Embed Size (px)

Citation preview

ICP 18B:Management of Key Risks

Basic-level Module

A Core Curriculum for Insurance Supervisors

Copyright © 2006 International Association of Insurance Supervisors (IAIS).All rights reserved.

The material in this module is copyrighted. It may be used for training by competent organi-zations with permission. Please contact the IAIS to seek permission.

This module was prepared by Stuart Wason, senior actuary with Assuris, Canada’s life insur-ance policyholder protection fund. He was director of Mercer Oliver Wyman, an operating company of Mercer, a subsidiary of Marsh and McLennan Companies. At Mercer, he served as an adviser on enterprise risk management, as the appointed actuary for several life insur-ers, as the valuation actuary for the liquidator of two life insurers, as the independent actuary in the purchase and sale of several blocks of life insurance business, as the independent actu-ary in the demutualization of Mutual Life, as the peer reviewer of the valuation of life insur-ers, and as an actuary responsible for preparing appraisals of life insurers. He has more than 30 years of experience in actuarial, financial reporting, and insurance company management positions. He has been involved in the work of the Canadian Institute of Actuaries, the Society of Actuaries, and the International Actuarial Association.

This module was reviewed by Anthony Asher, N. M. Govardhan, and Hauw-Quek Soo Hoon. Anthony Asher is a consulting actuary with Trowbridge Deloitte. His previous positions in-clude senior policy manager with the Australian Prudential Regulation Authority, professor of actuarial science and head of the School of Statistics and Actuarial Science at the University of Witwatersrand, Johannesburg, and before that chief actuary of the Prudential Assurance Company of South Africa. N. M. Govardhan served as internal actuary with the Insurance Regulation Department, Bank Negara Malaysia, from 1997 to 2003. He is currently doing re-view work for the Insurance Regulatory Development Authority of India as a member of the Actuarial Review Committee. Hauw-Quek Soo Hoon recently retired as executive director of the Insurance Group at the Monetary Authority of Singapore (MAS), where she represented MAS on several IAIS committees and subcommittees, including the Executive Committee and a period as chair of the Education Subcommittee.

iii

Contents

About the Core Curriculum . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . v

Note to learner . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . vii

Pretest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .ix

A. Insurer key risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

B. Underwriting (insurance) risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

C. Credit risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

D. Market risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

E. Operational risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

F. Putting it all together . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

G. Summary and Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

H. References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

Posttest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

Appendix I. ICP 18 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

Appendix II. Answer key . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

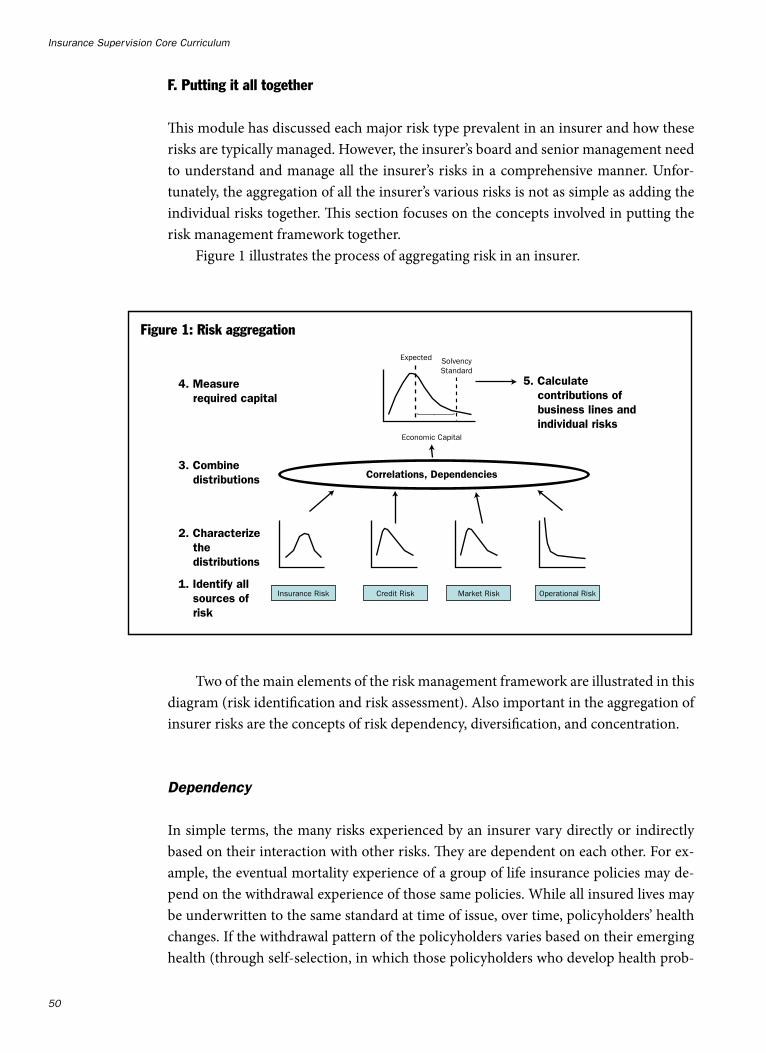

FiguresFigure 1. Risk aggregation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

v

About theCore Curriculum

A financially sound insurance sector contributes to economic growth and well-being by supporting the management of risk, allocation of resources, and mobilization of long-term savings. The insurance core principles (ICPs), developed by the International As-sociation of Insurance Supervisors (IAIS), are key international standards relevant for sound financial systems.

Effective implementation of the ICPs requires skilled and knowledgeable insurance supervisors. Recognizing this need, the World Bank and the IAIS partnered in 2002 to develop a “core curriculum” for insurance supervisors. The Core Curriculum Project, funded and supported by various sources, accelerates the learning process of both new and experienced supervisors. The ICPs provide the structure for the core curriculum, which consists of a set of modules that summarize the most relevant aspects of each topic, focus on the practical application of supervisory concepts, and cross-reference existing literature.

The core curriculum is designed to help those studying it to:

• Recognize the risks that arise from insurance operations• Know the techniques and tools used by private and public sector professionals• Identify, measure, and manage these risks• Operate effectively within a supervisory organization• Understand the ICPs and other IAIS principles, standards, and guidance• Recommend techniques and tools to help a particular jurisdiction observe the

ICPs and other IAIS principles, standards, and guidance• Identify the constraints and identify and prioritize supervisory techniques and

tools to best manage the existing risks in light of these constraints.

vii

Note to learner

Welcome to the ICP 18B: Management of Key Risks module. This is a basic-level module that focuses on each of the key risks faced by an insurer and how they can be managed within the framework described in module ICP 18A, Risk Management Fundamentals. It is recommended that you successfully complete module ICP 18A before studying this module. This module should be useful to new insurance supervisors or experienced supervisors who have not dealt extensively with the topic—or are simply seeking to refresh and update their knowledge.

Start by reviewing the objectives, which will give you an idea of what you will learn as a result of studying the module. Then answer the questions in the pretest to help gauge your prior knowledge of the topic. Proceed to study the module either on an independent, self-study basis or in the context of a seminar or workshop. The amount of time required for self-study will vary but it is recommended that the module be ad-dressed over a short time, broken into sessions on parts if desired.

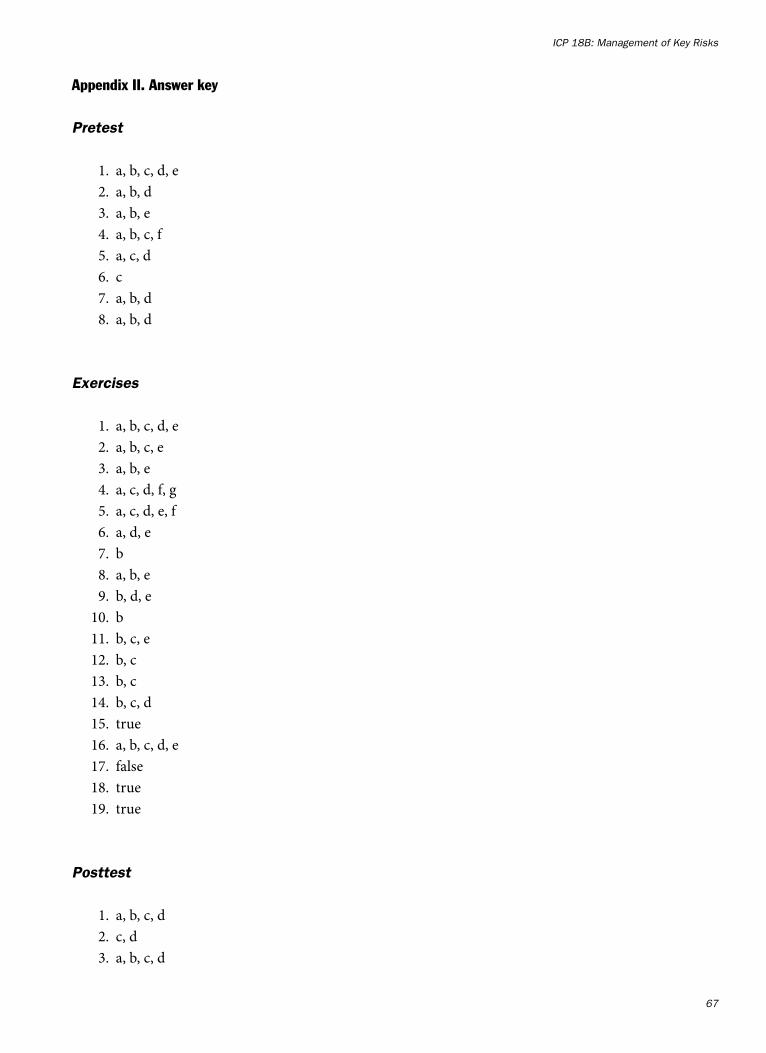

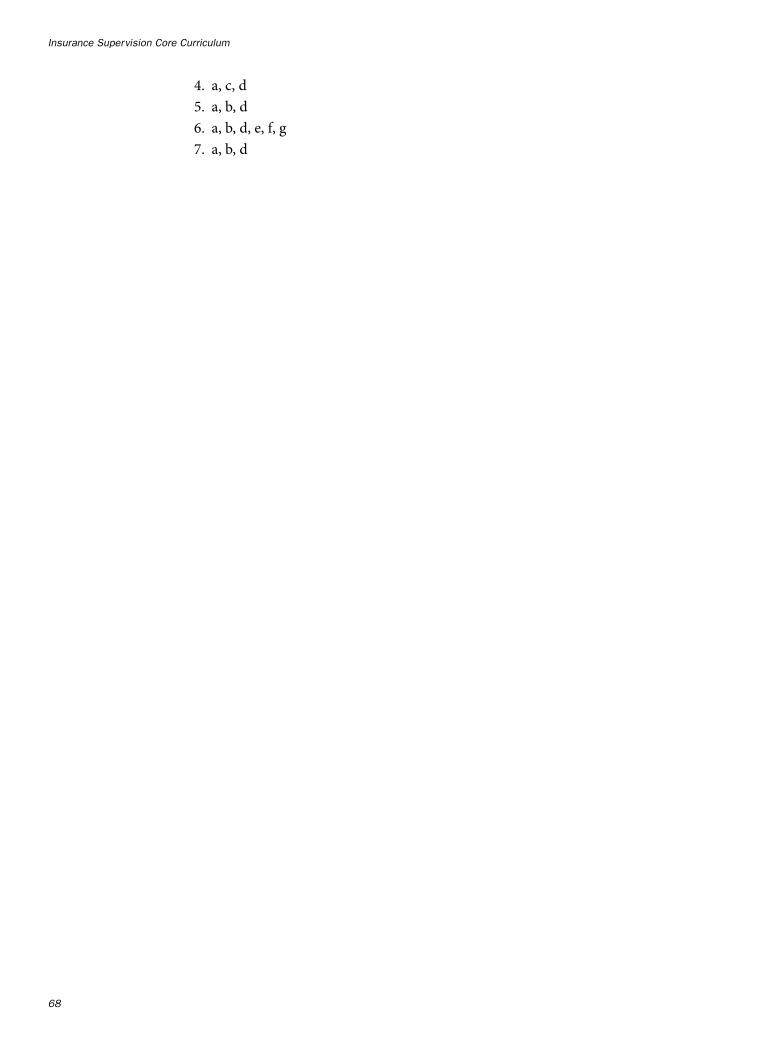

To help you engage and involve yourself in the topic, we have interspersed the module with a number of hands-on activities for you to complete. These exercises are intended to provide a checkpoint from time to time so that you can absorb and under-stand the material more readily and can apply the material to your local circumstances. You are encouraged to complete each of these activities before proceeding with the next section of the module. If you are working with others on this module, develop the answers through discussion and cooperative work methods. An answer key is provided in appendix II.

As a result of studying the material in this module, you will be able to do the fol-lowing:

Insurance Supervision Core Curriculum

viii

1. Explain how an insurer could apply each step of the risk management frame-work (objective setting, risk identification, risk assessment, strategy planning, risk monitoring, and controlling) to each of the following risks:

a. Underwriting (insurance) riskb. Credit riskc. Market riskd. Operational risk.

2. Provide examples of approaches commonly used by insurers to regularly review the market environment in which they operate in order to identify and draw ap-propriate conclusions about the risks posed.

3. Discuss the difference between risk control and risk financing and illustrate how each can contribute to the risk management process.

4. Define financial engineering and illustrate its application as a risk management tool.

5. Describe products commonly used for risk management purposes, including

a. Insuranceb. Contingent capitalc. Swapsd. Securitization.

6. Describe the statistical and analytic techniques commonly used in each step of the risk management steps framework.

7. Explain what is meant by the term “risk aggregation.”8. Discuss the relevance of dependency, concentration, and diversification to risk

aggregation.

ICP 18B: Management of Key Risks

ix

Pretest

Before studying this module on risk management, answer the following questions. The questions are designed to help you gauge your knowledge of ICP 18, Risk Assessment and Management, and the material presented in module ICP 18A, Risk Management Fundamentals, before beginning this module. The answer key is presented in appendix II.

For each of the following questions, circle the correct response(s); there may be more than one correct response.

1. Whichofthefollowingstatementsaboutriskmanagementaretrue?

a. Riskmanagementisimportantinensuringthataninsurermeetsitsobligationsnowandinthefuture.

b.Thebusinessofinsuranceisfundamentallyaboutthemanagementofrisk.

c. Likeotherbusinesses,insuranceissubjecttooperationalrisk.

d. Insurancesupervisorshaveidentifiedpoorriskmanagementasaleadingcauseofinsolvency.

e.Riskmanagementisimportantforoverallfinancialsystemstability.

Insurance Supervision Core Curriculum

x

2. WhichofthefollowingaretruestatementsforICP18,RiskAssessmentandManagement?

a. Aninsurershouldidentify,understand,andmanagethesignificantrisksthatitfaces.

b.Allinsurersshouldestablishriskmanagementfunctionsandriskmanagementcommittees.

c. Ultimateresponsibilityforthedevelopmentofbestpracticesandtheproperoperationoftheinsurerrestswithitsseniormanagement.

d.Thesupervisoryauthorityrequiresandchecksthatinsurershaveinplacecomprehensiveriskmanagementpoliciesandsystems.

e.Theriskmanagementpoliciesandriskcontrolsystemsthatshouldbeusedbyaninsurerarelargelyindependentofthenatureoftheinsurer’sbusiness

3. Whichofthefollowingpairsofinsurancestakeholderandstakeholderinterestareappropriatelymatched?

Stakeholder Primary stakeholder interest

a. Insurancesupervisor Insurersolvency

b. Insurerboardofdirectors Goodgovernance

c. Insureractuaries Riskcompliance

d. Insurerseniormanagement Riskappetiteapproval

e.Auditors Independentreviewofcontrols

4. Whatrolescansupervisorsplay?

a. Understandingtherisksfacedbyaninsurerandthemannerinwhichthoserisksaremanagedisamajorfocusofsupervision.

b.Supervisorsplayacriticalroleintheriskmanagementprocessbyreviewingthemonitoringandcontrolsexercisedbytheinsurer.

c. Thesupervisoryauthoritydevelopsprudentialregulationsandrequirementstocontaintheserisks.

d. Increasingly,supervisorsarerelyingonexpost(afterthefact)reviewsordisclosuresratherthanusingrisk-basedsupervisionwithanexante(early)detectionmannerofoperation.

e.Supervisorsshouldleavethereviewofinsurerstrategiestoinsurers’boardsofdirectorsbutshouldinsistoncompliancechecklistsshowingthatallriskshavebeenaddressed.

f. Boardsunwillingtoimplementappropriateriskmanagementpracticesposeconsiderablerisktopolicyholders,andsupervisorsshouldbepreparedtoconsideralloptionswithintheirlegalpowerstoinfluenceinsurersandtheirboardstotakecorrectiveaction.

ICP 18B: Management of Key Risks

xi

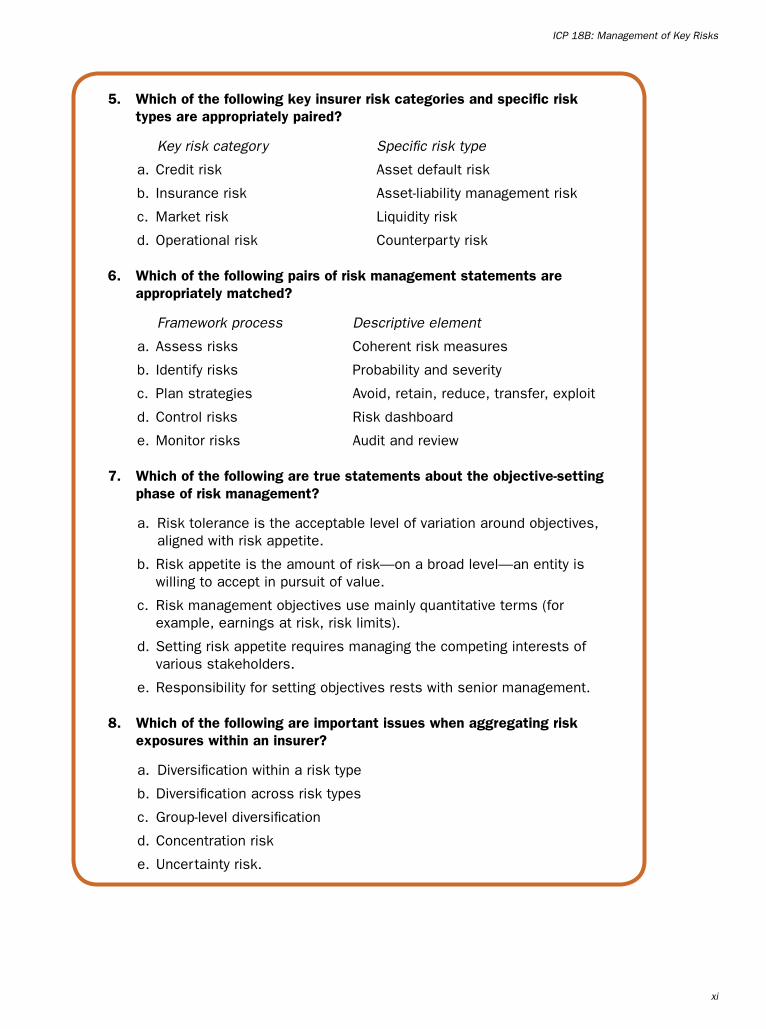

5. Whichofthefollowingkeyinsurerriskcategoriesandspecificrisktypesareappropriatelypaired?

Key risk category Specific risk type

a.Creditrisk Assetdefaultrisk

b. Insurancerisk Asset-liabilitymanagementrisk

c. Marketrisk Liquidityrisk

d.Operationalrisk Counterpartyrisk

6. Whichofthefollowingpairsofriskmanagementstatementsareappropriatelymatched?

Framework process Descriptive element

a.Assessrisks Coherentriskmeasures

b. Identifyrisks Probabilityandseverity

c. Planstrategies Avoid,retain,reduce,transfer,exploit

d.Controlrisks Riskdashboard

e.Monitorrisks Auditandreview

7. Whichofthefollowingaretruestatementsabouttheobjective-settingphaseofriskmanagement?

a. Risktoleranceistheacceptablelevelofvariationaroundobjectives,alignedwithriskappetite.

b.Riskappetiteistheamountofrisk—onabroadlevel—anentityiswillingtoacceptinpursuitofvalue.

c. Riskmanagementobjectivesusemainlyquantitativeterms(forexample,earningsatrisk,risklimits).

d.Settingriskappetiterequiresmanagingthecompetinginterestsofvariousstakeholders.

e.Responsibilityforsettingobjectivesrestswithseniormanagement.

8. Whichofthefollowingareimportantissueswhenaggregatingriskexposureswithinaninsurer?

a. Diversificationwithinarisktype

b.Diversificationacrossrisktypes

c. Group-leveldiversification

d.Concentrationrisk

e.Uncertaintyrisk.

1

ICP 18B:Management of Key Risks

Basic-level Module

A. Insurer key risks

Risk is the raison d’être for insurance. Through insurance contracts customers seek to transfer financial uncertainties to the insurer in exchange for a set of premiums lev-ied by the insurer. Life insurance contracts provide protection in the event of death, longevity, morbidity, critical illness, or health care costs. Contracts for other types of insurance afford protection against costs or losses to property, for example, owing to contingencies such as fire, theft, accident, and storms. Therefore, it is to be expected that an insurer’s core operations, the estimation of the amount and timing of policyholder payments, and the present value of their amount (taking account of the future costs to administer these obligations) are subject to risk. It is vital that insurers manage the risks inherent in the insurance contracts they assume.

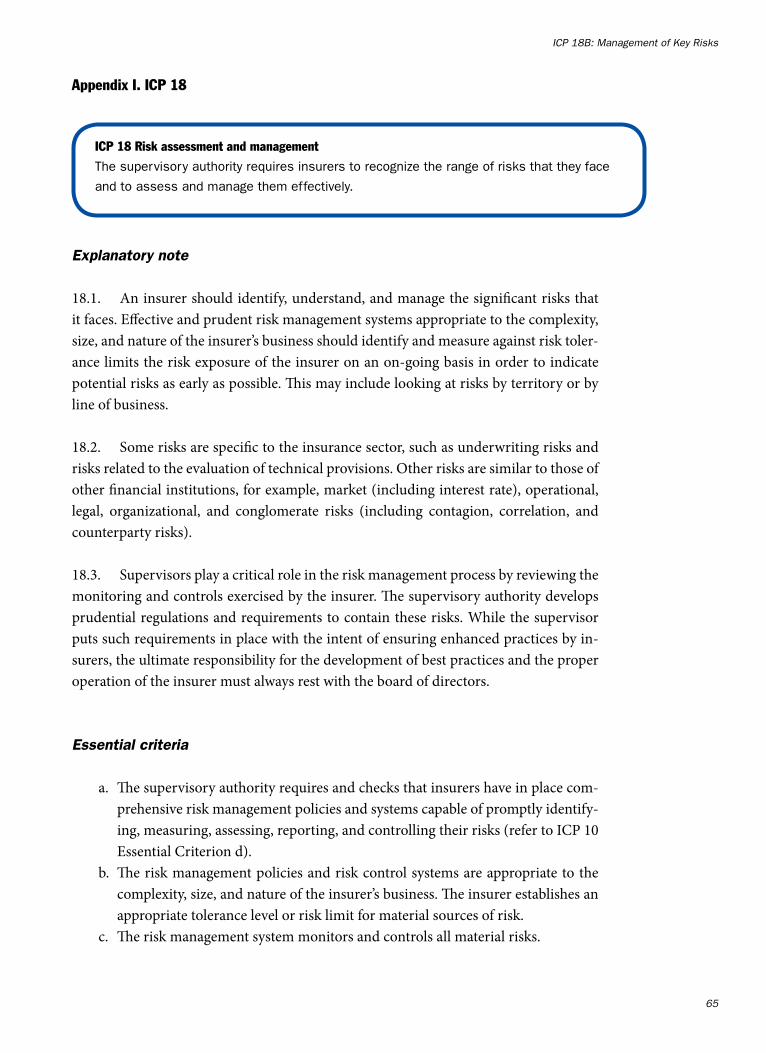

Like any business, the business of insurance involves many functions to be success-ful. The successful execution of these business functions also entails risk. In this regard, the explanatory note to ICP 18 states

Some risks are specific to the insurance sector, such as underwriting risks and risks related to the evaluation of technical provisions. Other risks are similar to those of other financial institutions, for example, market (including interest rate), opera-tional, legal, organizational, and conglomerate risks (including contagion, correla-tion, and counterparty risks).

Insurance Supervision Core Curriculum

�

In other words, insurers are subject to risks inherent in their core business as well as to general business risks applicable to any business. In the rapidly developing field of risk management, there is no single globally accepted manner of naming and categoriz-ing insurer risks. However, there is growing convergence on the key broad categories of insurer risk. The development of a common means of categorizing risks is most impor-tant to ensure clarity of communication among insurer stakeholders. Insurer key risks might be categorized under the following major headings:

• Underwriting • Credit • Market • Operational• Liquidity• Strategic.

This module introduces the reader to each of the major risk types prevalent in an insurer and the manner in which these risks are typically managed. This module builds on the concepts described in the companion module, ICP 18A, Risk Management Fun-damentals. This module also describes the process of integrating and aggregating risk exposures across risk types, products, and geographic areas. At the conclusion of both modules you will have had a comprehensive introduction to risk assessment and man-agement for an insurer.

Commonly used terms

EntErprisE risk managEmEnt

In “Overview of Enterprise Risk Management” (CAS 2004), the Casualty Actuarial So-ciety describes enterprise risk management as “the discipline by which an organization in any industry assesses, controls, exploits, finances, and monitors risk from all sources for the purposes of increasing the organization’s short- and long-term value to its stake-holders.”

In Enterprise Risk Management—Integrated Framework (2004), COSO (Commit-tee of Sponsoring Organizations of the Treadway Commission) defines enterprise risk management (ERM) as “a process, effected by an entity’s board of directors, manage-ment, and other personnel, applied in strategy setting and across the enterprise, de-signed to identify potential events that may affect the entity, and manage risks to be within its risk appetite, to provide reasonable assurance regarding the achievement of entity objectives.”

ICP 18B: Management of Key Risks

�

non-systEmatic risk

Non-systematic risk is also known as diversifiable risk or specific risk. It can be reduced or eliminated by aggregating entities that are less than 100% positively correlated with respect to a given risk factor. An entity could be, for example, a financial security, a li-ability, a corporation, an asset class, or a person’s life. In these examples, the risks could be default, policyholder withdrawals, bankruptcy, return volatility, or mortality, respec-tively.

risk

The IAIS Glossary defines risk as being “used to indicate a condition of the real world in which there is a possibility of loss; also used by insurance practitioners to indicate the property insured or the peril insured against.”

The 1995 Standard on Risk Management (ASNZS 4360:1995) released by Stan-dards Australia and Standards New Zealand states that “risk management is as much about identifying opportunities as avoiding or mitigating losses.”

risk managEmEnt

The IAIS Glossary defines risk management as “a scientific approach to the problem of dealing with the pure risks facing an individual or an organization, in which insurance is viewed as simply one of several approaches for dealing with such risks.”

The 1995 Standard on Risk Management (ASNZS 4360:1995) released by Stan-dards Australia and Standards New Zealand states that “risk management is as much about identifying opportunities as avoiding or mitigating losses.”

In Enterprise Risk Management (2003), James Lam states “[R]isk management is not only about reducing downside potential or the probability of pain, but also about increasing upside opportunity or the prospects for gain.”

systEmatic risk

Systematic risk is also known as non-diversifiable risk or market risk. It is the residual risk that cannot be eliminated by aggregating or pooling the same risk within a given market, but may be further reduced by aggregating the underlying risk with other im-perfectly correlated risks in the same market or other imperfectly correlated markets. For example, the relationship between a stock’s return and the return of the stock mar-ket as a whole represents that stock’s systematic risk.

Insurance Supervision Core Curriculum

�

systEmic risk

Systemic risk represents the danger that specific local problems may spread more broad-ly to affect the entire financial system. Examples affecting the banking sector include the liquidity and lending crises that rapidly escalated from local country problems to international crises. A flu pandemic or the failure of a sufficiently large global reinsurer are examples of local problems that might have systemic implications for the insurance industry.

ICP 18B: Management of Key Risks

�

B. Underwriting (insurance) risk

Insurance companies assume risk through the insurance contracts they underwrite. Underwriting risks are those associated with both the perils covered by the specific line of insurance (fire, death, motor accident, windstorm, earthquake, etc.) and the risk mitigation processes used to manage the insurance business. The types of perils that are insurable are limited perhaps only by one’s imagination and the judgment of an insurer that the risk is insurable.

Importance of good data

For each insurable peril it is vital for the insurer to understand the frequency and se-verity data. For the vast majority of perils, achieving this understanding requires gath-ering data on both exposure (the amount and number of insurable risks) and claim (the amount and number of claims arising from the exposure base). As mentioned in module ICP 18A, the study of the frequency and severity of claims arising from each peril can be used to prepare a claims distribution. This statistical information provides the insurer with much valuable information about the number and amount of claims arising from each peril (for example, mean, median, standard deviation, coefficient of variance, tail variance) that is used for pricing and valuing those risks.

It is vital that the insurer have as clear an understanding as possible of the key driv-ers behind each peril. For a peril such as automobile collision, key risk drivers might include the operator’s past accident record, the operator’s driving habits, the type of vehicle, the geographic region, and the demographics of the operator. For tradition-ally insured perils (such as mortality, disability, longevity, and many products in the personal and commercial lines of non-life insurance), considerable data are available to the insurer either from the insurer’s experience or from broader databases of industry experience. The data must be reliable, credible, and internally consistent. An insurer can gain much insight from such data.

Insurers naturally seek additional data on the risks they insure. A useful and com-mon technique is to combine the data gained from experience studies over several time periods. In so doing, however, the insurer needs to consider the possibility that com-bining data from additional time periods masks underlying volatility (random fluctua-tions), trends (such as mortality improvement), or periods of unusual activity (such as a flu epidemic for the peril of mortality, and severe floods in the case of property insur-ance). Therefore, when assessing experience studies, insurers must consider the impli-cations of prior experience for the future experience of the risks already underwritten, as well as for the future experience of the risks resulting from new business.

Another technique insurers use to gather more data is to consider relevant industry data. This is particularly helpful when the insurer does not yet have sufficient statis-tically credible data of its own on the peril being insured. However, in selecting this

Insurance Supervision Core Curriculum

�

technique, the insurer must consider the many possible differences between industry experience and its own experience (such as the perils being insured, the types of sub-jects being insured, and the trends inherent in each set of data).

In some situations (for example, a new product, an emerging market), little claims experience may be available to the insurer. In such situations, the insurer must rely on some combination of experience gained in related markets, the experience of local reinsurers, and industry experience (where available). Clearly, where there is a public interest need for these types of insurance products, the local insurance industry should be encouraged to provide such products. The local supervisory authority can be of as-sistance in supporting or encouraging the development of pools of experience data among insurers and within the local industry. Until credible experience data are ob-tained, insurers should value these risks conservatively, recognizing the uncertainties they have assumed.

Underwriting process

The gathering of accurate, credible, and relevant data is vital for the underwriting of risks by an insurer. There are many components to the underwriting process. Some of the generic processes involved with underwriting risks are as follows (IAAust 2003, 120):

• Underwriting process risk. Risk from exposure to financial losses related to the selection and approval of risks to be insured.

• Pricing risk. Risk that the prices charged by the company for insurance contracts will be ultimately inadequate to support the future obligations arising from those contracts.

• Product design risk. Risk that the company faces risk exposure under its insur-ance contracts that were unanticipated in the design and pricing of the insur-ance contract.

• Claims risk (for each peril). Risk that many more claims occur than expected or that some claims that occur are much larger than expected claims resulting in unexpected losses. This includes both the risk that a claim may occur, as well as the risk that the claim might develop adversely after it occurs.

• Economic environment risk. Risk that social conditions will change in a manner that has an adverse effect on the company.

• Net retention risk. Risk that higher retention of insurance loss exposures results in losses due to catastrophic or concentrated claims experience.

• Policyholder behavior risk. Risk that the insurance company’s policyholders will act in ways that are unanticipated and have an adverse effect on the company.

ICP 18B: Management of Key Risks

�

• Reserving [provisioning] risk. Risk that the provisions held in the insurer’s finan-cial statements for its policyholder obligations (also called claim liabilities, loss reserves, or technical provisions) will prove to be inadequate.

Underwriting risk management framework

This section applies the lessons learned about the general risk management framework in module ICP 18A, Risk Management Fundamentals, to underwriting risk. Sound cor-porate governance practices are presumed to be in place. To illustrate the concepts in this section, life insurance mortality risk is used as an example.

sEt objEctivEs

As with any set of risks, the process of establishing risk-related objectives (that is, risk appetite and risk tolerances) is essential in the development of any business strategy involving underwriting risks.

For life insurance mortality, an insurer might define its risk appetite in terms of

• Population segments in which it is willing to underwrite risks (that is, to focus on countries in which the insurer has experience)

• Maximum amount of life insurance the insurer is willing to underwrite on a single life, on a gross or net (of reinsurance) basis

• Type of underwriting to be used (that is, short form underwriting versus fully underwritten).

The insurer might also define its risk appetite for the life insurance line of business (or other lines of business) in terms of its ability to deliver a target risk-adjusted return on capital. Of course, to be effective, the “return” and “capital” components need to be clearly defined and communicated within the insurer. The return might be based on GAAP after-tax earnings. The capital might be based on risk-based capital appropriate for the risks assumed by the line of business (reflective of all of the risks undertaken by that line of business).

The insurer might further define its risk appetite and tolerance for life insurance mortality risk, using a combination of the following:

• Underwriting approval levels (a set of progressively higher limits for senior un-derwriters, the underwriting committee, the vice president of underwriting, the CEO, etc.)

• Reinsurance limits (the levels at which reinsurance is required for a life insur-ance risk)

Insurance Supervision Core Curriculum

8

• Substandard limits (the levels at which the insurer is comfortable underwriting the risk by itself, with the aid of a reinsurer or not)

• Medical condition limits (conditions, such as heart disease, that require a sub-standard rating or an exclusion)

• Occupation limits (occupations, such as mining, that require a substandard rat-ing or an exclusion)

• Activity limits (activities, such as skydiving, that require a substandard rating or an exclusion).

Various levels within the insurer will be involved in setting the risk appetite and tolerances:

• Board (for overall risk appetite and tolerances)• Underwriting committee, perhaps consisting of the CFO, CRO, actuary, medical

director, senior underwriters, business unit head, etc. (for example, for under-writing policies, high limit approvals, reinsurance limits, and complex under-writing decisions)

• Senior underwriter (for example, for second-level approvals and judgment of risks that require underwriting committee approval)

• Underwriter (for example, for routine and first-level approvals).

idEntify risks

When assuming underwriting risk for a specific peril (such as life insurance mortality) it is vital that the insurer capture sufficient relevant information about the characteris-tics or drivers of that risk, so that a fair price or value can be placed on the risk. The in-surer should maintain accurate, reliable, and verifiable systems to administer and track the emerging experience of its risks for purposes of risk management, pricing, financial reporting, policyholder service, and other efforts.

Of course, the primary purpose of insurance is to pool a large number of similar risks so that a fair price (premium) can be levied for each risk (or policyholder) in ex-change for a promise from the insurer to pay if the insured peril occurs. The insurer’s ability to determine the similarity of risks (which risk category they fit into) is linked to the insurer’s ability to discern the characteristics or drivers of each risk.

For individual life insurance, an insurer will likely keep a record, for each life in-sured, of several risk characteristics:

• Name of insured• Age• Gender• Country of residence

ICP 18B: Management of Key Risks

�

• Occupation• Product type (permanent, term, variable, universal life, etc.)• Smoking status• Type of underwriting (nonmedical, medical, short-form, etc.)• Substandard rating.

If the insurer fails to capture information about key risk characteristics at the time of underwriting, the insurer may inadvertently take on a disproportionate number of policyholders with that risk characteristic. Potential policyholders will naturally select the insurer offering the most favorable price. Taken to an extreme, an insurer may find that its underwriting experience steadily worsens and it may be forced to steadily in-crease its premium rates. This rate spiral will cause the insurer to become unprofitable and uncompetitive relative to its peers who attract policyholders with more favorable risk characteristics.

The public’s perception of what questions are appropriate and socially acceptable (nondiscriminatory) to ask policyholders at the time of underwriting can change. For example, in recent years policymakers in some jurisdictions have judged that certain insurance products should not differentiate their prices on the basis of gender. If the claims experience differs materially by gender for these products, undifferentiated pric-ing undermines the fundamental insurance principle of pooling similar risks.

Like any business, insurers are constantly under pressure to innovate by introduc-ing new features, differentiated pricing, and entirely new product introductions. These pressures arise from competitors, customers, sales representatives, and product design-ers. Unfortunately, the race to innovate frequently precedes the availability of solid data from experience on the risks entailed with these products. Examples of the challenges faced by insurers and supervisors in identifying new risks include the introduction of a “preferred” mortality risk underwriting class and the original versions of the critical illness product in North America.

Insurance supervisors should expect insurers to retain appropriately trained and experienced staff to identify and underwrite the insurer’s insurance risks. Such staff members are arguably the most important risk managers, because the claims experi-ence of the policies they underwrite can affect the insurer’s profitability for years to come.

assEss risks

The management of risk requires a clear understanding or assessment of its impact and behavior. Assessment involves consideration of a risk’s impact through a combination of its

• Probability (likelihood of its occurrence)• Severity (size if it does occur).

Insurance Supervision Core Curriculum

10

The assessment of underwriting risk is needed for many of the essential operations of an insurer: product design, product pricing, risk management, financial reporting, valuation of insurance liabilities, asset/liability management, etc. Skilled staff in each of these areas have useful perspectives on the assessment of underwriting risks.

Actuaries are skilled at assessing risk, especially underwriting risk. Actuaries are often members of a local actuarial association and are represented internationally by the International Actuarial Association (IAA). Actuaries generally must meet educa-tion and examination requirements established by their association and must abide by a code of conduct and binding standards of practice. Some jurisdictions reserve specified roles (such as valuation of insurance obligations) for actuaries.

Underwriting risks quite commonly have a term of many years. Life insurance mor-tality risk can be limited for a specified number of years in term insurance or be covered for a lifetime in permanent insurance. Therefore, when assessing underwriting risk (for life, health, or non-life insurance), it is frequently more important to understand the present value of the longer-term impact of experience changes than to react to short-term changes in experience. Although a sudden clustering of large life insurance claims will negatively affect the insurer’s earnings in the near term, there may be little future impact if the claims simply reflect normal volatility in experience. If instead they signal an adverse trend in experience, then the assumptions used to value all future claims may need strengthening and the adverse impact on earnings may be much greater.

In assessing underwriting risk, policyholder behavior (rate of policy surrender, rate of policy loans, usage of policy options, payment of premiums, etc.) must usu-ally be taken into account. The modeling of policyholder behavior is a complex topic. It requires considerable skill and care in its evaluation to determine the present value impact of long-term contracts.

When assessing underwriting risk it is frequently important to perform integrated assumption modeling (with all types of risks, not just underwriting risks). A change in one assumption can influence other assumptions, producing a different cumulative present value impact than that of one assumption alone. For example, the investment performance of the assets underlying a variable or unit-linked insurance policy can affect policyholder behavior in terms of their premium payments or their rates of with-drawals. In turn, this altered behavior may change the mix of remaining policyholders so that the mortality assumption for other policyholders is affected.

In the assessment of risk one important area of an insurer is the claims department. Typically responsible for claims approval, the claims department may also provide the first notice of large claims, unusual claim causes, claim epidemics, and the like. How-ever, emerging trends may not always be readily detected without examination of long periods (several months or years) of experience. Typically, such experience studies are conducted by actuaries within the insurer to facilitate the re-pricing of insurance prod-ucts and the revaluation of technical provisions.

Frequently, the actuary has sufficient exposure and claims experience for an un-derwriting risk to readily define the claims distribution. From this distribution, the

ICP 18B: Management of Key Risks

11

mean claim amount and the various useful risk measures (Tail Value at Risk, standard deviation, etc.) can be estimated. With this knowledge, actual claims can be compared on a regular basis with these risk measures to determine whether additional risk man-agement action is required.

Risk assessment requires studying the volatility, uncertainty, and catastrophic ele-ments of each risk. Risk assessment also requires a clear understanding of the root cause or drivers of each risk. Insurers should employ skilled risk specialists, such as actuaries, who have the expertise to address these topics on a daily basis.

The sophistication of the risk measures used by insurers to assess their risks varies considerably, from simple standardized formulaic techniques to sophisticated stochas-tic models requiring highly trained specialists. For risks that are well understood in the industry, fairly simple, and not material to the insurer, simple standardized formu-laic requirements are likely appropriate. For complex risks with considerable “tail” risk (unit-linked annuity products with material maturity amount guarantees if the under-lying asset values fall before maturity), it is inappropriate for the insurer to assume these risks without using appropriate advanced expertise and systems to assess and manage them on a regular basis. Therefore, a smaller insurer can use standardized approaches for its simpler risks, but it should be required to use an appropriate (advanced) level of expertise for any complex risks it assumes.

The supervisory authority should work with the insurance industry to determine guidelines for appropriate types of risk measures and assessment. An example is Pru-dential Standard GPS 220: Risk Management from the Australian Prudential Regulation Authority (APRA 2006), on risk management for general insurers.

plan stratEgiEs—an introduction

The need to manage underwriting risk is driven by some combination of the insurer’s risk appetite and risk tolerances, the risk versus reward tradeoff of potential risk re-sponses, the degree to which a response will reduce the risk’s severity or probability, and the impact of the response on the business unit’s return on equity.

As described in module ICP 18A, the general strategies for managing risk fall into five major categories:

• Avoid—eliminate, stop, prohibit, or sell the risk exposure• Retain—accept and self-insure the risk exposure (perhaps by integrating it with

other risks or by diversifying risks)• Reduce—mitigate or cap portions of the risk exposure• Transfer—reinsure, hedge, securitize, or outsource the risk exposure• Exploit—expand and diversify the risk exposure.

Insurance Supervision Core Curriculum

1�

The insurer tries to select the optimal combination of strategies from these cat-egories. Some of the examples in module ICP 18A used underwriting risk to illustrate their operation. Generally, all these strategies, except for risk transfer, depend solely on the actions of the insurer. Risk transfer uses a counterparty to assume some or all of the risk. In most cases, the policyholder relationship is unaffected by risk transfer. However, if the counterparty fails to perform, there are financial repercussions on the insurer and if any element of policyholder service is outsourced, policyholder relations may also be affected.

Whichever strategies are adopted by an insurer in managing its risks, the insurance supervisor should expect the insurer to demonstrate

• A sound level of understanding of the underlying risks as well as the risks en-tailed in the strategies adopted

• An appropriate level of expertise to manage the strategy adopted based on the complexity of the risks and strategies (for example, the use of professional rein-surers is a common strategy for transferring risk for all sizes of insurers, whereas the use of a dynamic hedging strategy requires sophisticated employee or exter-nal consultant expertise and software).

plan stratEgiEs—rEinsurancE

Reinsurance is one of the most important risk management tools available to all types of insurers. Reinsurance companies are specialized insurers that assume risk from direct writing insurers. Reinsurance refers to insurance purchased by an insurer to provide protection against some or all of certain risks (primarily, but not only, underwriting risks) of the insurance policies issued by the insurer. In exchange for assuming these risks, the reinsurer receives payment in the form of reinsurance premiums or allow-ances from the direct writer of the business, the insurer. (See module ICP 19B, Reinsur-ance, for a more complete discussion.)

In a reinsurance arrangement, the insurer cedes risks to the reinsurer. Reinsurers can do the same thing by a retrocession to other reinsurers. Reinsurance is purchased for several reasons:1

• Increase new business capacity. One of the most common reasons for purchas-ing reinsurance is to enable an insurer to issue larger insurance policies than it would prudently issue on its own, because the reinsurance will reduce the im-pact of several large claims occurring in a short period of time.

• Limit catastrophic claims. Catastrophic coverage generally provides for the rein-surer to pay claims in excess of a certain limit, subject to a minimum number of claims and a maximum amount of reinsurance per event. This coverage pro-

1. Refer to Tiller and Tiller (1995) for a discussion of reinsurance.

ICP 18B: Management of Key Risks

1�

vides protection against concentrated claims arising from a single event (such as storms, earthquakes, and plane crashes).

• Limit total claims. Some insurers, especially smaller ones, need stop-loss rein-surance to limit the aggregate cost of claims in a given year.

• Transfer investment risk. Insurers may reinsure a block of business to effect a transfer of investment risk from the insurer. This can occur because of the growth of interest-sensitive life and annuity products, either to take advantage of reinsurer asset management capabilities or to avoid a large concentration of assets arising from a single product or annuity.

• Gain product expertise. On entering a new product, territory, or line of business, an insurer may request the assistance of a reinsurer with experience in that mar-ket. In exchange for its advice, the reinsurer will participate through reinsurance in the future profitability of the business sold.

• Gain underwriting advice. One benefit that reinsurers provide is their experi-ence in underwriting. This can prove valuable during the design, pricing, and underwriting of products, especially new, novel, large, or complex ones.

• Divest a product line. An insurer wishing to exit a certain business, product, or territory may choose to cede that business through an assumption reinsurance agreement or through indemnity reinsurance.

• Manage financial results. Insurers may be able to use the financial reporting im-pact of reinsurance agreements to achieve earnings and surplus objectives and also to minimize taxes.

The most important types of reinsurance are as follows:

• Indemnity/assumption. A reinsurance agreement between an insurer and a re-insurer is called a reinsurance treaty. Most treaties are called indemnity agree-ments. Such agreements are binding only for the companies. The policyholders of the insurer have no contractual relationship with the reinsurer. Assumption reinsurance entails the permanent transfer of insurance liabilities to the reinsur-er. Policyholders are notified that the assumption reinsurer has assumed legal responsibility for the business and that all future premiums and claims are the responsibility of the assumption reinsurer.

• Proportional/nonproportional. Reinsurance may be offered on either a propor-tional or a nonproportional basis. Proportional reinsurance provides for the cession of a portion of the coverage through a formula based on the ceding insurer’s retention limit (for example, all amounts of life insurance in excess of the insurer’s retention limit will be reinsured). Common proportional rein-surance techniques include traditional coinsurance, for life insurance products with a savings element, whereby all risks and policy elements are shared with the reinsurer, including the investment risk; modified coinsurance, similar to traditional coinsurance except that the insurer retains the investment risk; and

Insurance Supervision Core Curriculum

1�

yearly renewable term (YRT) cover, whereby the insurer reinsures a specific risk, such as mortality, in exchange for a YRT premium. Nonproportional reinsur-ance provides protection that depends on the claims amount experienced (for example, stop-loss or catastrophe reinsurance).

• Automatic/facultative. An automatic reinsurance treaty allows an insurer to automatically cede risks in excess of its retention limit to its reinsurer, subject to predetermined conditions. Facultative treaties require that the reinsurer ap-prove each risk before assuming any liability for it. Facultative treaties tend to be used for larger risks that are more complex to underwrite.

• Excess/quota share. Excess treaties provide for risks in excess of the schedule of retention limits to be reinsured. Quota share treaties provide for a fixed percent-age of each risk to be reinsured.

According to the Institute of Actuaries of Australia (IAAust) (with some editing for emphasis),

From the perspective of the insurer, the direct writer of insurance policies, reinsur-ance provides for a transfer of risk to the reinsurer. The extent of the transfer depends on the specifics of the reinsurance agreement or treaty. It is important to note that re-insurance also creates risk for the insurer. The insurer must carefully evaluate these risks:

• Reinsurance exposes the insurer to the risk that the reinsurer defaults on its obligations through insolvency. Depending on local legislation or case law, the insurer may find that many other classes of creditors will rank higher for distri-bution of proceeds from the liquidated reinsurer.

• The terms of the reinsurance agreement may not match exactly those of the un-derlying insurance contracts.

• Heavy reliance on reinsurance may expose the insurer to increased costs in tightening reinsurance markets.

Beyond all of the risks normally associated with being an insurer, a reinsurer fac-es some unique challenges. Reinsurance products are difficult to price (especially in the general insurance market, where there are often complicated layers of reinsurance cover) owing to the limited data available on which to base the pricing. Additional risk arises in general insurance from the low claim frequency and high claim severity of many reinsurance coverages and from the lengthy time delays between the occurrence, reporting and settlement of many covered loss events (CAS 2001). It is especially im-portant for the reinsurer to understand the insurer’s target market, its pricing, and all of the layers involved in its reinsurance program. In addition, the reinsurer is exposed to the risk of default by the ceding insurer. Depending on local legislation or case law, the reinsurer may find that many other classes of creditors will rank higher for distribu-tion of proceeds from the liquidated insurer. Potentially critical to the reinsurer in this

ICP 18B: Management of Key Risks

1�

circumstance is the legal right (allowed in some cases) to offset any funds it owes to the liquidator by the amounts which the ceding insurer owes it.

Reinsurers must monitor the profile of their insurance risks very carefully, for pre-cisely the reasons that they were ceded in the first place. They will often retrocede a high proportion of the risks and, in turn, accept retrocessions from other reinsurers. Some of the most complex and significant risks thus become spread over a very large number of reinsurers in what is almost a reverse form of pooling. This is why major disasters seem to affect all major reinsurers, no matter where they are based. (IAAust 2003, 126-7)

Additional useful references on reinsurance include A Global Framework for In-surer Solvency Assessment (IAA 2004) and Prudential Standard GPS 230 Reinsurance Management (APRA 2006a).

plan stratEgiEs—policy adjustability or pass-through fEaturEs

Another form of risk transfer applicable for some types of insurance products is the ability to share emerging experience with policyholders. This ability is constrained or permitted by the provisions of the insurance contract, competition from other insurers, and policyholders’ expectations.

An example of such a product is a participating (sometimes called “with profits”) insurance policy. In its life insurance form, policyholders pay a higher premium than for a comparable nonparticipating insurance policy, in exchange for receiving an an-nual experience dividend (or bonus). The size of the dividend depends on the contri-butions made by the policyholder through increased premiums and on the experience of the insurer. Dividends are not guaranteed, but an insurer’s past practices and sales illustrations can create policyholder expectations.

An example of useful supervisory guidance in this area is provided by the U.K. Financial Services Authority in its Conduct of Business (COB) 6.10, Principles and Practices on Financial Management. (See ICP 25, Consumer Protection, and the related module for more information on communication with policyholders.)

Although these adjustability or pass-through features permit insurers to transfer or share risk with policyholders, insurers that deviate significantly from policyholder expectations or the practices of competing insurers risk confusing, alienating, or even angering their policyholders. In extreme cases, class action lawsuits brought by policy-holders can cause an insurer both financial loss and loss of reputation.

Many types of insurance products have some degree of product adjustability or pass-through of emerging experience feature, regardless of whether they are called par-ticipating, variable, unit-linked, adjustable nonparticipating, or other names. Regard-less of the type of policy, the best insurer practices entail:

• Clear communication between the insurer (and intermediaries) and the policy-holder regarding the nature of the adjustability or pass-through feature

Insurance Supervision Core Curriculum

1�

• Clear communication between the insurer (and intermediaries) and the policy-holder regarding how the insurer will act in the face of emerging experience

• Development of insurer policies related to the operation of these product fea-tures at the board level

• Well developed internal studies of emerging experience for these products, such as sophisticated contribution analyses (asset share or embedded value analy-ses)

• Formalized or written communications to policyholders regarding their emerg-ing experience.

monitor risks

The monitoring of underwriting risks depends on the timely availability of accurate data on the insurer’s exposure to each risk, as well as frequency and severity data for related claims. Skilled risk professionals seek to establish a statistically credible pool of experience. Where that is not possible, they seek industry experience from similar risks to supplement the insurer’s experience.

The risk professionals seek to understand the determinants of each risk, their ex-pected values, their (statistical) volatility, their inherent trends (for example, rate of improvement in mortality), uncertainty risks, etc. They compare the insurer’s emerging experience against that assumed at the time of product pricing, the experience expected from a prior period, or the experience of other insurers for similar risks.

For individual life insurance, larger insurers often conduct regular annual experi-ence studies of mortality, withdrawals, and expenses. Actual experience can then be compared with expected experience. It is important that these experience studies in-clude sufficient detail by product, size of policy, age, gender, and duration, so that ap-propriate risk management decisions can be made.

Monitoring claims experience helps the insurer make necessary modifications to its pricing, underwriting, provisioning, or claims management practices to better man-age its risks and to be alert to emerging trends as early as possible.

control activitiEs

The underwriting risk management framework would not be useable, reliable, or effec-tive without an appropriate set of control activities. Some examples of needed control mechanisms follow.

• Organization structure. Effective underwriting risk management requires the presence of an enabling corporate structure, typically requiring overall board responsibility for ERM, and including a CRO reporting to the CEO or CFO. It

ICP 18B: Management of Key Risks

1�

also requires the formation of executive and business unit underwriting com-mittees to develop, maintain, and monitor underwriting risk policies, limits, and approvals. Vital to controlling underwriting risk exposures is a skilled team of risk professionals, typically involving actuaries at a senior level within the insurer.

• Objectives. The insurer’s board should establish overall risk appetite and risk tolerance objectives for the insurer and all its business units. The detailed list of risk measures to be used by the insurer to track its progress should also require board approval. The insurer’s appetite for underwriting risk can be measured in several ways—for example, through premium volume, policy liabilities, or a form of value at risk.

• Approvals. The insurer should be expected to establish appropriate approval levels throughout the steps of the underwriting risk management framework. Those entrusted with approval authority must have appropriate experience and training to fully appreciate the possible consequences of their decisions (fi-nancial and organizational impacts on their own areas as well as on the entire company). Key underwriting approvals relate to experience rating decisions (declinations as well as claims approvals or denials). Other decisions relate to product repricing and changes to adjustable product features (for example, divi-dend scale changes).

• Limits. The insurer should be expected to establish appropriate limits on the risk decisions made by its managers, to control its exposure to risks. The ability of all key processes to operate within agreed limits and authorities must be monitored and exceptions examined for their causes and significance.

• Training and communication. The insurer should have regular programs for providing relevant staff training and ensuring that all underwriting risk man-agement staff members have an appropriate level of awareness of the risk man-agement policies and practices relevant to their business. The insurer should ensure that the level of training (especially for those involved with highly com-plex risks) is commensurate with industry and supervisory standards for such responsibilities.

• Change controls. Risk management depends on the consistent assessment of risks over time. Any change in source data, experience, models, assumptions, or the like should be subject to appropriate change control procedures so that their impact does not cloud a true assessment. Such changes can occur from a natural desire to better meet the insurer’s performance (for example, return on equity) targets.

• Models. It is common for insurers to use models to assess and manage material or complex risks. To avoid these models being viewed as a “black box,” insurers should be able to document and describe the key model assumptions, methods, and output. The models should be used regularly in the insurer’s operations. The models should also be subject to validation and review by knowledgeable

Insurance Supervision Core Curriculum

18

internal and external professionals. The models should conform to all relevant industry and supervisory norms and standards.

• Audit and review. All key processes of the insurer must be subject to periodic independent review by appropriate experts. An insurer’s internal audit func-tion plays a key role in this regard and should report directly to the board on these matters on a routine basis. In addition, several of the insurer’s key internal processes may involve significant judgment, outsourcing, or expert systems, ne-cessitating specialized independent (and perhaps external) reviews of specific aspects of the insurer’s operations.

Exercises

1. Whichofthefollowingareimportantconsiderationsinthereviewofdatausedtoassesstheexperiencefromunderwritingrisks?

a. Accuracyofthedata

b.Credibilityoftheinsurer’sdata

c. Relevanceofindustrydata

d.Underlyingvolatility,uncertainty,andextremeeventsinamultiyearstudy

e.Relevanceofexperienceforthefuture.

2. Whichofthefollowingunderwritingriskprocessesanddescriptionsareproperlymatched?

Process Description

a.Underwritingprocess Selectionandapprovalofriskstobe insured

b.Pricing Pricesproveinadequate

c. Productdesign Implicationsofdesignnotunderstood

d.Claims Provisionsforclaimsproveinadequate

e.Policyholderbehavior Actionsadverselyaffectsinsurer

f. Provisioning Frequencyandseverityaregreater

3. Whichofthefollowingaretruestatementsforunderwritingrisk?

a. Whenassessingunderwritingriskitisfrequentlyimportanttoperformintegratedassumptionmodeling.Achangeinoneassumptioncanreactwithotherassumptions,producingadifferentcumulativepresentvalueimpactthanthatofthesingleassumptionalone.

b.Themodelingofpolicyholderbehaviorisacomplextopic,requiringconsiderableskillandcareinitsevaluationtodeterminethepresentvalueimpactoflongtermcontracts.

ICP 18B: Management of Key Risks

1�

c. Productscontainingadjustabilityorpass-throughofemergingexperiencefeaturesrequirelittleinthewayofcommunicationbetweentherepresentativesoftheinsurerandthepolicyholder.

d. Fromtheperspectiveoftheinsurer,thedirectwriterofinsurancepolicies,reinsurancefrequentlyprovidesacompletetransferofrisktothereinsurer.

e. Failuretocaptureakeyriskcharacteristicatthetimeofunderwritingwillresultintheinsurerassumingadisproportionatenumberofriskswiththatcharacteristic,aspotentialpolicyholdersnaturallyselecttheinsurerofferingthemostfavorableprice.

4. Whichofthefollowingareamongthecommonreasonsforusingreinsuranceasastrategyformitigatingunderwritingrisk?

a. Limitclaims

b.Acquirenewblocksofbusiness

c. Increasenewbusinesscapacity

d.Gainproductexpertise

e.Gaininvestmentexpertise

f. Gainunderwritingexpertise

g. Financialresultmanagement.

Insurance Supervision Core Curriculum

�0

C. Credit risk

Defining credit risk

Credit risk is the inability or unwillingness of a counterparty to fully meet its on- or off-balance sheet contractual financial obligations. The counterparty could be an issuer, a debtor, a borrower, a broker, a policyholder, a reinsurer, or a guarantor.

The IAIS defines credit risk as “the risk that a counterparty to the insurer is unable or unwilling to meet their obligations causing a financial loss to the insurer. Sources of credit risk include investment counterparties, policyholders (through outstanding premiums), reinsurers, and derivative counterparties.”

Note that intermediaries can also be a potential source of credit risk to the extent that they do not properly forward policyholder premiums to the insurer. This risk can be particularly important for non-life insurers, where insufficient attention to outstand-ing premium levels can threaten the solvency position of the insurer.

A useful reference for this section is the IAIS Guidance Paper on Investment Risk Management (2004b).

Credit risk has traditionally been associated with assets. However, it can exist for any set of projected future cash flows. Credit risk is therefore also important in assess-ing the true relief provided by a counterparty to an insurance transaction, such as a reinsurer or a party to whom the insurer has outsourced some work functions.

Credit risk can be reflected in the present value of a set of cash flows, either implic-itly through a credit risk spread incorporated in the discount rate or explicitly through modeling of the cash flows themselves.

The market value of a stream of projected future cash flows (say, a bond) reflects the current market view of (among many things) the credit risk of the provider of the cash flows. Such a view might reflect a variety of information available to the market about the bond issuer, such as credit ratings provided by various agencies. Necessarily, such a view will likely reflect the current financial position of the issuer as well as the current economic environment. Such a view will consider the possibility of the issuer slipping in its ratings (and its ability to pay) as well as the probability of default and the amount of loss given that default occurs.

The Basel Committee for Banking Supervision sets international standards regard-ing the capital requirements for banks. Its April 2003 document, The New Basel Capital Accord, contains extensive materials related to the determination of credit risk capital requirements, including both standardized and advanced approaches. The IAA has rec-ommended that similar approaches be used for insurers.

ICP 18B: Management of Key Risks

�1

Credit risk management framework

This section applies the lessons learned about the general risk management framework to credit risk. Sound corporate governance practices are presumed to be in place.

sEt objEctivEs

As with any set of risks, establishing risk-related objectives (risk appetite and risk toler-ances) is essential in the development of any business strategy involving credit risks.

An insurer might define its credit risk appetite in terms of

• Asset classes in which it is willing to invest (government and corporate bonds, mortgages, equities, etc.)

• Type of credit activity, collateral security, or real estate and type of borrower• Range of exposures in each asset class (for example, government bonds 10–20%,

marketable corporate bonds 20–40%, mortgages 10–30%, equities 5–10%)• Maximum exposure to a given credit, issuer, industry sector, or counterparty

(chosen to limit the possible impact of a default on the surplus of the insurer)• Transactions or exposures involving connected or related entities.

The insurer might also define its risk appetite for credit risk in terms of a broader ability to deliver a target total return in excess of risk-free rates of return (for assets in-vested generally) or to deliver a total return in excess of various benchmark indices (for investments supporting variable or unit-linked policies).

The insurer might further define its risk appetite and tolerance for credit risk in a number of ways using a combination of the following:

• Credit approval levels (a set of progressively higher limits for investment manag-ers, senior investment officers, the vice president of investments, and the CEO)

• Portfolio limit approvals (required to increase the size of an asset class, exposure to a given credit, etc.)

• Target credit quality (expected average credit quality for debt instruments—per-haps single A quality)

• Minimum credit quality limits (for example, debt securities of all types must be no lower than triple BBB quality).

Various levels within the insurer will be involved in setting the credit risk appetite and tolerances:

• Board (for example, for overall risk appetite and tolerances)• Chief Investment Officer (CIO)

Insurance Supervision Core Curriculum

��

• Investment committee, perhaps consisting of insurer’s senior investment staff, CFO, CRO, actuary, business unit representatives, etc. (for example, to monitor credit risk experience across business units and to develop related policies and practices across business units)

• Senior investment staff (for example, first-line decisions regarding credit risk).

idEntify risks

Credit risk is assumed whenever the insurer selects investments to support its poli-cyholder obligations and its surplus or when it selects a counterparty for some of its activities. When assuming credit risk, it is vital that the insurer capture sufficient rel-evant information about the characteristics or drivers of that risk to manage the risk properly.

The principal sources of credit risk are:

• Direct default risk. Risk that a firm will not receive the cash flows or assets to which it is entitled because a party with which the firm has a bilateral contract defaults on one or more obligations.

• Downgrade or migration risk. Risk that changes in the possibility of a future de-fault by an obligor will adversely affect the present value of the contract with the obligor today.

• Indirect credit or spread risk. Risk due to market perception of increased risk (i.e., perhaps due to business cycle or perceived creditworthiness in relation to other market participants).

• Settlement risk. Risk arising from the lag between the value and settlement dates of securities transactions.

• Sovereign risk. Risk of exposure to losses due to the decreasing value of foreign assets or increasing value of obligations denominated in foreign currencies.

• Concentration risk. Risk of increased exposure to losses due to concentration of investments in a geographical area or other economic sector.

• Counterparty risk. Risk of changes in values of reinsurance, contingent assets and liabilities (i.e., such as swaps that are not otherwise reflected in the balance sheet). (IAA 2004, 29)

The insurer should maintain accurate, reliable, and verifiable systems to administer and track the performance of its assets and counterparties to manage its credit risks for purposes of asset valuation, measurement of investment returns, financial reporting, and the like. The exact nature of the data to be maintained will vary by specific asset class but for debt instruments might include

• Details of the loan amount, repayment terms, and effective interest rate

ICP 18B: Management of Key Risks

��

• Specifics of the collateral security behind each loan. In the case of real estate or mortgages this entails specific detail about the nature of the underlying prop-erty, its location, type of business, etc.

• Certain financial information from the borrower to ascertain the borrower’s ability to make all payments when due

• Credit rating of the borrower, either as determined by a rating agency or as de-termined by the insurer through a similar process

• Repayment history.

assEss risks

As described earlier, the management of credit risk requires a clear understanding and assessment of its impact and behavior. Assessment involves considering the impact of credit risk through a combination of its

• Probability (likelihood of its occurrence)• Severity (its size in the event that it does occur).

The assessment of credit risk is needed for many of the essential operations of an insurer—investment, product design, product pricing, risk management, financial re-porting, valuation of insurance liabilities, and asset-liability management. Skilled staff from each of these areas of the insurer have useful perspectives on the assessment of credit risks.

According to the IAA,

In general, life and health insurers purchase assets to support their liabilities. His-torically this has not been true for non-life insurers where there has been a tendency for insurers to manage separately the results from underwriting and investments. While all of the assets of an insurer are available to provide against adversity, it is common risk management practice for insurers to implicitly or explicitly allocate their assets for one of the following purposes:

• Support insurance contract liabilities• Represent economic capital• Represent free surplus.

The allocation of assets to support specific policy liabilities is especially im-portant for those insurance products whose performance depends directly on the performance of the underlying assets. In situations where the asset performance is shared directly or indirectly with the policyholder, then the impact of credit losses

Insurance Supervision Core Curriculum

��

can also likely be shared in a similar manner. Such credit must take into account policyholders’ reasonable expectations in this regard as well as the insurer’s prac-tices in sharing such experience with policyholders. Sizeable portions of an insurer’s liabilities can have durations comparable to readily available high-quality liquid assets in the local market. In these situations it is possible to select assets whose cash flows can provide a very close match to the liability cash flows. In other words, a replicating portfolio of assets is available in the market. In this situation, credit risk focuses on the actual assets held and the ability of the insurer to manage its credit loss position within the replicating port-folio horizon. This type of credit risk will be called Type A risk. The long-term duration of some insurance (especially life insurance) liabilities requires the consideration of long-term reinvestment of existing assets since a rep-licating portfolio of assets of sufficient duration may not be currently offered in the market. For this type of business appropriate account must be taken not only of credit risk in current assets (Type A credit risk) but also the credit risk involved with future reinvested assets as well. This latter aspect of credit risk will be called Type B risk. Assessing Type B credit risk entails considerable uncertainty about the composition of the replicating portfolio and the manner of its reinvestment to ma-ture the underlying cash flows. The length of the reinvestment period may extend through several economic periods. (IAA 2004, 146)

Allowance for Type A credit risk can be made through specific asset (loan loss) provisions, through conservative valuation of the assets (for example, at market value, reflecting higher credit spreads), and through credit risk provisioning in the policy li-abilities (that is, through conservative choice of the discount rate used in their valua-tion). Allowance for Type B credit risk can be made only through the policy liability discount rate.

Some considerations in the assessment of credit risk:

• Credit quality. Credit quality of an investment or an enterprise refers to the probability that the issuer will meet all contractual obligations. This assessment normally occurs at both the initial investment and at each renewal point. [For debt instruments] one of the common measurements used in assessing credit quality is the rating assigned to the issuer. A variety of ratings agencies provide these assessments to the public, giving the investor a perceived level of confi-dence in the issuer’s ability to make good on the repayment schedules to which it is committed.

• Maturity. The longer the term to maturity of an investment, the longer even a high-quality issuer has to potentially deteriorate.

• Concentration by industry. Conditions that trigger credit events have a tendency to impact on the entire economy simultaneously. Within this general charac-

ICP 18B: Management of Key Risks

��

teristic, however, the impact of economic development often varies between sectors of the economy. Within a sector, however, there tends to be uniformity between the entities participating in that sector. Degrees of separation within a sector will exist, but these are on a smaller scale than those that normally occur between sectors.

• Concentration by geography. Credit risk has been shown to carry a large de-gree of contagion. Periods of relatively few credit events are followed by periods where default experience is extremely high. Similarly, economically depressed regions tend to produce high levels of default experience in comparison with more prosperous areas. That these regions can and do change over time creates a challenge to the process of credit risk analysis

• Size of expected loss. The size of loss due to a credit event can vary widely, from loss of some or all of the return on an investment to loss of some, or all, of the inherent principal. Losses can also occur from a delay in the timing of a sched-uled payment, causing either a loss of return during the deferral period, a reduc-tion in available reinvestment rate during the deferral period, or both. When a scheduled payment is delayed for any reason, there is also the potential for an associated loss if the payment were needed to match a scheduled outflow. The investor would then be required to make good on its obligation by borrowing or selling other assets. They might need to delay payment of their own scheduled obligation, possibly incurring a penalty. (IAA 2004, 146; original source: Cana-dian Institute of Actuaries. 2003. “Report of the CIA Sub-Committee on Credit Risk”. October. Available only in the members section of the CIA website.)

An additional consideration in the assessment of credit risk is cyclicality. This re-fers to the tendency for credit losses to increase or diminish with each economic cycle. Provisioning for credit risk should take into account the insurer’s expected future posi-tion in the economic cycle. Frequently, higher credit losses are associated with a weak-ened economic situation; both the frequency and severity of default losses increase with a worsening economy.

Key to the assessment of credit risk is the rating of all exposures for their quality (the probability that the issuer of the exposure will meet its contractual obligations). For publicly traded exposures (such as corporate bonds), the ratings are assigned by various commercial rating agencies. For other credit exposures (such as mortgages), the insurer must develop a comparable internal rating process.

Once the ratings have been determined, commercially available credit risk soft-ware can assist the insurer in making provision for future credit risk events.

Insurance Supervision Core Curriculum

��

plan stratEgiEs

Important in the insurer’s management of credit risk are a combination of sound un-derwriting practices and appropriate lending limits.

A broad definition of hedging strategies used to offset credit risk includes

• Letters of credit• Contingency deposits • Securitization of mortgages (mortgage-backed securities)• Securitization of other assets (asset-backed securities)• Credit derivatives • Credit default swaps• Total return swaps• Collateralized debt obligations• Credit-linked notes• Credit spread options• Basket derivatives.

The investment performance features of some insurance products also permit some or all credit losses for assets deemed to be used to support the policyholder obligations of specific blocks of insurance products. (IAA 2004, 147)

However, if a full pass-through of credit losses is not required by the terms of the product, policyholders’ reasonable expectations will be relevant.

The insurer should have appropriate contingency plans to deal with worsening credit situations in a timely and disciplined manner. The assessment and management of distressed assets as well as the use of several of the credit-related strategies described above may require additional or specialized skills for effective management.

monitor risks

Important tools to monitor credit risk include

• Detailed reporting of new credit risk exposures assumed or purchased• Summary of all credit exposures assumed by rating• Exception reports identifying issuers whose rating has changed• Watch list reports for those exposures exhibiting early signs of distress• Delinquency reports for exposures in default.

Insurance supervisors should expect insurers to have sound procedures for select-ing, rating, and monitoring all credit risk exposures. These rating systems should be subject to periodic audit and expert external review. This includes insurer research (or

ICP 18B: Management of Key Risks

��

access to appropriate outside expert advice) into relevant credit risk trends for the expo-sures assumed. Insurance supervisors should also expect close control and preventive actions for all emerging credit risk events.

control activitiEs

In general, the control activities needed for credit risk are generally similar to those needed for other key insurer risks (as described earlier for underwriting risk). The fol-lowing are specific differences.

• Organization structure. Effective credit risk management requires the presence of an enabling corporate structure. This typically entails overall board respon-sibility for ERM, a CRO reporting to the CEO or CFO and the formation of a senior-level credit risk committee (typically chaired by the CIO; the CEO and CFO are often members) involving the lead credit risk specialists for each ma-jor asset class. The committee develops, maintains, and monitors the insurer’s credit risk policies, authorities, limits, and experience. Leading life insurers also maintain committees at the executive and business unit levels for asset-liability management (ALM). These committees develop, maintain, and monitor ALM risk policies, limits, and approvals. These asset-liability committees (ALCOs) bring together the top asset and liability managers to coordinate their actions. Credit risk is one of the risks discussed in an ALCO.