Embed Size (px)

Citation preview

1666 K Street, N.W.Washington, DC 20006

Telephone: (202) 207-9100Facsimile: (202) 862-8433

www.pcaobus.org

Report on

2015 Inspection of BDO USA, LLP(Headquartered in Chicago, IL)

Issued by the

Public Company Accounting Oversight Board

December 20, 2016

THIS IS A PUBLIC VERSION OF

PORTIONS OF THE COMPLFROM THIS DOCUMENT IN

SECTIONS 104(g)OF THE SARBANES

A PCAOB INSPECTION REPORT

ETE REPORT ARE OMITTEDORDER TO COMPLY WITH

(2) AND 105(b)(5)(A)

PCAOB RELEASE NO. 104-2017-030

-OXLEY ACT OF 2002

PCAOB Release No. 104-2017-030

2015 INSPECTION OF BDO USA, LLP

Preface

In 2015, the Public Company Accounting Oversight Board ("PCAOB" or "theBoard") conducted an inspection of the registered public accounting firm BDO USA, LLP("the Firm") pursuant to the Sarbanes-Oxley Act of 2002 ("the Act").

Inspections are designed and performed to provide a basis for assessing thedegree of compliance by a firm with applicable requirements related to auditing issuers.For a description of the procedures the Board's inspectors may perform to fulfill thisresponsibility, see Part I.D of this report (which also contains additional informationconcerning PCAOB inspections generally). The inspection included reviews of portionsof selected issuer audits. These reviews were intended to identify whether deficienciesexisted in the reviewed work, and whether such deficiencies indicated defects orpotential defects in the Firm's system of quality control over audits. In addition, theinspection included a review of policies and procedures related to certain quality controlprocesses of the Firm that could be expected to affect audit quality.

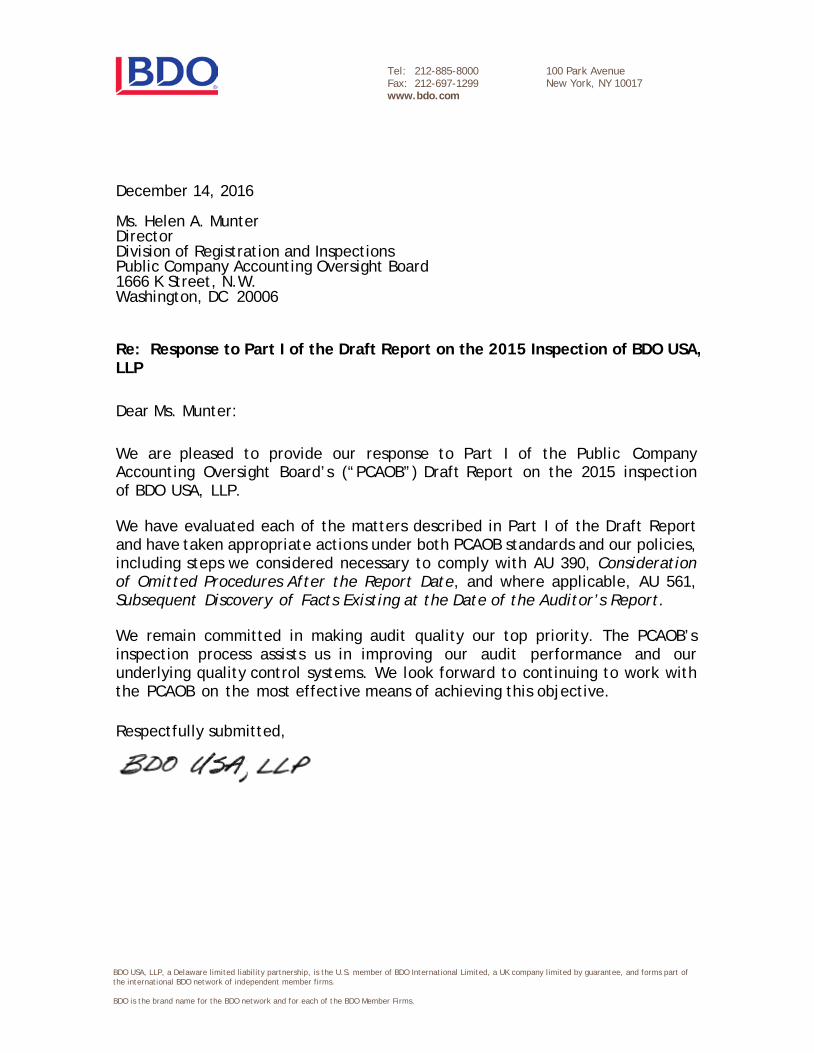

The Board is issuing this report in accordance with the requirements of the Act.The Board is releasing to the public Part I of the report, portions of Appendix B,Appendix C, and Appendix D. Appendix B consists of the Firm's comments, if any, on adraft of the report. If the nonpublic portions of the report discuss criticisms of or potentialdefects in the Firm's system of quality control, those discussions also could eventuallybe made public, but only to the extent the Firm fails to address the criticisms to theBoard's satisfaction within 12 months of the issuance of the report. Appendix C presentsthe text of the paragraphs of the auditing standards that are referenced in Part I.A inrelation to the description of auditing deficiencies there.

Note on this report's citations to auditing standards: On March 31, 2015, thePCAOB adopted a reorganization of its auditing standards using a topical structure anda single, integrated numbering system. See Reorganization of PCAOB AuditingStandards and Related Amendments to PCAOB Standards and Rules, PCAOB ReleaseNo. 2015-002 (Mar. 31, 2015). The reorganization will be effective as of December 31,2016, but the reorganized numbering system may be used before that date. In thisreport, citations to PCAOB auditing standards use the numbering system and titles ofstandards that were in effect at the time of the primary inspection procedures. A tablecross-referencing the section numbers of those standards included in Part I of thisreport as reorganized is included at Appendix D.

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 2

PART I

INSPECTION PROCEDURES AND CERTAIN OBSERVATIONS

Members of the Board's staff ("the inspection team") conducted primaryprocedures1 for the inspection from August 2015 to February 2016. The inspection teamperformed field work at the Firm's National Office and at 17 of its approximately 56 U.S.practice offices.2

A. Review of Audit Engagements

The inspection procedures included reviews of portions of 23 issuer auditsperformed by the Firm. The inspection team identified matters that it considered to bedeficiencies in the performance of the work it reviewed. Three of the deficiencies relateto auditing aspects of an issuer's financial statements that the issuer restated after theprimary inspection procedures.3 In addition, in three of the audits described below, afterthe primary inspection procedures, the Firm revised its opinion on the effectiveness ofthe issuer's internal control over financial reporting ("ICFR") to express an adverseopinion.

1 For this purpose, the time span for "primary procedures" includes fieldwork, other review of audit work papers, and the evaluation of the Firm's quality controlpolicies and procedures through review of documentation and interviews of Firmpersonnel. The time span does not include (1) inspection planning, which maycommence months before the primary procedures, and (2) inspection follow-upprocedures, wrap-up, analysis of results, and the preparation of the inspection report,which generally extend beyond the primary procedures.

2 This represents the Firm's total number of practice offices; however,approximately 36 of the Firm's practice offices have primary responsibility for issueraudit clients.

3 The 2015 inspection did not include review of any additional audit workrelated to the restatements.

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 3

The descriptions of the deficiencies in Part I.A of this report include, at the end ofthe description of each deficiency, references to specific paragraphs of the auditingstandards that relate to those deficiencies. The text of those paragraphs is set forth inAppendix C to this report. The references in this sub-Part include only standards thatprimarily relate to the deficiencies; they do not present a comprehensive list of everyauditing standard that applies to the deficiencies. Further, certain broadly applicableaspects of the auditing standards that may be relevant to a deficiency, such asprovisions requiring due professional care, including the exercise of professionalskepticism; the accumulation of sufficient appropriate audit evidence; and theperformance of procedures that address risks, are not included in the references to theauditing standards in this sub-Part, unless the lack of compliance with these standardsis the primary reason for the deficiency. These broadly applicable provisions aredescribed in Part I.B of this report.

Certain of the deficiencies identified were of such significance that it appeared tothe inspection team that the Firm, at the time it issued its audit report, had not obtainedsufficient appropriate audit evidence to support its opinion that the financial statementswere presented fairly, in all material respects, in accordance with the applicablefinancial reporting framework and/or its opinion about whether the issuer hadmaintained, in all material respects, effective internal control over financial reporting("ICFR"). In other words, in these audits, the auditor issued an opinion without satisfyingits fundamental obligation to obtain reasonable assurance about whether the financialstatements were free of material misstatement and/or the issuer maintained effectiveICFR.

The fact that one or more deficiencies in an audit reach this level of significancedoes not necessarily indicate that the financial statements are misstated or that thereare undisclosed material weaknesses in ICFR. It is often not possible for the inspectionteam, based only on the information available from the auditor, to reach a conclusion onthose points.

Whether or not associated with a disclosed financial reporting misstatement, anauditor's failure to obtain the reasonable assurance that the auditor is required to obtainis a serious matter. It is a failure to accomplish the essential purpose of the audit, and it

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 4

means that, based on the audit work performed, the audit opinion should not have beenissued.4

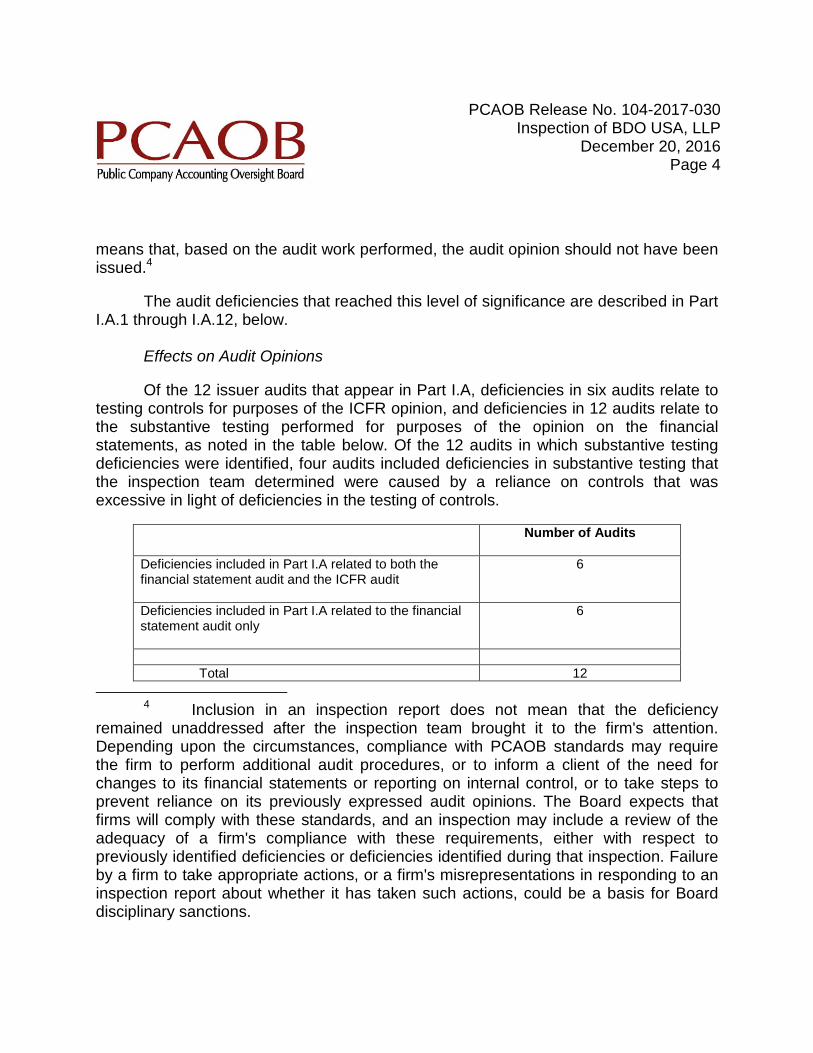

The audit deficiencies that reached this level of significance are described in PartI.A.1 through I.A.12, below.

Effects on Audit Opinions

Of the 12 issuer audits that appear in Part I.A, deficiencies in six audits relate totesting controls for purposes of the ICFR opinion, and deficiencies in 12 audits relate tothe substantive testing performed for purposes of the opinion on the financialstatements, as noted in the table below. Of the 12 audits in which substantive testingdeficiencies were identified, four audits included deficiencies in substantive testing thatthe inspection team determined were caused by a reliance on controls that wasexcessive in light of deficiencies in the testing of controls.

Number of Audits

Deficiencies included in Part I.A related to both thefinancial statement audit and the ICFR audit

6

Deficiencies included in Part I.A related to the financialstatement audit only

6

Total 12

4 Inclusion in an inspection report does not mean that the deficiencyremained unaddressed after the inspection team brought it to the firm's attention.Depending upon the circumstances, compliance with PCAOB standards may requirethe firm to perform additional audit procedures, or to inform a client of the need forchanges to its financial statements or reporting on internal control, or to take steps toprevent reliance on its previously expressed audit opinions. The Board expects thatfirms will comply with these standards, and an inspection may include a review of theadequacy of a firm's compliance with these requirements, either with respect topreviously identified deficiencies or deficiencies identified during that inspection. Failureby a firm to take appropriate actions, or a firm's misrepresentations in responding to aninspection report about whether it has taken such actions, could be a basis for Boarddisciplinary sanctions.

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 5

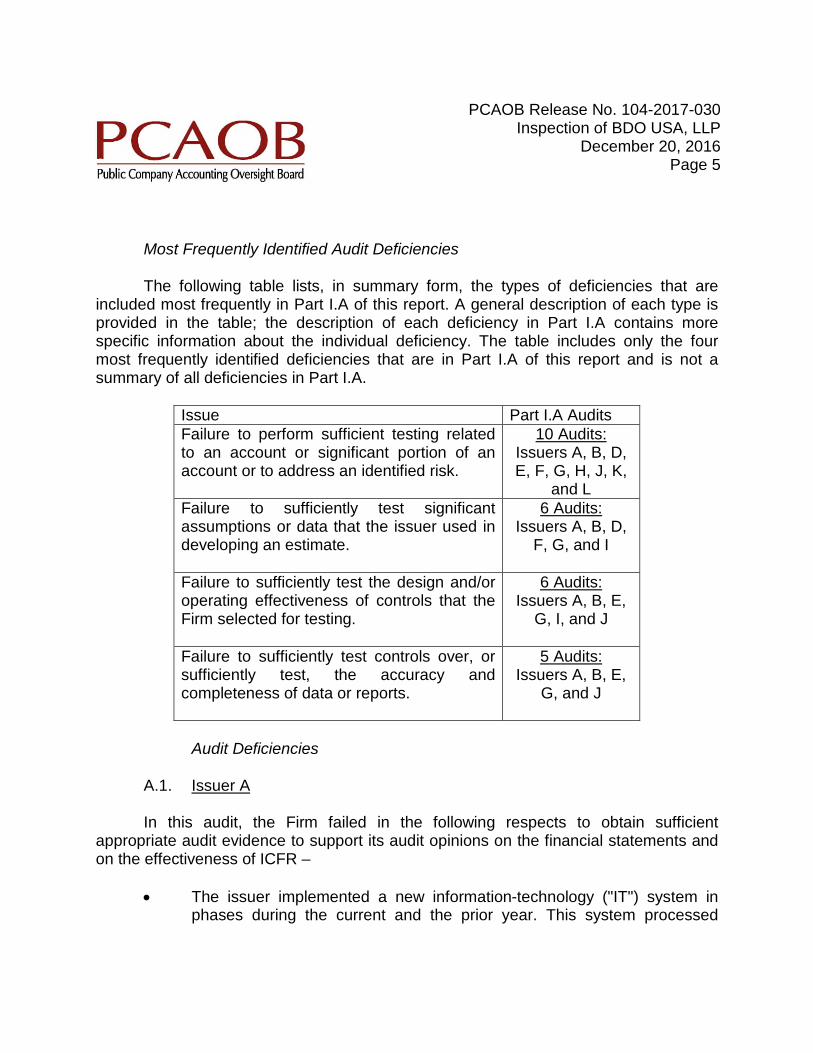

Most Frequently Identified Audit Deficiencies

The following table lists, in summary form, the types of deficiencies that areincluded most frequently in Part I.A of this report. A general description of each type isprovided in the table; the description of each deficiency in Part I.A contains morespecific information about the individual deficiency. The table includes only the fourmost frequently identified deficiencies that are in Part I.A of this report and is not asummary of all deficiencies in Part I.A.

Issue Part I.A AuditsFailure to perform sufficient testing relatedto an account or significant portion of anaccount or to address an identified risk.

10 Audits:Issuers A, B, D,E, F, G, H, J, K,

and LFailure to sufficiently test significantassumptions or data that the issuer used indeveloping an estimate.

6 Audits:Issuers A, B, D,

F, G, and I

Failure to sufficiently test the design and/oroperating effectiveness of controls that theFirm selected for testing.

6 Audits:Issuers A, B, E,

G, I, and J

Failure to sufficiently test controls over, orsufficiently test, the accuracy andcompleteness of data or reports.

5 Audits:Issuers A, B, E,

G, and J

Audit Deficiencies

A.1. Issuer A

In this audit, the Firm failed in the following respects to obtain sufficientappropriate audit evidence to support its audit opinions on the financial statements andon the effectiveness of ICFR –

The issuer implemented a new information-technology ("IT") system inphases during the current and the prior year. This system processed

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 6

revenue and inventory transactions and, in its testing of controls over thesales and inventory-management processes, the Firm selected a numberof application controls that depended on this system. The Firm identifiedmultiple deficiencies related to the IT general controls ("ITGCs") over thissystem, including issues related to segregation of duties, as well asdeficiencies that meant that individuals could access and changeunderlying data.

o The Firm failed to consider the potential effects of thesedeficiencies on the effectiveness of the application and IT-dependent manual controls on which the Firm relied when testingrevenue and inventory. (AS No. 13, paragraph 34)

o The Firm failed to perform sufficient procedures to evaluate theseverity of the deficiencies, as follows –

With respect to revenue, the Firm identified fourcompensating controls, operating as of year end, but failedto sufficiently evaluate whether these controls would mitigatethe risks related to revenue posed by the ITGC deficiencies.Specifically, (1) the Firm determined that one of thesecontrols was not operating effectively and (2) as describedbelow, the Firm failed to sufficiently test the other threecontrols, which consisted of (a) a review of order informationentered into the system used to process revenuetransactions, (b) the approval of both standard and non-standard pricing, and (c) reviews of the revenue disclosuresin the financial statements. (AS No. 5, paragraph 68)

With respect to inventory, the Firm asserted that there werecompensating controls in place, but failed to identify thespecific compensating controls and evaluate whether thosecontrols would operate at a level of precision that wouldprevent or detect a material misstatement. (AS No. 5,paragraph 68)

The issuer recognized revenue from sales directly to end customers andfrom transactions involving distributors. The transactions involving

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 7

distributors included both sales on a sell-in basis (for which revenue wasrecognized upon transfer of title to the distributor) and sales on aconsignment basis (for which revenue was generally recognized uponsubsequent transfer of title). The Firm failed to perform sufficientprocedures related to revenue, for which the Firm identified a fraud risk,and net accounts receivable, as follows –

o The Firm selected for testing a number of controls over the enteringof order information into, and processing of that information by, thesystem that was subject to the ITGC deficiencies described above.The Firm's procedures were insufficient. Specifically –

The Firm selected for testing a control that consisted of areview of the order information entered into the system. TheFirm failed to sufficiently test an important aspect of thecontrol that consisted of the review of the order codingentered into the system, which the system used to determinewhether revenue was recognized or deferred. Specifically,the Firm's procedures were limited to obtaining a checklistevidencing the review without understanding and evaluatingthe procedures that the control owner performed to reviewthe order coding. (AS No. 5, paragraphs 42 and 44)

The Firm failed to identify and test any controls thataddressed whether the system would correctly recognize ordefer revenue based on the order coding. (AS No. 5,paragraph 39)

For revenue transactions recognized either on the sale toend customers or on a sell-in basis to distributors, the Firmselected for testing a number of application controls thatwere based on the configuration of the system. The Firm'sprocedures were insufficient, as follows –

The Firm tested a control that generated an errormessage if the shipping and invoice date did notmatch in the system. The Firm, however, failed to

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 8

identify and test any controls over the accuracy of theproduct shipment dates. (AS No. 5, paragraph 39)

The Firm failed to identify and test any controls thataddressed whether the quantity of product recognizedas revenue agreed to the quantity of product shipped.(AS No. 5, paragraph 39)

The Firm selected for testing a manual control that consistedof the approval of both standard and non-standard pricing.The sample that the Firm used to test this control was toosmall to provide sufficient evidence because it was limited toone customer with non-standard pricing and one invoice withstandard pricing. (AS No. 5, paragraph 44)

o The Firm selected for testing a control consisting of reviews of theissuer's revenue disclosures. The Firm's procedures to test thiscontrol were limited to inquiring of one of the control owners andinspecting initials on the quarterly disclosure checklist as evidencethat a review had occurred. The Firm also pointed to its testing ofthe accuracy of the issuer's disclosures, but these procedures didnot directly test the control. The Firm's testing did not includeascertaining and evaluating the nature of the review proceduresthat the control owners performed. (AS No. 5, paragraphs 42, 44,and B9)

o The Firm designed certain of its substantive procedures – includingsample sizes – based on a level of control reliance that was notsupported due to the deficiencies in the Firm's testing of controlsthat are discussed above. As a result, certain of the samples thatthe Firm used to test revenue and accounts receivable were toosmall to provide sufficient evidence. (AS No. 13, paragraphs 16, 18,and 37; AU 350, paragraphs .19, .23, and .23A)

o In addition to the fraud risk related to revenue, the Firm identified afraud risk related to the potential for management override ofcontrols due to a small accounting department and multiple personswith administrative rights to the accounting system. The Firm

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 9

identified that the chief financial officer ("CFO") had the ability tocreate and post journal entries, and had created and postedmultiple entries to the cash and accounts receivable sub-ledgers inthe first half of the year. To address this fraud risk, the Firm testedonly a small number of the journal entries created and posted bythe CFO in the first half of the year. In addition, the Firm failed tosufficiently evaluate the appropriateness of the journal entriesselected for testing because its procedures were limited tocomparing the entries to the issuer's system without examining anysupporting documentation. Further, the Firm failed to performprocedures, beyond inquiry, to test whether the CFO had createdand posted journal entries during the last six months of the year.(AU 316, paragraph .61)

o The Firm failed to perform sufficient procedures related to theallowance for doubtful accounts, as follows –

The Firm's procedures to test the control that it selected,consisting of a review of the allowance for doubtful accounts,were limited to inquiring of management, tracing certainamounts to the general ledger, and inspecting emails asevidence that reviews had occurred. The Firm failed toascertain and evaluate the nature of the review proceduresthat the control owners performed, including the criteria usedby the control owners to identify matters for follow up andwhether those matters were appropriately resolved. Inaddition, the Firm failed to identify and test any controls overthe accuracy and completeness of the data used in theperformance of this control. (AS No. 5, paragraphs 39, 42,and 44)

The Firm's substantive procedures to test the allowance fordoubtful accounts were limited to testing the aging of asample of invoices and inquiring of management. (AU 342,paragraph .07)

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 10

o The Firm failed to perform sufficient procedures to evaluatewhether the issuer's accounting for revenue that was recognized ona sell-in basis was in conformity with GAAP, as follows –

The Firm's procedures to test this revenue were limited toobtaining the associated purchase orders, shippingevidence, invoices, and subsequent cash receipts. TheFirm's testing did not include evaluating whether these salesshould be recognized as revenue upon shipment rather thandeferred until the product was sold by the distributor. (ASNo. 14, paragraph 30)

For one significant transaction, the Firm failed to identify andappropriately address what appeared to the inspection teamto be an instance in which the financial statements were notpresented fairly, in all material respects, in conformity withGAAP. Specifically, the Firm failed to identify that the issuerhad incorrectly applied Financial Accounting StandardsBoard ("FASB") Accounting Standards Codification ("ASC")605, Revenue Recognition, as the issuer recognizedrevenue for this transaction even though there was nopersuasive evidence of an arrangement and collectibility wasnot reasonably assured. (AS No. 14, paragraph 30)

o The issuer recognized a significant amount of revenue fromtransactions involving consignments. The Firm failed to obtain anunderstanding of the issuer's process for recognizing this revenue,and the Firm also failed in the following respects to performsufficient procedures related to revenue recognized fromconsignment transactions –

The Firm failed to identify and test any controls over whetherrevenue recognized from consignment transactionsrepresented sales involving a transfer of title. (AS No. 5,paragraph 39)

The Firm failed to perform sufficient substantive proceduresto test this revenue. The Firm's procedures consisted of

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 11

obtaining the associated purchase orders, evidence that theproduct was shipped from the issuer to the consignmentlocation, invoices, and subsequent cash receipts. The Firm'stesting did not include an evaluation of whether the revenuerepresented transactions involving a transfer of title. (AS No.14, paragraph 30)

The Firm failed to identify and appropriately addressinaccuracies in the issuer's disclosures related toconsignment sales. (AS No. 14, paragraphs 30 and 31)

The issuer held inventory at its locations and also reported inventory heldat other locations that was subject to consignment arrangements. TheFirm failed to obtain an understanding of the issuer's process forassessing the existence of inventory, both at its own locations and atexternal locations, and the Firm also failed in the following respects toperform sufficient procedures related to the existence of inventory –

o The Firm failed to identify and test any controls over the existenceof inventory held on consignment. (AS No. 5, paragraph 39)

o The Firm failed to sufficiently test controls over the existence ofinventory held at the issuer's locations, as follows –

The Firm failed to identify and test any controls related tophysical counts of the inventory held by the issuer. (AS No.5, paragraph 39)

The only two controls that the Firm selected related to theexistence of this inventory consisted of scanning inventoryitems when they were received, modified, or shipped by theissuer and updating the inventory recorded in the IT system;the IT system was subject to the ITGC deficienciesdescribed above. The Firm failed to sufficiently test thesetwo controls, as its procedures consisted of inquiring ofmanagement and observing that the scanner indicated anerror when an item was packed for shipment that was notordered. In addition, in its evaluation of these controls, the

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 12

Firm considered the results of certain of its substantiveprocedures that consisted of obtaining the inventory detailand tracing the total to the general ledger and noting thatproducts appeared reasonably classified among rawmaterials, work-in-process, and finished goods, but thoseprocedures did not directly test the controls. (AS No. 5,paragraphs 42, 44, and B9)

o The Firm did not obtain an understanding of or observe any of theissuer's count procedures; its primary substantive procedure to testthe existence of inventory held at the issuer's locations consisted ofperforming an independent count of a judgmentally determinedsample of items at year end. (AU 331, paragraph .12)

The Firm failed to perform sufficient procedures related to the valuation ofinventory. Specifically –

o The one control that the Firm selected over the valuation ofinventory consisted of a review of the annual standard cost study,which the issuer used to allocate raw materials and overhead coststo each product. The Firm failed to sufficiently test this control, asits procedures were limited to inquiring of management, obtaining acopy of the standard cost study, and noting that costs appeared tobe reasonably allocated to each product. The Firm failed toascertain and evaluate the nature of the review procedures that thecontrol owner performed, including the criteria used by the controlowner to identify matters for follow up and whether those matterswere appropriately resolved. In addition, the Firm failed to identifyand test any controls over the accuracy and completeness of thedata used in the performance of this control. Further, the Firm failedto identify and test any controls that addressed whether theinventory costs that were the basis for the amount shown in thegeneral ledger were the same as the costs generated in the annualstandard cost study. (AS No. 5, paragraphs 39, 42, and 44)

o The Firm failed to perform sufficient substantive procedures to testthe valuation of inventory. The Firm tested a sample of the finishedgoods inventory values in the annual standard cost study. The

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 13

Firm, however, did not compare the inventory costs that it hadtested in the annual standard cost study to the inventory costs thatwere the basis for the amount shown in the general ledger. (AS No.13, paragraph 8)

The Firm failed to perform sufficient procedures related to investments.Specifically –

o To address the valuation of investments, the Firm selected fortesting two controls. These controls consisted of (1) reviews ofinvestment balances and transactions for compliance with theissuer's investment policy and (2) the reconciliation of investmentstatements to the general ledger; however, the Firm failed to testany aspects of these controls, or any other controls, that addressedthe risk related to whether the investments were recorded at fairvalue. (AS No. 5, paragraph 39)

o To address the issuer's disclosure of investments in the financialstatements, the Firm selected for testing a control consisting ofreviews of the issuer's financial statements. The Firm's proceduresto test this control were limited to tracing amounts in the financialstatements to the general ledger, considering the accuracy of thedisclosures based on the Firm's knowledge of events, andinspecting correspondence that indicated a review had occurred.The Firm's testing did not include ascertaining and evaluating thenature of the review procedures that the control owner performed,including how the control owner assessed whether disclosureswere in conformity with GAAP. (AS No. 5, paragraphs 42 and 44)

o The issuer classified certain securities as trading securities andentered into an amended purchase agreement related to thesesecurities. The Firm failed to sufficiently test these securities, asfollows –

The Firm failed to perform any procedures to test theexistence of these securities. (AS No. 13, paragraph 8)

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 14

The Firm failed to identify and appropriately address that theissuer's disclosures regarding these securities omitted thefact that the purchase agreement had been amended andwere inconsistent with the terms of the amended purchaseagreement. (AS No. 14, paragraphs 30 and 31)

o The Firm failed to perform sufficient substantive procedures to testthe existence of available-for-sale ("AFS") securities. The Firm'sprocedures were limited to (1) requesting a confirmation of all AFSsecurities from the investment manager, who did not have custodyof the securities, and (2) comparing the fair value of AFS securitiesfrom the returned confirmation in aggregate to a statement that theissuer had obtained from the custodian. The Firm, however, did notobtain that statement directly from the custodian. (AU 332,paragraph .21)

A.2. Issuer B

In this audit of a manufacturer of technology products, the Firm failed in thefollowing respects to obtain sufficient appropriate audit evidence to support its auditopinions on the financial statements and on the effectiveness of ICFR –

The issuer entered into contracts involving multiple elements andallocated consideration to the deliverables using vendor-specific objectiveevidence ("VSOE") of fair value or the best estimate of selling price("BESP"). The Firm identified a fraud risk related to the occurrence ofrevenue, but the Firm failed to perform sufficient procedures related torevenue, deferred revenue, and net accounts receivable, as follows –

o The Firm failed in the following respects to sufficiently test controls–

The Firm failed to test the operating effectiveness of thecontrol that it selected over the accuracy and completenessof sales order data that were input into the issuer's system.(AS No. 5, paragraph 44)

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 15

The Firm identified and tested a control that included theinternal audit department's ("IA") evaluation of theappropriateness of revenue recognition for a sample oftransactions each quarter. The Firm noted that IA identified anumber of exceptions in the sample of transactions that ithad tested each quarter. The Firm, however, failed to (1)evaluate the effect of these exceptions on its conclusionrelated to the design effectiveness of this control or (2)identify and test any other controls that addressed the riskthat revenue was not appropriately recognized. (AS No. 5,paragraph 48)

The Firm selected for testing two controls to address the riskrelated to the amount of revenue allocated to each of themultiple elements; these controls consisted of (1) the reviewof the sales contracts, including the approval of anydiscounts, and (2) the analysis of VSOE and BESP. TheFirm's procedures to test these controls were limited to, forthe first control, inspecting approvals as evidence that theactions performed as part of the control had occurred and,for the second control, obtaining the issuer's VSOE andBESP memoranda and analyses. The Firm failed toascertain and evaluate the nature of the review proceduresthat the control owners performed, including the criteria usedby the control owners to identify matters for follow up andwhether those matters were appropriately resolved. Inaddition, the Firm failed to identify and test any controls overthe accuracy and completeness of the data used in theperformance of these controls. (AS No. 5, paragraphs 39,42, and 44)

The Firm failed to identify and test any controls over theaccuracy and completeness of the accounts receivableaging report, which was used in the issuer's control over theallowance for doubtful accounts that the Firm selected fortesting. (AS No. 5, paragraph 39)

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 16

o The Firm failed to perform sufficient substantive procedures to testrevenue from contracts involving multiple elements, as follows –

The Firm failed to perform any procedures to evaluatewhether third-party evidence existed for elements that theissuer valued using BESP. (AS No. 14, paragraph 30)

The Firm failed to sufficiently evaluate the appropriatenessof the methodology and the reasonableness of theassumptions used in the issuer's VSOE and BESP analyses,as its procedures were limited to obtaining the issuer'sVSOE and BESP memoranda. (AU 342, paragraph .11)

The Firm failed to perform sufficient procedures to test theaccuracy and completeness of the data used in the issuer'sVSOE and BESP analyses. Specifically, the Firm'sprocedures were limited to comparing five items from itsrevenue testing to the analyses for each of the first andsecond quarters; for the other two quarterly analyses, theFirm performed no testing. (AU 342, paragraph .11)

The Firm's procedures to test a significant adjustment thatthe issuer made to revenue were not sufficient. Specifically,the Firm obtained the issuer's memorandum and comparedthe posted adjustment to the general ledger, but it failed toperform any procedures to determine whether the amount ofthe adjustment was accurate. (AS No. 13, paragraph 8)

o The Firm tested the existence of accounts receivable as of aninterim date. The Firm's procedures to extend its conclusion to yearend were not sufficient. Specifically, these procedures were limitedto obtaining schedules that rolled forward accounts receivable fromthe interim testing date to the year end and, for certain locations,testing (1) a very small sample of sales and (2) a sample of cashreceipts related to sales tested as of the interim date. (AS No. 13,paragraph 45)

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 17

The Firm failed to perform sufficient procedures related to inventory atcertain of the issuer's locations, which held approximately 75 percent ofthe issuer's total inventory. Specifically –

o The Firm failed to appropriately evaluate certain exceptionsidentified in its testing of ITGCs. Specifically, the Firm failed toevaluate the effect of these exceptions on the effectiveness ofautomated and IT-dependent manual controls over inventory that ithad tested. (AS No. 5, paragraphs 47 and 48)

o The issuer identified exceptions in its testing of a control over cashpayments and concluded that the control was not operatingeffectively. The Firm failed to consider the effect of theseexceptions on its own evaluation that this control was operatingeffectively. (AS No. 5, paragraph 48)

o The Firm failed to evaluate, in combination with the other identifieddeficiencies, the severity of a deficiency that it identified in aninventory control that it tested. (AS No. 5, paragraph 62)

o Although the Firm identified four compensating controls that itbelieved addressed the deficiencies that it had identified in controlsover inventory and related ITGCs, the Firm failed to sufficiently testthese controls. Specifically –

The Firm failed to test one of the compensating controls thatit had identified. (AS No. 5, paragraph 39)

Another of the compensating controls that the Firm hadidentified was the control over cash payments that the issuerhad determined was not operating effectively, as discussedabove. (AS No. 5, paragraph 68)

The Firm's procedures to test the other two compensatingcontrols – consisting of reviews of balance sheetreconciliations and the review of a comparison of thefinancial statements by region to prior periods – were limitedto inquiring of management, inspecting signatures as

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 18

evidence that reviews had occurred, inspecting a list of thegeneral review procedures to be performed for areconciliation, tracing the balance of a reconciliation to thegeneral ledger, and reading the explanations for significantdifferences identified through the financial statementcomparison. The Firm's testing did not include ascertainingand evaluating the nature of the specific review proceduresthat the control owners performed, including the criteria usedby the control owners to identify matters for investigation andwhether those matters were appropriately investigated andresolved. (AS No. 5, paragraph 68)

o The Firm failed to sufficiently test controls over the existence ofinventory. The Firm selected for testing a control that related to thephysical inventory count procedures; an aspect of this controlconsisted of management's evaluation of all physical countvariances to determine the adjustment to be recorded. The Firmfailed to test this aspect of the control. In addition, the Firm failed toidentify and test any controls over the report used in theperformance of this control. (AS No. 5, paragraphs 39, 42, and 44)

o The Firm failed in the following respects to sufficiently test controlsover the valuation of inventory –

The Firm failed to identify and test any controls over thedetermination of standard costs, including the capitalizationof labor and overhead costs into inventory. (AS No. 5,paragraph 39)

The Firm failed to test the operating effectiveness of certaincontrols that it selected for testing, which consisted of theapproval of changes to standard costs and the review ofmanufacturing variances. (AS No. 5, paragraph 44)

The Firm selected for testing a control that consisted of areview of inventory allowances and other valuationadjustments. The Firm's procedures to test this control werelimited to inquiring of the control owners regarding the nature

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 19

of the review procedures performed, comparing certainbalances to the general ledger, and inspecting signatures asevidence that the reviews had occurred. The Firm's testingdid not include evaluating the criteria used by the controlowners to identify matters for follow up and whether thosematters were appropriately resolved. In addition, the Firmfailed to identify and test any controls over the accuracy andcompleteness of the data used in the performance of thiscontrol. (AS No. 5, paragraphs 39, 42, and 44)

o The Firm failed to perform sufficient substantive procedures to testthe existence of inventory. In performing test counts of the issuer'sinventory, the Firm identified differences between its counts andmanagement's counts. For certain of these differences, there wasno evidence in the audit documentation, and no persuasive otherevidence, that the Firm had evaluated the reasons for thesedifferences or otherwise performed procedures to address theimplications of the differences. In addition, for certain of the testcounts, the Firm failed to trace the quantities that it had counted tothe quantities recorded in the issuer's system. (AU 331, paragraph.09)

o The Firm failed to perform sufficient substantive procedures to testthe valuation of inventory, as follows –

The Firm failed to test any of the labor and overhead coststhat were capitalized into inventory. (AS No. 13, paragraph8)

To test inventory pricing for manufactured goods, the Firmselected a sample of five items. The Firm tested only a verysmall number of the raw materials that were included inthese five manufactured goods. (AS No. 13, paragraph 8)

The Firm failed to investigate significant variances that itidentified between the bill of materials, which was intendedto be used to determine the inventory's recorded cost, andthe cost recorded in the inventory subsidiary ledger. In

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 20

addition, the Firm failed to sufficiently evaluate significantvariances that it identified between the standard and actualcosts, as it failed to evaluate whether these variances wereincluded in the purchase-price variance detail. (AS No. 15,paragraph 29)

The Firm failed to perform sufficient procedures to test theinventory allowance, which consisted of six separatecomponents. To test these components, the Firm obtainedan understanding of how the issuer determined thecomponents; inspected supporting worksheets for certain ofthe components; tested the mathematical accuracy of certaincalculations; considered changes in the balance for certainof the components as compared to previous periods;considered recent sales activity for one component; and, foranother component, considered total write-offs during theyear as compared to the component balance. The Firm,however, failed to evaluate the reasonableness of certainsignificant underlying assumptions for each of thecomponents. (AU 342, paragraph .11)

The Firm failed to sufficiently test the accuracy andcompleteness of data and reports used in calculating thecomponents of the inventory allowance. Specifically, theFirm failed to test the underlying data used for four of the sixcomponents. For one of the remaining components, theFirm's procedures were limited to testing one item on one ofthe supporting schedules. For the last component, the Firm'sprocedures were limited to, for one of the supportingschedules, (1) tracing a small number of items to theinventory subsidiary ledger and prior-year schedule and (2)tracing a small number of items from the prior-year scheduleto the current-year schedule. (AU 342, paragraph .11)

The Firm failed to sufficiently test the accuracy andcompleteness of a report prepared by the issuer that theFirm used to test the net realizable value of inventory, as theFirm's procedures were limited to comparing one invoice

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 21

from its revenue test of details to the report. (AS No. 15,paragraph 10)

The Firm designed certain of its substantive procedures – includingsample sizes – based on a level of control reliance that was not supporteddue to the deficiencies in the Firm's testing of controls that are discussedabove. As a result, certain of the samples that the Firm used to testrevenue, deferred revenue, accounts receivable, and the cost of inventorywere too small to provide sufficient evidence. In addition, the Firm'ssample to test the net realizable value of inventory was too small toprovide sufficient evidence because, in determining its sample size, theFirm did not appropriately consider relevant factors, including thecharacteristics of the population and the Firm's risk assessments. (AS No.13, paragraphs 16, 18, and 37; AU 350, paragraphs .23 and .23A)

During the year, the issuer completed a number of significant acquisitions,and it accounted for these acquisitions as business combinations. TheFirm identified a fraud risk related to these business combinations. TheFirm failed to perform sufficient procedures to test controls over thevaluation of the assets acquired and liabilities assumed in these businesscombinations. The Firm selected three controls for testing: these controlsincluded a review of the valuation report and the checklist for eachacquisition, the preparation of technical accounting memoranda, and theapproval of the business combination by the board of directors. The Firm'sprocedures to test these controls were limited to verifying that theacquisition checklists were completed for a sample of the businesscombinations; inspecting signatures as evidence that reviews hadoccurred; reading issuer-prepared technical accounting memoranda;reading minutes of meetings of the board of directors; and, for oneacquisition, reading emails from an external valuation specialist. The Firmfailed to evaluate whether these controls were designed and operated at alevel of precision that would prevent or detect material misstatements, asit failed to ascertain the nature of the review procedures that the controlowners performed, including the criteria used by the control owners toidentify matters for follow up and whether those matters wereappropriately resolved. (AS No. 5, paragraphs 42 and 44)

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 22

A.3. Issuer C

In this audit, the Firm failed to identify and appropriately address what appearedto the inspection team to be an instance in which the financial statements were notpresented fairly, in all material respects, in conformity with GAAP. Specifically, the Firmfailed to identify that (1) the issuer had incorrectly applied GAAP when it recorded achange in estimate on a prospective basis and (2) the issuer had omitted requireddisclosures regarding the change. (AS No. 14, paragraphs 30 and 31)

A.4. Issuer D

In this audit, the Firm failed in the following respects to obtain sufficientappropriate audit evidence to support its audit opinion on the financial statements –

The issuer recognized certain revenue using the percentage-of-completion("POC") method. The Firm identified a significant risk related to the use ofestimates in calculating revenue to be recognized using the POC methodand a fraud risk related to revenue. The Firm failed to perform sufficientprocedures related to the POC revenue as follows –

o The Firm selected a sample of 14 contracts for which to perform themajority of its substantive testing. Twelve of these contracts wereselected for testing based on contract size and risk criteria, andthese contracts represented approximately 50 percent of the totalPOC revenue. The other two contracts were selected from theremaining population. The Firm's sample for that remainingpopulation was too small to provide sufficient evidence, given theidentified significant risks and the amount of the POC revenuerelated to the remaining contracts, which was many times theFirm's established level of materiality. (AS No. 13, paragraphs 8and 42; AU 350, paragraphs .23 and .23A)

o The Firm failed to sufficiently evaluate the reasonableness of theestimated costs to complete the contracts that were open as of yearend, as the procedures it designed and performed to address thisestimate were limited to, as described more specifically below,inquiries, procedures that did not address the estimated costs, and

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 23

observations at the project site for one contract. (AU 342,paragraph .07) The Firm's procedures consisted of –

testing the total costs incurred for one item on one contract; inquiring of management related to the status of the project

for the sample of contracts described above, as well as forcertain additional contracts that exceeded a monetarythreshold, including inquiring about the reasons for certainchanges in estimated costs and gross margins that the Firmidentified when performing comparisons of those items toprior or subsequent periods;

for the sample of contracts described above, confirmingcertain terms – which did not include costs – with thecustomers and performing alternative procedures when therequested confirmations were not returned; and

for one contract, inquiring of the project team, observing theprogress at the project site, tracing the names of certainemployees observed onsite to the payroll records, andinspecting for any uninstalled materials.

o The Firm failed to sufficiently test the change orders that wereincluded in the POC calculations but had not yet been approved bythe customer as of year end. In determining the population ofchange orders from which to select its sample for testing, the Firmincluded only those change orders that were unapproved at yearend but had been approved by the customer by the later testingdate. As a result, the Firm failed to select any of its sample fromchange orders that remained unapproved at the testing date. (AU350, paragraph .17)

During the year, the issuer acquired a significant business. The Firm failedto sufficiently evaluate the reasonableness of the estimated costs tocomplete related to the contracts of this business; these costs were usedto calculate the value of the assets acquired and liabilities assumed thatrepresented the differences between the revenue that the acquiree hadpreviously recognized under the POC method and the billings per thecontractual terms. Specifically, the Firm's procedures related to theseestimated costs were limited to (1) reviewing the predecessor auditor's

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 24

work papers for the prior-year audit, (2) inquiring of management aboutthe reasons for certain changes in estimated costs and gross margins,and (3) performing the procedures that the Firm intended to test theestimated costs to complete for specific contracts that are describedabove. (AU 342, paragraph .07)

The Firm failed to identify and evaluate the significance to the financialstatements of the issuer having accounted for an acquisition other than inconformity with FASB ASC 805, Business Combinations. (AS No. 14,paragraph 30)

A.5. Issuer E

In this audit of a pharmaceutical company, the Firm failed in the followingrespects to obtain sufficient appropriate audit evidence to support its audit opinions onthe financial statements and on the effectiveness of ICFR –

The issuer initially recorded sales net of estimated rebates, expectedreturns, chargebacks, and other sales adjustments, and recorded theseamounts on the balance sheet, either as a reduction to accountsreceivable (a sales allowance) or as a liability (a price-concession reserveor sales return reserve). The issuer updated its sales allowance andreserve accounts quarterly if actual results differed from previousexpectations. The Firm identified a fraud risk related to the occurrence ofrevenue, but failed to perform sufficient procedures to test net sales, netaccounts receivable, and price-concession and sales return reserves forone subsidiary, as follows –

o The Firm failed to identify and test any controls over theidentification and consideration of contract terms that would affectrevenue recognition. (AS No. 5, paragraph 39)

o The Firm selected for testing controls that consisted of (1) amonthly review of the accounts receivable aging schedule in orderto assess collectibility and (2) a quarterly review of salesallowances and reserves, as well as certain of the reductionsrecorded when revenue was recognized, and the supporting

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 25

schedules. The Firm's procedures to test these controls werelimited to inquiring of management and inspecting signatures oremails as evidence that a review had occurred. The Firm failed toascertain and evaluate the nature of the review procedures that thecontrol owners performed, including the criteria used by the controlowners to identify matters for follow up and whether those matterswere appropriately resolved. In addition, the Firm failed to identifyand test any controls over the accuracy and completeness of thereport used in the performance of the sales allowance and reservecontrol. (AS No. 5, paragraphs 39, 42, and 44)

o The Firm designed certain of its substantive procedures to test netsales – including sample sizes – based on a level of controlreliance that was not supported due to the deficiencies in the Firm'stesting of controls that are discussed above. As a result, the samplethat the Firm used to test net sales was too small to providesufficient evidence. (AS No. 13, paragraphs 16, 18, and 37; AU350, paragraphs .19, .23, and .23A)

o The Firm's sample to test accounts receivable was too small toprovide sufficient evidence because, in determining its sample size,the Firm did not appropriately consider relevant factors, includingthe characteristics of the population being tested and the Firm's riskassessments. (AU 350, paragraphs .23 and .23A)

o The Firm failed to perform any substantive procedures to testcertain significant reductions recorded when revenue wasrecognized. (AS No. 13, paragraph 8)

o The Firm failed to sufficiently test the sales return reserve.Specifically, the Firm failed to perform any procedures to test theaccuracy and completeness of the unprocessed returns scheduleprovided to the issuer by an external administrator; the issuer usedthis schedule in calculating the sales return reserve. (AU 342,paragraph .11)

The Firm failed to perform sufficient procedures to test controls overincome taxes. The Firm selected for testing two controls that consisted of

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 26

reviews of the income tax provision and the effective tax ratereconciliation, as well as their supporting schedules. The Firm'sprocedures to test these controls were limited to inquiring of management,obtaining the schedules that were reviewed as part of the controls, andinspecting emails as evidence that the reviews had occurred. The Firmfailed to ascertain and evaluate the nature of the review procedures thatthe control owners performed, including the criteria used by the controlowners to identify matters for follow up and whether those matters wereappropriately resolved. In addition, the Firm failed to identify and test anycontrols over the accuracy and completeness of the data used in theperformance of these controls. (AS No. 5, paragraphs 39, 42, and 44)

A.6. Issuer F

In this audit of a financial institution, the Firm failed in the following respects toobtain sufficient appropriate audit evidence to support its audit opinion on the financialstatements –

The Firm identified a fraud risk related to the valuation of the allowance forloan losses ("ALL"). The Firm's procedures to test the specific componentof the ALL were insufficient, as they were limited to (1) for one significantimpaired loan, obtaining corroboration of its classification and paymentstatus, (2) for a small sample of impaired loans, examining documentationsupporting the issuer's impairment assessment, and (3) for three otherimpaired loans, testing the loan grades, examining documentationsupporting the loans' classification, and documenting that the recordedcarrying value and accrual status appeared appropriate. The Firm failed toevaluate the significant assumptions used in the issuer's impairmentassessments and to test the related calculation of the specific component.(AU 342, paragraph .11)

The Firm tested the existence of loans receivable as of an interim dateand performed procedures to extend its conclusions to the year end. TheFirm's procedures for testing the existence of loans were insufficient in thefollowing respects –

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 27

o The Firm's sample for testing at the interim date was too small toprovide sufficient evidence because the Firm increased thetolerable misstatement that it used to develop the sample to anamount that was multiple times the tolerable misstatement that wasbased on the Firm's established level of materiality. (AU 350,paragraphs .16, .18, .18A, and .23)

o The Firm's roll-forward procedures were limited to obtaining, for asub-set of the loans receivable tested at the interim date, thetransactions related to those loans from the issuer's records for theperiod between the interim testing date and the year end withoutperforming any procedures to test those transactions. (AS No. 13,paragraph 45)

The issuer acquired a business during the year and accounted for thisacquisition as a business combination. The Firm failed to performsufficient procedures to test certain assets acquired and liabilitiesassumed in this acquisition. Specifically, the Firm's procedures to test theloans receivable acquired and deposits assumed were limited to selectinga small sample from the population of loans and deposits outstanding asof a date approximately four months after the acquisition date, confirmingthese amounts, and rolling the amounts of those individual loan anddeposit accounts back to the acquisition date. The Firm failed to performany procedures to address changes in the populations of loans anddeposits between the acquisition date and the date of its testingprocedures. (AU 350, paragraph .17)

A.7. Issuer G

In this audit of a financial institution, the Firm failed in the following respects toobtain sufficient appropriate audit evidence to support its audit opinions on the financialstatements and on the effectiveness of ICFR –

The Firm failed to perform sufficient procedures related to the ALL, asfollows –

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 28

o The Firm selected for testing three controls that consisted ofreviews of the ALL by management and the audit committee. TheFirm's procedures to test these controls were limited to inquiring ofmanagement; obtaining certain documents and inspectingsignatures as evidence that reviews had occurred; comparingcertain amounts used in the calculation of the ALL to internallygenerated supporting documents or the general ledger; reading theminutes of the review committees, including the audit committee;and attending audit committee meetings. The Firm failed toascertain and evaluate the nature of the specific review proceduresthat the various control owners performed, including the criteriaused by those control owners to identify matters for follow up andwhether those matters were appropriately resolved. In addition, theFirm failed to test the aspects of these controls related to theaccuracy and completeness of the data and reports used in theperformance of these controls. (AS No. 5, paragraphs 42 and 44)

o The Firm failed to perform sufficient substantive procedures to testthe specific component of the ALL, as the Firm failed to sufficientlyevaluate the reasonableness of certain significant assumptionsused in the calculation of this component. Specifically, with respectto impaired collateral-dependent loans included in the specificcomponent, the Firm evaluated the significant assumptions used byappraisers in valuing the loan collateral based only on its generalexperience and knowledge of the banking industry and the realestate environment, without considering whether thoseassumptions reflected, or were not inconsistent with, existingmarket information relevant to those assets. (AU 328, paragraphs.26 and .28)

o The Firm decreased its sample size to test the impaired loansincluded in the specific component of the ALL based on theassurance it obtained from certain other substantive procedures;these procedures, however, related to the quantitative andqualitative components of the ALL, and did not address theimpaired loans or the specific component. As a result, the samplethat the Firm used to test impaired loans receivable was too small

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 29

to provide sufficient evidence. (AU 350, paragraphs .19, .23, and.23A)

The Firm tested the existence of loans receivable as of an interim dateand performed additional procedures to test loans originated in the periodbetween the interim testing date and the year end. Both the interimprocedures and the additional procedures were insufficient. Specifically –

o The Firm's sample to test loans receivable as of the interim datewas too small to provide sufficient evidence because, indetermining its sample size, the Firm did not appropriately considerrelevant factors, including the characteristics of the population andthe Firm's risk assessments. (AU 350, paragraphs .23 and .23A)

o The Firm selected key items that exceeded a monetary threshold totest the loans that originated in the period between its interimtesting date and year end. For the loans originated in this periodthat were not covered by the Firm's testing of key items, whichtotaled multiple times the Firm's established level of materiality, theFirm failed to perform any procedures. (AS No. 15, paragraph 27)

The Firm's samples to test the loans receivable for which the issuer ownedonly a portion of the loan were too small to provide sufficient evidencebecause the Firm increased the tolerable misstatement that it used todevelop the sample to an amount that was multiple times the tolerablemisstatement that was based on the Firm's established level of materiality.(AU 350, paragraphs .16, .18, .18A, and .23)

A.8. Issuer H

In this audit of a retailer of consumer products, the Firm failed in the followingrespects to obtain sufficient appropriate audit evidence to support its audit opinion onthe financial statements. The issuer acquired a significant business during the year, butthe Firm failed to perform sufficient testing related to the inventory and revenue for thisacquired component –

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 30

The Firm failed to perform sufficient procedures to test the quantity ofinventory acquired in the business combination at the acquisition date andthe quantity of inventory held by this component at year end. The Firm'sprocedures to test this inventory consisted of (1) reading the issuer'scycle-count instructions, (2) observing the issuer's cycle counts andperforming independent counts for a selection of the inventory at both theacquisition date and a date close to the year end, and (3) for its year-endtesting, performing procedures to extend its conclusions from the date ofits independent counts to year end. In determining that the cycle-countprocedures that the issuer used for this inventory were sufficiently reliable,the Firm failed to consider the extent of the inventory items counted, thefrequency of the counts, and the deviations identified in the counts. (AU328, paragraph .39; AU 331, paragraph .11)

The Firm failed to perform sufficient procedures to test the occurrence ofone type of revenue, for which the Firm identified a fraud risk. The Firmdetermined its sample size for testing the occurrence of this revenuebased on the assurance it had obtained from certain other substantiveprocedures. These other procedures consisted of performing an analyticalprocedure related to revenue cut-off, testing four journal entries related torevenue or the deferred revenue liability, testing subsequent aggregatedcash collections for accounts receivable outstanding as of year end, andtesting the deferred revenue liability. As these procedures were focusedon the year end, they did not provide sufficient assurance about theoccurrence of revenue throughout the period since the acquisition dateand, as a result, the sample that the Firm used to test this revenue wastoo small to provide sufficient evidence. (AU 350, paragraphs .19, .23, and.23A)

A.9. Issuer I

In this audit, the Firm failed in the following respects to obtain sufficientappropriate audit evidence to support its audit opinions on the financial statements andon the effectiveness of ICFR –

The Firm's testing of the fair value assigned to the intangible assetsresulting from a business combination during the year was insufficient.

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 31

Specifically, the Firm failed to sufficiently evaluate the reasonableness ofthe significant assumptions underlying the internally developed cash-flowforecast that the issuer used to determine the fair value of the assets, asits procedures were limited to (1) obtaining the forecast and relatedsignificant assumptions, (2) inquiring of management, and (3) testing themathematical accuracy of the forecast. (AU 328, paragraphs .26 and .28)

The Firm failed to perform sufficient procedures to test controls over theannual analyses of the possible impairment of goodwill and otherintangible assets. The Firm selected for testing a control that consisted ofan annual review of the impairment analyses; these analyses included theuse of cash-flow forecasts. The Firm's procedures to test the aspect of thiscontrol related to the cash-flow forecasts were limited to (1) obtaining theissuer's impairment memorandum, cash-flow forecasts, and relatedsupporting schedules; (2) inquiring of management; and (3) comparingcertain amounts to data, reports, and schedules prepared by the issuer.The Firm failed to ascertain and evaluate the nature of the reviewprocedures that the control owners performed related to this aspect of thecontrol, including the criteria used by the control owners to identify mattersfor follow up and whether those matters were appropriately resolved. (ASNo. 5, paragraphs 42 and 44)

The Firm failed to perform sufficient procedures to test the cash-flowforecast that the issuer used when performing its analysis of the possibleimpairment of goodwill. Specifically, the Firm's procedures to evaluate thereasonableness of the significant assumptions used in this forecast werelimited to (1) obtaining the issuer's impairment memorandum, cash-flowforecast, and related supporting schedules; (2) inquiring of management;(3) testing the mathematical accuracy of the cash-flow forecast; and (4)performing a sensitivity analysis. Through its sensitivity analysis, the Firmidentified that numerous scenarios could result in the reporting unit's fairvalue being less than its carrying value, but the Firm concluded that theassumptions used in the forecast were reasonable without performing anyadditional procedures. (AU 328, paragraphs .26 and .28)

The Firm failed to perform sufficient procedures to test the issuer'sanalysis of the possible impairment of intangible assets other than

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 32

goodwill. Specifically, the Firm's procedures to evaluate thereasonableness of the significant assumptions in this analysis were limitedto (1) obtaining the issuer's memorandum, (2) inquiring of management,and (3) comparing certain amounts to data, reports, or schedulesprepared by the issuer. (AU 328, paragraphs .26 and .28)

A.10. Issuer J

In this audit of a manufacturer of consumer products, the Firm failed to obtainsufficient appropriate audit evidence to support its audit opinions on the financialstatements and on the effectiveness of ICFR, as it failed to sufficiently test inventory forone of the issuer's significant geographic regions, as follows –

This inventory was subject to daily cycle counts, and the issuer maintaineda manual spreadsheet that summarized which items were counted eachday. The Firm's procedures to test the existence of, and the controls overthe existence of, this inventory were insufficient. Specifically, in testingwhether the cycle-count procedures that the issuer used for this inventorywere sufficiently reliable, the Firm failed to consider the extent of theinventory items counted, the frequency of the counts, and the deviationsidentified in the counts. (AS No. 5, paragraphs 42 and 44; AU 331,paragraph .11)

The Firm's approach for testing the valuation of this inventory includedtesting ITGCs over certain inventory applications to support the Firm'sconclusions regarding transaction-level controls that were part of, ordepended on, these applications. The Firm identified a control deficiencyrelated to users having inappropriate developer-level access to theseapplications. The Firm tested certain compensating controls that itconsidered to mitigate the deficiency; these controls consisted of (1) thereview of program changes made to the inventory applications, (2) thereview of certain account balances that involved judgment, and (3) thecomparison of the recorded results for each business unit to its budget.The Firm, however, failed to obtain sufficient evidence to support itsconclusion that the compensating controls would prevent or detectmaterial misstatements resulting from the ITGC access deficiency.Specifically –

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 33

o The Firm failed to identify and test any controls that addressed thecompleteness of the population of changes that was actuallyreviewed pursuant to the control over program changes. (AS No. 5,paragraph 39)

o The Firm's procedures to test the second and third compensatingcontrols were limited to inquiring of management, ascertaining thethresholds that were used by the control owners to identify mattersfor investigation, and inspecting signatures and notes as evidencethat reviews had occurred. The Firm's testing did not includeevaluating whether the thresholds used by the control owners toidentify matters for investigation were consistently applied orwhether the matters identified for investigation were appropriatelyinvestigated and resolved. (AS No. 5, paragraph 68)

o The Firm failed to identify and test any controls over the accuracyand completeness of the data used in the comparison of therecorded results to the budget. (AS No. 5, paragraph 39)

The Firm selected for testing a control that included the review ofinventory reserves. The Firm's procedures to test this review aspect of thecontrol consisted of inquiring of management and inspecting signatures asevidence that reviews had occurred. In addition, the Firm stated thatcertain of its substantive tests were dual-purpose in nature and providedevidence of the effectiveness of this aspect of the control. The Firm failedto test, however, through any of its procedures, whether this aspect of thecontrol operated at a level of precision that would prevent or detectmaterial misstatements. (AS No. 5, paragraphs 42, 44, and B9)

The Firm designed certain of its substantive procedures to test thevaluation of raw materials and work-in-process inventory – includingsample sizes – based on a level of control reliance that was not supporteddue to the deficiencies in the Firm's testing of controls that are discussedabove. As a result, certain of the samples that the Firm used to test thevaluation of this inventory were too small to provide sufficient evidence. Inaddition, the Firm's sample to test the valuation of finished goodsinventory was too small to provide sufficient evidence because, indetermining its sample size, the Firm did not appropriately consider

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 34

relevant factors, including the characteristics of the population and theFirm's risk assessments. (AS No. 13, paragraphs 16, 18, and 37; AU 350,paragraphs .19, .23, and .23A)

A.11. Issuer K

In this audit of a financial institution, the Firm failed to obtain sufficientappropriate audit evidence to support its audit opinion on the financial statements, asthe Firm failed to perform sufficient procedures to test loans receivable. Specifically, theFirm's sample to test the existence of loans receivable was too small to providesufficient evidence because, in determining its sample size, the Firm did notappropriately consider relevant factors, including the characteristics of the populationand the Firm's risk assessments. (AU 350, paragraphs .23 and .23A)

A.12. Issuer L

In this audit of a financial institution, the Firm failed to obtain sufficientappropriate audit evidence to support its audit opinion on the financial statements, asthe Firm failed to perform sufficient procedures to test loans receivable. Specifically, theFirm's sample to test the existence of loans receivable was too small to providesufficient evidence because, in determining its sample size, the Firm did notappropriately consider relevant factors, including the characteristics of the populationand the Firm's risk assessments. (AU 350, paragraphs .23 and .23A)

B. Auditing Standards

Each deficiency described in Part I.A above could relate to several provisions ofthe standards that govern the conduct of audits. The paragraphs of the standards thatare cited for each deficiency are those that most directly relate to the deficiency. Thedeficiencies also may relate, however, to other paragraphs of those standards and toother auditing standards, including those concerning due professional care, responsesto risk assessments, and audit evidence.

Many audit deficiencies involve a lack of due professional care. AU 230, DueProfessional Care in the Performance of Work, paragraphs .02, .05, and .06, requiresthe independent auditor to plan and perform his or her work with due professional careand sets forth aspects of that requirement. AU 230, paragraphs .07 through .09, and ASNo. 13, The Auditor's Responses to the Risks of Material Misstatement, paragraph 7,

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 35

specify that due professional care requires the exercise of professional skepticism.These standards state that professional skepticism is an attitude that includes aquestioning mind and a critical assessment of the appropriateness and sufficiency ofaudit evidence.

AS No. 13, paragraphs 3, 5, and 8, requires the auditor to design and implementaudit responses that address the risks of material misstatement. AS No. 15, AuditEvidence, paragraph 4, requires the auditor to plan and perform audit procedures toobtain sufficient appropriate audit evidence to provide a reasonable basis for the auditopinion. Sufficiency is the measure of the quantity of audit evidence, and the quantityneeded is affected by the risk of material misstatement (in the audit of financialstatements) or the risk associated with the control (in the audit of ICFR) and the qualityof the audit evidence obtained. The appropriateness of evidence is measured by itsquality; to be appropriate, evidence must be both relevant and reliable in providingsupport for the related conclusions.

The paragraphs of the standards that are described immediately above are notcited in Part I.A, unless those paragraphs are the most directly related to the relevantdeficiency.

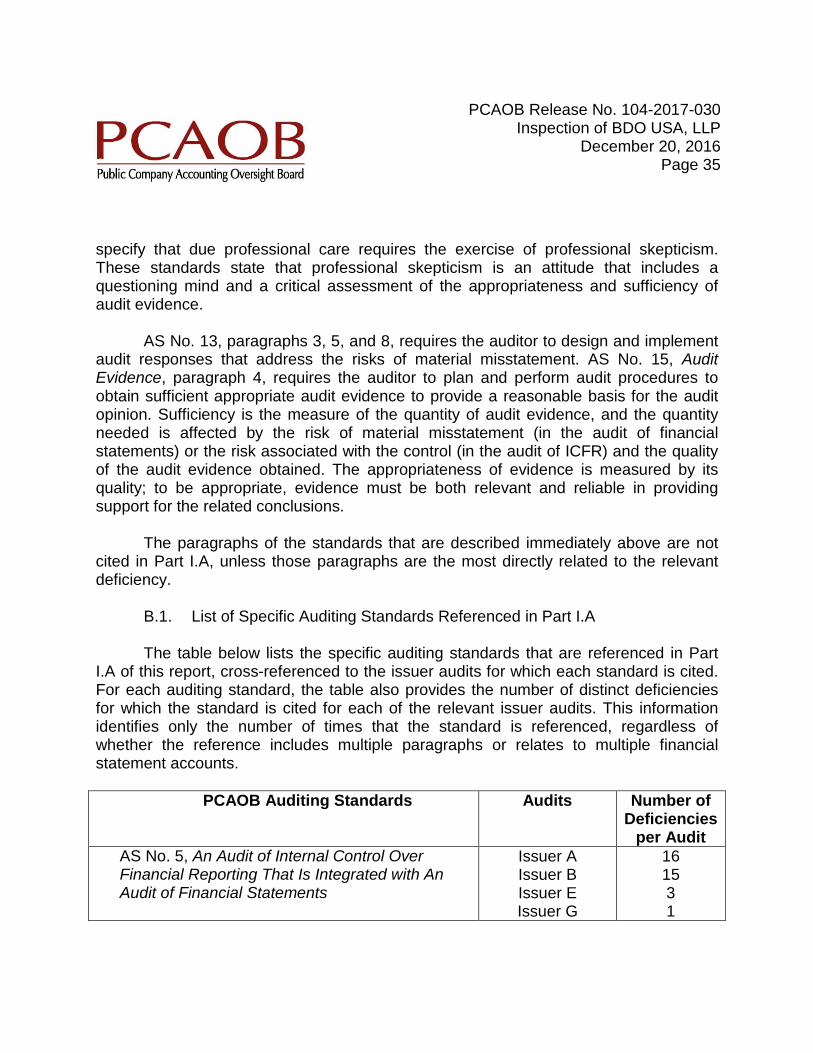

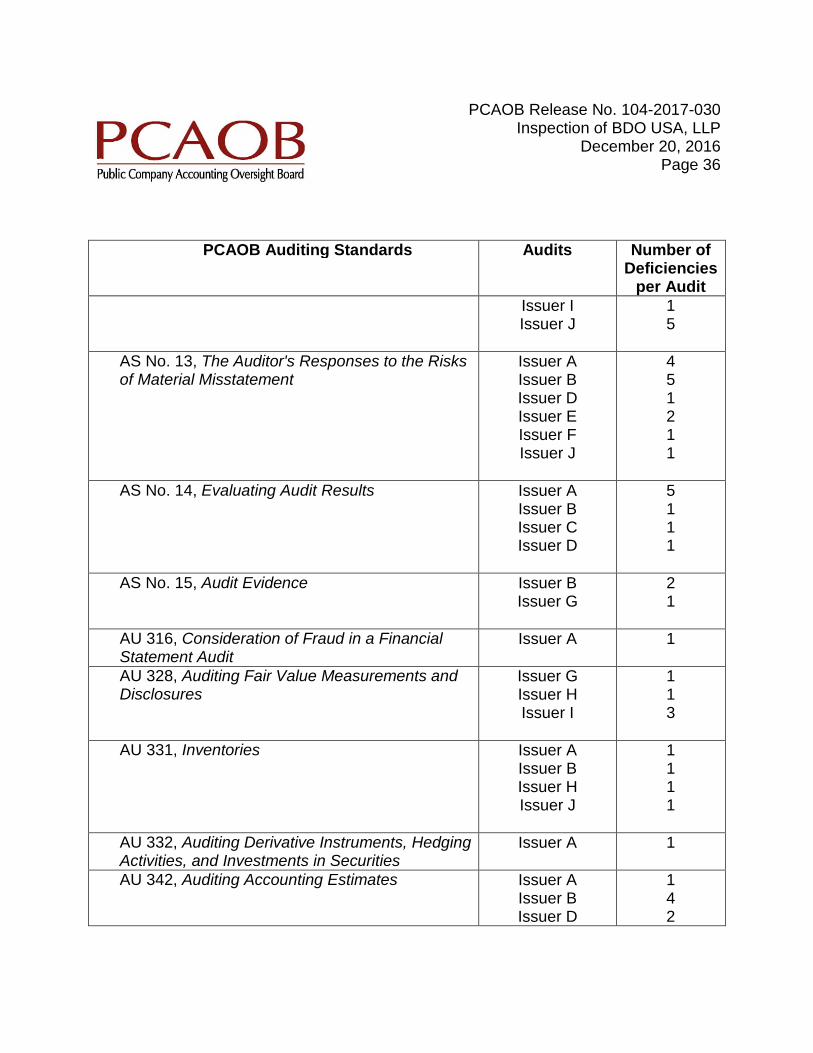

B.1. List of Specific Auditing Standards Referenced in Part I.A

The table below lists the specific auditing standards that are referenced in PartI.A of this report, cross-referenced to the issuer audits for which each standard is cited.For each auditing standard, the table also provides the number of distinct deficienciesfor which the standard is cited for each of the relevant issuer audits. This informationidentifies only the number of times that the standard is referenced, regardless ofwhether the reference includes multiple paragraphs or relates to multiple financialstatement accounts.

PCAOB Auditing Standards Audits Number ofDeficiencies

per AuditAS No. 5, An Audit of Internal Control OverFinancial Reporting That Is Integrated with AnAudit of Financial Statements

Issuer AIssuer BIssuer EIssuer G

161531

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 36

PCAOB Auditing Standards Audits Number ofDeficiencies

per AuditIssuer IIssuer J

15

AS No. 13, The Auditor's Responses to the Risksof Material Misstatement

Issuer AIssuer BIssuer DIssuer EIssuer FIssuer J

451211

AS No. 14, Evaluating Audit Results Issuer AIssuer BIssuer CIssuer D

5111

AS No. 15, Audit Evidence Issuer BIssuer G

21

AU 316, Consideration of Fraud in a FinancialStatement Audit

Issuer A 1

AU 328, Auditing Fair Value Measurements andDisclosures

Issuer GIssuer HIssuer I

113

AU 331, Inventories Issuer AIssuer BIssuer HIssuer J

1111

AU 332, Auditing Derivative Instruments, HedgingActivities, and Investments in Securities

Issuer A 1

AU 342, Auditing Accounting Estimates Issuer AIssuer BIssuer D

142

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 37

PCAOB Auditing Standards Audits Number ofDeficiencies

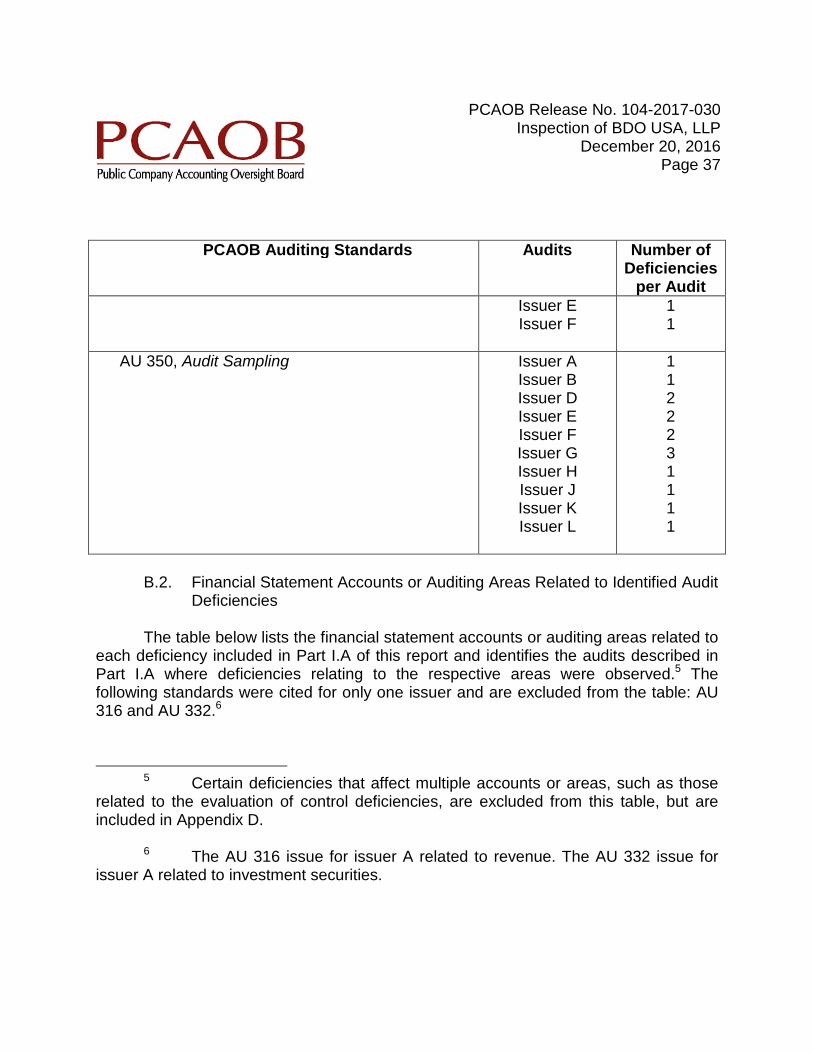

per AuditIssuer EIssuer F

11

AU 350, Audit Sampling Issuer AIssuer BIssuer DIssuer EIssuer FIssuer GIssuer HIssuer JIssuer KIssuer L

1122231111

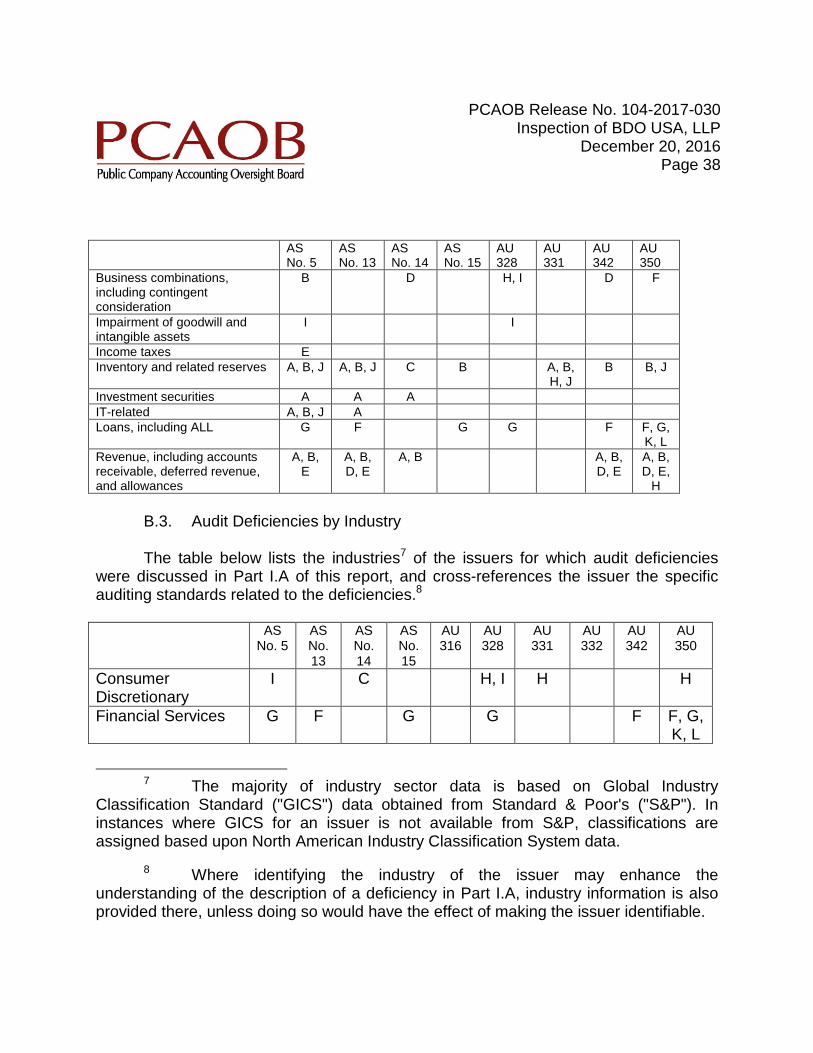

B.2. Financial Statement Accounts or Auditing Areas Related to Identified AuditDeficiencies

The table below lists the financial statement accounts or auditing areas related toeach deficiency included in Part I.A of this report and identifies the audits described inPart I.A where deficiencies relating to the respective areas were observed.5 Thefollowing standards were cited for only one issuer and are excluded from the table: AU316 and AU 332.6

5 Certain deficiencies that affect multiple accounts or areas, such as thoserelated to the evaluation of control deficiencies, are excluded from this table, but areincluded in Appendix D.

6 The AU 316 issue for issuer A related to revenue. The AU 332 issue forissuer A related to investment securities.

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 38

ASNo. 5

ASNo. 13

ASNo. 14

ASNo. 15

AU328

AU331

AU342

AU350

Business combinations,including contingentconsideration

B D H, I D F

Impairment of goodwill andintangible assets

I I

Income taxes EInventory and related reserves A, B, J A, B, J C B A, B,

H, JB B, J

Investment securities A A AIT-related A, B, J ALoans, including ALL G F G G F F, G,

K, LRevenue, including accountsreceivable, deferred revenue,and allowances

A, B,E

A, B,D, E

A, B A, B,D, E

A, B,D, E,

H

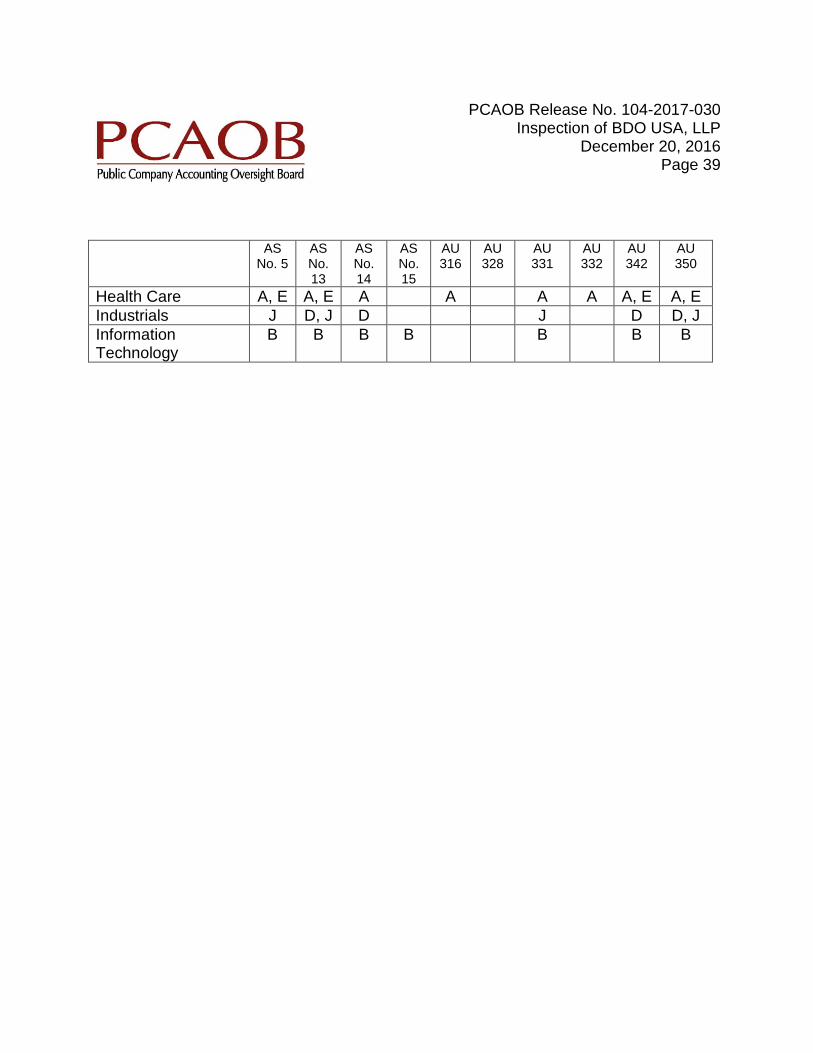

B.3. Audit Deficiencies by Industry

The table below lists the industries7 of the issuers for which audit deficiencieswere discussed in Part I.A of this report, and cross-references the issuer the specificauditing standards related to the deficiencies.8

ASNo. 5

ASNo.13

ASNo.14

ASNo.15

AU316

AU328

AU331

AU332

AU342

AU350

ConsumerDiscretionary

I C H, I H H

Financial Services G F G G F F, G,K, L

7 The majority of industry sector data is based on Global IndustryClassification Standard ("GICS") data obtained from Standard & Poor's ("S&P"). Ininstances where GICS for an issuer is not available from S&P, classifications areassigned based upon North American Industry Classification System data.

8 Where identifying the industry of the issuer may enhance theunderstanding of the description of a deficiency in Part I.A, industry information is alsoprovided there, unless doing so would have the effect of making the issuer identifiable.

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 39

ASNo. 5

ASNo.13

ASNo.14

ASNo.15

AU316

AU328

AU331

AU332

AU342

AU350

Health Care A, E A, E A A A A A, E A, EIndustrials J D, J D J D D, JInformationTechnology

B B B B B B B

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 40

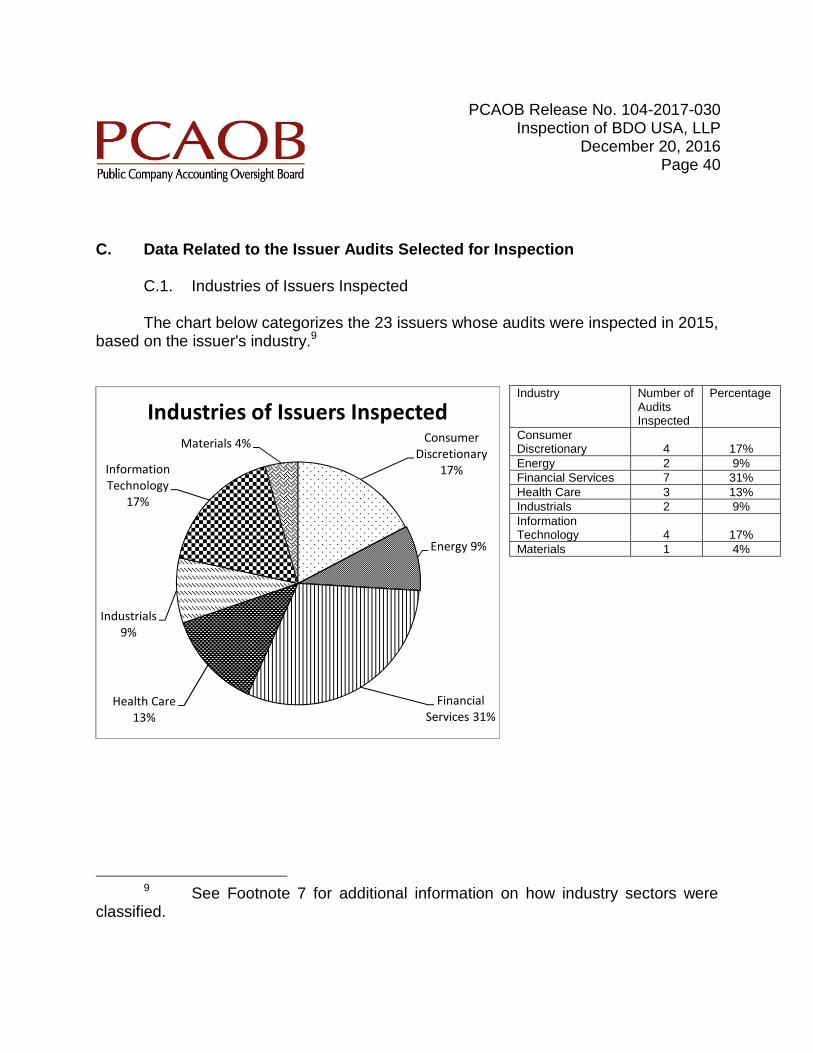

C. Data Related to the Issuer Audits Selected for Inspection

C.1. Industries of Issuers Inspected

The chart below categorizes the 23 issuers whose audits were inspected in 2015,based on the issuer's industry.9

9 See Footnote 7 for additional information on how industry sectors wereclassified.

ConsumerDiscretionary

17%

Energy 9%

FinancialServices 31%

Health Care13%

Industrials9%

InformationTechnology

17%

Materials 4%

Industries of Issuers InspectedIndustry Number of

AuditsInspected

Percentage

ConsumerDiscretionary 4 17%Energy 2 9%Financial Services 7 31%Health Care 3 13%Industrials 2 9%InformationTechnology 4 17%Materials 1 4%

PCAOB Release No. 104-2017-030Inspection of BDO USA, LLP

December 20, 2016Page 41

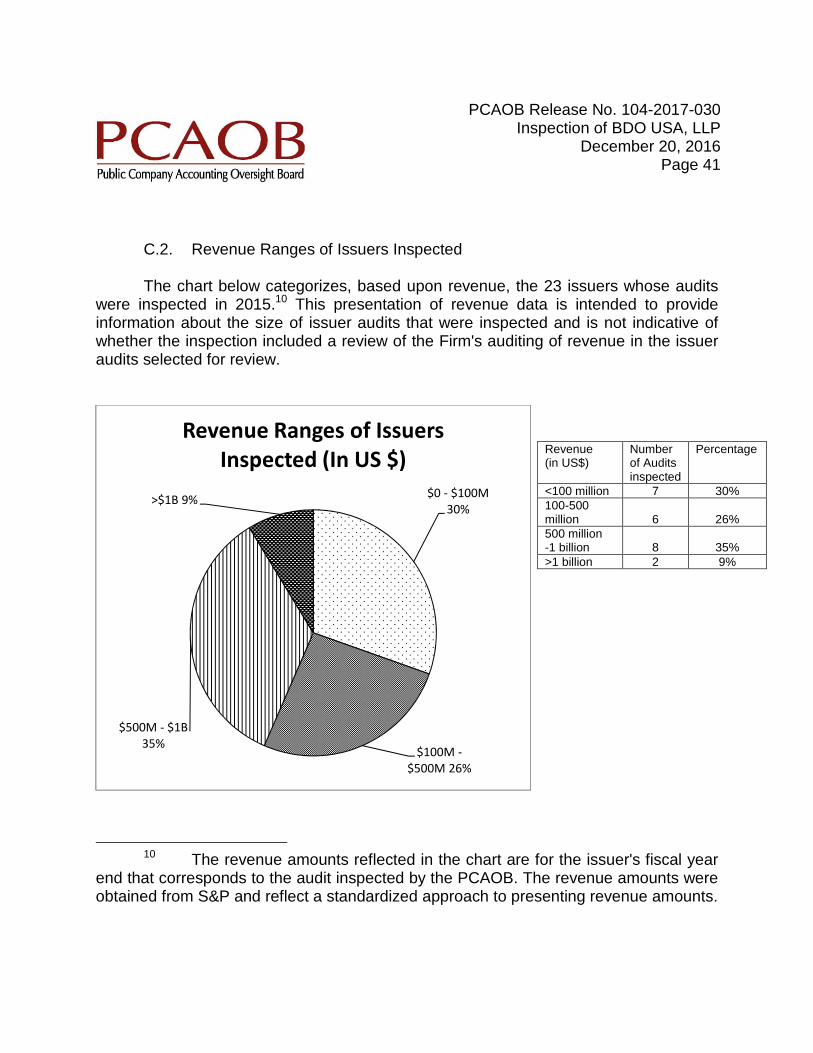

C.2. Revenue Ranges of Issuers Inspected