Embed Size (px)

Citation preview

Guide to preparing the 2015-16Portfolio Budget StatementsGovernance and Resource Management Group

ATTACHMENT A TO EM 2015/09 | MARCH 2015

Guide to preparing the 2015-16Portfolio Budget StatementsGovernance and Resource Management Group

ATTACHMENT A TO EM 2015/XX | MARCH 2015

Contents

Contents 2

1. Overview 41.1 Purpose 41.2 Who should prepare PB Statements 41.3 Structure 51.4 Sourcing information 71.5 Clearance processes 7

2. Publication requirements 92.1 Security requirements 92.2 Which printer to use and printing specifications 92.3 Delivery to Lockup, the Senate, House of Representatives, Treasury and

Finance 102.4 Online publication 13

Guidance on the preparation of the 2015-16 PB Statements 17

3. Portfolio Overview section 183.1 Minister(s) and portfolio responsibilities 183.2 Portfolio structure and outcomes 183.3 Portfolio resources made available in the Budget year 19

4. Entity Overview and Resources section 214.1 Strategic direction statement 214.2 Entity resource statement 214.3 Budget measures 24

5. Outcomes and planned performance section 285.1 Outcome strategy statement 295.2 Outcome expense statement 295.3 Programme reporting 315.4 Programme objective 335.5 Programme expenses 34

Contents

5.6 Programme components 365.7 Programme deliverables 365.8 Programme key performance indicators 37

6. Explanatory tables and budgeted financial statements section 396.1 Movement of administered funds between years 406.2 Estimates of special account flows and balances 406.3 Australian Government Indigenous expenditure 416.4 Budgeted financial statements 426.5 Departmental comprehensive income statement (showing net cost of

services) 436.6 Budgeted departmental balance sheet 446.7 Departmental statement of changes in equity 446.8 Budgeted statement of cash flows 446.9 Departmental capital budget statement 446.10 Departmental statement of asset movements 456.11 Schedule of budgeted income and expenses administered on behalf of

Government 456.12 Schedule of budgeted assets and liabilities administered on behalf of

Government 466.13 Schedule of budgeted administered cash flows 466.14 Schedule of administered capital budget statement 466.15 Schedule of administered asset movements 47

7. Related issues 487.1 Machinery of government changes 487.2 Programme and outcome changes 527.3 Working with the templates 527.4 Preparing the Word template for printing 567.5 Preparing the Word template for online publication 567.6 Web accessibility requirements 577.7 Additional guidance on ACM Reports and Appropriation Bills 58

8. Contacts 60

9. Glossary of terms 62

1.

Guide to preparing the 2015-16 Portfolio Budget Statements

1.1 PurposeThe Portfolio Budget Statements (PB Statements) are formal ministerial documents,. Together with the Budget Papers, PB Statements represent a package of documents tabled in Parliament on Budget night, which explain the Government’s budget decisions.

The Appropriation Acts refer to the PB Statements as ‘relevant documents’ to the interpretation of the Acts, according to section 15AB of the Acts Interpretation Act 1901. The PB Statements provide additional explanation to the Appropriation Bills and as a result, they must be consistent with the Bills, which once passed by Parliament, become law as Appropriation Acts. Should a discrepancy occur between the Appropriation Acts and the PB Statements, it is the Appropriation Acts that are definitive.

The PB Statements also provide further information (financial and non-financial) at the Portfolio and entity level about the ongoing policy and programme delivery initiatives of the Government.

PB Statements are signed by the respective Portfolio Minister. Signing and arrangements for PB Statements will be determined by the senior Portfolio Minister (the first minister shown in the current Ministry List issued by the Department of the Prime Minister and Cabinet at https://www.dpmc.gov.au/pmc/parliamentary- information).

1.2 Who should prepare PB StatementsAll Commonwealth entities which receive funding through the annual Appropriation Acts (whether directly or through a portfolio department) must be included in the PB Statements. Entities will normally be shown as separate chapters in the PB Statements, unless they are in the process of being merged or consolidated into another.

Where there is more than one department in a portfolio, senior Portfolio Ministers determine how the portfolio should be represented, i.e. whether there is to be a book for each department, or one consolidated book for the portfolio.

Entities are to use the following Portfolio numbers for the covers of their PB Statements:

Guide to preparing the 2015-16 Portfolio Budget Statements

1.1 Agriculture Portfolio

1.2 Attorney-General’s Portfolio

1.3 Communications Portfolio

1.4A Defence Portfolio

1.4B Defence Portfolio (Department of Veterans’ Affairs)

1.5 Education and Training Portfolio

1.6 Employment Portfolio

1.7 Environment Portfolio

1.8 Finance Portfolio

1.9 Foreign Affairs and Trade Portfolio

1.10 Health Portfolio

1.11 Immigration and Border Protection Portfolio

1.12 Industry and Science Portfolio

1.13 Infrastructure and Regional Development Portfolio

1.14 Prime Minister and Cabinet Portfolio

1.15A Social Services Portfolio

1.15B Social Services Portfolio (Department of Human Services)

1.16 Treasury Portfolio

1.17A Department of the House of Representatives

1.17B Department of the Senate

1.17C Department of Parliamentary Services

1.17D Parliamentary Budget Office

1.3 StructureThe PB Statements contain four levels of information: Portfolio, Entity, Outcome and Programme. To ensure that PB Statements are clear and concise, it is important for entities to include information where it is most relevant. Guidance on the information required in each section of the PB Statements is included throughout this document.

Entities should aim to produce PB Statements that presents three key messages:

What does the Government (through the entity) want to achieve? How and through what means it proposes to achieve this? How will it know if it is succeeding or making progress?

Entities can publish additional information that goes beyond the requirements of the PB Statements on their websites.

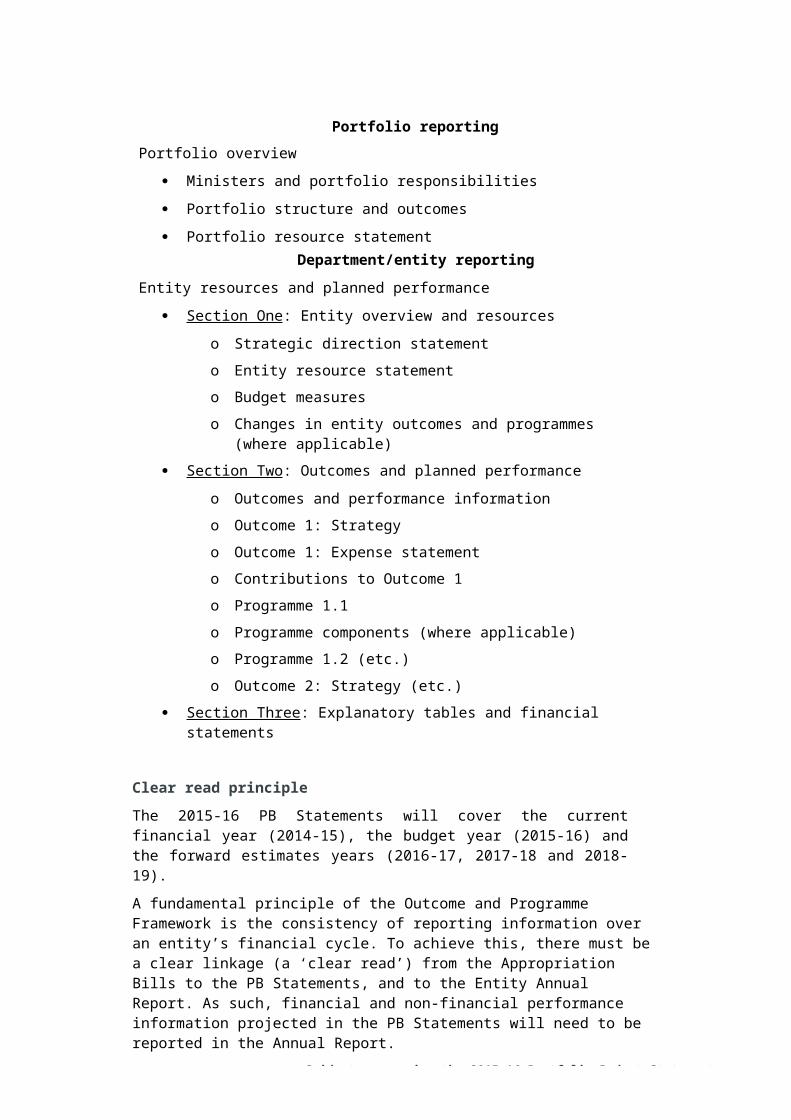

The 2015-16 Portfolio Budget Statements will have the following structure:

Guide to preparing the 2015-16 Portfolio Budget Statements

Portfolio reporting

Portfolio overview

Ministers and portfolio responsibilities

Portfolio structure and outcomes

Portfolio resource statement

Department/entity reporting

Entity resources and planned performance

Section One : Entity overview and resources

o Strategic direction statement

o Entity resource statement

o Budget measures

o Changes in entity outcomes and programmes (where applicable)

Section Two : Outcomes and planned performance

o Outcomes and performance information

o Outcome 1: Strategy

o Outcome 1: Expense statement

o Contributions to Outcome 1

o Programme 1.1

o Programme components (where applicable)

o Programme 1.2 (etc.)

o Outcome 2: Strategy (etc.)

Section Three : Explanatory tables and financial statements

o Explanatory tables

o Budgeted financial statements

Glossary (optional)

Clear read principleThe 2015-16 PB Statements will cover the current financial year (2014-15), the budget year (2015-16) and the forward estimates years (2016-17, 2017-18 and 2018-19).

A fundamental principle of the Outcome and Programme Framework is the consistency of reporting information over an entity’s financial cycle. To achieve this, there must be a clear linkage (a ‘clear read’) from the Appropriation Bills to the PB Statements, and to the Entity Annual Report. As such, financial and non-financial performance information projected in the PB Statements will need to be reported in the Annual Report.

From 2014-15, the new accounting standard AASB 1055 Budgetary Reportingrequires entities to include budgetary information for the original Budget (from the

Guide to preparing the 2015-16 Portfolio Budget Statements

PB Statements) and revised Budget (from a portfolio statement update) in their financial statements, accompanied with variance explanations. The explanations will be audited by the ANAO as part of their audit of the annual financial statements. Consequently, entities are reminded of the importance of maintaining internal documentation in order to substantiate the basis of the estimates included in the PB Statements.

1.4 Sourcing informationThe financial information reported in the PB Statements must match with the figures in the Central Budget Management System (CBMS).

CBMS is the central source of budget information and is the basis of whole-of- government figures, the Appropriation Bills, financial data and Budget Papers Nos. 1-4. As such, all appropriation figures must be sourced from CBMS to ensure consistency between the PB Statements, the Appropriation Bills and the Budget Papers.

An entity’s financial management information system may be used to supplement information in CBMS, particularly if information to be published as a lower level in the PB Statements.

1.5 Clearance processesPortfolios do not need to provide their whole PB Statements document to Finance for checking.

Certain material, however, needs to match exactly the information contained elsewhere in the Budget Papers for which the Treasurer and Minister for Finance are responsible. This includes information on the appropriations and the measures tables. To the extent that information in the PB Statements describes measures published in Budget Paper (BP) No.2, it must be consistent with the measures descriptions in BP No.2 and the PB Statements should not be printed until BP No.2 is cleared.

Table 1.2: Budget measures should be provided to your Finance Agency Advice Unit (AAU) for checking against measures descriptions and Appropriation Bills reports prior to the PB Statements being printed.

Portfolio entities are responsible for ensuring the accuracy and completeness of the information contained in their PB Statements, including the presentation of information that is consistent with CBMS. The following areas should be checked by entities prior to publication:

the PB Statements are completed in accordance with the guidance and templates provided;

the measures table matches the final measures list provided by your Finance AAU;

the Average Staffing Level (ASL) numbers match the numbers published in BP 4;

all Bills information matches to the Appropriation Bill Schedule produced by the Appropriation Bill report from BEAM; and

the relevant Chief Finance Officer (CFO) sign-offs on Bills and estimates have been provided to your Finance AAU.

Guide to preparing the 2015-16 Portfolio Budget Statements

Guide to preparing the 2015-16 Portfolio Budget Statements

2. Publication requirements

2.1 Security requirementsThe PB Statements are classified as Protected and under embargo up until the time they are tabled in Parliament and publicly released. The Treasurer has endorsed this classification and it is the responsibility of each portfolio entity to ensure appropriate security arrangements are made. If staff are unsure of the correct security processes during the budget preparation period, they should contact their entity security adviser.

Issues to keep in mind include:

PB Statements should be prepared in an area of the entity appropriate for managing Protected material.

PB Statements documentation should under no circumstances be distributed via unsecure electronic mail.

The ‘need to know’ principle should be applied in the distribution of all material.

PB Statements should not be prepared by external companies or contractors who cannot demonstrate that their premises meet the security standards for protected information as provided by the Protective Security Policy Framework (http://www.protectivesecurity.gov.au).

If you have any questions regarding security issues please speak to the security adviser in your entity.

2.2 Which printer to use and printing specifications

SpecificationsHard copies of the PB Statements must be produced on standard B5 size paper (17.6 cm x 25 cm) with a font point size of at least 10 point and using the styles provided in the templates (Attachments B to D) to ensure that the statements are consistent with other budget documents and related papers.

For the covers, entities must use ‘Tablex System Board 200gsm – Yellow” paper with the cover text in black.

For consistency, all portfolios must have the portfolio name made clearly visible on the spine of the documents.

Printer

It is strongly recommended that portfolio departments contact CanPrint to arrange printing for the PB Statements. If printing is carried out ‘in-house’, entities must liaise with Finance and CanPrint to ensure that cover stock, colour and text is consistent with all other Portfolio Entities.

Guide to preparing the 2015-16 Portfolio Budget Statements

It is the responsibility of each portfolio department to arrange the printing and secure freighting of their PB Statements. The contact officers for CanPrint Communications Pty Ltd are Peter Reid and Andrew Brien on (02) 6295 4450.

Portfolios should make sure they have sufficient hard copies of their PB Statements for their own internal needs, and make additional hard copies of their PB Statements available on request to other stakeholders, not including the distribution requirements listed below, such as:

Other departments and relevant entities;

Major client organisations; and

The libraries of tertiary institutions.

ClassificationPlease be aware that the PB Statements are classified as Protected documents until they are tabled in Parliament. Accordingly boxes of the PB Statements should be labelled as follows:

Protected – Budget 2015-16Under Embargo until 20:15 hours 12 May 2015

2.3 Delivery to Lockup, the Senate, House of Representatives, Treasury and Finance

Portfolio departments are to deliver printed copies of the PB Statements to the Senate and House of Representatives Tabling Offices, the Treasury lock-up and Finance by COB Monday, 11 May 2015.

Due to security measures that preclude access of non-authorised vehicles at the entrances to Parliament House, delivery arrangements for PB Statements will be as follows:

If a portfolio department prints in-house or with a printer other than CanPrint they must arrange for an officer of the entity to deliver the copies of PB Statements for the Senate and the House of Representatives to the Documents Officer, Senate Table Office, SG 25.

Entity officers who deliver the Statements will require Commonwealth Officer passes and trolleys to transfer the documents from the car park to SG 25. Boxes will have to be x-rayed by security at the entrance—entity officers will be required to unload and reload the boxes at this point.

If you have any queries about or difficulties with these arrangements, please contact the Documents Officer, Senate Table Office. (Phone: (02) 6277 3037)

Guide to preparing the 2015-16 Portfolio Budget Statements

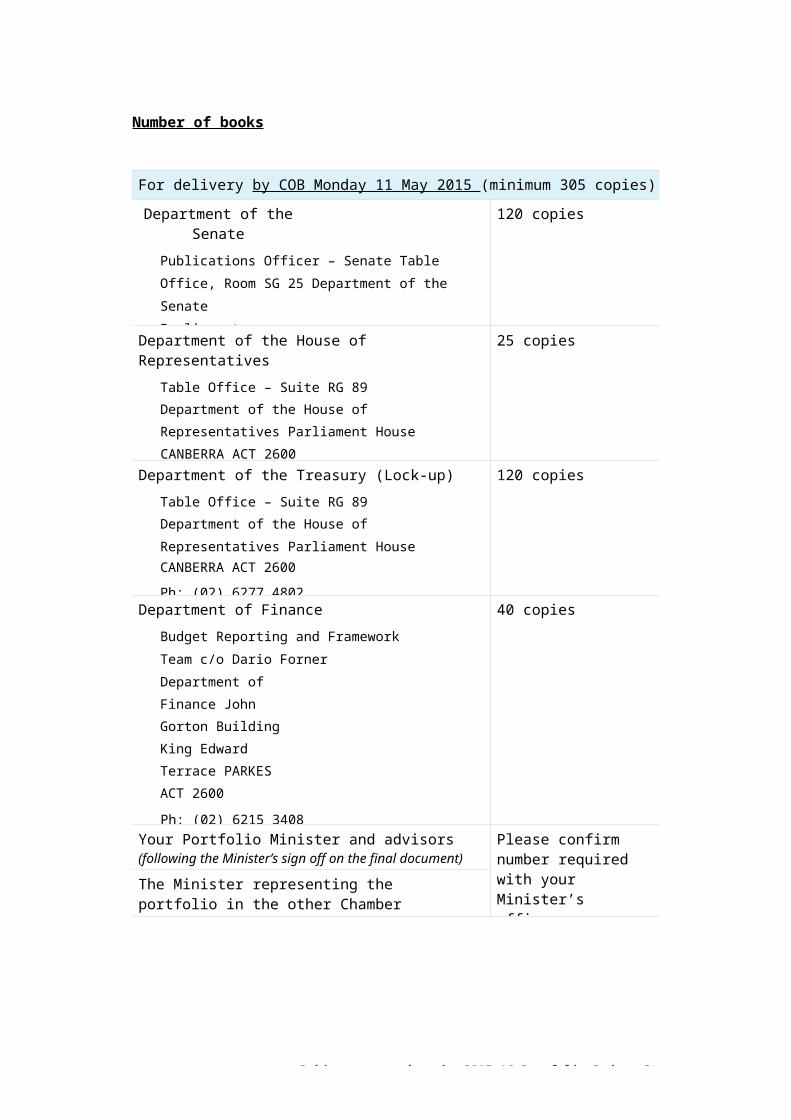

Number of books

For delivery by COB Monday 11 May 2015 (minimum 305 copies)

Department of the Senate

Publications Officer – Senate Table Office, Room SG 25

Department of the Senate

Parliament House

CANBERRA ACT 2600

Ph: (02) 6277 3037

120 copies

Department of the House of Representatives

Table Office – Suite RG 89

Department of the House of Representatives Parliament HouseCANBERRA ACT 2600

Ph: (02) 6277 4802

25 copies

Department of the Treasury (Lock-up)

Table Office – Suite RG 89

Department of the House of Representatives

Parliament HouseCANBERRA ACT 2600

Ph: (02) 6277 4802

120 copies

Department of Finance

Budget Reporting and Framework Team

c/o Dario Forner

Department of Finance John Gorton Building King Edward Terrace PARKES ACT 2600

Ph: (02) 6215 3408

NB: PB Statements must be delivered to the Budget Reporting and Framework Team – no PB Statements should be delivered to the AAU.

40 copies

Your Portfolio Minister and advisors (following the Minister’s sign off on the final document)

Please confirm number required with your Minister’s office

The Minister representing the portfolio in the other Chamber

Guide to preparing the 2015-16 Portfolio Budget Statements

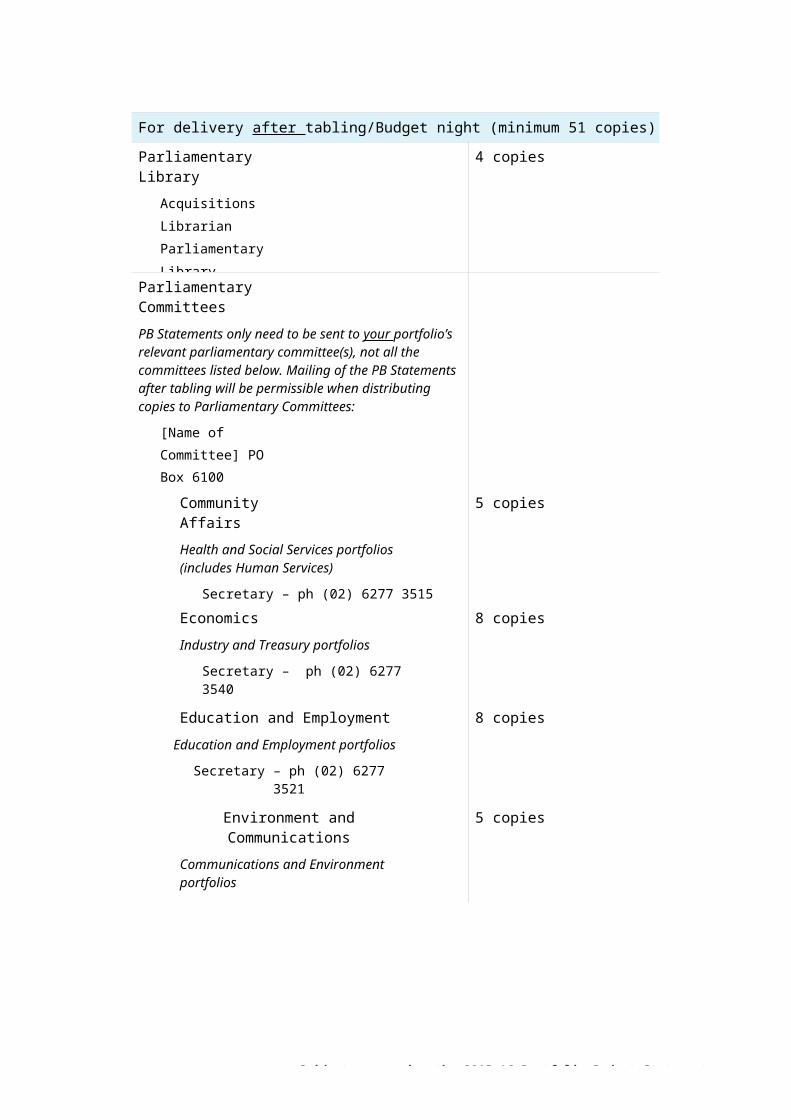

For delivery after tabling/Budget night (minimum 51 copies)

Parliamentary Library

Acquisitions Librarian

Parliamentary Library

Department of Parliamentary Services

Parliament HouseCANBERRA ACT 2600

4 copies

Parliamentary Committees

PB Statements only need to be sent to your portfolio’s relevant parliamentary committee(s), not all the committees listed below. Mailing of the PB Statements after tabling will be permissible when distributing copies to Parliamentary Committees:

[Name of Committee] PO Box 6100Parliament House Canberra ACT 2600 Australia

Community Affairs

Health and Social Services portfolios (includes Human Services)

Secretary – ph (02) 6277 3515

Estimates – ph (02) 6277 3515

5 copies

Economics

Industry and Treasury portfolios

Secretary – ph (02) 6277 3540

Estimates – ph (02) 6277 3540

8 copies

Education and Employment

Education and Employment portfolios

Secretary – ph (02) 6277 3521

Estimates – ph (02) 6277 3437

8 copies

Environment and Communications

Communications and Environment portfolios

Secretary – ph (02) 6277 3526

Estimates – ph (02) 6277 3528

5 copies

Guide to preparing the 2015-16 Portfolio Budget Statements

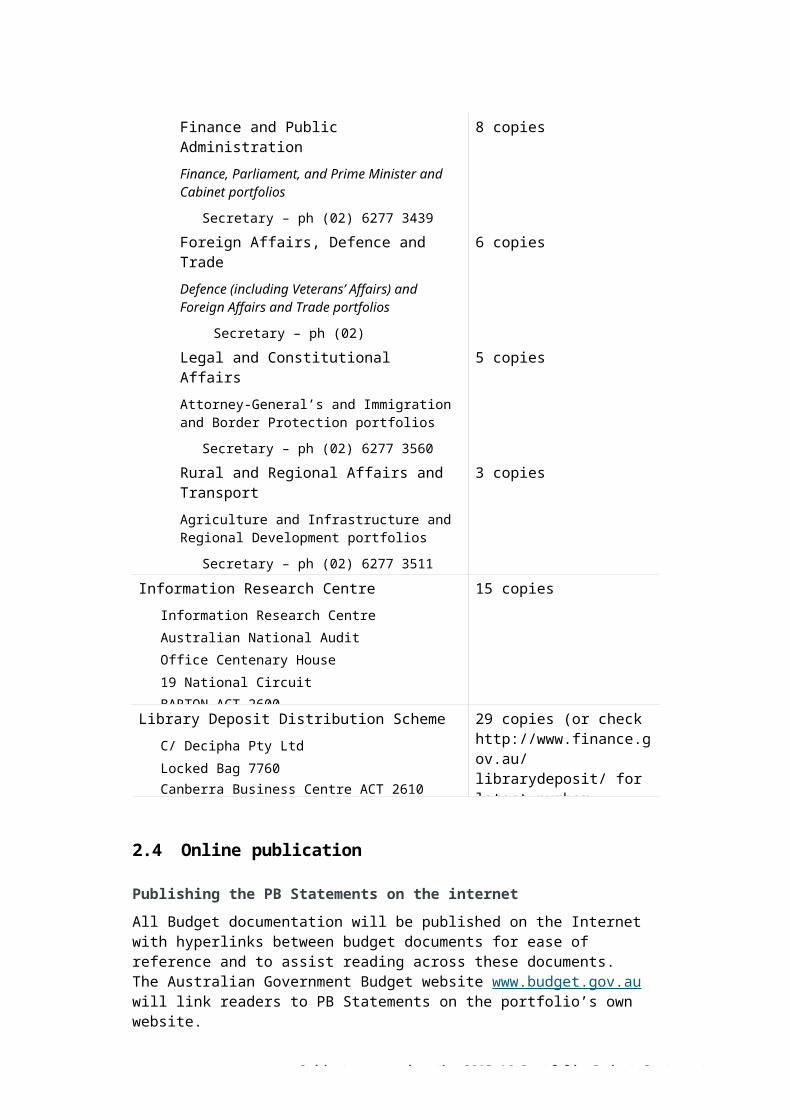

Finance and Public Administration

Finance, Parliament, and Prime Minister and Cabinet portfolios

Secretary – ph (02) 6277 3439

Estimates – ph (02) 6277 3534

8 copies

Foreign Affairs, Defence and Trade

Defence (including Veterans’ Affairs) and Foreign Affairs and Trade portfolios

Secretary – ph (02) 6277 3535

Estimates – ph (02) 6277 3536

6 copies

Legal and Constitutional Affairs

Attorney-General’s and Immigration and Border Protection portfolios

Secretary – ph (02) 6277 3560

Estimates – ph (02) 6277 3498

5 copies

Rural and Regional Affairs and Transport

Agriculture and Infrastructure and Regional Development portfolios

Secretary – ph (02) 6277 3511

Estimates – ph (02) 6277 3511

3 copies

Information Research Centre

Information Research Centre Australian National Audit Office Centenary House19 National Circuit

BARTON ACT 2600

15 copies

Library Deposit Distribution Scheme

C/ Decipha Pty Ltd

Locked Bag 7760Canberra Business Centre ACT 2610

29 copies (or check http://www.finance.gov.au/ librarydeposit/ for latest number required)

2.4 Online publication

Publishing the PB Statements on the internetAll Budget documentation will be published on the Internet with hyperlinks between budget documents for ease of reference and to assist reading across these documents. The Australian Government Budget website www.budget.gov.au will link readers to PB Statements on the portfolio’s own website.

All portfolios must to post their electronic copy of the PB Statements to their portfolio department’s website. This should be posted in an accessible format as

Guide to preparing the 2015-16 Portfolio Budget Statements

required by the Web Content Accessibility Guidelines issued by Finance (for example, post the document in multiple formats to be sure it can be read by screen readers). The Web Content Accessibility Guidelines and other publishing requirements and guidance are available at http://webguide.gov.au/accessibility- usability/accessibility/. See Section 7.6 of this guidance for more information on making the PB Statements web accessible.

Portfolios should email the Treasury Web Content team ([email protected]) by no later than close of business Monday, 11 May 2015 with details of:

the URL address where the portfolio will post its PB Statements;

contact details for the author of the PB Statements; and

contact details for the portfolio’s webmaster.

Portfolio departments should ensure the above information is forwarded on to their internal Web Publishing area for action.

PB Statements should not be uploaded onto portfolio departments ‘websites until they are tabled in the Senate (note, no PB Statements will be tabled in the Senate until the Appropriation Bills are tabled in the House of Representatives).

Entities can check the tabling status by referring to the Department of the Senate’s Dynamic Red page: http://www.aph.gov.au/Parliamentary_Business/Chamber_documents/Dynami c_Red

Portfolio departments are to scroll down the page until they find the note referencing the ‘2015-16 Portfolio Budget Statements’. The light red column on the right hand side of the entry will show the time the documents were tabled. Please note that no Portfolio will be separately identified.

It is anticipated that this notice will appear on the Dynamic Red website around 8.15pm on Tuesday, 12 May 2015. If there is any doubt as to whether the PB Statements have been tabled, please call the Senate enquiries number ((02) 6277 3010) who will be able to provide the necessary advice.

Please note that the PB Statements are not archived on the Budget.gov.au website – portfolio departments should ensure electronic copies of past PB Statements remain available on their websites.

Standard file-naming conventionPortfolios should follow a consistent file-naming convention for electronic copies of the PB Statements as outlined below to aid file comprehension and retrieval for readers who download the documents, and to remove the confusion that occurs when files are not clearly named or numbered.

An example of the recommended convention is:

FinancialYear + Portfolio + ’PBS’ + a file sequence number (i.e. 01, 02 etc)+Chapter Number (or entity name/acronym, etc)

Examples would be:

2014-15_DBCDE_PBS_01_Parts_A_and_B

Guide to preparing the 2015-16 Portfolio Budget Statements

2014-15_DBCDE_PBS_10_ABC

2014-15_Health_PBS_05_Outcome3

Note: The file sequence number simply indicates which file would be read first, second, third etc if the document was read like a book. Naming the files in this way means that the order of files downloaded into a sub-directory would be the same order as the order of presentation of chapters in the PB Statements.

This would result in the electronic files being listed in the same order as the printed chapters, and therefore easier and more intuitive navigation for those accessing the files.

Open Government Initiative – publication on data.gov.auAs part of the Government’s Open Government initiative to increase Budget transparency, portfolio departments are now required to provide a copy of finalised PB Statements tables for publication on Data.gov.au under the default Australian Government license (Creative Commons BY 3.0 AU).

The PB Statements tables, as received from portfolios, will be published on Data.gov.au in Excel workbook format, with a separate workbook for each entity.

The collection of PB Statements financial tables will be published on a single page for ease of discoverability and access, by the media and the public, managed by Finance.

This requirement is designed to satisfy the Government’s direction regarding the proactive publishing of government data in a format that facilitates public access and promotes more efficient data sharing and analysis across government, as detailed in the Coalition's E-Government and Digital Economy Policy.

The following financial tables with headings and footnotes will be published on data.gov.au:

Table 1.1: Entity resource statement;

Table 1.2: Entity 2015-16 Budget measures;

Table 2.1: Budgeted expenses for Outcome X;

Table 2.2: Programme expenses and Programme components;

Table 3.1.1: Movement of administered funds between years;

Table 3.1.2: Estimates of special account flows and balances;

Table 3.1.3: Australian Government Indigenous expenditure (AGIE);

Tables 3.2.1 to 3.2.6: Departmental budgeted financial statements; and

Tables 3.2.7 to 3.2.11: Administered budgeted financial statements.

As the Programme deliverables and Key performance indicators tables will not be published, entities are not required to send these tables to Finance.

Where an entity prepares two or more sets of tables, (for example Departmental budgeted financial statements consolidated and non-consolidated), these tables should be included and clearly marked.

As PB Statements information is under embargo until tabled in Parliament, portfolio departments are to coordinate and collate each Portfolio entity’s financial tables and

Guide to preparing the 2015-16 Portfolio Budget Statements

footnotes and send them to Finance either via CabNet (addressed Dario Forner) or Protected-rated email to [email protected] by close of business Monday, 11 May 2015.

Portfolios should ensure that all hidden sheets and cells, comments, links to databases, and other workings are removed from the workbooks before they are sent to Finance.

To check whether your entity has Protected-rated email, please refer to the Fedlink user list: http://www.fedlink.cybertrust.com.au/.

Portfolio departments should also ensure the following before sending the financial tables to Finance:

Tables should be provided in unlinked Excel (not picture) format with all totals hard coded;

Remove any working, calculations or notes that are outside the boundary of each table. We recommend entities use the Paste Special Values function in Excel before removing this data to ensure totals do not change;

Check that there are no hidden tabs containing ‘other workings or calculations’ and remove any unnecessary cell comments;

Check that workbooks / tabs are not password protected;

Entities will be able to and must provide updated files (as a result of a corrigendum) as necessary.

Finance will not quality assure the data in the tables provided for publishing on data.gov.au. It is the portfolio departments’ responsibility to check the integrity of the data provided in each table and that it matches the published PB Statements.

For advice on the machine readable file format for the PB Statement tables for data.gov.au or the Open Government initiative, please email [email protected].

Guide to preparing the 2015-16 Portfolio Budget Statements

Guidance on the preparation of the 2015-16 PB Statements

Guide to preparing the 2015-16 Portfolio Budget Statements

3. Portfolio Overview section

The Portfolio Overview section of the PB Statements is intended to provide the reader with a high-level summary of the portfolio, its Minister(s), portfolio entities, goals/objectives, structure and resources.

This section should include brief descriptions of portfolio entities and only include information which is relevant and specific from a portfolio perspective. This will avoid unnecessary duplication of entity-specific information presented in later sections.

Information at a department or entity level should be included only where it contributes to a broader understanding of portfolio goals and responsibilities.

Components of Portfolio overview:

Minister(s) and portfolio responsibilities – text description of portfolio of around two pages.

Portfolio structure and outcomes

o Figure 1: Portfolio structure and outcomes

Portfolio resources made available in the Budget year

o Table 1: Portfolio resources made available in the Budget year

3.1 Minister(s) and portfolio responsibilitiesThis section should provide a description of the Portfolio Ministers and the structure of the portfolio, as well as its objectives at a strategic and high level. Specifics of particular portfolio entities should be left to the relevant entity’s section.

It should include a brief discussion of common themes across the portfolio outcomes, for example, the broad impacts and/or trends of health policy on the Australian Community (Health portfolio), or improvements in Indigenous Affairs (Prime Minister and Cabinet portfolio). Portfolios should also take into account the following sources of information when preparing this section:

Major new Government policy or legislation affecting the portfolio and the intended results and impacts;

Portfolio department’s mission and/or vision statement; and

Ministerial statements by portfolio Ministers.

3.2 Portfolio structure and outcomesThe template for this figure can be found in the “Figure 1” tab of the Excel Tables workbook (Attachment B).

This figure is a graphical representation of the portfolio structure and the responsible Ministers. It should clearly indicate the names and titles of the

Guide to preparing the 2015-16 Portfolio Budget Statements

Ministers, the portfolio department(s) and Secretary, and the other portfolio entities and their Chief Executive Officers (CEOs), as well as the outcome statements for each entity.

All portfolio entities covered by the Public Governance, Performance and Accountability (PGPA) Act 2013 are to be included in the figure.

Portfolios should include the current outcome statements for each entity as agreed by the Minister for Finance. The outcome statement(s) included in Figure 1, and throughout the PB Statement, must be consistent with the Appropriation Bills.

Source of information:

A summary of portfolio entities which are subject to the PGPA Act can be found at http://www.finance.gov.au/resource-management/governance/#flipchart

3.3 Portfolio resources made available in the Budget yearThe template for this table can be found in the “Table 1” tab of the Excel Tables workbook (Attachment B).

This table shows the total new resources provided to the portfolio in the 2015-16 Budget year, broken down by entity and appropriation source. The table does not include amounts carried forward, nor opening special account balances.

The figures shown in this table should be consistent with figures reported in the Entity Resourcing Table in Budget Paper No. 4 (BP 4) and the Appropriation Bills, noting that some special accounts reported in BP4 may contain amounts considered special public money, whilst Table 1 should exclude special public moneys.

It is recommended that this table be completed by the portfolio department once all entities in the portfolio have completed their Entity resource statements (Table 1.1).

Source of information:

The information to be included in this table can be sourced by running the following CBMS report for the 2015-16 Budget year:

BEAM Reports > Appropriation Bills > Appropriation Bill Report > Agency Resourcing Table

The figures included for each entity must match the figures included in the Appropriation Bills and in the ‘Entity Resourcing Table’ in BP 4 as they are the authoritative documents. Using the figures from CBMS will ensure consistency as it is the central repository of budget information used for the production of the Appropriation Bills and Budget Papers.

The “Receipts” column in the Portfolio resources table is the sum of funds received from other sources, through section 74 PGPA Act Retained Revenue Receipts (or receipts from independent sources for corporate entities, i.e. corporate Commonwealth entities and Commonwealth companies) and non- appropriated credits to entity special accounts. These figures appear under the “Receipts” and “Special accounts” columns in the Entity Resourcing Table of BP 4, respectively.

Guide to preparing the 2015-16 Portfolio Budget Statements

The “Special” column in the Portfolio resources table is the sum of the “Special appropriations” columns in the Entity Resourcing Table in BP 4.

Payments to corporate entities that appear in the Bills are not to be shown in the portfolio department’s appropriation lines. They are to be reported by the corporate entity as “Departmental appropriations” under “Bill No. 1”, not in the receipts column.

The Portfolio total line will equal the Portfolio total line in the Entity Resourcing Table in BP 4. Transfers between agencies within the Portfolio are to be netted out (e.g. section 74 Retained revenue receipts from one entity to another) to show an accurate picture of the resources made available to the portfolio.

Guide to preparing the 2015-16 Portfolio Budget Statements

4. Entity Overview and Resources section

This section of the PB Statements is aimed at providing the reader with an overall picture of each entity’s objectives and resources across the budget and forward estimates period.

This section should also provide the reader with an overall picture of each entity’s strategic direction and planned performance, as well as a summary of new government measures.

There are four components to this section which together link the entity strategy with the resources available.

Components of Section 1: Entity overview and resources

Strategic direction statement;

Entity resource statement (including Table 1.1);

Budget measures (Table 1.2); and

4.1 Strategic direction statementThis section should be no longer than two pages.

The Strategic direction statement should outline an entity’s anticipated strategic direction for the budget and forward years.

The Strategic direction statement should describe an entity’s outcome statement(s) in a strategic, relevant and concise manner, as well as outline the broad strategies the entity intends to adopt in order to achieve these outcomes, and the planned results and goals to be achieved. The statement should also outline how these outcome statements contribute to the achievement of whole-of-government strategic priorities and outcomes.

The statement should identify major ongoing functions, new functions (or loss of functions) and measures allocated to the entity, and any significant challenges that will impact on the entity’s performance against its outcome(s) over the medium term.

The statement should be reasonably high level – a detailed discussion of operational issues can be covered in the entity’s corporate plan or on its website.

4.2 Entity resource statementThe template for this table can be found in the “Table 1.1” tab of the Excel Tables workbook (Attachment B). There is a template for non-corporate Commonwealth entities (coloured green) and a template for corporate Commonwealth entities and Commonwealth companies (coloured red).

Guide to preparing the 2015-16 Portfolio Budget Statements

The Entity resource statement provides a summary of all resources available to the entity over the budget year which it may draw upon in achieving government outcomes and objectives.

It provides a breakdown of these resources by funding source, and includes undrawn and unspent amounts from prior years as well as the balances of special accounts, but excludes amounts subject to quarantine or reduction.

Entities with special accounts will need to ensure amounts transferred to and from the special accounts and other funding sources are netted off so they are not double counted.

The “Actual Available Appropriation” column shows the estimated amount available to the entity in the 2014-15 financial year.

Prior year annual appropriation balancesPlease note that as a result of the Statute Stocktake (Appropriations) Act 2013 and the Omnibus Repeal Day (Autumn 2014) Act 2014, all unspent annual appropriations (both for ordinary annual services and for other services) from 2011-12 or earlier were extinguished.

Annual appropriations relating to the 2012-13 and 2013-14 financial years will be repealed two years after the end of the relevant financial years through future Omnibus Repeal Day Bills.

Amounts which have been extinguished should be excluded from the calculation of prior year balances for the purposes of the Entity resource statement.

A separate Estimates Memorandum will be issued on the repeal of prior year annual appropriations.

QuarantinesUnder the PGPA Act, the Minister for Finance is able to quarantine amounts under section 51. These quarantined amounts should not be recognised as appropriations in Table 1.1 nor in the financial statements.

Source of information:

Appropriation information in this table must be sourced from CBMS and an entity’s annual reports, and should be consistent with information captured in an entity’s financial management information system (FMIS).

The majority of the information can be sourced by running the following reports from CBMS:

BEAM Reports > Appropriation Bills > Appropriation Bill Report > Agency Resourcing Table

BEAM Reports > Appropriation Bills > Appropriation Bill Report > Appropriation Bill 1

BEAM Reports > Appropriation Bills > Appropriation Bill Report > Appropriation Bill 2

BEAM Reports > Appropriation Bills > Appropriation Bill Report > Estimated Expenses Special Appropriations

Guide to preparing the 2015-16 Portfolio Budget Statements

BEAM Reports > Appropriation Bills > Appropriation Bill Report > Estimated Cash Flows and Balances for Special Accounts

ACM Reports > Appropriation Balance Report

BEAM Reports > Appropriation Bills > AAA Audit Report – select the current financial year only to get the “Actual available appropriation” figure available on that day. This amount may not include amounts to be appropriated through Appropriation Bill (Nos. 5 and 6) 2014-15 nor Advances to the Minister for Finance.

The “prior year appropriation” rows should reflect unspent/undrawn appropriations available at the start of the financial year (i.e. the closing balance of the previous year).

For the “Actual available appropriation” column, this will be the closing unspent appropriation balance from the entity’s 2013-14 annual report.

For the “Estimate of prior year amounts” column, this will be the forecast closing unspent appropriation balance as at the end of the 2014-15 year.

Entities can also check unspent, undrawn balances by running the Appropriation Balance Report from CBMS for the relevant financial year and referring to the “Available – Hard Limit” lines. The “Available – Hard Limit” lines show how much of the amount which is still available to the entity but has yet to be drawn down.

Where there are unspent equity injections and Administered Assets and Liabilities appropriations available, they should also be shown in Table 1.1 as a separate line item.

The “Departmental appropriation” row should reflect the amount appropriated to the entity in the relevant year. This figure will be made up of:

Amounts appropriated through Appropriation Acts (Nos. 1, and 3) and Appropriation Bill (No. 5)

+ Advances to the Minister for Finance (AFM)

+/- section 75 transfers as a result of Machinery of Government changes

- administrative quarantines made by Finance

- any formal reductions in appropriation made by the Minister for Finance under s51 of the PGPA Act (such as for foreign exchange movements, savings measures and other quarantines).

Amounts under the “Actual Available Appropriation” column can be sourced by running the AAA Audit Report (which provides an estimate at a point in time) and including any amounts yet to be appropriated, e.g. amounts through Appropriation Bill (No. 5) and AFMs.

The “s74 Retained revenue receipts” row should reflect the entity’s forecast Receipts from Independent Sources. These figures should be sourced from the “Receipts” columns in the Entity Resourcing Table report from CBMS.

The “Administered expenses” rows should be taken from the Appropriation Bill 1 report from CBMS and match the “outcome” and “payments to corporate entities” splits outlined in the Bill.

Guide to preparing the 2015-16 Portfolio Budget Statements

For portfolio departments, the Appropriation Bill 1 report should be run at the portfolio rather than entity level.

Amounts under the “Actual Available Appropriation” column can be sourced by running the AAA Audit Report (which provides a point-in-time figure) and including any amounts yet to be appropriated, e.g. amounts through Appropriation Bill (No. 5) and AFMs.

This amount can also be sourced from the Appropriation note of the entity’s 2013-14 annual report, under the “Appropriations applied” column.

The “Other Services” rows should be taken from the Appropriation Bill 2 report from CBMS.

For portfolio departments, the Appropriation Bill 2 report should be run at the portfolio rather than entity level.

Amounts under the “Actual Available Appropriation” column can be sourced by running the AAA Audit Report (which provides a point-in-time figure) and including any amounts yet to be appropriated, e.g. amounts through Appropriation Bill (No. 5) and AFMs.

The “Special Appropriations” rows should reflect expenses expected to be incurred in relation to special appropriations. These figures should match the figures published in BP 4 (in both the Special Appropriations table and also the Entity Resource Table), and be sourced from the Estimated Expenses from Special Appropriations report from CBMS.

The “Special Accounts” rows should reflect the opening balances and receipts for all special accounts managed by the entity. These figures should be drawn from the “Estimated Cash Flows and Balances for Special Accounts” report from CBMS. Special public moneys held in “Services for Other Entities and Trust Moneys” (SOETM) accounts should be excluded from this figure as they do not constitute funds available to the entity.

The “Third Party Payments” information will be drawn from entities’ own records and should be agreed with the relevant entity. These figures should be prepared on a consistent basis, i.e. all resourcing (cash payments/appropriations received) or all expenses (and appropriation revenue), and the reader should be able to reconcile figures between entities.

4.3 Budget measuresThe template for this table can be found in the “Table 1.2” tab of the Excel Tables workbook (Attachment B).

The Budget measures section primarily highlights new government decisions taken since the tabling of the last set of Appropriation Bills, generally at Additional Estimates. It includes measure titles and estimates for the current financial year (2014-15), the budget year (2015-16) and forward years (2016-17 to 2018-19).

For completeness, all measures need to be reported at the entity level in a Portfolio statement, i.e. either the PB Statements, Portfolio Additional Estimates Statements (PAES), Portfolio Supplementary Estimates Statements (PSES), or Portfolio Supplementary Additional Estimates Statements (PSAES).

Guide to preparing the 2015-16 Portfolio Budget Statements

This complements the whole-of-government public reporting of all measures in either Budget Paper No. 2 (BP 2) or the Mid-Year Economic and Fiscal Outlook (MYEFO) and ensures a clear-read of Government decisions to entity level across key budget publications.

All details of 2015-16 Budget measures must match the final measures list provided by your AAU before being reported in Table 1.2. Measure figures are to be reported on a fiscal balance basis as this is the basis on which BP No.2 is prepared.

The wording for cross Portfolio measures should be the same in each PB Statements affected by the measure. To increase transparency, where an entity is not the lead entity in a measure package, they are required to name the lead entity in a footnote to the measure to allow easy cross reference to the measure description in BP No.2 and across PB Statements. This should be done with the following text:

The lead entity for measure xxxxxxx is entity xxxxxxx. The full measure description and package details appear in Budget Paper No. 2 under the xxxxxxx portfolio.

Table 1.2 is split into two parts – one part covers measures which will be announced in the 2015-16 Budget, and the other part covers those announced since the previous Budget which have not previously been reported in Portfolio Statement, such as those announced in an Economic Statement, in a Pre-Election Economic and Fiscal Outlook or MYEFO and which were not included in the 2014-15 PAES.

The most common reasons for excluding measures from the 2014-15 PAES are:

the measure did not require additional funding through Appropriation Bills (Nos. 3 and/or 4); or

the measure was for savings, or there was no additional appropriation required as the entity’s spending measures were fully offset by savings measures; or

the measure related to future year (i.e. 2015-16 or later years); or

the measure related to an alternative source of funding, such as a special appropriation and/or special account.

The Budget measures published in the first part of Table 1.2 should match the measures as printed in BP No.2. Where a measure was reported in PAES and also appears in BP 2, it does not need to be reported again in the PB Statements.Measures in BP No.2 will also include those that were Decisions taken but not yet announced at MYEFO.

Measures in the second part of Table 1.2 should match the measure as printed in the relevant economic statement/budget paper.

Measure reversalsWhere a measure reversal will be reported in BP 2, the measure reversal needs to be reported in Part 1 of the measures table.

Where a measure reversal has been reported in MYEFO, but has not been reported in PAES, the reversal needs to be reported in Part 2 of the measures table.

Measure reversals reported in either Part 1 of 2 of the measures table need to be reported on the following basis:

Guide to preparing the 2015-16 Portfolio Budget Statements

where it is a full reversal, the measure should include dashes in fiscal impact (as zero net fiscal impact); and

where it is a partial reversal, the measure should reflect the final amount to be appropriated, i.e. the difference between the initial measure and the partial reversal.

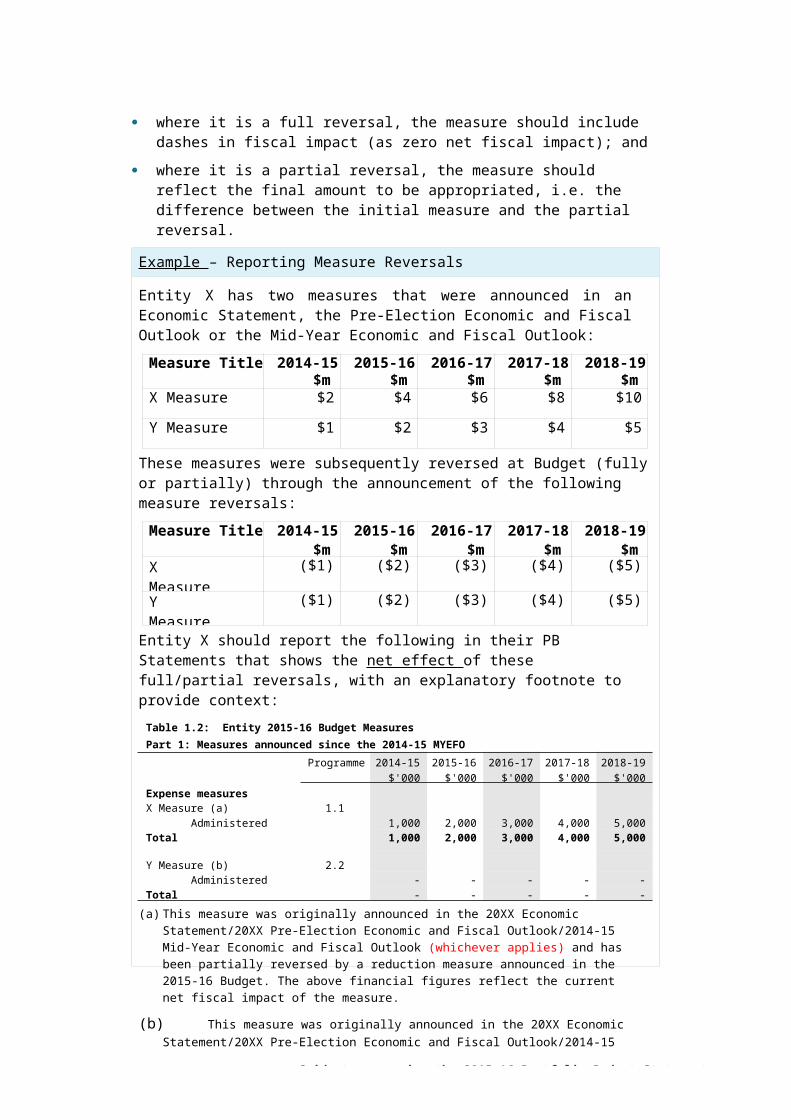

Example – Reporting Measure Reversals

Entity X has two measures that were announced in an Economic Statement, the Pre-Election Economic and Fiscal Outlook or the Mid-Year Economic and Fiscal Outlook:

Measure Title 2014-15$m

2015-16$m

2016-17$m

2017-18$m

2018-19$m

X Measure $2 $4 $6 $8 $10

Y Measure $1 $2 $3 $4 $5

These measures were subsequently reversed at Budget (fully or partially) through the announcement of the following measure reversals:

Measure Title 2014-15$m

2015-16$m

2016-17$m

2017-18$m

2018-19$m

X Measure – reduction

($1) ($2) ($3) ($4) ($5)

Y Measure - cessation

($1) ($2) ($3) ($4) ($5)

Entity X should report the following in their PB Statements that shows the net effect of these full/partial reversals, with an explanatory footnote to provide context:

Table 1.2: Entity 2015-16 Budget MeasuresPart 1: Measures announced since the 2014-15 MYEFO

Programme 2014-15 2015-16 2016-17 2017-18 2018-19$'000 $'000 $'000 $'000 $'000

Expense measuresX Measure (a) 1.1

Administered expenses 1,000 2,000 3,000 4,000 5,000Total 1,000 2,000 3,000 4,000 5,000

Y Measure (b) 2.2Administered expenses - - - - -

Total - - - - -

(a) This measure was originally announced in the 20XX Economic Statement/20XX Pre-Election Economic and Fiscal Outlook/2014-15 Mid-Year Economic and Fiscal Outlook (whichever applies) and has been partially reversed by a reduction measure announced in the 2015-16 Budget. The above financial figures reflect the current net fiscal impact of the measure.

(b) This measure was originally announced in the 20XX Economic Statement/20XX Pre-Election Economic and Fiscal Outlook/2014-15 Mid-Year Economic and Fiscal Outlook (whichever applies) and has been fully reversed by a cessation measure announced in the 2015-16 Budget. The above dashes reflect that the measure has no fiscal impact as it has ceased.

Guide to preparing the 2015-16 Portfolio Budget Statements

Decisions taken but not yet announcedWhere a measure has been published in an economic statement as a “Decision taken but not yet announced” (DTBNYA), it should be published in the next available budget statement.

Where the measure has been announced by the Government, the measure should be listed in Table 1.2 with its full measure title and associated costs.

Where the measure has not been or will not be (e.g. for national security reasons) announced publically at the next budget statement, the costs for measure should be included as part of the “Decisions taken but not yet announced” total line at the bottom of Table 1.2. The measure title should not be listed separately.

The exception is where the entity is preparing their PAES and the measure does not require funding through Appropriation Bills (No. 3, 4, 5 or 6) – in this case, the measure can be omitted from the PAES and published in the next PB Statements.

Measures with indicative costsWhere measures are published in an economic statement with indicative costs, these measures should be listed in Table 1.2 where costs for each affected entity are known.

Once final costs have been agreed, entities may republish the measure in Table1.2 of the PAES or PB Statements, and include a footnote stating that the measure was previously published in BP2/MYEFO/the relevant economic statement and the costs shown are now final.

For cross-portfolio measures where final costs have now been agreed for each entity, the measure should be listed in Table 1.2 with the final agreed costs, with a footnote noting that it is a cross-portfolio measure previously published in BP2/MYEFO/the relevant economic statement, and naming the lead entity.

Machinery of government changesWhere there are Machinery of Government changes, the gaining entity should publish any new measures relating to the function(s) being gained.

For further information on showing Machinery of Government changes in the PB Statements, please refer to Section 6.16 of this guidance.

Source of information

Figures should be presented on a fiscal balance basis – to confirm the correct amounts, please refer to the costing agreement letters provided by your AAU.

Information to be included in this table should be taken from estimates adjustments for measures (i.e. those entered against the reason code “Government decision or measure”) in CBMS.

Titles of measures are to be confirmed against the final agreed measures list provided by the Department of the Treasury (or the Department of Finance).

Guide to preparing the 2015-16 Portfolio Budget Statements

5. Outcomes and planned performance section

The Outcomes and planned performance section (Section 2) details the outcomes and programmes of an entity, its resourcing, deliverables and performance information.

The first part of Section 2 addresses the outcome statement level of reporting, with a focus on the Outcome strategy statement and an Outcome expense table, split by programme.

The 2015-16 PB Statements are used to provide structured reporting of an entity’s performance, focusing primarily on programmes. The reporting structure allows entities to demonstrate their performance in a logical and consistent manner, indicating to the public and the Parliament the resourcing provided and the deliverables produced.

As outlined in the Commonwealth’s Outcome Statements and Approval Policy (Outcomes Policy), outcome statements articulate Government objectives and serve three main purposes within the financial framework. They:

1. explain the purpose for which annual appropriations are approved by the Parliament for use by entities;

2. provide a basis for budgeting and reporting against the use of appropriated funds; and

3. measure and assess entity and programme non-financial performance in contributing to Government policy objectives:

For information on amending an entity’s existing outcome statement(s) or programmes, please refer to the Outcomes policy and Programmes policy available on the Finance website: http://www.finance.gov.au/resource- management/performance/

Entities are required to report Key Performance Indicators (KPIs) for their programme objectives. If a KPI changes from last year’s PB Statement or Portfolio

No changes will be made to the performance reporting requirements for the 2015-16 PB Statements. Further guidance will be issued in due course on the corporate plan requirements.

For advice on changing outcome statements or programmes, please contact your Agency Advice Unit in Finance in the first instance.

For advice on performance reporting in the PB Statements, please contact the Performance Reporting and Planning Branch in Finance ([email protected]).

Guide to preparing the 2015-16 Portfolio Budget Statements

Additional Estimates Statements (PAES), entities should footnote in the KPI table a summary of the change and whether they have met the previous KPI at the programme level. In order to assess programme performance over time, consistency in KPI reporting is encouraged.

Components of Section 2: Outcomes and planned performance

Outcome strategy statement

Changes in entity outcomes and programmes (where applicable – including Table 2).

Outcome expense statement (including Table 2.1 Budgeted expenses for Outcome X)

5.1 Outcome strategy statementThe Outcome strategy statement should be no longer than three quarters of a page in length.

When completing the Outcome strategy statement, entities may wish to indicate the timeframes relevant to the outcome and its supporting programme(s) (i.e. if outcomes are focusing on a 10-year timeframe then the strategy should take this into account). Entities may also wish to include evidence of actual and planned progress against their Outcome strategy statement to assist in explaining how it is being implemented.

The circumstances of the target group (as addressed by the Outcome strategy statement’s intended result) should be outlined with reference, where possible, to the evidence source to be used for measurement purposes (for example, Australian Bureau of Statistics (ABS) census data etc).

5.2 Outcome expense statementThe template for this table can be found in the “Table 2.1” tab of the Excel Tables workbook (Attachment B). There is a template for non-corporate Commonwealth entities (coloured green) and a template for corporate Commonwealth entities and Commonwealth companies (coloured red).

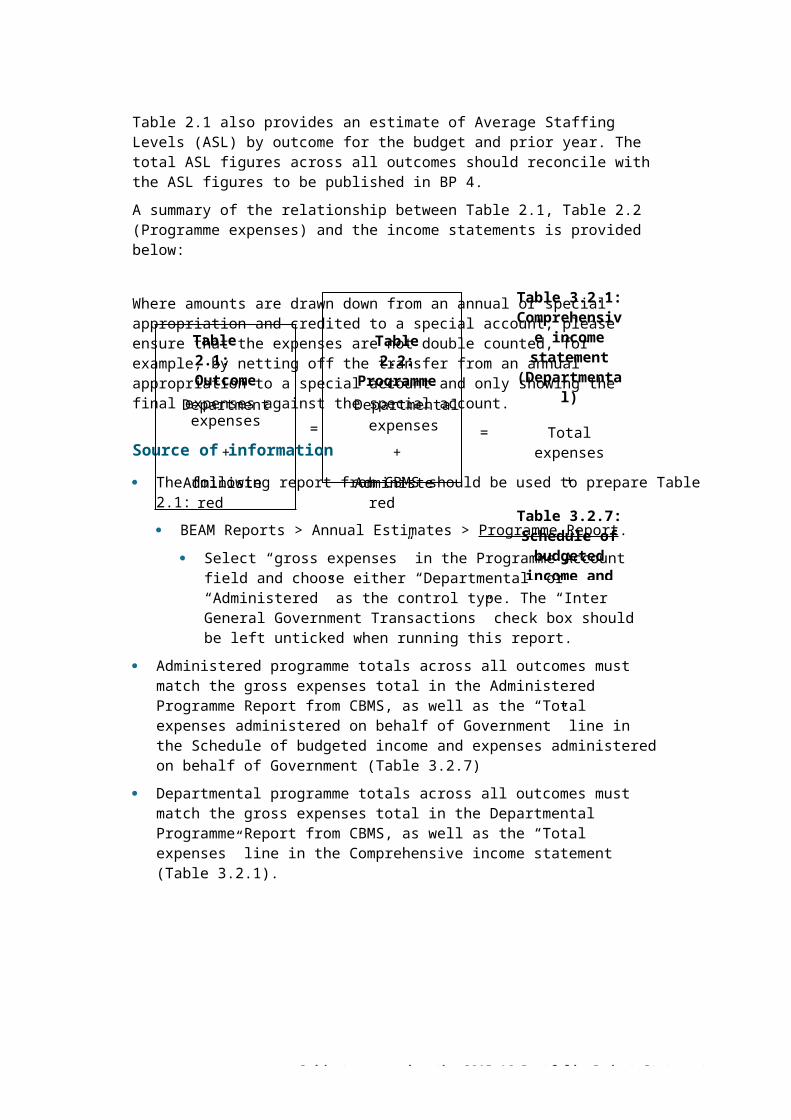

The Outcome expense statement (Table 2.1) provides the reader with further detail of an entity’s programmes and expenses, in particular, the proposed use of appropriations and links this expenditure to the entity’s financial statements (specifically the income statement). It provides a breakdown of total expenses for each outcome by funding source. This statement complements the Entity resource statement (Table 1.1), which in contrast provides a summary of funding sources but not forecast expenditure.

Entities are to report outcomes on an expenses basis, for each programme. Programme expenses are to be broken down further into the respective funding source/appropriation type. A separate table should be prepared for each outcome.

The total budgeted expenses for all outcomes must equal the aggregated of total Departmental and Administered expenses as outlined in the Comprehensive income statement (Table 3.2.1) and Schedule of budgeted income and expenses administered on behalf of Government (Table 3.2.7).

Guide to preparing the 2015-16 Portfolio Budget Statements

Table 2.1 also provides an estimate of Average Staffing Levels (ASL) by outcome for the budget and prior year. The total ASL figures across all outcomes should reconcile with the ASL figures to be published in BP 4.

A summary of the relationship between Table 2.1, Table 2.2 (Programme expenses) and the income statements is provided below:

Where amounts are drawn down from an annual or special appropriation and credited to a special account, please ensure that the expenses are not double counted, for example, by netting off the transfer from an annual appropriation to a special account and only showing the final expenses against the special account.

Source of information

The following report from CBMS should be used to prepare Table 2.1:

BEAM Reports > Annual Estimates > Programme Report .

Select “gross expenses” in the Programme Account field and choose either “Departmental” or “Administered” as the control type. The “Inter General Government Transactions” check box should be left unticked when running this report.

Administered programme totals across all outcomes must match the gross expenses total in the Administered Programme Report from CBMS, as well as the “Total expenses administered on behalf of Government” line in the Schedule of budgeted income and expenses administered on behalf of Government (Table 3.2.7)

Departmental programme totals across all outcomes must match the gross expenses total in the Departmental Programme Report from CBMS, as well as the “Total expenses” line in the Comprehensive income statement (Table 3.2.1).

Table 3.2.1: Comprehensive

income statement

(Departmental)

Total expenses

+

Table 3.2.7: Schedule of

budgeted income and

expenses administered on behalf of Government

Table 2.1: Outcome expenses

Table 2.2: Programme expenses

Departmental Departmentalexpenses = expenses =

+ +

Administered expenses

Administered expenses

Guide to preparing the 2015-16 Portfolio Budget Statements

For the “programme support” row in Table 2.1, this is not usually reported in CBMS as a separate programme. Entities are to use the gross expense figure for ‘Departmental—Other’.

Total expense figures for special appropriations must match those reported in BP 4 in the “Estimated Expenses from Special Appropriations” table.

The figures included in the “Programme expenses” section which follows the Outcome Expense section must reconcile to the totals included in the Outcome expenses statement by programme, appropriation type and Administered/Departmental classification.

Entities which maintain a special account(s) will need to ensure these amounts are not double counted at the outcome expense level. Special accounts which hold “special public monies” will not flow through to the Programme report in CBMS and should not be included in the Outcome Expense statement.

The “Expenses not requiring appropriation in Budget year” line is to be used by entities where there is a government policy not to fund those expenses; the funding has been provided in a prior year but the expense will be incurred in the current year; or the expenses reflect the usage of services provided free of charge.

For example, depreciation expenses which the Government has provided a separate capital budget/Collection Development Acquisition Budget should be shown in this line, along with expenses associated with audit services provided by the Australian National Audit Office.

Please note : The Entity resource statement (Table 1.1) focuses on funding/appropriations whereas the Outcome expense statement (Table 2.1) focuses on expenditure (expenses). These are not always the same amounts as differences can exist between appropriation amounts and the total expenses recognised against programmes.

Items which do not or will not involve a cash flow impact (such as write-offs, asset devaluations and bad debt expenses) are excluded from the calculation of appropriations, and hence the Entity resource statement (Table 1.1). As such, these expenses (i.e. expenses with no appropriation impact) are to be reported as “Expenses not requiring appropriation” at the appropriate line in Table 2.1 to show the total expenses for each programme, and to allow for reconciliation with the appropriation view of entity resources, the programme report in CBMS and the entity’s income statement(s).

Average staffing level figures across all outcomes are to be sourced from the entity’s own records, and match the figures to be published in BP 4. Please refer to the latest Estimates Memorandum on Average Staffing Levels (ASL) for more information.

5.3 Programme reportingThe aim of programme reporting is to provide transparent and consistent information to Parliament and the public about Government activities. The Commonwealth Programmes Policy and Approval Process (Programme Policy) sets

Guide to preparing the 2015-16 Portfolio Budget Statements

out guidance on establishing programmes (http://www.finance.gov.au/resource- management/performance/).

The Programme Policy states that “in addition to resourcing information, entities are required to provide details of the programme’s objectives and non-financial performance, including the deliverables and key performance indicators for each programme.” This information is required to provide an understanding of a programme’s purpose, how much funding it requires, what it will deliver to the community or specific target group and a measure of its effectiveness.

Deliverables and key performance indicators (KPIs) are two different concepts. The Performance Information and Indicators policy paper includes the following definitions:

1. Deliverables are:

Produced by the programme in meeting its objective; and

Tangible, quantifiable products of a programme (e.g. payments or a database).

2. KPIs:

Assist in determining if a programme is achieving its objectives. KPIs should measure the effectiveness and efficiency of the programme and clearly measure the programme’s success, particularly against the intended result of the relevant outcome statement.

Please note: ‘Other Departmental’ must not be used as a programme name in the PB Statements. The CBMS allocation line ‘Other Departmental’ should be reported in the PB Statements as:

1. Programme support - where departmental funding supports the delivery of existing Commonwealth Programmes; or

2. A single programme, with the entity name or similar used as the programme name - where departmental funding is not classed as programme support and the funding represents the functions of the entity (e.g. the Productivity Commission reports under a single programme titled ‘Productivity Commission’).

Entities that have a single outcome and single programme do not need to complete the outcome strategy section, as this information should be reflected in the strategic direction statement. These entities will still need to complete the Entity resource statement, Budget expense for outcomes table, and programme information section as these tables detail different information.

Components of Section 2 (Part 2): Outcomes and planned performance:

Programme reporting:

Programme objective

Programme expenses

Programme components (where applicable)

Programme deliverables

Programme key performance indicators

Guide to preparing the 2015-16 Portfolio Budget Statements

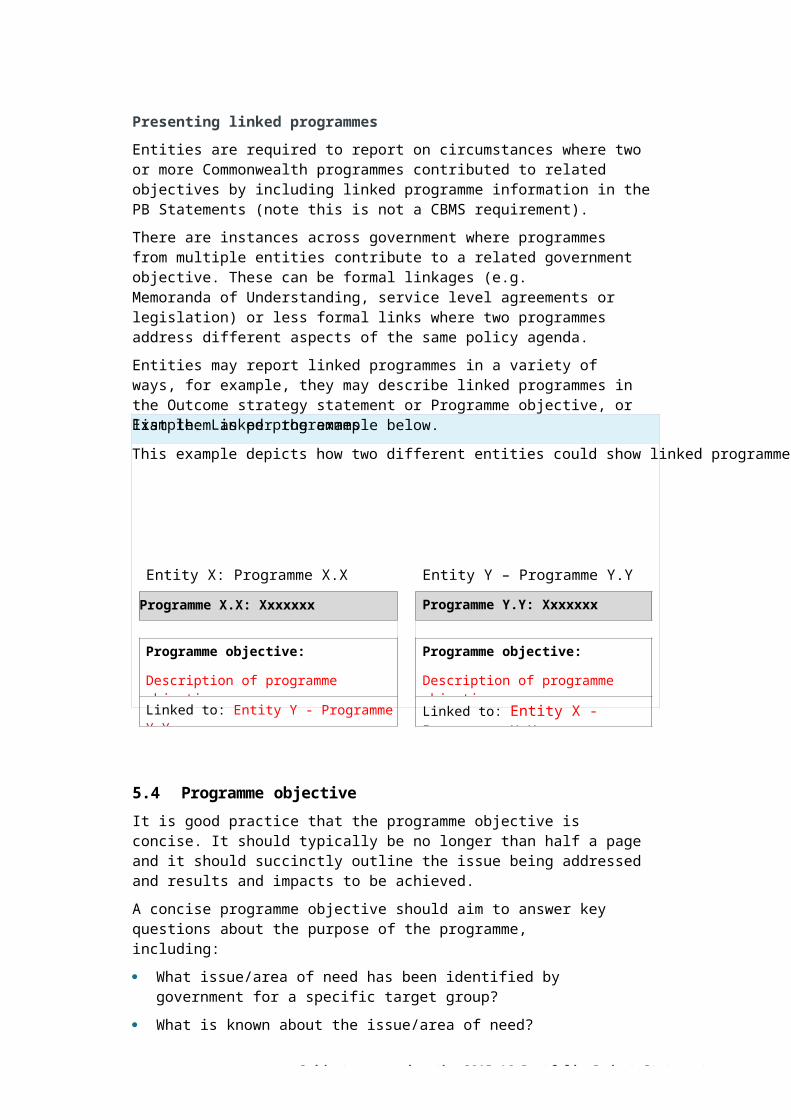

Example: Linked programmes

This example depicts how two different entities could show linked programmes in their PB Statements.

Presenting linked programmesEntities are required to report on circumstances where two or more Commonwealth programmes contributed to related objectives by including linked programme information in the PB Statements (note this is not a CBMS requirement).

There are instances across government where programmes from multiple entities contribute to a related government objective. These can be formal linkages (e.g.Memoranda of Understanding, service level agreements or legislation) or less formal links where two programmes address different aspects of the same policy agenda.

Entities may report linked programmes in a variety of ways, for example, they may describe linked programmes in the Outcome strategy statement or Programme objective, or list them as per the example below.

Entity X: Programme X.X Entity Y – Programme Y.Y

Programme X.X: Xxxxxxx Programme Y.Y: Xxxxxxx

Programme objective: Programme objective:

Description of programme objective. Description of programme objective.

Linked to: Entity Y - Programme Y.Y Linked to: Entity X - Programme X.X

5.4 Programme objectiveIt is good practice that the programme objective is concise. It should typically be no longer than half a page and it should succinctly outline the issue being addressed and results and impacts to be achieved.

A concise programme objective should aim to answer key questions about the purpose of the programme, including:

What issue/area of need has been identified by government for a specific target group?

What is known about the issue/area of need?

What is the scope of the issue/area of need?

How the programme will achieve its objectives (including linkages to other programmes)?

Entities are to link to Commonwealth programmes in other entities which contribute to similar or closely-related Government objectives.

The linked programme box is to be used where programmes undertaken by multiple entities contribute to the same Government objective. To ensure consistency across government, entities are to seek agreement with the other relevant entities on the

Guide to preparing the 2015-16 Portfolio Budget Statements

detail included, prior to including the linked programme information. Details such as the relevant entity name (if in another entity), and programme number (i.e. 1.2) should be included in the PB Statements, so that similar details may be easily found within the other entity’s PB Statements.

Those entities affected by Federal Financial Relations payments made by Treasury, should expand as necessary the non-financial information provided for the planned performance of these programmes, within the relevant section and also ensure that the affected programmes are linked or cross referenced to the payments made by Treasury within the “linked to” section and where appropriate a footnote under the Programme expense table.

A short sentence to explain the link is also recommended, such as:

Linked to Treasury Programme 1.10 for Federal Financial Relations National Partnership Agreement on Remote Indigenous Housing; or

DHS delivers the ABC programme payments on behalf of Entity Y for their GHI programme 1.2.

Where relevant, entities should reference the Council of Australian Government (COAG) agreements that their individual programmes contribute to, and provide the relevant web address for further information.

5.5 Programme expensesThe template for this table can be found in the “Table 2.2” tab of the Excel Tables workbook (Attachment B).

This table provides a breakdown of programme expenses by funding source/appropriation type and item/component as relevant. Programmes are to include prior year and forward year data.

Please note: Total expenses across all programmes are to match total expenses captured in CBMS, and reconcile to total expenses reported in the Outcome expense tables (Table 2.1). Total programme expenses should also reconcile to total expenses reported in the Comprehensive income statement (Table 3.2.1) and the Schedule of Budgeted income and expenses administered on behalf of government (Table 3.2.7).

Where programme expenses relate to transfers to special accounts, the following footnote must be included:

XXXXXX item is credited into the XXXXX Special Account. For full Special Account details see Table 3.1.3.

Departmental expenses in support of programme activities are to be allocated to programme support, indicating the full cost to government of delivering a specific programme. As programme support (and some departmental programmes) will typically include an apportionment of corporate/overhead expenses (in addition to direct costs), a reliable and consistent allocation methodology should be used by agencies to produce accurate information.

Expenses deemed to be programme support and other small departmental items, are likely to be included in the ‘Departmental—Other’ programme. Where these expenses are split between Programme expenses tables, they must, in aggregate, reconcile to the data in CBMS.

Guide to preparing the 2015-16 Portfolio Budget Statements

Programmes listed in the PB Statement must be consistent with those reported in CBMS. If changes in CBMS programme structures or reallocations are required, they should be completed in CBMS before the Budget estimates update so the PB Statements will match the data in CBMS. Entities should contact their AAUs as soon as practicable to discuss any programme changes.

Where relevant, entities may also wish to include a footnote to relevant tables which explains that the allocation of departmental expenses to programmes is notional only and based on attribution models maintained by entities.

Entities should use the text box in the template to outline very briefly any significant trends or variances in programme expenses for the budget and forward years.

Where amounts are drawn down from an annual or special appropriation and credited to a special account, please ensure that the expenses are not double counted, for example, by netting off the transfer from an annual appropriation to a special account and only showing the final expenses against the special account.

Source of information

The following report from CBMS should be used to prepare Table 2.2:

BEAM Reports > Annual Estimates > Programme Report .

Select “gross expenses” in the Programme Account field and choose either “Departmental” or “Administered” as the control type. The “Inter General Government Transactions” check box should be left unticked when running this report.

Administered expense totals across all programmes must match the gross expenses total in the Administered Programme Report from CBMS, as well as the “Total expenses administered on behalf of government” line in the Schedule of budgeted income and expenses administered on behalf of Government (Table 3.2.7)

Departmental expense totals across all programmes must match the gross expenses total in the Departmental Programme Report from CBMS, as well as the “Total expenses” line in the Comprehensive income statement (Table 3.2.1).

For the “programme support” row in Table 2.1, this is not usually reported in CBMS as a separate programme. Entities are to use the gross expense figure for ‘Departmental—Other’.

The figures included in Table 2.2 must reconcile to the totals included in the Outcome expenses statement by programme, appropriation type and Administered/Departmental classification.

Entities which maintain a special account(s) will need to ensure these amounts are not double counted at the programme expense level. Special accounts which hold “special public monies” will not flow through to the Programme report in CBMS and should not be included in the Programme expense statement.

The “Expenses not requiring appropriation in Budget year” line is to be used by entities where there is a government policy not to fund those expenses; the funding has been provided in a prior year but the expense will be incurred in the current year; or the expenses reflect the usage of services provided free of charge.

Guide to preparing the 2015-16 Portfolio Budget Statements

For example, depreciation expenses which the Government has provided a separate capital budget/Collection Development Acquisition Budget should be shown in this line, along with expenses associated with audit services provided by the Australian National Audit Office.

Please note that the Entity resource statement (Table 1.1) focuses on funding/appropriations whereas the Programme expense statement (Table 2.2) focuses on expenditure (expenses). These are not always the same amounts as differences can exist between appropriation amounts and the total expenses recognised against programmes.

Items which do not or will not involve a cash flow impact (such as write-offs, asset devaluations and bad debt expenses) are excluded from the calculation of appropriations, and hence the Entity resource statement (Table 1.1). As such, these expenses (i.e. expenses with no appropriation impact) are to be reported as “Expenses not requiring appropriation” at the appropriate line in Table 2.2 to show the total expenses for each programme, and to allow for reconciliation with the appropriation view of entity resources, the programme report in CBMS and the entity’s income statement(s).

5.6 Programme componentsThe template for this table can be found in the “Table 2.2 Programme Components” tab of the Excel Tables workbook (Attachment B).

Entities are not required to provide reporting below the programme level.

Programme component reporting is a subset of programme level reporting, and programme components can be funded through administered and departmental appropriations. If programme components are used, they should be clearly identified as such and not described as a programme. An example of a programme component could be an item of special public interest or political sensitivity.

Within the programme deliverables and programme key performance indicators (KPIs) information, sub headings for each programme component should be included and the relevant deliverables and KPIs for the specific programme component should also be identified.

Should entities choose to report on programme components, a programme component expense table should be provided for each programme component. The full programme expenses must still be provided in the initial programme expense table (Table 2.2). The itemised sub-set of expenses is then provided for each relevant programme component.

The expenses across all programme components should reconcile to the programme expense tables (Table 2.2) and outcome expense tables (Table 2.1).

5.7 Programme deliverablesThe purpose of the Programme deliverables table is to show the goods and services produced and delivered by a programme in meeting its objective.

Entities should use the text box to answer briefly the following questions about the deliverables of a programme:

What deliverables and services will the programme deliver to achieve its objective?

Guide to preparing the 2015-16 Portfolio Budget Statements

How will these deliverables and services bring about the desired change to address the objective?

The text in this section should typically be brief and not repeat information included in the Programme objective or KPIs sections.

As outlined in the Commonwealth’s Performance Information and Indicators guidance:

“Deliverables are the tangible, quantifiable products of a programme and include both the direct programme activities, (e.g. payments) and the support activities that deliver and manage the programme. However, agencies should focus on the impacts the programme will be making in the community more so than the support activities.

Some examples of programme deliverables include:

number of payments/transfers made;

number of days/hours of a service provided (either provided directly by the entity or through a third party); or

number of information sessions held/participants.”

Further information performance indicators can be found on the Finance website: http://www.finance.gov.au/resource-management/performance/.

5.8 Programme key performance indicatorsReporting on the KPIs associated with programmes provides stakeholders, including the Parliament, with an indication of progress made towards meeting the objectives of a programme. Entities should aim to select strategic and meaningful programme- level performance indicators.

The KPIs section provides information about the programme-level performance measures that will be used by an entity to assess the achievement of programme objectives. Measures may be quantitative or qualitative in nature. This information, most commonly reported in table form, reports on how the programme delivered against a target for the last Budget, in this case 2014-15, with data also provided about planned targets for the current Budget and forward years, where relevant. In many instances, programmes will have various KPIs due to the complexity or scope of the programme activities. Wherever possible, programme-level KPIs should remain consistent across reporting periods to assist with monitoring the achievement of programme objectives over time.

It is good practice for entities to maintain records of trend information and changes to their KPIs. It is recommended that entities advise their AAU in Finance if there are any changes to their KPIs.

If a KPI changes from last year’s budget or PAES, entities should also include a footnote in the KPI table, a summary of the change and whether they have met the previous KPI at the programme level. If it is likely the KPI will not be achieved, a brief explanation of the reasons should be noted in the PB Statements.

Entities are to use data sources and measurable samples of the relevant target groups to show the impact of the programme, where relevant, and support chosen indicators. The group of indicators chosen for a particular programme should collectively address the objective of the programme.

Guide to preparing the 2015-16 Portfolio Budget Statements

When setting performance targets within or beyond the forward estimates period, entities are to be conscious of previous years’ targets and their progress towards achieving them. Performance targets should not be static; they should evolve with improved practices and methods, and periodically be evaluated and revised to ensure entities are achieving the best possible results in contributing towards their outcomes.