Embed Size (px)

Citation preview

© 2016 Equirus. All rights reserved.

1QFY17 Earnings Preview

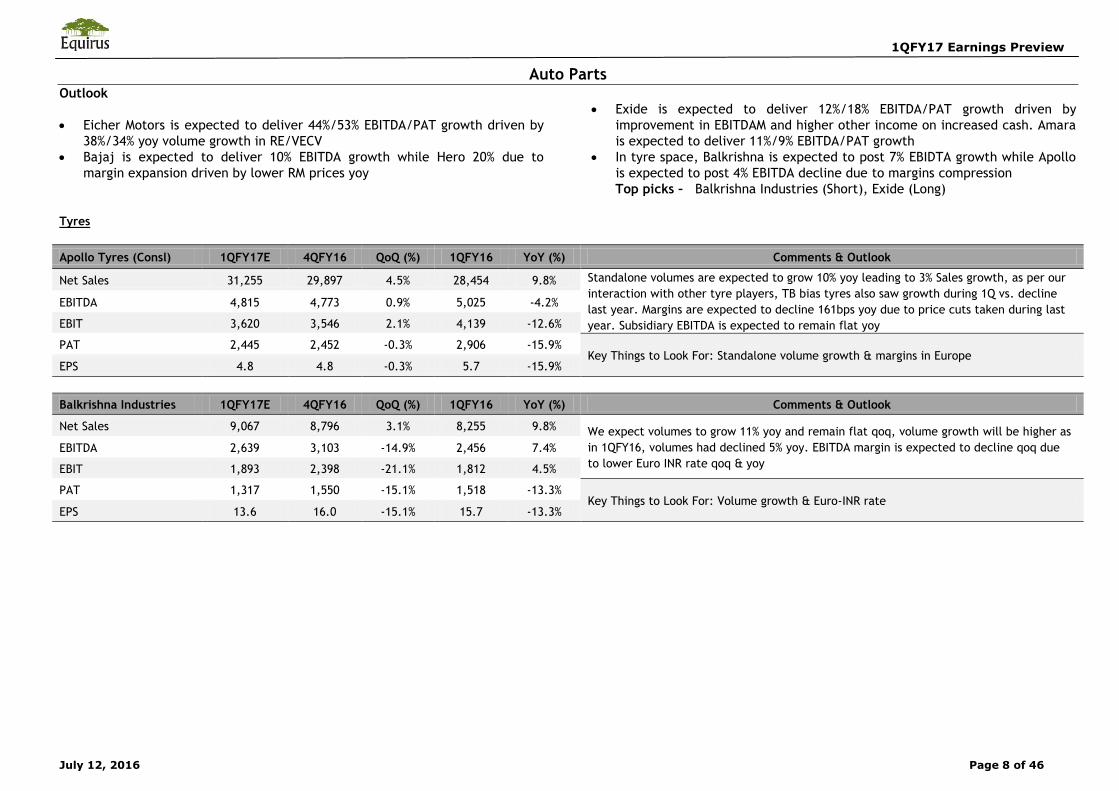

Auto Parts

Eicher Motors is expected to deliver 44%/53% EBITDA/PAT growth driven by

38%/34% yoy volume growth in RE/VECV

Bajaj is expected to deliver 10% EBITDA growth while Hero 20% due to

margin expansion driven by lower RM prices yoy

Exide is expected to deliver 12%/18% EBITDA/PAT growth driven by

improvement in EBITDAM and higher other income on increased cash. Amara

is expected to deliver 11%/9% EBITDA/PA\T growth

In tyre space, Balkrishna is expected to post 7% EBIDTA growth while Apollo

is expected to post 4% EBITDA decline due to margin compression

Capital Goods

We think that cap goods companies would continue to report results in

1QFY17 which would not reflect much change in the stressful conditions as

such. The cap goods and industrials space is struggling because of lack of

ordering activity and except for some select names in a few sub-sectors;

most other companies are finding it difficult to generate enough order flows

and seeing a decline in book to bill ratios. There are a few other things

which happen as a result, a) pressure on profitability, b) deterioration in

working capital cycle, and, c) unwillingness to undertake new investment in

building capacity. It is also important to note that Index of Industrial

Production (IIP) numbers which have been reported are bad (for the month

of April, after March which also reported flat IIP). Three key takeaways from

IIP data, 1) A sharp 3% dip in manufacturing was a clear sentiment dampener

we think, 2) The IIP data has been poor over last few months and this is

certainly not a good sign for recovery, and, 3) even a bad number this

month was possible because of a massive 15% yoy increase in Electricity.

Consumer Goods

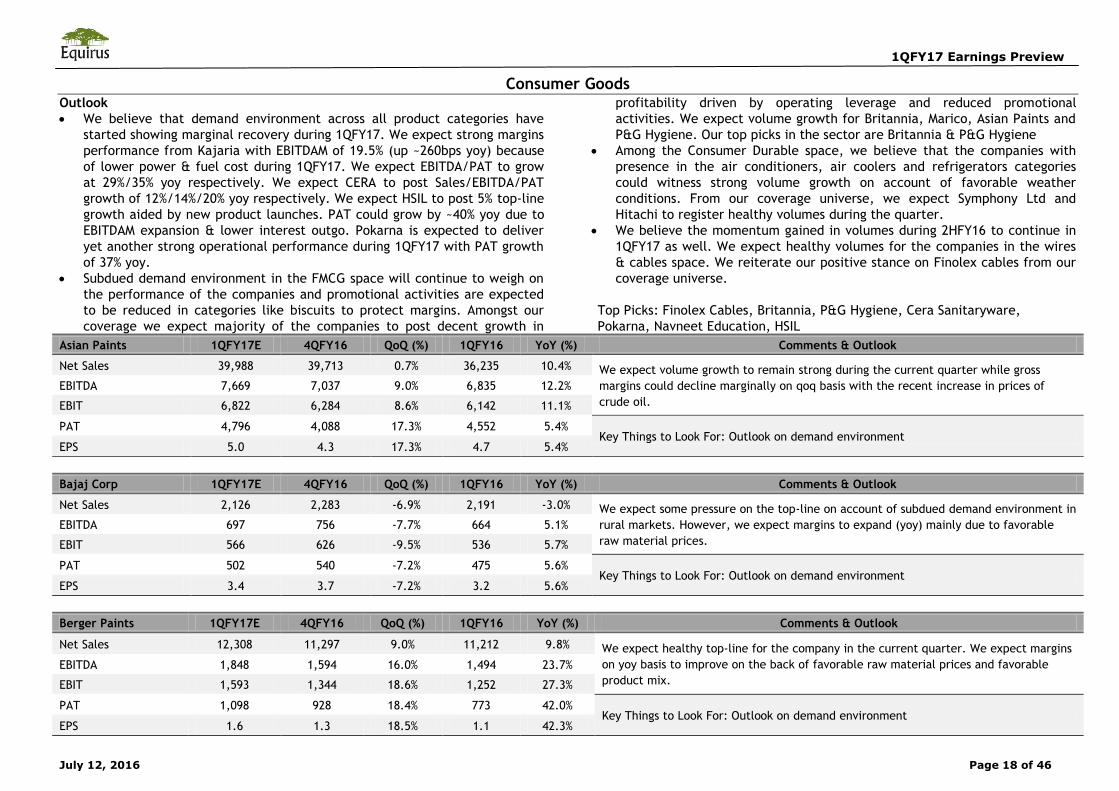

We believe that demand environment across all product categories have

started showing marginal recovery during 1QFY17. We expect strong margins

performance from Kajaria with EBITDAM of 19.5% (up ~260bps yoy) because

of lower power & fuel cost during 1QFY17. We expect EBITDA/PAT to grow

at 29%/35% yoy respectively. We expect CERA to post Sales/EBITDA/PAT

growth of 12%/14%/20% yoy respectively. We expect HSIL to post 5% top-line

growth aided by new product launches. PAT could grow by ~40% yoy due to

EBITDAM expansion & lower interest outgo. Pokarna is expected to deliver

yet another strong operational performance during 1QFY17 with PAT growth

of 37% yoy.

Subdued demand environment in the FMCG space will continue to weigh on

the performance of the companies and promotional activities are expected

to be reduced in categories like biscuits to protect margins. Amongst our

coverage we expect majority of the companies to post decent growth in

profitability driven by operating leverage and reduced promotional

activities. We expect volume growth for Britannia, Marico, Asian Paints and

P&G Hygiene. Our top picks in the sector are Britannia & P&G Hygiene

Among the Consumer Durable space, we believe that the companies with

presence in the air conditioners, air coolers and refrigerators categories

could witness strong volume growth on account of favorable weather

conditions. From our coverage universe, we expect Symphony Ltd and

Hitachi to register healthy volumes during the quarter.

We believe the momentum gained in volumes during 2HFY16 to continue in

1QFY17 as well. We expect healthy volumes for the companies in the wires

& cables space. We reiterate our positive stance on Finolex cables in our

coverage universe.

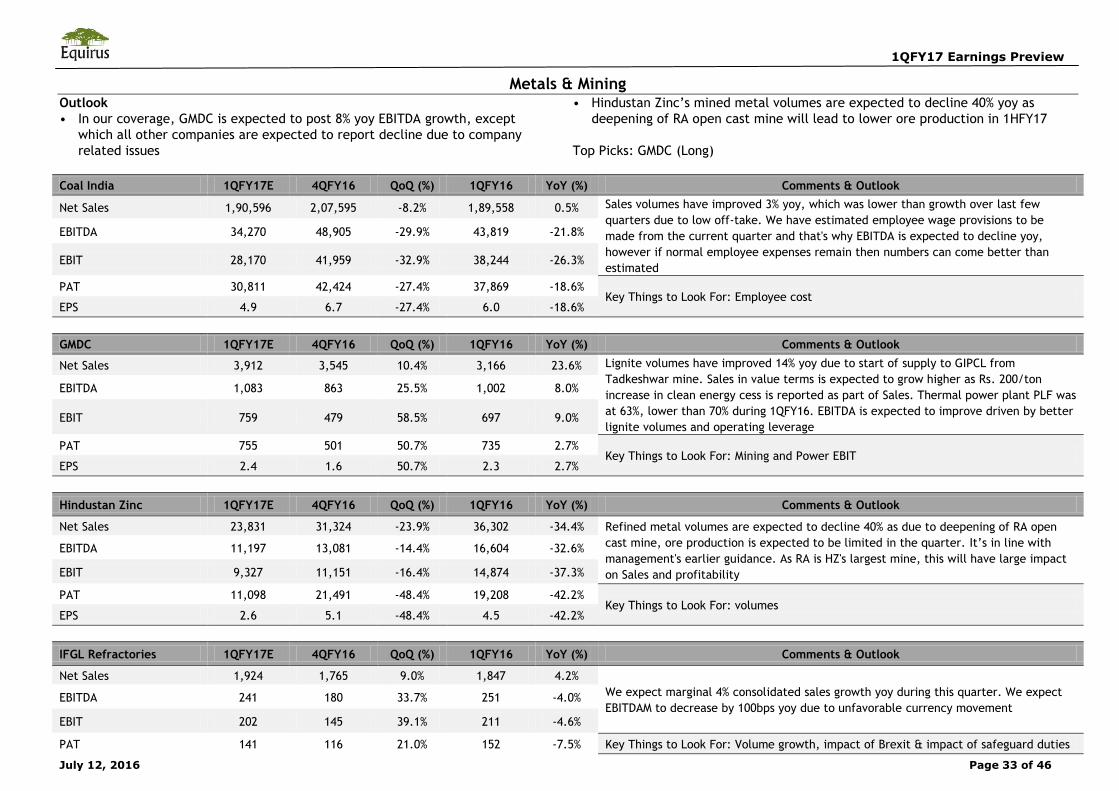

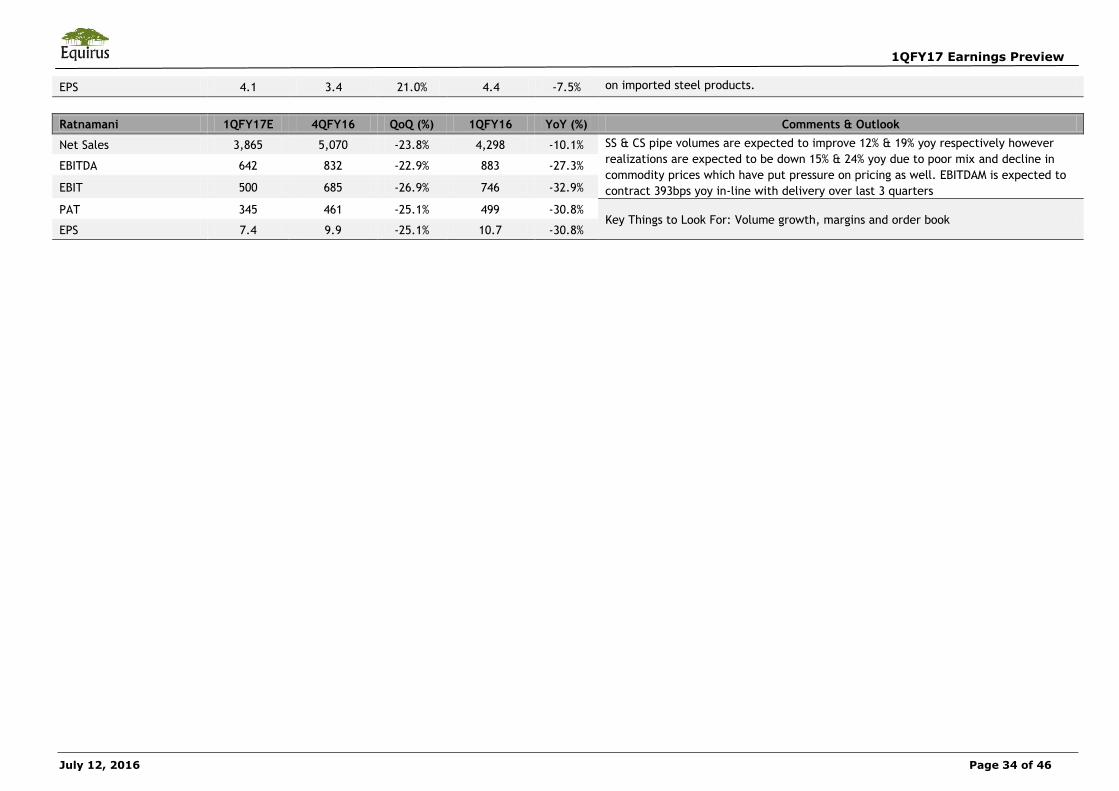

Metals and Mining

In our coverage, GMDC is expected to post 8% yoy EBITDA growth, except

which all other companies are expected to report decline due to company

related issues

Hindustan Zinc’s mined metal volumes are expected to decline 40% yoy as

deepening of RA open cast mine will lead to lower ore production in 1HFY17

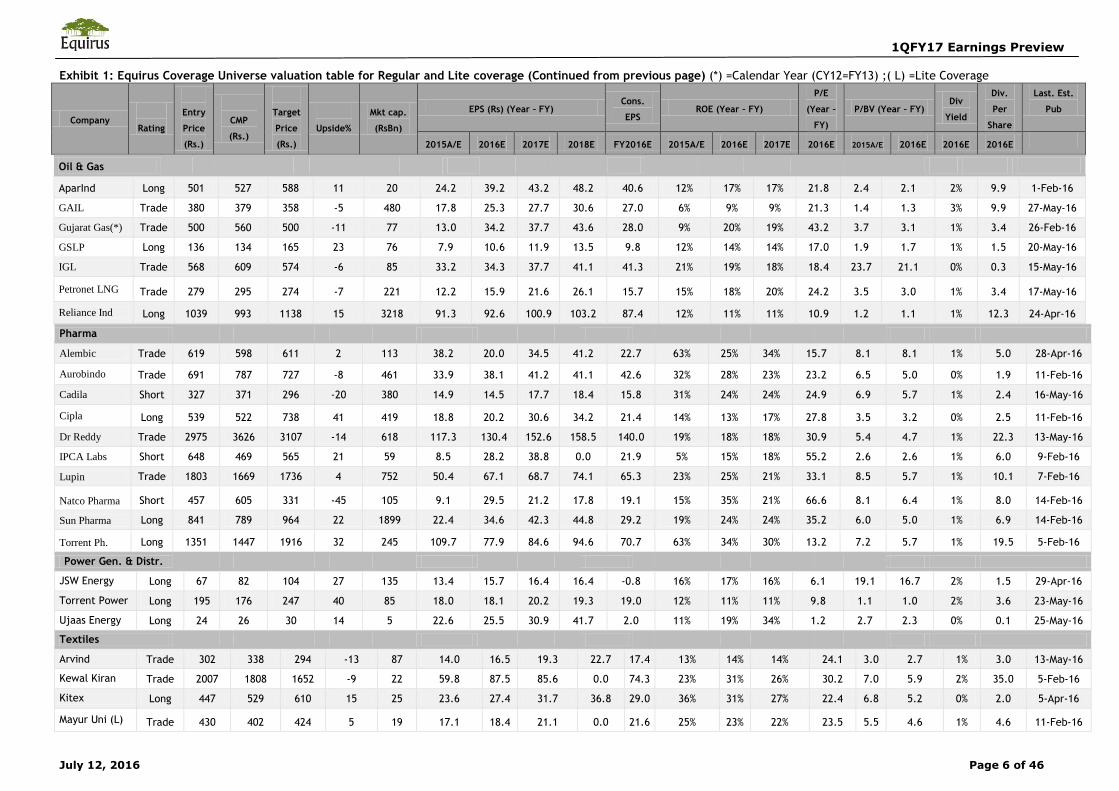

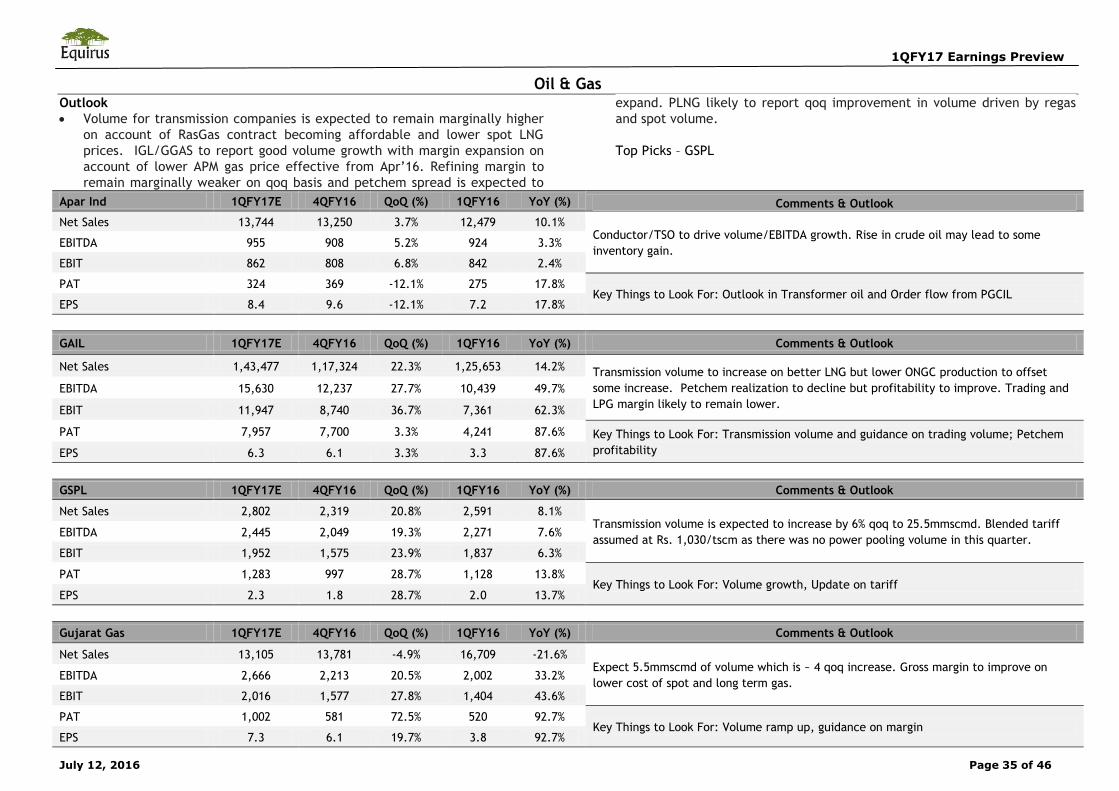

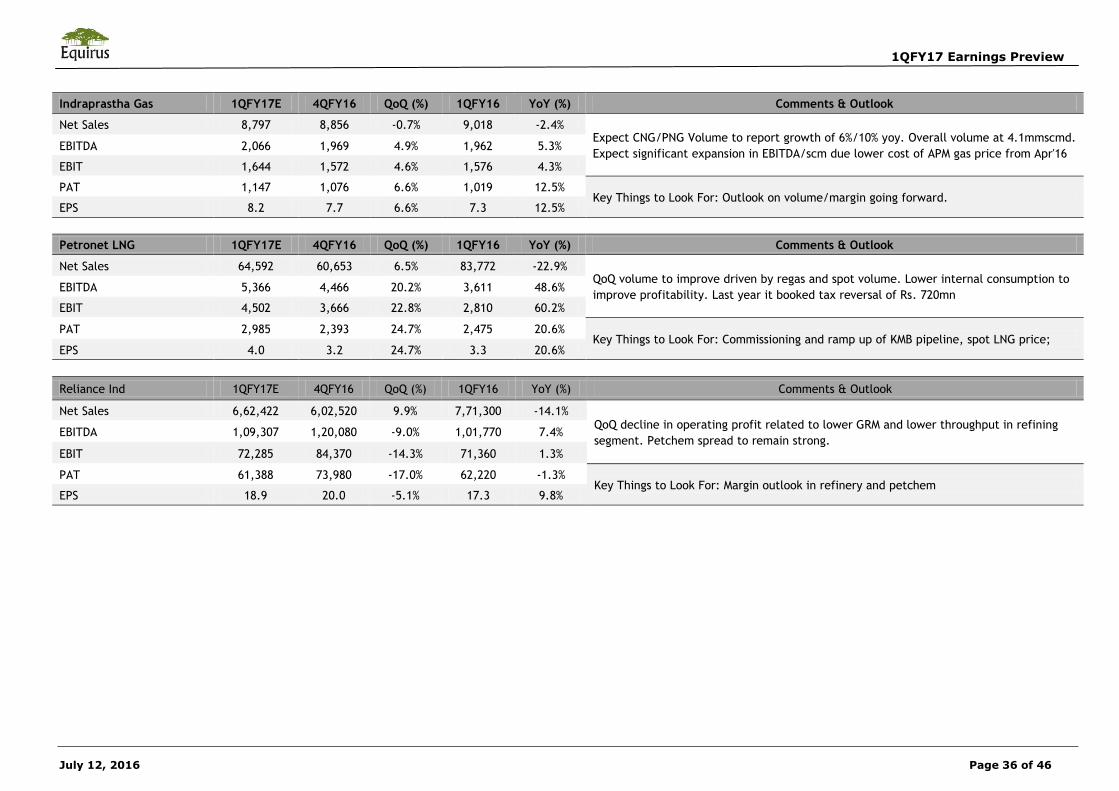

Oil & Gas

Volume for transmission companies is expected to remain marginally higher

on account of RasGas contract becoming affordable and lower spot LNG

prices. IGL/GGAS to report good volume growth with margin expansion on

account of lower APM gas price effective from Apr'16. Refining margin to

remain marginally weaker on qoq basis and petchem spread is expected to

expand. PLNG likely to report qoq improvement in volume driven by regas

and spot volume.

1QFY17 Earnings Preview

July 12, 2016 Page 2 of 46

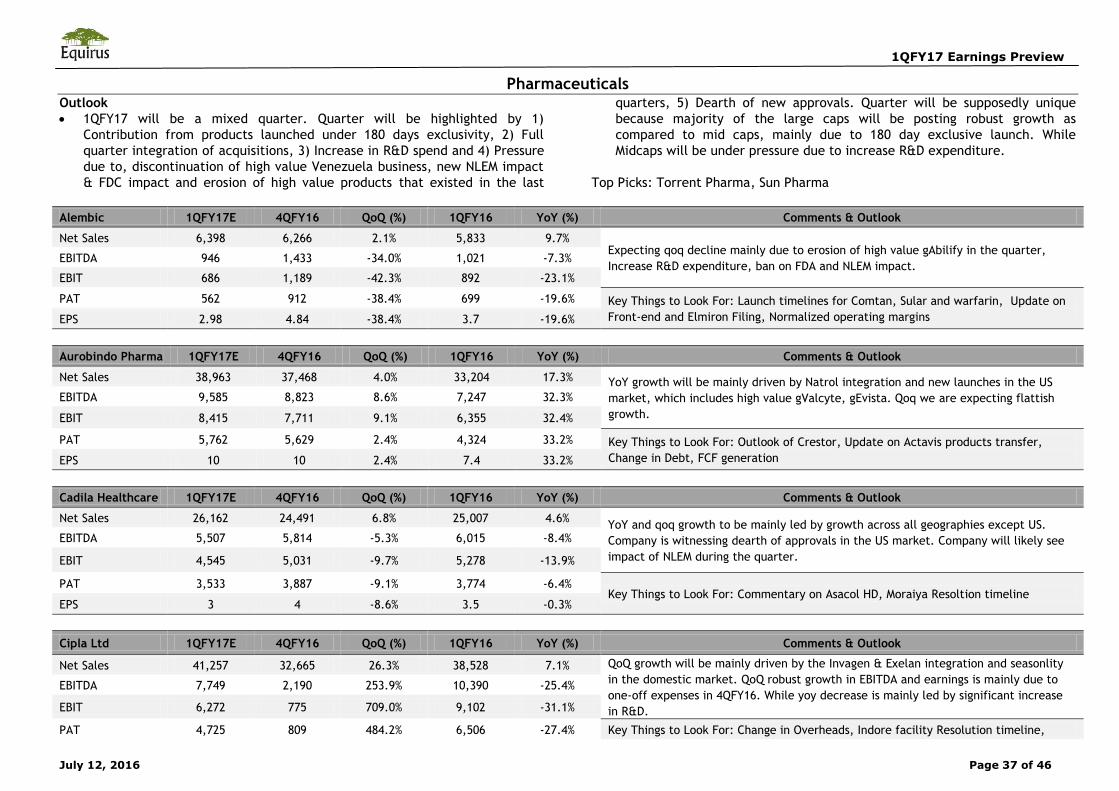

Pharmaceuticals

1QFY17 will be a mixed quarter. Quarter will be highlighted by 1)

Contribution from products launched under 180 days exclusivity, 2) Full

quarter integration of acquisitions, 3) Increase in R&D spend and 4) Pressure

due to discontinuation of high value Venezuela business, new NLEM impact

& FDC impact and erosion of high value products that existed in the last

quarters, 5) Dearth of new approvals. Quarter will be supposedly unique

because majority of the large caps will be posting robust growth as

compared to mid-caps, mainly due to 180 day exclusive launch. While

Midcaps will be under pressure due to increase R&D expenditure.

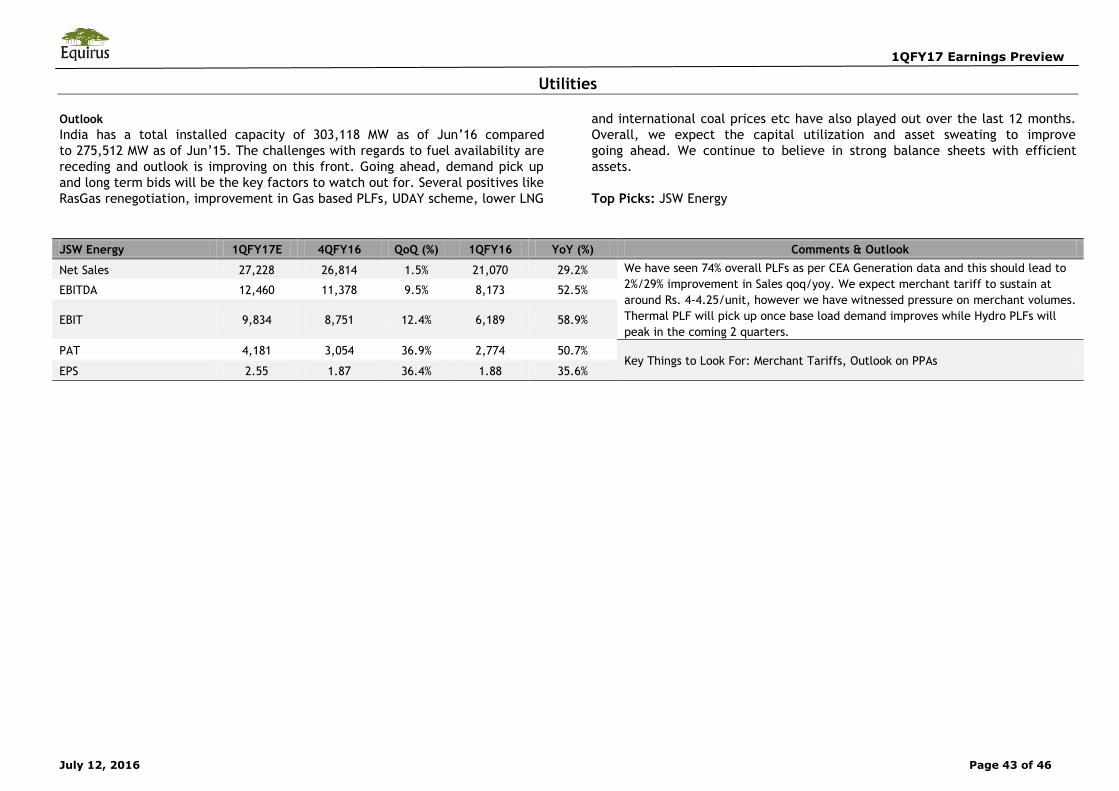

Utilities

India has a total installed capacity of 303,118 MW as of Jun’16

compared to 275,512 MW as of Jun’15. The challenges with regards to fuel

availability are receding and outlook is improving on this front. Going ahead,

demand pick up and long term bids will be the key factors to watch out for.

Several positives like RasGas renegotiation, improvement in Gas based PLFs,

UDAY scheme, lower LNG and international coal prices etc have also played

out over the last 12 months. Overall, we expect the capital utilization

and asset sweating to improve going ahead. We continue to believe in

strong balance sheets with efficient assets.

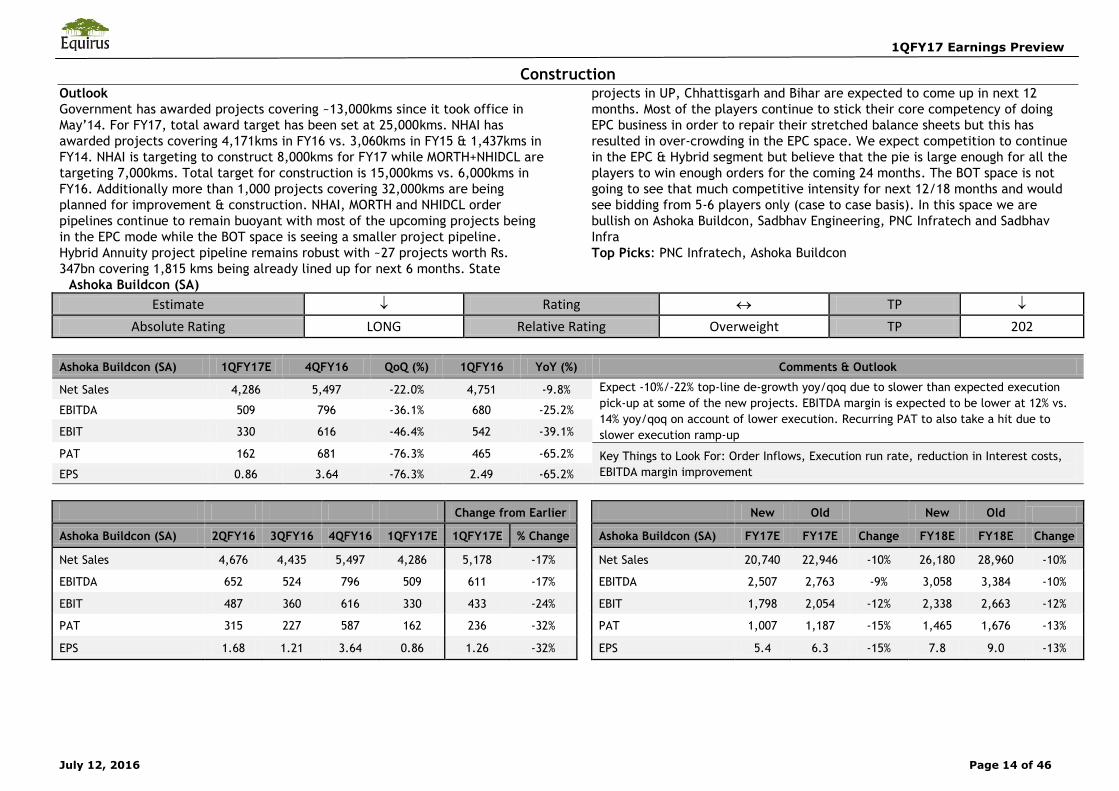

Construction

Government has awarded projects covering ~13,000kms since it took office

in May’14. For FY17, total award target has been set at 25,000kms. NHAI has

awarded projects covering 4,171kms in FY16 vs. 3,060kms in FY15 &

1,437kms in FY14. NHAI is targeting to construct 8,000kms for FY17 while

MORTH+NHIDCL are targeting 7,000kms. Total target for construction is

15,000kms vs. 6,000kms in FY16. Additionally more than 1,000 projects

covering 32,000kms are being planned for improvement & construction.

NHAI, MORTH and NHIDCL order pipelines continue to remain buoyant with

most of the upcoming projects being in the EPC mode while the BOT space is

seeing a smaller project pipeline. Hybrid Annuity project pipeline remains

robust with ~27 projects worth Rs. 347bn covering 1,815 kms being already

lined up for next 6 months. State projects in UP, Chhattisgarh and Bihar are

expected to come up in next 12 months. Most of the players continue to

stick their core competency of doing EPC business in order to repair their

stretched balance sheets but this has resulted in over-crowding in the EPC

space. We expect competition to continue in the EPC & Hybrid segment but

believe that the pie is large enough for all the players to win enough orders

for the coming 24 months. The BOT space is not going to see that much

competitive intensity for next 12/18 months and would see bidding from 5-6

players only (case to case basis). In this space we are bullish on Ashoka

Buildcon, Sadbhav Engineering, PNC Infratech and Sadbhav Infra.

IT Services

1QFY17 is expected to be seasonally strong quarter but this should include

moderate cross currency tailwinds too. However, 1Q has pressures in terms

of wage hikes and visa costs that could negatively impact margins.

Management commentaries on lower visa applications, impact of Brexit and

insights on spending across verticals should be interesting. We expect qoq $

Sales growth to be broadly in 1%-4% range and margin impact of upto

~150bps due to seasonality. Other key things to look include deal wins and

hiring trends.

1QFY17 Earnings Preview

July 12, 2016 Page 3 of 46

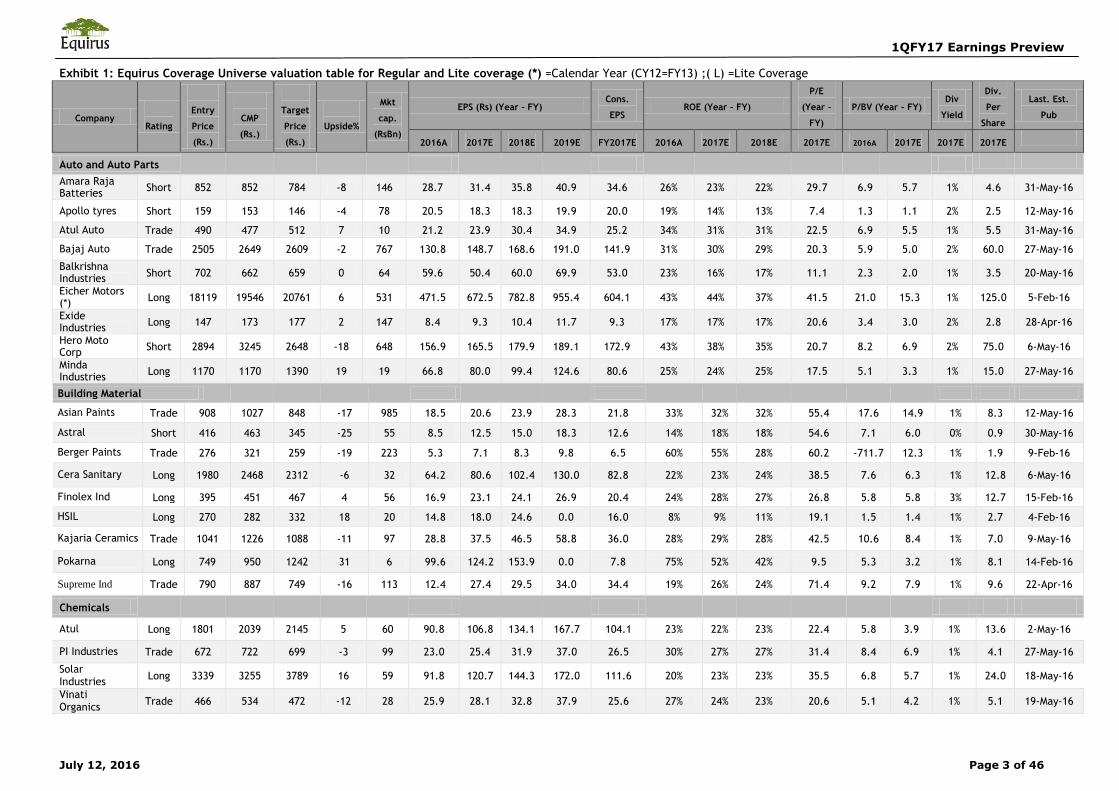

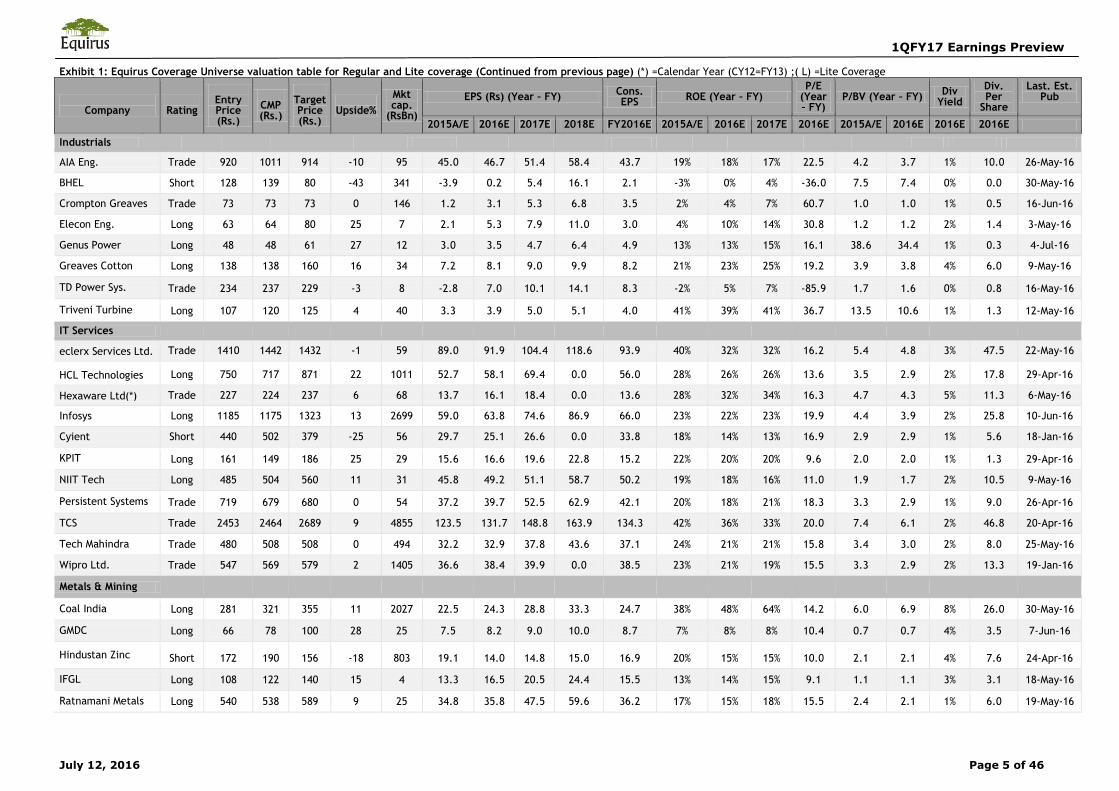

Exhibit 1: Equirus Coverage Universe valuation table for Regular and Lite coverage (*) =Calendar Year (CY12=FY13) ;( L) =Lite Coverage

Company

Rating

Entry

Price

(Rs.)

CMP

(Rs.)

Target

Price

(Rs.)

Upside%

Mkt

cap.

(RsBn)

EPS (Rs) (Year – FY) Cons.

EPS ROE (Year – FY)

P/E

(Year –

FY)

P/BV (Year – FY) Div

Yield

Div.

Per

Share

Last. Est.

Pub

2016A 2017E 2018E 2019E FY2017E 2016A 2017E 2018E 2017E 2016A 2017E 2017E 2017E

Auto and Auto Parts

Amara Raja Batteries

Short 852 852 784 -8 146 28.7 31.4 35.8 40.9 34.6 26% 23% 22% 29.7 6.9 5.7 1% 4.6 31-May-16

Apollo tyres Short 159 153 146 -4 78 20.5 18.3 18.3 19.9 20.0 19% 14% 13% 7.4 1.3 1.1 2% 2.5 12-May-16

Atul Auto Trade 490 477 512 7 10 21.2 23.9 30.4 34.9 25.2 34% 31% 31% 22.5 6.9 5.5 1% 5.5 31-May-16

Bajaj Auto Trade 2505 2649 2609 -2 767 130.8 148.7 168.6 191.0 141.9 31% 30% 29% 20.3 5.9 5.0 2% 60.0 27-May-16

Balkrishna Industries

Short 702 662 659 0 64 59.6 50.4 60.0 69.9 53.0 23% 16% 17% 11.1 2.3 2.0 1% 3.5 20-May-16

Eicher Motors (*)

Long 18119 19546 20761 6 531 471.5 672.5 782.8 955.4 604.1 43% 44% 37% 41.5 21.0 15.3 1% 125.0 5-Feb-16

Exide Industries

Long 147 173 177 2 147 8.4 9.3 10.4 11.7 9.3 17% 17% 17% 20.6 3.4 3.0 2% 2.8 28-Apr-16

Hero Moto Corp

Short 2894 3245 2648 -18 648 156.9 165.5 179.9 189.1 172.9 43% 38% 35% 20.7 8.2 6.9 2% 75.0 6-May-16

Minda Industries

Long 1170 1170 1390 19 19 66.8 80.0 99.4 124.6 80.6 25% 24% 25% 17.5 5.1 3.3 1% 15.0 27-May-16

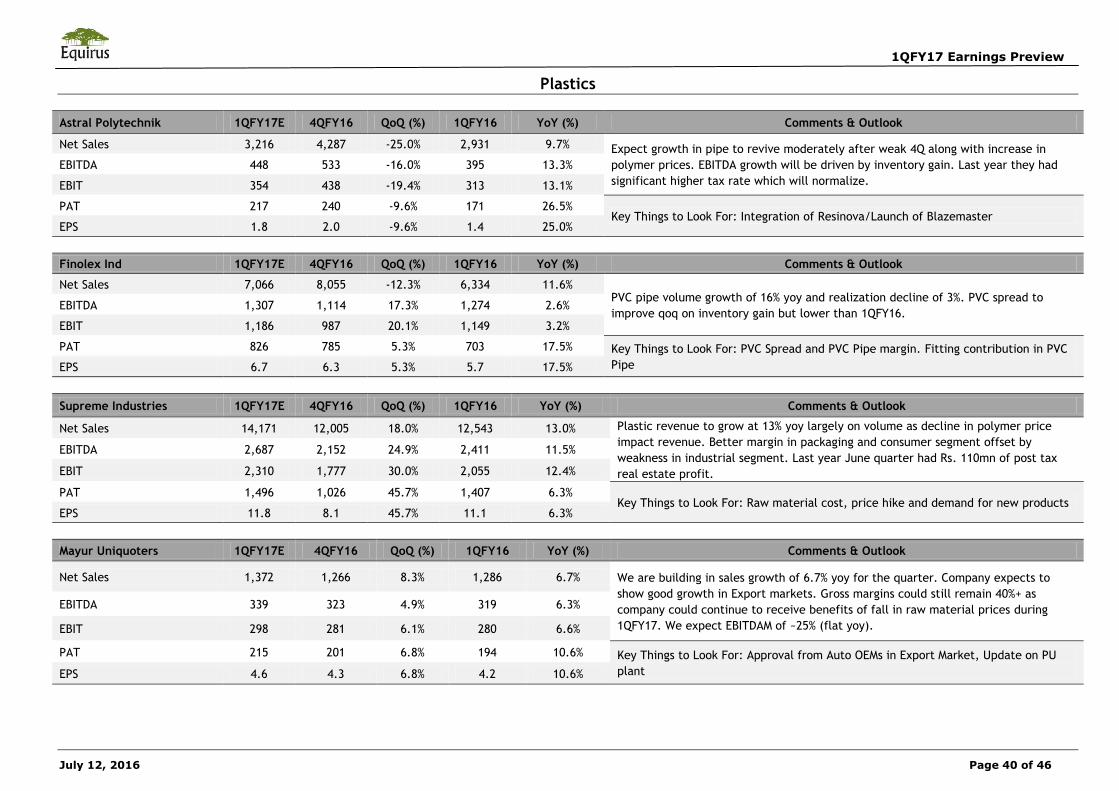

Building Material

Asian Paints Trade 908 1027 848 -17 985 18.5 20.6 23.9 28.3 21.8 33% 32% 32% 55.4 17.6 14.9 1% 8.3 12-May-16

Astral Short 416 463 345 -25 55 8.5 12.5 15.0 18.3 12.6 14% 18% 18% 54.6 7.1 6.0 0% 0.9 30-May-16

Berger Paints Trade 276 321 259 -19 223 5.3 7.1 8.3 9.8 6.5 60% 55% 28% 60.2 -711.7 12.3 1% 1.9 9-Feb-16

Cera Sanitary Long 1980 2468 2312 -6 32 64.2 80.6 102.4 130.0 82.8 22% 23% 24% 38.5 7.6 6.3 1% 12.8 6-May-16

Finolex Ind Long 395 451 467 4 56 16.9 23.1 24.1 26.9 20.4 24% 28% 27% 26.8 5.8 5.8 3% 12.7 15-Feb-16

HSIL Long 270 282 332 18 20 14.8 18.0 24.6 0.0 16.0 8% 9% 11% 19.1 1.5 1.4 1% 2.7 4-Feb-16

Kajaria Ceramics Trade 1041 1226 1088 -11 97 28.8 37.5 46.5 58.8 36.0 28% 29% 28% 42.5 10.6 8.4 1% 7.0 9-May-16

Pokarna Long 749 950 1242 31 6 99.6 124.2 153.9 0.0 7.8 75% 52% 42% 9.5 5.3 3.2 1% 8.1 14-Feb-16

Supreme Ind Trade 790 887 749 -16 113 12.4 27.4 29.5 34.0 34.4 19% 26% 24% 71.4 9.2 7.9 1% 9.6 22-Apr-16

Chemicals

Atul Long 1801 2039 2145 5 60 90.8 106.8 134.1 167.7 104.1 23% 22% 23% 22.4 5.8 3.9 1% 13.6 2-May-16

PI Industries Trade 672 722 699 -3 99 23.0 25.4 31.9 37.0 26.5 30% 27% 27% 31.4 8.4 6.9 1% 4.1 27-May-16

Solar Industries

Long 3339 3255 3789 16 59 91.8 120.7 144.3 172.0 111.6 20% 23% 23% 35.5 6.8 5.7 1% 24.0 18-May-16

Vinati Organics

Trade 466 534 472 -12 28 25.9 28.1 32.8 37.9 25.6 27% 24% 23% 20.6 5.1 4.2 1% 5.1 19-May-16

1QFY17 Earnings Preview

July 12, 2016 Page 4 of 46

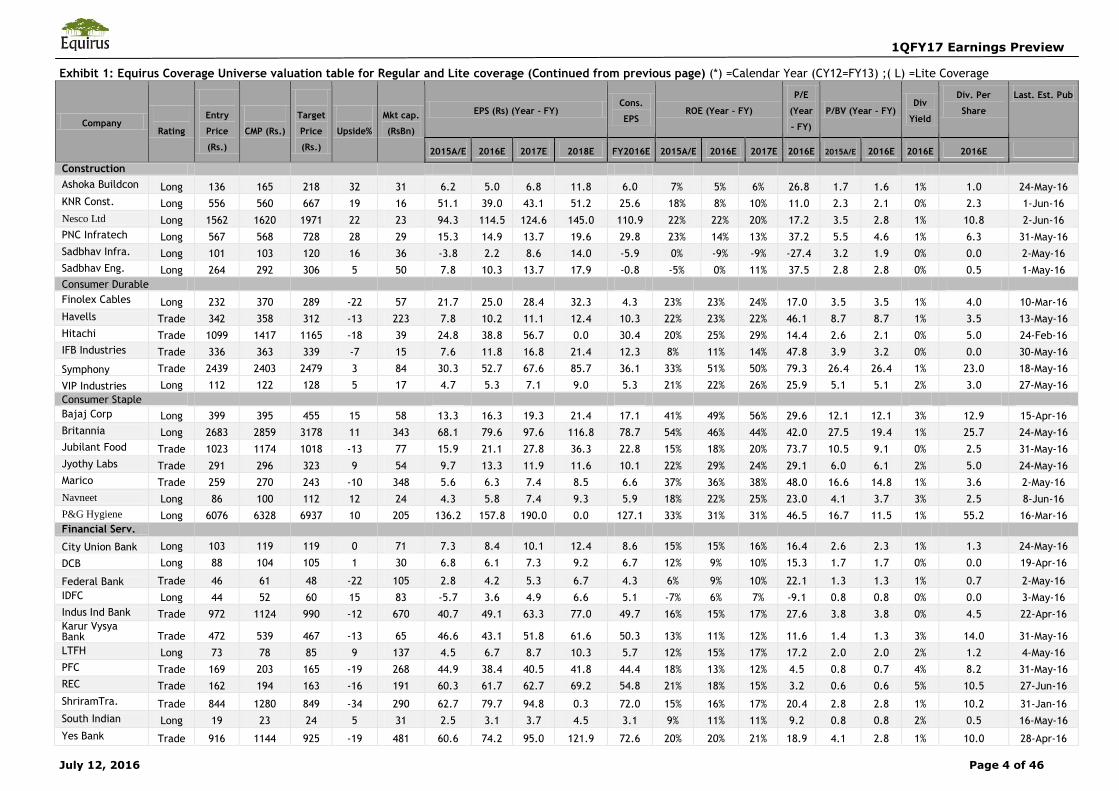

Exhibit 1: Equirus Coverage Universe valuation table for Regular and Lite coverage (Continued from previous page) (*) =Calendar Year (CY12=FY13) ;( L) =Lite Coverage

Company

Rating

Entry

Price

(Rs.)

CMP (Rs.)

Target

Price

(Rs.)

Upside%

Mkt cap.

(RsBn)

EPS (Rs) (Year – FY) Cons.

EPS ROE (Year – FY)

P/E

(Year

– FY)

P/BV (Year – FY) Div

Yield

Div. Per

Share

Last. Est. Pub

2015A/E 2016E 2017E 2018E FY2016E 2015A/E 2016E 2017E 2016E 2015A/E 2016E 2016E 2016E

Construction

Ashoka Buildcon Long 136 165 218 32 31 6.2 5.0 6.8 11.8 6.0 7% 5% 6% 26.8 1.7 1.6 1% 1.0 24-May-16

KNR Const. Long 556 560 667 19 16 51.1 39.0 43.1 51.2 25.6 18% 8% 10% 11.0 2.3 2.1 0% 2.3 1-Jun-16

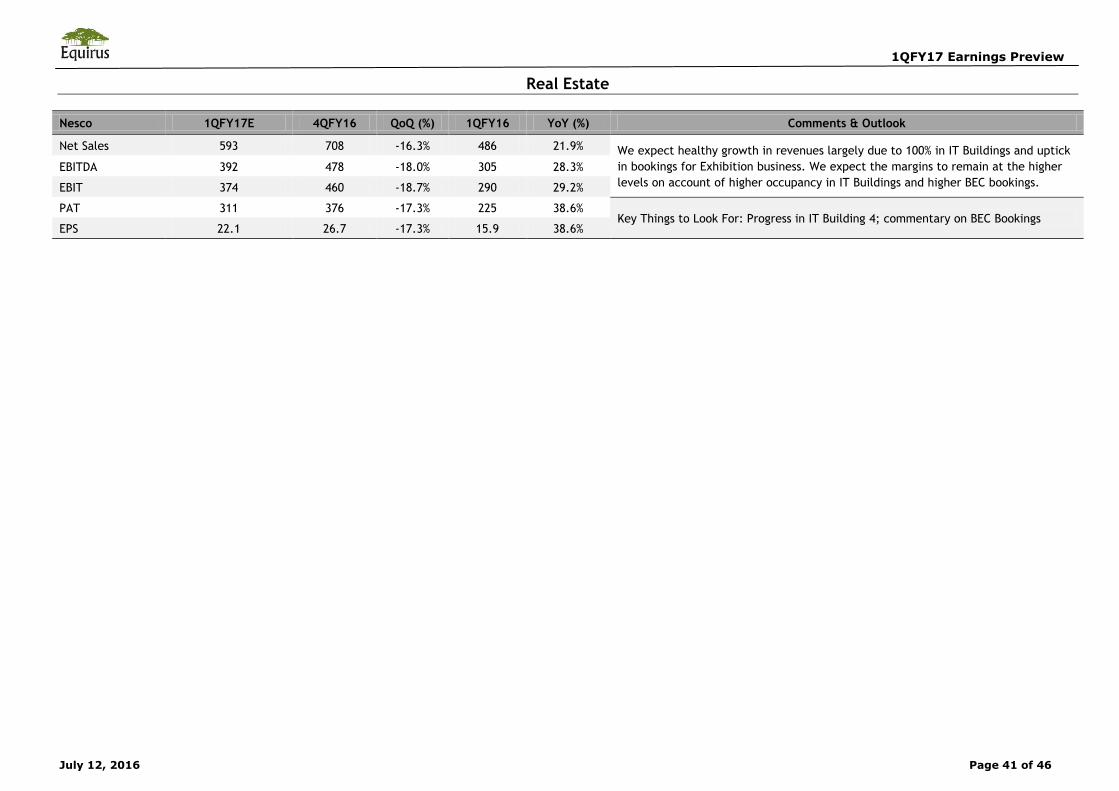

Nesco Ltd Long 1562 1620 1971 22 23 94.3 114.5 124.6 145.0 110.9 22% 22% 20% 17.2 3.5 2.8 1% 10.8 2-Jun-16

PNC Infratech Long 567 568 728 28 29 15.3 14.9 13.7 19.6 29.8 23% 14% 13% 37.2 5.5 4.6 1% 6.3 31-May-16

Sadbhav Infra. Long 101 103 120 16 36 -3.8 2.2 8.6 14.0 -5.9 0% -9% -9% -27.4 3.2 1.9 0% 0.0 2-May-16

Sadbhav Eng. Long 264 292 306 5 50 7.8 10.3 13.7 17.9 -0.8 -5% 0% 11% 37.5 2.8 2.8 0% 0.5 1-May-16

Consumer Durable

Finolex Cables Long 232 370 289 -22 57 21.7 25.0 28.4 32.3 4.3 23% 23% 24% 17.0 3.5 3.5 1% 4.0 10-Mar-16

Havells Trade 342 358 312 -13 223 7.8 10.2 11.1 12.4 10.3 22% 23% 22% 46.1 8.7 8.7 1% 3.5 13-May-16

Hitachi Trade 1099 1417 1165 -18 39 24.8 38.8 56.7 0.0 30.4 20% 25% 29% 14.4 2.6 2.1 0% 5.0 24-Feb-16

IFB Industries Trade 336 363 339 -7 15 7.6 11.8 16.8 21.4 12.3 8% 11% 14% 47.8 3.9 3.2 0% 0.0 30-May-16

Symphony Trade 2439 2403 2479 3 84 30.3 52.7 67.6 85.7 36.1 33% 51% 50% 79.3 26.4 26.4 1% 23.0 18-May-16

VIP Industries Long 112 122 128 5 17 4.7 5.3 7.1 9.0 5.3 21% 22% 26% 25.9 5.1 5.1 2% 3.0 27-May-16

Consumer Staple

Bajaj Corp Long 399 395 455 15 58 13.3 16.3 19.3 21.4 17.1 41% 49% 56% 29.6 12.1 12.1 3% 12.9 15-Apr-16

Britannia Long 2683 2859 3178 11 343 68.1 79.6 97.6 116.8 78.7 54% 46% 44% 42.0 27.5 19.4 1% 25.7 24-May-16

Jubilant Food Trade 1023 1174 1018 -13 77 15.9 21.1 27.8 36.3 22.8 15% 18% 20% 73.7 10.5 9.1 0% 2.5 31-May-16

Jyothy Labs Trade 291 296 323 9 54 9.7 13.3 11.9 11.6 10.1 22% 29% 24% 29.1 6.0 6.1 2% 5.0 24-May-16

Marico Trade 259 270 243 -10 348 5.6 6.3 7.4 8.5 6.6 37% 36% 38% 48.0 16.6 14.8 1% 3.6 2-May-16

Navneet Long 86 100 112 12 24 4.3 5.8 7.4 9.3 5.9 18% 22% 25% 23.0 4.1 3.7 3% 2.5 8-Jun-16

P&G Hygiene Long 6076 6328 6937 10 205 136.2 157.8 190.0 0.0 127.1 33% 31% 31% 46.5 16.7 11.5 1% 55.2 16-Mar-16

Financial Serv.

City Union Bank Long 103 119 119 0 71 7.3 8.4 10.1 12.4 8.6 15% 15% 16% 16.4 2.6 2.3 1% 1.3 24-May-16

DCB Long 88 104 105 1 30 6.8 6.1 7.3 9.2 6.7 12% 9% 10% 15.3 1.7 1.7 0% 0.0 19-Apr-16

Federal Bank Trade 46 61 48 -22 105 2.8 4.2 5.3 6.7 4.3 6% 9% 10% 22.1 1.3 1.3 1% 0.7 2-May-16

IDFC Long 44 52 60 15 83 -5.7 3.6 4.9 6.6 5.1 -7% 6% 7% -9.1 0.8 0.8 0% 0.0 3-May-16

Indus Ind Bank Trade 972 1124 990 -12 670 40.7 49.1 63.3 77.0 49.7 16% 15% 17% 27.6 3.8 3.8 0% 4.5 22-Apr-16 Karur Vysya Bank Trade 472 539 467 -13 65 46.6 43.1 51.8 61.6 50.3 13% 11% 12% 11.6 1.4 1.3 3% 14.0 31-May-16

LTFH Long 73 78 85 9 137 4.5 6.7 8.7 10.3 5.7 12% 15% 17% 17.2 2.0 2.0 2% 1.2 4-May-16

PFC Trade 169 203 165 -19 268 44.9 38.4 40.5 41.8 44.4 18% 13% 12% 4.5 0.8 0.7 4% 8.2 31-May-16

REC Trade 162 194 163 -16 191 60.3 61.7 62.7 69.2 54.8 21% 18% 15% 3.2 0.6 0.6 5% 10.5 27-Jun-16

ShriramTra. Trade 844 1280 849 -34 290 62.7 79.7 94.8 0.3 72.0 15% 16% 17% 20.4 2.8 2.8 1% 10.2 31-Jan-16

South Indian Long 19 23 24 5 31 2.5 3.1 3.7 4.5 3.1 9% 11% 11% 9.2 0.8 0.8 2% 0.5 16-May-16

Yes Bank Trade 916 1144 925 -19 481 60.6 74.2 95.0 121.9 72.6 20% 20% 21% 18.9 4.1 2.8 1% 10.0 28-Apr-16

1QFY17 Earnings Preview

July 12, 2016 Page 5 of 46

Exhibit 1: Equirus Coverage Universe valuation table for Regular and Lite coverage (Continued from previous page) (*) =Calendar Year (CY12=FY13) ;( L) =Lite Coverage

Company

Rating

Entry Price (Rs.)

CMP (Rs.)

Target Price (Rs.)

Upside%

Mkt cap.

(RsBn)

EPS (Rs) (Year – FY) Cons. EPS

ROE (Year – FY) P/E

(Year – FY)

P/BV (Year – FY) Div

Yield

Div. Per

Share

Last. Est. Pub

2015A/E 2016E 2017E 2018E FY2016E 2015A/E 2016E 2017E 2016E 2015A/E 2016E 2016E 2016E

Industrials

AIA Eng. Trade 920 1011 914 -10 95 45.0 46.7 51.4 58.4 43.7 19% 18% 17% 22.5 4.2 3.7 1% 10.0 26-May-16

BHEL Short 128 139 80 -43 341 -3.9 0.2 5.4 16.1 2.1 -3% 0% 4% -36.0 7.5 7.4 0% 0.0 30-May-16

Crompton Greaves Trade 73 73 73 0 146 1.2 3.1 5.3 6.8 3.5 2% 4% 7% 60.7 1.0 1.0 1% 0.5 16-Jun-16

Elecon Eng. Long 63 64 80 25 7 2.1 5.3 7.9 11.0 3.0 4% 10% 14% 30.8 1.2 1.2 2% 1.4 3-May-16

Genus Power Long 48 48 61 27 12 3.0 3.5 4.7 6.4 4.9 13% 13% 15% 16.1 38.6 34.4 1% 0.3 4-Jul-16

Greaves Cotton Long 138 138 160 16 34 7.2 8.1 9.0 9.9 8.2 21% 23% 25% 19.2 3.9 3.8 4% 6.0 9-May-16

TD Power Sys. Trade 234 237 229 -3 8 -2.8 7.0 10.1 14.1 8.3 -2% 5% 7% -85.9 1.7 1.6 0% 0.8 16-May-16

Triveni Turbine Long 107 120 125 4 40 3.3 3.9 5.0 5.1 4.0 41% 39% 41% 36.7 13.5 10.6 1% 1.3 12-May-16

IT Services

eclerx Services Ltd. Trade 1410 1442 1432 -1 59 89.0 91.9 104.4 118.6 93.9 40% 32% 32% 16.2 5.4 4.8 3% 47.5 22-May-16

HCL Technologies Long 750 717 871 22 1011 52.7 58.1 69.4 0.0 56.0 28% 26% 26% 13.6 3.5 2.9 2% 17.8 29-Apr-16

Hexaware Ltd(*) Trade 227 224 237 6 68 13.7 16.1 18.4 0.0 13.6 28% 32% 34% 16.3 4.7 4.3 5% 11.3 6-May-16

Infosys Long 1185 1175 1323 13 2699 59.0 63.8 74.6 86.9 66.0 23% 22% 23% 19.9 4.4 3.9 2% 25.8 10-Jun-16

Cyient Short 440 502 379 -25 56 29.7 25.1 26.6 0.0 33.8 18% 14% 13% 16.9 2.9 2.9 1% 5.6 18-Jan-16

KPIT Long 161 149 186 25 29 15.6 16.6 19.6 22.8 15.2 22% 20% 20% 9.6 2.0 2.0 1% 1.3 29-Apr-16

NIIT Tech Long 485 504 560 11 31 45.8 49.2 51.1 58.7 50.2 19% 18% 16% 11.0 1.9 1.7 2% 10.5 9-May-16

Persistent Systems Trade 719 679 680 0 54 37.2 39.7 52.5 62.9 42.1 20% 18% 21% 18.3 3.3 2.9 1% 9.0 26-Apr-16

TCS Trade 2453 2464 2689 9 4855 123.5 131.7 148.8 163.9 134.3 42% 36% 33% 20.0 7.4 6.1 2% 46.8 20-Apr-16

Tech Mahindra Trade 480 508 508 0 494 32.2 32.9 37.8 43.6 37.1 24% 21% 21% 15.8 3.4 3.0 2% 8.0 25-May-16

Wipro Ltd. Trade 547 569 579 2 1405 36.6 38.4 39.9 0.0 38.5 23% 21% 19% 15.5 3.3 2.9 2% 13.3 19-Jan-16

Metals & Mining

Coal India Long 281 321 355 11 2027 22.5 24.3 28.8 33.3 24.7 38% 48% 64% 14.2 6.0 6.9 8% 26.0 30-May-16

GMDC Long 66 78 100 28 25 7.5 8.2 9.0 10.0 8.7 7% 8% 8% 10.4 0.7 0.7 4% 3.5 7-Jun-16

Hindustan Zinc Short 172 190 156 -18 803 19.1 14.0 14.8 15.0 16.9 20% 15% 15% 10.0 2.1 2.1 4% 7.6 24-Apr-16

IFGL Long 108 122 140 15 4 13.3 16.5 20.5 24.4 15.5 13% 14% 15% 9.1 1.1 1.1 3% 3.1 18-May-16

Ratnamani Metals Long 540 538 589 9 25 34.8 35.8 47.5 59.6 36.2 17% 15% 18% 15.5 2.4 2.1 1% 6.0 19-May-16

1QFY17 Earnings Preview

July 12, 2016 Page 6 of 46

Exhibit 1: Equirus Coverage Universe valuation table for Regular and Lite coverage (Continued from previous page) (*) =Calendar Year (CY12=FY13) ;( L) =Lite Coverage

Company

Rating

Entry

Price

(Rs.)

CMP

(Rs.)

Target

Price

(Rs.)

Upside%

Mkt cap.

(RsBn)

EPS (Rs) (Year – FY) Cons.

EPS ROE (Year – FY)

P/E

(Year –

FY)

P/BV (Year – FY) Div

Yield

Div.

Per

Share

Last. Est.

Pub

2015A/E 2016E 2017E 2018E FY2016E 2015A/E 2016E 2017E 2016E 2015A/E 2016E 2016E 2016E

Oil & Gas

AparInd Long 501 527 588 11 20 24.2 39.2 43.2 48.2 40.6 12% 17% 17% 21.8 2.4 2.1 2% 9.9 1-Feb-16

GAIL Trade 380 379 358 -5 480 17.8 25.3 27.7 30.6 27.0 6% 9% 9% 21.3 1.4 1.3 3% 9.9 27-May-16

Gujarat Gas(*) Trade 500 560 500 -11 77 13.0 34.2 37.7 43.6 28.0 9% 20% 19% 43.2 3.7 3.1 1% 3.4 26-Feb-16

GSLP Long 136 134 165 23 76 7.9 10.6 11.9 13.5 9.8 12% 14% 14% 17.0 1.9 1.7 1% 1.5 20-May-16

IGL Trade 568 609 574 -6 85 33.2 34.3 37.7 41.1 41.3 21% 19% 18% 18.4 23.7 21.1 0% 0.3 15-May-16

Petronet LNG Trade 279 295 274 -7 221 12.2 15.9 21.6 26.1 15.7 15% 18% 20% 24.2 3.5 3.0 1% 3.4 17-May-16

Reliance Ind Long 1039 993 1138 15 3218 91.3 92.6 100.9 103.2 87.4 12% 11% 11% 10.9 1.2 1.1 1% 12.3 24-Apr-16

Pharma

Alembic Trade 619 598 611 2 113 38.2 20.0 34.5 41.2 22.7 63% 25% 34% 15.7 8.1 8.1 1% 5.0 28-Apr-16

Aurobindo Trade 691 787 727 -8 461 33.9 38.1 41.2 41.1 42.6 32% 28% 23% 23.2 6.5 5.0 0% 1.9 11-Feb-16

Cadila Short 327 371 296 -20 380 14.9 14.5 17.7 18.4 15.8 31% 24% 24% 24.9 6.9 5.7 1% 2.4 16-May-16

Cipla Long 539 522 738 41 419 18.8 20.2 30.6 34.2 21.4 14% 13% 17% 27.8 3.5 3.2 0% 2.5 11-Feb-16

Dr Reddy Trade 2975 3626 3107 -14 618 117.3 130.4 152.6 158.5 140.0 19% 18% 18% 30.9 5.4 4.7 1% 22.3 13-May-16

IPCA Labs Short 648 469 565 21 59 8.5 28.2 38.8 0.0 21.9 5% 15% 18% 55.2 2.6 2.6 1% 6.0 9-Feb-16

Lupin Trade 1803 1669 1736 4 752 50.4 67.1 68.7 74.1 65.3 23% 25% 21% 33.1 8.5 5.7 1% 10.1 7-Feb-16

Natco Pharma Short 457 605 331 -45 105 9.1 29.5 21.2 17.8 19.1 15% 35% 21% 66.6 8.1 6.4 1% 8.0 14-Feb-16

Sun Pharma Long 841 789 964 22 1899 22.4 34.6 42.3 44.8 29.2 19% 24% 24% 35.2 6.0 5.0 1% 6.9 14-Feb-16

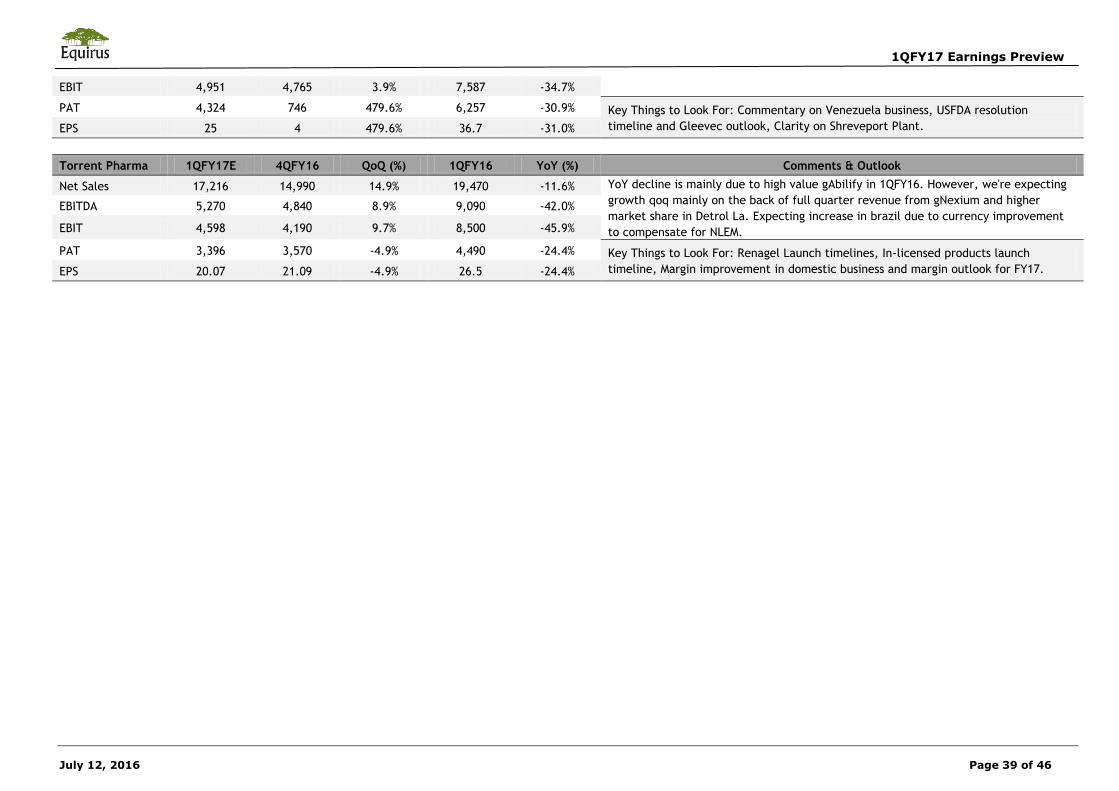

Torrent Ph. Long 1351 1447 1916 32 245 109.7 77.9 84.6 94.6 70.7 63% 34% 30% 13.2 7.2 5.7 1% 19.5 5-Feb-16

Power Gen. & Distr.

JSW Energy Long 67 82 104 27 135 13.4 15.7 16.4 16.4 -0.8 16% 17% 16% 6.1 19.1 16.7 2% 1.5 29-Apr-16

Torrent Power Long 195 176 247 40 85 18.0 18.1 20.2 19.3 19.0 12% 11% 11% 9.8 1.1 1.0 2% 3.6 23-May-16

Ujaas Energy Long 24 26 30 14 5 22.6 25.5 30.9 41.7 2.0 11% 19% 34% 1.2 2.7 2.3 0% 0.1 25-May-16

Textiles

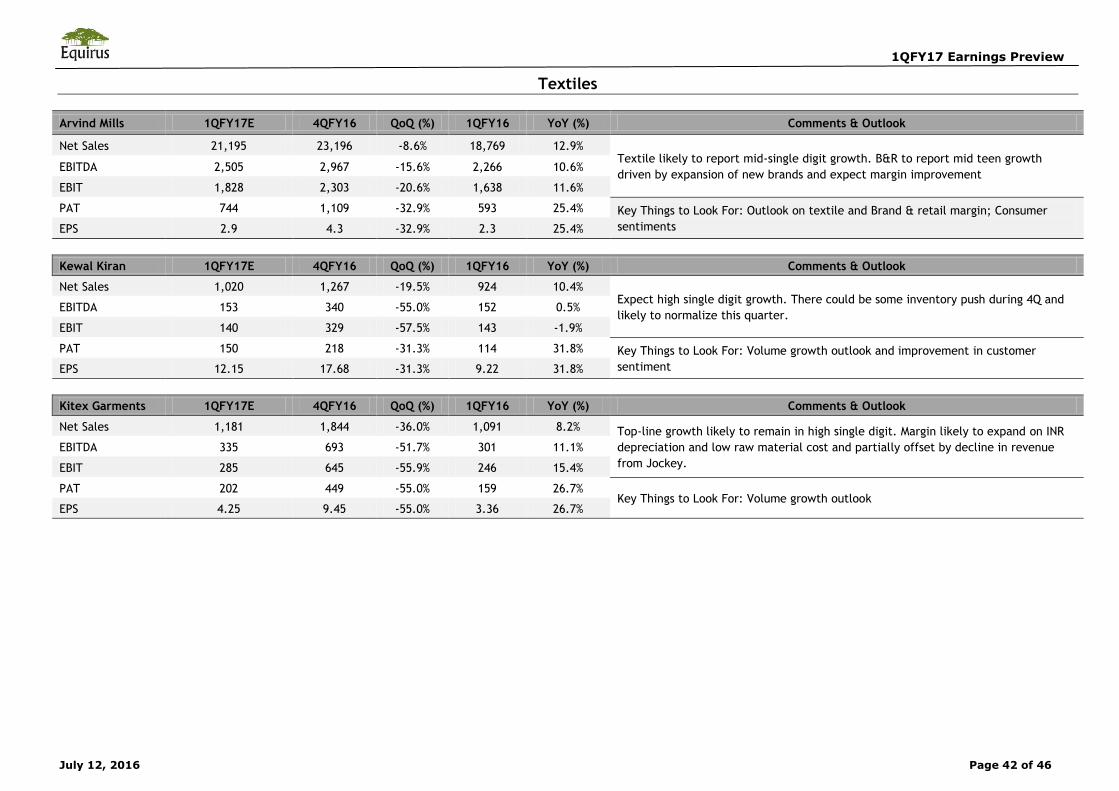

Arvind Trade 302 338 294 -13 87 14.0 16.5 19.3 22.7 17.4 13% 14% 14% 24.1 3.0 2.7 1% 3.0 13-May-16

Kewal Kiran Trade 2007 1808 1652 -9 22 59.8 87.5 85.6 0.0 74.3 23% 31% 26% 30.2 7.0 5.9 2% 35.0 5-Feb-16

Kitex Long 447 529 610 15 25 23.6 27.4 31.7 36.8 29.0 36% 31% 27% 22.4 6.8 5.2 0% 2.0 5-Apr-16

Mayur Uni (L) Trade 430 402 424 5 19 17.1 18.4 21.1 0.0 21.6 25% 23% 22% 23.5 5.5 4.6 1% 4.6 11-Feb-16

1QFY17 Earnings Preview

July 12, 2016 Page 7 of 46

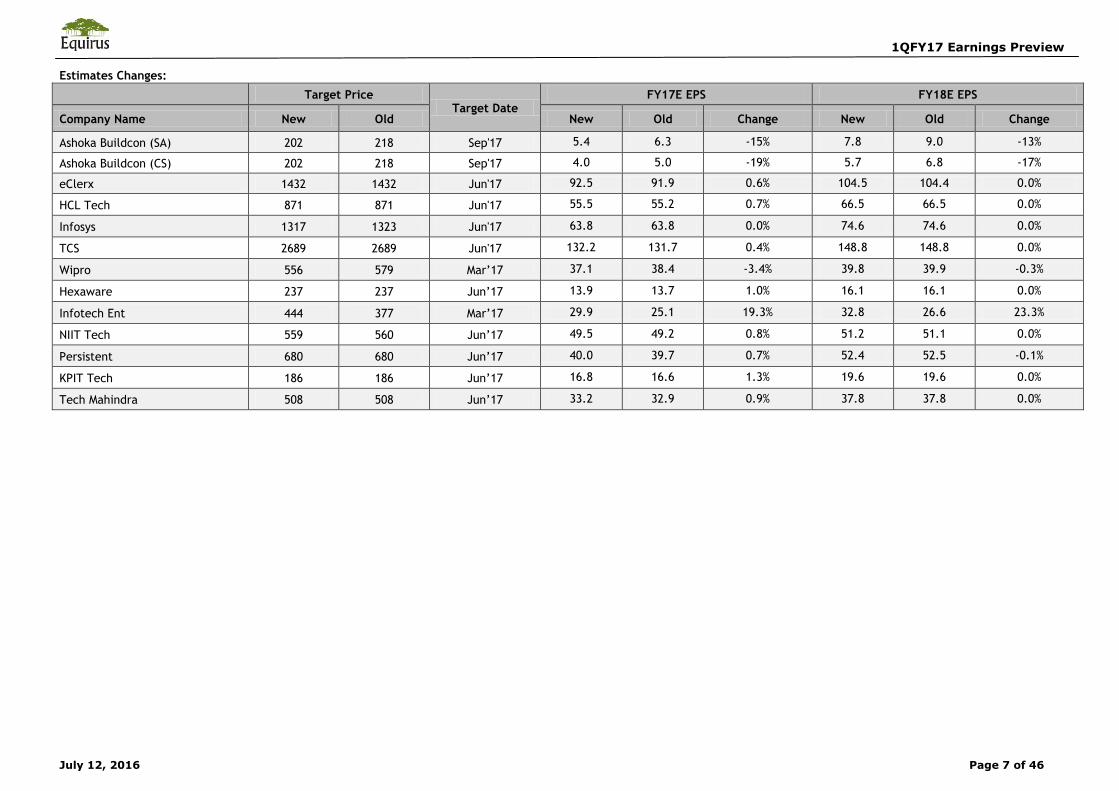

Estimates Changes:

Target Price

Target Date FY17E EPS FY18E EPS

Company Name New Old New Old Change New Old Change

Ashoka Buildcon (SA) 202 218 Sep'17 5.4 6.3 -15% 7.8 9.0 -13%

Ashoka Buildcon (CS) 202 218 Sep'17 4.0 5.0 -19% 5.7 6.8 -17%

eClerx 1432 1432 Jun'17 92.5 91.9 0.6% 104.5 104.4 0.0%

HCL Tech 871 871 Jun'17 55.5 55.2 0.7% 66.5 66.5 0.0%

Infosys 1317 1323 Jun'17 63.8 63.8 0.0% 74.6 74.6 0.0%

TCS 2689 2689 Jun'17 132.2 131.7 0.4% 148.8 148.8 0.0%

Wipro 556 579 Mar’17 37.1 38.4 -3.4% 39.8 39.9 -0.3%

Hexaware 237 237 Jun’17 13.9 13.7 1.0% 16.1 16.1 0.0%

Infotech Ent 444 377 Mar’17 29.9 25.1 19.3% 32.8 26.6 23.3%

NIIT Tech 559 560 Jun’17 49.5 49.2 0.8% 51.2 51.1 0.0%

Persistent 680 680 Jun’17 40.0 39.7 0.7% 52.4 52.5 -0.1%

KPIT Tech 186 186 Jun’17 16.8 16.6 1.3% 19.6 19.6 0.0%

Tech Mahindra 508 508 Jun’17 33.2 32.9 0.9% 37.8 37.8 0.0%

1QFY17 Earnings Preview

July 12, 2016 Page 8 of 46

Auto PartsOutlook

Eicher Motors is expected to deliver 44%/53% EBITDA/PAT growth driven by

38%/34% yoy volume growth in RE/VECV

Bajaj is expected to deliver 10% EBITDA growth while Hero 20% due to

margin expansion driven by lower RM prices yoy

Exide is expected to deliver 12%/18% EBITDA/PAT growth driven by

improvement in EBITDAM and higher other income on increased cash. Amara

is expected to deliver 11%/9% EBITDA/PAT growth

In tyre space, Balkrishna is expected to post 7% EBIDTA growth while Apollo

is expected to post 4% EBITDA decline due to margins compression

Top picks – Balkrishna Industries (Short), Exide (Long)

Tyres

Apollo Tyres (Consl) 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 31,255 29,897 4.5% 28,454 9.8% Standalone volumes are expected to grow 10% yoy leading to 3% Sales growth, as per our

interaction with other tyre players, TB bias tyres also saw growth during 1Q vs. decline

last year. Margins are expected to decline 161bps yoy due to price cuts taken during last

year. Subsidiary EBITDA is expected to remain flat yoy

EBITDA 4,815 4,773 0.9% 5,025 -4.2%

EBIT 3,620 3,546 2.1% 4,139 -12.6%

PAT 2,445 2,452 -0.3% 2,906 -15.9% Key Things to Look For: Standalone volume growth & margins in Europe

EPS 4.8 4.8 -0.3% 5.7 -15.9%

Balkrishna Industries 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 9,067 8,796 3.1% 8,255 9.8% We expect volumes to grow 11% yoy and remain flat qoq, volume growth will be higher as

in 1QFY16, volumes had declined 5% yoy. EBITDA margin is expected to decline qoq due

to lower Euro INR rate qoq & yoy EBITDA 2,639 3,103 -14.9% 2,456 7.4%

EBIT 1,893 2,398 -21.1% 1,812 4.5%

PAT 1,317 1,550 -15.1% 1,518 -13.3% Key Things to Look For: Volume growth & Euro-INR rate

EPS 13.6 16.0 -15.1% 15.7 -13.3%

1QFY17 Earnings Preview

July 12, 2016 Page 9 of 46

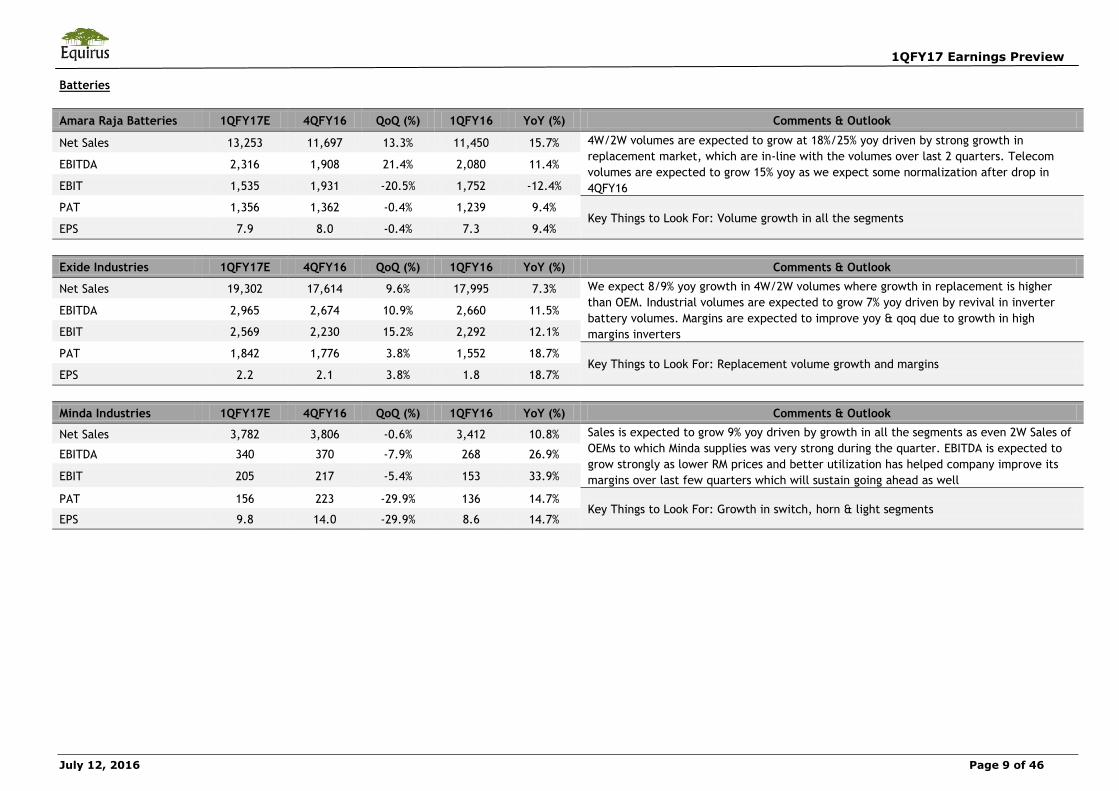

Batteries

Amara Raja Batteries 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 13,253 11,697 13.3% 11,450 15.7% 4W/2W volumes are expected to grow at 18%/25% yoy driven by strong growth in

replacement market, which are in-line with the volumes over last 2 quarters. Telecom

volumes are expected to grow 15% yoy as we expect some normalization after drop in

4QFY16

EBITDA 2,316 1,908 21.4% 2,080 11.4%

EBIT 1,535 1,931 -20.5% 1,752 -12.4%

PAT 1,356 1,362 -0.4% 1,239 9.4% Key Things to Look For: Volume growth in all the segments

EPS 7.9 8.0 -0.4% 7.3 9.4%

Exide Industries 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 19,302 17,614 9.6% 17,995 7.3% We expect 8/9% yoy growth in 4W/2W volumes where growth in replacement is higher

than OEM. Industrial volumes are expected to grow 7% yoy driven by revival in inverter

battery volumes. Margins are expected to improve yoy & qoq due to growth in high

margins inverters

EBITDA 2,965 2,674 10.9% 2,660 11.5%

EBIT 2,569 2,230 15.2% 2,292 12.1%

PAT 1,842 1,776 3.8% 1,552 18.7% Key Things to Look For: Replacement volume growth and margins

EPS 2.2 2.1 3.8% 1.8 18.7%

Minda Industries 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 3,782 3,806 -0.6% 3,412 10.8% Sales is expected to grow 9% yoy driven by growth in all the segments as even 2W Sales of

OEMs to which Minda supplies was very strong during the quarter. EBITDA is expected to

grow strongly as lower RM prices and better utilization has helped company improve its

margins over last few quarters which will sustain going ahead as well

EBITDA 340 370 -7.9% 268 26.9%

EBIT 205 217 -5.4% 153 33.9%

PAT 156 223 -29.9% 136 14.7% Key Things to Look For: Growth in switch, horn & light segments

EPS 9.8 14.0 -29.9% 8.6 14.7%

1QFY17 Earnings Preview

July 12, 2016 Page 10 of 46

Automobiles

Atul Auto 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 930 1,297 -28.3% 1,068 -12.9% Volumes have declined 14% yoy due to VAT issues in its largest market during the month

of April and demand weakness in Gujarat and Northern markets where Atul is stronger.

This will lead to Sales as well as PAT decline yoy EBITDA 106 173 -38.8% 119 -10.8%

EBIT 91 160 -43.2% 106 -13.8%

PAT 62 109 -42.6% 71 -12.3% Key Things to Look For: Gross margins

EPS 2.8 4.8 -42.6% 3.2 -14.1%

Bajaj Auto 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 59,480 54,114 9.9% 56,135 6.0% Domestic 2W/3W volumes improved 13%/48% but export 2W/3W volumes declined

17%/46% due to demand and currency availability issues in Africa. Export is expected to

contribute 36% of total Sales vs. 47% last year. We expect EBITDAM to contract 28bps qoq

due to poor mix

EBITDA 12,491 11,515 8.5% 11,397 9.6%

EBIT 11,706 10,754 8.8% 10,612 10.3%

PAT 9,588 8,031 19.4% 10,148 -5.5% Key Things to Look For: Margins

EPS 33.1 27.8 19.4% 35.1 -5.5%

Eicher Consol 1QFY17E 5QFY16 QoQ (%) 2QFY16 YoY (%) Comments & Outlook

Net Sales 37,093 37,649 -1.5% 29,167 27.2% RE volumes have grown 38% yoy, we expect EBITDAM to expand 278bps yoy due to RM

benefits and operating leverage. VECV volumes have grown 34% yoy led by growth in HD

and LMD segments, we expect subsidiary EBITDAM to improve 29bps yoy due to benefits of

operating leverage

EBITDA 6,211 6,399 -2.9% 4,316 43.9%

EBIT 5,123 5,313 -3.6% 3,522 45.5%

PAT 3,396 3,345 1.5% 2,218 53.1% Key Things to Look For: EBITDA Margins

EPS 125.3 123.4 1.5% 81.9 53.1%

Hero Motocorp 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 76,345 75,122 1.6% 69,553 9.8% Volumes have grown 6% yoy due to strong volume growth during the month of led driven

by demand revival in rural pockets. Margins are expected to improve 140bps yoy due to

gross margin expansion, margins will also likely improve 81bps qoq as marketing and other

expenses are lower in 1Q

EBITDA 12,567 11,758 6.9% 10,479 19.9%

EBIT 11,388 10,604 7.4% 9,449 20.5%

PAT 8,728 8,142 7.2% 7,503 16.3% Key Things to Look For: Margins

EPS 43.7 40.8 7.2% 37.6 16.3%

1QFY17 Earnings Preview

July 12, 2016 Page 11 of 46

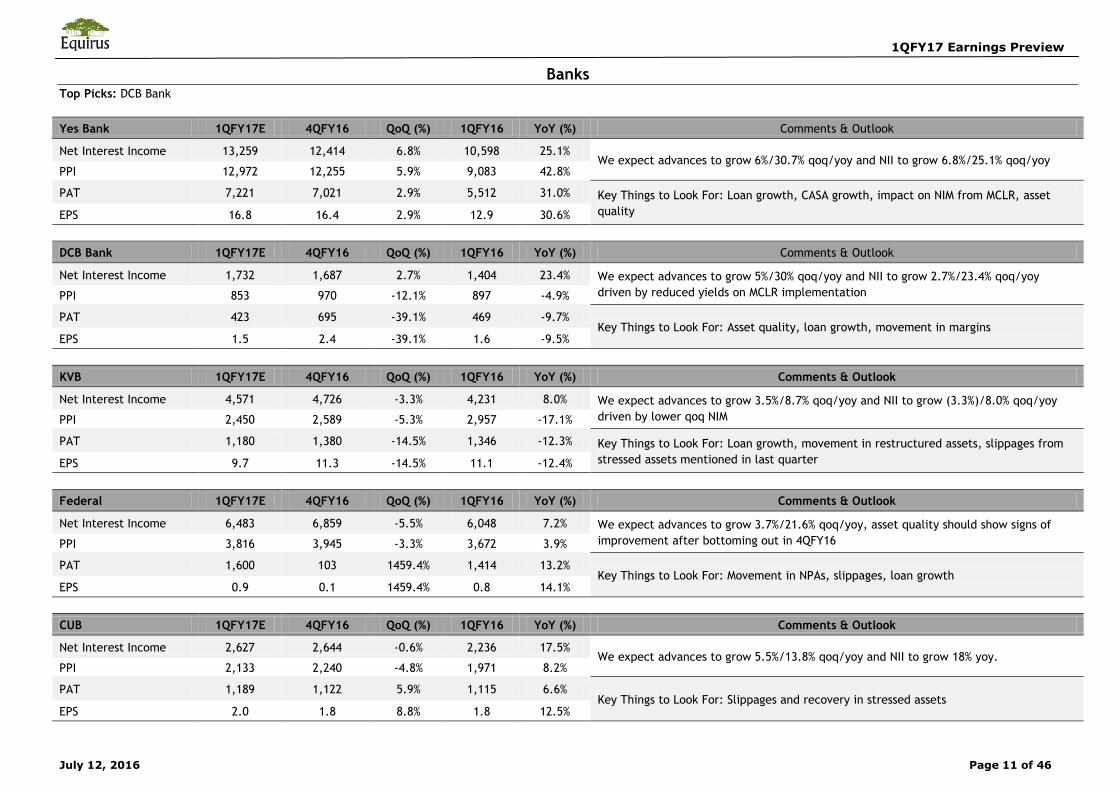

Banks

Top Picks: DCB Bank

Yes Bank 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Interest Income 13,259 12,414 6.8% 10,598 25.1% We expect advances to grow 6%/30.7% qoq/yoy and NII to grow 6.8%/25.1% qoq/yoy

PPI 12,972 12,255 5.9% 9,083 42.8%

PAT 7,221 7,021 2.9% 5,512 31.0% Key Things to Look For: Loan growth, CASA growth, impact on NIM from MCLR, asset

quality EPS 16.8 16.4 2.9% 12.9 30.6%

DCB Bank 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Interest Income 1,732 1,687 2.7% 1,404 23.4% We expect advances to grow 5%/30% qoq/yoy and NII to grow 2.7%/23.4% qoq/yoy

driven by reduced yields on MCLR implementation PPI 853 970 -12.1% 897 -4.9%

PAT 423 695 -39.1% 469 -9.7% Key Things to Look For: Asset quality, loan growth, movement in margins

EPS 1.5 2.4 -39.1% 1.6 -9.5%

KVB 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Interest Income 4,571 4,726 -3.3% 4,231 8.0% We expect advances to grow 3.5%/8.7% qoq/yoy and NII to grow (3.3%)/8.0% qoq/yoy

driven by lower qoq NIM PPI 2,450 2,589 -5.3% 2,957 -17.1%

PAT 1,180 1,380 -14.5% 1,346 -12.3% Key Things to Look For: Loan growth, movement in restructured assets, slippages from

stressed assets mentioned in last quarter EPS 9.7 11.3 -14.5% 11.1 -12.4%

Federal 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Interest Income 6,483 6,859 -5.5% 6,048 7.2% We expect advances to grow 3.7%/21.6% qoq/yoy, asset quality should show signs of

improvement after bottoming out in 4QFY16 PPI 3,816 3,945 -3.3% 3,672 3.9%

PAT 1,600 103 1459.4% 1,414 13.2% Key Things to Look For: Movement in NPAs, slippages, loan growth

EPS 0.9 0.1 1459.4% 0.8 14.1%

CUB 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Interest Income 2,627 2,644 -0.6% 2,236 17.5% We expect advances to grow 5.5%/13.8% qoq/yoy and NII to grow 18% yoy.

PPI 2,133 2,240 -4.8% 1,971 8.2%

PAT 1,189 1,122 5.9% 1,115 6.6% Key Things to Look For: Slippages and recovery in stressed assets

EPS 2.0 1.8 8.8% 1.8 12.5%

1QFY17 Earnings Preview

July 12, 2016 Page 12 of 46

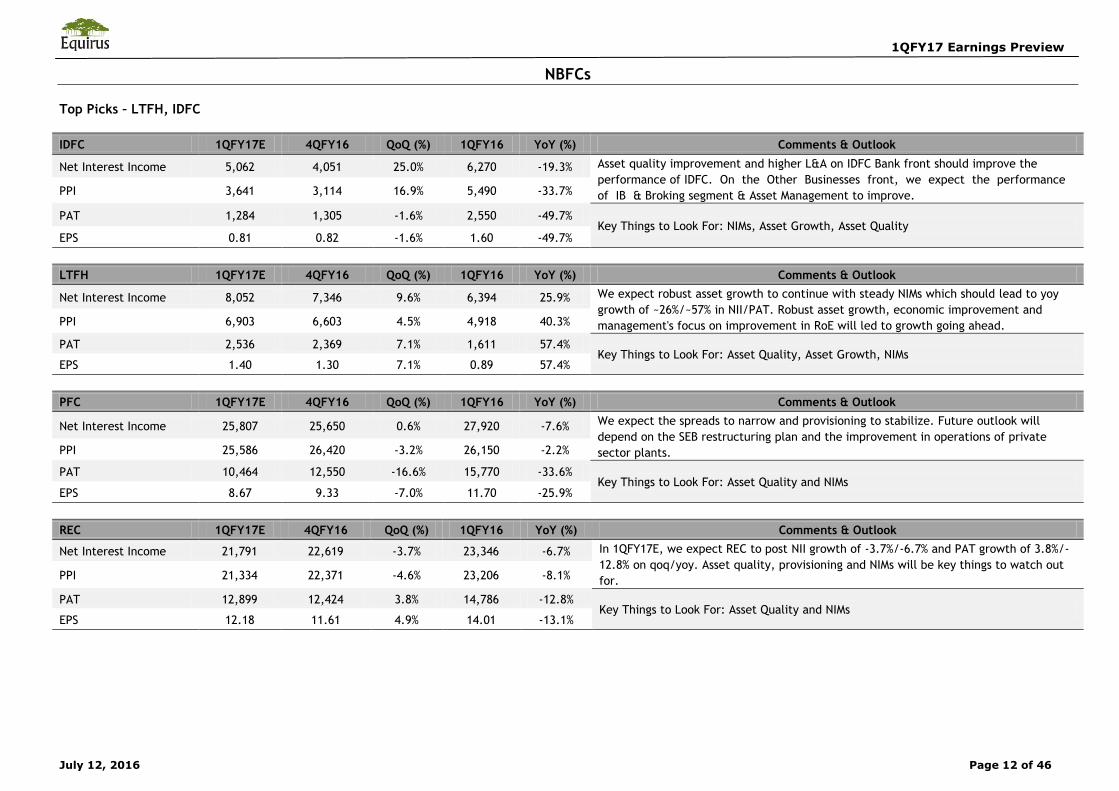

NBFCs

Top Picks – LTFH, IDFC

IDFC 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Interest Income 5,062 4,051 25.0% 6,270 -19.3% Asset quality improvement and higher L&A on IDFC Bank front should improve the

performance of IDFC. On the Other Businesses front, we expect the performance

of IB & Broking segment & Asset Management to improve. PPI 3,641 3,114 16.9% 5,490 -33.7%

PAT 1,284 1,305 -1.6% 2,550 -49.7% Key Things to Look For: NIMs, Asset Growth, Asset Quality

EPS 0.81 0.82 -1.6% 1.60 -49.7%

LTFH 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Interest Income 8,052 7,346 9.6% 6,394 25.9% We expect robust asset growth to continue with steady NIMs which should lead to yoy

growth of ~26%/~57% in NII/PAT. Robust asset growth, economic improvement and

management's focus on improvement in RoE will led to growth going ahead. PPI 6,903 6,603 4.5% 4,918 40.3%

PAT 2,536 2,369 7.1% 1,611 57.4% Key Things to Look For: Asset Quality, Asset Growth, NIMs

EPS 1.40 1.30 7.1% 0.89 57.4%

PFC 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Interest Income 25,807 25,650 0.6% 27,920 -7.6% We expect the spreads to narrow and provisioning to stabilize. Future outlook will

depend on the SEB restructuring plan and the improvement in operations of private

sector plants. PPI 25,586 26,420 -3.2% 26,150 -2.2%

PAT 10,464 12,550 -16.6% 15,770 -33.6% Key Things to Look For: Asset Quality and NIMs

EPS 8.67 9.33 -7.0% 11.70 -25.9%

REC 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Interest Income 21,791 22,619 -3.7% 23,346 -6.7% In 1QFY17E, we expect REC to post NII growth of -3.7%/-6.7% and PAT growth of 3.8%/-

12.8% on qoq/yoy. Asset quality, provisioning and NIMs will be key things to watch out

for. PPI 21,334 22,371 -4.6% 23,206 -8.1%

PAT 12,899 12,424 3.8% 14,786 -12.8% Key Things to Look For: Asset Quality and NIMs

EPS 12.18 11.61 4.9% 14.01 -13.1%

1QFY17 Earnings Preview

July 12, 2016 Page 13 of 46

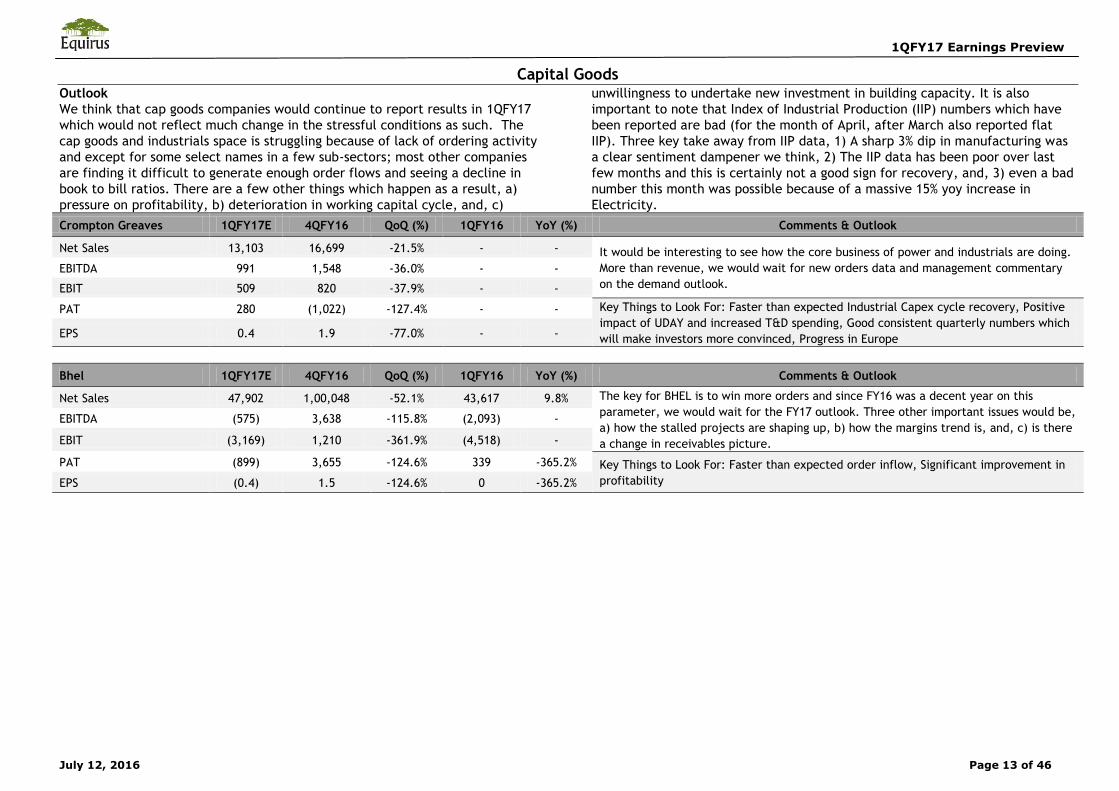

Capital GoodsOutlook

We think that cap goods companies would continue to report results in 1QFY17

which would not reflect much change in the stressful conditions as such. The

cap goods and industrials space is struggling because of lack of ordering activity

and except for some select names in a few sub-sectors; most other companies

are finding it difficult to generate enough order flows and seeing a decline in

book to bill ratios. There are a few other things which happen as a result, a)

pressure on profitability, b) deterioration in working capital cycle, and, c)

unwillingness to undertake new investment in building capacity. It is also

important to note that Index of Industrial Production (IIP) numbers which have

been reported are bad (for the month of April, after March also reported flat

IIP). Three key take away from IIP data, 1) A sharp 3% dip in manufacturing was

a clear sentiment dampener we think, 2) The IIP data has been poor over last

few months and this is certainly not a good sign for recovery, and, 3) even a bad

number this month was possible because of a massive 15% yoy increase in

Electricity.

Crompton Greaves 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 13,103 16,699 -21.5% - - It would be interesting to see how the core business of power and industrials are doing.

More than revenue, we would wait for new orders data and management commentary

on the demand outlook. EBITDA 991 1,548 -36.0% - -

EBIT 509 820 -37.9% - -

PAT 280 (1,022) -127.4% - - Key Things to Look For: Faster than expected Industrial Capex cycle recovery, Positive

impact of UDAY and increased T&D spending, Good consistent quarterly numbers which

will make investors more convinced, Progress in Europe EPS 0.4 1.9 -77.0% - -

Bhel 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 47,902 1,00,048 -52.1% 43,617 9.8% The key for BHEL is to win more orders and since FY16 was a decent year on this

parameter, we would wait for the FY17 outlook. Three other important issues would be,

a) how the stalled projects are shaping up, b) how the margins trend is, and, c) is there

a change in receivables picture.

EBITDA (575) 3,638 -115.8% (2,093) -

EBIT (3,169) 1,210 -361.9% (4,518) -

PAT (899) 3,655 -124.6% 339 -365.2% Key Things to Look For: Faster than expected order inflow, Significant improvement in

profitability EPS (0.4) 1.5 -124.6% 0 -365.2%

1QFY17 Earnings Preview

July 12, 2016 Page 14 of 46

ConstructionOutlook

Government has awarded projects covering ~13,000kms since it took office in

May’14. For FY17, total award target has been set at 25,000kms. NHAI has

awarded projects covering 4,171kms in FY16 vs. 3,060kms in FY15 & 1,437kms in

FY14. NHAI is targeting to construct 8,000kms for FY17 while MORTH+NHIDCL are

targeting 7,000kms. Total target for construction is 15,000kms vs. 6,000kms in

FY16. Additionally more than 1,000 projects covering 32,000kms are being

planned for improvement & construction. NHAI, MORTH and NHIDCL order

pipelines continue to remain buoyant with most of the upcoming projects being

in the EPC mode while the BOT space is seeing a smaller project pipeline.

Hybrid Annuity project pipeline remains robust with ~27 projects worth Rs.

347bn covering 1,815 kms being already lined up for next 6 months. State

projects in UP, Chhattisgarh and Bihar are expected to come up in next 12

months. Most of the players continue to stick their core competency of doing

EPC business in order to repair their stretched balance sheets but this has

resulted in over-crowding in the EPC space. We expect competition to continue

in the EPC & Hybrid segment but believe that the pie is large enough for all the

players to win enough orders for the coming 24 months. The BOT space is not

going to see that much competitive intensity for next 12/18 months and would

see bidding from 5-6 players only (case to case basis). In this space we are

bullish on Ashoka Buildcon, Sadbhav Engineering, PNC Infratech and Sadbhav

Infra

Top Picks: PNC Infratech, Ashoka Buildcon

Ashoka Buildcon (SA)

Estimate Rating TP

Absolute Rating LONG Relative Rating Overweight TP 202

Ashoka Buildcon (SA) 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 4,286 5,497 -22.0% 4,751 -9.8% Expect -10%/-22% top-line de-growth yoy/qoq due to slower than expected execution

pick-up at some of the new projects. EBITDA margin is expected to be lower at 12% vs.

14% yoy/qoq on account of lower execution. Recurring PAT to also take a hit due to

slower execution ramp-up

EBITDA 509 796 -36.1% 680 -25.2%

EBIT 330 616 -46.4% 542 -39.1%

PAT 162 681 -76.3% 465 -65.2% Key Things to Look For: Order Inflows, Execution run rate, reduction in Interest costs,

EBITDA margin improvement EPS 0.86 3.64 -76.3% 2.49 -65.2%

Change from Earlier

New Old

New Old

Ashoka Buildcon (SA) 2QFY16 3QFY16 4QFY16 1QFY17E 1QFY17E % Change

Ashoka Buildcon (SA) FY17E FY17E Change FY18E FY18E Change

Net Sales 4,676 4,435 5,497 4,286 5,178 -17%

Net Sales 20,740 22,946 -10% 26,180 28,960 -10%

EBITDA 652 524 796 509 611 -17%

EBITDA 2,507 2,763 -9% 3,058 3,384 -10%

EBIT 487 360 616 330 433 -24%

EBIT 1,798 2,054 -12% 2,338 2,663 -12%

PAT 315 227 587 162 236 -32%

PAT 1,007 1,187 -15% 1,465 1,676 -13%

EPS 1.68 1.21 3.64 0.86 1.26 -32%

EPS 5.4 6.3 -15% 7.8 9.0 -13%

1QFY17 Earnings Preview

July 12, 2016 Page 15 of 46

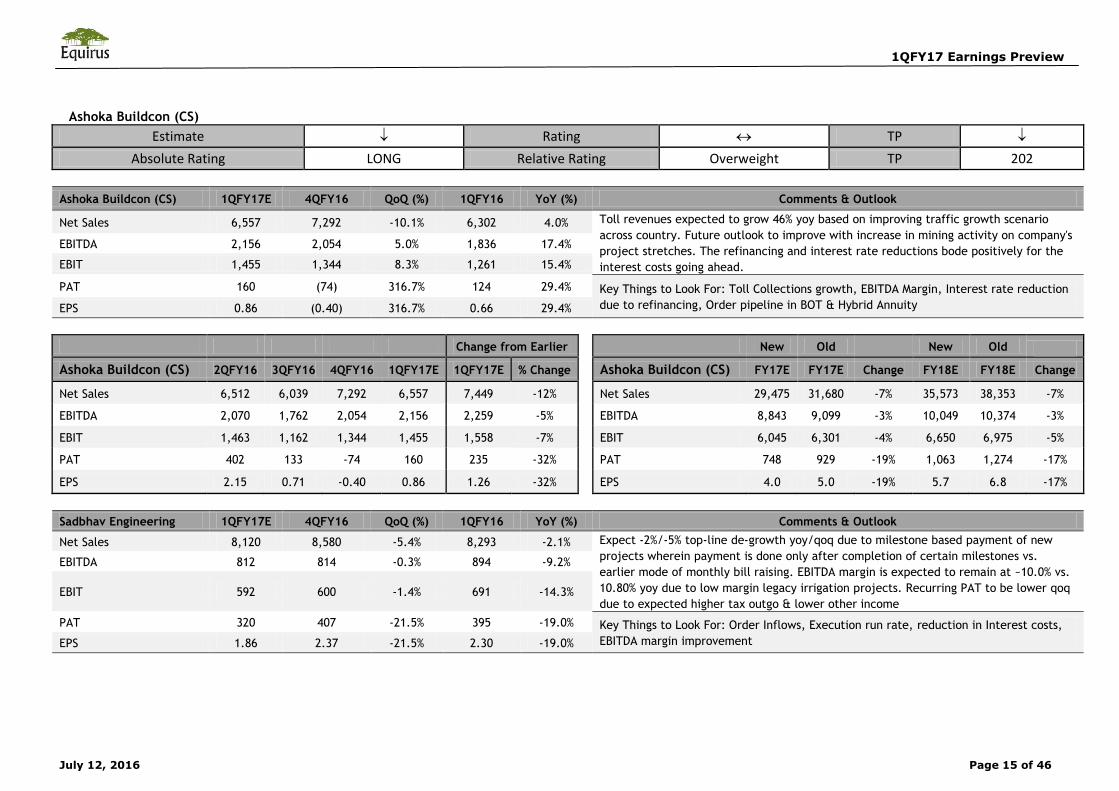

Ashoka Buildcon (CS)

Estimate Rating TP

Absolute Rating LONG Relative Rating Overweight TP 202

Ashoka Buildcon (CS) 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 6,557 7,292 -10.1% 6,302 4.0% Toll revenues expected to grow 46% yoy based on improving traffic growth scenario

across country. Future outlook to improve with increase in mining activity on company's

project stretches. The refinancing and interest rate reductions bode positively for the

interest costs going ahead.

EBITDA 2,156 2,054 5.0% 1,836 17.4%

EBIT 1,455 1,344 8.3% 1,261 15.4%

PAT 160 (74) 316.7% 124 29.4% Key Things to Look For: Toll Collections growth, EBITDA Margin, Interest rate reduction

due to refinancing, Order pipeline in BOT & Hybrid Annuity EPS 0.86 (0.40) 316.7% 0.66 29.4%

Change from Earlier

New Old

New Old

Ashoka Buildcon (CS) 2QFY16 3QFY16 4QFY16 1QFY17E 1QFY17E % Change

Ashoka Buildcon (CS) FY17E FY17E Change FY18E FY18E Change

Net Sales 6,512 6,039 7,292 6,557 7,449 -12%

Net Sales 29,475 31,680 -7% 35,573 38,353 -7%

EBITDA 2,070 1,762 2,054 2,156 2,259 -5%

EBITDA 8,843 9,099 -3% 10,049 10,374 -3%

EBIT 1,463 1,162 1,344 1,455 1,558 -7%

EBIT 6,045 6,301 -4% 6,650 6,975 -5%

PAT 402 133 -74 160 235 -32%

PAT 748 929 -19% 1,063 1,274 -17%

EPS 2.15 0.71 -0.40 0.86 1.26 -32%

EPS 4.0 5.0 -19% 5.7 6.8 -17%

Sadbhav Engineering 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 8,120 8,580 -5.4% 8,293 -2.1% Expect -2%/-5% top-line de-growth yoy/qoq due to milestone based payment of new

projects wherein payment is done only after completion of certain milestones vs.

earlier mode of monthly bill raising. EBITDA margin is expected to remain at ~10.0% vs.

10.80% yoy due to low margin legacy irrigation projects. Recurring PAT to be lower qoq

due to expected higher tax outgo & lower other income

EBITDA 812 814 -0.3% 894 -9.2%

EBIT 592 600 -1.4% 691 -14.3%

PAT 320 407 -21.5% 395 -19.0% Key Things to Look For: Order Inflows, Execution run rate, reduction in Interest costs,

EBITDA margin improvement EPS 1.86 2.37 -21.5% 2.30 -19.0%

1QFY17 Earnings Preview

July 12, 2016 Page 16 of 46

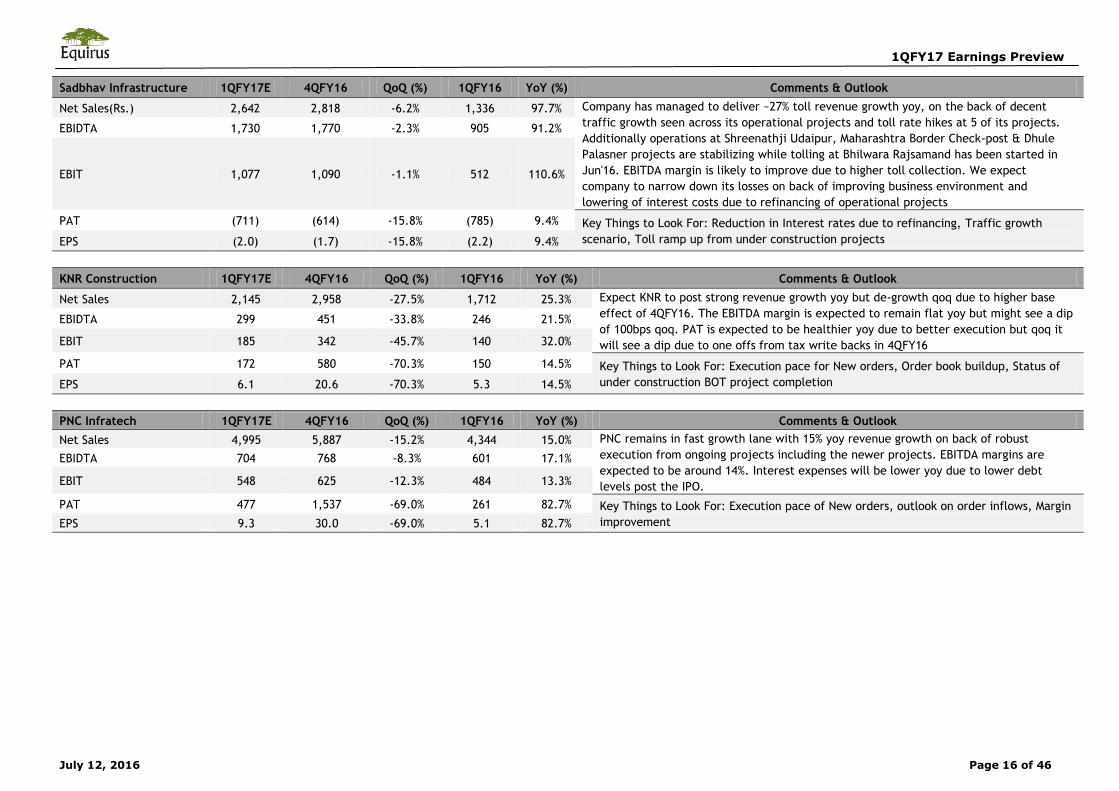

Sadbhav Infrastructure 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales(Rs.) 2,642 2,818 -6.2% 1,336 97.7% Company has managed to deliver ~27% toll revenue growth yoy, on the back of decent

traffic growth seen across its operational projects and toll rate hikes at 5 of its projects.

Additionally operations at Shreenathji Udaipur, Maharashtra Border Check-post & Dhule

Palasner projects are stabilizing while tolling at Bhilwara Rajsamand has been started in

Jun'16. EBITDA margin is likely to improve due to higher toll collection. We expect

company to narrow down its losses on back of improving business environment and

lowering of interest costs due to refinancing of operational projects

EBIDTA 1,730 1,770 -2.3% 905 91.2%

EBIT 1,077 1,090 -1.1% 512 110.6%

PAT (711) (614) -15.8% (785) 9.4% Key Things to Look For: Reduction in Interest rates due to refinancing, Traffic growth

scenario, Toll ramp up from under construction projects EPS (2.0) (1.7) -15.8% (2.2) 9.4% KNR Construction 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 2,145 2,958 -27.5% 1,712 25.3% Expect KNR to post strong revenue growth yoy but de-growth qoq due to higher base

effect of 4QFY16. The EBITDA margin is expected to remain flat yoy but might see a dip

of 100bps qoq. PAT is expected to be healthier yoy due to better execution but qoq it

will see a dip due to one offs from tax write backs in 4QFY16

EBIDTA 299 451 -33.8% 246 21.5%

EBIT 185 342 -45.7% 140 32.0%

PAT 172 580 -70.3% 150 14.5% Key Things to Look For: Execution pace for New orders, Order book buildup, Status of

under construction BOT project completion EPS 6.1 20.6 -70.3% 5.3 14.5% PNC Infratech 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 4,995 5,887 -15.2% 4,344 15.0% PNC remains in fast growth lane with 15% yoy revenue growth on back of robust

execution from ongoing projects including the newer projects. EBITDA margins are

expected to be around 14%. Interest expenses will be lower yoy due to lower debt

levels post the IPO.

EBIDTA 704 768 -8.3% 601 17.1%

EBIT 548 625 -12.3% 484 13.3%

PAT 477 1,537 -69.0% 261 82.7% Key Things to Look For: Execution pace of New orders, outlook on order inflows, Margin

improvement EPS 9.3 30.0 -69.0% 5.1 82.7%

1QFY17 Earnings Preview

July 12, 2016 Page 17 of 46

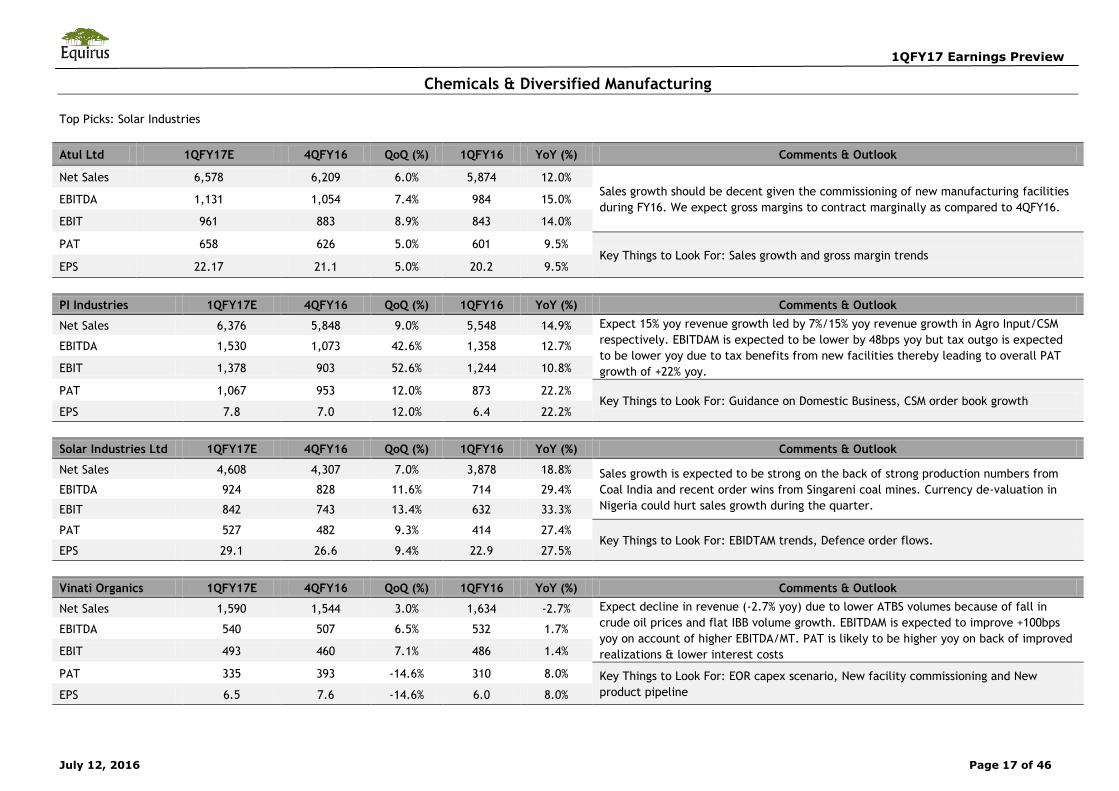

Chemicals & Diversified Manufacturing

Top Picks: Solar Industries

Atul Ltd 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 6,578 6,209 6.0% 5,874 12.0% Sales growth should be decent given the commissioning of new manufacturing facilities

during FY16. We expect gross margins to contract marginally as compared to 4QFY16. EBITDA 1,131 1,054 7.4% 984 15.0%

EBIT 961 883 8.9% 843 14.0%

PAT 658 626 5.0% 601 9.5% Key Things to Look For: Sales growth and gross margin trends

EPS 22.17 21.1 5.0% 20.2 9.5%

PI Industries 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 6,376 5,848 9.0% 5,548 14.9% Expect 15% yoy revenue growth led by 7%/15% yoy revenue growth in Agro Input/CSM

respectively. EBITDAM is expected to be lower by 48bps yoy but tax outgo is expected

to be lower yoy due to tax benefits from new facilities thereby leading to overall PAT

growth of +22% yoy.

EBITDA 1,530 1,073 42.6% 1,358 12.7%

EBIT 1,378 903 52.6% 1,244 10.8%

PAT 1,067 953 12.0% 873 22.2% Key Things to Look For: Guidance on Domestic Business, CSM order book growth

EPS 7.8 7.0 12.0% 6.4 22.2%

Solar Industries Ltd 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 4,608 4,307 7.0% 3,878 18.8% Sales growth is expected to be strong on the back of strong production numbers from

Coal India and recent order wins from Singareni coal mines. Currency de-valuation in

Nigeria could hurt sales growth during the quarter. EBITDA 924 828 11.6% 714 29.4%

EBIT 842 743 13.4% 632 33.3%

PAT 527 482 9.3% 414 27.4% Key Things to Look For: EBIDTAM trends, Defence order flows.

EPS 29.1 26.6 9.4% 22.9 27.5%

Vinati Organics 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 1,590 1,544 3.0% 1,634 -2.7% Expect decline in revenue (-2.7% yoy) due to lower ATBS volumes because of fall in

crude oil prices and flat IBB volume growth. EBITDAM is expected to improve +100bps

yoy on account of higher EBITDA/MT. PAT is likely to be higher yoy on back of improved

realizations & lower interest costs

EBITDA 540 507 6.5% 532 1.7%

EBIT 493 460 7.1% 486 1.4%

PAT 335 393 -14.6% 310 8.0% Key Things to Look For: EOR capex scenario, New facility commissioning and New

product pipeline EPS 6.5 7.6 -14.6% 6.0 8.0%

1QFY17 Earnings Preview

July 12, 2016 Page 18 of 46

Consumer Goods Outlook

We believe that demand environment across all product categories have

started showing marginal recovery during 1QFY17. We expect strong margins

performance from Kajaria with EBITDAM of 19.5% (up ~260bps yoy) because

of lower power & fuel cost during 1QFY17. We expect EBITDA/PAT to grow

at 29%/35% yoy respectively. We expect CERA to post Sales/EBITDA/PAT

growth of 12%/14%/20% yoy respectively. We expect HSIL to post 5% top-line

growth aided by new product launches. PAT could grow by ~40% yoy due to

EBITDAM expansion & lower interest outgo. Pokarna is expected to deliver

yet another strong operational performance during 1QFY17 with PAT growth

of 37% yoy.

Subdued demand environment in the FMCG space will continue to weigh on

the performance of the companies and promotional activities are expected

to be reduced in categories like biscuits to protect margins. Amongst our

coverage we expect majority of the companies to post decent growth in

profitability driven by operating leverage and reduced promotional

activities. We expect volume growth for Britannia, Marico, Asian Paints and

P&G Hygiene. Our top picks in the sector are Britannia & P&G Hygiene

Among the Consumer Durable space, we believe that the companies with

presence in the air conditioners, air coolers and refrigerators categories

could witness strong volume growth on account of favorable weather

conditions. From our coverage universe, we expect Symphony Ltd and

Hitachi to register healthy volumes during the quarter.

We believe the momentum gained in volumes during 2HFY16 to continue in

1QFY17 as well. We expect healthy volumes for the companies in the wires

& cables space. We reiterate our positive stance on Finolex cables from our

coverage universe.

Top Picks: Finolex Cables, Britannia, P&G Hygiene, Cera Sanitaryware,

Pokarna, Navneet Education, HSIL

Asian Paints 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 39,988 39,713 0.7% 36,235 10.4% We expect volume growth to remain strong during the current quarter while gross

margins could decline marginally on qoq basis with the recent increase in prices of

crude oil. EBITDA 7,669 7,037 9.0% 6,835 12.2%

EBIT 6,822 6,284 8.6% 6,142 11.1%

PAT 4,796 4,088 17.3% 4,552 5.4% Key Things to Look For: Outlook on demand environment

EPS 5.0 4.3 17.3% 4.7 5.4%

Bajaj Corp 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 2,126 2,283 -6.9% 2,191 -3.0% We expect some pressure on the top-line on account of subdued demand environment in

rural markets. However, we expect margins to expand (yoy) mainly due to favorable

raw material prices. EBITDA 697 756 -7.7% 664 5.1%

EBIT 566 626 -9.5% 536 5.7%

PAT 502 540 -7.2% 475 5.6% Key Things to Look For: Outlook on demand environment

EPS 3.4 3.7 -7.2% 3.2 5.6%

Berger Paints 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 12,308 11,297 9.0% 11,212 9.8% We expect healthy top-line for the company in the current quarter. We expect margins

on yoy basis to improve on the back of favorable raw material prices and favorable

product mix. EBITDA 1,848 1,594 16.0% 1,494 23.7%

EBIT 1,593 1,344 18.6% 1,252 27.3%

PAT 1,098 928 18.4% 773 42.0% Key Things to Look For: Outlook on demand environment

EPS 1.6 1.3 18.5% 1.1 42.3%

1QFY17 Earnings Preview

July 12, 2016 Page 19 of 46

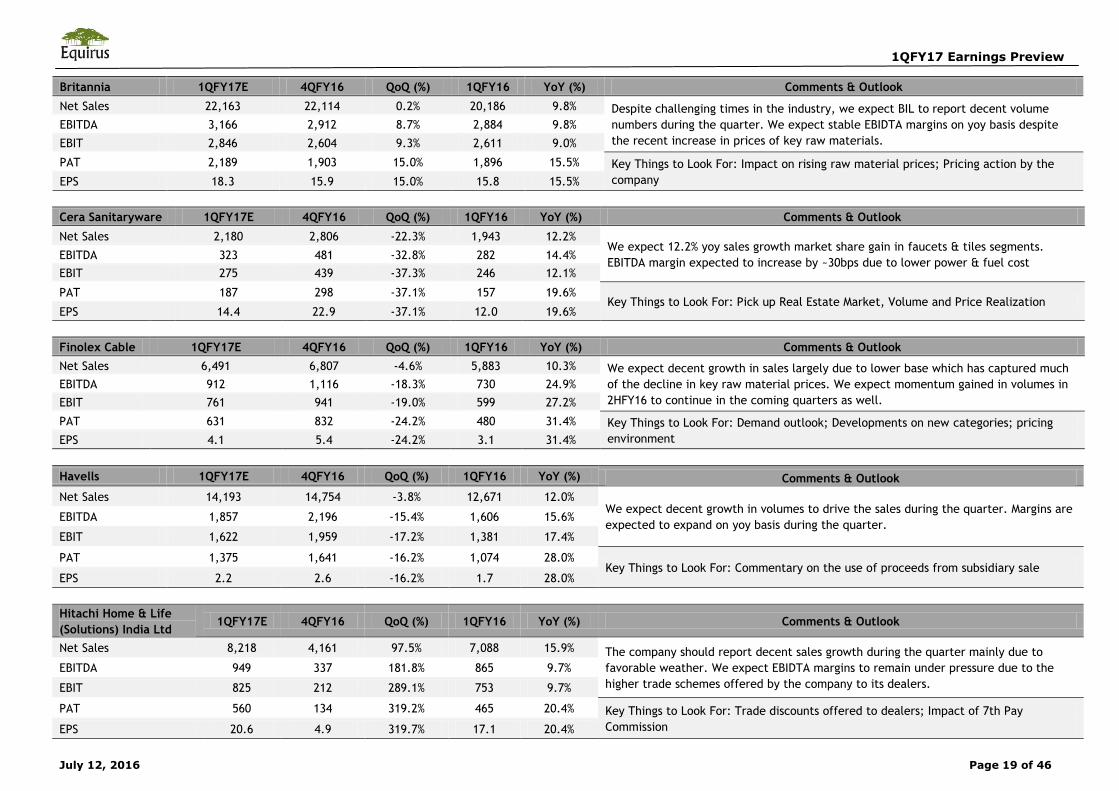

Britannia 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 22,163 22,114 0.2% 20,186 9.8% Despite challenging times in the industry, we expect BIL to report decent volume

numbers during the quarter. We expect stable EBIDTA margins on yoy basis despite

the recent increase in prices of key raw materials. EBITDA 3,166 2,912 8.7% 2,884 9.8% EBIT 2,846 2,604 9.3% 2,611 9.0%

PAT 2,189 1,903 15.0% 1,896 15.5% Key Things to Look For: Impact on rising raw material prices; Pricing action by the

company EPS 18.3 15.9 15.0% 15.8 15.5%

Cera Sanitaryware 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 2,180 2,806 -22.3% 1,943 12.2% We expect 12.2% yoy sales growth market share gain in faucets & tiles segments.

EBITDA margin expected to increase by ~30bps due to lower power & fuel cost EBITDA 323 481 -32.8% 282 14.4% EBIT 275 439 -37.3% 246 12.1%

PAT 187 298 -37.1% 157 19.6% Key Things to Look For: Pick up Real Estate Market, Volume and Price Realization

EPS 14.4 22.9 -37.1% 12.0 19.6% Finolex Cable 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 6,491 6,807 -4.6% 5,883 10.3% We expect decent growth in sales largely due to lower base which has captured much

of the decline in key raw material prices. We expect momentum gained in volumes in

2HFY16 to continue in the coming quarters as well. EBITDA 912 1,116 -18.3% 730 24.9% EBIT 761 941 -19.0% 599 27.2%

PAT 631 832 -24.2% 480 31.4% Key Things to Look For: Demand outlook; Developments on new categories; pricing

environment EPS 4.1 5.4 -24.2% 3.1 31.4%

Havells 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook Net Sales 14,193 14,754 -3.8% 12,671 12.0%

We expect decent growth in volumes to drive the sales during the quarter. Margins are

expected to expand on yoy basis during the quarter. EBITDA 1,857 2,196 -15.4% 1,606 15.6%

EBIT 1,622 1,959 -17.2% 1,381 17.4%

PAT 1,375 1,641 -16.2% 1,074 28.0% Key Things to Look For: Commentary on the use of proceeds from subsidiary sale

EPS 2.2 2.6 -16.2% 1.7 28.0%

Hitachi Home & Life

(Solutions) India Ltd 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 8,218 4,161 97.5% 7,088 15.9% The company should report decent sales growth during the quarter mainly due to

favorable weather. We expect EBIDTA margins to remain under pressure due to the

higher trade schemes offered by the company to its dealers. EBITDA 949 337 181.8% 865 9.7%

EBIT 825 212 289.1% 753 9.7%

PAT 560 134 319.2% 465 20.4% Key Things to Look For: Trade discounts offered to dealers; Impact of 7th Pay

Commission EPS 20.6 4.9 319.7% 17.1 20.4%

1QFY17 Earnings Preview

July 12, 2016 Page 20 of 46

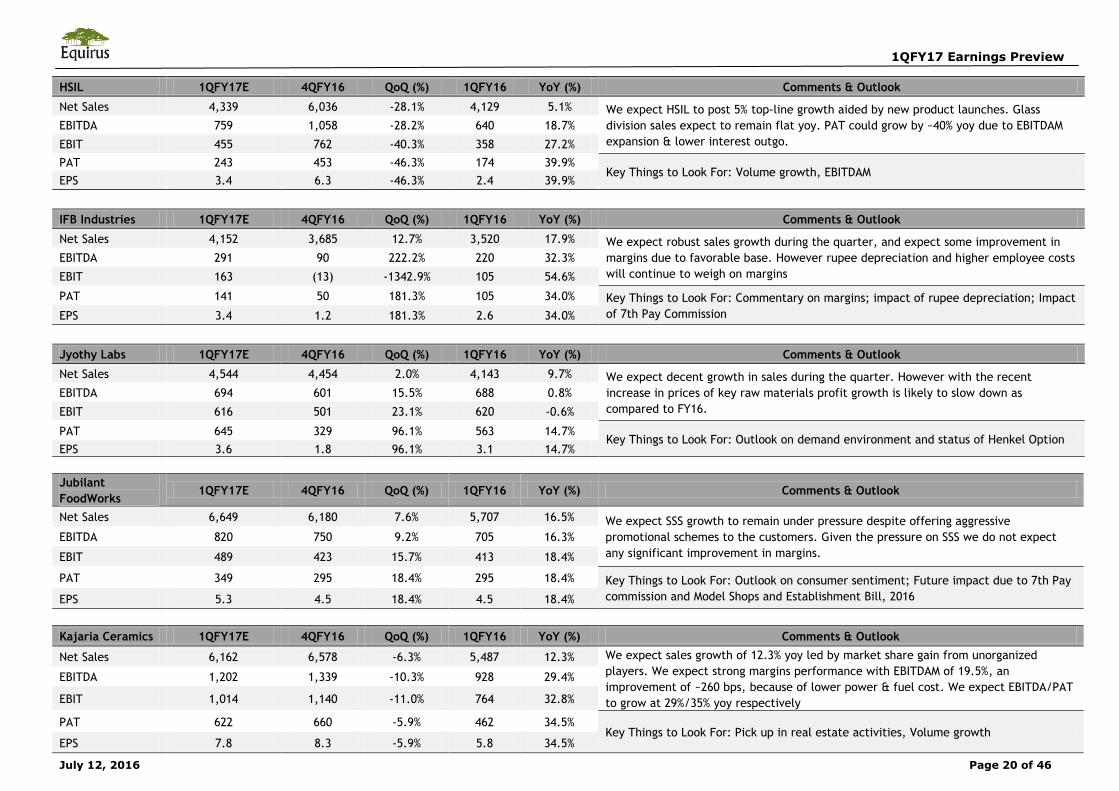

HSIL 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 4,339 6,036 -28.1% 4,129 5.1% We expect HSIL to post 5% top-line growth aided by new product launches. Glass

division sales expect to remain flat yoy. PAT could grow by ~40% yoy due to EBITDAM

expansion & lower interest outgo. EBITDA 759 1,058 -28.2% 640 18.7%

EBIT 455 762 -40.3% 358 27.2% PAT 243 453 -46.3% 174 39.9%

Key Things to Look For: Volume growth, EBITDAM EPS 3.4 6.3 -46.3% 2.4 39.9%

IFB Industries 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 4,152 3,685 12.7% 3,520 17.9% We expect robust sales growth during the quarter, and expect some improvement in

margins due to favorable base. However rupee depreciation and higher employee costs

will continue to weigh on margins EBITDA 291 90 222.2% 220 32.3%

EBIT 163 (13) -1342.9% 105 54.6%

PAT 141 50 181.3% 105 34.0% Key Things to Look For: Commentary on margins; impact of rupee depreciation; Impact

of 7th Pay Commission EPS 3.4 1.2 181.3% 2.6 34.0%

Jyothy Labs 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 4,544 4,454 2.0% 4,143 9.7% We expect decent growth in sales during the quarter. However with the recent

increase in prices of key raw materials profit growth is likely to slow down as

compared to FY16. EBITDA 694 601 15.5% 688 0.8%

EBIT 616 501 23.1% 620 -0.6%

PAT 645 329 96.1% 563 14.7% Key Things to Look For: Outlook on demand environment and status of Henkel Option

EPS 3.6 1.8 96.1% 3.1 14.7%

Jubilant

FoodWorks 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 6,649 6,180 7.6% 5,707 16.5% We expect SSS growth to remain under pressure despite offering aggressive

promotional schemes to the customers. Given the pressure on SSS we do not expect

any significant improvement in margins. EBITDA 820 750 9.2% 705 16.3%

EBIT 489 423 15.7% 413 18.4%

PAT 349 295 18.4% 295 18.4% Key Things to Look For: Outlook on consumer sentiment; Future impact due to 7th Pay

commission and Model Shops and Establishment Bill, 2016 EPS 5.3 4.5 18.4% 4.5 18.4%

Kajaria Ceramics 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 6,162 6,578 -6.3% 5,487 12.3% We expect sales growth of 12.3% yoy led by market share gain from unorganized

players. We expect strong margins performance with EBITDAM of 19.5%, an

improvement of ~260 bps, because of lower power & fuel cost. We expect EBITDA/PAT

to grow at 29%/35% yoy respectively

EBITDA 1,202 1,339 -10.3% 928 29.4%

EBIT 1,014 1,140 -11.0% 764 32.8%

PAT 622 660 -5.9% 462 34.5% Key Things to Look For: Pick up in real estate activities, Volume growth

EPS 7.8 8.3 -5.9% 5.8 34.5%

1QFY17 Earnings Preview

July 12, 2016 Page 21 of 46

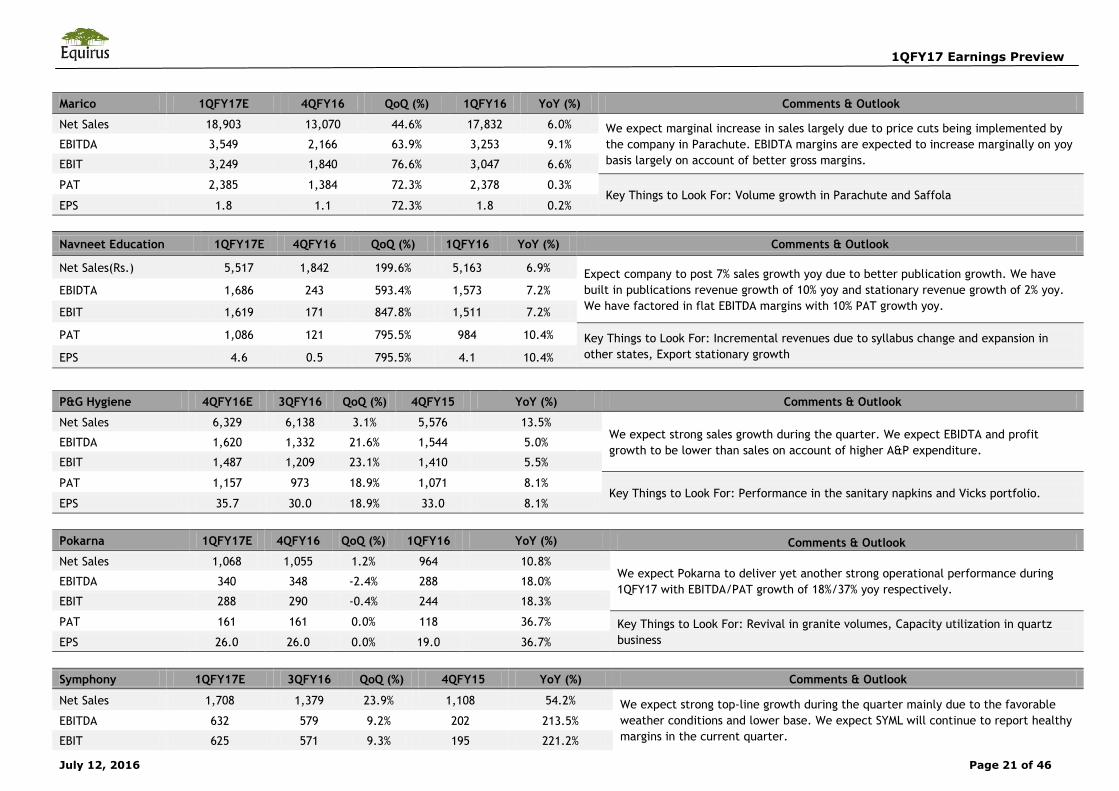

Marico 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 18,903 13,070 44.6% 17,832 6.0% We expect marginal increase in sales largely due to price cuts being implemented by

the company in Parachute. EBIDTA margins are expected to increase marginally on yoy

basis largely on account of better gross margins. EBITDA 3,549 2,166 63.9% 3,253 9.1%

EBIT 3,249 1,840 76.6% 3,047 6.6%

PAT 2,385 1,384 72.3% 2,378 0.3% Key Things to Look For: Volume growth in Parachute and Saffola

EPS 1.8 1.1 72.3% 1.8 0.2%

Navneet Education 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales(Rs.) 5,517 1,842 199.6% 5,163 6.9% Expect company to post 7% sales growth yoy due to better publication growth. We have

built in publications revenue growth of 10% yoy and stationary revenue growth of 2% yoy.

We have factored in flat EBITDA margins with 10% PAT growth yoy. EBIDTA 1,686 243 593.4% 1,573 7.2%

EBIT 1,619 171 847.8% 1,511 7.2%

PAT 1,086 121 795.5% 984 10.4% Key Things to Look For: Incremental revenues due to syllabus change and expansion in

other states, Export stationary growth EPS 4.6 0.5 795.5% 4.1 10.4%

P&G Hygiene 4QFY16E 3QFY16 QoQ (%) 4QFY15 YoY (%) Comments & Outlook

Net Sales 6,329 6,138 3.1% 5,576 13.5% We expect strong sales growth during the quarter. We expect EBIDTA and profit

growth to be lower than sales on account of higher A&P expenditure. EBITDA 1,620 1,332 21.6% 1,544 5.0%

EBIT 1,487 1,209 23.1% 1,410 5.5%

PAT 1,157 973 18.9% 1,071 8.1% Key Things to Look For: Performance in the sanitary napkins and Vicks portfolio.

EPS 35.7 30.0 18.9% 33.0 8.1%

Pokarna 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook Net Sales 1,068 1,055 1.2% 964 10.8%

We expect Pokarna to deliver yet another strong operational performance during

1QFY17 with EBITDA/PAT growth of 18%/37% yoy respectively. EBITDA 340 348 -2.4% 288 18.0%

EBIT 288 290 -0.4% 244 18.3%

PAT 161 161 0.0% 118 36.7% Key Things to Look For: Revival in granite volumes, Capacity utilization in quartz

business EPS 26.0 26.0 0.0% 19.0 36.7%

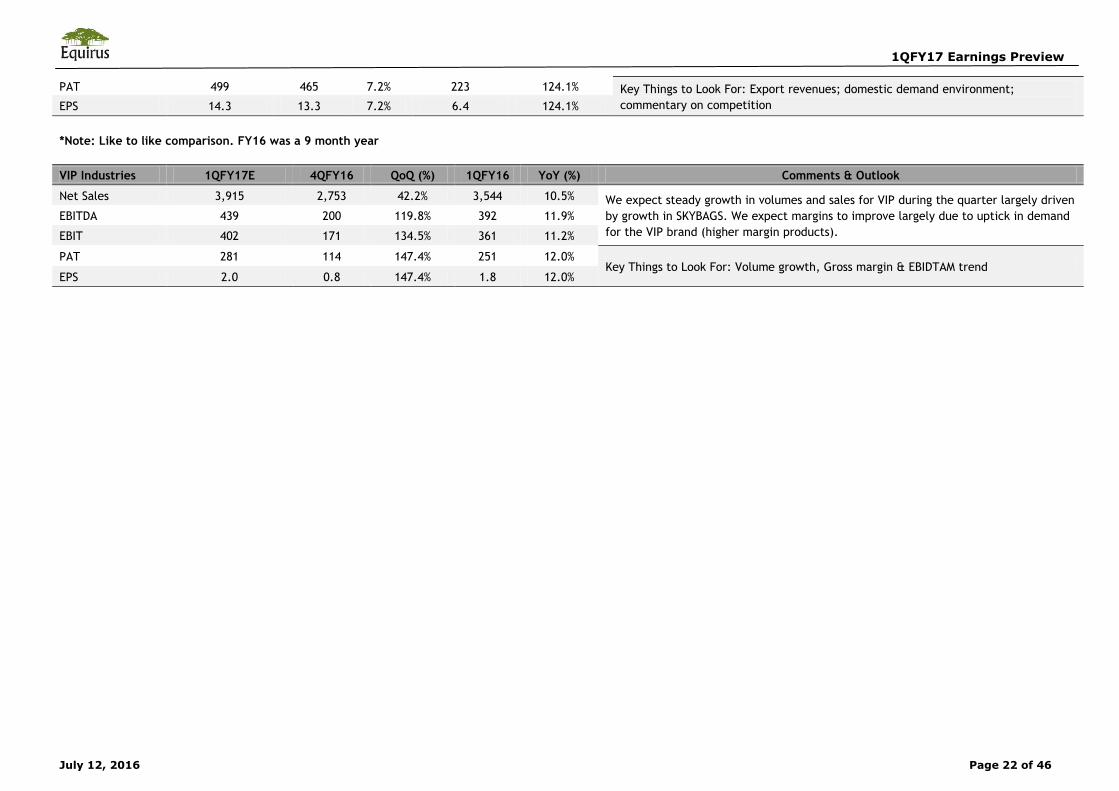

Symphony 1QFY17E 3QFY16 QoQ (%) 4QFY15 YoY (%) Comments & Outlook

Net Sales 1,708 1,379 23.9% 1,108 54.2% We expect strong top-line growth during the quarter mainly due to the favorable

weather conditions and lower base. We expect SYML will continue to report healthy

margins in the current quarter. EBITDA 632 579 9.2% 202 213.5%

EBIT 625 571 9.3% 195 221.2%

1QFY17 Earnings Preview

July 12, 2016 Page 22 of 46

PAT 499 465 7.2% 223 124.1% Key Things to Look For: Export revenues; domestic demand environment;

commentary on competition EPS 14.3 13.3 7.2% 6.4 124.1%

*Note: Like to like comparison. FY16 was a 9 month year

VIP Industries 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

Net Sales 3,915 2,753 42.2% 3,544 10.5% We expect steady growth in volumes and sales for VIP during the quarter largely driven

by growth in SKYBAGS. We expect margins to improve largely due to uptick in demand

for the VIP brand (higher margin products). EBITDA 439 200 119.8% 392 11.9%

EBIT 402 171 134.5% 361 11.2%

PAT 281 114 147.4% 251 12.0% Key Things to Look For: Volume growth, Gross margin & EBIDTAM trend

EPS 2.0 0.8 147.4% 1.8 12.0%

1QFY17 Earnings Preview

July 12, 2016 Page 23 of 46

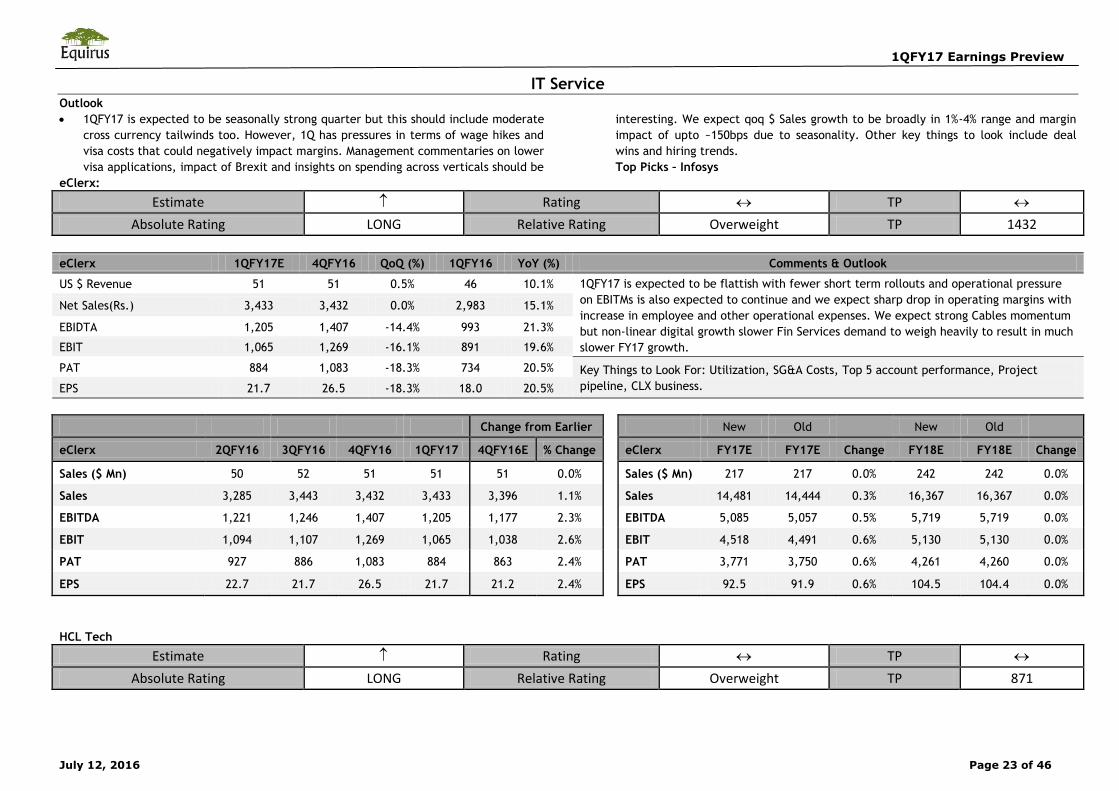

IT ServiceOutlook

1QFY17 is expected to be seasonally strong quarter but this should include moderate

cross currency tailwinds too. However, 1Q has pressures in terms of wage hikes and

visa costs that could negatively impact margins. Management commentaries on lower

visa applications, impact of Brexit and insights on spending across verticals should be

interesting. We expect qoq $ Sales growth to be broadly in 1%-4% range and margin

impact of upto ~150bps due to seasonality. Other key things to look include deal

wins and hiring trends.

Top Picks – Infosys

eClerx:

Estimate Rating TP

Absolute Rating LONG Relative Rating Overweight TP 1432

eClerx 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

US $ Revenue 51 51 0.5% 46 10.1% 1QFY17 is expected to be flattish with fewer short term rollouts and operational pressure

on EBITMs is also expected to continue and we expect sharp drop in operating margins with

increase in employee and other operational expenses. We expect strong Cables momentum

but non-linear digital growth slower Fin Services demand to weigh heavily to result in much

slower FY17 growth.

Net Sales(Rs.) 3,433 3,432 0.0% 2,983 15.1%

EBIDTA 1,205 1,407 -14.4% 993 21.3%

EBIT 1,065 1,269 -16.1% 891 19.6%

PAT 884 1,083 -18.3% 734 20.5% Key Things to Look For: Utilization, SG&A Costs, Top 5 account performance, Project

pipeline, CLX business. EPS 21.7 26.5 -18.3% 18.0 20.5%

Change from Earlier

New Old

New Old

eClerx 2QFY16 3QFY16 4QFY16 1QFY17 4QFY16E % Change

eClerx FY17E FY17E Change FY18E FY18E Change

Sales ($ Mn) 50 52 51 51 51 0.0%

Sales ($ Mn) 217 217 0.0% 242 242 0.0%

Sales 3,285 3,443 3,432 3,433 3,396 1.1%

Sales 14,481 14,444 0.3% 16,367 16,367 0.0%

EBITDA 1,221 1,246 1,407 1,205 1,177 2.3%

EBITDA 5,085 5,057 0.5% 5,719 5,719 0.0%

EBIT 1,094 1,107 1,269 1,065 1,038 2.6%

EBIT 4,518 4,491 0.6% 5,130 5,130 0.0%

PAT 927 886 1,083 884 863 2.4%

PAT 3,771 3,750 0.6% 4,261 4,260 0.0%

EPS 22.7 21.7 26.5 21.7 21.2 2.4%

EPS 92.5 91.9 0.6% 104.5 104.4 0.0%

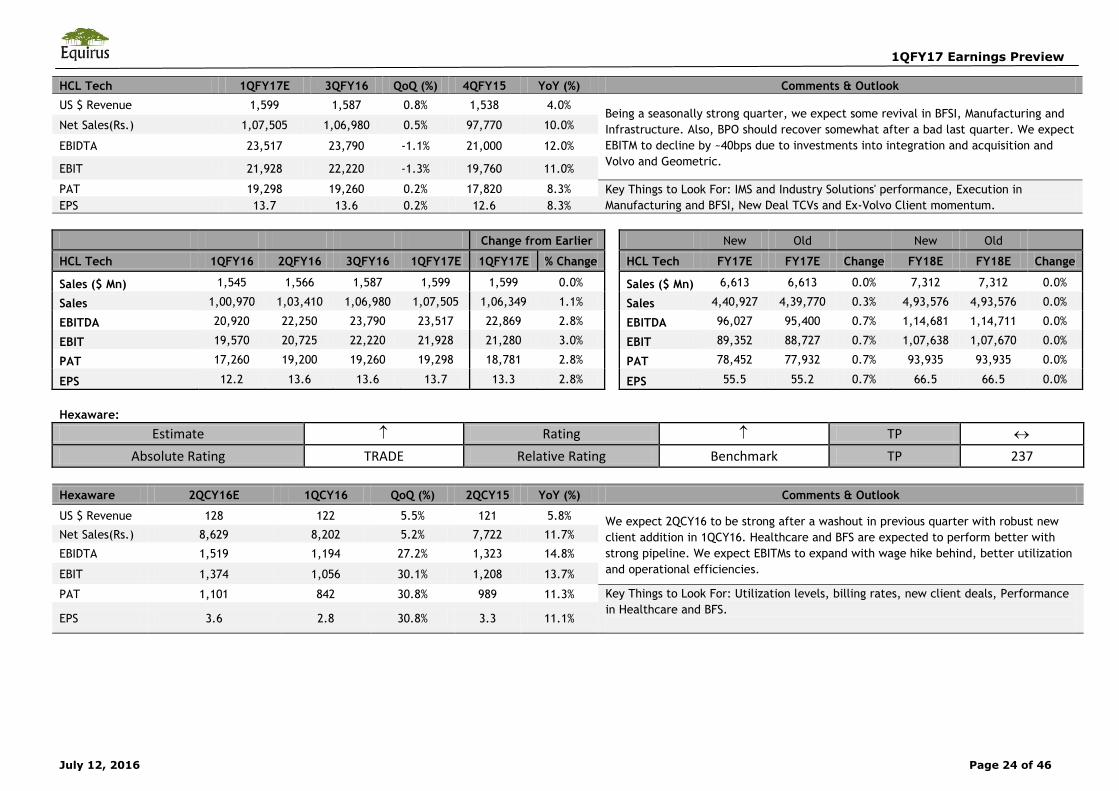

HCL Tech

Estimate Rating TP

Absolute Rating LONG Relative Rating Overweight TP 871

1QFY17 Earnings Preview

July 12, 2016 Page 24 of 46

HCL Tech 1QFY17E 3QFY16 QoQ (%) 4QFY15 YoY (%) Comments & Outlook

US $ Revenue 1,599 1,587 0.8% 1,538 4.0% Being a seasonally strong quarter, we expect some revival in BFSI, Manufacturing and

Infrastructure. Also, BPO should recover somewhat after a bad last quarter. We expect

EBITM to decline by ~40bps due to investments into integration and acquisition and

Volvo and Geometric.

Net Sales(Rs.) 1,07,505 1,06,980 0.5% 97,770 10.0%

EBIDTA 23,517 23,790 -1.1% 21,000 12.0%

EBIT 21,928 22,220 -1.3% 19,760 11.0%

PAT 19,298 19,260 0.2% 17,820 8.3% Key Things to Look For: IMS and Industry Solutions' performance, Execution in

Manufacturing and BFSI, New Deal TCVs and Ex-Volvo Client momentum. EPS 13.7 13.6 0.2% 12.6 8.3%

Change from Earlier

New Old

New Old

HCL Tech 1QFY16 2QFY16 3QFY16 1QFY17E 1QFY17E % Change

HCL Tech FY17E FY17E Change FY18E FY18E Change

Sales ($ Mn) 1,545 1,566 1,587 1,599 1,599 0.0%

Sales ($ Mn) 6,613 6,613 0.0% 7,312 7,312 0.0%

Sales 1,00,970 1,03,410 1,06,980 1,07,505 1,06,349 1.1%

Sales 4,40,927 4,39,770 0.3% 4,93,576 4,93,576 0.0%

EBITDA 20,920 22,250 23,790 23,517 22,869 2.8%

EBITDA 96,027 95,400 0.7% 1,14,681 1,14,711 0.0%

EBIT 19,570 20,725 22,220 21,928 21,280 3.0%

EBIT 89,352 88,727 0.7% 1,07,638 1,07,670 0.0%

PAT 17,260 19,200 19,260 19,298 18,781 2.8%

PAT 78,452 77,932 0.7% 93,935 93,935 0.0%

EPS 12.2 13.6 13.6 13.7 13.3 2.8%

EPS 55.5 55.2 0.7% 66.5 66.5 0.0%

Hexaware:

Estimate Rating TP

Absolute Rating TRADE Relative Rating Benchmark TP 237

Hexaware 2QCY16E 1QCY16 QoQ (%) 2QCY15 YoY (%) Comments & Outlook

US $ Revenue 128 122 5.5% 121 5.8% We expect 2QCY16 to be strong after a washout in previous quarter with robust new

client addition in 1QCY16. Healthcare and BFS are expected to perform better with

strong pipeline. We expect EBITMs to expand with wage hike behind, better utilization

and operational efficiencies.

Net Sales(Rs.) 8,629 8,202 5.2% 7,722 11.7%

EBIDTA 1,519 1,194 27.2% 1,323 14.8%

EBIT 1,374 1,056 30.1% 1,208 13.7%

PAT 1,101 842 30.8% 989 11.3% Key Things to Look For: Utilization levels, billing rates, new client deals, Performance

in Healthcare and BFS.

EPS 3.6 2.8 30.8% 3.3 11.1%

1QFY17 Earnings Preview

July 12, 2016 Page 25 of 46

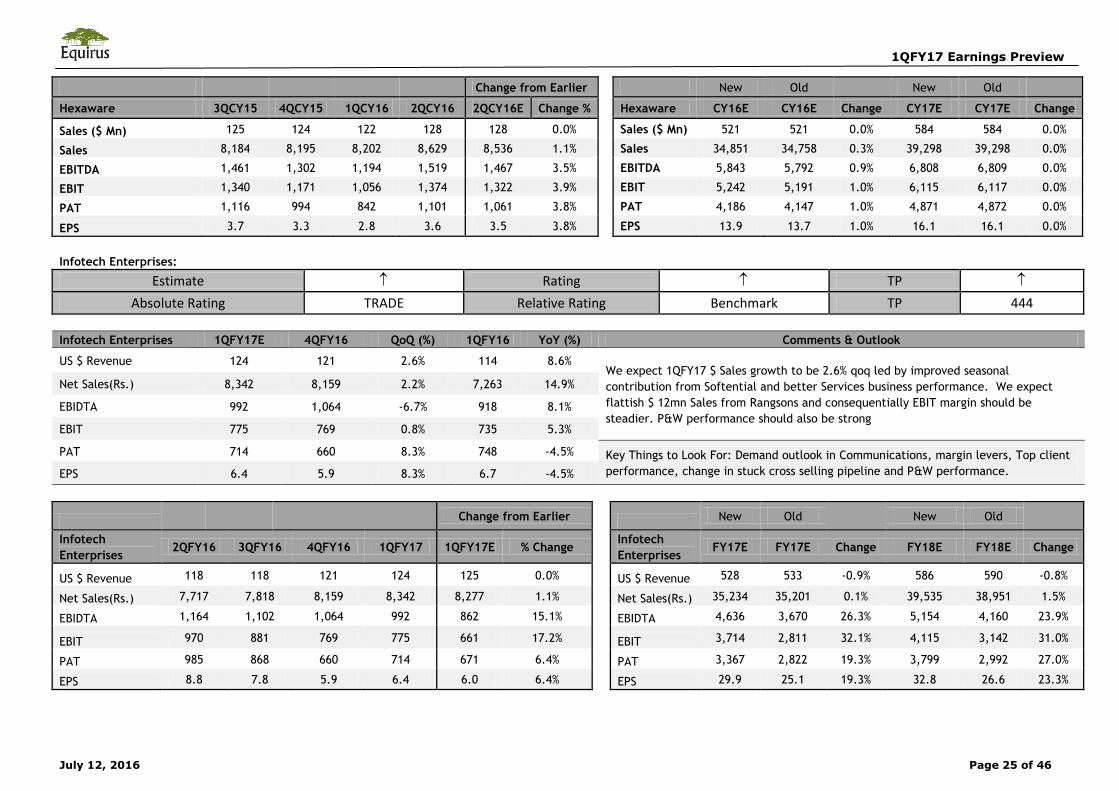

Change from Earlier

New Old

New Old

Hexaware 3QCY15 4QCY15 1QCY16 2QCY16 2QCY16E Change %

Hexaware CY16E CY16E Change CY17E CY17E Change

Sales ($ Mn) 125 124 122 128 128 0.0%

Sales ($ Mn) 521 521 0.0% 584 584 0.0%

Sales 8,184 8,195 8,202 8,629 8,536 1.1%

Sales 34,851 34,758 0.3% 39,298 39,298 0.0%

EBITDA 1,461 1,302 1,194 1,519 1,467 3.5%

EBITDA 5,843 5,792 0.9% 6,808 6,809 0.0%

EBIT 1,340 1,171 1,056 1,374 1,322 3.9%

EBIT 5,242 5,191 1.0% 6,115 6,117 0.0%

PAT 1,116 994 842 1,101 1,061 3.8%

PAT 4,186 4,147 1.0% 4,871 4,872 0.0%

EPS 3.7 3.3 2.8 3.6 3.5 3.8%

EPS 13.9 13.7 1.0% 16.1 16.1 0.0%

Infotech Enterprises:

Estimate Rating TP

Absolute Rating TRADE Relative Rating Benchmark TP 444

Infotech Enterprises 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

US $ Revenue 124 121 2.6% 114 8.6% We expect 1QFY17 $ Sales growth to be 2.6% qoq led by improved seasonal

contribution from Softential and better Services business performance. We expect

flattish $ 12mn Sales from Rangsons and consequentially EBIT margin should be

steadier. P&W performance should also be strong

Net Sales(Rs.) 8,342 8,159 2.2% 7,263 14.9%

EBIDTA 992 1,064 -6.7% 918 8.1%

EBIT 775 769 0.8% 735 5.3%

PAT 714 660 8.3% 748 -4.5% Key Things to Look For: Demand outlook in Communications, margin levers, Top client

performance, change in stuck cross selling pipeline and P&W performance. EPS 6.4 5.9 8.3% 6.7 -4.5%

Change from Earlier

New Old

New Old

Infotech

Enterprises 2QFY16 3QFY16 4QFY16 1QFY17 1QFY17E % Change

Infotech

Enterprises FY17E FY17E Change FY18E FY18E Change

US $ Revenue 118 118 121 124 125 0.0%

US $ Revenue 528 533 -0.9% 586 590 -0.8%

Net Sales(Rs.) 7,717 7,818 8,159 8,342 8,277 1.1%

Net Sales(Rs.) 35,234 35,201 0.1% 39,535 38,951 1.5%

EBIDTA 1,164 1,102 1,064 992 862 15.1%

EBIDTA 4,636 3,670 26.3% 5,154 4,160 23.9%

EBIT 970 881 769 775 661 17.2%

EBIT 3,714 2,811 32.1% 4,115 3,142 31.0%

PAT 985 868 660 714 671 6.4%

PAT 3,367 2,822 19.3% 3,799 2,992 27.0%

EPS 8.8 7.8 5.9 6.4 6.0 6.4%

EPS 29.9 25.1 19.3% 32.8 26.6 23.3%

1QFY17 Earnings Preview

July 12, 2016 Page 26 of 46

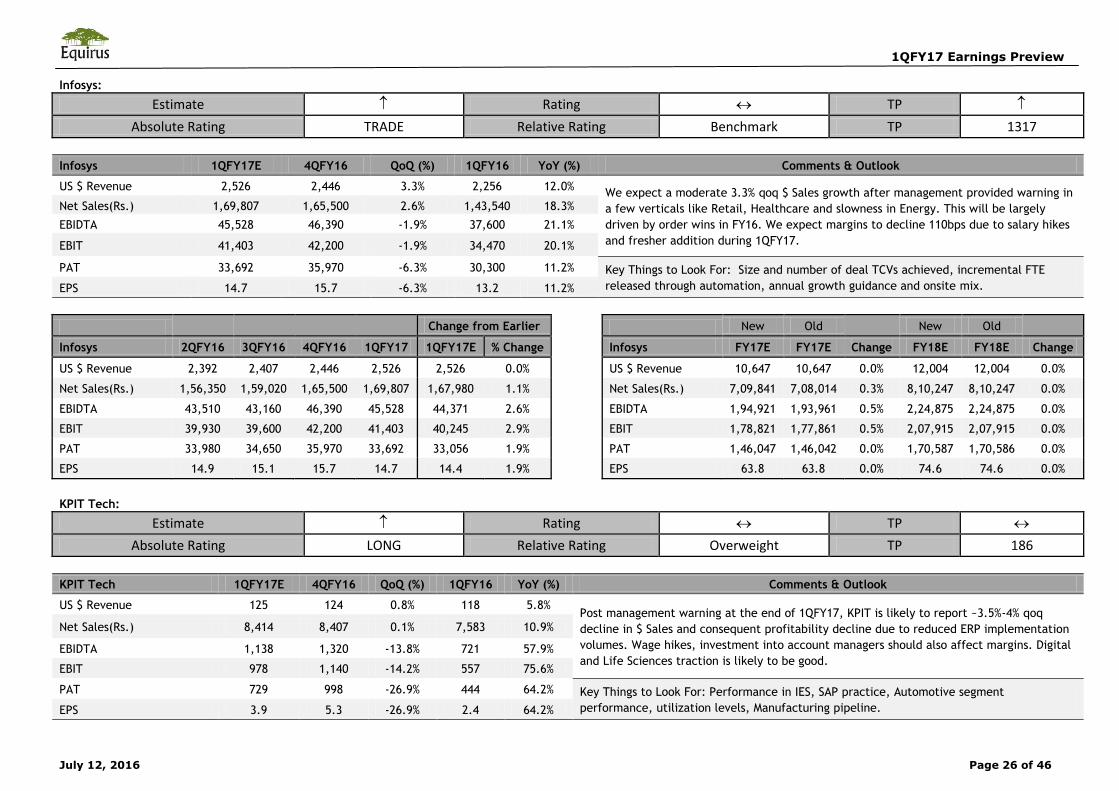

Infosys:

Estimate Rating TP

Absolute Rating TRADE Relative Rating Benchmark TP 1317

Infosys 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

US $ Revenue 2,526 2,446 3.3% 2,256 12.0% We expect a moderate 3.3% qoq $ Sales growth after management provided warning in

a few verticals like Retail, Healthcare and slowness in Energy. This will be largely

driven by order wins in FY16. We expect margins to decline 110bps due to salary hikes

and fresher addition during 1QFY17.

Net Sales(Rs.) 1,69,807 1,65,500 2.6% 1,43,540 18.3% EBIDTA 45,528 46,390 -1.9% 37,600 21.1%

EBIT 41,403 42,200 -1.9% 34,470 20.1%

PAT 33,692 35,970 -6.3% 30,300 11.2% Key Things to Look For: Size and number of deal TCVs achieved, incremental FTE

released through automation, annual growth guidance and onsite mix. EPS 14.7 15.7 -6.3% 13.2 11.2%

Change from Earlier

New Old

New Old

Infosys 2QFY16 3QFY16 4QFY16 1QFY17 1QFY17E % Change

Infosys FY17E FY17E Change FY18E FY18E Change

US $ Revenue 2,392 2,407 2,446 2,526 2,526 0.0%

US $ Revenue 10,647 10,647 0.0% 12,004 12,004 0.0%

Net Sales(Rs.) 1,56,350 1,59,020 1,65,500 1,69,807 1,67,980 1.1%

Net Sales(Rs.) 7,09,841 7,08,014 0.3% 8,10,247 8,10,247 0.0%

EBIDTA 43,510 43,160 46,390 45,528 44,371 2.6%

EBIDTA 1,94,921 1,93,961 0.5% 2,24,875 2,24,875 0.0%

EBIT 39,930 39,600 42,200 41,403 40,245 2.9%

EBIT 1,78,821 1,77,861 0.5% 2,07,915 2,07,915 0.0%

PAT 33,980 34,650 35,970 33,692 33,056 1.9%

PAT 1,46,047 1,46,042 0.0% 1,70,587 1,70,586 0.0%

EPS 14.9 15.1 15.7 14.7 14.4 1.9%

EPS 63.8 63.8 0.0% 74.6 74.6 0.0%

KPIT Tech:

Estimate Rating TP

Absolute Rating LONG Relative Rating Overweight TP 186

KPIT Tech 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

US $ Revenue 125 124 0.8% 118 5.8% Post management warning at the end of 1QFY17, KPIT is likely to report ~3.5%-4% qoq

decline in $ Sales and consequent profitability decline due to reduced ERP implementation

volumes. Wage hikes, investment into account managers should also affect margins. Digital

and Life Sciences traction is likely to be good.

Net Sales(Rs.) 8,414 8,407 0.1% 7,583 10.9%

EBIDTA 1,138 1,320 -13.8% 721 57.9%

EBIT 978 1,140 -14.2% 557 75.6%

PAT 729 998 -26.9% 444 64.2% Key Things to Look For: Performance in IES, SAP practice, Automotive segment

performance, utilization levels, Manufacturing pipeline. EPS 3.9 5.3 -26.9% 2.4 64.2%

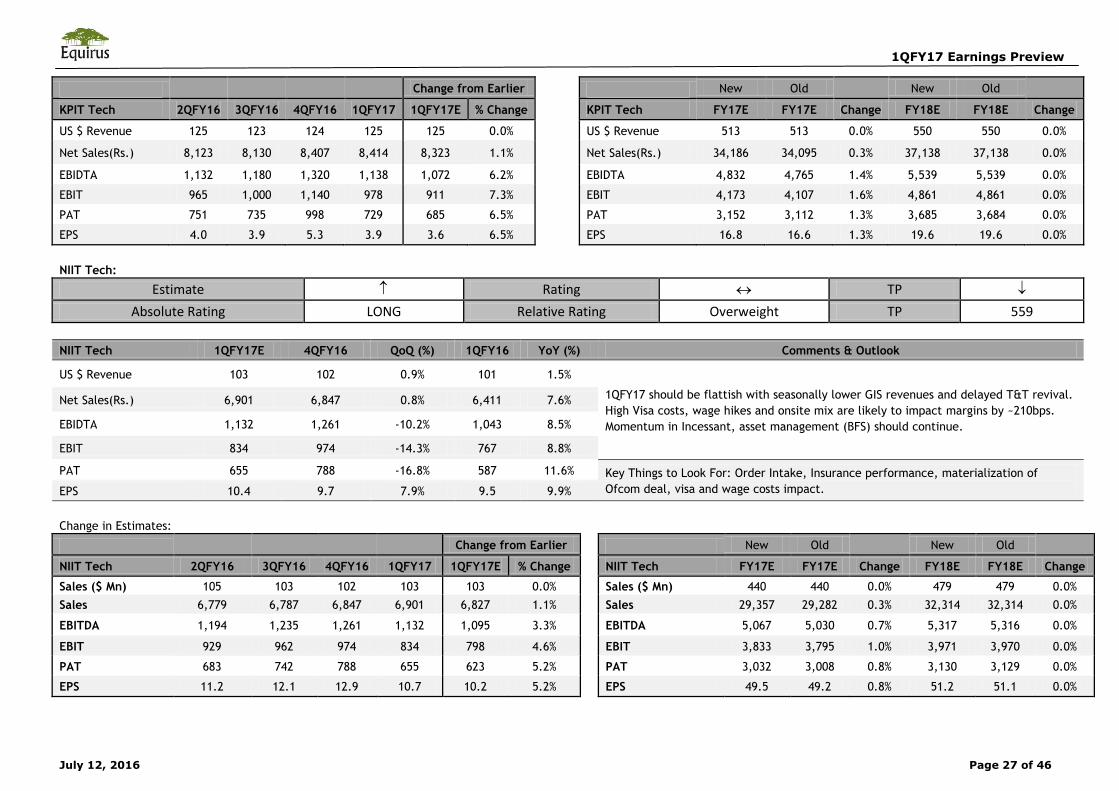

1QFY17 Earnings Preview

July 12, 2016 Page 27 of 46

Change from Earlier

New Old

New Old

KPIT Tech 2QFY16 3QFY16 4QFY16 1QFY17 1QFY17E % Change

KPIT Tech FY17E FY17E Change FY18E FY18E Change

US $ Revenue 125 123 124 125 125 0.0%

US $ Revenue 513 513 0.0% 550 550 0.0%

Net Sales(Rs.) 8,123 8,130 8,407 8,414 8,323 1.1%

Net Sales(Rs.) 34,186 34,095 0.3% 37,138 37,138 0.0%

EBIDTA 1,132 1,180 1,320 1,138 1,072 6.2%

EBIDTA 4,832 4,765 1.4% 5,539 5,539 0.0%

EBIT 965 1,000 1,140 978 911 7.3%

EBIT 4,173 4,107 1.6% 4,861 4,861 0.0%

PAT 751 735 998 729 685 6.5%

PAT 3,152 3,112 1.3% 3,685 3,684 0.0%

EPS 4.0 3.9 5.3 3.9 3.6 6.5%

EPS 16.8 16.6 1.3% 19.6 19.6 0.0%

NIIT Tech:

Estimate Rating TP

Absolute Rating LONG Relative Rating Overweight TP 559

NIIT Tech 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

US $ Revenue 103 102 0.9% 101 1.5%

1QFY17 should be flattish with seasonally lower GIS revenues and delayed T&T revival.

High Visa costs, wage hikes and onsite mix are likely to impact margins by ~210bps.

Momentum in Incessant, asset management (BFS) should continue.

Net Sales(Rs.) 6,901 6,847 0.8% 6,411 7.6%

EBIDTA 1,132 1,261 -10.2% 1,043 8.5%

EBIT 834 974 -14.3% 767 8.8%

PAT 655 788 -16.8% 587 11.6% Key Things to Look For: Order Intake, Insurance performance, materialization of

Ofcom deal, visa and wage costs impact. EPS 10.4 9.7 7.9% 9.5 9.9%

Change in Estimates:

Change from Earlier

New Old

New Old

NIIT Tech 2QFY16 3QFY16 4QFY16 1QFY17 1QFY17E % Change

NIIT Tech FY17E FY17E Change FY18E FY18E Change

Sales ($ Mn) 105 103 102 103 103 0.0%

Sales ($ Mn) 440 440 0.0% 479 479 0.0% Sales 6,779 6,787 6,847 6,901 6,827 1.1%

Sales 29,357 29,282 0.3% 32,314 32,314 0.0%

EBITDA 1,194 1,235 1,261 1,132 1,095 3.3%

EBITDA 5,067 5,030 0.7% 5,317 5,316 0.0%

EBIT 929 962 974 834 798 4.6%

EBIT 3,833 3,795 1.0% 3,971 3,970 0.0%

PAT 683 742 788 655 623 5.2%

PAT 3,032 3,008 0.8% 3,130 3,129 0.0%

EPS 11.2 12.1 12.9 10.7 10.2 5.2%

EPS 49.5 49.2 0.8% 51.2 51.1 0.0%

1QFY17 Earnings Preview

July 12, 2016 Page 28 of 46

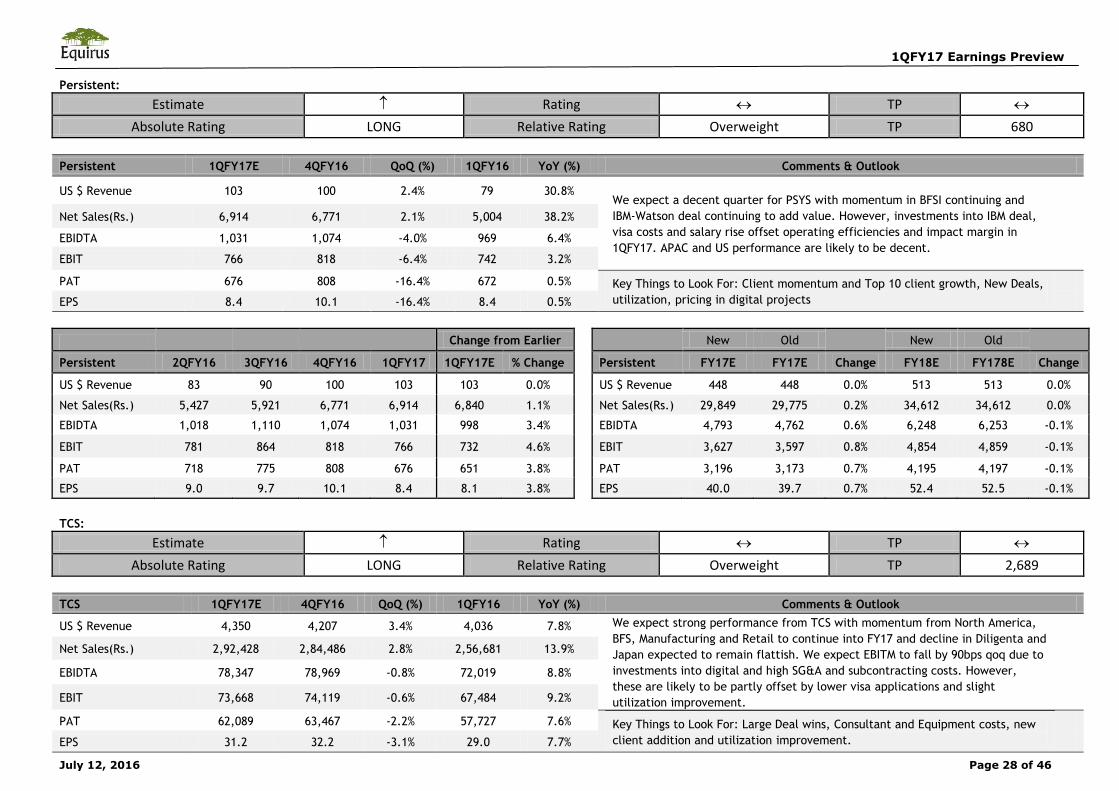

Persistent:

Estimate Rating TP

Absolute Rating LONG Relative Rating Overweight TP 680

Persistent 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

US $ Revenue 103 100 2.4% 79 30.8% We expect a decent quarter for PSYS with momentum in BFSI continuing and

IBM-Watson deal continuing to add value. However, investments into IBM deal,

visa costs and salary rise offset operating efficiencies and impact margin in

1QFY17. APAC and US performance are likely to be decent.

Net Sales(Rs.) 6,914 6,771 2.1% 5,004 38.2%

EBIDTA 1,031 1,074 -4.0% 969 6.4%

EBIT 766 818 -6.4% 742 3.2%

PAT 676 808 -16.4% 672 0.5% Key Things to Look For: Client momentum and Top 10 client growth, New Deals,

utilization, pricing in digital projects

EPS 8.4 10.1 -16.4% 8.4 0.5%

Change from Earlier

New Old

New Old

Persistent 2QFY16 3QFY16 4QFY16 1QFY17 1QFY17E % Change

Persistent FY17E FY17E Change FY18E FY178E Change

US $ Revenue 83 90 100 103 103 0.0%

US $ Revenue 448 448 0.0% 513 513 0.0%

Net Sales(Rs.) 5,427 5,921 6,771 6,914 6,840 1.1%

Net Sales(Rs.) 29,849 29,775 0.2% 34,612 34,612 0.0%

EBIDTA 1,018 1,110 1,074 1,031 998 3.4%

EBIDTA 4,793 4,762 0.6% 6,248 6,253 -0.1%

EBIT 781 864 818 766 732 4.6%

EBIT 3,627 3,597 0.8% 4,854 4,859 -0.1%

PAT 718 775 808 676 651 3.8%

PAT 3,196 3,173 0.7% 4,195 4,197 -0.1%

EPS 9.0 9.7 10.1 8.4 8.1 3.8%

EPS 40.0 39.7 0.7% 52.4 52.5 -0.1%

TCS:

Estimate Rating TP

Absolute Rating LONG Relative Rating Overweight TP 2,689

TCS 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

US $ Revenue 4,350 4,207 3.4% 4,036 7.8% We expect strong performance from TCS with momentum from North America,

BFS, Manufacturing and Retail to continue into FY17 and decline in Diligenta and

Japan expected to remain flattish. We expect EBITM to fall by 90bps qoq due to

investments into digital and high SG&A and subcontracting costs. However,

these are likely to be partly offset by lower visa applications and slight

utilization improvement.

Net Sales(Rs.) 2,92,428 2,84,486 2.8% 2,56,681 13.9%

EBIDTA 78,347 78,969 -0.8% 72,019 8.8%

EBIT 73,668 74,119 -0.6% 67,484 9.2%

PAT 62,089 63,467 -2.2% 57,727 7.6% Key Things to Look For: Large Deal wins, Consultant and Equipment costs, new

client addition and utilization improvement.

EPS 31.2 32.2 -3.1% 29.0 7.7%

1QFY17 Earnings Preview

July 12, 2016 Page 29 of 46

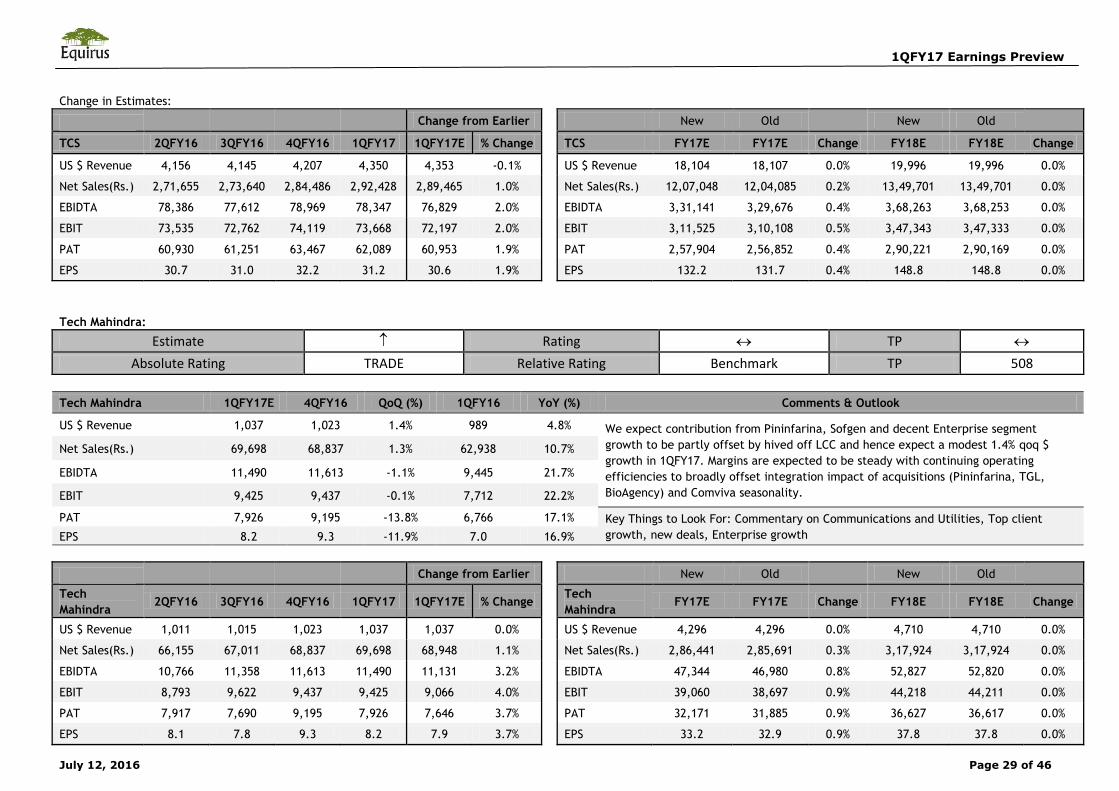

Change in Estimates:

Change from Earlier

New Old

New Old

TCS 2QFY16 3QFY16 4QFY16 1QFY17 1QFY17E % Change

TCS FY17E FY17E Change FY18E FY18E Change

US $ Revenue 4,156 4,145 4,207 4,350 4,353 -0.1%

US $ Revenue 18,104 18,107 0.0% 19,996 19,996 0.0%

Net Sales(Rs.) 2,71,655 2,73,640 2,84,486 2,92,428 2,89,465 1.0%

Net Sales(Rs.) 12,07,048 12,04,085 0.2% 13,49,701 13,49,701 0.0%

EBIDTA 78,386 77,612 78,969 78,347 76,829 2.0%

EBIDTA 3,31,141 3,29,676 0.4% 3,68,263 3,68,253 0.0%

EBIT 73,535 72,762 74,119 73,668 72,197 2.0%

EBIT 3,11,525 3,10,108 0.5% 3,47,343 3,47,333 0.0%

PAT 60,930 61,251 63,467 62,089 60,953 1.9%

PAT 2,57,904 2,56,852 0.4% 2,90,221 2,90,169 0.0%

EPS 30.7 31.0 32.2 31.2 30.6 1.9%

EPS 132.2 131.7 0.4% 148.8 148.8 0.0%

Tech Mahindra:

Estimate Rating TP

Absolute Rating TRADE Relative Rating Benchmark TP 508

Tech Mahindra 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

US $ Revenue 1,037 1,023 1.4% 989 4.8% We expect contribution from Pininfarina, Sofgen and decent Enterprise segment

growth to be partly offset by hived off LCC and hence expect a modest 1.4% qoq $

growth in 1QFY17. Margins are expected to be steady with continuing operating

efficiencies to broadly offset integration impact of acquisitions (Pininfarina, TGL,

BioAgency) and Comviva seasonality.

Net Sales(Rs.) 69,698 68,837 1.3% 62,938 10.7%

EBIDTA 11,490 11,613 -1.1% 9,445 21.7%

EBIT 9,425 9,437 -0.1% 7,712 22.2%

PAT 7,926 9,195 -13.8% 6,766 17.1% Key Things to Look For: Commentary on Communications and Utilities, Top client

growth, new deals, Enterprise growth EPS 8.2 9.3 -11.9% 7.0 16.9%

Change from Earlier

New Old

New Old

Tech

Mahindra 2QFY16 3QFY16 4QFY16 1QFY17 1QFY17E % Change

Tech

Mahindra FY17E FY17E Change FY18E FY18E Change

US $ Revenue 1,011 1,015 1,023 1,037 1,037 0.0%

US $ Revenue 4,296 4,296 0.0% 4,710 4,710 0.0%

Net Sales(Rs.) 66,155 67,011 68,837 69,698 68,948 1.1%

Net Sales(Rs.) 2,86,441 2,85,691 0.3% 3,17,924 3,17,924 0.0%

EBIDTA 10,766 11,358 11,613 11,490 11,131 3.2%

EBIDTA 47,344 46,980 0.8% 52,827 52,820 0.0%

EBIT 8,793 9,622 9,437 9,425 9,066 4.0%

EBIT 39,060 38,697 0.9% 44,218 44,211 0.0%

PAT 7,917 7,690 9,195 7,926 7,646 3.7%

PAT 32,171 31,885 0.9% 36,627 36,617 0.0%

EPS 8.1 7.8 9.3 8.2 7.9 3.7%

EPS 33.2 32.9 0.9% 37.8 37.8 0.0%

1QFY17 Earnings Preview

July 12, 2016 Page 30 of 46

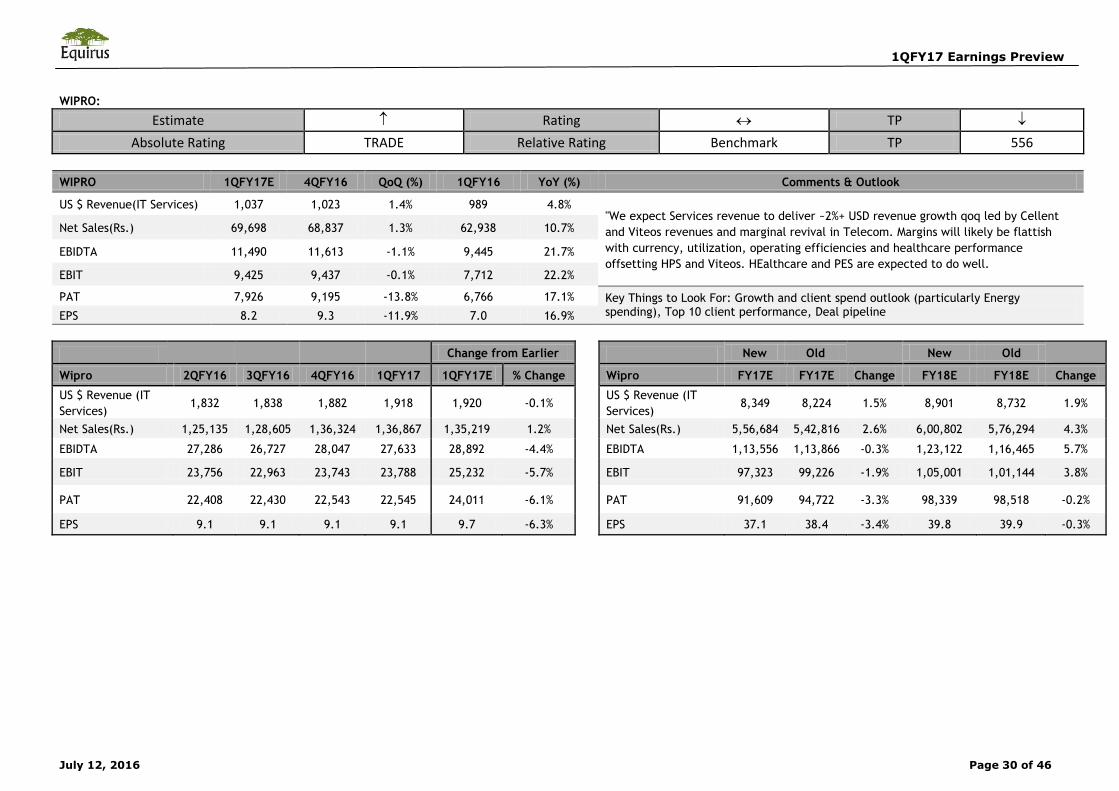

WIPRO:

Estimate Rating TP

Absolute Rating TRADE Relative Rating Benchmark TP 556

WIPRO 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook

US $ Revenue(IT Services) 1,037 1,023 1.4% 989 4.8% "We expect Services revenue to deliver ~2%+ USD revenue growth qoq led by Cellent

and Viteos revenues and marginal revival in Telecom. Margins will likely be flattish

with currency, utilization, operating efficiencies and healthcare performance

offsetting HPS and Viteos. HEalthcare and PES are expected to do well.

Net Sales(Rs.) 69,698 68,837 1.3% 62,938 10.7%

EBIDTA 11,490 11,613 -1.1% 9,445 21.7%

EBIT 9,425 9,437 -0.1% 7,712 22.2%

PAT 7,926 9,195 -13.8% 6,766 17.1% Key Things to Look For: Growth and client spend outlook (particularly Energy spending), Top 10 client performance, Deal pipeline EPS 8.2 9.3 -11.9% 7.0 16.9%

Change from Earlier

New Old

New Old

Wipro 2QFY16 3QFY16 4QFY16 1QFY17 1QFY17E % Change

Wipro FY17E FY17E Change FY18E FY18E Change

US $ Revenue (IT

Services) 1,832 1,838 1,882 1,918 1,920 -0.1%

US $ Revenue (IT

Services) 8,349 8,224 1.5% 8,901 8,732 1.9%

Net Sales(Rs.) 1,25,135 1,28,605 1,36,324 1,36,867 1,35,219 1.2%

Net Sales(Rs.) 5,56,684 5,42,816 2.6% 6,00,802 5,76,294 4.3%

EBIDTA 27,286 26,727 28,047 27,633 28,892 -4.4%

EBIDTA 1,13,556 1,13,866 -0.3% 1,23,122 1,16,465 5.7%

EBIT 23,756 22,963 23,743 23,788 25,232 -5.7%

EBIT 97,323 99,226 -1.9% 1,05,001 1,01,144 3.8%

PAT 22,408 22,430 22,543 22,545 24,011 -6.1%

PAT 91,609 94,722 -3.3% 98,339 98,518 -0.2%

EPS 9.1 9.1 9.1 9.1 9.7 -6.3%

EPS 37.1 38.4 -3.4% 39.8 39.9 -0.3%

1QFY17 Earnings Preview

July 12, 2016 Page 31 of 46

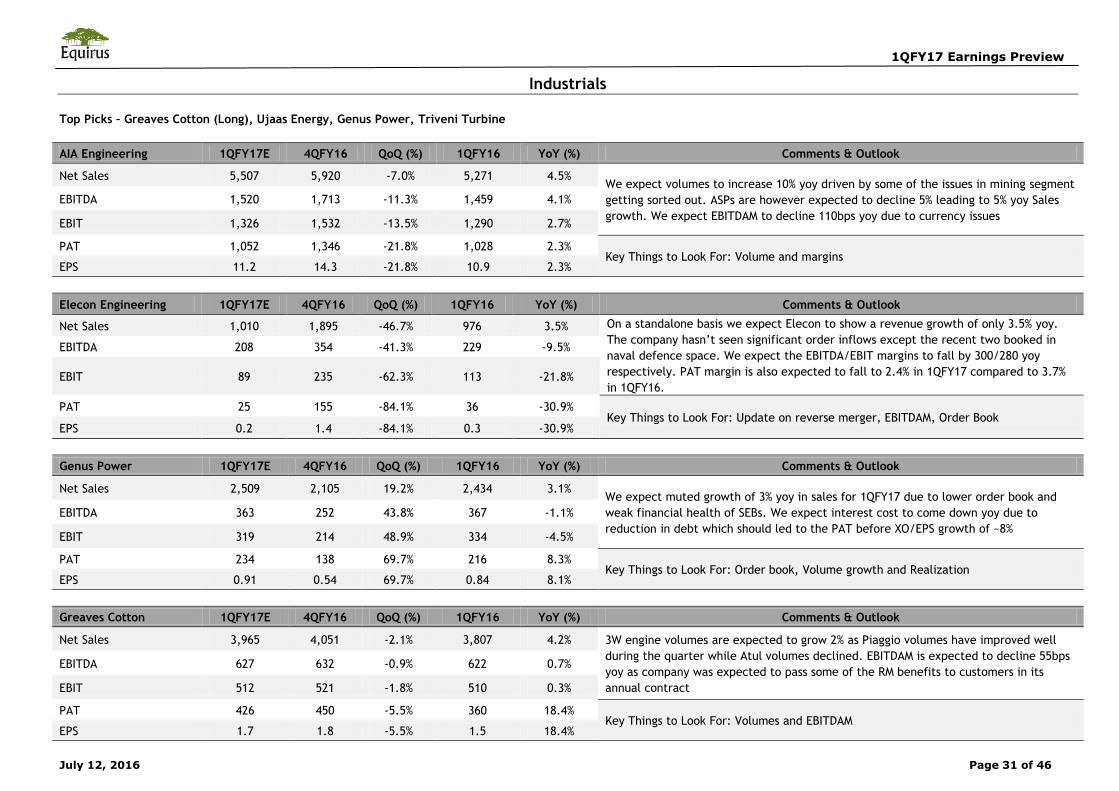

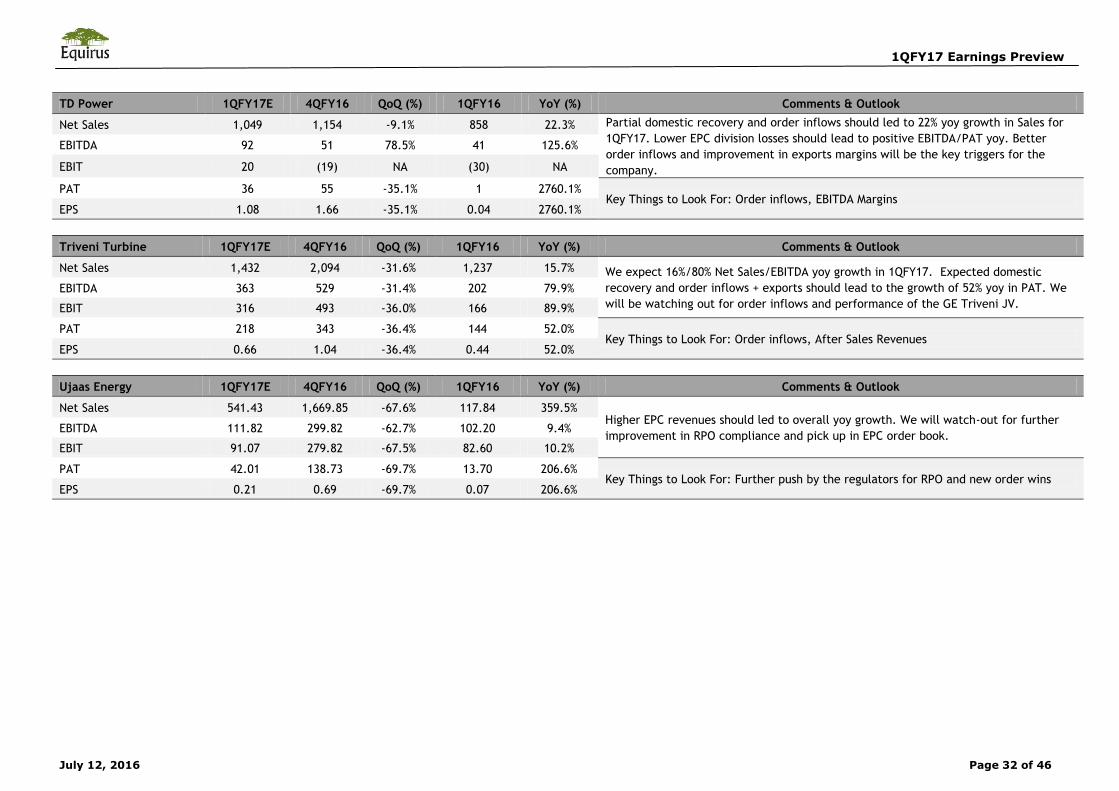

Industrials

Top Picks – Greaves Cotton (Long), Ujaas Energy, Genus Power, Triveni Turbine

AIA Engineering 1QFY17E 4QFY16 QoQ (%) 1QFY16 YoY (%) Comments & Outlook