Embed Size (px)

Citation preview

Asgard Tech bulletins – April 2016

Eligibility and process for claiming tax deductions for

personal super contributions made in 2015/16

1. In brief

The finer points of the tax deduction rules need to be followed to ensure your clients

don’t lose the ability to claim a deduction for their personal superannuation

contributions. Not following the rules can lead to a loss of deduction and in some cases

it can also lead to a breach of the contributions caps. This bulletin looks at the

eligibility, requirements and processes which must be followed to:

claim a personal tax deduction for personal superannuation contributions made in

2015/16

vary a previous personal tax deduction notice to reduce the amount of personal

superannuation contributions for which a tax deduction is claimed

claim a tax deduction for personal contributions if a partial withdrawal from

superannuation is intended.

2. Eligibility to contribute to super

In order to make a personal contribution to superannuation an individual needs to be

aged:

under 65 or

65 to 75 and satisfy the work test by being gainfully employed for at least 40 hours

over 30 consecutive days in the financial year in which the contribution is made.

Individuals who are turning 75 in the financial year (and meet the work test) must

contribute before the 28th day of the month following the month in which they turn 75

(for example, if a person’s 75th birthday is in April, the contribution needs to be made

by 28 May of the same year).

2.1 What is the right reason for making a personal contribution to super?

The primary purpose for making any contribution to superannuation must be to obtain

superannuation benefits for the member on retirement or for their dependants in the

event the member dies.

Importantly, any associated tax deduction should only be an ancillary or minor purpose,

not the primary purpose, otherwise the ATO may deny the tax deduction.

Asgard Tech bulletins – April 2016

2.2 What is the time period the contribution must be made in?

To be able to claim a tax deduction for personal contributions made in the 2015/16

financial year, an eligible person must ensure their superannuation fund has received

their personal contribution by Thursday 30 June 2016.

3. Who is eligible to claim a deduction for a personal contribution?

Tax law states that any individual can claim a deduction for their contribution provided

that either, they are not employee or, if they have been an employee during the year,

the ‘<10% test’ is met.

Effectively this means that a tax deduction can be claimed by:

a self employed person i.e. sole trader or a partner in a partnership,

a substantially self employed person provided that the total income1 they earn as

an employee is less than 10% of their total income from all sources for the

financial year in which the contribution is made or

a person who is not engaged in any employment activity during the financial year

aged 18 to 64 inclusive. Individuals under age 18 at the end of the financial year

cannot claim a tax deduction unless they earned income as an employee or

business operator in that financial year. Unemployed individuals aged 65 and over

would not meet the work test, so would be unable to contribute to super.

Further discussions on the ‘<10% test’ and the definition of ‘total income’ can be found

in the Appendix to this Bulletin.

3.1 Deduction may be limited

Eligible persons are able to claim a full tax deduction for the total amount of personal

contributions made to superannuation for a financial year. Note, however, that the

deduction cannot exceed the level of the individual’s taxable income for that financial

year.

3.2 How is the contribution treated for contribution cap purposes?

Personal contributions for which a personal tax deduction has been claimed are

included in an individual’s concessional contributions cap.

1 Total income = assessable income plus reportable fringe benefits plus reportable employer

superannuation contributions.

Asgard Tech bulletins – April 2016

4. Policy definitions and ancillary benefits

Individuals eligible to claim a deduction for personal contributions need to notify their

superannuation fund of their intention to claim the deduction, in an approved form,

within a restricted time period. If the notice is valid, the fund will provide the individual

with an acknowledgement of receipt of the notice which allows the individual to claim

the deduction in their tax return.

An individual cannot claim any deduction on their personal superannuation

contributions, in their tax return, unless acknowledgement of receipt of their notice is

received from their fund.

A copy of the ATO’s approved form, Notice of intent to claim or vary a deduction for

personal super contributions, is available on the ATO website.

Many superannuation funds also produce their own branded version of this ATO form.

4.1 Time-frame for lodging a notice

Individuals wishing to claim a tax deduction for personal contributions made during the

2015/16 financial year must:

a) meet the eligibility criteria to claim a deduction (outlined earlier) and

b) complete and return their Notice of intent to claim or vary a deduction for personal

super contributions to their superannuation fund by the earlier of:

the day they lodge their income tax return for the 2015/16 financial year or

30 June 2017.

Note, however, that many individuals will need to notify their superannuation fund prior

to the above date as their ability to claim a tax deduction will cease on the day:

they cease to be a member of the fund,

the superannuation fund trustee no longer holds the contributions or

the superannuation fund trustee begins to pay an income stream based in whole

or part on the contribution (i.e. when any amount of the member’s superannuation

benefit is used to commence an income stream within the same fund).

In addition, individuals should also notify their superannuation fund prior to making a

partial withdrawal as their ability to claim a deduction will be limited after a partial

withdrawal.2

2 For details of the treatment of tax deduction notices provided after a partial withdrawal– see section

7, Notices provided after partial withdrawals, of this bulletin.

Asgard Tech bulletins – April 2016

4.2 When will a notice to claim a tax deduction be invalid?

Under tax law, a superannuation fund cannot accept a personal tax deduction notice or

variation of a previous notice if it is received outside the restricted time period

described in section 4.1.

In these instances the notice would be invalid. For example, a notice received after the

member commenced a pension with (even a part of) their superannuation benefit

would be invalid.

These requirements place an onus on individuals and their advisers to be aware of the

timing implications of when they need to provide a notice to the superannuation fund.

Other occurrences causing the notice to be invalid are:

if the amount stated as a deduction is covered by a previous notice,

if the notice is incomplete or

if the information in the notice is not correct.

When signing the notice, the member is asked to make a declaration that none of

these apply.

Example 1: Valid notice

John makes $40,000 in personal superannuation contributions in the 2015/16

financial year. He checks and confirms he is ‘substantially self employed’ (i.e. less than

10% of his total income3 comes from employment). He wishes to claim a tax deduction

for $10,000 of personal contributions and intends to submit his tax return on 30

August 2016.

John must submit a personal tax deduction notice to his superannuation fund prior to

submitting his tax return on 30 August 2016. However, if John intends to make a full or

partial withdrawal or commence an income stream, he should provide his notice prior

to any of these events. His notice must be in the approved form.

John can only claim this deduction in his 2015/16 tax return after he receives a written

acknowledgment of his personal tax deduction notice from his superannuation fund.

Example 2: Invalid notice (lodged outside the permitted time-frame)

Karen has made personal super contributions in 2015/16. As she wishes to claim a

deduction on these contributions, she lodges a notice on 16 July 2017 and awaits the

acknowledgment from the trustee before lodging her tax return for 2015/16.

3 Total income = assessable income plus reportable fringe benefits plus reportable employer

superannuation contributions.

Asgard Tech bulletins – April 2016

The trustee cannot acknowledge the notice as it is invalid. The latest date Karen could

have lodged a valid notice was 30 June 2017. Karen has missed the opportunity to

claim a deduction on personal contributions made in 2015/16.

Example 3: Invalid notice (contributions no longer held)

Larry makes personal contributions of $10,000 to superannuation fund A in the

2015/16 financial year. He is self-employed and wishes to claim a tax deduction for the

full amount of these contributions. He intends to submit his tax return in October 2016.

In July 2016, Larry rolls over his entire superannuation account balance to

superannuation fund B. He provides a notice of intent to claim a tax deduction for

$10,000 to superannuation fund A in September 2016 prior to completing his tax

return. Superannuation fund A advises that the notice is invalid as they no longer hold

the contributions. Larry has lost the opportunity to claim a tax deduction for these

contributions, as he cannot provide a notice to either fund A or fund B.

Example 4: Invalid notice (income stream commenced)

Maxine is 62 and makes $20,000 in personal contributions to her superannuation fund

in the 2015/16 financial year. She is self-employed and wishes to claim a tax

deduction of $20,000 for these contributions. She intends to submit her tax return in

October 2016.

In August 2016, Maxine retires and commences a pension with the same provider,

using $140,000 of her $200,000 superannuation benefit in her accumulation account.

She provides a notice of intent to claim a tax deduction for $20,000 of personal

contributions to her superannuation fund in September 2016, prior to completing her

tax return. Her superannuation fund advises Maxine that her notice is invalid as the

trustee has begun to pay an income stream based in whole or part on the contribution.

Maxine has lost the opportunity to claim a tax deduction for these personal

contributions.

5. Multiple notices during the year

A member may lodge as many valid notices as they wish during the year, provided that

the amount stated as a deduction in any notice is not already covered by a previous

notice.

If a notice has been provided for contributions and further personal contributions are

made, a new notice can be provided in relation to the new contributions, provided that

it is given within the restricted time period and is otherwise valid.

Asgard Tech bulletins – April 2016

Example 5: Multiple notices

Deb made personal super contributions of $25,000 in 2015/16. Deb lodged a valid

notice in respect of $20,000 of these contributions, claiming the full $20,000 as a

deduction. She receives an acknowledgment of the notice from the trustee.

Deb now wishes to claim the entire year’s contributions as a deduction, an increase of

$5,000. Deb can lodge a second notice in respect of $5,000 of the contributions made

in 2015/16, claiming the full $5,000 as a deduction.

6. Varying a notice

A notice can only be varied to reduce the amount of personal contributions intended to

be claimed as a deduction, by giving notice to the superannuation fund in the approved

form within the restricted time period described above.

After this time, the notice cannot be varied unless all or part of the deduction is

disallowed by the Commissioner of Taxation.

A notice cannot be varied if:

the individual is no longer a member of the fund,

the superannuation fund trustee no longer holds the contributions or

the superannuation fund trustee begins to pay an income stream based in

whole or part on the contribution (i.e. when any amount of the member’s

superannuation benefit is used to commence an income stream within the

same fund).

In addition, if a person has given notice to their superannuation fund of their intention

to claim a deduction for personal contributions and has subsequently made a partial

withdrawal or requested to split those contributions with their spouse, the person’s

ability to vary the notice will be limited.

The ATO approved form Notice of intent to claim or vary a deduction for personal super

contributions is used to vary a notice previously submitted to the fund.

Example 6: Variation notice allowed

Lisa is 45 and makes $35,000 in personal superannuation contributions in the

2015/16 financial year. She is self-employed and wishes to claim a tax deduction for

the full amount of these contributions. She intends to submit her tax return on 20

October 2016.

Lisa provides a valid notice of intent to claim a tax deduction of $35,000 in August

2016 and receives an acknowledgement from her superannuation fund. She then

realises she will exceed her concessional contributions cap of $30,000 so she provides

a variation notice to her superannuation fund in September 2016 to reduce the

amount claimed to $30,000.

Asgard Tech bulletins – April 2016

Since providing her original notice Lisa has not made a full or partial withdrawal, has

not commenced an income stream and she confirms on the variation notice that she

has not yet lodged her tax return. As her variation notice is provided within the

restricted time period, it is acknowledged by the superannuation fund and the amount

advised in her previous notice is revised downwards to $30,000.

Example 7: Variation notice invalid (lodged outside the permitted time-frame)

James provides a valid notice of intent to claim a tax deduction of $5,000 for personal

contributions made during the 2015/16 financial year and receives an

acknowledgement from his superannuation fund. After lodging his income tax return,

James provides a variation notice to his superannuation fund requesting to vary the

amount advised in his previous notice down to $3,000.

The fund cannot accept the variation notice because it is outside the restricted time

period as James has already lodged his tax return. The fund can only accept a variation

outside the restricted time period if the ATO has disallowed the deduction on his

personal super contributions. Example 8: Variation notice allowed where deduction disallowed by Commissioner

Jenny provides a valid notice of intent to claim a tax deduction of $8,000 for personal

contributions made during the 2015/16 financial year and receives an

acknowledgement from her superannuation fund. Jenny’s taxable income for the year is

$5,000. When she lodges her 2015/16 tax return, $3,000 of Jenny’s deduction for

personal superannuation contributions is disallowed as this amount exceeds her

taxable income. Jenny can provide a variation notice to her superannuation fund

requesting to vary the amount advised in her previous notice down to $5,000 and this

variation will be allowed.

Example 9: Invalid notice (partial rollover)

Lauren makes $10,000 in personal contributions to superannuation fund A in the

2015/16 financial year. She is self-employed and wishes to claim a tax deduction of

$10,000 for these contributions when she submits her tax return in October 2016.

In July 2016, Lauren rolls over part of her account balance to superannuation fund B.

She provides a notice to superannuation fund A to claim a tax deduction for $10,000 in

September 2016 prior to completing her tax return. Superannuation fund A advises this

request is invalid as they no longer hold the all of the contribution. Lauren has lost the

opportunity to claim a tax deduction on the total contributions, but may be able to claim

a partial deduction, see discussion in next section.

7. Notices provided after partial withdrawals

On 25 February 2010, the ATO issued Taxation Ruling 2010/1 Income tax:

superannuation contributions. As a result of this ruling, individuals cannot claim a tax

deduction for the full amount of their personal contributions after making a partial

withdrawal (rollover or lump sum) from their superannuation benefit.

Asgard Tech bulletins – April 2016

After a member has made a partial withdrawal from their superannuation they can only

provide a valid personal tax deduction notice for an amount up to the proportion of

their personal contributions that remain in their account after the withdrawal. This

amount is determined using a formula provided in TR 2010/1:

Tax free component X Contribution .

of account after withdrawal Tax free component of account

before withdrawal

Example 10 demonstrates how this formula is applied.

Assuming a member makes further personal contributions after the partial withdrawal,

they can claim a deduction for the full amount of those contributions if a valid notice is

provided prior to making any further withdrawals and the notice is provided within the

restricted time period.

This rule applies in relation to contributions made from the 2007/08 financial year

however transitional relief has allowed most superannuation funds to apply this rule to

contributions received from 1 July 2011 only.

Example: 10: Impact of partial withdrawals on amount claimed

Rebecca has a superannuation account valued at $50,000. This account includes

a contributions segment of $10,000. She makes a $25,000 personal contribution

in March 2016. The fund records this contribution against the tax free component

of her superannuation account. The value of her superannuation account is

$75,000.

In June 2016, Rebecca rolls over $60,000 leaving her with $15,000 in the fund.

The $60,000 roll-over is comprised of a $28,000 tax free component and a

$32,000 taxable component.

Using the proportioning rule, the tax free component of the withdrawal is worked

out as follows:

Withdrawal amount x Tax free component of account before withdrawal/Value of

the superannuation account before withdrawal

= $60,000 x $35,000/$75,000

= $28,000

The tax free component of the superannuation account after withdrawal is $7,000

i.e. $35,000 - $28,000.

Rebecca then lodges a notice in September 2016 advising that she intends to

claim a deduction for the $25,000 contribution made in the 2015/16 year.

That notice is not valid. Rebecca’s superannuation fund no longer holds the entire

$25,000 contribution. However, Rebecca could give a valid deduction notice for an

Asgard Tech bulletins – April 2016

amount up to $5,000. That amount is worked out as follows:

Tax free component of account after withdrawal x Contribution/Tax free

component of account before withdrawal

= $7,000 x $25,000/$35,000

= $5,000

Due to her prior rollover, Rebecca was only able to claim a maximum of $5,000

even though she had contributed $25,000 to superannuation in 2015/16.

For simplicity, this example assumes no investment earnings and all results have been

rounded to the nearest dollar.

8. Variation notices provided after partial withdrawals

After a member has made a partial withdrawal from their superannuation, the amount

by which they wish to vary an earlier notice may be limited due to the guidance

provided in TR 2010/1 Income tax: superannuation contributions.

A formula is used to determine how much of the contribution remains in the account

and a variation up to that amount is permitted. The formula used is the same as that

used for new/original notices provided after partial withdrawals but the focus is on

determining the taxable component (rather than the tax-free component).

The amount up to which a person can vary a previous notice is determined using the

formula:

Taxable component of X Contribution subject of notice (net of 15%) . X 1.176

account after withdrawal Taxable component of account

before withdrawal

Example 11: Impact of partial withdrawals on a variation

In early August 2015, Marco’s super account balance is $478,750 including $50,000

tax free component.

On 10 August 2015, Marco makes two personal contributions: $25,000 and

$150,000. His account balance is now $653,750 including $225,000 tax free

component and $428,750 taxable component.

In November 2015, Marco provides a personal tax deduction notice advising his

intention to claim a tax deduction for $25,000 of personal contributions made earlier in

2015/16.

After contributions tax of $3,750 ($25,000 x 15%) is deducted, Marco’s account

balance is $650,000 including $200,000 tax free component and $450,000 taxable

component.

Asgard Tech bulletins – April 2016

In December 2015, Marco withdraws $260,000 which includes a tax free component

of $80,000 (calculated using the proportioning rule). Marco’s account balance is now

$390,000 including $120,000 tax free component and $270,000 taxable component.

In June 2016, Marco provides a variation notice to reduce the amount advised in his

previous notice to $12,000. To assess whether the notice is valid, the trustee must

determine the amount of personal contributions covered by the previous notice that

remain in the taxable component of Marco’s account following the partial withdrawal.

This is calculated as:

Taxable component of X Contribution subject of notice (net of 15%) . X 1.176

account after withdrawal Taxable component of account

before withdrawal

= $270,000 x ($21,250 / $450,000) x 1.176

= $14,994

Therefore, Marco is able to reduce the amount advised in his previous notice by up to

$14,994. As the variation notice requests to vary the amount to $12,000 (being a

reduction of $13,000) the notice is valid and can be acknowledged by the trustee.

For simplicity, this example assumes no investment earnings and all results have been

rounded to the nearest dollar.

9. Tips Checklist

If your client intends to claim a personal tax deduction for personal superannuation

contributions made during the 2015/16 financial year they need to ensure:

their superannuation fund receives their personal contribution by 30 June 2016

and

they are eligible to claim a personal tax deduction for personal superannuation

contributions made in 2015/16 (refer to section 3, Who is eligible to claim a

deduction on a personal contribution?)

they provide a personal tax deduction notice (and any subsequent request to vary

the notice) to their superannuation fund in the approved form within the restricted

time period. For contributions made in 2015/16, this period ceases on the earliest

of the following events:

o the super fund no longer holds the contributions,

o the client uses any amount of their super benefit to commence an income

stream in the same superannuation fund,

o the client ceases to be a member of the fund,

o the client lodges their tax return for the 2015/16 financial year and

o 30 June 2017.

Asgard Tech bulletins – April 2016

they consider providing a personal tax deduction notice (and any subsequent

request to vary the notice) prior to making a partial withdrawal to ensure they

are able to claim the full amount of their intended deduction. Following a

partial withdrawal your client’s ability to claim a deduction will be limited.

10. Tips and Traps

Ensure your client considers their concessional contributions cap when claiming a

deduction for personal contributions so they do not exceed their concessional

contributions cap.

Claim the correct amount, as there may be a restricted ability to vary a notice at a

later time.

Ensure your client provides a notice prior to any part or full withdrawal (lump sum

or rollover) or prior to using any amount of their super benefit to commence an

income stream in the same fund.

It is important to note that whilst claiming a tax deduction may reduce the tax an

individual pays personally, it increases the contributions tax payable from their

super account. As such, consideration should be given to the overall benefit of

claiming a tax deduction based on the individual’s specific financial circumstances.

Remember that different rules apply when claiming tax deductions for personal

contributions made in financial years prior to 1 July 2011 and also prior to 1 July

2007.

11. Legislative References

Income Tax Assessment Act 1997

Subdivision 290-C (ability to claim a personal tax deduction for contributions made

from 1 July 2007)

Related ATO Rulings/Determinations

Taxation Ruling 2010/1 Income tax: Superannuation Contributions

Asgard Tech bulletins – April 2016

12. Appendix

12.1 The <10% test

If an individual has been an employee during the year, they can claim a deduction

on their personal contribution if the <10% test is met for that financial year.

An individual is eligible to claim a deduction if the sum of their:

o assessable income from employment,

o reportable fringe benefits and

o reportable employer superannuation contributions is less than 10% of:

o their total assessable income from all sources

o their reportable fringe benefits and

o their reportable employer superannuation contributions for the financial

year.

If the individual has not been an employee at any time during the year, this test

does not apply.

12.2 Assessable income from employment

Amounts that are attributable to ‘employment’ activity are taken into account as

assessable income in the <10% test. These include the assessable amounts of:

salary or wages,

allowances and other payments earned by an employee,

other payments, such as commission, director’s remuneration and contract

payments, that are treated as salary or wages by section 11 of the SGAA4 for those

persons who engage in an ‘employment’ activity in a capacity other than a common

law employee,

payments received on termination of employment including accrued leave and

employment termination payments and

workers’ compensation and like payments made because of injury or illness

received by a person while holding the employment, office or appointment, the

performance of which gave rise to the entitlement to the compensation payments.

Employment activity need not be an activity in Australia. However, if income attributable

to overseas employment income is non-assessable in Australia then it will not be

counted towards the maximum earnings test. This needs to be distinguished from

employment activities where the person is an Australian resident and where the income

is assessable in Australia.

4 Superannuation Guarantee (Administration) Act 1992

Asgard Tech bulletins – April 2016

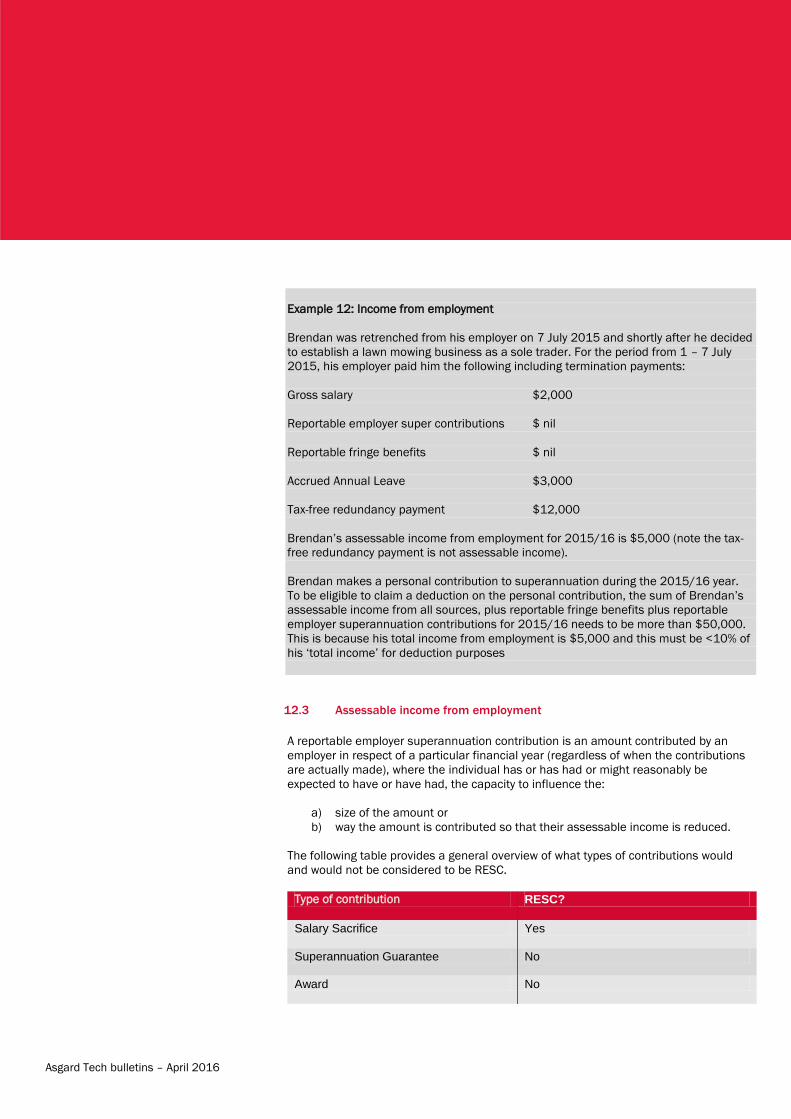

Example 12: Income from employment

Brendan was retrenched from his employer on 7 July 2015 and shortly after he decided

to establish a lawn mowing business as a sole trader. For the period from 1 – 7 July

2015, his employer paid him the following including termination payments:

Gross salary $2,000

Reportable employer super contributions $ nil

Reportable fringe benefits $ nil

Accrued Annual Leave $3,000

Tax-free redundancy payment $12,000

Brendan’s assessable income from employment for 2015/16 is $5,000 (note the tax-

free redundancy payment is not assessable income).

Brendan makes a personal contribution to superannuation during the 2015/16 year.

To be eligible to claim a deduction on the personal contribution, the sum of Brendan’s

assessable income from all sources, plus reportable fringe benefits plus reportable

employer superannuation contributions for 2015/16 needs to be more than $50,000.

This is because his total income from employment is $5,000 and this must be <10% of

his ‘total income’ for deduction purposes

12.3 Assessable income from employment

A reportable employer superannuation contribution is an amount contributed by an

employer in respect of a particular financial year (regardless of when the contributions

are actually made), where the individual has or has had or might reasonably be

expected to have or have had, the capacity to influence the:

a) size of the amount or

b) way the amount is contributed so that their assessable income is reduced.

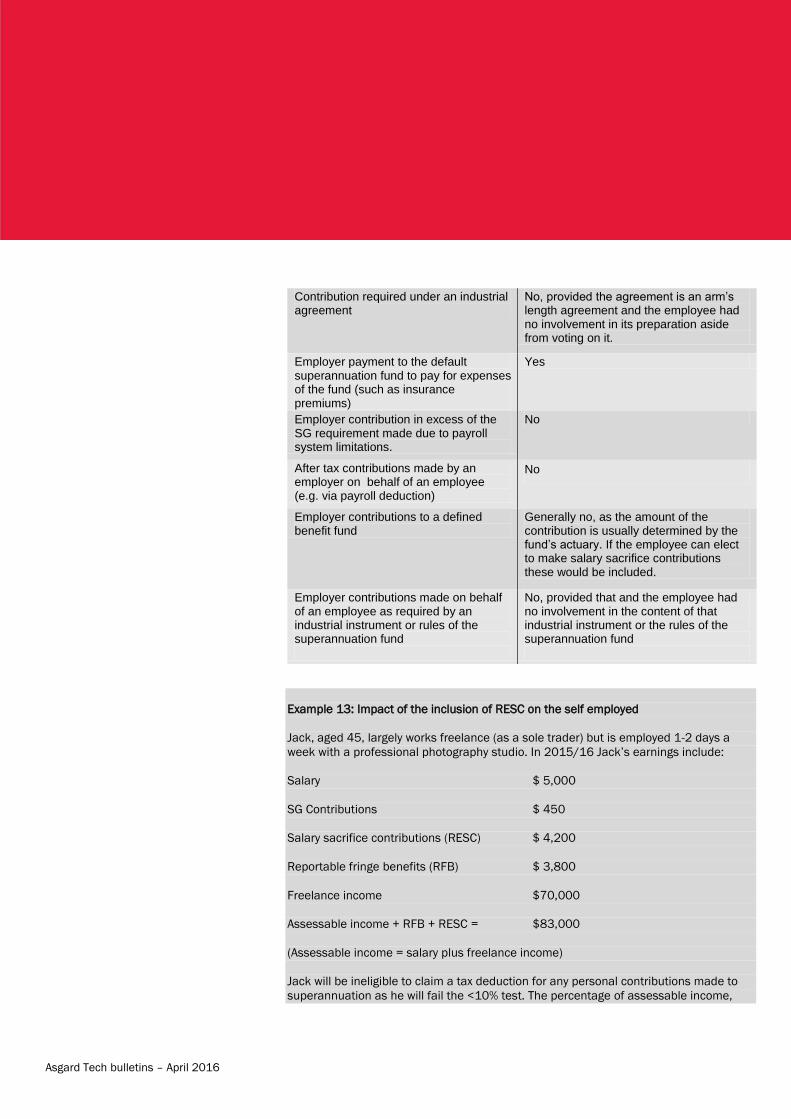

The following table provides a general overview of what types of contributions would

and would not be considered to be RESC.

Type of contribution RESC?

Salary Sacrifice Yes

Superannuation Guarantee No

Award No

Asgard Tech bulletins – April 2016

Example 13: Impact of the inclusion of RESC on the self employed

Jack, aged 45, largely works freelance (as a sole trader) but is employed 1-2 days a

week with a professional photography studio. In 2015/16 Jack’s earnings include:

Salary $ 5,000

SG Contributions $ 450

Salary sacrifice contributions (RESC) $ 4,200

Reportable fringe benefits (RFB) $ 3,800

Freelance income $70,000

Assessable income + RFB + RESC = $83,000

(Assessable income = salary plus freelance income)

Jack will be ineligible to claim a tax deduction for any personal contributions made to

superannuation as he will fail the <10% test. The percentage of assessable income,

Contribution required under an industrial agreement

No, provided the agreement is an arm’s length agreement and the employee had no involvement in its preparation aside from voting on it.

Employer payment to the default superannuation fund to pay for expenses of the fund (such as insurance premiums)

Yes

Employer contribution in excess of the SG requirement made due to payroll system limitations.

No

After tax contributions made by an employer on behalf of an employee (e.g. via payroll deduction)

No

Employer contributions to a defined benefit fund

Generally no, as the amount of the contribution is usually determined by the fund’s actuary. If the employee can elect to make salary sacrifice contributions these would be included.

Employer contributions made on behalf of an employee as required by an industrial instrument or rules of the superannuation fund

No, provided that and the employee had no involvement in the content of that industrial instrument or the rules of the superannuation fund

Asgard Tech bulletins – April 2016

RFB and RESC attributable to employment as an employee will not be less than 10% of

$83,000.

(Salary + RFB + RESC)/Total Income

= ($5,000 + $3,800 + $4,200) / $83,000 = 15.7%.

FOR GENERAL INFORMATION ONLY

This information has been prepared by BT Funds Management Ltd ABN 63 002916 458.

It is provided solely for the general information of external financial advisers and must not be relied on as a substitute for legal, tax

or other professional advice. Further, it must not be copied, used, reproduced or otherwise distributed or circulated to any retail

client or other party. The information is given in good faith and has been derived from sources believed to be accurate at its issue

date. However, it should not be considered a comprehensive statement on any matter nor relied upon as such. BT Funds

Management Ltd (including its related entities, employees and directors) does not give any warranty of reliability or accuracy or

accept any responsibility arising in any way including by reason of negligence for errors or omissions in the information.