Embed Size (px)

Citation preview

Executive Compensation, Tax Reporting Aggressiveness, and Future Firm Performance

Sonja Olhoft Rego University of Iowa

Ryan Wilson*

University of Iowa

December 22, 2008

Abstract

This study investigates the association between tax reporting aggressiveness and the level of CEO and CFO compensation, after controlling for standard economic determinants of such compensation. Across six different measures of tax aggressiveness, we consistently find a positive relation between aggressive tax reporting and the level of CEO and CFO compensation. We investigate whether this positive relation is due to optimal contracting or to managers extracting rents from firms. We find no evidence that aggressive tax strategies allow managers to extract rents from firms. In particular, we find no evidence that firms with aggressive tax reporting and weak corporate governance pay their CEOs and CFOs more than other firms. Moreover, we find no evidence that the positive relation between executive compensation and tax reporting aggressiveness leads to poor future firm performance. JEL Classifications: M41, M52, G34 Keywords: Tax aggressiveness, executive compensation, corporate governance. * We appreciate helpful comments from Dan Collins, Cristi Gleason, Leslie Hodder, Paul Hribar, Steve Kachelmeier, Sean McGuire, Rick Mergenthaler, Lillian Mills, Tom Omer, John Robinson, Terry Shevlin, Connie Weaver, and workshop participants at Indiana University, Texas A&M University, the University of Iowa, and the University of Texas.

Executive Compensation, Tax Reporting Aggressiveness, and Future Firm Performance 1. Introduction

Prior research links executive compensation to the economic determinants of such

compensation (e.g., Smith and Watts 1992; Core and Guay 1999), to governance characteristics

(e.g., Core, Holthausen, and Larcker 1999; Ashbaugh-Skaife, Collins, and LaFond 2006), and to

earnings management incentives (e.g., Erickson, Hanlon, and Maydew 2006; Armstrong,

Jagolinzer, and Larcker 2008). While Core and Guay (1999) generally conclude that

compensation contracts on average reflect incentive alignment, several recent studies suggest a

positive relation between executive compensation and accounting manipulation (e.g., Cheng and

Warfield 2005; Bergstresser and Philippon 2006). Despite a surge in both executive

compensation and tax shelter activity during the 1990’s and early 2000’s, few studies have

considered the link between executive compensation and tax reporting aggressiveness. We

examine the association between executive compensation and tax aggressiveness and the

implications of that association for future firm performance.

For purposes of our study, we consider tax aggressiveness to include standard tax

planning practices that do not necessarily violate income tax rules, as well as fraudulent tax

avoidance, including tax shelter transactions considered abusive by the IRS and the Treasury

Department. Firms may compensate managers for aggressive tax reporting for various reasons,

the most obvious of which is the tax savings associated with tax planning activities. These tax

savings often increase after-tax cash flows, book income, net assets, and more generally,

financial slack – attributes that typically have a positive impact on firm value. In addition, firms

may also compensate managers for aggressive tax reporting to reward risk-taking behaviors,

which managers may otherwise avoid (e.g., Rajgopal and Shevlin 2002).

1

Despite the considerable tax savings generated by corporate tax shelters, significant

cross-sectional variation exists in the degree to which firms pursue aggressive tax reporting

strategies. Shevlin (2007) calls for research examining why some firms enter into tax shelters

while other do not. Investigating the link between executive compensation and tax

aggressiveness provides insight into one potentially important determinant of observed cross-

sectional variation in tax shelter activity. In particular, managers may forego aggressive tax

sheltering unless such activities have a net positive impact on their total compensation. Our

study also provides insights into whether optimal contracting or opportunistic behavior by top

executives accounts for the association between executive compensation and aggressive tax

reporting.

Although we expect firms to compensate managers for some degree of tax

aggressiveness, we do not expect firms to compensate managers for tax aggressiveness that

imposes excess costs on the firm and thus reduces shareholder wealth. Highly aggressive tax

reporting can cause firms to incur additional costs, such as the costs of implementing the

aggressive tax plan (e.g., promoter and attorney fees), the costs associated with IRS audits and

subsequent litigation (e.g., accounting and legal fees), as well as reputational costs associated

with the public disclosure of tax shelter activity (e.g., negative stock price implications as in

Hanlon and Slemrod 2007). Moreover, to the extent that conformity exists between financial and

tax reporting, reporting lower taxable income can generate financial reporting costs (i.e., lower

financial income). In sum, we do not expect firms to compensate managers for tax

aggressiveness if the costs exceed the benefits. We investigate the extent that firms compensate

managers for aggressive tax planning using different measures of tax aggressiveness and we

2

examine chief executive officers (CEOs) separately from chief financial officers (CFOs), as

CFOs have greater responsibility for the accounting function, relative to CEOs.

Using compensation data obtained in a survey of corporate executives, Phillips (2003)

finds that compensating division managers (but not CEOs) on an after-tax basis leads to greater

tax planning effectiveness. Hanlon, Mills, and Slemrod (2005) find a positive association

between the level of equity incentives from exercisable stock options and proposed IRS

deficiencies. In contrast, Desai and Dharmapala (2006) find that increases in equity-based

incentives actually lead to a reduction in the level of tax avoidance. Desai and Dharmapala

conjecture that because tax shelters are intentionally designed to obscure the economic substance

of a transaction they therefore provide a shield for managers to engage in opportunistic behavior.

Consequently, they argue that increases in equity compensation reduce the level of tax sheltering

by better aligning the incentives of managers with those of shareholders. Desai and Dharmapala

argue this improved alignment is especially true in firms with poor corporate governance

structures where it is easier for managers to engage in opportunistic behavior through the use of

corporate tax shelters.

While it is possible tax shelters could be used opportunistically by managers, they often

generate significant tax savings that benefit shareholders. Examining a sample of 44 identified

tax shelter cases, Graham and Tucker (2006) find the average tax shelter generates an annual tax

deduction sufficient to shield income equal to approximately 9 percent of asset value. Also

consistent with tax shelters benefiting shareholders, Wilson (2008) finds firms with strong

governance structures that engage in tax shelter transactions exhibit positive abnormal stock

returns during the tax shelter period. Because aggressive tax reporting can result in significant

tax savings, but can also generate significant costs, including the potential for managerial

3

opportunism, it is not clear whether executive compensation contracts will be designed to reward

managers for aggressive tax reporting. We directly test this association using a number of

recently developed measures of tax reporting aggressiveness. Specifically, we utilize traditional

effective tax rates, cash effective tax rates, total book-tax differences, permanent book-tax

differences, discretionary book-tax differences, and predicted tax shelter firms. These six

measures reflect varying degrees of aggressiveness, with the latter two likely reflecting the most

aggressive tax strategies.

Our initial tests document a strong, positive association between total CEO and CFO

compensation and aggressive tax planning. This result is robust for all six measures of tax

aggressiveness, as well as controls for the economic determinants of executive compensation.

We infer that firms compensate managers for varying degrees of tax aggressiveness.

We then investigate whether this positive relation between CEO and CFO compensation

and tax aggressiveness is consistent with optimal contracting or with managers extracting rents

from firms. First, we build on Desai and Dharmapala (2006) and examine whether governance

structures moderate the positive relation between executive compensation and tax

aggressiveness. If firms with weaker governance mechanisms exhibit a more positive relation

between executive compensation and tax aggressiveness, then we would infer that managers at

firms with weaker governance structures are able to extract rents from those firms via aggressive

tax planning. On the other hand, if firms with stronger governance mechanisms exhibit a more

positive relation between executive compensation and tax aggressiveness, then we would

conclude that such managers are compensated for efficient tax sheltering choices. Contrary to

stories of managerial rent extraction, our results suggest that corporate governance structures do

4

not consistently moderate the relation between executive compensation and tax reporting

aggressiveness.

Our second test of ‘optimal contracting’ vs. ‘managerial rent extraction’ considers the

implications of the positive relation between executive compensation and tax aggressiveness for

future firm performance. Core et al. (1999) and Ashbaugh-Skaife et al. (2006) show that

measures of “excess” compensation are associated with negative future return on assets and

negative future stock returns.1 They interpret their results as consistent with managers at firms

with greater agency problems receiving higher compensation that leads to worse future firm

performance. We model our analyses after their empirical tests and calculate the portions of

CEO and CFO compensation that are related to tax reporting aggressiveness, which we refer to

as CEO and CFO ‘tax-based compensation.’ We then regress future return on assets and future

stock returns on CEO and CFO tax-based compensation and control variables. We find that tax-

based compensation is not associated with inferior future firm performance. Thus, we find no

evidence that aggressive tax strategies allow managers to extract rents from firms.

Our study contributes to several streams of research, including studies that investigate

whether executive compensation practices align managers’ incentives with those of shareholders,

and studies that examine the economic outcomes associated with tax reporting aggressiveness.

To our knowledge, this is the first study to link tax aggressiveness to executive compensation

and future firm performance. Our results have implications for corporate compensation

committees that determine that structure of executive compensation contracts, for regulators and

corporate stakeholders that monitor corporate tax practices, as well as researchers interested in

1 Core et al. (1999) and Ashbaugh-Skaife et al. (2006) calculate excess compensation as the portion of total compensation that is predicted by board and ownership structure variables. Core et al. argue that if contracting is optimal there should be no association between CEO compensation and governance structures, i.e., CEO compensation should only be a function of economic determinants.

5

understanding the factors that impact corporate tax aggressiveness. Specifically, our results

suggest tax reporting aggressiveness is an important determinant of total CEO (CFO)

compensation and that this association does not appear to be a result of managerial opportunism.

The remainder of this paper proceeds as follows. Section 2 describes prior studies that

we build upon and develops hypotheses. Section 3 explains our research design, while Section 4

discusses sample selection and empirical results. Section 5 concludes.

2. Background and Hypothesis Development

2.1 Prior Research

Our study builds on separate streams of prior research. One stream investigates the

valuation implications of aggressive tax reporting, as well as the links between managerial

compensation practices and tax reporting aggressiveness. The other stream examines the

determinants of executive compensation. We discuss each of these streams below.

2.1.1 Is Tax Avoidance a Value-Maximizing Activity?

Few studies directly investigate whether tax avoidance (aka tax planning or tax

aggressiveness) is a value-maximizing activity for firms to undertake. Bankman (1999) argues

that the dollar benefit of participating in a tax shelter far outweighs the cost, given the low

probability of detection by the tax authorities. Graham and Tucker (2006) state that tax

sheltering should affect stock prices since tax sheltering can “increase financial slack, reduce

expected bankruptcy costs, enhance credit quality, reduce the risk of covenant violation, and

reduce the cost of debt” (p. 566). They find that tax shelter firms’ credit ratings improve one

notch relative to those of matched, control firms, consistent with lower costs of debt for their

6

sample of tax shelter firms. In addition, Wilson (2008) finds that the average tax shelter

transaction generates federal income tax savings of $375.5 million.

Using a large sample of U.S. firms, Desai and Dharmapala (2007) investigate whether

corporate tax avoidance is valued by investors. They find a positive relation between their proxy

for corporate tax avoidance (as measured by book-tax differences adjusted for accruals) and firm

value (as proxied by Tobin’s Q). They also find that firms with higher levels of institutional

ownership (their proxy for strong corporate governance) exhibit a more positive relation between

those two variables than firms with less institutional ownership. Hanlon and Slemrod (2007)

investigate a similar research question but implement a different research design. They examine

how the stock market evaluates news of corporate tax aggressiveness by investigating stock price

reactions to the initial press mention that a firm was involved in a corporate tax shelter. The

stock price reactions should reflect competing stock price components, including the positive

impact of corporate tax planning and the negative impact of the direct costs associated with tax

sheltering, as well as indirect reputational costs associated with the negative publicity. Hanlon

and Slemrod find a small stock price decline associated with the initial tax shelter

announcements; however, the decline is relatively small compared to other accounting

transgressions. They also find the stock price decline is smaller for firms with stronger corporate

governance structures.

Based on a sample of firms identified ex post as having participated in tax shelter

transactions, Wilson (2008) develops a model of tax shelter participation and then uses the model

to identify a sample of predicted tax shelter firms. He relies on both samples to investigate

whether tax sheltering increases shareholder wealth or allows managers to extract rents from the

firm. Wilson finds that tax shelter firms with strong corporate governance exhibit positive

7

abnormal stock returns during the period of active tax sheltering, and these returns are

significantly greater than the returns of tax shelter firms with poor corporate governance.

Similar to Desai and Dharmapala (2007) and Hanlon and Slemrod (2007), the results in Wilson

(2008) suggest an interaction effect between tax aggressiveness, strength of corporate

governance, and their impact on firm value.

In sum, prior research shows that tax sheltering can be a value-maximizing activity, but

most likely for those firms with stronger corporate governance structures.

2.1.2 Linking Tax Aggressiveness to Compensation Practices

Few studies have examined the relation between executive compensation practices and

tax reporting aggressiveness. Shackelford, Slemrod, and Sallee (2007) develop a general model

of how taxes affect the real and accounting decisions of corporations. They note that financial

reports are a means by which managers convey their inside knowledge to external investors,

reducing information asymmetries and thus lowering the cost of obtaining capital. In their

model, there are at least two reasons why accounting information may be important to managers.

First, many contracts (including compensation contracts) rely on the firm’s accounting

information. Second, if users of financial statements cannot distinguish between low earnings

arising from poor profitability and low earnings arising from tax plans that increase cash flow at

the expense of accounting earnings, then managers may be unwilling to minimize real taxes paid.

This discussion highlights the fact that although tax aggressiveness can improve the cash flows

of the firm, managers may not engage in such activity if it will reduce their expected

compensation.

In an empirical study that more directly investigates the link between tax aggressiveness

and executive compensation, Phillips (2003) examines whether compensating managers based on

8

after-tax performance measures leads to lower effective tax rates, his proxy for tax planning

effectiveness. Phillips notes that firms should use after-tax performance measures to compensate

managers only if the expected benefits exceed the expected costs of doing so. Based on a sample

of 209 surveyed corporate executives, Phillips concludes that compensating business unit

managers, but not CEOs, on an after-tax basis leads to lower effective tax rates.

Desai and Dharmapala (2006) examine how equity-based compensation incentives

influence tax sheltering decisions. Because equity-based incentives should align managerial

interests with those of shareholders, Desai and Dharmapala predict that such incentives should

induce managers to reduce their diversion of rents and increase their tax sheltering activities.

However, Desai and Dharmapala also conjecture that complex tax shelter transactions that are

designed to obscure the economic substance of the transactions may also obscure a firm’s

financial reporting and increase the opportunities for managerial diversion.2 They test their

model across well-governed and weaker-governed firms and find that increases in incentive

compensation reduce the level of tax sheltering and this negative effect is driven primarily by

weaker-governed firms. Desai and Dharmapala conclude that incentive compensation better

aligns managerial incentives with those of shareholders and reduces opportunistic tax sheltering.

Our study extends Phillips (2003) and Desai and Dharmapala (2006) by directly

investigating whether CEOs and CFOs are compensated for tax reporting aggressiveness and

then linking these compensation practices to future firm performance. We consider various

definitions of tax aggressiveness and examine their interactions with different corporate

2 Desai and Dharmapala (2006) cite Dynegy as an example of a company that used an opaque, tax-motivated transaction to mislead the capital markets. Although the authors acknowledge that no evidence of managerial diversion exists in the Dynegy example, they claim that Dynegy illustrates how “misrepresentations destructive to shareholders can be facilitated by tax avoidance.” (p. 157)

9

governance structures. Importantly, our empirical tests are based on existing models of

executive compensation, which we discuss below.

2.1.3 Determinants of Executive Compensation

In a seminal study in finance, Smith and Watts (1992) examine the determinants of

corporate policy decisions, including the level of executive compensation. Smith and Watts

predict that a firm’s investment opportunity set, industry regulation, size, and accounting return

should explain the level of salary compensation. Their results indicate that larger firms with

greater growth opportunities, less regulation, and higher accounting return have significantly

higher salary compensation. The authors also find that firms with greater growth options have

higher salary compensation and use stock-based incentive plans more often.

Core, Holthausen, and Larcker (1999) extend Smith and Watts (1992) and model CEO

compensation as a function of the economic determinants of CEO compensation, as well as

board of director characteristics and ownership structure. Core et al. propose that the board and

ownership structures observed in practice should induce optimal CEO contracting and firm

performance. If firms engage in optimal contracting then the economic determinants of CEO

compensation should completely describe the cross-sectional variation in CEO compensation. In

this case, board and ownership structure variables should be unrelated to CEO compensation.

Contrary to expectations, after controlling for standard economic determinants of CEO

compensation, Core et al. find that board and ownership structure variables have a significant

impact on the level of CEO compensation. Subsequent tests indicate a negative relation between

the amount of excess compensation (calculated as the portion of total compensation predicted by

the board and ownership structure variables) and future operating and stock market performance.

Together, their results suggest that firms with weaker governance structures have greater agency

10

problems, that CEOs at firms with greater agency problems receive greater compensation, and

that these firms exhibit worse future firm performance. We rely on the theory and compensation

model underlying Core et al. (1999) to investigate our hypotheses, which we develop below.

2.2 Hypotheses

Core et al. (1999) contend that the board and ownership structures observed in practice

should induce optimal CEO contracting and firm performance.3 In this case, managers should

select the level of tax reporting aggressiveness that maximizes firm value.4 If Core et al.’s

model for the equilibrium wage of the CEO is well-specified (i.e., if the economic determinants

fully explain the level of CEO compensation), then tax aggressiveness should not predict the

level of CEO compensation. That is, tax aggressiveness should be a noisy proxy for the

variables that explain CEO compensation (e.g., after-tax return on assets). Thus, our first

hypothesis (stated in the alternative) examines the basic relation between tax aggressiveness and

the level of executive compensation:

H1: Tax reporting aggressiveness is incrementally useful in predicting the amount of

CEO and CFO compensation beyond standard economic determinants of such

compensation.

If hypothesis 1 is supported by our empirical results, then either: 1) managers are

compensated for tax planning activities that merit a higher equilibrium wage (i.e., optimal

contracting exists), or 2) there exist unresolved agency problems that allow managers to use

3 Their argument presumes that firms and managers engage in optimal contracting. Prior studies (e.g., Eaton and Rosen 1983 and Demsetz and Lehn 1985) assume that firms choose optimal compensation schemes that are based on unique firm characteristics and the characteristics of their executives. These studies contrast other studies in finance (e.g., Jensen and Murphy 1990) that conclude CEO compensation contracts in practice are less than optimal. 4 We do not claim that the CEO is directly involved in the tax planning process. Instead, we view the CEO as having a significant impact on corporate policies and decision-making, including tax planning. This view is consistent with results in Dyreng, Hanlon, and Maydew (2008) that suggest CEOs and CFOs influence a firm’s level of tax aggressiveness.

11

aggressive tax strategies to extract rents from the firm (i.e., optimal contracting does not exist).

If managers are compensated for tax planning activities that merit a higher equilibrium wage,

then our proxies for tax aggressiveness reflect economic determinants of CEO and CFO

compensation that are not captured by the variables included in the Core et al. (1999) model. For

example, our measures of tax aggressiveness may reflect long-term savings associated with tax

planning activities that extend over a multi-year period. Our measures of tax aggressiveness may

also reflect the negative relation between aggressive tax sheltering and a firm’s reliance on debt

as a tax shield. The results in Graham and Tucker (2006) suggest that firms with more

aggressive tax reporting are generally less levered, and thus likely have lower costs of debt, for

which managers may receive higher compensation.

On the other hand, if unresolved agency problems exist, then aggressive tax strategies

may allow executives to obtain levels of compensation in excess of those implied by standard

economic determinants. Desai and Dharmapala (2006) conjecture that complex tax shelter

transactions may obscure the financial reporting of a firm (i.e., increase the information

asymmetry between managers and shareholders) such that tax sheltering increases a manager’s

opportunity for the diversion of rents. For example, certain tax shelter transactions may generate

financial reporting benefits that are difficult to identify in the financial statements but

nonetheless generate bonus and/or stock-based compensation that the manager would not have

otherwise earned.5

The ‘rent extraction’ argument in Desai and Dharmapala (2006) hinges on unresolved

agency conflicts, such as those discussed in Core et al. (1999). If firms do not operate with

5 Enron is illustrative of this argument. Enron’s numerous tax-motivated transactions not only saved the corporation millions of dollars in Federal income taxes but also enhanced the net income and net assets shown in its financial statements. Enron reported near-zero taxable income between 1996 and 2000 but billions of dollars of book income over the same reporting period (Seida 2003). This divergence between book and taxable income likely had a direct (and positive) impact on Enron’s executives’ total compensation.

12

optimal corporate governance mechanisms in place, then managers may be able to engage in tax

sheltering that increases their personal wealth rather than shareholder wealth. If aggressive tax

reporting is associated with suboptimal contracting, we would expect this association to be

strongest in firms with weak corporate governance. This leads to our second hypothesis (also

stated in the alternative):

H2: Firms with weaker corporate governance structures and more aggressive tax

reporting pay more compensation to their executives.

Even if we do not find results that support hypotheses 2, there may still exist unresolved

agency problems that our corporate governance proxies are unable to capture. So we further try

to distinguish between the ‘optimal contracting’ and ‘rent extraction’ explanations for the

positive association between tax aggressiveness and executive compensation by examining the

relation between the portion of compensation predicted by tax aggressiveness (‘tax-based

compensation’) and future firm performance. Our tests are modeled after those in Core et al.

(1999). Specifically, if the association between managerial compensation and tax aggressiveness

reflects agency conflicts (e.g., sub-optimal governance structures that allow managerial rent

diversion), we expect to find a negative relation between tax-based compensation and future firm

performance. A negative relation would be consistent with managerial rent extraction that

reduces future firm performance. We expect no association (or perhaps a positive association)

between tax-based compensation and future firm performance if tax aggressiveness is an

economic determinant of executive compensation, consistent with optimal contracting. Thus,

our third hypothesis predicts (also stated in the alternative):

H3: Tax-based compensation is negatively associated with measures of future firm

performance.

13

3. Proxies for tax reporting aggressiveness

Before we describe our research design we provide a brief discussion of our measures of

tax reporting aggressiveness. Because of the difficulty in accurately measuring tax reporting

aggressiveness, we conduct our tests using six alternative measures. With the exception of the

final measure of tax aggressiveness (SHELTER), we rank each measure by year and two-digit

SIC code. We then create an indicator variable that is set equal to one for the firms in the top

(bottom for ETR and CASH_ETR) quintile of each respective tax aggressiveness measure, and

zero for all other firms. This approach allows us to identify the most aggressive tax reporting

firms according to each measure while controlling for industry effects that could cause

differences in these measures unrelated to aggressive tax reporting strategies.6 Each of the

measures has limitations which we discuss below. However, observing consistent results across

these measures supports the contention that our proxies capture a firm’s tax reporting

aggressiveness.

3.1 Effective Tax Rate (ETR)

We begin with a measure of the traditional effective tax rate (ETR), calculated as total tax

expense divided by pre-tax book income less special items. Numerous studies have used ETR as

a measure of corporate tax burden and firms are also required to disclose their ETR in their

financial statements. Zimmerman (1983) examines firm size and its association with effective

tax rates. Gupta and Newberry (1992) examine the associations between ETR and firm size,

capital structure, asset mix, and performance. Further, policy makers such as Citizens for Tax

Justice (CTJ) have used the ETR measure to identify which U.S. corporations have relatively low

total tax burdens.

6 Nonetheless, in untabulated analyses, we also perform all of our empirical tests using continuous measures of tax aggressiveness. Inferences from these tests are substantially the same as those based on our tabulated results.

14

Hanlon (2003) identifies a number of limitations of ETR as a measure of tax

aggressiveness. First, total tax expense is the sum of current and deferred taxes. Deferred taxes

represent taxes that will be paid (or refunded) in the future associated with temporary book-tax

differences. Including deferred taxes in the calculation means that the ETR measure will not

reflect aggressive tax planning that causes temporary book-tax differences. This limitation is

important because some aggressive tax reporting strategies involve accelerating expenses or

deferring revenue for tax purposes. Second, if firms are recording contingencies (i.e., tax

cushion) associated with uncertain tax benefits generated by aggressive tax positions, then ETR

will understate the firm’s true level of tax aggressiveness. This limitation occurs because the

firm may not record the benefit associated with uncertain tax positions in its financial statements

in the same year that it is taking the aggressive tax position on its returns. As a result, the firm’s

tax expense in that year is a noisy indicator of how aggressive the firm was on its actual

corporate tax return. Third, until recently, GAAP required firms to record the tax benefit

associated with the deduction for employee stock options directly into equity rather than

reducing the firm’s current tax expense.7 If a firm has significant stock option deductions then

ETR overstates the firm’s actual tax burden.

3.2 Cash Effective Tax Rate (CASH_ETR)

Our second tax aggressiveness measure is the long-run cash effective tax rate

(CASH_ETR) introduced by Dyreng et al. (2008). CASH_ETR is calculated as the ratio of the

five-year sum of cash taxes paid to the five-year sum of pretax financial accounting income less

special items. Dyreng et al. (2008) note this measure of tax aggressiveness has several

advantages over the traditional ETR measure. First, CASH_ETR is not affected by changes in

the firm’s tax contingencies. Regardless of whether the firm records a benefit associated with an 7 See Hanlon and Shevlin (2002) for a discussion of the accounting for the tax benefit of employee stock options.

15

aggressive tax position in its financial statements, the reduced cash tax payments that result from

the aggressive position will be reflected in a lower CASH_ETR. Second, to the extent firms

aggressively accelerate expenses or defer income for tax purposes, these activities will be

reflected in a lower CASH_ETR provided those timing differences do not reverse within the five-

year period over which CASH_ETR is calculated. Finally, the CASH_ETR measure will be

reduced by the tax benefit associated with employee stock options and therefore provides a better

measure of the firm’s true tax burden than the traditional ETR measure.

Despite these advantages, CASH_ETR still contains some measurement error, as this

measure does not control for nondiscretionary sources of book-tax differences (e.g., depreciable

and amortizable assets) and is biased downward for those firms that consistently manage their

pretax book-income upward over extended periods of time. Moreover, CASH_ETR is designed

to capture a broad array of tax planning activities, which may or may not be considered

aggressive in nature.

3.3 Book-tax Differences (BTDs)

Our third proxy for tax aggressiveness is an estimate of the difference between pretax

book income and taxable income (i.e., book-tax differences). There are a number of studies that

suggest book-tax differences can be used as a signal of tax aggressiveness. Mills (1998) finds

that proposed IRS audit adjustments are positively related to large positive book-tax differences.

Desai (2003) posits that the growing difference between book and taxable income during the

1990’s was caused by increased levels of tax sheltering. In addition, Wilson (2008) finds that

book-tax differences are positively associated with actual cases of tax sheltering.

Despite evidence that large positive book-tax differences are associated with aggressive

tax reporting, this measure also has limitations. Hanlon (2003) and Manzon and Plesko (2002)

16

identify firm specific characteristics that generate book-tax differences, but are not necessarily

reflective of aggressive tax reporting. For example, firms with large capital expenditures could

have significant book-tax differences associated with depreciation, but these differences would

not be reflective of aggressive tax strategies. In addition, Phillips, Pincus, and Rego (2003) and

Hanlon (2005) demonstrate how temporary book-tax differences can reflect earnings

management activities. To the extent that earnings management and innate firm characteristics

unrelated to aggressive tax reporting are the primary determinants of book-tax differences, book-

tax differences will be a noisy proxy for tax aggressiveness.

Book-tax differences (BTD) are computed as pre-tax book income less an estimate of

taxable income. We calculate taxable income by grossing up the sum of current federal tax

expense and current foreign tax expense and subtracting the change in net operating loss

carryforward. If the current federal tax expense is missing, total current tax expense is calculated

by subtracting deferred tax expense, state tax expense, and other income taxes from total tax

expense. We measure book income as pre-tax book income less minority interest.

3.4 Permanent BTDs (PERM_BTD)

Many aggressive tax reporting strategies result in permanent book-tax differences. The

majority of the cases of tax sheltering examined by Wilson (2008) resulted in permanent book-

tax differences. Further, the U.S. Congress Joint Committee on Taxation (1999), Weisbach

(2002), and Shevlin (2002) describe the ideal tax shelter as creating permanent, rather than

temporary, book-tax differences. Consequently, we also include permanent book-tax differences

(PERM_BTD) as a measure of tax aggressiveness in this study. The primary advantage of this

measure is its exclusion of temporary differences that can reflect earnings management activity

and/or book-tax rule differences unrelated to tax planning. We calculate PERM_BTD as total

17

book-tax differences less deferred tax expense grossed-up by the applicable federal statutory tax

rate.

3.5 Discretionary Permanent BTDs (DTAX)

Our fifth proxy for tax reporting aggressiveness is a measure of discretionary permanent

book-tax differences. Frank, Lynch, and Rego (2008) calculate discretionary permanent

differences (DTAX) by regressing permanent book-tax differences on nondiscretionary items

unrelated to tax planning that are known to cause permanent differences. The nondiscretionary

items include intangible assets and state tax expense, among others. The residual from this

regression is then used as a proxy for tax reporting aggressiveness. See Appendix A for a

complete description of the model used to calculate the DTAX variable. Similar to total book-tax

differences in Wilson (2008), Frank et al. (2008) find that their measure of discretionary

permanent differences is associated with actual cases of tax sheltering.

3.6 Predicted Tax Shelter Firms

Our final measure of tax aggressiveness is based on a model developed by Wilson (2008)

to identify active tax shelter participants. The model of tax sheltering was developed using a

sample of identified tax shelter participants and is composed of variables predicted to be

associated with tax shelter activity. We use the model of tax sheltering to rank firm-year

observations into quintiles based on the probability the firm is engaged in tax shelter activity in

year t. Firm-year observations ranked in the top quintile are then designated as predicted tax

shelter firms (SHELTER). See Appendix A for a complete description of the tax shelter model.

In summary, we utilize six different measures of tax reporting aggressiveness because no

single measure perfectly captures “tax aggressiveness”. Moreover, each measure captures

varying degrees of tax aggressiveness. The proxies discussed earlier (ETR, CASH_ETR, and

18

BTD) likely reflect less aggressive tax planning than the proxies discussed later (PERM_BTD,

DTAX, and SHELTER). Thus, to the extent we obtain similar results across these measures of

tax aggressiveness we can be confident that our results are highly robust.

4. Research Design

4.1 Tests Linking Executive Compensation and Tax Aggressiveness

Hypothesis 1 predicts that tax reporting aggressiveness is associated with the level of

executive compensation. We base our tests of hypothesis 1 on Core et al. (1999) and Core,

Guay, and Larcker (2008), which model total compensation as a function of the economic

determinants of such compensation. In particular, we regress the natural log (Log) of total CEO

(CFO) compensation on proxies for CEO and CFO experience, firm size, growth opportunities,

stock and accounting returns, and the standard deviation of stock and accounting returns in the

prior five years. Recall that we examine CEO compensation separately from CFO

compensation, as CFOs have greater responsibility for the accounting function, relative to CEOs.

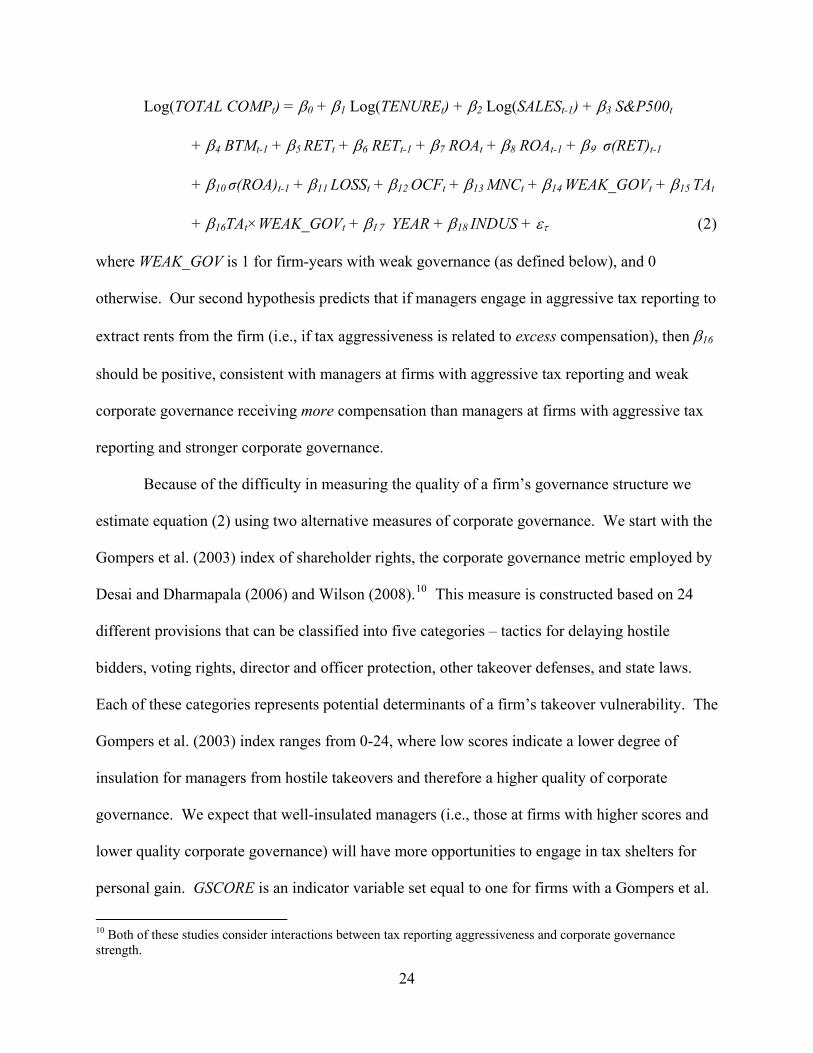

Log(TOTAL COMPt) = β0 + β1 Log(TENUREt) + β2 Log(SALESt-1) + β3 S&P500t

+ β4 BTMt-1 + β5 RETt + β6 RETt-1 + β7 ROAt + β8 ROAt-1 + β9 σ(RET)t-1

+ β10 σ(ROA)t-1 + β11 LOSSt + β12 OCFt + β13 MNCt + β14 TAt + β15 YEAR

+ β16 INDUS + ετ (1)

where TOTAL COMP is a measure of CEO (CFO) salary, bonus, long-term incentive plan

payouts, the value of restricted stock grants, the value of options grants during the year, and any

other annual pay; TENURE is the logarithm of the CEO’s (CFO’s) tenure at the firm; SALES is

the logarithm of total sales; S&P500 is 1 if the firm is in the S&P 500, and 0 otherwise; BTM is

the firm’s book-to-market ratio; RET is the firm’s stock return; ROA is income before

19

extraordinary items divided by average total assets; and σ(RET) [σ(ROA)] is the standard

deviation of annual stock returns (return on assets) over the five prior years. Core et al. (2008)

base their model on prior research that examines the economic determinants of executive

compensation, including Smith and Watts (1992), Core et al. (1999), and Murphy (1999). These

studies generally find that total CEO compensation is positively related to firm size (as measured

by total sales) and current and prior year stock returns, and negatively related to the standard

deviation of ROA and the book-to-market ratio. Core et al. (2008) also show that firms in the

S&P 500 pay more total compensation to their CEOs.

We expand the model developed by Core et al. (2008) to include additional variables that

could be associated with both executive compensation and our measures of tax aggressiveness,

including any current year losses, multinational activity, and net operating cash flows. In

particular, LOSS is 1 if the firm reports negative income before extraordinary items, and 0

otherwise; OCF is operating cash flow divided by average total assets; and MNC is 1 if the firm

reports income from foreign operations, and 0 otherwise. We also estimate equation (1) with

fixed-effects for year (YEAR) and 2-digit SIC codes (INDUS). The focus of our analysis is on

our measures of tax aggressiveness, TA. Our first hypothesis predicts that managerial

compensation is positively associated with tax reporting aggressiveness (i.e., β14 is significantly

greater than 0).

Our data comes from three sources. We obtain CEO and CFO compensation data from

the Execucomp database. We use CRSP data to calculate stock returns, while all other data are

obtained from the Compustat database. For a firm-year observation to be included in our sample

it must have all the data necessary to calculate the variables described in equation (1). The

sample for our first set of tests consists of 18,827 CEO-year observations from 1992 through

20

2006 that were successfully matched to CRSP and Compustat firm-year data. All variables are

winsorized at the 1st and 99th percentiles.

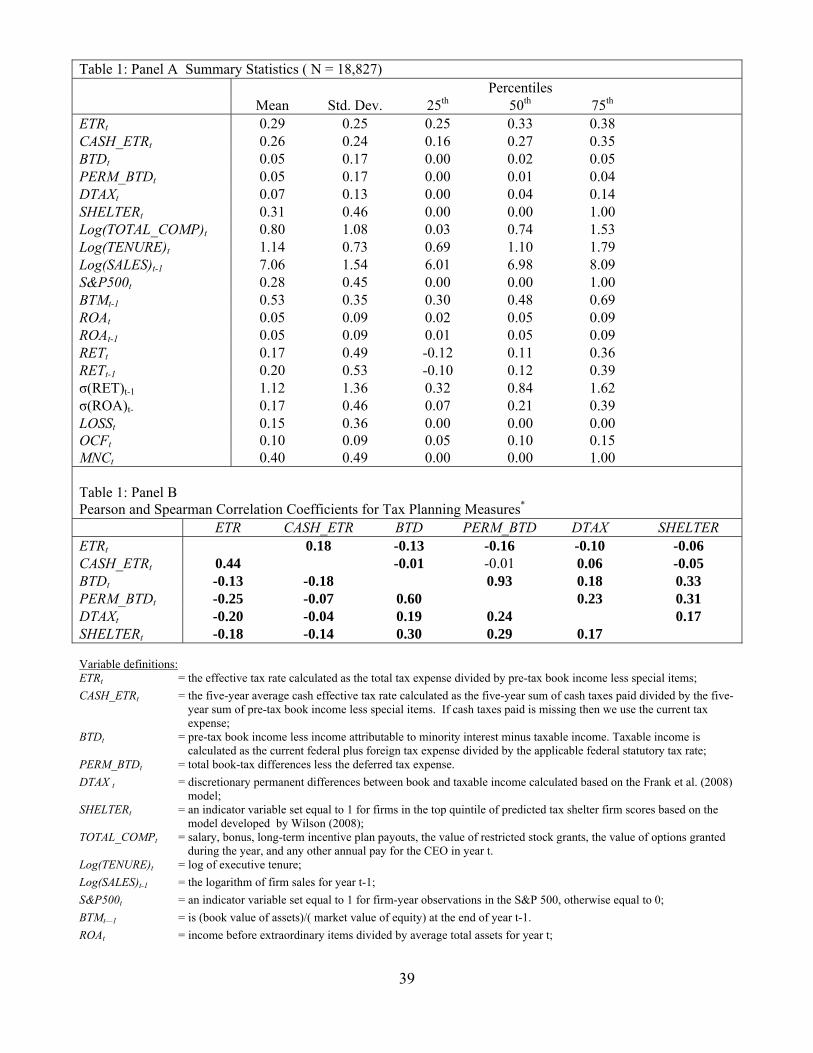

Panel A of Table 1 provides descriptive statistics for the variables used in our first set of

tests. We tabulate continuous data for our measures of tax aggressiveness in Table 1, but include

the quintile indicator variables for each measure of tax aggressiveness in all subsequent tables.

The median sample CASH_ETR is 27 percent, compared to a median ETR of 33 percent. The

median firm is profitable and has positive book-tax differences, BTD. We calculate the

SHELTER variable using all Compustat firm-years from 1992 through 2006 that have the

requisite data and then match these firm-years to the CEO (CFO) data on ExecuComp. As a

result, the SHELTER indicator variable is set equal to one for more than 20 percent of our sample

firm-years. Similarly, we calculate the DTAX variable using all Compustat firm-years from 1992

through 2006 that have the requisite data and then match these firm-years to the ExecuComp

observations. As a result, the mean DTAX is not equal to zero despite being the residual from

annual cross-sectional regressions.8 Panel B presents the Pearson and Spearman correlation

coefficients for each of the six tax aggressiveness measures. Consistent with expectations, each

of the measures is significantly correlated and in the anticipated direction.

INSERT TABLE 1 HERE

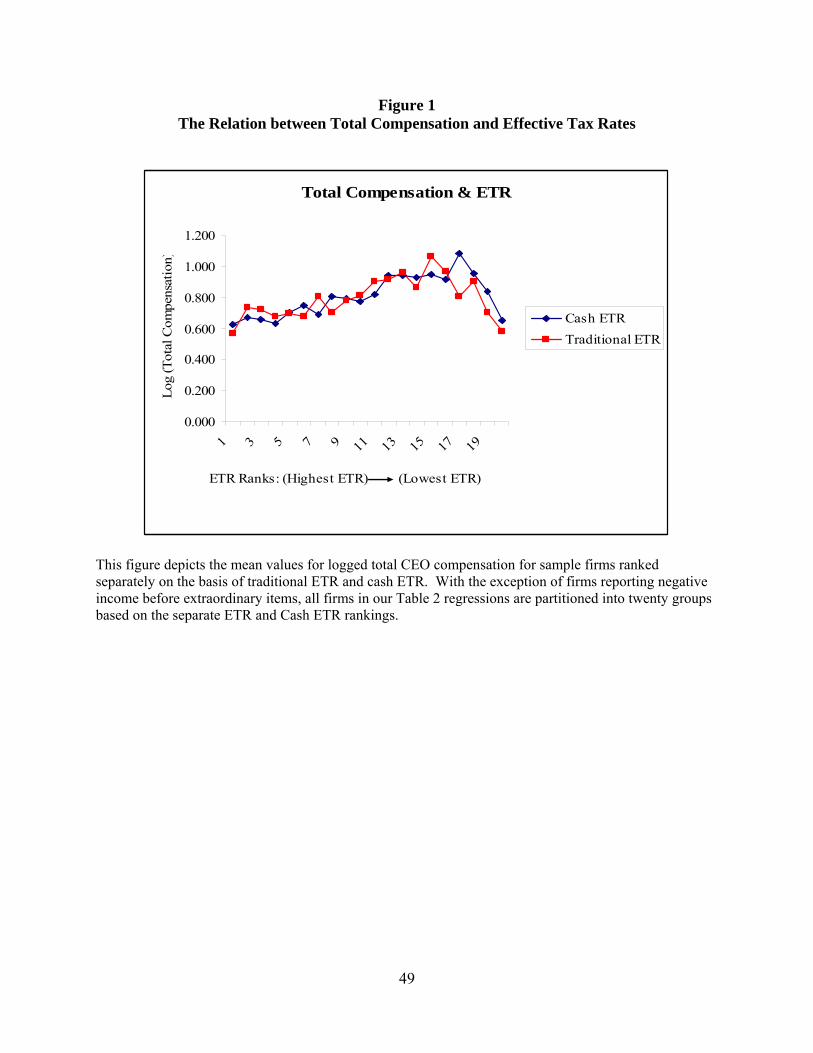

We examine the basic relation between CEO compensation and tax reporting

aggressiveness in Figure 1, which contains a graph of average (logged) total CEO compensation

across firms ranked based on two measures of tax aggressiveness, ETR and CASH_ETR. In

particular, all firm-year observations for CEO compensation are placed into 20 groups based on

8 See Appendix A for a complete discussion of the calculation of the SHELTER and DTAX variables.

21

separate rankings of ETR and CASH_ETR.9 Figure 1 shows that total CEO compensation

generally increases as the level of tax aggressiveness increases (i.e., as CASH ETR and ETR

decrease). However, for groups 18, 19, and 20, which contain the highest levels of tax

aggressiveness, this trend reverses and total compensation declines as tax aggressiveness

continues to increase. This result suggests that while compensation committees may generally

reward CEOs for more aggressive tax reporting, there appears to be a point at which this is no

longer the case. This decrease in CEO compensation for the highest levels of tax aggressiveness

is consistent with extreme levels of tax aggressiveness being viewed as value-destroying. At

such high levels, the costs of aggressive tax planning may outweigh the benefits and, as a result,

executives are actually punished in the form of lower compensation for engaging in overly

aggressive strategies.

INSERT FIGURE 1 HERE

Table 2 presents the results of our estimation of equation (1) for the CEO compensation

sample using each of the alternative measures of tax aggressiveness. Consistent with prior

research we find that total compensation is positively related to CEO tenure (Log(TENURE)),

firm size (Log(SALES)), S&P 500 membership, current and lagged annual stock returns (RETt,

RETt-1), and the standard deviation of stock returns σ(RET)t-1, and negatively related to the

standard deviation of return on assets (σ(ROA)t-1,) and the book-to-market ratio (BTM). Further,

we observe a significant positive relation between the existence of foreign operations (MNC) and

executive compensation. This finding is consistent with executives receiving greater

compensation for managing more complex, international operations. We also observe a

significant positive association between total compensation and tax aggressiveness for each of

9 We remove loss firms from this analysis prior to ranking the firms into the 20 groups because loss firms are likely to have very low ETR measures. However, the results are generally consistent with those in Figure 1 when the loss firms are included.

22

the tax aggressiveness measures. These findings support hypothesis 1, which predicts an

association between executive compensation and tax aggressiveness, even after controlling for

standard economic determinants of executive compensation. Thus, our measures of tax

aggressiveness do not simply reflect tax savings, since our measures of tax aggressiveness are

significant after controlling for current (ROA, OCF) and anticipated (RET) firm performance. We

explore the cause of this association when we test hypotheses 2 and 3 below.

INSERT TABLE 2 HERE

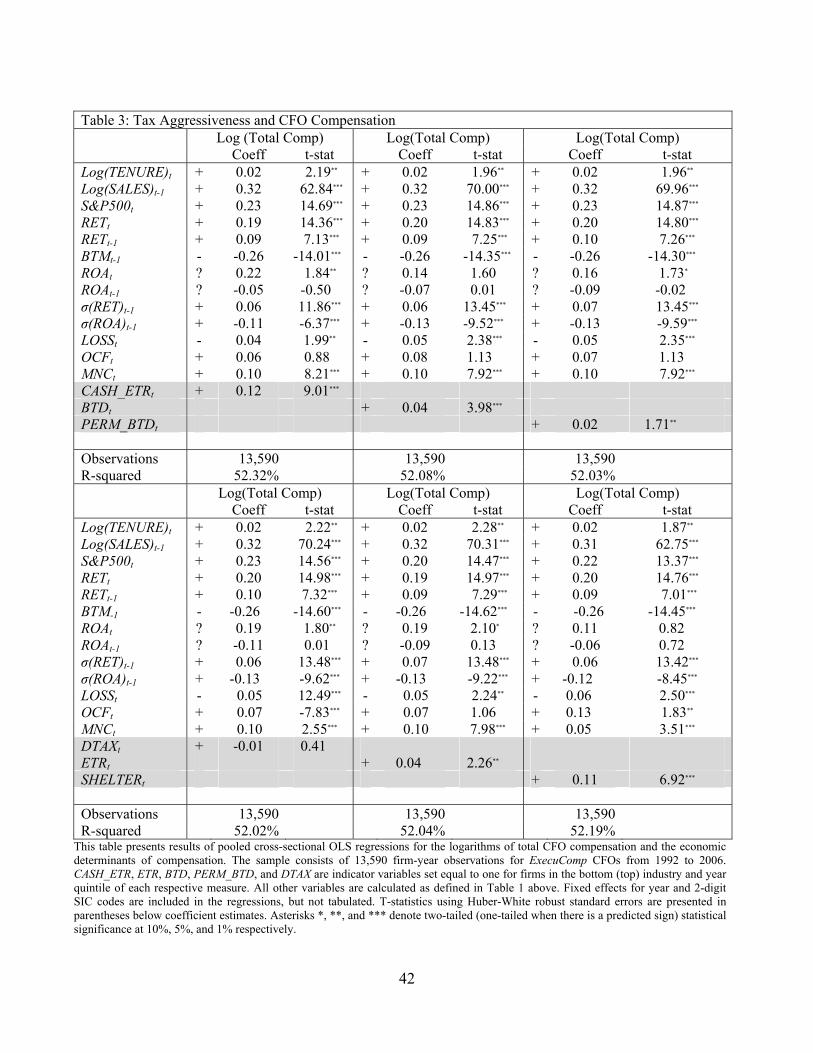

Table 3 presents the results for estimating equation (1) using the CFO compensation

sample, which is composed of 13,590 CFO-year observations that were successfully matched to

Compustat and CRSP firm-year data. Consistent with the results regarding CEO compensation,

we find that CFO total compensation is positively associated with CFO tenure, firm size, S&P

500 membership, stock returns, the standard deviation of stock returns, and the existence of

foreign operations, and negatively related to the standard deviation of return on assets and

growth opportunities. CFO compensation is significantly associated with five of the six

measures of tax aggressiveness, with the only exception being DTAX. Similar to the results for

CEOs, the results in Table 3 suggest that CFOs are also rewarded for engaging in aggressive tax

reporting.

INSERT TABLE 3 HERE

4.2 Tax-Related Compensation and Corporate Governance

To test our second hypothesis, we modify equation (1) to include a variable that indicates

the presence of weak corporate governance (WEAK_GOV), as well as that term’s interaction with

tax aggressiveness (TA×WEAK_GOV):

23

Log(TOTAL COMPt) = β0 + β1 Log(TENUREt) + β2 Log(SALESt-1) + β3 S&P500t

+ β4 BTMt-1 + β5 RETt + β6 RETt-1 + β7 ROAt + β8 ROAt-1 + β9 σ(RET)t-1

+ β10 σ(ROA)t-1 + β11 LOSSt + β12 OCFt + β13 MNCt + β14 WEAK_GOVt + β15 TAt

+ β16TAt×WEAK_GOVt + β17 YEAR + β18 INDUS + ετ (2)

where WEAK_GOV is 1 for firm-years with weak governance (as defined below), and 0

otherwise. Our second hypothesis predicts that if managers engage in aggressive tax reporting to

extract rents from the firm (i.e., if tax aggressiveness is related to excess compensation), then β16

should be positive, consistent with managers at firms with aggressive tax reporting and weak

corporate governance receiving more compensation than managers at firms with aggressive tax

reporting and stronger corporate governance.

Because of the difficulty in measuring the quality of a firm’s governance structure we

estimate equation (2) using two alternative measures of corporate governance. We start with the

Gompers et al. (2003) index of shareholder rights, the corporate governance metric employed by

Desai and Dharmapala (2006) and Wilson (2008).10 This measure is constructed based on 24

different provisions that can be classified into five categories – tactics for delaying hostile

bidders, voting rights, director and officer protection, other takeover defenses, and state laws.

Each of these categories represents potential determinants of a firm’s takeover vulnerability. The

Gompers et al. (2003) index ranges from 0-24, where low scores indicate a lower degree of

insulation for managers from hostile takeovers and therefore a higher quality of corporate

governance. We expect that well-insulated managers (i.e., those at firms with higher scores and

lower quality corporate governance) will have more opportunities to engage in tax shelters for

personal gain. GSCORE is an indicator variable set equal to one for firms with a Gompers et al.

10 Both of these studies consider interactions between tax reporting aggressiveness and corporate governance strength.

24

(2003) index score above the sample median (and thus indicates weaker governance), and set

equal to zero for all other observations.

Our second proxy for corporate governance measures the number of independent

blockholders with at least 5 percent stock ownership. In their study of the impact of corporate

tax avoidance on firm value, Desai and Dharmapala (2007) also rely on blockholder data as a

proxy for the strength of corporate governance. Jensen (1993) contends that blockholders play

an important role in a firm’s governance structure because they are independent and have a

financial interest that gives them incentives to monitor management. Because blockholders

control significant amounts of stock they can use their voting power to pressure management if

they believe managers are behaving opportunistically. BLOCK is an indicator variable set equal

to one for firm-years where the number of independent blockholders owning greater than 5

percent of the stock of a particular firm is below the sample median (and thus indicates weaker

governance). BLOCK is set equal to zero for all other observations. Blockholder data was

obtained from the Wharton Research Data Services website (WRDS) and is only available for

the years 1996 – 2001. Thus, when we match the blockholder data to our CEO-year

observations, our sample size is reduced to 5,147 observations.

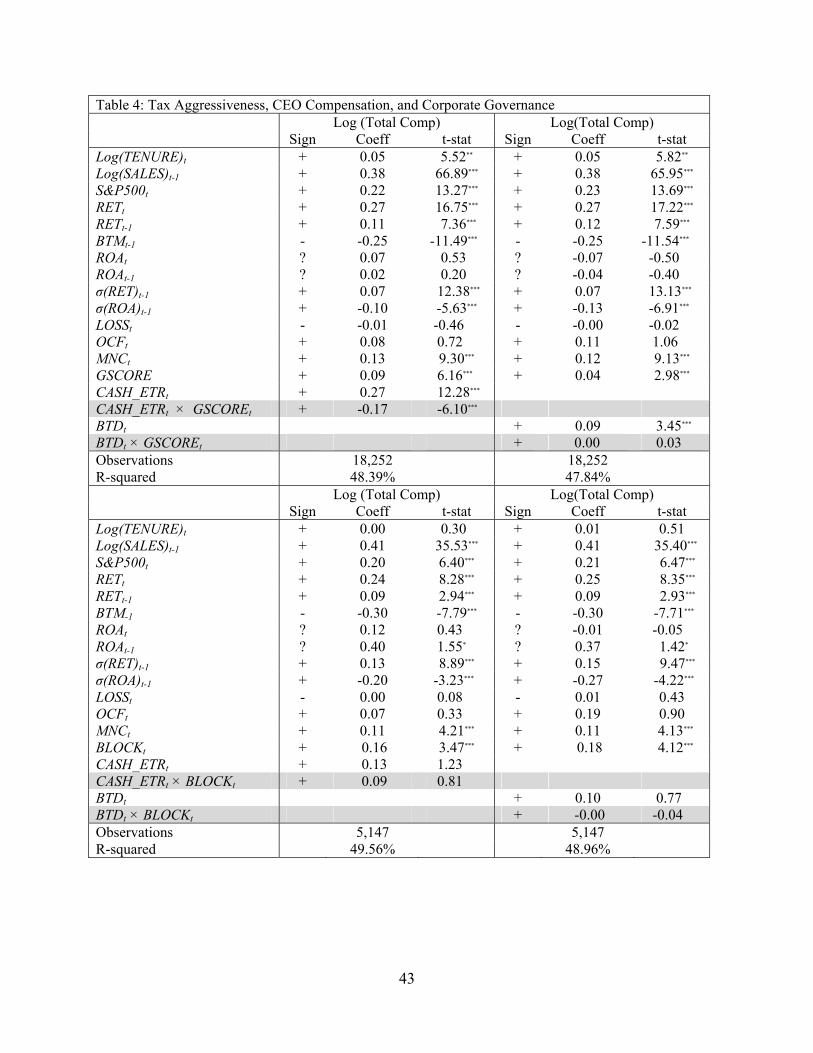

Table 4 presents the results of estimating equation (2) for the CEO sample, including two

of our six measures of tax aggressiveness.11 We first estimate equation (2) using the CASH_ETR

measure and find that it continues to be significantly positively associated with total

compensation. In contrast, its interaction with GSCORE (CASH_ETR × GSCORE) is negative

and significant. This result does not support our second hypothesis. In fact, it is consistent with

11 We tabulate results for just two of the six measures of tax aggressiveness to minimize the length of our manuscript. Consistent with the results reported in Table 4, the interaction terms between corporate governance and the remaining four measures of tax aggressiveness are not significant in the predicted direction for any of the four measures.

25

well-governed firms compensating CEOs for aggressive tax reporting more than weakly-

governed firms. In Column (2) of Table 4 we replace CASH_ETR with BTD as an alternative

proxy for tax aggressiveness. The coefficient on BTD continues to be significantly positive

while the coefficient on the interaction term (BTD × GSCORE) is not significant. In sum, the

results of the regressions containing GSCORE are not consistent with the positive relation

between total compensation and tax aggressiveness being driven by managers extracting rents

from firms with poor corporate governance.

INSERT TABLE 4 HERE

Next, we substitute BLOCK for GSCORE as an alternative measure of governance

quality. In these regressions the coefficients on our measures of tax aggressiveness, BTD and

CASH_ETR, are positive but no longer significant, and the coefficients on the BLOCK

interaction terms are also insignificant. We note that in the Table 4 regressions, we observe a

positive association between total compensation and our measures of weak corporate governance

(i.e., the GSCORE and BLOCK main effects). This finding is consistent with Core et al. (1999)

who find that CEOs earn greater compensation when governance structures are less effective.

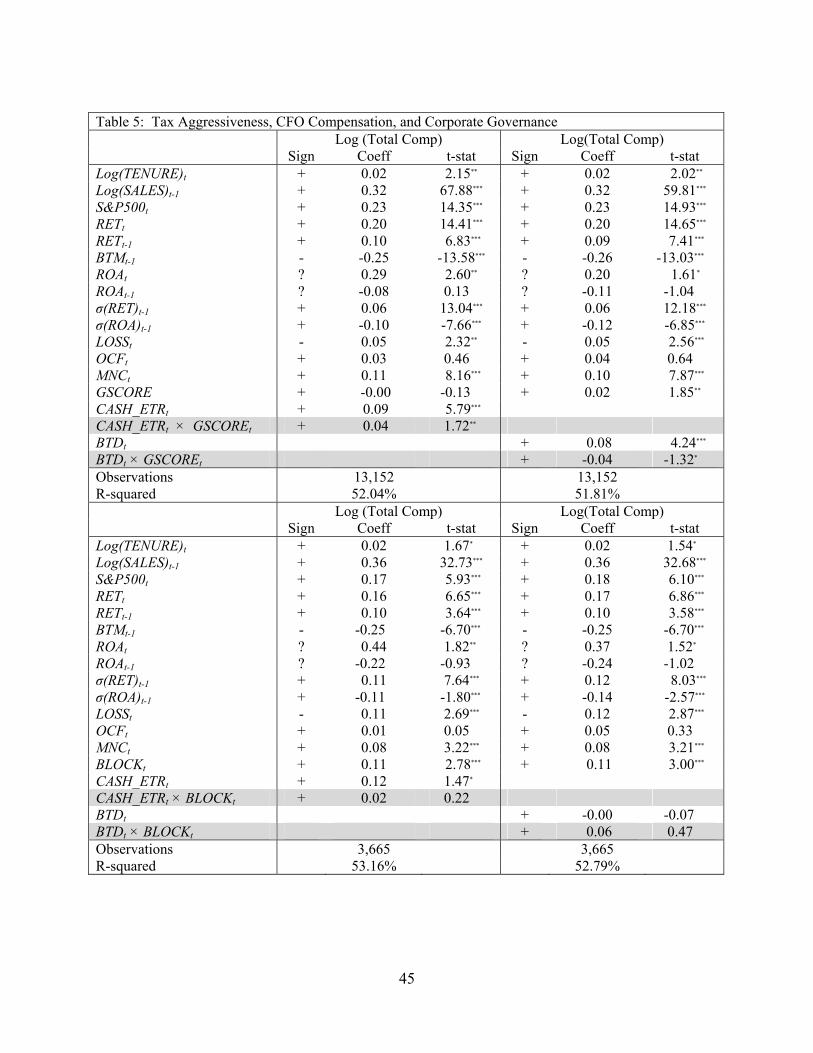

Table 5 presents the results of our estimation of equation (2) based on the CFO-year

sample. Similar to the results for CEO-years, the coefficients on CASH_ETR and BTD are

positive and significant when GSCORE is our proxy for corporate governance quality. The

coefficient on the interaction of GSCORE and CASH_ETR is also positive and significant,

consistent with hypothesis 2. In contrast, when we substitute BTD for CASH_ETR as a measure

of tax aggressiveness, the coefficient on the GSCORE interaction term becomes negative and

marginally significant, inconsistent with hypothesis 2. When we substitute each of the remaining

four measures of tax aggressiveness into equation (2), none of the coefficients on the GSCORE

26

interaction terms are significant in the predicted direction (results untabulated). We conclude

that the results based on GSCORE as a measure of governance quality generally do not support

hypothesis (2). When we substitute BLOCK for GSCORE as our corporate governance measure

in Table 5, the coefficients on the interaction of BLOCK and both measures of tax aggressiveness

(i.e., CASH_ETR and BTD) are not significant. In sum, the results in Tables 4 and 5 are not

consistent with hypothesis 2, which predicts that managers at firms with weaker corporate

governance use aggressive tax reporting strategies to increase their total compensation.

INSERT TABLE 5 HERE

It is possible that we did not find consistently positive and significant coefficients on our

corporate governance interaction terms because firms write optimal compensation contracts that

align managerial incentives with those of shareholders and those contracts act as substitutes for

other governance mechanisms. To explore this possibility, we decompose total CEO and CFO

compensation into: 1) salary and bonus, and 2) other compensation. This second component is

primarily composed of stock option and other stock-based compensation. We then re-estimate

equation (1) with each of these components of total compensation as the dependent variables.

The results (not tabulated) indicate that our measures of tax aggressiveness are related to “other”

CEO (CFO) compensation (i.e., stock-based compensation), but not related to salary and bonus.

These results are consistent with stock-based compensation aligning managerial incentives with

those of shareholders; thus, incentive alignment may indeed act as a substitute for other

governance mechanisms.12

12 Desai and Dharmapala (2006) find a significantly negative association between their measure of tax aggressiveness and the proportion of total compensation that is related to the value of stock options grants. Because we employ somewhat different research designs, we cannot directly compare our results to theirs. Nonetheless, their negative relation is not significant for firms with stronger corporate governance, consistent with incentive alignment at well-governed firms.

27

4.3 Tests Linking Future Firm Performance to Executive Compensation Practices

Our final set of tests continues to investigate whether the positive relation between

executive compensation and tax aggressiveness (as shown in Tables 2 and 3) exists because: 1)

tax aggressiveness is an economic determinant of executive compensation that has been omitted

from prior compensation models, or 2) there exist unresolved agency problems similar to those

in Core et al. (1999), which allow managers to use aggressive tax sheltering to extract rents from

the firm. To distinguish between these two alternative explanations, we examine the relation

between the portion of compensation predicted by tax aggressiveness (‘tax-based compensation’)

and future firm performance. Consistent with Core et al. (1999), a negative relation between tax-

based compensation and future firm performance would indicate agency conflicts, while an

insignificant or positive relation would suggest that managers are appropriately compensated for

their tax sheltering choices. We first consider the relation between tax-based compensation and

subsequent accounting operating performance. Similar to Core et al. (1999), we test hypothesis

(3) with the following OLS regression:

FUT_ROAt+1 = β0 + β1 TAX_COMPt + β2 STD_ROAt-1 + β3 SALESt-1 + β4 YEAR

+ β5 INDUS + ε (3),

where performance is measured as the return on assets for the subsequent year. STD_ROAt-1 is

the standard deviation of return on assets calculated over the five years prior to when

compensation is awarded. SALESt-1 are measured in the year prior to the compensation award.

TAX_COMP is the portion of total compensation predicted by our tax aggressiveness measures,

based on estimations of equation (1). We calculate TAX_COMP by multiplying the estimated

28

coefficient for a particular measure of tax aggressiveness (β14) by the firm’s actual measure of

tax aggressiveness.13

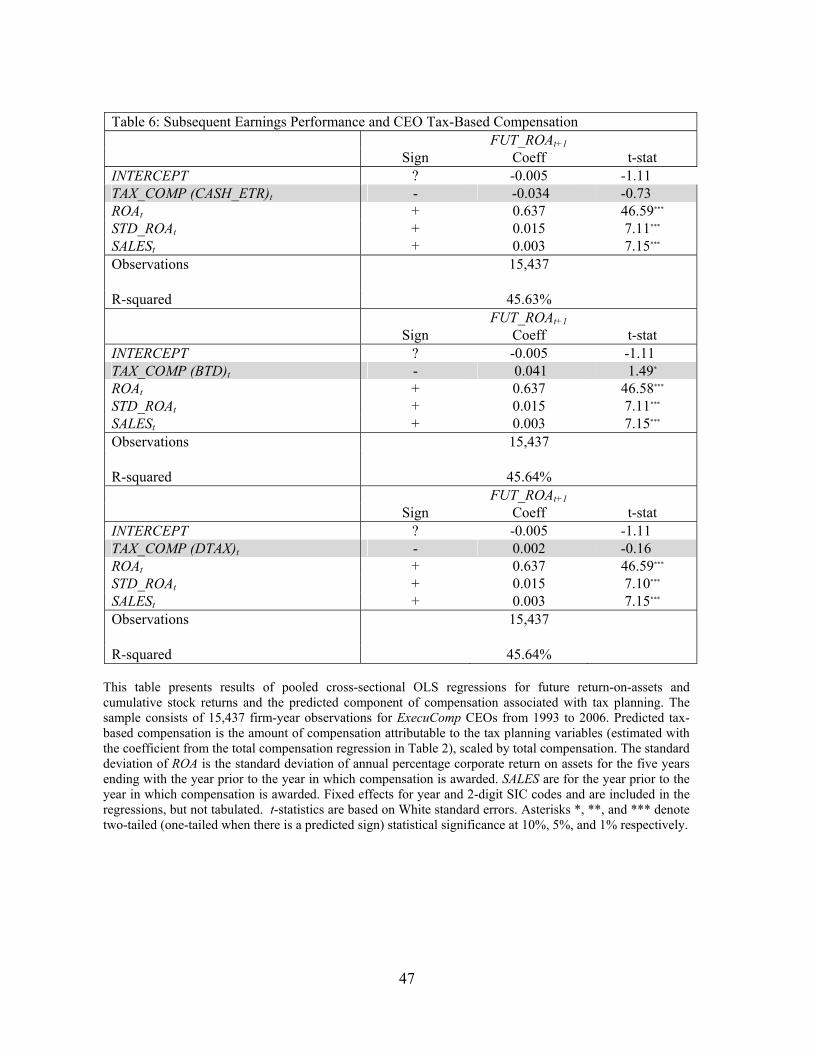

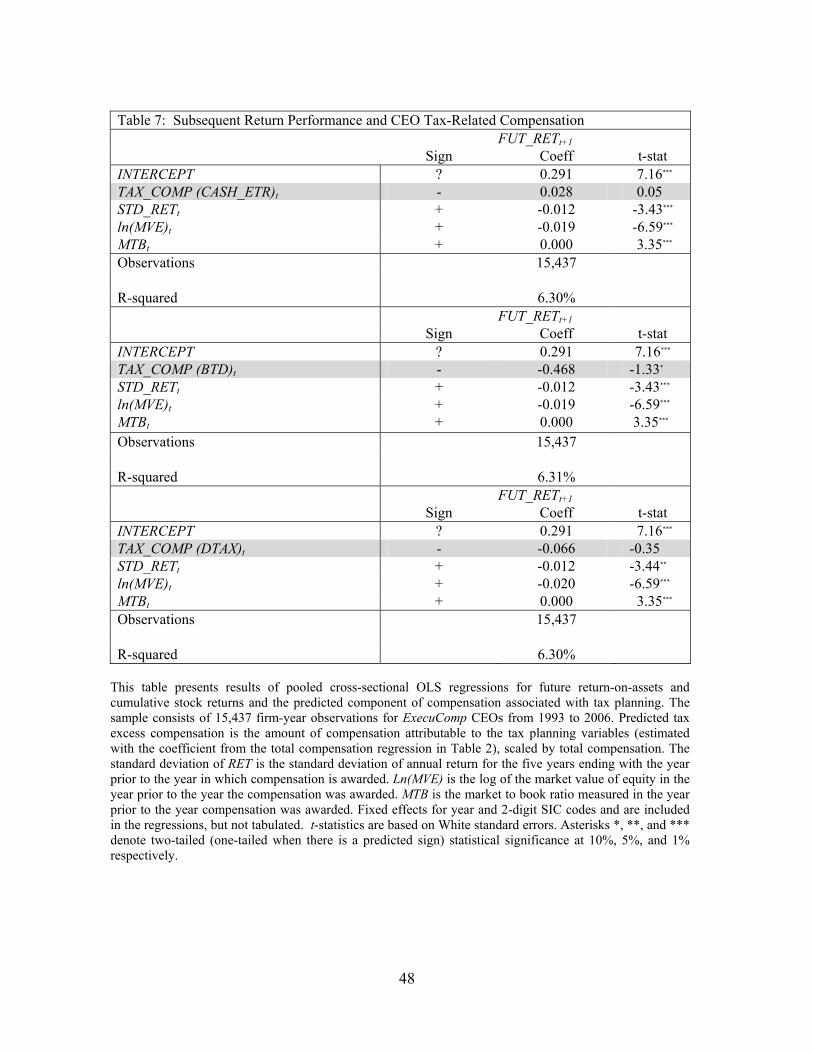

The results in Table 6 generally indicate that tax-based compensation (TAX_COMP) is

not significantly related to future operating performance. We estimate equation (3) using three

TAX_COMP calculations that are based on three alternative estimations of equation (1).

Specifically, we estimate separate regressions of equation (1) using the CASH_ETR, BTD, and

DTAX variables. The association between TAX_COMP and future return on assets is only

significant for one of the alternative proxies of tax aggressiveness.14 In particular, we find a

positive and marginally significant association between the portion of total compensation

predicted by tax aggressiveness, as measured by BTD, and future operating performance. These

results are not consistent with the conjecture that aggressive tax reporting obscures financial

reporting and allows managers to extract rents from firms, which would likely negatively impact

future operating performance.

INSERT TABLE 6 HERE

Next, we estimate the association between TAX_COMP and future stock returns. If

investors perceive compensation for tax aggressiveness as being associated with opportunistic

13 The results in Tables 2 and 3 are estimates of equation (1) using pooled cross-sectional regressions. For tests of our third hypothesis (Tables 6 and 7) we re-estimate equation (1) using firm-specific regressions. This estimation procedure allows us to obtain firm-specific coefficients for the relation between tax aggressiveness and total compensation. This coefficient is then multiplied by the firm’s actual measure of tax aggressiveness to calculate the portion of compensation predicted by tax aggressiveness for each firm. In contrast, pooled, cross-sectional estimation would not allow the coefficient on tax aggressiveness (β14) in equation (1) to vary across firms, which would essentially result in the multiplication of a constant (β14) and a firm’s actual measure of tax aggressiveness. In this case, the variation in ‘tax-based compensation’ would be driven entirely by a firm’s actual tax aggressiveness. We also substitute continuous measures of tax aggressiveness into this analysis in place of the indicator variables to allow for more variation of the tax aggressiveness measures across firm-year observations. 14 In untabulated tests we also examined the association between future earnings and TAX_COMP calculated using PERM_BTD and ETR. Because SHELTER is an indicator variable, we did not compute TAX_COMP based on SHELTER. While TAX_COMP based on PERM_BTD is positively associated with future earnings, TAX_COMP based on ETR is not significantly associated with future earnings. In sum, we do not find evidence consistent with hypothesis 3, when future performance is measured as future earnings.

29

behavior by managers, then the market may fully impound this information into stock prices as

investors become aware of tax planning activities. Consequently, even if TAX_COMP is

correlated with future firm performance, we may not observe a significant association between

TAX_COMP and future stock returns (since the information may have already been impounded

into stock price). Similar to Core et al. (1999), we test the relation between tax-based

compensation and future stock returns as follows:

FUT_RETt+1 = β0 + β1 TAX_COMPt + β2 STD_RETt-1 + β3 MVEt-1 + β4 MTBt-1 + β5

YEAR + β6 INDUS + ε (4),

where FUT_RETt+1 is the annual buy-and-hold stock return for the subsequent fiscal year. The

standard deviation of stock returns (STD_RET) is the annual standard deviation of return for the

five years prior to when compensation is awarded. The log of the market value of equity (MVEt-

1) and the market-to-book ratio (MTBt-1) are measured as of the end of the fiscal year prior to

when the compensation is awarded. Following Core et al. (1999), we include industry-indicator

variables to control for idiosyncratic returns within industry groups. We also include year fixed-

effects, which allow us to measure stock returns relative to the average sample return over the

same time period.

The results in Table 7 indicate that the relation between tax-based compensation

(TAX_COMP) and future stock returns is only significant for one of the alternative proxies of tax

aggressiveness. In particular, we find a negative and marginally significant association between

TAX_COMP, as measured by BTD, and future stock returns. In contrast, the coefficients on

TAX_COMP are not significant when CASH_ETR and DTAX are used as measures of tax

aggressiveness. Moreover, the signs of the coefficients on TAX_COMP are inconsistent across

30

the three estimations.15 In sum, the results in Table 7 are not consistent with unresolved agency

conflicts, where managers opportunistically engage in aggressive tax planning strategies that lead

to lower future stock returns.16

INSERT TABLE 7 HERE

5. Concluding Remarks

Despite the increase in elaborate tax shelter strategies during the 1990s and early 2000s,

little is known about whether CEOs are rewarded for engaging their firms in such activity. We

find that both CEO and CFO total compensation is positively linked to aggressive tax planning.

We propose two alternative explanations for this result. First, the link between aggressive tax

reporting and total compensation could reflect the opportunistic use of tax shelter transactions by

top executives to extract rents from the firm. This explanation would be consistent with the

assertion by Desai and Dharmapala (2006) that because tax shelters are designed to obscure the

underlying purpose of a transaction they can serve as a vehicle for rent extraction by

management. Alternatively, a positive link between total compensation and aggressive tax

reporting could reflect the fact that tax reporting aggressiveness is an additional economic

determinant of executive compensation that is not captured by the variables used in prior models

of CEO compensation.

In an effort to distinguish between these two alternative explanations we examine

whether the quality of a firm’s corporate governance moderates the relation between total 15 We also estimated TAX_COMP based on PERM_BTD and ETR and neither measure is significantly related to future stock returns. In sum, we do not find evidence consistent with hypothesis 3, when future performance is measured as future stock returns. 16 In supplemental tests (not tabulated) we also re-estimate equations (3) and (4) using return on assets and stock returns over a two-year period, since the consequences of opportunistic behavior may take some time to unravel and affect firm performance. Consistent with the results in Tables 6 and 7, we find no significant association between the portion of total compensation predicted by tax aggressiveness (TAX_COMP) and future firm performance.

31

compensation and tax aggressiveness. If this relation is a function of opportunistic behavior by

top managers then we would expect the association to be strongest in firms with poor corporate

governance. We find no evidence that firms with aggressive tax reporting and weak corporate

governance compensate their CEOs or CFOs more than other firms.

Next, we examine the relation between future firm performance and the portions of total

CEO and CFO compensation that are predicted by our measures of tax aggressiveness (‘tax-

based compensation’). If these associations are driven by managerial opportunism then we

would expect a negative relation between the component of total compensation predicted by tax

aggressiveness and future performance. In contrast, we find that tax-based compensation is not

related to future operating or stock performance. These findings suggest the relation between

total CEO and CFO compensation and tax aggressiveness is reflective of optimal contracting and

not managerial opportunism.

The strong positive association between CEO compensation and tax reporting

aggressiveness is somewhat surprising given the findings in Phillips (2003) that compensating

CEOs on an after-tax basis generally does not lead to greater tax planning effectiveness.

However, we rely on different proxies of tax aggressiveness and different measures of CEO

compensation schemes over a different time period. Moreover, recent evidence in Dyreng,

Hanlon, and Maydew (2008) indicates that CEOs, CFOs, and other top managers have a

significant impact on both traditional and cash effective tax rates. Thus, our investigation

complements their concurrent study of managers and tax reporting aggressiveness.

32

Appendix A

a. Discretionary Permanent Book-Tax Differences (DTAX)

Discretionary permanent book-tax differences (DTAX) are calculated using a model

developed by Frank, Lynch, and Rego (2008). We regress permanent book-tax differences on

nondiscretionary items unrelated to aggressive tax planning that are known determinants of

permanent book-tax differences. Specifically, we estimate equation (A1) below by two-digit SIC

code and fiscal year using all firm-years on Compustat for 1992 – 2006 with the necessary

available data. The residual from equation (1) is our estimate of discretionary permanent book-

tax differences:

PERMDIFFit = α0 + α1INTANGit + α2UNCONit + α3MIit + α4CSTEit + α5CHGNOLit +

LAGPERMit + εit (1)

Where:

PERMDIFFit = Total book-tax differences- temporary differences,

INTANGit = Goodwill and other intangibles (data 33) scaled by beginning of the year total

assets (data 6),

UNCONit = Income (loss) reported under the equity method (data 55) scaled by beginning

of the year total assets (data 6),

MIit = Income (loss) attributable to minority interest (data 49) scaled by beginning of

the year total assets (data 6),

CSTEit = Current state income tax expense (data 173) scaled by beginning of the year

total assets (data 6),

CHGNOLit = End of year NOL carryforwards (data 52) minus beginning of the year NOL

carryforwards, scaled by beginning of the year total assets (data 6).

LAGPERMit = One-year lagged PERMDIFF,

33

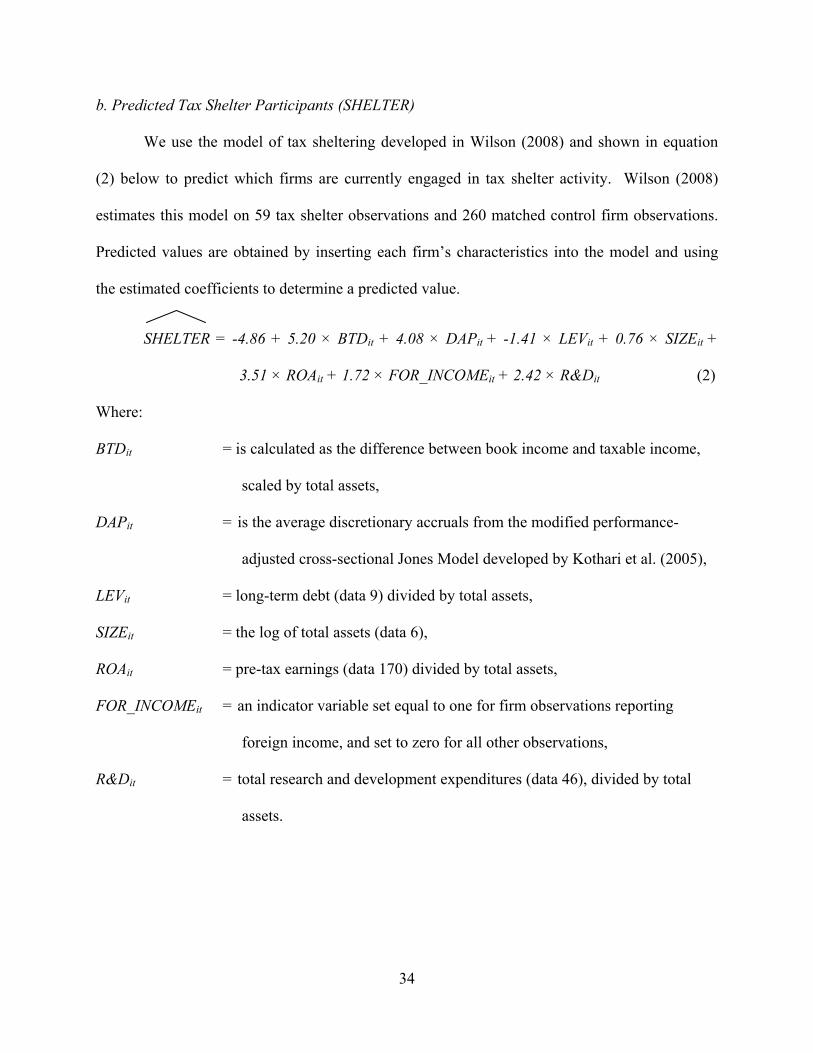

b. Predicted Tax Shelter Participants (SHELTER)

We use the model of tax sheltering developed in Wilson (2008) and shown in equation

(2) below to predict which firms are currently engaged in tax shelter activity. Wilson (2008)

estimates this model on 59 tax shelter observations and 260 matched control firm observations.

Predicted values are obtained by inserting each firm’s characteristics into the model and using

the estimated coefficients to determine a predicted value.

SHELTER = -4.86 + 5.20 × BTDit + 4.08 × DAPit + -1.41 × LEVit + 0.76 × SIZEit +

3.51 × ROAit + 1.72 × FOR_INCOMEit + 2.42 × R&Dit (2)

Where:

BTDit = is calculated as the difference between book income and taxable income,

scaled by total assets,

DAPit = is the average discretionary accruals from the modified performance-

adjusted cross-sectional Jones Model developed by Kothari et al. (2005),

LEVit = long-term debt (data 9) divided by total assets,

SIZEit = the log of total assets (data 6),

ROAit = pre-tax earnings (data 170) divided by total assets,

FOR_INCOMEit = an indicator variable set equal to one for firm observations reporting

foreign income, and set to zero for all other observations,

R&Dit = total research and development expenditures (data 46), divided by total

assets.

34

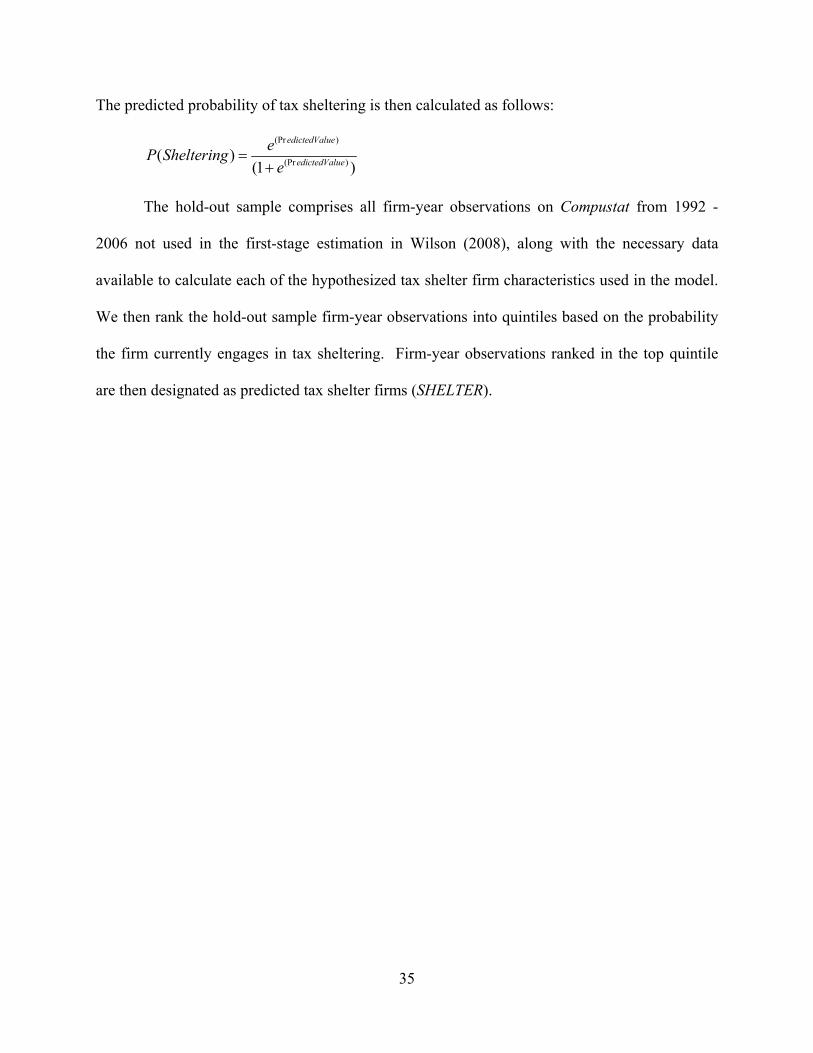

The predicted probability of tax sheltering is then calculated as follows:

(Pr )

(Pr )( )(1 )

edictedValue

edictedValue

eP Shelteringe

=+

The hold-out sample comprises all firm-year observations on Compustat from 1992 -

2006 not used in the first-stage estimation in Wilson (2008), along with the necessary data

available to calculate each of the hypothesized tax shelter firm characteristics used in the model.

We then rank the hold-out sample firm-year observations into quintiles based on the probability

the firm currently engages in tax sheltering. Firm-year observations ranked in the top quintile

are then designated as predicted tax shelter firms (SHELTER).

35

REFERENCES

Armstrong, Christopher S., A. Jagolinzer, and D. Larcker. 2008. Chief executive officer equity incentives and accounting irregularities. Stanford University working paper.

Ashbaugh-Skaife, Collins, and LaFond (2006) “The effects of corporate governance on firms’

credit ratings” Journal of Accounting and Economics 42 (1,2): pp. 203-243. Bankman, J. 1999. The new market in corporate tax shelters Tax Notes 83: 1775-1794.

Bergstresser, Daniel and T. Philippon. 2006. CEO incentives and earnings management. Journal of Financial Economics 80 pp. 511-529.

Cheng, Qiang and T. Warfield. 2005. Equity incentives and earnings management. The

Accounting Review 80 (2): 441-476. Cloyd, B. 1995. The effects of financial accounting conformity on recommendations of tax

preparers. Journal of the American Taxation Association 17 (2): 50-70. Core and Guay (1999) “The use of equity grants to maange optimal equity incentive levels”

Journal of Accounting and Economics 28 pp. 151-184. Core, Guay, and Larcker (2008) “The power of the pen and executive compensation” Journal of

Financial Economics 88 pp. 1-25. Core, Holthausen, and Larcker (1999) “Corporate governance, chief executive officer

compensation, and firm performance” Journal of Financial Economics 51 pp. 371-406. Demsetz, H., and K. Lehn. 1985. The structure of corporate ownership: Causes and

consequences. Journal of Political Economy 93 (6): 1155-77. Desai, M.A. 2003. The divergence between book and tax income, Tax Policy and Economy 17,

ed. J. Porterba, MIT press, 169-206.

Desai and Dharmapala. 2006. “Corporate tax avoidance and high-powered incentives” Journal of Financial Economics 79 pp. 145-179.

Desai and Dharmapala. 2007. “Corporate tax avoidance and firm value” Harvard University

working paper. Dyreng, S., M. Hanlon, and E. Maydew. 2008. Long-Run Corporate Tax Avoidance. The

Accounting Review 83 (1): 61-82. Eaton, J. and H. Rosen. 1983. Agency, delayed compensation, and the structure of executive

remuneration. Journal of Finance 38 (5): 1489-1505.

36

Efendi, J., Srivastava, A., and E.P. Swanson. 2007. Why do corporate managers misstate financial statements? The role of option compensation and other factors. Journal of Financial Economics 85 pp. 667-708.

Erickson, M., Hanlon, M., and E. Maydew. 2006. Is there a link between executive equity

incentives and accounting fraud? Journal of Accounting Research 44 (X): 113-143. Frank, Mary Margaret, L. Lynch, and S. Rego. 2009. Tax reporting aggressiveness and its

relation to aggressive financial reporting. The Accounting Review, forthcoming 2009. Gompers, P., J. Ishii, and A. Metrick. 2003. Corporation governance and equity prices. Quarterly

Journal of Economics, 118: 107-155.

Graham, J., and A. Tucker. 2006. Tax shelters and corporate debt policy. Journal of Financial Economics 81: 563-594.

Gupta, S., and K. Newberry. 1997. Determinants of the variability in corporate effective tax

rates: evidence from longitudinal study. Journal of Accounting and Public Policy. 16(1): 1-34.

Hanlon, M., and T. Shevlin. 2002. Accounting for tax benefit of employee stock options and implications for research. Accounting Horizons 16(1): 1-16.

Hanlon, M. 2003. What can we infer about a firm’s taxable income from its financial statements? National Tax Journal 56 (4): 831-863.

Hanlon, M. 2005. The persistence and pricing of earnings, accruals, and cash flows when firms

have large book-tax differences. The Accounting Review 80 (1): 137-166. Hanlon, M., L. Mills, and J. Slemrod. 2005. An Empirical examination of corporate tax

noncompliance. in Taxing Corporate Income in the 21st Century, A. Auerbach, J. R. Hines Jr., and J. Slemrod (eds.). Cambridge: Cambridge University Press, 2007.

Hanlon, M., and J. Slemrod. 2007. What does tax aggressiveness signal? Evidence from stock price reactions to news about tax aggressiveness. University of Michigan working paper.

Jensen, M., 1993. The modern industrial revolution, exit, and the failure of internal control systems. Journal of Finance 48:831–880.

Jensen, M. and K.J. Murphy. 1990. Performance pay and top-management incentives. Journal of

Political Economy 98 (2): 225-64. Manzon, G., and G. Plesko. 2002. The relation between financial and tax reporting measures of

income. Tax Law Review 55: 175-214.

37

Mills, L. 1998. Book-tax differences and Internal Revenue service adjustments. Journal of Accounting Research 36 (2): 343-356.

Murphy, K.J. (1999), “Executive Compensation,” In O. Ashenfelter and D. Card, eds., Handbook

of Labor Economics, Vol. 3. Amsterdam: North-Holland.

Phillips (2003) “Corporate tax planning effectiveness: The role of compensation-based incentives” The Accounting Review 78 (3): pp. 847-874.

Phillips, J., M. Pincus, and S. Rego. 2003. Earnings management: New evidence based on

deferred tax expense. The Accounting Review 78 (2): 491-521. Rajgopal, Shivaram and Terry Shevlin. 2002. Empirical evidence on the relation between stock

option compensation and risk taking. Journal of Accounting and Economics 33 (2): 145-171.