Embed Size (px)

Citation preview

Econometric MethodsIntroduction

Burcu Erdogan

Universitat Trier

WS 2011/2012

(Universitat Trier) Econometric Methods 26.10.2011 1 / 24

Moving on to ...

1 Overview

2 Introduction

3 Introduction to Ordinary Least Squares Regression

4 Quality of the Estimation Procedure

(Universitat Trier) Econometric Methods 26.10.2011 2 / 24

Time and Location

Lectures:

Wednesdays: 10:00 - 12:00 C 01 (German), Czapor:Wednesdays: 8:30 - 10:00 DM 131 (English), Erdogan

Tutorials:

Thursdays: 16:00 - 18:00 C 360 (German), Czapor:Thursdays: 16:00 - 18:00 C 106 (English), Erdogan

First tutorial on the 3rd November.

No lecture/tutorial on 21.12.11 and 22.12.2011.

(Universitat Trier) Econometric Methods 26.10.2011 3 / 24

Contact Information

Burcu Erdogan

Room: C 538

E-Mail: [email protected]

Lecture slides: http://www.uni-trier.de/index.php?id=30150

Office hours: On appointment

(Universitat Trier) Econometric Methods 26.10.2011 4 / 24

Literature and Grading

Lecture:

Ludwig von Auer (2011): Okonometrie, 5. Auflage

Jeffrey M. Wooldrigde (2008): Introductory Econometrics, 4th Edition

Stock and Watson (2006/2011): Introduction to Econometrics,2nd/3rd Edition

Tutorial:

Ulrich Kohler & Frauke Kreuter (2008): Datenanalyse mit Stata, 3.Auflage

Christopher F. Baum (2006): An Introduction to ModernEconometrics Using Stata

Grading:

Final Exam: 100%

(Universitat Trier) Econometric Methods 26.10.2011 5 / 24

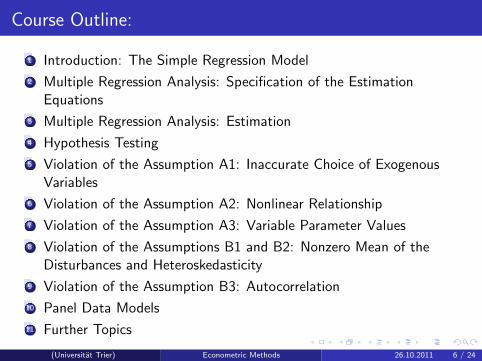

Course Outline:

1 Introduction: The Simple Regression Model

2 Multiple Regression Analysis: Specification of the EstimationEquations

3 Multiple Regression Analysis: Estimation

4 Hypothesis Testing

5 Violation of the Assumption A1: Inaccurate Choice of ExogenousVariables

6 Violation of the Assumption A2: Nonlinear Relationship

7 Violation of the Assumption A3: Variable Parameter Values

8 Violation of the Assumptions B1 and B2: Nonzero Mean of theDisturbances and Heteroskedasticity

9 Violation of the Assumption B3: Autocorrelation

10 Panel Data Models

11 Further Topics

(Universitat Trier) Econometric Methods 26.10.2011 6 / 24

Moving on to ...

1 Overview

2 Introduction

3 Introduction to Ordinary Least Squares Regression

4 Quality of the Estimation Procedure

(Universitat Trier) Econometric Methods 26.10.2011 7 / 24

Introduction

Econometrics serve to detect and quantify the causal relationships

Verification of the economic theory through the economic reality bymeans of measurement

The most important method is the ordinary least squares (OLS)regression

(Universitat Trier) Econometric Methods 26.10.2011 8 / 24

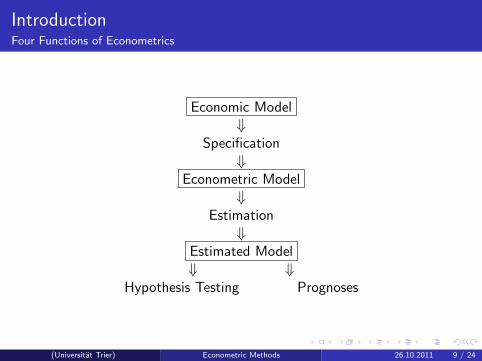

IntroductionFour Functions of Econometrics

Economic Model⇓

Specification⇓

Econometric Model⇓

Estimation⇓

Estimated Model⇓ ⇓

Hypothesis Testing Prognoses

(Universitat Trier) Econometric Methods 26.10.2011 9 / 24

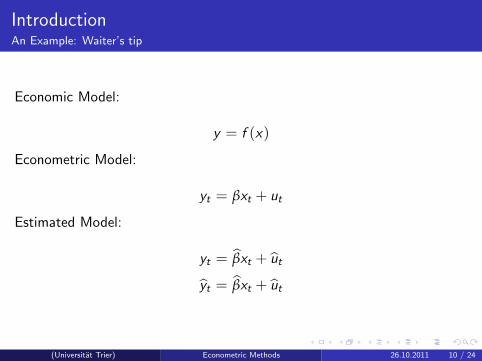

IntroductionAn Example: Waiter’s tip

Economic Model:

y = f (x)

Econometric Model:

yt = βxt + ut

Estimated Model:

yt = βxt + ut

yt = βxt + ut

(Universitat Trier) Econometric Methods 26.10.2011 10 / 24

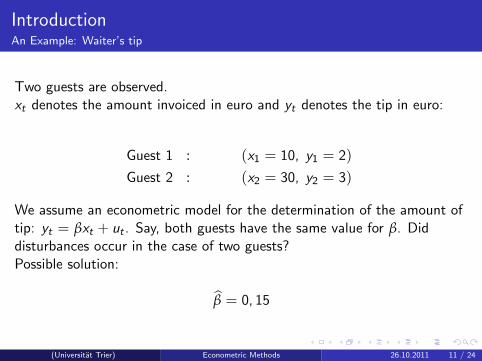

IntroductionAn Example: Waiter’s tip

Two guests are observed.xt denotes the amount invoiced in euro and yt denotes the tip in euro:

Guest 1 : (x1 = 10, y1 = 2)

Guest 2 : (x2 = 30, y2 = 3)

We assume an econometric model for the determination of the amount oftip: yt = βxt + ut . Say, both guests have the same value for β. Diddisturbances occur in the case of two guests?Possible solution:

β = 0, 15

(Universitat Trier) Econometric Methods 26.10.2011 11 / 24

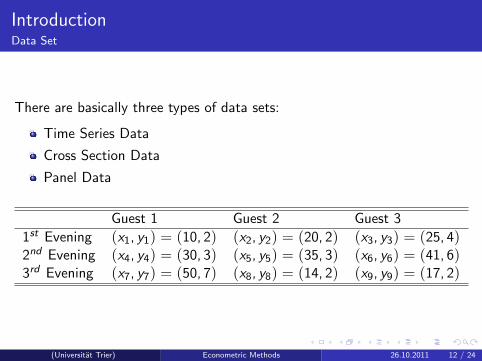

IntroductionData Set

There are basically three types of data sets:

Time Series Data

Cross Section Data

Panel Data

Guest 1 Guest 2 Guest 3

1st Evening (x1, y1) = (10, 2) (x2, y2) = (20, 2) (x3, y3) = (25, 4)2nd Evening (x4, y4) = (30, 3) (x5, y5) = (35, 3) (x6, y6) = (41, 6)3rd Evening (x7, y7) = (50, 7) (x8, y8) = (14, 2) (x9, y9) = (17, 2)

(Universitat Trier) Econometric Methods 26.10.2011 12 / 24

Moving on to ...

1 Overview

2 Introduction

3 Introduction to Ordinary Least Squares Regression

4 Quality of the Estimation Procedure

(Universitat Trier) Econometric Methods 26.10.2011 13 / 24

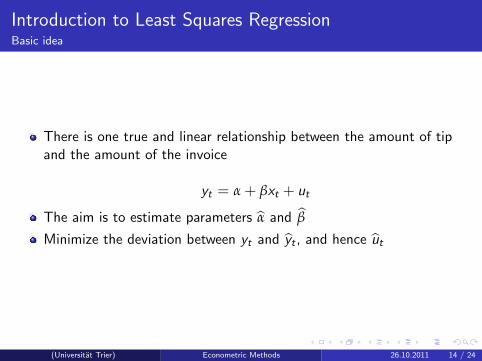

Introduction to Least Squares RegressionBasic idea

There is one true and linear relationship between the amount of tipand the amount of the invoice

yt = α + βxt + ut

The aim is to estimate parameters α and β

Minimize the deviation between yt and yt , and hence ut

(Universitat Trier) Econometric Methods 26.10.2011 14 / 24

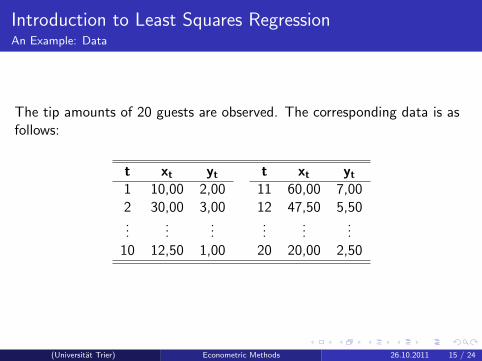

Introduction to Least Squares RegressionAn Example: Data

The tip amounts of 20 guests are observed. The corresponding data is asfollows:

t xt yt t xt yt

1 10,00 2,00 11 60,00 7,002 30,00 3,00 12 47,50 5,50...

......

......

...10 12,50 1,00 20 20,00 2,50

(Universitat Trier) Econometric Methods 26.10.2011 15 / 24

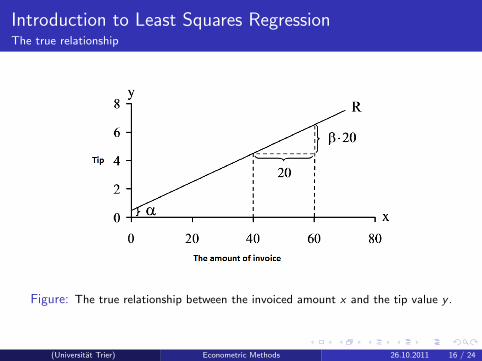

Introduction to Least Squares RegressionThe true relationship

Figure: The true relationship between the invoiced amount x and the tip value y .

(Universitat Trier) Econometric Methods 26.10.2011 16 / 24

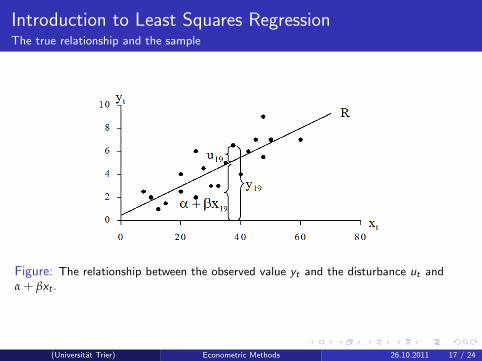

Introduction to Least Squares RegressionThe true relationship and the sample

Figure: The relationship between the observed value yt and the disturbance ut andα + βxt .

(Universitat Trier) Econometric Methods 26.10.2011 17 / 24

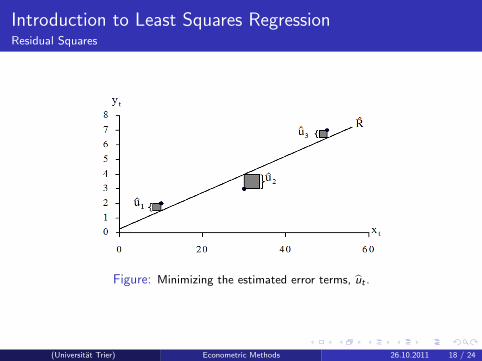

Introduction to Least Squares RegressionResidual Squares

Figure: Minimizing the estimated error terms, ut .

(Universitat Trier) Econometric Methods 26.10.2011 18 / 24

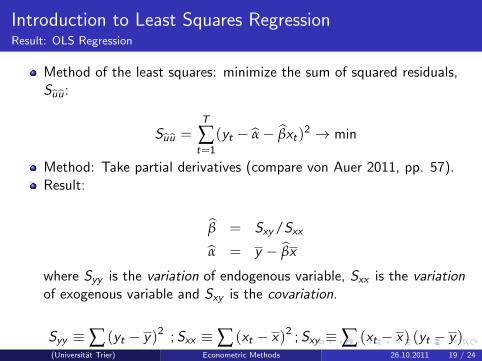

Introduction to Least Squares RegressionResult: OLS Regression

Method of the least squares: minimize the sum of squared residuals,Suu:

Suu =T

∑t=1

(yt − α− βxt)2 → min

Method: Take partial derivatives (compare von Auer 2011, pp. 57).Result:

β = Sxy/Sxx

α = y − βx

where Syy is the variation of endogenous variable, Sxx is the variationof exogenous variable and Sxy is the covariation.

Syy ≡∑ (yt − y)2 ; Sxx ≡∑ (xt − x)2 ; Sxy ≡∑ (xt − x) (yt − y)(Universitat Trier) Econometric Methods 26.10.2011 19 / 24

Moving on to ...

1 Overview

2 Introduction

3 Introduction to Ordinary Least Squares Regression

4 Quality of the Estimation Procedure

(Universitat Trier) Econometric Methods 26.10.2011 20 / 24

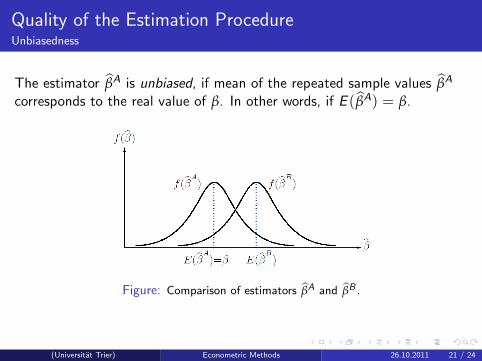

Quality of the Estimation ProcedureUnbiasedness

The estimator βA is unbiased, if mean of the repeated sample values βA

corresponds to the real value of β. In other words, if E (βA) = β.

Figure: Comparison of estimators βA and βB .

(Universitat Trier) Econometric Methods 26.10.2011 21 / 24

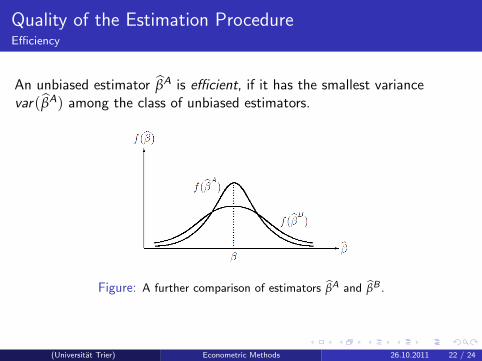

Quality of the Estimation ProcedureEfficiency

An unbiased estimator βA is efficient, if it has the smallest variancevar(βA) among the class of unbiased estimators.

Figure: A further comparison of estimators βA and βB .

(Universitat Trier) Econometric Methods 26.10.2011 22 / 24

Quality of the Estimation ProcedureOrdinary Least Squares Estimator I

It can be proved that under certain assumptions (A-, B- andC-Assumptions):

E (α) = α and E (β) = β

The OLS-Estimator α and β are linear estimators. One can show thattheir variances are the smallest among the class of unbiasedestimators.

Under certain assumptions, the OLS-Estimators α and β are efficientin the class of unbiased linear estimators (BLUE) - excluding thenonlinear estimators.

Under certain assumptions, the OLS-Estimators α and β are efficientin the class of unbiased estimators including the nonlinear estimators(BUE).

(Universitat Trier) Econometric Methods 26.10.2011 23 / 24

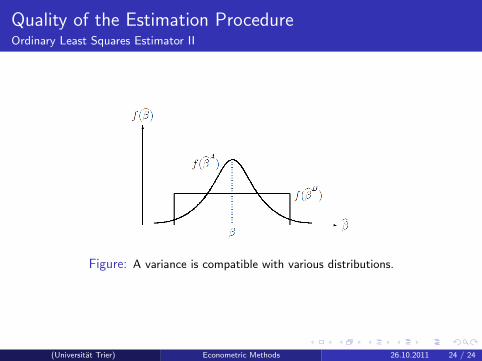

Quality of the Estimation ProcedureOrdinary Least Squares Estimator II

Figure: A variance is compatible with various distributions.

(Universitat Trier) Econometric Methods 26.10.2011 24 / 24