-

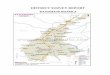

8/7/2019 Financial Inclusion in Rajasthan - A Case Study of

Rajsamand district

1/3

ck

40

|CAB CALLI NG |Janu ary - March, 2009|

Financial Inclusion in Rajasthan:A Case Study of Rajsamand

District

Subah Singh Yadav*

*Chief Manager, Bank of Baroda, Zonal Office, Lucknow

Financial

Inclusion which

flashed on the horizon

of banking industry in the

wake of inclusive growth

policies, has after crossing the

crucial tides of time, come to stay

to some extent in a comparatively less

developed State of Rajasthan. The state

has been a frontier, if not pioneer, in

searching for an alternate credit delivery

mechanism through Self Help Groups. Its Ajmermodel has been one

of the most popular and

illustrative device of reaching out to the poor. Financial

inclusion is not an end in itself as most of the people

having

a bank account or an insurance coverage, ipso facto, does

not mean an enhancement in their economic position, but it

should help, in some way, the process of economic development

in

the distribution of existing income pattern.

This is exactly in this context a pilot project on financial

inclusion was

triggered in Rajsamand district of Rajasthan. This is an average

size district,

with strong presence of Women & Child Development

Departments a initiatives

on SHG linkage program.

The sub committee of the SLBC identified Rajsamand district for

the purpose and the project was

launched on August 25,2006. It was decided to conduct house hold

survey and identity families

who are not within banking reach. The role of Panchayati Raj

institutions was also stressed upon in

view of easy access of these units operating at the grassroots

level. It was also resolved that household

survey must be completed by December 2006 and then the district

should be fully covered for inclusion by

March 2007.

Methodology

-

8/7/2019 Financial Inclusion in Rajasthan - A Case Study of

Rajsamand district

2/3

ck

41

|CAB CALLI NG |Janu ary - March, 2009|

Fifty nine branches were to cover 1004 villages and 90 wards in

their service area targeting 185721 families.The work was co-

ordinate by the Lead Bank Managers of SBBJ at Rajsamand.

Branches were advised to open no frill accounts as per the

Reserve Bank of India guidelines with a minimum of one account

per household as per the voter list. A record of families who

have migrated to other places or refused to open the account was

prepared and duly authenticated by sarpanch/ government

authorities.

Note: During the aforesaid household survey and identification

of families, number of families increased by 11335 from the

figure obtained in the 2001 census level due to increase in

population and sub-division of families.

The survey and opening of deposit/loan accounts in the entire

district was completed in the first week of January 2007. The

district administration had undertaken a sample check through

its field staff to ensure that the needful had been done. The

work

of data punching was done to update the various information and

future requirements.

SBBJ and Mewar Gramin Bank had the maximum branch network with

19 branches each (32 %) followed by Bank of Rajasthan

with 12 (20%). The remaining banks have one to three 3

branches.

The district is characterized by migratory population. As many

as 7101 families were not available and 5540 families refused

to

open bank account. Rest of the population was brought in the

fold of banking system. It appears that old persons and

pensioners prefer even late delivery of money order at their

doorstep rather than going to bank premises.

Progress of the Project

Analysis

-

8/7/2019 Financial Inclusion in Rajasthan - A Case Study of

Rajsamand district

3/3

ck

42

|CAB CALLI NG |Janu ary - March, 2009|

An analysis of the data reveals that

47.68 percent families were already

linked with banking system and for the

remaining 52.32 percent, new accounts

were opened during the financial

inclusion project.

Migratory nature of population is equally

evident with some variation in semi

urban area also. As many as 645

families who went in the nearby Gujarat

state in search of wage employment were not

available for account opening with banks.

However 1176 families were found reluctant for

opening bank account.

People in the semi urban area are better aware

of the advantages to be associated withbanking system.

Therefore, banks had to put

less efforts and by opening only 17.37 of new

account, all the ward were financially included.

The evaluation of the project in the district conducted by an

external agency found that 92.27 per cent households in the

villages

have a bank account but 52.39 per cent of the households had no

transactions in their accounts due to various reasons like,

distance of the branch (79.64%), illiteracy(6.60%) and not being

interested (10.04%). In towns, 98 per cent households had a

bank account and 86.94 per cent not carrying out transactions.

Non-availability of passbook (75.47%) was cited as the major

reason. Majority of the people contacted were not familiar with

the process of opening the account and could not get their

passbooks. However, despite these deterrents and disconnects,

the accounts opened under financial inclusion project weregainfully

utilized by the NREGA beneficiaries for effecting transactions. As

per the evaluation study, these accounts would have

been largely inoperative otherwise.

The experience of Rajsamand district brought out the following

issues to the forefront :

l Efficient delivery of services with low cost of

intermediation

l Substantial upscale of micro credit activities.

l Change attitude and aptitude of staff posted in rural

branches; rejuvenation of rural branches and making the rural

posting

more attractive

l Exploring collaborative support from hybrid channels like NGOs

/ NFIs / post offices / RUDSETIs / Educational Institutes.

l Fostering real sector linkage amongst farm activities and

leveraging technology to the maximum extent possible

This pilot project seems to have played a refreshing and

reassuring role in leading the way for creating supply of

financial

services and facilitate their distribution. However the men,

machinery and methodology have to be geared up for upgrading

quality of services and access. Simultaneously, there is a felt

need of extending the customers financial literacy and

counseling.

Banks might develop clients and demand through financial

literacy, education community development, business development

services for clients and increasing publicity as well as

developing brand recognition. Banks and local administration have

to

perform distinctly, but mutually reinforcing roles in achieving

social transformation through financial inclusion.

Evaluation Study

Conclusion

Status of existing and new accounts