Embed Size (px)

Citation preview

Public Relations Review, 24(4): 521-534 Copyright © 1998 by JAI Press Inc. ISSN: 0363-8111 All rights of reproduction in any form reserved.

Teresa Martin

Employees' Understanding of Employer-sponsored Retirement Plans, A Knowledge Gap Perspective ABSTRACT: The retirement benefit community is currently undergoing a paradigm shift as many organizations cast aside traditional defined benefit plans in favor of defined contribution plans. In other words, instead of employers providing defined benefit plans that are risk free to employees, many organizations have decided to offer defined contribution plans in which employees are responsible for both contributing to the plan and making the investment decisions required therein.

As employees are required to make decisions that will ultimately determine their fmancial security during retirement, it is crucial that employers develop materials that will equip all employees with knowledge about retirement-related issues. Therefore, this study examined the range of knowledge about retirement-related issues that exists among various employee groups within a particular organization. Results showed that education serves as a strong predictor in determining employees' knowledge about retirement-related concepts. Based on the study's findings, implications for future research regarding the development of materials designed to educate employees about employer-sponsored retirement plans are discussed.

Winter 1998 521

Public Relations Review

Teresa Mastin is an assistant professor in the College of Mass Communication at Middle Tennessee State University.

The retirement benefit community is currently undergo- ing a paradigm shift as many organizations cast aside traditional defmed benefit plans in favor of defined contribution plans. In other words, instead of employers providing defmed benefit plans that are risk free to employees, many organiza- tions have decided to offer defined contribution plans in which employees are responsible for both contributing to the plan and making the investment deci- sions required therein.

Requiring that employees become more involved in retirement planning is positive in many ways; however, it is also problematic as many employees do not understand the investment issues associated with employer-sponsored retirement plans well enough to make wise investment decisions. 1

Perhaps anticipating that many employees might not be qualified to make such weighty decisions, Congress outlined a voluntary guideline, in Section 404(c) of the Employee Retirement Income Security Act (ERISA) of i974, which recommends, among other suggestions, that employers provide under- standable information and education about each investment plan. 2

As employees are required to make decisions that will ultimately determine their fmancial security during retirement, it is crucial that employers develop materials that will equip all employees with knowledge about retirement-related issues. If employer-sponsored retirement plans are to fulfill a goal of encouraging and preparing employees to take personal responsibility for their retirement plan- ning, it is important that employer-provided supporting materials consider the range of knowledge about this topic that is likely to exist among a diverse group of employees.

Therefore, the purpose of this study is to examine the range of knowledge about retirement-related issues that exists among various employee groups within a particular organization.

REVIEW OF THE LITERATURE

Unlike most Western European countries, which have publicly mandated retirement programs designed to ensure that citizens can meet at least basic expenses after retirement, the American social security system was deliberately structured to provide only a bare-bones level of support for its citi- zens. Social security represents one leg of the U. S. three-legged stool of retire- ment income philosophy. According to this philosophy, social security should make up 40% of an individual's total retirement income, whereas funds generated from savings and pensions are to provide the remaining 60%. 3

Even though private pensions are mandated as one of three sources of retirees' income, 43% of all American workers are not covered by a pension plan. 4 When first introduced into the work place, pensions were created as rewards (i.e., a benefit) for a favored few. 5 However, by the 1940s, employee

522 Vol. 24, No. 4

Emph~yees' Understanding of Employer-sponsored Retirement Plans

benefits, which include pensions, had become a staple in many American organi- zations. In fact, benefits have become so prevalent that they now represent a major expense for employers. In particular in 1943, employee benefits repre- sented an average of five percent of wages and salaries. By 1990, the same bene- fits represented an average of 20% of wages and salaries. 6

Naturally employers sought ways to decrease continually increasing bene- fits costs. Employer-sponsored pre-tax savings plans as outlined in The Revenue Act of 1978 provided a form of relief. This Act authorized the use of employer- sponsored pre-tax savings plans.

Employer-sponsored pre-tax savings plans are popular because of their potential value to both employers and employees. Employers benefit because they can deduct any contributions made into the retirement plan at the time the con- tributions are made. Moreover, even if employers match employee contributions for some pre-determined amount, they match contributions only for employees who make contributions. 7

Pre-tax savings plans have the potential to benefit employees in three pri- mary ways:

1. an easy way for employees to save--contributions are automati- cally deducted from employees' salaries,

2. the employer-matching component provides a way for employees to make higher contributions without further reduction of their ascribed wages or salaries, and

3. pre-tax savings plans provide participants with substantial finan- cial gain realized from years of compounding.

The potential gains from pre-tax savings plans for employers are most always realized. Unfortunately potential employee gains are not as easily obtained. In the past, under the defined benefit umbrella, employers chose the retirement plan for their employees and shouldered the investment risks while providing employees with a specified monthly income upon retirement. 8

However, under the defined contribution umbrella, if employees are to achieve ultimate benefit (i.e., financial security in retirement) from pre-tax sav- ings plans, they must understand that it is primarily their responsibility to pre- pare for their financial security in retirement, and that the quality of their investment decisions will determine whether they have sufficient funds upon retirement. 9

THEORETICAL FRAMEWORK

Knowledge

Knowledge is crucial because it acts as a catalyst. This fact becomes extremely relevant in an information-oriented society because those in a position to access information are capable of using the information to enhance

Winter 1998 523

Public Relations Review

their knowledge in multiple areas. In contrast, individuals who do not frequently interact with information as a problem solver or as a knowledge enhancer often do not perceive information as a valuable commodity. The more education an individual has obtained, the more likely the individual will interact with a broad range of information and therefore perceive information as a tool to increase his or her knowledge in general.lo

In this study, information is defined as "that by which things are ascer- tained, certainty is increased and uncertainty is decreased. "11 Knowledge is defined as "that which has achieved some degree of exactness and precision by the substitution of ideas for concrete reality. ''12 That is, a distinction is made between knowledge of (i.e., common sense) and knowledge about (i.e., formal knowledge based on systematic observation).

Ironically, employees who are in the greatest need of employer-provided information about retirement-related issues are those who are least likely to bene- fit from provided information. That is, individuals who do not interact with a wide range of information on a daily basis are less likely to gain practical informa- tion from distributed materials. I f employees are not able to translate employer- provided retirement-related information into knowledge that will enable them to make wise investment decisions for the specific purpose of preparing for a finan- cially secure retirement, they are in danger of retiring with less than sufficient funds for their retirement years and as a result are more likely to become a finan- cial burden on society. 13

In addition, employees who are not successful in their retirement planning are more likely to initiate litigation against employers for not providing adequate investment education as outlined in ERISA. Recent judicial rulings suggest that courts are willing to favor individual employees in this manner.14

A substantial body of research supports the notion that the more education an individual has obtained, the more he or she tends to use information as a means of solving problems. 15 Tichenor, Donohue, and Olien 16 labeled the effect that results in differing levels of knowledge across various groups as knowledge gaps. Their knowledge gap hypothesis states that: "as the infusion of mass media information into a social system increases, segments of the population with higher socioeconomic status tend to acquire this information at a faster rate than the lower status segments, so that the gap in knowledge between these segments tends to increase rather than decrease. "17

Since introduction of the knowledge gap hypothesis in 1970, there has been a steady stream of research examining the hypothesis in various topical areas. Gaziano and Gaziano 18 developed a typology of theoretical perspectives and conceptual models in order to examine knowledge gap studies conducted during the past 25 plus years. The typology includes three competing concep- tions of the knowledge gap hypothesis.

The first conception, primarily developed by Tichenor, Donohue, and Olien 19, the social structural perspective--considers differential knowledge acquirement within a collective.

524 Vol. 24, No. 4

Employees" Understanding of Employer-sponsored Retirement Plans

The second conception, primarily developed by Ettema and Kline 2°, an individual-focused perspective--examines the knowledge gap in regards to situa- tional needs and motivations of individual actors. Arguing that the original knowledge gap hypothesis is not broad enough to explain the gap phenomenon, researchers in support of this perspective focus on an individual-level account of "subjectivity and agency. "21

A third conception, primarily developed by Dervin 22, the cybernetic model--considers varying levels of knowledge across groups as a function of the information delivery system. That is, knowledge gap studies that have been devel- oped in association with this conceptualization strive to redefine communication in a manner which favors the user through humanzing information delivery sys- tems.

All three competing perspectives have valid strengths; however, this study is developed on the assumption that differing knowledge levels among various groups emerge primarily from societal structural forces.

To date the knowledge gap effect has not been tested in respect to a finan- cial issue. It is of critical importance that the knowledge gap hypothesis be tested in this arena. In particular, the U. S. social security system as it currently stands is in no condition to support the massive baby boomer cohorts scheduled to retire within the next few decades. 23 Therefore, it is important that individuals become more actively involved in preparing for their fmancial security in retire- ment.

Based on the preceding discussion of the importance of financial knowl- edge and the generic knowledge gap phenomenon, the following hypotheses are posed:

HI: Less educated individuals are less likely than more educated individuals to possess knowledge about general retirement-related issues.

H2: Less educated individuals are less likely than more educated individuals to possess knowledge about the specifics of their employer-sponsored retirement plan.

M E T H O D

Independent and Dependent Variables. A correlational research design utilizing cross-sectional survey methodology was employed. Con- sistent with knowledge gap studies, the independent variable was education. The dependent variables were self-reported knowledge about general and specific retirement-related information and tested knowledge about general and specific retirement-related information.

Subjects. To determine the level of knowledge held among participants of an employer-sponsored retirement plan, a questionnaire was sent to a subset of employees enrolled in a sponsored retirement plan (N=500). All participants

Winter 1998 525

Public Relations Review

were employees of a large mid-western university. A stratified random sample was employed.

Item Generation. Development of the general and specific knowledge indi- ces for this study followed a thorough review of retirement-related materials made available to university employees through the university's Benefits Retire- ment office. In a similar manner, information provided by the Benefits Retire- ment office about the university-sponsored plan was perused.

Fifteen items emerged from this process. Seven of the items sought to measure respondents' general knowledge about retirement-related issues. The remaining eight items determined to tap into respondents' knowledge about the university-sponsored retirement plan. Responses were coded as either correct or incorrect (which included "don't knows"). The range of the general index was 0- 14, and the range of the specific index was 0-16. Cronbach's alpha was computed for each index (see Appendix for general and specific index questions). The reli- ability coefficient was .77 for the general index, and .65 for the specific index.

Survey Procedure. The questionnaire was developed based on Dillman's 24 mail survey total design method. The initial naailing included a cover letter detail- ing the nature of the study, a copy of the questionnaire, and a self-addressed return envelope. The cover letter noted that participants who returned a com- pleted questionnaire would be entered into a drawing for a cash prize of $100. The lottery was added to encourage increased participation.

The correspondences were mailed through campus mail. Employees not housed on campus (i.e., extension employees), and employees who were on leave received their correspondences via first-class mail. Two follow-up reminders were also mailed to participants.

The questionnaire. Before distribution, the questionnaire was pretested with approximately 30 people: individuals representative of those who would receive the questionnaire, and individuals familiar with questionnaire construction. Par- ticipants were instructed to look for potential problems. The questionnaire was revised based on suggestions.

Questionnaire items were designed to examine employees' knowledge about (self-reported and tested) retirement-related issues as a function of educa- tion.

RESULTS

Sample Characteristics. Overall, 286 usable question- naires-representing a 57% response rate--were returned. A response rate of 57% is more than adequate for a mail survey. 25

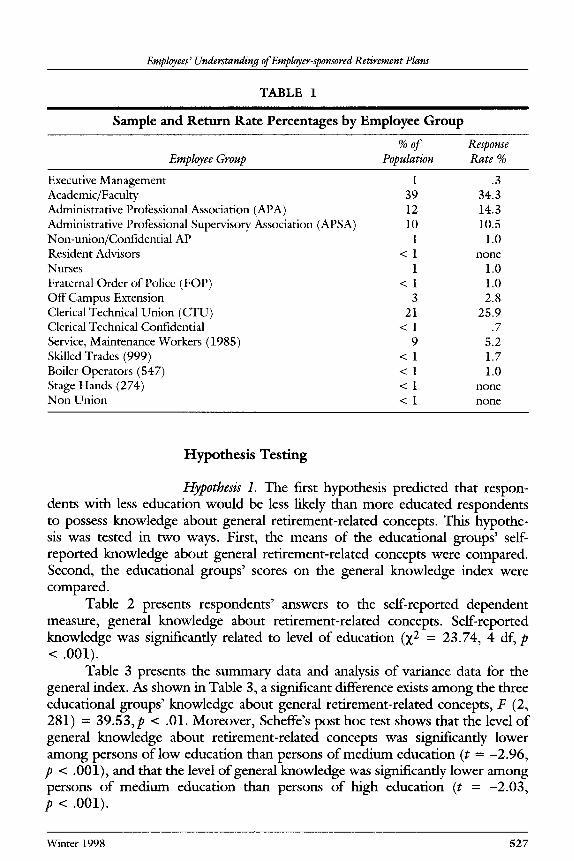

Respondents closely reflected the university employee population. Table 1 gives the percentage of university employees that comprise each employee group, and the percentages of usable questionnaires returned by each employee group.

526 Vol. 24, No. 4

Employees" Understanding of Employer-sponsored Retirement Plans

TABLE 1

Sample and Return Rate Percentages by Employee Group

% of Response Employee Group Population Rate %

Executive Management 1 Academic/Faculty 39 Administrative Professional Association (APA) 12 Administrative Professional Supervisory Association (APSA) 10 Non-union/Confidential AP 1 Resident Advisors < 1 Nurses 1 Fraternal Order of Police (FOP) < 1 Off Campus Extension 3 Clerical Technical Union (CTU) 21 Clerical Technical Confidential < 1 Service, Maintenance Workers (1985) 9 Skilled Trades (999) < 1 Boiler Operators (547) < 1 Stage Hands (274) < 1 Non Union < 1

.3 34.3 14.3 10.5

1.0 F l o n e

1.0 1.0 2.8

25.9 .7

5.2 1.7 1.0

n o n e

n o n e

Hypothesis Testing

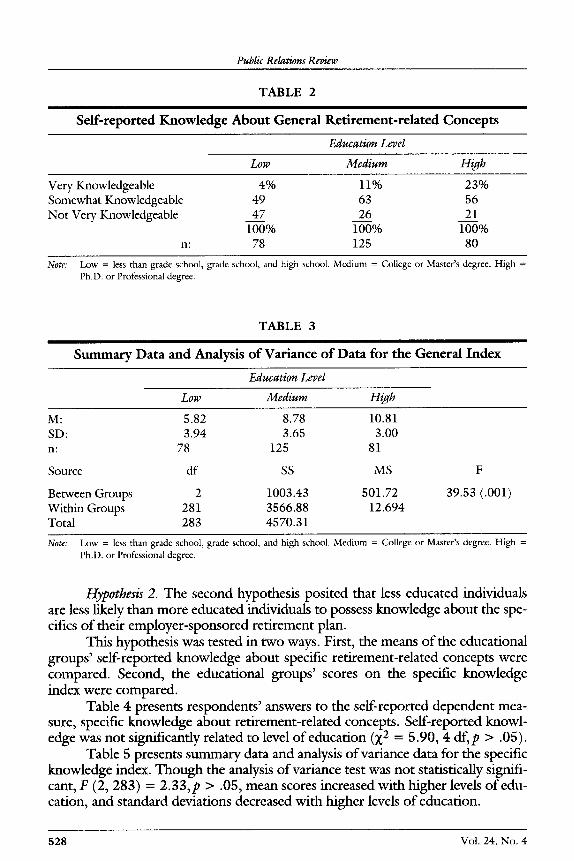

Hypothesis I. The first hypothesis predicted that respon- dents with less education would be less likely than more educated respondents to possess knowledge about general retirement-related concepts. This hypothe- sis was tested in two ways. First, the means of the educational groups' self- reported knowledge about general retirement-related concepts were compared. Second, the educational groups' scores on the general knowledge index were compared.

Table 2 presents respondents' answers to the self-reported dependent measure, general knowledge about retirement-related concepts. Self-reported knowledge was significantly related to level of education (~2 = 23.74, 4 df, p < .001).

Table 3 presents the summary data and analysis of variance data for the general index. As shown in Table 3, a significant difference exists among the three educational groups' knowledge about general retirement-related concepts, F (2, 281) = 39.53,p < .01. Moreover, Scheffe's post hoc test shows that the level of general knowledge about retirement-related concepts was significantly lower among persons of low education than persons of medium education (t = -2.96, p < .001), and that the level o f general knowledge was significantly lower among persons o f med ium education than persons o f high education (t = -2 .03 , p < .001).

Winter 1998 527

Public Relations Review

T A B L E 2

Self-reported Knowledge About General Retirement-related Concepts

Education Level

Low Medium High

Very Knowledgeable Somewha t Knowledgeable N o t Very Knowledgeable

n :

4 % 11% 23% 49 63 56 47 26 21

100% 100% 100% 78 125 80

Note: Low = less than grade school, grade school, and high school. Medium = College or Master's degree. High = Ph.D. or Professional degree.

T A B L E 3

Summary Data and Analysis of Variance of Data for the General Index

Education Level

Low Medium High

M: 5.82 8.78 10.81 SD: 3.94 3.65 3.00 n: 78 125 81

Source d f SS MS

Between Groups 2 1003.43 501.72 Wi th in Groups 281 3566.88 12.694 Total 283 4570.31

F

39.53 (.001)

Note: Low = less than grade school, grade school, and high school. Medium = College or Master's degree. High = Ph.D. or Professional degree.

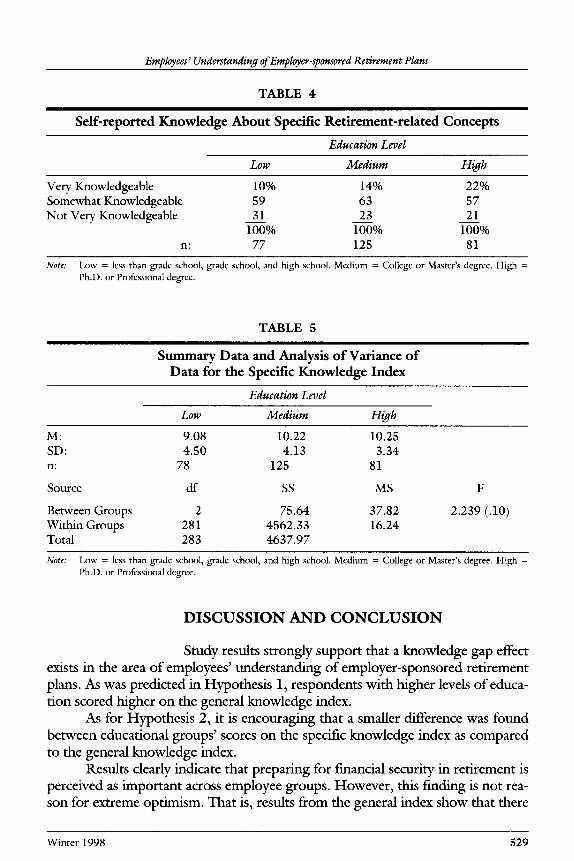

Hypothesis 2. The second hypothesis posited that less educated individuals are less likely than more educated individuals to possess knowledge about the spe- cifics of their employer-sponsored retirement plan.

This hypothesis was tested in two ways. First, the means of the educational groups' self-reported knowledge about specific retirement-related concepts were compared. Second, the educational groups' scores on the specific knowledge index were compared.

Table 4 presents respondents' answers to the self-reported dependent mea- sure, specific knowledge about retirement-related concepts. Self-reported knowl- edge was not significantly related to level of education (22 = 5.90, 4 df, p > .05).

Table 5 presents summary data and analysis of variance data for the specific knowledge index. Though the analysis of variance test was not statistically signifi- cant, F (2, 283) = 2.33,p > .05, mean scores increased with higher levels of edu- cation, and standard deviations decreased with higher levels of education.

528 Vol. 24, No. 4

Employees" Understanding of Employer-sponsored Retirement Plans

T A B L E 4

Self-reported Knowledge About Specific Retirement-related Concepts

Education Level

Low Medium High

Very Knowledgeable Somewha t Knowledgeable N o t Very Knowledgeable

n~

10% 14% 22% 59 63 57 31 23 21

100% 100% 100% 77 125 81

Note: Low = less than grade school, grade school, and high school. Medium = College or Master's degree. High = Ph.D. or Professional degree.

TABLE 5

Summary Data and Analysis of Variance of Data for the Specific Knowledge Index

Education Level

Low Medium High

M: 9.08 10.22 10.25 SD: 4 .50 4.13 3.34 n: 78 125 81

Source d f SS MS

Between Groups 2 75.64 37.82 Wi th in Groups 281 4562 .33 16.24 Total 283 4637 .97

F

2 .239 (.10)

Note: Low = less than grade school, grade school, and high school. Medium = College or Master's degree. High = Ph.D. or Professional degree.

DISCUSSION AND CONCLUSION

Study results strongly support that a knowledge gap effect exists in the area of employees' understanding of employer-sponsored retirement plans. As was predicted in Hypothesis 1, respondents with higher levels of educa- tion scored higher on the general knowledge index.

As for Hypothesis 2, it is encouraging that a smaller difference was found between educational groups' scores on the specific knowledge index as compared to the general knowledge index.

Results clearly indicate that preparing for financial security in retirement is perceived as important across employee groups. However, this finding is not rea- son for extreme optimism. That is, results from the general index show that there

Winter 1998 529

Public Relations Review

exists a substantial gap between employees' knowledge about investment-related concepts as a function of education. In particular, persons with higher levels of education were more knowledgeable about the investment concepts that enable people to make wise investment decisions in general, not just those decisions associated with a particular retirement plan.

Contemporary employees are becoming more aware of their responsibili- ties under the defined contribution umbrella. Unfortunately, the results of this study suggest that not all employees are in possession of retirement-related knowledge that will lead them to financially secure retirements. More specifically, results show that age, employee group, gender, household income, and racial identification strongly effect individuals' knowledge about general and specific retirement-related issues.

Practical Application. If employers are to achieve a goal of guiding all employees toward educated retirement-related decision making, it is crucial that they provide all employees with information that they understand based on their manner of interacting with information. Therefore, supporting materials should be developed with a goal of improving comprehension among group members who are less knowledgeable about retirement-related issues. Simply, materials developed to provide information to diverse groups should not assume a particu- lar level of knowledge. A concerted effort should be made to determine the level of knowledge held within various groups, then, materials should be tailored toward revealed knowledge levels.

Implications for Future Research. The results of this study are limited as the sample was drawn from a collective group and analyzed based on respondents' level of education. There are many factors, in addition to education, that rein- force information gaps. Some are----communication skills; amount of prior knowledge about specified topics; relevant social contact; selective exposure; acceptance and retention of information; and the nature of the mass media infor- mation-defivery subsystems. 26 However, all noted factors are to varying degrees a function of education.

Still, the results clearly support that a knowledge gap effect is at work in the area of employees' understanding of employer-sponsored retirement plans. Therefore, organizations that sponsor defined contribution plans should consider more closely the retirement-related materials distributed to employees. Merely providing all employees with typical retirement-related materials may not guaran- tee that all employee groups understand the concepts covered therein.

APPENDIX

General Index Item

Q6: In general, an asset allocation fund seeks high total return with reduced risk over the long term.

530 Vol. 24, No. 4

Employees" Understanding of Employer-sponsored Retirement Plans

Q7: In general, the greater the potential investment return, the lower the risk.

Q8: In general, bond investments often provide a lower return rate than stock investments.

Q9: Mutual funds provide a means of diversification for investors.

Q l l : Money market funds invest in short-term debt obligations, such as stocks and bonds.

Q12: Bond funds or income funds invest in securities that pay fixed rates, such as government, mortgage-backed, corporate or utility bonds.

Q13: An investment option prospectus details an option's objectives and the methods used to achieve those objectives.

Specific Index Items

Q10: Your contributions made to the BRP are pooled with other peo- ple's contributions in the investment option you choose.

Q14: The investment companies to which you can direct your BRP contributions are called vendors.

Q15: The only vendor choices available on campus are Fidelity Invest- ments and the Vanguard Group.

Q17: Fidelity Investments and the Vanguard Group offer mutual funds.

Q18: Only full-time employees can participate in the BRP.

Q19: Those who participate in the BRP contribute six percent of their salary to their BRP account.

Q20: Regular full-time employees age 30 or older are required to par- ticipate in the BRP after completing the indicated number of FTE ser- vice hours.

Q21: Tax-deferred distributions from the tmiversity's retirement plans are subject to federal income tax in the year of distribution.

1.

NOTES

Randy Myers, "Employee Education on 401(k) Plans," Nation's Business (June 1996), p. 66; Karen Ferguson and Kate Blackwell, Pensions in Crisis: Why the System is Failing American and How You Can Protect Your Future (New York: Arcade Pub- lishing, 1995); Raymond R. Maddock, "The Emergency of Customer Focus in

Winter 1998 531

Public Relations Review

Defined Contribution Plans," Compensation and Benefit Review 27 (January-Febru- ary 1995), pp. 33-37; John Wyatt, "401(k)s Must be Managed," Fortune (April 17, 1995), pp. 208-209; B. Douglas Bernheim, The Determinants and Consequences of Financial Illiteracy, study conducted for Merrill Lynch, Stanford University, Depart- ment of Economics (1994), pp. 33-40; &even K. Fine, "Research Roundup: Trends and Issues in 401(k) Plans," Compensation & Benefits Review 26 (March- April 1994), pp. 62-66; B. Douglas Bernheim and Lawrence Levin, "Social Security and Personal Savings: An Analysis of Expectations," American Economic Review 79 (1989), pp. 97-102; Olivia S. Mitchell, "Worker Knowledge of Pension Provi- sions," Journal of Labor Economics 6 (1988), pp. 21-39.

2. Ellie Williams, "Communicating Your 401(k): Guidelines to Choosing the Right Employee Education Program," Compensation & Benefits Review 26 (March-April 1995), pp. 54-61; Victor S. Barocas, Benefit Communications: Enhancing the Employer's Investment, Report Number 1035 (New York: The Conference Board, 1993).

3. Karen Ferguson and Kate Blackwell, Pensions in Crisis: Why the System is Failing America and How You Can Protect Your Future (New York: Arcade Publishing, 1995).

4. Pensions and Health Benefits of American Workers, New Findings From the April 1993 Current Population Survey, Office of Research and Economic Analysis (Washington, D.C., U.S. Department of Labor, Pension and Welfare Benefits Administration, 1994).

5. Robert M. McCaffery, "From Fringes to Flexible Compensation," Employee Benefit Programs: A Total Compensation Perspective, 2 nd ed.; Kent Series in Human Resource Management, PWS (Boston, MA: Kent Publishing Company, 1992), pp. 1-16.

6. Ibid. 7. Leslie E. Papke, "Participating in and Contributions to 401(k) Pension Plans, Evi-

dence From Plan Data," TheJournal of Human Resources 30 (1995), pp. 311-325; Luis R. Gomez-Meja and David B. Balkin, "Compensation: Breaking From the Past and Searching for New Directions," Compensation, Organizational Strategy, and Firm Performance, South-Western Series in Human Resources Management (Cincinnati, OH: College Division, South-Western Publishing, 1992), pp. 3-33; Ibid.

8. Judy A. Bischopink and Gail G. Meister, "Investment Education Under 401(k) Plans," Benefits Quarterly (Second Quarter 1994), pp. 33-40; Luis R. Gomez-Meja and David B. Balkin, op. cit., pp. 3-33; Robert M. McCaffery, op. cir., pp. 1-16.

9. Judy A. Bishopink and Gail G. Meister, op. cit., pp. 33-40; Ellie Williams, op. cit., pp. 54-61; Lisa M. Hoene, "Making Your Retirement Savings Plan Information a More Effective Package," Pension World 29 (1993), pp. 9-10; Will S. Bashan, "Case Study: Creating Lifestyle Portfolios for Defined Contribution Plans," Pension World 29 (1993), pp. 30-32; Olivia S. Mitchell, op. cit., pp. 21-39; Raymond R. Mad- dock, op. cit., pp. 33-37; Randy Myers, op. cit., p. 66; John Wyatt, op. cit., pp. 208-209.

10. Kjell Nowak, "From Information Gaps to Communication Potential," in Mie Berg, Pertti Hemanus, J. E. Kecran, Frands Mortensen, and Preben Septrup (eds.), Cur- rent Theories in Scandinavian Mass Communication Research (Grenaa, Denmark: GMT), pp. 231-258; Elina Suominen, "Who Needs Information and Why,"Journal of Communication 26 (1976), pp. 15-19; Alfred G. Smith, "The Primary Resource," Journal of Communication 25 (1975), pp. 15-20; Natan Katzman, "The Impact of

532 Vol. 24, No. 4

Employees' Understanding of Employer-~onsored Retirement Plans

Communication Technology: Promises and Prospects," Journal of Communication 24 (1974), pp. 47-58.

11. L. David Ritchie, Information, Communication Concepts 2 (Newbury Park, CA: Sage Publications).

12. Robert E. Park, "News as a Form of Knowledge: A Chapter in the Sociology of Knowledge," American Journal of Sociology 45 (1940), pp. 669-686.

13. "Landmark 404(c) Leads to a Surge of Activity in Nation's 401(k) Industry," Spe- cial Advertising Section, Pension World (June 1993), pp. 2-18; Ann C. Foster, "Defined Contribution Retirement Plans Become More Prevalent," Compensation and Working Conditions 1 (June 1996), pp. 42-44; Ann C. Foster, "Employee Par- ticipation in Savings and Thrift Plans," Monthly Labor Review 119 (March 1996), pp. 17-22; Olivia S. Mitchell, '~Fhe Hard Facts About Social Security," Challenge 39 (1996), pp. 16-18; B. Douglas Bernheim, "Will Baby Boomers be as Well-off in Retirement as Their Parents," CQ Researcher 41 (November 5, 1993), p. 977; B. Douglas Bernheim and John Karl Scholz," Do Americans Save Too Little?" Business Review, Federal Reserve Bank of Philadelphia (September-October 1993), pp. 3-20.

14. Donald C. Dilworth, "Employees Sue Companies to Recover 401(k) Loses," Trial 33 (1997), pp. 78-79; Mark R. Hornak, Judi A. Lewis, and P. Jerome Richey, "Modifying Employee Benefits, Third Circuit Places Employers on a Slippery Slope in Disclosing Amendment to Benefits Plans," The National Law Review 19 (1997),pp. C6,col 4, C7-C8; Constance B. DiCesare, "Benefits Fraud, (Varity Corp. v. Howe)," Monthly Labor Review 119 (1996), pp. 51-52.

15. Phillip J. Tichenor, George A. Donohue, and Clarice N. Olien, "Mass Media Flow and Differential Growth in Knowledge," Public Opinion Quarterly 34 (1970), pp. 159-170; Anne M. Thunberg, Kjell Nowak, Karl Erik Rosengren, and Bengt Sig- urd, Communication and Equality: A Swedish Perspective (Stockholm, Sweden: Alm- qvist & Wiksell International, 1982); Kjell Nowak, op. cit., pp. 231-258; Elina Suominen, op. cit., pp. 15-19; Alfred G. Smith, op. cit., pp. 15-20; Natan Katz- man, op. cit., pp. 47-58; Thomas Childers with Joyce A. Post, The Information Poor in America (Metuchen, NJ: The Scarecrow Press, 1975).

16. Phillip J. Tichenor, George A. Donohue, and Clarice N. Olien, op. cit., pp. 159- 170.

17. Ibid. 18. Cecilie Gaziano and Emanuel Gaziano, "Theories and Methods in Knowledge Gap

Research Since 1970," in Michael B. Salwen and Don W. Stacks (eds.), An Inte- grated Approach to Communication Theory and Research (Mahwah, NJ: Lawrence Erlbaum, 1996), pp. 127-143.

19. Phillip J. Tichenor, George A. Donohue, and Clarice N. Olien, op. cir., pp. 159- 170.

20. James S. Etteman and F. Gerald Kline, "Deficits, Differences, and Ceilings: Contin- gent Conditions for Understanding the Knowledge Gap," Communication Research 4 (1977), 179-202.

21. Cecile Gaziano and Emanuel Gaziano, op. cit., p. 131. 22. Brenda Dervin, "Communication Gaps and Inequalities: Moving Toward a Recon-

ceptualization," in Brenda Dervin and Melvin J. Voigt (eds.), Progress in Communi- cation Sciences 1 (Norwood, NJ: Ablex), pp. 73-112.

23. "A False Choice," The Economist 341 (December 14, 1996), pp. 20-21; "The Pen- sion Conspiracy," The Economist 341 (1996), pp. 27-28; Ann C. Foster op. cit., pp. 42 44; Ann C. Foster, op. cit., pp. 17-22; Olivia S. Mitchell, op. cit., pp. 16-18;

Winter 1998 533

Public Relations Review

24.

25.

26.

Karen Ferguson and Kate Blackwell, op. cit.; Vernon Kozlen, "The Future of Pen- sion Plans," Pension World 30 (1994), pp. 32-38; Landmark 404 (c), op. cir., pp. 2- 18; B. Douglas Bernheim and Lawrence Levin, op. cit., pp. 97-102. Don A. Dillman, Mail and Telephone Survey, The Total Design Method (New York: John Wiley & Sons, 1978). Earl R. Babbie, Survey Research Methods, 2 nd ed. (Belmont, CA: Wadsworth Pub- lishing, 1990). Phillip J. Tichenor, George A. Donohue, and Clarice N. Olien, op. cit., pp. 159- 170; Phillip J. Tichenor, Jane M. Rodenkirchen, Clarice N. Olien, and George A. Donohue, "Community Issues, Conflict, and Public Affairs Knowledge," in Peter Clarke (e&), New Models for Mass Communication Research (Beverly Hills, CA: Sage Publications), pp. 45-79; Cecilie Gaziano and Emanuel Gaziano, op. cit., pp. 127- 143; Cecilie Gaziano, "The Knowledge Gap an Analytical Review of Media Effects," Communication Research 10 (1983), pp. 447-486; Anne M. Thunberg, Kjell Nowak, Karl Erik Rosengren, and Bengt Sigurd, op. cit.

534 Vol. 24, No. 4