Embed Size (px)

Citation preview

With the compliments of

Limited Edition Protect your marketing budgets

FREE eTips at dummies.com®

Promotional Risk

Management

01_975725-ffirs.indd i 9/17/10 11:53 AM

By Mando

A John Wiley and Sons, Ltd, Publication

Promotional RiskManagement

FOR

DUMmIES‰

01_975725-ffirs.indd i 9/17/10 11:53 AM

Promotional Risk Management For Dummies®

Published byJohn Wiley & Sons, Ltd

The AtriumSouthern GateChichesterWest SussexPO19 8SQEnglandFor details on how to create a custom For Dummies book for your business or organisation, contact [email protected]. For information about licensing the For Dummies brand for products or services, contact BrandedRights&[email protected] our Home Page on www.customdummies.comCopyright © 2011 by John Wiley & Sons Ltd, Chichester, West Sussex, EnglandAll Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechani-cal, photocopying, recording, scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency Ltd, 90 Tottenham Court Road, London, W1T 4LP, UK, without the permission in writing of the Publisher. Requests to the Publisher for permission should be addressed to the Permissions Department, John Wiley & Sons, Ltd, The Atrium, Southern Gate, Chichester, West Sussex, PO19 8SQ, England, or emailed to [email protected], or faxed to (44) 1243 770620.Trademarks: Wiley, the Wiley Publishing logo, For Dummies, the Dummies Man logo, A Reference for the Rest of Us!, The Dummies Way, Dummies Daily, The Fun and Easy Way, Dummies.com and related trade dress are trademarks or registered trademarks of John Wiley & Sons, Inc. and/or its affiliates in the United States and other countries, and may not be used without written permission. All other trade-marks are the property of their respective owners. Wiley Publishing, Inc., is not associated with any product or vendor mentioned in this book.

LIMIT OF LIABILITY/DISCLAIMER OF WARRANTY: THE PUBLISHER, THE AUTHOR, AND

ANYONE ELSE INVOLVED IN PREPARING THIS WORK MAKE NO REPRESENTATIONS OR WAR-

RANTIES WITH RESPECT TO THE ACCURACY OR COMPLETENESS OF THE CONTENTS OF THIS

WORK AND SPECIFICALLY DISCLAIM ALL WARRANTIES, INCLUDING WITHOUT LIMITATION

WARRANTIES OF FITNESS FOR A PARTICULAR PURPOSE. NO WARRANTY MAY BE CREATED

OR EXTENDED BY SALES OR PROMOTIONAL MATERIALS. THE ADVICE AND STRATEGIES CON-

TAINED HEREIN MAY NOT BE SUITABLE FOR EVERY SITUATION. THIS WORK IS SOLD WITH

THE UNDERSTANDING THAT THE PUBLISHER IS NOT ENGAGED IN RENDERING LEGAL,

ACCOUNTING, OR OTHER PROFESSIONAL SERVICES. IF PROFESSIONAL ASSISTANCE IS

REQUIRED, THE SERVICES OF A COMPETENT PROFESSIONAL PERSON SHOULD BE SOUGHT.

NEITHER THE PUBLISHER NOR THE AUTHOR SHALL BE LIABLE FOR DAMAGES ARISING HERE-

FROM. THE FACT THAT AN ORGANIZATION OR WEBSITE IS REFERRED TO IN THIS WORK AS

A CITATION AND/OR A POTENTIAL SOURCE OF FURTHER INFORMATION DOES NOT MEAN

THAT THE AUTHOR OR THE PUBLISHER ENDORSES THE INFORMATION THE ORGANIZATION

OR WEBSITE MAY PROVIDE OR RECOMMENDATIONS IT MAY MAKE. FURTHER, READERS

SHOULD BE AWARE THAT INTERNET WEBSITES LISTED IN THIS WORK MAY HAVE CHANGED

OR DISAPPEARED BETWEEN WHEN THIS WORK WAS WRITTEN AND WHEN IT IS READ.

Wiley also publishes its books in a variety of electronic formats. Some content that appears in print may not be available in electronic books.ISBN: 978-0-470-97572-5Printed and bound in Great Britain by Page Bros, Norwich10 9 8 7 6 5 4 3 2 1

01_975725-ffirs.indd ii 9/17/10 11:53 AM

Introduction

W elcome to Promotional Risk Management For Dummies, your step-by-step guide to protecting your promotional budget.

Fixed fee. Over redemption cover. Prize indemnity. Assessing and evaluating insurance options for a pro-motional campaign, or whether you need to cover at all, can be a mind-boggling task. This book takes you through the process from a risk manager’s point of view so you can see what he sees, and understand the questions he might ask you.

The more you understand about managing the risk in a promotion, the more control you have over the sepa-rate budgetary elements of a campaign, and not just those connected with risk. By looking at the individual components you can see which ones really matter, and which are having the greatest influence over consumer behaviour.

About This BookThis book aims to provide you with information to make the right choices when it comes to managing promotional risk. It’s full of useful tips and hints about where the risk lies in your promotional strategy, and how you can use that risk to make your brand’s budget work harder.

02_975725-intro.indd 1 9/17/10 11:53 AM

Foolish AssumptionsIn writing this book, we made some assumptions about you:

✓ You work in promotional marketing.

✓ You work in an agency or for a brand.

✓ You know that some promotions carry financial risk that’s linked to the level of uptake of the offer by your target customers.

How This Book is OrganisedPromotional Risk Management For Dummies is divided into five small but perfectly-formed parts:

✓ Chapter 1: Identifying Risk. Go here to see where the risk is lurking in your strategy, and how to manage it to your advantage.

✓ Chapter 2: Assessing Risk. Understand what’s inside the head of your risk manager and why he’s asking you all those questions; we look at what’s in the quote.

✓ Chapter 3: Managing Risk. In this part we run through the ways you can manage risk and how to choose the right experts to help you.

✓ Chapter 4: Looking at Risk Management in Action. Here we give you examples of promotions such as scratch cards and coupons.

✓ Chapter 5: Ten Steps to Promotional Risk Management Success. This succinct list leads the way to success.

2

02_975725-intro.indd 2 9/17/10 11:53 AM

3

Icons Used in This BookWe highlight crucial text for you with the following icons:

The Dummies man indicates real-life examples to illustrate a point and inspire you.

The knotted string highlights important infor-mation to bear in mind.

Home in on the target for tips to enable you to understand your risk better.

Where to Go from HereAs with all For Dummies books, you can either read this guide from cover to cover or flick straight to the sec-tion that interests you. Whether you read it in small doses using the section headings or all in one go, you’ll find plenty of information to get you on your way to managing bigger, safer, better-protected promotion marketing campaigns.

02_975725-intro.indd 3 9/17/10 11:53 AM

Chapter 1

Identifying Risk

In This Chapter▶ Knowing why promotional marketing can be a risky

business▶ Understanding the different types of risk▶ Discovering how promotional risk management

works

The problem with promotional marketing is that if you do it really well, it can cost you a lot of money.

If you create an offer that consumers find irresistible, not only will your products fly off the shelves, but your costs for honouring that offer could run out of control.

Risk management isn’t just about financial risk; it also covers logistical issues surrounding your campaign and ensures you can deliver it within the terms of the promotion.

Effective use of risk management techniques can enhance the creative process, allowing you to make stunning offers within even modest budgets.

03_975725-ch01.indd 4 9/17/10 11:54 AM

5

Understanding Where Risk Comes FromYour risk management strategy depends on your pro-motion. You can determine the risk during the develop-ment of the campaign by looking at elements such as communication routes, brand history and the redemp-tion process. Most important of all is the budget.

Budget Your fixed costs often affect consumers’ aware-

ness of the promotion, but your variable costs are related to how much they like it. Intrigued? This section explains all.

Only some parts of your budget are open to risk. Your total campaign may include elements such as advertis-ing, pack printing and PR. These elements are ‘fixed’ irre-spective of the uptake of your promotion, so you need to put them to one side when deciding the proportion of your budget that can be allocated to ‘variable’ costs.

However, the risk assessor needs to know your fixed spend before agreeing a quote because these elements affect the audience awareness of your promotion and so affect its uptake. In fact, you’re likely to find your risk assessor can help you here, suggesting changes to fixed cost activities to enable you to meet your variable budget.

Some promotional costs are very much dependent on how many people participate in the offer. These include coupon refunds, data capturing applications and postage to send out prizes. If your promotion is successful, these costs can mount up quickly.

03_975725-ch01.indd 5 9/17/10 12:15 PM

6

It is this variable budget that dictates the rest of your promotion and how it is made up. It determines your prize fund or premium choice, it affects the participa-tion rates or winning rates you need to target, and it affects the redemption routes you have available to you.

Your risk assessor can advise you on budgets. Indeed, she could suggest changes to the pro-motion if your budget is too low for the type of offer in the brief.

Brand profileThe personality of your brand is a consideration in any promotion when determining the uptake of your offer. For example, a t-shirt with a Coca-Cola slogan may have more appeal than one from, say, Andrex. However, Andrex has pretty much cornered the market of cute puppies, so a plush toy Coca-Cola bottle may not excite your target audience as much.

Frequency of product usage or, more accurately, its purchase also affects the promotional uptake espe-cially on collector-led schemes or campaigns where the product must be fully consumed before entry (for example, where an entry form is included on the pack).

The type of productEach product sector has its own characteristics regard-ing product loyalty and usage rates. You can expect collector schemes on tea and coffee, where brand loy-alty is high, to redeem higher than one on frozen ready meals, where the consumer is more promiscuous.

Cereals, pet foods and nappies are also heavily pro-moted compared to white goods, for example. Look

03_975725-ch01.indd 6 9/17/10 11:54 AM

7

down the aisles at any supermarket and you will see the sectors where brand competition is high – if one cereal brand runs an on-pack, the rest will soon follow.

Historical resultsHindsight is a wonderful thing; never more so than in promotional risk management! Past history of similar promotions is invaluable in assessing the likely uptake of future campaigns. But remember that every cam-paign has its own unique elements – even one repeat-ing the same promotion as last year, because the consumer environment and economic climate will have changed. Also not all products within the same group have the same profile; for example, Heineken has a dif-ferent consumer profile and therefore behaviour from Grolsch.

Historical results affect not only the likely uptake of a promotion, but also how the insurance market will view the campaign. Since Hoover (see the nearby side-bar), alarm bells start to ring if ‘electrical white goods’ and ‘free flights’ appear together on a broker’s pro-posal form. In fact, any promotion that leads to a claim on insurance affects premiums for similar future campaigns.

This doesn’t mean you should avoid letting your risk assessor know of past campaigns. Far from it. Failure to disclose this kind of material information could lead to a difficult claim if your campaign over-redeems. And with fixed fee arrangements, it could nullify the con-tract completely, irrespective of the uptake. When in doubt, disclose everything.

03_975725-ch01.indd 7 9/17/10 11:54 AM

8

Method of communicationHow you communicate the offer greatly affects the uptake – and hence costs – of your promotion. Leaving TV and display advertising to one side for the moment, the consumers’ reaction to the campaign depends on whether they see the offer on a pack, on the Internet or by leaflet or coupon.

The entry route also affects the number of opportunities to enter, and so also the uni-verse on which the risk assessed.

Hoover’s Free Flights campaignThe Hoover Free Flights campaign was an important lesson in how not to manage promotional risk. In 1992, the household brand offered free return flights to Europe and USA with every appliance purchased.

It was a truly generous offer and the public were quick to spot that the value of the flights far exceeded the value of the appliance.

The company soon found itself overwhelmed with requests for tickets; a pressure group was formed specifically to pursue claims and the court cases continued until 1998. It’s estimated that the whole situation cost the company over £45 million to resolve and resulted in the British division of Hoover being sold to a competitor.

The promotion was completely uninsured, despite risk assessment advice that the offer was too rich.

03_975725-ch01.indd 8 9/17/10 11:54 AM

9

LeafletsLeaflet-led campaigns require the consumer to pick up and save a leaflet to enter the offer. Leaflets could be magazine inserts, enabling a well-targeted campaign, but separating the communication from the actual product. You can place in-store leaflets nearer the merchandise, but your offer is shown to everyone, whether or not they buy the product, and still requires extra effort from the consumer to enter. In all these cases the financial risk is directly linked to the number of leaflets printed.

InternetIf your promotion exists only online, the risk could become infinite if there are no other controls in the ‘real’ world. So if you invite users to ‘click to print a coupon’, the assessor might require forecasts of the product sales to give some sense-check to the redemp-tion forecasts. An alternative would be to switch off the web page once a certain number of visitors have printed a coupon.

On-pack offers On-pack communication gives the highest par-

ticipation rates of all routes. The offer is shown to the consumer each time he buys or uses the product and requires no further action to keep the entry route. The strength of the message on the pack also affects its uptake, both in terms of product pick up in store and application rate.

Break down on-pack communication further and redemption rates differ significantly according to how the offer appears. Fix-a-forms and neck collars may cause an uplift in responses because they interfere with the product usage in the home. You have to

03_975725-ch01.indd 9 9/17/10 11:54 AM

10

remove the collar before you pour the bottle, or peel off the fix-a-form to open the pack. This means the con-sumer is forced to look at the offer in his hand, making it more likely that he will enter.

Whichever communication route you choose, your risk assessor will ask to see artwork before confirming a level of cover and will advise on the message tone and strength in order to keep fees within your budget.

Coupons Coupons can be distributed in a number of ways, each with its own redemption pattern. For example, a coupon published in a free newspaper could be expected to redeem at around 1% due to the dispos-able nature of the medium. However, a coupon direct-mailed to known users of a specific product sector can reach as high as 40%. So it’s essential you know pre-cisely the means of communication and, for direct mail, what the source of the list is.

Supporting mediaYour campaign’s use of media affects the risk asses-sor’s perception of the promotion. She needs to have all the information you can give about how the promo-tion will be supported.

TV or display advertisements affect the sales of a product, but not necessarily the uptake of the offer. However, if the advertisement is itself an offer – such as a taste challenge, or try-me-free – then you can expect a significant uplift in participation.

Many promotions enjoy success without any media support; the on-pack offer being sufficiently well designed to work alone.

03_975725-ch01.indd 10 9/17/10 11:54 AM

11

Consider the value and purpose of the media spend before committing budget to this part of the campaign. Resources could perhaps be more targeted at boosting the offer itself through a better quality premium, higher win rates or easier entry routes.

Proof of purchase requirementFor most promotions, some degree of proof of pur-chase (POP) is required to ensure the consumer has bought the correct product. In some cases this may just be one or more pack tokens, ring pulls or unique numbers printed on the pack. In others the actual till receipt may be required.

In risk management terms, the till receipt does more than prove a purchase. Keeping a till receipt may put some consumers off applying (which can be a positive or negative thing). The receipt also carries a date which can be very important in validating the claim (see ‘Timescale’).

Similarly, a high requirement for token collection may be used to ensure a real effort on the part of the con-sumer to participate in the offer.

Perceived value of offerRemember Hoover? The free flights promotion is noto-rious because the perceived value of the offer far out-weighed the purchase price required to enter. Stories of consumers buying product to claim the tickets and then selling on their machine at car boot sales, and now eBay, should act as a constant reminder!

03_975725-ch01.indd 11 9/17/10 11:54 AM

12

If the perceived value of your offer is going to exceed the purchase price, ensure you have the budget and resources to fulfil that offer. This is where campaigns can fall down by inadequately planning the workload generated by a high response rate.

Conversely, you want to ensure the offer is sufficiently attractive to consumers to tempt them to purchase the product. A free CD with every test drive of the new Ford is more attractive than a free CD when you buy a new Ford. The former might create a change in behav-iour, the latter probably won’t.

The best way to avoid such issues is to ensure your offer has a reasonable perceived value, keep responses to a manageable level and keep costs within your budget. Risk managers can help here, as they want to avoid both a Hoover scenario and a campaign flop. They want a successful campaign. Their role is to recommend a promotional structure that meets your budget and ensures you can manage the responses and finances. They have good advice on the balance between offer value and purchase price.

Ease of participationYou want to make the promotion easy and fun for the consumer to engage with. So you need to strike a balance between making it too easy (leading to over-redemption) and too difficult (leading to a poor cam-paign and possibly unwanted customer service issues).

Your risk manager can advise on the route to entry you’re considering in order to meet the budget. In some cases this may require only minor changes. For

03_975725-ch01.indd 12 9/17/10 11:54 AM

13

example, a brief requiring the consumer to collect three tokens in exchange for a mug may be brought into budget by simply requiring four tokens. It may be that a postal contribution can be added, giving the dual effect of reducing applications and part-funding the offer.

With SMS (text) campaigns, remember to make it easy to enter with short initial mes-sages. If you need to confirm winner contact details, you can do so online later.

TimescaleThe time you give participants to respond to an offer affects total redemption levels and resourcing costs. Risk assessors like to have set parameters within which they can determine their exposure – start and end dates in other words.

You need to give consumers enough time to use up the required amount of product to enter your offer, but if you give them too long, you may incur unnecessary costs for handling, storage or coupon management. Your risk assessor can help to estimate the redemption rates over time, and decide a cut-off date at which point the level of applications becomes too low to warrant keeping the promotion open.

Coupon clearing houses usually have a minimum monthly charge for managing a promotion, and this can become significant once redemptions fall below this level. Talking to your risk assessor, or direct with the clearing house, helps you determine a cut-off date to print on the coupon. Remember that retailers don’t need any more than three months from the consumer cut-off date to send in their tokens.

03_975725-ch01.indd 13 9/17/10 11:54 AM

14

Setting a time limit for applications can help reduce cost too by asking the consumer to work a little harder. If the consumer has only 14 days from purchase to redeem, you can expect fewer responses than if they had, say, 30 days, or no limit at all.

The key is to make the time limit reasonable, fair and verifiable.

SecurityMany campaigns offer high value prizes in games of chance or skill. These campaigns not only carry their own risks associated with the prize being won, but also from fraudulent claims. If you plan to take out insur-ance or a fixed fee policy, the risk assessor wants to ensure you’ve built in sufficient security to control the chance of winning. For this she’ll probably appoint a loss adjuster before the campaign begins to oversee production and administrative issues.

The loss adjuster will want to be certain, for example, that only the specified number of winning bottle caps is produced in an instant-win promotion. He’ll want to witness their production, obtain audited statements from the manufacturers and will oversee the destruc-tion of any over-production. Once the top prize caps are produced, the loss adjuster may add a security mark to them to ensure they’re not reproduced (the consumer will be asked to describe this if the prize is claimed). The adjustor will also ensure the winning caps are seeded correctly and fairly into the main pro-duction run so there’s no chance of being able to iden-tify a winning batch.

03_975725-ch01.indd 14 9/17/10 11:54 AM

15

With scratch cards, the loss adjuster will assess the effectiveness of samples produced before giving the OK on a full run. He’ll ensure the cards aren’t see-through, even exposed to high-intensity lighting, and that the winning sequences on the cards are randomised, with enough scenarios to make predictive revealing impossible.

In games of skill, too, the loss adjuster needs to be present. ‘Kick-to-win’ competitions are conducted in the presence of an adjudicator, who’ll want to place the ball before each attempt and want to know the player is a bona fide member of the public, not a professional.

Loss adjusters are there to ensure the promo-tion runs fairly, as you planned it. Should a claim lead to an investigation, remember the adjuster is on your side even though it may not always seem that way!

Purchasing behaviourYou need to understand the demographics of your target market and how that interacts with the brand

Not a lotteryOne promotion famously sent a pub landlord a set of three-from-nine scratch cards, all of which carried the same pat-tern beneath the latex panels. The landlord was able to claim a full set of golf clubs and ten umbrellas for his trouble!

03_975725-ch01.indd 15 9/17/10 11:54 AM

16

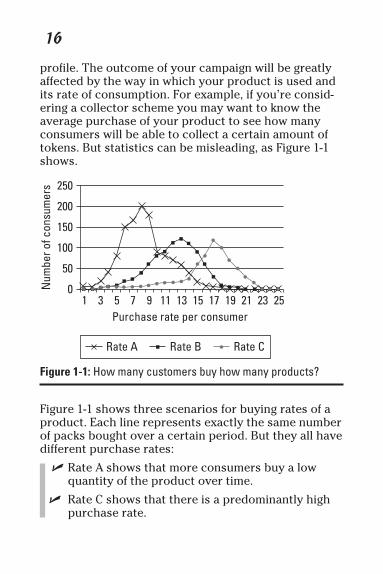

profile. The outcome of your campaign will be greatly affected by the way in which your product is used and its rate of consumption. For example, if you’re consid-ering a collector scheme you may want to know the average purchase of your product to see how many consumers will be able to collect a certain amount of tokens. But statistics can be misleading, as Figure 1-1 shows.

01

50

100

150

200

250

3 5 7 9 11 13 15Purchase rate per consumer

Rate A Rate B Rate C

Num

ber o

f con

sum

ers

17 19 21 23 25

Figure 1-1: How many customers buy how many products?

Figure 1-1 shows three scenarios for buying rates of a product. Each line represents exactly the same number of packs bought over a certain period. But they all have different purchase rates:

✓ Rate A shows that more consumers buy a low quantity of the product over time.

✓ Rate C shows that there is a predominantly high purchase rate.

03_975725-ch01.indd 16 9/17/10 11:54 AM

17

Or you can compare the average rate of purchase:

✓ Rate A has an average rate of 8 packs

✓ Rate B has an average of 12

✓ Rate C has an average of 16.

Rate C represents half the number of consumers as Rate A, while Rate B rate falls somewhere between the two.

This matters because if you’re estimating the redemption rates for a collector scheme based on manufacturer-supplied buying averages of 12, you may also decide to set the token requirement to 12.

Now, Rate B has an average of 12 so over half the con-sumers could collect enough tokens. And they would need to buy nearly three quarters of the total packs. But if consumers were closer to Rate C, with its higher average, nearly everyone would collect 12 and nearly all packs could be used.

So, for a collector on, say, biscuits you might provide an average frequency of purchase of 12 per year, but a range of between 2 and 120. While only the top 1 to 2% of consumers may be buying at the 100+ rate, in a col-lector or instant win mechanic they can represent a disproportionate amount of the risk.

Average means nothing without accurate information on the rate of purchase. And that means a comprehensive review of who’s going to buy the product and how many buyers will participate in the promotion.

03_975725-ch01.indd 17 9/17/10 11:54 AM

Chapter 2

Assessing Risk

In This Chapter▶ Knowing what risk managers look for in promotions▶ Considering the questions you might be asked▶ Grasping how mechanics makes a difference

When you’ve identified where the risk lies in your promotion, it then needs to be assessed to

show how much of a risk it presents. Your risk man-ager needs to know where it is on the scale between high and low risks.

During this assessment you’ll be asked questions about areas of the campaign you may not have considered. In this part we help you understand risk assessment and the level of detail you need to supply.

Asking the Right Questions to Offer the Right QuoteYour risk manager will ask for lots of information before calculating a quote. Here’s a taster.

04_975725-ch02.indd 18 9/17/10 11:54 AM

19

Product detailsThe product and the market it sits in give context to the offer you’re building, so it’s important to set the scene with this information.

Brand and manufacturerSome brands carry more loyalty than others; some have their own personalities that affect people’s perceptions of them. So this information helps the risk manager under-stand how consumers may react to the product or service even without a promotion. It’s also important to know whether this is a new product, an existing one enjoying a re-launch, or just part of a sustained programme.

Purchase priceThe spend:reward ratio is very important in determin-ing the likely uptake of a promotion, whether on-pack or as a result of a service or loyalty programme.

Buying patternsHow often people buy the product, and in what quanti-ties affects many promotional mechanics. This informa-tion might be hard to find, but most brands have research showing frequency and weight of purchase.

Averages can be misleading here so try to give the range of buying patterns to your risk manager.

Who buys and whereThe type of people who normally buy the product and where they buy affect the uptake. Products bought pre-dominantly by professionals online have a different promotional profile from fast-moving consumer goods (FMCGs) bought daily in a supermarket.

04_975725-ch02.indd 19 9/17/10 12:21 PM

20

Many brands have their target customers’ pro-files, so look to share this information with your risk manager so he has a better picture of who’s likely to be involved in the promotion.

The promotionExplaining a promotion – what it’s all about and why you’re doing it – is often quite simple but you need to expand on other details when looking at it from a risk manager’s point of view.

CommunicationWhere do consumers see the promotion and learn how to take part? It’s often on pack if space and production allow, but it could also be communicated on leaflets, TV, radio, or through sampling teams. And any combi-nation or variation of these is possible.

Whichever route you choose affects the promotional risk, so your risk manager needs to know your commu-nication method.

The gift, prize or give-awayThe reward you’re offering the consumer clearly affects their perception of the promotion. You need to con-sider how much they get back in return for their initial efforts, whether they actually want the reward, how well it fits with the product they’re buying and whether they already have one.

Your risk manager will also want to know if there are any supply issues with the rewards in terms of manu-facturing times and minimum order quantities. These can have a hidden and significant impact on the final costs of the campaign.

04_975725-ch02.indd 20 9/17/10 11:54 AM

21

If you have a coupon campaign, you need to determine the restrictions on its use in terms of the stores that might accept it and against which products.

The universeThe universe in this context is nothing to do with the stars, but all about the size of the risk. If you’re produc-ing one million coupons, the universe is one million coupons. But if the campaign is communicated on TV, with no special packs, the universe is harder to define.

Risk managers work with you to agree the limits of their liability, and the potential size of the campaign. Make sure any quantifiable measures you can provide are accurate and relevant.

The rulesAll promotions have terms and conditions and while many of these are there for legal reasons, you can work with your risk manager to ensure they match his under-standing of what the consumer can and can’t do to enter the campaign.

Of particular importance for application-based offers is whether the promotion is restricted to one per household, if there’s a time limit for entry and whether the consumer needs to submit any other material to validate the application.

Variable costsWith all this information, it can be easy to miss out exactly what the risk management company is liable for! This needs to be set out as clearly and in as much detail as possible.

04_975725-ch02.indd 21 9/17/10 11:54 AM

22

At its simplest you have a basic cost per application but the elements that make this up depend on the mechanic of the offer.

Supporting activitySome promotions work perfectly well on their own with the on-pack message, leaflet or website doing all the work. Others enjoy considerable cross-media support and risk managers need to know all about that too.

Trade supportStore staff can greatly assist a consumer product pro-motion if they’re aware of it, and possibly incentivised towards it. Let your risk manager know if this is your plan and he can factor in its effect.

Uncovering the hidden costsLurking in many campaigns are the hidden costs. These include, but are far from limited to:

✓ Stock risk (caused by minimum order quantities and pro-duction lead times)

✓ Text messaging

✓ Translation services if needed

✓ Complex data capture

✓ Set up costs such as SMS message responses or linking your website to the handling house systems.

04_975725-ch02.indd 22 9/17/10 11:54 AM

23

Consumer supportYou can help consumers find your promotion in store with floor markers or shelf barkers. You can have dem-onstrators handing out the promotional product. Or perhaps you might create a major TV campaign to sup-port the offer. Whichever route you choose, be sure to let your risk manager know so its effect can be determined.

Historical informationWhen you insure a car, one of the questions you need to answer is whether you’ve had any bumps or crashes in the past five years. The same is true for promotions. If your brand has a history of high, or low, redemp-tions, the risk manager needs to know in order to assess the risk accurately.

Similar promotionsTell your risk manager if the manufacturer has run the same mechanic on a different brand in the past. This is relevant because it gives an indication of the previous promotional performance of the company.

Same brand, different mechanicPerhaps this is the first time the brand has run a collec-tor scheme, having previously used prize mechanics. Let the risk manager know about the prize promotions because it gives some insight to the behaviour of the brand’s purchasers.

Past promotional data is highly relevant when a promotion is insured. As we’ve said before, when in doubt, disclose everything.

04_975725-ch02.indd 23 9/17/10 11:54 AM

Chapter 3

Managing Risk

In This Chapter▶ Understanding your options▶ Considering remaining risk▶ Choosing the right company

Broadly speaking, risk management can be applied in four ways to sales promotions, which we

explain in this chapter. Choosing the right level and type of protection is the final step to ensuring your promotion is covered.

Ways to Manage RiskThis section explains your options when it comes to managing risk in sales promotions.

Fixed FeeFixed fee insurance typically covers all costs of a promotion irrespective of the number of redemptions actually received, protecting the promoter up to 100% claim rate.

05_975725-ch03.indd 24 9/17/10 11:55 AM

25

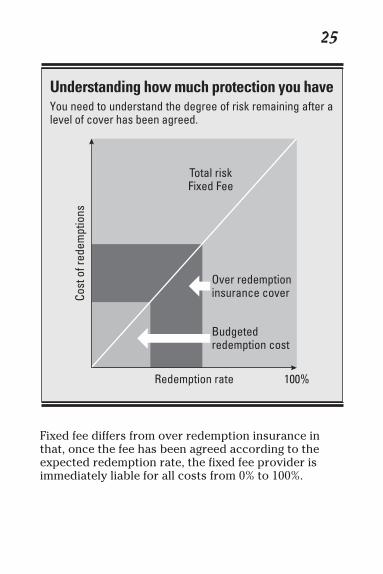

Fixed fee differs from over redemption insurance in that, once the fee has been agreed according to the expected redemption rate, the fixed fee provider is immediately liable for all costs from 0% to 100%.

Understanding how much protection you haveYou need to understand the degree of risk remaining after a level of cover has been agreed.

Total riskFixed Fee

Redemption rate 100%

Cost

of r

edem

ptio

ns

Over redemptioninsurance cover

Budgetedredemption cost

05_975725-ch03.indd 25 9/17/10 12:21 PM

26

Over redemption coverOver-redemption insurance, sometimes referred to as contingency insurance, means protecting the promoter in the event of participation being greater than the antici-pated, or budgeted, level, usually up to a pre-agreed maximum. So if you expect a 5% redemption level, you can take out over redemption insurance between 5% and 7.5%. But risk returns to you after 7.5%.

Over redemption insurance may appear to be the cheaper option for low-risk campaigns. It pays out after redemptions have reached a certain level, and contin-ues paying until a pre-set maximum has been exceeded. It’s a band of insurance – all costs either side of that band are your responsibility as the promoter.

Like any other kind of insurance, over redemption insurance is paid for through an insurance premium, which is subject to Insurance Premium Tax (IPT). Any claims may only be settled after the promotion has closed so you need to fund those costs, which may cover more than one financial year.

In order to meet loss adjuster requirements, your han-dling house needs to store all redemptions until the claim has been met. Some handling houses may charge for this service.

Fixed fee provides blanket cover for the promotion and as such may appear more expensive than over-redemption insurance. However, evaluate the two with caution to ensure a like for like comparison. Your promo-tion will be managed by the fixed fee company so you release responsibility for paying sup-plier invoices and dealing with loss adjusters to them.

05_975725-ch03.indd 26 9/17/10 11:55 AM

27

Prize indemnityPrize indemnity protects the promoter in the event of a particular prize, or prize fund, being won; normally Hole-In-One prizes.. Costs of processing applications aren’t covered in this insurance.

Promoter’s own riskIn this instance, the promoter takes on all risks and pays all costs.

Ensuring You Check Out the Risk Managers tooBefore handing over your promotion’s liabilities to a risk management company, ensure that they have the financial ability to take on that risk and fulfil your brand’s promise to its consumers whatever the redemption levels.

You can do this by checking the company’s balance sheet (last year’s financial statements will do); this shows you what immediate funds they could draw on if the promotion costs more than their fees.

Also check how they’ll re-insure themselves against the risk they’re taking on on your behalf. Make sure that they have enough funding or are adequately covered through a reputable and solid underwriter.

Any insurance documentation they provide must mention your promotion by name, otherwise it may not cover them against your activity.

05_975725-ch03.indd 27 9/17/10 11:55 AM

Chapter 4

Looking at Risk Management in Action

In This Chapter▶ Using scratch cards and coupons▶ Challenging tastebuds▶ Guaranteeing quality

Promotions can take many forms, so it follows that risk management varies from promotion to promo-

tion. This chapter runs through a few scenarios.

Free Prize DrawA chewing gum brand wants to run a prize draw offer-ing tickets to an exclusive concert by a major pop star. The offer is shown on outdoor posters and in store dump bins with leaflets. The entries to the draw must include three chewing gum wrappers in order to qual-ify. The wrappers aren’t specially marked. Applicants send their wrappers to a freepost address to enter the draw.

✓ There’s no risk on the ticket costs – all the tickets will be won.

06_975725-ch04.indd 28 9/17/10 11:56 AM

29

✓ There’s a risk on entry costs because each entry incurs a cost from the freepost rates and from ver-ifying the application is complete.

✓ The scale of the risk is proportionate to the sales of chewing gum over the time period.

Instant WinA fast food chain offers millions of prizes ranging from food to cash. Every burger and chips carton carries a win or lose message. Food prizes can be claimed in the store instantly. Other prize claims must be mailed in for verification.

✓ The risk is proportionate to the number of prizes on the packs, rather than the number of packs in total.

✓ Food prizes are outside a risk management arrangement due to their instant nature and low cost of redemption to the manufacturer.

✓ Costs would be incurred to verify the other prizes, particularly very high-value prizes which must be independently audited.

✓ The costs of the other prizes would be covered by the risk management company.

✓ There’d be a difference in claim rate between the lower value prizes and the very high value prizes because the higher value prizes are more desirable.

06_975725-ch04.indd 29 9/17/10 12:22 PM

30

CouponA soft drinks brand runs a promotion in a newspaper offering every reader a free bottle of soft drink on the day of publication. The offer is flashed on the front page of the paper and the coupon is printed within the main body of the paper. The coupon is only valid in one supermarket chain.

✓ The level of risk is proportionate to the circula-tion of newspaper on the day of publication.

✓ The coupon bar code would be set up to be valid only in the specific supermarket chain.

✓ The forecast redemptions based on the newspa-per circulation were sense-checked against daily sales of the product in the specific supermarket.

✓ Depending on the electronic point of sale (EPOS) systems at the supermarket chain, the single-day validity would be hard to verify, so reasonable judgement would need to be applied.

✓ The front page flash wouldn’t be guaranteed until the day of publication dependent on that day’s news. Risk managers would have to assume the flash would be used.

✓ The artwork for the coupon advert and the rest of the page are put together by the paper, with very little control from the brand or agency.

✓ The cost of each redemption is the face value of the coupon plus clearance at the coupon process-ing house.

06_975725-ch04.indd 30 9/17/10 11:56 AM

31

Quality GuaranteeA health yoghurt brand offers consumers their money back if they write in and say why they don’t feel better after trying the product for 14 days. The offer is pro-moted on special packs, two of which are required to complete a 14-day trial. Applications need to include till receipts showing purchase of the right number of packs as well as the promotion token from the special packs.

✓ The maximum number of applications is equal to half the number of special packs, because two packs are needed for each application.

✓ Verification costs include checking the till receipts, consumers’ statements and capturing the total cost of the consumer’s purchase (which could differ from store to store).

✓ Redemption costs would include the costs of pro-ducing branded cheques for the refund and all bank charges for clearing those cheques.

Collector SchemeA bread manufacturer wants to tie in to a major TV series by offering its consumers a range of branded goods. Consumers collect different numbers of tokens for each item and can reduce the token requirement by including a cash contribution with their application. Every pack of bread carries one token.

✓ The risk is related to the number of on-pack tokens that will enter the promotion, and then which gifts they’d be redeemed against.

06_975725-ch04.indd 31 9/17/10 11:56 AM

32

Explaining money-back offersThere are three types of money back offers, each redeeming at different rates:

✓ Try Me Free. The consumer must send in a till receipt to receive their money back. This typically redeems at between 10% to 40%.

✓ Quality or Taste Challenge. As well as a till receipt, con-sumers must write a short statement telling the brand what they think of the product. They receive their refund whether or not they like the product. Challenges normally redeem between 4% and 10%.

✓ Quality or Taste Guarantee. Like a Challenge, but refunds are only available if the consumer didn’t like the product, so the statement must be negative. Because consumers generally don’t like to complain, guarantees often redeem below 2%.

✓ Consumer’s cash contributions could be off-set against the costs of each gift.

✓ The branded gifts are only available in pro duction runs of 5,000 each, making the stock risk considerable.

✓ Redemption costs include lengthy verification of the number of tokens, the contribution and the gift required.

Collector schemes with just one gift carry far less stock risk than those with a range of gifts.

06_975725-ch04.indd 32 9/17/10 11:56 AM

33

Scratch CardA drinks manufacturer offers cash prizes on a scratch card included inside large packs of its major vodka-based brand. To play, consumers scratch off three from the seven panels. If they reveal three matching symbols they win a prize. Every card is a potential winner with prizes ranging from 50p coupons against the next purchase, to £2,000 cash.

✓ Every card is a potential winner so the liability is fairly high.

✓ The chances of successfully revealing 3 matching symbols from 7 panels are 1 in 35 so this helps to bring the risk down (see the nearby sidebar for more on statistics).

✓ Consumers are less likely to claim a 50p money off next purchase coupon than they would a £2,000 cash prize, so this is factored into the risk profile.

✓ Risk management costs need to include the secu-rity of the scratch card production to ensure the cards can’t be predicted or tampered with.

Statistical risks in promotionsSometimes the risks within a promotion are driven more by maths than human behaviour. You can consider a number of statistical scenarios in promotional mechanics:

✓ Scratch card. You have a scratch card with nine panels, but you can only scratch off three of them. If you reveal

(continued)

06_975725-ch04.indd 33 9/17/10 11:56 AM

34

three identical symbols you win a prize. The odds of matching three panels from nine is calculated like this: 9/3 x 8/2 x 7/1 or 3 x 4 x 7 = 84:1. So you have a 1 in 84 chance of being successful.

✓ Ranking statements in order (factorial). You’re pre-sented with seven statements about the product and need to rank them in order of importance. Forgetting per-sonal preferences, the chances of putting these state-ments in the same order as the judges entirely by chance is calculated as follows: 7 x 6 x 5 x 4 x 3 x 2 x 1 = 5040:1. So you have a 1 in 5,040 chance of ranking the state-ments correctly.

✓ Safe cracking. A safe has five dials that need to be cor-rectly aligned to open. Each dial has ten numbers on it, from zero to nine. The chances of opening the safe are calculated as follows: 10 x 10 x 10 x 10 x 10 = 100,000:1. So you’ve a 1 in 100,000 chance of opening the safe.

✓ Probability risks aren’t statistical, but the same princi-ples apply. So if you want to offer £100 off a product if England win the World Cup, you can take the percentage odds of this happening and apply it to your costs.

Once you’ve applied the statistical or probability odds to the promotion, you must then apply the play rate (how many people play the card) and, if relevant, claim rate (how many people apply for their prize) to calculate the risk.

(continued)

06_975725-ch04.indd 34 9/17/10 11:56 AM

Chapter 5

Ten Steps to Promotional Risk Management Success

If you remember nothing else from this book, remem-ber these tips:

✓ Get the risk manager in early.

✓ Be prepared to be flexible if the budget isn’t.

✓ Find out what promotions the brand has run before.

✓ Meet your risk manager face to face – don’t rely on phone quotes.

✓ Check the financial credentials of your risk manager.

✓ Share even the earliest versions of artwork to avoid surprises later on.

✓ Treat your risk manager as a partner, not just a supplier.

✓ Ensure your risk manager is insured with the correct documentation.

✓ If you’re not sure whether something is important, include it on the brief anyway.

✓ Don’t be scared of risk; use it as a creative tool.

07_975725-ch05.indd 35 9/17/10 11:56 AM

Making Everything Easier!TM

978-0-470-99468-9 978-0-470-51015-5

Dan GookinBestselling author of Word For Dummies and PCs For Dummies

Learn to:Make the most of the latest laptop features and capabilities

Synchronize your laptop with your desktop and cell phone

Set up security for mobility and social networking

Beef up your laptop’s memory and hard drive capacity

Laptops4th Edition

Making Everything Easier! ™

978-0-470-46542-4 978-0-470-57829-2

978-0-470-03077-6

978-0-470-49743-2

978-0-7645-5193-2 978-0-470-68815-1 978-0-471-77270-5

Available wherever books are sold

HISTORY

COMPUTER BASICS

LANGUAGES

risk is good.

09_975725-badvert02.indd 38 9/17/10 11:56 AM

some use risk to create fear.

Mando knows better than that.

You can trust our 30 years’ experience of identifying, assessing and managing promotional risk. Some of the world’s leading brands and agencies already have, and still do. Because it helps them create value.

call on 01296 717900 or email [email protected]

www.mando.co.uk

ISBN: 978-0-470-97572-5

Not for resale

Successfully protect your promotional budgets by getting the best

from risk management specialists

Make sense of the bewildering array of options and when you should be using them. By taking a risk manager’s point of view, this guide gets you into his mind, which helps you create more exciting, cost effective and, above all, budget-safe campaigns every time.

Spot your campaign’s risk

Effectively manage risk

Control your budget

� Find listings of all our books

� Choose from among many different subject categories

� Sign up for eTips at etips.dummies.com

Use risk as a creative tool

Explanations in plain

English

‘Get in, get out’

information

Icons and other

navigational aids

A dash of humour and fun

![[GUIDE] Link2SD for Dummies _ Samsung Galaxy Young - Xda-Developers](https://img.pdfslide.net/doc/110x75/55cf981e550346d03395b3ef/guide-link2sd-for-dummies-samsung-galaxy-young-xda-developers.jpg)