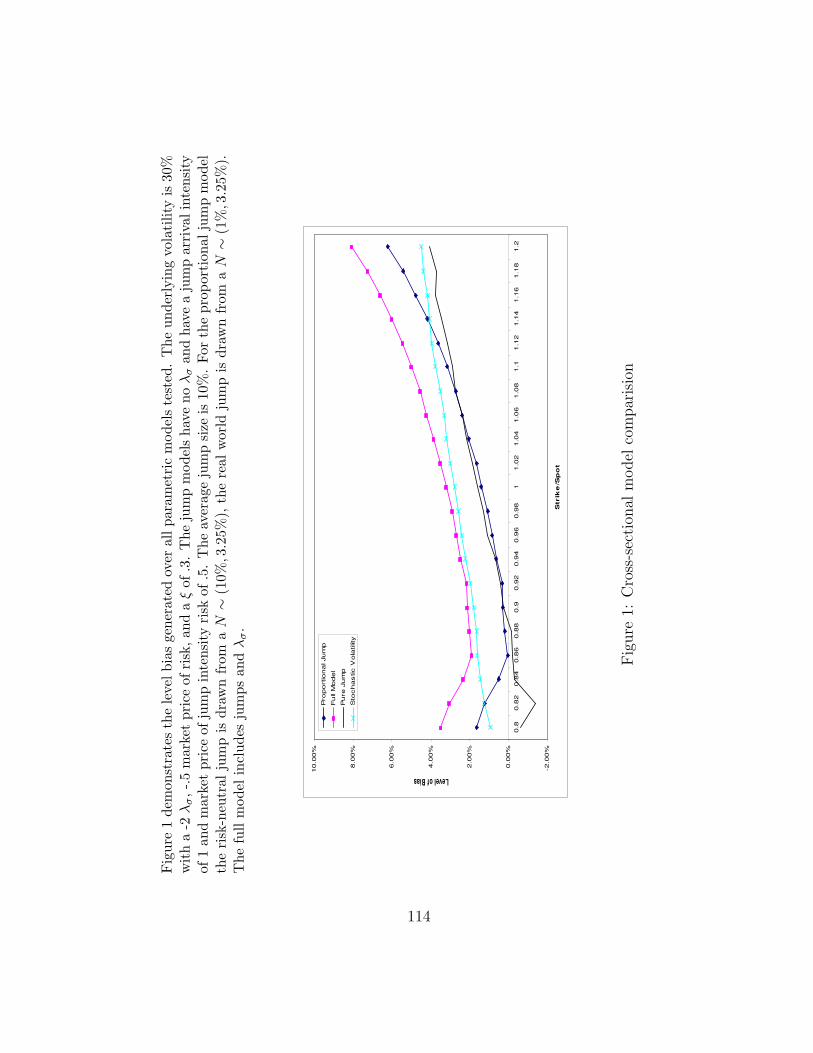

1 Cross-sectional model comparision . . . . . . . . . . . . . . . . 114

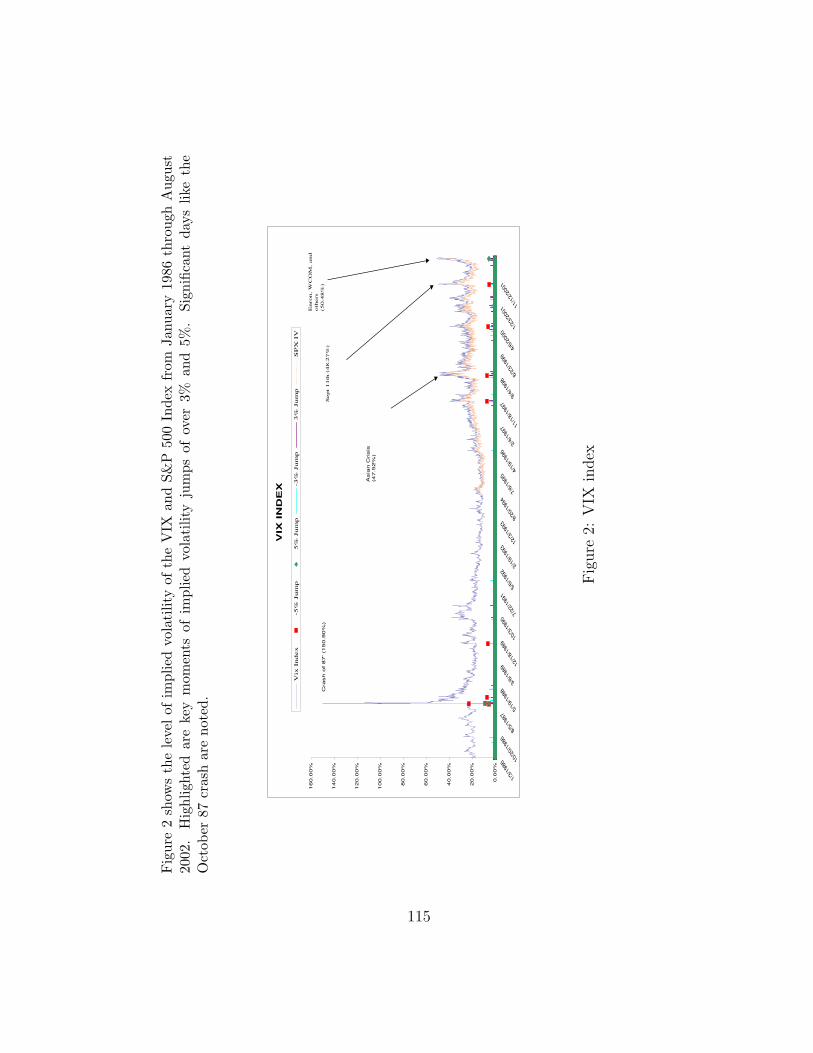

2 VIX index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115

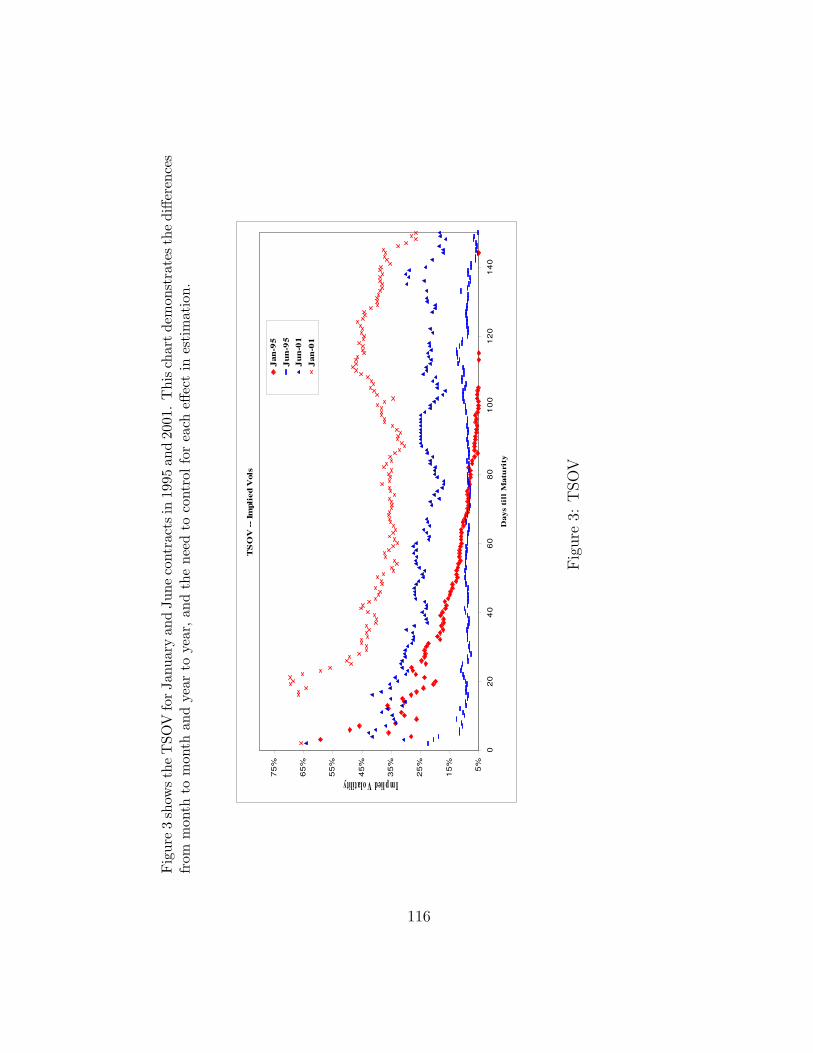

3 TSOV . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 116

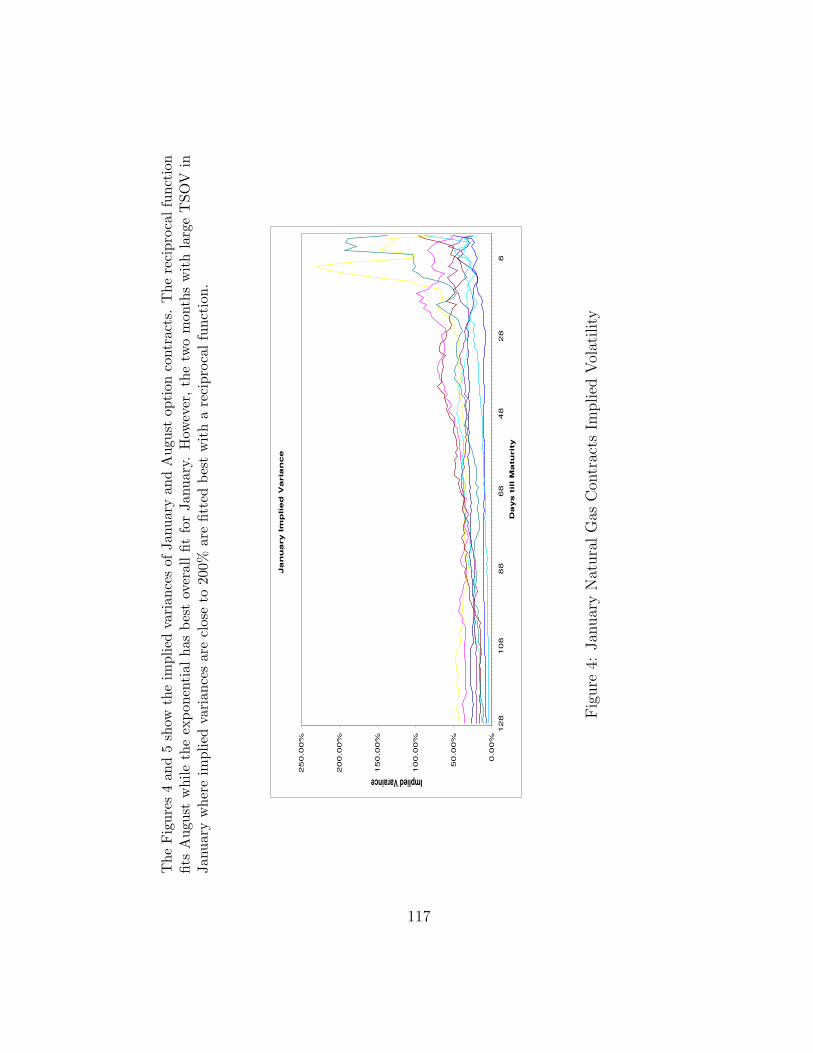

4 January Natural Gas Contracts Implied Volatility . . . . . . . 117

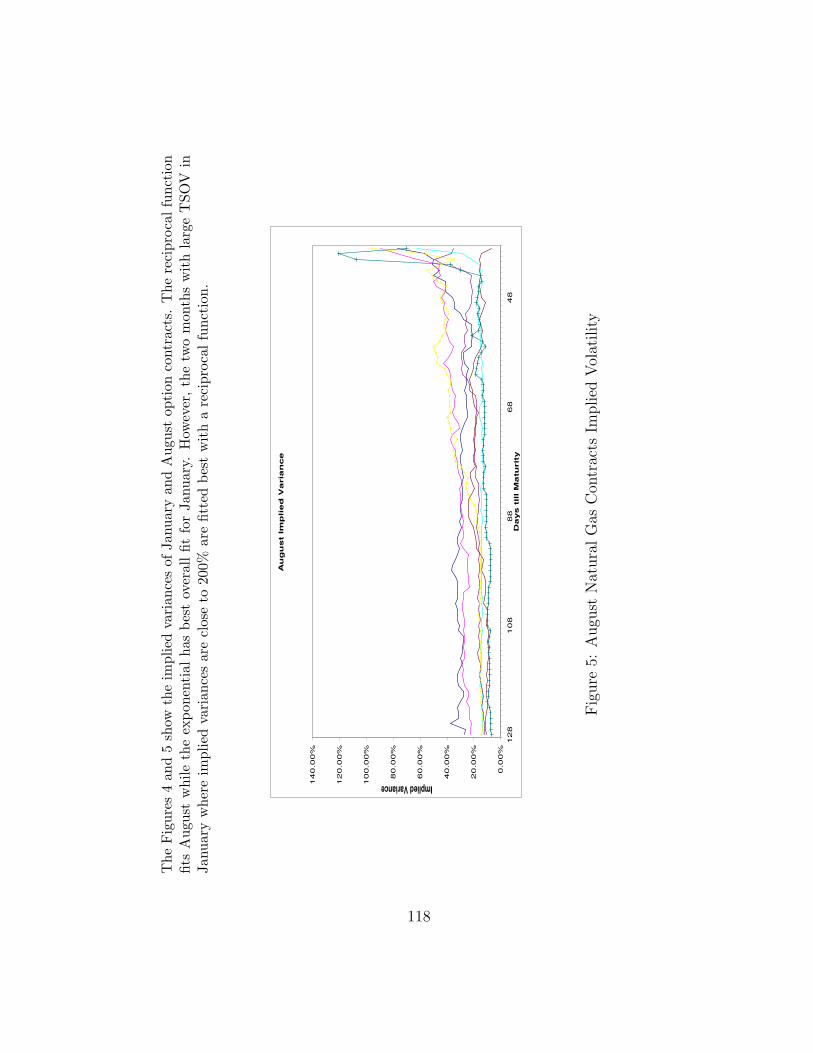

5 August Natural Gas Contracts Implied Volatility . . . . . . . 118

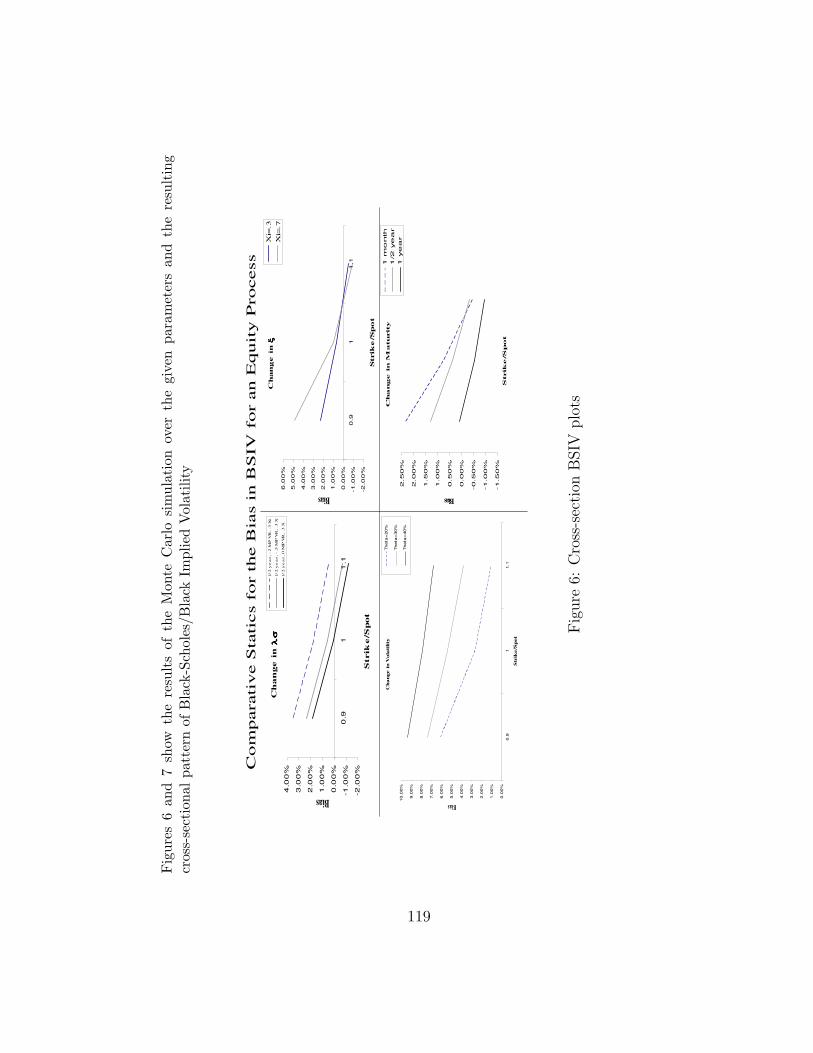

6 Cross-section BSIV plots . . . . . . . . . . . . . . . . . . . . . 119

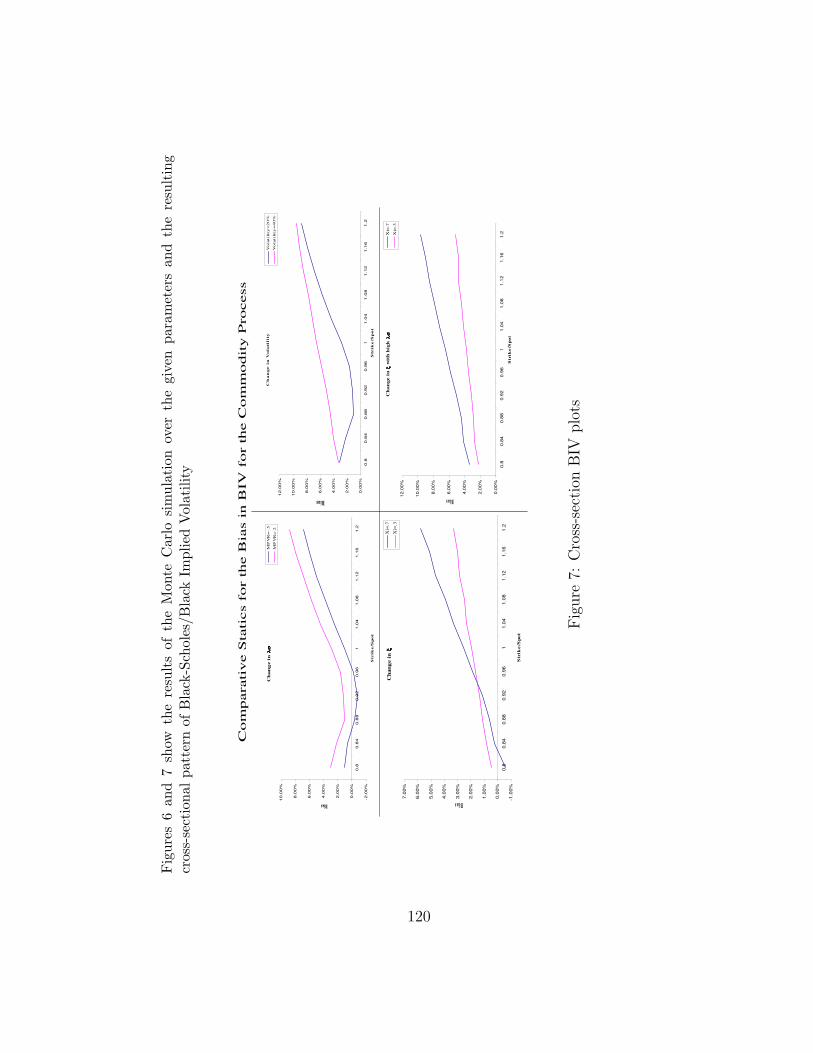

7 Cross-section BIV plots . . . . . . . . . . . . . . . . . . . . . . 120

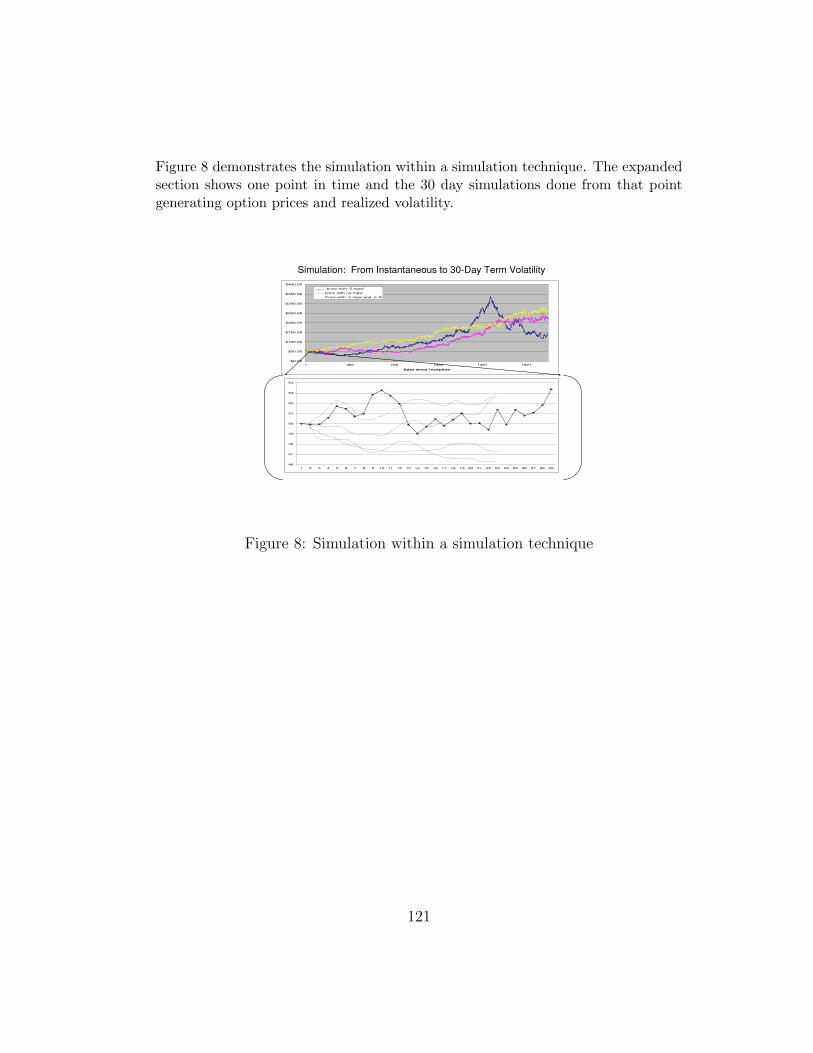

8 Simulation within a simulation technique . . . . . . . . . . . . 121

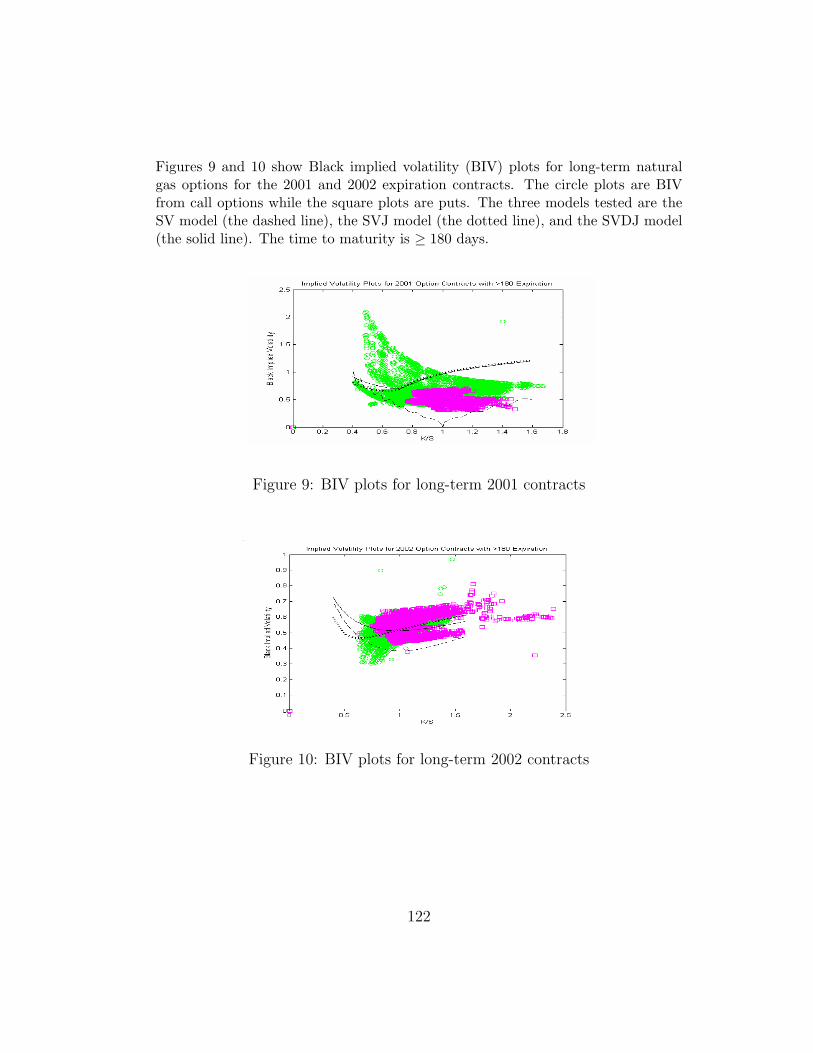

9 BIV plots for long-term 2001 contracts . . . . . . . . . . . . . 122

10 BIV plots for long-term 2002 contracts . . . . . . . . . . . . . 122

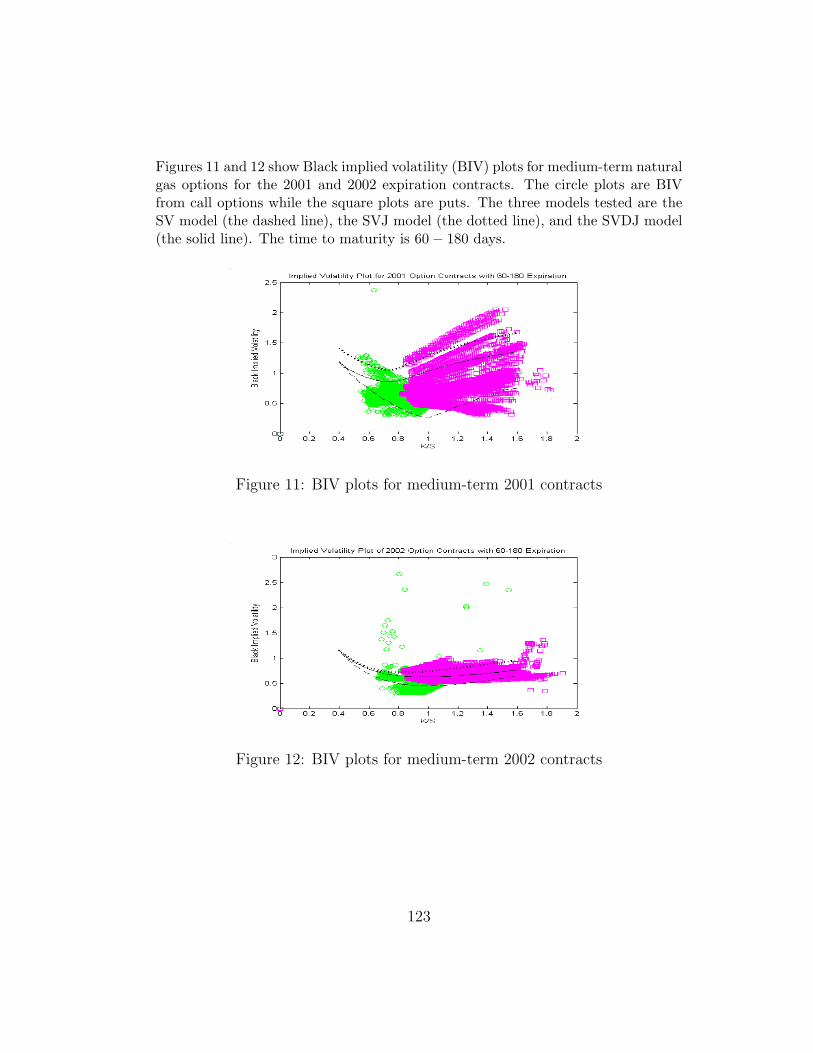

11 BIV plots for medium-term 2001 contracts . . . . . . . . . . . 123

12 BIV plots for medium-term 2002 contracts . . . . . . . . . . . 123

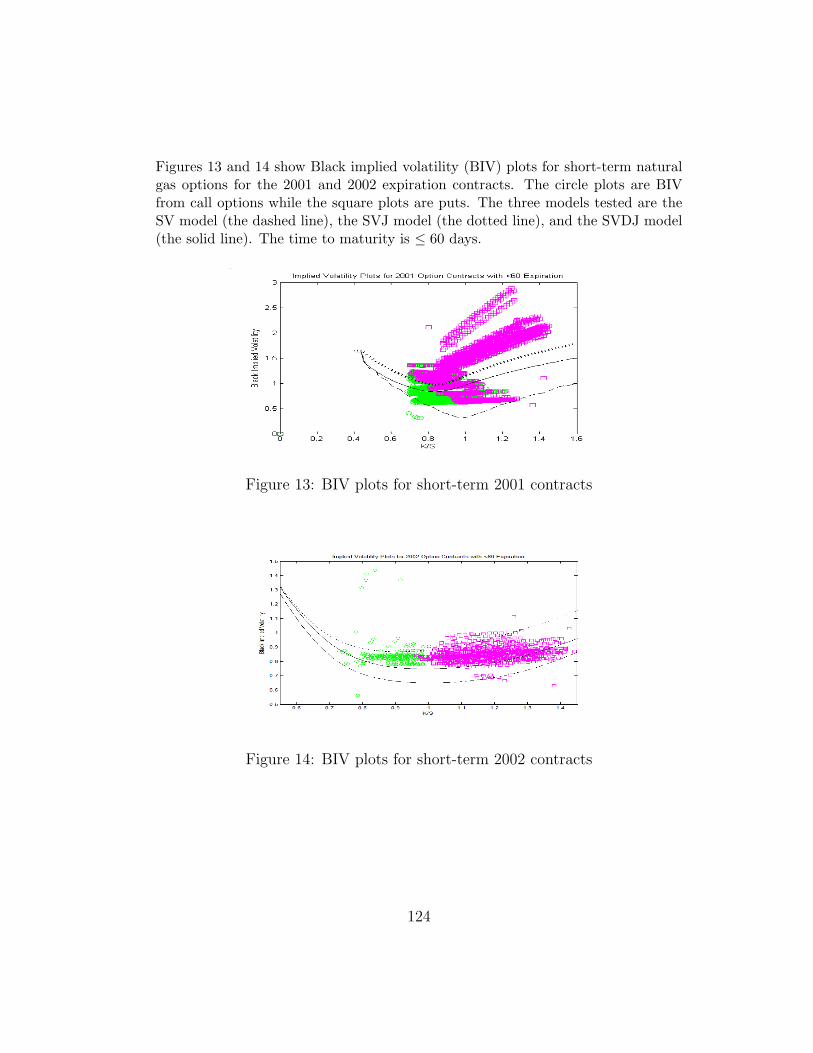

13 BIV plots for short-term 2001 contracts . . . . . . . . . . . . . 124

14 BIV plots for short-term 2002 contracts . . . . . . . . . . . . . 124

xiii

Chapter 1

Introduction

To what extent is implied volatility a biased or unbiased predictor of

future realized volatility? The answer to this question is important for a

variety of reasons, impacting option trading, volatility forecasting, and overall

risk management. Understanding this bias could lead to resolving issues such

as why option traders tend to be short and whether forward prices are upward-

or downward-biased predictors of spot prices. The predictive power of implied

volatility will be explored in both the equity and commodity markets, as one

of my objectives in this work is to understand this bias.

There exists a rich literature on the computation and interpretation

of implied volatility, following closely upon the heels of the derivation of the

Black-Scholes option pricing formula. Christensen and Prabhala (1998) com-

pared implied volatility to an ex-post estimate of return volatility. By per-

forming a time-series analysis of pre- and post-87 data, they suggest that the

implied volatility of S&P 100 index options is an unbiased and efficient predic-

tor of future volatility. They were able to show that implied volatility remains

an efficient estimator even when including past volatility in the specification.

Others, such as Jorion (1995) and Lamoureux and Lastrapes (1993), consid-

1

ered foreign currency options and have suggested that implied volatility, while

efficient, is a biased predictor of future realized volatility.

If Black-Scholes implied volatility is truly an unbiased predictor of fu-

ture realized term volatility, this is consistent with the hypothesis that the

Black-Scholes model is the “true” model for stock prices, and that there is

no model misspecification. Such a conclusion would appear inconsistent with

the volatility skew present in option prices. In fact, we should expect Black-

Scholes/Black implied volatility to be biased, when we account for the market

price of volatility risk within a jump and/or stochastic volatility framework.

The estimation will lead to the conclusion that Black-Scholes implied volatil-

ity is an upward-biased predictor, which I will relate to the underlying data

generating process.

The evolution of the commodity markets differs from the tradition eq-

uity/index markets, and reporting on the volatility bias and underlying pa-

rameters in this market is the next objective. I will use Black’s formula for

the implied volatility (BIV) for the commodity simulation case. Commodities

contracts add additional complexity not prevalent for equities. The presence

of a significant term structure of volatility (TSOV), as well as seasonality, re-

quires additional modeling, and further complicates estimation. Thus I resort

to estimating the necessary TSOV parameters that reduce pricing errors by

postulating three parametric forms for the term structure. The findings sug-

gest that a reciprocal specification for the TSOV best fits the model when

there is a severe “ramping up” of volatility, versus the traditional Schwartz

2

(1997) specification and a quadratic form. As for seasonality, it was necessary

to separate the contracts by months. This allows further insight into the effects

of stochastic volatility premiums on winter versus summer months. There is

an additional concern with liquidity issues, and/or sticky prices, due to low

turnover. Focusing on gas contracts versus oil or electricity, minimized these

concerns since the volume is sufficient and data is readily available. After

accounting for these idosyncrasies, demonstrating BIV is an upward-bias pre-

dictor of future realized volatility can be accomplished in similar methodology

to the upward-bias in BSIV.

After estimation, the intent is to examine current option pricing models

to determine how well each model can explain this bias. Whereas Black and

Scholes (1973) postulated a geometric Brownian motion, papers such as Hull

and White (1987), Heston (1993), and Bates (1994, 1996) introduced stochas-

tic volatility and jumps into the data generating process, with the intended

implication that prices may incorporate premiums for jumps and changes in

volatility. Incorporating both stochastic volatility and jumps in the formu-

lation, I consider the individual and combined effects of the underlying pa-

rameters and how they either contribute to, or diminish, the bias in implied

volatility.

Recent literature has expanded upon these models by incorporating

additional factors such as jumps in volatility, multiple volatility factors, and

alternative power coefficients. While these models help improve the under-

standing of the evolution of options markets, there are unanswered questions

3

that can be resolved without the need for such additional price-process model-

ing. In addition, there appears to be limited significant improvement to overall

model fit.1

The parameter of particular interest is the market price of volatility risk.

There is a wide body of literature on stochastic volatility models, but very lim-

ited information on the market price of volatility risk. Only recently, findings

in Bakshi and Kapadia (2001), Coval and Shumway (2001), Pan (2000), and

others address the direction and magnitude of market price of volatility risk.

The hypothesis is that the market price of volatility risk is indelibly linked

to the bias in Black-Scholes implied volatility: The process volatility and in-

teraction with the market price of volatility risk, determines the magnitude

of the bias. If market price of volatility risk is negative, this can potentially

explain the upward-bias we observe in Black-Scholes implied volatility as well

as contribute to Bates’ (1996) finding that out-of-the money (OTM) puts are

volatility skew expensive relative to other options. Traders short OTM puts

require compensation for volatility risk, independent of any jump intensity or

jump size risk that may also be included. Eraker (2001) and Bates (2000)

have documented the Sharpe ratios of OTM puts are approximately six times

higher than the Sharpe ratio of traditional equity portfolios. These results

suggest large premiums for exposure to volatility risk. However, fully under-

standing this parameter requires going beyond examining volatility changes

1A test of the double-jump model of Duffie, Pan, and Singelton (2002) performed by Bak-shi and Cao (2003), reveals no significant difference between this model and the traditionalstochastic volatility with jump model in terms of RMSE

4

through time. It is necessary to examine this parameter in conjunction with

jumps in the price process, since these are two separate effects. Regardless

of model specification, inferring significant estimates for the parameter is a

non-trivial exercise, that requires either extensive years of data or advanced

econometric techniques.

The commodity market is quite distinct from the equity market. First,

individuals are net consumers of energy, versus net savers in the equity mar-

ket. Secondly, forward prices may be upward-bias predictors of expected spot

prices in the energy markets while the reverse is true for equities.2 Third, we

observe implied volatility skews for out-of-the money calls and in-the-money

puts; this is possibly due to firms wishing to hedge against energy market price

spikes/positive jumps. This may suggest a positive market price of volatility

risk for energy commodities. However, if forward prices are upward-bias pre-

dictors of expected spot prices, it implies a negative market price of risk for

energy products.3 A positive skew, which is a possible indicator of positive

correlation between the price and volatility process, also leads to the conclu-

sion that the market price of volatility risk is negative, as it is in the equity

markets. Nevertheless, it is not clear that the market price of risk is negative in

commodity markets, and thus the claim that there are negative Sharpe ratios

for energy commodities is debatable. Through the estimation of a negative

market price of volatility risk for the gas markets, and establishing positive

2Since the expected rate of return is typically higher for equities than the risk free rate,one expects that forward prices are downward bias predictors of expected spot prices.

3As noted by Dincerler and Ronn (2001)

5

correlation between price and volatility, strengthens the argument for negative

values for the market price of risk in commodities. In addition, I can relate

the upward-bias predictive nature in BIV by showing that it necessary to have

a negative market price of volatility risk.

Central to the estimation for the market price of volatility risk is relat-

ing the bias in Black-Scholes/Black implied volatility to the underlying data

generating process. Accomplishing estimation required recovering the risk neu-

tral parameters by linking the instantaneous volatility to thirty day BSIV/BIV

through a simulation technique. Recent literature has focused on the appro-

priate way to estimate continuous time models. Chernov and Ghysels (2002)

use the Galant and Tauchen EMM technique, Pan (2000) applied an IS-GMM

framework, and Jones (2001)and Eraker (2001) have used Bayesian analysis to

arrive at their estimates. Through a simulation within a simulation technique,

the problem of estimating the latent spot volatility from the instantaneous pro-

cesses is avoided, using 30 day Black-Scholes implied volatility as a proxy for

instantaneous spot volatility. Using these results, and implementing a mean

reverting regression framework allows inference on the level of mean-reversion,

the long run mean, and the volatility of the volatility process. The market

price of volatility risk can then be deduced from the risk neutral parameters

and the level of bias in BSIV/BIV. This procedure focuses only on the volatil-

ity process and ignores the price process, reducing the problem to one equation

and one unknown. Initially, the focus is on the market price of volatility risk,

thus I do not concern myself with the full model, and restrict attention to the

6

volatility process in estimation.

While a strong focus is placed on Black-Scholes/Black model misspec-

ification, specifically focusing on the stochastic element in volatility, it is also

important to account for the possible measurement error in implied volatility

from the model. As Hentschel (2002) points out, it is possible to find positive

upward-bias in Black-Scholes and positive skew in index options even if Black-

Scholes is correctly specified. The problem lies in inverting BS to find implied

volatility since there is potential measurement error in discrete call prices,

stock prices, dividends, risk free rate, and time to maturity. For example,

non-syncronous reporting of the closing option price and the underlying price.

These small measurement errors can cause large errors in implied volatility due

to the non-linear amplification, especially for the OTM options, and options

with time to expiration close to zero. In addition to the measurement error,

Hentschel (2002) argues the implied volatilities estimates are upward- bias due

to the absence of lower arbitrage bounds eliminating low implied volatilities.

This results in truncation, causing a smile/smirk pattern. This truncation

occurs for options away from the money, because only the true prices at these

points approach the bounds. This particular problem will be minimized for

the ATM index options since there is infrequent activity that allows the option

price to go negative. In addition, the VIX sample appears to be fairly efficient

with minimal measurement error due to the averaging of implied volatilities

from puts and calls, low weights assigned to options near expiration, and the

7

focus on near ATM options.4 Hentschel (2002) reports ATM bias of around ±

1.25% in volatility for stock index options and this bias is considerable worse

for individual stock options. This bias seems to be independent of volatility

level, assuming high enough volatility levels, and increases with a decreasing

strike price. I will account for these potential measurement errors when it

comes to estimating how biased BSIV is to realized term volatility.

As noted in Heston (1993), Hull and White (1987), and others, the

payoff of a stochastic volatility process cannot be replicated, and therefore

the market is incomplete. Under the initial assumption of perfect correlation

between the processes, I reduce the two-factor model to a single factor, and

can use the Black-Scholes model to invert the call price and arrive at the

estimate of implied volatility (BSIV). Inverting the Black-Scholes formula to

find the implied volatility may seem inconsistent when volatility is stochastic,

since constant volatility is one of the strong assumptions of Black-Scholes.

However, if at all points in time, there exists an instantaneously maturing

option, using the closed form solution to find the volatility at any specific time

would not be in violation of the Black-Scholes assumption since instantaneous

volatility is constant. Additionally, this allows for replication of any payoff

and a complete market setting. This framework allows for easy analysis to

examine the effect of the market price of volatility risk. It is important to

note that a major goal is to examine the bias in Black-Scholes, as this is the

most prevalent and tractable analytical formula we have to price options. I

4Hentschel points out a confidence interval of ± .25% in volatility.

8

will relax the assumption of perfect correlation and complete markets in both

the simulation and estimation.

1.1 Evidence on the Market Price of Volatility Risk

Since the focus of this work is the market price of volatility risk, it is

necessary to review the current knowledge on this priced risk factor. There are

two issues that must be resolved when it comes to the market price of volatility

risk. The first is the sign of the risk factor, which is less problematic than the

second, showing that the risk factor contributes to the model. For equities, the

market price of volatility risk should be negative. Options are purchased as

hedges against significant declines in the market, and buyers of the options are

willing to pay a premium for downside protection. This could be interpreted

as buying market volatility, since high volatility coincides with falling market

prices [French, Schwert and Stambaugh(1987) and Nelson (1991)]. In addition

to the high Sharpe ratios in trading option, pointed out by Bates (2000) and

Eraker (2001), Jackwerth and Rubinstein (1996) have also suggested that at

the money (ATM) implied volatilities are systematically higher than realized

volatilities which could be explained by a negative volatility risk premium.5

For gas options this issue is less clear, since the dynamics of the energy market

differ from those of equity markets. These differences are:

1. Higher market prices tend to coincide with higher volatility.

5Jackwerth and Rubinstein (1996) demonstrate this by recovering the probability distri-butions from option prices.

9

2. Beta coefficients tend to be negative for commodities markets

3. There is a significant term structure of volatility and seasonality for gas

futures prices.

Nevertheless, even in the presence of these major differences I will show

that the market price of volatility risk for the gas contracts is also negative.

The evidence on the economic impact of market price of risk is some-

what mixed. While most concede that the presence of priced stochastic volatil-

ity risk results in more expensive options, it is not necessarily clear whether

the precise parameter value can be disentangled from other risk-factors. If the

various types of jump and price risk are accounted for, does the impact of the

market price of volatility risk become insignificant? In addition, the sensitiv-

ity of the volatility of volatility process significantly impacts the ability to fit

the model which may lead to overfitting and poor out-of-sample performance.

These two parameters, the market price of volatility risk and the volatility of

volatility process, are intertwined, making inference of precise estimates of the

market price of volatility risk challenging.

Bakshi, Cao, Chen (1997) and Buraschi and Jackwerth (2001) provide

evidence that equity index options are non-redundant securities and omitting

a volatility risk premium may be inconsistent with option pricing dynamics.

Pan (2000) however, refutes this finding, suggesting that a model without

a risk factor for stochastic volatility best explains the cross-section of option

prices. She suggests that jump size risk is the major component that allows for

10

the best model fit, while the market price of volatility risk, while negative, is

insignificant. Additionally, models that do not account for jumps or jump risk,

but include stochastic volatility, severely under-price medium and long dated

options in periods of high volatility and over-price the options on low volatility

days. She notes that these models can reconcile the difference between the spot

and option markets for indicies, but the inclusion of a significant market price

of market volatility risk does not improve model fit. These results seem to be

in direct contradiction with those of Bakshi and Kapadia (2001), and Coval

and Shumway (2000).

Both Bakshi and Kapadia (2001), and Coval and Shumway (2000) per-

form non-parametric tests on option data from the S&P 500 and S&P 100.

While these tests cannot enlighten us to the value of the pricing factor itself,

they do present strong evidence for the existence of a significant parameter.

Coval and Shumway (2000) examine option pricing returns, and set up zero-

delta straddle to test for the validity of the Black-Scholes model. If the Black-

Scholes model holds, then the return on the straddle on average should be the

risk-free rate. Their findings on both the S&P 100 and S&P 500 show signif-

icant negative returns on the straddle position, generating excess returns for

the short position. This could be explained by either some jump or stochastic

volatility priced factor. They conclude that it must be the stochastic volatility

factor after constructing a crash neutral straddle,6 showing that the position

6The crash neutral straddle holds an additonal OTM put to protect against downsiderisk.

11

still produces negative returns.

Bakshi and Kapadia (2001) provide more direct evidence for the exis-

tence of a priced stochastic volatility factor by also constructing delta-neutral

position, but controlling for positive Vega. This portfolio should on average

return the risk free rate, but if it does not, this is suggestive of a significant

market price of volatility risk. Their results for a Delta-Neutral, positive Vega

portfolio, that buys calls and hedges with the stock significantly underperforms

zero. The result is decreasing for options away from the money.7 Controlling

for the strike, the underperformance is greater for longer horizons. Addition-

ally, they show that for periods of higher volatility, the underperformance is

even more negative. They account for the argument for jump premium by

showing that the risk volatility premium can still retain its explanatory power

even in the presence of higher moments. This is important as the inclusion

of a jump premium tends to account for excess skewness and kurtosis. Thus

they provide this as strong evidence for a significantly negative market price

of volatility risk.

The question arises of where the breakdown occurred between the para-

metric model of Bates (1996), Pan (2000) and others and the conclusions drawn

from the non-parametric evidence of Bakshi and Kapadia (2001) and Coval and

Shumway (2000). Could it be that the non-parametric evidence was finding

7This is potentially an interesting result since OTM puts tends to have significant jumppremiums while OTM calls tend to have very little premium according to Bates (1996). Itis worth exploring the reverse hedge to see how the portfolio performs.

12

addition jump factors that have not been controlled for in the test specifica-

tion? Or could it be that parametric model is incomplete or mis-specified. My

conclusions from the work shown in the following chapters suggest that the

latter is incorrect for both the equity and gas processes, and that the market

price of volatility risk is negative and significant.

13

Chapter 2

The Bias in Black-Scholes/Black

Implied Volatility

2.1 Introduction

The work in this chapter will address the upward-bias in Black-Scholes

and Black implied volatility. First, I will proceed with a quick review of the

stochastic volatility data generating process to provide a theoretical founda-

tion for the following empirical tests. I will then incorporate term-structure

parameters for commodities to capture the increase in volatility for close to

maturing gas futures contracts. Finally, empirical tests will be conducted

showing that Black-Scholes/Black implied volatility is an efficient but biased

predictor of future realized volatility.

2.2 The Model

2.2.1 Stochastic Volatility

The data generating process for the equity process is given below. I

have adopted the familiar square root process developed by Heston (1993):

14

dSt

St

= µ dt+ σt dzs (2.1)

dσ2t = [κ(θ − σ2

t ) + λσξσ2t ] dt+ ξσt

(ρ dzs +

√1− ρ2 dzσ

)(2.2)

In equation 2.1, the price process is a function of the drift term, µ,

volatility rate, σ, and Brownian motion dzs. The variance is a mean-reverting

process with speed of mean-reversion κ,long run mean θ, and Brownian motion

dzσ. The drift in the price-process is governed by:

µ = r + λsσt (2.3)

where r is the risk free rate and λs is the market of price of risk. The market

price of volatility risk is λσ, and ξ represents volatility of volatility. ρ captures

the correlation betweeen the processes, allowing for the Black (1976) finding

that stock returns and changes in volatility are negatively correlated. Using the

Girsanov Theorem we can see the transformation from the real world to the risk

neutral world. In the risk-neutral world µ = r, because the expected growth

rate is equal to the risk-free rate. The risk-neutral process is governed by a

separate Wiener process under the transformed Q-measure denoted dz∗, dz∗σ:

dSt

St

= r dt+ σt dz∗s (2.4)

dσ2t = κ(θ − σ2

t ) dt+ ξσt

(ρ dz∗s +

√1− ρ2 dz∗σ

)(2.5)

15

For the commodity process, the futures price F follows the process

dFt

Ft

= υ dt+ σt dzF (2.6)

dσ2t = [κ(θt − σ2

t ) + λσξσ2t ] dt+ ξσt

(ρ dzF +

√1− ρ2 dzσ

)(2.7)

where υ = λsσ. is In the risk-neutral world υ = 0, since the market price of

riskis equal to zero. Note the subscript on θt where t represents the time to

maturity of the futures contract. Thus, the risk-neutral process is:

dFt

Ft

= σt dz∗F (2.8)

dσ2t = κ(θt − σ2

t ) dt+ ξσt

(ρ dz∗F +

√1− ρ2 dz∗σ

)(2.9)

For the equity process, the market price of risk and the market price

of volatility risk appear in the real world distributions. The speed of mean

reversion and long-term volatility are assumed identical in each distribution.

Assuming that the market price of volatility risk is zero, then regardless of

changes in the other parameters, the real world and risk neutral distributions

are identical.1 As previously noted, Bakshi and Kapadia (2001) and others

have shown that the market price of volatility risk is negative, implying that in

the specification the implied volatility coming from the risk neutral distribution

would be higher than the real world volatility. However, when the market price

1The same analysis can be applied to the futures process.

16

of volatility risk is held constant, the other parameters play an important role

in quantifying the bias, and cannot be ignored.

Initially, I reduce the two-factor process by making assumptions about

the correlation between the price and volatility process, and the market prices

of risk. This was done for two reasons: First, to provide simple intuition about

relating the effect of the parameters and the subsequent difference in volatility

between the option implied volatility and the realized term volatility; secondly,

reducing the equation to a one-factor process allows for the evaluation of the

problem in simple bushy lattice framework. Assume dzs = −dzσ which implies

λs = −λσ for the equity process, discretize equation (2.1) through (2.5) and

substitute:

(St − St−1)

St−1

= µdt+ σdzs

(St − St−1)

St−1

= (r + λσt−1)4t+ [−(σ2

t − σ2t−1 − [κ(θ − σ2

t−1) + λξσ2t−1]4t)

ξ)]

combining like terms:

4SS

= [A+ λBt]4t− Ct

17

with

A = r +κθ

ξ

Bt = (σt−1 − σ2t−1)

Ct =σ2

t − σ2t−1(1− κ)

ξ

For the risk neutral process, the equations combine in a similar fashion to

4SS

= A4t − Ct, since λ = 0. Within the reduced factor process it becomes

easy to interpret the effect of an increase in λ on the change in price, and

subsequently, the volatility process. If λ is equal to zero, then we should

expect exactly the same price movements in the risk neutral process and the

real world process. However, when there is positive market price of risk, as is

the case for equities, the two processes should diverge. To evaluate the effect of

λ, I use the bushy lattice framework since the volatility is not constant. Solving

for the bushy lattice, it is easy to see the evolution of the price tree for the two

processes.2 I combine the risk neutral process with the real world process and

am left with 4S∗

S∗= 4S

S− λB4t. Since λ is positive, and σ must always be

positive, the change in the real world price must be greater than that of the

risk neutral process. From the assumption of perfect negative correlation, it

should then hold that the volatility change is more volatile for the risk neutral

process. This is easily shown by substituting equations (2.2) into (2.3), and

2Please refer to appendix for discussion on the technique used for the bushy lattice.

18

(2.4) into (2.5). The proof is shown in the Appendix. Given that the market

price of risk is positive for equities, and that dzs, dzσ are perfectly negatively

correlated, there is a resulting negative effect on the volatility change due to a

negative market price of volatility risk. This results in a less volatile process for

the objective distribution. For commodities, the same intuition applies except

that there is a negative market price of risk and perfect positive correlation

between the processes.3

If there exists a negative market price of volatiltiy risk, then result-

ing risk-neutral and real-world volatilties should demonstrate the properties

shown above for both equites and commodities. Hereto, Black-Scholes (Black)

implied volatility should be greater than realized term volatility for equities

(commodities). This can be tested by regressing Black-Scholes implied volatil-

ity (BSIV) on realized-term volatility and showing that BSIV is an upward-bias

predictor of realized-term volatiltiy.

2.3 Estimation of the Bias in BSIV/BIV

2.3.1 Data

To test the bias in BSIV/BIV, and later for the data generating process,

I use the S&P 500 and S&P 100 Index for the equity/index process and ten

years of gas futures contracts that expire in each month of the year. I have

3The assumption of perfect correlation will be relaxed in the following chapter for bothsimulation of the model and estimation of the data. For the simulation, the bushy-latticetechnique will be replaced with a quasi-Monte Carlo procedure.

19

collected daily price and annualized daily-implied volatility from October 1994

until July 2001 for the S&P 500 and from January 1st 1986 to August 26th

2002 for the S&P 100. For the gas contracts, I have futures and options prices

for all the options contracts starting with a contract that expired January 1995

and finishing with a contract that expires December 2005. I will focus on all

the contracts and will control for seasonality issues. The option and price data

has come from Bloomberg. Bloomberg constructs an implied volatility based

on a weighted average of closing prices of call and put options with time to

maturity as close to 22 days. For estimating bias I look only at ATM forward

call and put options. I will address the potential measurement error issues

shortly. The gas contracts implied volatility comes from the actual contracts,

and thus the term-structure of volatility (TSOV) must be accounted for. The

implied volatility for the S&P 100 was collected from the VIX index.4 The

daily risk free rate comes from the Federal Reserve for the 1-month T-Bill.

The frequency of the data is daily. Currently there are 1959 days for the S&P

500, 4183 days for the S&P 100, and 5067 combined days for the gas futures

contracts. Table 1 provides the descriptive statistics for the both the implied

volatility and realized term volatility5 for the S&P 100 and the S&P500. The

sample clearly indicates that implied volatility has been higher than realized

volatility for both indices as well as the pre- and post- October 1987 crash.

4The implied volatility from the VIX index was caluclated using the old methodology.The method for calculating BSIV was changed in 2003.

5Please refer to equations 3.9-3.10 for reference on the calculation of realized term volatil-ity.

20

Figure 2 shows the time series of implied volatility for both the S&P 100

and S&P 500 with daily price movements of 3% and 5%. This is shown to

highlight how infrequently the index had moved in these amounts on a daily

basis over this period. In addition, tables 3-4 document how often gas prices

have jumped in daily movements of over 5% and 10%. Table 2 has descriptive

statistics of daily returns for the natural gas futures contracts. What is evident

is the degree of volatility present in gas prices, and to what extent that these

“jumps” are clustered in certain years and monthly contracts. Controlling for

these effects will be crucial in the estimation procedure. Figure 3 shows the

daily implied volatility level for each of the gas contracts for January and July

in years 1995 and 2001, which gives the best description of the effect of the

TSOV.

2.3.1.1 Measurement Error

As Hentschel (2002) points out, the potential measurement error in

implied volatility can range from insignificant to potentially disastrous. The

problem in inferring implied volatilities from the Black-Scholes formula is that

small pricing errors in the stock price and call price can lead to large distor-

tions in the inverted volatility. The problem is relatively insignificant for the

ATM options, especially for index options, but becomes exponentially worse

for deep ITM and OTM options.6 However, since for this particular estimation

I only look at a constructed estimates of implied volatility for all contacts, the

6Refer to table 2a,b in Hentschel (2002) for example.

21

concern with measurement error is minimized. The difference between VIX

and the GLS correction in Hentschel (2002) is insignificant, and since the

Bloomberg HIVG estimate is constructed in a similar manner, I am confident

in the precision of the results.

2.3.2 Estimating the bias

2.3.2.1 Equity Bias

The hypothesis that Black-Scholes is an efficient and unbiased predictor

of realized term volatility is assessed by estimating a regression of the form

ht = α0 + αiit + εt (2.10)

where ht denotes the realized term volatility for period t and it denotes the

implied volatility from the Black-Scholes closed form solution at the beginning

of period t.7 For BSIV to be unbiased, it must be the case that α0 = 0 and

αi = 1; for efficiency the residuals should be white noise and uncorrelated

with the independent variables. As Christiansen and Prabhala (1998) note,

there could be an errors-in-variables (EIV) problem with using BSIV, and use

prior-month BSIV as an instrument. This they feel helps resolve the issue of

7ht is Christensen and Prabhala definition of realized term volatility as given in equation2 of their paper and equations 3.9 and 3.10 in this chapter. Additional specification add inpast realized term volatility such that ht = α0 + αiit + αhht−1 + εt. This was run despitethe multi-collinearity problem. The correlation between it and ht−1 for the S&P 100 wasaround .8. For the S&P 500 the correlation was close to .4. This is independent of level orlog-level specification.

22

EIV.8

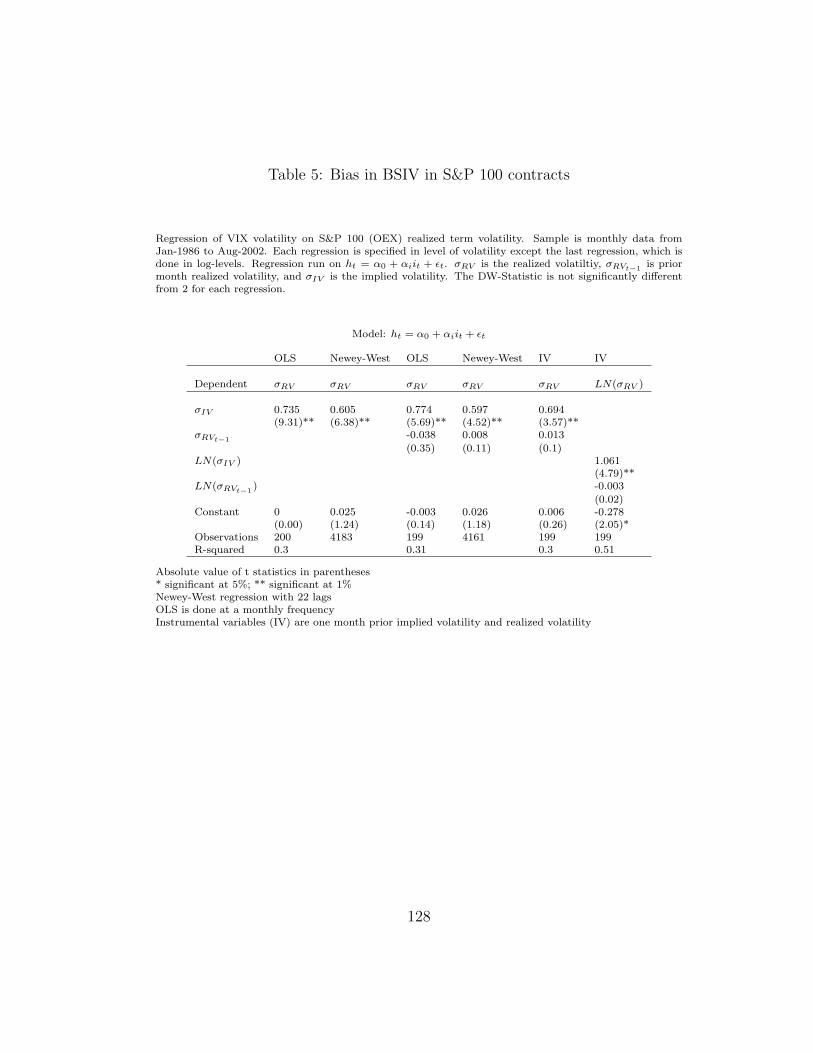

In table 5, I have replicated the results in Christensen and Prabhala

(1998), with data that extend their original sample to August 2002.9 Their

findings suggested that Black-Scholes implied volatility was an efficient and

unbiased predictor of future realized volatility, as shown in equations 3.9 and

3.10. To refute the findings I need only show that the intercept coefficient not

equal zero or the slope coefficient is not unity. It is my contention that if BSIV

is an upward-biased predictor of realized term volatility, the intercept term

should be negative or the slope coefficient less than unity. The OLS regression

on the sample is done with a non-overlapping monthly frequency similar to the

Christiansen and Prabhala study. The results show the slope coefficient is less

than unity for both specifications. Additionally, the coefficient is significantly

different from one, suggesting that BSIV is an upward-bias predictor. Since

I also have data for all closing days, tests were run similar to that of Jorion

(1995) and Canina and Figelweski (1993). However, the sample has high levels

of autocorrelation and must be corrected for. The results confirm that BSIV

coefficient is significantly less than one while doing a Newey-West correction

with 22 lags. By using the entire sample I avoided any bias using any one

particular day throughout the sample.

8Please refer to their paper for a discussion of the EIV problem. However, since Black-Scholes is mis-specified, one must assume that model-misspecification is a considerable prob-lem.

9Christiansen and Prabhala also ran their specification on pre and post 1987 crash data.Their finding suggested a regime shift around the time of the crash.

23

This particular specification was done on levels of volatility versus log-

levels. In this analysis I will examine both the levels and log-levels of volatil-

ity even though log-levels seem to be more appropriate. The Christiansen

and Prabhala (1998) study also notes that implied volatility may incorporate

measurement error, and uses the prior month’s implied volatility as well as

prior month realized term volatility as an instrument.10 The results on levels

show the slope term is significantly different for one. As for the results on

the log-levels, the intercept term is negative and significantly different from

zero, suggesting upward-bias in BSIV. I find these results give foundation for

relating this bias to the underlying parameters that drive stock prices and

volatility.

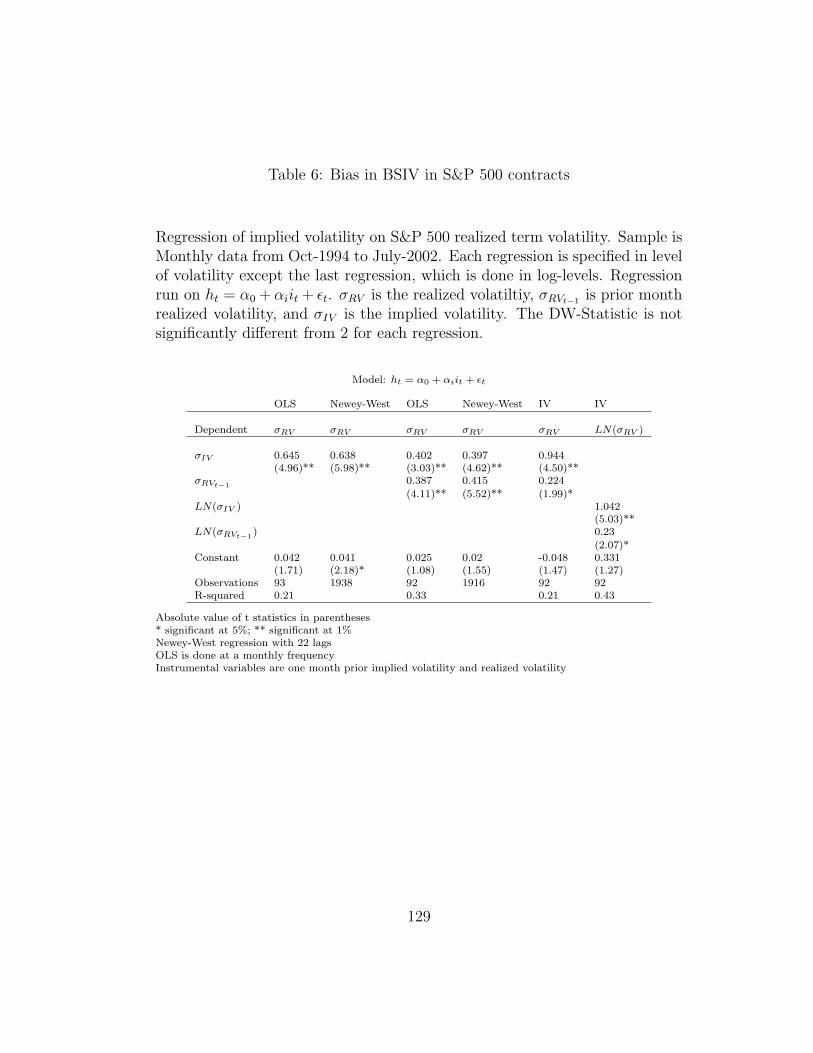

I additionally looked at the S&P 500, since I wanted to confirm that

it was not index specific. This data set, while smaller, will still give enough

data points to come up with significant results. The results are shown in

table 6 and are very similar to those on the S&P 100, with the exception of

the instrumental variables test on levels and log-levels. However a joint F-

test that the intercept term is equal to zero and the slope coefficient equal

to one is 5.84, resulting in rejection of the hypothesis that BSIV is unbiased.

For the log-level, the F-Statistic is 1.87, thus I cannot reject the hypothesis.

However, the log of prior month realized volatility is significant, which also

refutes the claim that BSIV is unbiased and efficient. These results should not

10Implied Volatility may be correlated with ht, but prior month implied volatility willnot.

24

be surprising given that we know that the data cannot be described by a pure

Black-Scholes model. If there is a negative market price of volatility risk, we

should expect that Black-Scholes implied volatility is an upward-bias predictor

of future realized volatility.

When adding prior month realized volatility to the specification, I still

find implied volatility as the best predictor for future realized volatility.11 The

estimates based on prior realized volatility tend to be insignificant at either

the statistic or economic level. This is an important result. Regardless of the

bias nature in implied volatility, it still appears to be the strongest forecast of

future volatility in the market. By providing these reliable estimates on the

bias in implied volatility I provide better forecasts of future market movements

with BSIV.

Interpreting the instrumental variables test for BSIV levels of 15%,

20%, and 30% on the S&P 100 translated into realized term volatility levels of

10.41%, 13.88%, and 20.82%. For the S&P 500 these BSIV levels translate into

9.36%, 14.08%, and 23.52% for realized term volatility. It is my contention

that as the volatility in the equity markets rises, the degree to which BSIV is

an upward-bias forecast of future volatility also increases.

11Canina and Figelweski (1993) suggest that prior month realized volatility is the efficientpredictor for future realized volatility

25

2.3.2.2 Modeling of the TSOV

Solving for the bias in implied volatility for gas contracts is compli-

cated by the significant presence of a term structure of volatility. As a results,

regressing the term implied volatility on realized term volatility does not gen-

erate comparable bias estimates. Controlling for the TSOV is crucial, and will

allow for a direct comparison to the equity markets if done correctly. This

requires specific modeling of the term structure that can handle the quick

“ramping up” of volatility in the last two to three months of the contract. I

have chosen to implement several parametric candidates while assuming cer-

tain fixed controls for the volatility and TSOV parameters. The relationship

between implied term volatility and instantaneous volatility is given by

σ2T =

1

T

∫ T

0

σ2t dT (2.11)

Since there is time-dependent volatility σt = σf(t), it is necessary

to come up with a functional form to express this particular relationship.

Schwartz (1997) exponential relationship between term volatility and instan-

taneous volatility is an obvious choice, but a one factor model is limited in

it success. Thus I choose two additional forms, a quadratic and reciprocal

relationship. Adding an additional factor will capture the long run mean of

volatility, while the other factors can fit the time dynamics. Given σt = σf(t),

the options for the functional form are listed below.

26

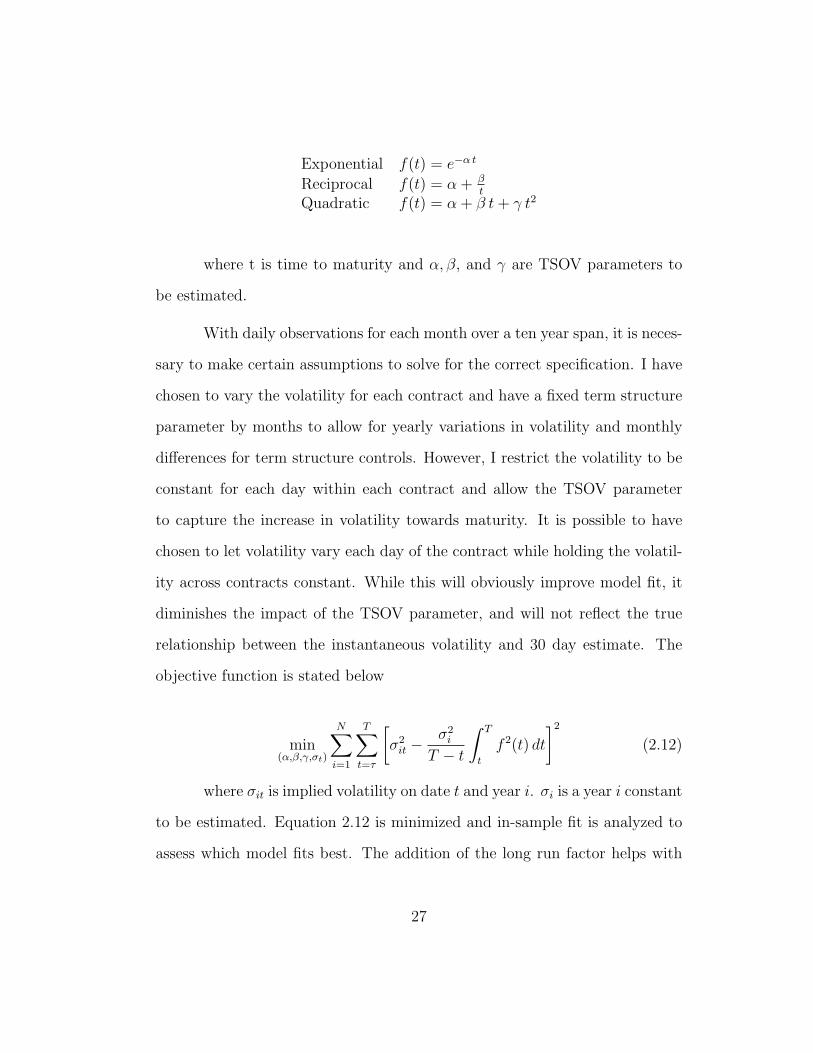

Exponential f(t) = e−α t

Reciprocal f(t) = α+ βt

Quadratic f(t) = α+ β t+ γ t2

where t is time to maturity and α, β, and γ are TSOV parameters to

be estimated.

With daily observations for each month over a ten year span, it is neces-

sary to make certain assumptions to solve for the correct specification. I have

chosen to vary the volatility for each contract and have a fixed term structure

parameter by months to allow for yearly variations in volatility and monthly

differences for term structure controls. However, I restrict the volatility to be

constant for each day within each contract and allow the TSOV parameter

to capture the increase in volatility towards maturity. It is possible to have

chosen to let volatility vary each day of the contract while holding the volatil-

ity across contracts constant. While this will obviously improve model fit, it

diminishes the impact of the TSOV parameter, and will not reflect the true

relationship between the instantaneous volatility and 30 day estimate. The

objective function is stated below

min(α,β,γ,σt)

N∑i=1

T∑t=τ

[σ2

it −σ2

i

T − t

∫ T

t

f 2(t) dt

]2

(2.12)

where σit is implied volatility on date t and year i. σi is a year i constant

to be estimated. Equation 2.12 is minimized and in-sample fit is analyzed to

assess which model fits best. The addition of the long run factor helps with

27

overall model fit, but the results are highly dependent on the given contract

month. The exponential function form performs well relative to the others

with either fitting the close-to-maturity or far-from-maturity dates depending

on the initial condition given. The quadratic tends force the curvature to fit

the close-to-maturity dates by implying negative volatilities for the 3-7 months

to maturity period. The reciprocal fits best in certain months because it allows

for the increasing convexity close-to-maturity without sacrificing earlier dates.

Figure 4 and 5 best demonstrates this.

I test for model misspecification of the TSOV by using 5-day before,

1-day before and 5-day after volatilities for each model on each day for each

contract. These tests are typical for model misspecification as discussed in

Arimya (1980) and have been used in tests of various option models as in Bak-

shi, Cao and Chen (1997). The typical argument is that with more structural

parameters it becomes easier to fit a given model, but can cause overfitting

which will result in poor out-of-sample performance. Again minimization was

done on the objective function as given before and tests each monthly con-

tract. The results are presented in table 7 along with the in-sample results.

The results suggest that either Schwartz (1997) exponential model or the re-

ciprocal functions are the best candidates for the TSOV for gas contracts.

For each month the apparent in-sample candidate model also performs best in

the out-of-sample tests. A closer look at the January results show the perfor-

mance of the exponential model is best in all three out-of-sample tests with

the reciprocal function showing large performance improvements when using

28

5-day behind volatilities. This is suggestive of a pontential problem either

with the final couple of days of volatility in a given contract or the reciprocal

model itself. One fault in the estimation relies on the taking the log of in-

finity, which requires an approximation, and this approximation can result in

large errors when maturity of a given contract approaches. This seems to be

apparent given the results for January, where there exists a large TSOV and

poor reciprocal fit, and the results for May, which are the opposite.12

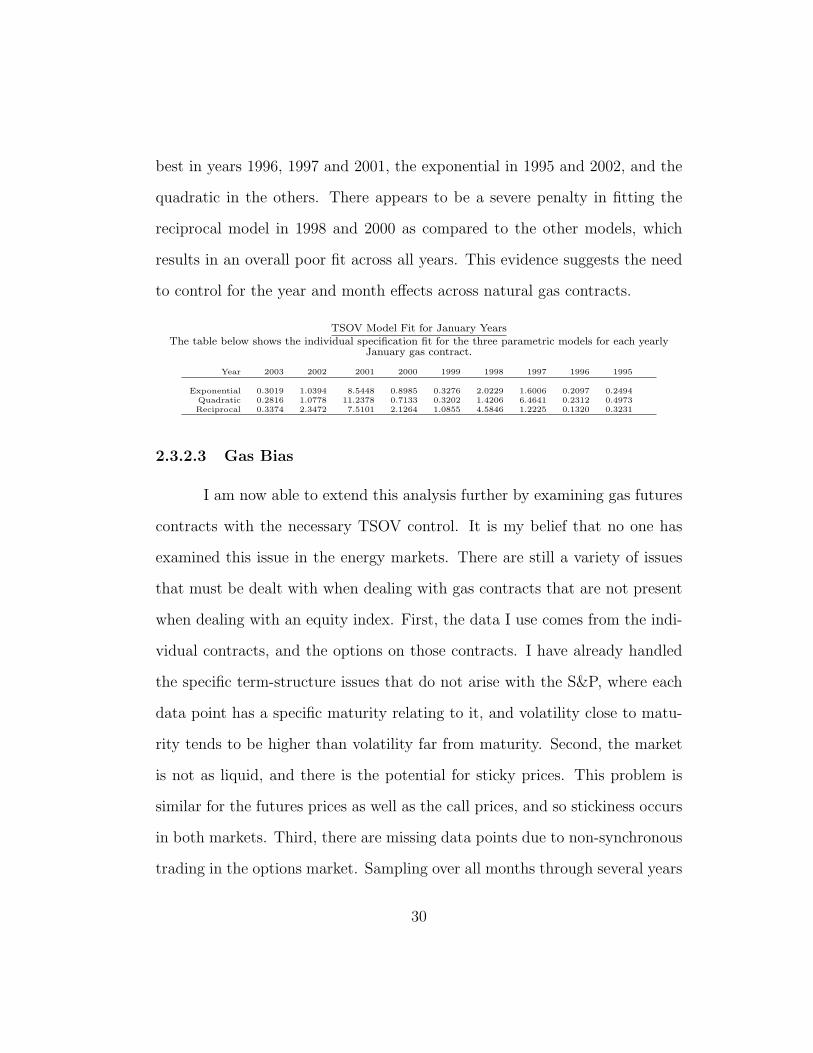

I extend the analysis by breaking up each test into individual years for a

given monthly contract and testing each model on those years. The concern is

that the results may hinge on the poor fit of one particular year thus distorting

the overall fit through the minimization of equation 2.12. For example, let year

1995 have no significant TSOV while other years have significant slopes. This

can result in a greater penalty for a given model, say the exponential, for

year 1995, while that same model fits the other years better than the other

potential parametric candidates. It may then be better to examine the years

one by one versus collectively since each year has a unique TSOV associated

with it. Below I break up the January estimation into individual years, and

examine the individual RMSE to asses the model fit. Initially it appears that

the exponential fit does best for the overall period, given the in and out-of-

sample fits. The table below suggests that the other models do better for

certain years. There is no apparent trend as the reciprocal model performs

12These particular months were choosen to shown the disparity between months that haslarge TSOV effects and months that did not. Likewise, December and April could have beenselected for this particular comparision.

29

best in years 1996, 1997 and 2001, the exponential in 1995 and 2002, and the

quadratic in the others. There appears to be a severe penalty in fitting the

reciprocal model in 1998 and 2000 as compared to the other models, which

results in an overall poor fit across all years. This evidence suggests the need

to control for the year and month effects across natural gas contracts.

TSOV Model Fit for January YearsThe table below shows the individual specification fit for the three parametric models for each yearly

January gas contract.

Year 2003 2002 2001 2000 1999 1998 1997 1996 1995

Exponential 0.3019 1.0394 8.5448 0.8985 0.3276 2.0229 1.6006 0.2097 0.2494Quadratic 0.2816 1.0778 11.2378 0.7133 0.3202 1.4206 6.4641 0.2312 0.4973Reciprocal 0.3374 2.3472 7.5101 2.1264 1.0855 4.5846 1.2225 0.1320 0.3231

2.3.2.3 Gas Bias

I am now able to extend this analysis further by examining gas futures

contracts with the necessary TSOV control. It is my belief that no one has

examined this issue in the energy markets. There are still a variety of issues

that must be dealt with when dealing with gas contracts that are not present

when dealing with an equity index. First, the data I use comes from the indi-

vidual contracts, and the options on those contracts. I have already handled

the specific term-structure issues that do not arise with the S&P, where each

data point has a specific maturity relating to it, and volatility close to matu-

rity tends to be higher than volatility far from maturity. Second, the market

is not as liquid, and there is the potential for sticky prices. This problem is

similar for the futures prices as well as the call prices, and so stickiness occurs

in both markets. Third, there are missing data points due to non-synchronous

trading in the options market. Sampling over all months through several years

30

to account for this deficiency. Additionally, since the estimation is more of a

cross-section than a time-series analysis, it does not matter how the prices

evolve, but that I have an implied volatility matched to a realized volatility

30 days or 22 trading days hence.

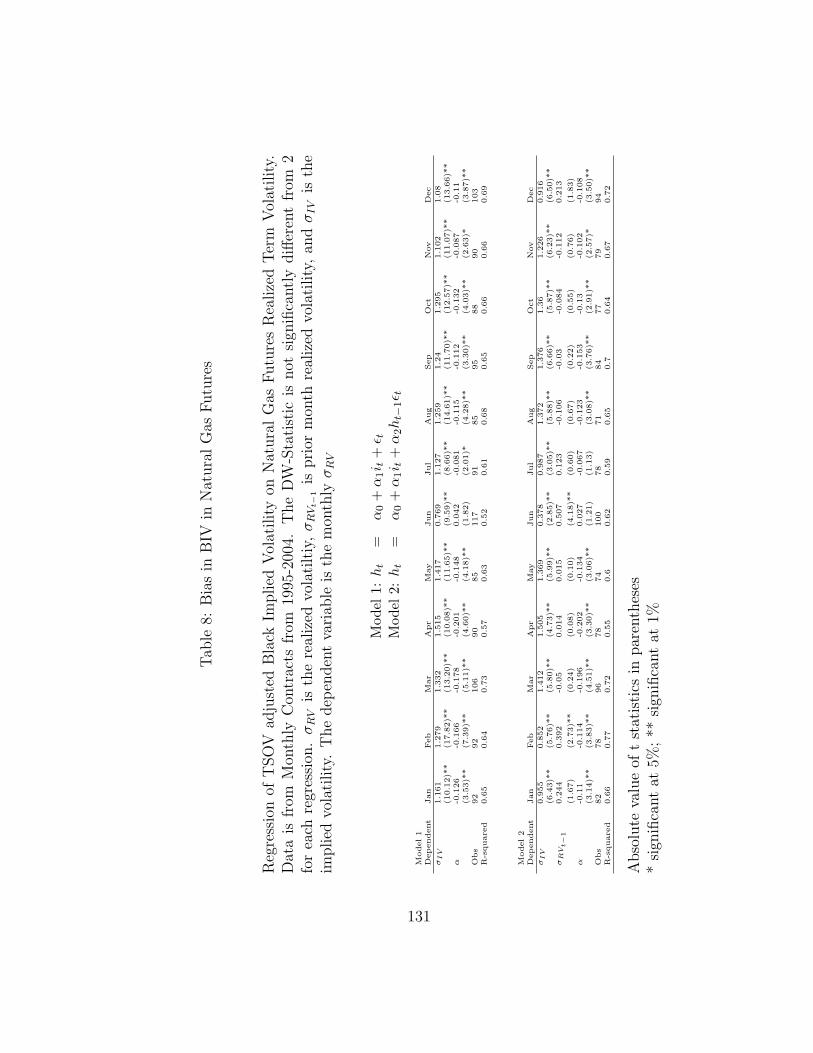

Estimating the degree of bias in Black (1976) implied volatility for gas

contracts involves accounting for these additional factors not present in index

options. From the prior TSOV estimation, intergrating up to a 30-day implied

volatility estimate allows for direct market comparison between the equity and

gas bias using the Christiansen and Prabhala (1998) estimate of realized term

volatility. Secondly, the impact of seasonality will require the estimation to

be done on a contract by contract basis. This is done not only to control for

monthly effects, but because the price and volatility estimates are a function

of the maturity of the contract. Unlike the S&P estimates, these estimates

are a function of the specific contract and the time to maturity. While the

TSOV control should account for the term effect, estimation on a contract

by contract basis will account for the seasonality. A fixed effects estimation

using all contracts could have been implemented, but requires specific modeling

of the variance-covariance matrix due to the high levels of cross-correlation

between the contracts. Since there are enough data points for each monthly

contract, and the individual monthly bias estimates are a foremost concern, a

fixed-effect regression is ommitted.

Given the high presence of seasonality in the energy markets I control

31

for each month of expiration for the futures contracts.13 This is accomplished

by running separate regressions for each month and accounting for the year

effects through the TSOV corrections. The results are shown in table 8. I

correct the heteroskedacity through a white correction as well as running a

weighted-least-squares using implied volatility as the weight.14 Regressions

were run using only the starting day in each month,15 and then using the full

sample with Newey-West corrected errors done at 22 day lags. This was done

for two reasons. First, the full sample cannot be used due to the high pres-

ence of auto-correlation at the daily level, and second, to have results that

were comparable to those for the equity regressions ran earlier. The findings

are quite different to those reported for the equity index regression, however,

result in the same conclusion that BIV would have to be upward-bias. What

is immediately obvious is that bias decreases as implied volatility increases.

This is not surprising since we observe the highest levels of volatility close to

maturity for these contracts. Typically, realized volatility increases as matu-

rity approaches and can even exceed implied volatility.16 However, even with

a slope coefficient greater than unity, the intercept coefficients are negative,

and significantly different from zero. For the January, July, November, and

December months, the intercept term is close to 1. A t-test on the slope coef-

13Summer and winter months tend to have more demand due to the excessive heat/cold.It is during these months that most price spikes occur.

14results suppressed.15I also ran this specification using the last day of every month, and the middle of each

month, with the results coming up similar to those reported16this can also be a function of how realized volatility is calculated. As maturity ap-

proaches, statistical variance increases.

32

ficients revealed that they were not significantly different from 1, but a joint

f-test with the intercept equal to zero was rejected.

This suggests an upward-bias in Black implied volatility (BIV) in pre-

dicting realized term volatility of gas futures contracts. We should expect that

this bias should be in the same direction as the equity market even though

the market price of risk for the energy markets tends to be negative. While

it is well documented that the price process is negatively correlated with the

volatility process for the S&P and other equity indices, this is not the case

for the energy process. As volatility increases, the price tends to increase.17

This can be seen by the positive correlation between the volatility of the gas

market and the changes in price. Additionally, it is my contention that the

market price of volatility risk is positively correlated with the market price of

risk for the energy process, and should also be negative. If this is the case, it

is can offered as an explanation for the upward-biased nature of BIV.

The table below presents the degree of bias for the monthly gas con-

tracts. There are clear cases (April, May) where realized volatility is higher

than that of implied volatility. However, these results are reflective of levels

where volatility is only observed close to maturity, and where end of month

effects are present. In these spring months volatility rarely goes above 35%,

and so it is unlikely that one would observe realized volatility above implied

volatility. June estimation from model 2 from table 8 must be interpreted

17Refer to Dincerler and Ronn for a more detailed discussion.

33

with caution because of the impact that prior month realized volatility had on

the estimate. However, the R2 from model 1 to model 2 only added 10% of

explanatory power and thus model 1 estimates may be more appropriate. By

comparison, at the 20% volatility level, the gas markets tend to exhibit greater

BSIV/BIV bias versus the equity markets, especially for the winter months.

Given that the energy markets are more volatile, and that we observe greater

BIV/BIV bias, could this tell us something about the proportional premium

placed on volatility in these markets? Should we expect that the market price

of volatility risk in the gas markets will be higher in absolute terms? A major

goal of this work is to determine this out by relating the bias to the parame-

ters that govern the volatility process. I have demonstrated the upward-bias

in BIV. This allows for testing the feasibility of various option pricing models

as well as prior estimated parameters from these models. If a model can attain

this level of bias, it further indicates the appropriateness of the specification.

Bias in BIVThe table below show the bias in BIV relative to realized term volatility. For a given level of BIV the table

shows for each month the difference between BIV and realized term volatility. Model 1 is the initialspecification given equation 2.12. Model 2 incorporates prior realized term volatility.

Model 1 Model 2

20.00% 30.00% 40.00% 20.00% 30.00% 40.00%

Jan 9.38% 7.77% 6.16% 11.90% 12.35% 12.80%Feb 11.02% 8.23% 5.44% 14.36% 15.84% 17.32%Mar 11.16% 7.84% 4.52% 11.36% 7.24% 3.12%Apr 9.80% 4.65% -0.50% 10.10% 5.05% 0.00%May 6.46% 2.29% -1.88% 6.02% 2.33% -1.36%Jun 0.42% 2.73% 5.04% 9.74% 15.96% 22.18%Jul 5.56% 4.29% 3.02% 6.96% 7.09% 7.22%

Aug 6.32% 3.73% 1.14% 4.86% 1.14% -2.58%Sep 6.40% 4.00% 1.60% 7.78% 4.02% 0.26%Oct 7.30% 4.35% 1.40% 5.80% 2.20% -1.40%Nov 6.66% 5.64% 4.62% 5.68% 3.42% 1.16%Dec 9.40% 8.60% 7.80% 12.48% 13.32% 14.16%

34

2.4 Conclusion

The implications of the findings in this section confirm two important

prior results; first, that the Black-Scholes model is misspecified, and second,

BSIV is still the efficient predictor of future realized volatiltiy. Additonally, the

results for the equities markets transfer directly to the commodities markets,

specifically for natural gas futures and the Black model. Controlling for the

term structure of volatility allows for a direct comparison between the equities

and the commodities markets, and the results reveal that both BSIV and BIV

are upward-bias predictors of σRTV .

This is highly relevant since the degree of the bias can be related to the

underlying data generating process that governs stock and futures prices. An

upward-bias in BSIV/BIV is suggestive of a negative market price of volatility

risk. The intent of the next section is to use these results and relate them

to various instantaneous structural models that incorporate both stochastic

volatility and jumps. Through Monte Carlo simulation and mean-reversion

estimation, the market price of volatiltiy risk can be extracted using the esti-

mated degree of bias found in tables 5, 6, and 8.

35

Chapter 3

Monte Carlo Simulation and Estimation of the

Market Price of Volatility Risk

3.1 Introduction

Using the knowledge attained through the upward- bias relationship be-

tween BSIV/BIV and realized-term volatility, I will calibrate the underlying

data generating process from both the risk-neutral and real-world processes

to the degree of bias using the sensitivity of the instantaneous structural pa-

rameters. The intent here is to demonstrate that the market price of volatility

risk, λσ, is negative and significant. The first will be accomplished through

Monte Carlo simulation. The second will be demonstrated by the simulations

incorporating many parameterizations, and showing that a large negative λσ is

necessary, and independent of model specification, to demonstrate the degree

of upward-bias shown in the previous chapter. Once this claim has been estab-

lished, the estimation of the market price of volatility risk will be conducted

using a stochastic volatility mean reverting framework. Using a time-series

of implied volatilities from short-term at-the-money (ATM) options and con-

structed realized-term volatilties, the market price of volatility risk can be

estimated via calibration.

36

3.2 Monte Carlo Simulation

I adopt Monte Carlo simulation to test for the sensitivity of the bias

in BSIV to realized term volatility in the underlying parameters of the model.

The stochastic volatility simulation is executed using equations (2.1)-(2.5) for

the equity process, and equations (2.6)-(2.9) for the commodity process. For

completeness, I present the real-world and risk-neutral price and volatility

processes below:1

Real-World Process:

dSt

St

= µ dt+ σt dzs (3.1)

dσ2t = [κ(θ − σ2

t ) + λσξσ2t ] dt+ ξσt

(ρ dzs +

√1− ρ2 dzσ

)(3.2)

Risk-Neutral Process:

dSt

St

= r dt+ σt dz∗s (3.3)

dσ2t = κ(θ − σ2

t ) dt+ ξσt

(ρ dz∗s +

√1− ρ2 dz∗σ

)(3.4)

where r is the risk free rate and λs is the market of price of risk. The market

price of volatility risk is λσ, and ξ represents volatility of volatility. κ is the

speed of mean-reversion, θ is the long run mean, and rho captures the corre-

lation between the price and volatility processes. dzs and dzσ are geometric

Brownian motions. dz∗s and dz∗σ are Brownian motions transformed under the

risk-neutral measure Q.

1For the futures processes, refer to the prior chapter.

37

Two variance reduction control techniques were implemented to help

reduce the standard error of the estimate and improve the efficiency of the

results.2 For each sample path, random shocks are drawn from N ∼ (0,√4t)

at 4t intervals over the life of the option. So with a 1-month to expiration

option, 22 random shocks are drawn for the price process for 22 business days.

This procedure is replicated for the volatility process and is governed by a

separate Brownian motion. Since the concern is with both the risk-neutral

and real-world processes, a total of four random draws are needed for the

evolution of one day. The option value for a call and put are then calculated

as,

Cnt = E∗t [e−rt max(SnT −K, 0)] (3.5)

Pnt = E∗t [e−rt max(−SnT +K, 0)] (3.6)

under the risk neutral measure, where n represents the particular path.

This process is repeated for 1,000,000 runs. This is slightly excessive, but, it

was important to reach an efficient estimator for the call value since inferring

the correct volatility relies on precise estimates of fractions of a cent.3 The

final call and put values are then:

2I have used the antithetic variable and control variate techniques using Black-Scholesas the know analytical solution. In addition, I have run quasi monte-carlo simulations usingthe Sobol sequence to generate results, this was done to determine the number of runs toachieve efficiency.

3As pointed out by Hentschel (2002) and others, pricing and implied volatility errors canbe large when call prices are measured inaccurately.

38

Ct =1

n

n∑i=1

Cit (3.7)

P t =1

n

n∑i=1

Pit (3.8)

By finding C, P and given the starting value for the stock price, risk-

free rate, time to expiration, and strike price, Black-Scholes, or Black for

the gas process, can be inverted and the estimate for BSIV/BIV solved. It

is important to note that the time interval for sampling the random shocks

is small, otherwise it could lead to an instantaneous shock to the volatility

process resulting in a negative variance. For current purposes, the shocks are

bound so that there are zero negative variance realizations. Nevertheless, even

without the bound the variance process infrequently dips below zero.4

To solve for the realized term volatility two methods are adopted. The

first is to sample the returns of the stock/future over the remaining life of the

option.

σrtv =

√√√√1

t

t∑i=1

(ri − rt) (3.9)

where t is number of days to expiration, ri is return on day i and rt

is the average daily return over the option’s life. Additionally, this volatility

4The large ξ is, the large the changes in variance. This can be countered by a smallersampling interval.

39

is annualize to make an easy comparison with the BSIV. This estimate of

realized volatility has been used by Christiansen and Prabhala(1998). The

second measure is

σrtv =

√∑ni=1[(ln(STi

S0)− r)2]

√T

(3.10)

where the period variance is calculated versus the daily variance within

the period. To annualize the volatility the square-root of the period was taken

versus the sampling interval. On average these two estimates should be equal.

While not reported, the bias of BSIV to either estimate of relative term volatil-

ity is not significantly different from one another, and thus only the second

estimate is reported. Calculating mean return, r, requires the transformation

from normal to log-normal.5 This requires knowledge of σ, which is unknown

prior to finding r. This is accomplished by transforming the starting normal

mean, and calculating σ2 from this initial estimate of r. From this first esti-

mate of σ2 the initial mean is then adjusted to a log-normal estimate. The

process to find σ2 with this transformed estimate of r is repeated until con-

vergence is achieved for both values, such that the σ2 is exactly the same for

the standard deviation and the log-normal adjustment for r.6

5The mean return is adjusted from µ to µ− σ2

2 .6No iteration required more than 4 loops to achieve convergence.

40

3.2.1 Stochastic Volatility Simulation

3.2.1.1 Perfect and Zero Correlation Cases

The first tests run were base cases using zero and perfect (negative for

equities) correlation. By examining the extremes in correlation it is possible

to separate out the effect of correlation and the market price of risk on the bias

in BSIV/BIV. In the zero correlation case there should be a limited skew and

minimal bias since there is no market price of volatility risk. In the perfect

negative correlation case, the positive market price of risk is transfered into a