Embed Size (px)

Citation preview

Digital Disruption

in InsuranceAndy Parton

Partner, Ernst & Young AustraliaMob: 0404 810 676

FST Future of Insurance, 10 March 2016

2 Copyright © 2016 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

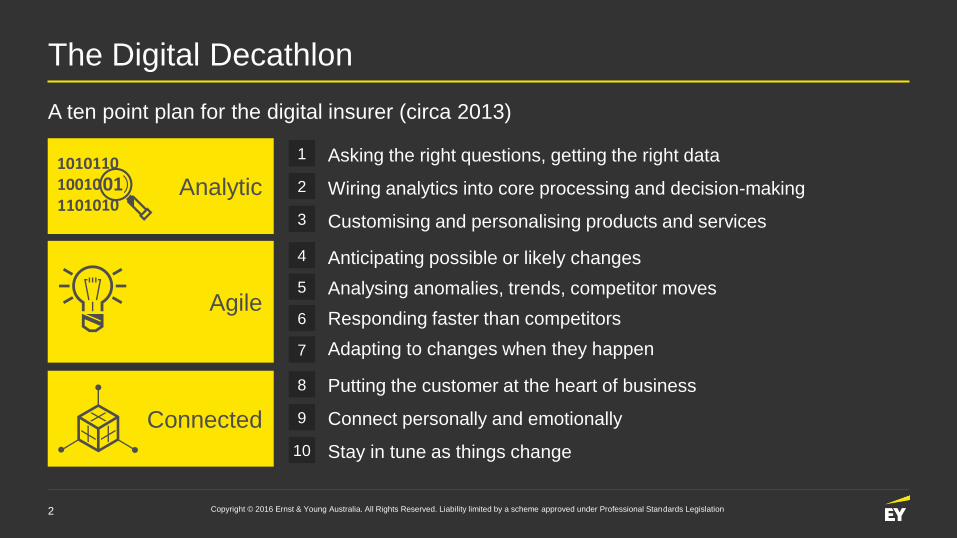

The Digital Decathlon

A ten point plan for the digital insurer (circa 2013)

Analytic

Agile

Connected

Asking the right questions, getting the right data

Wiring analytics into core processing and decision-making

Customising and personalising products and services

Anticipating possible or likely changes

Analysing anomalies, trends, competitor moves

Responding faster than competitors

Adapting to changes when they happen

Putting the customer at the heart of business

Connect personally and emotionally

Stay in tune as things change

1

2

3

4

5

6

7

8

9

10

3 Copyright © 2016 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

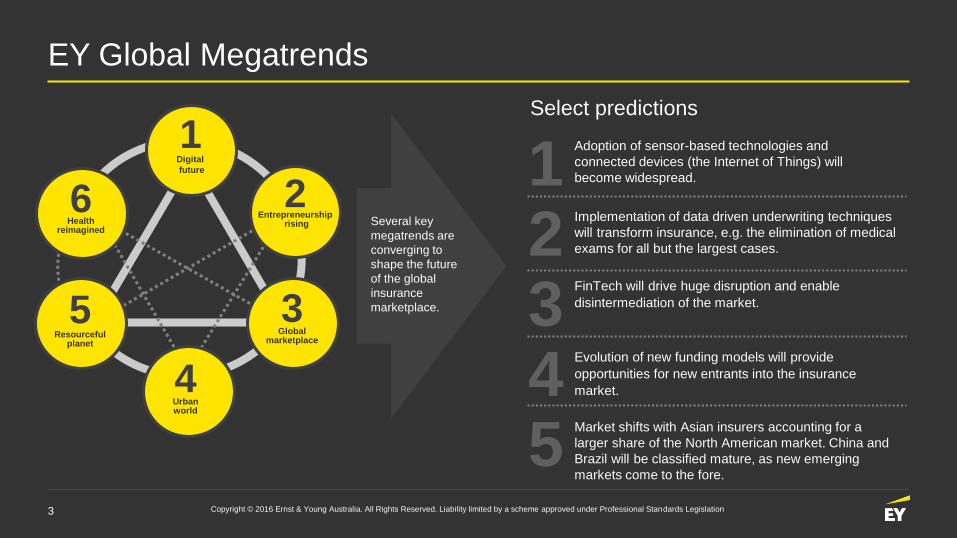

EY Global Megatrends

1

2

3

4

5

6

Digital

future

Entrepreneurshiprising

Globalmarketplace

Urban world

Resourcefulplanet

Healthreimagined

Several key

megatrends are

converging to

shape the future

of the global

insurance

marketplace.

Select predictions

Adoption of sensor-based technologies and

connected devices (the Internet of Things) will

become widespread.

Implementation of data driven underwriting techniques

will transform insurance, e.g. the elimination of medical

exams for all but the largest cases.

FinTech will drive huge disruption and enable

disintermediation of the market.

Evolution of new funding models will provide

opportunities for new entrants into the insurance

market.

Market shifts with Asian insurers accounting for a

larger share of the North American market. China and

Brazil will be classified mature, as new emerging

markets come to the fore.

12345

4 Copyright © 2016 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

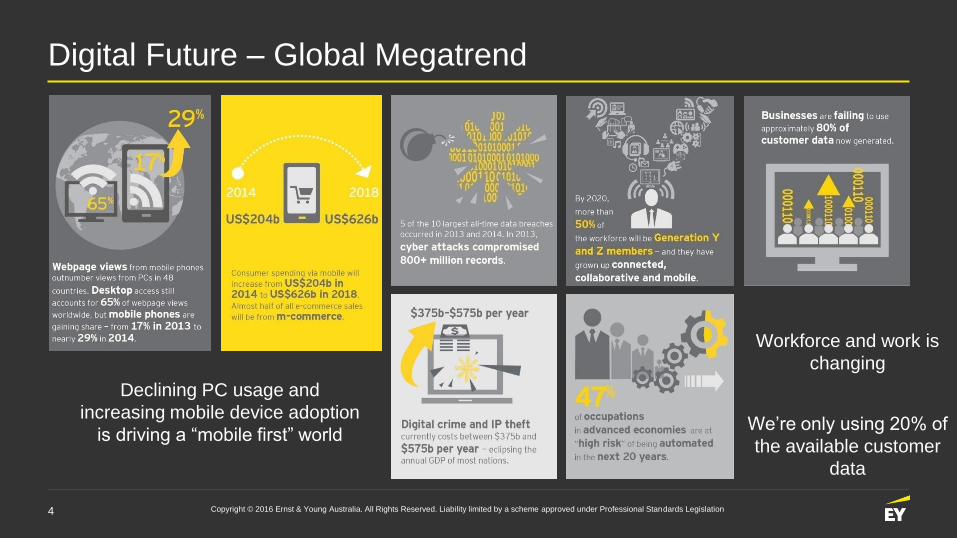

Digital Future – Global Megatrend

Declining PC usage and

increasing mobile device adoption

is driving a “mobile first” world

Workforce and work is

changing

We’re only using 20% of

the available customer

data

5 Copyright © 2016 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

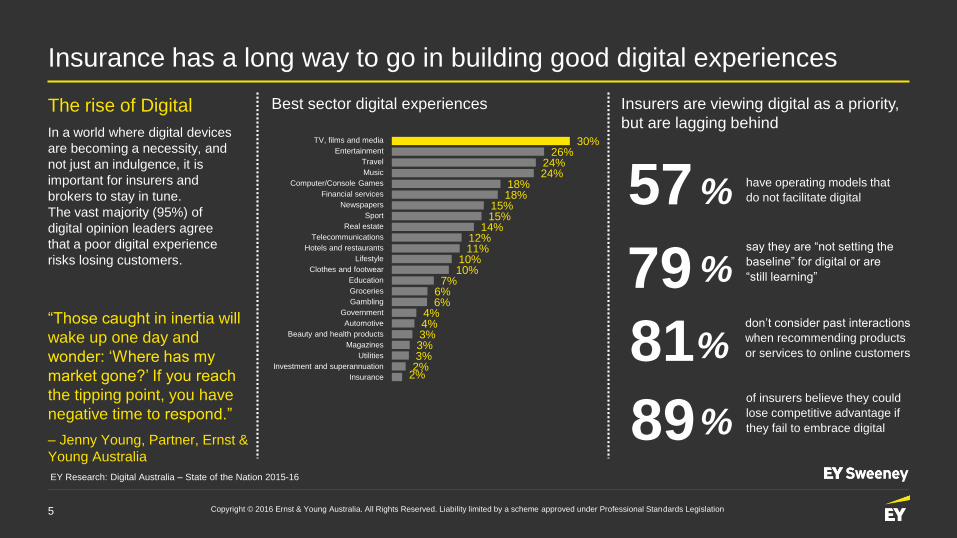

Insurance has a long way to go in building good digital experiences

The rise of Digital

In a world where digital devices

are becoming a necessity, and

not just an indulgence, it is

important for insurers and

brokers to stay in tune.

The vast majority (95%) of

digital opinion leaders agree

that a poor digital experience

risks losing customers.

57 %

89%

79 %

have operating models that

do not facilitate digital

say they are “not setting the

baseline” for digital or are

“still learning”

81%

of insurers believe they could

lose competitive advantage if

they fail to embrace digital

don’t consider past interactions

when recommending products

or services to online customers

“Those caught in inertia will

wake up one day and

wonder: ‘Where has my

market gone?’ If you reach

the tipping point, you have

negative time to respond.”

– Jenny Young, Partner, Ernst &

Young Australia

Insurers are viewing digital as a priority,

but are lagging behindTV, films and media

Entertainment

Travel

Music

Computer/Console Games

Financial services

Newspapers

Sport

Real estate

Telecommunications

Hotels and restaurants

Lifestyle

Clothes and footwear

Education

Groceries

Gambling

Government

Automotive

Beauty and health products

Magazines

Utilities

Investment and superannuation

Insurance

30%26%

24%24%

18%18%

15%15%

14%12%11%

10%10%

7%6%6%

4%4%3%3%3%

2%2%

Best sector digital experiences

EY Research: Digital Australia – State of the Nation 2015-16

6 Copyright © 2016 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

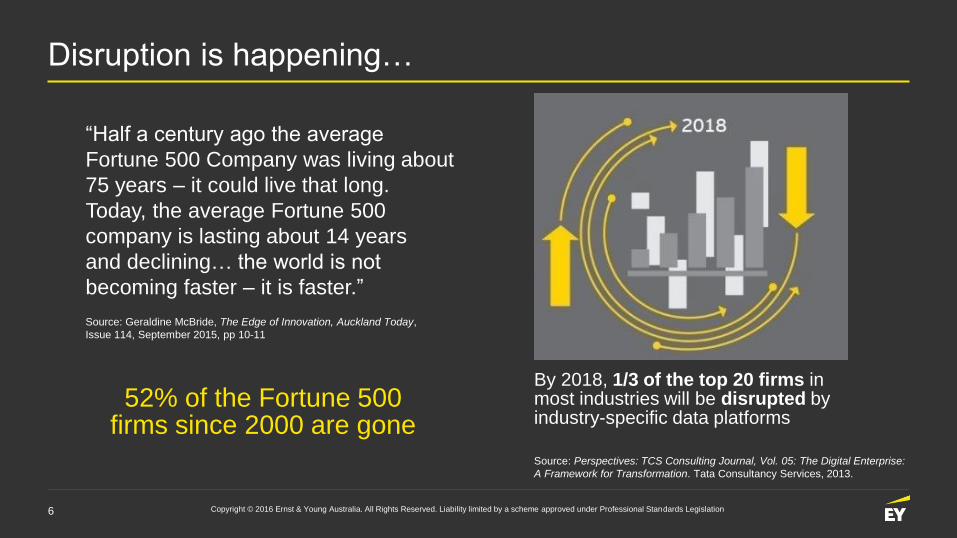

Disruption is happening…

52% of the Fortune 500 firms since 2000 are gone

Source: Perspectives: TCS Consulting Journal, Vol. 05: The Digital Enterprise:

A Framework for Transformation. Tata Consultancy Services, 2013.

“Half a century ago the average

Fortune 500 Company was living about

75 years – it could live that long.

Today, the average Fortune 500

company is lasting about 14 years

and declining… the world is not

becoming faster – it is faster.”

Source: Geraldine McBride, The Edge of Innovation, Auckland Today,

Issue 114, September 2015, pp 10-11

By 2018, 1/3 of the top 20 firms in most industries will be disrupted by industry-specific data platforms

7 Copyright © 2016 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

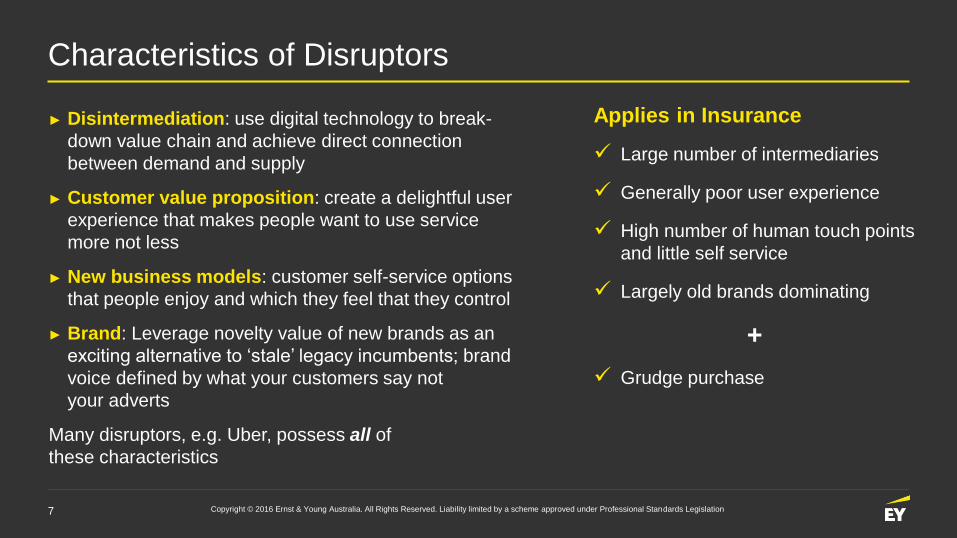

Characteristics of Disruptors

► Disintermediation: use digital technology to break-

down value chain and achieve direct connection

between demand and supply

► Customer value proposition: create a delightful user

experience that makes people want to use service

more not less

► New business models: customer self-service options

that people enjoy and which they feel that they control

► Brand: Leverage novelty value of new brands as an

exciting alternative to ‘stale’ legacy incumbents; brand

voice defined by what your customers say not

your adverts

Many disruptors, e.g. Uber, possess all of

these characteristics

Large number of intermediaries

Generally poor user experience

High number of human touch points

and little self service

Largely old brands dominating

+

Grudge purchase

Applies in Insurance

8 Copyright © 2016 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

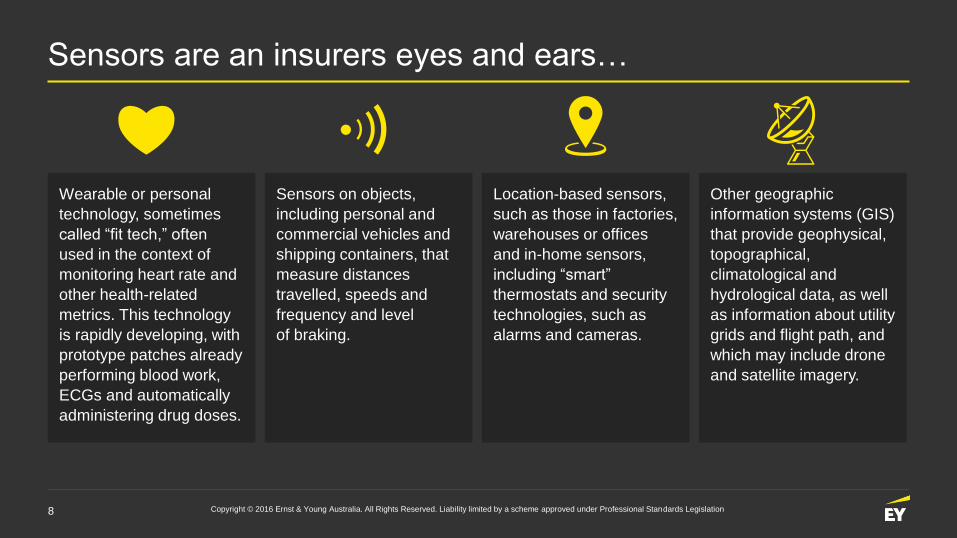

Sensors are an insurers eyes and ears…

Wearable or personal

technology, sometimes

called “fit tech,” often

used in the context of

monitoring heart rate and

other health-related

metrics. This technology

is rapidly developing, with

prototype patches already

performing blood work,

ECGs and automatically

administering drug doses.

Sensors on objects,

including personal and

commercial vehicles and

shipping containers, that

measure distances

travelled, speeds and

frequency and level

of braking.

Location-based sensors,

such as those in factories,

warehouses or offices

and in-home sensors,

including “smart”

thermostats and security

technologies, such as

alarms and cameras.

Other geographic

information systems (GIS)

that provide geophysical,

topographical,

climatological and

hydrological data, as well

as information about utility

grids and flight path, and

which may include drone

and satellite imagery.

9 Copyright © 2016 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Gartner says the Internet of Things will be at the plateau of productivity in

5-10 years along with the Connected Home and Autonomous Vehicle.

10 Copyright © 2016 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

The driverless car is on it’s way…

One Car =

100 TB/day

US Market

5,000,000 PB/day

(Facebook currently

stores 500 PB)

Google have

completed

500,000+km

Fleet of 10

different cars

Driverless car

4 US states

have

approved

Image source: still from Google video on Driverless Cars circa. April 2013 and republished

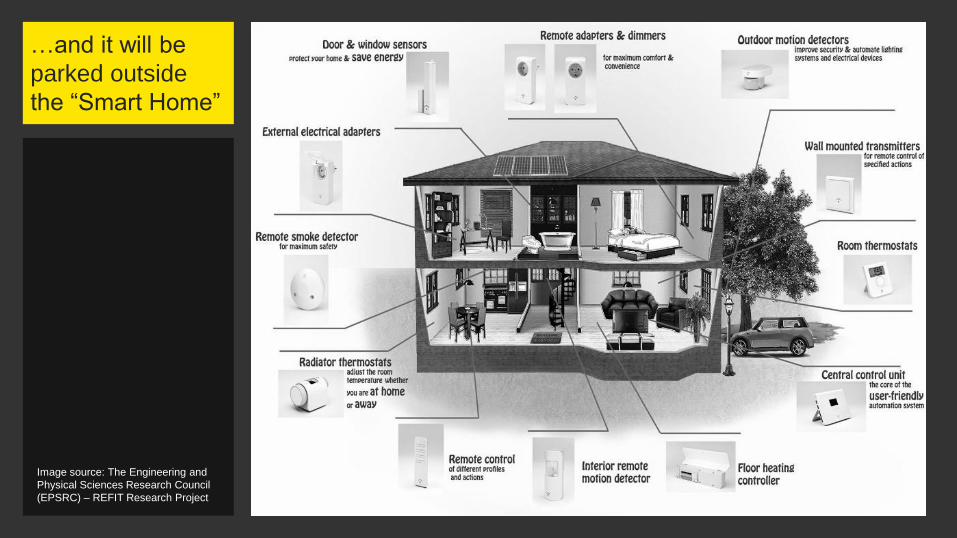

…and it will be

parked outside

the “Smart Home”

Image source: The Engineering and

Physical Sciences Research Council

(EPSRC) – REFIT Research Project

12 Copyright © 2016 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

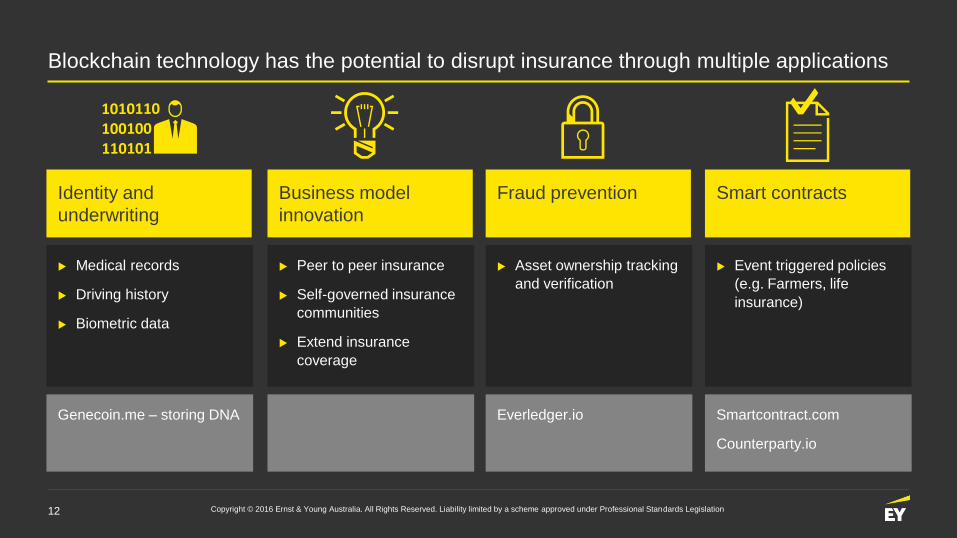

Blockchain technology has the potential to disrupt insurance through multiple applications

Identity and

underwriting

Fraud preventionBusiness model

innovation

Medical records

Driving history

Biometric data

Asset ownership tracking

and verification

Peer to peer insurance

Self-governed insurance

communities

Extend insurance

coverage

Genecoin.me – storing DNA Everledger.io

Smart contracts

Event triggered policies

(e.g. Farmers, life

insurance)

Smartcontract.com

Counterparty.io

13 Copyright © 2016 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

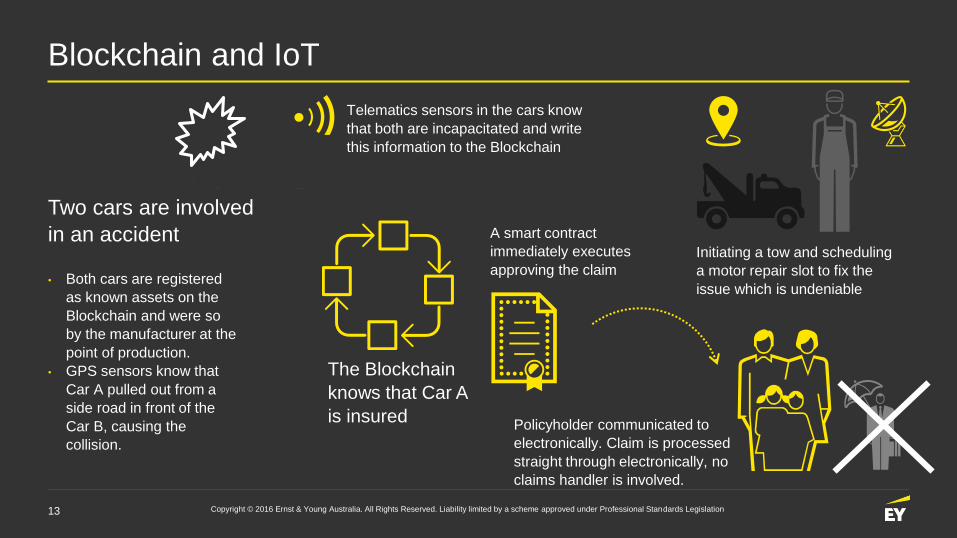

Blockchain and IoT

Two cars are involved

in an accident

• Both cars are registered

as known assets on the

Blockchain and were so

by the manufacturer at the

point of production.

• GPS sensors know that

Car A pulled out from a

side road in front of the

Car B, causing the

collision.

Telematics sensors in the cars know

that both are incapacitated and write

this information to the Blockchain

The Blockchain

knows that Car A

is insured

A smart contract

immediately executes

approving the claim

Initiating a tow and scheduling

a motor repair slot to fix the

issue which is undeniable

Policyholder communicated to

electronically. Claim is processed

straight through electronically, no

claims handler is involved.

14 Copyright © 2016 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Purpose galvanises people to ignite long-lasting positive change, driving growth and innovation

‘Purpose activated’ is the implementation of purpose

Purpose is an aspirational reason for being that is grounded in humanity and which inspires a call to action

The business world is placing a spotlight on purpose…

“Purpose: The secret

ingredient that drives

business success”,

Forbes

“Profits with purpose:

How organising for

sustainability can benefit

the bottom line”,

McKinsey & Company

“A shared purpose drives collaboration”, Harvard Business Review

“What Millennials

want most:

A career that

actually matters”,

Forbes

“How purpose drives revenue”,

Forbes

“Instil a sense of

purpose, unleash

better performance”, Wall Street Journal

15 Copyright © 2016 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

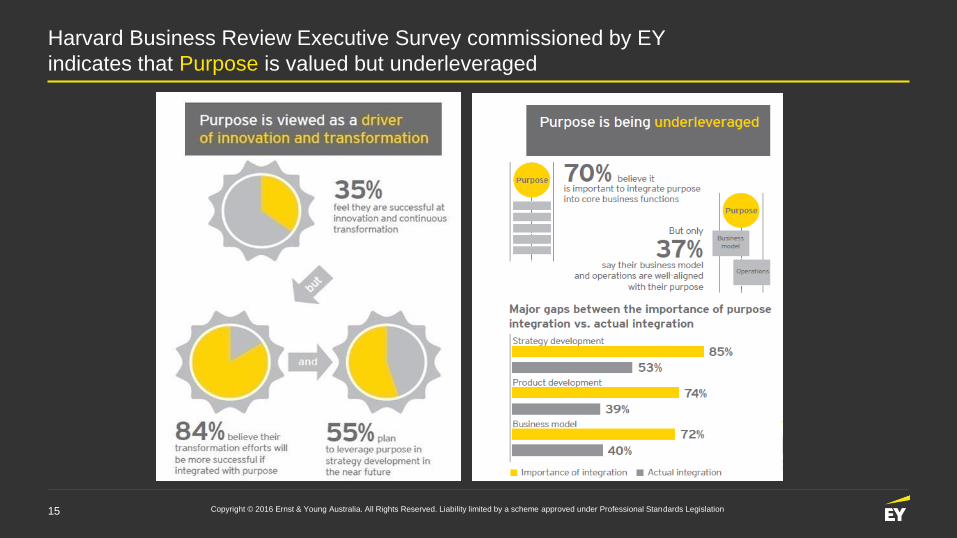

Harvard Business Review Executive Survey commissioned by EY

indicates that Purpose is valued but underleveraged

16 Copyright © 2016 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

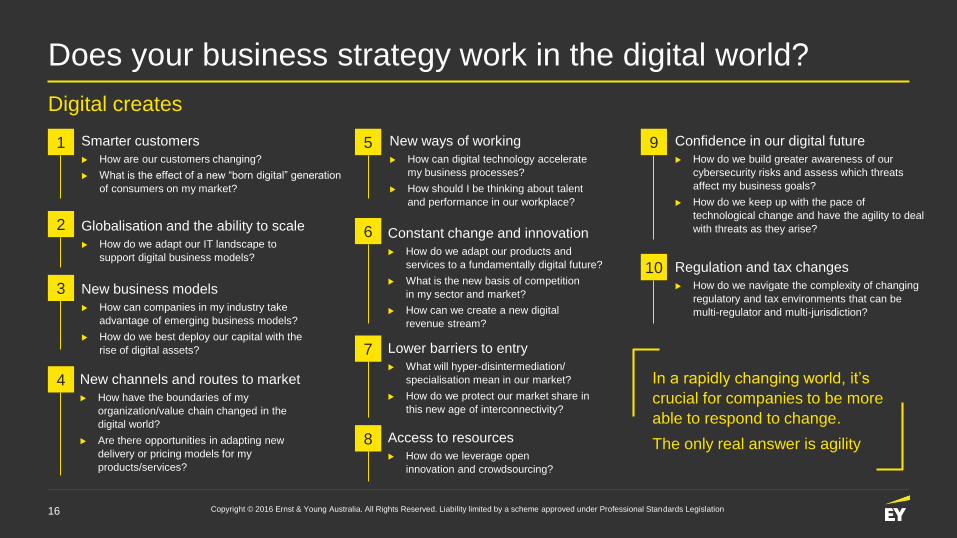

Smarter customers

How are our customers changing?

What is the effect of a new “born digital” generation

of consumers on my market?

In a rapidly changing world, it’s

crucial for companies to be more

able to respond to change.

The only real answer is agility

Does your business strategy work in the digital world?

Globalisation and the ability to scale

How do we adapt our IT landscape to

support digital business models?

New business models

How can companies in my industry take

advantage of emerging business models?

How do we best deploy our capital with the

rise of digital assets?

New channels and routes to market

How have the boundaries of my

organization/value chain changed in the

digital world?

Are there opportunities in adapting new

delivery or pricing models for my

products/services?

New ways of working

How can digital technology accelerate

my business processes?

How should I be thinking about talent

and performance in our workplace?

Confidence in our digital future

How do we build greater awareness of our

cybersecurity risks and assess which threats

affect my business goals?

How do we keep up with the pace of

technological change and have the agility to deal

with threats as they arise?

Regulation and tax changes

How do we navigate the complexity of changing

regulatory and tax environments that can be

multi-regulator and multi-jurisdiction?

Constant change and innovation

How do we adapt our products and

services to a fundamentally digital future?

What is the new basis of competition

in my sector and market?

How can we create a new digital

revenue stream?

Lower barriers to entry

What will hyper-disintermediation/

specialisation mean in our market?

How do we protect our market share in

this new age of interconnectivity?

Access to resources

How do we leverage open

innovation and crowdsourcing?

Digital creates

1

2

3

4

5

6

7

8

9

10

17 Copyright © 2016 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

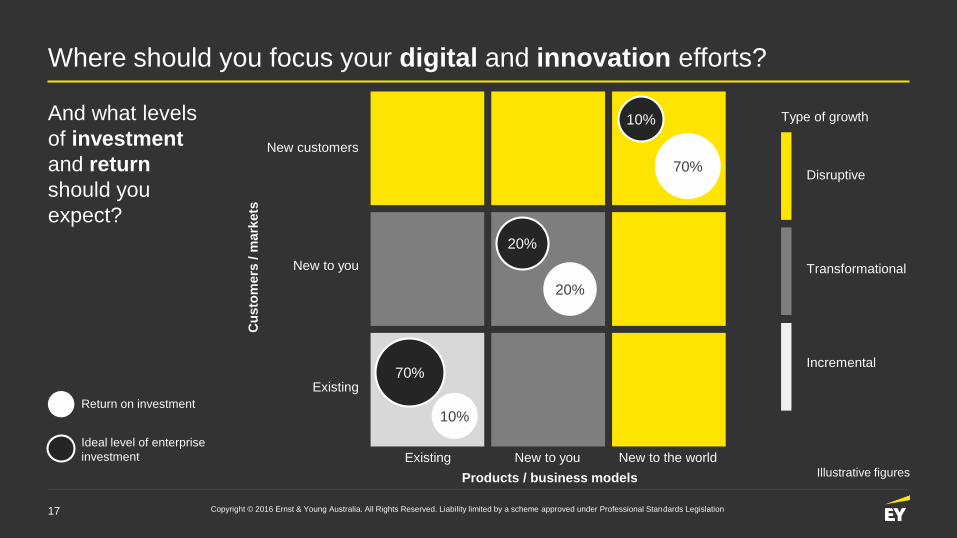

Type of growth

Disruptive

New customers

New to the world

TransformationalNew to you

New to you

Incremental

Existing

Existing

Where should you focus your digital and innovation efforts?

And what levels

of investment

and return

should you

expect?

10%

70%

20%

20%

70%

Ideal level of enterprise

investment

10%Return on investment

Illustrative figuresProducts / business models

Cu

sto

mers

/ m

ark

ets

18 Copyright © 2016 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

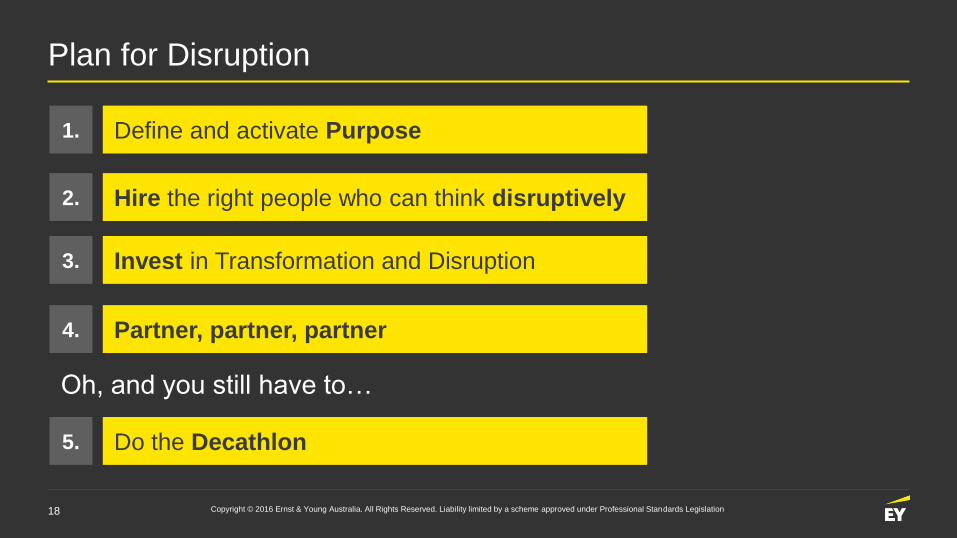

Plan for Disruption

Define and activate Purpose1.

Hire the right people who can think disruptively2.

Invest in Transformation and Disruption3.

Do the Decathlon5.

Oh, and you still have to…

Partner, partner, partner4.

The better the question. The better the answer.

The better the world works.

Is your business

strategy fit for

the digital world?

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights

and quality services we deliver help build trust and confidence in the capital markets

and in economies the world over. We develop outstanding leaders who team to deliver

on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms

of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst &

Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2016 Ernst & Young, Australia.All Rights Reserved.

APAC no. AU00002585

This communication provides general information which is current at the time of

production. The information contained in this communication does not constitute advice

and should not be relied on as such. Professional advice should be sought prior to any

action being taken in reliance on any of the information. Ernst & Young disclaims all

responsibility and liability (including, without limitation, for any direct or indirect or

consequential costs, loss or damage or loss of profits) arising from anything done or

omitted to be done by any party in reliance, whether wholly or partially, on any of the

information. Any party that relies on the information does so at its own risk. Liability limited by a scheme approved under Professional Standards Legislation.

ey.com