Embed Size (px)

Citation preview

THE VIRTUES AND VICES OF EQUILIBRIUM AND THE FUTURE OF FINANCIAL ECONOMICS

BY

J. DOYNE FARMER and JOHN GEANAKOPLOS

COWLES FOUNDATION PAPER NO. 1274

COWLES FOUNDATION FOR RESEARCH IN ECONOMICS YALE UNIVERSITY

Box 208281 New Haven, Connecticut 06520-8281

2009

http://cowles.econ.yale.edu/

J. DOYNE FARMER ANDJOHN GEANAKOPLOS

J. Doyne Farmer is affiliated with SantaFe Institute, Santa Fe, NM 87501 andLUISS Guido Carli, 00198, Roma, Italy(e-mail: [email protected])

John Geanakoplos is affiliated with YaleUniversity, New Haven, CT 06520 andSanta Fe Institute, Santa Fe, NM 87501.

The Virtues and Vices of Equilibriumand the Future of Financial Economics

The use of equilibrium models in economics springs from the desire for parsimoniousmodels of economic phenomena that take human reasoning into account. This approachhas been the cornerstone of modern economic theory. We explain why this is so, extollingthe virtues of equilibrium theory; then we present a critique and describe why thisapproach is inherently limited, and why economics needs to move in new directions if itis to continue to make progress. We stress that this shouldn’t be a question of dogma,and should be resolved empirically. There are situations where equilibrium modelsprovide useful predictions and there are situations where they can never provide usefulpredictions. There are also many situations where the jury is still out, i.e.,where so far theyfail to provide a good description of the world, but where proper extensions might changethis. Our goal is to convince the skeptics that equilibrium models can be useful, but alsoto make traditional economists more aware of the limitations of equilibrium models.Wesketch some alternative approaches and discuss why they should play an important rolein future research in economics. © 2008 Wiley Periodicals, Inc. Complexity 14: 11–38,2009

Key Words: equilibrium; rational expectations; efficiency; arbitrage; bounded ratio-nality; power laws; disequilibrium; zero intelligence; market ecology; agent-basedmodeling

1. INTRODUCTION

T he concept of equilibrium has dominated economics and finance for at least50 years. Motivated by the sound desire to find a parsimonious descriptionof the world, equilibrium theory has had an enormous impact on the way

that economists think, and indeed in many respects defines the way economiststhink. Nonetheless, its empirical validity and the extent of its scope still remains amatter of debate. Its proponents argue that it has been enormously successful, andthat it at least qualitatively explains many aspects of real economic phenomena.Its detractors argue that when one probes to the bottom, most of its predictionsare essentially unfalsifiable and therefore are not in fact testable scientific theories.We attempt to give some clarity to this debate. Our view is that while equilibriumtheory is useful, there are inherent limitations to what it can ever achieve. Economists

This is an invited article for the Special Issue—Econophysics, Guest Editors: MartinShubik and Eric Smith.

© 2008 Wiley Periodicals, Inc., Vol. 14, No. 3DOI 10.1002/cplx.20261Published online 10 November 2008 in Wiley InterScience(www.interscience.wiley.com)

C O M P L E X I T Y 11

must expand the scope of equilibriumtheory, explore entirely new approaches,and combine equilibrium methods withnew approaches.

This article is the outcome of an eight-year conversation between an economistand a physicist. Both of us have beeninvolved in developing trading strategiesfor hedge funds, giving us a deep appre-ciation of the difference between theo-ries that are empirically useful and thosethat are merely aesthetically pleasing.Our hedge funds use completely differ-ent strategies. The strategy the econo-mist developed uses equilibrium meth-ods with behavioral modifications totrade mortgage-backed securities; thestrategy the physicist developed usestime-series methods based on histori-cal patterns to trade stocks, an approachthat is in some sense the antithesis ofthe equilibrium method. Both strategieshave been highly successful. We initiallycame at the concept of equilibrium fromvery different points of view, one verysupportive and the other very skepti-cal. We have had many arguments overthe last eight years. Surprisingly, we havemore or less come to agree on the advan-tages and disadvantages of the equi-librium approach and the need to gobeyond it. The view presented here is theresult of this dialogue.

This article is organized as follows:In Section 2 we present a short qual-itative review of what equilibrium the-ory is and what it is not, and in Section3 we discuss the related idea of mar-ket efficiency and its importance infinance. In Section 4 we present whatwe think are the accomplishments andstrengths of equilibrium theory, and inSection 5 we discuss its inherent lim-itations from a theoretical perspective.In Section 6 we review the empiricalevidence for and against equilibriummodels. Then in Section 7 we developsome further motivation for nonequilib-rium models, illustrated by a few prob-lems that we think are inherently outof equilibrium. We also compare equi-librium in physics and economics anduse nonequilibrium models in physics

to motivate corresponding models ineconomics. In Section 8 we review sev-eral alternatives approaches, includingnow established approaches such asbehavioral and experimental economics.We also describe some less establishedapproaches to dealing with boundedrationality, specialization and heteroge-neous agents. We make a distinctionbetween the structural properties of amodel (those depend on the structureof institutions and interactions) vs. thestrategic properties (those that dependon the strategies of agents) and discussproblems in which structure dominates(so equilibrium may not be very impor-tant). We also discuss how ideas frombiology may be useful for understandingmarkets. Finally in Section 9 we presentsome conclusions.

2. WHAT IS AN EQUILIBRIUM THEORY?In this section we explain the basic ideaand the motivation for the neoclassi-cal concept of economic equilibrium,and discuss some variations on the basictheme.

Market equilibrium models aredesigned to describe the market interac-tions of rational agents in an economy.The prototype is the general equilibriumtheory of Arrow and Debreu [1, 2]. Theeconomy consists of a set of goods, suchas seed, corn, apples, and labor time,and a set of agents (households) whodecide what to buy and sell, how andwhat to produce, and how much to con-sume of each good. Agents are character-ized by their endowments, technologies,and utilities. The endowment of an agentis the set of all goods she inherits: forexample, her ability to labor, the appleson the trees in her backyard and so on.The technology of an agent is her col-lection of recipes for transforming goodsinto others, like seed into corn. She mightbuy the seed and hire the labor to do thejob, or use her own seed and labor. Somerecipes are better than others, and notall agents have access to the same tech-nologies. The utility of an agent describes

how much happiness she gets out of con-suming the goods. The agent does not getpleasure out of each good separately, butonly in the context of all the goods sheconsumes taken together.

The goal is to model the decisionsof agents incentivized solely by theirown selfish goals, and to deduce theconsequences for the production, con-sumption, and pricing of each good. Themodel of Arrow and Debrieu is based onfour assumptions:

1. Perfect competition (price taking).Each agent is small enough to havea negligible effect on prices. Agents“take” the prices as given, in the sensethat they are offered prices at whichthey can buy or sell as much as theywant, but the agents cannot do any-thing to change the prices.

2. Agent optimization of utility. At thegiven prices each agent indepen-dently chooses what to buy, what andhow to produce, and what to sell soas to maximize her utility. There is nofree lunch—the cost of all purchasesmust be financed by sales. An agentcan only buy corn, for example, byselling an equal value of her labor, orapples, or some other good from herendowment.

3. Market clearing. The aggregatedemand, i.e. the total quantity thatpeople wish to buy, must be equalto the aggregate supply, i.e. the totalquantity that people wish to sell.

4. Rational expectations. Agents makerational decisions based on perfectinformation. They have perfect mod-els of the world. They know the pricesof every good before they decide howmuch to buy or sell of any good.

To actually use this theory one mustof course make it concrete by specify-ing the set of goods in the economy, howproduction depends on labor and otherinputs, and a functional form for theutilities. General equilibrium theory wasrevolutionary because it provided clo-sure, giving a framework connecting thedifferent components of the economy to

12 C O M P L E X I T Y © 2008 Wiley Periodicals, Inc.DOI 10.1002/cplx

each other and providing a minimum setof assumptions necessary to get a solu-tion. The behavior of markets is an extra-ordinarily complicated and subtle phe-nomenon, but neoclassical economistsbelieve that most of it can be explainedon the basis of equilibrium.

The advent of general equilibriumtheory marked a major transition in thediscipline of economics. It gave hope fora quantitative explanation of the prop-erties of the economy in one grand the-ory, causing a sea change in the wayeconomics is done and in the kind ofpeople that do it. Mainstream econom-ics shifted from a largely qualitative pur-suit, often called “political economy,” toa highly mathematical field in whicharticles are often published in theorem-proof format.

We do not have the space todescribe the many applications and con-sequences of equilibrium in any detail.The most important consequence for ourpurposes is efficiency, which we shallcome to shortly. In the remainder of thissection we discuss some logical ques-tions one might raise about whetherequilibrium exists and how and whetherit is attainable. Then we give a fewexamples of how equilibrium models arebeing continuously extended to includemore phenomena, and develop the con-cept of financial equilibrium, our centraltopic here.

2.1. Existence of Equilibrium andFixed PointsIn equilibrium everybody’s plans are ful-filled. An agent who plans to buy threeears of corn by selling two apples at thegiven prices will find agents who wantto sell him the three ears of corn andothers who want to buy his two apples.A mother who goes to the store to buyher children bread will find as much asshe wants to buy at the going prices onthe shelves; yet at the end of the daythe store will not be left with extra breadthat goes to waste. One might well won-der how this could happen without anycentral coordinator. In short, why should

there be an equilibrium? This is calledthe existence problem.

In 1954 Arrow, Debreu, and McKen-zie simultaneously showed that therealways is an equilibrium, no matterwhat the endowments and technologiesand utilities, provided that each utilitydisplays diminishing marginal utility ofconsumption and each technology dis-plays diminishing marginal product. Themargin is a very famous concept in eco-nomics that was discovered by Jevons,Menger, and Walras in the so-called mar-ginal revolution of 1871. Apples displaydiminishing marginal utility if the moreapples an agent consumes, the less addi-tional happiness he achieves from onemore apple. Diminishing marginal prod-uct means that the more a good likelabor is used in production, the less extraoutput comes from one additional unit(hour) of input.

The method of proof used by allthese authors was first to guess a vec-tor of prices, one for each good, thento compute demand and supply at theseprices, and then to increase the pricesfor the goods with excess demand and todecrease the prices of goods with excesssupply. This defines a map from pricevectors to price vectors. A price vectorgenerates an equilibrium if and only ifit is mapped into itself by this map (forthen there is no excess demand or excesssupply). By a clever use of Brouwer’sfixed point theorem, it was shown thatthere must always be a fixed point andtherefore an equilibrium.

2.2. Getting to Equilibrium2.2.1. TatonnementWho sets the equilibrium prices? Howdoes the economy get to equilibrium?Just because there is an equilibrium doesnot mean it is easy to find. One sug-gestion of the marginalist Leon Walraswas that the equilibrium map could beiterated over and over. Starting from aguess, one could keep increasing anddecreasing prices depending on whetherthere was too much demand or sup-ply. He called this groping (tatonnement

in French) toward equilibrium. Unfortu-nately, after many years of analysis, itbecame clear that in general this taton-nement can cycle without ever gettingclose to equilibium.

2.2.2. OmniscienceAn alternative is that the agents know thecharacteristics of their competitors andknow that they are rational and will notsell their goods at less than they couldget elsewhere; if it is common knowl-edge that everybody is rational, and ifthe characteristics are common knowl-edge, then each agent will himself solvefor equilibrium and the prices will simplyemerge.

This explanation for the emergence ofprices has an analogue in Nash equilib-rium in game theory. A game is a con-test in which each player makes a moveand receives a payoff that depends onthis move as well as the moves of theother players. The question is how does aplayer know what move to make withoutknowing what moves his opponents willmake? And how can he guess what theywill do without knowing what they thinkhe will do? This circular conundrum wasresolved by Nash in 1951 who basicallyshowed that there is always at least oneself-consistent fixed point in the spaceof strategies. To be more specific, a Nashequilibrium is an assignment of movesto each player such that if each playerthought the others would follow theirassignments, then he would want to fol-low his. In game theory the question alsoarises: who announces this assignment?If the players are all perfectly logical, andare aware of all their characteristics, theyshould deduce the assignment.

2.3. Financial Equilibrium Models2.3.1. Time, Uncertainty, andSecuritiesOne of the main limitations of generalequilibrium theory (as described so far)is that it is cast in a nontemporal set-ting. There is only one time period, soagents don’t need to worry about thefuture. They don’t look ahead and they

© 2008 Wiley Periodicals, Inc.DOI 10.1002/cplx

C O M P L E X I T Y 13

don’t speculate. This simplifies mattersenormously but comes at the heavy costthat the theory is powerless to deal withtemporal change. Another limitation tothe theory so far is that agents onlytrade goods. In the real world they tradestocks and bonds and other financialsecurities. Financial equilibrium extendsgeneral equilibrium to allow for time,uncertainty, and financial securities.

Uncertainty about the future is mod-eled in terms of states of nature thatunfold as the nodes in a tree [2, 3]. Eachstate represents the condition of thingslike the weather or political events whosefuture behavior is unknown, but exoge-nous to the economy. States are given,and while they can affect the economy,the economy does not affect them. Achange in the state of nature is oftencalled a shock. The agents in the econ-omy do not know the future states ofnature, but they do know the tree fromwhich the future states of nature aredrawn and the probability for reachingeach node. For example, suppose weassume that the dividends of an agri-cultural company are made once a yearand take on only one of two possible val-ues, “high” or “low,” depending on theweather that year. Then we can orga-nize these as a binary tree in which thenth level with 2n nodes corresponds tothe nth year in the future, and a pathfrom the beginning to the end of the treecorresponds to a particular sequence ofhigh and low dividends.1 If the situa-tion was more complicated so that wehad to separate the weather in the west-ern hemisphere from the eastern hemi-sphere, then each node would have fourbranches instead of two and there wouldbe 4n paths. The agents assign proba-bilities to each branch of the tree, giv-ing a probability for reaching each nodeand thus a probability measure on theterminal states in the tree.

1Financial models can also be formu-lated with continuous states and/or incontinuous time.

Financial models also extend the

notion of equilibrium by generalizing

the notion of what can be traded to

include securities, which are promises to

deliver certain goods at certain points in

time. Such promises can be contingent

on future states of nature. Examples are

stocks (which promise future dividends

that change depending on the profits

of the firm), bonds (which promise the

same amount each period over a fixed

maturity) and so on. The existence of

such securities is important because it

allows agents to decrease their risk. It

also allows them to speculate in ways

that they might not otherwise be able

to. The implication of such securities for

social welfare has proved to be highly

controversial.

In the general equilibrium model

each agent is aware of her total con-

sumption of every good, and makes her

decisions in that context. That is why

every decision is a marginal decision:

an increase in her consumption of one

good must be evaluated in light of the

decrease in her consumption of some

other good that might be required to bal-

ance her budget. In the financial equilib-

rium extension we are describing, each

agent is assumed to be aware of what

her consumption will turn out to be at

every node, and to compute her utility

on that basis. One popular way to make

that calculation is to evaluate the util-

ity of consumption at any given node

exactly as agents evaluated their utility

of consumption in the general equilib-

rium model (which is basically a spe-

cial case of the financial model with

one node). One could then multiply the

utility of consumption at a given node

by the probability of ever reaching the

node. Finally, one could discount that

number again (i.e., multiply it by a fac-

tor less than 1), depending on how far

away from the origin of the tree the

node is, to account for the impatience of

consumers. Summing over all the nodes

gives the expected discounted utility of

consumption. An agent who contem-

plates increasing her consumption of

some good in some node in the finan-cial model must evaluate her utility inlight of the decrease in the holding ofsome financial security that might thenbe required for her to balance her bud-get, including the consequent loss ofconsumption in future states where thatsecurity would have paid dividends.

2.3.2. Financial EquilibriumOnce the model is extended to allow forthe tree of states of nature, and the trad-ing of securities, we need to extend thenotion of equilibrium. This is done byfollowing principles (1–4) above. Pricesmust now be given at every node of thetree. When agents optimize they mustchoose an entire action plan contem-plating what they will buy and sell at eachnode in the tree; part of their contem-plated trades will involve securities, andthe other part commodities.2 Any pur-chase at any node must be financed by asale of equal value at the same node. Thesale could be of other goods, or it couldbe of securities. The market for securi-ties, as well as for goods, must clear atevery node in the tree. Finally, the ratio-nal expectations hypothesis becomesmuch more demanding: Agents are notonly aware of the prices of all goods andsecurities today, but are also aware ofhow all the prices depend on each nodein the future.

2.4. Rational Expectations and UtilityMaximizationMaximizing a utility function alreadyembeds a large dose of rationality. Theutility function is defined over the entireconsumption plan. The agents are alsopresumed to know the tree of states ofnature, and the probabilities of everybranch, and to correctly forecast the

2As the path of future states unfolds theagents will carry out the trades they antic-ipated making on that path. Of courseonly one path will eventually material-ize, and the agents will never get a chanceto implement the plans they had made forunrealized branches.

14 C O M P L E X I T Y © 2008 Wiley Periodicals, Inc.DOI 10.1002/cplx

prices that will emerge at each node ifthey get there. So when an agent stopsto buy an apple today, she does so onlyafter considering what other fruit she willlikely have for dinner, how likely it is shewill pass the same shop tomorrow, whatelse she could spend the money on theday after tomorrow, and so on.

Not surprisingly, this rational utilitymaximization has received a great dealof attention and has been attacked frommany different directions. In 2002 Kah-neman received a Nobel prize for show-ing that real people do not have simpleutility functions such as those that aretypically assumed in standard economictheory, but instead have preferences thatdepend on context and even on fram-ing, i.e. on the way things are presented[4]. The field of behavioral economics,which Kahneman exemplifies, investi-gates psychologically motivated modi-fications of the rationality and utilityassumptions. There are a range of levelsat which one can do this. At the oppositeextreme from rational expectations, onecan simply assume that agents have fixedbeliefs, which might or might not corre-spond to reality [5–7]. At an in-betweenlevel one can use a so-called noise tradermodel in which some agents have fixedbeliefs while others are perfectly ratio-nal [8, 9] (This can actually make thetask of computing the equilibrium evenharder, since the rational agents have tohave perfect models of the noise tradersas well as of each other). At a higherlevel one can assume that agents are notgiven the probabilities of states of naturea priori, but need to learn them [10, 11].

2.5. Extensions of EquilibriumThe rational expectations equilibriummodel that we have described so far ishighly idealized, and in the next sectionswe will present a critique outlining itsproblems. The main agenda of cur-rent economic theory is to extend it bymodifying or generalizing the assump-tions. For example, in 1958 Samuel-son extended the finite tree equilibrium

model to an infinite number of time peri-ods, calling it the overlapping genera-tions model, in order to study intergener-ational issues like social security. In 2001Akerlof, Spence and Stiglitz received theNobel prize for their work on asymmetricinformation, i.e. for studying situationssuch as buying a used car, or negotia-tions between labor and management,in which the information sets of agentsdiffer [12–14]. Another significant exten-sion is to allow agents who sell secu-rities to default on delivering the divi-dends those securities promise [15, 16].This raises interesting problems such ashow the market determines the amountof collateral that must be put up forloans [17].

In view of all these extensions themeaning of the word “equilibrium” is notalways clear. One definition would beany model that could be interpreted assatisfying hypotheses (1–4) as describedin the introduction to this Section. Butwe also wish to allow for some bound-edly rational agents. Following the prac-tice of most economists, we will definean equilibrium model as one in whichat least some agents maximize prefer-ences and incorporate expectations ina self-consistent manner. So, for exam-ple, a noise trader model is an equilib-rium model as long as some of the agentsare rational, but models in which all theagents act according to fixed beliefs arenot equilibrium models.

3. EFFICIENCYIn equilibrium everyone is acting inhis own selfish interest, guided only bythe market prices, without any directionfrom a central planner. One wonders ifanything coherent can come from thisdecentralization of control. One mightexpect coordination failures and otherproblems to arise. If activities were orga-nized by rational cooperation, surelypeople could be made better off. Yet inthe general equilibrium model of Arrowand Debreu, equilibrium allocations arealways allocatively efficient. Allocativeefficiency means that the economy is

as productive as possible, or Pareto effi-cient, i.e. that there is no change in pro-duction choices and trades that wouldmake everyone better off. In equilibriumeveryone acts in his own selfish interest,yet the decisions they make are in thecommon good in the sense that not evena benevolent and wise dictator who toldeveryone what to produce and what totrade could make all the agents better off.

In financial equilibrium the situationis much more complicated and interest-ing. An important assumption underpin-ning much of the theory of financial eco-nomics is that of complete markets. Themarkets are complete if at any node inthe tree it is possible to offset any futurerisk, defined as a particular future state,by purchasing a security that pays if andonly if that state occurs. When all suchsecurities exist so that markets are com-plete, financial equilibrium is necessarilyPareto efficient.3

In contrast, when markets arenot complete, financial equilibrium isalmost never Pareto efficient. Worse still,the markets that do exist are not usedproperly. When markets are incomplete,a benevolent and wise dictator canalmost always make everyone better offsimply by taxing and subsidizing theexisting security trades [21]. What formsuch government interventions shouldtake is a matter for economic policy.Is it a good approximation to assumethat real markets are complete? If theyare not complete, does the governmenthave enough information to improve the

3This was proved by Arrow [18] andDebreu [19] under conditions (10-94),including the rationality hypothesis onagents. Brock, Hommes and Wagenerhave shown that when one deviatesfrom rational expectations, for exampleby assuming agents use reinforcementlearning, adding additional securitiescan destabilize prices [20]. This suggeststhat there are situations where mar-ket completeness can actually decreaseutility.

© 2008 Wiley Periodicals, Inc.DOI 10.1002/cplx

C O M P L E X I T Y 15

situation? These questions have been amatter of considerable debate.

Since allocative efficiency typicallyfails for financial economies, economiststurned to properties of security pricesthat must always hold. Informationalefficiency is the property that secu-rity prices are in some sense unpre-dictable. In its strongest form, informa-tional efficiency is the simple statementthat prices are a martingale [22, 23], i.e.that the current price is the best predic-tion of future prices.4 This is importantbecause it suggests that all the informa-tion held in the economy is revealed bythe prices. If weather forecasts cannotimprove on today’s price in predictingfuture orange prices, then one can saythat today’s orange price already incor-porates those forecasts, even if manytraders are unaware of the forecasts.5

Arbitrage efficiency means that throughbuying and selling securities it is notpossible for any trader to make profitsin some state without taking any risk(i.e. without losing money in some otherstate). Again this is important because itsuggests that there are no traders whocan always beat the market by takingadvantage of less informed traders. Thusthe uninformed should not feel afraidthat they are not getting a fair deal. Infor-mational efficiency and arbitrage effi-ciency are intimately related; in somecontexts they are equivalent.

A consequence of the martingaleproperty is that the price of every (finitely

4More precisely, if no security pays a divi-dend in period t +1, then there is a proba-bility measure on the branches out of anynode in period t such that the expectedprice in period t + 1 of any security (rela-tive to a fixed security), given its (relative)price in period t, is just the period t price.5Roll found in some Florida coun-ties that today’s orange prices predictedtomorrow’s orange prices better thantoday’s weather reports, and also thattoday’s orange prices predicted tomor-row’s weather better than today’s weatherforecasts [24].

lived) asset must be equal to its funda-mental value (also called present value ifthere is no uncertainty). The fundamen-tal value of an asset is the discountedexpected dividend payments of the assetover its entire life, where the expectationis calculated according to the martin-gale probabilities, and the discount is therisk free rate (the interest rate on secu-rities such as treasury bonds for whichthe chance of default can be taken tobe zero). This is important for investorswho might feel too ignorant to buystocks, because it suggests that on aver-age everybody will get what he pays for.

From the point of view of finance,arbitrage efficiency and informationalefficiency are particularly useful becausethey can be described without anyexplicit assumptions about utility. Manyresults in finance can be derived directlyfrom arbitrage efficiency. For exam-ple, the Black-Scholes model for pric-ing options is perhaps the most famousmodel in finance. The option price canbe derived from only two assumptions,namely that the price of the underlyingasset is a random walk and that neitherthe person issuing the option nor theperson buying it can make risk-free prof-its. Because it does not rely on utility, sev-eral people have suggested that arbitrageefficiency forms a better basis for finan-cial economics than equilibrium; see forexample Ross [25]. As we will argue later,because of all the problems with definingutility, this is a highly desirable feature.

4. THE VIRTUES OF EQUILIBRIUM

4.1. Agent-Based ModelingEquilibrium theory focuses on individ-ual actions and individual choices. Bycontrast Marx emphasized class strug-gles, without asking whether each indi-vidual in a class would have the incentiveto carry on the struggle. Similarly Key-nesian macroeconomics often positedreduced form relationships, such as apositive correlation between unemploy-ment and inflation (called the Phillipscurve), without deriving them from

individual actions. Equilibrium theory isan agent based approach which does notadmit any variables except those thatcan be explained in terms of individualchoices.

The advantages of the agent basedapproach can be seen in the macroeco-nomic correlation between inflation andoutput. At its face, such a correlation sug-gests that the monetary authority canstimulate increased output by engineer-ing higher inflation through printingmoney. According to equilibrium theory,if inflation causes higher output, theremust be an agent-based explanation. Forexample, it may be that workers see theirwages going up and are tempted to workharder, not realizing that the prices of thegoods they will want to buy are also goingup so that there is no real incentive towork harder. But if that is the explana-tion, then it becomes obvious that pol-icy makers will not be able to rely onthe Phillips curve to stimulate output byprinting more money. Agents will even-tually catch on that when their wages arerising, so are general prices.6 That skepti-cism was validated during the stagflationof the 1970s, when there was higher infla-tion and lower output. If printing moneysometimes causes higher output, it mustbe through a different channel, con-nected say to interest rates and liquidityconstraints. Finding what these are atthe agent level deepens the analysis andbrings it closer to reality.

4.2. The Need to Take Human Reasoninginto AccountThe fundamental difference betweeneconomics and physics is that atomsdon’t think. People are capable of rea-soning and of making strategic plansthat take each other’s ability to reasoninto account. Ultimately any economicmodel has to address this problem. Bygoing to a logical extreme, equilibriummodels provide a way to incorporate rea-soning without having to confront the

6This has come to be called the Lucascritique [26].

16 C O M P L E X I T Y © 2008 Wiley Periodicals, Inc.DOI 10.1002/cplx

messiness of real human behavior. Eventhough this approach is obviously unre-alistic, the hope is that it may nonethe-less be good enough for many purposes.

4.3. Parsimony

4.3.1. RationalityThe rationality hypothesis is a par-simonious description of the worldthat makes strong predictions. Rationalexpectations equilibrium models havethe advantage that agent expectationsare derived from a single, simple andself-consistent assumption. Without thisassumption one needs to confront thehard task of determining how agentsactually think, and how they think aboutwhat others think. This requires formu-lating a model of cognition or learn-ing, and thereby introducing additionalassumptions that are usually compli-cated and/or ad hoc. Without rationalityone needs either to introduce a set ofbehavioral rules of thumb or to intro-duce a learning model. While perfectrationality defines a unique or nearlyunique model of the world, there arean infinite number of boundedly ratio-nal models. To paraphrase ChristopherSims, once we depart from perfect ratio-nality, there are so many possible modelsit is easy to become lost in the wildernessof bounded rationality [27].

Perfect rationality is an impossiblestandard for any individual to attain,but the hope of the economist in mak-ing a rational expectations model is thatin aggregate, people behave “as if” theywere rational. This maybe true in somesituations, and it may not be true in oth-ers. In any case, rational expectationsmodels can provide a useful benchmarkfor understanding whether or not peo-ple are actually rational, which can serveas a starting point for more complicatedmodels that take bounded rationalityinto account.

4.3.2. SuccinctnessEquilibrium theory provides a unifyingframework from which many differentconclusions can be drawn. Rather than

having to invent a new method to attackeach problem, it provides a standardizedapproach, and a standardized languagein which to explain each conclusion.

A standardized model does not ruleout new theories. New equilibrium theo-ries are of two forms. First, one can spe-cialize the class of utilities, technologies,and endowments to try to draw a sharpand interesting conclusion that does nothold in general. If either the premiseor conclusion can be empirically vali-dated, one has found a law of economics.Second, one can extend the definitionof equilibrium (adding say asymmetricinformation or default). The second formfacilitates the discovery of many the-ories of the first form. Agreement ona unifying framework, such as equilib-rium and hypotheses (1–4), makes it eas-ier to evaluate new economic theories,and to make progress on applications.But of course it stultifies radically newapproaches.

4.4. The Normative Purpose of EconomicsOne of the principal differences betweenphysical and social science is that thelaws of the physical world are fixed,whereas the laws of society are mal-leable. As human beings we have thecapacity to change the world we live in.Economics thus has a normative as wellas a descriptive purpose. A descriptivemodel describes the world as it is, whilea normative model describes the worldas it might be under a change in socialinstitutions. The equilibrium model ismeant to allow us to describe both. Foreach arrangement of social institutions,such as those that prevail today, we com-pute the equilibrium. The representationof agents by utilities (as well as endow-ments) enables us to evaluate the bene-fits to each person of the resulting equi-librium, and thereby implicitly the utilityof the underlying institutions. Equilib-rium theory then recommends the insti-tutions that lead to the highest utilities.By contrast, consider a purely phenom-enological model that assumes behav-ioral rules for the agents without deriving

them from utility. Such a model is eithersilent on policy questions, or requires aseparate ad hoc notion of desireability inorder to recommend one institution overanother.

The rationality hypothesis allows usto define equilibrium succinctly. But asa byproduct it shapes the economist’sevaluation of the institutions. For exam-ple, one of the basic questions in eco-nomics is whether free markets orga-nize efficient sharing of risks, leading tosensible production decisions. The equi-librium model is often used to showthat under certain conditions, free mar-ket incentives lead selfish individuals tomake wise social decisions. We calledthis allocative efficiency or Pareto effi-ciency. But of course the rationality ofall the individuals is an indispensablehypothesis in the proof. If agents aremisinformed about future productionpossibilities, or act whimsically, the freemarket economy will obviously makebad decisions.

Even if rational expectations doesn’tprovide a good model of the present, itmay sometimes provide a good model ofthe future. The introduction of an equi-librium model can change the futurefor the simple reason that once peoplebetter understand their optimal strate-gies they may alter their behavior. Agood example of this is the Black-Scholesmodel; as people began using it to buyand sell mispriced options, the prices ofoptions more closely matched its pre-dictions. Another example is the capi-tal asset pricing model. In that modelthe optimal strategy for every investoris to hold a giant mutual fund of allstocks. Nowadays every investor who haslearned a little finance does indeed thinkfirst of holding exactly such an index(though few investors hold only that).

Unfortunately, many economistshave used the normative purpose of eco-nomics as an excuse to construct eco-nomic theories that are so far removedfrom reality that they are useless. For aneconomic theory to have useful norma-tive value it must be sufficiently closeto reality to inspire confidence that its

© 2008 Wiley Periodicals, Inc.DOI 10.1002/cplx

C O M P L E X I T Y 17

conclusions give useful advice. Unless atheory can give some approximation ofthe world as it is, it is hard to have confi-dence in its predictions of how the worldmight be.

4.5. Why Does Wall Street Like theEquilibrium Model?Many Wall Street professionals try tobeat the market by actively lookingfor arbitrages. Fundamental analysts,for example, believe that they can findstocks whose prices differ substantiallyfrom their fundamental values. Statis-tical arbitrageurs believe they can findinformation in previous stock move-ments that will help them predict therelative direction of future stock move-ments. The activities of these Wall Streetprofessionals seems proof that theythink the equilibrium model is flawed.If they believe the market is in equilib-rium, why are they pursuing strategiesthat cannot succeed in equilibrium?

Ironically, in fixed income and deriva-tive asset markets the arbitrageurs them-selves use the apparatus of equilibriummodels to find arbitrages. Many peoplemake good profits by betting that whenprices make large deviations from equi-librium these deviations will eventuallydie out and return to equilibrium.

There are many ways Wall Street prac-titioners use equilibrium models. Wereview some of them below.

4.5.1. Conditional Forecasting IsGood DisciplineMany pundits, and even some pro-fessional economists (and especiallymacroeconomists), make unconditionalforecasts. They say growth next quarterwill be slow, but by the fourth quar-ter it should pick up and unemploy-ment should start to decline. They donot often bother to say, for example,that their predictions might change ifthere is a messy war in Iraq. In theequilibrium model agents do not knowwhat state will prevail tomorrow, butthey do know what prices will prevailconditional on tomorrow’s state. Theymake conditional forecasts, based on

a tree of possible future states. WallStreet traders are trained in businessschools and economics departmentsacross the country to appreciate equi-librium models. Nowadays so many WallStreet traders make conditional forecastsusing concrete trees of future possibil-ities that this assumption has becomemore plausible as a descriptive model ofthe world.

One of the virtues of making con-ditional forecasts is that it stimulatestraders to find strategies (called risklessarbitrages) that will work no matter whatthe future holds. If one is lucky enough tofind a riskless arbitrage, success is inde-pendent of the probabilities of the futurestates of nature. In the real world risk-less arbitrages are rare (as equilibriumtheory says they should be). Most realarbitrageurs actually make their moneywith risky arbitrages, and in this casethe probabilities for branches of thetree become important. The estimationerrors that are inherent in estimatingthese probabilities compound the risk.Not only might the future bring a state inwhich money will be lost, but the tradermight also underestimate the probabil-ity of this state. But at least she can seethe scenarios that constitute the modelexplicitly, and can compute the sensitiv-ity of her expected profits to variations inthe probabilities of these scenarios.

4.5.2. The Power of theNo-Arbitrage HypothesisTree building is most useful when thefuture possibilities are easy to imagine,when they are not too numerous to com-pute, and when there is a reliable guide totheir probabilities. The hypothesis of no-arbitrage drastically reduces the num-ber of states, making the computationfeasible, and often even determines theprobabilities.

One reason that financial practition-ers like the no arbitrage assumptionis because it makes things much sim-pler. Arbitrage efficiency requires a con-sistency between prices that drasticallyreduces the size of the hypotheticaltree. For example, a mortgage derivative

trader might worry about future inter-est rates of all maturities, including theovernight (i.e one day) rate, the yearlyrate, the ten year rate, and so on. If thereare 20 such rates, and each rate can takeon 100 values, then each node in thetree will require 10020 branches! Usingthe overnight rate alone requires a muchsmaller tree with only 100 branches fromeach node. The crucial point is that ifthe trader assumes there will never beany arbitrage among interest rate securi-ties of different maturities in the future,then the smaller tree will be sufficient torecover all the information in the largertree even for a trader who cares about allthe rates. Given the smaller tree and theprobabilities of each branch, the tradercan deduce all the other future longrates, conditional on the future overnightrates, without adding any new nodes toher tree. (Today’s two day discount, forexample, can be deduced as the productof today’s one day discount and tomor-row’s one day discount, averaged over allpossible values of the one day discounttomorrow). Furthermore, if the traderassumes there is no arbitrage betweencurrent long maturity interest rate secu-rities and future short interest rate secu-rities and current interest rate options,then she can deduce the probabilitiesof each branch in the smaller overnightinterest rate tree.

The homage arbitrage traders pay toarbitrage efficiency is the most com-pelling evidence that in some respects itis true. Again we see the irony that theroad to arbitrage comes from assumingno arbitrage.7

7The mortgage trader assumes no arbi-trage in the class of interest rate securi-ties alone. By contrast, she does assumethere is an arbitrage involving interestrate securities and mortgage securities. Amortgage derivative trader might assumethere is no arbitrage involving interestrate securities and mortgage securities,but that there is an arbitrage once mort-gage derivatives are added to the mix.

18 C O M P L E X I T Y © 2008 Wiley Periodicals, Inc.DOI 10.1002/cplx

4.5.3. Risk ReductionHedging refers to the process of reduc-ing specific financial risks. To hedge thevalue of a particular security one cre-ates a combination of other securities,called a portfolio, that mimics the secu-rity that one wishes to hedge. By sellingthis combination of securities one cancancel or partially cancel the risk of buy-ing the original security. Statistical arbi-trageurs, for example, try to make bets onthe relative movements of stocks withoutmaking bets on the overall movement ofthe stock market. The market risk canbe hedged by making sure that the totalposition is market neutral, i.e. that undera movement of the market as a whole thevalue of the position is unaffected. Thisis typically done by maintaining con-straints on the overall position, and canalso be done by selling a security, such asa futures contract on a market index.

To properly hedge it is necessary tohave a set of scenarios for the future.Such scenarios can be represented bymeans of a tree, exactly as we describedfor equilibrium models. Thus, the samestructure we defined in order to discussequilibrium is central to hedging risks.Wall Street professionals are very con-cerned about risks, and for this reasonlike the financial framework for under-standing equilibrium.

Hedging and arbitrage are two sidesof the same coin. In both hedging andarbitrage, the trader looks for a portfolioof securities that will pay off exactly whatthe risky asset does. By buying the assetand selling the portfolio, the trader iscompletely hedged. If the trader discov-ers that the cost of the hedging portfoliois more than the security, then hedgingbecomes arbitrage: The arbitrageur canbuy the security and sell the portfolioand lock in a riskless profit.

5. DIFFICULTIES AND LIMITATIONS OFEQUILIBRIUMWhile equilibrium should be an impor-tant component of the economist’s toolkit, its dangers and limitations need to beunderstood (and all too often are not).

5.1. Falsifiability?Empirical laws in economics are muchharder to find than in physics or theother natural sciences. Realistic experi-ments for the economy as a whole arenearly impossible to conduct (though forsome small scale phenomena there isa thriving experimental research effortunderway) and many causal variablesare impossible to measure or evento observe. Economists usually do notdream of finding “constants of behav-ior,” analogous to the constants of naturefound in physics; when they do, they donot expect more than a couple of signifi-cant digits.8 We shall argue later that thismay be a mistake, and that it is possibleto find finely calibrated relationships ineconomic data.

Perhaps because of the difficulty ofempirical work, economic theory hasemphasized understanding over pre-dictability. For example, to economists,equilibrium theory itself is most impor-tant not for any empirical predictions,but for the paradoxical understandingit provides for markets: Without anycentralized coordination, all individualplans can perfectly mesh; though every-one is perfectly selfish, their actionspromote the common good; thougheverybody is spending lots of time hag-gling and negotiating over prices, theirbehavior can be understood as if every-body took all the prices as given andimmutable.

Equilibrium theory has not beenbuilt with an eye exclusively focusedon testability or on finding exact func-tional forms. Most equilibrium modelsare highly simplified at the sacrifice offeatures such as temporal dynamics orthe complexities of institutional struc-ture. When it comes time to test themodel, it is usually necessary to makeauxiliary assumptions that put in addi-tional features that are outside of the

8Okun’s Law for example, which statesthat every 1% increase in unemploymentis accompanied by a 3% decrease in GNP,has one significant digit.

theory. All these factors make equilib-rium theories difficult to test, and meanthat many of the predictions are not assharp as they seem at first. In manysituations, whether or not the predic-tions of equilibrium theory agree withreality remains controversial, even afterdecades of debate.

Not only are there few sharp eco-nomic predictions to test, but thehypotheses of economic equilibriumalso seem questionable, or hard toobserve. A long-standing dispute iswhether utility is a reasonable founda-tion for economic theory. The concept ofutility as it is normally used in economictheory is purely qualitative. The func-tional form of utility is generally cho-sen for convenience, without any empir-ical justification for choosing one formover another. No one takes the functionalform and the parameters of utility func-tions literally. This creates a vaguenessin economic theory that remains in itspredictions.

Psychologists have generally con-cluded that utility is not a good way todescribe preferences, and have proposedalternatives, such as prospect theory [4].Some economists have taken this seri-ously, as evidenced by the recent Nobelprize awarded to Kahneman. However,most theory is still built around con-ventional utility functions, and so farthe alternatives are not well-integratedinto the mainstream. Attempts that havebeen made to develop economic mod-els based on prospect theory still do notdetermine the parameters a priori (andin fact they have more free parameters).Thus so far it is still not clear whethermore general notions of preferences canbe used to make sharper and more quan-titative economic predictions.9

9One approach that has gained someattention is hyperbolic discounting [28].Hyperbolic agents care a lot more abouttoday than tomorrow, yet they act todayas if they will never care about the differ-ence between 30 days from today and 31days from today.

© 2008 Wiley Periodicals, Inc.DOI 10.1002/cplx

C O M P L E X I T Y 19

The other big problem that is intrinsicto equilibrium theories concerns expec-tations about the probabilities of futurestates. It is difficult to measure expecta-tions. In practice we only observe a singlepath through the tree of future states.Theparticular path that is observed histor-ically may be atypical, and may not bea good indication of what agents reallybelieved when they made their deci-sions. Thus, even when we have a goodhistorical record there is plenty of roomto debate the conclusions.

All these problems occur in testingthe assertion that markets are arbitrageefficient, as we discuss later. Real arbi-trages are rarely risk free. Instead, theyinvolve risk, and determining whetherone arbitrage is better than anotherinvolves measuring risk. Future risksmay not match historical risks. If a skill-ful trader produces excess returns (aboveand beyond the market as a whole)with a high level of statistical signifi-cance, a champion of market efficiencycan always argue that this was possibleonly because the asset had “unobservedrisk factors.” What seems like a power-ful scientific prediction from one pointof view can look suspiciously like anunfalsifiable belief system from another.

5.2. Parsimony and Tractability Are Notthe SameWhile we have argued that equilibriummodels are parsimonious this does notnecessarily mean that they are easyto use. The mathematical machineryrequired to set up and solve an equilib-rium model can be cumbersome. Find-ing fixed points is much more diffi-cult than iterating dynamic maps. Thusincorporating equilibrium into a modelcomes at a large cost, and may forceone to neglect other factors, such as thereal structure of market institutions. Asa result of this complexity most equi-librium models end up being qualitativetoy models, formulated over one or twotime periods, whose predictions are tooqualitative to be testable.

5.3. Realism of the RationalityHypothesis?It seems completely obvious that peo-ple are not rational. The economic modelof rationality not only requires themto be super-smart, it requires them tohave God-like powers of omniscience.This should make anyone skeptical thatsuch models can ever describe the realworld. Rational expectations (i.e., know-ing the probabilities of each branch inthe tree and knowing what the priceswill be at each node) is often justified bythe argument that people behave “as if”they were rational. Skeptics do not findsuch arguments convincing, particularlywithout supporting empirical evidence.There are many reasons to be suspiciousof equilibrium models, and many situa-tions where the cognitive tasks involvedare sufficiently complicated that the apriori expectation that an equilibriumtheory should work is not high.

The conceptual problems with per-fect rationality can be broken down intoseveral categories:

• Omniscience. To take each others’expectations into account agents musthave an accurate model of each other,including the cognitive abilities, util-ity, and information sets of all agents.All agents construct and solve the sametree. They must also agree on the prob-abilities of the branches. More real-istically one must allow for errors inmodel building, so that not all agentshave the same estimates or even thesame tree of possibilities.

• Excessive cognitive demands. The cog-nitive demands the equilibrium modelplaces on its agents can be prepos-terous in the sense that the calcu-lations the agents need to make areextremely time consuming to perform.Even given the tree and the prob-abilities and the conditional prices,it may be difficult for an agent tocompute her optimal plan. But howdoes the agent know the conditionalprices unless she herself computesthe entire equilibrium based on her

knowledge of all the other agents’ utili-ties and endowments? These compu-tational problems can be intractableeven if all agents are fully rational, andthey can become even worse if someagents are rational and others aren’t.

• Behavioral anomalies. There is perva-sive evidence of irrationality in bothpsychological experiments and realworld economic behavior. Even in sim-ple situations where people should beable to deal with the difficulties ofcomputing an equilibrium it seemsmany do not do so [29, 30].

• Modeling cognitive cost and het-erogeneity. Real agents have highlydiverse and context dependentnotions of rationality. Because modelsare expensive to create real agentstake shortcuts and ignore lots of infor-mation. They use specialized strate-gies. The resulting set of decisions maybe far from the rationality supposedin equilibrium, even when taken inaggregate.

5.4. Limited ScopeThere are many interesting problems infinancial economics that the equilibriumframework was never intended to solve.Under conditions that are rapidly evolv-ing, e.g. where there is insufficient timefor agents to learn good models of thesituation they are placed in, there is lit-tle reason to believe that the equilib-rium framework describes the real world.Some of the problems include

• Evolution of knowledge. In a real mar-ket setting the framework from whichwe view the world is constantly andunpredictably evolving. The modelsused by traders to evaluate mortgagesecurities in the 1980s were vastly moreprimitive than the models used to eval-uate the same securities today. Peo-ple have a difficult time imagining thepossible ways in which knowledge willevolve, much less assigning probabili-ties to all of its states.

• Lack of tatonnement. The fact that anequilibrium exists does not necessarily

20 C O M P L E X I T Y © 2008 Wiley Periodicals, Inc.DOI 10.1002/cplx

imply that it is stable. For stability it isnecessary to show that when a systemstarts out of equilibrium it will neces-sarily move toward equilibrium. Thisrequires the construction of a modelfor price formation out of equilibrium,a process that is called tatonnement.Such models suggest that there aremany situations where prices will failto converge to equilibrium [31].

• Inability to model deviations fromitself. Equilibrium can’t model devia-tions from itself. It provides no wayto pose questions such as “How inef-ficient is the economy?”. One wouldlike to be able to understand questionssuch as the timescale for violations ofarbitrage efficiency to disappear, butsuch questions are inherently outsideof the equilibrium framework. (See thediscussion in Section 7).

While the financial implications ofequilibrium theory are on one handextraordinarily powerful, on the otherhand, their very power makes themalmost empty. Economic theory says thatthere is very little to know about markets:An asset’s price is the best possible mea-sure of its fundamental value, and thebest predictor of future prices. If that istrue, there is no need to answer the kindsof questions that economists are askedall the time, such as “Are stocks going upor down?,” or“Is this a good time to investin real estate?.” Only by going outside theequilibrium model can one raise manypressing financial questions.

It is worth noting that the merefact that people so persistently asksuch questions puts equilibrium theoryinto doubt. There are three possibilities:Either the people that do this are irra-tional, but if they are, then how can weexpect equilibrium theory to describethem? Or they are rational, but if so, thentheir questions reflect that their under-standing is deeper than that of the equi-librium theorist. The only other expla-nation is that the people who ask suchquestions do not invest an economi-cally significant amount of money. But

this seems implausible—almost every-one asks such questions.

6. EMPIRICAL EVIDENCE FOR ANDAGAINSTEquilibrium theory teaches us thatexpectations are important, and this isno less true in evaluating the successor failure of equilibrium theory itself.The booster can point to significant suc-cesses and the detractor can point tosignificant failures.

The booster can assert that equilib-rium theory has made many practicalsuggestions that have been followed andhave been borne out as correct. Com-munism did not produce as much out-put as the free markets of capitalism.Diversifying your investments really isa good idea, and many index fundshave been created to accommodate thisdesire. A hedge fund that can showits returns are independent of muchof the rest of the economy can attractinvestors even if it promises a lowerrate of return than competitors whosereturns are highly correlated with themarket.10 Arbitrages are indeed hard tofind, and even harder to exploit. Stockoption prices are explained to a highdegree of accuracy by the Black-Scholesformula. Prepayment behavior for primemortgages can be explained by maximiz-ing the utility of individual households(with some allowances for inattentionand other irrational behaviors).

The skeptic counters that, with a fewexceptions, most of the predictions ofequilibrium theory are qualitative andhave not been strongly borne out empir-ically in an unambiguous manner. Toquote Ijiri and Simon: “To be sure, eco-nomics has evolved a highly sophisti-cated body of mathematical laws, but

10Though diversification is often sightedas evidence for equilibrium theory, theskeptic will point out that this onlydepends on portfolio theory, which is asimple result from variational calculusconcerning statistical estimation and hasnothing to do with equilibrium theory.

for the most part these laws bear arather distant relation to empirical phe-nomena, and usually imply only qual-itative relations among observables . . . .Thus, we know a great deal about thedirection of movement of one variablewith the movement of another, a littleabout the magnitudes of such move-ment, and almost nothing about thefunctional forms of the underlying rela-tions” [32]. Since they said this in 1977the situation has improved, but only a lit-tle. Apart from options and prime mort-gage pricing (but not subprime), thereare very few examples of economic the-ories that cleanly fit the data and alsounambiguously exclude nonequilibriumalternatives. While some of the predic-tions of equilibrium models are in quali-tative agreement with the data, there arefew that can be quantitatively verified ina really convincing manner.

One of the conclusions of equilibrumtheory is that relative prices should fol-low a martingale. It is well documentedthat over the long-term risky securi-ties like stocks have had higher returnsthan safe securities like short term gov-ernment bonds, at least in the UnitedStates.11 This would seem to contradictthe martingale pricing theorem. But themartingale pricing theorem says onlythat asset prices follow a martingale withrespect to some probability measure, notnecessarily with respect to the objectiveprobabilities. The skeptic naturally com-plains that this is giving the theory toomuch freedom, making it close to tauto-logical. Economists have responded bymaking more assumptions on the under-lying utilities in the equilibrium model tolimit how the set of allowable martingale

11Brown, Goetzmann and Ross point outthat averaged over all western countries,stocks have not outperformed bonds [33].An economic collapse, say during theRussian revolution, usually crushes stockprices more than bond prices. So theAmerican experience may not be repre-sentative. Of course this illustrates thedifficulty of testing the prediction.

© 2008 Wiley Periodicals, Inc.DOI 10.1002/cplx

C O M P L E X I T Y 21

probabilities can deviate from objectiveprobabilities, making the theory falsifi-able. The most famous model of thattype is the so-called capital asset pricingmodel (CAPM) developed by Markowitz,Tobin, Linter, and Sharpe [34–37]. Inone version of CAPM all utilities arequadratic.12 Under this assumption themartingale probabilities are not arbi-trary, but must lie in a one dimensionalset, making the theory more straight-forwardly testable. CAPM does explainwhy riskier securities should have higherreturns than safe securities, and also pro-vides a rigorous definition and quantifi-cation of the risk of a security. Data fromthe 1930s through the 1960s seemed toconfirm the CAPM theory of pricing.But little by little the empirical valid-ity of CAPM has unraveled. Of coursethere is always the possibility that adifferent specialization will give rise toanother model that matches the datamore closely. Or perhaps an extension ofthe equilibrium model involving defaultand collateral will be able to match thedata, without creating so many free para-meters as to make the theory unfalsifi-able.13

A similar story can be told aboutthe conclusion that asset prices shouldmatch fundamental values. Attemptsto independently compute fundamen-tal values based on dividend series donot match prices very well. For exam-ple, for the U.S. stock market Campbelland Shiller [38] show deviations betweenprices and fundamental values of morethan a factor of two over periods aslong as decades. This conclusion can

12This is an example of the first kindof progress equilibrium theory makes,in which specialized assumptions giverise to more precise conclusions, as wediscussed in Section 4.3.2.13If successful, this would be an exampleof the second kind of progress equilib-rium theory makes, when the model isextended to incorporate new concepts,butretains methodological premises 1-4, aswe discussed in Section 4.3.2.

be disputed on the grounds that funda-mental values are not easily measurable,and perhaps none of the measures theyuse are correct (though they tried sev-eral alternatives). But whether the theoryis wrong or whether it is merely unfal-sifiable, the failure to produce a goodmatch to fundamental values representsa major flaw in either case.

Perhaps even worse, there are situa-

tions where equilibrium makes predic-

tions that appear to be false. For exam-

ple, people seem to trade much more

than they should in equilibrium [39].

Global trading in financial markets is on

the order of a hundred times as large

as global production [40, 41]. If people

are properly taking each others’ expecta-

tions into account why should they need

to trade so much? One of the problems

is that the theoretical predictions of how

much people should trade are not very

sharp, due at least in part to the prob-

lems discussed in the previous section.

Nonetheless, it seems that even under

the most favorable set of assumptions

people trade far more than can be ratio-

nalized by an equilibrium model [42].

As already discussed in the previous

section, one of the key principles of ratio-

nal expectations is that investors should

correctly process information, and thus

price movements should occur only in

response to new information. Studies

that attempt to correlate news arrival

with large market moves do not support

this. For example, Cutler et al. exam-

ined the largest 100 daily price move-

ments in the S&P index during a 40

year period and showed that most of

the largest movements occur on days

where there is no discernable news,

and conversely, days that are partic-

ularly newsworthy are not particularly

likely to have large price movements

[43]. Other studies have shown that price

volatility when markets are closed, even

on non-holidays, is much lower than

when the market is open [44]. The evi-

dence seems to suggest that a substantial

fraction of price changes are driven by

factors unrelated to information arrival.

While news arrival and market move-

ments are clearly correlated, the correla-

tion is not nearly as strong as one would

expect based on rational expectations. As

asserted in the previous section, markets

appear to make their own news. One of

the problems in answering this question

empirically is that it is difficult to mea-

sure information arrival—“news” con-

tains a judgement about what is impor-

tant or not important, and is difficult

to objectively reduce to a quantitative

measure.14

7. MOTIVATION FOR NONEQUILIBRIUMMODELS: A FEW EXAMPLESWe begin by describing some empir-ical regularities in financial data thatseem salient yet which equilibrium the-ory does not seem able to explain. Ofparticular importance is price volatil-ity. Not only do many people think thatprices change more than they shouldunder equilibrium, but also volatilitydisplays an interesting temporal corre-lation structure that seems to be bet-ter explained by nonequilibrium mod-els. This correlation is an example of apower law, a functional form that seemsto underly many of the regularities infinancial economics. In physics powerlaws can’t be generated at equilibriumand are a signature of nonequilibriumbehavior. Economic and physical equi-librium are quite different, however, as

14Engle and Rangel [45] demonstrate thatthere is a positive correlation betweenlow frequency price volatility and macro-economic fundamentals. Because theirresults involve both a longtitudinal anda cross-sectional regression involvingboth developed and undeveloped coun-tries the interpretation of the correla-tions that they observe is not obvious.No one disputes that prices respond toinformation—the question is,“What frac-tion of price movements can be explainedby information?.” Timescale is clearlycritical, i.e. one expects more correla-tion to information arrival at lowerfrequencies.

22 C O M P L E X I T Y © 2008 Wiley Periodicals, Inc.DOI 10.1002/cplx

we try to make clear. Statistical testing forpower laws is difficult and the existenceof power laws and their relevance foreconomics have generated a great dealof debate, which we briefly review.

Next we observe that one of the mostfrequently cited pieces of evidence forequilibrium is that arbitrage opportuni-ties tend to disappear. There is substan-tial evidence that real markets are effi-cient at some level of approximation. Butwe present anecdotal evidence that effi-ciencies disappear surprisingly slowly.We would like a theory of the transi-tion to equilibrium, or of tatonnementas it has sometimes been called. We endthis section with a brief discussion ofone of the most remarkable episodes infinancial markets of the last ten years,which illustrates both the value and thelimitations of the equilibrium model.

7.1. Some Economically ImportantPhenomena May Not Depend on EquilibriumThere are many empirically observedproperties of markets that have so farnot been explained under the equilib-rium framework. One famous exam-ple is called clustered volatility. Thisrefers to the fact that there are sub-stantial and strongly temporally corre-lated changes in the size of price move-ments at different points in time [46].If prices move a lot on a Tuesday, theywill probably move a lot the Wednesdayafter, and probably (but not as likely)move a lot on Thursday.15 The hardcore rational expectations booster would

15Mandelbrot and Clark suggest that itis possible to describe clustered volatitlityas if time gradually speeds up and slowsdown, according to some random processthat is independent of the direction ofprices [47–49]. It has also been suggestedthat the correct notion of trading timecan be measured by either transactionvolume or frequency of transactions [50];more careful analysis reveals that thisis not correct, and that fluctuations ofvolume are dominated by fluctuations inliquidity [51].

say that there is nothing to explain. Ifthe standard equilibrium theory is cor-rect, changes in price are caused by thereceipt of new information, so clusteredvolatility is simply a reflection of non-uniform information arrival. The rate ofinformation arrival has to do with mete-orology, sociology, political science, etc.It is exogenous to financial econom-ics and so it is someone else’s job toexplain it, if such a question is eveninteresting.

An alternative point of view is that,

due to a lack of a perfect rationality,

the market is not in perfect equilibrium

and thus prices do not simply passively

reflect new information. Under this view

the market acts as a nonlinear dynam-

ical system: agents process information

via decision-making rules that respond

to prices and other inputs, and prices

are formed as a result of agent deci-

sions. Since this information processing

is imperfect, the resulting feedback loop

amplifies noise. As a result a significant

component of volatility is generated by

the market itself. This point of view is

supported by the fact that there are now

many examples of nonequilibrium mod-

els that generate clustered volatility, and

in some cases there is a good match to

empirical data. For many of these mod-

els it is possible to include equilibrium as

a special case; when this is done the over-

all volatility level drops and clustered

volatility disappears (see Section 8.3).

Another relevant point is that volatility is

widely believed to exhibit long-memory,

which we discuss shortly in the section

on power laws.

Since the discussion of properties of

markets that are not currently explained

by equilibrium makes more sense in

the context of alternative models, we

will return to review this in more depth

when we discuss nonequilibrium het-

erogeneous agent models in Section 8.3.

As we discuss in the next section, the

questions of when equilibrium theory

is irrelevant or simply wrong can blur

together.

7.2. Power LawsAs we already mentioned, clusteredvolatility and many other phenomena ineconomics are widely believed to displaypower laws. Loosely speaking, a powerlaw is a relationship of the form y =kxα , where k and α are constants, thatholds for asymptotic values of a vari-able x, such as x → ∞ [52, 53]. Thefirst observation of a power law (in anyfield) was made by Pareto, who claimedthat this functional form fit the distri-bution of the incomes of the wealthi-est people in many different countries[54]. Power laws are reported to occurin many aspects of financial economics,such as the distribution of large pricereturns16 [47, 55–66], the size of trans-actions [67, 68], the autocorrelation ofvolatility [69–74] the prices where ordersare placed relative to the best prices[75–77], the autocorrelation of signs oftrading orders [78–81], the growth rate ofcompanies [82–84], and the scaling of theprice impact of trading with market cap-italization [85]. The empirical evidencefor power laws in economics and theirrelevance for economic theory remainscontroversial [86]. But there is a large lit-erature claiming that power laws existin economics and unless one is will-ing to cast aside this entire literature, itseems a serious problem that there is noexplanation based on equilibrium.

This problem might be resolved inone of several ways: Either as in physics,(1) power laws represent nonequilibriumphenomena from an economic point ofview and thus provide a motivation fornonequilibrium theory, or (2) power lawsare consistent with economic equilib-rium, but still need to be explained bysome other means, or (3) equilibrium isa key concept in understanding power

16Under time varying volatility the dis-tribution of returns can be interpreted asa mixture of normal distributions withvarying standard deviations. This gener-ically fattens the tails, and for the rightdistribution of standard deviations canproduce a power law.

© 2008 Wiley Periodicals, Inc.DOI 10.1002/cplx

C O M P L E X I T Y 23

laws but we just don’t know how todo this yet.17 Or perhaps the exis-tence of power laws is just an illusion.But it seems that power laws fit thedata to at least a reasonable degree ofapproximation. Furthermore, there aremany nonequilibrium models that nat-urally generate power laws, and for suchmodels it is easy to test that the phenom-ena they generate are indeed real powerlaws.

It may seem strange to single outa particular functional form for specialattention. There are several reasons forviewing power laws as important. Oneof them comes from extreme value the-ory [89], which says that in a certainsense there are only four possible con-vergent forms for the tail of a probabilitydistribution,18 and power laws are oneof them. The main motivation for look-ing at tail distributions is that they pro-vide a clue to underlying mechanisms:different mechanisms or behaviors tendto generate different classes of taildistributions.

Statistically classifying a tail distribu-

tion is inherently difficult because one

does not know a priori where the tail

begins. In extreme value theory a power

law is more precisely stated as a rela-

tion of the form y = K (x)xα , where

K (x) is a slowly varying function. A

slowly varying function K (x) satisfies

limx→∞ K (tx)/K (x) = 1, for every pos-

itive constant t . There is a great variety of

17See articles by Calvet and Fisher forexamples where power laws seem to beconsistent with equilibrium [87, 88].18The four possible tail behaviors ofprobability distributions correspond todistributions with finite support; thintailed distributions such as Gaussians,exponentials or log-normals; distribu-tions where there is a critical cutoffabove which moments don’t exist (namelypower laws); and distributions that lackany regular tail behavior at all. Almost allcommonly used distributions are in one ofthe first three categories.

possible slowly varying functions; with

a finite amount of data it is only possi-

ble to probe to a finite value of x and

the slowly varying function may con-

verge slowly. In practice one tends to

look for a threshhold x beyond which

the points (log x, log y) almost lie on a

straight line. (This can be made pre-

cise using maximum likelihood estima-

tion, including the estimation of the

threshold x [90]).

In the last 20 years or so the phe-

nomenon of power laws has received a

great deal of attention in physics. Power

laws are special because they are self-

similar, i.e. under a scale change of the

dependent variable x′ = cx, treating K

as a constant, the function f (x′) = cαf (x)

remains a power law with the same expo-

nent α but a modified scale K ′ = cαK .

One of the places where power laws are

widespread is at phase transitions, such

as the point where a liquid changes into a

solid. Self-similarity proved to be a pow-

erful clue to understanding the physics

of phase transitions and led to the devel-

opment of the renormalization group,

which made it possible to compute the

properties of phase transitions precisely.

The main assumption of the renormal-

ization group is that the physics is invari-

ant across different scales, i.e. the rea-

son the observed phenomena are power

laws is because their underlying physics

is self-similar. This is an important clue

about mechanism.In physics power laws are associ-

ated with nonequilibrium behavior andare viewed as a possible signature ofnonequilibrium dynamics [52, 53, 91]. Itwas shown more than 100 years ago byBoltzmann and Gibbs that in physicalequilibrium, energies obey an exponen-tial distribution; thus a power law indi-cates nonequilibrium behavior. As dis-cussed in Section 7.4, equilibrium inphysics is quite different from equilib-rium in economics, but it seems tellingthat the current set of financial models inwhich power laws appear are (economic)nonequilibrium models, as discussed inSection 8.3.

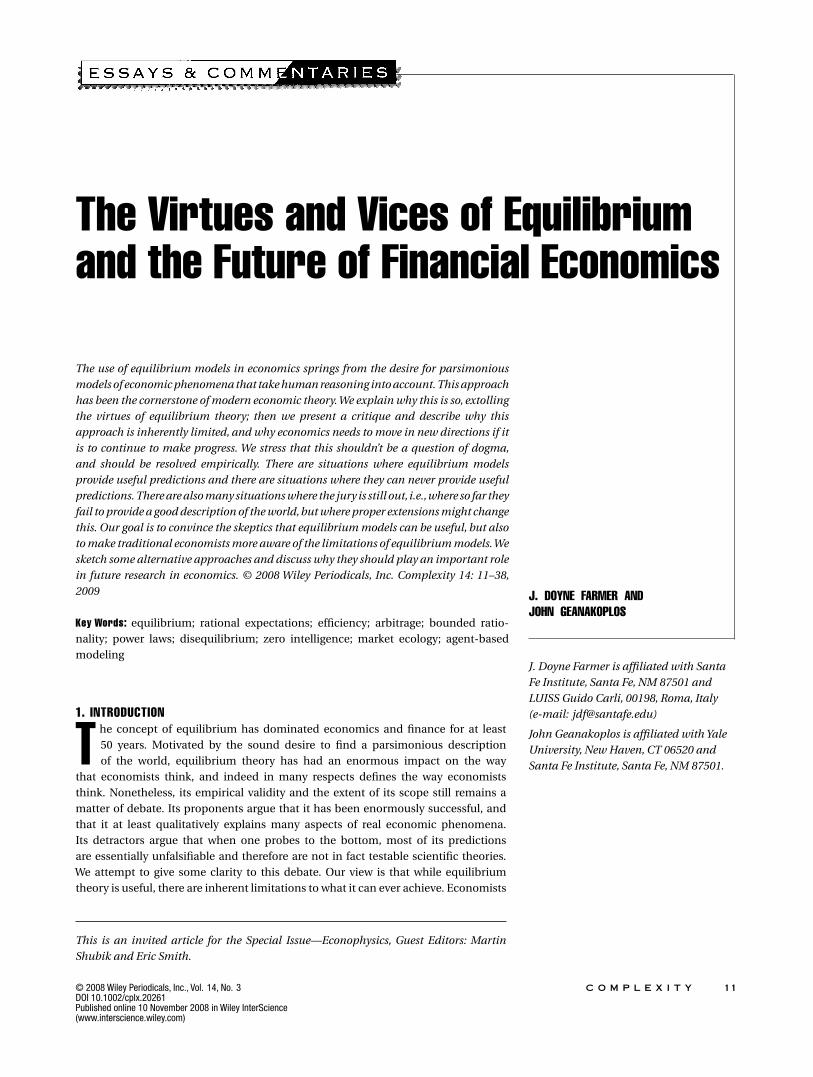

7.3. The Progression Toward MarketEfficiencyThe theory of market (arbitrage) effi-ciency is justified by the assertion thatif there were profit-making opportuni-ties in markets, they would be quicklyfound and exploited, and the resultingtrading activity would change prices inways that would remove them. But isthis really true? Anecdotal empirical evi-dence suggests otherwise, as illustratedin Figure 1, where we plot the per-formance of two proprietary predictivetrading signals developed by PredictionCompany (where one of the authors wasemployed). The performance of the sig-nals is measured in terms of their correla-tion to future price movements on a twoweek time scale over a twenty three yearperiod.19 In the case of signal 1 we seea gradual degradation in performanceover the twenty three year period. Thecorrelation to future prices is variable butthe overall trend is clear. At the begin-ning of the period in 1975 it averagesabout 14% and by 1998 it has declinedto roughly 4%. Nonetheless, even in 1998the signal remains strong enough to beprofitably tradeable.