Embed Size (px)

Citation preview

Dorel Home Furnishings

• Norman Braunstein ‐ President, Dorel Home Furnishings

• Our vision: To be the product, innovation, and volume market leaders in the supply of Home Furnishings to the major North American retailers

• Five individual business units

– Great product diversity

– Currently take advantage of shared services to reduce cost and increase efficiency within IT, SG&A, supply chain and distribution

2

Today’s agenda

• Overview of the furniture industryy

• Dorel Home Furnishings Divisions– Cosco Home and Office

A i d– Ameriwood

– Altra

– DHP

– Dorel Asia

• E‐Commerce

C l i• Conclusion

$

3

Note: amounts are in US$

Overview of US Furniture Market

Aft t f d li th US f it k t 4% i 2010 d• After two years of decline, the US furniture market grew 4% in 2010 and 2.4% in 2011.

• Furniture demand is strongly tied to new home and home sale increases.Furniture demand is strongly tied to new home and home sale increases. Both of these data points have been fairly stagnant in the US., but are now showing signs of improvement.

• Upholstery is expected to be the fastest growing segment as home owners invest in their homes. Bedroom is the largest segment.

• Furniture stores continue to be the largest sales channel however non• Furniture stores continue to be the largest sales channel, however non‐traditional channels such as Internet and mass merchants are growing at a much faster rate.

• Walmart, including Sam’s Club, is US’s largest furniture retailer.

• Ashley (furniture store), Walmart (mass merchant) and IKEA (specialty) are the three largest retailers of furniture.

4

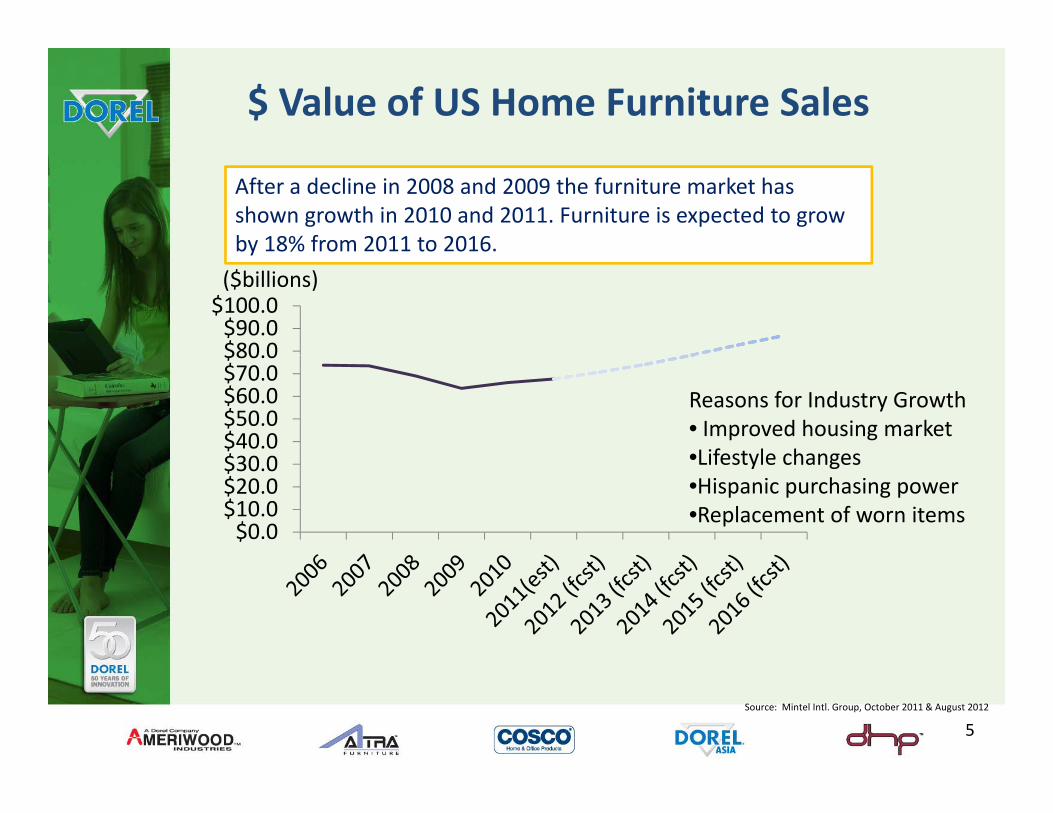

$ Value of US Home Furniture Sales

After a decline in 2008 and 2009 the furniture market has shown growth in 2010 and 2011. Furniture is expected to grow by 18% from 2011 to 2016.

$80.0$90.0$100.0

y

($billions)

$30 0$40.0$50.0$60.0$70.0$80.0

Reasons for Industry Growth• Improved housing market•Lifestyle changes

$0.0$10.0$20.0$30.0 •Lifestyle changes

•Hispanic purchasing power•Replacement of worn items

Source: Mintel Intl. Group, October 2011 & August 2012

5

Where do people buy furniture?

70 2004

2007

Dorel HF sales via Internet presents a big opportunity

Dorel well positioned To take advantage in

40

50

60en

t 2007

2011these three categories

20

30Perce

0

10

Internet Furniture Mass Home* Club Department tstore

Based on a survey of 1000 people who have bought furniture in the last year * No data for 2004

Source: Mintel Intl. Group, October 2011

6

US Distribution of Retail FurniturePeople are buying furniture outside of the traditional channelsPeople are buying furniture outside of the traditional channels

$20

$30

$40

$50

20082009

(in billions)

$0

$10

$20

Furniture Stores Mass Merc. All Other*

20102011

* All other includes Internet, catalogue, office superstores, home centers and specialty stores

Source: Mintel Intl. Group, October 2011

7

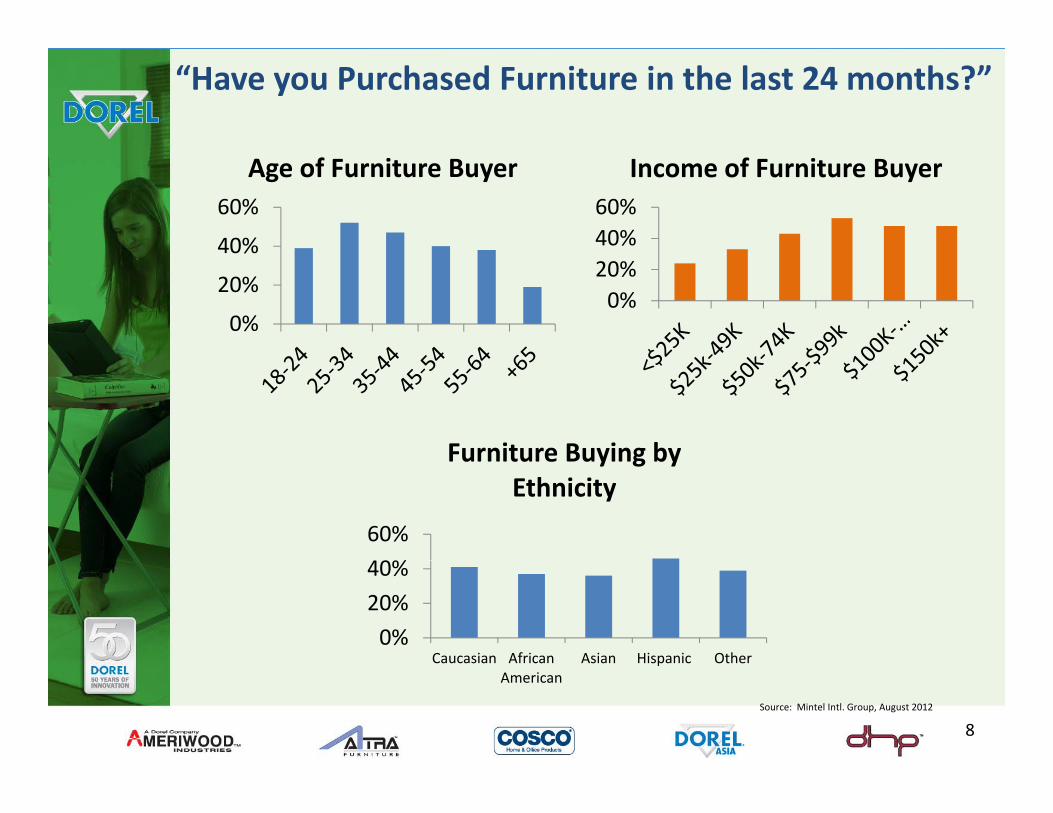

“Have you Purchased Furniture in the last 24 months?”

40%

60%

Age of Furniture Buyer

40%60%

Income of Furniture Buyer

0%

20%

40%

0%20%

Furniture Buying by

40%

60%

Furniture Buying by Ethnicity

0%

20%

40%

Caucasian African Asian Hispanic Other

Source: Mintel Intl. Group, August 2012

Caucasian AfricanAmerican

Asian Hispanic Other

8

Leading US Furniture Retailers2011

$3.0(in billions)

$1 5

$2.0

$2.5

$0.5

$1.0

$1.5

$0.0

= Current Dorel HF CustomerSource: Furniture Today, Aug 2012

9

Manufacturer Sales of Furniture into the US2009‐2010

$

$3.5(in billions)

$

$2.0

$2.5

$3.0

$0 0

$0.5

$1.0

$1.5 2009

2010

$0.0

Source: Furniture Today: November, 2011

10

Dorel Home Furnishings

11

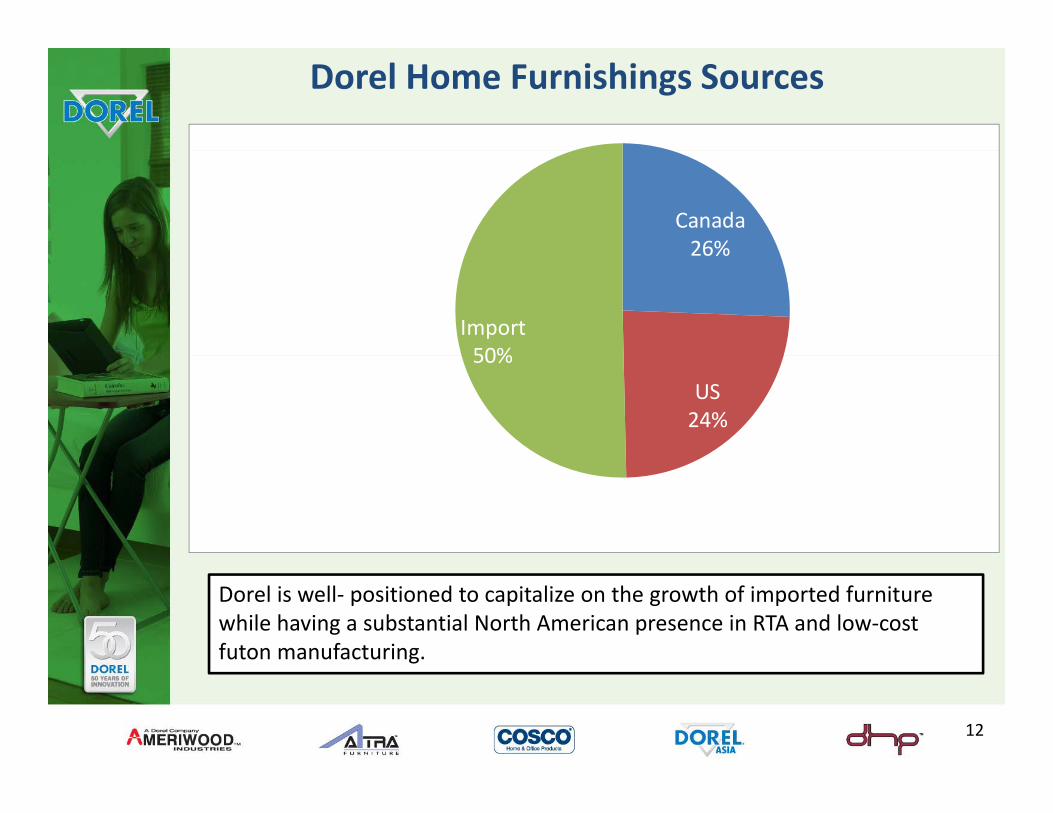

Dorel Home Furnishings Sources

Canada26%26%

Import50%

US24%

50%

Dorel is well‐ positioned to capitalize on the growth of imported furniture while having a substantial North American presence in RTA and low‐cost futon manufacturing.g

12

Home Furnishings Segment Asia Operations

Asia:

—Investment in “on the ground” resources—Product Development—Engineering—Quality Control—Order Flow and LogisticsOrder Flow and Logistics—Sourcing—60 Employees

Kunshan

Xiamen

DongguanHo Chi Minh

13

Home Furnishings Geographic Strategy

• Canada

– Reorganized our Canadian Home Furnishings organization in 2009

– Substantial growth in the last three years

– Sell product from all Dorel Home Furnishings divisions

– Target Canada opportunity

• Exploring sales opportunities outside North America

– South America/Central America

– Europe

– Australia/ New Zealand

– China

14

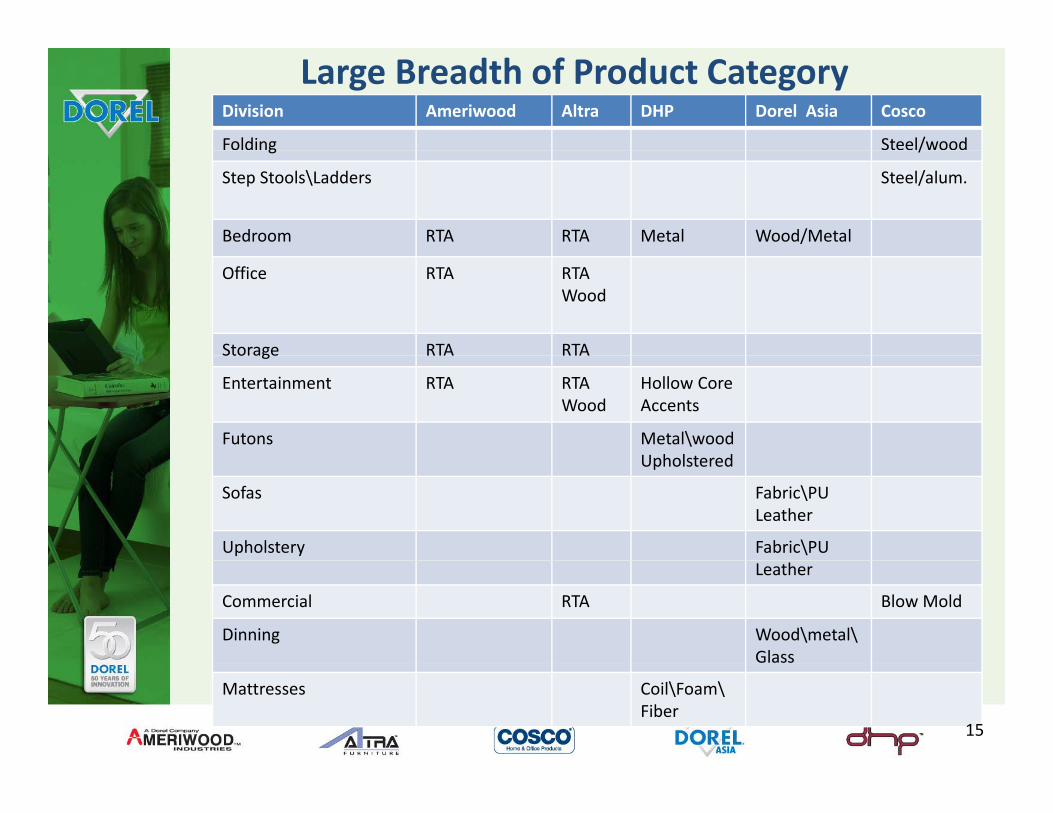

Large Breadth of Product CategoryDivision Ameriwood Altra DHP Dorel Asia Cosco

Folding Steel/woodg /

Step Stools\Ladders Steel/alum.

Bedroom RTA RTA Metal Wood/Metal

Office RTA RTAWood

Storage RTA RTAStorage RTA RTA

Entertainment RTA RTAWood

Hollow CoreAccents

Futons Metal\woodUpholsteredUpholstered

Sofas Fabric\PULeather

Upholstery Fabric\PULeather

Commercial RTA Blow Mold

Dinning Wood\metal\Glass

Mattresses Coil\Foam\Fiber

15

Cosco Home & Office

• Location ‐ Columbus, IN,

• Imports – folding furniture, step stools, hand trucks and specialty ladders

• Import distribution facilities – Ontario, California and Savannah, Georgia

• Main customers‐Mass merchants clubs home centersMain customers‐Mass merchants, clubs, home centers, commercial office suppliers, hardware chains

16

Folding Furniture:

17

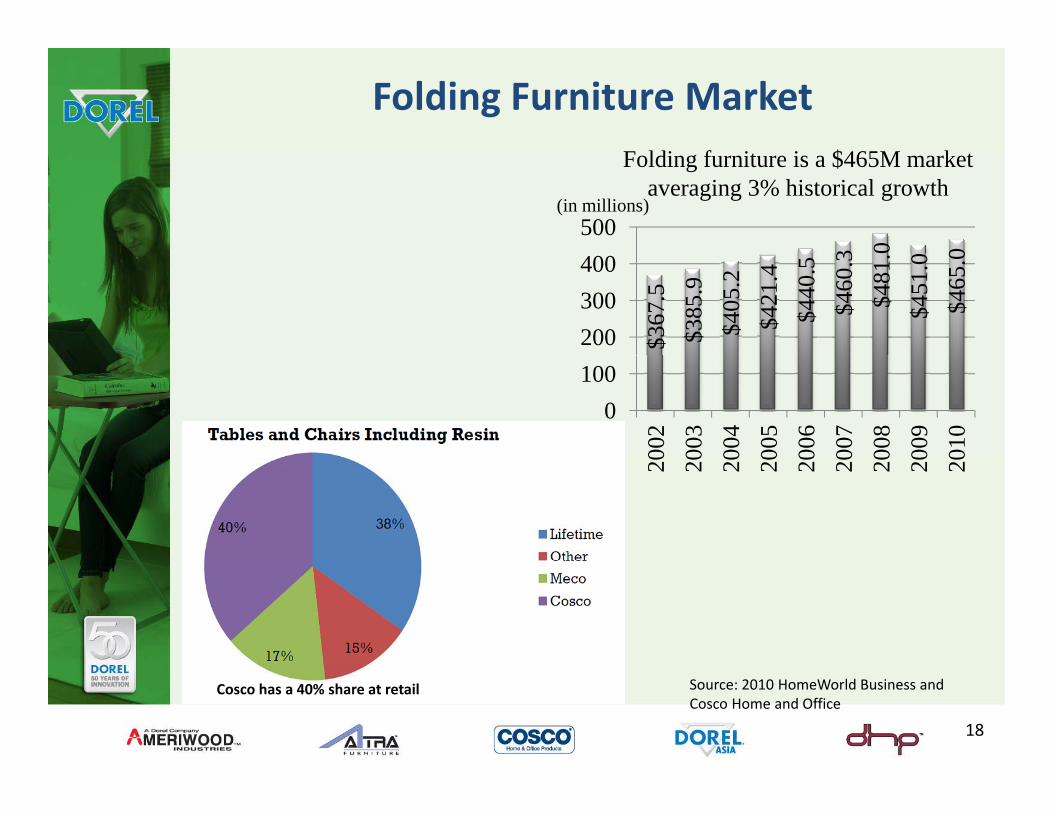

Folding Furniture Marketldi f i i $ kFolding furniture is a $465M market averaging 3% historical growth

3 0 0

500(in millions)

$367

.5$3

85.9

$405

.2$4

21.4

$440

.5$4

60. 3

$481

.0$4

51.0

$465

.0

200300400

0100

002

003

004

005

006

007

008

009

010

20 20 20 20 20 20 20 20 20

Source: 2010 HomeWorld Business and Cosco Home and Office

Cosco has a 40% share at retail

18

Step Stools and Ladders:

19

Step Stool Market

Retail Dollar Sales of Step Stools ( in millions)

200

250

167178 187

199211

179164 166

150

167 164 166

50

100

Source: 2010 HomeWorld Business and

02004 2005 2006 2007 2008 2009 2010 2011

Source: 2010 HomeWorld Business and Cosco Home and Office

20

Product Line Expansions: :

21

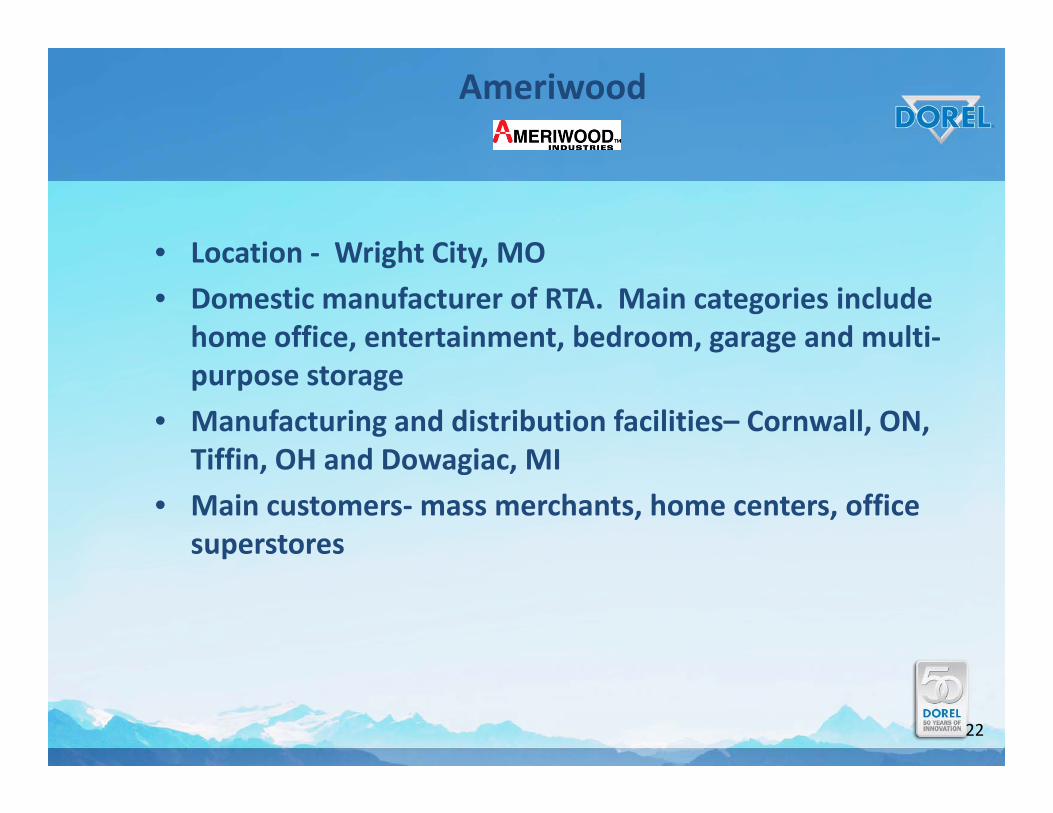

Ameriwood

• Location Wright City MO• Location ‐ Wright City, MO

• Domestic manufacturer of RTA. Main categories include home office, entertainment, bedroom, garage and multi‐purpose storage

• Manufacturing and distribution facilities– Cornwall, ON, Tiffin OH and Dowagiac MITiffin, OH and Dowagiac, MI

• Main customers‐mass merchants, home centers, office superstores

22

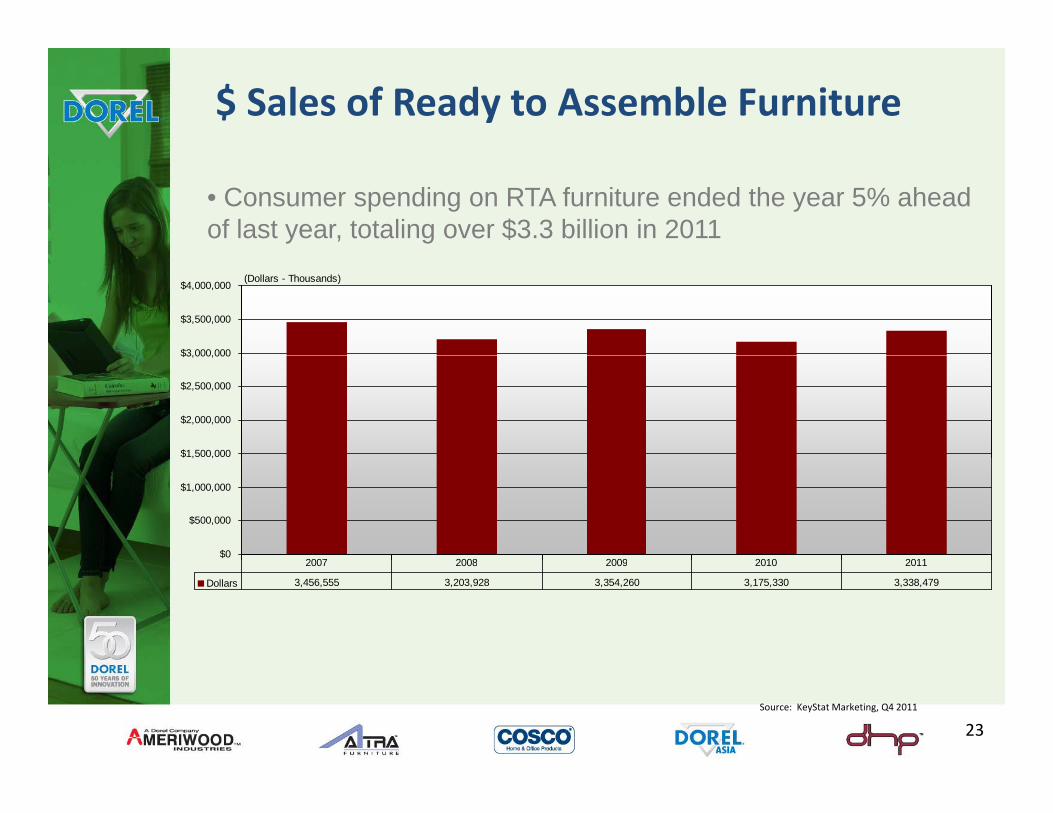

$ Sales of Ready to Assemble Furniture

• Consumer spending on RTA furniture ended the year 5% ahead of last year, totaling over $3.3 billion in 2011

$3,000,000

$3,500,000

$4,000,000(Dollars - Thousands)

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$0

$500,000

$1,000,000

, ,

2007 2008 2009 2010 2011

Dollars 3,456,555 3,203,928 3,354,260 3,175,330 3,338,479

2007 2008 2009 2010 2011

Source: KeyStat Marketing, Q4 2011

23

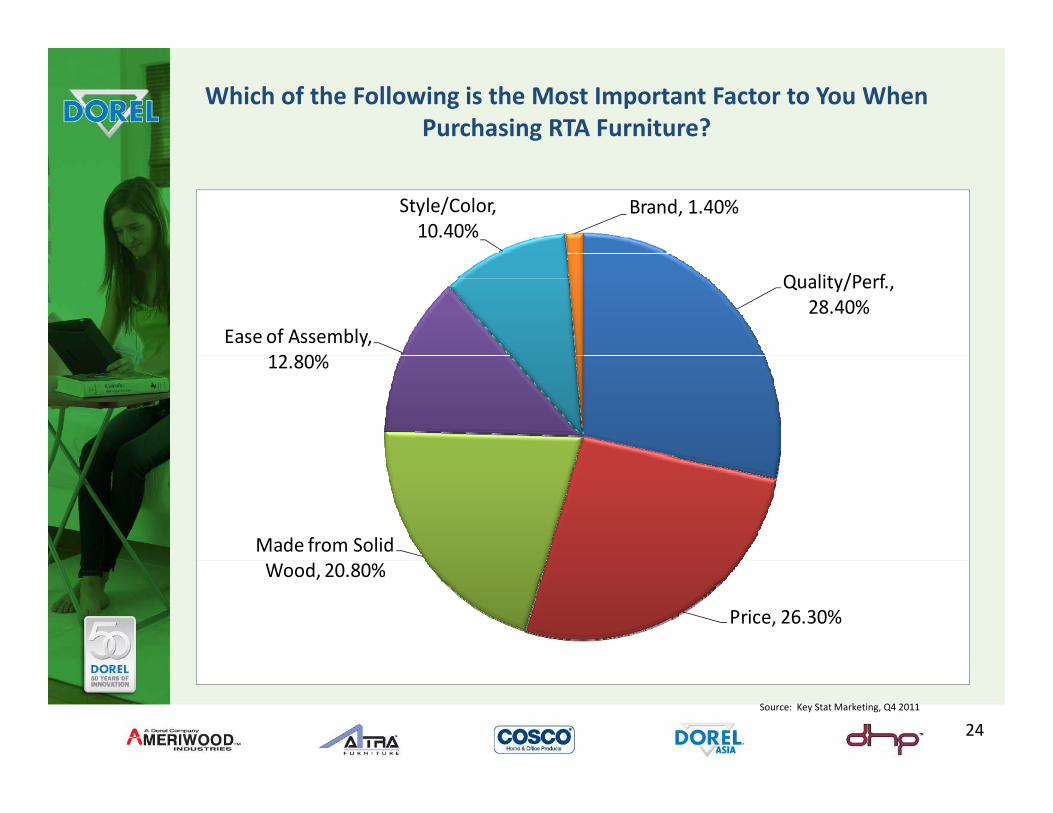

Which of the Following is the Most Important Factor to You When Purchasing RTA Furniture?

Style/Color, 10.40%

Brand, 1.40%

Quality/Perf., 28.40%

Ease of Assembly, 12 80%12.80%

Made from Solid

Price, 26.30%

Wood, 20.80%

Source: Key Stat Marketing, Q4 2011

24

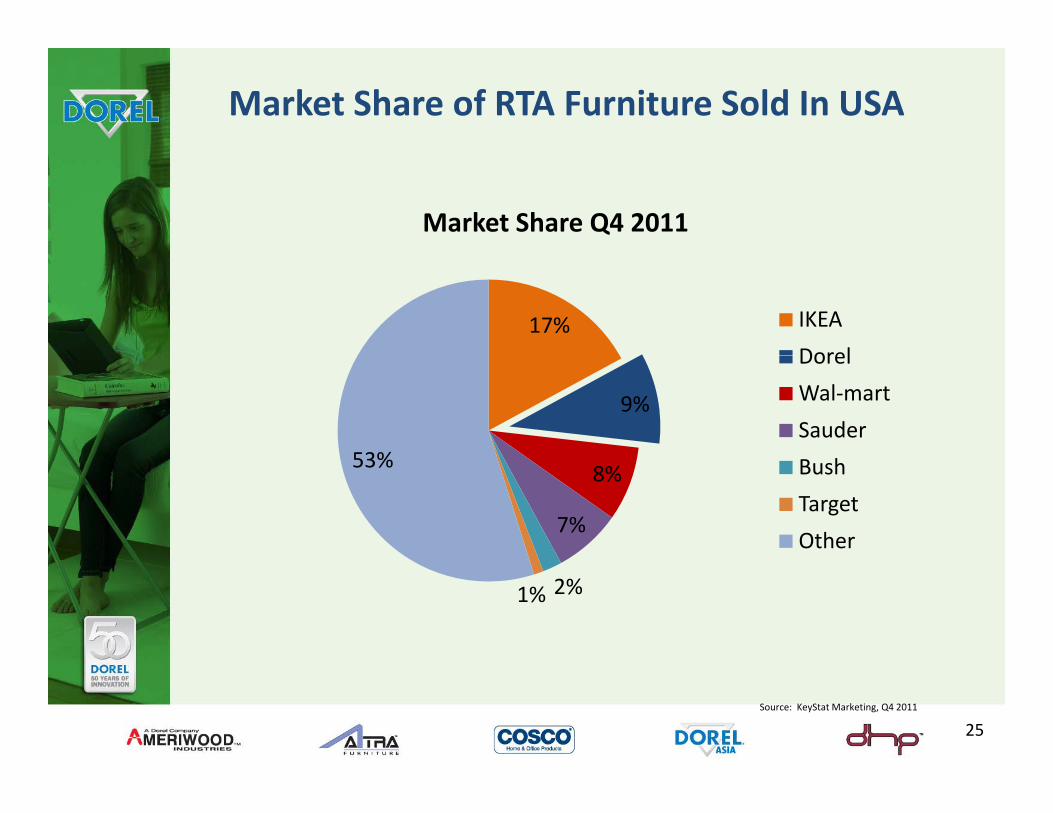

Market Share of RTA Furniture Sold In USA

Market Share Q4 2011

17% IKEA

Dorel

9%

53%

Dorel

Wal‐mart

Sauder

h8%

7%

53% Bush

Target

Other

2%1%

Source: KeyStat Marketing, Q4 2011

25

RTA‐Storage: Ameriwood

26

RTA‐Bedroom/Office: Ameriwood

27

Dorel has the Advantage of Domestically Produced RTA

• Ameriwood, through its domestic manufacturing facilities, is a significant source of cash generation and revenue for Dorel Home FurnishingsFurnishings.

• Ameriwood operates three highly efficient/low CAPEX manufacturing and distribution facilities

Cornwall ON– Cornwall, ON

– Tiffin, OH

– Dowagiac, MI• Retailers recognize the advantages of domestic production

– Shorter lead‐times– Reduced inventory costs– Reduced freight costs

• More stable cost environment compared to import• “Made in North America”

28

Altra Furniture

• Location ‐ Wright City, MOg y,

• Importer of RTA with concentration in home entertainment, home office, commercial office, and storage furniture

• Importer of case pieces for home office and home entertainment

• Import distribution facilities– Ontario California andImport distribution facilities Ontario, California and Savannah, Georgia

• Main customers‐mass merchants, office superstores, home entertainment superstores, clubs

29

RTA – Ready to Assemble: Altra

30

Case Pieces: Altra

31

RTA/Back to College: Altra

32

Dorel Home Products

• Location ‐ Montreal, QC

• Manufacturer and importer of futons, mattresses, baby mattresses

• Importer of futons accent tables leisure seating and metal• Importer of futons, accent tables, leisure seating and metal bunk and loft beds

• Import distribution facility– Ontario, California, Savannah, Georgia

• Domestic distribution facility‐Montreal, QC

M i t h t di t h i I t t• Main customers‐mass merchants, discount chains, Internet

33

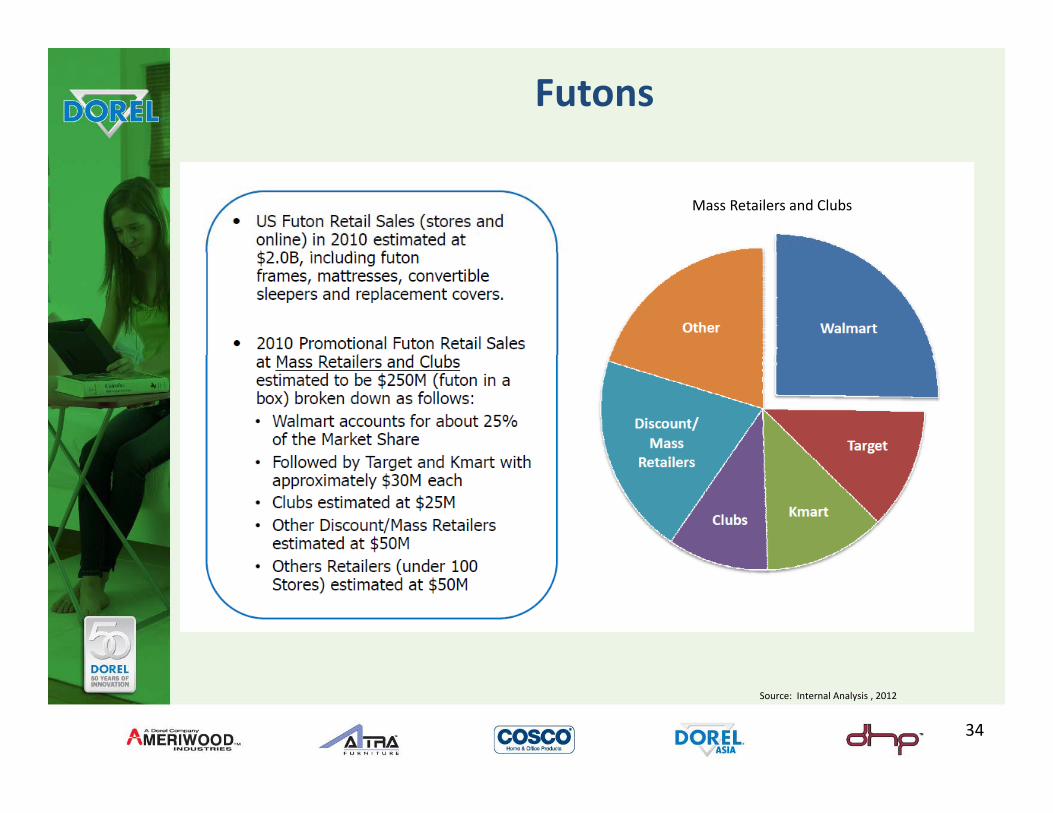

Futons

Mass Retailers and Clubs

Source: Internal Analysis , 2012

34

Futons: DHP

35

Mattresses: DHP

36

Mattress Sales Starting to Rebound

$

$17

s

Sales of Mattresses & Other Sleep Environments

$14

$15

$16es $billion

s Environments

l$12

$13

$14

attress Sale

$3$10

$16 $19Dorel Mattress Sales $ millions

$10

$11

$12

US Ma

$102007 2008 2009 2010 2011 2012 est

Source: Mintel International, Oct 2011 & Internal

37

38

Metal Bunk Beds: DHP

39

Dorel Asia

• Importer

Upholstery– Upholstery

– Bedroom

– Dining and KitchenDining and Kitchen

– Youth

– Accent

• Import distribution facility– Ontario, California, Savannah,

GeorgiaGeorgia

• Main customers‐mass merchants, clubs, Internet

40

Upholstery: Dorel Asia

41

Bedroom Furniture: Dorel Asia

42

Dining/ Accent: Dorel Asia

43

E‐Commerce• On‐line research now very important for comparison shopping

• “Free Ship” sights or “free pick‐up at store” driving on‐line purchasespurchases

• Importance of on‐line reviews in buying decision

• Physical footprint of furniture at “brick and mortar” retailers is d l ldriving on‐line line extensions

• Ability to use video and animation will allow for increases on‐line

• 2/3rds of consumers still want to touch and feel furniture before purchase, especially at the higher end

• Younger consumers increasingly likely to buy on‐line

44

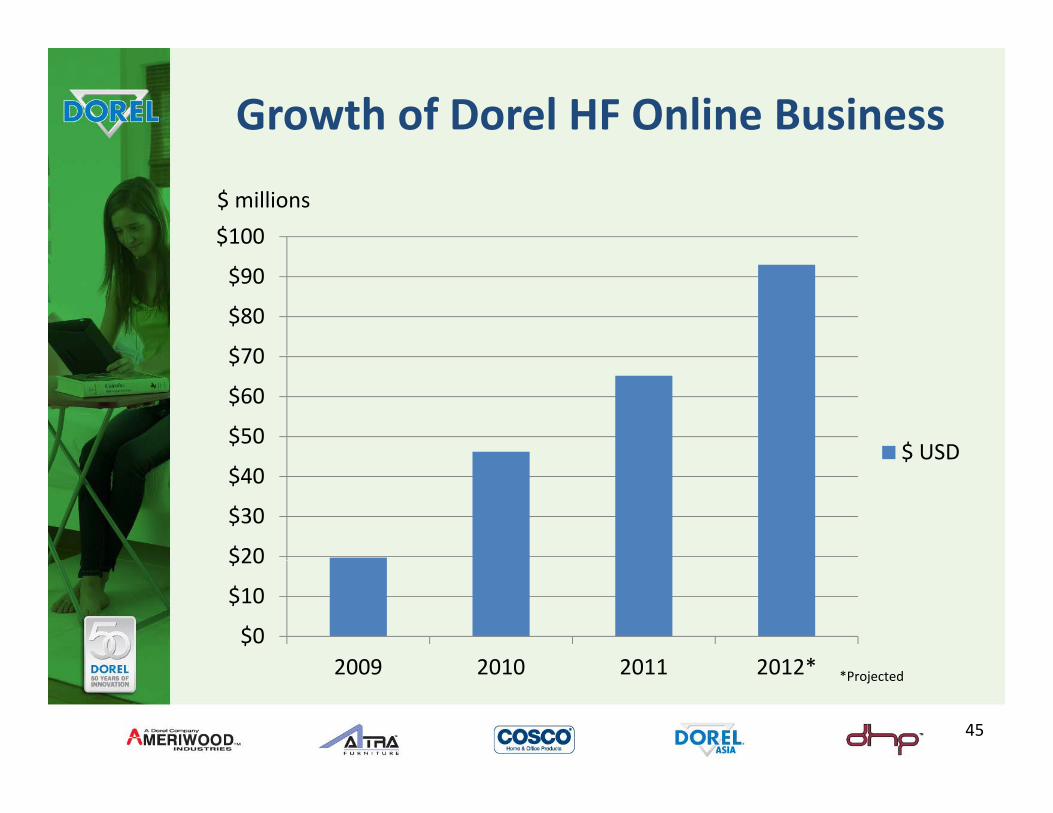

Growth of Dorel HF Online Business

$100

$ millions

$70

$80

$90

$50

$60

$70

$ USD

$20

$30

$40$ USD

$0

$10

$20

2009 2010 2011 2012*2009 2010 2011 2012* *Projected

45

Home Furnishings Online Strategy

“To deliver to the front door of the consumer the best value in furniture”

New online distribution f lfacility in Savannah,Georgia

Existing West Coast Distribution

46

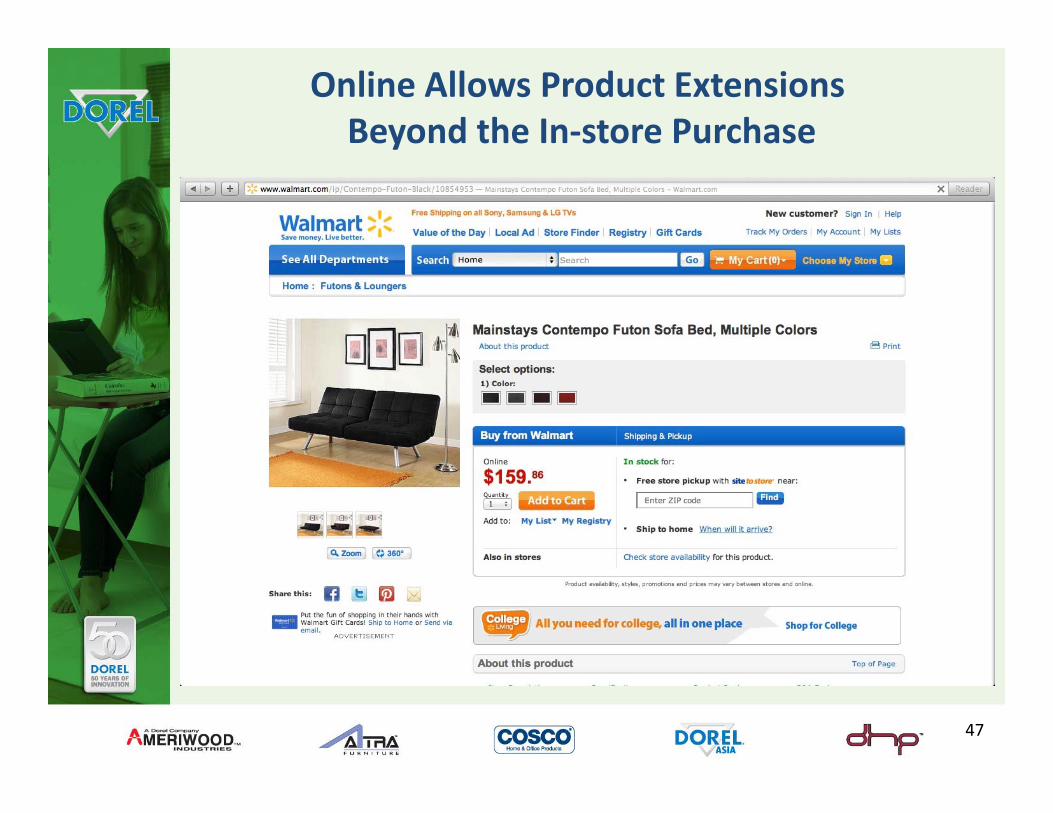

Online Allows Product ExtensionsBeyond the In‐store Purchase

47

Online Allows Product ExtensionsBeyond the In‐store Purchase

In‐store Nolan Item at Target

Nolan Extensions offered on Target.com

48

Online Allows Product ExtensionsBeyond the In‐store Purchase

In‐store desk at Office Depot

Line extensions at Officedepot.com

49

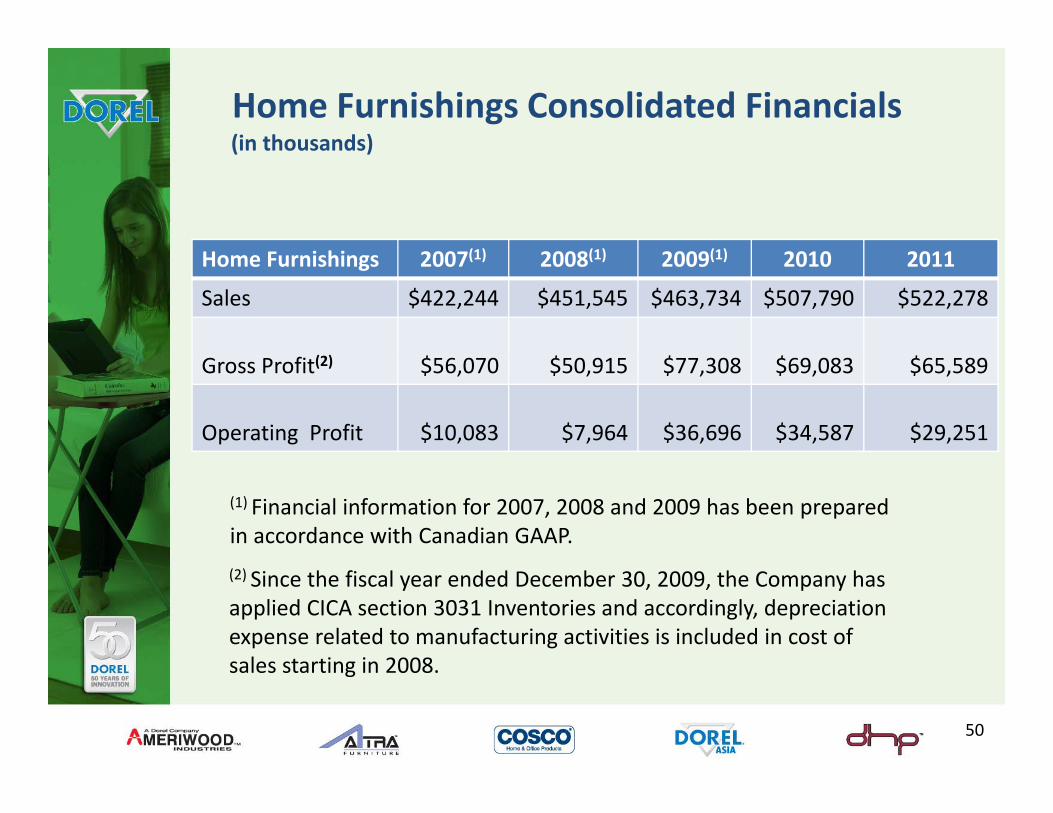

Home Furnishings Consolidated Financials(in thousands)

H F i hi 2007(1) 2008(1) 2009(1) 2010 2011

(in thousands)

Home Furnishings 2007(1) 2008(1) 2009(1) 2010 2011

Sales $422,244 $451,545 $463,734 $507,790 $522,278

( ) $ $ $ $ $Gross Profit(2) $56,070 $50,915 $77,308 $69,083 $65,589

Operating Profit $10,083 $7,964 $36,696 $34,587 $29,251

(1) Financial information for 2007, 2008 and 2009 has been prepared in accordance with Canadian GAAP.

(2) Since the fiscal year ended December 30, 2009, the Company has applied CICA section 3031 Inventories and accordingly, depreciation expense related to manufacturing activities is included in cost of sales starting in 2008

50

sales starting in 2008.

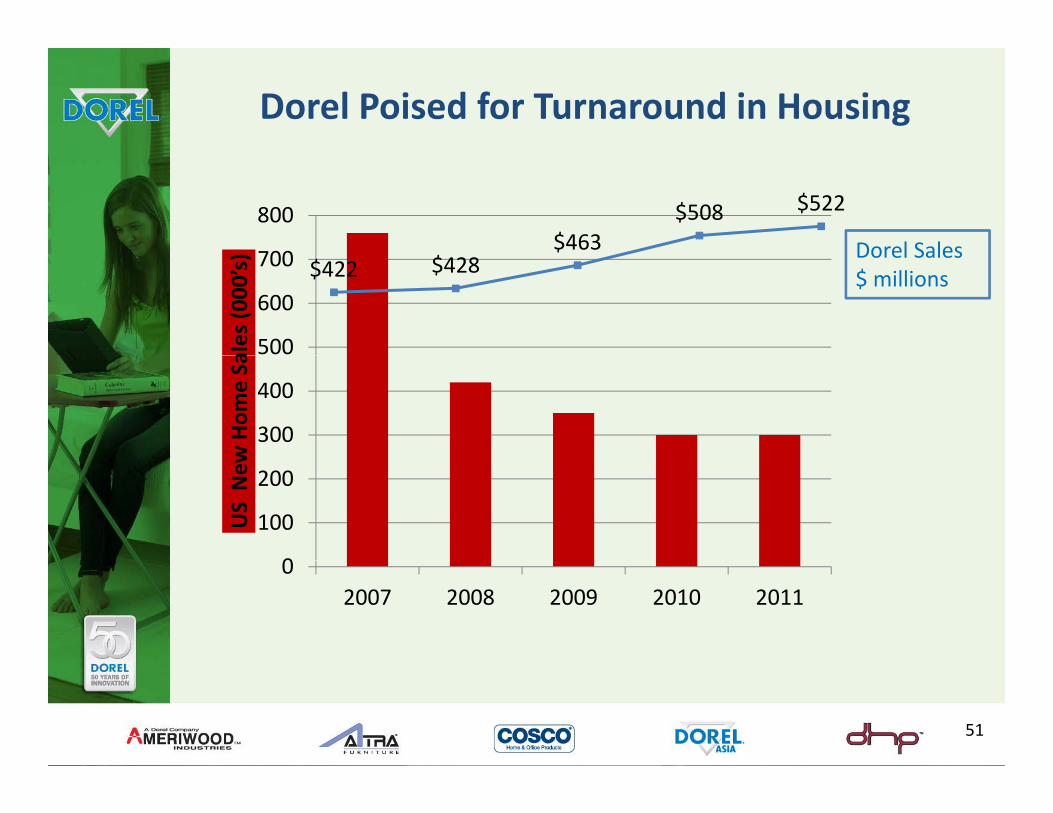

Dorel Poised for Turnaround in Housing

700

800$463

$508 $522

Dorel Sales

500

600

700ales (0

00’s)

$422 $428Dorel Sales $ millions

300

400

w Hom

e Sa

0

100

200

US New

02007 2008 2009 2010 2011

51

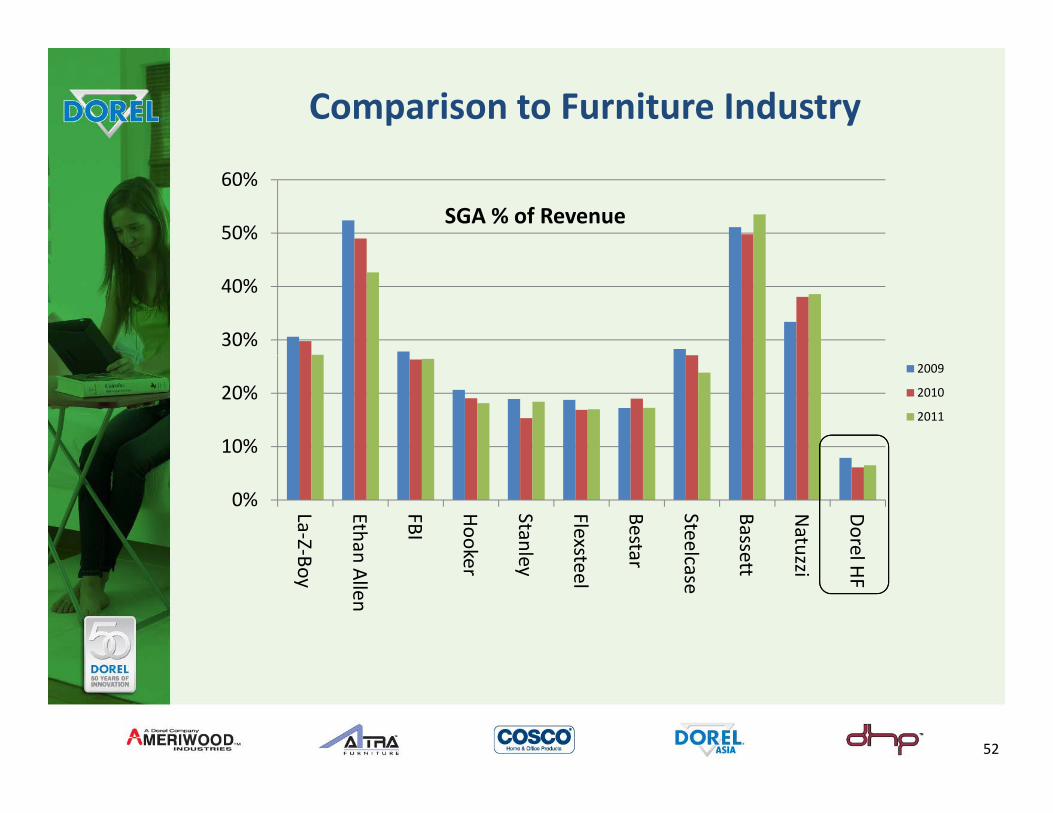

Comparison to Furniture Industry

50%

60%

SGA % of Revenue

30%

40%

10%

20%2009

2010

2011

0% La‐Z‐B

Ethan

FBI

Hooke

Stanle

Flexst

Besta

Steelc

Basse

Natuz

Dorel Boy

n Allen

er

ey

teel

r case

ett

zzi HF

52

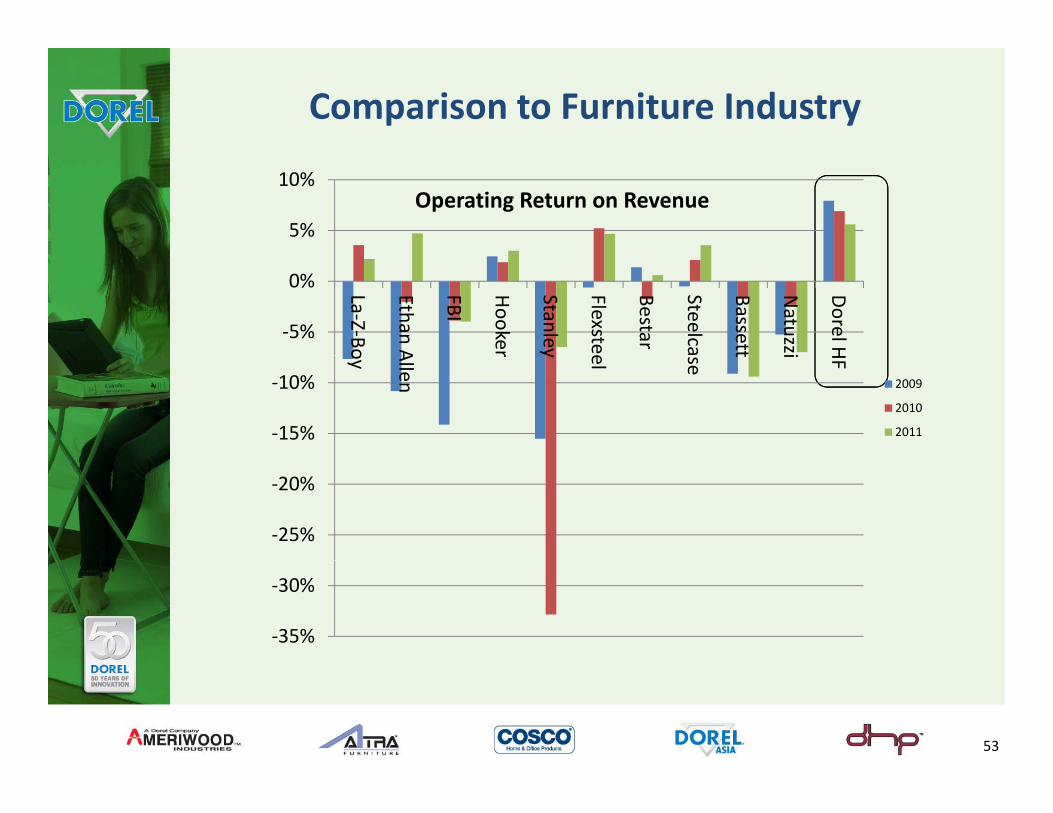

Comparison to Furniture Industry

5%

10%Operating Return on Revenue

‐5%

0% La‐Z‐Bo

Ethan A

FBI

Hooke r

Stanley

Flexstee

Bestar

Steelca

Basset t

Natuzzi

Dorel H

‐15%

‐10%

oy

Allen

r y el

se

t i HF

2009

2010

2011

‐25%

‐20%

‐35%

‐30%

53

The Next Three Years

• Continue to generate significant cash flow for Dorel Industries

• Revenue growth through the development of value‐ oriented, ell designed prod ctwell‐designed product

• Increased penetration: additional customers and channels Strong effort to increase on‐line sales

• Possible consolidation of divisions to increase profitability, efficiencies and effectiveness in product development, sourcing, and customer presentations

• Possible acquisitions in order to drive revenue, expand our product line, or enable vertical integration

• Continued focus on bottom line profitability while increasing d lrevenue and return on capital

54

In Conclusion: The Dorel Advantage

• Diversification

• Domestic manufacturing and import distribution footprint

• Industry leaders in folding furniture, step stools, futons, and among the leaders in RTA

• Customer Base: Focus on big box retailers‐ fastest growing furniture segment. Provide product, sourcing, and logistics expertise

• Taking advantage of consumer trends

• Potential to leverage cross‐divisional synergies through administrative, distribution, and sales/marketing consolidation

• Strong divisional management teamg g

• Corporate strength

THANK YOU.....ANY QUESTIONS?55