Embed Size (px)

Citation preview

DOMESTIC TRANSFER PRICING

By CA Ramesh S Iyer

04-08-2013

1

Reasons for introduction

• The SC in the case of CIT vs. Glaxo Smithkline Asia Pvt Ltd [2010]195Taxman 35(SC) recommended introduction of domestic TP provisions. The Court has stated in Para 4 of its order-

• The main issue which needs to be addressed is, whether Transfer Pricing Regulations should be limited to cross-border transactions or whether the Transfer Pricing Regulations be extended to domestic transactions. In the case of domestic transactions, the under-invoicing of sales and over-invoicing of expenses ordinarily will be revenue neutral in nature, except in two circumstances having tax arbitrage—

• (i)If one of the related Companies is loss making and the other is profit making and profit is shifted to the loss making concern; and

• (ii)If there are different rates for two related units (on account of different status, area based incentives, nature of activity, etc.) and if profit is diverted towards the unit on the lower side of tax arbitrage. For example, sale of goods or services from non-SEZ area (taxable division) to SEZ unit (non-taxable unit) at a price below the market price so that taxable division will have less profit taxable and non-taxable division will have a higher profit exemption.

2

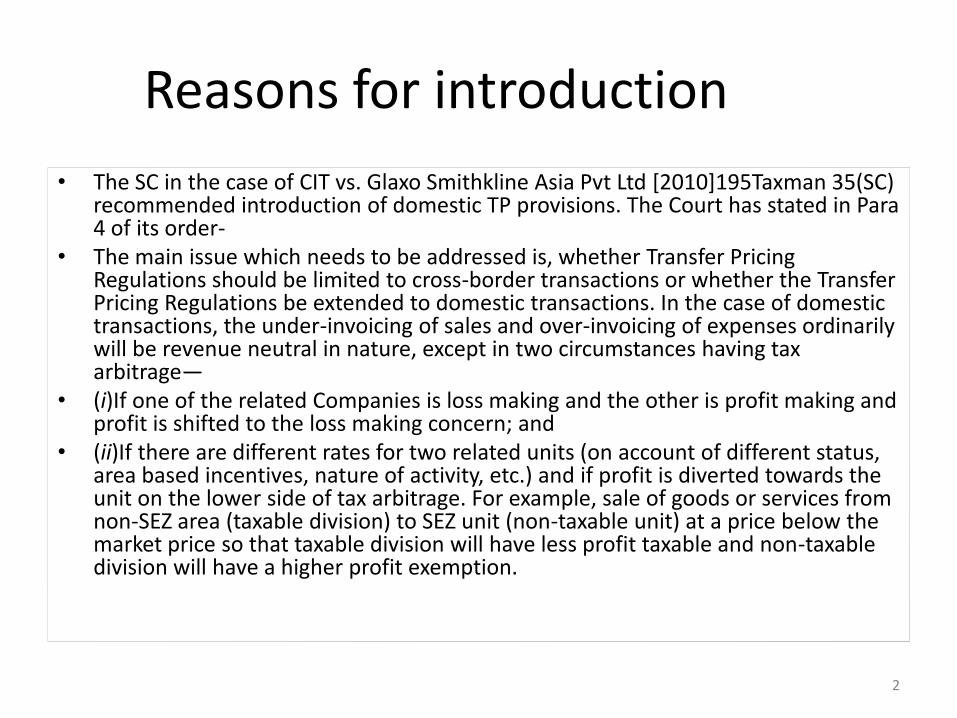

Examples of Tax Arbitrage in Domestic Transactions due

to Differential tax rates

India India

Shifting of Expenses/losses

Shifting of Income/profits

3

Tax Holiday entity

Related DTA entity

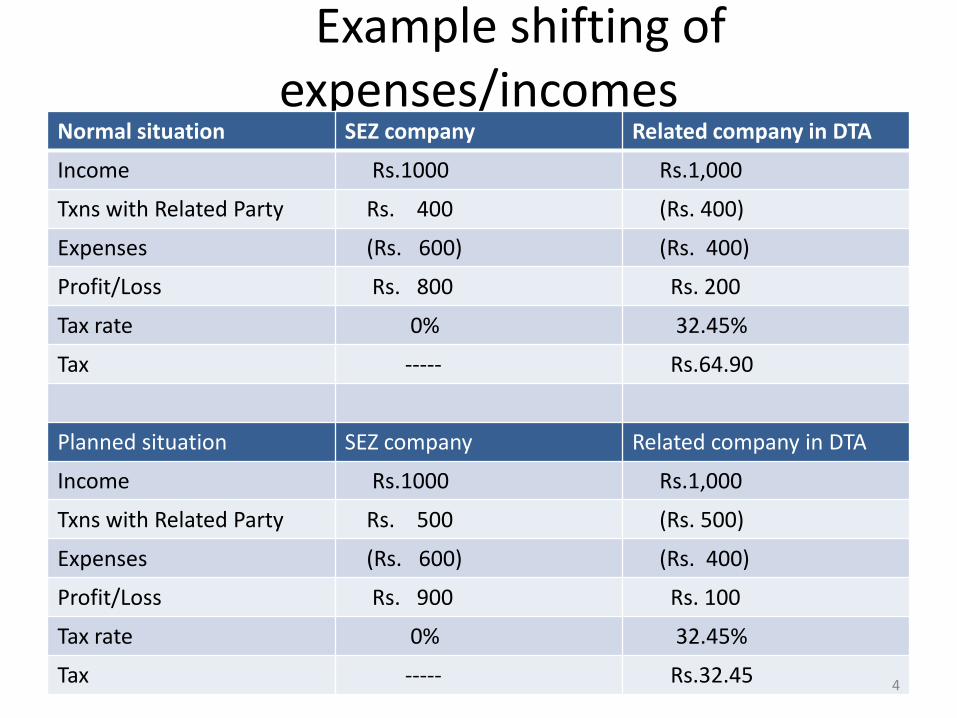

Example shifting of expenses/incomes

Normal situation SEZ company Related company in DTA

Income Rs.1000 Rs.1,000

Txns with Related Party Rs. 400 (Rs. 400)

Expenses (Rs. 600) (Rs. 400)

Profit/Loss Rs. 800 Rs. 200

Tax rate 0% 32.45%

Tax ----- Rs.64.90

Planned situation SEZ company Related company in DTA

Income Rs.1000 Rs.1,000

Txns with Related Party Rs. 500 (Rs. 500)

Expenses (Rs. 600) (Rs. 400)

Profit/Loss Rs. 900 Rs. 100

Tax rate 0% 32.45%

Tax ----- Rs.32.45 4

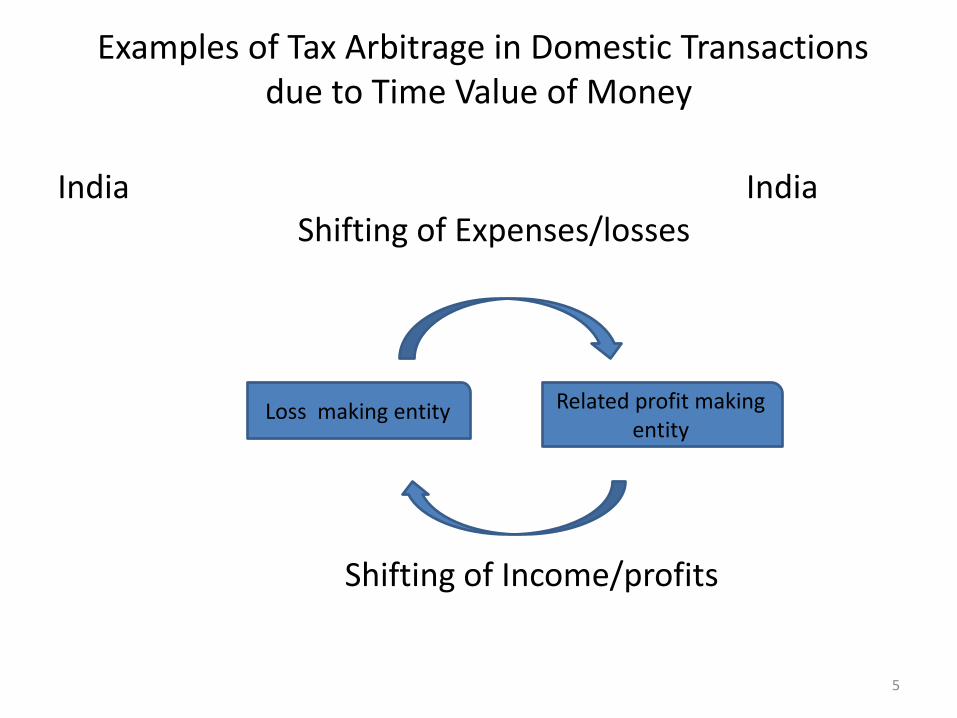

Examples of Tax Arbitrage in Domestic Transactions due to Time Value of Money

India India Shifting of Expenses/losses Shifting of Income/profits

5

Loss making entity

Related profit making entity

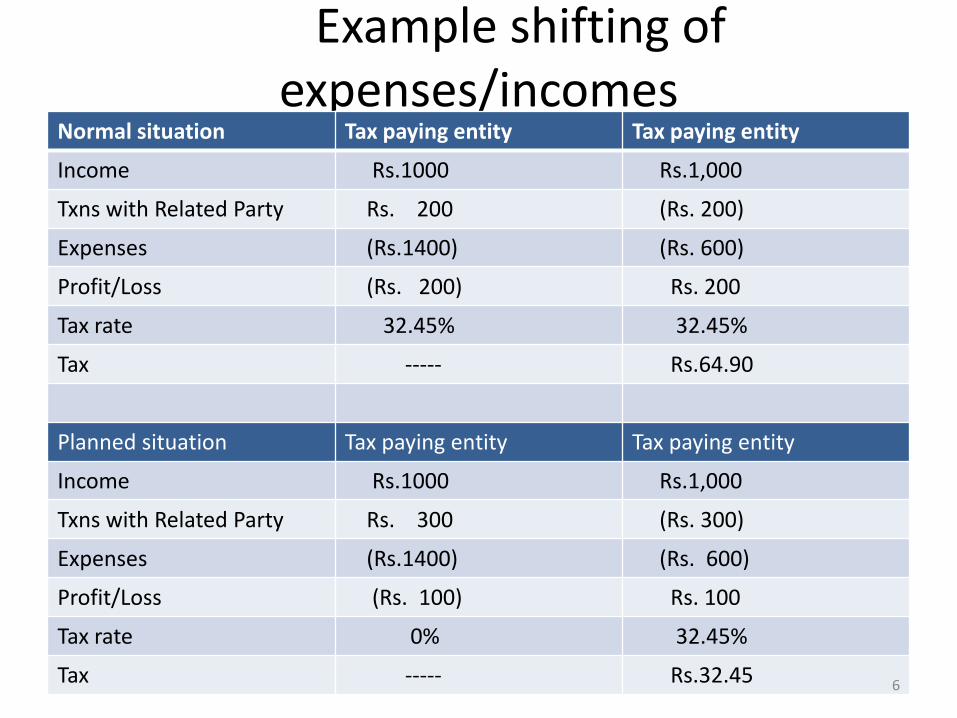

Example shifting of expenses/incomes

Normal situation Tax paying entity Tax paying entity

Income Rs.1000 Rs.1,000

Txns with Related Party Rs. 200 (Rs. 200)

Expenses (Rs.1400) (Rs. 600)

Profit/Loss (Rs. 200) Rs. 200

Tax rate 32.45% 32.45%

Tax ----- Rs.64.90

Planned situation Tax paying entity Tax paying entity

Income Rs.1000 Rs.1,000

Txns with Related Party Rs. 300 (Rs. 300)

Expenses (Rs.1400) (Rs. 600)

Profit/Loss (Rs. 100) Rs. 100

Tax rate 0% 32.45%

Tax ----- Rs.32.45 6

Brief Background

Legislative history

• To ensure that Taxpayers carrying on business with related persons do not make excessive and unreasonable expenditure to such persons, provisions of section 40A(2) was introduced to ensure that payments are made to related persons in an amount not exceeding the Fair Market Value (FMV). • To ensure that the profits of eligible units for availing the deduction under section 80A, 80IA, 10AA etc are not over stated , provisions were introduced in section 80A, 80IA, 10AA • However, there was no effective system in place in the Statute to monitor/deal with the transactions with the related parties

7

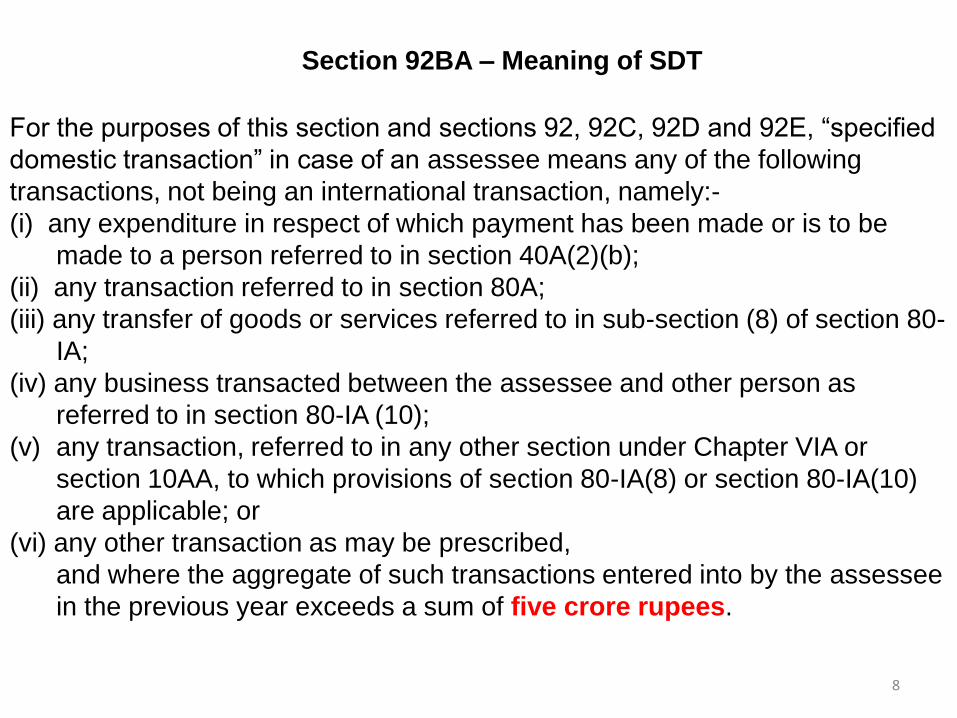

Section 92BA – Meaning of SDT

For the purposes of this section and sections 92, 92C, 92D and 92E, “specified

domestic transaction” in case of an assessee means any of the following

transactions, not being an international transaction, namely:-

(i) any expenditure in respect of which payment has been made or is to be

made to a person referred to in section 40A(2)(b);

(ii) any transaction referred to in section 80A;

(iii) any transfer of goods or services referred to in sub-section (8) of section 80-

IA;

(iv) any business transacted between the assessee and other person as

referred to in section 80-IA (10);

(v) any transaction, referred to in any other section under Chapter VIA or

section 10AA, to which provisions of section 80-IA(8) or section 80-IA(10)

are applicable; or

(vi) any other transaction as may be prescribed,

and where the aggregate of such transactions entered into by the assessee

in the previous year exceeds a sum of five crore rupees.

8

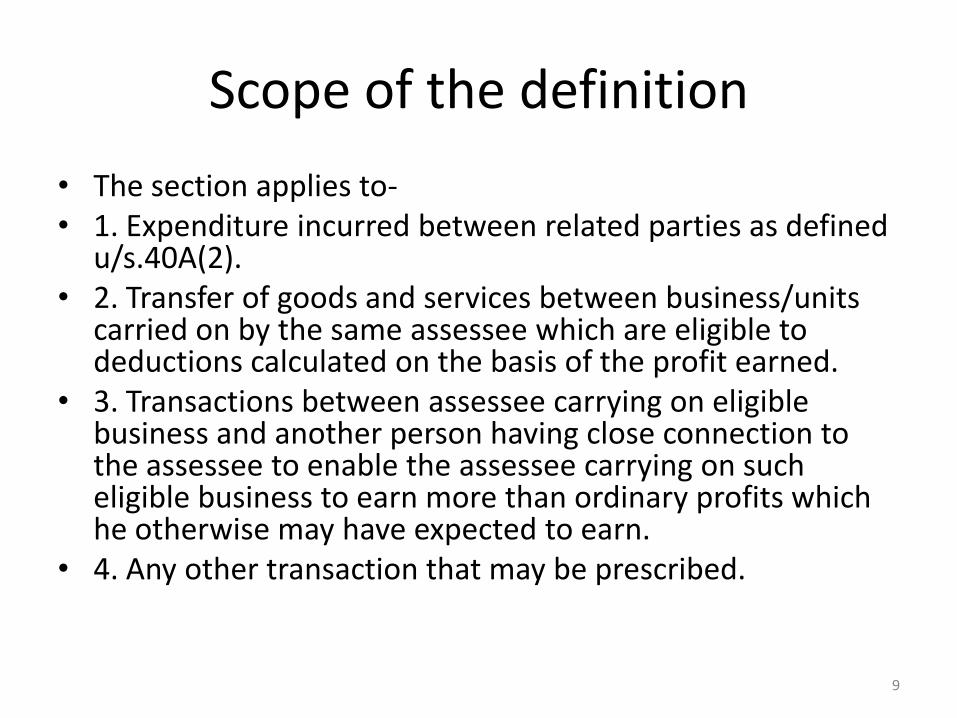

Scope of the definition

• The section applies to- • 1. Expenditure incurred between related parties as defined

u/s.40A(2). • 2. Transfer of goods and services between business/units

carried on by the same assessee which are eligible to deductions calculated on the basis of the profit earned.

• 3. Transactions between assessee carrying on eligible business and another person having close connection to the assessee to enable the assessee carrying on such eligible business to earn more than ordinary profits which he otherwise may have expected to earn.

• 4. Any other transaction that may be prescribed.

9

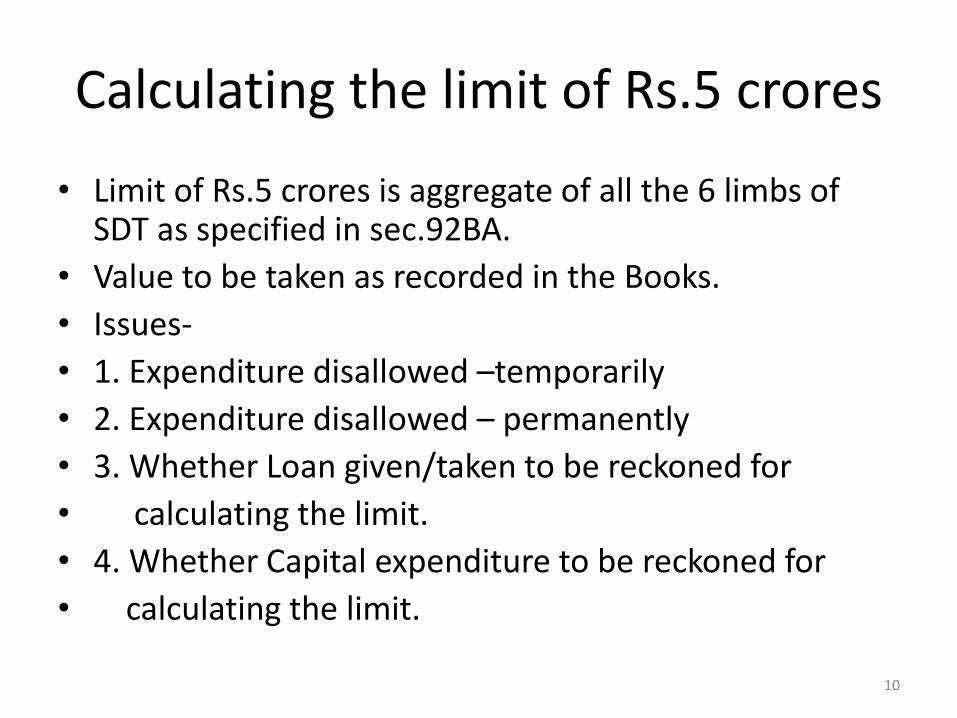

Calculating the limit of Rs.5 crores

• Limit of Rs.5 crores is aggregate of all the 6 limbs of SDT as specified in sec.92BA.

• Value to be taken as recorded in the Books.

• Issues-

• 1. Expenditure disallowed –temporarily

• 2. Expenditure disallowed – permanently

• 3. Whether Loan given/taken to be reckoned for

• calculating the limit.

• 4. Whether Capital expenditure to be reckoned for

• calculating the limit.

10

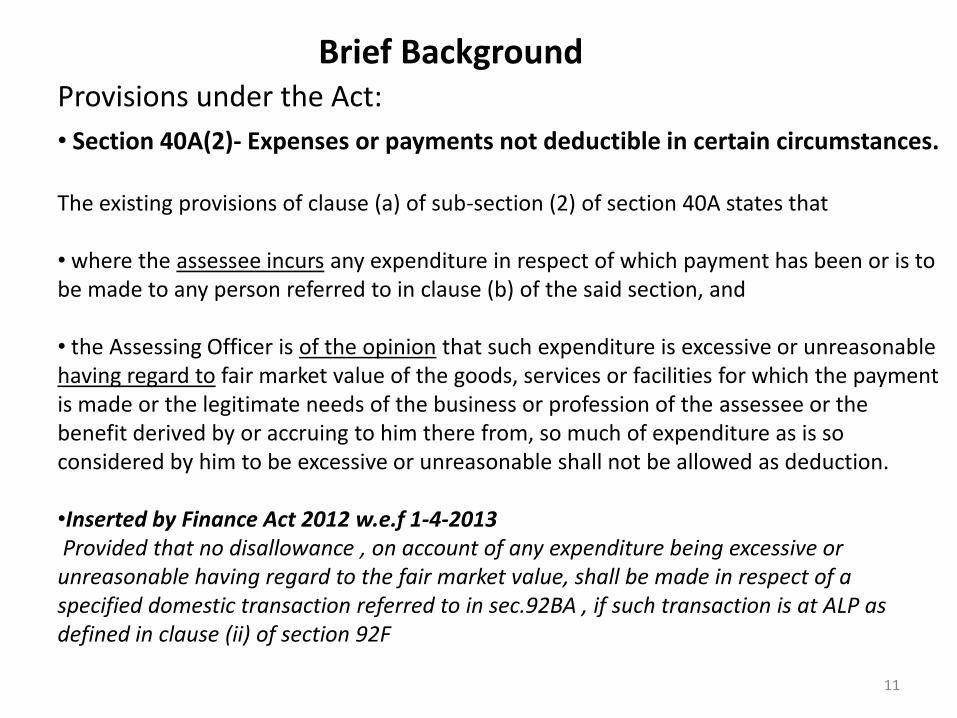

Brief Background Provisions under the Act:

• Section 40A(2)- Expenses or payments not deductible in certain circumstances. The existing provisions of clause (a) of sub-section (2) of section 40A states that • where the assessee incurs any expenditure in respect of which payment has been or is to be made to any person referred to in clause (b) of the said section, and • the Assessing Officer is of the opinion that such expenditure is excessive or unreasonable having regard to fair market value of the goods, services or facilities for which the payment is made or the legitimate needs of the business or profession of the assessee or the benefit derived by or accruing to him there from, so much of expenditure as is so considered by him to be excessive or unreasonable shall not be allowed as deduction. •Inserted by Finance Act 2012 w.e.f 1-4-2013 Provided that no disallowance , on account of any expenditure being excessive or unreasonable having regard to the fair market value, shall be made in respect of a specified domestic transaction referred to in sec.92BA , if such transaction is at ALP as defined in clause (ii) of section 92F

11

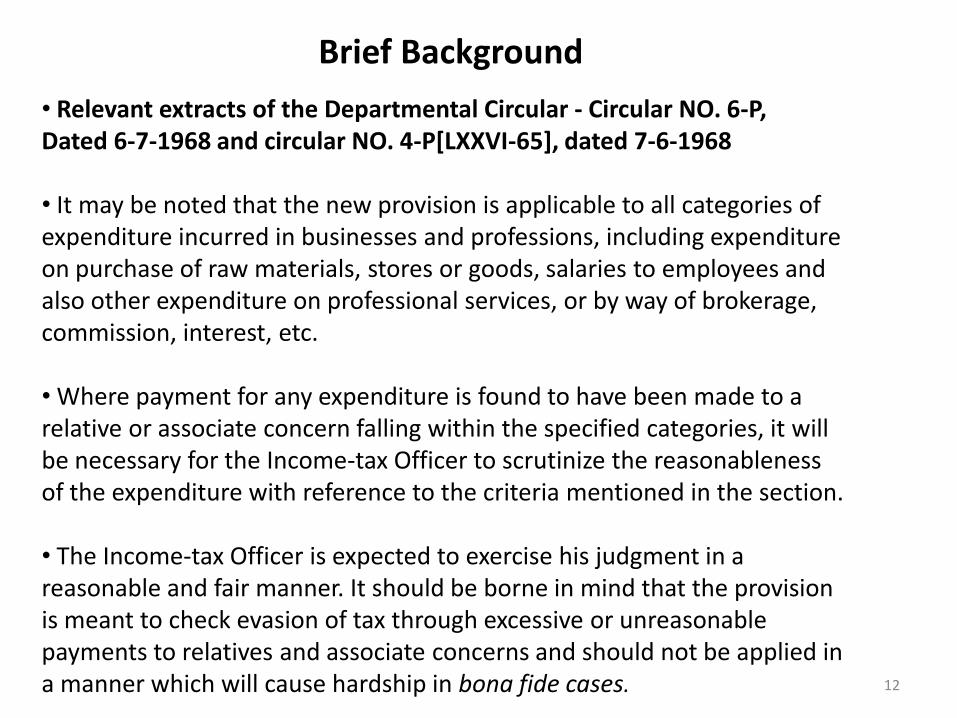

Brief Background

• Relevant extracts of the Departmental Circular - Circular NO. 6-P, Dated 6-7-1968 and circular NO. 4-P[LXXVI-65], dated 7-6-1968 • It may be noted that the new provision is applicable to all categories of expenditure incurred in businesses and professions, including expenditure on purchase of raw materials, stores or goods, salaries to employees and also other expenditure on professional services, or by way of brokerage, commission, interest, etc. • Where payment for any expenditure is found to have been made to a relative or associate concern falling within the specified categories, it will be necessary for the Income-tax Officer to scrutinize the reasonableness of the expenditure with reference to the criteria mentioned in the section. • The Income-tax Officer is expected to exercise his judgment in a reasonable and fair manner. It should be borne in mind that the provision is meant to check evasion of tax through excessive or unreasonable payments to relatives and associate concerns and should not be applied in a manner which will cause hardship in bona fide cases. 12

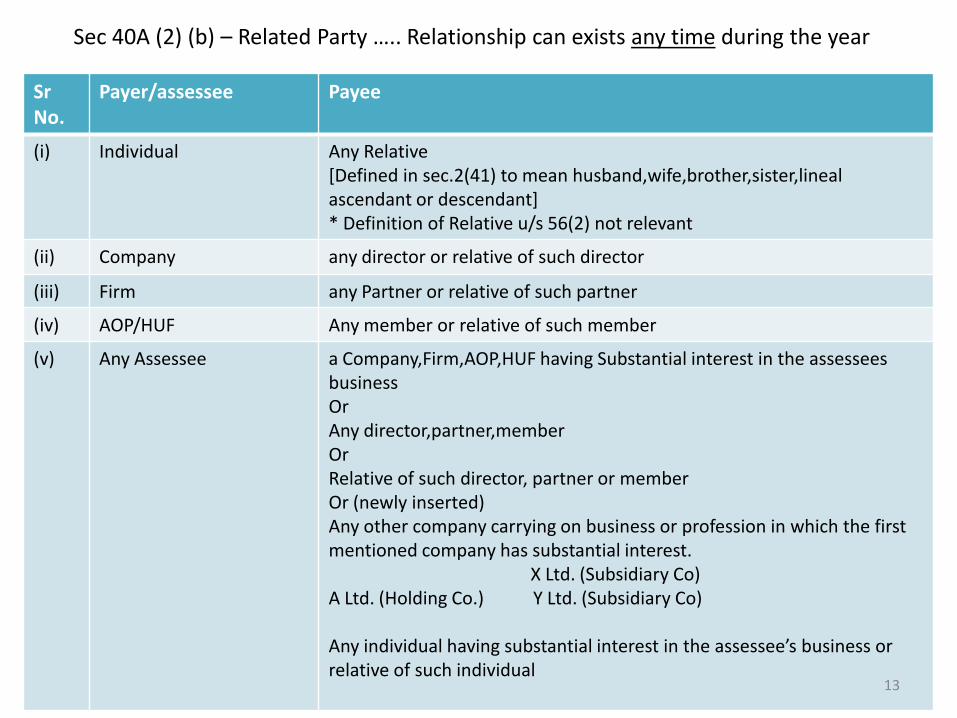

Sr No.

Payer/assessee Payee

(i) Individual Any Relative [Defined in sec.2(41) to mean husband,wife,brother,sister,lineal ascendant or descendant] * Definition of Relative u/s 56(2) not relevant

(ii) Company any director or relative of such director

(iii) Firm any Partner or relative of such partner

(iv) AOP/HUF Any member or relative of such member

(v) Any Assessee a Company,Firm,AOP,HUF having Substantial interest in the assessees business Or Any director,partner,member Or Relative of such director, partner or member Or (newly inserted) Any other company carrying on business or profession in which the first mentioned company has substantial interest. X Ltd. (Subsidiary Co) A Ltd. (Holding Co.) Y Ltd. (Subsidiary Co) Any individual having substantial interest in the assessee’s business or relative of such individual

Sec 40A (2) (b) – Related Party ….. Relationship can exists any time during the year

13

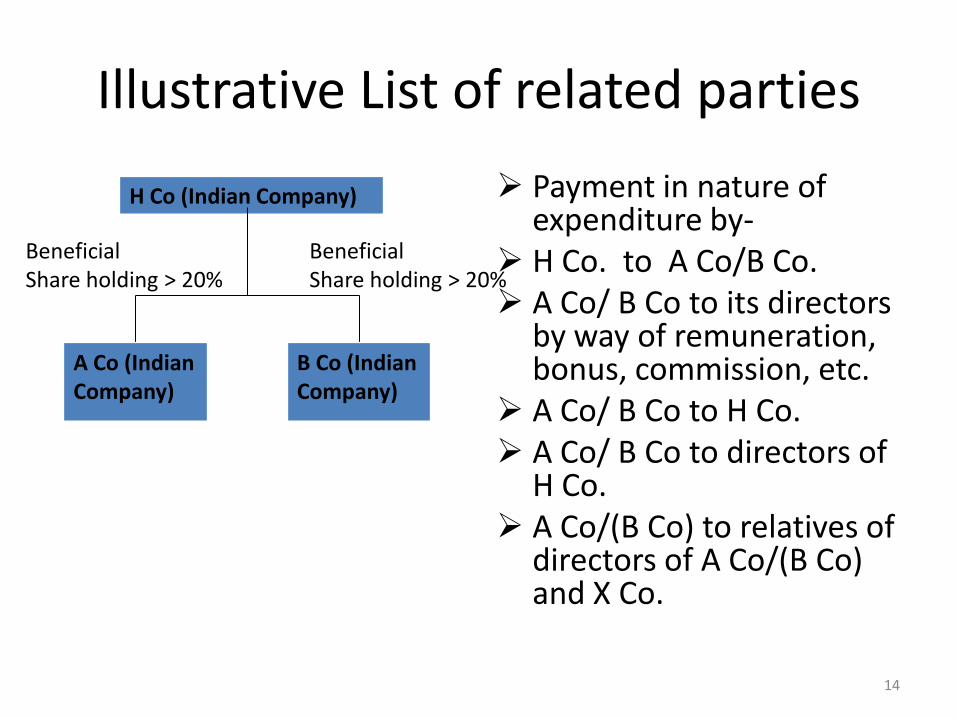

Illustrative List of related parties

H Co (Indian Company) Payment in nature of expenditure by-

H Co. to A Co/B Co. A Co/ B Co to its directors

by way of remuneration, bonus, commission, etc.

A Co/ B Co to H Co. A Co/ B Co to directors of

H Co. A Co/(B Co) to relatives of

directors of A Co/(B Co) and X Co.

14

A Co (Indian Company)

B Co (Indian Company)

Beneficial Share holding > 20%

Beneficial Share holding > 20%

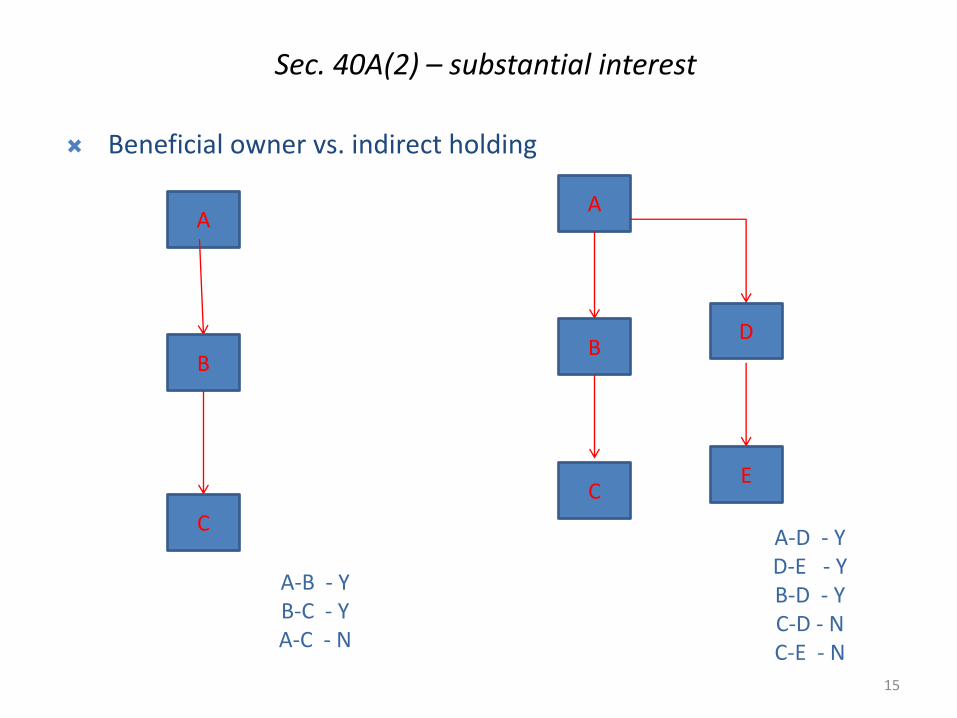

Sec. 40A(2) – substantial interest

Beneficial owner vs. indirect holding

A

B

C

A-B - Y B-C - Y A-C - N

A

B D

C E

A-D - Y D-E - Y B-D - Y C-D - N C-E - N

15

Indirect interest

• “Substantial Interest” as defined in Explanation to Sec 40A(2) refers to in case of a company “a person who is the beneficial owner of shares carrying not less than 20 % of the voting power, in any other case “ a person who is beneficially entitled to not less than 20% of the profits of such business or profession”.

• Can “C” be treated as related enterprise to “A” since “A” indirectly controls “C”

• Argument for – Circular 6 P dated 6-7-1968 refers to “direct or indirect” substantial interest.

• Argument against- If “indirect interest” is to be covered then it should be specifically mentioned in the Act as was mentioned in the case of Sec. 92A.

•

16

Issues and Challenges

- Whether Capital expenditure is covered by SDT ? - Whether payments to Subsidiaries is covered u/s.40A(2) ? - Whether transactions with non-resident covered by SDT ? - Whether applies to Government companies ? - Service provided Gratis whether to be evaluated for

computation of ALP ? - Whether Beneficial ownership is akin to Indirect ownership

covered? - Whether applies to “ Income from other Sources” ? - Whether Corresponding adjustments can be made ?

17

Issues and Challenges (contd)

- Benchmarking of-

a. Payment to Directors

b. Salary and Interest to partners

c. Allocation of common expenses

- Whether GAAR (if and when it applies) can override Transfer Pricing ?

- Litigation ?

- Transactions not leading to base erosion whether requires SDT compliance ?

18

Brief Background Provisions under the Act: • Section 80A - Deductions To Be Made In Computing Total Income

•The provision of the Explanation to sub-section (6) (inserted by Finance Act 2009, w.r.e.f.1-4-2009) of the aforesaid section 80A provides the definition of expression “market value” in relation to any goods or services sold or supplied and in relation to goods or services acquired as under: (i) in relation to any goods or services sold or supplied, means the price that such goods or services would fetch if these were sold by the undertaking or unit or enterprise or eligible business in the open market, subject to statutory or regulatory restrictions, if any; (ii) in relation to any goods or services acquired, means the price that such goods or services would cost if these were acquired by the undertaking or unit or enterprise or eligible business from the open market, subject to statutory or regulatory restrictions, if any. • Inserted by Finance Act, 2012 w.e.f.1-4-2013 (iii) In relation to any goods or services supplied or acquired means the ALP as defined in clause (ii) of sec.92Fof such goods or services, if it is a specified domestic transaction referred to in sec. 92BA

19

Brief Background

Provisions under the Act: • Section 80IA - Deductions in respect of profits and gains from industrial undertakings or enterprises engaged in infrastructure development, etc •Sec.80-IA(8) – Provides for adjustment of consideration paid to/received by, an eligible business of the assessee from any other business of the same assessee for receipt / provision of goods and services . Where the consideration does not correspond to the market value of such goods or services as on the date of the transfer, then for the purposes of deduction under this section, the profits of such eligible business shall be calculated as if the transfer was made at market value of such goods and services on that date. •The Explanation to sub-section (8) of the aforesaid section 80-IA provides for the definition of “market value” in relation to goods or services, as the price that such goods or services would ordinarily fetch in the open market. •Inserted by Finance Act, 2012 w.e.f 1-4-2013 Explanation – For the purposes of this sub-section “market value” , in relation to any goods or services means- (i). The price that such goods or services would ordinarily fetch in the open market ; or (ii). The ALP as defined in clause (ii) of sec.92F, where the transfer of such goods or services is a specified domestic transaction referred to in sec.92BA

20

Sec 80A(6)/ 80IA(8)

• Covers intra division transfer of goods or services between eligible enterprises and non-eligible enterprises of the same assessee.

• Applies when consideration recorded in the accounts do not correspond to the market value of such goods or services as on the date of the transfer.

• This section envisages dealings between businesses carried on by the assessee.

• Non business activities like HO expenses, IT support , compliance , use of common resources , etc ,which may be charged , to be out of purview of SDT. However, expenses on non-business activities should be distributed in a fair and commercial manner with proper justification for the same.

• Thus only marketable services rendered by inter units will have to be at ALP.

• Envisages both favourable as well as adverse adjustment.

21

Brief background • Provisions under the Act

• Sec.80-IA(10) -The existing provisions provide that where it appears to the

Assessing Officer, owing to the close connection between the assessee carrying on the eligible business to which this section applies and any other person, or for any other reason, the course of business between them is so arranged that the business transacted between them produces to the assessee more than the ordinary profits which might be expected to arise in such eligible business, the Assessing Officer shall, in computing the profits and gains of such eligible business for the purposes of the deduction under this section, take the amount of profits as may be reasonably deemed to have been derived there from.

• Inserted by Finance Act 2012 w.e.f 1-4-2013 • Provided that in case the aforesaid arrangement involves a specified domestic

transaction referred to in sec.92BA, the amount of profits from such transaction shall be determined having regard to the ALP as defined in clause (ii) of sec.92F

22

Other sections under chapter VIA to which 80IA(8) and 80IA(10) applies

• 80IAB- Income of an undertaking or enterprise engaged in development of SEZ.

• 80IB- Income from certain Industrial undertaking and Housing Projects etc.

• 80IC- Income from certain Industrial undertaking set up in Sikkim, HP...etc.

• 80ID- Income from hotels etc in Delhi, Faridabad and other specified districts

• 80IE- Income from eligible business undertaking in North Eastern States

23

Provisions under the Act:

• Section 10AA - Special provisions in respect of newly established Units in Special Economic Zones. •The provisions of sub-section (8) and sub-section (10) of section 80-IA shall, so far as may be, apply in relation to the undertaking referred to in this section as they apply for the purposes of the undertaking referred to in section 80-IA. •Hence by applying the provisions of sub-section (8) and sub-section (10) of section 80-IA, any transfer of goods/ services by an undertaking to another group company will be measured on arm’s length basis.

Brief Background

24

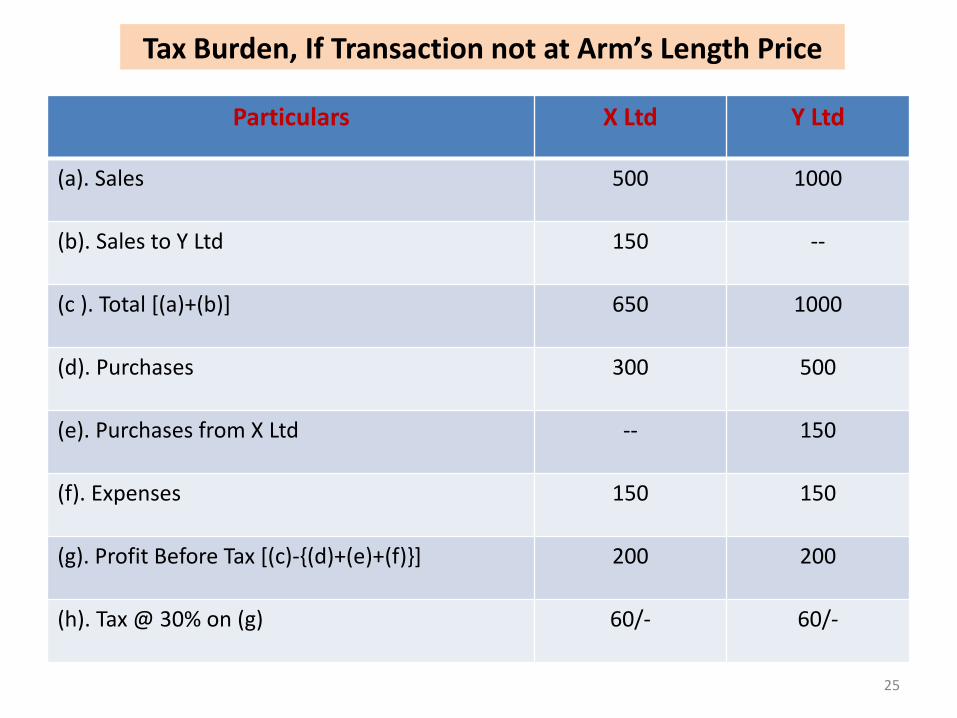

Particulars X Ltd Y Ltd

(a). Sales 500 1000

(b). Sales to Y Ltd 150 --

(c ). Total [(a)+(b)] 650 1000

(d). Purchases 300 500

(e). Purchases from X Ltd -- 150

(f). Expenses 150 150

(g). Profit Before Tax [(c)-{(d)+(e)+(f)}] 200 200

(h). Tax @ 30% on (g) 60/- 60/-

Tax Burden, If Transaction not at Arm’s Length Price

25

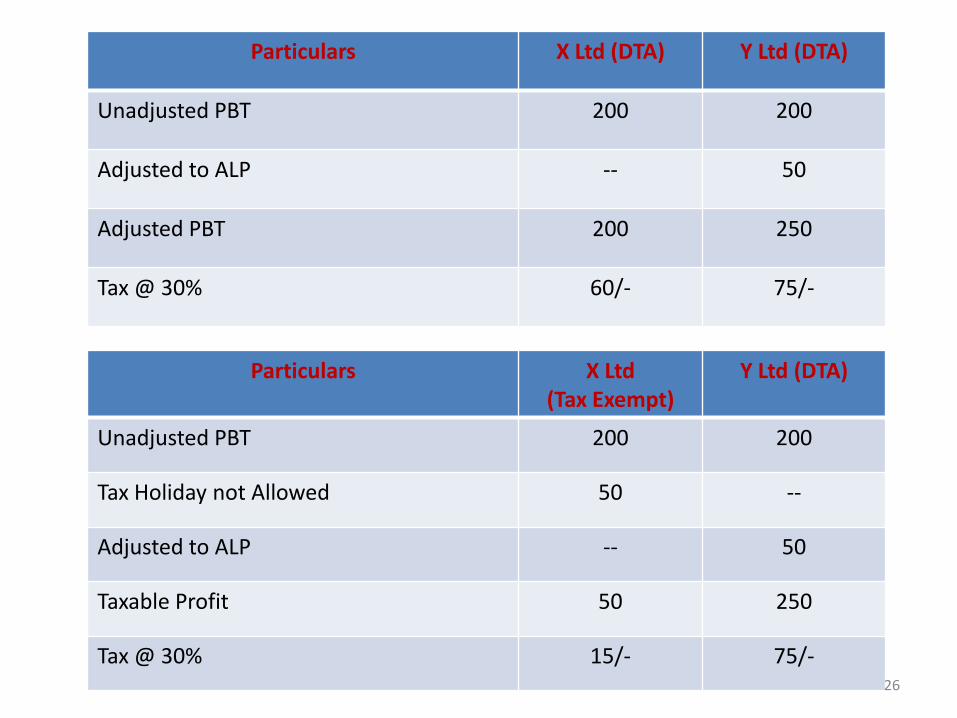

Particulars X Ltd (DTA) Y Ltd (DTA)

Unadjusted PBT 200 200

Adjusted to ALP -- 50

Adjusted PBT 200 250

Tax @ 30% 60/- 75/-

Particulars X Ltd (Tax Exempt)

Y Ltd (DTA)

Unadjusted PBT 200 200

Tax Holiday not Allowed 50 --

Adjusted to ALP -- 50

Taxable Profit 50 250

Tax @ 30% 15/- 75/- 26

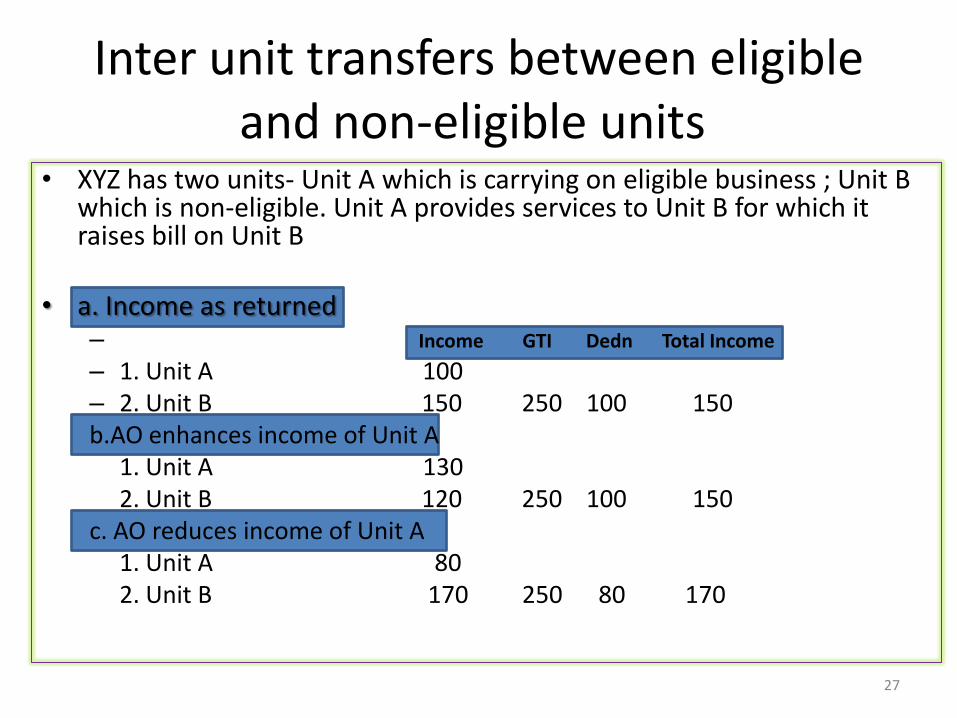

Inter unit transfers between eligible and non-eligible units

• XYZ has two units- Unit A which is carrying on eligible business ; Unit B which is non-eligible. Unit A provides services to Unit B for which it raises bill on Unit B

• a. Income as returned – Income GTI Dedn Total Income – 1. Unit A 100 – 2. Unit B 150 250 100 150 b.AO enhances income of Unit A 1. Unit A 130 2. Unit B 120 250 100 150 c. AO reduces income of Unit A 1. Unit A 80 2. Unit B 170 250 80 170

27

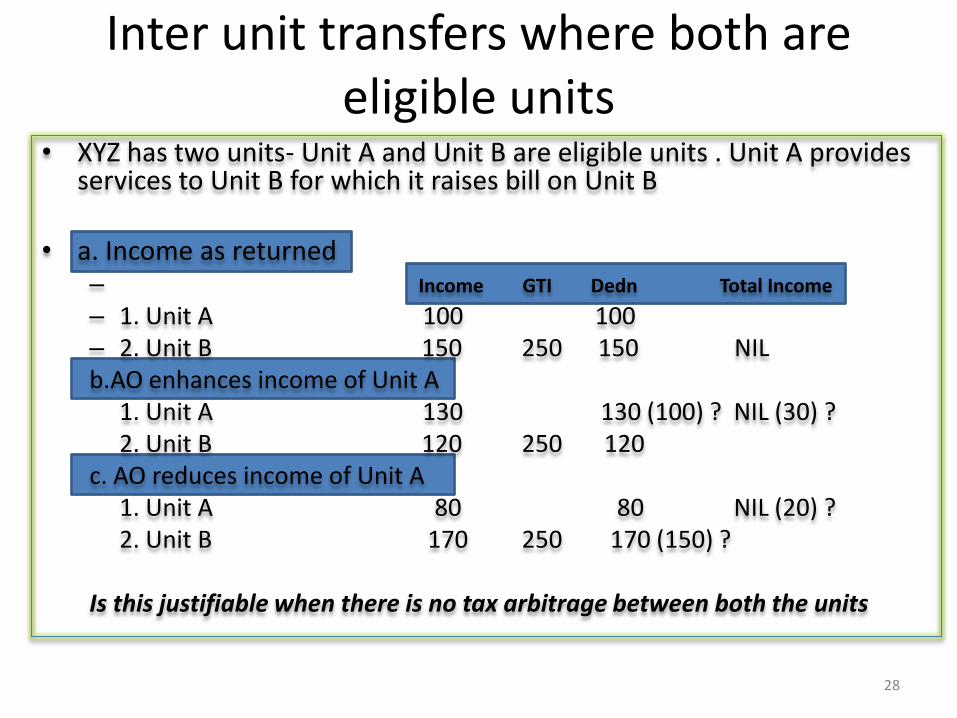

Inter unit transfers where both are eligible units

• XYZ has two units- Unit A and Unit B are eligible units . Unit A provides services to Unit B for which it raises bill on Unit B

• a. Income as returned – Income GTI Dedn Total Income – 1. Unit A 100 100 – 2. Unit B 150 250 150 NIL b.AO enhances income of Unit A 1. Unit A 130 130 (100) ? NIL (30) ? 2. Unit B 120 250 120 c. AO reduces income of Unit A 1. Unit A 80 80 NIL (20) ? 2. Unit B 170 250 170 (150) ? Is this justifiable when there is no tax arbitrage between both the units

28

Effect of TP adjustment

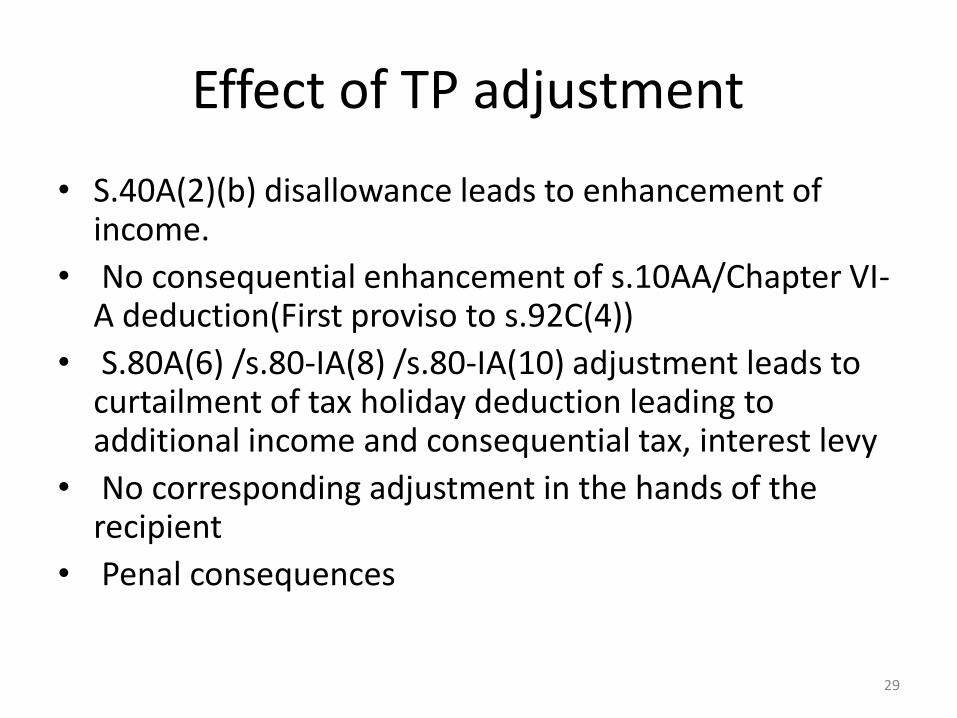

• S.40A(2)(b) disallowance leads to enhancement of income.

• No consequential enhancement of s.10AA/Chapter VI-A deduction(First proviso to s.92C(4))

• S.80A(6) /s.80-IA(8) /s.80-IA(10) adjustment leads to curtailment of tax holiday deduction leading to additional income and consequential tax, interest levy

• No corresponding adjustment in the hands of the recipient

• Penal consequences

29

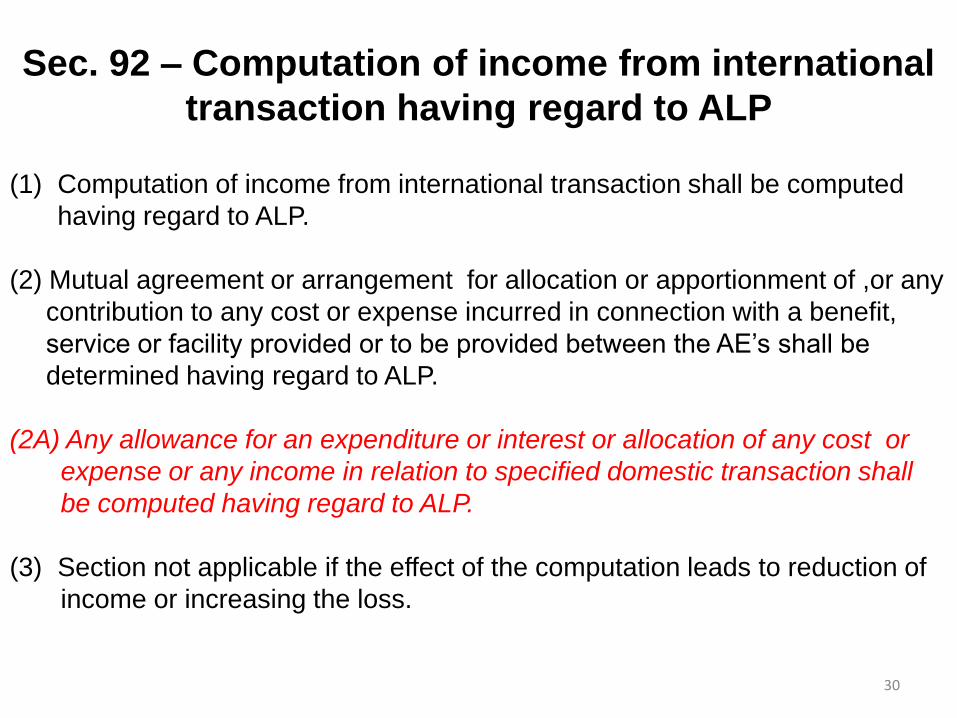

Sec. 92 – Computation of income from international

transaction having regard to ALP

(1) Computation of income from international transaction shall be computed

having regard to ALP.

(2) Mutual agreement or arrangement for allocation or apportionment of ,or any

contribution to any cost or expense incurred in connection with a benefit,

service or facility provided or to be provided between the AE’s shall be

determined having regard to ALP.

(2A) Any allowance for an expenditure or interest or allocation of any cost or

expense or any income in relation to specified domestic transaction shall

be computed having regard to ALP.

(3) Section not applicable if the effect of the computation leads to reduction of

income or increasing the loss.

30

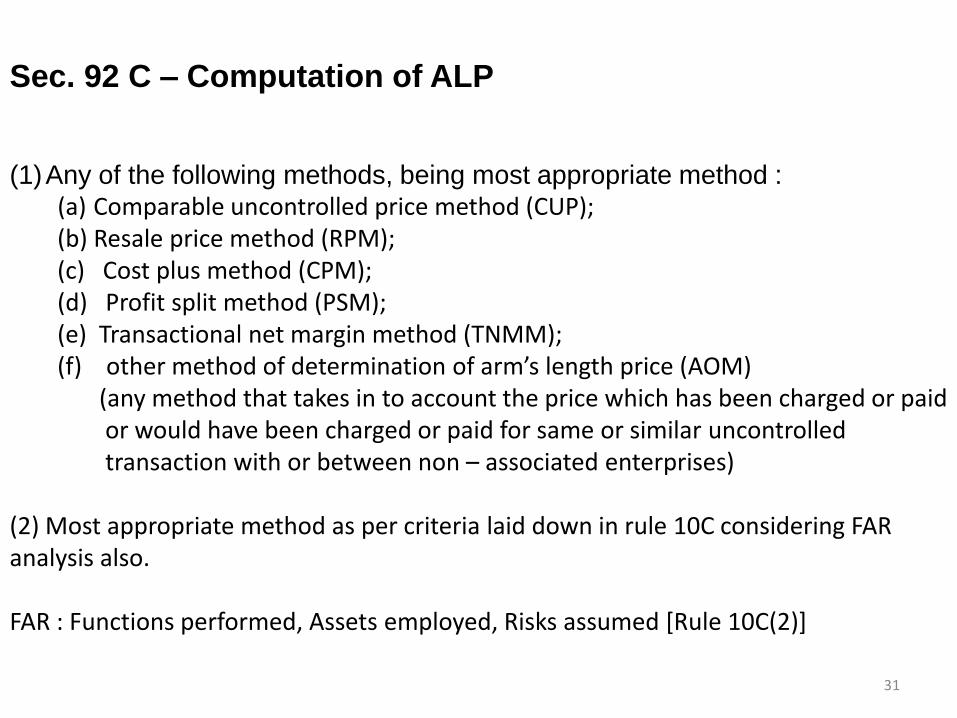

Sec. 92 C – Computation of ALP

(1)Any of the following methods, being most appropriate method : (a) Comparable uncontrolled price method (CUP);

(b) Resale price method (RPM); (c) Cost plus method (CPM); (d) Profit split method (PSM); (e) Transactional net margin method (TNMM); (f) other method of determination of arm’s length price (AOM) (any method that takes in to account the price which has been charged or paid or would have been charged or paid for same or similar uncontrolled transaction with or between non – associated enterprises) (2) Most appropriate method as per criteria laid down in rule 10C considering FAR analysis also. FAR : Functions performed, Assets employed, Risks assumed [Rule 10C(2)]

31

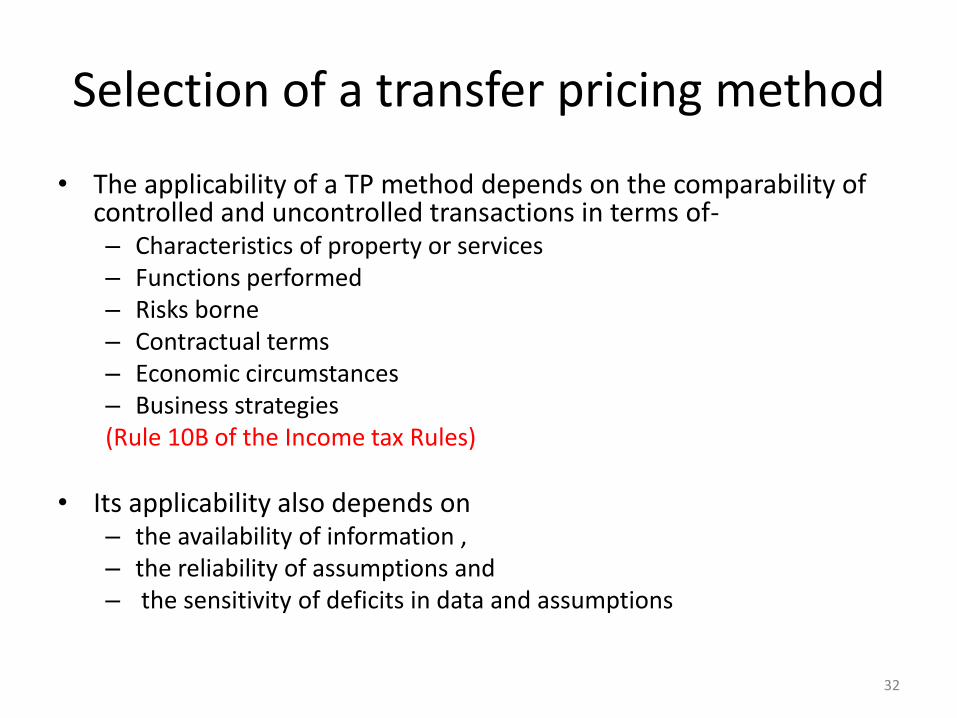

Selection of a transfer pricing method

• The applicability of a TP method depends on the comparability of controlled and uncontrolled transactions in terms of- – Characteristics of property or services – Functions performed – Risks borne – Contractual terms – Economic circumstances – Business strategies (Rule 10B of the Income tax Rules)

• Its applicability also depends on – the availability of information , – the reliability of assumptions and – the sensitivity of deficits in data and assumptions

32

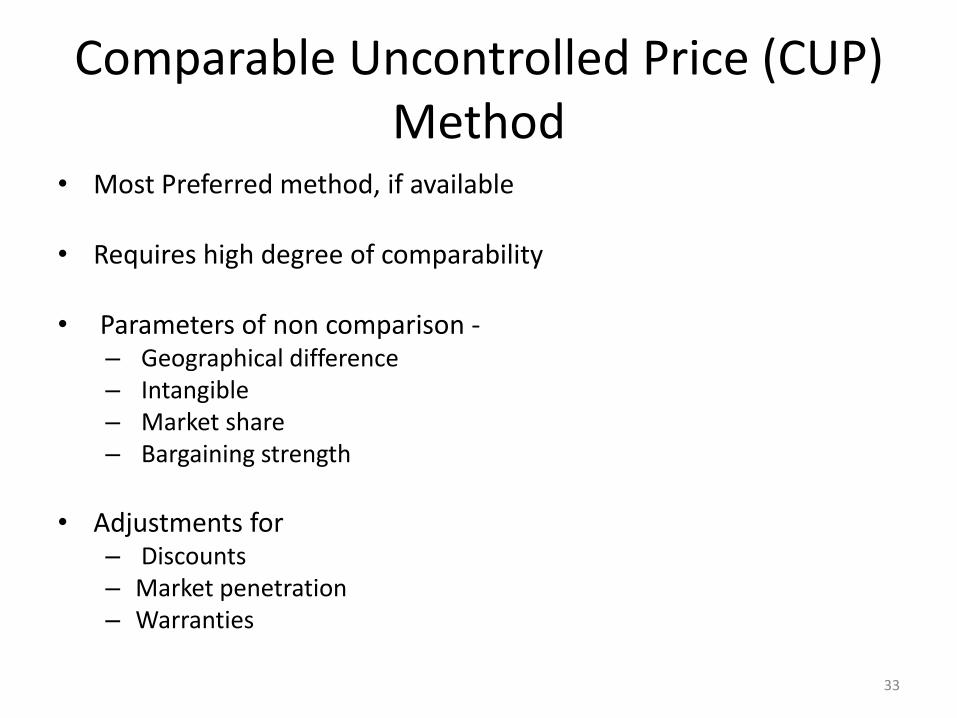

Comparable Uncontrolled Price (CUP) Method

• Most Preferred method, if available

• Requires high degree of comparability

• Parameters of non comparison - – Geographical difference – Intangible – Market share – Bargaining strength

• Adjustments for

– Discounts – Market penetration – Warranties

33

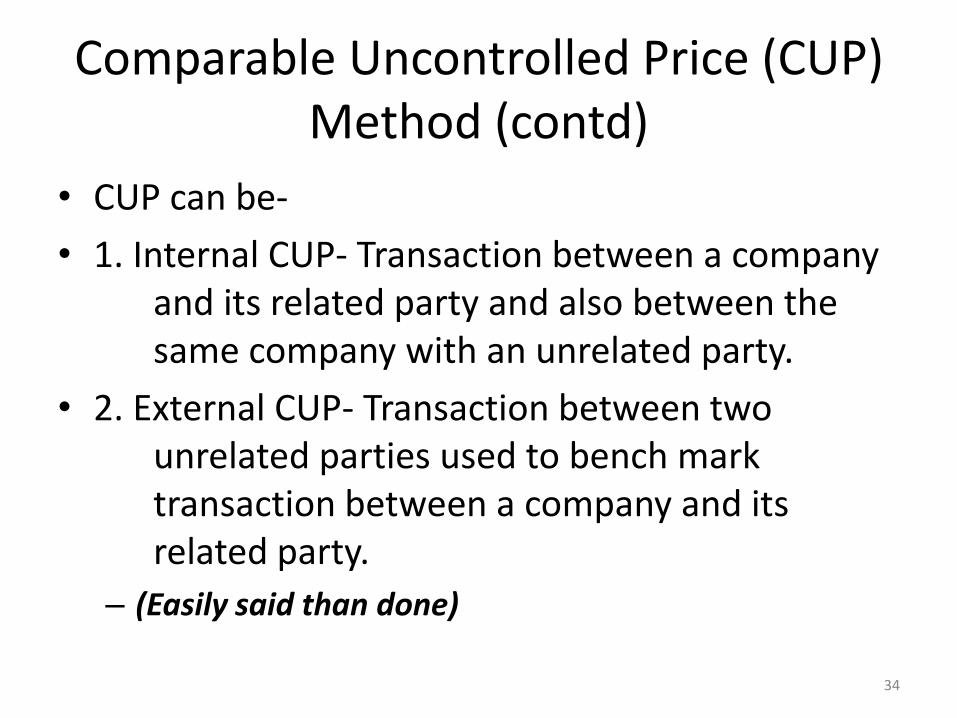

Comparable Uncontrolled Price (CUP) Method (contd)

• CUP can be-

• 1. Internal CUP- Transaction between a company and its related party and also between the same company with an unrelated party.

• 2. External CUP- Transaction between two unrelated parties used to bench mark transaction between a company and its related party.

– (Easily said than done)

34

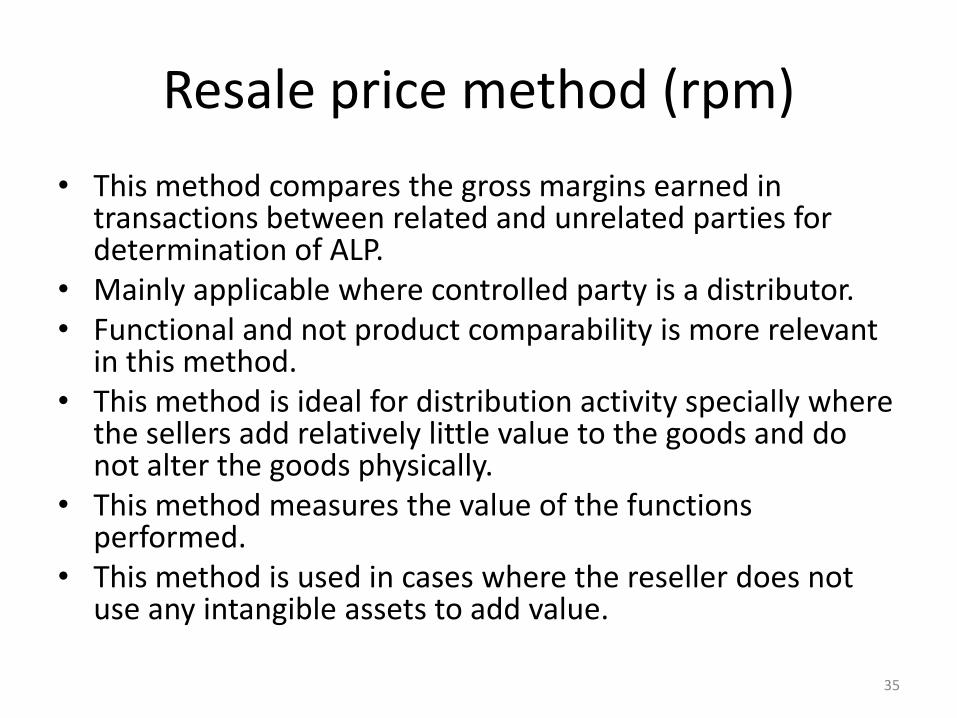

Resale price method (rpm)

• This method compares the gross margins earned in transactions between related and unrelated parties for determination of ALP.

• Mainly applicable where controlled party is a distributor. • Functional and not product comparability is more relevant

in this method. • This method is ideal for distribution activity specially where

the sellers add relatively little value to the goods and do not alter the goods physically.

• This method measures the value of the functions performed.

• This method is used in cases where the reseller does not use any intangible assets to add value.

35

Cost plus method (CPM)

• Used mainly when a company works for its AE as a contract manufacturer.

• Applies to low risk bearing manufacturers.

• The ALP is calculated by adding a comparable profit margin to the Direct and Indirect Costs of product/service.

36

Transactional net margin method

• The comparable Net profit margin is adopted to compare profits of the assessee with that of comparable companies.

• The comparability can based on either the costs incurred, sales , assets employed, etc.

37

Profit split method

• This method is generally used when the transactions involve –

– 1. Transfer of unique intangibles

– 2. Transactions between the AE’s are so closely

– interconnected that the profits of each AE cannot

– be evaluated independent of the other.

The overall profit of the entire group are split between

the various group entities based on their relative

contribution.

38

Other unspecified methods

• For the purposes of clause (f) of sub-section (1) of section 92C, the other method for determination of the arms' length price in relation to an international transaction or a specified domestic transaction shall be any method which takes into account the price which has been charged or paid, or would have been

• charged or paid, for the same or similar uncontrolled transaction, with or between non-associated enterprises, under similar circumstances, considering all the relevant facts.

39

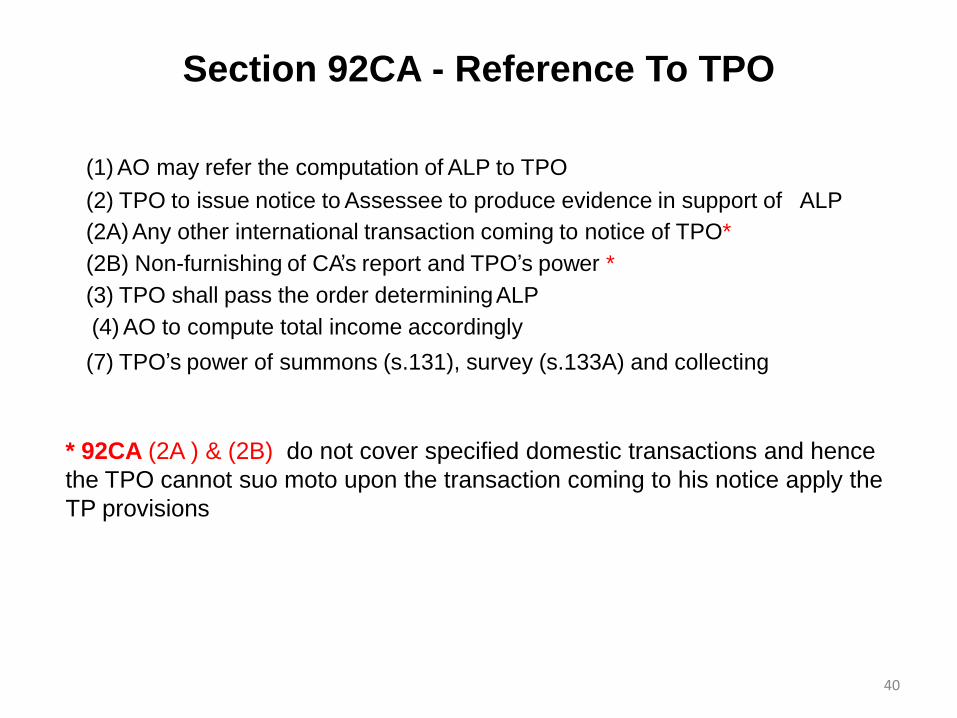

(1) AO may refer the computation of ALP to TPO

(2) TPO to issue notice to Assessee to produce evidence in support of ALP

(2A) Any other international transaction coming to notice of TPO*

(2B) Non-furnishing of CA’s report and TPO’s power *

(3) TPO shall pass the order determining ALP

(4) AO to compute total income accordingly

(7) TPO’s power of summons (s.131), survey (s.133A) and collecting

Section 92CA - Reference To TPO

* 92CA (2A ) & (2B) do not cover specified domestic transactions and hence

the TPO cannot suo moto upon the transaction coming to his notice apply the

TP provisions

40

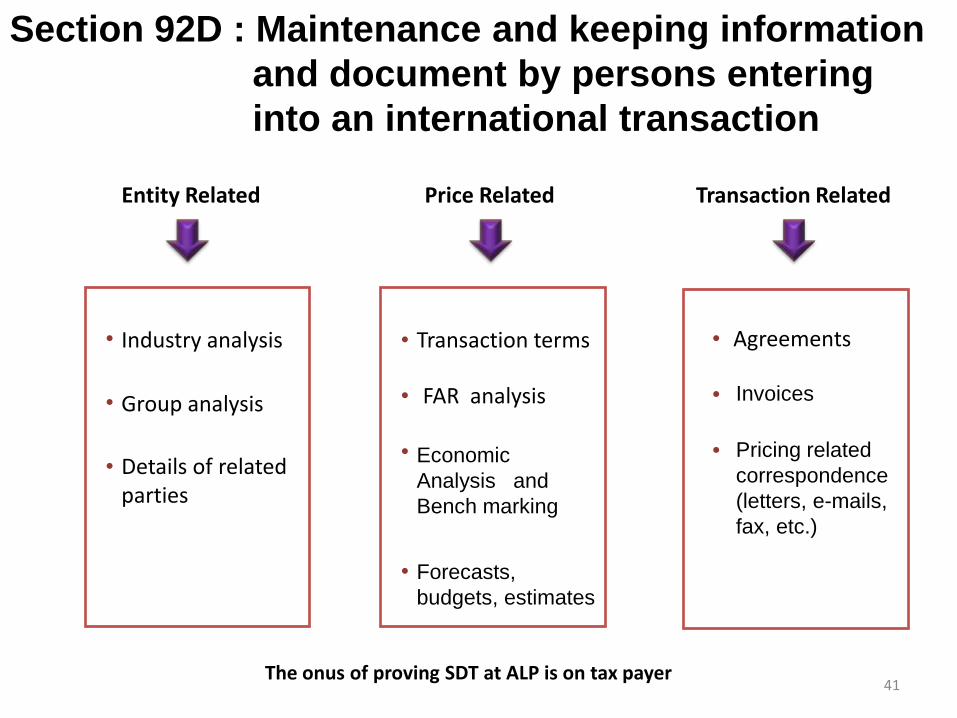

Section 92D : Maintenance and keeping information

and document by persons entering

into an international transaction

Entity Related Price Related Transaction Related

•

•

•

•

•

•

•

•

•

•

Industry analysis

Group analysis

Details of related parties

Transaction terms

FAR analysis

Economic

Analysis and

Bench marking

Forecasts,

budgets, estimates

Agreements

Invoices

Pricing related

correspondence

(letters, e-mails,

fax, etc.)

The onus of proving SDT at ALP is on tax payer 41

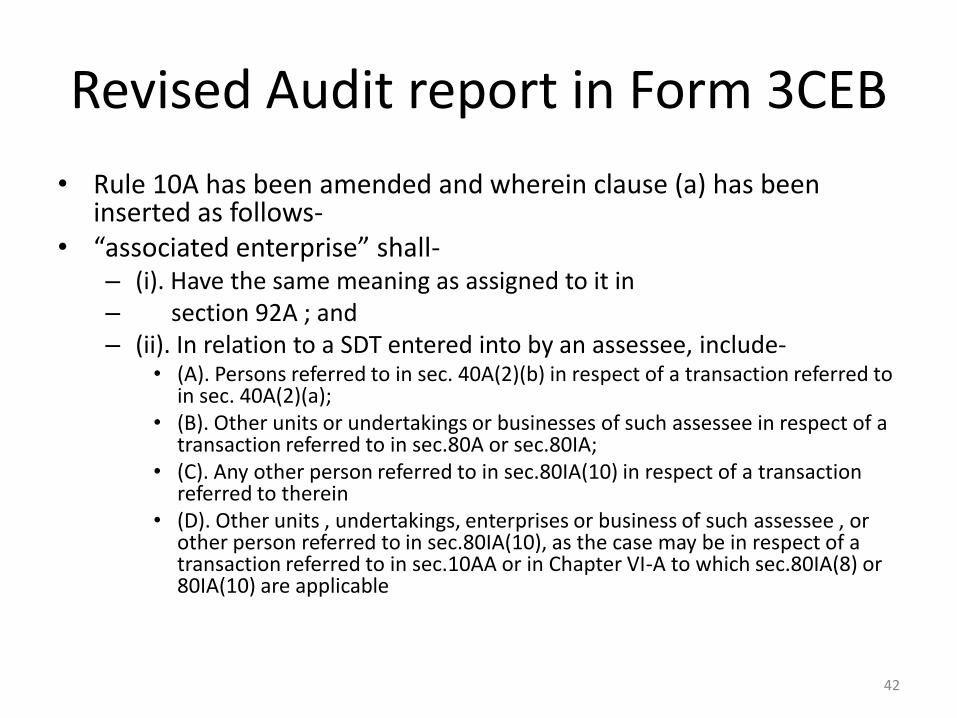

Revised Audit report in Form 3CEB

• Rule 10A has been amended and wherein clause (a) has been inserted as follows-

• “associated enterprise” shall- – (i). Have the same meaning as assigned to it in – section 92A ; and – (ii). In relation to a SDT entered into by an assessee, include-

• (A). Persons referred to in sec. 40A(2)(b) in respect of a transaction referred to in sec. 40A(2)(a);

• (B). Other units or undertakings or businesses of such assessee in respect of a transaction referred to in sec.80A or sec.80IA;

• (C). Any other person referred to in sec.80IA(10) in respect of a transaction referred to therein

• (D). Other units , undertakings, enterprises or business of such assessee , or other person referred to in sec.80IA(10), as the case may be in respect of a transaction referred to in sec.10AA or in Chapter VI-A to which sec.80IA(8) or 80IA(10) are applicable

42

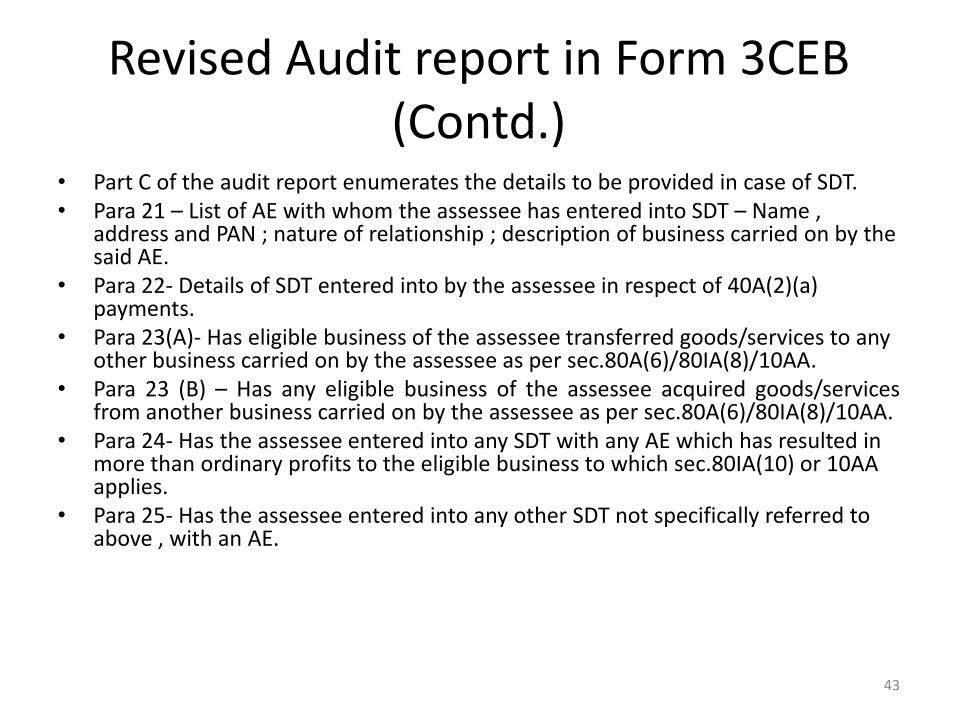

Revised Audit report in Form 3CEB (Contd.)

• Part C of the audit report enumerates the details to be provided in case of SDT. • Para 21 – List of AE with whom the assessee has entered into SDT – Name ,

address and PAN ; nature of relationship ; description of business carried on by the said AE.

• Para 22- Details of SDT entered into by the assessee in respect of 40A(2)(a) payments.

• Para 23(A)- Has eligible business of the assessee transferred goods/services to any other business carried on by the assessee as per sec.80A(6)/80IA(8)/10AA.

• Para 23 (B) – Has any eligible business of the assessee acquired goods/services from another business carried on by the assessee as per sec.80A(6)/80IA(8)/10AA.

• Para 24- Has the assessee entered into any SDT with any AE which has resulted in more than ordinary profits to the eligible business to which sec.80IA(10) or 10AA applies.

• Para 25- Has the assessee entered into any other SDT not specifically referred to above , with an AE.

43

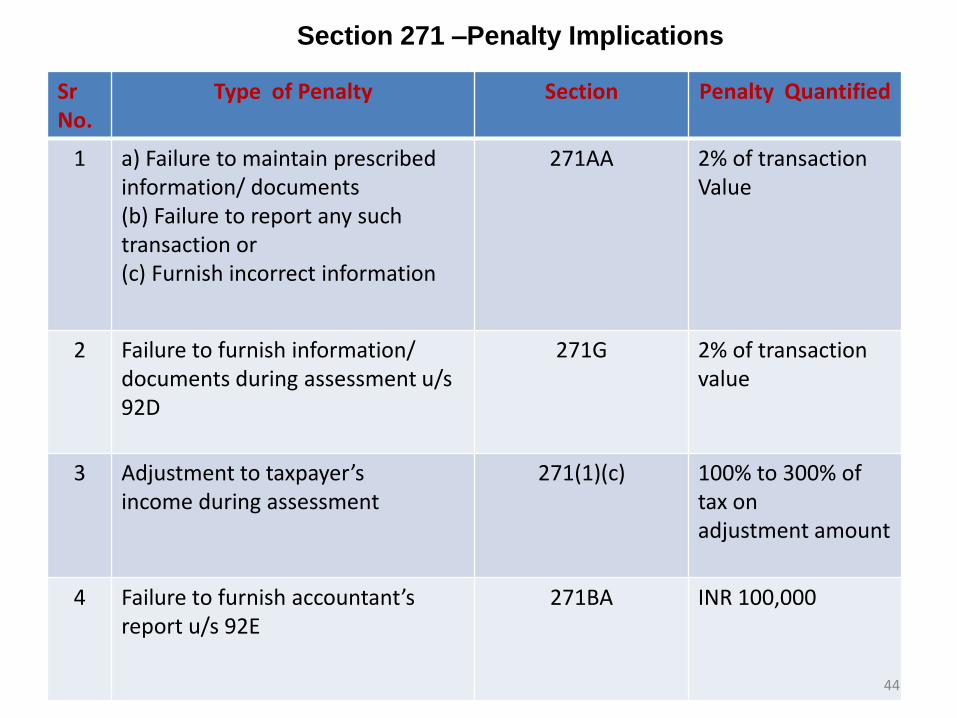

Section 271 –Penalty Implications

Sr No.

Type of Penalty Section Penalty Quantified

1 a) Failure to maintain prescribed information/ documents (b) Failure to report any such transaction or (c) Furnish incorrect information

271AA 2% of transaction Value

2 Failure to furnish information/ documents during assessment u/s 92D

271G 2% of transaction value

3 Adjustment to taxpayer’s income during assessment

271(1)(c) 100% to 300% of tax on adjustment amount

4 Failure to furnish accountant’s report u/s 92E

271BA INR 100,000

44

Thank you

Information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is

received or that it will Continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

45