Embed Size (px)

Citation preview

Euromoney Markets1

Euro-money Markets

Euromoney Markets 2

(concept of euromoney)

Eurodollar is a dollar deposit outside the US

Euroyen is a yen deposit outside Japan

Eurosterling is a sterling deposit outside the UK

The key point to note here is that these deposits are outside the regulation of the respective central banks

Euromoney Markets 3

Origins of the Euromarket

A most unlikely source

The former Soviet Union, a big importer of food grains from the US

Had dollars ready for payment to the US exporter

Deposited these dollars in a French bank in Paris, rather than in a bank in the US

This is supposed to have been the origin of eurodollars

Euromoney Markets 4

Major stimuli for the growth of euro-markets

Excessive regulation of banking in the US and the UK

Growth of transnational corporations

Convertibility of currencies

Euromoney Markets 5

Euro-markets (Contd.,)

A large and efficient market, in which a firm can raise large amounts (say $ 500 million) in about three months, as compared with :

World Bank : 2-3 years

Bilateral Loans : 2-3 years

Euromoney Markets 6

Eurocurrency Market

Involves a chain of deposits and a chain of borrowers and lenders

There is a chain of ownership between the original dollar depositor and the US bank

There is a changing control over the deposit and the use to which the money is put

Euromoney Markets 7

Question

How does the euro-market survive, as a market, separate from the domestic dollar market?

Euromoney Markets 8

Possible answer to question on the previous slide

Absence of central bank regulation enables euro-banks to survive on a lower spread than banks in the domestic dollar market

Euromoney Markets 9

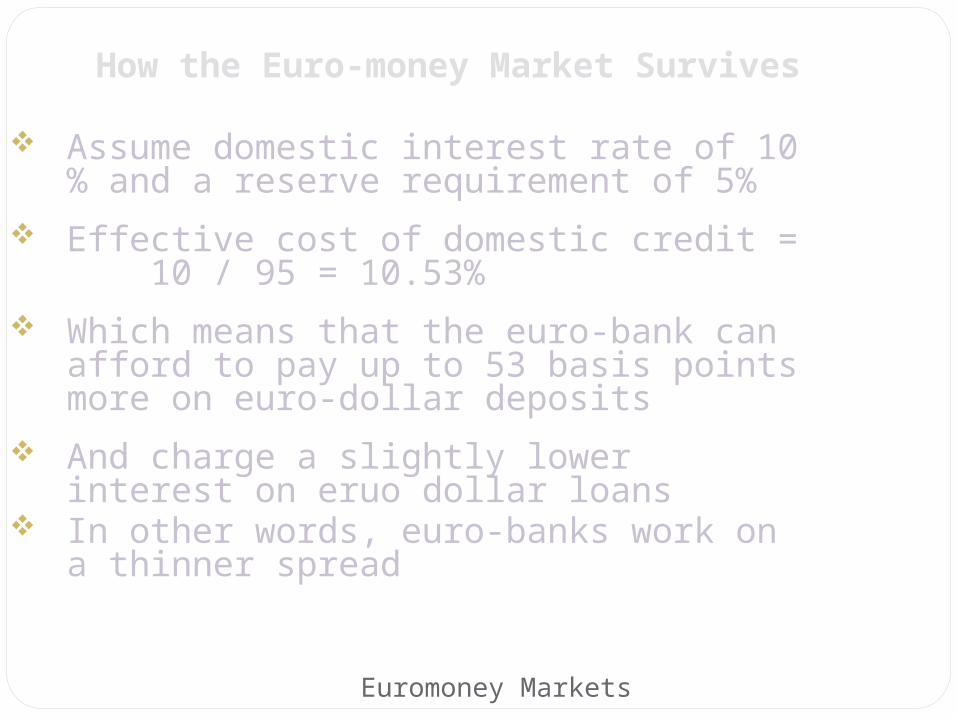

How the Euro-money Market Survives

Assume domestic interest rate of 10 % and a reserve requirement of 5%

Effective cost of domestic credit = 10 / 95 = 10.53%

Which means that the euro-bank can afford to pay up to 53 basis points more on euro-dollar deposits

And charge a slightly lower interest on eruo dollar loans

In other words, euro-banks work on a thinner spread

Euromoney Markets 10

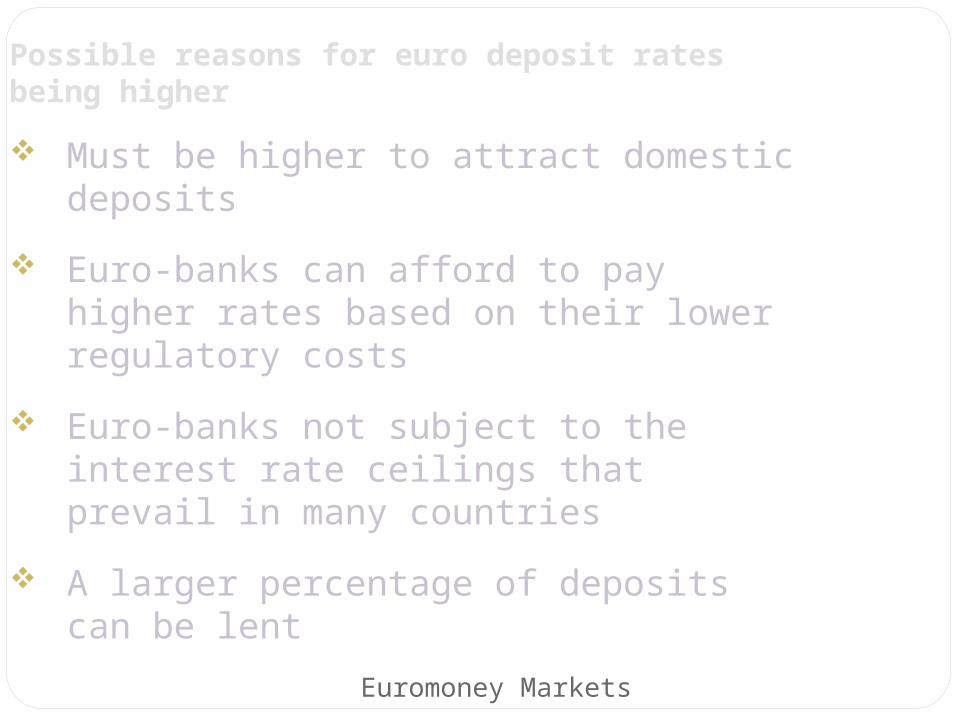

Possible reasons for euro deposit rates being higher

Must be higher to attract domestic deposits

Euro-banks can afford to pay higher rates based on their lower regulatory costs

Euro-banks not subject to the interest rate ceilings that prevail in many countries

A larger percentage of deposits can be lent

Euromoney Markets 11

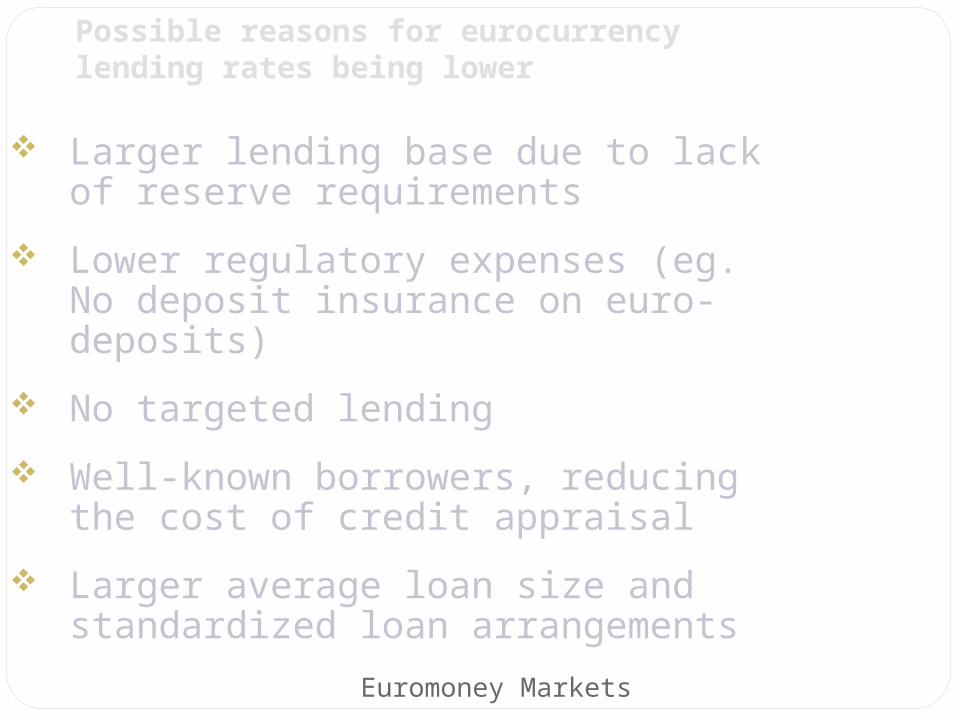

Possible reasons for eurocurrency lending rates being lower

Larger lending base due to lack of reserve requirements

Lower regulatory expenses (eg. No deposit insurance on euro-deposits)

No targeted lending

Well-known borrowers, reducing the cost of credit appraisal

Larger average loan size and standardized loan arrangements

Euromoney Markets 12

Loan Syndications

Loan syndications are common in the euro-market

A loan syndicate normally consists of the following

A lead bank

Co-managers

Participating banks

Euromoney Markets 13

Element of cost

Front-end fee (paid upfront to the lead bank)

Commitment fee (charged on the un-drawn amount)

Spread over the base rate (normally Libor) In the case of euro-loans, this reflects country risk, in addition to credit risk

Question : What should be the bargaining posture of a borrowing firm? Where to give in and where to stand firm?

Euromoney Markets 14

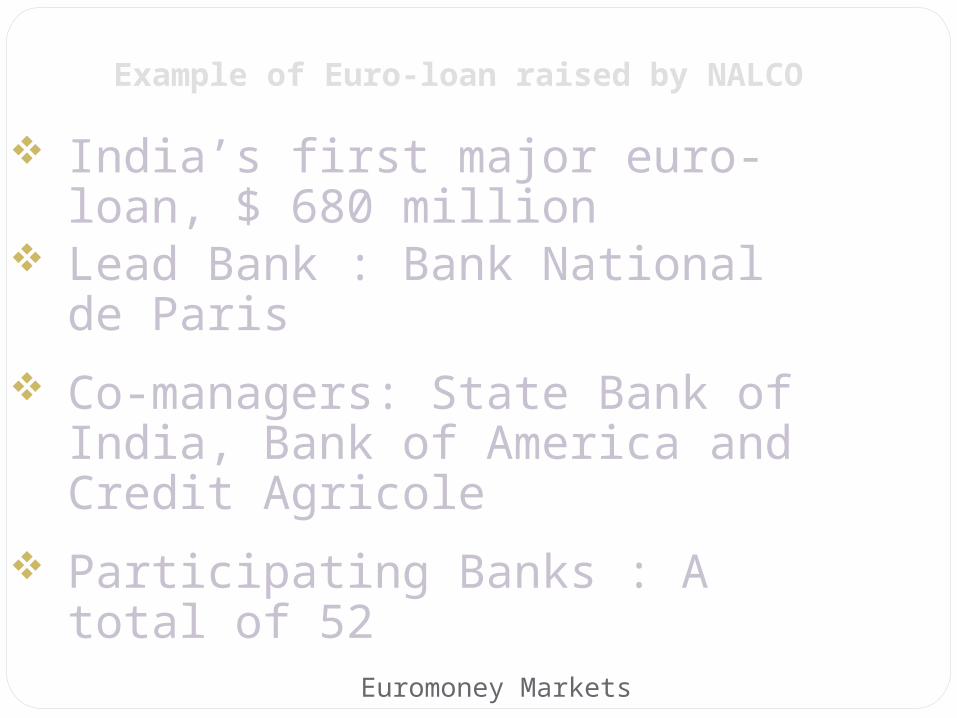

Example of Euro-loan raised by NALCO

India’s first major euro-loan, $ 680 million

Lead Bank : Bank National de Paris

Co-managers: State Bank of India, Bank of America and Credit Agricole

Participating Banks : A total of 52

Euromoney Markets 15

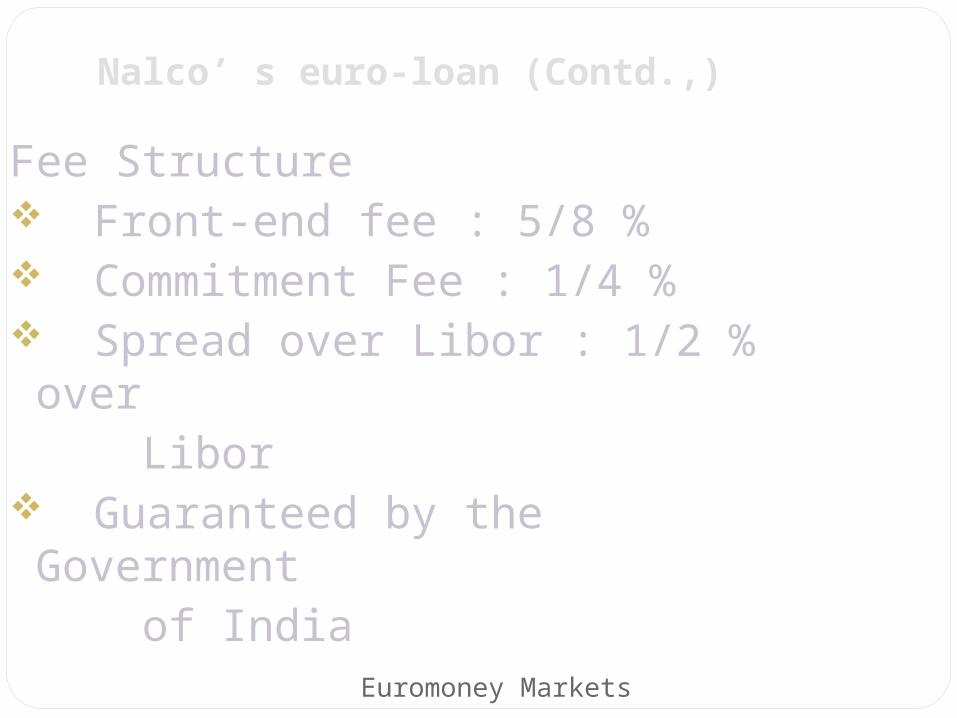

Nalco’ s euro-loan (Contd.,)

Fee Structure Front-end fee : 5/8 % Commitment Fee : 1/4 % Spread over Libor : 1/2 % over Libor Guaranteed by the Government of India

Euromoney Markets 16

Government PolicyIn recent years, the Indian government has encouraged the

use of euro-loans by Indian companies, particularly in infrastructure and other priority sectors of the economy

Government’s major concerns seem to be to minimize short-term ( maturity less than one year ) loans and to encourage end use in terms of expansion, modernization and up-gradation of technology

A liberal policy regime that permits companies to borrow ( or to prepay ) upto $ 500 million on the automatic route

Euromoney Markets 17

International Bonds

All international bonds are sold initially to investors outside the country of the borrower

Major Instruments Euro-bonds Foreign bonds Floating rate notes (FRNs) Euro-commercial paper

Euromoney Markets 18

Eurobond

Is underwritten by an international syndicate of bankers and security firms

Is sold exclusively in countries other than the one in whose currency the issue is denominated

Example : IBM issuing dollar bonds in Europe and Japan

Euromoney Markets 19

Foreign Bond

Is underwritten by a syndicate composed of members from a single country

Sold principally within that country

Denominated in the currency of that countryExample : A Swedish company issuing dollar bonds in the US Proliferation of terms in this area:Example: Yankee Bonds, Samurai Bonds, and Bull-

dog Bonds

Euromoney Markets 20

Floating Rate Notes

Are issued by sovereign nations, state enterprises and other high-quality borrowers

Underwritten by investment bankers, as an alternative to medium and long-term syndicated bank loans

Sells at lower interest margins over Libor, and have slightly longer maturities than syndicate loans

Euromoney Markets 21

A borrower’s graduation

Stage 1 : Syndicate Loans

Stage 2 : Floating Rate Notes

Stage 3 : Fixed Rate Bonds

As a borrower’s credit rating improves and he becomes better known, he moves up the ladder from syndicated loans to FRNs to fixed rate bonds. (Example : ONGC)

Euromoney Markets 22

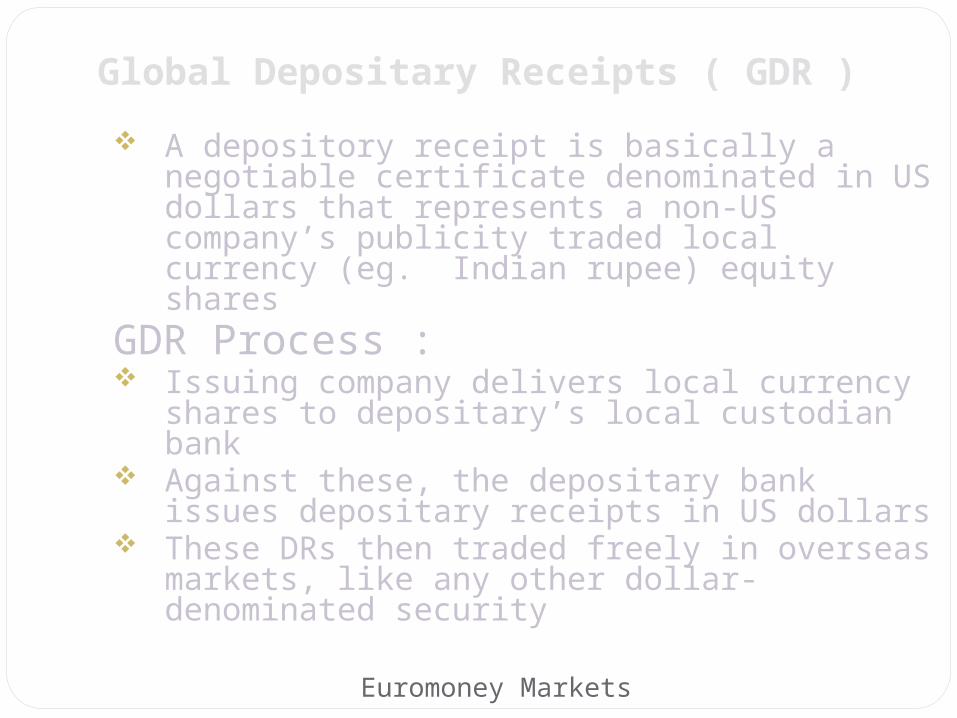

Global Depositary Receipts ( GDR )

A depository receipt is basically a negotiable certificate denominated in US dollars that represents a non-US company’s publicity traded local currency (eg. Indian rupee) equity shares

GDR Process : Issuing company delivers local currency shares

to depositary’s local custodian bank Against these, the depositary bank issues

depositary receipts in US dollars These DRs then traded freely in overseas

markets, like any other dollar-denominated security

Euromoney Markets 23

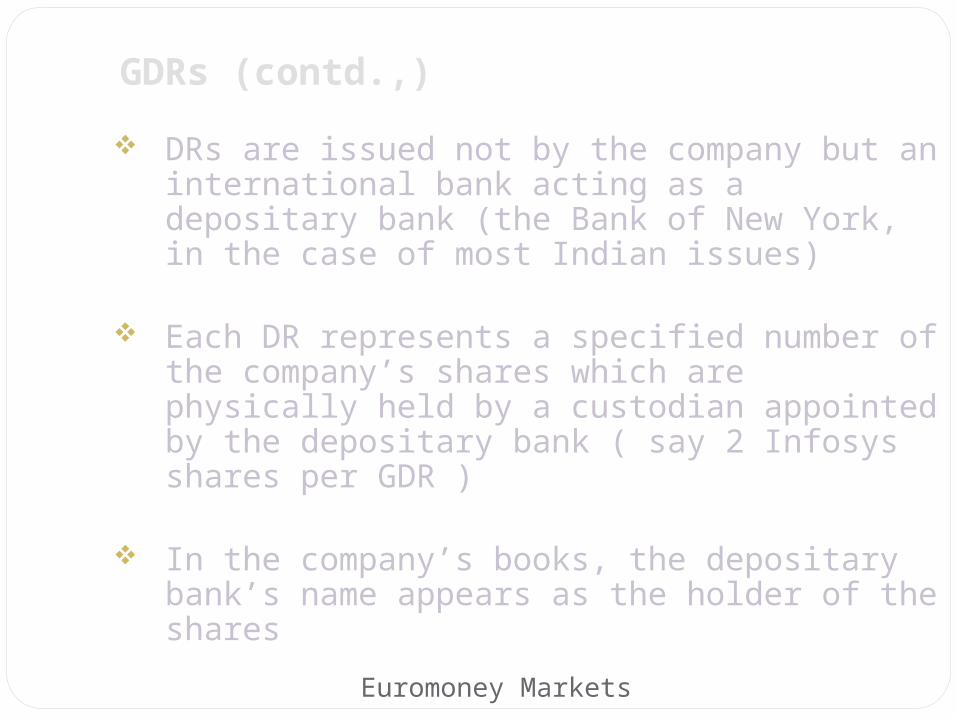

GDRs (contd.,)

DRs are issued not by the company but an international bank acting as a depositary bank (the Bank of New York, in the case of most Indian issues)

Each DR represents a specified number of the company’s shares which are physically held by a custodian appointed by the depositary bank ( say 2 Infosys shares per GDR )

In the company’s books, the depositary bank’s name appears as the holder of the shares

Euromoney Markets 24

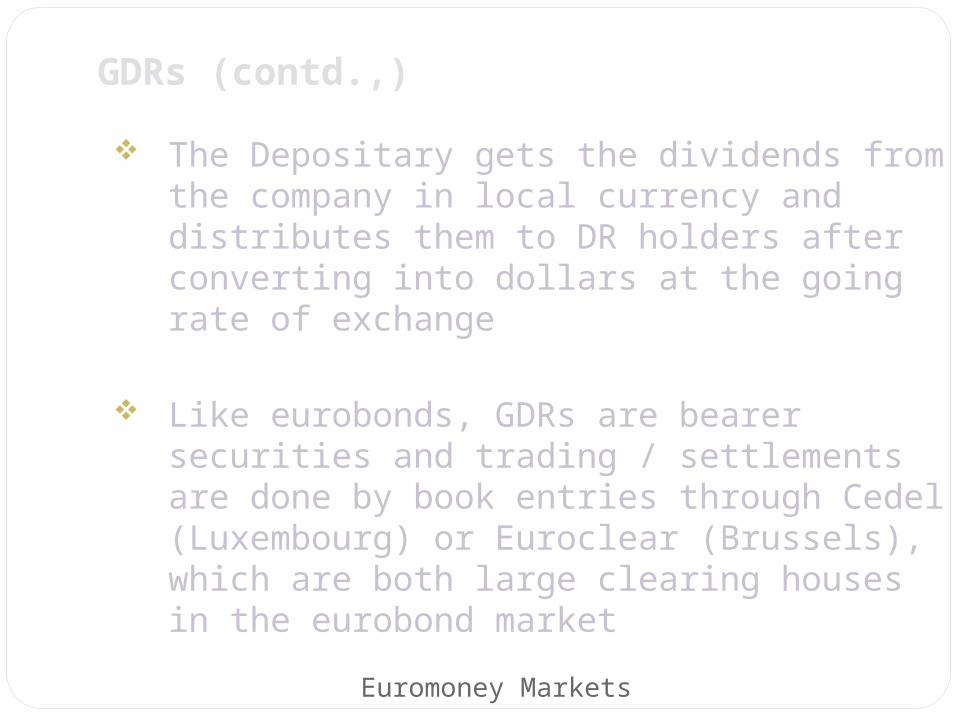

GDRs (contd.,)

The Depositary gets the dividends from the company in local currency and distributes them to DR holders after converting into dollars at the going rate of exchange

Like eurobonds, GDRs are bearer securities and trading / settlements are done by book entries through Cedel (Luxembourg) or Euroclear (Brussels), which are both large clearing houses in the eurobond market

Euromoney Markets 25

GDRs (contd.,)

The DRs are exchangeable with the underlying shares either at any time or after the lapse of a specified period of time ( say one year )

The exchanged shares could then be traded in the local stock market

The issue price depends on the market price of the underlying shares at the time of issue

Underwriting fees and commission typically work out to around 4% with other expenses being similar to those in the case of bond issues

Euromoney Markets 26

QuestionWhat are the major roles of a depositary bank ?

Euromoney Markets 27

The roles of a depositary bankProgramme managerCustodianIssuer of depositary receiptsRegistrar and transfer agentPaying agent ( dividends, proceeds on sale of DRs etc)Information agent

Euromoney Markets 28

QuestionWhat are the likely benefits of a GDR issue to the issuer

?

Euromoney Markets 29

GDR : Potential benefits to issuers

Access to global markets Raising foreign currency equity Perceived advantages of raising equity over

debt :No repayment of principalGenerally lower servicing costs

(In quite a few cases) Higher prices than would have been possible in a domestic issue

No currency risk to issuer The convenience of dealing with one

shareholder, the depository bank

Euromoney Markets 30

QuestionWhat are some of the potential benefits to investors in

a GDR issue?

Euromoney Markets 31

GDR :Potential benefits to investorsPortfolio diversification ( regional returns are

cyclical, much of the long-term growth is outside the developed world b/o demographics, many global markets outperform indices such as the S & P 500 )

Instrument denominated in a convertible currencyTraded in developed stock markets( contd.. Next slide )

Euromoney Markets 32

GDR :Potential benefits to investors

On the other hand :Currency riskRisks inherent in equity investments ( dividend

uncertainty and capital loss)Withholding taxes ( not in India )Tax on capital gains ( now limited to 10% on ST

capital gains ), applicable only in case of conversion to underlying shares and sale in the secondary market

Euromoney Markets 33

American Depositary Receipt (ADR)What is an ADR?A negotiable certificate or “receipt” issued in the

US representing ownership of securities of a non-US based company issued in a foreign market

They are considered a US domestic security under US law and are quoted and traded in US dollars offering a convenient and simple means to invest in overseas companies

(contd. Next slide)

Euromoney Markets 34

American Depositary Receipt (ADR)ADRs offer the benefit of protections and transparency

offered by US securities regulationsADRs normally offer lower trading and custody costs

than shares bought directly in the foreign market

Euromoney Markets 35

A brief history of ADRs1927 : First DR progamme created. Selfridges, UK-

based Department Store, established to facilitate investment in overseas stocks by large US institutions

1950s : Several large MNCs in Western Europe, Australia and Japan, started to list in the US

1970s : Dozens of ADR programmes developed for mining companies

(contd. Next slide)

Euromoney Markets 36

A brief history of ADRs1980s : Market experienced tremendous growth1990s : Established in global markets ( ADRs and

GDRs)2004 : ADRs accounted for 35% of global equities (

total global USD 2.4 trillion)2009 : More than 2000 sponsored DR programmes

from over 77 countries

Euromoney Markets 37

American Depositary Receipt (ADR)Issuer ( say Infosys Technologies ) assigns a bank

( say the Bank of New York ) as depositary for its sponsored DR programme

Depositary issues and cancels ADRS and acts as registrar, transfer agent and paying agent for the DR programme

Investor generally uses broker or depositary’s direct investment plan as the intermediary to issuer ( eg. Bank of New York – Direct Programme )

Euromoney Markets 38

ADR structures

Objective: Broaden investor baseLevel 1 : over-the-counter ( eg. Deutsche Bank, a

large bank as well as depositary )Level 2 : Exchange-listedObjective : Raise capitalLevel 3 : Public offeringLevel 4 : Rule 144 A ( Private placement)Levels 2 and 3 must comply with US GAAP and full

disclosure

Euromoney Markets 39

Where do ADRs trade?Like other US securities, ADRs can trade on the

NYSE, NASDAQ and AMEX, or may be over the counter ( OTC) . NYSE –Euronext is by far the largest ,with over 60% of volumes

If an ADR is listed, you can benefit from readily available price and trading information

An ADR can represent any number or fraction of underlying shares ( say 2 Infosys shares for every ADR )

Euromoney Markets 40

ADR TrendsAt end of year 2008, a record 2132 sponsored DR

programmes were available to investorsDR liquidity reached an all-time high in 2008Trading value reached nearly $ 4.4 trillion

Euromoney Markets 41

Benefits of ADRs to investorsConvenienceQuoted and traded in US dollars Trade, clear and settle in accordance with US

regulations permitting prompt dividend payments and timely corporate action notifications

Easy access to markets that have some of the world’s best companies

Contd. Next slide

Euromoney Markets 42

Benefits of ADRs to investorsOpportunity to diversify portfolio while using US

dollarsADRs tend to outperform their home marketsADRs offer lower trading and custody charges

Euromoney Markets 43

Benefits of ADRs to IssuerAdhere to transparency and disclosure standards of

the world’s largest equity marketIncrease retail and institutional investor acceptanceAccess to US investors who are unable to invest

overseas

Euromoney Markets 44

Benefits of ADRs to IssuerEnhance share valuationIncrease liquidity by enlarging the market for the

company’s shareStock option programme for US employees

Euromoney Markets 45

QuestionWhat might be some of the risks involved in investing

in ADRs?

Euromoney Markets 46

Possible RisksInvesting in any security involves a certain amount

of risk, along with rewardsAs ADRs are backed by non-US securities, the

following specific risks apply:Currency riskCountry risk – political, economic and social

conditions in the home market may impact the stock price

Also accounting standards vis-à-vis US GAAP