Embed Size (px)

Citation preview

Global Back Office / Operational Efficiency Summit

NEW PAYMENTS REGULATION ACCELERATING DIGITAL TRANSFORMATION

Nils Jung I November 2016

2 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

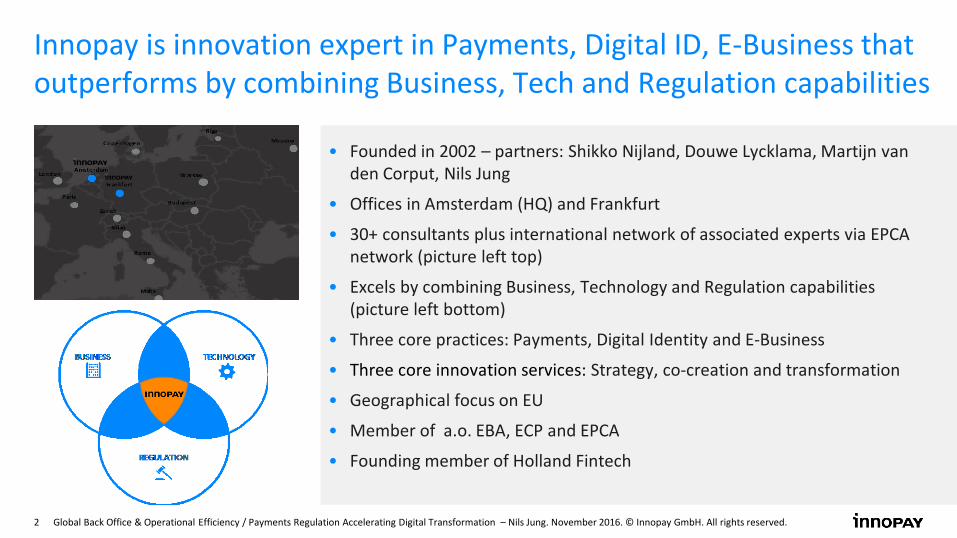

• Founded in 2002 – partners: Shikko Nijland, Douwe Lycklama, Martijn van den Corput, Nils Jung

• Offices in Amsterdam (HQ) and Frankfurt

• 30+ consultants plus international network of associated experts via EPCA network (picture left top)

• Excels by combining Business, Technology and Regulation capabilities (picture left bottom)

• Three core practices: Payments, Digital Identity and E-Business

• Three core innovation services: Strategy, co-creation and transformation

• Geographical focus on EU

• Member of a.o. EBA, ECP and EPCA

• Founding member of Holland Fintech

Innopay is innovation expert in Payments, Digital ID, E-Business that outperforms by combining Business, Tech and Regulation capabilities

3 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

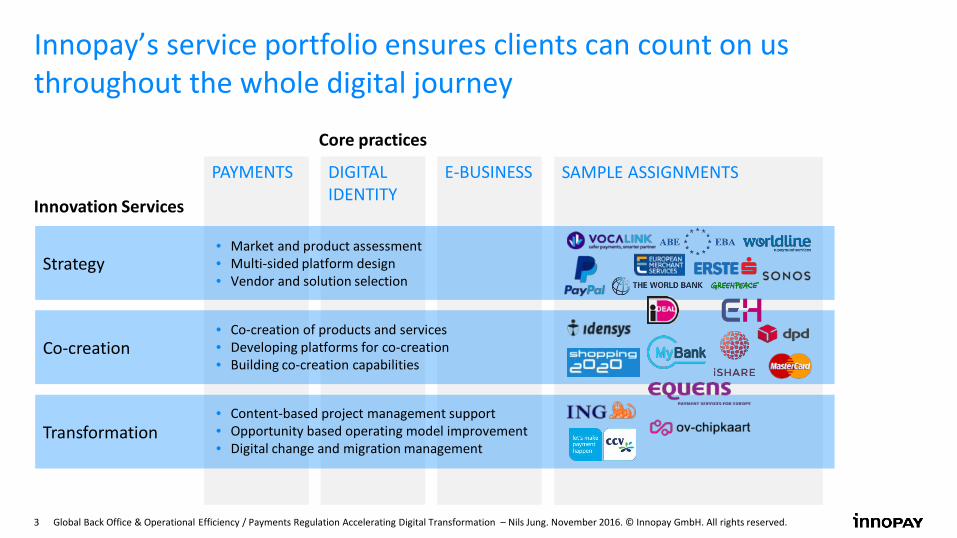

PAYMENTS DIGITAL IDENTITY

E-BUSINESS SAMPLE ASSIGNMENTS

Innovation Services

Core practices

Strategy

Co-creation

Transformation

• Market and product assessment • Multi-sided platform design • Vendor and solution selection

• Co-creation of products and services • Developing platforms for co-creation • Building co-creation capabilities

• Content-based project management support • Opportunity based operating model improvement • Digital change and migration management

Innopay’s service portfolio ensures clients can count on us throughout the whole digital journey

4 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

Topics for today

• Overview payments regulation and other key industry drivers

• Deep dive into PSD2 including strategic scenarios

• Considerations to successfully execute digital transformation

5 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

1 I Overview payments regulation and other key industry drivers

6 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

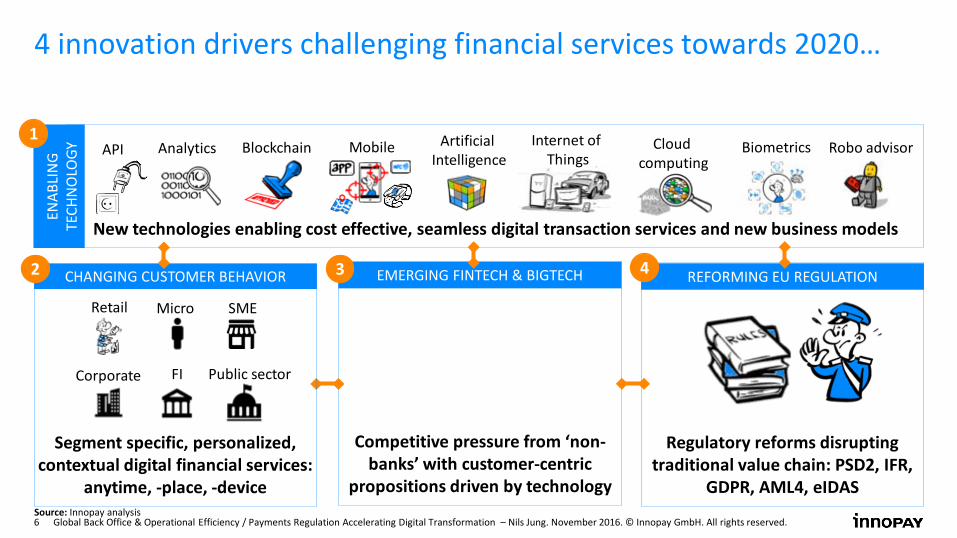

4 innovation drivers challenging financial services towards 2020…

Source: Innopay analysis

New technologies enabling cost effective, seamless digital transaction services and new business models

ENAB

LIN

G

TECH

NO

LOGY

1 Analytics Blockchain Mobile Artificial

Intelligence Cloud

computing Biometrics Robo advisor Internet of

Things API

Competitive pressure from ‘non-banks’ with customer-centric

propositions driven by technology

EMERGING FINTECH & BIGTECH 3

Regulatory reforms disrupting traditional value chain: PSD2, IFR,

GDPR, AML4, eIDAS

REFORMING EU REGULATION 4

Segment specific, personalized, contextual digital financial services:

anytime, -place, -device

SME Micro

Corporate Public sector FI

Retail

CHANGING CUSTOMER BEHAVIOR 2

7 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

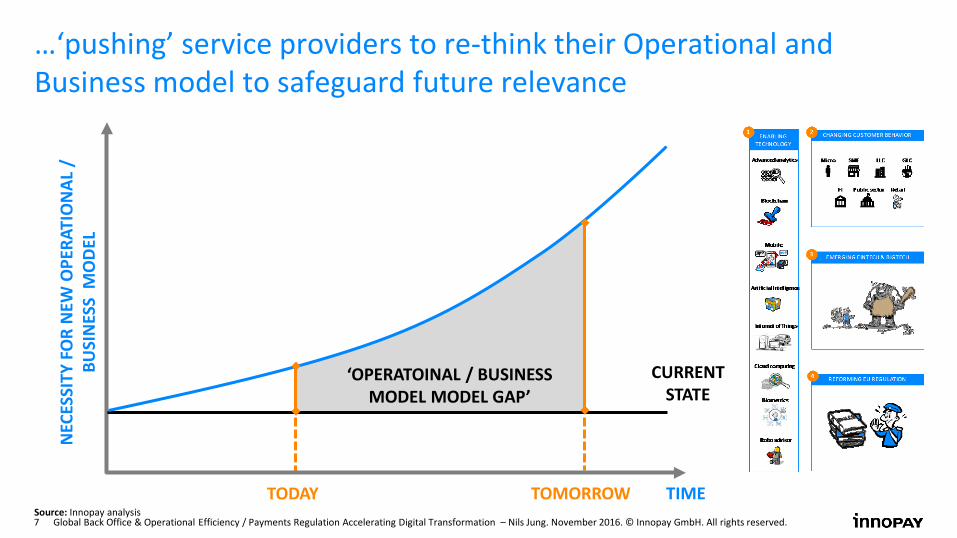

…‘pushing’ service providers to re-think their Operational and Business model to safeguard future relevance

TIME

NEC

ESSI

TY F

OR

NEW

OPE

RATI

ON

AL /

BU

SIN

ESS

MO

DEL

TODAY TOMORROW

‘OPERATOINAL / BUSINESS MODEL MODEL GAP’

CURRENT STATE

Source: Innopay analysis

8 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

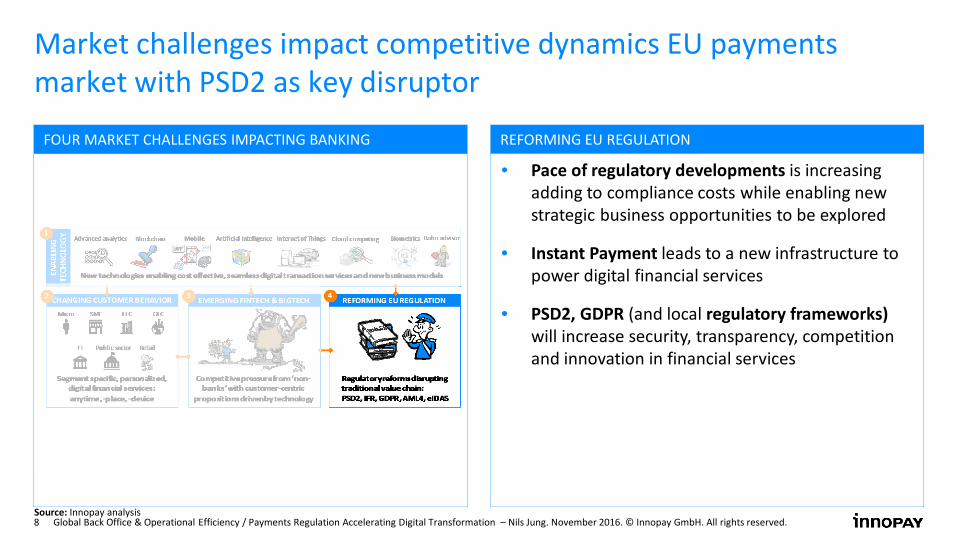

Market challenges impact competitive dynamics EU payments market with PSD2 as key disruptor

REFORMING EU REGULATION

• Pace of regulatory developments is increasing adding to compliance costs while enabling new strategic business opportunities to be explored

• Instant Payment leads to a new infrastructure to power digital financial services

• PSD2, GDPR (and local regulatory frameworks) will increase security, transparency, competition and innovation in financial services

FOUR MARKET CHALLENGES IMPACTING BANKING

Source: Innopay analysis

9 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

2 I Deep dive into PSD2 including strategic scenarios

10 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

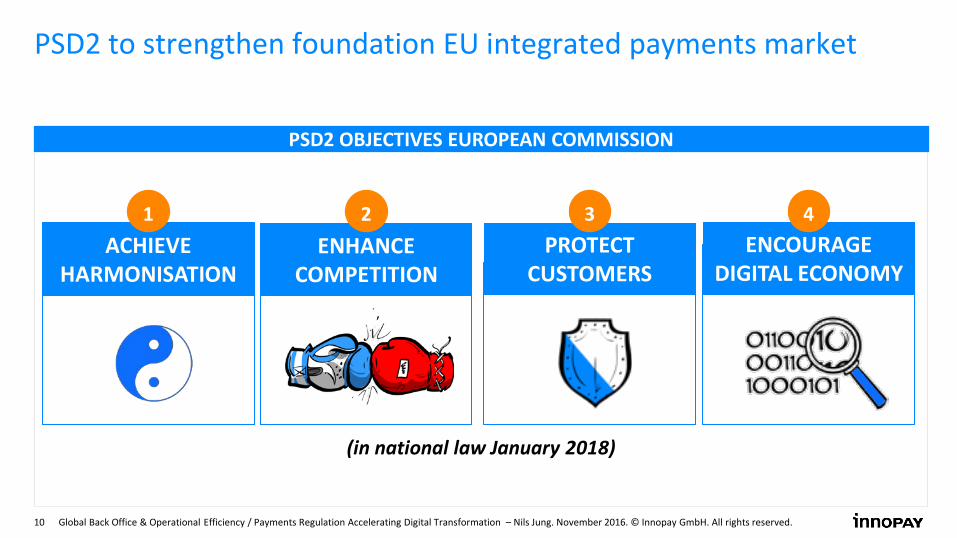

ACHIEVE

HARMONISATION

PSD2 to strengthen foundation EU integrated payments market

(in national law January 2018)

PSD2 OBJECTIVES EUROPEAN COMMISSION

1 ENHANCE

COMPETITION PROTECT

CUSTOMERS ENCOURAGE

DIGITAL ECONOMY

2 3 4

11 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

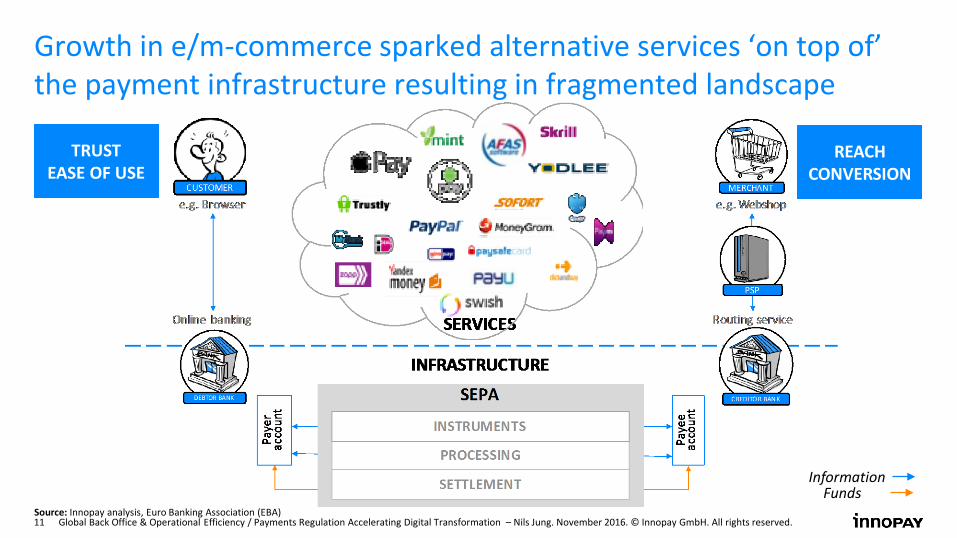

Growth in e/m-commerce sparked alternative services ‘on top of’ the payment infrastructure resulting in fragmented landscape

Information

Funds

Source: Innopay analysis, Euro Banking Association (EBA)

TRUST EASE OF USE

REACH CONVERSION

12 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

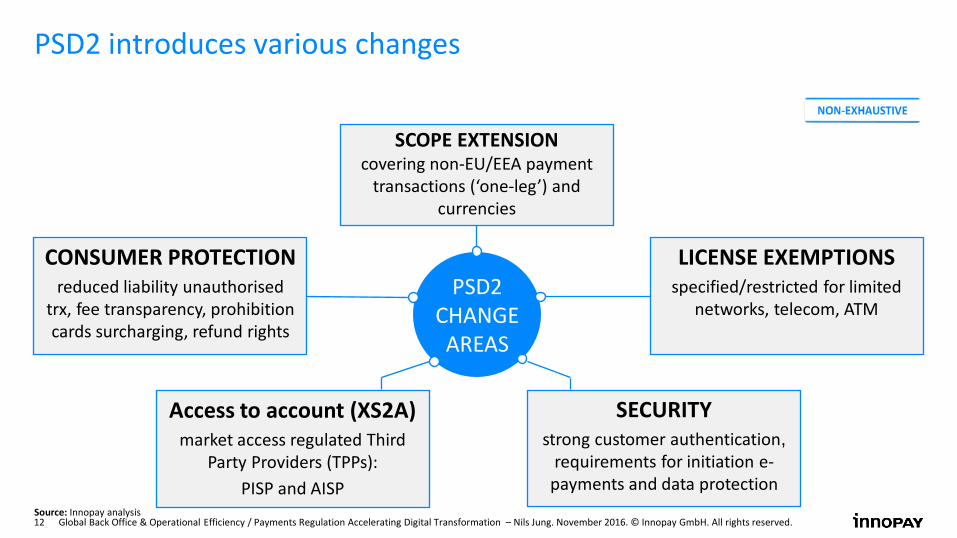

PSD2 introduces various changes

Source: Innopay analysis

PSD2 CHANGE AREAS

SCOPE EXTENSION covering non-EU/EEA payment

transactions (‘one-leg’) and currencies

LICENSE EXEMPTIONS specified/restricted for limited

networks, telecom, ATM

CONSUMER PROTECTION reduced liability unauthorised

trx, fee transparency, prohibition cards surcharging, refund rights

SECURITY strong customer authentication,

requirements for initiation e-payments and data protection

Access to account (XS2A) market access regulated Third

Party Providers (TPPs): PISP and AISP

13 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

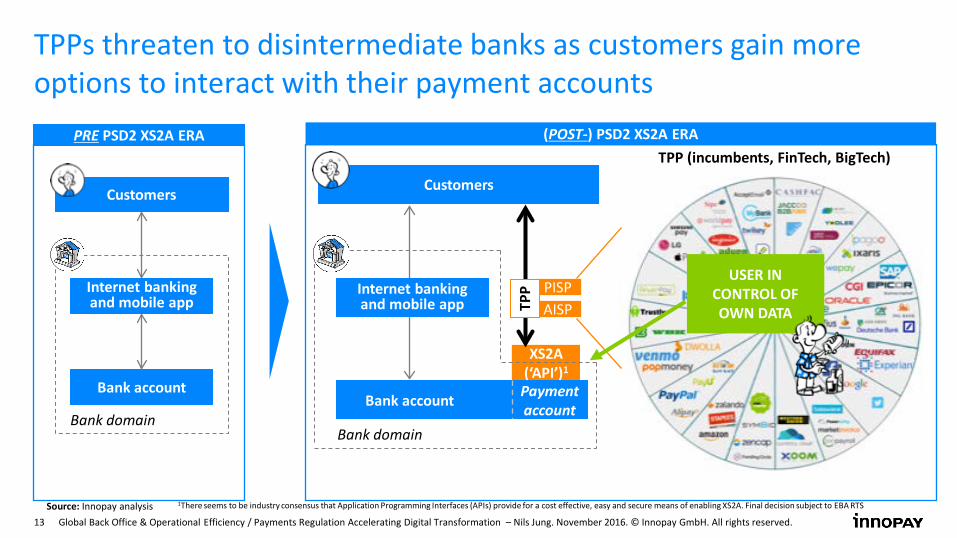

XS2A (‘API’)1

TPPs threaten to disintermediate banks as customers gain more options to interact with their payment accounts

Customers

Bank domain

PRE PSD2 XS2A ERA (POST-) PSD2 XS2A ERA

Payment account

TPP (incumbents, FinTech, BigTech)

Bank account

Internet banking and mobile app

1There seems to be industry consensus that Application Programming Interfaces (APIs) provide for a cost effective, easy and secure means of enabling XS2A. Final decision subject to EBA RTS

Bank account

Internet banking and mobile app

Customers

Bank domain

PISP AISP TP

P Source: Innopay analysis

USER IN CONTROL OF OWN DATA

14 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

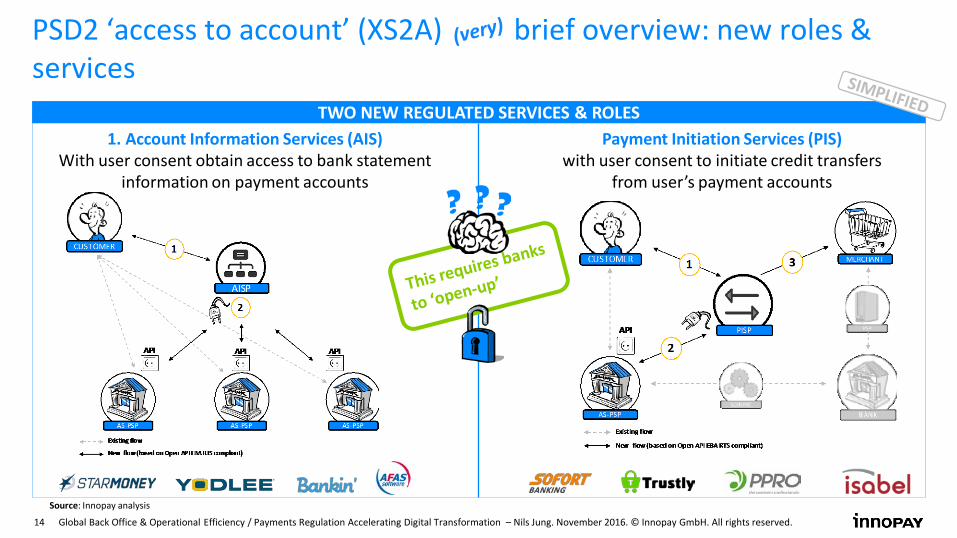

PSD2 ‘access to account’ (XS2A) brief overview: new roles & services

1. Account Information Services (AIS) With user consent obtain access to bank statement

information on payment accounts

TWO NEW REGULATED SERVICES & ROLES Payment Initiation Services (PIS)

with user consent to initiate credit transfers from user’s payment accounts

Source: Innopay analysis

15 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

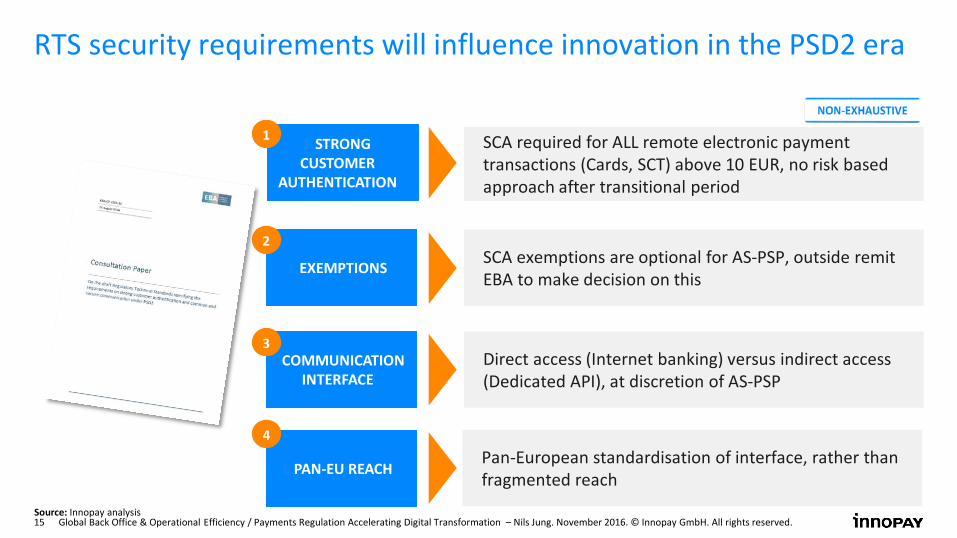

RTS security requirements will influence innovation in the PSD2 era

SCA required for ALL remote electronic payment transactions (Cards, SCT) above 10 EUR, no risk based approach after transitional period

1.STRONG CUSTOMER

AUTHENTICATION

1.EXEMPTIONS

1.COMMUNICATION INTERFACE

1.PAN-EU REACH

SCA exemptions are optional for AS-PSP, outside remit EBA to make decision on this

Direct access (Internet banking) versus indirect access (Dedicated API), at discretion of AS-PSP

Pan-European standardisation of interface, rather than fragmented reach

1

2

3

4

Source: Innopay analysis

16 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

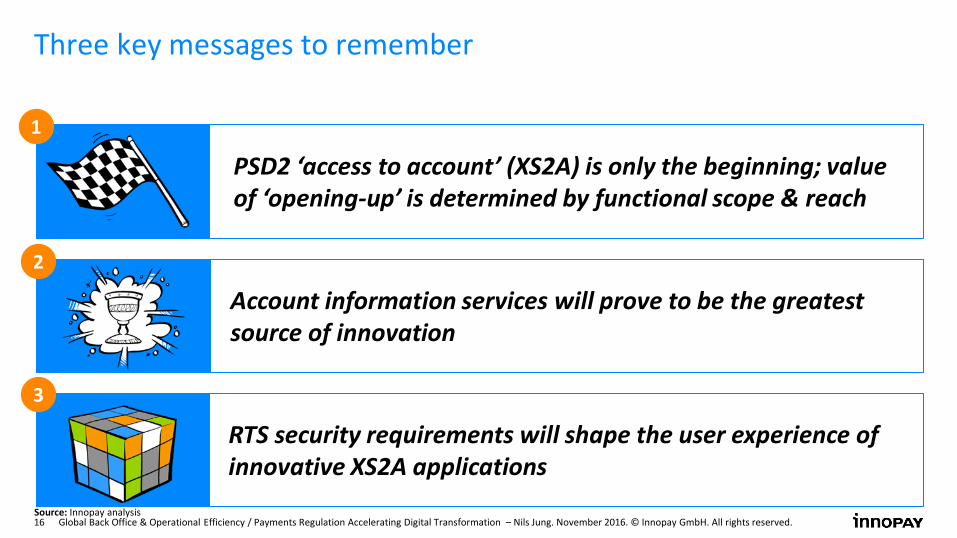

PSD2 ‘access to account’ (XS2A) is only the beginning; value of ‘opening-up’ is determined by functional scope & reach

Three key messages to remember

Account information services will prove to be the greatest source of innovation

RTS security requirements will shape the user experience of innovative XS2A applications

1

2

3

Source: Innopay analysis

17 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

3 I Considerations to successfully execute digital transformation

18 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

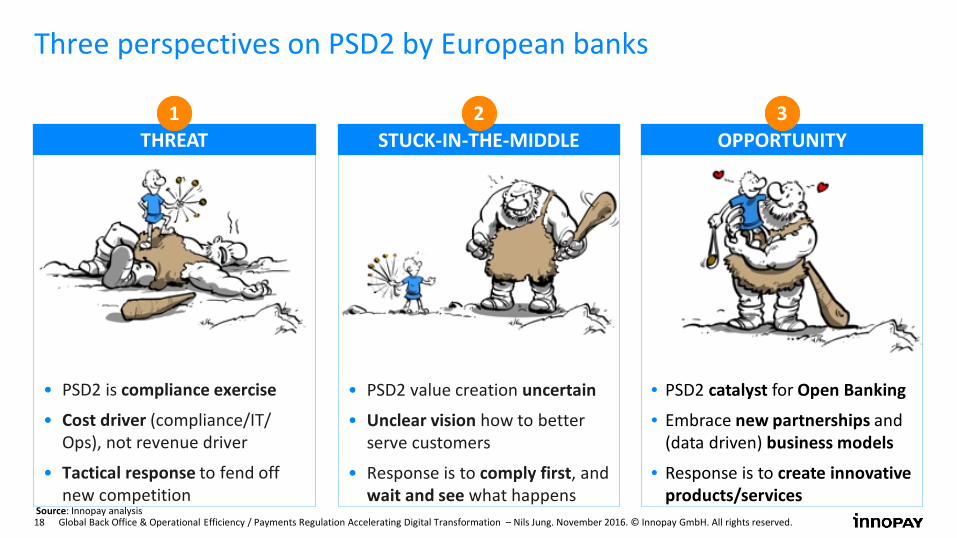

• PSD2 is compliance exercise

• Cost driver (compliance/IT/ Ops), not revenue driver

• Tactical response to fend off new competition

THREAT

Three perspectives on PSD2 by European banks

• PSD2 value creation uncertain

• Unclear vision how to better serve customers

• Response is to comply first, and wait and see what happens

STUCK-IN-THE-MIDDLE

• PSD2 catalyst for Open Banking

• Embrace new partnerships and (data driven) business models

• Response is to create innovative products/services

OPPORTUNITY

Source: Innopay analysis

1 2 3

19 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

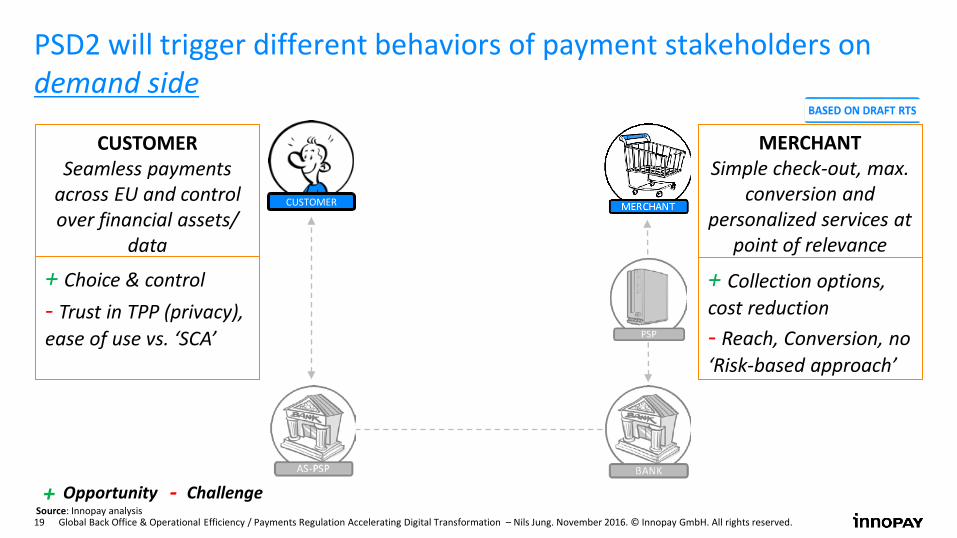

PSD2 will trigger different behaviors of payment stakeholders on demand side

CUSTOMER

CUSTOMER Seamless payments

across EU and control over financial assets/

data

MERCHANT Simple check-out, max.

conversion and personalized services at

point of relevance

Source: Innopay analysis

+ Choice & control - Trust in TPP (privacy), ease of use vs. ‘SCA’

+ Collection options, cost reduction - Reach, Conversion, no ‘Risk-based approach’

+ - Opportunity Challenge

20 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

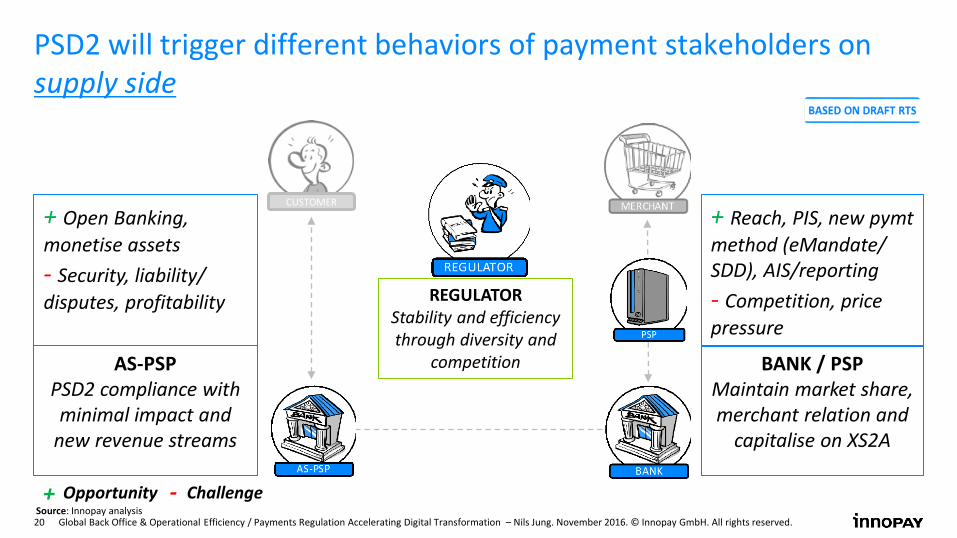

PSD2 will trigger different behaviors of payment stakeholders on supply side

CUSTOMER

Source: Innopay analysis

AS-PSP PSD2 compliance with minimal impact and

new revenue streams

+ Open Banking, monetise assets - Security, liability/ disputes, profitability

BANK / PSP Maintain market share, merchant relation and

capitalise on XS2A

+ Reach, PIS, new pymt method (eMandate/ SDD), AIS/reporting - Competition, price pressure

REGULATOR Stability and efficiency through diversity and

competition

+ - Opportunity Challenge

21 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

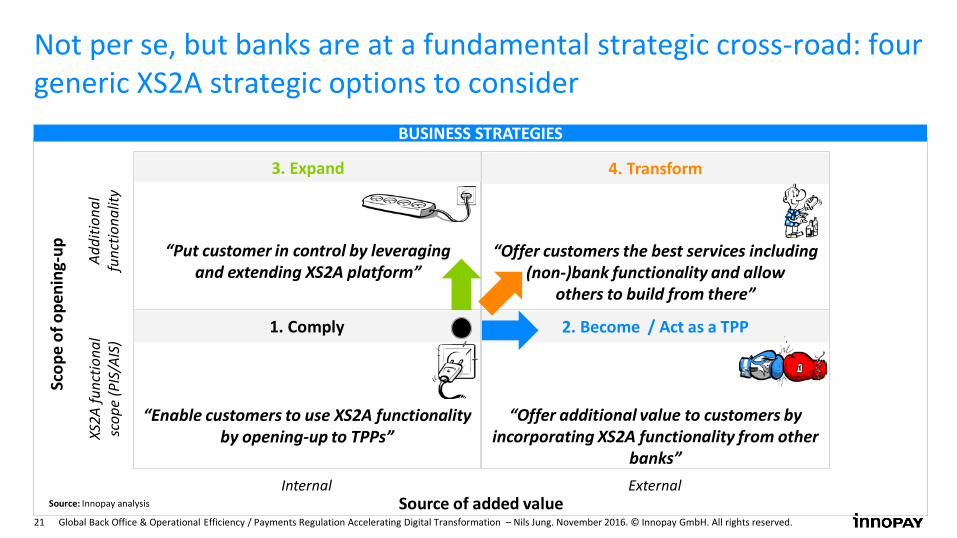

Internal External Source of added value

2. Become / Act as a TPP

3. Expand 4. Transform

1. Comply

XS2A

func

tiona

l sc

ope

(PIS

/AIS

) Ad

ditio

nal

func

tiona

lity

Scop

e of

ope

ning

-up

Source: Innopay analysis

Not per se, but banks are at a fundamental strategic cross-road: four generic XS2A strategic options to consider

BUSINESS STRATEGIES

“Offer additional value to customers by incorporating XS2A functionality from other

banks”

“Enable customers to use XS2A functionality by opening-up to TPPs”

“Put customer in control by leveraging and extending XS2A platform”

“Offer customers the best services including (non-)bank functionality and allow

others to build from there”

22 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

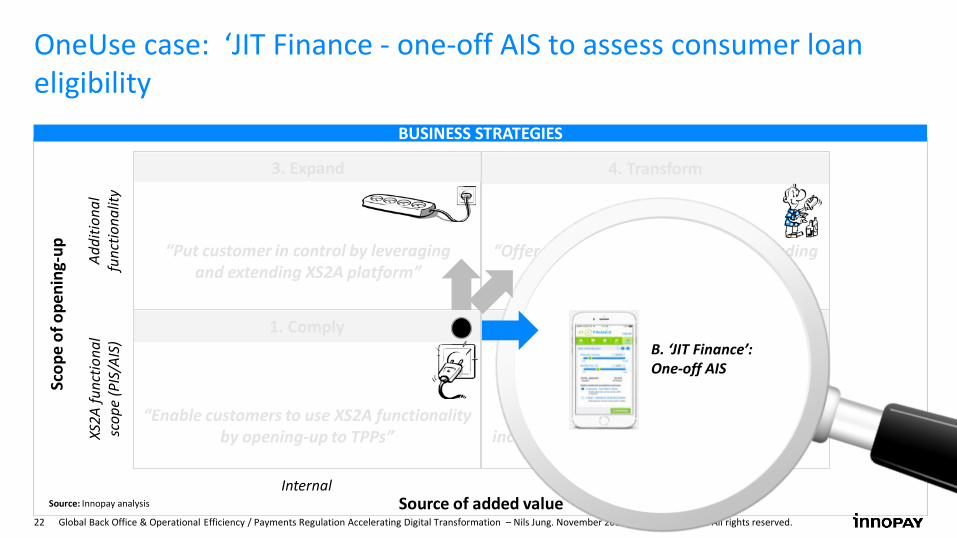

Internal External Source of added value

2. Become / Act as a TPP

3. Expand 4. Transform

1. Comply

XS2A

func

tiona

l sc

ope

(PIS

/AIS

) Ad

ditio

nal

func

tiona

lity

Scop

e of

ope

ning

-up

Source: Innopay analysis

OneUse case: ‘JIT Finance - one-off AIS to assess consumer loan eligibility

BUSINESS STRATEGIES

“Offer additional value to customers by incorporating XS2A functionality from other

banks”

“Enable customers to use XS2A functionality by opening-up to TPPs”

“Put customer in control by leveraging and extending XS2A platform”

“Offer customers the best services including (non-)bank functionality and allow

others to build from there”

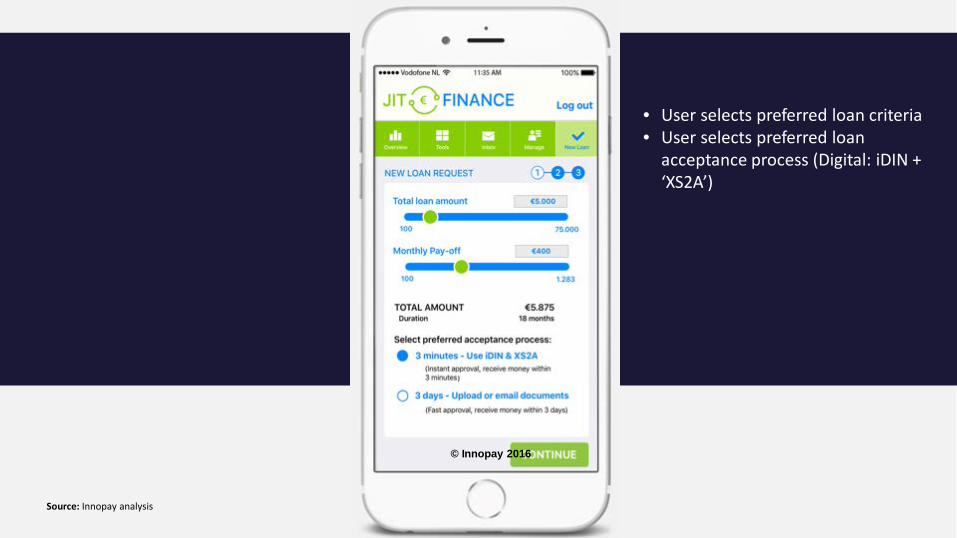

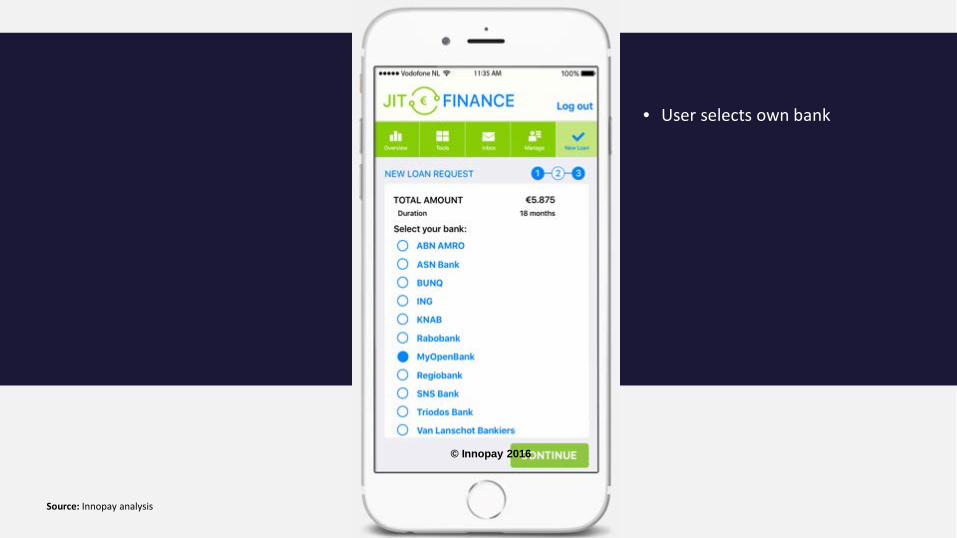

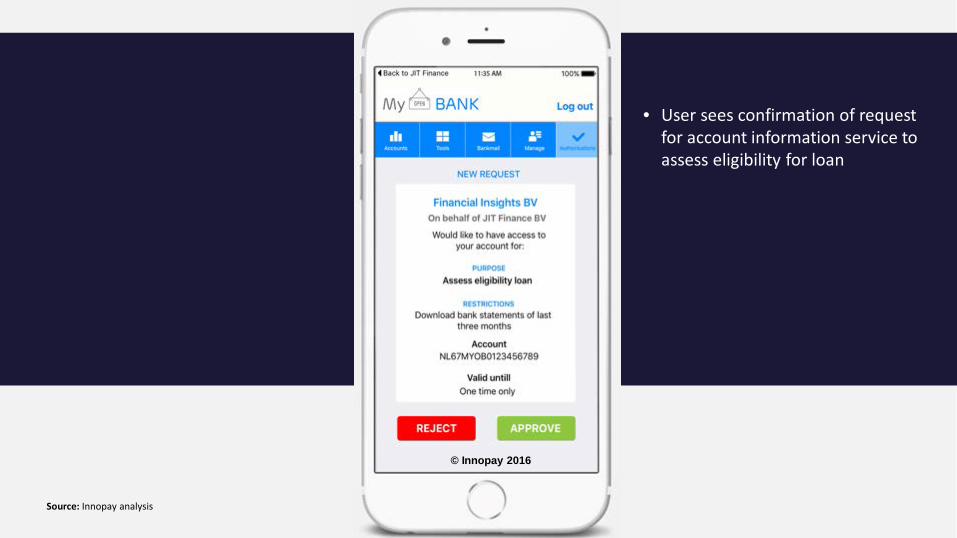

B. ‘JIT Finance’: One-off AIS

23 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

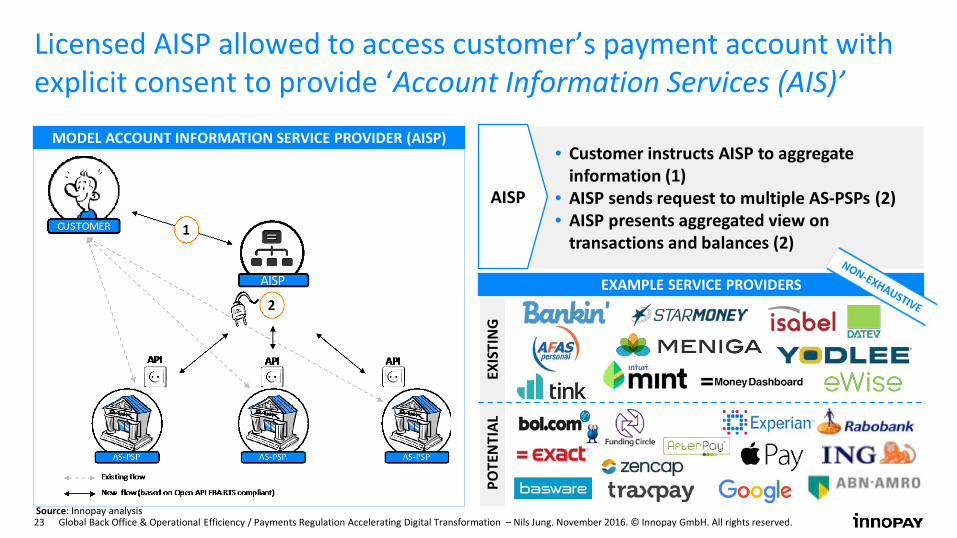

Licensed AISP allowed to access customer’s payment account with explicit consent to provide ‘Account Information Services (AIS)’

MODEL ACCOUNT INFORMATION SERVICE PROVIDER (AISP) • Customer instructs AISP to aggregate

information (1) • AISP sends request to multiple AS-PSPs (2) • AISP presents aggregated view on

transactions and balances (2)

AISP

EXAMPLE SERVICE PROVIDERS

EXIS

TIN

G

POTE

NTI

AL

Source: Innopay analysis

24 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved. Source: Innopay analysis

© Innopay 2016

• User selects preferred loan criteria • User selects preferred loan

acceptance process (Digital: iDIN + ‘XS2A’)

25 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved. Source: Innopay analysis

© Innopay 2016

• User selects own bank

26 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved. Source: Innopay analysis

© Innopay 2016

• User sees confirmation of request for account information service to assess eligibility for loan

27 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved. Source: Innopay analysis

© Innopay 2016

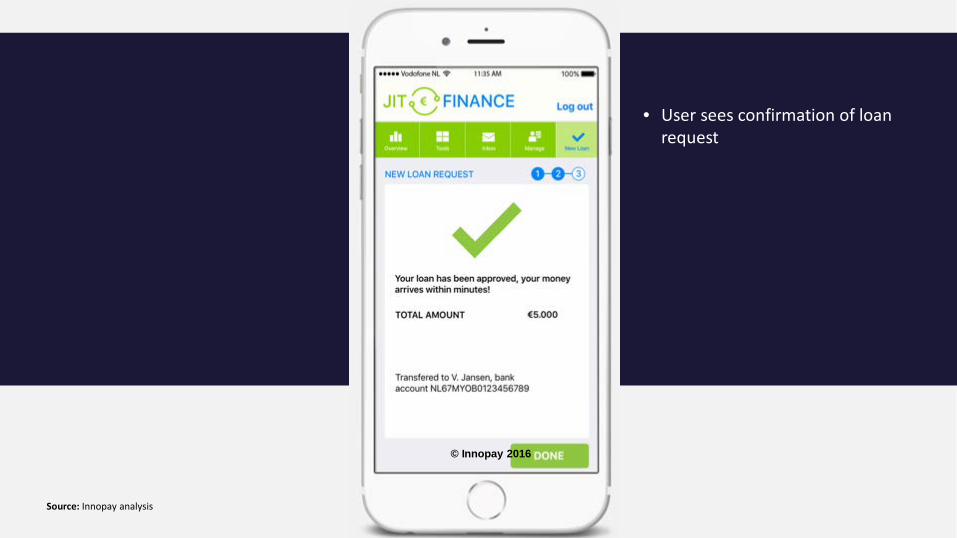

• User sees confirmation of loan request

28 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved. Source: Innopay analysis

© Innopay 2016

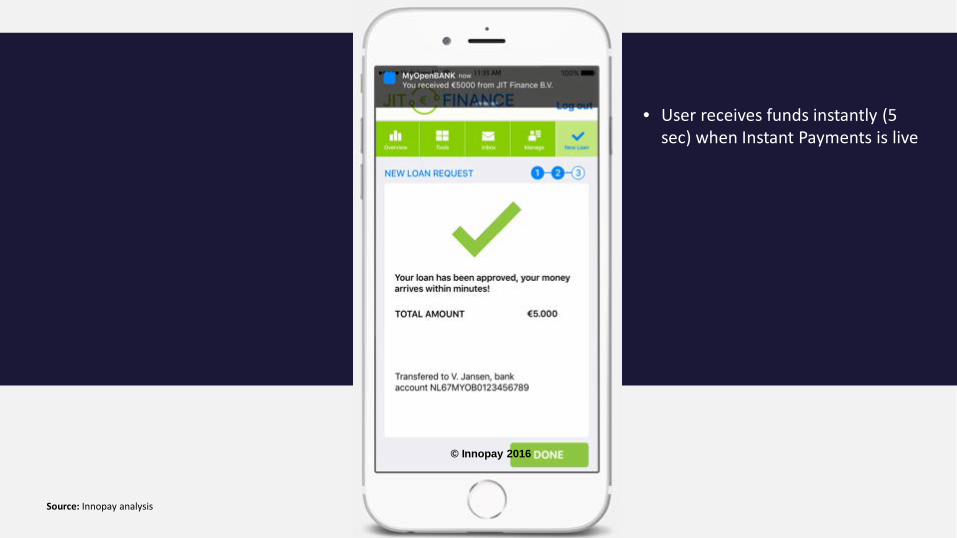

• User receives funds instantly (5 sec) when Instant Payments is live

29 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

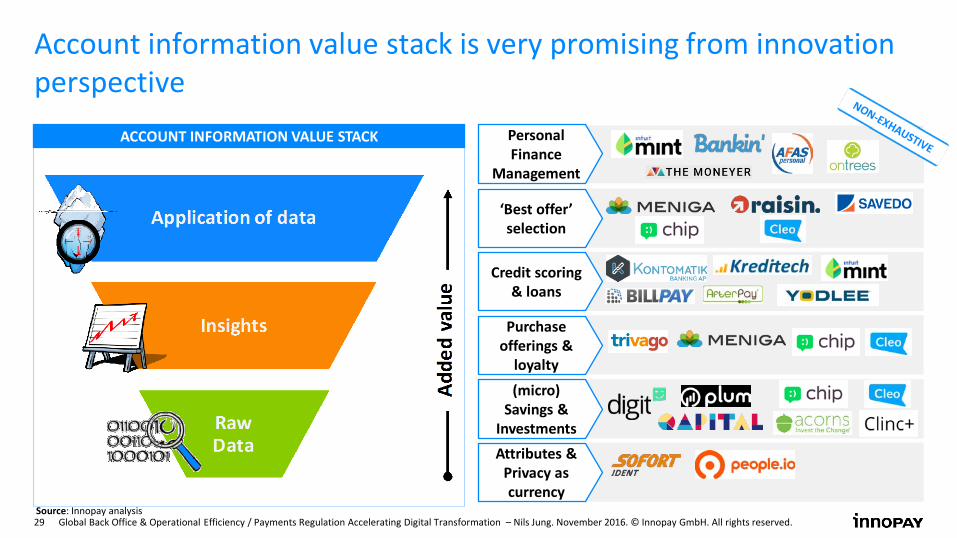

Account information value stack is very promising from innovation perspective

Personal Finance

Management

‘Best offer’ selection

Credit scoring & loans

Purchase offerings &

loyalty

(micro) Savings &

Investments Attributes &

Privacy as currency

Source: Innopay analysis

ACCOUNT INFORMATION VALUE STACK

30 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

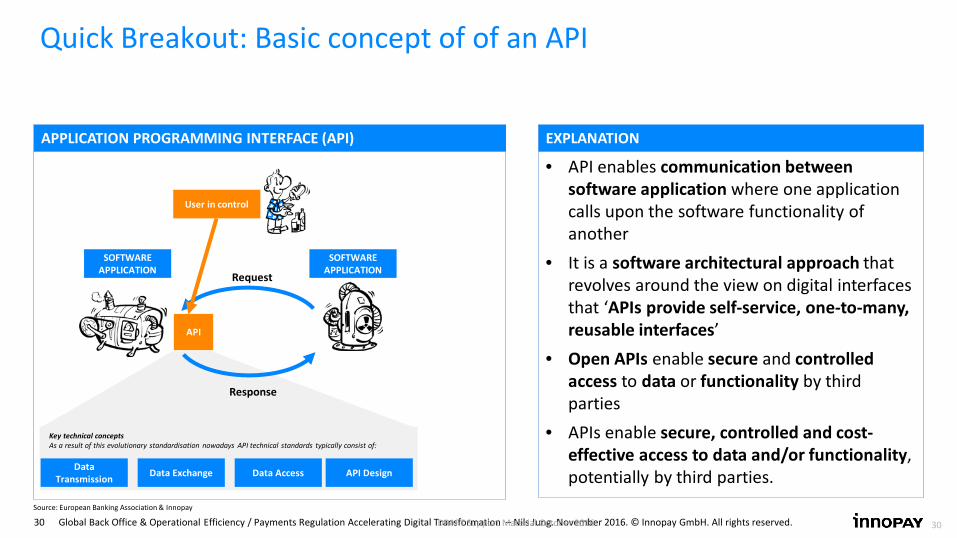

Quick Breakout: Basic concept of of an API

30

APPLICATION PROGRAMMING INTERFACE (API)

• API enables communication between software application where one application calls upon the software functionality of another

• It is a software architectural approach that revolves around the view on digital interfaces that ‘APIs provide self-service, one-to-many, reusable interfaces’

• Open APIs enable secure and controlled access to data or functionality by third parties

• APIs enable secure, controlled and cost-effective access to data and/or functionality, potentially by third parties.

EXPLANATION

API

SOFTWARE APPLICATION

SOFTWARE APPLICATION

Response

Request

User in control

Source: European Banking Association & Innopay

DRAFT Support Material October 2016

Data Transmission Data Exchange Data Access API Design

Key technical concepts As a result of this evolutionary standardisation nowadays API technical standards typically consist of:

31 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

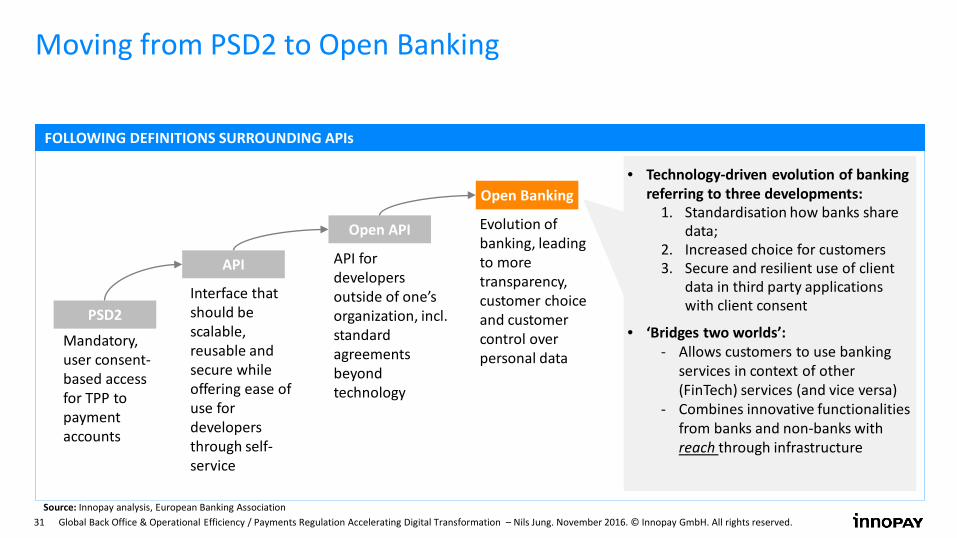

Moving from PSD2 to Open Banking

API

Interface that should be scalable, reusable and secure while offering ease of use for developers through self-service

Open API

API for developers outside of one’s organization, incl. standard agreements beyond technology

Open Banking

Evolution of banking, leading to more transparency, customer choice and customer control over personal data

PSD2

Mandatory, user consent- based access for TPP to payment accounts

FOLLOWING DEFINITIONS SURROUNDING APIs

Source: Innopay analysis, European Banking Association

• Technology-driven evolution of banking referring to three developments:

1. Standardisation how banks share data;

2. Increased choice for customers 3. Secure and resilient use of client

data in third party applications with client consent

• ‘Bridges two worlds’: - Allows customers to use banking

services in context of other (FinTech) services (and vice versa)

- Combines innovative functionalities from banks and non-banks with reach through infrastructure

32 PSD2 - accelerating innovation beyond compliance. August 2016. © Innopay GmbH. All rights reserved.

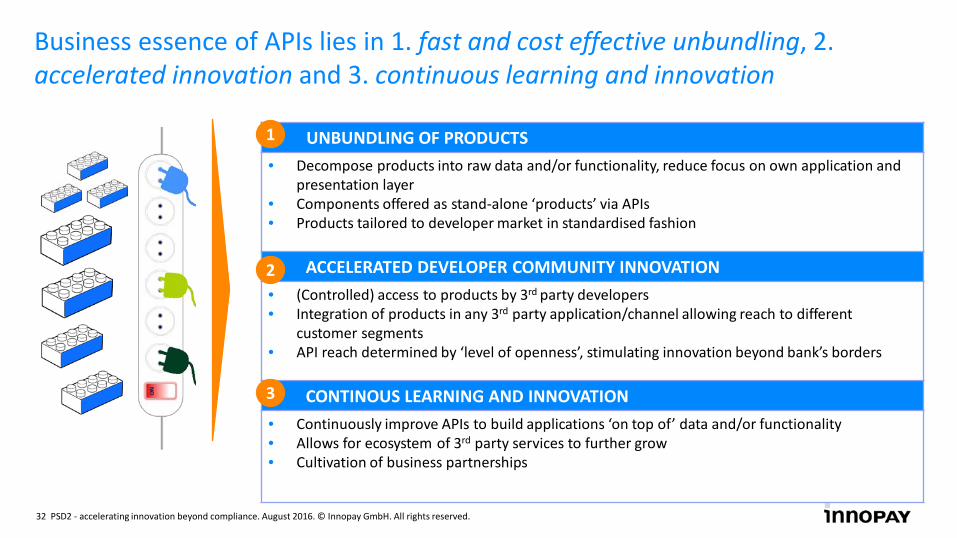

Business essence of APIs lies in 1. fast and cost effective unbundling, 2. accelerated innovation and 3. continuous learning and innovation

UNBUNDLING OF PRODUCTS • Decompose products into raw data and/or functionality, reduce focus on own application and

presentation layer • Components offered as stand-alone ‘products’ via APIs • Products tailored to developer market in standardised fashion

ACCELERATED DEVELOPER COMMUNITY INNOVATION • (Controlled) access to products by 3rd party developers • Integration of products in any 3rd party application/channel allowing reach to different

customer segments • API reach determined by ‘level of openness’, stimulating innovation beyond bank’s borders

CONTINOUS LEARNING AND INNOVATION • Continuously improve APIs to build applications ‘on top of’ data and/or functionality • Allows for ecosystem of 3rd party services to further grow • Cultivation of business partnerships

1

2

3

33 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

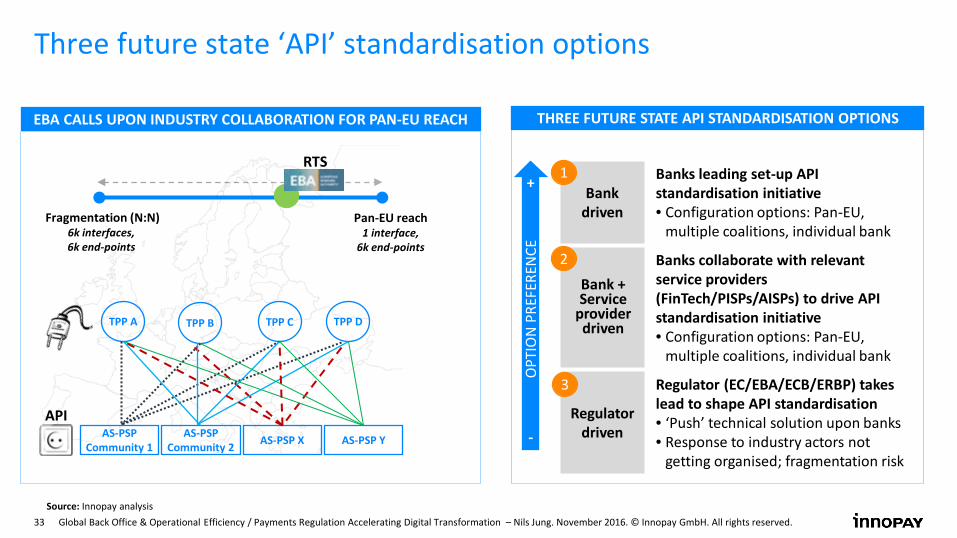

Three future state ‘API’ standardisation options

Bank driven

Banks leading set-up API standardisation initiative • Configuration options: Pan-EU,

multiple coalitions, individual bank

Bank + Service

provider driven

Banks collaborate with relevant service providers (FinTech/PISPs/AISPs) to drive API standardisation initiative • Configuration options: Pan-EU,

multiple coalitions, individual bank

Regulator driven

Regulator (EC/EBA/ECB/ERBP) takes lead to shape API standardisation • ‘Push’ technical solution upon banks • Response to industry actors not

getting organised; fragmentation risk

EBA CALLS UPON INDUSTRY COLLABORATION FOR PAN-EU REACH

TPP A

AS-PSP Community 1

AS-PSP Community 2

TPP B TPP C TPP D

AS-PSP X AS-PSP Y

Fragmentation (N:N) 6k interfaces, 6k end-points

Pan-EU reach 1 interface,

6k end-points

THREE FUTURE STATE API STANDARDISATION OPTIONS

1

2

3

OPT

ION

PRE

FERE

NCE

-

+

API

RTS

Source: Innopay analysis

34 Global Back Office & Operational Efficiency / Payments Regulation Accelerating Digital Transformation – Nils Jung. November 2016. © Innopay GmbH. All rights reserved.

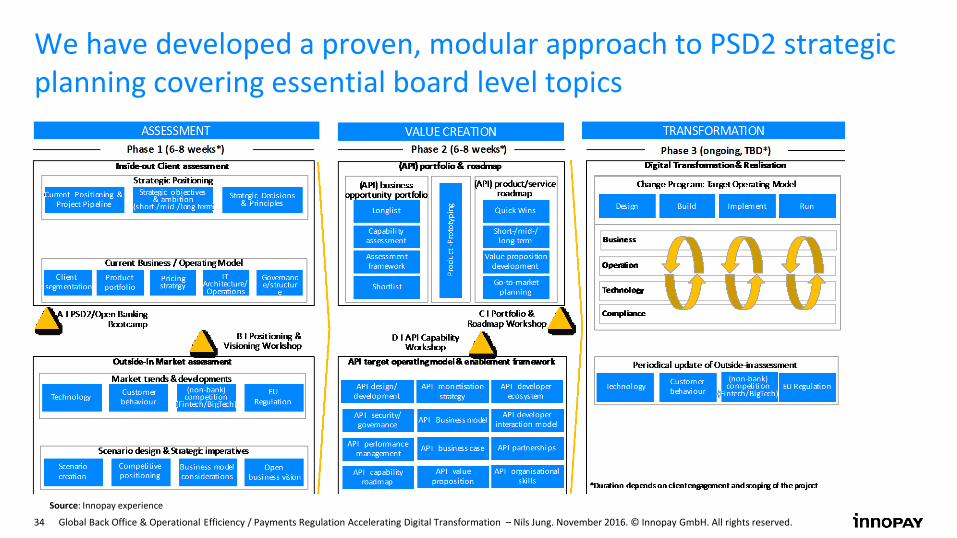

We have developed a proven, modular approach to PSD2 strategic planning covering essential board level topics

Source: Innopay experience

![[BACK OFFICE SERVICES] The 5 Biggest Benefits In Outsourcing Back Office Accounting](https://img.pdfslide.net/doc/110x75/55a631ba1a28abf8398b45ba/back-office-services-the-5-biggest-benefits-in-outsourcing-back-office-accounting.jpg)

![[Back office services] how to empower your back office services team](https://img.pdfslide.net/doc/110x75/5480bd6ab4795946578b4788/back-office-services-how-to-empower-your-back-office-services-team.jpg)