Embed Size (px)

Citation preview

Fubon Financial 2015 Q1 Interim Results

and

2015.05.13

and

2014 Embedded Value of Fubon Life

Disclaimer

This meeting may contain forward-looking statements with respect to the financial

condition, results of operations and business of the company. These forward-looking

statements represent the company’s expectations or beliefs concerning future events

and involve known and unknown risks and uncertainty that could cause actual

results, performance or events to differ materially from those expressed. Certain

statements, such as those that include the words “potential”, “estimated”, and similar

2

expressions or variations on such expressions may be considered “forward-looking

statements”. Financial numbers in this report may include preliminary unaudited

numbers or management accounts.

� Performance review by subsidiary

• Fubon Life

� Performance highlights of Fubon Financial Holdings

Agenda

• Taipei Fubon Bank

3

• Fubon Life

• Fubon Securities

• Fubon Insurance

•Fubon Bank (China)

� 2014 Embedded Value of Fubon Life

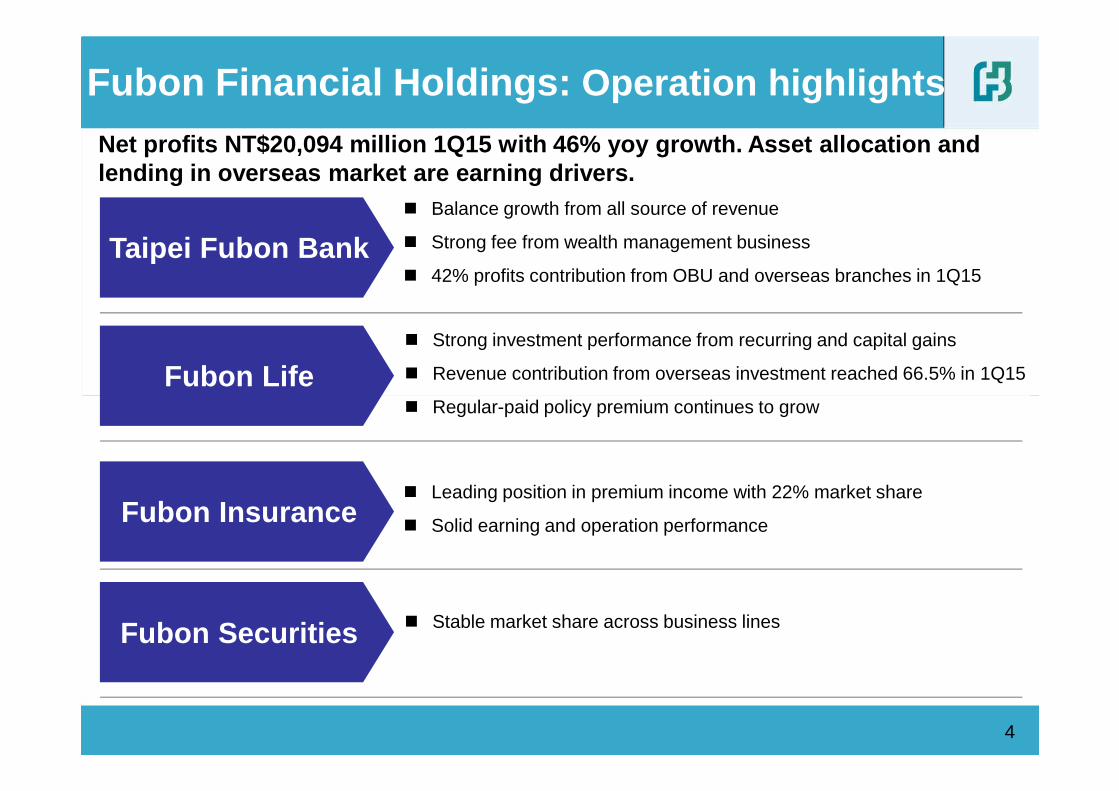

Fubon Financial Holdings: Operation highlights

Taipei Fubon Bank

Fubon Life

Net profits NT$20,094 million 1Q15 with 46% yoy gro wth. Asset allocation and lending in overseas market are earning drivers.

� Strong investment performance from recurring and capital gains

� Revenue contribution from overseas investment reached 66.5% in 1Q15

� Balance growth from all source of revenue

� Strong fee from wealth management business

� 42% profits contribution from OBU and overseas branches in 1Q15

4

� Stable market share across business lines

Fubon Insurance

Fubon Securities

� Regular-paid policy premium continues to grow

� Leading position in premium income with 22% market share

� Solid earning and operation performance

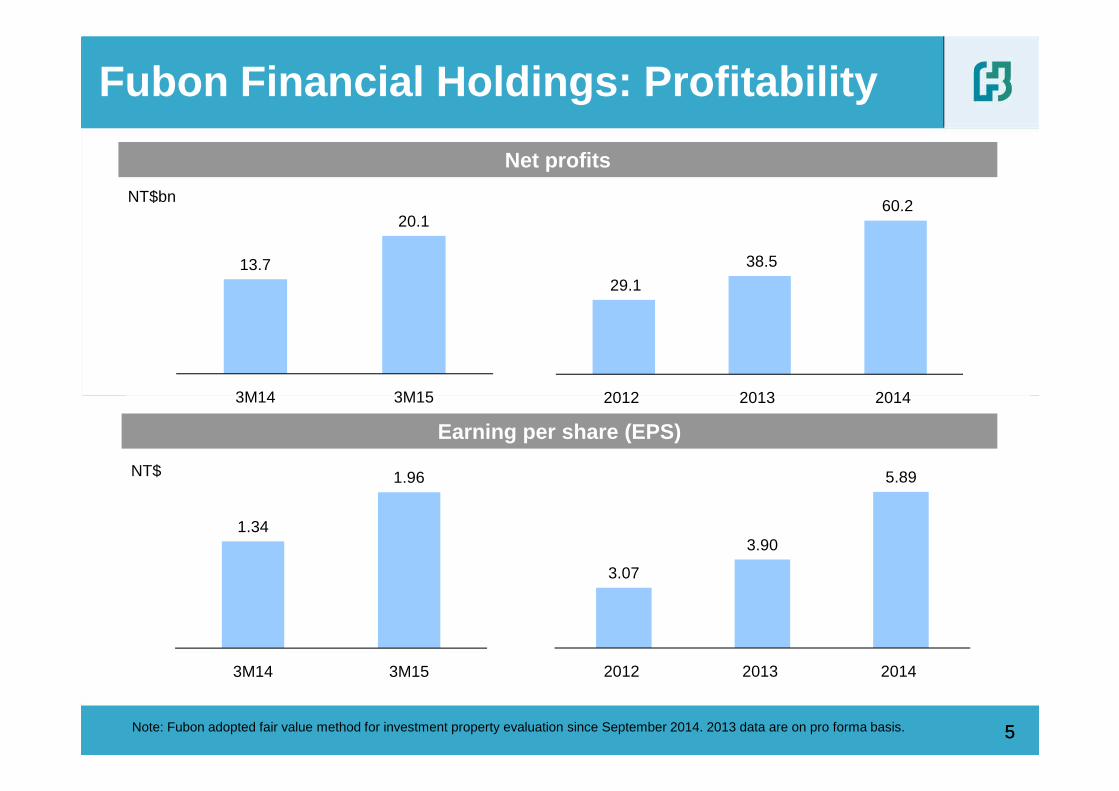

13.7

20.1

3M14 3M15

Net profits

NT$bn

29.1

38.5

60.2

2012 2013 2014

Fubon Financial Holdings: Profitability

3M14 3M15

3.07

3.90

5.89

2012 2013 2014

1.34

1.96

3M14 3M15

5

Earning per share (EPS)

NT$

Note: Fubon adopted fair value method for investment property evaluation since September 2014. 2013 data are on pro forma basis. 5

2012 2013 2014

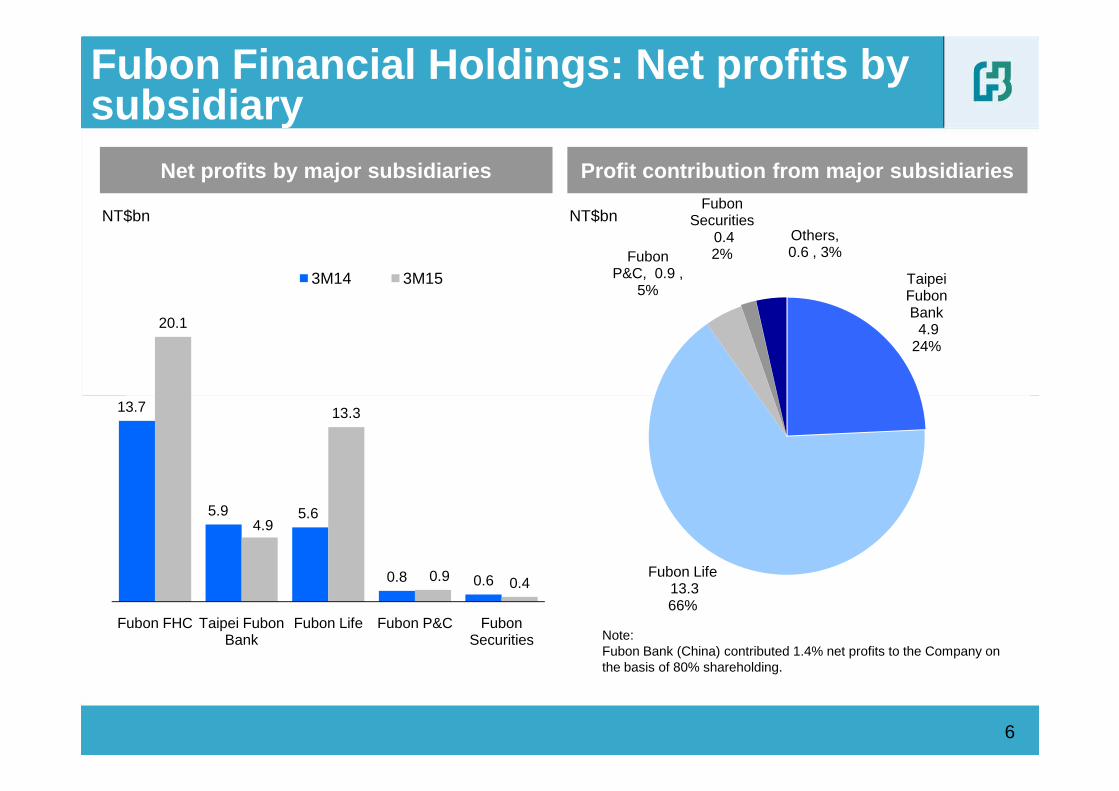

Fubon Financial Holdings: Net profits by subsidiary

Net profits by major subsidiaries Profit contribution from major subsidiaries

NT$bn NT$bn

20.1

3M14 3M15 Taipei Fubon Bank

4.9 24%

Fubon P&C, 0.9 ,

5%

Fubon Securities

0.4 2%

Others, 0.6 , 3%

6

Note: Fubon Bank (China) contributed 1.4% net profits to the Company on the basis of 80% shareholding.

13.7

5.9 5.6

0.8 0.6

4.9

13.3

0.9 0.4

Fubon FHC Taipei Fubon Bank

Fubon Life Fubon P&C Fubon Securities

Fubon Life13.3 66%

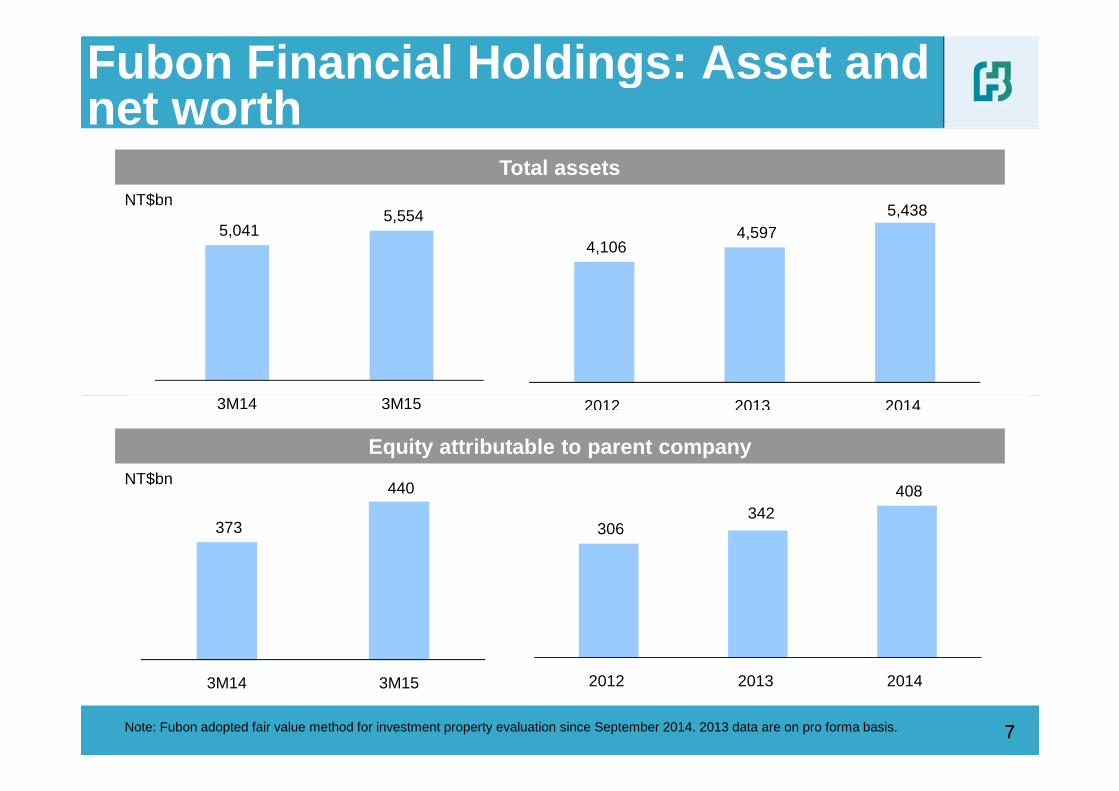

Total assetsNT$bn

4,106 4,597

5,438 5,041

5,554

3M14 3M15

Fubon Financial Holdings: Asset and net worth

77

Equity attributable to parent companyNT$bn

2012 2013 2014

306 342

408

2012 2013 2014

3M14 3M15

373

440

3M14 3M15

Note: Fubon adopted fair value method for investment property evaluation since September 2014. 2013 data are on pro forma basis.

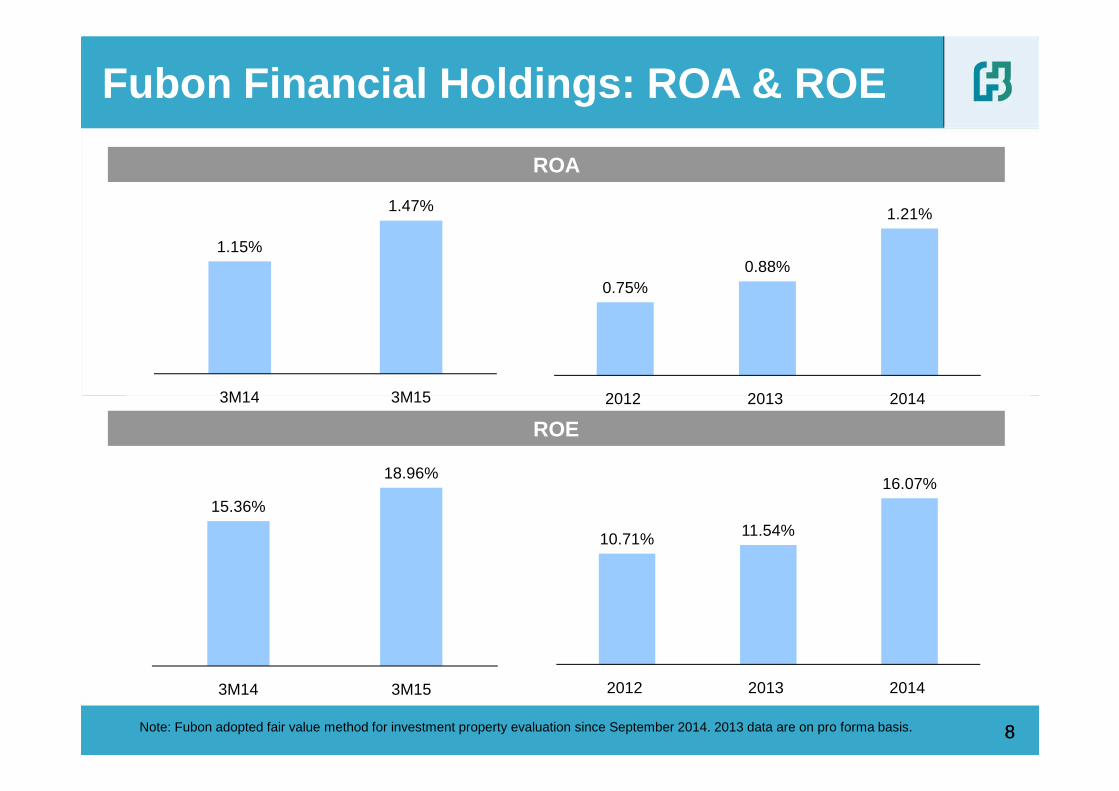

ROA

Fubon Financial Holdings: ROA & ROE

0.75%0.88%

1.21%

2012 2013 2014

1.15%

1.47%

3M14 3M15

88

ROE

2012 2013 2014

10.71% 11.54%

16.07%

2012 2013 2014

3M14 3M15

15.36%

18.96%

3M14 3M15

Note: Fubon adopted fair value method for investment property evaluation since September 2014. 2013 data are on pro forma basis.

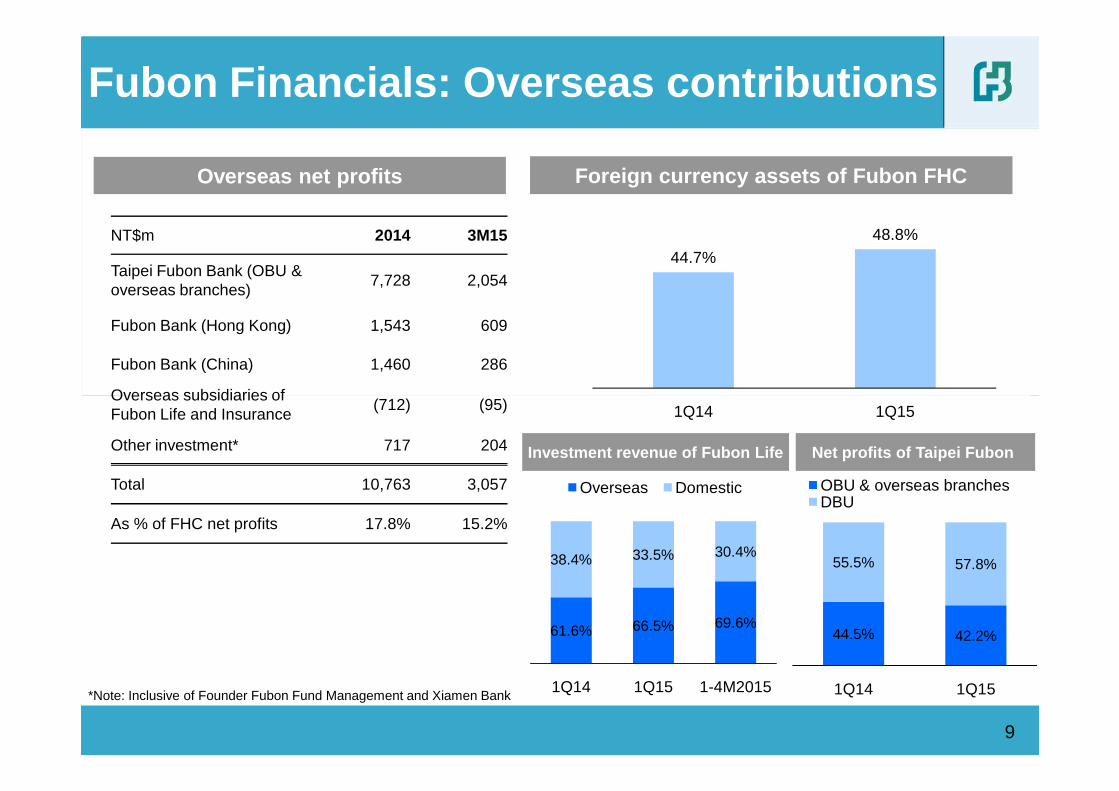

Fubon Financials: Overseas contributions

Foreign currency assets of Fubon FHC

44.7%48.8%

Overseas net profits

NT$m 2014 3M15

Taipei Fubon Bank (OBU & overseas branches)

7,728 2,054

Fubon Bank (Hong Kong) 1,543 609

Fubon Bank (China) 1,460 286

Overseas subsidiaries of

9

Investment revenue of Fubon Life

1Q14 1Q15

*Note: Inclusive of Founder Fubon Fund Management and Xiamen Bank

Overseas subsidiaries of Fubon Life and Insurance

(712) (95)

Other investment* 717 204

Total 10,763 3,057

As % of FHC net profits 17.8% 15.2%

Net profits of Taipei Fubon

61.6% 66.5% 69.6%

38.4% 33.5% 30.4%

1Q14 1Q15 1-4M2015

Overseas Domestic

44.5% 42.2%

55.5% 57.8%

1Q14 1Q15

OBU & overseas branchesDBU

� Performance review by subsidiary

• Fubon Life

� Performance highlights of Fubon Financial Holdings

Agenda

• Taipei Fubon Bank

10

• Fubon Life

• Fubon Securities

• Fubon Insurance

• Fubon Bank (China)

� 2014 Embedded Value of Fubon Life

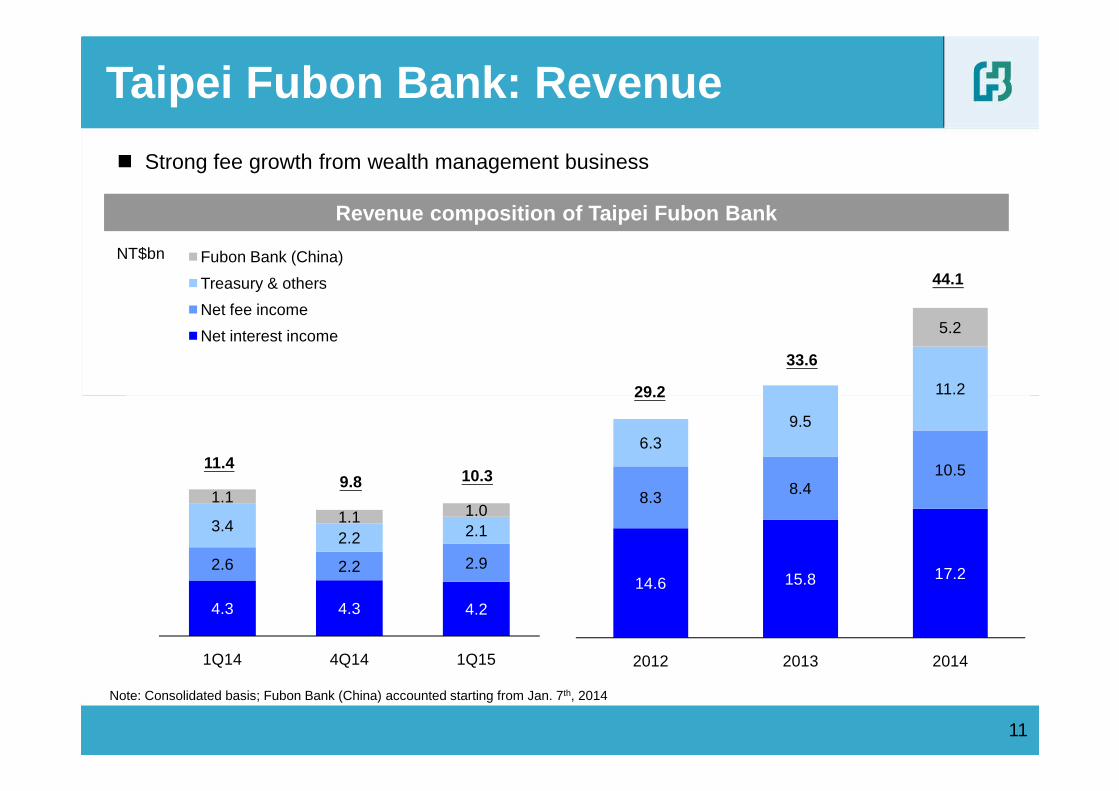

Fubon Bank (China)

Treasury & others

Net fee income

Net interest income

Taipei Fubon Bank: Revenue

Revenue composition of Taipei Fubon Bank

NT$bn

� Strong fee growth from wealth management business

29.2

33.6

44.1

11.2

5.2

4.3 4.3 4.2

2.6 2.2 2.9

3.42.2 2.1

1.11.1 1.0

1Q14 4Q14 1Q15

11

29.2

Note: Consolidated basis; Fubon Bank (China) accounted starting from Jan. 7th, 2014

10.311.4

9.8

14.6 15.8 17.2

8.3 8.410.5

6.39.5

11.2

2012 2013 2014

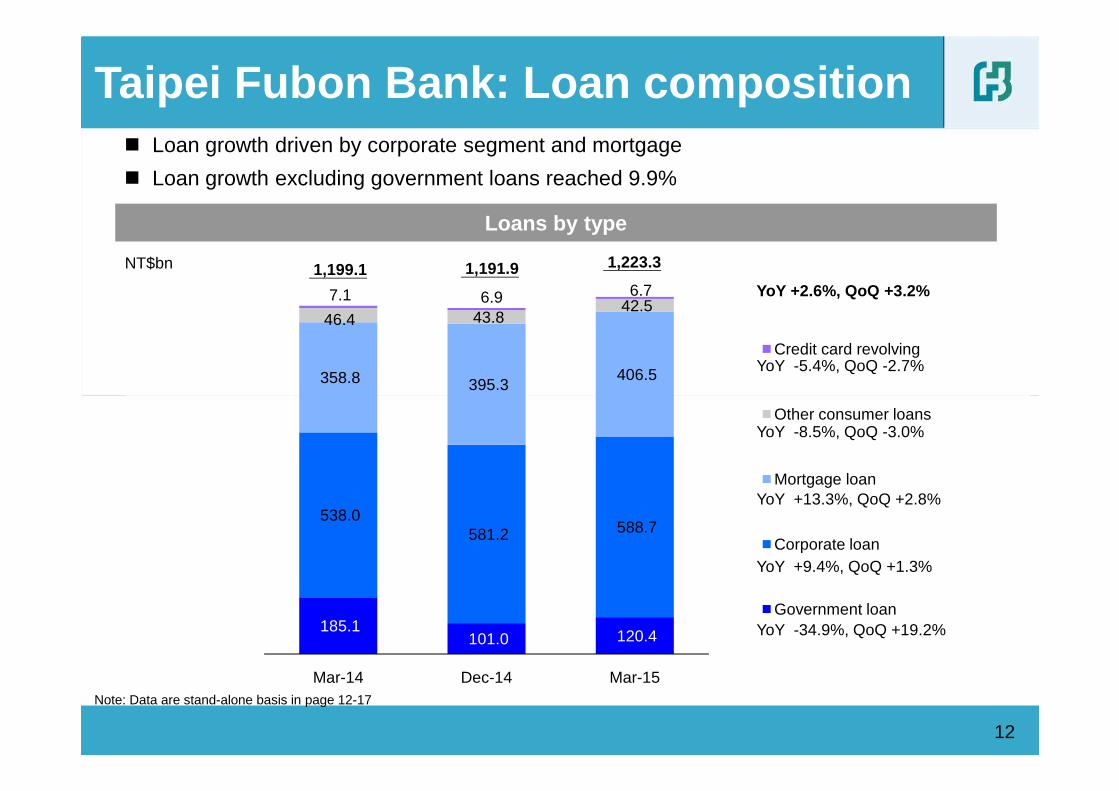

358.8 395.3 406.5

46.4 43.8 42.5

7.1 6.9 6.7

Credit card revolving

Taipei Fubon Bank: Loan composition

Loans by type

NT$bn 1,199.1 1,223.3

YoY +2.6%, QoQ +3.2%

YoY -5.4%, QoQ -2.7%

� Loan growth driven by corporate segment and mortgage

� Loan growth excluding government loans reached 9.9%

1,191.9

185.1 101.0 120.4

538.0 581.2 588.7

Mar-14 Dec-14 Mar-15

Other consumer loans

Mortgage loan

Corporate loan

Government loan

12

YoY -8.5%, QoQ -3.0%

YoY +13.3%, QoQ +2.8%

YoY +9.4%, QoQ +1.3%

YoY -34.9%, QoQ +19.2%

Note: Data are stand-alone basis in page 12-17

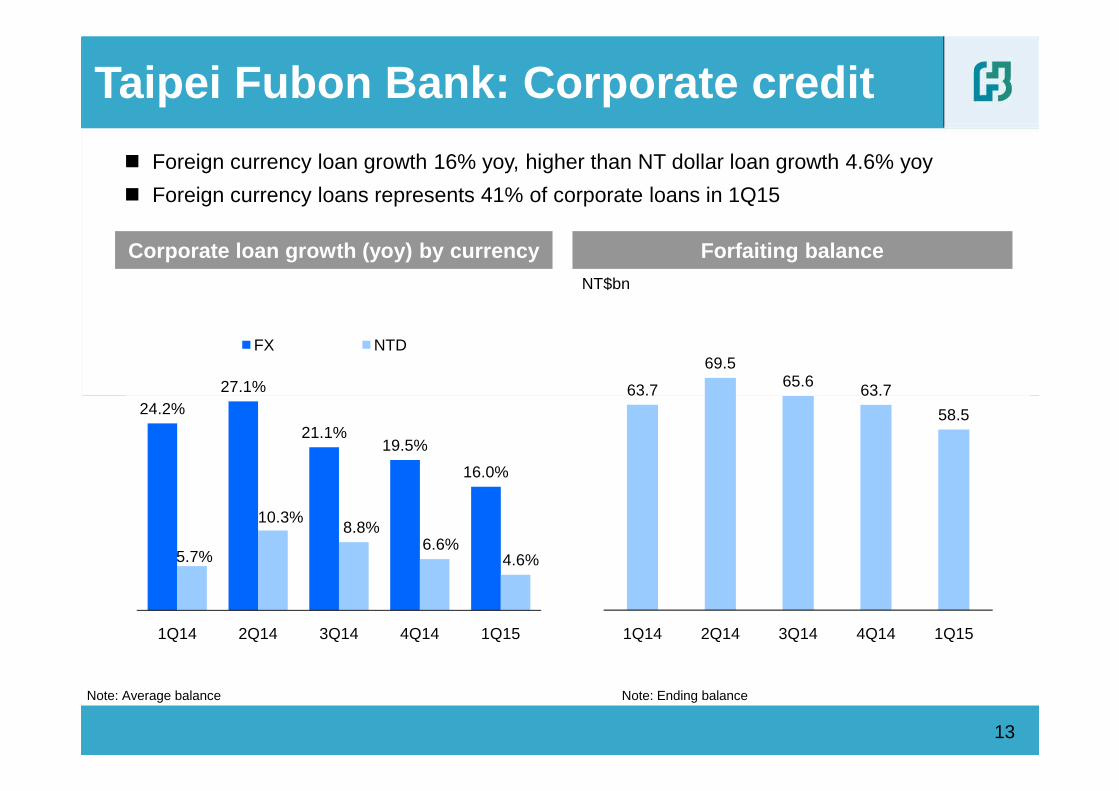

Taipei Fubon Bank: Corporate credit

Corporate loan growth (yoy) by currency Forfaiting balance

27.1%

FX NTD

63.7

69.5 65.6 63.7

NT$bn

� Foreign currency loan growth 16% yoy, higher than NT dollar loan growth 4.6% yoy

� Foreign currency loans represents 41% of corporate loans in 1Q15

13

Note: Average balance

24.2%

21.1%19.5%

16.0%

5.7%

10.3%8.8%

6.6%4.6%

1Q14 2Q14 3Q14 4Q14 1Q15

63.7 63.7

58.5

1Q14 2Q14 3Q14 4Q14 1Q15

Note: Ending balance

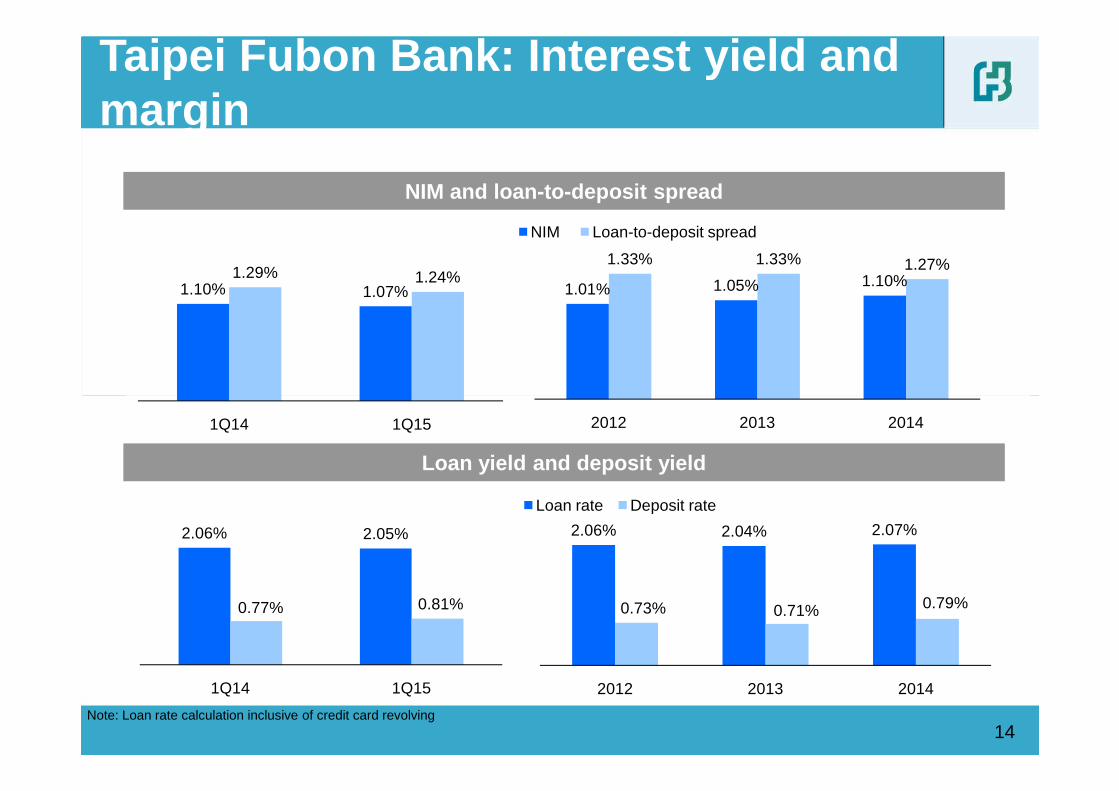

Taipei Fubon Bank: Interest yield and margin

NIM and loan-to-deposit spread

1.01% 1.05% 1.10%1.33% 1.33% 1.27%

NIM Loan-to-deposit spread

1.10% 1.07%1.29% 1.24%

14

Loan yield and deposit yield

Note: Loan rate calculation inclusive of credit card revolving

2012 2013 2014

2.06% 2.04% 2.07%

0.73% 0.71% 0.79%

2012 2013 2014

Loan rate Deposit rate

1Q14 1Q15

2.06% 2.05%

0.77% 0.81%

1Q14 1Q15

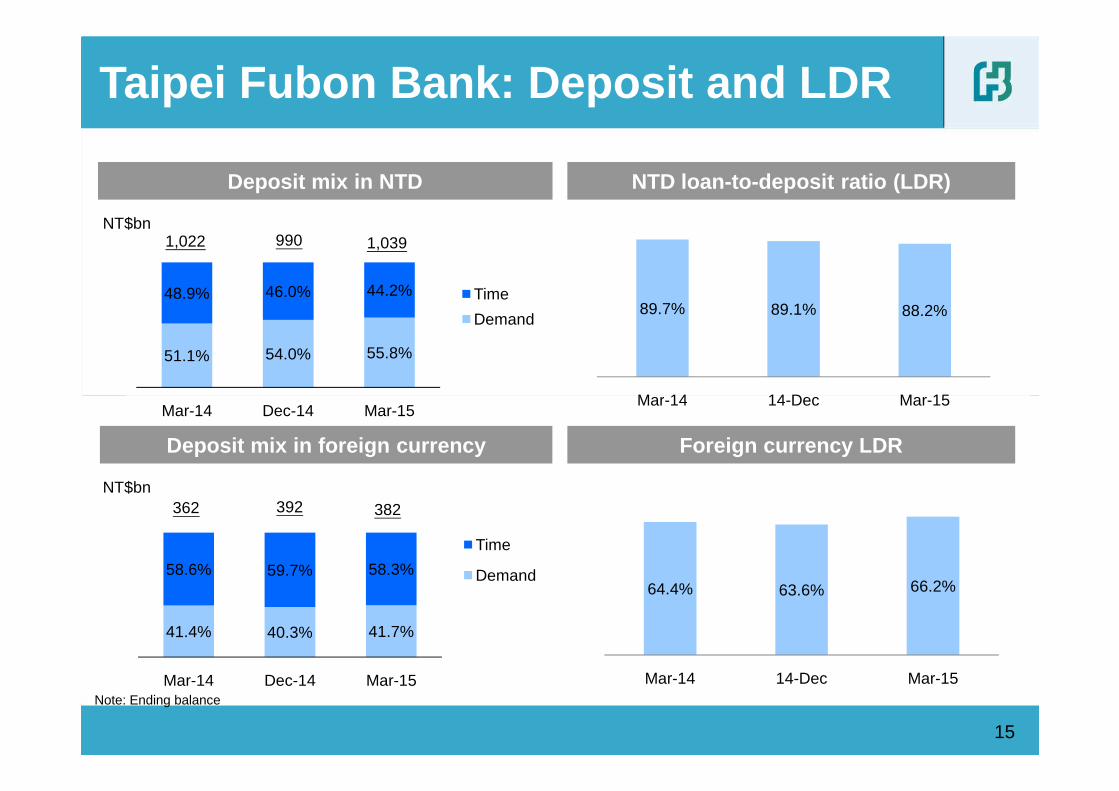

89.7% 89.1% 88.2%

Mar-14 14-Dec Mar-15

51.1% 54.0% 55.8%

48.9% 46.0% 44.2% Time

Demand

Taipei Fubon Bank: Deposit and LDR

NTD loan-to-deposit ratio (LDR)Deposit mix in NTD

NT$bn1,022 990 1,039

64.4% 63.6% 66.2%

Mar-14 14-Dec Mar-15

Mar-14 14-Dec Mar-15

41.4% 40.3% 41.7%

58.6% 59.7% 58.3%

Mar-14 Dec-14 Mar-15

Time

Demand

Mar-14 Dec-14 Mar-15

15

Deposit mix in foreign currency

NT$bn

Note: Ending balance

Foreign currency LDR

362 392 382

379

DCI,SI,SN and others

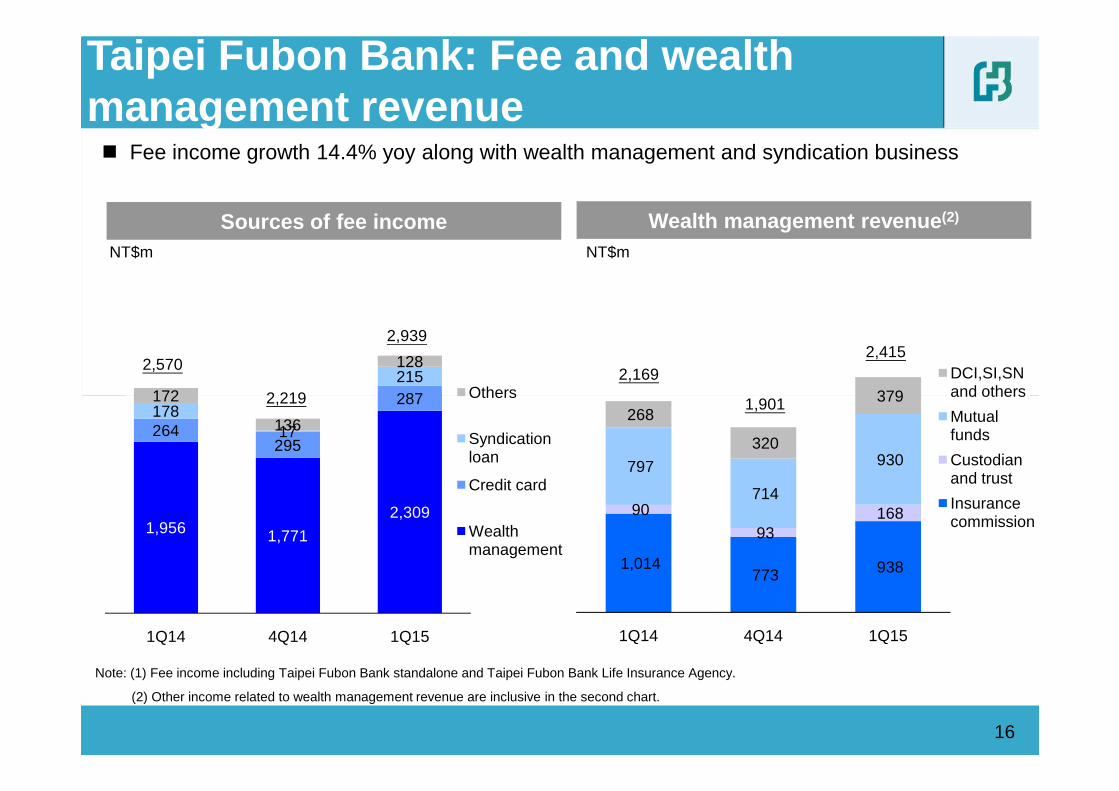

Taipei Fubon Bank: Fee and wealth management revenue

Sources of fee income Wealth management revenue (2)

NT$m NT$m

� Fee income growth 14.4% yoy along with wealth management and syndication business

2,570

2,939

2,1692,415

2,219 1,901287 215

172

128

Others

1,014 773 938

90

93 168

797

714

930

268

320

379

1Q14 4Q14 1Q15

and others

Mutual funds

Custodian and trust

Insurance commission

16

Note: (1) Fee income including Taipei Fubon Bank standalone and Taipei Fubon Bank Life Insurance Agency.

(2) Other income related to wealth management revenue are inclusive in the second chart.

2,219 1,901

1,956 1,771

2,309

264 295

287 178

17

172

136

1Q14 4Q14 1Q15

Others

Syndication loan

Credit card

Wealth management

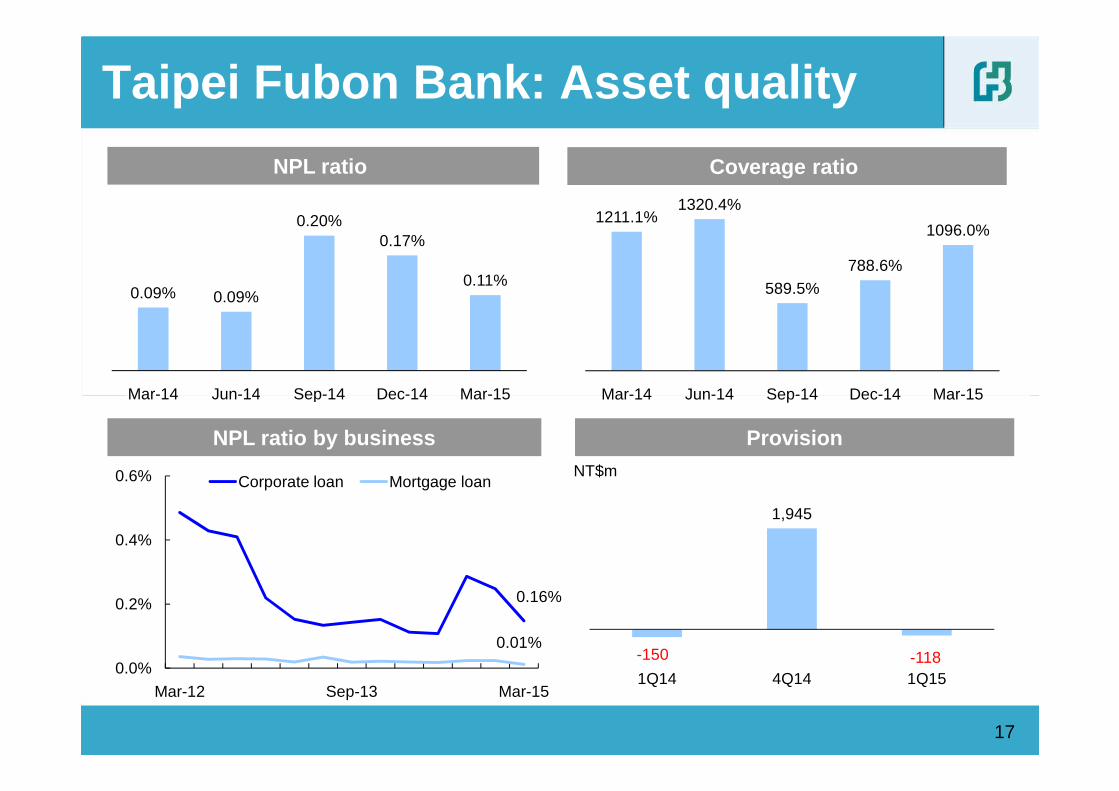

Taipei Fubon Bank: Asset quality

NPL ratio Coverage ratio

1211.1%1320.4%

589.5%788.6%

1096.0%

Mar-14 Jun-14 Sep-14 Dec-14 Mar-15

0.09% 0.09%

0.20%0.17%

0.11%

Mar-14 Jun-14 Sep-14 Dec-14 Mar-15

0.0%

0.2%

0.4%

0.6%

Mar-12 Sep-13 Mar-15

Corporate loan Mortgage loan

17

NPL ratio by business Provision

0.16%

0.01%

NT$m

Mar-14 Jun-14 Sep-14 Dec-14 Mar-15Mar-14 Jun-14 Sep-14 Dec-14 Mar-15

-150

1,945

-1181Q14 4Q14 1Q15

� Performance review by subsidiary

• Fubon Life

� Performance highlights of Fubon Financial Holdings

Agenda

• Taipei Fubon Bank

18

• Fubon Life

• Fubon Securities

• Fubon Insurance

• Fubon Bank (China)

� 2014 Embedded Value of Fubon Life

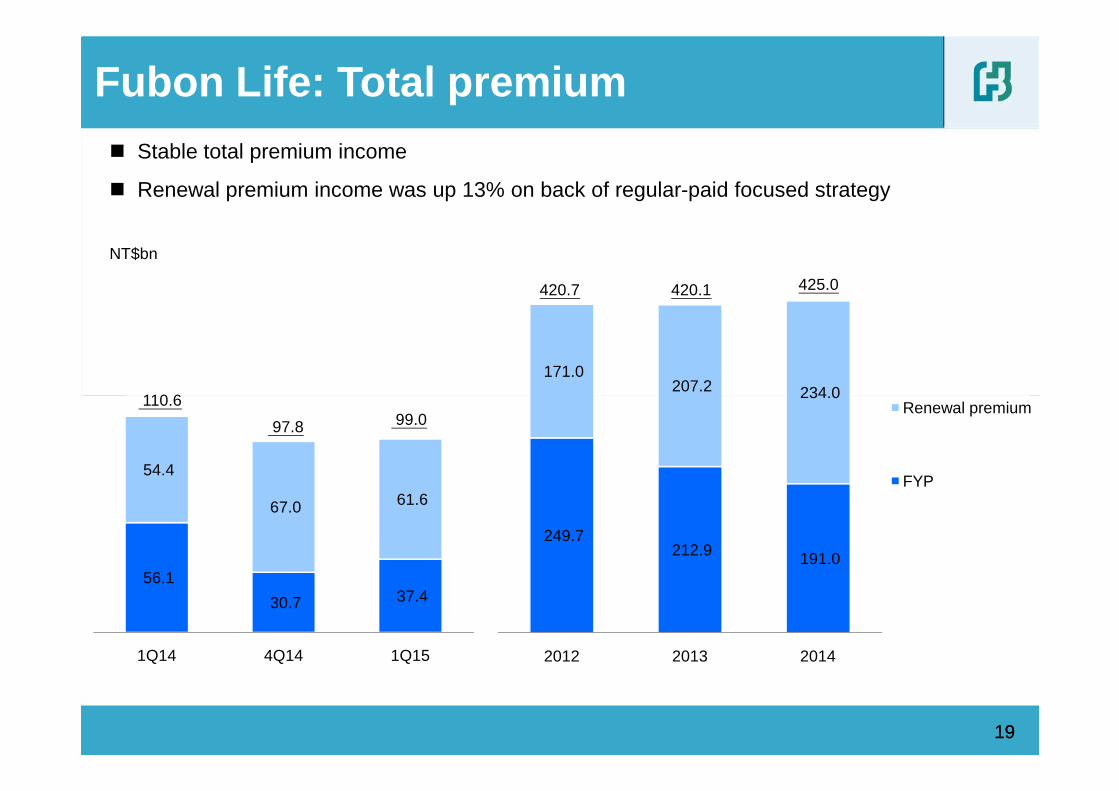

171.0 207.2 234.0

420.7

NT$bn

420.1 425.0

� Stable total premium income

� Renewal premium income was up 13% on back of regular-paid focused strategy

Fubon Life: Total premium

110.6

56.1

30.7 37.4

54.4

67.0 61.6

1Q14 4Q14 1Q15

249.7 212.9 191.0

234.0

2012 2013 2014

Renewal premium

FYP

1919

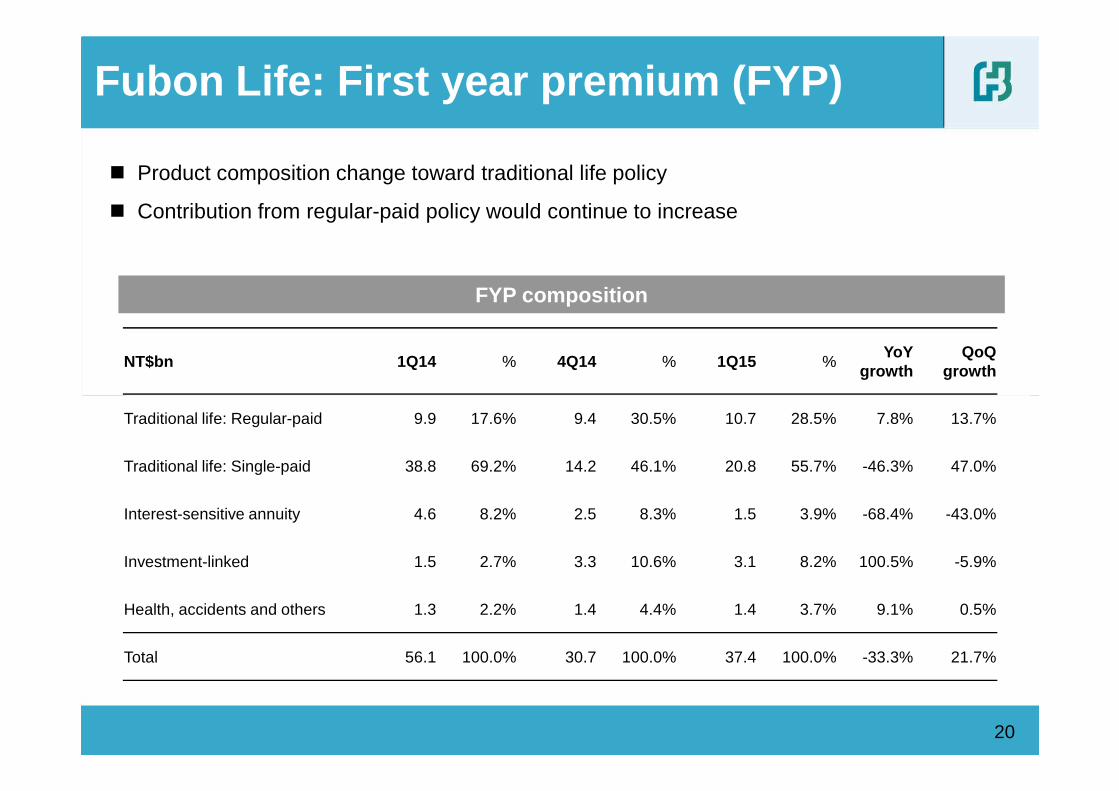

110.6 99.0 97.8

FYP composition

Fubon Life: First year premium (FYP)

� Product composition change toward traditional life policy

� Contribution from regular-paid policy would continue to increase

NT$bn 1Q14 % 4Q14 % 1Q15 %YoY

growthQoQ

growth

20

Traditional life: Regular-paid 9.9 17.6% 9.4 30.5% 10.7 28.5% 7.8% 13.7%

Traditional life: Single-paid 38.8 69.2% 14.2 46.1% 20.8 55.7% -46.3% 47.0%

Interest-sensitive annuity 4.6 8.2% 2.5 8.3% 1.5 3.9% -68.4% -43.0%

Investment-linked 1.5 2.7% 3.3 10.6% 3.1 8.2% 100.5% -5.9%

Health, accidents and others 1.3 2.2% 1.4 4.4% 1.4 3.7% 9.1% 0.5%

Total 56.1 100.0% 30.7 100.0% 37.4 100.0% -33.3% 21.7%

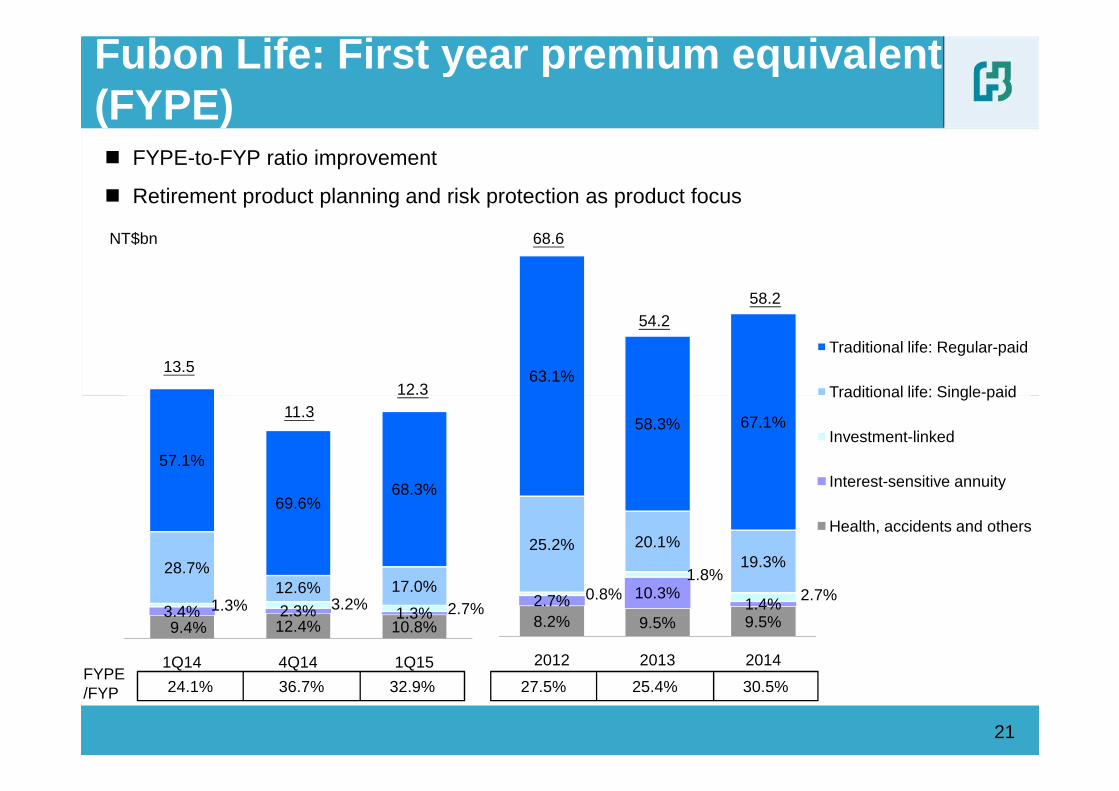

� FYPE-to-FYP ratio improvement

� Retirement product planning and risk protection as product focus

63.1%

Traditional life: Regular-paid

Traditional life: Single-paid

54.2

68.6NT$bn

Fubon Life: First year premium equivalent (FYPE)

58.2

12.313.5

9.4% 12.4% 10.8%3.4% 2.3% 1.3% 1.3% 3.2% 2.7%

28.7%12.6% 17.0%

57.1%

69.6%68.3%

1Q14 4Q14 1Q15

8.2% 9.5% 9.5%2.7% 10.3%

1.4% 0.8%

1.8%2.7%

25.2% 20.1%19.3%

58.3% 67.1%

2012 2013 2014

Traditional life: Single-paid

Investment-linked

Interest-sensitive annuity

Health, accidents and others

21

12.311.3

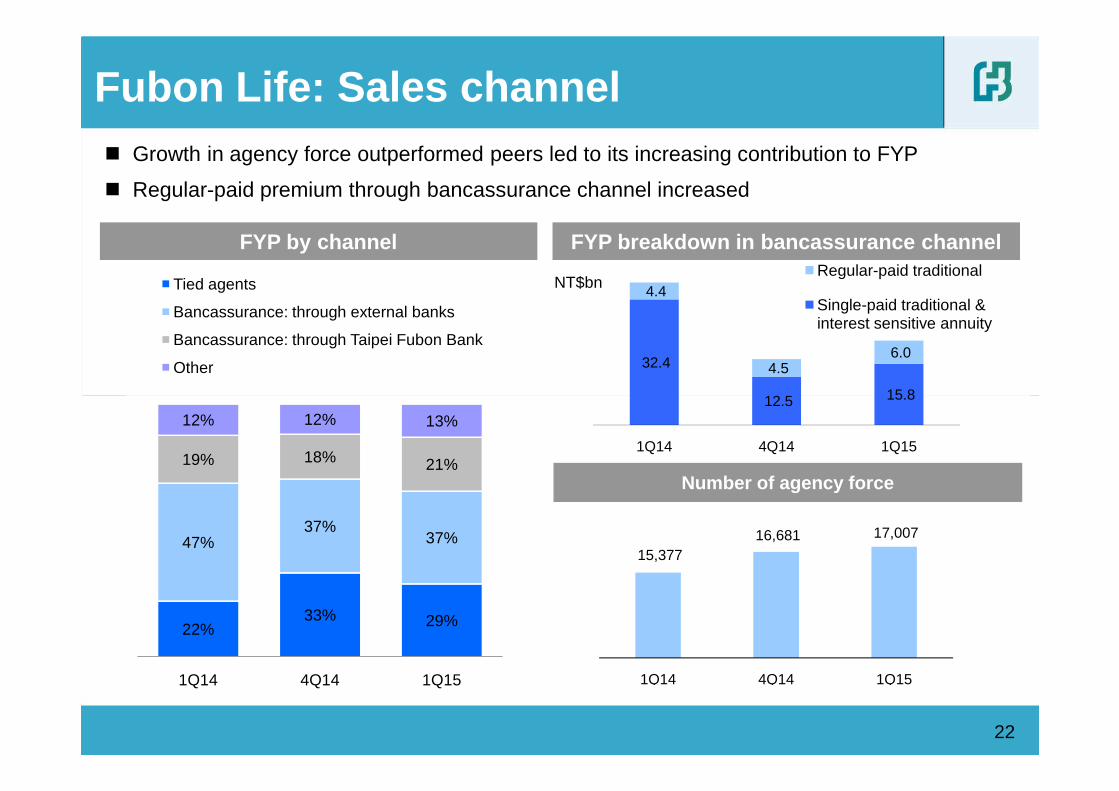

24.1% 36.7% 32.9%FYPE/FYP 27.5% 25.4% 30.5%

Tied agents

Bancassurance: through external banks

Bancassurance: through Taipei Fubon Bank

Other

FYP by channel

Fubon Life: Sales channel� Growth in agency force outperformed peers led to its increasing contribution to FYP

� Regular-paid premium through bancassurance channel increased

FYP breakdown in bancassurance channel

NT$bn

32.4

12.5 15.8

4.4

4.5 6.0

Regular-paid traditional

Single-paid traditional & interest sensitive annuity

22%33% 29%

47%37%

37%

19% 18% 21%

12% 12% 13%

1Q14 4Q14 1Q15

22

Number of agency force

15,377 16,681 17,007

1Q14 4Q14 1Q15

12.5 15.8

1Q14 4Q14 1Q15

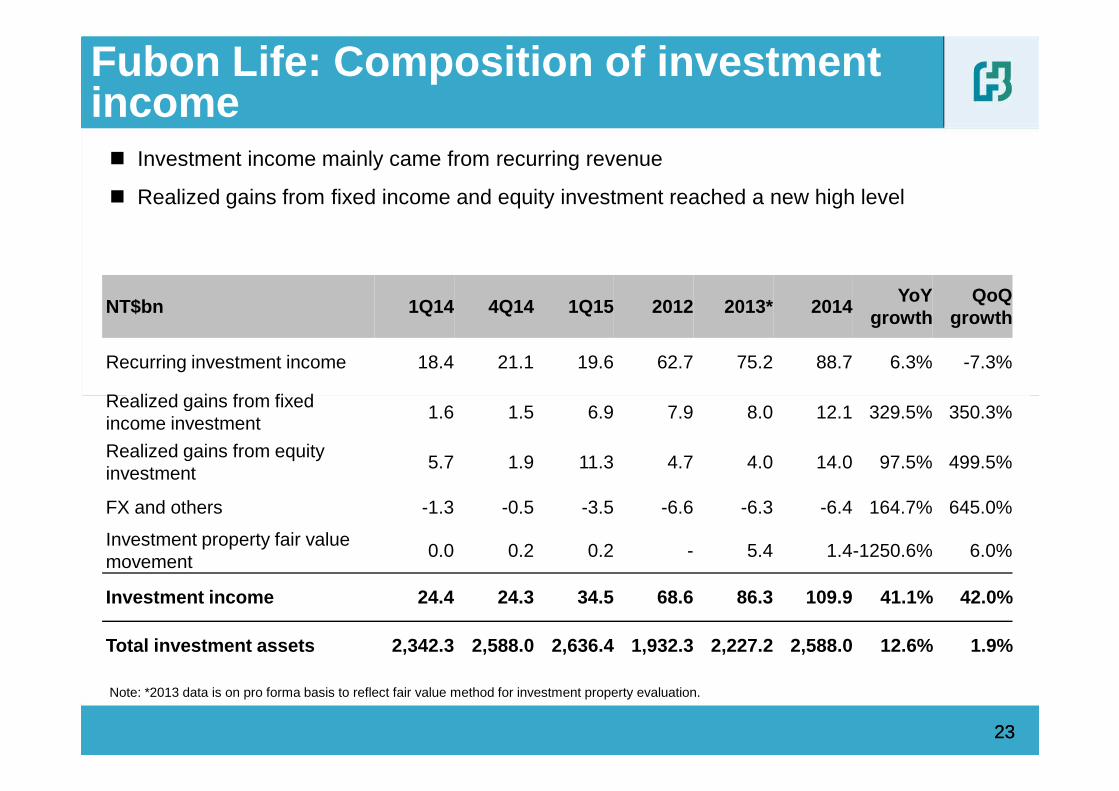

� Investment income mainly came from recurring revenue

� Realized gains from fixed income and equity investment reached a new high level

Fubon Life: Composition of investment income

NT$bn 1Q14 4Q14 1Q15 2012 2013* 2014YoY

growthQoQ

growth

Recurring investment income 18.4 21.1 19.6 62.7 75.2 88.7 6.3% -7.3%

Realized gains from fixed

2323

Note: *2013 data is on pro forma basis to reflect fair value method for investment property evaluation.

Realized gains from fixed income investment

1.6 1.5 6.9 7.9 8.0 12.1 329.5% 350.3%

Realized gains from equity investment

5.7 1.9 11.3 4.7 4.0 14.0 97.5% 499.5%

FX and others -1.3 -0.5 -3.5 -6.6 -6.3 -6.4 164.7% 645.0%

Investment property fair value movement

0.0 0.2 0.2 - 5.4 1.4-1250.6% 6.0%

Investment income 24.4 24.3 34.5 68.6 86.3 109.9 41.1% 42.0 %

Total investment assets 2,342.3 2,588.0 2,636.4 1,932.3 2,227.2 2,588.0 12.6% 1.9%

Overseas Domestic

Overseas investment income

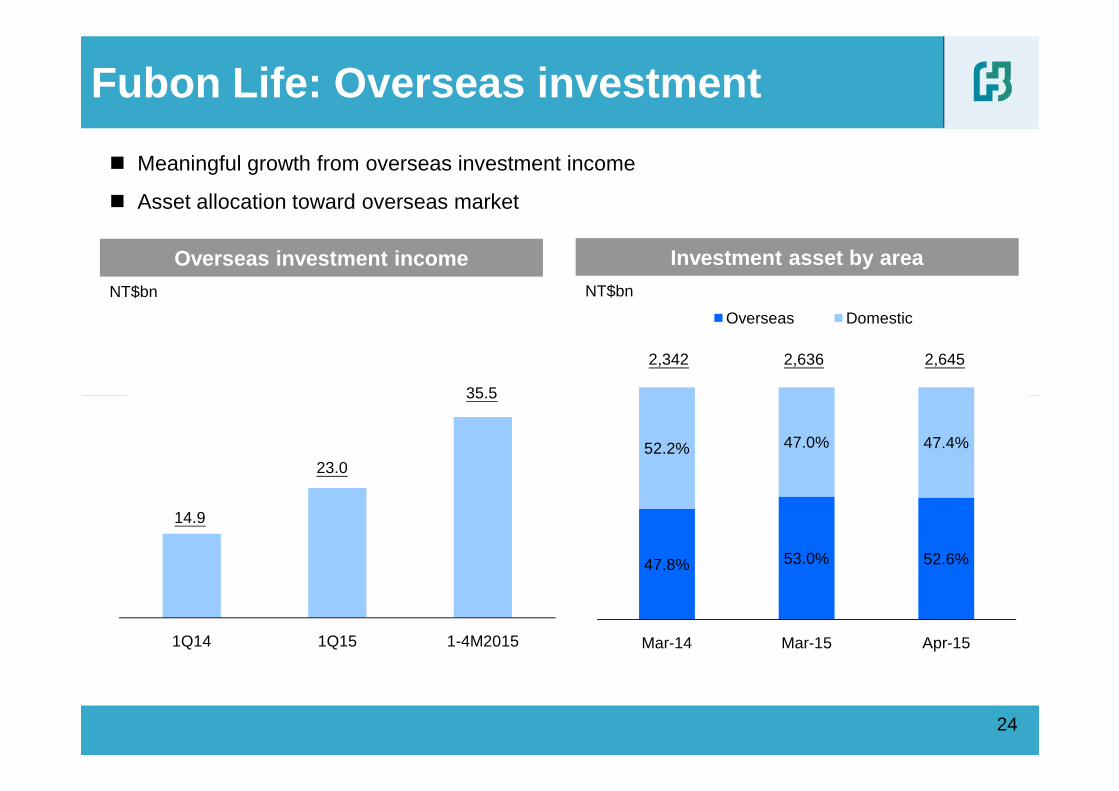

Fubon Life: Overseas investment

Investment asset by area

NT$bn NT$bn

35.5

2,342 2,636 2,645

� Meaningful growth from overseas investment income

� Asset allocation toward overseas market

47.8% 53.0% 52.6%

52.2% 47.0% 47.4%

Mar-14 Mar-15 Apr-151Q14 1Q15 1-4M2015

24

14.9

23.0

35.5

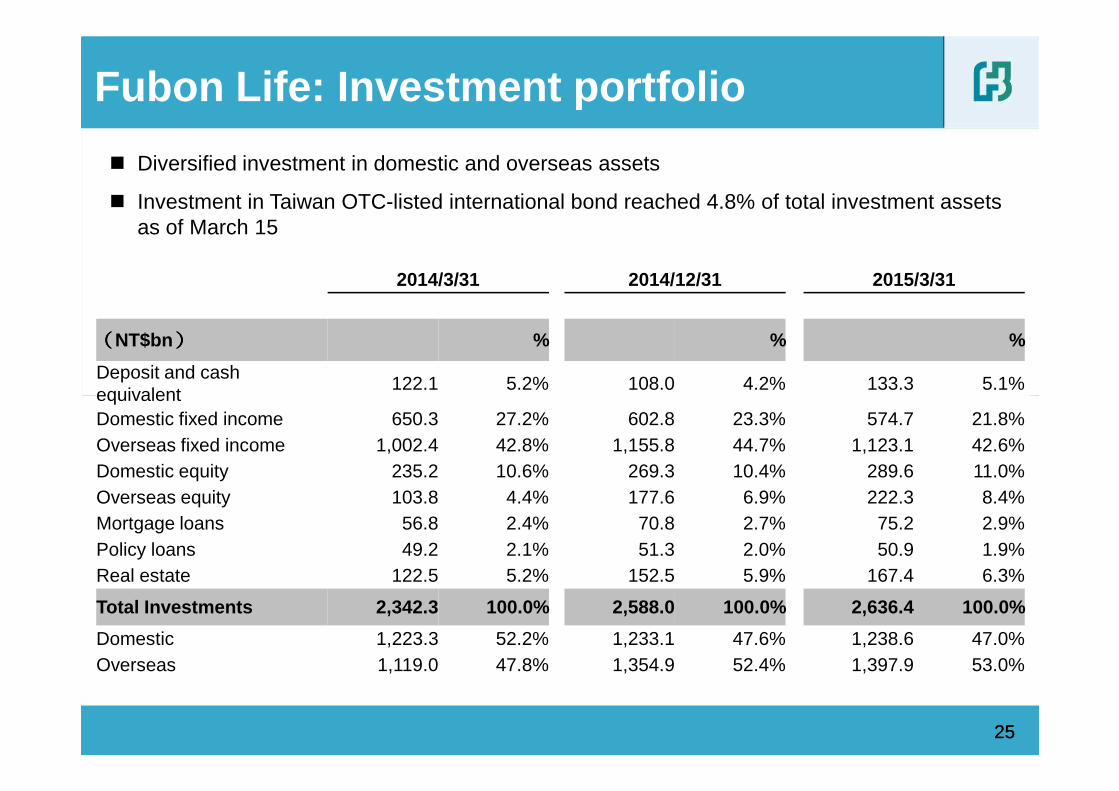

� Diversified investment in domestic and overseas assets

� Investment in Taiwan OTC-listed international bond reached 4.8% of total investment assets as of March 15

Fubon Life: Investment portfolio

2014/3/31 2014/12/31 2015/3/31

((((NT$bn)))) % % %

Deposit and cash equivalent

122.1 5.2% 108.0 4.2% 133.3 5.1%

2525

equivalentDomestic fixed income 650.3 27.2% 602.8 23.3% 574.7 21.8%Overseas fixed income 1,002.4 42.8% 1,155.8 44.7% 1,123.1 42.6%Domestic equity 235.2 10.6% 269.3 10.4% 289.6 11.0%Overseas equity 103.8 4.4% 177.6 6.9% 222.3 8.4%Mortgage loans 56.8 2.4% 70.8 2.7% 75.2 2.9%Policy loans 49.2 2.1% 51.3 2.0% 50.9 1.9%Real estate 122.5 5.2% 152.5 5.9% 167.4 6.3%

Total Investments 2,342.3 100.0% 2,588.0 100.0% 2,636. 4 100.0%

Domestic 1,223.3 52.2% 1,233.1 47.6% 1,238.6 47.0%Overseas 1,119.0 47.8% 1,354.9 52.4% 1,397.9 53.0%

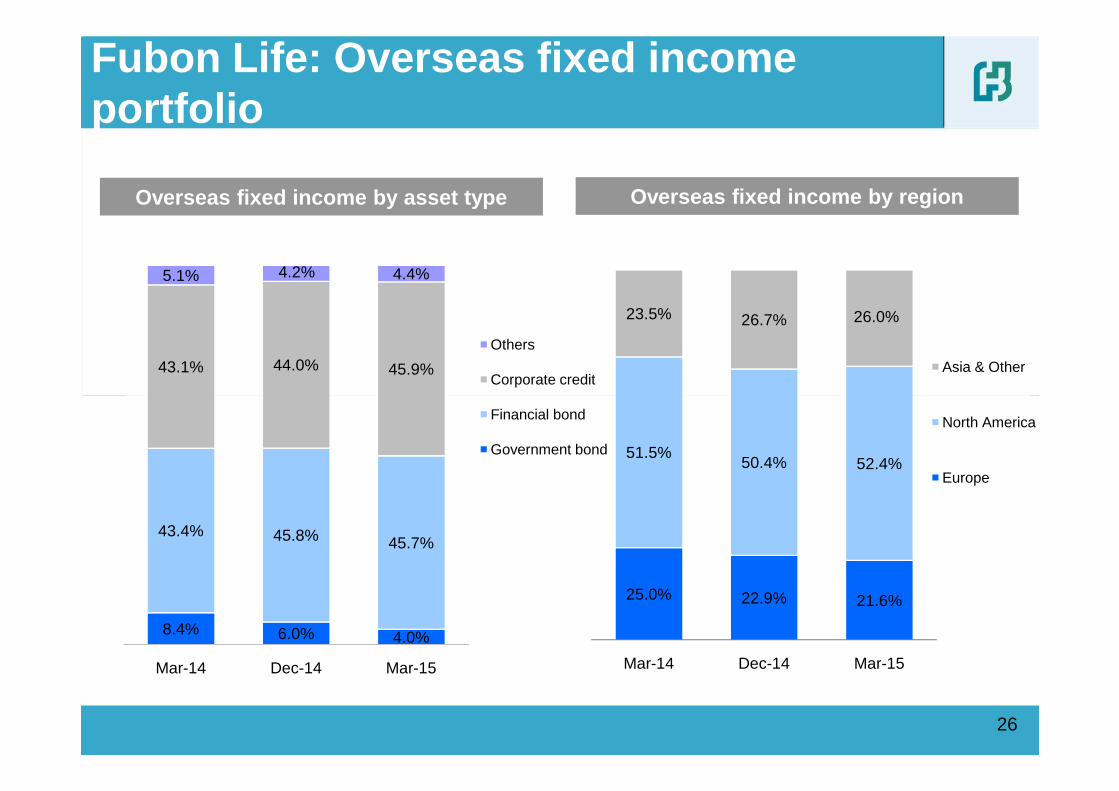

Overseas fixed income by asset type

Fubon Life: Overseas fixed income portfolio

Overseas fixed income by region

23.5% 26.7% 26.0%

Asia & Other43.1% 44.0% 45.9%

5.1% 4.2% 4.4%

Others

Corporate credit

26

25.0% 22.9% 21.6%

51.5%50.4% 52.4%

Mar-14 Dec-14 Mar-15

North America

Europe

8.4% 6.0% 4.0%

43.4% 45.8% 45.7%

Mar-14 Dec-14 Mar-15

Financial bond

Government bond

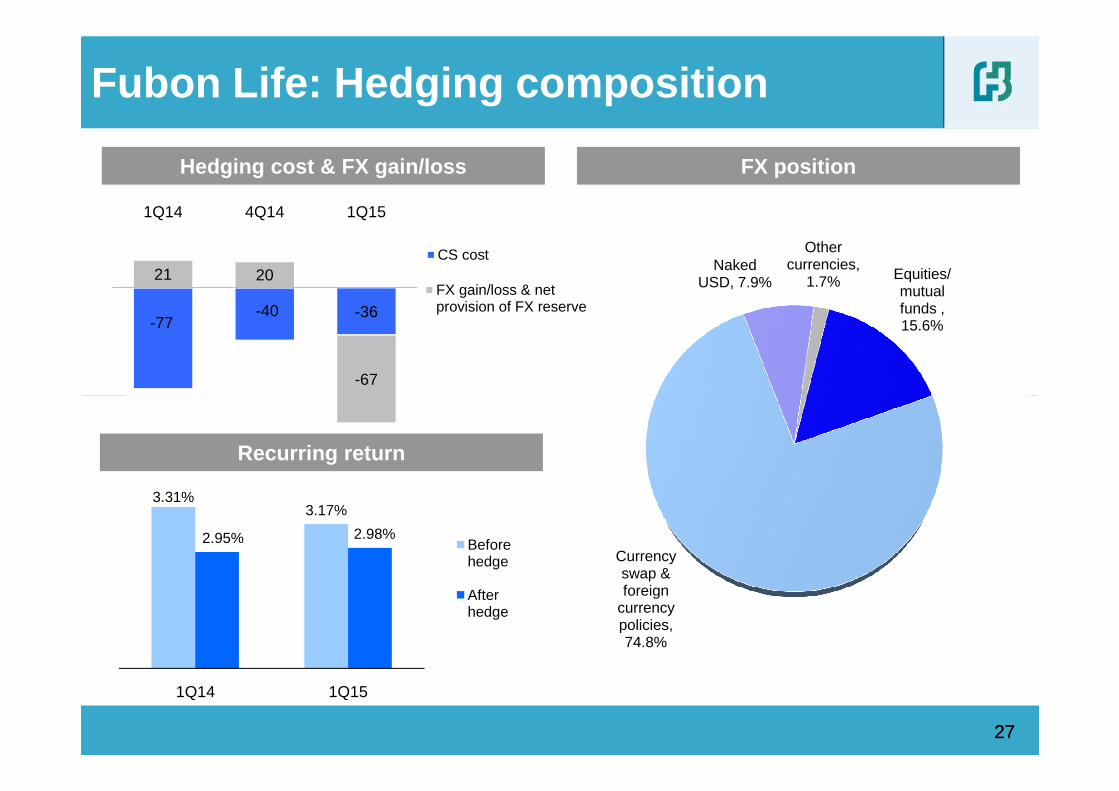

Hedging cost & FX gain/loss FX position

Fubon Life: Hedging composition

CS cost

FX gain/loss & netprovision of FX reserve

Naked USD, 7.9%

Other currencies,

1.7% Equities/ mutual funds , 15.6%-77

-40 -36

21 20

-67

1Q14 4Q14 1Q15

2727

Recurring return

Currency swap & foreign

currency policies, 74.8%

3.31%3.17%

2.95% 2.98%

1Q14 1Q15

Before hedge

After hedge

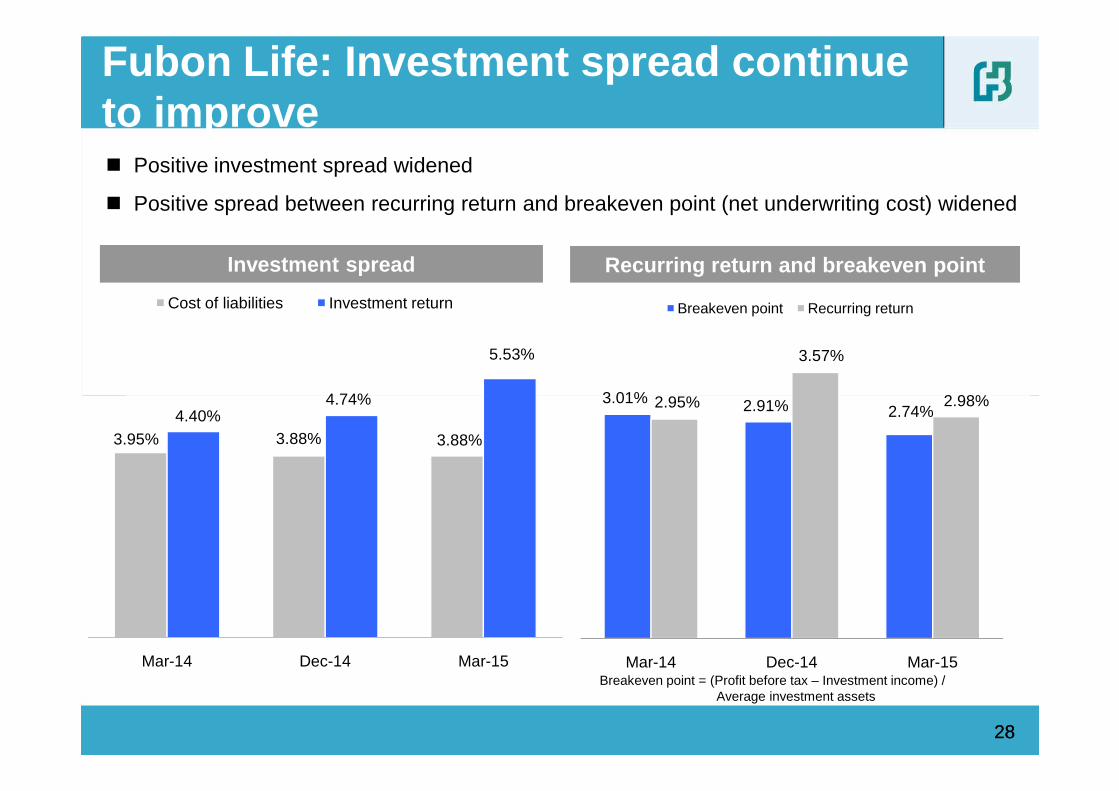

Fubon Life: Investment spread continue to improve� Positive investment spread widened

� Positive spread between recurring return and breakeven point (net underwriting cost) widened

Investment spread Recurring return and breakeven point

3.01% 2.95%

3.57%

2.98%

Breakeven point Recurring return

4.74%

5.53%

Cost of liabilities Investment return

2828

Breakeven point = (Profit before tax – Investment income) / Average investment assets

3.01% 2.91% 2.74%2.95% 2.98%

Mar-14 Dec-14 Mar-15

3.95% 3.88% 3.88%

4.40%4.74%

Mar-14 Dec-14 Mar-15

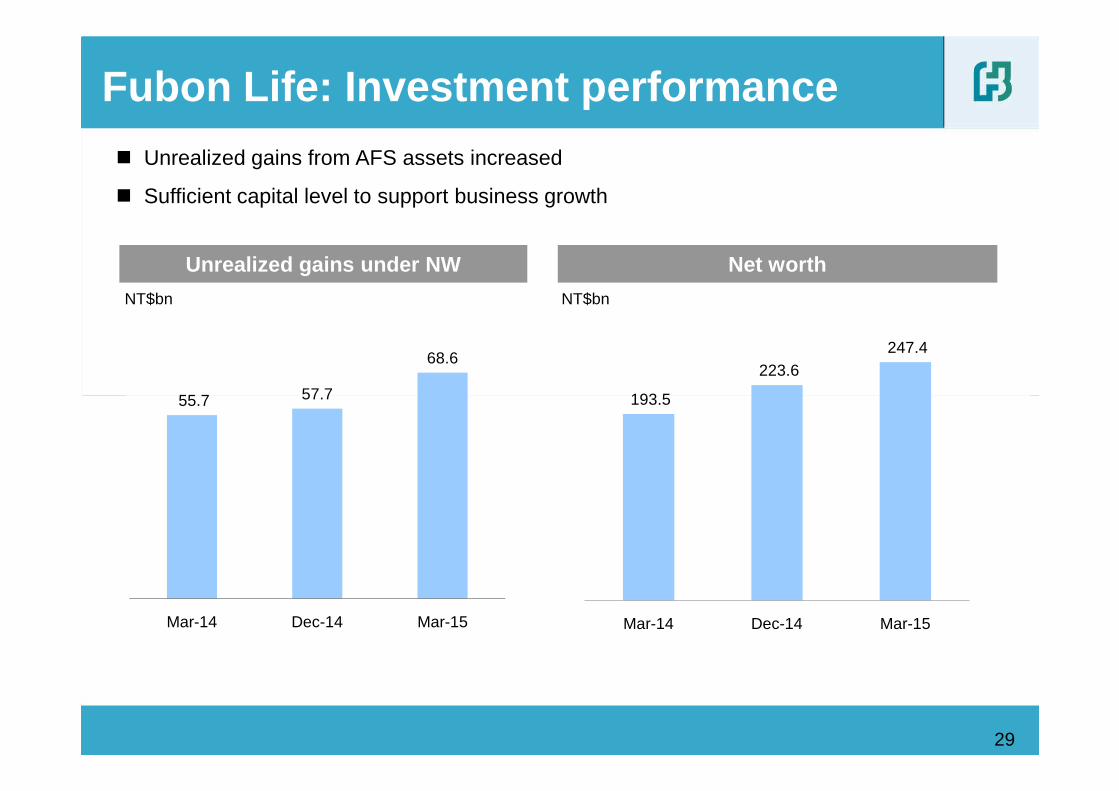

Net worthUnrealized gains under NW

NT$bn

� Unrealized gains from AFS assets increased

� Sufficient capital level to support business growth

Fubon Life: Investment performance

55.7 57.7

68.6

NT$bn

193.5

223.6 247.4

29

55.7 57.7

Mar-14 Dec-14 Mar-15

193.5

Mar-14 Dec-14 Mar-15

� Performance review by subsidiary

• Fubon Life

� Performance highlights of Fubon Financial Holdings

Agenda

• Taipei Fubon Bank

30

• Fubon Life

• Fubon Securities

• Fubon Insurance

• Fubon Bank (China)

� 2014 Embedded Value of Fubon Life

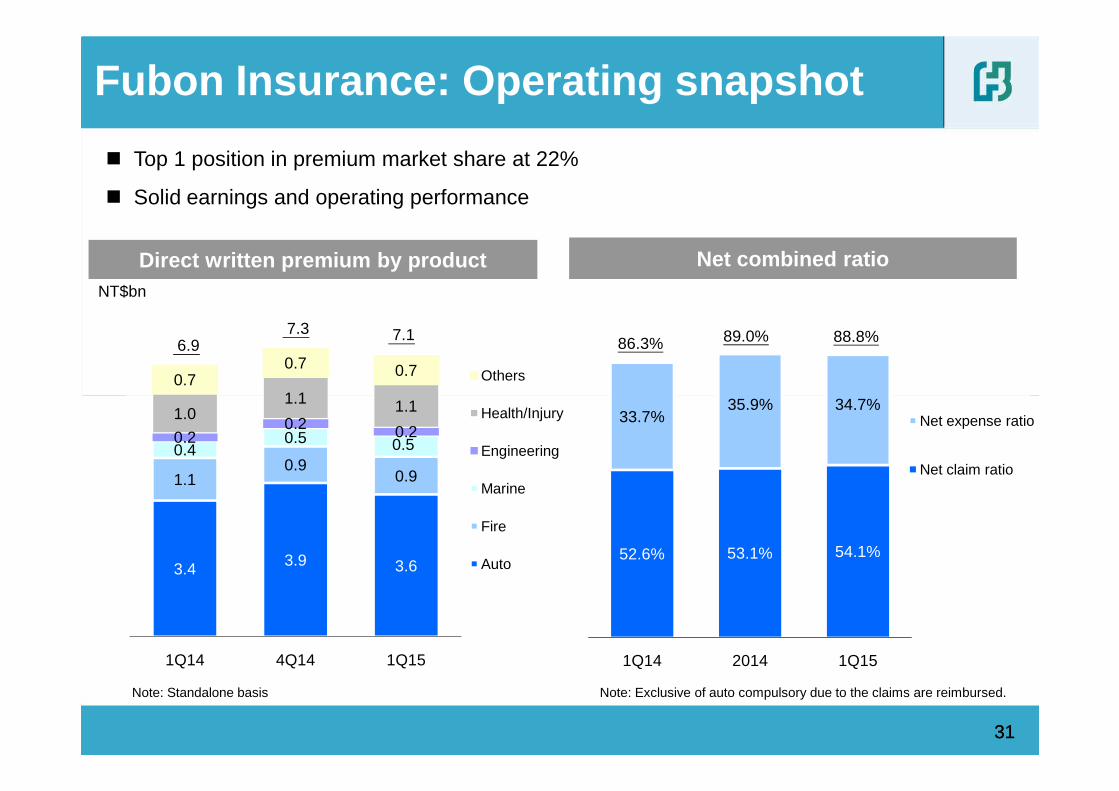

35.9% 34.7%1.10.7

0.7 0.7 Others

Net combined ratioNT$bn

� Top 1 position in premium market share at 22%

� Solid earnings and operating performance

Fubon Insurance: Operating snapshot

Direct written premium by product

86.3%6.9 7.1 7.3 89.0% 88.8%

52.6% 53.1% 54.1%

33.7%35.9% 34.7%

1Q14 2014 1Q15

Net expense ratio

Net claim ratio

3.4 3.9 3.6

1.10.9

0.9

0.40.5 0.50.20.2 0.2

1.01.1 1.1

1Q14 4Q14 1Q15

Health/Injury

Engineering

Marine

Fire

Auto

3131

Note: Standalone basis Note: Exclusive of auto compulsory due to the claims are reimbursed.

� Performance review by subsidiary

• Fubon Life

� Performance highlights of Fubon Financial Holdings

Agenda

• Taipei Fubon Bank

32

• Fubon Life

• Fubon Securities

• Fubon Insurance

• Fubon Bank (China)

� 2014 Embedded Value of Fubon Life

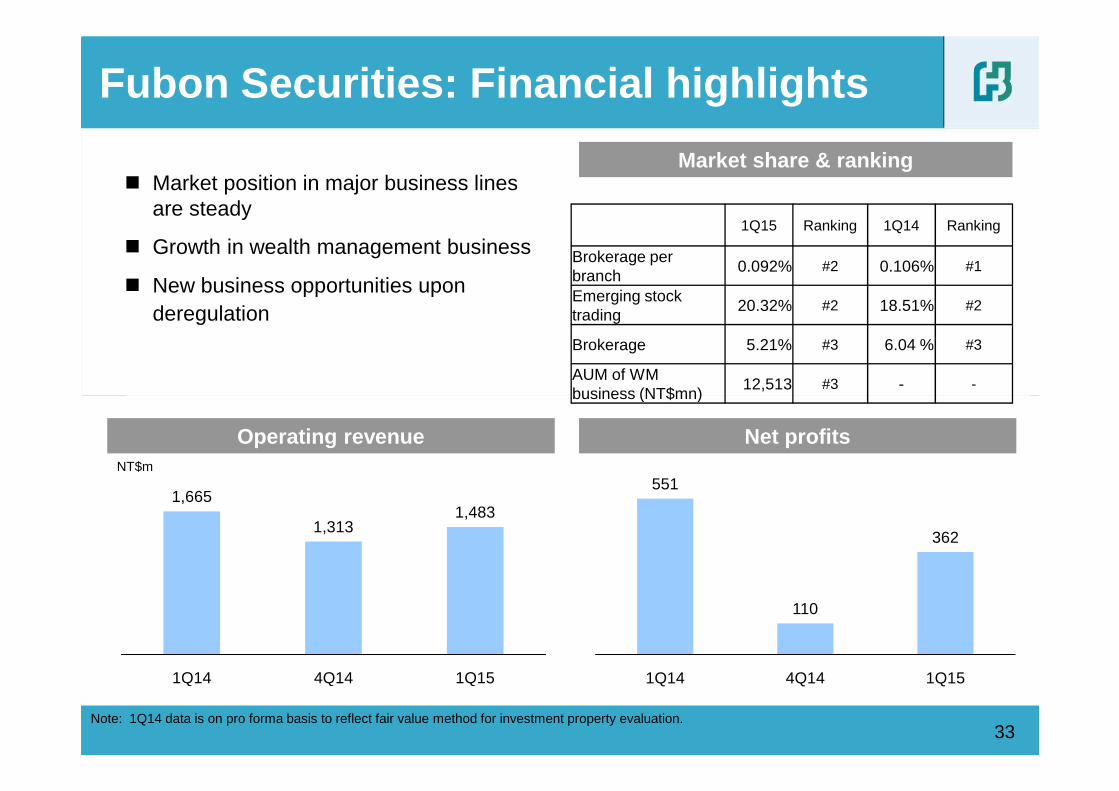

Fubon Securities: Financial highlights

Market share & ranking� Market position in major business lines

are steady

� Growth in wealth management business

� New business opportunities upon deregulation

1Q15 Ranking 1Q14 Ranking

Brokerage per branch

0.092% #2 0.106% #1

Emerging stock trading

20.32% #2 18.51% #2

Brokerage 5.21% #3 6.04 % #3

AUM of WM business (NT$mn)

12,513 #3 - -

33

Operating revenueNT$m

Net profits

business (NT$mn)

Note: 1Q14 data is on pro forma basis to reflect fair value method for investment property evaluation.

1,665

1,3131,483

1Q14 4Q14 1Q15

551

110

362

1Q14 4Q14 1Q15

� Performance review by subsidiary

• Fubon Life

� Performance highlights of Fubon Financial Holdings

Agenda

• Taipei Fubon Bank

34

• Fubon Life

• Fubon Securities

• Fubon Insurance

• Fubon Bank (China)

� 2014 Embedded Value of Fubon Life

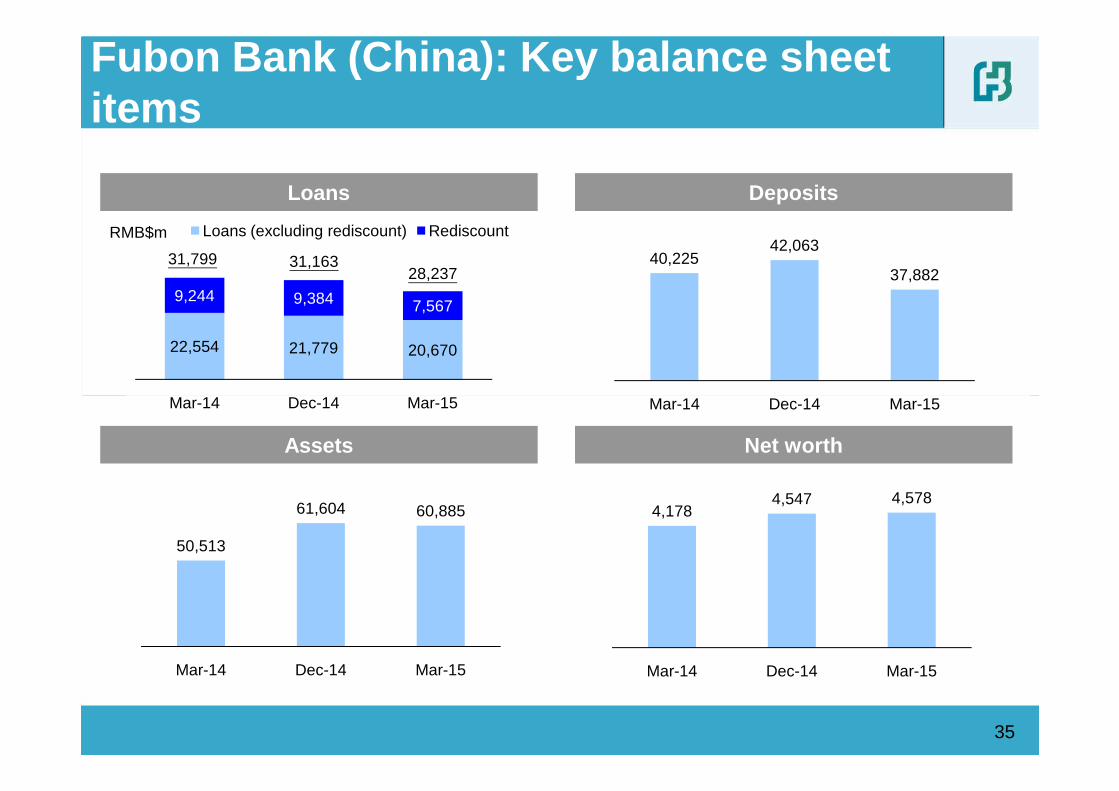

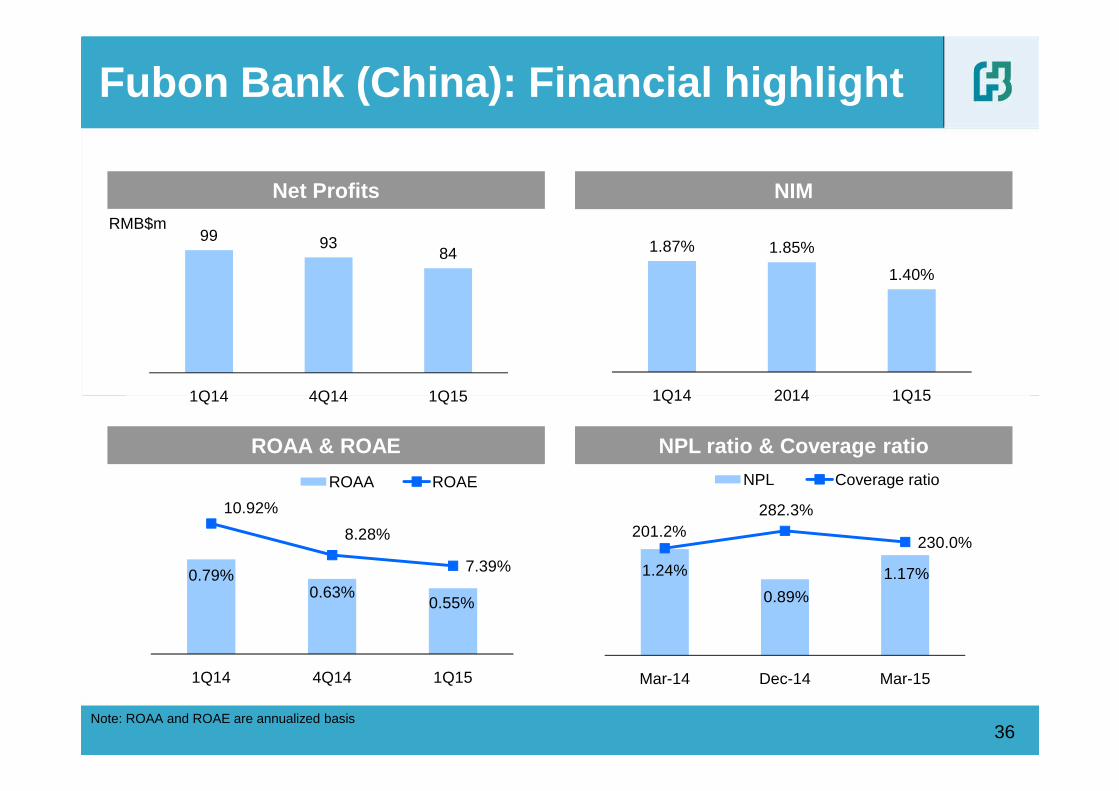

22,554 21,779 20,670

9,244 9,384 7,567

Mar-14 Dec-14 Mar-15

Loans (excluding rediscount) Rediscount

Fubon Bank (China): Key balance sheet items

DepositsLoans

RMB$m

40,22542,063

37,882

Mar-14 Dec-14 Mar-15

31,799 31,16328,237

Mar-14 Dec-14 Mar-15

35

Assets Net worth

4,1784,547 4,578

Mar-14 Dec-14 Mar-15

Mar-14 Dec-14 Mar-15

50,513

61,604 60,885

Mar-14 Dec-14 Mar-15

99 9384

1Q14 4Q14 1Q15

Fubon Bank (China): Financial highlight

NIMNet ProfitsRMB$m

1.87% 1.85%

1.40%

1Q14 2014 1Q151Q14 4Q14 1Q15

36

ROAA & ROAE NPL ratio & Coverage ratio

1Q14 2014 1Q15

Note: ROAA and ROAE are annualized basis

0.79%0.63%

0.55%

10.92%

8.28%

7.39%

1Q14 4Q14 1Q15

ROAA ROAE

1.24%

0.89%

1.17%

201.2%282.3%

230.0%

Mar-14 Dec-14 Mar-15

NPL Coverage ratio

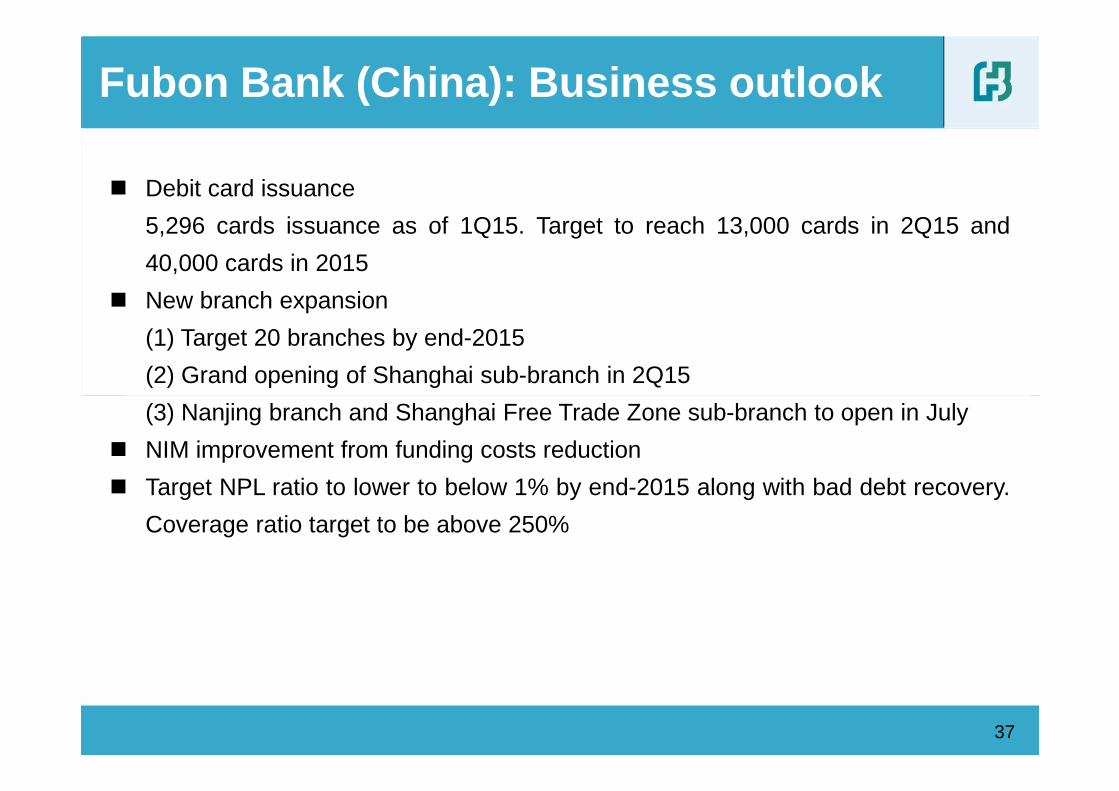

� Debit card issuance

5,296 cards issuance as of 1Q15. Target to reach 13,000 cards in 2Q15 and

40,000 cards in 2015

� New branch expansion

(1) Target 20 branches by end-2015

(2) Grand opening of Shanghai sub-branch in 2Q15

Fubon Bank (China): Business outlook

37

(3) Nanjing branch and Shanghai Free Trade Zone sub-branch to open in July

� NIM improvement from funding costs reduction

� Target NPL ratio to lower to below 1% by end-2015 along with bad debt recovery.

Coverage ratio target to be above 250%

� Performance review by subsidiary

• Fubon Life

� Performance highlights of Fubon Financial Holdings

Agenda

• Taipei Fubon Bank

38

• Fubon Life

• Fubon Securities

• Fubon Insurance

• Fubon Bank (China)

� 2014 Embedded Value of Fubon Life

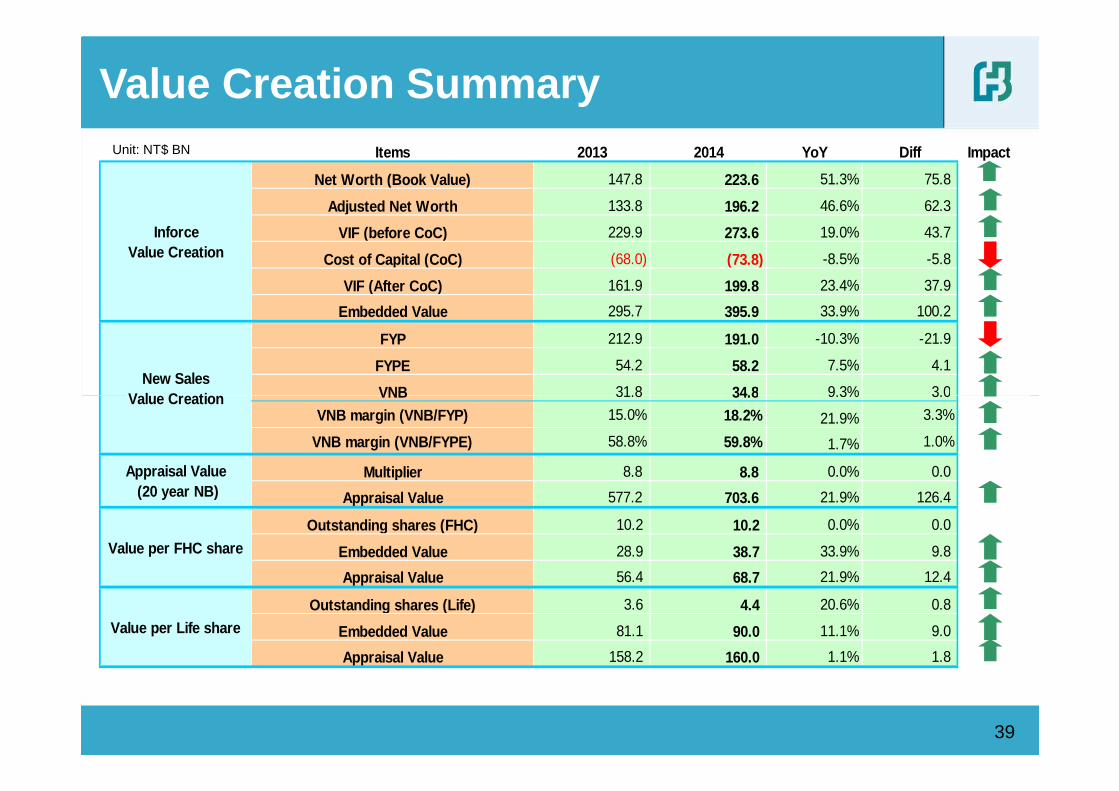

Value Creation SummaryUnit: NT$ BN Items 2013 2014 YoY Diff Impact

Net Worth (Book Value) 147.8 223.6 51.3% 75.8

Adjusted Net Worth 133.8 196.2 46.6% 62.3

VIF (before CoC) 229.9 273.6 19.0% 43.7

Cost of Capital (CoC) (68.0) (73.8) -8.5% -5.8

VIF (After CoC) 161.9 199.8 23.4% 37.9

Embedded Value 295.7 395.9 33.9% 100.2

FYP 212.9 191.0 -10.3% -21.9

FYPE 54.2 58.2 7.5% 4.1

VNB 31.8 34.8 9.3% 3.0

InforceValue Creation

New SalesValue Creation

39

VNB 31.8 34.8 9.3% 3.0

VNB margin (VNB/FYP) 15.0% 18.2% 21.9% 3.3%

VNB margin (VNB/FYPE) 58.8% 59.8% 1.7% 1.0%

Multiplier 8.8 8.8 0.0% 0.0

Appraisal Value 577.2 703.6 21.9% 126.4

Outstanding shares (FHC) 10.2 10.2 0.0% 0.0

Embedded Value 28.9 38.7 33.9% 9.8

Appraisal Value 56.4 68.7 21.9% 12.4

Outstanding shares (Life) 3.6 4.4 20.6% 0.8

Embedded Value 81.1 90.0 11.1% 9.0

Appraisal Value 158.2 160.0 1.1% 1.8

Value per FHC share

Value per Life share

Value Creation

Appraisal Value (20 year NB)

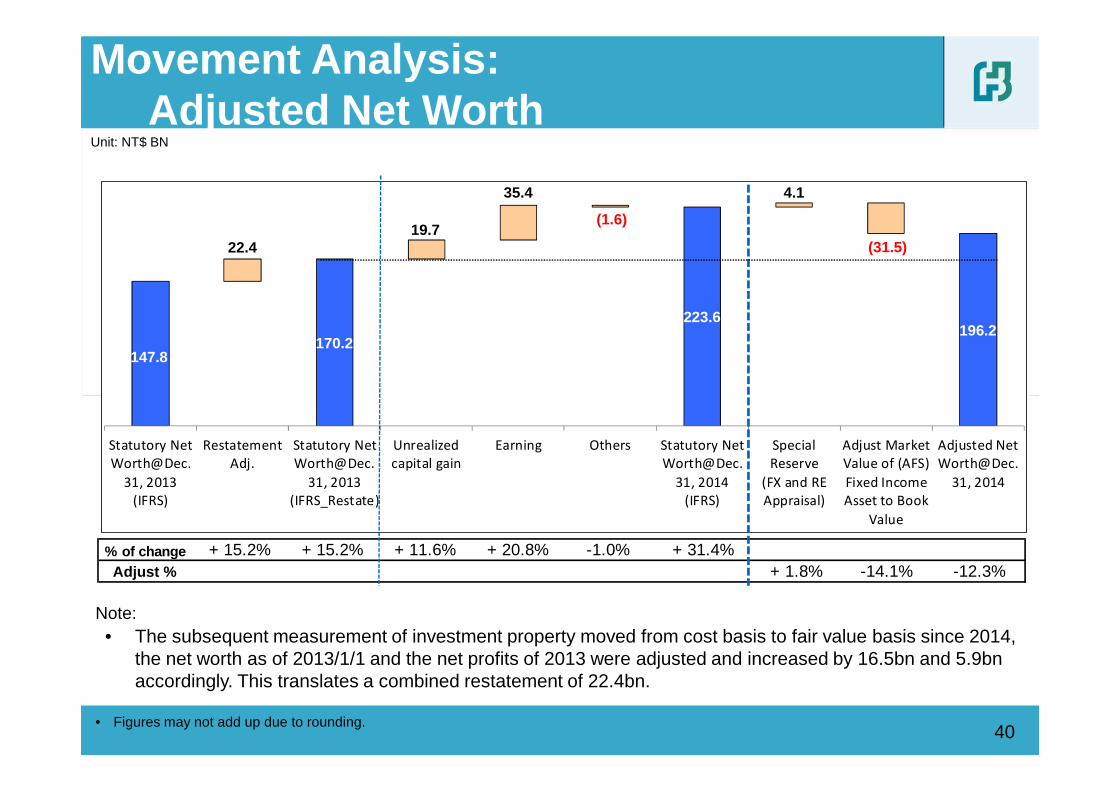

Movement Analysis: Adjusted Net Worth

Unit: NT$ BN

147.8

22.4

170.2

19.7

35.4

(1.6)

223.6

4.1

(31.5)

196.2

40

% of change + 15.2% + 15.2% + 11.6% + 20.8% -1.0% + 31.4%Adjust % + 1.8% -14.1% -12.3%

Statutory NetWorth@Dec.

31, 2013(IFRS)

RestatementAdj.

Statutory NetWorth@Dec.

31, 2013(IFRS_Restate)

Unrealizedcapital gain

Earning Others Statutory NetWorth@Dec.

31, 2014(IFRS)

SpecialReserve

(FX and REAppraisal)

Adjust MarketValue of (AFS)Fixed IncomeAsset to Book

Value

Adjusted NetWorth@Dec.

31, 2014

• Figures may not add up due to rounding.

Note:• The subsequent measurement of investment property moved from cost basis to fair value basis since 2014,

the net worth as of 2013/1/1 and the net profits of 2013 were adjusted and increased by 16.5bn and 5.9bn accordingly. This translates a combined restatement of 22.4bn.

229.9

(1.4) (24.6)

27.2

(0.3) (1.6)

2.5 1.3

40.5

273.6

50.0

100. 0

150. 0

200. 0

250. 0

300. 0

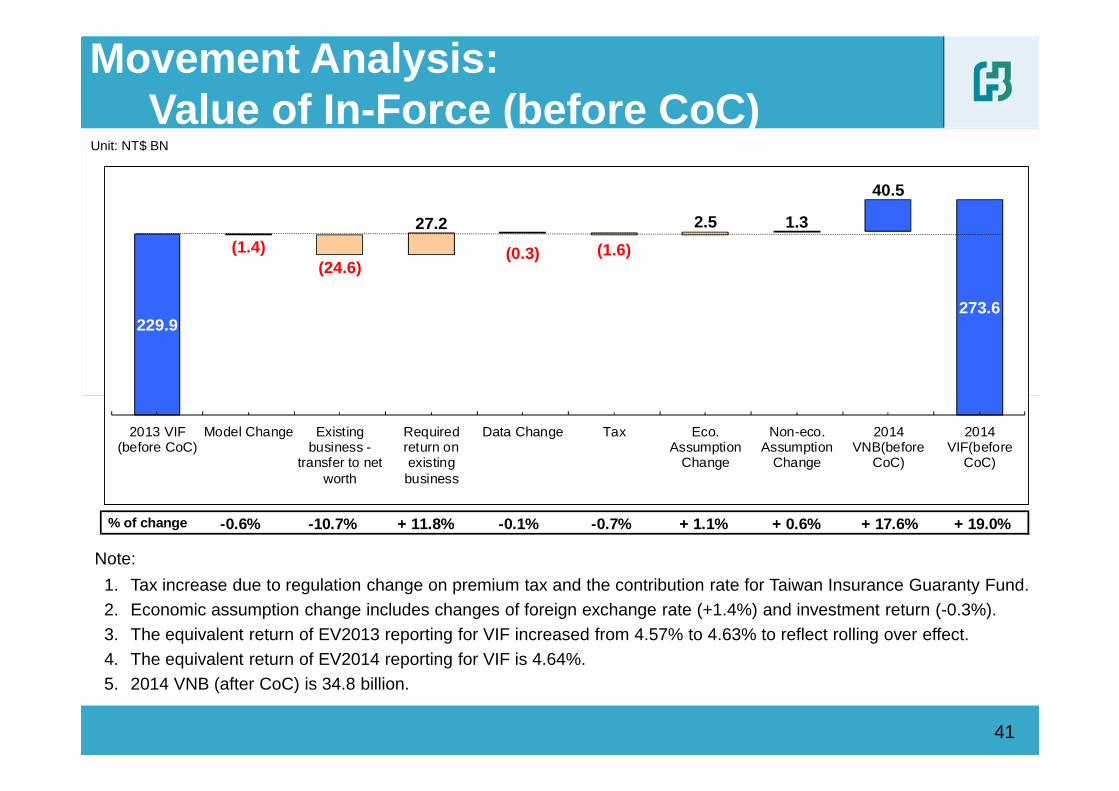

Movement Analysis:Value of In-Force (before CoC)

Unit: NT$ BN

% of change -0.6% -10.7% + 11.8% -0.1% -0.7% + 1.1% + 0.6% + 17.6% + 19.0%

- 50.0

0.0

2013 VIF(before CoC)

Model Change Existingbusiness -

transfer to networth

Requiredreturn onexistingbusiness

Data Change Tax Eco.Assumption

Change

Non-eco.Assumption

Change

2014VNB(before

CoC)

2014VIF(before

CoC)

41

Note:

1. Tax increase due to regulation change on premium tax and the contribution rate for Taiwan Insurance Guaranty Fund.2. Economic assumption change includes changes of foreign exchange rate (+1.4%) and investment return (-0.3%).3. The equivalent return of EV2013 reporting for VIF increased from 4.57% to 4.63% to reflect rolling over effect.4. The equivalent return of EV2014 reporting for VIF is 4.64%.5. 2014 VNB (after CoC) is 34.8 billion.

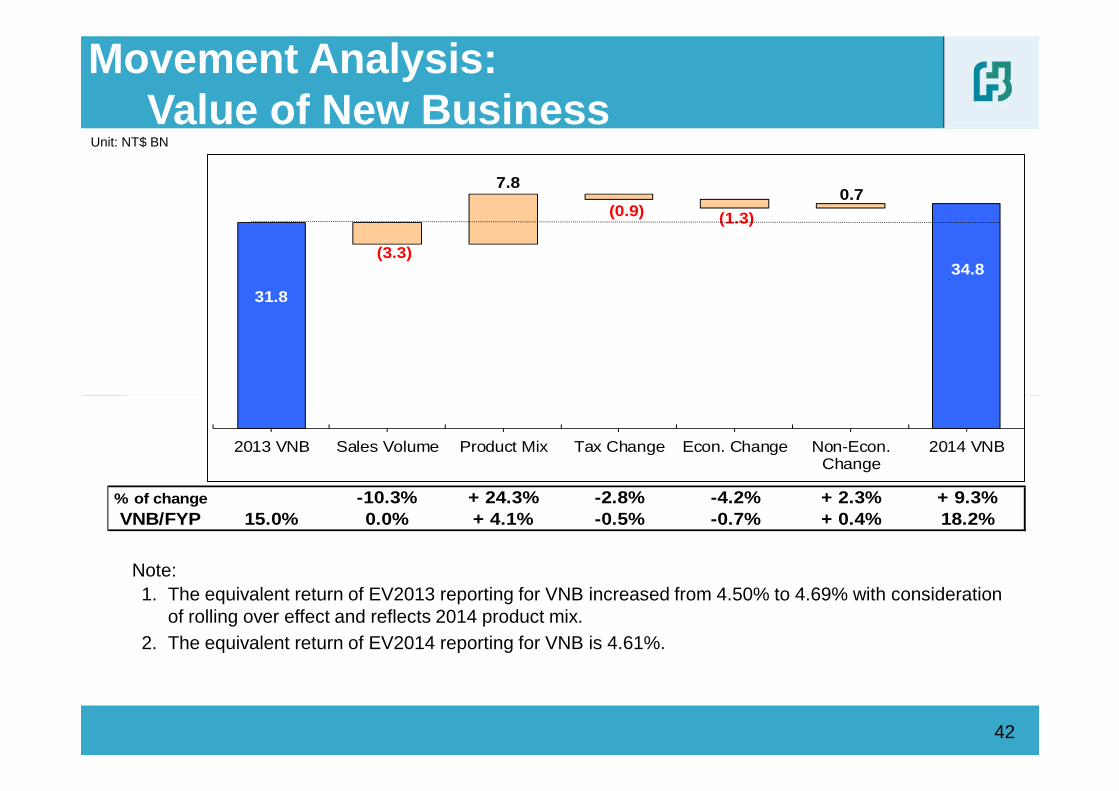

Movement Analysis: Value of New Business

Unit: NT$ BN

31.8

(3.3)

7.8

(0.9) (1.3)

0.7

34.8

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

26.0

28.0

30.0

32.0

34.0

36.0

38.0

40.0

42

% of change -10.3% + 24.3% -2.8% -4.2% + 2.3% + 9.3%VNB/FYP 15.0% 0.0% + 4.1% -0.5% -0.7% + 0.4% 18.2%

-8. 0

-6. 0

-4. 0

-2. 0

0.0

2.0

4.0

2013 VNB Sales Volume Product Mix Tax Change Econ. Change Non-Econ.Change

2014 VNB

Note:1. The equivalent return of EV2013 reporting for VNB increased from 4.50% to 4.69% with consideration

of rolling over effect and reflects 2014 product mix.2. The equivalent return of EV2014 reporting for VNB is 4.61%.

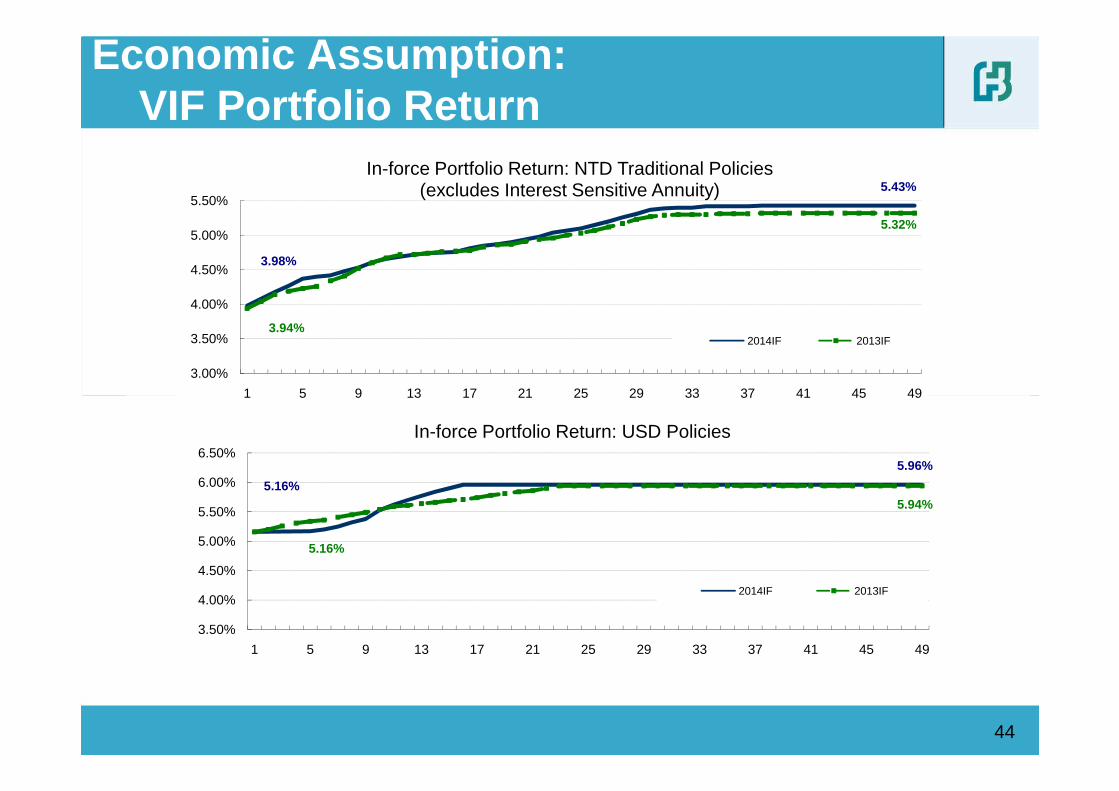

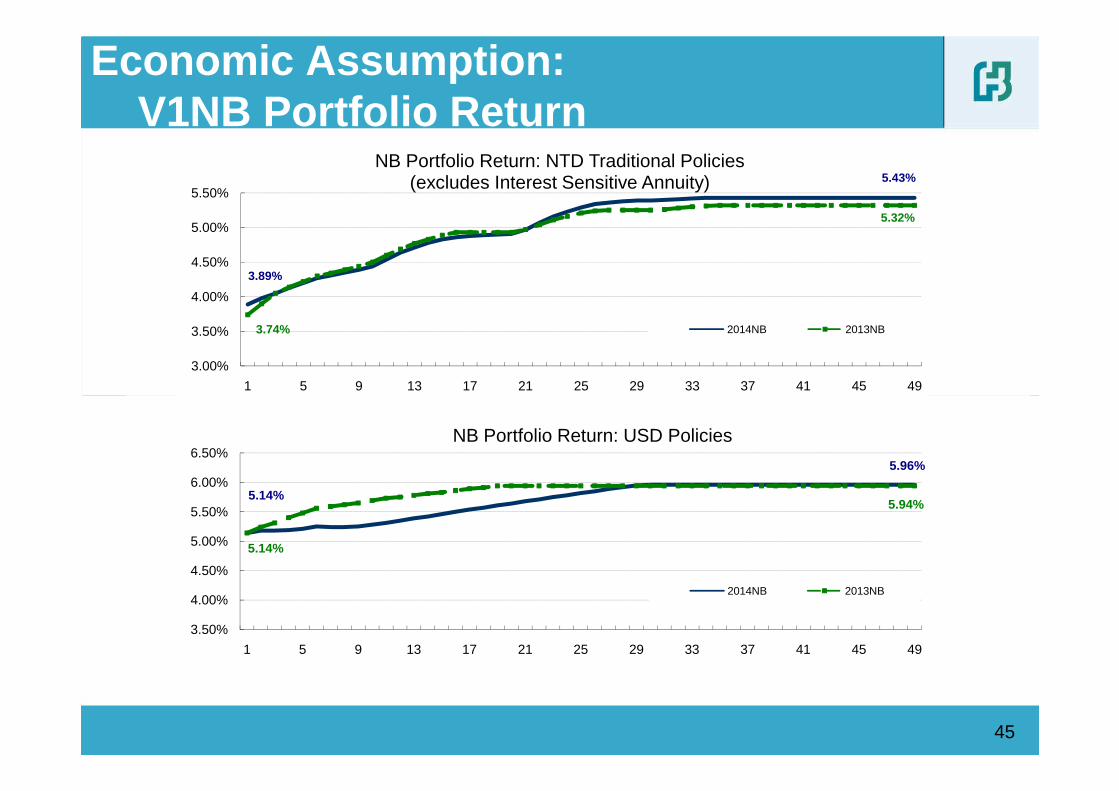

Economic AssumptionYear 2013 Year 2014

Investment return

VIF

NTD Traditional Policies :

Year 2014 to Year 2051 at 3.94%~5.32%(2052+)

USD Policies :

Year 2014 to Year 2036 at 5.16%~5.94%(2037+)

V1NB

NTD Traditional Policies :

Year 2014 to Year 2048 at 3.74%~5.32%(2049+)

USD Policies :

Year 2014 to Year 2032 at 5.14%~5.94%(2033+)

VIF

NTD Traditional Policies :

Year 2015 to Year 2052 at 3.98%~5.43%(2053+)

USD Policies :

Year 2015 to Year 2030 at 5.16%~5.96%(2031+)

V1NB

NTD Traditional Policies :

Year 2015 to Year 2048 at 3.89%~5.43%(2049+)

USD Policies :

Year 2015 to Year 2044 at 5.14%~5.96%(2045+)

43

ISAAverage retained spread for the Interest sensitive business is around 100bps.

ISAAverage retained spread for the Interest sensitive business is around 100bps.

Risk Discount Rate VIF: 11.0%

V1NB: 10.5%

VIF: 11.0%

V1NB: 10.5%

Equivalent ReturnVIF: 4.57% (rolling over to 2014: 4.63%)

V1NB: 4.50% (rolling over to 2014: 4.69%)

VIF: 4.64%

V1NB: 4.61%

YC (10 year)

Initial / ultimate

TWD: 1.72% / 3.50%

USD : 3.09% / 5.25%

TWD: 1.64% / 3.50%

USD : 2.28% / 5.25%

Note:• The FX reserve mechanism was stipulated from 2012, its respective cost is reflected in the derivation

of portfolio return.

Economic Assumption:VIF Portfolio Return

3.98%

5.43%

3.94%

5.32%

3.00%

3.50%

4.00%

4.50%

5.00%

5.50%

1 5 9 13 17 21 25 29 33 37 41 45 49

In-force Portfolio Return: NTD Traditional Policies(excludes Interest Sensitive Annuity)

2014IF 2013IF

44

1 5 9 13 17 21 25 29 33 37 41 45 49

5.16%

5.96%

5.16%

5.94%

3.50%

4.00%

4.50%

5.00%

5.50%

6.00%

6.50%

1 5 9 13 17 21 25 29 33 37 41 45 49

In-force Portfolio Return: USD Policies

2014IF 2013IF

Economic Assumption:V1NB Portfolio Return

3.89%

5.43%

3.74%

5.32%

3.00%

3.50%

4.00%

4.50%

5.00%

5.50%

1 5 9 13 17 21 25 29 33 37 41 45 49

NB Portfolio Return: NTD Traditional Policies(excludes Interest Sensitive Annuity)

2014NB 2013NB

45

5.14%

5.96%

5.14%

5.94%

3.50%

4.00%

4.50%

5.00%

5.50%

6.00%

6.50%

1 5 9 13 17 21 25 29 33 37 41 45 49

NB Portfolio Return: USD Policies

2014NB 2013NB

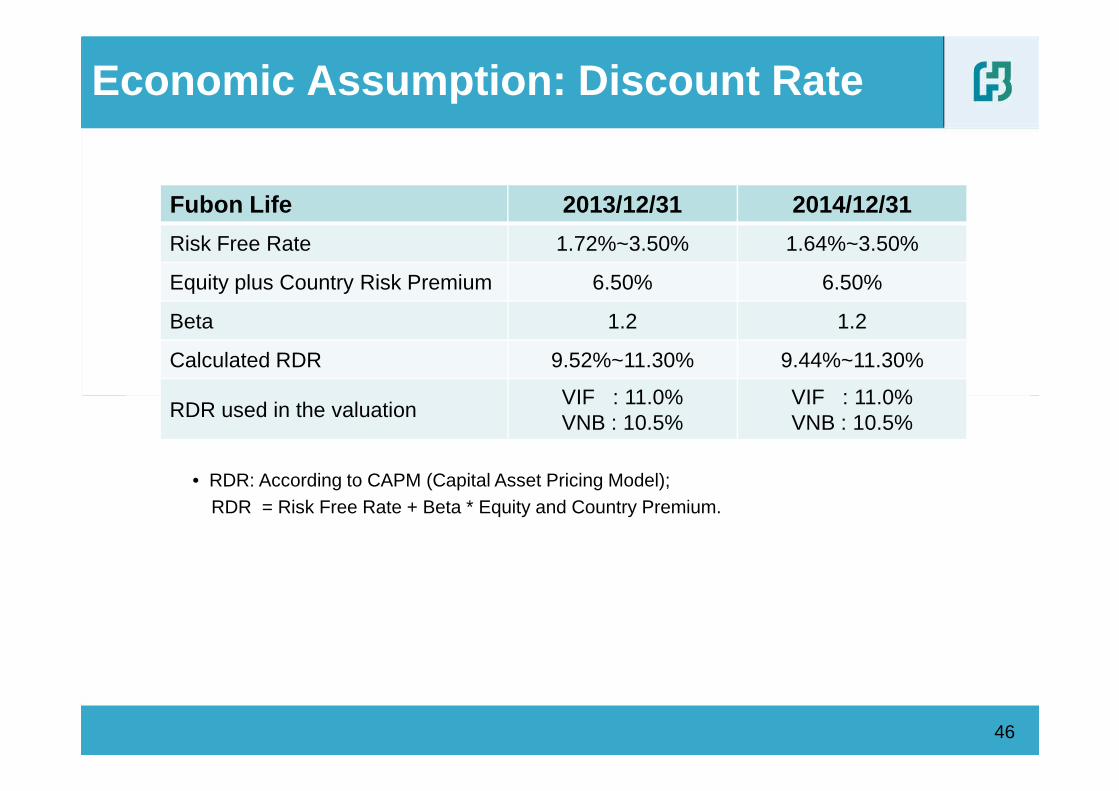

Economic Assumption: Discount Rate

Fubon Life 2013/12/31 2014/12/31

Risk Free Rate 1.72%~3.50% 1.64%~3.50%

Equity plus Country Risk Premium 6.50% 6.50%

Beta 1.2 1.2

Calculated RDR 9.52%~11.30% 9.44%~11.30%

VIF : 11.0% VIF : 11.0%

46

• RDR: According to CAPM (Capital Asset Pricing Model);RDR = Risk Free Rate + Beta * Equity and Country Premium.

RDR used in the valuationVIF : 11.0%VNB : 10.5%

VIF : 11.0%VNB : 10.5%

Cost of Capital

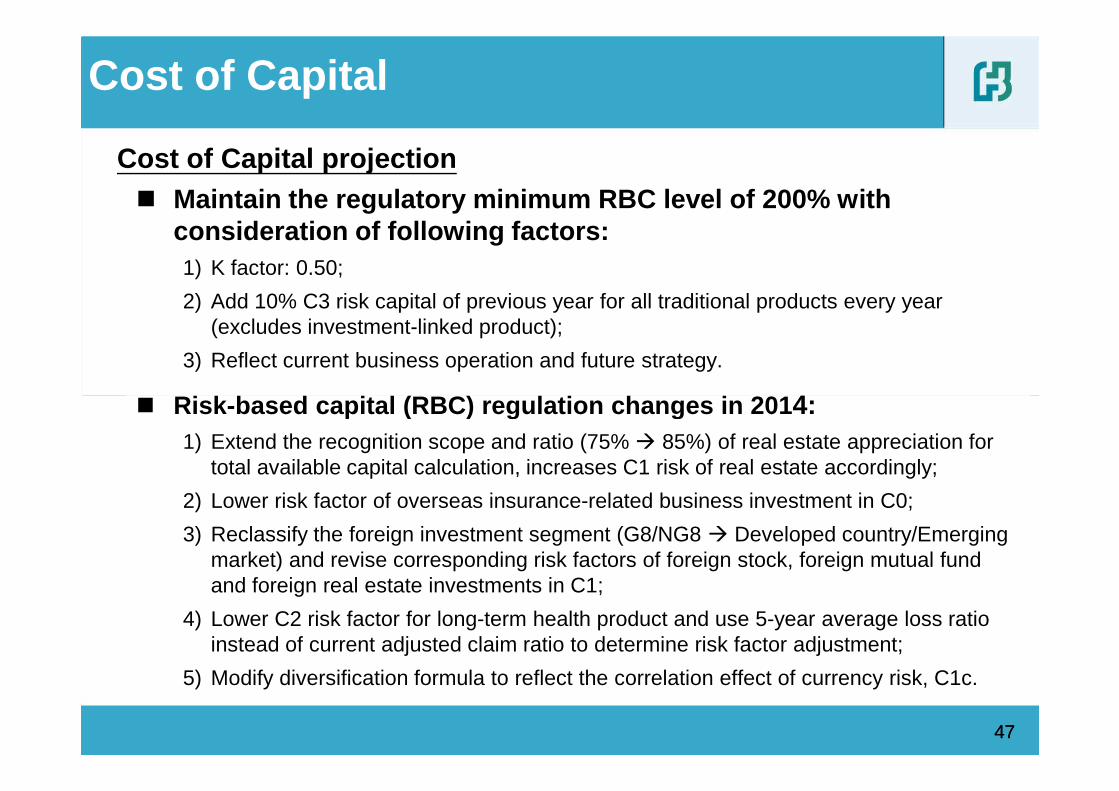

Cost of Capital projection� Maintain the regulatory minimum RBC level of 200% w ith

consideration of following factors: 1) K factor: 0.50;

2) Add 10% C3 risk capital of previous year for all traditional products every year (excludes investment-linked product);

3) Reflect current business operation and future strategy.

� Risk -based capital (RBC) regulation changes in 201 4:

47

� Risk -based capital (RBC) regulation changes in 201 4:1) Extend the recognition scope and ratio (75% � 85%) of real estate appreciation for

total available capital calculation, increases C1 risk of real estate accordingly;

2) Lower risk factor of overseas insurance-related business investment in C0;

3) Reclassify the foreign investment segment (G8/NG8 � Developed country/Emerging market) and revise corresponding risk factors of foreign stock, foreign mutual fund and foreign real estate investments in C1;

4) Lower C2 risk factor for long-term health product and use 5-year average loss ratio instead of current adjusted claim ratio to determine risk factor adjustment;

5) Modify diversification formula to reflect the correlation effect of currency risk, C1c.

47

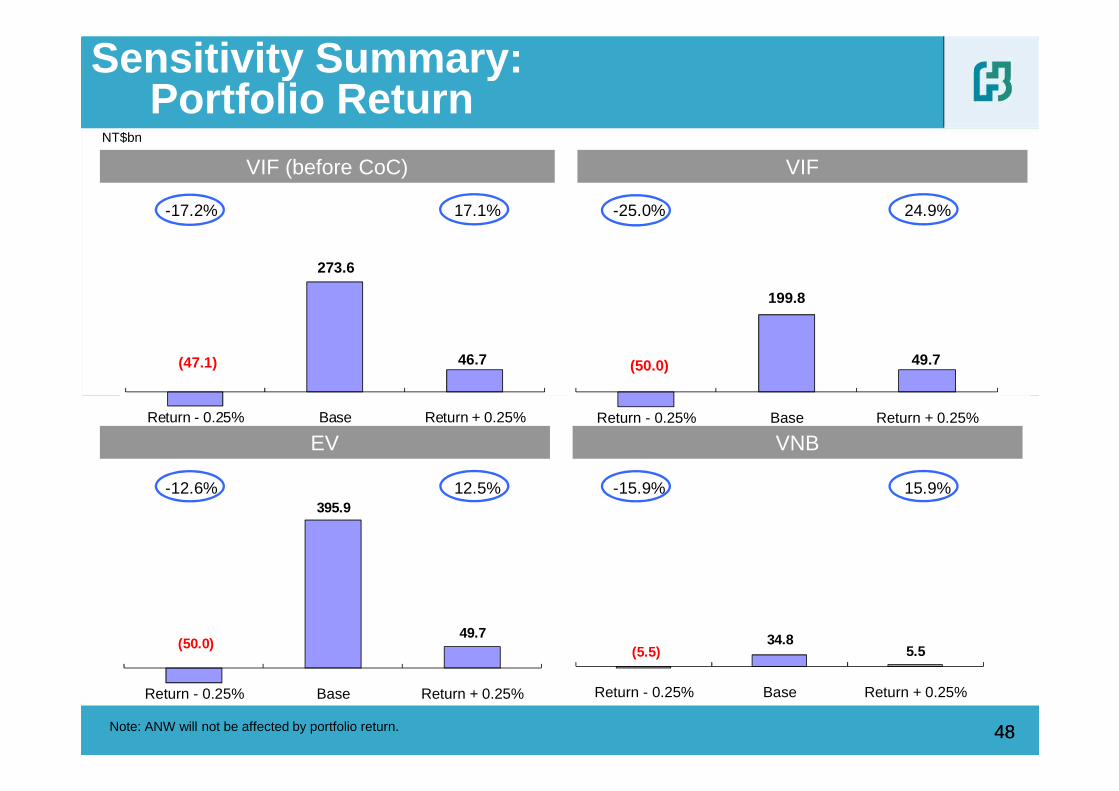

-17.2% 17.1% -25.0% 24.9%

(47.1)

273.6

46.7 (50.0)

199.8

49.7

Sensitivity Summary:Portfolio Return

VIF (before CoC) VIF

NT$bn

-12.6% 12.5% -15.9% 15.9%

Return - 0.25% Base Return + 0.25%

(50.0)

395.9

49.7

Return - 0.25% Base Return + 0.25%

Return - 0.25% Base Return + 0.25%

(5.5)34.8

5.5

Return - 0.25% Base Return + 0.25%

48Note: ANW will not be affected by portfolio return.

EV VNB

48

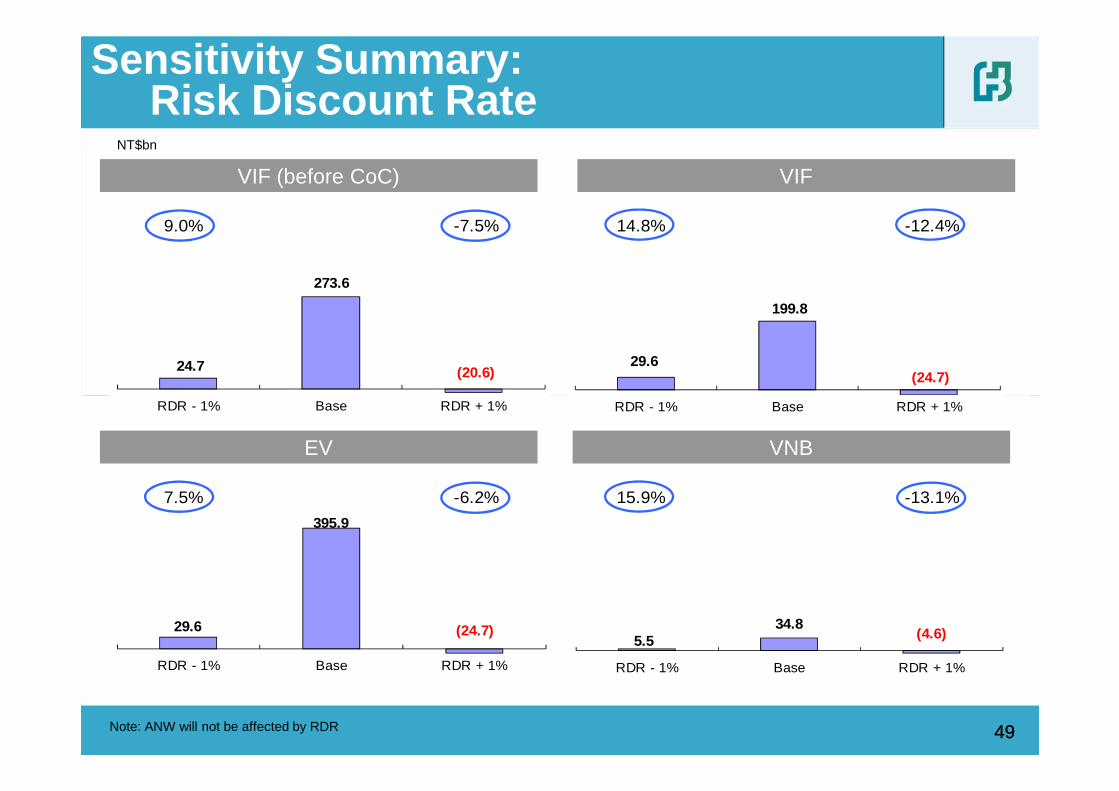

9.0% -7.5% 14.8% -12.4%

24.7

273.6

(20.6)29.6

199.8

(24.7)

VIF (before CoC) VIF

Sensitivity Summary: Risk Discount Rate

NT$bn

49

7.5% -6.2% 15.9% -13.1%

RDR - 1% Base RDR + 1%

29.6

395.9

(24.7)

RDR - 1% Base RDR + 1%

RDR - 1% Base RDR + 1%

5.5 34.8

(4.6)

RDR - 1% Base RDR + 1%

Note: ANW will not be affected by RDR

EV VNB

49

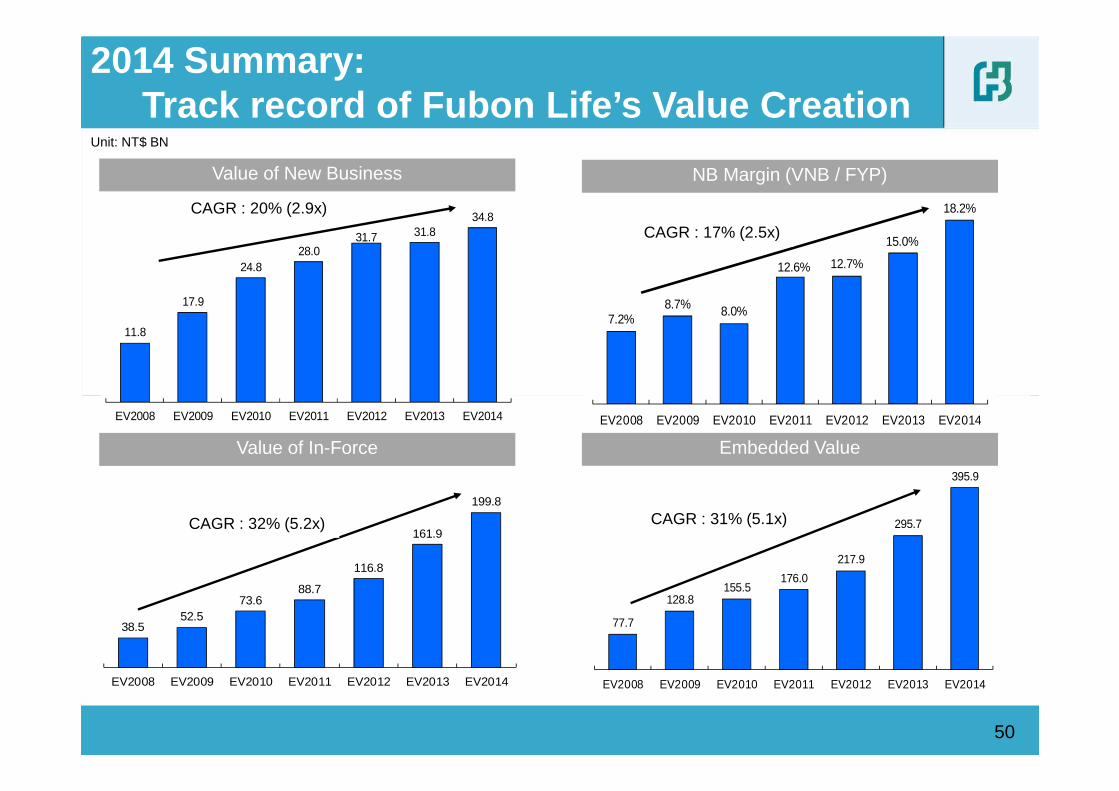

7.2%8.7% 8.0%

12.6% 12.7%

15.0%

18.2%

CAGR: 17%

Unit: NT$ BN

NB Margin (VNB / FYP)

11.8

17.9

24.8 28.0

31.7 31.8 34.8 CAGR: 20%

Value of New Business

CAGR : 20% (2.9x)

CAGR : 17% (2.5x)

2014 Summary: Track record of Fubon Life’s Value Creation

77.7

128.8 155.5

176.0

217.9

295.7

395.9

EV2008 EV2009 EV2010 EV2011 EV2012 EV2013 EV2014

CAGR: 31%

EV2008 EV2009 EV2010 EV2011 EV2012 EV2013 EV2014

50

EV2008 EV2009 EV2010 EV2011 EV2012 EV2013 EV2014

38.5 52.5

73.6 88.7

116.8

161.9

199.8

EV2008 EV2009 EV2010 EV2011 EV2012 EV2013 EV2014

CAGR: 32%

Value of In-Force Embedded Value

CAGR : 32% (5.2x) CAGR : 31% (5.1x)

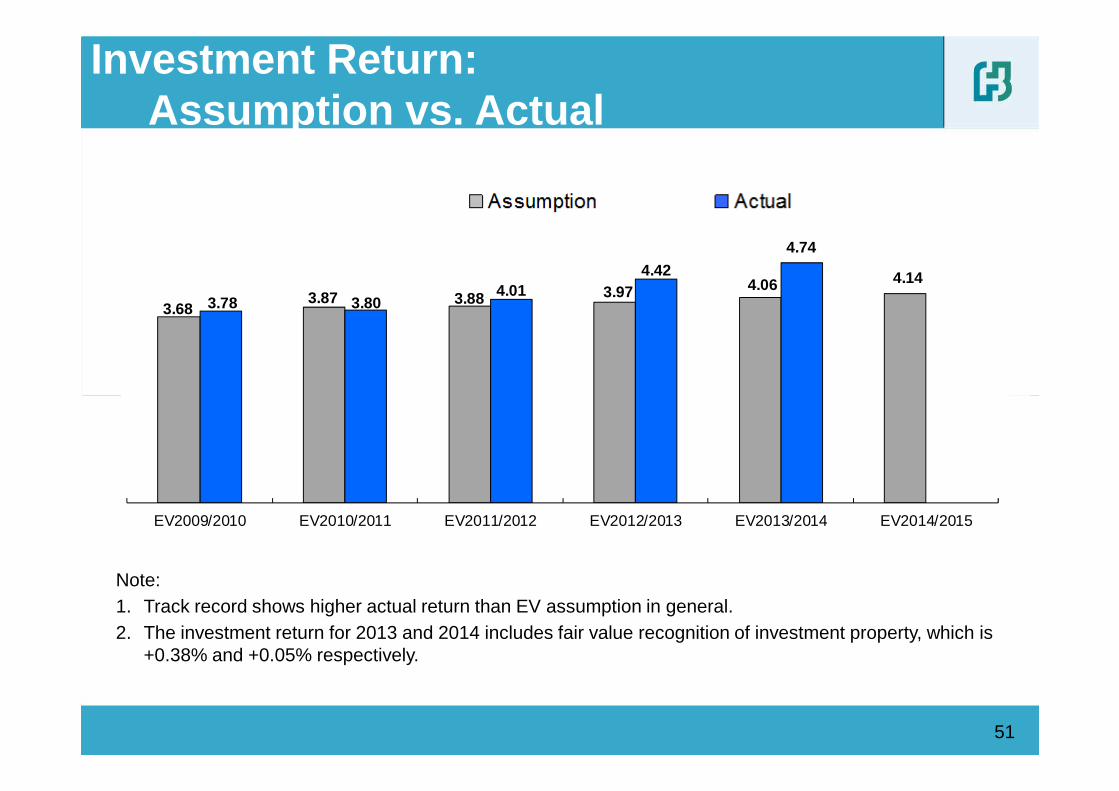

Investment Return:Assumption vs. Actual

3.68 3.87 3.88 3.97 4.06 4.14

3.78 3.80 4.01

4.42

4.74

51

Note:1. Track record shows higher actual return than EV assumption in general.2. The investment return for 2013 and 2014 includes fair value recognition of investment property, which is

+0.38% and +0.05% respectively.

EV2009/2010 EV2010/2011 EV2011/2012 EV2012/2013 EV2013/2014 EV2014/2015

Independent Review by Deloitte Consulting

Deloitte ConsultingThe Engagement• Deloitte Consulting (Hong Kong) Limited (“Deloitte Consulting”) were retained by Fubon Life to perform an

independent review of the Embedded Value (EV) as at 31 December 2014 and the Value of One Year’s NewBusiness (V1NB) written over the period of 1 January 2014 to 31 December 2014.

Scope of Deloitte Consulting’s Involvement• Review and opine on the reasonableness of the EV and V1NB as calculated by the Company;

• Review of the reasonableness of the assumptions used in the calculations, taking into consideration both theCompany’s recent experience and the experience of the Taiwanese life insurance market;

5252

Company’s recent experience and the experience of the Taiwanese life insurance market;

• Review, at a high-level, model changes to the actuarial projection model since the previous valuation date;• Review of the Company’s projection approach of the Cost of Capital;• Review of the data put through the model compared to the policy data on the Company’s policy

administration systems to judge the extent to which the business has been valued in the financial model and to identify the portion (if any) omitted and how that was valued;

• Review of the approach used to determine the Adjusted Net Worth (“ANW”), in particular, the adjustments made in deriving the ANW, and any other adjustments made outside of the actuarial projection model;

• Review of the Company's analysis of change in the Value of In-Force Business (“VIF”) between 31 December 2013 and 31 December 2014.

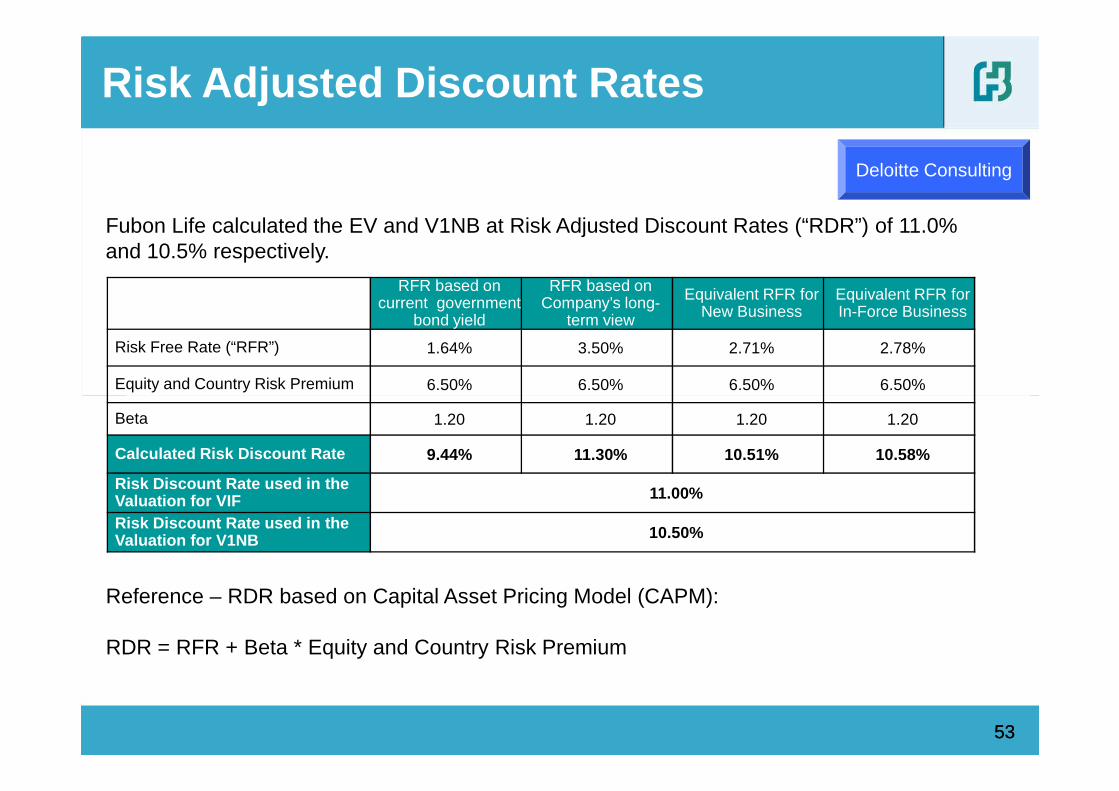

Risk Adjusted Discount Rates

Fubon Life calculated the EV and V1NB at Risk Adjusted Discount Rates (“RDR”) of 11.0% and 10.5% respectively.

RFR based on current government

bond yield

RFR based on Company’s long-

term view

Equivalent RFR for New Business

Equivalent RFR for In-Force Business

Risk Free Rate (“RFR”) 1.64% 3.50% 2.71% 2.78%

Equity and Country Risk Premium 6.50% 6.50% 6.50% 6.50%

Deloitte Consulting

5353

Beta 1.20 1.20 1.20 1.20

Calculated Risk Discount Rate 9.44% 11.30% 10.51% 10.58%

Risk Discount Rate used in the Valuation for VIF 11.00%

Risk Discount Rate used in the Valuation for V1NB 10.50%

Reference – RDR based on Capital Asset Pricing Model (CAPM):

RDR = RFR + Beta * Equity and Country Risk Premium

Comments on the Risk Adjusted Discount Rates

Deloitte Consulting independently derived a range of RDRs using the CAPM approach:

� The low end of the RDR is developed based on the current yield on 10-year Taiwan government bonds.

� The high end of the RDR is developed based on the Company’s view of the 10-year Taiwan government bond in the future.

� The equivalent RFR is the RFR equivalent to using a set of graded-up RFR from 1.64% to 3.50% that derives the same VIF and V1NB.

� The Equity and Country Risk Premium was developed based on the Country Default Spreads and Risk Premiums research published by New York University.

Deloitte Consulting

5454

Premiums research published by New York University.

� The Beta of 1.2 was set using a risk profiling approach which considers risks related to the product range, distribution diversification/vulnerability, regulatory intervention and investments. Note that this beta value is consistent with that used in previous valuations.

� The RDR assumption applied by Fubon Life in the valuation lies within the range of RDR that we derived.

� In particular, we feel comfortable with different RDRs being used for the valuation of the in-force and new business, given the specific market conditions in Taiwan: it is well-known that the legacy business has a much riskier profile than the current new business, and hence it is reasonable for shareholders to be expecting a higher rate of return for the higher risk level. We feel that Fubon Life has taken a good approach in splitting up the RDR assumption for the two distinctively different blocks of business.

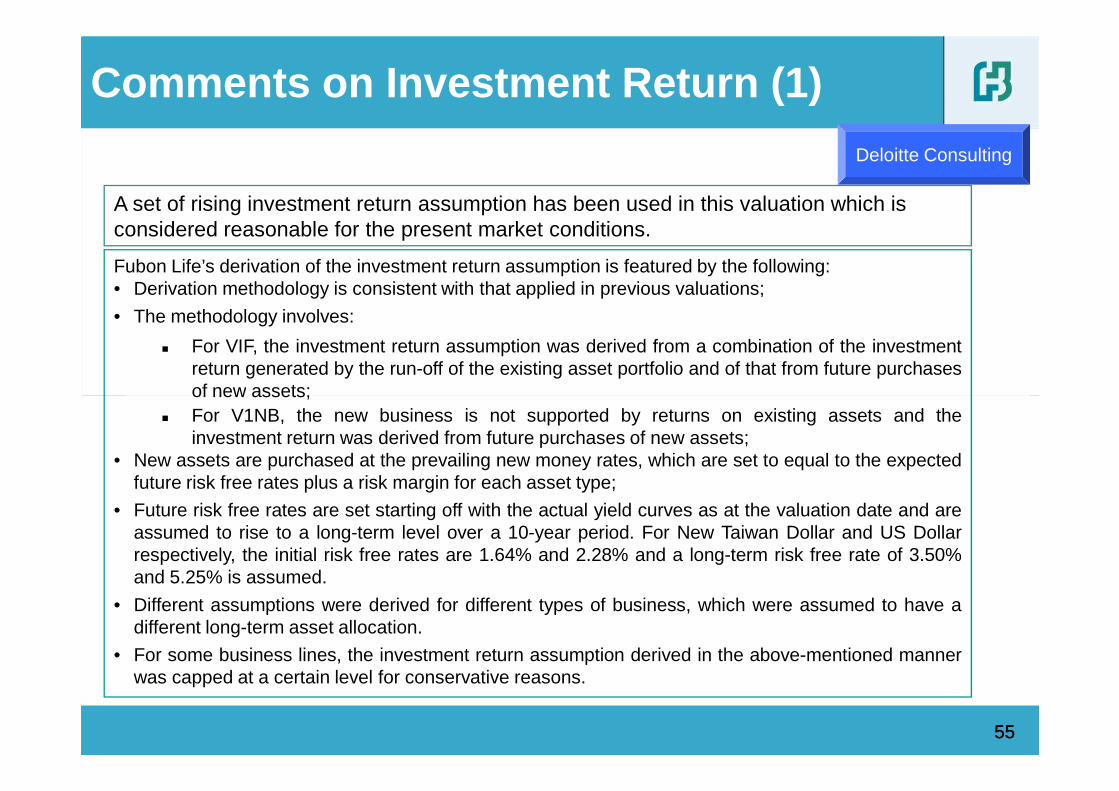

Comments on Investment Return (1)

A set of rising investment return assumption has been used in this valuation which is considered reasonable for the present market conditions.

Fubon Life’s derivation of the investment return assumption is featured by the following:• Derivation methodology is consistent with that applied in previous valuations;

• The methodology involves:

� For VIF, the investment return assumption was derived from a combination of the investmentreturn generated by the run-off of the existing asset portfolio and of that from future purchasesof new assets;

Deloitte Consulting

5555

of new assets;� For V1NB, the new business is not supported by returns on existing assets and the

investment return was derived from future purchases of new assets;• New assets are purchased at the prevailing new money rates, which are set to equal to the expected

future risk free rates plus a risk margin for each asset type;

• Future risk free rates are set starting off with the actual yield curves as at the valuation date and areassumed to rise to a long-term level over a 10-year period. For New Taiwan Dollar and US Dollarrespectively, the initial risk free rates are 1.64% and 2.28% and a long-term risk free rate of 3.50%and 5.25% is assumed.

• Different assumptions were derived for different types of business, which were assumed to have adifferent long-term asset allocation.

• For some business lines, the investment return assumption derived in the above-mentioned mannerwas capped at a certain level for conservative reasons.

Comments on Investment Return (2)

It is in Deloitte Consulting’s view that:

Methodology• Fubon Life’s derivation methodology for the investment return assumption is reasonable and

consistent with the way that the ANW is calculated;

Economic Assumptions• The expected long-term risk-free rate for New Taiwan Dollar yield and US Dollar yield are

maintained at 3.5% and 5.25% respectively.

Deloitte Consulting

5656

• We note that taking a view on the future capital market is not uncommon under the traditionalEmbedded Value methodology. On a macro-economic level the arguments put forward forrising interest rates are plausible, and we note that the expected future rise in yields is spreadout over a reasonably long period of 10 years.

• Readers should be aware that capital market conditions are subject to the impact of manyforces. Yields and prices of financial instruments can move dramatically in a short period oftime. As a result, it is difficult to predict the interest rate level in the future with great certainty.Readers should refer to the sensitivity tests to develop a broader understanding of the impact ofthe investment return assumption on the assessment of the economic value of Fubon Life.

• Overall, the economic assumptions appear to be reasonable.

Comments on Non-Economic Assumptions

Non - Economic Assumptions• The non-economic assumptions reflect Fubon Life’s best estimate of future operating

experience, and are appropriately supported by the company’s historical operating experience.

Deloitte Consulting

5757

Comments on EV and V1NB Results

Deloitte Consulting have reviewed the Embedded Value and Value of OneYear’s New Business results at a high-level under the generally acceptedmethod for calculating traditional embedded values in Taiwan:

• Review of the changes in the VIF relative to the assumption changes and modelchanges from 2013 to 2014;

• Review of the changes in the new business profit margin relative to that in 2013 based

Deloitte Consulting

5858

• Review of the changes in the new business profit margin relative to that in 2013 basedon information on changes in sales mix, sales volume and valuation assumptions;

• Review of the sensitivities relative to the base case results.

The Embedded Value and Value of One Year’s New Business results appear tobe reasonable within the above context.Deloitte Consulting’s detailed opinion can be found in their opinion letter.

Thank you

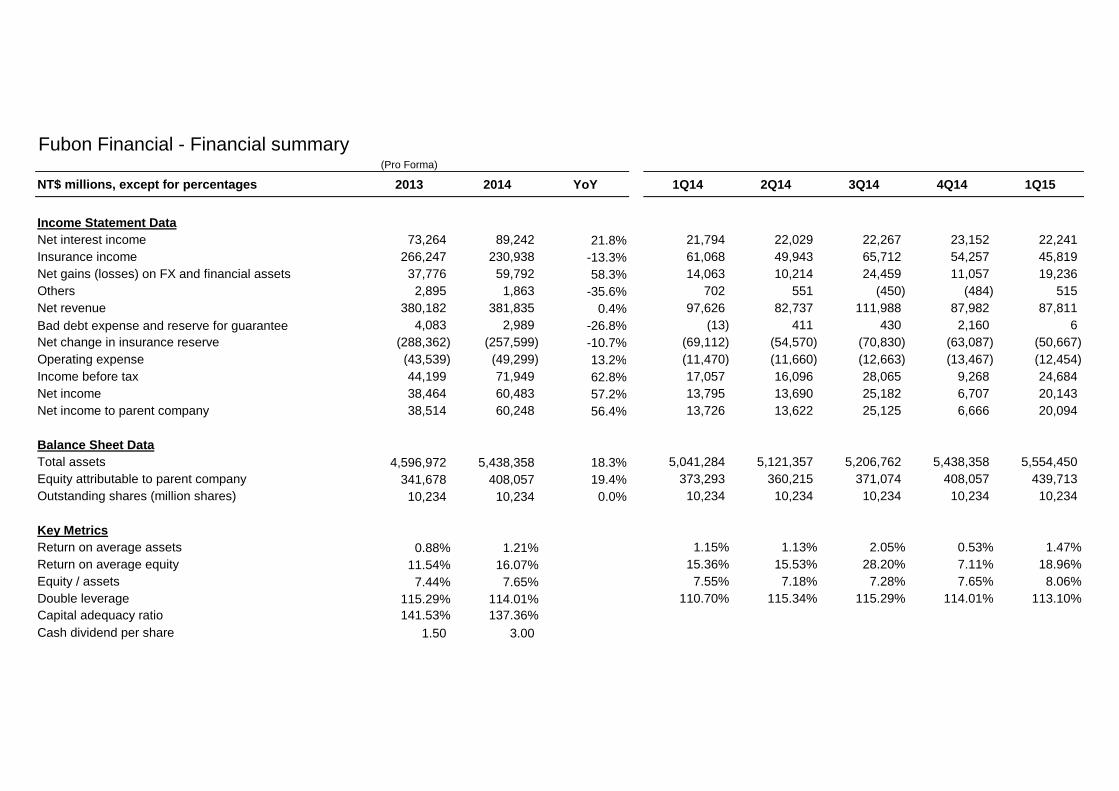

Fubon Financial - Financial summary(Pro Forma)

NT$ millions, except for percentages 2013 2014 YoY 1Q14 2Q14 3Q14 4Q14 1Q15

Income Statement DataNet interest income 73,264 89,242 21.8% 21,794 22,029 22,267 23,152 22,241Insurance income 266,247 230,938 -13.3% 61,068 49,943 65,712 54,257 45,819Net gains (losses) on FX and financial assets 37,776 59,792 58.3% 14,063 10,214 24,459 11,057 19,236Others 2,895 1,863 -35.6% 702 551 (450) (484) 515Net revenue 380,182 381,835 0.4% 97,626 82,737 111,988 87,982 87,811Bad debt expense and reserve for guarantee 4,083 2,989 -26.8% (13) 411 430 2,160 6Net change in insurance reserve (288,362) (257,599) -10.7% (69,112) (54,570) (70,830) (63,087) (50,667)Operating expense (43,539) (49,299) 13.2% (11,470) (11,660) (12,663) (13,467) (12,454)Operating expense (43,539) (49,299) 13.2% (11,470) (11,660) (12,663) (13,467) (12,454)Income before tax 44,199 71,949 62.8% 17,057 16,096 28,065 9,268 24,684Net income 38,464 60,483 57.2% 13,795 13,690 25,182 6,707 20,143Net income to parent company 38,514 60,248 56.4% 13,726 13,622 25,125 6,666 20,094

Balance Sheet DataTotal assets 4,596,972 5,438,358 18.3% 5,041,284 5,121,357 5,206,762 5,438,358 5,554,450Equity attributable to parent company 341,678 408,057 19.4% 373,293 360,215 371,074 408,057 439,713Outstanding shares (million shares) 10,234 10,234 0.0% 10,234 10,234 10,234 10,234 10,234

Key MetricsReturn on average assets 0.88% 1.21% 1.15% 1.13% 2.05% 0.53% 1.47%Return on average equity 11.54% 16.07% 15.36% 15.53% 28.20% 7.11% 18.96%Equity / assets 7.44% 7.65% 7.55% 7.18% 7.28% 7.65% 8.06%Double leverage 115.29% 114.01% 110.70% 115.34% 115.29% 114.01% 113.10%Capital adequacy ratio 141.53% 137.36%Cash dividend per share 1.50 3.00

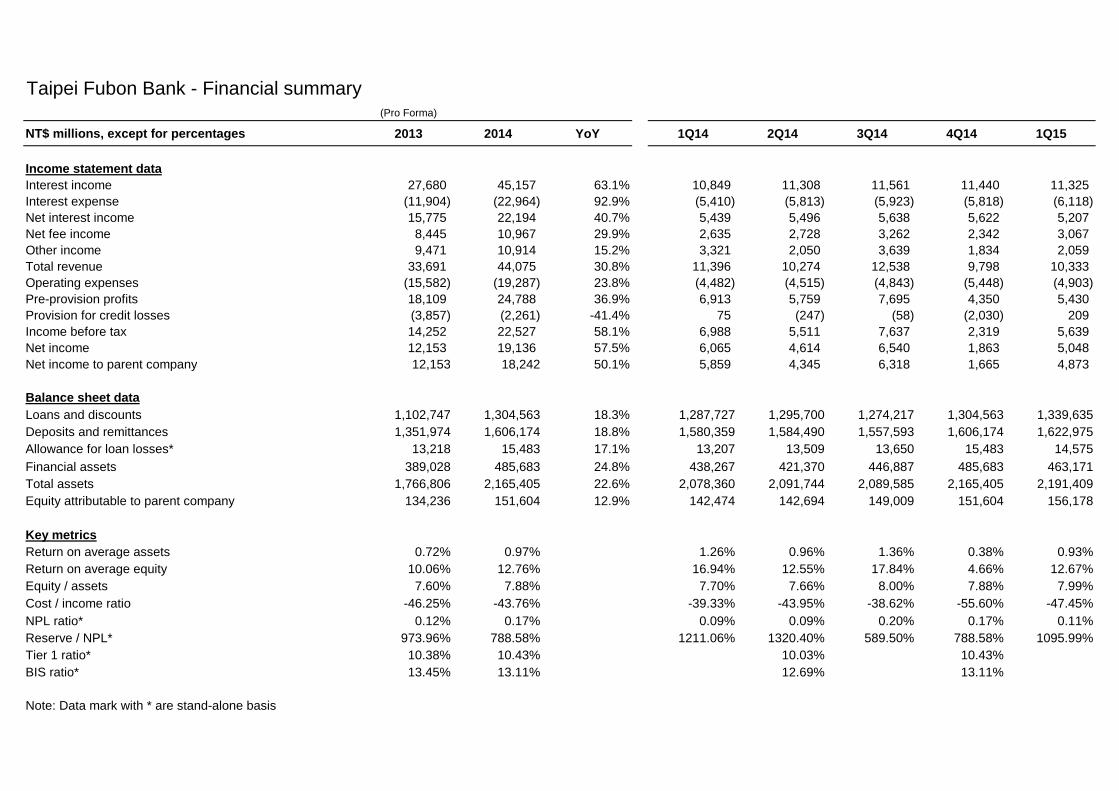

Taipei Fubon Bank - Financial summary(Pro Forma)

NT$ millions, except for percentages 2013 2014 YoY 1Q14 2Q14 3Q14 4Q14 1Q15

Income statement dataInterest income 27,680 45,157 63.1% 10,849 11,308 11,561 11,440 11,325Interest expense (11,904) (22,964) 92.9% (5,410) (5,813) (5,923) (5,818) (6,118)Net interest income 15,775 22,194 40.7% 5,439 5,496 5,638 5,622 5,207Net fee income 8,445 10,967 29.9% 2,635 2,728 3,262 2,342 3,067Other income 9,471 10,914 15.2% 3,321 2,050 3,639 1,834 2,059Total revenue 33,691 44,075 30.8% 11,396 10,274 12,538 9,798 10,333Operating expenses (15,582) (19,287) 23.8% (4,482) (4,515) (4,843) (5,448) (4,903)Pre-provision profits 18,109 24,788 36.9% 6,913 5,759 7,695 4,350 5,430Provision for credit losses (3,857) (2,261) -41.4% 75 (247) (58) (2,030) 209Income before tax 14,252 22,527 58.1% 6,988 5,511 7,637 2,319 5,639Net income 12,153 19,136 57.5% 6,065 4,614 6,540 1,863 5,048Net income to parent company 12,153 18,242 50.1% 5,859 4,345 6,318 1,665 4,873Net income to parent company 12,153 18,242 50.1% 5,859 4,345 6,318 1,665 4,873

Balance sheet dataLoans and discounts 1,102,747 1,304,563 18.3% 1,287,727 1,295,700 1,274,217 1,304,563 1,339,635Deposits and remittances 1,351,974 1,606,174 18.8% 1,580,359 1,584,490 1,557,593 1,606,174 1,622,975Allowance for loan losses* 13,218 15,483 17.1% 13,207 13,509 13,650 15,483 14,575Financial assets 389,028 485,683 24.8% 438,267 421,370 446,887 485,683 463,171Total assets 1,766,806 2,165,405 22.6% 2,078,360 2,091,744 2,089,585 2,165,405 2,191,409Equity attributable to parent company 134,236 151,604 12.9% 142,474 142,694 149,009 151,604 156,178

Key metricsReturn on average assets 0.72% 0.97% 1.26% 0.96% 1.36% 0.38% 0.93%Return on average equity 10.06% 12.76% 16.94% 12.55% 17.84% 4.66% 12.67%Equity / assets 7.60% 7.88% 7.70% 7.66% 8.00% 7.88% 7.99%Cost / income ratio -46.25% -43.76% -39.33% -43.95% -38.62% -55.60% -47.45%NPL ratio* 0.12% 0.17% 0.09% 0.09% 0.20% 0.17% 0.11%Reserve / NPL* 973.96% 788.58% 1211.06% 1320.40% 589.50% 788.58% 1095.99%Tier 1 ratio* 10.38% 10.43% 10.03% 10.43%BIS ratio* 13.45% 13.11% 12.69% 13.11%

Note: Data mark with * are stand-alone basis

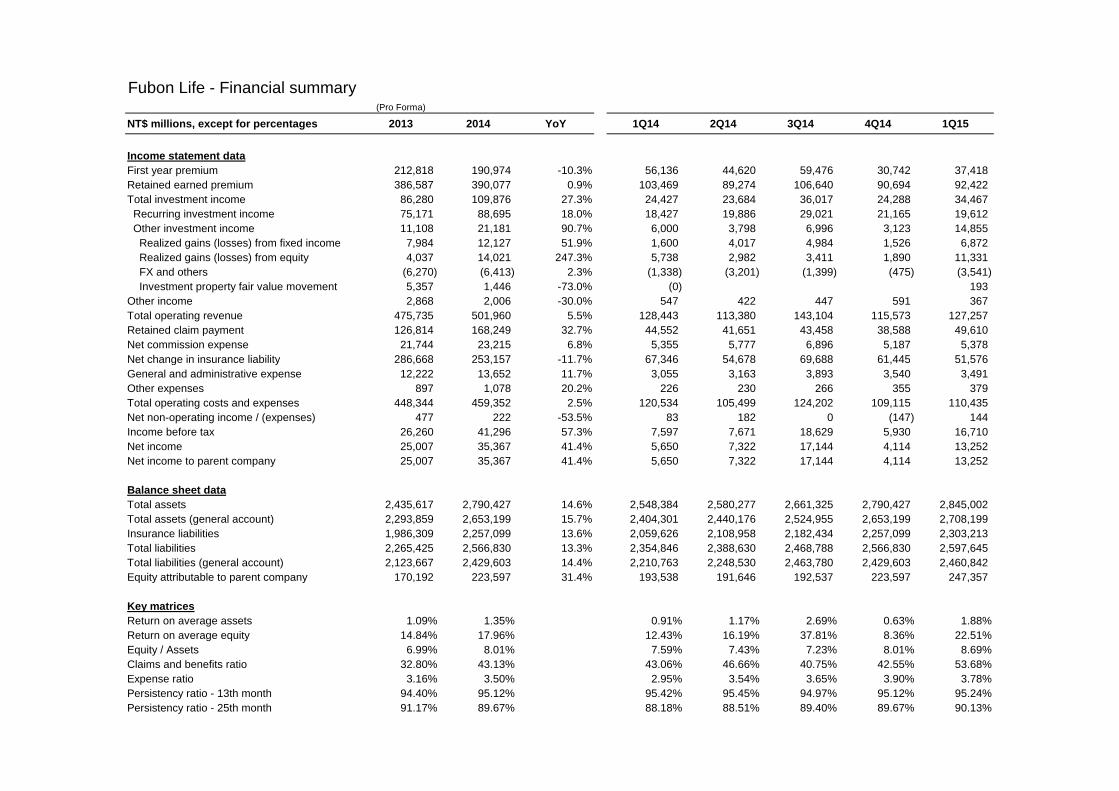

Fubon Life - Financial summary(Pro Forma)

NT$ millions, except for percentages 2013 2014 YoY 1Q14 2Q14 3Q14 4Q14 1Q15

Income statement dataFirst year premium 212,818 190,974 -10.3% 56,136 44,620 59,476 30,742 37,418Retained earned premium 386,587 390,077 0.9% 103,469 89,274 106,640 90,694 92,422Total investment income 86,280 109,876 27.3% 24,427 23,684 36,017 24,288 34,467 Recurring investment income 75,171 88,695 18.0% 18,427 19,886 29,021 21,165 19,612 Other investment income 11,108 21,181 90.7% 6,000 3,798 6,996 3,123 14,855 Realized gains (losses) from fixed income 7,984 12,127 51.9% 1,600 4,017 4,984 1,526 6,872 Realized gains (losses) from equity 4,037 14,021 247.3% 5,738 2,982 3,411 1,890 11,331 FX and others (6,270) (6,413) 2.3% (1,338) (3,201) (1,399) (475) (3,541) Investment property fair value movement 5,357 1,446 -73.0% (0) 193Other income 2,868 2,006 -30.0% 547 422 447 591 367Total operating revenue 475,735 501,960 5.5% 128,443 113,380 143,104 115,573 127,257Retained claim payment 126,814 168,249 32.7% 44,552 41,651 43,458 38,588 49,610Net commission expense 21,744 23,215 6.8% 5,355 5,777 6,896 5,187 5,378Net change in insurance liability 286,668 253,157 -11.7% 67,346 54,678 69,688 61,445 51,576Net change in insurance liability 286,668 253,157 -11.7% 67,346 54,678 69,688 61,445 51,576General and administrative expense 12,222 13,652 11.7% 3,055 3,163 3,893 3,540 3,491Other expenses 897 1,078 20.2% 226 230 266 355 379Total operating costs and expenses 448,344 459,352 2.5% 120,534 105,499 124,202 109,115 110,435Net non-operating income / (expenses) 477 222 -53.5% 83 182 0 (147) 144Income before tax 26,260 41,296 57.3% 7,597 7,671 18,629 5,930 16,710Net income 25,007 35,367 41.4% 5,650 7,322 17,144 4,114 13,252Net income to parent company 25,007 35,367 41.4% 5,650 7,322 17,144 4,114 13,252

Balance sheet dataTotal assets 2,435,617 2,790,427 14.6% 2,548,384 2,580,277 2,661,325 2,790,427 2,845,002Total assets (general account) 2,293,859 2,653,199 15.7% 2,404,301 2,440,176 2,524,955 2,653,199 2,708,199Insurance liabilities 1,986,309 2,257,099 13.6% 2,059,626 2,108,958 2,182,434 2,257,099 2,303,213Total liabilities 2,265,425 2,566,830 13.3% 2,354,846 2,388,630 2,468,788 2,566,830 2,597,645Total liabilities (general account) 2,123,667 2,429,603 14.4% 2,210,763 2,248,530 2,463,780 2,429,603 2,460,842Equity attributable to parent company 170,192 223,597 31.4% 193,538 191,646 192,537 223,597 247,357

Key matricesReturn on average assets 1.09% 1.35% 0.91% 1.17% 2.69% 0.63% 1.88%Return on average equity 14.84% 17.96% 12.43% 16.19% 37.81% 8.36% 22.51%Equity / Assets 6.99% 8.01% 7.59% 7.43% 7.23% 8.01% 8.69%Claims and benefits ratio 32.80% 43.13% 43.06% 46.66% 40.75% 42.55% 53.68%Expense ratio 3.16% 3.50% 2.95% 3.54% 3.65% 3.90% 3.78%Persistency ratio - 13th month 94.40% 95.12% 95.42% 95.45% 94.97% 95.12% 95.24%Persistency ratio - 25th month 91.17% 89.67% 88.18% 88.51% 89.40% 89.67% 90.13%

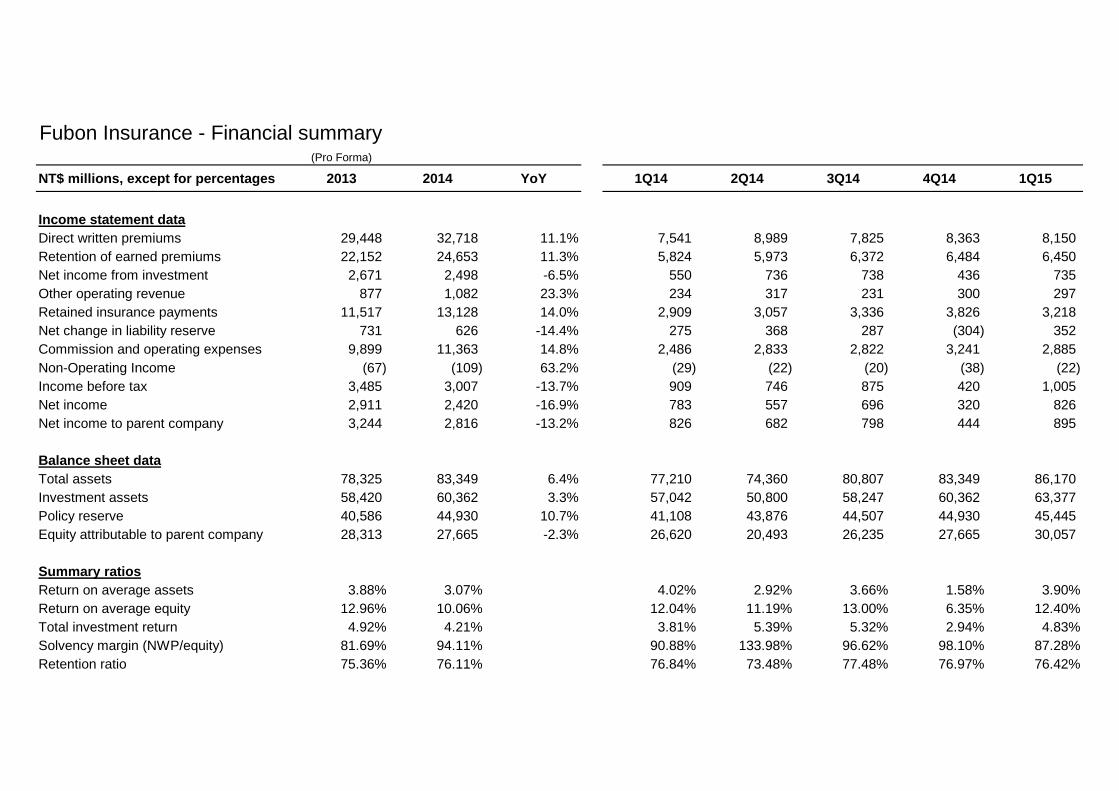

Fubon Insurance - Financial summary(Pro Forma)

NT$ millions, except for percentages 2013 2014 YoY 1Q14 2Q14 3Q14 4Q14 1Q15

Income statement dataDirect written premiums 29,448 32,718 11.1% 7,541 8,989 7,825 8,363 8,150Retention of earned premiums 22,152 24,653 11.3% 5,824 5,973 6,372 6,484 6,450Net income from investment 2,671 2,498 -6.5% 550 736 738 436 735Other operating revenue 877 1,082 23.3% 234 317 231 300 297Retained insurance payments 11,517 13,128 14.0% 2,909 3,057 3,336 3,826 3,218Net change in liability reserve 731 626 -14.4% 275 368 287 (304) 352Commission and operating expenses 9,899 11,363 14.8% 2,486 2,833 2,822 3,241 2,885Non-Operating Income (67) (109) 63.2% (29) (22) (20) (38) (22)Income before tax 3,485 3,007 -13.7% 909 746 875 420 1,005Net income 2,911 2,420 -16.9% 783 557 696 320 826Net income to parent company 3,244 2,816 -13.2% 826 682 798 444 895

Balance sheet dataTotal assets 78,325 83,349 6.4% 77,210 74,360 80,807 83,349 86,170Investment assets 58,420 60,362 3.3% 57,042 50,800 58,247 60,362 63,377Policy reserve 40,586 44,930 10.7% 41,108 43,876 44,507 44,930 45,445Equity attributable to parent company 28,313 27,665 -2.3% 26,620 20,493 26,235 27,665 30,057

Summary ratiosReturn on average assets 3.88% 3.07% 4.02% 2.92% 3.66% 1.58% 3.90%Return on average equity 12.96% 10.06% 12.04% 11.19% 13.00% 6.35% 12.40%Total investment return 4.92% 4.21% 3.81% 5.39% 5.32% 2.94% 4.83%Solvency margin (NWP/equity) 81.69% 94.11% 90.88% 133.98% 96.62% 98.10% 87.28%Retention ratio 75.36% 76.11% 76.84% 73.48% 77.48% 76.97% 76.42%

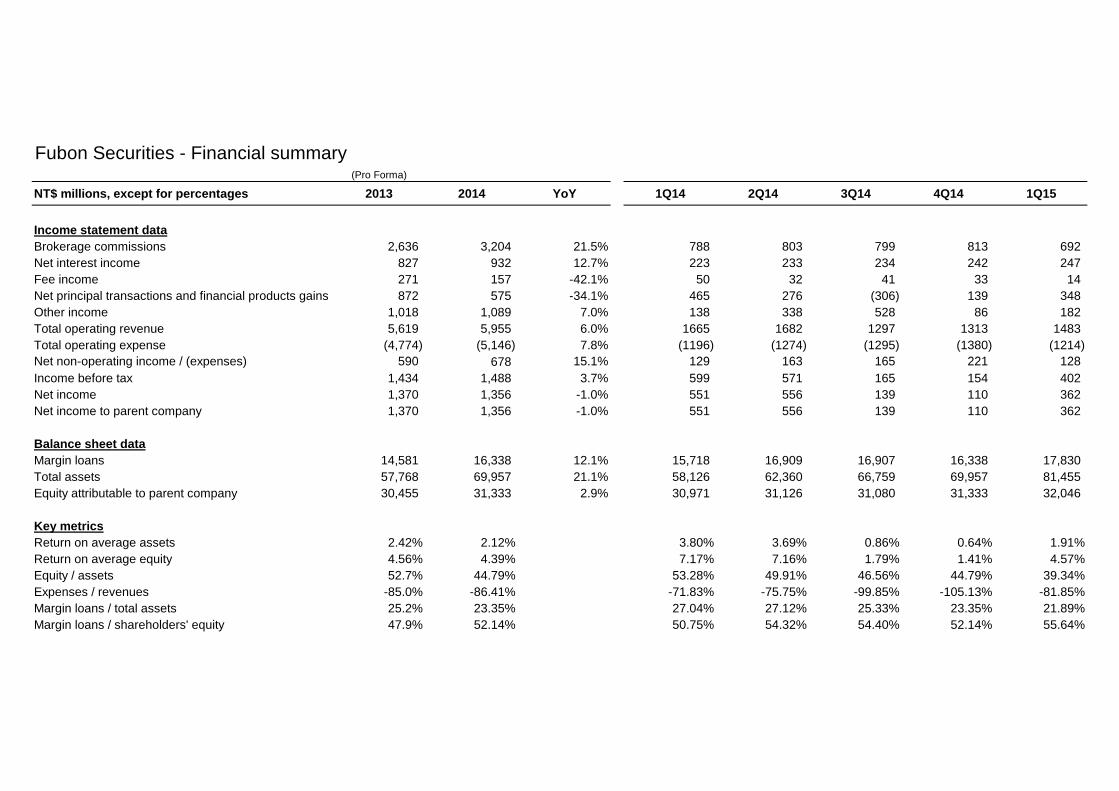

Fubon Securities - Financial summary(Pro Forma)

NT$ millions, except for percentages 2013 2014 YoY 1Q14 2Q14 3Q14 4Q14 1Q15

Income statement dataBrokerage commissions 2,636 3,204 21.5% 788 803 799 813 692Net interest income 827 932 12.7% 223 233 234 242 247Fee income 271 157 -42.1% 50 32 41 33 14Net principal transactions and financial products gains 872 575 -34.1% 465 276 (306) 139 348Other income 1,018 1,089 7.0% 138 338 528 86 182Total operating revenue 5,619 5,955 6.0% 1665 1682 1297 1313 1483Total operating expense (4,774) (5,146) 7.8% (1196) (1274) (1295) (1380) (1214)Net non-operating income / (expenses) 590 678 15.1% 129 163 165 221 128Net non-operating income / (expenses) 590 678 15.1% 129 163 165 221 128Income before tax 1,434 1,488 3.7% 599 571 165 154 402Net income 1,370 1,356 -1.0% 551 556 139 110 362Net income to parent company 1,370 1,356 -1.0% 551 556 139 110 362

Balance sheet dataMargin loans 14,581 16,338 12.1% 15,718 16,909 16,907 16,338 17,830 Total assets 57,768 69,957 21.1% 58,126 62,360 66,759 69,957 81,455 Equity attributable to parent company 30,455 31,333 2.9% 30,971 31,126 31,080 31,333 32,046

Key metricsReturn on average assets 2.42% 2.12% 3.80% 3.69% 0.86% 0.64% 1.91%Return on average equity 4.56% 4.39% 7.17% 7.16% 1.79% 1.41% 4.57%Equity / assets 52.7% 44.79% 53.28% 49.91% 46.56% 44.79% 39.34%Expenses / revenues -85.0% -86.41% -71.83% -75.75% -99.85% -105.13% -81.85%Margin loans / total assets 25.2% 23.35% 27.04% 27.12% 25.33% 23.35% 21.89%Margin loans / shareholders' equity 47.9% 52.14% 50.75% 54.32% 54.40% 52.14% 55.64%

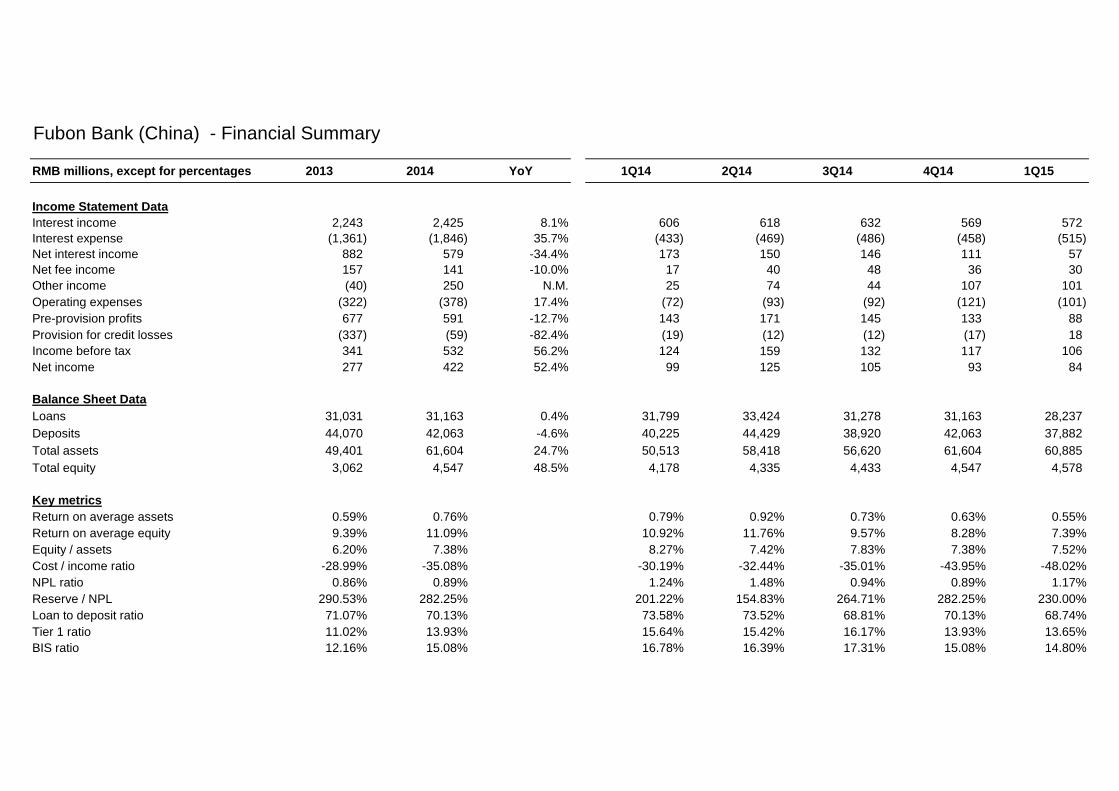

Fubon Bank (China) - Financial Summary

RMB millions, except for percentages 2013 2014 YoY 1Q14 2Q14 3Q14 4Q14 1Q15

Income Statement DataInterest income 2,243 2,425 8.1% 606 618 632 569 572Interest expense (1,361) (1,846) 35.7% (433) (469) (486) (458) (515)Net interest income 882 579 -34.4% 173 150 146 111 57Net fee income 157 141 -10.0% 17 40 48 36 30Other income (40) 250 N.M. 25 74 44 107 101Operating expenses (322) (378) 17.4% (72) (93) (92) (121) (101)Pre-provision profits 677 591 -12.7% 143 171 145 133 88Provision for credit losses (337) (59) -82.4% (19) (12) (12) (17) 18Income before tax 341 532 56.2% 124 159 132 117 106Income before tax 341 532 56.2% 124 159 132 117 106Net income 277 422 52.4% 99 125 105 93 84

Balance Sheet DataLoans 31,031 31,163 0.4% 31,799 33,424 31,278 31,163 28,237 Deposits 44,070 42,063 -4.6% 40,225 44,429 38,920 42,063 37,882 Total assets 49,401 61,604 24.7% 50,513 58,418 56,620 61,604 60,885 Total equity 3,062 4,547 48.5% 4,178 4,335 4,433 4,547 4,578

Key metricsReturn on average assets 0.59% 0.76% 0.79% 0.92% 0.73% 0.63% 0.55%Return on average equity 9.39% 11.09% 10.92% 11.76% 9.57% 8.28% 7.39%Equity / assets 6.20% 7.38% 8.27% 7.42% 7.83% 7.38% 7.52%Cost / income ratio -28.99% -35.08% -30.19% -32.44% -35.01% -43.95% -48.02%NPL ratio 0.86% 0.89% 1.24% 1.48% 0.94% 0.89% 1.17%Reserve / NPL 290.53% 282.25% 201.22% 154.83% 264.71% 282.25% 230.00%Loan to deposit ratio 71.07% 70.13% 73.58% 73.52% 68.81% 70.13% 68.74%Tier 1 ratio 11.02% 13.93% 15.64% 15.42% 16.17% 13.93% 13.65%BIS ratio 12.16% 15.08% 16.78% 16.39% 17.31% 15.08% 14.80%

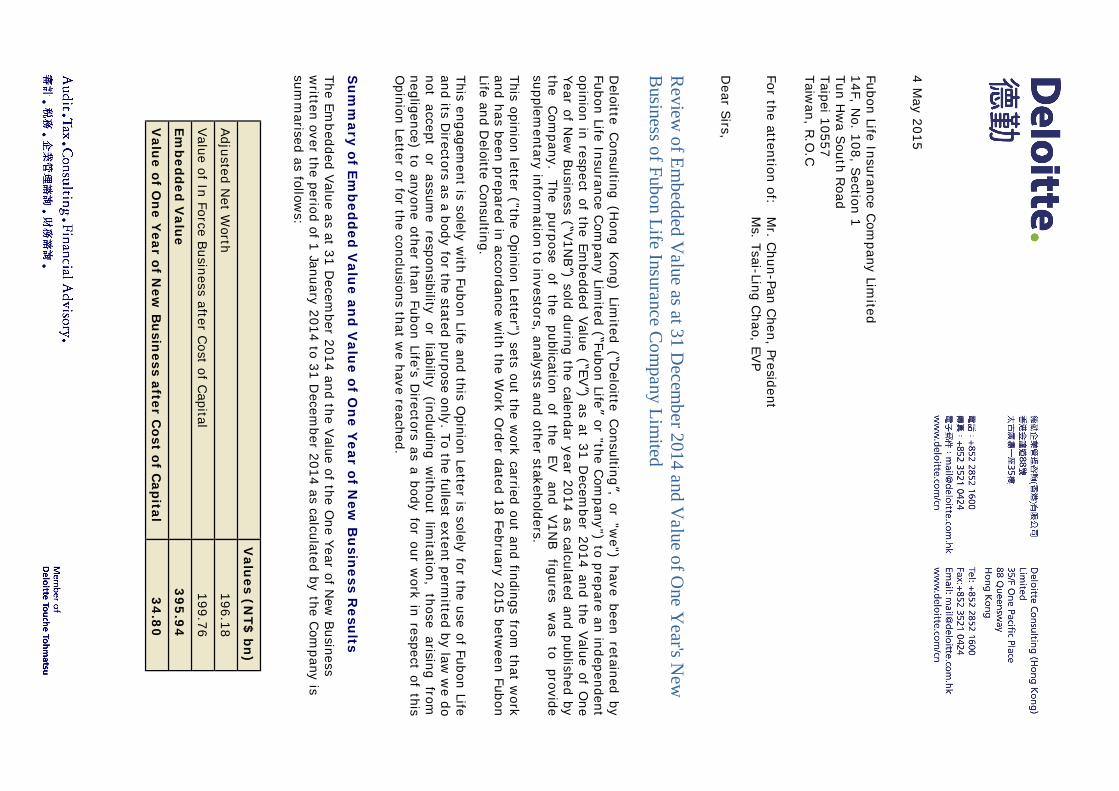

4 M

ay 2015

Fubon Life Insurance Com

pany Limited

14F, No. 108, Section 1

Tun Hw

a South Road

Taipei 10557 Taiw

an, R.O.C

For the attention of: M

r. Chun-Pan C

hen, President

Ms. Tsai-Ling C

hao, EVP D

ear Sirs,

Review

of Embedded V

alue as at 31 Decem

ber 2014 and Value of O

ne Year's N

ew

Business of Fubon Life Insurance C

ompany Lim

ited D

eloitte Consulting (H

ong Kong) Lim

ited (“Deloitte C

onsulting”, or "we") have been retained by

Fubon Life Insurance Com

pany Limited (“Fubon Life” or "the C

ompany") to prepare an independent

opinion in respect of the Embedded Value (“EV”) as at 31 D

ecember 2014 and the Value of O

ne Year of N

ew Business (“V1N

B”) sold during the calendar year 2014 as calculated and published by the

Com

pany. The

purpose of

the publication

of the

EV and

V1NB

figures w

as to

provide supplem

entary information to investors, analysts and other stakeholders.

This opinion letter ("the Opinion Letter") sets out the w

ork carried out and findings from that w

ork and has been prepared in accordance w

ith the Work O

rder dated 18 February 2015 between Fubon

Life and Deloitte C

onsulting.

This engagement is solely w

ith Fubon Life and this Opinion Letter is solely for the use of Fubon Life

and its Directors as a body for the stated purpose only. To the fullest extent perm

itted by law w

e do not accept or assum

e responsibility or liability (including without lim

itation, those arising from

negligence) to anyone other than Fubon Life's Directors as a body for our w

ork in respect of this O

pinion Letter or for the conclusions that we have reached.

Su

mm

ary of Em

bed

ded

Valu

e and

Valu

e of On

e Year of N

ew B

usin

ess Resu

lts The Em

bedded Value as at 31 Decem

ber 2014 and the Value of the One Year of N

ew Business

written over the period of 1 January 2014 to 31 D

ecember 2014 as calculated by the C

ompany is

summ

arised as follows:

V

alues (N

T$ bn)

Adjusted Net W

orth 196.18

Value of In Force Business after Cost of C

apital 199.76

Emb

edded V

alue

39

5.9

4

Valu

e of On

e Year of N

ew B

usin

ess after Cost of C

apital 3

4.8

0

2

Defin

ition

s A num

ber of specific terms are used in this O

pinion Letter. They are defined as follows:

• Em

bedded Value ("EV"): this is the sum of the Adjusted N

et Worth and Value of In Force

Business as at the valuation date. It includes no allowance for the value of future business yet

to be written;

• Adjusted N

et Worth ("AN

W"): this represents the shareholder equity in the enterprise as at the

valuation date. This is equal to the shareholder equity as reported in its Taiwan statutory

balance sheet plus several adjustment item

s. The purpose of the adjustments is to m

ake the Adjusted N

et Worth consistent w

ith the projection of future profits and Cost of C

apital;

• Value of In Force Business ("VIF"): this is equal to the present value as at valuation date of the future statutory profits from

the business in force as at the valuation date using a risk adjusted discount rate, less the C

ost of Capital associated with such business;

• Appraisal Value ("AV"): this is the sum

of the Embedded Value and Value of Future N

ew

Business as at the valuation date. It represents an assessment of the econom

ic value of the com

pany on a going concern basis using best estimate assum

ptions and a discounted cash flow

approach;

• Value of O

ne Year of New

Business ("V1NB"): this is equal to the present value as at the policy

issue dates of the future statutory profits from the policies sold in 2014 less the C

ost of Capital associated w

ith such business;

• Value of Future N

ew Business ("VN

B"): this is equal to the present value as at the issue date of the future statutory profits from

policies assumed to be sold in the future less the C

ost of Capital associated w

ith such business. One of the com

mon calculation approaches is to m

ultiply the Value of O

ne Year of New

Business by a new business m

ultiplier. The new business

multiplier reflects an assessm

ent of the company's future new

business volume, the profitability

of such new business and the uncertainty in achieving such volum

e and profitability.

• Cost of C

apital: this is defined as the amount of capital required to be held at the valuation date

less the present value of future releases of such capital and after-tax earnings on the assets backing it. The level of capital required depends on the C

ompany's internal target of capital

level but is subject to the minim

um of statutory requirem

ent.

This Opinion Letter does not give any opinion on the “fair m

arket value” of any part or the whole of

the Com

pany. Actual market values are determ

ined by investors based on a variety of information

available to them and their ow

n investment criteria.

The techniques for calculating a company’s Em

bedded Value and the Value of One Year of N

ew

Business have

been evolving

over the

last 20

years.

The Com

pany has

used “traditional”

techniques. This is a comm

on approach in Taiwan w

hich is consistent with the m

ethodology used by all local dom

estically-owned com

panies which publish their Em

bedded Values. This method does

not include an explicit allowance for the cost of options and guarantees w

ithin the business. Instead,

this approach

makes

an im

plicit allow

ance for

the tim

e value

cost of

options and

guarantees and other risks associated with the realisation of the projected future profits through the

use of a risk adjusted discount rate.

Sco

pe of R

eview

The scope of our review is outlined as follow

s:

• Review

and opine on the reasonableness of the EV and V1NB as calculated by the C

ompany;

• Review

of the reasonableness of the assumptions used in the calculations, taking into

consideration both Com

pany’s recent experience and the experience of the Taiwanese life

insurance market;

• Review

of the Com

pany’s projection approach of the Cost of C

apital;

• Review

, at a high-level, of the changes made to the actuarial projection m

odel by the Com

pany since the previous valuation date of 31 D

ecember 2013;

3

• Review

of the data put through the model com

pared to the policy data on the Com

pany’s policy adm

inistration systems to judge the extent to w

hich the business has been valued in the financial m

odel and to identify the portion (if any) omitted and how

that was valued;

• Review

of the approach used to determine the Adjusted N

et Worth (“AN

W”), in particular, the

adjustments m

ade in deriving the ANW

, and any other adjustments m

ade outside of the actuarial projection m

odel;

• Review

of the Com

pany's analysis of change in the VIF between 31 D

ecember 2013 and 31

Decem

ber 2014.

The scope of our review did not include the follow

ing aspects:

• Review

of the policy data on the Com

pany’s administration system

s;

Our review

did not cover an audit of the accuracy or completeness of the policy data item

s and w

e offer no comm

ent on the quality of the policy data used by the Com

pany in the valuation, and readers should not assum

e our review verifies the data is free from

error.

• Review

or audit of the valuation of the assets or any items unless specifically stated on the

Com

pany’s balance sheet;

We referred to the C

ompany’s audited financial statem

ents and placed reliance on them.

• Review

of the calculation of the RBC

(risk based capital) of the Com

pany as at 31 Decem

ber 2014; and

Whilst w

e reviewed the projection of the R

BC into future periods, w

e relied on the accuracy and com

pleteness of the starting RBC

figures as at 31 Decem

ber 2014 as submitted by the C

ompany

to the Taiwanese regulator.

• Any other actuarial or other valuation figures, such as an Appraisal Value, Value of Future N

ew

Business, New

Business Multiplier, or any “Fair Value” or potential transaction price.

Only the EV

and V1NB fell in the scope of our review

, and we offer no opinion on any other

values.

Our review

was conducted in accordance w

ith current generally accepted actuarial practices and processes for review

s of traditional Embedded Value calculations. In particular, w

e made reference

to the methods, approach and other considerations as set out in:

• The relevant parts of Practice G

uideline 199.03 of the Institute of Actuaries of Australia entitled “Econom

ic Valuations”; and

• Professional C

onduct Standards as defined by the Professional Affairs Board of the Institute and Faculty of Actuaries in the U

K.

Find

ing

s from

ou

r Review

O

ur findings are summ

arised as follows:

• W

ith respect to the calculation methodology adopted by the C

ompany in the calculations:

− The chosen traditional EV m

ethodology used by the Com

pany has been applied in line with

generally accepted actuarial practice and relevant guidance; and

− The m

ethodology was in line w

ith the purpose stated by the Com

pany, and is consistent w

ith a “going concern” approach.

• W

ith respect to the policy data used in the calculations:

− The C

ompany has used policy data that is, in aggregate, consistent w

ith the policy data held on the C

ompany's adm

inistration systems as at the appropriate dates.

• W

ith respect to the actuarial projection and valuation systems and the results produced by the

Com

pany:

4

− O

ver 99% of the policy data has been included in the valuation and a zero value has been

assigned to that part which w

as not included in the valuation;

− At the aggregate level, the m

odel outputs for each major block of business that w

e reviewed

appear to be consistent with the assum

ptions applied in the calculations, the features of the products

included in

each block

of business,

the prevailing

applicable and

relevant regulations in Taiw

an.

• W

ith respect to the assumptions used in the calculations:

− The assum

ptions, taken as a whole, are reasonable for the C

ompany and the environm

ent in w

hich it conducts business;

− The econom

ic assumptions, including rate of investm

ent return, risk adjusted discount rate and inflation rate, w

ere set consistently with one another and w

ith the way in w

hich the adjusted net w

orth was calculated;

− The econom

ic assumptions represent plausible future outcom

es for expected future total returns (including the release of risk m

argins) and lie within a reasonable range of such

plausible future outcomes; and

− The non-econom

ic assumptions have been set w

ith regard to relevant actual historical experience of both the C

ompany and the industry, and the C

ompany has provided plausible,

reasoned arguments in relation to their expectations of future trends and developm

ents for these assum

ptions.

• W

ith respect to the calculation of the Adjusted Net W

orth:

− The C

ompany has m

ade adjustments to the N

et Worth as reported on the statutory balance

sheet which are appropriate for the purpose of this valuation.

In conclusion, we find the results of the Em

bedded Value and Value of One Year of N

ew Business

calculated by the Com

pany to be reasonable within the purpose and chosen m

ethodology of their calculation,

and that

the m

ethodology is

consistent w

ith the

approach taken

by all

local dom

estically-owned life insurers w

hich publish similar figures in Taiw

an and with one generally

accepted method for their calculation.

In stating the above opinion, we draw

attention to the uncertainty related to such calculations.

The calculations of EV and V1NB results necessarily m

ake numerous assum

ptions with respect to

economic conditions, operating conditions, taxes and other m

atters, many of w

hich are not fully w

ithin the control of the Com

pany. Although the assumptions used represent estim

ates which fall

within a reasonable range of expectations, actual experience in the future is alm

ost certain to vary from

that assumed in the calculation of the results and any such variations m

ay be material.

Deviations from

assumed experience are norm

al and are to be expected.

We note, and draw

the attention of readers to the sensitivity of the results to assumptions, and in

particular, to the assumed rate of future investm

ent return and the risk discount rate; this is illustrated quantitatively in the C

ompany's disclosures. A deviation from

the assumed future

investment return, even still w

ithin a reasonably plausible range of such assumptions, m

ay lead to a m

aterially different result. We note that future investm

ent returns are subject to market factors

beyond the control of the Com

pany and hence it is not possible for the Com

pany to fully imm

unise future profitability against m

ovements in future investm

ent returns.

Yours faithfully,

Deloitte C

onsulting (Hong K

ong) Limited