Embed Size (px)

Citation preview

Exploring switching behavior of USmobile service customers

Arvind Malhotra and Claudia Kubowicz Malhotra

Kenan-Flagler Business School, University of North Carolina at Chapel Hill, Chapel Hill, North Carolina, USA

AbstractPurpose – The purpose of this paper is to explore the switching behavior of mobile service customers in the USA with a focus on service quality,innovation and lock-in strategies as deterrents of switching.Design/methodology/approach – A thorough literature review coupled with two focus group interviews provided the impetus for the design anddevelopment of a survey instrument that was then administered to graduate and undergraduate students in the Southeast USA.Findings – The paper finds that: mobile service quality (m-SERVQUAL) is a significant detractor of switching intentions of customers – if customersperceive their provider to be innovative, they are less likely to switch to another provider; the perception of being innovative is equally as important asthe perception of the service quality delivered by the provider; hard lock-in (unreasonable contract length) leads customers to increase their intention toswitch, which is completely counter to its intended purpose; and service quality perceptions and perceptions of the innovativeness of the companypositively impact consumers’ intent to buy more add-on services.Practical implications – Delivering high service quality as well as being perceived as an innovator are key determinants in reducing consumerswitching. Each has a unique role to play, but understanding the impact of the interplay between them is critical. Important innovation factors forproviders include creating new services, especially data services, and working with hardware manufacturers to provide new phone models morefrequently. Lastly, hard lock-in (e.g. long contracts, contract breaking fees, etc.) may backfire with a higher reported propensity to switch in the long run.Originality/value – The study draws attention to the importance of innovation in retaining customers. Counter to the literature, it also finds that hardlock-ins may be detrimental in the long run and a practice to be avoided.

Keywords Mobile services, Service quality, Innovation, Lock-in, Mobile communication systems, Service quality assurance

Paper type Research paper

An executive summary for managers and executive

readers can be found at the end of this article.

Mobile phones have not only changed the way we

communicate with our friends and family (video calls,

SMS), but also the way we access and share information

(SMS, social networking), consume media (mobile web,

games, music) and navigate our world (GPS, mobile web,

applications). Mobile phones have evolved into multi-tasking

devices where on average 70 percent of usage is voice and the

remaining 30 percent is data, with internet analyst Mary

Meeker predicting that data usage will increase by almost

4,000 percent by 2014 (Ingram, 2010). In 2009, 285.6

million people in the USA (half a billion people around the

world) accessed the internet through a mobile device, and

usage is expected to double within five years as more people

will access the web through a mobile phone than a

computer[1].

To meet the high market demand for mobile connectivity

(voice and data), mobile service providers have made

substantial investments in upgrading their infrastructure and

thus improving the clarity of the voice calls and integrity of

data transfer. This “technical quality” or quality that comes

from the base infrastructure is clearly important to consumers

as it serves as the minimum requirement for positive customer

service perceptions. Going further, mobile service providers

have found opportunities to partner with hardware and

software providers to create devices that are not only fast and

reliable, but also provide attractive data capabilities to

consumers. On the hardware side, manufacturers continue

to improve device capabilities such as speed (migration from

3G to 4G), photo quality (advancement from five to eight

megapixels and higher), video (better quality and length of

video capture) and face-to-face calling (voice and video phone

calls). Smart phones, such as Research in Motion’s

Blackberry, Apple’s iPhone, and Samsung’s Galaxy, are

helping to shift the entire paradigm of the mobile industry

from a voice-driven to a data-driven model. On the service

side, software and applications designed for the mobile

environment have also contributed to the immense growth in

this industry. Services, such as GPS and thousands of

applications and games (on both the Apple and Android

platforms), have increased the value consumers can derive

from the mobile devices themselves. Together, infrastructure

investment coupled with considerable advancements in both

hardware and software has resulted in tremendous growth in

the mobile services industry.

Sustaining such positive growth requires companies in this

industry to retain their current customers. Further, to drive

future revenue and market share growth, mobile service

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/0887-6045.htm

Journal of Services Marketing

27/1 (2013) 13–24

q Emerald Group Publishing Limited [ISSN 0887-6045]

[DOI 10.1108/08876041311296347]

13

providers must also attract new customers. Intense

competition is prevalent not only for truly new customers in

the market, but also existing ones in the marketplace who are

continually incentivized with attractive offers to switch

providers. In such a dynamic industry, it would be expected

that service quality among the providers of mobile services

would be high. It is not. Compared with other US industries

selling goods and services, mobile phone services rank “well

below the average” in customer satisfaction (Hamblen, 2010).

Only 49 percent of the subscribers at Verizon, perceived to be

the “best” service provider, are “very satisfied” with the

services received. At the lowest-rated service provider, AT&T,

only 23 percent of the subscribers claim to be “very satisfied”

with its services (Campbell, 2010). With such low levels of

customer satisfaction, the legion of dissatisfied customers is

ever increasing in size. Moreover, these dissatisfied consumers

have begun to voice their grievances with the company and

other customers. One open letter from such a customer (see

the Appendix) is clearly indicative of the poor quality of

service that plagues the industry today.

In the academic literature, service quality has been shown

to have a direct impact on customer satisfaction (Negi, 2009)

as well as switching intentions (Zeithaml et al., 1996) and

service loyalty (de Ruyter et al., 1998). In the mobile services

industry specifically, it has been shown that service quality

impacts customer satisfaction and loyalty through both

economic and emotional factors (Lim et al., 2006). Thus,

with such low service quality perceptions, it is not surprising

to see then see high switching intentions (Shin and Kim,

2008) as well as high switching activity in both developed as

well as developing economies (Rahman and Azhar, 2011). As

many as 10 percent of customers surveyed recently stated that

they plan to switch providers within 90 days, a number that is

at highest level in the last 18 months (Carton, 2011).

Several factors that lead to switching have been identified,

including pricing, inconvenience, core service failure, service

encounter failure, response to service failure, competition,

ethical problems, and involuntary switching (Keaveney,

1995). In the mobile services industry, poor technical

reliability and weakening competitive positioning as an

innovator (e.g. AT&T is no longer going to be the exclusive

iPhone provider) has been shown to be instrumental in the

increase in customers’ switching propensity (Carton, 2011).

We would like to extend this literature on switching,

specifically in the mobile services industry, by exploring the

factors above and beyond service quality that impact

consumers’ switching behavior. Specifically, we seek to

explore how two popular strategies among mobile service

providers: lock-in and innovation; impact switching

intentions.

We seek to gain a better understanding of how mobile

service providers create lock-in for their consumers (as a way

of deterring switching behavior), and whether some lock-in

strategies (hard versus soft lock-in) are more effective than

others. Additionally, we explore whether customers place a

premium on innovation and reward mobile service providers

who continually innovate. Lastly, we conclude by examining

whether the interaction/interplay between service quality

perceptions and innovativeness is driving demand for

additional services from mobile service providers.

Lock-in strategies: creating switching barriers

There are positive and negative switching barriers (Vazquez-

Carrasco and Foxall, 2006). Egan (2001) considers certain

switching barriers – based on the personal relationship with

the service provider and created by customers’ own initiatives

(such as providing preference information to the provider) –

to be acceptable to customers. While financial switching

barriers can be construed as coercive (Vazquez-Carrasco and

Foxall, 2006). Hard lock-ins can be considered as negative

switching barriers, while soft lock-ins can be considered as

positive switching barriers. Soft lock-ins can be seen as

relational benefits enjoyed by the customer by a continued

relationship with the provider. Negative switching costs (such

as financial ones) create what is labeled as “spuriously loyal”

customers who are not willing to churn just because of

switching costs (Kim and Yoon, 2004), while positive

switching barriers (which we label “soft-lock in”), where

customers see the relational value of continuing with the

provider, create “relationally loyal” customers.

Mobile service providers rely on two primary business

models: “pay as you go” and contracts. Both rely on plans

where consumers choose usage plans based on predicted

usage of voice, data or a combination thereof for the

coming month. The difference between them is solely in the

contract commitment. With the “pay” as you go” model,

which has been adopted by the smaller and newer entrants

into the industry (e.g. Virgin Mobile, Boost Mobile,

TracFone), there is no formal lock-in through a signed

contract for a predetermined length of time. Consumers can

opt in to one plan one month, opt in to another plan a

different month, or opt out of service altogether at any time.

Flexibility is the differentiator and the draw for the

consumer to these mobile service providers. The larger

competitors within the industry, or Big Four (AT&T,

Sprint, T Mobile and Verizon), have overwhelmingly

adopted the contractual model. This is the case because

companies know that the more experience a customer has

with a service, the less likely he/she is to switch (Keaveney

and Parthasarathy, 2001). With a more stable customer

base, companies can better forecast demand and revenue.

Consequently, creating lock-in to ensure customer longevity

is a critical element of the business practices of this

industry. To combat the new entrants into the market, some

of the larger players have also added a “pay as you go”

option (e.g. T Mobile To Go), but overwhelmingly the large

mobile service providers use the contract model and entice

customers into contracts (new and renewed) by offering

incentives such a free or heavily discounted phones/mobile

devices. Incentives may be appealing for consumers, but

contracts can be long (often two years or longer), and they

can be complex with numerous confusing specifications of

what is or is not included in the contract. In addition to

binding consumers to contracts, mobile service providers

have been resorting to financially punitive ways to keep their

customers in their contracts. The contractual business

model is increasingly a form of a formal or “hard” lock-in

where the company dictates the terms and conditions of the

relationship.

When service providers force customers into unreasonable

contractual obligations, it makes customers feel a great deal of

Exploring switching behavior of US mobile service customers

Arvind Malhotra and Claudia Kubowicz Malhotra

Journal of Services Marketing

Volume 27 · Number 1 · 2013 · 13–24

14

power imbalance, in that the provider is taking away the

choice of walking away if the service is unsatisfactory. The

feeling of powerlessness in a customer-provider relationship

can result in severe “grudge-holding” on the part of customer.

Grudge holding in service relationships is defined as “as a

psychological process: maintaining a victim role and

perpetuating negative emotions associated with rehearsing

some hurtful offense” (Bunker and Ball, 2008, p. 37). When

customers sense a lack of ability to exit from a service

relationship – especially one that is also punitive – they tend

to hold a grudge against the provider (Bunker and Ball,

2008). Forcing customers into long and punitive contracts

may result in grudge-holding by customers. If customers find

themselves in “grudge-holding” situations, even if they do not

switch services immediately, they continue a downward trend

in their interaction with the company (Malhotra and

Kubowicz Malhotra, 2009). As a consequence, customers

who hold a grudge may be “falsely loyal” and harbor the

desire for retaliation (Bunker and Ball, 2008). Therefore,

when faced with hard lock-in like unreasonable contracts,

customers may start to increase their propensity to switch as a

retaliatory consequence of “grudge-holding” against their

mobile service providers.

Given the fact that most contracts in the industry today are

perceived by customers as punitive in nature, we hypothesize

that contracts create “hard” lock-in perceptions and lead to a

higher propensity to switch. Further, if this is true, we wanted

to explore whether there could be an alternative method of

capturing “soft” lock-in with fewer negative service

perceptions. For example, being on the same network as

one’s friends makes consumers less inclined to switch

providers. This type of soft lock-in created through a

network of friends could be encouraged through incentives,

not restrictions (e.g. T Mobile provided free mobile-to-mobile

calling to those on the same network). Loyalty is achieved

through the value of the network, whereby family and friends

are all on the same network, and financially it is better to be

on the same network than a different network. With greater

network value, consumers may not be inclined to switch and

have a greater positive attitude toward their wireless service

provider at the same time. Thus, we hypothesize that soft

lock-in strategies acting as a positive switching barrier will

lead to lesser customer propensity to switch.

Therefore, more formally, we hypothesize the following:

H1A. Hard lock-ins such as mobile service contractual

agreements increase the customer’s propensity to

switch providers.

H1B. Soft lock-ins such as social network effects reduce the

customer’s propensity to switch.

Innovativeness of service providers

Prior research has found that brand leadership and

differentiation can be signaled to customers through

product and process innovation (Gehlar et al., 2009). As a

result, companies have moved beyond competing on price

and the delivery of the core services to the promotion of

their value-added services and service quality offerings. That

said, perceived service quality has been found to be a

necessary – but not sufficient – condition for customer

loyalty (Aydin and Ozer, 2005). In addition to perceived

service quality, brand image has been found to reduce

customers’ intention to switch (Kim and Yoon, 2004). The

innovativeness of the company is an important facet of

consumers’ perception of brand image perceptions.

Consequently, innovation needs to be evaluated with an

eye on its impact not only on brand perceptions, but also

more directly on customer loyalty.

Innovation is a key driver of growth in the mobile services

industry. Evidence of innovation is prevalent in all areas of the

industry from the infrastructure to the hardware and service

offerings. In the infrastructure arena, innovation is visible with

the introduction of the next generation of connectivity

paradigms to the market, for example the fourth-generation

LTE technology that Verizon Wireless is deploying

throughout its network and Sprint’s 4G network. On the

hardware side, many providers have entered into exclusive

arrangements with hardware manufacturers to bring new

exclusive devices to the market. These devices are a source of

disruption in the industry, such as AT&T’s introduction of

the iPhone, because the phone is only available through one

service provider. In terms of innovative services, Sprint

recently brought to market a new service offering in which

consumer were allowed to make unlimited calls on the Sprint

network to 250 million wireless phone numbers, regardless of

carrier (e.g. Break Free of Calling Circles with Any Mobile,

Anytime SM), which was a major change from competitors

who offered free calling to numbers with the same carrier.

Other innovative service offerings include location-based

services that provide customers with real-time information

that is relevant to their current location and expressed need

(such as weather or traffic reports). In the future, service

innovation will include relevancy based services that use time,

location, and past behavioral data to anticipate a future need

that can be fulfilled (i.e. delivering a coupon prior to coffee

break to the local coffee shop; Malhotra and Kubowicz

Malhotra, 2009). Innovation is a key element of growth in this

industry, and we seek to gain a better understanding of

consumers’ perceptions of innovativeness of their mobile

service providers and how those perceptions in turn impact

their switching behavior or lack thereof.

In addition to the innovations themselves, companies must

communicate these advancements in innovation and

differentiation to consumers in order to drive greater market

performance (e.g. perceived service quality, customer

satisfaction, brand perceptions) and in turn, higher financial

performance (e.g. profit, market share) of the company (Zhou

et al., 2009). Specifically, the more innovative a provider is

perceived to be, the more likely that customers are going to

stay with the provider and consume additional services. For

example, the American Customer Satisfaction Index (ACSI)

revealed an increase in customer satisfaction with new

wireless services, such as Sprint Nextel’s “Beyond Talk”

plan, which combines unlimited text, e-mail and internet for

$25 a month (Hamblen, 2010). Service quality has been

found to impact purchase intentions positively (for a review,

see Zeithaml, 2000). In this paper, we wanted to examine

whether there would be a link between innovativeness

perceptions and consumers’ interest and intent to purchase

additional services from their mobile services provider. Being

innovative may not be enough to sell more services effectively

Exploring switching behavior of US mobile service customers

Arvind Malhotra and Claudia Kubowicz Malhotra

Journal of Services Marketing

Volume 27 · Number 1 · 2013 · 13–24

15

to consumers, but coupled with high service quality, purchase

intent may be enhanced above and beyond service quality.

Therefore, we hypothesize the following:

H2. Higher innovativeness perceptions of their mobile

service provider reduce customers’ propensity to

switch.

H3. Higher innovativeness perceptions will moderate the

impact of service quality on consumers’ intentions to

buy more services.

Method

Data collection

The survey instrument was administered in two waves and

yielded 442 total respondents. The respondents were a mix of

graduate and undergraduate students (covering the 18-24 age

range) at a large public university in the Southeastern USA.

We chose to focus on this demographic as this is one of the

demographics most coveted by mobile service providers in

terms of their purchasing behavior.

The items for the propensity to switch (dependent) variable

were derived from the work of Burnham et al. (2003). A five-

item scale (see Table I) with high reliability (a ¼ 0:91) was

used to measure propensity to switch. Hard lock-in was

measured by whether the service provider required an

unreasonable length of contract. Soft lock-in was measured

as the extent to which a customer’s friends were on the same

network as the customers themselves. The items for

measuring the innovativeness of service providers were

derived from our qualitative data collection phase. A four

item scale (see Table I) with high reliability (a ¼ 0:89) was

used to measure innovativeness of the service provider.

Intention to buy more services was measured using a

composite of nine items (see Table I) to gauge if customers

were willing to buy additional services from their current

service provider.

To develop a comprehensive scale for mobile service

quality, we applied a two-phase approach. In the first phase,

in order to develop a preliminary scale, we reviewed articles in

the popular press related to the service quality of mobile

service providers (e.g. AT&T, Sprint, etc.), blogs and

comments on various websites, and J.D. Power wireless

service reports. Next, we conducted two focus group

interviews to understand what matters most to customers in

terms of their impressions of service quality of their own

mobile service providers. Ideally, an existing scale could have

been leveraged for this purpose. Our search revealed only one

scale – a three-item scale developed by Shin and Kim (2008)

to measure service quality of mobile service providers. This

scale was inadequate to capture the essence of quality of

mobile services, especially given the channel complexity and

dynamic nature of the mobile services industry. We also

considered the SERVQUAL scale (Parasuraman et al., 1988)

given how well established it is, and also its comprehensive

nature, highlighting the five underlying dimensions of service

quality. However, SERVQUAL was developed to measure

service quality delivered by traditional service providers

(e.g. appliance repair and maintenance, retail banking, credit

cards, etc.). Only one study was found in the mobile service

industry that used an adapted SERVQUAL scale to measure

service quality (Negi, 2009). However, even with the industry

adaption, SERVQUAL still did not fully capture the

intricacies of service quality as applicable to mobile services

today. Finally, the e-SERVQUAL scale, created to measure

service quality delivered solely by companies online, was also

considered (Parasuraman et al., 2005). In order to measure

service quality across channels, both scales could have been in

conjunction with one another to measure both online and

offline service. However, we still did not feel that this would

help us a capture the nuances of the mobile services industry.

Seth et al. (2008) conducted a thorough review of the

service quality literature and argue that traditional service

quality measures need to be modified to be applicable to the

mobile services industry. They proposed that traditional

measures of service quality need to be augmented to include

dimensions that measure customers’ perceptions of network

quality as well as convenience. In a modified instrument, they

used all the dimensions of traditional service quality and

added a few items to reflect convenience and network

(technical) quality. While this is a step in the right direction,

through our initial field interviews we found that it did not

capture the multi-channel nature of mobile services and

providers. Our preliminary observations showed that the

availability of multiple channels for contact is what is

perceived as “convenient” by customers. Therefore, any

measure of mobile service quality should explicitly measure

the quality of service in each of these channels. Further, the

nature of “digital” services provided by mobile service

providers (such as contracts, plans, hardware, etc.) also

requires explicit measurement of the “flexibility” related to

such services. Therefore we made the effort to develop a new

scale (m-SERVQUAL) to capture these differences and

provide a comprehensive way to measure service quality

within the complex multi-channel service environment of the

mobile service industry.

Data analysis

The data was analyzed in a three-step procedure. As a first

step, we took a hold-out sample (150 respondents) from the

data and conducted an exploratory factor analysis (shown in

Table I) to determine the preliminary factor structure of items

and dimensions of the mobile service quality scale (m-

SERVQUAL). Next, the factor structure and items of the m-

SERVQUAL scale derived through exploratory factor analysis

were submitted to a confirmatory factor analysis using the

AMOS statistical software. The results of the confirmatory

factor analysis are shown in Table II. The x2 statistic and fit

indices (a . 0:90) demonstrate the robustness of the m-

SERVQUAL scale. A five-factor structure was uncovered as a

result of our factor analysis methodology. The five factors that

determine perceptions of mobile service providers’ service

quality are:

1 technical reliability of service;

2 in-store responsiveness;

3 on-phone responsiveness;

4 online self-service facilitation; and

5 flexibility of service.

It is clear that customers evaluate their mobile service

provider from a multi-channel perspective, i.e. by how the

customers’ needs are met in-store, on the phone, and through

Exploring switching behavior of US mobile service customers

Arvind Malhotra and Claudia Kubowicz Malhotra

Journal of Services Marketing

Volume 27 · Number 1 · 2013 · 13–24

16

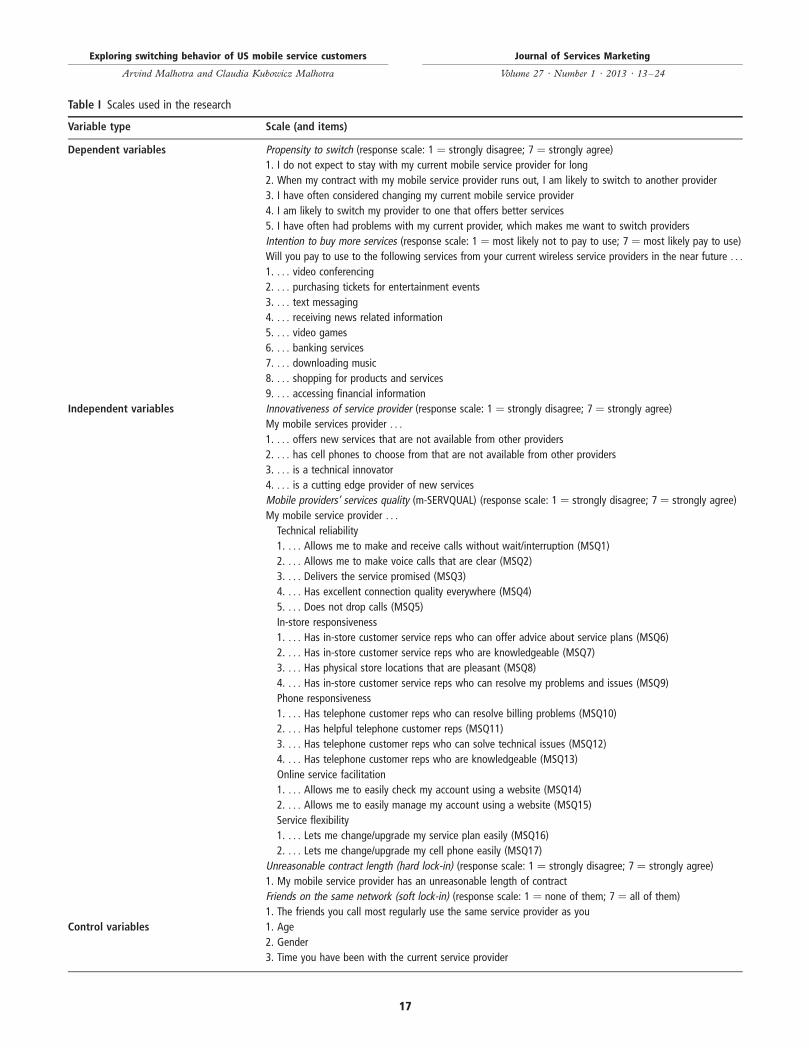

Table I Scales used in the research

Variable type Scale (and items)

Dependent variables Propensity to switch (response scale: 1 ¼ strongly disagree; 7 ¼ strongly agree)

1. I do not expect to stay with my current mobile service provider for long

2. When my contract with my mobile service provider runs out, I am likely to switch to another provider

3. I have often considered changing my current mobile service provider

4. I am likely to switch my provider to one that offers better services

5. I have often had problems with my current provider, which makes me want to switch providers

Intention to buy more services (response scale: 1 ¼ most likely not to pay to use; 7 ¼ most likely pay to use)

Will you pay to use to the following services from your current wireless service providers in the near future . . .

1. . . . video conferencing

2. . . . purchasing tickets for entertainment events

3. . . . text messaging

4. . . . receiving news related information

5. . . . video games

6. . . . banking services

7. . . . downloading music

8. . . . shopping for products and services

9. . . . accessing financial information

Independent variables Innovativeness of service provider (response scale: 1 ¼ strongly disagree; 7 ¼ strongly agree)

My mobile services provider . . .

1. . . . offers new services that are not available from other providers

2. . . . has cell phones to choose from that are not available from other providers

3. . . . is a technical innovator

4. . . . is a cutting edge provider of new services

Mobile providers’ services quality (m-SERVQUAL) (response scale: 1 ¼ strongly disagree; 7 ¼ strongly agree)

My mobile service provider . . .

Technical reliability

1. . . . Allows me to make and receive calls without wait/interruption (MSQ1)

2. . . . Allows me to make voice calls that are clear (MSQ2)

3. . . . Delivers the service promised (MSQ3)

4. . . . Has excellent connection quality everywhere (MSQ4)

5. . . . Does not drop calls (MSQ5)

In-store responsiveness

1. . . . Has in-store customer service reps who can offer advice about service plans (MSQ6)

2. . . . Has in-store customer service reps who are knowledgeable (MSQ7)

3. . . . Has physical store locations that are pleasant (MSQ8)

4. . . . Has in-store customer service reps who can resolve my problems and issues (MSQ9)

Phone responsiveness

1. . . . Has telephone customer reps who can resolve billing problems (MSQ10)

2. . . . Has helpful telephone customer reps (MSQ11)

3. . . . Has telephone customer reps who can solve technical issues (MSQ12)

4. . . . Has telephone customer reps who are knowledgeable (MSQ13)

Online service facilitation

1. . . . Allows me to easily check my account using a website (MSQ14)

2. . . . Allows me to easily manage my account using a website (MSQ15)

Service flexibility

1. . . . Lets me change/upgrade my service plan easily (MSQ16)

2. . . . Lets me change/upgrade my cell phone easily (MSQ17)

Unreasonable contract length (hard lock-in) (response scale: 1 ¼ strongly disagree; 7 ¼ strongly agree)

1. My mobile service provider has an unreasonable length of contract

Friends on the same network (soft lock-in) (response scale: 1 ¼ none of them; 7 ¼ all of them)

1. The friends you call most regularly use the same service provider as you

Control variables 1. Age

2. Gender

3. Time you have been with the current service provider

Exploring switching behavior of US mobile service customers

Arvind Malhotra and Claudia Kubowicz Malhotra

Journal of Services Marketing

Volume 27 · Number 1 · 2013 · 13–24

17

online self-service facilitation. This multiple-touch element is

both a challenge and opportunity for mobile service providers.

They can escalate the service problem resolution from online

to phone to in-store based on the complexity of the problem/

issue faced by the customer. It is also evident that the more

flexibility the service provider can build into their service, the

better their quality is perceived to be. This flexibility is in

terms of being able to change the plan as well as the phone.

Finally, technical reliability is always the key to service quality

perceptions for mobile service providers.

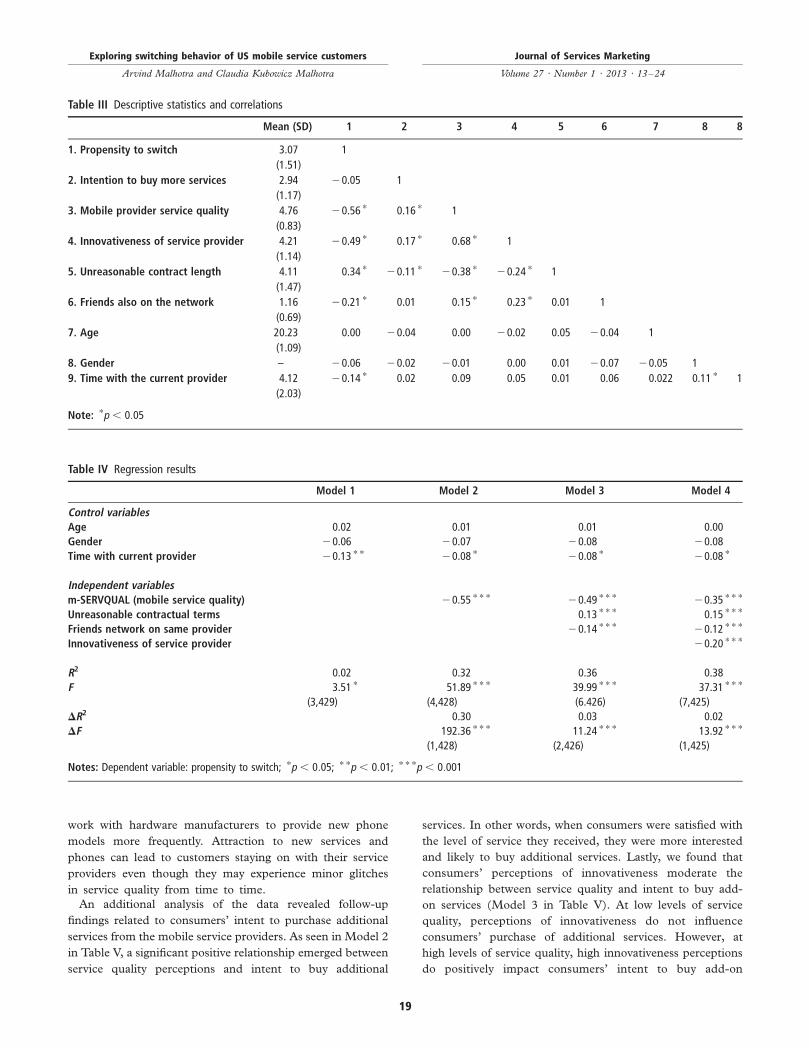

The means and standard deviations for the constructs in the

study are shown in Table III. Table III also includes the

correlations between the constructs of the study.

Next, we conducted a regression analysis using OLS to

determine what factors decrease the propensity to switch for

mobile service customers. The results are shown in Table IV.

Using hierarchical regression, we introduced the variables in

four stages to test the significance of each set of variables one

by one in determining their influence on propensity to switch.

First, as shown in Model 1 of Table IV, we introduced three

control variables (gender, age and time with current service

provider). Next (Model 2 of Table IV), we introduced the

aggregated m-SERVQUAL score (i.e. the mean of item scores

of the five dimensions of m-SERVQUAL). Third, we

introduced the variables associated with hard lock-in

(unreasonable contract length) and soft lock-in (friends and

family on the same network). Finally, in Model 4 of Table IV,

we introduced the variable “perception of innovativeness of

service provider”.

Results

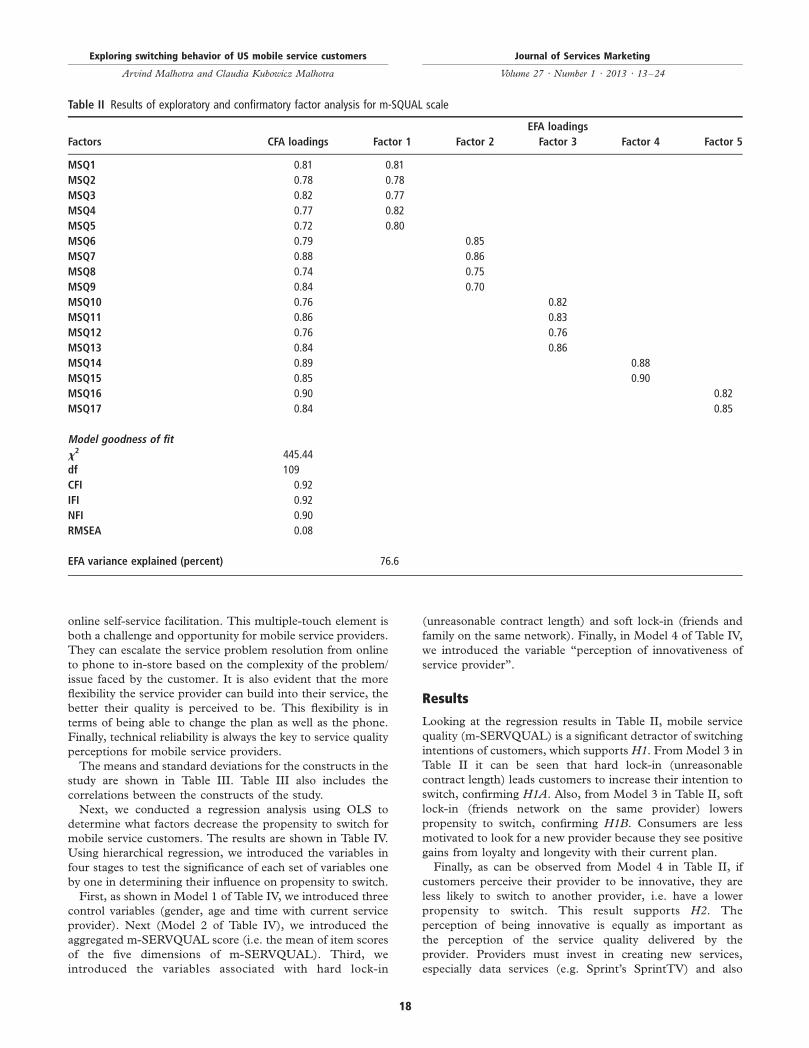

Looking at the regression results in Table II, mobile service

quality (m-SERVQUAL) is a significant detractor of switching

intentions of customers, which supports H1. From Model 3 in

Table II it can be seen that hard lock-in (unreasonable

contract length) leads customers to increase their intention to

switch, confirming H1A. Also, from Model 3 in Table II, soft

lock-in (friends network on the same provider) lowers

propensity to switch, confirming H1B. Consumers are less

motivated to look for a new provider because they see positive

gains from loyalty and longevity with their current plan.

Finally, as can be observed from Model 4 in Table II, if

customers perceive their provider to be innovative, they are

less likely to switch to another provider, i.e. have a lower

propensity to switch. This result supports H2. The

perception of being innovative is equally as important as

the perception of the service quality delivered by the

provider. Providers must invest in creating new services,

especially data services (e.g. Sprint’s SprintTV) and also

Table II Results of exploratory and confirmatory factor analysis for m-SQUAL scale

EFA loadings

Factors CFA loadings Factor 1 Factor 2 Factor 3 Factor 4 Factor 5

MSQ1 0.81 0.81

MSQ2 0.78 0.78

MSQ3 0.82 0.77

MSQ4 0.77 0.82

MSQ5 0.72 0.80

MSQ6 0.79 0.85

MSQ7 0.88 0.86

MSQ8 0.74 0.75

MSQ9 0.84 0.70

MSQ10 0.76 0.82

MSQ11 0.86 0.83

MSQ12 0.76 0.76

MSQ13 0.84 0.86

MSQ14 0.89 0.88

MSQ15 0.85 0.90

MSQ16 0.90 0.82

MSQ17 0.84 0.85

Model goodness of fit

x2 445.44

df 109

CFI 0.92

IFI 0.92

NFI 0.90

RMSEA 0.08

EFA variance explained (percent) 76.6

Exploring switching behavior of US mobile service customers

Arvind Malhotra and Claudia Kubowicz Malhotra

Journal of Services Marketing

Volume 27 · Number 1 · 2013 · 13–24

18

work with hardware manufacturers to provide new phone

models more frequently. Attraction to new services and

phones can lead to customers staying on with their service

providers even though they may experience minor glitches

in service quality from time to time.

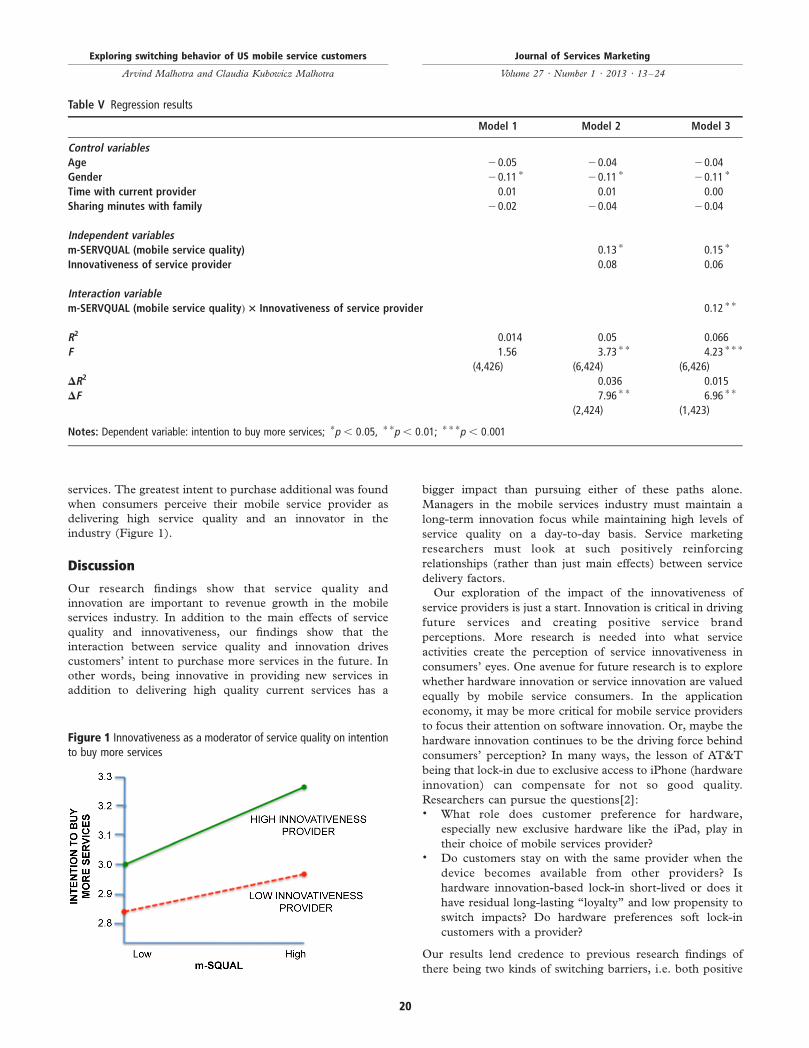

An additional analysis of the data revealed follow-up

findings related to consumers’ intent to purchase additional

services from the mobile service providers. As seen in Model 2

in Table V, a significant positive relationship emerged between

service quality perceptions and intent to buy additional

services. In other words, when consumers were satisfied with

the level of service they received, they were more interested

and likely to buy additional services. Lastly, we found that

consumers’ perceptions of innovativeness moderate the

relationship between service quality and intent to buy add-

on services (Model 3 in Table V). At low levels of service

quality, perceptions of innovativeness do not influence

consumers’ purchase of additional services. However, at

high levels of service quality, high innovativeness perceptions

do positively impact consumers’ intent to buy add-on

Table IV Regression results

Model 1 Model 2 Model 3 Model 4

Control variablesAge 0.02 0.01 0.01 0.00

Gender 20.06 20.07 20.08 20.08

Time with current provider 20.13 * * 20.08 * 20.08 * 20.08 *

Independent variablesm-SERVQUAL (mobile service quality) 20.55 * * * 20.49 * * * 20.35 * * *

Unreasonable contractual terms 0.13 * * * 0.15 * * *

Friends network on same provider 20.14 * * * 20.12 * * *

Innovativeness of service provider 20.20 * * *

R2 0.02 0.32 0.36 0.38

F 3.51 * 51.89 * * * 39.99 * * * 37.31 * * *

(3,429) (4,428) (6.426) (7,425)

DR2 0.30 0.03 0.02

DF 192.36 * * * 11.24 * * * 13.92 * * *

(1,428) (2,426) (1,425)

Notes: Dependent variable: propensity to switch; *p , 0:05; * *p , 0:01; * * *p , 0:001

Table III Descriptive statistics and correlations

Mean (SD) 1 2 3 4 5 6 7 8 8

1. Propensity to switch 3.07 1

(1.51)

2. Intention to buy more services 2.94 20.05 1

(1.17)

3. Mobile provider service quality 4.76 20.56 * 0.16 * 1

(0.83)

4. Innovativeness of service provider 4.21 20.49 * 0.17 * 0.68 * 1

(1.14)

5. Unreasonable contract length 4.11 0.34 * 20.11 * 20.38 * 20.24 * 1

(1.47)

6. Friends also on the network 1.16 20.21 * 0.01 0.15 * 0.23 * 0.01 1

(0.69)

7. Age 20.23 0.00 20.04 0.00 20.02 0.05 20.04 1

(1.09)

8. Gender – 20.06 20.02 20.01 0.00 0.01 20.07 20.05 1

9. Time with the current provider 4.12 20.14 * 0.02 0.09 0.05 0.01 0.06 0.022 0.11 * 1

(2.03)

Note: *p , 0:05

Exploring switching behavior of US mobile service customers

Arvind Malhotra and Claudia Kubowicz Malhotra

Journal of Services Marketing

Volume 27 · Number 1 · 2013 · 13–24

19

services. The greatest intent to purchase additional was found

when consumers perceive their mobile service provider as

delivering high service quality and an innovator in the

industry (Figure 1).

Discussion

Our research findings show that service quality and

innovation are important to revenue growth in the mobile

services industry. In addition to the main effects of service

quality and innovativeness, our findings show that the

interaction between service quality and innovation drives

customers’ intent to purchase more services in the future. In

other words, being innovative in providing new services in

addition to delivering high quality current services has a

bigger impact than pursuing either of these paths alone.

Managers in the mobile services industry must maintain a

long-term innovation focus while maintaining high levels of

service quality on a day-to-day basis. Service marketing

researchers must look at such positively reinforcing

relationships (rather than just main effects) between service

delivery factors.

Our exploration of the impact of the innovativeness of

service providers is just a start. Innovation is critical in driving

future services and creating positive service brand

perceptions. More research is needed into what service

activities create the perception of service innovativeness in

consumers’ eyes. One avenue for future research is to explore

whether hardware innovation or service innovation are valued

equally by mobile service consumers. In the application

economy, it may be more critical for mobile service providers

to focus their attention on software innovation. Or, maybe the

hardware innovation continues to be the driving force behind

consumers’ perception? In many ways, the lesson of AT&T

being that lock-in due to exclusive access to iPhone (hardware

innovation) can compensate for not so good quality.

Researchers can pursue the questions[2]:. What role does customer preference for hardware,

especially new exclusive hardware like the iPad, play in

their choice of mobile services provider?. Do customers stay on with the same provider when the

device becomes available from other providers? Is

hardware innovation-based lock-in short-lived or does it

have residual long-lasting “loyalty” and low propensity to

switch impacts? Do hardware preferences soft lock-in

customers with a provider?

Our results lend credence to previous research findings of

there being two kinds of switching barriers, i.e. both positive

Figure 1 Innovativeness as a moderator of service quality on intentionto buy more services

Table V Regression results

Model 1 Model 2 Model 3

Control variablesAge 20.05 20.04 20.04

Gender 20.11 * 20.11 * 20.11 *

Time with current provider 0.01 0.01 0.00

Sharing minutes with family 20.02 20.04 20.04

Independent variablesm-SERVQUAL (mobile service quality) 0.13 * 0.15 *

Innovativeness of service provider 0.08 0.06

Interaction variablem-SERVQUAL (mobile service qualityÞ3 Innovativeness of service provider 0.12 * *

R2 0.014 0.05 0.066

F 1.56 3.73 * * 4.23 * * *

(4,426) (6,424) (6,426)

DR2 0.036 0.015

DF 7.96 * * 6.96 * *

(2,424) (1,423)

Notes: Dependent variable: intention to buy more services; *p , 0:05, * *p , 0:01; * * *p , 0:001

Exploring switching behavior of US mobile service customers

Arvind Malhotra and Claudia Kubowicz Malhotra

Journal of Services Marketing

Volume 27 · Number 1 · 2013 · 13–24

20

and negative (Vazquez-Carrasco and Foxall, 2006). Egan

(2001) considers certain switching barriers – based on the

personal relationship with the service provider and created by

customers’ own initiatives (such as providing preference

information to the provider) – to be acceptable to customers.

Soft lock-ins provide benefits to consumers that accrue from a

long-term relationship with a company. Consumers can see

the relational value of continuing with the provider, and thus

evaluate these switching barriers positively. Although by

definition barriers, some switching barriers have positive

outcomes and can result in “relationally loyal” customers

(Kim and Yoon, 2004). However, others – including financial

switching barriers – can be construed as coercive and negative

(Vazquez-Carrasco and Foxall, 2006).

We also hope to have alerted researchers and practitioners

to the opposite than desired consequence of hard lock-in

strategies. It is generally thought that the more you raise the

switching barrier, the longer the customers will stay with the

provider when faced with high barriers. Several providers

resort to financial switching barriers (e.g. contract termination

fees in mobile service industries). However, researchers have

found that there may not be a correlation between financial

switching barriers and intention to switch (Hu and Hwang,

2006). These financial switching barriers create a hard lock-in

because switching would entail financial penalties for

customers. As a result, the switching costs achieve their

objective, but consumers are “spuriously loyal”, not loyal by

the true definition of the word (Kim and Yoon, 2004).

Further, based on the “grudge-holding” behavior (Bunker

and Ball, 2008), our research shows that there is a sign that

“negative” switching barriers may be having a contradictory

effect – rather than increasing customers’ intention to stay,

such barriers maybe increasing customers’ “retaliatory

intention” to switch at the next most convenient/feasible

time. As a result, a company may keep the customer the first

time around with an unreasonable contract length, but when

the initial contract expires, the mobile service provider will see

a backlash from imposing an unreasonable initial contractual

length and/or adding punitive monetary penalties for breaking

the contract.

Similar to prior research in the same context of mobile

service quality (Rahman and Azhar, 2011), our sample is

limited to a young demographic (18-24 year olds). The

younger generation tend to be a coveted demographic for

service providers and early adopters of technology-based

services. Future research is encouraged to test the

generalizability of our findings with a more diverse sample,

including a wider age range. One interesting question is

whether older business-oriented users behave differently to

our younger demographic sample. An additional limitation of

our survey is the focus on consumers’ future intentions rather

than actual past behavior. We do not know whether

consumers will do what they say they will do. Future

research is encouraged to use actual purchase and consumer

activity data.

In our study, the subtle benefits of soft lock-ins are

highlighted, i.e. providers can create switching barriers

without inciting customers into grudge-holding. We focused

on the network effect – friends also on the same network – as

one type of soft lock-in. Researchers may want to explore

other types of soft lock-in and the relative strengths (switching

barriers) of the different soft lock-ins. One type of soft lock-in

that may be interesting to explore in greater detail is

“information lock-in”, whereby customers provide (or

producers infer) their preference data to service providers

who in turn customize services to the taste of the customers

(Malhotra and Kubowicz Malhotra, 2009). The growing

cloud-based offerings highlight this business trend. For

example, Amazon offers music streaming where customers

who buy music get storage space on Amazon’s servers so as to

listen to their music from anywhere with any device. Such

technology-based soft lock-ins can also result in higher

switching barriers. Future researchers can pursue the study of

interplay between hard lock-ins and soft lock-ins. It is quite

possible for several customers that both types of lock-ins exist

in parallel. Do positive feelings induced by soft lock-ins

compensate for negative feelings induced by hard lock-ins?

Does the existence of high levels of both type of lock-ins

results in a higher switching barrier than just high levels of one

or the other?

Conclusion

As the mobile industry continues to grow, we contend that the

three switching deterrents explored in this study (service

quality, lock-in and innovation) will continue to have a large

impact on the bottom line (Figure 2). Service quality,

innovation and creative forms of “positively perceived” lock-

in (which positively influence the customer, not penalize him/

her) will be integral factors (alone and more importantly

together) for success in the mobile services industry.

Notes

1 See http://mobithinking.com/mobile-marketing-tools/

latest-mobile-stats2 The authors would like to thank the anonymous reviewer

for pointing out this direction of enquiry.

Figure 2 Key switching deterrent in mobile services industry

Exploring switching behavior of US mobile service customers

Arvind Malhotra and Claudia Kubowicz Malhotra

Journal of Services Marketing

Volume 27 · Number 1 · 2013 · 13–24

21

References

Aydin, S. and Ozer, G. (2005), “The analysis of antecedents

of customer loyalty in the Turkish mobile

telecommunication market”, European Journal ofMarketing, Vol. 39 Nos 7/8, pp. 910-25.

Bunker, M.P. and Ball, A.D. (2008), “Causes and

consequences of grudge-holding in service relationships”,

Journal of Services Marketing, Vol. 22 No. 1, pp. 37-47.Burnham, T.A., Frels, J.K. and Mahajan, V. (2003),

“Consumer switching costs: a typology, antecedents, and

consequences”, Journal of the Academy of Marketing Science,Vol. 31 No. 2, pp. 109-26.

Campbell, S.J. (2010), “AT&T: poor service with low

customer churn: the Midas touch of the iPhone”,

available at http://voice-quality.tmcnet.com/topics/voice-

quality/articles/84236-att-poor-service-with-low-customer-

churn-midas.htm (accessed December 20, 2010).Carton, P. (2011), “New survey shows Verizon iPhone will

have major impact on US wireless service providers: can

AT&T forestall large-scale defections?”, available at www.

investorplace.com/28029/impact-verizon-apple-iphone-

wireless-service-providers/ (accessed January 31, 2011).de Ruyter, K., Wetzels, M. and Bloemer, J. (1998), “On the

relationship between perceived service quality, service

loyalty and switching costs”, International Journal ofService Industry Management, Vol. 9 No. 5, pp. 436-53.

Egan, J. (2001), Relationship Marketing. Exploring RelationalStrategies in Marketing, Financial Times Prentice Hall,

London.Gehlar, M.J., Regmi, A., Stefanou, S.E. and Zoumas, B.L.

(2009), “Brand leadership and product innovation as firm

strategies in global food markets”, Journal of Product& Brand Management, Vol. 18 No. 2, pp. 115-26.

Hamblen, M. (2010), “Subscribers more satisfied with cell-

phone carriers: Sprint jumps 11% in customer satisfaction

survey”, available at: www.computerworld.com/s/article/

9176935/Subscribers_more_satisfied_with_cell_phone_

carriers (accessed 20 December 2010).Hu, A.W.-L. and Hwang, I.S. (2006), “Measuring the effects

of consumer switching costs on switching intention in

Taiwan mobile telecommunication services”, The Journal ofAmerican Academy of Business, Cambridge, Vol. 9 No. 1,

pp. 75-85.Ingram, M. (2010), “Mary Meeker: mobile internet will soon

overtake fixed internet”, available at: http://gigaom.com/

2010/04/12/mary-meeker-mobile-internet-will-soon-

overtake-fixed-internet/ (accessed 20 December 2010).Keaveney, S.M. (1995), “Customer switching behavior in

service industries: an exploratory study”, Journal ofMarketing, Vol. 59 No. 2, pp. 71-83.

Keaveney, S.M. and Parthasarathy, M. (2001), “Customer

switching behavior in online services: an exploratory study

of the role of selected attitudinal, behavioral, and

demographic factors”, Journal of the Academy of MarketingScience, Vol. 29 No. 4, pp. 374-90.

Kim, H. and Yoon, C. (2004), “Determinants of subscriber

churn and customer loyalty in the Korean mobile telephony

market”, Telecommunications Policy, Vol. 28 Nos 9/10,

pp. 751-65.Lim, H., Widdows, R. and Park, J. (2006), “M-loyalty:

winning strategies for mobile carriers”, Journal of ConsumerMarketing, Vol. 23 No. 4, pp. 208-18.

Malhotra, A. and Kubowicz Malhotra, C. (2009),

“A relevancy-based services view for driving adoption of

wireless web services in the US”, Communications of theACM, Vol. 52 No. 7, pp. 130-4.

Negi, R. (2009), “Perceived service quality: a study of

Ethiopian mobile users”, International Journal of MobileMarketing, Vol. 4 No. 1, pp. 31-8.

Parasuraman, P., Zeithaml, V.A. and Berry, L.L. (1988),

“SERVQUAL: a multiple-item scale for measuring service

quality”, Journal of Retailing, Vol. 64 No. 1, pp. 12-40.Parasuraman, P., Zeithaml, V.A. and Malhotra, A. (2005),

“e-SERVQUAL: a multiple-item scale for assessing

electronic service quality”, Journal of Service Research,Vol. 7 No. 3, pp. 213-33.

Rahman, S. and Azhar, S. (2011), “Xpressions of generation

Y: perceptions of the mobile phone service industry in

Pakistan”, Asia Pacific Journal of Marketing and Logistics,Vol. 23 No. 1, pp. 91-107.

Seth, A., Momaya, K., Gupta, H. and Vikalpa, M. (2008),

“Managing the customer perceived service quality for

cellular mobile telephony: an empirical investigation”, TheJournal for Decision Makers, Vol. 33 No. 1, pp. 19-34.

Shin, D. and Kim, W. (2008), “Forecasting customer

switching intention in mobile service: an exploratory

study of predictive factors in mobile number portability”,

Technological Forecasting & Social Change, Vol. 75 No. 6,

pp. 854-87.Vazquez-Carrasco, R. and Foxall, G.R. (2006), “Positive vs

negative switching barriers: the influence of service

consumers’ need for variety”, Journal of ConsumerBehavior, Vol. 5 No. 4, pp. 367-79.

Zeithaml, V. (2000), “Service quality, profitability, and the

economic worth of customers: what we know and what we

need to learn”, Journal of the Academy of Marketing Science,Vol. 28 No. 1, pp. 67-85.

Zeithaml, V.A., Berry, L.L. and Parasuraman, A. (1996),

“The behavioral consequences of service quality”, Journalof Marketing, Vol. 60 No. 2, pp. 31-46.

Zhou, K.Z., Brown, J.R. and Dev, C.S. (2009), “Market

orientation, competitive advantage, and performance:

a demand-based perspective”, Journal of Business Research,Vol. 62 No. 11, pp. 1063-70.

Appendix. A customer grievance letter

To Whom It May Concern:

I have had numerous defective devices from [mobile service

provider] over the past couple of months as well as extremely

poor customer service from in store (corporate) reps and call

center reps. I have taken the phones into the store for repair

and get treated like an * * *hole the entire time that I am in the

store. I have called customer support numerous times as well,

and just get passed from person to person and nobody will

accept responsibility for the issues. At times, the phone will

not accept or make calls out. . . It is quite obvious that [mobile

service provider] is only concerned with their churn rate, as

well as sales of anciliary products such as visual voicemail,

insurance, [name of proprietary software], 7! rhapsody.

Once you are a customer of [mobile service provider], they

don’t care at all- if you have problems, you get blown off and

told to get lost. It’s VERY frustrating to have a phone that the

company will not service or take care of. I’m sorry that I

Exploring switching behavior of US mobile service customers

Arvind Malhotra and Claudia Kubowicz Malhotra

Journal of Services Marketing

Volume 27 · Number 1 · 2013 · 13–24

22

already have a fully optioned out account and don’t purchase

any extra services when I’m in the store. At this point, I have a

phone that eats through the battery in 2 hours, with very

minimal calling/use . . . If I cannot get any satisfaction out of

[mobile service provider], I will be getting in contact with the

Better Business Bureau as well as the FCC, so they can both

investigate the issues that I and others are having with this

device and the complete lack of support that [mobile service

provider] is providing to me. I cannot believe that I was

bamboozled into a contract and phone from [mobile service

provider]. I have a friend that has had nothing but horrid

service from [mobile service provider], as well as many

devices that have been defective from the get go.

(Available at: http://www.planetfeedback.com/verizon+

w i r e l e s s+%28ce l l+phone s%29 / o t h e r / c omp l e t e+

dissatisfaction+and+extremely+poor+service+from+verizon+

wireless/325440)

About the authors

Arvind Malhotra’s research is focused in the areas of market

impact of digital innovations and evolving organizational

forms. His research projects include studying successful

innovative structures, adoption of innovative technologies,

and knowledge management in interorganizational contexts.

His work has been published in leading journals such as

Harvard Business Review, Sloan Management Review, MIS

Quarterly, Information Systems Research, Journal of Service

Research, and Journal of the Academy of Marketing Science. He

received his PhD in Business Administration and his MS in

Industrial and Systems Engineering from the University of

Southern California and his BE in Electronics and

Communications Engineering from the University of Delhi.

Claudia Kubowicz Malhotra’s research interests are in the

area of consumer behavior. Specifically, her research focus is

on service failures and service recovery strategies, consumer

privacy issues, and new product marketing. She has also

examined how consumers adopt and use web and mobile

technologies with a focus on the evolution and effectiveness of

advertising in these contexts. Her work has been published in

Communications of the ACM and Journal of Service Research.

She received her PhD and MBA from UNC’s Kenan-Flagler

Business School and her BSBA from Georgetown University.

Claudia Kubowicz Malhotra is the corresponding author and

can be contacted at: [email protected]

Executive summary and implications formanagers and executives

This summary has been provided to allow managers and executives

a rapid appreciation of the content of the article. Those with a

particular interest in the topic covered may then read the article in

toto to take advantage of the more comprehensive description of the

research undertaken and its results to get the full benefit of the

material present.

If you think you’ve got the most up-to-date, top-of-the-range,

all-singing-all-dancing mobile phone there is, blink and you’ll

find there are others out there with even better capabilities. At

least that’s how it seems as they come on the market with

breathtaking speed. Did we say “phone”? Well, you know

what we mean. True, they are telephones but cameras,

computers, calculators, calendars, office organizers, radios,

videos, games consoles, music players, GPS systems – you

name it, they’ll probably do it.

Manufacturers amaze us with their innovativeness, falling

over themselves to be the smartest, quickest, best. They have

to, of course, to keep ahead of the game and persuade us to

choose their products over others. But in doing so, aren’t they

missing a trick? Isn’t there something else that consumers like

that is being overlooked in the headlong rush to technological

superiority? Here’s a clue. How many times do you hear

people (not the young, savvy amateur experts maybe, but the

majority of us) saying they’ve a problem they’re having

difficulty getting fixed? Or they don’t use much of the stuff

their “phones” do because they don’t know how? And doesn’t

there seem to be an assumption, perhaps unique in the world

of techno-offerings, that people have an innate knowledge of

how to use the products without the benefit of a simple book

of instructions?

True, mobile service providers have made substantial

investments in amazing us with the versatility of their

products and improving their infrastrcuture, increasing

speeds, enhancing photo quality, voice call quality, etc. All

this has resulted in tremendous growth in the industry. But,

sustaining such growth requires companies to retain their

current customers and attract new ones. In such a dynamic

industry, it would be expected that service quality would be

high. It is not.

In “Exploring switching behavior of US mobile service

customers”, Arvind Malhotra and Claudia Kubowicz

Malhotra say that, compared with other US industries

selling goods and services, mobile phone services rank well

below the average in customer satisfaction. Moreover,

dissatisfied consumers have begun to voice their grievances

with the company and other customers about poor customer

service, being treated badly and being passed from person to

person.

So switch providers. There’s plenty of competition. Well

that’s good advice, but consumers are often “locked in” to a

long contract. The authors explore factors above and beyond

service quality that impact consumers’ switching behavior.

Specifically, they consider how two popular strategies among

mobile service providers (lock-in and innovation) impact

switching intentions, and try to find out whether customers

place a premium on innovation, and reward mobile service

providers who continually innovate.

As the mobile industry continues to grow, they conclude

that service quality, lock-in and innovation will continue to

have a large impact on the bottom line. Service quality,

innovation and creative forms of “positively perceived” lock-

in (which positively influence the customer, not penalize him/

her) will be integral factors for success. Being innovative in

providing new services in addition to delivering high-quality

current services has a bigger impact than pursuing either of

these paths alone. Managers must maintain a long-term

innovation focus while maintaining high levels of service

quality on a day-to-day basis.

This study’s results lend credence to previous research

findings of there being two kinds of switching barriers, both

positive and negative. Certain switching barriers – based on

the personal relationship with the service provider and created

Exploring switching behavior of US mobile service customers

Arvind Malhotra and Claudia Kubowicz Malhotra

Journal of Services Marketing

Volume 27 · Number 1 · 2013 · 13–24

23

by customers’ own initiatives (such as providing preference

information to the provider) – are considered to be acceptable

to customers. Soft lock-ins provide benefits to consumers that

accrue from a long-term relationship with a company.

Consumers can see the relational value of continuing with

the provider, and thus evaluate these switching barriers

positively. While some switching barriers have positive

outcomes and can result in “relationally loyal” customers,

others, including financial switching barriers, can be

construed as coercive and negative.

It is generally thought that the more you raise the switching

barrier, the longer the customers will stay with the provider.

Several providers resort to financial switching barriers

(e.g. contract termination fees). However, researchers have

found that there may not be a correlation between financial

switching barriers and intention to switch. These financial

switching barriers create a hard lock-in because switching

would entail financial penalties. As a result, the switching

costs achieve their objective, but consumers are “spuriously

loyal”, not loyal by the true definition of the word.

There is evidence that “negative” switching barriers may

have a contradictory effect – rather than increasing

customers’ intention to stay, such barriers maybe increasing

customers’ “retaliatory intention” to switch at the next most

convenient/feasible time. As a result, a company may keep the

customer the first time around with an unreasonable contract

length, but when the initial contract expires, the provider will

see a backlash.

(A precis of the article “Exploring switching behavior of US mobile

service customers”. Supplied by Marketing Consultants for

Emerald.)

Exploring switching behavior of US mobile service customers

Arvind Malhotra and Claudia Kubowicz Malhotra

Journal of Services Marketing

Volume 27 · Number 1 · 2013 · 13–24

24

To purchase reprints of this article please e-mail: [email protected]

Or visit our web site for further details: www.emeraldinsight.com/reprints