Embed Size (px)

Citation preview

Financial Reporting Update

Recent developments in financial reporting presentation

July 2021

Facilitators

July 2021 Financial Reporting Update Page 2

Laura ElliottAfrica IFRS Desk

Abigail PaulusAfrica IFRS Desk

Marieke FourieAfrica IFRS Desk

Agenda

Page 3

1) Presentation matters

• Disclosure initiative

• Management commentary

• Materiality

• Going concern

• Significant judgements, estimation uncertainty & policies

• Financing arrangement disclosures

• Sustainability reporting

2) Practical presentation application

• IFRS 15: presentation of rebates

• IAS 7: statement of cash flows

3) Other presentation issues

July 2021 Financial Reporting Update

Presentation matters

July 2021 Financial Reporting UpdatePage 4

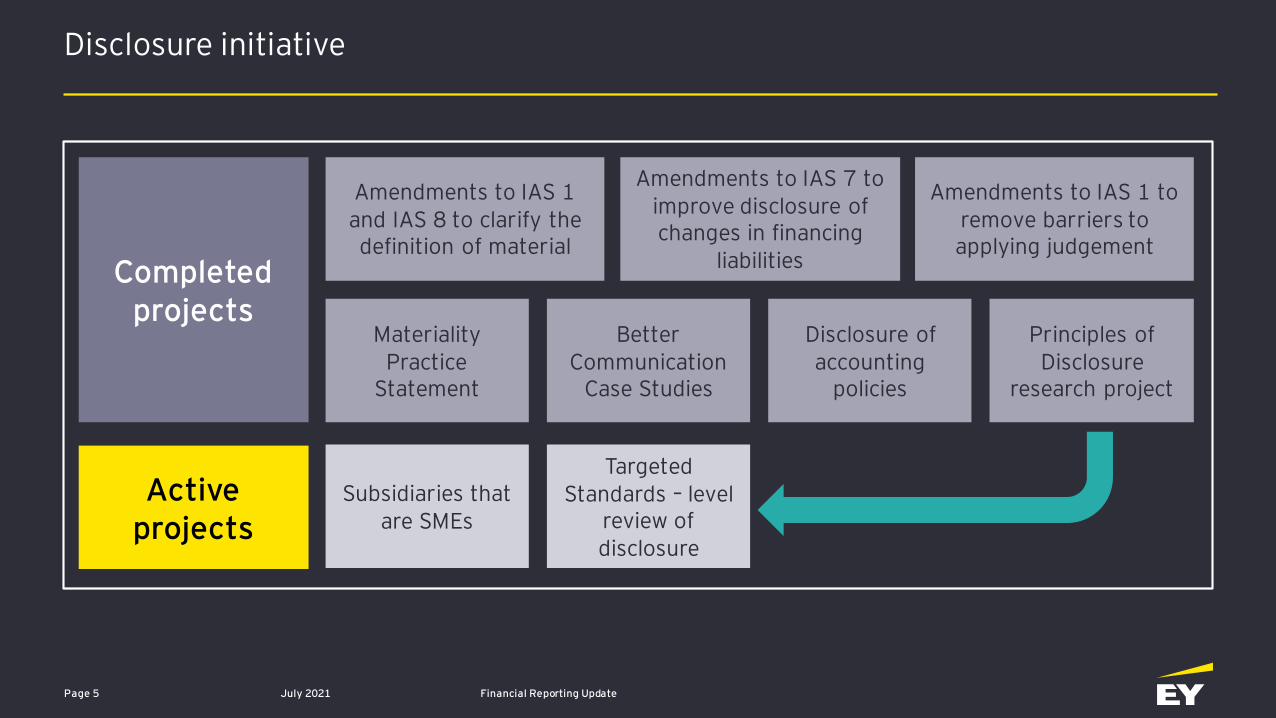

Disclosure initiative

July 2021 Financial Reporting Update Page 5

Completed projects

Active projects

Amendments to IAS 1 and IAS 8 to clarify the definition of material

Materiality Practice

Statement

Amendments to IAS 7 to improve disclosure of changes in financing

liabilities

Amendments to IAS 1 to remove barriers to applying judgement

Better Communication

Case Studies

Disclosure of accounting

policies

Principles of Disclosure

research project

Subsidiaries that are SMEs

Targeted Standards – level

review of disclosure

Items of information

Specific disclosure objectives

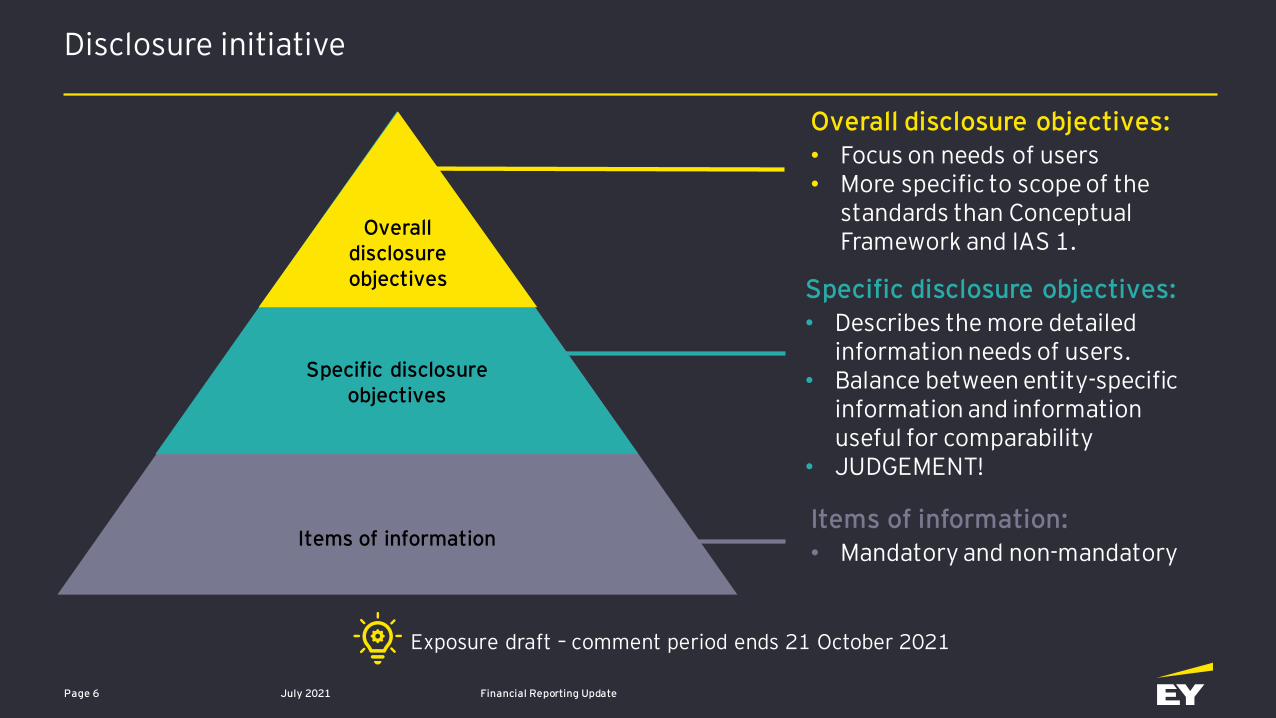

Disclosure initiative

July 2021 Financial Reporting UpdatePage 6

Overall disclosure objectives

Overall disclosure objectives:• Focus on needs of users• More specific to scope of the

standards than Conceptual Framework and IAS 1.

Specific disclosure objectives:• Describes the more detailed

information needs of users. • Balance between entity-specific

information and information useful for comparability

• JUDGEMENT!

Items of information:• Mandatory and non-mandatory

Exposure draft – comment period ends 21 October 2021

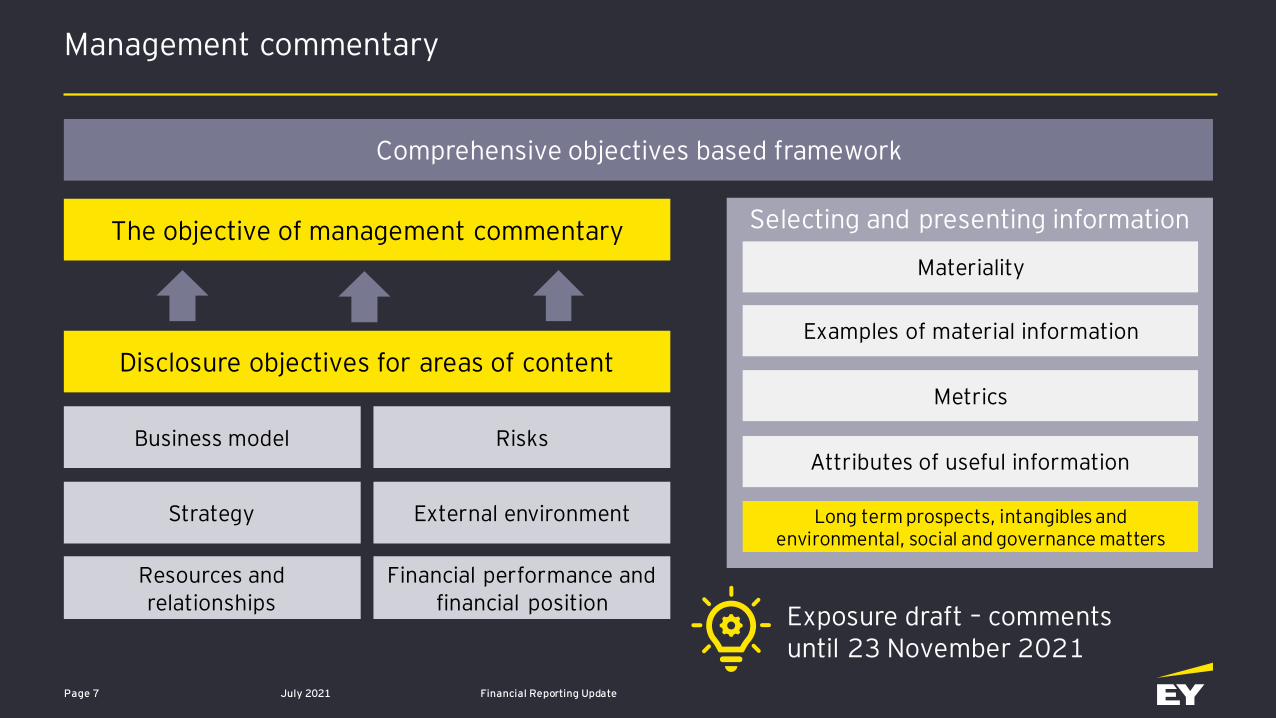

Management commentary

July 2021 Financial Reporting UpdatePage 7

Exposure draft – comments until 23 November 2021

Comprehensive objectives based framework

The objective of management commentary

Disclosure objectives for areas of content

Business model Risks

Strategy External environment

Resources and relationships

Financial performance and financial position

Selecting and presenting information

Materiality

Examples of material information

Metrics

Attributes of useful information

Long term prospects, intangibles and environmental, social and governance matters

July 2021

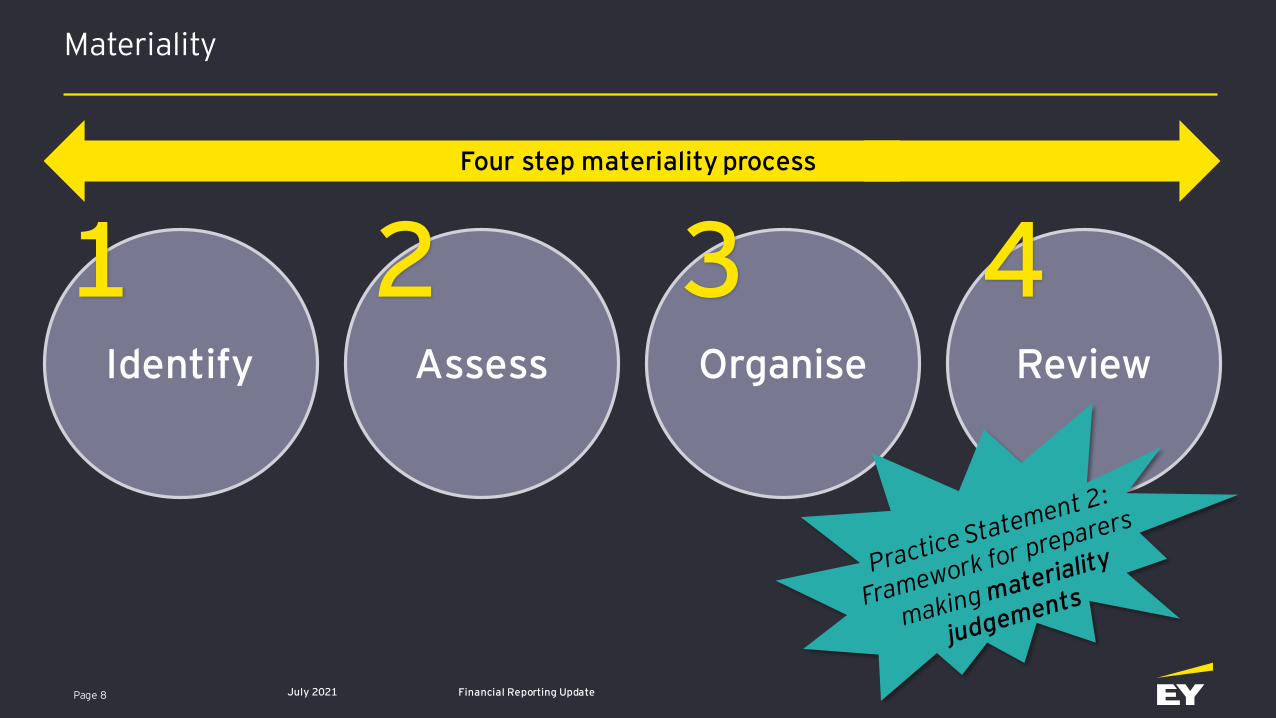

Identify Assess Organise Review

1 2 3 4Four step materiality process

Page 8 Financial Reporting Update

Materiality

July 2021 Financial Reporting UpdatePage 9

JSE internal controls statement

❑ Change to JSE listing requirements

❑ Statement in Annual Report regarding reliance on adequacy and effectiveness of internal financial controls in compiling the annual financial statements

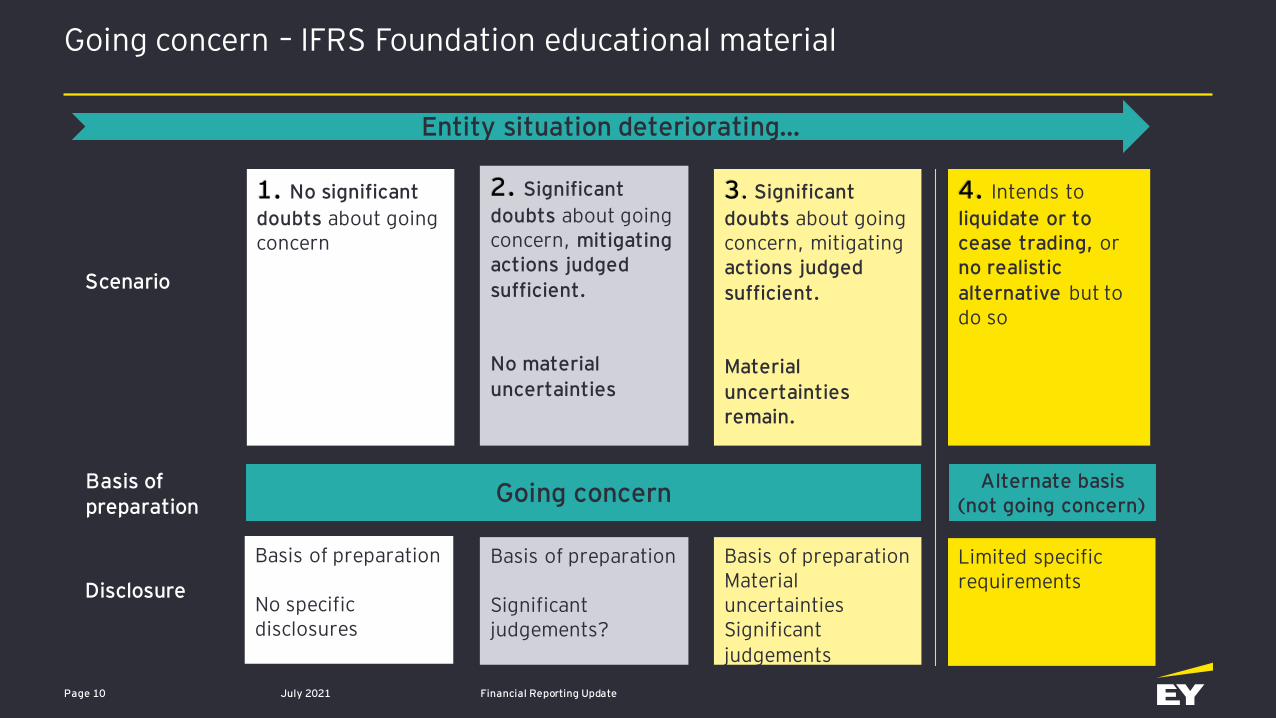

Going concern – IFRS Foundation educational material

Financial Reporting UpdatePage 10 July 2021

1. No significant

doubts about going concern

2. Significant

doubts about going concern, mitigating actions judged

sufficient.

No material

uncertainties

3. Significant

doubts about going concern, mitigatingactions judged

sufficient.

Material

uncertainties remain.

4. Intends to

liquidate or to cease trading, or no realistic

alternative but to do so

Going concernAlternate basis

(not going concern)

Basis of preparation

No specific disclosures

Basis of preparation

Significant judgements?

Basis of preparationMaterial uncertaintiesSignificant

judgements

Limited specific requirements

Scenario

Basis of preparation

Disclosure

Entity situation deteriorating…

Going concern

July 2021 Financial Reporting UpdatePage 11

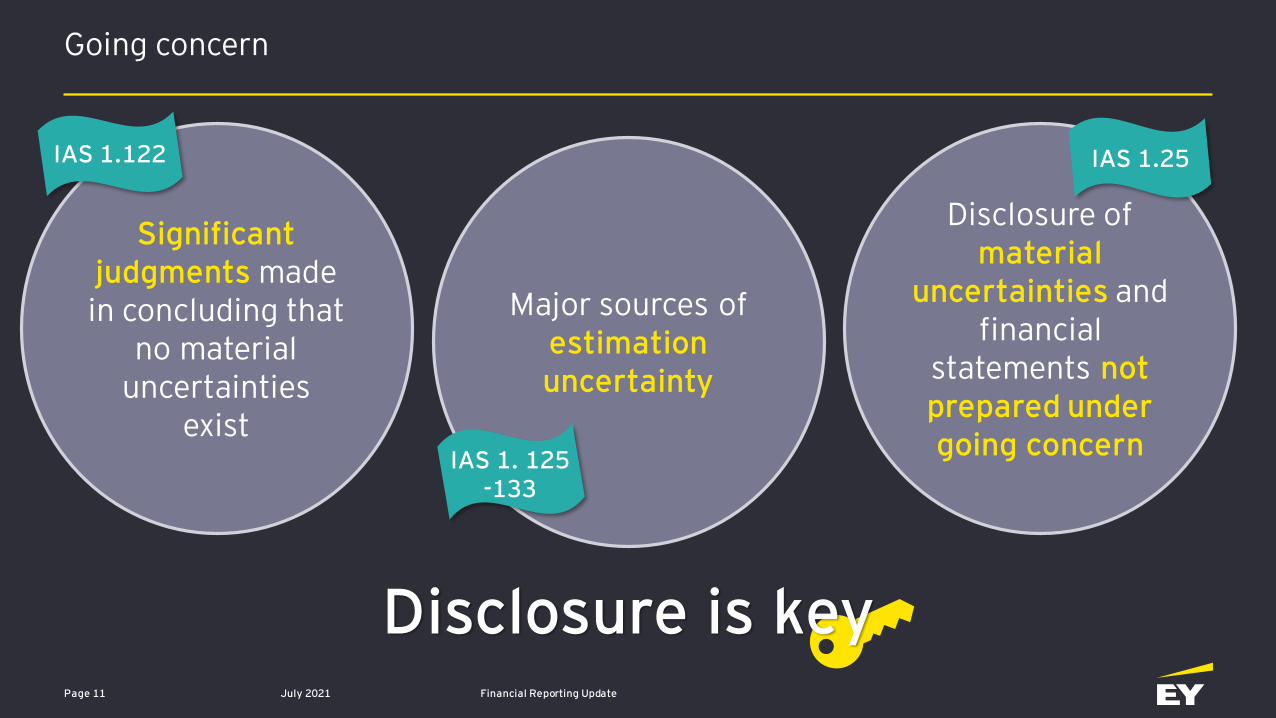

Significant judgments made in concluding that

no material uncertainties

exist

Major sources of estimation uncertainty

Disclosure of material

uncertainties and financial

statements not prepared under going concern

IAS 1.122

IAS 1. 125 -133

IAS 1.25

Disclosure is key

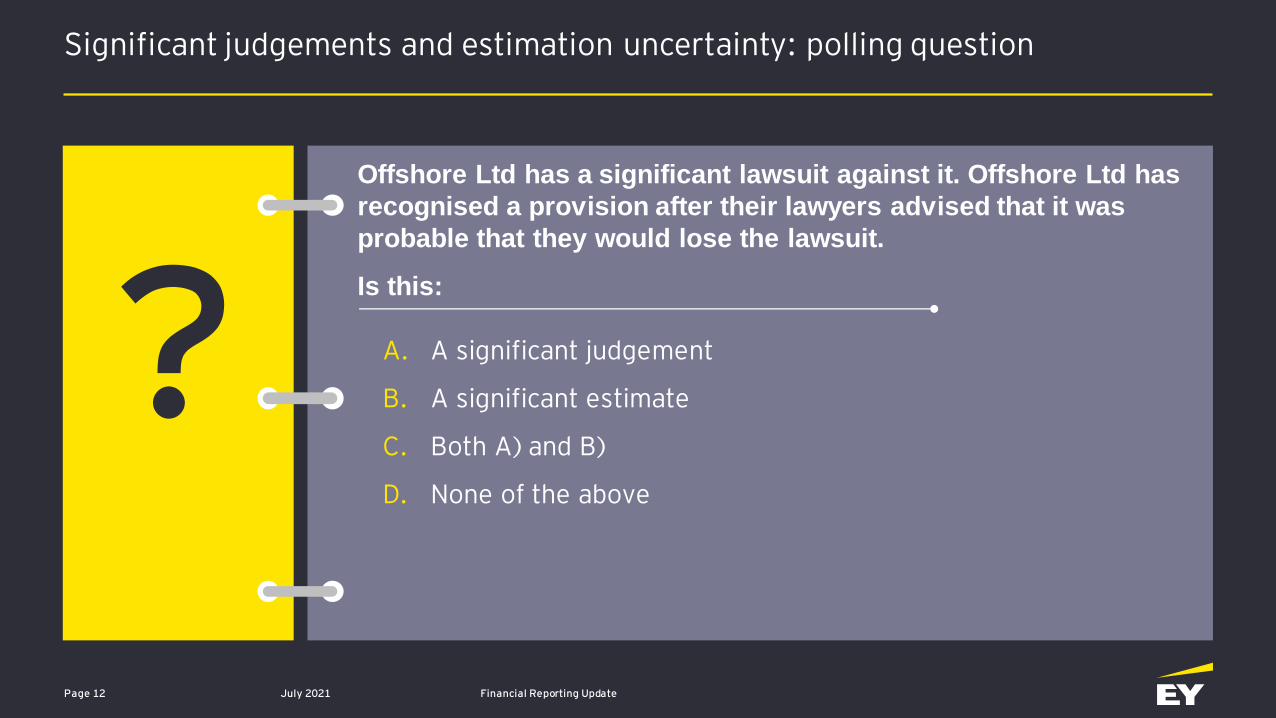

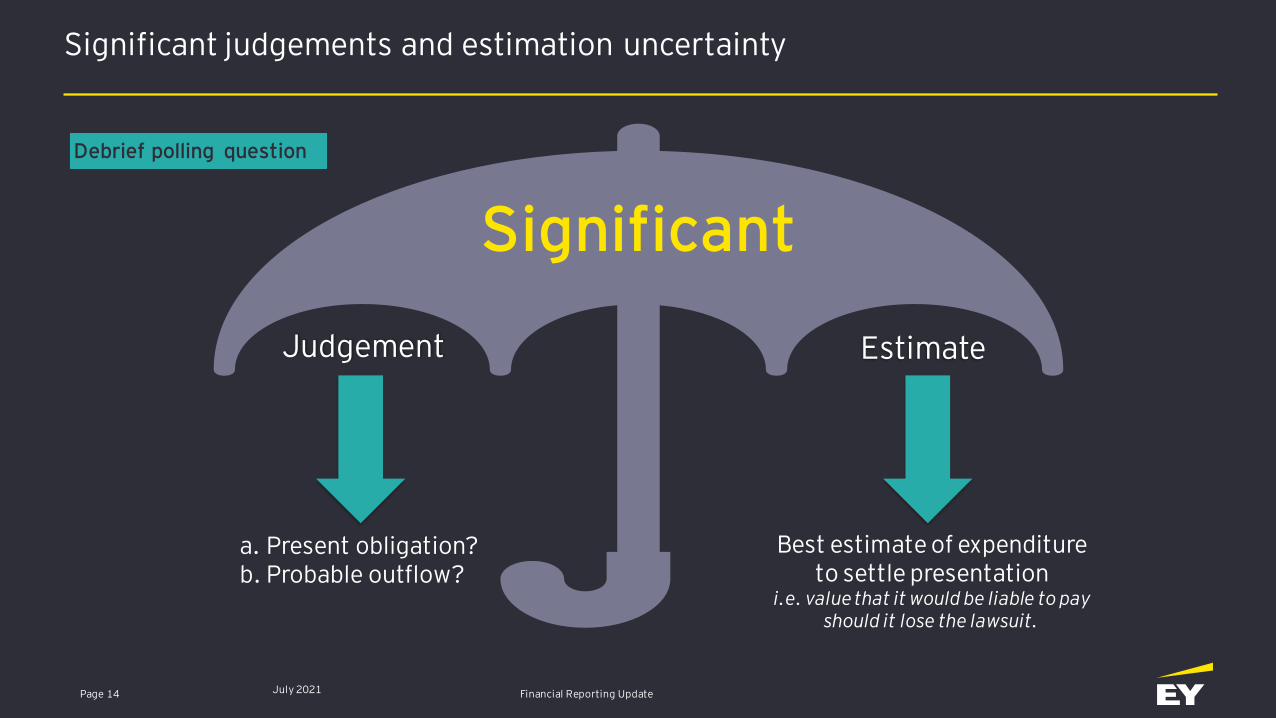

Significant judgements and estimation uncertainty: polling question

July 2021 Financial Reporting Update Page 12

A. A significant judgement

B. A significant estimate

C. Both A) and B)

D. None of the above

Offshore Ltd has a significant lawsuit against it. Offshore Ltd has

recognised a provision after their lawyers advised that it was

probable that they would lose the lawsuit.

Is this:

?

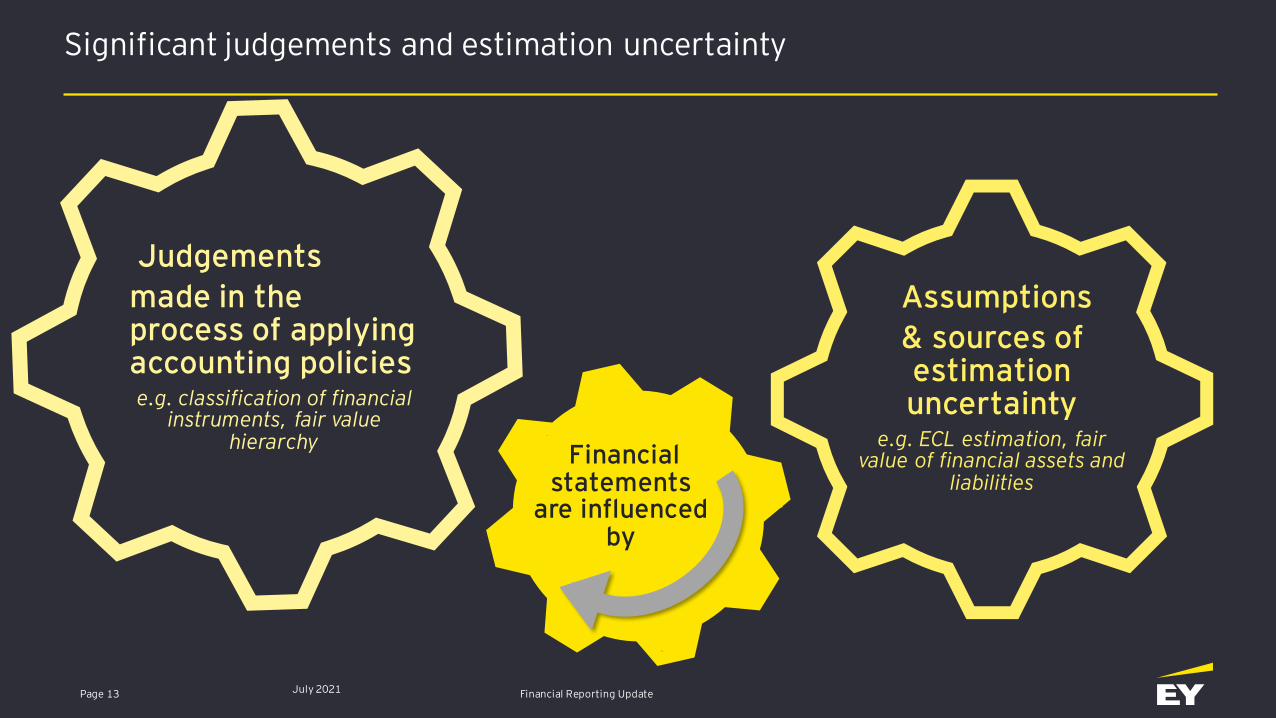

Significant judgements and estimation uncertainty

Assumptions

& sources of estimation uncertainty

e.g. ECL estimation, fair value of financial assets and

liabilities

Judgements

made in the process of applying accounting policies e.g. classification of financial

instruments, fair value hierarchy

Financial statements

are influenced by

Page 13 July 2021 Financial Reporting Update

Judgement Estimate

a. Present obligation?b. Probable outflow?

Best estimate of expenditure to settle presentation

i.e. value that it would be liable to pay should it lose the lawsuit.

Significant

Page 14 July 2021 Financial Reporting Update

Debrief polling question

Significant judgements and estimation uncertainty

July 2021 Financial Reporting UpdatePage 15

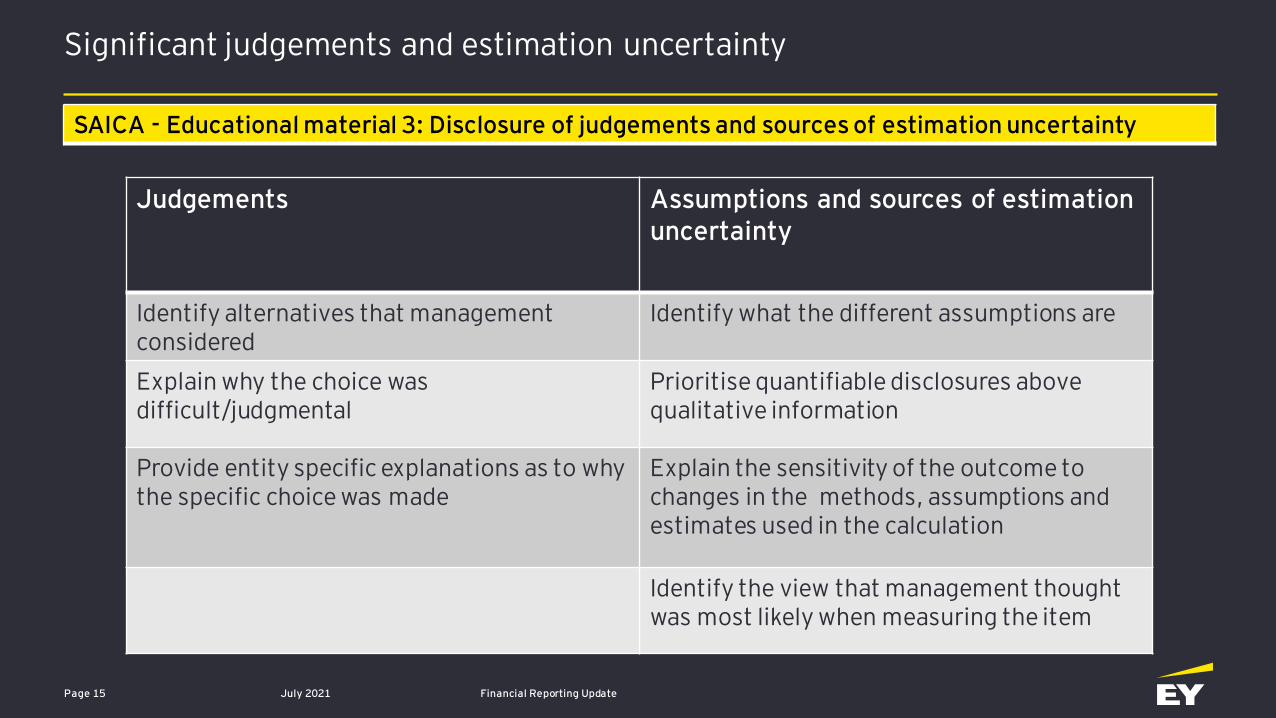

SAICA - Educational material 3: Disclosure of judgements and sources of estimation uncertainty

Judgements Assumptions and sources of estimation uncertainty

Identify alternatives that management considered

Identify what the different assumptions are

Explain why the choice was difficult/judgmental

Prioritise quantifiable disclosures above qualitative information

Provide entity specific explanations as to why the specific choice was made

Explain the sensitivity of the outcome to changes in the methods, assumptions and estimates used in the calculation

Identify the view that management thought was most likely when measuring the item

Significant judgements and estimation uncertainty

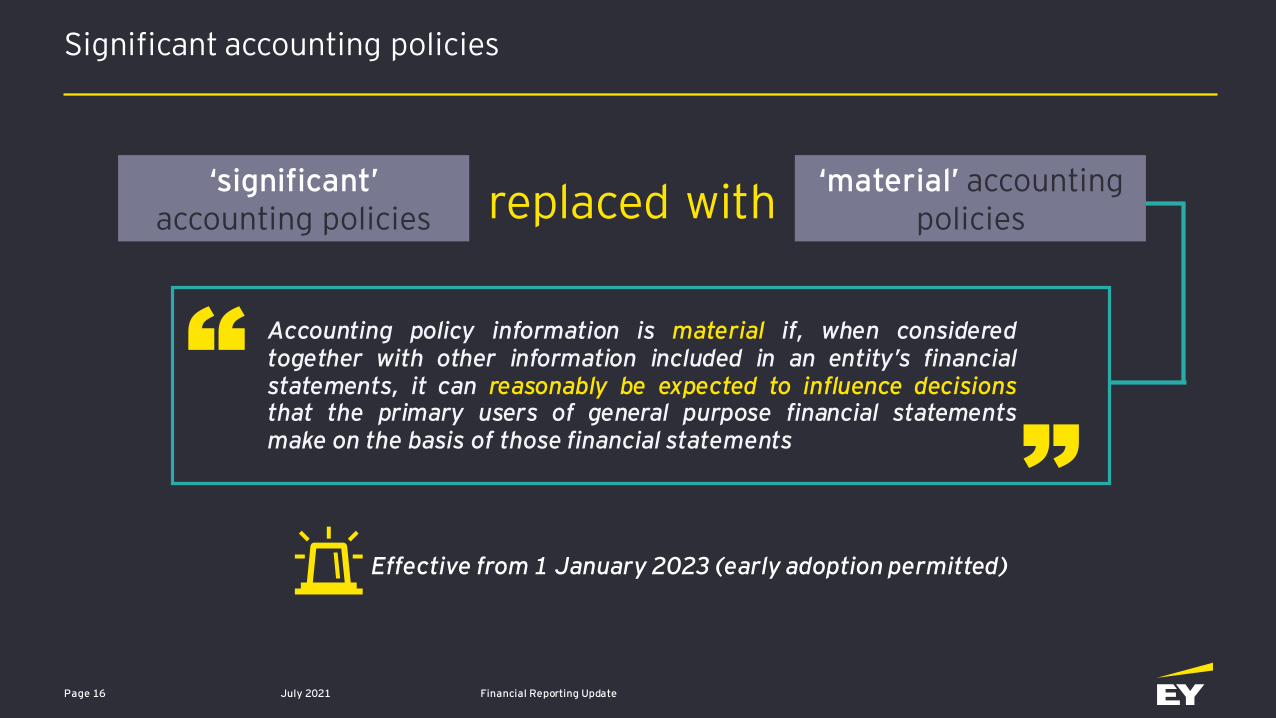

Accounting policy information is material if, when consideredtogether with other information included in an entity’s financialstatements, it can reasonably be expected to influence decisionsthat the primary users of general purpose financial statementsmake on the basis of those financial statements

Effective from 1 January 2023 (early adoption permitted)

July 2021 Financial Reporting UpdatePage 16

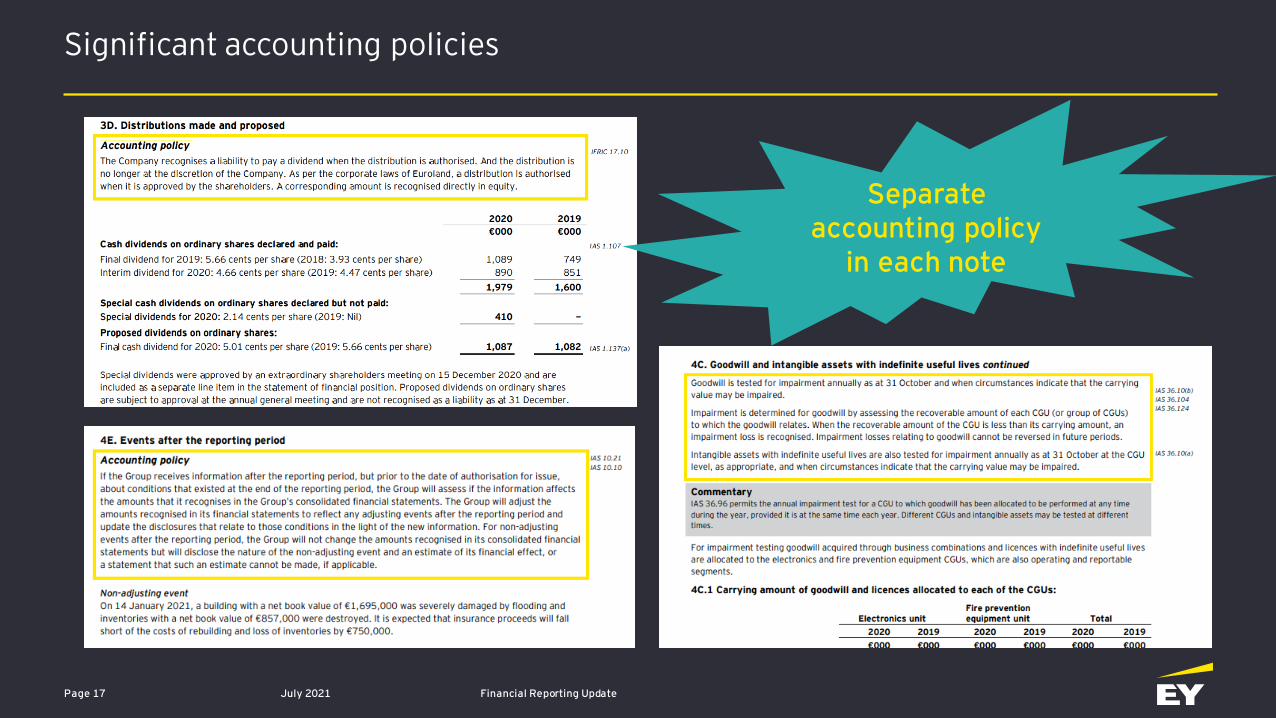

Significant accounting policies

‘significant’ accounting policies replaced with

‘material’ accounting policies

Significant accounting policies

July 2021 Financial Reporting UpdatePage 17

Separate accounting policy

in each note

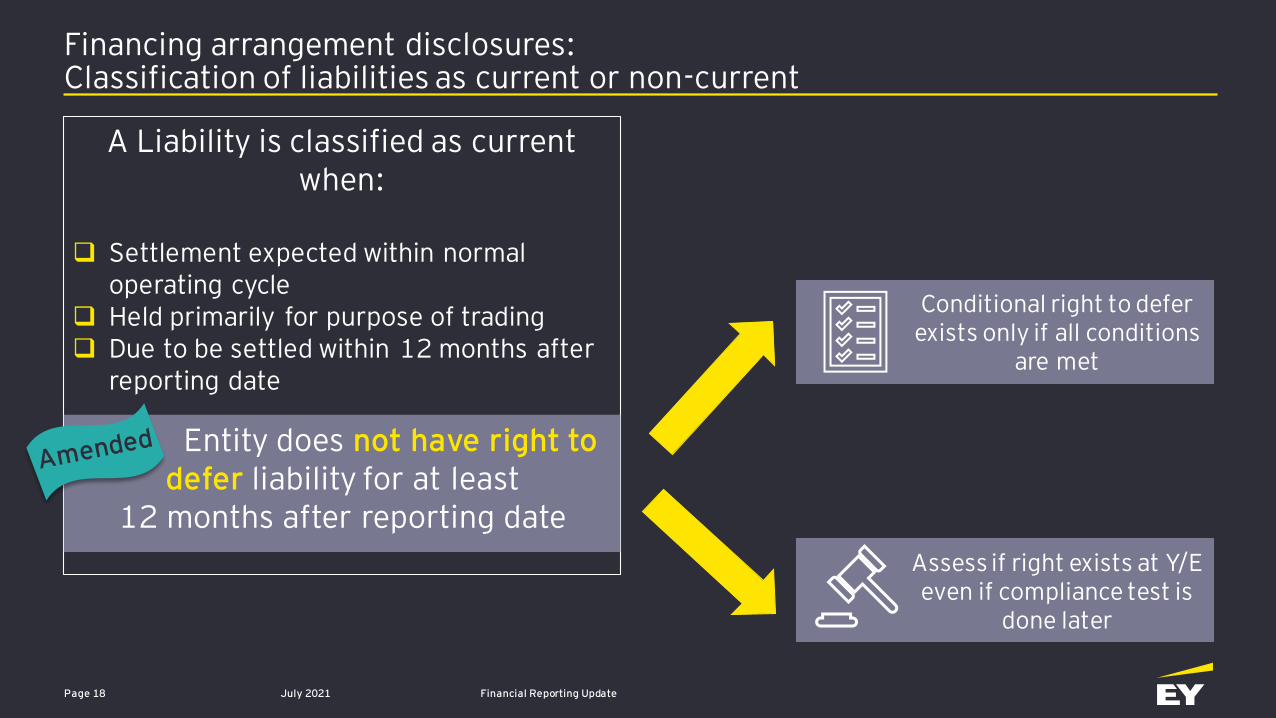

Financing arrangement disclosures:Classification of liabilities as current or non-current

July 2021 Financial Reporting UpdatePage 18

A Liability is classified as current when:

❑ Settlement expected within normal operating cycle

❑ Held primarily for purpose of trading❑ Due to be settled within 12 months after

reporting date

Entity does not have right to defer liability for at least

12 months after reporting date

Conditional right to defer exists only if all conditions

are met

Assess if right exists at Y/E even if compliance test is

done later

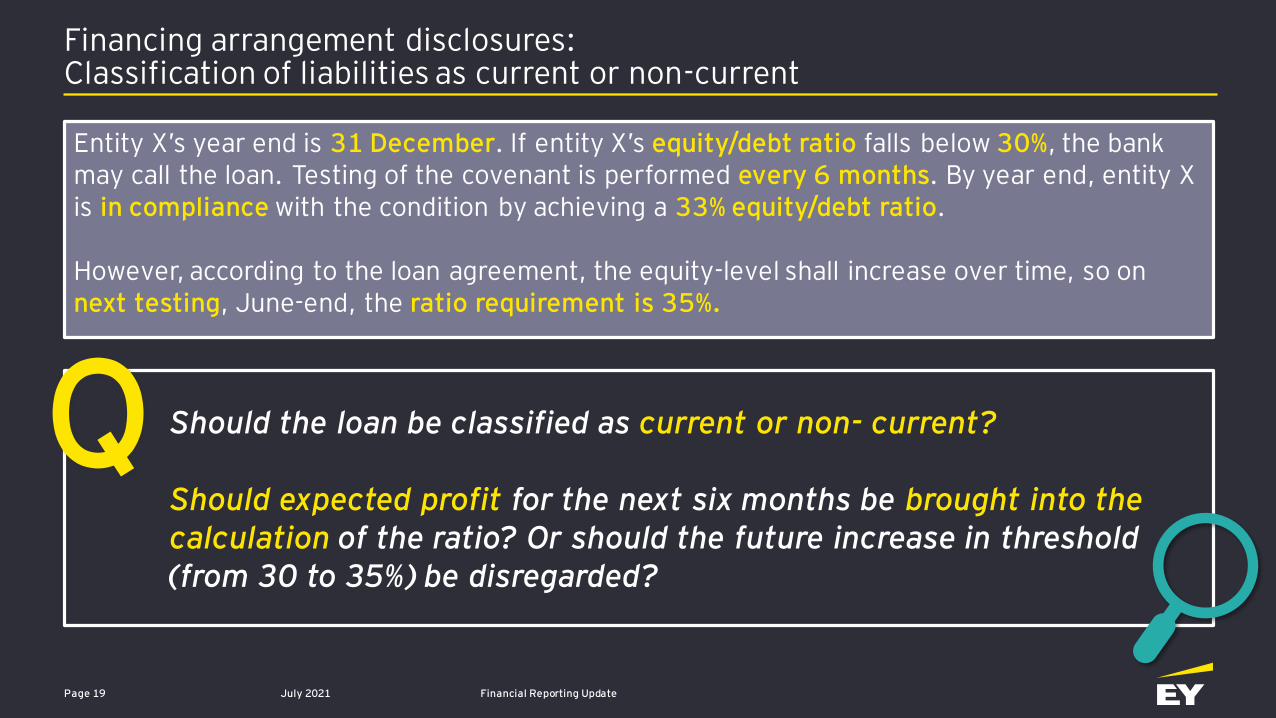

Entity X’s year end is 31 December. If entity X’s equity/debt ratio falls below 30%, the bank may call the loan. Testing of the covenant is performed every 6 months. By year end, entity X is in compliance with the condition by achieving a 33% equity/debt ratio.

However, according to the loan agreement, the equity-level shall increase over time, so on next testing, June-end, the ratio requirement is 35%.

Financing arrangement disclosures:Classification of liabilities as current or non-current

Page 19 July 2021 Financial Reporting Update

Should the loan be classified as current or non- current?

Should expected profit for the next six months be brought into the calculation of the ratio? Or should the future increase in threshold (from 30 to 35%) be disregarded?

Q

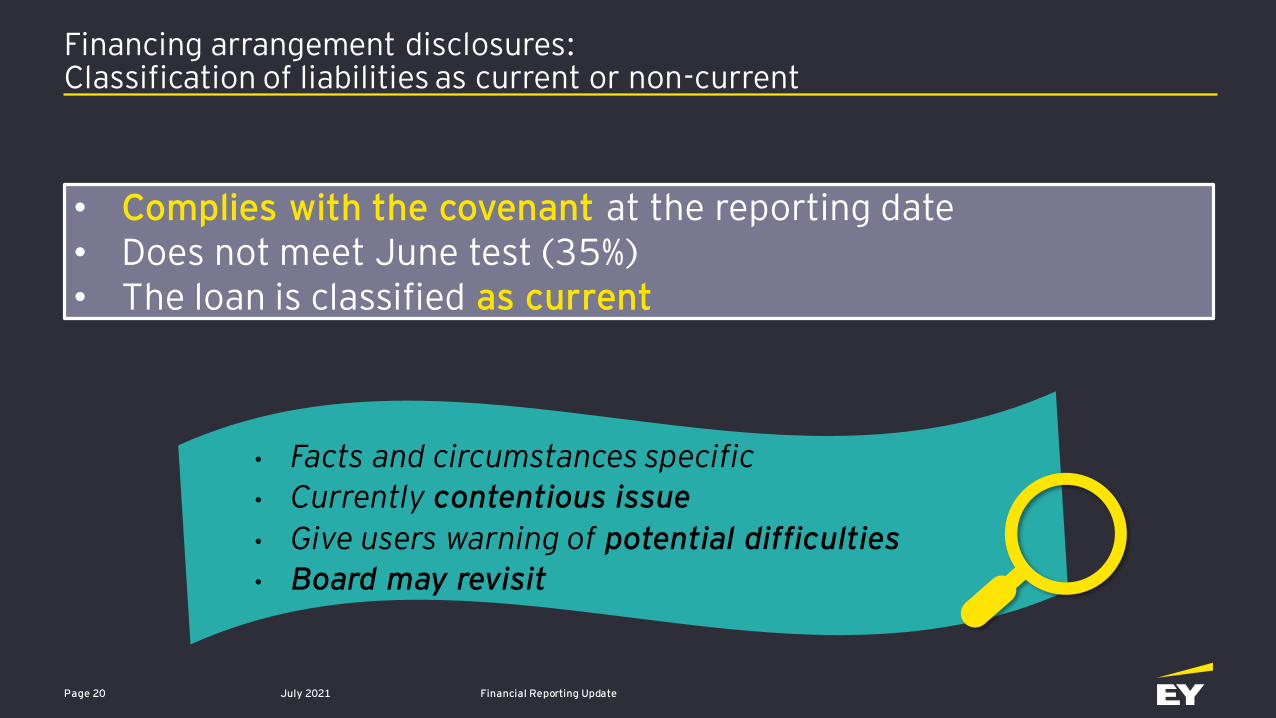

• Complies with the covenant at the reporting date• Does not meet June test (35%)• The loan is classified as current

Financing arrangement disclosures:Classification of liabilities as current or non-current

July 2021 Financial Reporting UpdatePage 20

• Facts and circumstances specific

• Currently contentious issue

• Give users warning of potential difficulties

• Board may revisit

Financing arrangement disclosures: covenants

Page 21 July 2021 Financial Reporting Update

Headroom?

JSE COVID-19: effective communication with investors

JSE communication provides users with early warning with respect to possible difficulties

Sustainability reporting: polling question

July 2021 Financial Reporting Update Page 22

?In which area of your annual reports do you expect environmental related matters to be disclosed?

A. IAS 1 Presentation of financial statements disclosures

B. IAS 16 Property, plant and equipment disclosures

C. IAS 36 Impairment of assets disclosures

D. Management Commentary

E. I do not know or another area

Sustainability reporting

July 2021 Financial Reporting UpdatePage 23

• Trustees of the IFRS Foundation published a proposal to amend the IFRS Foundation Constitution to accommodate a sustainability standards board.

• If proposal is well received, the Trustees intend to announce their plans to create a new board in November 2021.

• Comment period for the Exposure Draft ends on 29 July 2021.

Monitoring Board

Trustees

IASB ISSB

Sustainability reporting: debrief

July 2021 Financial Reporting UpdatePage 24

?In which area of your annual reports do you expect environmental related matters to be disclosed?

A. IAS 1 Presentation of financial statements disclosures

B. IAS 16 Property, plant and equipment disclosures

C. IAS 36 Impairment of assets disclosures

D. Management Commentary

E. I do not know or another area

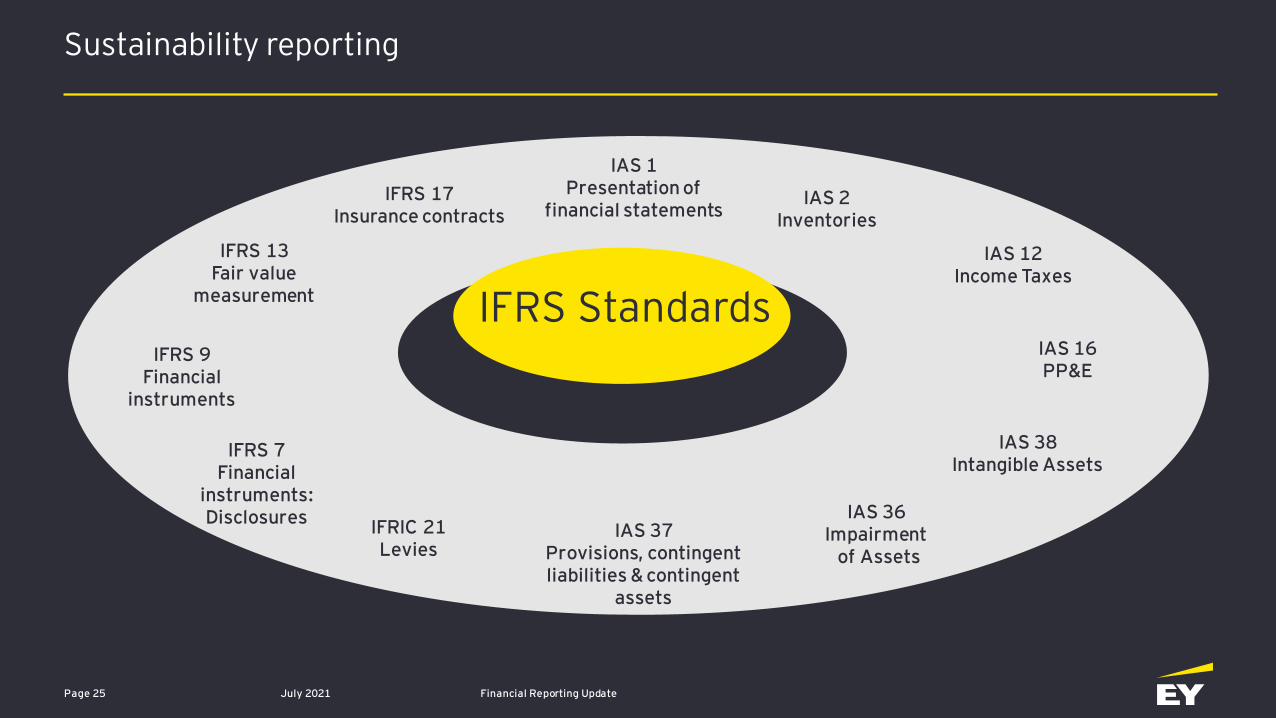

Sustainability reporting

July 2021 Financial Reporting UpdatePage 25

Monitoring Board

IFRS Standards

IFRS 7 Financial

instruments: Disclosures

IFRS 13 Fair value

measurement

IFRIC 21Levies

IAS 37 Provisions, contingent liabilities & contingent

assets

IAS 36 Impairment

of Assets

IAS 38 Intangible Assets

IAS 16 PP&E

IAS 12 Income Taxes

IAS 2 Inventories

IAS 1 Presentation of

financial statements

IFRS 9 Financial

instruments

IFRS 17 Insurance contracts

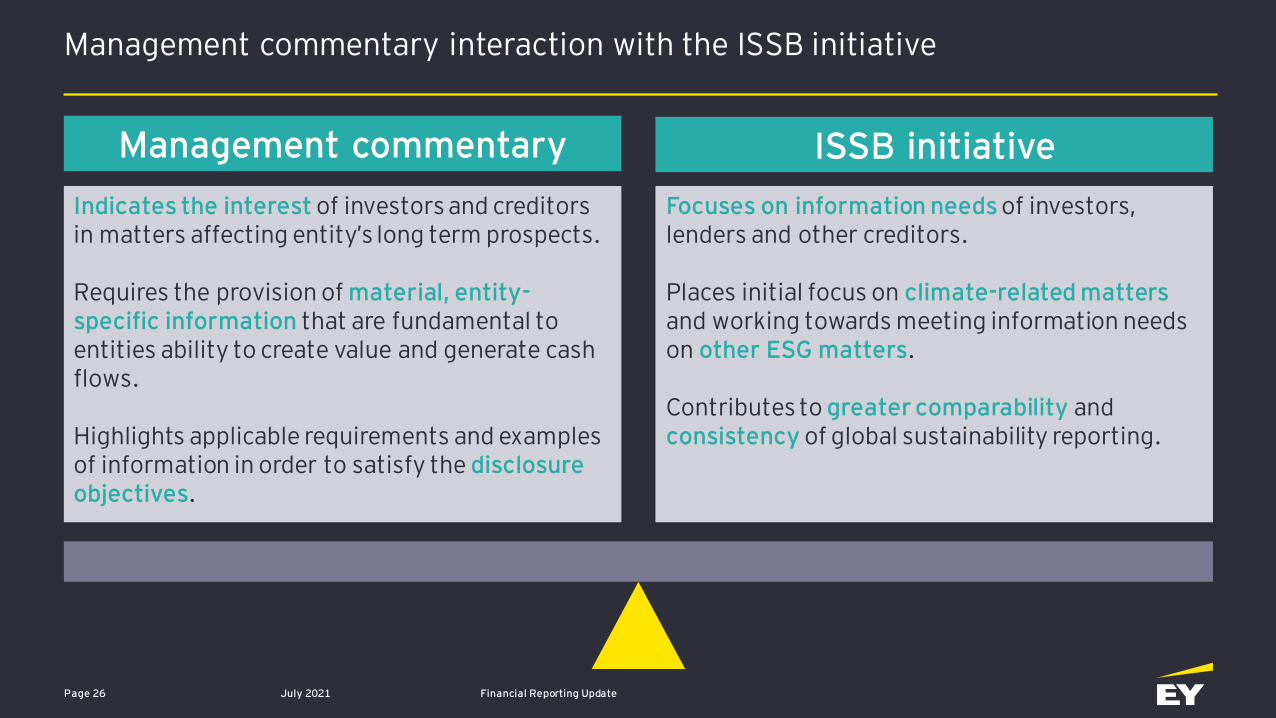

Management commentary interaction with the ISSB initiative

July 2021 Financial Reporting UpdatePage 26

Management commentary ISSB initiative

Indicates the interest of investors and creditors in matters affecting entity’s long term prospects.

Requires the provision of material, entity-specific information that are fundamental to entities ability to create value and generate cash flows.

Highlights applicable requirements and examples of information in order to satisfy the disclosure objectives.

Focuses on information needs of investors, lenders and other creditors.

Places initial focus on climate-related matters and working towards meeting information needs on other ESG matters.

Contributes to greater comparability and consistency of global sustainability reporting.

Practical presentation application

Page 27 July 2021 Financial Reporting Update

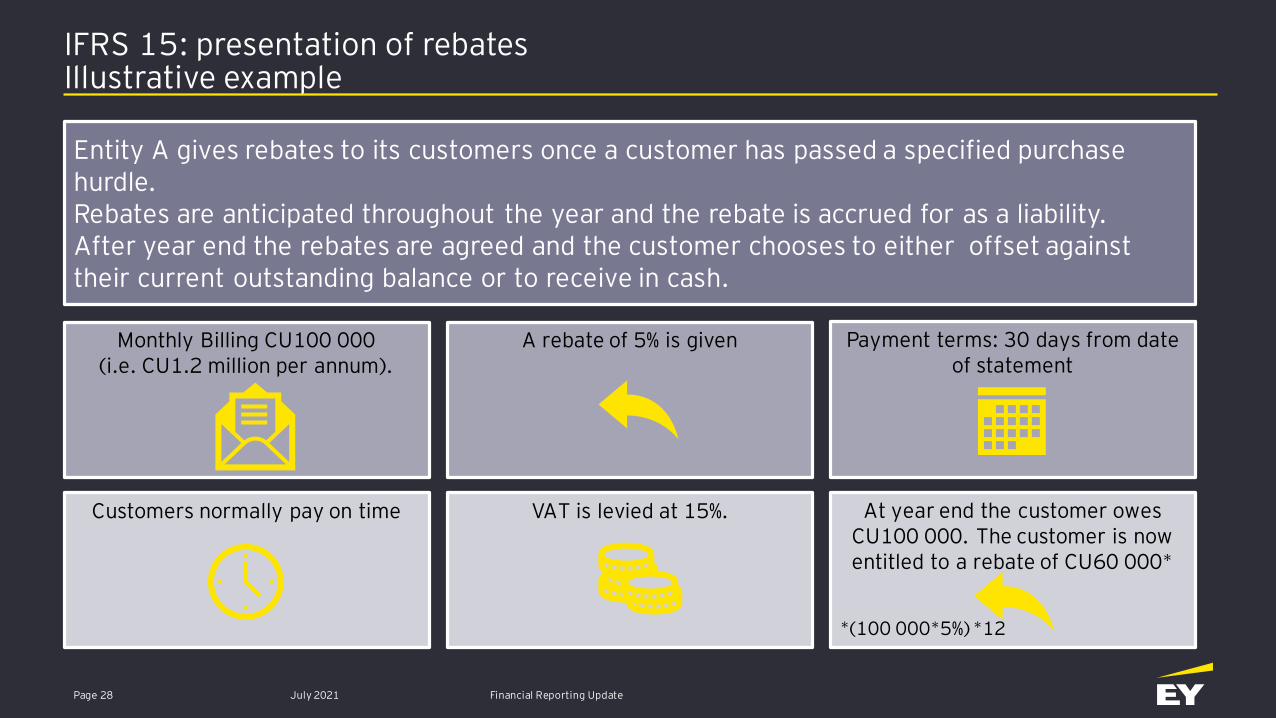

IFRS 15: presentation of rebatesIllustrative example

Entity A gives rebates to its customers once a customer has passed a specified purchase hurdle.Rebates are anticipated throughout the year and the rebate is accrued for as a liability.After year end the rebates are agreed and the customer chooses to either offset against their current outstanding balance or to receive in cash.

Monthly Billing CU100 000 (i.e. CU1.2 million per annum).

A rebate of 5% is given Payment terms: 30 days from date of statement

Customers normally pay on time VAT is levied at 15%. At year end the customer owes CU100 000. The customer is now entitled to a rebate of CU60 000*

*(100 000*5%) *12

July 2021 Financial Reporting UpdatePage 28

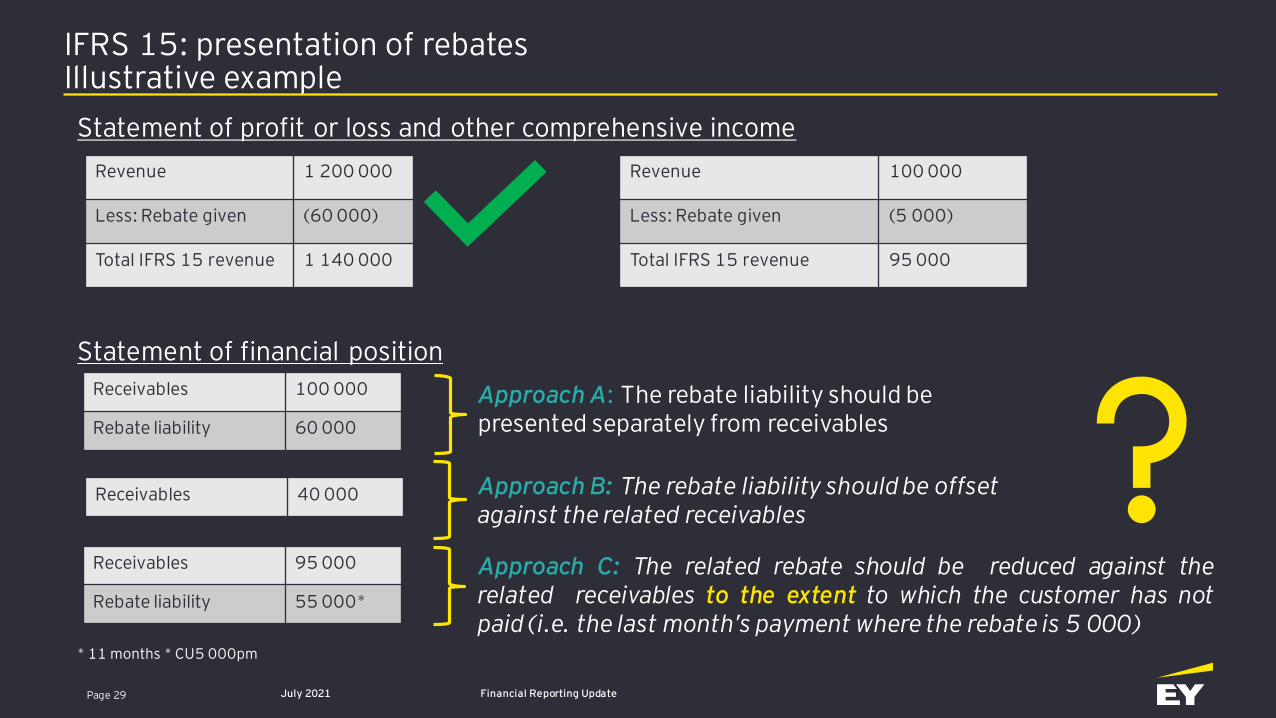

IFRS 15: presentation of rebatesIllustrative example

Statement of profit or loss and other comprehensive income

Statement of financial position

* 11 months * CU5 000pm

Revenue 1 200 000

Less: Rebate given (60 000)

Total IFRS 15 revenue 1 140 000

Receivables 100 000

Rebate liability 60 000

Receivables 40 000

Receivables 95 000

Rebate liability 55 000*

Approach A: The rebate liability should bepresented separately from receivables

Approach B: The rebate liability should be offsetagainst the related receivables

Approach C: The related rebate should be reduced against therelated receivables to the extent to which the customer has notpaid (i.e. the last month’s payment where the rebate is 5 000)

Revenue 100 000

Less: Rebate given (5 000)

Total IFRS 15 revenue 95 000

PaJuly 2021 Financial Reporting UpdatePage 29

IFRS 15: presentation of rebatesIllustrative example

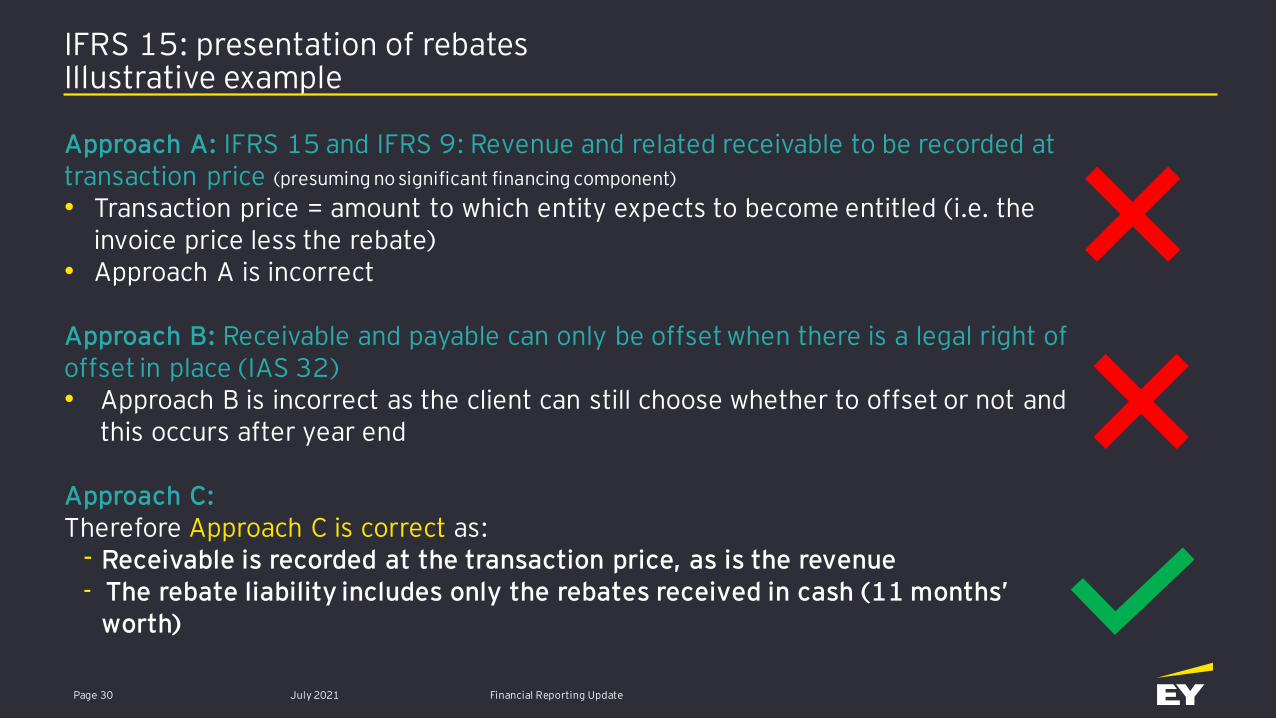

Approach A: IFRS 15 and IFRS 9: Revenue and related receivable to be recorded at transaction price (presuming no significant financing component)

• Transaction price = amount to which entity expects to become entitled (i.e. the invoice price less the rebate)

• Approach A is incorrect

Approach B: Receivable and payable can only be offset when there is a legal right of offset in place (IAS 32)• Approach B is incorrect as the client can still choose whether to offset or not and

this occurs after year end

Approach C:Therefore Approach C is correct as:

- Receivable is recorded at the transaction price, as is the revenue- The rebate liability includes only the rebates received in cash (11 months’

worth)

July 2021 Financial Reporting UpdatePage 30

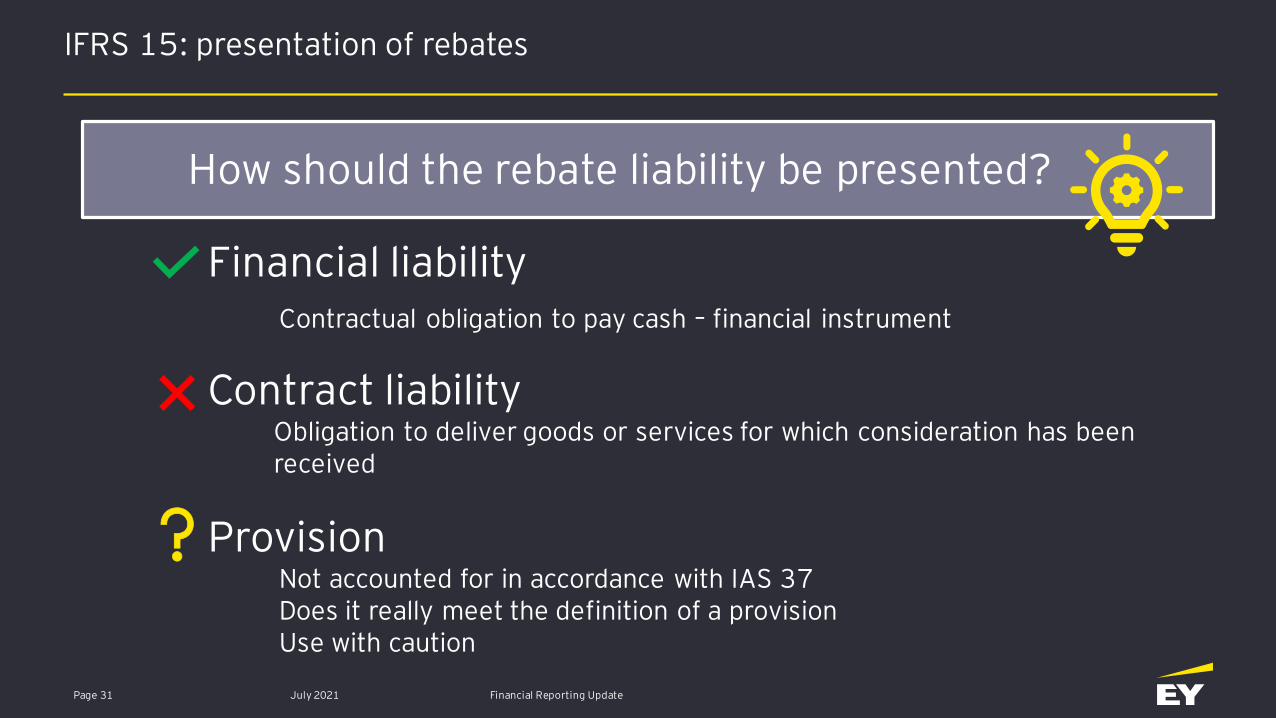

IFRS 15: presentation of rebates

Financial liabilityContractual obligation to pay cash – financial instrument

Contract liabilityObligation to deliver goods or services for which consideration has been received

Provision Not accounted for in accordance with IAS 37Does it really meet the definition of a provisionUse with caution

How should the rebate liability be presented?

July 2021 Financial Reporting UpdatePage 31

IAS 7: statement of cash flows

July 2021 Financial Reporting UpdatePage 32

Effective interest

----------------------------

------------------------

-------------------------

--------------------------

--------------------------

---------------------------

----------------------------

------------------------

-------------------------

--------------------------

--------------------------

---------------------------%

Page 33

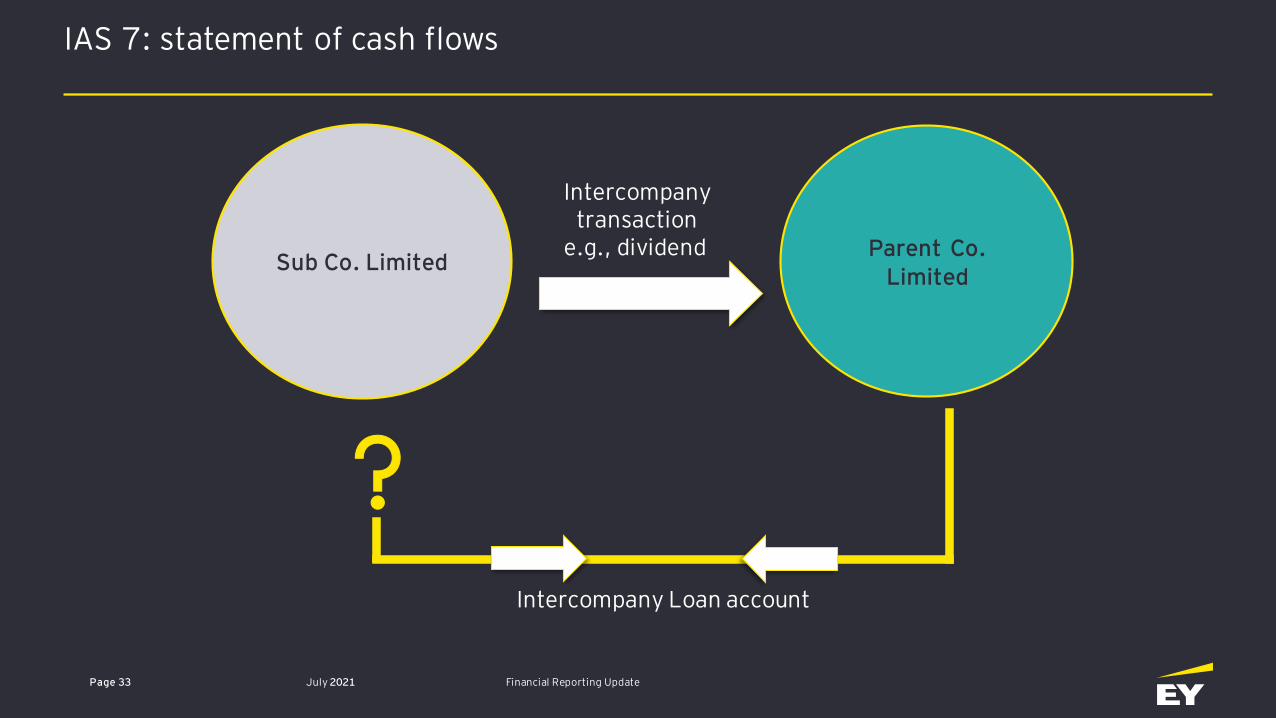

Intercompany transaction

e.g., dividend

Intercompany Loan account

Parent Co. Limited

Sub Co. Limited

July 2021 Financial Reporting UpdatePage 33

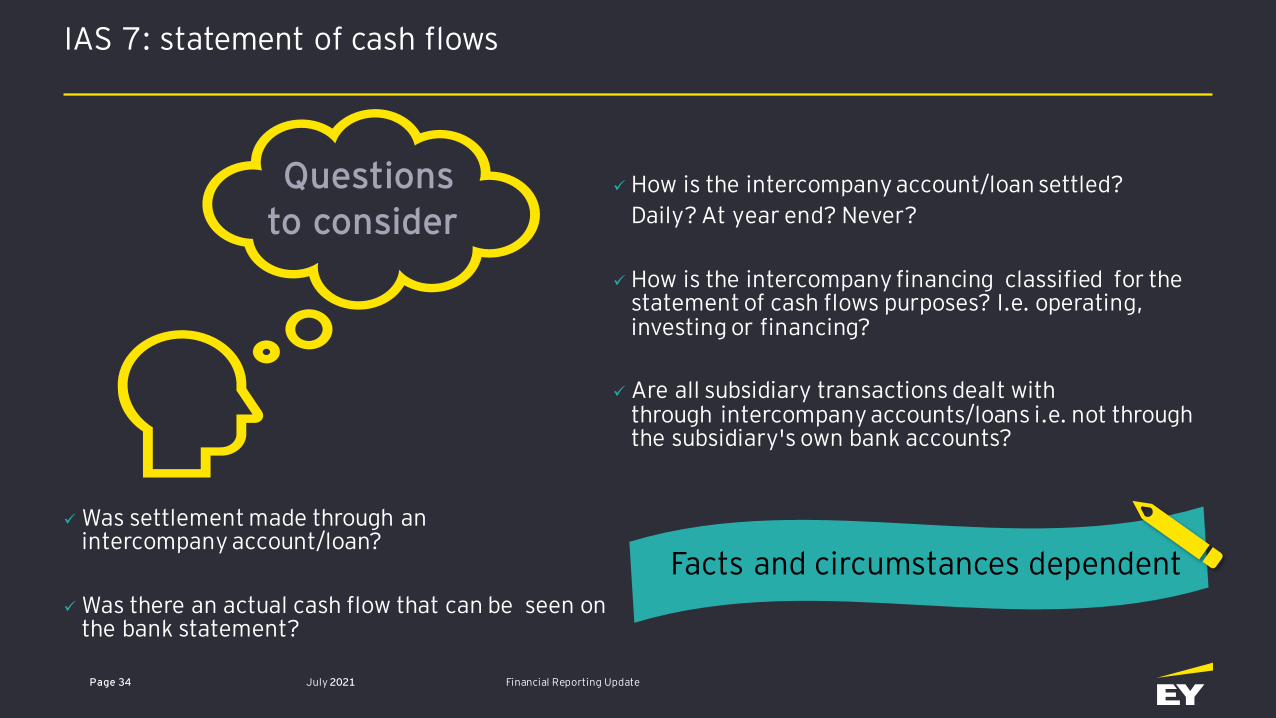

IAS 7: statement of cash flows

WEM IFRS desk technical call - Climate change and sustainabilityPage 34

✓ How is the intercompany account/loan settled?

Daily? At year end? Never?

✓ How is the intercompany financing classified for the statement of cash flows purposes? I.e. operating, investing or financing?

✓ Are all subsidiary transactions dealt with through intercompany accounts/loans i.e. not through the subsidiary's own bank accounts?

Questions to consider

Facts and circumstances dependent

✓ Was settlement made through an intercompany account/loan?

✓ Was there an actual cash flow that can be seen on the bank statement?

July 2021 Financial Reporting UpdatePage 34

IAS 7: statement of cash flows

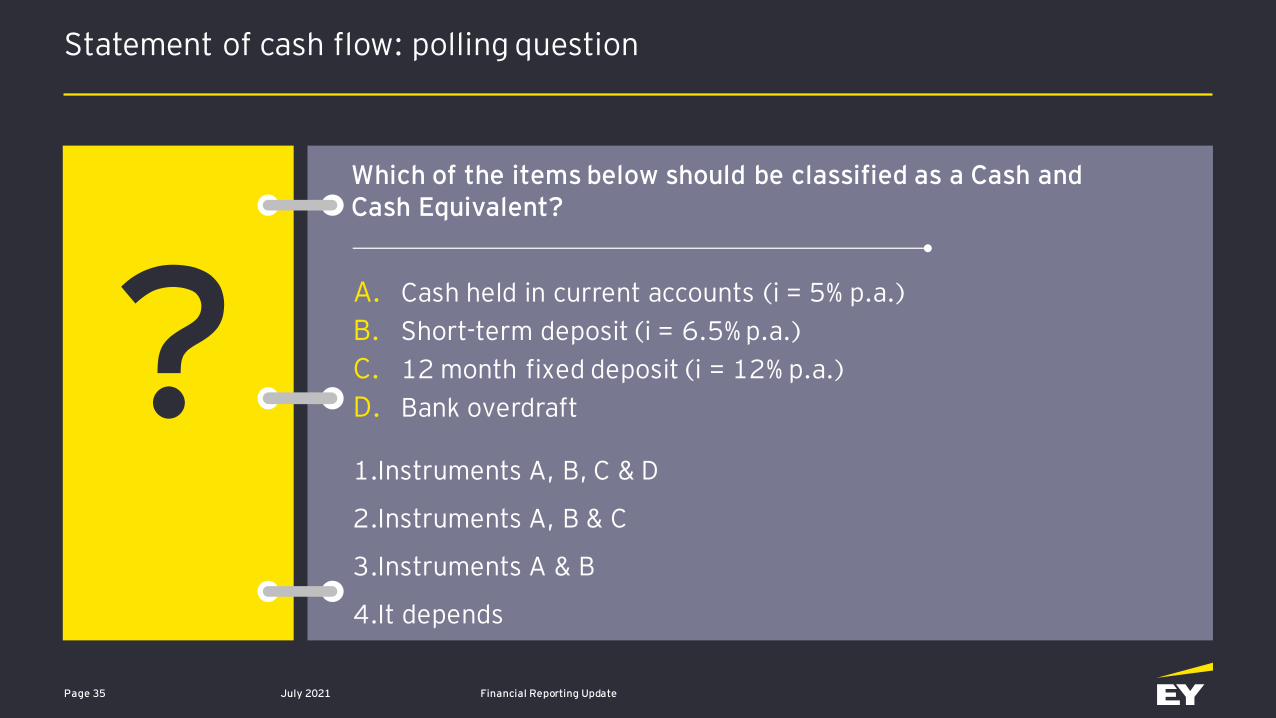

Statement of cash flow: polling question

July 2021 Financial Reporting UpdatePage 35

A. Cash held in current accounts (i = 5% p.a.)

B. Short-term deposit (i = 6.5% p.a.)

C. 12 month fixed deposit (i = 12% p.a.)

D. Bank overdraft

1.Instruments A, B, C & D

2.Instruments A, B & C

3.Instruments A & B

4.It depends

Which of the items below should be classified as a Cash and Cash Equivalent?

?

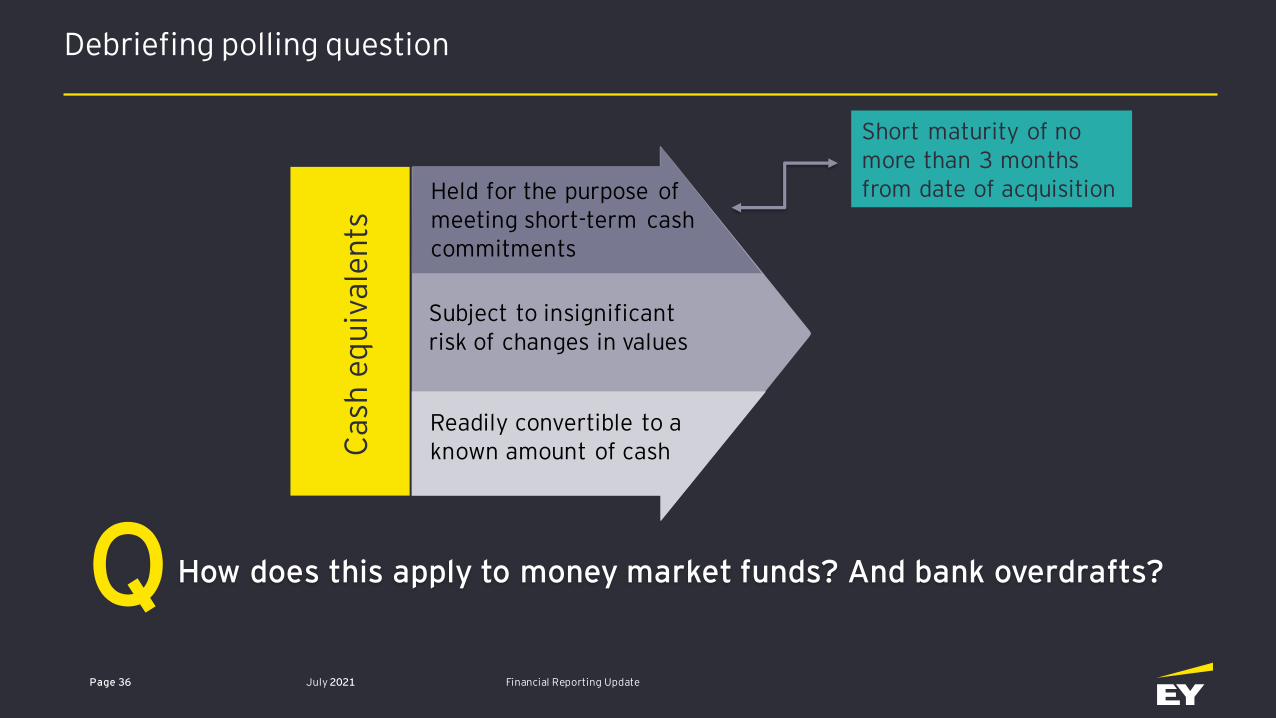

Held for the purpose of meeting short-term cash commitments

Readily convertible to aknown amount of cash

Subject to insignificant risk of changes in values

How does this apply to money market funds? And bank overdrafts?

Ca

sh e

qu

iva

len

ts

Short maturity of no more than 3 months from date of acquisition

July 2021 Financial Reporting UpdatePage 36

Debriefing polling question

Q

Statement of cash flows

Page 37 July 2021 Financial Reporting Update

Statement of Cash Flows

Cash and cash

equivalents

Investing

activities

Financing

activities

Other presentation issues

Page 38 July 2021 Financial Reporting Update

Amendment to IFRS 16 COVID-19 related rent concessions

Entities are required to apply the practical expedient consistentlyto contracts with similar characteristics and in similar circumstances.

• Update to condition to apply relief to a change in lease payments originally due on or before 30 June 2021 to 30 June 2022

• Modified retrospective application to annual reporting periods beginning on or after 1 April 2021, with earlier application permitted

July 2021 Financial Reporting UpdatePage 39

One minute recap

Page 40 July 2021 Financial Reporting Update

Page 41

Resources

• www.ey.com/ifrs

• Applying IFRS

• EY IFRS Core Tools

• IFRS Update

• Good Group illustrative financial statements

• Good Group alternative illustrative financial statements

• International GAAP® Disclosure Checklist

• EY International GAAP publication

• For additional recordings visit: https://www.ey.com/en_za/assurance/financial-reporting-quarterly-updates

July 2021 Financial Reporting Update

EY | Assurance | Tax | Strategy and Transactions | Consulting

About EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our p eople, for our clients and for our communities.

EY refers to the global organisation and may refer to one or more of the member firms of Ernst & Young Global Limited, each o f which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organisation, please visit ey.com.

© 2020 EYGM Limited.

All Rights Reserved. Creative Services ref. 6499. Artwork by Shangase.

In line with EY’s commitment to minimise its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com