Embed Size (px)

Citation preview

FOCUS: MITIGATIONCompliance and voluntary

marketsLouis Perroy, ClimatEkos

30 August 2011, Vientiane, Lao PDR

Content

• Climate change mitigation and carbon markets• Regulatory markets• Voluntary markets• Comparison of regulatory and voluntary markets• The AFOLU Sector and Carbon markets

Content

• Climate change mitigation and carbon markets• Regulatory markets• Voluntary markets• Comparison of regulatory and voluntary markets• The AFOLU Sector and Carbon markets

What is climate change mitigation?

‘An anthropogenic intervention to reduce the

sources or enhance the sinks of greenhouse gases.’IPCC Glossary

Where do GHG emissions come from in the agricultural, rural and land use sector?

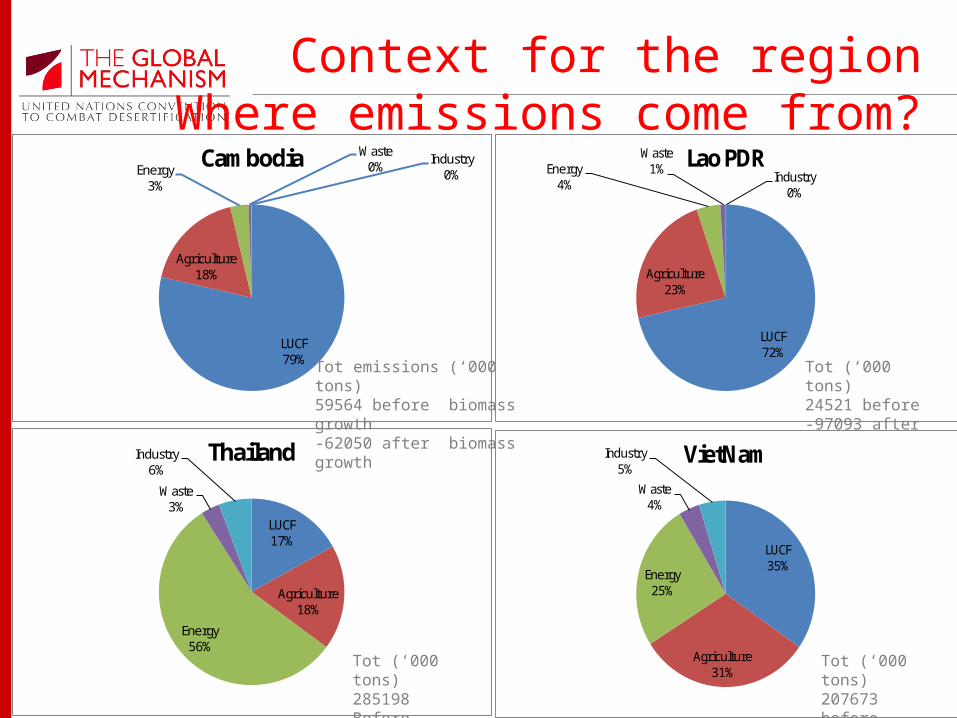

Context for the region Where emissions come from?

LUCF79%

Agriculture18%

Energy3%

Waste0%

Industry0%

Cambodia

LUCF72%

Agriculture23%

Energy4%

Waste1%

Industry0%

Lao PDR

LUCF17%

Agriculture18%

Energy56%

Waste3%

Industry6%

Thailand

LUCF35%

Agriculture31%

Energy25%

Waste4%

Industry5%

VietNam

Tot emissions (‘000 tons)59564 before biomass growth-62050 after biomass growth

Tot (‘000 tons)24521 before-97093 after

Tot (‘000 tons)207673 before150673 after

Tot (‘000 tons)285198 Before232798 after

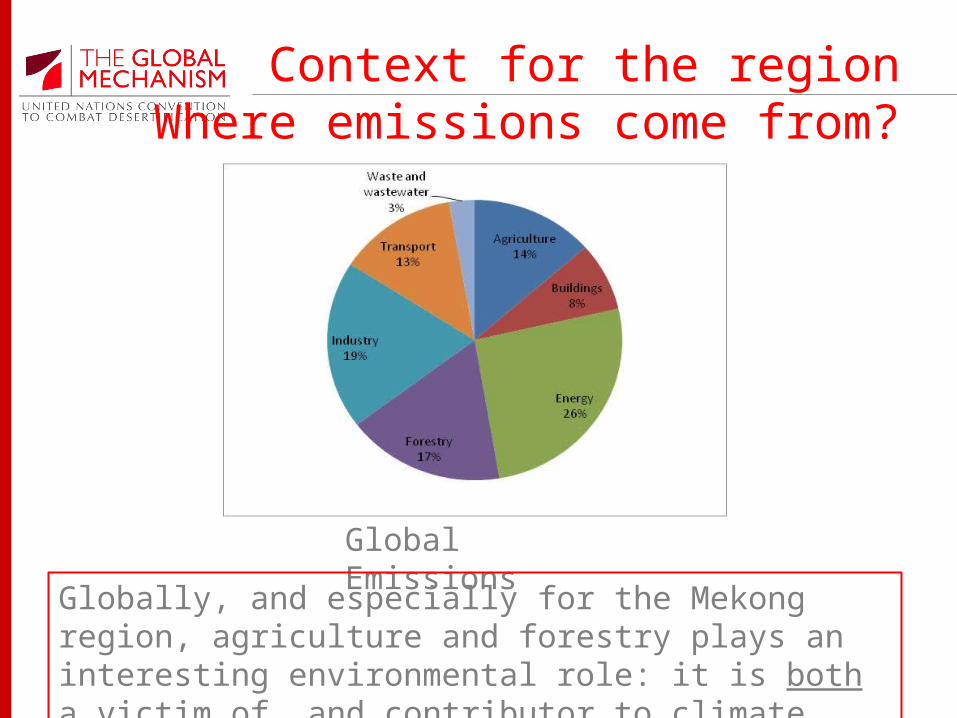

Context for the region Where emissions come from?

Global Emissions

Globally, and especially for the Mekong region, agriculture and forestry plays an interesting environmental role: it is both a victim of, and contributor to climate change.

What is climate change mitigation?

AGRICULTUREA. Domestic livestock (methane produced from intensive livestock,

enteric fermentation), B. Rice cultivation (nitrogen fertilizer use (20% of global use),

methane emissions from fermentation of organic matter in flooded rice paddies)

C. Grassland burningD. Agricultural residue burningE. Agricultural soils(almost entirely A and B)LAND USE CHANGE AND FORESTRYA. Change in forest/woody biomassB. Forest/land use change(mostly clearing of forests and draining of

wetlands)

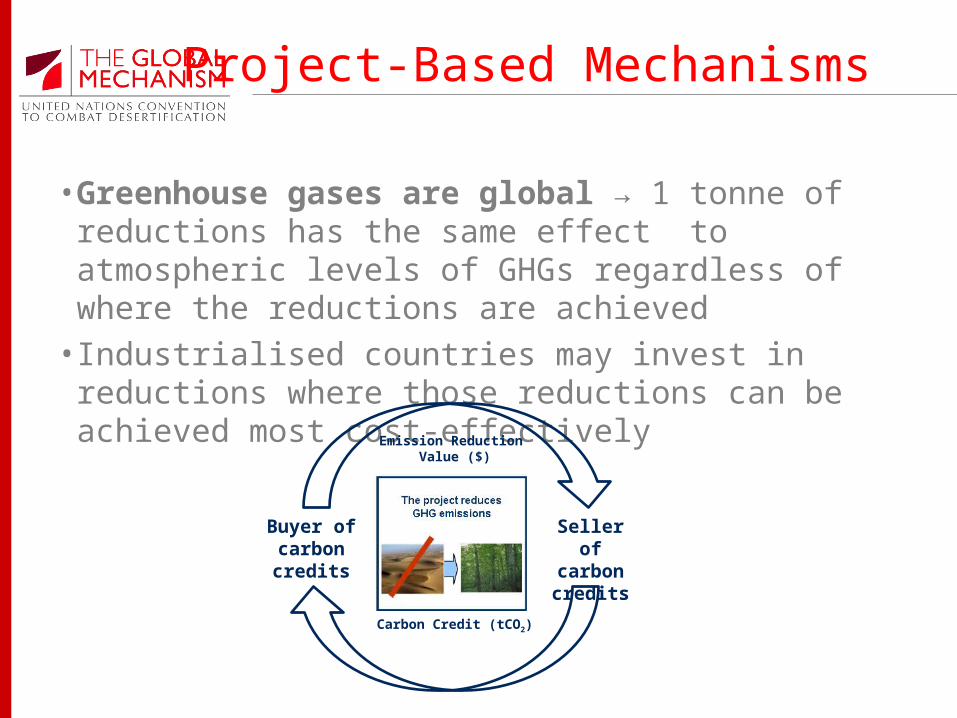

Project-Based Mechanisms

• Greenhouse gases are global → 1 tonne of reductions has the same effect to atmospheric levels of GHGs regardless of where the reductions are achieved

• Industrialised countries may invest in reductions where those reductions can be achieved most cost-effectively

Buyer of carbon credits

Seller of carbon credits

Emission Reduction Value ($)

Carbon Credit (tCO2)

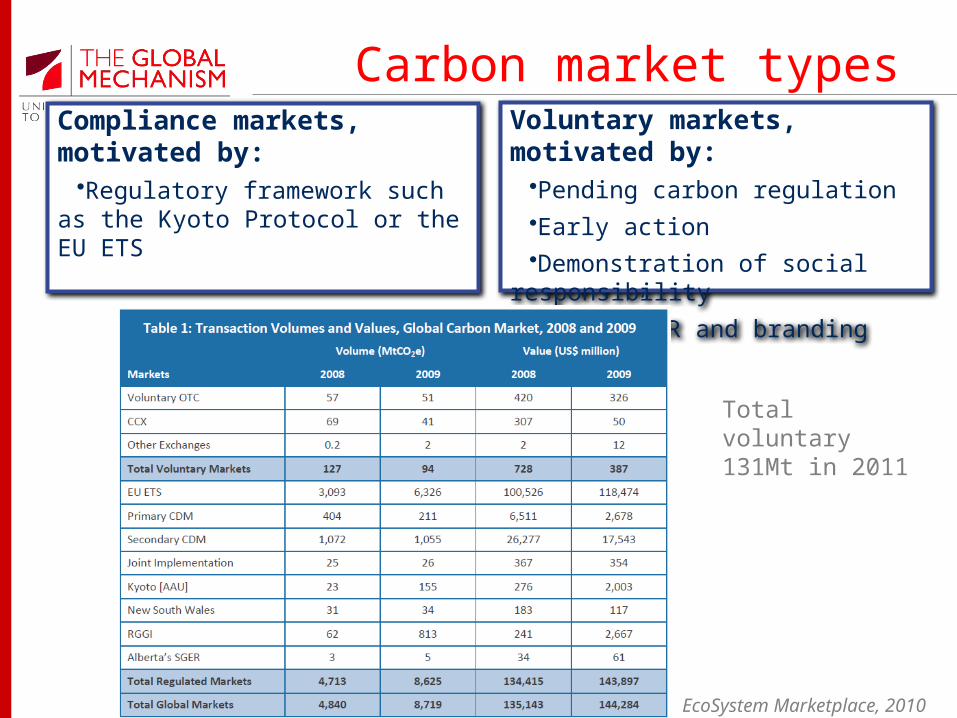

Carbon market typesCompliance markets, motivated by:

•Regulatory framework such as the Kyoto Protocol or the EU ETS

Voluntary markets, motivated by:

•Pending carbon regulation•Early action•Demonstration of social

responsibility•“Green” PR and branding

EcoSystem Marketplace, 2010

Total voluntary 131Mt in 2011

Content

• Climate change mitigation and carbon markets• Regulatory markets• Voluntary markets• Comparison of regulatory and voluntary markets• The AFOLU Sector and Carbon markets

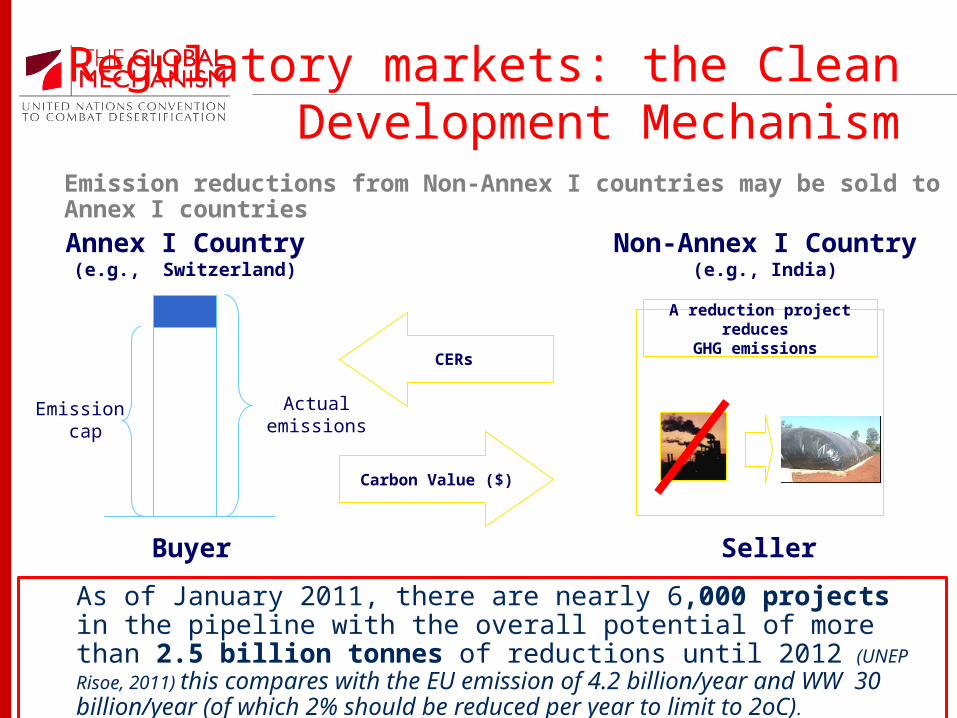

Emission reductions from Non-Annex I countries may be sold to Annex I countries

Emission cap

Actual emissions

Buyer

CERs

Carbon Value ($)

Annex I Country(e.g., Switzerland)

Non-Annex I Country(e.g., India)

Seller

A reduction project reduces GHG emissions

As of January 2011, there are nearly 6,000 projects in the pipeline with the overall potential of more than 2.5 billion tonnes of reductions until 2012 (UNEP Risoe, 2011) this compares with the EU emission of 4.2 billion/year and WW 30 billion/year (of which 2% should be reduced per year to limit to 2oC).

Regulatory markets: the Clean Development Mechanism

Content

• Climate change mitigation and carbon markets• Regulatory markets• Voluntary markets• Comparison of regulatory and voluntary markets• The AFOLU Sector and Carbon markets

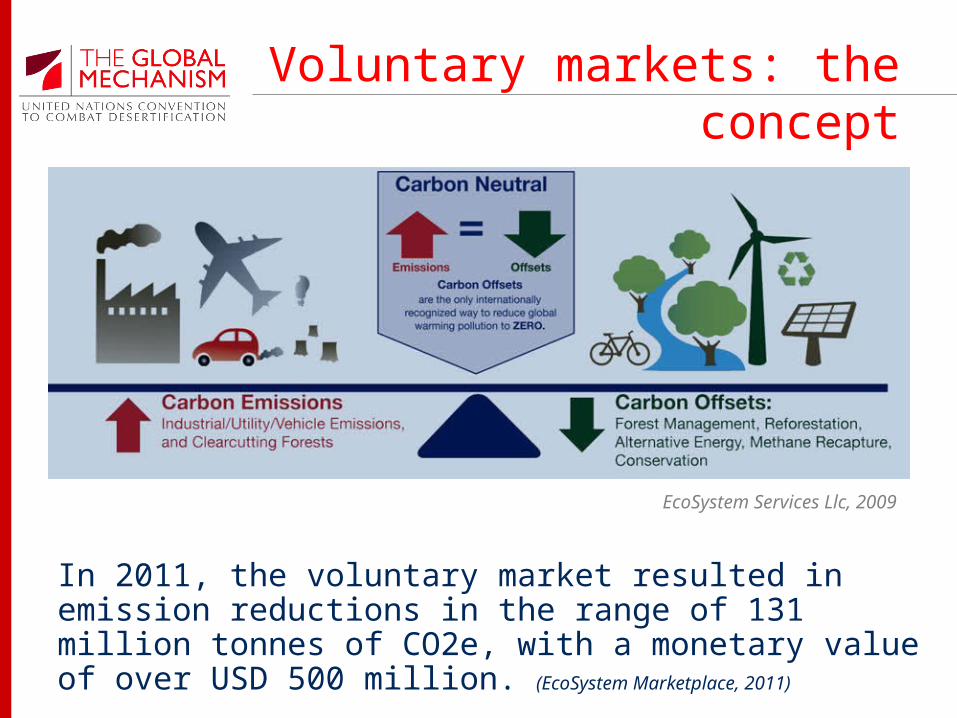

Voluntary markets: the concept

EcoSystem Services Llc, 2009

In 2011, the voluntary market resulted in emission reductions in the range of 131 million tonnes of CO2e, with a monetary value of over USD 500 million. (EcoSystem Marketplace, 2011)

Content

• Climate change mitigation and carbon markets• Regulatory markets• Voluntary markets• Comparison of regulatory and voluntary markets• The AFOLU Sector and Carbon markets

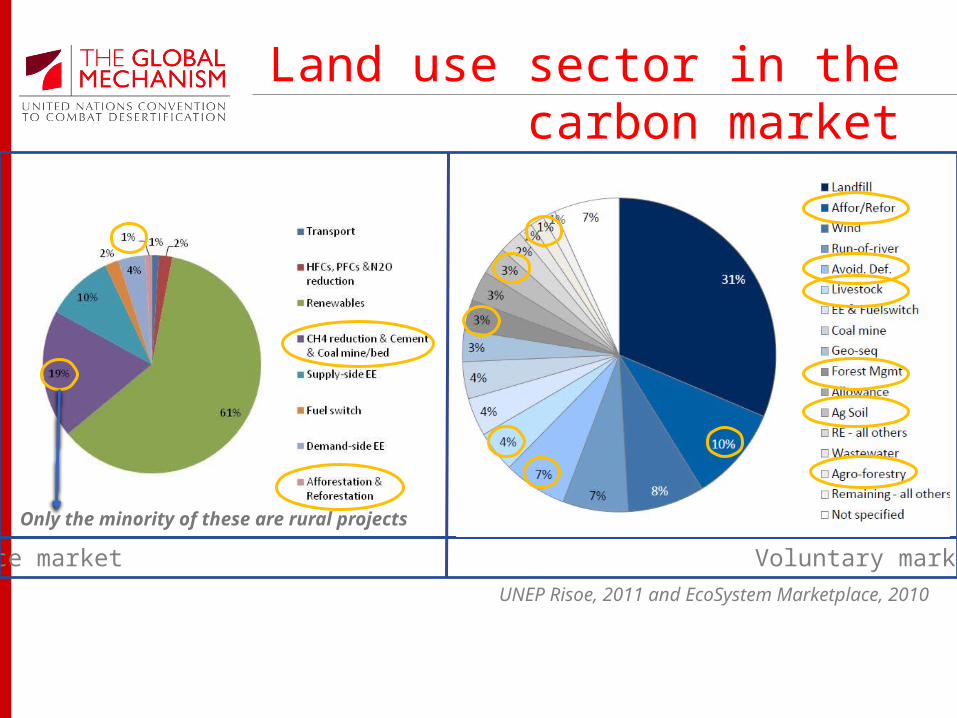

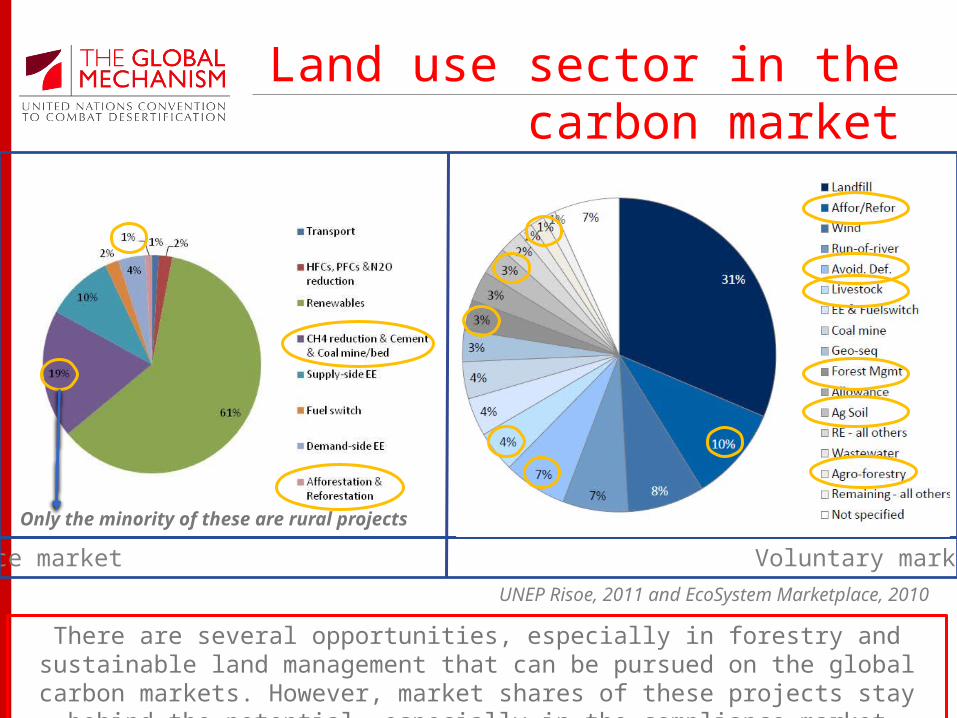

Land use sector in the carbon market

UNEP Risoe, 2011 and EcoSystem Marketplace, 2010

Compliance market Voluntary market

Only the minority of these are rural projects

Compliance market Voluntary market

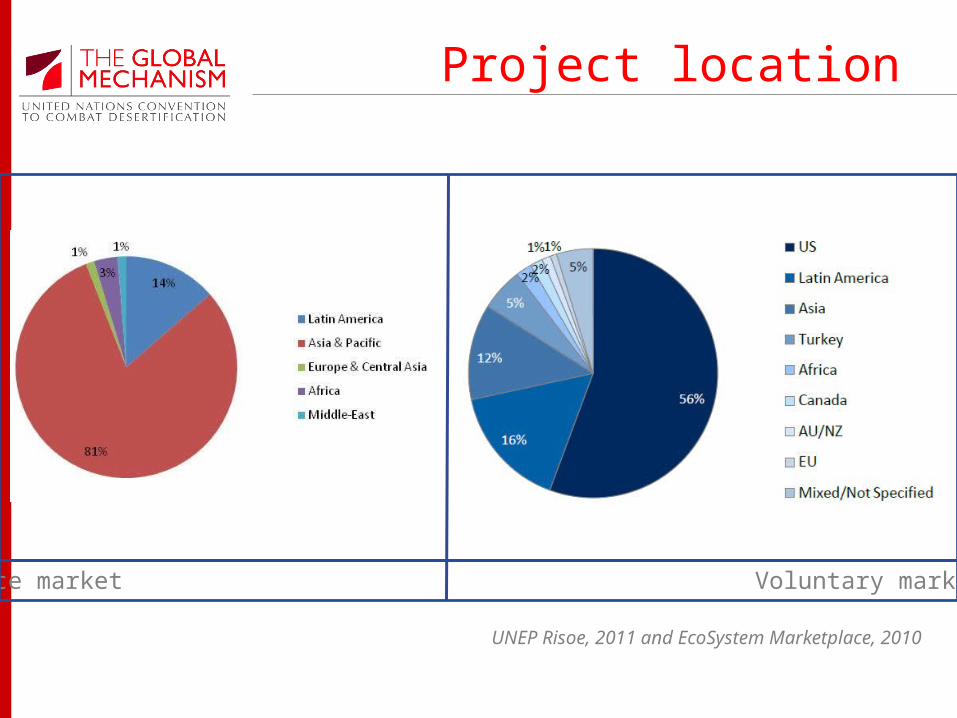

Project location

UNEP Risoe, 2011 and EcoSystem Marketplace, 2010

Content

• Climate change mitigation and carbon markets• Regulatory markets• Voluntary markets• Comparison of regulatory and voluntary markets• The AFOLU Sector and Carbon markets

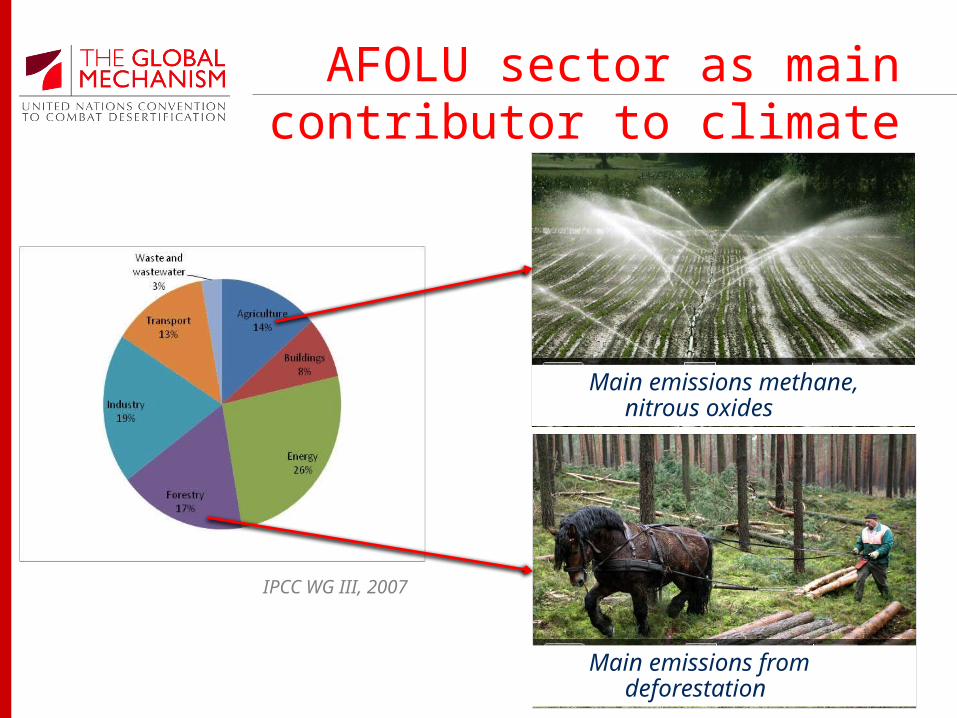

AFOLU sector as main contributor to climate change

• Sector is important in several aspects:

• In addition, sector with highest potential • for synergies with other ConventionsMain emissions methane,

nitrous oxides

Main emissions from deforestation

IPCC WG III, 2007

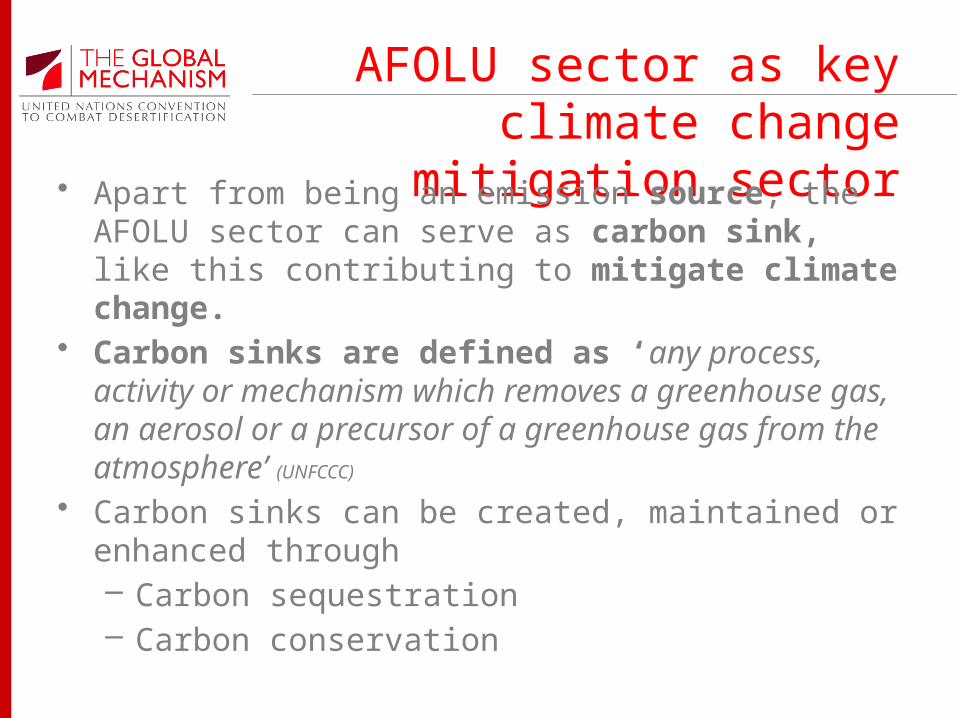

AFOLU sector as key climate change mitigation sector

• Apart from being an emission source, the AFOLU sector can serve as carbon sink, like this contributing to mitigate climate change.

• Carbon sinks are defined as ‘any process, activity or mechanism which removes a greenhouse gas, an aerosol or a precursor of a greenhouse gas from the atmosphere’ (UNFCCC)

• Carbon sinks can be created, maintained or enhanced through – Carbon sequestration– Carbon conservation

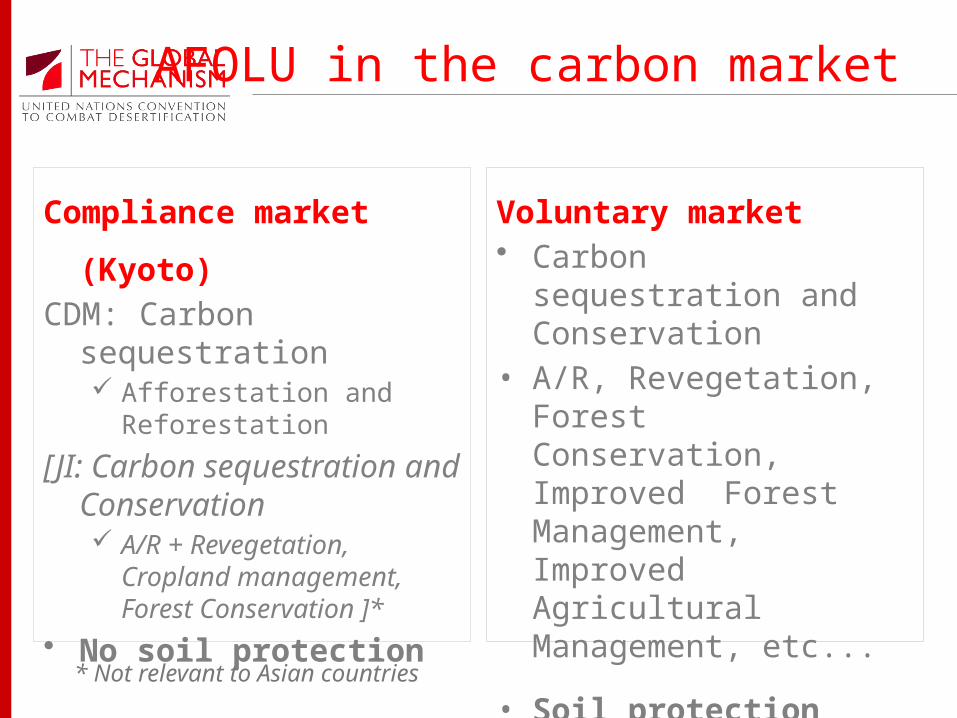

AFOLU in the carbon market

Compliance market (Kyoto)

CDM: Carbon sequestration Afforestation and

Reforestation

[JI: Carbon sequestration and Conservation A/R + Revegetation,

Cropland management, Forest Conservation ]*

• No soil protection

Voluntary market• Carbon sequestration and

Conservation • A/R, Revegetation, Forest

Conservation, Improved Forest Management, Improved Agricultural Management, etc...

• Soil protection eligible

* Not relevant to Asian countries

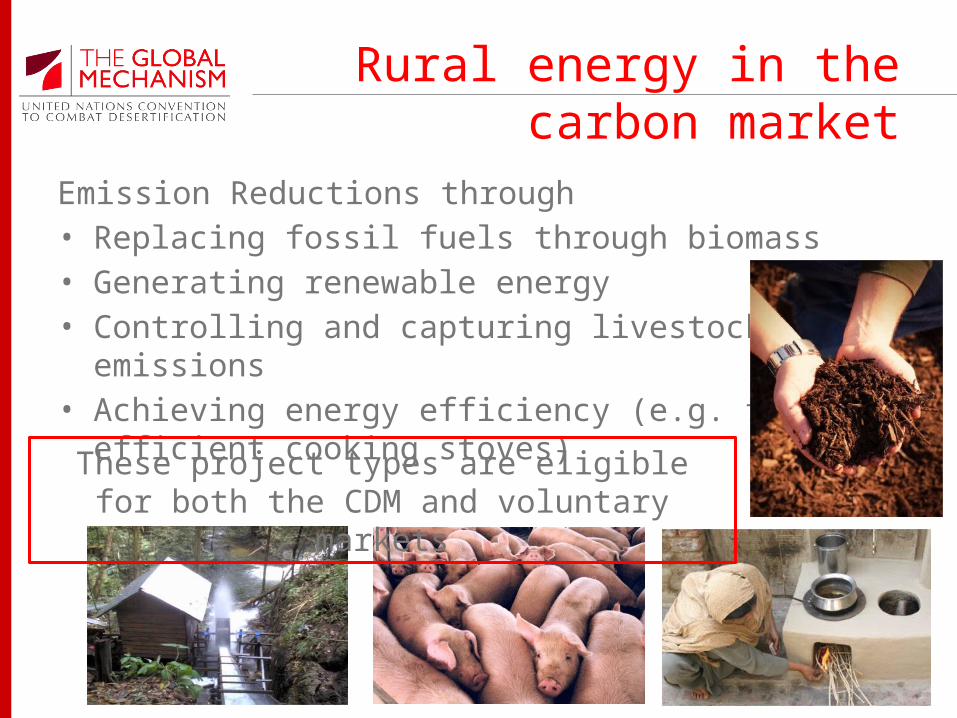

Rural energy in the carbon market

Emission Reductions through• Replacing fossil fuels through biomass• Generating renewable energy• Controlling and capturing livestock emissions • Achieving energy efficiency (e.g. fuel efficient

cooking stoves)

These project types are eligible for both the CDM and voluntary markets

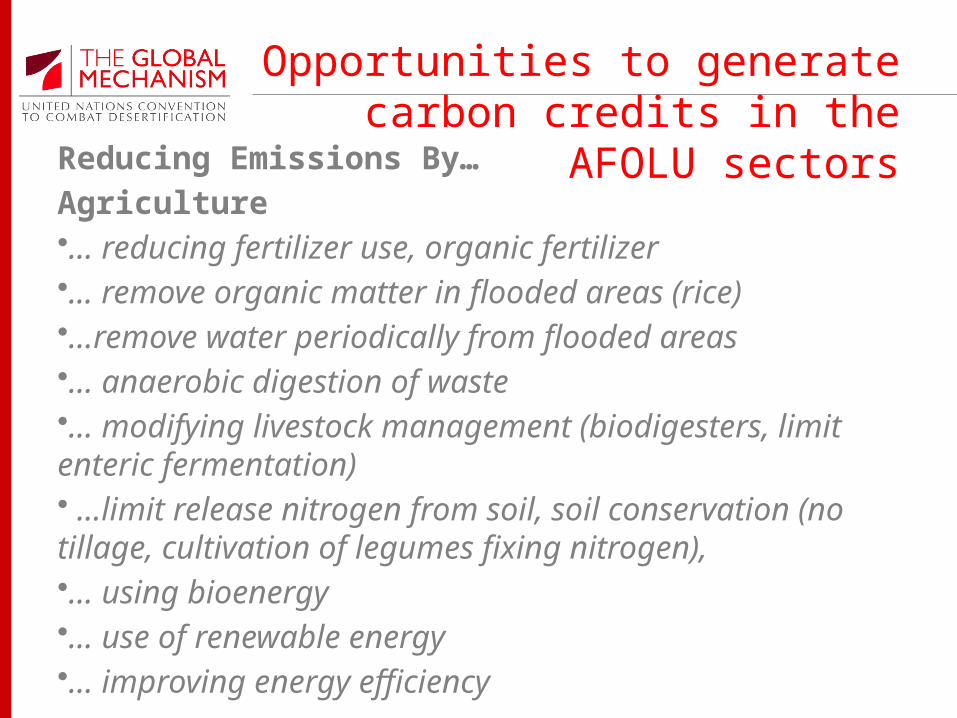

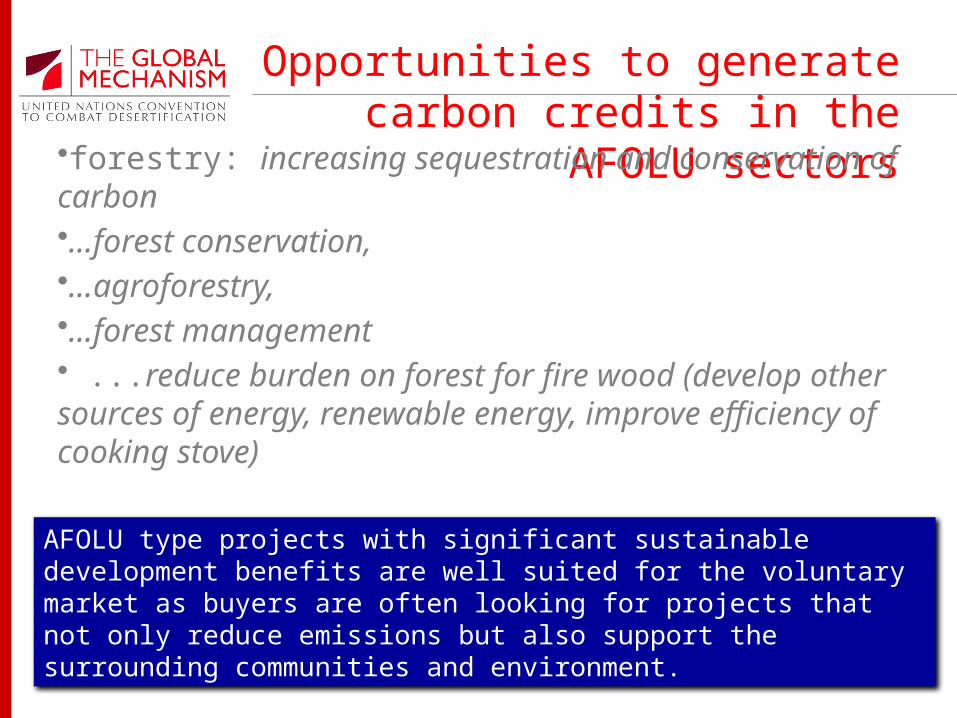

Opportunities to generate carbon credits in the AFOLU sectors

Reducing Emissions By…

Agriculture•… reducing fertilizer use, organic fertilizer•... remove organic matter in flooded areas (rice)•…remove water periodically from flooded areas•… anaerobic digestion of waste•… modifying livestock management (biodigesters, limit enteric fermentation)• ...limit release nitrogen from soil, soil conservation (no tillage, cultivation of legumes fixing nitrogen), •… using bioenergy•… use of renewable energy •… improving energy efficiency

Opportunities to generate carbon credits in the AFOLU sectors

•forestry: increasing sequestration and conservation of carbon•...forest conservation, •...agroforestry, •...forest management• ...reduce burden on forest for fire wood (develop other sources of energy, renewable energy, improve efficiency of cooking stove)

AFOLU type projects with significant sustainable development benefits are well suited for the voluntary market as buyers are often looking for projects that not only reduce emissions but also support the surrounding communities and environment.

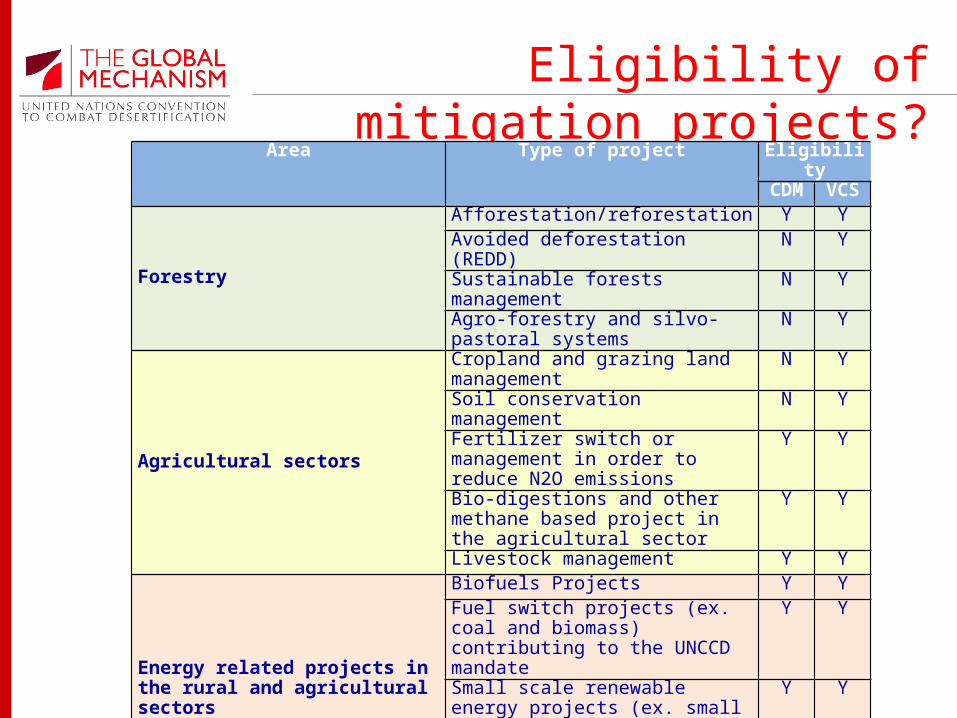

Eligibility of mitigation projects?

Area Type of project EligibilityCDM VCS

Forestry

Afforestation/reforestation Y YAvoided deforestation (REDD) N YSustainable forests management N YAgro-forestry and silvo-pastoral systems

N Y

Agricultural sectors

Cropland and grazing land management

N Y

Soil conservation management N Y

Fertilizer switch or management in order to reduce N2O emissions

Y Y

Bio-digestions and other methane based project in the agricultural sector

Y Y

Livestock management Y Y

Energy related projects in the rural and agricultural sectors

Biofuels Projects Y YFuel switch projects (ex. coal and biomass) contributing to the UNCCD mandate

Y Y

Small scale renewable energy projects (ex. small hydro combined with forestry activities for protection of watersheds)

Y Y

Energy efficiency Y Y

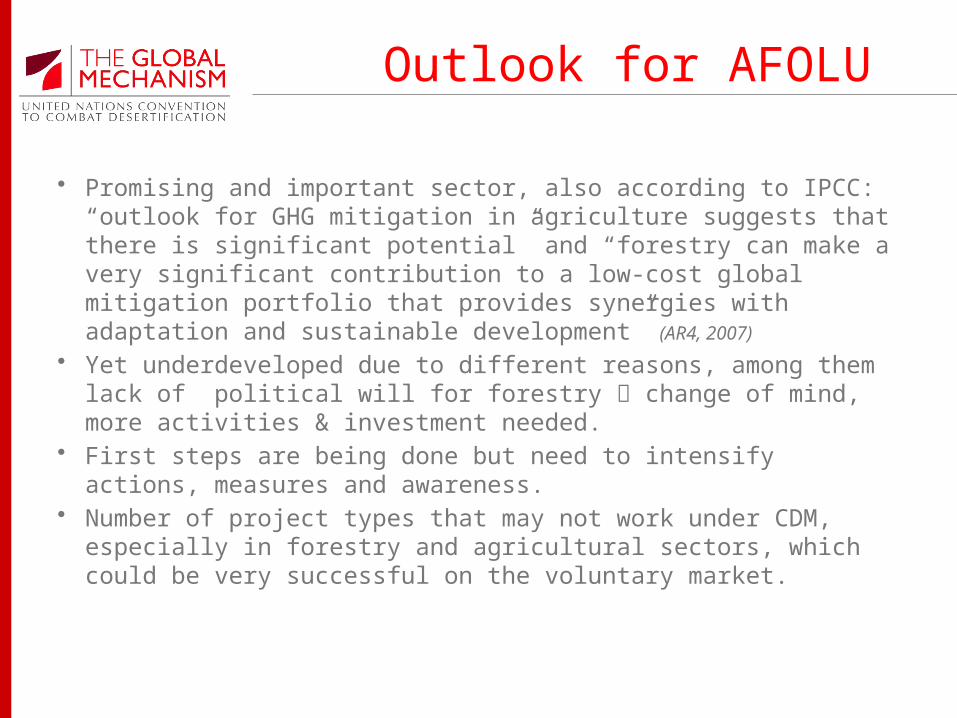

Outlook for AFOLU

• Promising and important sector, also according to IPCC: “outlook for GHG mitigation in agriculture suggests that there is significant potential” and “forestry can make a very significant contribution to a low-cost global mitigation portfolio that provides synergies with adaptation and sustainable development” (AR4, 2007)

• Yet underdeveloped due to different reasons, among them lack of political will for forestry change of mind, more activities & investment needed.

• First steps are being done but need to intensify actions, measures and awareness.

• Number of project types that may not work under CDM, especially in forestry and agricultural sectors, which could be very successful on the voluntary market.

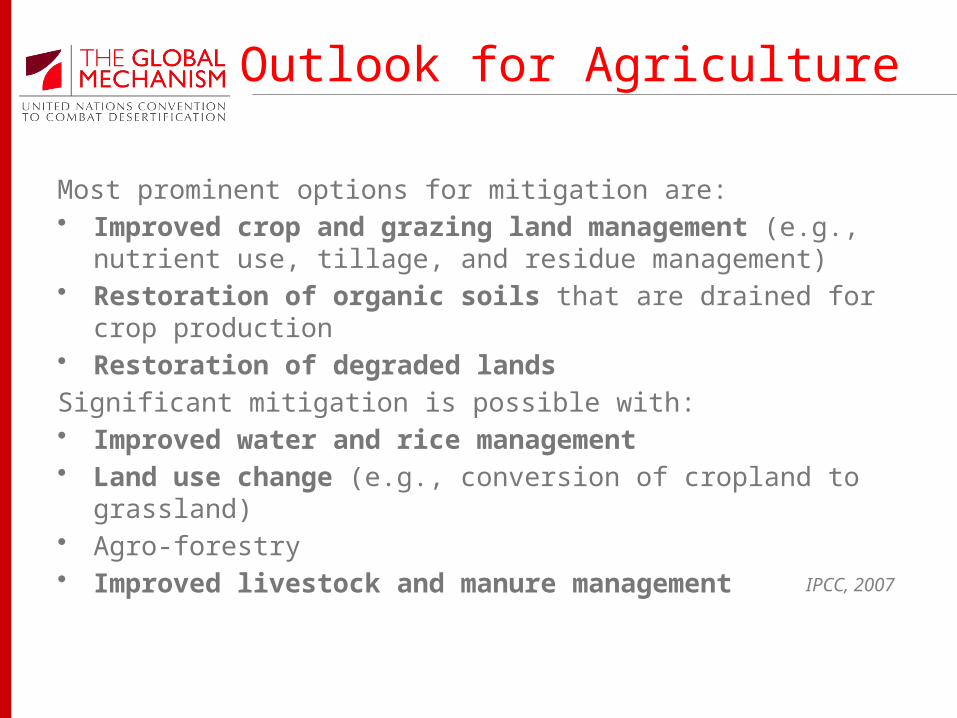

Outlook for Agriculture

Most prominent options for mitigation are:• Improved crop and grazing land management (e.g., nutrient use,

tillage, and residue management) • Restoration of organic soils that are drained for crop production• Restoration of degraded lands

Significant mitigation is possible with:• Improved water and rice management• Land use change (e.g., conversion of cropland to grassland) • Agro-forestry• Improved livestock and manure management

IPCC, 2007

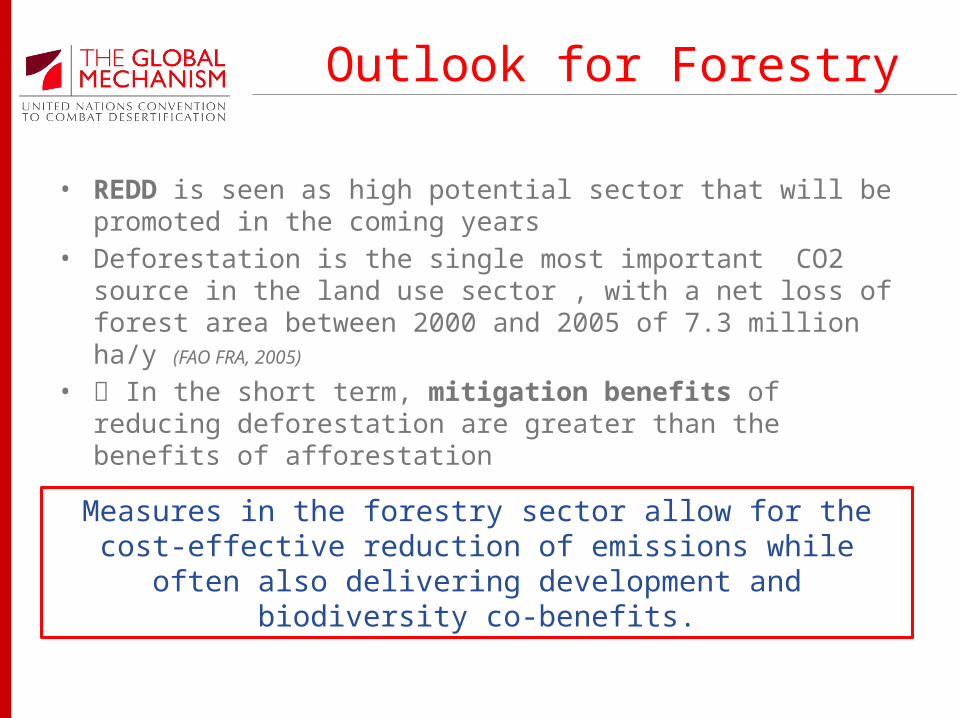

Outlook for Forestry

• REDD is seen as high potential sector that will be promoted in the coming years

• Deforestation is the single most important CO2 source in the land use sector , with a net loss of forest area between 2000 and 2005 of 7.3 million ha/y (FAO FRA, 2005)

• In the short term, mitigation benefits of reducing deforestation are greater than the benefits of afforestation

Measures in the forestry sector allow for the cost-effective reduction of emissions while often also

delivering development and biodiversity co-benefits.

Climate change mitigation Cambodia

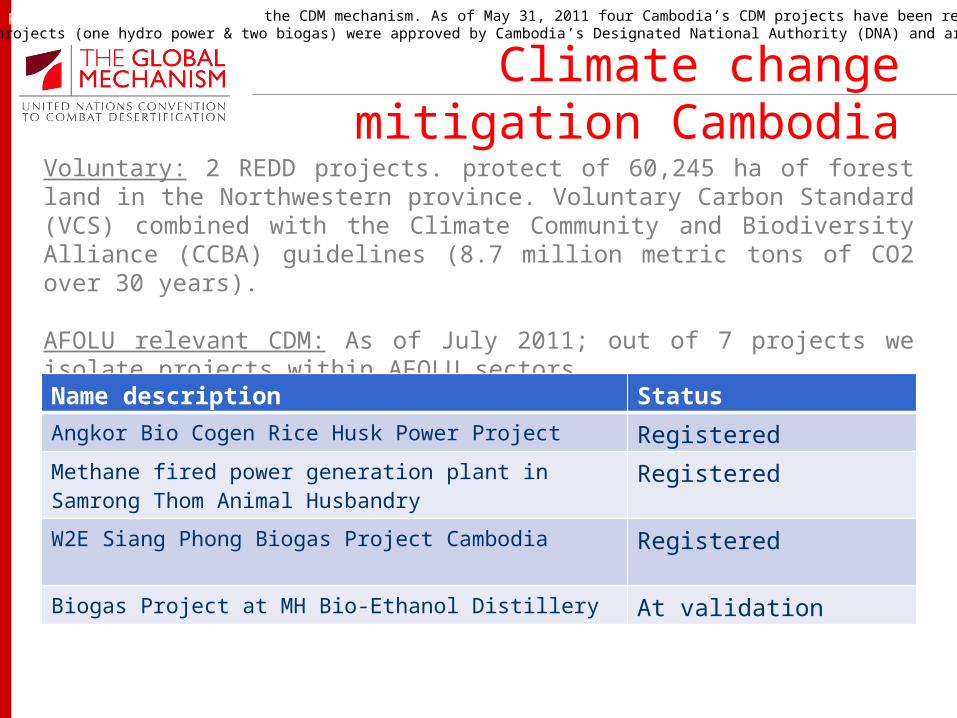

Cambodia approved its first CDM project in early January 2006, an important step to show that even a small and least developed country (LD) like Cambodia can participate and benefit from the CDM mechanism. As of May 31, 2011 four Cambodia’s CDM projects have been registered at the CDM Executive Board (EB): rice husk biomass cogeneration project in Kandal Province; biogas project at tapioca starch factory in Kampong Cham Province; methane recovery and utilization at a pig farm in Kandal Province, and Kampot cement waste heat power generation project in Kampot Province. Three projects (one hydro power & two biogas) were approved by Cambodia ’s Designated National Authority (DNA) and are currently under validation.

Voluntary: 2 REDD projects. protect of 60,245 ha of forest land in the Northwestern province. Voluntary Carbon Standard (VCS) combined with the Climate Community and Biodiversity Alliance (CCBA) guidelines (8.7 million metric tons of CO2 over 30 years).

AFOLU relevant CDM: As of July 2011; out of 7 projects we isolate projects within AFOLU sectors.

Name description Status

Angkor Bio Cogen Rice Husk Power Project Registered

Methane fired power generation plant in Samrong Thom Animal Husbandry

Registered

W2E Siang Phong Biogas Project Cambodia Registered

Biogas Project at MH Bio-Ethanol Distillery At validation

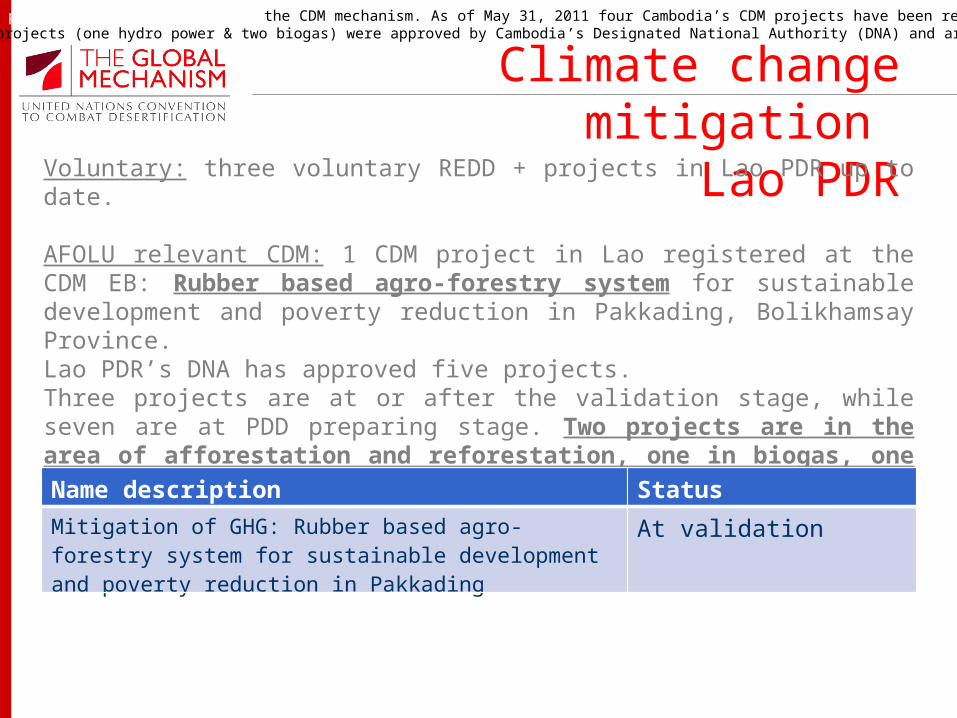

Climate change mitigation Lao PDR

Cambodia approved its first CDM project in early January 2006, an important step to show that even a small and least developed country (LD) like Cambodia can participate and benefit from the CDM mechanism. As of May 31, 2011 four Cambodia’s CDM projects have been registered at the CDM Executive Board (EB): rice husk biomass cogeneration project in Kandal Province; biogas project at tapioca starch factory in Kampong Cham Province; methane recovery and utilization at a pig farm in Kandal Province, and Kampot cement waste heat power generation project in Kampot Province. Three projects (one hydro power & two biogas) were approved by Cambodia ’s Designated National Authority (DNA) and are currently under validation.

Voluntary: three voluntary REDD + projects in Lao PDR up to date.

AFOLU relevant CDM: 1 CDM project in Lao registered at the CDM EB: Rubber based agro-forestry system for sustainable development and poverty reduction in Pakkading, Bolikhamsay Province. Lao PDR’s DNA has approved five projects. Three projects are at or after the validation stage, while seven are at PDD preparing stage. Two projects are in the area of afforestation and reforestation, one in biogas, one in biomass.

Name description Status

Mitigation of GHG: Rubber based agro-forestry system for sustainable development and poverty reduction in Pakkading

At validation

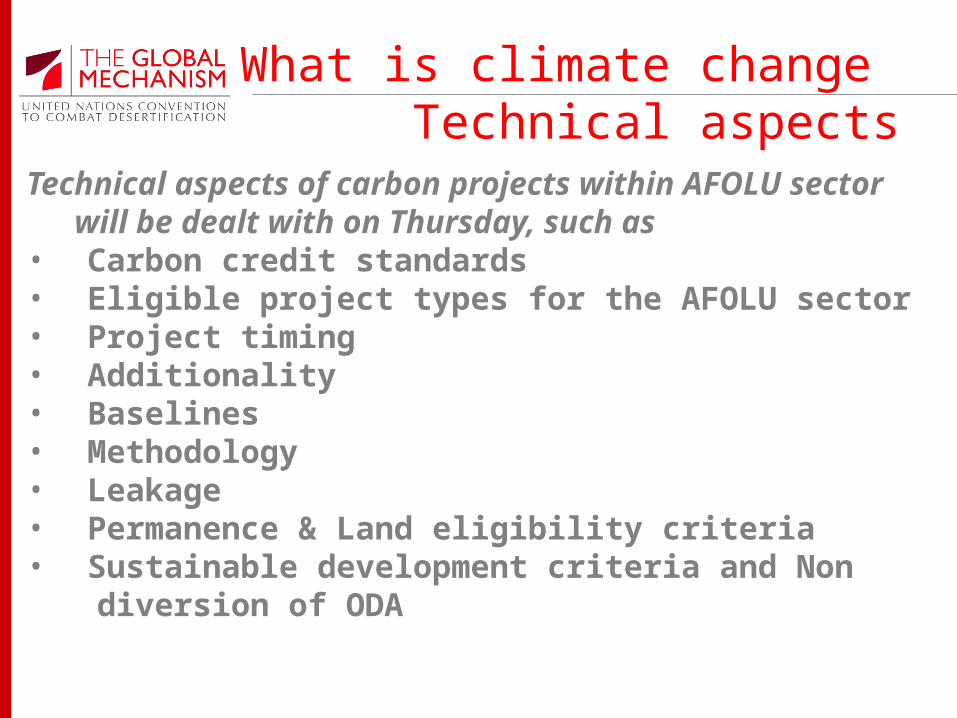

What is climate change Technical aspects

Technical aspects of carbon projects within AFOLU sector will be dealt with on Thursday, such as

• Carbon credit standards• Eligible project types for the AFOLU sector• Project timing• Additionality• Baselines• Methodology• Leakage • Permanence & Land eligibility criteria• Sustainable development criteria and Non

diversion of ODA

Land use sector in the carbon market

UNEP Risoe, 2011 and EcoSystem Marketplace, 2010

Compliance market Voluntary market

Only the minority of these are rural projects

There are several opportunities, especially in forestry and sustainable land management that can be pursued on the global carbon markets. However, market shares of these projects stay behind the potential, especially in the

compliance market