Embed Size (px)

Citation preview

December 2011

Hotels & Tourism Conference

Section Particulars

Section – I Tourism & Hospitality Industry Overview

Table of Contents

Section – I Tourism & Hospitality Industry Overview

Section – II Investment Rationale & Change in Business Model

Section – III Government Initiatives & Investments in the Industry

Section – IV Financial Norms from a Debt and Equity Perspective

Section – V Emerging Financing Opportunities in Hospitality

Section – VI Case Studies

Section – I: Tourism & Hospitality Industry Overview

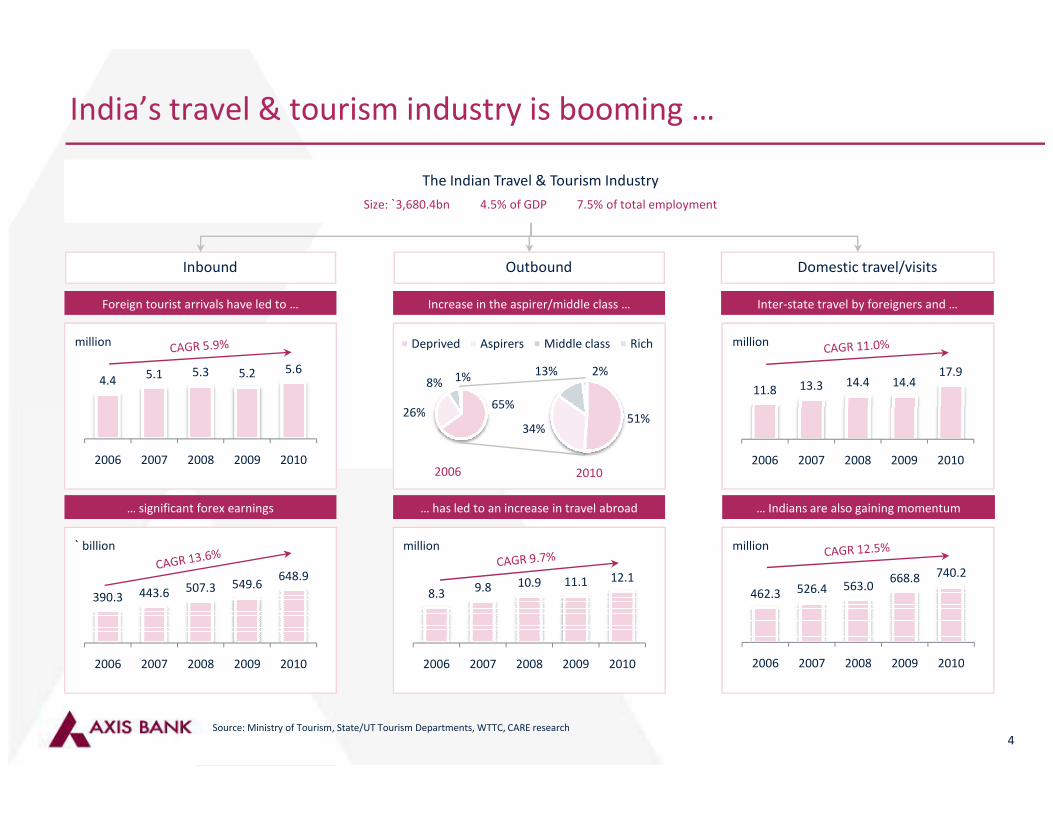

65%26%

8% 1%

Deprived Aspirers Middle class Rich

13% 2%

India’s travel & tourism industry is booming …

Inbound Outbound Domestic travel/visits

4.4 5.1 5.3 5.2 5.6

million million

Foreign tourist arrivals have led to … Increase in the aspirer/middle class … Inter-state travel by foreigners and …

The Indian Travel & Tourism Industry

Size: `3,680.4bn 4.5% of GDP 7.5% of total employment

11.8 13.3 14.4 14.4 17.9

million

65%26% 51%

34%

4Source: Ministry of Tourism, State/UT Tourism Departments, WTTC, CARE research

2006 2007 2008 2009 2010

390.3 443.6 507.3 549.6 648.9

2006 2007 2008 2009 2010

8.3 9.8 10.9 11.1 12.1

2006 2007 2008 2009 2010

` billion million

… significant forex earnings … has led to an increase in travel abroad

2006 20102006 2007 2008 2009 2010

462.3 526.4 563.0 668.8 740.2

2006 2007 2008 2009 2010

… Indians are also gaining momentum

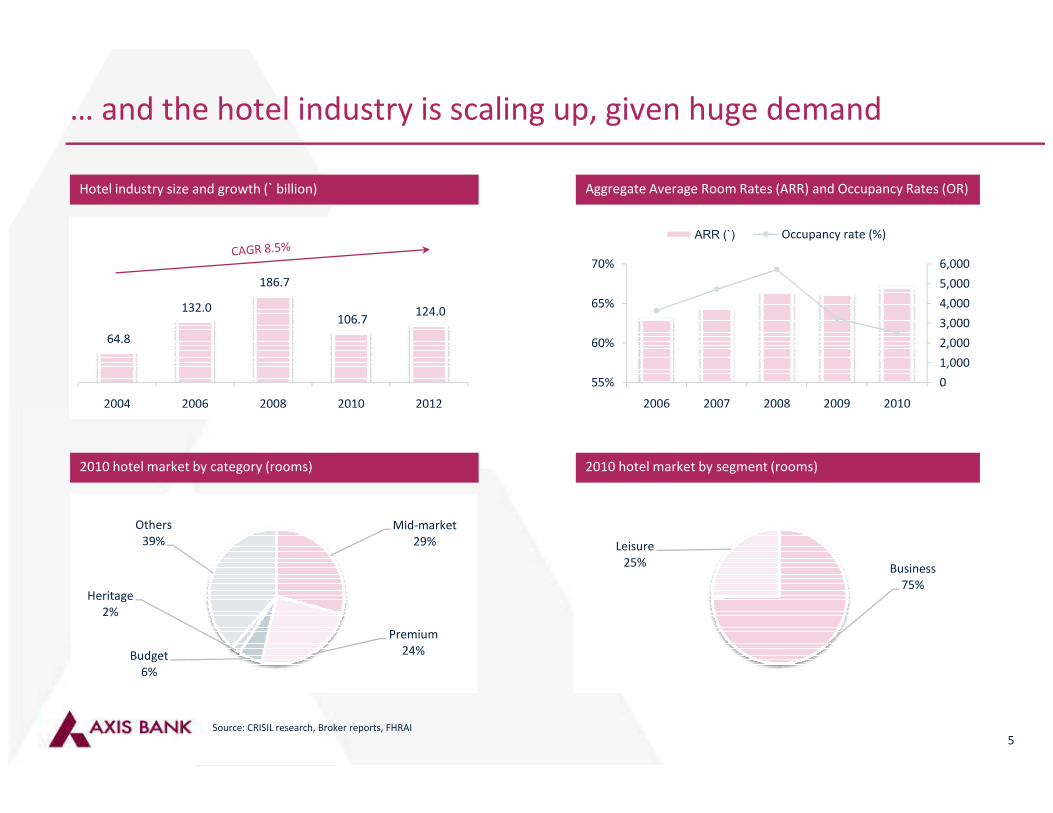

… and the hotel industry is scaling up, given huge demand

Hotel industry size and growth (` billion) Aggregate Average Room Rates (ARR) and Occupancy Rates (OR)

64.8

132.0

186.7

106.7 124.0

2004 2006 2008 2010 2012

55%

60%

65%

70%

2006 2007 2008 2009 2010

0

1,000

2,000

3,000

4,000

5,000

6,000

ARR (`) Occupancy rate (%)

5Source: CRISIL research, Broker reports, FHRAI

2010 hotel market by category (rooms) 2010 hotel market by segment (rooms)

2004 2006 2008 2010 2012 2006 2007 2008 2009 2010

Mid-market

29%

Premium

24%Budget

6%

Heritage

2%

Others

39%

Business

75%

Leisure

25%

Section – II: Investment Rationale & Change in Business Model

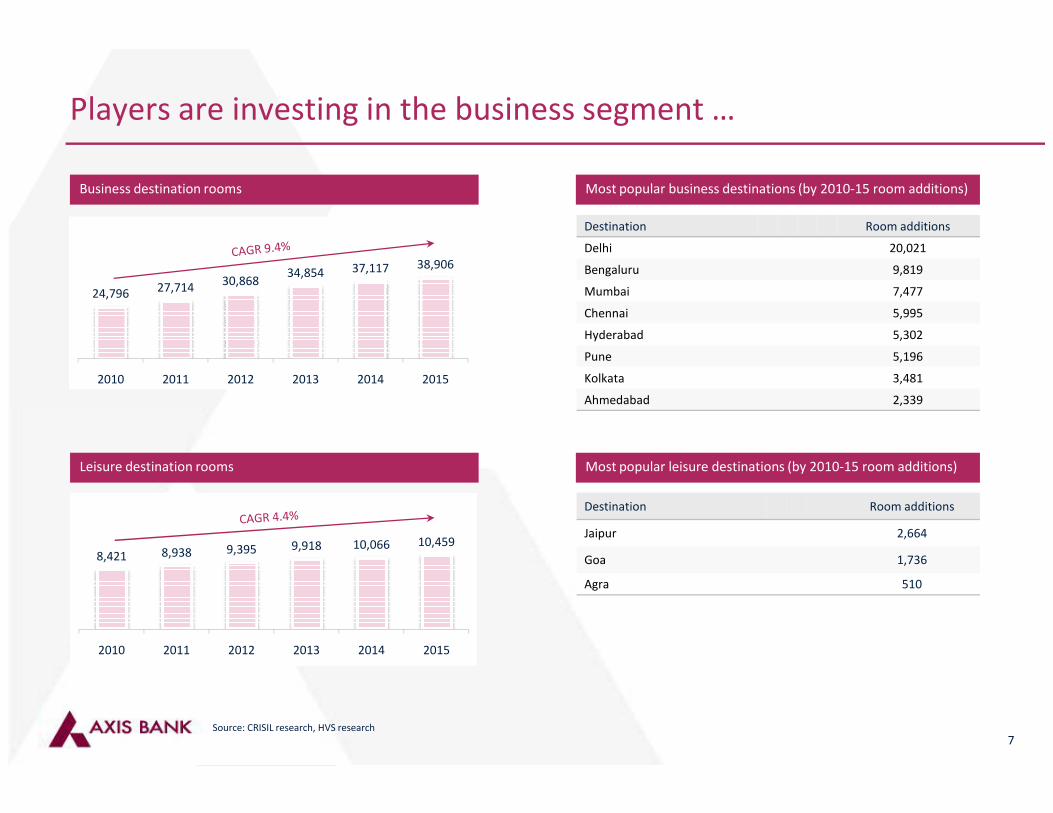

Players are investing in the business segment …

Business destination rooms Most popular business destinations (by 2010-15 room additions)

24,796 27,714 30,868

34,854 37,117 38,906

2010 2011 2012 2013 2014 2015

Destination Room additions

Delhi 20,021

Bengaluru 9,819

Mumbai 7,477

Chennai 5,995

Hyderabad 5,302

Pune 5,196

Kolkata 3,481

Ahmedabad 2,339

7

Leisure destination rooms Most popular leisure destinations (by 2010-15 room additions)

Destination Room additions

Jaipur 2,664

Goa 1,736

Agra 510

Source: CRISIL research, HVS research

8,421 8,938 9,395 9,918 10,066 10,459

2010 2011 2012 2013 2014 2015

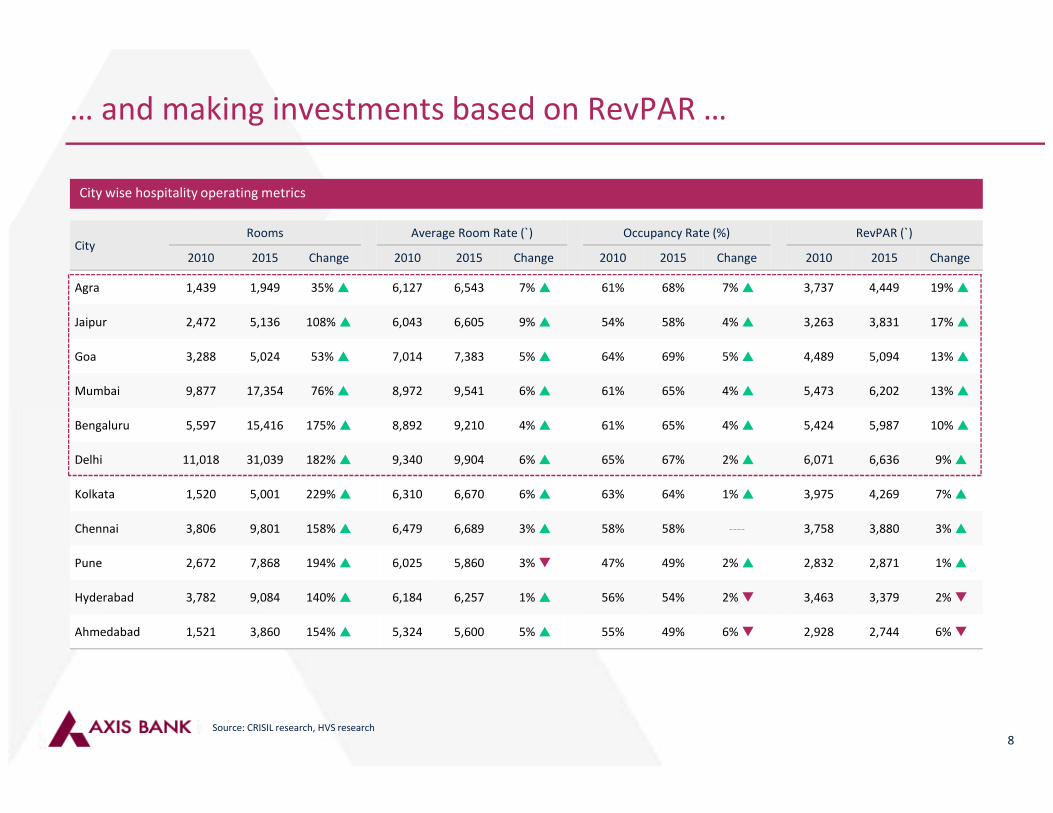

… and making investments based on RevPAR …

CityRooms Average Room Rate (`) Occupancy Rate (%) RevPAR (`)

2010 2015 Change 2010 2015 Change 2010 2015 Change 2010 2015 Change

Agra 1,439 1,949 35% � 6,127 6,543 7% � 61% 68% 7% � 3,737 4,449 19% �

Jaipur 2,472 5,136 108% � 6,043 6,605 9% � 54% 58% 4% � 3,263 3,831 17% �

Goa 3,288 5,024 53% � 7,014 7,383 5% � 64% 69% 5% � 4,489 5,094 13% �

Mumbai 9,877 17,354 76% � 8,972 9,541 6% � 61% 65% 4% � 5,473 6,202 13% �

City wise hospitality operating metrics

8

Bengaluru 5,597 15,416 175% � 8,892 9,210 4% � 61% 65% 4% � 5,424 5,987 10% �

Delhi 11,018 31,039 182% � 9,340 9,904 6% � 65% 67% 2% � 6,071 6,636 9% �

Kolkata 1,520 5,001 229% � 6,310 6,670 6% � 63% 64% 1% � 3,975 4,269 7% �

Chennai 3,806 9,801 158% � 6,479 6,689 3% � 58% 58% ---- 3,758 3,880 3% �

Pune 2,672 7,868 194% � 6,025 5,860 3% � 47% 49% 2% � 2,832 2,871 1% �

Hyderabad 3,782 9,084 140% � 6,184 6,257 1% � 56% 54% 2% � 3,463 3,379 2% �

Ahmedabad 1,521 3,860 154% � 5,324 5,600 5% � 55% 49% 6% � 2,928 2,744 6% �

Source: CRISIL research, HVS research

… with a focus on management contracts …

� Ownership model

� Franchise model� Management contract � Management contract

Business

model focus

1991-20011991-20012002-20102002-2010 2010 onwards2010 onwards

� Tier I cities

� Tourist destinations� Tier II cities

� Multi tourism optionsGeography

9

� Tourist destinations�

� Tier III cities� Multi tourism optionsGeography

� Luxury category

� Unclassified category

� Mid-level category

� Individual profit centres

� Budget category

� Mixed land usageFocus area

� Top-line growth

� Customer acquisition

� Customer segmentation

� Diversification of base

� Customer retention

� Value added service offerings

Customer

strategy

� Conventional funding

� Tie-ups with international brands

� Tie-ups with construction, real

estate companies & PE players

� Acquisition/expansion under sub-

brands

� Refurbishments

Investments

Source: Technopak, Broker reports

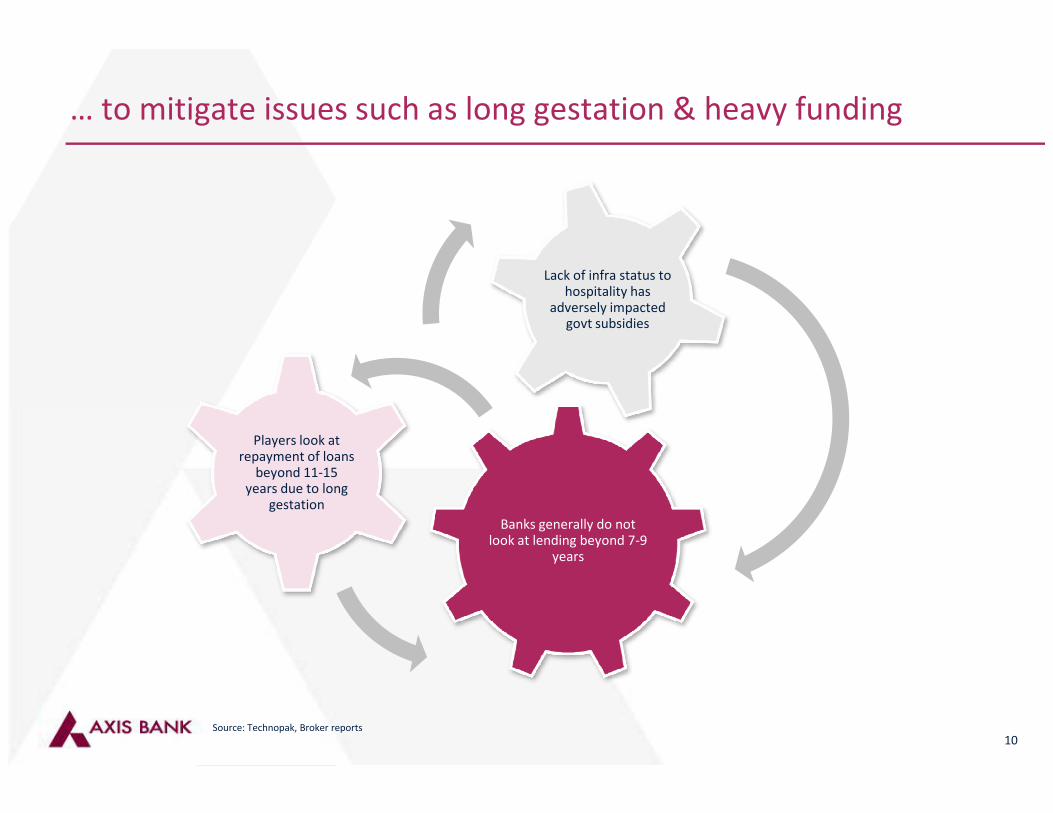

… to mitigate issues such as long gestation & heavy funding

Lack of infra status to hospitality has

adversely impacted govt subsidies

10

Banks generally do not look at lending beyond 7-9

years

Players look at repayment of loans

beyond 11-15 years due to long

gestation

Source: Technopak, Broker reports

Section – III: Government Initiatives & Investments in the Industry

The Government has initiated several promotional activities

Visa on arrival &

medical visa

Hospitality Development

& Promotion Board

Foreign Direct Investments (FDI)

Tax incentives &

subsidies

� Introduction of Medical

Visa (M-Visa) to

encourage Indian medical

� In some cases more than

65 clearances are

required to set up a hotel

� 100% FDI is permitted in

hotels & tourism including

restaurants, resorts, and

� Under Section 35 of the

Income Tax Act, a co is

permitted to claim

12

encourage Indian medical

tourism

� Introduction of visa-on-

arrival for persons from

Japan, Finland, Singapore,

Luxembourg & New

Zealand. Plans to

introduce visa-on-arrival

for 16 more countries

required to set up a hotel

in India

� The Union Cabinet of

India has approved

creation of Hospitality

Development and

Promotion Board (HDPB)

for single window

processing of clearances

and approvals

restaurants, resorts, and

other tourist complexes

providing accommodation

and/or catering and food

facilities to tourists, travel

agencies, tour operating

agencies and tourist

transport operating

agencies, etc

permitted to claim

deduction for investments

in new hotels to set off

against profits from other

existing hotels

� 5 year income tax holiday

granted to 2-4 star hotels

in specified districts

having UNESCO declared

“World Heritage Sites”

Source: Technopak, Broker reports

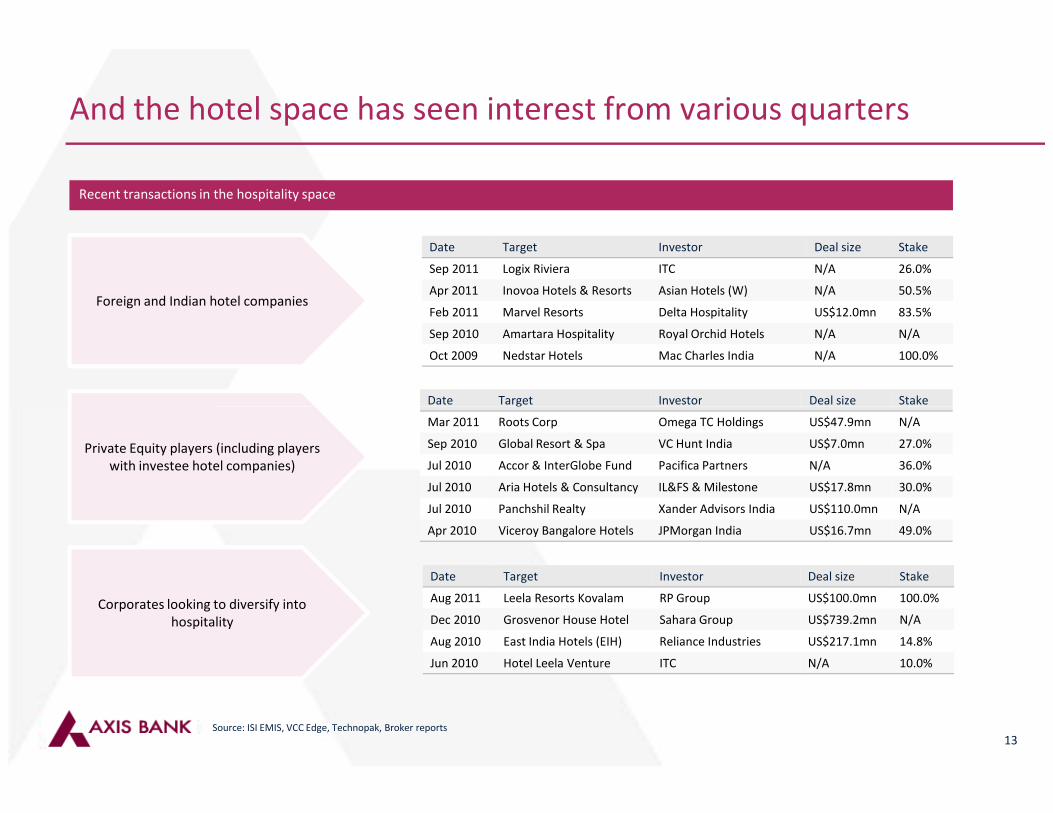

And the hotel space has seen interest from various quarters

Date Target Investor Deal size Stake

Sep 2011 Logix Riviera ITC N/A 26.0%

Apr 2011 Inovoa Hotels & Resorts Asian Hotels (W) N/A 50.5%

Feb 2011 Marvel Resorts Delta Hospitality US$12.0mn 83.5%

Sep 2010 Amartara Hospitality Royal Orchid Hotels N/A N/A

Oct 2009 Nedstar Hotels Mac Charles India N/A 100.0%

Date Target Investor Deal size Stake

Foreign and Indian hotel companies

Recent transactions in the hospitality space

13Source: ISI EMIS, VCC Edge, Technopak, Broker reports

Mar 2011 Roots Corp Omega TC Holdings US$47.9mn N/A

Sep 2010 Global Resort & Spa VC Hunt India US$7.0mn 27.0%

Jul 2010 Accor & InterGlobe Fund Pacifica Partners N/A 36.0%

Jul 2010 Aria Hotels & Consultancy IL&FS & Milestone US$17.8mn 30.0%

Jul 2010 Panchshil Realty Xander Advisors India US$110.0mn N/A

Apr 2010 Viceroy Bangalore Hotels JPMorgan India US$16.7mn 49.0%

Date Target Investor Deal size Stake

Aug 2011 Leela Resorts Kovalam RP Group US$100.0mn 100.0%

Dec 2010 Grosvenor House Hotel Sahara Group US$739.2mn N/A

Aug 2010 East India Hotels (EIH) Reliance Industries US$217.1mn 14.8%

Jun 2010 Hotel Leela Venture ITC N/A 10.0%

Private Equity players (including players

with investee hotel companies)

Corporates looking to diversify into

hospitality

Section – IV: Financial Norms from a Debt and Equity Perspective

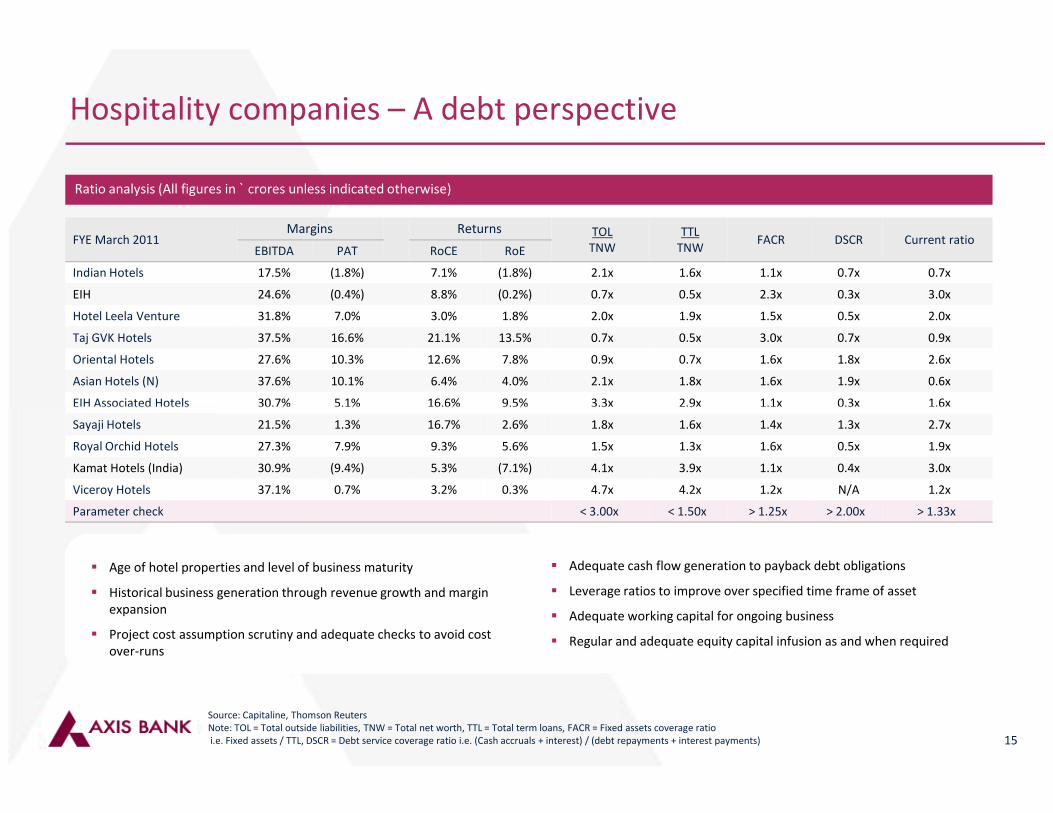

Hospitality companies – A debt perspective

FYE March 2011Margins Returns TOL

TNW

TTL

TNWFACR DSCR Current ratio

EBITDA PAT RoCE RoE

Indian Hotels 17.5% (1.8%) 7.1% (1.8%) 2.1x 1.6x 1.1x 0.7x 0.7x

EIH 24.6% (0.4%) 8.8% (0.2%) 0.7x 0.5x 2.3x 0.3x 3.0x

Hotel Leela Venture 31.8% 7.0% 3.0% 1.8% 2.0x 1.9x 1.5x 0.5x 2.0x

Taj GVK Hotels 37.5% 16.6% 21.1% 13.5% 0.7x 0.5x 3.0x 0.7x 0.9x

Oriental Hotels 27.6% 10.3% 12.6% 7.8% 0.9x 0.7x 1.6x 1.8x 2.6x

Asian Hotels (N) 37.6% 10.1% 6.4% 4.0% 2.1x 1.8x 1.6x 1.9x 0.6x

EIH Associated Hotels 30.7% 5.1% 16.6% 9.5% 3.3x 2.9x 1.1x 0.3x 1.6x

Ratio analysis (All figures in ` crores unless indicated otherwise)

15

EIH Associated Hotels 30.7% 5.1% 16.6% 9.5% 3.3x 2.9x 1.1x 0.3x 1.6x

Sayaji Hotels 21.5% 1.3% 16.7% 2.6% 1.8x 1.6x 1.4x 1.3x 2.7x

Royal Orchid Hotels 27.3% 7.9% 9.3% 5.6% 1.5x 1.3x 1.6x 0.5x 1.9x

Kamat Hotels (India) 30.9% (9.4%) 5.3% (7.1%) 4.1x 3.9x 1.1x 0.4x 3.0x

Viceroy Hotels 37.1% 0.7% 3.2% 0.3% 4.7x 4.2x 1.2x N/A 1.2x

Parameter check < 3.00x < 1.50x > 1.25x > 2.00x > 1.33x

� Age of hotel properties and level of business maturity

� Historical business generation through revenue growth and margin

expansion

� Project cost assumption scrutiny and adequate checks to avoid cost

over-runs

� Adequate cash flow generation to payback debt obligations

� Leverage ratios to improve over specified time frame of asset

� Adequate working capital for ongoing business

� Regular and adequate equity capital infusion as and when required

Source: Capitaline, Thomson Reuters

Note: TOL = Total outside liabilities, TNW = Total net worth, TTL = Total term loans, FACR = Fixed assets coverage ratio

i.e. Fixed assets / TTL, DSCR = Debt service coverage ratio i.e. (Cash accruals + interest) / (debt repayments + interest payments)

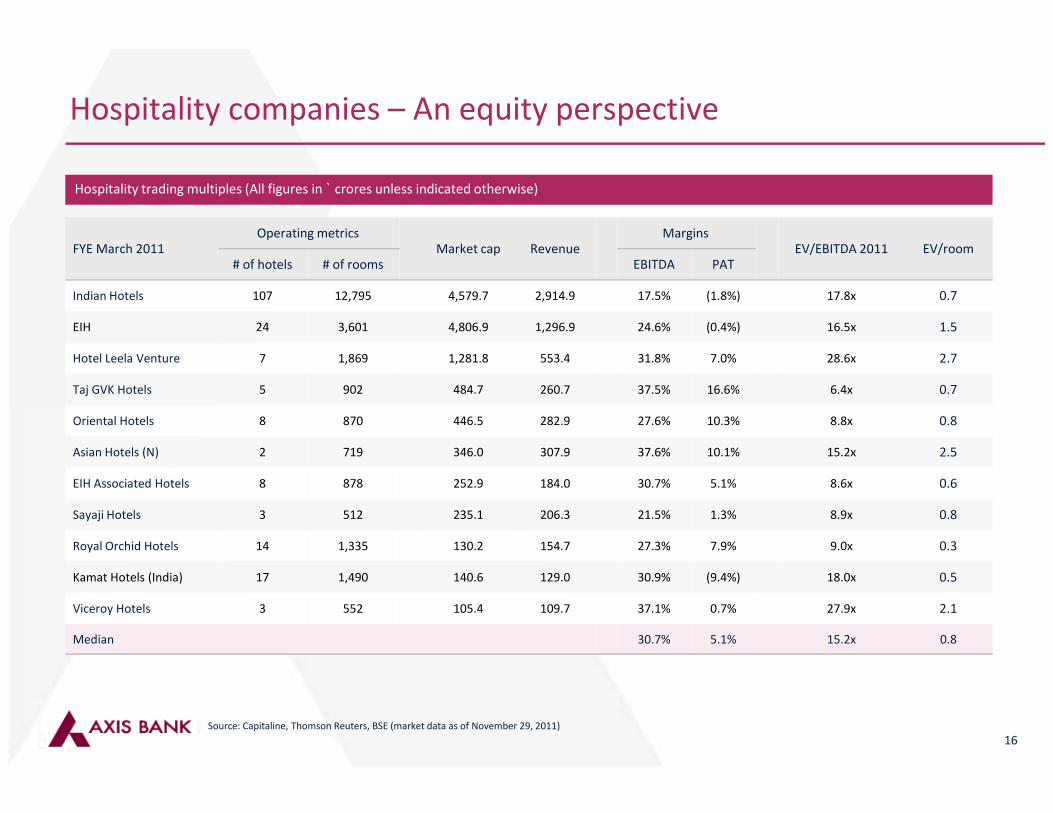

Hospitality companies – An equity perspective

FYE March 2011Operating metrics

Market cap RevenueMargins

EV/EBITDA 2011 EV/room# of hotels # of rooms EBITDA PAT

Indian Hotels 107 12,795 4,579.7 2,914.9 17.5% (1.8%) 17.8x 0.7

EIH 24 3,601 4,806.9 1,296.9 24.6% (0.4%) 16.5x 1.5

Hotel Leela Venture 7 1,869 1,281.8 553.4 31.8% 7.0% 28.6x 2.7

Taj GVK Hotels 5 902 484.7 260.7 37.5% 16.6% 6.4x 0.7

Hospitality trading multiples (All figures in ` crores unless indicated otherwise)

16

Oriental Hotels 8 870 446.5 282.9 27.6% 10.3% 8.8x 0.8

Asian Hotels (N) 2 719 346.0 307.9 37.6% 10.1% 15.2x 2.5

EIH Associated Hotels 8 878 252.9 184.0 30.7% 5.1% 8.6x 0.6

Sayaji Hotels 3 512 235.1 206.3 21.5% 1.3% 8.9x 0.8

Royal Orchid Hotels 14 1,335 130.2 154.7 27.3% 7.9% 9.0x 0.3

Kamat Hotels (India) 17 1,490 140.6 129.0 30.9% (9.4%) 18.0x 0.5

Viceroy Hotels 3 552 105.4 109.7 37.1% 0.7% 27.9x 2.1

Median 30.7% 5.1% 15.2x 0.8

Source: Capitaline, Thomson Reuters, BSE (market data as of November 29, 2011)

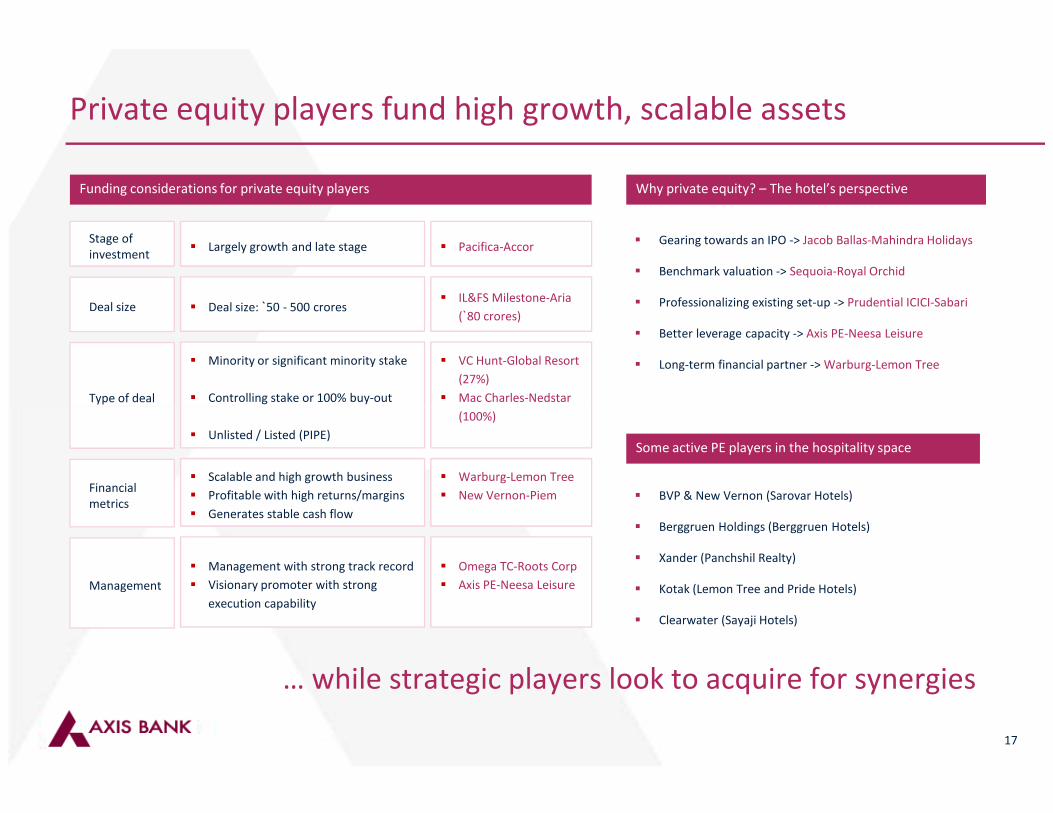

Private equity players fund high growth, scalable assets

Funding considerations for private equity players

� Largely growth and late stageStage of

investment

� Deal size: `50 - 500 croresDeal size

� Minority or significant minority stake

� Controlling stake or 100% buy-outType of deal

� Pacifica-Accor

� IL&FS Milestone-Aria

(`80 crores)

� VC Hunt-Global Resort

(27%)

� Mac Charles-Nedstar

� Gearing towards an IPO -> Jacob Ballas-Mahindra Holidays

� Benchmark valuation -> Sequoia-Royal Orchid

� Professionalizing existing set-up -> Prudential ICICI-Sabari

� Better leverage capacity -> Axis PE-Neesa Leisure

� Long-term financial partner -> Warburg-Lemon Tree

Why private equity? – The hotel’s perspective

17

… while strategic players look to acquire for synergies

� Unlisted / Listed (PIPE)

� Scalable and high growth business

� Profitable with high returns/margins

� Generates stable cash flow

Financial

metrics

� Management with strong track record

� Visionary promoter with strong

execution capability

Management

(100%)

� Warburg-Lemon Tree

� New Vernon-Piem

� Omega TC-Roots Corp

� Axis PE-Neesa Leisure

Some active PE players in the hospitality space

� BVP & New Vernon (Sarovar Hotels)

� Berggruen Holdings (Berggruen Hotels)

� Xander (Panchshil Realty)

� Kotak (Lemon Tree and Pride Hotels)

� Clearwater (Sayaji Hotels)

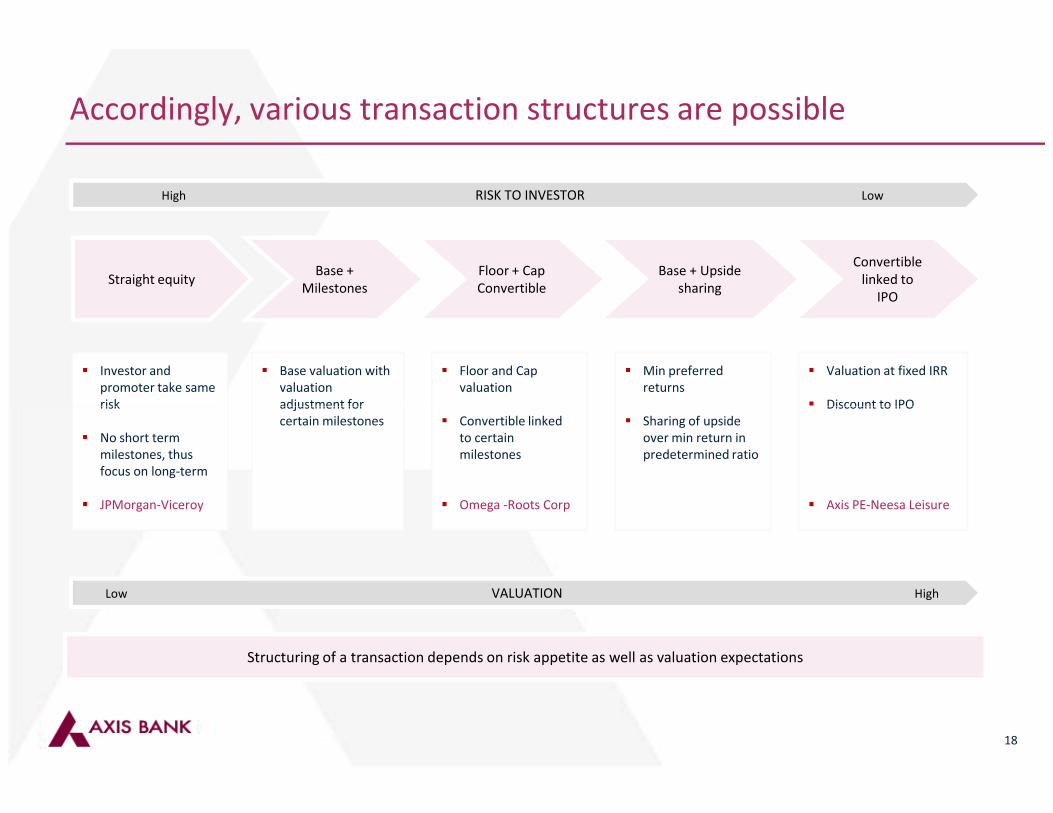

Accordingly, various transaction structures are possible

Straight equityBase +

Milestones

Floor + Cap

Convertible

Convertible

linked to

IPO

� Investor and

promoter take same

risk

Base + Upside

sharing

� Base valuation with

valuation

adjustment for

� Floor and Cap

valuation

� Min preferred

returns

� Valuation at fixed IRR

� Discount to IPO

High RISK TO INVESTOR Low

18

risk

� No short term

milestones, thus

focus on long-term

� JPMorgan-Viceroy

adjustment for

certain milestones � Convertible linked

to certain

milestones

� Omega -Roots Corp

� Sharing of upside

over min return in

predetermined ratio

� Discount to IPO

� Axis PE-Neesa Leisure

Low VALUATION High

Structuring of a transaction depends on risk appetite as well as valuation expectations

Section – V: Emerging Financing Opportunities in Hospitality

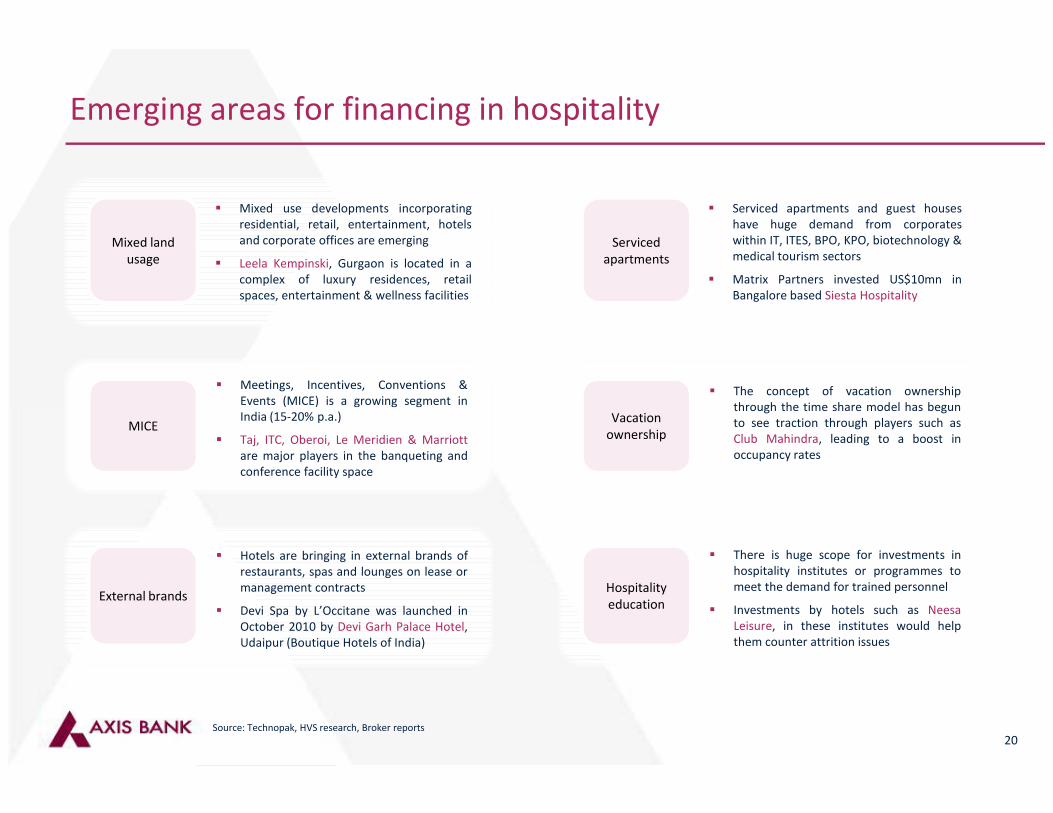

Emerging areas for financing in hospitality

Mixed land

usage

� Mixed use developments incorporating

residential, retail, entertainment, hotels

and corporate offices are emerging

� Leela Kempinski, Gurgaon is located in a

complex of luxury residences, retail

spaces, entertainment & wellness facilities

� Meetings, Incentives, Conventions &

Events (MICE) is a growing segment in

Serviced

apartments

� Serviced apartments and guest houses

have huge demand from corporates

within IT, ITES, BPO, KPO, biotechnology &

medical tourism sectors

� Matrix Partners invested US$10mn in

Bangalore based Siesta Hospitality

� The concept of vacation ownership

through the time share model has begun

20

MICE

Events (MICE) is a growing segment in

India (15-20% p.a.)

� Taj, ITC, Oberoi, Le Meridien & Marriott

are major players in the banqueting and

conference facility space

External brands

� Hotels are bringing in external brands of

restaurants, spas and lounges on lease or

management contracts

� Devi Spa by L’Occitane was launched in

October 2010 by Devi Garh Palace Hotel,

Udaipur (Boutique Hotels of India)

Vacation

ownership

through the time share model has begun

to see traction through players such as

Club Mahindra, leading to a boost in

occupancy rates

Hospitality

education

� There is huge scope for investments in

hospitality institutes or programmes to

meet the demand for trained personnel

� Investments by hotels such as Neesa

Leisure, in these institutes would help

them counter attrition issues

Source: Technopak, HVS research, Broker reports

Section – VI: Case Studies

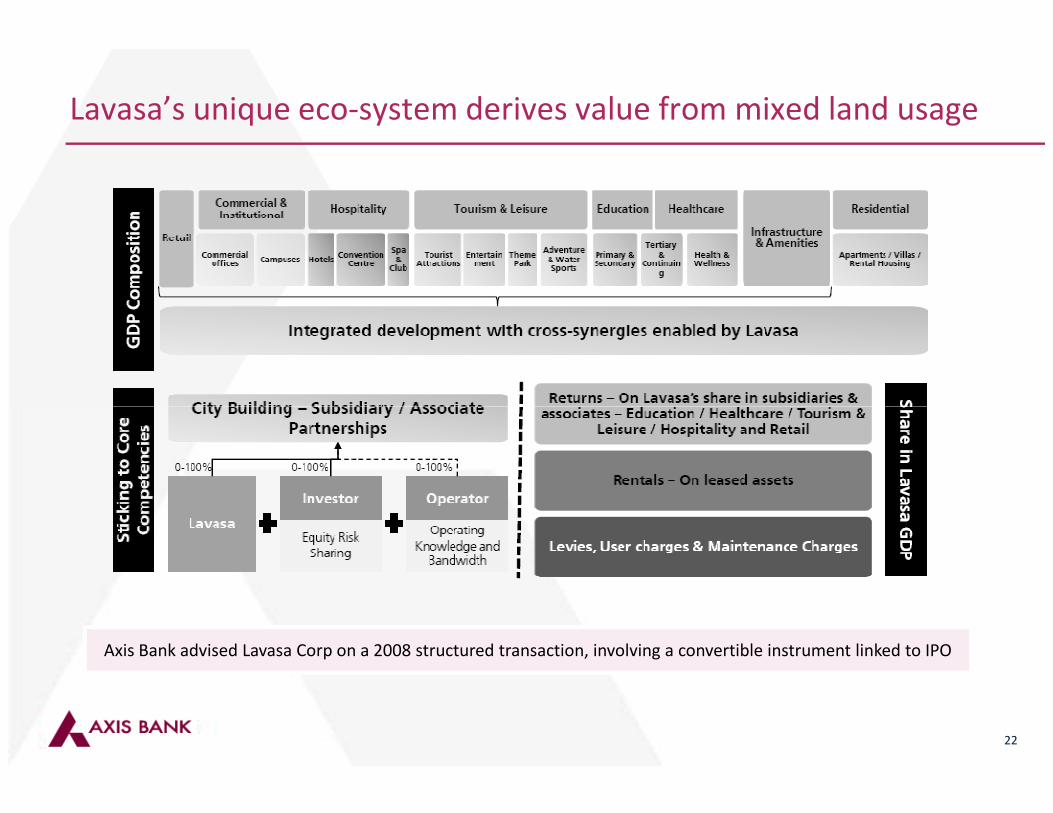

Lavasa’s unique eco-system derives value from mixed land usage

22

Axis Bank advised Lavasa Corp on a 2008 structured transaction, involving a convertible instrument linked to IPO

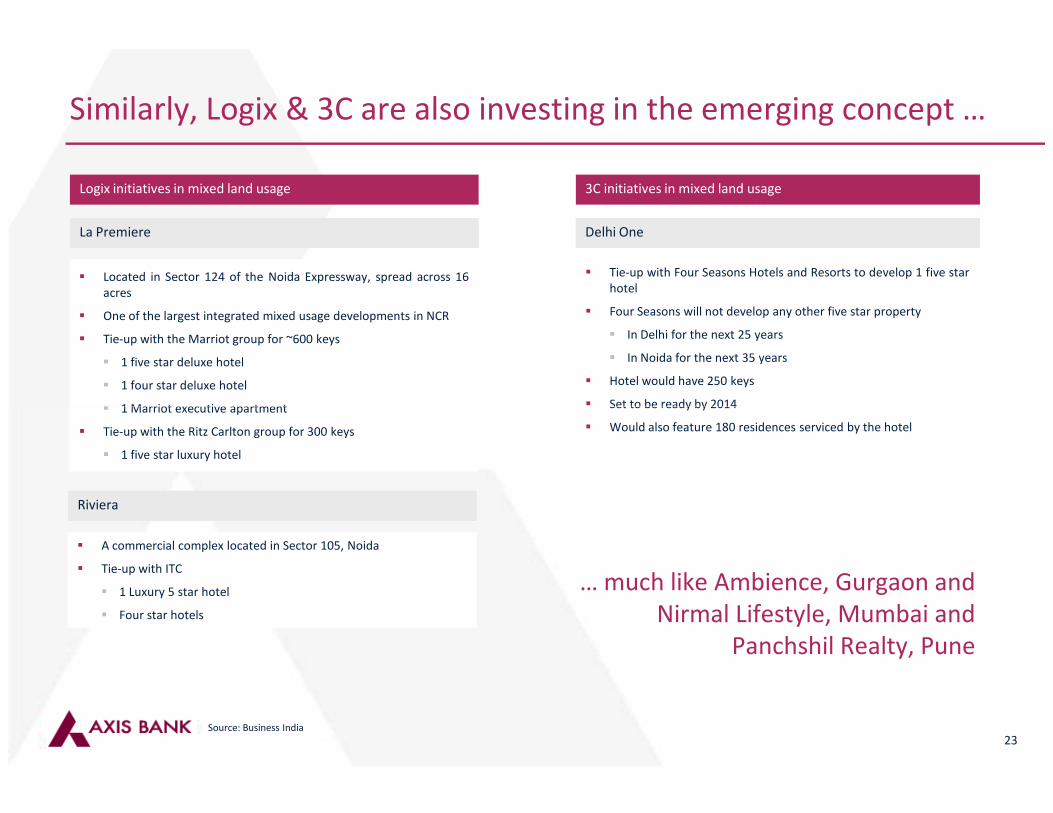

Similarly, Logix & 3C are also investing in the emerging concept …

Logix initiatives in mixed land usage 3C initiatives in mixed land usage

� Located in Sector 124 of the Noida Expressway, spread across 16

acres

� One of the largest integrated mixed usage developments in NCR

� Tie-up with the Marriot group for ~600 keys

� 1 five star deluxe hotel

� 1 four star deluxe hotel

� 1 Marriot executive apartment

La PremiereLa Premiere Delhi OneDelhi One

� Tie-up with Four Seasons Hotels and Resorts to develop 1 five star

hotel

� Four Seasons will not develop any other five star property

� In Delhi for the next 25 years

� In Noida for the next 35 years

� Hotel would have 250 keys

� Set to be ready by 2014

23

� 1 Marriot executive apartment

� Tie-up with the Ritz Carlton group for 300 keys

� 1 five star luxury hotel

� Set to be ready by 2014

� Would also feature 180 residences serviced by the hotel

� A commercial complex located in Sector 105, Noida

� Tie-up with ITC

� 1 Luxury 5 star hotel

� Four star hotels

RivieraRiviera

… much like Ambience, Gurgaon and

Nirmal Lifestyle, Mumbai and

Panchshil Realty, Pune

Source: Business India

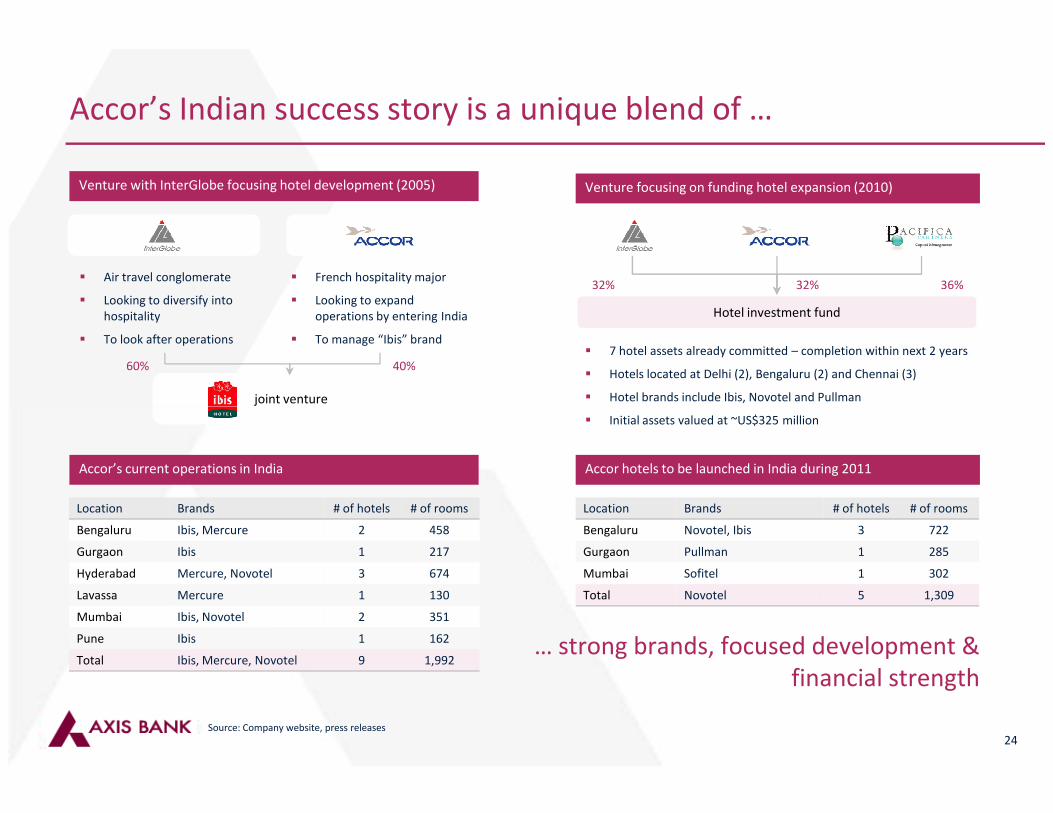

Accor’s Indian success story is a unique blend of …

� Air travel conglomerate

� Looking to diversify into

hospitality

� To look after operations

� French hospitality major

� Looking to expand

operations by entering India

� To manage “Ibis” brand

joint venture

Venture with InterGlobe focusing hotel development (2005) Venture focusing on funding hotel expansion (2010)

60% 40%

Hotel investment fund

� 7 hotel assets already committed – completion within next 2 years

� Hotels located at Delhi (2), Bengaluru (2) and Chennai (3)

� Hotel brands include Ibis, Novotel and Pullman

32% 36%32%

24

Accor’s current operations in India

Location Brands # of hotels # of rooms

Bengaluru Ibis, Mercure 2 458

Gurgaon Ibis 1 217

Hyderabad Mercure, Novotel 3 674

Lavassa Mercure 1 130

Mumbai Ibis, Novotel 2 351

Pune Ibis 1 162

Total Ibis, Mercure, Novotel 9 1,992

Accor hotels to be launched in India during 2011

Location Brands # of hotels # of rooms

Bengaluru Novotel, Ibis 3 722

Gurgaon Pullman 1 285

Mumbai Sofitel 1 302

Total Novotel 5 1,309

� Initial assets valued at ~US$325 million

Source: Company website, press releases

… strong brands, focused development &

financial strength

100.0%

56.7%

33.3%20.0%

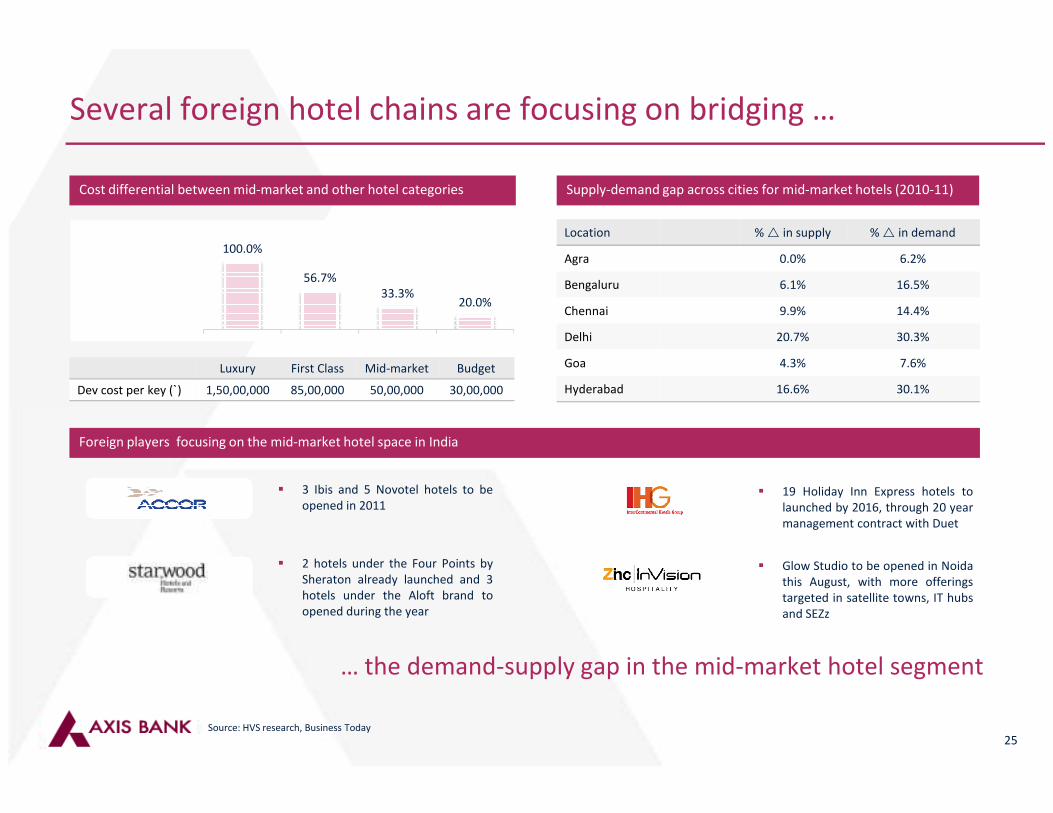

Several foreign hotel chains are focusing on bridging …

Supply-demand gap across cities for mid-market hotels (2010-11)

Location % � in supply % � in demand

Agra 0.0% 6.2%

Bengaluru 6.1% 16.5%

Chennai 9.9% 14.4%

Delhi 20.7% 30.3%

Goa 4.3% 7.6%

Hyderabad 16.6% 30.1%

Cost differential between mid-market and other hotel categories

Luxury First Class Mid-market Budget

Dev cost per key (`) 1,50,00,000 85,00,000 50,00,000 30,00,000

25

… the demand-supply gap in the mid-market hotel segment

Source: HVS research, Business Today

� 3 Ibis and 5 Novotel hotels to be

opened in 2011

� 2 hotels under the Four Points by

Sheraton already launched and 3

hotels under the Aloft brand to

opened during the year

� 19 Holiday Inn Express hotels to

launched by 2016, through 20 year

management contract with Duet

� Glow Studio to be opened in Noida

this August, with more offerings

targeted in satellite towns, IT hubs

and SEZz

Foreign players focusing on the mid-market hotel space in India

Several players are working together to increase industry pie size

Financial Investors focused on hospitality Players who only focus on managing hotels

26

New hotel

projects

Corporates with a stake in the hospitality space Players who own as well as manage hotels

Funding capability, land bank Operational expertise, branding

Axis Bank Limited, Investment Banking Department, Corporate Office,

Axis House, Wing C - Level 1. Bombay Dyeing Mills Compound,

Pandurang Budhkar Marg, Worli. Mumbai 400 025.

www.axisbank.com

Thank you

Disclaimer

� The presentation is only for restricted circulation to the addressed parties. This presentation does not constitute an engagement or offer for the engagement

from Axis Bank Limited or any of its subsidiaries or affiliates (“Axis”) to any party and the information contained herein will not form the basis of any contract.

� Neither Axis Bank nor any of their respective affiliates, shareholders, directors, employees, agents or representatives makes any warranty or representation as

to the accuracy or completeness of the information contained herein (including statements of opinion and expectation, whether communicated in written,

oral, visual or electronic form) or as to the reasonableness of any assumptions contained herein. In particular, no representation or warranty is given as to the

achievement or reasonableness of, any information.

� Consequently, neither Axis Bank nor any of their respective affiliates, shareholders, directors, employees, agents or advisors shall be liable for any loss or

damage (direct or indirect) suffered as a result of reliance upon any statements contained in, or any omission from this presentation and expressly disclaim any

and all liability relating to or resulting from the use of this presentation.

� This presentation should not be distributed, reproduced, or used without the express consent of Axis Bank.

� Nothing contained in this presentation should be relied upon as a promise or representation as to the future. The pro forma and information contained herein

28

� Nothing contained in this presentation should be relied upon as a promise or representation as to the future. The pro forma and information contained herein

was prepared expressly for use herein and is based on certain assumptions and management's analysis of information available at the time this presentation

was prepared. There is no representation, warranty or other assurance in this regard.