Embed Size (px)

Citation preview

INTERNATIONAL FEDERATION OF AGRICULTURAL PRODUCERS (IFAPIFAP)

Philippe Jachnik

PresidentInternational Dairy Federation (IDF)

4th IFAP COMMODITIES CONFERENCE

DAIRY PRODUCTS GROUP

PRETORIA, 10.05.2003

WORLD MARKET SITUATION AND WORLD MARKET SITUATION AND OUTLOOK FOR DAIRY PRODUCTSOUTLOOK FOR DAIRY PRODUCTSWORLD MARKET SITUATION AND WORLD MARKET SITUATION AND OUTLOOK FOR DAIRY PRODUCTSOUTLOOK FOR DAIRY PRODUCTS

TABLE OF CONTENTS

1. WORLD DAIRY ECONOMY: MAIN DATA AND TRENDS

2. IDF WDS 2003 FIRST PREVIEW

1. WORLD DAIRY ECONOMY: MAIN DATA AND TRENDS

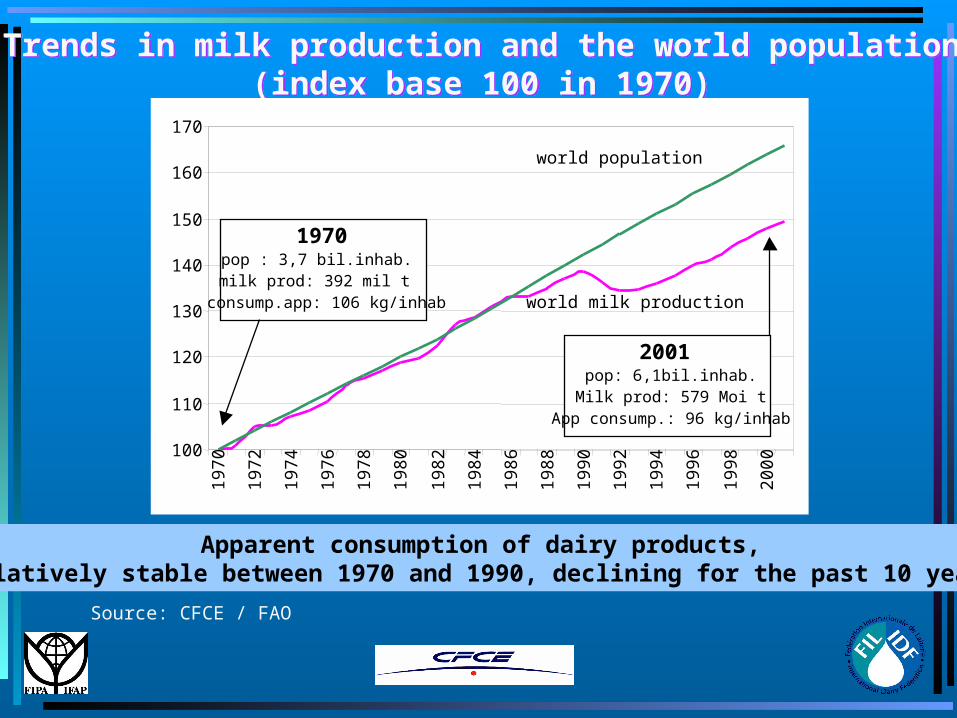

Trends in milk production and the world population(index base 100 in 1970)

Trends in milk production and the world population(index base 100 in 1970)

Apparent consumption of dairy products,Relatively stable between 1970 and 1990, declining for the past 10 years

Source: CFCE / FAO

100

110

120

130

140

150

160

170

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

world population

world milk production

1970pop : 3,7 bil.inhab.milk prod: 392 mil t

consump.app: 106 kg/inhab

2001pop: 6,1bil.inhab.

Milk prod: 579 Moi tApp consump.: 96 kg/inhab

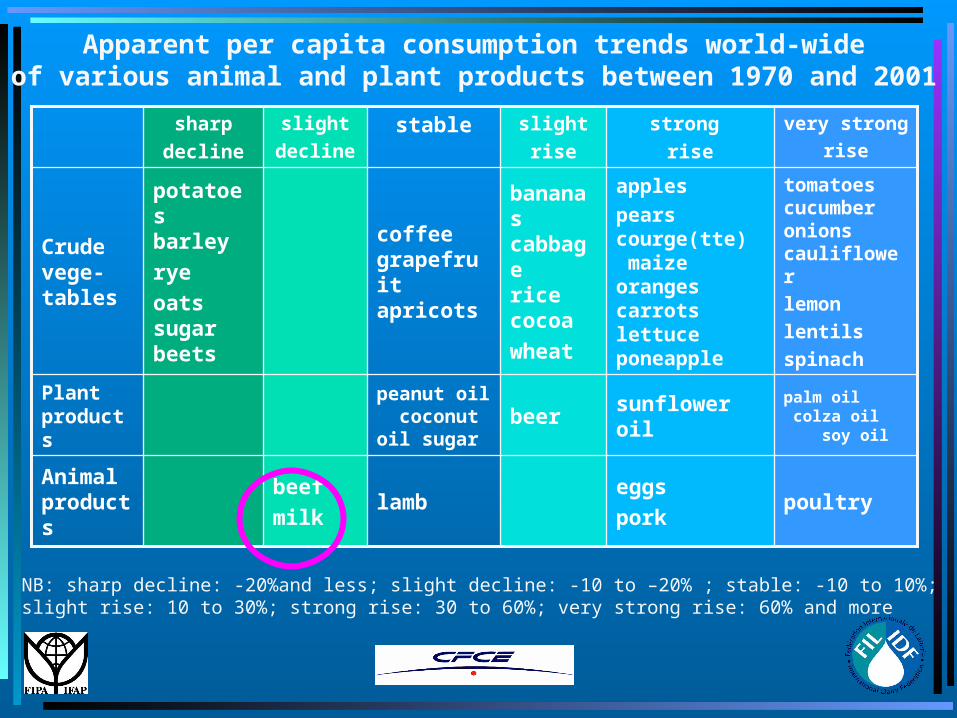

Apparent per capita consumption trends world-wideof various animal and plant products between 1970 and 2001

poultryeggs

porklamb

beef

milkAnimal products

palm oil colza oil soy oil

sunflower oilbeerpeanut oil coconut oil sugar

Plant products

tomatoes cucumber onions cauliflower

lemon

lentils

spinach

apples

pears courge(tte) maize oranges carrots lettuce poneapple

bananas cabbage rice cocoa

wheat

coffee grapefruit apricots

potatoes barley

rye

oats sugar beets

Crude vege-tables

very strong

rise

strong

rise

slight

risestableslight

decline

sharp

decline

NB: sharp decline: -20%and less; slight decline: -10 to –20% ; stable: -10 to 10%;slight rise: 10 to 30%; strong rise: 30 to 60%; very strong rise: 60% and more

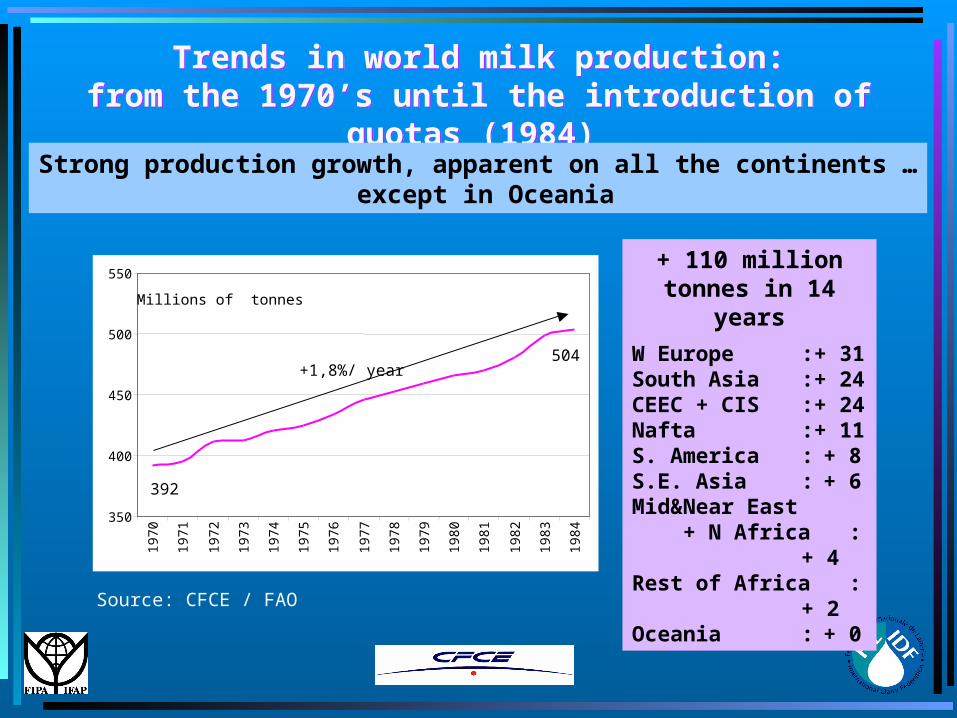

Trends in world milk production:from the 1970’s until the introduction of quotas

(1984)

Trends in world milk production:from the 1970’s until the introduction of quotas

(1984) Strong production growth, apparent on all the continents …

except in Oceania

W Europe :+ 31South Asia :+ 24CEEC + CIS :+ 24Nafta :+ 11S. America : + 8S.E. Asia : + 6Mid&Near East + N Africa : + 4Rest of Africa : + 2Oceania : + 0

+ 110 million tonnes in 14

years

Source: CFCE / FAO

350

400

450

500

550

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

392

Millions of tonnes

504 +1,8%/ year

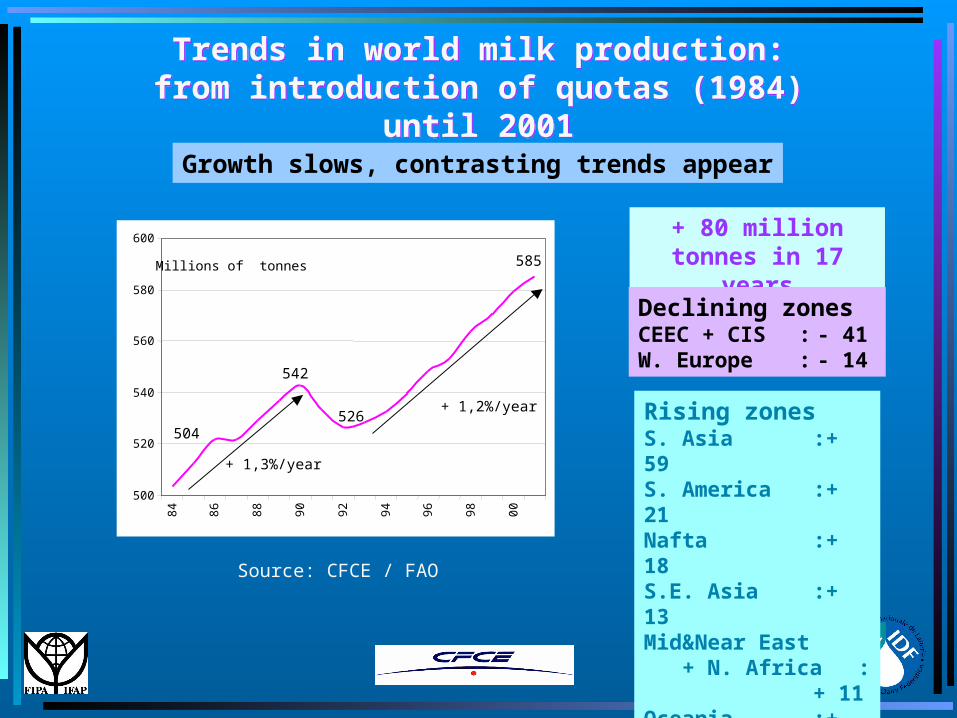

Trends in world milk production:from introduction of quotas (1984) until

2001

Trends in world milk production:from introduction of quotas (1984) until

2001Growth slows, contrasting trends appear

+ 80 million tonnes in 17

yearsDeclining zonesCEEC + CIS : - 41W. Europe : - 14

Rising zonesS. Asia :+ 59S. America :+ 21Nafta :+ 18S.E. Asia :+ 13Mid&Near East + N. Africa :+ 11Oceania :+ 11

Source: CFCE / FAO

500

520

540

560

580

600

84

86

88

90

92

94

96

98

00

585

504

Millions of tonnes

526

542

+ 1,3%/year

+ 1,2%/year

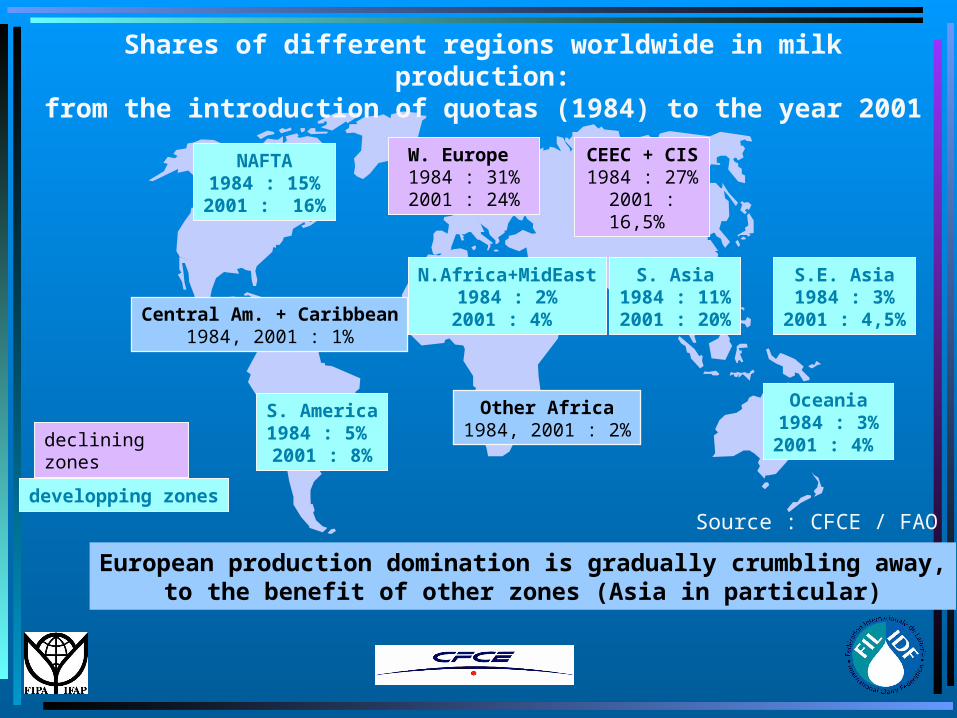

S. Asia1984 : 11%2001 : 20%

Source : CFCE / FAO

W. Europe 1984 : 31%2001 : 24%

CEEC + CIS1984 : 27%

2001 : 16,5%

N.Africa+MidEast1984 : 2%2001 : 4%

NAFTA1984 : 15%2001 : 16%

Central Am. + Caribbean1984, 2001 : 1%

S. America1984 : 5% 2001 : 8%

Other Africa1984, 2001 : 2%

Oceania1984 : 3%2001 : 4%

Shares of different regions worldwide in milk production:from the introduction of quotas (1984) to the year 2001

declining zones

developping zones

European production domination is gradually crumbling away,to the benefit of other zones (Asia in particular)

S.E. Asia1984 : 3%

2001 : 4,5%

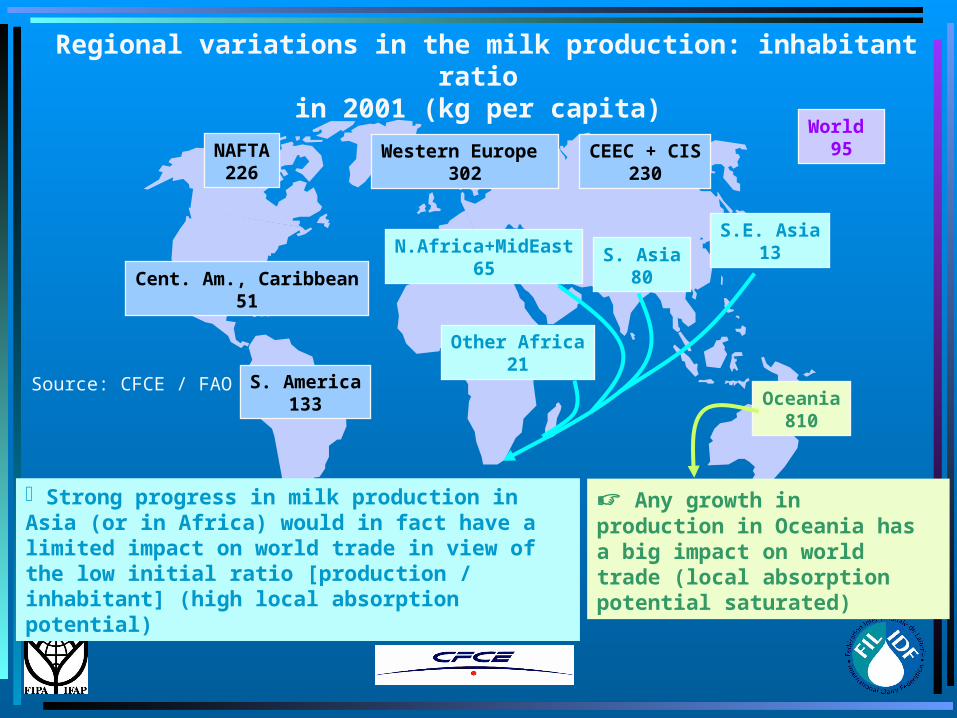

Western Europe 302

CEEC + CIS230

N.Africa+MidEast65

NAFTA226

S. America133

Other Africa21

S. Asia80

Oceania810

World 95

Source: CFCE / FAO

Regional variations in the milk production: inhabitant ratio

in 2001 (kg per capita)

Any growth in production in Oceania has a big impact on world trade (local absorption potential saturated)

S.E. Asia13

Cent. Am., Caribbean51

Strong progress in milk production in Asia (or in Africa) would in fact have a limited impact on world trade in view of the low initial ratio [production / inhabitant] (high local absorption potential)

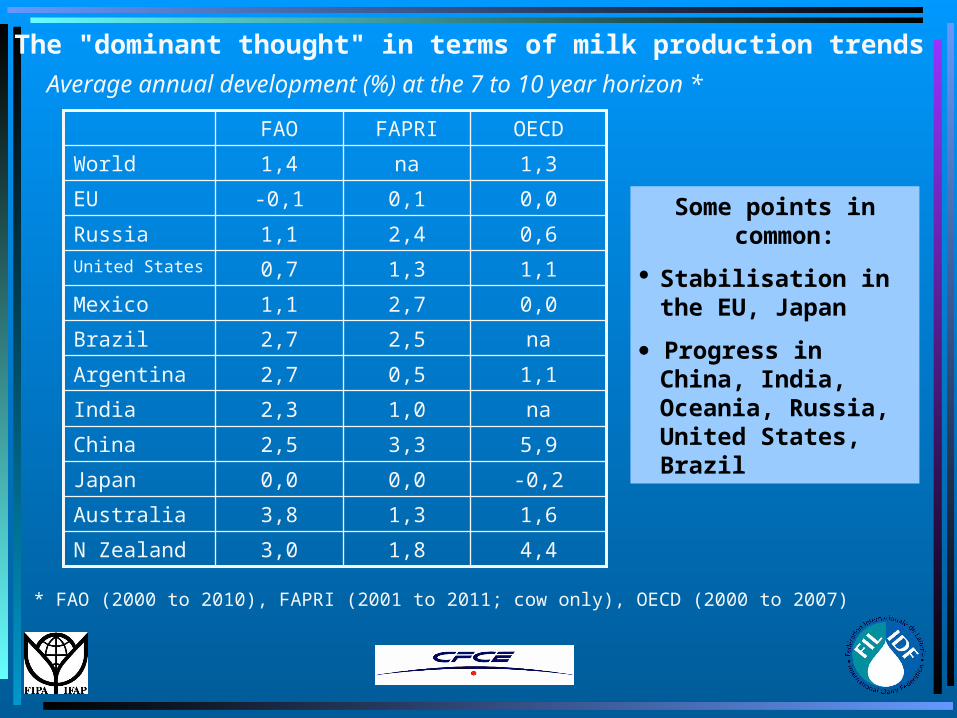

The "dominant thought" in terms of milk production trends

-0,20,00,0Japan

1,61,33,8Australia

na1,02,3India

5,93,32,5China

na2,52,7Brazil

1,10,52,7Argentina

4,41,83,0N Zealand

0,02,71,1Mexico

1,11,30,7United States

0,62,41,1Russia

0,00,1-0,1EU

1,3na1,4World

OECDFAPRIFAO

Average annual development (%) at the 7 to 10 year horizon *

* FAO (2000 to 2010), FAPRI (2001 to 2011; cow only), OECD (2000 to 2007)

Some points in common:

Stabilisation in the EU, Japan

Progress in China, India, Oceania, Russia, United States, Brazil

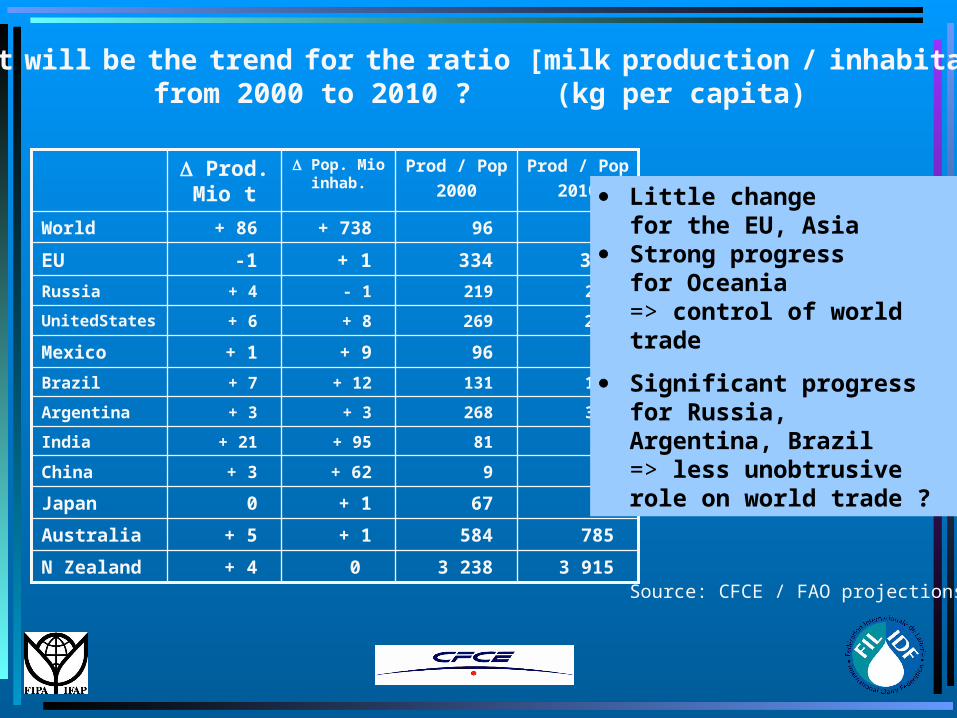

What will be the trend for the ratio [milk production / inhabitant]from 2000 to 2010 ? (kg per capita)

3 238

584

67

9

81

268

131

96

269

219

334

96

Prod / Pop

2000

67+ 10Japan

785+ 1+ 5Australia

89+ 95+ 21India

11+ 62+ 3China

153+ 12+ 7Brazil

313+ 3+ 3Argentina

3 9150 + 4N Zealand

93+ 9+ 1Mexico

275+ 8+ 6UnitedStates

246- 1+ 4Russia

333+ 1-1EU

98+ 738+ 86World

Prod / Pop

2010

Pop. Mio inhab.

Prod. Mio t

Source: CFCE / FAO projections

Little changefor the EU, Asia

Strong progressfor Oceania

=> control of world trade

Significant progress for Russia, Argentina, Brazil=> less unobtrusive role on world trade ?

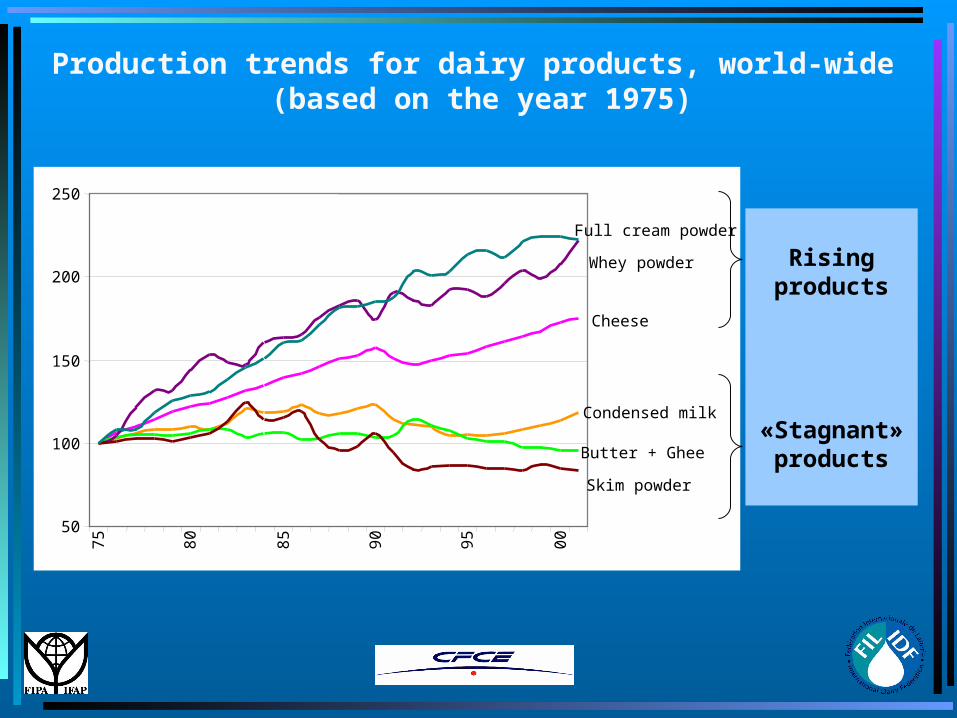

50

100

150

200

250

75

80

85

90

95

00

Whey powder

Full cream powder

Cheese

Condensed milk

Butter + Ghee

Skim powder

Production trends for dairy products, world-wide (based on the year 1975)

Rising products

«Stagnant» products

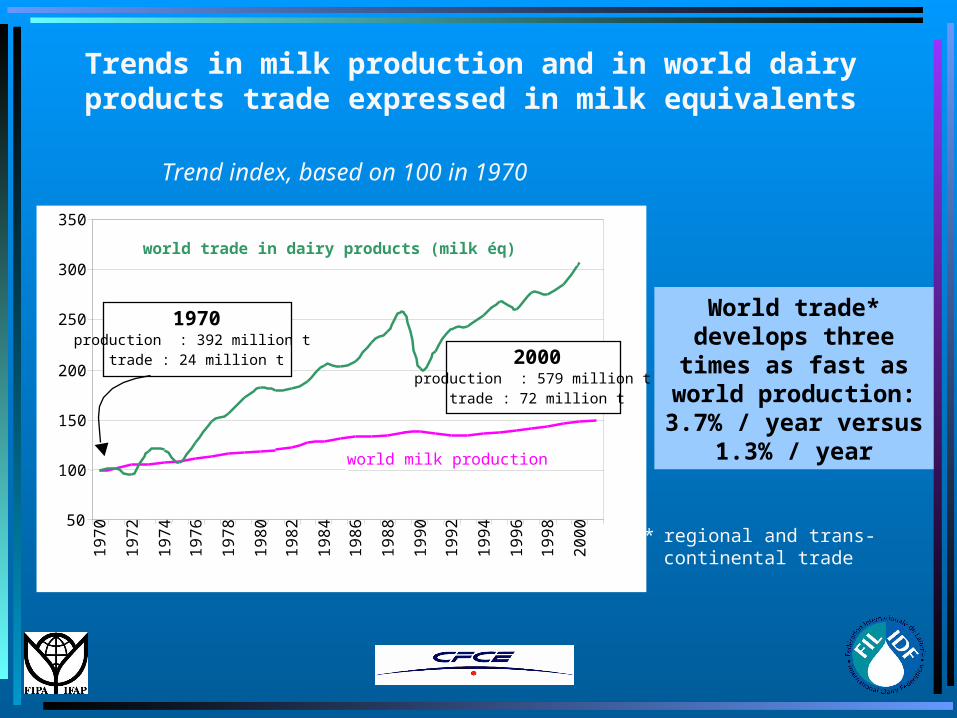

Trends in milk production and in world dairyproducts trade expressed in milk equivalents

Trend index, based on 100 in 1970

World trade* develops three times as fast as

world production:3.7% / year versus

1.3% / year

50

100

150

200

250

300

350

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

world trade in dairy products (milk éq)

world milk production

1970production : 392 million t

trade : 24 million t 2000production : 579 million t

trade : 72 million t

* regional and trans-continental trade

Intra-EU trade and world trade in 2000Intra-EU trade and world trade in 2000

Regional trade dominates trade in consumer products.

Intra-EU trade alone accounts for the vast majority of world flows in retail-pack milk and cream, yogurt and cheese.

132201 710Full-cream milk powder

305401 810Skimmed milk powder

39490 1 260Butter

581 8603 180Cheese

505101 050Condensed milks

701 0501 500Yogurt, fermented milk

85600710Cream

885 1105 780Liquid milk

% intra EU

Intra-EU

trade

World

trade*

* intra-EU included

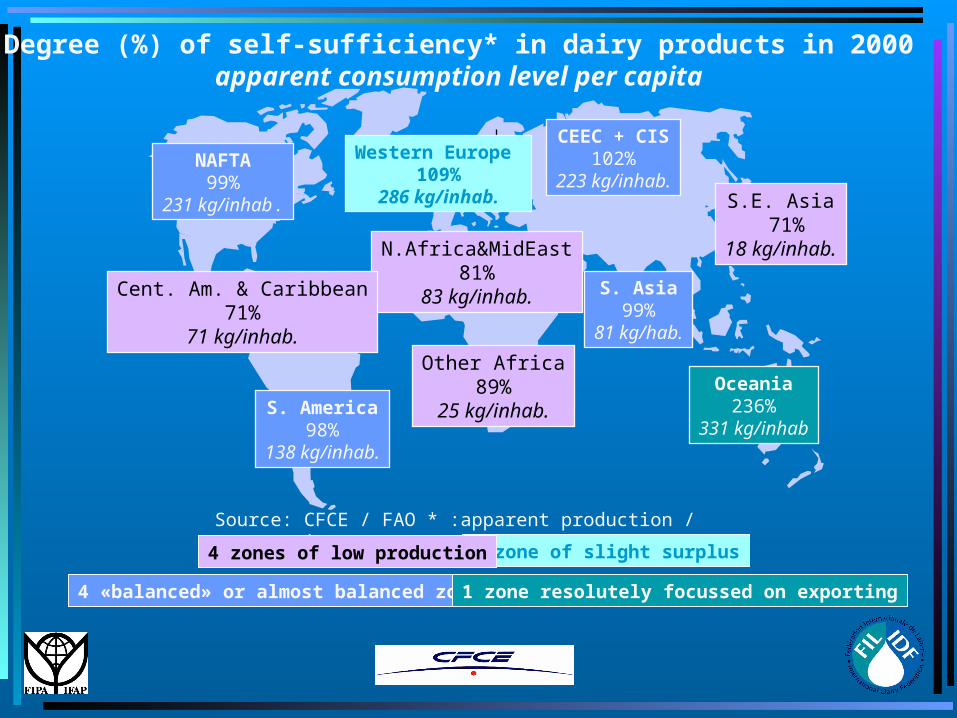

1 zone of slight surplus

CEEC + CIS102%

223 kg/inhab.S.E. Asia

71%18 kg/inhab.N.Africa&MidEast

81%83 kg/inhab.

NAFTA99%

231 kg/inhab.

Cent. Am. & Caribbean71%

71 kg/inhab.

S. America98%

138 kg/inhab.

Other Africa89%

25 kg/inhab.

S. Asia99%

81 kg/hab.

Oceania236%

331 kg/inhab

Source: CFCE / FAO * :apparent production / consumption

Degree (%) of self-sufficiency* in dairy products in 2000apparent consumption level per capita

4 zones of low production

4 «balanced» or almost balanced zones1 zone resolutely focussed on exporting

Western Europe 109%

286 kg/inhab.

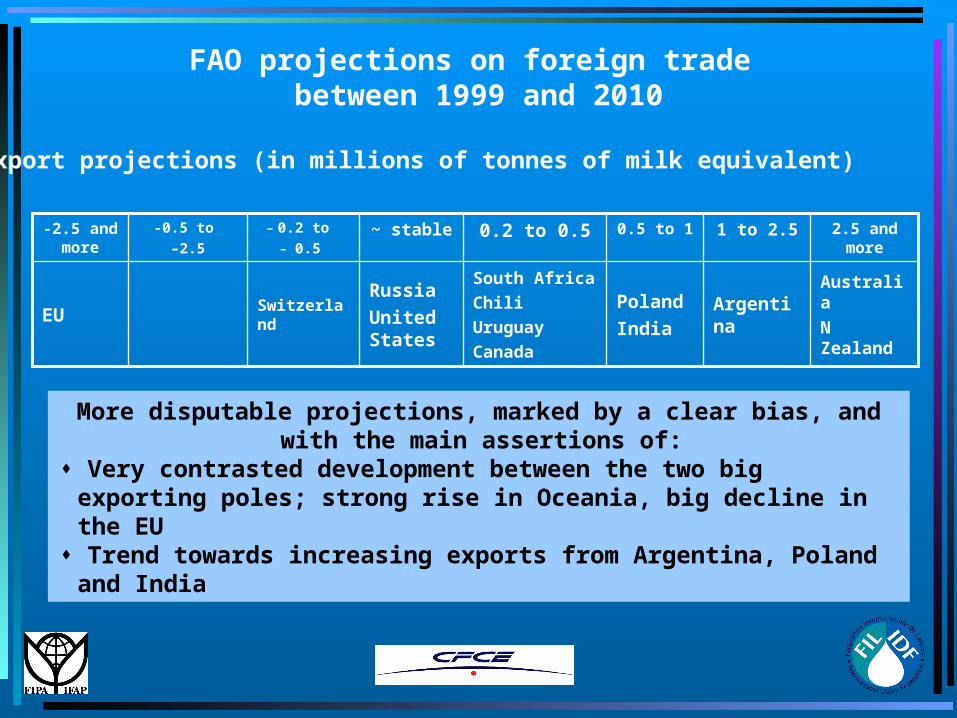

FAO projections on foreign trade between 1999 and 2010

Growth in trade (intra-EU trade excl.) from 10 to 11 million tonnes

Russia

Mexico

Thaïland

China

South Korea

Japan

Morocco

Egypt

Nigeria

Malaisia

Venezuela

Algeria

EU

IndiaSaudiArabia

Poland

BrazilUnited States

1 to 2.50.5 to 10.2 to 0.5~ stable- 0.2 to –0.5

Import projections (in millions of tonnes of milk equivalent)

Nothing really upsetting in these projections, where the main assertions are:

Mexico, Russia and the Far East would be the most dynamic import zones

No country would show a sharp decline in its imports

FAO projections on foreign trade between 1999 and 2010

-0.5 to

–2.5

EU

-2.5 and more

Argentina

1 to 2.5

Australia

N Zealand

Poland

India

South Africa

Chili

Uruguay

Canada

Russia

United States

Switzerland

2.5 and more

0.5 to 10.2 to 0.5~ stable- 0.2 to

- 0.5

Export projections (in millions of tonnes of milk equivalent)

More disputable projections, marked by a clear bias, and with the main assertions of:

Very contrasted development between the two big exporting poles; strong rise in Oceania, big decline in the EU

Trend towards increasing exports from Argentina, Poland and India

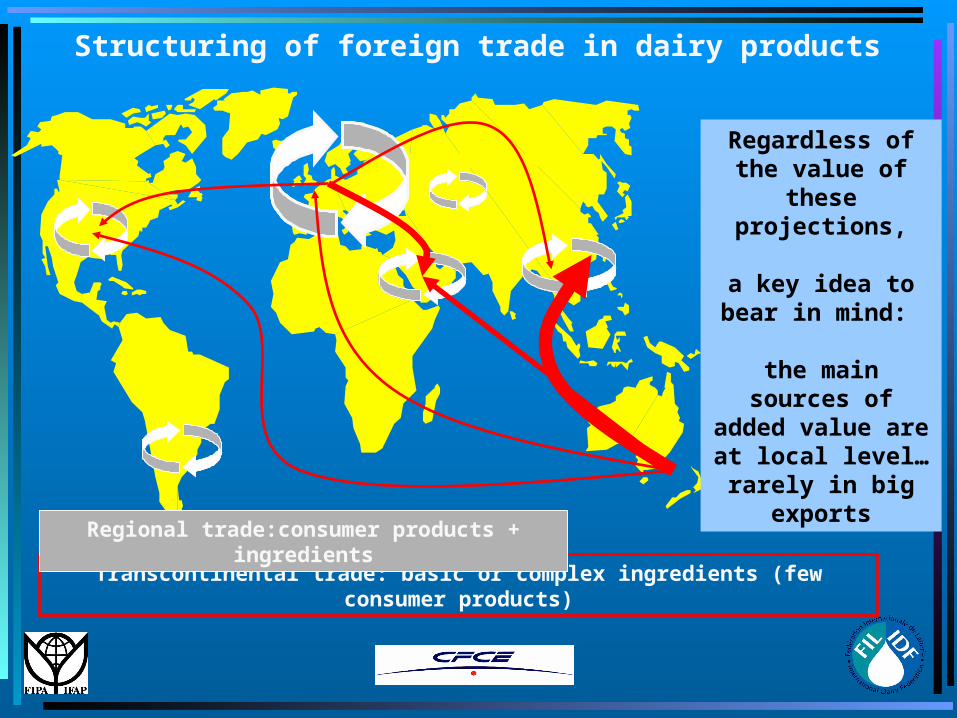

Transcontinental trade: basic or complex ingredients (few consumer products)

Regional trade:consumer products + ingredients

Structuring of foreign trade in dairy products

Regardless of the value of

these projections,

a key idea to bear in mind:

the main sources of

added value are at local level…

rarely in big exports

Top 40 EU dairy companies 2001, ranked by total amount of milk processed *

Rabobank International (update May 2001)

EU milk pro-cessed m kg

1 ArlaFoods (Denmark/Sweden) 7,100 21 Ebro-Puleva (Spain)1,000

2 Lactalis (France) 6,540 22 Berglandmilch (Austria)920

3 Friesland Coberco DF (Netherlands) 5,90023 3A (France) 9004 Campina Melkunie (Netherlands) 4,700

24 Dairygold (Ireland) 8685 Nordmilch (Germany) 4,482 25 Omira/Neub. (Germany)

8506 Bongrain (France) 3,700 26 Hochwald-Eifelperle (Germany)

8507 Dairy Crrest (Great Britain) 3,100 27 CAPSA (Spain)

8068 Nestlé (Switzerland) 2,800 28 Eurial (France)

8009 Humana Milchunion (Germany) 2,536 29 R. Wiseman (Great Britain)

78010 Sodiaal (France) 2,400 30 Leerdammer (Bel) (Netherlands)

75111 Glanbia (Ireland) 2,150 31 Galbani (Italy)

75012 Danone (France) 2,150 32 BMI/BMU (Germany)

73613 Express Dairies (Great Britain) 2,100 33 Belgomilk (Belgium)

70014 Entremont (France) 1,900 34 Unicopa (France)

70015 Valio (Finland) 1,660 35 ACC (Great Britain)

70016 Laïta (France) 1,650 36 Goldsteig (Germany)

60017 Aloïs Müller (Germany) 1,517 37 Golden Vale (Kerry) (Ireland)

59018 Parmalat (Italy) 1,270 38 D.O.C. (Netherlands)

58019 Lactogal (Portugal) 1,100 39 Milchunion Hocheiffel (Germany)

57020 Fromageries Bel (France) 1,000 40 Hansa Milch (Germany)

569

EU milk pro-cessed m kg

* excluding Kraft Foods because proper figures are not available

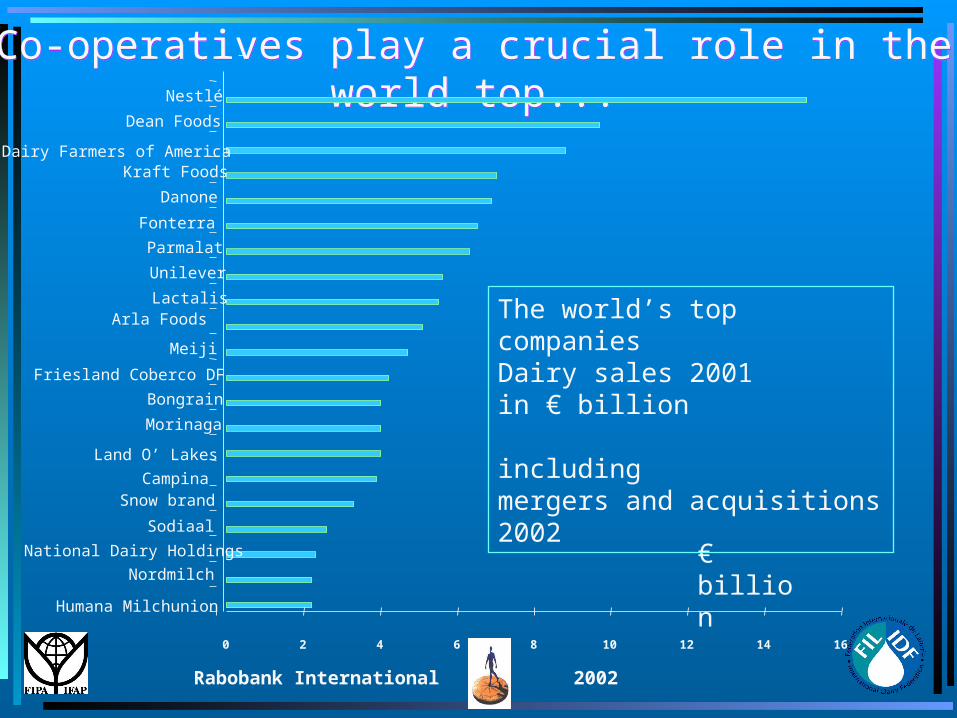

Co-operatives play a crucial role in the world top...

Co-operatives play a crucial role in the world top...

0 2 4 6 8 10 12 14 16

National Dairy Holdings

Snow brand

Morinaga

Bongrain

Meiji

Lactalis

Unilever

Parmalat

Danone

Kraft Foods

Dean Foods

Nestlé

€ billion

The world’s top companiesDairy sales 2001in € billion

including mergers and acquisitions 2002

Friesland Coberco DF

Dairy Farmers of America

Fonterra

Arla Foods

Sodiaal

Nordmilch

Land O’ Lakes

Humana Milchunion

Campina

Rabobank International 2002

Top 10 retailers(total sales)

1. Wal-Mart Stores 218 2. Carrefour 62 3. Ahold 60 4. Kroger 50 5. Metro AG 44 6. Albertson’s 38 7. Safeway (USA) 34 8. Rewe 34 9. Tesco 3410.Aldi 32

Total USD 606

Top 10 foodservice (total sales)

1. McDonald’s 41 2. Yum! Brands (Tricon) 22 3. Compass 13 4. Burger King 11 5. Sodexho Alliance 11 6. Wendy’s 8 7. Aramark 8 8. Accor 7 9. Six Continents (Bass) 610.Whitbread 4

Total USD 131

Ranked by total sales, 2001 (in USD billion)

Top 10 manufacturers(food&drinks sales only)

1. Nestlé 41 2. Kraft Foods 34 3. PepsiCo 27 4. Unilever 26 5. Tyson Foods 25 6. ConAgra 22 7. Coca Cola Co. 20 8. Diageo 14 9. General Mills 1310.Danone 13

Total USD 235

Food manufacturers have to deal with increasingly powerful customers

Food manufacturers have to deal with increasingly powerful customers

Rabobank International 2002

2. IDF WORLD DAIRY SITUATION 2003 FIRST PREVIEW

Short Term Market TrendsShort Term Market Trends

domestic producers and Oceanian suppliers took most advantage from growing demand

Europe and North America: Slower growth of cheese demand

International trade continues to grow, but

Short Term Market TrendsShort Term Market Trends

however the international trade is growing by volume, it has not increased its share of overall consumption in percentage terms

these shares vary widely according the products‘ nature and are also changing by origin and destination

Short Term Market TrendsShort Term Market Trends

because prices are attractive again therefore the international trade, though growing

by volume, does not increase its share in percentage terms

but these shares vary widely according the products‘ nature

International trade continues to grow

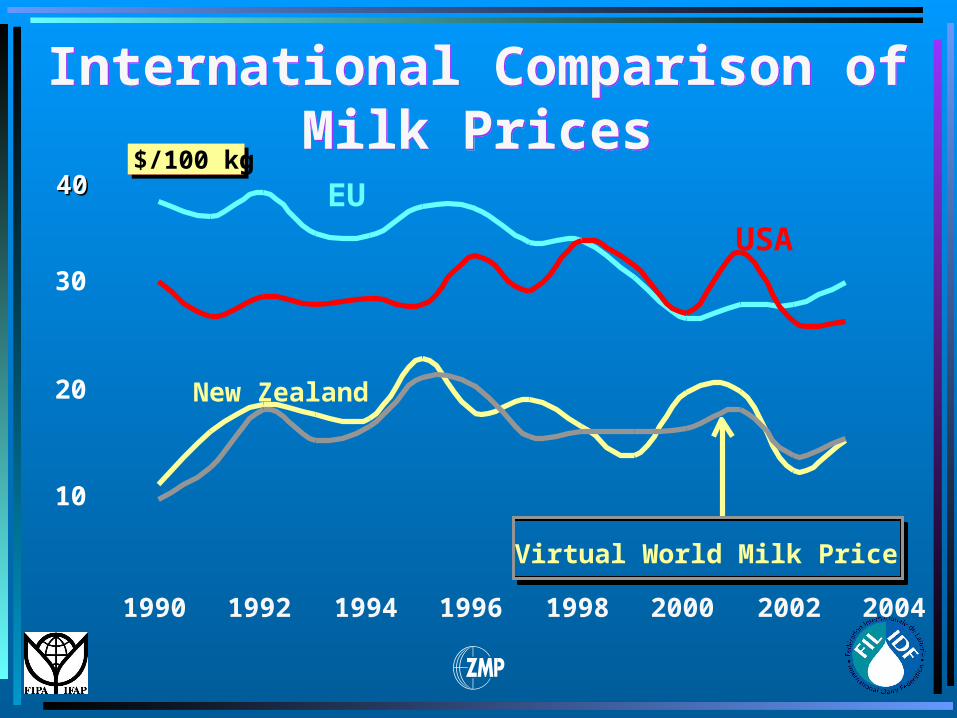

International Comparison of

Milk Prices International Comparison of

Milk Prices

4040$/100 kg

10

20

30

1990 1992 1994 1996 1998 2000 2002 2004

EUUSA

New Zealand

Virtual World Milk Price

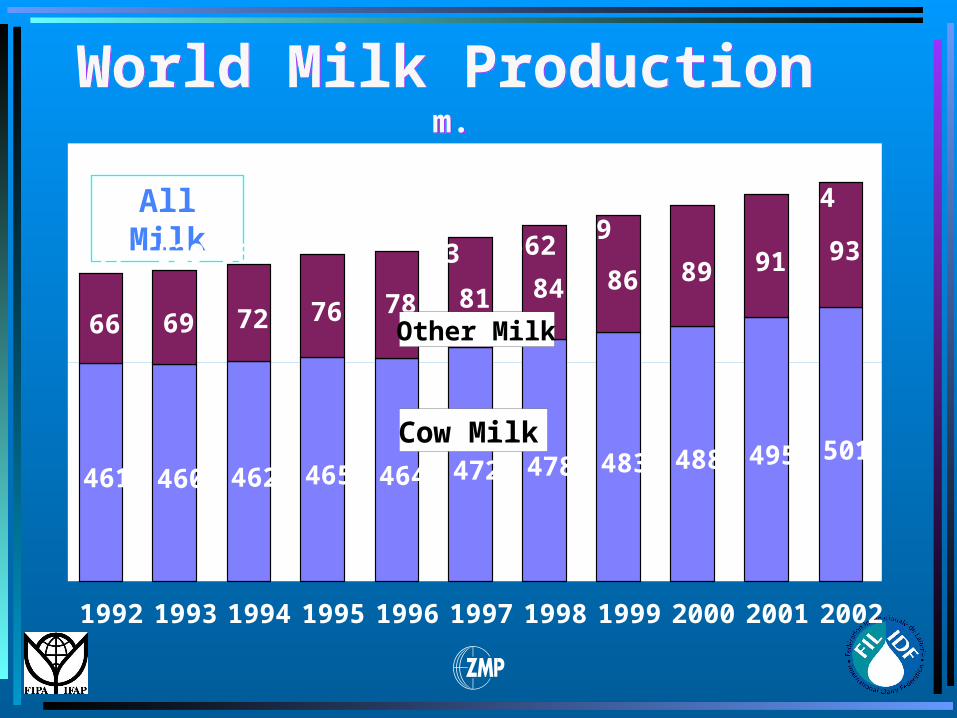

World Milk ProductionWorld Milk Productionm. t.m. t.

461 460 462 465 464 472 478 483 488 495 501

66 69 72 76 81 84 86 89 91 93

78

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Cow Milk

Other Milk

All Milk

527 529 534541 543

553 562569 577

585 594

7

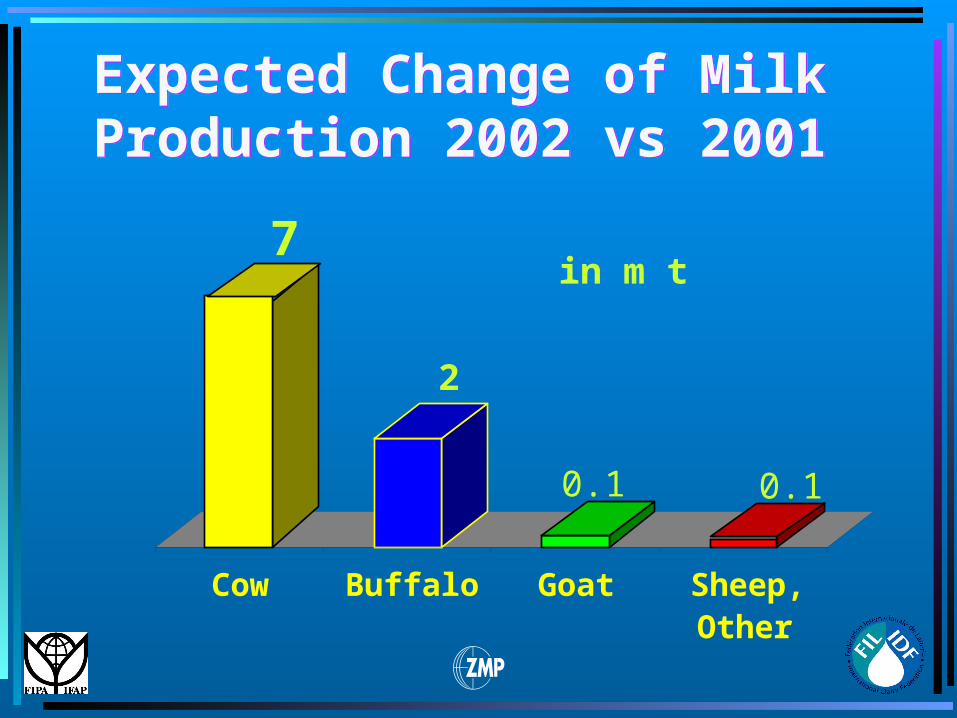

2

0.1 0.1

Cow Buffalo Goat Sheep,Other

Expected Change of Milk Production 2002 vs 2001 Expected Change of Milk Production 2002 vs 2001

in m t

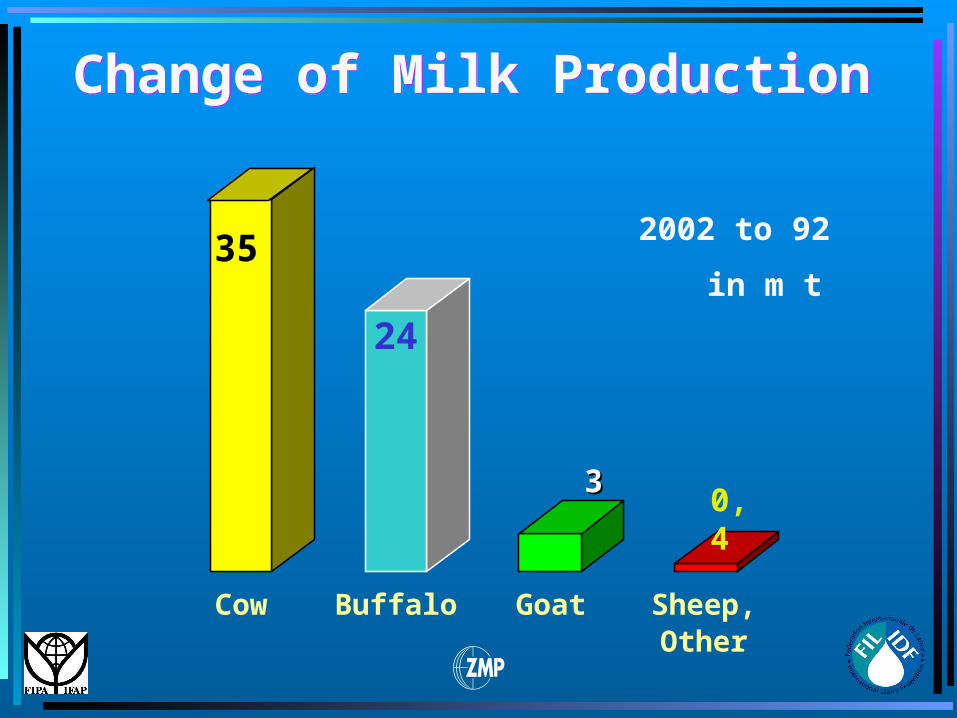

35

24

0,4

Cow Buffalo Goat Sheep,Other

Change of Milk Production Change of Milk Production

2002 to 92

in m t

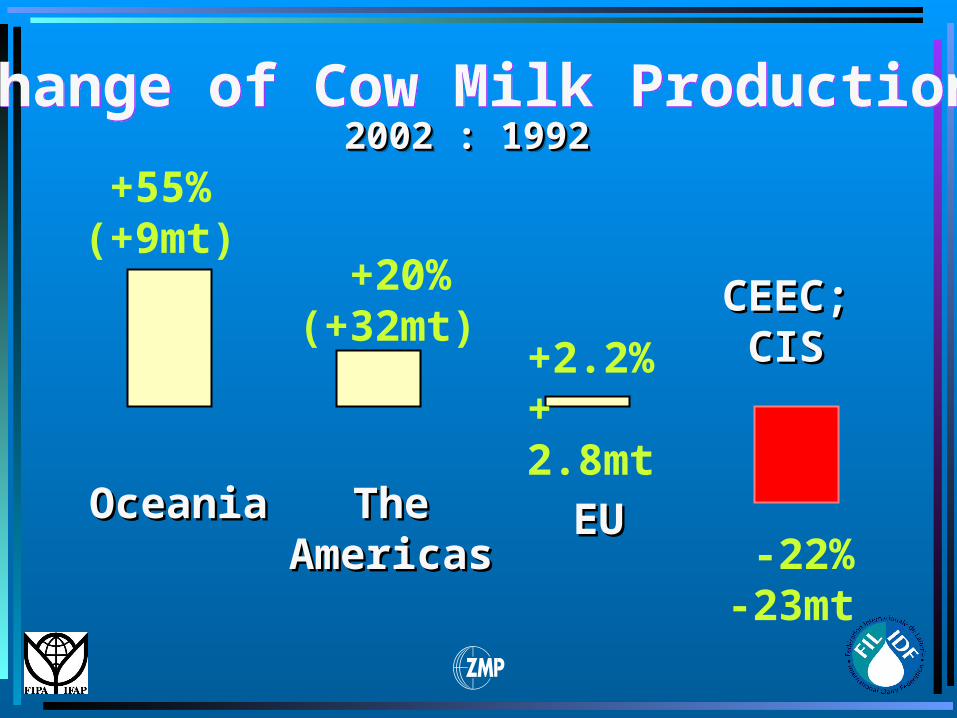

33

Change of Cow Milk Production Change of Cow Milk Production 2002 : 19922002 : 19922002 : 19922002 : 1992

-22%-23mt

+2.2%+ 2.8mt

+20%(+32mt)

+55%(+9mt)

OceaniaOceania The The AmericasAmericas

EUEU

CEEC; CEEC; CISCIS

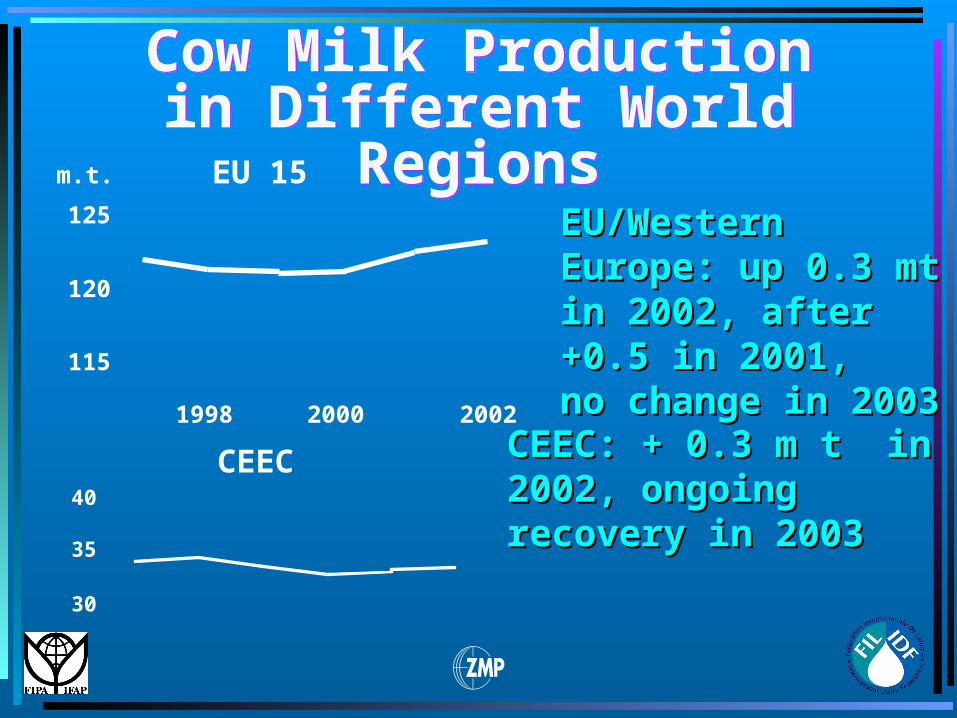

EU 15

115

120

125

m.t.

Cow Milk Production in Different World RegionsCow Milk Production in Different World Regions

EU/Western Europe: EU/Western Europe: up 0.3 mt in 2002, up 0.3 mt in 2002, after +0.5 in 2001,after +0.5 in 2001,no change in 2003no change in 2003

CEEC

30

35

40

CEEC: + 0.3 m t in CEEC: + 0.3 m t in 2002, ongoing 2002, ongoing recovery in 2003 recovery in 2003

1998 2000 2002

Cow Milk Production in Different World RegionsCow Milk Production in Different World Regions

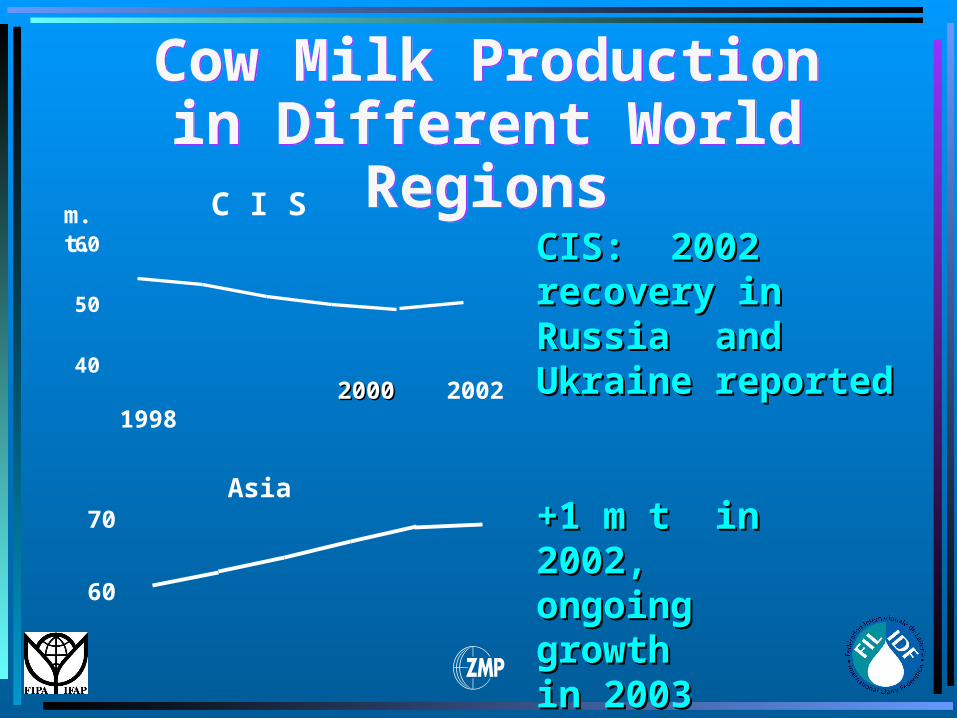

C I S

40

50

60 CIS: 2002 recovery CIS: 2002 recovery in Russia and in Russia and Ukraine reportedUkraine reported

Asia

60

70

1998 20002000 2002

+1 m t in 2002,+1 m t in 2002,ongoing growthongoing growthin 2003 likelyin 2003 likely

m.t.

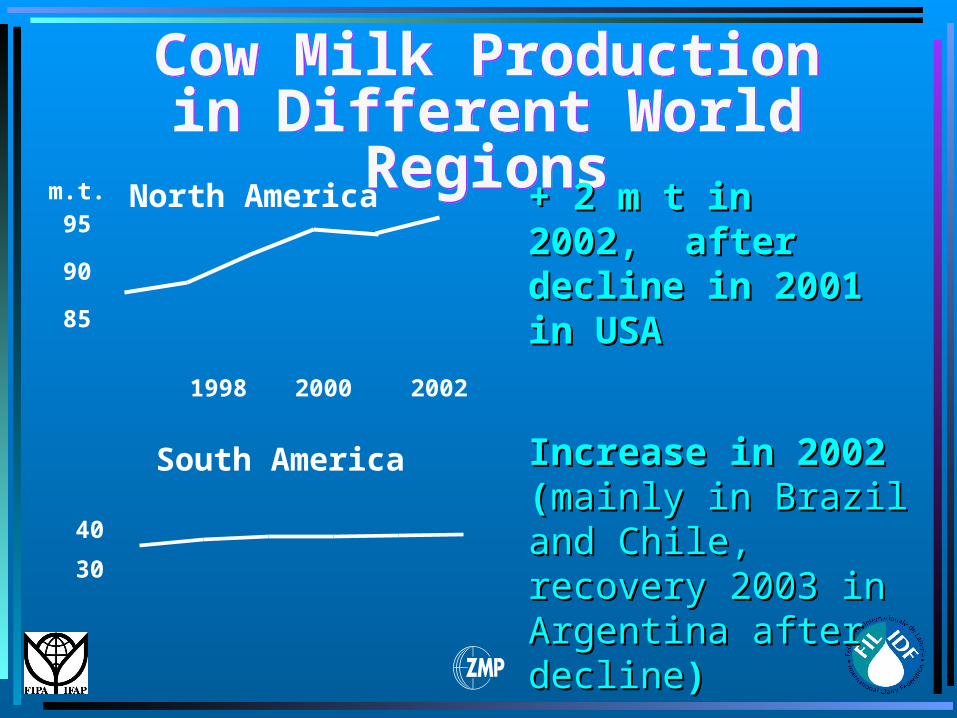

North America

85

90

95

1998 2000 2002

m.t.

Cow Milk Production in Different World RegionsCow Milk Production in Different World Regions

+ 2 m t in 2002, + 2 m t in 2002, after decline in after decline in 2001 in USA2001 in USA

South America

30

40

Increase in 2002 Increase in 2002 ((mainly in Brazil and mainly in Brazil and Chile, recovery 2003 Chile, recovery 2003 in Argentina after in Argentina after declinedecline))

Cow Milk Production in Different World RegionsCow Milk Production in Different World Regions

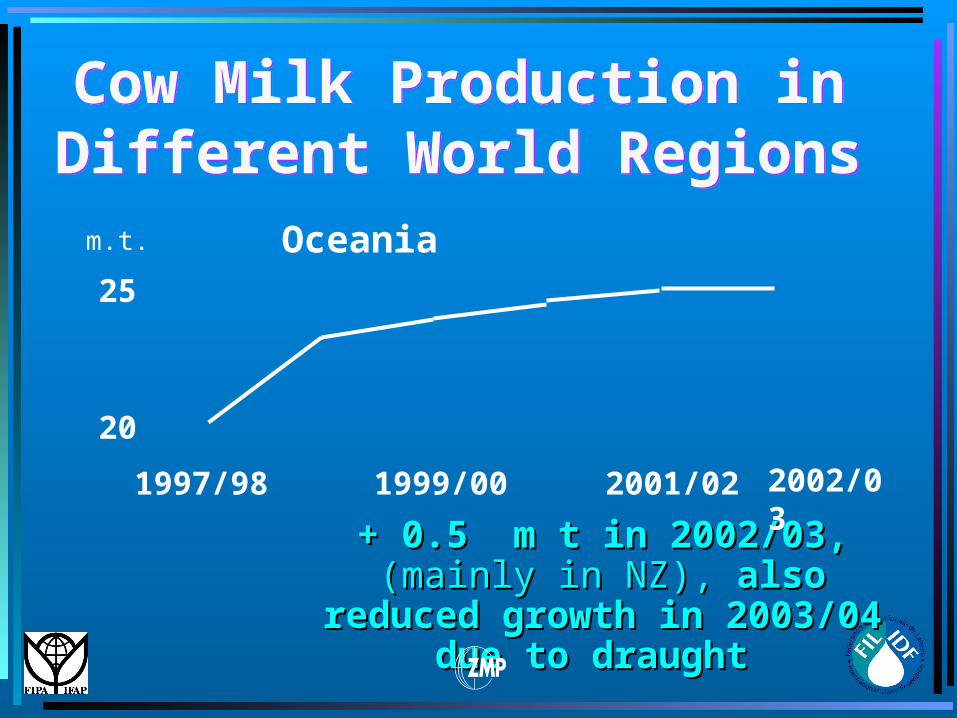

+ 0.5 m t in 2002/03, + 0.5 m t in 2002/03, (mainly in (mainly in NZ), NZ), also reduced growth in also reduced growth in

2003/04 due to draught 2003/04 due to draught

Oceania

20

25

1997/98 1999/00 2001/02

m.t.

2002/03

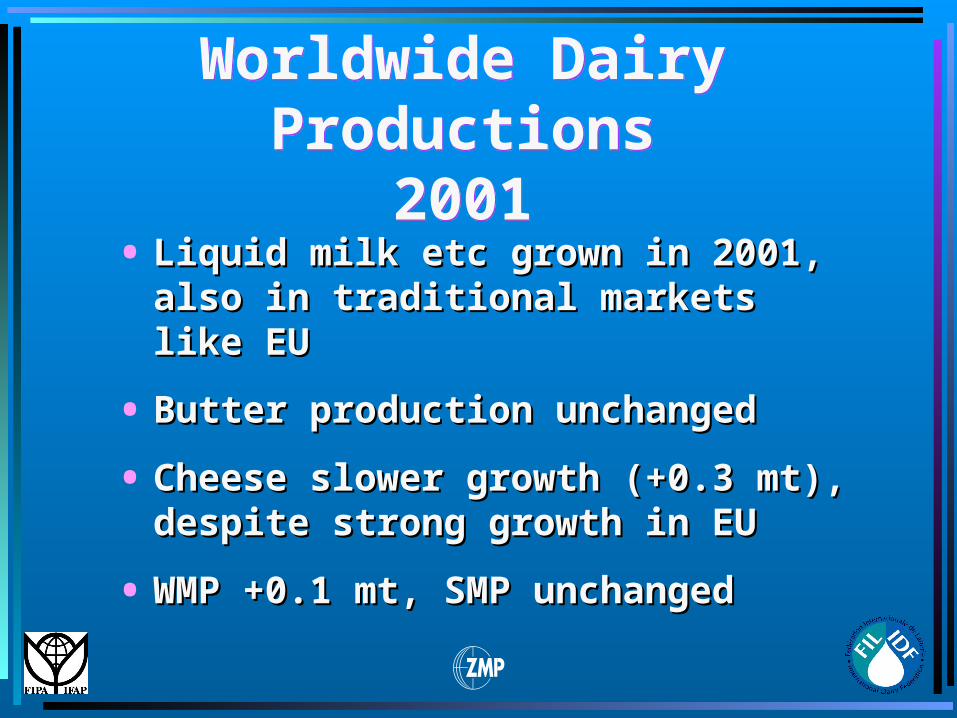

Worldwide Dairy Productions2001

Worldwide Dairy Productions2001

• Liquid milk etc grown in 2001, also in Liquid milk etc grown in 2001, also in traditional markets like EUtraditional markets like EU

• Butter production unchangedButter production unchanged

• Cheese slower growth (+0.3 mt), Cheese slower growth (+0.3 mt), despite strong growth in EUdespite strong growth in EU

• WMP +0.1 mt, SMP unchangedWMP +0.1 mt, SMP unchanged

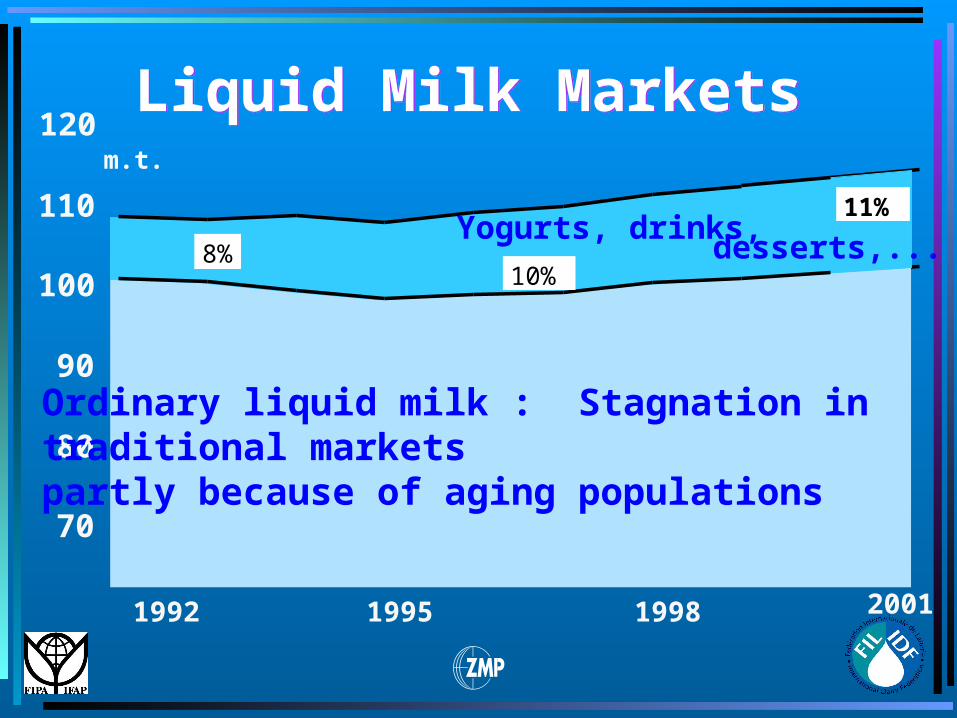

Liquid Milk Markets Liquid Milk Markets

70

80

90

100

110

120

1992 1995 1998 2001

m.t.

Yogurts, drinks, desserts,...

Ordinary liquid milk : Stagnation in traditional marketspartly because of aging populations

8%10%

11%

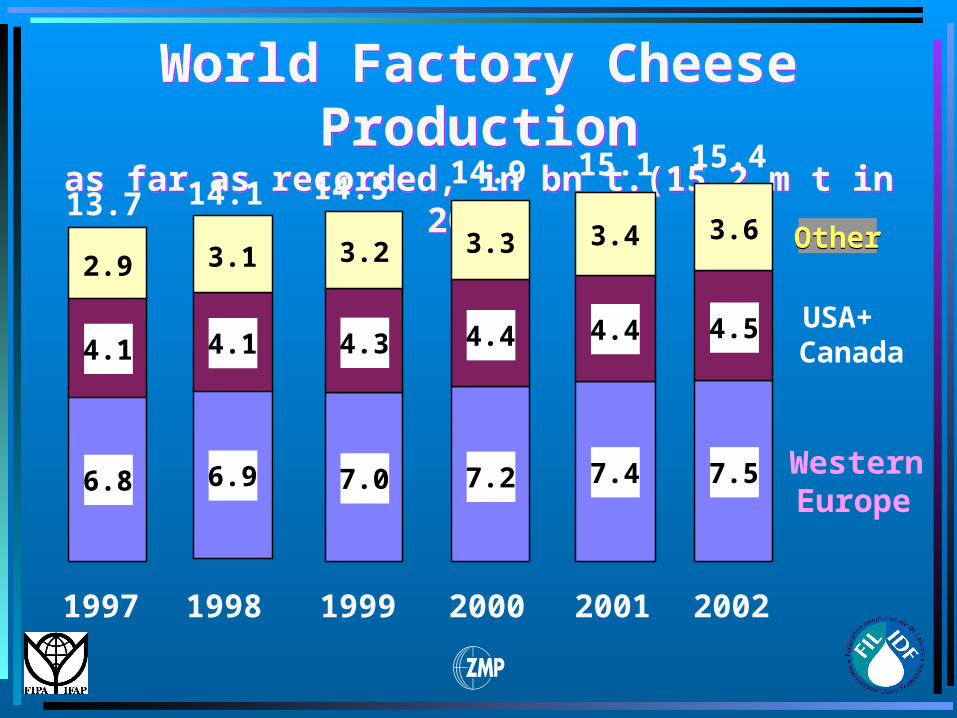

World Factory Cheese Productionas far as recorded, in bn t.(15.2 m t in 2002)

World Factory Cheese Productionas far as recorded, in bn t.(15.2 m t in 2002)

Western Europe

USA+Canada

OtherOther

1997

13.7

6.8

4.1

2.9

1999

14.5

7.0

4.3

3.2

2001

15.1

7.4

4.4

3.4

2002

15.4

7.5

4.5

3.6

2000

14.9

4.4

3.3

7.2

14.1

6.9

4.1

3.1

1998

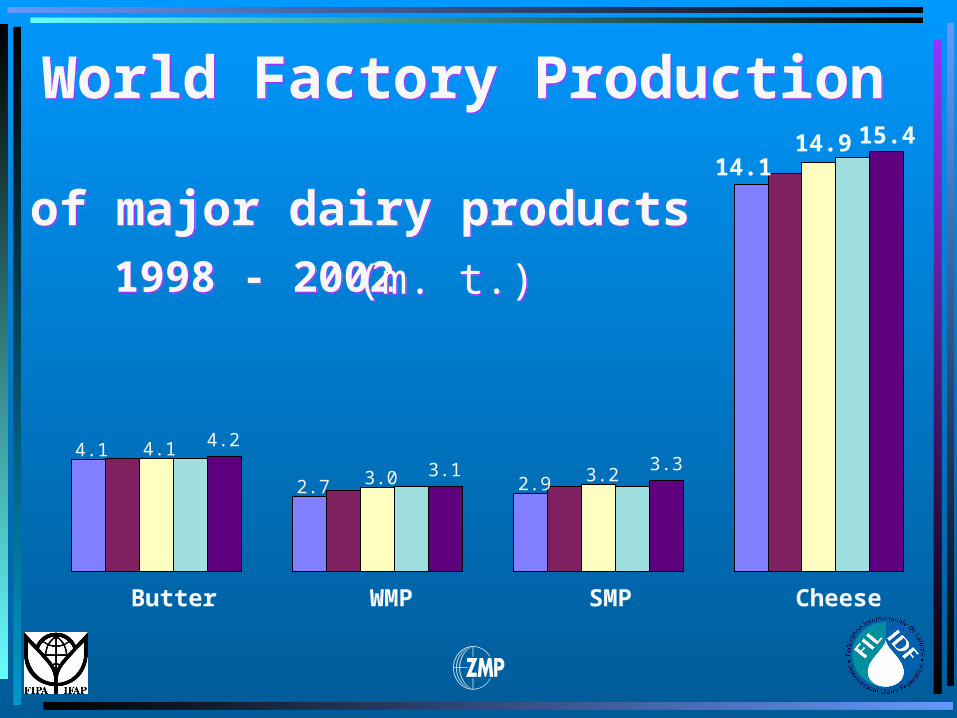

World Factory ProductionWorld Factory Production

of major dairy products of major dairy products

1998 - 2002 1998 - 2002 (m. t.)(m. t.)

4.1

2.7 2.9

14.1

4.1

3.0 3.2

14.9

4.2

3.1 3.3

15.4

Butter WMP SMP Cheese

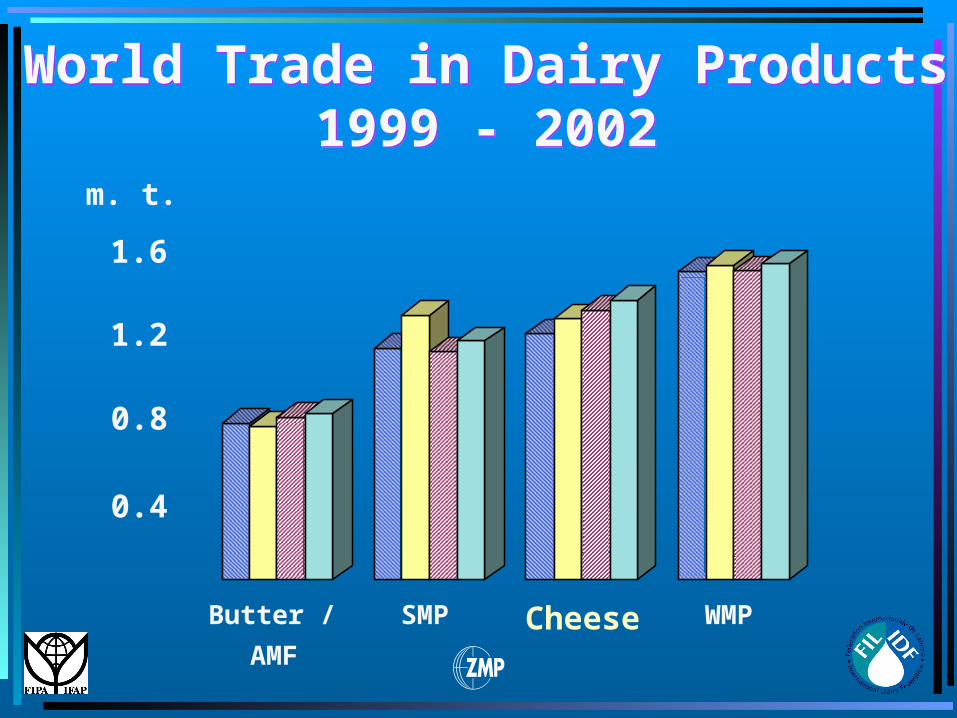

World Trade in Dairy ProductsWorld Trade in Dairy Products1999 - 20021999 - 2002

0.4

0.8

1.2

1.6

Butter /

AMF

SMP Cheese WMP

m. t.

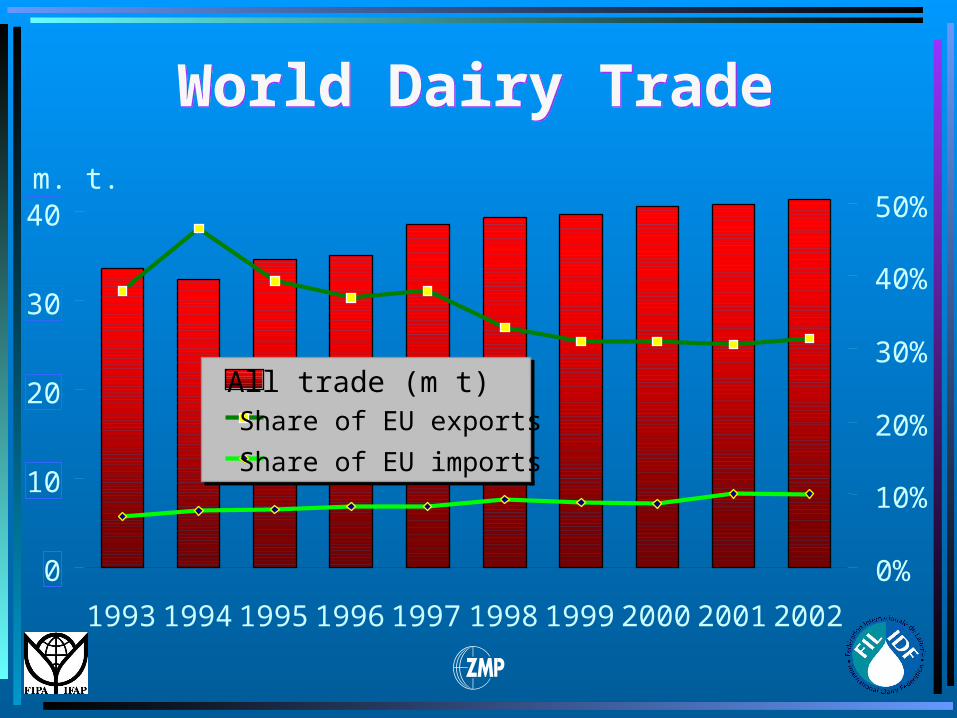

World Dairy Trade World Dairy Trade

0

10

20

30

40

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

0%

10%

20%

30%

40%

50%

All trade (m t)Share of EU exports

Share of EU imports

m. t.

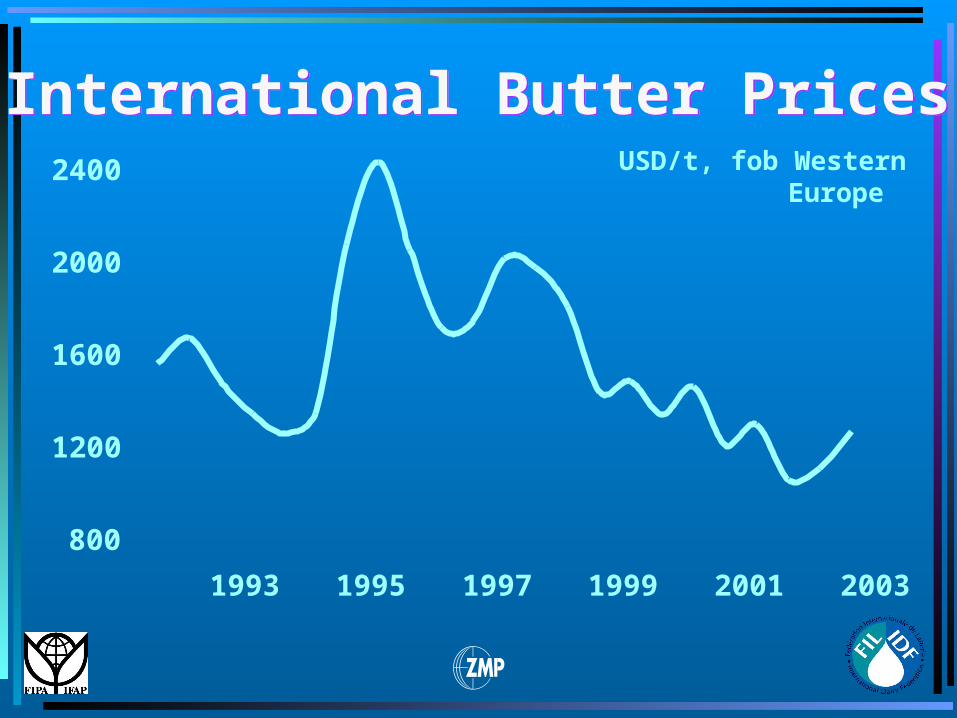

International Butter PricesInternational Butter Prices

800

1200

1600

2000

2400

1993 1995 1997 1999 2001 2003

USD/t, fob Western Europe

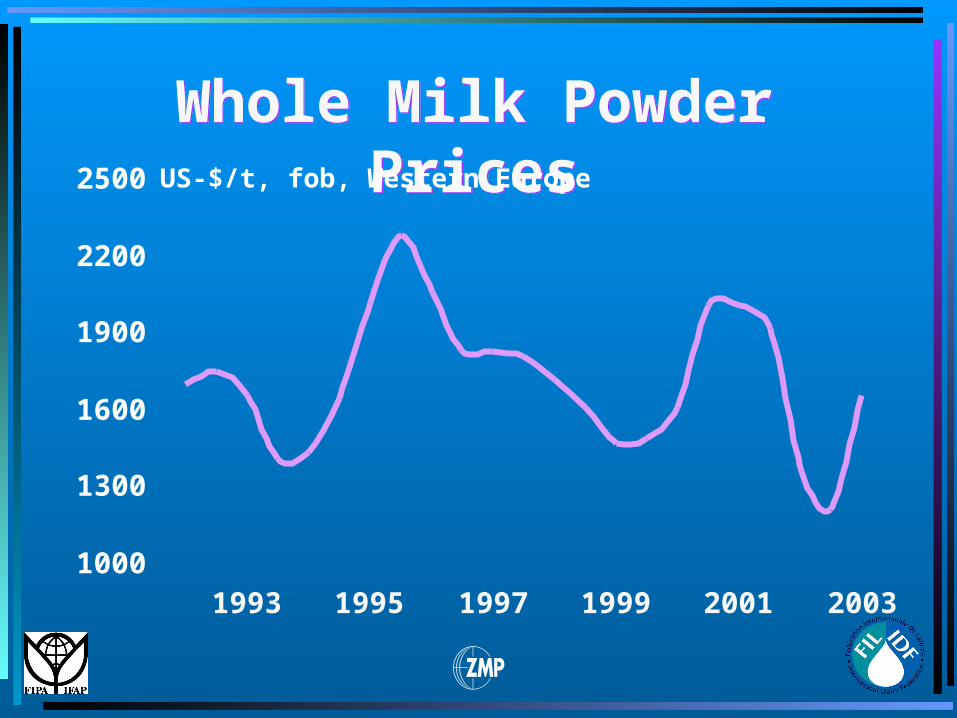

Whole Milk Powder PricesWhole Milk Powder Prices

1000

1300

1600

1900

2200

2500

1993 1995 1997 1999 2001 2003

US-$/t, fob, Western Europe

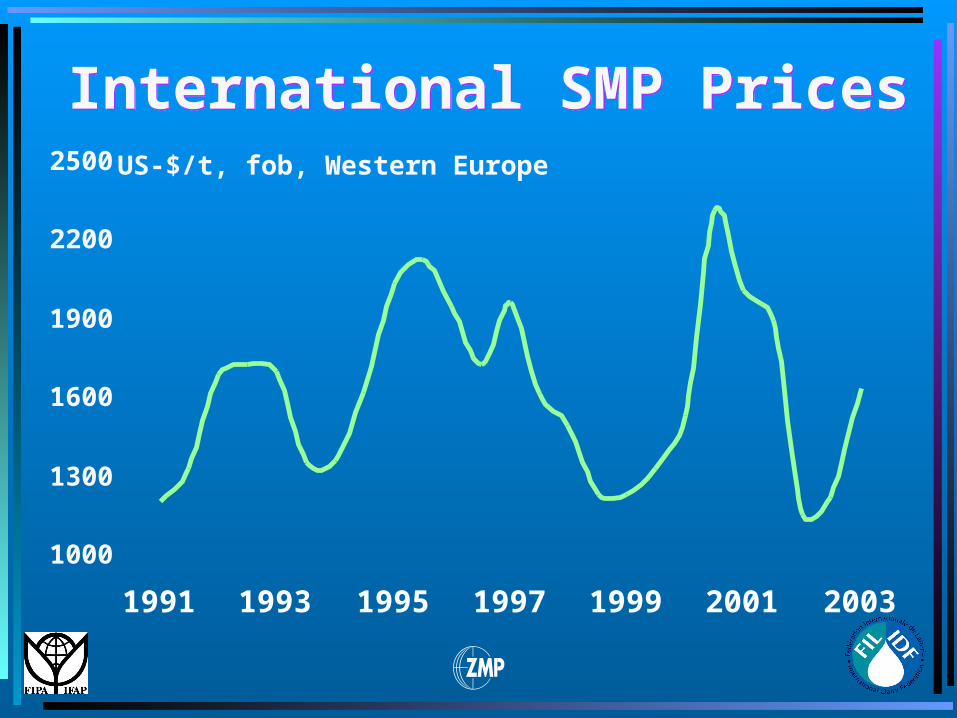

International SMP PricesInternational SMP Prices

1000

1300

1600

1900

2200

2500

1991 1993 1995 1997 1999 2001 2003

US-$/t, fob, Western Europe

1000

2000

3000

4000

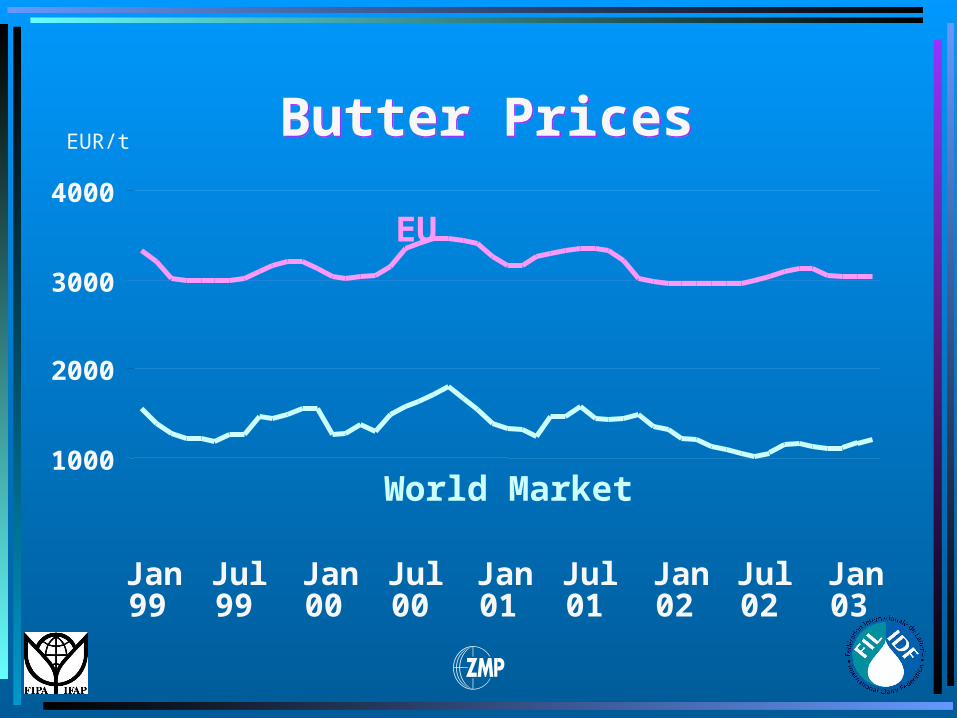

Jan99

Jul99

Jan00

Jul00

Jan01

Jul01

Jan02

Jul02

Jan03

Butter PricesButter PricesEUR/t

EU

World Market

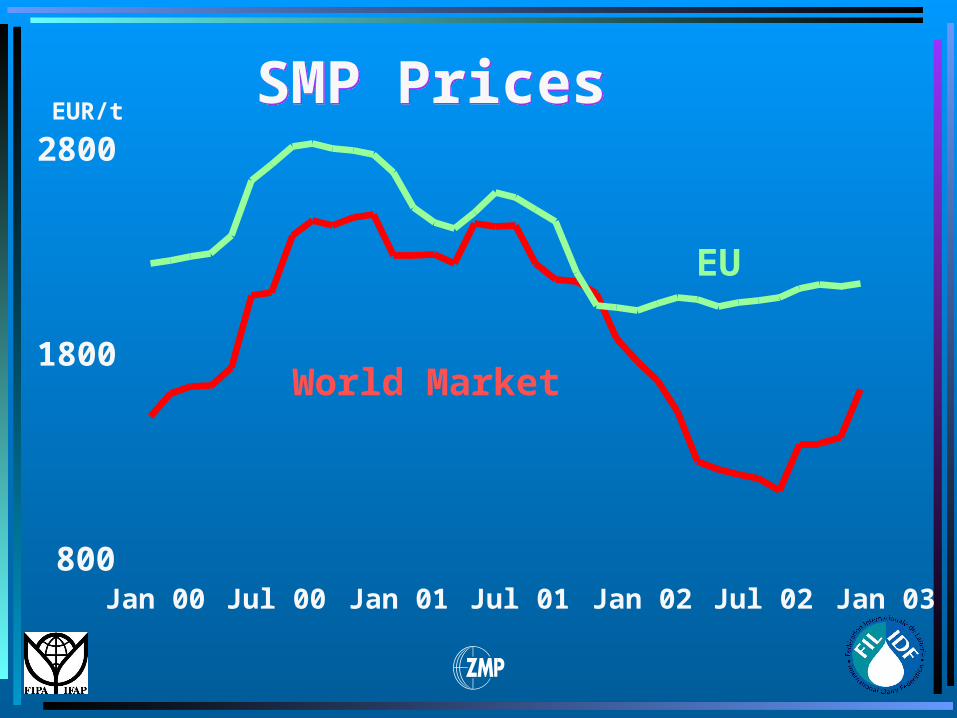

SMP Prices SMP Prices

800

1800

2800

Jan 00 Jul 00 Jan 01 Jul 01 Jan 02 Jul 02 Jan 03

EUR/t

EU

World Market

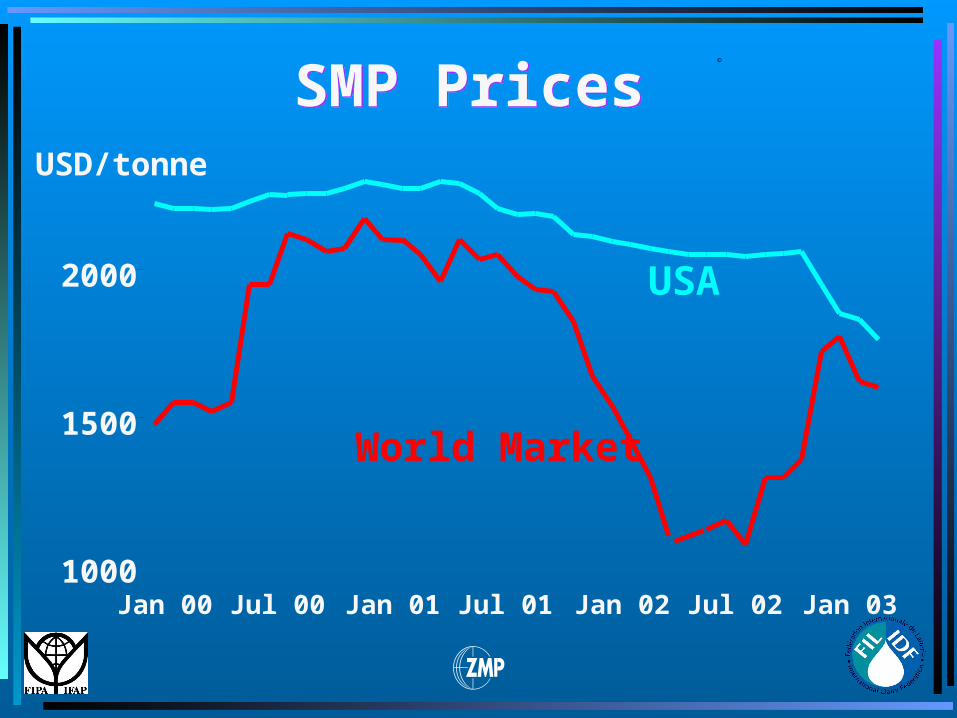

1000

1500

2000

Jan 00 Jul 00 Jan 01 Jul 01 Jan 02 Jul 02 Jan 03

SMP Prices SMP Prices USD/tonne

©

USA

World Market

0.80

0.90

1.00

1.10

Jan

99

Apr JulOct Jan

00

Apr JulOct Jan

01

Apr JulOct Jan

02

Apr JulOct Jan

03

Apr

USD/EURUSD/EUR

World Dairy Situation 2003First Preview

World Dairy Situation 2003First Preview

Thank You For Thank You For

Your AttentionYour Attention

World Dairy Situation 2003World Dairy Situation 2003

This new issue will be presented in greater detail at the IDF Centenary in Bruges in September 2003. It will be published as an IDF Bulletin and will

be made available through IDF