Embed Size (px)

Citation preview

Sharper Insight. Smarter Investing.

AUTOMATED INVESTING PLATFORM STUDY

HIGH-TECH AND HIGH-TOUCH

Investors Make the Case for Converging Automated Investing Platforms and Financial Planning

Summary and Methodology Page 1

Key Finding #1: Investors require both high-tech and high-touch forms of advice to satisfy today’s complex financial needs. Pages 2-3

Key Finding #2: Investors are equally satisfied with automated investing platforms and financial planners/advisors, but appear to be more satisfied when utilizing both.

Pages 4-9

Key Finding #3: There is a growing opportunity for automated investing platforms and financial planners/advisors to work together. Pages 10-11

Respondent Demographics Pages 12-13

WHAT’S INSIDE?

Today’s fast-paced, digital world is presenting new opportunities for investors to get low-cost, more accessible advice for their investments through automated investing platforms (a.k.a. robo advisors). With the number of solutions seemingly growing by the day, what’s clear is that while investors have an increasing interest in these high-tech advice providers, they also have a need for the high-touch level of advice offered by financial planners/advisors.

High-Tech and High-Touch: Investors Make the Case for Converging Automated Investing Platforms and Financial Planning, new research by Investopedia and the Financial Planning Association® (FPA®), reveals three primary findings:

1

Investopedia and Financial Planning Association® (FPA®) Page 1

SUMMARY AND METHODOLOGY

2

3

Investors are equally satisfied with automated investing platforms and financial planners/advisors, but appear to be more satisfied when utilizing both.

Investors require both high-tech and high-touch forms of advice to satisfy today’s financial needs.

There is a growing opportunity for automated investing platforms and financial planners/advisors to work together.

Investopedia and the Financial Planning Association® (FPA®) conducted a survey among users of Investopedia.com to better understand their opinions about automated investing platforms and financial planners/advisors. The web-based survey on investopedia.com was fielded between Aug. 25 and Sept. 14, 2016 and resulted in 2,002 completed responses from investors meeting the following criteria:

• Live in the United States • Age 21+ • Have input in household investment decisions

The data was weighted to match Investopedia.com demographics on ComScore.

METHODOLOGY

Investors require both high-tech and high-touch forms of advice to satisfy today’s complex financial needs.

Investopedia and Financial Planning Association® (FPA®) Page 2

KEY FINDINGS1

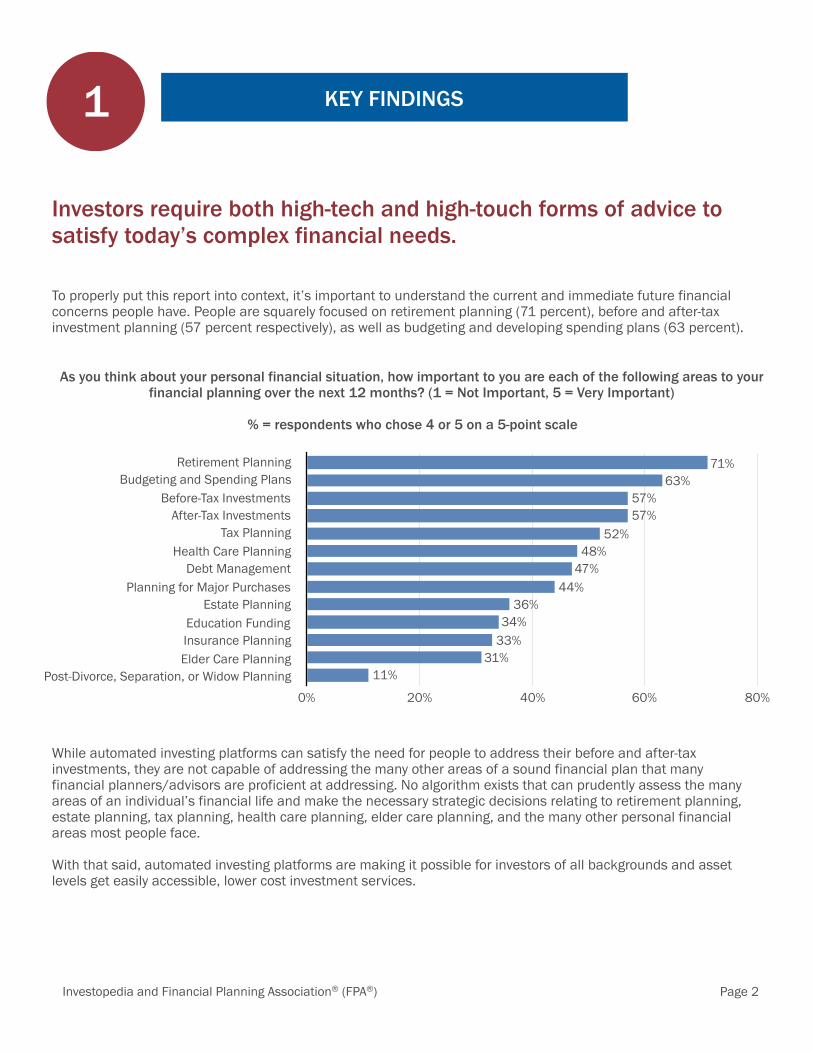

To properly put this report into context, it’s important to understand the current and immediate future financial concerns people have. People are squarely focused on retirement planning (71 percent), before and after-tax investment planning (57 percent respectively), as well as budgeting and developing spending plans (63 percent).

Retirement PlanningBudgeting and Spending Plans

Before-Tax InvestmentsAfter-Tax Investments

Tax PlanningHealth Care Planning

Debt ManagementPlanning for Major Purchases

Estate PlanningEducation FundingInsurance PlanningElder Care Planning

Post-Divorce, Separation, or Widow Planning0% 20% 40% 60% 80%

11%31%

33%34%

36%44%

47%48%

52%57%57%

63%71%

As you think about your personal financial situation, how important to you are each of the following areas to your financial planning over the next 12 months? (1 = Not Important, 5 = Very Important)

% = respondents who chose 4 or 5 on a 5-point scale

While automated investing platforms can satisfy the need for people to address their before and after-tax investments, they are not capable of addressing the many other areas of a sound financial plan that many financial planners/advisors are proficient at addressing. No algorithm exists that can prudently assess the many areas of an individual’s financial life and make the necessary strategic decisions relating to retirement planning, estate planning, tax planning, health care planning, elder care planning, and the many other personal financial areas most people face.

With that said, automated investing platforms are making it possible for investors of all backgrounds and asset levels get easily accessible, lower cost investment services.

Investopedia and Financial Planning Association® (FPA®) Page 3

KEY FINDINGS1

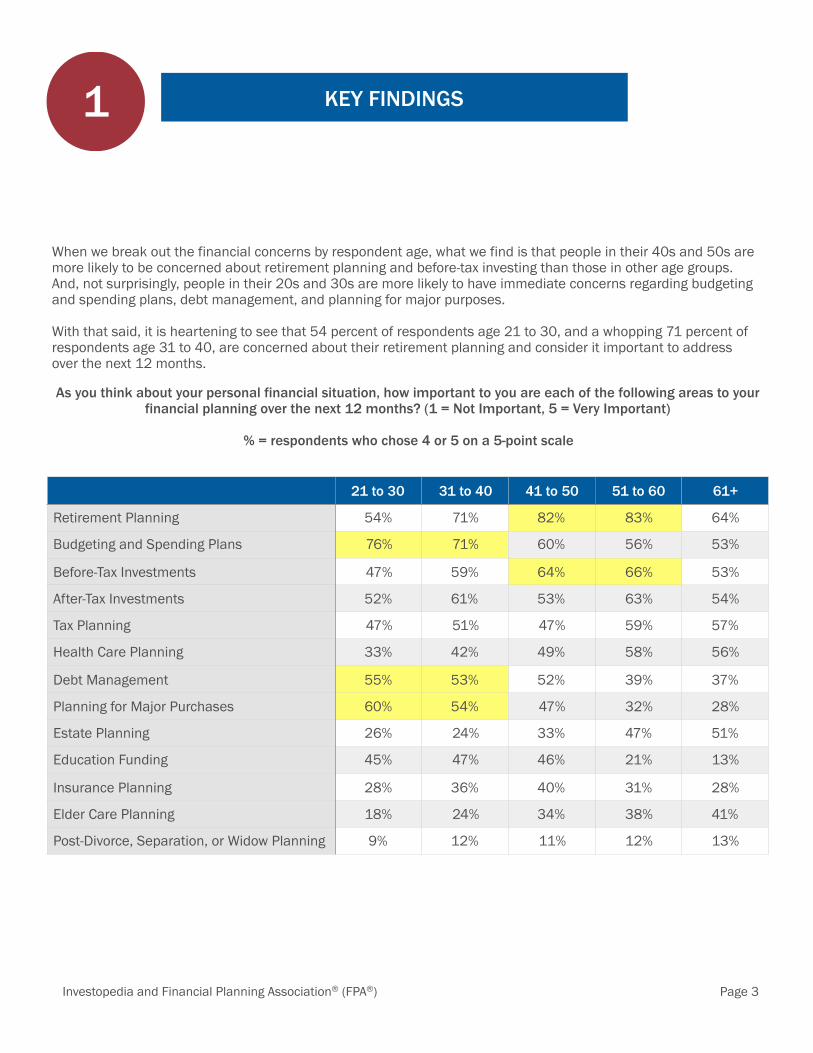

When we break out the financial concerns by respondent age, what we find is that people in their 40s and 50s are more likely to be concerned about retirement planning and before-tax investing than those in other age groups. And, not surprisingly, people in their 20s and 30s are more likely to have immediate concerns regarding budgeting and spending plans, debt management, and planning for major purposes.

With that said, it is heartening to see that 54 percent of respondents age 21 to 30, and a whopping 71 percent of respondents age 31 to 40, are concerned about their retirement planning and consider it important to address over the next 12 months.

As you think about your personal financial situation, how important to you are each of the following areas to your financial planning over the next 12 months? (1 = Not Important, 5 = Very Important)

% = respondents who chose 4 or 5 on a 5-point scale

21 to 30 31 to 40 41 to 50 51 to 60 61+

Retirement Planning 54% 71% 82% 83% 64%

Budgeting and Spending Plans 76% 71% 60% 56% 53%

Before-Tax Investments 47% 59% 64% 66% 53%

After-Tax Investments 52% 61% 53% 63% 54%

Tax Planning 47% 51% 47% 59% 57%

Health Care Planning 33% 42% 49% 58% 56%

Debt Management 55% 53% 52% 39% 37%

Planning for Major Purchases 60% 54% 47% 32% 28%

Estate Planning 26% 24% 33% 47% 51%

Education Funding 45% 47% 46% 21% 13%

Insurance Planning 28% 36% 40% 31% 28%

Elder Care Planning 18% 24% 34% 38% 41%

Post-Divorce, Separation, or Widow Planning 9% 12% 11% 12% 13%

Investopedia and Financial Planning Association® (FPA®) Page 4

KEY FINDINGS2

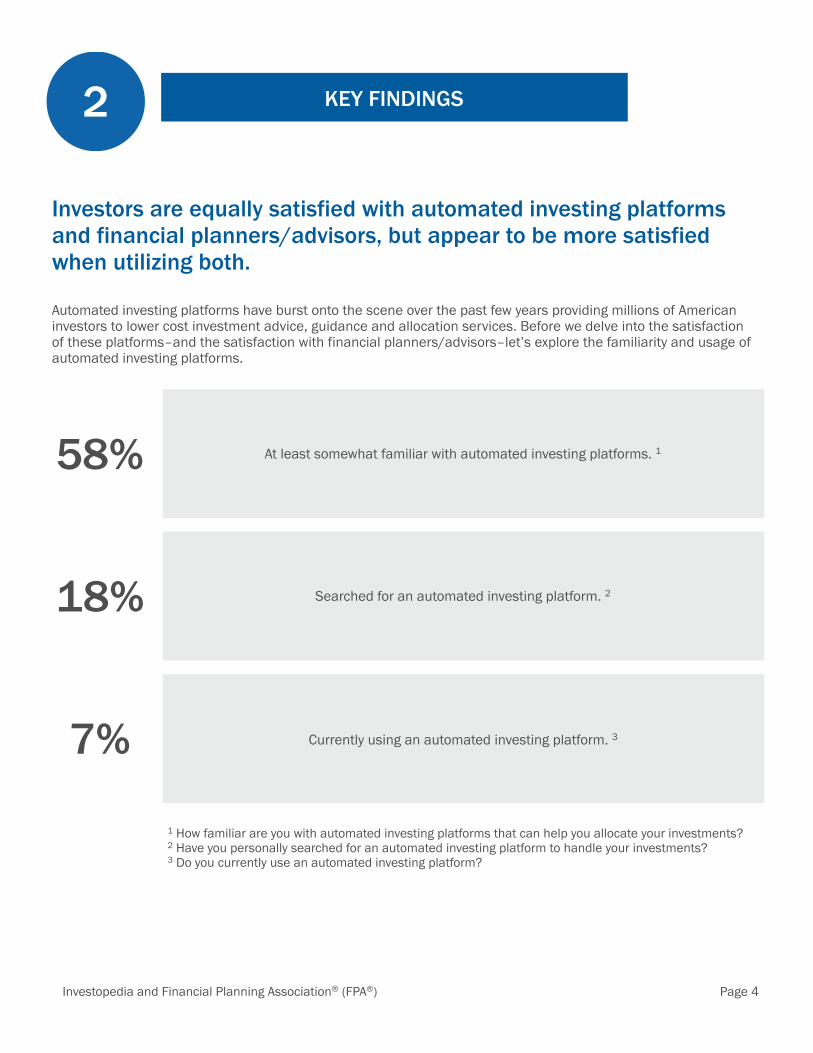

Automated investing platforms have burst onto the scene over the past few years providing millions of American investors to lower cost investment advice, guidance and allocation services. Before we delve into the satisfaction of these platforms–and the satisfaction with financial planners/advisors–let’s explore the familiarity and usage of automated investing platforms.

Investors are equally satisfied with automated investing platforms and financial planners/advisors, but appear to be more satisfied when utilizing both.

At least somewhat familiar with automated investing platforms. 1

Searched for an automated investing platform. 2

Currently using an automated investing platform. 3

58%

18%

7%

1 How familiar are you with automated investing platforms that can help you allocate your investments? 2 Have you personally searched for an automated investing platform to handle your investments? 3 Do you currently use an automated investing platform?

Investopedia and Financial Planning Association® (FPA®) Page 5

KEY FINDINGS2

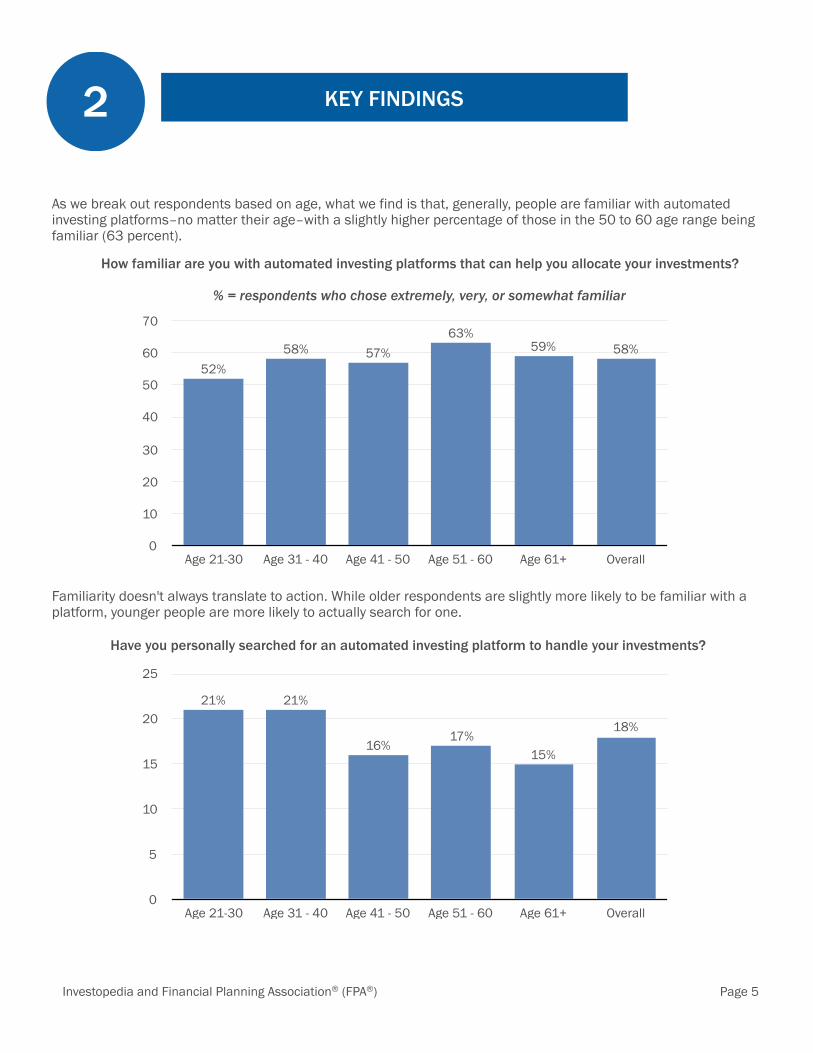

As we break out respondents based on age, what we find is that, generally, people are familiar with automated investing platforms–no matter their age–with a slightly higher percentage of those in the 50 to 60 age range being familiar (63 percent).

How familiar are you with automated investing platforms that can help you allocate your investments?

% = respondents who chose extremely, very, or somewhat familiar

0

10

20

30

40

50

60

70

Age 21-30 Age 31 - 40 Age 41 - 50 Age 51 - 60 Age 61+ Overall

58%59%63%

57%58%52%

Familiarity doesn't always translate to action. While older respondents are slightly more likely to be familiar with a platform, younger people are more likely to actually search for one.

Have you personally searched for an automated investing platform to handle your investments?

0

5

10

15

20

25

Age 21-30 Age 31 - 40 Age 41 - 50 Age 51 - 60 Age 61+ Overall

18%

15%17%

16%

21%21%

Investopedia and Financial Planning Association® (FPA®) Page 6

KEY FINDINGS2

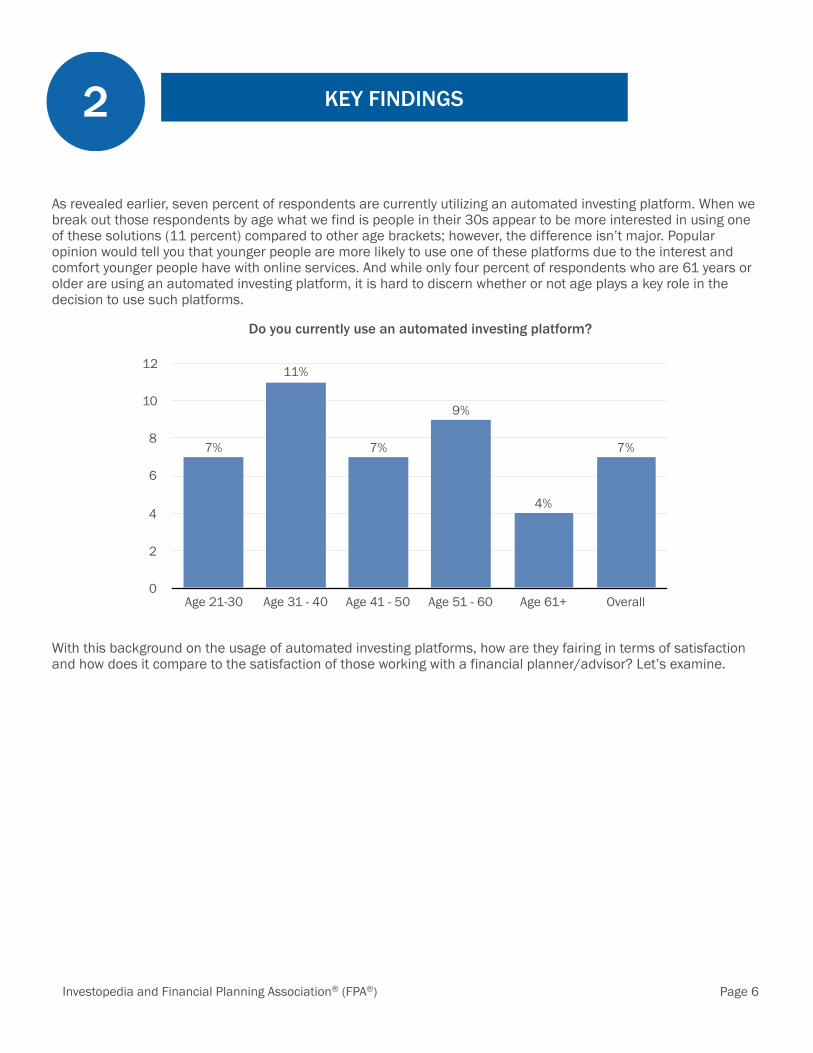

As revealed earlier, seven percent of respondents are currently utilizing an automated investing platform. When we break out those respondents by age what we find is people in their 30s appear to be more interested in using one of these solutions (11 percent) compared to other age brackets; however, the difference isn’t major. Popular opinion would tell you that younger people are more likely to use one of these platforms due to the interest and comfort younger people have with online services. And while only four percent of respondents who are 61 years or older are using an automated investing platform, it is hard to discern whether or not age plays a key role in the decision to use such platforms.

Do you currently use an automated investing platform?

0

2

4

6

8

10

12

Age 21-30 Age 31 - 40 Age 41 - 50 Age 51 - 60 Age 61+ Overall

7%

4%

9%

7%

11%

7%

With this background on the usage of automated investing platforms, how are they fairing in terms of satisfaction and how does it compare to the satisfaction of those working with a financial planner/advisor? Let’s examine.

Investopedia and Financial Planning Association® (FPA®) Page 7

KEY FINDINGS2

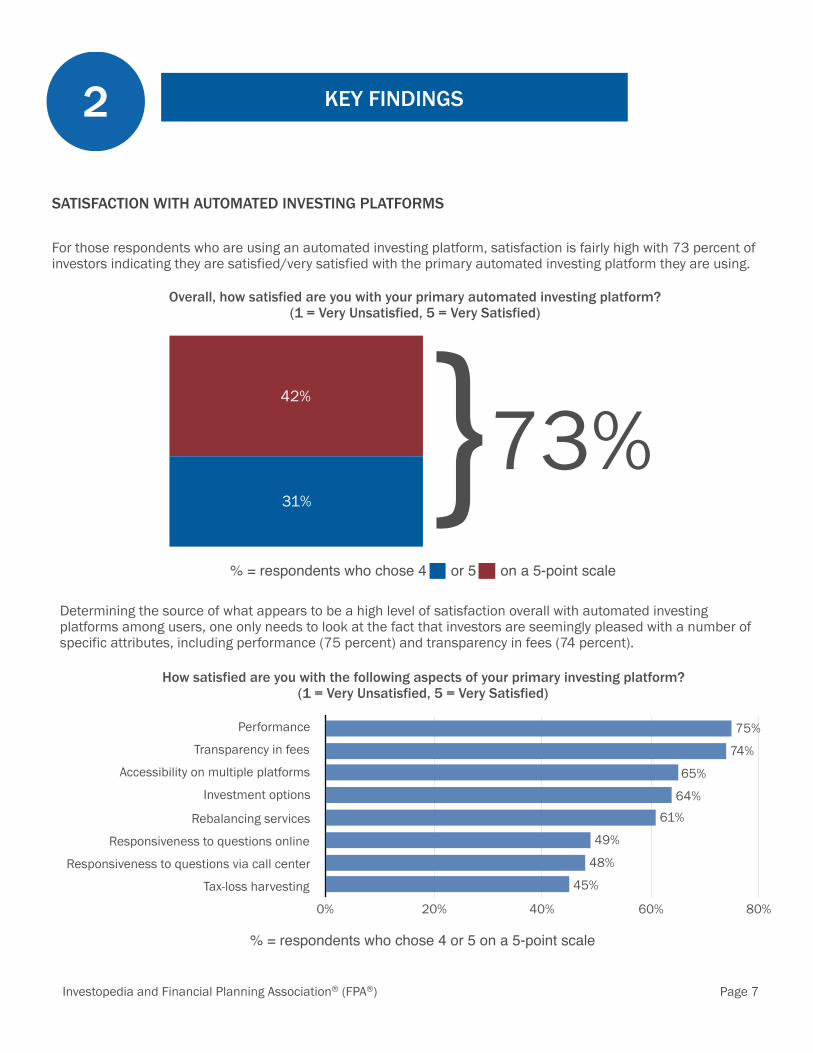

For those respondents who are using an automated investing platform, satisfaction is fairly high with 73 percent of investors indicating they are satisfied/very satisfied with the primary automated investing platform they are using.

Performance

Transparency in fees

Accessibility on multiple platforms

Investment options

Rebalancing services

Responsiveness to questions online

Responsiveness to questions via call center

Tax-loss harvesting

0% 20% 40% 60% 80%

45%

48%

49%

61%64%

65%

74%

75%

Overall, how satisfied are you with your primary automated investing platform? (1 = Very Unsatisfied, 5 = Very Satisfied)

42%

31%

% = respondents who chose 4 or 5 on a 5-point scale

}73%

Determining the source of what appears to be a high level of satisfaction overall with automated investing platforms among users, one only needs to look at the fact that investors are seemingly pleased with a number of specific attributes, including performance (75 percent) and transparency in fees (74 percent).

How satisfied are you with the following aspects of your primary investing platform? (1 = Very Unsatisfied, 5 = Very Satisfied)

% = respondents who chose 4 or 5 on a 5-point scale

SATISFACTION WITH AUTOMATED INVESTING PLATFORMS

Investopedia and Financial Planning Association® (FPA®) Page 8

KEY FINDINGS2

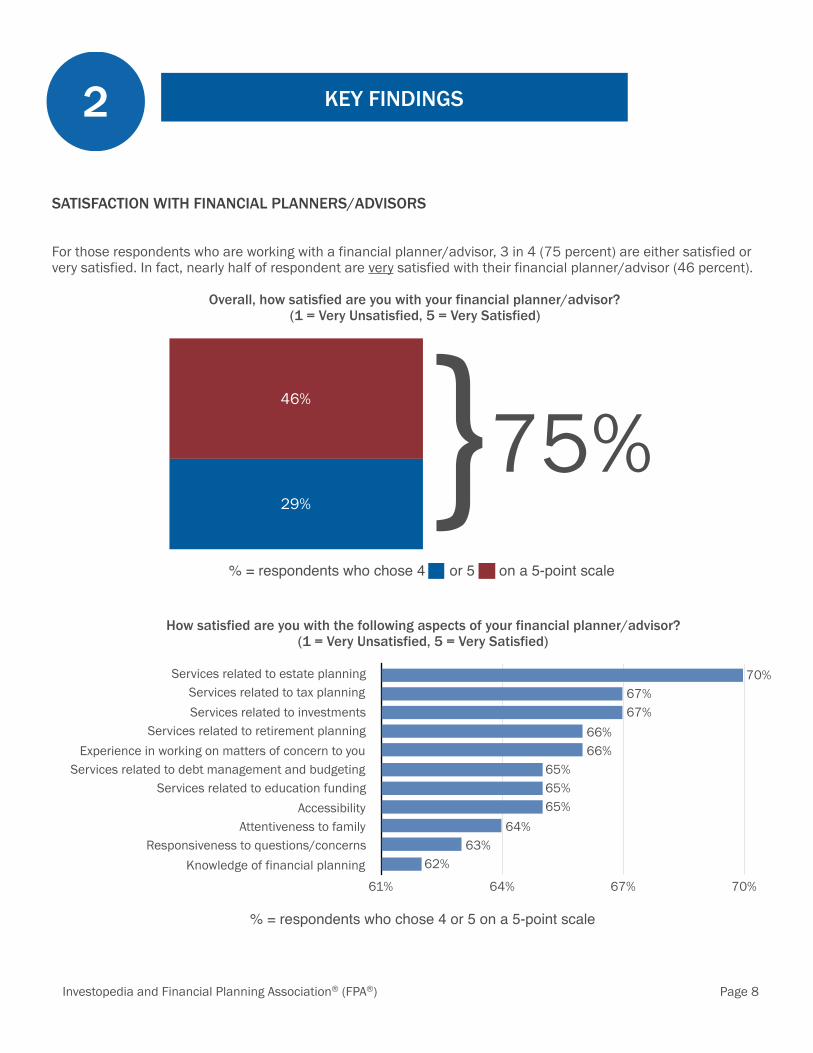

SATISFACTION WITH FINANCIAL PLANNERS/ADVISORS

For those respondents who are working with a financial planner/advisor, 3 in 4 (75 percent) are either satisfied or very satisfied. In fact, nearly half of respondent are very satisfied with their financial planner/advisor (46 percent).

Overall, how satisfied are you with your financial planner/advisor? (1 = Very Unsatisfied, 5 = Very Satisfied)

46%

29%}75%

Services related to estate planningServices related to tax planningServices related to investments

Services related to retirement planningExperience in working on matters of concern to you

Services related to debt management and budgetingServices related to education funding

AccessibilityAttentiveness to family

Responsiveness to questions/concernsKnowledge of financial planning

61% 64% 67% 70%

62%63%

64%65%65%65%

66%66%

67%67%

70%

How satisfied are you with the following aspects of your financial planner/advisor? (1 = Very Unsatisfied, 5 = Very Satisfied)

% = respondents who chose 4 or 5 on a 5-point scale

% = respondents who chose 4 or 5 on a 5-point scale

Investopedia and Financial Planning Association® (FPA®) Page 9

KEY FINDINGS2

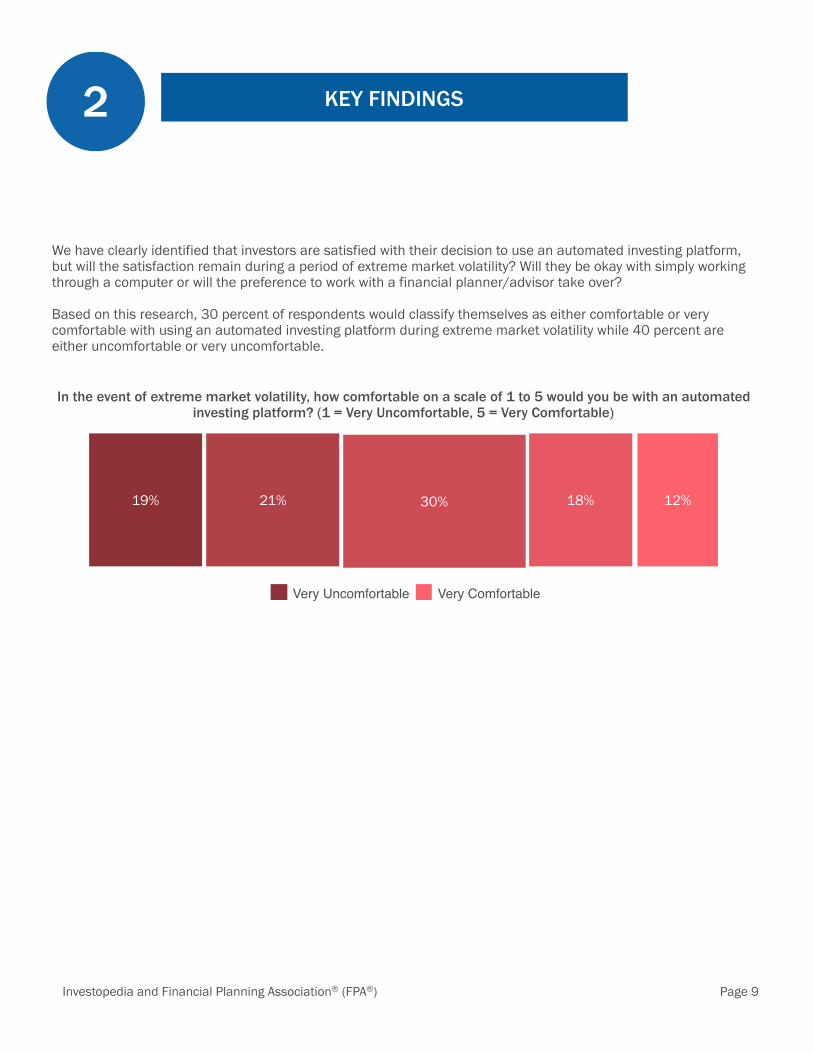

We have clearly identified that investors are satisfied with their decision to use an automated investing platform, but will the satisfaction remain during a period of extreme market volatility? Will they be okay with simply working through a computer or will the preference to work with a financial planner/advisor take over?

Based on this research, 30 percent of respondents would classify themselves as either comfortable or very comfortable with using an automated investing platform during extreme market volatility while 40 percent are either uncomfortable or very uncomfortable.

In the event of extreme market volatility, how comfortable on a scale of 1 to 5 would you be with an automated investing platform? (1 = Very Uncomfortable, 5 = Very Comfortable)

19% 21% 30% 18% 12%

Very Uncomfortable Very Comfortable

Investopedia and Financial Planning Association® (FPA®) Page 10

There is a growing opportunity for automated investing platforms and financial planners/advisors to work together.

KEY FINDINGS3

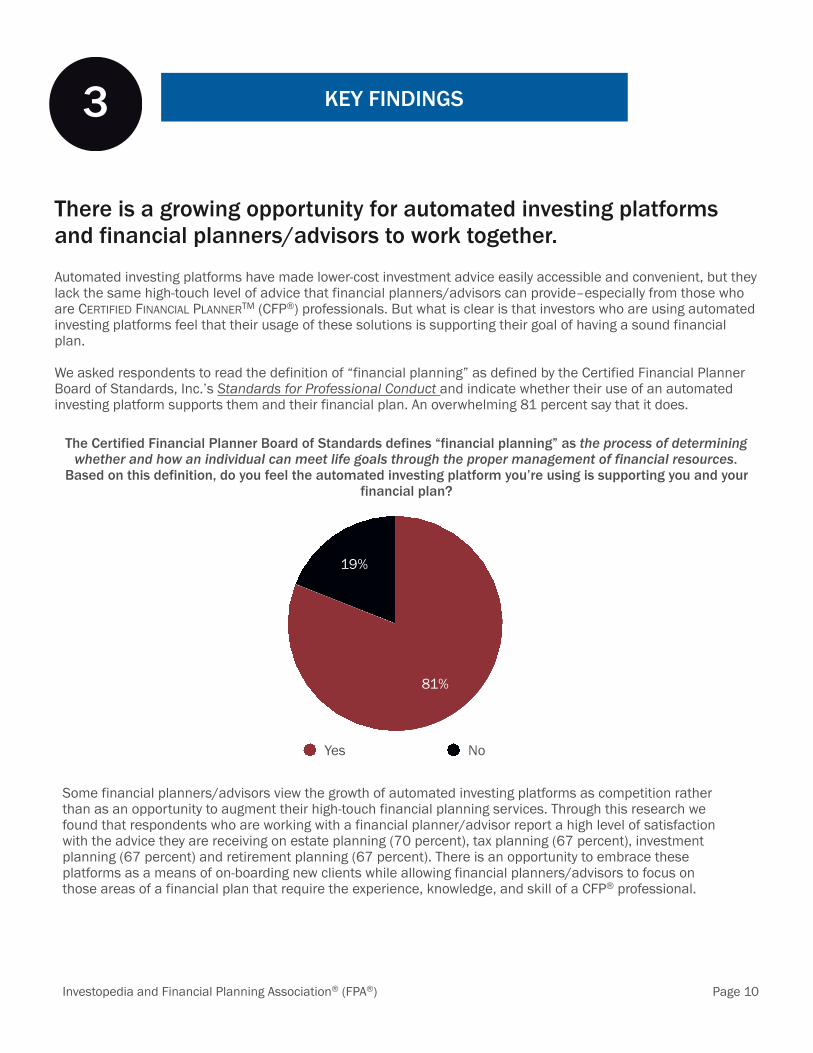

Automated investing platforms have made lower-cost investment advice easily accessible and convenient, but they lack the same high-touch level of advice that financial planners/advisors can provide–especially from those who are CERTIFIED FINANCIAL PLANNERTM (CFP®) professionals. But what is clear is that investors who are using automated investing platforms feel that their usage of these solutions is supporting their goal of having a sound financial plan.

We asked respondents to read the definition of “financial planning” as defined by the Certified Financial Planner Board of Standards, Inc.’s Standards for Professional Conduct and indicate whether their use of an automated investing platform supports them and their financial plan. An overwhelming 81 percent say that it does.

19%

81%

Yes No

The Certified Financial Planner Board of Standards defines “financial planning” as the process of determining whether and how an individual can meet life goals through the proper management of financial resources.

Based on this definition, do you feel the automated investing platform you’re using is supporting you and your financial plan?

Some financial planners/advisors view the growth of automated investing platforms as competition rather than as an opportunity to augment their high-touch financial planning services. Through this research we found that respondents who are working with a financial planner/advisor report a high level of satisfaction with the advice they are receiving on estate planning (70 percent), tax planning (67 percent), investment planning (67 percent) and retirement planning (67 percent). There is an opportunity to embrace these platforms as a means of on-boarding new clients while allowing financial planners/advisors to focus on those areas of a financial plan that require the experience, knowledge, and skill of a CFP® professional.

Investopedia and Financial Planning Association® (FPA®) Page 11

KEY FINDINGS3

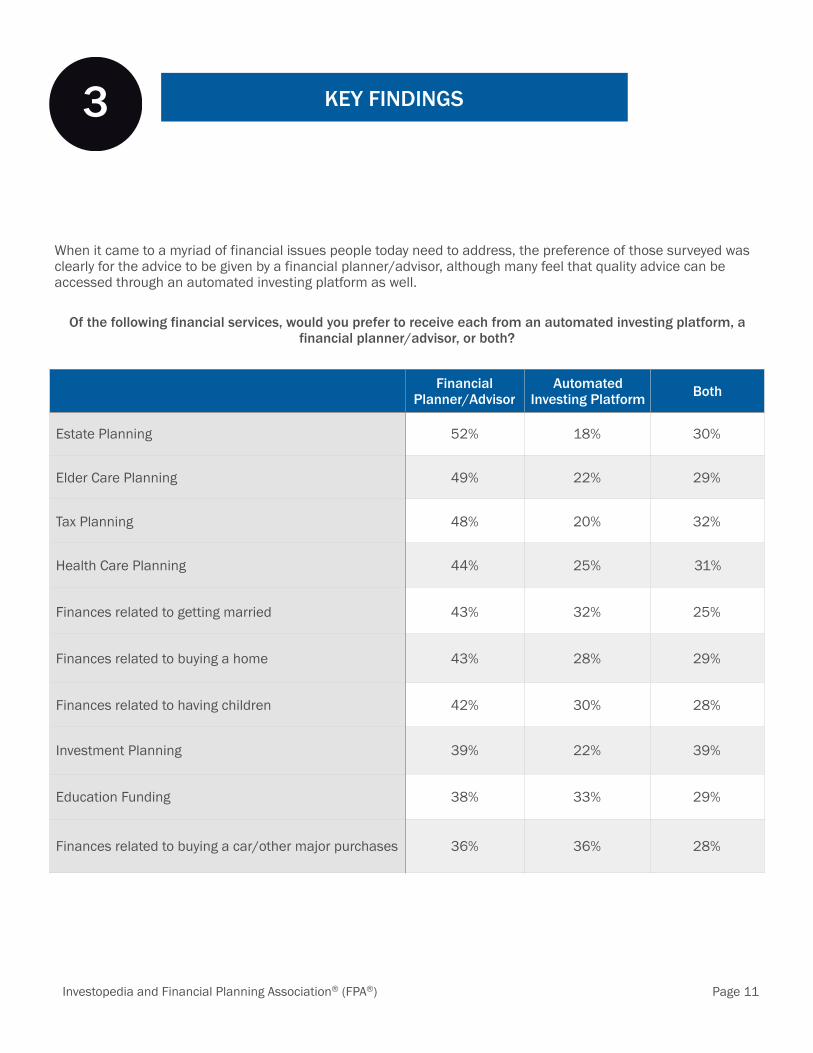

When it came to a myriad of financial issues people today need to address, the preference of those surveyed was clearly for the advice to be given by a financial planner/advisor, although many feel that quality advice can be accessed through an automated investing platform as well.

Of the following financial services, would you prefer to receive each from an automated investing platform, a financial planner/advisor, or both?

Financial Planner/Advisor

Automated Investing Platform Both

Estate Planning 52% 18% 30%

Elder Care Planning 49% 22% 29%

Tax Planning 48% 20% 32%

Health Care Planning 44% 25% 31%

Finances related to getting married 43% 32% 25%

Finances related to buying a home 43% 28% 29%

Finances related to having children 42% 30% 28%

Investment Planning 39% 22% 39%

Education Funding 38% 33% 29%

Finances related to buying a car/other major purchases 36% 36% 28%

Investopedia and Financial Planning Association® (FPA®) Page 12

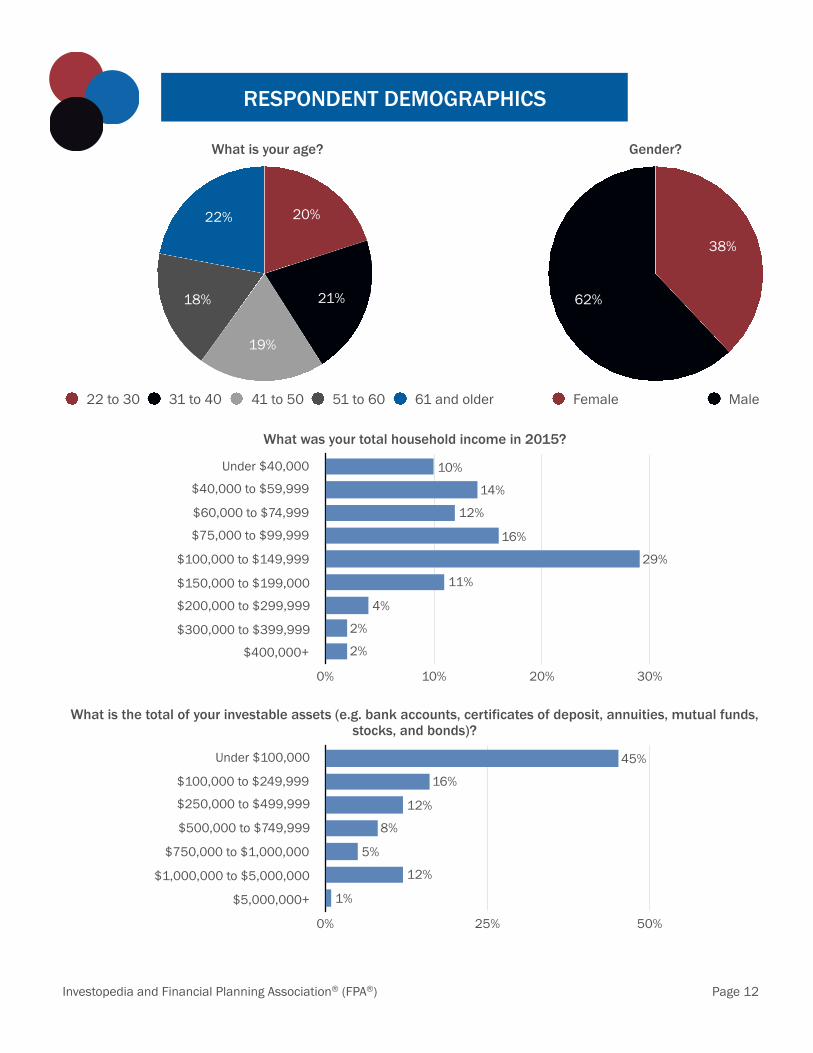

22%

18%

19%

21%

20%

22 to 30 31 to 40 41 to 50 51 to 60 61 and older

What is your age?

62%

38%

Female Male

Gender?

Under $40,000

$40,000 to $59,999

$60,000 to $74,999

$75,000 to $99,999

$100,000 to $149,999

$150,000 to $199,000

$200,000 to $299,999

$300,000 to $399,999

$400,000+

0% 10% 20% 30%

2%

2%

4%

11%

29%

16%

12%

14%

10%

What was your total household income in 2015?

What is the total of your investable assets (e.g. bank accounts, certificates of deposit, annuities, mutual funds, stocks, and bonds)?

Under $100,000

$100,000 to $249,999

$250,000 to $499,999

$500,000 to $749,999

$750,000 to $1,000,000

$1,000,000 to $5,000,000

$5,000,000+

0% 25% 50%

1%

12%

5%

8%

12%

16%

45%

RESPONDENT DEMOGRAPHICS

Investopedia and Financial Planning Association® (FPA®) Page 13

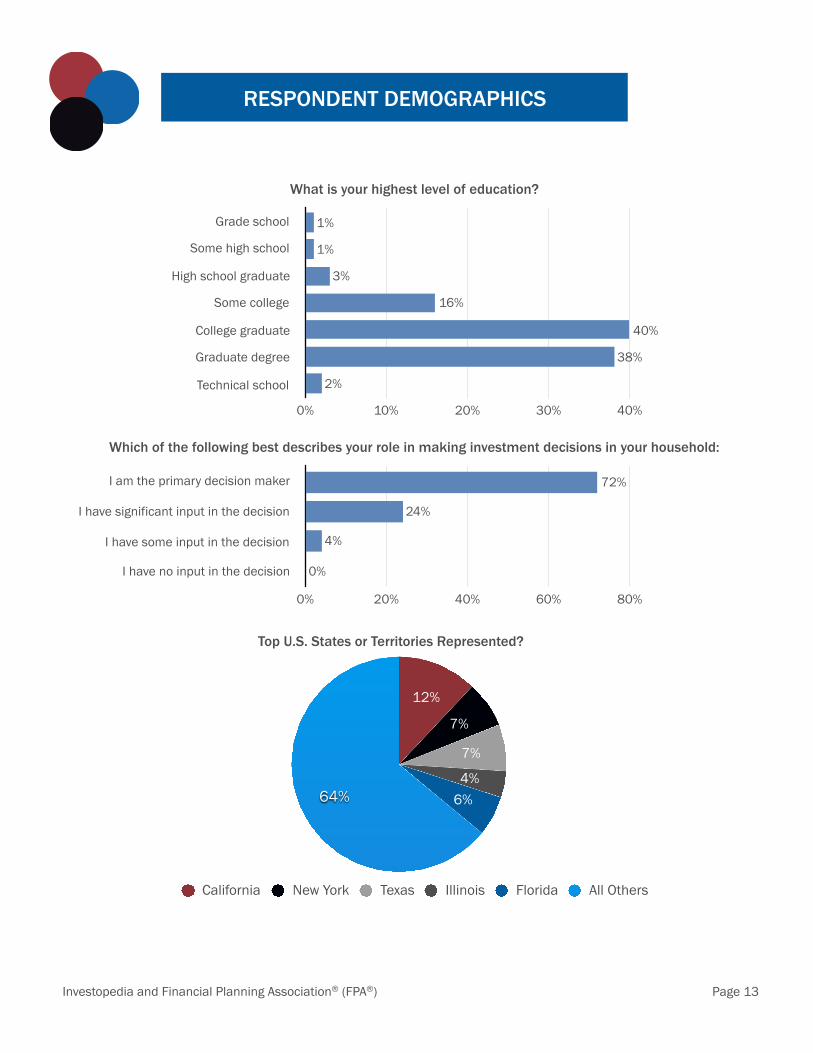

What is your highest level of education?

Grade school

Some high school

High school graduate

Some college

College graduate

Graduate degree

Technical school

0% 10% 20% 30% 40%

2%

38%

40%

16%

3%

1%

1%

Which of the following best describes your role in making investment decisions in your household:

I am the primary decision maker

I have significant input in the decision

I have some input in the decision

I have no input in the decision

0% 20% 40% 60% 80%

0%

4%

24%

72%

64% 6%4%

7%

7%

12%

California New York Texas Illinois Florida All Others

Top U.S. States or Territories Represented?

RESPONDENT DEMOGRAPHICS

Sharper Insight. Smarter Investing.

AUTOMATED INVESTING PLATFORM STUDY

HIGH-TECH AND HIGH-TOUCHInvestors Make the Case for Converging Automated

Investing Platforms and Financial Planning

Members of the media interested in talking with a representative of Investopedia or the Financial Planning Association® (FPA®) can contact the following.

FOR INVESTOPEDIA:

Kevin Moogan Public Relations Representative 917.765.8720 [email protected]

FOR FPA:

Ben Lewis Director of Public Relations 303.867.7190 [email protected]

Access great additional content of personal finance and financial planning through Investopedia at www.Investopedia.com and through FPA at www.PlannerSearch.org.