Embed Size (px)

Citation preview

FINANCING

THE FUTURE OF THE GLOBAL

PHARMACEUTICAL INDUSTRY

Philipp Gutzwiller

November 2014

Is the Pharma Market moving

from Monopoly to Monopsony?

2

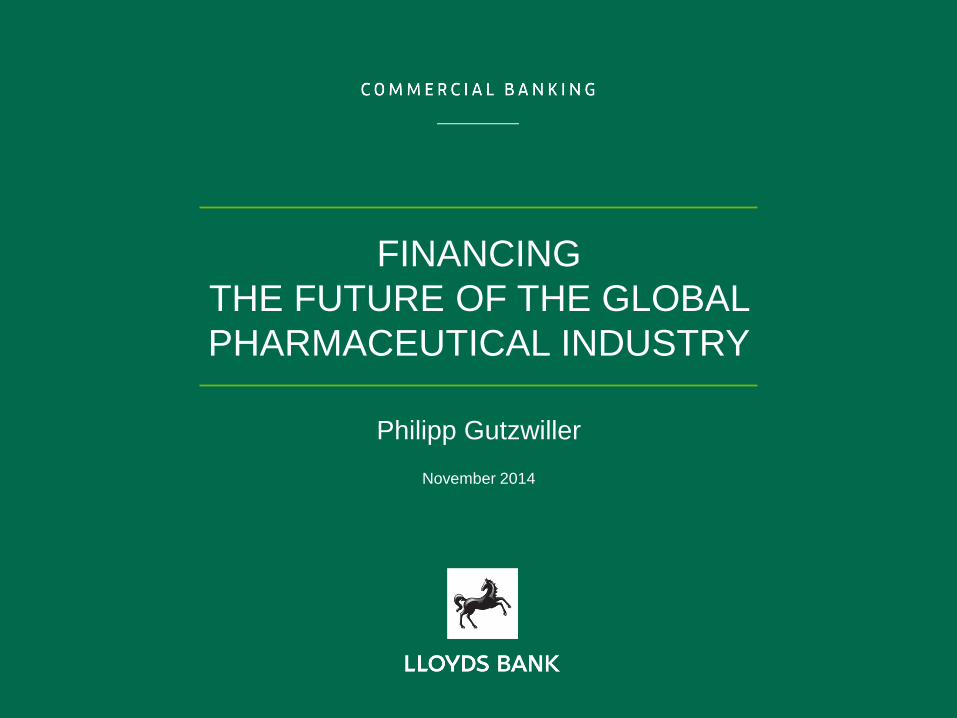

2.8

0.6

1.2

0.5

0.8

0.0

0.5

1.0

1.5

2.0

2.5

3.0

US Japan EU Top 5 EU Other BRIC

Health expenditure, total US$trn (absolute)

Healthcare Spend by Geography

3

Developed Economies Emerging Markets

2%

11%

5%

0.5%

USDtrn

Sources: WorldBank: 2012 data; Bain & Company

Expected growth 2012-2020 Health Expenditure

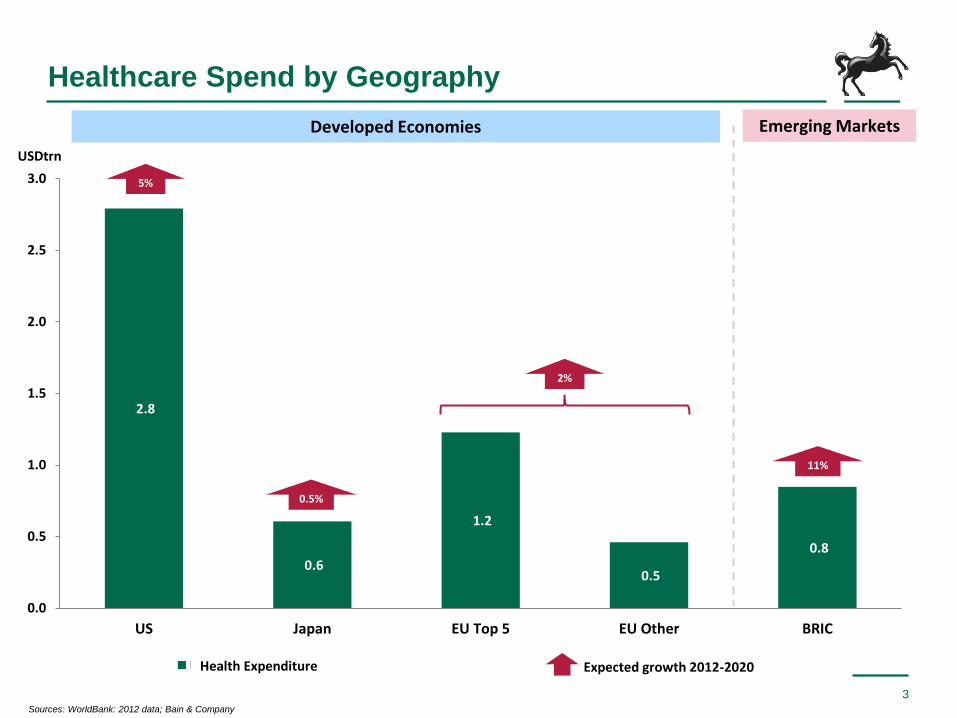

Healthcare Spend in % of GDP

4

Developed Economies Emerging Markets

8.3 8.3 7.9

6.0

3.1

9.6

1.8 2.3

2.4

3.1

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

US Japan EU Top 5 EU Other BRIC

Public Private

% GDP

Sources: WorldBank: 2012 data

Spend Spend

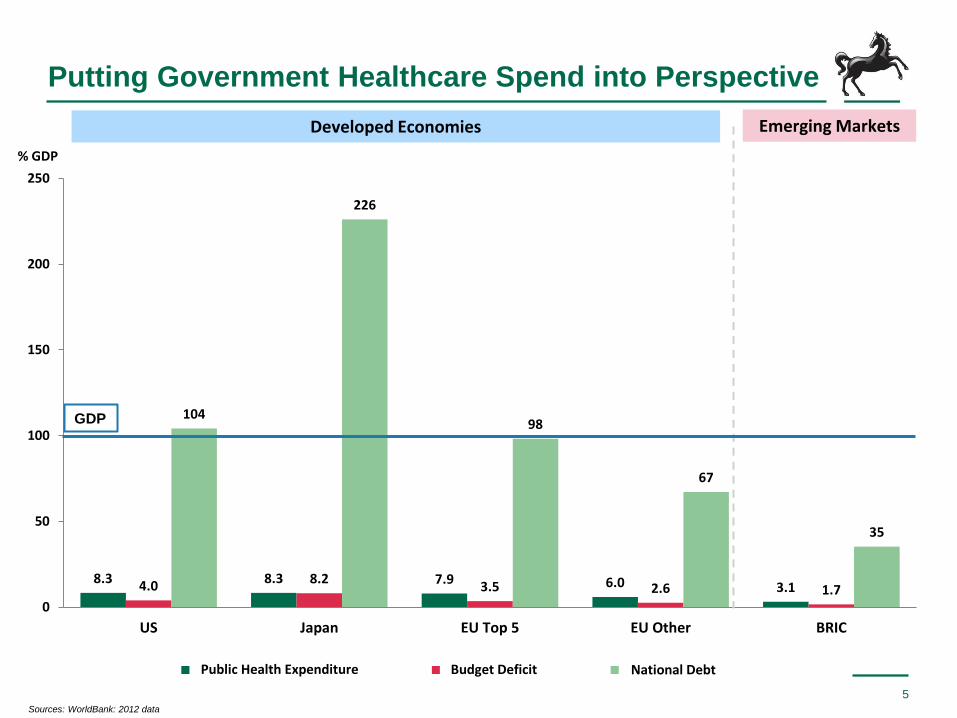

8.3 8.3 7.9 6.0 3.1 4.0 8.2 3.5 2.6 1.7

104

226

98

67

35

0

50

100

150

200

250

US Japan EU Top 5 EU Other BRIC

Public Health expenditure (%GDP) Budget Deficit (%GDP) National debt (% of GDP)

Putting Government Healthcare Spend into Perspective

5

Developed Economies Emerging Markets

GDP

% GDP

Sources: WorldBank: 2012 data

Public Health Expenditure Budget Deficit National Debt

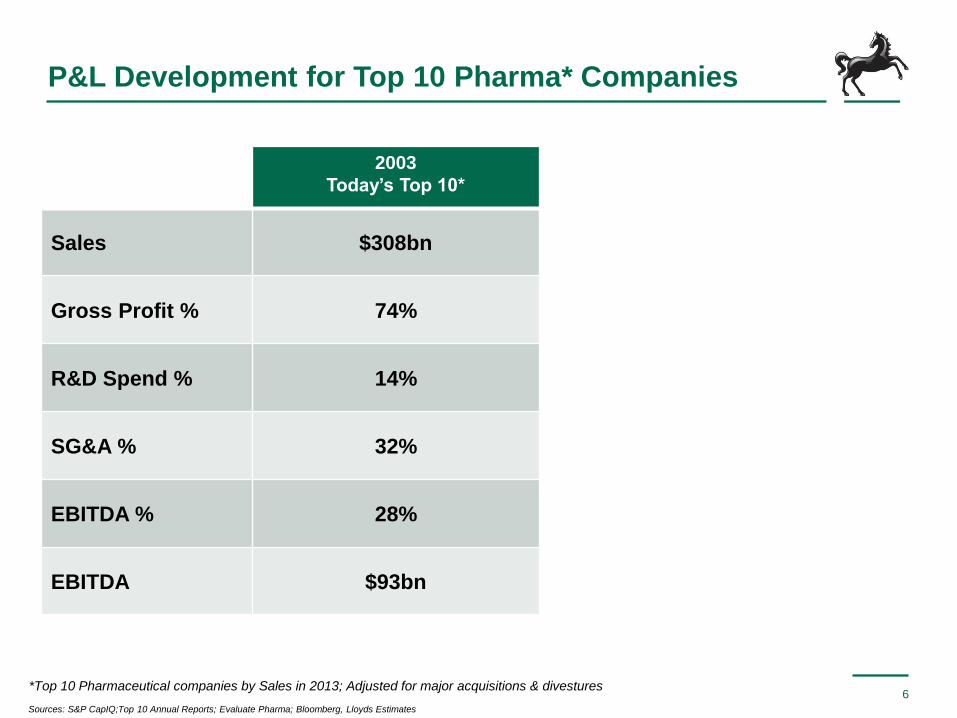

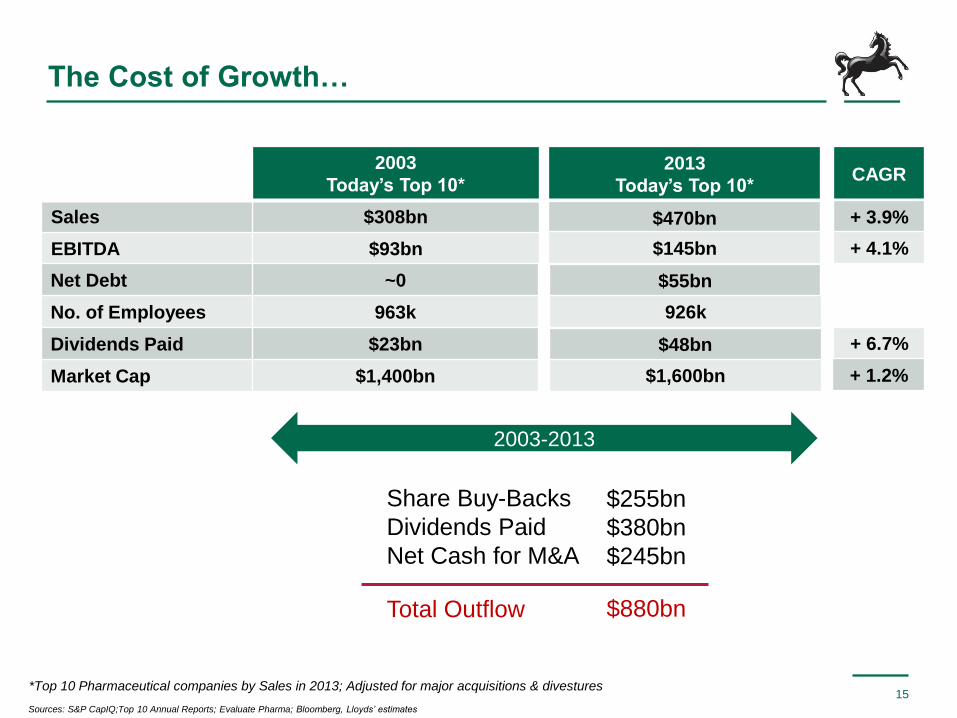

P&L Development for Top 10 Pharma* Companies

6

2003

Today’s Top 10*

Sales $308bn

Gross Profit % 74%

R&D Spend % 14%

SG&A % 32%

EBITDA % 28%

EBITDA $93bn

Sources: S&P CapIQ;Top 10 Annual Reports; Evaluate Pharma; Bloomberg, Lloyds Estimates

*Top 10 Pharmaceutical companies by Sales in 2013; Adjusted for major acquisitions & divestures

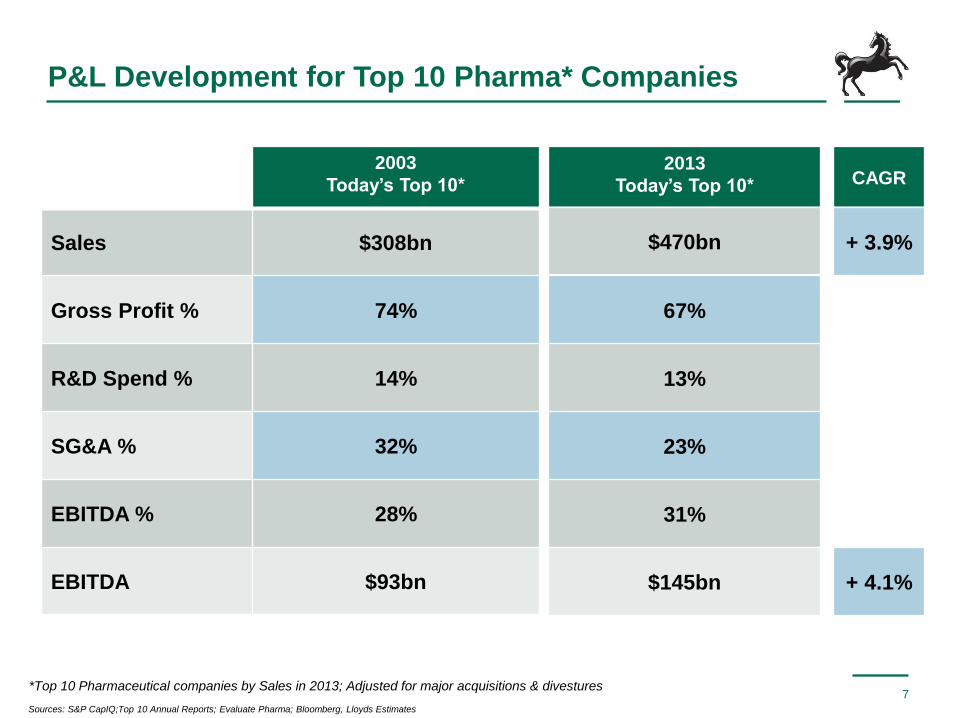

P&L Development for Top 10 Pharma* Companies

7

2003

Today’s Top 10*

Sales $308bn

Gross Profit % 74%

R&D Spend % 14%

SG&A % 32%

EBITDA % 28%

EBITDA $93bn

Sources: S&P CapIQ;Top 10 Annual Reports; Evaluate Pharma; Bloomberg, Lloyds Estimates

2013

Today’s Top 10* CAGR

$470bn

67%

13%

23%

31%

$145bn

+ 3.9%

+ 4.1%

*Top 10 Pharmaceutical companies by Sales in 2013; Adjusted for major acquisitions & divestures

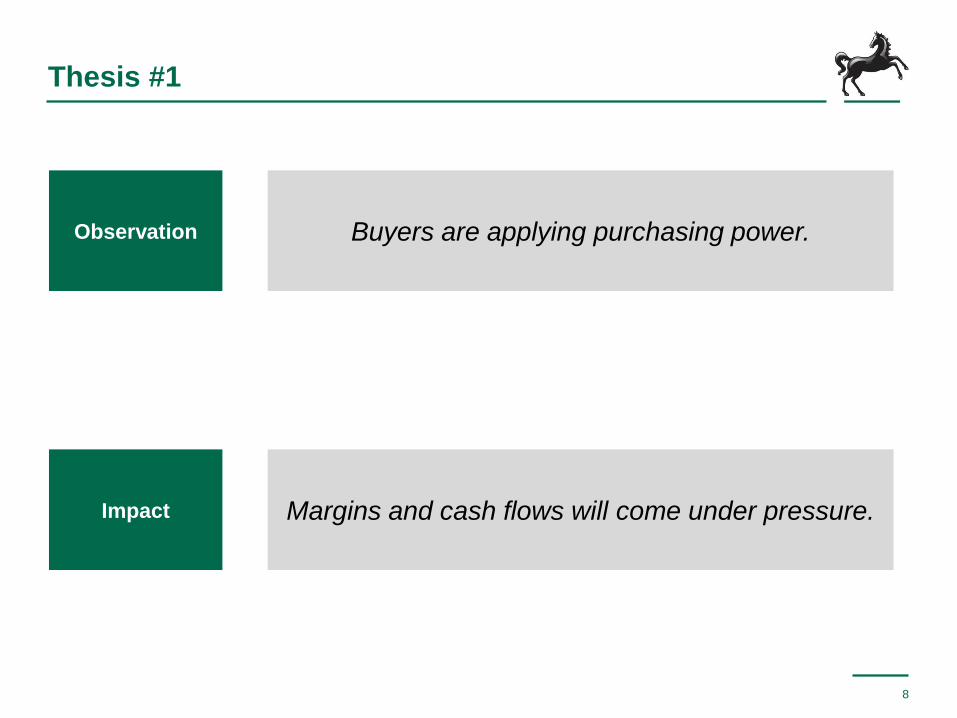

Thesis #1

8

Observation

Impact

Buyers are applying purchasing power.

Margins and cash flows will come under pressure.

More Volatility, Anyone?

9

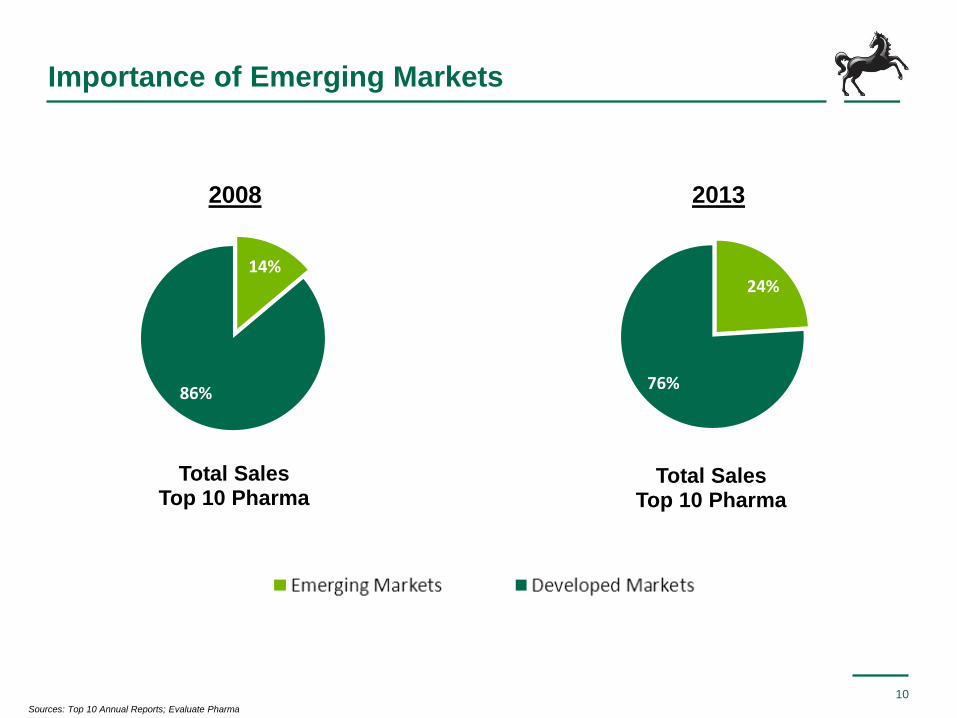

Importance of Emerging Markets

10

14%

86%

Total Sales Top 10 Pharma

Sources: Top 10 Annual Reports; Evaluate Pharma

24%

76%

Total Sales Top 10 Pharma

2008 2013

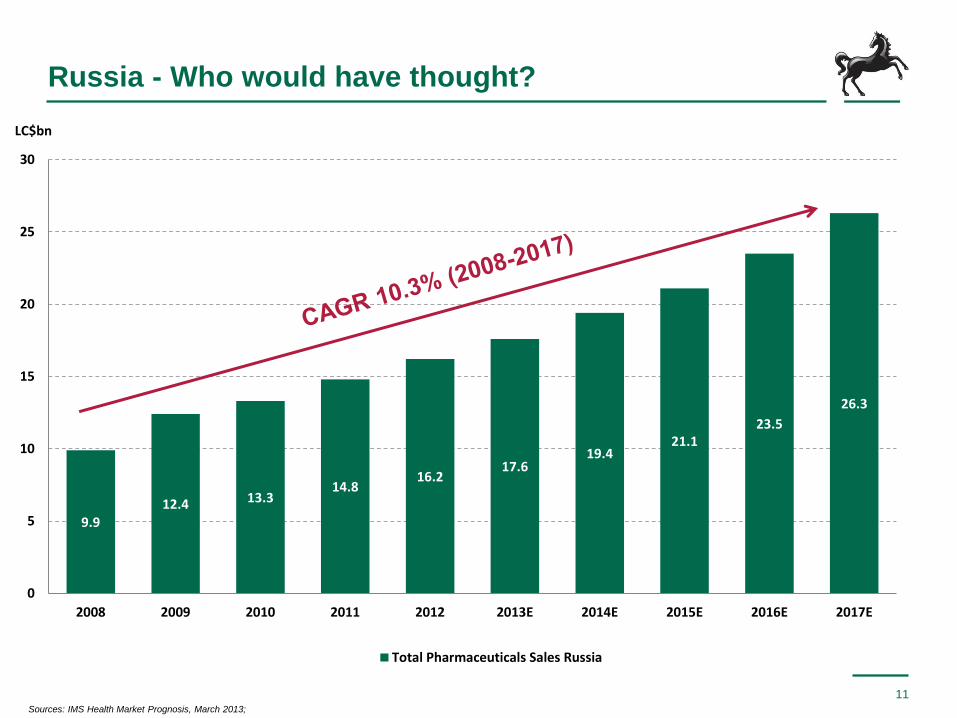

Russia - Who would have thought?

11

9.9 12.4 13.3

14.8 16.2

17.6 19.4

21.1 23.5

26.3

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E 2017E

Total Pharmaceuticals Sales Russia

Sources: IMS Health Market Prognosis, March 2013;

LC$bn

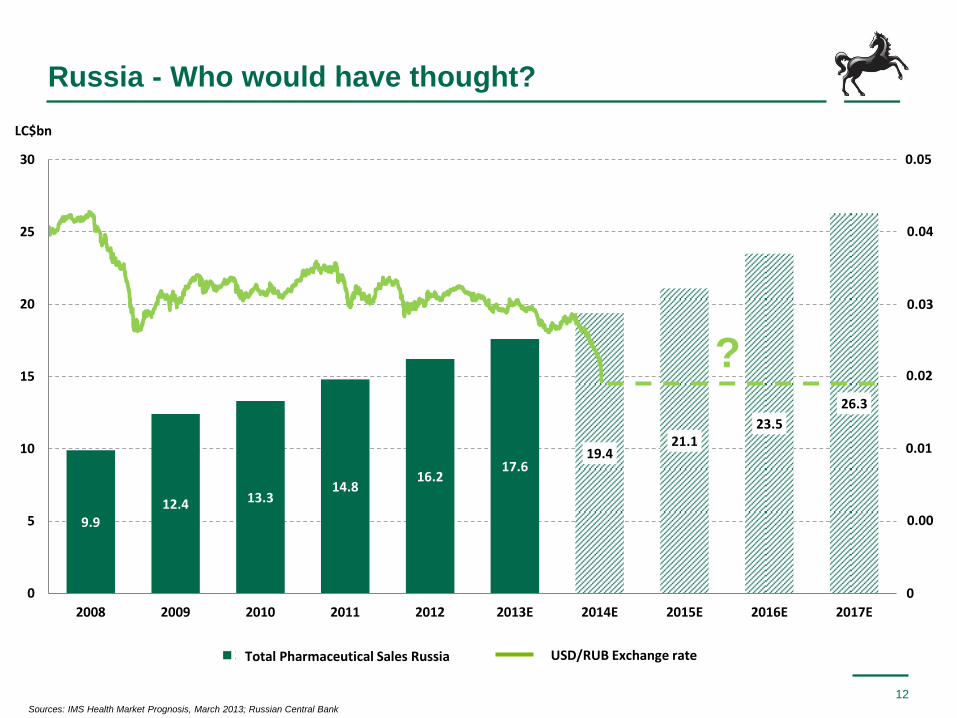

Russia - Who would have thought?

12

9.9 12.4 13.3

14.8 16.2

17.6 19.4

21.1 23.5

26.3

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E 2017E

2008 2016E USD/RUB Exchange rate

? 0.02

0.04

0.03

0.05

0.01

0.00

0

Sources: IMS Health Market Prognosis, March 2013; Russian Central Bank

LC$bn

Total Pharmaceutical Sales Russia

Thesis #2

13

Observation

Impact

Emerging Markets are here to stay.

Increased volatility will need to be managed.

Can Pharma afford the Cost of Growth?

14

The Cost of Growth…

15

2003

Today’s Top 10*

Sales $308bn

EBITDA $93bn

2003-2013

Share Buy-Backs

Dividends Paid

Net Cash for M&A

$255bn

$380bn

$245bn

$880bn Total Outflow

Sources: S&P CapIQ;Top 10 Annual Reports; Evaluate Pharma; Bloomberg, Lloyds’ estimates

2013

Today’s Top 10* CAGR

$470bn

$145bn

$55bn

926k

$48bn

$1,600bn

+ 3.9%

+ 6.7%

+ 1.2%

+ 4.1%

*Top 10 Pharmaceutical companies by Sales in 2013; Adjusted for major acquisitions & divestures

Net Debt ~0

No. of Employees 963k

Dividends Paid $23bn

Market Cap $1,400bn

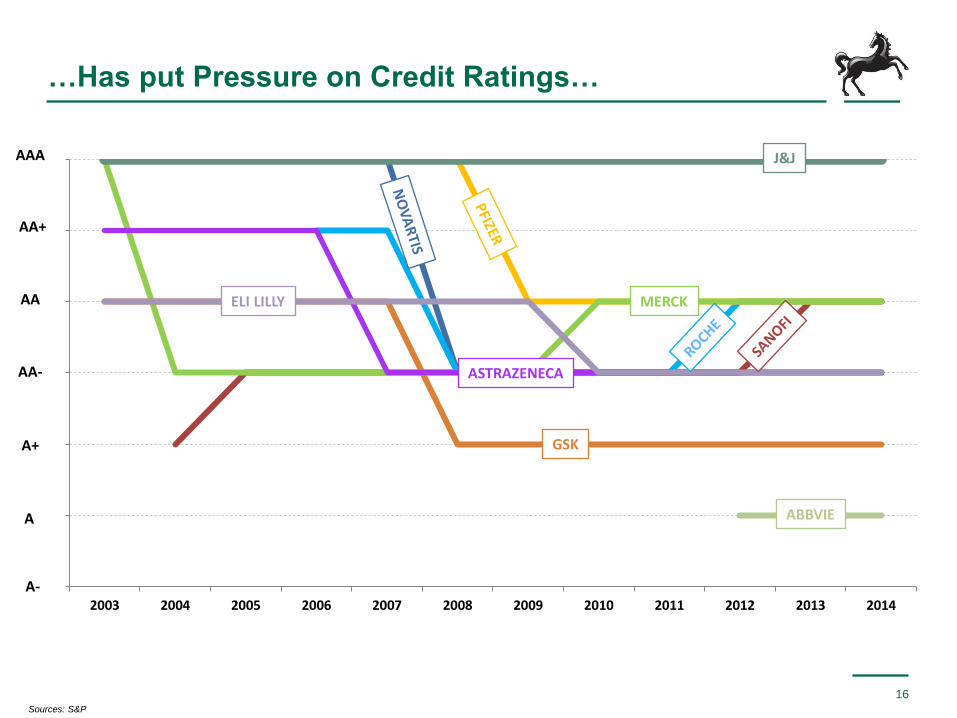

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

…Has put Pressure on Credit Ratings…

16

J&J

MERCK

ASTRAZENECA

GSK

ABBVIE

ELI LILLY

AAA

AA+

AA

AA-

A+

A

A-

Sources: S&P

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

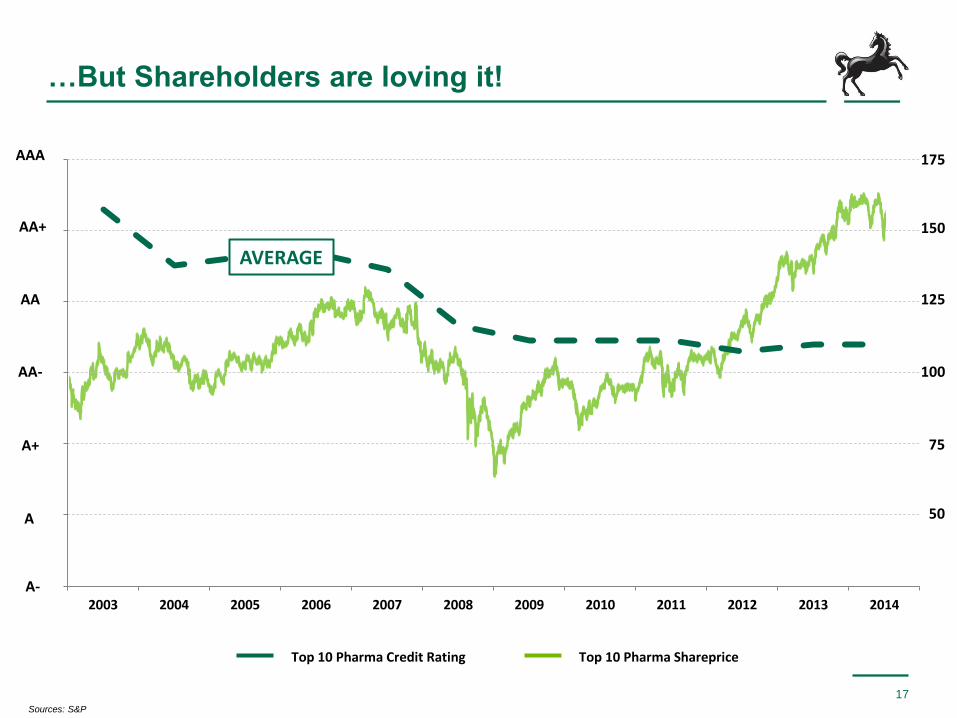

…But Shareholders are loving it!

17

AVERAGE

AAA

AA+

AA

AA-

A+

A

A-

Sources: S&P

Top 10 Pharma Shareprice Top 10 Pharma Credit Rating

100

150

125

175

75

50

Thesis #3

18

Observation

Impact

Shareholders expect growth AND return of cash.

How long is this sustainable for?

Possible Solutions

19

Defensive

Neutral

Innovative

Cost reduction

Mega mergers

Increased outsourcing

Divestment of non-core assets

Market-based risk mitigation

Break-up of corporate structures

Alternative pricing models

‘Emerging Markets First’ policy

Ruthless application of digital technology

Crowd funding

20