Embed Size (px)

Citation preview

Everything you need to know about trended credit data

LendIt USA 2017

LendIt USA 2017

About our speaker:

Paul DeSaulniers Sr. Director, Experian Email: [email protected] Phone: 714.830.7580

28/02/2017

LendIt USA 20174

1. Trended data 101

2. How Trended Data helps lenders

3. Leverage the power of trended data

4. Best practices

5. Q&A

Agenda

28/02/2017

LendIt USA 20175

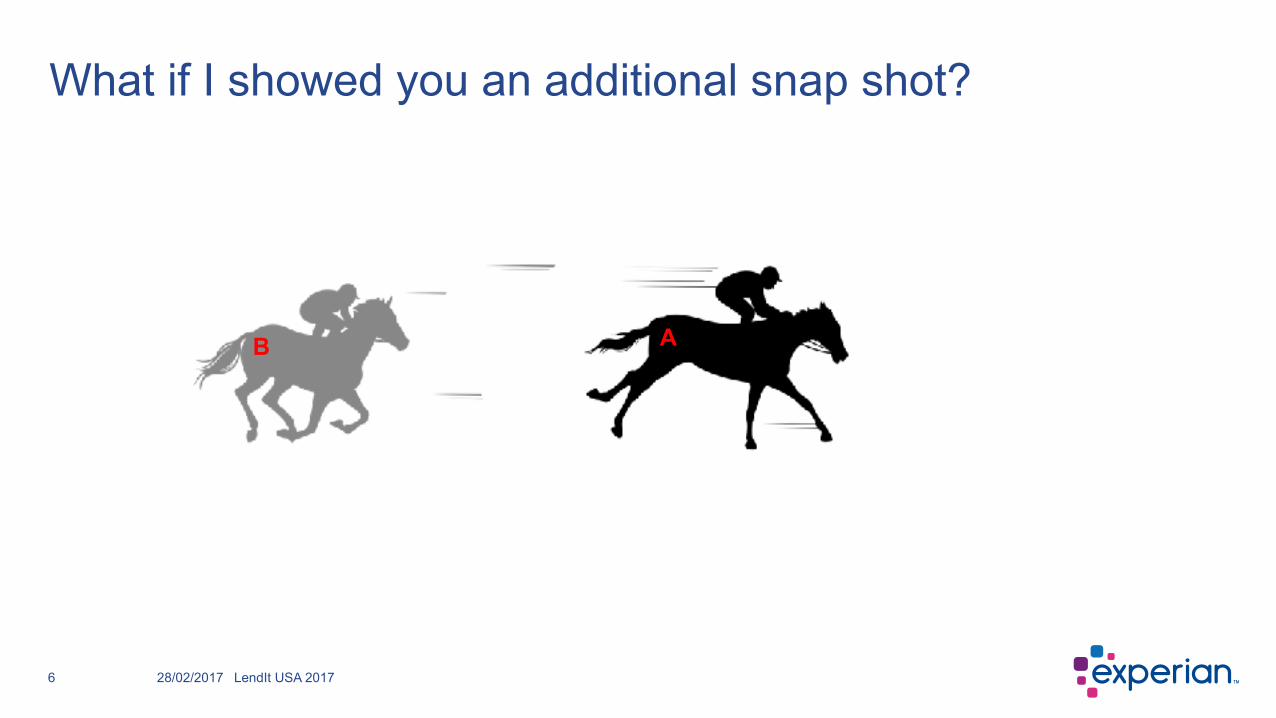

Who is going to win?

28/02/2017

AB

Finish Line

LendIt USA 20176

What if I showed you an additional snap shot?

28/02/2017

B A

LendIt USA 20177

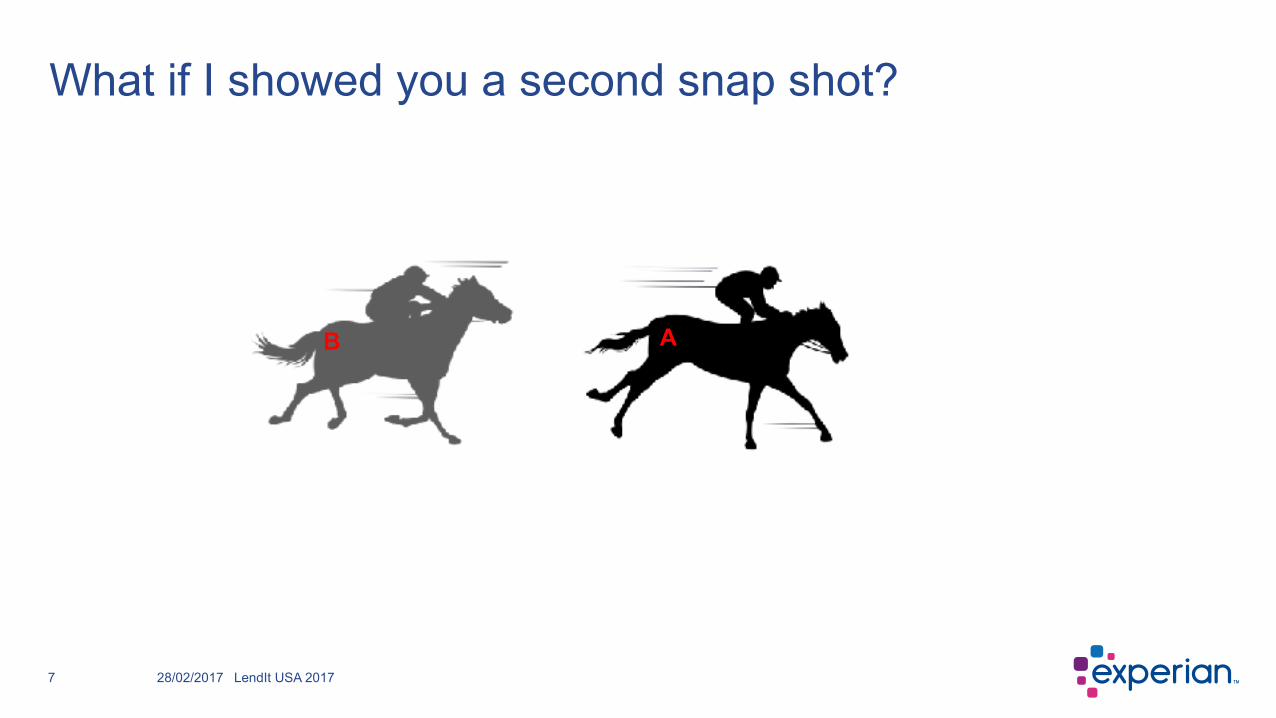

What if I showed you a second snap shot?

28/02/2017

B A

LendIt USA 20178

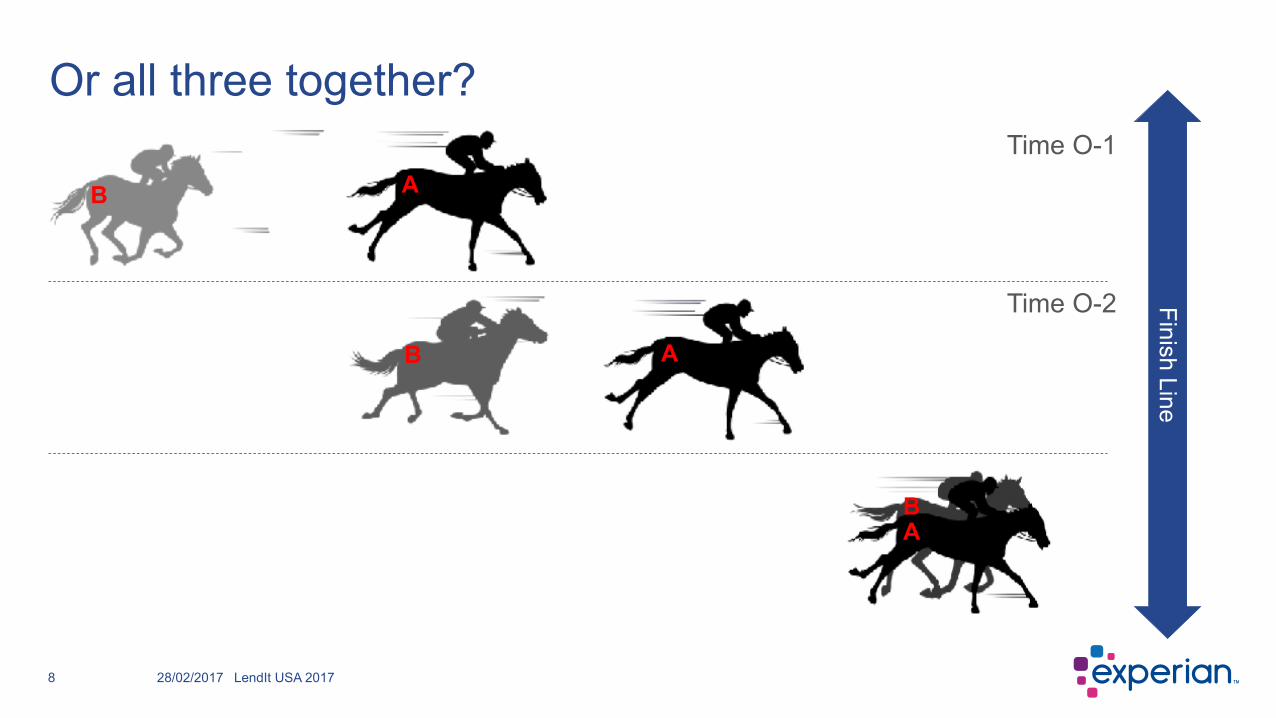

Or all three together?

28/02/2017

AB

Finish Line

B A

B A

Time O-2

Time O-1

LendIt USA 20179

Who would you bet on?

28/02/2017

Image source: www.sport-it.net

LendIt USA 201710

Market perspective on trended data

28/02/2017

An underutilized tool today due to technology barriers

Intuitively ‘trended data’ sounds like a no-brainer (with value seen across the credit chain of acquisitions, origination and account management) but the limitations of technology have historically prevented its widespread use. Change after all requires people, process and technology; and “trended data” has historically been difficult to deploy with a lot of testing required – and ultimately needs the customers to adjust their decisioning, acquisition, offering and other strategies.

Barclays Research October 6, 2016

“

”

LendIt USA 201711

• Understand trended data beyond the buzz word

• Learn what trended data can tell you across the Customer Life Cycle to improve your business

• Most effective uses of trended data

• How to use trended data to solve your most pressing business challenges

Objective

28/02/2017

LendIt USA 201712

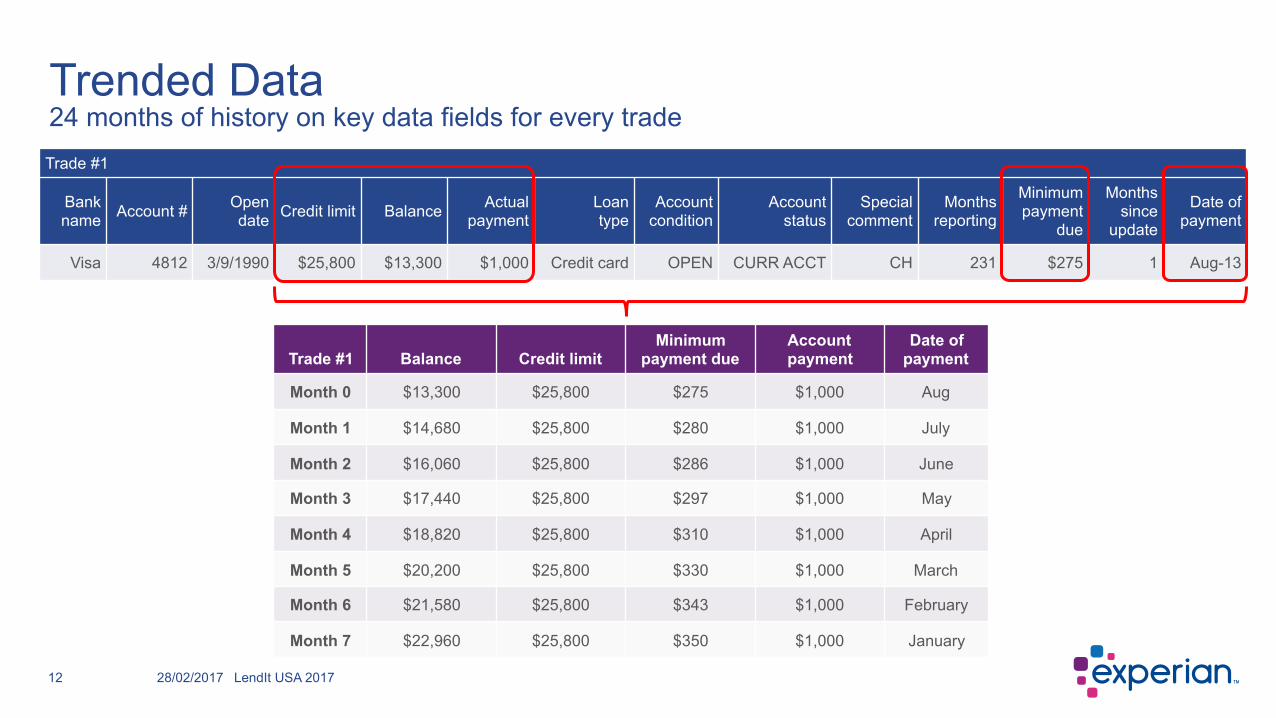

Trended Data24 months of history on key data fields for every trade

28/02/2017

Trade #1 Balance Credit limitMinimum

payment dueAccount payment

Date of payment

Month 0 $13,300 $25,800 $275 $1,000 Aug

Month 1 $14,680 $25,800 $280 $1,000 July

Month 2 $16,060 $25,800 $286 $1,000 June

Month 3 $17,440 $25,800 $297 $1,000 May

Month 4 $18,820 $25,800 $310 $1,000 April

Month 5 $20,200 $25,800 $330 $1,000 March

Month 6 $21,580 $25,800 $343 $1,000 February

Month 7 $22,960 $25,800 $350 $1,000 January

Trade #1

Bank name Account # Open

date Credit limit Balance Actual payment

Loan type

Account condition

Account status

Special comment

Months reporting

Minimum payment

due

Months since

update

Date of payment

Visa 4812 3/9/1990 $25,800 $13,300 $1,000 Credit card OPEN CURR ACCT CH 231 $275 1 Aug-13

LendIt USA 201713

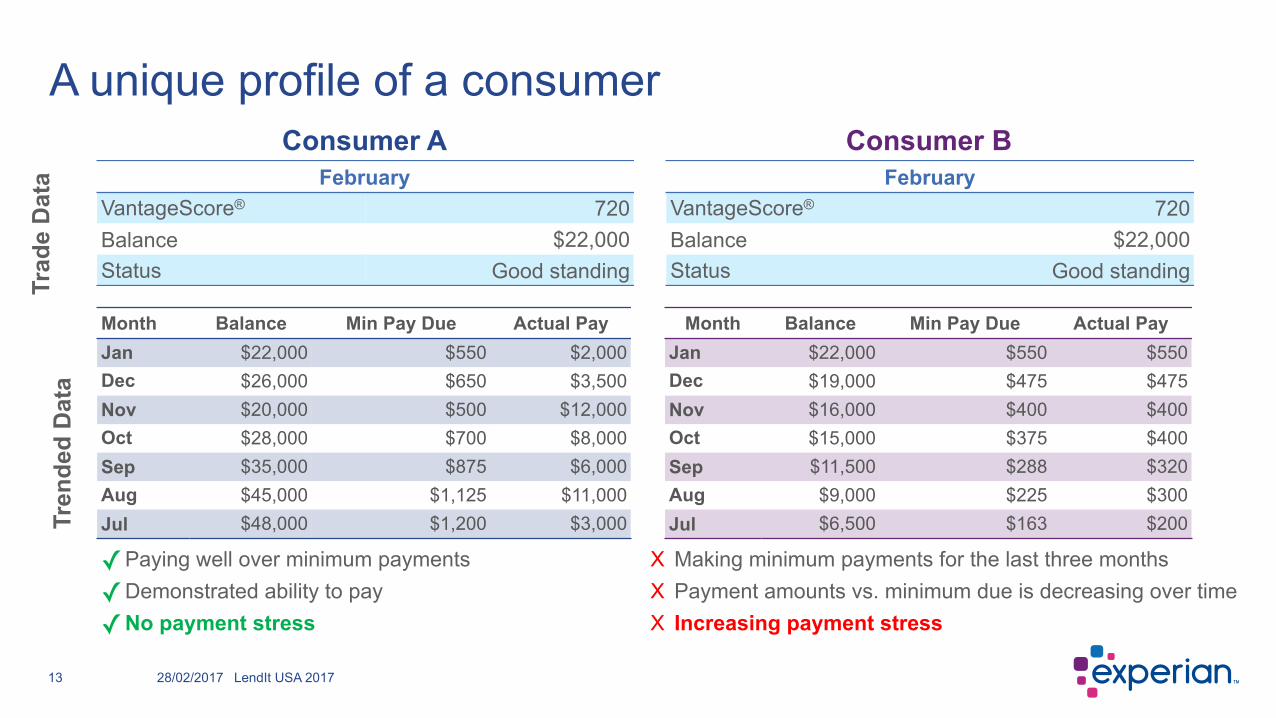

A unique profile of a consumer

28/02/2017

FebruaryVantageScore® 720Balance $22,000 Status Good standing

Month Balance Min Pay Due Actual PayJan $22,000 $550 $2,000 Dec $26,000 $650 $3,500 Nov $20,000 $500 $12,000 Oct $28,000 $700 $8,000 Sep $35,000 $875 $6,000 Aug $45,000 $1,125 $11,000 Jul $48,000 $1,200 $3,000

Month Balance Min Pay Due Actual PayJan $22,000 $550 $550 Dec $19,000 $475 $475 Nov $16,000 $400 $400 Oct $15,000 $375 $400 Sep $11,500 $288 $320 Aug $9,000 $225 $300 Jul $6,500 $163 $200

Consumer A Consumer BFebruary

VantageScore® 720Balance $22,000 Status Good standing

✓Paying well over minimum payments

✓Demonstrated ability to pay

✓No payment stress

X Making minimum payments for the last three months X Payment amounts vs. minimum due is decreasing over time X Increasing payment stress

Trad

e D

ata

Tren

ded

Dat

a

LendIt USA 201714

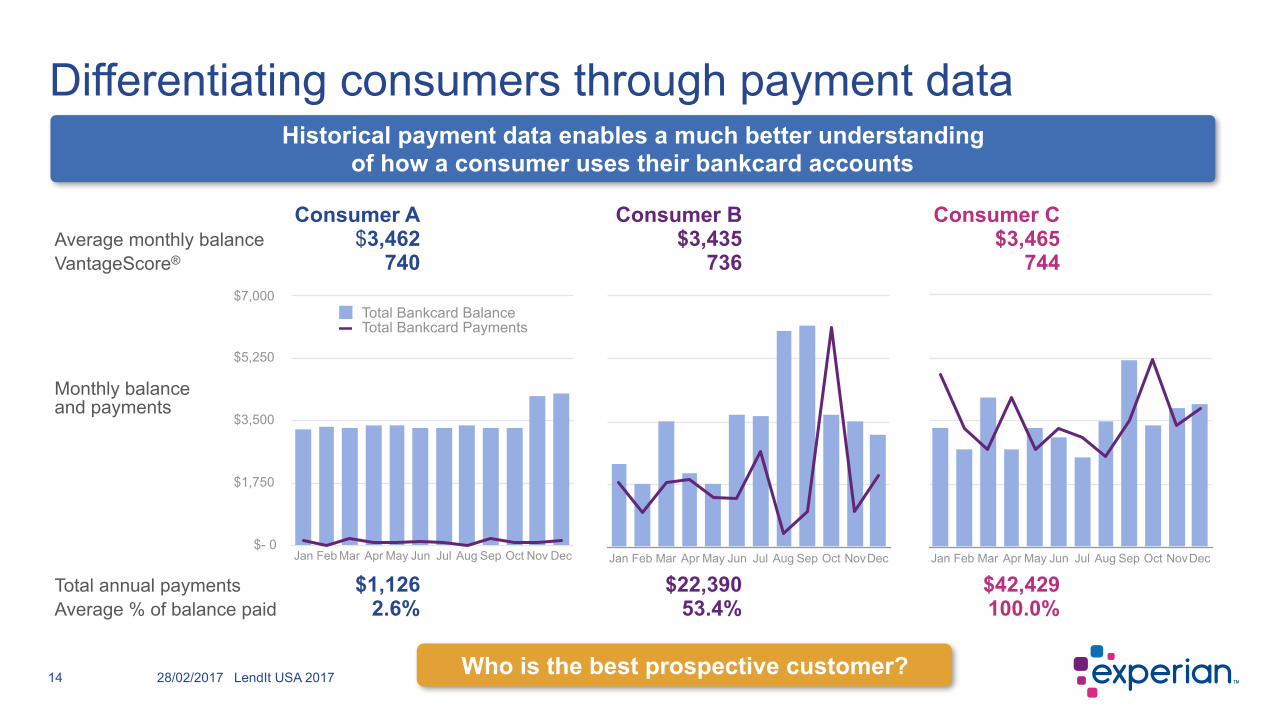

Differentiating consumers through payment data

28/02/2017

Consumer A Consumer B Consumer C Average monthly balance $3,462 $3,435 $3,465 VantageScore® 740 736 744

Monthly balanceand payments

Total annual payments $1,126 $22,390 $42,429 Average % of balance paid 2.6% 53.4% 100.0%

Who is the best prospective customer?

$- 0

$1,750

$3,500

$5,250

$7,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Total Bankcard BalanceTotal Bankcard Payments

Jan Feb Mar Apr May Jun Jul Aug Sep Oct NovDec Jan Feb Mar Apr May Jun Jul Aug Sep Oct NovDec

Historical payment data enables a much better understanding of how a consumer uses their bankcard accounts

LendIt USA 201715

Problem:

Solution:

Benefit:

How trended data helps lenders

28/02/2017

Knowing a consumer’s credit information at a single point in time only tells part of the story

To understand the whole story, lenders need the ability to assess a consumer’s credit behavior over time

Understanding how a consumer uses credit or pays back debt over time can help lenders: • Offer the right products & terms to increase response rates • Determine up sell and cross sell opportunities • Prevent attrition • Identify profitable customers • Avoid consumers with payment stress • Limit loss exposure

LendIt USA 201716 28/02/2017

LendIt USA 201717

The challenge with trended data

28/02/2017

How do you find the payment pattern?

LendIt USA 201718

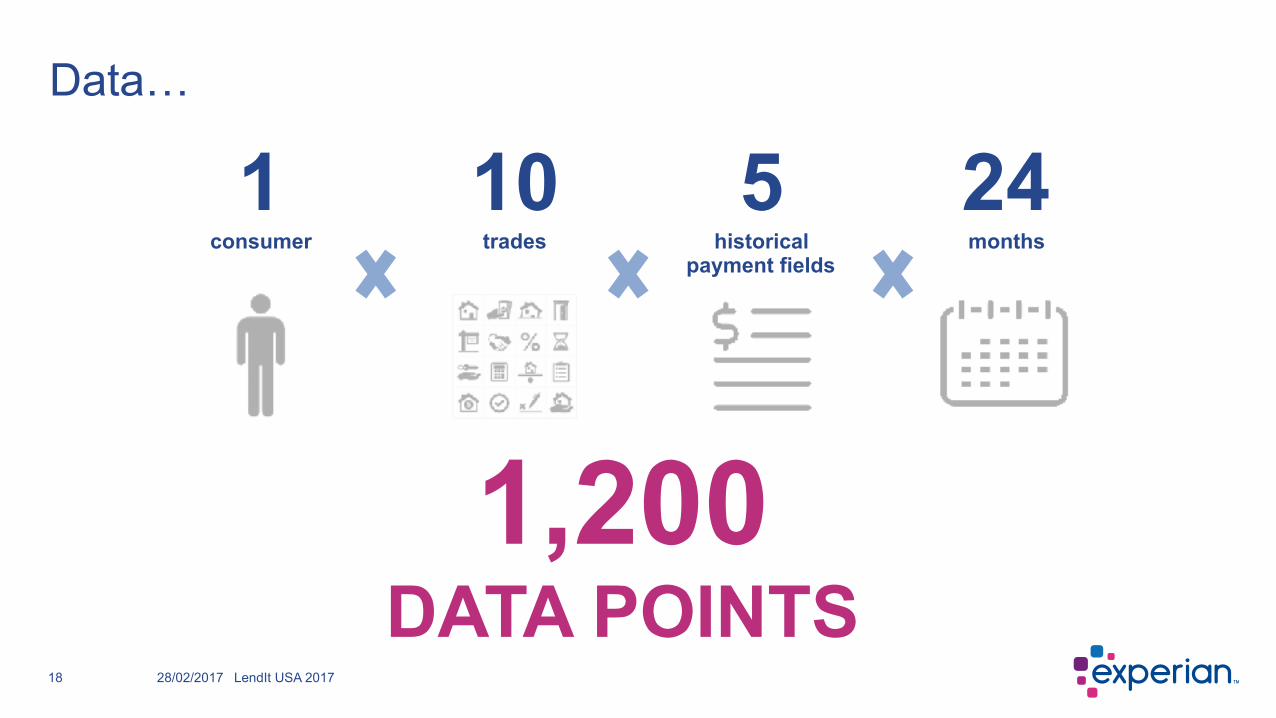

Data…

28/02/2017

10

trades

24 months

1,200 DATA POINTS

1 consumer

5 historical

payment fields

LendIt USA 201719

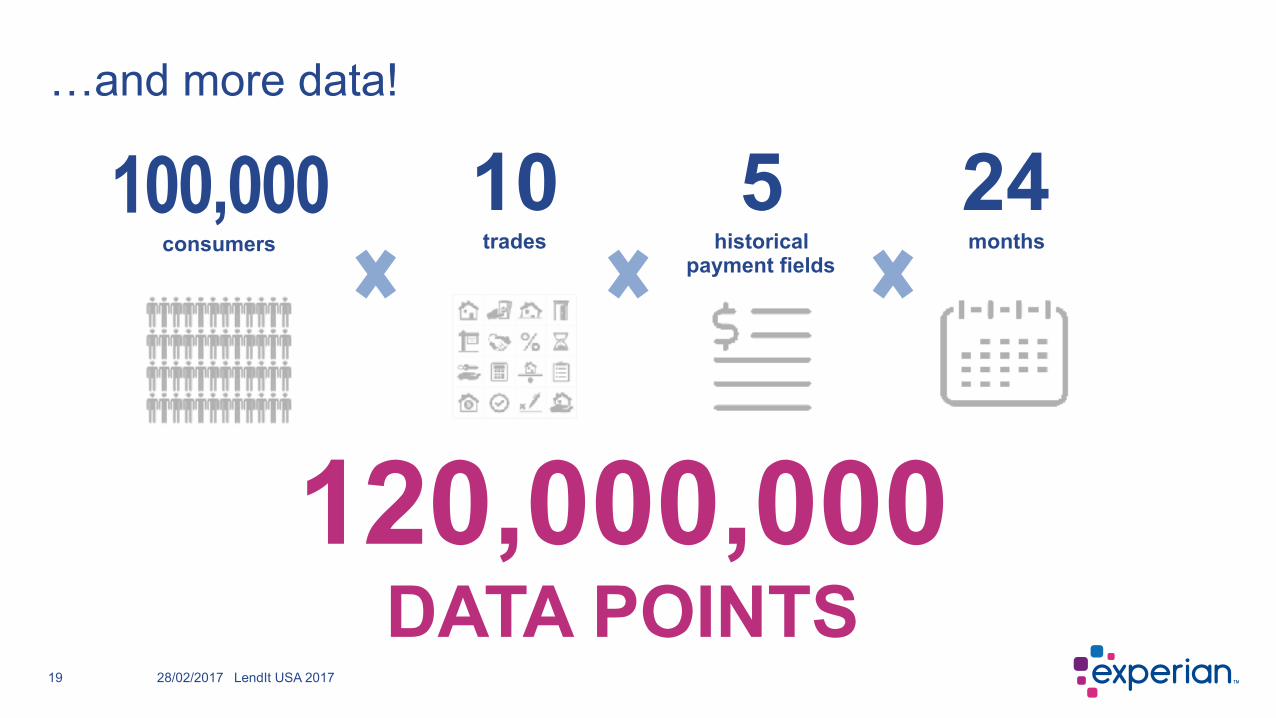

…and more data!

28/02/2017

10

trades

24 months

120,000,000 DATA POINTS

100,000 consumers

5 historical

payment fields

LendIt USA 201720

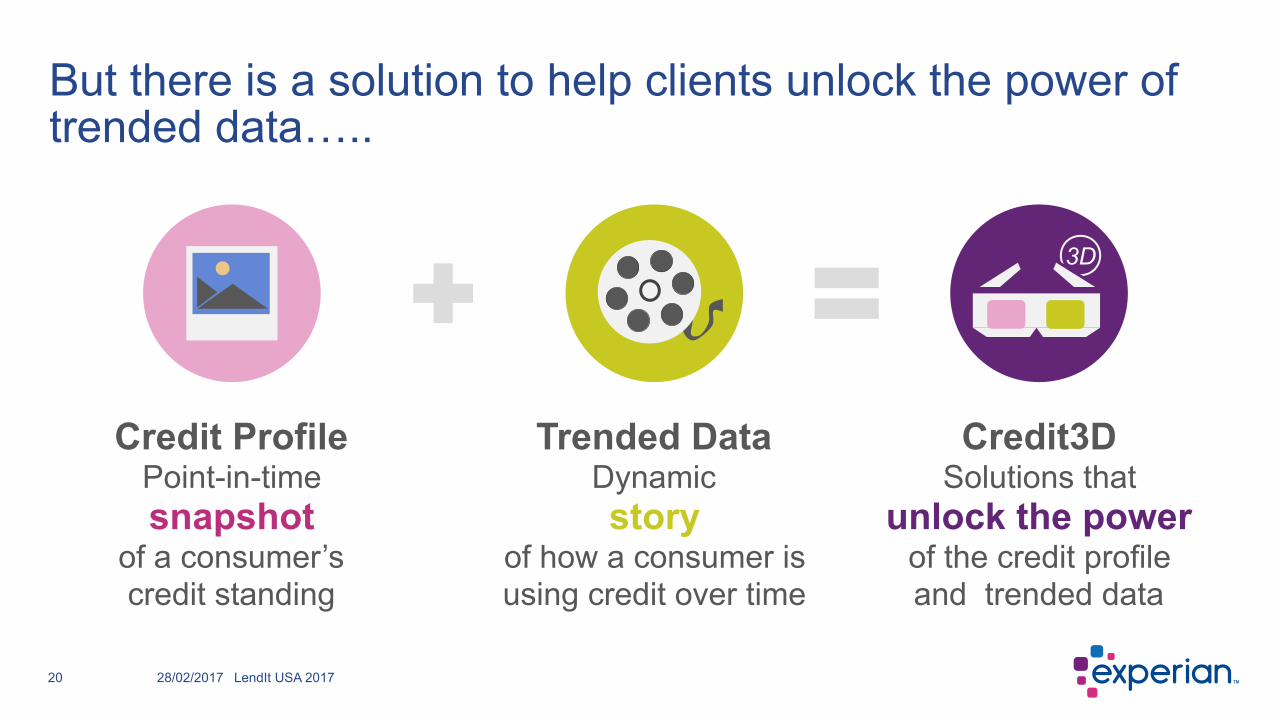

But there is a solution to help clients unlock the power of trended data…..

28/02/2017

Credit Profile Point-in-time snapshot

of a consumer’s credit standing

Trended Data Dynamic story

of how a consumer is using credit over time

Credit3D Solutions that

unlock the power of the credit profile and trended data

3D

LendIt USA 201721

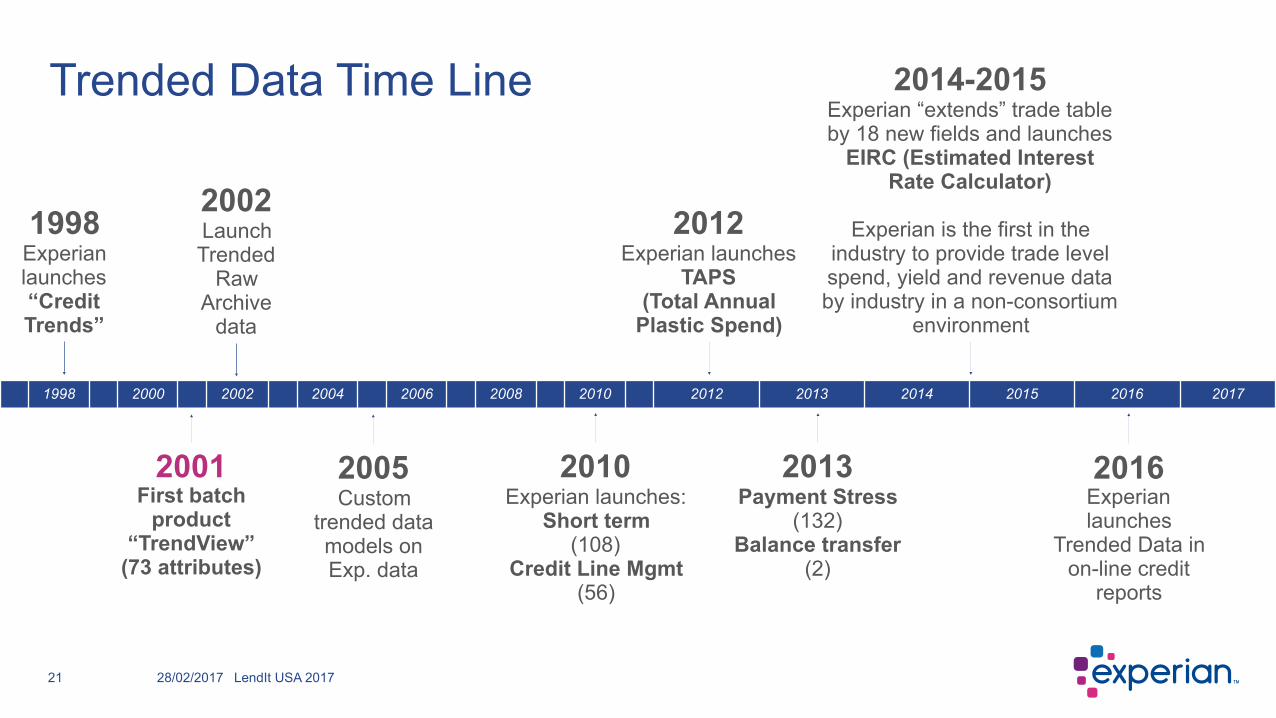

Trended Data Time Line

28/02/2017

1998 2000 2002 2004 2006 2008 2010 2012 2013 2014 2015 2016 2017

1998 Experian launches “Credit Trends”

2001 First batch

product “TrendView”

(73 attributes)

2002 Launch Trended

Raw Archive

data

2005 Custom

trended data models on Exp. data

2010 Experian launches:

Short term (108)

Credit Line Mgmt (56)

2012 Experian launches

TAPS (Total Annual

Plastic Spend)

2013 Payment Stress

(132) Balance transfer

(2)

2014-2015Experian “extends” trade table by 18 new fields and launches

EIRC (Estimated Interest Rate Calculator)

Experian is the first in the industry to provide trade level spend, yield and revenue data by industry in a non-consortium

environment

2016 Experian launches

Trended Data in on-line credit

reports

LendIt USA 201722

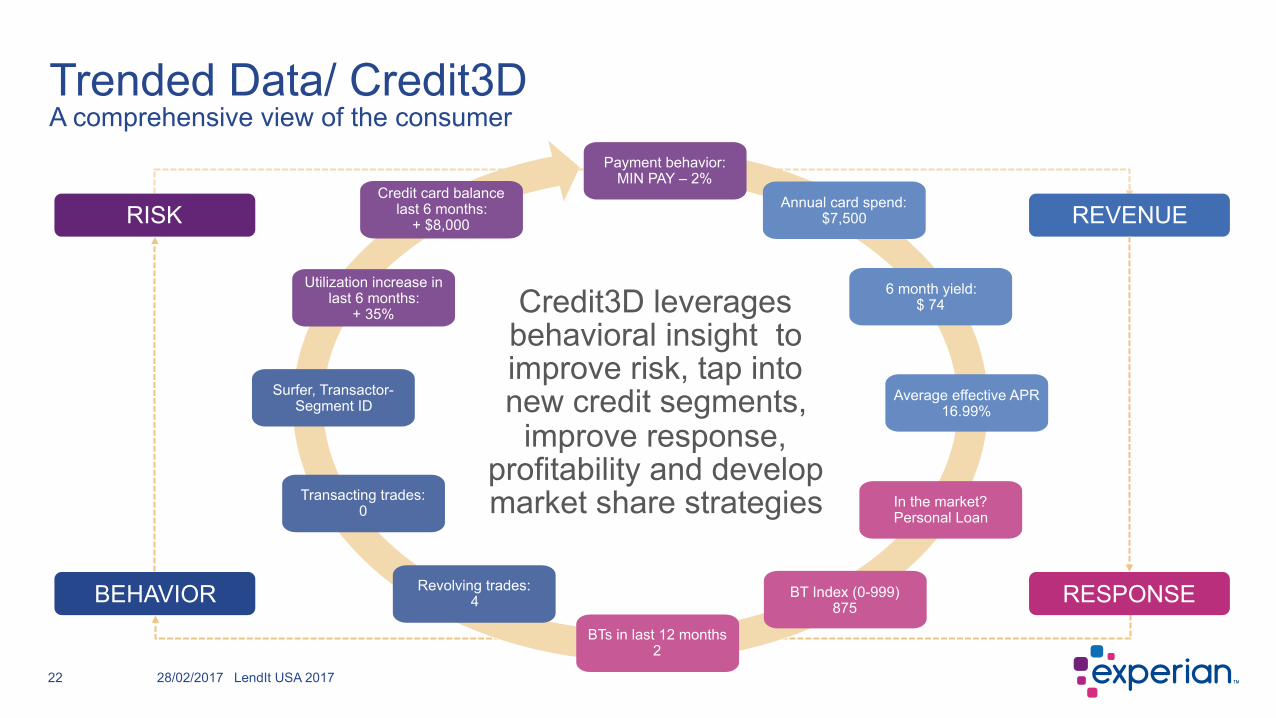

Trended Data/ Credit3D A comprehensive view of the consumer

28/02/2017

Payment behavior: MIN PAY – 2%

Annual card spend: $7,500

6 month yield: $ 74

Average effective APR 16.99%

In the market? Personal Loan

BT Index (0-999) 875

BTs in last 12 months 2

Revolving trades: 4

Transacting trades: 0

Surfer, Transactor- Segment ID

Utilization increase in last 6 months:

+ 35%

Credit card balance last 6 months:

+ $8,000

BEHAVIOR

RISK REVENUE

RESPONSE

Credit3D leverages

behavioral insight to improve risk, tap into new credit segments,

improve response, profitability and develop market share strategies

LendIt USA 201723

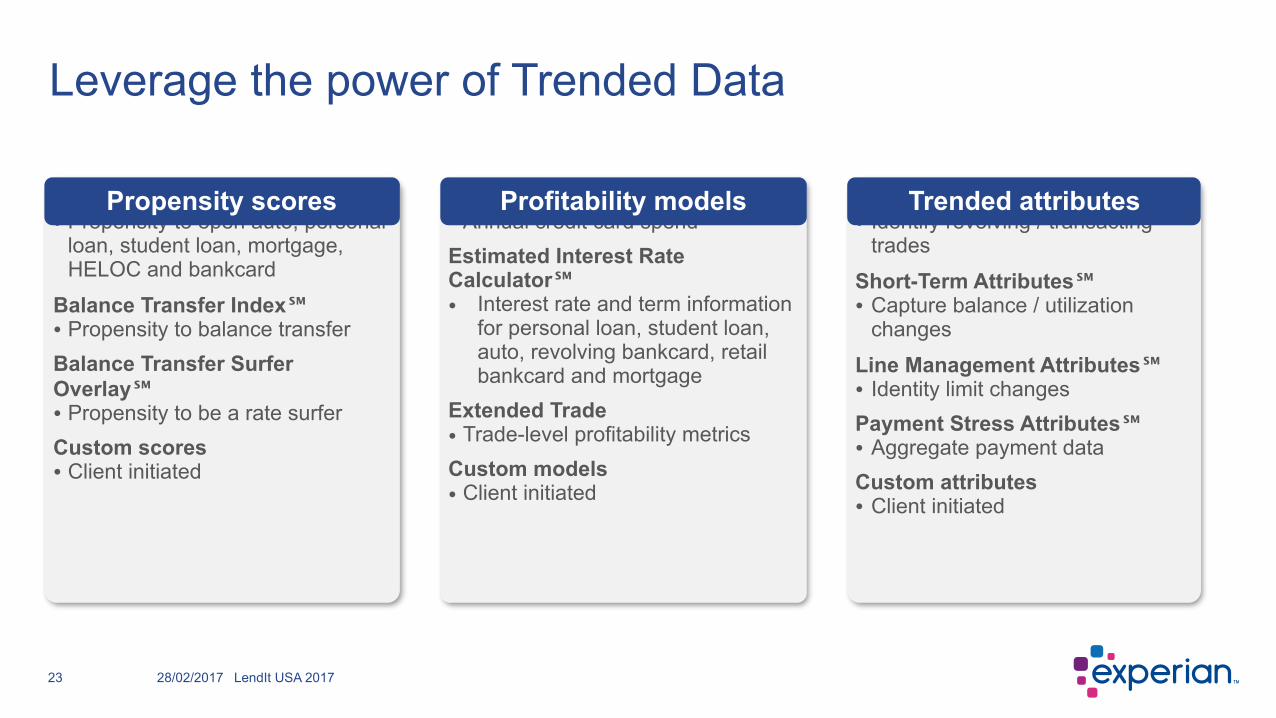

Experian TAPS℠ • Annual credit card spend Estimated Interest Rate Calculator℠ • Interest rate and term information

for personal loan, student loan, auto, revolving bankcard, retail bankcard and mortgage

Extended Trade • Trade-level profitability metrics Custom models • Client initiated

Trend View℠ • Identify revolving / transacting

trades

Short-Term Attributes℠ • Capture balance / utilization

changes

Line Management Attributes℠ • Identity limit changes Payment Stress Attributes℠ • Aggregate payment data Custom attributes • Client initiated

In the Market Models℠ • Propensity to open auto, personal

loan, student loan, mortgage, HELOC and bankcard

Balance Transfer Index℠ • Propensity to balance transfer Balance Transfer Surfer Overlay℠ • Propensity to be a rate surfer Custom scores • Client initiated

Leverage the power of Trended Data

28/02/2017

Trended attributesProfitability modelsPropensity scores

LendIt USA 201724

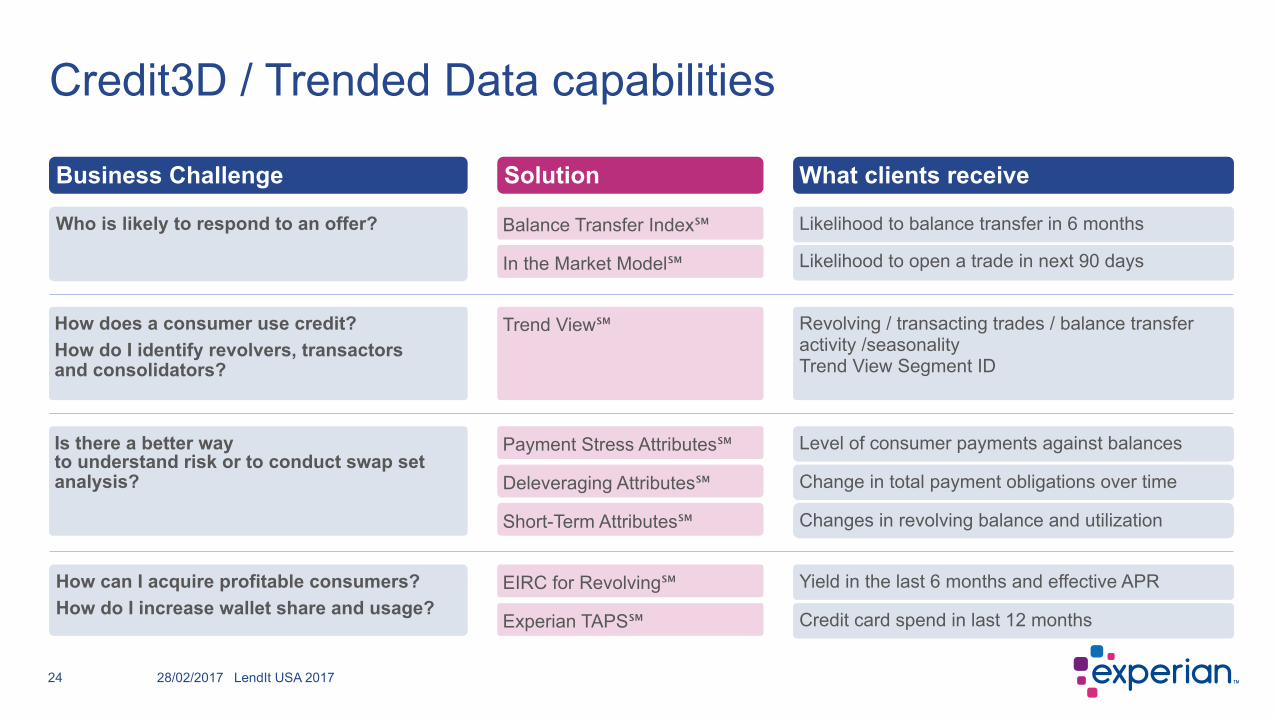

Credit3D / Trended Data capabilities

28/02/2017

Who is likely to respond to an offer? Balance Transfer Index℠

In the Market Model℠

Likelihood to balance transfer in 6 months

Likelihood to open a trade in next 90 days

Is there a better way to understand risk or to conduct swap set analysis?

Payment Stress Attributes℠

Deleveraging Attributes℠

Level of consumer payments against balances

Change in total payment obligations over time

Short-Term Attributes℠ Changes in revolving balance and utilization

How can I acquire profitable consumers? How do I increase wallet share and usage?

EIRC for Revolving℠

Experian TAPS℠

Yield in the last 6 months and effective APR

Credit card spend in last 12 months

How does a consumer use credit? How do I identify revolvers, transactors and consolidators?

Trend View℠ Revolving / transacting trades / balance transfer activity /seasonality Trend View Segment ID

Business Challenge Solution What clients receive

LendIt USA 201725

Comprehensive Credit Marketing using Trended Data/Credit 3D

28/02/2017

LendIt USA 201726

Marketing strategy should be about more than just response rate. A comprehensive approach can ensure quality originations and healthy portfolio growth. ➢Response Rate ➢Risk Expansion ➢Long-term Value

Three Pillars of Comprehensive Prescreen

28/02/2017

LendIt USA 201727

How do you reach receptive audiences to get the most out of your marketing campaigns?

Offer timing Offer relevance

Combine propensity models and offer relevance to get the right consumers the right offer at the right time.

Response Rate: Make an ImpactMost people don’t need your product; are you effectively finding those that do?

28/02/2017

LendIt USA 201728

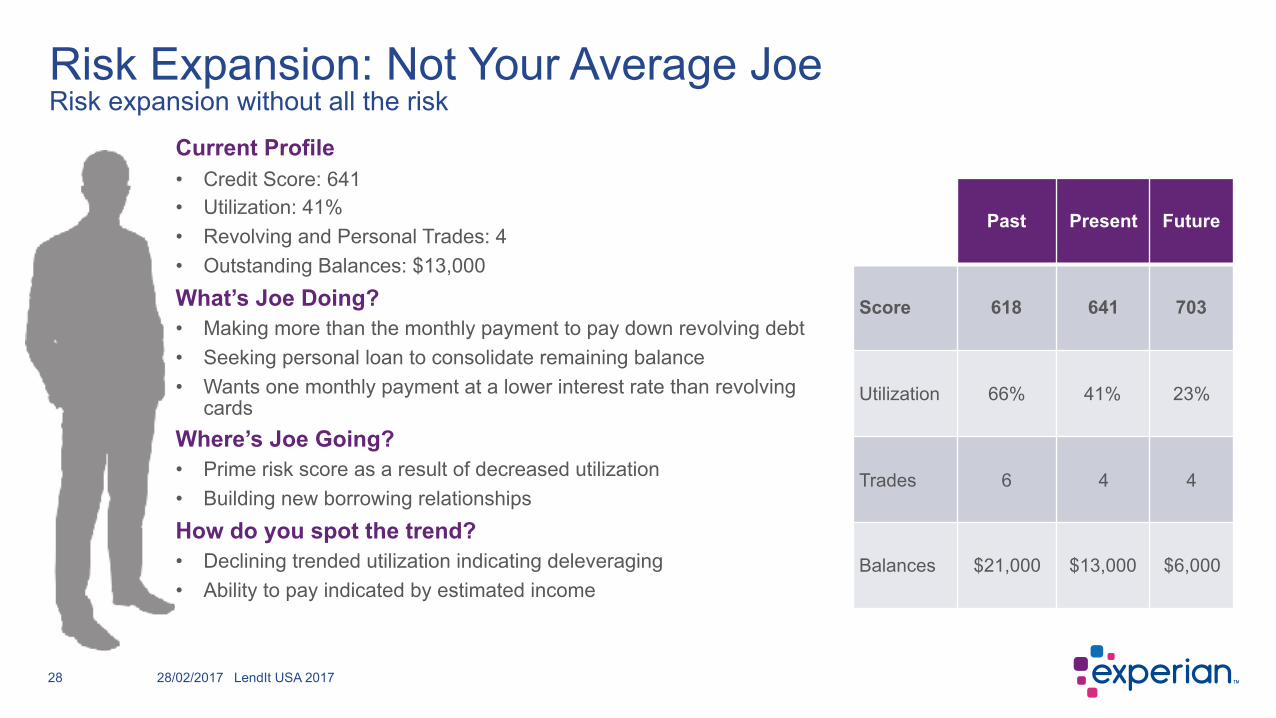

Risk Expansion: Not Your Average JoeRisk expansion without all the risk

28/02/2017

Current Profile • Credit Score: 641 • Utilization: 41% • Revolving and Personal Trades: 4 • Outstanding Balances: $13,000 What’s Joe Doing? • Making more than the monthly payment to pay down revolving debt • Seeking personal loan to consolidate remaining balance • Wants one monthly payment at a lower interest rate than revolving

cards Where’s Joe Going? • Prime risk score as a result of decreased utilization • Building new borrowing relationships How do you spot the trend? • Declining trended utilization indicating deleveraging • Ability to pay indicated by estimated income

` Past Present Future

Score 618 641 703

Utilization 66% 41% 23%

Trades 6 4 4

Balances $21,000 $13,000 $6,000

LendIt USA 201729

• Maximize response rates: Propensity tools aren’t enough. Layering credit attributes can further refine results and improve campaign performance.

• Risk expansion: Expand risk score cutoffs without taking on incremental risk. Trended data helps identify trends in credit behavior. Find candidates in lower score ranges who are deleveraging and trending up.

• Long-term value: Understanding how a consumer uses credit enables long-term loyalty building. Give your team the edge by identifying likely short-term and long-term borrowers.

Think comprehensive

28/02/2017

LendIt USA 201730

Questions

28/02/2017

LendIt USA 2017

Paul DeSaulniers Sr. Director, Experian Email: [email protected] Phone: 714.830.7580

28/02/2017

![Everything you need to know about blogging]](https://img.pdfslide.net/doc/110x75/54964bf5b47959e1148b463c/everything-you-need-to-know-about-blogging.jpg)