Embed Size (px)

DESCRIPTION

DETAIL DESCRIPTION OF EURO BONDS

Citation preview

Carl‐Erik Torgersen

LL.M. Program

April, 2012

International Finance: Seminar

Professor Hal Scott

EUROBONDS

LL.M. short paper

Table of Contents

I. Introduction ........................................................................................................................ 3

II. Background ......................................................................................................................... 4

A. History of Eurobonds .......................................................................................................... 4

B. Eurobonds and the current European sovereign debt crisis .............................................. 6

C. Legal issues ......................................................................................................................... 7

III. Summary of different Eurobond proposals .................................................................... 9

A. Gros/Micossi .................................................................................................................... 9

B. De Grauwe/Mösen ........................................................................................................ 10

C. Hild/Herz/Bauer ............................................................................................................ 12

D. Muellbauer .................................................................................................................... 14

E. Delpla/von Weizsäcker .................................................................................................. 16

IV. An alternative Eurobond proposal ................................................................................ 19

V. Conclusion ......................................................................................................................... 23

VI. References ..................................................................................................................... 24

I. Introduction

This paper discusses the major Eurobond proposals put forth by politicians, scholars and

bankers. The paper analyzes the benefits and weaknesses of the various proposals, critically

assesses the concept of Eurobonds, and finally proposes a different Eurobond system.

The paper is structured in the following way: Following this brief introduction, the second

section presents a brief background on Eurobonds, explaining their history and their

implications for the current sovereign debt crisis. It then discusses the legal issues and myths

about Eurobonds.

The third section reviews different Eurobond proposals. Proceeding in chronological order,

the section starts with the first proposal, made by Daniel Gros and Stefano Micossi in spring

2009. It then analyzes the proposal made by Paul De Grauwe and Wim Moesen later the

same year. Next, it considers the 2011 proposal by the German legal scholars Alexandra Hild,

Bernhard Herz and Christian Bauer, which uses modern financing instruments. It then turns

to John Muellbauer’s conditional Eurobond proposal in October 2011. The section concludes

by discussing the most elaborate proposal, made by the two economists Jacques Delpla and

Jacob von Weizsäcker.

The last section presents a new Eurobond proposal, which tries to solve the major

drawbacks of the various existing proposals.

II. Background

A. History of Eurobonds

Eurobonds are debt instruments or loans jointly and severally guaranteed by the 27 EU

member states or by the 17 member states of the European Monetary Union. The guarantee

means that if an issuing country cannot service its Eurobonds, the creditors can demand

payment from all other member states.

The concept of such bonds is not new. The first real Eurobond proposal was made by

Jacques Delors, the former president of the European Commission. Delors suggested issuing

Eurobonds to finance the budget of the European Union in 1993. Although this idea was

backed by Romano Prodi, another former president of the European Commission, the

majority of the member states feared an increase in their current debt level and opposed

the idea.1 In 2000, Giovannini Group issued a report that intensified the debate on the

integration of government bond market. However the report concluded that “co‐ordination

involving a joint or single debt instrument was not regarded as a practical option for the Euro

area as a whole.”2 Between 2000 and 2008, there were not any proposals about Eurobonds.

This changed, however, with the beginning of the European sovereign debt crisis in late

2009. The crisis prompted many different proposals, which are discussed in detail below, in

section III.

Some scholars argue3 that despite this seemingly unresolved debate, Eurobonds already

exist. As an example, such scholars cite the “New Community Instruments,” which were

developed in the 1970s and 80s to help European member states recover from a natural

1 EURACTIV, EU bonds spark debate as recession hits. 2 Report of the Giovannini Group (2000), Co‐ordinated Public Debt Issuance in the Euro Area, November 3 E.g. CAHIER COMTE BOEL, The creation of a common European bond market § 14 (European League for Economic Cooperation ed., 2010).

disaster or fund projects.4 The New Community Instrument is secured by the European

budget.

Buiter and Rahbari5 describe the European Investment Bank bonds as being close to

Eurobonds. The European Investment Bank is a European institution created to finance long‐

term investment projects by issuing debt. Although the Bank’s founding documents statues

do not refer to joint and several guarantees, Buiter and Rahbari argue that “there is a clear

perception in the markets that the support provided by the 27 EU member states would go

beyond their contribution of the EIB’s subscribed capital.”6 This conclusion is clearly

supported by practice; as the S&P has reported, “[a]bout 90 percent of the loan portfolio [of

the European Investment Bank] was on projects within EU member countries, and nearly all

of the remainder was guaranteed by either the EU or EU member states.”7

Finally, some scholars argue that borrowing under the European Financial Stabilization

Mechanism (EFSM),8 whose object is to preserve financial stability of the European

monetary union, is essentially the same as issuing Eurobonds.9 Under the EFSM, the

Commission is allowed to borrow up to €60 billion in financial markets on behalf of the

Union under an implicit EU budget guarantee.10 This guarantee means that borrowing under

the EFSM is a direct and unconditional obligation, which is guaranteed jointly and severally

by the 27 member states of the European Union. Currently Ireland (with up to €22.5 billion)

4 EURACTIV. 5 BUITER WILLEM. & RAHBARI EBRAHIM., Global Economics View: The future of the euro area. (Citi Group 2011). 6 , 34. 7 BUTT LEILA., Ratings On European Investment Bank Affirmed At 'AAA/A‐1+'; Off Watch Neg; Outlook Negative, S&P (2012). 8 Council Regulation (EU) No 407/2010 of 11 May 2010 establishing a European financial stabilization mechanism. 9 WILLEM. & EBRAHIM. 10 Council Regulation (EU) No 407/2010 of 11 May 2010 establishing a European financial stabilization mechanism.

and Portugal (with up to €26 billion) are using money from the EFSM; if either country

defaults, the debt will be paid out of the European Union’s budget.

B. Eurobonds and the current European sovereign debt crisis

The most comprehensive solution to the current sovereign debt crisis would be a full fiscal

union for the Euro area, in which a central authority controls spending, taxes, and most

important debts. The political climate across Europe, however, means such a union would

face strong oppositions in almost all member states.11 Because the will to keep the Euro

intact is very strong, alternative, less sweeping solutions, such as Eurobonds, have drawn

increasing attention in the past months.

It is essential to note that Eurobonds would not solve the problems of the European Union.

While Eurobonds might help secure short term funding and liquidity, they would not address

the underlying fiscal problems. Specifically, Eurobonds would not increase fiscal discipline,

reduce the sovereign debt level, or help refinance European banks. These are crucial

considerations, and the most sensible approach would be to introduce Eurobonds only in

conjunction with laws that strengthen the enforcement of budgetary rules.12

Given the limits of Eurobonds, proposals should address the problem of fiscal discipline and

create incentives for member states to fulfill their obligations and have their government

finances fundamentally in order.13

11 Member states in the following article is defined as one of the 17 states which currently have the Euro as their currency, unless otherwise indicated. 12 BOONSTRA WIM., Can Eurobonds solve EMU's problems (European League for Economic Cooperation 2011). 13 Id. at

C. Legal issues

There is a great deal of debate among scholars and in the media whether Eurobonds would

be possible at all under the current legal framework of the European Union. One key

argument is that any provision for joint and several liability would contravene Art. 125 of the

Lisbon Treaty (ex Art. 103 TEC), which is commonly known as the “no bail‐out clause”:14

1. The Union shall not be liable for or assume the commitments of central governments, regional, local or other public authorities, other bodies governed by public law, or public undertakings of any Member State, without prejudice to mutual financial guarantees for the joint execution of a specific project. A Member State shall not be liable for or assume the commitments of central governments, regional, local or other public authorities, other bodies governed by public law, or public undertakings of another Member State, without prejudice to mutual financial guarantees for the joint execution of a specific project. 2. The Council, on a proposal from the Commission and after consulting the European Parliament, may, as required, specify definitions for the application of the prohibitions referred to in Articles 123 and 124 and in this Article.

Buiter and Rahbari argue that this article is often misread.15 Because Art. 125 of the Lisbon

Treaty states that neither the EU nor the individual member states are liable for or can

assume the commitments or public undertakings of any other member state, “without

prejudice to mutual financial guarantees for the joint execution of a specific project,”16

Buiter and Rahbari conclude that mutual financial guarantees are permitted as long as it is

“for the joint execution of a specific project.”17 The Article does not define “specific project,”

and thus under paragraph 2, the Council, acting on a proposal from the Commission and

after consulting the European Parliament, can define the term.18 Buiter and Rahbari thus

suggest that Eurobonds could be a “project” to reinforce sovereign debt sustainability in the

14See e.g. GROS DANIEL., Eurobonds: Wrong solution for legal, political, and economic reasons. (Vox 2011). 15 WILLEM. & EBRAHIM. 16 Art. 125 of the Lisbon Treaty 17 Art. 125 of the Lisbon Treaty 18 WILLEM. & EBRAHIM.

Euro area or a “project” to recapitalize systemically important EU banks. As anything can be

declared a “specific project,” Art. 125 does not create any legal obstacles to Eurobonds.

On another reading, Art. 125 of the Lisbon Treaty might only prohibit situations in which

individual member states are made liable against their will. If Eurobonds were created

pursuant to a voluntary guarantee by some member states, then there would be no treaty

limitation.

Without going into too much detail in the legal discussion, it is safe to say that there are thus

at least different approaches to comply with the legal framework. Additionally,

notwithstanding the foregoing, it would certainly be possible to change Art. 125 of the

Lisbon Treaty if this should be the will of the European Union.

III. Summary of different Eurobond proposals

Regardless of any legal concerns — and notwithstanding Eurobonds’ inability to address the

full range of fiscal problems confronting Europe — the current sovereign debt crisis sparked

renewed interest in the concept of Eurobonds. This section reviews the major proposals and

critiques the drawbacks of each of them.

A. Gros/Micossi

In the spring of 2009, Gros and Micossi identified two factors of the crisis as particularly

concerning: the extreme volatility of financial markets, which leads companies to cut back on

investments, and the difficulties of the banking sector.19 They suggested that the EU set up a

massive European Financial Stability Fund (EFSF) on the scale of the Troubled Assets Relief

Program in the US. Gros and Micossi argue that the EFSF should issue bonds “on the

international market with the explicit guarantee of member states, and as the rationale for

the EFSF would be crisis management, its operations should be wound down after a pre‐

determined period, perhaps of five years.”20 Under this proposal, the money from the EFSF

would be used either to recapitalize banks or to strengthen the existing EU instruments for

balance of payments assistance in the European region.21

Gros and Micossi conclude that there would be no risk for global investors, as these EFSF

bonds would be practically riskless. Further, they estimate that there would be a huge

demand, because investors everywhere have developed a strong preference for public debt.

19 GROS DANIEL. & MICOSSI STEFANO., A bond‐issuing EU stability fund could rescue Europe (2009). 20 Id. at 21 Id. at

This would develop a unified market for Eurobonds, guaranteed jointly by the EU member

states; with this development, the Euro could become a leading reserve currency like the

dollar.

The authors were aware of the moral hazard problem their proposal could generate and

address this concern by specifying that a common guarantee would not necessarily imply

that stronger member countries would have to pay for the mistakes of others. They explain

that losses could be distributed across member countries according to where they arose.

Under the proposal, the European Investment Bank would be used for issuing the bonds as it

has the necessary expertise and is an agency of EU government.

Gros and Micossi offered the first proposal after the crisis of 2008. Notably, they correctly

anticipated the EFSF, which was established more than a year later. However, they

recommend creating Eurobonds only temporarily to solve the crisis. To create a sustainable

and liquid Eurobond market, as they suggest, it is essential to issue Eurobonds not only

temporarily but permanently.

Further, the moral hazard problem is not addressed completely, as strong member states

would have to pay for weak member states in a default. In fact, weak member states would

also have no incentives for financial discipline.

B. De Grauwe/Mösen

De Grauwe and Mösen argue that the dramatic increase of credit spreads on certain

member states’ debt in the beginning of 2009 created distortions. A low response to fiscal

stimuli and a growing perception of likely default with negative externalities and spillover

made it impossible for the member states to find a way out of the recession22. To solve these

problems, the authors propose two different solutions.

First, they propose that the European Central Bank buy government bonds of distressed

states (quantitative easing). This would reduce the spreads in government bonds in the

Eurozone and would therefore reduce the distortions and the externalities that these

spreads created.

Second, the authors propose that member states replace national bonds with euro

denominated bonds guaranteed collectively by the governments of the Eurozone. The bonds

would be issued either by the European Investment Bank or by the member states

themselves.

The authors argue that the advantage of their plan is that countries facing high spreads

would have easier access to funding. In turn, this access should give those states more time

to implement new fiscal mechanisms to reduce their sovereign debt.

De Grauwe and Mösen address the free riding problem by adding several characteristics to

the issue of Eurobonds. In a first step, each member state would participate in the issue on

the basis of its equity share in the European Investment Bank. The coupon of the Eurobonds

would be a weighted average of the yields observed in each government bond market at the

moment of the issue. The resources from the Eurobonds then would be allocated to each

member state using the same weights. However, each member state would still pay the

yearly interest rate on its portion of the bond.23

22 DE GRAUWE PAUL. & MÖSEN WIM., Gains for all: A proposal for a common euro bond (May‐June 2009 ed. 2009). 23 Id. at

As an illustrative example, the authors use the February 2009 data and conclude that Greece

would pay a yearly interest rate of 5.7 percent on its portion of the hypothetical bond, while

Germany would pay only 3.1 percent. The only reason countries such as Greece would

participate in such a system would be if they could not sell their bonds and were completely

shut out from the market. On the other hand, strong countries like Germany would not have

to fear a free riding problem by weaker member states.

There are two limitations to this proposal: First, weak countries would only join if they could

not finance themselves on the capital market, which would mean that they were practically

insolvent. If such countries joined, there would be a high chance that they would default

soon afterwards, leaving the other countries with the joint liability.

Second, interest rates for countries such as Greece and Italy would be too high a five‐year

maturity bond would have a rate of over 7 percent. (Admittedly, at the time of the proposal

the interest rate would not have been so high.) In addition, fiscal reforms, which normally

would be reflected in the yearly interest rate on bonds, would not have any effect because

the rates would “frozen” to a certain level when the bonds were issued. Accordingly,

member states would have less incentive to implement them such reforms.

C. Hild/Herz/Bauer

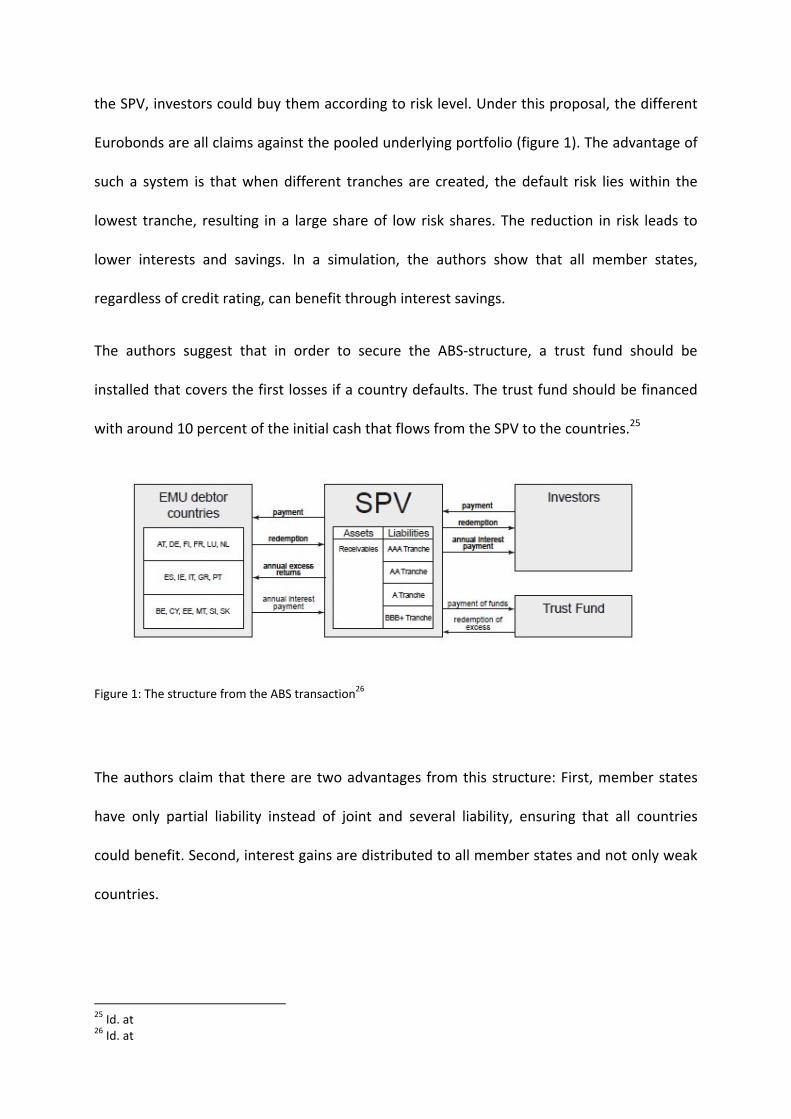

The authors propose a Eurobond structure using asset‐backed securities.24 A special purpose

vehicle would buy a portfolio of member states’ debt instruments and then issue Eurobonds

with varying risk and rating. Once the Eurobonds were subdivided into different tranches by

24 ALEXANDRA. HILD, et al., Structured Eurobonds (11.07.2011 ed. 2011).

the SPV, investors could buy them according to risk level. Under this proposal, the different

Eurobonds are all claims against the pooled underlying portfolio (figure 1). The advantage of

such a system is that when different tranches are created, the default risk lies within the

lowest tranche, resulting in a large share of low risk shares. The reduction in risk leads to

lower interests and savings. In a simulation, the authors show that all member states,

regardless of credit rating, can benefit through interest savings.

The authors suggest that in order to secure the ABS‐structure, a trust fund should be

installed that covers the first losses if a country defaults. The trust fund should be financed

with around 10 percent of the initial cash that flows from the SPV to the countries.25

Figure 1: The structure from the ABS transaction26

The authors claim that there are two advantages from this structure: First, member states

have only partial liability instead of joint and several liability, ensuring that all countries

could benefit. Second, interest gains are distributed to all member states and not only weak

countries.

25 Id. at 26 Id. at

This proposal’s main focus is generating liquidity for member states that have difficulty

accessing the debt market. While all member states could benefit under this proposal, there

is unfortunately still no incentive for member states to keep their future budgets balanced.

As explained above, access to liquidity must be linked to fiscal reforms so that weak member

states have a strong incentive to reduce their debts.

D. Muellbauer

Muellbauer argues that “conditional Eurobonds, coordinated nominal wage cuts linked with

limited debt writedowns and bank recapitalization are the lynch‐pin of a successful

resolution”.27 He correctly identifies the need for strong incentives to adopt the fundamental

structural and financial reforms that have yet to move forward in the weak member states.

Conditional Eurobonds are defined as Eurobonds “with a collective underwriting guarantee

which limits the country risk faced by investors and where administratively set spreads

determine the annual side‐payments at below AAA rated countries pay to the AAA‐countries

currently Germany, France the Netherlands, Austria, Finland and Luxembourg. The spreads

would compensate the taxpayers in these countries for their risk in underwriting the bonds

of the riskier countries and would be paid in proportion to the outstanding government

bond issuance of the receiving countries.”28

Muellbauer further suggests that the spread should be set in accordance with the European

monetary and fiscal authority (EMFA), which would set a performance target for each

country.

27 JOHN MUELLBAUER, Resolving the Eurozone crisis: Time foe conditional eurobonds, 59 Policy Insight (2011). 28 Id. at

The EMFA would use a mix of fixed rules and discretionary judgment in a respective weight

of 80 percent to 20 percent. The fixed rules would be based on four indicators that

Muellbauer discusses in detail: (i) unit labor costs, (ii) the sovereign debt to GDP ratio, (iii)

the current account to GDP ratio, and (iv) the World Bank’s “Doing Business” indicator.

To illustrate the conditional Eurobonds proposal, Muellbauer describes a hypothetical 10

year government bond from Portugal that faces a spread of around 8 percent relative to

German treasury bonds. The EMFA would set the spread to 5 percent in the first year, but

only if Portugal committed itself to serious fiscal reforms. Additionally, there would be an

option to reduce Portugal’s spread if the country made satisfactory progress in its fiscal

reforms. The advantage of this plan is that Portugal can refinance itself at lower costs, while

strong incentives still encourage the country to implement fiscal reforms.

This combination of fiscal reform and cheaper debt for distressed states thus correctly

identifies one of the main problems facing Europe. However, since Muellbauer first made

the proposal, all member states except Germany lost their triple A credit ratings, which

could alter the scenario he describes.

Additionally, the EMFA might not be a suitable institution for deciding debt spreads and

supervising member states’ progress instituting fiscal reforms. First, the EMFA would need a

great deal of resources to oversee the performance indicators. Second, the EMFA likely

would need a much higher degree of discretionary decisionmaking authority than 20

percent. The problems in each member state are so different that a fix set of rules might be

too inflexible.

E. Delpla/von Weizsäcker

The “Blue” and “Red” Eurobond proposal by Jacques Delpla and Jacob von Weizsäcker is one

of the most discussed and elaborate proposals. 29 The proposal envisions dividing the

sovereign debt of each country into senior (Blue) and junior (Red) tranches. The senior

tranche of Blue bonds would represent up to 60 percent of a state’s GDP and would be

jointly and severally guaranteed by all participating countries to ensure that it was a very

safe asset (the authors like to call it “AAAA”). It is important to emphasize that this senior

tranche would have to be repaid before any other public debt except IMF bonds.

Delpla and von Weizsäcker propose that the annual allocation of Blue bonds be done by an

independent stability council. This council would consist of members with a degree of

professional independence similar to that of European Central Bank board members.

Following this council’s decision, its allocation would be voted on by each national

parliament of all the participating countries. If a parliament voted against the council’s

decision, the parliament’s member state would be barred from issuing its own Blue bonds

and excused from guaranteeing other state’s Blue bonds. As the authors explain, “full

participation in the Blue Bond scheme should not be regarded as an entitlement but as

something earned through enhanced fiscal credibility, by means of low debt levels or

credible institutional guarantees (credible national fiscal rules in particular) that put public

finances on a sustainable path”.30 The authors conclude that the Eurobond, because of its

size and the liquidity of its market (the Blue bond market could have size of round €5.6

29 JACQUES. DELPLA & JAKOB. VON WEIZSÄCKER, Eurobonds: The blue bond concept and its implications (2010). 30 JACQUES. DELPLA & JAKOB. VON WEIZSÄCKER, Eurobonds: The blue bond concept and its implications II (2011).

trillion) would have a significantly lower yield than the weighted average of the national

bond yields.31

Any debt beyond the 60 percent of GDP threshold for Blue bonds could be issued only as

Red bonds, which would have junior status and be guaranteed only nationally. The Red

bonds should help to guarantee fiscal discipline because they “would make borrowing more

expensive at the margin and strengthen market signals in the absence of a credible fiscal

stance, thereby complementing the Stability and Growth Pact rules.”32 The authors further

propose that in order to allow an orderly default of Red bonds, such bonds should be kept

out of the banking system. This should be achieved with two restrictions: First, Red bonds

should not be allowed for use refinancing ECB operations. Second, regulators should

demand high capital requirements for banks that wish to hold Red bonds.

This proposal actively enforces fiscal discipline as member states can only issue a certain

amount of Blue bonds. Member states are encouraged to stay below 60 percent debt to GDP

because borrowing is much cheaper. Moreover, strong states like Germany would also get

the benefit of lower rates. With the opt‐out option for the Blue bond allocation, there is a

further way to force high deficit states to keep their spending in balance.

One major drawback could be the implementation of the Blue bond proposal. Currently the

following member states have sovereign debts exceeding 60 percent of their GDP and

therefore are violating the Stability and Growth Pact (SGP) criteria:

31 DELPLA & VON WEIZSÄCKER, Eurobonds: The blue bond concept and its implications. 32 DELPLA & VON WEIZSÄCKER, Eurobonds: The blue bond concept and its implications II.

Table 1: GDP of European Member states based on the World Economic Outlook from the International Monetary Fund, September 2011. http://en.wikipedia.org/wiki/Economy_of_the_European_Union#cite_note‐8

If member states can only issue Blue bonds up to 60 percent of their GDP, the states listed in

table 1 would need to issue costly Red bonds. The authors suggest a transition period but do

not go into detail how this problem could be solved. The average European member state

has a sovereign debt to GDP ratio of 80.1 percent, and it could take years to reduce this

debt. In addition, it is still possible that in the next two or three years an increase in

sovereign debt could occur.

Such an increase would make it hard to implement the Blue bond proposal in the short run.

Strong member states would use the opt out option (or would not even join in the

beginning) once defaults of weak states like Greece, Portugal, and Spain began to seem

possible.

IV. An alternative Eurobond proposal

As explained above, it is important to establish Eurobonds only in a way that ensures true

fiscal discipline. The most effective solution is one that the existing proposals have

overlooked: all future debt issuance of each member state should be controlled at the EU

level to ensure that individual member states do not make any borrowing decisions alone. In

return of giving up the right to issue debt, member states should be allowed to issue

Eurobonds. All Eurozone member states would be jointly and severally liable for these

bonds. This guarantee would be preferable to proportional liability since it would ensure

that member states could meet their obligations even in fiscal straits.

Under such a system, any member state would have the right to issue as many Eurobonds as

it wanted up to the current SGP limit of 60 percent debt to GDP. There should be no

constraints in terms of how the money is spent. However, once the 60 percent limit is

reached, a member state should not be allowed to issue any further debt unless it received

approval from an EU body, such as the Council. The Council should use the EU qualified

majority voting procedures to avoid coalitions in which member states joint together to

approve each other’s debt. Under Article I‐25 of the Constitutional Treaty, a qualified

majority is defined as at least 55 percent of the members of the Council that together

represent at least 65 percent of the population of the Union. A blocking minority must

include at least four Council members.

The Council should only allow debt issuance above the 60 percent SGP limit if additional

debt is absolutely necessary. In such cases, the Council could condition its approval on the

debtor state meeting certain fiscal requirements. This system would not be a fiscal union

and therefore member states would still have the power to tax and make their own

budgeting decisions. However, it certainly would be possible – and indeed recommended –

to restrict these powers in exchange for additional money. Such outside controls on member

states’ fiscal policies already have been discussed; for example, Chancellor Merkel proposed

in late January 2012 that it might be useful to take over authority of the Greek budget.33

There are certainly some challenges facing this proposed Eurobond system and thus it is

essential to have a transition period. Member states with weak economies would be pleased

to join the system, as the EU‐wide guarantee would ensure they paid less interest on their

bonds. Strong member states, on the other hand, would have fewer incentives to join the

new Eurobond system; the risk of other member states defaulting would force the strong

states to pay more interest on Eurobonds than if they issued their own bonds.

Ultimately, however, it is important to keep the overall picture in mind: there is a strong

political will to keep the Eurozone and its members together. Further, it is far from clear how

much more small strong countries, like Finland, would have to pay to issue Eurobonds

instead of issuing their own bonds. There are some scholars34 who believe that the increased

liquidity of the Eurobond market would outweigh the risk premium for small strong

countries, leaving such countries without any increase in costs.

For Germany and France, there most likely would be an increase in debt costs. These key EU

members might accept such an increase for multiple reasons. First, the proposed Eurobond

system should be seen as a fiscal support for weak countries. Second, the Eurobond system

would decrease the risk of complete euro area to collapse – a catastrophe that would be

especially costly for Germany and France. Finally, the system would mean EU emergency

measures would no longer be needed. For example the EFSF, which has a EUR 440 billion

33 MARIA. MARGARONIS, European Summit: German Austerity Blues(2012). 34 CARLO. FAVERO & ALESSANDRO. MISSALE, EU public debt management and Eurobonds (European Parliament 2010).

lending capacity and is jointly and severally guaranteed by the Eurozone, could be phased

out, as could the EFSM, from which distressed member states can borrow up combined

loans up to €60 billion – with the EU budget as collateral.

With regard to the transition period, it is important to take the current situation into

account. This is a weakness of most of the published Eurobond proposals and therefore

merits close attention. As pointed out in table 1, the percentage of debt to GDP is far above

60 percent on average in the Eurozone. Therefore a transition period for the new Eurobond

system would need to allow member states to issue guaranteed debt over the 60 percent

limit without seeking E.U. approval in order to bring their budget in balance. Currently this

might be between 10 to 20 percent on top of the SGP’s 60 percent debt to GPD limit.

There would be no additional cost to this guarantee, unlike the EFSM and the EFSM, which

required raising capital, as all member states would simply be liable for the debt issued. A

transition period between 3 to 5 years should give member states time to fix their budgets

and significantly reduce their spending, which would not be converted to Eurobonds.

After this transition period, member states only would be allowed to issue Eurobonds up to

60 percent of GDP. If they need more debt, approval would be subject to qualified majority

voting in the Council. The same approval also would be required if member states needed

more debt during the transition period than the 10 to 20 percent above the 60 percent SGP

ceiling.

This Eurobond proposal would help weak member state gain access to cheaper debt while

ensuring that fiscal reforms are implemented. Furthermore, it would avoid creating

additional institutions either for issuing bonds or for supervising fiscal reforms. All decisions

could be made by the Council, and qualified majority voting would ensure that there were

no coalitions of smaller member states trying to expand their debt at the expense of

stronger member states.

Finally, if member states stay below the 60 percent debt to GDP ratio, issuing Eurobonds

does not affect their taxing or spending at all. Only if a member state violates the SGP and is

therefore a potential danger for the whole Eurozone would other member states have a

right to intervene in the issuance of Eurobonds.

V. Conclusion

It comes as no surprise that Eurobonds are an active topic of discussion since 2009. The

ongoing public debate reflects the pressure on weaker countries to finance their debt under

current conditions. Those weak member states, like Greece, could infect other member

states and therefore endanger the Euro.

As this paper has emphasized, Eurobonds do not release weak member states from their

obligation to keep their budgets in balance. However, there is an option that combines the

right incentives in a Eurobond system that gives weak member states time to put their

affairs in order without forcing the Eurozone into another crisis.

It is possible to create a Eurobond system which avoids the free riding problem while giving

weak member states the incentives to adopt much needed financial reforms. The idea is

simple: member states whose debt is below 60 percent to the GDP can issue Eurobonds

themselves, while any issuance above that ceiling would require an approval by the Council

according to the qualified majority voting. This would strengthen the Stability and Growth

Pact and does not require a fiscal union. Countries are free in taxing and spending as long as

they keep their budget in balance.

VI. References

EURACTIV, EU bonds spark debate as recession hits.

CAHIER COMTE BOEL, The creation of a common European bond market § 14 (European League

for Economic Cooperation ed., 2010).

BUITER WILLEM. & RAHBARI EBRAHIM., Global Economics View: The future of the euro area. (Citi

Group 2011).

BUTT LEILA., Ratings On European Investment Bank Affirmed At 'AAA/A‐1+'; Off Watch Neg;

Outlook Negative, S&P(2012).

BOONSTRA WIM., Can Eurobonds solve EMU's problems (European League for Economic

Cooperation 2011).

GROS DANIEL., Eurobonds: Wrong solution for legal, political, and economic reasons. (Vox

2011).

GROS DANIEL. & MICOSSI STEFANO., A bond‐issuing EU stability fund could rescue Europe (2009).

DE GRAUWE PAUL. & MÖSEN WIM., Gains for all: A proposal for a common euro bond (May‐June

2009 ed. 2009).

ALEXANDRA. HILD, et al., Structured Eurobonds (11.07.2011 ed. 2011).

JOHN MUELLBAUER, Resolving the Eurozone crisis: Time foe conditional eurobonds, 59 Policy

Insight (2011).

JACQUES. DELPLA & JAKOB. VON WEIZSÄCKER, Eurobonds: The blue bond concept and its

implications (2010).

JACQUES. DELPLA & JAKOB. VON WEIZSÄCKER, Eurobonds: The blue bond concept and its

implications II (2011).

MARIA. MARGARONIS, European Summit: German Austerity Blues(2012).

CARLO. FAVERO & ALESSANDRO. MISSALE, EU public debt management and Eurobonds (European

Parliament 2010).