Embed Size (px)

Citation preview

FINANCIAL REPORTING UPDATES

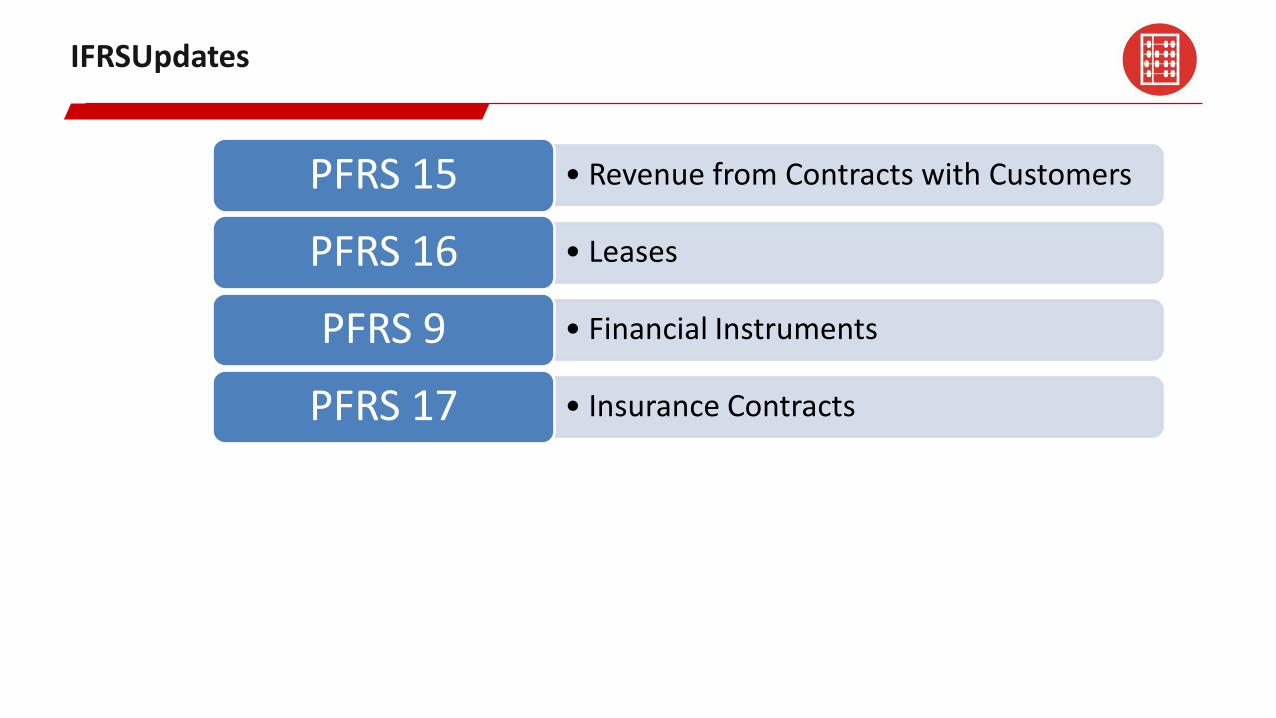

IFRSUpdates

• Revenue from Contracts with CustomersPFRS 15• Leases PFRS 16• Financial InstrumentsPFRS 9• Insurance ContractsPFRS 17

IPSAS Updates

• Service Concession ArrangementIPSAS 32

• Initial Adoption of Accrual Basis IPSASIPSAS 33

PFRS 15: Revenue from Contracts with CustomersEffective beginning on or after January 1, 2018

Introduction to PFRS 15An Overview of PFRS 15

When to recognize revenue?

• Entities should recognise revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange.

PFRS 15: Revenue from Contracts with Customers

The Revenue Recognition StandardThe Five-Step Model Framework

1 • Identify the contract with the customer

2 • Identify the separate performance obligations

3 • Determine the transaction price

4• Allocate the transaction price to the separate performance

obligations

5• Recognize revenue when a performance obligation is

satisfied

Steps to apply the core principle:

PFRS 15: Revenue from Contracts with Customers

The Revenue Recognition StandardThe Five-Step Model Framework

Step 1: Identify the contract(s)

• A contract should meet the following criteria:– Approval of the parties– Rights and obligations.– Payment terms– Commercial substance– Collectability is reasonably assured

PFRS 15: Revenue from Contracts with Customers

Step 2: Identify the separate performance obligation(s)

Two-step model to identify which goods or services are distinct

Part 1:Focus on whether the good or service is capable of being distinct

Part 2: Focus on whether the good or service is distinct in the context of the contract

Customer can benefit from the individual good or service on its own

In combination with other goods or services available to the customer

OR

The good or service is not highly dependent on, is not highly interrelated with, or does not

significantly modify or customize other promised goods or services in the contract

The Revenue Recognition StandardThe Five-Step Model Framework

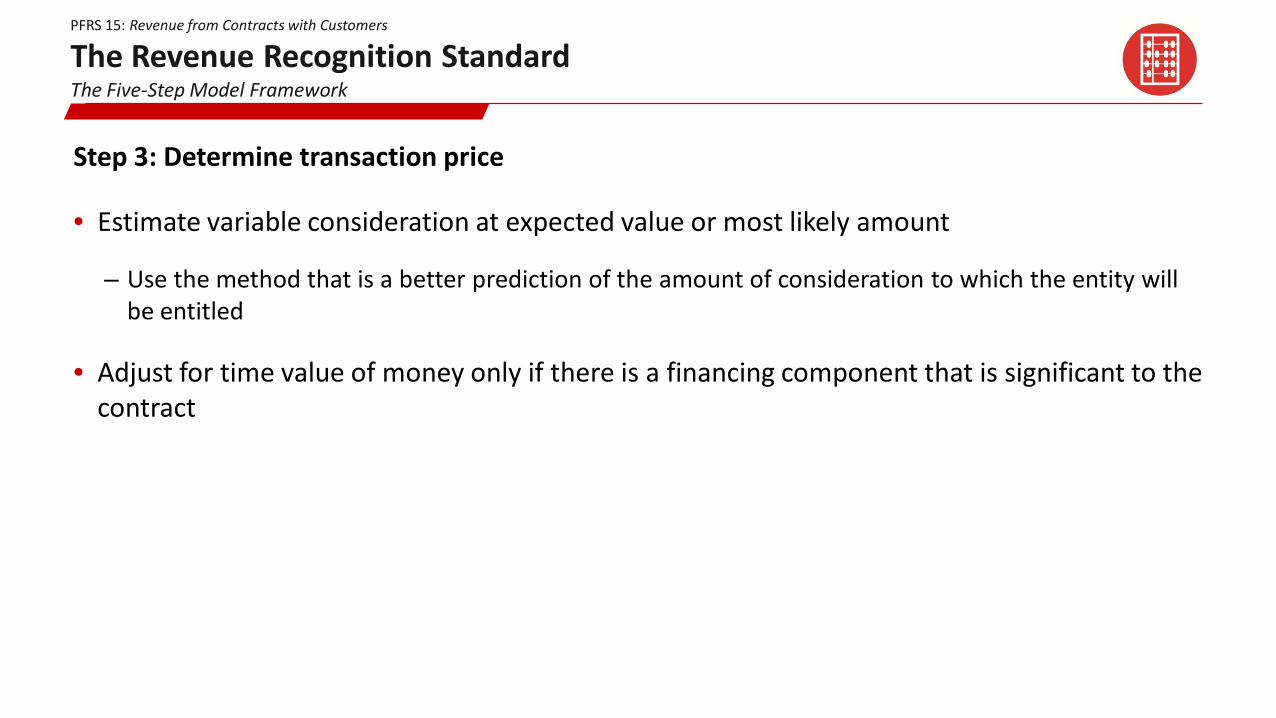

Step 3: Determine transaction price

• Estimate variable consideration at expected value or most likely amount

– Use the method that is a better prediction of the amount of consideration to which the entity will be entitled

• Adjust for time value of money only if there is a financing component that is significant to the contract

PFRS 15: Revenue from Contracts with Customers

The Revenue Recognition StandardThe Five-Step Model Framework

Step 4: Allocate the transaction price

• Allocating on a relative standalone selling price basis will generally meet the objective

– Estimate selling prices if they are not observable

– Residual estimation techniques may be appropriate in rare circumstances

PFRS 15: Revenue from Contracts with Customers

The Revenue Recognition StandardThe Five-Step Model Framework

Step 5: Recognize revenue

• Revenue is recognised at the point in time when the customer obtains control of the promised asset.

– Indicators of control include:• a present right to payment• legal title• physical possession• risks and rewards of ownership• customer acceptance

PFRS 15: Revenue from Contracts with Customers

The Revenue Recognition StandardThe Five-Step Model Framework

Recognize revenue over a period of time

• the customer simultaneously receives and consumes the benefits provided by the entity’s performance as the entity performs

• the entity’s performance creates or enhances an asset that the customer controls as the asset is created or enhanced; OR

• the entity’s performance does not create an asset with an alternative use to the entity AND the entity has an enforceable right to payment for performance completed to date

PFRS 15: Revenue from Contracts with Customers

The Revenue Recognition StandardThe Five-Step Model Framework

Transition and effective date

• Retrospective application• Effective date: 1 January 2018

PFRS 15: Revenue from Contracts with Customers

PFRS 16: LeasesEffective beginning on or after January 1, 2019

What is a lease?

• A lease is a contract that conveys the right to use an identified asset for a period of time in exchange for consideration.

Amendments to PFRS 16What’s changing

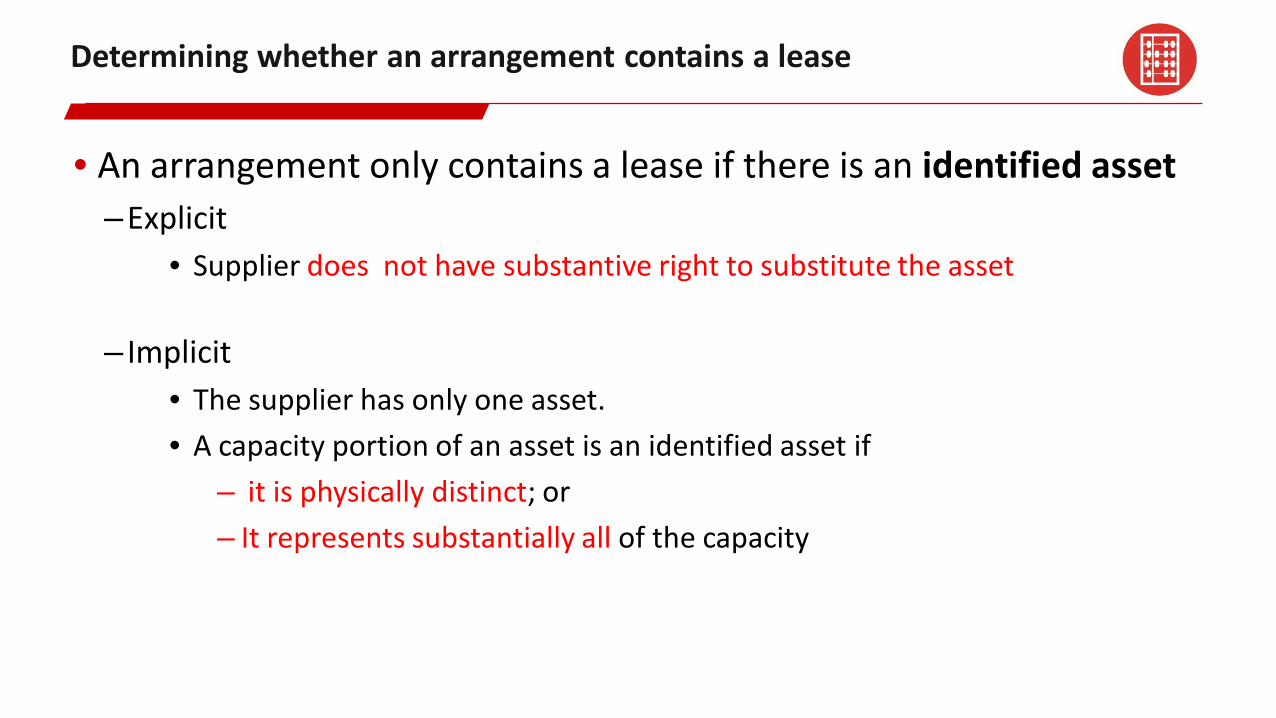

Determining whether an arrangement contains a lease

• An arrangement only contains a lease if there is an identified asset–Explicit

• Supplier does not have substantive right to substitute the asset

– Implicit• The supplier has only one asset.• A capacity portion of an asset is an identified asset if

– it is physically distinct; or – It represents substantially all of the capacity

Determining whether an arrangement contains a lease

• CONVEYS THE RIGHT TO USE THE ASSET–The customer must have the right to obtain substantially all of the economic

benefits from the use of the identified asset; and –The customer must have the right to direct the use of the identified asset.

• The customer has the right to direct how and for what purpose the asset is used; or• The relevant decisions about how and for what purpose an asset is used are

predetermined; and– The customer has the right to operate the asset or direct others to operate the

asset in a manner that it determines without the supplier having the right to change those operating instructions; or

– The customer designed the asset in a way that predetermines how and for what purpose the asset will be used

PFRS 16- LeasesLease vs. Service

•When the customer controls the use of an asset

Lease

•When the supplier controls the use of an asset

Service

Assessment of the Contract

• An assessment of whether an arrangement contains a lease shall be made at the inception of the lease.

• A reassessment is made only if the terms and conditions of the contract are changed.

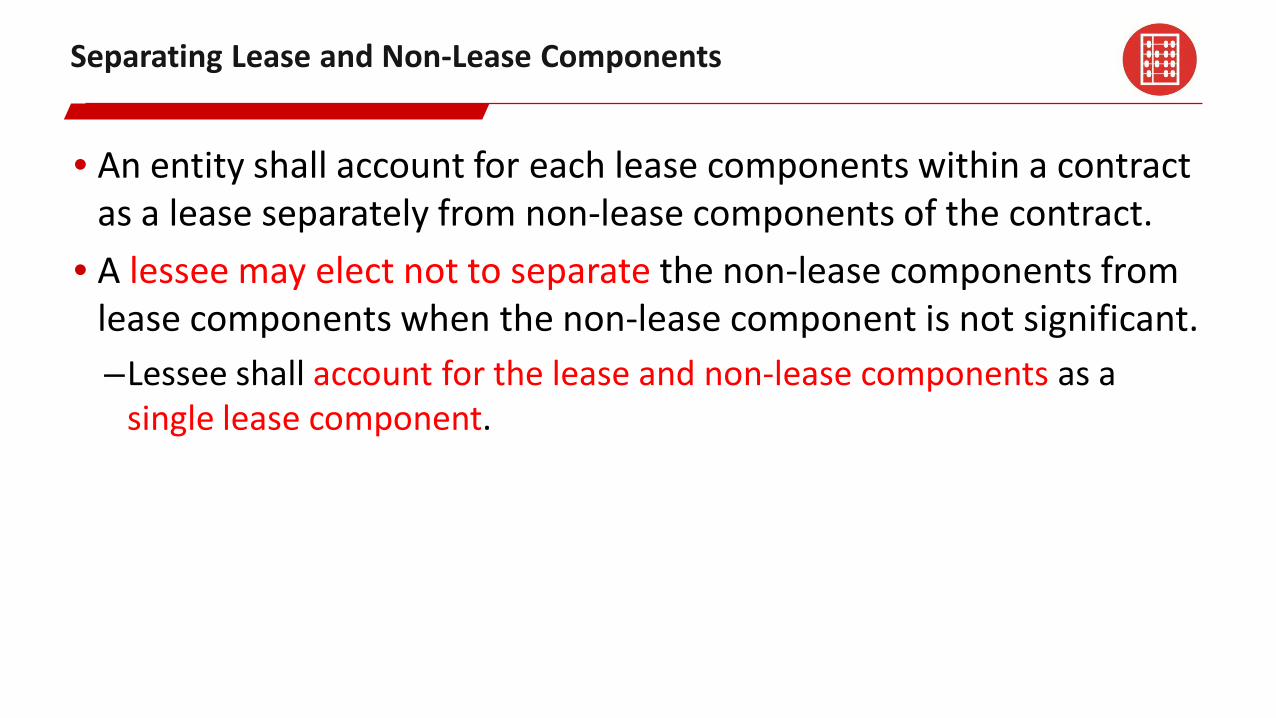

Separating Lease and Non-Lease Components

• An entity shall account for each lease components within a contract as a lease separately from non-lease components of the contract.

• A lessee may elect not to separate the non-lease components from lease components when the non-lease component is not significant.–Lessee shall account for the lease and non-lease components as a

single lease component.

Determining the Lease Term

• An entity determines the lease term as the–Non-cancellable period of the lease; plus–Period covered by an option to extend (if the lessee is reasonably certain to

exercise the option); and–Periods covered by an option to terminate (if the lessee is reasonably certain

not to exercise the option.)

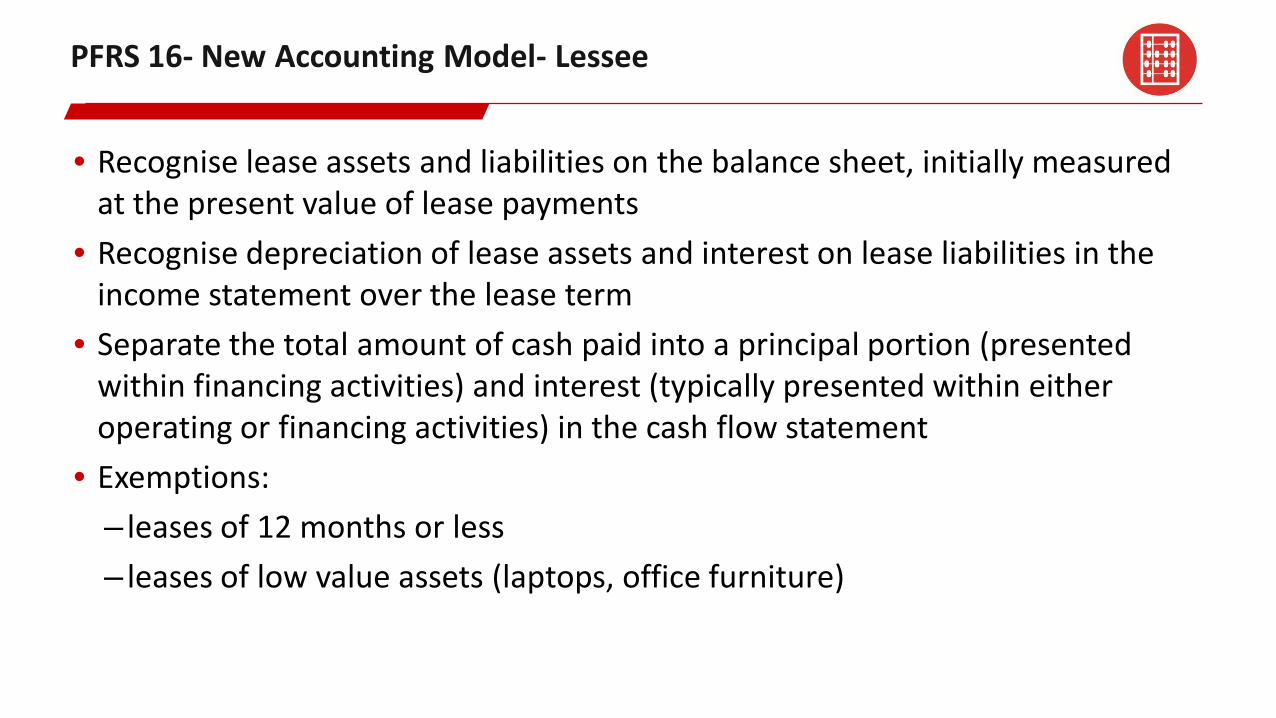

PFRS 16- New Accounting Model- Lessee

• Recognise lease assets and liabilities on the balance sheet, initially measured at the present value of lease payments

• Recognise depreciation of lease assets and interest on lease liabilities in the income statement over the lease term

• Separate the total amount of cash paid into a principal portion (presented within financing activities) and interest (typically presented within either operating or financing activities) in the cash flow statement

• Exemptions:– leases of 12 months or less– leases of low value assets (laptops, office furniture)

Amendments to PFRS 16Lessee - Transition

Changed to focus on the most relevant information• Existing finance leases: may choose to retain existing accounting • Existing operating leases: choose either full retrospective or modified

retrospective approach (consistently for all leases) • Modified retrospective approach

–Exemption for leases ending within 12 months of transition date –No restatement of comparatives –Choice of measurement of ROU assets (i.e. retrospective basis or equal to

lease liabilities) on a lease-by-lease basis

Amendments to PFRS 16What does PFRS 16 change for lessors?

There is little change for lessors

• Applying PFRS 16, a lessor continues to classify its leases as operating leases or finance leases and to account for those two types of leases differently.

• PFRS 16 also requires lessors to provide enhanced disclosures about their risk exposure arising from leasing activities

PFRS 9- Financial Instruments

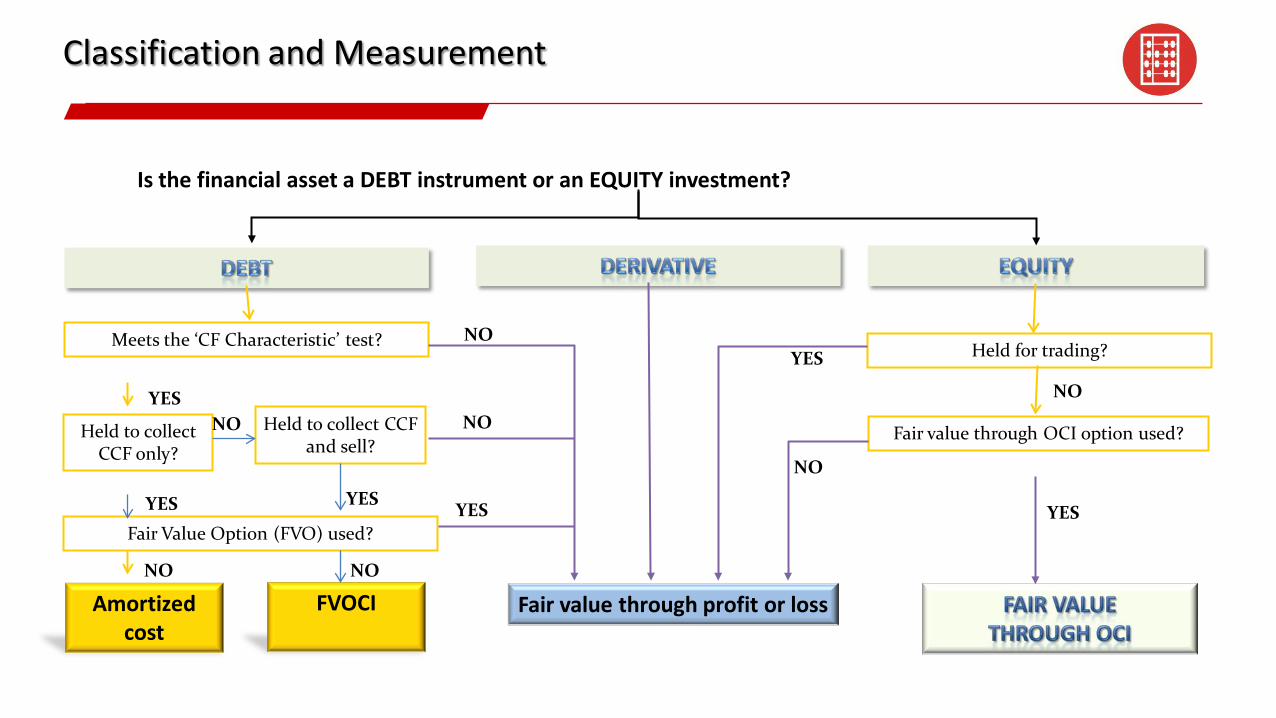

Classification and Measurement

Is the financial asset a DEBT instrument or an EQUITY investment?

Meets the ‘CF Characteristic’ test?

Amortized cost

Held to collect CCF only?

Fair Value Option (FVO) used?

Fair value through profit or loss

Fair value through OCI option used?

Held for trading?

NO

NO

YES

YES

YES

NO

NO

YES

YES

NO

Held to collect CCF and sell?

NO

FVOCINO

YES

Impairment- Expected Loss Model

• Objective:–To provide users of financial statements with more useful information about

an entity’s expected credit losses on financial instruments.

• Requirement:–Recognize expected credit losses at all times and– Update the amount of expected credit losses recognized at each reporting

date to reflect changes in the credit risk of financial instruments.

OVERVIEW of Impairment Requirement

Stage 1• Recognize 12-month expected credit loss in P&L• EIR is based on Gross Receivables

Stage 2

• Recognize lifetime expected credit losses if credit risk significantly increases

• EIR is based on Gross Receivables

Stage 3

• There is objective evidence of impairment;• Individual assessment is made;• EIR is based on Net Receivables

Simplified Approach- Impairment

IFRS 17- Insurance Contracts

IFRS 17 Income Statement

IFRS 17 Balance Sheet

Measuring insurance liabilities

Future cash flows

Discount rates

Risk adjustment

Contractual Service Margin

IPSAS 32: Service Concession Arrangements

Recognition

• A grantor recognizes a service concession asset if the following conditions are met:– The grantor controls or regulates

• The type of services that operator must provide;• To whom it must provide them; and• At what price

– The grantor controls any significant residual interest in the asset at the end of the arrangement term through

• Ownership; or • Beneficial entitlement.

Measurement of Asset

• A grantor shall initially measure a service concession asset at its fair value.• Subsequently, service concession asset shall be accounted for as a separate

class of asset in accordance with PPSAS 17 or PPSAS 31 as appropriate.

Measurement of Liability

• A grantor shall initially measure a service concession liability at fair value of the service concession asset.–The financial liability model

The grantor compensates the operator by paying cash or other financial asset

–The grant of right modelThe grantor compensates the operator by granting the operator to

earn revenue from the users of the service concession asset

Financial Liability Model

Where the grantor has an unconditional obligation to pay cash or anotherfinancial asset to the operator for the construction, development, acquisition,or upgrade of a service concession asset, the grantor shall account for theliability recognized as a financial liability

Grant of Right Model

Where the grantor does not have an unconditional obligation to pay cash andgrants the operator the right to earn revenue from third-party users, the grantorshall account for the liability recognized as the unearned portion of the revenuearising from the exchange of assets.

The grantor shall recognize revenue and reduce the liability recognized accordingto the economic substance of the service concession arrangement.

IPSAS 33- First Time Adoption of Accrual Basis IPSAS

FIRST-TIME ADOPTER

• An entity is a first-time adopter if it prepares financial statements in accordance with this IPSAS for the first time and the entity– Did not present financial statements in the previous period;– Presented its most recent previous financial statements in conformity with IPSAS;

or– Presented its most recent previous financial statements using other GAAP.

Opening Statement of Financial Position

• At transition date, an entity shall prepare an opening statement of financial position.

Transition Date

• Transition date is the beginning of the period of the earliest financial statement presented.

PROCEDURES AT DATE OF TRANSITION

• Prepare an opening statement of financial position in accordance with IPSAS– Recognize– Derecognize– Reclassify– Remeasure

• Treat the cumulative effect/adjustments resulting from the above transition directly to opening Surplus (or, if appropriate, other equity account)

RECOGNIZE

• Service Concession Assets• Service Concession Liabilities• Provision for terminal leave benefits• Deferred taxes• Allowance for impairment of receivables

DERECOGNIZE

• Deferred Charges• Training costs• Development costs

RECLASSIFY

• Deferred tax assets and liabilities• Investment property• Inventory

REMEASURE

• Property, plant and equipment• Investment property• Provision for terminal benefits• Allowance for impairment

DISCLOSURES

• Explain how the transition has affected its financial statements– Description of the nature of each change in accounting policy– Reconciliation of profit or loss for the most recent financial statements determined

in accordance with its previous financial reporting framework– Reconciliation of its equity for both

• The date of transition; and• End of the latest period presented in the entity’s most recent annual financial

statements determined in accordance with its previous financial reporting framework

End of Presentation

Thank you

![$ EDUCATIONAL FACILITIES REVENUE [AND REVENUE REFUNDING… · EDUCATIONAL FACILITIES REVENUE [AND REVENUE REFUNDING] ... Educational Facilities Revenue [and Revenue ... Aeronautical](https://img.pdfslide.net/doc/110x75/5b16e1207f8b9a686d8e7aa7/-educational-facilities-revenue-and-revenue-refunding-educational-facilities.jpg)

![VMW Earnings Press Release[1] - VMware · During May 2014, the Financial Accounting Standards Board issued updates to accounting standards related to revenue recognition ("ASC 606")](https://img.pdfslide.net/doc/110x75/5ed43e211e109569e121442d/vmw-earnings-press-release1-vmware-during-may-2014-the-financial-accounting.jpg)