Embed Size (px)

DESCRIPTION

“CONSUMER BUYING BEHAVIOUR TOWARDS FINANCIAL PRODUCTS OF IDBI FEDERAL”

Citation preview

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 1/68

“CONSUMER BUYING BEHAVIOUR TOWARDS

FINANCIAL PRODUCTS OF IDBI FEDERAL”

(Summer Traii! Pr"#e$% Re&"r% 'umi%%e) i &ar%ia* +u*+i*me% "+ %,e

re-uireme%' +"r %,e P"'% Gra)ua%e Di&*"ma i Maa!eme%.

A%

/ai&uria I'%i%u%e "+ Maa!eme%0 Lu$1"2

B3

Sa!ar Sari

/L45PGDM657

Su&er8i'"r9

I)u'%r39 M': S,a%,i Ya!3aa%,

C"**e!e9 Pr"+: /a%i Sri8a'%a8a

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 2/68

CERTIFICATE OF FACULTY MENTOR

This is to certify that the Summer Project Study Report, Titled “C"'umer Bu3i!

Be,a8i"ur %"2ar)' Fia$ia* Pr")u$%' "+ IDBI Fe)era*” submitted by Mr: Sa!ar Sari as partial fulfilment of requirement of the two year PGDM (!"#$!"%& is a bonafide wor'carried out by the student at our nstitute)

This Summer Project Study is his ori*inal wor' and has not been submitted to any other+niersity-nstitute)

Pr"+: ;;;;;;;;;; Pr"+: ;;;;;;;;;;:

Pr"#e$% Su&er8i'"r Pr"!ram Dire$%"r< PGDM

Da%e9

P*a$e9

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 3/68

STUDENT DECLERATION

Sa*ar Sarin student of PGDM batch (!"#$"!"%& declare that the project entitled

“C"'umer Bu3i! Be,a8i"ur %"2ar)' +ia$ia* &r")u$%' "+ IDBI Fe)era*” is my own

wor' conducted under the superision of Pr"+: /a%i Sri8a'%a8a as a partial fulfilment of

Summer nternship Pro*ram for the course of PGDM submitted to D. /ederal 0ife

nsurance 1o 0TD and 2aipuria nstitute of Mana*ement, 0uc'now)

further declare that to the best of my 'nowled*e the project does not contain any part of any

wor' which has been submitted for any other project either in this institute or in any other

without proper citation)

P*a$e9 Lu$1"2

Da%e9 Si!a%ure "+ %,e Ca)i)a%e

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 4/68

AC=NOWLEDGEMENT

e3press heartfelt *ratitude to my institution /ai&uria I'%i%u%e "+ Maa!eme% and the

company hae wor'ed in IDBI Fe)era* Li+e I'ura$e C": LTD: for allowin* a aluable

chance to do a research on “C"'umer Bu3i! Be,a8i"ur %"2ar)' Fia$ia* Pr")u$%' "+

IDBI Fe)era*”

also *ie my sincere *ratitude to my faculty mentor Pr"+: /a%i Sri8a'%a8a who *uided me

throu*hout the project, motiated, supported and helped in the successful completion of this

project)

4et importantly, would li'e to e3press my heartfelt than's to my industry *uide M':

S,a%,i Ya!3aa%,0 Bra$, Hea)0 IDBI Fe)era* Li+e I'ura$e C": L%): for *uidin* me

in successfully completin* this project)

would also li'e to than' my +rie)' a) m3 &are%' who helped me a lot durin* this

project and supported me)

am *rateful to you all for supportin*, encoura*in* and helpin* me throu*hout this project)5ithout you all, this project would hae not been a success) Than' you all)

Sa!ar Sari

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 5/68

E>ECUTIVE SUMMARY

My internship in D. /ederal 0ife nsurance 1o 0td started on 6th 7pril, !"8) 7s per the

pro*ram we had trainin* for RD7 and the different products offered by the company to pitch

for our prospectie clients)

The wor' assi*ned to me was to achiee a sales tar*et of 9 policies each of minimum

Rs)"%!!! annually in terms of premium collected) mana*ed to conert my pitches into sales

and sell 9 policies for the company)

7lon* with sellin* also wor'ed on the project :1onsumer .uyin* .ehaiour towards

financial products of D. /ederal); The project is focused on analy<in* the factors which

aim at determinin* the customers buyin* behaiour towards financial products of D.

/ederal) .uyin* behaiour is a ast and important mar'etin* subject) t is mainly focused in

tryin* to understand the arious 'ey factors which influence a prospectie consumer of life

insurance the most when considerin* the purchase of an insurance product) +nderstandin*

these factors is a critical tas') 7 questionnaire was prepared and sureyed "!! respondents

to understand their buyin* behaiour and pattern)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 6/68

Contents

CHAPTER 1: INTRODUCTION..................................................................................1

1.1) Problem Statement.....................................................................................2

1.2) Rationale of the Problem.............................................................................

1.) !etho"olo#$................................................................................................%

1.%) S&o'e of the St("$......................................................................................

1.) *imitation+ of the St("$..............................................................................,

CHAPTER 2: DETAI*S O- THE ORANI/ATION........................................................0

2.1) Hi+tor$ of In+(ran&e....................................................................................

2.2) In"(+tr$ a&3#ro(n".................................................................................14

2.2.1) A rief Hi+tor$ of In+(ran&e Se&tor in In"ia.........................................11

2.2.2) In"ian In+(ran&e !ar3et......................................................................12

2.2.) In"(+tr$ D$nami&+..............................................................................1

2.2.%) T$'e+ of In+(ran&e+.............................................................................1%

2.) IDI -e"eral *ife In+(ran&e Co. *t"............................................................1

2..1) Pro"(&t+ in rief..................................................................................1

2..2) Or#ani5ational Str(&t(re.....................................................................24

2..) HR Pra&ti&e+........................................................................................22

2.%) S6ot Anal$+i+............................................................................................ 2%

CHAPTER : RE*E7ANT *ITERATURE RE7IE8.......................................................2

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 7/68

Con+(mer ($in# eha9io(r............................................................................2,

Re9ie6 of Rele9ant *iterat(re...........................................................................20

CHAPTER %: DATA CO**ECTION AND ANA*SIS....................................................2;

%.1) Sam'lin# Plan............................................................................................4

%.2) Data Colle&tion !etho".............................................................................4

%.) Pre+entation of Data an" Anal$+i+.............................................................2

CHAPTER : DATA ANA*SIS AND INTERPRETATION.............................................%2

.1 -in"in#+ an" Inter'retation of -in"in#+.......................................................%

.2) Con&l(+ion.................................................................................................%

CHAPTER ,: RECO!!ENDATIONS........................................................................%0

,.1) De+&ri'tion of Re&ommen"ation+<S(##e+tion+.........................................%

CHAPTER 0:..........................................................................................................4

CONC*UDIN RE!AR=S.......................................................................................4

0.1) ain+ from the Pro>e&t...............................................................................1

0.2) *imitation+ of the Pro>e&t...........................................................................2

0.) S&o'e for -(rther 8or3..............................................................................

Referen&e+<iblio#ra'h$......................................................................................%

APPENDICES.........................................................................................................

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 8/68

Li'% "+ Ta*e'

Table =o) Title Pa*e =o)

" >ccupation of respondents 9

Major sources of awareness in re*ard to insurance policies 999 /eatures inestors consider before ta'in* an insurance policy 9#

# Percenta*e of respondents hain* insurance policy 98

8 Reasons behind not inestin* in insurance policies 9%

% Most preferred ban's of inestors 96

6 Reasons behind ta'in* an insurance policy 9?

Li'% "+ Fi!ure'

1hart =o) Title Pa*e =o)

Pie " >ccupation of Respondents 9

.ar " Major sources of awareness in re*ard to insurance policies 99

.ar /eatures inestors consider before ta'in* an insurance policy 9#

Pie Percenta*e of respondents hain* insurance policy 98

.ar 9 Reasons behind not inestin* in insurance policies 9%

Graph " Most preferred ban's of inestors 96

.ar# Reasons behind ta'in* an insurance policy 9?

Dou*hnut

"

7wareness leel about D. /ederal 9@

Graph 1ustomers of D. /ederal #!

Pie 9 nestors who would li'e to inest in D. /ederal in future #"

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 9/68

P a # e ? 1

CHAPTER 1:

INTRODUCTION

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 10/68

P a # e ? 2

1.1) Problem Statement

D. /ederal life insurance is still a *rowin* company in the insurance sector and has many

tou*h competitors so it is ery important for the company to 'now the perception of the

potential customers and there buyin* behaiour) Therefore the mana*erial decision problem

or the problem at hand is to understand the consumer buyin* behaiour of consumers towards

the financial products of D. /ederal 0ife nsurance and reactions towards the same) The

main objecties of this project areA

To analy<e the inestors perception about D. /ederal)

To study the consumers buyin* behaior towards financial products of D.

/ederal)

To study the reactions of the consumers with reference to D. /ederal)

To su**est ways for creatin* awareness about the products of D. /ederal)

To find the arious competitors of D. /ederal)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 11/68

P a # e ? 3

1.2) Rationale o t!e Problem

n todayBs corporate and competitie world, the insurance sector has a potential of hu*e

*rowth as compared to other sectors) nsurance has ma3imum *rowth rate of 6!$?!C

accordin* to the report by Mar'et Research /irm R=1>S, analy<in* the ndian nsurance

Mar'et) 0ar*e insurance sector is a sector which is lar*ely drien by propensity of people to

sae)

4et nearly ?!C of ndian population is without life insurance coer and this part of the

population is also subject to wea' social security and pension systems with hardly any old

a*e income security) Thus it is an indicator that *rowth potential for the insurance sector is

immense)

n the introduction sta*e of the product life cycle a firm see's to create awareness and

deelop a mar'et for the product and D. /ederal 0ife nsurance 1o 0td is in its

introduction sta*e of its P01)

Thus this report will help me in understandin* what are the consumerBs perception and

buyin* behaiour towards D. /ederal and will help me to recommend those crucial factors

which influence a prospectie life insurance inestor the most when they *o ahead in

purchasin* a life insurance product, so that they can create ma3imum awareness and attract

ma3imum customers and thus deelop a mar'et for their customers)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 12/68

P a # e ? "

1.3) #et!o$olo%&

• Re'ear$, De'i!9 7 research desi*n is a framewor' that has been created to see'

answers to research questions) t is based on a framewor' and proides a direction to

the inesti*ation bein* conducted in the most efficient manner)Since this study see's to identify the buyin* behaiour of consumers and their

perception towards the products offered by D. /ederal, thus this research will be

conducted based on descriptie research)

• Re'ear$, I'%rume%9 uestionnaire for surey will be used to collect information

related to the project) The questionnaire will include both open and close ended

questions to 'now what the different perceptions of customers are)

• S"ur$e' "+ Da%a C"**e$%i"9 Data collection is an important aspect of any type of

research study) t is a term used to describe a process of preparin* and collectin* data

from all sources and obserations) Data has been collected from both primary and

secondary resources)

a& Primar3 Da%a9 >btainin* first hand by spea'in* to customers and *ettin*

the questionnaire form filled by them about the insurance products of D.

/ederal and obserin* their iews, reactions and beliefs about the oerall

insurance products)

. Se$")ar3 Da%a9 Secondary data will be collected throu*h company

websites, journals and ma*a<ines to find about the history of the or*ani<ations

their position in the mar'et and their competitors)

•

Da%a Aa*3'i' Te$,i-ue97nalysis will be carried out throu*h with help of

software li'e MS$E3cel, SPSS, etc) 0i'ert scale multiple choice questions will be

used in the questionnaire)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 13/68

P a # e ? '

1.") S(oe o t!e St*$&

The scope of a subject refers to eerythin* that is studied as part of that subject) 5hen we set

out to e3plain the scope of consumer behaiour we need to refer to all that which forms part

of consumer behaiour)

1onsumer behaiour includes not only the actual buyer and his act of buyin* but also the

arious roles played by different indiiduals and the influence they e3ert on the final

purchase decision)

To define the scope of a subject it is important to set parameters or a framewor' within which

it shall be studied) This framewor' is made up of three main sections$the decision process as

represented by the inner$most circle, the indiidual determinants on the middle 1ircle and the

e3ternal enironment which is represented by the outer circle) The study of all these three

sections constitutes the scope of consumer behaiour)

n this project will discoer what are the featured that people consider before buyin* an

insurance policy and what is their buyin* behaiour towards the products of D. /ederal)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 14/68

P a # e ? +

1.') ,imitations o t!e St*$&

Due to constraints of time and resources, the study is li'ely to suffer from certain limitations)

Some of these are mentioned here under so that the findin*s of the study may be understood

in a proper perspectie)

The limitations of the study areA

• Some of the respondents of the surey were unwillin* to share information) People

refrain from *iin* personal details)

• The research was carried out in a short period of ? wee's) Therefore the sample

si<e and other parameters were selected accordin*ly so as to finish the wor' within

the *ien time frame)

• The information *ien by the respondents mi*ht be biased because some of them

mi*ht not be interested to *ie correct information)

• The research was confined to 0uc'now city only)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 15/68

P a # e ? -

CHAPTER 2: DETAI,S

O THE

OR/ANI0ATION

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 16/68

P a # e ?

2.1) Histor& o Ins*ran(e

n some sense we can say that insurance appeared simultaneously with appearance of human

society) n earlier economies, we can see insurance in the form of people helpin* each other)

/or e3ample, if a house is burnt, the members of the community help build a new one) Should

the same thin* happen to oneBs nei*hbour, the other nei*hbours must come to helpF

>therwise, nei*hbours will not receie help in the future) nsurance in the modern sense,

started as a methods of transferrin* or distributin* ris', were practiced by 1hinese and

.abylonian traders as lon* a*o as the 9rd and nd millennia .1, respectiely) 1hinese

merchants traellin* treacherous rier rapids would redistribute their car*o across many

essels to limit the loss due to any sin*le esselBs capsi<in*) The .abylonians deeloped a

system which was recorded in the famous 1ode of ammurabi, c)"68! .1, and practiced by

early Mediterranean sailin* merchants) f a merchant receied a loan to fund his shipment, he

would pay the lender an additional sum in e3chan*e for the lenderBs *uarantee to cancel the

loan should the shipment be stolen)

Gree' monarchs were the first to insure their people and made it official by re*isterin* the

insurin* process in *oernmental notary offices) They inented the concept of the *eneral

aera*e) Merchants whose *oods were bein* shipped to*ether would pay a proportionally

diided premium which would be used to reimburse any merchant whose *oods

were jettisoned durin* storm or sin'in* of the essel in the sea) The Gree's and Romans

introduced the ori*ins of health and life insurance in %!! 7D when they or*ani<ed *uilds

called Hbeneolent societies which cared for the families and paid funeral e3penses of

members upon death) Guilds in the middle 7*es sered a similar purpose) .efore insurance

was established in the late "6th century, friendly societies e3isted in En*land, in which people

donated amounts of money to a *eneral sum that could be used for emer*encies) Separate

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 17/68

P a # e ?

insurance contracts (i)e), insurance policies not bundled with loans or other 'inds

of contracts& were inented in Gree's rulers in the "#th century, as were insurance pools

bac'ed by pled*es of landed estates) These new insurance contracts allowed insurance to be

separated from inestment, a separation of roles that first proed useful in marine insurance)

nsurance became far more sophisticated in post$Renaissance Europe, and speciali<ed

arieties deeloped) nsurance as we 'now it today can be traced to the Great /ire of

0ondon, which in "%%% 7)D deoured "9,!! houses) n the aftermath of this disaster,

=icholas .arbon opened an office to insure buildin*s) n "%?!, he established En*landIs first

fire insurance company, The /ire >ffice to insure bric' and frame homes) The first insurance

company in the +nited States underwrote fire insurance and was formed in 1harles Town

(modern$day 1harleston&, South 1arolina, in "69)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 18/68

P a # e ? 1

2.2) In$*str& 4a(5%ro*n$

The insurance industry of ndia consists of 8" insurance companies of which # are in life

insurance business and 6 are non$life insurers) 7mon* the life insurers, 0ife nsurance

1orporation (01& is the sole public sector company) 7part from that, amon* the non$life

nsurers, there are si3 public sector insurers) n addition to these, there is sole national

reinsurer, namely, General nsurance 1orporation of ndia) >ther sta'eholders in ndian

nsurance mar'et include 7*ents (ndiidual and 1orporate&, .ro'ers, Sureyors and Third

Party 7dministrators sericin* ealth nsurance claims) >ut of 6 non$life insurance

companies, # priate sector insurers are re*istered to underwrite policies e3clusiely in

ealth, Personal 7ccident and Trael insurance se*ments) They are Star ealth and 7llied

nsurance 1ompany 0td, 7pollo Munich ealth nsurance 1ompany 0td, Ma3 .upa ealth

nsurance 1ompany 0td and Reli*are ealth nsurance 1ompany 0td) There are two more

speciali<ed insurers belon*in* to public sector, namely, E3port 1redit Guarantee 1orporation

of ndia for 1redit nsurance and 7*riculture nsurance 1ompany 0td for 1rop nsurance)

nsurance penetration of ndia i)e) Premium collected by ndian insurers is #)"!C of GDP in

/4 !""$") Per capita premium underwritten i)e) insurance density in ndia durin* /4 !""$

" is +SJ 8@)!)

The insurance sector in ndia has come to a full circle from bein* an open competitie mar'et

to nationali<ation and bac' to a liberali<ed mar'et a*ain) Tracin* the deelopments in the

ndian insurance sector reiles the 9%!$de*re turn witnessed oer a period of almost two

centuries)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 19/68

P a # e ? 11

2.2.1) A 4rie Histor& o Ins*ran(e Se(tor in In$ia

0ife nsurance in its modern form came to ndia from En*land in the year "?"?) >riental 0ife

nsurance 1ompany started by Europeans in 1alcutta was the first life insurance company on

ndian Soil) 7ll the insurance companies established durin* that period were brou*ht up with

the purpose of loo'in* after the needs of European community and ndian naties were not

bein* insured by these companies) oweer, later with the efforts of eminent people li'e

.abu Muttylal Seal, the forei*n life insurance companies started insurin* ndian lies) .ut

ndian lies were bein* treated as sub$standard lies and heay e3tra premiums were bein*

char*ed on them) .ombay Mutual 0ife 7ssurance Society heralded the birth of first ndian

life insurance company in the year "?6!, and coered ndian lies at normal rates)

nsurance is an Rs #8! billion industry in ndia) The life insurance se*ment writes about ?!C

of the oerall mar'et alue) ndian nsurance mar'et was at its all time hi*h in !!9 with a

*rowth of about "6)#C oer the preious year) Since !!" nsurance is *rowin* at the rate of

"8$! C annually) The *rowth in the insurance industry is affected by olatility in real estate

rates, GDP rates and lon* term interest rates) /luctuations in e3chan*e rates also affect the

*rowth in this sector) The *ross premium as a percenta*e of the GDP has *one up from )9 in

the year !!! to #)? in !!%) The premium as percenta*e of the countryBs *ross domestic

product (GDP& has increased from #)? percent in !!% to 8) percent in !"") To*ether with

ban'in* serices, it adds about 6C to the countryBs GDP)

Some of the important milestones in the life insurance business in ndia areA

• "?"?A >riental 0ife nsurance 1ompany, the first life insurance company on ndian

soil started functionin*)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 20/68

P a # e ? 12

• "?6!A .ombay Mutual 0ife 7ssurance Society, the first ndian life insurance company

started its business

• "@"A The ndian 0ife 7ssurance 1ompanies 7ct enacted as the first statute to re*ulate

the life insurance business)• "@?A The ndian nsurance 1ompanies 7ct enacted to enable the *oernment to

collect statistical information about both life and non$life insurance businesses)

• "@9?A Earlier le*islation consolidated and amended to by the nsurance 7ct with the

objectie of protectin* the interests of the insurin* public)

• "@8%A #8 ndian and forei*n insurers and proident societies are ta'en oer by the

central *oernment and nationali<ed) 01 formed by an 7ct of Parliament, i<) 01

7ct, "@8%, with a capital contribution of Rs) 8 crores from the Goernment of ndia)

I)ia I'ura$e i 74'% Ce%ur39

!!!A RD7 starts *iin* licenses to priate insurersA 11 prudential and D/1 Standard

0ife insurance first priate insurers to sell a policy

!!A .an's allowed sellin* insurance plans) 7s TP7s enter the scene, insurers start settin*

non$life claims in the cashless mode

!!6A /irst >nline nsurance portal, www)insurancemall)in set up by an ndian nsurance

.ro'er, .onsai nsurance .ro'in* Pt) 0td)

2.2.2) In$ian Ins*ran(e #ar5et

The insurance sector which stood at a stron* +SJ 6 billion in !" has the potential to *row

to +SJ ?! billion by !!) This *rowth is drien by ndiaBs faourable re*ulatory

enironment which *uarantees stability and fair play) This enironment has *ien rise to an

insurance mar'et which encoura*es forei*n inestors to tap into the sectorBs massie

potential) Eer since the ndian *oernment liberalised the insurance sector in !!! and

opened the doors for priate participation, the sector has *one from stren*th to stren*th) The

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 21/68

P a # e ? 13

resultant competition has proided the consumer with a neer$before$seen ran*e of products

and proiders, and also enhanced serice leels mar'edly) The health of the insurance sector

reflects a countryBs economy) This sector not only *enerates lon*$term funds for

infrastructure deelopment, but also increases a countryBs ris'$ta'in* capacity) ndiaBs

economic *rowth since the turn of the century is iewed as a si*nificant deelopment in the

*lobal economy) This iew is helped in no small part by a boomin* insurance industry

2.2.3) In$*str& D&nami(s

/actors that influence consistent *rowth in insurance sector areA

• Effectie distribution channels K The efficiency and cost of the arious distribution

strate*ies used by companies are si*nificant to their success in the insurance business)

This particularly holds true for the retail business)

• /ocus on oerall financial inclusion K 7s time eoles, so must the approach of the

insurance sector in ndia) The objectie of the insurance sector should ideally be to

offer a broader ran*e of actiities to a wider populace)• 1onsumer needs and preferences K The *rowth of ndiaBs insurance industry can be

attributed to product innoation, dynamic distribution channels, and ibrant publicity

and promotional campai*ns run by insurance companies) .enefits attached to the

products and the manner in which they are deliered (throu*h arious mar'etin* tie$

ups& hae helped brin* customers and insurance companies closer to each other and

made the latter more releant)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 22/68

P a # e ? 1"

2.2.") T&es o Ins*ran(es

nsurance business is diided into four classesA

"& 0ife nsurance& /ire9& Marine#& Miscellaneous nsurance)

0ife insurers underta'e the 0ife nsurance businessL *eneral insurers handle the rest) The

.usiness of insurance essentially means defrayin* ris's attached to an actiity (includin* life&

and sharin* the ris's between arious entities, both persons and or*ani<ations) nsurance

companies are important players in financial mar'ets as they collect and inest lar*e amounts

of premium in arious inestment instruments)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 23/68

P a # e ? 1'

2.3) ID4I e$eral ,ie Ins*ran(e Co. ,t$.

D. /ederal 0ife nsurance 1o 0td is a joint$enture of D. .an', ndiaBs premier

deelopment and commercial ban', /ederal .an', one of ndiaBs leadin* priate sector ban's

and 7*eas, a multinational insurance *iant based out of Europe) n this enture, D. .an'

owns #?C equity while /ederal .an' and 7*eas own %C equity each) 7t D. /ederal, we

endeaour to delier products that proide alue and conenience to the customer) Throu*h a

continuous process of innoation in product and serice deliery we intend to delier world$

class wealth mana*ement, protection and retirement solutions to ndian customers) ain*

started in March !!?, in just fie months of inception we became one of the fastest *rowin*

new insurance companies to *arner Rs "!! 1r in premiums) The company offers its serices

throu*h a ast nationwide networ' across the branches of D. .an' and /ederal .an' in

addition to a si<eable networ' of adisors and partners) 7s on 2anuary 9"st !"", the

company has issued oer )%? la'h policies with oer Rs "#, 9! 1r in Sum 7ssured )

A"u% %,e '&"'"r' "+ IDBI Fe)era* Li+e I'ura$e C" L%)

IDBI Ba1 L%): continues to be, since its inception, ndiaBs premier industrial deelopment

ban') 1reated in "@8% to support ndiaBs industrial bac'bone, D. .an' has since eoled

into a powerhouse of industrial and retail finance) Today, it is amon*st ndiaBs foremost

commercial ban's, with a wide ran*e of innoatie products and serices, serin* retail and

corporate customers in all corners of the country from 6?9 branches and "9? 7TMs) The

.an' offers its customers an e3tensie ran*e of diersified serices includin* project

financin*, term lendin*, wor'in* capital facilities, lease finance, enture capital, loan

syndication, corporate adisory serices and le*al and technical adisory serices to its

corporate clients as well as mort*a*es and personal loans to its retail clients) 7s part of its

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 24/68

P a # e ? 1+

deelopment actiities, D. .an' has been instrumental in sponsorin* the deelopment of

'ey institutions inoled in ndiaBs financial sector K=ational Stoc' E3chan*e of ndia

0imited (=SE& and =ational Securities Depository 0td, S10 (Stoc' oldin* 1orporation

of ndia 0td&, 17RE (1redit 7nalysis and Research 0td&

Fe)era* Ba1 is one of ndiaBs leadin* priate sector ban's, with a dominant presence in the

state of erala) t has a stron* networ' of oer 69@ branches and 6@6 7TMs spread across

ndia) The ban' proides oer four million retail customers with a wide ariety of financial

products) /ederal .an' is one of the first lar*e ndian ban's to hae an entirely automated

and interconnected branch networ') n addition to interconnected branches and 7TMs, the

.an' has a wide ran*e of serices li'e nternet .an'in*, Mobile .an'in*, Tele .an'in*, 7ny

5here .an'in*, debit cards, online bill payment and call centre facilities to offer round the

cloc' ban'in* conenience to its customers) The .an' has been a pioneer in proidin*

innoatie technolo*ical solutions to its customers and the .an' has won seeral awards and

recommendations)

A!ea' is an international insurance company with a herita*e spannin* more than "?! years)

Ran'ed amon* the top ! insurance companies in Europe, 7*eas has chosen to concentrate

its business actiities in Europe and 7sia, which to*ether ma'e up the lar*est share of the

*lobal insurance mar'et) They are *rouped around four se*mentsA .el*ium, +nited in*dom,

1ontinental Europe and 7sia) t is an undisputed leader in the .el*ian mar'et for indiidual

life and employee benefits, as well as a leadin* non$life player, throu*h 7G nsurance)

nternationally 7*eas has a stron* presence in the +, where it is the second lar*est player in

priate car insurance) The company also has subsidiaries in /rance, Germany and on*

on*) 7*eas has a trac' record in deelopin* partnerships with stron* financial institutions

and 'ey distributors in different mar'ets around the world and successfully operates

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 25/68

P a # e ? 1-

partnerships in 0u3embour*, taly, Portu*al,1hina, Malaysia, ndia and Thailand) 7*eas

employs more than "9,!!! people and has annual inflows of almost E+R "?billion)

Vi'i"0 Mi''i" a) Va*ue' "+ %,e IDBI Fe)era*

Vi'i"9

To be the leadin* proider of wealth mana*ement, protection and retirement solutions that

meets the needs of our customers and adds alue to their lies)

Mi''i"9

• To continually strie to enhance customer e3perience throu*h innoatie product

offerin*s, dedicated relationship mana*ement and superior serice deliery while

striin* to interact with our customers in the most conenient and cost effectie

manner)

• To be transparent in the way we deal with our customers and to act with inte*rity)

• To inest in and build quality human capital in order to achiee their mission)

Va*ue'9

• TransparencyA 1rystal 1lear communication to our partners and sta'eholders

• Nalue to 1ustomersA 7 product and serice offerin* in which customers perceie

alue

• Roc' Solid and Deliery on PromiseA This translates into bein* financially stron*,

operationally robust and hain* clarity in claims

• 1ustomer$friendlyA 7dice and support in wor'in* with customers and partners

• Profit to Sta'eholdersA .alance the interests of customers, partners, employees,

shareholders and the community at lar*e

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 26/68

P a # e ? 1

2.3.1) Pro$*(ts in 4rie

4. IDBI Fe)era* Li+e'ura$e Sa8i!' I'ura$e P*a9 is a fi3ed term non$lin'ed plan

that proides twin benefits of lon*$term sain*s and life coer) 5ith customers small

sain*s will help them to reali<e their bi* dreams that they hae for their family) The

benefits of life coer will proide financial security to their family in their absence)

7. IDBI Fe)era* C,i*)'ura$e Sa8i! Pr"%e$%i" I'ura$e P*a is a non$lin'ed

endowment plan that ensures a child future) 1hildsurance plan is desi*ned to *ie

their customers *uaranteed annual payouts) n the unfortunate eent of the parents not

around the policy would continue e3actly as they hae planned it without any further

premium bein* paid) n other words the plan ensures that their child *ets to lie

his-her dream e3actly they hae planned)

?. IDBI Fe)era* I$"me'ura$e Guara%ee) M"e3 Ba$1 I'ura$e P*a is non$

lin'ed non$participatin* money bac' plan which *ies *uaranteed return on an

inestment so that the customers stop worryin* about their future) This plan also

*uarantees a secure future for their families een when they are not around)

5. Wea*%,'ura$e Gr"2%, I'ura$e P*a is a unit$lin'ed plan that *ies customer the

freedom to build his wealth e3actly the way he wants) The D. /ederal

5ealthsurance Growth nsurance Plan is a re*ular premium unit$lin'ed insurance

plan) 7 plan that *ies you freedom to decide how much you want to inest and for

how lon* you want to stay inested) 5ith a bouquet of @ fund offerin*s, it *ies you

the freedom to inest in one or more funds, basis your ris' appetite and financial *oals

in life) Plus it comes with a life coer benefit that ensures financial security for your

loed ones) n a nutshell, a smart inestment plan that helps you desi*n your

inestments, your wayO

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 27/68

P a # e ? 1

@. Wea*%,'ura$e Su8i),a Gr"2%, I'ura$e P*a is a simple unit$lin'ed plan that

helps to build wealth with ease and een protects your loed ones with a life coer in

your absence) t is a plan that helps you ta'e your first step towards wealth creation

and that too, with ease) 5hatBs more, the life coer with this plan proides financial

protection to your loed ones)

. Wea*%,'ura$e Fu%ure S%ar I'ura$e P*a is a unit$lin'ed insurance plan that

enables the customer to fulfill his childBs dream) This plan with its e3clusie Iwaier

of premiumB benefit ensures that the plan continues een in the case of an eentuality

and proides the maturity benefit as you had initially planned)

. Wea*%,'ura$e Gr"2%, I'ura$e P*a SP9 The D. /ederal 5ealthsurance SP is

a sin*le premium unit$lin'ed insurance plan) 7 one$time inestment plan, whereby

payin* the premium once, you allow your inestment to enjoy returns of the selected

funds) The plan also offers you life coer proidin* your loed ones with financial

protection in case of any eentuality) n a nutshell, it is a smart inestment plan that

helps you ma3imi<e the potential of your windfall, rather than let it sit idle)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 28/68

P a # e ? 2

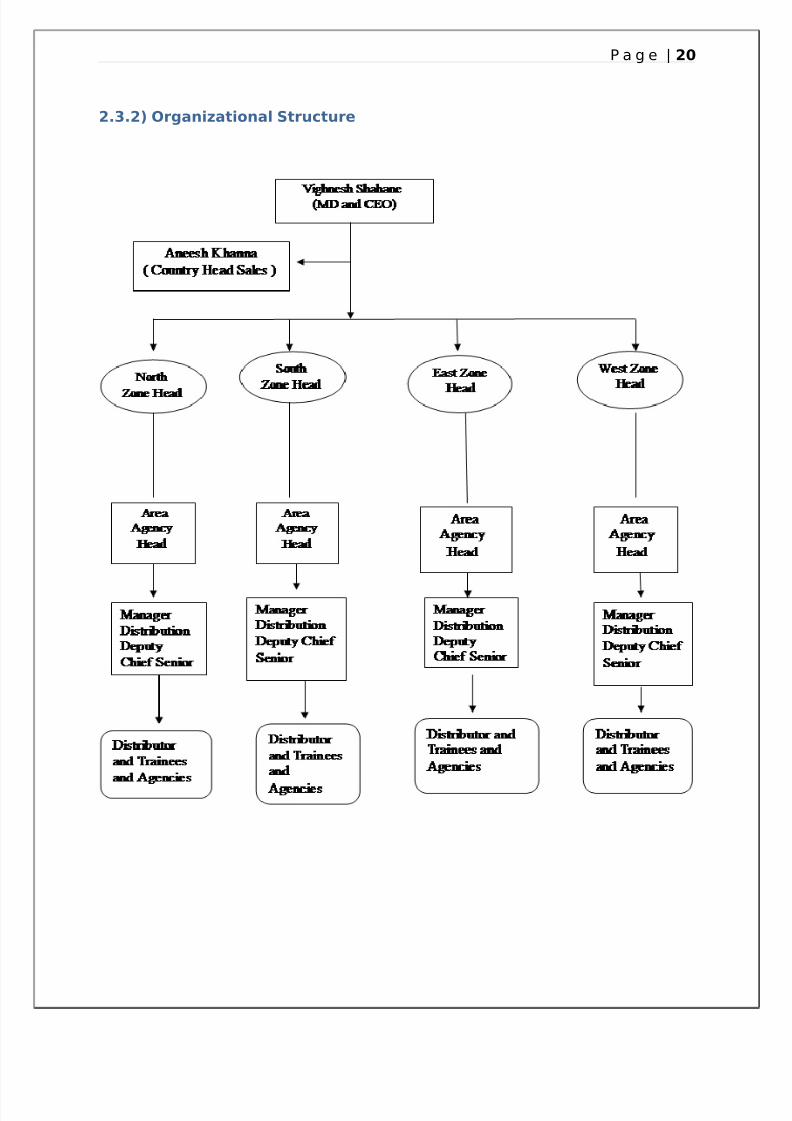

2.3.2) Or%ani6ational Str*(t*re

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 29/68

P a # e ? 21

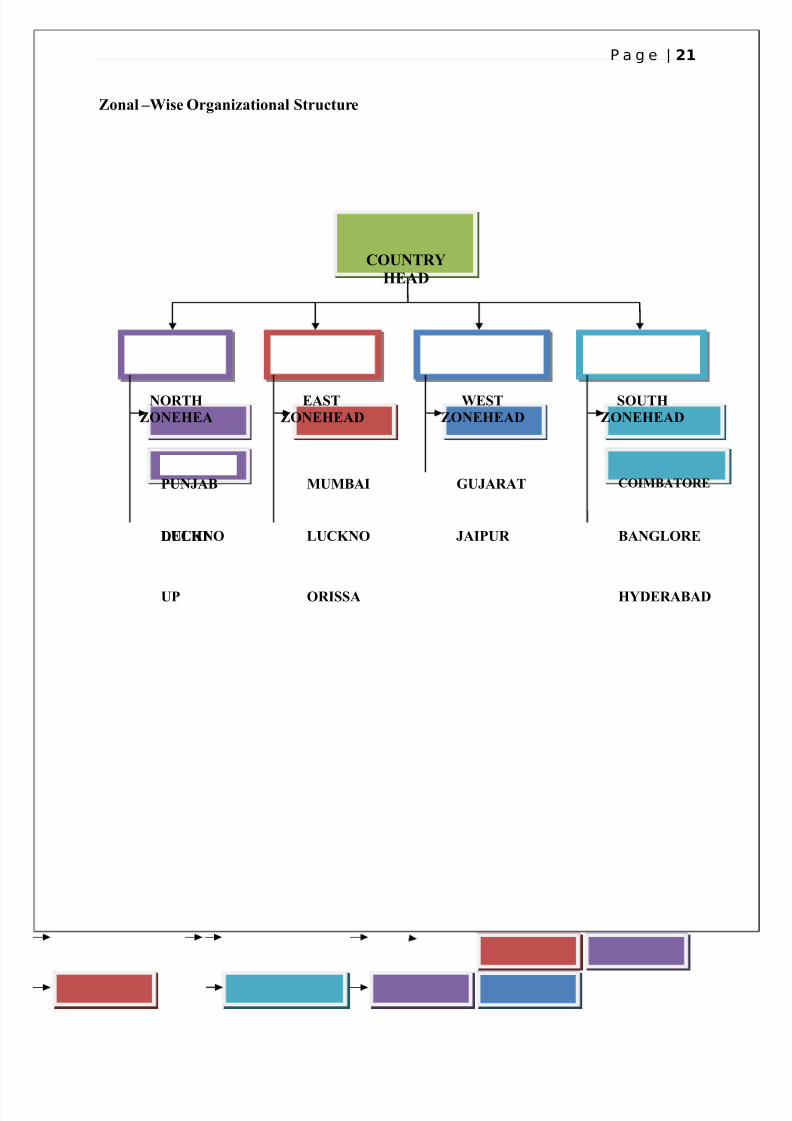

"a* Wi'e Or!aia%i"a* S%ru$%ure

COUNTRY

HEAD

WEST

ONEHEAD

SOUTH

ONEHEAD

EAST

ONEHEAD

NORTH

ONEHEA

COIMBATOREGU/ARATMUMBAIPUN/AB

BANGLOREDELHILUC=NO LUC=NO /AIPUR

HYDERABADUP ORISSA

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 30/68

P a # e ? 22

2.3.3) HR Pra(ti(es

7round !! Employees and about 68!! a*ents are wor'in* for the or*ani<ation) D.

federal .an' proides many facilities to the employees as well as a*ents) 0et us see the

uman resource department structure, recruitment process, Trainin* process and other

priile*es of the >r*ani<ation) 7t D. /ederal, the mana*erial style is Participatie in

nature)

Recruitment Process

The Recruitment process of D. federal is completely throu*h the resume screenin* and

interiew methods) .ased on the Real time e3perience the candidates are recruited to the

or*ani<ation) The selected candidates are proposed to 7chiee tar*et policies) The Tar*et of

the each employee is 8 products sale) So, each candidate should sell 8 products to ma'e him

as the employee of the or*ani<ation) This is the selection method where the or*ani<ation is

recruitin* the lower leel mana*ers which are based on the tas' performin*)

Training

Trainin* is must for eery indiidual when he enters into the or*ani<ation) Een thou*h the

candidate has e3perience he also should *et trainin*) 5hy because the or*ani<ation culture,

alues and beliefs are different from one or*ani<ation to other) ThatBs why the trainin*

pro*ram plays a 'ey role in eery or*ani<ation) Trainin* pro*ram followin* by D. /ederal

is different at arious leels) Mainly in trainin* pro*ram the company concentrates on sales

mana*ers, a*ents, operations e3ecuties and tele$callers)

Performance Appraisal

The Performance appraisal of D. federal is based upon types)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 31/68

P a # e ? 23

") Employees 7ppraisal)

) 7*ents 7ppraisal)

Em&*"3ee' A&&rai'a*9 The Employee appraisal is based upon the tar*et system) There are

three leels in the performance appraisal)

• L"2er *e8e*9 /or the Post of Mana*er leel, the employee must achiee the product

sales worth of 6)la'hs at the 7nnual period of the year)

• Hi!,er *e8e*9 /or the Post of Senior Mana*er 0eel, the employee must achiee the

product sales worth of )la'hs at the 7nnual period of the year)

A!e%' A&&rai'a*9 The 7*ents are paid with commission percenta*e for eery sale which is

dependin* upon the products)

AWARDS

The awards and the other *rieances are proided only based upon the indiidual

performance) The 1ompany Proides free forei*n trip for the employees all the year and best

performer 7wards of the year)

OTHER RELAVANT INFORATION

The 1ompany proides non$interest loan for the employees in the D. .an' and /ederal

.an') t also proides health insurance to the family members of the employee) Pro*rams li'e

uic' Starter 'in*-ueen, ero March, Super 7pril, .est performer and .est Project

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 32/68

P a # e ? 2"

au*mented the morale of the interns) Monetary compensation in the form of commission and

non monetary compensation (Stature oriented& li'e .est performer and .est project really

*ae us the drie to wor' in for the company)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 33/68

P a # e ? 2'

2.") S7ot Anal&sis

S%re!%,'9<

• 5ide ran*e of products to suit the need of each type of customer • Sufficient cash base and stable forei*n shareholders)

• 1an learn from the mista'es of the first "6 life insurance companies of ndia)

• +ses a unique method of e3pansion, in which its ne3t branch in a re*ion is opened

only when, the earlier one reaches its brea'$een point)

Wea1e''e'9<

• 0ate entrant in the mar'et)

• 0ac' of 'nowled*e about the company and the products of the company) =eed brand

awareness and promotional actiities)

O&&"r%ui%ie'9<

• 7bilities to tap the *rowin* internet space for mar'etin* and sellin* the products)

• Prospectie easin* up of the /D in insurance industry to #@C from the current %C)

T,rea%'9<

• Presence of hi*hly competitie mar'et) Presence of established players such as 01,

S. life, 11 prudential etc)

• ncreasin* e3penses and lowerin* mar*ins due to cut throat competition are hittin*

hart companies with low mar'et share)• The insurance companies are bein* oer re*ulated by RD7) t is hamperin* the

companies)

• Goernment re*ulations on issues li'e health care and terrorism can quic'ly chan*e

the direction of insurance)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 34/68

P a # e ? 2+

CHAPTER 3:

RE,E8ANT

,ITERATURE RE8IE9

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 35/68

P a # e ? 2-

Cons*mer 4*&in% 4e!aio*r

1onsumer .uyin* .ehaiour may be defined as :the interplay of forces that ta'es place

durin* a consumption process, within a consumersB self and his enironment)

$ This interaction ta'es place between three elements i<) 'nowled*e, affect and behaiourL

$ t continues throu*h pre$purchase actiity to the post purchase e3perienceL

$ it includes the sta*es of ealuatin*, acquirin*, usin* and disposin* of *oods and serices;)

The :consumer; includes both personal consumers and business-industrial-or*ani<ational

consumers) 1onsumer behaiour e3plains the reasons and lo*ic that underlie purchasin*

decisions and consumption patternsL it e3plains the processes throu*h which buyers ma'e

decisions)

The study includes within its puriew, the interplay between co*nition, affect and behaiour

that *oes on within a consumer durin* the consumption processA selectin*, usin* and

disposin* of *oods and serices)

• C"!i%i"A This includes within its ambit the :'nowled*e, information processin*

and thin'in*; partL t includes the mental processes inoled in processin* of

information, thin'in* and interpretation of stimuli (people, objects, thin*s, places and

eents&) n our case, stimuli would be product or serice offerin*)• A++e$%A This is the :feelin*s; part) t includes the faourable or unfaourable feelin*s

and correspondin* emotions towards stimuli (e)*) towards a product or serice

offerin* or a brand&) These ary in direction, intensity and persistence)

• Be,a8i"urA This is the :isible; part) n our case, this could be the purchase actiityA

to buy or not a buy (a*ain specific to a product or serice offerin*, a brand or een

related to any of the # Ps&)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 36/68

P a # e ? 2

Reie7 o Releant ,iterat*re

• Ra8i&a L: Mar1 S: (7665. state that customer perceied that life insurance is a

lon*$term inestment) 5ith the lon*$term policy of life insurance, customers want to

confirm that they understand how to receie their money bac' when the maturity date

of insurance policy in the future, or that their family 'nows how to *et it when they

hae any unfortunately happen) /undamentally, customers need personal commitment

from salespeople whom they trust to ma'e sure their money will not be lost cause of

the poor inestment by the insurance company) .esides that, customers want to hae

someone who will help them ta'e care their interest and can be contacted easily when

they need claim for themseles)

• M"**er (7665. found that income and social security which are the own wa*es, ability

to proide for family, insurance a*ainst illness and death, and income in old a*e hae

been re*arded as one of the major pointers of quality of life, this point of iew

stresses the importance of insurance to human life)

• Ta#u)ee0 A3a%u#i a) Da**a, (766. belieed that people with education hae

more positie attitude toward insurance than people who less education ones) .esides

that, they also find out the respondents who hae hi*hest positie attitude towards

insurance is the people in a*e *roup between 8% and %8 years than other a*e *roups

this is due to the people in this a*e *roup are at the end of the actie life and they are

more aware of their retirement life) They also found that hi*h household income

*roups hae hi*hest positie attitude toward insurance than the low household

incomes *roups, in fact, the wealthy household comparatiely feel protected

commonly in =i*erian economic enironment) /rom the other point of iew, the low

household income *roups are less authori<ed and usually they feel that the insurance

is further than their reach)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 37/68

P a # e ? 2

• =ureu%,er (4. :t is not the ma*nitude of a potential loss that inspires people to

buy insurance oluntarily K it is the frequency with which a loss is li'ely to occur;)

• R"!er: A: F"rmi'a" (44. e3amined, ia consumer interiews, the impact of the

=ational 7ssociation of nsurance 1ommissioners Model 0ife nsurance Solicitation

Re*ulation as implemented in =ew 2ersey) 7 substantial portion of the insurance

buyers sampled did not become aware of the proisions of the re*ulation aimed to

improe their buyin* ability) /urther, many life insurance buyers were not well

informed concernin* the nature and operation of life insurance contracts, and in

particular, the life insurance policies that they had purchased)

• Dr: Pra8ee Sa,u0 Gaura8 /ai'2a* Vi#a3 =umar Pa)e3 (766. stated that the

consumerBs perception towards 0ife nsurance Policies is positie) t deeloped a

positie mind sets for their inestment pattern, in insurance policies) Still some

actions are needed for deelopin* insurance mar'et) The major factors playin* the

role in deelopin* consumerBs perception towards 0ife nsurance Policies are

1onsumer 0oyalty, Serice uality, Ease of Procedures, Satisfaction 0eel, 1ompany

ma*e, and 1ompany$1lient Relationship)

•

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 38/68

P a # e ? 3

CHAPTER ": DATA

CO,,ECTION AND

ANA,;SIS

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 39/68

P a # e ? 31

".1) Samlin% Plan

• Sam&*e Frame9 Due to the nature of the study, people residin* or wor'in* in

0uc'now hae been ta'en into consideration)

Sam&*e Ui%9 People belon*in* to any a*e *roup with or without an insurance policy

hae been ta'en into consideration)

Sam&*e Sie9 eepin* in mind all the constraints the si<e of the sample of the study

was selected as "!!)

• Sam&*i! Me%,")9 Simple Random Samplin* method has been used wherein people

were ta'en into consideration on a completely random basis and questions were as'ed

from them) Research was conducted on clear assumptions that the respondents would

*ie fran' and fair answers in a pra*matic way and without any bias)

Time Frame9 %! days time frame was ta'en to conduct the research)

".2) Data Colle(tion #et!o$

Data for the research has been collected by obtainin* first hand information by spea'in* to

customers and *ettin* the surey form filled by them about the insurance products of D.

/ederal and obserin* their iews, reactions and beliefs about the oerall insurance products)

This will help us in recordin* their reaction towards the products of financial products by

D. /ederal and will help in 'nowin* the major stren*th areas and also in findin* out the

wea'nesses where the company can wor' towards for increasin* customer satisfaction and

increase the business of the company)

.oth primary and secondary methods hae been used for data collectionA$

Primar3 Da%a9 < Primary data includes questionnaire hain* open and close ended

questions for the purpose of understandin* the perception and buyin* behaior of

inestors towards insurance policies proided by D. /ederal 0ife nsurance 1o)

0td)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 40/68

P a # e ? 32

• Se$")ar3 Da%a9 < Secondary data will be collected throu*h company websites,

journals and ma*a<ines to find about the history of the or*ani<ations and their

position in the mar'et and their competitors)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 41/68

P a # e ? 33

".3) Presentation o Data an$ Anal&sis

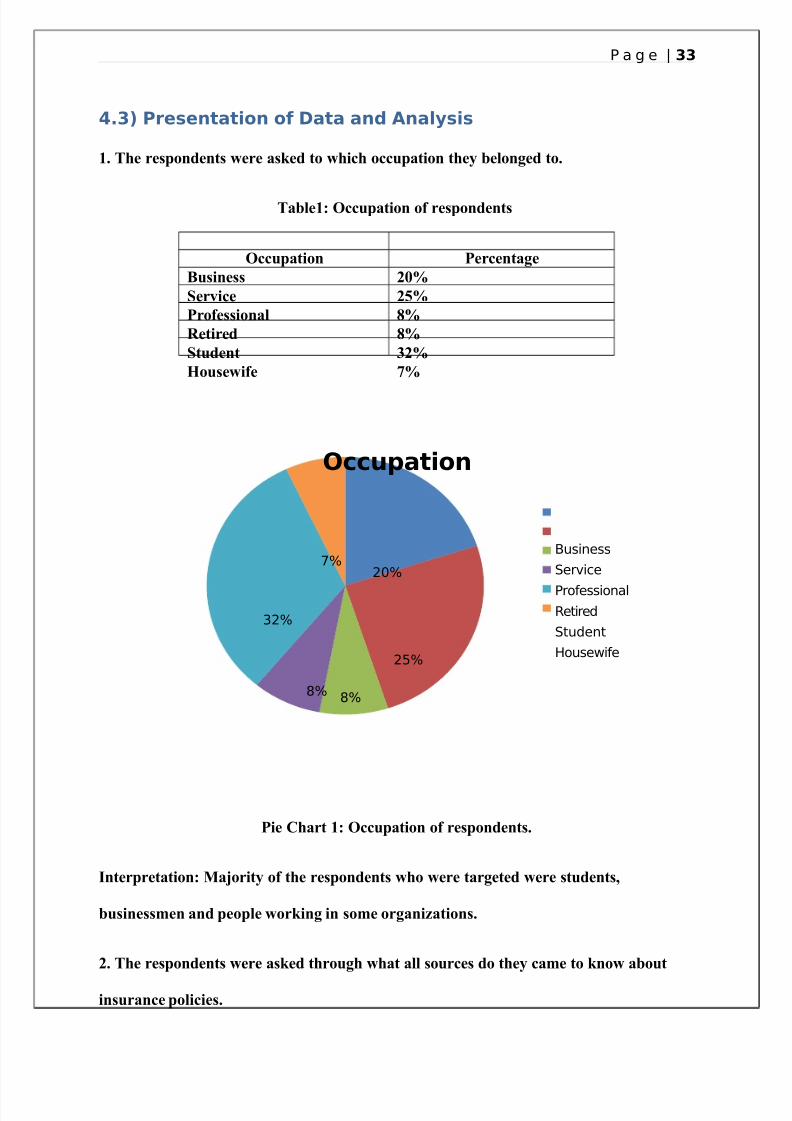

4: T,e re'&")e%' 2ere a'1e) %" 2,i$, "$$u&a%i" %,e3 e*"!e) %":

Ta*e49 O$$u&a%i" "+ re'&")e%'

O$$u&a%i" Per$e%a!e

Bu'ie'' 76

Ser8i$e 7@

Pr"+e''i"a*

Re%ire)

S%u)e% ?7

H"u'e2i+e

24@

2@

@@

2@

0@

O((*ation

(+ine++

Ser9i&e

Profe++ionalRetire"

St("ent

Ho(+e6ife

Pie C,ar% 49 O$$u&a%i" "+ re'&")e%':

I%er&re%a%i"9 Ma#"ri%3 "+ %,e re'&")e%' 2," 2ere %ar!e%e) 2ere '%u)e%'0

u'ie''me a) &e"&*e 2"r1i! i '"me "r!aia%i"':

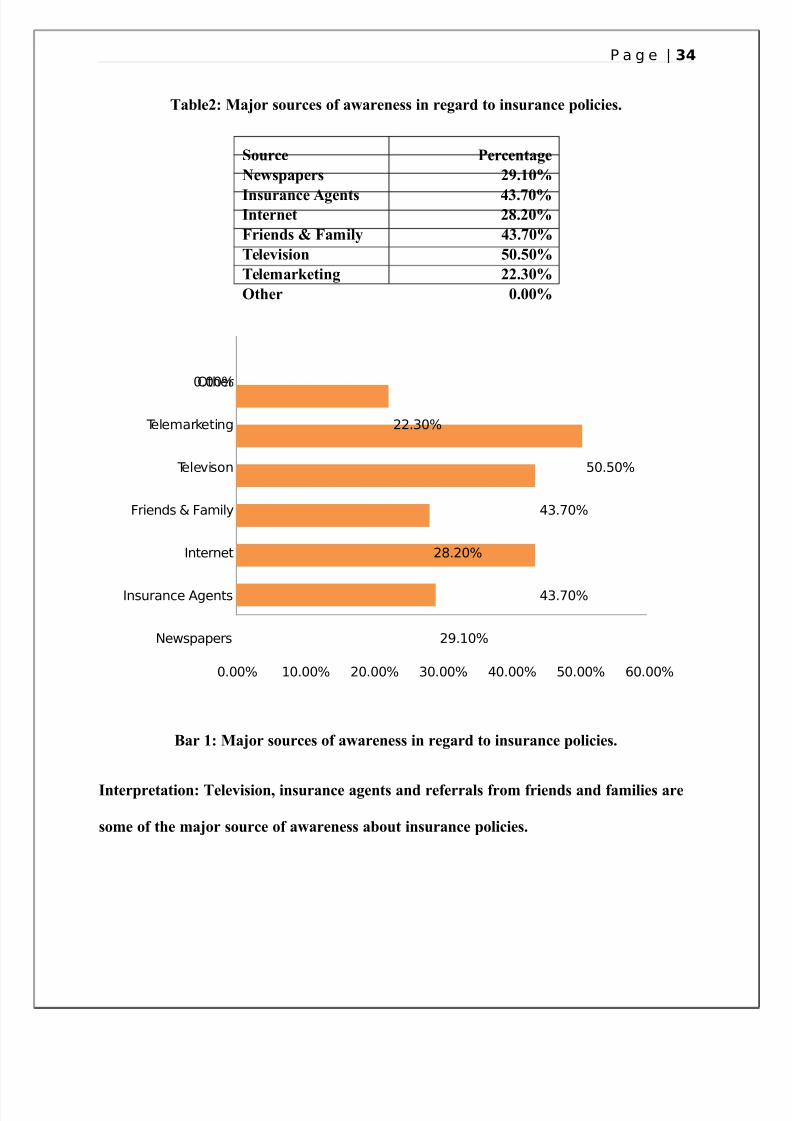

7: T,e re'&")e%' 2ere a'1e) %,r"u!, 2,a% a** '"ur$e' )" %,e3 $ame %" 1"2 a"u%

i'ura$e &"*i$ie':

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 42/68

P a # e ? 3"

Ta*e79 Ma#"r '"ur$e' "+ a2aree'' i re!ar) %" i'ura$e &"*i$ie':

S"ur$e Per$e%a!e

Ne2'&a&er' 7:46

I'ura$e A!e%' 5?:6I%ere% 7:76

Frie)' Fami*3 5?:6

Te*e8i'i" @6:@6

Te*emar1e%i! 77:?6

O%,er 6:66

Ne6+'a'er+

In+(ran&e A#ent+

Internet

-rien"+ -amil$

Tele9i+on

Telemar3etin#

Other

4.44@ 14.44@ 24.44@ 4.44@ %4.44@ 4.44@ ,4.44@

2;.14@

%.04@

2.24@

%.04@

4.4@

22.4@

4.44@

Bar 49 Ma#"r '"ur$e' "+ a2aree'' i re!ar) %" i'ura$e &"*i$ie':

I%er&re%a%i"9 Te*e8i'i"0 i'ura$e a!e%' a) re+erra*' +r"m +rie)' a) +ami*ie' are

'"me "+ %,e ma#"r '"ur$e "+ a2aree'' a"u% i'ura$e &"*i$ie':

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 43/68

P a # e ? 3'

?: T,e re'&")e%' 2ere a'1e) 2,a% +ea%ure' %,e3 $"'i)er e+"re %a1i! a i'ura$e

&"*i$3:

Ta*e ?9 Fea%ure' i8e'%"r' $"'i)er e+"re %a1i! a i'ura$e &"*i$3:

Fea%ure' Per$e%a!e

I'ura$e C"8era!e 4:6

Hi!, Re%ur' @@:?6

L"2 Premium ?:6

F*eJi*e Wi%,)ra2a*' 7@:76

Ri'1 I8"*8e) 76:56

O%,er 6:66

In+(ran&e Co9era#e

Hi#h Ret(rn+

*o6 Premi(m

-leBible 8ith"ra6al+

Ri+3 In9ol9e"

Other

4.44@ [email protected]@4.44@%[email protected]@,[email protected]@4.44@

01.4@

.4@

,.;4@

2.24@

24.%4@

4.44@

Bar79 Fea%ure' i8e'%"r' $"'i)er e+"re %a1i! a i'ura$e &"*i$3:

I%er&re%a%i"9 I'ura$e $"8era!e a) ,i!, re%ur' are '"me "+ %,e mai +ea%ure' %,a%

a i8e'%"r 2a%' %" ,a8e i a i'ura$e &"*i$3:

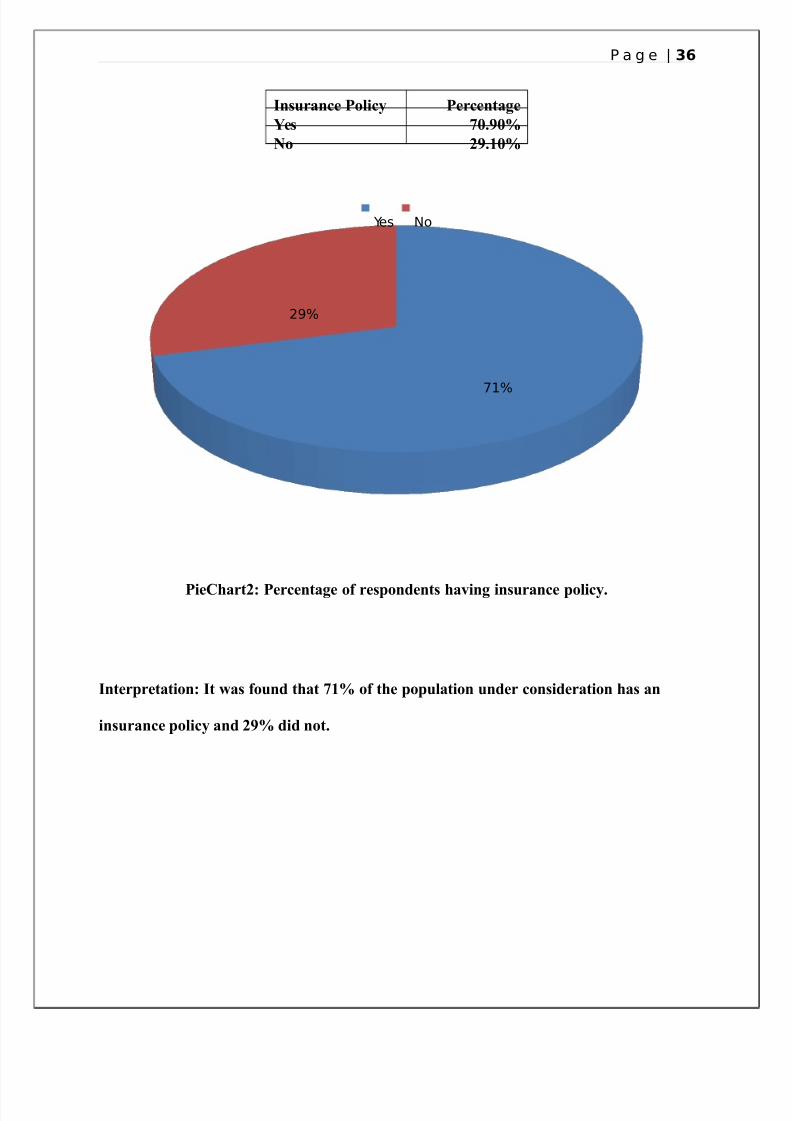

5: T,e re'&")e%' 2ere 2,e%,er %,e3 ,a8e a i'ura$e &"*i$3:

Ta*e59 Per$e%a!e "+ re'&")e%' ,a8i! i'ura$e &"*i$3:

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 44/68

P a # e ? 3+

I'ura$e P"*i$3 Per$e%a!e

Ye' 6:6

N" 7:46

01@

2;@

e+ No

PieC,ar%79 Per$e%a!e "+ re'&")e%' ,a8i! i'ura$e &"*i$3:

I%er&re%a%i"9 I% 2a' +"u) %,a% 4 "+ %,e &"&u*a%i" u)er $"'i)era%i" ,a' a

i'ura$e &"*i$3 a) 7 )i) "%:

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 45/68

P a # e ? 3-

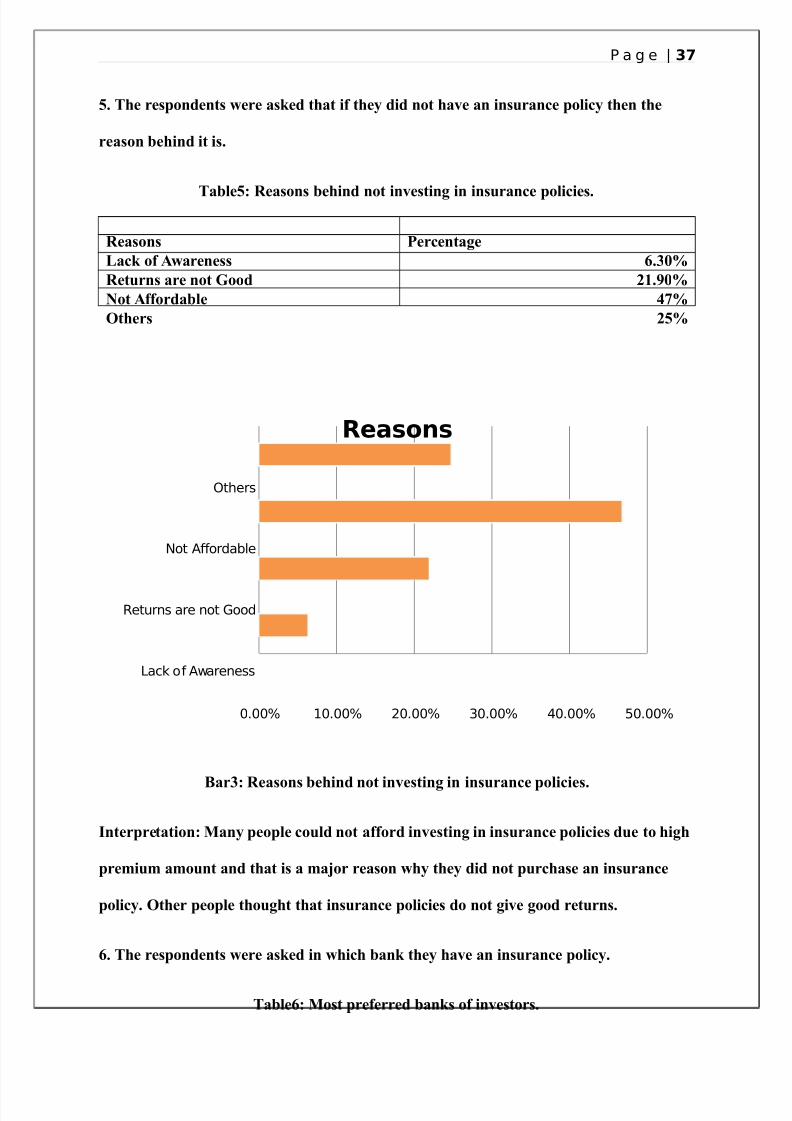

@: T,e re'&")e%' 2ere a'1e) %,a% i+ %,e3 )i) "% ,a8e a i'ura$e &"*i$3 %,e %,e

rea'" e,i) i% i':

Ta*e@9 Rea'"' e,i) "% i8e'%i! i i'ura$e &"*i$ie':

*a&3 of A6arene++

Ret(rn+ are not oo"

Not Aor"able

Other+

4.44@ 14.44@ 24.44@ 4.44@ %4.44@ 4.44@

Reasons

Bar?9 Rea'"' e,i) "% i8e'%i! i i'ura$e &"*i$ie':

I%er&re%a%i"9 Ma3 &e"&*e $"u*) "% a++"r) i8e'%i! i i'ura$e &"*i$ie' )ue %" ,i!,

&remium am"u% a) %,a% i' a ma#"r rea'" 2,3 %,e3 )i) "% &ur$,a'e a i'ura$e

&"*i$3: O%,er &e"&*e %,"u!,% %,a% i'ura$e &"*i$ie' )" "% !i8e !"") re%ur':

: T,e re'&")e%' 2ere a'1e) i 2,i$, a1 %,e3 ,a8e a i'ura$e &"*i$3:

Ta*e9 M"'% &re+erre) a1' "+ i8e'%"r':

Rea'"' Per$e%a!e

La$1 "+ A2aree'' :?6

Re%ur' are "% G"") 74:6

N"% A++"r)a*e 5

O%,er' 7@

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 46/68

P a # e ? 3

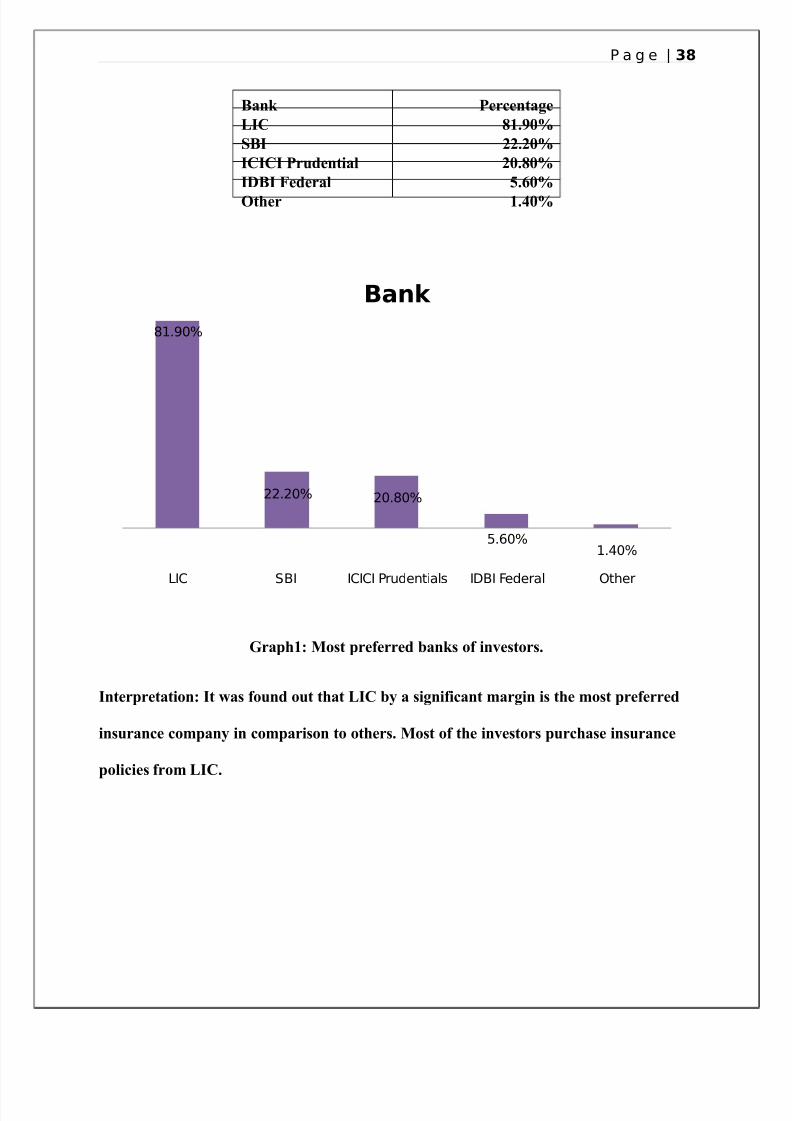

Ba1 Per$e%a!e

LIC 4:6

SBI 77:76

ICICI Pru)e%ia* 76:6

IDBI Fe)era* @:6

O%,er 4:56

*IC SI ICICI Pr("ential+ IDI -e"eral Other

1.;4@

22.24@ 24.4@

.,4@1.%4@

4an5

Gra&,49 M"'% &re+erre) a1' "+ i8e'%"r':

I%er&re%a%i"9 I% 2a' +"u) "u% %,a% LIC 3 a 'i!i+i$a% mar!i i' %,e m"'% &re+erre)

i'ura$e $"m&a3 i $"m&ari'" %" "%,er': M"'% "+ %,e i8e'%"r' &ur$,a'e i'ura$e

&"*i$ie' +r"m LIC:

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 47/68

P a # e ? 3

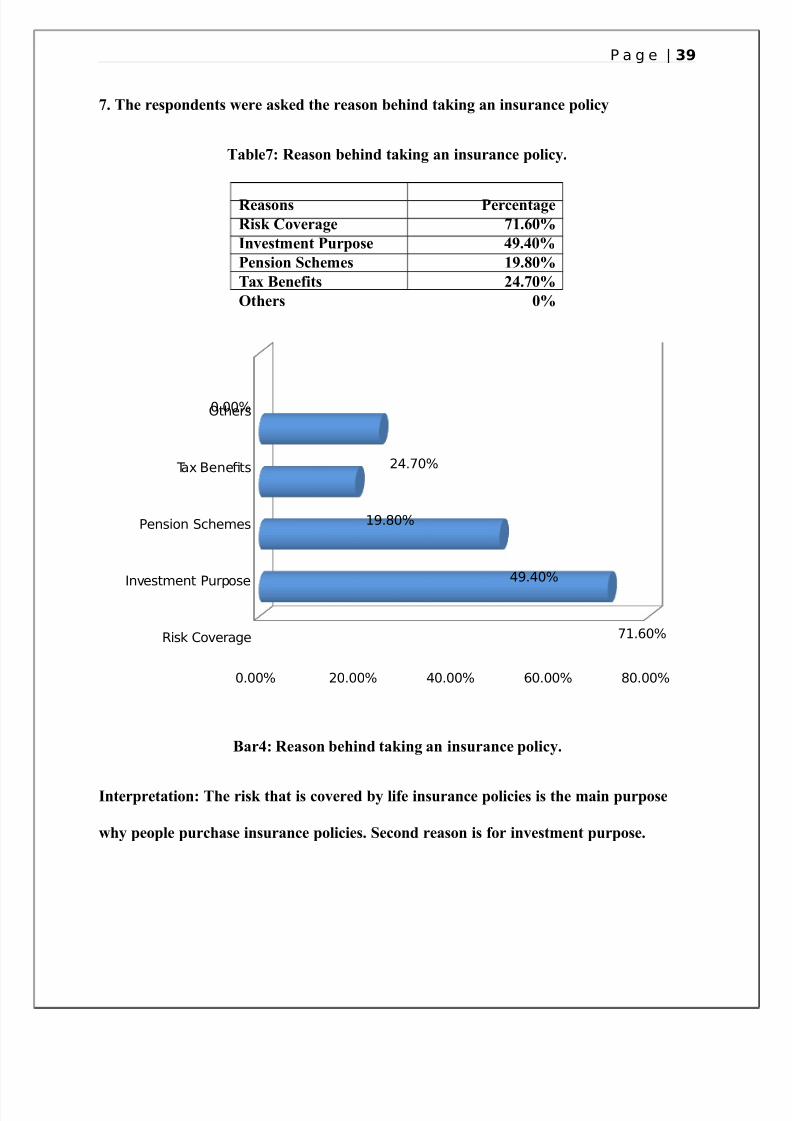

: T,e re'&")e%' 2ere a'1e) %,e rea'" e,i) %a1i! a i'ura$e &"*i$3

Ta*e9 Rea'" e,i) %a1i! a i'ura$e &"*i$3:

Rea'"' Per$e%a!e

Ri'1 C"8era!e 4:6

I8e'%me% Pur&"'e 5:56

Pe'i" S$,eme' 4:6

TaJ Bee+i%' 75:6

O%,er' 6

Ri+3 Co9era#e

In9e+tment P(r'o+e

Pen+ion S&heme+

TaB enet+

Other+

4.44@ 24.44@ %4.44@ ,4.44@ 4.44@

01.,4@

%;.%4@

1;.4@

2%.04@

4.44@

Bar59 Rea'" e,i) %a1i! a i'ura$e &"*i$3:

I%er&re%a%i"9 T,e ri'1 %,a% i' $"8ere) 3 *i+e i'ura$e &"*i$ie' i' %,e mai &ur&"'e

2,3 &e"&*e &ur$,a'e i'ura$e &"*i$ie': Se$") rea'" i' +"r i8e'%me% &ur&"'e:

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 48/68

P a # e ? "

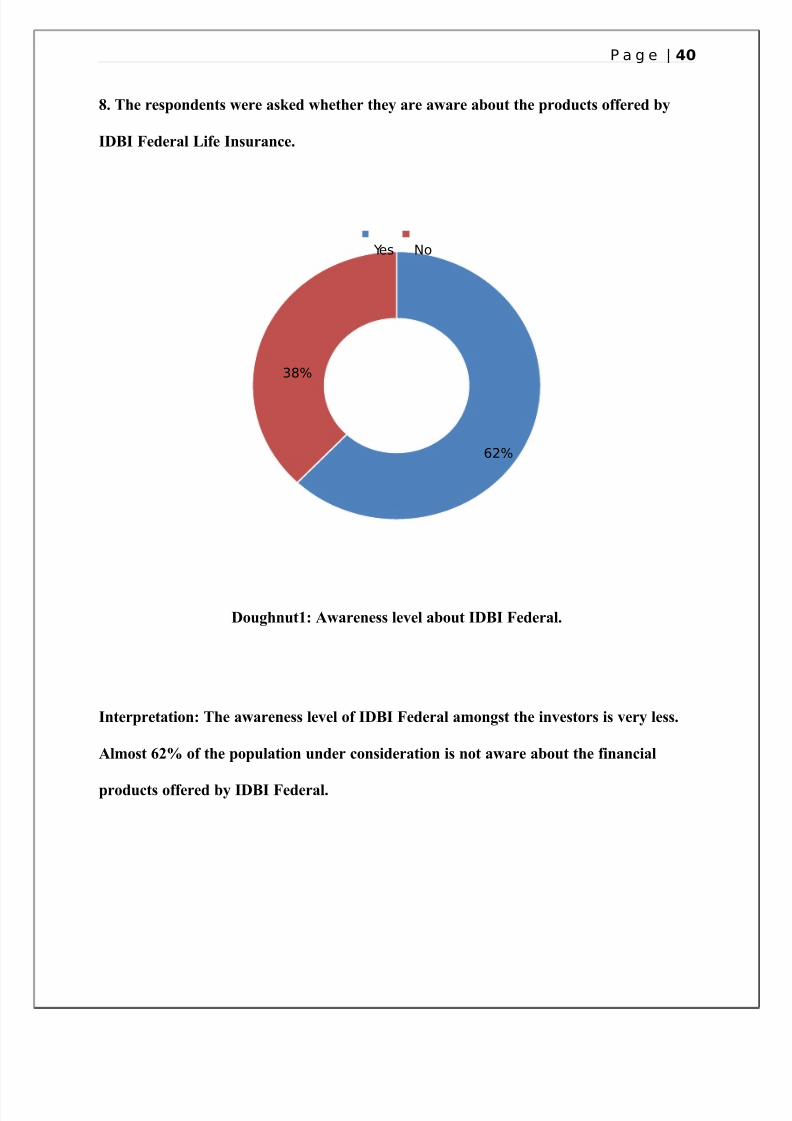

: T,e re'&")e%' 2ere a'1e) 2,e%,er %,e3 are a2are a"u% %,e &r")u$%' "++ere) 3

IDBI Fe)era* Li+e I'ura$e:

,2@

@

e+ No

D"u!,u%49 A2aree'' *e8e* a"u% IDBI Fe)era*:

I%er&re%a%i"9 T,e a2aree'' *e8e* "+ IDBI Fe)era* am"!'% %,e i8e'%"r' i' 8er3 *e'':

A*m"'% 7 "+ %,e &"&u*a%i" u)er $"'i)era%i" i' "% a2are a"u% %,e +ia$ia*

&r")u$%' "++ere) 3 IDBI Fe)era*:

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 49/68

P a # e ? "1

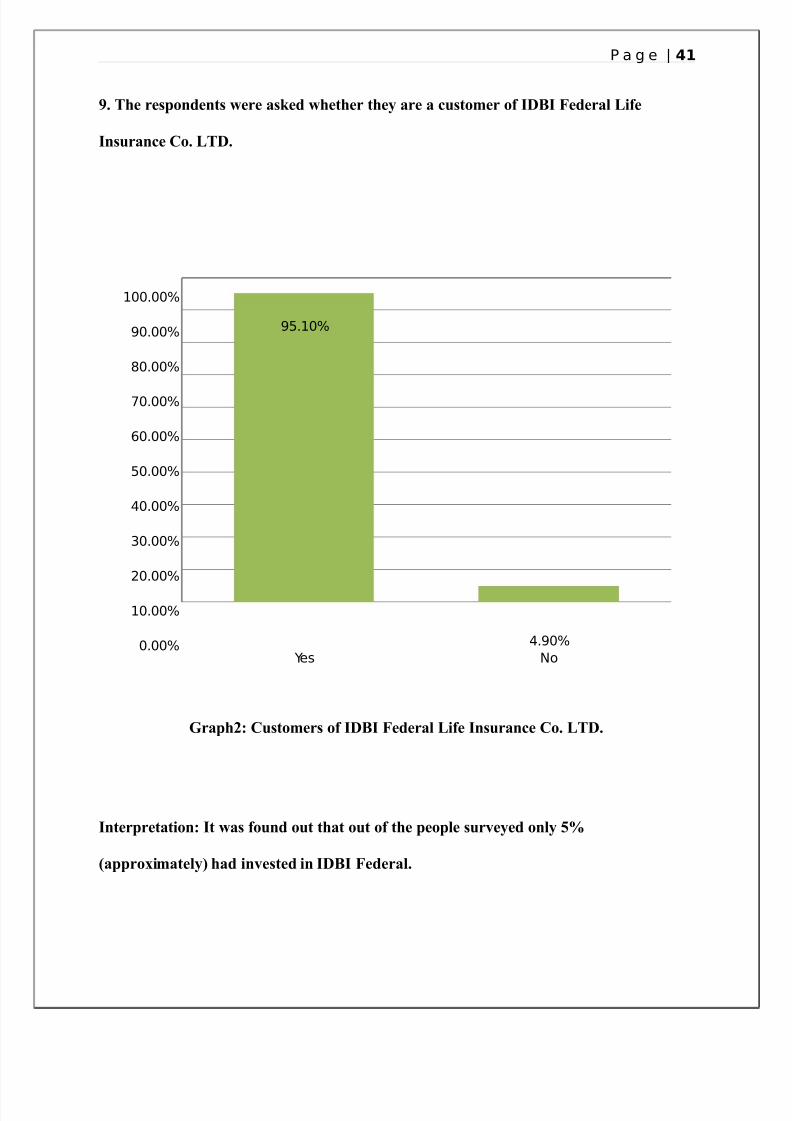

: T,e re'&")e%' 2ere a'1e) 2,e%,er %,e3 are a $u'%"mer "+ IDBI Fe)era* Li+e

I'ura$e C": LTD:

e+ No4.44@

14.44@

24.44@

4.44@

%4.44@

4.44@

,4.44@

04.44@

4.44@

;4.44@

144.44@

;.14@

%.;4@

Gra&,79 Cu'%"mer' "+ IDBI Fe)era* Li+e I'ura$e C": LTD:

I%er&re%a%i"9 I% 2a' +"u) "u% %,a% "u% "+ %,e &e"&*e 'ur8e3e) "*3 @

(a&&r"Jima%e*3. ,a) i8e'%e) i IDBI Fe)era*:

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 50/68

P a # e ? "2

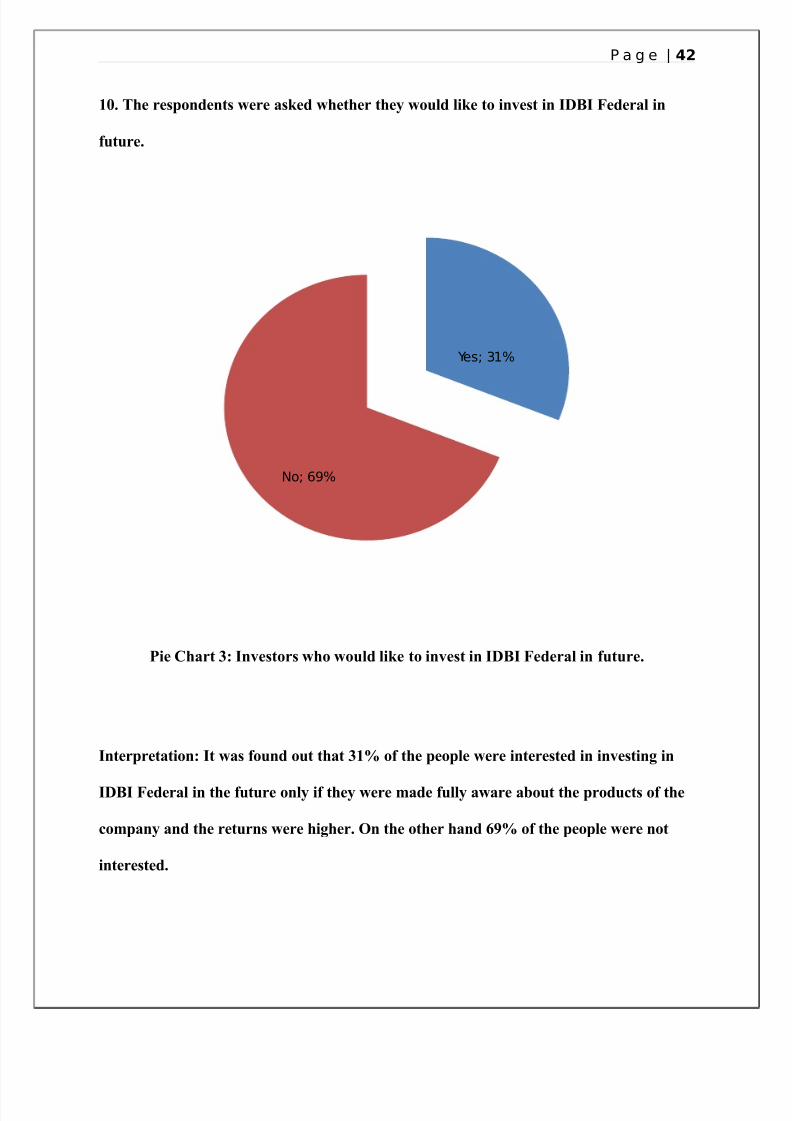

46: T,e re'&")e%' 2ere a'1e) 2,e%,er %,e3 2"u*) *i1e %" i8e'% i IDBI Fe)era* i

+u%ure:

e+ 1@

No ,;@

Pie C,ar% ?9 I8e'%"r' 2," 2"u*) *i1e %" i8e'% i IDBI Fe)era* i +u%ure:

I%er&re%a%i"9 I% 2a' +"u) "u% %,a% ?4 "+ %,e &e"&*e 2ere i%ere'%e) i i8e'%i! i

IDBI Fe)era* i %,e +u%ure "*3 i+ %,e3 2ere ma)e +u**3 a2are a"u% %,e &r")u$%' "+ %,e

$"m&a3 a) %,e re%ur' 2ere ,i!,er: O %,e "%,er ,a) "+ %,e &e"&*e 2ere "%

i%ere'%e):

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 51/68

P a # e ? "3

CHAPTER ': DATA

ANA,;SIS AND

INTERPRETATION

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 52/68

P a # e ? ""

'.1 in$in%s an$ Interretation o in$in%s

• Majority of the respondents who were tar*eted were students, businessmen and

people wor'in* in some or*ani<ations belon*in* to the serice sector)

• Shares and debentures are the most preferred option of inestors to inest in as

proide *reater returns than insurance policies)

• Teleision, insurance a*ents are some of the major source of awareness about

insurance policies) /riends and family are major influencers on customers when it

comes to the decision of buyin* a life insurance policy)

•

The main features that inestors consider before ta'in* an insurance policy is the life

coer that insurance proides and also would li'e to *et hi*h returns from their

insurance policies)

• 0ow premium amount is the also another which people consider before inestin* in

insurance schemes) Payin* premium annually is the most preferred mode of payment

accordin* to inestors)

• 7ppro3imately 6"C of the respondents were insured and rest @C had not inested in

insurance policies)

• There is a *ood amount of people in the a*e *roup "?$9! who hae not bothered to

buy a life insurance policy because they are ery sure that nothin* would happen to

them as they are fit and fine)

• Those who had not inested in insurance policies said that they could not afford

purchasin* an insurance policy and wanted the annual premium amount to be low

while others did not feel the need of it at the moment)

• 01 by a si*nificant mar*in is the most preferred company by the inestors and

almost ?C of the respondents hae purchased insurance policies from 01) .rand

ima*e and word of mouth in faor of 01 has had si*nificant impact on the selection

of inestors)

• The ris' that is coered by insurance policies is the main purpose or reason why

people purchase insurance policies) Second reason is inestment purpose)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 53/68

P a # e ? "'

• The awareness leel amon*st the consumers is ery low) 7ppro3imately %9C of the

respondents were not aware about the products offered by D. /ederal) Some were

not een aware about the companyBs e3istence as well)

• >ut of the 96C that are aware about more than @8C of the respondents are not

customers of D. /ederal)

• 0ac' of 'nowled*e or awareness about the products, other companies hae better

returns are some of the major reasons why people are not inestin* in D. /ederal)

Some already hae enou*h insurance policies and hence do not want to buy another

policy)

•

Some hae not heard concrete positie reiews about the returns or performance of

the company from their friends or family members) 01 or other priate ban's

proides much better and beneficial plans in comparison to D. /ederal)

• Some were hesitant in *iin* their mobile or other contact numbers because they did

not wanted to be disturbed by the calls from the companyBs side)

• t was found out that 9"C of the people were interested in inestin* in D. /ederal

in the future only if they were made fully aware about the products of the company

and the returns were hi*her) >n the other hand %@C of the people were not interested)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 54/68

P a # e ? "+

'.2) Con(l*sion

5hile the fresh air of competition in eery sector of economy brin*s in major chan*es in

consumer e3pectations, the insurance industry has e3perienced a few unique aspects, such as

re*ulation$inspired efforts to educate insurance buyers and a ast chan*e of s'ills and

capabilities of the intermediaries inoled in the distribution) The life insurance industry in

ndia has immense potential with nearly ?!C of the population without insurance coer) 0ife

insurance is a sector which is lar*est drien by propensity of people to sae and in

comparison to the west, ndians hae a hi*her propensity to sae) +nderstandin* the

consumer buyin* behaiour pattern can *ie the companies a sli*ht as to what a customer

wants before inestin* in an insurance policy) People are hain* *ood 'nowled*e about

insurance companies throu*h adertisements and insurance a*ents and most of the

respondents at least once in their life hae been approached by an insurance a*ent)

5ith respect to life insurance, potential buyers are driers of buyin* a policy for one or more

of these 9 major reasonsA ris' that is coered by insurance policies, for inestment purpose or

for the aailability of ta3 benefits) The challen*e for the insurance companies is to address

the motiatin* factors of customers and come up with *enuine solutions) The potential buyer

primarily e3pects that the sain* should be a painless process and that the money saed

should be absolutely safe) The challen*e is to proide not only conenient payment options,

but also mechanisms that could offer some measure of protection and relief to the customer if

he is forced to disrupt the payment arran*ement for unforeseen reasons) People iew

insurance as ta3 sain* and inestment instrument as much as a protectie one)

The comparatiely new player D. /ederal will hae to and must adertise well enou*h to

ma'e the people aware about their products and schemes because most of the time a

prospectie insurance customer will loo' for a brand name li'e that of 01) The company has

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 55/68

P a # e ? "-

a potential of *rowin* in the comin* years as still more than half the population of ndia is

still not insured) Thus here lies the opportunity for D. /ederal to increase their customer

base by increasin* the awareness leel of potential inestors in re*ard to their products and

by proidin* schemes accordin* to the needs and requirements of the customers)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 56/68

P a # e ? "

CHAPTER +:

RECO##ENDATIONS

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 57/68

P a # e ? "

+.1) Des(rition o Re(ommen$ations<S*%%estions

• Most of the respondents had only one su**estion to ma'e, and that is to increase

awareness throu*h adertisements and promotional actiities and 'eep them updated

about the products and their respectie benefits from time to time)

• ncreasin* awareness about the products offered by D. /ederal is the first and the

foremost important aspect that D. should focus upon as a lar*e chun' of people are

still not aware about the products of D., and the company een)

• 7s teleision and friends Q families are major sources of awareness about insurance

policies, adertisements should be broadcasted on teleisions which hae an

emotional appeal) The adertisements or promotional actiities should be friends and

family centred and tri**er a feelin* on uncertainty)

• There are still a lot of people in the a*e *roup of !$98 who has not inested in

insurance policies and D. should try to conince them life is full of uncertainties

and is ery unpredictable) =ew schemes can be launched which are affordable by

students or fresherBs who do not earn much)

• The rural areas are more also quite heaily populated) Thus this rural population must

be made aware about the company and its offerin*s and *ain their trust by appointin*

a*ents from the rural areas itself) The plans should be affordable by these se*ments of

the society)

• nsurance a*ents must be able to clearly tell all the benefits and features attached to a

particular policy to its customers and also proide after sales serice to them to

increase customer satisfaction) 7pproach and coniction of a*ents is ery important

and so the best efforts should be made to recruit and train their clients and handle

potential customers)

• 7nother su**estion from the respondents was that the returns are too low and the

annual premium amount is quite hi*h in comparison) Thus plans can be introduced

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 58/68

P a # e ? '

which hae low premium amount alon* with fle3ible withdrawals and also proide

*ood returns)

• Since M$1ommerce is the ne3t bi* thin* in the ban'in* or insurance industry, D.

/ederal should launch a mobile application of its own to ma'e the inestors aware

about their schemes and products)

• The app will also help the customers in 'nowin* about the ne3t premium due dates

and also pay the premiums) This will sae the time of the customers)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 59/68

P a # e ? '1

CHAPTER -:

CONC,UDIN/ RE#AR=S

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 60/68

P a # e ? '2

-.1) /ains rom t!e Pro>e(t

Durin* my internship with D. /ederal 0ife nsurance 1o 0TD *ot aluable 'nowled*e

about the insurance sector and *rowth potential in this sector is quite hi*h) 7 lar*e part of the

population is still not insured)

7s had some sales tar*et as well, reali<ed how difficult it was to approach, demonstrate

and conince a customer especially in the insurance industry while wor'in* for D. which

is still in its *rowin* phase) Some people already hae life insurance policies and wonBt buy

another one) Sellin* of life insurance indeed is ery difficult and one can only master it by

meetin* more and more customers daily)

7nother important thin* that learned is that it is not important what the company thin's

about a product) 5hat is important is that how the customers perceie your products or

serices in my case) The consumer has to be told how your product will proide them more

benefits and alue added serices in comparison to other companies)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 61/68

P a # e ? '3

-.2) ,imitations o t!e Pro>e(t

Due to constraints of time and resources, the study is li'ely to suffer from certain limitations)

Some of these are mentioned here under so that the findin*s of the study may be understood

in a proper perspectie)

The limitations of the study areA

• Some of the respondents of the surey were unwillin* to share information) People

refrain from *iin* personal details)

• The research was carried out in a short period of ? wee's) Therefore the sample

si<e and other parameters were selected accordin*ly so as to finish the wor' within

the *ien time frame)

• The information *ien by the respondents mi*ht be biased because some of them

mi*ht not be interested to *ie correct information)

• The research was confined to 0uc'now city only)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 62/68

P a # e ? '"

-.3) S(oe or *rt!er 9or5

The data collected for this research was from a sample si<e of "!!) 7lthou*h the sample si<e

is quite small, still the responses are quite consistent) The same questionnaires can used to

surey a lar*er sample to study the consumer behaior towards the insurance industry at

lar*e)

This research was carried out in the city of 0uc'now and hence the results reflect the

sentiments of the urban population) This research could be further carried out in tier$ and

tier$9 cities) The questionnaire can be translated in the local lan*ua*e to conduct the same

surey in illa*es where the illa*e dwellers are not proficient in En*lish lan*ua*e)

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 63/68

P a # e ? ''

Reeren(es<4iblio%ra!&

• www)idbifederal)com

• www)idbifederal)com-Press-PressRelease

• httpA--www)insidebusiness9%!)com-inde3)php-why$it$is$important$to$study$

consumer$behaior$?#6?-

• httpsA--en)wi'ipedia)or*-wi'i-D./ederal0ifensurance

• httpA--www)policyba<aar)com-life$insurance-companies-idbi$federal$life$

insurance$company$ltd-• httpsA--apps)aima)in-ejournalnew-articlespdf-*aurajaiswalnrc9#!?!@@!!

@99?@@#)pdf

•

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 64/68

P a # e ? '+

APPENDICES

KUESTIONNAIRE

(He**" P*ea'e ,e*& u' 3 1i)*3 +i**i! u& %,e +"**"2i! i+"rma%i": We a&&re$ia%e 3"ur

re'&"'e a) %,a1 3"u +"r 3"ur &re$i"u' %ime:.

4: Name9

7: A!e9

?: Ge)er9 Ma*e ( . Fema*e ( .

5: Te*e&,"e9

@: O$$u&a%i"9

a. Bu'ie'' ( .

. Ser8i$e ( .

$. Pr"+e''i"a* ( .

). Re%ire) ( .

e. S%u)e% ( .

+. H"u'e2i+e ( .

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 65/68

P a # e ? '-

:. H"2 )i) 3"u $"me %" 1"2 a"u% i'ura$e &"*i$ie' (3"u $a $,""'e m"re %,a

"e.

a. Ne2'&a&er' ( .

. I'ura$e a!e%' ( .

$. I%ere% ( .

). Frie)' +ami*ie' ( .

e. Te*e8i'i" ( .

+. Te*emar1e%i! ( .

: W,a% are %,e +ea%ure' 3"u $"'i)er e+"re %a1i! a i'ura$e &"*i$3 ( 3"u $a

$,""'e m"re %,a "e.

a. I'ura$e C"8era!e ( .

. Hi!, Re%ur' ( .

$. L"2 Premium Am"u% ( .

). F*eJi*e Wi%,)ra2a*' ( .

e. Ri'1 I8"*8e) ( .

+. O%,er'9

: D" 3"u "2 a I'ura$e P"*i$3

a. Ye' ( . . N" ( .

I+ "%0 2,3 "%

La$1 "+ a2aree'' ( .

Re%ur' are "% !"") ( .

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 66/68

P a # e ? '

N"% a++"r)a*e ( .

O%,er'9

I+ 3e'0 2,i$, $"m&a3

LIC ( .

ICICI Pru)e%ia* ( .

SBI ( .

IDBI Fe)era* ( .

O%,er'9

: Rea'"' e,i) %a1i! a i'ura$e &"*i$3

a. Ri'1 C"8era!e

. I8e'%me% &ur&"'e

$. Pe'i" '$,eme'

). TaJ Bee+i%

e. O%,er'9

46: W,a% &r"m&%e) 3"u %" u3 +r"m %,a% $"m&a3 (Y"u $a $,""'e m"re %,a "e.

a. Bra) Ima!e ( .

. W"r) "+ m"u%, ( .

$. A)8er%i'eme%' ( .

). A!e%' ( .

e. O%,er9

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 67/68

P a # e ? '

44: Are 3"u a2are "+ %,e &r")u$%' "++ere) 3 IDBI Fe)era*

a. Ye' ( . . N" ( .

47: Are 3"u a $u'%"mer "+ IDBI Fe)era*

a. Ye' ( . . N" ( .

I+ "%0 2,a% i' %,e rea'" e,i) i%

I+ 3e'0 me%i" %,e &*a

4?. W"u*) 3"u *i1e %" i8e'% i IDBI Fe)era* i +u%ure

a. Ye' ( . . N" ( .

45: A3 'u!!e'%i"' +"r IDBI Fe)era*

7/18/2019 IDBI Fedral

http://slidepdf.com/reader/full/idbi-fedral 68/68

P a # e ? +

(T,a1 3"u +"r 3"ur %ime %a1e i $"m&*e%i! %,i' -ue'%i"aire: T,e re'u*%' "+ %,i'

2"r1 2i** e im&"r%a% +"r )e%ermii! %,e $"'umer u3i! e,a8i"r %"2ar)' %,e

+ia$ia* &r")u$%' "+ IDBI Fe)era*.