Embed Size (px)

DESCRIPTION

Complete information & FAQ regarding Employee's Provident Funds Act 1952.

Citation preview

1

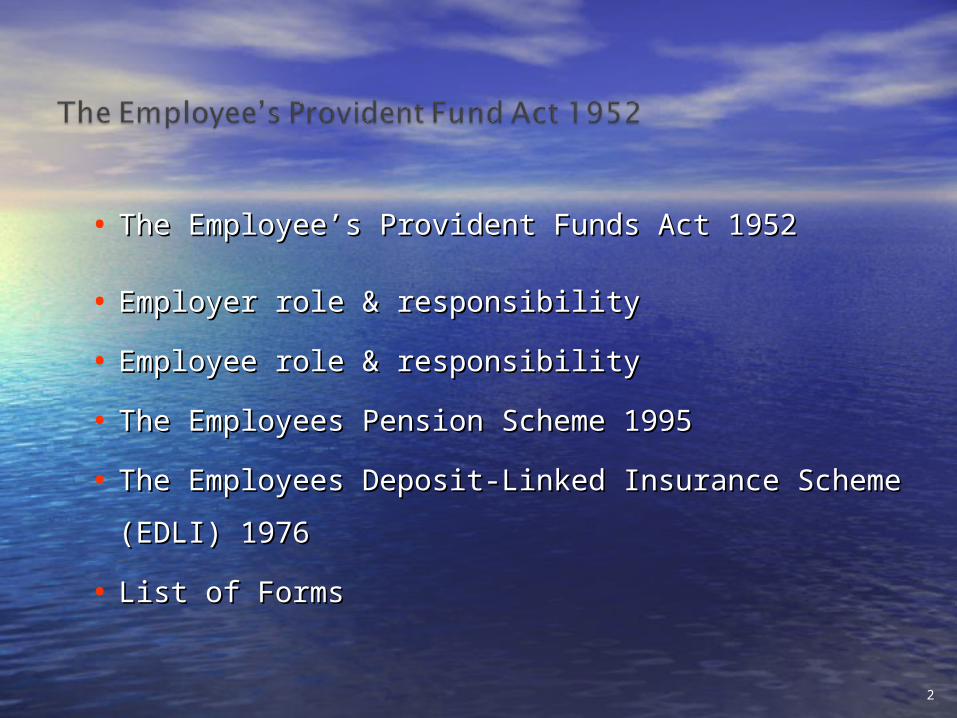

• The Employee’s Provident Funds Act 1952 The Employee’s Provident Funds Act 1952

• Employer role & responsibility Employer role & responsibility

• Employee role & responsibility Employee role & responsibility

• The Employees Pension Scheme 1995The Employees Pension Scheme 1995

• The Employees Deposit-Linked Insurance Scheme (EDLI) The Employees Deposit-Linked Insurance Scheme (EDLI)

19761976

• List of FormsList of Forms

2

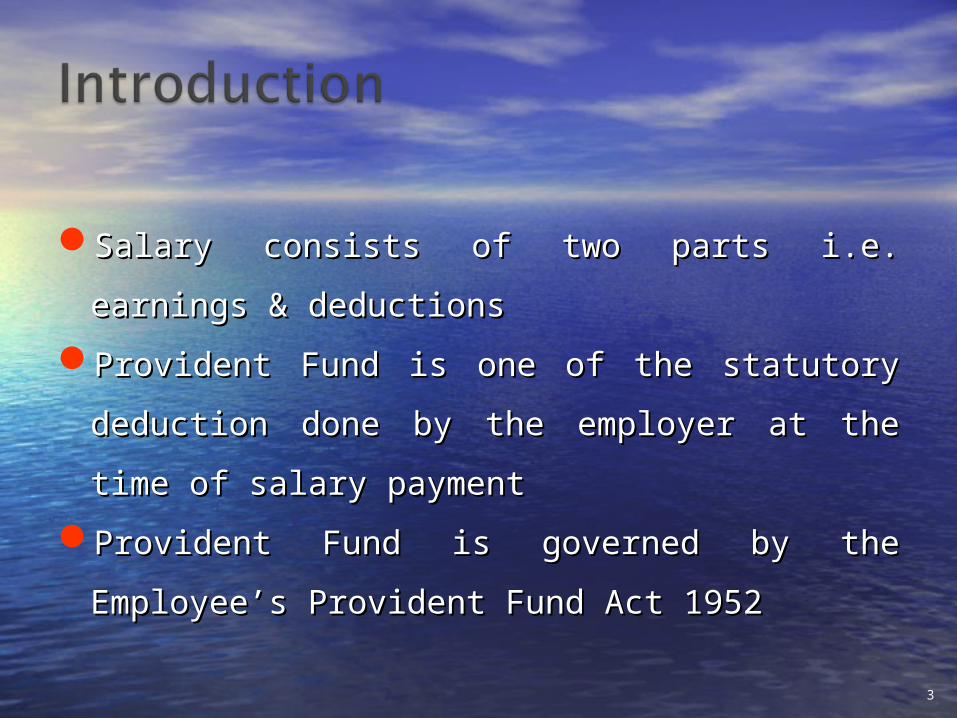

Salary consists of two parts i.e. earnings & Salary consists of two parts i.e. earnings &

deductionsdeductions

Provident Fund is one of the statutory deduction Provident Fund is one of the statutory deduction

done by the employer at the time of salary payment done by the employer at the time of salary payment

Provident Fund is governed by the Employee’s Provident Fund is governed by the Employee’s

Provident Fund Act 1952 Provident Fund Act 1952

3

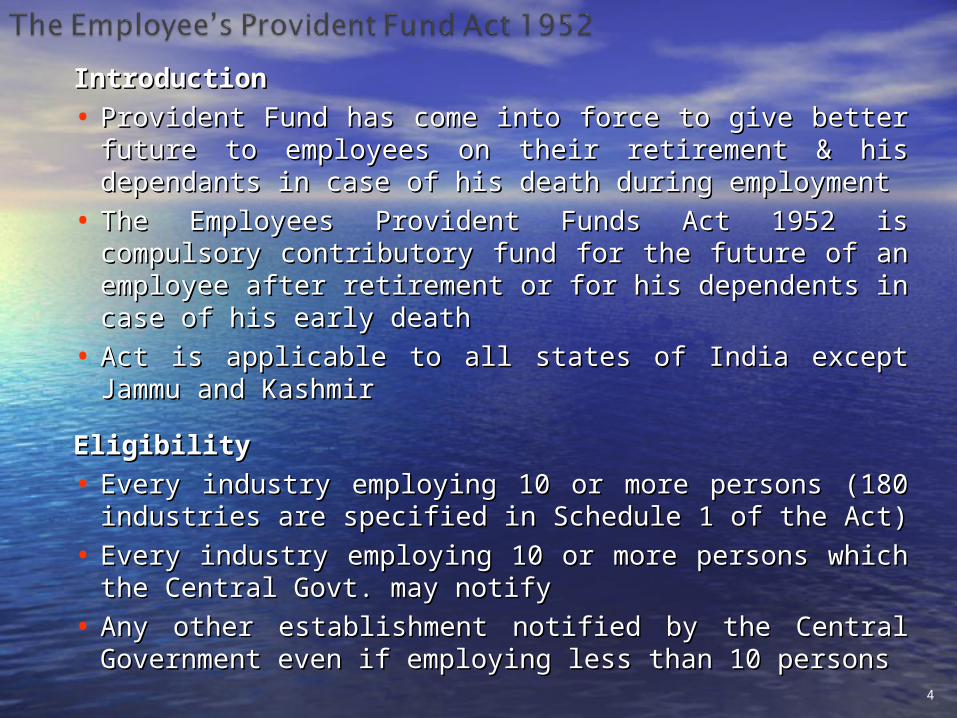

IntroductionIntroduction

• Provident Fund has come into force to give better future to Provident Fund has come into force to give better future to employees on their retirement & his dependants in case of employees on their retirement & his dependants in case of his death during employmenthis death during employment

• The Employees Provident Funds Act 1952 is compulsory The Employees Provident Funds Act 1952 is compulsory contributory fund for the future of an employee after contributory fund for the future of an employee after retirement or for his dependents in case of his early deathretirement or for his dependents in case of his early death

• Act is applicable to all states of India except Jammu and Act is applicable to all states of India except Jammu and KashmirKashmir

EligibilityEligibility

• Every industry employing 10 or more persons (180 Every industry employing 10 or more persons (180 industries are specified in Schedule 1 of the Act) industries are specified in Schedule 1 of the Act)

• Every industry employing 10 or more persons which the Every industry employing 10 or more persons which the Central Govt. may notify Central Govt. may notify

• Any other establishment notified by the Central Government Any other establishment notified by the Central Government even if employing less than 10 personseven if employing less than 10 persons 4

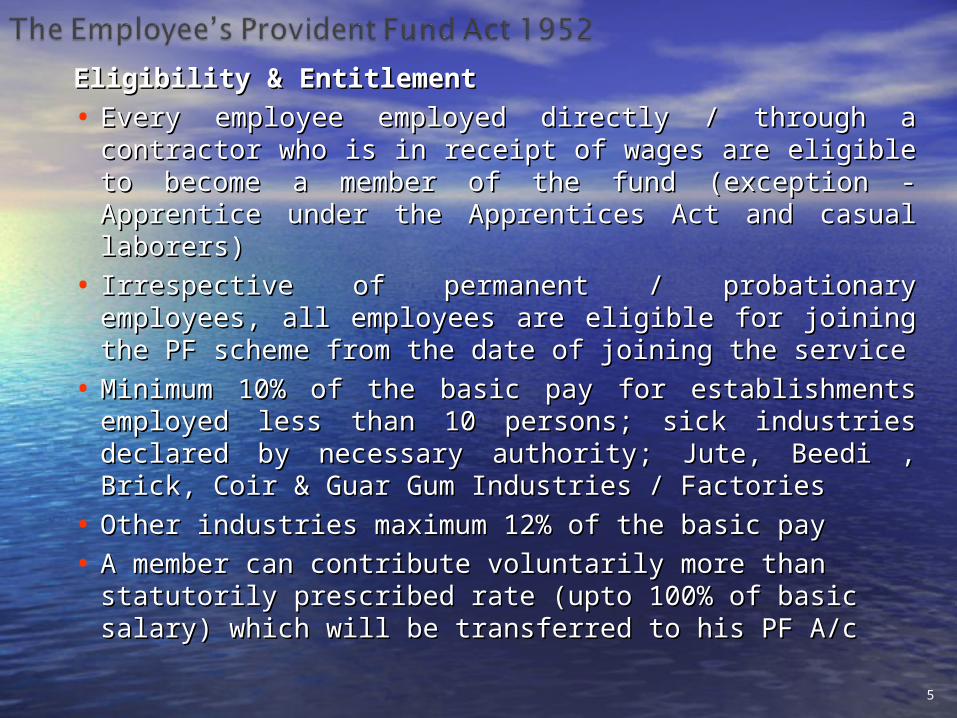

Eligibility & EntitlementEligibility & Entitlement

• Every employee employed directly / through a contractor Every employee employed directly / through a contractor who is in receipt of wages are eligible to become a who is in receipt of wages are eligible to become a member of the fund (exception - Apprentice under the member of the fund (exception - Apprentice under the Apprentices Act and casual laborers) Apprentices Act and casual laborers)

• Irrespective of permanent / probationary employees, all Irrespective of permanent / probationary employees, all employees are eligible for joining the PF scheme from the employees are eligible for joining the PF scheme from the date of joining the servicedate of joining the service

• Minimum 10% of the basic pay for establishments Minimum 10% of the basic pay for establishments employed less than 10 persons; sick industries declared by employed less than 10 persons; sick industries declared by necessary authority; Jute, Beedi , Brick, Coir & Guar Gum necessary authority; Jute, Beedi , Brick, Coir & Guar Gum Industries / FactoriesIndustries / Factories

• Other industries maximum 12% of the basic payOther industries maximum 12% of the basic pay

• A member can contribute voluntarily more than statutorily A member can contribute voluntarily more than statutorily prescribed rate (upto 100% of basic salary) which will be prescribed rate (upto 100% of basic salary) which will be transferred to his PF A/c transferred to his PF A/c

5

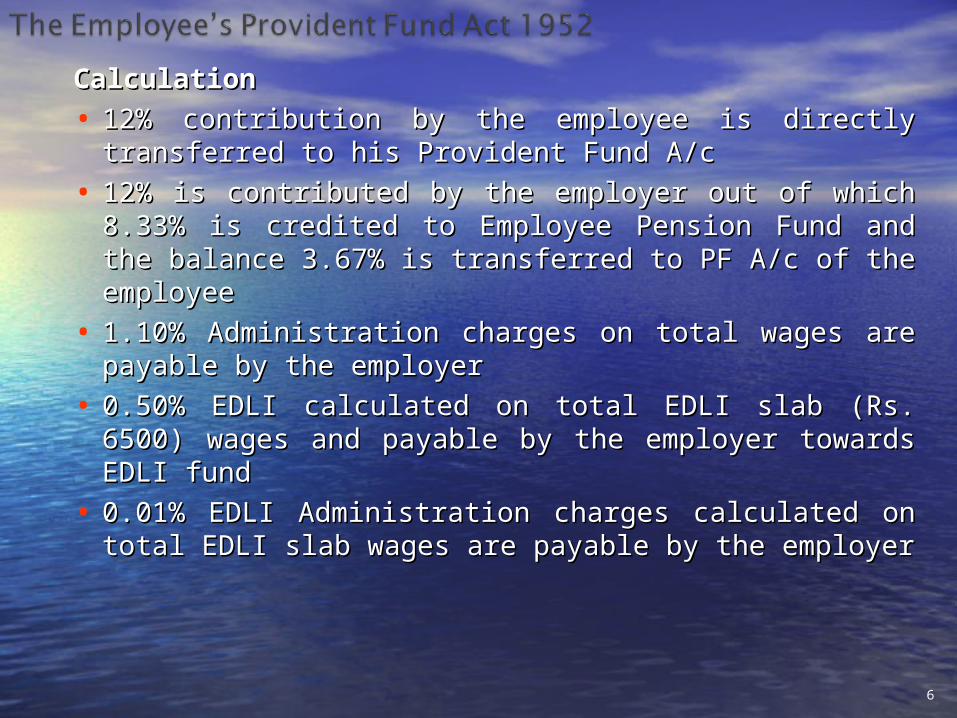

CalculationCalculation

• 12% contribution by the employee is directly 12% contribution by the employee is directly transferred to his Provident Fund A/ctransferred to his Provident Fund A/c

• 12% is contributed by the employer out of which 8.33% 12% is contributed by the employer out of which 8.33% is credited to Employee Pension Fund and the balance is credited to Employee Pension Fund and the balance 3.67% is transferred to PF A/c of the employee3.67% is transferred to PF A/c of the employee

• 1.10% Administration charges on total wages are 1.10% Administration charges on total wages are payable by the employerpayable by the employer

• 0.50% EDLI calculated on total EDLI slab (Rs. 6500) 0.50% EDLI calculated on total EDLI slab (Rs. 6500) wages and payable by the employer towards EDLI fundwages and payable by the employer towards EDLI fund

• 0.01% EDLI Administration charges calculated on total 0.01% EDLI Administration charges calculated on total EDLI slab wages are payable by the employerEDLI slab wages are payable by the employer

6

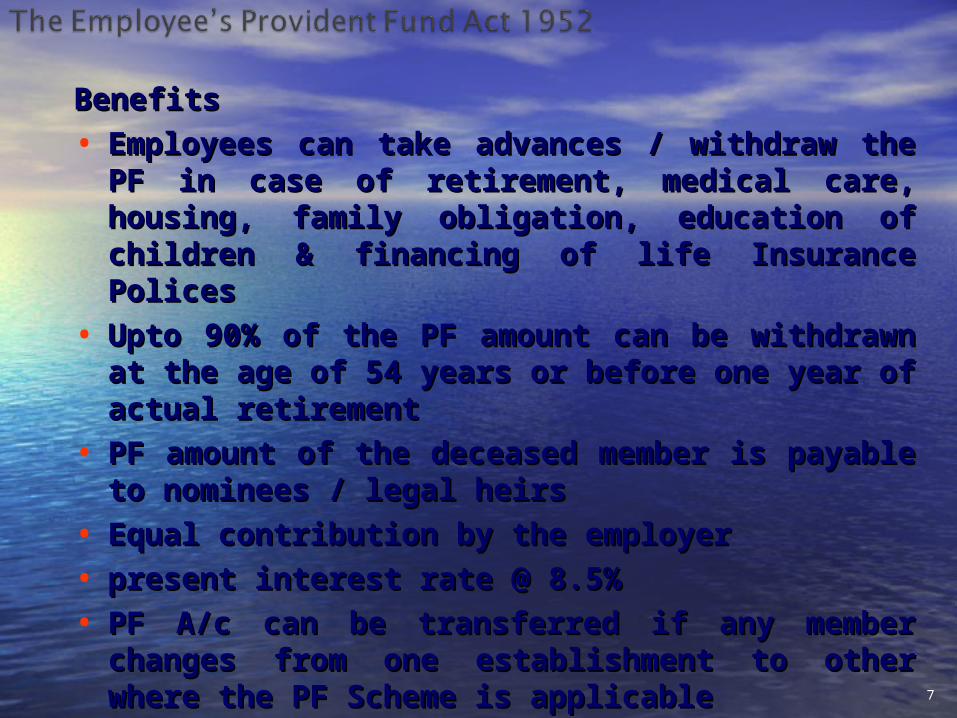

BenefitsBenefits

• Employees can take advances / withdraw the PF in Employees can take advances / withdraw the PF in case of retirement, medical care, housing, family case of retirement, medical care, housing, family obligation, education of children & financing of life obligation, education of children & financing of life Insurance Polices Insurance Polices

• Upto 90% of the PF amount can be withdrawn at the Upto 90% of the PF amount can be withdrawn at the age of 54 years or before one year of actual age of 54 years or before one year of actual retirementretirement

• PF amount of the deceased member is payable to PF amount of the deceased member is payable to nominees / legal heirsnominees / legal heirs

• Equal contribution by the employerEqual contribution by the employer

• present interest rate @ 8.5% present interest rate @ 8.5%

• PF A/c can be transferred if any member changes PF A/c can be transferred if any member changes from one establishment to other where the PF from one establishment to other where the PF Scheme is applicableScheme is applicable 7

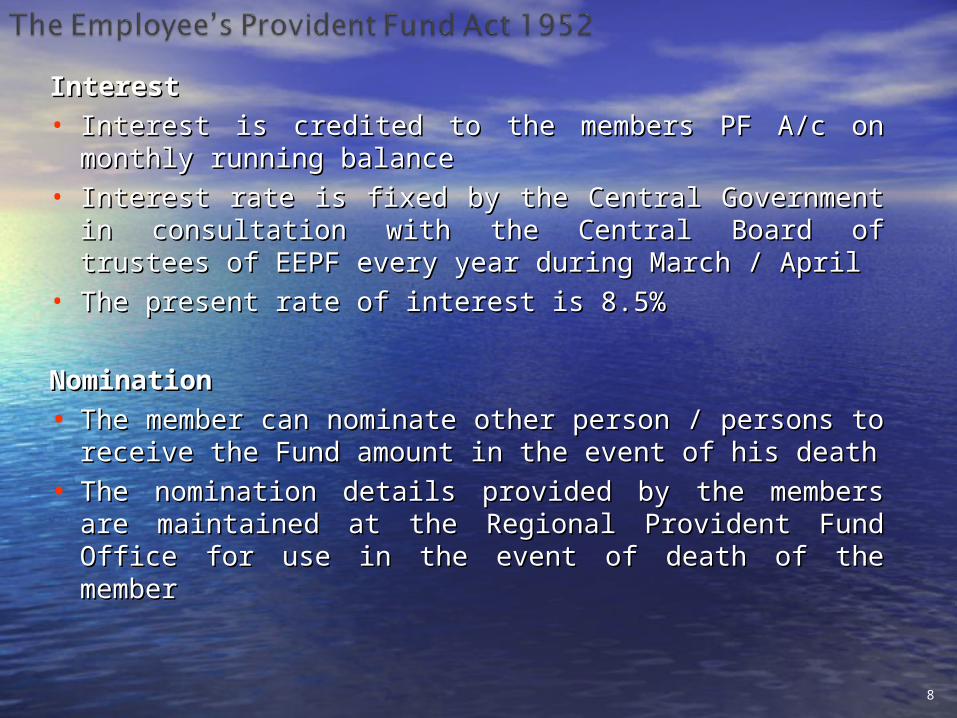

Interest Interest • Interest is credited to the members PF A/c on monthly Interest is credited to the members PF A/c on monthly

running balance running balance • Interest rate is fixed by the Central Government in Interest rate is fixed by the Central Government in

consultation with the Central Board of trustees of EEPF consultation with the Central Board of trustees of EEPF every year during March / Aprilevery year during March / April

• The present rate of interest is 8.5%The present rate of interest is 8.5%

NominationNomination

• The member can nominate other person / persons to The member can nominate other person / persons to receive the Fund amount in the event of his deathreceive the Fund amount in the event of his death

• The nomination details provided by the members are The nomination details provided by the members are maintained at the Regional Provident Fund Office for maintained at the Regional Provident Fund Office for use in the event of death of the memberuse in the event of death of the member

8

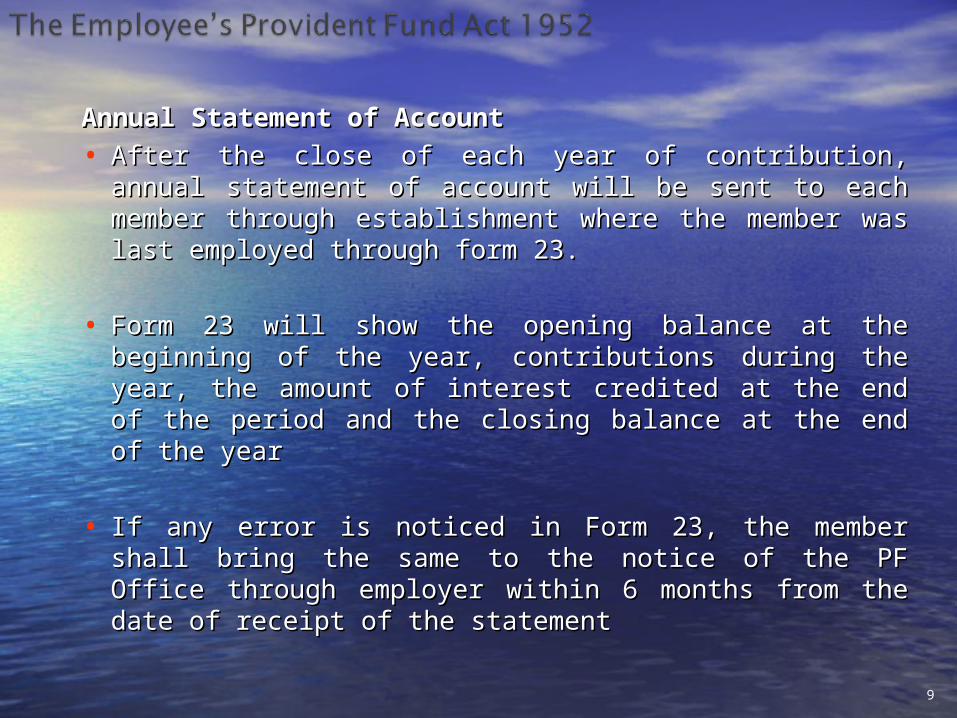

Annual Statement of AccountAnnual Statement of Account

• After the close of each year of contribution, annual After the close of each year of contribution, annual statement of account will be sent to each member through statement of account will be sent to each member through establishment where the member was last employed establishment where the member was last employed through form 23.through form 23.

• Form 23 will show the opening balance at the beginning of Form 23 will show the opening balance at the beginning of the year, contributions during the year, the amount of the year, contributions during the year, the amount of interest credited at the end of the period and the closing interest credited at the end of the period and the closing balance at the end of the yearbalance at the end of the year

• If any error is noticed in Form 23, the member shall bring If any error is noticed in Form 23, the member shall bring the same to the notice of the PF Office through employer the same to the notice of the PF Office through employer within 6 months from the date of receipt of the statementwithin 6 months from the date of receipt of the statement

9

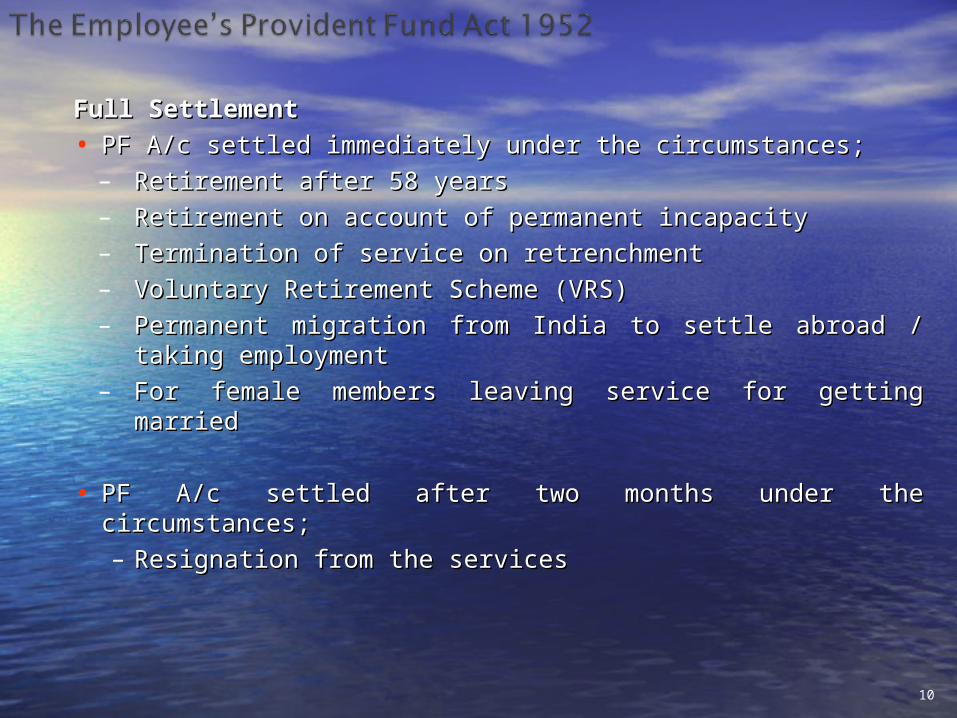

Full Settlement Full Settlement

• PF A/c settled immediately under the circumstances;PF A/c settled immediately under the circumstances;– Retirement after 58 yearsRetirement after 58 years– Retirement on account of permanent incapacity Retirement on account of permanent incapacity – Termination of service on retrenchmentTermination of service on retrenchment– Voluntary Retirement Scheme (VRS)Voluntary Retirement Scheme (VRS)– Permanent migration from India to settle abroad / taking Permanent migration from India to settle abroad / taking

employmentemployment– For female members leaving service for getting married For female members leaving service for getting married

• PF A/c settled after two months under the circumstances;PF A/c settled after two months under the circumstances;– Resignation from the services Resignation from the services

10

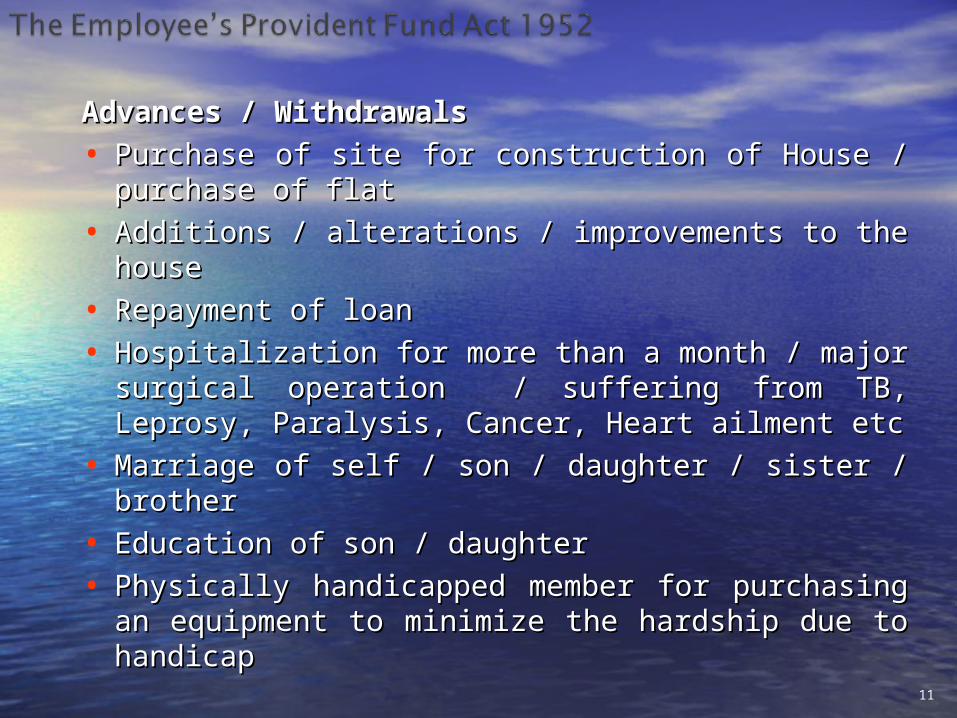

Advances / WithdrawalsAdvances / Withdrawals

• Purchase of site for construction of House / purchase of Purchase of site for construction of House / purchase of flat flat

• Additions / alterations / improvements to the house Additions / alterations / improvements to the house

• Repayment of loan Repayment of loan

• Hospitalization for more than a month / major surgical Hospitalization for more than a month / major surgical operation / suffering from TB, Leprosy, Paralysis, operation / suffering from TB, Leprosy, Paralysis, Cancer, Heart ailment etcCancer, Heart ailment etc

• Marriage of self / son / daughter / sister / brotherMarriage of self / son / daughter / sister / brother

• Education of son / daughter Education of son / daughter

• Physically handicapped member for purchasing an Physically handicapped member for purchasing an equipment to minimize the hardship due to handicapequipment to minimize the hardship due to handicap

11

Employer Role & ResponsibilityEmployer Role & Responsibility

12

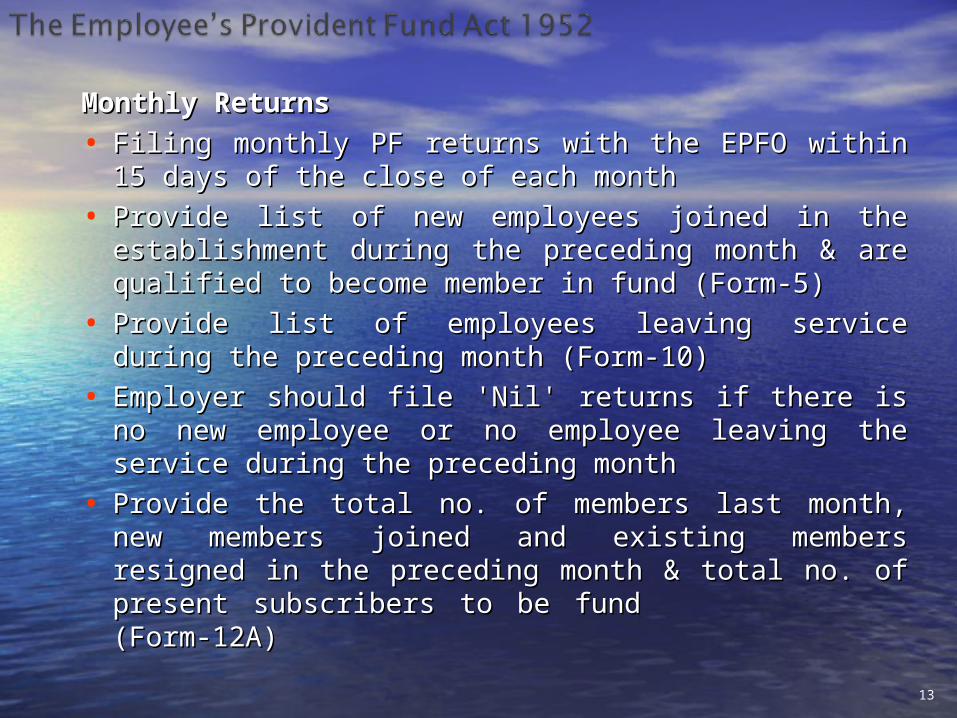

Monthly Returns Monthly Returns

• Filing monthly PF returns with the EPFO within 15 days of Filing monthly PF returns with the EPFO within 15 days of the close of each month the close of each month

• Provide list of new employees joined in the establishment Provide list of new employees joined in the establishment during the preceding month & are qualified to become during the preceding month & are qualified to become member in fund (Form-5)member in fund (Form-5)

• Provide list of employees leaving service during the Provide list of employees leaving service during the preceding month (Form-10)preceding month (Form-10)

• Employer should file 'Nil' returns if there is no new Employer should file 'Nil' returns if there is no new employee or no employee leaving the service during the employee or no employee leaving the service during the preceding monthpreceding month

• Provide the total no. of members last month, new Provide the total no. of members last month, new members joined and existing members resigned in the members joined and existing members resigned in the preceding month & total no. of present subscribers to be preceding month & total no. of present subscribers to be fund (Form-12A)fund (Form-12A)

13

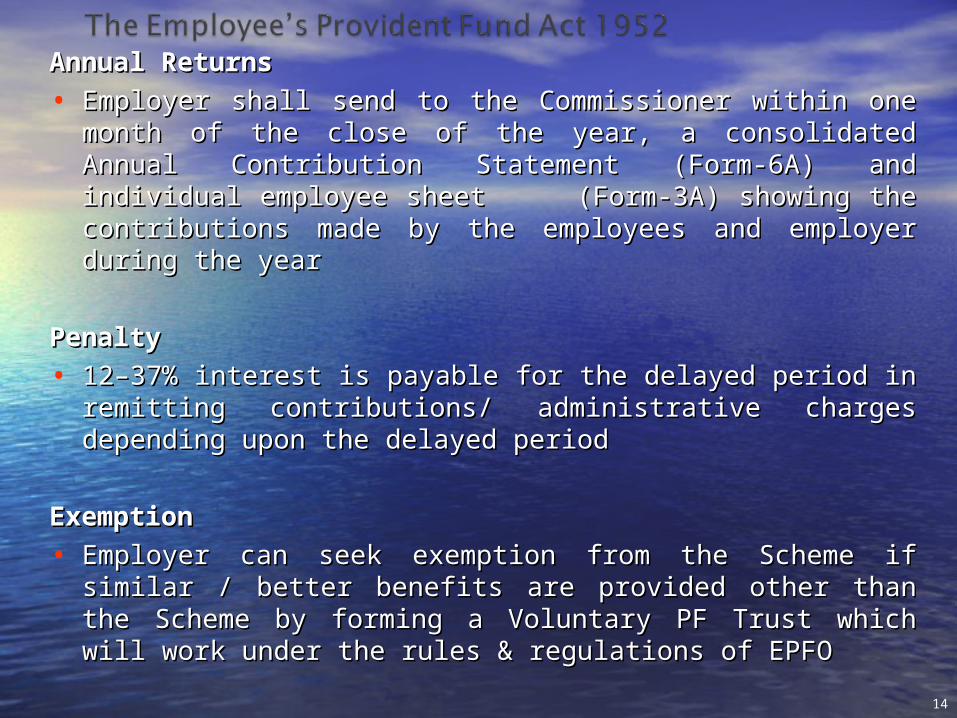

Annual Returns Annual Returns

• Employer shall send to the Commissioner within one month of Employer shall send to the Commissioner within one month of the close of the year, a consolidated Annual Contribution the close of the year, a consolidated Annual Contribution Statement (Form-6A) and individual employee sheet (Form-Statement (Form-6A) and individual employee sheet (Form-3A) showing the contributions made by the employees and 3A) showing the contributions made by the employees and employer during the yearemployer during the year

PenaltyPenalty

• 12–37% interest is payable for the delayed period in remitting 12–37% interest is payable for the delayed period in remitting contributions/ administrative charges depending upon the contributions/ administrative charges depending upon the delayed perioddelayed period

ExemptionExemption

• Employer can seek exemption from the Scheme if similar / Employer can seek exemption from the Scheme if similar / better benefits are provided other than the Scheme by forming a better benefits are provided other than the Scheme by forming a Voluntary PF Trust which will work under the rules & regulations Voluntary PF Trust which will work under the rules & regulations of EPFOof EPFO

14

Employee Role & ResponsibilityEmployee Role & Responsibility

15

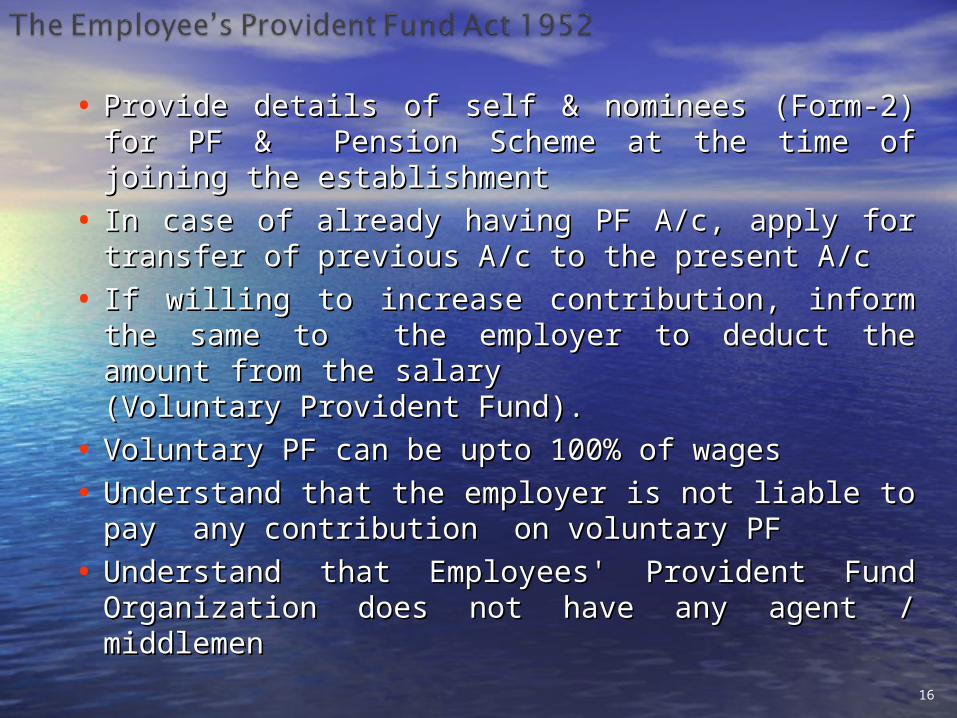

• Provide details of self & nominees (Form-2) for PF & Provide details of self & nominees (Form-2) for PF & Pension Scheme at the time of joining the Pension Scheme at the time of joining the establishmentestablishment

• In case of already having PF A/c, apply for transfer In case of already having PF A/c, apply for transfer of previous A/c to the present A/cof previous A/c to the present A/c

• If willing to increase contribution, inform the same to If willing to increase contribution, inform the same to the employer to deduct the amount from the salary the employer to deduct the amount from the salary (Voluntary Provident Fund). (Voluntary Provident Fund).

• Voluntary PF can be upto 100% of wagesVoluntary PF can be upto 100% of wages

• Understand that the employer is not liable to pay Understand that the employer is not liable to pay any contribution on voluntary PFany contribution on voluntary PF

• Understand that Employees' Provident Fund Understand that Employees' Provident Fund Organization does not have any agent / middlemenOrganization does not have any agent / middlemen

16

Employees Pension Scheme 1995Employees Pension Scheme 1995

17

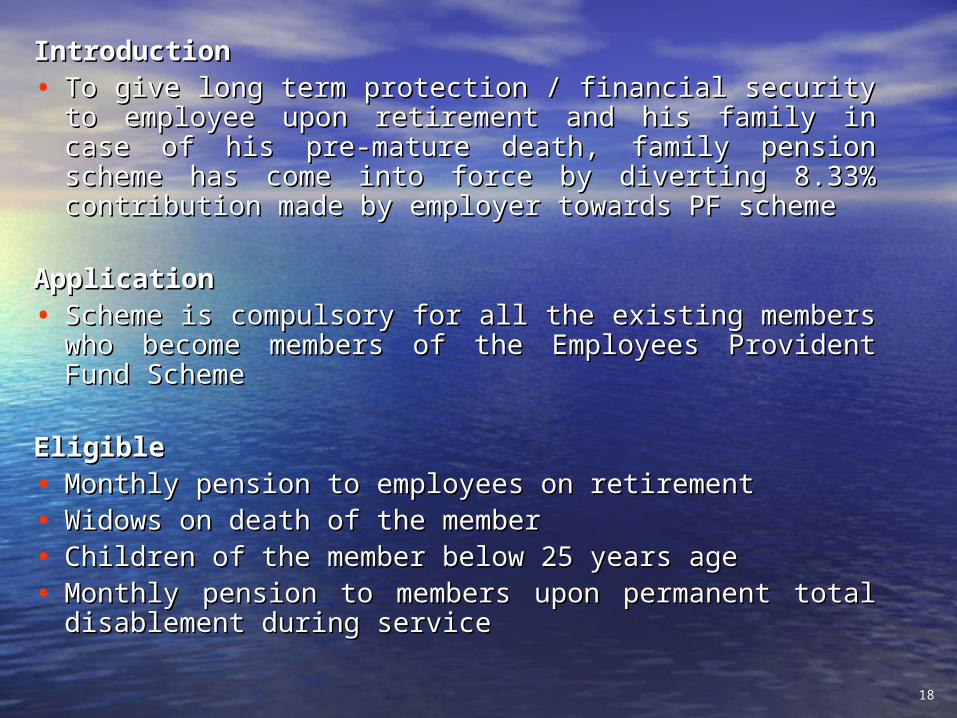

IntroductionIntroduction• To give long term protection / financial security to employee To give long term protection / financial security to employee

upon retirement and his family in case of his pre-mature upon retirement and his family in case of his pre-mature death, family pension scheme has come into force by death, family pension scheme has come into force by diverting 8.33% contribution made by employer towards PF diverting 8.33% contribution made by employer towards PF schemescheme

ApplicationApplication• Scheme is compulsory for all the existing members who Scheme is compulsory for all the existing members who

become members of the Employees Provident Fund Schemebecome members of the Employees Provident Fund Scheme

EligibleEligible• Monthly pension to employees on retirementMonthly pension to employees on retirement• Widows on death of the memberWidows on death of the member• Children of the member below 25 years age Children of the member below 25 years age • Monthly pension to members upon permanent total Monthly pension to members upon permanent total

disablement during servicedisablement during service

18

19

The Employees Deposit-Linked Insurance Scheme 1976

(EDLI)

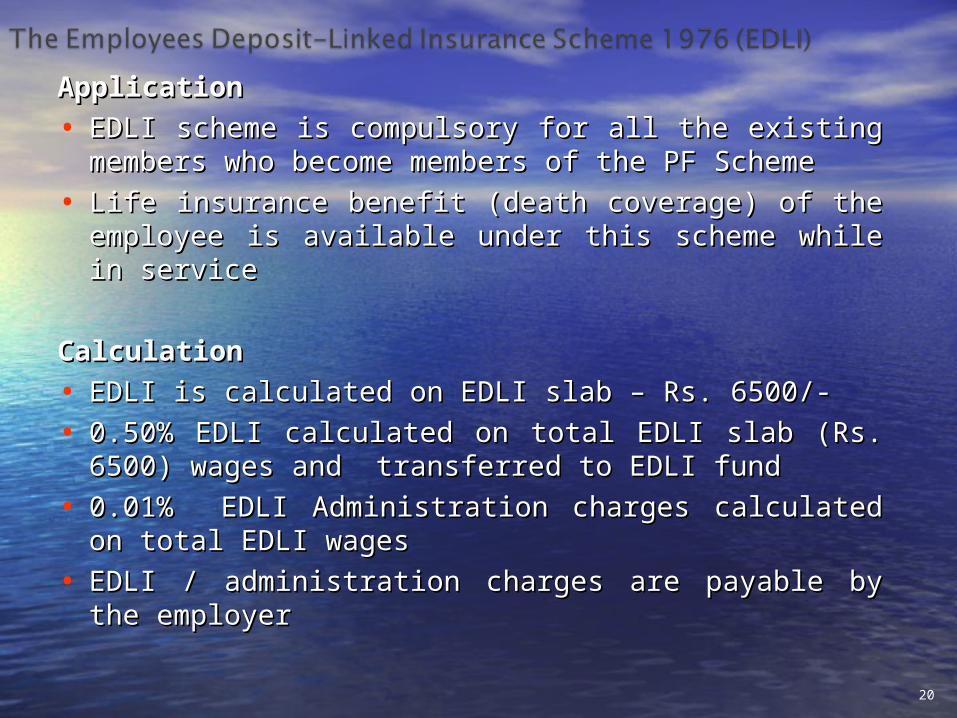

ApplicationApplication

• EDLI scheme is compulsory for all the existing members EDLI scheme is compulsory for all the existing members who become members of the PF Schemewho become members of the PF Scheme

• Life insurance benefit (death coverage) of the employee Life insurance benefit (death coverage) of the employee is available under this scheme while in serviceis available under this scheme while in service

CalculationCalculation

• EDLI is calculated on EDLI slab – Rs. 6500/-EDLI is calculated on EDLI slab – Rs. 6500/-

• 0.50% EDLI calculated on total EDLI slab (Rs. 6500) 0.50% EDLI calculated on total EDLI slab (Rs. 6500) wages and transferred to EDLI fundwages and transferred to EDLI fund

• 0.01% EDLI Administration charges calculated on total 0.01% EDLI Administration charges calculated on total EDLI wagesEDLI wages

• EDLI / administration charges are payable by the EDLI / administration charges are payable by the employer employer

20

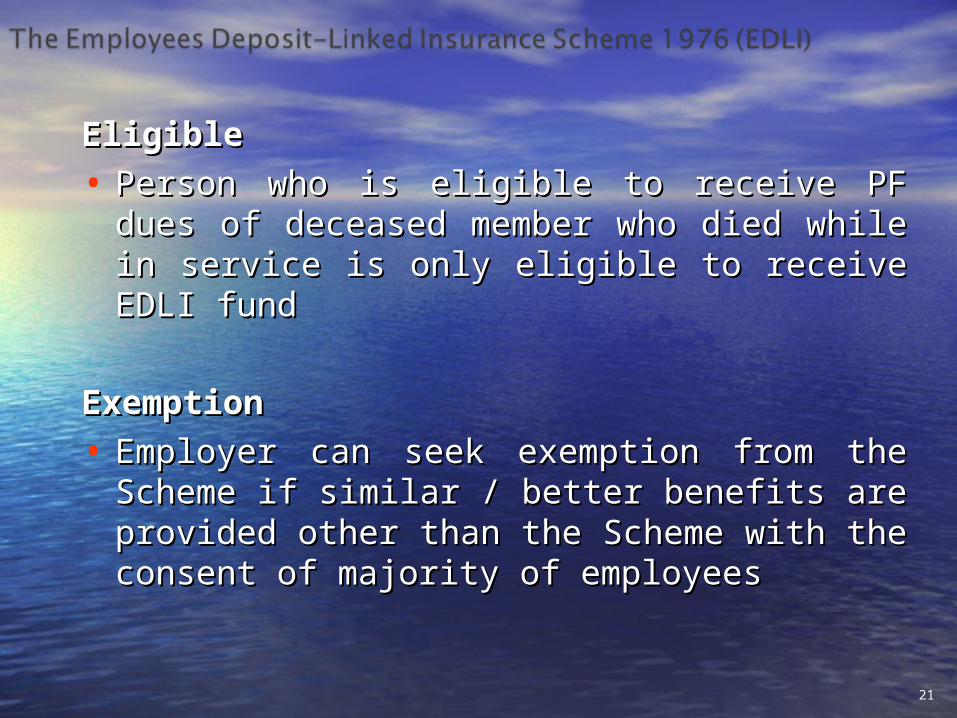

EligibleEligible

• Person who is eligible to receive PF dues of Person who is eligible to receive PF dues of deceased member who died while in service is deceased member who died while in service is only eligible to receive EDLI fundonly eligible to receive EDLI fund

Exemption Exemption

• Employer can seek exemption from the Scheme Employer can seek exemption from the Scheme if similar / better benefits are provided other than if similar / better benefits are provided other than the Scheme with the consent of majority of the Scheme with the consent of majority of employees employees

21

List of FormsList of Forms

22

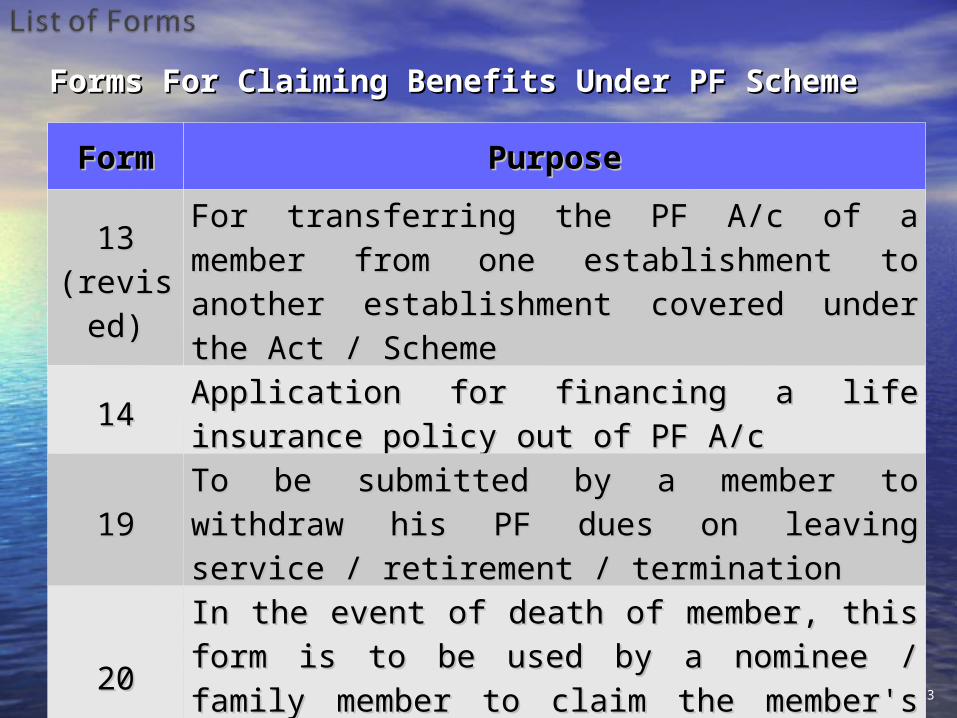

Forms For Claiming Benefits Under PF SchemeForms For Claiming Benefits Under PF Scheme

23

FormForm PurposePurpose1313

(revise(revised)d)

For transferring the PF A/c of a member from For transferring the PF A/c of a member from one establishment to another establishment one establishment to another establishment covered under the Act / Schemecovered under the Act / Scheme

1414Application for financing a life insurance Application for financing a life insurance policy out of PF A/cpolicy out of PF A/c

1919To be submitted by a member to withdraw To be submitted by a member to withdraw his PF dues on leaving service / retirement / his PF dues on leaving service / retirement / terminationtermination

2020In the event of death of member, this form is In the event of death of member, this form is to be used by a nominee / family member to to be used by a nominee / family member to claim the member's PF accumulationclaim the member's PF accumulation

3131For the use of PF members to avail advances For the use of PF members to avail advances / withdrawals as provided in the scheme/ withdrawals as provided in the scheme

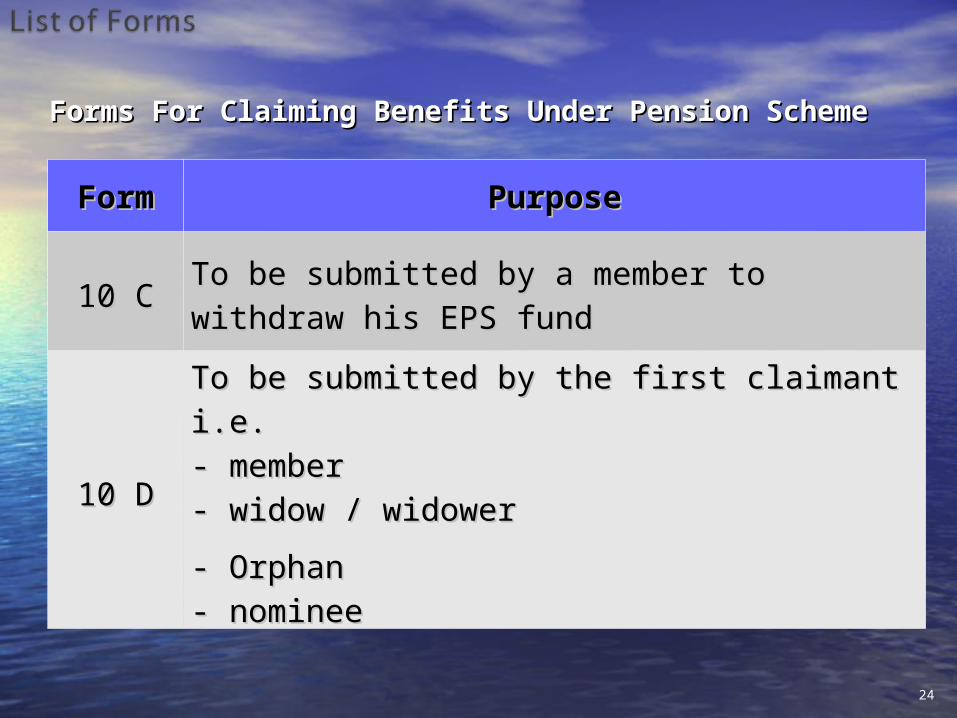

Forms For Claiming Benefits Under Pension SchemeForms For Claiming Benefits Under Pension Scheme

24

FormForm PurposePurpose

10 C10 CTo be submitted by a member to withdraw To be submitted by a member to withdraw his EPS fundhis EPS fund

10 D10 D

To be submitted by the first claimant i.e.To be submitted by the first claimant i.e.- member - member - widow / widower- widow / widower

- Orphan- Orphan- nominee- nominee

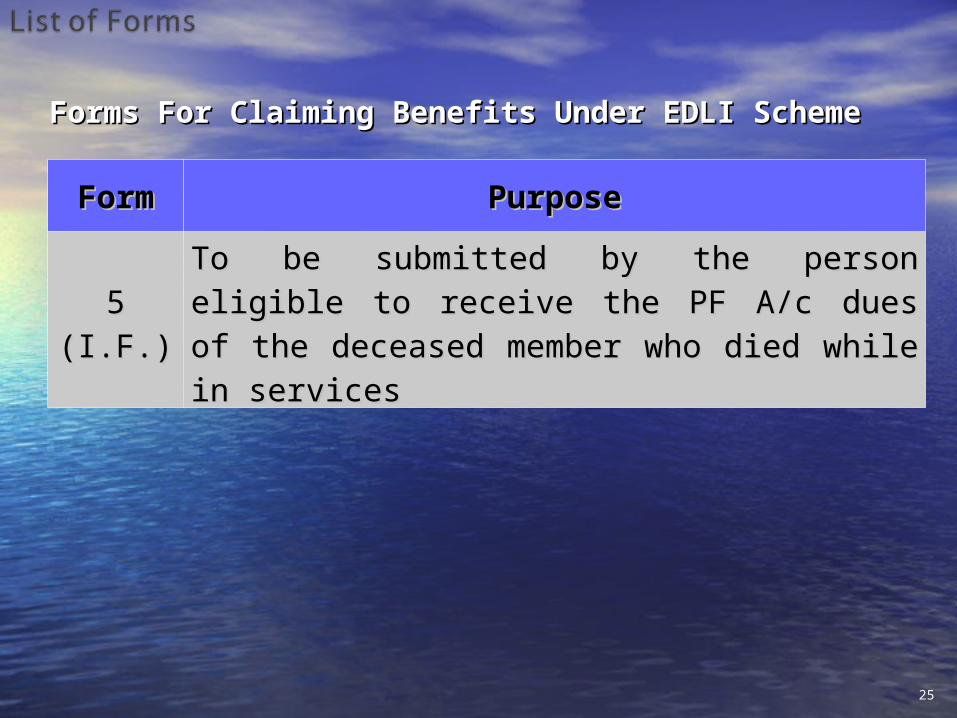

Forms For Claiming Benefits Under EDLI SchemeForms For Claiming Benefits Under EDLI Scheme

25

FormForm PurposePurpose

5 (I.F.)5 (I.F.)To be submitted by the person eligible to To be submitted by the person eligible to receive the PF A/c dues of the deceased receive the PF A/c dues of the deceased member who died while in servicesmember who died while in services

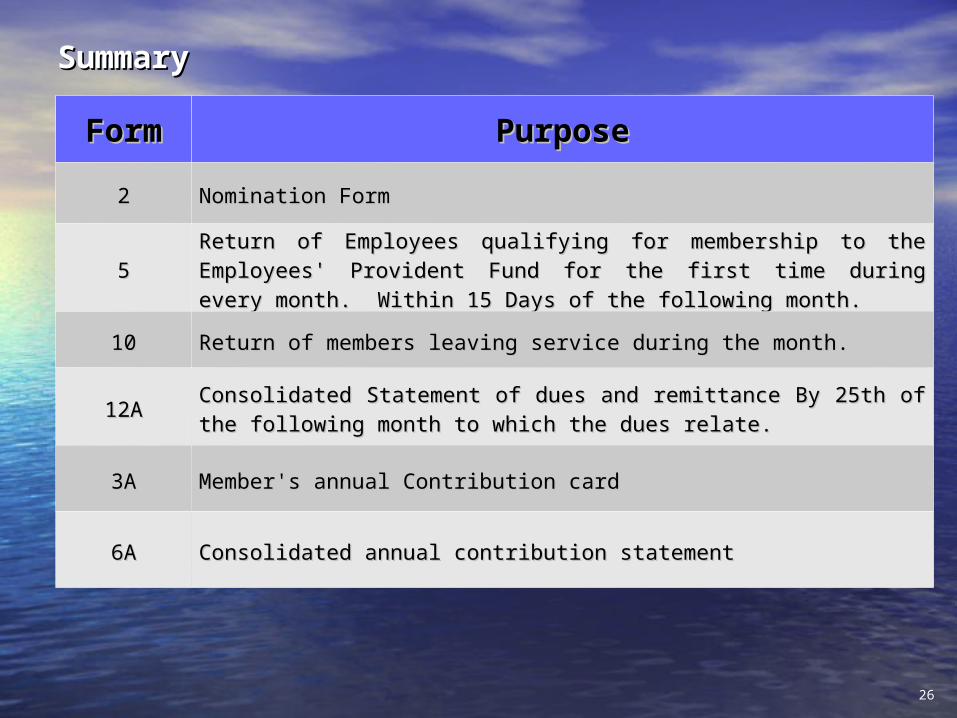

SummarySummary

26

FormForm PurposePurpose

22 Nomination FormNomination Form

55Return of Employees qualifying for membership to the Employees' Provident Return of Employees qualifying for membership to the Employees' Provident

Fund for the first time during every month. Within 15 Days of the following Fund for the first time during every month. Within 15 Days of the following

month.month.

1010 Return of members leaving service during the month.Return of members leaving service during the month.

12A12AConsolidated Statement of dues and remittance By 25th of the Consolidated Statement of dues and remittance By 25th of the following month to which the dues relate.following month to which the dues relate.

3A3A Member's annual Contribution card Member's annual Contribution card

6A6A Consolidated annual contribution statement Consolidated annual contribution statement

27

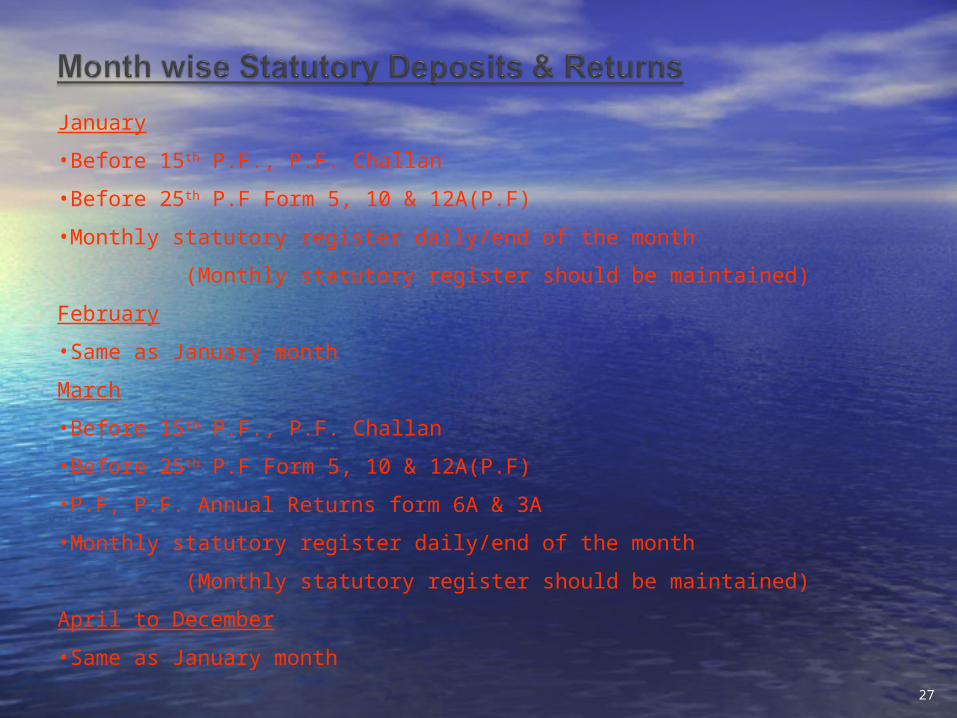

January

•Before 15th P.F., P.F. Challan

•Before 25th P.F Form 5, 10 & 12A(P.F)

•Monthly statutory register daily/end of the month

(Monthly statutory register should be maintained)

February

•Same as January month

March

•Before 15th P.F., P.F. Challan

•Before 25th P.F Form 5, 10 & 12A(P.F)

•P.F, P.F. Annual Returns form 6A & 3A

•Monthly statutory register daily/end of the month

(Monthly statutory register should be maintained)

April to December

•Same as January month

28

FAQFAQ

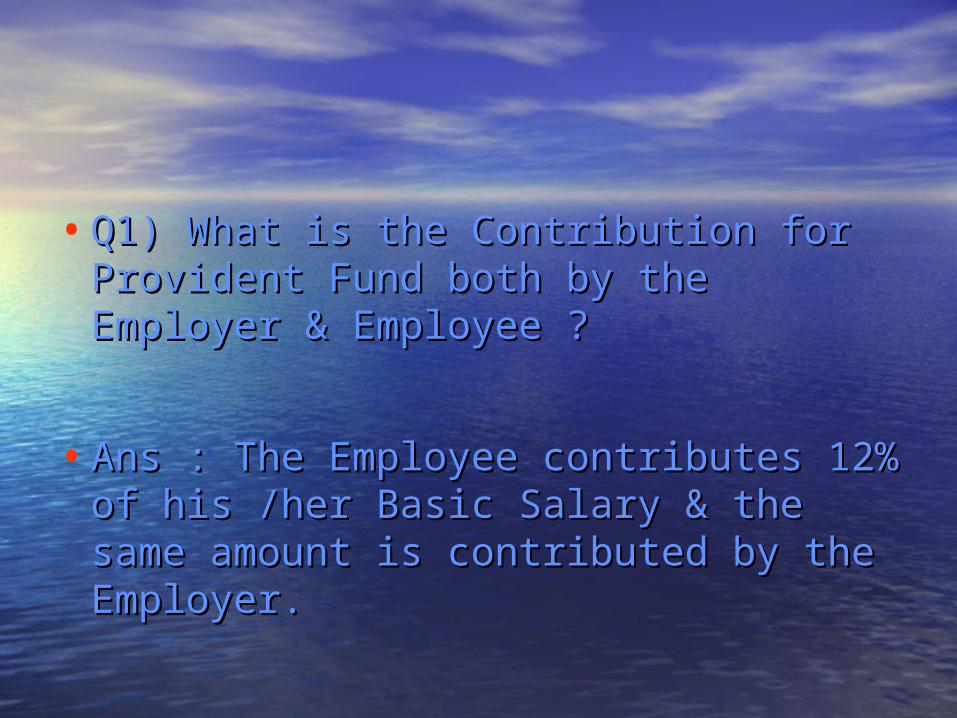

• Q1) What is the Contribution for Provident Q1) What is the Contribution for Provident Fund both by the Employer & Employee ?Fund both by the Employer & Employee ?

• Ans : The Employee contributes 12% of his Ans : The Employee contributes 12% of his /her Basic Salary & the same amount is /her Basic Salary & the same amount is contributed by the Employer.contributed by the Employer.

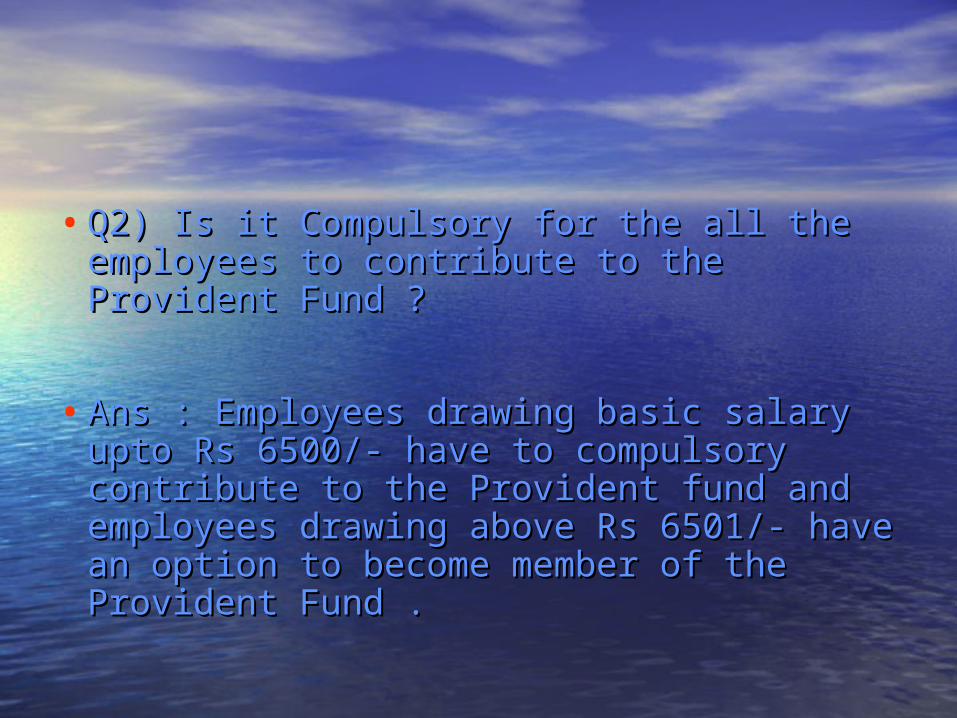

• Q2) Is it Compulsory for the all the employees Q2) Is it Compulsory for the all the employees to contribute to the Provident Fund ?to contribute to the Provident Fund ?

• Ans : Employees drawing basic salary upto Rs Ans : Employees drawing basic salary upto Rs 6500/- have to compulsory contribute to the 6500/- have to compulsory contribute to the Provident fund and employees drawing above Provident fund and employees drawing above Rs 6501/- have an option to become member Rs 6501/- have an option to become member of the Provident Fund .of the Provident Fund .

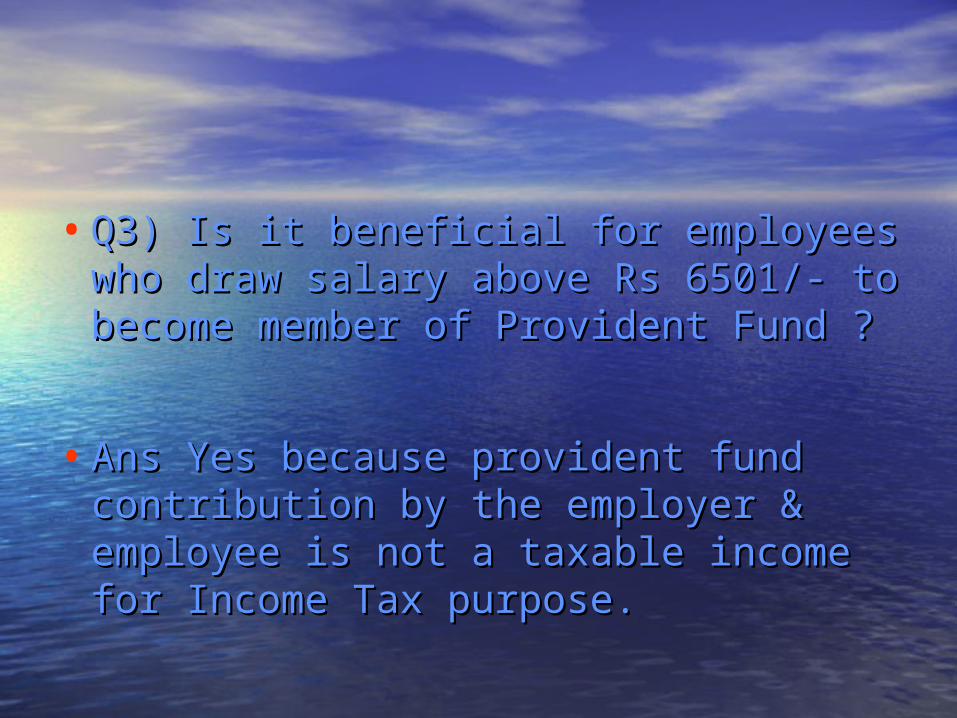

• Q3) Is it beneficial for employees who draw Q3) Is it beneficial for employees who draw salary above Rs 6501/- to become member of salary above Rs 6501/- to become member of Provident Fund ?Provident Fund ?

• Ans Yes because provident fund contribution Ans Yes because provident fund contribution by the employer & employee is not a taxable by the employer & employee is not a taxable income for Income Tax purpose.income for Income Tax purpose.

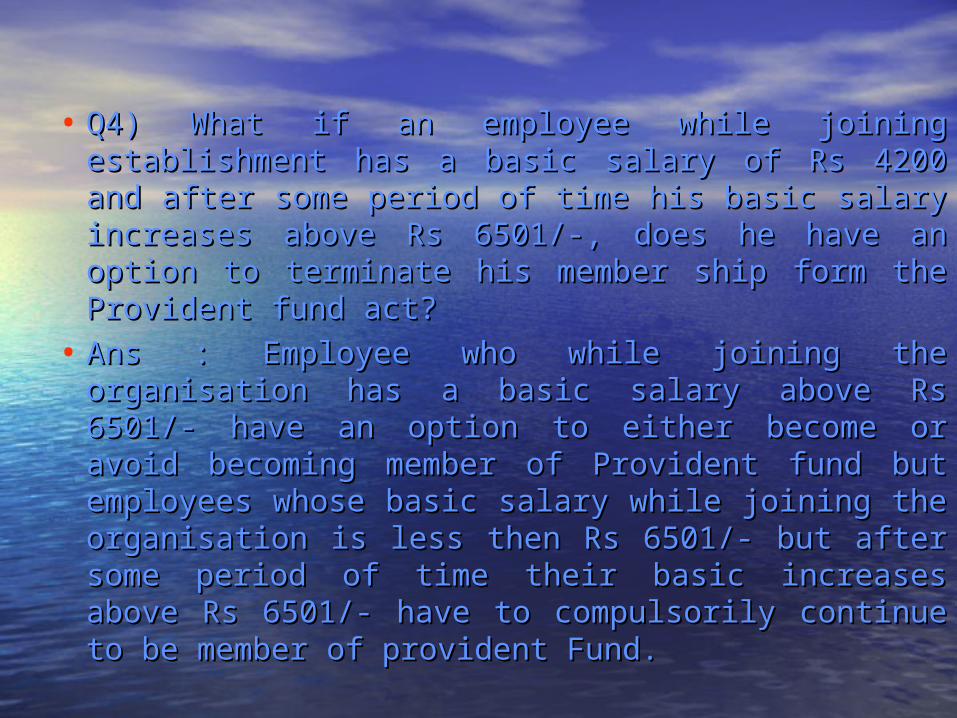

• Q4) What if an employee while joining establishment Q4) What if an employee while joining establishment has a basic salary of Rs 4200 and after some period of has a basic salary of Rs 4200 and after some period of time his basic salary increases above Rs 6501/-, does he time his basic salary increases above Rs 6501/-, does he have an option to terminate his member ship form the have an option to terminate his member ship form the Provident fund act?Provident fund act?

• Ans : Employee who while joining the organisation has Ans : Employee who while joining the organisation has a basic salary above Rs 6501/- have an option to either a basic salary above Rs 6501/- have an option to either become or avoid becoming member of Provident fund become or avoid becoming member of Provident fund but employees whose basic salary while joining the but employees whose basic salary while joining the organisation is less then Rs 6501/- but after some period organisation is less then Rs 6501/- but after some period of time their basic increases above Rs 6501/- have to of time their basic increases above Rs 6501/- have to compulsorily continue to be member of provident Fund.compulsorily continue to be member of provident Fund.

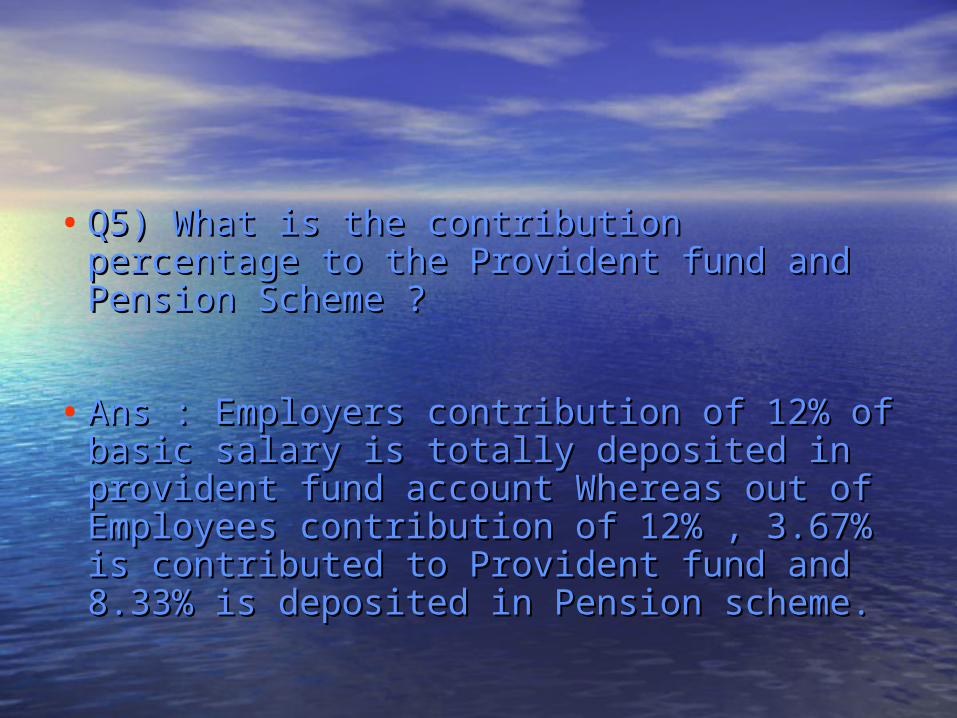

• Q5) What is the contribution percentage to the Q5) What is the contribution percentage to the Provident fund and Pension Scheme ?Provident fund and Pension Scheme ?

• Ans : Employers contribution of 12% of basic Ans : Employers contribution of 12% of basic salary is totally deposited in provident fund salary is totally deposited in provident fund account Whereas out of Employees contribution account Whereas out of Employees contribution of 12% , 3.67% is contributed to Provident fund of 12% , 3.67% is contributed to Provident fund and 8.33% is deposited in Pension scheme.and 8.33% is deposited in Pension scheme.

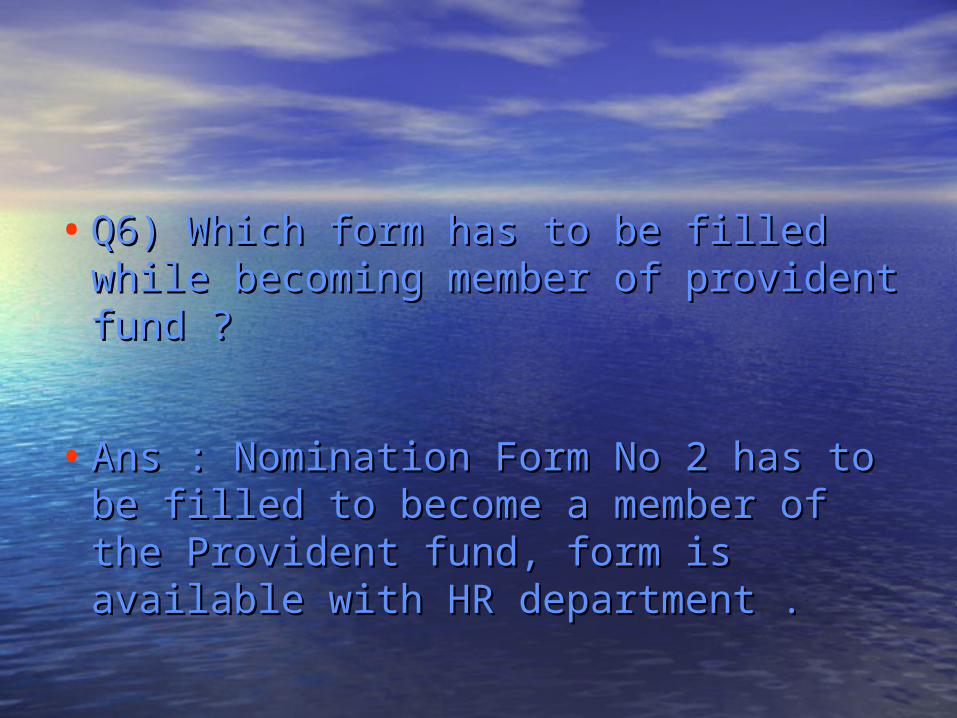

• Q6) Which form has to be filled while Q6) Which form has to be filled while becoming member of provident fund ?becoming member of provident fund ?

• Ans : Nomination Form No 2 has to be filled Ans : Nomination Form No 2 has to be filled to become a member of the Provident fund, to become a member of the Provident fund, form is available with HR department .form is available with HR department .

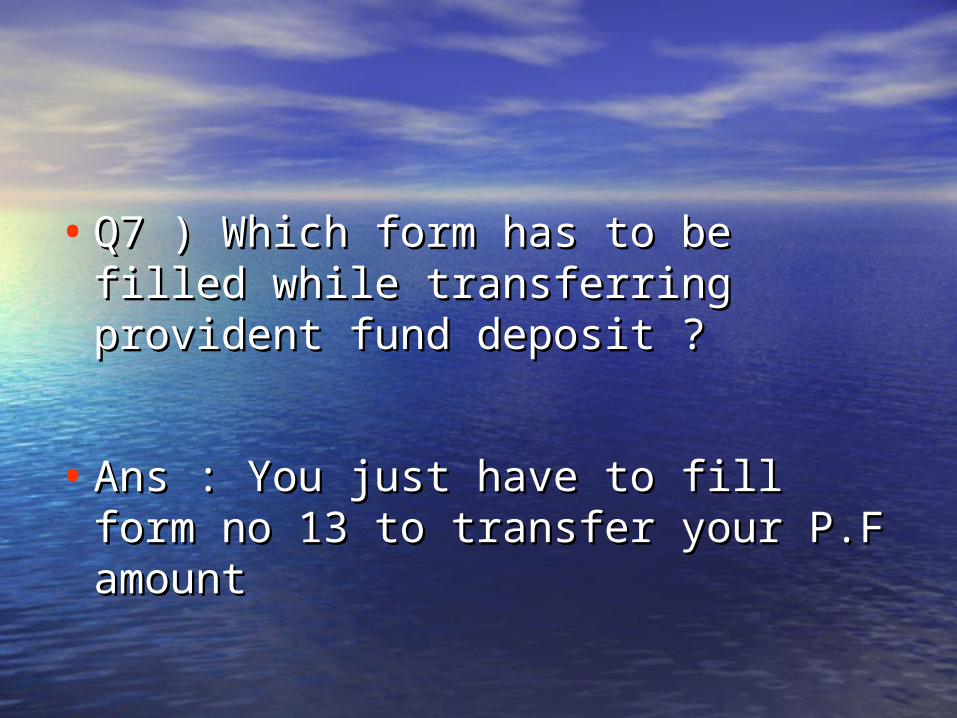

• Q7 ) Which form has to be filled while Q7 ) Which form has to be filled while transferring provident fund deposit ?transferring provident fund deposit ?

• Ans : You just have to fill form no 13 to Ans : You just have to fill form no 13 to transfer your P.F amounttransfer your P.F amount

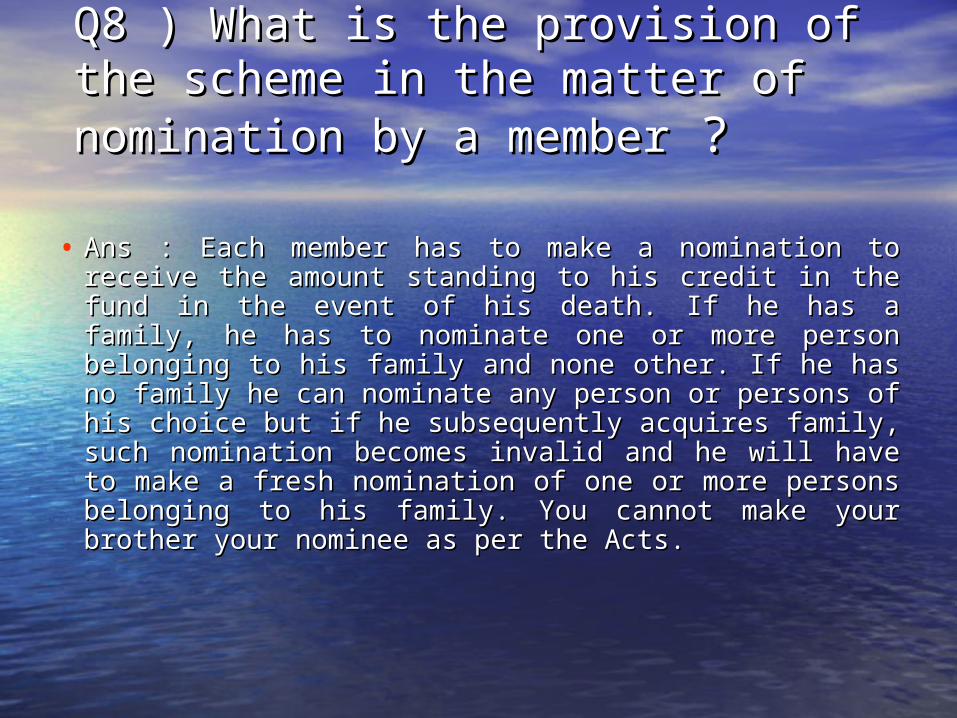

Q8 ) What is the provision of the scheme in Q8 ) What is the provision of the scheme in the matter of nomination by a memberthe matter of nomination by a member ? ?

• Ans : Each member has to make a nomination to receive the Ans : Each member has to make a nomination to receive the amount standing to his credit in the fund in the event of his amount standing to his credit in the fund in the event of his death. If he has a family, he has to nominate one or more death. If he has a family, he has to nominate one or more person belonging to his family and none other. If he has no person belonging to his family and none other. If he has no family he can nominate any person or persons of his choice family he can nominate any person or persons of his choice but if he subsequently acquires family, such nomination but if he subsequently acquires family, such nomination becomes invalid and he will have to make a fresh becomes invalid and he will have to make a fresh nomination of one or more persons belonging to his family. nomination of one or more persons belonging to his family. You cannot make your brother your nominee as per the You cannot make your brother your nominee as per the Acts.Acts.

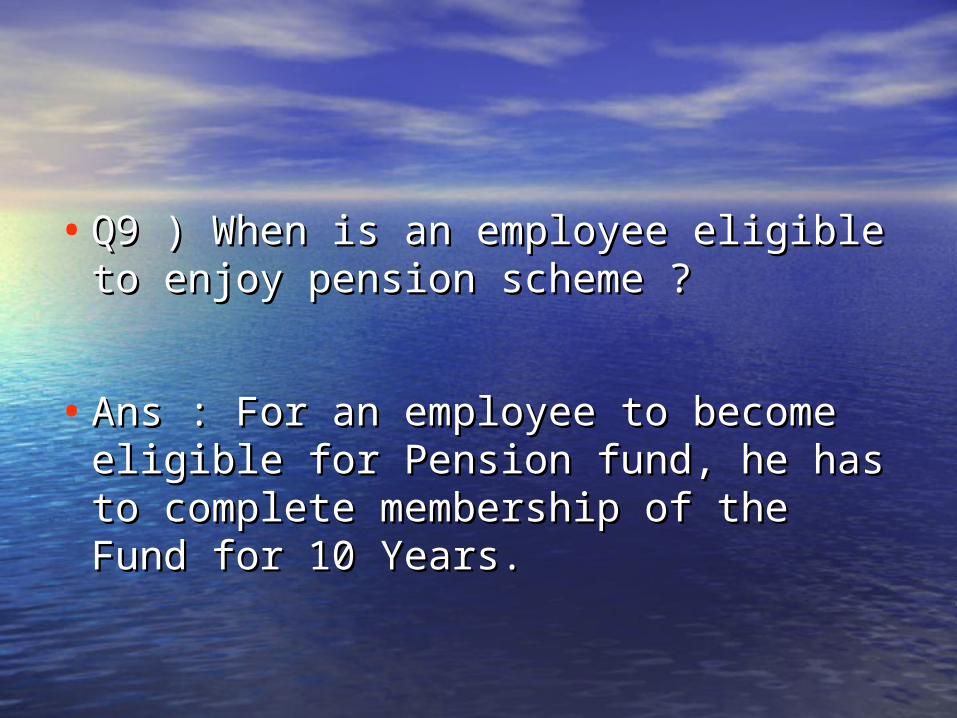

• Q9 ) When is an employee eligible to enjoy Q9 ) When is an employee eligible to enjoy pension scheme ?pension scheme ?

• Ans : For an employee to become eligible for Ans : For an employee to become eligible for Pension fund, he has to complete membership Pension fund, he has to complete membership of the Fund for 10 Years.of the Fund for 10 Years.

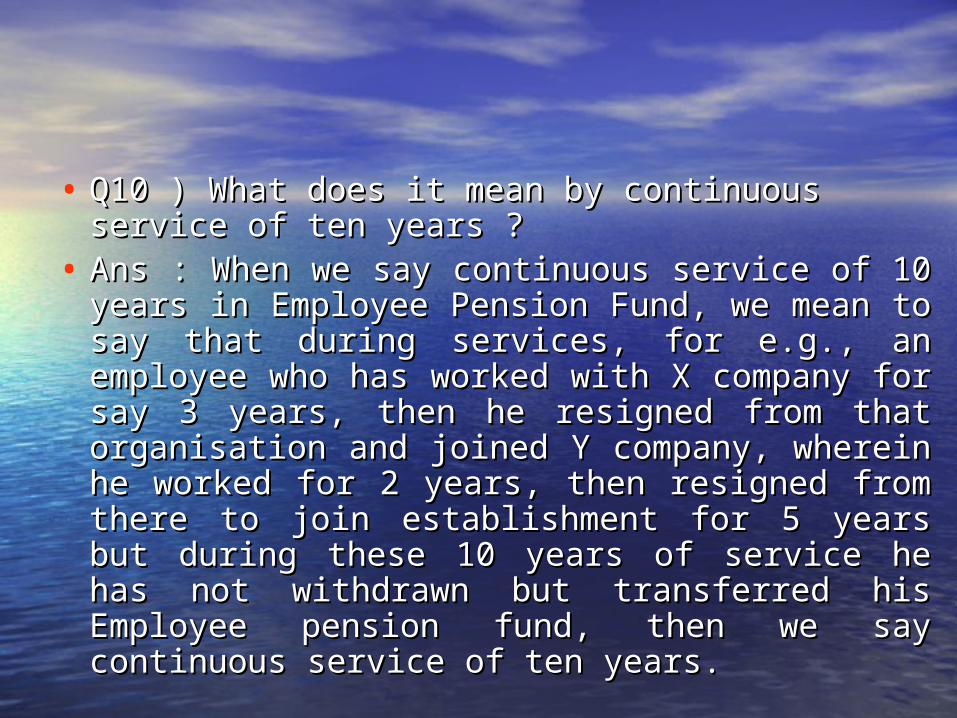

• Q10 ) What does it mean by continuous service of ten Q10 ) What does it mean by continuous service of ten years ?years ?

• Ans : When we say continuous service of 10 years in Ans : When we say continuous service of 10 years in Employee Pension Fund, we mean to say that during Employee Pension Fund, we mean to say that during services, for e.g., an employee who has worked with X services, for e.g., an employee who has worked with X company for say 3 years, then he resigned from that company for say 3 years, then he resigned from that organisation and joined Y company, wherein he worked organisation and joined Y company, wherein he worked for 2 years, then resigned from there to join for 2 years, then resigned from there to join establishment for 5 years but during these 10 years of establishment for 5 years but during these 10 years of service he has not withdrawn but transferred his service he has not withdrawn but transferred his Employee pension fund, then we say continuous service Employee pension fund, then we say continuous service of ten years.of ten years.

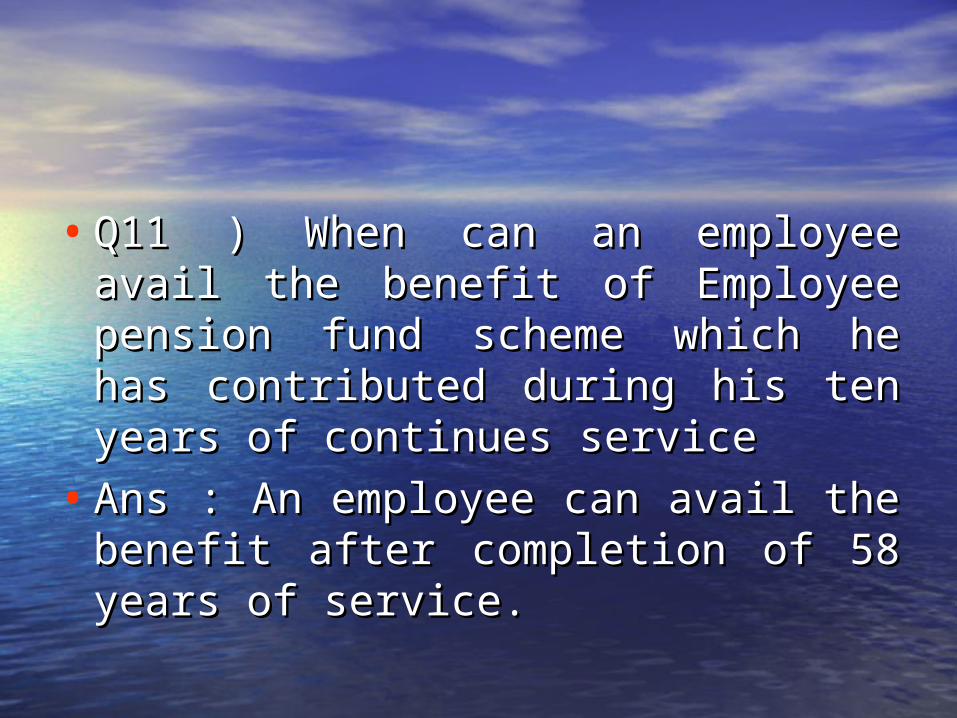

• Q11 ) When can an employee avail the benefit Q11 ) When can an employee avail the benefit of Employee pension fund scheme which he of Employee pension fund scheme which he has contributed during his ten years of has contributed during his ten years of continues service continues service

• Ans : An employee can avail the benefit after Ans : An employee can avail the benefit after completion of 58 years of service.completion of 58 years of service.

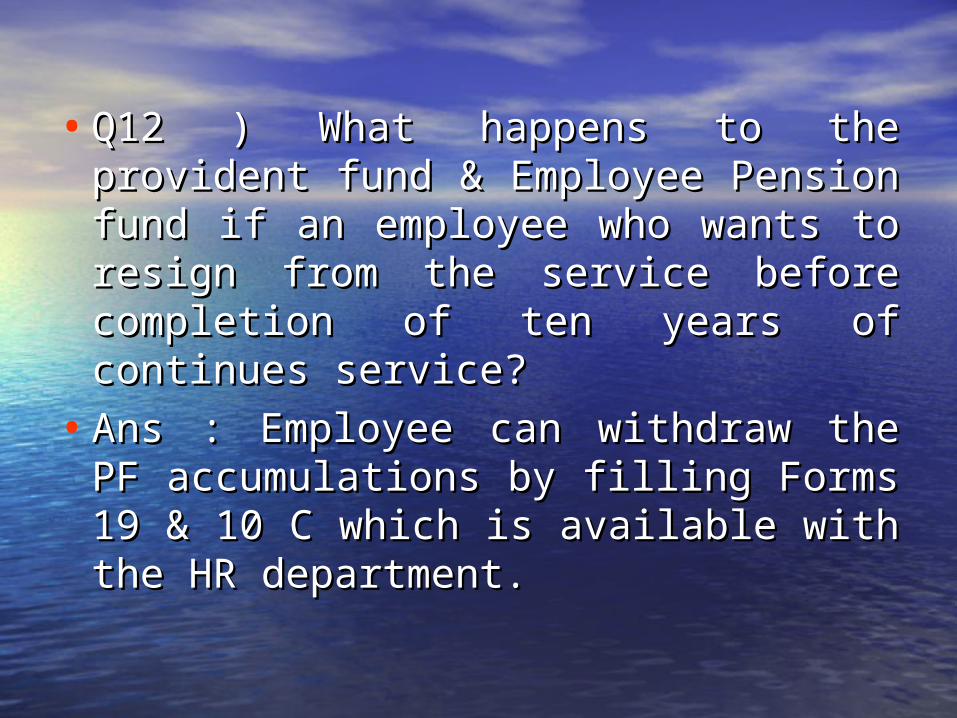

• Q12 ) What happens to the provident fund & Q12 ) What happens to the provident fund & Employee Pension fund if an employee who Employee Pension fund if an employee who wants to resign from the service before wants to resign from the service before completion of ten years of continues service?completion of ten years of continues service?

• Ans : Employee can withdraw the PF Ans : Employee can withdraw the PF accumulations by filling Forms 19 & 10 C accumulations by filling Forms 19 & 10 C which is available with the HR department.which is available with the HR department.

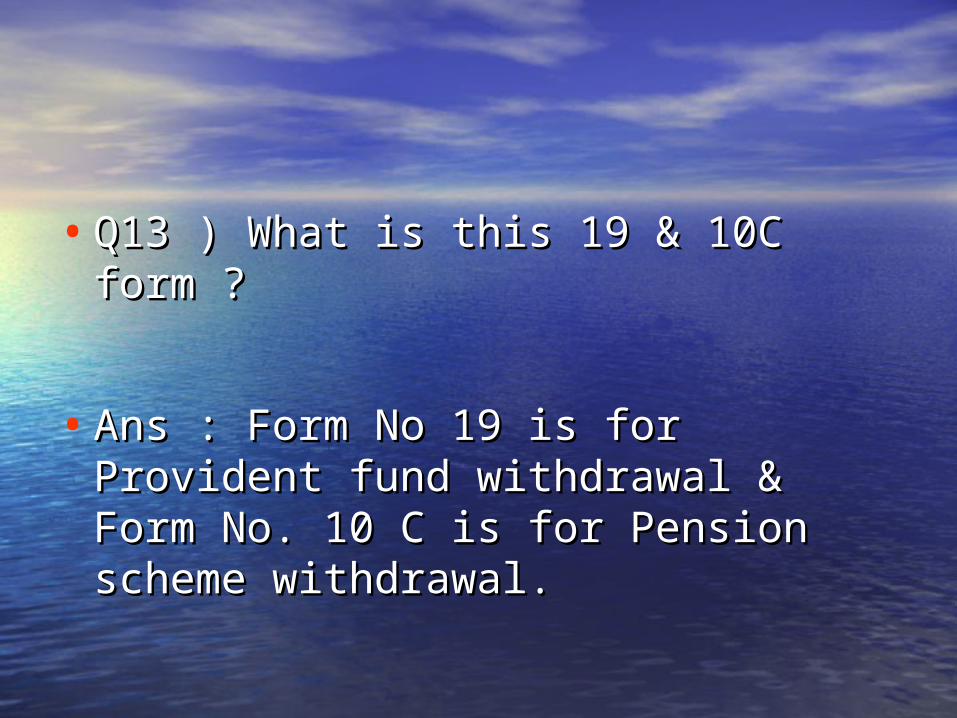

• Q13 ) What is this 19 & 10C form ?Q13 ) What is this 19 & 10C form ?

• Ans : Form No 19 is for Provident fund Ans : Form No 19 is for Provident fund withdrawal & Form No. 10 C is for Pension withdrawal & Form No. 10 C is for Pension scheme withdrawal.scheme withdrawal.

• Q14 ) Do we get any interest on the amount Q14 ) Do we get any interest on the amount which is deposited in the Provident Fund which is deposited in the Provident Fund account?account?

• Ans : Compound interest as declared by the Ans : Compound interest as declared by the Govt. is given for every year of service.Govt. is given for every year of service.

• Q15 ) What is the accounting year for Q15 ) What is the accounting year for Provident fund account?Provident fund account?

• Ans : Accounting year is from March to Ans : Accounting year is from March to February.February.

• Q16 ) What are the benefits provided under Q16 ) What are the benefits provided under Employee Provident Fund Scheme?Employee Provident Fund Scheme?

• Ans : Two kinds of benefits are provided under Ans : Two kinds of benefits are provided under the scheme-the scheme-

• a) Withdrawal benefita) Withdrawal benefit

• b) Benefit of non -Refundable advancesb) Benefit of non -Refundable advances

• Q17 ) What is the interest on the PF Q17 ) What is the interest on the PF accumulations ?accumulations ?

• Ans : Compound interest as declared by Ans : Compound interest as declared by Central Govt. is paid on the amount standing Central Govt. is paid on the amount standing to the credit of an employee as on 1st April to the credit of an employee as on 1st April every year.every year.

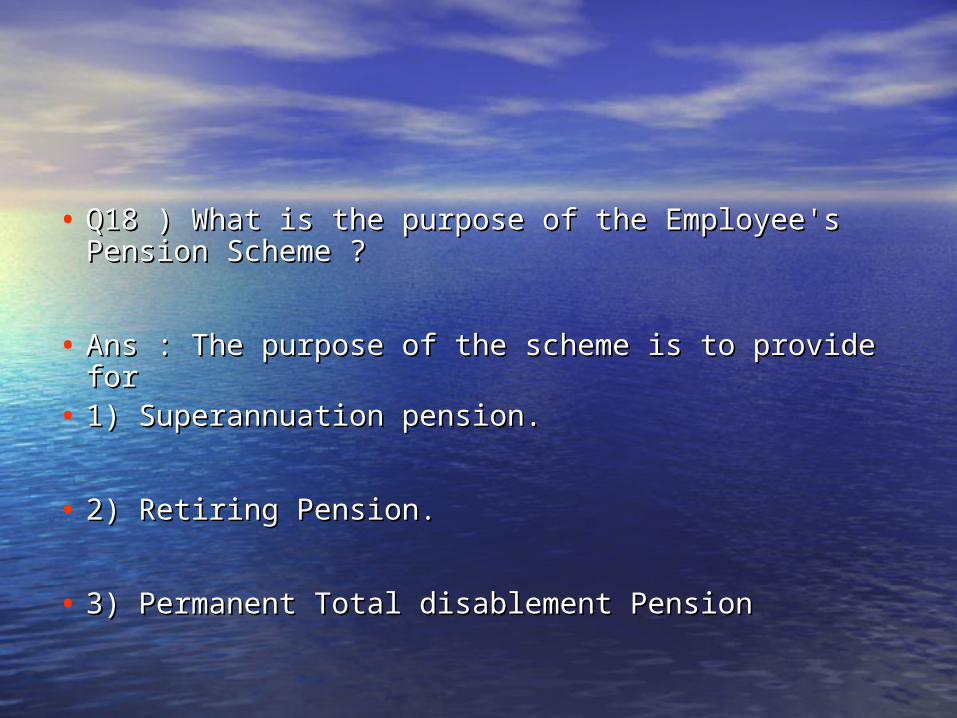

• Q18 ) What is the purpose of the Employee's Pension Q18 ) What is the purpose of the Employee's Pension Scheme ?Scheme ?

• Ans : The purpose of the scheme is to provide forAns : The purpose of the scheme is to provide for• 1) Superannuation pension.1) Superannuation pension.

• 2) Retiring Pension.2) Retiring Pension.

• 3) Permanent Total disablement Pension3) Permanent Total disablement Pension

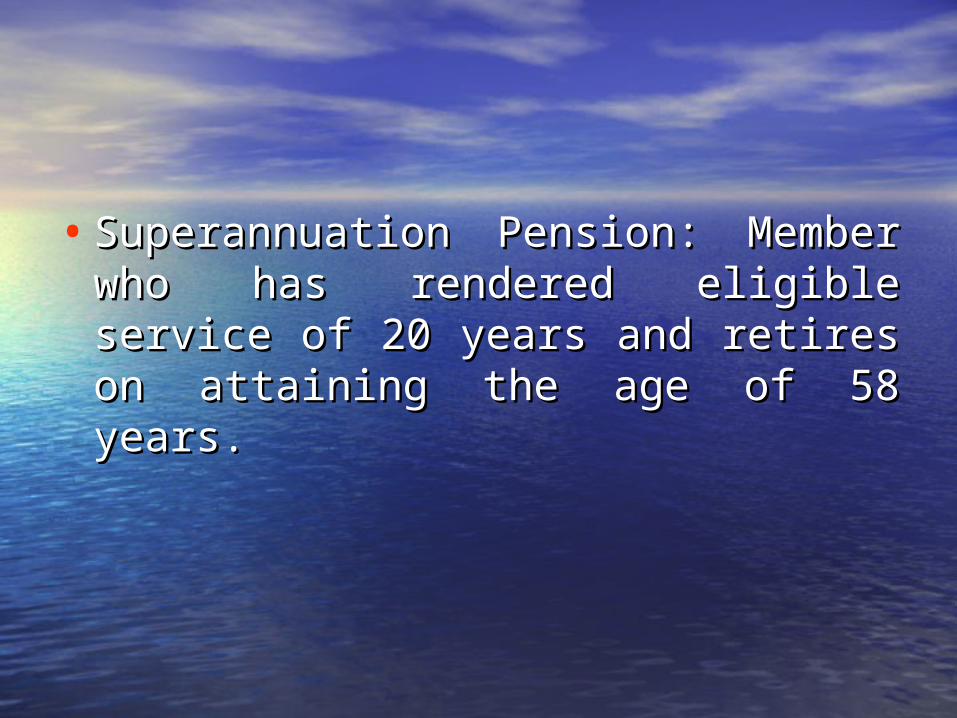

• Superannuation Pension: Member who has Superannuation Pension: Member who has rendered eligible service of 20 years and rendered eligible service of 20 years and retires on attaining the age of 58 years.retires on attaining the age of 58 years.

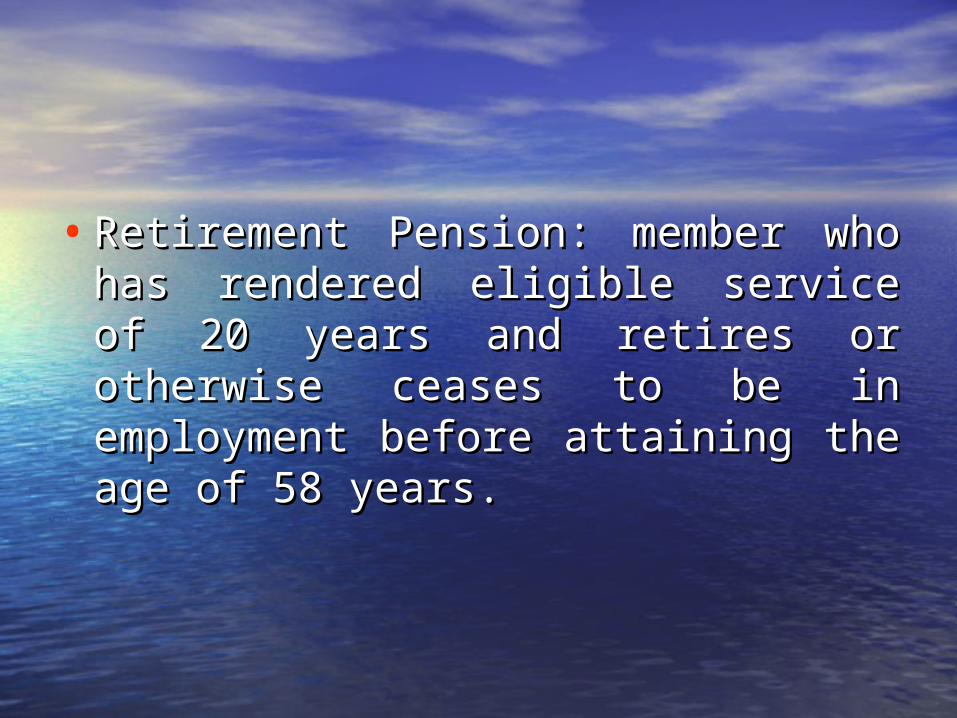

• Retirement Pension: member who has Retirement Pension: member who has rendered eligible service of 20 years and rendered eligible service of 20 years and retires or otherwise ceases to be in retires or otherwise ceases to be in employment before attaining the age of 58 employment before attaining the age of 58 years.years.

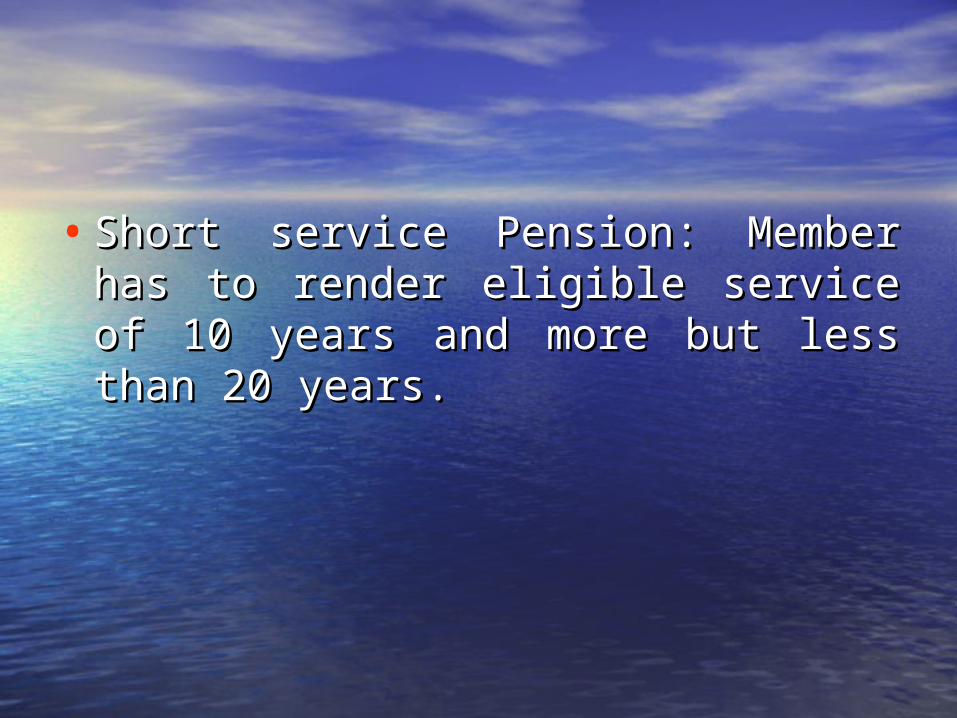

• Short service Pension: Member has to render Short service Pension: Member has to render eligible service of 10 years and more but less eligible service of 10 years and more but less than 20 years.than 20 years.

• Q19 ) How much time does it take to receive P.F & Q19 ) How much time does it take to receive P.F & pension money if an employee resigns from the pension money if an employee resigns from the Service?Service?

• Ans : Normally the procedure for receiving P.F & Ans : Normally the procedure for receiving P.F & Pension money is , the employee has to fill 19 & 10 c Pension money is , the employee has to fill 19 & 10 c Form and submit the same to PF Desk , which is then Form and submit the same to PF Desk , which is then submitted to the P.F office after two months, this two submitted to the P.F office after two months, this two months is nothing but a waiting period as the rules are months is nothing but a waiting period as the rules are that an employee should not be in employment for that an employee should not be in employment for two months after resigning if he has to withdraw his two months after resigning if he has to withdraw his P.F amount. After completion of two months the form P.F amount. After completion of two months the form is submitted to the regional provident fund is submitted to the regional provident fund Commissioner office after which the employee Commissioner office after which the employee receives his amount along with interest within a receives his amount along with interest within a period of 90 days.period of 90 days.

• Q20 ) Do we receive money through postal Q20 ) Do we receive money through postal order ?order ?

• Ans Previously there was a procedure wherein Ans Previously there was a procedure wherein member use to get P.F through Postal order but member use to get P.F through Postal order but now While submitting the P.F form withdrawal now While submitting the P.F form withdrawal form you have to mention your saving Bank form you have to mention your saving Bank account No. & the complete address of the account No. & the complete address of the Bank where you hold the account.Bank where you hold the account.

Q21 ) How would I know the amount of Q21 ) How would I know the amount of accumulations in my PF account ?accumulations in my PF account ?

• Ans : PF office sends an annual statement Ans : PF office sends an annual statement through the employer which gives details about through the employer which gives details about the PF accumulations. The statement contains the PF accumulations. The statement contains details like, Opening balance, amount details like, Opening balance, amount contributed during the year, withdrawal during contributed during the year, withdrawal during the year, interest earned and the closing balance the year, interest earned and the closing balance in the PF account. This statement is sent by the in the PF account. This statement is sent by the PF department on completion of the financial PF department on completion of the financial year.year.

Q22 ) Which establishments are covered by Q22 ) Which establishments are covered by the Act ?the Act ?

• Ans : Any establishment which employs 20 or Ans : Any establishment which employs 20 or more employees. Except apprentice and casual more employees. Except apprentice and casual laborers, every Employee including contract laborers, every Employee including contract labour who is in receipt of basic salary up to labour who is in receipt of basic salary up to Rs. 6500 p.m. is covered by the Act.Rs. 6500 p.m. is covered by the Act.

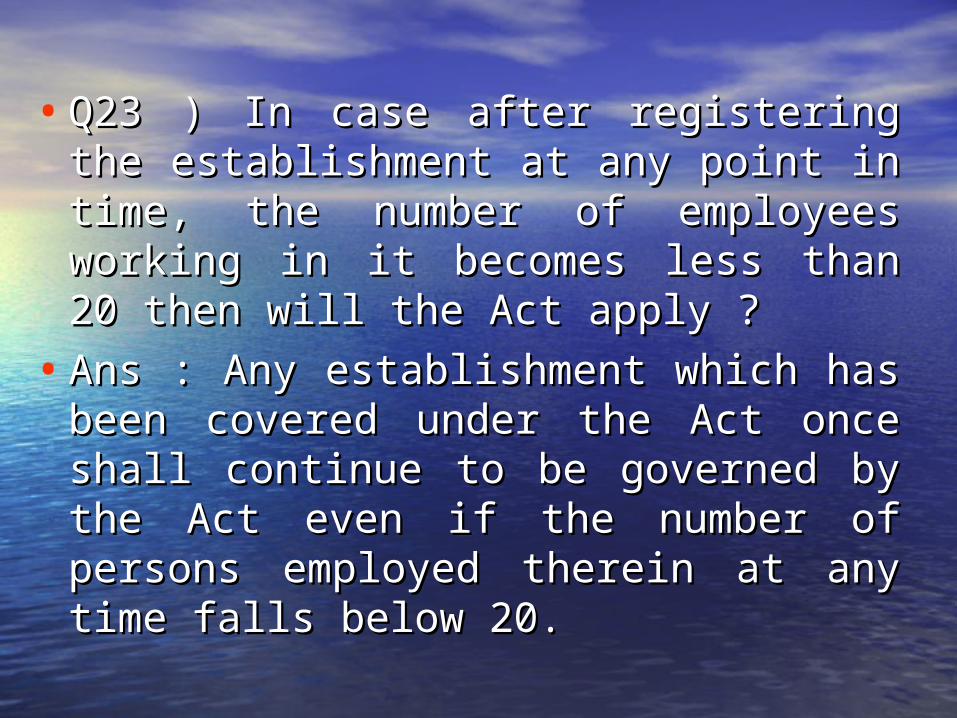

• Q23 ) In case after registering the establishment Q23 ) In case after registering the establishment at any point in time, the number of employees at any point in time, the number of employees working in it becomes less than 20 then will the working in it becomes less than 20 then will the Act apply ?Act apply ?

• Ans : Any establishment which has been Ans : Any establishment which has been covered under the Act once shall continue to be covered under the Act once shall continue to be governed by the Act even if the number of governed by the Act even if the number of persons employed therein at any time falls persons employed therein at any time falls below 20.below 20.

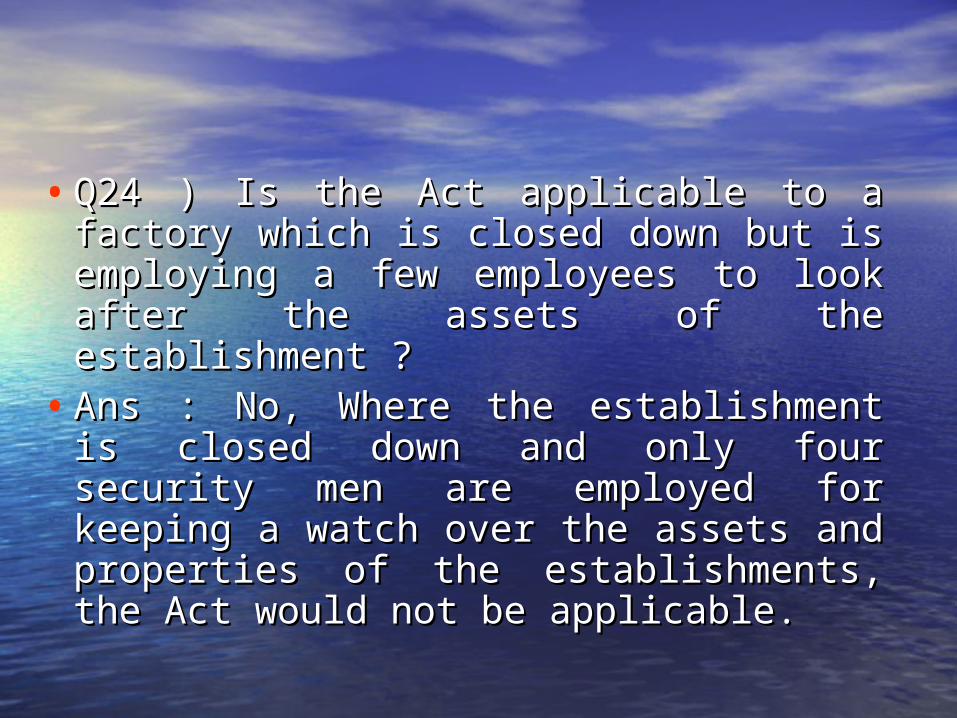

• Q24 ) Is the Act applicable to a factory which Q24 ) Is the Act applicable to a factory which is closed down but is employing a few is closed down but is employing a few employees to look after the assets of the employees to look after the assets of the establishment ?establishment ?

• Ans : No, Where the establishment is closed Ans : No, Where the establishment is closed down and only four security men are down and only four security men are employed for keeping a watch over the assets employed for keeping a watch over the assets and properties of the establishments, the Act and properties of the establishments, the Act would not be applicable.would not be applicable.

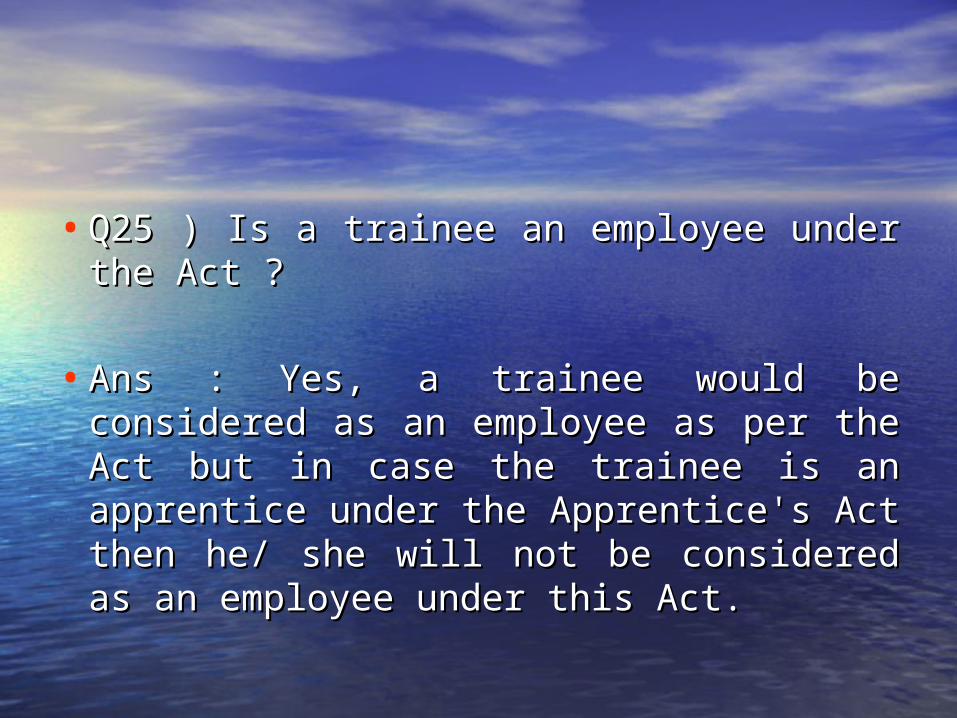

• Q25 ) Is a trainee an employee under the Act ?Q25 ) Is a trainee an employee under the Act ?

• Ans : Yes, a trainee would be considered as an Ans : Yes, a trainee would be considered as an employee as per the Act but in case the trainee employee as per the Act but in case the trainee is an apprentice under the Apprentice's Act is an apprentice under the Apprentice's Act then he/ she will not be considered as an then he/ she will not be considered as an employee under this Act.employee under this Act.

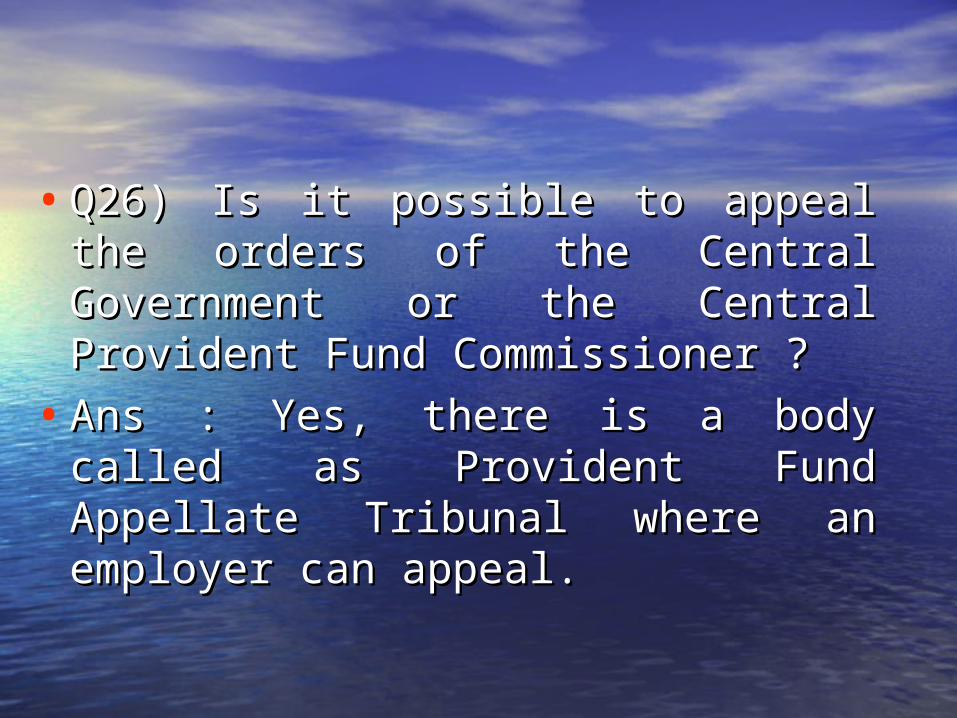

• Q26) Is it possible to appeal the orders of the Q26) Is it possible to appeal the orders of the Central Government or the Central Provident Central Government or the Central Provident Fund Commissioner ?Fund Commissioner ?

• Ans : Yes, there is a body called as Provident Ans : Yes, there is a body called as Provident Fund Appellate Tribunal where an employer Fund Appellate Tribunal where an employer can appeal.can appeal.

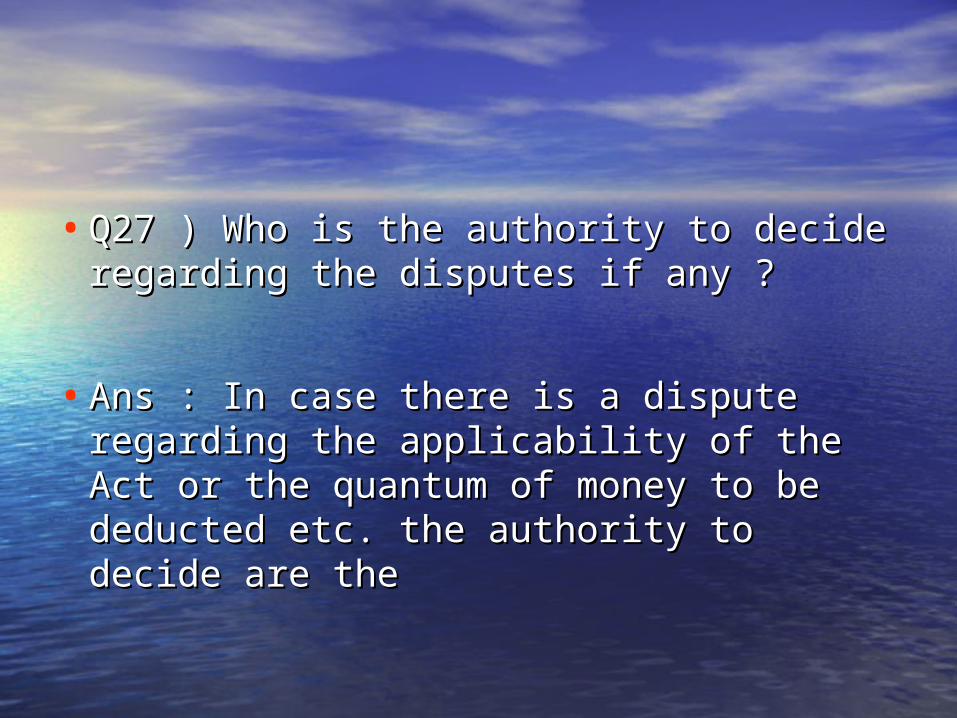

• Q27 ) Who is the authority to decide regarding Q27 ) Who is the authority to decide regarding the disputes if any ?the disputes if any ?

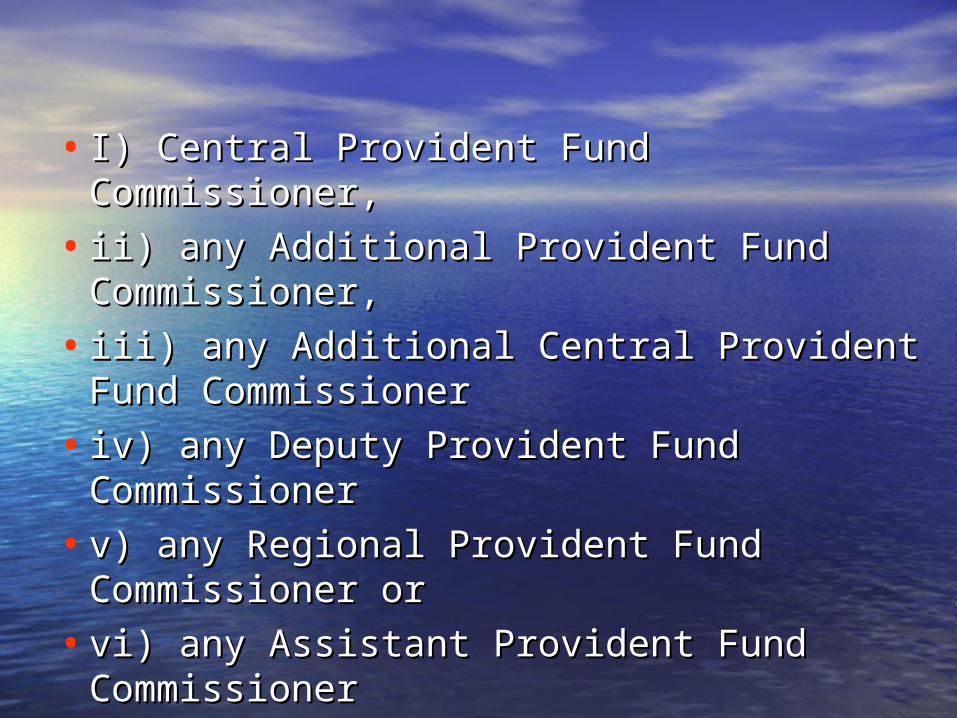

• Ans : In case there is a dispute regarding the Ans : In case there is a dispute regarding the applicability of the Act or the quantum of applicability of the Act or the quantum of money to be deducted etc. the authority to money to be deducted etc. the authority to decide are thedecide are the

• I) Central Provident Fund Commissioner,I) Central Provident Fund Commissioner,

• ii) any Additional Provident Fund ii) any Additional Provident Fund Commissioner,Commissioner,

• iii) any Additional Central Provident Fund iii) any Additional Central Provident Fund CommissionerCommissioner

• iv) any Deputy Provident Fund Commissioneriv) any Deputy Provident Fund Commissioner

• v) any Regional Provident Fund Commissioner v) any Regional Provident Fund Commissioner oror

• vi) any Assistant Provident Fund Commissionervi) any Assistant Provident Fund Commissioner

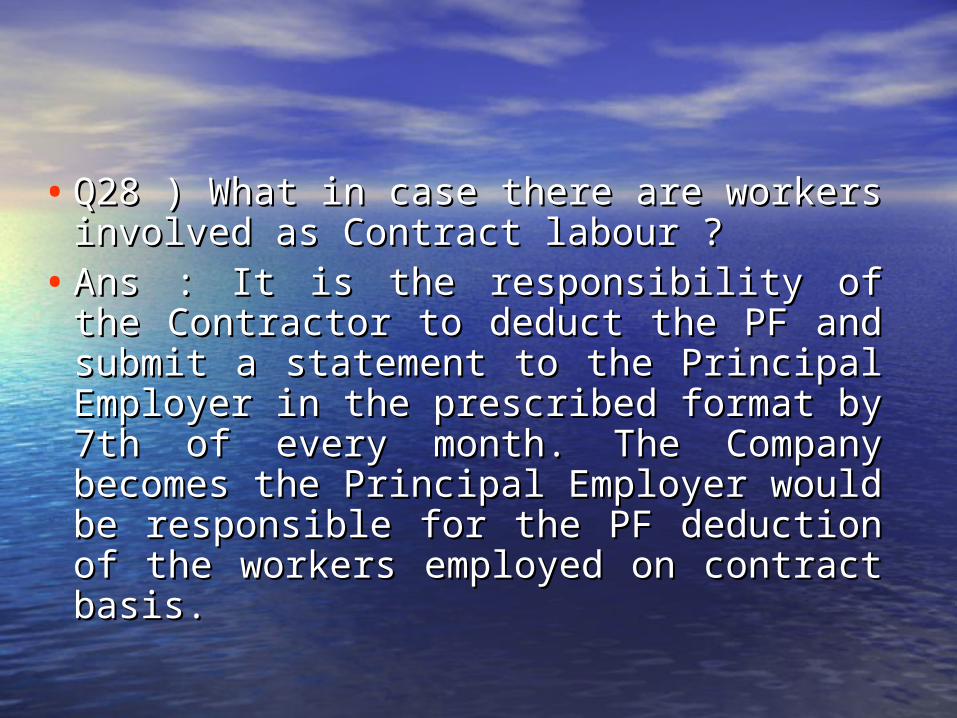

• Q28 ) What in case there are workers involved Q28 ) What in case there are workers involved as Contract labour ?as Contract labour ?

• Ans : It is the responsibility of the Contractor Ans : It is the responsibility of the Contractor to deduct the PF and submit a statement to the to deduct the PF and submit a statement to the Principal Employer in the prescribed format by Principal Employer in the prescribed format by 7th of every month. The Company becomes 7th of every month. The Company becomes the Principal Employer would be responsible the Principal Employer would be responsible for the PF deduction of the workers employed for the PF deduction of the workers employed on contract basis.on contract basis.

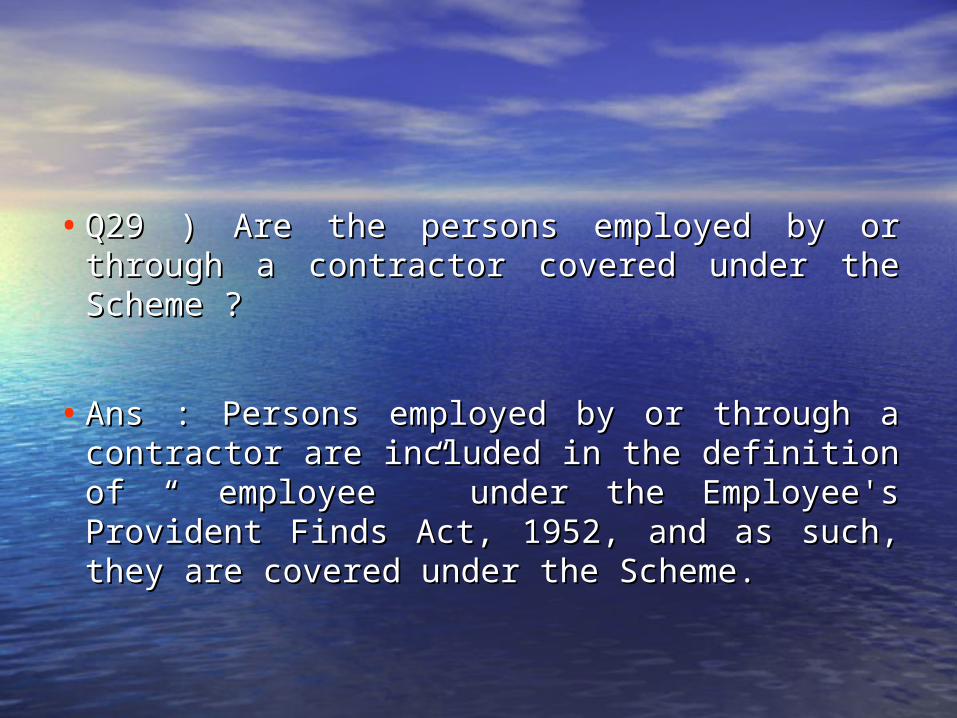

• Q29 ) Are the persons employed by or through Q29 ) Are the persons employed by or through a contractor covered under the Scheme ?a contractor covered under the Scheme ?

• Ans : Persons employed by or through a Ans : Persons employed by or through a contractor are included in the definition of “ contractor are included in the definition of “ employee ” under the Employee's Provident employee ” under the Employee's Provident Finds Act, 1952, and as such, they are covered Finds Act, 1952, and as such, they are covered under the Scheme.under the Scheme.

• Q30 ) In case the Contractor fails to deduct and Q30 ) In case the Contractor fails to deduct and submit the PF amount from the contract workers then submit the PF amount from the contract workers then what is to be done ?what is to be done ?

• Ans : The Company being the Principal employer is Ans : The Company being the Principal employer is responsible for the PF to be deducted from the responsible for the PF to be deducted from the Contract workers as well. In case the Contractors fails Contract workers as well. In case the Contractors fails to deduct and submit the PF dues then the Company to deduct and submit the PF dues then the Company has to pay the amount and can later on recover the has to pay the amount and can later on recover the amount from the Contractor.amount from the Contractor.

• Q31 ) Could the employer be punished in case Q31 ) Could the employer be punished in case the remittance of contribution by him is the remittance of contribution by him is delayed in a Bank or post office ?delayed in a Bank or post office ?

• Ans : Employer cannot be punished or Ans : Employer cannot be punished or penalized in case there is a delay in the penalized in case there is a delay in the remittance of the contribution on account of remittance of the contribution on account of delay in Bank or post office.delay in Bank or post office.

• Q32 ) What happens in case there is a salary Q32 ) What happens in case there is a salary revision and a raise in the basic salary of the revision and a raise in the basic salary of the employee and arrears need to be paid, Do we employee and arrears need to be paid, Do we need to deduct PF from the arrears as well ?need to deduct PF from the arrears as well ?

• Ans : Arrears are considered to be emoluments Ans : Arrears are considered to be emoluments earned by the employee and PF is to be earned by the employee and PF is to be deducted from such arrears.deducted from such arrears.

• Q33 ) Is it possible for an employee to contribute at a Q33 ) Is it possible for an employee to contribute at a higher rate of interest than 12 % ?higher rate of interest than 12 % ?

• Ans : Yes, if an employee desires to contribute an Ans : Yes, if an employee desires to contribute an amount at a higher rate of interest than 12 % of basic amount at a higher rate of interest than 12 % of basic salary then they can do so but it does not become salary then they can do so but it does not become obligatory for the employer to pay anything above obligatory for the employer to pay anything above than 12 %.This is called voluntary contribution and a than 12 %.This is called voluntary contribution and a Joint Declaration Form needs to be filled up where Joint Declaration Form needs to be filled up where the employer and the employee both have to give a the employer and the employee both have to give a declaration as to the rate at which PF would be declaration as to the rate at which PF would be deducted.deducted.

Thank YouThank You

![THE EMPLOYEES' PROVIDENT FUNDS AND MISCELLANEOUS ... · THE EMPLOYEES' PROVIDENT FUNDS AND MISCELLANEOUS PROVISIONS ACT, 1952 1[(Act No. 19 of 1952)] [4th March, 1952 An Act to Provide](https://img.pdfslide.net/doc/110x75/601a43dd90cd75726758f324/the-employees-provident-funds-and-miscellaneous-the-employees-provident-funds.jpg)

![THE EMPLOYEES' PROVIDENT FUNDS AND ......AND MISCELLANEOUS PROVISIONS ACT, 1952 1[(Act No. 19 of 1952)] [4th March, 1952 An Act to Provide for the institution of provident funds, 2[3[Pension](https://img.pdfslide.net/doc/110x75/5f36f4d099d5ca4ef767c70c/the-employees-provident-funds-and-and-miscellaneous-provisions-act-1952.jpg)

![THE EMPLOYEES’ PROVIDENT FUNDS AND MISCELLANEOUS ...(ACT NO. 19 OF 1952) 1 (4th March, 1952) An Act to provide for the Institution of Provident Funds 2[***] 3[Pension Fund], and](https://img.pdfslide.net/doc/110x75/5e75200229a76e1d5f211bdf/the-employeesa-provident-funds-and-miscellaneous-act-no-19-of-1952-1-4th.jpg)

![THE EMPLOYEES‟ PROVIDENT FUNDS AND MISCELLANEOUS … · 2020. 6. 29. · ACT, 1952 ACT NO. 19 OF 19521 [4th March, 1952.] An Act to provide for the institution of provident funds](https://img.pdfslide.net/doc/110x75/60f98c991965ad084f51585c/the-employeesa-provident-funds-and-miscellaneous-2020-6-29-act-1952-act.jpg)