Embed Size (px)

Citation preview

FEASIBILITY STUDY

Proposed Hotel Condominiums and Cottages

7376 MAIN STREET PORT SANILAC, MICHIGAN

SUBMITTED TO:PR OPOSED

Mr. Tim Cheek Port Sanilac Downtown Development Authority 56 North Ridge Street, Post Office Box 628 Port Sanilac, Michigan, 48469 +1 (586) 531-2304

PREPARED BY:

HVS Consulting and Valuation Services Division of CCG Holdings, LLC 111 North Wabash Avenue, Suite 1717 Chicago, Illinois, 60602 +1 (312) 526-3885

August-2014

September 2, 2014

Mr. Tim Cheek Port Sanilac Downtown Development Authority 56 North Ridge Street, Post Office Box 628 Port Sanilac, Michigan, 48469

Re: Proposed Hotel Condominiums and Cottages

Port Sanilac, Michigan

HVS Reference: 2014410051

Dear Mr. Cheek:

At your request, we are pleased to submit our feasibility study pertaining to the above-captioned property. We have inspected the real estate and analyzed the lodging market conditions in the Port Sanilac, Michigan area. We have studied the proposed project, and the results of our fieldwork and analysis are presented in this report. We have also reviewed the proposed improvements for this site. Our report was prepared in accordance with the Uniform Standards of Professional Appraisal Practice (USPAP), as provided by the Appraisal Foundation.

We certify that we have no undisclosed interest in the property, and our employment and compensation are not contingent upon our findings. This study is subject to the comments made throughout this report and to all assumptions and limiting conditions set forth herein.

Sincerely,

CCG Holdings, LLC

Hans Detlefsen, MPP, MAI, Managing Director

[email protected], +1 (312) 526-3885

State Appraiser License (MI) 1201074194

Appraisers are required to be licensed and are regulated by the

Michigan Department of Labor and Economic Growth, P.O. Box

30018, Lansing, MI 48909.

HVS CHICAGO

111 North Wabash Avenue, Suite 1717

Chicago, Illinois, 60602

+1 (312) 526-3885

+1 (213) 285-4958 FAX

www.hvs.com

Atlanta

Boston

Boulder

Chicago

Dallas

Denver

Houston

Las Vegas

Los Angeles

Mexico City

Miami

Minneapolis

Nassau

New York

Newport

Philadelphia

San Francisco

St. Louis

Toronto

Vancouver

Washington

Athens

Beijing

Buenos Aires

Dubai

Hong Kong

Lima

London

Milan

Moscow

Mumbai

New Delhi

Sao Paulo

Shanghai

Singapore

Superior results through unrivaled hospitality intelligence. Everywhere.

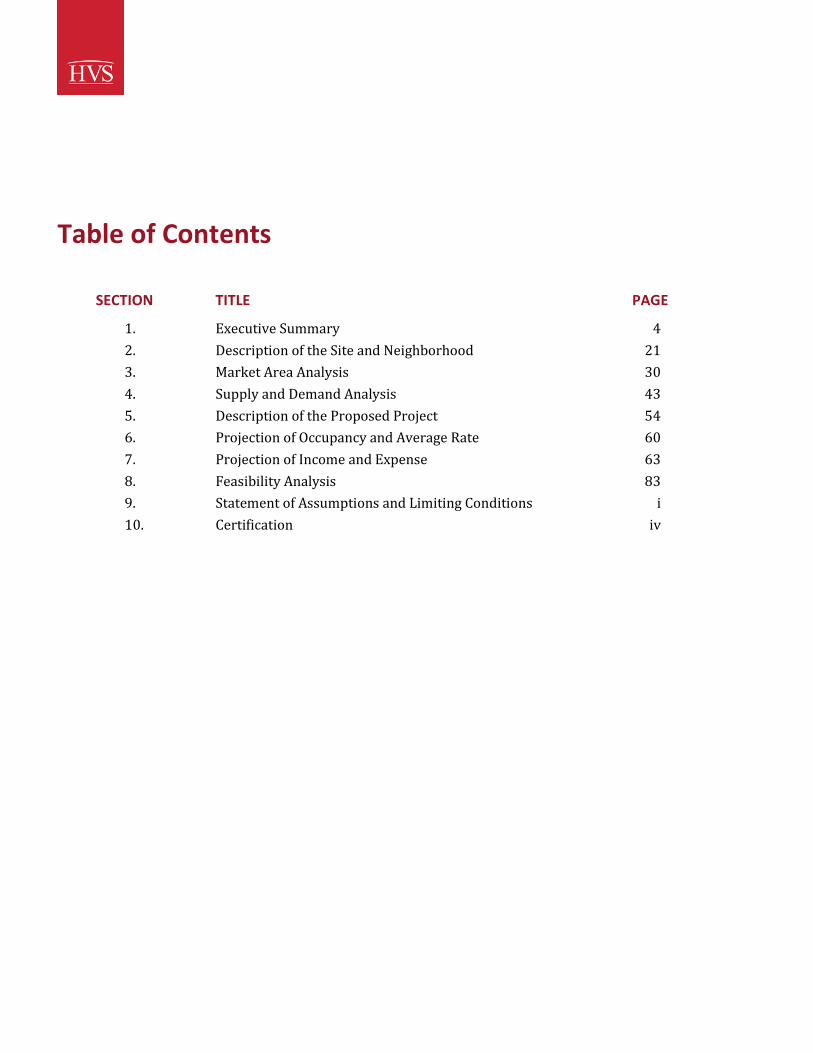

Table of Contents

SECTION TITLE PAGE

1. Executive Summary 4

2. Description of the Site and Neighborhood 21

3. Market Area Analysis 30

4. Supply and Demand Analysis 43

5. Description of the Proposed Project 54

6. Projection of Occupancy and Average Rate 60

7. Projection of Income and Expense 63

8. Feasibility Analysis 83

9. Statement of Assumptions and Limiting Conditions i

10. Certification iv

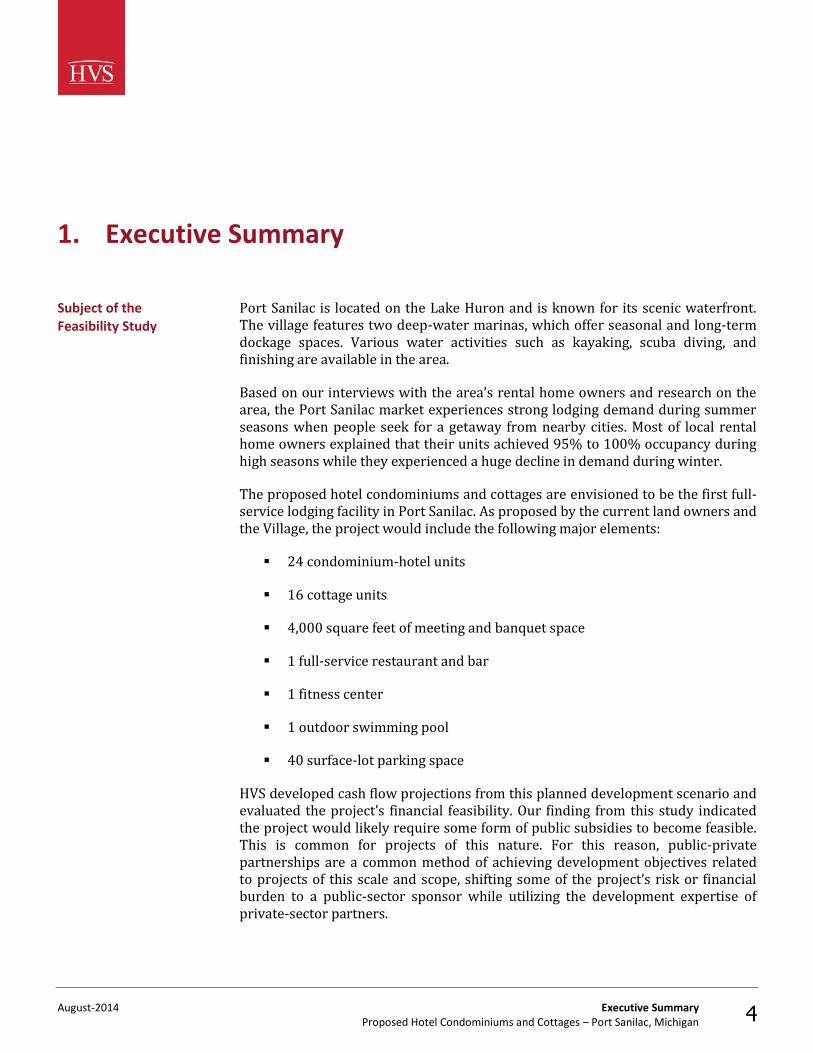

August-2014 Executive Summary Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 4

1. Executive Summary

Port Sanilac is located on the Lake Huron and is known for its scenic waterfront. The village features two deep-water marinas, which offer seasonal and long-term dockage spaces. Various water activities such as kayaking, scuba diving, and finishing are available in the area.

Based on our interviews with the area’s rental home owners and research on the area, the Port Sanilac market experiences strong lodging demand during summer seasons when people seek for a getaway from nearby cities. Most of local rental home owners explained that their units achieved 95% to 100% occupancy during high seasons while they experienced a huge decline in demand during winter.

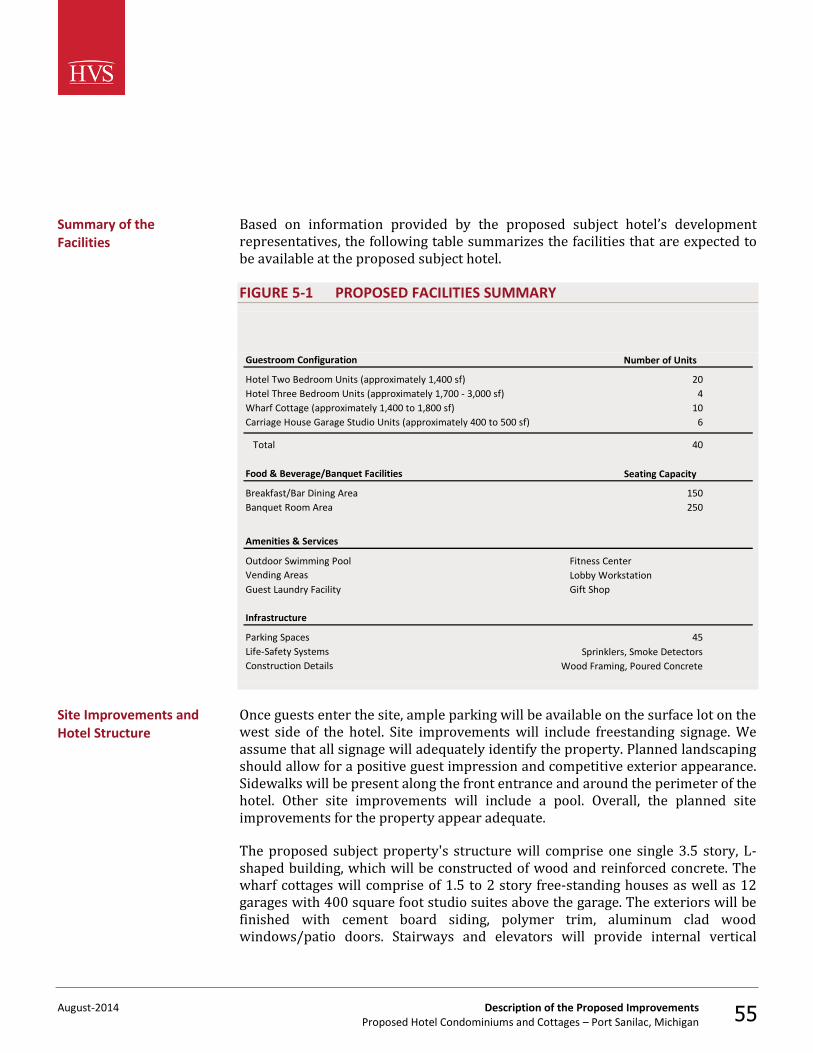

The proposed hotel condominiums and cottages are envisioned to be the first full-service lodging facility in Port Sanilac. As proposed by the current land owners and the Village, the project would include the following major elements:

24 condominium-hotel units

16 cottage units

4,000 square feet of meeting and banquet space

1 full-service restaurant and bar

1 fitness center

1 outdoor swimming pool

40 surface-lot parking space

HVS developed cash flow projections from this planned development scenario and evaluated the project’s financial feasibility. Our finding from this study indicated the project would likely require some form of public subsidies to become feasible. This is common for projects of this nature. For this reason, public-private partnerships are a common method of achieving development objectives related to projects of this scale and scope, shifting some of the project’s risk or financial burden to a public-sector sponsor while utilizing the development expertise of private-sector partners.

Subject of the Feasibility Study

August-2014 Executive Summary Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 5

To reduce or eliminate the project’s feasibility gap, a range of potential solutions could be considered. For example, the client could consider one or more of the following options:

Reduce the project size and scope to focus more on the revenue-generating spaces and reduce the amount of amenities and common areas currently envisioned.

Refine the project budget and obtain competitive bids to see if development costs can be reduced below current estimates.

Finance the entire project through tax-exempt bond financing, which reduces the overall cost of capital for the project, thereby adding to the project’s feasibility or reducing its feasibility gap.

Require private-sector partner to obtain land and contribute the value of the land as equity to the project, thereby subordinating the developer’s investment to the bond investors’ repayments.

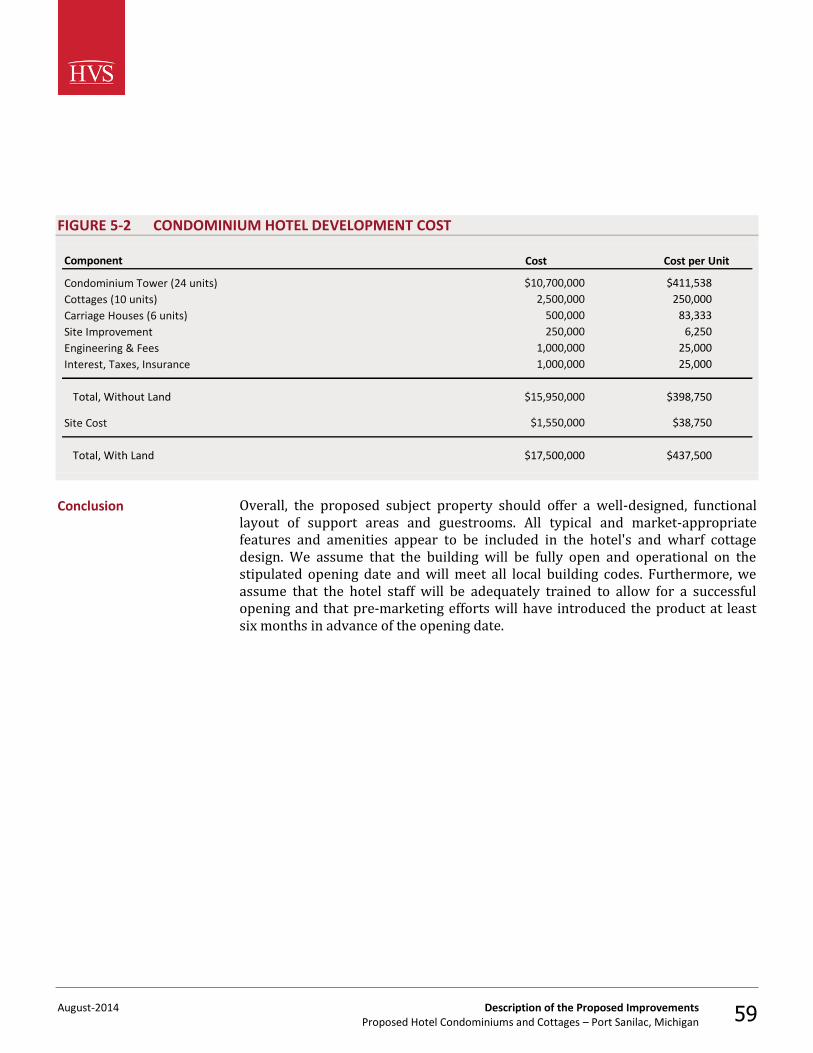

Based on the preliminary development cost provided by Shoreline Architecture Design, Inc., the cost to develop the condominium-hotel tower is $10,700,000, or $445,833 per unit, which is resulting in a feasibility gap for the project based on its expected cash flow as shown later in this report. Revising the proposed concept could substantially narrow the feasibility gap. This strategy would aim to reduce project costs by a greater amount than the reduction in project value resulting from such changes. Such a reduction of costs may be attainable through reducing or eliminating some envisioned amenities such as the spa, salon, banquet facilities, and retail areas, as well as potentially scaling back some of the features and amenities of the restaurant/bar and the condominium and wharf cottage units.

Creating a “63-20” non-profit corporation, sponsored by the City, to issue bonds to fund the project’s construction costs could also significantly close or eliminate a feasibility gap, if one remains. Bond financing shifts investment risk away from the private-sector developer and onto the public-sector sponsor, thereby taking advantage of the better credit rating available to municipal governments. While this strategy can substantially augment the feasibility of the project, we recommend that the public-sector sponsor also consider implementing various risk-mitigation strategies, such as requiring a project reserve and subordinating some component of investment derived from the private-sector partner.

For example, the municipal sponsor may require the private-sector partner to contribute project equity in the form of cash or land or both, which would be subordinated to the bond investments. The developer’s fee could potentially be

August-2014 Executive Summary Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 6

subordinated as well and structured to pay out only if the project’s financial performance reaches a certain threshold.

A combination of these options, or others like them, could substantially reduce or eliminate the feasibility gap of the project and potentially make the project feasible. We recommend evaluating which forms of public-sector participation would be most politically feasible. By measuring the market value of any potential incentives that could be available for the project, one can estimate the degree to which these factors contribute to the project’s market feasibility.

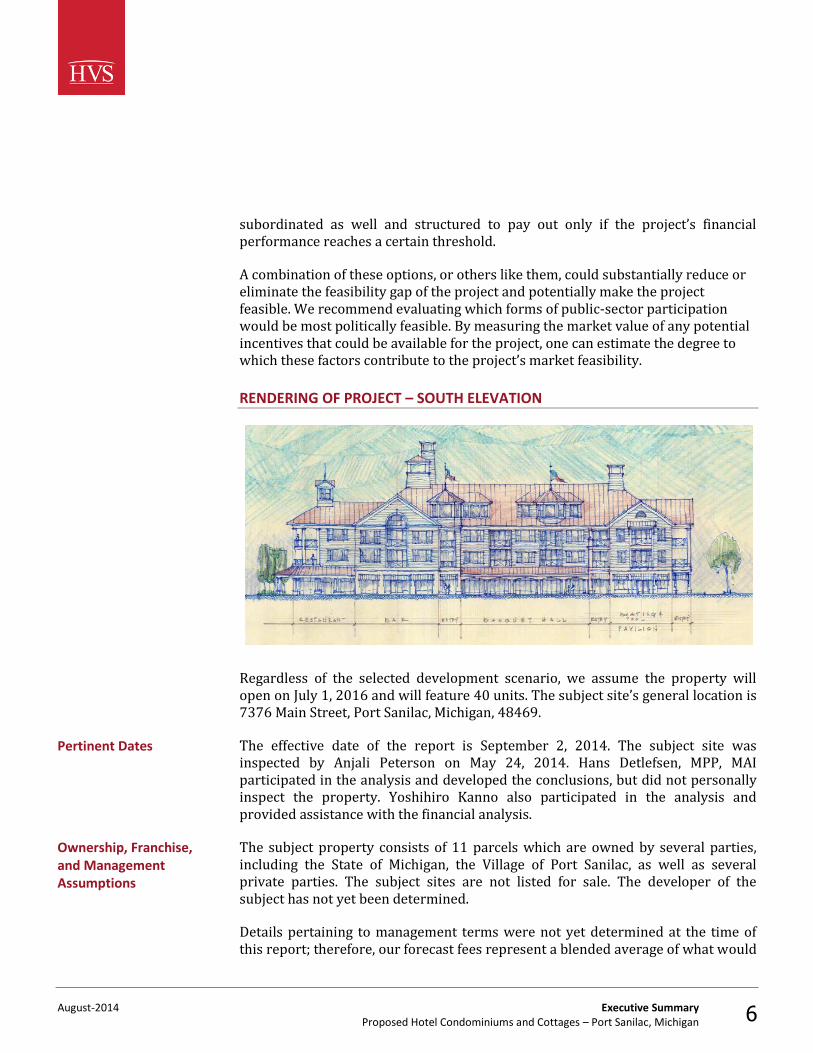

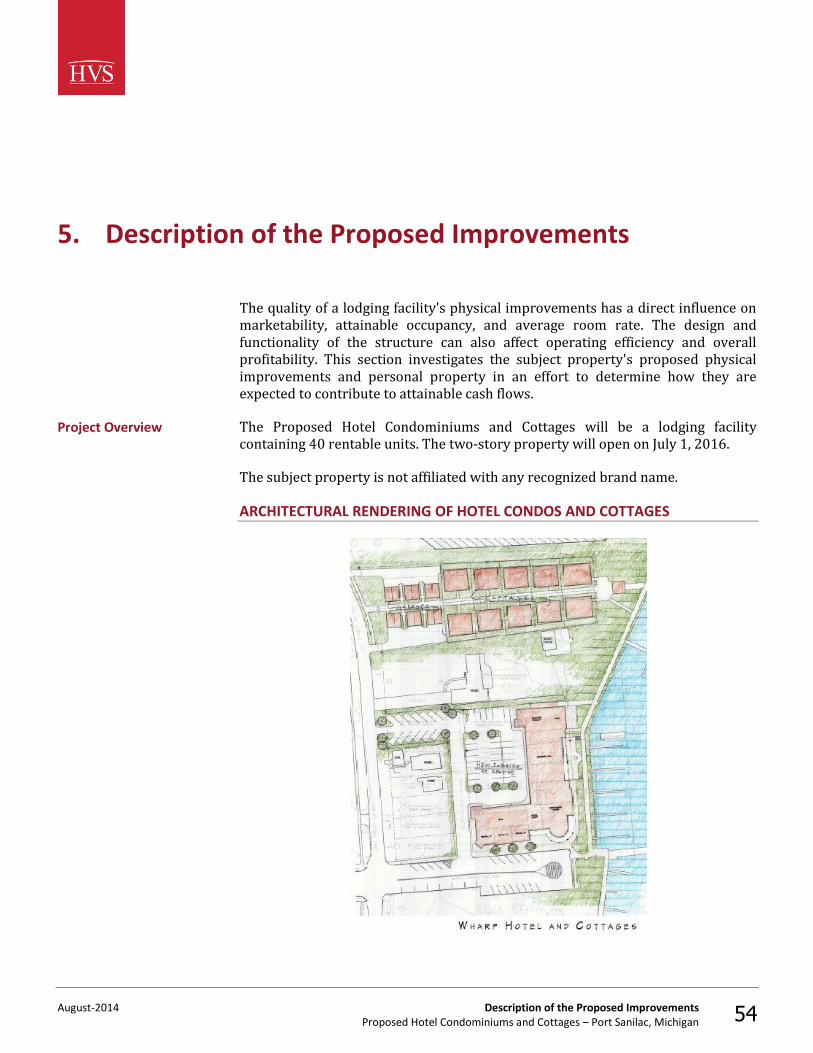

RENDERING OF PROJECT – SOUTH ELEVATION

Regardless of the selected development scenario, we assume the property will open on July 1, 2016 and will feature 40 units. The subject site’s general location is 7376 Main Street, Port Sanilac, Michigan, 48469.

The effective date of the report is September 2, 2014. The subject site was inspected by Anjali Peterson on May 24, 2014. Hans Detlefsen, MPP, MAI participated in the analysis and developed the conclusions, but did not personally inspect the property. Yoshihiro Kanno also participated in the analysis and provided assistance with the financial analysis.

The subject property consists of 11 parcels which are owned by several parties, including the State of Michigan, the Village of Port Sanilac, as well as several private parties. The subject sites are not listed for sale. The developer of the subject has not yet been determined.

Details pertaining to management terms were not yet determined at the time of this report; therefore, our forecast fees represent a blended average of what would

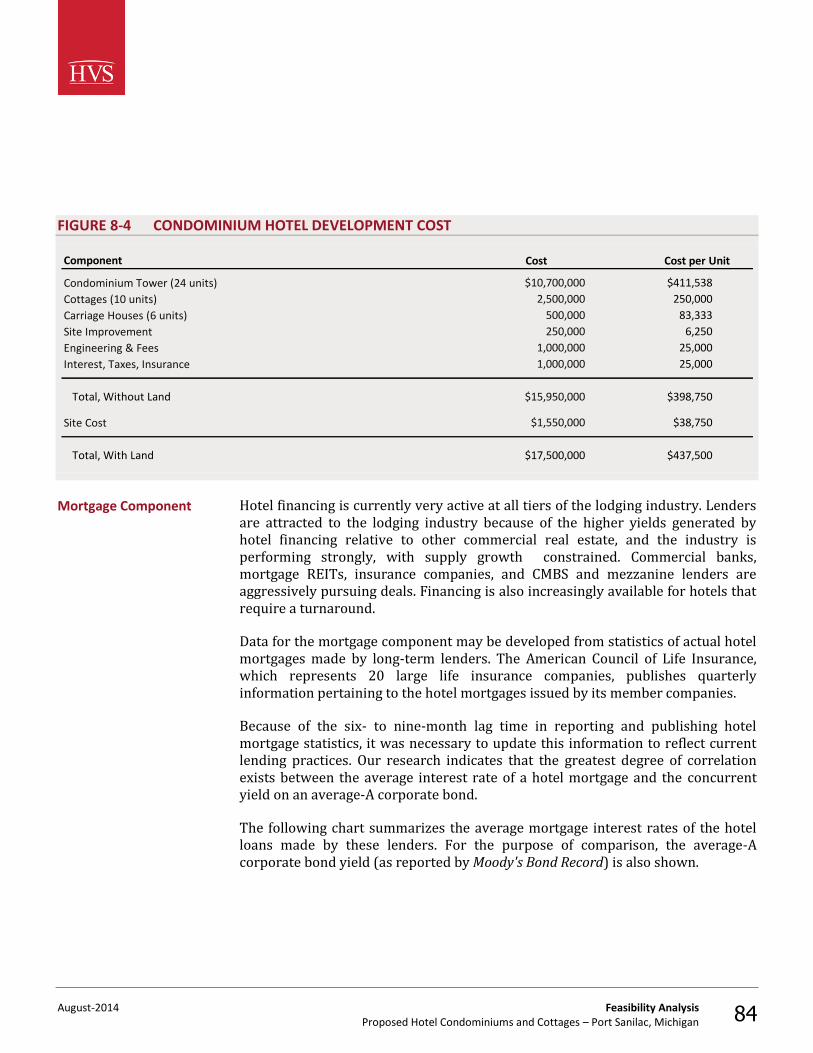

Pertinent Dates

Ownership, Franchise, and Management Assumptions

August-2014 Executive Summary Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 7

be expected on a base-fee and incentive-fee basis. We have assumed a market-appropriate total management fee of 3.0% of total revenues in our study.

The proposed condominium hotel and neighboring cottages are not expected to be franchised with a national brand and are planned to remain independently operated throughout the forecast period; therefore, the hotel and cottages will not be subject to franchise fees.

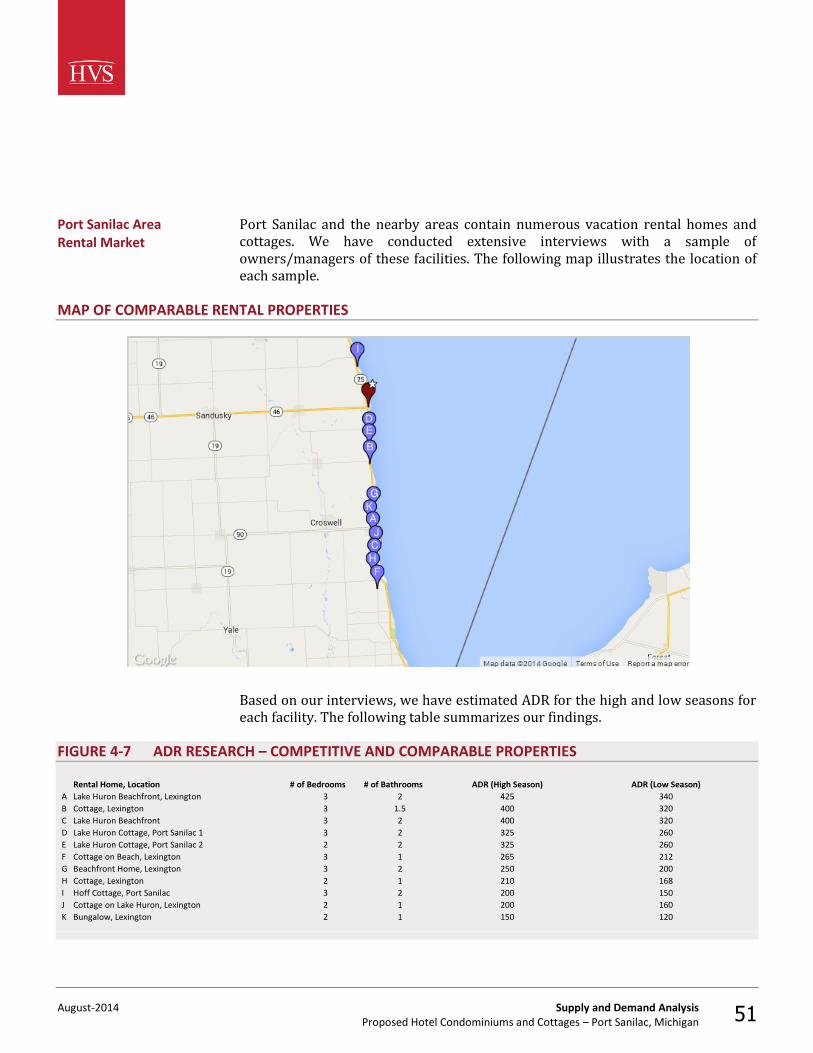

Lake Huron, the primary boat docking facilities in Port Sanilac, and the recreational events in Port Sanilac offer the primary sources of demand. Our research and interviews of owners with rental properties indicated strong occupancy trends through the summer months, and that occupancy during the winter months was primarily during the weekends. These market participants indicated that the renters were primarily from the Detroit metropolitan area and surrounding smaller markets throughout Michigan.

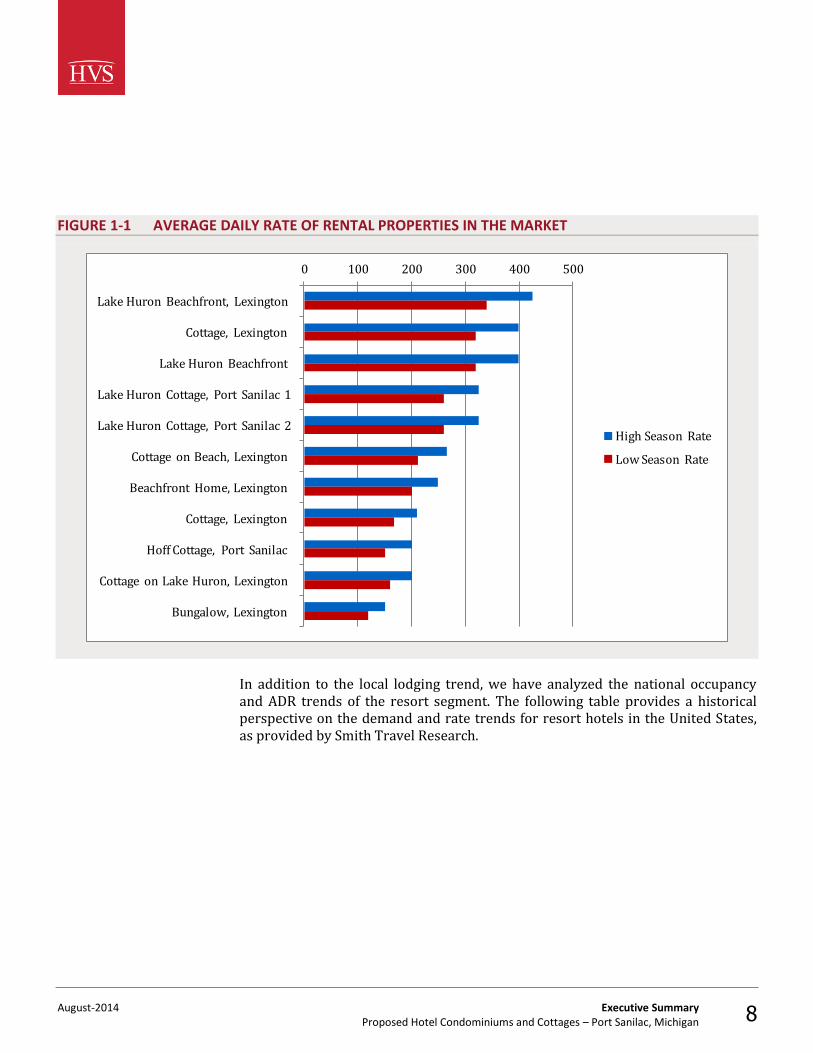

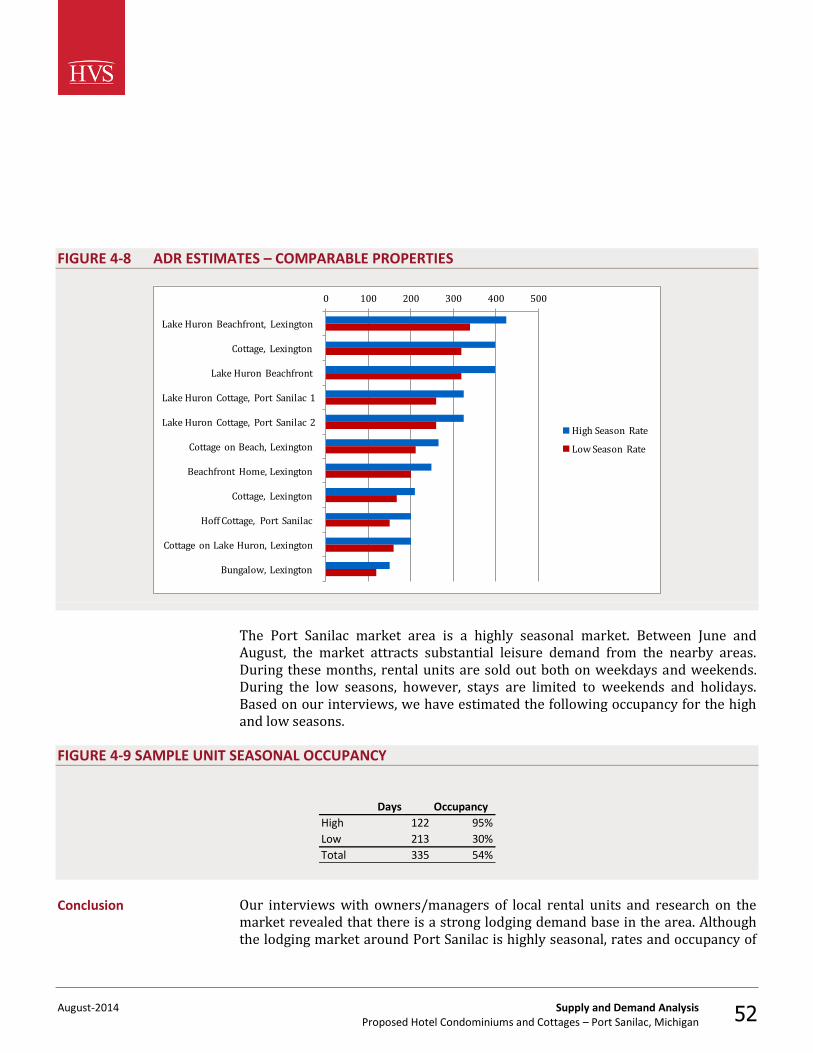

The following figure illustrates the average daily rate (ADR) of rental properties in the market. During low season, ADR in the market is typically 20% lower than during the high season due to this market’s seasonality.

Summary of Lodging Market Trends

August-2014 Executive Summary Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 8

FIGURE 1-1 AVERAGE DAILY RATE OF RENTAL PROPERTIES IN THE MARKET

0 100 200 300 400 500

Lake Huron Beachfront, Lexington

Cottage, Lexington

Lake Huron Beachfront

Lake Huron Cottage, Port Sanilac 1

Lake Huron Cottage, Port Sanilac 2

Cottage on Beach, Lexington

Beachfront Home, Lexington

Cottage, Lexington

Hoff Cottage, Port Sanilac

Cottage on Lake Huron, Lexington

Bungalow, Lexington

High Season Rate

Low Season Rate

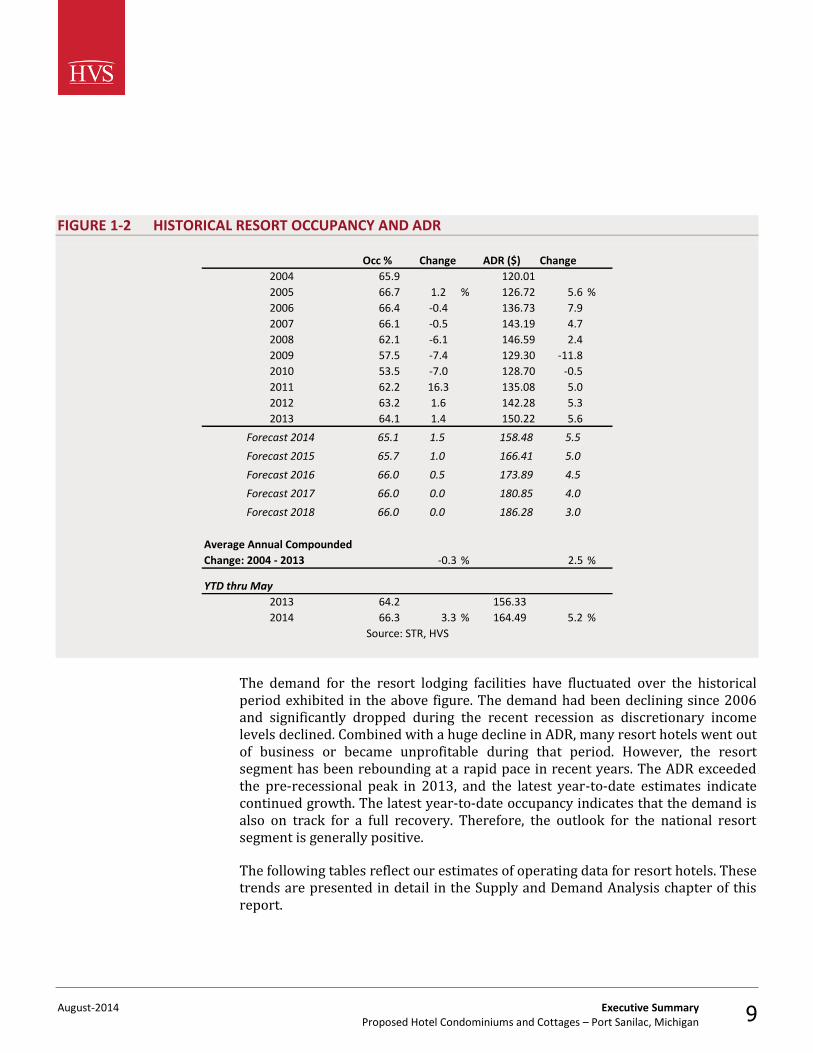

In addition to the local lodging trend, we have analyzed the national occupancy and ADR trends of the resort segment. The following table provides a historical perspective on the demand and rate trends for resort hotels in the United States, as provided by Smith Travel Research.

August-2014 Executive Summary Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 9

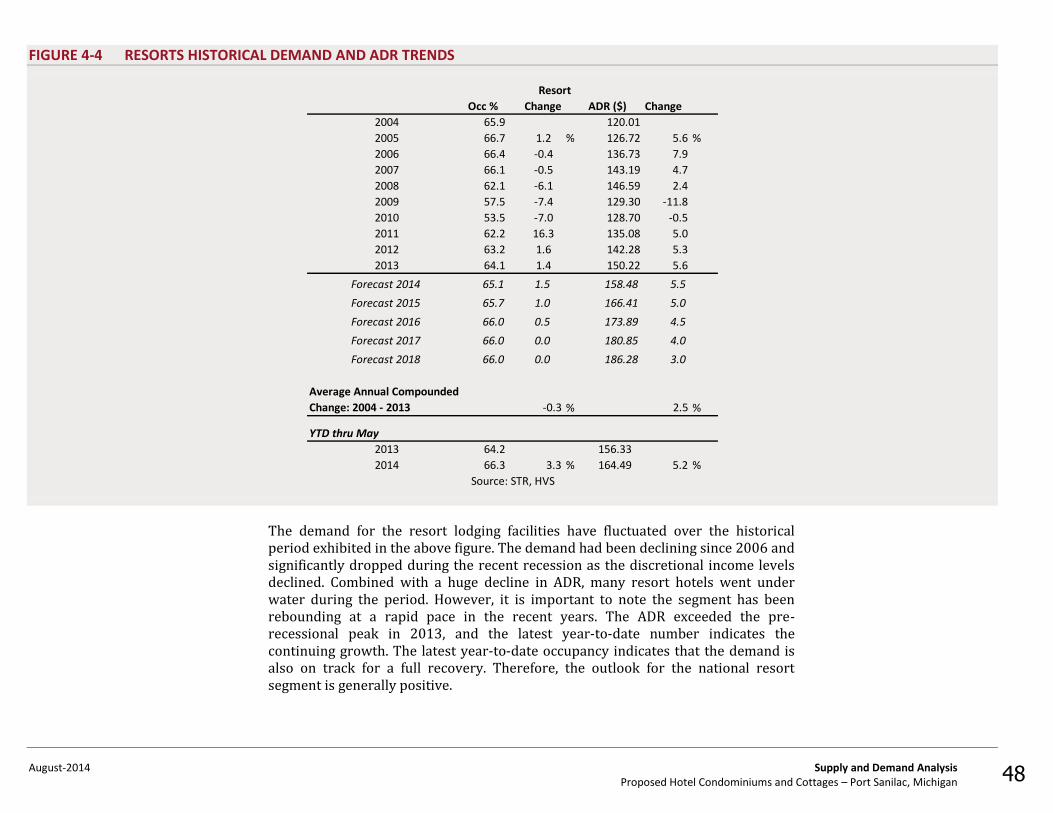

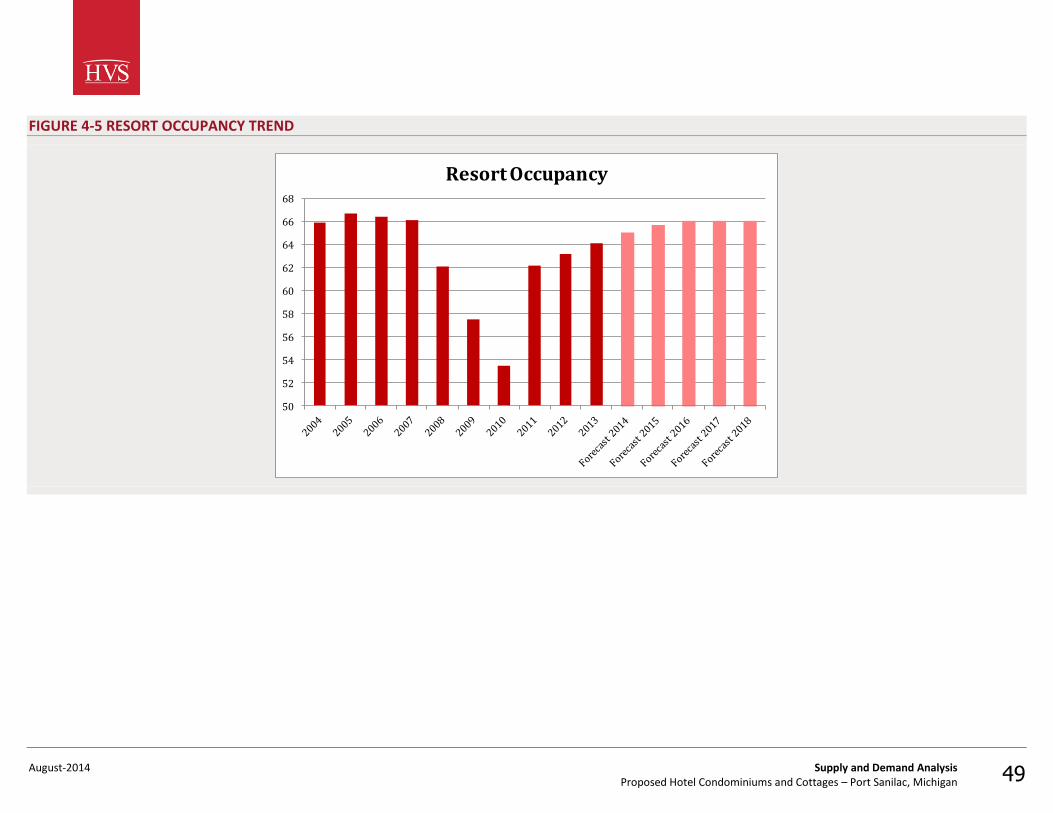

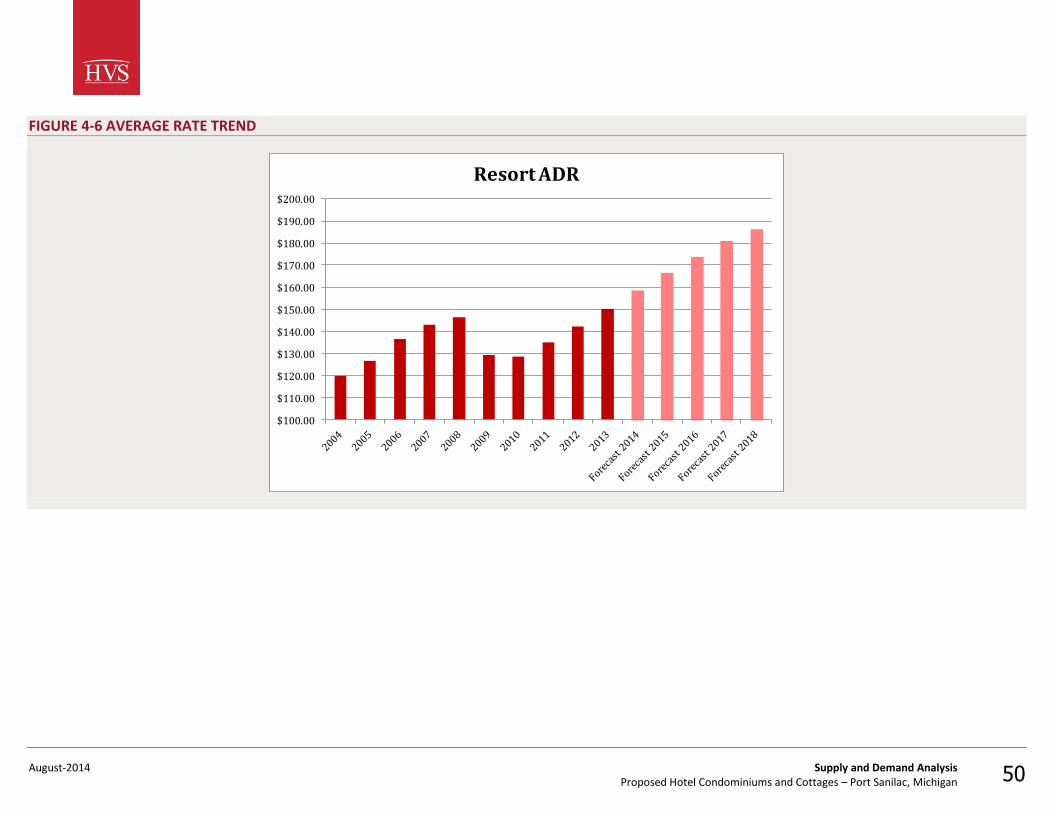

FIGURE 1-2 HISTORICAL RESORT OCCUPANCY AND ADR

Occ % Change ADR ($) Change

2004 65.9 120.01

2005 66.7 1.2 % 126.72 5.6 %

2006 66.4 -0.4 136.73 7.9

2007 66.1 -0.5 143.19 4.7

2008 62.1 -6.1 146.59 2.4

2009 57.5 -7.4 129.30 -11.8

2010 53.5 -7.0 128.70 -0.5

2011 62.2 16.3 135.08 5.0

2012 63.2 1.6 142.28 5.3

2013 64.1 1.4 150.22 5.6

Forecast 2014 65.1 1.5 158.48 5.5

Forecast 2015 65.7 1.0 166.41 5.0

Forecast 2016 66.0 0.5 173.89 4.5

Forecast 2017 66.0 0.0 180.85 4.0

Forecast 2018 66.0 0.0 186.28 3.0

Average Annual Compounded

Change: 2004 - 2013 -0.3 % 2.5 %

YTD thru May

2013 64.2 156.33

2014 66.3 3.3 % 164.49 5.2 %

Source: STR, HVS

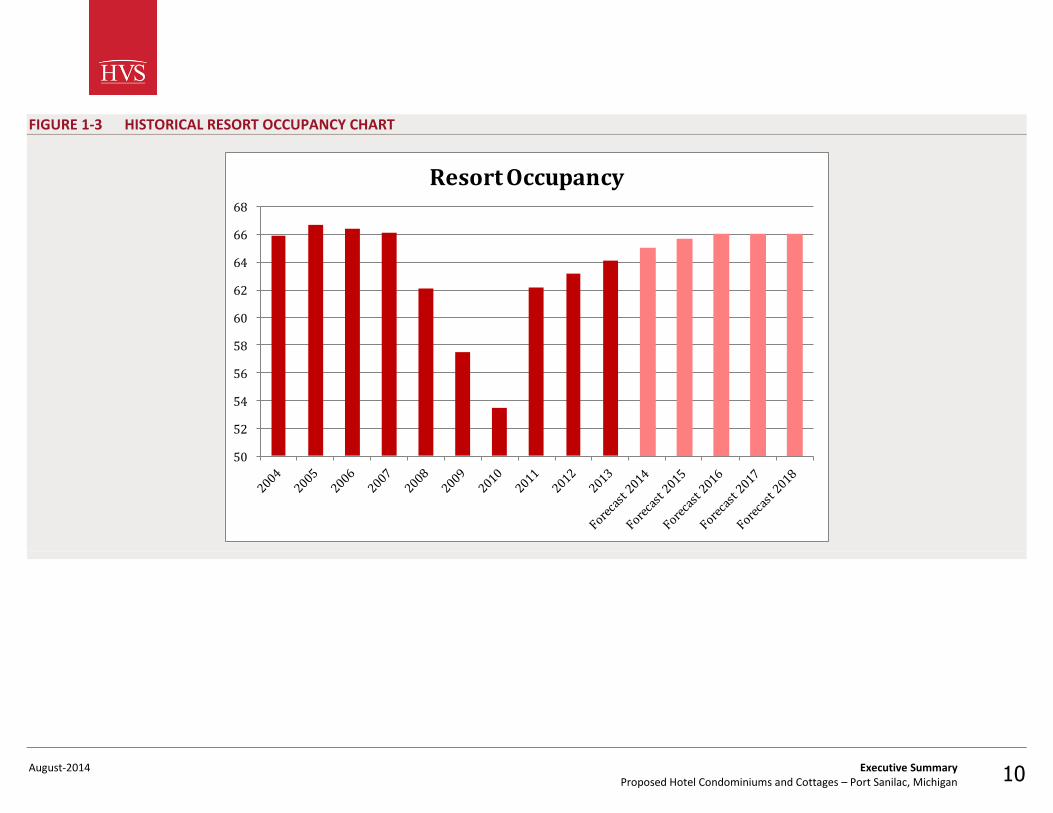

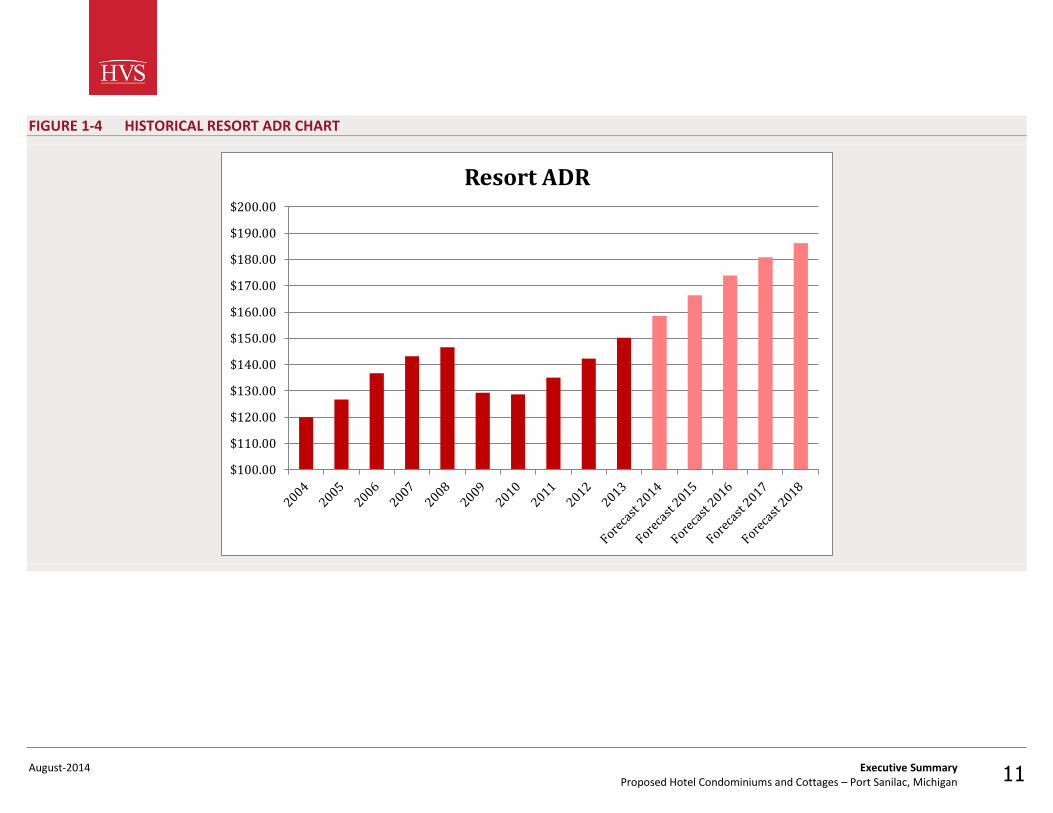

The demand for the resort lodging facilities have fluctuated over the historical period exhibited in the above figure. The demand had been declining since 2006 and significantly dropped during the recent recession as discretionary income levels declined. Combined with a huge decline in ADR, many resort hotels went out of business or became unprofitable during that period. However, the resort segment has been rebounding at a rapid pace in recent years. The ADR exceeded the pre-recessional peak in 2013, and the latest year-to-date estimates indicate continued growth. The latest year-to-date occupancy indicates that the demand is also on track for a full recovery. Therefore, the outlook for the national resort segment is generally positive.

The following tables reflect our estimates of operating data for resort hotels. These trends are presented in detail in the Supply and Demand Analysis chapter of this report.

August-2014 Executive Summary Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 10

FIGURE 1-3 HISTORICAL RESORT OCCUPANCY CHART

50

52

54

56

58

60

62

64

66

68

Resort Occupancy

August-2014 Executive Summary Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 11

FIGURE 1-4 HISTORICAL RESORT ADR CHART

$100.00

$110.00

$120.00

$130.00

$140.00

$150.00

$160.00

$170.00

$180.00

$190.00

$200.00

Resort ADR

August-2014 Executive Summary Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 12

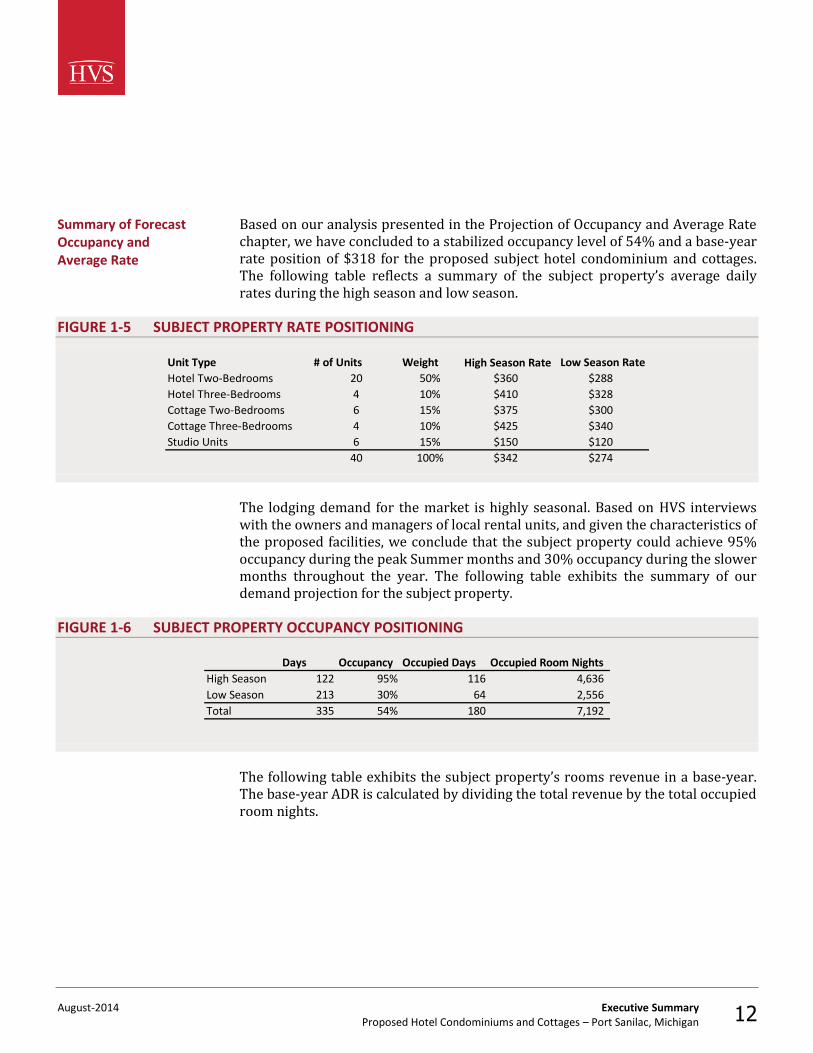

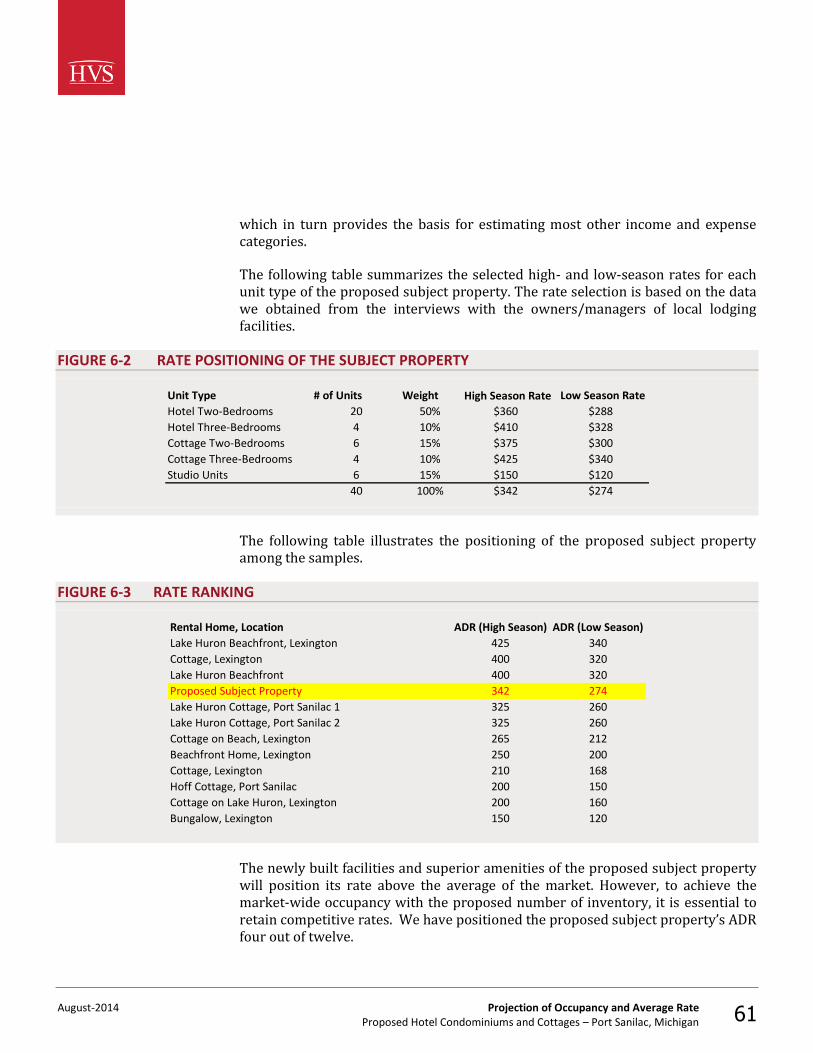

Based on our analysis presented in the Projection of Occupancy and Average Rate chapter, we have concluded to a stabilized occupancy level of 54% and a base-year rate position of $318 for the proposed subject hotel condominium and cottages. The following table reflects a summary of the subject property’s average daily rates during the high season and low season.

FIGURE 1-5 SUBJECT PROPERTY RATE POSITIONING

Unit Type # of Units Weight High Season Rate Low Season Rate

Hotel Two-Bedrooms 20 50% $360 $288

Hotel Three-Bedrooms 4 10% $410 $328

Cottage Two-Bedrooms 6 15% $375 $300

Cottage Three-Bedrooms 4 10% $425 $340

Studio Units 6 15% $150 $120

40 100% $342 $274

The lodging demand for the market is highly seasonal. Based on HVS interviews with the owners and managers of local rental units, and given the characteristics of the proposed facilities, we conclude that the subject property could achieve 95% occupancy during the peak Summer months and 30% occupancy during the slower months throughout the year. The following table exhibits the summary of our demand projection for the subject property.

FIGURE 1-6 SUBJECT PROPERTY OCCUPANCY POSITIONING

Days Occupancy Occupied Days Occupied Room Nights

High Season 122 95% 116 4,636

Low Season 213 30% 64 2,556

Total 335 54% 180 7,192

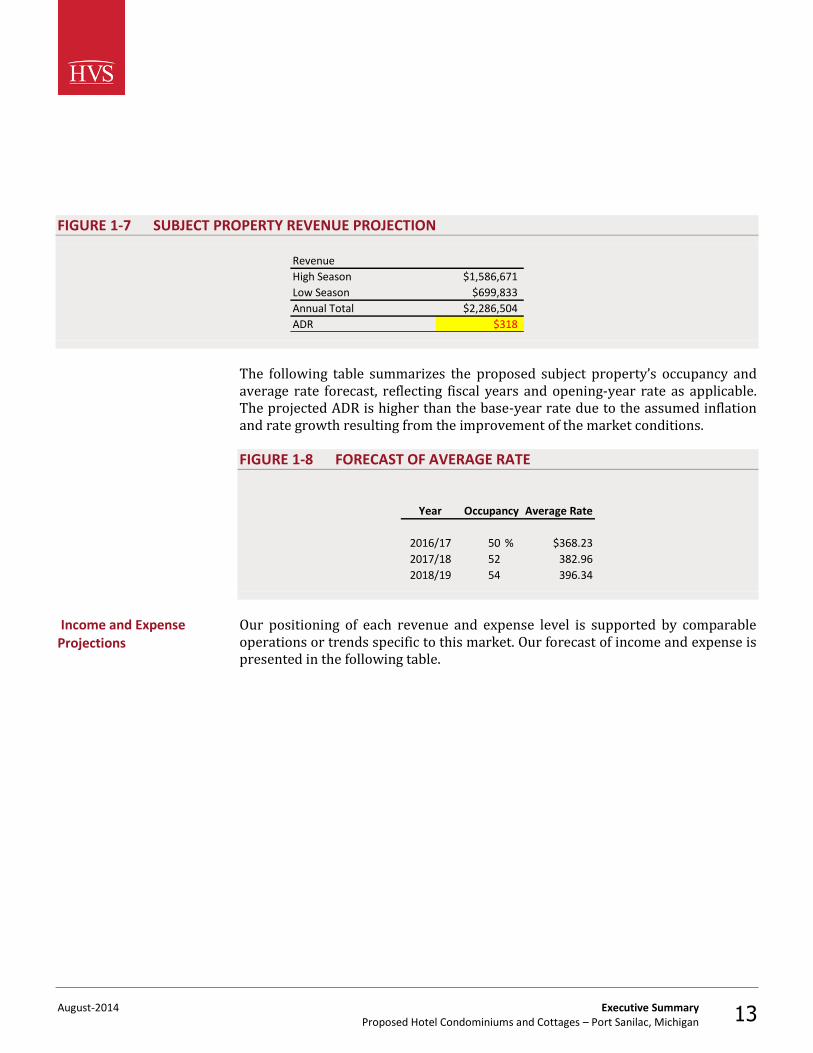

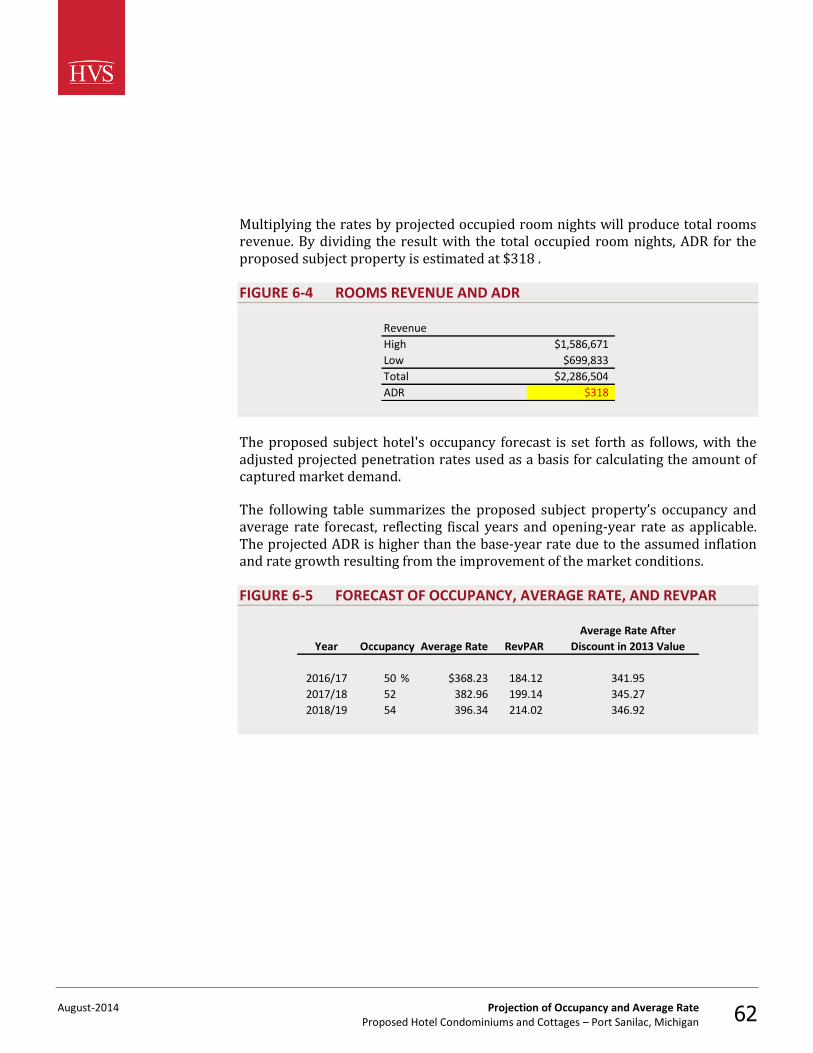

The following table exhibits the subject property’s rooms revenue in a base-year. The base-year ADR is calculated by dividing the total revenue by the total occupied room nights.

Summary of Forecast Occupancy and Average Rate

August-2014 Executive Summary Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 13

FIGURE 1-7 SUBJECT PROPERTY REVENUE PROJECTION

Revenue

High Season $1,586,671

Low Season $699,833

Annual Total $2,286,504

ADR $318

The following table summarizes the proposed subject property’s occupancy and average rate forecast, reflecting fiscal years and opening-year rate as applicable. The projected ADR is higher than the base-year rate due to the assumed inflation and rate growth resulting from the improvement of the market conditions.

FIGURE 1-8 FORECAST OF AVERAGE RATE

Year

2016/17 50 % $368.23

2017/18 52 382.96

2018/19 54 396.34

Occupancy Average Rate

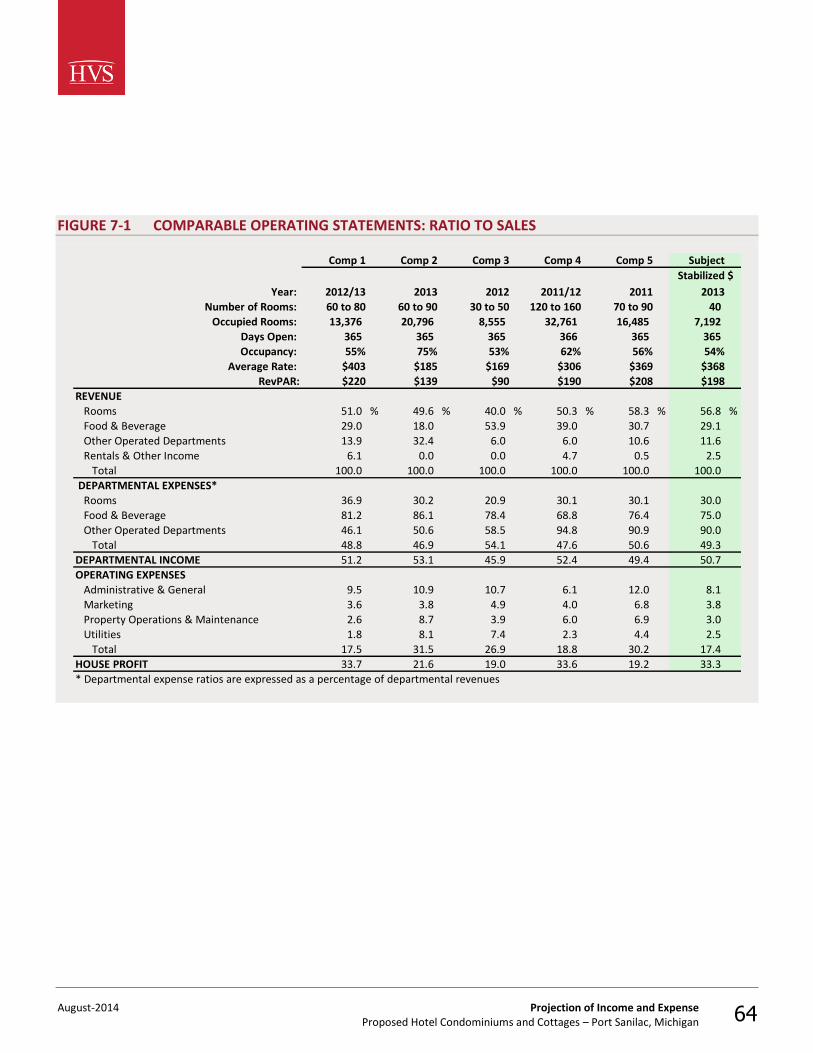

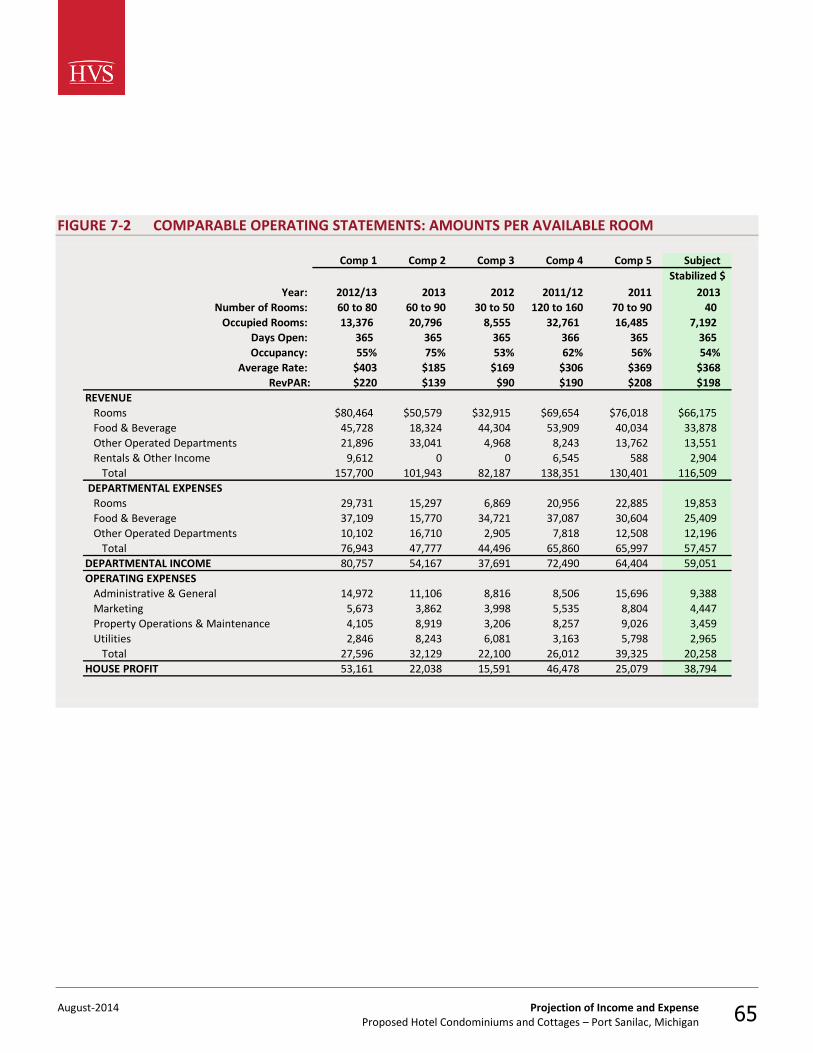

Our positioning of each revenue and expense level is supported by comparable operations or trends specific to this market. Our forecast of income and expense is presented in the following table.

Income and Expense Projections

August-2014 Executive Summary Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 14

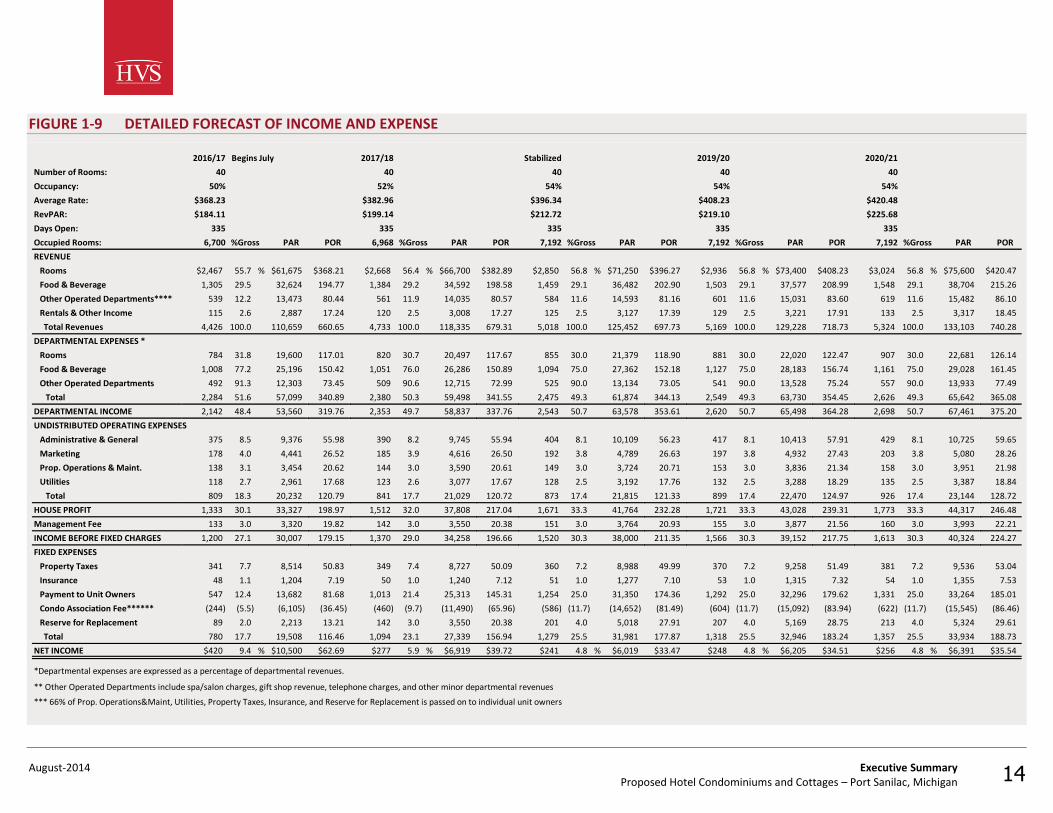

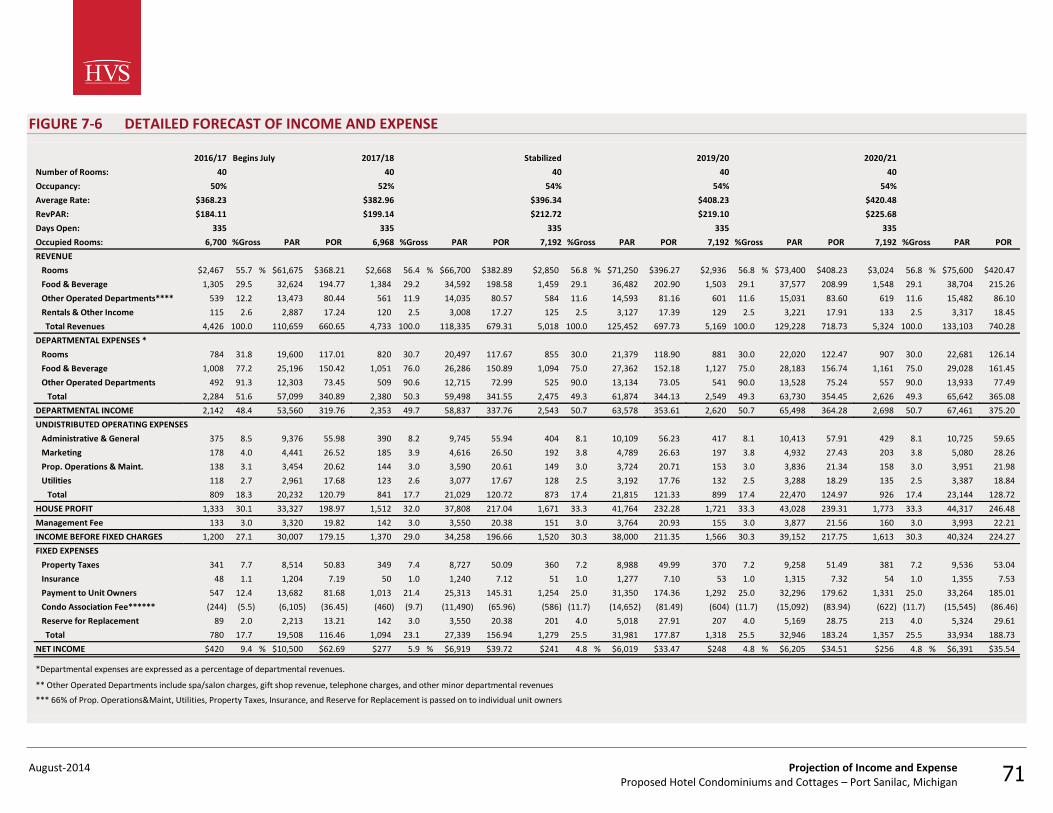

FIGURE 1-9 DETAILED FORECAST OF INCOME AND EXPENSE

2016/17 Begins July 2017/18 Stabilized 2019/20 2020/21

Number of Rooms: 40 40 40 40 40

Occupancy: 50% 52% 54% 54% 54%

Average Rate: $368.23 $382.96 $396.34 $408.23 $420.48

RevPAR: $184.11 $199.14 $212.72 $219.10 $225.68

Days Open: 335 335 335 335 335

Occupied Rooms: 6,700 %Gross PAR POR 6,968 %Gross PAR POR 7,192 %Gross PAR POR 7,192 %Gross PAR POR 7,192 %Gross PAR POR

REVENUE

Rooms $2,467 55.7 % $61,675 $368.21 $2,668 56.4 % $66,700 $382.89 $2,850 56.8 % $71,250 $396.27 $2,936 56.8 % $73,400 $408.23 $3,024 56.8 % $75,600 $420.47

Food & Beverage 1,305 29.5 32,624 194.77 1,384 29.2 34,592 198.58 1,459 29.1 36,482 202.90 1,503 29.1 37,577 208.99 1,548 29.1 38,704 215.26

Other Operated Departments**** 539 12.2 13,473 80.44 561 11.9 14,035 80.57 584 11.6 14,593 81.16 601 11.6 15,031 83.60 619 11.6 15,482 86.10

Rentals & Other Income 115 2.6 2,887 17.24 120 2.5 3,008 17.27 125 2.5 3,127 17.39 129 2.5 3,221 17.91 133 2.5 3,317 18.45

Total Revenues 4,426 100.0 110,659 660.65 4,733 100.0 118,335 679.31 5,018 100.0 125,452 697.73 5,169 100.0 129,228 718.73 5,324 100.0 133,103 740.28

DEPARTMENTAL EXPENSES *

Rooms 784 31.8 19,600 117.01 820 30.7 20,497 117.67 855 30.0 21,379 118.90 881 30.0 22,020 122.47 907 30.0 22,681 126.14

Food & Beverage 1,008 77.2 25,196 150.42 1,051 76.0 26,286 150.89 1,094 75.0 27,362 152.18 1,127 75.0 28,183 156.74 1,161 75.0 29,028 161.45

Other Operated Departments 492 91.3 12,303 73.45 509 90.6 12,715 72.99 525 90.0 13,134 73.05 541 90.0 13,528 75.24 557 90.0 13,933 77.49

Total 2,284 51.6 57,099 340.89 2,380 50.3 59,498 341.55 2,475 49.3 61,874 344.13 2,549 49.3 63,730 354.45 2,626 49.3 65,642 365.08

DEPARTMENTAL INCOME 2,142 48.4 53,560 319.76 2,353 49.7 58,837 337.76 2,543 50.7 63,578 353.61 2,620 50.7 65,498 364.28 2,698 50.7 67,461 375.20

UNDISTRIBUTED OPERATING EXPENSES

Administrative & General 375 8.5 9,376 55.98 390 8.2 9,745 55.94 404 8.1 10,109 56.23 417 8.1 10,413 57.91 429 8.1 10,725 59.65

Marketing 178 4.0 4,441 26.52 185 3.9 4,616 26.50 192 3.8 4,789 26.63 197 3.8 4,932 27.43 203 3.8 5,080 28.26

Prop. Operations & Maint. 138 3.1 3,454 20.62 144 3.0 3,590 20.61 149 3.0 3,724 20.71 153 3.0 3,836 21.34 158 3.0 3,951 21.98

Utilities 118 2.7 2,961 17.68 123 2.6 3,077 17.67 128 2.5 3,192 17.76 132 2.5 3,288 18.29 135 2.5 3,387 18.84

Total 809 18.3 20,232 120.79 841 17.7 21,029 120.72 873 17.4 21,815 121.33 899 17.4 22,470 124.97 926 17.4 23,144 128.72

HOUSE PROFIT 1,333 30.1 33,327 198.97 1,512 32.0 37,808 217.04 1,671 33.3 41,764 232.28 1,721 33.3 43,028 239.31 1,773 33.3 44,317 246.48

Management Fee 133 3.0 3,320 19.82 142 3.0 3,550 20.38 151 3.0 3,764 20.93 155 3.0 3,877 21.56 160 3.0 3,993 22.21

INCOME BEFORE FIXED CHARGES 1,200 27.1 30,007 179.15 1,370 29.0 34,258 196.66 1,520 30.3 38,000 211.35 1,566 30.3 39,152 217.75 1,613 30.3 40,324 224.27

FIXED EXPENSES

Property Taxes 341 7.7 8,514 50.83 349 7.4 8,727 50.09 360 7.2 8,988 49.99 370 7.2 9,258 51.49 381 7.2 9,536 53.04

Insurance 48 1.1 1,204 7.19 50 1.0 1,240 7.12 51 1.0 1,277 7.10 53 1.0 1,315 7.32 54 1.0 1,355 7.53

Payment to Unit Owners 547 12.4 13,682 81.68 1,013 21.4 25,313 145.31 1,254 25.0 31,350 174.36 1,292 25.0 32,296 179.62 1,331 25.0 33,264 185.01

Condo Association Fee****** (244) (5.5) (6,105) (36.45) (460) (9.7) (11,490) (65.96) (586) (11.7) (14,652) (81.49) (604) (11.7) (15,092) (83.94) (622) (11.7) (15,545) (86.46)

Reserve for Replacement 89 2.0 2,213 13.21 142 3.0 3,550 20.38 201 4.0 5,018 27.91 207 4.0 5,169 28.75 213 4.0 5,324 29.61

Total 780 17.7 19,508 116.46 1,094 23.1 27,339 156.94 1,279 25.5 31,981 177.87 1,318 25.5 32,946 183.24 1,357 25.5 33,934 188.73

NET INCOME $420 9.4 % $10,500 $62.69 $277 5.9 % $6,919 $39.72 $241 4.8 % $6,019 $33.47 $248 4.8 % $6,205 $34.51 $256 4.8 % $6,391 $35.54

*Departmental expenses are expressed as a percentage of departmental revenues.

** Other Operated Departments include spa/salon charges, gift shop revenue, telephone charges, and other minor departmental revenues

*** 66% of Prop. Operations&Maint, Utilities, Property Taxes, Insurance, and Reserve for Replacement is passed on to individual unit owners

August-2014 Executive Summary Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 15

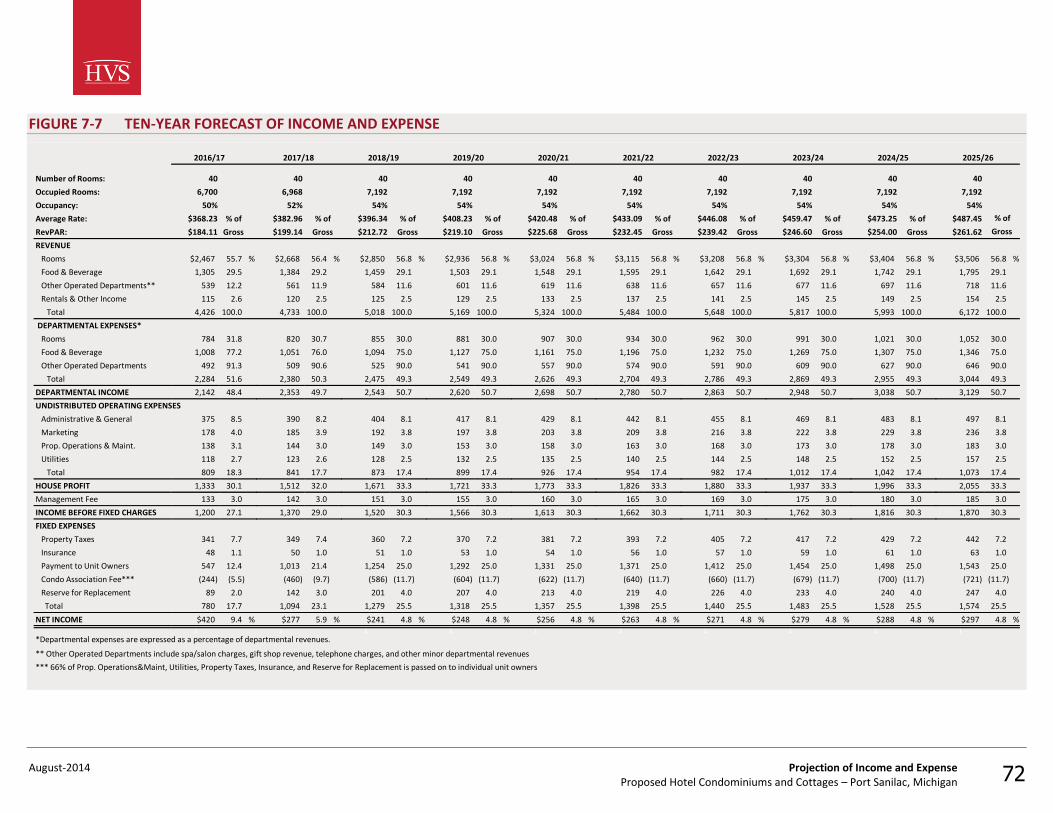

FIGURE 1-10 TEN-YEAR FORECAST OF INCOME AND EXPENSE

2016/17 2017/18 2018/19 2019/20 2020/21 2021/22 2022/23 2023/24 2024/25 2025/26

Number of Rooms: 40 40 40 40 40 40 40 40 40 40

Occupied Rooms: 6,700 6,968 7,192 7,192 7,192 7,192 7,192 7,192 7,192 7,192

Occupancy: 50% 52% 54% 54% 54% 54% 54% 54% 54% 54%

Average Rate: $368.23 % of $382.96 % of $396.34 % of $408.23 % of $420.48 % of $433.09 % of $446.08 % of $459.47 % of $473.25 % of $487.45

RevPAR: $184.11 Gross $199.14 Gross $212.72 Gross $219.10 Gross $225.68 Gross $232.45 Gross $239.42 Gross $246.60 Gross $254.00 Gross $261.62

REVENUE

Rooms $2,467 55.7 % $2,668 56.4 % $2,850 56.8 % $2,936 56.8 % $3,024 56.8 % $3,115 56.8 % $3,208 56.8 % $3,304 56.8 % $3,404 56.8 % $3,506 56.8 %

Food & Beverage 1,305 29.5 1,384 29.2 1,459 29.1 1,503 29.1 1,548 29.1 1,595 29.1 1,642 29.1 1,692 29.1 1,742 29.1 1,795 29.1

Other Operated Departments** 539 12.2 561 11.9 584 11.6 601 11.6 619 11.6 638 11.6 657 11.6 677 11.6 697 11.6 718 11.6

Rentals & Other Income 115 2.6 120 2.5 125 2.5 129 2.5 133 2.5 137 2.5 141 2.5 145 2.5 149 2.5 154 2.5

Total 4,426 100.0 4,733 100.0 5,018 100.0 5,169 100.0 5,324 100.0 5,484 100.0 5,648 100.0 5,817 100.0 5,993 100.0 6,172 100.0

DEPARTMENTAL EXPENSES*

Rooms 784 31.8 820 30.7 855 30.0 881 30.0 907 30.0 934 30.0 962 30.0 991 30.0 1,021 30.0 1,052 30.0

Food & Beverage 1,008 77.2 1,051 76.0 1,094 75.0 1,127 75.0 1,161 75.0 1,196 75.0 1,232 75.0 1,269 75.0 1,307 75.0 1,346 75.0

Other Operated Departments 492 91.3 509 90.6 525 90.0 541 90.0 557 90.0 574 90.0 591 90.0 609 90.0 627 90.0 646 90.0

Total 2,284 51.6 2,380 50.3 2,475 49.3 2,549 49.3 2,626 49.3 2,704 49.3 2,786 49.3 2,869 49.3 2,955 49.3 3,044 49.3

DEPARTMENTAL INCOME 2,142 48.4 2,353 49.7 2,543 50.7 2,620 50.7 2,698 50.7 2,780 50.7 2,863 50.7 2,948 50.7 3,038 50.7 3,129 50.7

UNDISTRIBUTED OPERATING EXPENSES

Administrative & General 375 8.5 390 8.2 404 8.1 417 8.1 429 8.1 442 8.1 455 8.1 469 8.1 483 8.1 497 8.1

Marketing 178 4.0 185 3.9 192 3.8 197 3.8 203 3.8 209 3.8 216 3.8 222 3.8 229 3.8 236 3.8

Prop. Operations & Maint. 138 3.1 144 3.0 149 3.0 153 3.0 158 3.0 163 3.0 168 3.0 173 3.0 178 3.0 183 3.0

Utilities 118 2.7 123 2.6 128 2.5 132 2.5 135 2.5 140 2.5 144 2.5 148 2.5 152 2.5 157 2.5

Total 809 18.3 841 17.7 873 17.4 899 17.4 926 17.4 954 17.4 982 17.4 1,012 17.4 1,042 17.4 1,073 17.4

HOUSE PROFIT 1,333 30.1 1,512 32.0 1,671 33.3 1,721 33.3 1,773 33.3 1,826 33.3 1,880 33.3 1,937 33.3 1,996 33.3 2,055 33.3

Management Fee 133 3.0 142 3.0 151 3.0 155 3.0 160 3.0 165 3.0 169 3.0 175 3.0 180 3.0 185 3.0

INCOME BEFORE FIXED CHARGES 1,200 27.1 1,370 29.0 1,520 30.3 1,566 30.3 1,613 30.3 1,662 30.3 1,711 30.3 1,762 30.3 1,816 30.3 1,870 30.3

FIXED EXPENSES

Property Taxes 341 7.7 349 7.4 360 7.2 370 7.2 381 7.2 393 7.2 405 7.2 417 7.2 429 7.2 442 7.2

Insurance 48 1.1 50 1.0 51 1.0 53 1.0 54 1.0 56 1.0 57 1.0 59 1.0 61 1.0 63 1.0

Payment to Unit Owners 547 12.4 1,013 21.4 1,254 25.0 1,292 25.0 1,331 25.0 1,371 25.0 1,412 25.0 1,454 25.0 1,498 25.0 1,543 25.0

Condo Association Fee*** (244) (5.5) (460) (9.7) (586) (11.7) (604) (11.7) (622) (11.7) (640) (11.7) (660) (11.7) (679) (11.7) (700) (11.7) (721) (11.7)

Reserve for Replacement 89 2.0 142 3.0 201 4.0 207 4.0 213 4.0 219 4.0 226 4.0 233 4.0 240 4.0 247 4.0

Total 780 17.7 1,094 23.1 1,279 25.5 1,318 25.5 1,357 25.5 1,398 25.5 1,440 25.5 1,483 25.5 1,528 25.5 1,574 25.5

NET INCOME $420 9.4 % $277 5.9 % $241 4.8 % $248 4.8 % $256 4.8 % $263 4.8 % $271 4.8 % $279 4.8 % $288 4.8 % $297 4.8 %1 1 1 1 1 1 1 1 1 1

*Departmental expenses are expressed as a percentage of departmental revenues.

** Other Operated Departments include spa/salon charges, gift shop revenue, telephone charges, and other minor departmental revenues

*** 66% of Prop. Operations&Maint, Utilities, Property Taxes, Insurance, and Reserve for Replacement is passed on to individual unit owners

% of

Gross

August-2014 Executive Summary Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 16

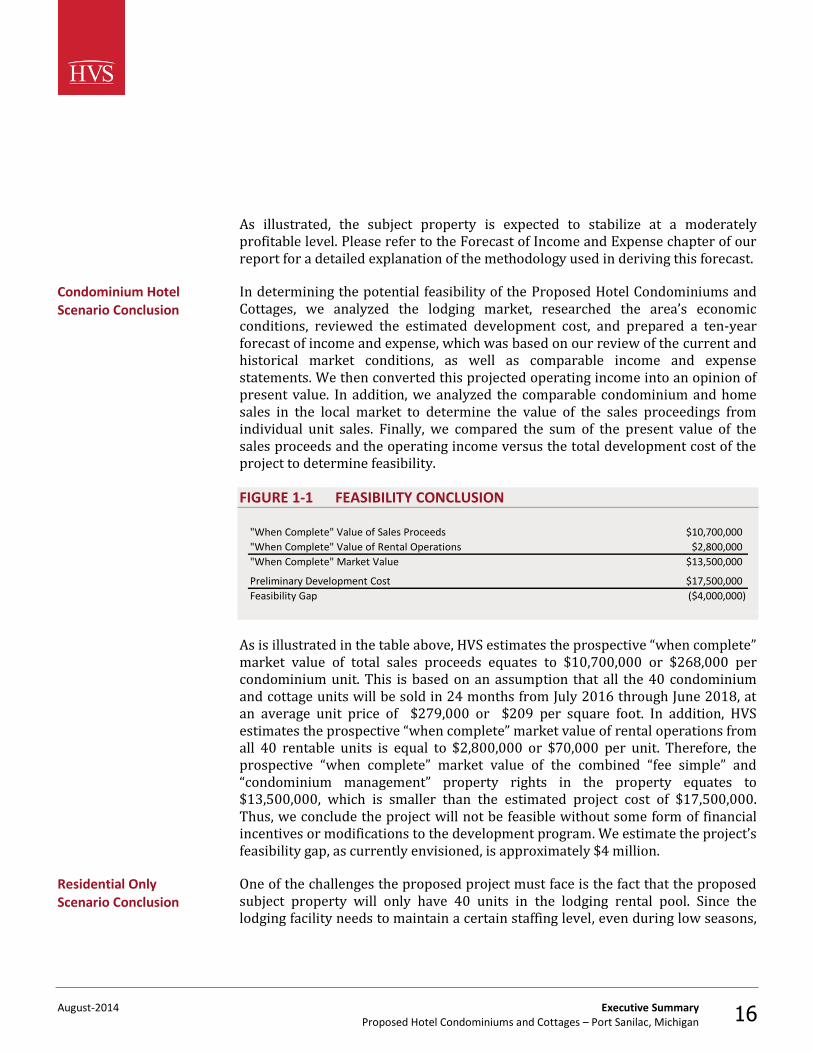

As illustrated, the subject property is expected to stabilize at a moderately profitable level. Please refer to the Forecast of Income and Expense chapter of our report for a detailed explanation of the methodology used in deriving this forecast.

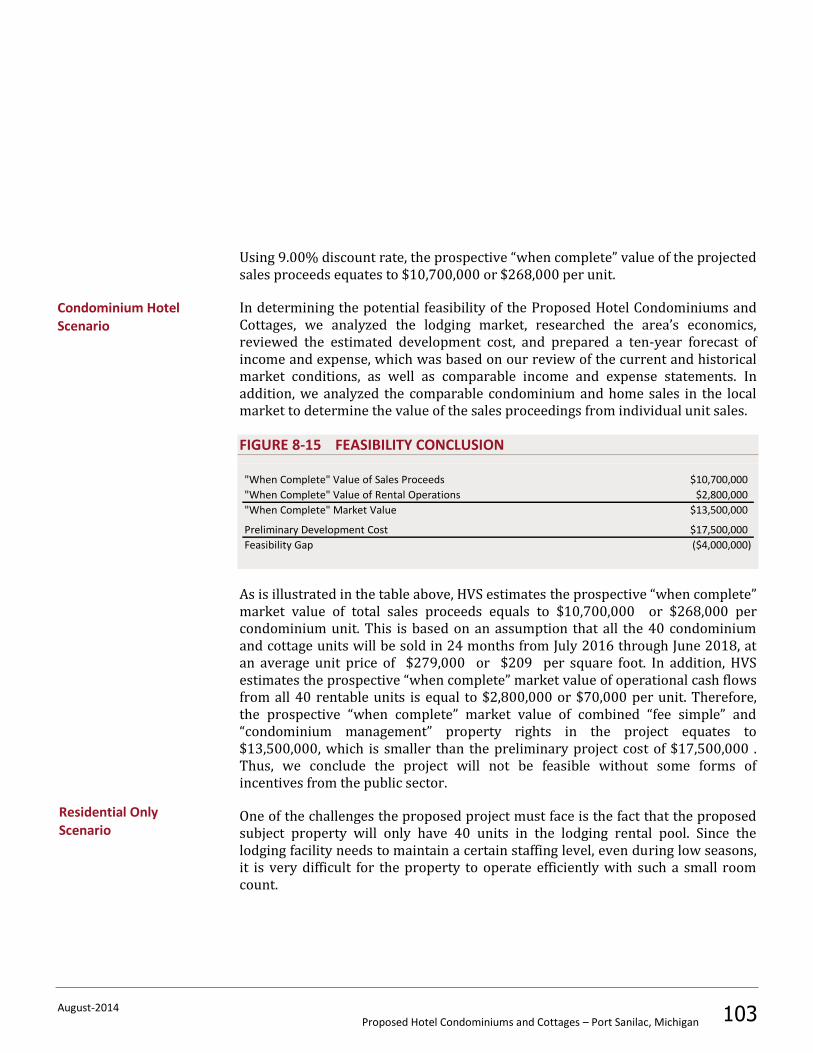

In determining the potential feasibility of the Proposed Hotel Condominiums and Cottages, we analyzed the lodging market, researched the area’s economic conditions, reviewed the estimated development cost, and prepared a ten-year forecast of income and expense, which was based on our review of the current and historical market conditions, as well as comparable income and expense statements. We then converted this projected operating income into an opinion of present value. In addition, we analyzed the comparable condominium and home sales in the local market to determine the value of the sales proceedings from individual unit sales. Finally, we compared the sum of the present value of the sales proceeds and the operating income versus the total development cost of the project to determine feasibility.

FIGURE 1-1 FEASIBILITY CONCLUSION

"When Complete" Value of Sales Proceeds $10,700,000

"When Complete" Value of Rental Operations $2,800,000

"When Complete" Market Value $13,500,000

Preliminary Development Cost $17,500,000

Feasibility Gap ($4,000,000)

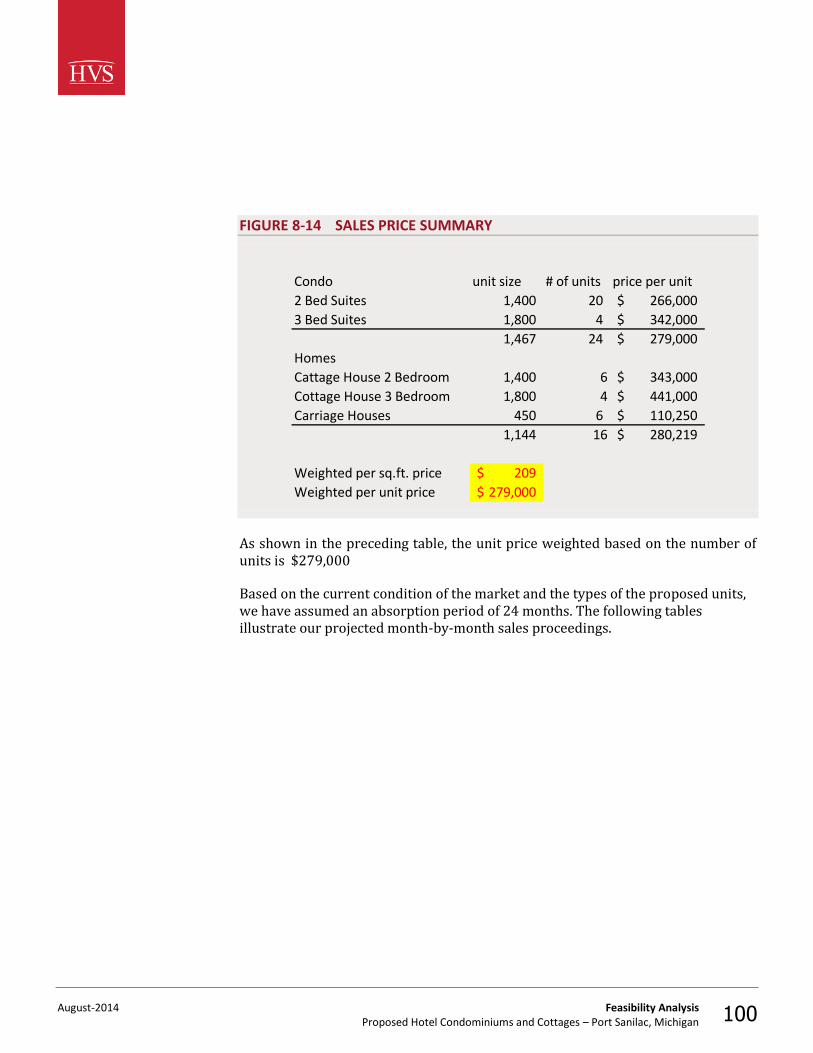

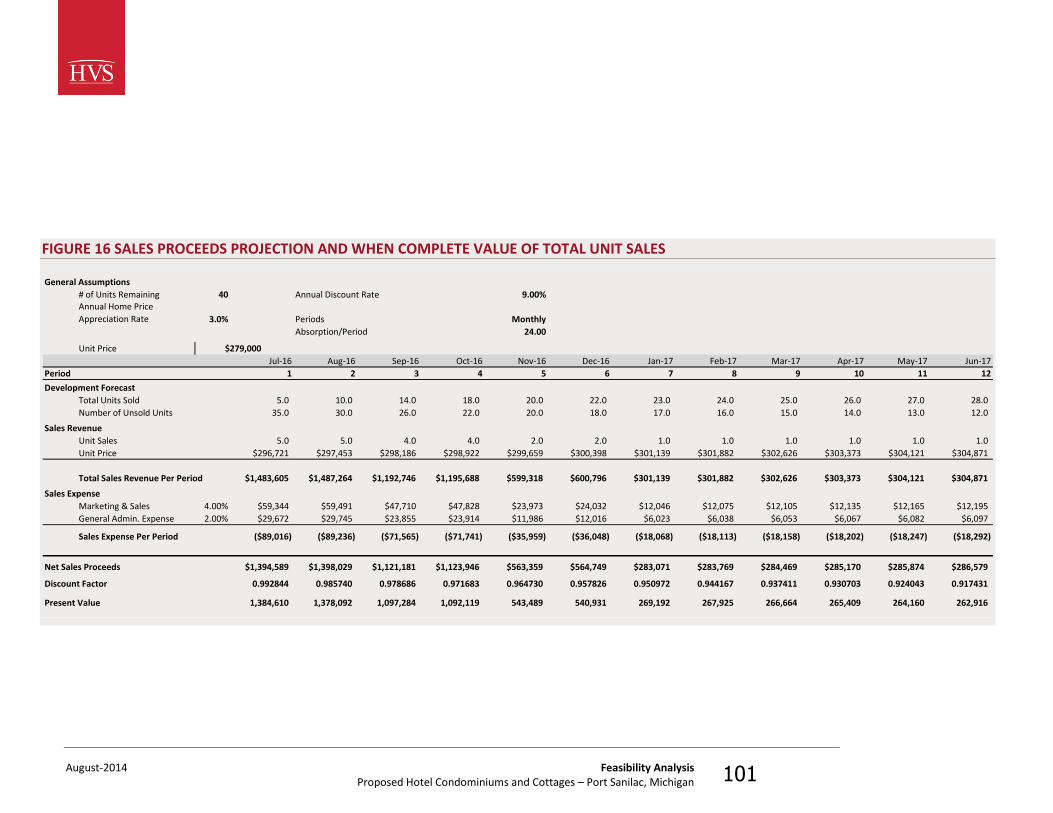

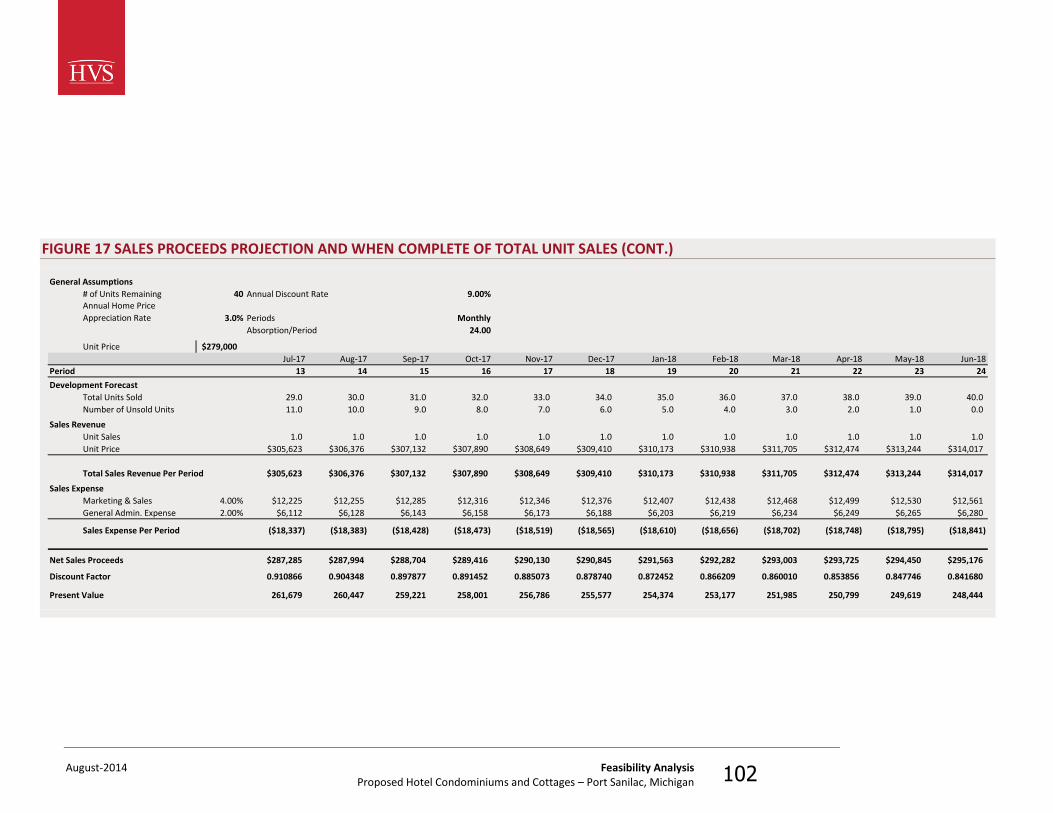

As is illustrated in the table above, HVS estimates the prospective “when complete” market value of total sales proceeds equates to $10,700,000 or $268,000 per condominium unit. This is based on an assumption that all the 40 condominium and cottage units will be sold in 24 months from July 2016 through June 2018, at an average unit price of $279,000 or $209 per square foot. In addition, HVS estimates the prospective “when complete” market value of rental operations from all 40 rentable units is equal to $2,800,000 or $70,000 per unit. Therefore, the prospective “when complete” market value of the combined “fee simple” and “condominium management” property rights in the property equates to $13,500,000, which is smaller than the estimated project cost of $17,500,000. Thus, we conclude the project will not be feasible without some form of financial incentives or modifications to the development program. We estimate the project’s feasibility gap, as currently envisioned, is approximately $4 million.

One of the challenges the proposed project must face is the fact that the proposed subject property will only have 40 units in the lodging rental pool. Since the lodging facility needs to maintain a certain staffing level, even during low seasons,

Condominium Hotel Scenario Conclusion

Residential Only Scenario Conclusion

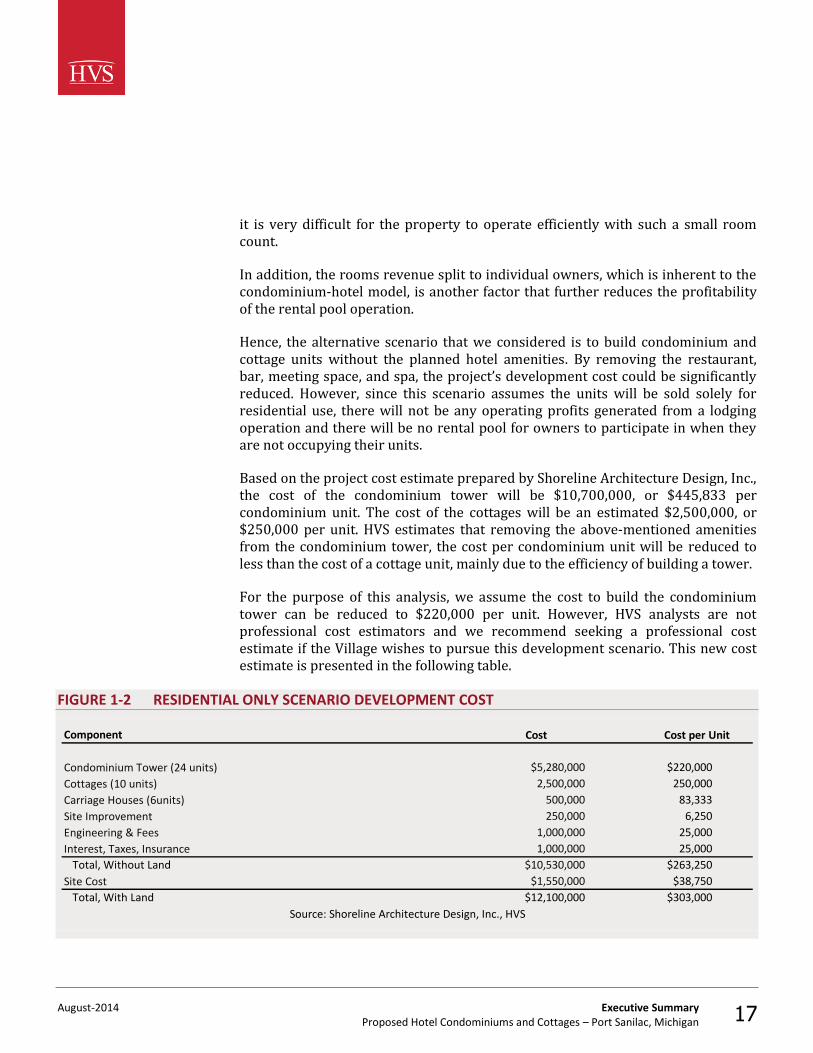

August-2014 Executive Summary Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 17

it is very difficult for the property to operate efficiently with such a small room count.

In addition, the rooms revenue split to individual owners, which is inherent to the condominium-hotel model, is another factor that further reduces the profitability of the rental pool operation.

Hence, the alternative scenario that we considered is to build condominium and cottage units without the planned hotel amenities. By removing the restaurant, bar, meeting space, and spa, the project’s development cost could be significantly reduced. However, since this scenario assumes the units will be sold solely for residential use, there will not be any operating profits generated from a lodging operation and there will be no rental pool for owners to participate in when they are not occupying their units.

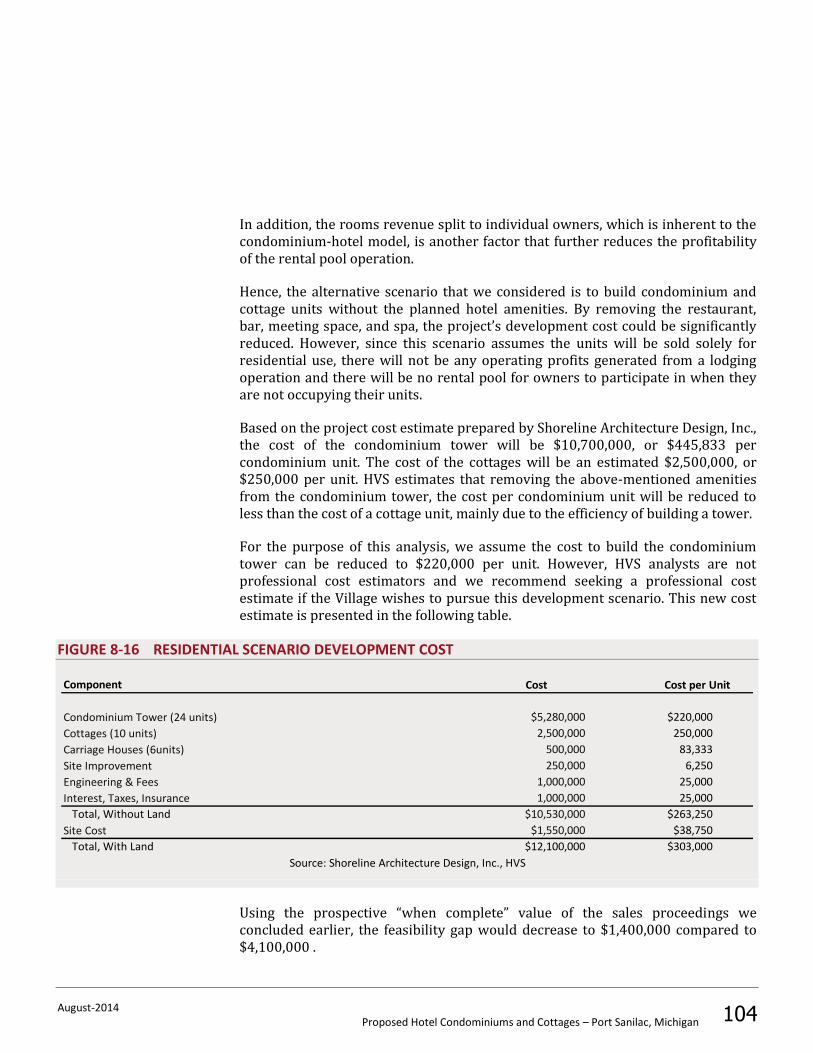

Based on the project cost estimate prepared by Shoreline Architecture Design, Inc., the cost of the condominium tower will be $10,700,000, or $445,833 per condominium unit. The cost of the cottages will be an estimated $2,500,000, or $250,000 per unit. HVS estimates that removing the above-mentioned amenities from the condominium tower, the cost per condominium unit will be reduced to less than the cost of a cottage unit, mainly due to the efficiency of building a tower.

For the purpose of this analysis, we assume the cost to build the condominium tower can be reduced to $220,000 per unit. However, HVS analysts are not professional cost estimators and we recommend seeking a professional cost estimate if the Village wishes to pursue this development scenario. This new cost estimate is presented in the following table.

FIGURE 1-2 RESIDENTIAL ONLY SCENARIO DEVELOPMENT COST

Component

$5,280,000 $220,000

2,500,000 250,000

500,000 83,333

250,000 6,250

1,000,000 25,000

1,000,000 25,000

Total, Without Land $10,530,000 $263,250

$1,550,000 $38,750

Total, With Land $12,100,000 $303,000

Cost Cost per Unit

Condominium Tower (24 units)

Cottages (10 units)

Carriage Houses (6units)

Site Improvement

Engineering & Fees

Interest, Taxes, Insurance

Site Cost

Source: Shoreline Architecture Design, Inc., HVS

August-2014 Executive Summary Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 18

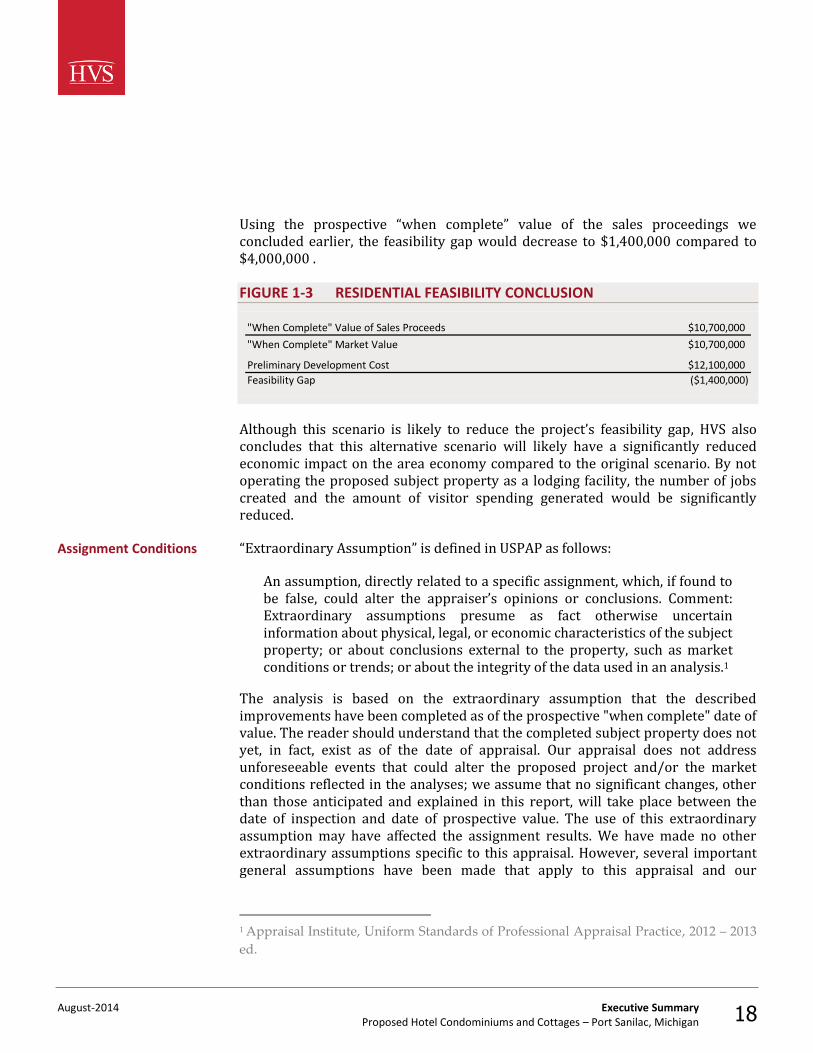

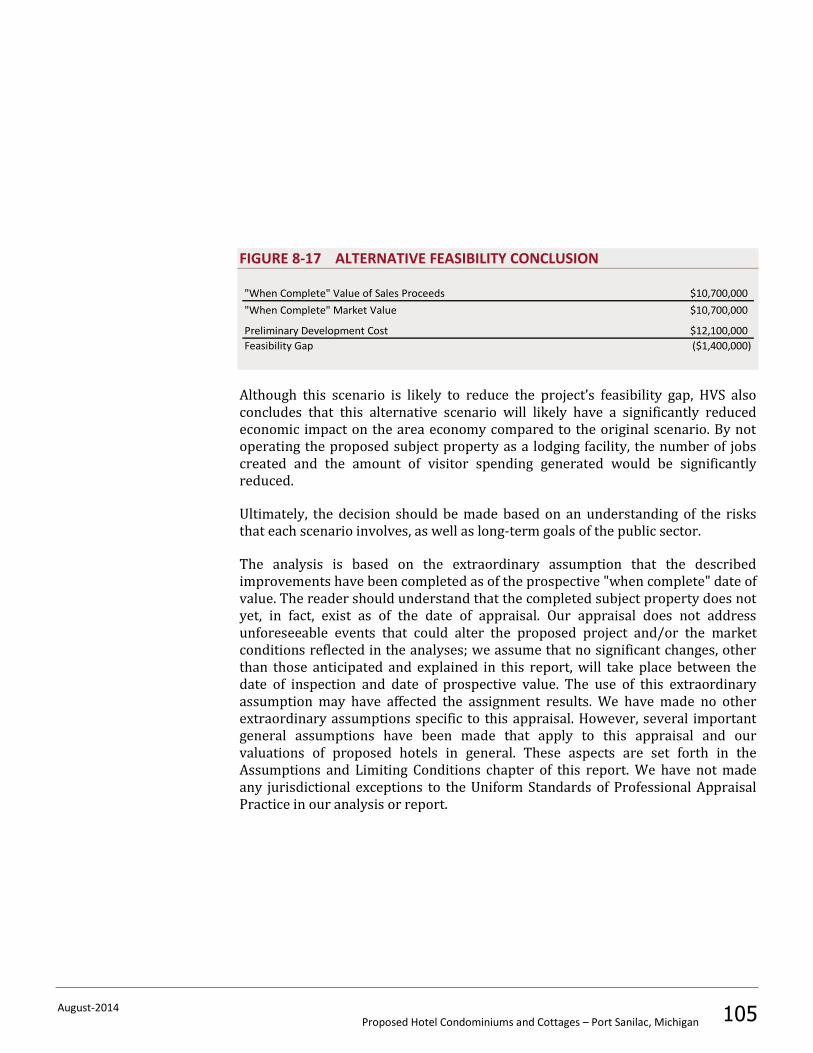

Using the prospective “when complete” value of the sales proceedings we concluded earlier, the feasibility gap would decrease to $1,400,000 compared to $4,000,000 .

FIGURE 1-3 RESIDENTIAL FEASIBILITY CONCLUSION

"When Complete" Value of Sales Proceeds $10,700,000

"When Complete" Market Value $10,700,000

Preliminary Development Cost $12,100,000

Feasibility Gap ($1,400,000)

Although this scenario is likely to reduce the project’s feasibility gap, HVS also concludes that this alternative scenario will likely have a significantly reduced economic impact on the area economy compared to the original scenario. By not operating the proposed subject property as a lodging facility, the number of jobs created and the amount of visitor spending generated would be significantly reduced.

“Extraordinary Assumption” is defined in USPAP as follows:

An assumption, directly related to a specific assignment, which, if found to be false, could alter the appraiser’s opinions or conclusions. Comment: Extraordinary assumptions presume as fact otherwise uncertain information about physical, legal, or economic characteristics of the subject property; or about conclusions external to the property, such as market conditions or trends; or about the integrity of the data used in an analysis.1

The analysis is based on the extraordinary assumption that the described improvements have been completed as of the prospective "when complete" date of value. The reader should understand that the completed subject property does not yet, in fact, exist as of the date of appraisal. Our appraisal does not address unforeseeable events that could alter the proposed project and/or the market conditions reflected in the analyses; we assume that no significant changes, other than those anticipated and explained in this report, will take place between the date of inspection and date of prospective value. The use of this extraordinary assumption may have affected the assignment results. We have made no other extraordinary assumptions specific to this appraisal. However, several important general assumptions have been made that apply to this appraisal and our

1 Appraisal Institute, Uniform Standards of Professional Appraisal Practice, 2012 – 2013

ed.

Assignment Conditions

August-2014 Executive Summary Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 19

valuations of proposed hotels in general. These aspects are set forth in the Assumptions and Limiting Conditions chapter of this report.

“Hypothetical Condition” is defined in USPAP as follows:

That which is contrary to what exists but is supposed for the purpose of analysis. Comment: Hypothetical conditions assume conditions contrary to known facts about physical, legal, or economic characteristics of the subject property; or about conditions external to the property, such as market conditions or trends; or about the integrity of data used in an analysis. 2

We have made no assumptions of hypothetical conditions in our report.

We have not made any jurisdictional exceptions to the Uniform Standards of Professional Appraisal Practice in our analysis or report.

This feasibility report is being prepared for use in the development of the proposed subject hotel condominiums and cottages.

The client for this engagement is Port Sanilac Downtown Development Authority. The client is also this report's intended user and the report should not be distributed to or relied upon by other persons or entities.

The methodology used to develop this study is based on the market research and valuation techniques set forth in the textbooks authored by Hospitality Valuation Services for the American Institute of Real Estate Appraisers and the Appraisal Institute, entitled The Valuation of Hotels and Motels,3 Hotels, Motels and Restaurants: Valuations and Market Studies,4 The Computerized Income Approach to Hotel/Motel Market Studies and Valuations,5 Hotels and Motels: A Guide to

2 Appraisal Institute, Uniform Standards of Professional Appraisal Practice, 2012 – 2013

ed. 3 Stephen Rushmore, The Valuation of Hotels and Motels. (Chicago: American Institute of

Real Estate Appraisers, 1978). 4 Stephen Rushmore, Hotels, Motels and Restaurants: Valuations and Market Studies.

(Chicago: American Institute of Real Estate Appraisers, 1983). 5 Stephen Rushmore, The Computerized Income Approach to Hotel/Motel Market Studies and

Valuations. (Chicago: American Institute of Real Estate Appraisers, 1990).

Intended Use of the Feasibility Study

Identification of the Client and Intended User

Scope of Work

August-2014 Executive Summary Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 20

Market Analysis, Investment Analysis, and Valuations,6 and Hotels and Motels – Valuations and Market Studies.7

1. All information was collected and analyzed by the staff of CCG Holdings, LLC. Information was supplied by the client and/or the property’s development team.

2. The subject site has been evaluated from the viewpoint of its physical utility for the future operation of a hotel, as well as access, visibility, and other relevant factors.

3. The subject property's proposed improvements have been reviewed for their expected quality of construction, design, and layout efficiency.

4. The surrounding economic environment, on both an area and neighborhood level, has been reviewed to identify specific hostelry-related economic and demographic trends that may have an impact on future demand for hotels.

5. Dividing the market for hotel accommodations into individual segments defines specific market characteristics for the types of travelers expected to utilize the area's hotels. The factors investigated include purpose of visit, average length of stay, facilities and amenities required, seasonality, daily demand fluctuations, and price sensitivity.

6. An analysis of existing and proposed competition provides an indication of the current accommodated demand, along with market penetration and the degree of competitiveness. Unless noted otherwise, we have inspected the competitive lodging facilities summarized in this report.

7. Documentation for an occupancy and average rate projection is derived utilizing the build-up approach based on an analysis of lodging activity.

8. A detailed projection of income and expense made in accordance with the Uniform System of Accounts for the Lodging Industry sets forth the anticipated economic benefits of the subject property.

9. A feasibility analysis is performed that compares the net present value of the forecast cash flows to the development cost of the hotel.

6 Stephen Rushmore, Hotels and Motels: A Guide to Market Analysis, Investment

Analysis, and Valuations (Chicago: Appraisal Institute, 1992). 7 Stephen Rushmore and Erich Baum, Hotels and Motels – Valuations and Market Studies.

(Chicago: Appraisal Institute, 2001).

August-2014 Description of the Site and Neighborhood Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 21

2. Description of the Site and Neighborhood

The suitability of the land for the operation of a lodging facility is an important consideration affecting the economic viability of a property and its ultimate marketability. Factors such as size, topography, access, visibility, and the availability of utilities have a direct impact on the desirability of a particular site.

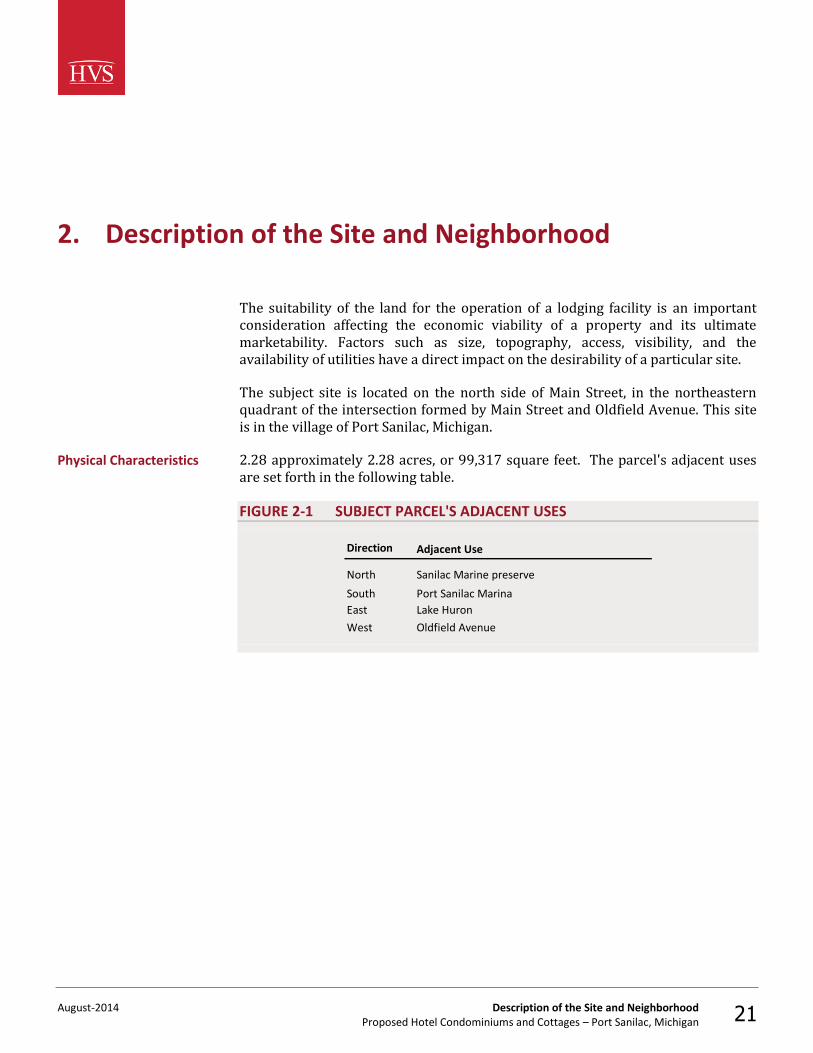

The subject site is located on the north side of Main Street, in the northeastern quadrant of the intersection formed by Main Street and Oldfield Avenue. This site is in the village of Port Sanilac, Michigan.

2.28 approximately 2.28 acres, or 99,317 square feet. The parcel's adjacent uses are set forth in the following table.

FIGURE 2-1 SUBJECT PARCEL'S ADJACENT USES

Direction

North Sanilac Marine preserve

South Port Sanilac Marina

East Lake Huron

West Oldfield Avenue

Adjacent Use

Physical Characteristics

August-2014 Description of the Site and Neighborhood Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 22

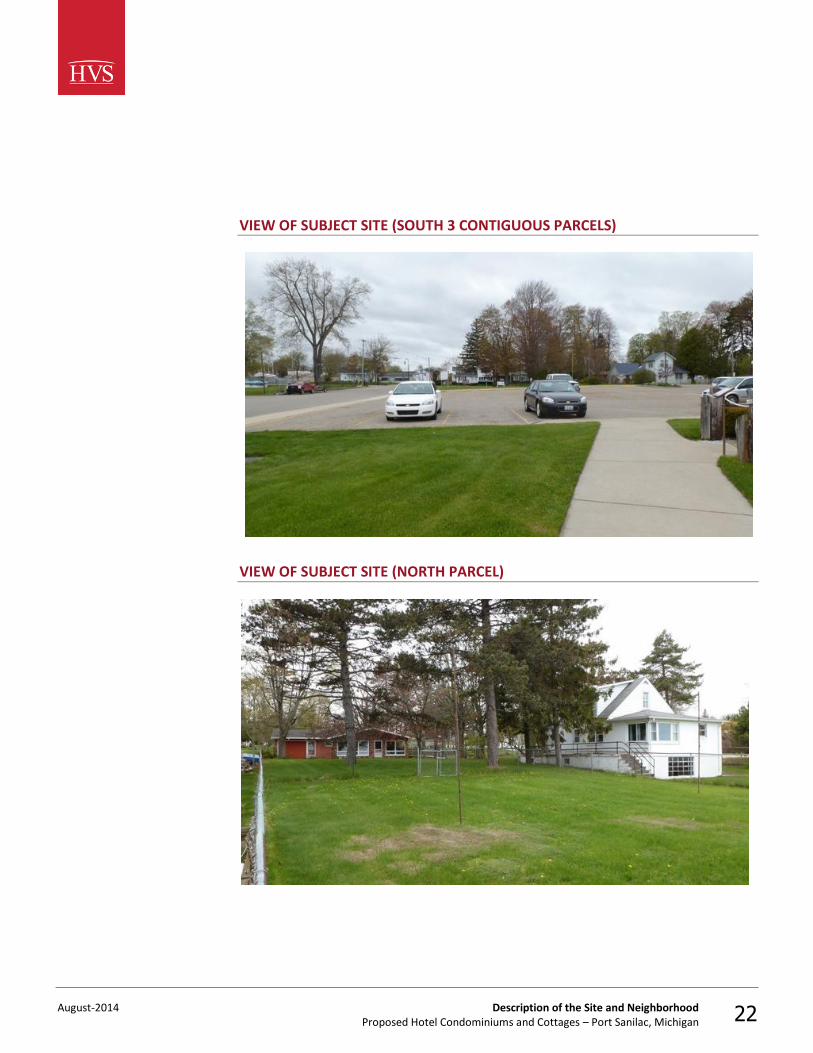

VIEW OF SUBJECT SITE (SOUTH 3 CONTIGUOUS PARCELS)

VIEW OF SUBJECT SITE (NORTH PARCEL)

August-2014 Description of the Site and Neighborhood Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 23

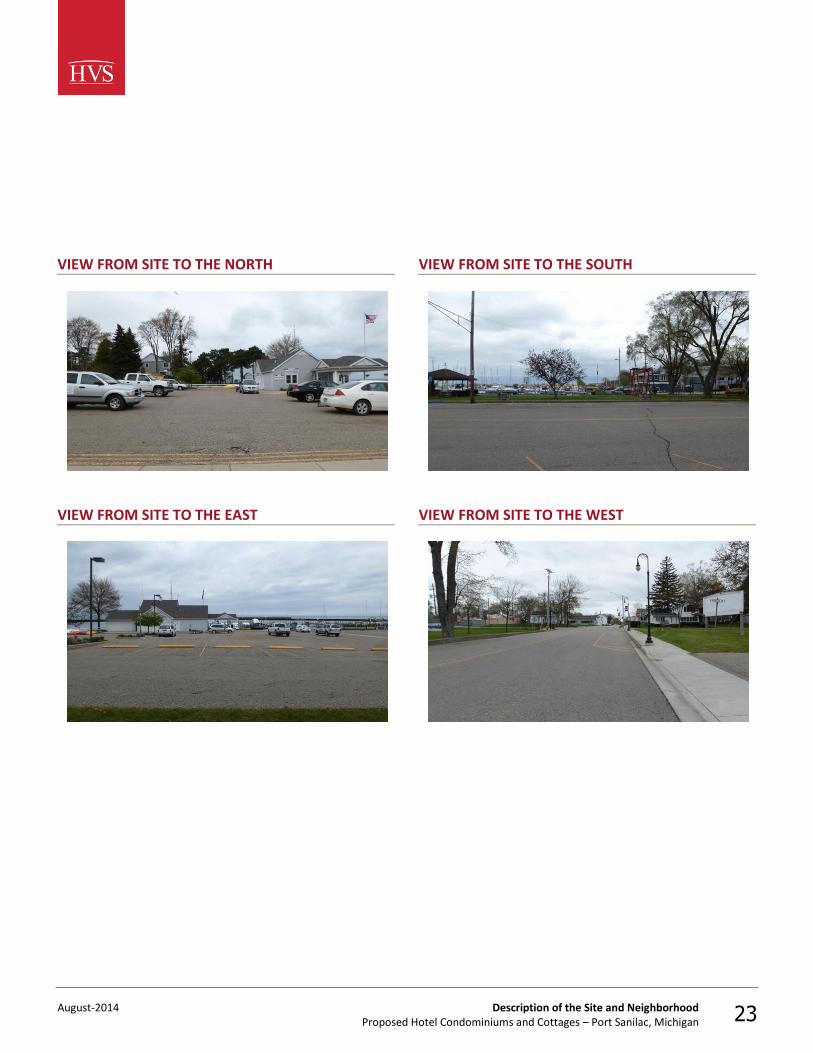

VIEW FROM SITE TO THE NORTH

VIEW FROM SITE TO THE SOUTH

VIEW FROM SITE TO THE EAST

VIEW FROM SITE TO THE WEST

August-2014 Description of the Site and Neighborhood Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 24

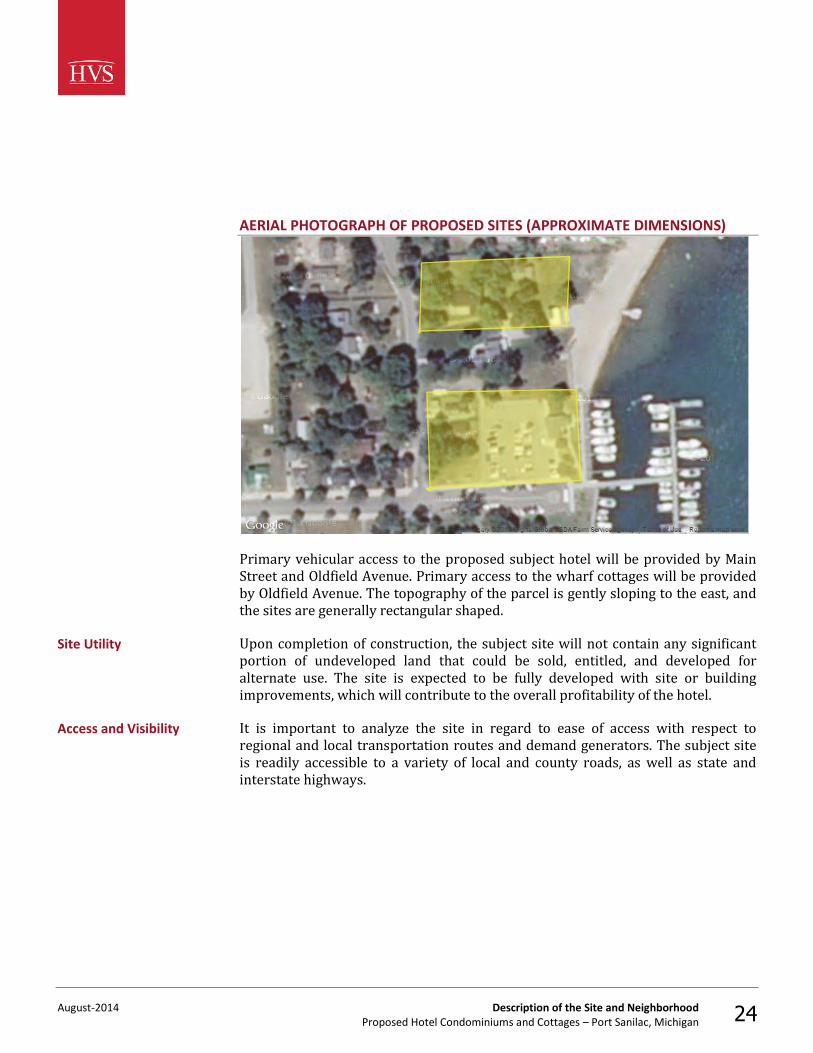

AERIAL PHOTOGRAPH OF PROPOSED SITES (APPROXIMATE DIMENSIONS)

Primary vehicular access to the proposed subject hotel will be provided by Main Street and Oldfield Avenue. Primary access to the wharf cottages will be provided by Oldfield Avenue. The topography of the parcel is gently sloping to the east, and the sites are generally rectangular shaped.

Upon completion of construction, the subject site will not contain any significant portion of undeveloped land that could be sold, entitled, and developed for alternate use. The site is expected to be fully developed with site or building improvements, which will contribute to the overall profitability of the hotel.

It is important to analyze the site in regard to ease of access with respect to regional and local transportation routes and demand generators. The subject site is readily accessible to a variety of local and county roads, as well as state and interstate highways.

Site Utility

Access and Visibility

August-2014 Description of the Site and Neighborhood Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 25

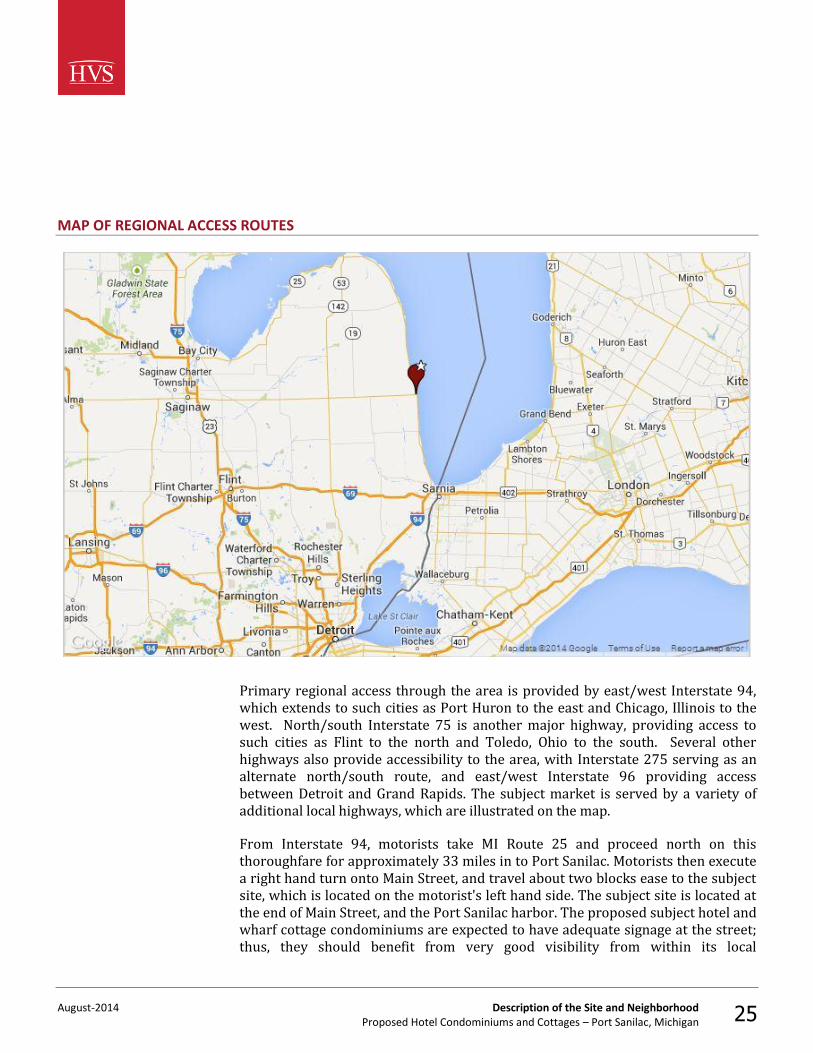

MAP OF REGIONAL ACCESS ROUTES

Primary regional access through the area is provided by east/west Interstate 94, which extends to such cities as Port Huron to the east and Chicago, Illinois to the west. North/south Interstate 75 is another major highway, providing access to such cities as Flint to the north and Toledo, Ohio to the south. Several other highways also provide accessibility to the area, with Interstate 275 serving as an alternate north/south route, and east/west Interstate 96 providing access between Detroit and Grand Rapids. The subject market is served by a variety of additional local highways, which are illustrated on the map.

From Interstate 94, motorists take MI Route 25 and proceed north on this thoroughfare for approximately 33 miles in to Port Sanilac. Motorists then execute a right hand turn onto Main Street, and travel about two blocks ease to the subject site, which is located on the motorist's left hand side. The subject site is located at the end of Main Street, and the Port Sanilac harbor. The proposed subject hotel and wharf cottage condominiums are expected to have adequate signage at the street; thus, they should benefit from very good visibility from within its local

August-2014 Description of the Site and Neighborhood Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 26

neighborhood. Overall, the subject site benefits from excellent accessibility, and the proposed development is expected to enjoy very good visibility attributes.

The proposed subject hotel will be served by the Detroit Metropolitan Wayne County Airport, which is located approximately 110 miles to the south-west of the subject site. From the airport, motorists will follow signs to Interstate 94 and travel east on this thoroughfare towards the City of Detroit and then northeast to Port Huron. Motorists will then proceed north on MI Route 25 for approximately 25 miles until its intersection with MI 46 (aka Main Street) in Port Sanilac. Motorists will then execute a right hand turn on Main Street, and travel two blocks to the subject site, which will be on motorists' left-hand side.

The neighborhood surrounding a lodging facility often has an impact on a hotel's status, image, class, style of operation, and sometimes its ability to attract and properly serve a particular market segment. This section of the report investigates the subject neighborhood and evaluates any pertinent location factors that could affect its future occupancy, average rate, and overall profitability.

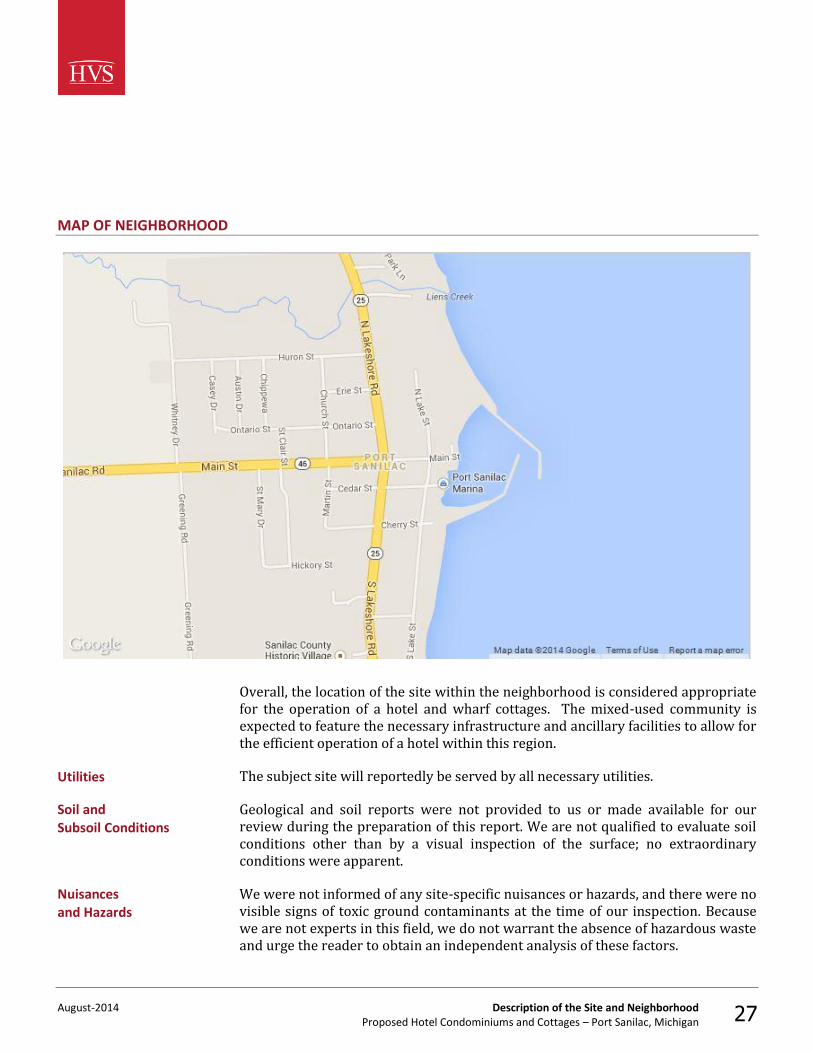

The neighborhood surrounding the subject site is generally defined by Park Lane to the north, Lake Huron to the east, Sanilac County historic village to the south, and Whitney Drive/Greening Road to the west. This neighborhood is in the stable stage of its life cycle, with pockets of moderate growth occurring in the commercial sector. Within the immediate proximity of the site, land use is primarily commercial and residential in nature. The neighborhood is characterized by smaller/older single family homes, two marinas, and retail stores along the primary, main thoroughfares, with additional residential areas located along the secondary roadways.

Some specific businesses and entities in the area include the Port Sanilac and Bark Shanty Marina's, Uri waterfront restaurant, Blue Water Sports Bar and the Stone Lodge restaurant. Other entities in the area include the Port Sanilac historic museum and the Barn Theatre. In general, we would characterize the neighborhood as 30% residential use, 30% retail/restaurant use, 10% vacant, and 30% other. The proposed subject hotel's opening should be a positive influence on the area.

Airport Access

Neighborhood

August-2014 Description of the Site and Neighborhood Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 27

MAP OF NEIGHBORHOOD

Overall, the location of the site within the neighborhood is considered appropriate for the operation of a hotel and wharf cottages. The mixed-used community is expected to feature the necessary infrastructure and ancillary facilities to allow for the efficient operation of a hotel within this region.

The subject site will reportedly be served by all necessary utilities.

Geological and soil reports were not provided to us or made available for our review during the preparation of this report. We are not qualified to evaluate soil conditions other than by a visual inspection of the surface; no extraordinary conditions were apparent.

We were not informed of any site-specific nuisances or hazards, and there were no visible signs of toxic ground contaminants at the time of our inspection. Because we are not experts in this field, we do not warrant the absence of hazardous waste and urge the reader to obtain an independent analysis of these factors.

Utilities

Soil and Subsoil Conditions

Nuisances and Hazards

August-2014 Description of the Site and Neighborhood Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 28

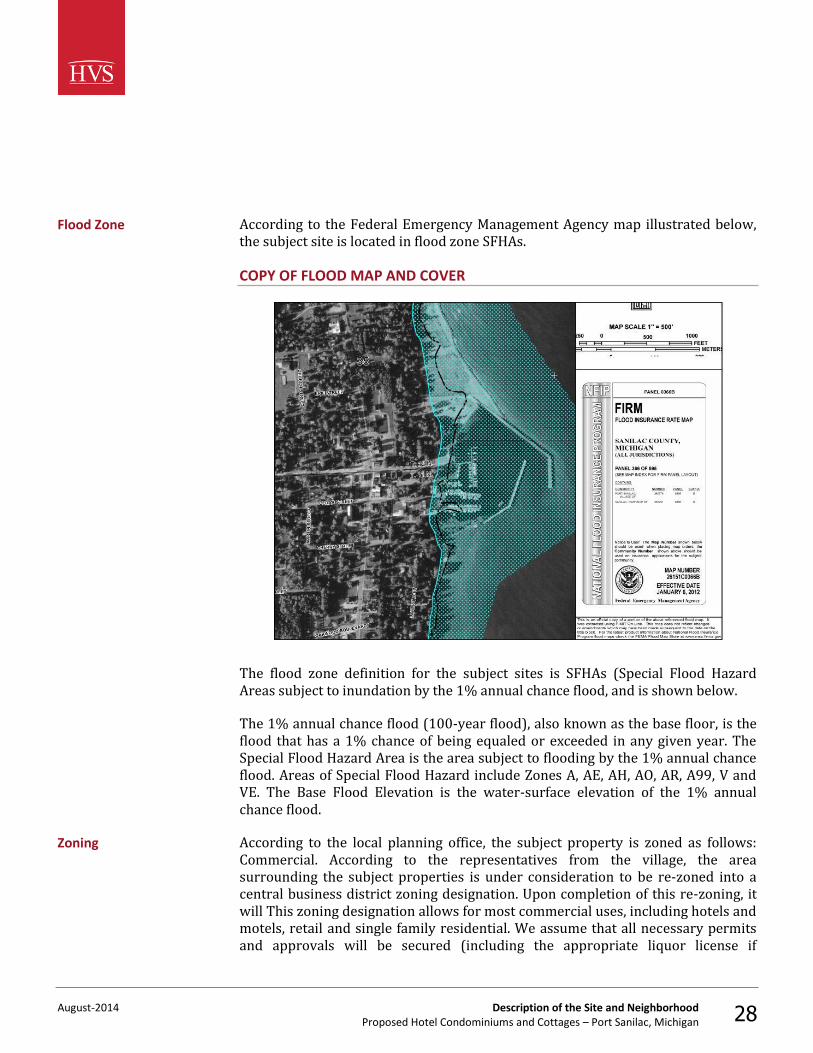

According to the Federal Emergency Management Agency map illustrated below, the subject site is located in flood zone SFHAs.

COPY OF FLOOD MAP AND COVER

The flood zone definition for the subject sites is SFHAs (Special Flood Hazard Areas subject to inundation by the 1% annual chance flood, and is shown below.

The 1% annual chance flood (100-year flood), also known as the base floor, is the flood that has a 1% chance of being equaled or exceeded in any given year. The Special Flood Hazard Area is the area subject to flooding by the 1% annual chance flood. Areas of Special Flood Hazard include Zones A, AE, AH, AO, AR, A99, V and VE. The Base Flood Elevation is the water-surface elevation of the 1% annual chance flood.

According to the local planning office, the subject property is zoned as follows: Commercial. According to the representatives from the village, the area surrounding the subject properties is under consideration to be re-zoned into a central business district zoning designation. Upon completion of this re-zoning, it will This zoning designation allows for most commercial uses, including hotels and motels, retail and single family residential. We assume that all necessary permits and approvals will be secured (including the appropriate liquor license if

Flood Zone

Zoning

August-2014 Description of the Site and Neighborhood Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 29

applicable) and that the subject property will be constructed in accordance with local zoning ordinances, building codes, and all other applicable regulations. Our zoning analysis should be verified before any physical changes are made to the site.

We are not aware of any easements attached to the property that would significantly affect the utility of the site or marketability of this project.

We have analyzed the issues of size, topography, access, visibility, and the availability of utilities. The subject site is ideally located about two blocks east of the main downtown area of the Village of Port Sanilac, in a mixed-use commercial/residential area. It is adjacent to the Port Sanilac harbor and docks, as well as existing general retail/commercial buildings and restaurants. In general, the site should be well suited for future hotel/condominium, wharf cottage use, with acceptable access, visibility, and topography for an effective operation.

Easements and Encroachments

Conclusion

August-2014 Market Area Analysis Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 30

3. Market Area Analysis

The economic vitality of the market area and neighborhood surrounding the subject site is an important consideration in forecasting lodging demand and future income potential. Economic and demographic trends that reflect the amount of visitation provide a basis from which to project lodging demand. The purpose of the market area analysis is to review available economic and demographic data to determine whether the local market will undergo economic growth, stabilize, or decline. In addition to predicting the direction of the economy, the rate of change must be quantified. These trends are then correlated based on their propensity to reflect variations in lodging demand, with the objective of forecasting the amount of growth or decline in visitation by individual market segment (e.g., commercial, meeting and group, and leisure).

The market area for a lodging facility is the geographical region where the sources of demand and the competitive supply are located. The subject site is located in the city of Port Sanilac, the county of Sanilac, and the state of Michigan. The Village of Port Sanilac is located approximately 90 miles northeast of the City of Detroit, Michigan, on the shores of Lake Huron, which is one of the Great Lakes. The primary economic drivers and engine for the village is generated by the three harbors and restaurants, as well as tourist attractions which include the Port Sanilac Lighthouse built in 1886; the Port Sanilac historic museum, which consists of Victorian and Edwardian buildings and exhibits where events are held to provide visitors with a look back at the way life used to be at the turn of the century as well as arts and crafts and fairs; and the Barn Theatre, which is a non-profit summer theatre providing plays and local musical entertainment venues. The three harbors are reported to have a total of 201 slips.

Market Area Definition

August-2014 Market Area Analysis Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 31

PORT SANILAC HARBOR

The following exhibit illustrates the market area.

August-2014 Market Area Analysis Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 32

MAP OF MARKET AREA

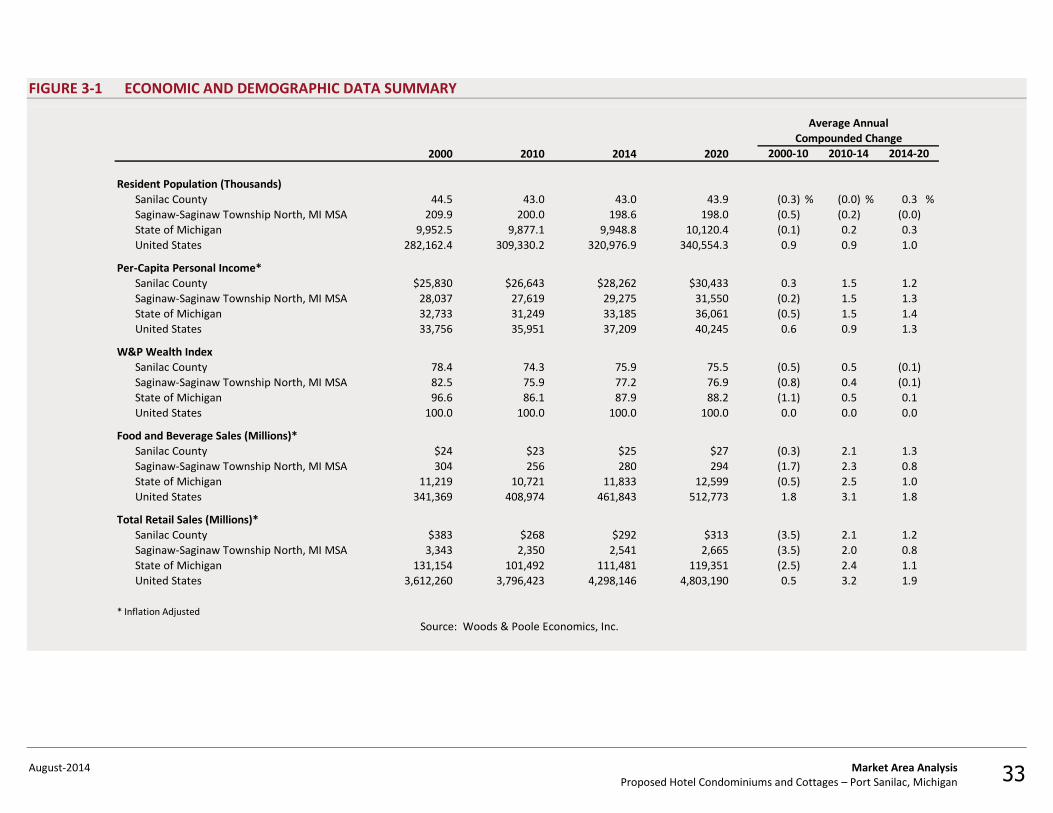

A primary source of economic and demographic statistics used in this analysis is the Complete Economic and Demographic Data Source published by Woods & Poole Economics, Inc., a well-regarded forecasting service based in Washington, D.C. Using a database containing more than 900 variables for each county in the nation, Woods & Poole employs a sophisticated regional model to forecast economic and demographic trends. Historical statistics are based on census data and information published by the Bureau of Economic Analysis. Projections are formulated by Woods & Poole, and all dollar amounts have been adjusted for inflation, thus reflecting real change.

These data are summarized in the following table.

Economic and Demographic Review

August-2014 Market Area Analysis Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 33

FIGURE 3-1 ECONOMIC AND DEMOGRAPHIC DATA SUMMARY

Average Annual

Compounded Change

2000 2010 2014 2020 2000-10 2010-14 2014-20

Resident Population (Thousands)

Sanilac County 44.5 43.0 43.0 43.9 (0.3) % (0.0) % 0.3 %

Saginaw-Saginaw Township North, MI MSA 209.9 200.0 198.6 198.0 (0.5) (0.2) (0.0)

State of Michigan 9,952.5 9,877.1 9,948.8 10,120.4 (0.1) 0.2 0.3

United States 282,162.4 309,330.2 320,976.9 340,554.3 0.9 0.9 1.0

Per-Capita Personal Income*

Sanilac County $25,830 $26,643 $28,262 $30,433 0.3 1.5 1.2

Saginaw-Saginaw Township North, MI MSA 28,037 27,619 29,275 31,550 (0.2) 1.5 1.3

State of Michigan 32,733 31,249 33,185 36,061 (0.5) 1.5 1.4

United States 33,756 35,951 37,209 40,245 0.6 0.9 1.3

W&P Wealth Index

Sanilac County 78.4 74.3 75.9 75.5 (0.5) 0.5 (0.1)

Saginaw-Saginaw Township North, MI MSA 82.5 75.9 77.2 76.9 (0.8) 0.4 (0.1)

State of Michigan 96.6 86.1 87.9 88.2 (1.1) 0.5 0.1

United States 100.0 100.0 100.0 100.0 0.0 0.0 0.0

Food and Beverage Sales (Millions)*

Sanilac County $24 $23 $25 $27 (0.3) 2.1 1.3

Saginaw-Saginaw Township North, MI MSA 304 256 280 294 (1.7) 2.3 0.8

State of Michigan 11,219 10,721 11,833 12,599 (0.5) 2.5 1.0

United States 341,369 408,974 461,843 512,773 1.8 3.1 1.8

Total Retail Sales (Millions)*

Sanilac County $383 $268 $292 $313 (3.5) 2.1 1.2

Saginaw-Saginaw Township North, MI MSA 3,343 2,350 2,541 2,665 (3.5) 2.0 0.8

State of Michigan 131,154 101,492 111,481 119,351 (2.5) 2.4 1.1

United States 3,612,260 3,796,423 4,298,146 4,803,190 0.5 3.2 1.9

* Inflation Adjusted

Source: Woods & Poole Economics, Inc.

August-2014 Market Area Analysis Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 34

The U.S. population has grown at an average annual compounded rate of 0.9% from 2010 through 2014. The county’s population has declined slightly when compared to the nation’s population; the average annual growth rate of 0.0% between 2010 and 2014 reflects a relatively stable area. Following this population trend, per-capita personal income increased slowly, at 1.5% on average annually for the county between 2010 and 2014. Local wealth indexes have remained stable in recent years, registering a relatively low 75.9 level for the county in 2014.

Food and beverage sales totaled $25 million in the county in 2014, versus $23 million in 2010. This reflects a 2.1% average annual change, which is stronger than the -0.3% pace recorded in the prior decade, the latter years of which were adversely affected by the recession. Over the long term, the pace of growth is forecast to moderate to a more sustainable level of 1.3%, which is forecast through 2020. The retail sales sector demonstrated an annual decline of -3.5% registered in the decade 2000 to 2010, followed by an increase of 2.1% in the period 2010 to 2014. An increase of 1.2% average annual change is expected in county retail sales through 2020.

The characteristics of an area's workforce provide an indication of the type and amount of transient visitation likely to be generated by local businesses. Sectors such as finance, insurance, and real estate (FIRE); wholesale trade; and services produce a considerable number of visitors who are not particularly rate-sensitive. The government sector often generates transient room nights, but per-diem reimbursement allowances often limit the accommodations selection to budget and mid-priced lodging facilities. Contributions from manufacturing, construction, transportation, communications, and public utilities (TCPU) employers can also be important, depending on the company type.

The following table sets forth the county workforce distribution by business sector in 2000, 2010, and 2014, as well as a forecast for 2020.

Workforce Characteristics

August-2014 Market Area Analysis Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 35

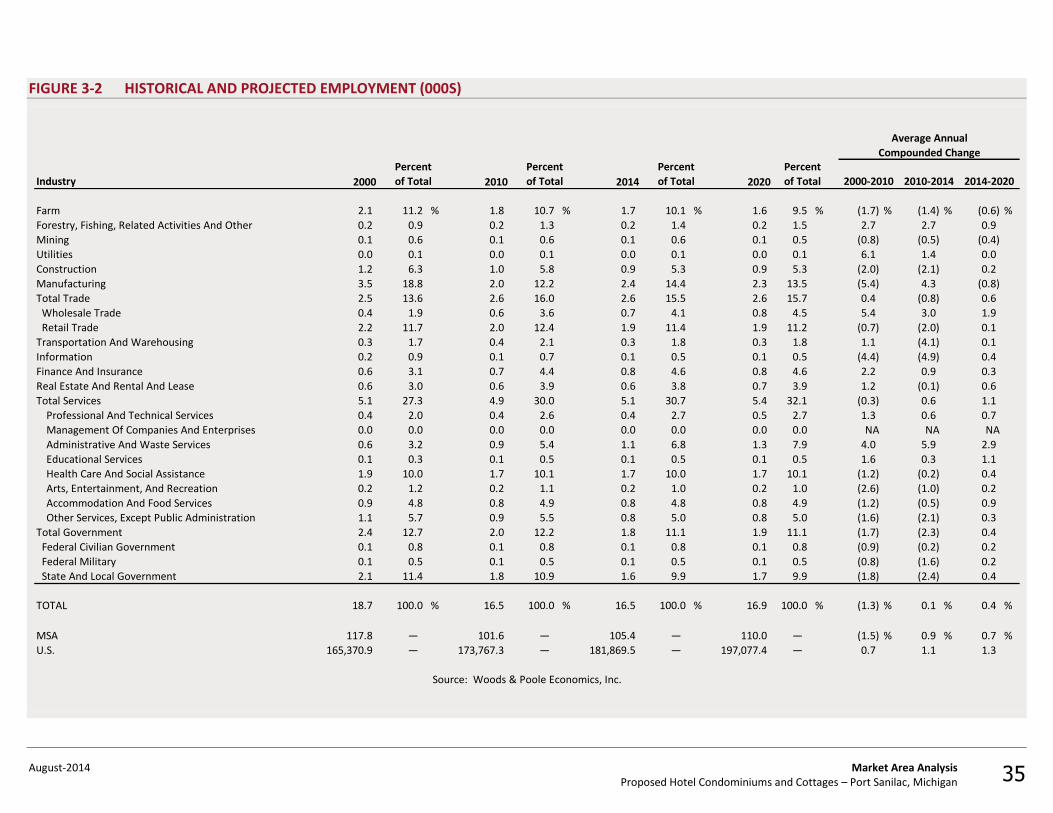

FIGURE 3-2 HISTORICAL AND PROJECTED EMPLOYMENT (000S)

Average Annual

Compounded ChangePercent Percent Percent Percent

Industry 2000 of Total 2010 of Total 2014 of Total 2020 of Total

Farm 2.1 11.2 % 1.8 10.7 % 1.7 10.1 % 1.6 9.5 % (1.7) % (1.4) % (0.6) %

Forestry, Fishing, Related Activities And Other 0.2 0.9 0.2 1.3 0.2 1.4 0.2 1.5 2.7 2.7 0.9

Mining 0.1 0.6 0.1 0.6 0.1 0.6 0.1 0.5 (0.8) (0.5) (0.4)

Utilities 0.0 0.1 0.0 0.1 0.0 0.1 0.0 0.1 6.1 1.4 0.0

Construction 1.2 6.3 1.0 5.8 0.9 5.3 0.9 5.3 (2.0) (2.1) 0.2

Manufacturing 3.5 18.8 2.0 12.2 2.4 14.4 2.3 13.5 (5.4) 4.3 (0.8)

Total Trade 2.5 13.6 2.6 16.0 2.6 15.5 2.6 15.7 0.4 (0.8) 0.6

Wholesale Trade 0.4 1.9 0.6 3.6 0.7 4.1 0.8 4.5 5.4 3.0 1.9

Retail Trade 2.2 11.7 2.0 12.4 1.9 11.4 1.9 11.2 (0.7) (2.0) 0.1

Transportation And Warehousing 0.3 1.7 0.4 2.1 0.3 1.8 0.3 1.8 1.1 (4.1) 0.1

Information 0.2 0.9 0.1 0.7 0.1 0.5 0.1 0.5 (4.4) (4.9) 0.4

Finance And Insurance 0.6 3.1 0.7 4.4 0.8 4.6 0.8 4.6 2.2 0.9 0.3

Real Estate And Rental And Lease 0.6 3.0 0.6 3.9 0.6 3.8 0.7 3.9 1.2 (0.1) 0.6

Total Services 5.1 27.3 4.9 30.0 5.1 30.7 5.4 32.1 (0.3) 0.6 1.1

Professional And Technical Services 0.4 2.0 0.4 2.6 0.4 2.7 0.5 2.7 1.3 0.6 0.7

Management Of Companies And Enterprises 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 NA NA NA

Administrative And Waste Services 0.6 3.2 0.9 5.4 1.1 6.8 1.3 7.9 4.0 5.9 2.9

Educational Services 0.1 0.3 0.1 0.5 0.1 0.5 0.1 0.5 1.6 0.3 1.1

Health Care And Social Assistance 1.9 10.0 1.7 10.1 1.7 10.0 1.7 10.1 (1.2) (0.2) 0.4

Arts, Entertainment, And Recreation 0.2 1.2 0.2 1.1 0.2 1.0 0.2 1.0 (2.6) (1.0) 0.2

Accommodation And Food Services 0.9 4.8 0.8 4.9 0.8 4.8 0.8 4.9 (1.2) (0.5) 0.9

Other Services, Except Public Administration 1.1 5.7 0.9 5.5 0.8 5.0 0.8 5.0 (1.6) (2.1) 0.3

Total Government 2.4 12.7 2.0 12.2 1.8 11.1 1.9 11.1 (1.7) (2.3) 0.4

Federal Civilian Government 0.1 0.8 0.1 0.8 0.1 0.8 0.1 0.8 (0.9) (0.2) 0.2

Federal Military 0.1 0.5 0.1 0.5 0.1 0.5 0.1 0.5 (0.8) (1.6) 0.2

State And Local Government 2.1 11.4 1.8 10.9 1.6 9.9 1.7 9.9 (1.8) (2.4) 0.4

TOTAL 18.7 100.0 % 16.5 100.0 % 16.5 100.0 % 16.9 100.0 % (1.3) % 0.1 % 0.4 %

MSA 117.8 — 101.6 — 105.4 — 110.0 — (1.5) % 0.9 % 0.7 %

U.S. 165,370.9 — 173,767.3 — 181,869.5 — 197,077.4 — 0.7 1.1 1.3

Source: Woods & Poole Economics, Inc.

2000-2010 2010-2014 2014-2020

August-2014 Market Area Analysis Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 36

Woods & Poole Economics, Inc. reports that during the period from 2000 to 2010, total employment in the county contracted at an average annual rate of -1.3%. This trend was above the growth rate recorded by the MSA and also lagged the national average. More recently, the pace of total employment growth in the county accelerated to 0.1% on an annual average from 2010 to 2014, reflecting the initial years of the recovery.

Of the primary employment sectors, Manufacturing recorded the highest increase in number of employees during the period from 2010 to 2014, increasing by 372 people, or 18.5%, and rising from 12.2% to 14.4% of total employment. Of the various service sub-sectors, Health Care And Social Assistance and Administrative And Waste Services were the largest employers. Strong growth was also recorded in the Total Services sector, as well as the Finance And Insurance sector, which expanded by -8.2% and -8.2%, respectively, in the period 2010 to 2014. Forecasts developed by Woods & Poole Economics, Inc. anticipate that total employment in the county will change by 0.4% on average annually through 2020. The trend is below the forecast rate of change for the U.S. as a whole during the same period.

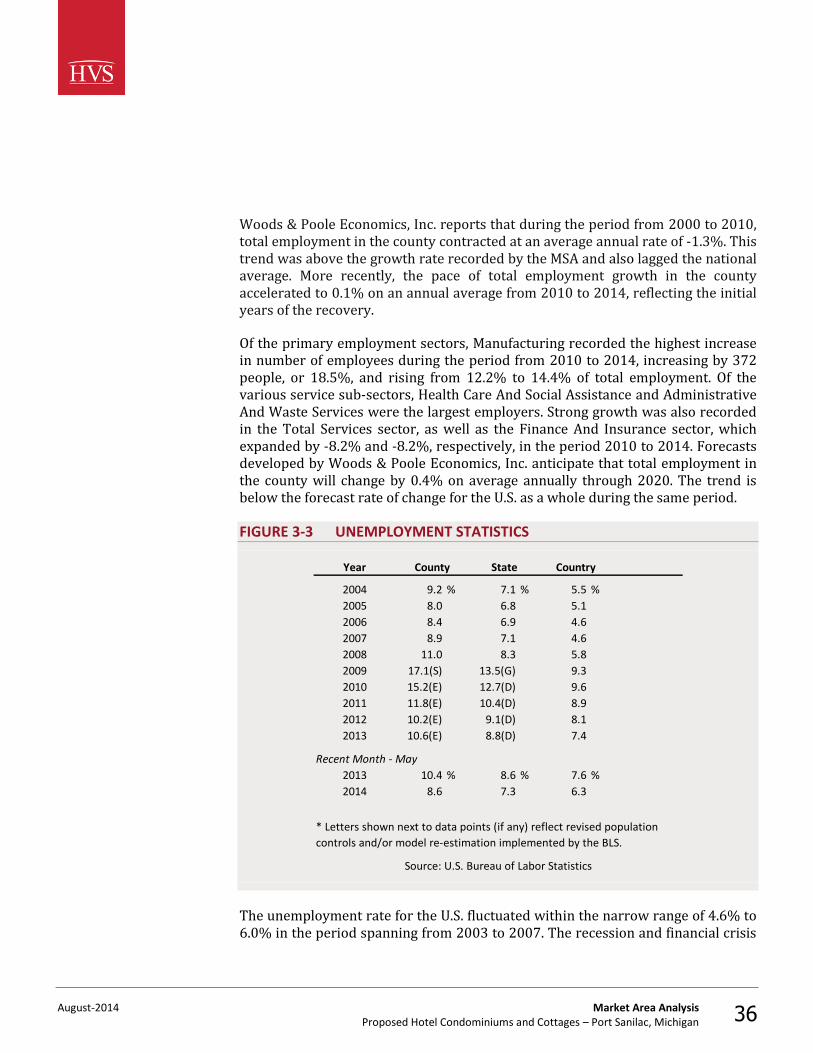

FIGURE 3-3 UNEMPLOYMENT STATISTICS

Year

2004 9.2 % 7.1 % 5.5 %

2005 8.0 6.8 5.1

2006 8.4 6.9 4.6

2007 8.9 7.1 4.6

2008 11.0 8.3 5.8

2009 17.1(S) 13.5(G) 9.3

2010 15.2(E) 12.7(D) 9.6

2011 11.8(E) 10.4(D) 8.9

2012 10.2(E) 9.1(D) 8.1

2013 10.6(E) 8.8(D) 7.4

Recent Month - May

2013 10.4 % 8.6 % 7.6 %

2014 8.6 7.3 6.3

County State

Source: U.S. Bureau of Labor Statistics

Country

* Letters shown next to data points (if any) reflect revised population

controls and/or model re-estimation implemented by the BLS.

The unemployment rate for the U.S. fluctuated within the narrow range of 4.6% to 6.0% in the period spanning from 2003 to 2007. The recession and financial crisis

August-2014 Market Area Analysis Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 37

in 2007 and 2008 resulted in heightened unemployment rates, which peaked at 10.0% in October of 2009. Job growth resumed in late 2009; the national unemployment rate has steadily declined since 2010. Total nonfarm payroll employment increased by 75,000, 113,000, and 175,000 jobs in December of 2013 and January and February of 2014, respectively, which brought the unemployment rate to 6.7%, remaining near the lowest level in over four years. Job growth has averaged 189,000 per month over the last twelve months. In February of 2014, job growth was strongest in professional and business services, as well as wholesale trade. This positive trend reflects steady progress by the U.S. economy.

Locally, the unemployment rate for the county was 10.6(E)% in 2013; for this same area in 2014, the most recent month’s unemployment rate was registered at 8.6%, versus 10.4% for the same month in 2013. Local employment is highly dependent on the automobile and manufacturing sectors, with over 4,000 manufacturing plants in the Metro Detroit area. Unemployment rates in the area remained relatively stable from 2003 through 2007. However, unemployment notably increased in 2008 as the nation entered an economic slowdown; this negative trend continued into 2009, illustrated by the extraordinarily high unemployment figures that year. In 2009, General Motors and Chrysler emerged from bankruptcy restructurings with funding provided in part by the U.S. and Canadian governments. The general strengthening of the world's traditional automotive center led the local economy with significant decreases in unemployment rates from 2010 through 2012. The most recent comparative period illustrates further improvement, as indicated by the latest available data for 2014, primarily due to growing employment in the manufacturing, professional services, and trade and transportation sectors.

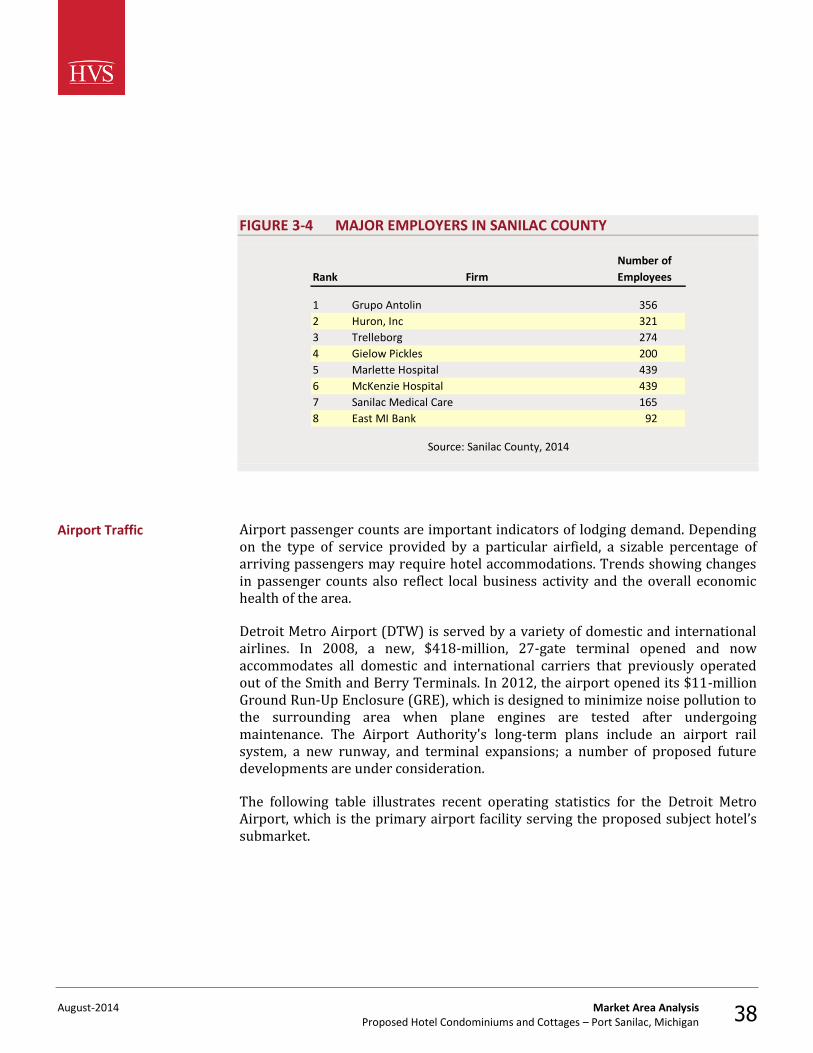

Providing additional context for understanding the nature of the regional economy, the following table presents a list of the major employers in the subject property’s market.

Major Business and Industry

August-2014 Market Area Analysis Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 38

FIGURE 3-4 MAJOR EMPLOYERS IN SANILAC COUNTY

Number of

Rank Firm Employees

1 Grupo Antolin 356

2 Huron, Inc 321

3 Trelleborg 274

4 Gielow Pickles 200

5 Marlette Hospital 439

6 McKenzie Hospital 439

7 Sanilac Medical Care 165

8 East MI Bank 92

Source: Sanilac County, 2014

Airport passenger counts are important indicators of lodging demand. Depending on the type of service provided by a particular airfield, a sizable percentage of arriving passengers may require hotel accommodations. Trends showing changes in passenger counts also reflect local business activity and the overall economic health of the area.

Detroit Metro Airport (DTW) is served by a variety of domestic and international airlines. In 2008, a new, $418-million, 27-gate terminal opened and now accommodates all domestic and international carriers that previously operated out of the Smith and Berry Terminals. In 2012, the airport opened its $11-million Ground Run-Up Enclosure (GRE), which is designed to minimize noise pollution to the surrounding area when plane engines are tested after undergoing maintenance. The Airport Authority's long-term plans include an airport rail system, a new runway, and terminal expansions; a number of proposed future developments are under consideration.

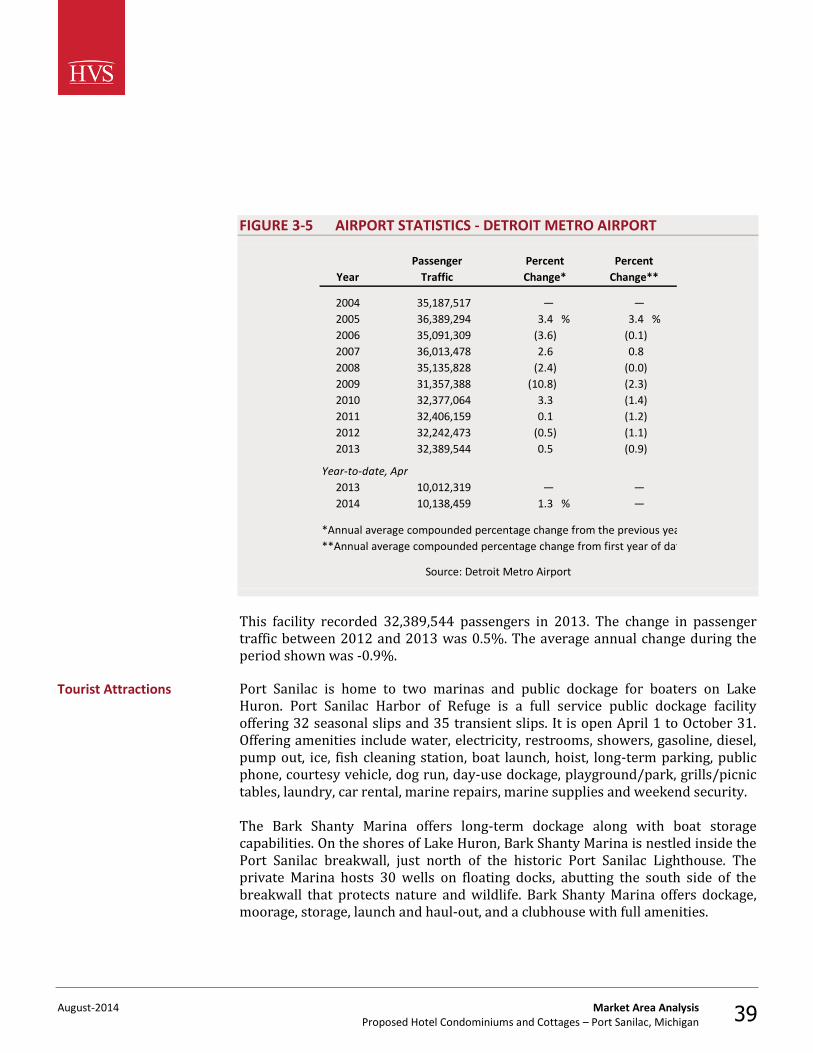

The following table illustrates recent operating statistics for the Detroit Metro Airport, which is the primary airport facility serving the proposed subject hotel’s submarket.

Airport Traffic

August-2014 Market Area Analysis Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 39

FIGURE 3-5 AIRPORT STATISTICS - DETROIT METRO AIRPORT

Year

2004 35,187,517 — —

2005 36,389,294 3.4 % 3.4 %

2006 35,091,309 (3.6) (0.1)

2007 36,013,478 2.6 0.8

2008 35,135,828 (2.4) (0.0)

2009 31,357,388 (10.8) (2.3)

2010 32,377,064 3.3 (1.4)

2011 32,406,159 0.1 (1.2)

2012 32,242,473 (0.5) (1.1)

2013 32,389,544 0.5 (0.9)

Year-to-date, Apr

2013 10,012,319 — —

2014 10,138,459 1.3 % —

*Annual average compounded percentage change from the previous year

**Annual average compounded percentage change from first year of data

Source: Detroit Metro Airport

Passenger

Change*Traffic

Percent Percent

Change**

This facility recorded 32,389,544 passengers in 2013. The change in passenger traffic between 2012 and 2013 was 0.5%. The average annual change during the period shown was -0.9%.

Port Sanilac is home to two marinas and public dockage for boaters on Lake Huron. Port Sanilac Harbor of Refuge is a full service public dockage facility offering 32 seasonal slips and 35 transient slips. It is open April 1 to October 31. Offering amenities include water, electricity, restrooms, showers, gasoline, diesel, pump out, ice, fish cleaning station, boat launch, hoist, long-term parking, public phone, courtesy vehicle, dog run, day-use dockage, playground/park, grills/picnic tables, laundry, car rental, marine repairs, marine supplies and weekend security. The Bark Shanty Marina offers long-term dockage along with boat storage capabilities. On the shores of Lake Huron, Bark Shanty Marina is nestled inside the Port Sanilac breakwall, just north of the historic Port Sanilac Lighthouse. The private Marina hosts 30 wells on floating docks, abutting the south side of the breakwall that protects nature and wildlife. Bark Shanty Marina offers dockage, moorage, storage, launch and haul-out, and a clubhouse with full amenities.

Tourist Attractions

August-2014 Market Area Analysis Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 40

Port Sanilac is home to the Sanilac Shores Underwater Preserve. This marine museum is home to a number of historical shipwrecks, including the Regina, a 250-foot steel package freighter that sank in a fierce gale in 1913. The Regina, which was discovered in 1986, and some of its cargo rests in 80 feet of water, with the ship rising 25 feet from the bottom. Other shipwrecks include Mary Alice B, North Star, F.B. Gardner, Charles Street, F.B. Gardner, Col A.B. Williams, Checotah and New York. Diving charters are available from Port Sanilac Harbor. Sanilac Shores Underwater Preserve offers some shipwreck diving in Michigan within a 163 square mile area in Lake Huron.

Port Sanilac is fast becoming a desired fishing destination for perch in Michigan. From late June through mid-August the perch abound. The rest of the year the area has everything from perch off the break wall for the most novice of fishers to salmon and walleye for the big game fishermen with large boats.

The Huron Shores Golf Club & Restaurants’ golf course is located just three miles north of the main downtown area of the Village of Port Sanilac. The 18-hole regulation course offers challenging golf with its rolling hills, water hazards, and tight fairways to the experienced golfer, yet and also be played by the beginner just learning the game.

The Sanilac County Historic Village and Museum is home to more than a dozen historic buildings. The ten-acre site is part of the estate of Dr. Joseph Loop and boasts gardens and Victorian, Edwardian vintage buildings and exhibits. The museum society also hosts a number of events throughout the year. A visit to the museum gives you a look back in time to the way life used to be in this lumbering, farming, and seafaring community. Highlights include seeing how children learned their ABCs in the one-room 19th century schoolhouse, the General Store, period-furnished mansion, marine shipwreck items, military memorabilia, and Native American artifacts.

The Barn Theatre is a non-profit summer stock theatre that prides itself on providing entertainment to local residents as well as visitors, and doing it all on a shoestring budget. The Theatre pulls in talented volunteers from all over eastern Michigan.

August-2014 Market Area Analysis Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 41

PORT SANILAC LIGHTHOUSE

This section discussed a wide variety of economic indicators for the pertinent market area. Port Sanilac is experiencing a period of economic recovery and strength, buoyed by tourism related attractions being developing in the village. The village is planning large development projects to implement at the Port Sanilac Harbor and the surrounding infrastructure. Once completed, the area is expected to transform to a beautiful leisure destination with a quaint atmosphere. The outlook for the market area is generally positive.

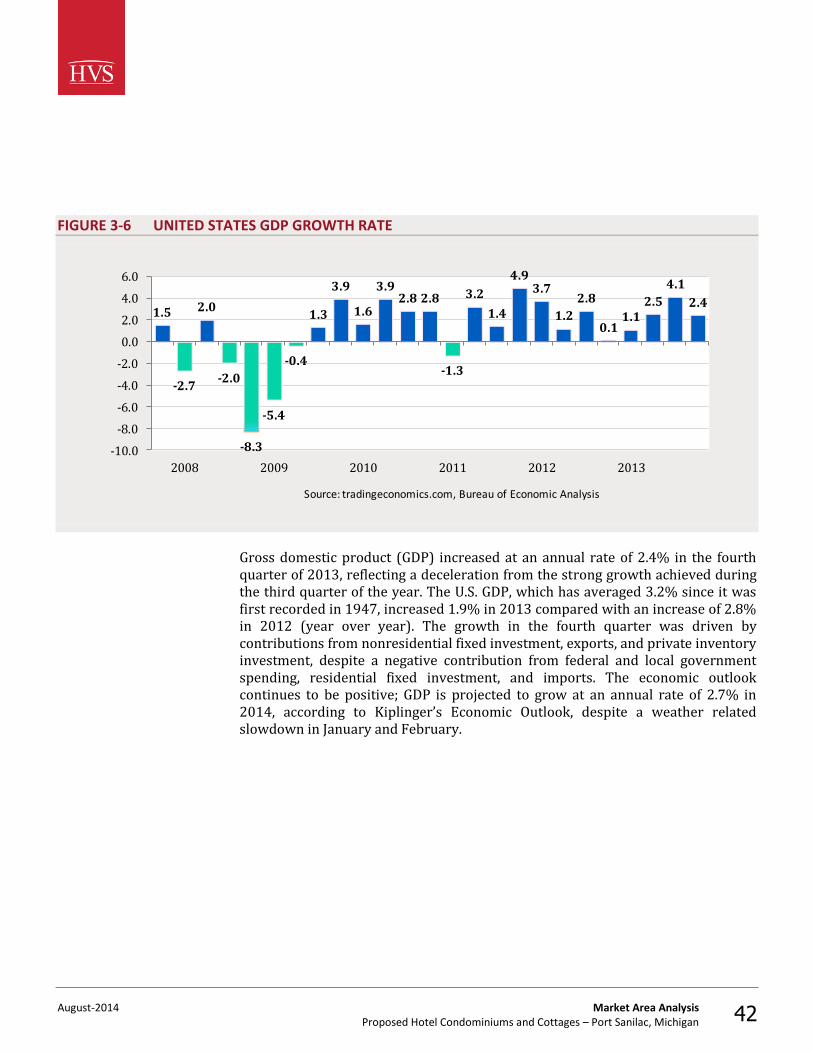

Our analysis of the outlook for this specific market also considers the broader context of the national economy. The U.S. economy entered a recession in December of 2007, which worsened in the fall of 2008 when the financial crisis shocked the world economy. The U.S. fell into economic decline for most of 2009, but the nation’s gross domestic product (GDP) and corporate profits began to grow again in the third quarter of 2009. In 2010, the economy experienced four consecutive quarters of economic growth, reflecting a rebound from the recession. Following a slight contraction in the first quarter of 2011, the economy has grown at positive, albeit fluctuating rates, as evidenced in the following table.

Conclusion

National GDP

August-2014 Market Area Analysis Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 42

FIGURE 3-6 UNITED STATES GDP GROWTH RATE

1.5

-2.7

2.0

-2.0

-8.3

-5.4

-0.4

1.3

3.9

1.6

3.92.8 2.8

-1.3

3.2

1.4

4.93.7

1.2

2.8

0.11.1

2.5

4.1

2.4

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

2008 2009 2010 2011 2012 2013

Source: tradingeconomics.com, Bureau of Economic Analysis

Gross domestic product (GDP) increased at an annual rate of 2.4% in the fourth quarter of 2013, reflecting a deceleration from the strong growth achieved during the third quarter of the year. The U.S. GDP, which has averaged 3.2% since it was first recorded in 1947, increased 1.9% in 2013 compared with an increase of 2.8% in 2012 (year over year). The growth in the fourth quarter was driven by contributions from nonresidential fixed investment, exports, and private inventory investment, despite a negative contribution from federal and local government spending, residential fixed investment, and imports. The economic outlook continues to be positive; GDP is projected to grow at an annual rate of 2.7% in 2014, according to Kiplinger’s Economic Outlook, despite a weather related slowdown in January and February.

August-2014 Supply and Demand Analysis Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 43

4. Supply and Demand Analysis

In the lodging industry, price varies directly, but not proportionately, with demand and inversely, but not proportionately, with supply. Supply is measured by the number of guestrooms available, and demand is measured by the number of rooms occupied; the net effect of supply and demand toward equilibrium results in a prevailing price, or average rate. The purpose of this section is to investigate current supply and demand trends, as indicated by the current competitive market, and to set forth a basis for the projection of future supply and demand growth.

The 40-room Proposed Hotel Condominiums and Cottages will be located in Port Sanilac, Michigan. The greater market surrounding the subject site offers no hotel condos; however, there are numerous rental cottages in the immediate Port Sanilac and nearby Lexington areas, which are located to the south of Port Sanilac.

The proposed subject hotel condominium and wharf cottages are expected to compete with a smaller set of lodging facilities based on various factors. These factors may include location, price point, product quality, length of stay (such as an extended-stay focus vs. non-extended-stay focus), room type, or age of the units, among other factors. We have reviewed these pertinent attributes and established an expected competitive set based upon this review. Our review of the proposed subject hotel’s specific competitive set within the Port Sanilac area begins after our review of national occupancy, average rate, and RevPAR trends.

The proposed subject hotel condominium and wharf cottage rental market is most directly affected by the supply and demand trends within the immediate area. However, individual markets are also influenced by conditions in the national lodging market. We have reviewed national lodging trends to provide a context for the forecast of the supply and demand for the proposed subject hotel’s competitive set.

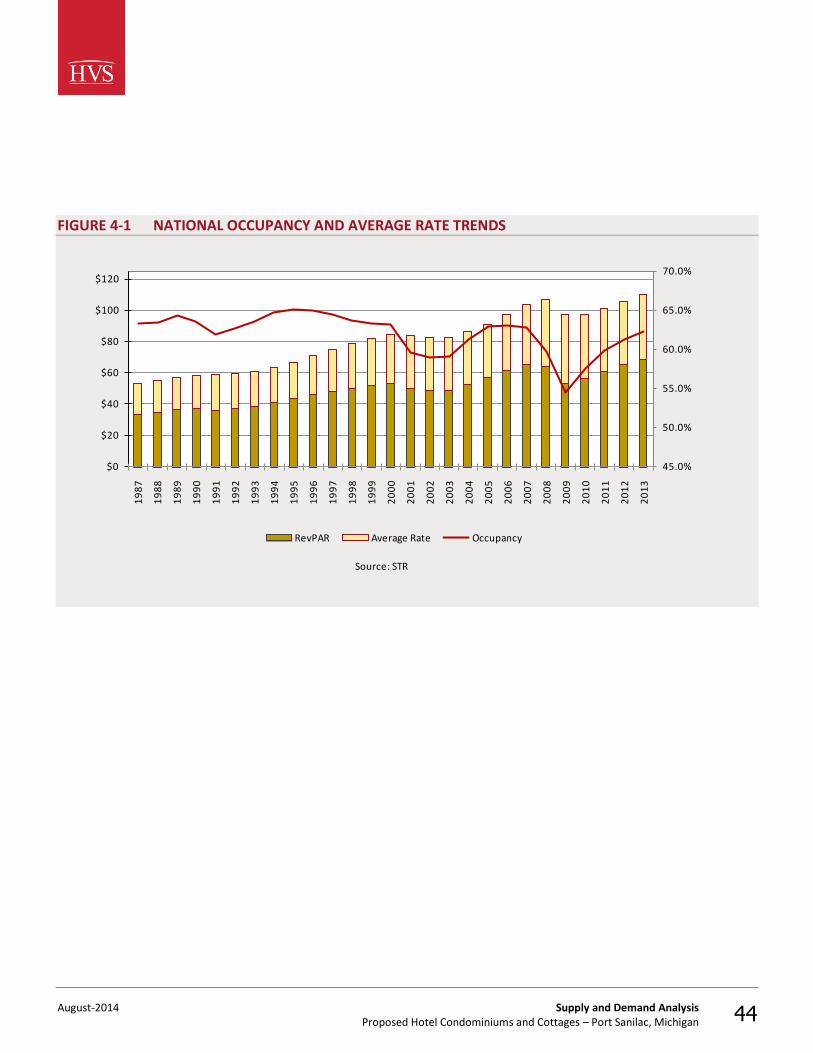

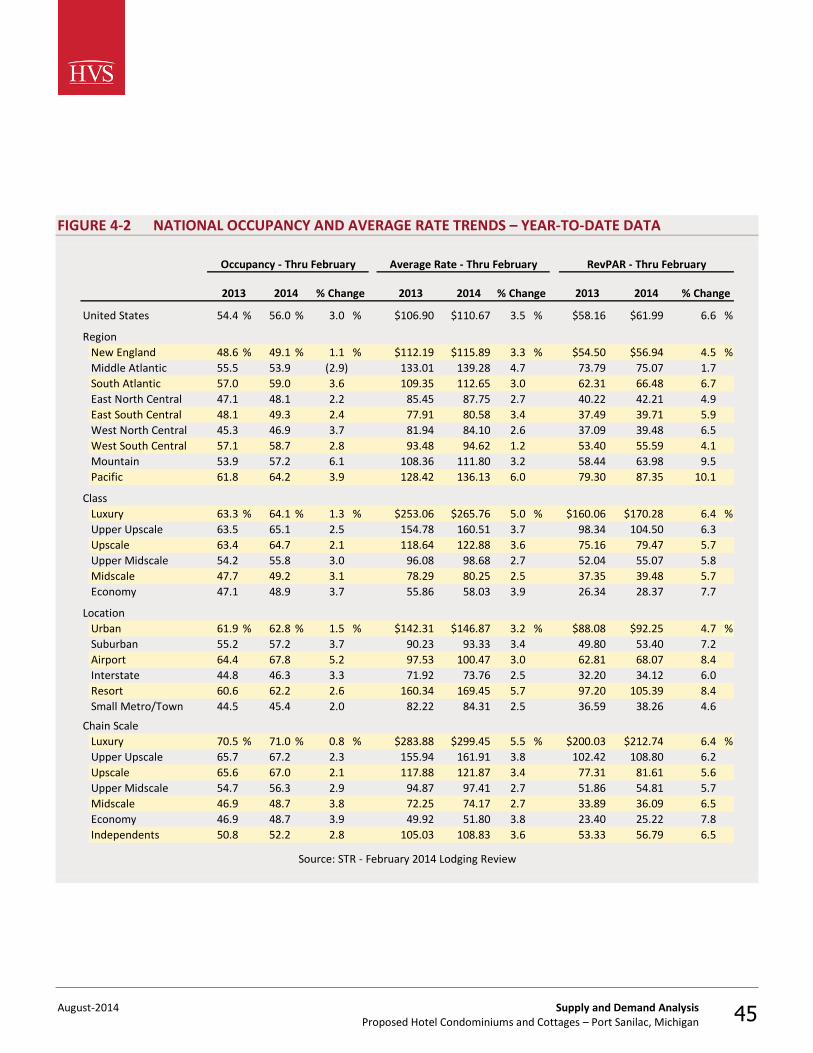

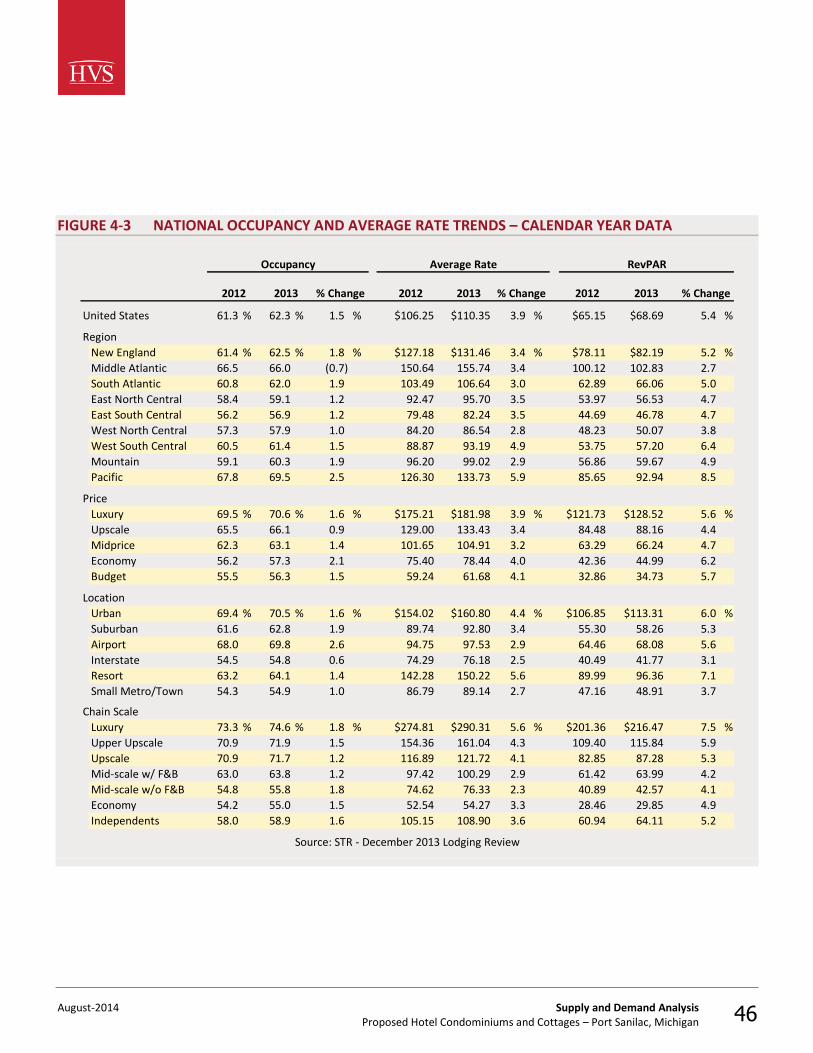

Smith Travel Research (STR) is an independent research firm that compiles data on the lodging industry, and this information is routinely used by typical hotel buyers. Figure 4-1 presents annual hotel occupancy and average rate data since 1987. Figures 4-2 and 4-3 illustrate the more recent trends, categorized by geography, price point, type of location, and chain scale. The statistics include occupancy, average rate, and rooms revenue per available room (RevPAR). RevPAR is calculated by multiplying occupancy by average rate and provides an indication of how well rooms revenue is being maximized.

Definition of Subject Hotel Market

National Trends Overview

August-2014 Supply and Demand Analysis Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 44

FIGURE 4-1 NATIONAL OCCUPANCY AND AVERAGE RATE TRENDS

45.0%

50.0%

55.0%

60.0%

65.0%

70.0%

$0

$20

$40

$60

$80

$100

$120

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Source: STR

RevPAR Average Rate Occupancy

August-2014 Supply and Demand Analysis Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 45

FIGURE 4-2 NATIONAL OCCUPANCY AND AVERAGE RATE TRENDS – YEAR-TO-DATE DATA

United States 54.4 % 56.0 % 3.0 % $106.90 $110.67 3.5 % $58.16 $61.99 6.6 %

Region

New England 48.6 % 49.1 % 1.1 % $112.19 $115.89 3.3 % $54.50 $56.94 4.5 %

Middle Atlantic 55.5 53.9 (2.9) 133.01 139.28 4.7 73.79 75.07 1.7

South Atlantic 57.0 59.0 3.6 109.35 112.65 3.0 62.31 66.48 6.7

East North Central 47.1 48.1 2.2 85.45 87.75 2.7 40.22 42.21 4.9

East South Central 48.1 49.3 2.4 77.91 80.58 3.4 37.49 39.71 5.9

West North Central 45.3 46.9 3.7 81.94 84.10 2.6 37.09 39.48 6.5

West South Central 57.1 58.7 2.8 93.48 94.62 1.2 53.40 55.59 4.1

Mountain 53.9 57.2 6.1 108.36 111.80 3.2 58.44 63.98 9.5

Pacific 61.8 64.2 3.9 128.42 136.13 6.0 79.30 87.35 10.1

Class

Luxury 63.3 % 64.1 % 1.3 % $253.06 $265.76 5.0 % $160.06 $170.28 6.4 %

Upper Upscale 63.5 65.1 2.5 154.78 160.51 3.7 98.34 104.50 6.3

Upscale 63.4 64.7 2.1 118.64 122.88 3.6 75.16 79.47 5.7

Upper Midscale 54.2 55.8 3.0 96.08 98.68 2.7 52.04 55.07 5.8

Midscale 47.7 49.2 3.1 78.29 80.25 2.5 37.35 39.48 5.7

Economy 47.1 48.9 3.7 55.86 58.03 3.9 26.34 28.37 7.7

Location

Urban 61.9 % 62.8 % 1.5 % $142.31 $146.87 3.2 % $88.08 $92.25 4.7 %

Suburban 55.2 57.2 3.7 90.23 93.33 3.4 49.80 53.40 7.2

Airport 64.4 67.8 5.2 97.53 100.47 3.0 62.81 68.07 8.4

Interstate 44.8 46.3 3.3 71.92 73.76 2.5 32.20 34.12 6.0

Resort 60.6 62.2 2.6 160.34 169.45 5.7 97.20 105.39 8.4

Small Metro/Town 44.5 45.4 2.0 82.22 84.31 2.5 36.59 38.26 4.6

Chain Scale

Luxury 70.5 % 71.0 % 0.8 % $283.88 $299.45 5.5 % $200.03 $212.74 6.4 %

Upper Upscale 65.7 67.2 2.3 155.94 161.91 3.8 102.42 108.80 6.2

Upscale 65.6 67.0 2.1 117.88 121.87 3.4 77.31 81.61 5.6

Upper Midscale 54.7 56.3 2.9 94.87 97.41 2.7 51.86 54.81 5.7

Midscale 46.9 48.7 3.8 72.25 74.17 2.7 33.89 36.09 6.5

Economy 46.9 48.7 3.9 49.92 51.80 3.8 23.40 25.22 7.8

Independents 50.8 52.2 2.8 105.03 108.83 3.6 53.33 56.79 6.5

2013 2014 % Change

Occupancy - Thru February Average Rate - Thru February RevPAR - Thru February

Source: STR - February 2014 Lodging Review

2013 % Change2013 20142014 % Change

August-2014 Supply and Demand Analysis Proposed Hotel Condominiums and Cottages – Port Sanilac, Michigan 46

FIGURE 4-3 NATIONAL OCCUPANCY AND AVERAGE RATE TRENDS – CALENDAR YEAR DATA

United States 61.3 % 62.3 % 1.5 % $106.25 $110.35 3.9 % $65.15 $68.69 5.4 %

Region

New England 61.4 % 62.5 % 1.8 % $127.18 $131.46 3.4 % $78.11 $82.19 5.2 %

Middle Atlantic 66.5 66.0 (0.7) 150.64 155.74 3.4 100.12 102.83 2.7

South Atlantic 60.8 62.0 1.9 103.49 106.64 3.0 62.89 66.06 5.0

East North Central 58.4 59.1 1.2 92.47 95.70 3.5 53.97 56.53 4.7

East South Central 56.2 56.9 1.2 79.48 82.24 3.5 44.69 46.78 4.7

West North Central 57.3 57.9 1.0 84.20 86.54 2.8 48.23 50.07 3.8

West South Central 60.5 61.4 1.5 88.87 93.19 4.9 53.75 57.20 6.4

Mountain 59.1 60.3 1.9 96.20 99.02 2.9 56.86 59.67 4.9

Pacific 67.8 69.5 2.5 126.30 133.73 5.9 85.65 92.94 8.5

Price

Luxury 69.5 % 70.6 % 1.6 % $175.21 $181.98 3.9 % $121.73 $128.52 5.6 %

Upscale 65.5 66.1 0.9 129.00 133.43 3.4 84.48 88.16 4.4

Midprice 62.3 63.1 1.4 101.65 104.91 3.2 63.29 66.24 4.7

Economy 56.2 57.3 2.1 75.40 78.44 4.0 42.36 44.99 6.2

Budget 55.5 56.3 1.5 59.24 61.68 4.1 32.86 34.73 5.7

Location

Urban 69.4 % 70.5 % 1.6 % $154.02 $160.80 4.4 % $106.85 $113.31 6.0 %

Suburban 61.6 62.8 1.9 89.74 92.80 3.4 55.30 58.26 5.3

Airport 68.0 69.8 2.6 94.75 97.53 2.9 64.46 68.08 5.6

Interstate 54.5 54.8 0.6 74.29 76.18 2.5 40.49 41.77 3.1

Resort 63.2 64.1 1.4 142.28 150.22 5.6 89.99 96.36 7.1

Small Metro/Town 54.3 54.9 1.0 86.79 89.14 2.7 47.16 48.91 3.7

Chain Scale

Luxury 73.3 % 74.6 % 1.8 % $274.81 $290.31 5.6 % $201.36 $216.47 7.5 %

Upper Upscale 70.9 71.9 1.5 154.36 161.04 4.3 109.40 115.84 5.9

Upscale 70.9 71.7 1.2 116.89 121.72 4.1 82.85 87.28 5.3

Mid-scale w/ F&B 63.0 63.8 1.2 97.42 100.29 2.9 61.42 63.99 4.2

Mid-scale w/o F&B 54.8 55.8 1.8 74.62 76.33 2.3 40.89 42.57 4.1

Economy 54.2 55.0 1.5 52.54 54.27 3.3 28.46 29.85 4.9

Independents 58.0 58.9 1.6 105.15 108.90 3.6 60.94 64.11 5.2

2013% Change % Change