Embed Size (px)

Citation preview

FROM UPPER MIDDLE INCOME TO BUILDING A MORE SECURE MIDDLE CLASS:

CRITICAL STEPS

WORLD BANK GROUP

Systematic Country Diagnostics

AEF June 15, 2017

• Setting the stage and identifying challenges..

..to growth, jobs, and building a more secure middle class

• Getting back on course – 4 interconnected and interdependent paths:

Economic management for diversification

Private sector development

Integration and connectivity

Competitive and adaptive human capital

• Concluding thoughts: looking forward

OUTLINE

SETTING THE STAGE: GROWTH, JOBS,

AND BUILDING A SECURE MIDDLE CLASS

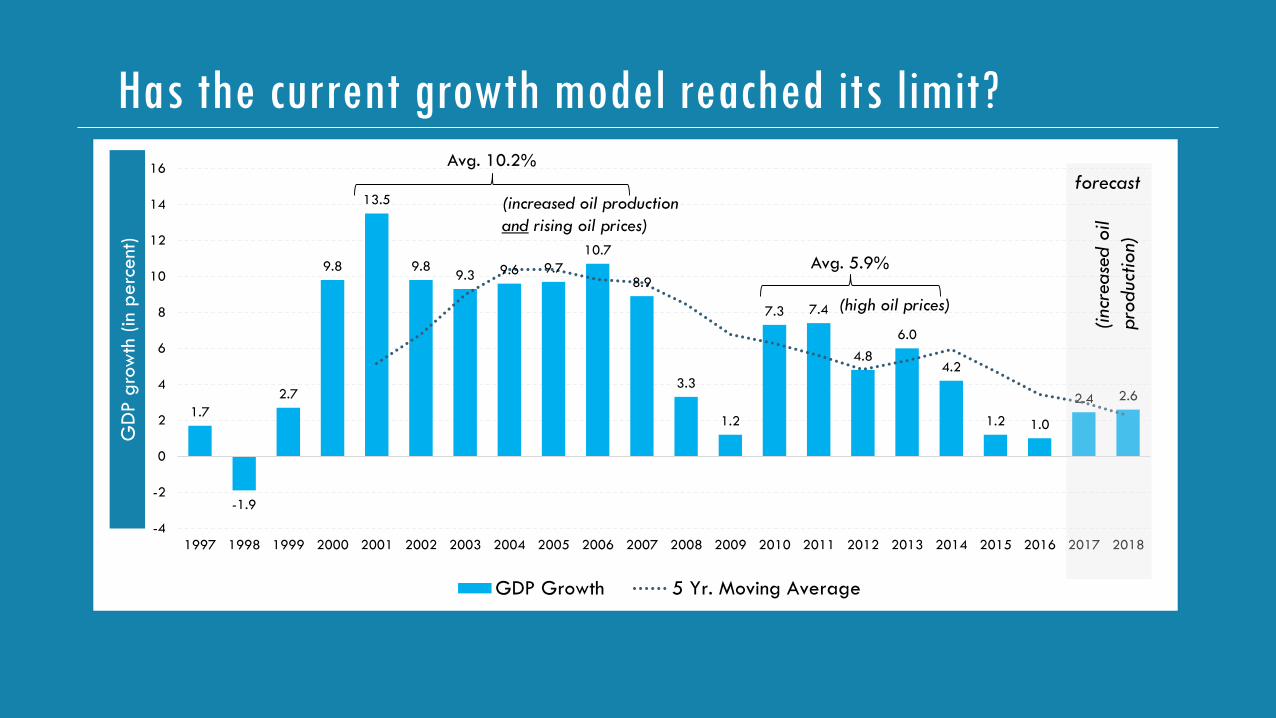

Has the current growth model reached its limit?

1.7

-1.9

2.7

9.8

13.5

9.8 9.3 9.6 9.7

10.7

8.9

3.3

1.2

7.3 7.4

4.8

6.0

4.2

1.2 1.0

2.4 2.6

-4

-2

0

2

4

6

8

10

12

14

16

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

GDP Growth 5 Yr. Moving Average

Avg. 10.2%

Avg. 5.9%

(high oil prices)

(increased oil production

and rising oil prices)

forecast

GD

P g

row

th (

in p

erc

ent

)

(inc

rease

d o

il

pro

duc

tion)

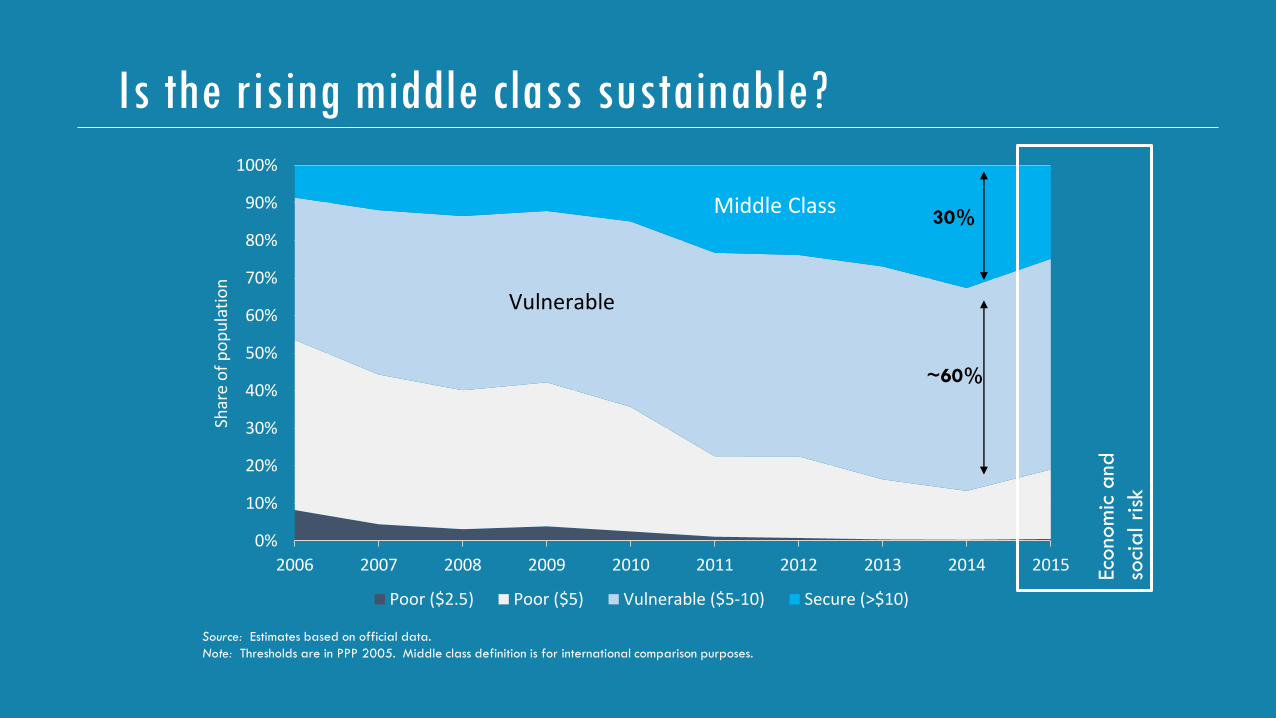

Is the rising middle class sustainable?

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Shar

e o

f p

op

ula

tio

n

Poor ($2.5) Poor ($5) Vulnerable ($5-10) Secure (>$10)

Vulnerable

Middle Class30%

~60%

Source: Estimates based on official data.

Note: Thresholds are in PPP 2005. Middle class definition is for international comparison purposes.

Econo

mic

and

soci

al ri

sk

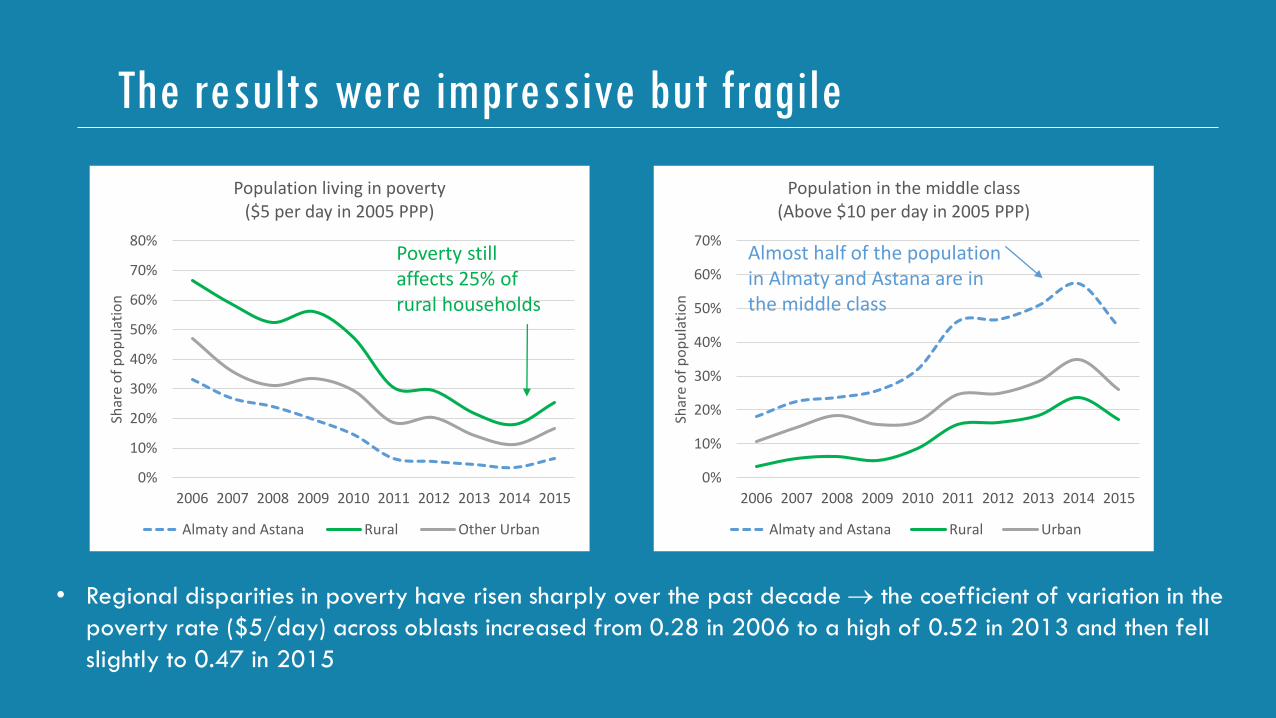

The results were impressive but fragile

0%

10%

20%

30%

40%

50%

60%

70%

80%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Shar

e o

f p

op

ula

tio

n

Population living in poverty($5 per day in 2005 PPP)

Almaty and Astana Rural Other Urban

0%

10%

20%

30%

40%

50%

60%

70%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Shar

e o

f p

op

ula

tio

n

Population in the middle class(Above $10 per day in 2005 PPP)

Almaty and Astana Rural Urban

• Regional disparities in poverty have risen sharply over the past decade the coefficient of variation in the

poverty rate ($5/day) across oblasts increased from 0.28 in 2006 to a high of 0.52 in 2013 and then fell

slightly to 0.47 in 2015

Poverty still affects 25% of rural households

Almost half of the population in Almaty and Astana are in the middle class

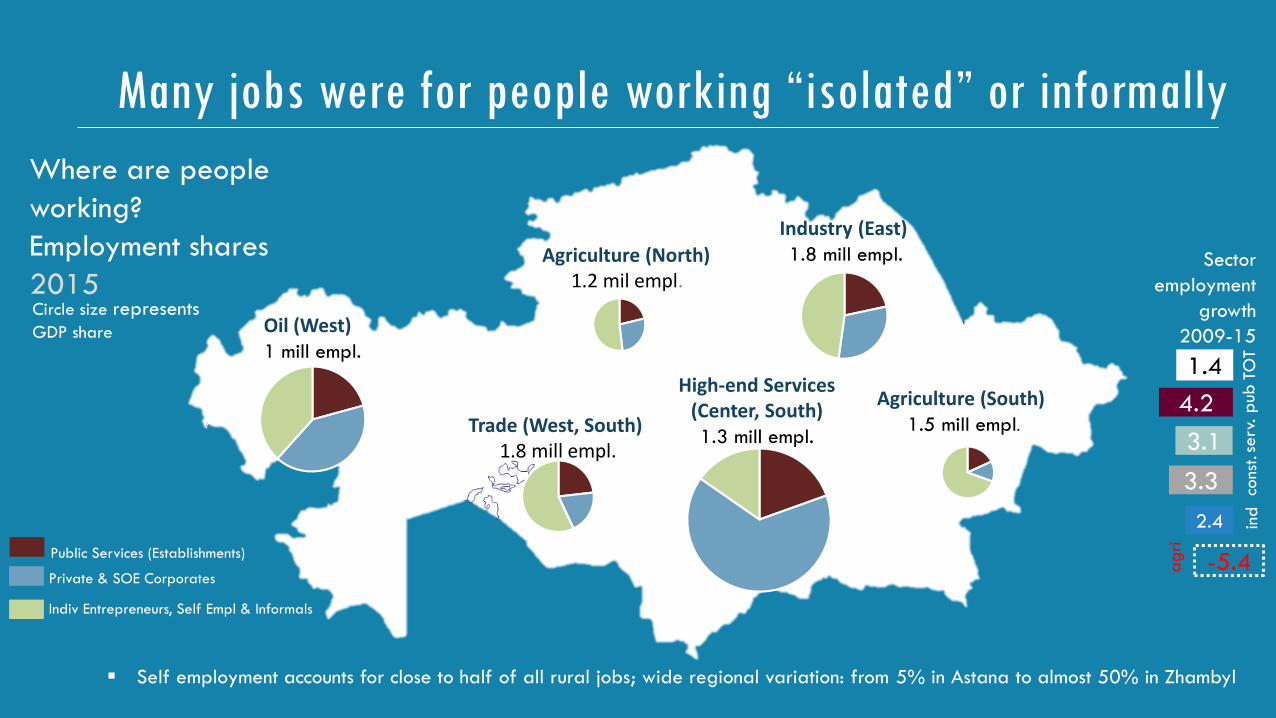

Many jobs were for people working “isolated” or informally

Where are people

working?

Employment shares

2015Circle size representsGDP share

Public Services (Establishments)

Private & SOE Corporates

Indiv Entrepreneurs, Self Empl & Informals

3.1

2.4

1.4

-5.4

3.3

Sector

employment

growth

2009-15

ag

ri

ind

pub

serv

.co

nst.

TOT

4.2

Self employment accounts for close to half of all rural jobs; wide regional variation: from 5% in Astana to almost 50% in Zhambyl

Oil (West)1 mill empl.

Agriculture (North)1.2 mil empl.

Agriculture (South) 1.5 mill empl.Trade (West, South)

1.8 mill empl.

Industry (East) 1.8 mill empl.

High-end Services (Center, South) 1.3 mill empl.

PUBLIC

SECTOR

NON-

TRADABLES

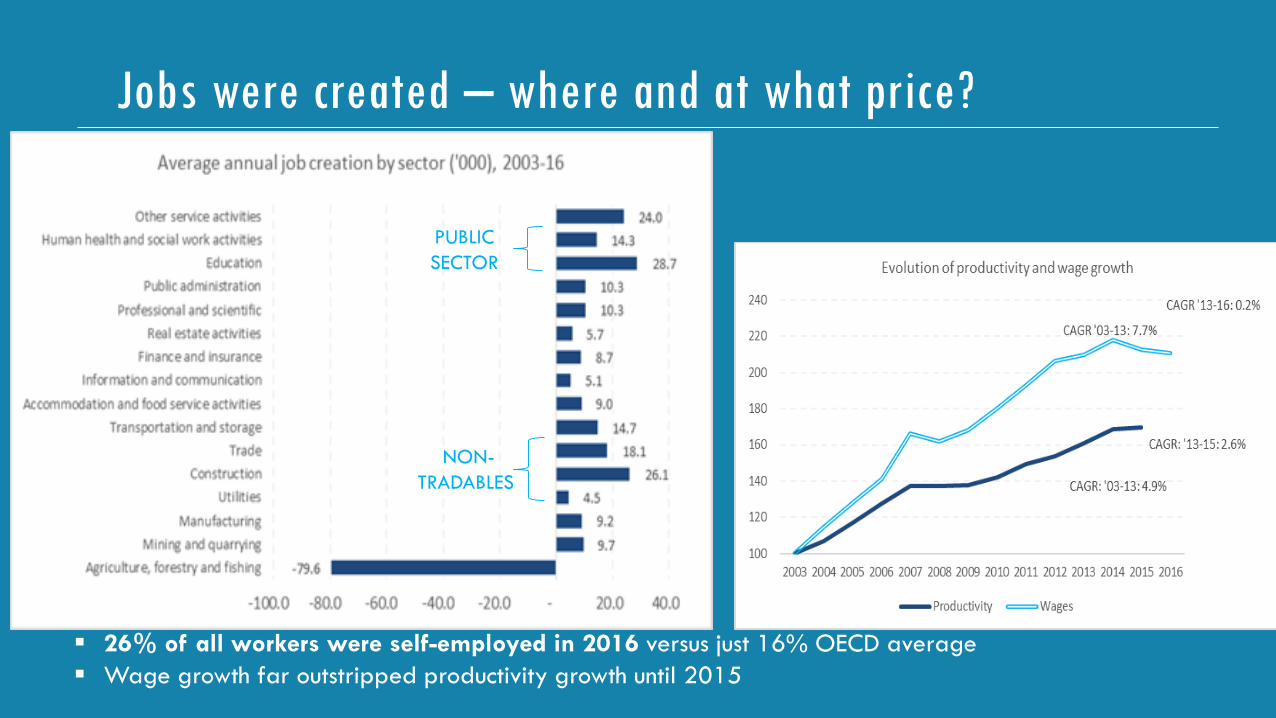

Jobs were created – where and at what price?

26% of all workers were self-employed in 2016 versus just 16% OECD average

Wage growth far outstripped productivity growth until 2015

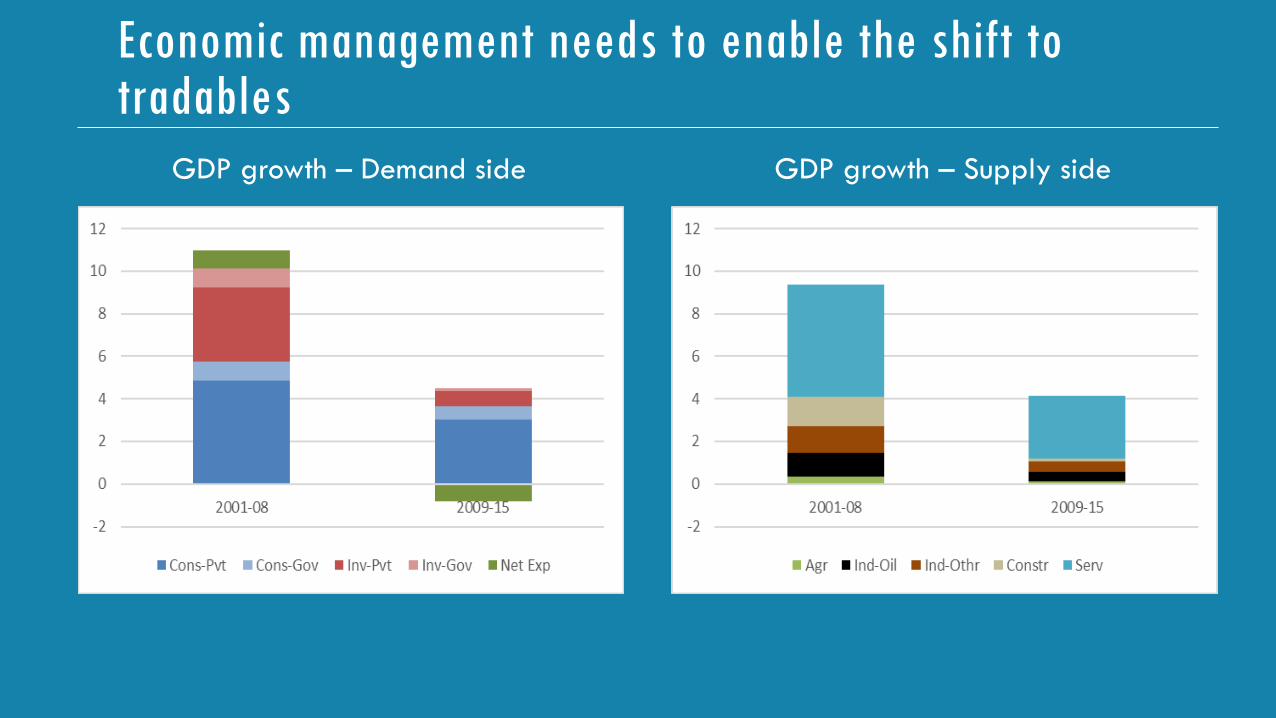

Economic management needs to enable the shift to tradables

GDP growth – Supply sideGDP growth – Demand side

PATHWAY #1

ECONOMIC MANAGEMENT

FOR DIVERSIFICATION

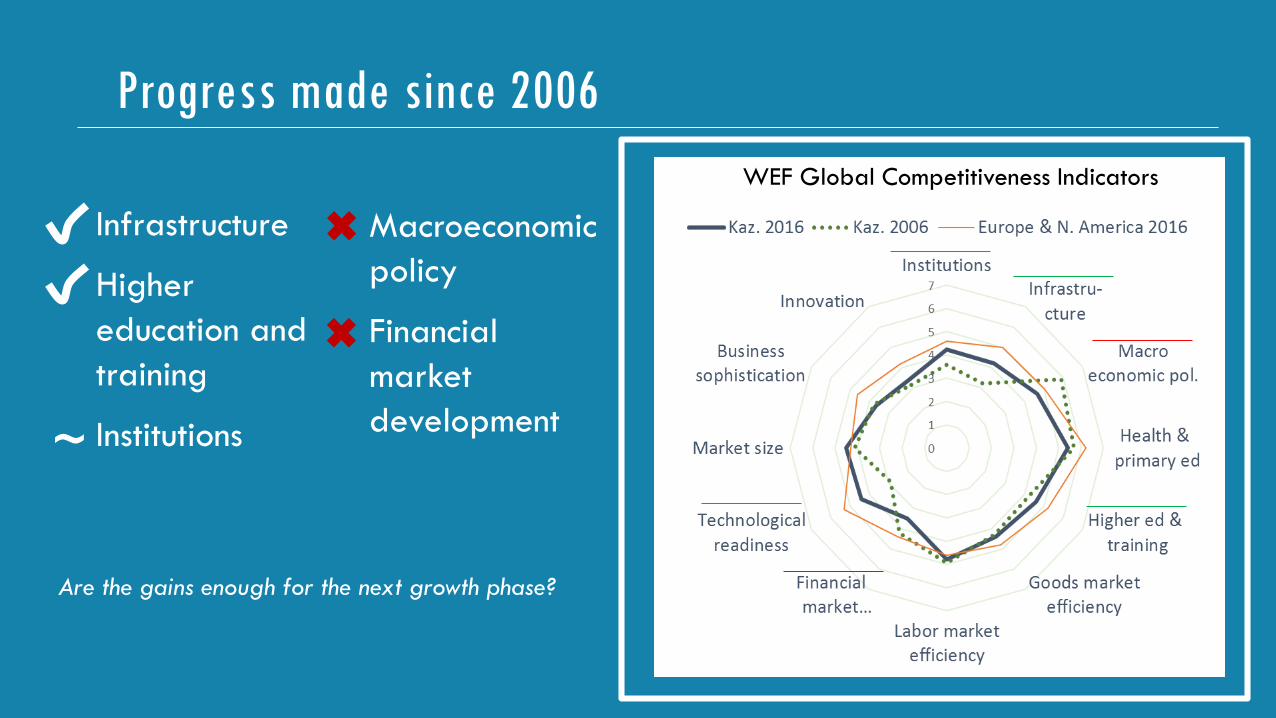

Progress made since 2006

Infrastructure

Higher

education and

training

Institutions

Macroeconomic

policy

Financial

market

development

Are the gains enough for the next growth phase?

WEF Global Competitiveness Indicators

~

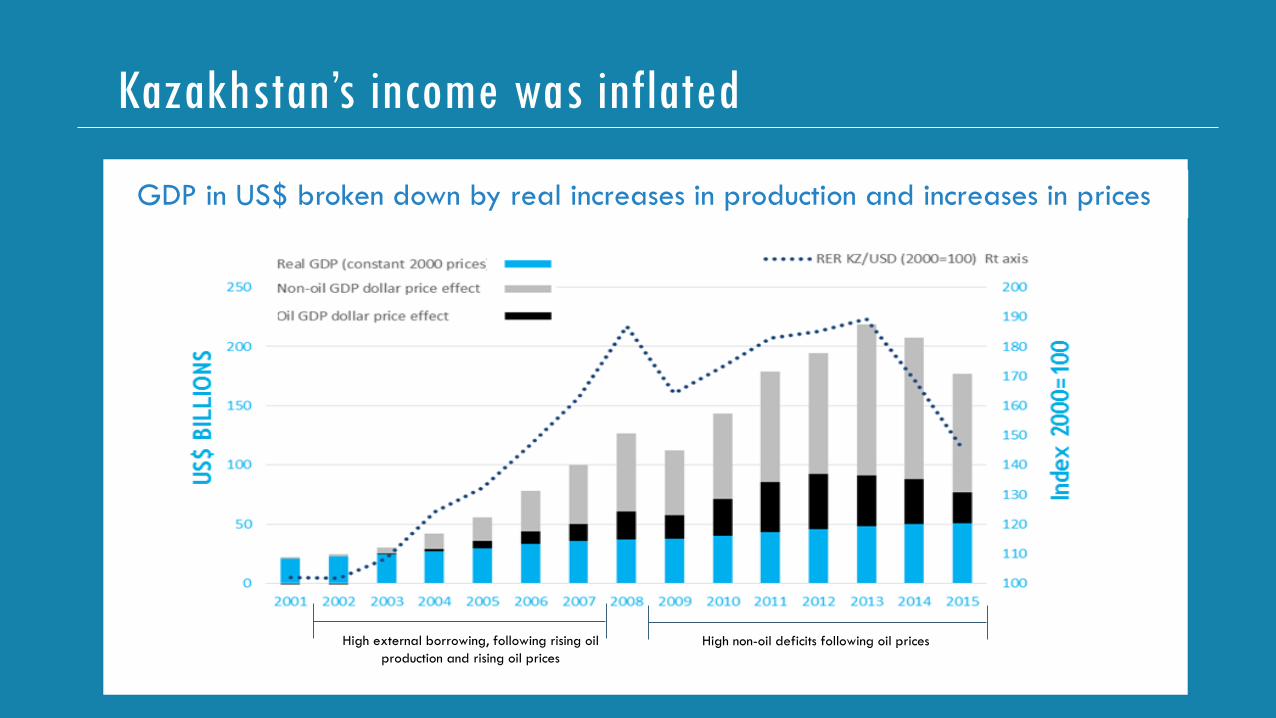

Kazakhstan’s income was inflated

High non-oil deficits following oil pricesHigh external borrowing, following rising oil

production and rising oil prices

GDP in US$ broken down by real increases in production and increases in prices

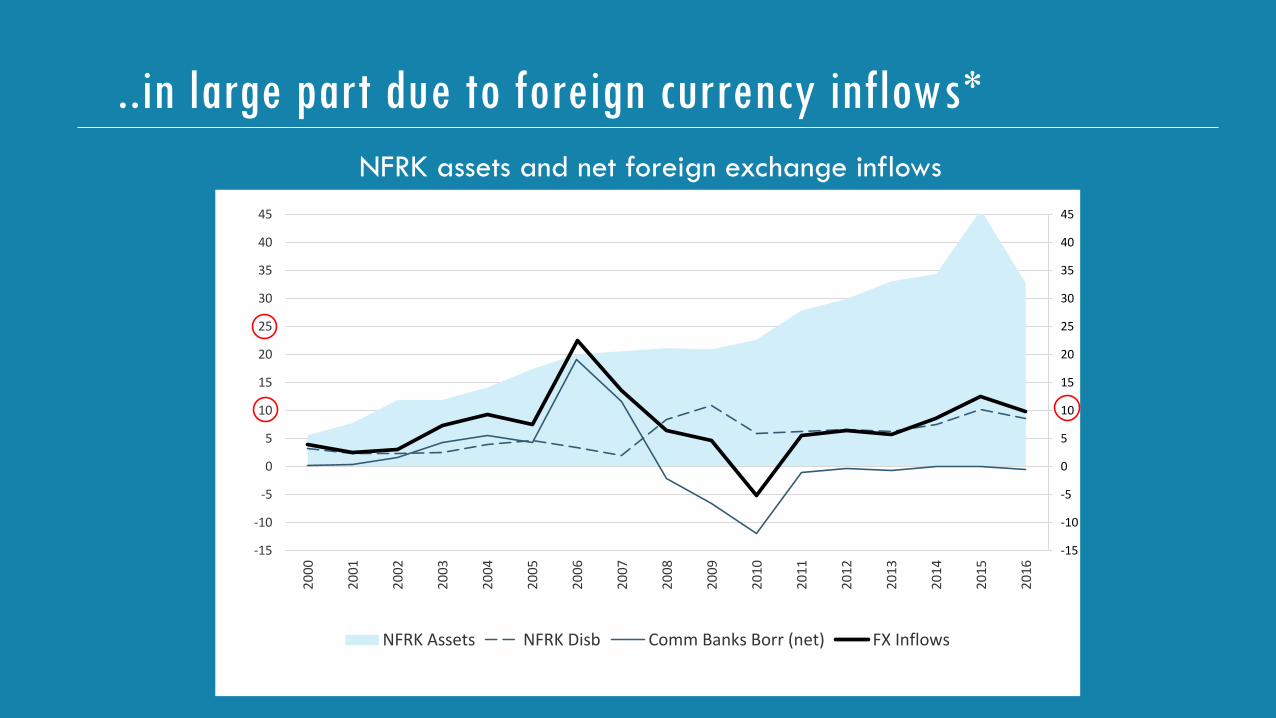

..in large part due to foreign currency inflows*

NFRK assets and net foreign exchange inflows

-15

-10

-5

0

5

10

15

20

25

30

35

40

45

-15

-10

-5

0

5

10

15

20

25

30

35

40

45

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

NFRK Assets NFRK Disb Comm Banks Borr (net) FX Inflows

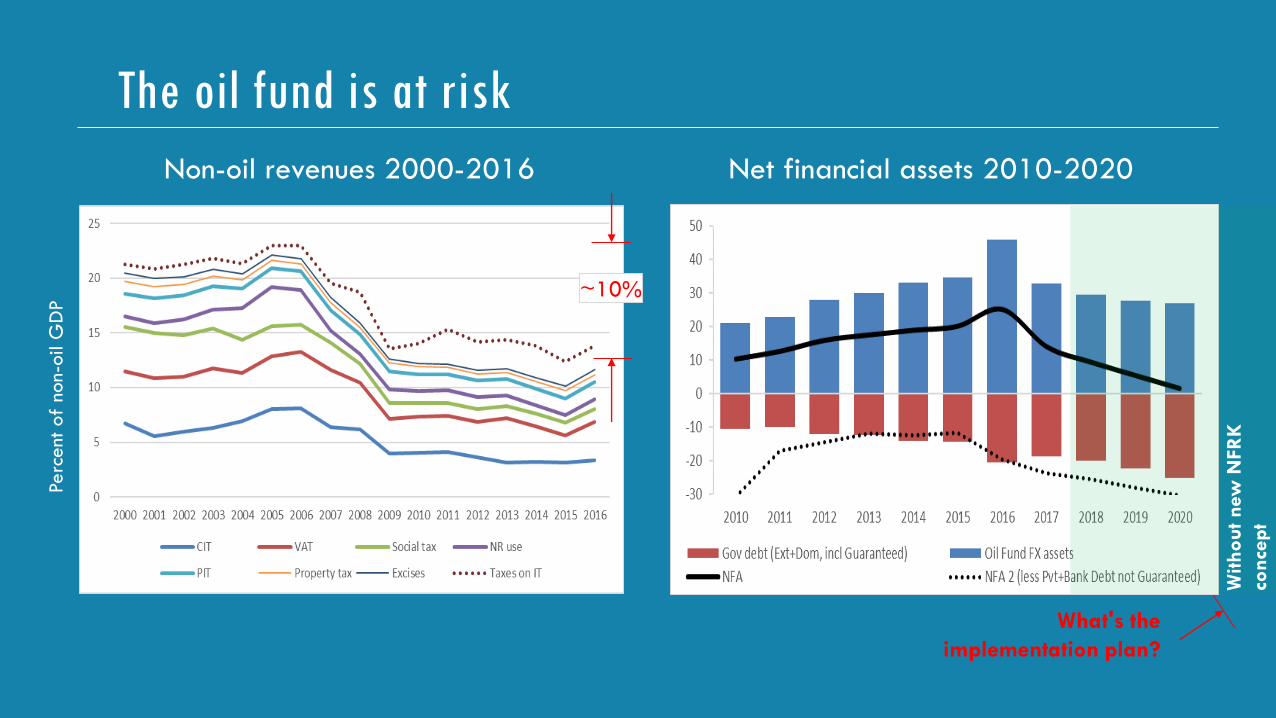

The non-oil deficit after 2008 was too large*

-5

0

5

10

15

20

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Perc

ent

of

no

n-o

il G

DP

OF guaranteed transfer OF TT+Cust. Duty

OF direct lending to SOEs Net borrowing

50

75

100

125

150

175

200

Jan

Au

g

Mar

Oct

May

De

c

Jul

Feb

Sep

Ap

r

No

v

Jun

Jan

Au

g

Mar

Oct

May

De

c

Jul

Feb

Sep

Ap

r

No

v

Jun

Jan

Au

g

Mar

Oct

May

De

c

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

RER KZT/Ruble RER KZT/USD RER KZT/CNY

~8-10%

What's the

implementation plan?

Non-oil deficit financing 2001-2016Real exchange rates 2001-2016

The oil fund is at risk

Net financial assets 2010-2020Non-oil revenues 2000-2016

~10%

Witho

ut new

NFR

K

conce

pt

What's the

implementation plan?

Perc

ent

of

non-o

il G

DP

Problems with corruption persist

Corruption experience in transition economies

Households

• Education quality

• Health access

• Health quality

• Utilities access

Businesses

• SOE procurement

• GOK procurement

• Licenses

• Inspections

Things to look at

Source: Life In Transition Survey III (2016)

PATHWAY #2

PRIVATE SECTOR

DEVELOPMENT

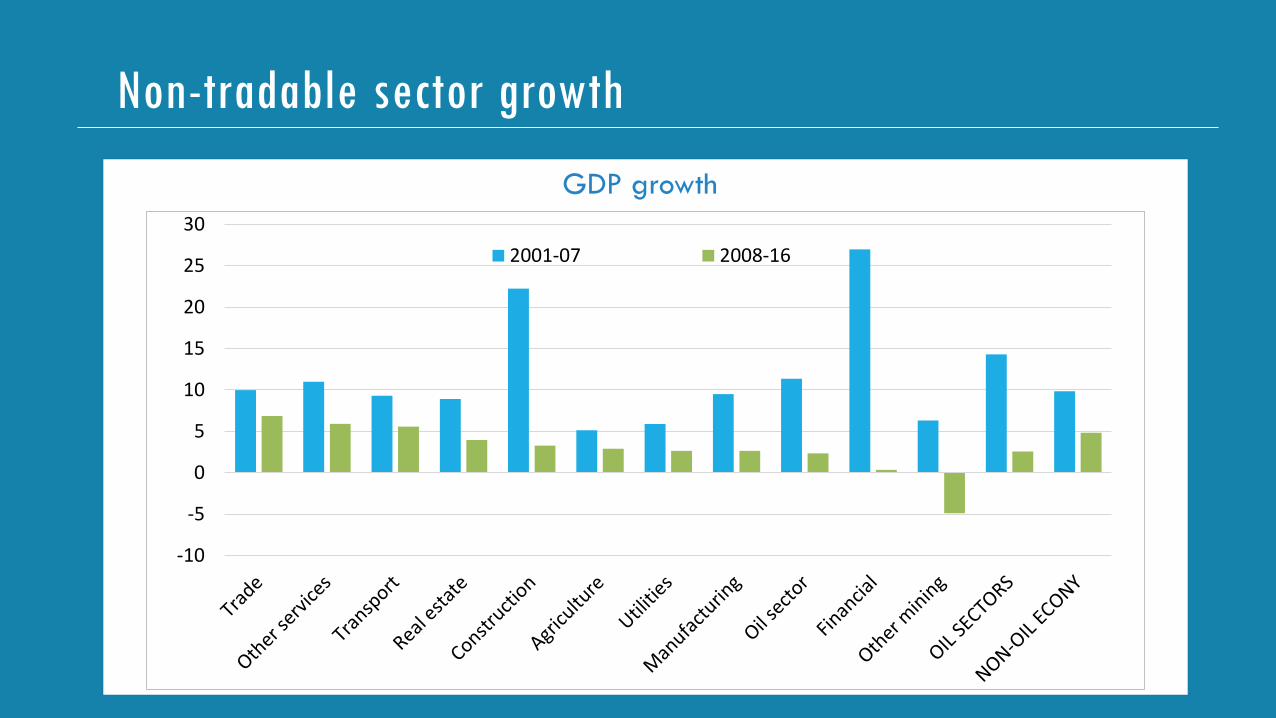

Non-tradable sector growth

-10

-5

0

5

10

15

20

25

30

2001-07 2008-16

GDP growth

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Credit to the economy (percent of GDP)

Real growth of credit to rest of economy (percent change)

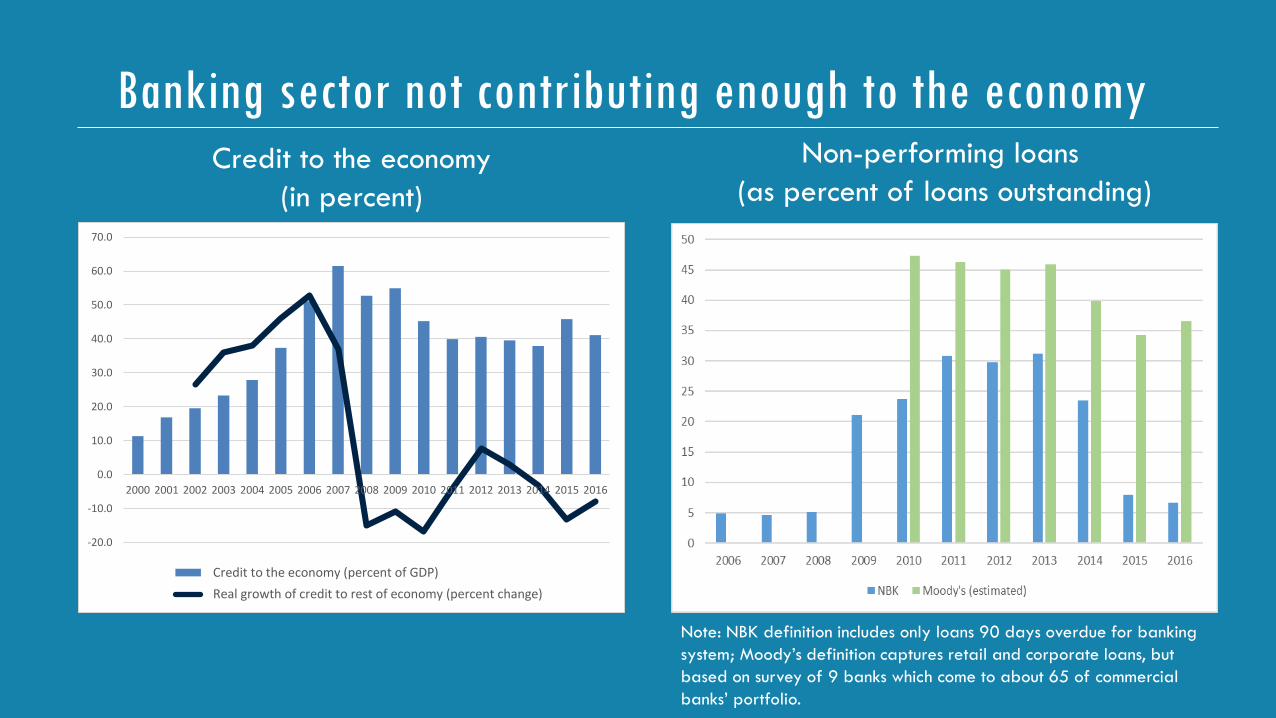

Banking sector not contributing enough to the economyNon-performing loans

(as percent of loans outstanding)Credit to the economy

(in percent)

Note: NBK definition includes only loans 90 days overdue for banking

system; Moody’s definition captures retail and corporate loans, but

based on survey of 9 banks which come to about 65 of commercial

banks’ portfolio.

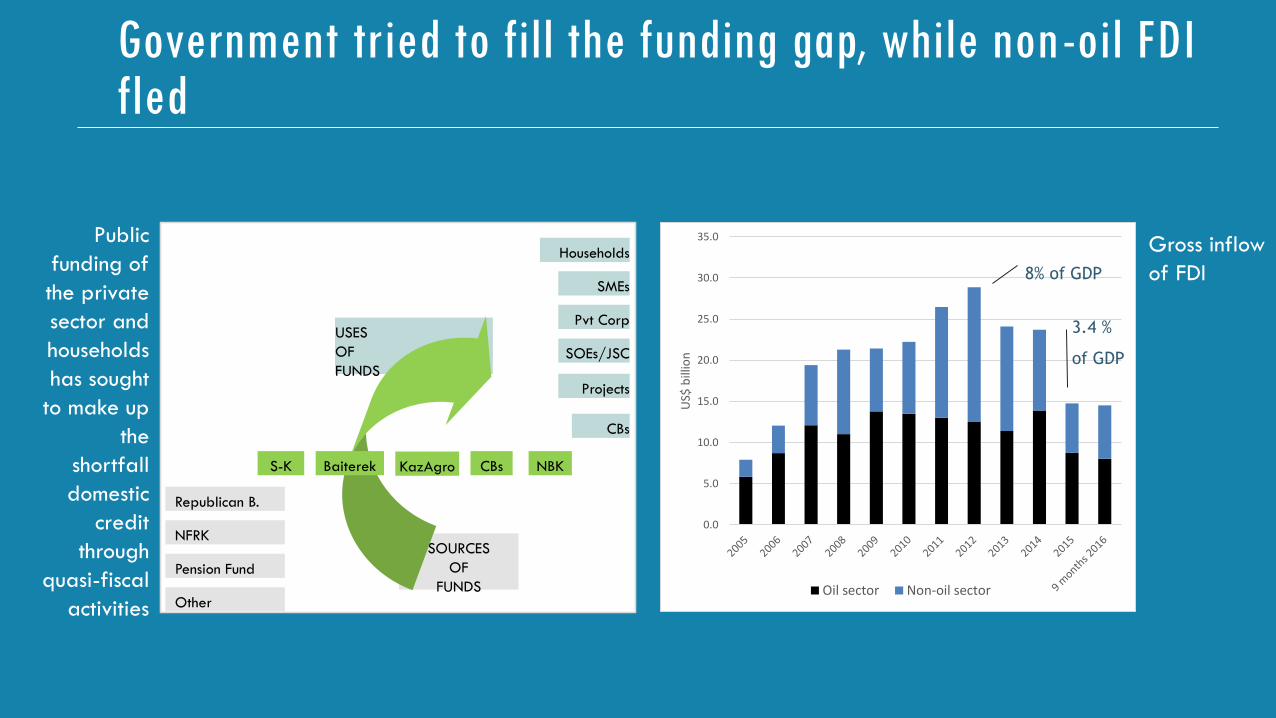

USES

OF

FUNDS

SOURCES

OF

FUNDS

Republican B.

NFRK

Pension Fund

Other

S-K KazAgro CBs NBK

Households

SMEs

Pvt Corp

SOEs/JSC

Projects

CBs

Baiterek

Public

funding of

the private

sector and

households

has sought

to make up

the

shortfall

domestic

credit

through

quasi-fiscal

activities

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

US$

bill

ion

Oil sector Non-oil sector

8% of GDP

3.4 %

of GDP

Gross inflow

of FDI

Government tried to fill the funding gap, while non-oil FDI fled

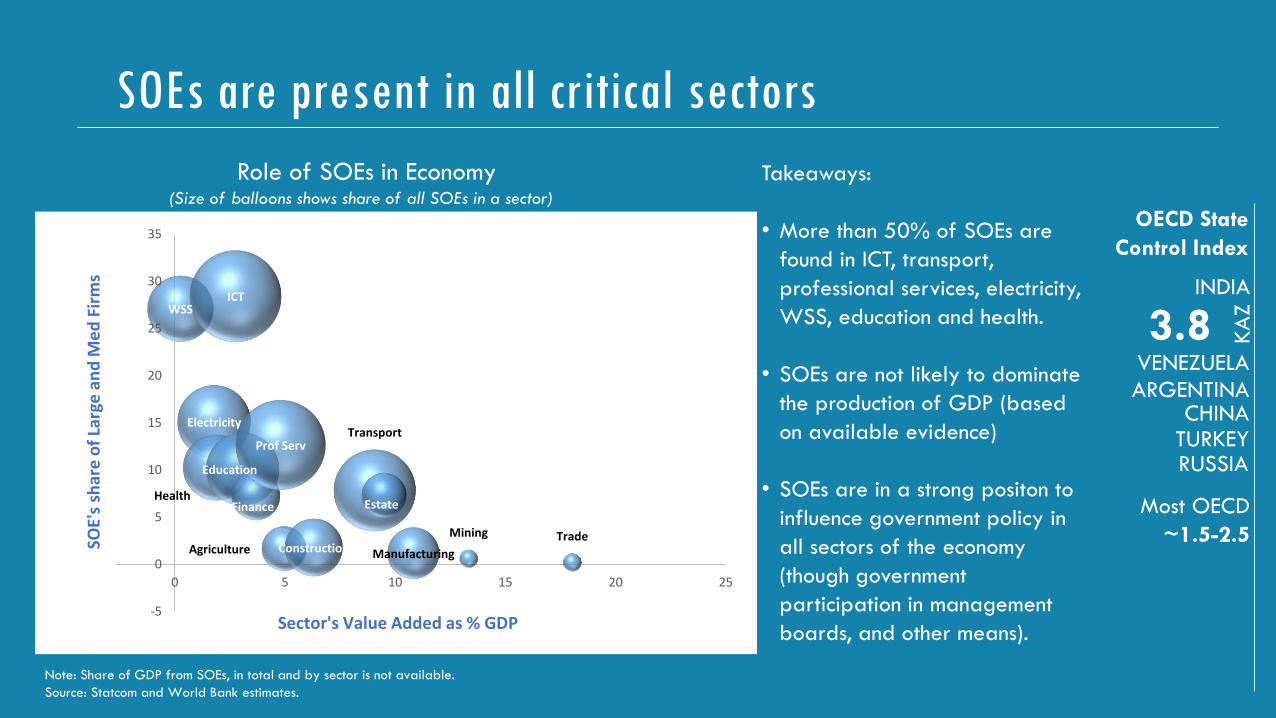

SOEs are present in all critical sectors

WSS

Electricity

Health

ICT

Education

Finance

Prof Serv

Agriculture Construction

Transport

Estate

Manufacturing

Mining Trade

-5

0

5

10

15

20

25

30

35

-5 0 5 10 15 20 25

Series1Sector's Value Added as % GDP

SOE'

s sh

are

of

Larg

e a

nd

Me

dFi

rms

Role of SOEs in Economy(Size of balloons shows share of all SOEs in a sector)

Takeaways:

• More than 50% of SOEs are

found in ICT, transport,

professional services, electricity,

WSS, education and health.

• SOEs are not likely to dominate

the production of GDP (based

on available evidence)

• SOEs are in a strong positon to

influence government policy in

all sectors of the economy

(though government

participation in management

boards, and other means).

3.8

OECD State

Control Index

KA

Z

INDIA

VENEZUELA

ARGENTINACHINA

TURKEYRUSSIA

Most OECD

~1.5-2.5

Note: Share of GDP from SOEs, in total and by sector is not available.

Source: Statcom and World Bank estimates.

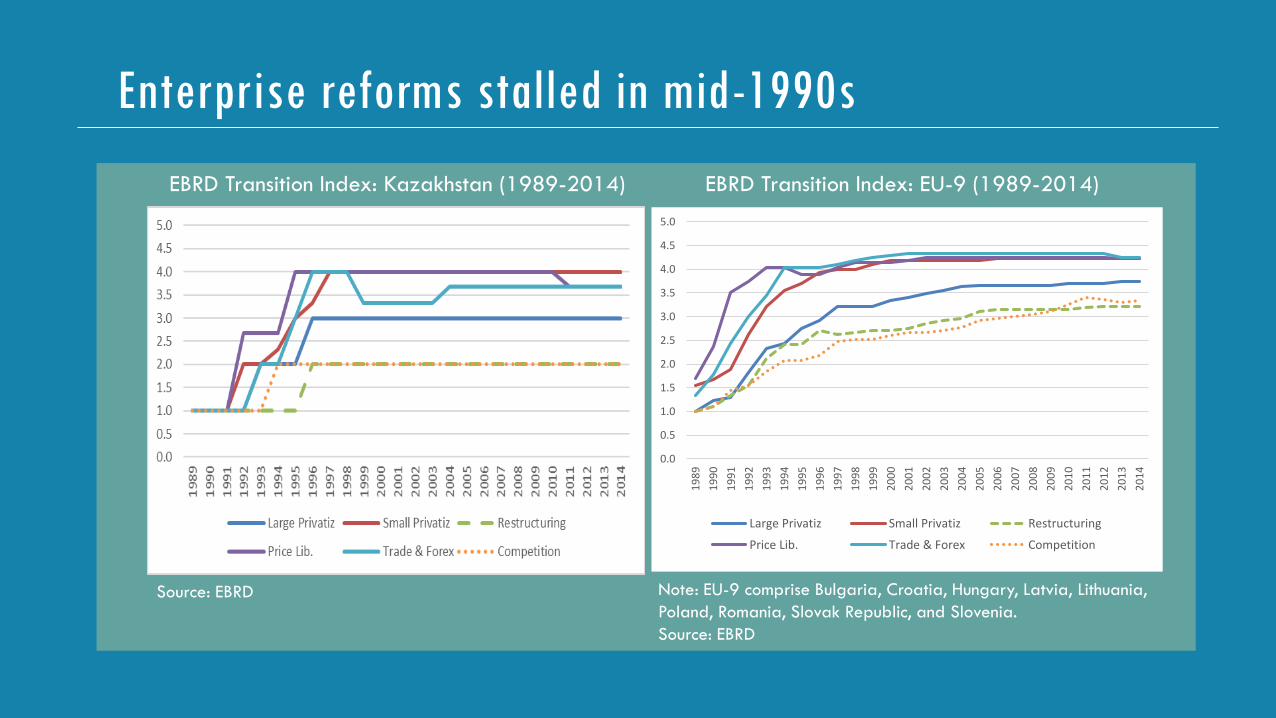

Enterprise reforms stalled in mid-1990s

EBRD Transition Index: Kazakhstan (1989-2014) EBRD Transition Index: EU-9 (1989-2014)

Source: EBRD Note: EU-9 comprise Bulgaria, Croatia, Hungary, Latvia, Lithuania,

Poland, Romania, Slovak Republic, and Slovenia.

Source: EBRD

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Large Privatiz Small Privatiz Restructuring

Price Lib. Trade & Forex Competition

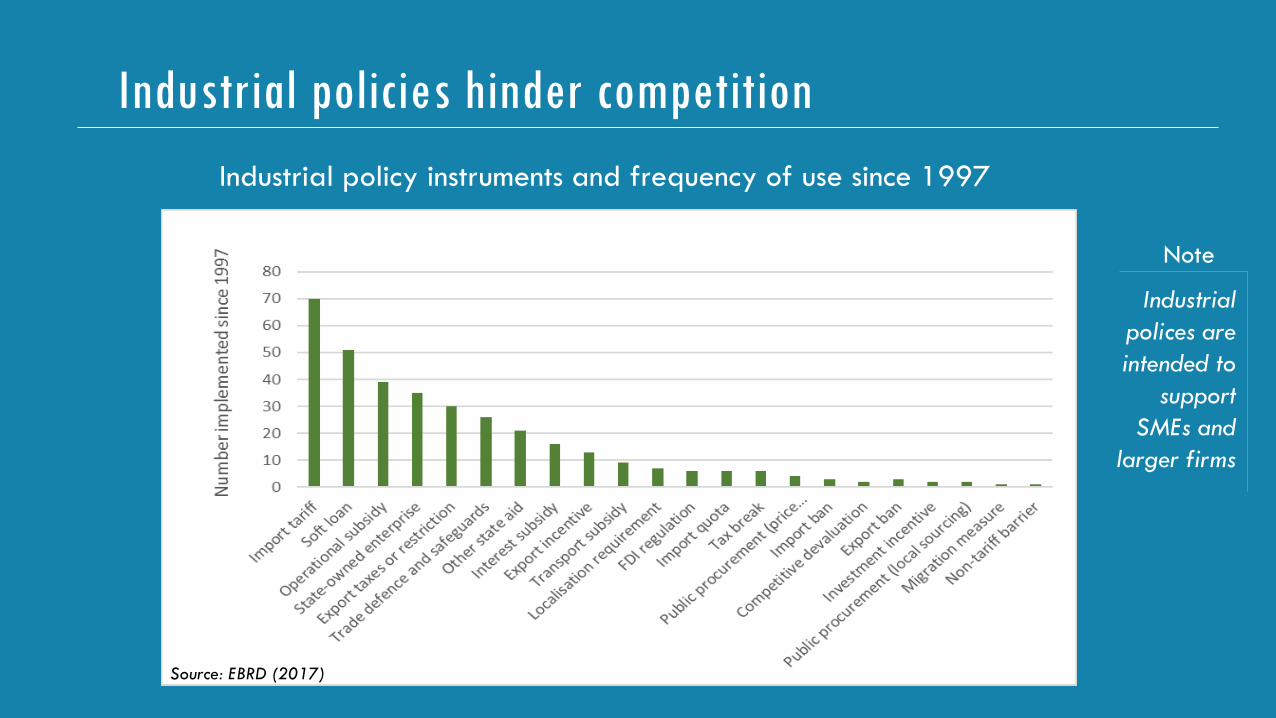

Industrial policies hinder competition

Industrial policy instruments and frequency of use since 1997

Source: EBRD (2017)

Industrial

polices are

intended to

support

SMEs and

larger firms

Note

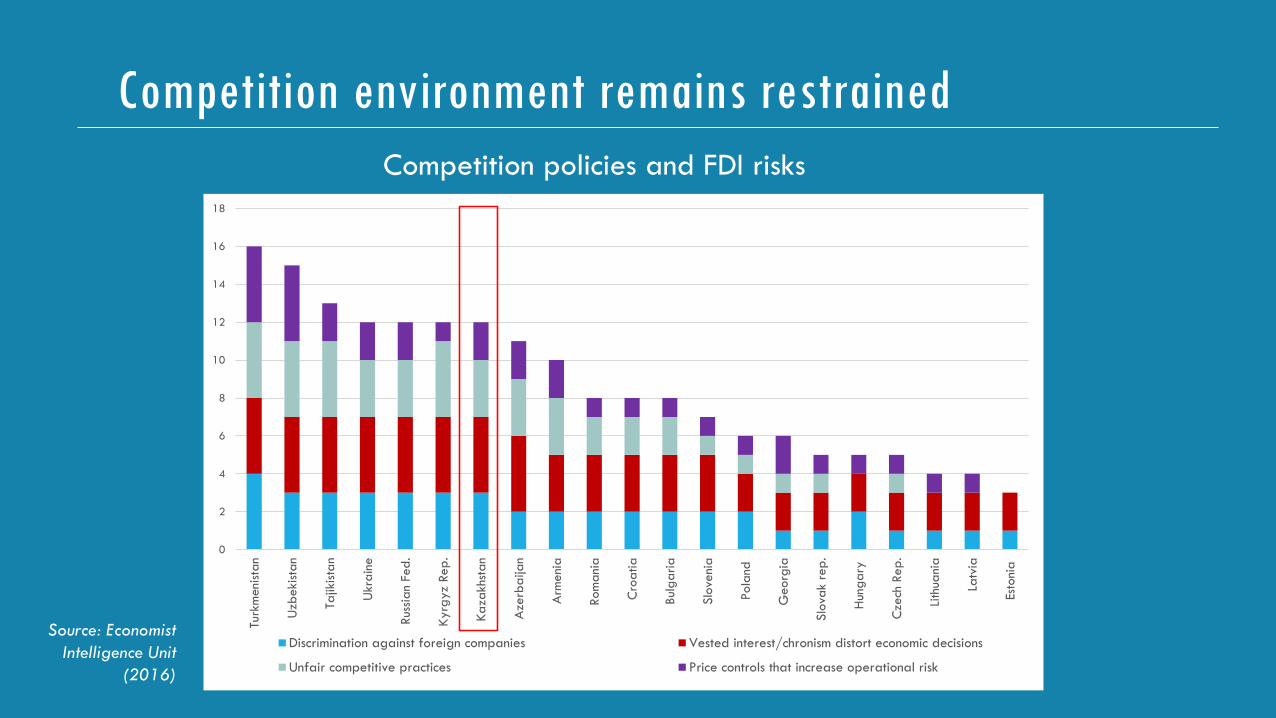

Competition environment remains restrained

0

2

4

6

8

10

12

14

16

18

Turk

menista

n

Uzb

ekista

n

Tajik

ista

n

Ukr

ain

e

Rus

sian

Fed

.

Kyrg

yz R

ep

.

Ka

zakhs

tan

Aze

rba

ijan

Arm

eni

a

Rom

ania

Cro

atia

Bul

garia

Slo

veni

a

Pola

nd

Georg

ia

Slo

vak r

ep.

Hun

gary

Cze

ch R

ep.

Lith

uani

a

Latv

ia

Esto

nia

Discrimination against foreign companies Vested interest/chronism distort economic decisions

Unfair competitive practices Price controls that increase operational risk

Competition policies and FDI risks

Source: Economist

Intelligence Unit

(2016)

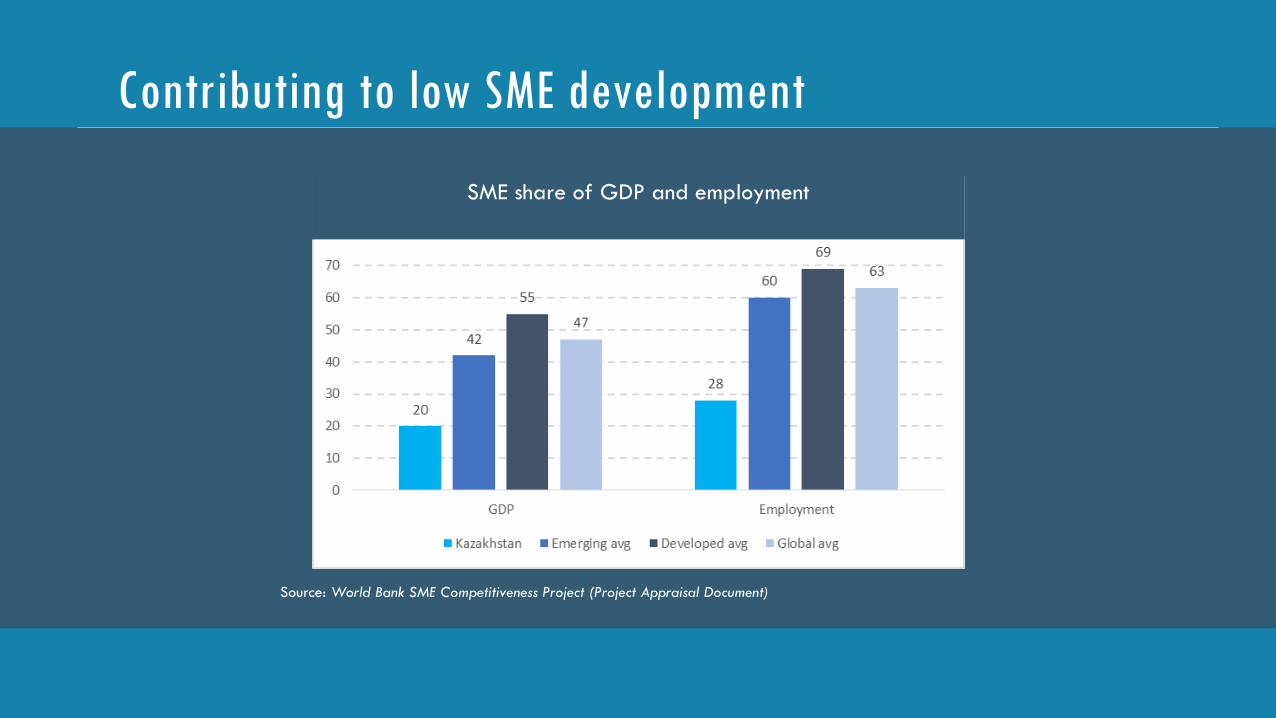

Contributing to low SME development

Source: World Bank SME Competitiveness Project (Project Appraisal Document)

SME share of GDP and employment

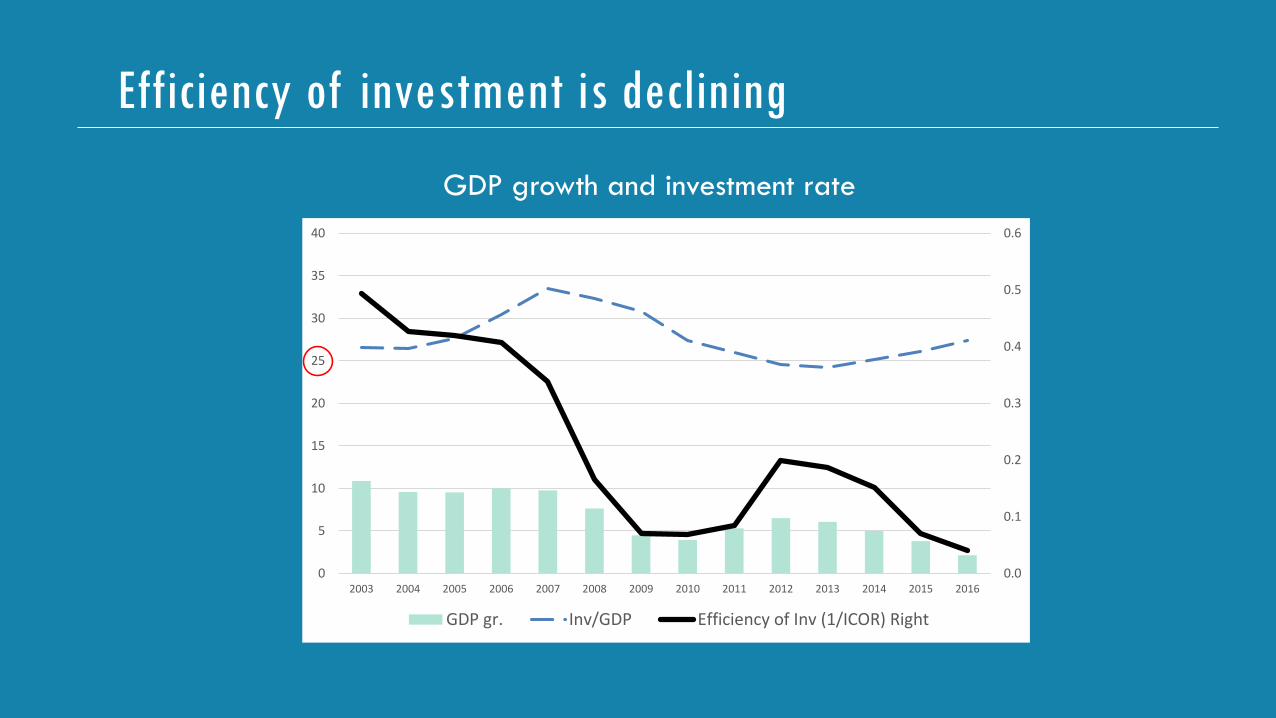

Efficiency of investment is declining

GDP growth and investment rate

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0

5

10

15

20

25

30

35

40

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

GDP gr. Inv/GDP Efficiency of Inv (1/ICOR) Right

PATHWAY #3

TRADE, CONNECTIVITY

AND INTEGRATION

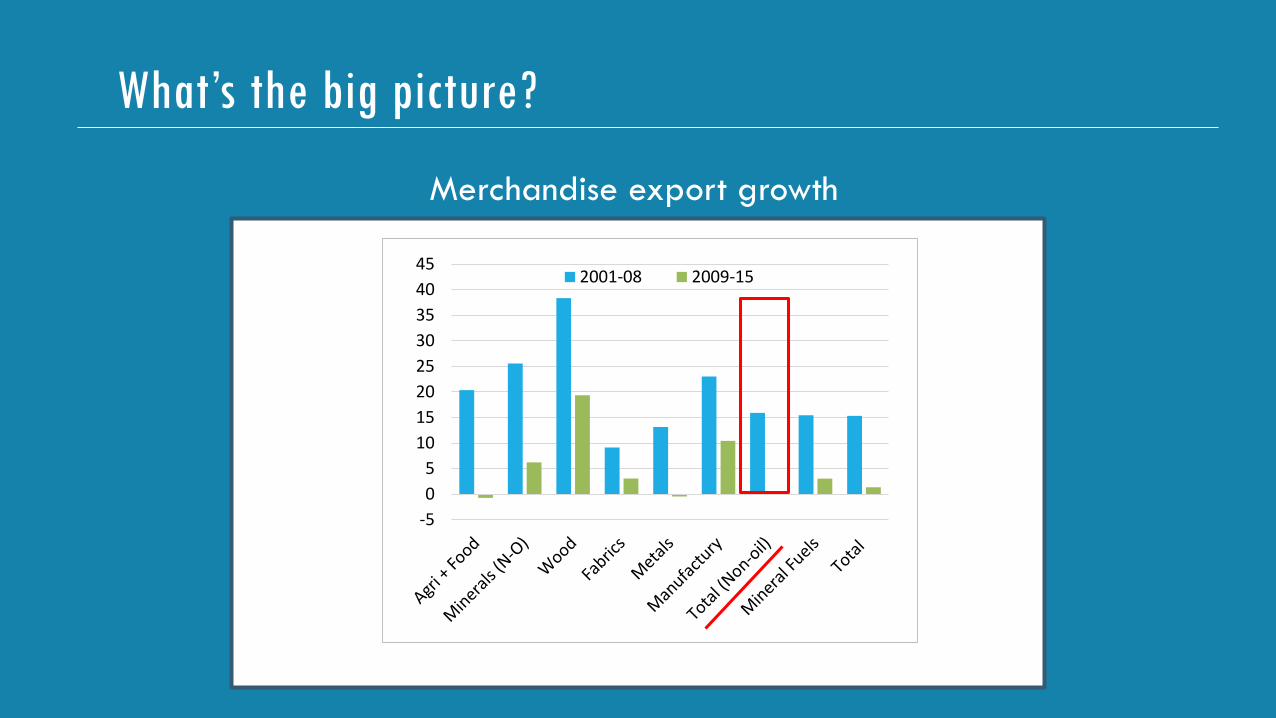

What’s the big picture?

-5

0

5

10

15

20

25

30

35

40

452001-08 2009-15

Merchandise export growth

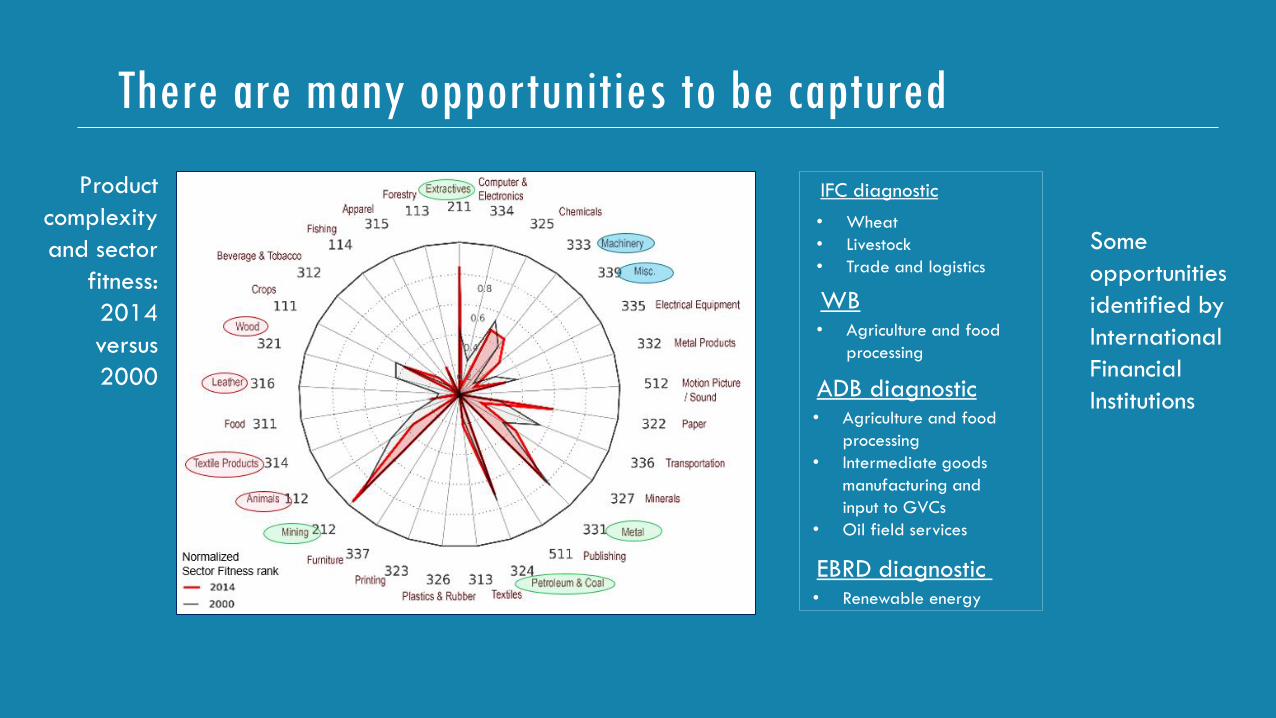

There are many opportunities to be captured

• Wheat

• Livestock

• Trade and logistics

IFC diagnostic

• Agriculture and food

processing

WB

• Agriculture and food

processing

• Intermediate goods

manufacturing and

input to GVCs

• Oil field services

ADB diagnostic

• Renewable energy

EBRD diagnostic

Some

opportunities

identified by

International

Financial

Institutions

Product

complexity

and sector

fitness:

2014

versus

2000

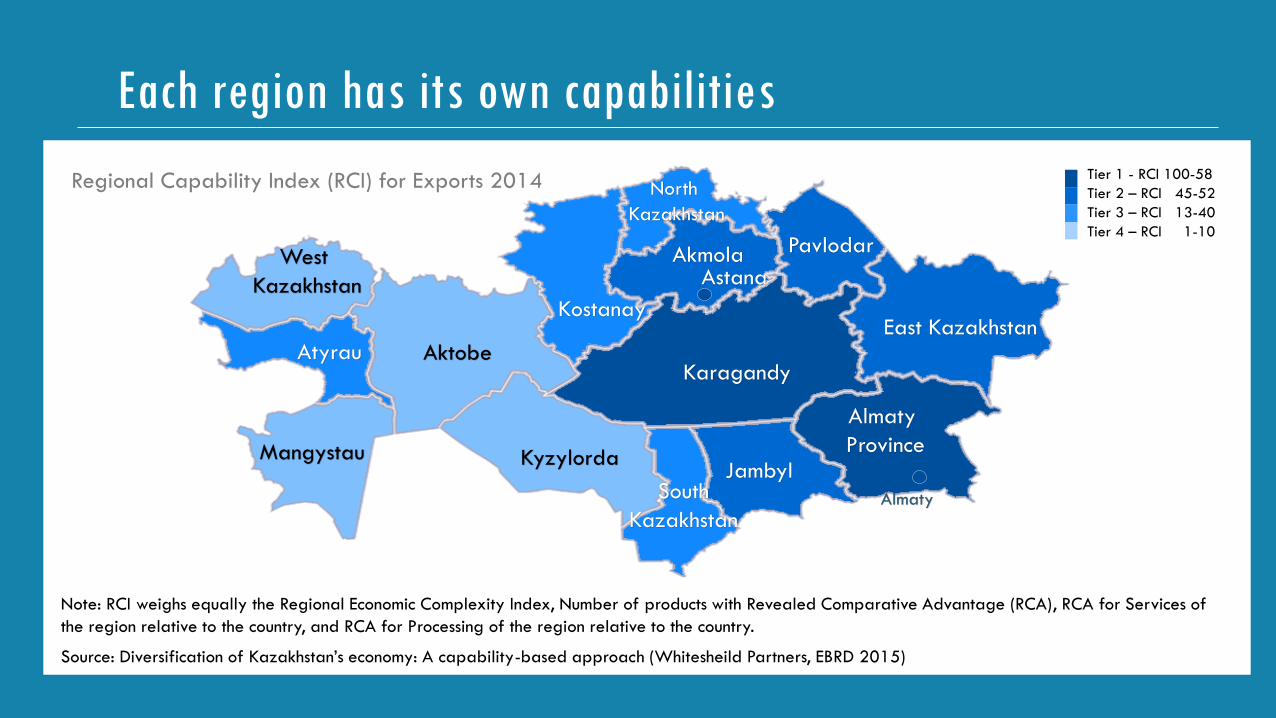

West

Kazakhstan

AktobeAtyrau

Mangystau Kyzylorda

South

Kazakhstan

Jambyl

Almaty

Province

Almaty

Karagandy

East Kazakhstan

Pavlodar

North

Kazakhstan

Kostanay

AstanaAkmola

Tier 1 - RCI 100-58

Tier 2 – RCI 45-52

Tier 3 – RCI 13-40

Tier 4 – RCI 1-10

Note: RCI weighs equally the Regional Economic Complexity Index, Number of products with Revealed Comparative Advantage (RCA), RCA for Services of

the region relative to the country, and RCA for Processing of the region relative to the country.

Source: Diversification of Kazakhstan’s economy: A capability-based approach (Whitesheild Partners, EBRD 2015)

Regional Capability Index (RCI) for Exports 2014

Each region has its own capabilities

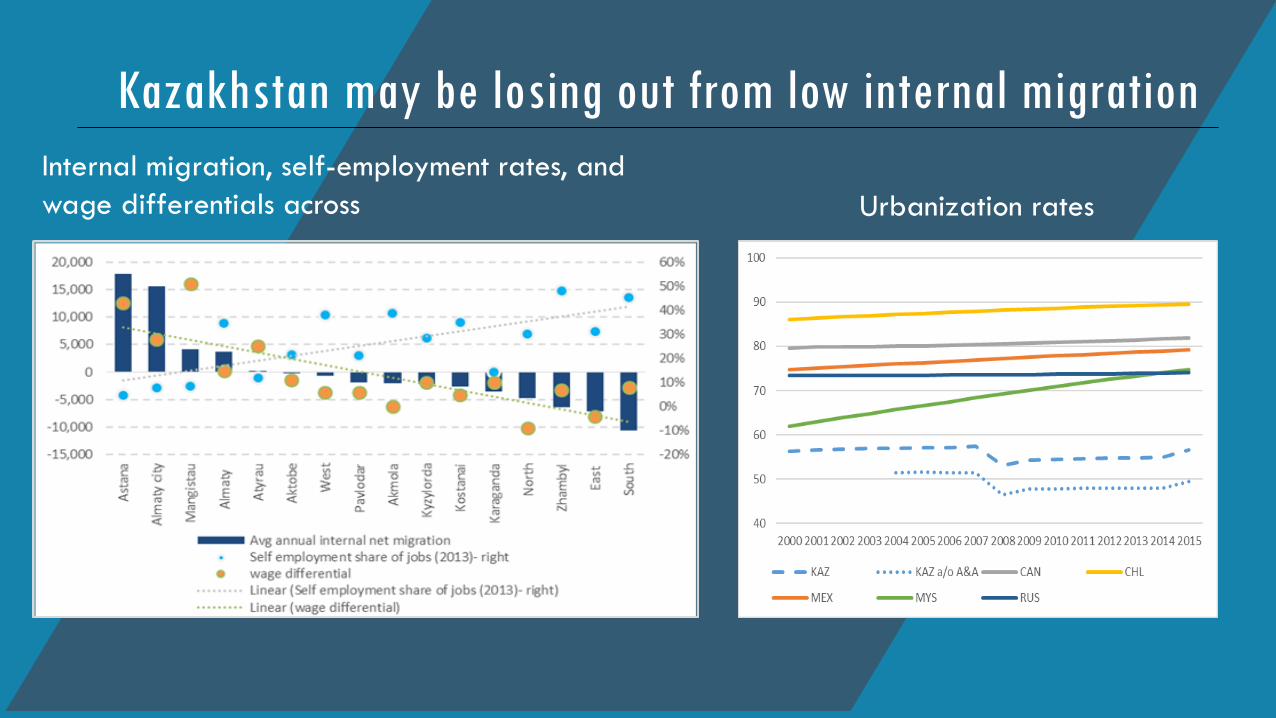

Kazakhstan may be losing out from low internal migration

Urbanization rates

Internal migration, self-employment rates, and

wage differentials across

FUTURE

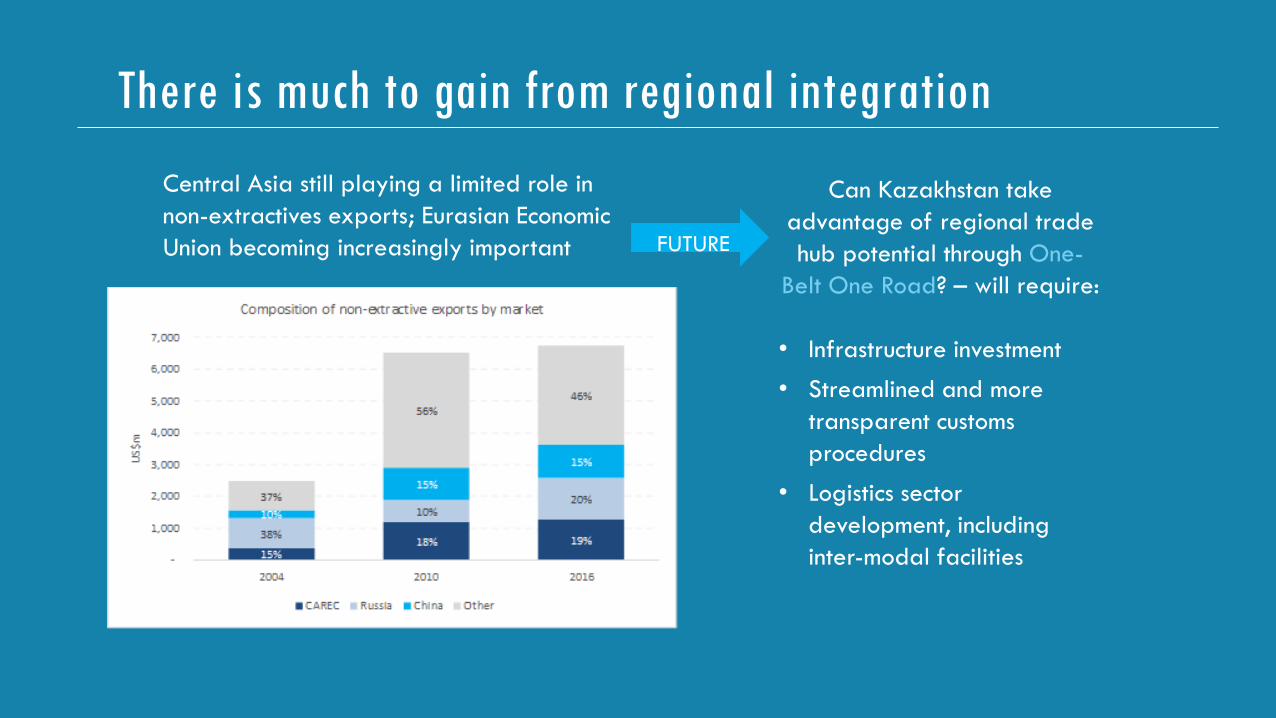

Central Asia still playing a limited role in

non-extractives exports; Eurasian Economic

Union becoming increasingly important

Can Kazakhstan take

advantage of regional trade

hub potential through One-

Belt One Road? – will require:

• Infrastructure investment

• Streamlined and more

transparent customs

procedures

• Logistics sector

development, including

inter-modal facilities

There is much to gain from regional integration

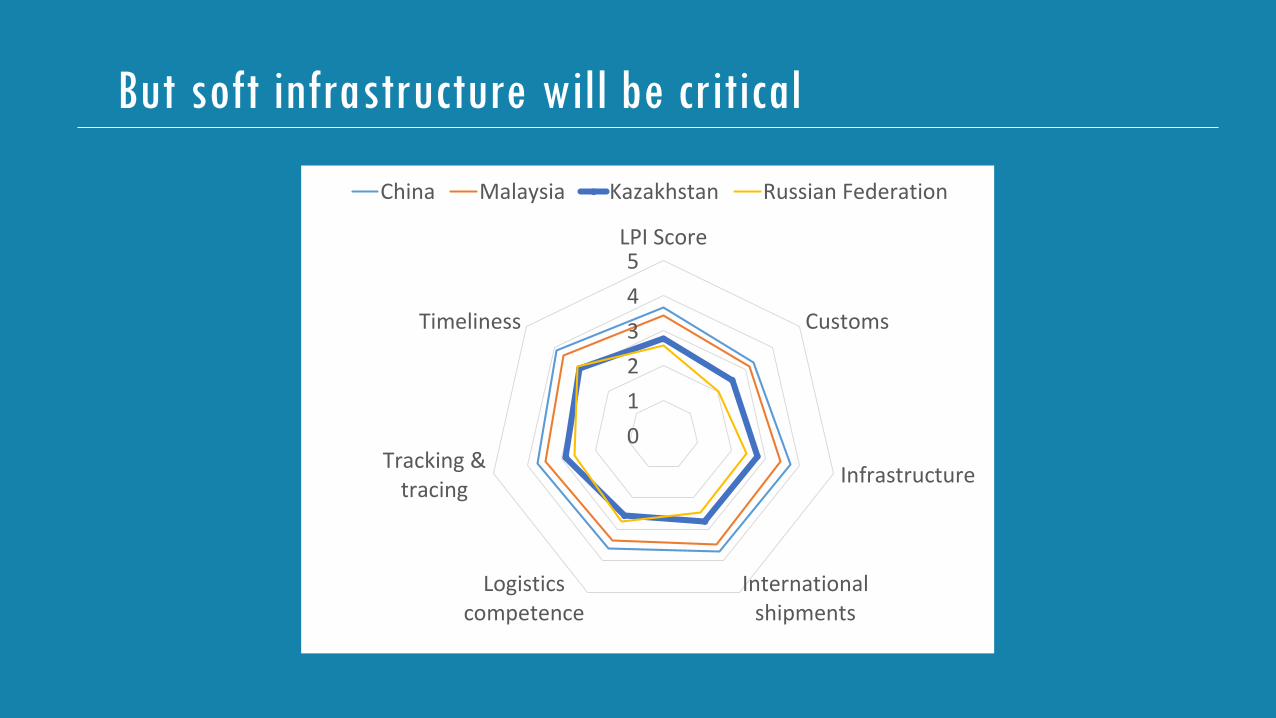

But soft infrastructure will be critical

0

1

2

3

4

5LPI Score

Customs

Infrastructure

Internationalshipments

Logisticscompetence

Tracking &tracing

Timeliness

China Malaysia Kazakhstan Russian Federation

PATHWAY #3

COMPETITIVE AND ADAPTIVE

HUMAN CAPITALEducation

Job market

linkages

Health

outcomesSocial

protection

related to

job market

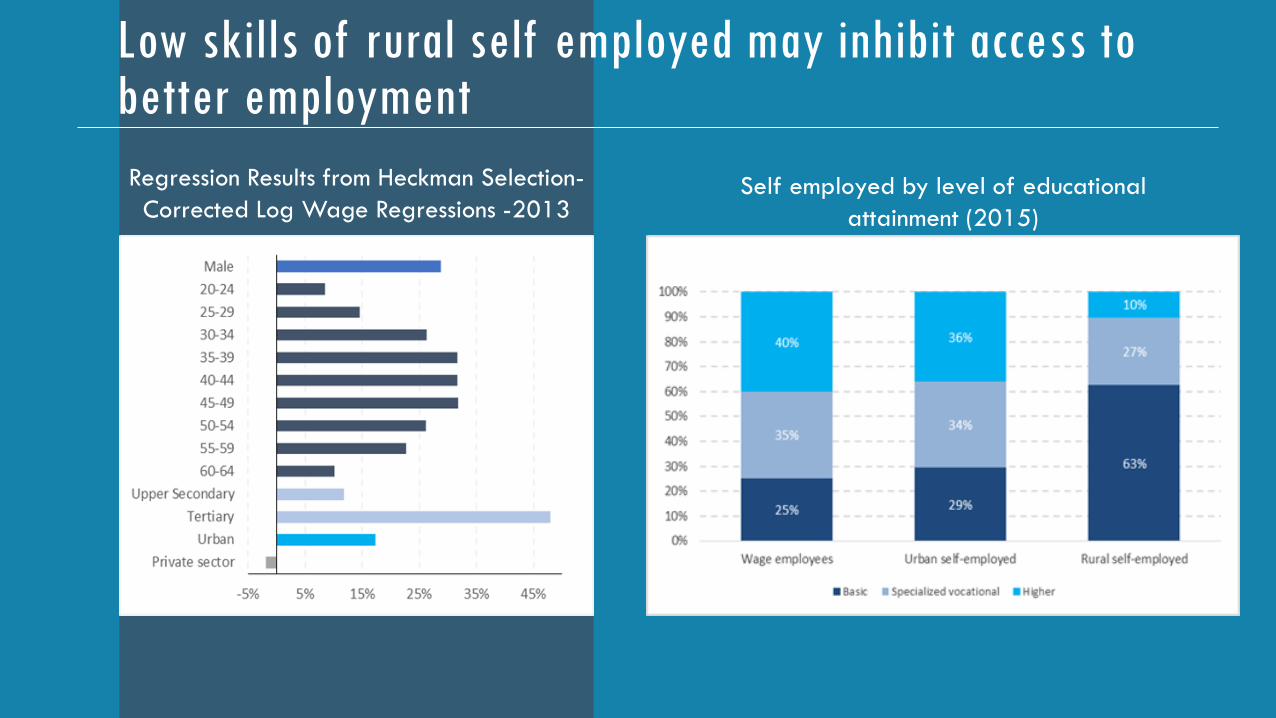

Low skills of rural self employed may inhibit access to better employment

Regression Results from Heckman Selection-

Corrected Log Wage Regressions -2013Self employed by level of educational

attainment (2015)

Distribution of educational attainment of youth population

(15-28)

Evolution of Kazakhstan’s PISA

performance

Despite overall progress made on education

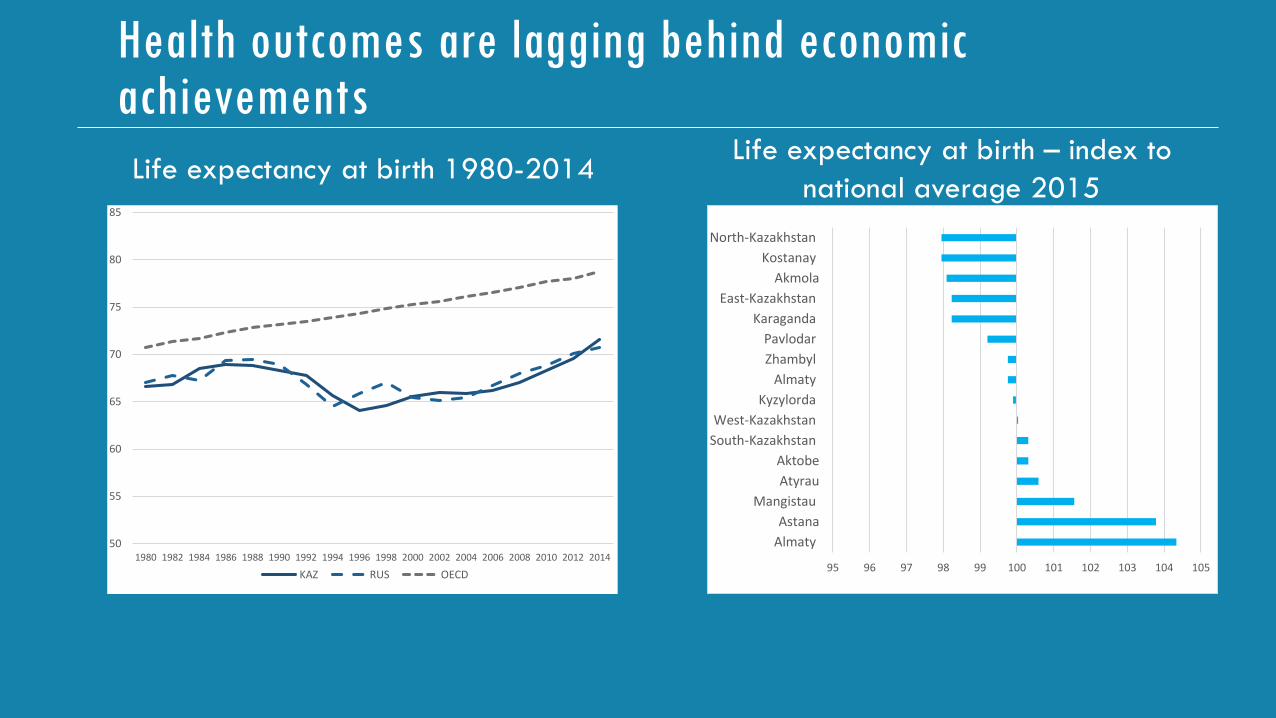

Health outcomes are lagging behind economic achievements

95 96 97 98 99 100 101 102 103 104 105

Almaty

Astana

Mangistau

Atyrau

Aktobe

South-Kazakhstan

West-Kazakhstan

Kyzylorda

Almaty

Zhambyl

Pavlodar

Karaganda

East-Kazakhstan

Akmola

Kostanay

North-Kazakhstan

50

55

60

65

70

75

80

85

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

KAZ RUS OECD

Life expectancy at birth – index to

national average 2015Life expectancy at birth 1980-2014

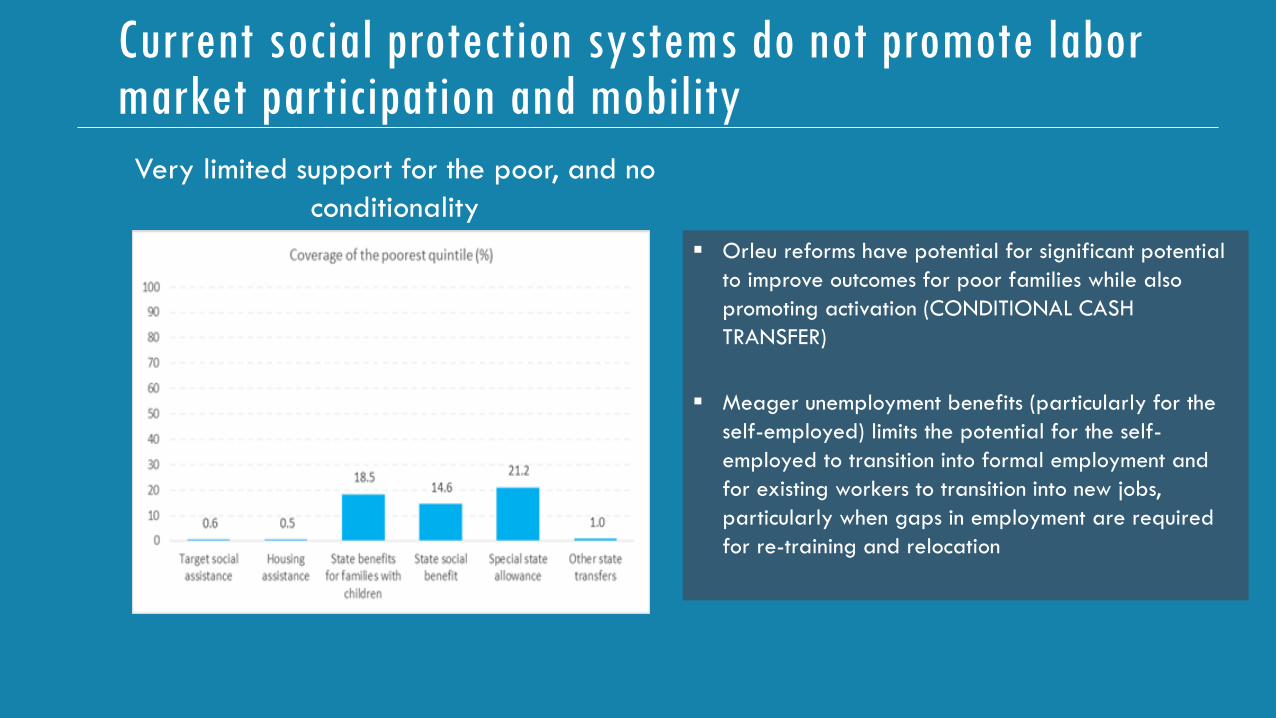

Current social protection systems do not promote labor market participation and mobility

Very limited support for the poor, and no

conditionality

Orleu reforms have potential for significant potential

to improve outcomes for poor families while also

promoting activation (CONDITIONAL CASH

TRANSFER)

Meager unemployment benefits (particularly for the

self-employed) limits the potential for the self-

employed to transition into formal employment and

for existing workers to transition into new jobs,

particularly when gaps in employment are required

for re-training and relocation

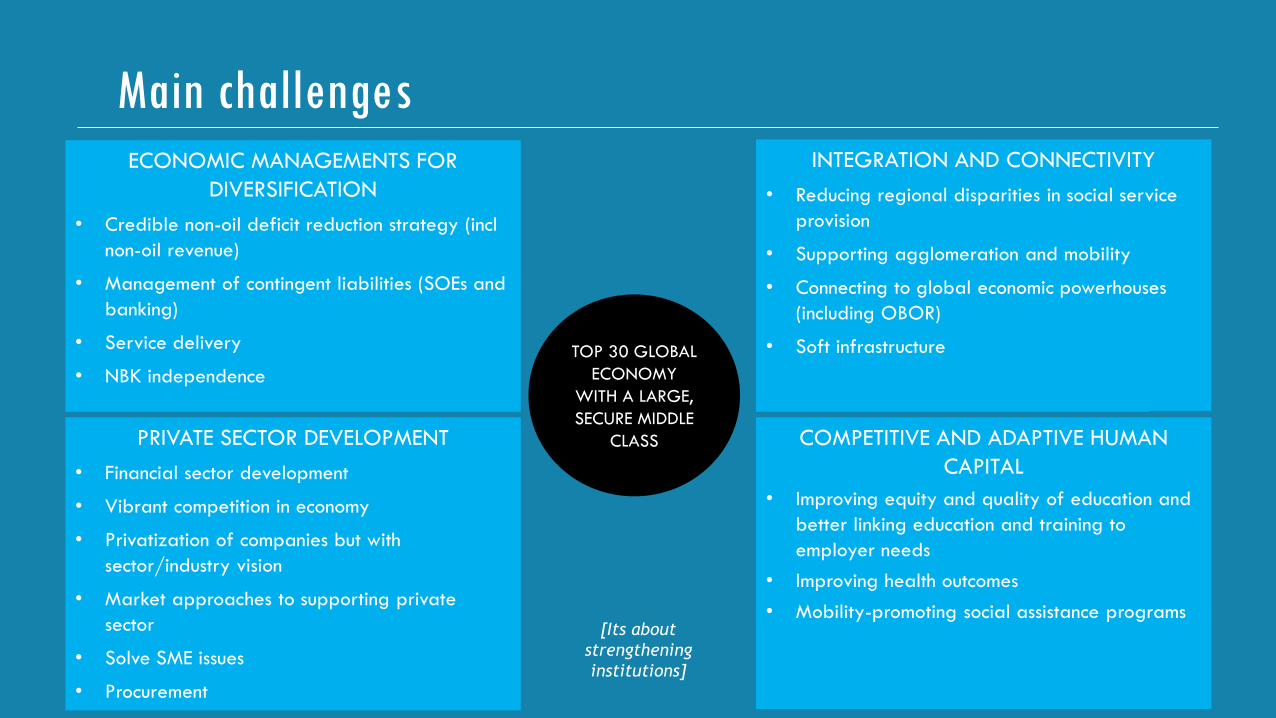

ECONOMIC MANAGEMENTS FOR

DIVERSIFICATION

• Credible non-oil deficit reduction strategy (incl

non-oil revenue)

• Management of contingent liabilities (SOEs and

banking)

• Service delivery

• NBK independence

PRIVATE SECTOR DEVELOPMENT

• Financial sector development

• Vibrant competition in economy

• Privatization of companies but with

sector/industry vision

• Market approaches to supporting private

sector

• Solve SME issues

• Procurement

COMPETITIVE AND ADAPTIVE HUMAN

CAPITAL

• Improving equity and of education

and better linking education and

training to employer needs

• Improving health outcomes

• Mobility-promoting social assistance

programs

COMPETITIVE AND ADAPTIVE HUMAN

CAPITAL

• Improving equity and quality of education and

better linking education and training to

employer needs

• Improving health outcomes

• Mobility-promoting social assistance programs

TOP 30 GLOBAL

ECONOMY

WITH A LARGE,

SECURE MIDDLE

CLASS

[Its about

strengthening

institutions]

Main challengesINTEGRATION AND CONNECTIVITY

• Reducing regional disparities in social service

provision

• Supporting agglomeration and mobility

• Connecting to global economic powerhouses

(including OBOR)

• Soft infrastructure

THANK YOU FOR YOUR ATTENTION