Embed Size (px)

Citation preview

Financial Engineering and Actuarial Science In the Life Insurance Industry Presentation at University of California at Santa Barbara February 21, 2014 Frank Zhang, CFA, FRM, FSA, MSCF, PRM Vice President, Risk Management Pacific Life Insurance Company

2 2

Disclaimer

This presentation contains the current opinions of the author and not of my employer Pacific Life Insurance Company or the Society of Actuaries. Any such opinions are subject to change without notice. This presentation is distributed for educational purposes only.

3 3

Table of contents

Traditional insurance and risk management Variable annuities as a newer generation of hybrid products Financial engineering and actuarial science as a new practice for variable

annuities

4 4

Traditional insurance based on averages

Traditional insurance products with mortality, longevity, morbidity, etc. may be diversified

Most products can be safely priced based on actuarial expected values (averages) and standard deviation

Typical actuarial risk management techniques ⇒ Test sensitivities of assumptions ⇒ Test of distributions and tails

5 5

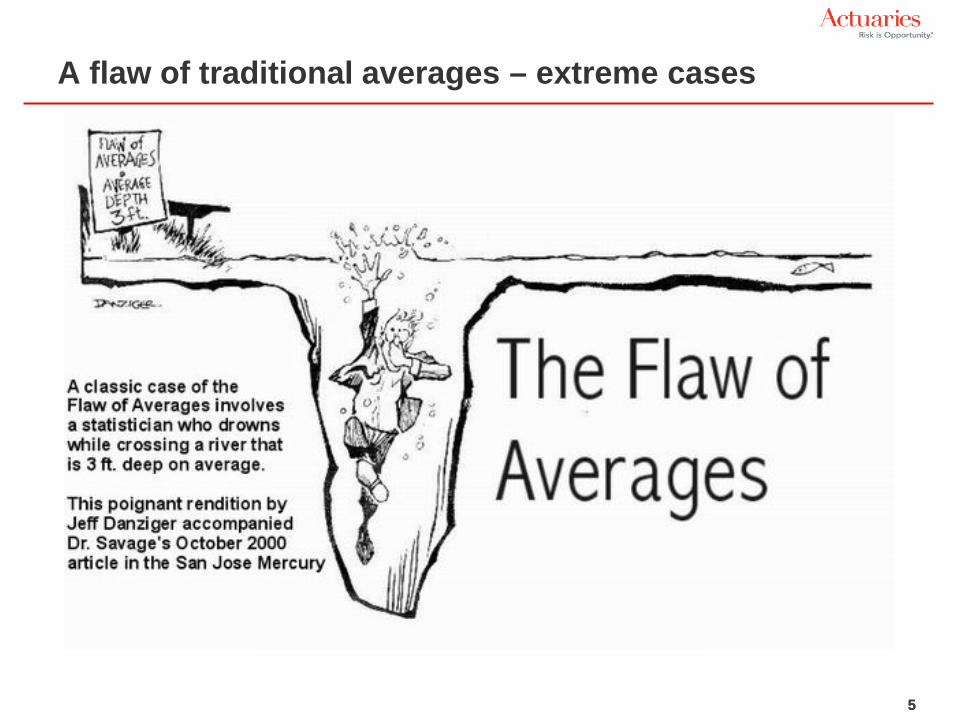

A flaw of traditional averages – extreme cases

6 6

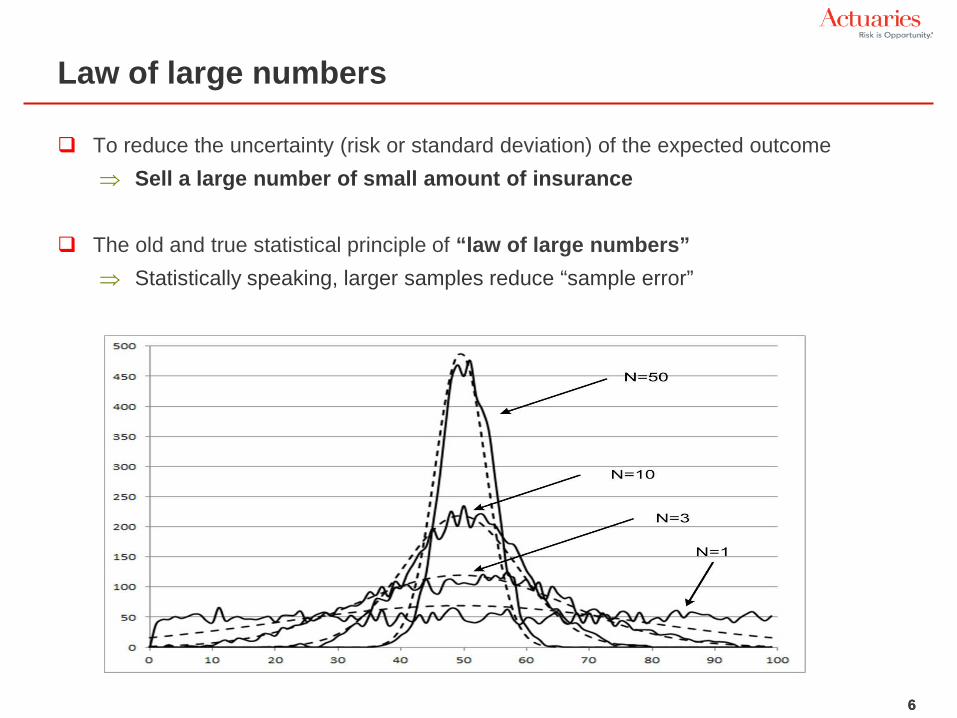

Law of large numbers

To reduce the uncertainty (risk or standard deviation) of the expected outcome ⇒ Sell a large number of small amount of insurance

The old and true statistical principle of “law of large numbers”

⇒ Statistically speaking, larger samples reduce “sample error”

7 7

Worked well with tail risk management, until …

Risk mitigations ⇒ Cut off the tails with caps in insurance coverage (to make sure no single case is

too large to kill like the crossing river example) ⇒ Sell more to diversify ⇒ Be prepared for rare but extreme pandemic events (systemic)

Actuarial risk analysis

⇒ Stochastic simulations and principle-based valuation ⇒ Look at more than the averages but also the distributions ⇒ Look at percentiles and use CTEs for tail risk

Worked well with traditional life and annuity products, until recently

⇒ Core insurance expertise is to pool diversifiable risks ⇒ How about newer generation of products, such as variable annuities?

8 8

Table of contents

Traditional insurance and risk management Variable annuities as a newer generation of hybrid products Financial engineering and actuarial science as a new practice for variable

annuities

9 9

Variable annuity (VA)

Life insurance products are increasingly derivatives oriented and many of the same derivatives valuation techniques apply

The hybrid products also create unique challenges and opportunities to actuaries and financial engineers

Variable annuity is a retirement investment account sold by life insurers ⇒ Underlying investments are generally “mutual funds” of various asset classes ⇒ Contract holders pay insurer and mutual fund manager fees over time ⇒ The account value can go higher or lower due to investment results ⇒ Guarantee payoffs = f( guaranteed amount - total basket value of mutual funds) ⇒ Death benefit is paid when

a) The account value is lower than principal and b) Policyholder died

⇒ Living benefits can be paid without having to die, based on different designs such as accumulation guarantees (wait for 10 years), withdrawal benefits (guaranteed withdrawal amounts, regardless of investment performance), etc.

⇒ Policyholders keep upside potential of the account performance – and insurance company provides the downside guarantees (put options!)

⇒ Many VA contracts have much more exotic benefits ⇒ Traditionally, policyholder may or may not exercise optimally

10

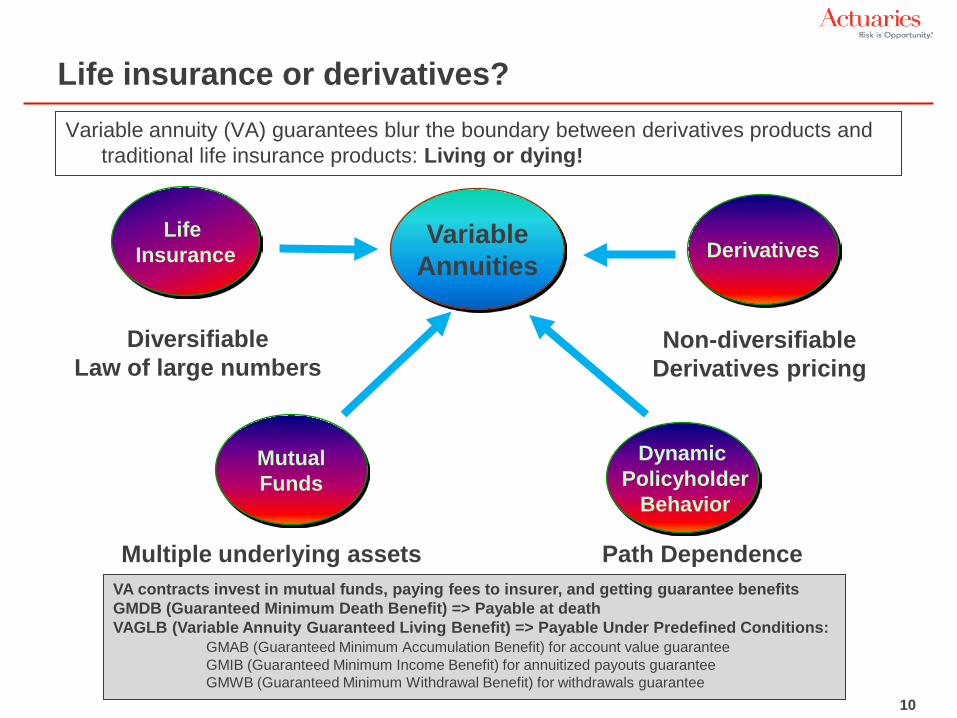

Life insurance or derivatives? Variable annuity (VA) guarantees blur the boundary between derivatives products and

traditional life insurance products: Living or dying!

Variable Annuities Derivatives

Life Insurance

Mutual Funds

Diversifiable Law of large numbers

Non-diversifiable Derivatives pricing

Multiple underlying assets

Dynamic Policyholder

Behavior

Path Dependence VA contracts invest in mutual funds, paying fees to insurer, and getting guarantee benefits GMDB (Guaranteed Minimum Death Benefit) => Payable at death VAGLB (Variable Annuity Guaranteed Living Benefit) => Payable Under Predefined Conditions: GMAB (Guaranteed Minimum Accumulation Benefit) for account value guarantee GMIB (Guaranteed Minimum Income Benefit) for annuitized payouts guarantee GMWB (Guaranteed Minimum Withdrawal Benefit) for withdrawals guarantee

11

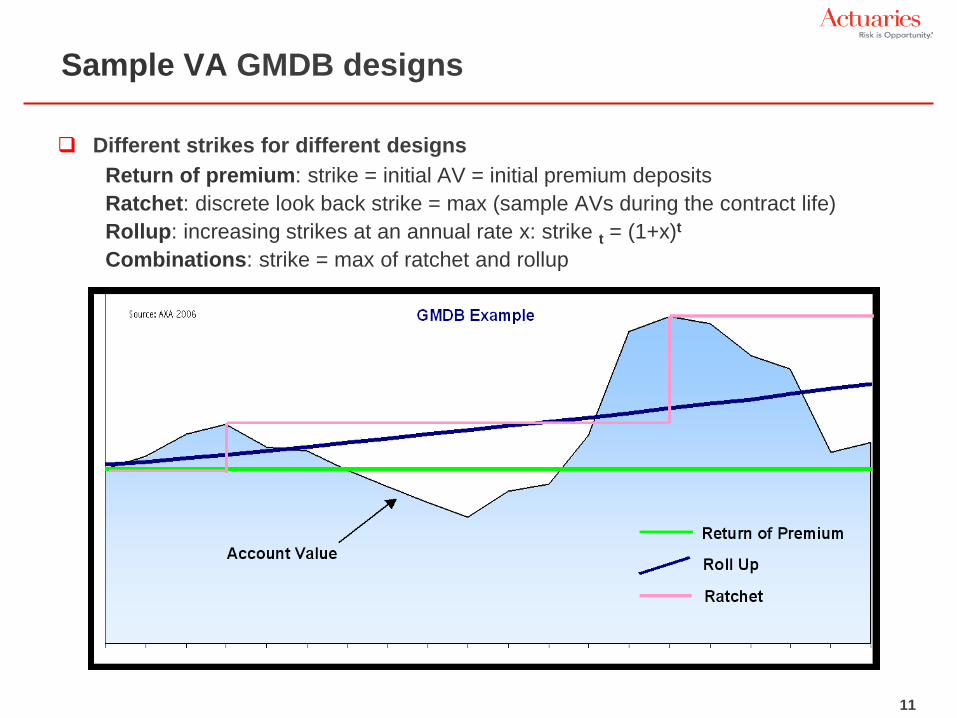

Sample VA GMDB designs

Different strikes for different designs Return of premium: strike = initial AV = initial premium deposits Ratchet: discrete look back strike = max (sample AVs during the contract life) Rollup: increasing strikes at an annual rate x: strike t = (1+x)t Combinations: strike = max of ratchet and rollup

12

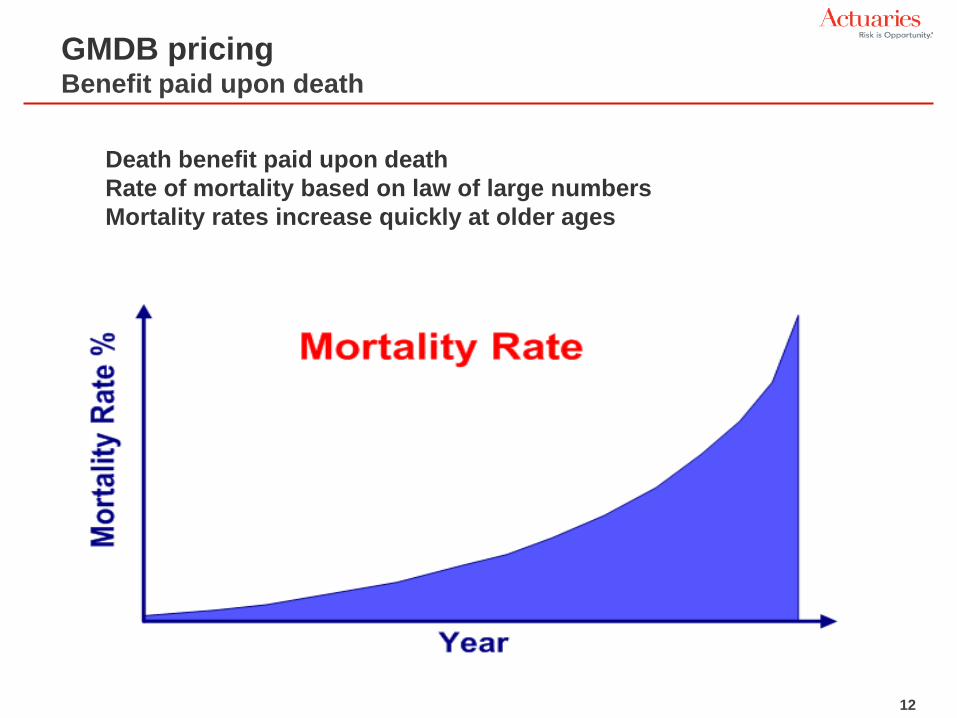

GMDB pricing Benefit paid upon death

Death benefit paid upon death Rate of mortality based on law of large numbers Mortality rates increase quickly at older ages

13

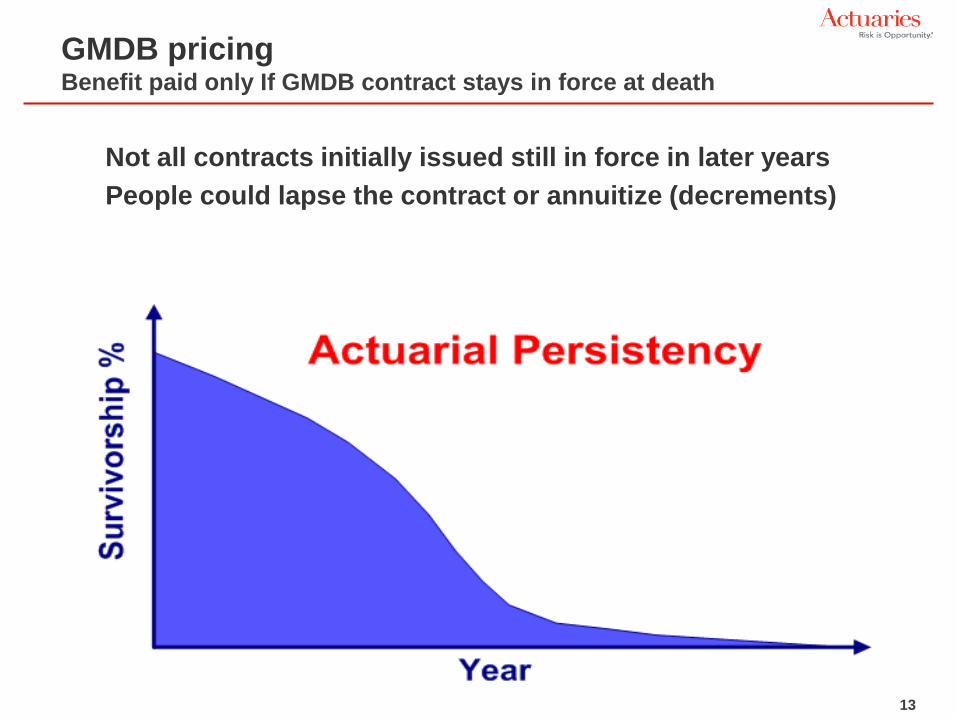

GMDB pricing Benefit paid only If GMDB contract stays in force at death

Not all contracts initially issued still in force in later years People could lapse the contract or annuitize (decrements)

14

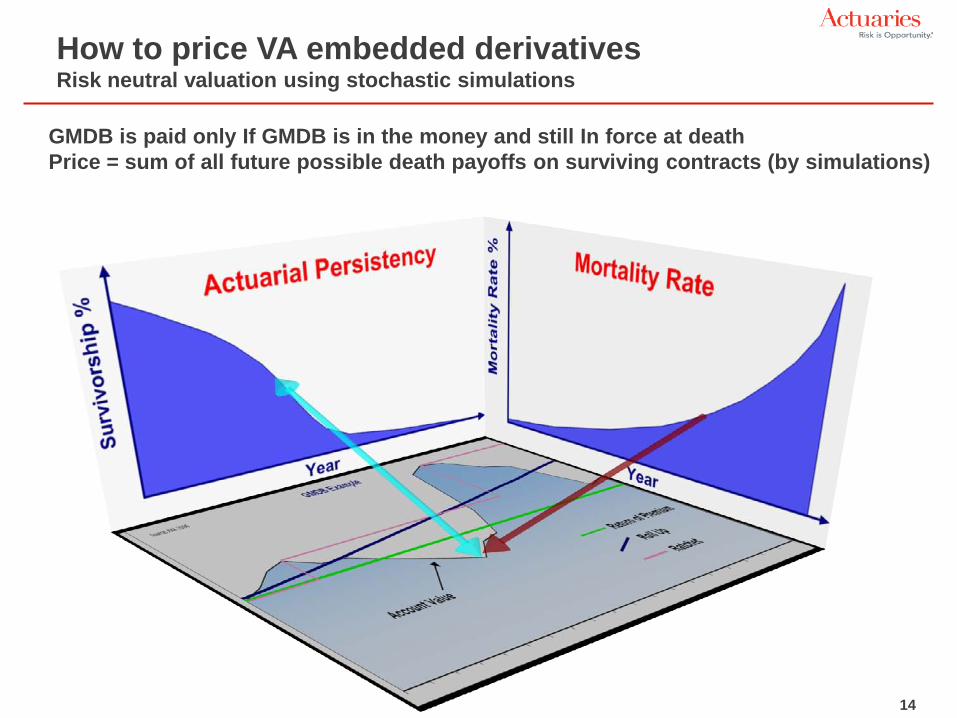

How to price VA embedded derivatives Risk neutral valuation using stochastic simulations

GMDB is paid only If GMDB is in the money and still In force at death Price = sum of all future possible death payoffs on surviving contracts (by simulations)

15 15

Table of contents

Traditional insurance and risk management Variable annuities as a newer generation of hybrid products Financial engineering and actuarial science as a new practice for

variable annuities

16 16

Capital market risk management

Capital markets represented by Wall Street and portfolio investments Traditional investments in fixed income (bonds), equity (stocks), and

modern derivatives (options) ⇒ Fixed income portfolio management focuses on interest rate risk and credit risk ⇒ Equity investment focuses on systematic risk (measured by beta) ⇒ Derivatives are priced using financial engineering techniques

Financial engineering is based on “law of one number” or no arbitrage Wall Street has used financial engineering to price and manage the risks for

derivatives

17 17

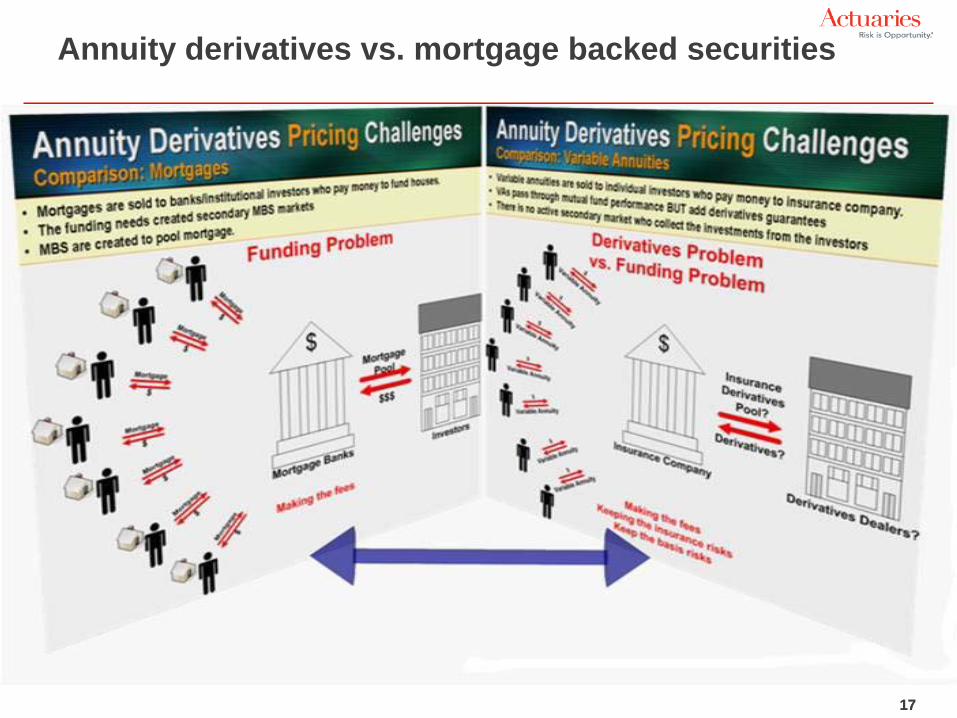

Annuity derivatives vs. mortgage backed securities

18

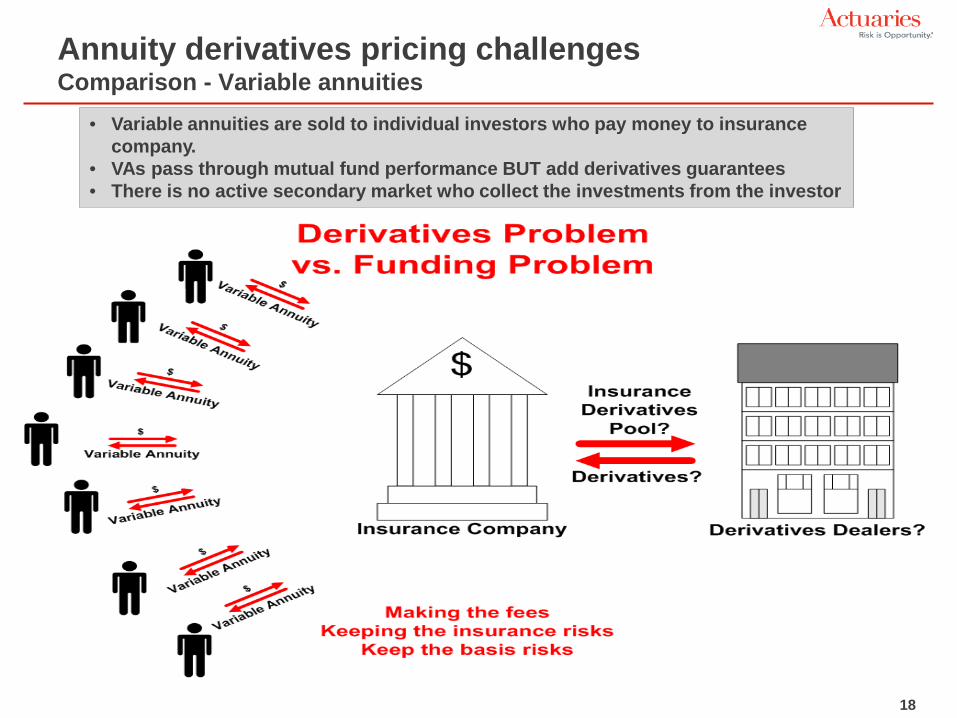

Annuity derivatives pricing challenges Comparison - Variable annuities

• Variable annuities are sold to individual investors who pay money to insurance company.

• VAs pass through mutual fund performance BUT add derivatives guarantees • There is no active secondary market who collect the investments from the investor

19

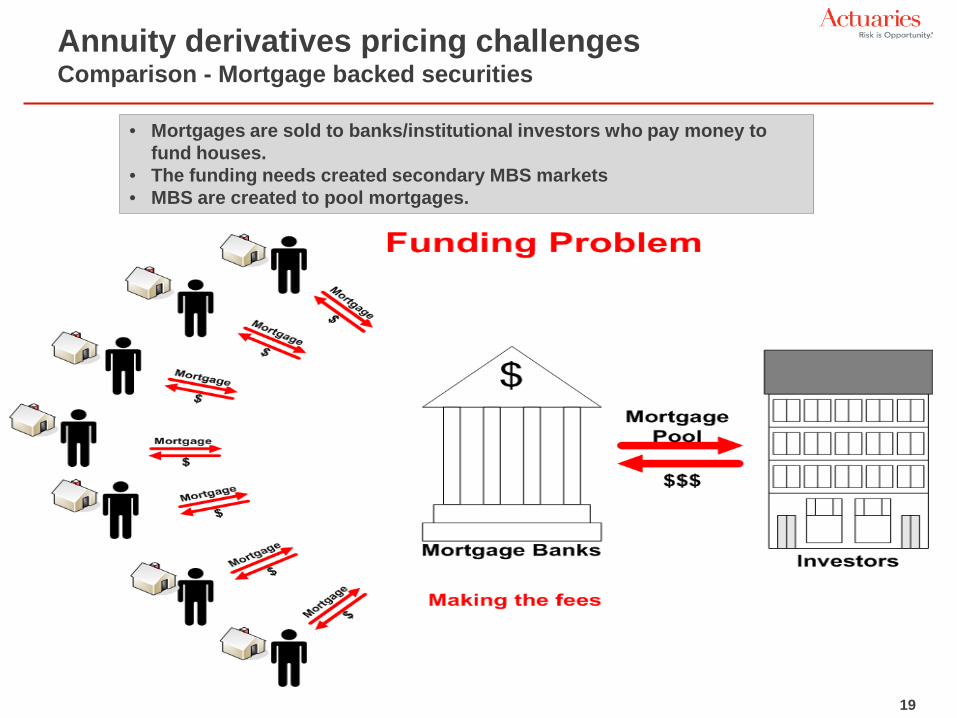

Annuity derivatives pricing challenges Comparison - Mortgage backed securities

• Mortgages are sold to banks/institutional investors who pay money to fund houses.

• The funding needs created secondary MBS markets • MBS are created to pool mortgages.

20 20

Dynamic policyholder behavior modeling is critical & difficult ⇒ Key driver for pricing but options not always exercised optimally ⇒ Mortality risk managed by pool of large numbers but living benefits much more challenging ⇒ Behavior very difficult to predict and with little or no experience ⇒ Policyholder dynamics causing significant gamma exposure ⇒ Capital market risks not diversifiable as insurance risks

MBS prepayment vs. annuities dynamic policyholder behavior modeling

⇒ MBS prepayments based on real world experience or expectations but validated by active capital market MBS prices, unlike annuities

⇒ Risk neutral pricing standard in financial engineering, but transition from actuarial expectations to risk neutral pricing caused confusions about probability distributions and stochastic simulations

⇒ MBS markets not usually concerned with nested stochastic projections that mix risk neutral world and risk neutral valuations, unlike annuities

Annuity derivatives pricing challenges Dynamic policyholder behavior modeling

21

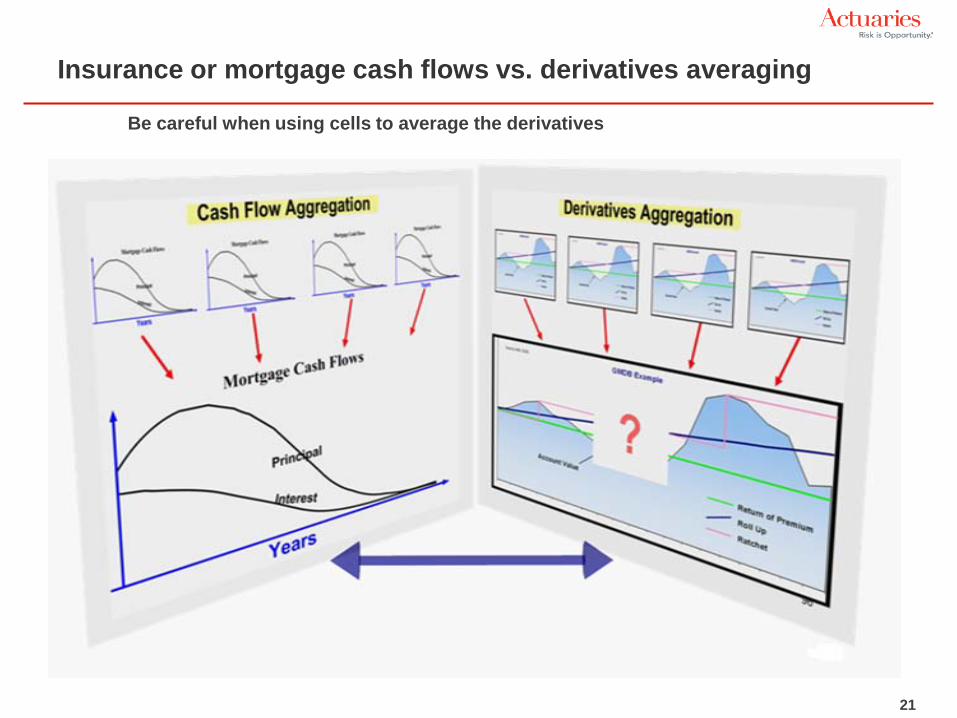

Insurance or mortgage cash flows vs. derivatives averaging

Be careful when using cells to average the derivatives

22

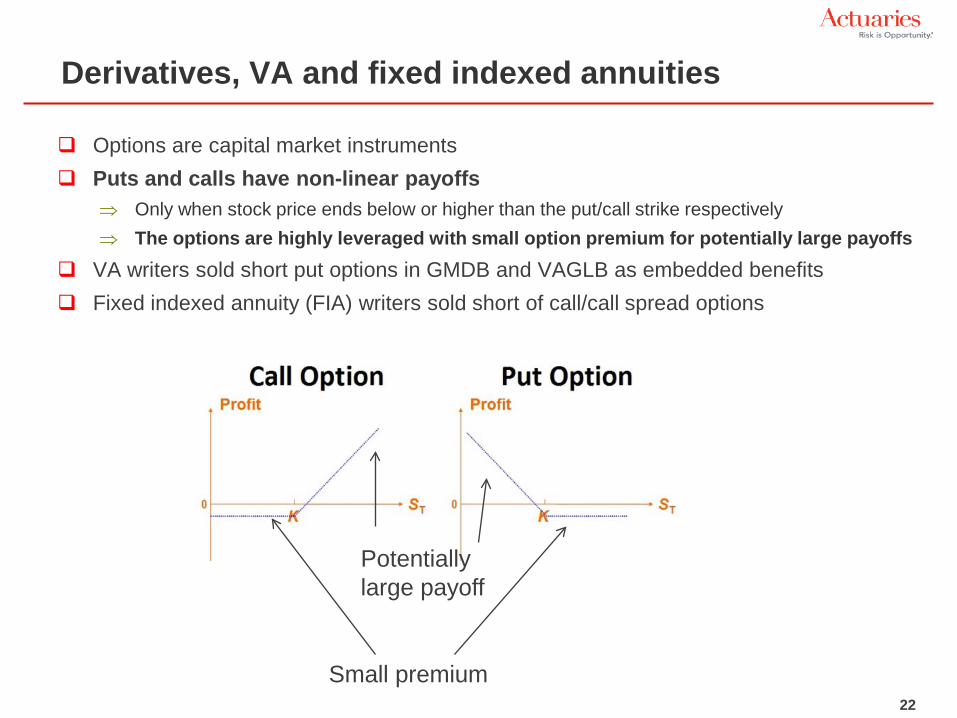

Derivatives, VA and fixed indexed annuities

Options are capital market instruments Puts and calls have non-linear payoffs

⇒ Only when stock price ends below or higher than the put/call strike respectively ⇒ The options are highly leveraged with small option premium for potentially large payoffs

VA writers sold short put options in GMDB and VAGLB as embedded benefits Fixed indexed annuity (FIA) writers sold short of call/call spread options

Small premium

Potentially large payoff

23 23

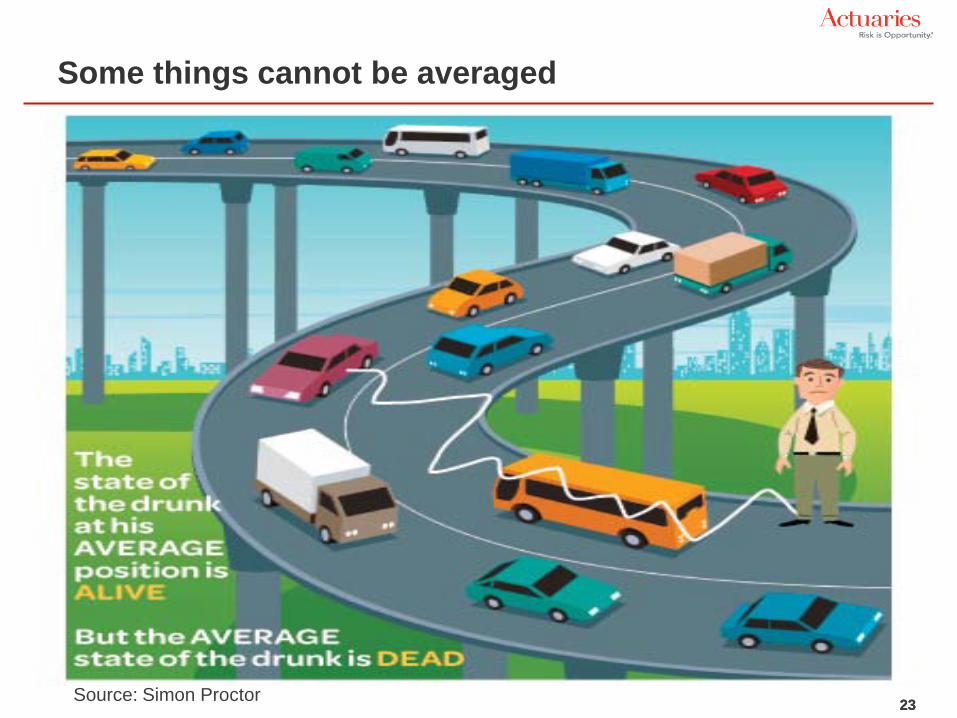

Some things cannot be averaged

Source: Simon Proctor

24

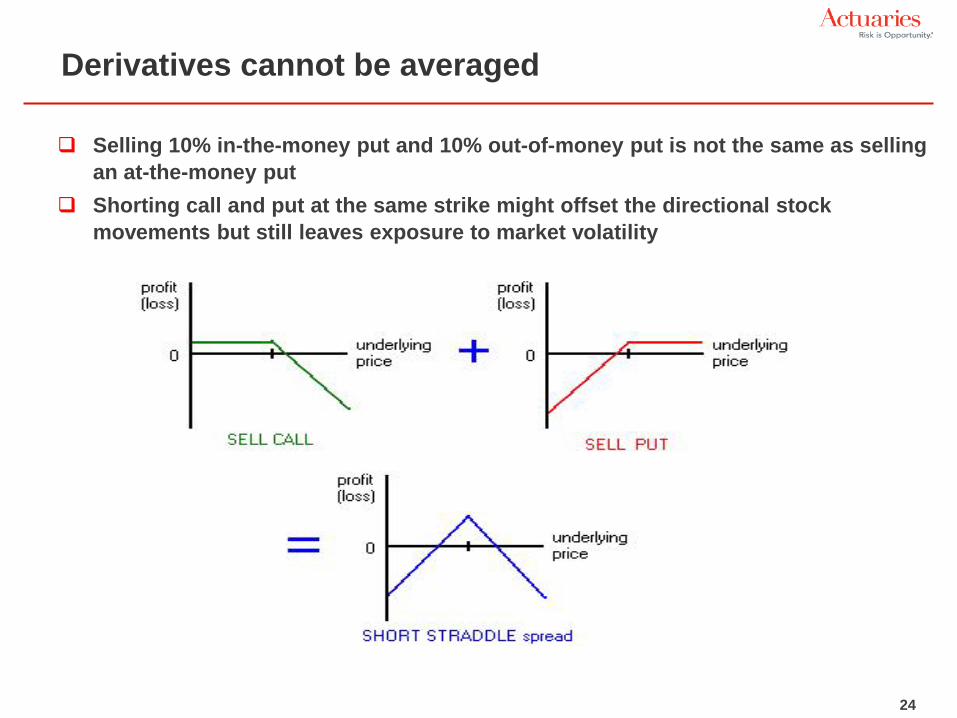

Derivatives cannot be averaged

Selling 10% in-the-money put and 10% out-of-money put is not the same as selling an at-the-money put

Shorting call and put at the same strike might offset the directional stock movements but still leaves exposure to market volatility

25 25

Capital market law of one number (price)

Financial engineering is based on “law of one number” or no arbitrage No arbitrage means no risk-free way of making money and there is only one price

that is the market price

26 26

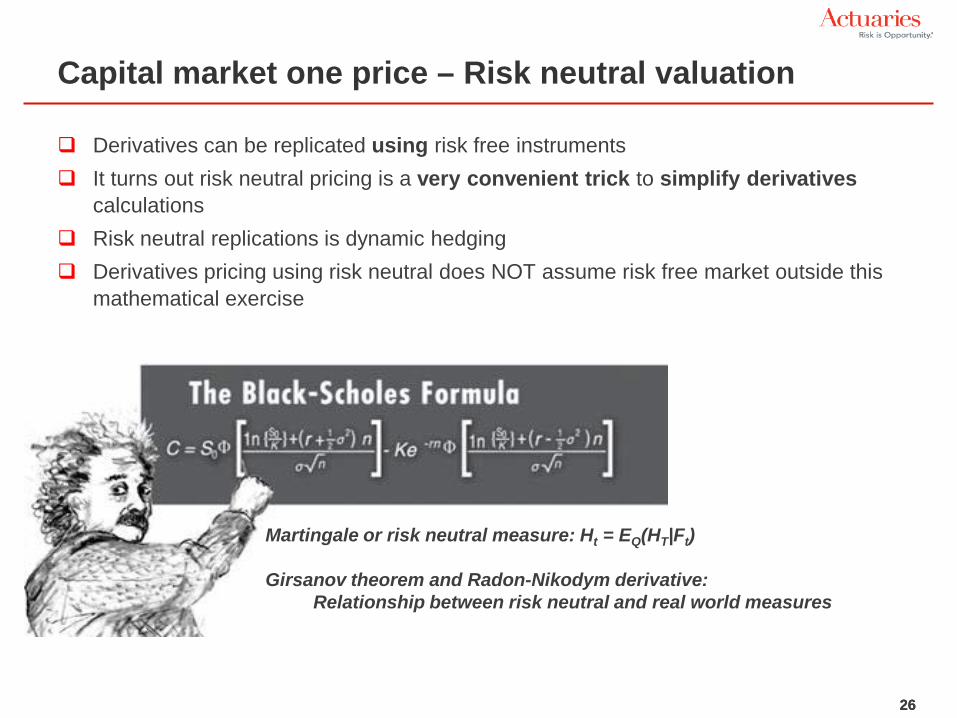

Capital market one price – Risk neutral valuation

Derivatives can be replicated using risk free instruments It turns out risk neutral pricing is a very convenient trick to simplify derivatives

calculations Risk neutral replications is dynamic hedging Derivatives pricing using risk neutral does NOT assume risk free market outside this

mathematical exercise

Martingale or risk neutral measure: Ht = EQ(HT|Ft) Girsanov theorem and Radon-Nikodym derivative:

Relationship between risk neutral and real world measures

27

Derivatives cannot be diversified

Diversification by derivatives product offering is very limited ⇒ Shorting 100,000 put options with varying strikes and maturity dates

Add, but not reduce, the main exposure to the block – systemic exposure to equity

⇒ Selling VA and FIA Might offset to some degree of the directional exposure to equity but not the

volatility

Derivatives risks are systemic ⇒ Time diversification is not very reliable – still the same market exposure

28

Derivatives are hedged but not diversified

Sound risk management practice is ⇒ To neutralize the systemic capital market exposure by hedging (hope we have priced

adequately) ⇒ The best “diversification” for derivatives is hedging

Hedging with risk neutral valuation is the most reliable way to offload the risks

⇒ Risk neutral valuation of derivatives ensures consistent results ⇒ No matter what happens - real world or risk neutral path or good/bad scenario ⇒ Without taking any bets of market directions

Hedging is to create opposite economic payoffs of the liability guarantees • Through matching the sensitivities (Greeks) of the VA/FIA • Greeks are capital market drivers of equity, interest rates, volatility, etc.

29 29

Annuity derivatives challenges Stochastic simulations

Simulations are often the only choice ⇒ No closed form solutions ⇒ Path dependency ⇒ Amortizing options ⇒ Multiple underlying assets ⇒ Very complex rules ⇒ Individual modeling ⇒ Option premiums (fees) collected over time ⇒ Policies are not uniform, i.e. everything is customized by individual investments

A lot of exciting challenges and opportunities ahead ⇒ Most existing theoretic researches can’t deal with path dependency ⇒ Passport optionality ⇒ American optionality ⇒ Lattice approach rarely used ⇒ Large scale grid computing (i.e. thousands of CPUs) typical ⇒ Model efficiency critical

30 30

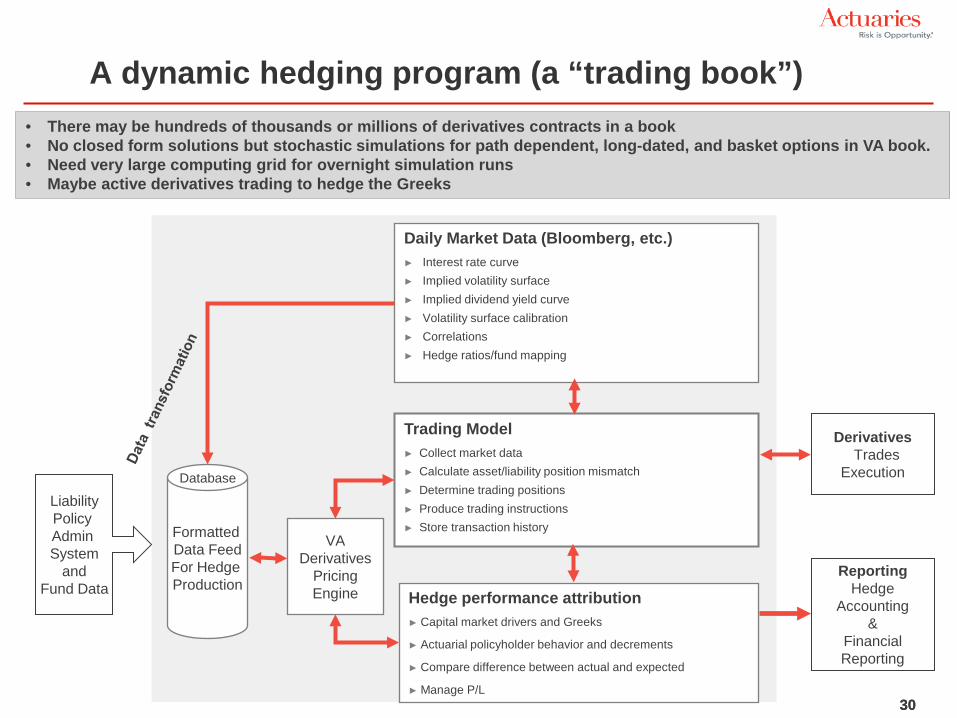

A dynamic hedging program (a “trading book”)

Formatted Data Feed For Hedge Production

Database

Trading Model ► Collect market data ► Calculate asset/liability position mismatch ► Determine trading positions ► Produce trading instructions ► Store transaction history

VA Derivatives

Pricing Engine

Derivatives Trades

Execution

Liability Policy Admin System

and Fund Data Hedge performance attribution

► Capital market drivers and Greeks

► Actuarial policyholder behavior and decrements

► Compare difference between actual and expected

► Manage P/L

Reporting Hedge

Accounting &

Financial Reporting

Daily Market Data (Bloomberg, etc.) ► Interest rate curve ► Implied volatility surface ► Implied dividend yield curve ► Volatility surface calibration ► Correlations ► Hedge ratios/fund mapping

• There may be hundreds of thousands or millions of derivatives contracts in a book • No closed form solutions but stochastic simulations for path dependent, long-dated, and basket options in VA book. • Need very large computing grid for overnight simulation runs • Maybe active derivatives trading to hedge the Greeks

31 31

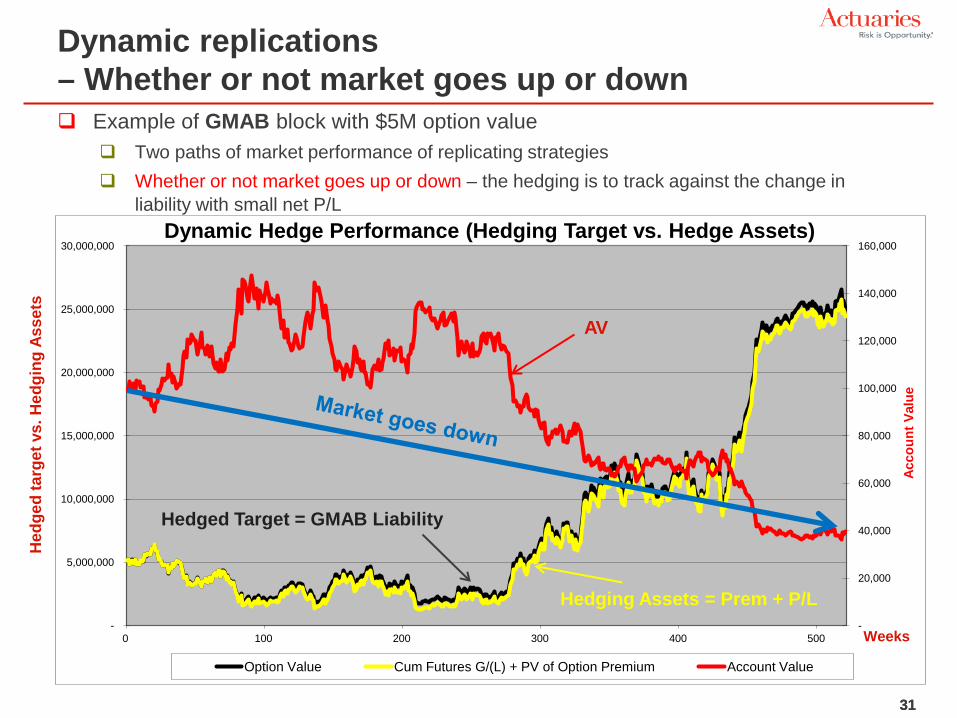

Dynamic replications – Whether or not market goes up or down Example of GMAB block with $5M option value

Two paths of market performance of replicating strategies Whether or not market goes up or down – the hedging is to track against the change in

liability with small net P/L

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

0 100 200 300 400 500

Acco

unt V

alue

Dynamic Hedge Performance (Hedging Target vs. Hedge Assets)

Option Value Cum Futures G/(L) + PV of Option Premium Account Value

Weeks

Hed

ged

targ

et v

s. H

edgi

ng A

sset

s

AV

Hedged Target = GMAB Liability

Hedging Assets = Prem + P/L

32 32

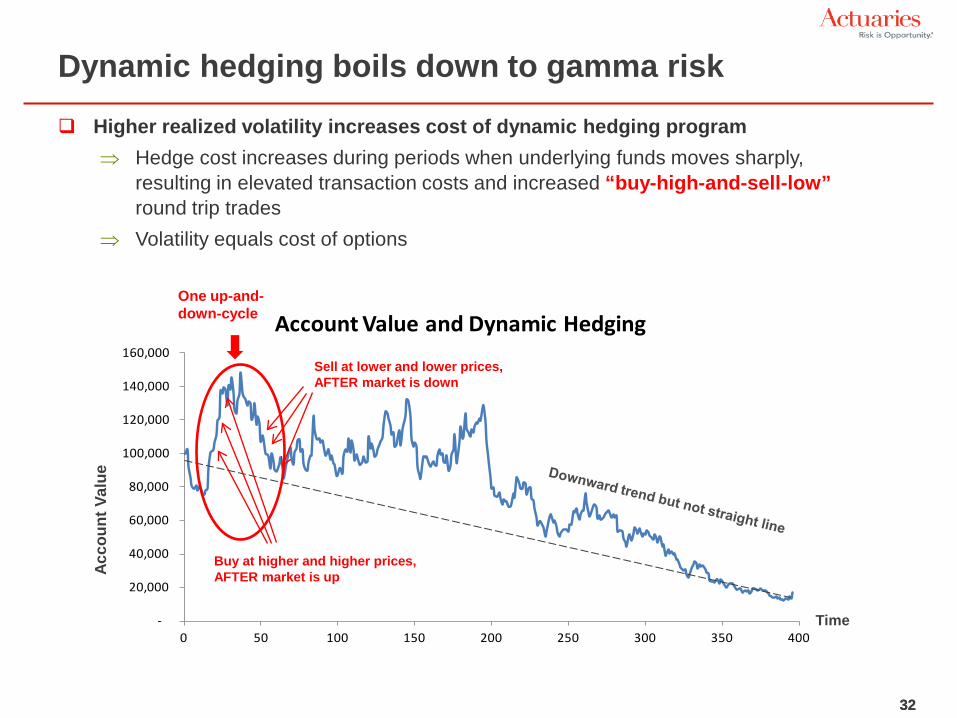

Higher realized volatility increases cost of dynamic hedging program ⇒ Hedge cost increases during periods when underlying funds moves sharply,

resulting in elevated transaction costs and increased “buy-high-and-sell-low” round trip trades

⇒ Volatility equals cost of options

Dynamic hedging boils down to gamma risk

2. Why volatility m

atters

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

0 50 100 150 200 250 300 350 400

Account Value and Dynamic Hedging

Acco

unt V

alue

Time

Buy at higher and higher prices, AFTER market is up

Sell at lower and lower prices, AFTER market is down

One up-and-down-cycle

33

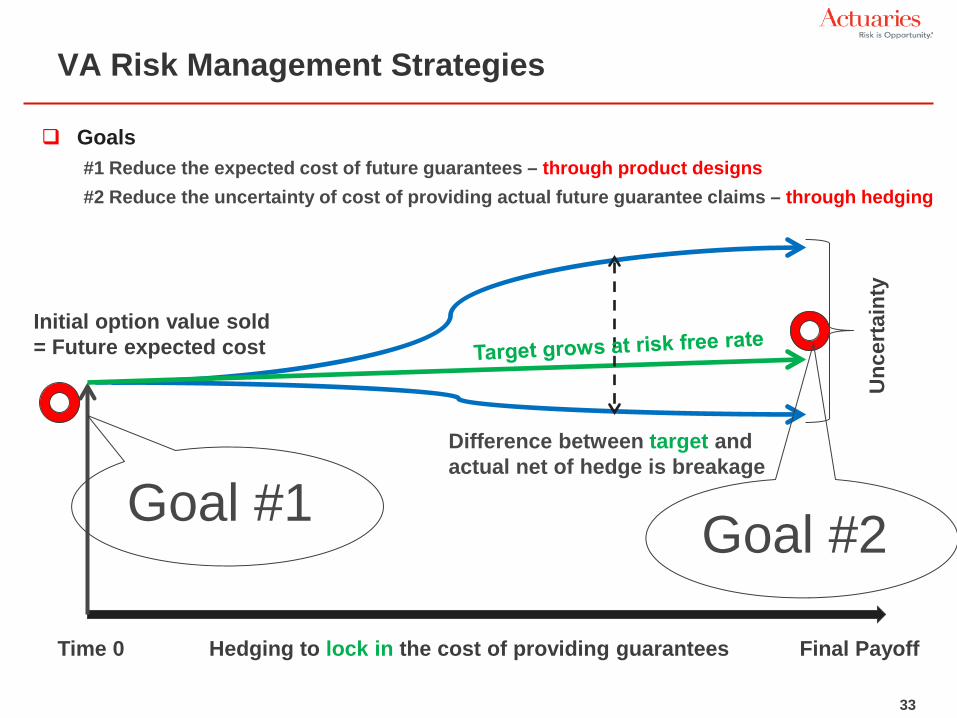

VA Risk Management Strategies

Goals #1 Reduce the expected cost of future guarantees – through product designs #2 Reduce the uncertainty of cost of providing actual future guarantee claims – through hedging

Time 0 Hedging to lock in the cost of providing guarantees

Initial option value sold = Future expected cost

Final Payoff

Unc

erta

inty

Difference between target and actual net of hedge is breakage

Goal #1 Goal #2

34 34

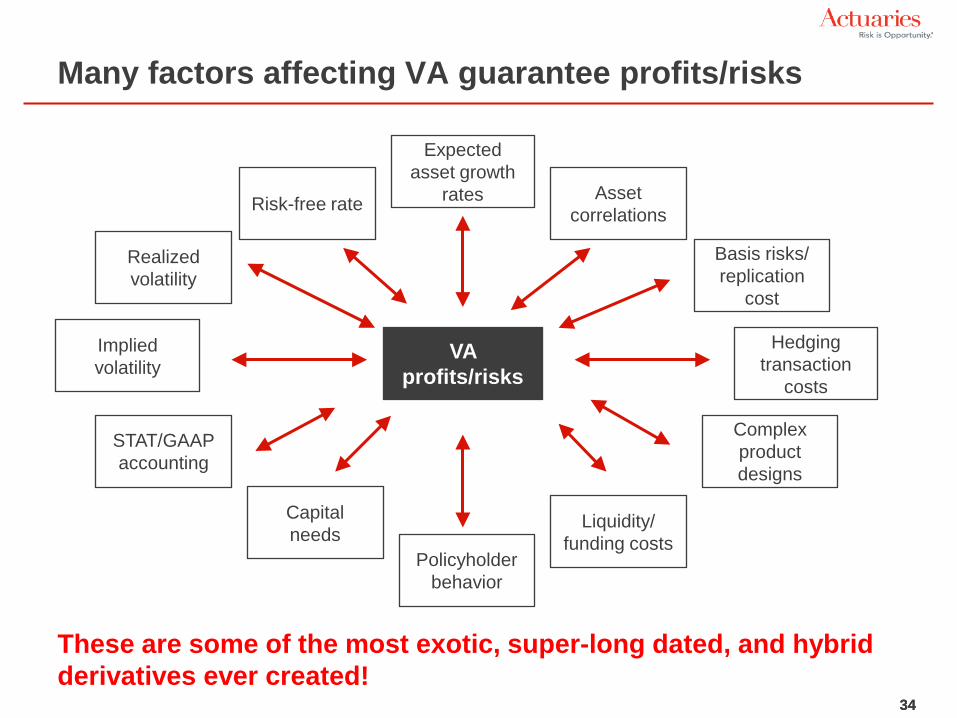

Many factors affecting VA guarantee profits/risks

VA profits/risks

Risk-free rate

Hedging transaction

costs

Expected asset growth

rates Asset correlations

Implied volatility

Basis risks/ replication

cost

Realized volatility

Capital needs

STAT/GAAP accounting

Complex product designs

Liquidity/ funding costs

Policyholder behavior

These are some of the most exotic, super-long dated, and hybrid derivatives ever created!

35 35

36 36

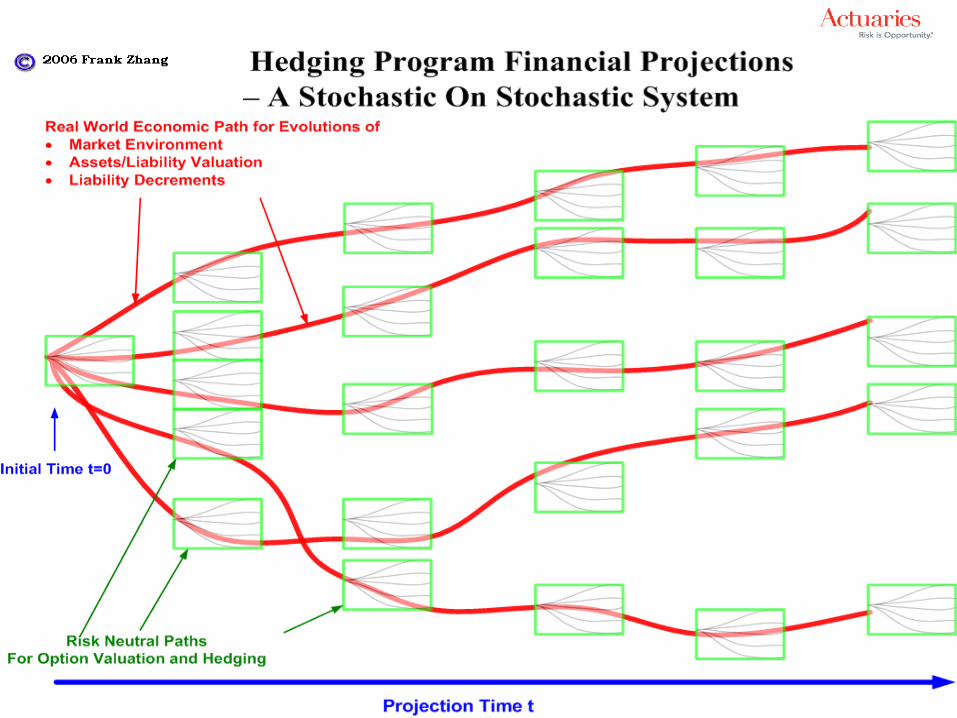

Long term financial and hedging projections There is something better than back testing

Long term financial projections are core of actuarial technology

Stochastic-on-stochastic real world and risk neutral projections

For projecting VaR and economic capital into the future and testing different techniques for efficient financial and capital managements under different accounting rules and capital rules

Required for regulatory capital and reserve

CTE calculations

To test optimized hedge strategies and derivatives positions under different

market scenarios

“Realistic” projections of the future more dynamic and comprehensive than simple back testing or stress testing

Calculate option values and Greeks along the paths of real

world financial projections

37

Summary – Financial engineering and actuarial science

Law of large numbers does not work effectively with derivatives ⇒ Capital market risks are now dominate risks in many life insurance companies

Law of one number is critical for insurance derivatives products

⇒ Derivative contracts will be priced and risk is mitigated individually (not by average) ⇒ Derivatives are priced with no-arbitrage and risk neutral hedging replication ⇒ Dynamic hedging is used to manage the derivatives risks sold

Variable annuities need both law of large numbers and law of one numbers

⇒ New practice requires both financial engineering and actuarial science ⇒ The non-market components are somewhat diversifiable ⇒ Capital market derivatives exposure long dated and path dependent ⇒ Imperfectly defined derivatives with many moving parts ⇒ New practical and theoretical challenges and opportunities

Contact: Email: [email protected] LinkedIn: www.linkedin.com/in/zhangfrank