Embed Size (px)

Citation preview

©2017

EMERGING TRENDS AND ISSUES

SHELL COMPANIES, CORRUPT PRACTICES, AND HOW TO UNCOVER THEM

Shell companies are used for many reasons; some are legal while others are not. They act as the

intermediaries, while the real owners remain hard to trace. As such, they are an ideal mechanism

for concealing identity and aiding fraudulent transactions to appear legitimate. This session will

provide a practical breakdown of what constitutes a shell company and provide tools to identify

when shells are being used for illegal purposes.

LISA DUKE, CFE, CPA, MAFF

Supervisor Forensic Accountant

U.S. Department of Justice

Federal Bureau of Investigation

Prior to her current appointment, for the past 10 years, Ms. Duke worked as a subject matter

expert at the New York State Comptroller’s Office. In her current role, she leads a team of

forensic accountants who provide financial investigative support to cross programmatic threats,

which requires financial analysis, documentation of analysis, and expert testimony by employing

surge based response. Her engagements have included cases involving fraud investigations,

conflict of interest, waste and abuse of multiple government agencies, contractors, public

authorities, and nonprofit organizations. Duke is a certified trainer by the NYS Governor’s

Office of Employee Relations (GOER) and Rutgers University. She has done multiple

presentations on a variety of audit and fraud related topics for the NYS Office of the State

Comptroller, as well as the NY Chapter of Association of Government Auditors (AGA), the NY

& NJ Intergovernmental Audit Forum, and the Association of Certified Fraud Examiners

(ACFE). She is a member of ACFE, AGA, the Institute of Internal Auditors (IIA), and the

National Association of Certified Valuators and Analyst (NACVA).

“Association of Certified Fraud Examiners,” “Certified Fraud Examiner,” “CFE,” “ACFE,” and the

ACFE Logo are trademarks owned by the Association of Certified Fraud Examiners, Inc. The contents of

this paper may not be transmitted, republished, modified, reproduced, distributed, copied, or sold without

the prior consent of the author.

SHELL COMPANIES, CORRUPT PRACTICES, AND HOW TO UNCOVER THEM

28th Annual ACFE Global Fraud Conference ©2017 1

NOTES Module 1: Program Introduction

Course Overview

This presentation will provide forensic accountants,

government investigators, auditors, and regulators with best

practice and skills for understanding what constitutes a

shell company and how it can be used to commit fraud and

other nefarious activities, as well as some investigative

tools for cases involving shell companies.

Objective

What are shell companies and how are they revlevant

for fraudulent acts?

Ways people abuse shell companies for fraud

Legitimate reasons to set up shell companies

Tools to detect whether a shell company is being used

for illegitimate purposes

What Are Shell Companies and Why Are They

Relevant for Fraudulent Acts?

Objectives:

What Is a Shell Company and Is It Legal?

Shells can be legitimate, legal entities that do not possess

actual assets or run business operations. They function as

transactional vehicles. They give the appearance of being a

legitimate business, but are just empty shells. They hide the

true ownership of the money that they manage. They can

also be called letter box or mail box companies as they are

no more than an address to post documents to.

SHELL COMPANIES, CORRUPT PRACTICES, AND HOW TO UNCOVER THEM

28th Annual ACFE Global Fraud Conference ©2017 2

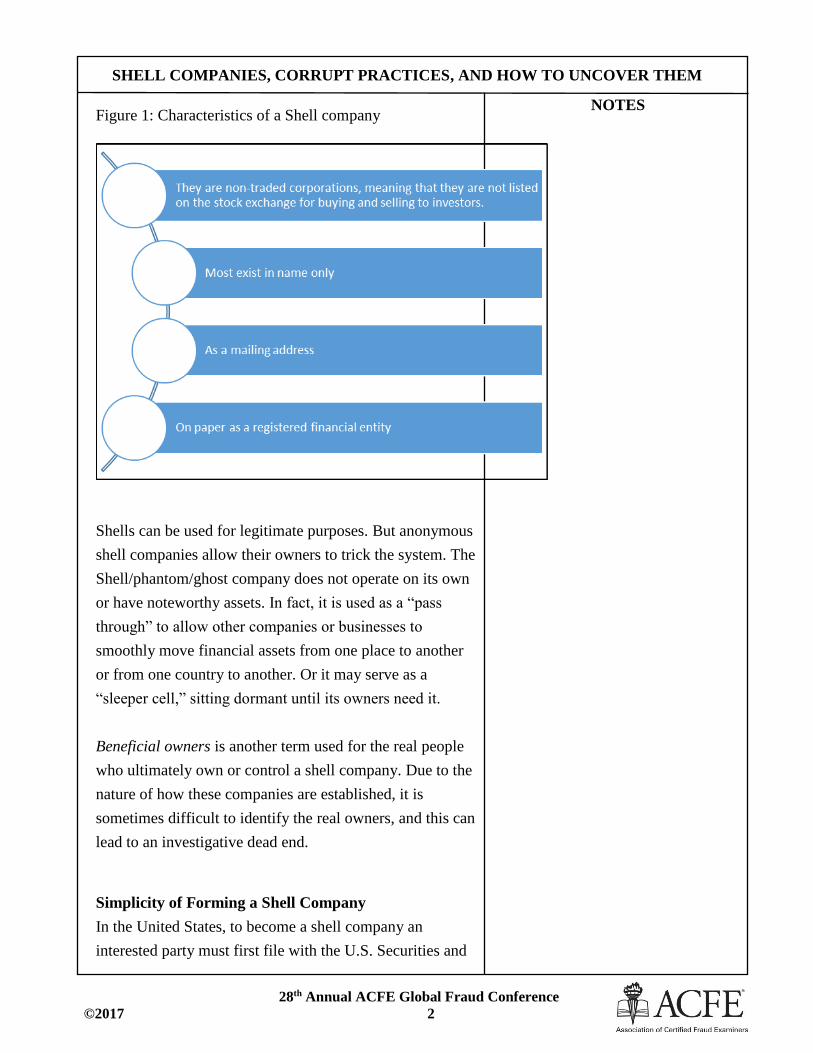

NOTES Figure 1: Characteristics of a Shell company

Shells can be used for legitimate purposes. But anonymous

shell companies allow their owners to trick the system. The

Shell/phantom/ghost company does not operate on its own

or have noteworthy assets. In fact, it is used as a “pass

through” to allow other companies or businesses to

smoothly move financial assets from one place to another

or from one country to another. Or it may serve as a

“sleeper cell,” sitting dormant until its owners need it.

Beneficial owners is another term used for the real people

who ultimately own or control a shell company. Due to the

nature of how these companies are established, it is

sometimes difficult to identify the real owners, and this can

lead to an investigative dead end.

Simplicity of Forming a Shell Company

In the United States, to become a shell company an

interested party must first file with the U.S. Securities and

SHELL COMPANIES, CORRUPT PRACTICES, AND HOW TO UNCOVER THEM

28th Annual ACFE Global Fraud Conference ©2017 3

NOTES Exchange Commission (SEC). Each state has statutes

governing the formation and operation of a Shell. Examples

of shell companies include:

Limited liability companies (LLCs) and trusts,

corporations

Any start-up firm that files with the SEC is technically

a shell corporation.

In some states, only minimal information is required to

register articles of incorporation or to establish and

maintain “good standing” for business entities. Owners can

distance themselves from the actual formation of the

company by using registered agents or nominee

incorporation services to create them. They can be set up

online in many countries for a few hundred dollars by using

law firms or accounting firms that specializes in this

business.

They are established all over the world but are concentrated

in tax havens, or Offshore Financial Centers (OFC).1 Many

OFCs have limited organizational disclosure and

recordkeeping requirements for establishing foreign

business entities. OFCs are normally small countries with

very low or non-existent tax on financial transactions. For

example, the British Virgin islands, Bahamas, Panama,

Cyprus.

The secrecy of the true owners is what makes them

attractive to criminals, money launderers, and tax evaders.

Within the United States, Delaware, Wyoming, and Nevada

are the top three states for shell formation, with Delaware

being number one. Their secrecy rules are especially tight

1 For general discussion on Offshore Financial Centers refer to

Resource Documents of the Board of Governors of the Federal Reserve

System

https://www.ffiec.gov/bsa_aml_infobase/pages_manual/OLM_097.htm

SHELL COMPANIES, CORRUPT PRACTICES, AND HOW TO UNCOVER THEM

28th Annual ACFE Global Fraud Conference ©2017 4

NOTES in comparison to other states. They have similarly lax

corporate registration laws and have attracted large

numbers of shell companies, along with registration fees

that contribute to the state’s funds. As a general practice,

states do not collect the names of beneficial owners through

their incorporation process. But Delaware and the majority

of states require disclosure of the names of the natural

persons who serve as director. 2 They also require each

corporation to disclose the names and addresses of its

directors on its annual franchise tax report.3

Foreign Business Companies

Similarly, foreign business entities that pose the greatest

risk are International Business Corporations (IBC) and

Private Investment Companies (PIC) opened in offshore

financial centers (OFC). IBCs are companies formed

outside of a person’s country of residence.

2 Refer to statute at

http://corplaw.delaware.gov/eng/facts_myths.shtml#fn:50 3 Further reference for studies of the State of Delaware and company

formation refer to

http://corplaw.delaware.gov/eng/facts_myths.shtml#fn:50

SHELL COMPANIES, CORRUPT PRACTICES, AND HOW TO UNCOVER THEM

28th Annual ACFE Global Fraud Conference ©2017 5

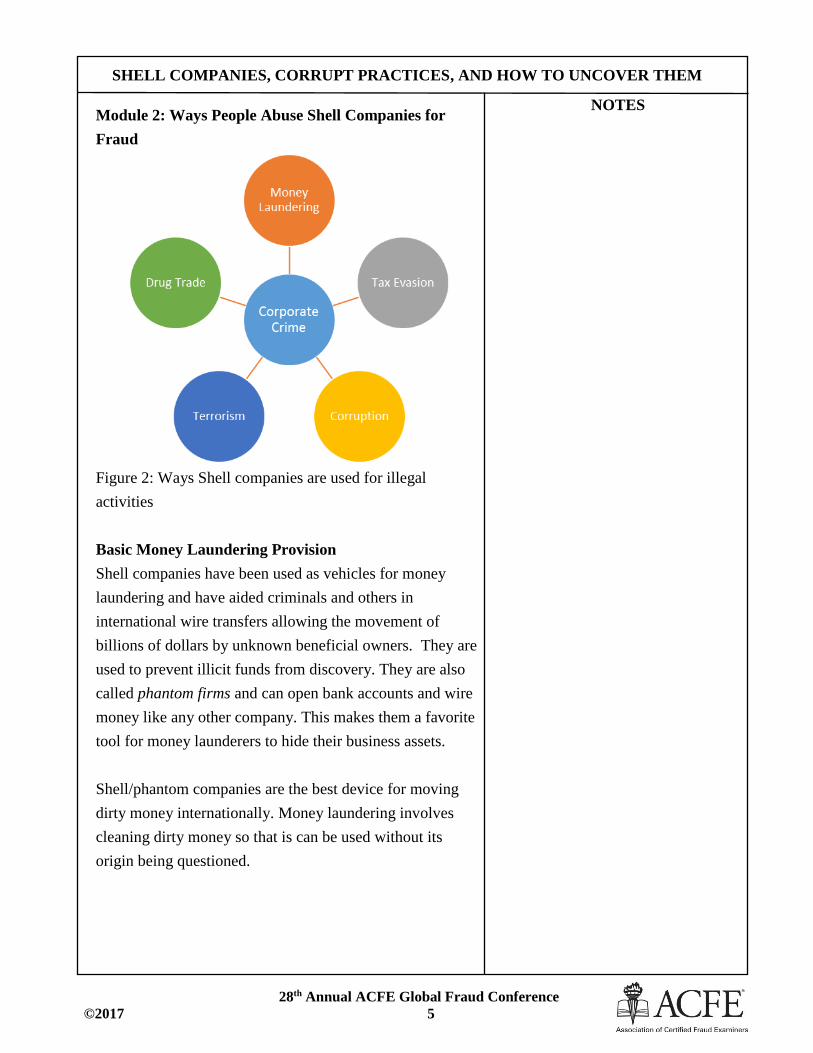

NOTES Module 2: Ways People Abuse Shell Companies for

Fraud

Figure 2: Ways Shell companies are used for illegal

activities

Basic Money Laundering Provision

Shell companies have been used as vehicles for money

laundering and have aided criminals and others in

international wire transfers allowing the movement of

billions of dollars by unknown beneficial owners. They are

used to prevent illicit funds from discovery. They are also

called phantom firms and can open bank accounts and wire

money like any other company. This makes them a favorite

tool for money launderers to hide their business assets.

Shell/phantom companies are the best device for moving

dirty money internationally. Money laundering involves

cleaning dirty money so that is can be used without its

origin being questioned.

SHELL COMPANIES, CORRUPT PRACTICES, AND HOW TO UNCOVER THEM

28th Annual ACFE Global Fraud Conference ©2017 6

NOTES

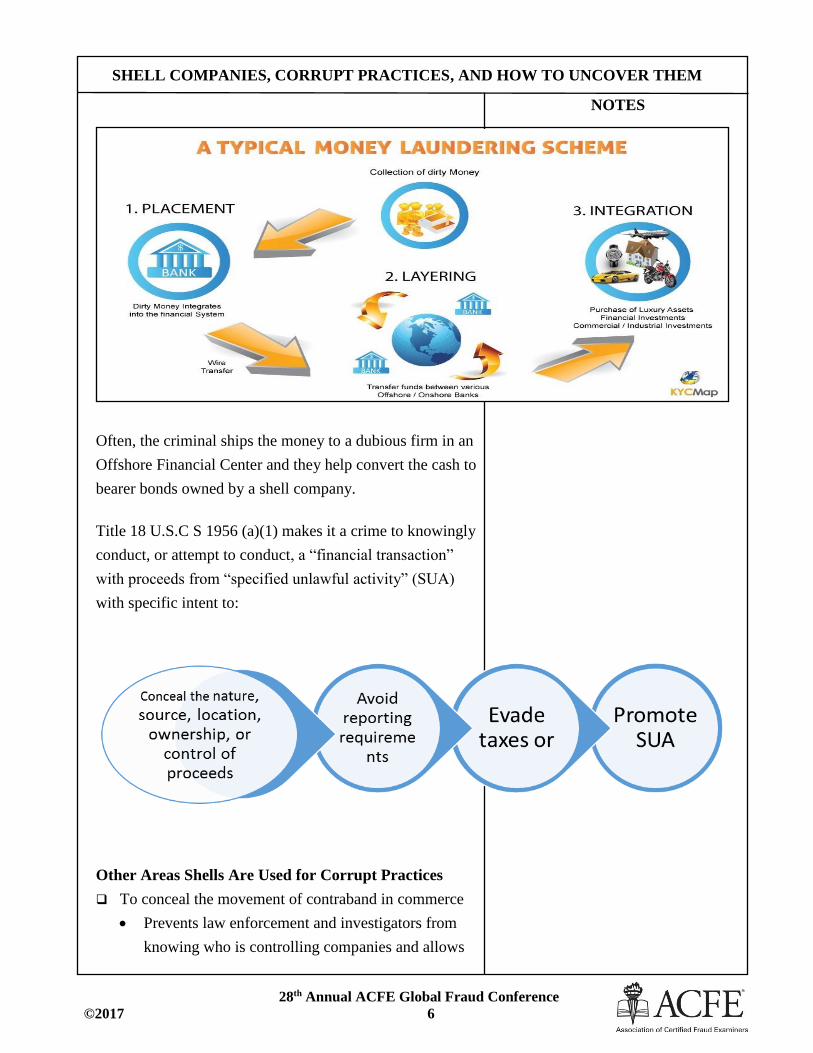

Often, the criminal ships the money to a dubious firm in an

Offshore Financial Center and they help convert the cash to

bearer bonds owned by a shell company.

Title 18 U.S.C S 1956 (a)(1) makes it a crime to knowingly

conduct, or attempt to conduct, a “financial transaction”

with proceeds from “specified unlawful activity” (SUA)

with specific intent to:

Other Areas Shells Are Used for Corrupt Practices

To conceal the movement of contraband in commerce

Prevents law enforcement and investigators from

knowing who is controlling companies and allows

SHELL COMPANIES, CORRUPT PRACTICES, AND HOW TO UNCOVER THEM

28th Annual ACFE Global Fraud Conference ©2017 7

NOTES bad actors to maintain plausible deniability and

operating freedom

Circumvent regulations and tax fraud—smaller

countries have established themselves as offshore

financial centers to stimulate economic development.

They attract investors and private individuals by

offering low or nonexistent tax rates. As such, they

attract deposits from individuals who are trying to

evade taxes through concealing much of their wealth.

Sanctions and sanctions busting

Sanctions are imposed on many countries,

businesses, and individuals to limit importation of

military equipment or ammunitions, or ban the

export of oil and other commodities. This is an

incentive for these bad actors to provide secret bank

accounts and shell companies in areas where

regulators turn a blind eye and, as a result, facilitate

sanction busting.

Module 3: Legitimate Reasons to Set Up Shell

Companies

To save up funds to open a business

As a front for product development that a well-

established company may want to keep private until it

is ready.

Facilitate financial institutions to perform financial

activity in foreign markets

To obtain financing, maintaining control over

conglomerate company

Realize a “tax haven” abroad

Module 4: Tools to Detect Whether a Shell Company Is

Being Used for Illegitimate Purposes

SHELL COMPANIES, CORRUPT PRACTICES, AND HOW TO UNCOVER THEM

28th Annual ACFE Global Fraud Conference ©2017 8

NOTES Investigative Red Flags of Suspicious Fund Transfers

Using Shells

There are several red flags that show potential suspicious

activities that may be associated with a Shell. These include

the following:

Payments that have no stated purpose, do not reference

goods or services, or identify only a contract or invoice

number

Purpose of the company is unknown or unclear

Goods or services identified do not match company

profile

Or responding bank provides dissimilar goods and

services in relations to the company transferring the

funds, or explanation given by respondent bank is

inconsistent with observed funds transfer activity

Fund transfers are sent in large, round dollar amounts.

Insufficient information available to positively identify

originators or beneficiaries of funds transfers

Company has little or no internet presence

Unusually large number of beneficiaries receiving

transfers from one company

Payments flow from one shell company to another with

no apparent legitimate business purpose.

Funds usually pass through jurisdictions or

beneficiaries located in high risk jurisdictions.

Transacting businesses share the same address, provide

only a registered agent’s address, or other

inconsistencies.

Other Areas to Review

Conduct due diligence research utilizing various

software to obtain affiliation for shells with suspicious

fund transfers. Utilize resources available to assist with ownership

identity and information on shell companies. This

SHELL COMPANIES, CORRUPT PRACTICES, AND HOW TO UNCOVER THEM

28th Annual ACFE Global Fraud Conference ©2017 9

NOTES includes conducting global research in various

databases and company registries. An initial search may show individuals in control of

the company.

Many companies list names and phone numbers for

their executives and board of directors on their

website to appear accountable and legitimate.

Companies don’t have websites and create a short

paper trail.

Web history

“Follow the Money”—Reviewing the flow of funds that

pass through one entity to another is useful in

identifying some individuals involved. Work with regulators and auditors in determining

whether constituents are complying with regulations.

“Know your customer.” Become familiar with evolving legislation regarding

beneficial ownership. Phantom companies shield the

veil of conduct.

International Standards Governing Shell Companies

The Financial Action Task Force (FATF) is the world

standard setter and enforcer of anti-money laundering

standards. More than 180 countries have committed to

FATF. It provides that “Countries should take measures to

prevent the misuse of legal persons [companies] for money

laundering or terrorist financing. Countries should ensure

that there is adequate, accurate and timely information on

the beneficial ownership and control of legal persons that

can be obtained or assessed in a timely fashion by

competent authorities.”4

4 Further studies on FATA can be viewed on

http://www.transparency.org/whatwedo/publication/doors_wide_open_

corruption_and_real_estate_in_four_key_markets

SHELL COMPANIES, CORRUPT PRACTICES, AND HOW TO UNCOVER THEM

28th Annual ACFE Global Fraud Conference ©2017 10

NOTES What Is Being Done to Eliminate Anonymous

Companies?

The UK has established a public beneficial ownership

information for all UK companies.

The European Parliament voted in March 2014 to create

a similar registry for all EU companies and trusts, but

further action by the EU commission and European

Council is pending.

All companies should be required to disclose their ultimate,

beneficial owner when they are created. This information

should be listed in a central registry.

Ways to Establish Beneficial Ownership of Shell

Companies

European Savings Directive

Banks in the EU countries collect the tax due on bank

accounts held by citizens of other EU countries.

U.S. Policies on Beneficial Ownership

On May 4, 2016, Financial Crimes Enforcement Network

(FinCEN) issued its long awaited final rule on beneficial

ownership with respect to customer due diligence. The final

rule required covered financial institutions to adopt due

diligence procedure to identify and verify a legal entity

customer’s beneficial owner(S) at the time a new account is

opened. The final rule creates a fifth “pillar” for anti-money

laundering (AML) programs required under FinCEN’ s

rules for banks.5

5 FinCEN releases Final rule on Beneficial Ownership and Risk based

Customer Due Diligence on May 10, 2016.

SHELL COMPANIES, CORRUPT PRACTICES, AND HOW TO UNCOVER THEM

28th Annual ACFE Global Fraud Conference ©2017 11

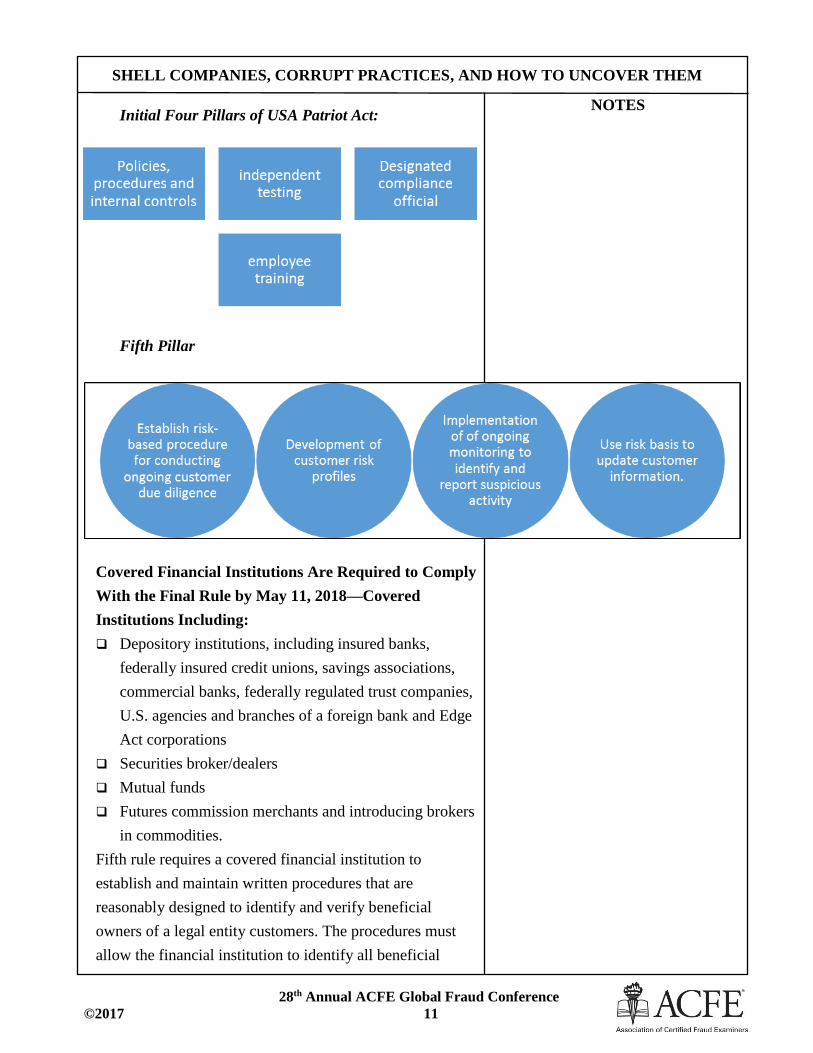

NOTES Initial Four Pillars of USA Patriot Act:

Fifth Pillar

Covered Financial Institutions Are Required to Comply

With the Final Rule by May 11, 2018—Covered

Institutions Including:

Depository institutions, including insured banks,

federally insured credit unions, savings associations,

commercial banks, federally regulated trust companies,

U.S. agencies and branches of a foreign bank and Edge

Act corporations

Securities broker/dealers

Mutual funds

Futures commission merchants and introducing brokers

in commodities.

Fifth rule requires a covered financial institution to

establish and maintain written procedures that are

reasonably designed to identify and verify beneficial

owners of a legal entity customers. The procedures must

allow the financial institution to identify all beneficial

SHELL COMPANIES, CORRUPT PRACTICES, AND HOW TO UNCOVER THEM

28th Annual ACFE Global Fraud Conference ©2017 12

NOTES owners of each legal entity customer at the time of account

opening unless an exclusion or exemption applies to the

customer or account.

Summary

Shell companies (Shell) are used for many reasons, some

are legal and others are not. They act as the intermediaries,

where the real owners remain hard to trace. As such, they

are an ideal mechanism for concealing identity and aiding

fraudulent transactions to appear legitimate. This training

provides a practical breakdown on what constitutes a Shell

and tools to identify when Shells are being used for illegal

purposes.

Abstract

Reason for writing: What is the importance of the

research? Why would a reader be interested in the

larger work?

Problem: What problem does this work attempt to

solve? What is the scope of the project? What is the

main argument/thesis/claim?

Methodology: An abstract of a scientific work may

include specific models or approaches used in the larger

study. Other abstracts may describe the types of

evidence used in the research.

Results: Again, an abstract of a scientific work may

include specific data that indicates the results of the

project. Other abstracts may discuss the findings in a

more general way.

Implications: What changes should be implemented as

a result of the findings of the work? How does this

work add to the body of knowledge on the topic?

Shells can be complex! A Shell can be owned by another

Shell, which in turn is owned by another Shell, weaving a

web of Shells with unknown beneficial ownership. The

SHELL COMPANIES, CORRUPT PRACTICES, AND HOW TO UNCOVER THEM

28th Annual ACFE Global Fraud Conference ©2017 13

NOTES ease with which they are created and the lack of

information required on the ownership makes them an ideal

mechanism for fraudulent activities. Don’t be a player or a

victim of “The Web of Shells.”

This session will provide participants with an

understanding of Shell Companies and it will provide some

tools on how to map and untangle The Web of Shells.

Target Audience

Forensic accountants

Regulators

Government investigators/auditors

Contractors and NPO (CEOs, CFOs) who receive

government funding

State registrants

Anti-money laundering specialist