Embed Size (px)

Citation preview

SOME PERSPECTIVES ON THE NATIONAL ECONOMY:

Enjoy the Party While it Lasts

Uwe E. Reinhardt

Woodrow Wilson School of Public and International Affairs

and

Department of Economics

Princeton University

CLASS OF 2000

2008 MILLENIAL LECTURE

May 31, 2008

This is an expanded and slightly updated version of a

presentation made to Princeton Alumni on May 31, 2008.

Slides containing text have been added to substitute for the

oral commentary made during the presentation. They were

not in the original presentation.

OUTLINE OF THE PRESENTATION:

I. A BRIEF REVIEW OF FRESHMAN ECON 101

II. SOME MACRO-ECONOMIC NUMBERS

A. Year-to-year growth in GDP

B. Inflation over time

C. Private investment in the U.S.

D. Taxes and economic growth

E. How was U.S. Investment financed?

1. Private savings by U.S. business and households

2. Savings (Dis-Savings) by government (esp. federal fiscal policy)

3. Importing the savings of foreigners (the Current Account)

I. A BRIEF REVIEW OF ECON 101

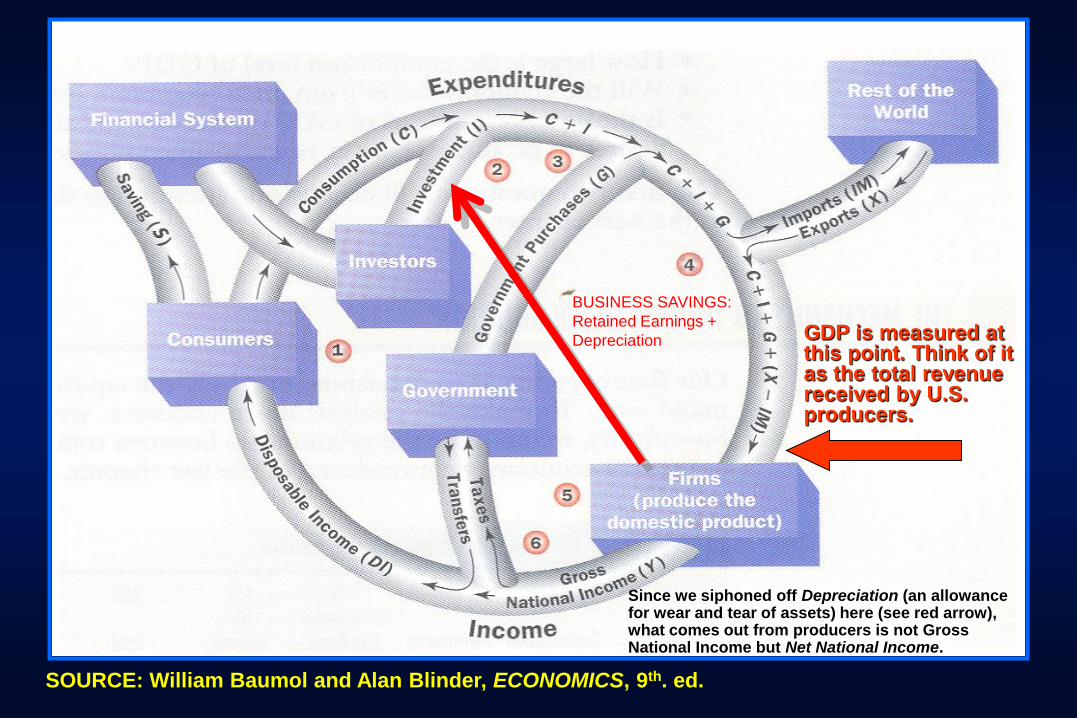

The first sketch economics professors put on the board in the

first lecture in introductory macro-economics courses is the

famous Circular Flow of Economic Activity, also known as the

Circular Money Flow, because economic activity is measured in

monetary terms.

In this circular flow the nation’s Gross Domestic Product (GDP)

is measured by the total revenues received by U.S. producers.

GDP thus measures all valuable output produced in a nation, but

only as long as that output was traded in the commercial market

place.

Thus, the highly valuable output produced by volunteer workers

and by parents – especially mothers – is not counted in GDP. It is

a major measurement error, leaving out much productive activity.

SOURCE: William Baumol and Alan Blinder, ECONOMICS, 9th. ed.

GDP is measured at this point. Think of it as the total revenue received by U.S. producers.

BUSINESS SAVINGS:

Retained Earnings +

Depreciation

Since we siphoned off Depreciation (an allowance for wear and tear of assets) here (see red arrow), what comes out from producers is not Gross National Income but Net National Income.

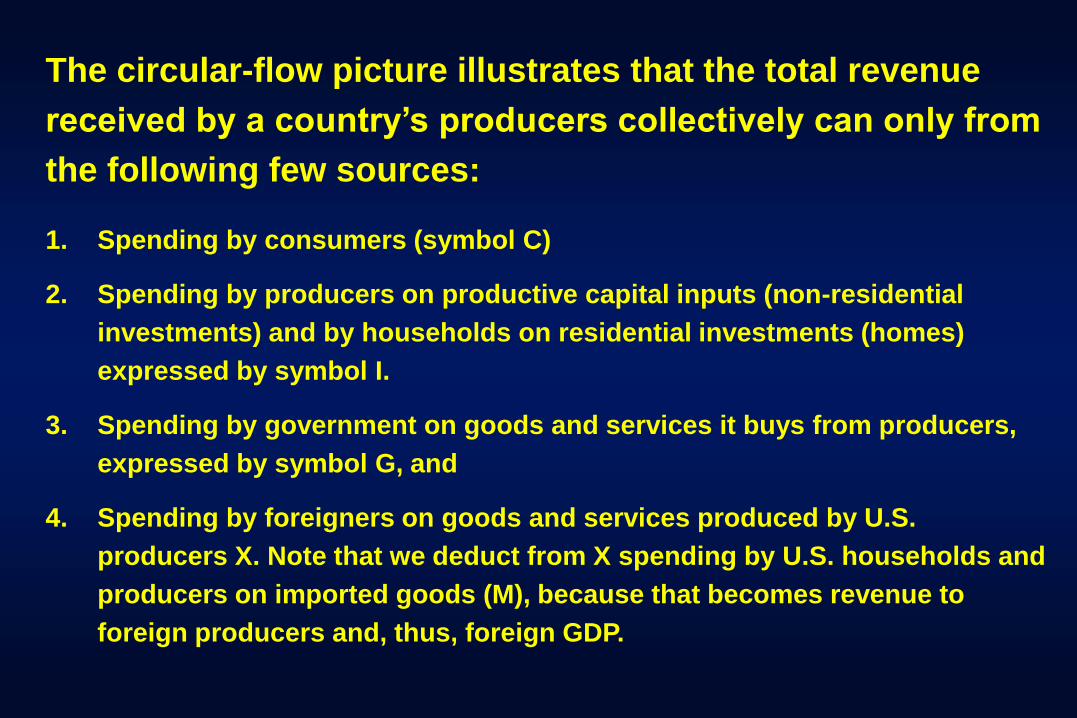

The circular-flow picture illustrates that the total revenue

received by a country’s producers collectively can only from

the following few sources:

1. Spending by consumers (symbol C)

2. Spending by producers on productive capital inputs (non-residential

investments) and by households on residential investments (homes)

expressed by symbol I.

3. Spending by government on goods and services it buys from producers,

expressed by symbol G, and

4. Spending by foreigners on goods and services produced by U.S.

producers X. Note that we deduct from X spending by U.S. households and

producers on imported goods (M), because that becomes revenue to

foreign producers and, thus, foreign GDP.

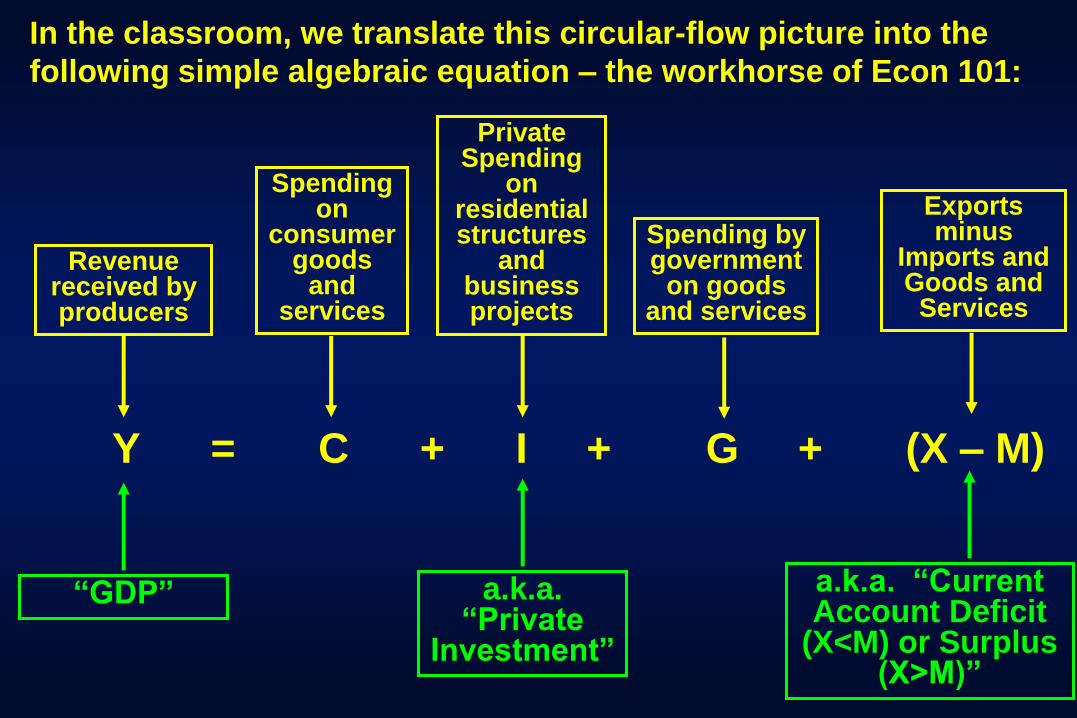

Y = C + I + G + (X – M)

Revenue received by producers

“GDP”

Spending on

consumer goods

and services

Private Spending

on residential structures

and business projects

Spending by government

on goods and services

Exports minus

Imports and Goods and

Services

a.k.a. “Current Account Deficit

(X<M) or Surplus (X>M)”

In the classroom, we translate this circular-flow picture into the

following simple algebraic equation – the workhorse of Econ 101:

a.k.a. “Private

Investment”

Now, before jumping from here into data from the real world,

let me first offer some gentle criticism of macro-economics,

as we professors teach it to our students.

Y = C + I + G + (X – M)

Spending on

residential structures

and business projects

Spending by government

on goods and services

To their shame, macro economists rarely ever

distinguish explicitly between government

spending on current operations and on long-

lived capital investments.

CONSIDER AGAIN THE MACRO EQUATION:

Perhaps because of our sloppy teaching, over the years it has

become part of American folklore that increases in Private

Investment (I) are always good for the economy, as it is apt to

increase labor productivity, while increases in government

expenditures on goods and services (G) tend to be a drag on the

economy, because much of it is considered wasteful.

That folklore is as silly as it is harmful. The term G includes

government spending on airports, bridges, basic research in

physics and medicine, defense equipment, schools and so on, all

of which are investments in long-lived, highly productive assets.

On the other hand, the Private Investment term I includes residential

real estate and golf resorts, which produce valued services over the

year but are not likely to enhance labor productivity.

Not splitting G into current government operations and government

investments can easily seduce people into thinking that cutting

taxes and reducing government spending on schools or research

(i.e., cutting G) and using those tax savings to build more private

golf resorts (i.e., increasing I) somehow makes America’s economy

stronger. Many people seem to believe it. It is pure bull shine.

Future generations of Americans are likely to pay a price for this

sloppy work in the form of a deteriorating infrastructure, in an

inadequate supply and composition of human capital and in a

reduced number of valuable patents.

Where is John Kenneth Galbraith when we need him? He famously

drew attention in his early writings to the bias whereof I speak.

II. SOME MACRO-ECONOMIC NUMBERS

All taken from the “Statistical Tables” section of the Economic

Report of the President to the Congress, February, 2008, found

at the website

http://www.gpoaccess.gov/eop/download.html

A. Data on the growth of Gross Domestic Product (GDP)

In the next few slides, I present data on the year-to-year growth in

“real” GDP, where “real” means “adjusted for inflation” or, in other

words, “expressed in US dollars with a constant purchasing power.”

Broadly speaking, we can think of these “constant dollars” as

dollars that buy the same amount of GDP over time.

Although, in fact, U.S. Presidents have at best a minor

influence on the growth of GDP (which is driven my numerous

variables often outside the President’s control) I superimpose

on most of the data to follow the regimes of Presidents,

because that is so often done in punditry on TV and in the

press.

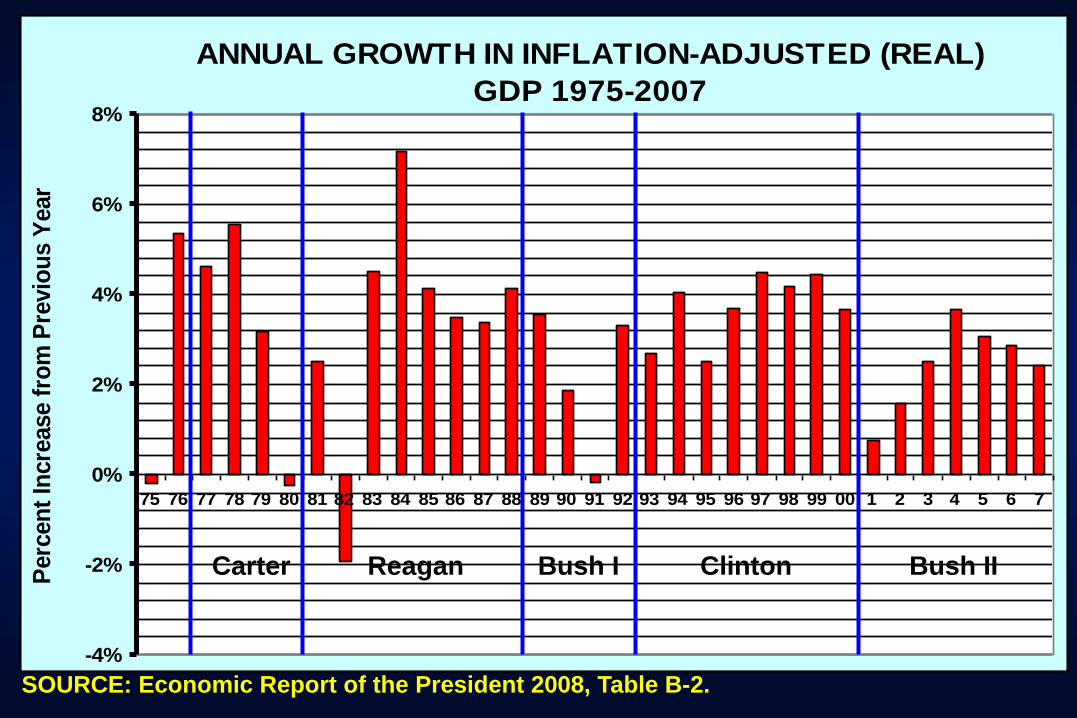

For example, there now are almost mythical references to President

Reagan’s allegedly miraculous, economic prowess. The late Robert

Bartley, Editor of the Wall Street Journal, celebrated it in his book

The Seven Fat Years: And How to do it again (1995).

However, with all respect due to President Reagan, I have trouble

seeing the miracle in the data found in the Economic Report to the

President to Congress cited here.

There was only one spectacular year (1984), but it followed an

earlier decline of GDP – that is, climbing out of a hole.

The rest of the Reagan years strike me as rather ordinary, if we

compare it to the Carter years and especially the Clinton years.

Indeed, I have long been bothered by the disrespect so many

Americans—especially on the right of center– show toward

President Carter.

The high oil prices and general inflation rates of the late 1970s eand

early 1980s can hardly be blamed on his economic policies.

Specifically, what policies would they have been?

It was at President Carter’s initiative – not President Reagan’s -- that

the airline and trucking industries were deregulated—now generally

viewed as sound policy.

It was President Carter—not President Reagan—who boldly

appointed Paul Volker to head the Federal Reserve, full well

knowing that Volker’s approach would entail some harsh but

needed medicine.

Finally, as you will see in the data, the Reagan years passed onto

the years of President George H. Bush (the Elder) a rather weak

economy.

At the beginning of the Reagan presidency, the supply-side

economists then in the saddle heralded an increase in savings and

investment in the US, in response to sharp cuts in income tax rates.

Judge for yourself in the slides (further on) plotting investment and

savings as a percentage of GDP over time. Investment and savings

as percent of GDP tended to decline during the Reagan years and

increase during the Clinton years.

Again, we should not overestimate the impact President’s have on

GDP – nor, however, should we create myths on fictional data.

ANNUAL GROWTH IN INFLATION-ADJUSTED (REAL)

GDP 1975-2007

-4%

-2%

0%

2%

4%

6%

8%

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 1 2 3 4 5 6 7

Perc

en

t In

cre

ase f

rom

Pre

vio

us Y

ear

Carter Reagan Bush I Clinton Bush II

SOURCE: Economic Report of the President 2008, Table B-2.

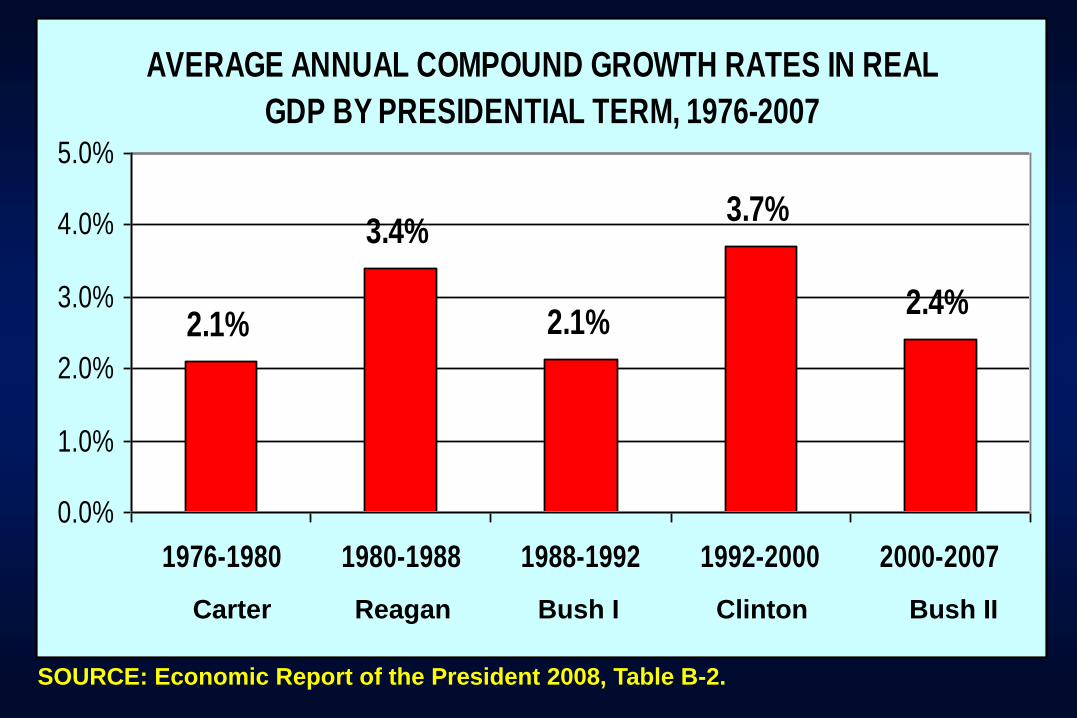

AVERAGE ANNUAL COMPOUND GROWTH RATES IN REAL

GDP BY PRESIDENTIAL TERM, 1976-2007

2.1%

3.4%

2.1%

3.7%

2.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

1976-1980 1980-1988 1988-1992 1992-2000 2000-2007

Carter Reagan Bush I Clinton Bush II

SOURCE: Economic Report of the President 2008, Table B-2.

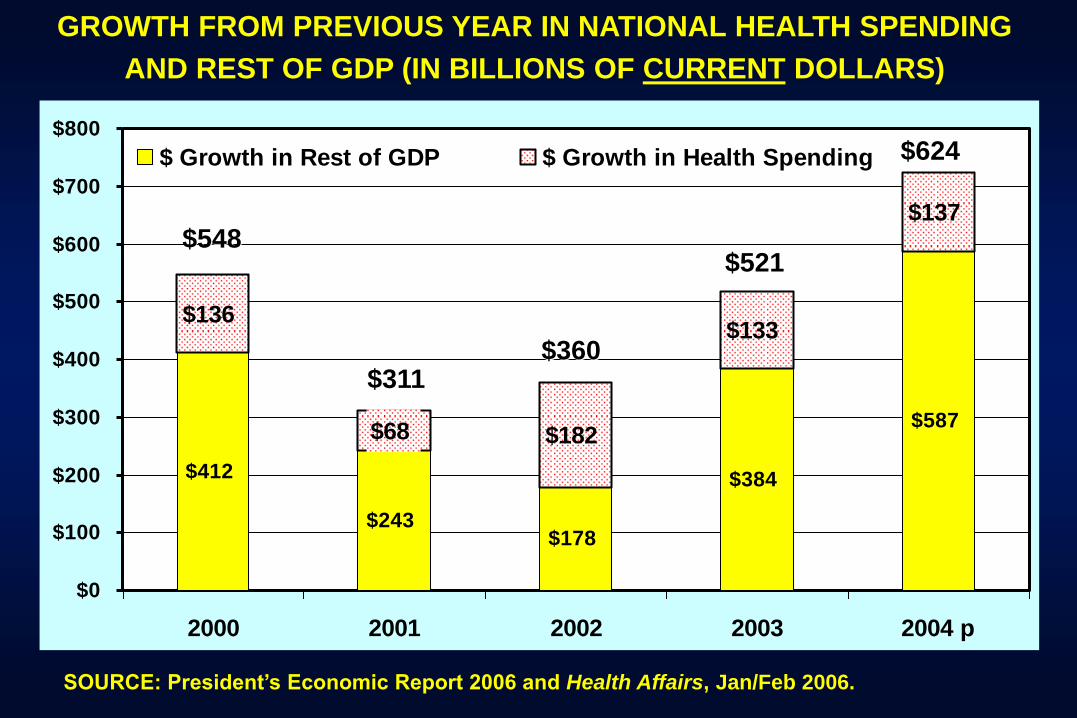

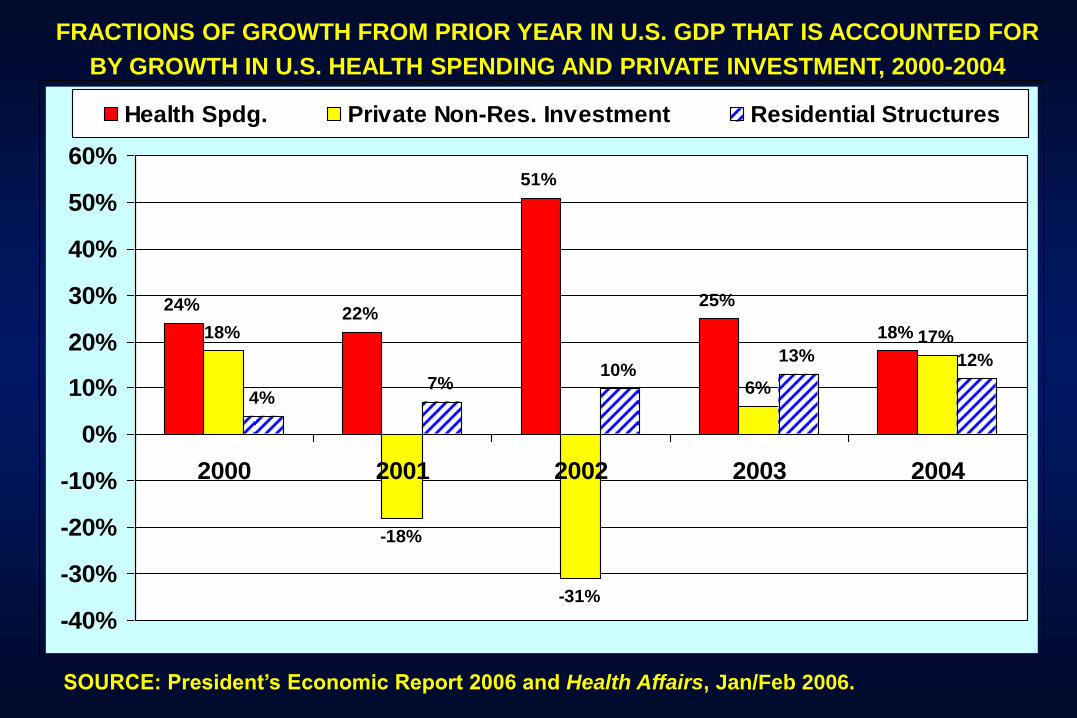

The much maligned U.S. health-care sector – so often decried by

economists and pundits alike decried as a drag on the economy

– actually became the economy’s most powerful economic

locomotive during the recessionary first term of President Bush,

as the next two slides illustrates, creating more new jobs than

any other sector of the economy.

As far as growth on GDP is concerned, the health-care sector

left both the housing boom and business investment in the dust.

On the next, the bold numbers atop the columns represent the

dollar growth in GDP over the previous year. The red portion of

the bar represents health spending.

AN INTERESTING ASIDE:

HEALTH CARE AS OUR ECONOMY’S ECONOMIC LOCOMOTIVE

$412

$243$178

$384

$587

$136

$68 $182

$133

$137

$0

$100

$200

$300

$400

$500

$600

$700

$800

2000 2001 2002 2003 2004 p

$ Growth in Rest of GDP $ Growth in Health Spending

GROWTH FROM PREVIOUS YEAR IN NATIONAL HEALTH SPENDING

AND REST OF GDP (IN BILLIONS OF CURRENT DOLLARS)

$548

$311 $360

$521

$624

SOURCE: President’s Economic Report 2006 and Health Affairs, Jan/Feb 2006.

24%22%

51%

25%

18%18%

-18%

-31%

6%

17%

4%7%

10%13% 12%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

2000 2001 2002 2003 2004

Health Spdg. Private Non-Res. Investment Residential Structures

FRACTIONS OF GROWTH FROM PRIOR YEAR IN U.S. GDP THAT IS ACCOUNTED FOR

BY GROWTH IN U.S. HEALTH SPENDING AND PRIVATE INVESTMENT, 2000-2004

SOURCE: President’s Economic Report 2006 and Health Affairs, Jan/Feb 2006.

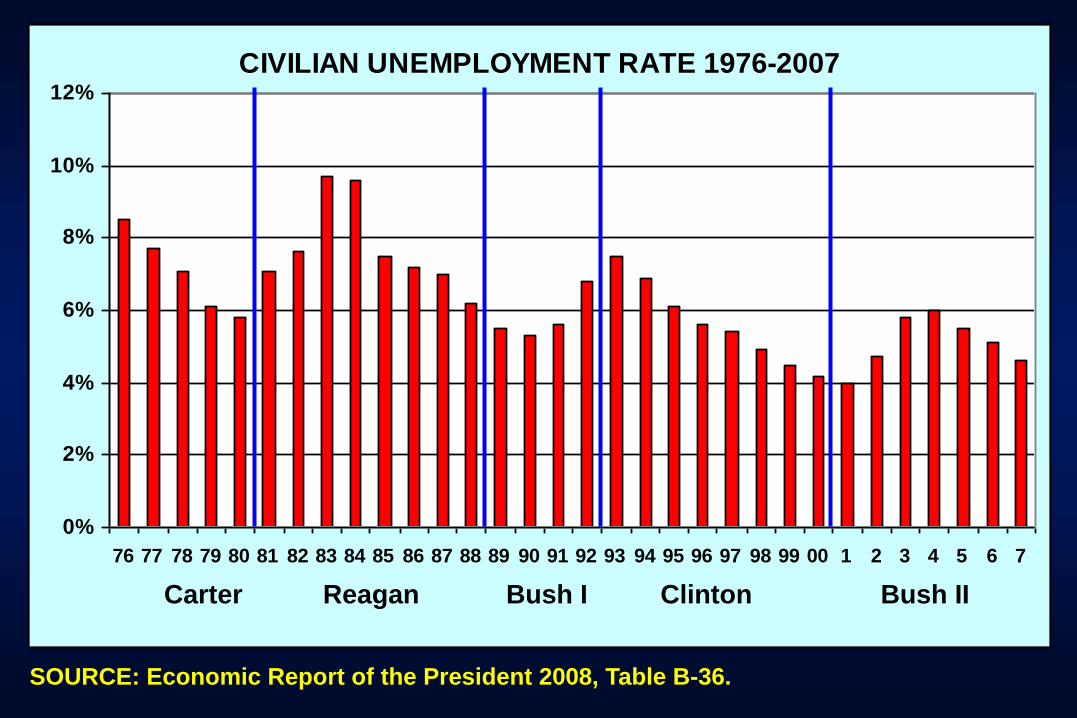

While on the topic of jobs, here are some data on unemployment,

also taken from the President’s Economic Report to Congress

2008.

B. Unemployment

CIVILIAN UNEMPLOYMENT RATE 1976-2007

0%

2%

4%

6%

8%

10%

12%

76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 1 2 3 4 5 6 7

Carter Reagan Bush I Clinton Bush II

SOURCE: Economic Report of the President 2008, Table B-36.

C. Data on Inflation

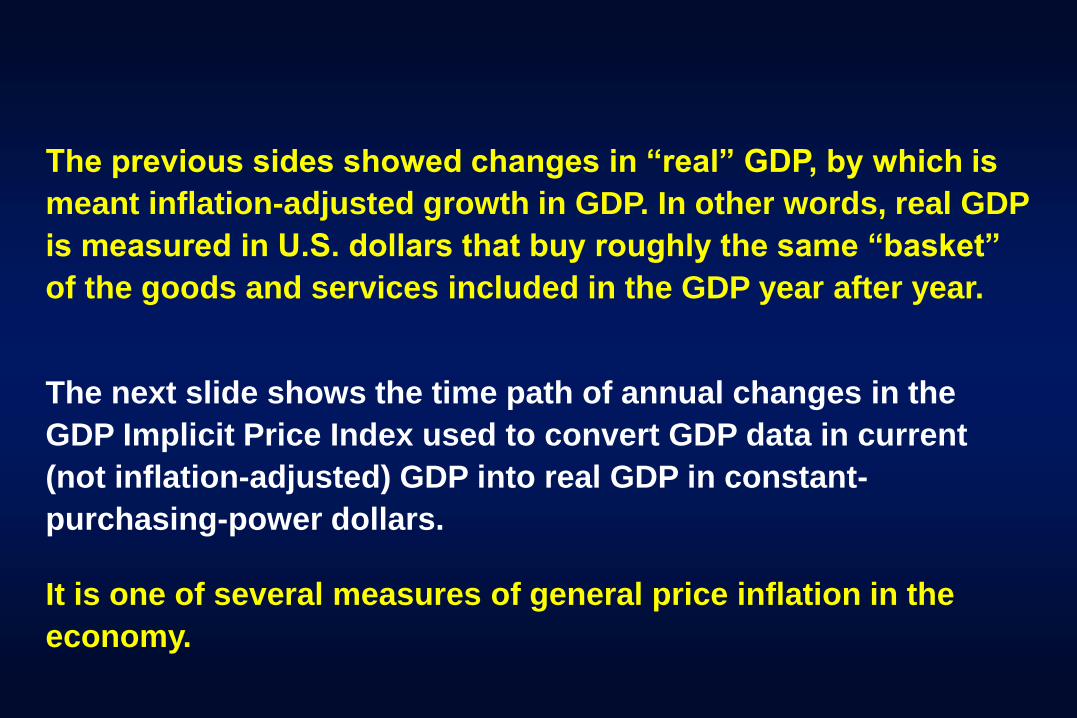

The previous sides showed changes in “real” GDP, by which is

meant inflation-adjusted growth in GDP. In other words, real GDP

is measured in U.S. dollars that buy roughly the same “basket”

of the goods and services included in the GDP year after year.

The next slide shows the time path of annual changes in the

GDP Implicit Price Index used to convert GDP data in current

(not inflation-adjusted) GDP into real GDP in constant-

purchasing-power dollars.

It is one of several measures of general price inflation in the

economy.

ANNUAL GROWTH IN THE GDP PRICE INDEX 1961-2007

0%

2%

4%

6%

8%

10%

12%

14%

61 63 65 67 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 1 3 5 7

% IN

CR

EA

SE

OV

ER

PR

EV

IOU

S Y

EA

R

SOURCE: Economic Report of the President 2008, Table B-7.

The next slide present data on annual changes in the Consumer

Price Index (CPI).

Broadly speaking, this index tracks the dollar cost, year after

year, of a constant basked of consumer goods (with some

adjustments for changes in quality and new products). The

inflation rate is then inferred from annual changes in the total

dollar cost of that fixed basket.

The basket of goods and services being priced out in this way is

selected to be representative of what a typical American family

buys in a year.

In fact, because different socio-demographic groups buy

different baskets of goods and services, one could construct

CPIs for each such group, each with its own basket.

SOURCE: Economic Report of the President 2008, Table B-60.

ANNUAL GROWTH IN CONSUMER PRICE INDEX (CPI) 1961-2007

0%

2%

4%

6%

8%

10%

61 63 65 67 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 1 3 5 7

% IN

CR

EA

SE

OV

ER

PR

EV

IOU

S Y

EA

R

TAKE-AWAY POINT ON INFLATION

It has become part of the American folklore on talk shows and

in media punditry that President Jimmy Carter is uniquely

responsible for the high inflation rates of the late 1970s.

A fair minded observer, however, would note that the inflation

experience during the late 1970s was the culmination of a long

trend that began as early as 1963. If any one President were to

be blamed for it, Presidents Johnson and Nixon would be better

candidates.

The back of inflation was not broken until President Carter

appointed Paul Volcker as Chairman of the Federal Reserve. His

very tight money policy deserves the major credit for the sharp

decline in inflation during the 1980s.

OVERALL TAKE-AWAY POINTS THE GROWTH OF GDP,

ON UNEMPLOYMENT AND ON INFLATION OVER THE

PAST THREE TO FOUR DECADES:

1. As noted, individual presidents and their administrations have

much less influence on macro-economic variable -- such as

GDP, the unemployment rate and inflation -- than seems widely

supposed, even though journalists and pundits pretend that

presidents do have powerful sway over these numbers (and

presidents themselves do so as well, but only when the

numbers are good and flatter them).

2. But if one wants to play that political game – as so often it is on

talk shows -- then certainly the picture that emerges is mixed.

D. Data on the Investment (I) in business capital and homes

Let us, next, look at private investment (I) in the U.S.

economy and the sources of funds (savings in the U.S.

and abroad) that have financed that investment.

We begin with another famous equation from Econ 101.

By “private investments” economists mean investments

by business firms in their capacity plus investments by

households in residential structures.

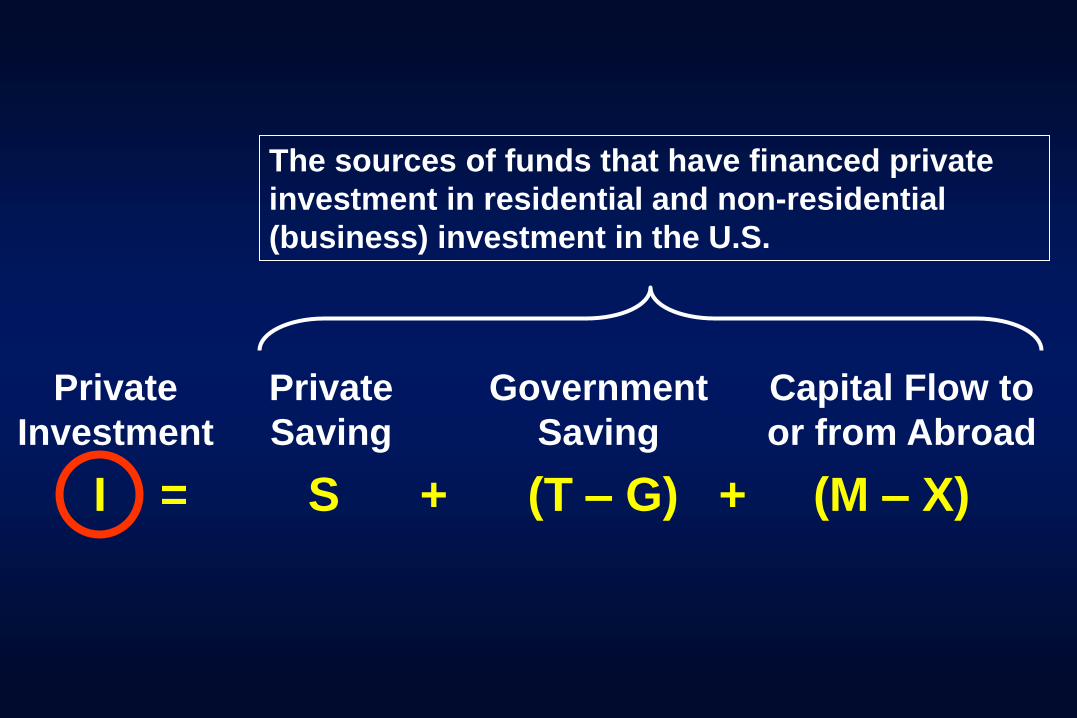

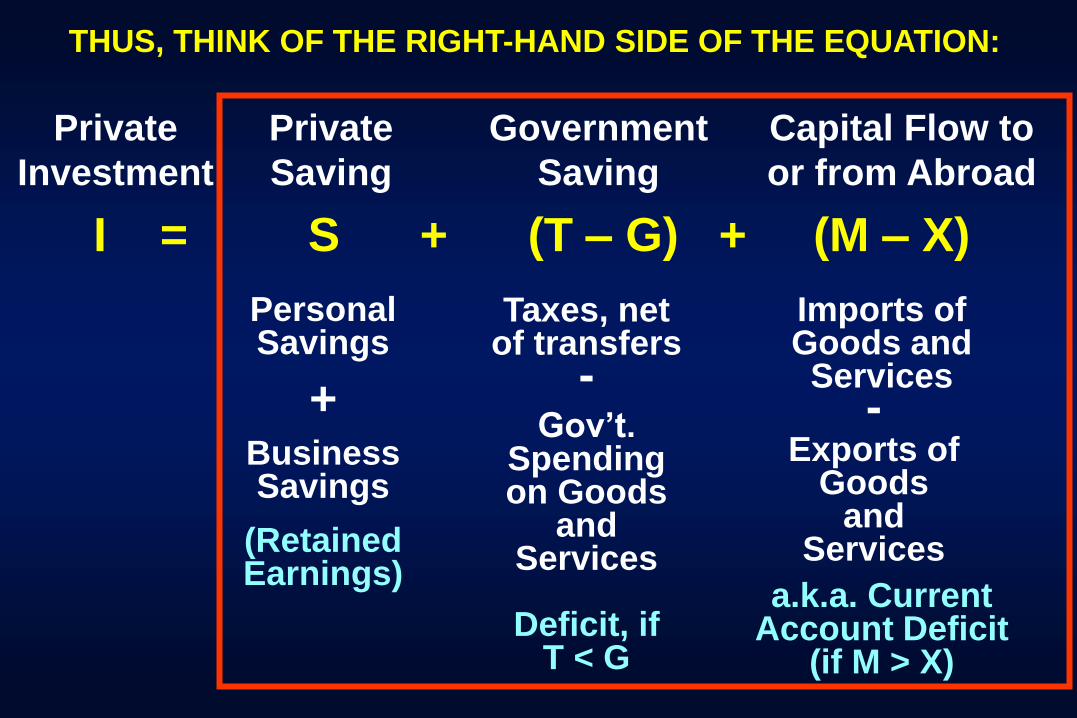

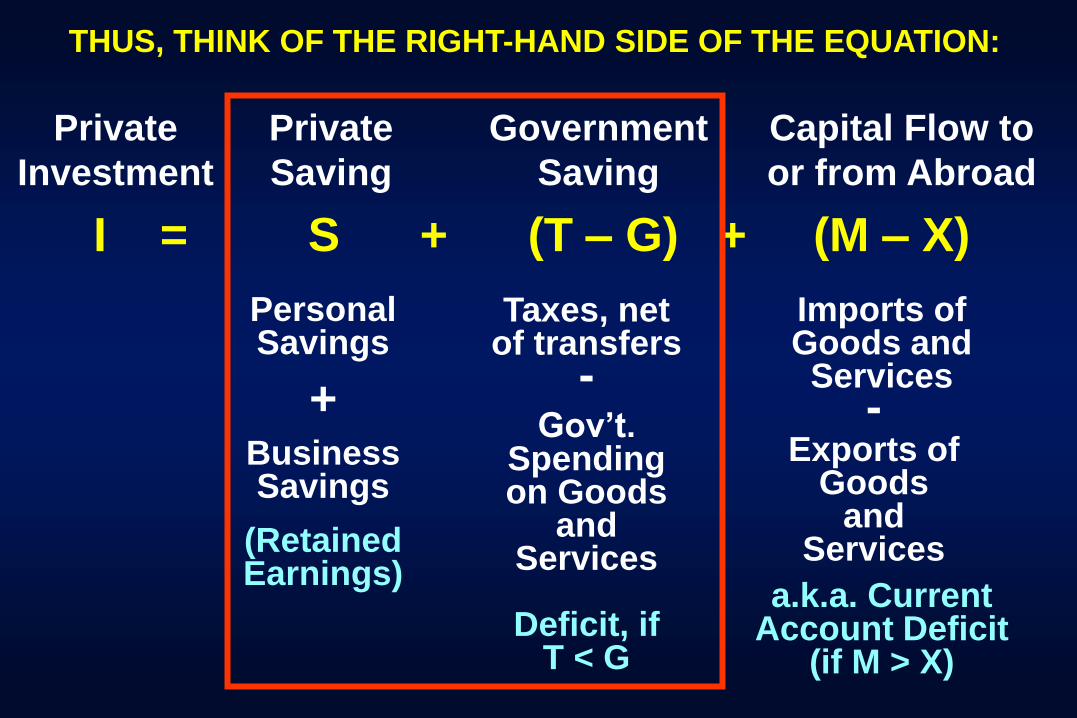

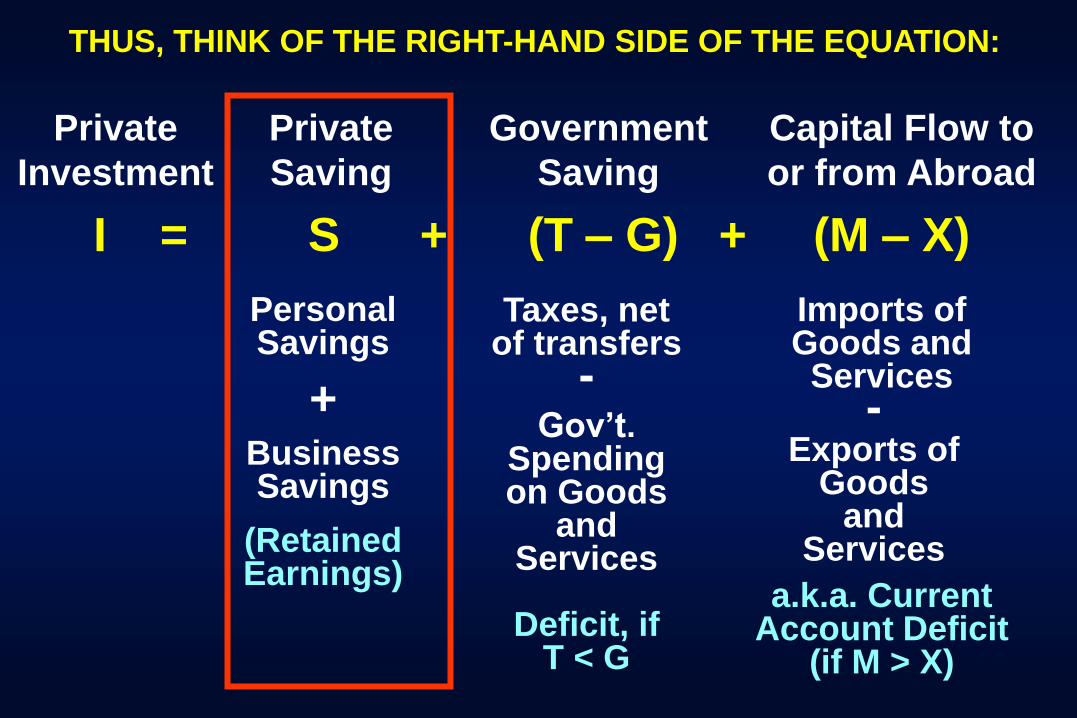

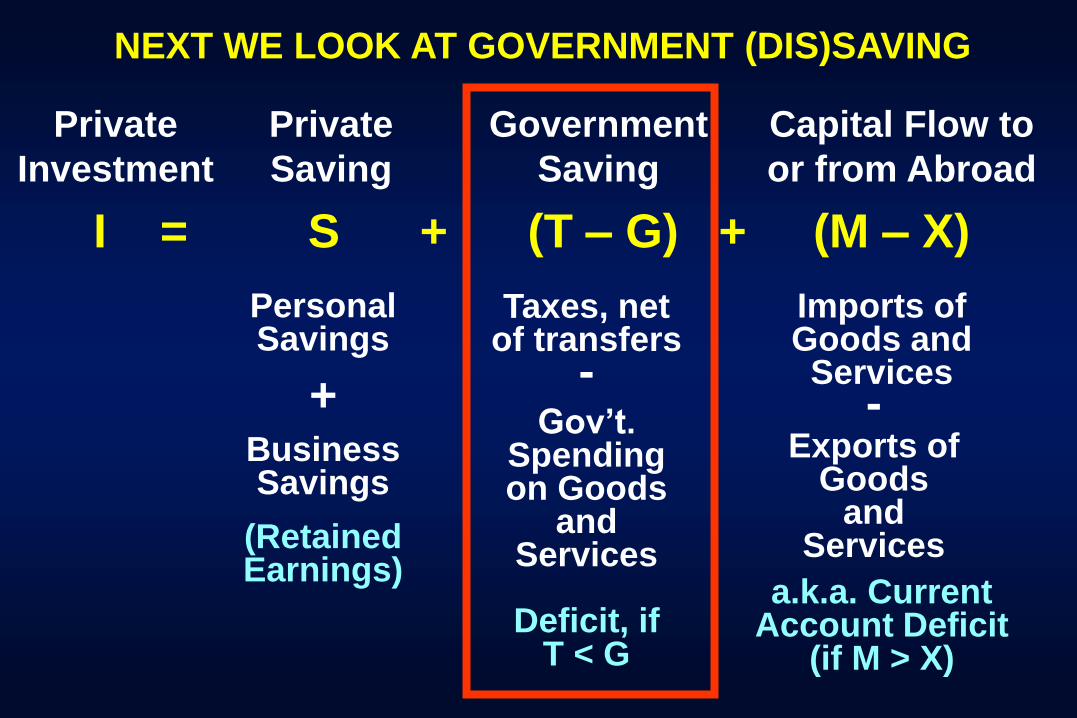

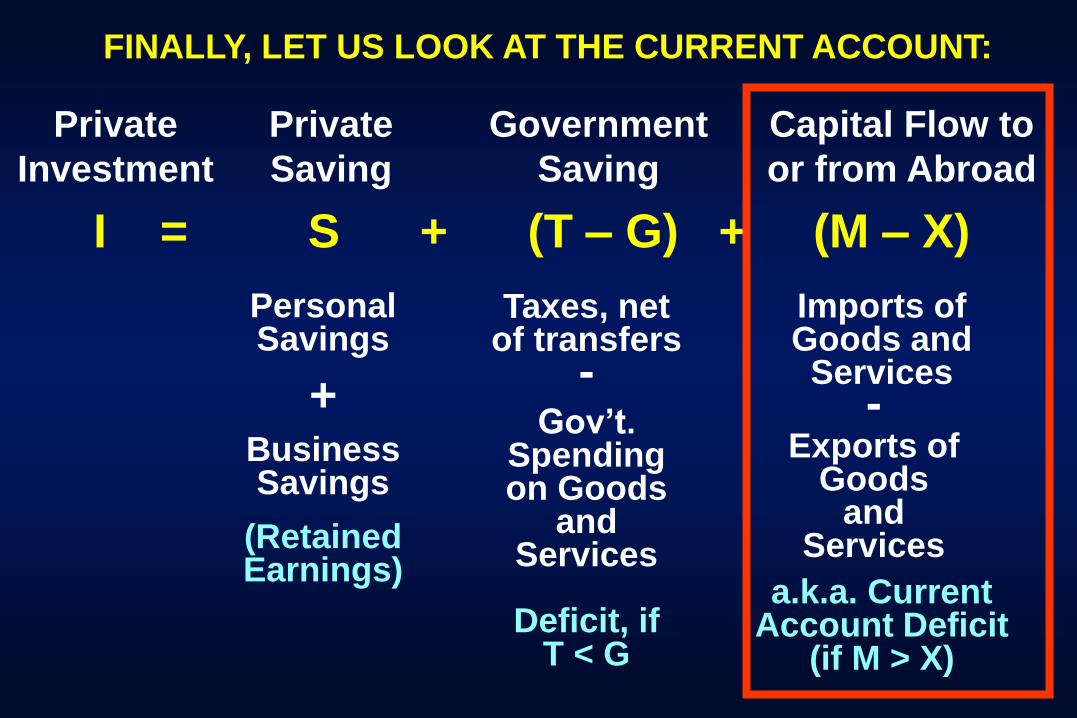

I = S + (T – G) + (M – X)

Private

Saving

Government

Saving

Capital Flow to

or from Abroad

Private

Investment

The sources of funds that have financed private

investment in residential and non-residential

(business) investment in the U.S.

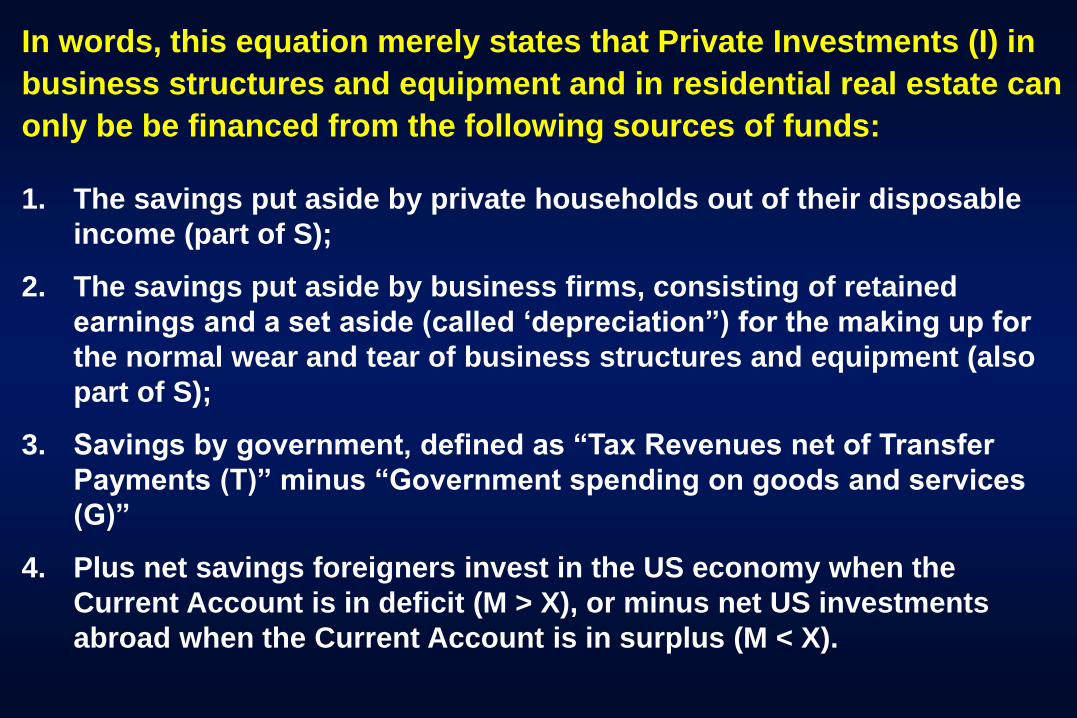

In words, this equation merely states that Private Investments (I) in

business structures and equipment and in residential real estate can

only be be financed from the following sources of funds:

1. The savings put aside by private households out of their disposable

income (part of S);

2. The savings put aside by business firms, consisting of retained

earnings and a set aside (called ‘depreciation”) for the making up for

the normal wear and tear of business structures and equipment (also

part of S);

3. Savings by government, defined as “Tax Revenues net of Transfer

Payments (T)” minus “Government spending on goods and services

(G)”

4. Plus net savings foreigners invest in the US economy when the

Current Account is in deficit (M > X), or minus net US investments

abroad when the Current Account is in surplus (M < X).

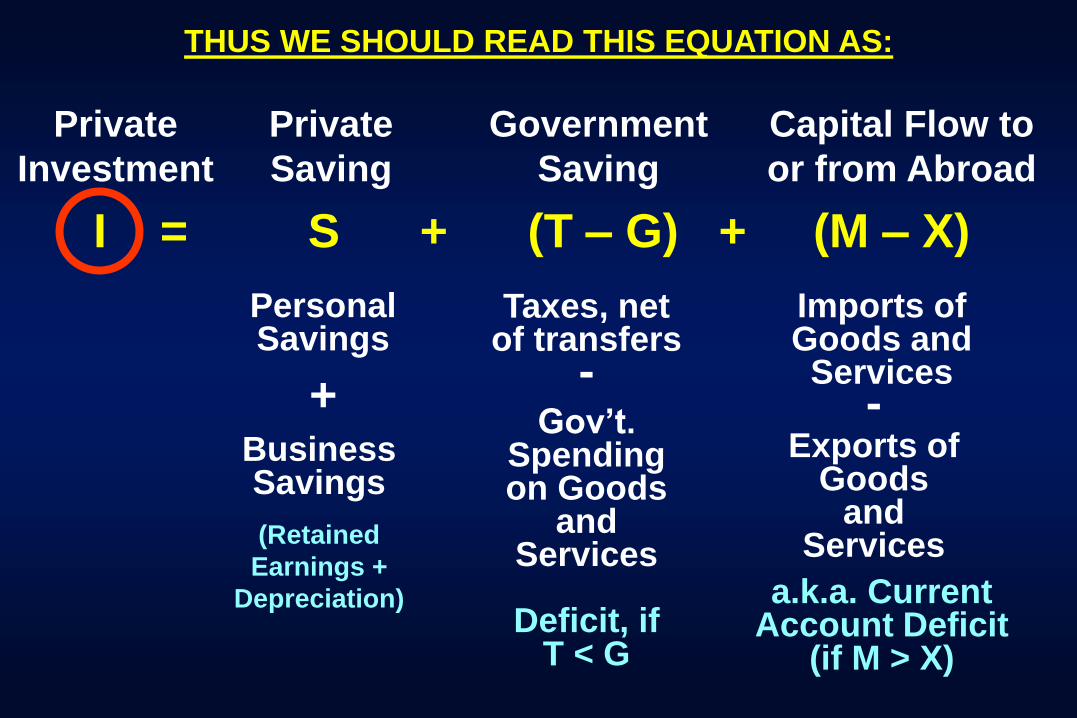

I = S + (T – G) + (M – X)

Private

Saving

Government

Saving

Capital Flow to

or from Abroad

Private

Investment

Personal Savings

+ Business Savings

(Retained

Earnings +

Depreciation)

Taxes, net of transfers

- Gov’t.

Spending on Goods

and Services

Imports of Goods and Services

- Exports of

Goods and

Services

a.k.a. Current Account Deficit

(if M > X) Deficit, if

T < G

THUS WE SHOULD READ THIS EQUATION AS:

Let us first look at the time-path of private investment in the U.S.,

broken down as follows:

The picture that emerges is fascinating, given the widely held

supply-side theory that cuts in personal income-tax rates will

drive up private business investment and thus economic growth,

while tax increases will reduce such investments.

1. total private investment in the US economy and its

components (the black line in the next slide),

2. business investments, i.e. non-residential investments (the

red line) and

3. investment in residential structures (the blue line).

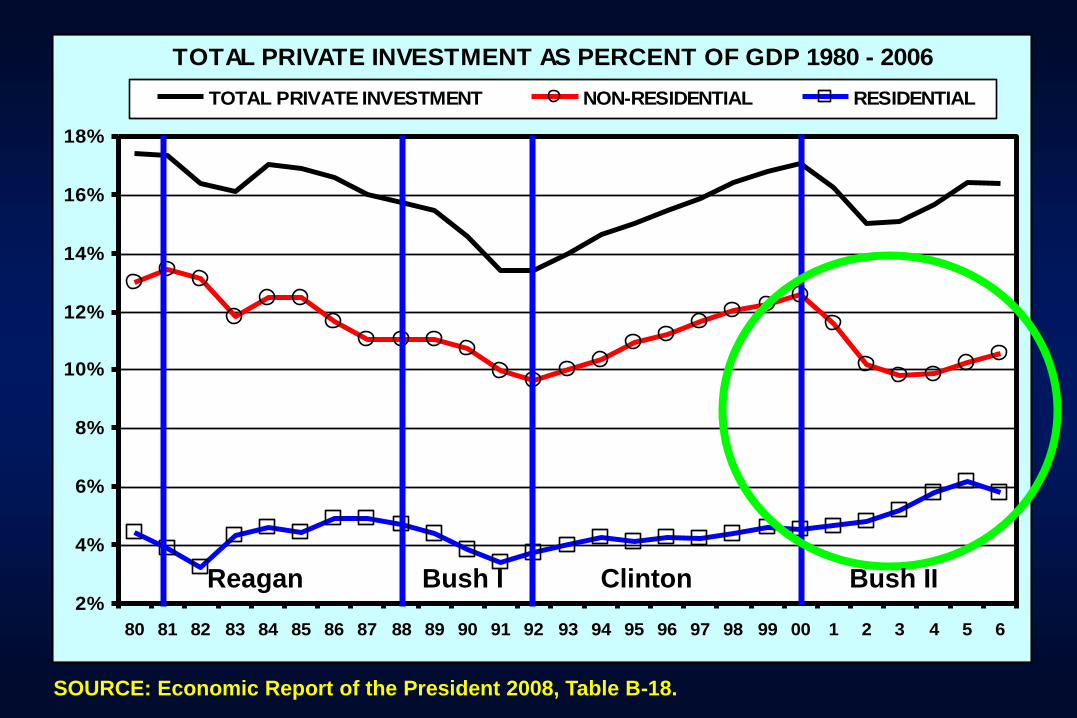

TOTAL PRIVATE INVESTMENT AS PERCENT OF GDP 1980 - 2006

2%

4%

6%

8%

10%

12%

14%

16%

18%

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 1 2 3 4 5 6

TOTAL PRIVATE INVESTMENT NON-RESIDENTIAL RESIDENTIAL

SOURCE: Economic Report of the President 2008, Table B-18.

Reagan Bush I Clinton Bush II

SOURCE: Economic Report of the President 2008, Table B-18.

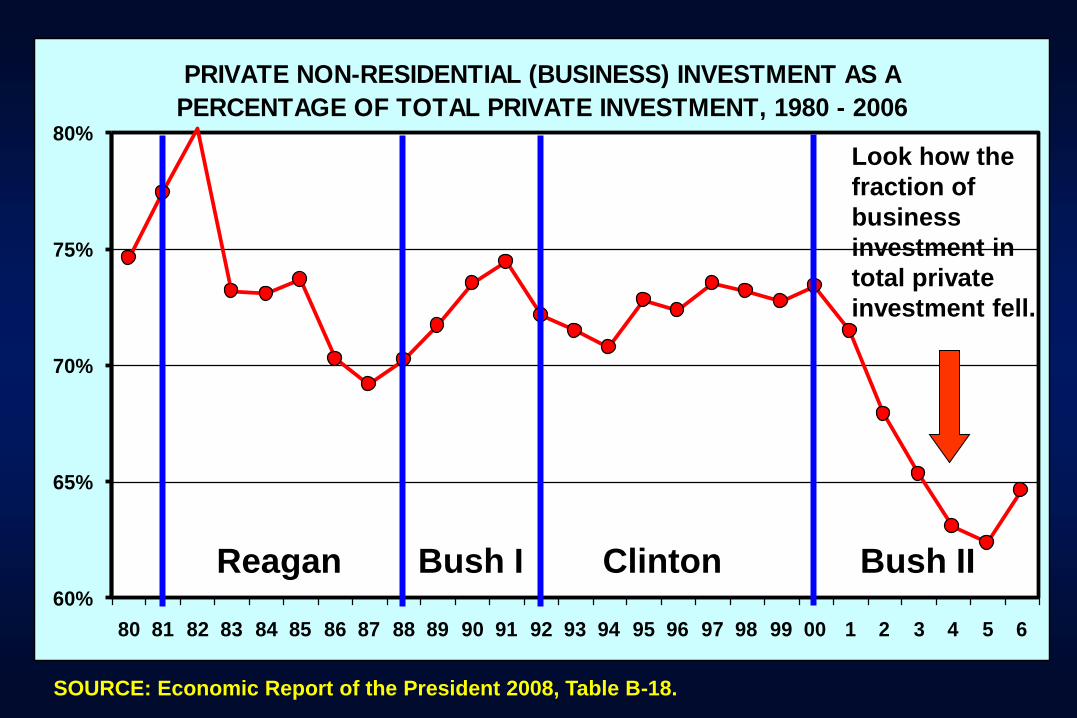

PRIVATE NON-RESIDENTIAL (BUSINESS) INVESTMENT AS A

PERCENTAGE OF TOTAL PRIVATE INVESTMENT, 1980 - 2006

60%

65%

70%

75%

80%

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 1 2 3 4 5 6

Reagan Bush I Clinton Bush II

Look how the

fraction of

business

investment in

total private

investment fell.

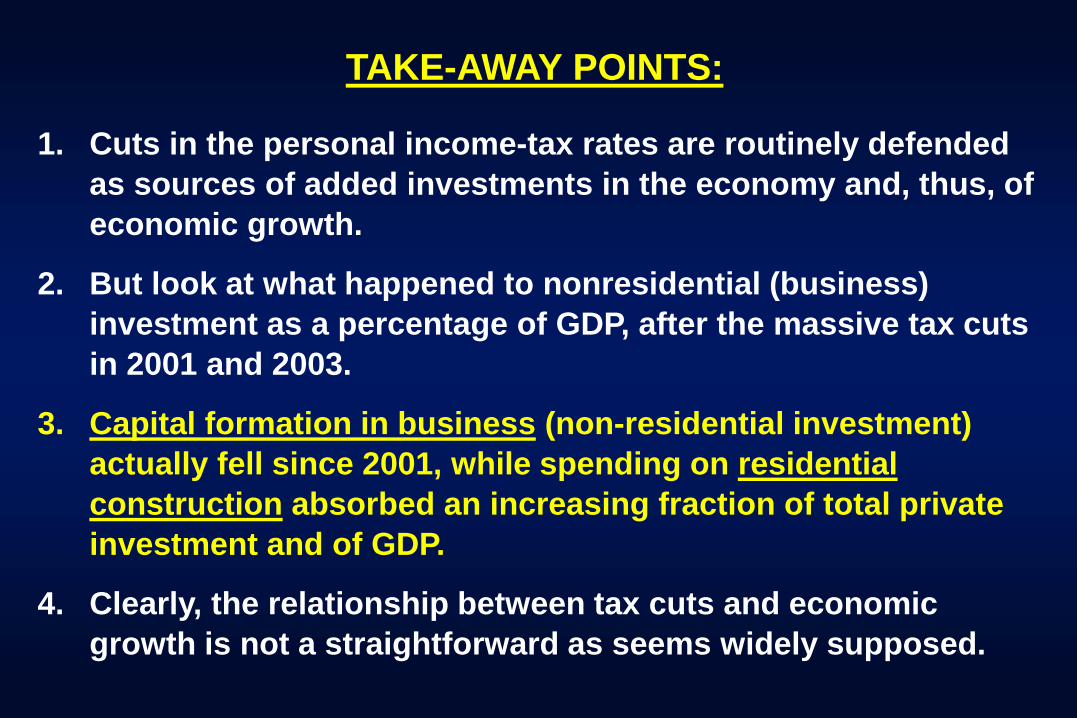

TAKE-AWAY POINTS:

1. Cuts in the personal income-tax rates are routinely defended

as sources of added investments in the economy and, thus, of

economic growth.

2. But look at what happened to nonresidential (business)

investment as a percentage of GDP, after the massive tax cuts

in 2001 and 2003.

3. Capital formation in business (non-residential investment)

actually fell since 2001, while spending on residential

construction absorbed an increasing fraction of total private

investment and of GDP.

4. Clearly, the relationship between tax cuts and economic

growth is not a straightforward as seems widely supposed.

E. Taxes and Economic Growth

As every freshman in economics is taught, taxes on any base

that can be altered by human decisions usually affect how these

decisions are made.

Among lay persons, it is usually assumed that if such a base

e.g., earned income or profits – is taxed, then the activity

generating that base (hours worked or dollars invested for profit)

will shrink.

That is often true, but, as every freshman learns, it is not always

true.

For example, earned income is taxed, then one effect is that

people earn less per hour of leisure given up for work and

therefore people work less – they will substitute more leisure for

hours worked. Economists call this the substitution effect.

On the other hand, because the taxed earners are now poorer,

they may also work harder to make up for the lost income.

Economist call this the income effect of taxing earned income.

Whether raising income taxes makes people work harder or work

less depends on the relative strength of these opposing effects.

In other words, counter-intuitive though it may be, we can never

predict with certainty what effect an increase in income taxes will

have on hours worked.

I added the next slide to this 2008 talk in 2011, when 2009

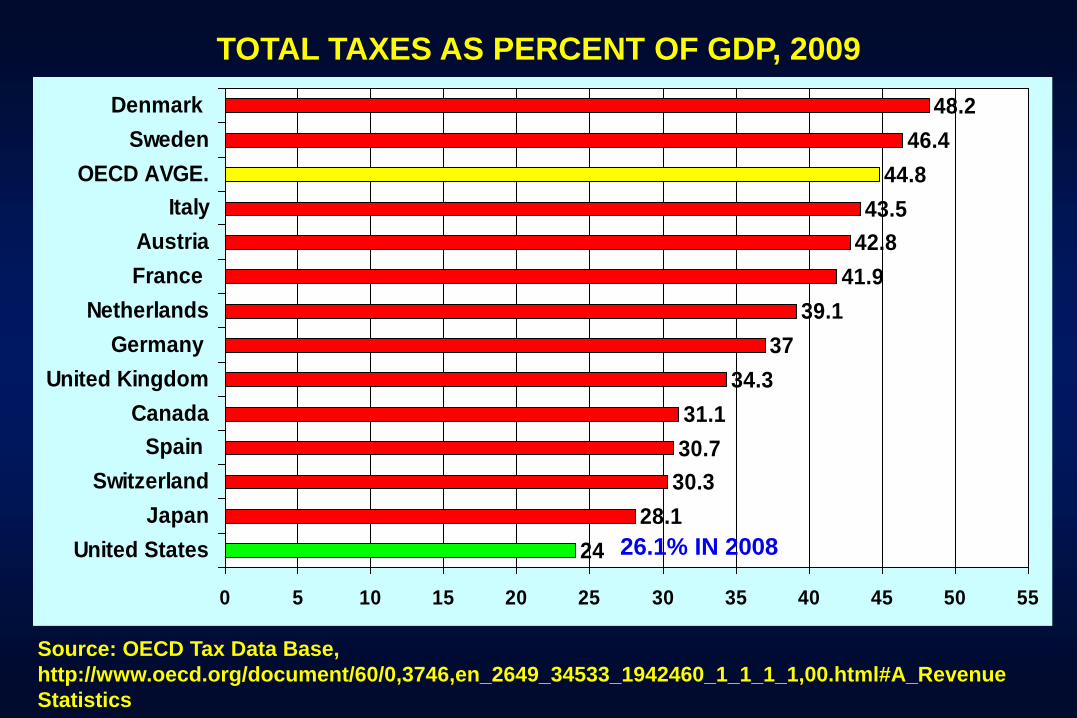

OECD data on taxation became available.

It shows the sum of taxes of all forms levied at all levels of

government as a percentage of GDP.

Unbeknownst it seems to many commentator5s in the US,

Americans actually are not heavily taxed by international

standards.

24

28.1

30.3

30.7

31.1

34.3

37

39.1

41.9

42.8

43.5

44.8

46.4

48.2

0 5 10 15 20 25 30 35 40 45 50 55

United States

Japan

Switzerland

Spain

Canada

United Kingdom

Germany

Netherlands

France

Austria

Italy

OECD AVGE.

Sweden

Denmark

Source: OECD Tax Data Base,

http://www.oecd.org/document/60/0,3746,en_2649_34533_1942460_1_1_1_1,00.html#A_Revenue

Statistics

TOTAL TAXES AS PERCENT OF GDP, 2009

26.1% IN 2008

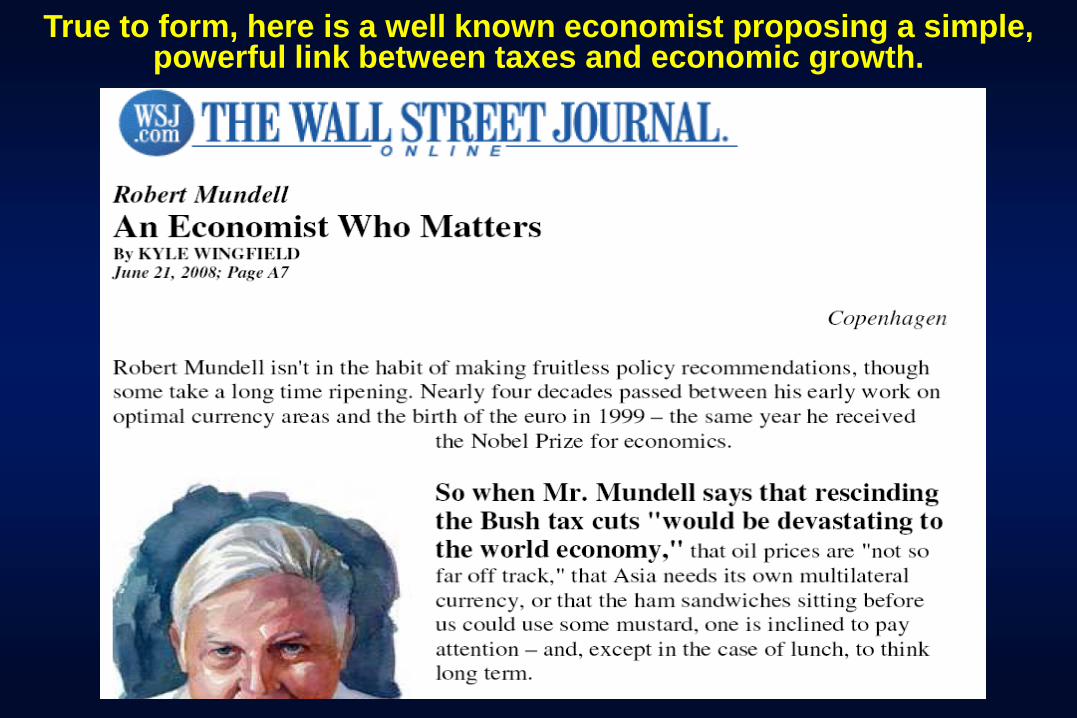

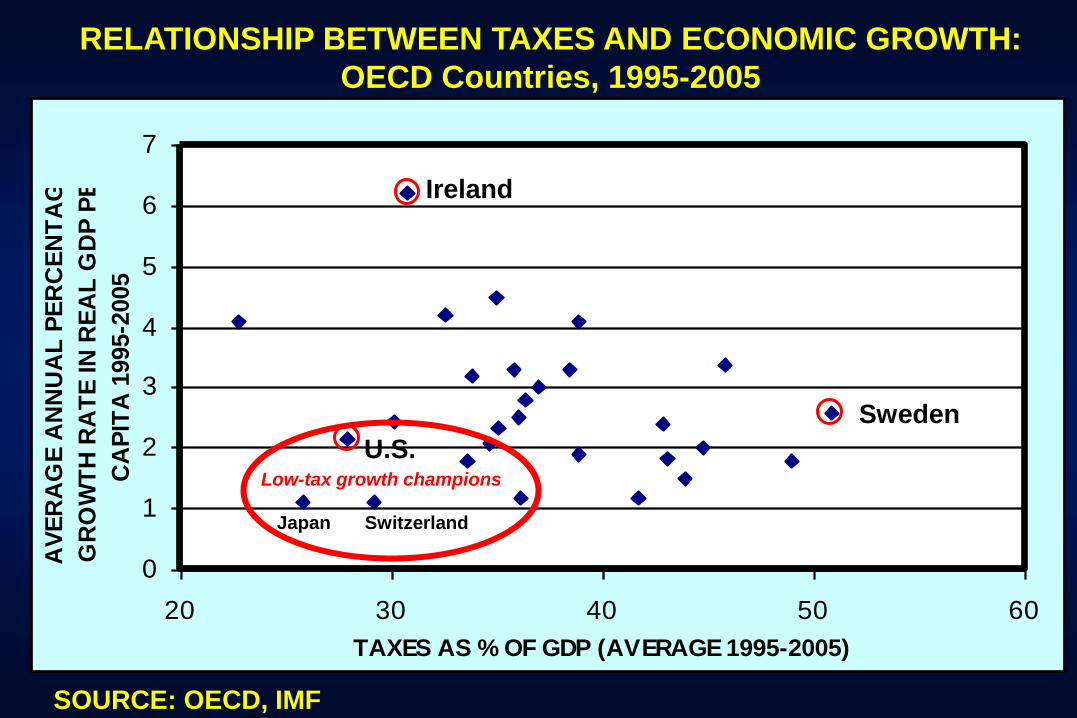

If one looks at the relationship between tax rates and economic

growth across entire economies in the OECD countries, that

relationship is not nearly as apparent as economist Mundell

would have us believe.

True to form, here is a well known economist proposing a simple, powerful link between taxes and economic growth.

0

1

2

3

4

5

6

7

20 30 40 50 60

TAXES AS % OF GDP (AVERAGE 1995-2005)

AV

ER

AG

E A

NN

UA

L P

ER

CE

NT

AG

E

GR

OW

TH

RA

TE

IN

RE

AL

GD

P P

ER

CA

PIT

A 1

995-2

005

Ireland

U.S.

Sweden

SOURCE: OECD, IMF

RELATIONSHIP BETWEEN TAXES AND ECONOMIC GROWTH:

OECD Countries, 1995-2005

Switzerland Japan

Low-tax growth champions

SOURCE: OECD, Statistics Brief No. 7, December 2003, http://www.oecd.org/dataoecd/5/11/22413472.pdf

TAKE-AWAY MESSAGE

1. Economists know that macro-economic magnitudes -- such as

GDP, total savings and total investment, etc., -- are driven by

numerous variables among which the tax-rate is only one.

2. Therefore, one cannot explain the changes in these variables

over time just by levels of tax rates, any more than one can

predict what will happen to the economy when tax-rates are

lowered or increased.

3. Note, for example, that the fraction of GDP devoted to non-

residential investment rose steadily over the Clinton era, in

spite of the tax increases he successfully urged on the

Congress and in fell since 2001, after the huge 2001-03 tax cuts.

TAKE-AWAY MESSAGE continued

4. All economists can do is theorize what might happen to these

macro-economic variables if tax rates were changed and

everything else did not change (the “ceteris paribus” clause in

Econ 101.)

5. Unfortunately, empirical research on what might happen under

such mental experiments remain controversial and are all over

the map among economists.

6. Sadly, quite often such empirical research itself is strongly

influenced by the ideological bent of the researching economist.

F. How was investment (I) in the U.S. financed?

Having looked at the time path of private investment in the U.S.,

let us now examine the sources of funds used to finance these

investments, to wit:

1. Private U.S. saving in the U.S., which consists of

a. personal (household) savings, and

b. savings by business firms

2. Government saving (or dis-saving), that is taxes (T) minus

government spending on goods and services (G)

3. savings by foreigners lent to the US, which is done through the so-

called CURRENT ACCOUNT of the Balance of International

Payments and is defined as “money Americans earn by exporting

U.S. goods and services (X) minus money Americans spent on

imports of foreign-made goods and services” (M).”

The first two items represent Total National Domestic Savings.

I = S + (T – G) + (M – X)

Private

Saving

Government

Saving

Capital Flow to

or from Abroad

Private

Investment

Personal Savings

+ Business Savings

(RetainedEarnings)

Taxes, net of transfers

- Gov’t.

Spending on Goods

and Services

Imports of Goods and Services

- Exports of

Goods and

Services

a.k.a. Current Account Deficit

(if M > X) Deficit, if

T < G

THUS, THINK OF THE RIGHT-HAND SIDE OF THE EQUATION:

TOTAL U.S. DOMESTIC SAVINGS: S + (T – G)

I = S + (T – G) + (M – X)

Private

Saving

Government

Saving

Capital Flow to

or from Abroad

Private

Investment

Personal Savings

+ Business Savings

(RetainedEarnings)

Taxes, net of transfers

- Gov’t.

Spending on Goods

and Services

Imports of Goods and Services

- Exports of

Goods and

Services

a.k.a. Current Account Deficit

(if M > X) Deficit, if

T < G

THUS, THINK OF THE RIGHT-HAND SIDE OF THE EQUATION:

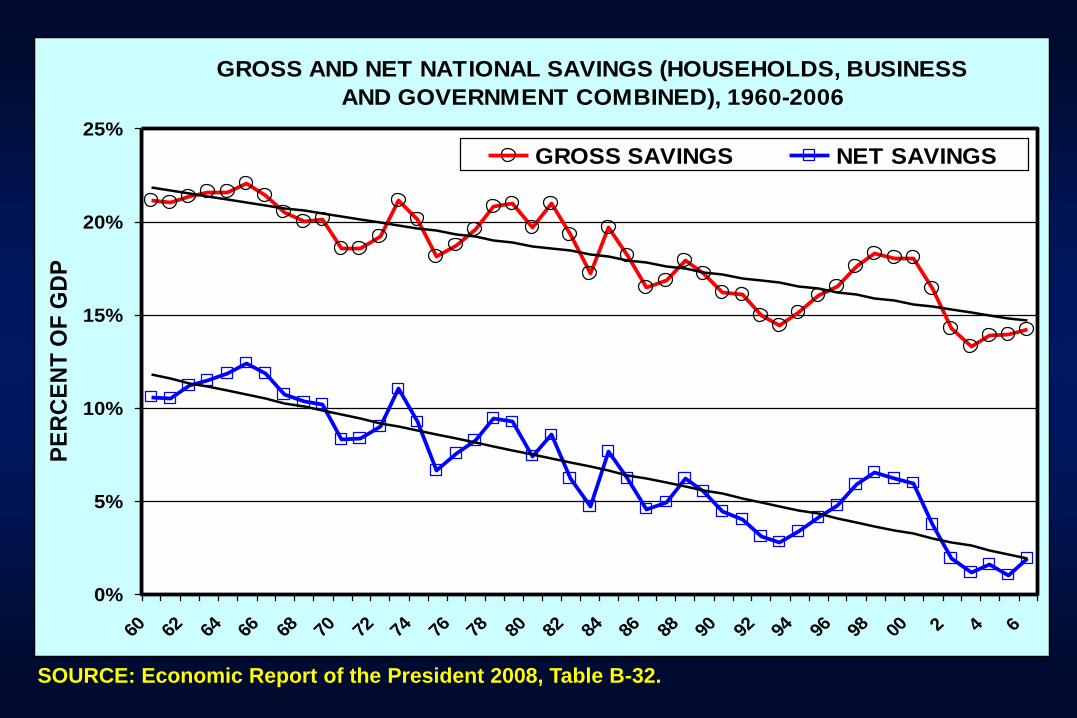

In looking at total domestic (National) U.S. savings, the national

accounts distinguish between

1. Gross National Savings, prior to deducting an allowance for the

wear and tear of capital equipment and structures (also known

as ‘depreciation”), and

2. Net National Savings, which is net of that allowance for the

wear and tear of structures and equipment.

We can think of Net National Savings the nation set aside to put in

place new structures and equipment.

The next slide shows the difference between these two savings

concepts.

GROSS AND NET NATIONAL SAVINGS (HOUSEHOLDS, BUSINESS

AND GOVERNMENT COMBINED), 1960-2006

0%

5%

10%

15%

20%

25%

60 62 64 66 68 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 2 4 6

PE

RC

EN

T O

F G

DP

GROSS SAVINGS NET SAVINGS

SOURCE: Economic Report of the President 2008, Table B-32.

Notice on the preceding slide how, over the long hall, both the

gross- and the net U.S. national savings rate has declined,

although not steadily.

Notice also that, after 1994, both savings rates increased (in

good part because the federal deficit then shrank and turned

into a surplus) and how it fell again after 2000 (in large part

because the federal deficit then began rising again.)

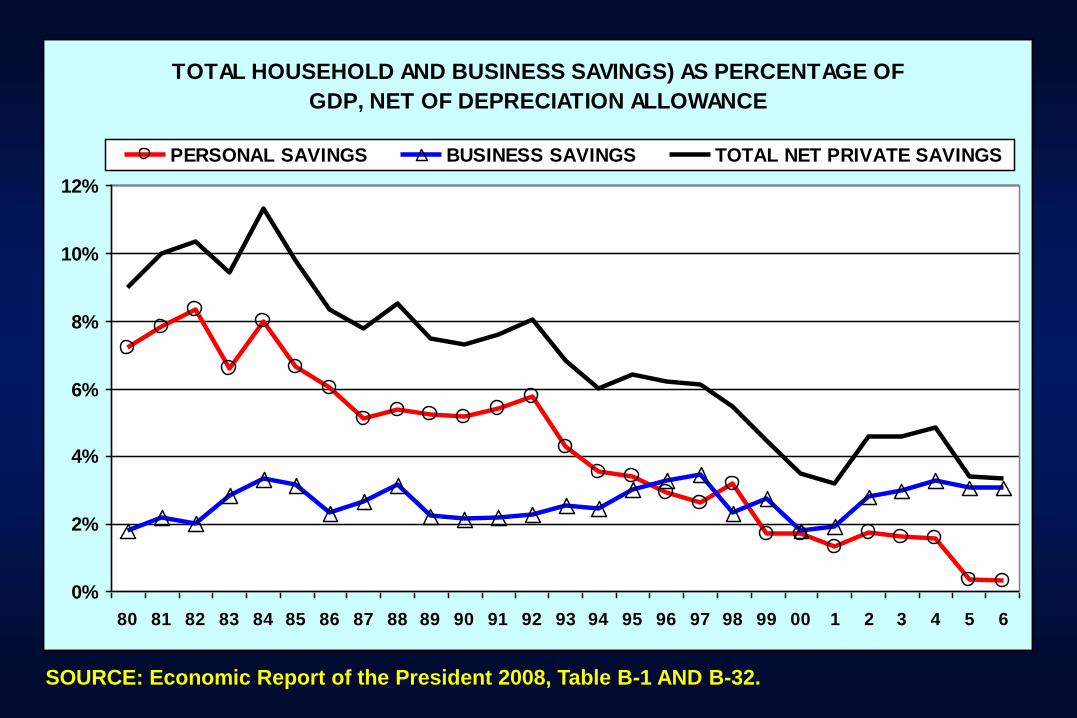

Private Saving (Business and Household) in the U.S. : S

Let us now turn to private savings, S, the first term on the right-

hand side of the equation. We recall that it is the sum of

business savings in the U.S. and of personal (household)

savings.

In the graphs that follows, business savings is on a “net” basis,

that is, excluding a set aside for depreciation. In other words,

business savings in these graphs represent retained profits

that have been reinvested in the business sector on behalf of

owners..

I = S + (T – G) + (M – X)

Private

Saving

Government

Saving

Capital Flow to

or from Abroad

Private

Investment

Personal Savings

+ Business Savings

(RetainedEarnings)

Taxes, net of transfers

- Gov’t.

Spending on Goods

and Services

Imports of Goods and Services

- Exports of

Goods and

Services

a.k.a. Current Account Deficit

(if M > X) Deficit, if

T < G

THUS, THINK OF THE RIGHT-HAND SIDE OF THE EQUATION:

SOURCE: Economic Report of the President 2008, Table B-1 AND B-32.

TOTAL HOUSEHOLD AND BUSINESS SAVINGS) AS PERCENTAGE OF

GDP, NET OF DEPRECIATION ALLOWANCE

0%

2%

4%

6%

8%

10%

12%

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 1 2 3 4 5 6

PERSONAL SAVINGS BUSINESS SAVINGS TOTAL NET PRIVATE SAVINGS

SOURCE: Economic Report of the President 2008, Table B-1 AND B-32.

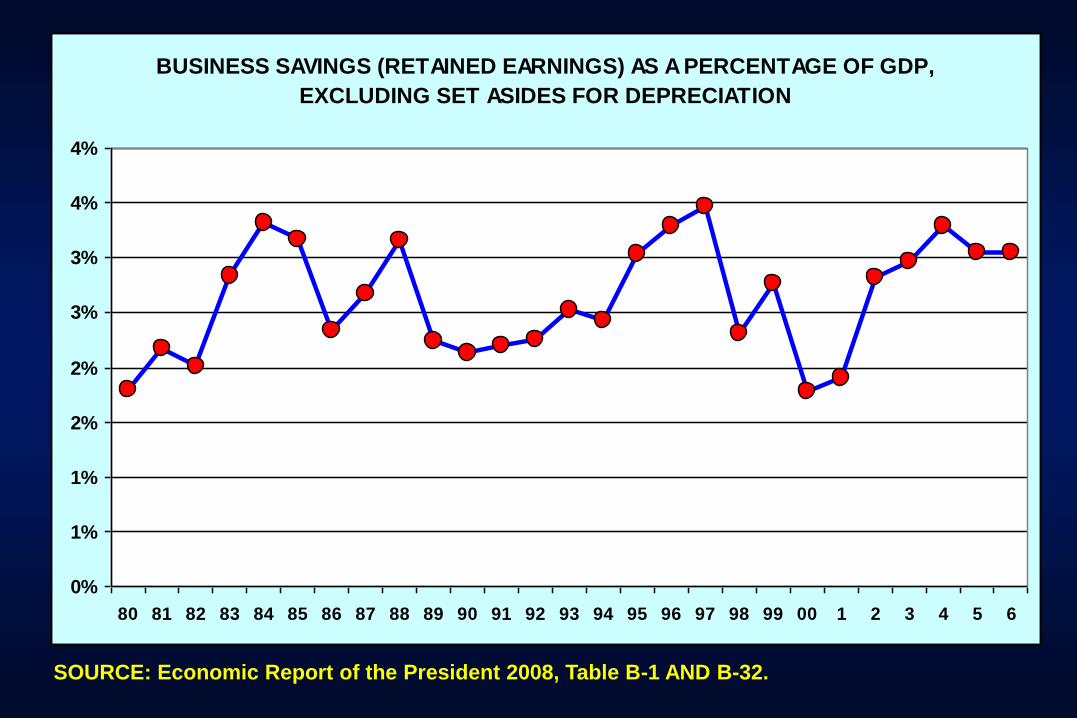

BUSINESS SAVINGS (RETAINED EARNINGS) AS A PERCENTAGE OF GDP,

EXCLUDING SET ASIDES FOR DEPRECIATION

0%

1%

1%

2%

2%

3%

3%

4%

4%

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 1 2 3 4 5 6

SOURCE: Economic Report of the President 2008, Table B-1 AND B-32.

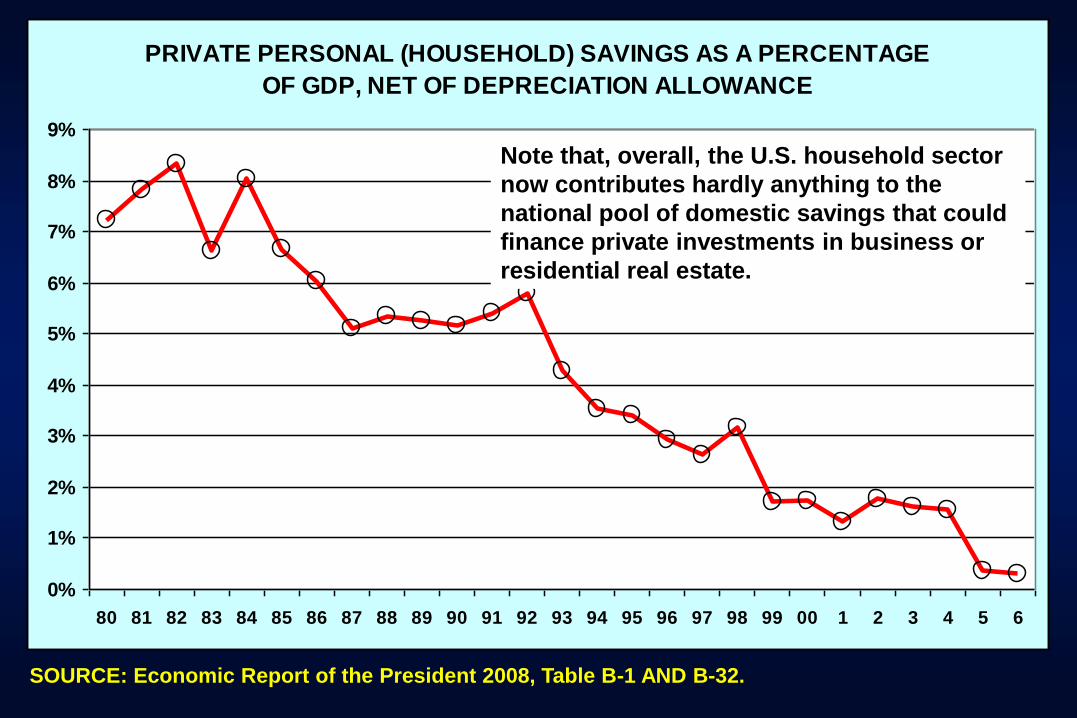

PRIVATE PERSONAL (HOUSEHOLD) SAVINGS AS A PERCENTAGE

OF GDP, NET OF DEPRECIATION ALLOWANCE

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 1 2 3 4 5 6

Note that, overall, the U.S. household sector

now contributes hardly anything to the

national pool of domestic savings that could

finance private investments in business or

residential real estate.

OBSERVATION ON HOUSEHOLD SAVINGS:

1. Apparently completely exhausted from the travails of our parents –

the hard fighting, hard-working, hard-saving-and-investing WWII

generation – we, the Baby Boom generation, decided that we

deserved a break in the form of a huge consumption binge. Thus we

invented credit cards, stopped saving (see the red line in the

previous graph), and gave ourselves huge tax cuts, borrowing

abroad to fund the resulting federal government deficits.

2. Next, we gave our children – among them you, the Class of 2000 and

your peers – free iPods, computers and toys like that, hoping you

would remain other-world-oriented and not notice that your parents

where having a ball on credit that you young ones will have to pay

back later on. It has been, like, a truly cool policy (for your parents).

“Tant pis pour vous,” as the French would put it. You deserve that

sorry fate for your attention deficit in this matter.

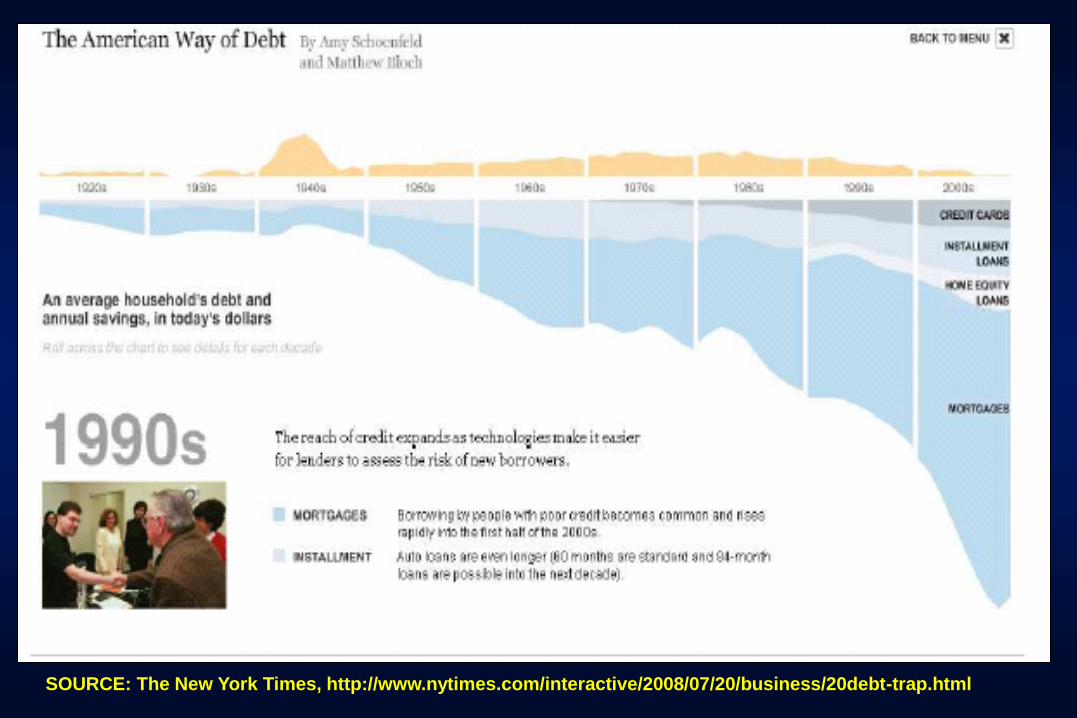

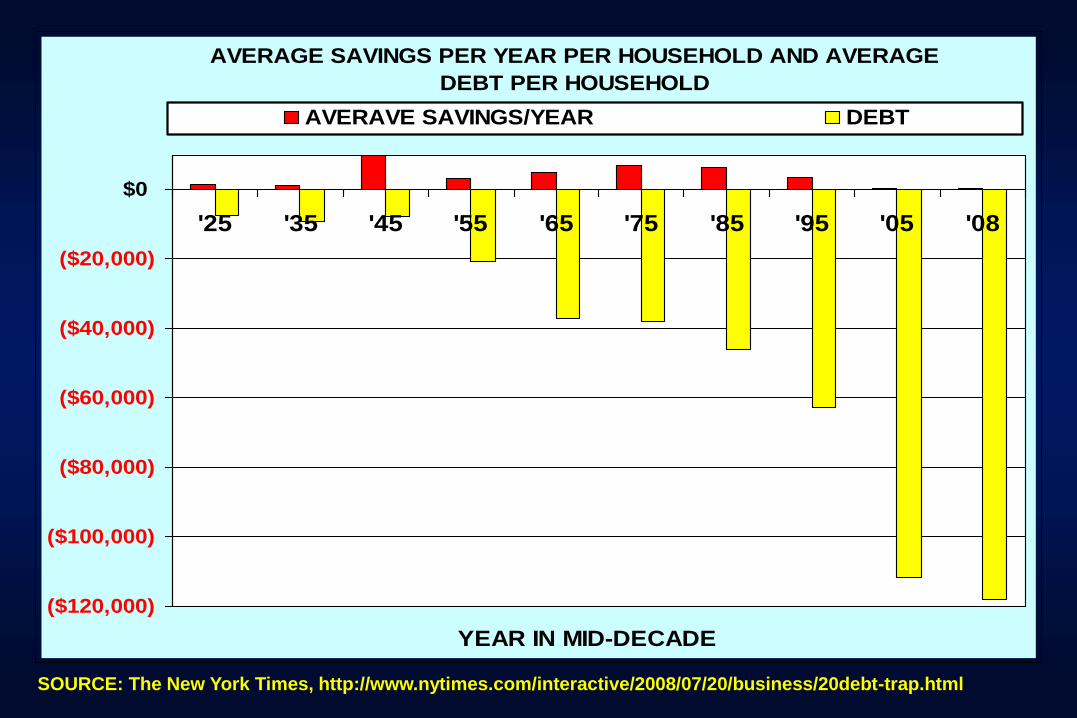

July 20, 2008: I add ex post two additional and revealing slides

on the financial position of U.S. households, taken from a

report in The New York Times, July 20, 2008

Apparently, much of the savings Americans traditionally had in

their homes was tapped through second mortgages to finance

additional consumption.

SOURCE: The New York Times, http://www.nytimes.com/interactive/2008/07/20/business/20debt-trap.html

SOURCE: The New York Times, http://www.nytimes.com/interactive/2008/07/20/business/20debt-trap.html

AVERAGE SAVINGS PER YEAR PER HOUSEHOLD AND AVERAGE

DEBT PER HOUSEHOLD

($120,000)

($100,000)

($80,000)

($60,000)

($40,000)

($20,000)

$0

'25 '35 '45 '55 '65 '75 '85 '95 '05 '08

YEAR IN MID-DECADE

AVERAVE SAVINGS/YEAR DEBT

Next, let us look a government savings -- Tax Revenue (T) minus

Government Expenditures on Goods and Services (G) in the

equation. Together, the management of T and G is known as

“fiscal policy.”

Because the federal government since 2001 has consistently

spent more than the tax revenue it took in – it consistently ran

deficits – we must think here not of “savings” but of “dis-

savings.”

We shall first look at fiscal policy over the long span 1980 to 2008

and then at fiscal policy since 2001.

Government Savings (mainly Dis-savings) in the U.S. : T - G

NEXT WE LOOK AT GOVERNMENT (DIS)SAVING

I = S + (T – G) + (M – X)

Private

Saving

Government

Saving

Capital Flow to

or from Abroad

Private

Investment

Personal Savings

+ Business Savings

(RetainedEarnings)

Taxes, net of transfers

- Gov’t.

Spending on Goods

and Services

Imports of Goods and Services

- Exports of

Goods and

Services

a.k.a. Current Account Deficit

(if M > X) Deficit, if

T < G

A LITTLE PRIMER ON THE FEDERAL BUDGET

The federal budget comes in two flavors:

1. A budget that excludes the Social Security and Medicare (and yet

other) trust funds (the purple line in the next slide) – moneys that

really are like pension-fund contributions in business. This is

called the “ON BUDGET” budget (the red line in the next slide).

2. A budget that includes these trust funds, called the UNIFIED

budget (the green line in the next slide).

President typically cite only the UNIFIED budget, which seems

less ominous than the ON BUDGET budget when, as has been

the case for decades, annual payments into the trust funds

exceed annual withdrawals from them. In the next slide, I

illustrate these distinctions.

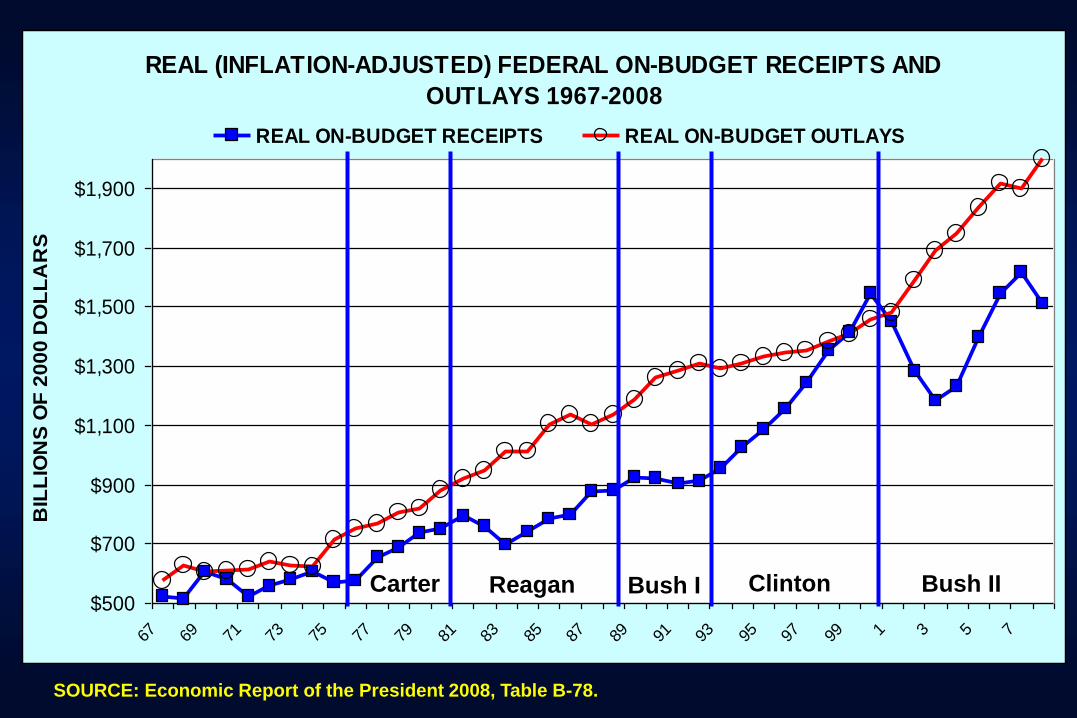

Let us begin by looking at the time path, from 1968 to 2008, of

federal ON-BUDGET receipts and outlays, adjusted for inflation by

the GDP Price Deflator set to 100 for the year 2000 (next slide).

We see that the Reagan-Bush I era does not stand out as one

under which real federal ON-BUDGET spending was under tight

control. It rose apace.

There is, however, a slight downward kink in the real spending line

under the earlier Clinton years.

Note also the large ON-BUDGET federal annual deficits started

under the Reagan years, shrank noticeably under the Clinton years

(and even turned into a surplus), but grew again under the Bush II

years.

SOURCE: Economic Report of the President 2008, Table B-78.

REAL (INFLATION-ADJUSTED) FEDERAL ON-BUDGET RECEIPTS AND

OUTLAYS 1967-2008

$500

$700

$900

$1,100

$1,300

$1,500

$1,700

$1,900

67 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 1 3 5 7

BIL

LIO

NS

OF

20

00

DO

LL

AR

S

REAL ON-BUDGET RECEIPTS REAL ON-BUDGET OUTLAYS

Carter Reagan Bush I Clinton Bush II

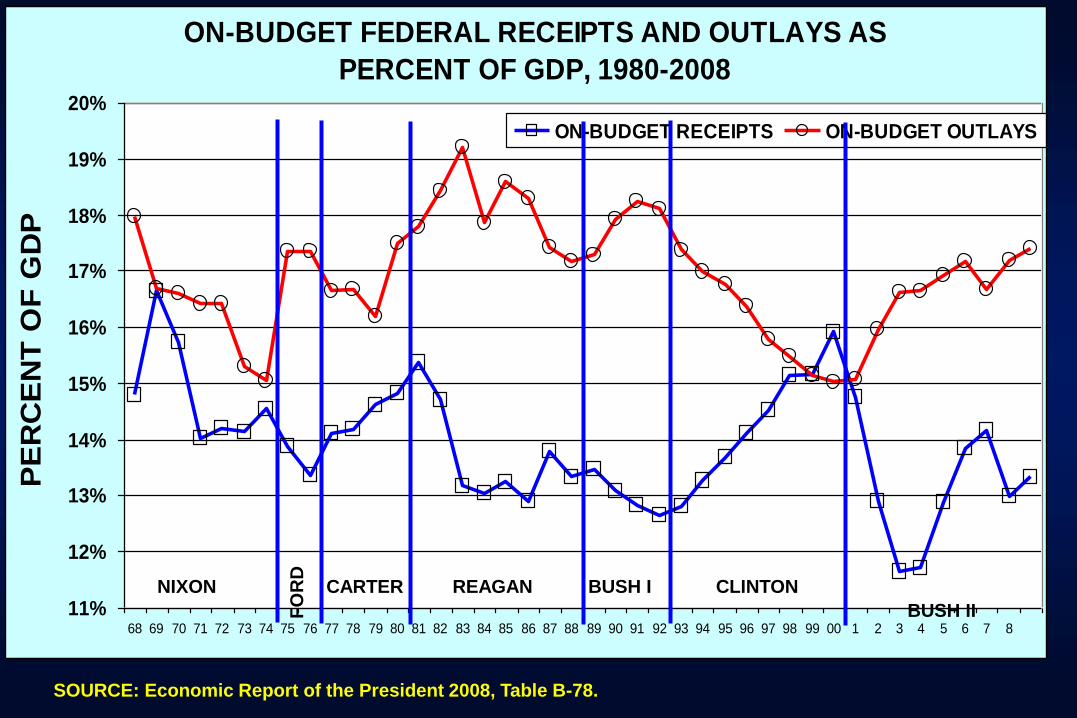

An alternative way of beholding federal fiscal policy is to

express both receipts and outlays as a percentage of GDP,

which is done in the next slide.

We see that federal ON-BUGDET receipts (i.e., excluding Social

Security and Medicare Trust Fund contributions) fell below 13%

of GDP in the Reagan-Bush I years but rose again sharply in the

Clinton years.

By contrast, federal ON-BUDGET spending was high in the

Reagan-Bush I era, certainly relative to the Carter and Clinton

years.

SOURCE: Economic Report of the President 2008, Table B-78.

ON-BUDGET FEDERAL RECEIPTS AND OUTLAYS AS

PERCENT OF GDP, 1980-2008

11%

12%

13%

14%

15%

16%

17%

18%

19%

20%

68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 1 2 3 4 5 6 7 8

PE

RC

EN

T O

F G

DP

ON-BUDGET RECEIPTS ON-BUDGET OUTLAYS

NIXON CARTER

FO

RD

REAGAN BUSH I

BUSH II

CLINTON

10%

12%

14%

16%

18%

20%

22%

24%

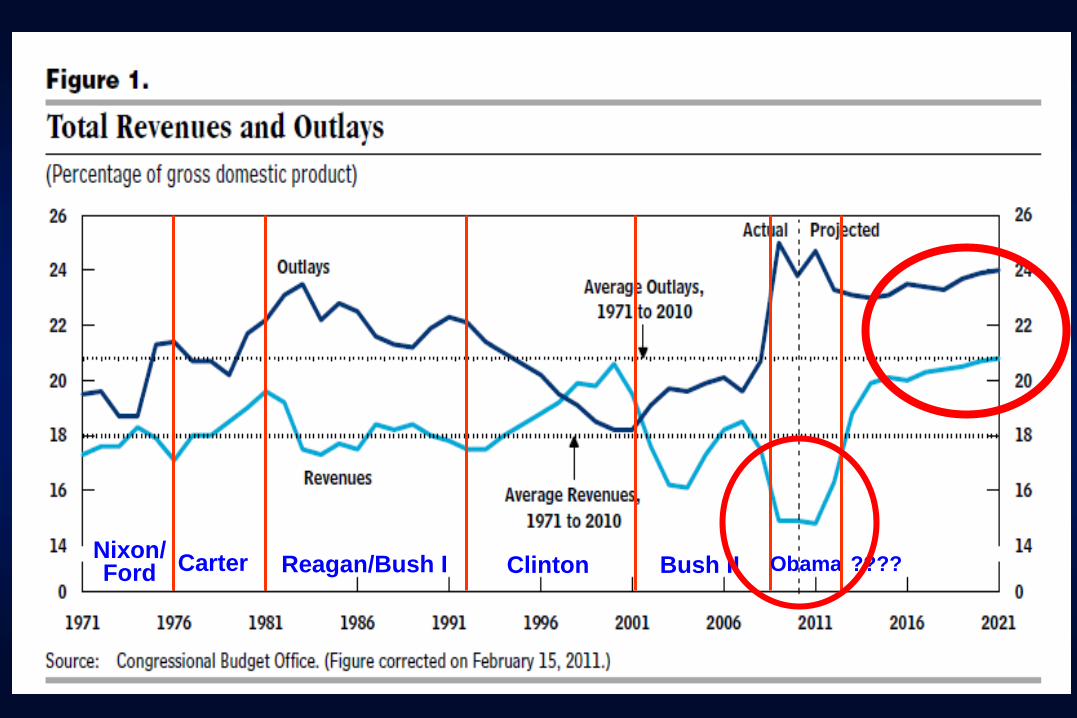

68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 0 1 2 3 4 5 6 7 8 9 10

ON-BUDGET RECEIPTS ON-BUDGET OUTLAYS

FEDERAL RECEIPTS AND OUTLAYS AS A PERCENT OF GDP, 1968 – 2010

(Excludes the Social Security and Medicare Trust Fund Operations)

Nixon Fo

rd

Carter Reagan Bush I Clinton Bush II Ob

am

a

SOURCE: Economic Report of the President 2010, Table B-78.

The next 2 slides were added to the 2008 talk in early 2012.

They make two points:

Our major federal-debt addiction – and that is what it is – started in

the early 1980s. Over that decade our gross federal debt

quadrupled.

The current debt crisis is a combination of higher spending as a

percent of GDP and of lower taxes as a percent of GDP.

Furthermore, over 2008—2009, GDP actually FELL by over $400

billion, which would have driven up the Spending/GDP ratio even if

spending had remained constant.

U.S.FEDERAL GROSS DEBT 1980-2011

$909

$2,600

$4,000

$5,600

$9,986

$15,000

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

1980 1988 1992 2000 2008 2011

SOURCE: Economic Report of the President 2011, Table B78.

Reagan/Bush I Clinton Bush II Obama Carter Nixon/Ford ????

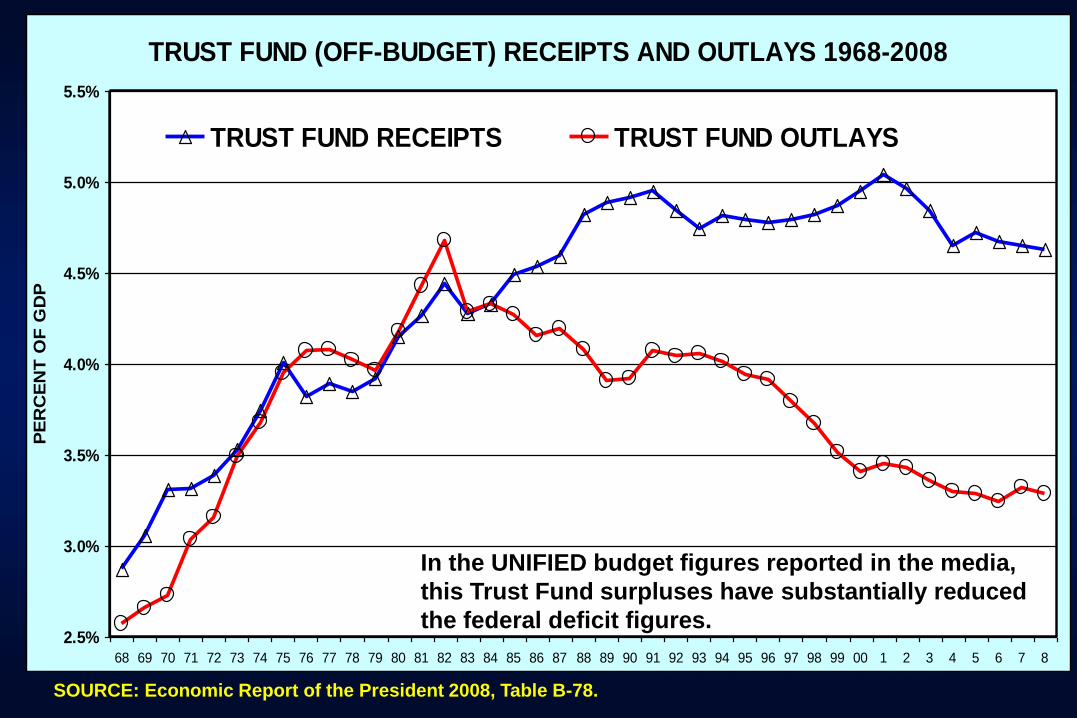

Finally, for good measure I show the time path of contributions to

and withdrawals from the Social Security-, Medicare- and other

trust funds.

We see that these trust funds developed large surpluses, starting

in the Reagan era (in response to the Greenspan report on Social

Security).

SOURCE: Economic Report of the President 2008, Table B-78.

TRUST FUND (OFF-BUDGET) RECEIPTS AND OUTLAYS 1968-2008

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 1 2 3 4 5 6 7 8

PE

RC

EN

T O

F G

DP

TRUST FUND RECEIPTS TRUST FUND OUTLAYS

In the UNIFIED budget figures reported in the media,

this Trust Fund surpluses have substantially reduced

the federal deficit figures.

Finally, the next slide shows how the time paths of federal receipts

and spending reflect themselves in the size of the annual federal

deficits or surpluses over time, both on an ON-BUDGET and

UNIFIED BUDGET basis. We see that these trust funds developed

large surpluses, starting in the Reagan era.

Note how much larger the ON-BUDGET deficit is than the UNIFIED

DEFICIT that is reported by the Administration and in the press.

For example, in 2004 the reported UNIFIED federal budget deficit

was $413 billion, while the ON-BUDGET deficit, excluding the trust

fund surpluses of $152 billion, was $568 billion.

Alert journalists would report all of these numbers and explain

them to the public.

THE FEDERAL SURPLUS (DEFICIT) 1980 - 2009

$(650)

$(550)

$(450)

$(350)

$(250)

$(150)

$(50)

$50

$150

$250

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 1 2 3 4 5 6 7 8 9

ON-BUDGET TRUST FUNDS UNIFIED BUDGET

SOURCE: Economic Report of the President 2008, Table B-78.

Bush I Bush II Reagan Clinton

As the previous slide shows, the ON BUDGET deficit is much

larger than the UNIFIED budget deficit.

Imagine if had had routinely invested the Social Security and

Medicare Trust Fund surpluses in a diversified portfolio of foreign

assets. Then, in the future, instead of paying people in Japan,

China and Dubai interest on the US Treasury bonds we sold them

and paying back those bonds, our children would face lower

taxes because these foreign citizens would pay our children

interest and profits and repaid debt. Alas, for our children, we

spend the Trust Fund surpluses on routine government

operations (G) and borrowed billions on top of it from abroad.

For fiscal year 2004, for example, the White House and the press

would have been talking about a deficit of roughly $400 billion,

when the true federal budget deficit was in excess of $550 billion.

Federal fiscal policy in recent years

At the beginning of 2001, the Congressional Budget Office (CBO)

projected a sizeable cumulative federal budget surplus for the

decade 2001-2010, based on tax- and revenue-trends and the

budget surpluses that had been achieved in the latter half of the

1990s.

The media spoke and wrote about a cumulative projected surplus

of $5.6 trillion for 2001-10; but $2.5 trillion of that surplus

represented cumulative projected surpluses in the Social

Security and Medicare trust funds, so that the cumulative federal

operating surplus (the so-called “on-budget” surplus) was only

$3.1 trillion (see next slide).

As noted, in principle, the Social Security surplus should have

been invested and not been spent as if it were spendable annual

operating revenue.

SOURCE: Congressional Budget Office (www.CBO.gov), various dates.

2.5

3.1

0.9

2.5

$0

$1

$2

$3

$4

$5

$6

JAN. 2001 AUG. 2001

TR

ILL

ION

S O

F D

OL

LA

RS

ON-BUDGET SOCIAL SECURITY

CUMULATIVE, PROSPECTIVE 10-YEAR FEDERAL BUDGET

SURPLUS/DEFICIT 2001-2011

Before 9/11 !

$5.6 tr

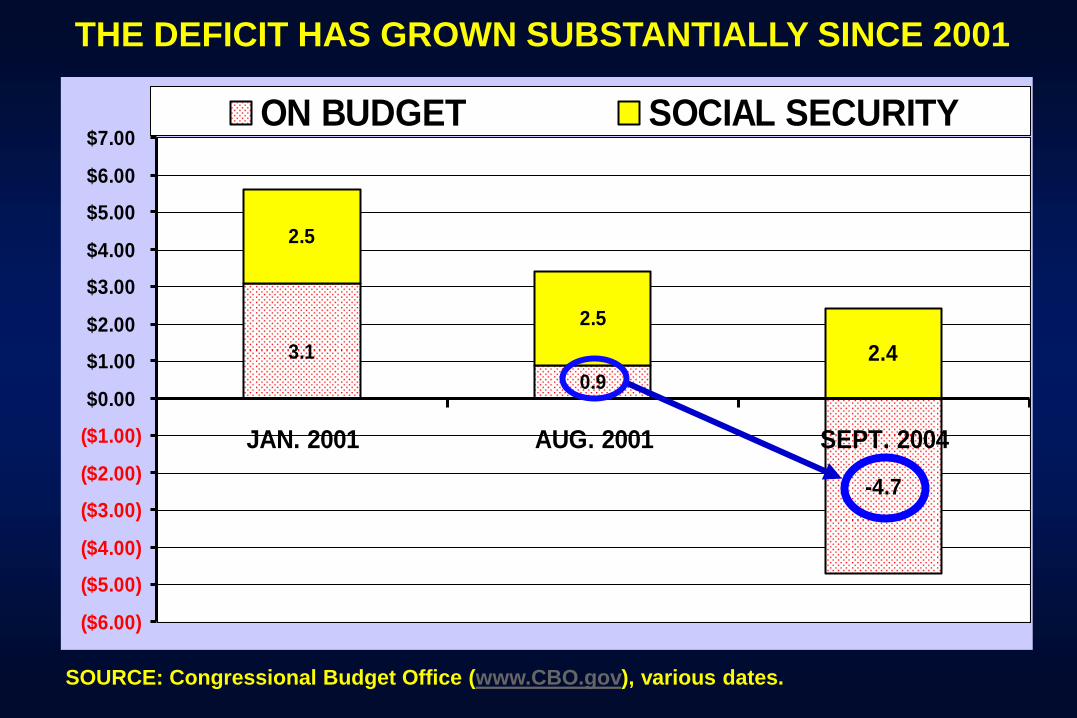

As can be seen in the previous slide, as early as August 1, 2001 –

fully one month before that fateful day of September 11, 2001 –

the operating (“on-budget”) surplus of $3.1 trillion as of the

beginning of 2001 had melted down to only $0.9 trillion, largely

as the result of the massive income-tax cut passed in early 2001.

The next slide shows that by September 2004, that operating

(“on-line” surplus of $09.tr had turned into a projected 10-year

cumulative deficit of $4.7 trillion, as a result of further tax cuts,

added outlays for defense and homeland security and down-

scaled expectations of future economic growth.

By then, even the combined Trust Funds and “on-budget”

budgets – the so-called “unified budget” reported in the media –

had swung into highly negative.

SOURCE: Congressional Budget Office (www.CBO.gov), various dates.

2.5

3.1

-4.7

0.9

2.5

2.4

($6.00)

($5.00)

($4.00)

($3.00)

($2.00)

($1.00)

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

JAN. 2001 AUG. 2001 SEPT. 2004

ON BUDGET SOCIAL SECURITY

THE DEFICIT HAS GROWN SUBSTANTIALLY SINCE 2001

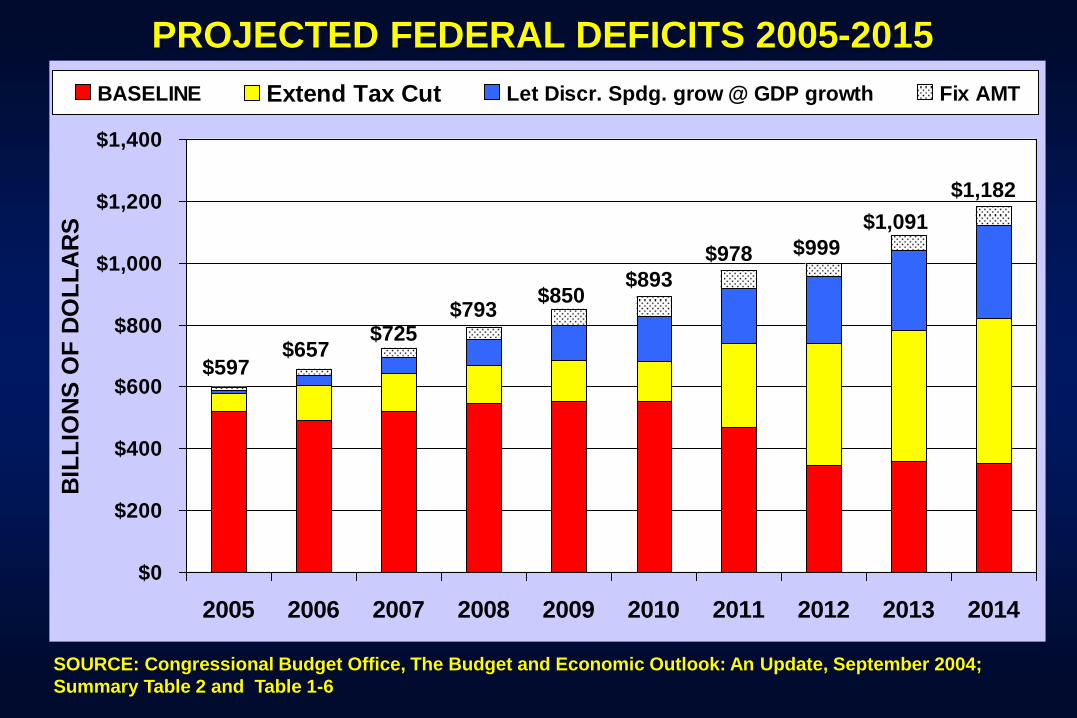

The next two slides show the projected cumulative federal

budget deficits under various assumed scenarios, including an

extension of the Bush tax cuts of 2001 and 2003 beyond 2010,

when the original tax cuts would expire unless they were formally

extended beyond 2010 by legislation.

The next slide shows that by September 2004, that operating

(“on-line” surplus of $09.tr had turned into a projected 10-year

cumulative deficit of $4.7 trillion, as a result of further tax cuts,

added outlays for defense and homeland security and down-

scaled expectations of future economic growth.

By then, even the combined Trust Funds and “on-budget”

budgets – the so-called “unified budget” reported in the media –

had swung into highly negative.

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

BIL

LIO

NS

OF

DO

LL

AR

SBASELINE Extend Tax Cut Let Discr. Spdg. grow @ GDP growth Fix AMT

$597 $657

$725 $793

$850 $893

$978 $999

$1,091

$1,182

SOURCE: Congressional Budget Office, The Budget and Economic Outlook: An Update, September 2004;

Summary Table 2 and Table 1-6

PROJECTED FEDERAL DEFICITS 2005-2015

-$7,832

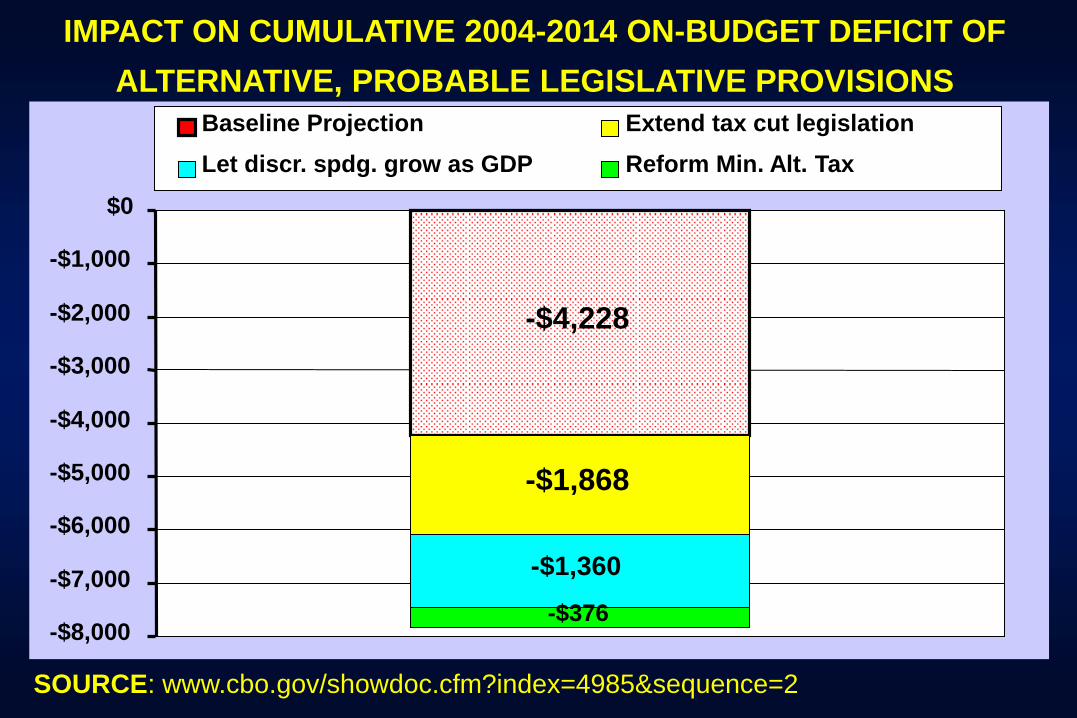

IMPACT ON CUMULATIVE 2004-2014 ON-BUDGET DEFICIT OF

ALTERNATIVE, PROBABLE LEGISLATIVE PROVISIONS

SOURCE: www.cbo.gov/showdoc.cfm?index=4985&sequence=2

-$4,228

-$1,868

-$1,360

-$376 -$8,000

-$7,000

-$6,000

-$5,000

-$4,000

-$3,000

-$2,000

-$1,000

$0

Baseline Projection Extend tax cut legislation

Let discr. spdg. grow as GDP Reform Min. Alt. Tax

Should we have cut personal income taxes or corporate

taxes in 2001?

3. As I have remarked for years in micro-economics course (Econ

100), a much better supply-side policy in 2001 would have been

to use the huge prospective, cumulative ten-year federal budget

surplus that was anticipated in 2001 -- $3.1 trillion, excluding the

Social Security Surplus of $2.5 trillion -- to eliminate once and

for all times the corporate income tax, which mainly falls on

labor in any event and distorts many business decisions.

4. It was a great opportunity missed, which makes me doubt the

sincerity of supply-side school. I believe they are just for

redistributing wealth upwards, rather than genuine economic

growth.

For the sake of completeness, the next slide shows the

time path of the annual state budgets during the longer

period 1980 to 2008.

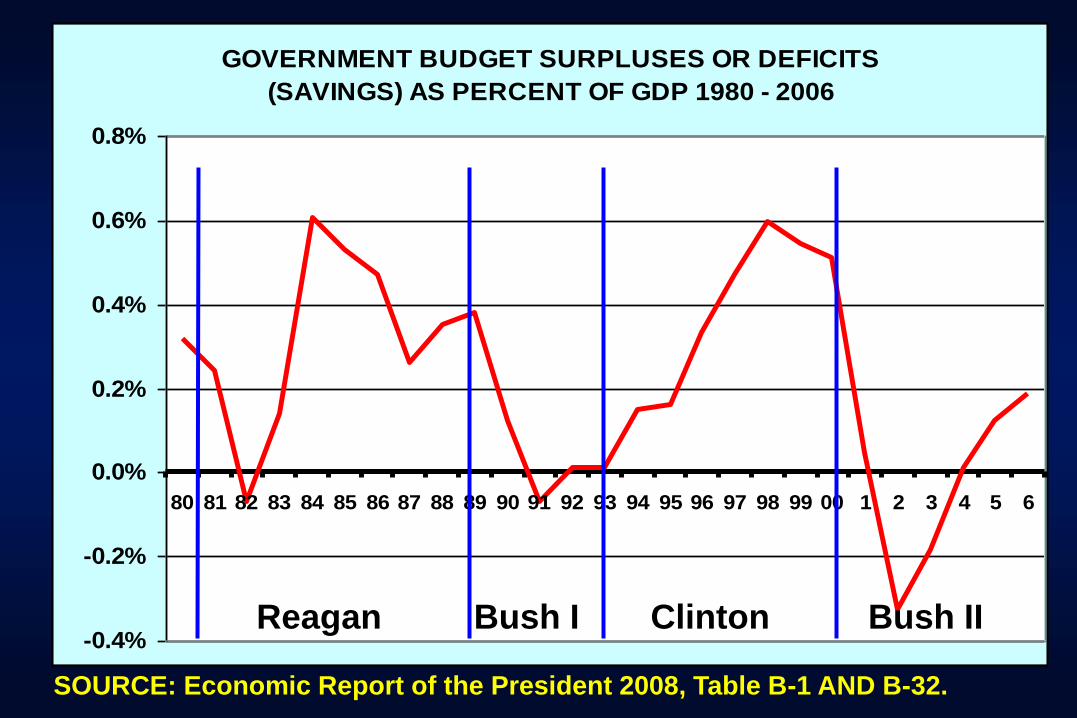

GOVERNMENT BUDGET SURPLUSES OR DEFICITS

(SAVINGS) AS PERCENT OF GDP 1980 - 2006

-0.4%

-0.2%

0.0%

0.2%

0.4%

0.6%

0.8%

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 1 2 3 4 5 6

SOURCE: Economic Report of the President 2008, Table B-1 AND B-32.

Reagan Bush I Clinton Bush II

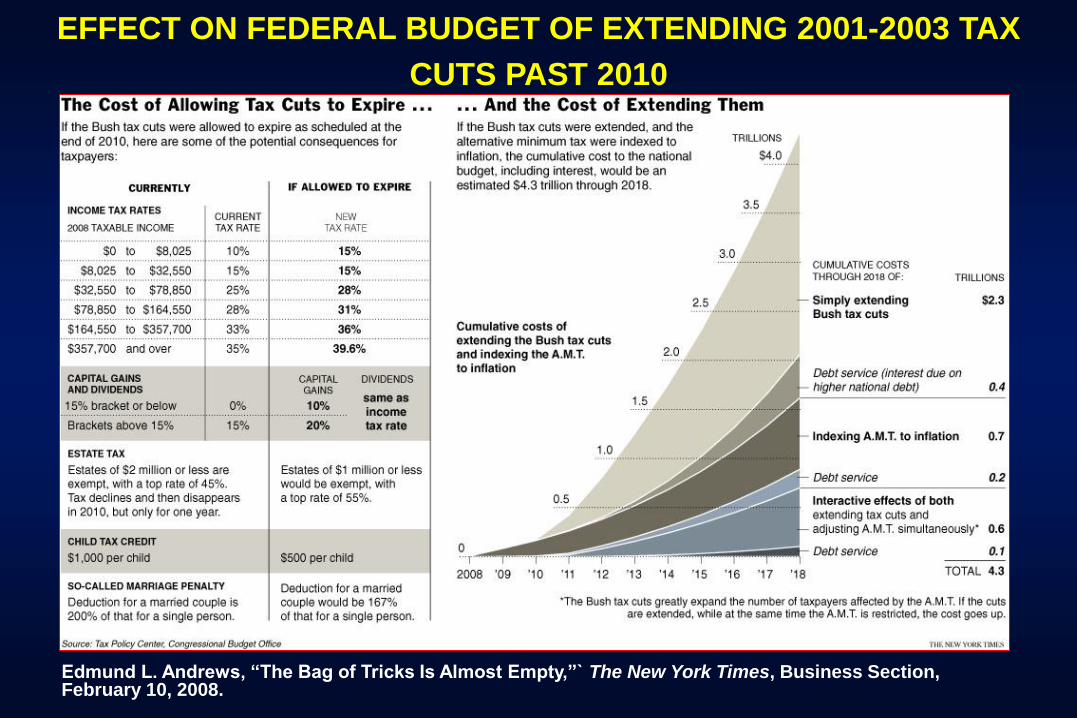

A major question in the upcoming election is whether

the tax cuts enacted in 2001 and 2003 – most of which

were set to expire in 2010-2011 – should be made

permanent.

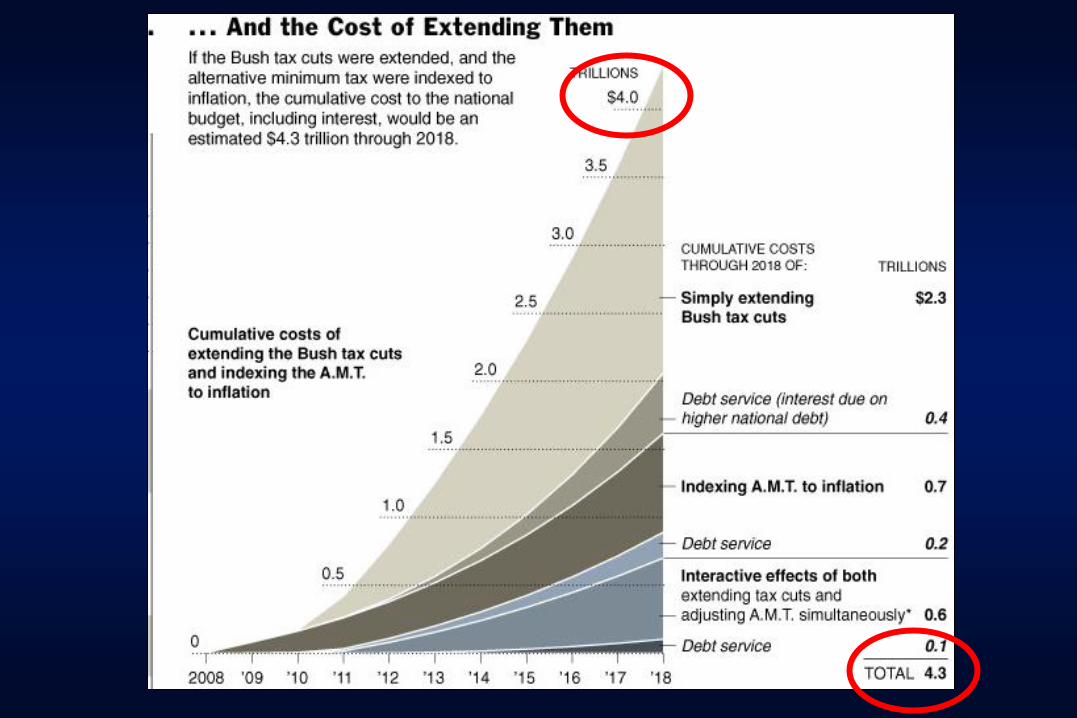

As the next slide, based on Congressional Budget Office

data, shows, extending the tax cuts would add an estimated

$4 trillion to our federal debt.

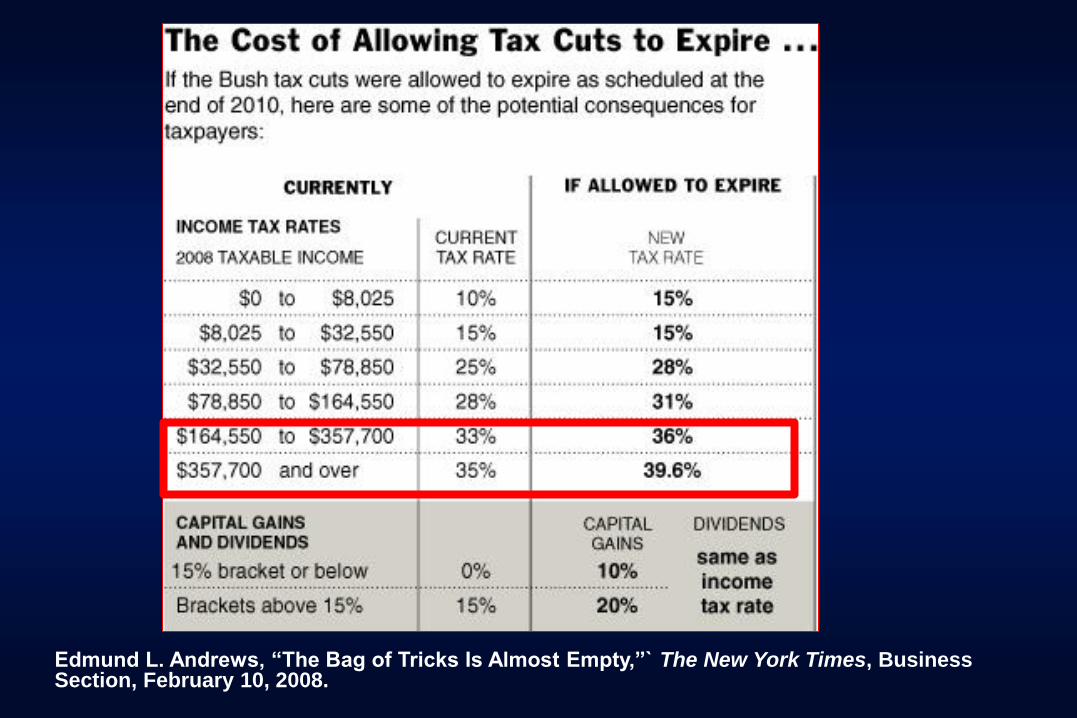

Edmund L. Andrews, “The Bag of Tricks Is Almost Empty,”` The New York Times, Business Section, February 10, 2008.

EFFECT ON FEDERAL BUDGET OF EXTENDING 2001-2003 TAX

CUTS PAST 2010

Edmund L. Andrews, “The Bag of Tricks Is Almost Empty,”` The New York Times, Business Section, February 10, 2008.

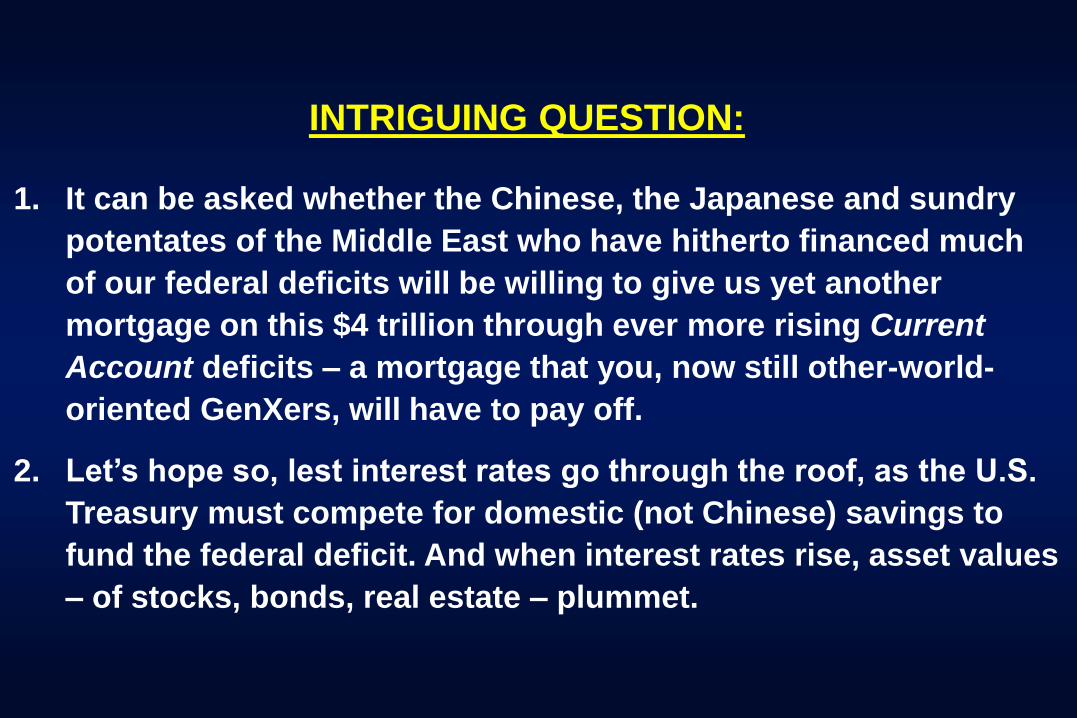

INTRIGUING QUESTION:

1. It can be asked whether the Chinese, the Japanese and sundry

potentates of the Middle East who have hitherto financed much

of our federal deficits will be willing to give us yet another

mortgage on this $4 trillion through ever more rising Current

Account deficits – a mortgage that you, now still other-world-

oriented GenXers, will have to pay off.

2. Let’s hope so, lest interest rates go through the roof, as the U.S.

Treasury must compete for domestic (not Chinese) savings to

fund the federal deficit. And when interest rates rise, asset values

– of stocks, bonds, real estate – plummet.

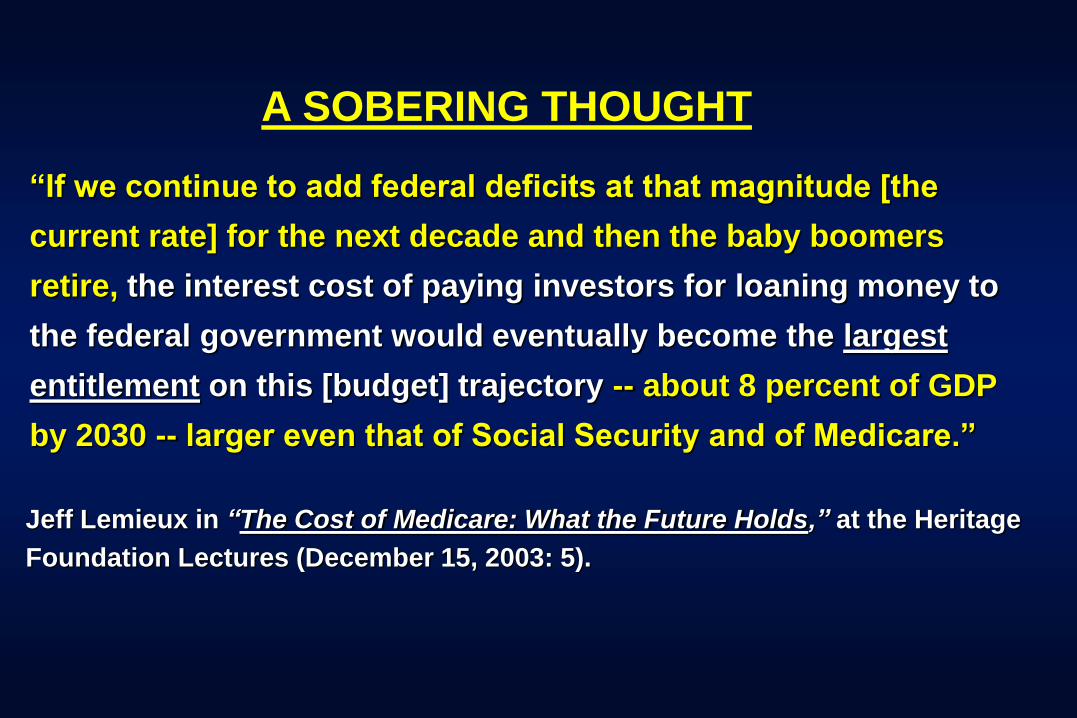

“If we continue to add federal deficits at that magnitude [the

current rate] for the next decade and then the baby boomers

retire, the interest cost of paying investors for loaning money to

the federal government would eventually become the largest

entitlement on this [budget] trajectory -- about 8 percent of GDP

by 2030 -- larger even that of Social Security and of Medicare.”

Jeff Lemieux in “The Cost of Medicare: What the Future Holds,” at the Heritage

Foundation Lectures (December 15, 2003: 5).

A SOBERING THOUGHT

A truly ironic part of this fiscal policy that in the future, foreign

lenders, which hold hundreds of billions of US Treasury bonds, will

have a prior claim on US tax dollars -- prior even to America’s

children and elderly.

It is ironic that Communist China is now helping to finance our

Baby Boom party and that, in the future, China’s entitlement to

being paid interest and repaid principal on that debt by us stands

ahead of the claims America’s children and aged might make on

the U.S. Treasury?

Cool! They hooked us on opium; we’ll hook them on credit.

Importing the savings of foreigners to help finance

consumption and investment in the United States.

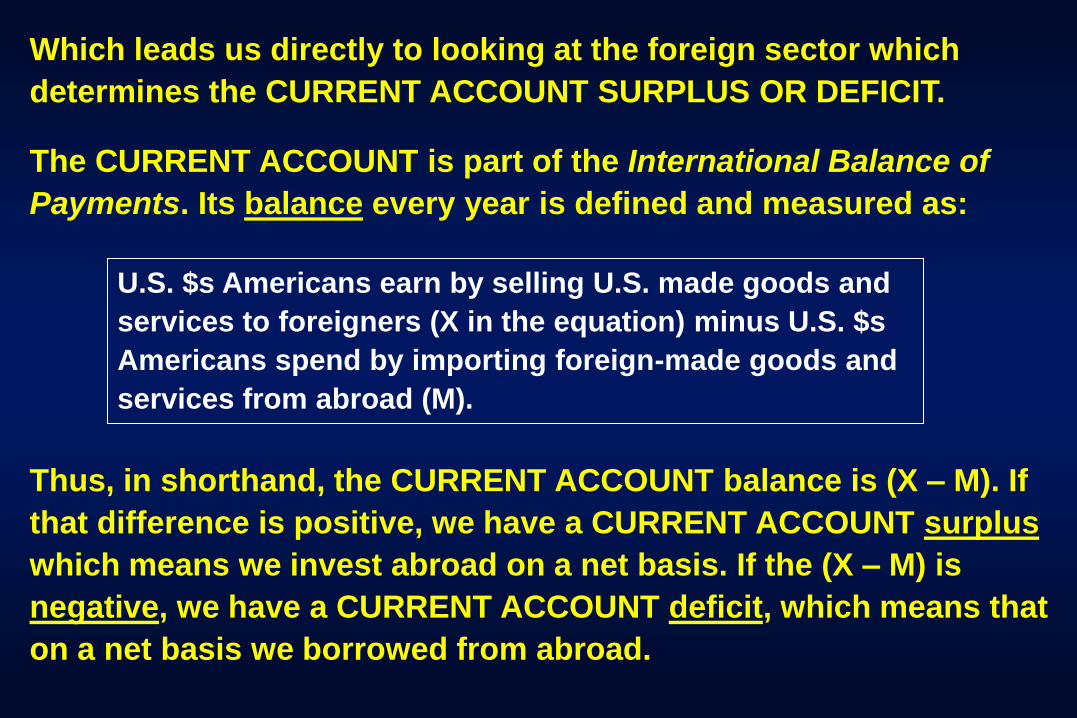

Which leads us directly to looking at the foreign sector which

determines the CURRENT ACCOUNT SURPLUS OR DEFICIT.

Thus, in shorthand, the CURRENT ACCOUNT balance is (X – M). If

that difference is positive, we have a CURRENT ACCOUNT surplus

which means we invest abroad on a net basis. If the (X – M) is

negative, we have a CURRENT ACCOUNT deficit, which means that

on a net basis we borrowed from abroad.

The CURRENT ACCOUNT is part of the International Balance of

Payments. Its balance every year is defined and measured as:

U.S. $s Americans earn by selling U.S. made goods and

services to foreigners (X in the equation) minus U.S. $s

Americans spend by importing foreign-made goods and

services from abroad (M).

FINALLY, LET US LOOK AT THE CURRENT ACCOUNT:

I = S + (T – G) + (M – X)

Private

Saving

Government

Saving

Capital Flow to

or from Abroad

Private

Investment

Personal Savings

+ Business Savings

(RetainedEarnings)

Taxes, net of transfers

- Gov’t.

Spending on Goods

and Services

Imports of Goods and Services

- Exports of

Goods and

Services

a.k.a. Current Account Deficit

(if M > X) Deficit, if

T < G

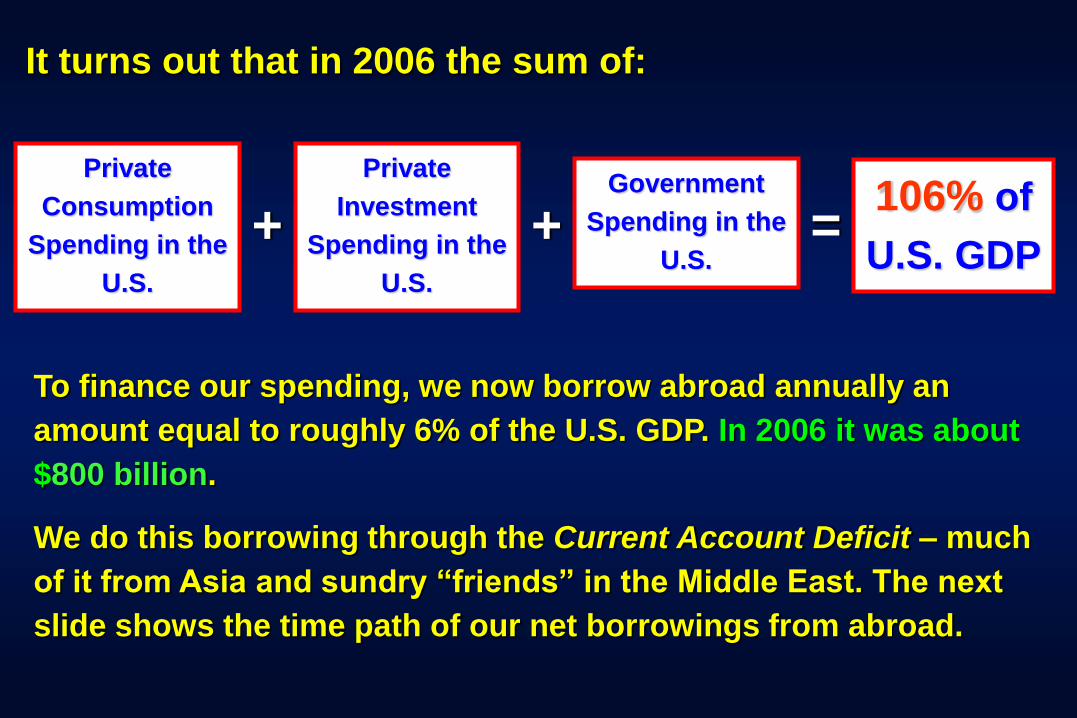

It turns out that in 2006 the sum of:

Private

Consumption

Spending in the

U.S.

Private

Investment

Spending in the

U.S.

+ Government

Spending in the

U.S. + =

106% of

U.S. GDP

To finance our spending, we now borrow abroad annually an

amount equal to roughly 6% of the U.S. GDP. In 2006 it was about

$800 billion.

We do this borrowing through the Current Account Deficit – much

of it from Asia and sundry “friends” in the Middle East. The next

slide shows the time path of our net borrowings from abroad.

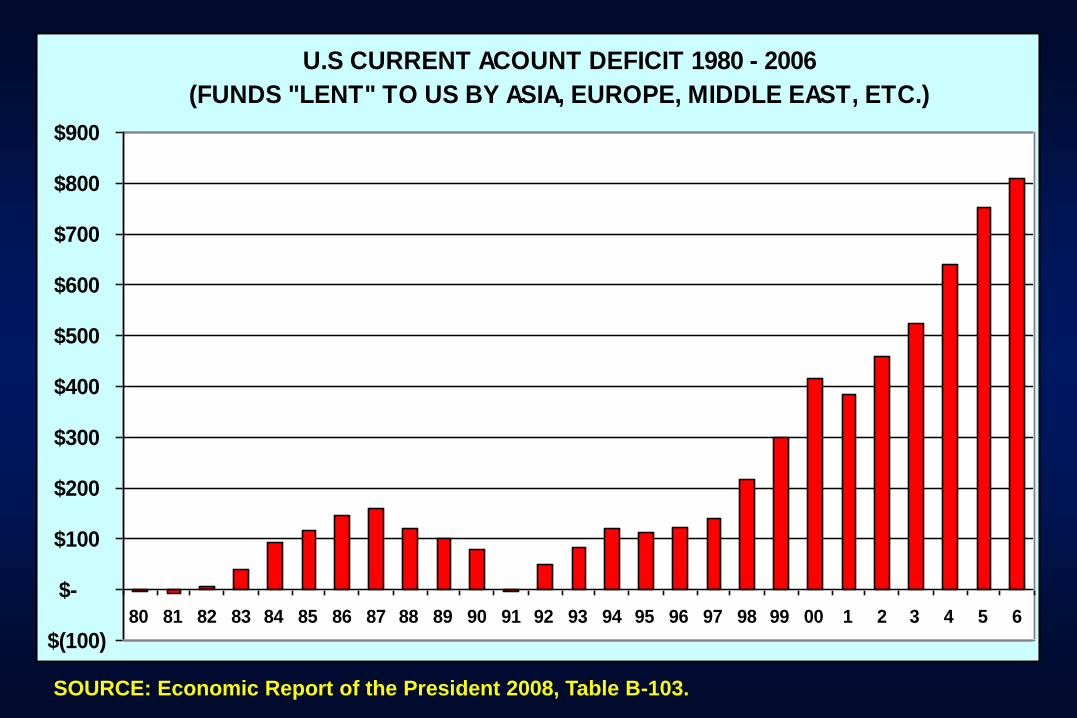

U.S CURRENT ACOUNT DEFICIT 1980 - 2006

(FUNDS "LENT" TO US BY ASIA, EUROPE, MIDDLE EAST, ETC.)

$(100)

$-

$100

$200

$300

$400

$500

$600

$700

$800

$900

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 1 2 3 4 5 6

SOURCE: Economic Report of the President 2008, Table B-103.

INDEBTEDNESS TO FOREIGNERS AND U.S. FOREIGN POLICY

1. The U.S. has long been dependent for energy on nations not

necessarily friendly to us.

2. Increasingly, we also now depend on these nations to finance our

consumption, government spending and private investment in

the U.S.

3. If anyone believes that our heavy reliance on borrowing from

abroad does not hem in our degrees of freedom in foreign policy,

I have some nice ocean-front property in Iowa I’d be happy to sell

them.

INDEBTEDNESS TO FOREIGNERS AND U.S. FOREIGN POLICY

4. For example, we claim to hate dictators who brutally violate

human rights. With our sophisticated drones and laser guided

missiles, we certainly could have persuaded the oppressive junta

ruling Myanmar to free its people from its current oppression. Yet

we did not even attempt to do so.

5. For a clue why it might be so, study the map on the next slide.

6. Chances are that a subtle hint from Beijing discouraged the U.S.

from even thinking about that option, lest China absent itself

from the next auction at which U.S. Treasuries are auctioned off

or shift its portfolio from $s to Euros.

7. We shall never know, but we can guess.

Myanmar is China’s

coveted window to

the Bay of Bengal

THE END